Fourth Capitalism: the Real Driver of Italian Growth

50

Fourth capitalism: the real driver of Italian growth Fulvio Coltorti, Director Emeritus , Mediobanca Research Area CUOA, meeting with supporting partners 3 July 2014

-

Upload

independent -

Category

Documents

-

view

6 -

download

0

Transcript of Fourth Capitalism: the Real Driver of Italian Growth

Fourth capitalism: the real driver of Italian growth Fulvio Coltorti, Director Emeritus , Mediobanca Research Area CUOA, meeting with supporting partners

3 July 2014

Section 1

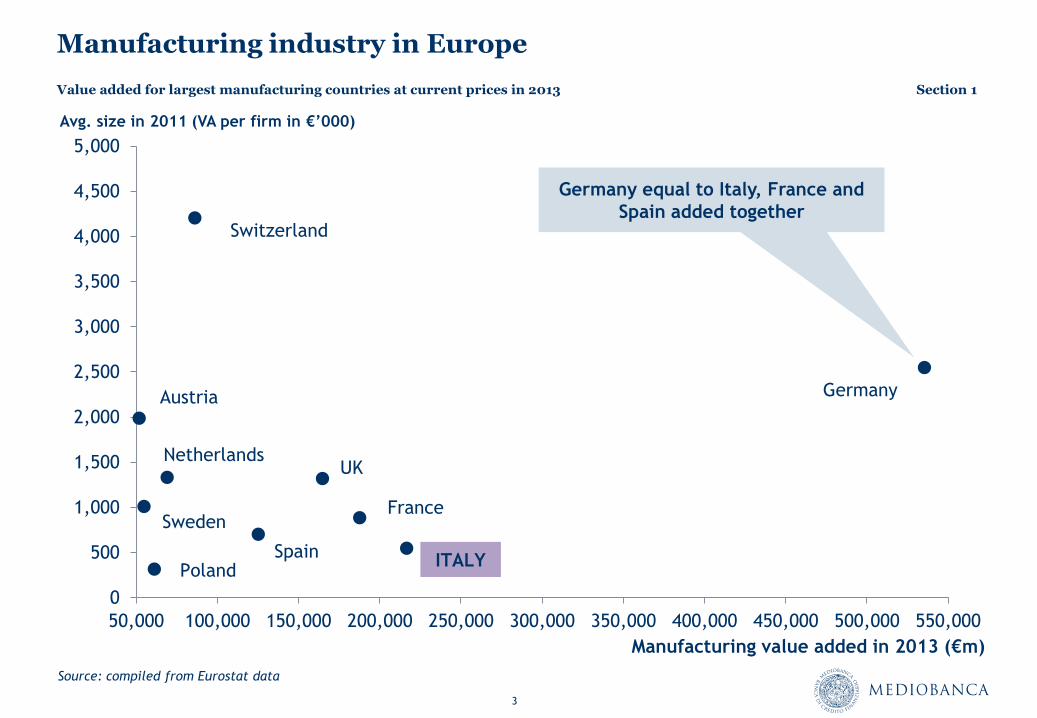

European manufacturing: who matters?

3

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

50,000 100,000 150,000 200,000 250,000 300,000 350,000 400,000 450,000 500,000 550,000

Manufacturing value added in 2013 (€m)

Germany

Switzerland

UK

ITALY

France

Spain

Netherlands

Sweden

Poland

Austria

Manufacturing industry in Europe

Value added for largest manufacturing countries at current prices in 2013 Section 1

Source: compiled from Eurostat data

Avg. size in 2011 (VA per firm in €’000)

Germany equal to Italy, France and

Spain added together

4

Italy vs European competitors: still at the bottom of the barrel … strong impulse needed to bounce back

23.1

23.5

24.0 24.2 24.2

23.9 23.9

24.4

24.9 25.2

24.1

23.2

21.6 21.6 21.6 21.9

20.3

21.1 21.1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2013 Q1

2013 Q2

2013 Q3

2013 Q4

2014 Q1

Relative VA indicators calculated based on Eurostat data - VA as % of aggregated European competitors (France, Germany, UK and Spain)

5

Geography of future growth …

Real GDP – 2011 index = 100 – Source: IMF

95

97

99

101

103

105

107

109

111

2011 2012 2013 2014 2015 2016 2017 2018 2019

Germany Italy Eurozone

+1.4%

+1.5%

+1%

2014-19

World: 2.5%...3.4% p.a.

Emerging: 4.9%...5.4%

Emerging Asia: 6.4%...6.8%

Sub-Saharan Africa: 5.4%...5.8%

Section 2

Italy does not stand out because of its excess of small businesses, but because of the crisis and the decline of its large industries

7

Crisis and decline of large enterprise in Italy

Percentage of GDP accounted for by leading Italian companies (based on Mediobanca and Istat data at current prices)

0.55

0.65

0.75

0.85

0.95

1.05

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Value added by LE/Italian GDP

First restructuring

Rescues and bailouts

Robots; group organization

Second restructuring

Rescues and bailouts

Lean production;

relocations

Technological decline

Loss of market shares

Relocations

Wrong investments

Lack of research

Financial crises

8

Dualism reversed: fewer and fewer large companies

Istat – Manufacturing industry census: firms with 1,000 staff and more

339

324

241

223

176

3,877

3,631 3,228

2,503 2,438

1971 1981 1991 2001 2011

No. of firms Avg. size (no. of staff)

9

Italy: four capitalisms

First large companies (late 1900s)

State capitalism (1933)

Industrial Districts (1960-70)

Medium-sized companies and others (1990s)

1

2

3

4

Section 3

What has happened in the territories?

11

Manufacturing in the provinces: % shares of staff

51.9 50.3

39.8

36.0

31.4 31.9

0.6 0.8 1.2

3.3

6.7 7.2

2.1

8.2

19.3

24.7

41.8 43.9

1951 1961 1971 1981 1991 1996

LE LE LI ID

LE=Large Enterprise areas; LI=low industrialization areas; ID = districts areas

Source: Becattini-Coltorti 2004

12

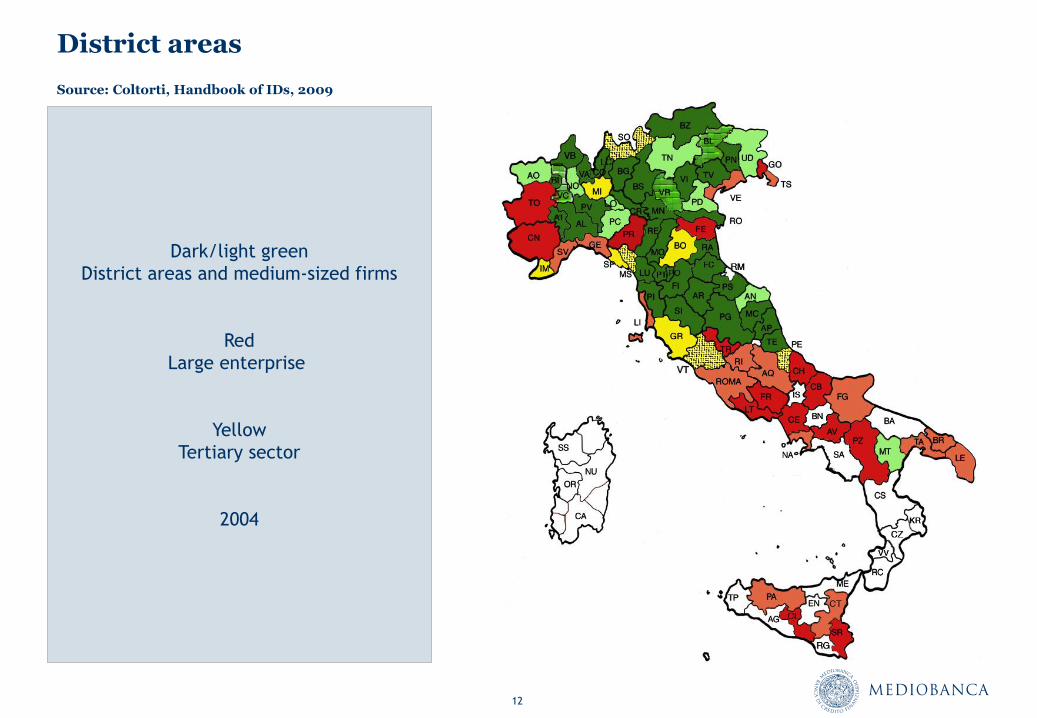

District areas

Source: Coltorti, Handbook of IDs, 2009

Dark/light green

District areas and medium-sized firms

Red

Large enterprise

Yellow

Tertiary sector

2004

13

Manufacturing: value added in 2011

Largest groups 6.1

Non-Italian LEs 12.4

Medium-large 12.6

Medium-sized 15.6

Small 53.3

Fourth capitalism

Medium-large,

medium

and small firms

50-60%

Mediobanca Research Area estimates based on Mediobanca and Istat data

Section 4

Methods of production change: end of Fordism

15

Lean production: the Apple iPad

Apple margin 25%

US non-Apple suppliers' margins

2%

Retail distribution and sale

23%

Korean suppliers' margins

7%

Taiwanese suppliers' margins

2%

Japanese suppliers' margins

2%

Costs of unknown origin

4%

Direct labour costs for suppliers

10%

Cost of acquiring input 25%

Source: Linden, Dedrick, Kraemer, Rassweiler (Who captures value in the Apple iPad?; 2011)

Plus margin for retail

distribution if sold online or

at own stores

LG and Samsung

(display and memory chip)

Breakdown of value generated by iPad 16GB, cost $499 (2009)

Manufacturing: Asia

Section 5

Can one be competitive without being large?

17

District effect: trust, filières, networks, entrepreneurialism

Districts are based on trust

Industry is concentrated in places

Places = communities of people, agglomerations of enterprises

High degree of division of labour enables specialization

Filières (short and long, to produce and acquire knowledge)

Many SMEs compete and co-operate with each other

Competition (= innovation, quality and appropriate production costs)

There are local markets for goods and services

Networks (informal and formal, short and long)

The strengthening of relations and technical/behavioural codes on a local basis facilitates the circulation of

information and reduces barriers to entry

Turnover between entrepreneurs and integrated division of labour

18

How does the fourth capitalism work?

1. Competition engaged in on basis of “systems” of companies

2. Impact of production scale felt at system level (network of relations; external economies leveraged)

3. Reliance on territory which provides and regenerates the resources and on network of social relations

4. Companies specialize

5. Firms create niches in which they have a virtual monopoly, innovating continuously and avoiding the

large multinationals’ practices

External economies and product differentiation

Carel: total sales €169m per annum

19

Fourth capitalism: governance

Competition takes place on product market rather than at level of

ownership structure

Decisions taken by market of consumers, not by financial markets

(institutional investors, banks, advisors, analysts, etc.)

Company survives and prospers to the extent that it remains

efficient

Quest for beauty is fundamental

NICE – Oderzo (Treviso)

20

Medium-sized enterprises in 2012

Source: Centro Studi Unioncamere

3,528 medium-sized firms

(3,463 considering groups)

50-499 employees

Annual total sales €15m-€330m

Limited companies

Independently-owned

21

Size: growth trends

-59 -59 -69 -50 -22 -55 -38 -55 -70

-44

8

-21 -34 -11

248

438

214

98 44

169 122

333 301

-81

-598

271 250

-50

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

MSEs become large Small firms become MSEs

Net changes, 1999-2012. A total of 334 companies was excluded in 2008 following adoption of new parameters

Section 6

Medium-sized firms qualify districts

23

More medium-sized companies in Istat districts

36.5 26.8

21.0 16.9

47.5

40.1

36.6

31.1

14.3

24.7

30.7

35.9

1.7 8.4 11.7 16.1

(0-49) > 74.9% (0-49) 62.5%-74.9% (0-49) 50%-62.5% (0-49) < 50%

Categories based on % presence of micro and small firms

Micro 0-9 Small 10-49 Medium-size I 50-249 Medium-size II + LEs >250

% breakdown of total staff employed, 2001 – Source: Coltorti (Handbook of IDs, 2009)

% of total staff 34% 44% 8% 14%

24

More staff in medium-sized firms in district areas

Compiled from M. Bellandi & F. Coltorti, “Distretti industriali e medium-sized companies, tra declino e traiettorie di sviluppo industriale in Italia”, Artimino report 2012-14, Bologna, Il Mulino (forthcoming); indexes 2001 = 100 – no. of staff

100

90.6 86.2

81.5

100

107.4

90.7 94.9

2001 2007 2009 2011

Total Medium-sized businesses

25

District areas between 2001 and 2011

MSE consolidation 72%

District restructuring 22%

District crisis 3%

District growth 3%

Source: M. Bellandi & F. Coltorti, 2014

26

District areas with high concentration of medium-sized companies

Source: M. Bellandi & F. Coltorti, op. cit. 2014 – KIS = Knowledge Intensive Services; LKIS = Low KIS

0

500

1000

1500

2000

2500

3000

2001 2007 2009 2011

Manufacturing staff Services: KIS Services: LKIS

No. of staff (000)

27

Changes in value added by medium-sized companies

614

1,357

1,289

2,859

2,498

6,592

8,232

191

325

577

2,006

2,422

-211

5,804

Other industries

Metallurgical

Paper, printing & Publishing

Food and drinks

Chemicals & pharmaceuticals

Personal and households goods

Mechanical engineering

in 1996 Change 1996-2012

Value added 1996-2012 – universe of medium-sized companies

“Made in Italy” turnover 62% (65.8% in 1996)

Exports 40.4% (32.5% in 1996)

Section 7

International orientation

29

Fourth capitalism: the happy many …

Categories of firms based on % share of exports in 2012; Source: Mediobanca Research Area

126 m

ediu

m-s

ized/la

rge >

75%

175 m

ediu

m-s

ized/la

rge 4

1-

74%

131 m

ediu

m-s

ized/la

rge 0

-40%

651 m

ediu

m-s

ized >

75%

467 m

ediu

m-s

ized 6

1-7

4%

628 m

ediu

m-s

ized 4

1-6

0%

708 m

ediu

m-s

ized 1

6-4

0%

504 m

ediu

m-s

ized <

15%

505 m

ediu

m-s

ized z

ero

%

Italy Elsewhere

3,463 medium-sized companies 432 medium-large firms

30

0

50

100

150

200

250

300

350

400

450

500

550

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0 100.0

No. of staff

% Sales abroad

Exports: size is NOT a conditio sine qua non

Universe of medium-sized companies 2012: shares of exports and no. of staff

Section 8

Growth drivers and brakes

32

The two drivers of value added: data by class of good

Index number of value added based on current prices (2000 = 100; Istat database with estimates for 2012-13)

100.0 99.3 100.0

98.9

103.2 104.8

108.9

116.2

111.7

93.1

102.3 103.1

96.9 96.3

100.0

104.7 106.2

105.3

107.1 107.3

111.9

118.9 117.4

103.8

108.2

110.0

103.5 102.2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Goods produced by large enterprise Goods produced by districts and fourth capitalism

33

The two drivers of value added: data by companies

Index number of value added based on current prices; Mediobanca data for companies with production facilities in Italy

100.0

86.1

77.6

85.3 86.6

83.4

94.7

108.6

98.2

83.3

94.9

88.5 85.9

100.0

104.2 106.4 107.2

113.0 115.9

125.1

136.7 136.8

124.9

132.9

137.9

134.2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Large groups Medium-sized companies

Section 9

Medium-size enterprise in Europe: a comparison

35

Where?

Medium Sized Enterprises in Europe (2013)

36

Medium-sized companies: size, productivity and CLUP

Size increases left to right (staff); median values based on rolling sets of 200 observations

Net VA per employee CLUP

Source: Confindustria, R&S, Unioncamere, Medium-Sized Enterprises in Europe, 2013

37

Medium-sized companies: productivity, wages and tax

Germany Italy France Spain

Net VA per employee (€'000) 56.1 51.0 52.1 47.9

DE index no. = 100 100.0 90.9 92.9 85.4

Unit labour cost (€'000) 46.7 39.6 43.6 36.8

DE index no. = 100 100.0 84.8 93.4 78.8

EBITDA as % of VA 14.9 18.6 14.9 19.2

DE index no. = 100 100.0 124.8 100.0 128.9

Tax rate* 27.4 38.2 24.5 23.5

FY 2009 - Confindustria – R&S Mediobanca – Unioncamere survey

* Tax rate in Italy in 2012

Medium-sized firms 37.0%

Large groups: 23.5%

38

Lots of it net worth, little of it working capital

-27.5 -12.8 -16.9 -21.3

-20.1

-19.6 -13.3 -21.0

-52.4 -67.6 -69.8

-57.7

44.2 30.2

38.1 38.8

38.4

36.0 34.6 35,7

17.4 33.8 27.3 25.5

Itay France Germany Spain

Short-term debt Medium-term debt Tangible net worth Fixed assets Working capital Financial assets

Assets

Loans

MSEs in Europe (2013) – Data as at 2009 - tangible net capital includes provisions set aside in medium/long term

39

If tax was less aggressive in Italy?

% of firms by class of financial solidity

Source: compiled by R&S based on R&S-Unioncamere scoring model

76.3

69.0 68.6

56.6

78.0

19.3

26.4 25.0

35.3

18.2

4.4 4.6 6.4 8.1 3.9

Germany France Spain Italy Italy 2

Investment grade Intermediate Distressed

Assuming tax rates equivalent to

those for large groups

(last ten years)

Section 10

What to do to exit the crisis

41

Promote fourth capitalism in district areas

Net flows of exports/imports in Euros by territories classified based on Becattini-Coltorti method (2004ff– UA = Turin/Milan/Rome/Naples)

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

€ mln

District areas Large enterprise areas Urban areas Remainder

42

Stimulate investments: Italy vs FR, DE and UK

Gross fixed investments in manufacturing sector, relative values (% of Eurostat national accounting data based on current prices)

50

60

70

80

90

100

110

120

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% of France % of Germany % of UK

43

Italy vs Germany

Data as at 2012

Italy Germany Italy vs

Germany

Population 59.4 m 81.7 m 73%

Balance of exports-imports:

districts + fourth capitalism/Mittelstand €86.2bn €102.9bn 84%

large groups €7.9bn €203.5bn 4%

Attract investment from large foreign groups /win back those which have fled

44

Keys to success: focus on revenues, not costs

1) Quality of work force (measured via unit wage levels): companies which use low-cost staff are less

productive than those which use a workforce which are more expensive when measured by unit cost but

matched with the stock of capital per staff member and against high-quality production. A work force

which is “worth” salary levels which are €1 higher produces, ceteris paribus, an increase of €1.4 in value

terms in productivity

2) Inverse relationship between size and productivity: a winning strategy involves production

specialization and a commercial policy geared towards creating and exploiting market niches, which are

dominated through skill and innovative ability (confirmed by the data shown in the previous slides)

3) Knowledge Intensive Services (KIS): there is a need for companies which provide high knowledge-

intensive services

4) Positive impact of managerial capabilities and infrastructure: the former is a product of training; the

latter tends to differentiate between performance (e.g. deteriorating in Southern Italy)

Source: econometric analysis based on data for medium-sized companies taken from Mediobanca-Unioncamere surveys produced in the last ten years

(F. Coltorti and D.Venanzi, “Produttività, competitività e territori delle medie imprese italiane”; in I nuovi distretti industriali. Rapporto di Artimino

sullo sviluppo locale 2012-13; ed. by M. Bellandi and A. Caloffi, Bologna, Il Mulino (forthcoming).

45

Indicators of attractiveness of fourth capitalism

Compiled by Mediobanca Reearch Area

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Veneto

Lom

bard

ia

Em

ilia

-Rom

agna

Marc

he

Fri

uli V

G

Um

bri

a

Trenti

no A

A

Pie

monte

+

VdA

Abru

zzo

Tosc

ana

Cam

pania

Lig

uri

a

Puglia

Basi

licata

Sic

ilia

Molise

Sard

egna

Lazio

Cala

bri

a

Blue indicates territories identified

by Giorgio Fuà in his North-East-

Centre model (NEC) - 1981

Normalized average of 7 indexes calculated based on data for medium-sized companies

46

Roll up our sleeves …

A proposal to recover use of resources which are currently wasted

47

Most important districtions: selected using KPIs

Source: F. Coltorti & L. Mastromarino, Per un piano strategico a sostegno dei distretti (OND report, 2014)

1

2

3

4

5

6

7 8 9

10

11

12

13

14

15

16

17 18 19

20

21

22 23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41 42

43

44 45

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

-3.5% -1.5% 0.5% 2.5% 4.5% 6.5% 8.5%

EBITDA/sales, % avg. 2010-12

Q1

Q2

Q3

Q4

Chg. in sales, 2010-12

48

Strategic plan with pivotal companies

ACTIVITIES RESPONSIBILITY

MAPPING DISTRICTS UNIONCAMERE

DISTRICTS CLASSIFIED BY KPIs (SALES, EBITDA, VA) MISE/REGIONAL AUTHORITY/UNIONCAMERE

DISTRICT COMMITTEE SET UP MISE/REGIONAL AUTHORITY

DISTRICT STRATEGIC PLAN DRAWN UP (DSP) DISTRICT COMMITTEE AND PIVOTAL COMPANIES

PSD APPROVED

DISTRICT COMMITTEE, PIVOTAL COMPANIES, TRADE

UNIONS, CATEGORY ASSOCIATIONS, LOCAL

ADMINISTRATION

START OF ACTIVITY AND MONITORING DISTRICT COMMITTEE/ REGIONAL AUTHORITY/MISE

Coltorti-Mastromarino methodological proposal: plan stages

49

Bibliography

R&S and Mediobanca, various publications (www.mbres.it)

Mediobanca-Unioncamere, Le medie imprese industriali italiane (www.mbres.it)

G. Becattini-F. Coltorti, “Aree di grande impresa ed aree distrettuali nello sviluppo post-bellico

dell’Italia” (Rivista Italiana degli Economisti, 2004); “Areas of large enterprise and industrial districts in

the development of post-war Italy: a preliminary study” (European Planning Studies 8, 2006)

F. Coltorti, “Medium-Sized Firms, Groups and Industrial Districts: an Italian Perspective”; in A Handbook

of Industrial Districts, ed. by G. Becattini, M. Bellandi e L. De Propris; Edward Elgar 2009

Confindustria, R&S and Unioncamere, Medium-Sized Enterprises in Europe; 2013 (www.mbres.it)

F. Coltorti-G. Garofoli, “Le medie imprese in Europa” (Economia Italiana 1, 2011); “Medium-Sized

Enterprises in Europe” (Review of Economic Conditions in Italy 1, 2011)

F. Coltorti, R. Resciniti, A. Tunisini, R. Varaldo (eds), Mid-Sized Manufacturing Companies: The New

Driver of Italian Competitiveness; Springer 2013

F. Coltorti, “Italian Industry, Decline or Transformation? A Framework”; (European Planning Studies, 21 ,

2013)

Osservatorio Nazionale Distretti Italiani, 2014 report (www.osservatoriodistretti.org)

M. Bellandi-F. Coltorti, “Distretti industriali e medie imprese, tra declino e traiettorie di sviluppo

industriale in Italia”; F. Coltorti-D. Venanzi, “Produttività, competitività e territori delle medie imprese

italiane”; in I nuovi distretti industriali, ed. by M. Bellandi and A. Caloffi, Il Mulino 2014 (forthcoming)

F. Coltorti-L. Mastromarino, Per un piano strategico a sostegno dei distretti industriali; 2014

(forthcoming)