HFT and risk management final version R Fernandez FEBELFIN march2013

65

1 Rue d'Arlon 80 / Aarlenstraat 80 B 1040 Brussels Professional Certificate in Risk Management “High Frequency Trading and the risk monitoring of automated trading.” Robert Fernandez Ferrandiz Prudential Supervision Analyst (NBB) & Assistant (Solvay) [email protected] [email protected] Brussels, March 2013 Agenda Executive Summary.................................................................................................... p2 Introduction.....................................................................................................................p4 Chapter I The key challenges to monitor risk in automated trading............................p5 Chapter II Case study of NYSE Euronext HFT & Chicago Stock Exchange patent....p18 Conclusion ....................................................................................................................p35 Bibliography..................................................................................................................p36 Appendix..................................................................................................................p37-65. o Appendix I Algorithm trading and HFT definition o Appendix II Patent research in USPTO o Appendix III Chicago Board Options Exchange patent to define how organize the IT architecture of the risk monitoring of automated trading. o Appendix IV Research questions on HFT and Algorithm trading. o Appendix V Lessons learned from the Flash Crash o Appendix VI CFTC Audit Trail o Appendix VII CFTC Electronic trading analysis o Appendix VIII The Global Financial Network o Appendix IX NYSE Technologies - Market Access Gateway Inventory (January 2013) Key words : Financial innovation, Systemic risk, IT monitoring, High Frequency Trading, Financial stability.

-

Upload

solvaybrussels -

Category

Documents

-

view

3 -

download

0

Transcript of HFT and risk management final version R Fernandez FEBELFIN march2013

1

Rue d'Arlon 80 / Aarlenstraat 80

B 1040 Brussels

Professional Certificate in Risk Management

“High Frequency Trading and the

risk monitoring of automated trading.”

Robert Fernandez Ferrandiz Prudential Supervision Analyst (NBB) & Assistant (Solvay)

[email protected] [email protected]

Brussels, March 2013

Agenda

Executive Summary.................................................................................................... p2

Introduction.....................................................................................................................p4

Chapter I The key challenges to monitor risk in automated trading............................p5

Chapter II Case study of NYSE Euronext HFT & Chicago Stock Exchange patent....p18

Conclusion ....................................................................................................................p35

Bibliography..................................................................................................................p36

Appendix..................................................................................................................p37-65. o Appendix I Algorithm trading and HFT definition o Appendix II Patent research in USPTO o Appendix III Chicago Board Options Exchange patent to define how organize the IT

architecture of the risk monitoring of automated trading. o Appendix IV Research questions on HFT and Algorithm trading. o Appendix V Lessons learned from the Flash Crash o Appendix VI CFTC Audit Trail o Appendix VII CFTC Electronic trading analysis o Appendix VIII The Global Financial Network o Appendix IX NYSE Technologies - Market Access Gateway Inventory (January 2013)

Key words: Financial innovation, Systemic risk, IT monitoring, High Frequency Trading, Financial stability.

2

Executive Summary Automated and algorithm trading are nowadays important drivers in financial markets. High Frequency trading (as a subdivision of automated trading) is also an important driver in US and EU automated trading platforms. This new paradigm involves important questions on risks, monitoring and regulation. The High Frequency Trading evolution underlines three keys questions:

How High Frequency traders could improve risk management tools to manage operational risks (algorithm issues) and market risks (price manipulation, liquidity and volatility)?

How stocks markets (and brokers-dealers) could improve and contribute to prevent individual failure but also systemic risks (including interdependencies and correlations from HFT algorithms)?

How supervisory authorities could / should regulate high frequency technology in financial markets in a risk monitoring perspective?

Based on case study and regulatory guidelines, this paper analyses key specifications on the automated trading risk monitoring tools. In an automated trading environment, a certain amount of control is lost when a market-maker has issued quotes in a large number of option series. The quotes are typically recorded in the automated and computer-based trading system, and matched up automatically with orders that enter the system electronically. IOSCO has clearly identified the risk of "black box" regarding the evolution of automated trading and ultra-speed trading. Regulators (as ESMA and CFTC) call for monitoring tools implemented not only by High Frequency Traders but also by stock exchanges and all professional traders. ESMA asks that trading platforms should monitor in real time their electronic trading systems (a real time audit trail). Additionally, ESMA asks that investment firms should prior to deploying an electronic trading system (or a trading algorithm) and prior to deploying updates, make use of clearly delineated development and testing methodologies. For algorithms, these might include performance simulations/back testing or off line testing within a trading platform testing environment (where market operators make testing available). CFTC encourages development of more industry-wide testing procedures (to test algorithms in “real life” conditions), including scenario and stress testing. Based on the NYSE Technologies platform case study, we can observe that audit trail from NYSE automated platforms is limited to the timeframe of hundredth of a second (1/100sec). In the same time, NYSE platforms provide total end-to-end latency (including inter-process and inter-server communications) of approximately 70 microseconds (1/1000.000 sec). This case study illustrates the current gap existing between the capacity of trading and the real capacity of monitoring HFT. This gap is creating a "shadow trading" where supervisors would not have the possibility to analyze what is really happening. Volume is also increasing with HFT. In Europe, before MiFID went live back in 2007, It was observed rates of 5,000 to 10,000 messages per second. Nowadays, the automated trading platform Chi-X alone can peak at over 80,000 messages per second. In the US the rates have already exploded, with total equity, options and futures markets topping 4 million messages per second. Additionally to the end-to-end latency issue, HFT increases the volume "message queue" creating a new challenge in the implementation of automated risk trading monitoring. The case study of the Chicago Board Options Exchange patent provides some useful ideas. This patent is dedicated to an automated risk monitoring IT architecture (including automated revision or cancellation of quotes based on risk thresholds).

Additionally to individual risk (For example, the crash of Knight Capital Group in August 2011), Algorithm trading (with direct access to the market and with a high frequency trading

3

timeframe) could also involve systemic risk due to correlation between algorithms. CFTC underlines the importance of testing. For CFTC, It is possible that code rollouts related to small changes in market structure (e.g. new order types) involve important risks due to the fact that many market participants affected simultaneously the condition of the market and that these new trading algorithms were potentially never employed before.

The conclusion of this paper is to support the idea that the new worldwide trading architecture should be articulated around Stock exchanges as regulated Hub. There are worldwide around 50 major stock exchanges. Stock exchange could be responsible to organize "Quality Acceptance" test environment to challenge algorithms in an individual perspective but also in a systemic approach (linked to potential correlation of algorithms).

4

Introduction: The declining costs of technology have led to its widespread adoption throughout financial industries. The resulting technological change has revolutionized financial markets and the way financial assets are traded. Many institutions now trade via algorithms and High Frequency Trading (more than 70% of Equity volume US markets, around 30/40% for European markets). Automated and algorithm trading are nowadays important drivers in financial markets. High Frequency trading (as a subdivision of automated trading) is also nowadays a driver in US and EU automated trading platforms. Based on lessons learned from the Flash Crash of May 2010 and the state of art on algorithmic trading and High Frequency Trading (see appendix), this paper provides an analysis to understand how to improve risk monitoring of automated trading. HFT is subject of many interrogations on net social benefice in the point of view of market efficiency (liquidity, volatility & pricing) but also potential risks for regulators (manipulation & systemic risk) but also for traders. The rise of HFT is a result of two important changes that have increased the ability and desirability of trading fast and frequently. First, the decimalization of quotes, the change from having bid and offer prices being quoted in eighths to having them quoted in pennies, has allowed for more minutes price variation. The smaller price increments makes trading during short horizons less risky as a tick in the wrong direction now can cause a penny per-stock loss whereas previously it would cost an eight of a dollar. Second, there have been technological advances in the ability to quickly analyze information and to rapidly transport data between locations. This evolution has involved the migration from floor-based to electronic (point-and-click) to high speed trading (or high frequency trading). This change also has involved the possibility to have direct access to the markets for a growing number of operators in a multitude of decentralized automatic trading platforms. In the present paper, we will run through key specifications from scholar to supervisory bodies regarding algorithm and High Frequency Trading and the creation of a “shadow trading” area. This paper is articulates on supervisory guidelines and case studies. Firstly, I examine the keys specifications from ESMA and CFTC. Secondly, as hub in the financial market, I challenge stock market regarding this issue. I examine the NYSE Euronext as case study and I present the Chicago Stock Exchange Board patent as illustration of IT architecture on risk monitoring of automated trading. The purpose of this paper is not to provide, as the majority of scholar paper, an exhaustive summary of the current debate on algorithm and HFT trading. The added value of this analysis is to present key ideas on the monitoring of automated trading. The main limit of this paper is due to the absence of possibility to challenge the analyzed specifications with experts from Stock market, dealing room and brokers. The second important limit of this research is the absence of additional analysis regarding the challenge to register and to audit algorithms used in HFT. The main innovative part of this study, regarding previous paper on the topic of HFT, comes from the presentation of a patent specification. This patent, from the Chicago Stock Exchange, deals with technical specifications of risk monitoring implemented in automated trading platforms. I hope that the singularity of this approach will provide a personal added-value on HFT risk management debate.

US stock exchange automated trading timeline

1980s – First electronic trading systems appeared.

1992 – The Chicago Mercantile Exchange (CME) launched

its first electronic platform, Globex.

1993 – Systematic/electronic trading was enabled for CME

equity futures.

2000 – New York-based International Securities Exchange

(ISE), the first fully electronic U.S. options exchange, was

launched.

2003 – NYSE introduced automated quote dissemination.

2010 – All seven U.S. exchanges offered either fully

electronic or a hybrid mix of floor and electronic trading in

options.

5

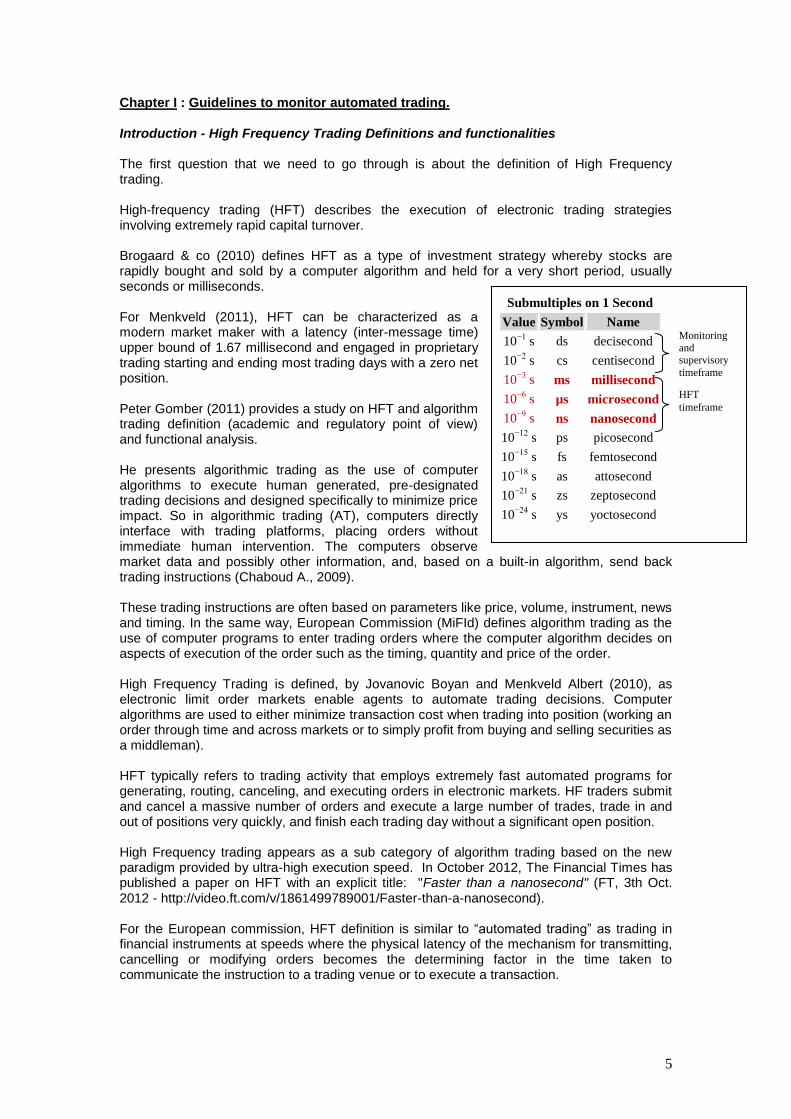

Submultiples on 1 Second

Value Symbol Name

10−1

s ds decisecond

10−2

s cs centisecond

10−3

s ms millisecond

10−6

s µs microsecond

10−9

s ns nanosecond

10−12

s ps picosecond

10−15

s fs femtosecond

10−18

s as attosecond

10−21

s zs zeptosecond

10−24

s ys yoctosecond

HFT

timeframe

Monitoring

and supervisory

timeframe

Chapter I : Guidelines to monitor automated trading. Introduction - High Frequency Trading Definitions and functionalities The first question that we need to go through is about the definition of High Frequency trading. High-frequency trading (HFT) describes the execution of electronic trading strategies involving extremely rapid capital turnover. Brogaard & co (2010) defines HFT as a type of investment strategy whereby stocks are rapidly bought and sold by a computer algorithm and held for a very short period, usually seconds or milliseconds. For Menkveld (2011), HFT can be characterized as a modern market maker with a latency (inter-message time) upper bound of 1.67 millisecond and engaged in proprietary trading starting and ending most trading days with a zero net position. Peter Gomber (2011) provides a study on HFT and algorithm trading definition (academic and regulatory point of view) and functional analysis. He presents algorithmic trading as the use of computer algorithms to execute human generated, pre-designated trading decisions and designed specifically to minimize price impact. So in algorithmic trading (AT), computers directly interface with trading platforms, placing orders without immediate human intervention. The computers observe market data and possibly other information, and, based on a built-in algorithm, send back trading instructions (Chaboud A., 2009). These trading instructions are often based on parameters like price, volume, instrument, news and timing. In the same way, European Commission (MiFId) defines algorithm trading as the use of computer programs to enter trading orders where the computer algorithm decides on aspects of execution of the order such as the timing, quantity and price of the order. High Frequency Trading is defined, by Jovanovic Boyan and Menkveld Albert (2010), as electronic limit order markets enable agents to automate trading decisions. Computer algorithms are used to either minimize transaction cost when trading into position (working an order through time and across markets or to simply profit from buying and selling securities as a middleman). HFT typically refers to trading activity that employs extremely fast automated programs for generating, routing, canceling, and executing orders in electronic markets. HF traders submit and cancel a massive number of orders and execute a large number of trades, trade in and out of positions very quickly, and finish each trading day without a significant open position. High Frequency trading appears as a sub category of algorithm trading based on the new paradigm provided by ultra-high execution speed. In October 2012, The Financial Times has published a paper on HFT with an explicit title: "Faster than a nanosecond" (FT, 3th Oct. 2012 - http://video.ft.com/v/1861499789001/Faster-than-a-nanosecond). For the European commission, HFT definition is similar to “automated trading” as trading in financial instruments at speeds where the physical latency of the mechanism for transmitting, cancelling or modifying orders becomes the determining factor in the time taken to communicate the instruction to a trading venue or to execute a transaction.

6

Gomber (2011) classifies the functionalities of algorithmic trading and High Frequency Trading as follow: According Gomber (P. Gomber, 2011), the key related concepts to HFT are the Market making characteristic, the Quantitative Portfolio Management (QPM) tools, and the Smart Order Routing (SOR) technology. Peter Gomber (2011) provides the following picture who summarizes also the specifications between Algorithm trading and HFT.

Common for HFT and AT

1) Pre-designed trading decisions 2) Used by professional traders

3) Observing market data in real-time 4) Automated order submission

5) Automated order management 6) Without human intervention 7) Use of direct market access

Specific for AT excl. HFT 1) Agent trading 2) Minimize market impact (for large orders) 3) Goal is to achieve a particular benchmark 4) Holding periods possibly days/weeks/months 5) Working an order through time and across markets

Specific for HFT 1) Very high number of orders 2) Rapid order cancellation 3) Proprietary trading 4) Profit from buying and selling (as middleman) 5) No significant position at end of day (flat position) 6) Very short holding periods 7) Extracting very low margins per trade 8) Low latency requirement 9) Use of co-location/proximity services and individual data feeds 10) Focus on high liquid instruments

7

The US Commodity Futures Trading Commission provides also an useful definition (October 2012). According this definition, High frequency trading is a form of automated trading that employs:

o algorithms for decision making, order initiation, generation, routing, or execution, for each individual transaction without human direction;

o low-latency technology that is designed to minimize response times, including proximity and co-location services;

o high speed connections to markets for order entry; and

o recurring high message rates (orders, quotes or cancellations) determined using one or

more objective forms of measurement, including:

cancel-to-fill ratios; participant-to-market message ratios; or participant-to-market trade volume ratios.

(source: http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/tac103012_wg1.pdf)

The ESMA 2012 Guidelines for automated trading platforms. In May 2012, the European Security and Markets Authority (ESMA) has published his “Guidelines - Systems and controls in an automated trading environment for trading platforms, investment firms and competent authorities”. For ESMA guidelines, trading platforms should, within their overall governance and decision-making framework, develop, procure (including outsourcing) and monitor their electronic trading systems through a clear and formalized governance process. On regulated markets and multilateral trading facilities, electronic trading systems should also for the ESMA have sufficient capacity to accommodate reasonably foreseeable volumes of messaging. They must be able to increase capacity in order to respond to rising message flow and emergency conditions that might threaten their proper operations. Regarding risks issues involved by the development of HFT, ESMA asks that trading platforms should monitor in real time their electronic trading systems. They should deal adequately with problems identified as soon as reasonably possible in order of priority and be able when necessary to adjust, wind down, or shut down the electronic trading system. Regarding their testing obligations, investment firms should prior to deploying an electronic trading system or a trading algorithm (and prior to deploying updates), make use of clearly delineated development and testing methodologies. For algorithms, these might include performance simulations/back testing or off line testing within a trading platform testing environment (where market operators make testing available). To ensure that there is orderly trading on the platform, trading platforms should have minimum requirements for members’/participants’ and users’ pre- and post-trade controls on their trading activities (including controls to ensure that there is no unauthorized access to trading systems). In particular, trading automated platforms should implement controls on filtering order price and quantity (this requirement is without prejudice to the responsibility of members/participants or users to implement their own pre and post-trade controls). ESMA guidelines also impose that trading platforms should have arrangements to prevent the excessive flooding of the order book at any one moment in time, notably through limits per participant on order entry capacity.

8

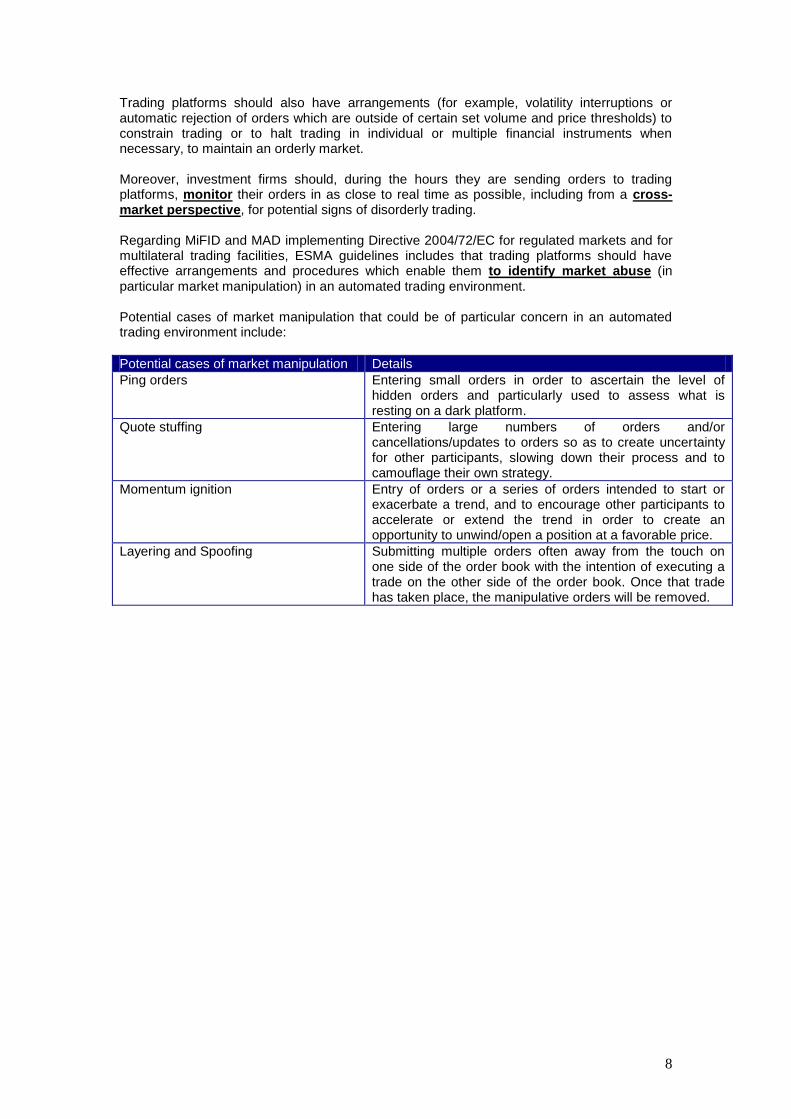

Trading platforms should also have arrangements (for example, volatility interruptions or automatic rejection of orders which are outside of certain set volume and price thresholds) to constrain trading or to halt trading in individual or multiple financial instruments when necessary, to maintain an orderly market. Moreover, investment firms should, during the hours they are sending orders to trading platforms, monitor their orders in as close to real time as possible, including from a cross-market perspective, for potential signs of disorderly trading. Regarding MiFID and MAD implementing Directive 2004/72/EC for regulated markets and for multilateral trading facilities, ESMA guidelines includes that trading platforms should have effective arrangements and procedures which enable them to identify market abuse (in particular market manipulation) in an automated trading environment. Potential cases of market manipulation that could be of particular concern in an automated trading environment include:

Potential cases of market manipulation Details

Ping orders Entering small orders in order to ascertain the level of hidden orders and particularly used to assess what is resting on a dark platform.

Quote stuffing Entering large numbers of orders and/or cancellations/updates to orders so as to create uncertainty for other participants, slowing down their process and to camouflage their own strategy.

Momentum ignition Entry of orders or a series of orders intended to start or exacerbate a trend, and to encourage other participants to accelerate or extend the trend in order to create an opportunity to unwind/open a position at a favorable price.

Layering and Spoofing Submitting multiple orders often away from the touch on one side of the order book with the intention of executing a trade on the other side of the order book. Once that trade has taken place, the manipulative orders will be removed.

9

New European legislative initiative: MiFID II proposal Under the new MiFID II proposal, European regulators are focusing greater scrutiny on high-speed trading. MiFID already covered Multilateral Trading Facilities and regulated markets, but the revision will now bring a new type of trading venue into its regulatory framework: the Organized Trading Facility (OTF). These are organized platforms which are currently not regulated but are playing an increasingly important role. MiFID will introduce new safeguards for algorithmic and high frequency trading activities which have drastically increased the speed of trading and pose possible systemic risks. These safeguards include the requirement for all algorithmic traders to become properly regulated, provide appropriate liquidity and rules to prevent them from adding to volatility by moving in and out of markets. Finally, the proposals will improve conditions for competition in essential post-trade services such as clearing, which may otherwise frustrate competition between trading venues. The proposals will reinforce the role and powers of regulators. In coordination with the European Securities and Markets Authority (ESMA) and under defined circumstances, supervisors will be able to ban specific products, services or practices in case of threats to investor protection, financial stability or the orderly functioning of markets.

Unsatisfied with delays to MiFID II, a draft legislation in Germany is set to curb high-frequency trading (HFT), bringing it under the control of Germany’s Federal Financial Supervisory Authority (BaFin) probably by the end of 2013. Under a new law known as the “Act for the prevention of risks and the abuse of high-frequency trading”, the definition of proprietary trading would be widened to include HFT firms, forcing them to be licensed, and compelling trading venues to enforce minimum tick sizes and order-to-trade ratios.

The draft of MiFID II contained a provision requiring all those operating automated trading strategies to be continuous market-makers whatever the market conditions. This proposed requirement will only apply (if adopted) to those operating a "high frequency strategy" and which has at least one of the four of the following characteristics:

it uses co-location facilities; it relates to a daily portfolio turnover of at least 50%; the ratio of orders to trades exceeds 4:1; the proportion of orders cancelled exceeds 20%; the majority of positions taken are unwound within the same day; over 50% of the orders are made on trading venues offering discounts or

rebates to orders which provide liquidity.

In this new European regulation, it is proposed that ESMA shall be tasked with developing regulatory technical standards for general position limits. It is also proposed that a minimum resting period for all orders is imposed at 500 milliseconds. European Parliament’s financial committee decided in September 2012 to rein in the velocity of high-frequency trading (a half-second speed limit on those using computers to execute lightning-fast stock deals).

An important remark is to understand that not only speed but also volume traded is growing very fast. Hirander Misra, co-founder and chief executive of Algorithm Technologies, notes that, collectively across all the major equity exchanges in Europe, It was observed rates of 5,000 to 10,000 messages per second before MiFID went live back in 2007. Nowadays, the automated trading platform Chi-X alone can peak at over 80,000 messages per second and it's anounced total market peaks approaching 150,000. In the US the rates have, of course, already exploded, with total equity, options and futures markets topping 4 million messages per second according to marketdatapeaks.com. (Source: http://www.automatedtrader.net/online-exclusive/80415/market-data-maelstrom).

10

US Commodity Futures Trading Commission (CFTC)

In October 2012, the US Commodity Futures Trading Commission (CFTC) has adopted the following HFT Draft Definition: => High frequency trading is a form of automated trading that employs:

algorithms for decision making, order initiation, generation, routing, or execution, for each individual transaction without human direction;

low-latency technology that is designed to minimize response times, including proximity and co-location services;

high speed connections to markets for order entry; and

recurring high message rates (orders, quotes or cancellations) determined using one or more objective forms of measurement, including:

o cancel-to-fill ratios; o participant-to-market message ratios; or o participant-to-market trade volume ratios.

=> High frequency trading is a mechanism utilized by a variety of trading strategies [including - but not limited to - liquidity provision and statistical arbitrage]. For CFTC, the objective forms of measurement are determined by a regulator for specific financial instruments or classes of instruments and provide a benchmark for comparing activity that is higher than normal. Such benchmarks should be published on a periodic basis and applied for a specified time period following publication. These measurements should be applied to the participant responsible for the recurring high message rates. The forms of measurement chosen are intended to allow a regulator to measure activity without direct access to the trading algorithms employed to generate the high message rates. CFTC October 2012 definition of HFT can be illustrated by the following flow Chart and Automated Trading process:

11

(CFTC source)

CFTC also has defined the key specifications of an audit trail regarding automated trading (see appendix). Pre-trade risk controls are now required in US equity markets. Equity markets require (limited) risk checks for all participants. Brokers are allowed to self-check. For CFTC, Exchange should expand the pre-trade risk checks available on their systems. CFTC also estimated that Exchange based risk checks should be applied equally to all participants including ensuring that they are applied with equal latency for all participants. Additionally, CFTC underlines the fact that all participants need risk controls, and not just firms specializing in automated trading. Substantial trading errors generated in electronic systems can happen in trading systems used by brokers and end investors. Coding, data, and procedural errors may be more dependent on the trading technology than on the purpose of the trading strategy. Also CFTC underlines the key role used by post-trade risk controls. Post-trade risk controls in the form of drop copies of orders to third parties or brokers can enable useful near real-time risk calculations that cannot be done with ultra-low latency pre-trade risk controls. Post-trade risk controls must:

Provide an alternative pathway for trade positioning;

Enable further data gathering for post-event analysis. CFTC also underlines the importance of testing. For CFTC, It is possible that code rollouts related to small changes in market structure (e.g. new order types) are particularly risky:

Many market participants could affected simultaneously market parameters;

New trading mechanics are potentially never employed before.

On testing topic, CFTC encourages development of more industry-wide testing procedures (to test algorithms in “real life” conditions), including scenario and stress testing. But in the same time, CFTC says to be not optimistic that regulatory certification of algorithms or testing methods can be practical or effective.

In the field of HFT registration, CFTC suggests to make the following distinctions:

Distinctions in degree of automation, latency, messaging and volume;

Distinctions across products, contract months, and range of strategies;

12

Distinctions in time horizon over which messaging/volume is measured.

In this approach, HFT participants can be identified and differentiated as desired to serve surveillance objectives using current data:

Distinguish ATS (Automated Trading System) from non-ATS activity;

Distinguish users’ type of connectivity;

Identify high messaging/volume participants at many levels (e.g. firm, account,…) for any instrument over any time period.

To the question to know if each algorithm should be registered, CFTC underlines the following limits:

Algorithms, inputs and parameters change frequently;

Difficult to consistently define what constitutes a unique algorithm;

No empirical basis to support need for strategy registration.

To the question to know if algorithms should be audited, CFTC underlines the following limits:

Enormous numbers of algorithms deployed;

Inefficient use of limited regulatory resources even assuming expertise were available in regulatory bodies to assess each algorithm;

Foresight economic impact study estimated cost of $1.3 billion/year in US if full descriptions of algorithmic trading strategies were collected and analyzed by regulators;

Entity employing the algorithm should be responsible for appropriate evaluation and testing.

The position of CFTC is to support robust and effective controls and supervision; established at all levels of the infrastructure (to mitigate any single point of failure) and not limited to post-deployment operation. CFTC considers that this controls and supervision should also be considered during every deployment phases. In this approach, it is important to conduct appropriate testing (internal & external conformance) in the following dimensions:

Administrative (user, product and market setup);

Quantitative (back testing algorithm changes against historic trade data);

Technical (connection logic, disconnect/reconnect management);

Functional (order entry, trade & market data processing, market support);

Error (trade bust/adjust management);

Alerting (exchange message & internal alerting notification and display);

Regulatory (clearing and regulatory tag validation);

Stress (load, capacity, performance under unusual market conditions);

Pre-trade risk management (order validation, position management,..). As other IT development, supervision need to implement a clear control framework on:

acceptance, installation and deployment/validation of ATS and HFT; and

Maintenance and monitoring (including an Audit trail tool for Supervision purpose).

13

CFTC Control Recommendation Summary

The audit trail data should be collected, for CFTC, in a way that enables meaningful aggregation, reconstruction, and analysis. The audit trail is also a critical tool to enhancing regulators’ ability to reconstruct and properly sequence activities include:

uniform market participant identifiers,

consistent approaches to the type of data to be collected,

and the use of accurate time-stamp mechanisms. CFTC Audit Trail Data Model (Oct.2012)

14

Examples of derived data (CFTC)

The CFTC Rule 536.B. fixes the “Recordkeeping Requirements" for US Stock exchanges as Chicago Mercantile Exchange Inc. (“CME”), The Board of Trade of the City of Chicago, Inc. (“CBOT”), The New York Mercantile Exchange, Inc. (“NYMEX”) and Commodity Exchange, Inc. (“COMEX”). To illustrate key specification, we have analyzed a regulation certification regarding Chicago Mercantile Exchange (CME Globex). (source:http://www.cftc.gov/stellent/groups/public/@rulesandproducts/documents/ifdocs/rul091912cmecbotnymexandcomex1.pdf) The regulatory requirement asks that orders entered into CME Globex must contain an accurate identification of whether the order is entered via automated or manual means (since June 2011). Inaccurate submission of this regulatory requirement may result in disciplinary action. Core principles of this regulatory requirement are also identified as follows:

An accurate audit trail must be able to identify trading activity that may be disruptive;

Clearing member firms will be required to maintain the front-end audit trail which will include trade information;

The Exchanges (as CME Globex) are formally adopting this regulatory requirements in order to ensure that each Exchange has accurate information concerning whether orders entered are done by automated or manual means.

So entering orders (into CME Globex) shall input for each order:

the user ID assigned him by the Exchange;

a clearing member or other authorized entity;

the price, quantity, product, expiration month, CTI code (Customer Type Indicator);

automated or manual indicator;

and account number;

and, for options, put or call and strike price. The order must be entered (into CME Globex) when it becomes executable. The electronic audit trail must be maintained for a minimum of 5 years and clearing members must have the ability to produce this data in a standard format.

15

For executed orders, the audit trail must record the execution time of the trade along with all fill information. So a record of all fields relating to order entry must be produced (including transaction date, product, Exchange code, expiration month, quantity, order type, order qualifier, price, buy/sell indicator, stop/trigger price, order number, unique transaction number, account number, session ID, automated or manual indicator, host order number, trader order number, clearing member, type of action, action status code, customer type indicator, origin, and timestamps). This electronic audit trail must contain all order receipt, order entry, order modification, and response receipt times to the highest level of precision achievable by the operating system, but at least to the hundredth of a second (1/100sec). The times captured must not be able to be modified by the person entering the order. According CFTC publications (see appendix), the HFT timeline is around 3.6 milliseconds in 2012 on average.

High Frequency Traders website (http://highfrequencytraders.com/news/2309/traders-look-wireless-lowest-latency) estimates that latency, due to wireless technology, could reach 13.3 milliseconds between the markets of Chicago and New York. Hibernia Atlantic (www.hiberniaatlantic.com/gfn.html - see appendix) provides the following worldwide vision of low latency:

24,000 Kilometers of Fiber Optic Cable

Access to over 120 key financial cities around the globe

Connection between London and New York City, with <60 ms latency, the fastest in transatlantic cable history

These examples underline the key challenge to monitor risk management in the high speed automated trading. Audit trail is expected to record and track orders in a timeline of 1/100 sec when transatlantique latency (London/NY) is less of 60/1000sec and with a HFT technology running to the nanosecond according the Financial Times. In this context, the question for regulators is to define how it would be possible to implement an audit trail monitoring HFT and covering the “shadow automated trading" due to ultra-fast trading (from the millisecond to the nanosecond). In October 2011, IOSCO issued its report on "Regulatory Issues Raised by the Impact of Technological Changes on Market Integrity and Efficiency". This report explicitly addresses the need for regulators to continuously evaluate the regulatory challenges related to new and evolving trading strategies. In this report, IOSCO issued the following recommendations:

16

Recommendation 4: “Regulators should continue to assess the impact on market integrity and efficiency of technological developments and market structure changes, including algorithmic and high frequency trading. Based on this, regulators should seek to ensure that suitable measures are taken to mitigate any related risks to market integrity and efficiency, including any risks to price formation or to the resiliency and stability of markets, to which such developments give rise” (source: http://www.iosco.org/library/pubdocs/pdf/IOSCOPD407.pdf) In his report "Regulatory Issues Raised by the Impact of Technological Changes on Market Integrity and Efficiency", IOSCO underlines also that HFT and algorithmic trading have arguably played a significant role in the developments of the new trading environment. IOSCO supports also the need for changes to the way competent authorities monitor trading. (source: http://www.iosco.org/library/pubdocs/pdf/IOSCOPD354.pdf) Regarding market access for automated trading, IOSCO has clearly identified the risk of "black box" due to algorithm and HFT trading: "Facilitating algorithmic trading through automated systems, which raises issues of capacity and the potential need for rationing bandwidth. Indeed, some “black box” trading systems are capable of transmitting several thousand order messages to a market in less than a second". (source: http://www.iosco.org/library/pubdocs/pdf/IOSCOPD284.pdf)

17

Few Comments... Many trading systems utilize what is known as an open outcry method of trading. In the open outcry system, market-makers are required to make a two-sided market by providing a bid and offer quote in all option series. The market-makers typically communicate verbally or visually with contra traders indicating their willingness to buy and sell various quantities of securities. Because the market-makers have personal control over the types and number of contracts traded, they can adjust their trading strategies as their positions change. In this way, the market-makers can manage their exposure, or risk, associated with their holdings by adjusting their quotes to favor trades that would tend to hedge away unwanted exposure. In an automated trading environment, a certain amount of control is lost when a market-maker has issued quotes in a large number of option series. The quotes are typically recorded in the automated and computer-based trading system, and matched up automatically with orders that enter the system electronically. With the proliferation of computer trading systems and increased communication speeds, the rate at which trades may be executed by an automated system far surpass the rate of trades that occur in an open outcry system. The speeds are such that the rapidity of trades may exceed the market-maker's ability to adapt his or her position. Specifically, one disadvantage of automated trading systems is that a number of automatic trades may occur within a very short time that result in an unacceptable risk being assumed by a market-maker. That is, the trades may occur so rapidly that the market-maker is unable to withdraw or modify his quotes in a timely manner (e.g. Knigh Capital crash in August 2012). There exist software tools that can analyze stock and option portfolios in close to real time. Market data is provided to the software analysis tools and used to evaluate the risk associated with stock and option portfolios. In addition, the tools may provide recommendations for trades and quotes and automated submission of those trades and quotes. However, even if a market-maker utilizes such a computer-implemented automated position analysis tool to revise or cancel quotes, the software tools may be unable to act in time given the speed at which an automated trading exchange system is capable of executing incoming orders. In particular, one aspect of existing exchange systems is that transactions are received and processed in the order received. Thus, even if a market-maker responds immediately using an automated software tool, the exchange may have a message queue containing additional orders that will be processed before the exchange system receives and processes the market-maker's quote cancellation request. The result is that a market-maker who is willing to take on a predetermined level of risk must limit the number of quotes or the depth (quantity) of each quote to ensure that rapid trades do not result in an unacceptable aggregate risk, rather than issuing quotes having greater depth and breadth (where the filling of a single quote might reach the market-maker's risk limit). Thus, a market-maker's limited control over risk management may have the undesirable effect of hindering the liquidity of the market. It would therefore be desirable to have a trading exchange system and method for automatically canceling, regenerating, or modifying quotes under certain trading conditions. The Chicago Board Options Exchange patent on risk monitoring of automated trading provides few ideas on the IT architecture needed to avoid "message queue" in automated revision or cancellation of quotes.

18

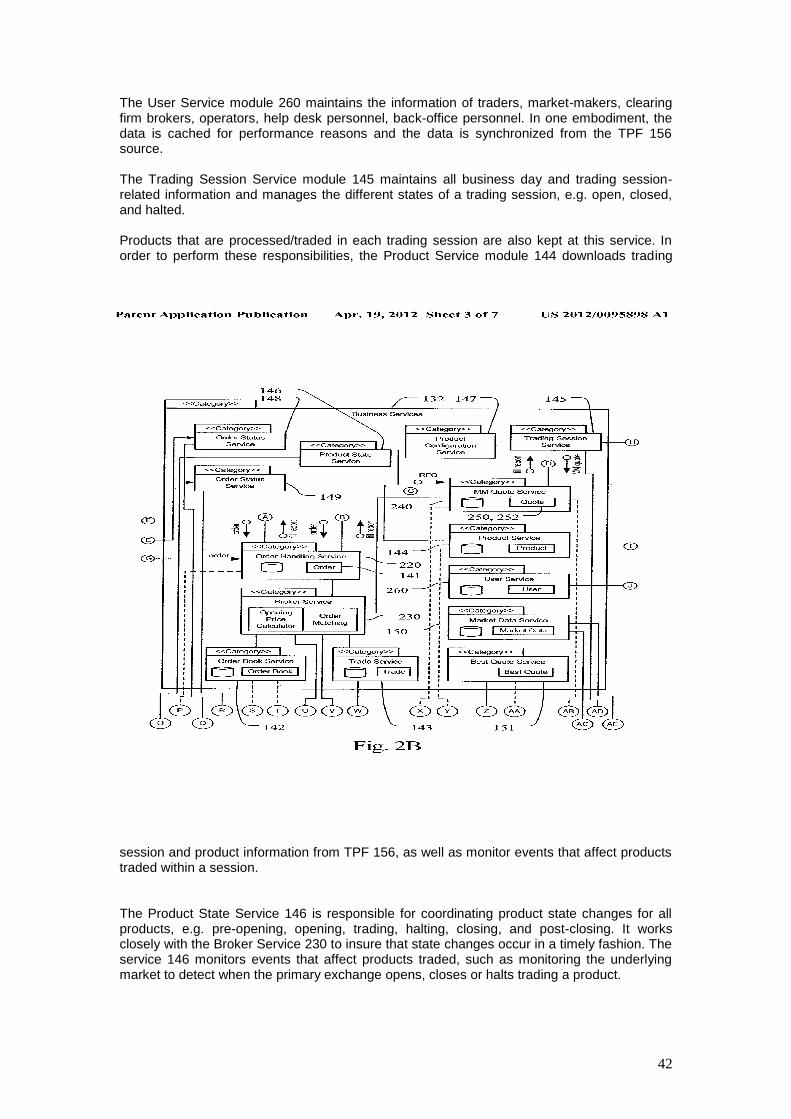

Chapter II: Case study of NYSE Euronext HFT & Chicago Stock Exchange patent In this section, we propose to analyze information from stock market regarding the implementation of automated trading and High Frequency technology. Acting as node in the financial network, stock markets are key actors in the risk management specifications. Also, stock market must incorporate very fast processing to stay competitive in a very fragmented and changing environment. This paper will focus on two case studies. One will analyze the specifications from the implementation of High speed trading technology in HFT NYSE Euronext. The other one will analyze the patent from Chicago Stock Exchange on the risk monitoring of automated trading. The case study of the NYSE Euronext HFT services NYSE Euronext (NYX) is a leading global operator of financial markets and a provider of innovative trading technologies. With exchanges in the US and Europe, NYSE Euronext equities marketplaces represent one-third of equities trading worldwide. NYSE Euronext is also one of the world’s leading futures and options trading venues, with four markets based in the US and Europe offering derivatives on commodities, FX, equities, bonds, interest rates, indices and swaps. Its commercial technology division, NYSE Technologies, provides transaction, data, and infrastructure management services and solutions. From a single global business, NYSE Technologies delivers best of breed products using world-class technology connected to all the world major markets. NYSE Technologies is one of the world's leading providers of end-to-end electronic trading solutions. Through leading edge software, combined with high performance connectivity, NYSE Technologies engages the global trading community with innovative tools, access to liquidity and worldwide markets.. NYSE Technologies provides High Frequency Trading services, also through Market Access Gateway (MAG) and Risk Management Gateway (RMG). For an investment firm to enter the arena of algorithmic trading, it must have reliable systems capable of moving tremendous volume in microseconds. NYSE Technologies combines these elements into a single normalized messaging interface. Market Access Gateway (MAG) is an extremely low-latency order routing platform, that offers high-frequency traders, institutional investors and broker-dealers a scalable connection to global execution venues. MAG provides high speed messaging on commodity hardware, with deployment specific fine-tuning to maximize performance and throughput. Regarding Risk management tools, MAG provides optional pre-trade risk checks to allow to mitigate operational risk (fat finger checks) and keeps orders compliance in real-time. MAG technology easily integrates with other NYSE Technologies products to provide complete trading solutions. The diagram below shows typical integration examples, providing low latency Direct Market Access (DMA) in both broker-managed and hosted/co-located environments.

19

NYSE Technologies Market Data Platform feed handlers normalize the incoming market data with very low latency and pass the updates to SuperBook and to OneTick. SuperBook builds a consolidated view of all open orders for stocks while. OneTick captures the updates and stores them for historical processing. The OneTick (as Complex Event

DMA = Direct Market Access providing low latency

MAMA or open MAMA = Open Middleware Agnostic

Messaging APITM

LDMA = physical box as the trading engine providing

sub- microsecond transport latency, at throughputs

approaching millions of messages per second.

MAG = Market Access Gateway

RMG = Risk Management Gateway

FH = Feed Handlers

SFTI= Secure Financial Transaction Infrastructure

20

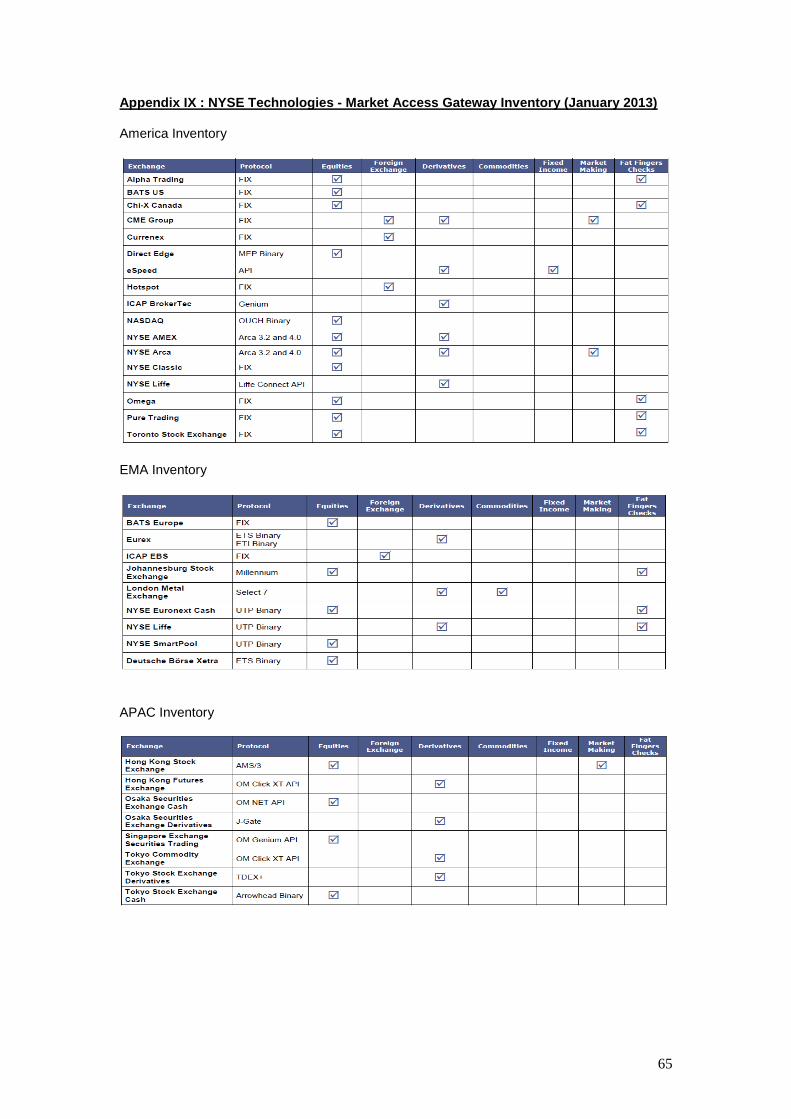

Processing Engine) calculates a range of mathematical analytics, which are delivered to the Client’s algorithmic engine. Finally, when the algorithm decides it’s time to trade, it issues the order to the NYSE Technologies (Market Access Gateway); which converts the trade to the format required by the corresponding Trading Venue. All this communication is handled at sub-microsecond latency via NYSE Technologies LDMA (Local Direct Memory Access = messaging platform). NYSE Technologies has published his Market Access Gateway Inventory for January 10, 2013 (see appendix). The total end-to-end latency introduced by the NYSE Technologies platform, including inter-process and inter-server communications, was approximately 70 microseconds

(1/1000.000 sec). The NYSE Technologies tests were designed to measure key factors of relevance to algorithmic traders:

the latency and throughput characteristics of the market data and market access infrastructure;

platform performance under varying market data update rates; and platform performance while varying the rate that orders are sent to market.

A logical view of the components in the test environment and the measurement points is shown in the following figure.

In a supervisory point of view, it’s

fundamental to assess the impact of

exchange simulator testing on

latency.

21

LATENCY MEASUREMENT – CLASSIC MISTAKES 1. Measuring the parts, not the whole. Measuring the

performance of components in isolation does not provide a true picture of how they will perform in combination. 2. Not using representative test data. Testing with

artificial data, or data from a different market, can produce results that do not accurately characterize real world performance. 3. Measuring only what can easily be captured.

Often, the metrics reported are those that are easy to measure, rather than those that are critical to trading system performance. 4. Not measuring what is important to business. If the

trading strategy is sensitive to latency outliers, there is little benefit in measuring averages. Similarly, capturing network round-trip times or single-component delays may not be particularly relevant in a business context.

The performance of the components shown in grey with dashed outlines was not measured in the tests. Latency was measured across three different segments of the platform:

the inbound components, the trading application, and the outbound components.

Inbound latency measures the time between a market data update being sent by the exchange simulator and the corresponding update being received by the algo engine code. This measures the end-to-end latency of the market data platform from the point of view of an algorithmic trader in the most stringent way: this is the total interval between a packet of market data entering the trader’s network from the exchange, and the time that the algorithm code can act upon it. Application latency measures the internal latency of the algorithm engine, defined as the time between it receiving a market data update and it being about to send an order message to the MAG. It was measured in order to be able to exclude the effect of the test code from the results and, therefore, is not included in the reported figures from NYSE Technologies. Outbound latency measures the time between the algorithm engine sending an order to the MAG and the network packet containing the order being sent to the exchange simulator. This measures the end-to-end latency of the market access platform from the point of view of an algorithmic trader. The first test (the market data test) was designed to determine the maximum rate at which the market data infrastructure could perform without introducing excessive latency. The algorithm engine was configured to send an order message to the MAG in response to every thousand price updates it received, and the multicast publisher was configured to send data at between 5,000 and 80,000 packets per second. This corresponds to approximately 2,300 to 37,000 market data updates per second. The second test (the Market Access test) was designed to determine the maximum order volume that the market access infrastructure could support. The algorithm engine was configured to send an order message to the MAG for every single market data update it received, and the multicast publisher was configured to send data at rates between 1,000 and 15,000 packets per second. These results correspond to market data update rates, and hence also order rates, between 450 and 7,000 per second. The test was run for ten minutes (five million packets for the market data test or half a million packets for the market access test). The entire day’s capture file contained 19.8 million packets, so the higher-rate market data tests correspond to consuming a quarter of a day’s data in just over a minute. The market data test showed consistent average inbound latency of between 46.7 and 50.1 microseconds for all data rates up to the maximum rate of 36,925 packets per second (and never exceeded 290.1 microseconds). The market access test showed very consistent average outbound latency of between 19.8 and 21.5 microseconds. The results of these tests are useful to understand the total end-to-end performance that can be achieved with a set of trading platform components that have been designed to work together.

22

NYSE Technologies - Test and results specifications.

As we can observe in this case study, testing on latency doesn’t cover the fundamental part of Stock exchange simulation. NYSE Technologies has created the industry standard for one of the highest-performance, lowest-latency global networks. It gives a single point of connection to a wide array of markets, through infrastructure reliable enough to power every NYSE Euronext market around the world. With over 1,600 potential counterparties and a wealth of third-party markets, It is one of the largest networks in the world. NYSE Technologies deploy Access Centers in London, Paris, Amsterdam, Brussels, Lisbon and Frankfurt. The Access Centers are housed in telco-neutral, third party data centers and are located a minimum distance apart. The speed of the cross connect is dependent on the bandwidth of the connection the costumer has ordered (this could be 10Mb, 100Mb, 1Gb). NYSE Euronext provides the equipment to be hosted. Most Tier 1 carriers have a presence within these facilities. To conclude this NYSE case study presentation, we would like focus on the "NYSE TECHNOLOGIES TERMS AND CONDITIONS". These Terms and conditions are useful to understand how a stock exchange defines responsibilities with his customers:

The Supplier may at any time, for any reason (except where prohibited by applicable law), deny the Client’s request for the Service or limit the available facilities of the Service as determined in the Supplier’s sole discretion.

The Client is responsible for making separate arrangements for use of any services (other than the Service) provided by the Supplier and its Affiliates (including

23

trading platform and market data services) and nothing in this Agreement entitles the Client or any other party to use or receive such services.

Only the Client (and not any third party) may use and access the Service, and the Client may not resell the Service (in whole or in part) or permit any third party to use or access the Service without the prior written consent of the Supplier.

Prior to allowing any of its Affiliates to use and access the Service, Client shall submit to the Supplier, for the Supplier’s approval, notice of such use and access and the identity of the Affiliates of the Client that would use and access the Service. The Supplier shall promptly notify the Client of its approval or disapproval of such use and access by such Affiliates of the Client.

A “Client User” means any third party, other than an Affiliate of the Client, who the Client permits to use and access the Service in accordance with this Agreement.

The Supplier reserves the right to make Policies governing the use of the Service (the “Policies”) and specifications concerning connection of systems to the Service (the “Specifications”) and to amend the Policies and the Specifications from time to time.

The Client agrees to comply with the Policies and Specifications and the rules and regulations of the Supplier as are notified by the Supplier to the Client from time to time.

The Supplier exercises no control over, and accepts no responsibility for, the content of any information transmitted using the Service. Use of such information is at the Client’s own risk. The Client is solely responsible for maintaining the accuracy and integrity of its own data.

24

Chicago Board Options Exchange as case study - A patent to define how organize the IT architecture of the risk monitoring of automated trading. In the fields of Patents, US market gives the originality to allow corporate to patent business model or organization. This section will analyze the Chicago Board Options Exchange patent as case study on what kind of IT architecture could be implemented in a risk management perspective for automated trading. This patent also provides IT architecture specification to help in managing "message queue" for High Frequency quotes revision or cancellation regarding Risk thresholds. To select the Chicago Board Options Exchange patent, we conduct a research in the US Patent & Trademark Office data base. This research has used key "words" to filter patents with the target to find patents related to risk monitoring of automated trading:

On the filter “Title&Abstract&Document” for the key words “automated trading”, we have found 92 patents;

If we include an additional filter on the key words “Risk management”, we have 15 patents;

If we include an additional filter on keys words “monitoring” or “risk monitoring”, we have 4 patents.

On these 4 patents, one patent comes from the Chicago Board Options on Exchange and his content covers the purpose of this paper. (see appendix)

This patent was approved in 2012 with the ID number 20020082967. It was submitted by Chicago Board Options Exchange (CBOE) and coverts the following organization topic: “Automated trading exchange system having integrated quote risk monitoring and integrated quote modification services”. CBOE sum up his patent as follow: “An automated trading exchange having integrated quote risk monitoring and quote modification services. An apparatus is implemented using at least one computer, having memory, and a processor. The computer is configured to receive orders and quotes, wherein specified ones of the quotes are contained in a quote group, and have associated trading parameters such as a risk threshold. Not all received quotes are required to have trading parameters as described herein. Preferably, the quote group contains all the quotes, or a subset of quotes, belonging to an individual market-maker for a given class of options contracts, or possibly the quotes of two or more market-makers that have identified themselves as belonging to a group for the purposes of risk monitoring and quote modification. The computer typically generates a trade by matching the received orders and quotes to previously received orders and quotes, and otherwise stores each of the received orders and quotes if a trade is not generated. The computer then determines whether a quote within the quote group has been filled as a result of the generated trade, and if so, determines a risk level and an aggregate risk level associated with said trade. The computer then compares the aggregate risk level with the market-maker's risk threshold, and if the threshold is exceeded, automatically modifies at least one of the remaining quotes in the quote group. The computer may also automatically regenerate quotes that have been filled”. CBOE has structured his patent on fhe following 30 claims: 1. A system for processing trades of securitized instruments based on security orders and quotes received from client computers, comprising:

at least one server computer comprising a memory, and a processor, said server computer configured to perform the steps of:

25

o receiving orders and quotes, wherein specified ones of said quotes belong to a quote group, and wherein said specified ones of said quotes have associated trading parameters comprising a risk threshold;

o generating a trade by matching said received orders and quotes to previously received orders and quotes;

o storing each of said orders and quotes when a trade is not generated; o determining whether a quote having associated trading parameters has been

filled as a result of the generated trade, and if so, determining a risk level and an aggregate risk level associated with said trade;

o comparing said aggregate risk level with said risk threshold; o and, automatically modifying at least one of the remaining said specified ones

of said quotes in the quote group if said threshold is exceeded.

2. The apparatus of claim 1 further comprising a quote data structure stored in said first memory, said data structure containing a plurality of quotes fields and at least one risk threshold field. 3. The apparatus of claim 2, wherein said plurality of quote fields comprises a bid quote field and an offer quote field. 4. The apparatus of claim 2, wherein said data structure further comprises a group indicator field. 5. The apparatus of claim 2, wherein said data structure further comprises a quote modification increment field. 6. The apparatus of claim 2, wherein said data structure further comprises a quote regeneration increment field. 7. The apparatus of claim 2, wherein said data structure further comprises an owner field. 8. A method of :

modifying quotes in an automated exchange trading system that receives orders and quotes from remote computers, matches the orders and quotes to generate trades, and stores orders and quotes that are unmatched, comprising the steps of:

receiving trading parameters comprising a risk threshold;

associating said trading parameters with specified ones of received quotes;

determining whether a quote having associated trading parameters has been filled as a result of a generated trade, and if so,

determining a risk level and an aggregate risk level associated with said trade;

comparing said aggregate risk level with said risk threshold;

and, automatically modifying at least one of the specified ones of received quotes if said threshold is exceeded.

9. The method of claim 8 wherein the step of determining a risk level comprises calculating a delta value for the generated trade. 10. The method of claim 8 wherein the step of determining a risk level comprises calculating a trading volume for the generated trade. 11. The method of claim 8 wherein the step of determining an aggregate risk level comprises determining a net delta. 12. The method of claim 8 wherein the trading parameters further comprise a time duration, and wherein the step of determining an aggregate risk level comprises summing the deltas from trades involving at least a subset of quotes contained in said quote group that were executed within the time duration. 13. The method of claim 8 wherein the trading parameters further comprise an integer N, and

26

wherein the step of determining an aggregate risk level comprises summing the deltas from the most recent N trades involving at least a subset of quotes contained in said quote group. 14. The method of claim 8 wherein the step of determining an aggregate risk level comprises determining a net contract volume. 15. The method of claim 8 wherein the step of determining an aggregate risk level comprises determining a weighted sum of contract volumes. 16. The method of claim 8 wherein the step of determining an aggregate risk level comprises determining an aggregate volume quantity. 17. The method of claim 8 wherein the step of automatically modifying at least one of the specified ones of said received quotes comprises canceling all said specified ones of said received quotes. 18. The method of claim 8 wherein the step of automatically modifying at least one of the specified ones of said received quotes comprises reducing the quantity associated with the specified ones of received quotes. 19. The method of claim 8 wherein the step of automatically modifying at least one of the specified ones of said quotes comprises revising at least one of the bid and offer values of each of the specified ones of received quotes. 20. The method of claim 8 wherein the trading parameters comprise a positive risk threshold and a negative risk threshold. 21. The method of claim 20 wherein the step of comparing the aggregate risk level with the risk threshold comprises comparing the aggregate risk level to the positive risk threshold if the aggregate risk level is positive, and comparing the aggregate risk level to the negative risk threshold if the aggregate risk level is negative. 22. The method of claim 8 wherein the step of comparing the aggregate risk level with the risk threshold comprises comparing the absolute value of the aggregate risk level to the risk threshold. 23. The method of claim 8 wherein each of the specified ones of received quotes are associated with one of a first subgroup and second subgroup, and wherein the step of automatically modifying at least one of the specified ones of received quotes in the quote group comprises reducing the offer values of the quotes in the first subgroup and raising the bid values of the quotes in the second subgroup. 24. The method of claim 23 wherein the first subgroup comprises quotes on call series options and the second subgroup comprises quotes on put series options, and wherein the aggregate risk is positive. 25. The method of claim 23 wherein the first subgroup comprises quotes on put series options and the second subgroup comprises quotes on call series options, and wherein the aggregate risk is negative. 26. The method of claim 23 where the amount of said reducing and raising is determined in response to a modification increment parameter. 27. The method of claim 8 further comprising the step of automatically modifying a quote comprises regenerating a quote having associated trading parameters that has been filled as a result of the generated trade. 28. The method of claim 27 wherein the step of regenerating a quote is performed utilizing a regeneration increment.

27

29. In a system, for processing trades of a security, that includes a computer that receives orders and quotes, executes a trade by matching the received orders and quotes, and stores received orders and quotes for which a trade is not executed, a computer-based risk monitoring apparatus, comprising:

a quote service module that associates market-maker trading parameters comprising a risk threshold with at least one received quote; and

a broker service module that communicates with the quote service module, wherein the broker service module automatically executes trades and provides corresponding fill reports to said quote service module, and wherein the quote service module modifies received quotes in accordance with the trading parameters and the fill reports.

30. In a system for processing trades of securitized instruments, the system including:

a computer having a memory and a processor, said computer being configured to perform the steps of receiving orders and quotes, generating a trade by matching said received orders and quotes to previously received orders and quotes, and storing each of said orders and quotes if a trade is not generated,

a method for managing risk comprising the steps of: o identifying specified ones of said quotes as belonging to a quote group; o associating trading parameters comprising a risk threshold with specified

ones of said quotes; o determining whether a quote having associated trading parameters has

been filled as a result of the generated trade, and if so, determining an aggregate risk level associated with said trade;

o comparing said aggregate risk level with said risk threshold; and o automatically modifying at least one of the remaining said specified ones of

said quotes in the quote group if said threshold is exceeded. So the CBOE's invention is based on a method and apparatus for an automated trading exchange having integrated quote risk monitoring and quote modification services. The computer is configured to receive orders and quotes, wherein specified ones of the quotes are contained in a quote group, and have associated trading parameters such as a risk threshold. All received quotes are required to have trading parameters as described herein. Preferably, the quote group contains all the quotes belonging to an individual market-maker for a given class of options contracts, or possibly the quotes of two or more market-makers that have identified themselves as belonging to a group for the purposes of risk monitoring and quote modification. The computer typically generates a trade by matching the received orders and quotes to previously received orders and quotes, and otherwise stores each of the received orders and quotes if a trade is not generated. The computer then determines whether a quote within the quote group has been filled as a result of the generated trade, and if so, determines a risk level and an aggregate risk level associated with said trade. The computer then compares the aggregate risk level with the market-maker's risk threshold, and if the threshold is exceeded, automatically modifies at least one of the remaining quotes in the quote group. The computer may also automatically regenerate quotes, that is, automatically issue new quotes when trades have occurred against previous quotes.

28

CBOE provides the following illustration of his architecture:

In this CBOE's figure, a preferred embodiment of the system 100 utilized for trading and quote modification is described. The system 100 (also referred to herein as a screen-based trading system, or SBT system) includes a plurality of computers, which may be one or more workstations, servers, mainframes, or other computer hardware platforms that provide sufficient resources to meet the desired trading volume and desired transaction-processing rate. The system includes a number of computer clusters such as cluster 102 (although only one is depicted in the figure), where each cluster 102 handles trading for a number of securities, such as one or more classes of options. In the preferred embodiment, each cluster 102 is made up of two servers (104 & 106). The servers 104 and 106 in cluster 102 communicate with a plurality of client servers (110 & 112) that are typically located at remote locations, such as at a brokerage house, but may also be located in the same facility as the clusters 102. Network 108 facilitates communication between the clusters 102 and the client servers (Two clients are showed in CBOE figure: 110 & 112). For CBOE, the network 108 is preferably a private LAN/WAN configuration, but a public network may be utilized, if it provided sufficient redundancies and message security. Each client server (110 & 112) may be provided with a predetermined message throughput rate into network (108), where the throughput rate may be a maximum rate determined by various parameters, including the volume of orders sent by the client server (110 & 112), the volume of quotes sent by the client server (110 & 112), the number of option series for which quotes are provided, communication/connection fees paid by the brokerage house or other entity utilizing the client server (110 & 112), the overall capacity of the trading system 100, etc.

29

The client servers (110 & 112) preferably communicate with other elements of the automated exchange system using a client application server module (210), as further described below, running on client servers (110 & 112). Each client server (110 & 112) is capable of serving a number of clients (shown in the figure as terminals 114, 116, 118, 120, 122, and 124). The client terminals may be "dumb" terminals, stand alone computing devices (PCs or workstations), or even portable wireless terminals. The client servers (110 & 112) may communicate with the client terminals (114-124) using a proprietary protocol or one of many standard public domain protocols. The automated exchange system 100 is comprised of the following five logical software modules:

Presentation Services Graphical User Interface (130- GUI);

Application Services (210 - Client Application Server, Gateway);

Business Services (132) - see appendix;

External Integration Services (133) - see appendix;

and, Infrastructure Services (134) - see appendix.

30

The Presentation Services (GUI module 130) is constituted by applications that interact with the exchange system (100) via the Member Interface (API 135). There are two types of client applications, those that provide a GUI to allow user interaction with the system directly and applications that automate trading functions. An SBT-GUI module (131) (screen-based trading - Graphical User Interface) is responsible for displaying the contents of a particular model to the screen and updating the display if the model's contents change. This module 131 contains several GUI applications, one for each of the major classes of human actors that use the system 100: traders, market-makers, clearing firm brokers, and system operators. The Application Services module 210 contains subordinate modules that forward requests initiated by human or automated actors, to be executed by the appropriate Business Services module(s) 132 (see appendix). These applications submit requests to Business Services components 132, notify clients of business events, and maintain user-specific views of information in the Business Services 132. This module also encompasses a Member Interface (MI) API 135 that provides a single entry point to the system exposing the applications in the Application Services Module 210 (i.e., Trader, Market-Maker). In addition, the Application Services Module 210 maintains instantaneously updated views that reflect the prevailing state of each actor's information in the Business Services module 132. The Trader Application module 136 has the following specific responsibilities:

submit, cancel, update, and cancel/replace orders;

submit requests for quotes;

present the current status of the trader's orders;

present fill and cancel reports;

present Market Best Bids and Offers for selected products;

set the trader's defaults and preferences;

present Book Depths for selected products;

and, present underlying quotes/last sales and news alerts. The Market-Maker module 137 inherits the Trader App module's 136 responsibilities and adds the following:

submit and modify market-maker quotes;

present requests for quotes;

set the market-maker's defaults and parameters;

set autoquote parameters; submit autoquotes. The Clearing Firm Broker module 138 inherits the Trader App module's 136 responsibilities and adds the following: assume control of a trader's privileges. A Clearing Firm Broker can:

force the logout of a market-maker;

set a maximum order quantity for quotes and orders of the clearing firm's market-makers.

The BackOffice application 139 is responsible for reporting order status information. This can include fill reports, cancel reports and new order notifications. The Operations application 140 has the following responsibilities:

start and shutdown the SBT system;

start and stop trading of a product;

change the status of a product's market (pre-open, open, close, halt, etc.);

present logged system events;

maintain SBT-specific trader information;

maintain SBT-specific product information;

maintain trading parameters (minimum market-maker order default size, required percent of responses to a request for quote (RFQ), maximum response time to an RFQ, etc).

The functionality of the Trader 136, Market-Maker 137, Clearing Firm Broker 138, and Back Office 139 modules is exposed by the Member Interface (MI) Application Programming

31

Interface (API) 135. The Member Interface 135 exposes different subsets of functionality depending on the user that logged on to the system. The intention behind sharing a common API among the different trader classes is to allow workstations to service all of them. Separate API's may alternatively be used for the different user classes. The Business Services module 132 (see appendix) contains the core functionality of the automated exchange system 100. It includes components that correspond to the key business object model entities of the automated trading system such as members, orders, books, products, quotes, et cetera. In addition, it includes components to administer and operate the system 100. CBOE's Risk Measurements and Risk Thresholds... In a preferred embodiment of the automated trading system 100 having integrated order modification and quote risk monitoring, the aggregate risk of a market-maker's recent trades is calculated after each trade. The measurement preferably includes either:

calculating an equivalent stock position, i.e., a net delta (by, for example, summing delta values for all contracts traded by the market-maker associated with the option series in the class),

or calculating a net gamma, theta, or vega. In particular, the aggregate risk measurement is preferably the net delta of all the trades for a specific market-maker or a designated group of market-makers in a given class in a given period of time. The quotes in a given class submitted by a market-maker (or a group of market-makers) are referred to herein as a quote group. The aggregate risk measurement is preferably based on the net delta for the entire class of options, which is the sum of all the deltas for a given market-maker's trades in all series of a class. The delta contribution for each trade is calculated every time a trade occurs for any series in the class. The aggregate risk is then calculated by summing delta contributions from only the most recent trades. Autoquote systems provide pricing information, and specifically theoretical delta values, using algorithms that utilize standard parameters. Most of the parameters associated with calculating an individual series delta value are objective data, such as the date, strike price, the price of the underlying security, etc. Other autoquote parameters have acceptable default values that may be used, such as using the broker loan rate for the interest rate, etc. One parameter that may be more subjective among individual market-makers is the volatility parameter. Thus, the system 100 may be designed such that each quote submitted by a market-maker includes a volatility field to be used by the system in determining the individual theoretical delta value. The theoretical delta value may then be calculated either:

as part of the threshold test,

or may be periodically updated at a rate sufficient to provide a fairly accurate delta value .