Full Board Packet 05_21_2019.pdf - Brown County

297

BOARD OF BROWN COUNTY COMMISSIONERS REGULAR MEETING –May 21, 2019 AGENDA: 9:00 AM 1. Approve County Board Official Proceedings and Synopsis of 05-07-19 9:01 AM Sheriff Jason Seidl Chief Deputy Steve Depew 2. Monthly Report of Activity 9:03 AM Auditor/Treasurer Jean Prochniak 3. General Government Claims 4. Cash Management/Investment Report 5. Resolution−Delegate Authority for EFT Transfers to the Auditor/Treasurer 9:08 AM Auditor/Treasurer Jean Prochniak Assistant Highway Engineer Andrew Lang 6. Drainage Ditch Repair Requests 9:10 AM Highway Engineer Wayne Stevens Assistant Highway Engineer Andrew Lang 7. SAP 008-607-014 Shoulder Widen & Regrade Project on CSAH 7 8. Storm Sewer Repair Project on CSAH 29 9:15 AM Assistant Zoning Administrator Robert Santaella Feedlot Technician Amanda Lang 9. 2018 Annual County Feedlot Report 9:20 AM Public Health Director Karen Moritz 10. Public Health Update 9:30 AM HR Director Ruth Schaefer 11. Public Health RN Resignation 12. Appoint 2019 Summer Highway Engineering/Maintenance Student 13. Salary Administration Plan 9:55 AM BREAK 10:00 AM Zoning Administrator Laine Sletta 14. Planning Commission Recommendations Brown County, Minnesota Board of Commissioners P.O. Box 248 Center & State Streets New Ulm, MN 56073 Telephone (507) 233-6600 District 1: David Borchert 405 South Broadway St. New Ulm, MN 56073 District 2: Anton Berg 20218 195 th Ave New Ulm, MN 56073 District 3: Scott Windschitl 10 Doris Drive New Ulm, MN 56073 District 4: Dean Simonsen 28711 310 th Ave. Sleepy Eye, MN 56085 District 5: Jeff Veerkamp 205 East George St. Comfrey, MN 56019

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Full Board Packet 05_21_2019.pdf - Brown County

BOARD OF BROWN COUNTY COMMISSIONERS REGULAR MEETING –May 21, 2019

AGENDA:

9:00 AM 1. Approve County Board Official Proceedings and Synopsis of 05-07-19

9:01 AM Sheriff Jason Seidl Chief Deputy Steve Depew 2. Monthly Report of Activity 9:03 AM Auditor/Treasurer Jean Prochniak 3. General Government Claims 4. Cash Management/Investment Report 5. Resolution−Delegate Authority for EFT Transfers to the Auditor/Treasurer 9:08 AM Auditor/Treasurer Jean Prochniak Assistant Highway Engineer Andrew Lang 6. Drainage Ditch Repair Requests 9:10 AM Highway Engineer Wayne Stevens Assistant Highway Engineer Andrew Lang 7. SAP 008-607-014 Shoulder Widen & Regrade Project on CSAH 7 8. Storm Sewer Repair Project on CSAH 29 9:15 AM Assistant Zoning Administrator Robert Santaella Feedlot Technician Amanda Lang 9. 2018 Annual County Feedlot Report 9:20 AM Public Health Director Karen Moritz 10. Public Health Update 9:30 AM HR Director Ruth Schaefer 11. Public Health RN Resignation 12. Appoint 2019 Summer Highway Engineering/Maintenance Student 13. Salary Administration Plan 9:55 AM BREAK 10:00 AM Zoning Administrator Laine Sletta 14. Planning Commission Recommendations

B r o w n C o u n t y , M i n n e s o t a B o a r d o f C o m m i s s i o n e r s

P.O. Box 248 Center & State Streets New Ulm, MN 56073 Telephone (507) 233-6600

District 1: David Borchert

405 South Broadway St. New Ulm, MN 56073

District 2: Anton Berg

20218 195th Ave New Ulm, MN 56073

District 3: Scott Windschitl 10 Doris Drive

New Ulm, MN 56073

District 4: Dean Simonsen 28711 310th Ave.

Sleepy Eye, MN 56085

District 5: Jeff Veerkamp

205 East George St. Comfrey, MN 56019

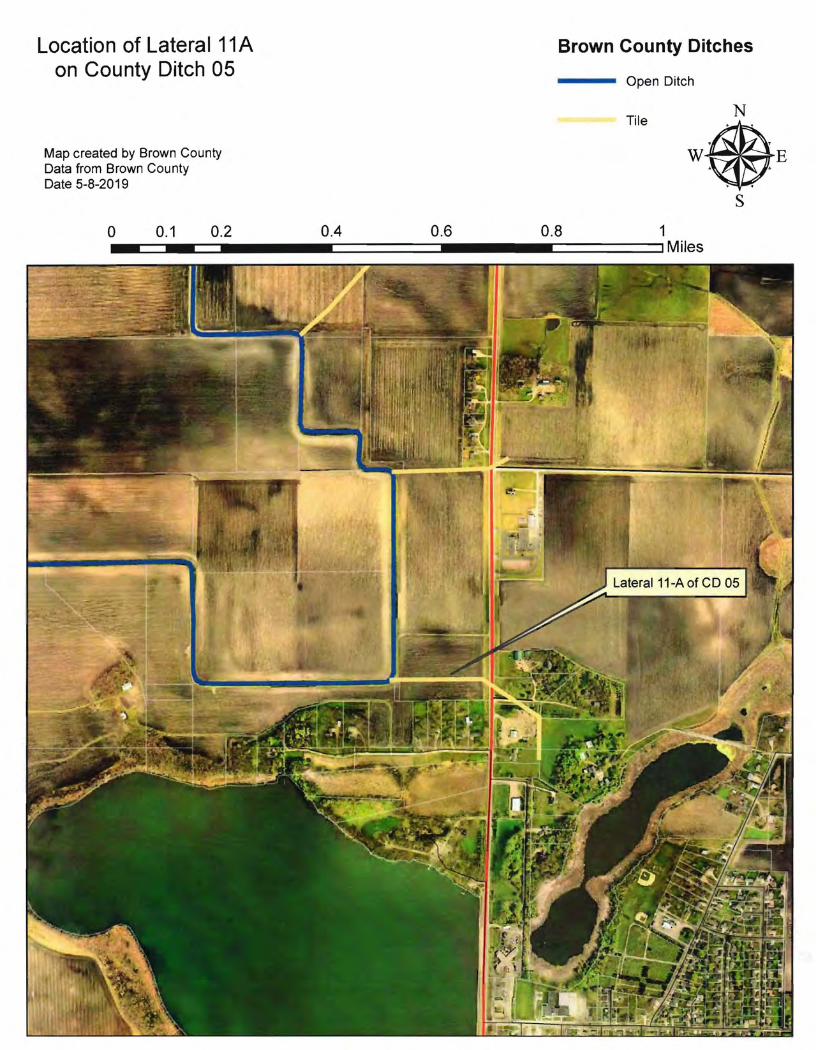

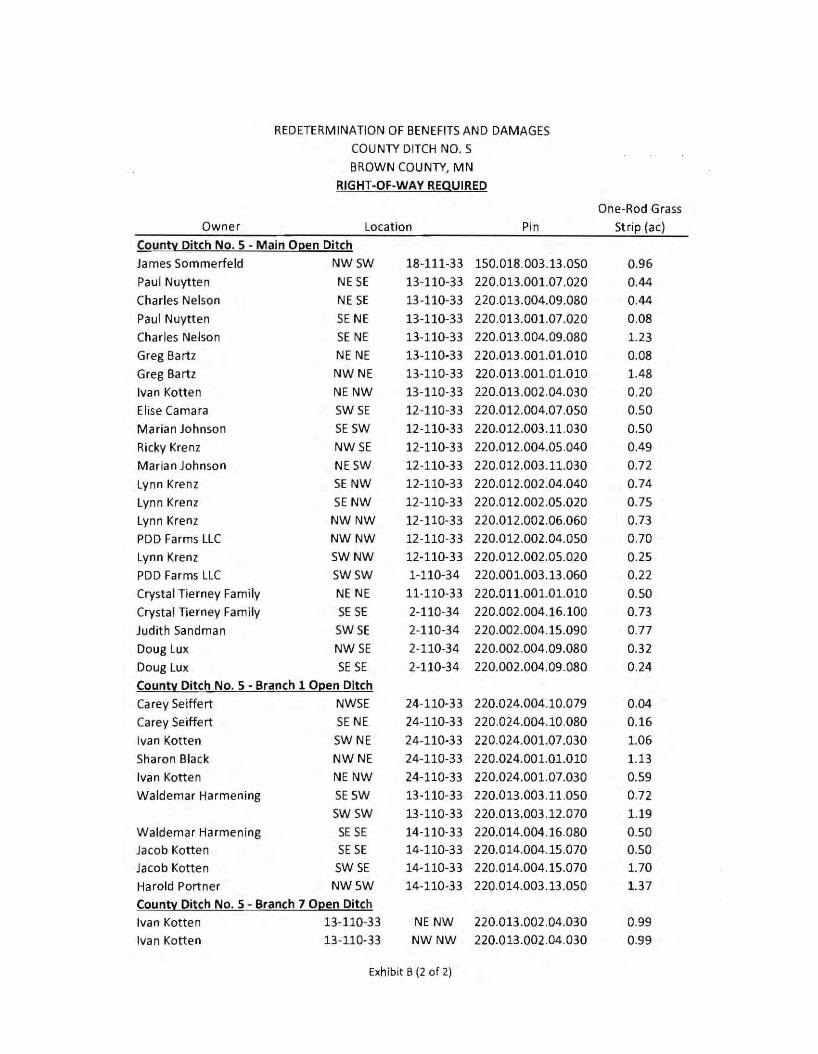

10:30 AM Auditor/Treasurer Jean Prochniak 15. Selection of Audit Firm 11:00 AM Auditor/Treasurer Jean Prochniak Highway Engineer Wayne Stevens 16. PUBLIC HEARING – Consolidation of Lateral 11A to CD 5 and

Redetermination of Benefits CD 5 11:15 AM Auditor/Treasurer Jean Prochniak 17. PUBLIC HEARING – Redetermination of Benefits CD 72 11:40 AM Human Services Director Tom Henderson 18. Payment of Human Services Claims 11:45 AM 19. CLOSED SESSION – Social Service Payments 11:50 AM County Administrator Charles Enter 20. April 2019 Budget Report 21. Other Business

22. Correspondence C-1 thru C-4 23. Coordinate Calendar Events

24. Adjournment Additional items may be added as Addenda and approved with Agenda or with a Suspension of Rules

NEXT COUNTY BOARD MEETING DATES

05-28-19 06-04-19 06-18-19 06-25-19

County Administrator’s E-Mail Address: [email protected] Home Page Address: www.co.brown.mn.us

May 7, 2019

75

At 9:00 AM, on Tuesday, May 7, 2019, the Board of Brown County Commissioners met in Regular Session in Room #204 of the Brown County Courthouse located in New Ulm, Minnesota 56073. Commissioners present were David Borchert, Anton Berg, Scott Windschitl, Dean Simonsen, and Jeff Veerkamp along with County Administrator Charles Enter and County Attorney Charles Hanson. Also present was County Administrator-Designee Sam Hansen. NUCAT staff was present, and Media Representatives Abby Berg of KNUJ Radio and Fritz Busch of the Journal (at 9:08 AM) were also present.

______________________________ Chairman Borchert convened the Regular Meeting at 9:00 AM, at which time the printed agenda was accepted along with the following addenda: 25a) Appraiser Resignation; 25b) PAC Pointing of License Bureau Technician Position Description; 25c) License Bureau Technician Appointment; C-9) South Country Health Alliance Capital Call Final Payment; C-10) Commissioner Berg report with Commissioner Windschitl on the Ad Hoc Audit Committee, with Commissioner Simonsen on CD#5 meetings, and with all Commissioners on the Hazard Mitigation work session; C-11) Commissioner Windschitl reports on Drug Court, Enterprise North, and South Country Health Alliance; C-12) Commissioner Simonsen report on the Underage Substance Abuse Coalition; C-13) Commissioner Veerkamp report on the Redwood-Cottonwood Rivers Control Area, Area II, and the Community Health Board meeting.

______________________________ A motion was offered by Commissioner Berg, and was seconded by Commissioner Simonsen, to accept the Minutes of 04-23-2019 and authorize publication of the Synopsis of same. This motion carried unanimously.

______________________________ At 9:02 AM, a motion was offered by Commissioner Windschitl, and was seconded by Commissioner Berg, to schedule a closed session for labor negotiation strategy planning to be held in the Commissioners Room 204 of the Brown County Courthouse, New Ulm, MN at approximately 10:40 AM this date 5-7-2019 for the AFSCME Courthouse and Highway Collective Bargaining Units, and for the LELS Locals #94 and #98 Collective Bargaining Units, pursuant to M.S. 13D.03. The motion passed unanimously.

______________________________ At 9:04 AM, Auditor/Treasurer Jean Prochniak met with the County Board. A motion was offered by Commissioner Windschitl, and was seconded by Commissioner Simonsen, to authorize payment of General Government claims in the amount of $341,581.50 as follows: Revenue $275,631.72 Public Health $1,803.59 Road and Bridge $27,477.70 Human Services $770.23 Park Fund $1,334.12 Ditch $7,650.05 Capital Improvement Fund $3,679.00 Landfill $22,492.57 Score $232.52 Forfeited Tax Fund $510.00 In accordance with MS 375.12, the following claims exceeding $2,000 are included in the Fund totals above: Area II MN River Basin Projects $12,971.00; Bode Collision & Glass $2,923.00; Bridging Brown County $3,250.00; Brown Co Agricultural Society $14,250.00; Brown Co Editorial Assn $5,679.66; Brown Co Historical Society $45,713.50; Brown Co Humane Society $4,037.50; Brown Co Library Board $40,757.50; Brown Co Soil & Water Cons Dist $48,700.00; Erickson Engineering Co, LLC $7,172.00; GEI Consultants Inc $8,769.25; Gemini Research $3,321.24; Hildi Inc $3,600.00; I & S Group Inc $6,438.00; Liberty Tire Recycling LLC $3,572.53; Miesen's Color Center $7,997.00; Mn Valley Action Council $3,317.00; Mn Valley Testing Laboratories $5,742.10; Optics Planet Inc $3,592.4; Ranger Chevrolet - Cadillac $36,448.16; Red Rock Quarry $9,414.32; River Bend Business Products $8,648.78; Ron'S Recycling $2,680.00; Trane U.S. Inc $3,346.25 101 Payments Less Than $2000.00 49,240.31; Final Total: $341,581.50. This motion carried unanimously.

______________________________ At 9:08 AM, Highway Engineer Wayne Stevens and Assistant Engineer Andrew Lang met with the County Board. A motion was offered by Commissioner Berg, and was seconded by Commissioner Borchert, to authorize the Highway Department to request quotes for the replacement of 2500 feet of tile in CD#58. This motion carried unanimously.

______________________________

gbode

Typewritten Text

# 1a

gbode

Oval

gbode

Draft

May 7, 2019

76

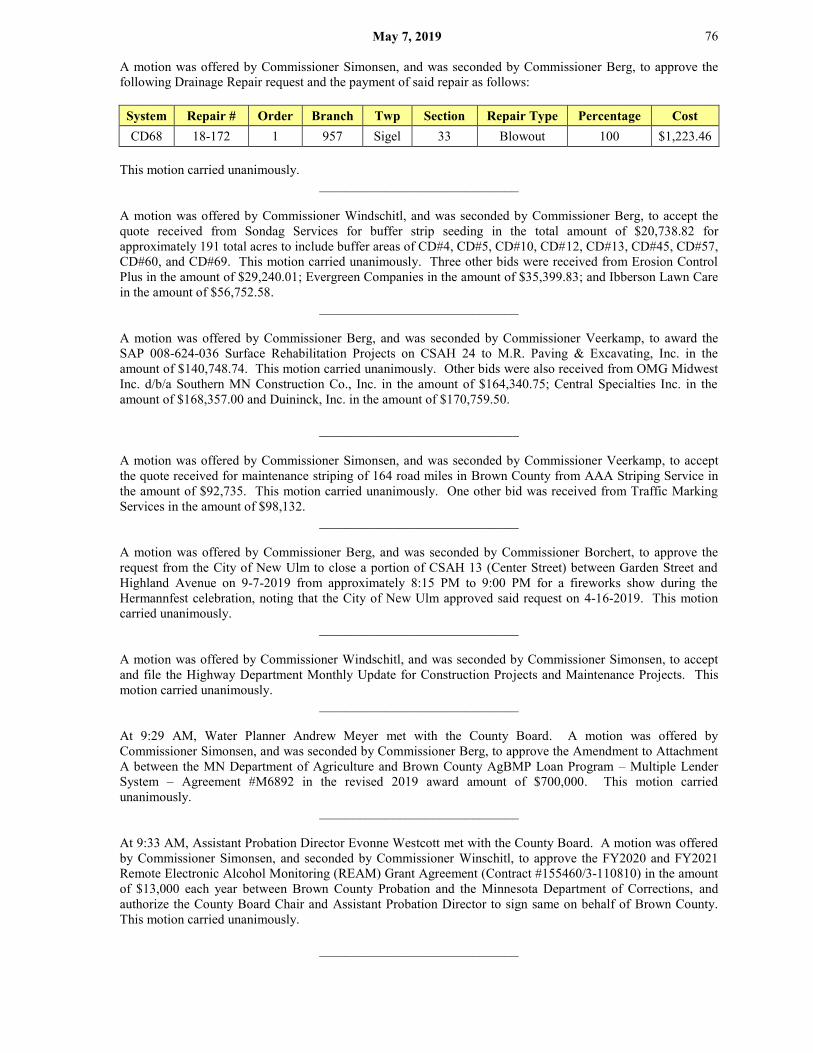

A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Berg, to approve the following Drainage Repair request and the payment of said repair as follows: System Repair # Order Branch Twp Section Repair Type Percentage Cost CD68 18-172 1 957 Sigel 33 Blowout 100 $1,223.46

This motion carried unanimously.

______________________________ A motion was offered by Commissioner Windschitl, and was seconded by Commissioner Berg, to accept the quote received from Sondag Services for buffer strip seeding in the total amount of $20,738.82 for approximately 191 total acres to include buffer areas of CD#4, CD#5, CD#10, CD#12, CD#13, CD#45, CD#57, CD#60, and CD#69. This motion carried unanimously. Three other bids were received from Erosion Control Plus in the amount of $29,240.01; Evergreen Companies in the amount of $35,399.83; and Ibberson Lawn Care in the amount of $56,752.58.

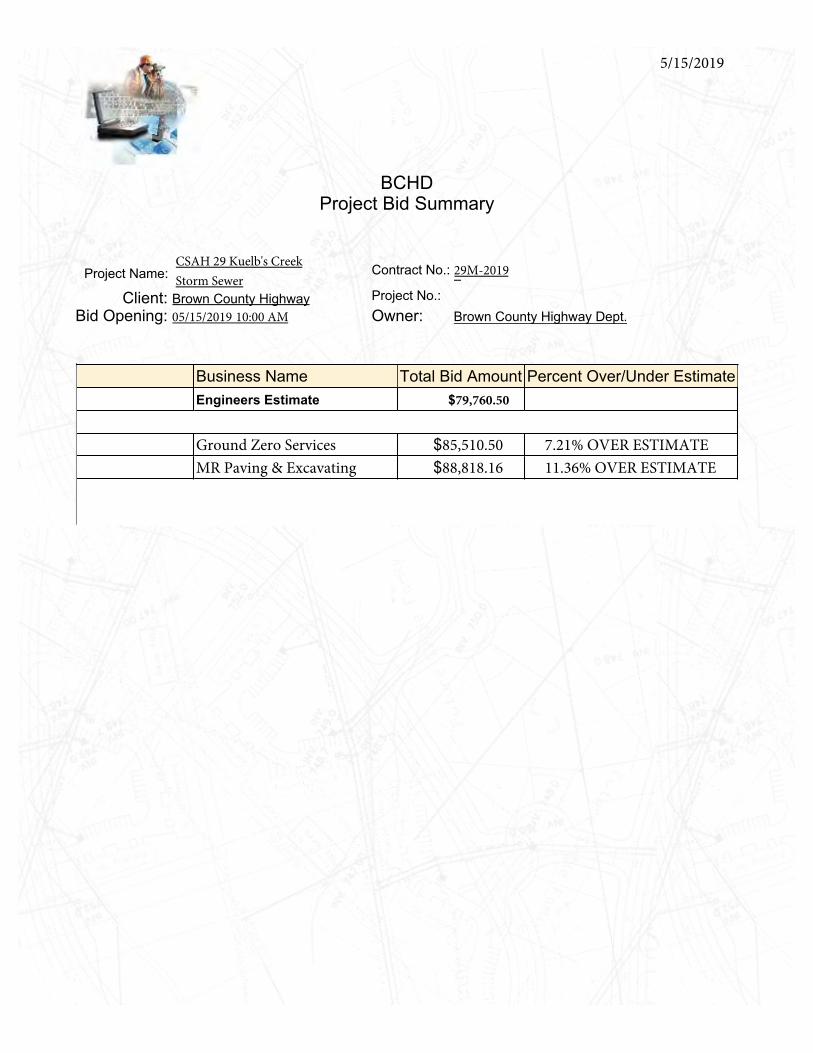

______________________________ A motion was offered by Commissioner Berg, and was seconded by Commissioner Veerkamp, to award the SAP 008-624-036 Surface Rehabilitation Projects on CSAH 24 to M.R. Paving & Excavating, Inc. in the amount of $140,748.74. This motion carried unanimously. Other bids were also received from OMG Midwest Inc. d/b/a Southern MN Construction Co., Inc. in the amount of $164,340.75; Central Specialties Inc. in the amount of $168,357.00 and Duininck, Inc. in the amount of $170,759.50.

______________________________ A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Veerkamp, to accept the quote received for maintenance striping of 164 road miles in Brown County from AAA Striping Service in the amount of $92,735. This motion carried unanimously. One other bid was received from Traffic Marking Services in the amount of $98,132.

______________________________ A motion was offered by Commissioner Berg, and was seconded by Commissioner Borchert, to approve the request from the City of New Ulm to close a portion of CSAH 13 (Center Street) between Garden Street and Highland Avenue on 9-7-2019 from approximately 8:15 PM to 9:00 PM for a fireworks show during the Hermannfest celebration, noting that the City of New Ulm approved said request on 4-16-2019. This motion carried unanimously.

______________________________ A motion was offered by Commissioner Windschitl, and was seconded by Commissioner Simonsen, to accept and file the Highway Department Monthly Update for Construction Projects and Maintenance Projects. This motion carried unanimously.

______________________________ At 9:29 AM, Water Planner Andrew Meyer met with the County Board. A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Berg, to approve the Amendment to Attachment A between the MN Department of Agriculture and Brown County AgBMP Loan Program – Multiple Lender System – Agreement #M6892 in the revised 2019 award amount of $700,000. This motion carried unanimously.

______________________________ At 9:33 AM, Assistant Probation Director Evonne Westcott met with the County Board. A motion was offered by Commissioner Simonsen, and seconded by Commissioner Winschitl, to approve the FY2020 and FY2021 Remote Electronic Alcohol Monitoring (REAM) Grant Agreement (Contract #155460/3-110810) in the amount of $13,000 each year between Brown County Probation and the Minnesota Department of Corrections, and authorize the County Board Chair and Assistant Probation Director to sign same on behalf of Brown County. This motion carried unanimously.

______________________________

May 7, 2019

77

At 9:37 AM, Probation Director Les Schultz met with the County Board. A motion was offered by Commissioner Windschitl, and seconded by Commissioner Berg, to approve the State of MN Grant Agreement #155714/3-110982 for Caseload/Workload programming for FY 2020 in the amount of $62,750 and for FY 2021 in the amount of $62,750; and authorize the County Board Chair and Probation Director to sign same on behalf of Brown County. This motion carried unanimously.

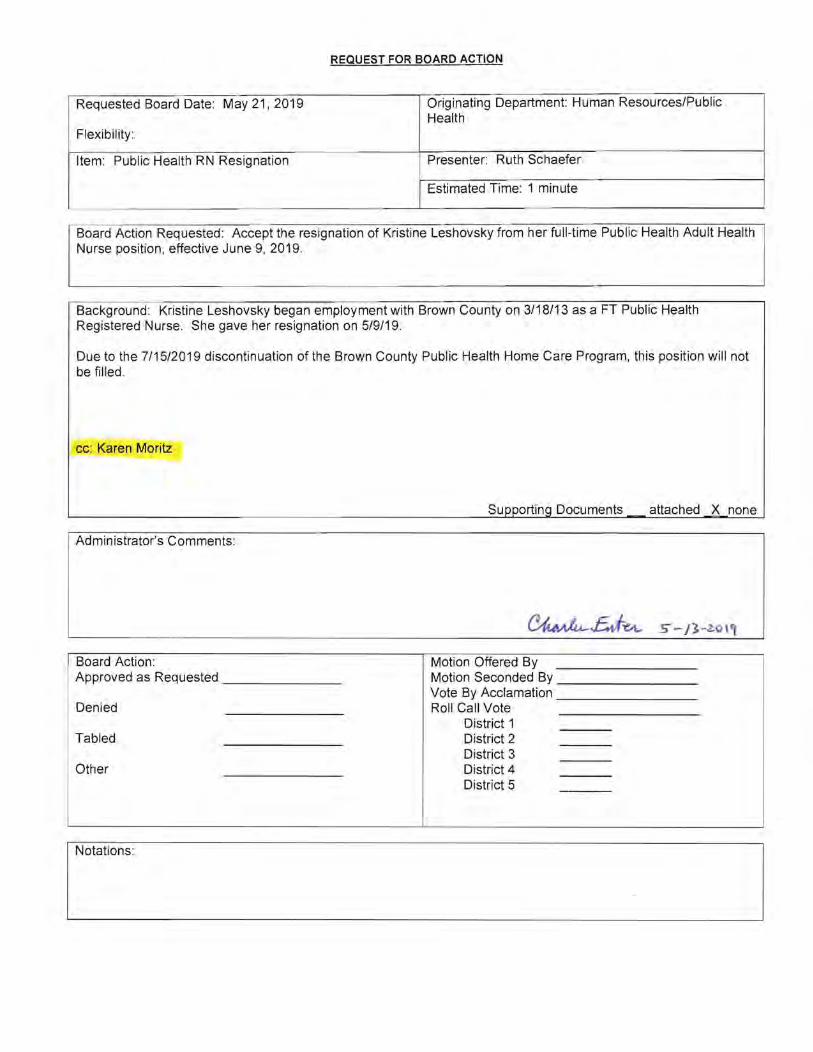

______________________________ At 9:47 AM, Public Health Director Karen Moritz and Public Health Administrative Supervisor Ann Gieseke met with the County Board. A motion was offered by Commissioner Windschitl, and was seconded by Commissioner Berg, to authorize the discontinuation of the Brown County Public Health Home Care Program with a sunset date of 7-15-2019, with the understanding that the Adult Health Program areas will include Jail Health, Public Health Nurse Clinic, SCHA Care Coordination, SCHA Connector, Community Health Education, MN Choice Assessments, Coalition and Community Engagement, Community Health Assessment, Community Health Improvement Planning, Quality Improvement, Performance Measurement, Disease Prevention & Control, Emergency Preparedness, and Case Management for Human Services Clients. This motion passed on a roll-call vote of 5-0.

______________________________ At 10:08 AM, HR Director Ruth Schaefer met with the County Board. A motion was offered by Commissioner Berg, and was seconded by Commissioner Borchert, to authorize to post the vacancy for one FT Public Health Supervisor according to policy. This motion passed unanimously.

______________________________ A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Veerkamp, to appoint Joan Wieneke as Full Time License Bureau Technician, at the hourly rate of $17.4124, Grade VIII, Step 4, with a start date of 5-13-2019. This motion carried unanimously.

______________________________ A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Berg, to appoint Steve Kissner as FT Information Technology Network & Systems Administrator at the hourly wage of $25.6421, Grade XV, Step 2, effective 5-21-2019. This motion carried unanimously.

______________________________ A motion was offered by Commissioner Berg, and was seconded by Commissioner Veerkamp, to appoint Luke Zellmer and Collin Ludewig for the 2019 Summer Highway Engineering/Maintenance Student positions with an anticipated start date of 5-13-2019 and 5-20-2019 respectively, at the first year hourly wage of $11.00 pending results of pre-employment drug screen and physical exam. This motion passed unanimously.

______________________________ A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Windschitl, to appoint Jeffrey Spessard as an Intermittent Part-Time Heartland Express Bus Driver at $16.3562/hour (Grade VIII, Step 2) with a start date contingent on the passage of the pre-employment background checks, and a DOT physical and drug screen. This motion passed unanimously.

______________________________ A motion was offered by Commissioner Windschitl, and was seconded by Commissioner Berg, to approve with respect to the Employment Agreement, Section 5. Outside Employment and Activities, Sam Hansen’s request to intermittently act as a Sports Official – Umpire with time off in accordance with the Employment Agreement dated 4-23-2019 and the Brown County Personnel Policy. This motion carried unanimously.

______________________________ A motion was offered by Commissioner Berg, and was seconded by Commissioner Simonsen, to approve and refer to PAC the following Planning and Zoning Department Position Descriptions, with adjustment to Section 8 in each position description to equal 40 hours : 1) Zoning Administrator/Emergency Management Director, 2) Assistant Zoning Administrator/Emergency Management Director, 3) Environmental Specialist, 4) County Feedlot Officer, 5) Emergency Manager, 6) Office Support Specialist, 7) Resident Park Caretaker, and 8) Park Maintenance Worker. This motion passed unanimously.

______________________________

May 7, 2019

78

A motion was offered by Commissioner Berg, and was seconded by Commissioner Windschitl, to table consideration of the resignation of Sean Gremmels, FT Appraiser, until later this date. This motion passed unanimously.

______________________________ A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Berg, to approve the PAC assigned 237 points, to be effective 5-7-2019, for the License Bureau Technician position presented through the 2018 Rotational Review process. This motion passed unanimously.

______________________________ At 10:20 AM, County Attorney Chuck Hanson presented a request. A motion was offered by Commissioner Veerkamp, and was seconded by Commissioner Windschitl, to ratify Assistant Attorney Daniel Kalk’s lodging cost in the amount of $345.86 for the Bureau of Alcohol, Tobacco, Firearms, and Explosives Arson for Prosecutors Training which was held on 4-23-19 through 4-25-19. This motion carried unanimously.

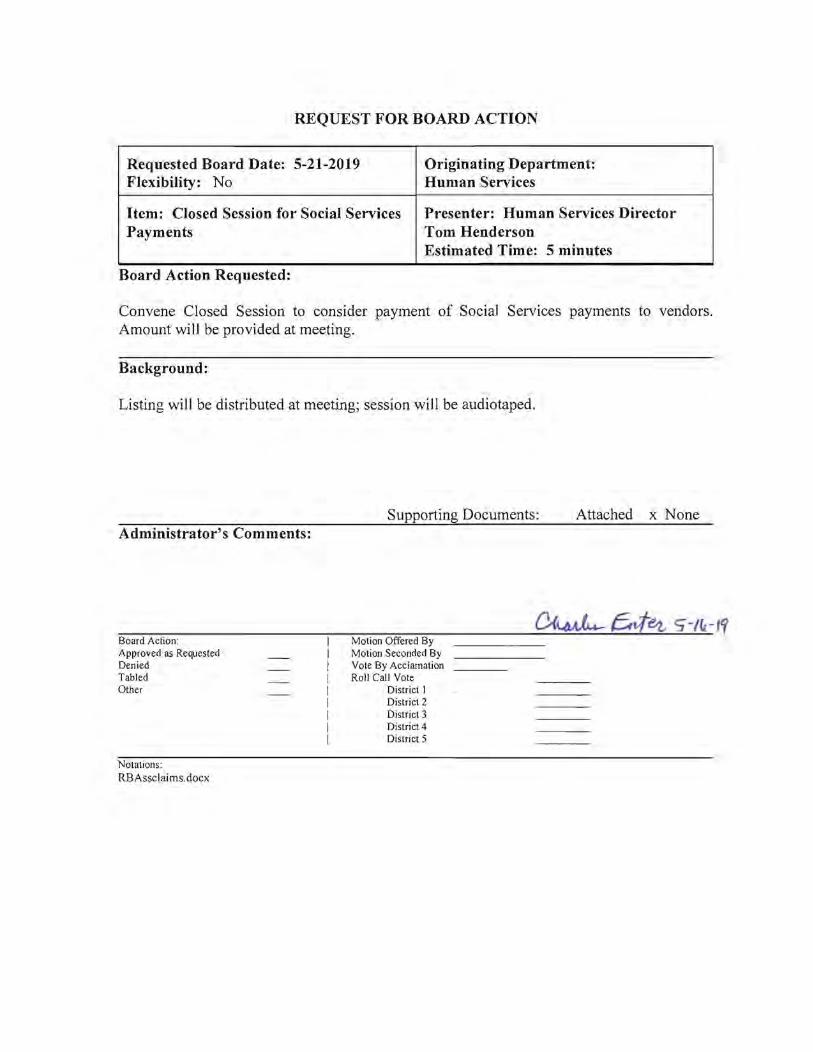

______________________________ At 10:21 AM, County Administrator Charles Enter presented the quarterly county budget report. A motion was made by Commissioner Berg, and seconded by Commissioner Simonsen, to accept and file the 2019 1st Quarter (Cash Basis and Unaudited) Budget Report which reflects activity at 25% of the budget year as follows: Expenditures of $8,355,697.85 or 22.4%, and revenues of $5,260,650.34 or 16.0%; and the 2019 1 st Quarter Supplemental Budgets Report noting expenditures of $492,912.87 or 23.8%, and revenues of $316,052.28 or 16.2% of budgeted activity. This motion carried unanimously.

______________________________ A motion was offered by Commissioner Simonsen, and was seconded by Commissioner Borchert, to accept the resignation of Sean Gremmels, FT Appraiser, effective 5-17-2019, and approve posting of this position according to policy and contract. This motion passed unanimously.

______________________________ A motion was made by Commissioner Berg, and seconded by Commissioner Borchert, to approve the Memorandum of Agreement between the County of Brown and AFSCME Council 65, Local 1204 Courthouse Unit through which, pursuant to M.S. 352.98, Brown County agrees to sponsor a Post Retirement Health Care Savings Program that allows aforementioned employees to save money to pay medical expenses and/or health insurance premiums after termination of public service, with payroll deductions not beginning until the full two-week pay period following HCSP Contract completion with the Minnesota State Retirement System (MSRS). This motion carried unanimously.

______________________________ At 10:32 AM, Chairman Borchert convened a Closed Session pursuant to M.S. 13D.03 for labor negotiation strategy planning in the Commissioners Room 204 of the Brown County Courthouse, New Ulm, MN for the AFSCME Courthouse and Highway Collective Bargaining Units, and for the LELS Locals #94 and #98 Collective Bargaining Units. This session was attended by Commissioners Borchert, Berg, Windschitl, Simonsen, and Veerkamp, along with County Administrator Enter, County Attorney Hanson, HR Director Schaefer, and County Administrator-Designee Sam Hansen. A motion was made by Commissioner Berg, and was seconded by Commissioner Simonsen, to end the closed session at 11:28 AM. The motion passed unanimously and Chairman Borchert declared the closed session ended at 11:28 AM.

______________________________ At 11:28 AM, Correspondence C-1 thru C-13 were accepted and filed. C-10) Commissioner Berg reported on the Community Health Board, with Commissioner Windschitl on the Ad Hoc Audit Committee, with Commissioner Simonsen on CD#5 meetings, and with all Commissioners on the Hazard Mitigation work session; C-11) Commissioner Windschitl reported on Brown/Nicollet/Watonwan Drug Court, Enterprise North, and South Country Health Alliance; C-12) Commissioner Simonsen reported on the Underage Substance Abuse Coalition meeting on 4-27-2019; C-13) Commissioner Veerkamp reported on the Redwood-Cottonwood Rivers Control Area, Area II, and the Community Health Board meeting.

______________________________ At 11:56 AM, Calendars were coordinated for the next two week period.

______________________________

May 7, 2019

79

There being no further business, a motion was made by Commissioner Simonsen, and was seconded by Commissioner Veerkamp, to adjourn the meeting. The motion passed unanimously and Chairman Borchert declared the Meeting adjourned at 12:03 PM.

______________________________

___________________________ David Borchert , Chair

Board of Brown County Commissioners Brown County, Minnesota

ATTEST: Charles Enter Brown County Administrator Brown County, Minnesota

36

SYNOPSIS OF COUNTY BOARD MEETING May 7, 2019

Members present: Borchert, Berg, Windschitl, Simonsen, and Veerkamp, along with County Administrator Enter, County Attorney Hanson and County Administrator-Designee Sam Hansen. M/Berg, S/Simonsen, to accept the Minutes of 04-23-2019 and authorize publication of the Synopsis of same; carried. M/Windschitl, S/Berg, to schedule a closed session for labor negotiation strategy planning to be held in the Commissioners Room 204 of the Brown County Courthouse, New Ulm, MN at approximately 10:40 AM this date 5-7-2019 for the AFSCME Courthouse and Highway Collective Bargaining Units, and for the LELS Locals #94 and #98 Collective Bargaining Units, pursuant to M.S. 13D.03; passed. M/Windschitl, S/Simonsen, to authorize payment of General Government claims in the amount of $341,581.50 as follows: Revenue $275,631.72; Public Health $1,803.59; Road and Bridge $27,477.70; Human Services $770.23; Park Fund $1,334.12; Ditch $7,650.05; Capital Improvement Fund $3,679.00; Landfill $22,492.57; Score $232.52; Forfeited Tax Fund $510.00. In accordance with MS 375.12, the following claims exceeding $2,000 are included in the Fund totals above: Area II MN River Basin Projects $12,971.00; Bode Collision & Glass $2,923.00; Bridging Brown County $3,250.00; Brown Co Ag Society $14,250.00; Brown Co Editorial Assn $5,679.66; Brown Co Historical Society $45,713.50; Brown Co Humane Society $4,037.50; Brown Co Library Board $40,757.50; Brown Co Soil & Water Cons Dist $48,700.00; Erickson Engineering Co, LLC $7,172.00; GEI Consultants Inc $8,769.25; Gemini Research $3,321.24; Hildi Inc $3,600.00; I & S Group Inc $6,438.00; Liberty Tire Recycling LLC $3,572.53; Miesen's Color Center $7,997.00; Mn Valley Action Council $3,317.00; Mn Valley Testing Laboratories $5,742.10; Optics Planet Inc $3,592.4; Ranger Chevrolet - Cadillac $36,448.16; Red Rock Quarry $9,414.32; River Bend Business Products $8,648.78; Ron'S Recycling $2,680.00; Trane U.S. Inc $3,346.25 101 Payments Less Than $2000.00 49,240.31; Final Total: $341,581.50; carried. M/Berg, S/Borchert, to authorize the Highway Dept. to request quotes for the replacement of 2500 feet of tile in CD#58; carried. M/Simonsen, S/Berg, to approve one (1) Drainage Repair request and the payment of said repair; carried. M/Windschitl, S/Berg, to accept the quote received from Sondag Services for buffer strip seeding in the total amount of $20,738.82 for approximately 191 total acres to include buffer areas of CD#4, CD#5, CD#10, CD#12, CD#13, CD#45, CD#57, CD#60, and CD#69; carried. Three other bids were received from Erosion Control Plus; Evergreen Companies; and Ibberson Lawn Care. M/Berg, S/Veerkamp, to award the SAP 008-624-036 Surface Rehabilitation Projects on CSAH 24 to M.R. Paving & Excavating, Inc. in the amount of $140,748.74; carried. Other bids were also received from OMG Midwest Inc. d/b/a Southern MN Construction Co., Inc.; Central Specialties Inc.; and Duininck, Inc. M/Simonsen, S/Veerkamp, to accept the quote received for maintenance striping of 164 road miles in Brown County from AAA Striping Service in the amount of $92,735; carried. One other bid was received from Traffic Marking Services. M/Berg, S/Borchert, to approve the request from the City of New Ulm to close a portion of CSAH 13 (Center Street) between Garden St. and Highland Ave. on 9-7-2019 from approximately 8:15 PM to 9:00 PM for a fireworks show during the Hermannfest celebration, noting that the City of New Ulm approved said request on 4-16-2019; carried. M/Windschitl, S/Simonsen, to accept and file the Highway Dept. Monthly Update for Construction Projects and Maintenance Projects; carried. M/Simonsen, S/Berg, to approve the Amendment to Attachment A between the MN Dept. of Agriculture and Brown County AgBMP Loan Program – Multiple Lender System – Agreement #M6892 in the revised 2019 award amount of $700,000; carried. M/Simonsen, S/Winschitl, to approve the FY2020 and FY2021 Remote Electronic Alcohol Monitoring (REAM) Grant Agreement (Contract #155460/3-110810) in the amount of $13,000 each year between Brown County Probation and the MN Dept. of Corrections, and authorize the County Board Chair and Assistant Probation Director to sign same on behalf of Brown County; carried. M/Windschitl, S/Berg, to approve the State of MN Grant Agreement #155714/3-110982 for Caseload/Workload programming for FY 2020 in the amount of $62,750 and for FY 2021 in the amount of $62,750; and authorize the County Board Chair and Probation Director to sign same on behalf of Brown County; carried. M/Windschitl, S/Berg, to authorize the discontinuation of the Brown County Public Health Home Care Program with a sunset date of 7-15-2019, with the understanding that the Adult Health Program areas will include Jail Health, Public Health Nurse Clinic, SCHA Care Coordination, SCHA Connector, Community

gbode

Typewritten Text

# 1b

gbode

Oval

gbode

Draft

37

Health Education, MN Choice Assessments, Coalition and Community Engagement, Community Health Assessment, Community Health Improvement Planning, Quality Improvement, Performance Measurement, Disease Prevention & Control, Emergency Preparedness, and Case Management for Human Services Clients; passed 5-0. M/Berg, S/Borchert, to authorize to post the vacancy for one FT Public Health Supervisor according to policy; passed. M/Simonsen, S/Veerkamp, to appoint Joan Wieneke as FT License Bureau Technician, at the hourly rate of $17.4124, Grade VIII, Step 4, with a start date of 5-13-2019; carried. M/Simonsen, S/Berg, to appoint Steve Kissner as FT Information Technology Network & Systems Administrator at the hourly wage of $25.6421, Grade XV, Step 2, effective 5-21-2019; carried. M/Berg, S/Veerkamp, to appoint Luke Zellmer and Collin Ludewig for the 2019 Summer Highway Engineering/Maintenance Student positions with an anticipated start date of 5-13-2019 and 5-20-2019 respectively, at the first year hourly wage of $11.00 pending results of pre-employment drug screen and physical exam; passed. M/Simonsen, S/Windschitl, to appoint Jeffrey Spessard as an IPT Heartland Express Bus Driver at $16.3562/hour (Grade VIII, Step 2) with a start date contingent on the passage of the pre-employment background checks, and a DOT physical and drug screen; passed. M/Windschitl, S/Berg, to approve with respect to the Employment Agreement, Section 5. Outside Employment and Activities, Sam Hansen’s request to intermittently act as a Sports Official – Umpire with time off in accordance with the Employment Agreement dated 4-23-2019 and the Brown County Personnel Policy; carried. M/Berg, S/Simonsen, to approve and refer to PAC the following Planning and Zoning Dept. Position Descriptions, with adjustment to Section 8 in each position description to equal 40 hours: 1) Zoning Administrator/Emergency Management Director, 2) Assistant Zoning Administrator/Emergency Management Director, 3) Environmental Specialist, 4) County Feedlot Officer, 5) Emergency Manager, 6) Office Support Specialist, 7) Resident Park Caretaker, and 8) Park Maintenance Worker; passed. M/Berg, S/Windschitl, to table consideration of the resignation of Sean Gremmels, FT Appraiser, until later this date; passed. M/Simonsen, S/Berg, to approve the PAC assigned 237 points, to be effective 5-7-2019, for the License Bureau Technician position presented through the 2018 Rotational Review process; passed. M/Veerkamp, S/Windschitl, to ratify Assistant Attorney Daniel Kalk’s lodging cost in the amount of $345.86 for the Bureau of Alcohol, Tobacco, Firearms, and Explosives Arson for Prosecutors Training which was held on 4-23-19 through 4-25-19; carried. M/Berg, S/Simonsen, to accept and file the 2019 1st Quarter (Cash Basis and Unaudited) Budget Report which reflects activity at 25% of the budget year as follows: Expenditures of $8,355,697.85 or 22.4%, and revenues of $5,260,650.34 or 16.0%; and the 2019 1st Quarter Supplemental Budgets Report noting expenditures of $492,912.87 or 23.8%, and revenues of $316,052.28 or 16.2% of budgeted activity; carried. M/Simonsen, S/Borchert, to accept the resignation of Sean Gremmels, FT Appraiser, effective 5-17-2019, and approve posting of this position according to policy and contract; passed. M/Berg, S/Borchert, to approve the Memorandum of Agreement between the County of Brown and AFSCME Council 65, Local 1204 Courthouse Unit through which, pursuant to M.S. 352.98, Brown County agrees to sponsor a Post Retirement Health Care Savings Program that allows aforementioned employees to save money to pay medical expenses and/or health insurance premiums after termination of public service, with payroll deductions not beginning until the full two-week pay period following HCSP Contract completion with the MN State Retirement System (MSRS); carried. At 10:32 AM, Chairman Borchert convened a Closed Session pursuant to M.S. 13D.03 for labor negotiation strategy planning in the Commissioners Room 204 of the Brown County Courthouse, New Ulm, MN for the AFSCME Courthouse and Highway Collective Bargaining Units, and for the LELS Locals #94 and #98 Collective Bargaining Units. This session was attended by Commissioners Borchert, Berg, Windschitl, Simonsen, and Veerkamp, along with County Administrator Enter, County Attorney Hanson, HR Director Schaefer, and County Administrator-Designee Hansen. M/Berg, S/Simonsen, to end the closed session at 11:28 AM; passed Chairman Borchert declared the closed session ended at 11:28 AM. At 11:28 AM, Correspondence C-1 thru C-13 were accepted and filed. Berg reported on the Community Health Board, with Windschitl on the Ad Hoc Audit Committee, with Simonsen on CD#5 meetings, and with all Commissioners on the Hazard Mitigation work session; Windschitl reported on Brown/Nicollet/Watonwan Drug Court, Enterprise North, and South Country Health Alliance; Simonsen reported on the Underage Substance Abuse Coalition meeting on 4-27-2019; Veerkamp reported on the Redwood-Cottonwood Rivers Control Area, Area II, and the Community Health Board meeting. At 11:56 AM, Calendars were coordinated for the next two week period.

38

There being no further business, M/Simonsen, S/Veerkamp, to adjourn the meeting; passed and Chairman Borchert declared the Meeting adjourned at 12:03 PM. The Official Minutes of the Regular Meeting of 5-7-2019 are on file in the County Administrator’s Office and may be viewed during normal business hours, M-F, 8AM-4:30PM. Correspondence and requests for additional information may be directed to the County Administrator’s E-Mail Address: [email protected] Home Page Address: www.co.brown.mn.us

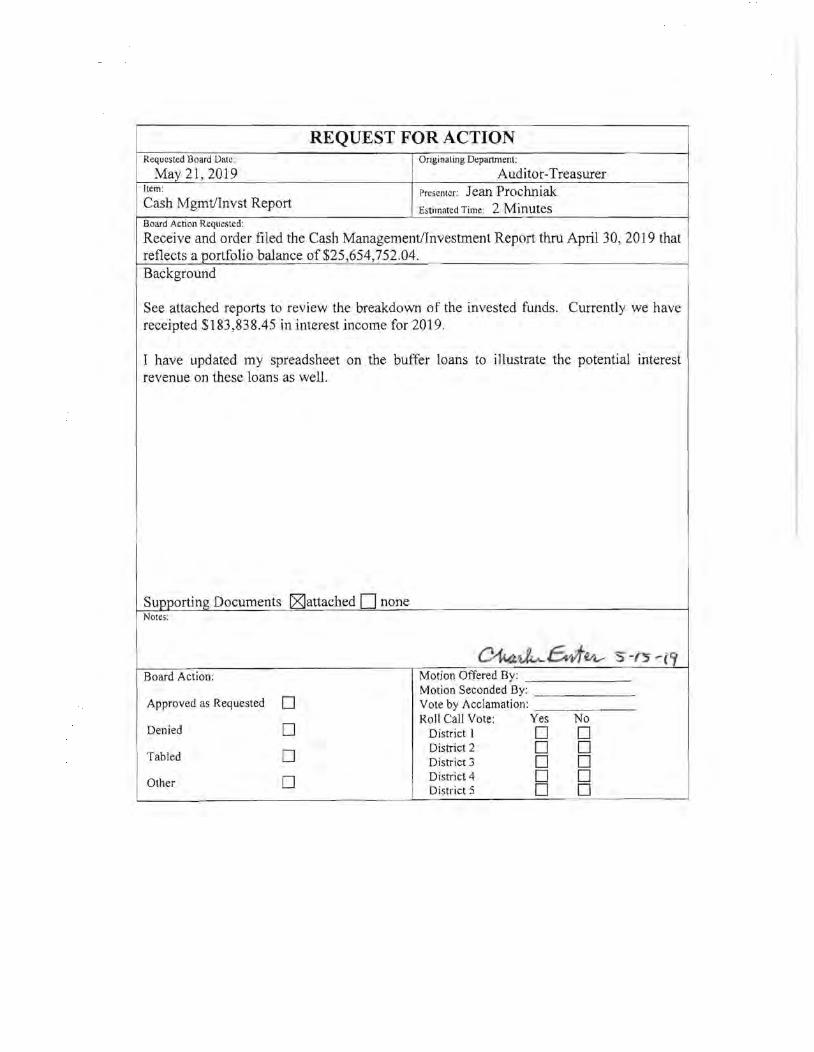

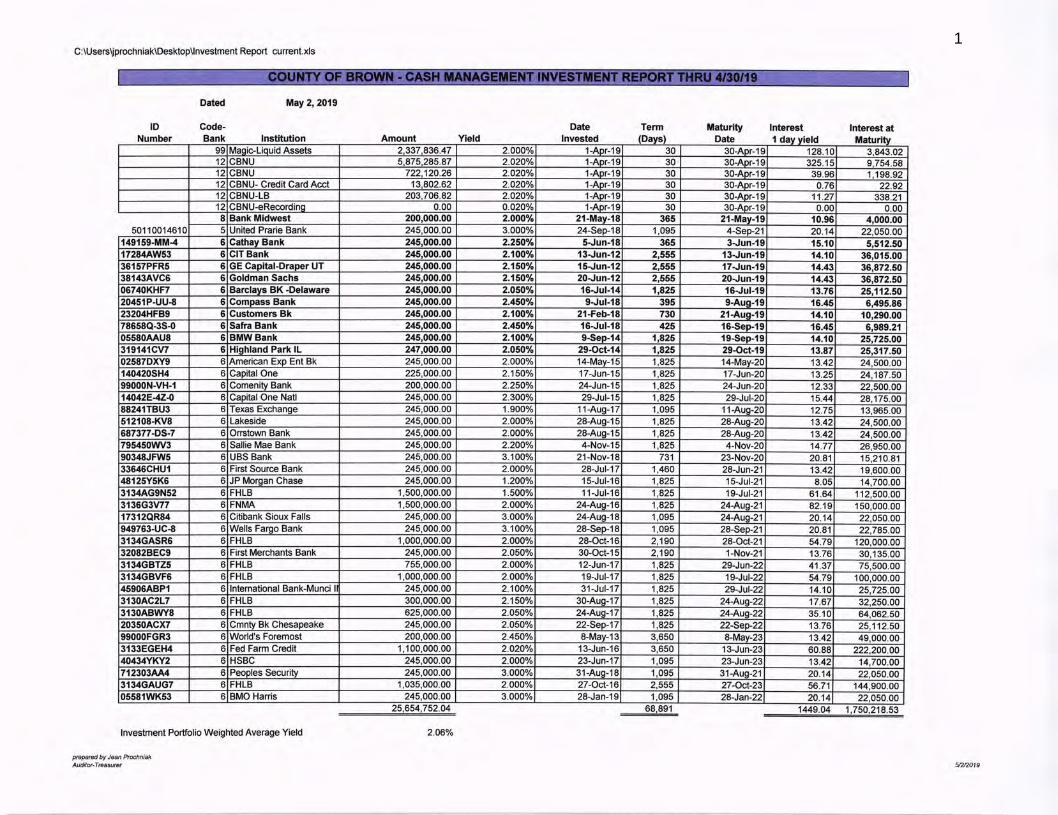

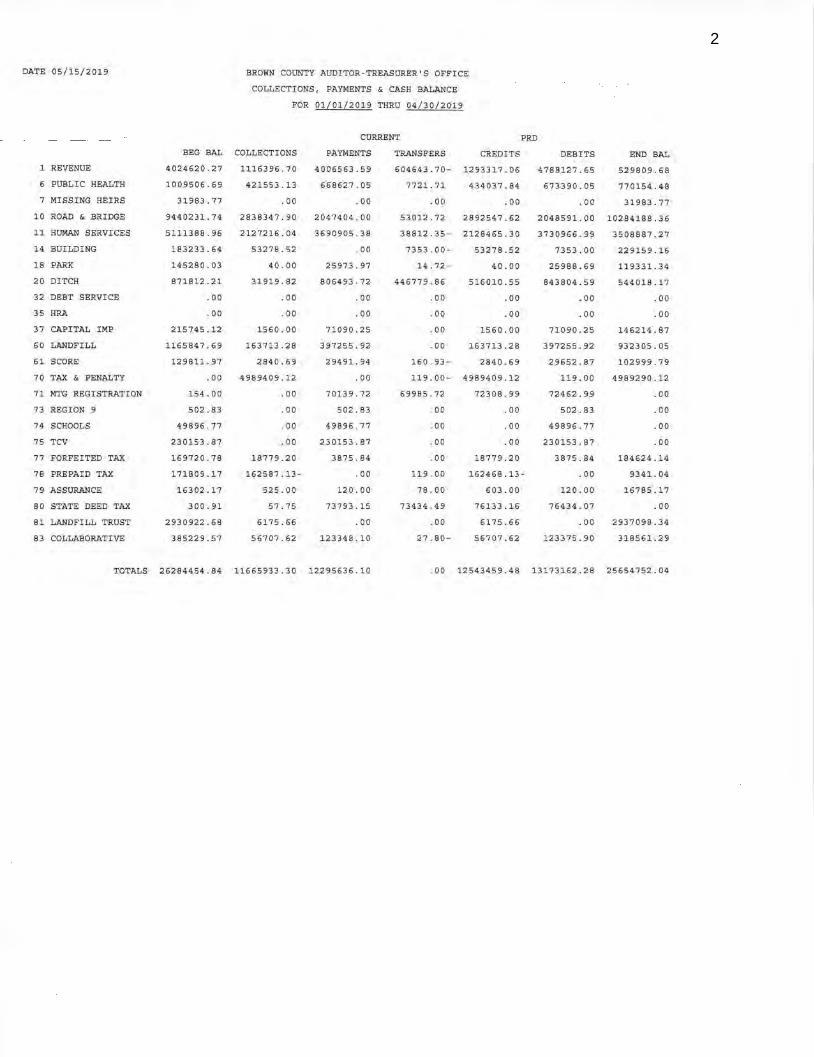

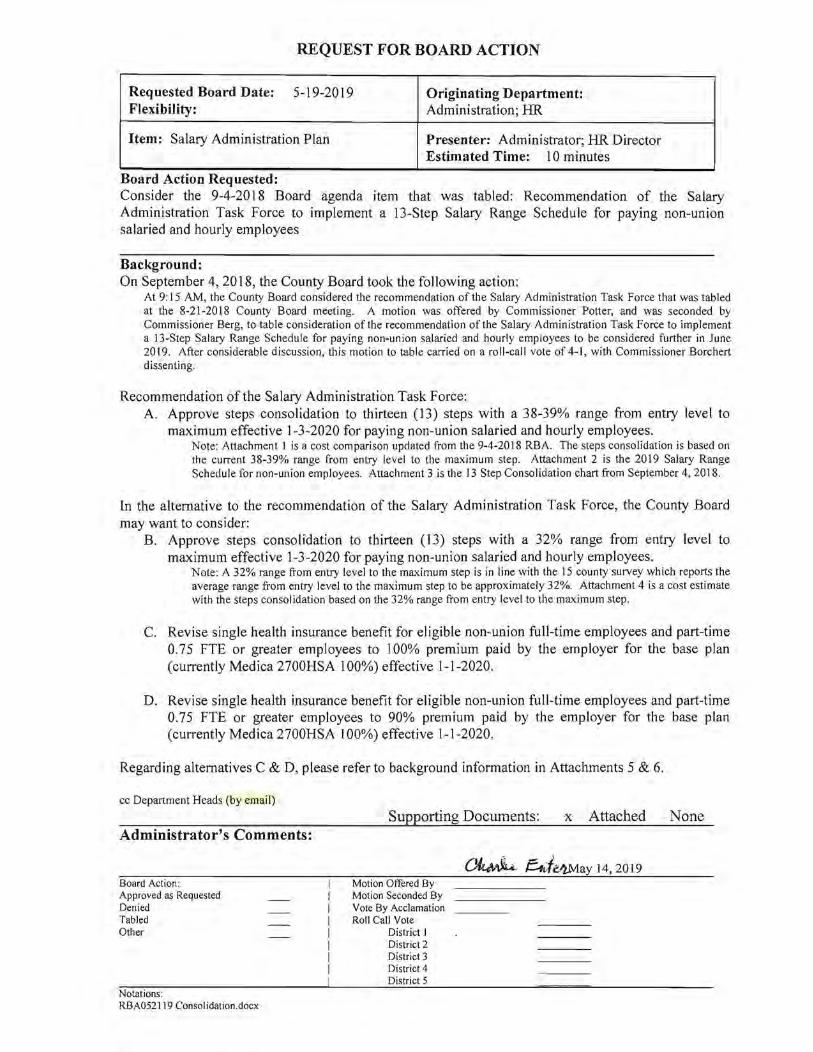

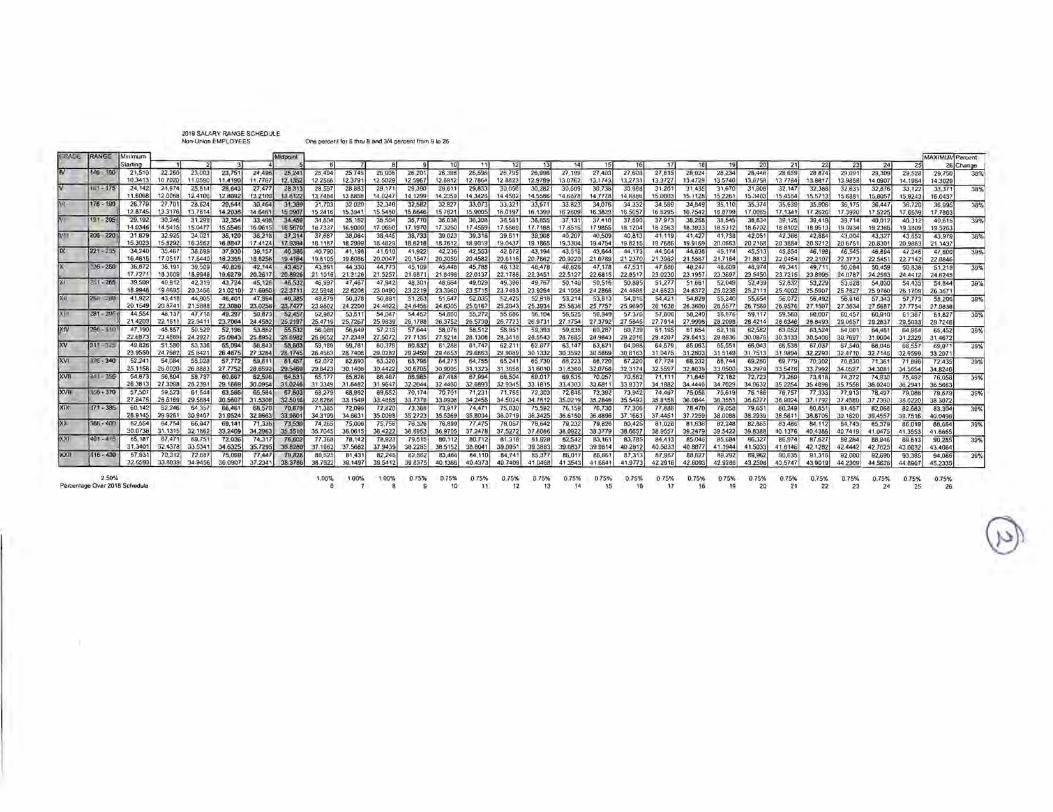

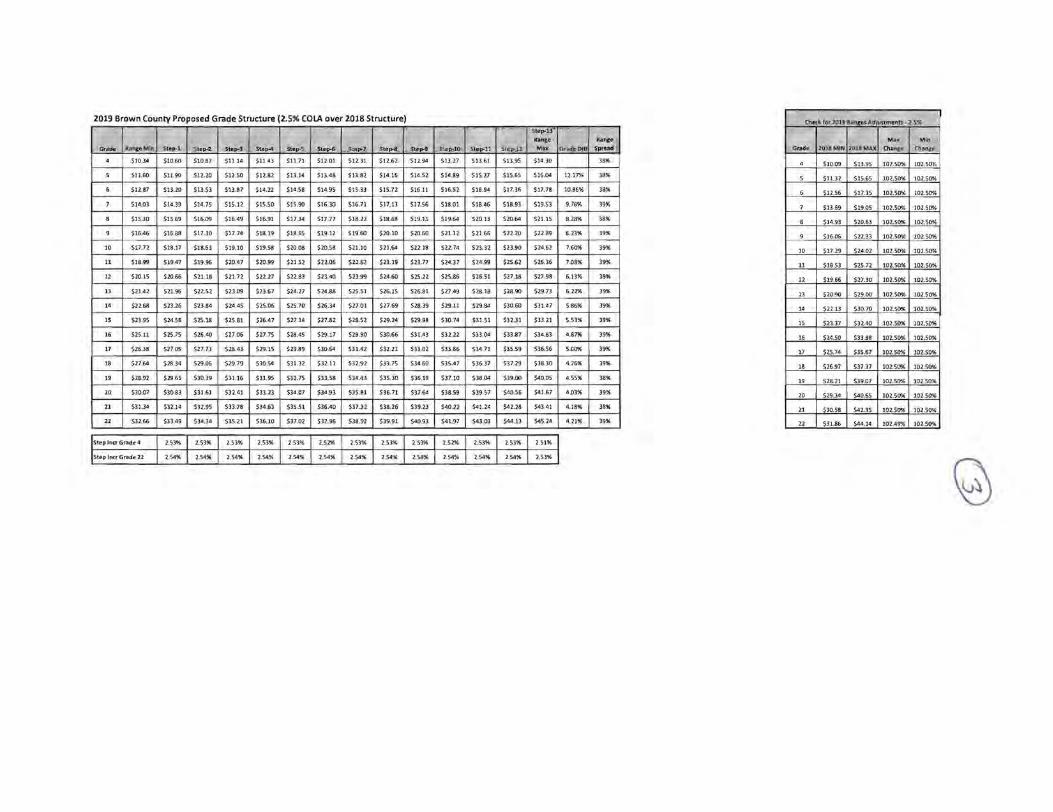

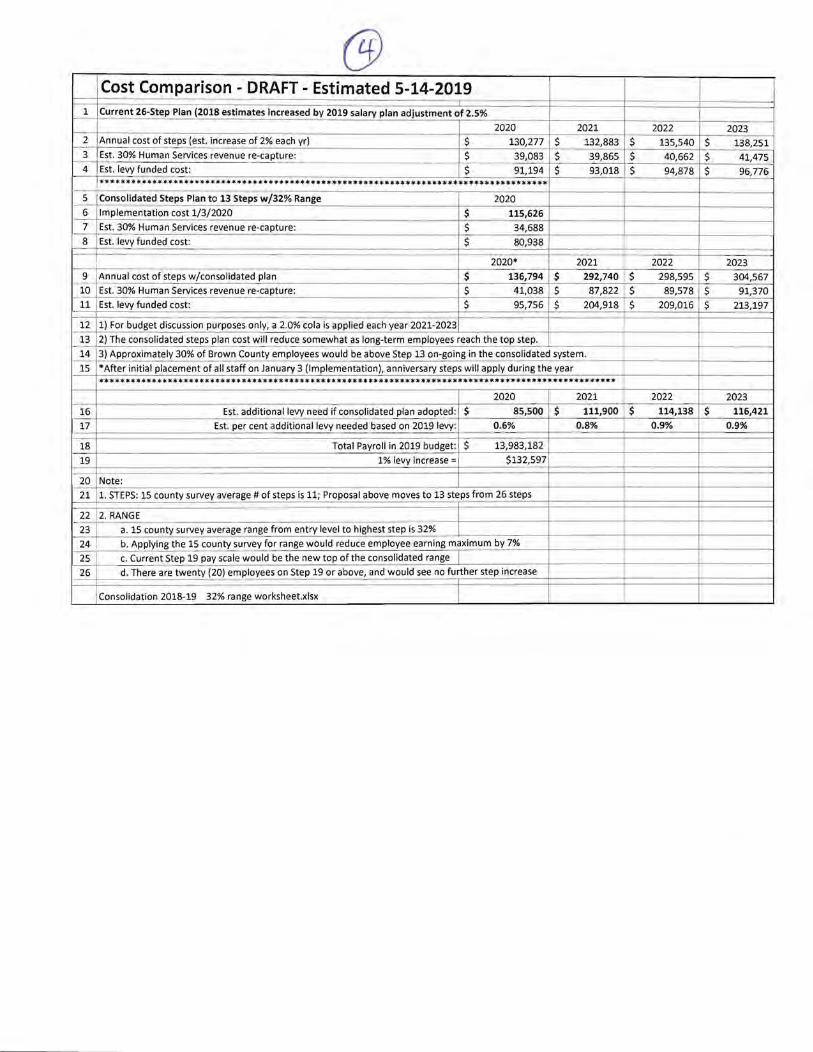

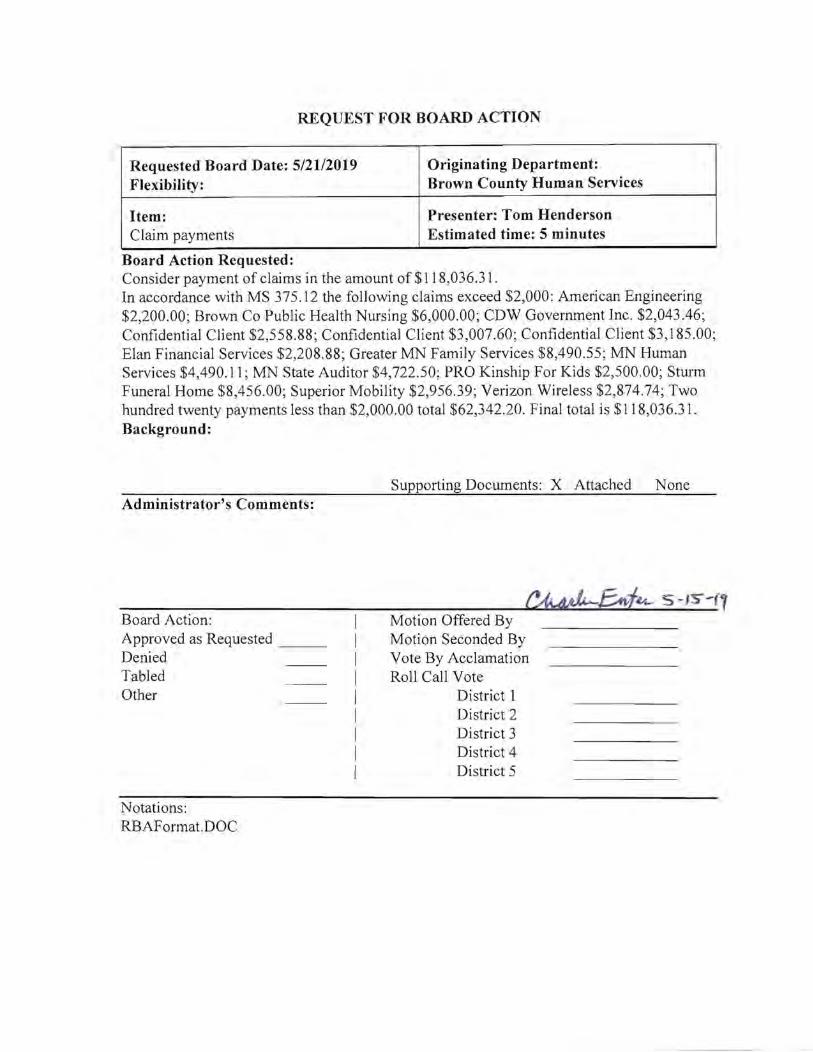

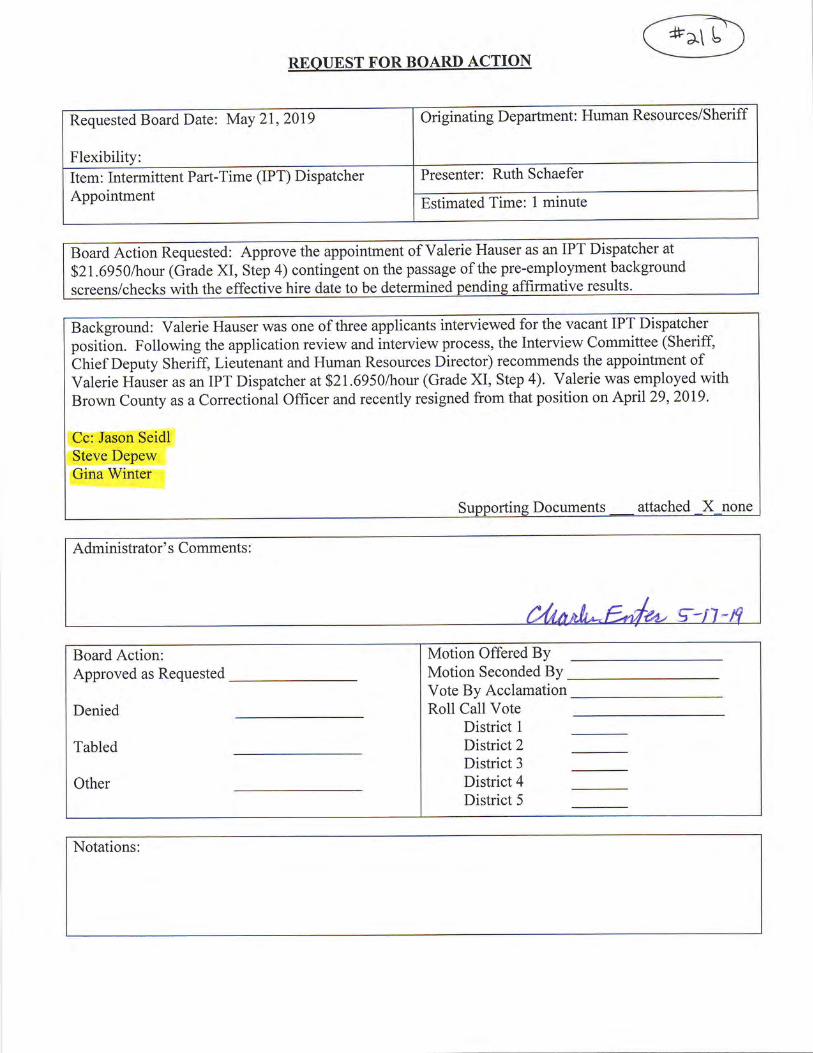

REQUEST FOR BOARD ACTION

Requested Board Date: 5-21-2019 Originating Department: Sheriff Flexibility: No

Item: Monthly Report of Activity Presenter: Jason Seidl- County Sheriff Estimated Time: 5 minutes

Board Action Requested: Accept and order filed the April 2019 Monthly Report of Activity for the Brown County Sheriffs Department.

Background:

See attachments.

cc Chief Deputy Depew

Administrator's Comments:

Board Action: Approved as Requested Denied Tabled Other

Notations: RBAsheriffrep 17.docx

Supporting Documents: x Attached None

Motion Offered By Motion Seconded By Vote By Acclamation Roll Call Vote

District I District 2 District 3 District 4 District 5

gbode

Typewritten Text

# 2

gbode

Oval

BROWN COUNTY SHERIFFS REPORT TO THE COUNTY COMMISSIONERS

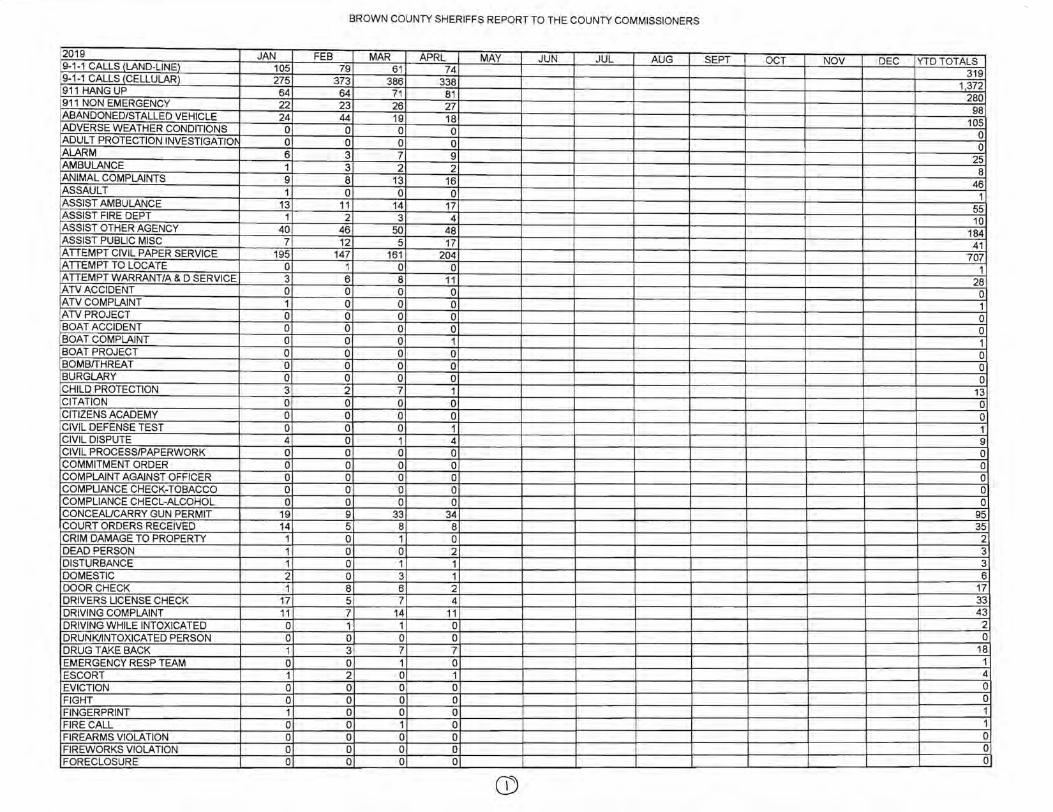

2019 JAN FEB MAR APRL MAY JUN JUL AUG SEPT OCT NOV DEC YTDTOTALS 9-1-1 CALLS (LAND-LINE) 105 79 61 74 319 9-1 -1 CALLS (CELLULAR) 275 373 386 338 1372 911 HANG UP 64 64 71 81 280 911 NON EMERGENCY 22 23 26 27 98 ABANDONED/STALLED VEHICLE 24 44 19 18 105 ADVERSE WEATHER CONDITIONS 0 0 0 0 0 ADULT PROTECTION INVESTIGATIGt 0 0 0 0 0 ALARM 6 3 7 9 25 AMBULANCE 1 3 2 2 8 ANIMAL COMPLAINTS 9 8 13 16 46 ASSAULT 1 0 0 0 1 ASSIST AMBULANCE 13 11 14 17 55 ASSIST FIRE DEPT 1 2 3 4 10 ASSIST OTHER AGENCY 40 46 50 48 184 ASSIST PUBLIC MISC 7 12 5 17 41 ATTEMPT CIVIL PAPER SERVICE 195 147 161 204 707 ATTEMPT TO LOCATE 0 1 0 0 1 ATTEMPT WARRANT/A & D SERVICE 3 6 8 11 28 ATVACCIDENT 0 0 0 0 0 ATV COMPLAINT 1 0 0 0 1 ATVPROJECT 0 0 0 0 0 BOAT ACCIDENT 0 0 0 0 0 BOAT COMPLAINT 0 0 0 1 1 BOAT PROJECT 0 0 0 0 0 BOMBITHREAT 0 0 0 0 0 BURGLARY 0 0 0 0 0 CHILD PROTECTION 3 2 7 1 13 CITATION 0 0 0 0 0 CITIZENS ACADEMY 0 0 0 0 0 CIVIL DEFENSE TEST 0 0 0 1 1 CIVIL DISPUTE 4 0 1 4 9 CIVIL PROCESSIPAPERWORK 0 0 0 0 0 COMMITMENT ORDER 0 0 0 0 0 COMPLAINT AGAINST OFFICER 0 0 0 0 0 COMPLIANCE CHECK-TOBACCO 0 0 0 0 0 COMPLIANCE CHECL-ALCOHOL 0 0 0 0 0 CONCEAUCARRY GUN PERMIT 19 9 33 34 95 COURT ORDERS RECEIVED 14 5 8 8 35 CRIM DAMAGE TO PROPERTY 1 0 1 0 2 DEAD PERSON 1 0 0 2 3 DISTURBANCE 1 0 1 1 3 DOMESTIC 2 0 3 1 6 DOOR CHECK 1 8 6 2 17 DRIVERS LICENSE CHECK 17 5 7 4 33 DRIVING COMPLAINT 11 7 14 11 43 DRIVING WHILE INTOXICATED 0 1 1 0 2 DRUNK/INTOXICATED PERSON 0 0 0 0 0 DRUG TAKE BACK 1 3 7 7 18 EMERGENCY RESP TEAM 0 0 1 0 1 ESCORT 1 2 0 1 4

EVICTION 0 0 0 0 0 FIGHT 0 0 0 0 0

FINGERPRINT 1 0 0 0 1 FIRE CALL 0 0 1 0 1 FIREARMS VIOLATION 0 0 0 0 0 FIREWORKS VIOLATION 0 0 0 0 0 FORECLOSURE 0 0 0 0 0

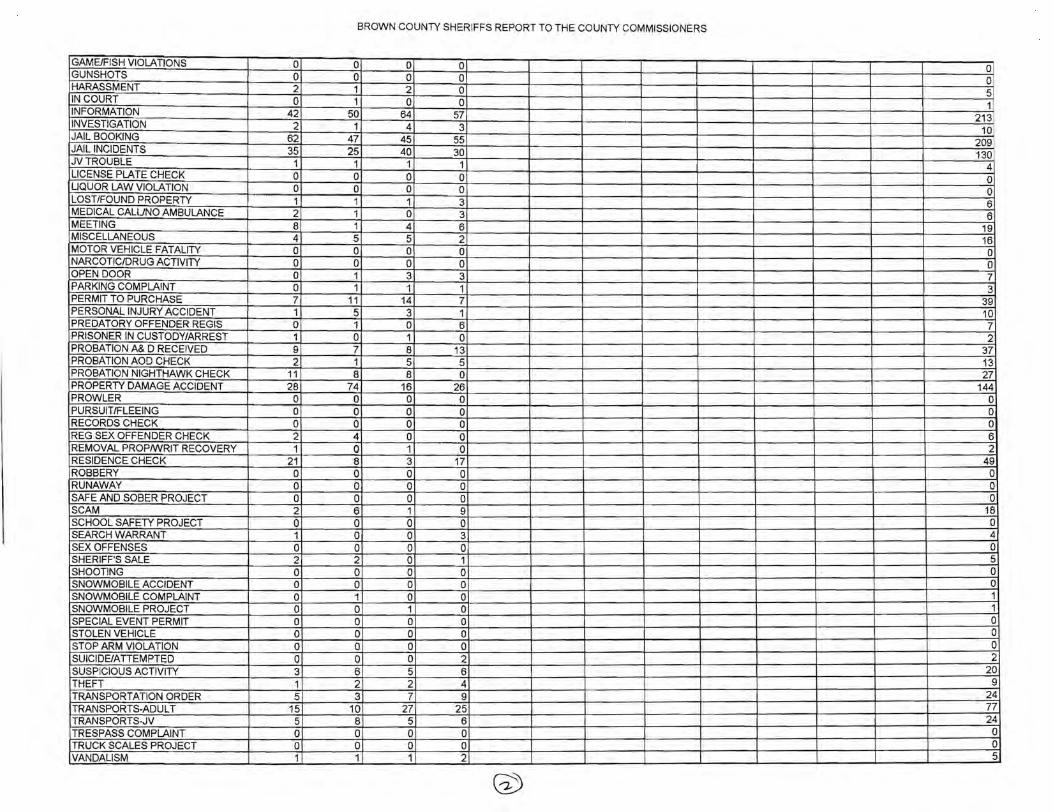

BROWN COUNTY SHERIFFS REPORT TO THE COUNTY COMMISSIONERS

GAMEIFISH VIOLATIONS 0 0 0 0 0 GUNSHOTS 0 0 0 0 0 HARASSMENT 2 1 2 0 5 IN COURT 0 1 0 0 1 INFORMATION 42 50 64 57 213 INVESTIGATION 2 1 4 3 10 JAIL BOOKING 62 47 45 55 209 JAIL INCIDENTS 35 25 40 30 130 JVTROUBLE 1 1 1 1 4 LICENSE PLATE CHECK 0 0 0 0 0 LlaUOR LAW VIOLATION 0 0 0 0 0 LOST/FOUND PROPERTY 1 1 1 3 6 MEDICAL CALUNO AMBULANCE 2 1 0 3 6 MEETING 8 1 4 6 19 MISCELLANEOUS 4 5 5 2 16 MOTOR VEHICLE FATALITY 0 0 0 0 0 NARCOTIC/DRUG ACTIVITY 0 0 0 0 0 OPEN DOOR 0 1 3 3 7 PARKING COMPLAINT 0 1 1 1 3 PERMIT TO PURCHASE 7 11 14 7 39 PERSONAL INJURY ACCIDENT 1 5 3 1 10 PREDATORY OFFENDER REGIS 0 1 0 6 7 PRISONER IN CUSTODY/ARREST 1 0 1 0 2 PROBATION A& D RECEIVED 9 7 8 13 37 PROBATION AOD CHECK 2 1 5 5 13 PROBATION NIGHTHAWK CHECK 11 8 8 0 27 PROPERTY DAMAGE ACCIDENT 28 74 16 26 144 PROWLER 0 0 0 0 0 PURSUITIFLEEING 0 0 0 0 0 RECORDS CHECK 0 0 0 0 0 REG SEX OFFENDER CHECK 2 4 0 0 6 REMOVAL PROPIWRIT RECOVERY 1 0 1 0 2 RESIDENCE CHECK 21 8 3 17 49 ROBBERY 0 0 0 0 0 RUNAWAY 0 0 0 0 0 SAFE AND SOBER PROJECT 0 0 0 0 0 SCAM 2 6 1 9 18 SCHOOL SAFETY PROJECT 0 0 0 0 0 SEARCH WARRANT 1 0 0 3 4 SEX OFFENSES 0 0 0 0 0 SHERIFF'S SALE 2 2 0 1 5 SHOOTING 0 0 0 0 0 SNOWMOBILE ACCIDENT 0 0 0 0 0 SNOWMOBILE COMPLAINT 0 1 0 0 1 SNOWMOBILE PROJECT 0 0 1 0 1 SPECIAL EVENT PERMIT 0 0 0 0 0 STOLEN VEHICLE 0 0 0 0 0 STOP ARM VIOLATION 0 0 0 0 0 SUICIDEIA TTEMPTED 0 0 0 2 2 SUSPICIOUS ACTIVITY 3 6 5 6 20 THEFT 1 2 2 4 9 TRANSPORTATION ORDER 5 3 7 9 24 TRANSPORTS-ADULT 15 10 27 25 77 TRANSPORTS-JV 5 8 5 6 24 TRESPASS COMPLAINT 0 0 0 0 0 TRUCK SCALES PROJECT 0 0 0 0 0 VANDALISM 1 1 1 2 5

BROWN COUNTY SHERIFFS REPORT TO THE COUNTY COMMISSIONERS

VEHIPROP FORFEITURE 0 0 0 0 0 VEHICLE STOP 43 27 44 104 218 WARRANT RECEIVED 26 28 20 27 101 WELFARE CHECK 6 5 6 3 20

0 0

TOTAL BROWN COUNTY CFS 816 766 818 972 0 0 0 0 0 0 0 0 3372 TOTAL CALLS FOR SERVICE-ALL 2060 1816 2154 2342 8372

CIVIL FEES PAID TO COUNTY $2647.35 $2667.79 $1425.00 $1 375.00 $8115.14 HUBER PAYMENTS $1095.00 $650.00 $930.00 $670.00 $3345.00 TOTAL JAIL AD.P. 30.87 26.75 27.58 28.50 37.90 OUT OF COUNTY AD.P. 3.20 3.80 2.87 3.70 4.52 BRN CO INMATE AD.P. 27.67 22.95 24.71 24 .80 33.38 BROWN COUNTY HUBER ADP 2.37 0.70 1.06 1.26 1.80 OIC INMATE BILLINGS $6402.00 $5568.00 $3948.00 $5416.00 $21334.00 TOTAL JAIL BOOKINGS 63 43 44 56 206 OUT OF COUNTY HUBER AD.P. 0 0 0 0 0

BROWN COUNTY SHERIFFS REPORT TO THE COUNTY COMMISSIONERS

2019 JAN FEB MAR APRL MAY JUN JUL AUG SEPT OCT NOV DEC YTDTOTALS 330 SHERIFF SEIDL 23567 24468 25297 26151 2017 Ford Explorer 459 901 829 854 3043

331 CHIEF DEPUTY DEPEW 43380 44624 46328 47818 2016 Ford Explorer 700 1244 1704 1490 5138

332 DEPUTY STUEBER 123054 124456 126695 129165 2014 ChevY CCl,Drice PPV 636 1402 2239 2470 6747

333 DEPUTY FAIRBAIRN 128100 128500 129350 129600 2011 Ford Crown Victoria 712011 1472 400 850 250 2972

334 DEPUTY REED 77652 78799 79740 80532 2015 Ford Explorer 1636 1147 941 792 4516

335 SCHWARZROCK 109832 111 440 115174 117278 2015 Ford Explorer 3261 1608 3734 2104 10707 2015 Ford Explorer

336 DEPUTY MURPHY 135700 136200 137930 139800 2013 ChevY Caprice PPV 1565 500 1730 1870 5665

337 SGT BENTZ 163956 164,918 166584 169040 2013 ChevyGaprice Classic 1 31 1 962 1666 2456 6395

338 DEPUTY KITZBERGER 140340 142572 144 805 147885 2014 ChevY Caprice Classic 3202 2232 2233 3080 10747

339 DEPUTY SHAW 134 126 136556 139893 142628 2015 Ford Explorer 2880 2430 3337 2735 11382

TRANSPORT SQUAD 126425 127706 128505 129931 2012 Ford Explorer-June 1 2013 2,014 1 281 799 1426 5520

340 DEPUTY BAUER 78393 80366 82529 85389 2016 FORD EXPLORER 2230 1973 2163 2860 9226

EXPEDITION 64503 65086 65693 67031 4 583 607 1338 2532

SPARE SQUAD 161760 161823 161880 162951 428 63 57 1071 1619

2003 FORD EXCURSION 60690 61375 61474 61884 397 685 99 410 1 591

MONTHLY TOTALS 19965 15438 20825 22346 0 0 0 0 0 0 0 0 78574

Agenda # _____ _ Date: ______ _

REQUEST FOR BOARD ACTION

Requested Board Date: 05/21/19 Originating Department: Auditor-Treasurer Flexibility:

Items: General Government Claims Presenter: Jean Prochniak Estimated Time:

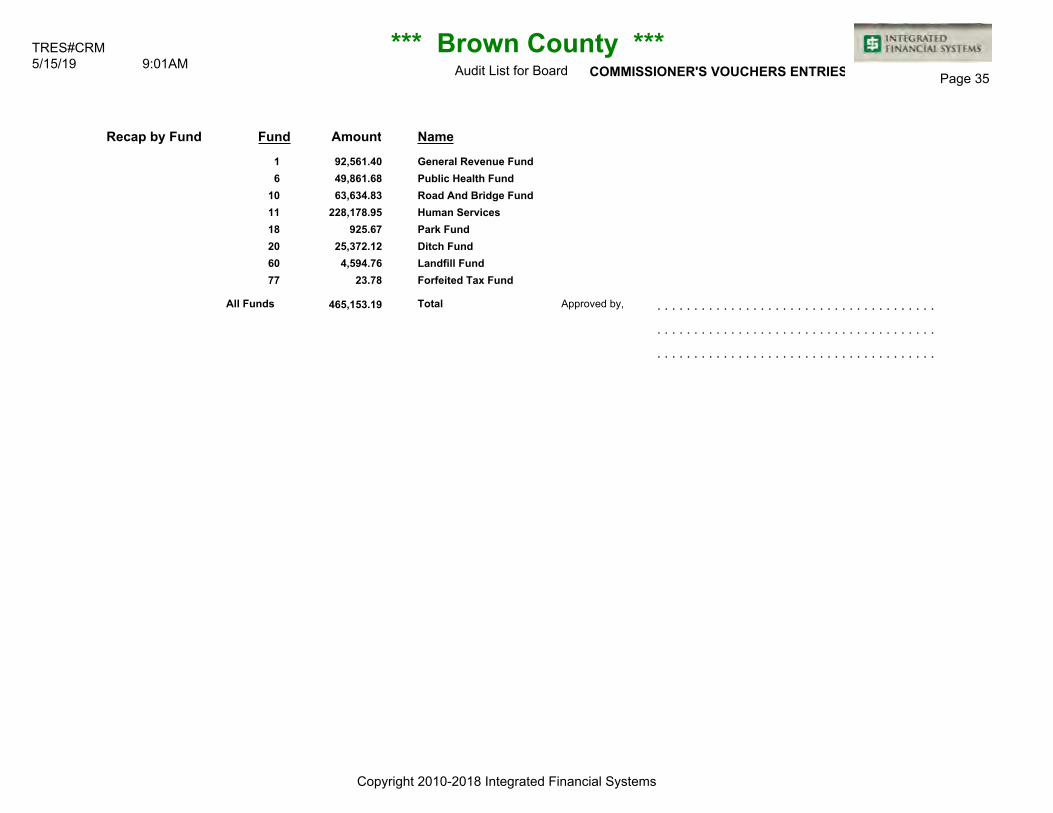

Board Action Requested: Consider payment of general government claims in the amount of $465, 153.19

Background:

Supporting Documents [g] attached D none

Administrator's Comments:

Gl~5?fG1, 5" -15"-(q

Board Action: Motion Offered By: Approved as Requested -- Motion Seconded By: Denied Vote By Acclamation: --Tabled Roll Call Vote --Other District 1 -- --

District 2 --District 3 - -District 4 --District 5 --

Notations:

IIC RT _SERVERIS YSIAUDTRESIOFFICElMYDOCSIAUDTR ES4IFORMICOMM_RBA.DOC

gbode

Typewritten Text

# 3

gbode

Oval

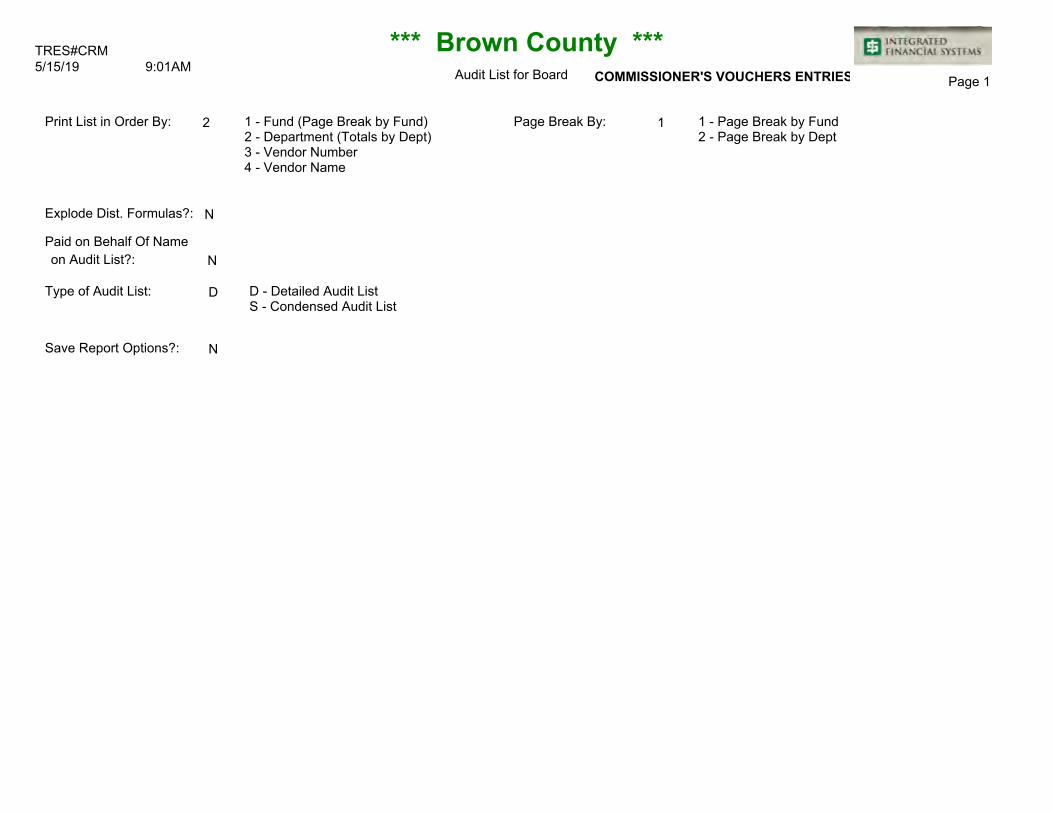

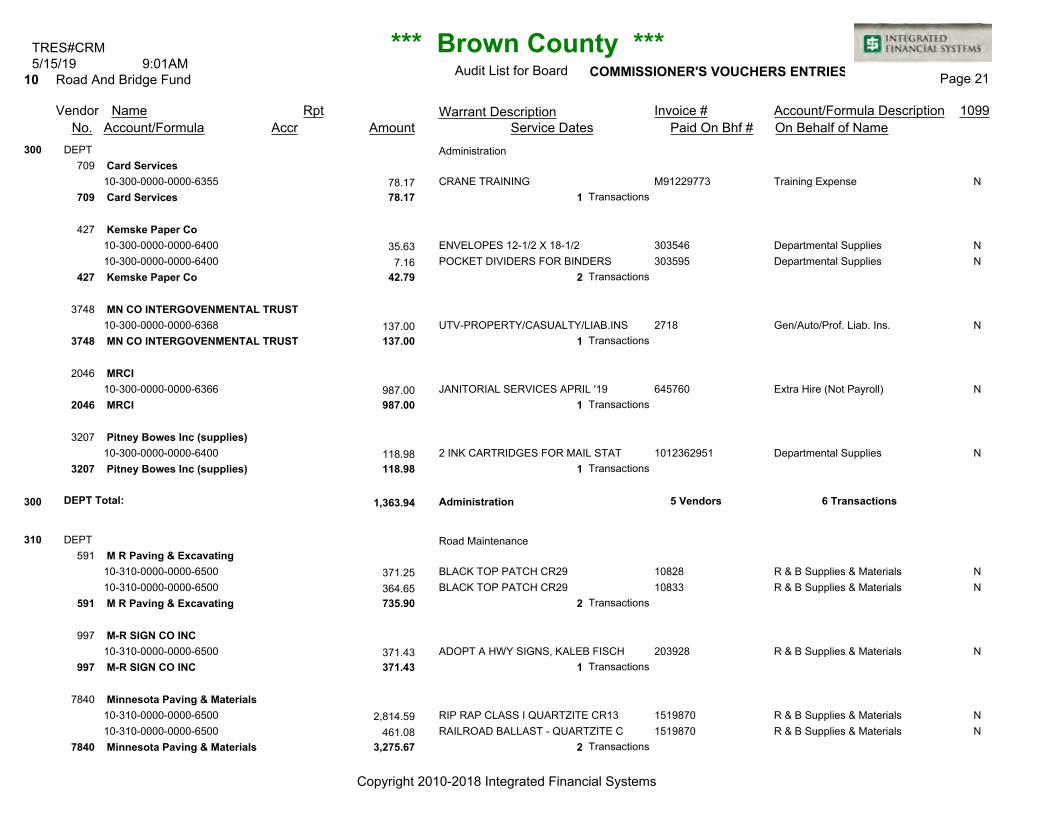

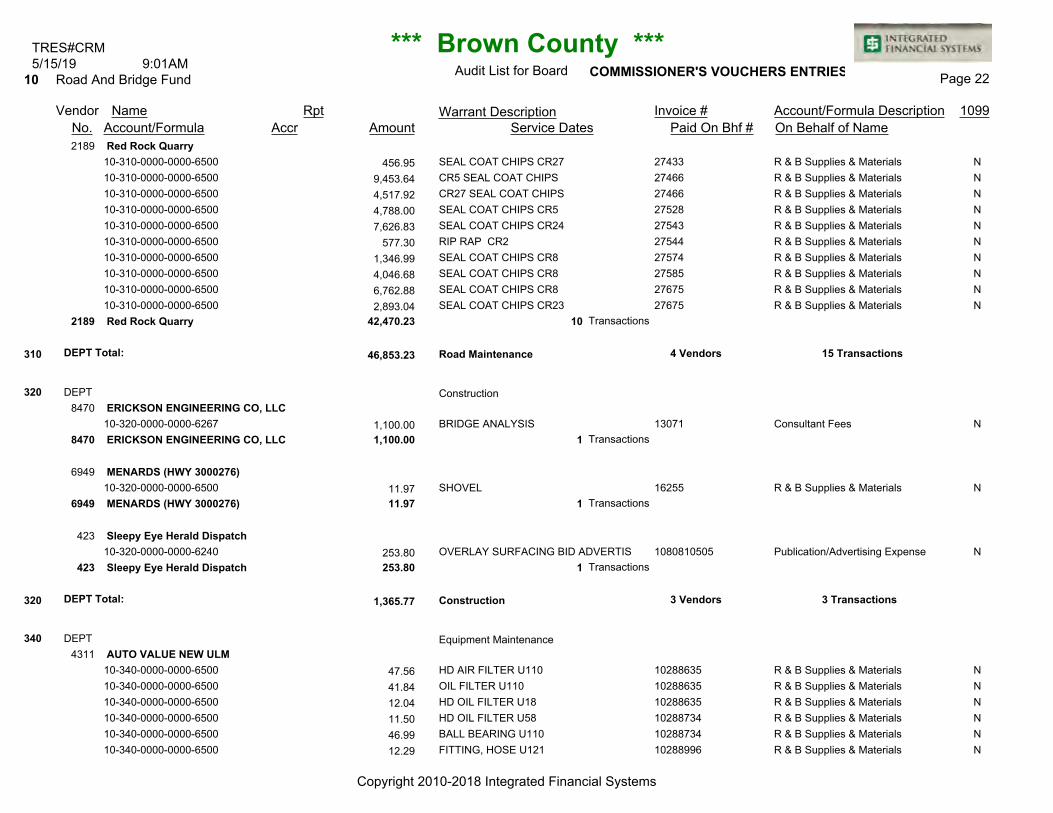

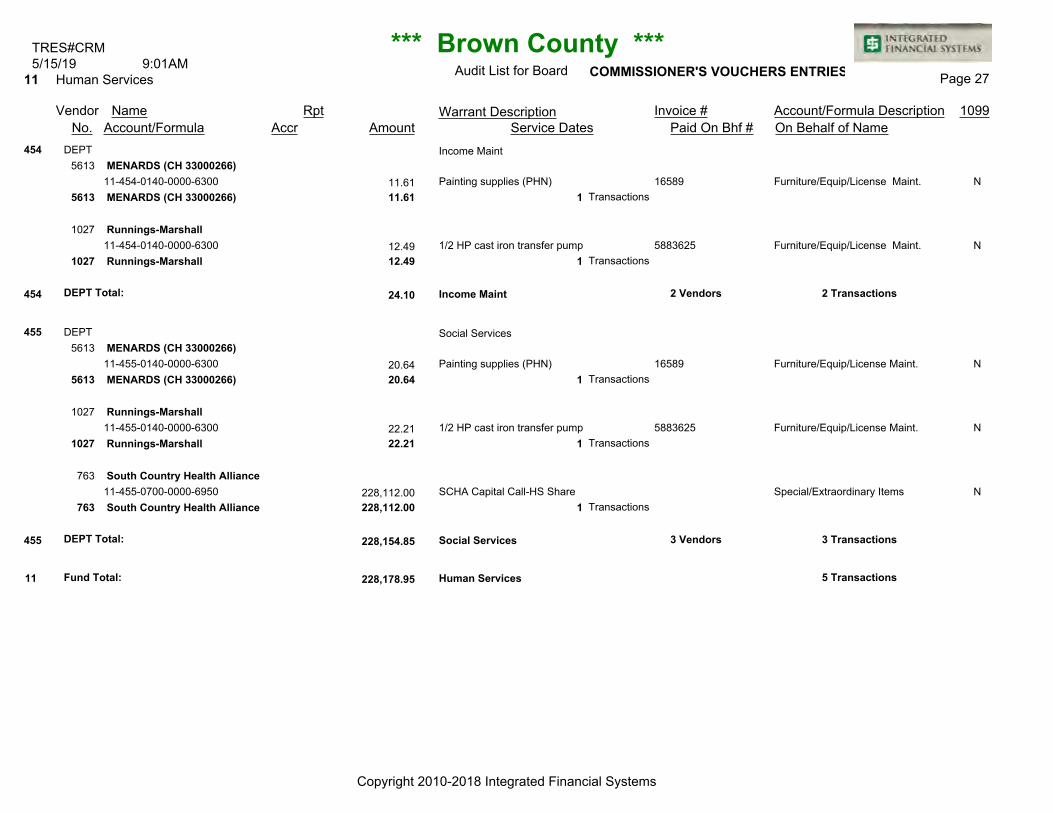

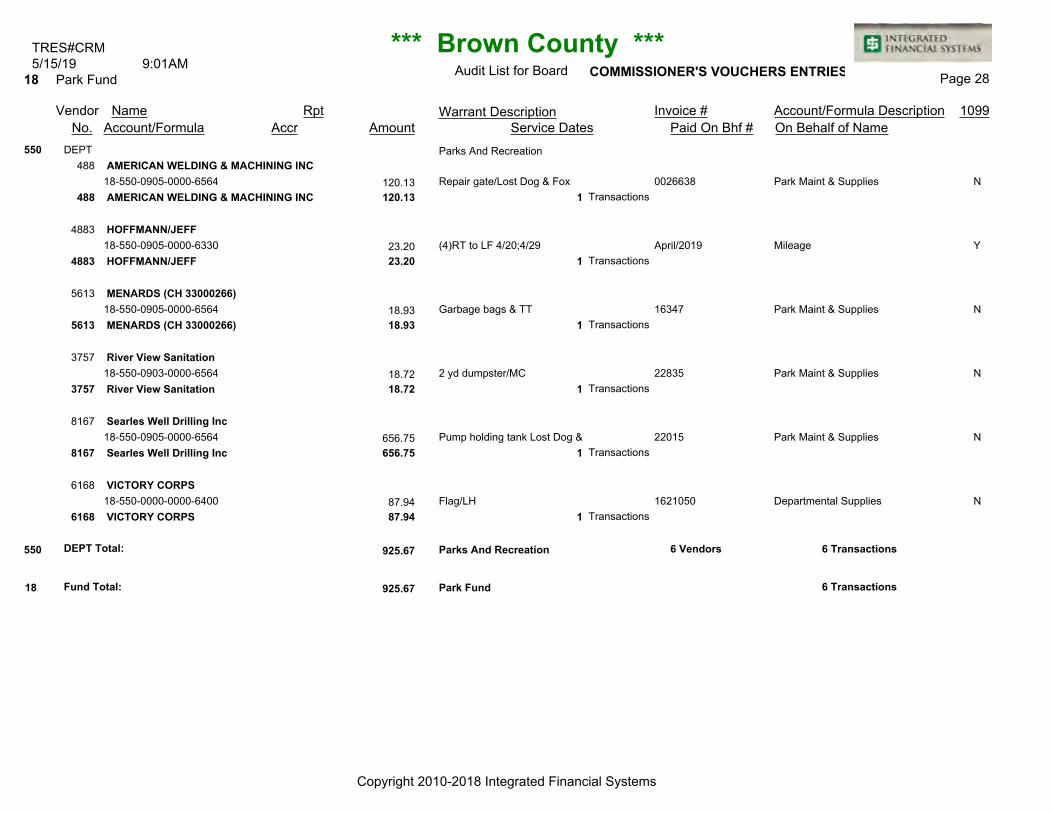

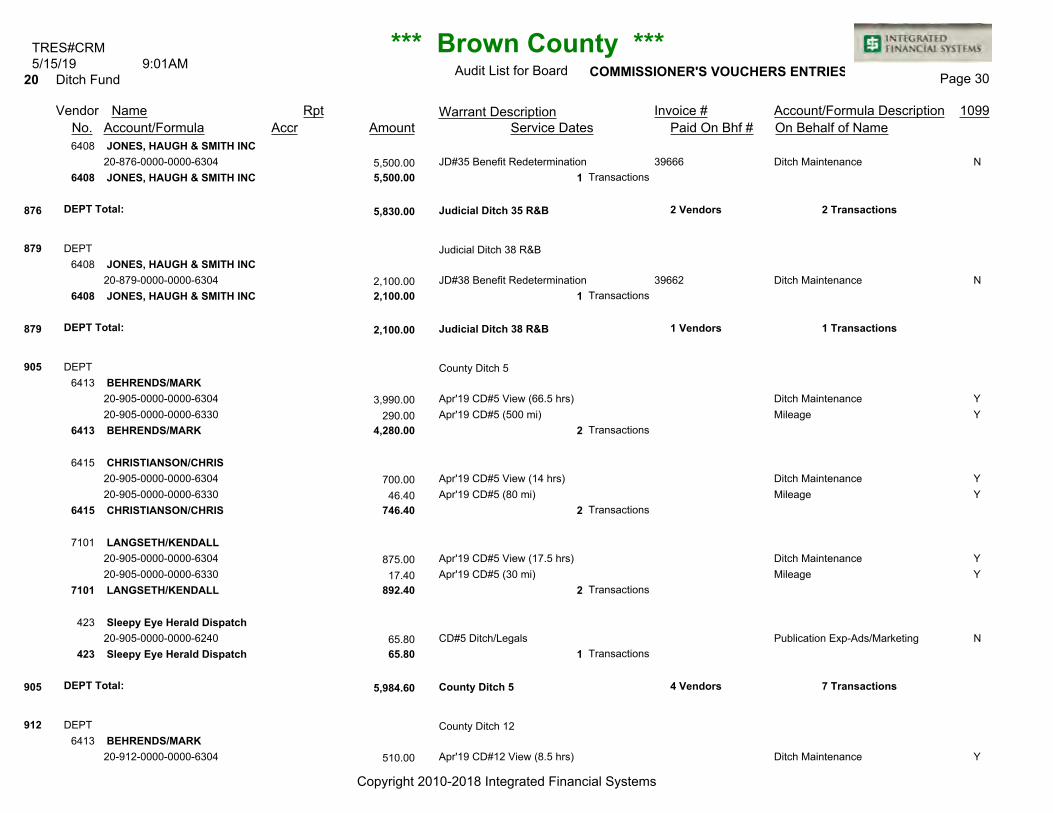

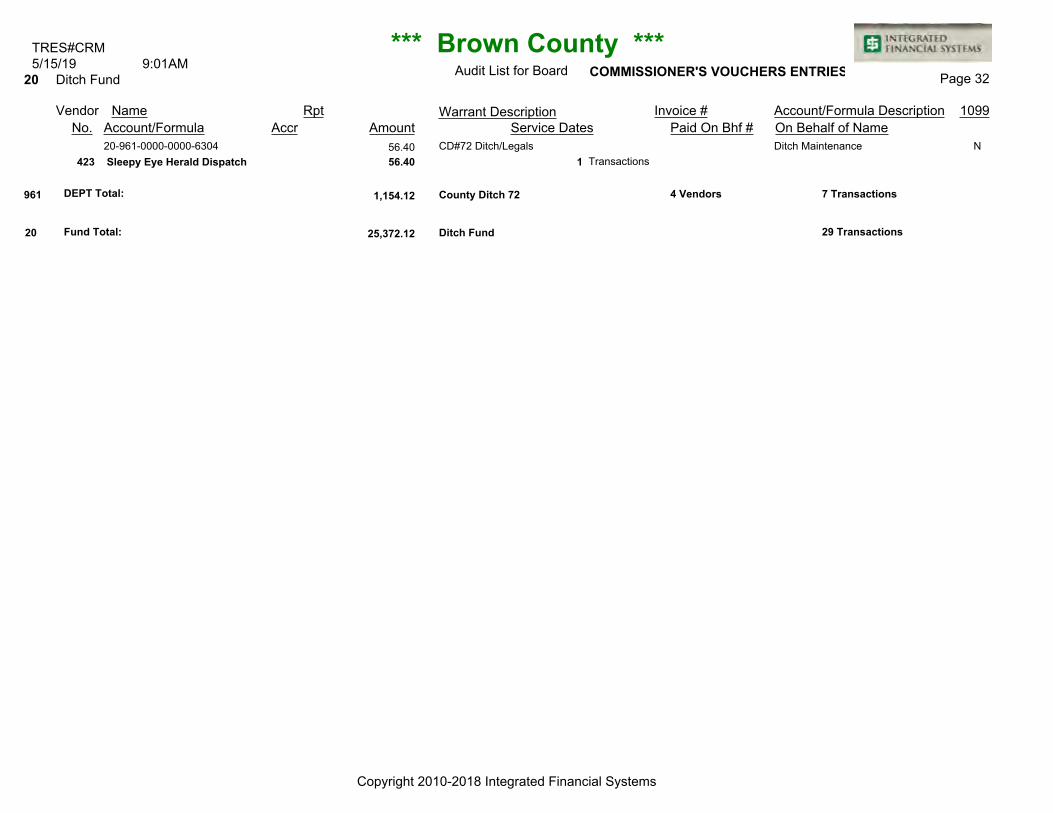

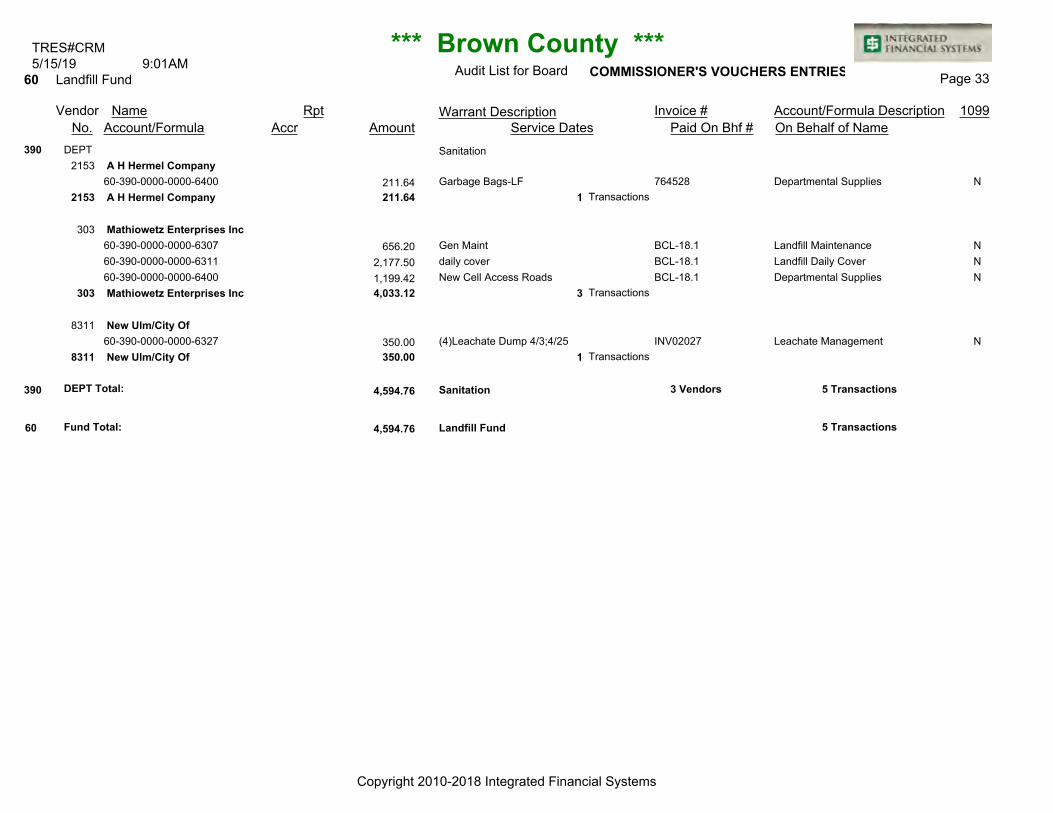

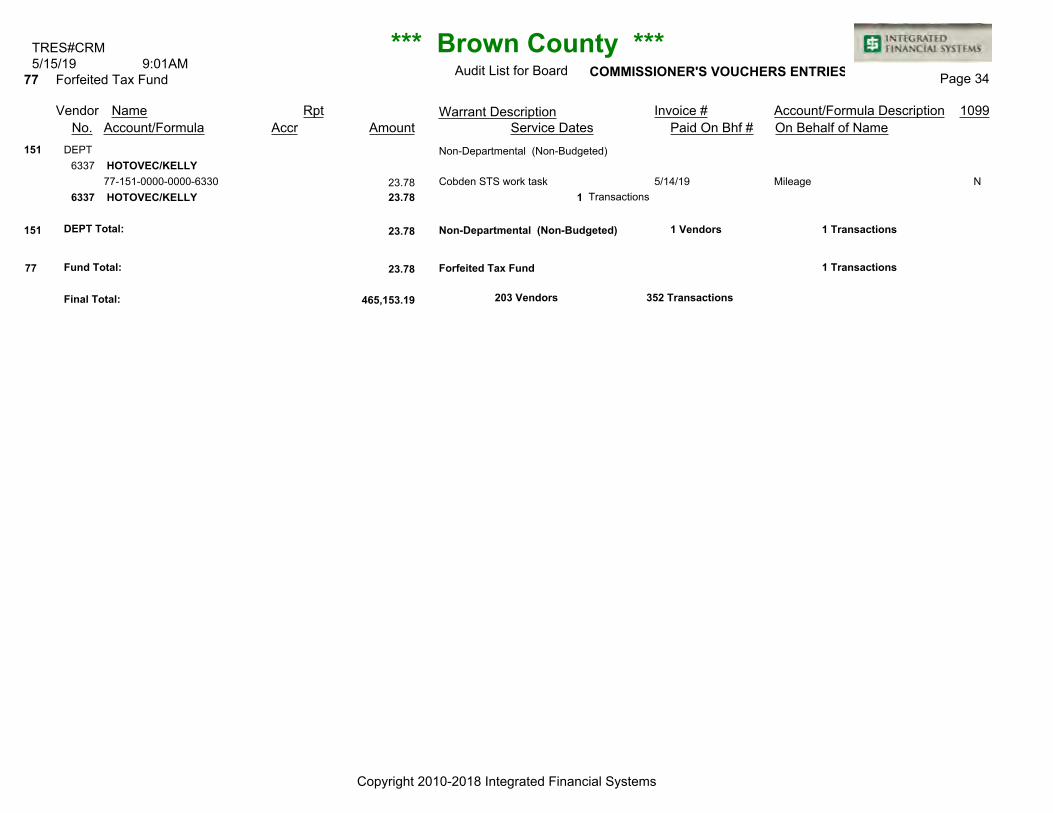

COMMISSIONER'S VOUCHERS ENTRIES

TRES#CRM 9:01AM5/15/19

N

N

D

2

N

1

Audit List for Board Page 1

Print List in Order By:

Explode Dist. Formulas?:

Paid on Behalf Of Nameon Audit List?:

Type of Audit List:

Save Report Options?:

D - Detailed Audit ListS - Condensed Audit List

1 - Fund (Page Break by Fund)2 - Department (Totals by Dept) 3 - Vendor Number4 - Vendor Name

Page Break By: 1 - Page Break by Fund2 - Page Break by Dept

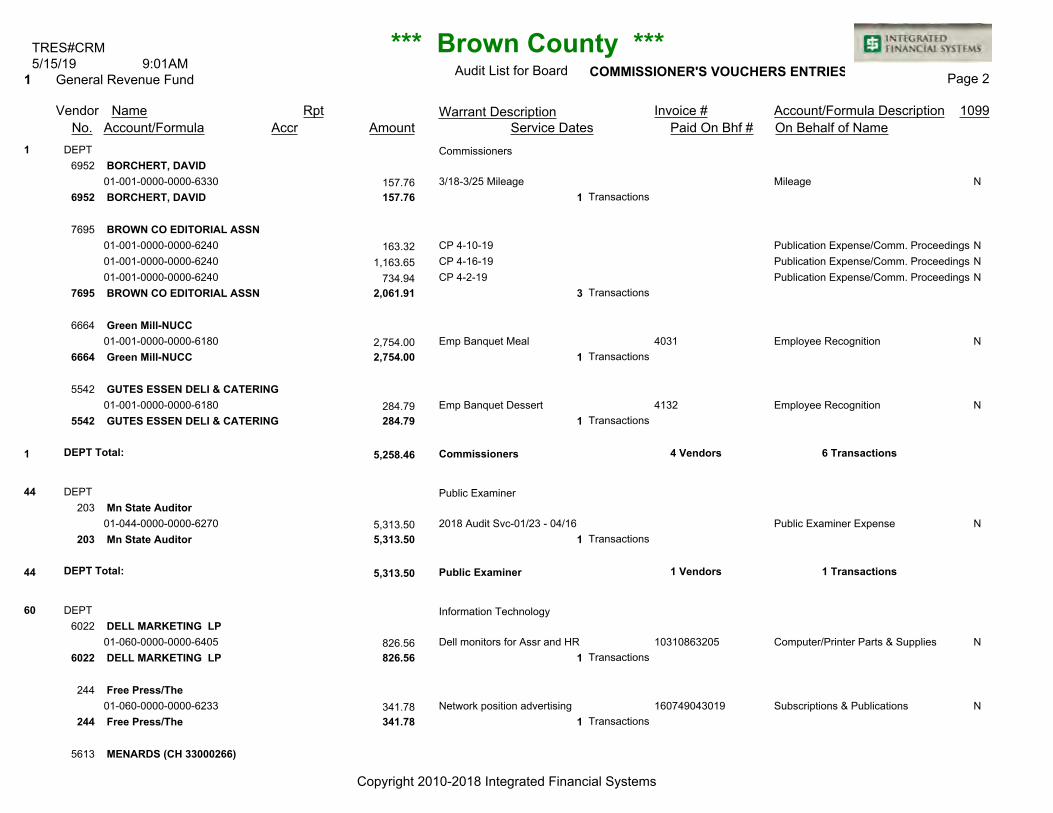

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

1

BORCHERT, DAVID

BORCHERT, DAVID 157.76 16952

BROWN CO EDITORIAL ASSN

BROWN CO EDITORIAL ASSN 2,061.91 37695

Green Mill-NUCC

Green Mill-NUCC 2,754.00 16664

GUTES ESSEN DELI & CATERING

GUTES ESSEN DELI & CATERING 284.79 15542

1 Commissioners5,258.46

44

Mn State Auditor

Mn State Auditor 5,313.50 1203

44 Public Examiner5,313.50

60

DELL MARKETING LP

DELL MARKETING LP 826.56 16022

Free Press/The

Free Press/The 341.78 1244

MENARDS (CH 33000266)

CommissionersDEPT

6952

01-001-0000-0000-6330 157.76 3/18-3/25 Mileage Mileage N

7695

01-001-0000-0000-6240 163.32 CP 4-10-19 Publication Expense/Comm. Proceedings N

01-001-0000-0000-6240 1,163.65 CP 4-16-19 Publication Expense/Comm. Proceedings N

01-001-0000-0000-6240 734.94 CP 4-2-19 Publication Expense/Comm. Proceedings N

6664

01-001-0000-0000-6180 2,754.00 Emp Banquet Meal 4031 Employee Recognition N

5542

01-001-0000-0000-6180 284.79 Emp Banquet Dessert 4132 Employee Recognition N

Public ExaminerDEPT

203

01-044-0000-0000-6270 5,313.50 2018 Audit Svc-01/23 - 04/16 Public Examiner Expense N

Information TechnologyDEPT

6022

01-060-0000-0000-6405 826.56 Dell monitors for Assr and HR 10310863205 Computer/Printer Parts & Supplies N

244

01-060-0000-0000-6233 341.78 Network position advertising 160749043019 Subscriptions & Publications N

5613

Page 2Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

4 Vendors 6 TransactionsDEPT Total:

Transactions

1 Vendors 1 TransactionsDEPT Total:

Transactions

Transactions

Account/Formula

*** Brown County ***

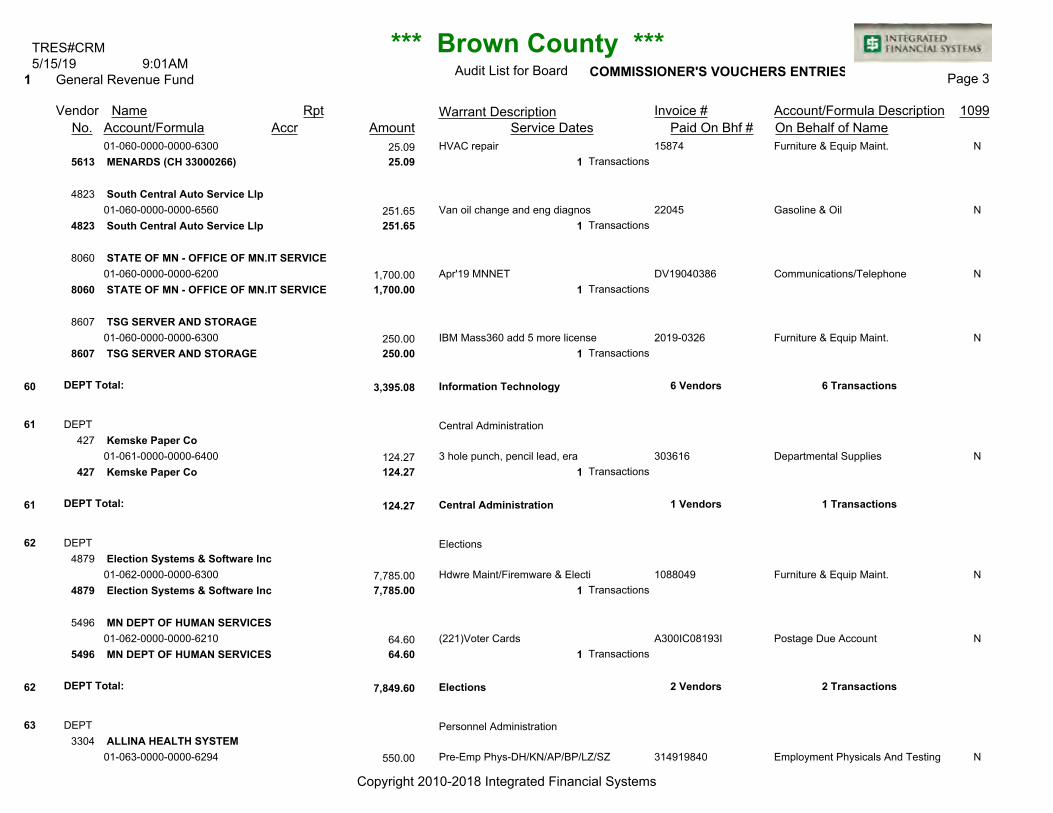

STATE OF MN - OFFICE OF MN.IT SERVICES

STATE OF MN - OFFICE OF MN.IT SERVICES

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

MENARDS (CH 33000266) 25.09 15613

South Central Auto Service Llp

South Central Auto Service Llp 251.65 14823

1,700.00 18060

TSG SERVER AND STORAGE

TSG SERVER AND STORAGE 250.00 18607

60 Information Technology3,395.08

61

Kemske Paper Co

Kemske Paper Co 124.27 1427

61 Central Administration124.27

62

Election Systems & Software Inc

Election Systems & Software Inc 7,785.00 14879

MN DEPT OF HUMAN SERVICES

MN DEPT OF HUMAN SERVICES 64.60 15496

62 Elections7,849.60

63

ALLINA HEALTH SYSTEM

01-060-0000-0000-6300 25.09 HVAC repair 15874 Furniture & Equip Maint. N

4823

01-060-0000-0000-6560 251.65 Van oil change and eng diagnos 22045 Gasoline & Oil N

8060

01-060-0000-0000-6200 1,700.00 Apr'19 MNNET DV19040386 Communications/Telephone N

8607

01-060-0000-0000-6300 250.00 IBM Mass360 add 5 more license 2019-0326 Furniture & Equip Maint. N

Central AdministrationDEPT

427

01-061-0000-0000-6400 124.27 3 hole punch, pencil lead, era 303616 Departmental Supplies N

ElectionsDEPT

4879

01-062-0000-0000-6300 7,785.00 Hdwre Maint/Firemware & Electi 1088049 Furniture & Equip Maint. N

5496

01-062-0000-0000-6210 64.60 (221)Voter Cards A300IC08193I Postage Due Account N

Personnel AdministrationDEPT

3304

01-063-0000-0000-6294 550.00 Pre-Emp Phys-DH/KN/AP/BP/LZ/SZ 314919840 Employment Physicals And Testing N

Page 3Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

6 Vendors 6 TransactionsDEPT Total:

Transactions

1 Vendors 1 TransactionsDEPT Total:

Transactions

Transactions

2 Vendors 2 TransactionsDEPT Total:

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

ALLINA HEALTH SYSTEM 550.00 13304

FSSOLUTIONS

FSSOLUTIONS 259.10 14394

Innovative Office Solutions

Innovative Office Solutions 18.12 11609

Kemske Paper Co

Kemske Paper Co 292.76 2427

MnCCC MI 33

MnCCC MI 33 1,643.00 1214

RVS SHREDDING

RVS SHREDDING 15.00 11682

TREBESCH/DONITTA

TREBESCH/DONITTA 34.80 16532

63 Personnel Administration2,812.78

90

BACHMAN PRINTING

BACHMAN PRINTING 192.00 15572

Bock/Theresa M

Bock/Theresa M 56.00 16185

RVS SHREDDING

4394

01-063-0000-0000-6294 259.10 Pre-Emp Drg Srn-DH/AP/JS/BP/KN FL00293469 Employment Physicals And Testing 6

1609

01-063-0000-0000-6400 18.12 Labels 2487899 Departmental Supplies N

427

01-063-0000-0000-6400 198.00 Chair 303680 Departmental Supplies N

01-063-0000-0000-6400 94.76 Chairmat 303687 Departmental Supplies N

214

01-063-0000-0000-6605 1,643.00 Optimum Pyrl Supt 6/30/19-7/1/ 1905017 Software Expense $5,000 or > N

1682

01-063-0000-0000-6400 15.00 Apr'19 Shred Svcs 22187 Departmental Supplies N

6532

01-063-0000-0000-6330 34.80 Mileage Mileage N

County AttorneyDEPT

5572

01-090-0000-0000-6360 192.00 Appellate Brief 71855 Trial & Investigation Exp N

6185

01-090-0000-0000-6360 56.00 Transcript/CR-19-163 2220 Trial & Investigation Exp Y

1682

Page 4Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

7 Vendors 8 TransactionsDEPT Total:

Transactions

Transactions

Account/Formula

*** Brown County ***

THOMSON REUTERS - WEST PAYMENT CENTER

THOMSON REUTERS - WEST PAYMENT CENTER

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

RVS SHREDDING 5.00 11682

278.44 2262

90 County Attorney531.44

100

Innovative Office Solutions

Innovative Office Solutions 194.25 11609

Kemske Paper Co

Kemske Paper Co 472.66 4427

NORTHSTAR

NORTHSTAR 347.12 16546

100 County Recorder1,014.03

101

DUNN/DIANE

DUNN/DIANE 83.49 16816

HEIL/JAMES

HEIL/JAMES 229.68 27672

01-090-0000-0000-6800 5.00 Shredding 22185 Shredding N

262

01-090-0000-0000-6260 249.55 Apr'19 West Law Info 840201691 Legal Research N

01-090-0000-0000-6260 28.89 Apr'19 Library Plan Chrg 840283509 Legal Research N

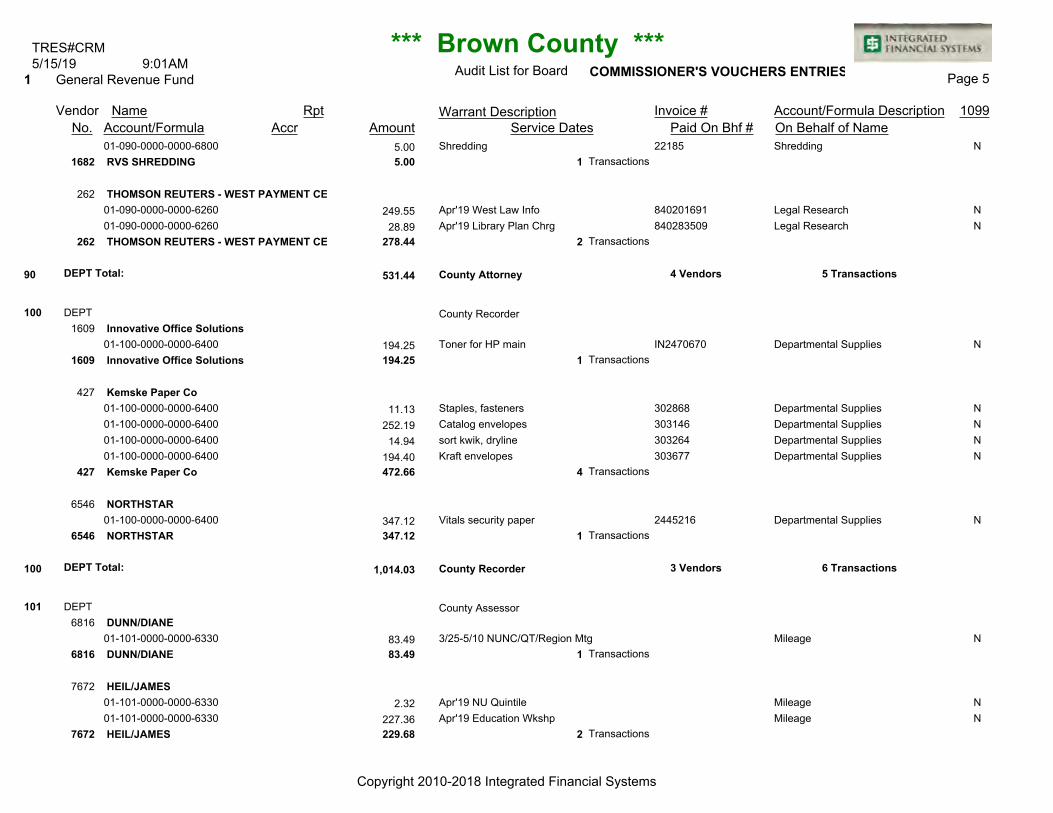

County RecorderDEPT

1609

01-100-0000-0000-6400 194.25 Toner for HP main IN2470670 Departmental Supplies N

427

01-100-0000-0000-6400 11.13 Staples, fasteners 302868 Departmental Supplies N

01-100-0000-0000-6400 252.19 Catalog envelopes 303146 Departmental Supplies N

01-100-0000-0000-6400 14.94 sort kwik, dryline 303264 Departmental Supplies N

01-100-0000-0000-6400 194.40 Kraft envelopes 303677 Departmental Supplies N

6546

01-100-0000-0000-6400 347.12 Vitals security paper 2445216 Departmental Supplies N

County AssessorDEPT

6816

01-101-0000-0000-6330 83.49 3/25-5/10 NUNC/QT/Region Mtg Mileage N

7672

01-101-0000-0000-6330 2.32 Apr'19 NU Quintile Mileage N

01-101-0000-0000-6330 227.36 Apr'19 Education Wkshp Mileage N

Page 5Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

4 Vendors 5 TransactionsDEPT Total:

Transactions

Transactions

Transactions

3 Vendors 6 TransactionsDEPT Total:

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

Innovative Office Solutions

Innovative Office Solutions 26.08 11609

Kemske Paper Co

Kemske Paper Co 14.42 1427

MnCCC MI 33

MnCCC MI 33 360.00 1214

River Bend Business Products

River Bend Business Products 28.56 17040

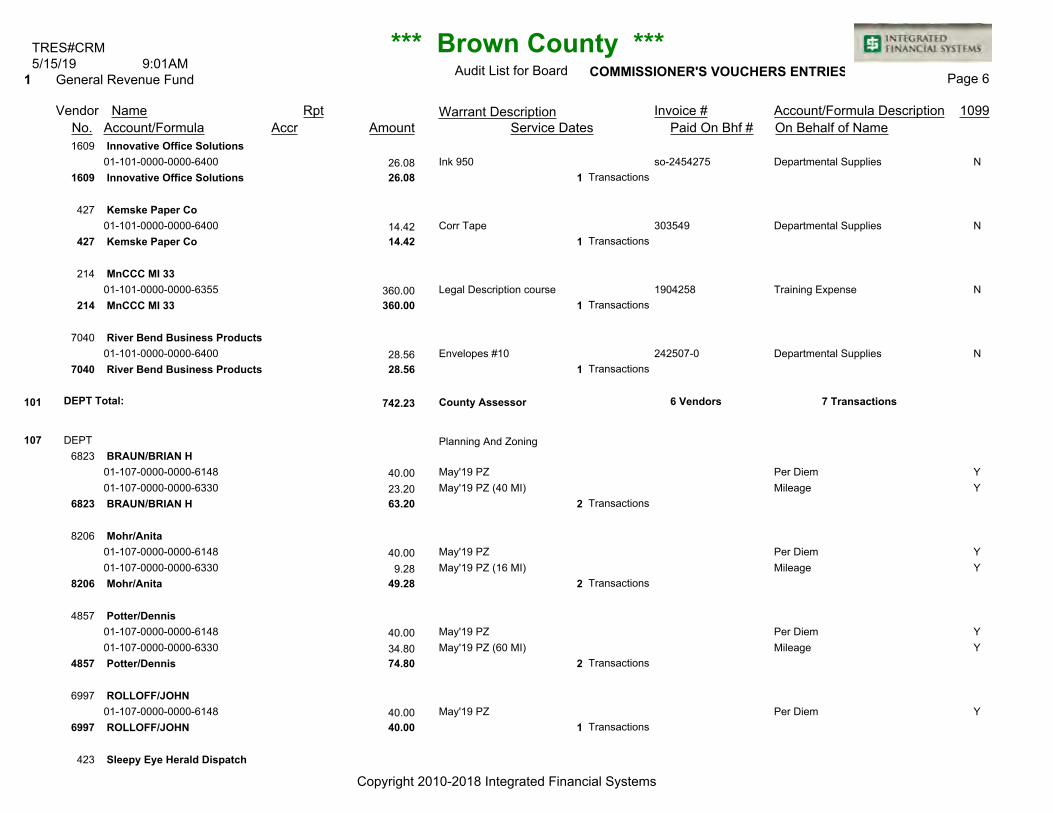

101 County Assessor742.23

107

BRAUN/BRIAN H

BRAUN/BRIAN H 63.20 26823

Mohr/Anita

Mohr/Anita 49.28 28206

Potter/Dennis

Potter/Dennis 74.80 24857

ROLLOFF/JOHN

ROLLOFF/JOHN 40.00 16997

Sleepy Eye Herald Dispatch

1609

01-101-0000-0000-6400 26.08 Ink 950 so-2454275 Departmental Supplies N

427

01-101-0000-0000-6400 14.42 Corr Tape 303549 Departmental Supplies N

214

01-101-0000-0000-6355 360.00 Legal Description course 1904258 Training Expense N

7040

01-101-0000-0000-6400 28.56 Envelopes #10 242507-0 Departmental Supplies N

Planning And ZoningDEPT

6823

01-107-0000-0000-6148 40.00 May'19 PZ Per Diem Y

01-107-0000-0000-6330 23.20 May'19 PZ (40 MI) Mileage Y

8206

01-107-0000-0000-6148 40.00 May'19 PZ Per Diem Y

01-107-0000-0000-6330 9.28 May'19 PZ (16 MI) Mileage Y

4857

01-107-0000-0000-6148 40.00 May'19 PZ Per Diem Y

01-107-0000-0000-6330 34.80 May'19 PZ (60 MI) Mileage Y

6997

01-107-0000-0000-6148 40.00 May'19 PZ Per Diem Y

423

Page 6Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

6 Vendors 7 TransactionsDEPT Total:

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

Sleepy Eye Herald Dispatch 244.40 1423

107 Planning And Zoning471.68

110

CARROLL CONSTRUCTION SUPPLY

CARROLL CONSTRUCTION SUPPLY 19.99 26761

Fastenal Company

Fastenal Company 71.28 12904

Johnstone Supply

Johnstone Supply 186.48 12359

MENARDS (CH 33000266)

MENARDS (CH 33000266) 157.06 55613

New Ulm Tire

New Ulm Tire 59.57 21999

Runnings-Marshall

01-107-0000-0000-6240 244.40 Apr/May BOA mtgs/P&Z 1005590505 Publication/Advertising Expense N

Government BuildingsDEPT

6761

01-110-0000-0000-6300 21.56 10 oz. caulk gun NU029259 Furniture & Equip Maint. N

01-110-0000-0000-6300 1.57 Exempt/sales tax adj NU029259 Furniture & Equip Maint. N

2904

01-110-0000-0000-6400 71.28 Anchors/bolts MNNEW163071 Departmental Supplies N

2359

01-110-0000-0000-6300 186.48 Crimper/notcher/cutter/snip me S100708817.001 Furniture & Equip Maint. N

5613

01-110-0140-0000-6300 11.34 Painting supplies (PHN) 16589 Furniture & Equip Maint. N

01-110-0000-0000-6400 116.65 3 hook rails/primer/key organi 16673 Departmental Supplies N

01-110-0135-0000-6300 10.73 Fem hose adapter/5 ft. flex ho 16703 Furniture & Equip Maint. N

01-110-0136-0000-6300 3.35 Fem hose adapter/5 ft. flex ho 16703 Furniture & Equip Maint. N

01-110-0041-0000-6300 14.99 60 qt. utility box (for ceilin 16704 Furniture & Equip Maint. N

1999

01-110-0000-0000-6310 30.13 2007 F150 patch front tire (dr 247242 Vehicle Maintenance N

01-110-0000-0000-6310 29.44 Lube/oil/filter 1999 F150 247243 Vehicle Maintenance N

1027

01-110-0000-0000-6400 12.58 Tri-flow lock spray 2ea. 5874866 Departmental Supplies N

01-110-0000-0000-6300 46.91 1/2 HP cast iron transfer pump 5883625 Furniture & Equip Maint. N

01-110-0135-0000-6300 35.74 1/2 HP cast iron transfer pump 5883625 Furniture & Equip Maint. N

01-110-0136-0000-6300 11.16 1/2 HP cast iron transfer pump 5883625 Furniture & Equip Maint. N

01-110-0140-0000-6300 12.20 1/2 HP cast iron transfer pump 5883625 Furniture & Equip Maint. N

Page 7Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

5 Vendors 8 TransactionsDEPT Total:

-

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

Runnings-Marshall 118.59 51027

110 Government Buildings612.97

120

Innovative Office Solutions

Innovative Office Solutions 635.59 11609

120 Veteran Services635.59

141

COMFREY TIMES/THE

COMFREY TIMES/THE 7.50 16188

JOURNAL INC/THE

JOURNAL INC/THE 578.45 2382

Kemske Paper Co

Kemske Paper Co 6.35 1427

KNUJ Radio Station

KNUJ Radio Station 57.00 16459

River Bend Business Products

River Bend Business Products 6,180.30 27040

RVS SHREDDING

RVS SHREDDING 33.50 11682

Veteran ServicesDEPT

1609

01-120-0000-0000-6400 635.59 Toner Cartridiges for Printer SO-2508113 Departmental Supplies N

License BureauDEPT

6188

01-141-0000-0000-6240 7.50 FT LB Tech Ad Publication/Advertising Expense N

382

01-141-0000-0000-6240 287.35 FT LB Tech Ad 008488 Publication/Advertising Expense N

01-141-0000-0000-6240 291.10 PT LB Tech Ad 438808 Publication/Advertising Expense N

427

01-141-0000-0000-6400 6.35 Take a # sign 303574 Departmental Supplies N

6459

01-141-0000-0000-6240 57.00 FT LB Tech Ad 67289-1 Publication/Advertising Expense N

7040

01-141-0000-0000-6400 6,097.00 Office Furniture 220335-0 Departmental Supplies N

01-141-0000-0000-6400 83.30 Envelopes 236748 Departmental Supplies N

1682

01-141-0000-0000-6800 33.50 Shredding Cabinet and boxes 22195 Other Expense N

Page 8Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

6 Vendors 16 TransactionsDEPT Total:

Transactions

1 Vendors 1 TransactionsDEPT Total:

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

Sleepy Eye Herald Dispatch

Sleepy Eye Herald Dispatch 106.26 1423

Springfield Advance Press

Springfield Advance Press 53.60 2441

VAN HEE MEDIA L.L.C

VAN HEE MEDIA L.L.C 61.50 26470

141 License Bureau7,084.46

149

MENARDS (CH 33000266)

MENARDS (CH 33000266) 165.38 25613

NOZCO INC

NOZCO INC 246.20 15644

River Bend Business Products

River Bend Business Products 152.78 27040

149 Other General Government564.36

200

ALPHA WIRELESS COMMUMICATIONS

ALPHA WIRELESS COMMUMICATIONS 1,361.40 1187

423

01-141-0000-0000-6240 106.26 FT/PT LB Tech Ad 1005430505 Publication/Advertising Expense N

441

01-141-0000-0000-6240 26.80 FT LB Tech Ad 196403 Publication/Advertising Expense N

01-141-0000-0000-6240 26.80 PT LB Tech Ad 196523 Publication/Advertising Expense N

6470

01-141-0000-0000-6240 30.00 FT LB Tech Ad 14011 Publication/Advertising Expense N

01-141-0000-0000-6240 31.50 PT LB Tech Ad 14210 Publication/Advertising Expense N

Other General GovernmentDEPT

5613

01-149-0000-0000-6889 59.47 1/2x4x8 Homasote board (PR) 16359 Contingency Fund N

01-149-0000-0000-6889 105.91 (2)4x4x8 birch Nom/(5)clr box 16568 Contingency Fund N

5644

01-149-0000-0000-6889 246.20 Lock Pocket door(PR) 4992 Contingency Fund N

7040

01-149-0000-0000-6320 110.92 MR: Canon Copier Maintenance B 241056-0 Copy Machine Maint. & Supply N

01-149-0000-0000-6320 41.86 HW: Canon Copier Maintenance B 241448-0 Copy Machine Maint. & Supply N

SheriffDEPT

187

01-200-0000-0000-6300 1,361.40 May19 Maint, console, paging, 698264 Maint for Bldg, Furn & Eq/Maint Cntrct N

Page 9Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

9 Vendors 13 TransactionsDEPT Total:

Transactions

Transactions

Transactions

3 Vendors 5 TransactionsDEPT Total:

Transactions

Account/Formula

*** Brown County ***

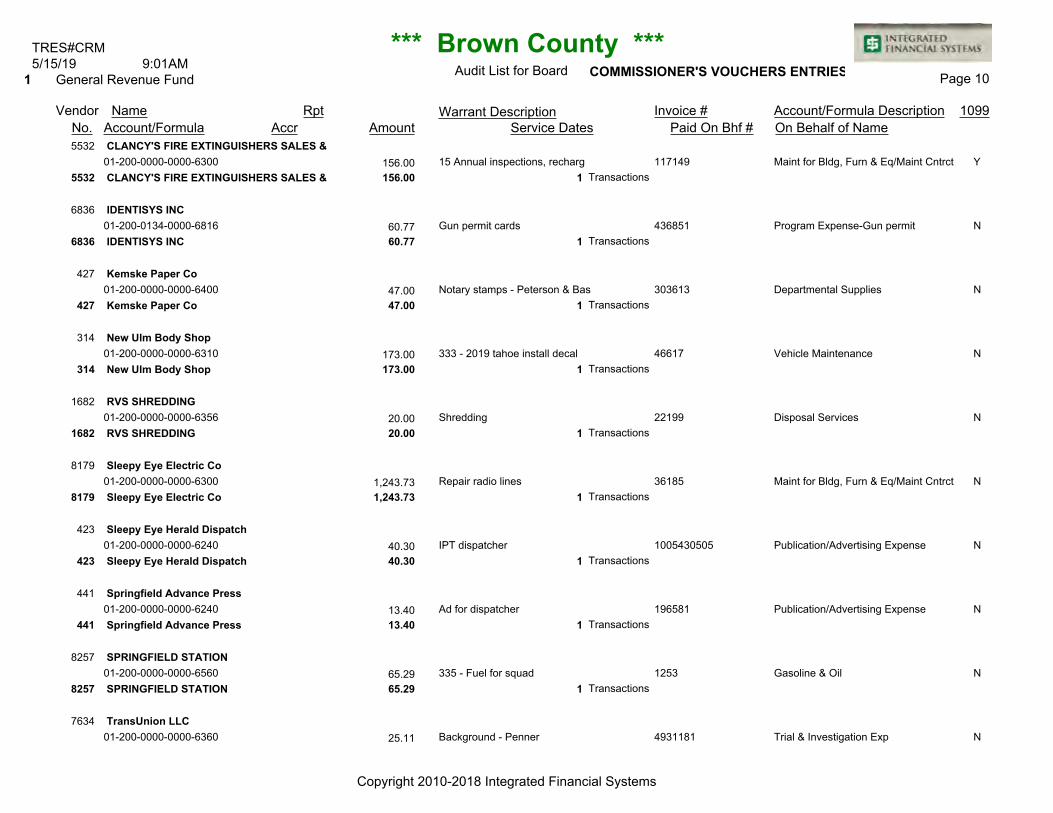

CLANCY'S FIRE EXTINGUISHERS SALES & SERV

CLANCY'S FIRE EXTINGUISHERS SALES & SERV

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

156.00 15532

IDENTISYS INC

IDENTISYS INC 60.77 16836

Kemske Paper Co

Kemske Paper Co 47.00 1427

New Ulm Body Shop

New Ulm Body Shop 173.00 1314

RVS SHREDDING

RVS SHREDDING 20.00 11682

Sleepy Eye Electric Co

Sleepy Eye Electric Co 1,243.73 18179

Sleepy Eye Herald Dispatch

Sleepy Eye Herald Dispatch 40.30 1423

Springfield Advance Press

Springfield Advance Press 13.40 1441

SPRINGFIELD STATION

SPRINGFIELD STATION 65.29 18257

TransUnion LLC

5532

01-200-0000-0000-6300 156.00 15 Annual inspections, recharg 117149 Maint for Bldg, Furn & Eq/Maint Cntrct Y

6836

01-200-0134-0000-6816 60.77 Gun permit cards 436851 Program Expense-Gun permit N

427

01-200-0000-0000-6400 47.00 Notary stamps - Peterson & Bas 303613 Departmental Supplies N

314

01-200-0000-0000-6310 173.00 333 - 2019 tahoe install decal 46617 Vehicle Maintenance N

1682

01-200-0000-0000-6356 20.00 Shredding 22199 Disposal Services N

8179

01-200-0000-0000-6300 1,243.73 Repair radio lines 36185 Maint for Bldg, Furn & Eq/Maint Cntrct N

423

01-200-0000-0000-6240 40.30 IPT dispatcher 1005430505 Publication/Advertising Expense N

441

01-200-0000-0000-6240 13.40 Ad for dispatcher 196581 Publication/Advertising Expense N

8257

01-200-0000-0000-6560 65.29 335 - Fuel for squad 1253 Gasoline & Oil N

7634

01-200-0000-0000-6360 25.11 Background - Penner 4931181 Trial & Investigation Exp N

Page 10Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

CLANCY'S FIRE EXTINGUISHERS SALES & SERV

CLANCY'S FIRE EXTINGUISHERS SALES & SERV

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

TransUnion LLC 25.11 17634

WEELBORG CHEVROLET

WEELBORG CHEVROLET 111.98 12813

Winter/Gina

Winter/Gina 240.24 38529

200 Sheriff3,558.22

201

17.00 15532

201 Boat & Water Safety Enforcement17.00

221

Ramsey County (Medical Examiner)

Ramsey County (Medical Examiner) 3,608.25 2469

221 County Coroner3,608.25

250

A H Hermel Company

A H Hermel Company 266.91 22153

Cashwise Pharmacy

2813

01-200-0000-0000-6310 111.98 338 - oil change, filter, pla 83562 Vehicle Maintenance N

8529

01-200-0000-0000-6331 10.50 Parking fees St. Cloud trainin 04/29/19 Travel Expense N

01-200-0000-0000-6330 204.74 Mileage to conference St Cloud 04/30/19 Mileage N

01-200-0000-0000-6450 25.00 Uniform hemming for dispatch 05/02/19 Uniform Supply N

Boat & Water Safety EnforcementDEPT

5532

01-201-0212-0201-6310 17.00 (4) annual inspections 117150 Vehicle Maintenance Y

County CoronerDEPT

469

01-221-0000-0000-6266 1,876.25 Postmortem Exam/Toxicology (C Coroner Expense 6

01-221-0000-0000-6266 1,732.00 Postmortem Exam/Toxicology (C Coroner Expense 6

Corrections-JailDEPT

2153

01-250-0207-0000-6814 163.77 Commissary 768835 Jail Canteen Account N

01-250-0000-0000-6400 103.14 Cleaning supplies 768919 Departmental Supplies N

3261

01-250-0000-0000-6363 82.79 Apr'19 Jail Imate RX Apr Stmt Medical Care Of Prisoners N

Page 11Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

13 Vendors 15 TransactionsDEPT Total:

Transactions

1 Vendors 1 TransactionsDEPT Total:

Transactions

1 Vendors 2 TransactionsDEPT Total:

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

Cashwise Pharmacy 82.79 13261

Johnstone Supply

Johnstone Supply 251.00 22359

Keefe Supply Company

Keefe Supply Company 641.78 25175

Kemske Paper Co

Kemske Paper Co 14.25 1427

KNUJ Radio Station

KNUJ Radio Station 57.00 16459

MENARDS (CH 33000266)

MENARDS (CH 33000266) 50.67 15613

NOZCO INC

NOZCO INC 325.00 15644

Premier Biotech Inc

Premier Biotech Inc 373.45 16115

Reliance Telephone Inc

Reliance Telephone Inc 600.00 13183

RVS SHREDDING

2359

01-250-0000-0000-6300 145.86 Tools/parts for Jail tower A/C S100708817.001 Furniture & Equip Maint. N

01-250-0000-0000-6400 105.14 Dryer - repair parts S100710661.001 Departmental Supplies N

5175

01-250-0207-0000-6814 629.84 Jail Commissary 1138747 Jail Canteen Account N

01-250-0000-0000-6400 11.94 Shampoo 1138748 Departmental Supplies N

427

01-250-0000-0000-6400 14.25 Receipt books - jail 303609 Departmental Supplies N

6459

01-250-0000-0000-6240 57.00 FT Correction Officer Ad 67619-1 Publication/Advertising Expense N

5613

01-250-0000-0000-6400 50.67 Casters for jail med cart 16341 Departmental Supplies N

5644

01-250-0000-0000-6300 325.00 Jail sallyport door repair 4969 Furniture & Equip Maint. N

6115

01-250-0000-0000-6363 373.45 April 2019 - Drug Testing L3315354 Medical Care Of Prisoners N

3183

01-250-0207-0000-6814 600.00 Phone cards $10 - 20 ct, $20 - D-22993 Jail Canteen Account Y

1682

01-250-0000-0000-6356 10.00 Shredding 22192 Disposal Services N

Page 12Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMUNITY COMPLIANCE MONITORING SERVICES

COMMUNITY COMPLIANCE MONITORING SERVICES

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

RVS SHREDDING 10.00 11682

Sleepy Eye Herald Dispatch

Sleepy Eye Herald Dispatch 44.30 1423

Springfield Advance Press

Springfield Advance Press 20.10 1441

250 Corrections-Jail2,737.25

251

31.00 16537

DESIGN HOME CENTER

DESIGN HOME CENTER 598.69 71090

GROCHOW/MATTHEW ELROY

GROCHOW/MATTHEW ELROY 1,908.08 17254

Homeward Bound Therapeutic Services

Homeward Bound Therapeutic Services 90.00 17692

Innovative Office Solutions

Innovative Office Solutions 126.21 11609

423

01-250-0000-0000-6240 44.30 FT correction officer 1005430505 Publication/Advertising Expense N

441

01-250-0000-0000-6240 20.10 FT Correction Officer Ad 196568 Publication/Advertising Expense N

ProbationDEPT

6537

01-251-0295-0000-6354 31.00 Ream grant participants Apr19A Electronic Monitoring Y

1090

01-251-0000-0000-6400 95.98 Paint 126961 Departmental Supplies N

01-251-0000-0000-6400 49.08 Paint supplies 126983 Departmental Supplies N

01-251-0000-0000-6400 25.46 Paint supplies 127108 Departmental Supplies N

01-251-0000-0000-6400 14.36 Paint supplies 127113 Departmental Supplies N

01-251-0000-0000-6400 117.97 Paint 127185 Departmental Supplies N

01-251-0000-0000-6400 55.89 Paint supplies 127199 Departmental Supplies N

01-251-0000-0000-6400 239.95 Paint 127276 Departmental Supplies N

7254

01-251-0298-0000-6816 1,908.08 DC surveillance reimb - April Program Expense Y

7692

01-251-0270-0253-6816 90.00 Group Therapy, CJ 3 Program Expense N

1609

01-251-0000-0000-6320 126.21 Toner IN2498400 Copy Mach. Maint/Supplies N

Page 13Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

13 Vendors 16 TransactionsDEPT Total:

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

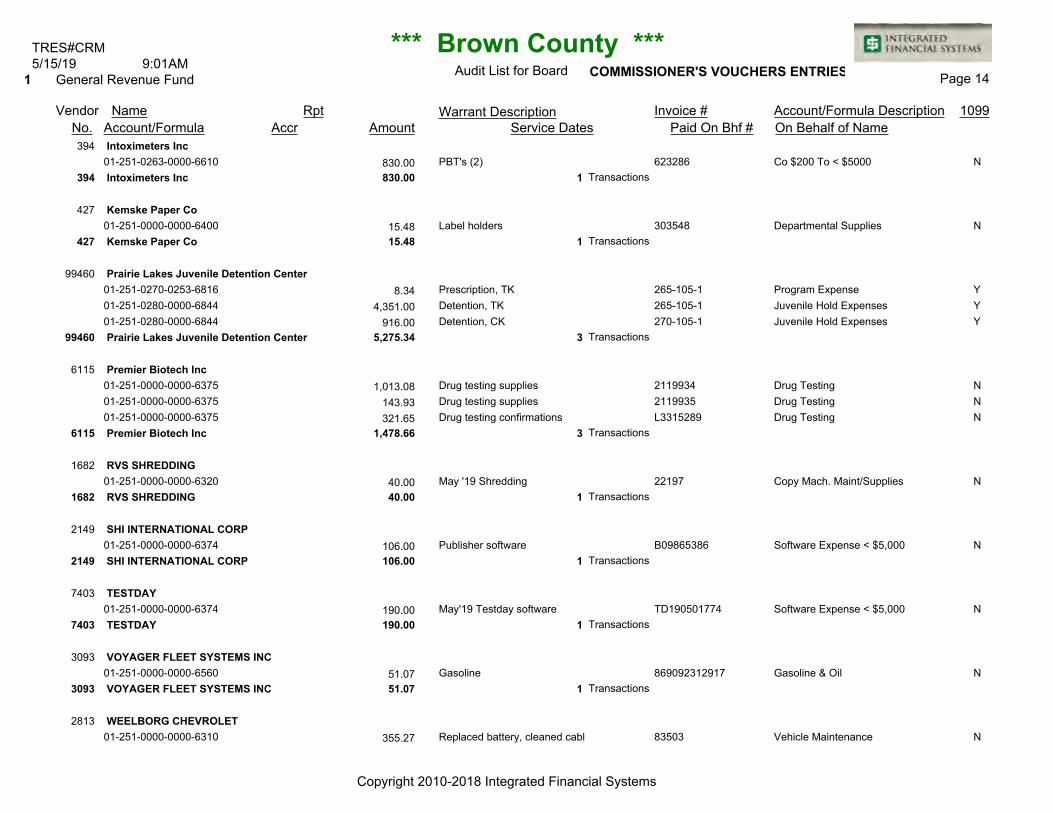

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

Intoximeters Inc

Intoximeters Inc 830.00 1394

Kemske Paper Co

Kemske Paper Co 15.48 1427

Prairie Lakes Juvenile Detention Center

Prairie Lakes Juvenile Detention Center 5,275.34 399460

Premier Biotech Inc

Premier Biotech Inc 1,478.66 36115

RVS SHREDDING

RVS SHREDDING 40.00 11682

SHI INTERNATIONAL CORP

SHI INTERNATIONAL CORP 106.00 12149

TESTDAY

TESTDAY 190.00 17403

VOYAGER FLEET SYSTEMS INC

VOYAGER FLEET SYSTEMS INC 51.07 13093

WEELBORG CHEVROLET

394

01-251-0263-0000-6610 830.00 PBT's (2) 623286 Co $200 To < $5000 N

427

01-251-0000-0000-6400 15.48 Label holders 303548 Departmental Supplies N

99460

01-251-0270-0253-6816 8.34 Prescription, TK 265-105-1 Program Expense Y

01-251-0280-0000-6844 4,351.00 Detention, TK 265-105-1 Juvenile Hold Expenses Y

01-251-0280-0000-6844 916.00 Detention, CK 270-105-1 Juvenile Hold Expenses Y

6115

01-251-0000-0000-6375 1,013.08 Drug testing supplies 2119934 Drug Testing N

01-251-0000-0000-6375 143.93 Drug testing supplies 2119935 Drug Testing N

01-251-0000-0000-6375 321.65 Drug testing confirmations L3315289 Drug Testing N

1682

01-251-0000-0000-6320 40.00 May '19 Shredding 22197 Copy Mach. Maint/Supplies N

2149

01-251-0000-0000-6374 106.00 Publisher software B09865386 Software Expense < $5,000 N

7403

01-251-0000-0000-6374 190.00 May'19 Testday software TD190501774 Software Expense < $5,000 N

3093

01-251-0000-0000-6560 51.07 Gasoline 869092312917 Gasoline & Oil N

2813

01-251-0000-0000-6310 355.27 Replaced battery, cleaned cabl 83503 Vehicle Maintenance N

Page 14Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

WEELBORG CHEVROLET 355.27 12813

251 Probation11,095.80

280

MENARDS (CH 33000266)

MENARDS (CH 33000266) 5.49 25613

280 Emergency Services5.49

282

ALPHA WIRELESS COMMUMICATIONS

ALPHA WIRELESS COMMUMICATIONS 1,066.25 1187

E-911 Independent Emergency Services

E-911 Independent Emergency Services 32.31 15365

282 911 Emergency Telephone System1,098.56

500

American Legion Post 7

American Legion Post 7 50.00 18100

American Legion Post 132

American Legion Post 132 50.00 13227

American Legion Post 244

American Legion Post 244 50.00 16256

American Legion Post 257

Emergency ServicesDEPT

5613

01-280-0000-0000-6400 13.48 Adhesive & PVC (Shawn) 16254 Departmental Supplies N

01-280-0000-0000-6400 7.99 Return divider 16337 Departmental Supplies N

911 Emergency Telephone SystemDEPT

187

01-282-0000-0000-6358 1,066.25 May19 Maint, console, paging, 698264 Contract Services N

5365

01-282-0000-0000-6300 32.31 May'19 - 911 Services 400-0168 Furniture & Equip Maint. N

Cultural ActivitiesDEPT

8100

01-500-0000-0000-6802 50.00 Memorial Day Reimbursement Memorial Day Expense N

3227

01-500-0000-0000-6802 50.00 Memorial Day Reimbursement Memorial Day Expense N

6256

01-500-0000-0000-6802 50.00 Memorial Day Reimbursement Memorial Day Expense N

745

01-500-0000-0000-6802 50.00 Memorial Day Reimbursement Memorial Day Expense N

Page 15Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

14 Vendors 24 TransactionsDEPT Total:

-

Transactions

1 Vendors 2 TransactionsDEPT Total:

Transactions

Transactions

2 Vendors 2 TransactionsDEPT Total:

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES1

9:01AM5/15/19TRES#CRM

General Revenue Fund

Copyright 2010-2018 Integrated Financial Systems

American Legion Post 257 50.00 1745

American Legion Post 365

American Legion Post 365 50.00 18113

500 Cultural Activities250.00

601

Innovative Office Solutions

Innovative Office Solutions 31.79 11609

601 County Extension31.79

611

Mn Pollution Control Agency 20000988700

Mn Pollution Control Agency 20000988700 33,681.91 38170

611 Septic Loan Program33,681.91

615

Innovative Office Solutions

Innovative Office Solutions 66.68 31609

615 Water Plan66.68

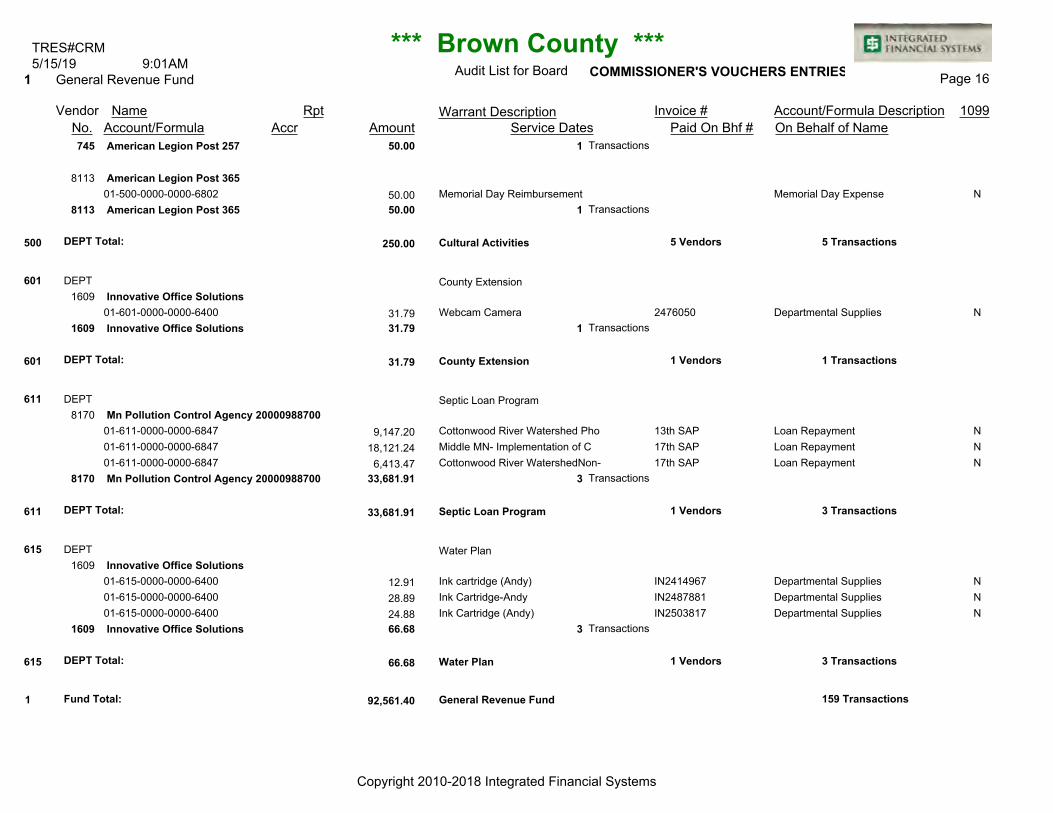

1 General Revenue Fund92,561.40

8113

01-500-0000-0000-6802 50.00 Memorial Day Reimbursement Memorial Day Expense N

County ExtensionDEPT

1609

01-601-0000-0000-6400 31.79 Webcam Camera 2476050 Departmental Supplies N

Septic Loan ProgramDEPT

8170

01-611-0000-0000-6847 9,147.20 Cottonwood River Watershed Pho 13th SAP Loan Repayment N

01-611-0000-0000-6847 18,121.24 Middle MN- Implementation of C 17th SAP Loan Repayment N

01-611-0000-0000-6847 6,413.47 Cottonwood River WatershedNon- 17th SAP Loan Repayment N

Water PlanDEPT

1609

01-615-0000-0000-6400 12.91 Ink cartridge (Andy) IN2414967 Departmental Supplies N

01-615-0000-0000-6400 28.89 Ink Cartridge-Andy IN2487881 Departmental Supplies N

01-615-0000-0000-6400 24.88 Ink Cartridge (Andy) IN2503817 Departmental Supplies N

Page 16Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

5 Vendors 5 TransactionsDEPT Total:

Transactions

1 Vendors 1 TransactionsDEPT Total:

Transactions

1 Vendors 3 TransactionsDEPT Total:

Transactions

1 Vendors 3 TransactionsDEPT Total:

Fund Total: 159 Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES6

9:01AM5/15/19TRES#CRM

Public Health Fund

Copyright 2010-2018 Integrated Financial Systems

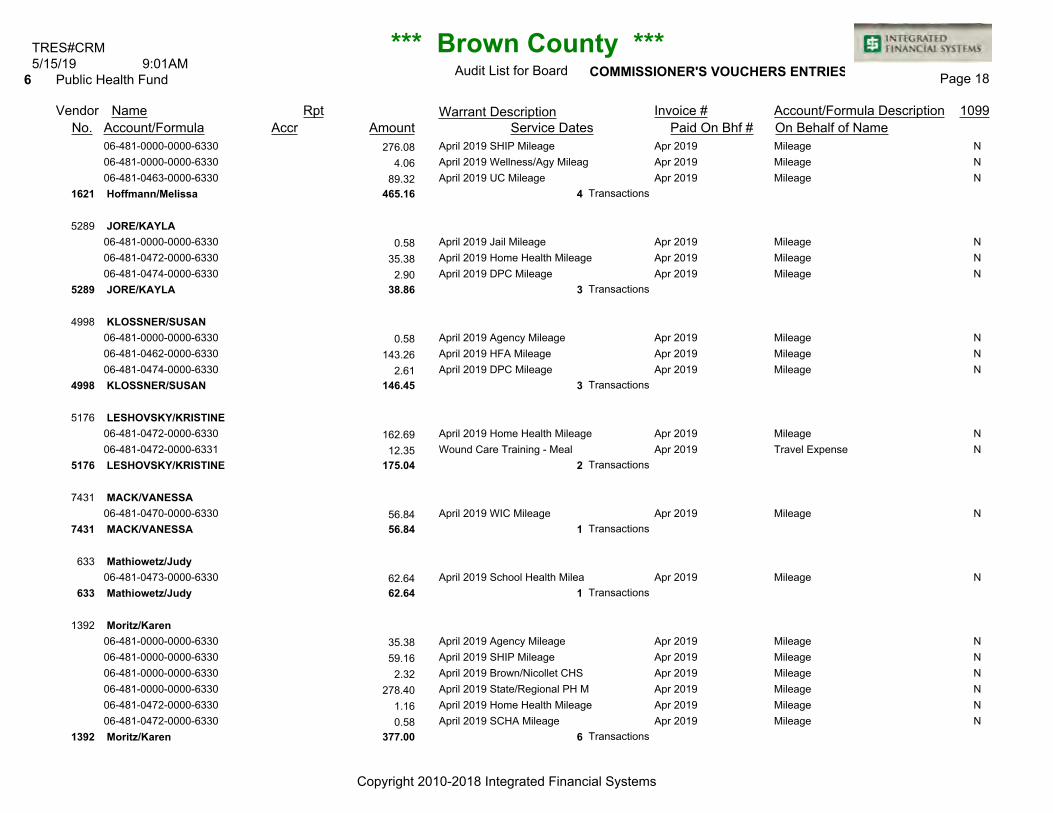

481

Andrews/Danielle

Andrews/Danielle 175.45 17541

Availity LLC

Availity LLC 50.00 17852

COMPTON, LISA

COMPTON, LISA 244.18 26400

DALLENBACH/MELISSA

DALLENBACH/MELISSA 186.18 25662

Fausch/Tara

Fausch/Tara 165.30 26477

Gilb/Stacy

Gilb/Stacy 11.02 22297

Grosklags/Chelsea

Grosklags/Chelsea 21.46 17486

GUTES ESSEN DELI & CATERING

GUTES ESSEN DELI & CATERING 150.11 15542

Hoffmann/Melissa

Public Health NursingDEPT

7541

06-481-0472-0000-6330 175.45 April 2019 HHA Mileage Apr 2019 Mileage N

7852

06-481-0000-0000-6374 50.00 Claim Submission Fee INV00479811 Software Expense < $5,000 Y

6400

06-481-0462-0000-6330 127.60 April 2019 HFA Mileage Apr 2019 Mileage N

06-481-0462-0000-6330 116.58 April 2019 MCH Mileage Apr 2019 Mileage N

5662

06-481-0472-0000-6330 78.30 April 2019 Home Health Apr 2019 Mileage N

06-481-0472-0000-6330 107.88 April 2019 SCHA Mileage Apr 2019 Mileage N

6477

06-481-0462-0000-6330 24.36 April 2019 HFA Mileage Apr 2019 Mileage N

06-481-0462-0000-6330 140.94 April 2019 MCH Mileage Apr 2019 Mileage N

2297

06-481-0000-0000-6330 9.28 April 2019 Agency Mileage Apr 2019 Mileage N

06-481-0474-0000-6330 1.74 April 2019 DPC Mileage Apr 2019 Mileage N

7486

06-481-0472-0000-6330 21.46 April 2019 HHA Mileage Apr 2019 Mileage N

5542

06-481-0000-0000-6355 150.11 Catering - All staff inservice 4123 Training Expense N

1621

06-481-0000-0000-6330 95.70 April 2019 Agency Mileage Apr 2019 Mileage N

Page 17Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES6

9:01AM5/15/19TRES#CRM

Public Health Fund

Copyright 2010-2018 Integrated Financial Systems

Hoffmann/Melissa 465.16 41621

JORE/KAYLA

JORE/KAYLA 38.86 35289

KLOSSNER/SUSAN

KLOSSNER/SUSAN 146.45 34998

LESHOVSKY/KRISTINE

LESHOVSKY/KRISTINE 175.04 25176

MACK/VANESSA

MACK/VANESSA 56.84 17431

Mathiowetz/Judy

Mathiowetz/Judy 62.64 1633

Moritz/Karen

Moritz/Karen 377.00 61392

06-481-0000-0000-6330 276.08 April 2019 SHIP Mileage Apr 2019 Mileage N

06-481-0000-0000-6330 4.06 April 2019 Wellness/Agy Mileag Apr 2019 Mileage N

06-481-0463-0000-6330 89.32 April 2019 UC Mileage Apr 2019 Mileage N

5289

06-481-0000-0000-6330 0.58 April 2019 Jail Mileage Apr 2019 Mileage N

06-481-0472-0000-6330 35.38 April 2019 Home Health Mileage Apr 2019 Mileage N

06-481-0474-0000-6330 2.90 April 2019 DPC Mileage Apr 2019 Mileage N

4998

06-481-0000-0000-6330 0.58 April 2019 Agency Mileage Apr 2019 Mileage N

06-481-0462-0000-6330 143.26 April 2019 HFA Mileage Apr 2019 Mileage N

06-481-0474-0000-6330 2.61 April 2019 DPC Mileage Apr 2019 Mileage N

5176

06-481-0472-0000-6330 162.69 April 2019 Home Health Mileage Apr 2019 Mileage N

06-481-0472-0000-6331 12.35 Wound Care Training - Meal Apr 2019 Travel Expense N

7431

06-481-0470-0000-6330 56.84 April 2019 WIC Mileage Apr 2019 Mileage N

633

06-481-0473-0000-6330 62.64 April 2019 School Health Milea Apr 2019 Mileage N

1392

06-481-0000-0000-6330 35.38 April 2019 Agency Mileage Apr 2019 Mileage N

06-481-0000-0000-6330 59.16 April 2019 SHIP Mileage Apr 2019 Mileage N

06-481-0000-0000-6330 2.32 April 2019 Brown/Nicollet CHS Apr 2019 Mileage N

06-481-0000-0000-6330 278.40 April 2019 State/Regional PH M Apr 2019 Mileage N

06-481-0472-0000-6330 1.16 April 2019 Home Health Mileage Apr 2019 Mileage N

06-481-0472-0000-6330 0.58 April 2019 SCHA Mileage Apr 2019 Mileage N

Page 18Audit List for Board

Account/Formula Description Rpt Invoice #Warrant DescriptionVendor Name 1099Paid On Bhf #Accr Amount On Behalf of NameNo. Service Dates

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Transactions

Account/Formula

*** Brown County ***

COMMISSIONER'S VOUCHERS ENTRIES6

9:01AM5/15/19TRES#CRM

Public Health Fund

Copyright 2010-2018 Integrated Financial Systems

O'NEILL/REBECCA

O'NEILL/REBECCA 95.70 26888

PIPPERT/TAMMY

PIPPERT/TAMMY 47.30 36134

RVS SHREDDING

RVS SHREDDING 5.00 11682

SEVERSON/TERESA

SEVERSON/TERESA 190.24 46538

SOUKUP/LINDA

SOUKUP/LINDA 128.47 18552

Springfield Area Community Center

Springfield Area Community Center 100.00 14723

Stark/Elen

Stark/Elen 162.40 22255

Steinbeisser/Michelle

6888

06-481-0472-0000-6330 94.54 April 2019 Home Health Mileage Apr 2019 Mileage N

06-481-0474-0000-6330 1.16 April 2019 DPC Mileage Apr 2019 Mileage N

6134

06-481-0000-0000-6330 1.16 April 2019 Agency Mileage Apr 2019 Mileage N

06-481-0000-0000-6432 6.41 Ribbon for the Audiometers Apr 2019 Program Supplies N

06-481-0473-0000-6330 39.73 April 2019 School Health Milea Apr 2019 Mileage N

1682

06-481-0000-0000-6358 5.00 Shredding 22198 Contract Services N

6538

06-481-0000-0000-6330 1.16 April 2019 Agency Mileage Apr 2019 Mileage N

06-481-0462-0000-6330 5.80 April 2019 HFA Mileage Apr 2019 Mileage N

06-481-0462-0000-6330 164.14 April 2019 MCH Mileage Apr 2019 Mileage N

06-481-0468-0000-6330 19.14 April 2019 CTC Mileage Apr 2019 Mileage N

8552

06-481-0472-0000-6330 128.47 April 2019 HHA Mileage Apr 2019 Mileage N

4723

06-481-0470-0000-6342 100.00 JUN'19 WIC Rent June 2019 Office Space Rent N

2255

06-481-0000-0000-6330 3.19 April 2019 Agency Mileage Apr 2019 Mileage N

06-481-0473-0000-6330 159.21 April 2019 School Health Milea Apr 2019 Mileage N

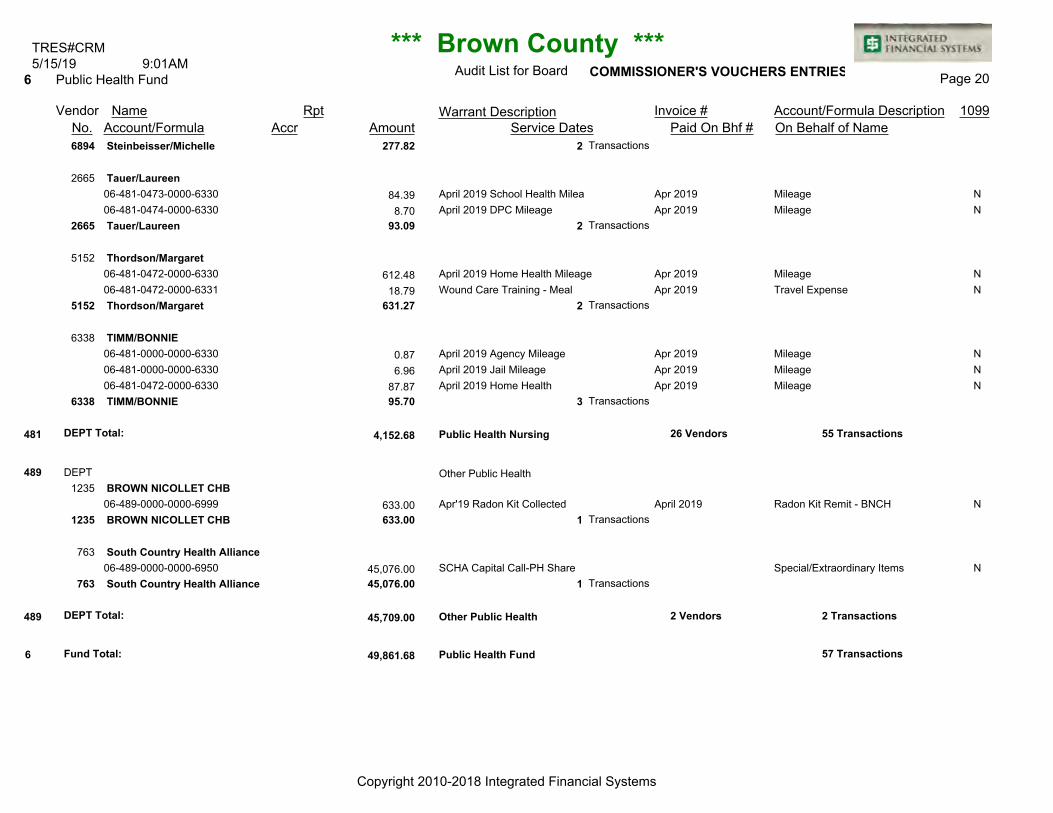

6894