FMCG Market in Pakistan - GreekPakistaniChamber

37

FMCGMarket in Pakistan

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of FMCG Market in Pakistan - GreekPakistaniChamber

FMCG Market in Pakistan

FMCG Market ofPakistan

• Rapidly Growing

• Double DigitGrowth

• 2016 PKR 450Billion

• Average 15% Growth over theyear

• Considerable increasein growth after2010

ü Usage of Internet

ü Opening of IMTs &LMTs

ü Changing Lifestyle&

Different Shopping

Experience

Trade Landscape

PA KI S T A N The Land Of Opportunities

Pakistan-TradeLandscape

Pakistan Urban Semi-Rural/RuralOutlets 290,000 360,000Outlet Buysfrom Distributor/wholesaler Nearest urban town

Assortment Wide – all categories Strong/Established Categories -LUPs

Company Direct Sales* 95% 5%*These are distributor sales to trade and do not reflectconsumption

Urban Channels

General Stores

Kiryana Stores

Wholesale Medical / Gen Med Stores

Self-Service/MT

Others*

% of Universe

48% 14% 4% 11% 0.2% 23%

Sales Contributi

on**

36% 11% 21% 10% 18% 4%

StoreCount FLAT FLAT FLAT* Others: Pan/cigarette shops, tea stalls, juice corners andHoreca** Of major FMCG companies. For pharma companies, 100% contribution comes through the MSchannel

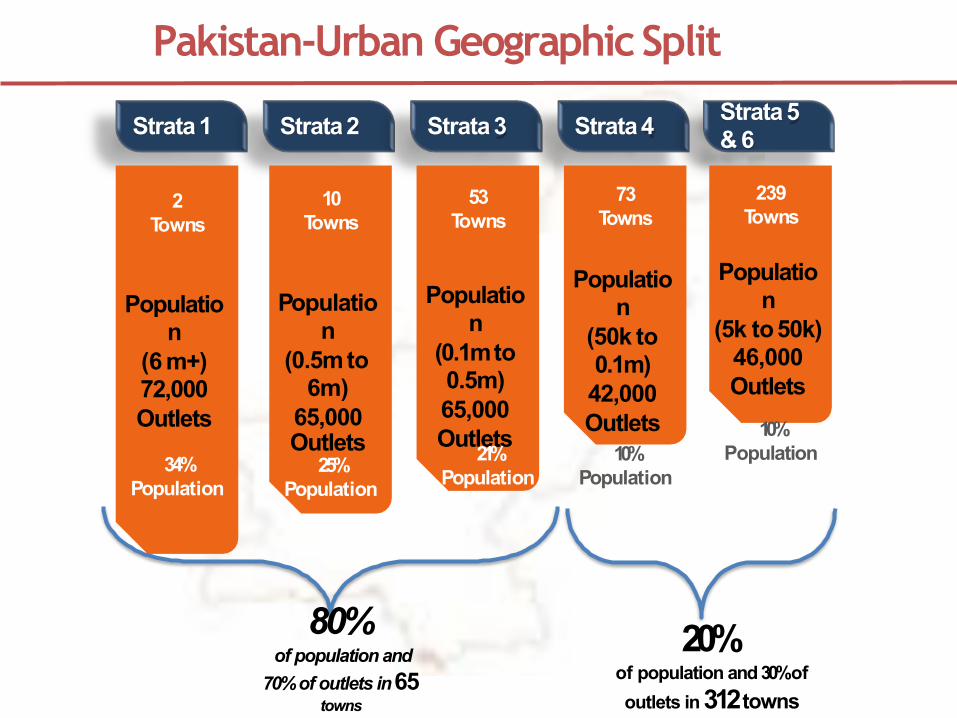

Strata1 Strata2 Strata3 Strata4 Strata5& 6

2Towns

Population

(6 m+)72,000Outlets

34%Population

10Towns

Population

(0.5mto6m)

65,000Outlets25%

Population

53Towns

Populatio n

(0.1mto 0.5m)65,000Outlets21%Population

73Towns

Populatio n

(50k to0.1m)

42,000Outlets10%

Population

239Towns

Populatio n

(5k to50k) 46,000Outlets10%

Population

20%of population and 30% of outlets in 312towns

80%of population and

70% of outlets in65 towns

Pakistan-Urban GeographicSplit

RTMStructure

RTMStructure

Modern Trade(IMT, LMT,

TER)

Self ServiceStores

Pharmacies (MS, GMS)

Wholesale

General Stores(GS,KS,Others)

Distributors

SelfService Stores

Pharmacies(MS, GMS)

Wholesale

GeneralStores (GS,KS,Others)

SubDistributors

Institutional Distributors

Company

USC/CSD

InstitutionalSupplies

Modern Trade Channel and

Shopper Characteristics

▪Female/male

, looking to stock-up; mainly SEC A &B

▪Looking for a

safe, comfortable,pleasurableexperience

▪Operateswith a list but likes to comparison shop

▪Experimenta

l – wants to explore new categories

▪Shopswith c

reditcards/cash

▪Expectsbarg

▪Motivatedby

ains/value

width of product mixavailable

▪Trusts thequ

▪Oftenforms

ality of thestore

a relationship of trust with storeowner

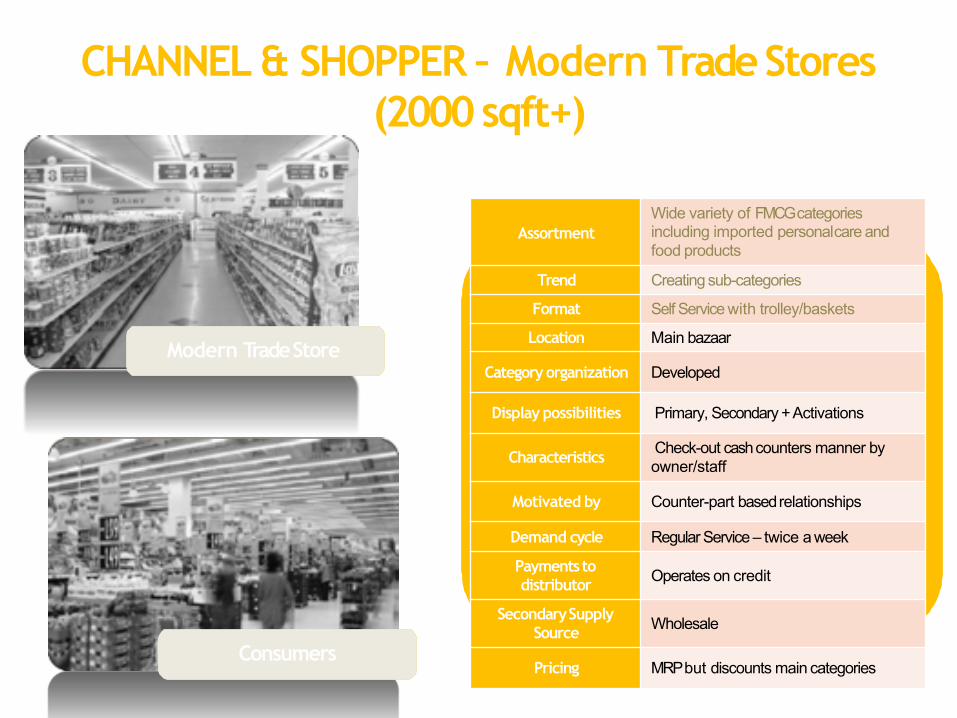

CHANNEL & SHOPPER – Modern TradeStores (2000sqft+)

Modern TradeStore

Consumers

Modern TradeStore

Consumers

AssortmentWide variety of FMCG categories including imported personalcare and food products

Trend Creating sub-categories

Format Self Service with trolley/baskets

Location Main bazaar

Categoryorganization Developed

Display possibilities Primary, Secondary +Activations

Characteristics Check-out cash counters manner by owner/staff

Motivated by Counter-part basedrelationships

Demand cycle Regular Service – twice a week

Paymentsto distributor Operates on credit

SecondarySupply Source Wholesale

Pricing MRP but discounts main categories

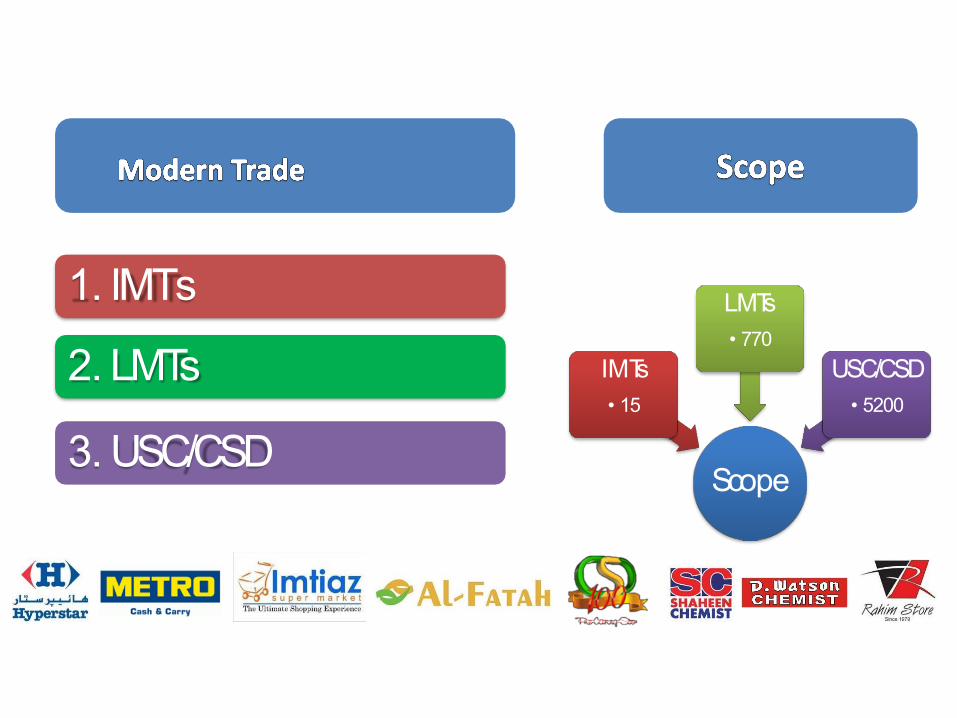

Modern Trade Landscape

Channels Introduction

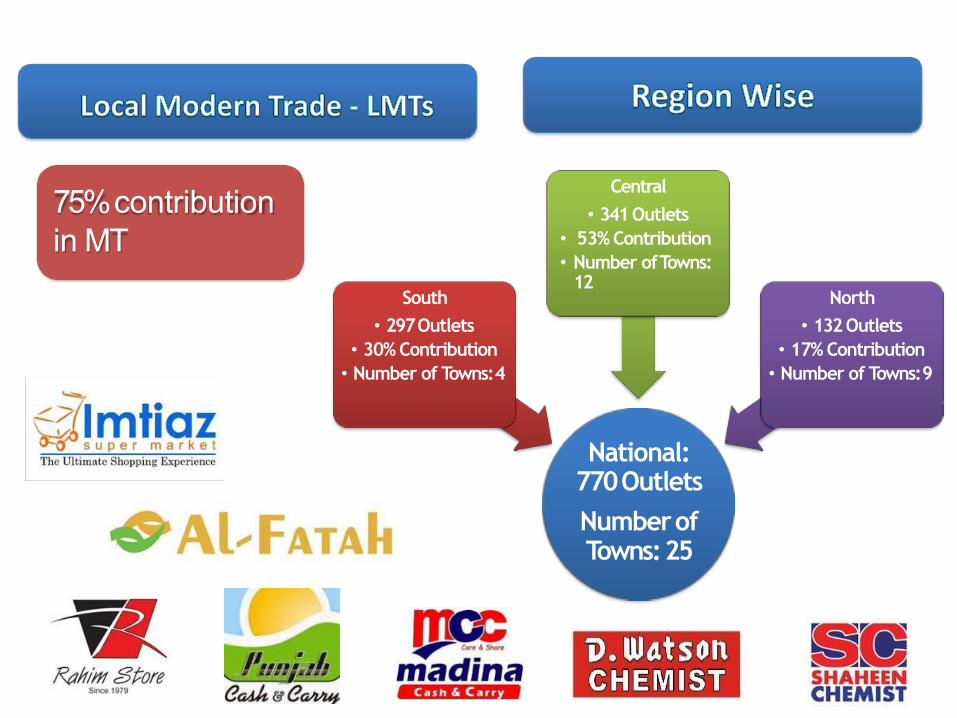

LMT• Local Modern Trade (Chain Stores, Cash & Caries)

IMT• International Modern Trade (Hyper, Metro)

USC• Utility Stores Corporation of Pakistan ( Ministry of

Industries)

CSD• Canteen Stores Department (Ministry Of Defense)

Retail• Retail Sales Sector through Distributions and

Shops

Scope

IMTs• 15

LMTs• 770

USC/CSD• 5200

1. IMTs

2. LMTs

3.USC/CSD

Scope

Karachi

• 5

Lahore

• 7Islamabad

• 2

Faisalabad

• 1

15% contribution in MT

National: 770OutletsNumberof Towns:25

South• 297Outlets

• 30% Contribution• Number of Towns:4

Central• 341 Outlets

• 53% Contribution• Number ofTowns:

12North

• 132 Outlets• 17% Contribution• Number of Towns:9

75% contribution in MT

CSD• 10 Shopping Mall• 109Outlets

USC• 50 Shopping Mall• 4650 Small Store• 1100Franchises

10% contribution in MT

Channel Introduction

Commenced Operations in Pakistan in the year 1971.

Total Turnover exceeded PKR 70 Billion.

Main business is commodities.

Branded segment sales cont 40-45%

Main shopper mission :Subsidized purchases of Commodities.More than 6000 Outlets

Turning Into Local Modern Trade

Visual Representation of USC operated outlets vs USC Franchises

523

429

434

605 64

2

785

322

606

420

86

216

46

187 22

3

148

18

82

12

ABT ISB KCHI LHR MLTN PSWR QUITA SRGHA SUKH

Main Franchise

Who are already in Race?Who are ahead of us?

We can be a step ahead ofthem…

Game is ON! MT Warriors

Modern Trade

Objectives & KeyDrivers

ChannelObjectives

ChannelObjectives Modern Trade General Trade

Penetration √ √

Merchandising √ √

Activations √

JBPs/Counter parts √

1919191919

Objectives MT GT

Penetration •OSA•MSL – ProfitMax

•Credit•Dedicated servicing model

•FCSimplementation•MSL - ‘Star’SKUs•Strengthening RTM•DSRIncentives/TPRs

Merchandising •Shelf dress-ups•Planograming

•SecondaryPlacements

•Product Placement• (POSM)

•HangerDisplays•Counter branding•Display drives

Activations •CPs•Shopper Intercepts

Market Storms

JBPs/Counter parts

•Target Incentives•Shelf rentals

•AdvertisingAllowances•Negotiation Skills

•Disproportionate ShelfShare

• Robust MIS System• Building relevant capability for meeting channelobjectives

KeyDrivers

Best Practices in Market

PenetrationCategories Defined

Stock Depth onShelves

Wide Range ofAssortment

Merchandisers

Twice a week in LMTs & Twice a Day Shelf Filling in IMTs

MerchandisingShelf dress-ups

Planograming

Secondary Placements

In Store Branding

ToolsDeployment

ActivationsConsumer Promotions

Shopper Interceptions

Shopper Engagement

Live Testing – Free Set up

Wet / Free Sampling

Podium for Promotions

Brand Ambassador Program

Brand Ambassador Program

Tools

Trade Partners Role/Participation

Consumer Offers From Trade

Digital Marketing FromTrade

Gifts ForConsumers

ThankYou

Tahir Siddiq General Manager

Sales & Corporate AffairsAsian Kings Associates Private Limited

Tahir Siddiq

Senior Vice PresidentGreek-Pakistan Chamber of Commerce