How Legal Restrictions on Collateral Limit Access to Credit in ...

147

Report No. 13873-BO How LegalRestrictions on Collateral Limit Access to Credit in Bolivia December1 994 Office of the Chief Economist LatinAmericaand the CaribbeanRegion Document of the World Bank Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

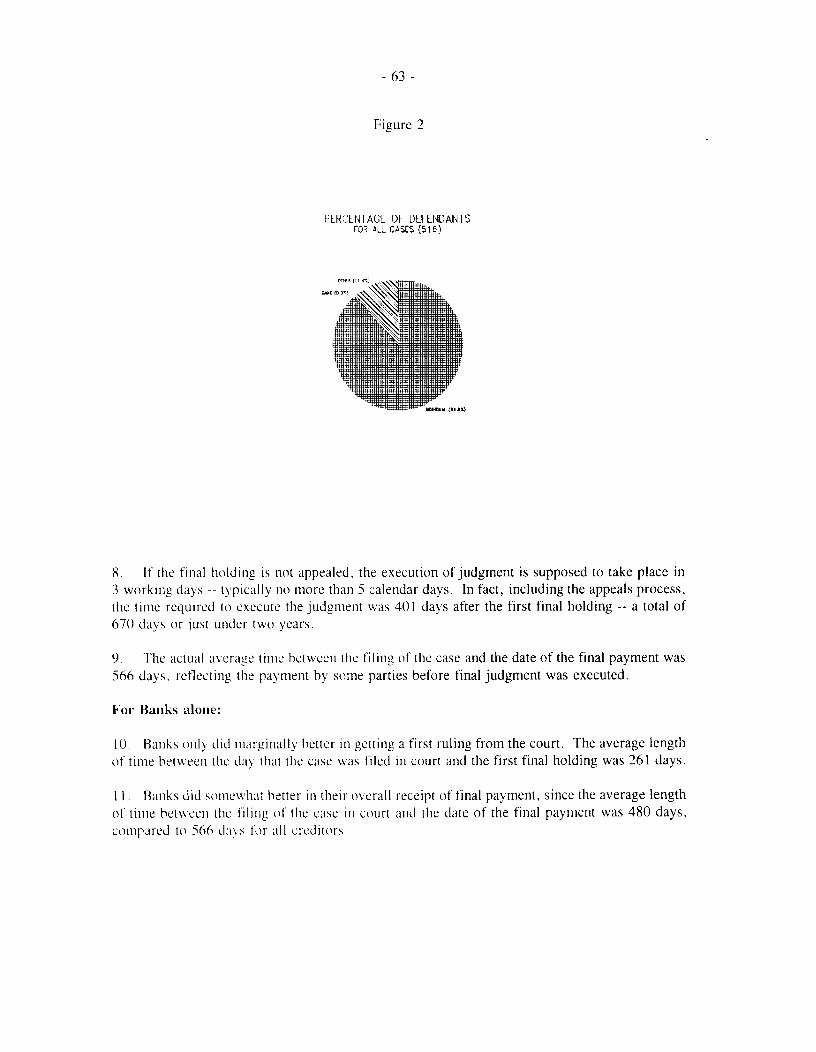

Documents

-

view

0 -

download

0

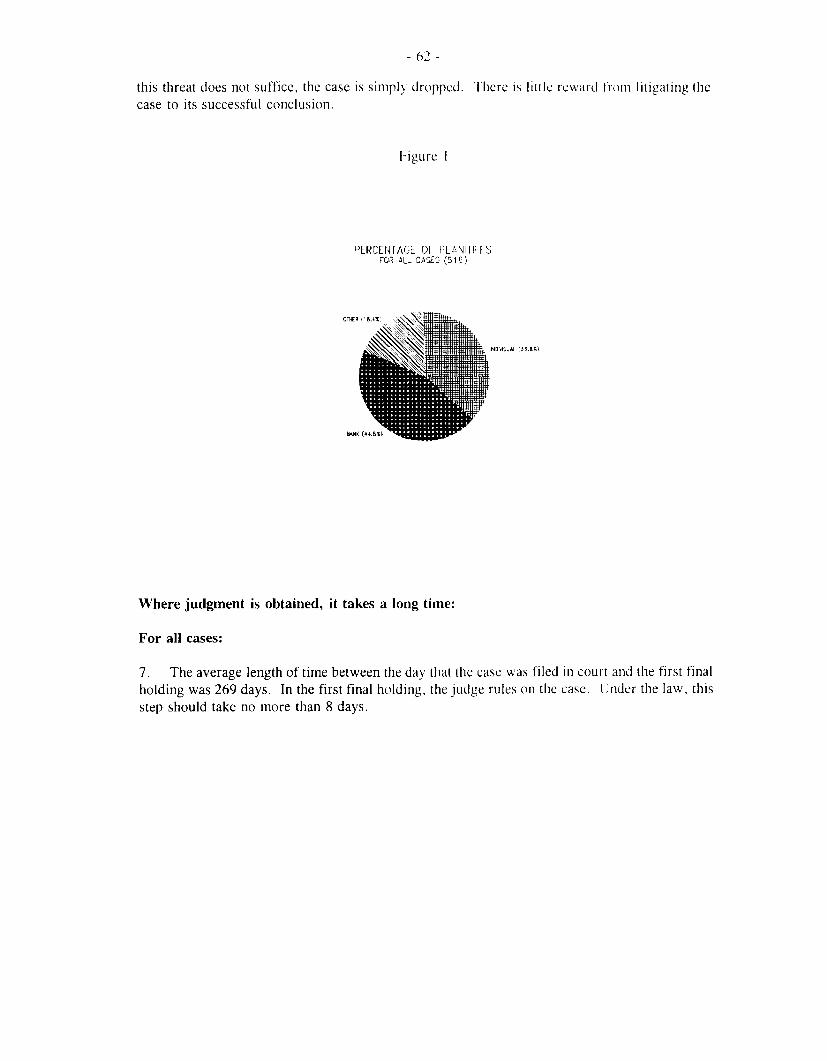

Transcript of How Legal Restrictions on Collateral Limit Access to Credit in ...

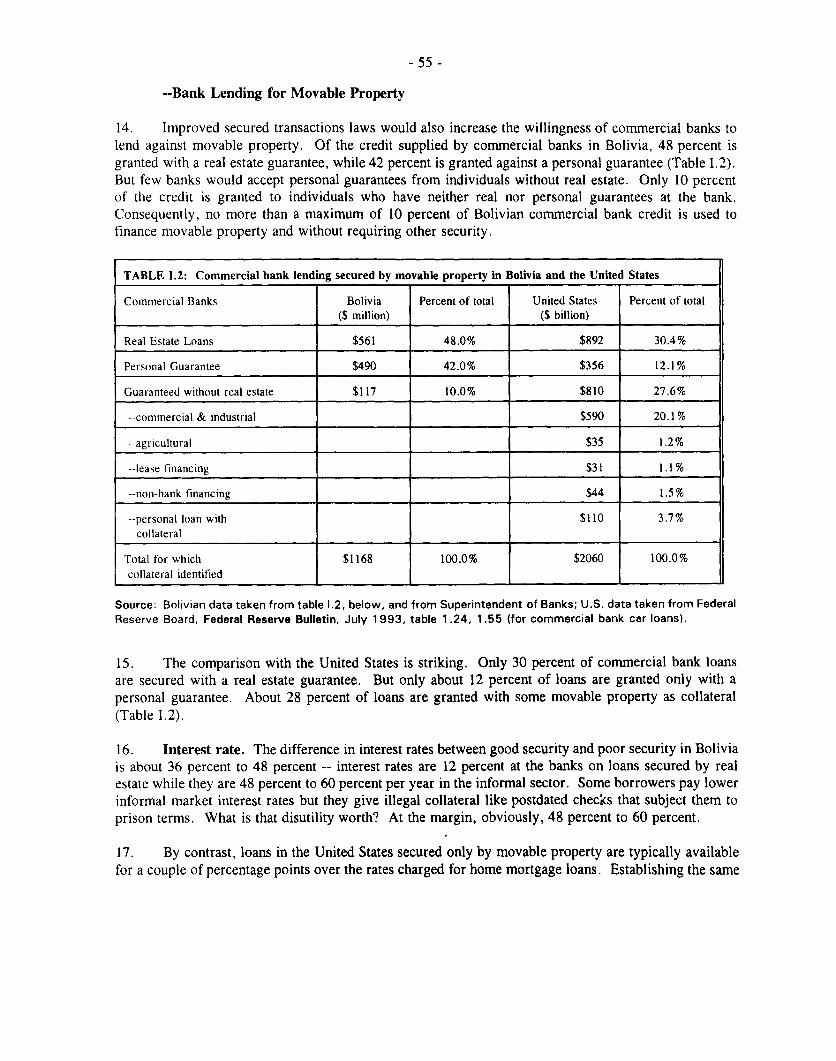

Report No. 13873-BO

How Legal Restrictions on CollateralLimit Access to Credit in BoliviaDecember1 994

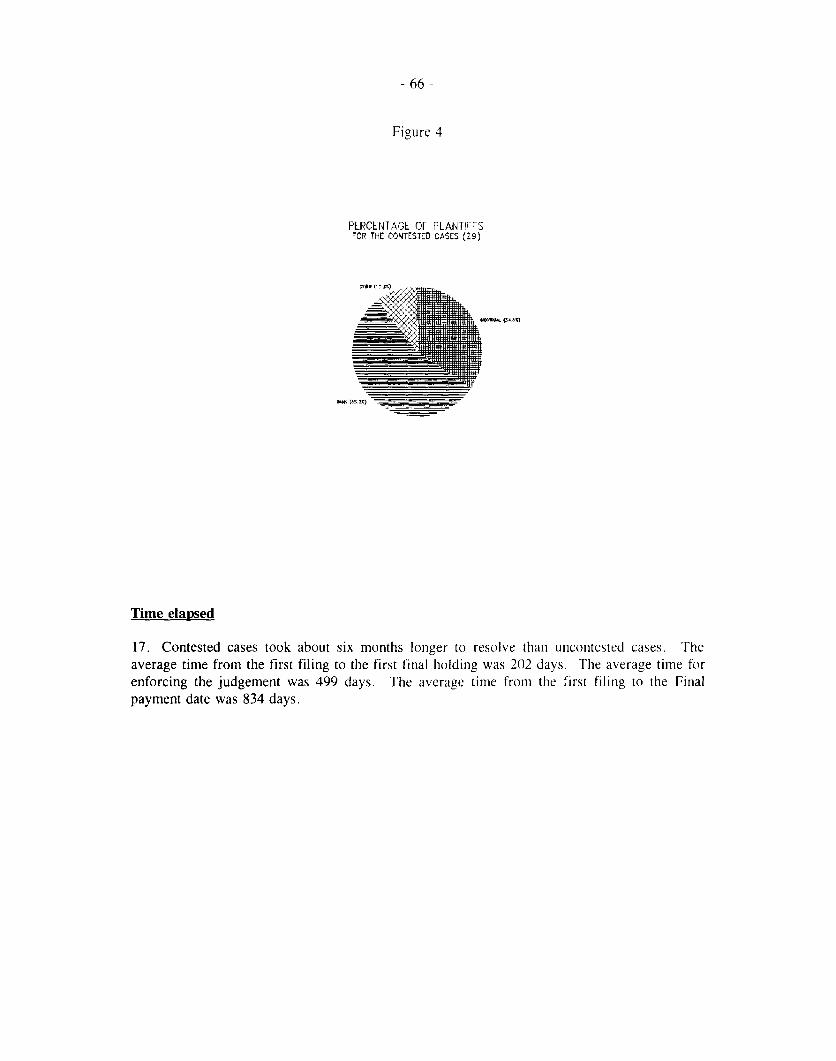

Office of the Chief EconomistLatin America and the Caribbean Region

Document of the World Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

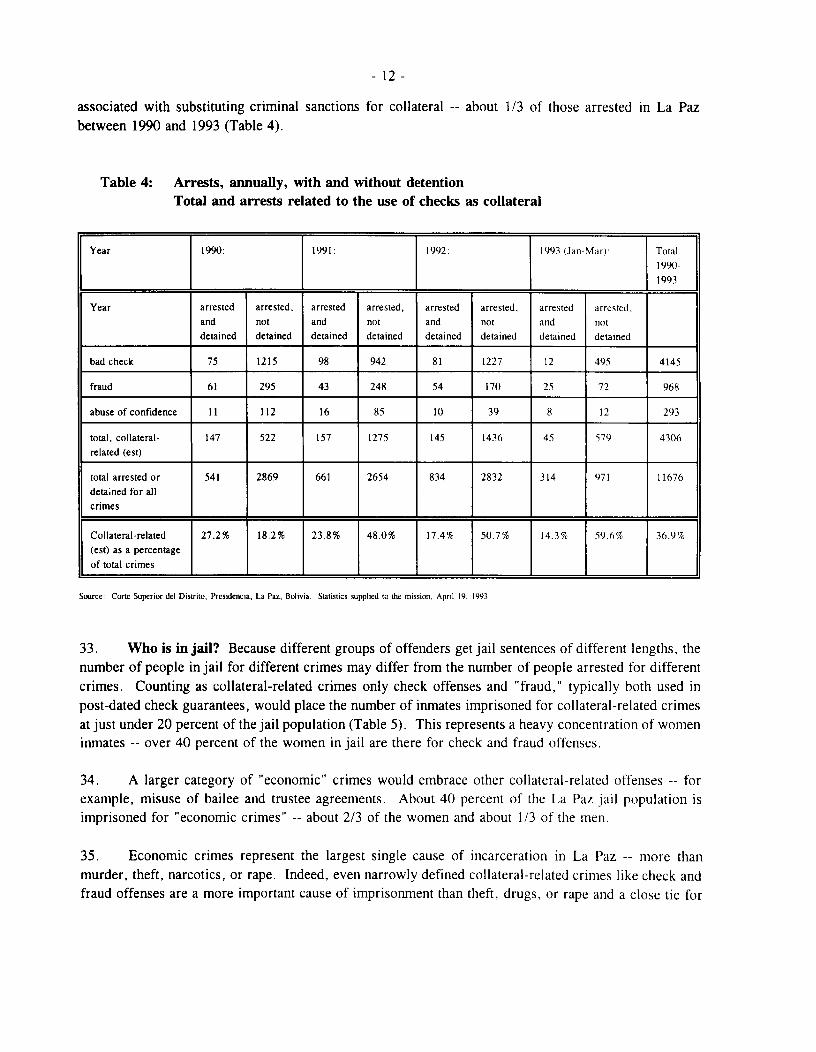

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

HOW LEGAL RESTRICTIONS ON COLLATERALLIMIT ACCESS TO CREDIT IN BOLIVIA

December 1994

*This report is based on the findings of two missions to Bolivia in March 1991 and March 1992.The team was led by Heywood W. Fleisig of the Bank and included Juan Carlos Aguilar, economist atthe La Paz Resident Mission, and Nuria de la Pefia, laywer and consultant to the Bank. The authors areobliged to Robert Effros of the International Monetary Fund for his early guidance about the economicimportance of these legal provisions, and to Alejandro Garro and Andrew Spanogle for extensive adviceon the legal issues. Marcelo Selowsky advised throughout on the economic analysis and its bearing onthe Bank's credit line operations. William Shaw worked closely with us and advised us from theinception of the project. Roberto Cucullu, Mark Dorfman, Graciela Rodriguez Ferrand, Lance Girton,Thomas Glaessner, Roberto Laver, and Hal Scott made many helpful comments. Many Bolivians havegenerously given their time to explain their perspectives on these problems. Any errors are entirely theresponsibility of the authors.

CONTENTS

Executive Summary ............. -

I. Introduction.. 1 -

II. How the Laws Governing Financial Instruments Affect Credit and EconomicGrowth .- 3-

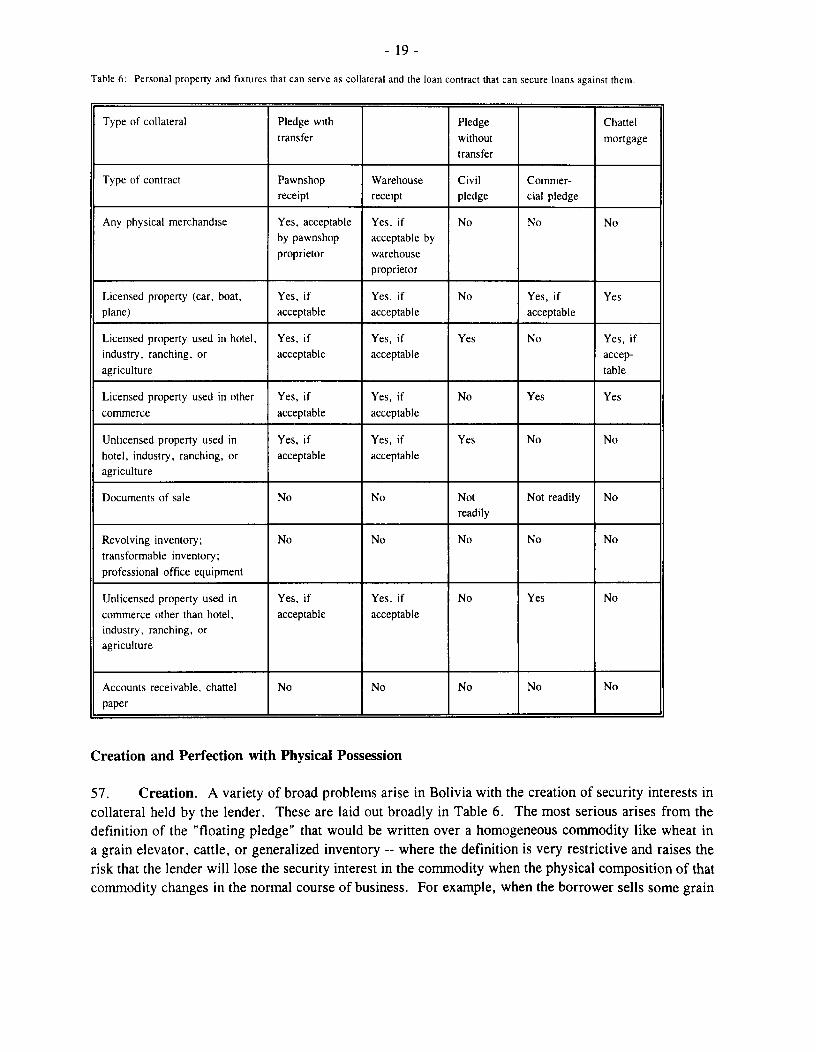

How Do Borrowers Back Their Loans? .- 3-Collateral Problems Reduce Investment and Growth .- 4 -

Collateral Problems Distort Credit Allocation. -6-CoHateral Problems Narrow the Distribution of Credit. -6-Conclusion.. 8-

III. Extralegal Repossession and Sale of Collateral .- 10 -

IV. Financial Instruments and Collateral: Overview of Legal Issues .- 14 -

Definition of Property .- 14 -Structuring Claims Against Property .- 15 -Establishing the Existence of a Claim Against Collateral in Bolivia .- 17 -Obtaining and Enforcing Judgment.. 17 -

V. Creation and Perfection of Security Interests .- 18 -

Creation and Perfection with Physical Possession .- 19 -Creation and Perfection without Physical Possession and without Written

Registration .- 22 -Creation and Perfection without Physical Possession and with Written

Registration .- 23 -The Registries .- 24 -

Problems and Options for Solutions .- 26 -Pass a Comprehensive Law of Secured Transactions .- 27 -

Improve the Operation of Legal Registries .- 29 -

VI. Obtainine Judgment in Bolivia .- 31-

Judicial Procedures .- 31 -Problems and Options for Solution .- 35 -

Permitting Private NonJudicial Enforcement of Loan Contracts .- 36 -Improve the Administration of Justice.- 37 -

VII. Enforcin2 Judoment .......................... - 41 -

Determining the Amount Owed . .......................... - 42 -Attachment and Seizure . ..........................- 43 -Public Auction ...........................- 44 -Problems and Options for Solution .......................... - 45 -

Appendix I: Economic Cost of Deficiencies in Bolivia's Collateral Law ....- 49 -

Appendix II: Results of an Analysis of Bolivian Debt Collection Cases ... - 61 -

Appendix III: le2islacion Sobre Garantias Reales Mobiliarias: Terininos de Referencia . - 71 -

Appendix IV: Legislacion Sobre Acceso Publico a los Registros. Bienes Inembargables vContratos Modelos para el Credito Mobiliario: Terminos de Referencia - 107 -

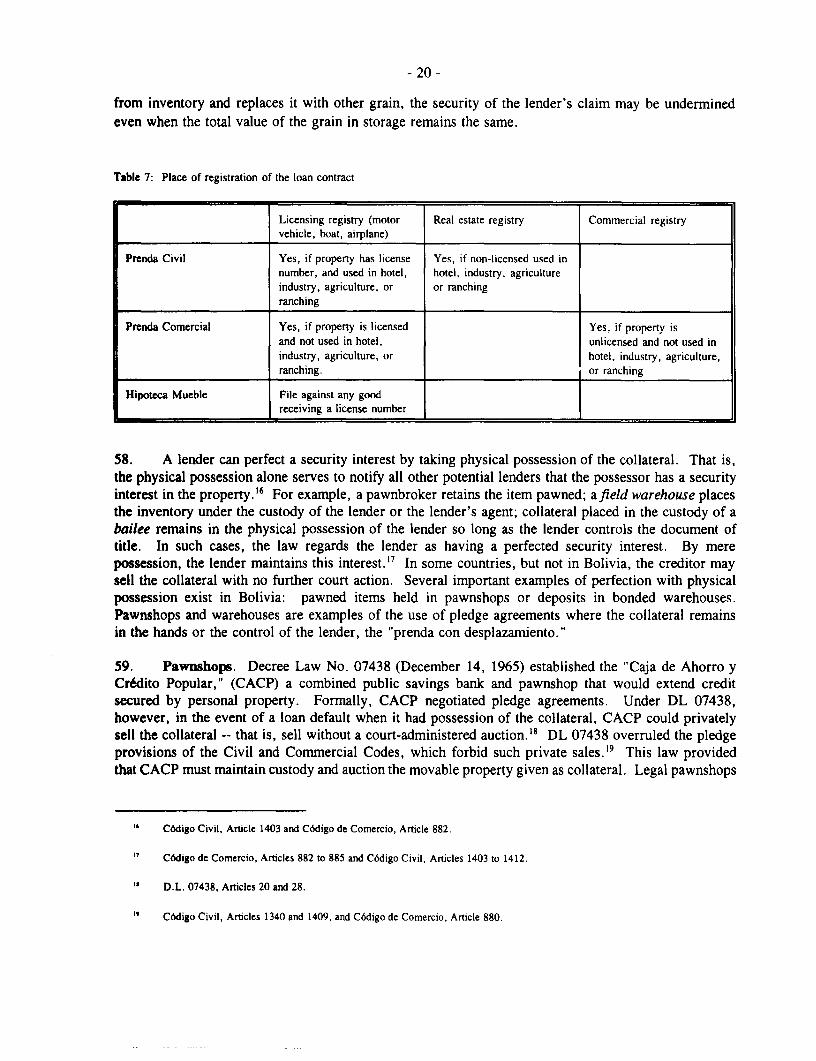

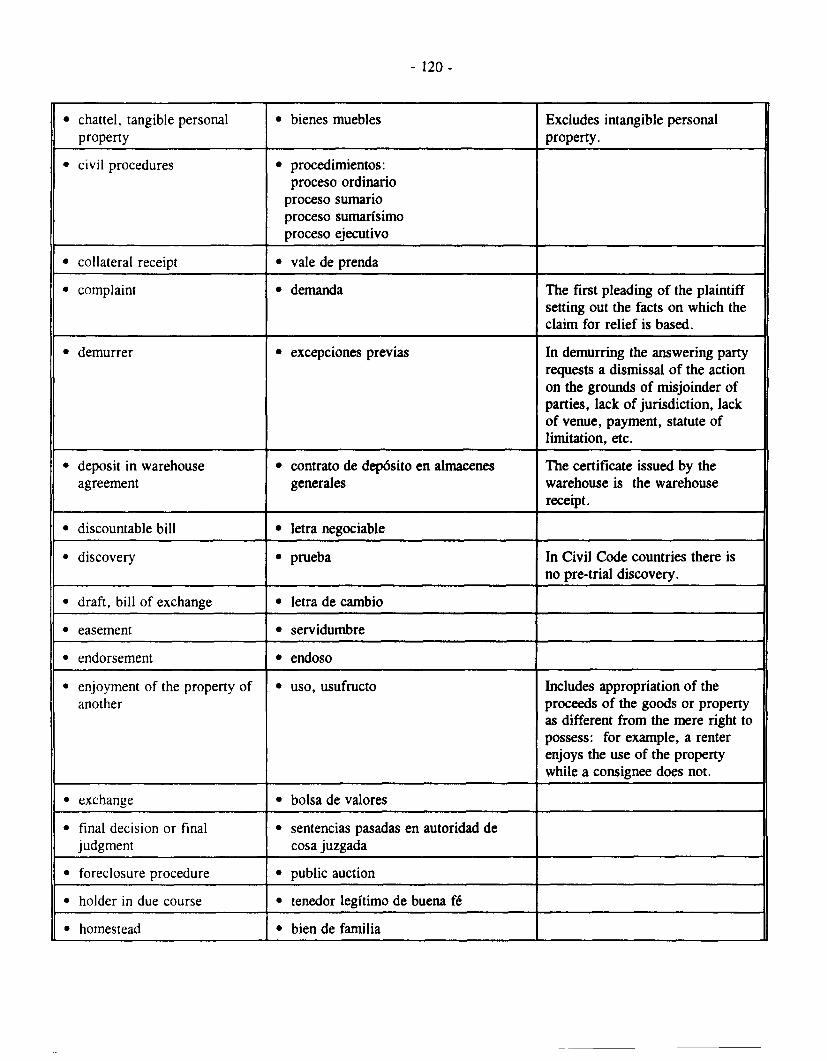

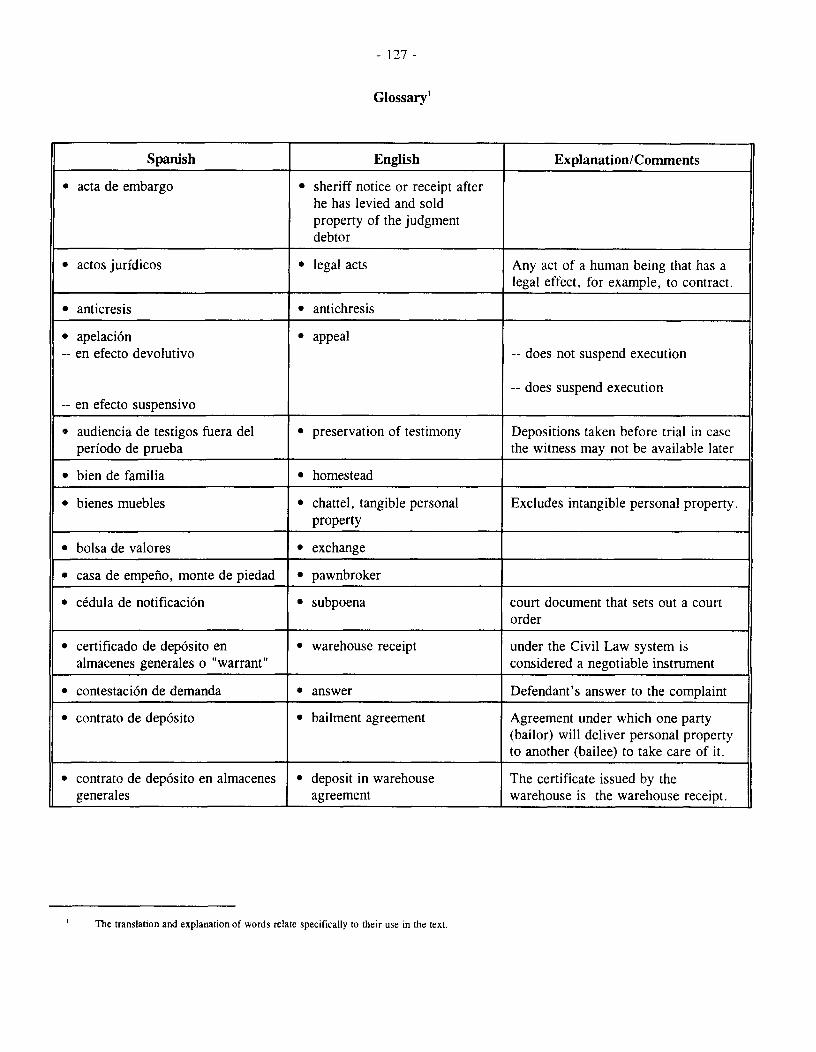

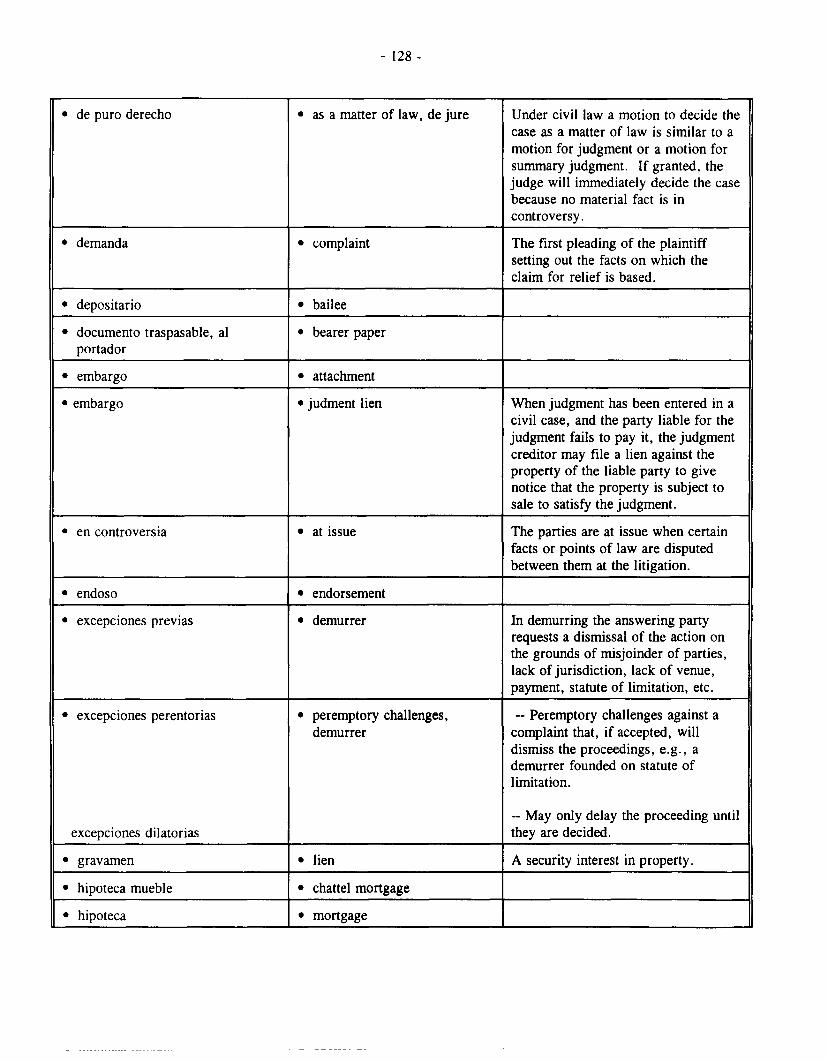

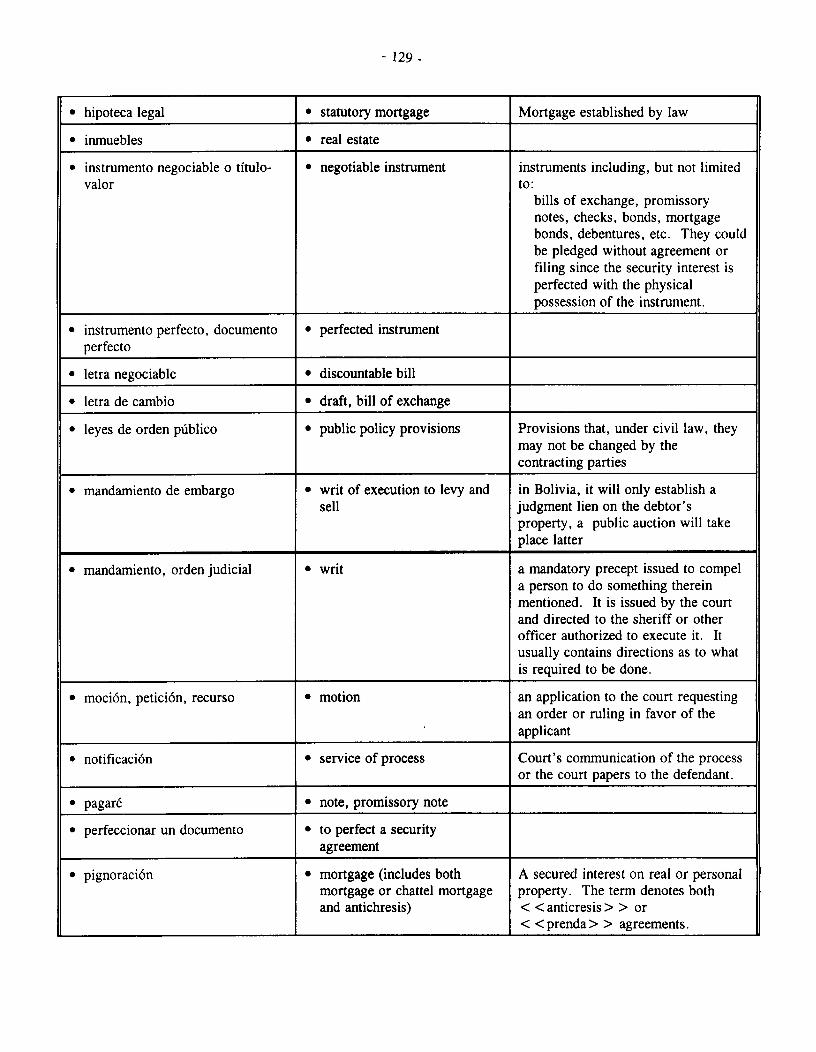

Glossaries: English/Spanish .. . - 119 -

Spanish/English .. . - 127 -

MAP (IBRD 16591)

Executive Summaary

i. In Bolivia, banks supply most of the loans to the private sector. Bolivian banks usuallyaccept only real estate as collateral for these loans, or the personal guarantee of someone whoowns real estate. They usually will not accept inventory, accounts receivable, livestock orindustrial equipment as collateral without demanding a supplemental guarantee based directly orindirectly on the ownership of real estate.

ii. These policies:

* Make it difficult for anyone without real estate to finance the purchase ofequipment, inventory, or livestock.

Limit access to credit by business enterprises in rented quarters, by farmers whowork rented land or have unclear title, and by all who don't own real estate.

* Limit profitable and socially useful lending by banks, as well as credit sales byindustrialists, importers, and merchants.

Make non-bank credit expensive, because lenders find collateral other than realestate very risky.

Deprive lenders and borrowers of due process of law, by misusing the punitivesanctions of the criminal law to substitute for inadequate civil enforcement ofcontracts.

Broadly, these lending policies lead to high interest rates, low volumes of lending,investment rates that fall short of socially profitable needs, and lower output and incomes.

Problems in Securing Loans Against Movable Property

iii. Why is credit so tightly linked to urban real estate and large rural land holdings inBolivia? Not because of low income, low growth rates, or the relatively small size of thecountry. Nor is there evidence of excessive conservatism by commercial banks, disinterest inthe needs of commerce, or excessive restriction by the Superintendency of Banks. Rather, thislink arises from Bolivian law and legal procedures.

iv. Lenders regard loans secured only by movable property and equipment as more risky thanloans secured by real estate; this is correct:

- ii -

* Inadequate legal definition of collateral and guarantees makes it impossible tocover some important economic transactions with legally-recognized agreements.

* The law permits only complex and time-consuming measures for repossessingcollateral, procedures that take longer than the economic life of many movableproperty.

* Inadequate registries make it hard for lenders to trace claims, pledges andmortgages and to identify their collateral in the eyes of the court.

v. Movable property typically depreciates rapidly with time and use. If collection procedurestake too long, such property has little value as collateral. In an examnination of over 500 debtcollection cases, the average collection time was over two years. Lenders, understandably,require other forms of collateral.

Ad Hoc Solutions to the Collateral Problem Have Failed in Bolivia

vi. Lenders and borrowers, struggling to make profitable and socially beneficial deals despitethe inadequacies of laws and legal institutions, go beyond the law. They use postdated checksto guarantee payment and send the borrower to jail in the event of default. They use baileeagreements that subject the bailee, typically a family member of the borrower, to jail if thecollateral is not delivered. Nearly a third of the people in jail in La Paz -- and 60 percent of thewomen -- are there because debt collection has been criminalized. Debt-related "crimes" accountfor more prisoners than murder, theft, drugs, or rape.

vii. Because these ad hoc solutions convert ordinary commercial risk into criminal risk, theseare not good remedies. Where ordinary businessmen outside Bolivia face the prospect of lossif they default on a loan, Bolivian businessmen face the prospect of jail. Understandably,potential sellers hesitate to sell on credit, and potential buyers hesitate to buy on credit. Lenderswith important reputations to protect, like banks, will not use these illegal methods to protectclaims on movable property; for banks, illegal solutions are not solutions at all.

The High Economic Cost of the Collateral Problem

viii. Breaking this tight link between access to credit and ownership of real estate requireschanging the law so that more lenders would find it profitable to make loans secured by movableproperty. This change could provide large and broadly distributed economic benefits.

Banks would gain from undertaking profitable loans presently closed to thembecause of excessive collateral risk.

- ill -

* Manufacturers and dealers in equipment, fertilizer, seeds, and grains couldextend their own credit to buyers.

* Banks could accept the loans arising from such credit sales as collateral for otherloans that would let these manufacturers and dealers sell more on credit.

* Other financial intermediaries such as leasing companies could borrow to financesales, accounts receivables, and machinery.

* Potential buyers who now lack access to credit because they cannot offer realestate collateral could borrow in the private sector for productive loans using themovable property itself as collateral.

ix. The overall benefit to the Bolivian economy would arise from the wider use of equipmentand working capital in projects where it is profitable but, at present, difficult to finance. A roughestimate of this benefit indicates that -- with the drop in interest rates that might be expected fromimproved collateral -- the demand for equipment could rise by about $1 billion. That expandeduse of equipment could increase output by an estimated $230 million to $330 million, about3 percent - 4 percent of Bolivian GDP.

Options for Solutions

x. Addressing this problem requires revising Bolivia's Laws, improving legal registrysystems for those commercial and civil contracts that create security interests, and speeding upthe process for settling claims. The government of Bolivia has several options.

Change the Law to Permit a Broader Range of Security Interests to Cover all EconomicallyImportant Transactions:

xi. Enact a new law on secured transactions for business and consumer borrowers thatincludes substantive and procedural rules that:

* Expand the range of assets that can serve as collateral.

* Regulate floating security interests for all secured transactions and agreements,using commercial inventory as collateral.

* Regulate accounts receivable as collateral, avoiding the transfer of accountsrequirement.

* Give a clear perfection of security interest in the goods sold on credit.

- iv -

* Establish clear regulations for disclosure of fees, interest rates, and other termnsof lending.

Accelerate the repossession and sale of collateral:

In the short-tern:

* Apply rapid resale to all movable collateral. Regulate or amend Article 171of the Civil Code to clarify that its application is not limited to fruits andvegetables, but applies to all movable property that decline in value (si hubierepeligro de perdida o desvalorizaci6n) in an amount sufficient to endanger thecollateral because of the long time required to litigate repossession and sale.Regulate or amend the law to clarify that the judicial power to order sale in themost convenient way (podra ordenar la venta en la forma mas conveniente)should include sale controlled by the creditor.

* Clarify rapid repossession procedures. Regulate or amend Article 162 of theCivil Code, which gives the court the power to act rapidly, to set specificprocedures for the rapid repossession of movable property.

(Clarify which contracts pernit rapid repossession and sale. Regulate oramend the law to provide that rapid repossession and sale procedures can applyto several important secured transactions contracts such as right of retention(Commercial Code, Article 812); the right of adjudication related to the pledgewithout transfer of possession (Civil Code, Article 1427); and to the conditionalsale or sale with retention of title (Commercial Code, Article 839).

Draft sample contracts. Include model standard contract forms for seller credit,specifically a standard contract for business borrowers, negotiated under freedomof contract (Commercial Code, Article 786 and Civil Code, Article 454),providing that the seller can retain title to the goods. For bank credit: usepledge-without-transfer and chattel mortgage agreements when lending againstmovable property.

In the long-term:

* Change the law. Let private parties bypass the court procedure for executionof judgment by allowing them to write contracts permitting harmless repossessionso that the creditor may repossess collateral, to sell it through private salecontrolled by the aggrieved lender or through judicial sale without appraisal.This procedure will also let private parties bypass existing auction procedures.

Improve Legal Registries:

xii. After the law has been changed to make it economically useful to register security interestagainst movable property, reform the registries:

* Index and computerize the registries in which secured claims are registered.* Computerize and modernize the Commercial Registry.* Expand the use of equipment registration at the Real Estate Registry.* Strictly enforce the public access requirements to government registries.* Set targets for improved performance and maintain public records of the amount

of time required for each step in the registration process.

How Legal Restrictions on CollateralLinit Access to Credit in Bolivia

I. Introduction

1. In Bolivia, most lenders require real estate as collateral. This practice makes it very difficultfor merchants, mine owners, industrialists, professionals, and farmers to borrow againstequipment, inventory, crops, or anything else they might use in the course of their trade orbusiness.

2. This paper asks why such a limited range of property should serve as collateral for loans.It finds the answer in the Bolivian legal, judicial, and regulatory systems: the court systemoperates very slowly and the system of laws makes it difficult for parties to make loan contractsthat can bypass the courts for their full enforcement.

3. This paper aims at both economists and lawyers. The economic problem is relatively simple:collecting any debt in Bolivia is expensive and takes a long time. Only the most durable andvaluable collateral is worth anything in such a system; therefore, most loans are ultimatelysecured by urban real estate, which will last beyond the time expected for a court decision andhas great enough value to cover at least the minimum cost of collection. The typical piece ofindustrial or agricultural equipment is worth less than the typical real estate holding and, unlikereal estate, typically falls in value with age. For lenders facing high fixed legal costs ofrepossession and sale, equipment is much less attractive as collateral than land.

4. This problem has complex legal and judicial roots. Consequently, this paper covers theseissues at a level of detail that may seem tedious to some legal readers; this is regrettable butunavoidable. It is important to distinguish technical legal terms from common usage. To indicatetechnical legal terms for the non-legal reader, italics are used for English legal terms, withSpanish terms in parentheses. This also identifies legal terms for lawyers trained in only one ofthe legal systems, civil or common law, relevant to discussions in this paper. In most cases,these terms appear in the appended glossary. In some cases, differences between the civil andcommon law usage means that no equivalent term exists in the other language. In that case, theglossary sets out the sense in which the term is used in this paper.

- 2 -

5. Chapter II discusses how Bolivian lenders actually secure their loans in the face of thesesevere problems that restrict the use of collateral. Chapter III discusses how the legal treatmentof collateral affects credit and, in turn, the financing of investment and economic growth.Chapter IV introduces the legal issues: it defines property, explains how claims are secured bycollateral, and discusses how the legal and judiciary system in Bolivia enforces those claims.Chapter V presents the general issue of the creation and perfection of security interests and howthey are handled in Bolivia. Chapter VI describes how a Bolivian creditor would obtain judgmentfrom the court in the event of a breach of a financial contract; it explains why the process takesa long time and sets out some options for shortening the process. Chapter VI discusses how aBolivian creditor would enforce such a judgment; it also explains why that process is soprotracted and discusses options for reform.

6. Appendix I sets out a back-of-the envelope estimate of the economic cost of the collateralproblem in Bolivia. Appendix II presents the analysis of debt collection cases in Bolivian courts.Appendix III contains the terms of reference for a general law of secured transactions for Bolivia,prepared by Professor Alejandro Garro. Appendix IV has the terms of reference for a series ofshort-term solutions that address aspects of the collateral problem.

II. How the Laws Governiig Financial Instruments Affect Credit and Economic Growth

7. Bolivian law envisions two broad classes of private borrowers: commercial banks andeveryone else. As a practical matter, the debt of non-bank private borrowers is backed by realestate: property other than real estate cannot readily serve as collateral. This system limits thevolume of credit available for productive transactions. It allocates credit away from farmers whorent, from farmers with unclear title to land, and from manufacturers who need large amountsof machinery relative to their real estate holdings. It allocates credit toward real estatedevelopment, and keeps credit out of the hands of those without land. This credit system reduceseconomic growth and directs the benefits of growth away from the poor.

How Do Borrowers Back Their Loasm?

8. Private lenders care deeply about how their debts will be repaid. Therefore, they care aboutwhat backing the borrower offers. Commercial banks borrow by taking deposits, by sellingcertificates of deposit, or by issuing bonds. They back their debts with their real property, theirinvestment assets, and their expected profits. At one level, these anticipated profits depend onthe bank's expected interest costs, interest receipts, and loan performance. At a deeper level,however, the quality of the backing that the bank offers depends indirectly on the quality ofclaims against the government. First, because the de facto and de jure policy of the Boliviangovernment on insuring depositors effectively provides a state guarantee to some of the debt ofcommercial banks. The state does not offer comparable guarantees for non-bank privateborrowers. Second, because how well a commercial bank services its own debt will depend ongovernment policies -- how freely the Central Bank rediscounts the private loans presented to itby the commercial banks, and how aggressively the bank regulators force banks to recognizelosses.

9. What backs the promises to repay by other borrowers -- consumers, industrialists, merchants,and farmers? For some loans to individuals, collateral is not necessary. To some degree,individuals, like nations, will service debts because the gain from future, larger loans exceeds theburden of servicing past, smaller loans. Accordingly, revolving funds that lend for recurringneeds, like seeds for farmers, often show high servicing rates. In other cases, communitypressure ensures repayment. Often community or church cooperative lenders show high servicingrates, and, no doubt, some individuals can be counted on to repay loans because they have strongmoral views that loans should be repaid. These loans are unsecured but they have good backing.

10. But, even while some lenders will make unsecured loans, if they have intimate knowledgeof the borrower, few lenders will make substantial loans under such conditions. For lenders inmost countries, good collateral and good collection make good loans. In most cases in Bolivia,

- 4 -

such borrowers secure their promises to pay by either mortgaging real estate to secure theirloans' or by giving evidence of the ownership of real estate that could be attached to pay loans.Such borrowers give personal guarantees,2 which involve a generalized pledge of their wealth,or use a surety of the wealth of another. Few Bolivian borrowers secure their loans by pledgingdurable equipment or personal belongings. This situation has roots in problems of Bolivian lawand legal procedures.

Collateral Problems Reduce Investment and Growth

11. How important are these legal obstacles compared to other factors in explaining highinterest rates or reduced investment? Do legal problems in creating collateral explain the highinterest rates facing borrowers who secure loans with real estate? Most likely, they do. Considersome frequently offered alternative explanations:

12. Macroeconomic instability and high bank intermediation margins. Only a smallamount of the high interest rates facing Bolivian borrowers arises from macroeconomic factorsor high bank intermediation spreads. Loans to individuals without real estate in Bolivia runbetween 36 percent and 72 percent per year, versus a range of 9 percent to 14 percent in theUnited States -- a difference of 22 - 63 percentage points (Table 1).

13. Of that difference, about 8.5 percentage points arises from the risk of macroeconomicinstability in Bolivia and another 5.5 percentage points arise from higher bank intermediationspreads. The additional interest rate differential -- 14 to 50 percentage points -- arises fromproblems with movable property as collateral.

14. Put a different way, half to three-quarters of the higher interest rates observed in Boliviaarise from the collateral problem.

For lawyers, "real property" refers to real estate as distinct from other physical or 'personal property.' For economists, "realproperty" connotes both real estate and 'personal property,' as distinct from "nominal" assets like paper securities.

Broadly speaking, under Bolivian lav, borrowers can give lenders one of two guarantees: a real guarantee or a personal guarantee.Under a real guarantee, the creditor has a security interest in a specific asset of the debtor, such as a mortgage on the debtor's houseor a pledge on the debtor's equipment. The lender is then a secured creditor who holds a position in the line of priority to recoverthe amount that he is owed from the proceeds of the eventual sale of that specific piece of property. tJnder a personal guarantee,the lender is an unsecured creditor because the borrower will [respond] with any and all of his property, giving the creditor no specificinterest, priority, or security interest against any specific property (C(6digo Civil, Art. 1335). In such a situatiol, the lender-creditorwill be unsecured until a court orders an attachment or a judgment lien recorded in the appropriate registry. Whetn the creditorrecords such a court order, the creditor creates a specific lien on a specific asset of the debtor; the lender then becomes a lien creditorwith respect to that specific asset, and will remain an unsecured creditor for any deficiency judgment (the creditor will have a personalguarantee on any of debtor's assets until the total balance due is paid). Under Bolivian law, the parties need not stipulate in theircontracts the debtor's personal guarantee: a personal guarantee of the debtor always exists under the law. without the need to providefor it specifically.

Table 1: Explaining High Interest Rates for Loans in Bolivia

United States Bolivia Difference

I. Greater Macroeconomic Risk in Bolivia:[7There is no risk that the U.S. government will be unable to pay its bonds in dollars, because it has the legal monopoly onprinting dollars. The government of Bolivia must get its dollars by raising taxes or cutting spending. These are politically

difficult actions and lead to perceptions of macroeconomic risk. The differnce between the U.S. interest rate on dollar bonds

and the Bolivian interest rate on dollar bonds is entirely macroeconomic risk.

Government borrowing rate in dollars | 3.5% 12.0% 8.5%

2. Higher commercial bank intermediation spreads in Bolivia:[Commercial banks in Bolivia have less competition than do U.S. banks so they charge more to intermediate funds. Reserverequirements are similar and do not explain differences in intermediation spreads]

Prime business rate 6.0% 20.0% l

--Spread over govemment borrowing rate 2.5% 8.0% 5.5%

3. Movable property is less adequate collateral for loans in Bolivia:

[Differences in macroeconomic risk and intermediation cost apply equally to loans secured by real estate and loans secured bymovable property. In the United States, loans secured by movable property have interest rates close to the interest rates onmortgages; in Bolivia, banks do not make loans secured only by movable property and informal lenders charge rates of 36percent to 72 percent]

Mortgage Interest Rate 8.25% (25 year) 18% (5-10 years)

Equipment/Automobile Loan 9.30% (4 yr) - 12.7% (10 yr) 36% - 72%

FSpread 1.05% - 4,45% | 18.00% - 54.00% 13.55% - 50.00%

Source: U.S. data taken from Federal Reserve Bulletin, July 1993, tables 1.35, 1.53, 1.56; Bolivian data from the Bulletin of the CentralBank. Rates for loans secured by movable collateral based on evidence given during interviews.

15. High transactions costs relative to loan size. One explanation offered for the reluctance to lendfor equipment rests on the supposed small size of such loans. This doesn't hold up well underexamination. In fact, about three-fourths of the loans made by Bolivian commercial banks are forUS$10,000 or less. Loans of that size for movable equipment are common in the United States, wherethe labor costs of loan processing are higher. High transactions costs can't explain the reluctance of theBolivian banks to make these loans. Their reluctance, rather, arises, as the bankers themselves repeatedlyand consistently stress, from their belief that the movable property do not offer much value as guaranteesfor loans.

16. Structure of banking. Some explanations of high interest rates rest on allegations ofconservative bank lending policies. But banks cannot substantially liberalize their policies regardingcollateral unless the underlying quality of collateral policy is changed. Without reform, loans securedonly by movable property do present substantial additional risks. Where high bank intermediation spreadsarise from too little competition, the collateral problem limits development of non-bank lenders that couldcompete with banks and lend for movable equipment.

- 6 -

Collateral Problems Distort Credit Allocation

17. Restrictions on collateral distort Bolivian economic activity. Economic sectors in Bolivia, aselsewhere, differ substantially in their most profitable combinations of real estate, equipment, and humancapital. Since real estate security is better in Bolivia, the legal and regulatory environment for lendingoperates to lower the risk of lending for real estate; this permits lower interest rates for such loans andleads the market to allocate more capital toward operations intensive in real estate. Hotels andcommercial buildings will be relatively easy to finance. By contrast, though, a factory operating in rentedspace will find it difficult to finance machinery because it cannot mortgage the real estate. A servicecompany -- such as a bus, taxi, or road transport company -- that requires large inputs of durableequipment and relatively little real estate will also find financing difficult. A landless farmer, or onewhose land is covered by murky homestead provisions, will have trouble financing equipment.

18. How much is it worth to address this problem? Appendix I sets out a rough estimate. In Bolivia,about 10 percent of commercial bank loans are granted using movable equipment as collateral; in theUnited States, about 40 percent. If fixing the problem of collateral led to a similar expansion in lendingand drop in interest rates, total lending for equipment could rise by as much as $675 million. Thatincrease in equipment use could increase Bolivian GDP by as much as $200 million a year, an increaseof about 2 percent.

Collateral Problems Narrow the Distribution of Credit

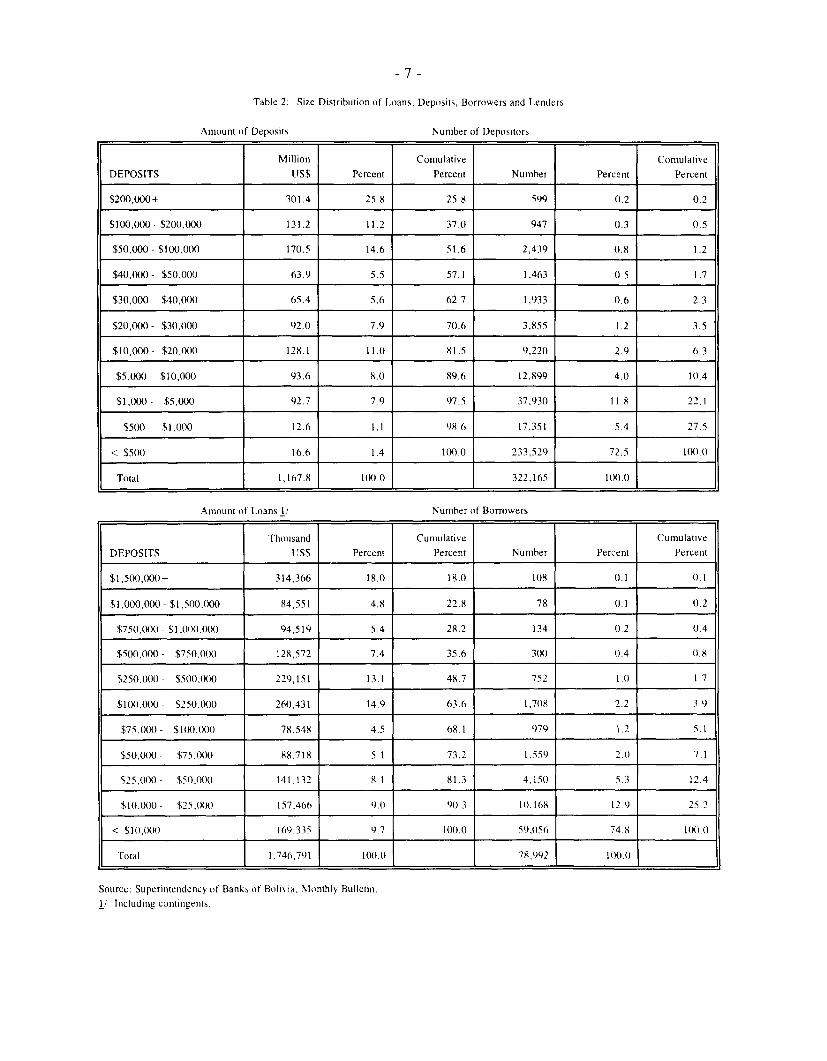

19. While both wealth and income are distributed quite unevenly in Bolivia, real estate is distributedeven more unequally. Indeed, Bolivia has one of the most concentrated patterns of land ownership inLatin America, with about 5 percent of the people owning about 95 percent of the land (Table 2).Problems with using movable property as collateral, therefore, lead the present system to distribute crediteven more narrowly than the distribution of wealth. In countries with different credit-granting systems,an employed person without wealth can borrow using movable property as security: a businessman inrented quarters might borrow to buy equipment or inventory, using these goods as security for the loan;a farmer on rented or inalienable land might pledge his equipment or his crop as collateral. PresentBolivian laws and legal procedures make such transactions nearly impossible. Not surprisingly, smallfarmers, small businessmen, and the poor cannot borrow in the formal banking sector. Nor can they getmuch credit from merchants or machinery dealers because those businesses, in turn, cannot get credit tofinance their movable property: inventories and accounts receivables. Instead, they must borrow in theinformal or illegal sector, where rates are higher than they would be if the legal framework permittedcompetition, and where borrowers are often subject to extralegal collection techniques.

Table 2: Size Distribution of Loans, Deposits, Borrowers and Lenders

Amount of Deposits Number of Depositors

Million Comulative Comulative

DEPOSITS US$ Percent Percent Number Percent Percent

$200,000+ 301.4 25.8 25.8 599 0.2 0.2

$100,000 - $200,00() 131.2 11.2 37.0 947 0.3 0.5

$50,000 - $100,000 170.5 14.6 51.6 2,439 (.8 1.2

$40,000- $50,(0() 63.9 5.5 57.1 1,463 0.5 1.7

$30,000- $40,000 65.4 5.6 62.7 1,933 0.6 2.3

$20,001)- $30,000 92.0 7.9 70.6 3,855 1.2 3.5

$10,00(0- $20,000 128.1 11.( 81.5 9,220 2.9 6.3

$5,00) - $10,000 93.6 8.( 89.6 12,899 4.0 1(0.4

$1,000 - $5,000 92.7 7.9 97.5 37,93() 11.8 22.1

$500- $1,00(0 12.6 1.1 98.6 17,351 5.4 27.5

< $500 16.6 1.4 1((.( 233,529 72.5 10().(

Total 1,167.8 1(XI.0 322,165 1()(1.()

Amount of Loans 1/ Number of Borrowers

Thousand Cumulative Cunmulative

DEPOSITS US$ Percent Percent Number Percent Percent

$1,500,0(0)(+ 314,366 18.0 18.0 108 (1.1 (.1

$1,0(0,(X)( - $1,500,000 84,551 4.8 22.8 78 ().1 0.2

$750,000 - $1,0)0).0()(( 94,519 5.4 28.2 134 (0.2 (1.4

$500,00) - $750,000 128,572 7.4 35.6 30)0) 1).4 ().8

$250,0(X) - $5(0,((( 229,151 13.1 48.7 752 1.() 1 7

$1(0),00) - $250,000 260,431 14.9 63.6 1,71)8 2.2 3 9

$75,0(0) - $10(1),1000 78,548 4.5 68 1 979 1.2 5.1

$50,)0 - $75,0(00 88,718 5.1 73.2 1,559 2.( 7.1

$25,000 - $50,000 141,132 8.1 81.3 4,15(0 5.3 12.4

$1(0010 - $25,(0(N) 157.466 9.() 90.3 1(),168 12 9 25.2

< $1(,0(1() 109,335 9.7 1()().() 59.056 74.8 10.()

Total 1,746,791 1()().() 78,992 1()().()

Source: Superiltelldenley of Banks of Bolivia, Monthlv Bulletih.

I/ Including contingents.

-8 -

Conclusion

20. These effects of law on the allocation and distribution of credit reflect the rational responses ofborrowers and lenders to the legal structure of the country. These allocative and distributive effectswould not, however, follow in an environment where the legal structure made personal property bettercollateral, as it does, for example, in Trinidad, Jamaica, the United States, and Germany. A differentlegal structure would yield lower interest rates without lowering risk to lenders. That would permit moreinvestment in equipment at the same level of profit and, consequently, produce a higher rate of economicgrowth.

21. The policy question facing Bolivia revolves around devising an alternative legal structure thatcould meet these economic needs and yet remain at least as politically acceptable as the current structure.Setting up public institutions that lend for the purchase of movable property despite these legal problemswill not solve the problem -- such institutions would simply find themselves with non-collectable loans.They would fail for precisely the same reasons that private lenders originally refused to make such loans.

- 9 -

Table 3: Gini index values for concentraion of land ownership

in 54 couz,ties a!

Number of countries in range

Range of index values Latin American countries Other non-industrial countries b/ Industrial counries cl

.80 and over 12 3 3

.70to .79 5 4 4

.60to.69 0 7 4

.50 to .59 0 4 3

.40 to .50 0 3 3

Total 17 21 17

Gini values for selected Latin American countries

Bolivia .94 Brazil .84

Venezuela .89 El Salvador .83

Peru .88 Uruguay .82

Guatemala .86 Dominican Republic .79

Ecuador .86 Honduras .76

Colombia .86 Nicaragua .76

Argentina .86 Panama .74

Mexico .69

a Most available data are frouitn e 1960s For three countries, irtdex values before and after land reform were available. Pre- and post-refoim valucs are, respecsely:Mexico, 0 96-0 69, Egypt, 0 81-0 67; Taiwan, 0.65.0.46

b/ Countries in Asia, North Africa, Southern Europe, plus Jamaica.

c/ Less than 30 percent of labor force employed in agriculture.

Source Samuel P Huntington, Political Order in Changing Societies (New Haven, Conn Yale University Press, 1968); Table 6.2, p. 382, cited an Malcolm Bale, LATenare in Venezuela, IBRD 1992

- 10 -

III. Extralegal Repossession and Sale of Collateral

22. If Bolivia could use property other than real estate as collateral, it would open up a large numberof profitable transactions between lenders and borrowers. These transactions would increase Bolivianeconomic efficiency, production, and incomes. Not surprisingly, Bolivians have devised ways to bolsterthe value of personal property as collateral, but these solutions are not legal: the postdated check (chequepostdativo), theft of collateral, police harassment, misuse of the bailment (depositario) agreement, misuseof sale with an option to repurchase (venta con pacto de retroventa), and illegal pawnshops. This chapterexplains how these Bolivian laws and legal procedures criminalize these business transactions.

23. The postdated check. The borrower writes a check to the lender for the amount of the loan butdoes not date the check. If the borrower does not pay the lender, the lender can threaten to deposit thecheck. If the borrower has insufficient funds, the check bounces; the borrower who wrote the check hascommitted a criminal offense.3 The lender can present the returned check to the police station and havethe borrower arrested. While using postdated checks to guarantee loans is a criminal offense for bothborrower and lender, respondents could cite no case of a person jailed for accepting a postdated check.

24. The postdated check, Dickensian though it is in its workings, is a major form of guarantee inBolivian lending. Half the inmates in La Paz jails are imprisoned for non-drug offenses; of these, halfare imprisoned for the crime of writing checks without funds. The mission interviewed approximately15 of these inmates. In each case, the "check without funds" had been written as the guarantee of abusiness transaction and in each case the prisoner was a small business operator. Those imprisonedtypically lacked the family connections necessary to raise the funds necessary to cover the check. Theyremain in prison until the check is covered, even if that means staying imprisoned beyond the four-yearmaximum penalty for crimes related to the use of the check. For imprisoned women this can take on aparticularly disturbing dimension, as they bring their children to the jail.

25. Abuse of the bailment (dep6sito). Under a bailment agreement, a third person is named bailee(depositario). The lender drafts the agreement requiring the borrower to name a close relative as thebailee, such as the wife, mother or child. That person is responsible for turning over the collateral inthe event of nonpayment. Failure to turn over the collateral is a criminal offense and the bailee can bejailed.

26. Misuse of the sale with reservation of title (venta con reserva de propiedad). The lender hasthe borrower execute a sale document granting the lender ownership until the total purchase price ispaid.4 If the borrower fails to repay, the lender gets a summary judgment and the property is passed

Codigo de Comercio, Art. 602, 640; C6digo Penal, Art. 204-205. See also D.S. 1943, March 6, 1950 which defines checks drawnwithout funds as a swindle (estafa) punishable under the C6digo Penal, Art. 637.

4 The sales agreement under reservation of title does not constitute a security interest, but merely an agreement specifying the time atwhich ownership passes to the buyer. See Alejandro M. Garro, 1990. "The Reform and Harmonization of Personal Property SecurityLaw in Latin America," Revista Juridica de la U.P.R., V59:1:90.

- 11 -

to the lender. Sometimes the amount of the loan is a small fraction of the value of the collateral, so thedebtor loses far more equity than would be the case with legal foreclosure procedures. The abuse arisesfrom the frequent occurrence of unconscionable contracts where the loan is for only a small fraction ofthe value of the property. Under conventional foreclosure procedures, the borrower receives thedifference between the selling price of the collateral and the loan due; in this case, the borrower does not.Such contracts are typically unenforceable because they are unconscionable, but a borrower withinsufficient funds to exercise the option to repurchase may also lack the funds for a lawyer to press thecase and will lose the property anyway.

27. Police harassment. Some lenders avoid judicial proceedings by requesting police investigationof a person whose payments are in arrears. Such investigations can lead to the debtor being jailed forminor infractions, apparently unrelated to the debt. Such harassment continues until the debt is servicedor the collateral returned. Legally, the police have no such function; in practice, creditors prepared topay the police can sometimes obtain their cooperation in such efforts.

28. Forcible repossession of collateral. Some industrial countries permit harmless repossession:a creditor may seize collateral for a loan so long as there is no breach of the peace, and a debtor wrongedin the process can sue for redress. In Bolivia such peaceful seizure would, strictly speaking, be theft.Nonetheless, creditors on occasion simply seize the collateral. In some cases, repossession is doneharmlessly; in other cases, bands of armed men are sent to collect equipment. It is then up to the debtorto use the painfully slow legal system to recover the property if it was wrongfully seized.

29. Illegal pawnshops. Informal lenders apparently grant loans with personal property as collateral.They charge interest rates above the usury ceiling and illegally privately sell collateral. It is difficult topass and enforce consumer protection legislation stipulating publicly quoted rates and clear proceduresfor privately selling collateral. The current practice ensures that the poor pay higher interest rates thanthey would if legal lenders competed under clear disclosure rules.

30. Extralegal solutions are socially undesirable; lenders averse to taking risks will avoid them,making interest rates and transactions costs higher than they would be otherwise. Borrowers averse totaking risks will also avoid them, because sanctions in the extralegal market expose them to far greaterrisks to person and property than would sanctions in a country whose laws facilitated these transactions.The fundamental issue is that private parties can contract around many defects in governmentperformance, but they will have great difficulty contracting around defects in the government's provisionof a legal framework in which to exercise the right to contract.

31. Arrest and imprisonment of debtors. A credible criminalized debt collection mechanism mustactually imprison debtors who fail to pay. In Bolivia, those who used the foregoing security devices aretypically jailed for check without funds, fraud, or abuse of confidence.

32. Who gets arrested? Offenders can be arrested and detained or they can be arrested andsubsequently freed. Over the period 1990-1993, about 20 percent of those arrested and detained andabout 40 percent of those arrested and freed were arrested in connection with an offense broadly

- 12 -

associated with substituting criminal sanctions for collateral -- about 1/3 of those arrested in La Pazbetween 1990 and 1993 (Table 4).

Table 4: Arrests, annually, with and without detentionTotal and arrests related to the use of checks as collateral

Year 1990: 1991: 1992: 1993 (Jan-Mar): Total

19993)

Year arrested arrested, arrested arrested, arrested arrested, arrested arrested,and not and not and not and notdetained detained detained detained detained detained detained detained

bad check 75 1215 98 942 81 1227 12 495 4145

fraud 61 295 43 248 54 170 25 72 968

abuse of confidence 11 112 16 85 10 39 8 12 293

total, collateral- 147 522 157 1275 145 1436 45 579 4306related (est)

total arrested or 541 2869 661 2654 834 2832 314 971 11676detained for allcrimes

| Collateral-related 27.2% 18.2% 23.8% 48.0% 17.4% 50.7% 14.3% 59.6% 36.9%(es() as a percentage|lllllllllof total crimes l l l l l l l l l

Source: Corte Superior del Distrito, Presidencia, La Paz, Bolivia. Statistics supplied to the mission, April 19, 1993

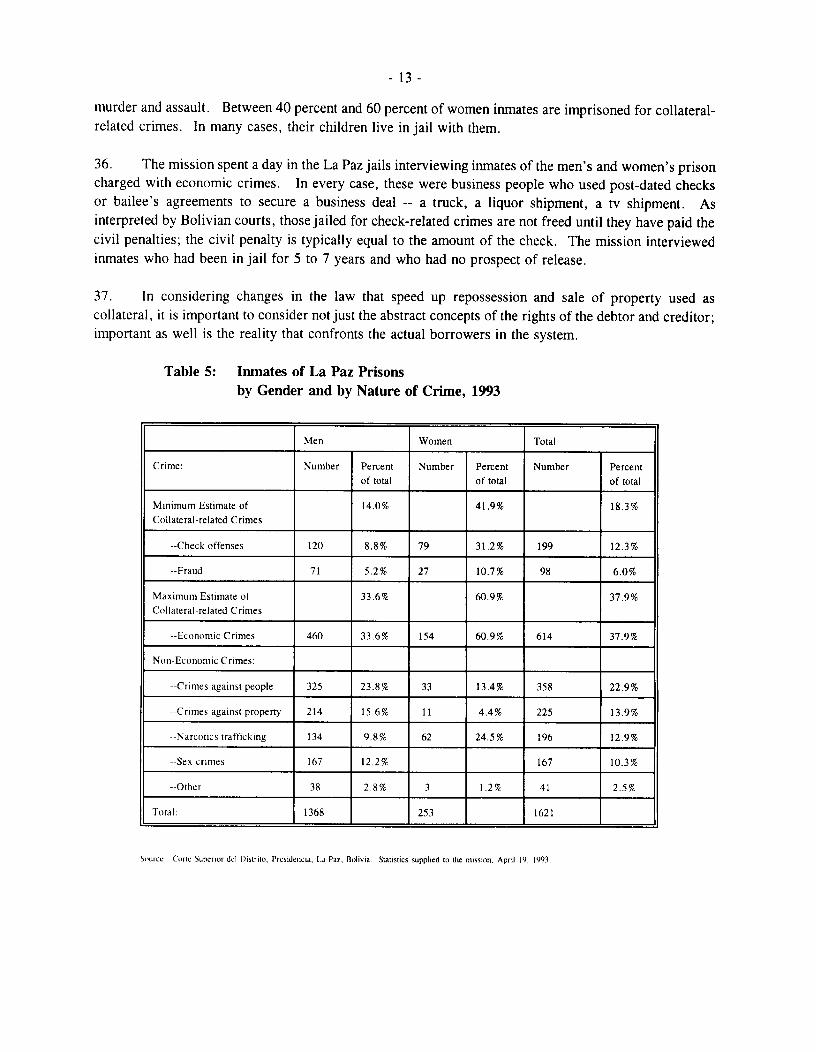

33. Who is in jail? Because different groups of offenders get jail sentences of different lengths, thenumber of people in jail for different crimes may differ from the number of people arrested for differentcrimes. Counting as collateral-related crimes only check offenses and "fraud," typically both used inpost-dated check guarantees, would place the number of inmates imprisoned for collateral-related crimesat just under 20 percent of the jail population (Table 5). This represents a heavy concentration of womeninmates -- over 40 percent of the women in jail are there for check and fraud offenses.

34. A larger category of "economic" crimes would embrace other collateral-related offenses -- forexample, misuse of bailee and trustee agreements. About 40 percent of the La Paz jail population isimprisoned for "economic crimes" -- about 2/3 of the women and about 1/3 of the men.

35. Economic crimes represent the largest single cause of incarceration in La Paz -- more thanmurder, theft, narcotics, or rape. Indeed, even narrowly defined collateral-related crimes like check andfraud offenses are a more important cause of imprisonment than theft, drugs, or rape and a close tie for

- 13 -

murder and assault. Between 40 percent and 60 percent of women inmates are imprisoned for collateral-related crimes. In many cases, their children live in jail with them.

36. The mission spent a day in the La Paz jails interviewing inmates of the men's and women's prisoncharged with economic crimes. In every case, these were business people who used post-dated checksor bailee's agreements to secure a business deal -- a truck, a liquor shipment, a tv shipment. Asinterpreted by Bolivian courts, those jailed for check-related crimes are not freed until they have paid thecivil penalties; the civil penalty is typically equal to the amount of the check. The mission interviewedinmates who had been in jail for 5 to 7 years and who had no prospect of release.

37. In considering changes in the law that speed up repossession and sale of property used ascollateral, it is important to consider not just the abstract concepts of the rights of the debtor and creditor;important as well is the reality that confronts the actual borrowers in the system.

Table 5: Inmates of La Paz Prisonsby Gender and by Nature of Crime, 1993

Men Women Total

Crime: Number Percent Number Percent Number Percentof total of total of total

Minimum Estimate of 14.0% 41.9% 18.3%Collateral-related Crimes

--Check offenses 120 8.8% 79 31.2 % 199 12.3 %

--Fraud 71 5.2% 27 10.7% 98 6.0%

Maximum Estimate of 33.6% 60.9% 37.9%Collateral-related Crimes

--Economic Crimes 460 33.6% 154 60.9% 614 37.9%

Non-Economic Crimes:

--Crimes against people 325 23.8% 33 13.4% 358 22.9%

--Crimes against property 214 15.6% 11 4.4% 225 13.9%

--Narcotics trafficking 134 9.8% 62 24.5% 196 12.9%

--Sex crimes 167 12.2% 167 10.3%

--Other 38 2 8% 3 1.2% 41 2.5%

Total: 1368 253 1621 .

Sotircc Coret Superior del Disirito, Presideiscia, La Paz, Bolivia. Statistics supplied to die missioin. April 19, 1993.

- 14 -

IV. Financial Instruments and Collateral: Overview of Leal Issues

38. Assets may have great economic value but be useless in credit transactions if the law does notpermit transfer of property rights in those assets. For example, mining machinery could representexcellent collateral for a loan in a legal system that permits the pledge of mining equipment, but not ina legal system that forbids it.5 Agricultural land may produce a good yield but be useless as collateralif the terms of occupancy forbid transfer of land rights or the seizure of the crop. For assets technicallyacceptable as collateral, such as a car or a lettuce crop, collection procedures may be so slow that thecollateral loses its economic value during the collection process.

39. Such restrictive legal institutions can have major effects on credit markets. Land reform thatmakes land inalienable makes farmers better off by ensuring they will always own land. It makes themworse off by preventing them from borrowing against the land. Under such a land policy, othercompensating measures are necessary to make it possible to seize collateral like cash crops or farnequipment, if the farmer is to receive secured credit at all. Similarly, when lengthier and more extensivelegal procedures are introduced to protect the rights of debtors, compensatory policies to maintain thespeed of these legal processes are necessary if those protected are to have access to credit.

40. These legal issues raise several general questions: What does the law view as property? Howcan individuals establish claim to property when they secure a transaction with an interest in thatproperty? If the borrower does not perform under the contract, how does the creditor obtaincompensation? If compensation is necessary, how does the creditor arrange for it, including seizure andsale of the collateral? When a court judgement is required for compensation, how does the creditorexecute that judgment?

Definition of Property

41. The law defines property. This paper follows the following definitions, typical in common andcivil law:

* Real Property -- real estate.

* Fixtures -- property physically attached to but not incorporated into real estate, like carpetsor most production machinery in a factory.

Bolivian law exempts mining equipment from the reach of all creditors. Bolivian lenders cannot legally accept movable personalproperty used in mining activities as collateral. Articles I to 10, 27 and 28 of the C6digo de Mineria states that they are 'goods ofpublic utility" (bienes de utilidad publica). Article 179 (Clauses9 and 10) of the Code of Civil Procedure, in conjunctionwith Article449 and 456 of the Commercial Code, states that property indispensable for the operation of the mine (or any business) cannot beattached to satisfy creditors' claims. So "protected," these citizens cannot buy such equipment on credit without offering otherproperty as a guarantee.

- 15 -

* Tangible Personal Property -- inventory, equipment, farm products, or consumer goods.

* Intangible Personal Property -- assignments of rights for payment of money, such as theaccounts receivable, promissory notes or documents of title (a warehouse receipt, apromissory note, or a bill of lading); intangible assets of a business may include its value asan on-going concern, good will, or the right to use a trademark, copyright, or patent.6

Structuring Claims Against Property

42. Claimants against property fall into two classes:

* General creditors having a general claim against a debtor's property.

* Secured creditors having a security interest in a specifically designated property of the debtor.

43. A security interest7 is "a right of satisfaction" from the property -- the collateral -- to which thesecurity interest is attached. When the collateral is sold or exchanged, the claim of the secured creditorwill be paid or "satisfied" in the order of its priority among all claims against the collateral.8 A securedcreditor has a security interest in the designated property of the debtor. This secured claim must besatisfied before any claim of the general creditor.9 The general creditor has a general claim against allpast, present or future properties of the debtor, but has no security interest in any specific property ofthe debtor."' A security interest in a designated property has priority over the general claim of a generalcreditor. "

44. Using security interests, firms can borrow from suppliers, merchants, or banks, and can offertheir inventory as security; they can borrow to buy equipment and secure their promises to pay with that

'This paper uses the term "movable property" to include tangible, intangible, and fixtures property.

7 The term security interest should be distinguished from securities. Securities are instruments that represent a general claim againstall the nonexempt assets and income of the issuing agent or corporation, such as stocks, bonds, commercial paper, certificates ofdeposit, or bank deposits.

Under U.S. concepts, a security interest is also an ownership interest in the property itself but less than full ownership.

For example, a mortgagee or pledgee is a secured creditor (Bolivian Civil Code, Articles 1360, 1397, 1398, 1405, 1406, 1427, and1428).

'° Bolivian Civil Code, Article 1335.

" Some important public-policy exceptions exist to this general rule: government liens for unpaid taxes, property that is exempt fromseizure for debts, and workers claims for severance pay and back wages are the most important] In the event that the securedcreditor's claim is not satisfied by sale of the collateral, the secured creditor has a general claim against the debtor's other propertyfor any deficiency balance.

- 16 -

equipment; they can borrow with loans secured by warrants that are issued by warehouses and representclaims on merchandise in the warehouse.

45. Security interests need not be created only against tangible personal property. They may becreated against intangible property, such as commercial contracts that economic agents use to assigndifferent property rights to the goods and services in which they deal. In most civil and common lawcountries, many types of commercial contracts exist: sales contracts to move goods from producer toconsumer; leases of goods that permit their use without ownership; consignments of goods that permittheir sale without use; contracts with carriers for the shipment of goods conveying no right to use or sell;contracts with warehouses for the storage of goods; assignments of accounts receivable; promissory notesissued as evidence of debt; documents of title; and rights to payment under letters of credit that ensurethat shipped goods are paid for before delivery.' 2 Security interests may also be created using a security(titulo-valor) as collateral: a lender could have a security interest in stock, bond, or a certificate ofdeposit. "

46. Each contract assigns property rights in a way that solves some economic problem; each contractmakes some improvement in economic efficiency. A commercially useful mechanism for secured loansmust minimally accomplish the following five basic tests:

1. It must cost little to create an enforceable security interest.2. It must cost little to enforce the security interest.3. The security must produce real commercial value for the lender when enforced.4. The lender must be able to determine before the loan is made, with certainty and

at little cost, whether any other lender has better claims to the security.5. The lender must be protected from claims of third parties, including secured and

unsecured creditors, the trustee in bankruptcy, and some purchasers of thesecurity. 14

47. Bolivian law permits many contracts with which creditors can secure a debt with movableproperty. Nothing in the Bolivian system is inconsistent with a commercially useful law system, but theBolivian secured transactions system does not meet the five tests. Moreover, Bolivian law unnecessarilyrestricts the types of collateral that may be covered by security interests, especially concerning thesecurity interests in fixtures and personal property on which this paper focuses.'5

12 Richard E. Speidel. Sales and Sales Financing. 1984. St. Paul; West's Publishing Co. 28.

'3 Usually this refers to a security agreement used as collateral (chattel paper). A lender may take as collateral all of another lender'ssecurity interests in equipment from the second lender's secured loans to its borrowers. Legal constraints in Bolivia give limited,almost non-existent use to chattel paper.

'' John A. Spanogle, Proposed Polish Charges Act (1992).

IS Uider Bolivian law, parties cannot fully contract security interests on any collateral they choose. The asset must be specificallymentioned in the law. Moreover, the law must also define the type of contract to be used. See Bolivian Civil Code, Articles 1417and 1418 and Bolivian Commercial Code, Articles 878 and 886.

- 17 -

Establishing the Existence of a Claim Against Collateral in Bolivia

48. When a creditor and debtor agree that a loan will be secured with some interest in the debtor'sproperty, the creditor obtains a security interest in the debtor's property. The agreement that creates thissecurity interest is the security agreement, and the transaction is a secured transaction.

49. The creditor gains public recognition of the security interest by giving effective public notice ofthat interest; if public notice is effected in accordance with the local laws, the creditor's interest isperfected. The process of perfecting an interest is crucial for the lender: it establishes the priority of thelender's claim among all claims against the property, and it permits the lender to legally defend this claimagainst the claims of other creditors. In some cases, the creditor must perfect an interest by filing it ina public registry. In others, the creditor is presumed to have a perfected interest by possessing thecollateral. Chapter V discusses how security interests are created and perfected in Bolivia.

Obtaining and Enforcing Judgment

50. If one of the parties to a contract believes that a contract has been breached, what proceduralsteps must be taken to give that party relief? For example, if a creditor makes a loan to a debtor topermit the debtor to buy a truck and the contract specifies that the creditor may repossess the truck ifpayment is not made in a timely way. If the borrower falls into arrears on the loan, what procedurecertifies that payment was not made and establishes the right of the creditor to take the truck?

51. Broadly speaking, that procedure is obtaining judgment; Chapter VI discusses it. But if a courtrules that the creditor is entitled to the truck, how does the creditor actually seize it? What distinguishesthe creditor in seizing the truck from a thief? Can the creditor physically take the truck? If the borrowerobjects, can the creditor use physical force? Will the judicial police enforce the judgment? How doesthe creditor enforce his rights? Chapter VII discusses enforcing judgment in Bolivia.

- 18 -

V. Creation and Perfection of Security Interests

52. The law determines what property can serve as collateral -- the object of a security interest. Thelaw also determines the circumstances under which that property can serve as the object of a securityinterest. Broadly speaking, these two features of the law set out how a security interest may be created.The law also establishes the procedure for determining the position, ranking, or seniority of differentsecurity interests in the same property. This takes place through perfection -- the legal process thatwarns all other potential creditors that a prior claim exists on the asset. This chapter sets out a briefoverview of Bolivian practices and then discusses the processes of creation and perfection in more detail.

53. Creation. Lenders may create security interests in goods that remain il the hands of theborrowers with three instruments: the civil pledge (prenda civil), the commercial pledge (prenidacomercial), and the chattel mortgage (hipoteca mueble). The law states that the civil pledge may be usedfor goods used by hotels, industries, agriculture and ranching. The commercial pledge must he used forother goods in commercial use that do not involve those sectors. The chattel mortgage regulates licensedpersonal property. Table 6 spells out the relationships among these instruments and types of contracts.

54. There are many "gaps" in Table 6 -- many economic agents, types of property, and types ofcontracts that are economically useful but not envisioned under the law. Any lender who, nonetheless.writes a loan contract will run a heightened risk of not collecting his loan.

55. Perfection. A lender may have a security interest in a property, but what prevents another lenderfrom taking another, more senior, security interest in the same property? Perfection is the legal processthat warns all other potential creditors that a prior claim exists on the assets and ranks the claims oflenders. In Bolivia, creditors may perfect the order of priority of their interests, either with or withoutphysical possession. When an interest is perfected with physical possession, the secured party physicallyholds the collateral, as does a pawnshop or bonded warehouse. This physical possession warns all otherpotential creditors that a prior claim exists on the asset. When an interest is perfected without physicalpossession, however, the creditor usually must file a notice of the security interest in a public registrymaintained for that purpose.

56. For both economic and legal reasons, the publicity is crucial for perfection. When lenders canreadily determine who else has a claim against the personal property or fixture, they can also know withconfidence that they can defend their claims against other potential claimants. They know the law willreject the claims of those who have failed to post their claims to the collateral publicly. The general rulethat all claims must be publicly registered permits a workable ranking system in which lenders can haveconfidence, and permits an economically superior outcome. By contrast, a system that permitted secretclaims would raise the risk to all lenders, reduce lending, and produce an economically inferior outcome.

- 19 -

Table 6: Personal property and fixtures that can serve as collateral and the loan contract that can secure loans against them.

Type of collateral Pledge with Pledge Chatteltransfer without mortgage

transfer

Type of contract Pawnshop Warehouse Civil Commer-receipt receipt pledge cial pledge

Any physical merchandise Yes, acceptable Yes, if No No Noby pawnshop acceptable byproprietor warehouse

proprietor

Licensed property (car, boat, Yes, if Yes, if No Yes, if Yesplane) acceptable acceptable acceptable

Licensed property used in hotel, Yes, if Yes, if Yes No Yes, ifindustry, ranching, or acceptable acceptable accep-agriculture table

Licensed property used in other Yes, if Yes, if No Yes Yescommerce acceptable acceptable

Unlicensed property used in Yes, if Yes, if Yes No Nohotel, industry, ranching, or acceptable acceptableagriculture

Documents of sale No No Not Not readily Noreadily

Revolving inventory; No No No No Notransformable inventory;professional office equipment

Unlicensed property used in Yes, if Yes, if No Yes Nocommerce other than hotel, acceptable acceptableindustry, ranching, oragriculture

Accounts receivable, chattel No No No No Nopaper

Creation and Perfection with Physical Possession

57. Creation. A variety of broad problems arise in Bolivia with the creation of security interests incollateral held by the lender. These are laid out broadly in Table 6. The most serious arises from thedefinition of the "floating pledge" that would be written over a homogeneous commodity like wheat ina grain elevator, cattle, or generalized inventory -- where the definition is very restrictive and raises therisk that the lender will lose the security interest in the commodity when the physical composition of thatcommodity changes in the normal course of business. For example, when the borrower sells some grain

- 20 -

from inventory and replaces it with other grain, the security of the lender's claim may be underminedeven when the total value of the grain in storage remains the same.

Table 7: Place of registration of the loan contract

Licensing registry (motor Real estate registry Commercial registryvehicle, boat, airplane)

Prenda Civil Yes, if property has license Yes, if non-licensed used innumber, and used in hotel, hotel, industry, agricultureindustry, agriculture, or or ranchingranching

Prenda Comercial Yes, if property is licensed Yes, if property isand not used in hotel, unlicensed and not used inindustry, agriculture, or hotel, industry, agriculture,ranching. or ranching

Hipoteca Mueble File against any goodreceiving a license number

58. A lender can perfect a security interest by taking physical possession of the collateral. That is,the physical possession alone serves to notify all other potential lenders that the possessor has a securityinterest in the property.'6 For example, a pawnbroker retains the item pawned; afield warehouse placesthe inventory under the custody of the lender or the lender's agent; collateral placed in the custody of abailee remains in the physical possession of the lender so long as the lender controls the document oftitle. In such cases, the law regards the lender as having a perfected security interest. By merepossession, the lender maintains this interest.'" In some countries, but not in Bolivia, the creditor maysell the collateral with no further court action. Several important examples of perfection with physicalpossession exist in Bolivia: pawned items held in pawnshops or deposits in bonded warehouses.Pawnshops and warehouses are examples of the use of pledge agreements where the collateral remainsin the hands or the control of the lender, the "prenda con desplazamiento."

59. Pawnshops. Decree Law No. 07438 (December 14, 1965) established the "Caja de Ahorro yCr6dito Popular," (CACP) a combined public savings bank and pawnshop that would extend creditsecured by personal property. Formally, CACP negotiated pledge agreements. Under DL 07438,however, in the event of a loan default when it had possession of the collateral, CACP could privatelysell the collateral -- that is, sell without a court-administered auction."8 DL 07438 overruled the pledgeprovisions of the Civil and Commercial Codes, which forbid such private sales.'9 This law providedthat CACP must maintain custody and auction the movable property given as collateral. Legal pawnshops

1" C6digo Civil, Article 1403 and C6digo de Comercio, Article 882.

1' C6digo de Comercio, Articles 882 to 885 and C6digo Civil, Articles 1403 to 1412.

II D.L. 07438, Articles 20 and 28.

" C6digo Civil, Articles 1340 and 1409, and C6digo de Comercio, Article 880.

- 21 -

no longer exist in Bolivia: the combination of usury ceilings20 and interest rates that soared withinflation made private pawnshops unprofitable; nor could private pawnshops use the private saleprovisions accorded to CACP. The CACP closed when the losses from its subsidized operation becameunmanageable.21

60. Bonded warehouses. Bolivian law authorizes general deposit warehouses (almacenes generales)for the storage of goods; warehouses have the power to issue warehouse receipts (certificados dedep6sito) which banks may accept as collateral.22

61. A warehouse receipt demonstrates ownership of the goods deposited in the warehouse. Endorsingthe warehouse receipt can transfer ownership of the goods. Attached to the warehouse receipt is acollateral receipt (bono de prenda). Endorsing the collateral receipt can transfer the security interest inthe goods.'

62. If the debtor does not pay the pledge credit when due, the holder of the collateral receipt for thegoods held as collateral can request that the warehouse manager sell them at a private auction.24 Thisauction may not be suspended except by order of a competent judge, or by payment of the amount dueplus interest and costs. The creditor will be paid from the proceeds of the auction. The secured creditorhas priority over any other creditor; no legal action is required to document this priority, as the lawdeems the fact of the goods being in the warehouse as constituting such notice.' Warehouse receiptsare readily accepted as collateral by Bolivian banks. They represent good collateral because, in the eventof default on a loan, the collateral may be quickly sold.6

63. This is important evidence against the charge that Bolivian banks are excessively conservative andunreasonably unwilling to lend on collateral other than mortgages and personal guarantees. Their

20 Usury laws prevent Bolivian consumers from not legally contracting to pay more than 3 % in monthly interest. 'De acuerdo a loprevisto por los Articulos 409 y 410 del C.C., que por ser imperativas de orden puiblico, el interes convencional no puede excederdel 3 % mensual y si se estipula una suma superior debe reducirse a dicha tasa...." (G.J. No. 1646, A.S. No. 120 de S.C. Ia., de 24-VII-80).

21 The law for the restructure of the Agrarian Bank contains similar provisions for private sale, arid it includes provisions for harmlessrepossession (Decreto Supremo 16699, July 5, 1979, Articles 57 and 58). See also D.S. 11658, Article 64.

22 C6digo de Comercio, Articles 689 to 711, and D.L. of January 15, 1931.

u C6digo de Comercio, Article 692(7), 694(1) and 698. Article 699 also requires giving notice, underthe responsibility of the endorser,that the security interest has been transferred to the endorsee. However, it seems that failure to give this notice would not affect theeffectiveness of the endorsement.

24 C6digo de Comercio, Article 706.

25 C6digo de Comercio, Articles 706-711. Also, and more importantly, constitutes notice the fact that the warehouse receipt, which

represents the stored goods, indicates that the collateral receipt has been negotiated (C6digo de Comercio, Articles 692(7), 694(1)and 698).

26 See also, Banking law (1928), Article 147; D.S. No. 06456, D.S. No. 07507, D.S. No. 7878, D.S. No. 8351, D.S. No. 8768, D.S.

No. 9229, D.S. No. 9733, D.S. No. 10326, D.S. No. 11658 (Article 64), D.S. No. 13100, D.S. No. 11536, D.S. No. 16699(Articles 57 and 58), D.S. No. 19534, D.S. No. 20252; and D. L. No. 07070 (2.3.65).

- 22 -

acceptance of warehouse receipts as collateral supports the view that lending would broaden if proceduresto repossess and sell collateral were improved for other classes of property.

64. Other types of possession. Aside from pawnshops and warehouses, Bolivian law broadly permitsbusinesses to make loans secured by personal property and fixtures in the lender's physical possessionunder the Commercial Code; non-business individuals can make similar loans under the Civil Code. Inthese cases, however, the provisions of the Commercial and Civil Codes prohibiting private sale apply.If the borrower defaults, the creditor must go through the full court procedure for obtaining and executingjudgment. These court processes are expensive and lengthy, reducing the usefulness of movable propertyas collateral from the perspective of the lender.

65. The parties to the loan contract could privately agree to private sale and shorter procedures; butsuch a private agreement would be contrary to the Civil and Commercial Codes and, therefore, void.27

The lender would be unable to enforce this right in court if the debtor objected. As the objection of thedebtor is not improbable, the lender would not view this extra-legal agreement as substantially reducinghis risk. The collateral, therefore, would not make the loan substantially less risky than an unsecuredloan to the same borrower.

66. Economic problems. Loans that rely on perfection with physical possession can severely restrictthe economic usefulness of collateral to the debtor, especially where the debtor needs to use the collateralsuch as retail inventory, a farm tractor, a truck, or woodworking machinery. Nor would physicalpossession reduce the lender's risk where the collateral was intangible; for example, physically possessingthe accounts receivable of a company would yield little advantage to the debtor.28

67. Summary. Perfection with physical possession plays an important role where the borrower doesnot need to retain physical possession of the collateral. Where it works in Bolivia, in warehouses andformerly in pawnshops, it works well even though gaps in the law could be closed and permit itsexpansion. This type of lending underscores the substantial role that movable collateral could play inBolivia if the problems surrounding obtaining and executing judgment (see below) could be solved orcircumvented.

Creation and Perfection without Physical Possession and without Written Registration

68. In Bolivia, as in most countries, security interests are never created automatically by the law.Only a formal agreement between the parties can create a security interest. However, in some othercountries, the law specifies that the underlying features of the transaction give a creditor a perfectedinterest without registration. Moreover, if a security agreement accompanied the credit or sale, and ifthe seller discovers that the buyer did not pay for the goods, the seller may satisfy the debt byrepossessing or selling the goods without going to court. Under Section 9-503 of the UniformCommercial Code (U.C.C.), the seller has the right of harmless repossession -- the seller/creditor canphysically take the collateral from the debtor so long as the seller/creditor does not breach the peace.

27 Bolivian Civil Code, Articles 1340 and 1409, and Commercial Code, Article 880 void any contract stipulation for private sale.

2M See, Alejandro M. Garro. 1987. "Security Interests in Personal Property in Latin America: A Comparison with Article 9 and a

Model for Reform," Houston Journal of International La v 157:171.

- 23 -

For example, a truck that serves as collateral for a loan in default can be towed from its parking placeand returned to the lender.

69. Bolivia's secured transactions law does not have similar provisions. In no case does a securityinterest arise automatically for the seller of goods against a debtor who has not paid for those goods.Typically, however, upon default the creditor gets a preference (privilegio) or statutory lien on paymentof the amount due, as a landlord would if a tenant failed to honor a lease, or seller if a buyer failed topay.'9 However, this statutory lien is much weaker than that implied by a perfected interest in theUnited States because it does not imply priority over other creditors.3 0

70. In Bolivia, the creditor without possession of the goods can only sell them judicially -- that is,get a court order to sell them.3' The creditor could not, as in the United States, repossess and privatelysell the goods and avoid going to court.

Creation and Perfection without Physical Possession and with Written Registration

71. In Bolivia, when the collateral stays in the possession of the debtor, the only legal way to createa security interest is by using one of the formal agreements specified in the law. The Civil and theCommercial Code regulate two such agreements: the pledge without transfer of possession and the chattelmortgage. The chattel mortgage requires a more specific identification of the property than does thepledge and is typically used for licensed movable property. The pledge can be used for some movableproperty. For any loan contemplated, whether the chattel mortgage or the pledge is most appropriatedepends on the nature of the property and the transactors. The criteria are set out in the Civil and theCommercial code.

72. To be perfected, these contracts must be recorded in the appropriate registry designated by thegovernment.32 Filing such claims with the state establishes priority of claims, because potential lendersknow where to look to discover whether other lenders have prior, conflicting claims to the samecollateral. In the simplest example, perfection would give notice to other creditors that a senior securityinterest exists in the same collateral. The borrower could grant another security interest, but only onewith less seniority than the first perfected security interest.

29 Besides the vendor's privilege, Bolivian law recognizes the lessor's privilege in the goods of the tenant, the repairman's lien privilegeover the property repaired, and the privilege of the innkeeper in the baggage of his guest. Bolivian Civil Code, Articles 1349, 1350,and 1351.

30 `[The privilege] comes into existence by operation of law if a seller is not paid for the goods sold; and its effects are generally limitedto the time during which the goods sold remain in the hands of the buyer. However, even during this period the privilege is generallynot effective in the buyer's bankruptcy. It is this lack of effectiveness vis-a-vis all third persons which diminishes the practical valueof the seller's privilege, making it merely a second-rate security device." Drobnig, Ulrich, 1977. Report of the Secretary General:study on security interests (A/NC.91131), Yearbook of the United Nations Commission on International Trade Law [hereinafterUNCITRAL Yearbook], 3:175.

31 C6digo Civil, Articles 1340 and 1341; C6digo de Comercio, Article 880.

32 C6digo Civil, Articles 1424, and C6digo de Comercio, Article 887.

- 24 -

The registries33

73. Bolivian law directs that different claims be registered in different registries (see Table 7). Mostclaims in Bolivia will be registered in one of three registries: the Real Estate Registry,34 the MotorVehicles Registry,35 or the Comnmercial Registry.36 Other registries exist, however, for licensedpersonal property; for example, title and security interests in an aircraft are registered in a separateregistry for aircraft, and title to some copyrights and trademarks are registered in the Registro de Patentesy Marcas.

74. Registering a claim in the wrong registry typically represents a fatal defect in perfection, becausea convincing case can be made that public notice is incomplete if notice is filed in a registry in whichinterested parties would not normally look. A creditor who misfiled a claim could, therefore, losepriority on the collateral.

75. All registries in Bolivia present major obstacles to the filing of claims against personal propertyand fixtures. The most important arises from the general barrier to public access, the key in establishingthe general credibility of claims against personal property and fixtures. In addition, registries typicallylack adequate computerized indexes or document retrieval systems. Consequently, retrieving documentsis time-consuming, expensive, and subject to great uncertainty about priority and authenticity.

76. The Real Estate Registry (Registro de los Derechos Reales). Located in the real estate office(oficina de los derechos reales), is the legally-designated registry for mortgages and for some agriculturalcredit instruments, like crop security interests and security interests on farm equipment. This registryfiles security interests according to the location of the property.37 Since physical location isunambiguous, a lender searching for security interests on a property offered as collateral has a clearindication of where to look. In principle, the record is public and can be inspected by any citizen.38

In practice. the system has been computerized, but searches can only be conducted by staff. This cansometimes involve a lengthy wait. Although the filing system is not fast, it is a workable way of locatingmortgages or other encumbrances in real estate.

77. Security interests against agricultural movable property such as tractors or grain driers, as wellas security interests against crops orfixtures -- equipment attached to the land -- are also filed in the real

33 Bolivia's legal registries are examined at greater length in Nuria de la Pefa, Heywood Fleisig and Frederick Miller, "Improving LegalRegistries in Bolivia to Facilitate Lending" (Govemment of Bolivia, 1992).

34 Registro de los Derechos Reales, C6digo Civil, Articles 1538 and 1566.

35 D.S., No. 15191, 12-15-77.

36 C6digo de Comercio, Article 26.

37 Generally, the real estate registry is the proper place to file documents affecting the financial status of property that can be easilylocated.

M C6digo Civil, Articles 1523 and 1562, Clauses I and 11.

- 25 -