Hans Thorborgs dilemma-3

22

Hans Thorborg’s dilemma Prepared by Alla Wagner, Erzhena Rinchinova, Maria Rybina

Transcript of Hans Thorborgs dilemma-3

Hans Thorborg’s dilemma

Prepared byAlla Wagner,

Erzhena Rinchinova,

Maria Rybina

APPEARANCE OF THE PROBLEM

Business of PWI:• Manufacturing industrial machines and

equipment for sale in numerous countries

Late May, 2013The General Manager of the German Plant of Precision Worldwide, Inc. (PWI) Hans Thorborg meets his Sales Manager, Accountant and Development Engineer to discuss a new product – plastic rings that could be a very good substitute for steel rings produced by PWI.Plastic rings were recently developed by a competing company Henri Poulenc from France.It was learned by PWI managers that plastic rings had• a much longer life;• a much lower manufacturing cost.The PWI problem is that they have a large quantity of steel rings on hand and the substantial amount of special steel inventory. Hence they have to find a way WHAT TO DO WITH ALL OF IT.

The different models of the machines priced between $18,900 and $28,900

• Providing repair services and replacement parts

Facts about the steel rings

Steel versus PlasticThe steel ring

is a spare part of PWI’s industrial machines, has a normal life of about 2 months, different models of machines require from two to six rings, the sales rate 690 rings per week, costs $1,107.9 per hundred,is priced at $1,350 per hundred

Facts about the plastic ringsThe plastic ring

is a substitute for the steel rings, has a normal life of about 8 months, costs $279.65 per hundred,Is priced at $1,350 per hundred .

Considering the rate of steel rings sales, there will be

15,100 finished rings on hand by mid-September in case we produce

no rings. Thus, we have 110,400 finished

rings in late May.

PWI is able to start manufacturing the plastic rings from mid-September.

PWI Europe Operations Geography

Some approaches for decision making process

• ABSORPTION(mainly for Financial

Accounting purposes)

Manufacturing costs Direct Material Direct Labor Variable Overhead Fixed Overhead

Calculate “Gross Margin”By Revenue (minus) Cost of Goods

Sold

• CONTRIBUTION(mainly for Managerial

Accounting purposes)

Manufacturing costs Direct Material Direct Labor Variable Overhead

Calculate “Contribution Margin”BySales (minus) Variable Expenses

Exactly our case

THE STARTING POINT

Per 100 rings Plastic rings

Steel rings

Price $ 1,350.00 $ 1,350.00

Material $ 17.65 $ 321.90Direct labor $ 65.50 $ 196.50Overhead*

Departmental $ 131.00 $ 393.00

Administrative $ 65.50 $ 196.50

Total costs $ 279.65 $ 1,107.90Contribution

Margin $ 1,070.35 $ 242.10

* The variable overhead costs (fringe benefits) amounted to 0,8¢ per direct labor dollar or about 40% of the departmental amounts.

MANUFACTURING COSTS =

PRODUCT COSTS

• DM steel inventory - $ 321.90

• DL wages of the workers manufacturing steel rings – $ 196.50

• OH (Departmental & Administrative)

Fringe benefits – Direct OH

80% of DLOther overhead – Indirect OH ($393.00 + $196.50)-(0.8*$ 196.50)

Direct Materials (DM)

Direct Labor (DL)

Overhead (OH) = mostly indirect costs

Variable costsFixed Costs

Getting rid of all fixed costs

Per 100 Rings Plastic rings Steel rings

Price $1,350.00 $1,350.00

Material $ 17.65 $ 321.90Direct labor $ 65.50 $ 196.50

Direct Overhead $ 52.40 $ 157.20Total costs $ 135.55 $ 675.60

Contribution Margin$

1,214.45 $ 674.40

Only Relevant Costs

Per 100 Rings Plastic rings Steel rings

Steel rings

(Opportunity

Costs)

Price$

1,350.00 $ 1,350.00 $ 1,350.00

Material $ 17.65 0 0

Direct labor $ 65.50 $ 196.50 $ 58.95Direct Overhead $ 52.40 $ 157.20 $ 47.16Total costs $ 135.55 $ 353.70 $ 106.11Contribution

Margin$

1,214.45 $ 996.30 $ 1,243.89

Discount Pricing Policy

Per 100 Rings Plastic rings

Steel rings (without

using excess labor)

Steel rings (with using excess labor)

Price$

1,350.00 $ 337.50 $ 337.50

Material $ 17.65 0 0

Direct labor $ 65.50 $ 196.50 $ 58.95Direct Overhead $ 52.40 $ 157.20 $ 47.16Total costs $ 135.55 $ 353.70 $ 106.11Contribution

Margin$

1,214.45 $ -16.2 $ 231.39

SALES75% OFF

Possible decisions Begin to produce plastic rings as soon as possible.

• Until the inventory and steel were exhausted it would be sold in the markets where it was offered by competitors. But this manipulation could harm the sale of PWI machines.

• Sell the inventory and steel (or throw away): the profit from plastic ring would recover the value of the steel inventory within less than a year.

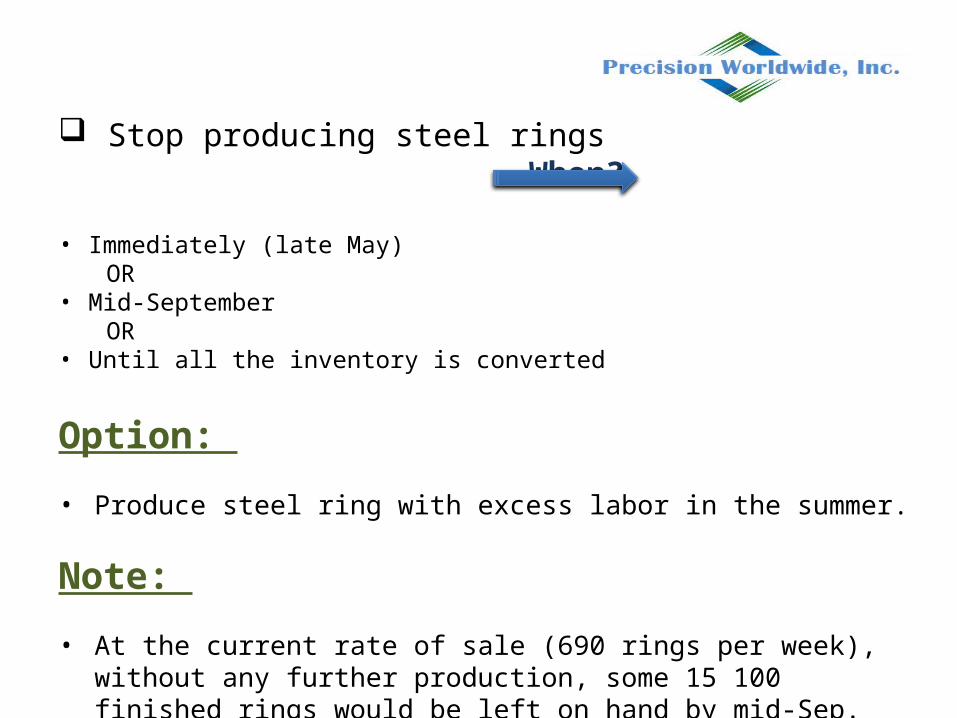

Stop producing steel rings When?

• Immediately (late May)OR

• Mid-September OR

• Until all the inventory is converted

Option: • Produce steel ring with excess labor in the summer.

Note: • At the current rate of sale (690 rings per week),

without any further production, some 15 100 finished rings would be left on hand by mid-Sep.

Solution: • To implement production of

plastic rings immediately.

• Continue producing and selling steel rings till mid-September.

• Employ excess labor in summer for the production of steel rings.

• In the mid-September introduce plastic rings at least in those markets where Henri Poulenc is present and to consider the idea of selling the steel rings with a discount of 75% on our markets.

Assumptions• Steel rings manufacturing rate = rate of sales (690 rings per week) in order to save on warehouse facilities

• Starting of plastic rings doesn’t affect steel rings sales rate, for the share of the markets where we are going to introduce our new kind of spare parts is too small compared to the rest.

Operating plan

SR Usual Manufacturing

SR Usual Manufacturing prior to Day X*

SR Manufacturing using excess labor with implementing Discount

Policy

May

27,

2013

July

16,

201

3

Sept

embe

r 04

, 20

13

Octo

ber

24,

2013

Dece

mber

13,

201

3

Febr

uary

01,

201

4

Marc

h 23

, 20

14

May

12,

2014

July

01,

201

4

Augu

st 2

0, 2

014

2 weeks

12 weeks

2 weeks

37 weeks

13 weeks

50 weeks

* Mid-September

Opportunity Plan

SR Usual Manufacturing

SR Manufacturing using excess labor

SR Usual Manufacturing prior to Day X*

Plastic Rings Manufacturing

May 27, 2013

July 16, 2013

September 4, 2013

October 24, 2013

December 13, 2013

February 1, 2014

March 23, 2014

May 12, 2014

July 1, 2014

August 20, 2014

2 weeks

12 weeks

2 weeks

50 weeks

Coefficient of use

# of rings needed for the market per week, hundred rings

Steel Rings 4 6.9Plastic rings for Operating Plan

1 (6.9/4)*10% ==0.1725

Plastic rings for Opportunity Plan

1 6.9/4*100%==1.725

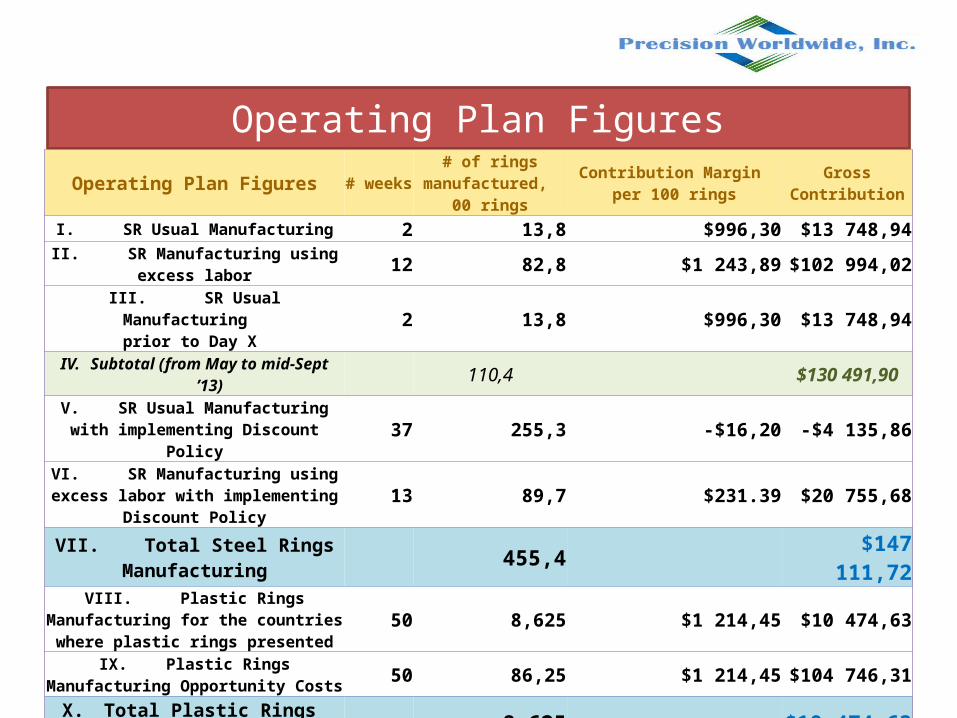

Operating Plan FiguresOperating Plan Figures # weeks

# of rings manufactured,

00 rings

Contribution Margin per 100 rings

Gross Contribution

I. SR Usual Manufacturing 2 13,8 $996,30 $13 748,94II. SR Manufacturing using

excess labor 12 82,8 $1 243,89 $102 994,02III. SR Usual Manufacturing prior to Day X

2 13,8 $996,30 $13 748,94

IV. Subtotal (from May to mid-Sept ’13) 110,4 $130 491,90

V. SR Usual Manufacturing with implementing Discount

Policy37 255,3 -$16,20 -$4 135,86

VI. SR Manufacturing using excess labor with implementing

Discount Policy13 89,7 $231.39 $20 755,68

VII. Total Steel Rings Manufacturing 455,4 $147

111,72VIII. Plastic Rings

Manufacturing for the countries where plastic rings presented

50 8,625 $1 214,45 $10 474,63

IX. Plastic Rings Manufacturing Opportunity Costs 50 86,25 $1 214,45 $104 746,31X. Total Plastic Rings

in Operating Plan 8,625 $10 474,63XI. Total Plastic Rings

in Opportunity Plan 86,25 $104 746,31

Operating plan (VII+X) $157 586,35

Opportunity Plan (IV+XI) $223

523,74

Thank you for your

attention!