Forwards response re NEDO-24708, "Addl Info Required for ...

Upload

khangminh22Category

view

0download

0

REGULATORY FORMATION DISTRIBUTION SY EM <RIDS)

ACCESQLPN sNBR: 85111103'IP5 DOC. DATE: 85/11/04 NOTARIZED: NO DOCKET 0FAG IL:STN-50-528 Palo Verde Nuclear Stationf Unit if Arizona Publi 05000528

AUTH. NAME AUTHOR AFFILIATIONTOY I T. M. Mudgef Rose. Guthrie LOB Alexander

RECIP. NAME RECIPIENT AFFILIATIONDENTONI H. R ~ Office of Nuclear Reactor Regulationp Director

SUBJECT: Forwards N*pp lication in Respect of Bale 2 Leaseback Ico~~cme o(Financing Transaction bg Public Svc Co of New Mexico" dtd ~~851018 5 supp or ting dtd 851104.

DIBTRIBUTION CODE: Y002D COPIEB RECEIVED: LTR Q ENCL ~ SIZE:TITLE: Distribution for Atypical 50 Dkt Material

NOTES: Standardized plant.OL: 12/31/84

05000528

REC IP IENTID CODE/NAME

NRR/DL/ADL 09NRR LB3 LA 08DENTONp H. R. 06

INTERNAL: 20EG F 04.

RM/DDAMI/MI8 17

COPIESLTTR ENCL

1

1 1

1 1

1 1

1 '11

RECIPIENTID CODE/NAME

NRR LB3 BC 07LIC ITRAf'E 01

ELD/HDS3RGN5

COPIESLTTR ENCL

1 1

1 1

1 1

1

FXTERNAL: 24X, ..NRC PDR 02

LPDRNSI C

0305

1

1 1

E~b ~o

TOTAL NUMBER OF COPIES REQUIRED: LTTR ~ ENCL

' 'ff

g".1, I

t.'

~t" i

I"

I

gt

"'II

I.

4

P'

1I

'3C il',s4"g

A

1<

P

~ v'" (,(

IW

h

t

„5,, f)~)g „"

C',

(f

ht

I I

n i~g g i

5 ~ y ~ $ 4I f, ~[ II

')x *'e '<

1,

Id II f ~

MUDGE ROSE GUTHRIE ALEXANDER 6 FERDON

I8O MAIDEN LANK

NEW YORK. N. Y. IOO38

2I2I K STRCET, H.W,

WASHINOTON» 0 C 20037202 429 9355

2 I 2- 5IO- /OOO

CASLC ADDRESS: BAITVCHIHS NEW YORK

TCLCXI WV 703729; WU I2'7889

TCLCCOPICR: 2I2 ~ 2A8 ~ 2dSS

SUITE 2020$ 3$ SOUTH ORAHD AVENUE

LOS ANOELCS. CALIF, 9007I2I3 813 'II2

I2, RUC DC LA PAIX

75002 PARIS. FRANCE

Cdl 87 ~ 7I

November 4, 1985

Mr. Harold C. DentonDirector,Office of Nuclear Reactor RegulationNuclear Regulatory CommissionWashington, D.C. 20555

Application in Respect of aSale and Leaseback Financing Transaction by

Public Service Company of New Mexico

Dear Mr. Denton:

On behalf of Public Service Company of New Mexico (RPNM"),its counsel Keleher 6 McLeod and Snell & Wilmer, Kidder, Peabody 6

Co. Incorporated and this firm, I enclose herewith one copy of eachof the above-captioned Application and memorandum in support thereof,both dated October 18, 1985, and a brief with respect thereto onbehalf PNM dated November 4, 1985.

Thank you for your attention to this transaction.

'85111103»15 851104PDR ADOCK 05000M8I PDR

Sincerely,

~i~4LU~!Timothy Michael Toy

boO: ~~/'~~~<, a.s7-

g+p . gVC+

QO

T

~'- .:'e '..-..";~.:>.„~~".<:i ~C~ ~n.~vv,:>;";~-"aR =-~caus'lls

'I V

I

Ji

C,

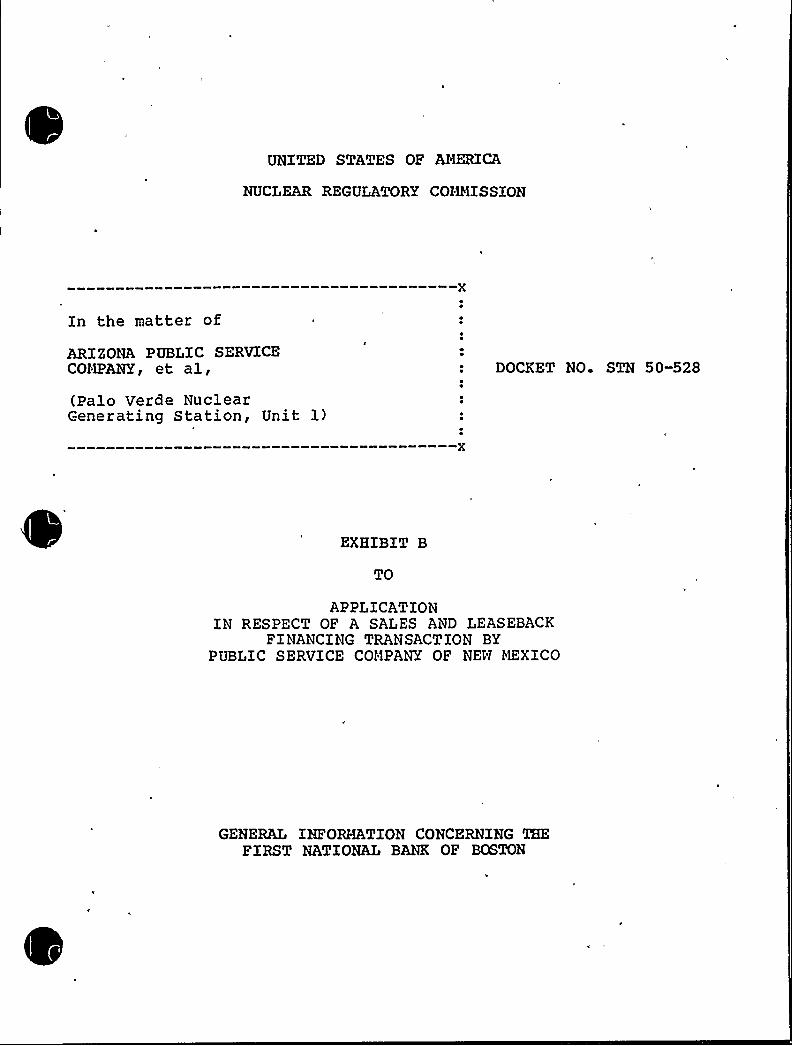

UNITED STATES OF AMERICA

NUCLEAR REGULATORY COMMISSION

In the matter of .

ARIZONA r'UBLIC SERVICE COMPANY,et al., DOCKET NO. STN

50-528

(Palo Verde Nuclear Generating Station, Unit 1)

APPLICATION IN RESPECT OF A SALE ANDLEASEBACK FINANCING TRANSACTION BY

PUBLIC SERVICE COMPANY OF NEW MEXICO

October 18, 1985

!f

TABLE OF CONTENTS

Relief Requested

Pacae

2 0 Purpose of the Financing Transaction .. 3

3 ~ Description of the Proposed Sale andLeaseback Financing Transaction .... 4

4 ~ Conditions Precedent to theFinancing Transaction ......... 6

5. 'Schedule of the FinancingTransaction ~ ~ 7

6.

7.

8.

Supporting Xnformation ......... 8

'Environmental Considerations ......10No Significant Hazards Consideration ..10

9. Responsibility for Management ofPVNGS Unit 1 ..............11

TABLE OF - CONTENTS, Continued

EXEIBITS

ExhibitDesi nation Descri tion

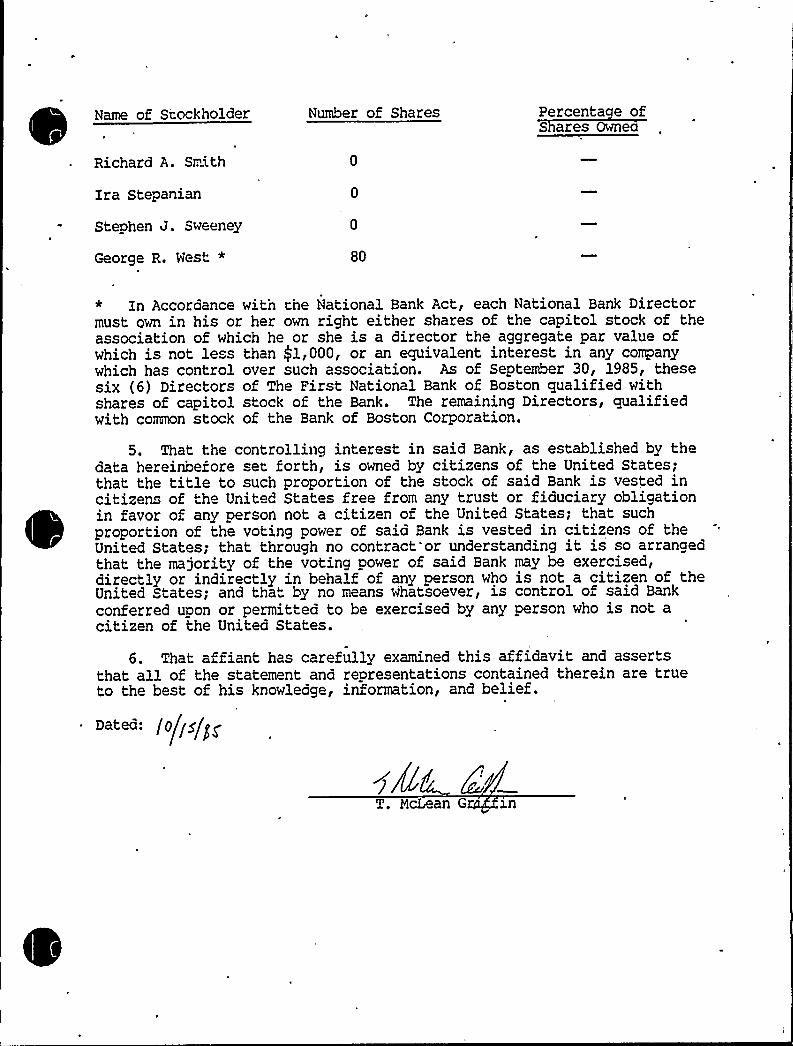

,.General Information ConcerningPublic Service Company of New Mexico

Attachment A: 1984 Annual Report of PublicService Company of New Mexicoand Annual Report on Form10-K for the Fiscal YearEnded December 31, 1984

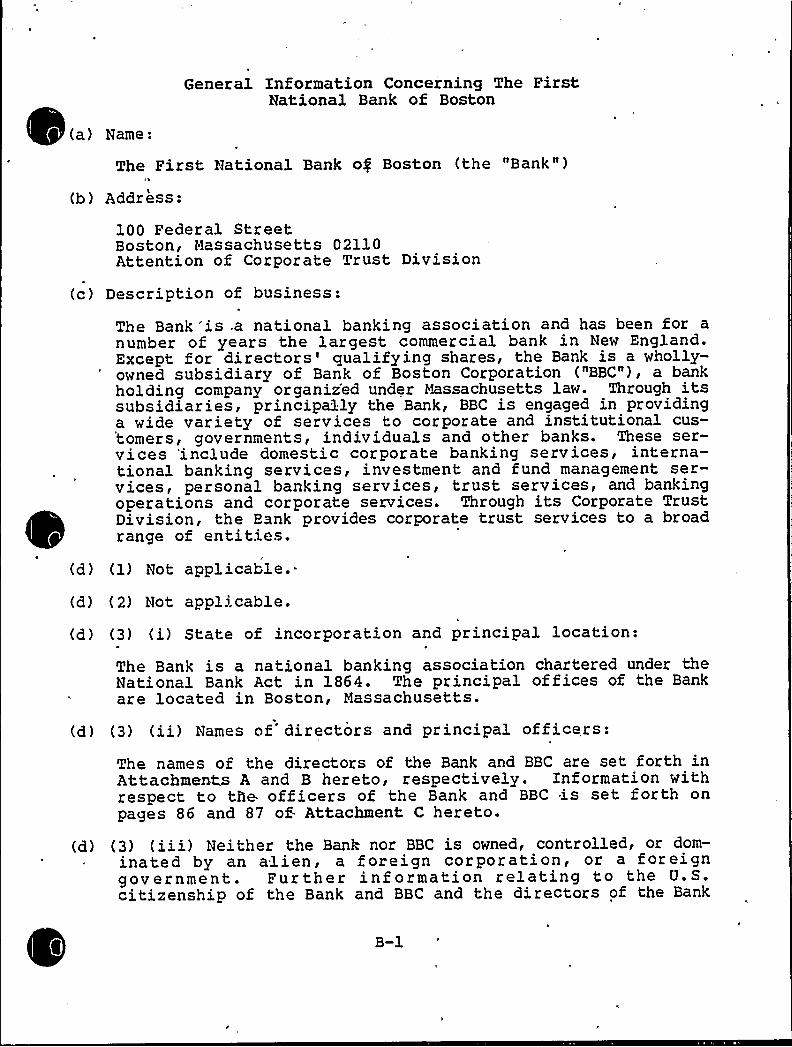

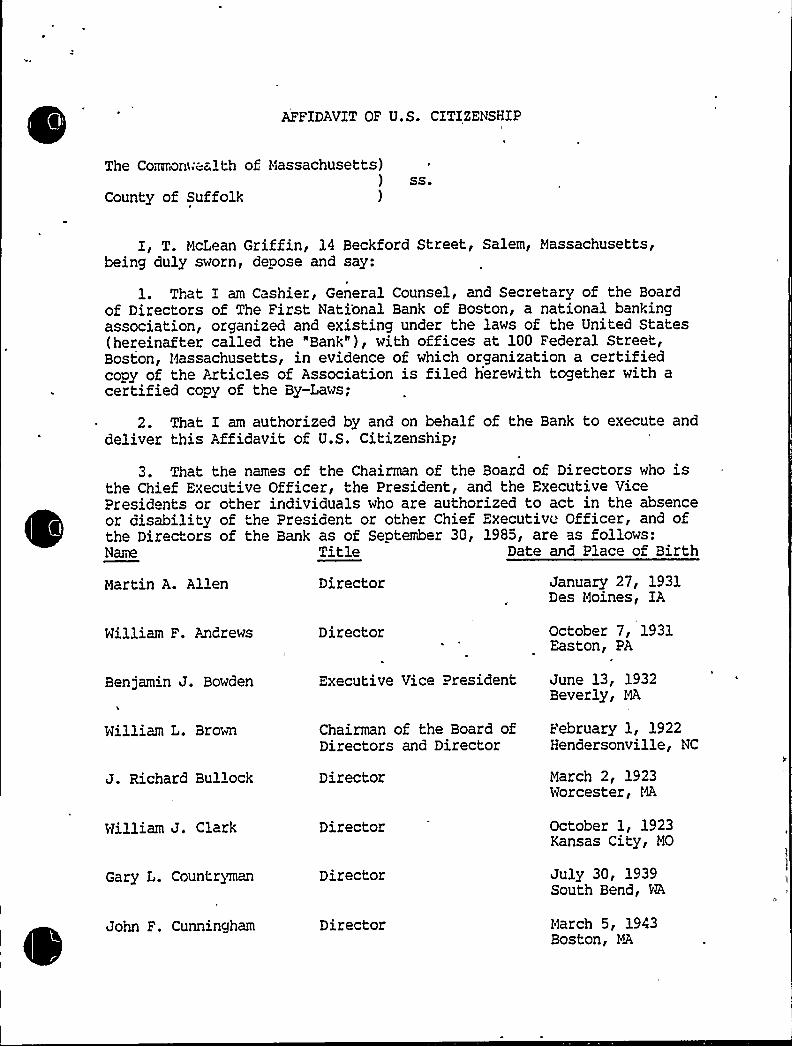

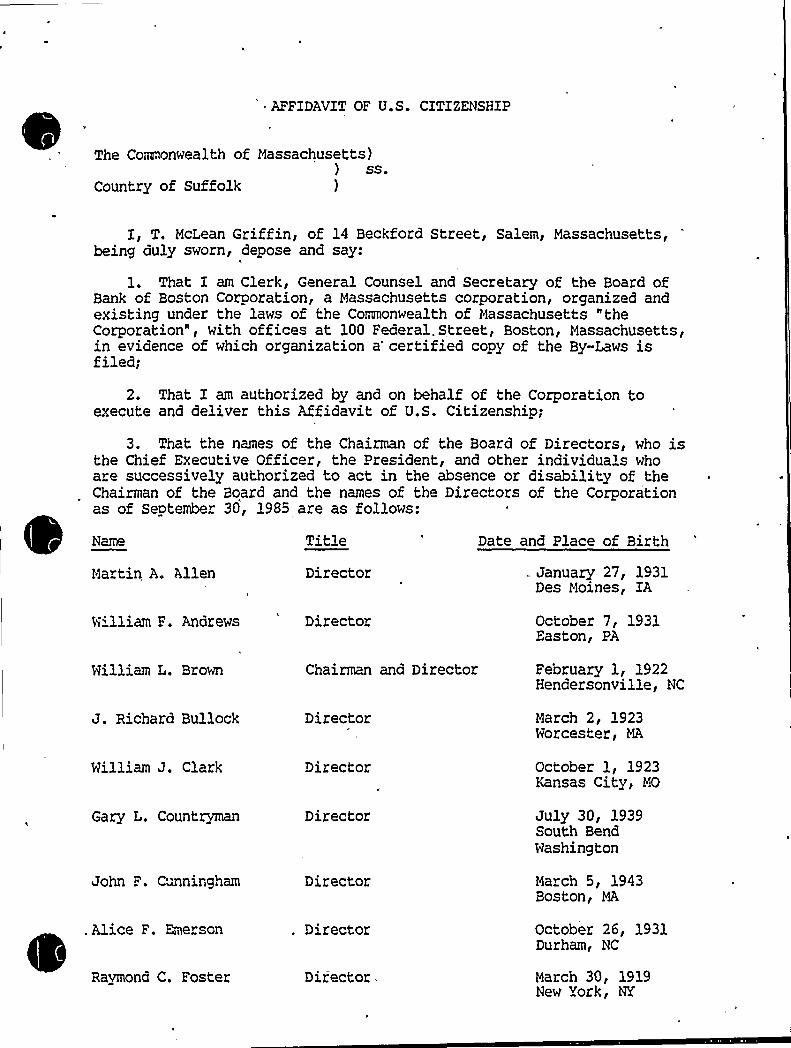

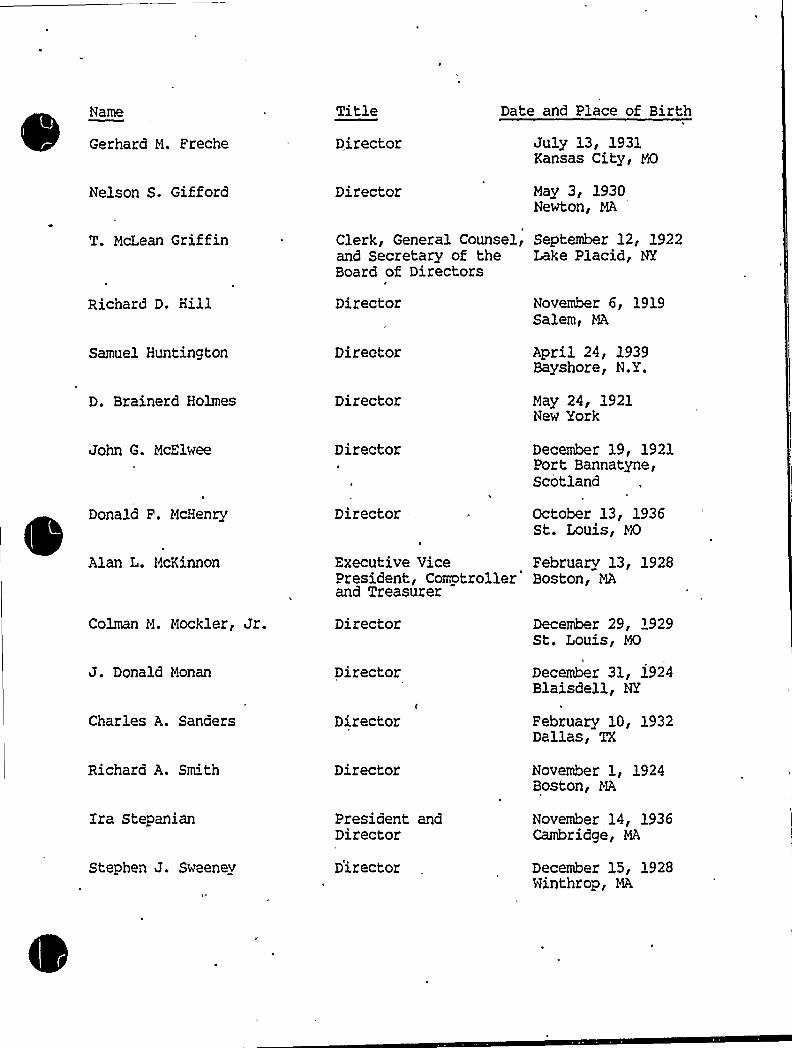

General Information Concerning:TheFirst National Bank of Boston

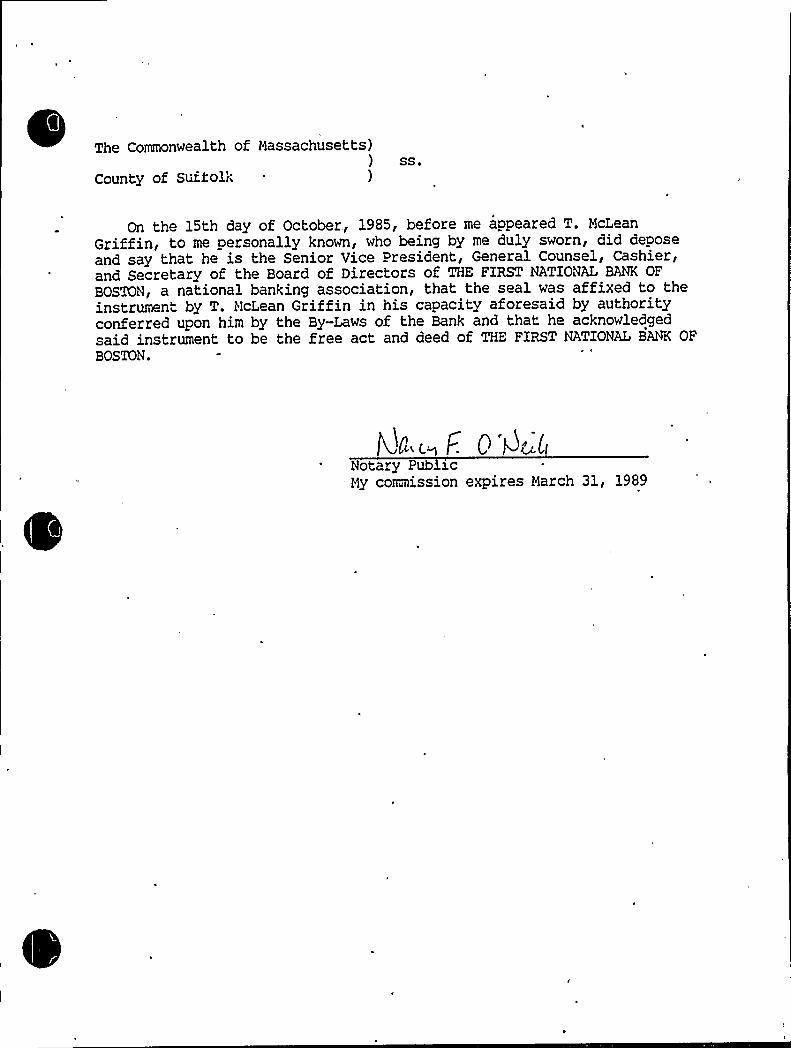

Attachment A: Affidavit of U.S. Citizenshipof The First National Bank ofBoston

Attachment B: Affidavit of U.S. Citizenshipof Bank of Boston Corporation

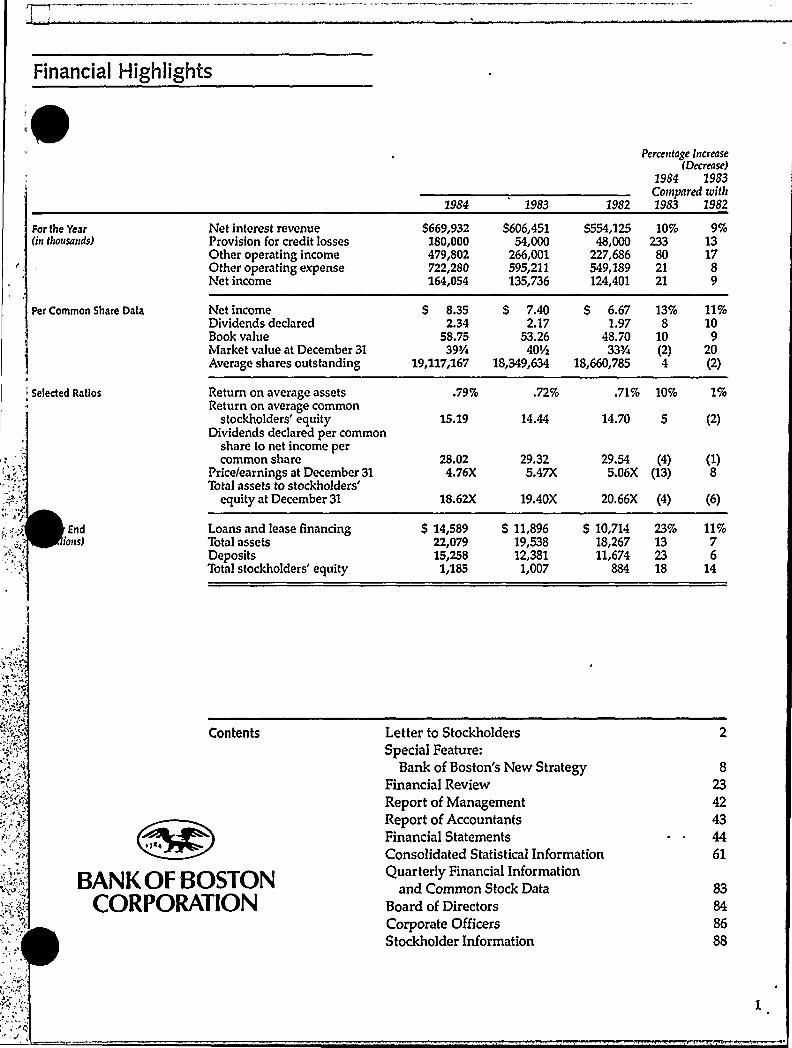

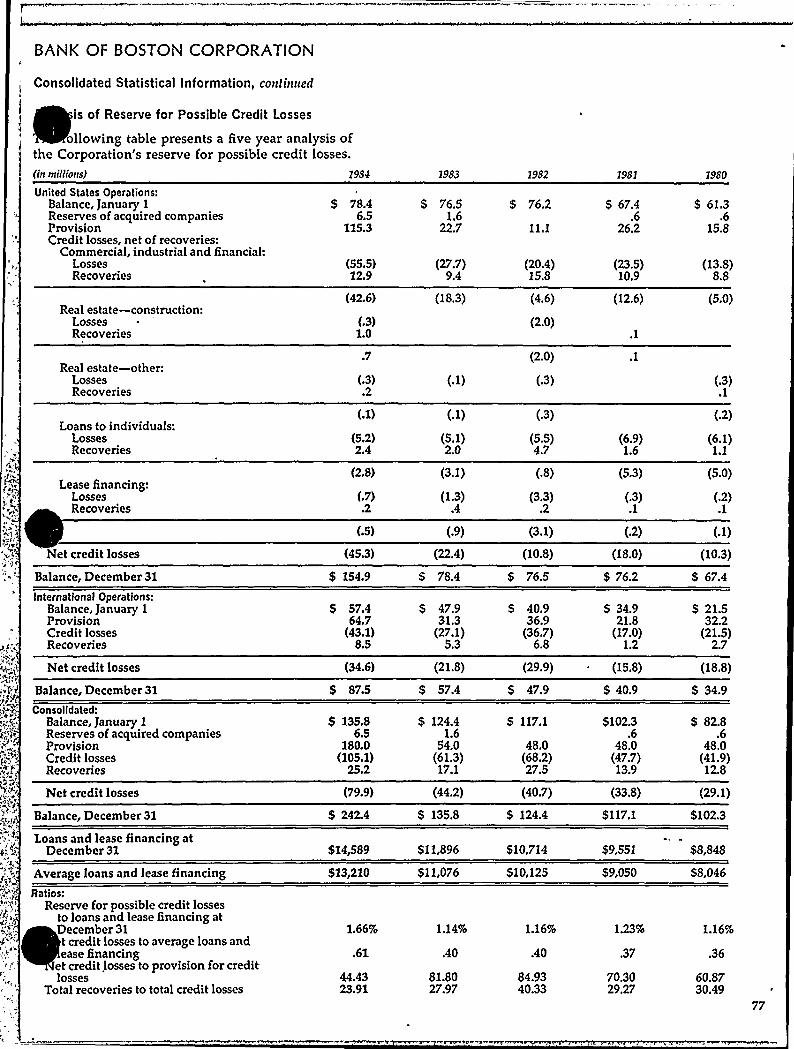

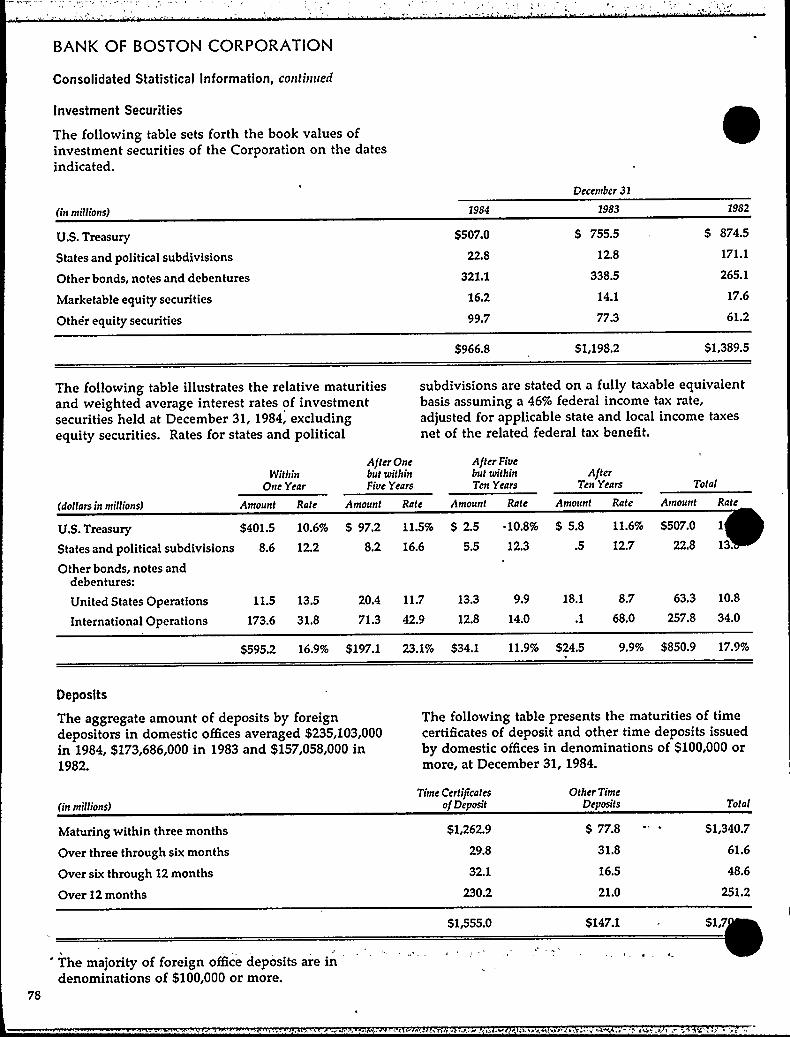

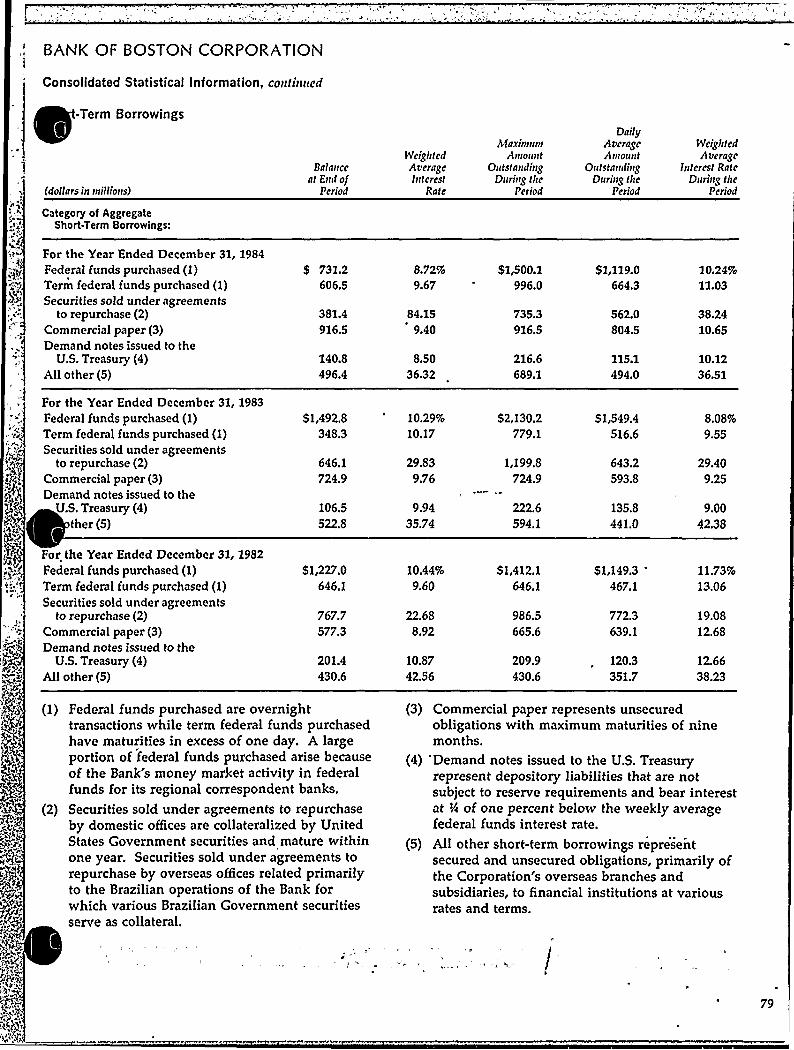

Attachment C: 1984 Annual Report of Bank ofBoston Corporation.

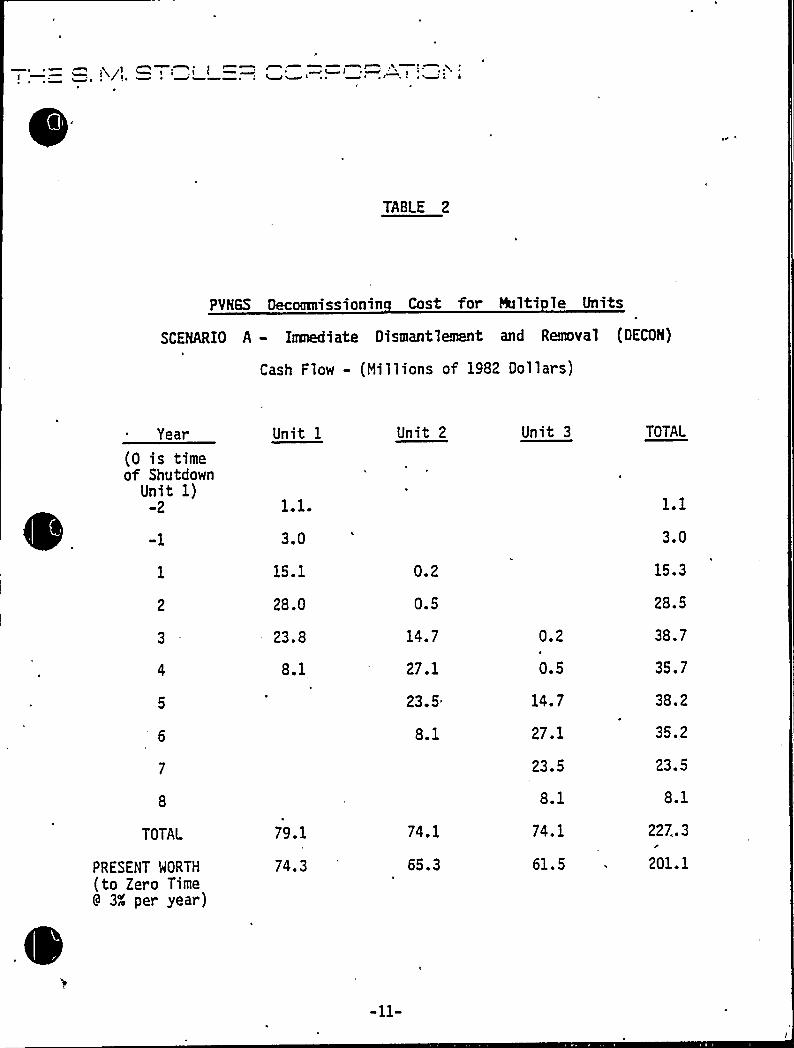

Final Report of the S.M. StollerCorporation dated August 3, 1982,entitled "Estimated Cost forDecommissioning Palo Verde NuclearGenera ting Sta tion (PVNGS) "

-11-

p

UNITED STATES OF AHERICA

NUCLEAR REGULATORY COHMISSION

In the matter of

ARIZONA PUBLIC SERVICECOMPANY, et al(Palo Verde NuclearGenerating Station', Unit 1)

X

DOCKET NO. STN 50-528

APPLICATION IH RESPECT OF ASALE AND LEASEBACK PIMANCIEG TRANSACTION BY

PUBLIC SERVICE COHPAHY OF NEN MEXICO

Pursuant to Section 103 of the Atomic Energy Act of 1954,

as amended, and 10 CFR 50.22 and 50 .54(c), Arizona Public Service

Company (APS), as Project Manager and Operating Agent of Palo Verde

Nuclear Generating Station (PVKGS) Units 1, 2 and 3, submits thisapplication, under 10 CFR 2.206> on behalf of Public Service Company

of New Mexico (PP1H), licensee under Facility Operating License No.

NPF-41, and The First National Bank of Boston, as Owner Trustee under

two or more separate grantor trust agreements (hereinafter Owner

Trustee) . Accompanying this Application is a Memorandum in Support

thereof (the Menorandum) .

l. Relief Requested

PNM proposes to refinance its construction financing forPVNGS Unit= 1 by entering into two or more sale and leaseback

financing transactions relating to all or a portion of PNM's 10.2%

undivided ownership interest in Unit 1 and all or a proportionate

share of one-th'ird .of PNM' 10.2% undivided ownership interest inPVNGS common facilities (said interest in Unit 1 and in the common

E

facilities being hereinafter collectively referred to as the

Faci1ities) .1 The relief requested by this Application is the issu-

ance of an order (i) authorizing the transfers of. the Facilitiesthrough the sale and leaseback financing transactions, pursuant to

Sections 50.22 and 50.54(c) of the Commission's regulations (10

CFR 50.22 and 50.54(c)), subject to the conditions that:

(a) The rights acquired by the Owner Trustee andany equity investor and any successors and assigns(including any mortgagee or secured party of suchOwner Trustee) in and to PVMS Unit 1 may be exercisedonly in compliance with and subject to the samerequirements and restrictions as would apply to PNMpursuant to the provisions of Facility OperatingLicense No. NPF-41 (the License), the Atomic EnergyAct of 1954, as amended (the Act), and the regulationsissued by the Commission pursuant to the Act; and

(b) Neither the Owner Trustee nor any quityinvestor nor any of their respective successors orassigns may take possession of any interest in PVNGSUnit 1 prior to either (1) the issuance o.". a licensefrom the Commission authorizing such possession or(2) the transfer of the License authorizing PNM topossess an interest in PVNGS Unit 1 upon an applica-tion for transfer of such License filed pursuant to 10CFR 50.80(b);

1. PNM will retain, however, ownership of easements, rights-of-wayand certain other real property rights associated with theFacilities, including property referred to under the Internal RevenueCode as "Section 1250 property" (such as the AdministrationBuilding) . PNM will also retain ownership of the nuclear fuel andelectric transmission facilities asso'ciated with PVNGS.

and (ii) acknowledging that neither the Owner Trustee nor any equity~

~investor nor any of their respective successors and assigns is or

shall become a licensee under the License unless and until the

Commission shall have issued an amendment of the License authorizing

such Owner Trustee, equity investor, successor or assign to take pos-

session of an interest in PVNGS Unit 1 or shall have approved a

transfer of PNM's license to such Owner Trustee, equity investor,

successor or assign.

2. Purpose of the Financing Transaction

The proposed sale and leaseba'ck financing transactions willprovide benefits to PNM's customers through two channels. First, the

net present value of capital costs (and the total nominal costs) willbe reduced Ly the transfer of tax benefits and by the recapitaliza-

tion of the p..ant financing with greater debt leverage. Second, the

revenue requ'ements associated with PNM's capital costs in PVNG's

Unit 1 wi3.1 be levelized over the life of the Unit.

Because the lessors in the proposed sale and leaseback

transactions will recapitalize the Unit with greater debt leverage,

the required lease payments represent a lower cost of capital than

would PNM's composite cost of capital. Also, PNM's tax situation is

such that it cannot take full advantage of tax benef its at the

present time. The sale will transfer the benefits of tax

depreciation to such lessors.

0

r.

The leveling of revenue requirements over time yieldsseveral benefits. Under conventional utility regulation, carrying

charges are determined by the asset's net book value which declines

over time as the asset is depreciated. This produces so-called

"front-end" loading —the familiar situation in which the stream of

revenue requirements falls'ver time while the actual value of the

plant output rises over time. Front-end loading is eliminated with

the proposed sale and leaseback transaction because a fixed lease

payment replaces'the conventional "high front-end" revenue require-

ments stream, thus benefitting PNM's ratepayers and insulating them

from potential "rate shock".

3 . Description of the Proposed Sa3.e and Leaseback Financing

Transaction

PNM proposes to sell to grantor trusts, the beneficiari. "

of which will be institutional equity investors, the Facilities,including without limitation PNM's 10.2% Generation Entitlement

Share> in PVNGS Unit 1. Such investors will enter into one or more

trust agreements with the Owner Trustee who will take and hold titleto the Facilities sold by PNM. The Owner Trustee will in turn

lease'he

Facilities back to PNM for a term of approximately 28-1/2 yea-s

2. "Generation Entitlement Share" is defined in Section 3.28 of theArizona Nuclear Power Project Participation Agreement as amended (seeAppendix D attached to the Memorandum) as: "The percentage entitle-ment of each Participant to the Net Energy Generation and to theAvailable Generating Capability..."

for a'tipulated basic rent. [See Section 4 of the Memorandum for a

more complete description of certain signif icant terms of the

leases.]

Under the ANPP Participation Agreement [see Appendices D

and E to the Memorandum] which governs the ownership and operation of

Unit 1, PNM will be empowered with respect to the Facilities to be

and act as the "Participant" with full power and authority, to the

exclusion of the Owner Trustee and/or the equity investors, to exer-

cise all the rights and perform all the duties and responsibilities

under such Agreement. The leases will confirm this authorization to

PNM. The Owner Trustee, as lessor under the leases, will be subject

only to typical financing risks and not to operational risks or

responsibilities.Sale and leas back financing is a recognized and accepted

t

mechanism that has been csed for many years by a number of* commercial

institutions involving a wide variety of property types. APS and a

number of other electric utilities have used this mechanism to

f inance or ref inance their investments in non-nuclear generating

facilities. In the past year PNM refinanced its investment in one of

its transmission lines, known as the Eastern Interconnection Project

(EIP), using sale and 2 easeback documentation similar to that pro-

posed for refinancing its interest in PVNGS Unit 1. Nhen used by

electric utilities, sale and leaseback transactions have been

subjected to review and approval of state and/or federal regulatory

t'

agencies. [See, for example, Appendices A and B attached to the

Memorandum.l

While this will be the first occasion of the use of a sale

and leaseback transaction in financing a nuclear power facility, the

secured financing of the nuclear fuel used in such facilities utiliz-ing a lease format is not unique.

4. Conditions Precedent to the Financing Transaction

The proposed financing transaction is subject to the fol-lowing conditions precedent, in addition to others commonly associ-

ated with any financial transaction of th'is nature:

4.1 The approval of the transaction by the New Mexico

Public Service Commission as required by the laws of the State of New

Mexico, such approval to be in form and substance satisfactory to allparties to such transaction.

4.2 The issuance of a declaratory order by the Federal

Energy Regulatory Commission (FERC), satisfactory in form and sub-

stance to all parties to the transaction, ruling that the equity

investors and the Owner Trustee will not, as a result of their hold-

ing title to the Leased Interests, become "public utilities" as

defined in section 203(a) of the Federal Power Act.

4.3 The actions of the Commission as applied for in this

Application.

4.4 Ownership and operation of PIGS Unit 1, together with

Units 2 and 3, is governed by the Arizona Nuclear Power Project

C

Participation Agreement, as amended. [See Appendices D and E

attached to the Memorandum.) The ANPP Administrative Committee cre-

ated by such Agreement will be required to make a determination that

the conditions to the proposed sale and leaseback transaction speci-

fied in proposed Amendment No. 10- to such Participation Agreement

have been met.

5. Schedule of the Financing Transaction

5 .1 The viability of the proposed financing transaction

hinges upon its consummation on or before December 31, 1985. To meet

this date it is planned that preliminary conditional commitments willbe obtained from the equity investors and the Owner Trustee on or

. about October 22, 1985. Thereafter, it is expected that on or about

November 15, 1985, approval of the proposed sale and leaseback from

the New Mexico Public Service Commis'ion and the requisite order from

FERC will be obtained. Finally, i~ is very desirable that the clos-

ing of the sale and leaseback transactions take place on or about

December 18, 1985. This is necessary to provide the equity investors

with the 1985 available tax benefits without which the proposed

transactions will fail to close. A December 18 closing will ensure

that the associated public debt o.".'fering can be sold in the public

market prior to the Christmas holidays.

5.2 To achieve this schedule it will be necessary that the

Commission i:ssue its final order not later than November 20, 1985,

authorizing the transfers of the Facilities by PNM to the Owner

Trustee and by the Owner Trustee back to PNM. [See Section 1

hereof.)

6. Supporting Information

6.1 The general information respecting applicant PNM

required by 10 CFR 50.33 (a) through (d) is provided by Exhibit A

attached to this Application.

6.2 The general information respecting applicant Owner

Trustee required by 10 CFR 50.33 (a) through (d) is provided, as

appropriate, by Exhibit B attached to this Application.

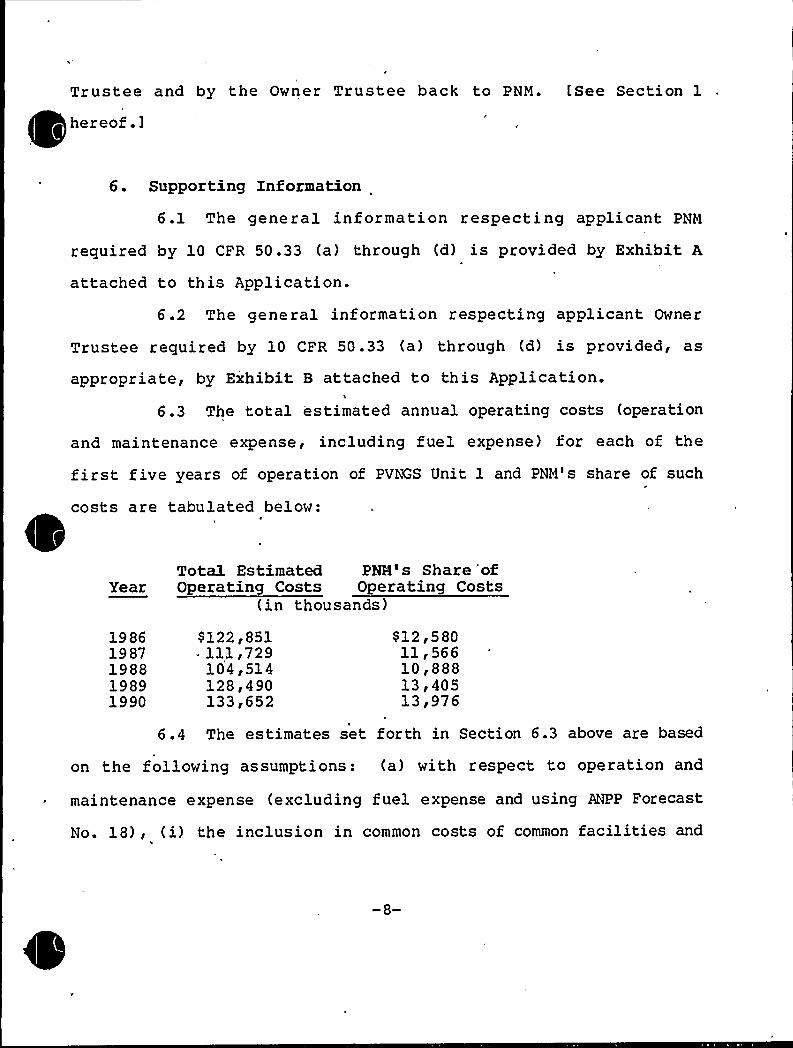

6.3 The total estimated annual operating costs (operation

and maintenance expense, including fuel expense) for each of the

first five years of operation of PVNGS Unit 1 and PNM's share of such

costs are tabulated below:

Tota1 Estimated PNN's Share ofYear Operating Costs Operating Costs

(in thousands)

19861987198819891990

$ 122 i 851- 111,729

104,514128,490133,652

812 F58011,56610,88813 i 40513,976

6.4 The estimates set forth in Section 6.3 above are based

on the following assumptions: (a) with respect to operation and

maintenance expense (excluding fuel expense and using ANPP Forecast

No. 18), (i) the inclusion in common costs of common facilities and

P

water reclamation facilities, (ii) inclusion of only Unit 1's share

of common costs with even allocation across all units (using APS's

date of firm power operation for Unit 2), (iii) loads have been

included (payroll, with the exception of taxes, materials and service

and outside services), and insurance and administrative and general

expense have been excluded, (iv) the projection of all dollars atyear's cost (escalation at 6% per year), and (v) the exclusion of PNM

legal fees, replacement power insurance costs and other PNM in-house

costs.; and (b) with respect to fuel expense (using the June 1985

nuclear fuel financial forcast) > (i) the subtracting out of Western

Nuclear's cash flow for 1985, (ii) the assignment to Unit 1 of one

third of each of U308 cash flows and conversion cash flows, (iii) the

use of the ratio of the current SWU price projection to the old SNU

price projection times Unit 1 enrichment cash flows to calculate

enrichment, (iv) no change in either fabrication or spent fuel dis-

posal fees and (v) recalculation of use tax assuming 5% of U308 costs

instead of 5% of total fuel assembly costs.

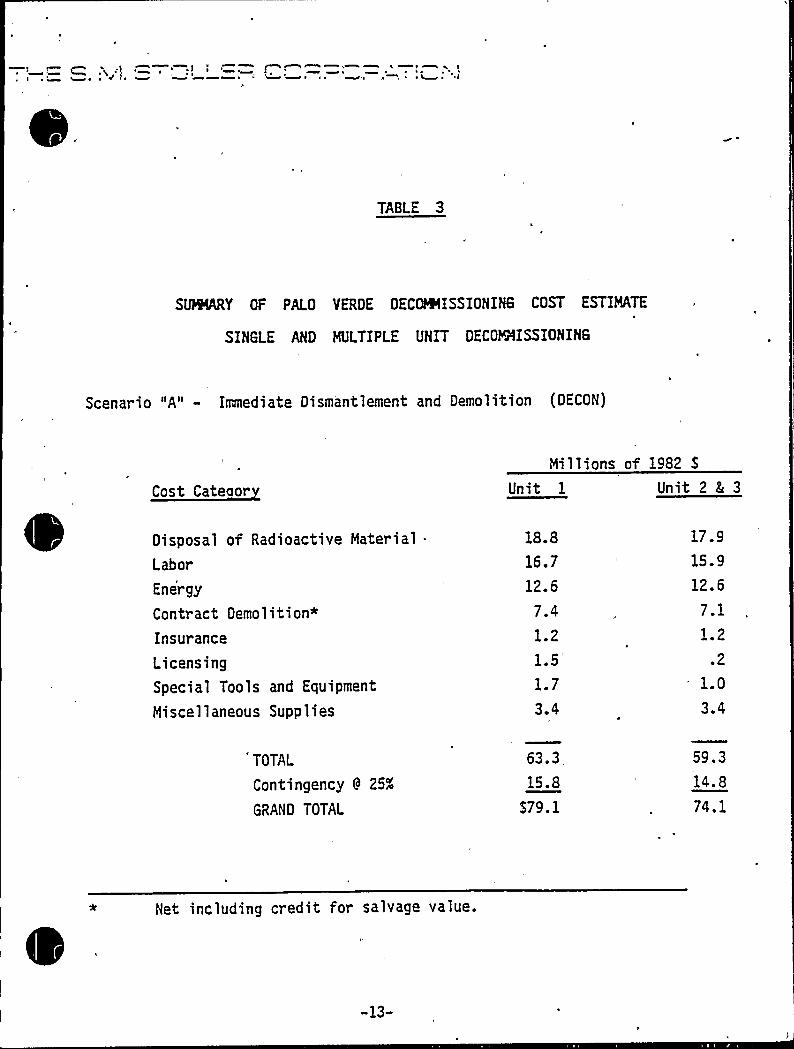

6.5 As Exhibit, C attached to this Application indicates,

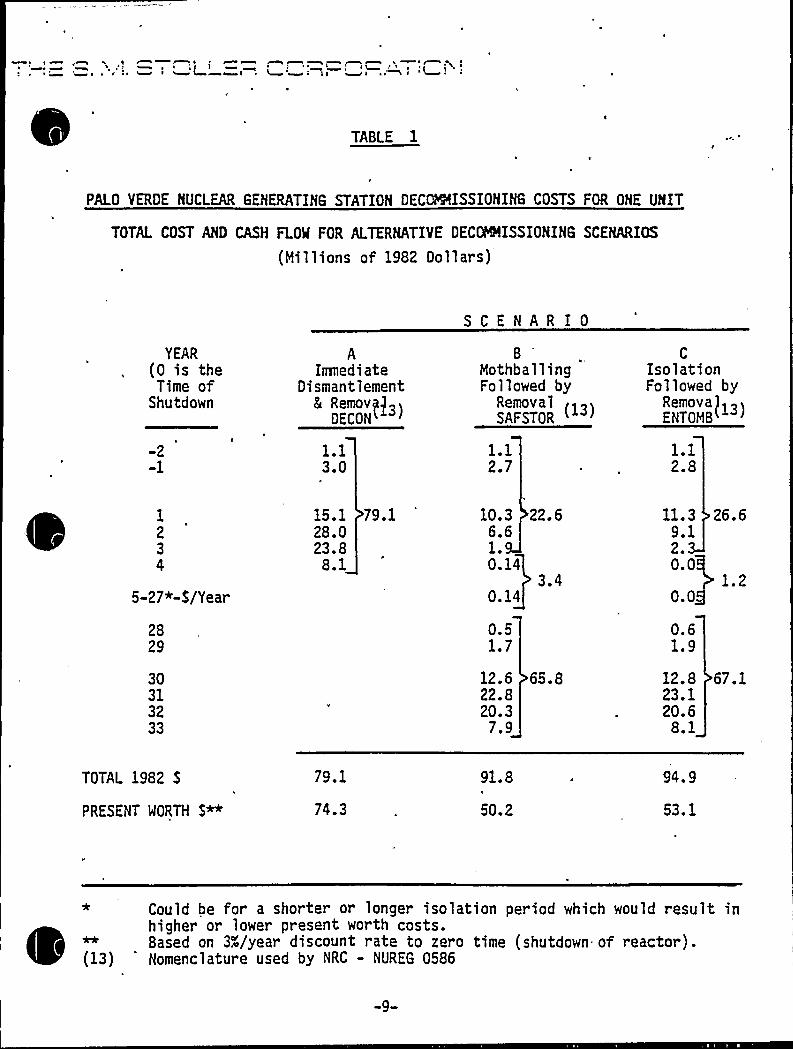

the cost of decommissioning PVHGS Unit 1 using the DECON alternative

(as described in the notice of proposed rulemaking published in the

Federal Register on February 11, 1985, at pages 23025 ~et e .) is

879 million (expressed in 1982 dollars). PNM is now and, pursuant to

the proposed leases, will continue to be-obligated to pay 10.2$ of

the costs of decommissioning PVNGS Unit l.

t

J

l

0

7. Environmental Considerations

The proposed conveyances of the Facilities to the Owner

Trustee and the leasebacks of the Facilities to PNM by the Owner

Trustee do not involve any design or physical change to PVNGS Unit 1,

any change in the transmission or other facilities associated with

PVNGS Unit 1, any change in types or amounts of effluents from PVNGS

Unit 1, any change in the potential for accidental releas s from

PVNGS Unit 1 or any change in the authorized power level of PVNGS

Unit l. Accordingly, the grant of the relief requested by thisApplication does not present an unreviewed environmental impact.

Pursuant to 10 CFR 51.5(d)(4), no environmental impact statement,

negative declaration, or environmental impact appraisal need be pre-

pared in connection with this Application.

3. No Significant Hazards Consideration

The consummation of the proposed sale and leaseback financ-

ing transactions will not involve any increase in the probability„or

consequences of an accident previously evaluated, or create the pos-

sibility of a new or different kind of accident from any accident

previously evaluated, or involve any reduction in a margin of

saf ety. Accordingly, the consummation of the transfers of the

Facilities as contemplated by the proposed sale and leaseback financ-

ing transactions does not involve a "significant hazards

consideration" within the meaning of that phrase as defined in 10 CFR

50.92.

-10-

9. Responsibility for Management of PVHGS Unit 1

9.1 The consummation of the proposed sale and leaseback

financing transactions 'will not result in any change in the responsi-

bilities, obligations or authorities of APS as licensee under the

License authorized to operate and maintain PVNGS Unit 1, nor as

Operating Agent under the ANPP Participation Agreement.

9.2 Under the terms of the proposed leases and pursuant to

the proposed amendment of the ANPP Participation Agreement, PNM shall

continue throughout the term of the leases to be a Participant under

the ANPP Participation Agreement, entitled to a 10.2% Generation

Entitlement Share of the power and energy generated by PVNGS Unit 1,

entitled to a full vote on all Unit 1 business and obligated to pay

10.2% of the costs of operating, maintaining and decomissioning such

9.3 It is not necessary to issue a license to the Owner

Trustee and/or equity investors since only APS, as Operating Agent,

and the other Unit 1 licensees, including PNM, are .ble to insure

that Unit 1's operation is consistent with the Commission's licensing

responsibilities. APS and the other Unit 1 licensees alone have con-

trol of and responsibility for the Operating Agent with respect to

the operation and maintenance of Unit 1. The ownership rights of 'the

Owner Trustee and/or the equity investors are far too limited in this

regard to require a license, as the Memorandum makes abundantly

clear. The Owner Trustee and/or the equity investors will have (i)

no ability to restrict or inhibit compliance with the security,

safety or other regulations of the Commission, (ii) no capacity to

control the use of Unit 1 nuclear fuel or to dispose of special

nuclear material generated by Unit 1, and (iii) no right to use or

direct the use of the Facilities. Although legal title to the

Facilities will reside with the Owner Trustee, the current regime of

control, supervision and responsibility is unaltered by the proposed

'transaction. APS is and will remain responsible to the Commission

for the proper operation and maintenance of Unit 1.

-12-

0

WHEREFORE, APS requests on behalf of PNM and the Owner

Trustee that the Commission grant the reliefhereof or in such other form and/or subject to

requested in Section 1

conditions in addition

to those stated in such Section as the Commission may deem

appropriate..

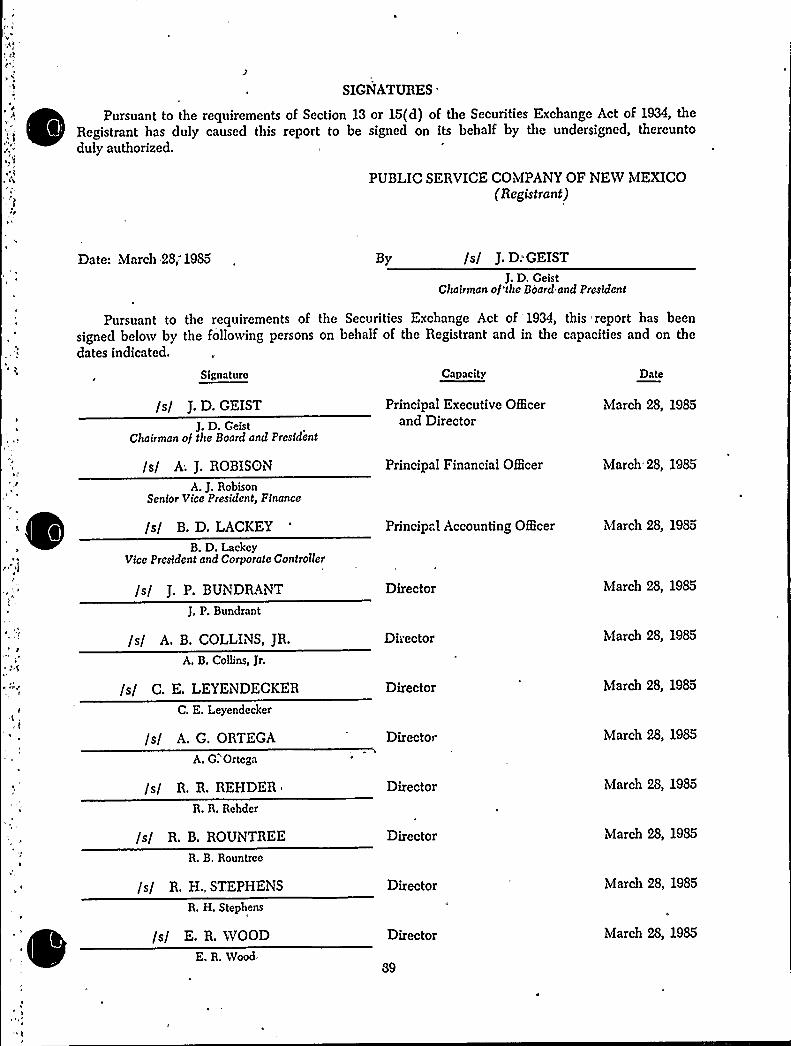

Respectfully submitted,

ARIZONA PUBLIC SERVICE COIG'ANY

ByEdwin E. Van Brunt, Jr./DBKEdwin E. Van Brunt, Jr.Executive Vice President-ANPP

Dated: October 18, 1985

-13-

STATE OP ARIZOHK )) ss.

COUNTY OP HARICOPA )

I, Donald B. Karner, represent that I am Assistant VicePresident, Nuclear Production of Arizona Nuclear Power Project, thatthe foregoing document has been signed by me on behalf of ArizonaPublic Service Company with full authority to do so, that I have readsuch document and know its contents, and that to the best of myknowledge and belief, the statements made therein are true.

Donald B. KarnerDonald B. Karner

Sworn before me this 17th day of October, 198S.

J.M. AllenNotary Public

My Commission Expires:

My Commission Ex ires Jan. 23, 1987

-14-

UNITED STATES OF AMERICA

NUCLEAR REGULATORY COMMISSION

In the matter of

ARIZONA PUBLIC SERVICECOMPANY, et al,(Palo Verde NuclearGenerating Station, Unit l)

DOCKET NO STN 50-528

EXHIBIT A

TO

APPLICATIONIN RESPECT OF A SALES AND LEASEBACK

FINANCING TRANSACTION BYPUBLIC SERVICE COMPANY OF NEW MEXICO

GENERAL INFORMATION CONCERNINGPUBLIC SERVICE COMPANY OF NEW. MEXICO

General Information Concerning Public ServiceCompany of New iLexico

(a) Name of applicant:Public Service Company of New Mexico ("PNM")

(b) Address of applicant:Alvarado SquareAlbuquerque, New Mexico 87158

(c) Description of business of applicant:PNM is a. public utility engaged principally in the generation,transmission, distribution and sale of electricity and, sinceJanuary 28, 1985, in the gathering, transmission, distributionand sale of natural gas within the State of New Mexico. PNMalso owns facilities for the pumping, storage, transmission,distribution and sale o'f water. In addition, PNM through itssubsidiaries, is engaged in a program of diversification intonon-utility areas.

(d) (1) Not applicable.(d) (2) Not applicable.

y(d) (3) (i) State 'of incorporation and principal location:PNM is an investor-owned corporation organized and existingunder and by virtue of the laws of the State of New Me-'co.Its principal offices are in Albuquerque, New Mexico. PNM pro-vides electric service to (1) a large area of north central NewMexico, including the cities of Albuquerque, Belen, Bernalillo,Santa Fe and Las Vegas, (2) Deming in southwestern New Mexicoand (3) Clayton in northeastern New Mexico. PNM also provideswholesale electric service to the the City of Gallup, the Cityof Farmington, Plains Electric Generation & TransmissionCooperative, Inc., and Texas-New Mexico Power Company.

(d) (3) (ii) Names of directors and principal officers:Directors of Public Service Company of New Mexico

F

. J.P. BundrantPresident, Electric OperationsPublic Service Company of New Mexico

A-1

A.B. Collins, Jr.PresidentReddy Communications, Inc.Albuquerque, NM

J.D. GeistChairman and PresidentPublic Service Company of New Mexico

C.E. Leyendec!cerChairman of the Board andChief Executive Officer,United New Mexico Bank at Mimbres ValleyDeming, NH

A.G. OrtegaAttorney at LawOrtega 6 Snead, P.A.Alburquerque, NM

R.R. RehderProfessor of ManagementRobert O. Anderson Graduate School of ManagementUniversity of New MexicoAlbuquerque, NM

R.B. RountreeSenior Vice PresidentPublic Service Company of New Mexico

R.H. StephensPresidentStephens-Irish Agency,

Inc.'as

Vegas, NM

E.R. Mood'icePresident and General Manager

Wood 5. Hill CorporationSanta Fe, NM

H.L. Gall s, Jr.Director EmeritusChairman of the BoardGalles Chevrolet CompanyAlbuquerque, NM

Principal Officers of Public Service Company of New Mexico

PNH CORPORATE

A-2

0

J.D. GeistChairman and President

B. Hulcock, Jr.Senior Vice President<Corporate Affairs andSecretary

A.J. RobisonSenior Vice Presidentand Chief Financial Officer

R.B. RountreeSenior Vice President

H.A. CliftonVice President,Financial Planning

B.D. LackeyVice. President andCorporate Controller

J.K. MurphyVice President, Regulatoryand Business Policy

N.C. ITygantVice President,Corporate Services

P.J. ArchibeckTreasurer and Assistant Secretary

H.L. Hitchins, Jr.Assistant Secretary andAssistant Treasurer

M.J. NarzecAssistant Treasurer

H. Mason-PlunkettAssistant Secretary

PHH ELECTRIC

J.P. BundrantPresident and Chief Operating Officer

A-3

I

0

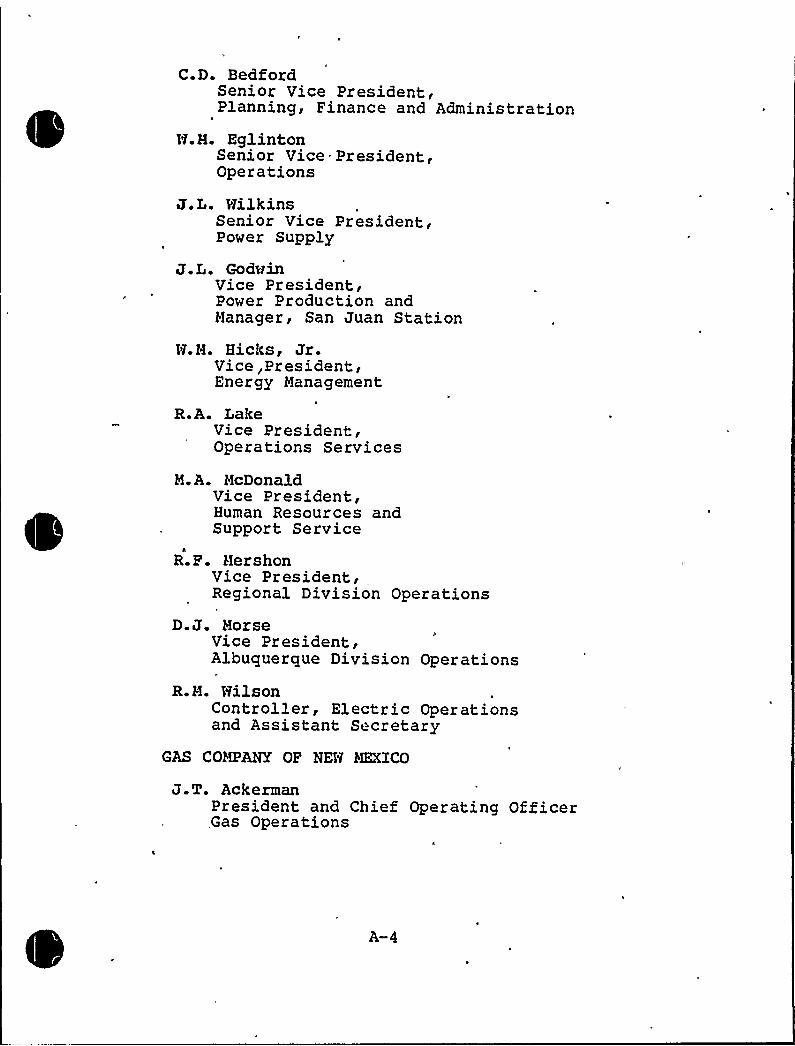

C.D. BedfordSenior Vice President,Planning, Finance and Administration

H.H. EglintonSenior Vice President,Operations

J.L. TlilkinsSenior Vice President,Power Supply

J.L. God@inVice President,Power Production andNanager, San Juan Station

N.N. Hicks, Jr.Vice,President,Energy Nanagement

R.A. LakeVice President,Operations Services

N.A. NcDonaldVice President,Human Resources andSupport Service

R.P. HershonVice President,Regional Division Operations

D.J. NorseVice President<Albuquerque Division Operations

R.M. WilsonController, Electric Operationsand Assistant Secretary

GAS COMPANY OF NEW &IEXICO

J.T. AckermanPresident and Chief Operating OfficerGas Operations

A-4

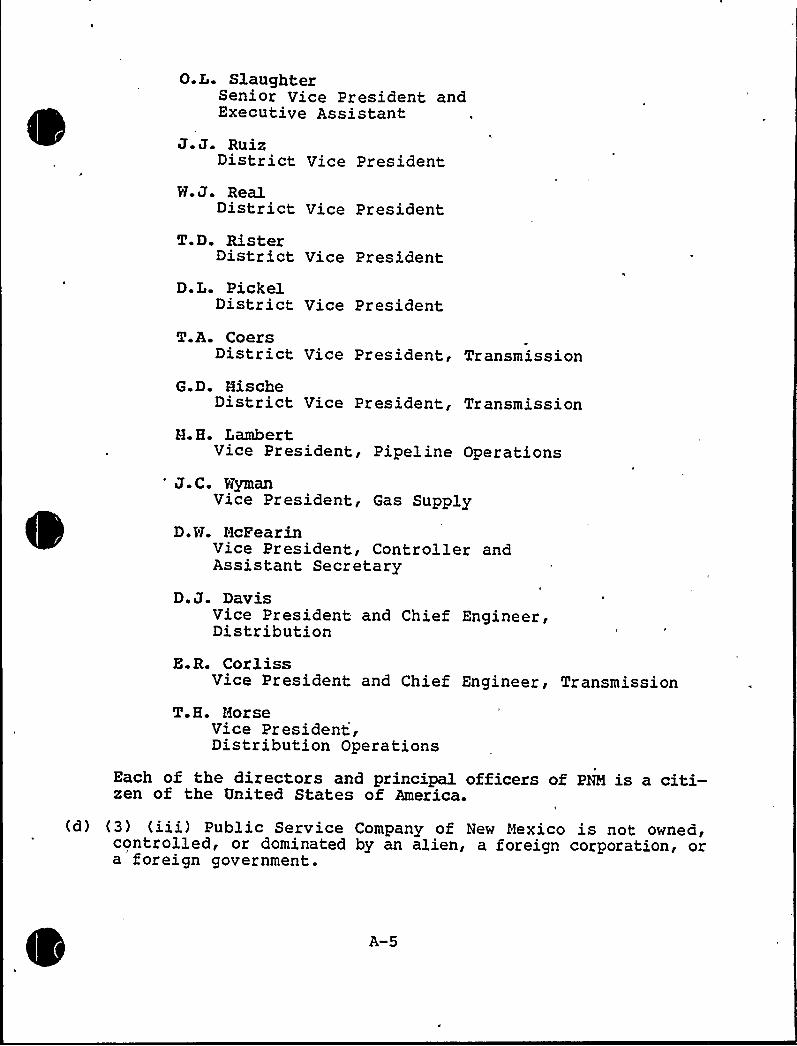

O.L. SlaughterSenior Vice President andExecutive Assistant

J J RuizDistrict Vice President

H.J. RealDistrict Vice President

T.D. RisterDistrict Vice President

D.L. PickelDistrict Vice President

T.A. CoersDistrict Vice President, Transmission

G.D. HischeDistrict Vice President, Transmission

H.H. LambertVice President, Pipeline Operations

J.C. omanVice President, Gas Supply

D.WT. HcPearinVice President, Controller andAssistant Secretary

D.J. DavisVice President and Chief Engineer,Distribution

E.R. CorlissVice President and Chief Engineer, Transmission

T.H. HorseVice President,Distribution Operations

Each of the directors and principal officers of PNM is a citi-zen of the United States of America.

(d) (3) (iii) Public Service Company of New Mexico is not owned,controlled, or dominated by an alien, a foreign corporation, ora foreign government.

A-5

(d) (4) Public Service Company of New Mexico is not acting as agentor representative of another person in -respect of thisapplication.(e) See the Application to which this document is attached asExhibi t A.

(f) Xn accordance with 10 CFR 50, Appendix C, a copy of PublicService Company of New Mexico's 1984 Annual Report and itsAnnual Report on Form 10-K for the f iscal year endedDecember 31, 1984, are attached hereto as Attachment A.

(g) Not applicable.(h) Not applicable.

(i) The names and addresses of regulatory agencies which have juris-diction over Public Service Company of New Mexico's rates andservices are:

New Mexico Public Service CommissionMarian Hall224 East Palace AvenueSanta Fe, New Mexico 87503

Federal Energy Regulatory CommissionNashington, D.C. 20426

News publications which circulate in the area in which thefacility is located are:

The Arizona Republic120 East Van BurenPhoenix, Arizona 85004

The Phoenix Gazette120 East Van BurenPhoenix, Arizona 85004

Buckeye Valley NewsP.O. Box 217Buckeye, Arizona 85326

News publications which circulate in Public Service Company ofNew Mexico's service area include the following:

Las Uegas Daily OpticLas Vegas, New Mexico 87701

The New Mexican, Inc.Post Oifice Box 2048Santa Fe, New Mexico 87501

A-6

Los Alamos MonitorPost Office Box 899Los Alamos, New Mexico 87544

Albuquerque JournalAlbuquerque Publishing Company.Post Office Drawer J-TAlbuquerque, New Mexico

87103'allup

Daily IndependentPost Office Box 1210Gallup, New Mexico 87301

(j) Not applicable.

A-7

UNITED STATES OF AHERXCA

NUCLEAR REGULATORY COKCISSION

In the matter of

ARIZONA PUBLIC SERVICECOMPANY, et

al,'Palo

Verde NuclearGenerating Station, Unit 1)

DOCKET NO STN 50-528

ATTACHHENT A TO EXHIBIT A

TO

APPLICATIONIN RESPECT OF A SALES AND LEASEBACK

FINANCING TRANSACTXON BYPUBLIC SERVICE COHPANY OF NEW HEXXCO

1984 ANNUAL REPORT OF

PUBLIC SERVICE COHPANY OF NEÃ MEXICOAND ANNUAL REPORT ON FORH10-K FOR THE FISCAL YEARENDED DECEHBER 31'984

"A fine wind is blowing the new direction of time"—D.H. Lawrence

PNM ANNUAL REPORT 1984

Changing, Yet Unchanged

The Southwest is a land of sharpcontrasts-modern cities rising fromtimeless deserts, multistory granite andglass office buildings standing withinsight of adobe Indian villages.

Laura Gilpin's "Storm From LaBajada Hill,New Mexico," on the coverof this year's annual report, reveals adramatic landscape. Since the Gilpinphotograph was taken in 1946, amodern interstate has been built acrossLa Pqjada's weather-beaten, highmountain desert. Wise travelers have ahealthy respect for the storms thatoften rack the otherwise serene hill.

As you turn the pages of the reportyou'l see other vintage photographsthat convey the ageless quality of NewMexico. They are accompanied byquotes from well-known authors andothers whose work has been deeplyinfluenced by experiences inthe Southwest.

PNM has also been influenced by thenatural beauty and the rich culturalheritage ofNew Mexico and theSouthwest. As we'e grown, as we'echanged to meet the chaHenges andtake advantage of the opportunitiesof the 1980s, we'e retained ourdose affinity for the land and for thepeople we serve.

"STORM FROM lABAJADAHILI„NEWMEXICO,"Laura Grlpln 1946 O 1985 Amon Caner,.

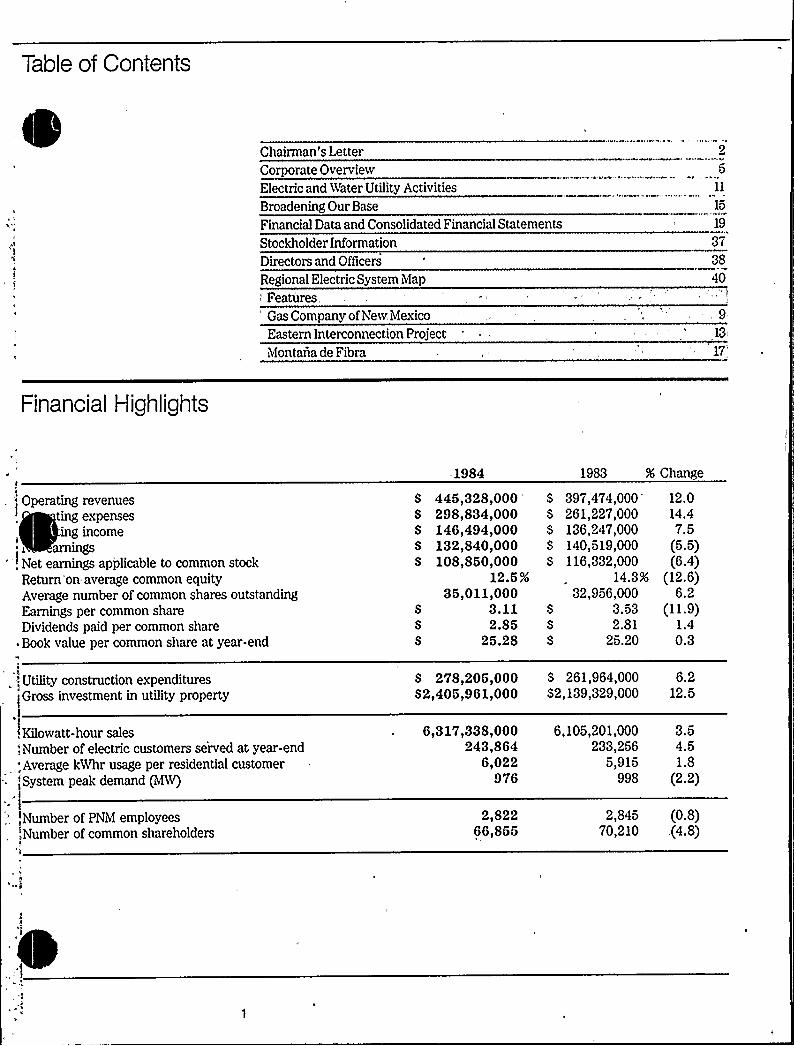

Table of Contents

Chair man's LetterCorporate OverviewElectric and Water UtilityActivitiesBroadening Our Base

Financial Data and Consolidated Financial Statements

Stockholder InformationDirectors and Officers

Regional Electric System MapFeatures

'as Company ofNew. Mexico

Eastern Interconnection ProjectMontaiia de Fibra

15

19

37

40

9

13

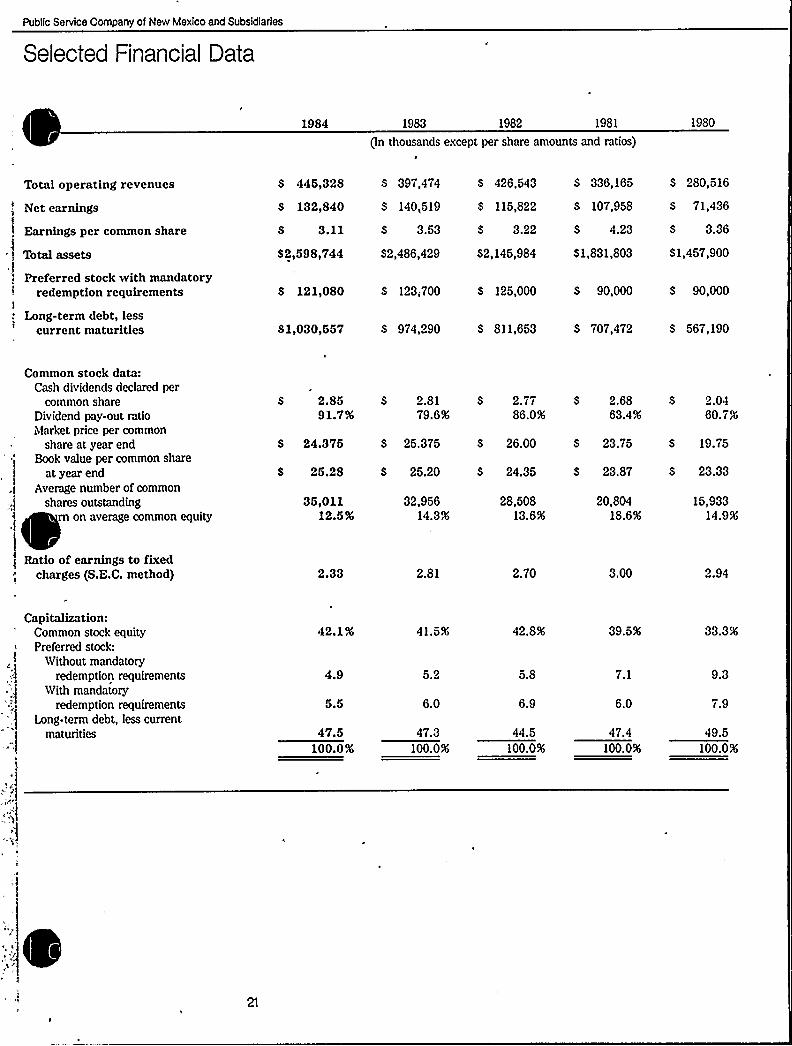

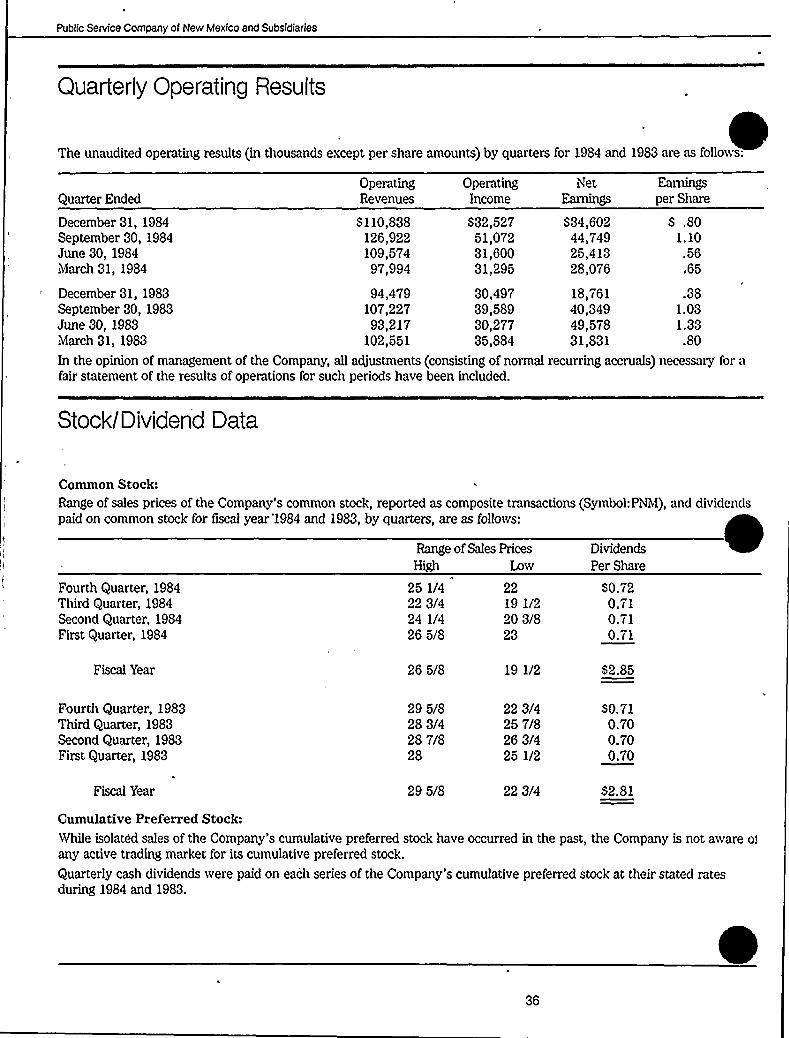

17'inancial

Highlights

" Operating revenuesting expensesing income

arnings' Net earnings applicable to common stock

Return on=average common equityAverage number of common shares outstandingEarnings per common shareDividends paid per common shareBook value per common share at year-end

1984

S 445,328,000 '

S 298,834,000 S

S 146,494,000 S

S 132,840,000 S

S 108,850,000 S

12.5%35,011,000

S 311 S

S 2.85 S

S 25 28 S

1983 % Change

397,474,000 12.0261,227,000 14.4136,247,000 7.5140,519,000 (5.5)116,332,000 (6.4)

14.3% (12.6)32,956,000 6.2

3.53 (11.9)281 14

25.20 0.3

, -; Utilityconstruction expendituresGross investment in utility property

S 278,205,000 S 261,964,000 6.2S2,405,961,000 $2,139,329,000 12.5

, Kilowatt-hour sales

. iVumber of electric customers served at year-end;Average kWhr usage per residential customer

-. -'System peak demand (MW)

6,317,338,000243,864

6,022976

6,105,201,000 3.5233,256 4.5

5,915 1.8998 (2.2)

Number of PNM employees,,Number of common shareholders

2,82266,855

2,845 (0.8)70,210 .(4.8)

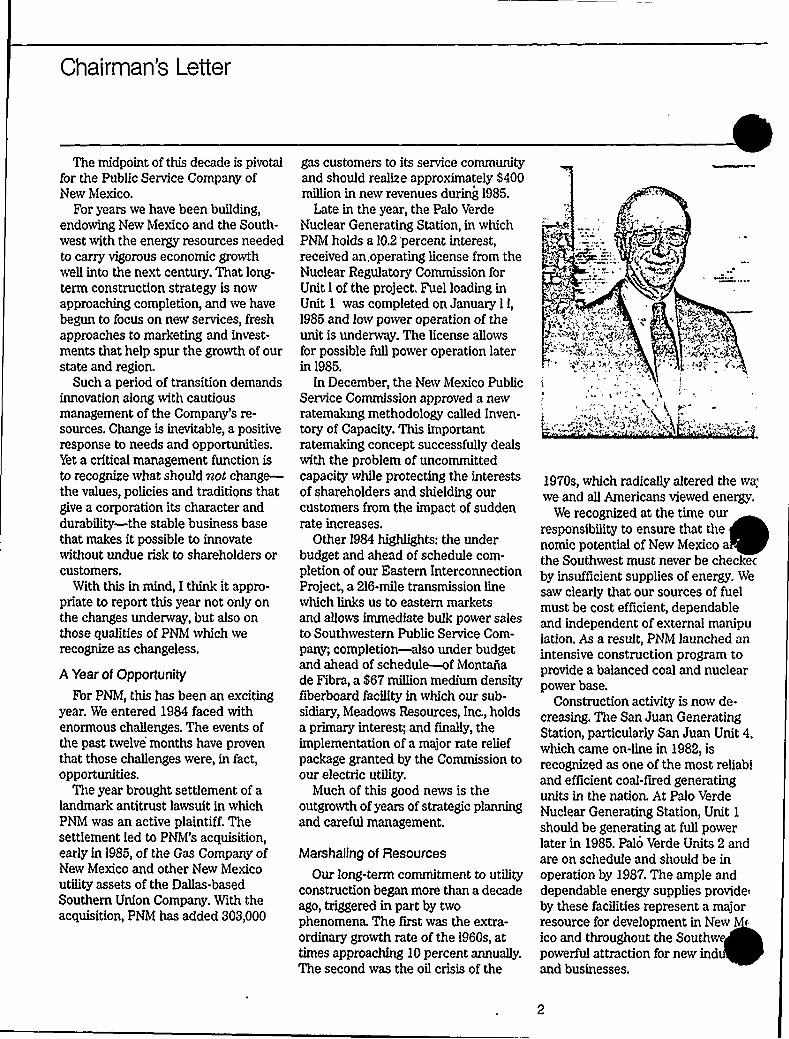

Chairman's Letter

The midpoint of this decade is pivotalfor the Public Service Company ofNew Mexico.

For years we have been building,endowing New Mexico and the South-west with the energy resources neededto carry vigorous economic growthwell into the next century. That long-term construction strategy is nowapproaching completion, and we havebegun to focus on new services, freshapproaches to marketing and invest-ments that help spur the growth of ourstate and region.

Such a period of transition demandsinnovation along with cautiousmanagement of the Company's re-sources. Change is inevitable, a positiveresponse to needs and opportunities.Yet a critical management function isto recognize what should not change-the values, policies and traditions thatgive a corporation its character anddurability—the stable business basethat makes it possible to innovatewithout undue risk to shareholders orcustomers.

With this in mind, I think it appro-priate to report this year not only onthe changes underway, but also onthose qualities of PNM which werecognize as changeless.

A Year of Opportunity

For PNM, this has been an excitingyear. We entered 1984 faced withenormous challenges. The events ofthe past twelve months have proventhat those challenges were, in fact,opportunities.

The year brought settlement of alandmark antitrust lawsuit in whichPNM was an active plaintiff. Thesettlement led to PNM's acquisition,early in 1985, of the Gas Company ofNew Mexico and other New Mexicoutilityassets of the Dallas-basedSouthern Union Company. With theacquisition, PNM has added 303,000

gas customers to its service communityand should realize approximately $400million in new revenues during 1985.

Late in the year, the Palo VerdeNuclear Generating Station, in whichPNM holds a 10.2 percent interest,received an. operating license from theNuclear Regulatory Commission forUnit 1 of the project. Fuel loading inUnit 1 was completed on January I 1,

1985 and low power operation of theunit is underway. The license allowsfor possible full power operation laterin 1985.

In December, the New Mexico PublicService Commission approved a newratemakmg methodology called Inven-tory of Capacity. This importantratemaking concept successfully dealswith the problem of uncommittedcapacity while protecting the interestsof shareholders and shielding ourcustomers from the impact of suddenrate increases.

Other 1984 highlights: the underbudget and ahead of schedule com-pletion of our Eastern InterconnectionProject, a 216-mile transmission linewhich links us to eastern marketsand allows immediate bulk power salesto Southwestern Public Service Com-pany; completion—also under budgetand ahead of schedule —of Montanade Fibra, a 867 millionmedium densityfiberboard facility in which our sub-sidiary, Meadows Resources, Inc., holdsa primary interest; and finally, theimplementation of a major rate reliefpackage granted by the Commission toour electric utility.

Much of this good news is theoutgrowth ofyears of strategic planningand careful management.

Marshaling of Resources

Our long-term commitment to utilityconstruction began more than a decadeago, triggered in part by twophenomena. The first was the extra-ordinary growth rate of the 1960s, attimes approaching 10 percent annually.The second was the oil crisis of the

~.p,CP,,)

1970s, which radically altered thewa.'e

and all Americans viewed energy.We recognized at the time our

responsibility to ensure that thenomic potential of New Mexico athe Southwest must never be checksby insufficient supplies of energy. Wesaw clearly that our sources of fuelmust be cost efficient, dependableand independent of external manipulation. As a result, PNM launched anintensive construction program toprovide a balanced coal and nuclearpower base.

Construction activity is now de-creasing. The San Juan GeneratingStation, particularly San Juan Unit 4,which came on-line in 1982, isrecognized as one of the most reliabland efficient coal-fired generatingunits in the nation. At Palo VerdeNuclear Generating Station, Unit 1

should be generating at full powerlater in 1985. Palo Verde Units 2 andare on schedule and should be inoperation by 1987. The ample anddependable energy supplies provide~by these facilities represent a majorresource for development in New M~

ico and throughout the Southwepowerful attraction for new indand businesses.

I

: SS ilange isinevi tab!e,a,oosiiive

',response to needs andopportunities. Ye1 a criiicai

. fnenaeernent ionction is-'" '"-~~~"'"-~ "f~sf ~i oulcf

'arketing: The Future Challenge

Added capacity brings with it a

ne 'ty for new emphasis on market-'ii the Eastern InterconnectionPi complete, PNM is now linkedwith power systems to the east. We are

also seeking markets to the north andin California. The early results of theseefforts are notable. The Company has

in-hand contracts to sell nearly three-quarters of our capacity in excess ofthat demanded by our New Mexicocustomers from 1985 through 1987.

An important element of our mar-

)eting program is the recognition that,. by promoting the success of our cus-

tomers, we ensure our own success.

We are listening more closely thanver to what our customers are telling

us about their energy needs.'] Our marketing program is gainingmomentum, but to protect our share-

holders and customers against the'oossible negative impact of uncom-mitted capacity, we have embracedinventory of Capacity. Inventoryingorotects customers from "stairstep"

'ate increases by holding uncommitted"a ity out of the rate base until it is

At the same time, this new'

concept recognizes the,egitimate interests of shareholders by

allowing capital costs to earn a fairreturn and to be recovered in thefuture.

Broadening Our Base

PNM is now a diversified businessfamily, organized to accomplish twocomplementary tasks. Our electric andgas utilitydivisions serve as NewMexico's primary energy resources.Our investment group, headed byMeadows Resources, Inc., enhancescorporate profitabilitywhile it spreadsour investment risk and creates eco-nomic opportunities in New Mexicoand the Southwest.

Our investment subsidiary, Meadows,accounted for 14 percent of our netearnings applicable to common stockfor the year. Meadows has developed abroad base of interests with invest-ments in forest products, minerals,land and new technologies.

Montana de Fibra, completed in 1984,is expected to produce as much as 88million square feet of medium densityfiberboard annually. It has also gen-erated 200 new jobs in an economicallydepressed area of New Mexico.

Meadows is tapping into South-western real estate markets throughits active partnership with BellamahAssociates, Ltd., a New Mexico-basedland development firm. The success ofreal estate activities has far exceededour expectations, with total sales during1984 amounting to $83.0 million.

The Meadows venture capital port-folio includes investments in gas lasersand other exciting technologies. Onlyabout 4 percent of Meadows'ssetsare dedicated to venture investments,but we expect good returns.

Changing, Yet Unchanged

These key events and accomplish-ments of 1984 and early 1985 representmajor milestones in the Company'sstrategic plan for the 1980s and beyond.But underlying the developments thatI have briefly described, which haveaccelerated the evolution of PNM, there

are solid principles of Company practicethat do not change.

Among those principles is our com-mitment to strong leadership. Therecent appointment of John Bundrantas President and Chief OperatingOfficer of our Electric Operations andJohn Ackerman as President and ChiefOperating Officer of our Gas Operationsreaffirms that commitment. These newappointments clearly separate ourelectric utilityfrom our gas operationsand assure a strengthening of activecompetition between the two utilities.'e seek only the best employees.The early completion of major projectssuch as Eastern InterconnectionProject and Montana de Fibra—at lessthan projected cost —is a testament totheir skill and dedication.

A tough but fair regulatory atmos-phere has yielded rate relief—$38.5million in relief became available lastJuly with another $ 7.5 million madeavailable on February 1, 1985 —andmade possible ratemaking innovationssuch as Inventory of Capacity.

Finally, we are firmlycommitted toour customers, our state and our region.Our enduring goals are to help preservean irreplaceable way of life and toenhance it through new opportunities.

Our shareholders, employees andcustomers recognize the importanceof these goals and commitments. ThePNM management and directors thankthem all for their confidence andsupport.

J. D. GeistChairman and President

"The wind lay upon me. The monoliths were therein the long light, standing cleanly apart from time."

—N. Scott Motttaday

~ .

\rCI

47'-~g

atv e

"NAVAJOCHURCH NEAR FORT WINGATE(New Mexico)," John K. Hitters. Citca 1880. Albumen Print

Corporate Overview

In the decades ahead, the Public.Se 'ompany of New Mexico

( nticipates a continuing popu-la 'o the Southwestern Sunbelt.A land of rich cultural heritage andburgeoning economic development, theSouthwest willrequire a steady andreliable supply of energy to match thisexpansion. As New Mexico and theSouthwest region grow, the Com-pany is committed to meet increasingcustomer demand —with its electric,'gas, and water utilities.,'ecognizing its obligation to promotethe success of its customers as well as

Its shareholders, PNM plays a uniqueiole in the development of the region.PNM believes in the importance ofoeneficial traditions —of development,of goals shared with the citizens itierves, and of a special concern for'he land and the resources with which.t is entrusted.

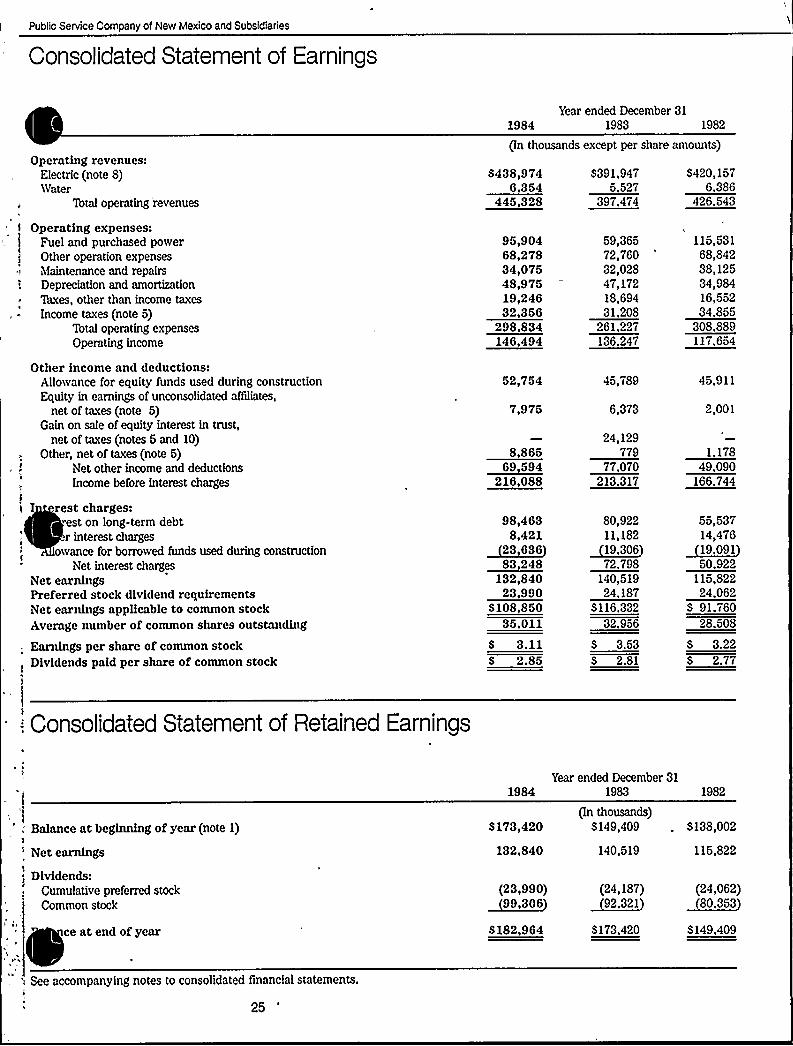

1 984 Earnings

„Careful management of Company..'esources is reflected in revenues and

s. Net earnings for 1984 totaled'on. This represented a 14

;: )e t increase in earnings over 1983,

after eliminating a nonrecurring gainof $24.1 million, in 1983, on the sale ofthe equity interest in a trust whichheld certain coal leases.

Earnings per share of common stockwere $3.11 in 1984. The average numberof shares outstanding was 35.0 million,up 6.2 percent from the 33.0 millionshares outstanding in 1983. Return onaverage common equity was 12.5

percent.

Regulatory Environment

During 1984, PNM was successfulin negotiating settlements of severalimportant cases before the New MexicoPublic Service Commission (Commis-sion). PNM believes that vigorousnegotiation in good faith better servesall interests —the shareholder's, thecustomer's and the public's —than doesprolonged and adversarial litigation.

Rate Filings

In 1984, the Commission approvedthe stipulated settlement of a raterelief request filed in August 1983, theCompany's first electric rate filingsinceOctober 1981. The April 1984 settle-ment allowed PNM's electric utilitytocollect approximately $300 million inannualized revenues (excluding fueladjustment clause revenues). The raterelief amounted to $46 million to beimplemented in two steps. The firstincrease, of $38.5 million, was imple-mented in July 1984. An additionalincrease of $7.5 million was effectivein February 1985.

The bulk of the overall rate adjust-ment reflects inclusion in the ratebase of PNM's portion of constructioncosts for the fourth and final unit atthe Company's coal-fired San JuanGenerating Station (San Juan), locatedin northwest New Mexico.

Inventory of Capacity

The Commission also approved inDecember 1984 a stipulation between

PNM, the Commission staff and otherparties that established a ratemakingmethodology called "Inventory of Ca-

pacity." This methodology places newgenerating facilities into the rate basegradually. Inventorying protects share-holder investment in new generatingplant, while shielding customers fromthe sudden rate impacts that wouldotherwise occur ifa new plant wereput into the rate base all at once.

Faced with the challenge of placingnew, capital intensive plant on-linewhile minimizing the impact on custo-mers, the Company and the Commissionbegan, in 1982, to study this newratemaking concept, which placescertain portions of uncommitted plantcapacity into "inventory." In 1983 theCommission established a task forcerepresenting the Commission staff,PNM, the Attorney General's staff andthree customer groups. This task forcewas charged with examining the in-ventorying concept and providing arecommendation on its application as

a ratemaking method.Inventorying defers certain costs

associated with uncommitted capacityabove a 20 percent reserve margin. Italso defers some of the cash return onshareholders'nvestment and accruesnon-cash earnings while the plant isin inventory. Such deferred carryingcosts willbe recovered from futurecustomers when the inventoried plantis placed into the rate base.

Inventorying includes other cost-recovery methods. Revenues from bulksales of inventoried capacity willbeused first to pay fuel costs and othervariable operating costs, then to payup to half of the depreciation andproperty tax costs. Any additionalrevenues willbe allocated to thesecosts and carrying charges, whichwould otherwise be paid by futurecustomers.

The plan also contains a cap whichlimits the cost that customers willpay in the future.

"Wherever humanity has made the hardest of all startsand lifteditselfout of mere brutality, is a sacred spot."

—Willa Cather

QYg e,qXg (p AJ v w ~%,f(vga'v'gPp i w QJ )'gv '%v'u'.

A

"CLIFF PERCHED ACOMA,"Edward S. Curtis. 190s. Glass Plate Negative

Securities Transactions

Bonds issued in 1984 were comprised" of first mortgage bonds and pollution

control revenue bonds. In August,PNM sold $ 65 million of its FirstMortgage Bonds, 13 I/8% Series due1994. Proceeds were applied to reduceshort-term debt. In September, approx-imately $77 mBlion of first mortgagebonds was issued to secure PNM'sguarantee of an equal amount of 5.9%Pollution Control Revenue RefundingBonds, Series 1977 due 2007, issuedby the City of Farmington, New Mexico.

- The refunding bonds were issued in1977 to provide funds to pay two prior

'ssues of pollution control revenuebonds which matured October 1, 1984.

ecember, a total of $38.5 milliontion control revenue bonds

was sold in two series through theMaricopa County, Arizona PollutionControl Corporation. The bonds wereissued to defray a portion of cost toPNM of certain pollution control facil-ities associated with the Palo VerdeNuclear Generating Station (Palo Verde)Units 1, 2, and 3. Of the $38.5 million,$23 millionwas Annual Tender Bonds

,maturing in 2009 which were sold in a'ublic offering and secured by the', Company's first mortgage bonds, and„$15.5 million was in a separate series,'sold as a private placement on an'unsecured basis.

Approximately $48 millionof newequity capital was raised through theCompany's special stock plans through-,out the year. About 2.2 million sharesof PNM common stock were issued,through such plans, including the.Company's Dividend Reinvestment

!

Plan.As of December 31, 1984, on a

'dated basis, commercial paperrt-term notes totaling $30.3

n had been borrowed under PNM'sI

$ 164 millionof bank lines of creditand revolving credit arrangements.

During the year, four rating agenciesreviewed the Company's securities.Standard & Poor's Corp. and FitchInvestors Service, Inc. reaffirmedtheir ratings. Duffand Phelps, Inc.removed the Company from its credit-watch list, maintaining its prior rating.Moody's Investors Service loweredits rating on the Company's firstmortgage bonds and secured pollutioncontrol revenue bonds from Al to A2.Unsecured pollution control revenuebond ratings have been lowered fromA2 to A3, with preferred stock ratingsreduced from a2 to a3.

PNM Acquires Gas Company of NewMexico

Among the most significant develop-ments in PNM's history is the recentsubstantial broadening of its utilitycommitment. In January 1985, PNMcompleted the acquisition of Gas

Company of New Mexico (GCNM) fromthe Texas-based Southern UnionCompany (Southern Union) as partialsettlement of an antitrust suit. Withthe acquisition PNM anticipates thattotal utilityrevenues willnearly doublein 1985.

PNM purchased Southern Union'sNew Mexico gas utilityassets for netbook value (less assumed liabilities)of approximately $224.3 million, withSouthern Union to receive $ 172.8 mil-lion. The $51.5 million differencerepresents Southern Union's settlementof the suit with all parties, includingPNM. As part of the settlement, PNMfunded $ 15.6 million, in cash and byissuing a note for $20 million, of thetotal $ 51.5 millionsettlement amountto the other plaintiffs. The remaining$ 15.9 million of the settlement, lessexpenses, willbe refunded to PNM'selectric customers by PNM.

Customers willbenefit from directrefunds made as part of the settlementand by PNM negotiations, made pos-sible through the acquisition, for lowergas prices at the wellhead.

Planning for the Future: New MexicoGenerating Station

PNM is considering a project withextraordinary potential for serving newmarkets while contributing to thequality of life in the region. In August,the Company entered into an agreementin principle with the Navajo Nation,General Electric Company and BechtelPower Corporation to explore thepossibility ofjointlybuilding and op-erating a major regional power projectin New Mexico. Participants willbeevaluating markets, design, fuel sourcesand financing to determine whetherthe project would be economicallyviable in the 1990s.

The proposed coal-fired plant, NewMexico Generating Station, would notbe designed as generating capacity forPNM's New Mexico electric customers,but would position the Company torespond to growing regional powerneeds. The project would complementelectric operations with associated newtransmission lines and facilities thatwould enhance the Company's abilityto market and deliver power.

"Itis the same now, as a thousand years ago once you overlook the cities:The desert begins just beyond those lights it crouches."

—Keith Wi(son

u l E''4

'K

s

IF

l ''; 'b.'.,: ''F

r'-*

"CHURCH BUTTRESS. RANCHOS DE TAOS CHURCH," Paul Strand, t 932, Silver Print

Gas Company ofNew Mexico

'0

Attorney Gene Gallegos argued one ofthe strongest cases of his career at analtitude of 85,000 feet. In 1981, chanceplaced the Santa Fe lawyer in an airlineseat beside Al Robison, PNM's VicePresident of Finance. Itwas a meetingwith far-reaching consequences forhundreds of thousands of New Mexicogas and electric customers, for PNMand, ultimately, for PM I shareholders.

Rvo years earlier, a group of NewMexico school teachers had hiredGallegos to challenge natural gas pricingpractices in court. Gallegos believed hecould make a credible antitrust price-fixing case against Southern UnionCompany, the Dallas-based owner of theGas Company af New Mexico, andseveral major natural gas producers andsuppliers. An antitrust lawsuit was filedon behalf of residential gas consumerspurchasing natural gas from GCNM.Certain agencies of the State of NewMexico, all large volume purchasers ofnatural gas, joined the lawsuit,

The battle dragged on far 23 monthsthrough depositions and hearings. Then„on an east-bound airliner, Gallegos foundan "attentive ear" in Robison, and laidout the facts of his case.

"As I listened, I realized PNM neededto lool at this case very, very carefully,"says Robison.

Some of PNM's generating plants werefired by natural gas. Ifallegations ofprice fang were true, PMI was payingtoo much for its gas and, worse, passingthe higher costs along to its own electriccustomers.

When Robison returned to Albuquer-que, he discussed the matter with JenyGeist, PNI I's President', wha authorizeda further investigation. A few weekslater, PNM joined the suit on the side ofthe residential gas consumers.

Shortly after PNM entered the case,two defendants, Southland Royalty Com-

pany and Supron Energy Corporation,settled out of court. After seven weeksof trial in Las Cruces, New hiexico, thejury ruled against Southern Union andthe remaining defendants. However, theliabilityverdict was overturned on a

technicality and a new trial ordered.Conoco and Consolidated Oil and Gas,also defendants, then settled, bringingthe settlement total to S70.3 million forPNM and the other plaintiffs.

By the faIIof 1983, all defend antsexcept Southern Union had settled. Witha second trial scheduled for the springof 1984, settlement negotiations withSouthern Union were conducted over aperiod ofweeks. When these negotiationsfailed, Sherman G. Finesilver, ChiefJudge of the United States District Courtfor the District of Colorado, ordered topofficials of Southern Union and PNI I toDenver for a face-to-face talk.

Only a few days before the case wasslated for trial, a series af around-the-clock discussions was held. Terms of asettlement were worked out, includingan understanding that Sauthern Unionwould sell its New Mexico gas utiTityassets to PNM.

The residential plaintiffs had wantedfor several months to bring ownershipand control of the gas utih*ty "home toNew Mexico.'" Many months before,Gallegos had suggested to PNM officialsthat acquisition of GCNM by PNMwould be af value to New Mexico andall gas consumers in the state, Aftercareful investigation of the gas utilitybusiness, PNM became convinced thatthe purchase was iri the best interest ofNew Mexico, residential gas customersand the corporation and agreed to thesettlement. For PÃM, the settlementincreases total Campany assets,broadens its earnings base and shouldimprove cash Ilaw.

The settlement benefits Nev Mexicansin a variety of ways. Itwillprovidemillions ofdollars in refunds to utiTitycustomers. And along with bringingcontrol of the state's gas utiTityback toNew Mexico, itmay bring lower gasrates as welL According to settlementterms, PNM willrenegotiate natural gas

supply contracts.

"From any distance itis all by itself... Risen alone off the dry Plateau,this rock or a mountain of a rock has seemed as alive as itis dead."

—Joseph McEiroy

tt

E

It)t

(ftT

t tt

T

Z,

"SHIPRCCK, NEW MEXICO,"Jody Forsrer. 1979. Sihrer Prinr

10

Electric and WaterUtilityActivities

The social, political and economic

, environment has changed over the,

>years, and the utilityindustry has

I adapted in a number of ways. Utilities..'„have changed fuel sources to limit

t dependence on foreign supply. Theyhave broadened resource bases andestablished nonutility subsidiaries to

l ensure stability. And they now function,I in much more competitive markets.

Operating in a changing marketplace,PNM has adapted successfully. Amidstthese changes, however, PNM continuesto balance its commitments to share-

: holders, customers and the region withtough productivity goals and innovativemarketing.

Electric and Water UtilityReport

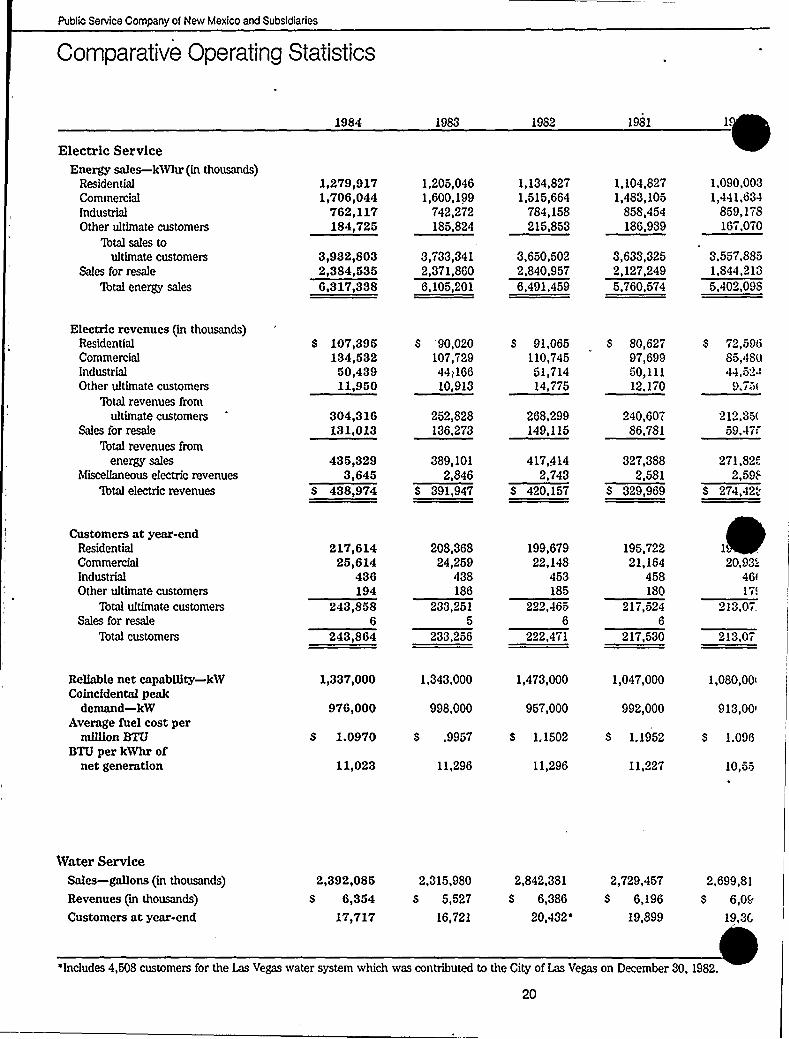

operating revenues for 1984sed 12.0 percent from $397

million in 1983 to $445 million in 1984.This increase in total operating revenuesresulted primarily from rate reliefgranted by the Commission andincreased fuel clause revenues.

Due to significant cost containmentefforts, utilityoperation and main-tenance expenses, excluding fuel andpurchased power expenses, decreased2.3 percent from $ 105 million in 1983to $ 102 million in 1984. However, totaloperating expenses in 1984 increased14.4 percent over 1983, largely becauseof higher fuel and purchased powercosts.

Kilowatt-hour sales increased 3.5percent in 1984, while retail saleswere up 5.3 percent. Sales to wholesalecustomers increased slightly over 1983levels. The average number of electriccustomers rose to 238,000, up from228,000 in 1983.

Marshaling Resources For The Future

In the 1960s, PNM recognized twofactors in the utilityindustry that wouldaffect the way the Company operates.Sharply rising demand for electricityindicated that it was time to buildadditional generating capacity, andfluctuating fuel prices cautioned againstreliance upon one fuel source.

In response to these signals, PNMlaunched a construction program toprepare for anticipated rising con-sumption. It also began to shift its fuelbase away from a dependence on oiland gas to a greater reliance on coaland nuclear fuels.

As the Company enters 1985, it hasmet these objectives. Net operatingcapacity for 1984 was 1,337 megawatts.Energy is supplied by two coal-firedplants, as well as by reserve oil-firedand natural gas-fired plants. A majornuclear power plant, in which PNMholds an interest, is nearing completion.

Palo Verde Unit 1 Licensed

Beginning in 1985, PNM's system isscheduled to receive its first energy

from a 10.2 percent interest in PaloVerde, located 55 miles west of Phoeni~,Arizona.

In December, the Nuclear RegulatoryCommission issued a 40-year operatinglicense for Palo Verde Unit 1. Thelicense temporarily restricts powerproduction to 5 percent, with successfullow-power testing leading to possiblefullpower operation by the end of1985. Units 2 and 3 are scheduledfor operation in 1986 and 1987,respectively.

When all units are complete, PaloVerde willgenerate 3,810 megawatts.PNM's share willbe 390 megawatts.The projected cost for the Company'stotal interest in the three units is $938million.

The new inventorying method ofratemaking willallow shareholders torecover the significant capital invest-ment in Palo Verde, while protectingPNM customers from the "rate shock"attributed to sudden rate increases.More important, Palo Verde is securingenergy independence for PNM wellinto the next centmy.

San Juan Surpasses Expectations

San Juan represents PNM's earlycommitment to end its reliance onunstable oil and gas markets. Locatedadjacent to a rich coal supply, SanJuan has surpassed Company expec-tations for cost, reliability andefficiency.

San Juan Unit 4 stands among themost reliable generating units of itstype and size in the country. SinceApril 1982, when Unit 4 was placed inservice, it has been available for service89.5 percent of the time. This comparesto an industry average of about 79percent.

Much of PNM's pride in San Juanstems from its environmental record.The coal-fired plant is equipped withpollution control equipment thatmeets or exceeds state and federalregulations.

11

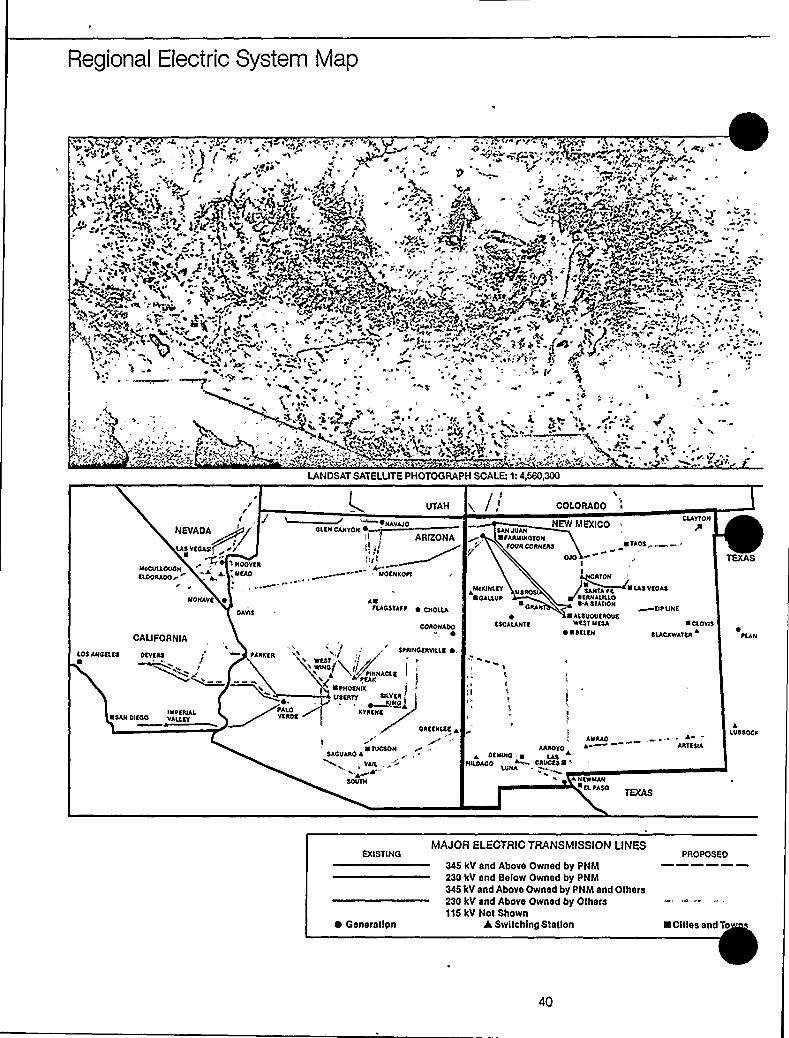

Eastern Interconnection ProjectOpens New Markets

With capacity additions in place,PNM is looking ahead toward a periodof expanded marketing. One importantstep in reaching new markets is toimprove PNM's transmission capabilitythrough efforts such as the constructionof the Eastern Interconnection Project(EIP). This 216-mile, 345-kilovolt lineruns from just north of Albuquerqueto an AC/DC converter station locatednear Clovis, New Mexico and willlinkthe Company with Texas.

In January 1985, PNM began thesale of up to 220 megawatts per hourof surplus energy to SouthwesternPublic Service Company (SPS). Thisenergy sale willend in 1989, whichSPS may extend into 1990. Starting in1991, the Company willpurchase 100megawatts of interruptible power fromSPS, thus improving system reliabilityand power mix. Between 1995 and2011, PNM willpurchase up to 200megawatts of interruptible power fromSPS.

To speed recovery of investment,the Company sold the facilities asso-ciated with the EIP to private investorsin February 1985. The facilities havebeen leased back to PNM, reducingrevenue requirements by approximately310 million in 1984, or 335 million inpresent value over the life of the project.

Sangre de Cristo Water Company

In January 1985, the Commissionapproved an additional N million rateincrease for PNM's Sangre de CristoWater Company, to be placed intoeffect in three-steps: one immediateincrease, a second scheduled for April1985 and a third for October 1985.

In November 1984, at the request ofthe City of Santa Fe, discussionsopened regarding a possible sale ofthis division to the city. Ifanagreement is reached, the sale couldbe completed during 1985.

~ /

k4

Developing New Markets

PNM recognizes that utilities operatein an increasingly competitive market.Today's customers have the option tochoose energy from a sizeable assort-ment of alternatives, including wood,propane, solar and cogeneration.

To compete effectively in this market,PNM has stepped up its retail marketingefforts. Anew marketing program basedon the concept of "customer success"willenable PNM to improve its alreadystrong market position by providingmore responsive, flexible services tocustomers.

The business of the electric ut'is service. For PNM's electric utility,customer success means finding waysto assist customers with their energymanagement needs and seeking newways to help industrial customersincrease their profit margins. The netresult of this marketing approach forPNM willbe increased profitabilityand enhanced credibility with itscustomers.

Marketing New Capacity

The Company initiated a marketingprogram six years ago to increase sakto wholesale customers. During thisperiod, PNM negotiated long- termcontracts and annual sales agreement.representing approximately 73 percei.of what was projected to be availableas uncommitted capacity from 1985through 1987.

Ongoing sales include contracts toseH as much as 236 megawatts oJuan Unit 4 capacity to San Dieand Electric Company. Also, P icontracted with Arizona Public ServicCompany to sell 60 megawatts dur~the 1985 summer peak. Plains ElectriGeneration and 'Aansmission Cooperative, Inc. willreceive 15 megawattsof peaking power until 1989.

During 1984, PNM also sold blocksof energy on the wholesale market tosuch diverse entities as El Paso ElectriCompany, Texas-New Mexico PowerCompany, Nevada Power Companyand the California cities of Burbankand Pasadena.

The creative challenge that lies ahe;for PNM is to design energy productsthat improve the Company's marketiiability. For example, the InterutilityMarketing Department is developinginnovative energy packages to attracbulk power purchasers. At the sametime, the Company is studying im-piovements for the transmission system

that would open up entirely new

12

Eastern InterconnectionProject

North of Albuquerque, along the RioGrande, stands PÃi's Bernalillo-Algodones transmission switching sta-tion. Eastward, beyond the majesticcentral mountains of New Mexico,stretch rambling plains and many-fingered gulches, reaching for Texas.To motorists traveling the smoothribbons of eastbound interstate, thepower lines darting in and out ofviewappear almost part of the landscape.

For the people who surveyed andstrung the miles of PiVih's EasternInterconnection Project from Algodonesto Clovis, New Mexico, those hightransmission lines represent two yearsof hard work in dramatic terrain.

Piei announced the project in No-vember 1982. Plans called for 216 milesof 345-kilovolt transmission line to bestrung and operational in less than twoyears —about half the normal construc-tion time fora project this size.

Southwestern Public Service Companyhad agreed to purchase up to 220megawatts per hour ofsurplus energyfrom PNM starting in January 1985 andcontinuing to at, least 1989. In 1991,PNM willbegin the purchase of 100megawatts of interruptible power fromSPS, and from 1995 through the remain-ing life of the contract, SPS willprovidePNI I with up to 200 megawatts ofinterruptible power.

PNM builtboth the line and theACIDCBlackwater Converter Station(Blaclnvater). Completed late in 1984the project, linked. PNM for the firsttime withpower systems ta the east.

Not only does the project enablePNM to sell available power not currentIydemanded by customers in New Mexico,but, says PNM Senior Vice PresidentJack Wilkins, "The interconnectiongives us fle~bili*tyin planning futuregenerating projects to meet New Mex-ico's energy needs. Italso providesboth PNM and SPS with additionalreliability."

One immediate consideration for theEIP team was to solve the problem ofinterconnecting the systems of PNMand SPS. The generators of the twosystems do not rotate identically, sothey needed an "interpreter" to completethe connection. The ultimate solution

was the Blackwater high voltage direct:current (HVDC) converter station whichconverts the AC of one system to auniform HVDC and then to a compatibleACsystem. Thisrathersimple-soundingconversion at Blaciovater is accom-plished with complex, state-of-the-artequipment.

Looking back on the project, PNM'sEIP Project Manager, Larry Sullivansees some advantages to working undersuch a tight construction schedule. "We

knew going into the project that wewould have to be flexible and creativeto meet the extremely short

deadline,*'ays

Sullivan.The EIP team devised faster, more

efficien ways to perform environmentalstudies, land surveys, right-of-way ne-gotiations and construction. Even withthe tight schedule, the team conductedcareful route and environmental studies,consulting withmore than a dozenfederal, state and, local agencies andcommunity leaders. Along the way„ theproject turned up such unexpectedtreasures as historical. artifacts, ancientarchaeological sites and rare flora—allfinds ofvalue to scientists and archae-ologists.

Looking for innovative ways to speedup construction, the project team re-placed plodding truck caravans withhelicopters and increased the pace oftower emplacements from 6 to 30 aday. The 8,000-pound towers wereassembled at staging areas about everysix miles along the line and liftedby helicopters to their precise con-crete foundations where ground crewsanchored them with guy wires. Thehelicopters not only saved time butminimized, the amount ofneeded accessland and reduced the project's environ-mental impact,

With such methods, some of whichhad never before been used by PNIII,the EIP team completed the projectahead of schedule and under budget."Alot of the innovations just came outofpeople's enthusiasm," Sullivan says."We tried to anticipate problems as wewent along. Anyone with an idea knewit was going to be heard. Itwas theenthusiasm of the people involved thatmade ita success."

13

"... I found that l was no longer lost in the enormous landscape of hills and sky.l was a veryimportant part of the teeming life of the llano and the river."

-Rudolfo A. Anaya

l1

~a~

0

l

h.w f

a

"LAMESITA. NEW MEXfco," filtttamC'itt, l978, Silver Pnnt

14

Broadening Our Base

At the core of PNM's long-termbusiness philosophy is a diversiTicationstrategy aimed at improving return onequity and stimulating economic growth.The broadening of PNM's revenue base

" willhelp stabilize earnings in the years" ahead, while enabling the Company to'ontribute to the economic development

, of the region. PNM is examining an'rray of nonutility investments with

"",exciting future earnings potentiaLt

Sunbelt Acquires GasGathering Company

Pl&I's mining subsidiary, SunbeltMining Company, Inc., (Sunbelt)acquires, markets and develops coaland other mineral resources and pro-

"

vides contract mining services. Underthe GCNM settlement agreement,

' Sunbelt acquired the stock ofSouthernUnion Gathering Company (Gathering

i C any), which purchases and trans-atural gas for GCNM. Gathering

plant and equipment assets

I are in excess of $ 19 million.Suribelt also purchased the stock of

'ranswestern Mining, Inc. (Trans-western). Transwestern's subsidiary,Calgom Mining Inc. is the operator ofGoldstripe joint venture, a surface gold

. mining project located in California.I

,'nvestment Subsidiary~ Creates Opportunities

The Company's nonutility arm,Meadows Resources, Inc. (Meadows),invests in nonutility ventures with highgrowth potential. Its real estate activi-

,ties have contributed to overall earnings

'or three years, while in July its first'ajor New Mexico project, Montanade Fibra (MdF), began creatingrevenues and jobs. Examining a widevariety of potential investment oppor-tunities, from manufacturing plants tohigh technology products, Meadows

'eeks to enhance PNM's earnings while'buting to the economic develop-

New Mexico and the Southwest.,I

Land Partnership DevelopsNew Potential

Three years ago Meadows entered aland development partnership calledBellamah Community Development(BCD). Meadows owns 50 percent ofBCD, and a successor to BellamahLand Company, a long-time New Mex-ico-based real estate company, ownsthe other 50 percent.

BCD's activities range from realestate acquisition, planning and devel-opment to the marketing of residentiallots or commercial and industrial tractsto builders. While approximately 26percent of the land owned by BCD isin New Mexico, development activitiesreach into Arizona, Texas, Oklahoma,and Colorado.

BCD has earned a respected placein the Southwestern real estate devel-opment market with two large-scaleprojects in Dallas, Texas. In 1982;BCDacquired Flower Mound, a 3,018 acredevelopment in northwest Dallas. Bythe end of 1984 almost all FlowerMound acreage had been sold todevelopers and builders. This successled the partners to purchase the4,377 acre Mountain Creek develop-ment, 10 miles southwest ofdowntown Dallas.

Both developments involve multi-purpose residential, commercial andindustrial land use with sales of parcelsto smaller developers who build inaccordance with BCD specifications.The projects are also similar in twoother important respects: (1) theyinvolve very large, previously un-developed acreage which allows forcomprehensive master planning andzoning; and (2) they are large enoughto-provide a wide mix of land uses andthus eliminate dependence on a singlesegment of the real,estate market.

Montana de Fibra, Inc.

Meadows has invested approxi-mately $67 million in the Las Vegas,New Mexico MdF facilitywhich

manufactures a wood substitute calledmedium density fiberboard. Construc-tion of the project was completed in1984.

Formerly a joint venture betweenPonderosa Products Inc. and Meadows,MdF is now a corporation in whichMeadows holds a 90 percent ownership.In October, Meadows entered into asale-leaseback transaction with MdFinvolving assets of about $55 million.

Meadows Invests Capital

One of Meadows'ost excitingactivities is its venture capital portfolio.By year-end Meadows held interests ineleven companies, representing a totalinvestment of nearly $7.6 million.

The primary investment focus is incompanies with high growth potential.These include a range of medium tohigh technology enterprises, both instart-up and later stages of develop-ment. Most such investments rangefrom $250,000 to $ 1 million.

Meadows has also joined with otherventure capital firms located in Texas,New York and California. This networkis providing a new channel for capital,contacts and expertise to supportdevelopment in New Mexico, whileexpanding Meadows'nvestment op-portunities outside the state and region.

Further development ofMeadows'enture

capital portfolio should increasereturn on equity, whBe contributing tothe New Mexico economy. Wheneverpossible, Meadows invests in companiesthat either operate in New Mexico orplan expansion into the state. Meadowsalso lends its expertise and capitalsupport to state economic develop-ment efforts, such as the BusinessDevelopment Corporation, the TechnicalInnovation Center, New MexicoEntrepreneurs'lub and New MexicoTechnet, Inc.

15

"You should understand the way it was back then,becauseitis the same even now."

—Leslie Mattnon Siiko

g f, ~tgC @Qf,

'a ~> k k''a"f'i

"-" M~~~ tti'"=" «-'Vg."tt~~~~$~$I'ot~"'~g~~~>(

~ ' p~QiI

harv~

. ~

>kg

r

r

rI

r

~~

"CAVE DWELLING,BANDELIERNATIONALMONUMENT,NEW MEXICO," David Noble. 1982. Silver Print

Montana de Fibra

* t

P

I

The eastern slopes of the Sangre deCristo mountains are covered with pinetrees. At the point where the tall,mountain forest meets the broad NewMexico plains stands the once-frontiertown of Las Vegas. Tlus historic com-munity has a new and beneficialneighbor.

Montana de Fibra-that's Spanish for"mountain of fiber"—is also the nameof an exciting, new manufacturingfacility located a short distance fromLas Vegas, New Mexico within view ofthe mountains and the pine forest ituses as a resource. Completed in1984-under budget and six monthsahead of schedule —the $67 millionfacility is a source of pride for the townand for Meadows Resources, Inc.,PNM's wholly-owned, nonutilityinvestment subsidiary.

MdF takes wood chips, shavings andsawdust —waste from local sawmills,including its own nearby sawmill—andturns them into a highly marketableproduct called medium density fiber-board. EVhen fullyoperational, the250,000-square-foot plant willproducefiberboard at a rate of up to 88 millionsquare feet annually.

You may be more familiar with me-dium density fiberboard than you think.It's free of knots, saws cleanly andholds a screw just as snugly as thewood in your favorite rocking chair.Unlike particle board, it does not chipor splinter easily. Fiberboard is a highquality product used to manufacture a

host of common items, such as furni-ture, cabinets, heavy-duty crates andeven church pews.

Meadows has the majority interest inthe plant Ponderosa Products, Inc.,the operating partner, is a companywith many years of experience in thewood products industry. Strategicallysituated near major transportationroutes, emerging markets, and thenecessary raw materials, the plant maysoon capture as much as 10 percent ofthe national fiberboard market.

Meadows'ontribution to the projectincludes its financial strength, construc-tion experience and knowledge of NewMexico. Ponderosa brought to the joint

venture extensive operating experiencein forest products, lumber manufactur-ing, and marketing. The combinationhas produced an efficient plantoperation.

Ecology and efficiency go hand-in-hand at MdF. Use of sawmill waste tomanufacture fiberboard eliminates anenvironmental nuisance, which other-wise must be burned, buried or dumped.MdF plant waste is used to fuel a boilerin the manufacturing process, and theboiler ash is sold to Las Vegas forfertilizer.

For PNM and its shareholders, MdFis a milestone in a carefully wroughtnonutility investment strategy, of wluchan important element is economicdevelopment in New Mexico and theSouthwest. The plant already employsover 200 people, and many other newemployment possibilities exist becauseof anciHary businesses attracted to Las

Vegas by h IdF. A modest estimate in-dicates this increased employment willgenerate $3.5 million in income, $2 mB-lion in retail sales and $ 1.7 million inbank deposits for the area. Demand forelectricity from the hfdF plant alone isexpected to generate revenues forPNM's electric utilityof about $300,000a month.

Las Vegas Mayor Steve Franken saysMdF not only has "contributed signif-icantly to the economy of the town, butalso has enhanced our image as a goodhome for industry."

Indeed, the industry has brought anew kind of thinking to the community,says MdF Personnel Manager AbelinoMontoya. "More than in buildings andsteel, the shareholders of PNM havemade a wise investment in the peopleof New Mexico."

17

"Black thunder-storms used to roll up from behindit and pounce on us like apanther without warning. The lightning would play round it and jab into it so thatwe were always expecting it would fire the brush. I'e never heard thunder so loudasit was there." —WillaCather

"."~ ~

"(««W»-'jest'4«r&r««tt«7«~xge~',0" 7'pt7cc., +~~a'.. 7

I( tw+fi7«z «~~)~~ » s«j'j «» '. 'i''.~ 'll

7

It'7

"LIGHTNINGOVER THE RIO GRANDE VALLEY,NEW MEXICO,"Jim Bones, f983, Dye Transfer

No reproduction of the works contained herein should be made without first obtaining express permission from the copyright holders.

18

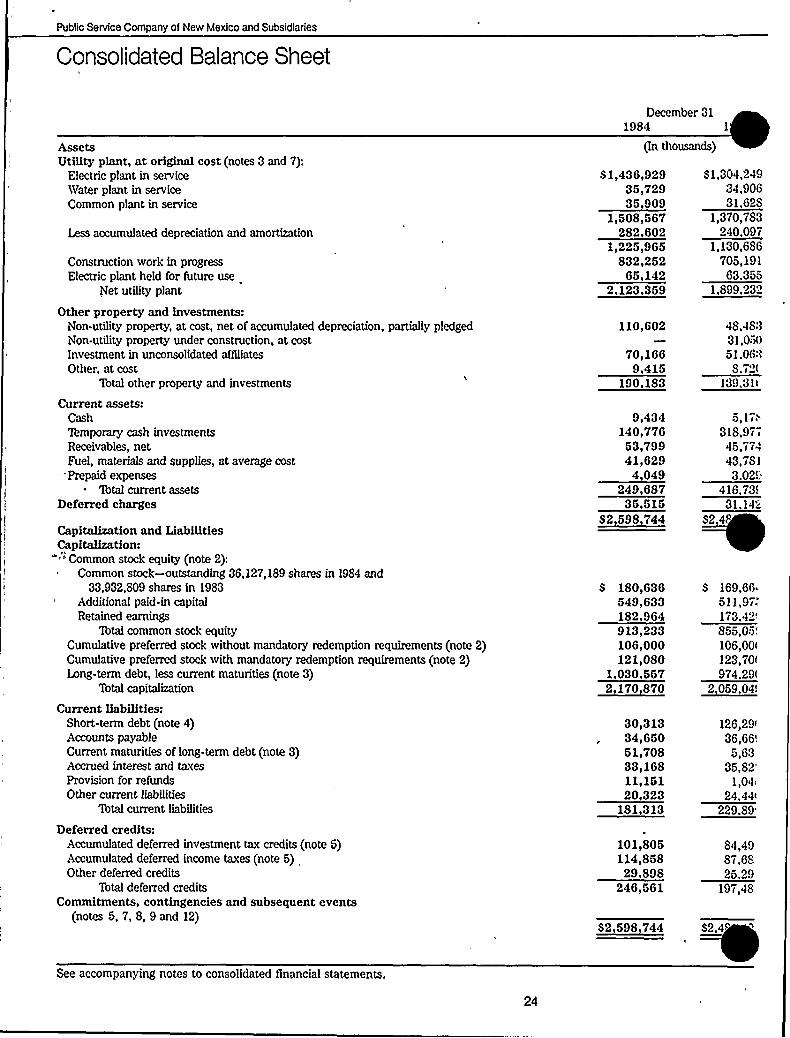

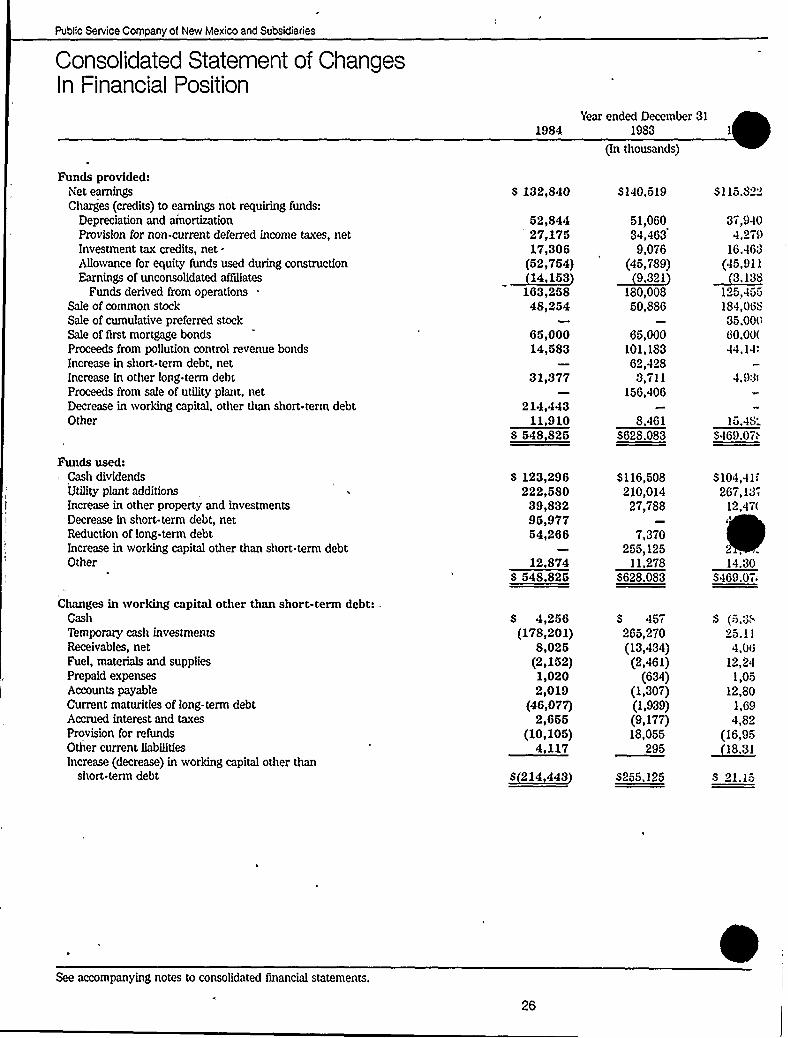

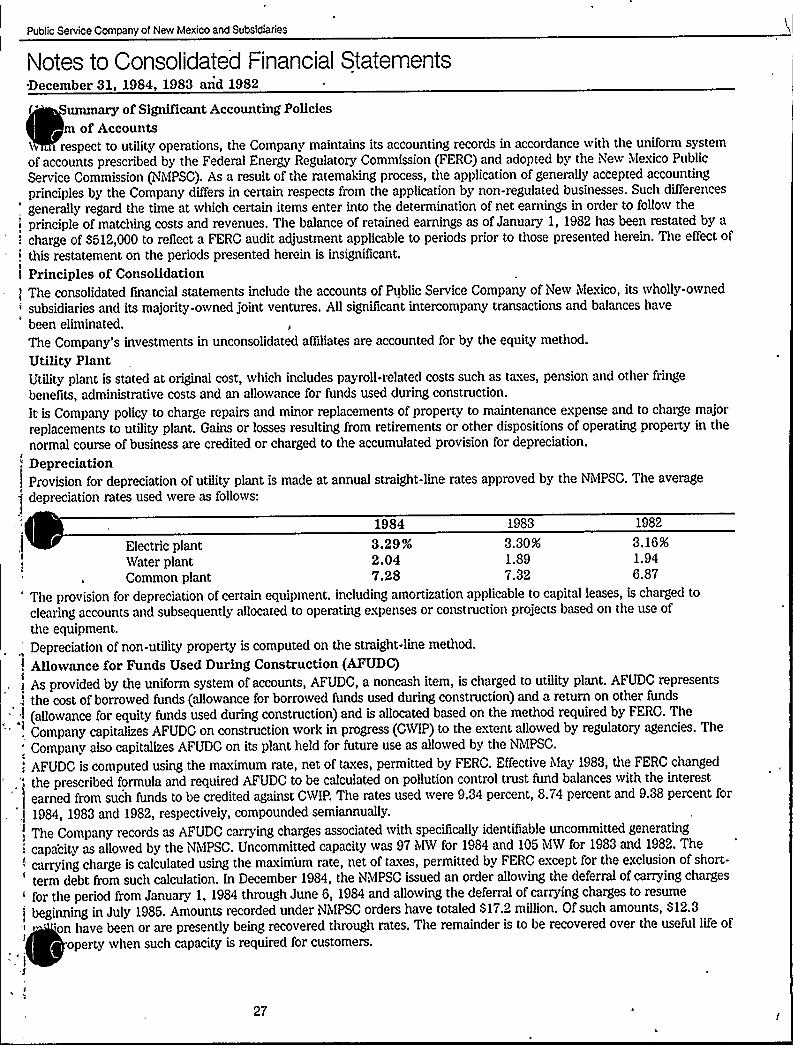

Financial Data and Consolidated Financial Statements

Comparative Operating Statistics

Selected Financial DataManagement's Discussion and Analysis of Financial Condition

and Results ofOperationsManagement's Responsibility for Financial Statements

Auditors'eportConsolidated Balance Sheet

Consolidated Statement ofEarnings

Consolidated Statement ofRetained Earnings

Consolidated Statement ofChanges in Financial Position

iVotes to Consolidated Financial Statements

Supplementary Information Concerning the Effects ofChanging Prices

Quarterly Operating Results

Stock/Dividend Data

2021

22

23