How far has open access enabled the growth of cross border pan European rail freight? A case study

10

How far has open access enabled the growth of cross border pan European rail freight? A case study Thomas Hagen Zunder, Dewan Md Zahurul Islam, Phil N. Mortimer, Paulus Teguh Aditjandra ⁎ NewRail, Newcastle Centre for Railway Research, School of Mechanical and Systems Engineering, Newcastle University, Stephenson Building, Claremont Road, Newcastle upon Tyne, NE1 7RU, United Kingdom abstract article info Article history: Received 31 May 2012 Received in revised form 30 November 2012 Accepted 10 December 2012 Available online 11 January 2013 Keywords: Rail freight Transport policy Logistics Railways This paper analyses the extent to which an open access rail freight market has enabled new pan European rail freight services, using a case study within the context of policy. Methodology was: desk top analysis of European Union freight policy, from the Railway Directives, through successive White Papers, to the recent 2011 White Paper; review of rail freight market performance; semi-structured interviews with rail regulators; operational records from a novel, cross-border rail freight service from Western Europe to the Black Sea. Evidence to date is mixed. The research finds that new entrants can operate within imperfect open access environment, facing many barriers from incumbents, infrastructure managers, rail regulators, and terminal operators. Examples of issues are: infrastructure discrimination; non-transparent or liberalised energy supply; monopolistic shunting services; safety certification; terminal access restricting trade; weak or discriminatory regulatory authorities. The research identified key barriers: trust between partners, wagon availability, lack of single European driver certification and access to non-path infrastructure and services. The pilot was successful and is commercially viable, and succeeded in a hybrid block and single wagon-load train service, integrating new private entrants and Eastern state railways. The research identified a research agenda and implications for practitioners and policy makers. © 2012 Elsevier Ltd. All rights reserved. 1. Introduction Nowadays, it is possible for people and goods to travel and trade freely within the European Union (EU). The gross domestic product (GDP) of the EU in 2009 was circa €11.7 billion; larger than the USA. With 7% of the world's population, the EU's trade with the rest of the world accounts for around 20% of global exports and imports, in value terms. It is the world's biggest exporter and its second biggest importer (after the USA). Around two thirds of EU countries' total trade is done within EU countries. The value of intra- and extra-EU trade has risen by 55% since 1999. This growth has come about through European integration and liberalisation and through the relatively low cost of freight transport, which has led to changes in production and trade patterns, both inside the EU and globally (European Commission, 2007). The United States is the EU's most important external trading partner, followed by China. In 2005, the EU accounted for 18.1% of world exports and 18.9% of imports (European Commission, 2011a). Estimates put the share of the freight transport industry in Europe at close to 14% of GDP. Until the recession started in 2008, the freight transport industry had growth rates above the average of European economies (European Commission Statistical Pocketbook, 2011). GDP grew at an average rate of 2.5% annually over the period 1995 to 2007. Over the same period, freight transport grew at an average rate of 2.7% annually. For 2009, total intra-EU27 goods transport activities are estimated as 3632 billion tkm, of which modal shares are: road 46.6%; maritime (including coastal) 36.80%; rail 10.0%; inland waterways 3.3%; oil pipelines 3.3%; and air 0.1% (European Commission Statistical Pocketbook, 2011). Over the years, the rail freight transport system in the EU has been transformed – in law, economics and policy – from separate, state- owned, incumbent monopolies, intended to service customers within national borders (with a few bilateral exceptions), into an integrated and open access European rail freight market, separated vertically be- tween infrastructure and operations and horizontally between passen- gers and freight. The methodology utilised is a desk top analysis of European Union freight policy, from the 1991 Railway Directives, through successive White Papers, to the recent 2011 White Paper; a review of railfreight market performance; a semi-structured interviews with rail regulators; and the operational records from a novel, cross-border rail freight ser- vice from Western Europe to the Black Sea. This paper is organised into seven sections: Introduction; a review of EU transport policy; a re- view of the EU rail freight market; interviews with rail regulators; the Research in Transportation Business & Management 6 (2013) 71–80 ⁎ Corresponding author. Tel.: +44 1912225997; fax: +44 1912228600. E-mail address: [email protected] (P.T. Aditjandra). 2210-5395/$ – see front matter © 2012 Elsevier Ltd. All rights reserved. http://dx.doi.org/10.1016/j.rtbm.2012.12.005 Contents lists available at SciVerse ScienceDirect Research in Transportation Business & Management

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of How far has open access enabled the growth of cross border pan European rail freight? A case study

Research in Transportation Business & Management 6 (2013) 71–80

Contents lists available at SciVerse ScienceDirect

Research in Transportation Business & Management

How far has open access enabled the growth of cross border pan European railfreight? A case study

Thomas Hagen Zunder, Dewan Md Zahurul Islam, Phil N. Mortimer, Paulus Teguh Aditjandra ⁎NewRail, Newcastle Centre for Railway Research, School of Mechanical and Systems Engineering, Newcastle University, Stephenson Building, Claremont Road,Newcastle upon Tyne, NE1 7RU, United Kingdom

⁎ Corresponding author. Tel.: +44 1912225997; fax:E-mail address: [email protected] (P.T. Ad

2210-5395/$ – see front matter © 2012 Elsevier Ltd. Allhttp://dx.doi.org/10.1016/j.rtbm.2012.12.005

a b s t r a c t

a r t i c l e i n f oArticle history:Received 31 May 2012Received in revised form 30 November 2012Accepted 10 December 2012Available online 11 January 2013

Keywords:Rail freightTransport policyLogisticsRailways

This paper analyses the extent to which an open access rail freight market has enabled new pan European railfreight services, using a case studywithin the context of policy. Methodologywas: desk top analysis of EuropeanUnion freight policy, from the Railway Directives, through successive White Papers, to the recent 2011 WhitePaper; review of rail freight market performance; semi-structured interviews with rail regulators; operationalrecords from a novel, cross-border rail freight service from Western Europe to the Black Sea. Evidence to dateis mixed. The research finds that new entrants can operate within imperfect open access environment, facingmany barriers from incumbents, infrastructure managers, rail regulators, and terminal operators. Examples ofissues are: infrastructure discrimination; non-transparent or liberalised energy supply; monopolistic shuntingservices; safety certification; terminal access restricting trade; weak or discriminatory regulatory authorities.The research identified key barriers: trust between partners, wagon availability, lack of single European drivercertification and access to non-path infrastructure and services. The pilot was successful and is commerciallyviable, and succeeded in a hybrid block and single wagon-load train service, integrating new private entrantsand Eastern state railways. The research identified a research agenda and implications for practitioners andpolicy makers.

© 2012 Elsevier Ltd. All rights reserved.

1. Introduction

Nowadays, it is possible for people and goods to travel and tradefreely within the European Union (EU). The gross domestic product(GDP) of the EU in 2009 was circa €11.7 billion; larger than the USA.With 7% of the world's population, the EU's trade with the rest of theworld accounts for around 20% of global exports and imports, in valueterms. It is the world's biggest exporter and its second biggest importer(after the USA). Around two thirds of EU countries' total trade is donewithin EU countries. The value of intra- and extra-EU trade has risenby 55% since 1999. This growth has come about through Europeanintegration and liberalisation and through the relatively low cost offreight transport, which has led to changes in production and tradepatterns, both inside the EU and globally (European Commission,2007). The United States is the EU's most important external tradingpartner, followed by China. In 2005, the EU accounted for 18.1% ofworld exports and 18.9% of imports (European Commission, 2011a).

Estimates put the share of the freight transport industry in Europe atclose to 14% of GDP. Until the recession started in 2008, the freight

+44 1912228600.itjandra).

rights reserved.

transport industry had growth rates above the average of Europeaneconomies (European Commission Statistical Pocketbook, 2011). GDPgrew at an average rate of 2.5% annually over the period 1995 to 2007.Over the same period, freight transport grew at an average rate of 2.7%annually. For 2009, total intra-EU27 goods transport activities areestimated as 3632 billion tkm, of which modal shares are: road 46.6%;maritime (including coastal) 36.80%; rail 10.0%; inland waterways3.3%; oil pipelines 3.3%; and air 0.1% (European Commission StatisticalPocketbook, 2011).

Over the years, the rail freight transport system in the EU has beentransformed – in law, economics and policy – from separate, state-owned, incumbent monopolies, intended to service customers withinnational borders (with a few bilateral exceptions), into an integratedand open access European rail freight market, separated vertically be-tween infrastructure and operations and horizontally between passen-gers and freight.

The methodology utilised is a desk top analysis of European Unionfreight policy, from the 1991 Railway Directives, through successiveWhite Papers, to the recent 2011 White Paper; a review of railfreightmarket performance; a semi-structured interviews with rail regulators;and the operational records from a novel, cross-border rail freight ser-vice from Western Europe to the Black Sea. This paper is organisedinto seven sections: Introduction; a review of EU transport policy; a re-view of the EU rail freight market; interviews with rail regulators; the

72 T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

case study of the RETRACK pilot; key results, barriers and successes ofthat pilot; and discussion and conclusion.

2. Review of EU transport policy leading to a rail freight case study

Reform in the freight transport sector began in 1957 with the Treatyof Rome – the establishment of what is now called the European Union –

and its Common Transport Policy. The role of freight transport policywas, and remains, a crucial component of the planning, practice, com-petitiveness and sustainability of freight transport in Europe. Whilstmuch of policy is enacted at the national level, the EU has variousmethods in which a pan-European policy can be promulgated. Forexample, the potential gains from full market opening in rail transport(both passenger and freight) were acknowledged (CopenhagenEconomics, 2007) following lessons learnt from the market failure inrail transport since the 1960s. This was largely due to monopolistic op-erations, economies of density, safety, asymmetries of information(Pietrantonio & Pelkmans, 2004), and the loss of contact with emergingand changing shipper requirements and expectations. As the way for-ward, a complete separation of infrastructure and transport services op-erationwas proposed, to overcome the structural obstacles to achievinga competitive European railway market at EU level (Stehmann &Zellhofer, 2004). Yet this model has not been fully implemented at thenational level and remains a point of contention regarding its validityand applicability.

For clarity, we note that the EU has a variety of instruments of differ-ing force: the regulation and the decision – which have direct effect;the directive – a legislative act of the EU requiring member statesto achieve a particular result without dictating the means; and thecommunication — which is an opinion or recommendation which hasno legal effect (Borchardt, 2010). In all cases we shall focus on thefreight elements policy, save where broader policies have had a signifi-cant effect on rail freight.

The Railway Directive 91/440/EEC of 1991 is the important turningpoint for rail liberalisation in Europe. It was the beginning of the endof national railways' state-owned and operated monopolies. It laiddown the first milestone for the creation of a European railway mar-ket. The Directive required that the national railways be operated ona commercial basis, driven by market demand, and be manageriallyindependent from the state (CER, 2008). The Common Transport Pol-icy of the European Commission (1992) set out the basic principles ofthe formation of the internal market to meet increased traffic volumedemand. This policy was part of the emergence of a new liberal eco-nomic model for the EU, the single European market, and of themove from state intervention and mandated cartels to free trade(Sandholtz & Zysman, 1989). The main themes of this policy werethe deregulation and liberalisation of the market for transport in theEU and the development of Trans-European Networks (TEN-T): stra-tegic, cross border transport corridors, highlighted for mutual devel-opment. The document noted the incompatibilities between nationaltransport systems, inadequate interconnections, missing links andbottlenecks and obstacles to interoperations, that resulted in ineffi-ciencies. Some of the measures encouraged by the 1991 Directivewere the liberalisation of quantitative restrictions and the eliminationof various administrative constraints — in combined transport as wellas in the field of road transport. Examples were: the reduction of tax-ation on the use, or possession, of commercial vehicles (to the extentthat they are carried by rail) and the exemption from compulsory tar-iff regulations of the initial and final road haulage journey legs. Whilstthe implementation of these measures boosted European free trade,competitiveness and prosperity, the open freight market may haveled to the strengthening of road's position at the expense of rail andinland waterways (Woodburn & Whiteing, 2010). It is widely accept-ed that this reflects the relative flexibility of the road freight industry,in contrast to rail's failure to adapt to the liberalised market and is

borne out by various reports, such as the Rail Liberalisation Index2011 (IBM, 2011).

In May 1997 the EU issued a Communication document entitled“Intermodality and Intermodal Freight Transport in the EU” (COM 97/243) that emphasises key strategies to stimulate the development of in-termodal transport, in the overall context of the Common Transport(Lowe, 2005). Such strategies include: refining of the TEN-T and nodesthat was aimed to improve the integration of the Community transportsystem, but not the improvement of the transport infrastructure in gen-eral (Banister et al., 2000); harmonising the regulations and competi-tion rules towards a single transport market; removing obstacles tointermodality and the associated costs (i.e. cost that make intermodaltransport uncompetitive in comparison to uni-modal); and introducingthe Information Society in transport. In 2002, a roundtable meeting, in-volving European ministers of transport, pointed to the need for an in-tervention – of whatever sort – in the growing share of road freight(European Conference of Ministers of Transport, 2002). This led to thedevelopment of three Railway packages.

The First Railway Packagewas launched on 15March 2003, based onthe provisions of the RailwayDirective 91/440/EEC of 1991, and permit-ted open access for national rail services across the EU, as well asannouncing a Trans-European Rail Freight Network (TERFN). This Pack-age comprised the following three directives:

• Directive 2001/12/EU is designed clarify the formal relationship be-tween the state and the infrastructure manager and the railway un-dertakings (operators);

• Directive 2001/13/EU sets out the conditions for freight operators tobe granted a license to operate services on the European rail network;

• Directive 2001/14/EU introduces a defined policy for capacity alloca-tion and infrastructure charging.

The Second Railway Package, adopted on 23 January 2002, is madeup ofmeasures to revitalise the railways by building an integrated Euro-pean railway area; in particular, by opening up the pan Europeanrail-freight market more quickly; by proposing a new directive on rail-way safety; and by the establishment of a European Railway Agency.This second package comprised the following three directives, plusone regulation:

• Directive 2004/51/EU (a revision to Railway Directive 91/440/EEC)opens up both national and pan European freight services on theentire European network from 1 January 2007;

• Directive 2004/49/EU (the Railway Safety Directive) lays down a pro-cedure to obtain a safety certificate for every railway company to runon the European rail network;

• Directive 2004/50/EU (on interoperability) harmonises and clarifiesinteroperability requirements;

• Regulation (EU) 881/2001 sets up the European Railway Agency tocoordinate groups of technical experts seeking common solutionson safety and interoperability.

The Third Railway Package was adopted by the EU on 3March 2004and opened up the pan European passenger rail services, within theCommunity, from 2010, whilst also introducing a certification systemfor locomotive drivers. This Package comprised the following twoDirec-tives and one regulation:

• Directive 2007/59/EU introduces the conditions and procedure forthe certification of train drivers (and crews) operating locomotivesand trains;

• Directive 2007/58/EU sets up the allocation of railway infrastructurecapacity and the charging system for using the railway infrastruc-tures; it also envisages opening the market for pan European passen-ger services to competition from 1 January 2010;

• Regulation 1371/2007 on rail passengers' rights and obligations, toensure passengers' basic rights are met in regard to insurance and

73T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

ticketing matters and also the needs of passengers with reducedmobility.

Despite the progress made through policies supporting an open ac-cess rail freight system, none of these directives required a completevertical separation of train ‘ownership’ operations from infrastructure.This has led to a contradictory problem between continued nationallevel freight monopolists and a single dominant Europe-wide carriersuch as Deutsche Bahn (DB) (Pittman, 2011; Stehmann & Zenger,2011). This problem echoes the experience of other network industriese.g. the telecommunications and electricity sectors (Stehmann&Zenger,2011). By the early years of the 21st century, evidence of the use of a‘vertical separation’ model to reform pan-European, cross border railfreight was starting to emerge, with the arrival of new freightoperators across Europe and Russia (Pittman, Diacony, Sip, Tomova, &Wronka, 2007).

There has been an on-going discussion about the launch of a fourthRailway Package, designed to ‘recast’ the first railway package, to ad-dress the slow uptake and non-compliance of some member states(Knieps & Zenhäusern, 2011; New Europe, 2010). According to a studyabout the potential recast it was identified that ‘weak finances ofmany Railway Undertakings (RU) in newmember States and low infra-structure quality’ are the main barriers to the development of the openaccess, 2009). This is followed by the need for non-discriminatory provi-sion of service facilities; for pricing and access transparency; and for fi-nancial and political incentives to support new entrants. The latterpoint is based upon the view that, the higher the number of railway un-dertakings in a country, the higher the liberalisation (IBM, 2011).

Rail has been explicitly supported in EU transport policy since the2001 Transport White Paper promoting a pro modal shift (from roadto other more sustainable modes) which explicitly proposed a stateinterventionist approach to achieving demand changes and the activepromotion of intermodality (Zunder, Aditjandra, & Islam, 2012). In2006 the EU published a mid-term review of the 2001 TransportWhite Paper (European Commission, 2006) that was an attempt to rec-ognise that all transport needs to be sustainable and that policy shouldoptimise eachmode separately, integrate themodes for seamless trans-port, and then look formodal shift in specific areas: long-distance, urbanareas and congested corridors (European Commission, 2006). The 2011

18.3

17.3

16.116.2

15.515.315.8

15.214.915

20.920.720.9

19.7

18.819

11

13

15

17

19

21

% o

f tk

m

Rail modal share of inland freighSource: Eurostat 2012

2002 data explicitly excluded due to unreliability o

Fig. 1. Percentage modal share of inland freight in EU (tkm

White Paper (European Commission, 2011b) reiterates the policy of1992 onwards, that rail shall liberalise, separate operations and infra-structure and allow an open access rail freight market as the mostappropriatemethod in Europe for rail to competewith road and achievemodal shift. The new targets for modal shift are even more ambitiousthan those of 2001 and, in line with co-modality, the rail is projectedto adopt a dominant role in long haul freight above 300 km. This is tobe achieved by and alongside better modal choice, greater integrationof the modes' networks and hubs and the development of pan-European green freight corridors. The targets are that 30% of roadfreight over 300 km should shift to other modes, such as rail transport,by 2030 and that more than 50% should shift by 2050.

3. Recent rail freight market in Europe

Despite the scepticism over rail freight market prospects, the poten-tial for growth has been recognised (Thompson, 2009). Recent studiescommissioned by CER (Community of European Railway and Infrastruc-ture Companies) and UIC (International Union of Railways) suggest thatrail freight transport in Europe has the potential to reach a maximummarket share of heavy land surface freight (this market excludes inlandbarges and trucks below 16 tonnes) of 31–36%, as compared to 18% atpresent (Boer, Essen, Brouwer, Pastori, & Moizo, 2011). Furthermore, itwas reported that the average Green House Gas Emission (GHG) reduc-tion potential of modal shift is higher in freight transport than in thecase of passenger transport (European Commission, 2006).

Actual rail freight performance as a share of the market has beenvariable. At EU level, rail has consistently fallen as a share of freight,against a background of rising absolute volumes, with the newmemberstates – many of which had dominant rail freight under Communism –

exhibiting the same downward trend. The EU-25 figures were used be-cause they are almost identical with EU-27, but the EU-25 data extendsfurther back in time. From 1991 to 2010 EU-15 share has fallen from18.3% to 14.9% and has then seen a slower recovery to 2010. For theEU-25 we see a similar picture but, rather than a recovery 2003–2008,a plateau (see Fig. 1). The impact of the ‘crisis’ of 2008–2009 is clearfrom the graph.

This aggregate view is nuanced by examples from some of the coun-tries within the EU, where we see differences. Countries viewed as

.114.5

14 13.914.114.7

1515.3

14.314.9

.1

18.217.817.617.5

17.817.817.8

16.517

t as a % of tkm(http://ec.europa.eu/eurostat): f French data for that year EU (15 countries)

EU (25 countries)

), Source Eurostat 2012 (http://ec.europa.eu/eurostat).

74 T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

having fully implemented rail liberalisation, such as Sweden and theUK, have seen growth since the start of the century (see Fig. 2). France,a country that is seen as highly resistant to change, has seen collapsingshares. However the simple correlation is deceptive, since Poland,which has implemented liberalisation, has seen massive falls, perhapsdue to the reorientation of the economy to face Germany rather thanRussia. The German rail market is perhaps the most complex to inter-pret; it is noted as a country slow to accept the liberalisation and yethas seen growth over the last decade, as Deutsche Bahn (DB) havebought into markets surrounding the home network and continuedwith a vertically integrated railway.

Fig. 2 suggests that the different approaches to liberalisation cannotalone explain fully the changes in rail freight performance and that thismust be considered alongside the organizational andmanagerial bottle-necks identified. These include limited share of dedicated freight traffic;interoperability; productivity-limiting infrastructure; as well as an in-sufficiently open market (Vassallo & Fagan, 2007) and also the way op-erators have addressed the key sectors of full train, intermodal trainsand single wagon services (Wolff, 2006). It is important to note thatrail freight growth has been particularly strong in states that performa transit role such as the Netherlands (Preston, 2009) and Austria. How-ever, Poland and Hungary that play a similar role show the opposite.This is due to market reorientation, and the shortage of investment(PwC, 2009). Rolling stock acquisition and bureaucracy were also iden-tified as barriers to rail freightmarket entry in Poland (Laisi, Mäkitalo, &Hilmola, 2012).

Following the endorsement of the TEN-T corridor policy, a number ofpanEuropean rail freight corridors have been investigated. One exampleis the Rotterdam–Genoa corridor that has benefited from the opening ofa dedicated pan European rail freight line from Rotterdam to Germany(Betuwe Route) (Peijs, 2006). Despite controversy, at the beginning ofthe project, due to the line passing through some densely populatedareas, recent statistics demonstrate an increase in rail freight volumeon the corridor (Government of the Netherlands, no date). Another ex-ample is the Madrid–Berlin corridor that was selected because of itschallenging nature for rail freight to gain share from road and shortsea shipping (Castagnetti, 2008). The TEN-T programme on the corridorwould better connect pan European rail systems that still now have dif-ferent track gauges and also the geography of the Pyrenees to overcome.

A number of successful case studies of rail freight modal shift arewell documented, including the rise of fresh produce delivery using

35.7

41.839

18.6

22.2

36.5

28.3

60.5

38.3

19.421

13.5

8.710.6 11.2

2.8 3.44.9

2

12

22

32

42

52

62

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

% o

f tk

m

Modal share of inland freight as a % of tkmSource: Eurostat 2012 (http://ec.europa.eu/eurostat)2002 French data excluded due to unreliabilty

Sweden

Austria

Germany

Hungary

Poland

France

United KingdomNetherlands

Fig. 2. Modal share of inland freight as a % of tkm, selected countries, Source Eurostat 2012(http://ec.europa.eu/eurostat).

‘reefer’ containers, for flowers, fruit and vegetables, from the Netherlandsto Italy and from Romania and Spain to the UK (Boer et al., 2011).Switzerland introduced a Heavy Vehicle Fee, similar to the Eurovignette:a road user charge aimed at Heavy Goods Vehicles with a gross vehicleweight of 12 tons or more to use motorways and toll highways in theEurovignette countries: Belgium, Denmark, Luxembourg, theNetherlandsand Sweden. Since its introduction in 2001, this has led to a 9%decrease intruck journeys through the Swiss Alps between 2000 and 2008 and, overthe same period, the volume of rail freight increased by 25% (Boer et al.,2011). EU rail policies are recognised to have contributed to the growthof the cross border rail freight market (Nash, 2011), although there areconsiderable variations in the way the Directives are applied acrossdifferent countries (Deville & Verduyn, 2012). The success stories aredue to several factors, reducing to two overarching objectives: improvedavailability of quality services and a political willingness to supportmodalshift. Achievement of the first objective depends partially on theenhancement of technology, such as the implementation of EuropeanRail Traffic Management System (ERTMS), new infrastructures invest-ment and the availability of reliable, attractive, cost effective andcompetitive services. The second objective depends more on the imple-mentation of EU policy, such as equitable infrastructure charging for allmodes and directmarket interventions, such asMarco Polo, fundingmar-ket start-ups, moving freight transport from road to sea, rail and inlandwaterways (European Commission, 2011b). It also requires train opera-tors to present and sustain attractive, competitive, efficient and secureservices that are capable of matching the competing road based competi-tion. In the following case study we examine just such a rail freightservice.

4. Rail regulators interviews

Interviews with policy makers and rail regulators in the Nether-lands, Germany, Austria and Hungary were carried out before the open-ing of the operational service and following in two cases. Full details ofthe interviewees can be found in the Appendix A. Interviews were un-dertaken with the national railway infrastructure managers, capacitymanagers, rail regulators and relevant ministries and agencies, in eachcountry through which the new service was intended to or did operate.At the time of the interviews, each nation was developing its own su-perstructure and administrative systems. Despite generic similarities,there were major identified differences in terms of the models usedand deployed. The positionwas further complicated by the varying dis-tance and independence of the regulatory arms from the national gov-ernment and the incumbent rail operator. Table 1 lists the questionsposed to the interviewees.

All five of the countries through which the RETRACK train wasplanned to and did ultimately operate were open to pan Europeanfreight services operating to/from and through their territories. Howev-er, it was clear from interviews that the levels of understanding and in-terpretation of the various directives from the EU varied. The positionwas most completely developed within the Netherlands and was fullycompliant with the requirements of the EU. The composite model ofrail operations and infrastructure management in Germany made theposition more opaque, although the rail regulatory body in Germanyhad been pressing DB to accommodate and reflect the requirements ofthe EU in a more positive way. It was heavily involved in judicial issuesrelating to energy charges at the time of the first interview round. Inboth Germany and the Netherlands, the structures of an independentregulatory arm were in evidence and working. Concerns from inGermany were mainly focused on issues of:

• Predatory energy pricing for electric traction,• Limitations on access to sidings and terminals,• Preferential treatment of the incumbent in relation to access to infra-structure and train paths during major reconstruction activities

Table 1Core rail regulator questions and the policy(s) in context.

Questions Policy(s) incontext

1 Do you think the formal relationship between the state and theinfrastructuremanager and the railway undertakings, to achievea competitive and commercial rail freightmarket in Europe havebeen established?

Directive 91/440/EECDirective 2001/12/EUDirective 2007/58/EU

2 Do you think is there still any issue regarding ‘licences’ tooperate that prevents a potential competitor from enteringthe market unfairly?

Directive 2001/13/EU

3 Do you think there is still any issue on the ‘transparency’ incapacity allocation to licensed operators?

Directive 2001/14/EU

4 Has the infrastructure manager/operator made available anexplicit scale of charges that are applied to all train operators?Are there any examples where charges have not been applied inany uniform or consistent manner?

Directive 2001/14/EU

5 Are there still any countries’ networks which are not open forthe European rail freight market operation?

Directive 2004/51/EU

6 Has there been any issue with the procedure to obtain a safetycertificate, for every rail freight operator including newentrants?

Directive 2004/49/EU

7 Has there been any issuewith the conditions and procedures forthe certification of train drivers?

Directive 2007/59/EU

75T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

The position in Austria was less well developed and the relationshipbetween the regulator and the national government and incumbent railoperator was opaque and potentially contentious. The incumbent at thetime was known to be intent on keeping new entrants from themarket,either by pricing, or by other means to constrain access. In Hungary theposition before the start of commercial operations by RETRACK appearedto be promising and compliant with the EU requirements. Initial contactwith the national rail regulator indicated a developing understanding ofthe role and requirements of a regulator. This position was overturnedshortly afterwards, due to changes in political positions within Hungary,and the position has remained opaque since then. The position in Roma-nia was the least well developed and understood at the first round ofinterviews.

The requirements set out by the EU to clarify and establish the roleand relationship between the train operators, infrastructure managerand capacity allocators,were understood at a differential level in the na-tional territories through which the trains were planned operate. Thelevel of development and implementation diminished progressively to-wards the eastern end of the planned route of RETRACK. The varyingmodels of ownership of infrastructure and operations also confusedthe position.

For new train services to be set up and operated, the operators haveto be compliantwith the network requirements of the domains throughwhich the trains operate and the new entrant must be certified and ap-proved technically, commercially and operationally before beinggranted access to the systems. The barriers to entry are potentiallyconstraining in relation to the scale of the entry requirements for roadfreight operators, but provide a barrier to non-compliant proposalsand also to services that are not supported financially and with the req-uisite safety and competence credentials.

In relation to transparency of allocation to tracks for train operations,there were concerns that this may be predatory in some rail domains.There were causes for concern in Germany, in relation to the priority al-located to new entrants versus the incumbent, in relation to planned in-frastructure modification and engineering work, with concerns that theincumbent was favoured.

In terms of barriers to market entry, the cost, complication and timerequired to secure approval is, asmentioned previously, on a larger scalethan equivalent new road freight service applications. New entrants are

primarily already compliant as railway operators or undertakings andare aware of the requirements to ensure approval to operate.

In relation to driver skills, competence and knowledge, thiswas seeninitially as a potential constraint and, in reality, securing competenttrain crew, able to operate across borders, was a constant issue to bemanaged. Language and technically skilled crew availability remains aproblem. This dimension cannot be ignored, given the more complexsafety requirements of the industry at a generic level, compared toother modes - particularly in operations on mixed traffic routes.

5. The case study of RETRACK pilot rail freight operation

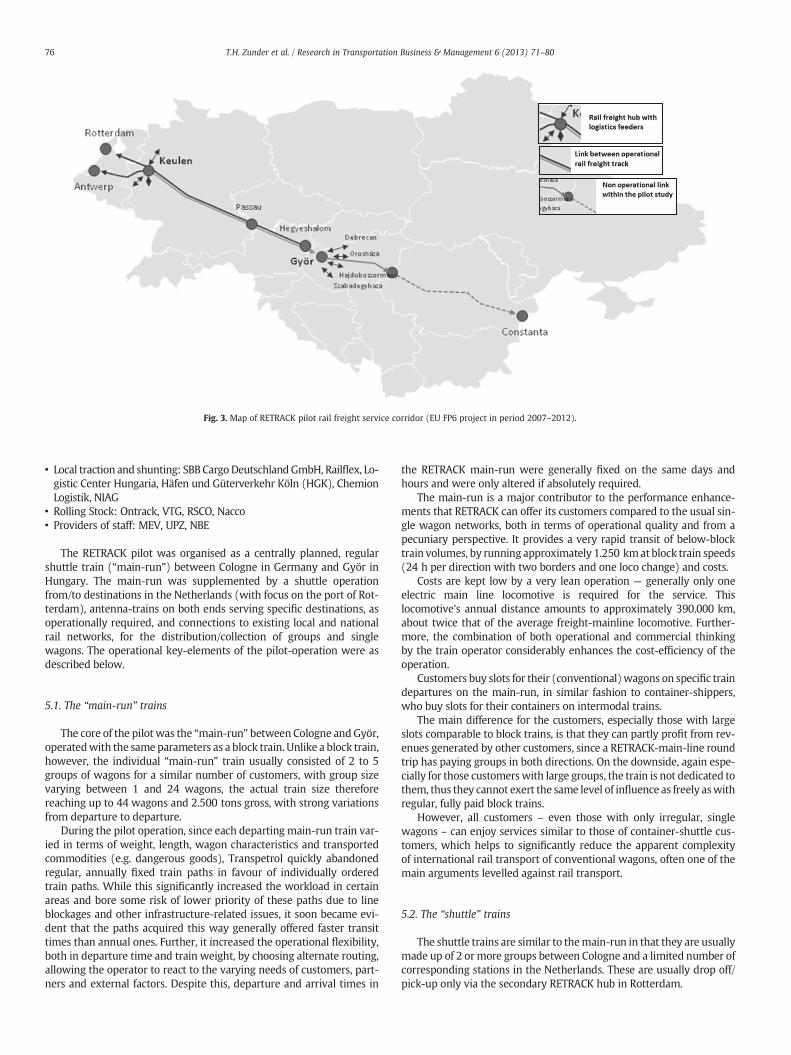

The overall objectives of the RETRACK project were to conduct re-search, develop, commission and implement pan-European privatelyoperated (not the national incumbents) rail freight services to achievethe EU key objective: modal shift to rail, operating between Rotterdamin The Netherlands and Constanza in Romania, through Germany, Aus-tria and Hungary (see Fig. 3). The results of the pilot are documented inboth public and confidential data collated and analysed by the authorsas part of the pilot process (Marg, Mauck, Zunder, & Mortimer, 2012)and in Zunder, Islam, and Mortimer (2012) that concluded that singlewagon load pan-European services can be operated profitably.

During the long implementation period of the project, RETRACK hadsuffered a number of major setbacks including the economic recessionin 2008 and beyond. By the second half of 2008, the project wasmakingonly limited and slow progress. Finally, the trading house Glencoreagreed to commit certain volumes out of its existing corn transportflows, from Hungary to Benelux, to the RETRACK Pilot, enabling thestart of the first train on 28th February 2010, nearly a year behindschedule.

NewRail Railway Research Centre project-managed the pilot and, aspart of it, four consortium members were tasked with the actual pilotoperation:

• LTE Logistik GmbH (LTE), Austria: The responsibility of LTE in the op-eration of the pilot consisted of the provision of the requiredmainlineelectric locomotives able to operate across networks based on 1.5 kvdc., 3 kv dc., 15 kv ac, and 25 kv ac and the provision of all requiredservices for the train operations through and within Austria.

• Central European Railways (CER), Hungary: CER was responsible forthe Hungarian part of the pilot's main line operation (Hegyeshalomborder to Györ) and the organisation and operation of antenna-trains from/to sites within Hungary to the RETRACK-hub in Györ.

• Servtrans, Romania: the Servtrans role was to provide traction ser-vices in Romania but, due to the actual operational concept (seebelow) and due to general inactivity in the project after 2009, no ac-tive part was played by Servtrans during the involvement of the au-thor in the RETRACK Project.

• Transpetrol GmbH, Germany (TP): TP was responsible for sales (incl.price calculation); train and capacity management; provision of rail-cars as part of the VTG leasing group; organisation of all required trac-tion services west of the Austrian border, including hub, antenna andmainline operations in Germany and Benelux. TP was in charge oforganising transports of single wagons and wagon groups from Györto their final destination in south eastern Europe and vice versa; com-munication with customers; sending and receiving terminals etc.From December 2010 onwards TP provided traction services, as rail-way operator for the main line operation on the German part of theservices, including the ordering of train paths, local infrastructure, op-erational staff and maintenance issues for all rolling stock.

In the course of the project, various service providers were involvedin the daily operations, at one time or another. Most notable amongthese were:

• Main-Line traction: Rurtalbahn, Rurtalbahn Benelux,Mittelweserbahn,Rotterdam Rail Feeding, Trainsport, Gysev, MÁV, GFR

Fig. 3. Map of RETRACK pilot rail freight service corridor (EU FP6 project in period 2007–2012).

76 T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

• Local traction and shunting: SBB CargoDeutschlandGmbH, Railflex, Lo-gistic Center Hungaria, Häfen und Güterverkehr Köln (HGK), ChemionLogistik, NIAG

• Rolling Stock: Ontrack, VTG, RSCO, Nacco• Providers of staff: MEV, UPZ, NBE

The RETRACK pilot was organised as a centrally planned, regularshuttle train (“main-run”) between Cologne in Germany and Györ inHungary. The main-run was supplemented by a shuttle operationfrom/to destinations in the Netherlands (with focus on the port of Rot-terdam), antenna-trains on both ends serving specific destinations, asoperationally required, and connections to existing local and nationalrail networks, for the distribution/collection of groups and singlewagons. The operational key-elements of the pilot-operation were asdescribed below.

5.1. The “main-run” trains

The core of the pilot was the “main-run” between Cologne andGyör,operatedwith the same parameters as a block train. Unlike a block train,however, the individual “main-run” train usually consisted of 2 to 5groups of wagons for a similar number of customers, with group sizevarying between 1 and 24 wagons, the actual train size thereforereaching up to 44 wagons and 2.500 tons gross, with strong variationsfrom departure to departure.

During the pilot operation, since each departing main-run train var-ied in terms of weight, length, wagon characteristics and transportedcommodities (e.g. dangerous goods), Transpetrol quickly abandonedregular, annually fixed train paths in favour of individually orderedtrain paths. While this significantly increased the workload in certainareas and bore some risk of lower priority of these paths due to lineblockages and other infrastructure-related issues, it soon became evi-dent that the paths acquired this way generally offered faster transittimes than annual ones. Further, it increased the operational flexibility,both in departure time and train weight, by choosing alternate routing,allowing the operator to react to the varying needs of customers, part-ners and external factors. Despite this, departure and arrival times in

the RETRACK main-run were generally fixed on the same days andhours and were only altered if absolutely required.

The main-run is a major contributor to the performance enhance-ments that RETRACK can offer its customers compared to the usual sin-gle wagon networks, both in terms of operational quality and from apecuniary perspective. It provides a very rapid transit of below-blocktrain volumes, by running approximately 1.250 kmat block train speeds(24 h per direction with two borders and one loco change) and costs.

Costs are kept low by a very lean operation — generally only oneelectric main line locomotive is required for the service. Thislocomotive's annual distance amounts to approximately 390.000 km,about twice that of the average freight-mainline locomotive. Further-more, the combination of both operational and commercial thinkingby the train operator considerably enhances the cost-efficiency of theoperation.

Customers buy slots for their (conventional)wagons on specific traindepartures on the main-run, in similar fashion to container-shippers,who buy slots for their containers on intermodal trains.

The main difference for the customers, especially those with largeslots comparable to block trains, is that they can partly profit from rev-enues generated by other customers, since a RETRACK-main-line roundtrip has paying groups in both directions. On the downside, again espe-cially for those customerswith large groups, the train is not dedicated tothem, thus they cannot exert the same level of influence as freely aswithregular, fully paid block trains.

However, all customers – even those with only irregular, singlewagons – can enjoy services similar to those of container-shuttle cus-tomers, which helps to significantly reduce the apparent complexityof international rail transport of conventional wagons, often one of themain arguments levelled against rail transport.

5.2. The “shuttle” trains

The shuttle trains are similar to themain-run in that they are usuallymade up of 2 ormore groups between Cologne and a limited number ofcorresponding stations in the Netherlands. These are usually drop off/pick-up only via the secondary RETRACK hub in Rotterdam.

77T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

The main difference, compared to the main run, is that these trainsaremore flexible in their departure times and the number ofweekly de-partures. This is basically an attempt to save costs,where possible. How-ever, due to the growing necessity of providing Rotterdamwith reliablesingle wagon services, the frequency of this shuttle train is increasinglymore stable. In the near future, it is anticipated that shuttle trains willbecome an integral part of the main-run.

5.3. The “antenna” trains

The third operational key element, antenna trains, connects the re-spective RETRACK-hub with the final destination, or the loading sitefor one group/customer, on a purely demand-driven basis. The trainsconsist of only one group of wagons, since they usually connect specificcustomer sites to the RETRACK system. A good example is the on-goingcorn transports from various loading sites throughout Hungary. Arriv-ing empty in Györ, the corn wagons (usually 20–24 wagons) arebeing transported by CER to the loading site requested by the customerin the order-phase, there to be loaded and transported back as a region-al block train, to the RETRACK hubs.

6. Key results, barriers and successes

6.1. Operational results

RETRACK has so far transported 255.000 net tons, in 5.289 loadedwagons, as well as 4.773 empty wagons and 25 locomotives in thecourse of the demonstrator operation. An average of 3–4 groups arecombined in one train. The commodities carried have been a mix ofbulk, corn and soya pellets, white wine, aluminium slabs, aluminiumoxide, automotive, chemicals, Ethylene oxide, Butane, Sulphur Dioxide(RID), Polyethylene, Acrylonitrile, Vegetable Oil, Styrene, Ethanol, androlling stock itself. The origins and destinations of the core loads havebeen Benelux to Hungary, with automotive parts from the Balkansinto Germany. Chemicals have run from one end of the corridor tothe other; indeed one notorious train was a single chemical wagon,run whilst the grain wagons were removed from service for bearingsfaults.

6.2. Barriers

Certain key barriers face new entrants in the open access market inEurope and the case study highlighted several of interest to practitionersand policy makers. The first is the complexity. The pilot involved up to8 railways in mainline and local operation, up to 8 customers withtheir own schedules andneeds, up to 10different loading and unloadingsites, in more than seven countries, 4 to 6 rail infrastructure providerswith different rules and regulations and potentially 4 different electricalpower systems.

Trust within the consortium itself was a barrier. Most of the partnersinvolved were simultaneously partners, customers and competitors ofeach other. Transpetrol, as a forwarding agent, was the best party tolead the consortium but was also seen as a potential competitor by therest. Establishing a business model that used a third party ‘honest bro-ker’ to manage the revenue collection and allocation allowed a degreeof commercial confidentiality, whilst still allowing a single joint ventureto operate. All costs were pooled and reallocated against the pooled rev-enue share. Resolving this mix took over 2 years.

Rolling stock availability was variable. Electric main-line locomo-tives for Austria and Germany are available, but the availability of loco-motives for the Netherlands is hampered by the need for additionalspecial requirements for the Betuwe line, both in actual availabilityand the leasing cost.

Wagon availability was a major bottleneck and – especially grain-wagons – has been a major source of trouble due to the age and poorcondition of the equipment. The differing interpretation of what should

be a single safety system across the EU alsomeant that wagon problemsresulted in some cases in slow running and, in other countries, the com-plete halt of the service.

Personnel: The availability of highly qualified operational staff is aconstant problem on the whole corridor served by RETRACK. This prob-lem is especially apparent in theNetherlands and in Belgium, but also inGermany, Austria andHungary. This is both a supply problem (there is ashortage of drivers in much of Europe), but also hampered by the factthat there is no single drivers licence that covers the whole of the EU,nor a common language to ensure operation (Marinov, Zunder,Arnoldus, & Moolen, 2012). Therefore, drivers need to be multiple-certified and multilingual. During the 2.5 years of operation, the pilotwas unable to realise border-crossing services with its electric locomo-tives (which are homologated and licensed for Hungarian operation)from Hegyeshalom to Györ due to the lack of qualified drivers. Shuttleand antenna-trains suffered from lack of drivers as much as they suf-fered from technical problems.

Onemajor drawback for the RETRACK operation is the lack of a suit-able ICT solution capable of covering the full scope of necessaryplanning and control tools required by the train operator.Whilst, with-in the project, a suitable and apparently very successful solution wasdeveloped for the railway operation as originally envisioned, the com-plexity of RETRACK's operations as a whole are beyond the scope ofthe software. As a result, the workload for the RETRACK team has attimes been tremendous, simply due to the lack of sophisticated ITsupport.

Access to Train paths: While no real discrimination was encoun-tered during the RETRACK pilot operation regarding train paths, theoverall process of obtaining a train path is extremely cumbersomeand difficult to co-ordinate for an international rail freight productsuch as RETRACK. Whilst the TEN-T and railway packages created a‘One-Stop-Shop’, whereby a single train path can be booked across allinfrastructures, the pilot found the process so slow and cumbersomethat all trains ran on multiple national train paths, often allocated onan ad hoc basis.

Access to non-path based infrastructure: As a private operator, thepilot faced discrimination, of varying degrees, connected to non-pathinfrastructure allocation. Transpetrol noted the practice of DBSchenker (DBS) Rail to block prime infrastructure by parking oldwagons. Obvious attempts by DBS and DB Netz to discriminateconcerning local infrastructurewere encountered, in various instances,and required - at least in some cases - institutional pressure. In Hungary,RETRACK was thus never able to secure the required infrastructureto wholly fulfil the functions of a true hub. All shunting, storageetc. had to be organised uniquely for each single transport. Wagonsmight be parked all over the station at Györ, instead of being collect-ed on a specific track, thus requiring additional shunting and increas-ing the possibility of operational mistakes. This is connected to theHungarian policy of not allowing the permanent rental of tracks atall. Tracks can only be reserved in connection with train runs, thusfavouring state railways with their de facto continuous train runs.It is therefore both a policy concern and an operational one forpractitioners.

Shunting: Inmost countries of Western Europe, the infrastructure isin the responsibility of specialised infrastructure companies. However,the locomotives and the staff effecting shunting services on theshunting yards and minor stations are usually not under the control ofthe infrastructure companies, but are part of the ‘operational’ parts ofthe former state railways. Thus, the operational support by thoseshunting is usually not available to private operators. While it is inmost cases technically possible to organise an alternative shunting solu-tionwith private operators, it is usually only possible at prohibitive cost.If local shunting servicesweremade available as an additional service ofthe rail infrastructure, available to every user of the infrastructure, a farmore efficient use of train and track capacity would be possible for newentrants.

78 T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

6.3. Successes

Themajor success of the RETRACK Pilot was in proving that it is pos-sible to set up privately operated, trans-European and complex railtransport systems for serving the market, not only with block train ser-vices, but also single wagon and wagon-group services. This wasachievedwith aminimumof resources and despite unfavourable gener-al conditions. The operators are confident that, with more favourableconditions (infrastructure availability, improved co-ordination alsowith western incumbents, ICT-System etc.), the model set by RETRACKcan be successfully implemented elsewhere. Although the traction wassplit between partners, it was split for operational and logistical reasons,not for country borders, and only for traction. The access to market andthe locomotives allow a single operator on the route, but the staff issuesdo not.

One of the clear achievements of RETRACK was the set-up of a con-nection to the network of the Eastern-European state railways. Whilethese railways adopted a very pragmatic approach in accepting wagonsfrom private carriers, the western railways (especially Deutsche Bahnand Rail Cargo Austria and their affiliates) adopted an aggressive, pro-tectionist stance.

Since completion of the pilot rail freight operation (February 2010 –

July 2012), the RETRACK service has achieved commercial viability andhas continued with a growing pool of customers and additional trainruns (Woroniuk, Marinov, Zunder, & Mortimer, 2013). Fig. 4 demon-strates the increasing volume ofwagons and trains over the pilot period.The partners have continued to run the servicewith no external fundingand it appears viable at the time of writing.

7. Discussion

7.1. Contribution to scholarly knowledge

There are few case studies of pan European rail freight operations inthe newly liberalisedmarket, and very few fromanacademic viewpoint.Whilst the papermust by its nature focus on a single case, it expands thebody of knowledge. Further case studies are needed to allow both as-sessment of the EU policy in this area but also cross comparisons ofthe EU and North America, in that it is not clear that single continentalrail system (USA and Canada) is easily compared with the EU-27when there is little evidence of continental scale rail freight in Europe.

Fig. 4. RETRACK demonstrator operations: volumes Feb

The research calls for a new research agenda that broadens the expe-riential data available, interviewing customers, operators and regulatorsalong the various TEN-T corridors. This research also calls for better un-derstanding of howopen access is delivered across Europe andassessingthe correlation of liberalisation and rail freight growth and decline indifferent markets, offset by other factors such as market reorientation,wider government policy and the different approaches of actors to thefull train, intermodal block train and single wagon load sectors.

7.2. Implications for managerial practice

The recent European transport policy (i.e. 2011 Transport WhitePaper) realises that the freight shipments over short and medium dis-tances (below 300 km) will largely, but not exclusively, remain ontrucks. There is a concern that this sort of prescriptive cut off distancebecomes a self-fulfilling mantra and that it is based on existing techni-cal, commercial and operational models that may be subject to majorchange. Therefore, it suggests that the services of other transportmodels (rail, waterborne transport) have to achieve efficiency, cost-effectiveness, availability and reliability, at the level (if not better) oftruck service.

Currently, rail freight is sometimes seen as anunattractivemode. Ex-amples in some Member States (e.g. Switzerland, The Netherlands)prove that it can offer quality service. The challenge is to ensure struc-tural change, to enable rail to compete effectively and take a significant-ly greater proportion of the medium and long distance freight market.Considerable investmentwill be needed to expandor to upgrade the ca-pacity of the rail network. The use of electric traction for rail freightendows a massive advantage, by virtue of the ability to use power gen-erated from a cocktail of fuel and primary sources. The ability to com-mercially exploit this, together with the inherent energy efficiency ofrail, compared to road, also needs to be addressed.

Rail freight can and should benefit from the reforms driven throughby the EU. The rail industry has been forced to respond to externallydriven changes. This can be seen as worrying, as the industry shouldhave been moving proactively to modernize itself (like the road freightsubsector) in response to competitive and context changes governingthe movement of cargo. The railways need to be much more pro-active in the development of new product and service offerings andmust also begin to recognise that the established view of the longevityof railway assets is no longer tenable in the face of the faster renewalcycle of trucks.

ruary 2010 to January 2012 (Source: Transpetrol).

79T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

The RETRACK service has managed to compete, rail-on-rail, utilisingthe market openings created and has thrived, being able to offer betterservice and transit time in cross border rail freight. It has managed todo so inmarkets such as Germany, that has partial observance of the di-rectives, facing many barriers from the incumbents, infrastructuremanagers, rail regulators, and terminal operators. This suggests that,with some caveats, an open access freightmarket does exist in the Euro-pean Union, and that it has created new opportunities for organisationsto focus on international rail freight. It is still difficult to say, from theRETRACK study, that rail freight has gained some market share fromroad freight, but it has at least proved that a cross border, pan European,privately driven rail freight offering can operate commercially, exploitingthe emergent open access position in Europe.

The availability of an alternative operator (RETRACK), offering equiv-alent or better services, without recourse to pricing action (traditionallythe method used to secure market share and then price up) has provedattractive to cargo interests and shippers. Flexibility, responsiveness,better asset management and, above all, pro-active links to the shipperswith real time information on train location, status and timings, is some-thing the shippers appear to have valued highly. The RETRACK projecthas developed with these facets well to the fore. It demonstrates whatcan be and needs to be done to attract shippers to alternative services,without recourse to loss making pricing activities to secure and retainmarket share. This should bring rail into contention with road-dominated services (national and international), where these require-ments are routinely met as part of the commercial and operationalpositioning.

Managers looking to develop a similar pan European service in thefuture should take care to address the issues raised in the pilot; asound business model that enables all parties to both co-operate andcompete; look to trainmultiply licensed and lingual driving staff; securenon path services and infrastructure; compete on service and not price;to ignore the supposed single infrastructure management system andaccess train paths at the national level; and look to develop hybrid logis-tics structures than enable hybrid block train and singlewagon business,accessing base volumes (grain in the case of the pilot) and high returnsingle or wagon group business such as chemicals.

7.3. Policy implications

The reforms instituted and driven by the EU to change the capabili-ties of the European railway industry have met with partial success.The biggest problem has been the differential speed of adoption of thereformmeasures, varying fromwholesale adoption tominimal incorpo-ration. Themodels of reform adopted have in some cases (Germany andFrance) left the incumbent operators in a very strong position, with di-rect government involvement in the direction and ownership and fi-nancing of the enterprises. The limited power of the various nationalrail regulators to intervene and curb the powers of the incumbents in re-lation to pricing, access limitations to sidings and facilities, power andaccess charges, also reflects the proximity of the incumbent railwaysto their sponsoring governments. The lack of willingness to drivethrough essential reforms for the long-term commercial well-being ofthe rail sector, at a uniform level and pace across Europe, is worrying.The resistance, by some of the larger and smaller incumbents, to theadoption of clearly desirable changes, puts the railways into a situationwhereby their traffic is being eroded by the failure to reform at a funda-mental level. The strength and near universality of the road freight sec-tor is something that some of the incumbents have clearly failed torecognise as being a threat to their long-term viability.

The development of RETRACK services by new entrant operators hasbeen constrained by the activities of some of the incumbents either di-rectly (pricing) or by the use of measures designed to obstruct or im-pede smooth operations. The denial or limitation of train paths, accessto sidings and terminals are all examples of where the ‘big battalions’have sought to exercise their powers to limit competition. The close

relationship between the incumbent operators, infrastructure man-agers, rail regulators, governments, ministries and other agencies, cre-ates a real barrier and resistance to externally generated (and agreed)changes. The EU should take a strong position with clear roles, respon-sibilities, status, timelines etc. and also take action against thosewho donot comply on time and properly.

For domestic national operations, the appearance of new competingentities for train operation, shunting and service provision has been atangible and visible sign that things are changing, albeit at a variablepace. There has already been some consolidation amongst the new en-trant operators. More worrying is the acquisition of the new entrants,by the incumbents, as a means of maintaining market share as an alter-native to the adoption of the required reforms, or to being prepared toadapt and modernise (see for example: Railway Gazettes, 2009, 2010for references). The competitive response by incumbents on pricinghas been muted to date. Certainly the incumbents are known to be pre-pared to retain their ‘core business’ bypricing to zero, if necessary. Againthis cuts across the requirement to become more competitive (rail onrail) and to break the umbilical link between the support of the stateand the long term financing of the incumbent.

At a strategic level, the EU's initiatives cannot be left in a part-appliedstate across the EU with massive disparity in the level to which the re-quired reforms have been implemented. The EU has taken actionsagainst those states identified as being non-compliant and it is regretta-ble that this was a necessary response to the lamentably slow introduc-tion of these measures. The variable standard and capability of therailway regulators is something that also causes concern. The disparitybetween the regulators at a national level is something that potentiallycompromises new pan European services. The opaque relationship be-tween regulators, infrastructure managers, incumbent operators andsome national governments is troubling. The fear is that the incumbentoperators are able to secure behind the scenes advantages over theircommercial rivals and suppress real, rail-on-rail competition.

For rail to succeed in both the domestic and pan European markets,under the new rules of engagement, it has to be able to match andoutperform road freight options, on price and service, on a sustainedbasis. Rail-on-rail competition, as envisaged by the EU, has to be seenas a transition towards more effective competition with the primarymodal competition from road transport. To achieve modal shift impliesa significant improvement of rail's capabilities and competence. The in-cumbents appear, at present, to be unwilling or unable to recognise thescale of the changes they will have to make to be able to compete withroad and win traffic and retain it on merit.

The deregulated rail freight market in Europe is still distorted bystructural inequalities. Examples along the RETRACK corridor in Centraland Eastern Europe are: infrastructure discrimination; non transparentor liberalised energy supply;monopolistic shunting services; safety cer-tifications barriers; terminal access is used to restrict trade; regulatoryauthorities can be weak or discriminatory; incumbent (often state-owned) railways being protected against bankruptcy; subsidies givento the national state railway alone; and, in some member states, an in-cumbent acting as de facto legislator, regulator and operator.

The key conclusions policymakers from the interviews and the pilotare that an open access policy regimehas been implemented imperfect-ly but it has allowed, in this pilot, for a pan European rail freight corridorservice to emerge. The key issues to address are the continued work onreinforcing the original railway package, and addressing the key issuesof personnel training and licensing and the open and equal availabilityof non path infrastructure and services.

Acknowledgment

The authors acknowledge the funding of this research by the Euro-pean Commission Sixth Framework Programme contract: TREN-06-FP6TR-SO7-69821.

80 T.H. Zunder et al. / Research in Transportation Business & Management 6 (2013) 71–80

Appendix A

RETRACK based study rail regulators' interviewee.

No Country Date of interview Company/Institution Name and position

1 Germany 14/10/2007 DZB Professor Dr Karsten Otte and Christopher Dobbe2 Germany 23/07/2007 DB Netz Duisberg Ulrich Weinberg and Michaela Kraus3 Germany 25/05/2012 Matthias Bruch Legal & Economics Wolfgang Gross, Head of Section Rail Access4 Hungary 19/09/2007 Ministry of Transport Pakozdi Istvan, Ministry of Transport; and Lajos Szucs,

Deputy Director General — Capacity Allocation Office5 Hungary 20/09/2007 Rail Regulator Antal Daniel6 Hungary 11/06/2012 Rail Regulator Dr Gabor Racz, Head of Rail Regulation Unit; and Istvan Pakozdi,

CEO Rail Capacity Allocation Office7 The Netherlands 01/08/2007 Ministry of Transport, Public Works

and Waterways (Civil Aviation and Freight)Hinne de Groot, policy officer

8 The Netherlands 02/08/2007 RNE Utrecht P.J. Brugts9 Austria 11/09/2007 Ministry of Transport Klaus Gsettenbauer, OBB Infrastructure Management — Network Access10 Austria 13/09/2007 Rail Regulator Dr Harald Hotz11 Romania 05/10/2007 Ministry of Transport Dr Marin Stancu

References

Banister, D., Stead, D., Steen, P., Akerman, J., Dreborg, K., Nijkamp, P., et al. (2000). Europeantransport policy and sustainable development. London: Spon.

Boer, E. d., Essen, H. v., Brouwer, F., Pastori, E., & Moizo, A. (2011). Potential of modalshift to rail transport — Study of the projected effects on GHG emissions and transportvolumes, Community of European Railway and Infrastructure Companies (CER). Delft:CE Delft 2011.

Borchardt, K. -D. (2010). The ABC of European Law, publications office of the European.Luxembourg: Union.

NEWOPERA The rail freight dedicated lines concept. Castagnetti, F. (Ed.). (2008). Finalreport, the European freight and logistics leaders forum (F&L), Brussels.

CER: Community of European Railway and Infrastructure Companies (2008). European rail-way legislation handbook (2ndedition).Hamburg: Eurailpress, DVVMediaGroupGmbH.

Copenhagen Economics (2007). The potential economic gains from full market openingin network industries. A study for the UK Department of Trade and Industry, DTI URN07/622.

Deville, X., & Verduyn, F. (2012). Implementation of EU legislation on rail liberalisationin Belgium, France and the Netherlands. National Bank of BelgiumWorking Paper No221, March 2012.

European Commission (1992). The future development of the common transport policy,COM 92/494 (final), Brussels.

European Commission (2006). Keep Europe moving — Sustainable mobility for our conti-nent mid-term review of the European Commission's 2001 Transport White Paper,COM (2006) 314 final.

European Commission (2007). Freight transport logistics action plan, Brussels.European Commission (2011a). EUROPA: About the EU: Facts and figures. retrieved July

29, 2011, from. http://europa.eu/about-eu/facts-figures/index_en.htm.European Commission (2011b). A roadmap for moving to a competitive low carbon econo-

my in 2050, Brussels.European Commission Statistical Pocketbook (2011). EU transport in figures, EU. retrieved

May 17, 2012, from. http://ec.europa.eu/transport/publications/statistics/pocketbook-2011_en.htm.

European Conference of Ministers of Transport (2002). The European integration of railfreight transport. Conclusion of Round Table # 125, Paris, 28-29 November 2002.

Government of the Netherlands (no date). Freight transport by rail, accessed 27 September2012 from http://www.government.nl/issues/freight-transportation/freight-transport-by-rail.

IBM (2011). Rail Liberalisation Index 2011, Market opening: comparison of the rail mar-kets of the Member States of the European Union, Switzerland and Norway. A studyconducted by IBM Deutchland GmbH in collaboration with Prof. Dr. Dr. Dr. h.c. ChristianKirchner, Humboldt-University Berlin, Brussels, 20 April 2011.

Knieps, G., & Zenhäusern, P. (2011). The reform process of the railway sector in Europe:A disaggregated regulatory approach. Discussion Paper No 141. Institut fürVerkehrswissenschaft und Regionalpolitik.

Laisi, M., Mäkitalo, M., & Hilmola, O. -P. (2012). Stimulating competition in the liberalizedrailway freight market. Baltic Journal of Management, 7(1), 68–85.

Lowe, D. (2005). Intermodal freight transport. Oxford: Elsevier Butterworth-Heinemann.Marg, J., Mauck, R., Zunder, T., & Mortimer, P. (2012). Demonstration of a viable new rail

freight service concept, 13th September 2012, Delft, restricted document.Marinov, M., Zunder, T., Arnoldus, R., & Moolen, C. A. (2012). Standardised language

code for rail freight operations. Transport problems, 7(2), 141–148.

Nash, C. (2011). How effective if EU Rail Policy. Presentation at the Transport EconomicsGroup (TEG) Meeting, 27 April 2011, London.

New Europe (2010). Rail freight liberalisation: A New Europe policy report, issue 868, 17November 2010.

Peijs, K. (2006). Developing European freight corridors — Making the Rotterdam–Genoarail freight corridor a success for the European economy in Europe's rail freight mar-ket. Community of European Railway and Infrastructure Companies (CER) (pp. 65–78).Eurailpress.

Pietrantonio, L., & Pelkmans, J. (2004). The Economics of EU railway reform, Bruges Europe-an economic policy briefings no 8, September 2004.

Pittman, R. (2011). Mergers and alliances in railways in emerging issues. In A. Estache(Ed.), Competition, collusion and regulation in network industries. Brussels: CEPR.

Pittman, R., Diacony, O., Sip, E., Tomova, A., & Wronka, J. (2007). Competition in freightrailways: “Above-the rail” operators in Central Europe and Russia. Journal of CompetitionLaw and Economics, 3(4), 673–687.

Preston, J. (2009). Trend in European railways over the last two decades. Built Environ-ment, 35(1), 11–23.

PwC – PriceWaterhouseCoopers (2009). Amendments to the rail access legislation in theframework of the recast of the 1st railway package. EU DG-TREN.

Railway Gazettes (2009). Veolia agrees sale of freight division. accessed 3 September2009. http://www.railwaygazette.com/news/single-view/view/veolia-agrees-sale-of-freight-division.html.

Railway gazettes (2010). Captrain completes ITL acquisition. accessed 29November 2010.http: //www.railwaygazette.com/nc/news/single-view/view/captrain-completes-itl-acquisition.html.

Sandholtz, W., & Zysman, J. (1989). 1992: Recasting the European bargain.World politics,42(1). (pp. 95–128).

Stehmann, O., & Zellhofer, G. (2004). Dominant rail undertakings under European com-petition policy. European Law Journal, 10(3), 327–353.

Stehmann, O., & Zenger, H. (2011). The competitive effects of rail freight mergers in thecontext of European liberalization. Journal of Competition Law and Economics, 7(2),455–479.

Thompson, L. S. (2009). Liberalization and commercialization of theworld's railways: Progressand key regulatory issues. Forum Paper 6. International Transport Forum, OECD.

Vassallo, J. M., & Fagan, M. (2007). Nature or nurture: Why do railroads carry greaterfreight share in the United States than in Europe? Transportation, 34, 177–193.

Wolff, C. (2006). Overview of rail freight markets – Europe and beyond in Competitionin Europe's rail freight market. Community of European Railway and InfrastructureCompanies (CER) (pp. 15–34). Eurailpress.

Woodburn, A., & Whiteing, A. (2010). Transferring freight to ‘greener’ transport sector. InA. McKinnon, S. Cullinane,M. Browne, & A.Whiteing (Eds.), Green logistics— Improvingthe environmental sustainability of logistics (pp. 124–139). CILT (UK): Kogan Page.

Woroniuk, C., Marinov, M., Zunder, T. H., & Mortimer, P. (2013). Time series analysis ofrail freight services by the private sector in Europe. Transport Policy, 25, 81–93.

Zunder, T. H., Aditjandra, P. T., & Islam, D. M. Z. (2012a). Europe's freight transport policy:White paper 2001 to white paper 2011. Proceedings of the 91st Annual Meeting of theTransportation Research Board, Washington, DC, USA.

Zunder, T. H., Islam, D. M. Z., & Mortimer, P. N. (2012b). Pan-European Rail freighttransport — Evidence from a pilot demonstration result. Procedia — Social and Be-havioral Sciences Special Issue: TRA Conference, 2012(48), 1346–1355.