Annual Report and Financial Statements for the year ended ...

Upload

khangminh22Category

view

2download

0

THE TOPEKA COMMUNITY FOUNDATION

FINANCIAL STATEMENTS YEARS ENDED DECEMBER 31, 2019 AND 2018

THE TOPEKA COMMUNITY FOUNDATION

Financial Statements December 31, 2019 and 2018

Table of Contents Page Independent Auditors’ Report 1 - 2 Financial Statements:

Statements of Financial Position 3 Statements of Activities 4 - 5 Statements of Functional Expenses 6 - 7 Statements of Cash Flows 8 Summary of Significant Accounting Policies 9 - 11 Notes to Financial Statements 12 - 21

INDEPENDENT AUDITORS’ REPORT The Board of Directors The Topeka Community Foundation Report on the Financial Statements We have audited the accompanying financial statements of The Topeka Community Foundation (the Foundation), which comprise the statements of financial position as of December 31, 2019 and 2018, and the related statements of activities, functional expenses, and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Foundation’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Foundation’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

-2-

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Foundation as of December 31, 2019 and 2018, and the changes in its net assets and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America. Emphasis of Matter As described in Note 1 to the financial statements, the Organization has changed its method of accounting for revenue recognition effective January 1, 2019 due to the adoption of Financial Accounting Standards Board (FASB) Accounting Standards Update (ASU) 2018-08, Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made. Our opinion is not modified with respect to this matter.

October 20, 2020 Topeka, Kansas

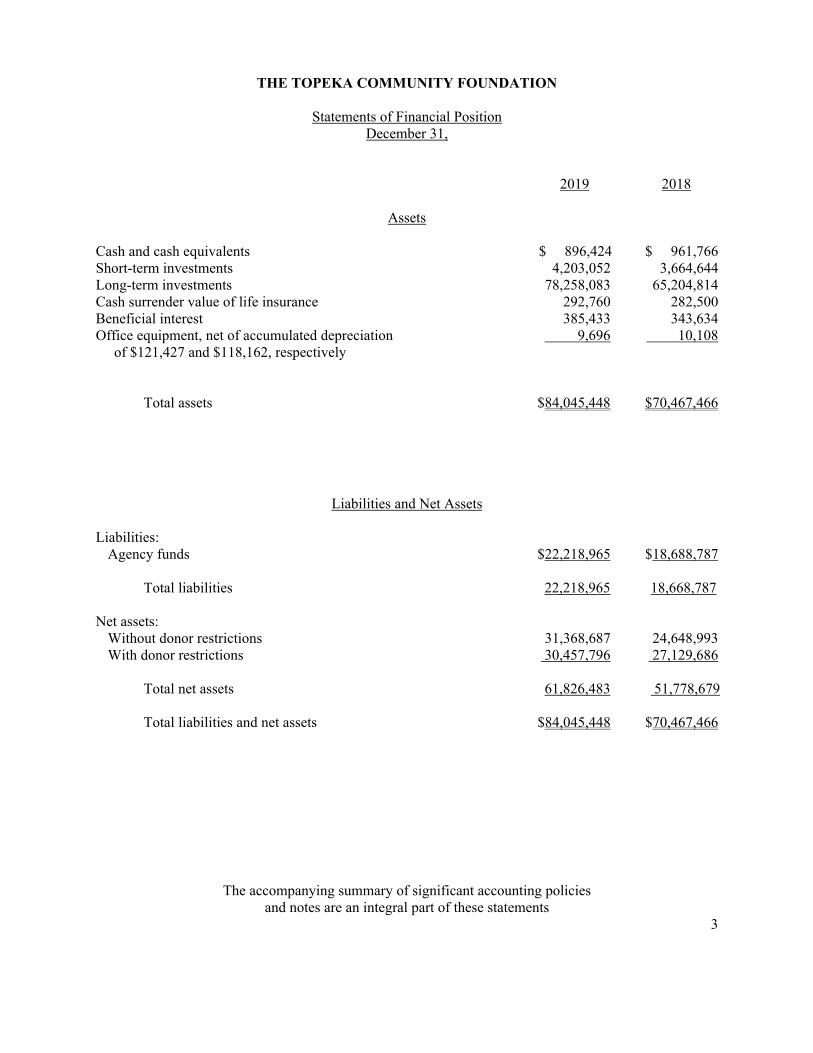

THE TOPEKA COMMUNITY FOUNDATION

Statements of Financial Position December 31,

2019 2018

Assets

Cash and cash equivalents $ 896,424 $ 961,766 Short-term investments 4,203,052 3,664,644 Long-term investments 78,258,083 65,204,814 Cash surrender value of life insurance 292,760 282,500 Beneficial interest 385,433 343,634 Office equipment, net of accumulated depreciation 9,696 10,108 of $121,427 and $118,162, respectively

Total assets $84,045,448 $70,467,466

Liabilities and Net Assets Liabilities:

Agency funds $22,218,965 $18,688,787

Total liabilities 22,218,965 18,668,787 Net assets:

Without donor restrictions 31,368,687 24,648,993 With donor restrictions 30,457,796 27,129,686

Total net assets 61,826,483 51,778,679 Total liabilities and net assets $84,045,448 $70,467,466

The accompanying summary of significant accounting policies and notes are an integral part of these statements

3

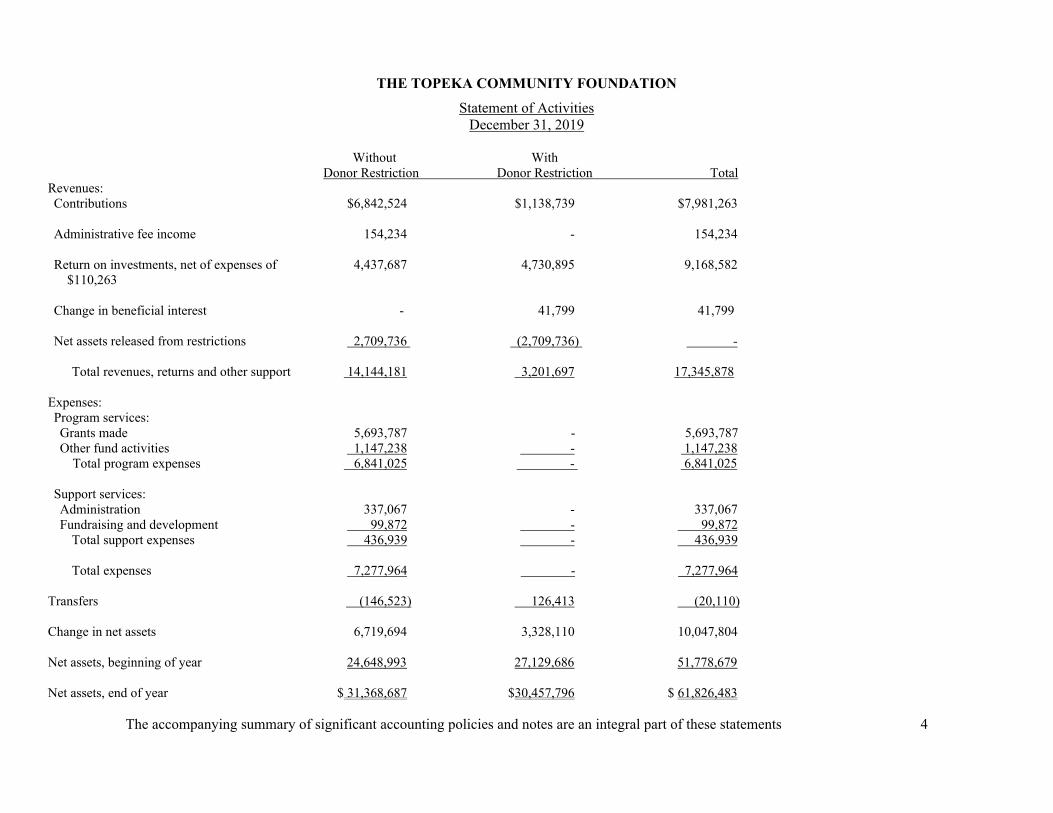

THE TOPEKA COMMUNITY FOUNDATION

Statement of Activities December 31, 2019

Without With Donor Restriction Donor Restriction Total Revenues: Contributions $6,842,524 $1,138,739 $7,981,263 Administrative fee income 154,234 - 154,234 Return on investments, net of expenses of 4,437,687 4,730,895 9,168,582 $110,263 Change in beneficial interest - 41,799 41,799 Net assets released from restrictions 2,709,736 (2,709,736) -

Total revenues, returns and other support 14,144,181 3,201,697 17,345,878

Expenses: Program services: Grants made 5,693,787 - 5,693,787 Other fund activities 1,147,238 - 1,147,238

Total program expenses 6,841,025 - 6,841,025 Support services: Administration 337,067 - 337,067 Fundraising and development 99,872 - 99,872

Total support expenses 436,939 - 436,939 Total expenses 7,277,964 - 7,277,964

Transfers (146,523) 126,413 (20,110) Change in net assets 6,719,694 3,328,110 10,047,804 Net assets, beginning of year 24,648,993 27,129,686 51,778,679 Net assets, end of year $ 31,368,687 $30,457,796 $ 61,826,483 The accompanying summary of significant accounting policies and notes are an integral part of these statements 4

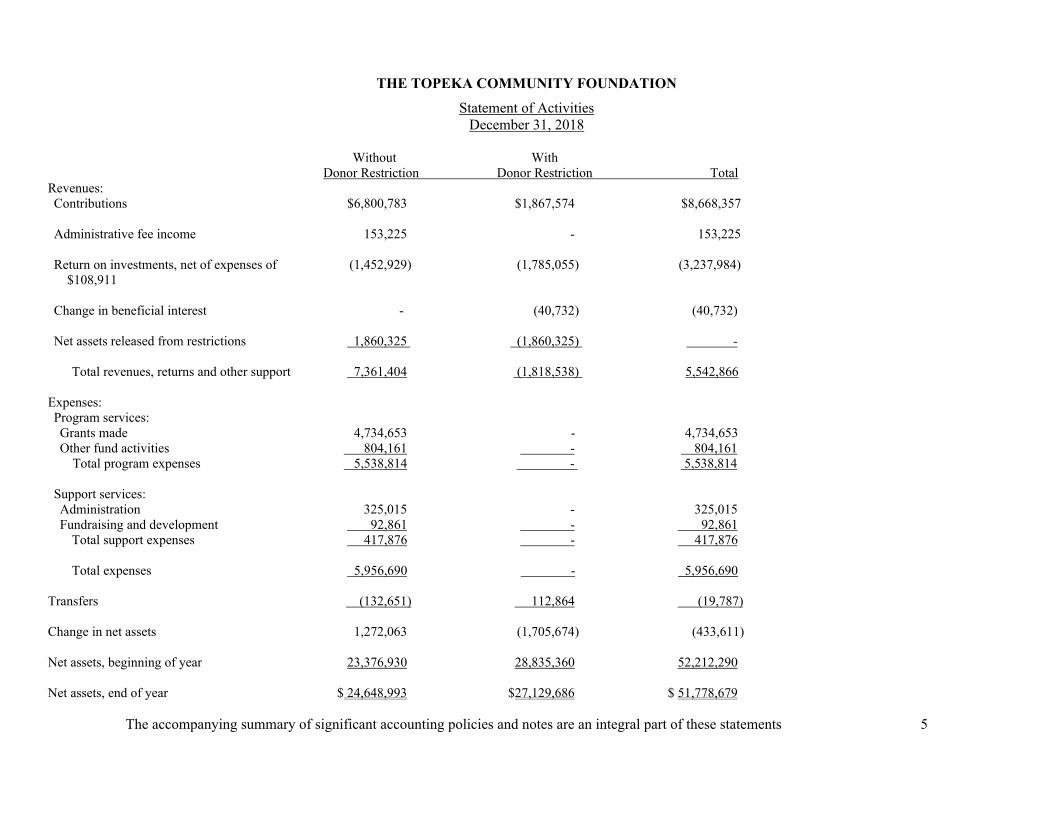

THE TOPEKA COMMUNITY FOUNDATION

Statement of Activities December 31, 2018

Without With Donor Restriction Donor Restriction Total Revenues: Contributions $6,800,783 $1,867,574 $8,668,357 Administrative fee income 153,225 - 153,225 Return on investments, net of expenses of (1,452,929) (1,785,055) (3,237,984) $108,911 Change in beneficial interest - (40,732) (40,732) Net assets released from restrictions 1,860,325 (1,860,325) -

Total revenues, returns and other support 7,361,404 (1,818,538) 5,542,866

Expenses: Program services: Grants made 4,734,653 - 4,734,653 Other fund activities 804,161 - 804,161

Total program expenses 5,538,814 - 5,538,814 Support services: Administration 325,015 - 325,015 Fundraising and development 92,861 - 92,861

Total support expenses 417,876 - 417,876 Total expenses 5,956,690 - 5,956,690

Transfers (132,651) 112,864 (19,787) Change in net assets 1,272,063 (1,705,674) (433,611) Net assets, beginning of year 23,376,930 28,835,360 52,212,290 Net assets, end of year $ 24,648,993 $27,129,686 $ 51,778,679 The accompanying summary of significant accounting policies and notes are an integral part of these statements 5

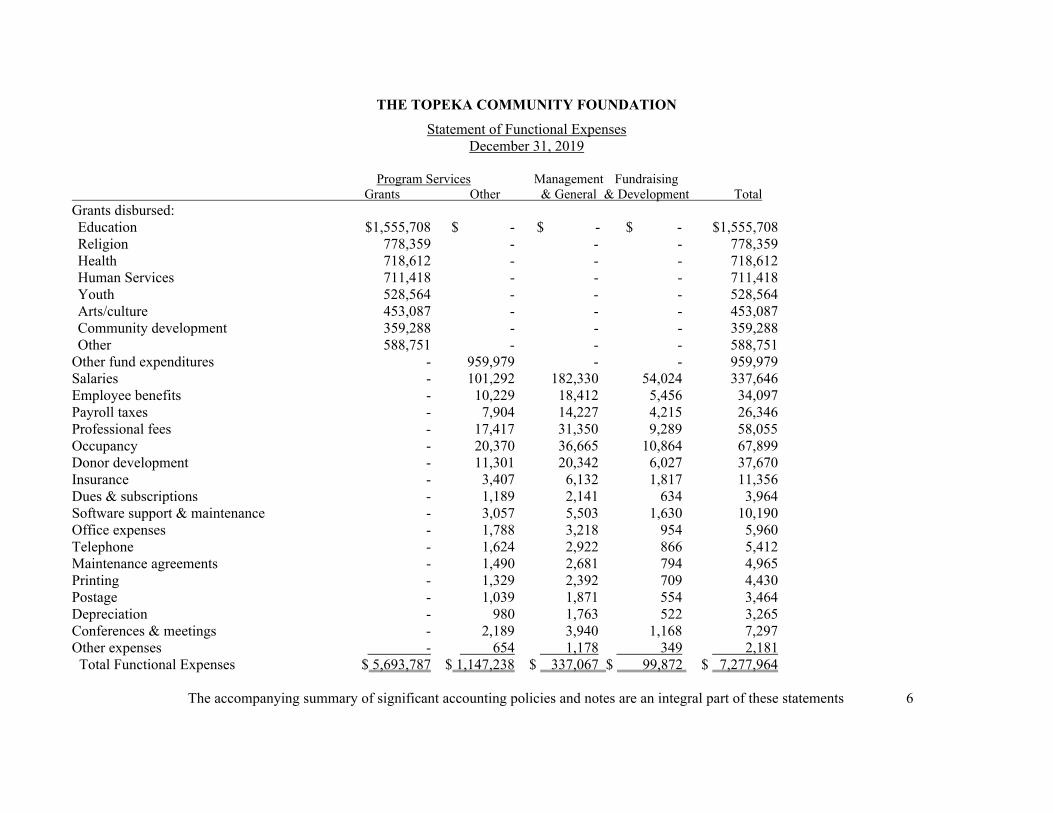

THE TOPEKA COMMUNITY FOUNDATION

Statement of Functional Expenses December 31, 2019

Program Services Management Fundraising Grants Other & General & Development Total Grants disbursed: Education $1,555,708 $ - $ - $ - $1,555,708 Religion 778,359 - - - 778,359 Health 718,612 - - - 718,612 Human Services 711,418 - - - 711,418 Youth 528,564 - - - 528,564 Arts/culture 453,087 - - - 453,087 Community development 359,288 - - - 359,288 Other 588,751 - - - 588,751

Other fund expenditures - 959,979 - - 959,979 Salaries - 101,292 182,330 54,024 337,646 Employee benefits - 10,229 18,412 5,456 34,097 Payroll taxes - 7,904 14,227 4,215 26,346 Professional fees - 17,417 31,350 9,289 58,055 Occupancy - 20,370 36,665 10,864 67,899 Donor development - 11,301 20,342 6,027 37,670 Insurance - 3,407 6,132 1,817 11,356 Dues & subscriptions - 1,189 2,141 634 3,964 Software support & maintenance - 3,057 5,503 1,630 10,190 Office expenses - 1,788 3,218 954 5,960 Telephone - 1,624 2,922 866 5,412 Maintenance agreements - 1,490 2,681 794 4,965 Printing - 1,329 2,392 709 4,430 Postage - 1,039 1,871 554 3,464 Depreciation - 980 1,763 522 3,265 Conferences & meetings - 2,189 3,940 1,168 7,297 Other expenses - 654 1,178 349 2,181 Total Functional Expenses $ 5,693,787 $ 1,147,238 $ 337,067 $ 99,872 $ 7,277,964 The accompanying summary of significant accounting policies and notes are an integral part of these statements 6

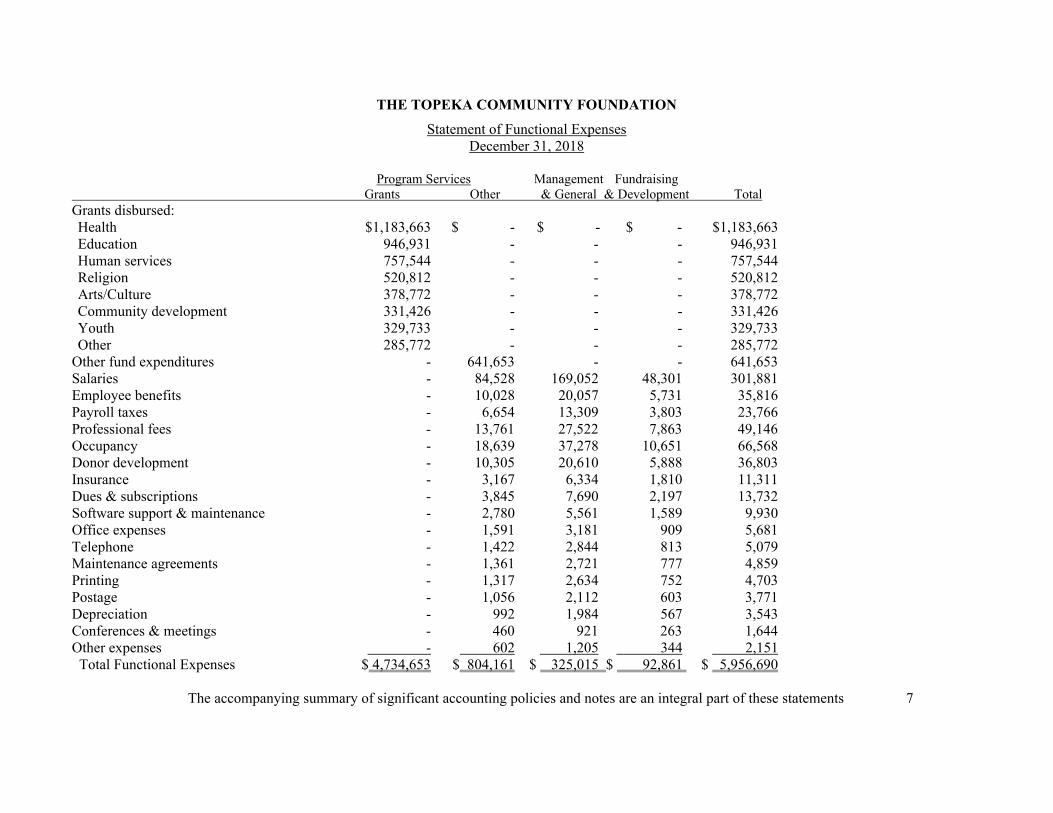

THE TOPEKA COMMUNITY FOUNDATION

Statement of Functional Expenses December 31, 2018

Program Services Management Fundraising Grants Other & General & Development Total Grants disbursed: Health $1,183,663 $ - $ - $ - $1,183,663 Education 946,931 - - - 946,931 Human services 757,544 - - - 757,544 Religion 520,812 - - - 520,812 Arts/Culture 378,772 - - - 378,772 Community development 331,426 - - - 331,426 Youth 329,733 - - - 329,733 Other 285,772 - - - 285,772

Other fund expenditures - 641,653 - - 641,653 Salaries - 84,528 169,052 48,301 301,881 Employee benefits - 10,028 20,057 5,731 35,816 Payroll taxes - 6,654 13,309 3,803 23,766 Professional fees - 13,761 27,522 7,863 49,146 Occupancy - 18,639 37,278 10,651 66,568 Donor development - 10,305 20,610 5,888 36,803 Insurance - 3,167 6,334 1,810 11,311 Dues & subscriptions - 3,845 7,690 2,197 13,732 Software support & maintenance - 2,780 5,561 1,589 9,930 Office expenses - 1,591 3,181 909 5,681 Telephone - 1,422 2,844 813 5,079 Maintenance agreements - 1,361 2,721 777 4,859 Printing - 1,317 2,634 752 4,703 Postage - 1,056 2,112 603 3,771 Depreciation - 992 1,984 567 3,543 Conferences & meetings - 460 921 263 1,644 Other expenses - 602 1,205 344 2,151 Total Functional Expenses $ 4,734,653 $ 804,161 $ 325,015 $ 92,861 $ 5,956,690 The accompanying summary of significant accounting policies and notes are an integral part of these statements 7

THE TOPEKA COMMUNITY FOUNDATION

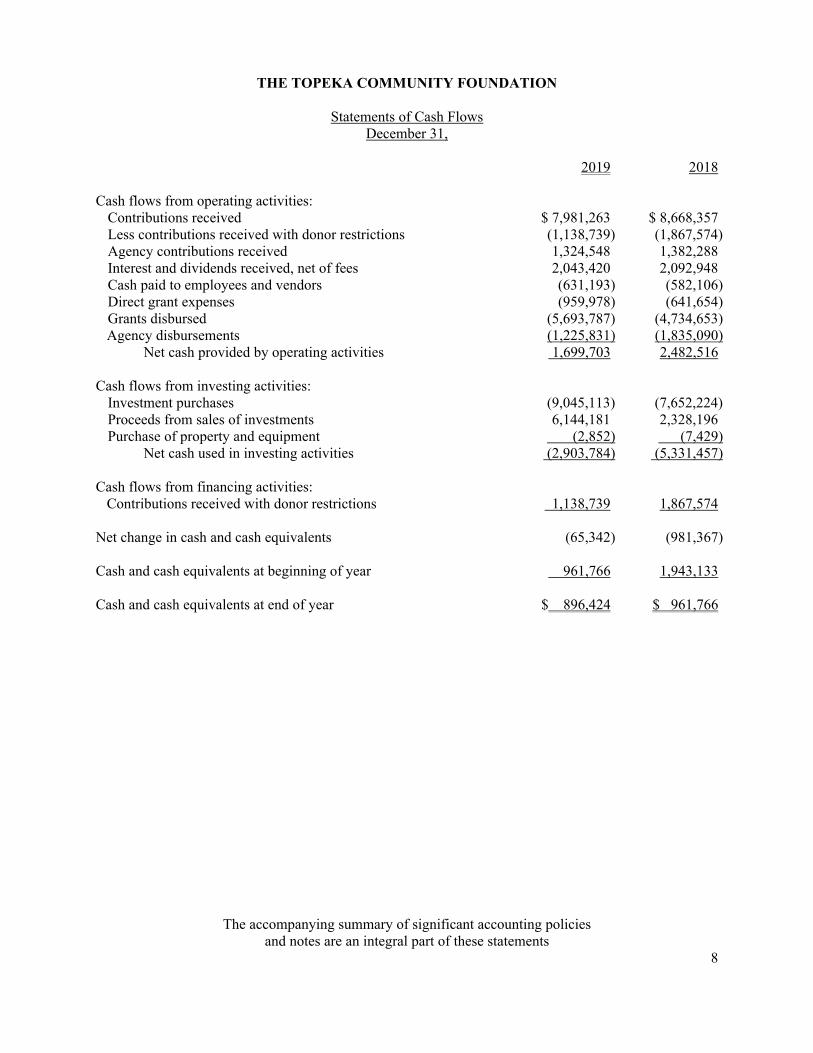

Statements of Cash Flows December 31,

2019 2018 Cash flows from operating activities:

Contributions received $ 7,981,263 $ 8,668,357 Less contributions received with donor restrictions (1,138,739) (1,867,574) Agency contributions received 1,324,548 1,382,288 Interest and dividends received, net of fees 2,043,420 2,092,948 Cash paid to employees and vendors (631,193) (582,106) Direct grant expenses (959,978) (641,654) Grants disbursed (5,693,787) (4,734,653)

Agency disbursements (1,225,831) (1,835,090) Net cash provided by operating activities 1,699,703 2,482,516

Cash flows from investing activities: Investment purchases (9,045,113) (7,652,224) Proceeds from sales of investments 6,144,181 2,328,196 Purchase of property and equipment (2,852) (7,429)

Net cash used in investing activities (2,903,784) (5,331,457) Cash flows from financing activities: Contributions received with donor restrictions 1,138,739 1,867,574 Net change in cash and cash equivalents (65,342) (981,367) Cash and cash equivalents at beginning of year 961,766 1,943,133 Cash and cash equivalents at end of year $ 896,424 $ 961,766

The accompanying summary of significant accounting policies and notes are an integral part of these statements

8

THE TOPEKA COMMUNITY FOUNDATION

Summary of Significant Accounting Policies December 31, 2019 and 2018

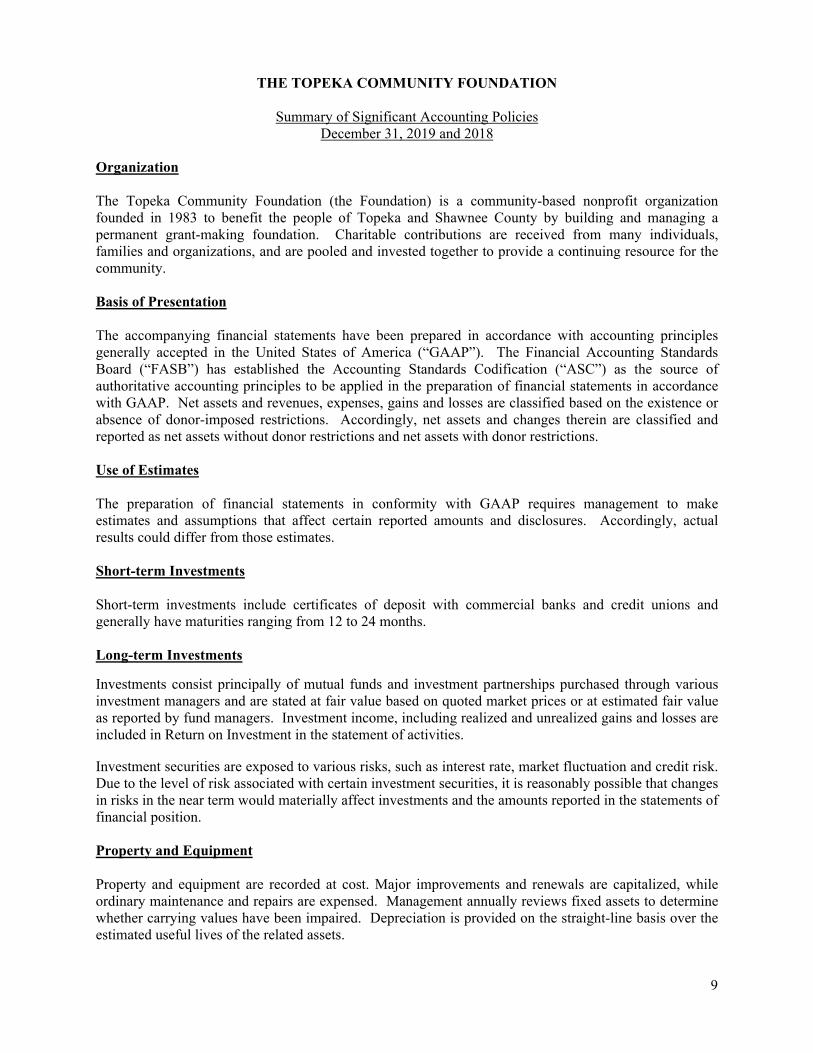

Organization The Topeka Community Foundation (the Foundation) is a community-based nonprofit organization founded in 1983 to benefit the people of Topeka and Shawnee County by building and managing a permanent grant-making foundation. Charitable contributions are received from many individuals, families and organizations, and are pooled and invested together to provide a continuing resource for the community. Basis of Presentation The accompanying financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). The Financial Accounting Standards Board (“FASB”) has established the Accounting Standards Codification (“ASC”) as the source of authoritative accounting principles to be applied in the preparation of financial statements in accordance with GAAP. Net assets and revenues, expenses, gains and losses are classified based on the existence or absence of donor-imposed restrictions. Accordingly, net assets and changes therein are classified and reported as net assets without donor restrictions and net assets with donor restrictions. Use of Estimates The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect certain reported amounts and disclosures. Accordingly, actual results could differ from those estimates. Short-term Investments Short-term investments include certificates of deposit with commercial banks and credit unions and generally have maturities ranging from 12 to 24 months. Long-term Investments

Investments consist principally of mutual funds and investment partnerships purchased through various investment managers and are stated at fair value based on quoted market prices or at estimated fair value as reported by fund managers. Investment income, including realized and unrealized gains and losses are included in Return on Investment in the statement of activities. Investment securities are exposed to various risks, such as interest rate, market fluctuation and credit risk. Due to the level of risk associated with certain investment securities, it is reasonably possible that changes in risks in the near term would materially affect investments and the amounts reported in the statements of financial position. Property and Equipment Property and equipment are recorded at cost. Major improvements and renewals are capitalized, while ordinary maintenance and repairs are expensed. Management annually reviews fixed assets to determine whether carrying values have been impaired. Depreciation is provided on the straight-line basis over the estimated useful lives of the related assets. 9

THE TOPEKA COMMUNITY FOUNDATION

Summary of Significant Accounting Policies

December 31, 2019 and 2018 Agency Funds The Foundation recognizes a liability for funds received from and held for the sole benefit of other non-profit organizations. Contributions and Bequests The Foundation recognizes contributions when cash, securities or other assets, an unconditional promise to give, or notification of a beneficial interest is received. Conditional promises to give, that is, those with a measurable performance or other barrier, and a right of return, are not recognized until the conditions on which they depend have been substantially met. Contributions and bequests received are recorded as without donor restrictions or with donor restrictions, depending on the existence or nature of any restrictions. Donor-restricted contributions and bequests are reported as increases in with donor restrictions net assets, depending on the nature of the restriction. Some donor-imposed restrictions are temporary in nature that may or will be met, either by actions of the Foundation and/or the passage of time. Other donor-imposed restrictions are perpetual in nature, where the donor stipulates resources be maintained in perpetuity. As of December 31, 2019, the Foundation’s net assets with donor restrictions are restricted for funding various health, education and community philanthropic programs specified by the donors. Non-cash contributions are recorded at the estimated fair value at the time of donation. Functional Allocation of Expenses The costs of providing the various programs and other activities have been summarized on a functional basis in the statement of activities and the consolidated statements of functional expenses. Accordingly, certain costs have been allocated among the programs and supporting services benefited. Expenses reported in the financial statements are attributed to more than one program or supporting function and require allocation based on the full-time employee equivalent method and management estimates of time and effort. Statement of Cash Flows For purposes of the statement of cash flows, all interest-bearing deposits at commercial banks and money market funds at commercial banks and brokerage houses, purchased with initial maturity dates of three months or less, are considered to be cash equivalents. 10

THE TOPEKA COMMUNITY FOUNDATION

Summary of Significant Accounting Policies December 31, 2019 and 2018

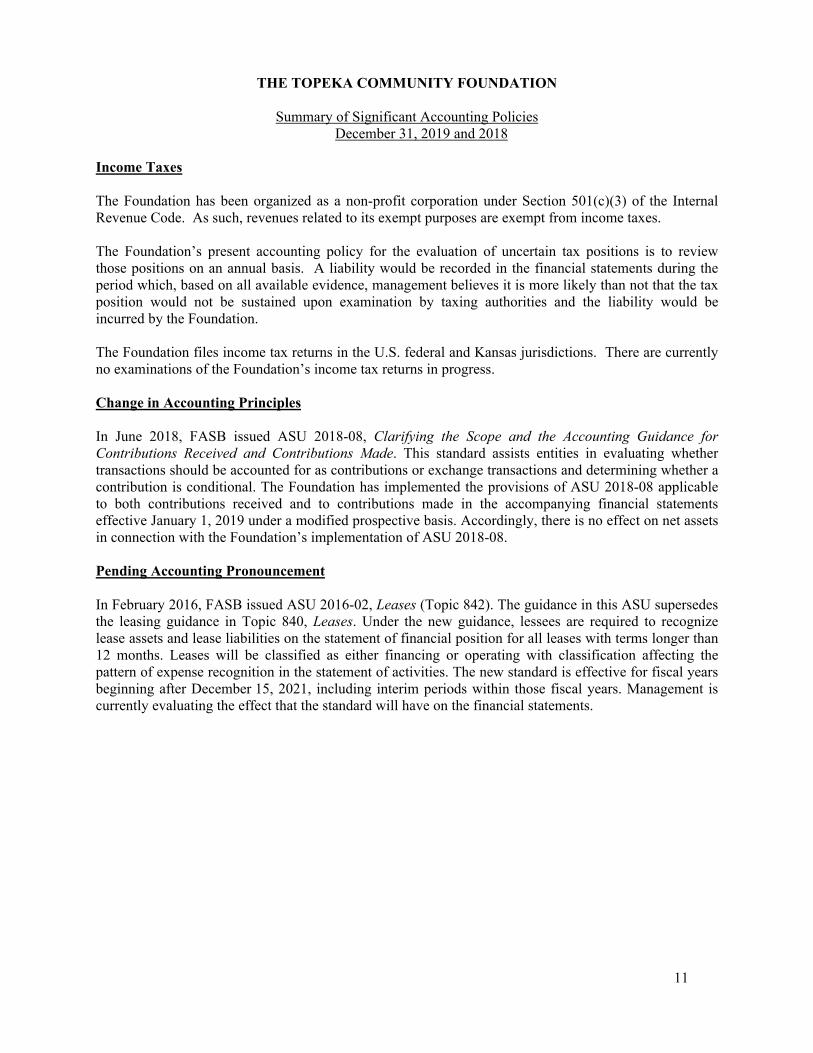

Income Taxes The Foundation has been organized as a non-profit corporation under Section 501(c)(3) of the Internal Revenue Code. As such, revenues related to its exempt purposes are exempt from income taxes. The Foundation’s present accounting policy for the evaluation of uncertain tax positions is to review those positions on an annual basis. A liability would be recorded in the financial statements during the period which, based on all available evidence, management believes it is more likely than not that the tax position would not be sustained upon examination by taxing authorities and the liability would be incurred by the Foundation. The Foundation files income tax returns in the U.S. federal and Kansas jurisdictions. There are currently no examinations of the Foundation’s income tax returns in progress.

Change in Accounting Principles In June 2018, FASB issued ASU 2018-08, Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made. This standard assists entities in evaluating whether transactions should be accounted for as contributions or exchange transactions and determining whether a contribution is conditional. The Foundation has implemented the provisions of ASU 2018-08 applicable to both contributions received and to contributions made in the accompanying financial statements effective January 1, 2019 under a modified prospective basis. Accordingly, there is no effect on net assets in connection with the Foundation’s implementation of ASU 2018-08. Pending Accounting Pronouncement In February 2016, FASB issued ASU 2016-02, Leases (Topic 842). The guidance in this ASU supersedes the leasing guidance in Topic 840, Leases. Under the new guidance, lessees are required to recognize lease assets and lease liabilities on the statement of financial position for all leases with terms longer than 12 months. Leases will be classified as either financing or operating with classification affecting the pattern of expense recognition in the statement of activities. The new standard is effective for fiscal years beginning after December 15, 2021, including interim periods within those fiscal years. Management is currently evaluating the effect that the standard will have on the financial statements.

11

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

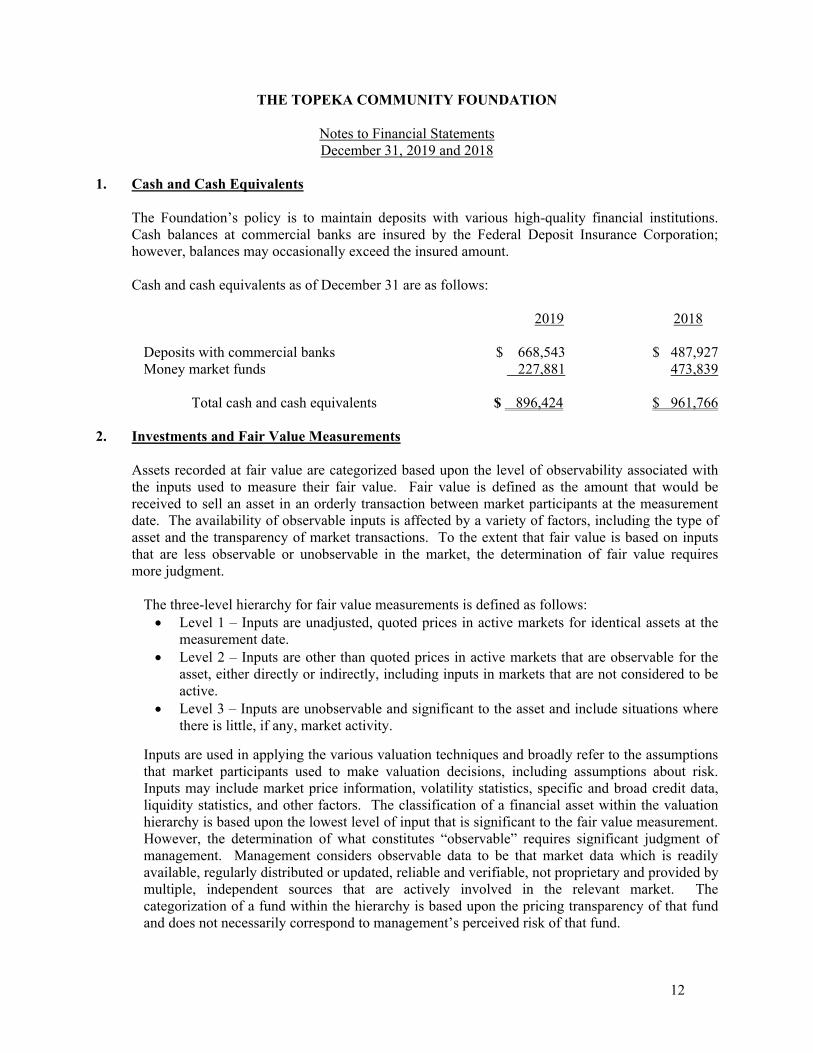

1. Cash and Cash Equivalents

The Foundation’s policy is to maintain deposits with various high-quality financial institutions. Cash balances at commercial banks are insured by the Federal Deposit Insurance Corporation; however, balances may occasionally exceed the insured amount. Cash and cash equivalents as of December 31 are as follows:

2019 2018

Deposits with commercial banks $ 668,543 $ 487,927 Money market funds 227,881 473,839

Total cash and cash equivalents $ 896,424 $ 961,766 2. Investments and Fair Value Measurements Assets recorded at fair value are categorized based upon the level of observability associated with the inputs used to measure their fair value. Fair value is defined as the amount that would be received to sell an asset in an orderly transaction between market participants at the measurement date. The availability of observable inputs is affected by a variety of factors, including the type of asset and the transparency of market transactions. To the extent that fair value is based on inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. The three-level hierarchy for fair value measurements is defined as follows:

Level 1 – Inputs are unadjusted, quoted prices in active markets for identical assets at the measurement date.

Level 2 – Inputs are other than quoted prices in active markets that are observable for the asset, either directly or indirectly, including inputs in markets that are not considered to be active.

Level 3 – Inputs are unobservable and significant to the asset and include situations where there is little, if any, market activity.

Inputs are used in applying the various valuation techniques and broadly refer to the assumptions that market participants used to make valuation decisions, including assumptions about risk. Inputs may include market price information, volatility statistics, specific and broad credit data, liquidity statistics, and other factors. The classification of a financial asset within the valuation hierarchy is based upon the lowest level of input that is significant to the fair value measurement. However, the determination of what constitutes “observable” requires significant judgment of management. Management considers observable data to be that market data which is readily available, regularly distributed or updated, reliable and verifiable, not proprietary and provided by multiple, independent sources that are actively involved in the relevant market. The categorization of a fund within the hierarchy is based upon the pricing transparency of that fund and does not necessarily correspond to management’s perceived risk of that fund.

12

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

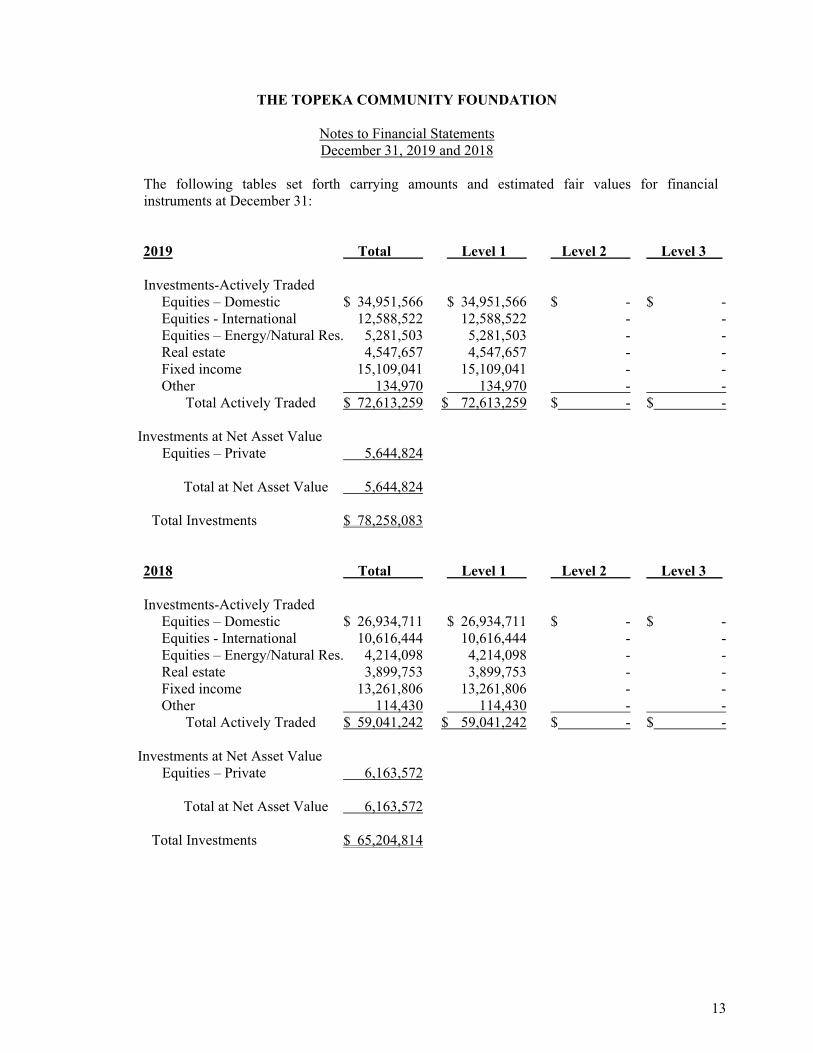

The following tables set forth carrying amounts and estimated fair values for financial instruments at December 31:

2019 Total Level 1 Level 2 Level 3

Investments-Actively Traded Equities – Domestic $ 34,951,566 $ 34,951,566 $ - $ - Equities - International 12,588,522 12,588,522 - -

Equities – Energy/Natural Res. 5,281,503 5,281,503 - - Real estate 4,547,657 4,547,657 - - Fixed income 15,109,041 15,109,041 - - Other 134,970 134,970 - -

Total Actively Traded $ 72,613,259 $ 72,613,259 $ - $ - Investments at Net Asset Value Equities – Private 5,644,824 Total at Net Asset Value 5,644,824

Total Investments $ 78,258,083

2018 Total Level 1 Level 2 Level 3

Investments-Actively Traded Equities – Domestic $ 26,934,711 $ 26,934,711 $ - $ - Equities - International 10,616,444 10,616,444 - -

Equities – Energy/Natural Res. 4,214,098 4,214,098 - - Real estate 3,899,753 3,899,753 - - Fixed income 13,261,806 13,261,806 - - Other 114,430 114,430 - -

Total Actively Traded $ 59,041,242 $ 59,041,242 $ - $ - Investments at Net Asset Value Equities – Private 6,163,572 Total at Net Asset Value 6,163,572

Total Investments $ 65,204,814 13

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

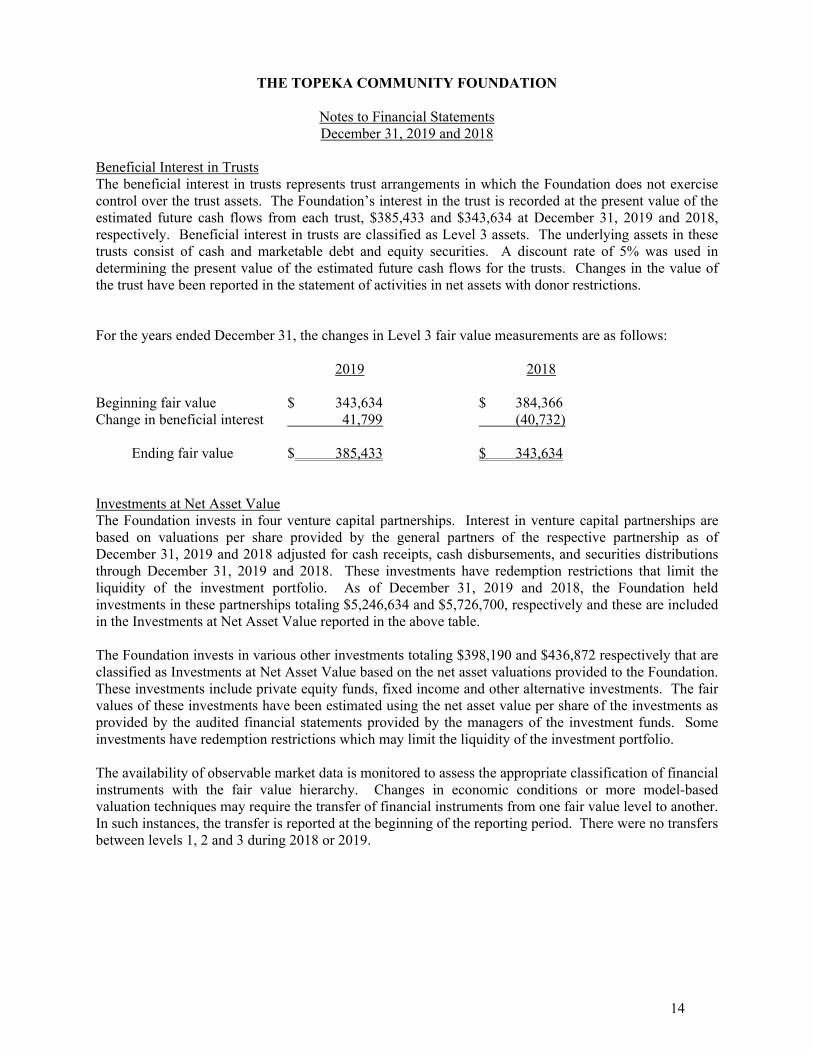

Beneficial Interest in Trusts The beneficial interest in trusts represents trust arrangements in which the Foundation does not exercise control over the trust assets. The Foundation’s interest in the trust is recorded at the present value of the estimated future cash flows from each trust, $385,433 and $343,634 at December 31, 2019 and 2018, respectively. Beneficial interest in trusts are classified as Level 3 assets. The underlying assets in these trusts consist of cash and marketable debt and equity securities. A discount rate of 5% was used in determining the present value of the estimated future cash flows for the trusts. Changes in the value of the trust have been reported in the statement of activities in net assets with donor restrictions. For the years ended December 31, the changes in Level 3 fair value measurements are as follows: 2019 2018 Beginning fair value $ 343,634 $ 384,366 Change in beneficial interest 41,799 (40,732) Ending fair value $ 385,433 $ 343,634 Investments at Net Asset Value The Foundation invests in four venture capital partnerships. Interest in venture capital partnerships are based on valuations per share provided by the general partners of the respective partnership as of December 31, 2019 and 2018 adjusted for cash receipts, cash disbursements, and securities distributions through December 31, 2019 and 2018. These investments have redemption restrictions that limit the liquidity of the investment portfolio. As of December 31, 2019 and 2018, the Foundation held investments in these partnerships totaling $5,246,634 and $5,726,700, respectively and these are included in the Investments at Net Asset Value reported in the above table. The Foundation invests in various other investments totaling $398,190 and $436,872 respectively that are classified as Investments at Net Asset Value based on the net asset valuations provided to the Foundation. These investments include private equity funds, fixed income and other alternative investments. The fair values of these investments have been estimated using the net asset value per share of the investments as provided by the audited financial statements provided by the managers of the investment funds. Some investments have redemption restrictions which may limit the liquidity of the investment portfolio. The availability of observable market data is monitored to assess the appropriate classification of financial instruments with the fair value hierarchy. Changes in economic conditions or more model-based valuation techniques may require the transfer of financial instruments from one fair value level to another. In such instances, the transfer is reported at the beginning of the reporting period. There were no transfers between levels 1, 2 and 3 during 2018 or 2019.

14

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

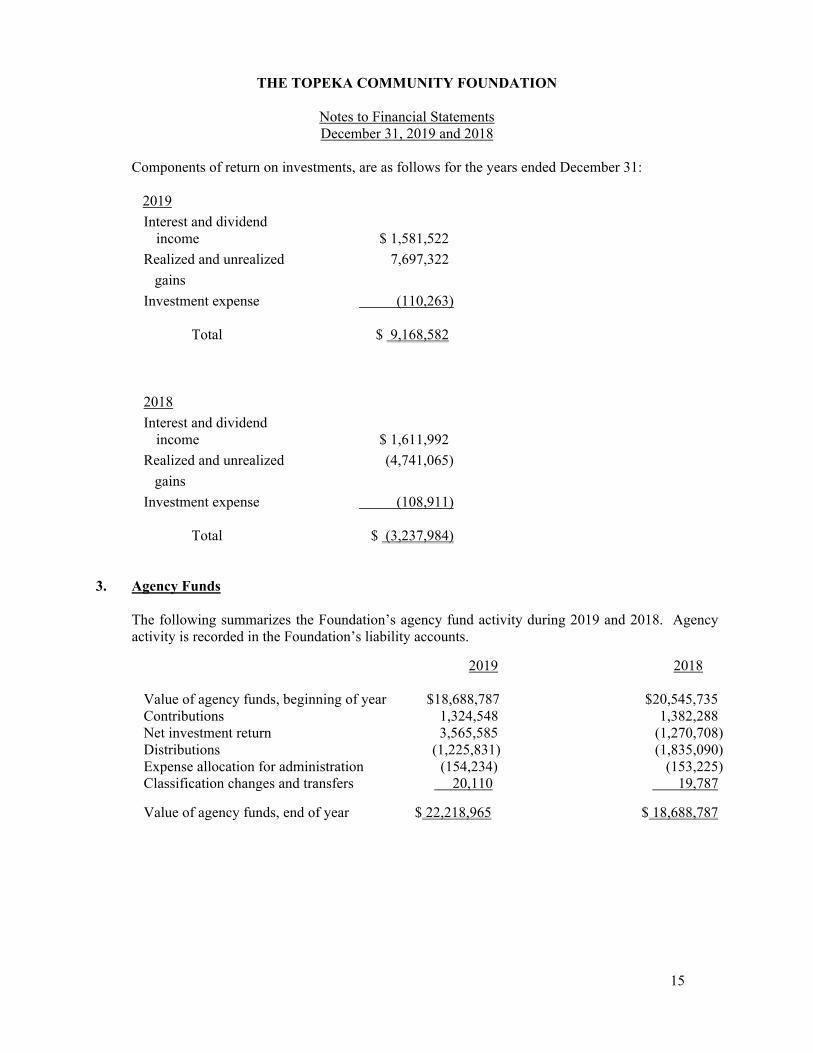

Components of return on investments, are as follows for the years ended December 31: 2019

Interest and dividend income $ 1,581,522

Realized and unrealized 7,697,322

gains

Investment expense (110,263)

Total $ 9,168,582

2018

Interest and dividend income $ 1,611,992

Realized and unrealized (4,741,065)

gains

Investment expense (108,911)

Total $ (3,237,984) 3. Agency Funds

The following summarizes the Foundation’s agency fund activity during 2019 and 2018. Agency activity is recorded in the Foundation’s liability accounts.

2019 2018

Value of agency funds, beginning of year $18,688,787 $20,545,735 Contributions 1,324,548 1,382,288 Net investment return 3,565,585 (1,270,708) Distributions (1,225,831) (1,835,090) Expense allocation for administration (154,234) (153,225) Classification changes and transfers 20,110 19,787

Value of agency funds, end of year $ 22,218,965 $ 18,688,787 15

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

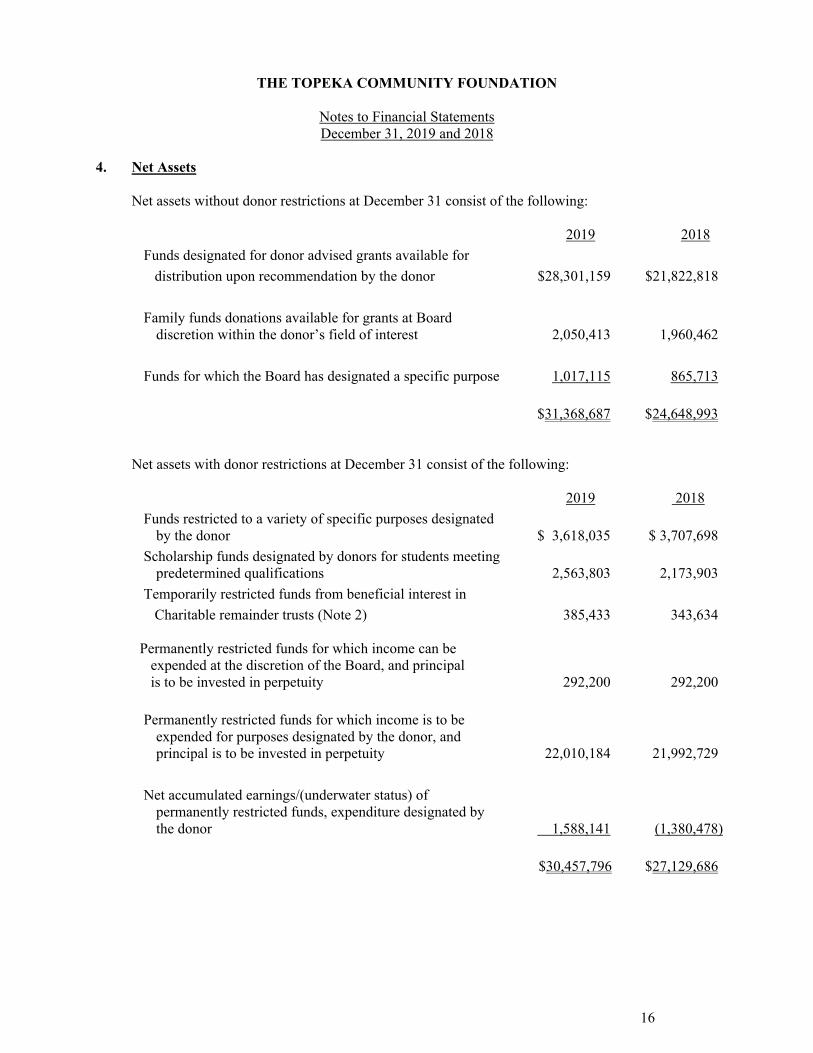

4. Net Assets

Net assets without donor restrictions at December 31 consist of the following:

2019 2018

Funds designated for donor advised grants available for

distribution upon recommendation by the donor $28,301,159 $21,822,818

Family funds donations available for grants at Board discretion within the donor’s field of interest 2,050,413 1,960,462

Funds for which the Board has designated a specific purpose 1,017,115 865,713

$31,368,687 $24,648,993

Net assets with donor restrictions at December 31 consist of the following:

2019 2018

Funds restricted to a variety of specific purposes designated by the donor $ 3,618,035 $ 3,707,698

Scholarship funds designated by donors for students meeting predetermined qualifications 2,563,803 2,173,903

Temporarily restricted funds from beneficial interest in

Charitable remainder trusts (Note 2) 385,433 343,634

Permanently restricted funds for which income can be expended at the discretion of the Board, and principal is to be invested in perpetuity 292,200 292,200

Permanently restricted funds for which income is to be expended for purposes designated by the donor, and principal is to be invested in perpetuity 22,010,184 21,992,729

Net accumulated earnings/(underwater status) of permanently restricted funds, expenditure designated by the donor 1,588,141 (1,380,478)

$30,457,796 $27,129,686 16

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

5. Endowment funds

The Foundation’s endowment funds have been established for a variety of purposes to provide income in support of certain designated activities. Endowments include both Board and donor-designated funds, and are classified and reported in net assets based on the existence or absence of donor-imposed restrictions. The State of Kansas has adopted the Uniform Prudent Management of Institutional Funds Act (UPMIFA), which provides guidance and authority to charitable organizations regarding the management and investment of endowment funds. The Board of Directors has interpreted UPMIFA as requiring the preservation of the fair value of the original gift as of the gift date of the donor-restricted endowment funds absent explicit donor stipulations to the contrary. The Foundation generally retains in perpetuity (a) the original value of the gifts donated to permanent endowments, (b) the original value of subsequent gifts to the permanent endowment, and (c) accumulations to the permanent endowment made in accordance with the direction of the applicable donor gift instrument at the time the accumulation is added to the fund. Donor restricted amounts not retained in perpetuity are subject to appropriation for expenditure by the Foundation. In accordance with UPMIFA, the organization considers the following factors in making a determination to appropriate or accumulate donor-restricted endowment funds:

The duration and preservation of the funds The purpose of the Foundation and the donor-restricted endowment fund General economic conditions The possible effects of inflation or deflation The expected total return from income and the appreciation of investments Other resources of the Foundation The investment policies of the Foundation

Endowment net assets as of December 31 are as follows: 2019 Without With Donor Restriction Donor Restriction Total Donor restricted $ 2,779,806 $25,513,622 $28,293,428 Board designated 1,012,356 - 1,012,356 Total endowment funds $ 3,792,162 $25,513,622 $29,305,784 2018 Without With Donor Restriction Donor Restriction Total Donor restricted $ 2,490,259 $22,371,658 $24,861,917 Board designated 861,697 - 861,697 Total endowment funds $ 3,351,956 $22,371,658 $25,723,614 17

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

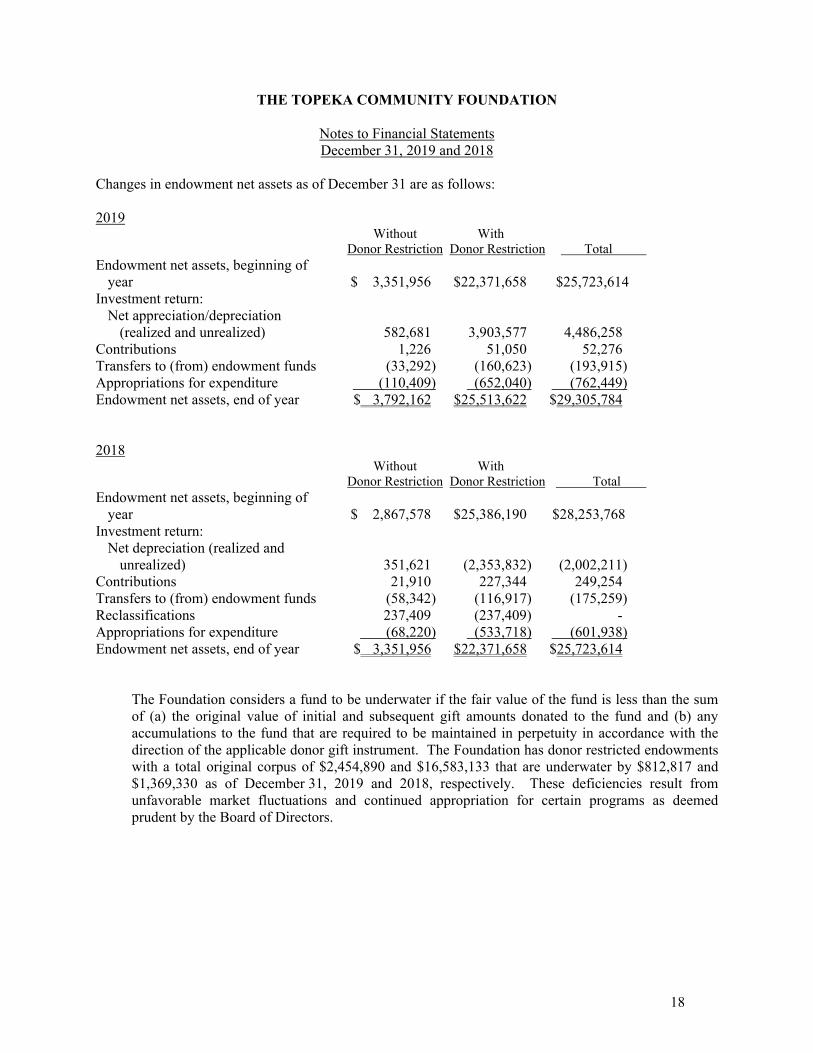

Changes in endowment net assets as of December 31 are as follows: 2019 Without With Donor Restriction Donor Restriction Total Endowment net assets, beginning of

year $ 3,351,956 $22,371,658 $25,723,614 Investment return:

Net appreciation/depreciation (realized and unrealized) 582,681 3,903,577 4,486,258

Contributions 1,226 51,050 52,276 Transfers to (from) endowment funds (33,292) (160,623) (193,915) Appropriations for expenditure (110,409) (652,040) (762,449) Endowment net assets, end of year $ 3,792,162 $25,513,622 $29,305,784 2018 Without With Donor Restriction Donor Restriction Total Endowment net assets, beginning of

year $ 2,867,578 $25,386,190 $28,253,768 Investment return:

Net depreciation (realized and unrealized) 351,621 (2,353,832) (2,002,211)

Contributions 21,910 227,344 249,254 Transfers to (from) endowment funds (58,342) (116,917) (175,259) Reclassifications 237,409 (237,409) - Appropriations for expenditure (68,220) (533,718) (601,938) Endowment net assets, end of year $ 3,351,956 $22,371,658 $25,723,614

The Foundation considers a fund to be underwater if the fair value of the fund is less than the sum of (a) the original value of initial and subsequent gift amounts donated to the fund and (b) any accumulations to the fund that are required to be maintained in perpetuity in accordance with the direction of the applicable donor gift instrument. The Foundation has donor restricted endowments with a total original corpus of $2,454,890 and $16,583,133 that are underwater by $812,817 and $1,369,330 as of December 31, 2019 and 2018, respectively. These deficiencies result from unfavorable market fluctuations and continued appropriation for certain programs as deemed prudent by the Board of Directors.

18

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

The Foundation has adopted investment and spending policies for endowment assets that provide for a predictable stream of funding to programs supported by its endowment while seeking to maintain the purchasing power of the endowment assets. Endowment funds are pooled with other investment funds held by the Foundation. Investment gains and losses are allocated in proportion to the endowment funds’ portion of the investment pool. The Foundation investment policy includes both a growth component and an income component. The long-term investment objective of the growth component is to earn a rate of return, net of all fees, in excess of commonly used endowment benchmarks over rolling five and ten-year periods. The income component objective is to earn a competitive short-term interest rate. The spending policy allows for a percentage distribution based on the average three-year September 30 balance. The percent for 2019 and 2018 was 4.5%.

On a case by case basis, the Foundation’s policy is to appropriate for expenditure of the endowment earnings in accordance with the donor restrictions and/or as approved by the Board of Directors. The Board designated unrestricted endowment assets represent a fund established to support the operations of the Foundation.

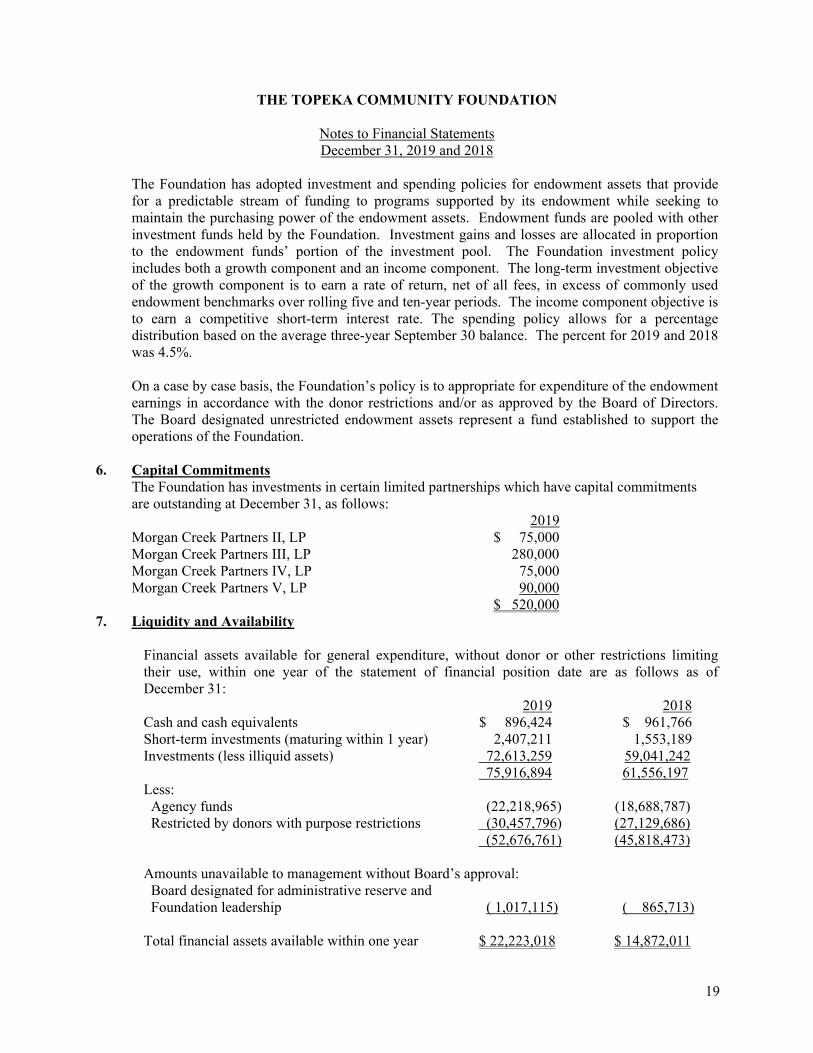

6. Capital Commitments The Foundation has investments in certain limited partnerships which have capital commitments are outstanding at December 31, as follows: 2019 Morgan Creek Partners II, LP $ 75,000 Morgan Creek Partners III, LP 280,000 Morgan Creek Partners IV, LP 75,000 Morgan Creek Partners V, LP 90,000 $ 520,000 7. Liquidity and Availability

Financial assets available for general expenditure, without donor or other restrictions limiting their use, within one year of the statement of financial position date are as follows as of December 31:

2019 2018 Cash and cash equivalents $ 896,424 $ 961,766 Short-term investments (maturing within 1 year) 2,407,211 1,553,189 Investments (less illiquid assets) 72,613,259 59,041,242 75,916,894 61,556,197 Less: Agency funds (22,218,965) (18,688,787) Restricted by donors with purpose restrictions (30,457,796) (27,129,686) (52,676,761) (45,818,473) Amounts unavailable to management without Board’s approval: Board designated for administrative reserve and Foundation leadership ( 1,017,115) ( 865,713) Total financial assets available within one year $ 22,223,018 $ 14,872,011

19

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

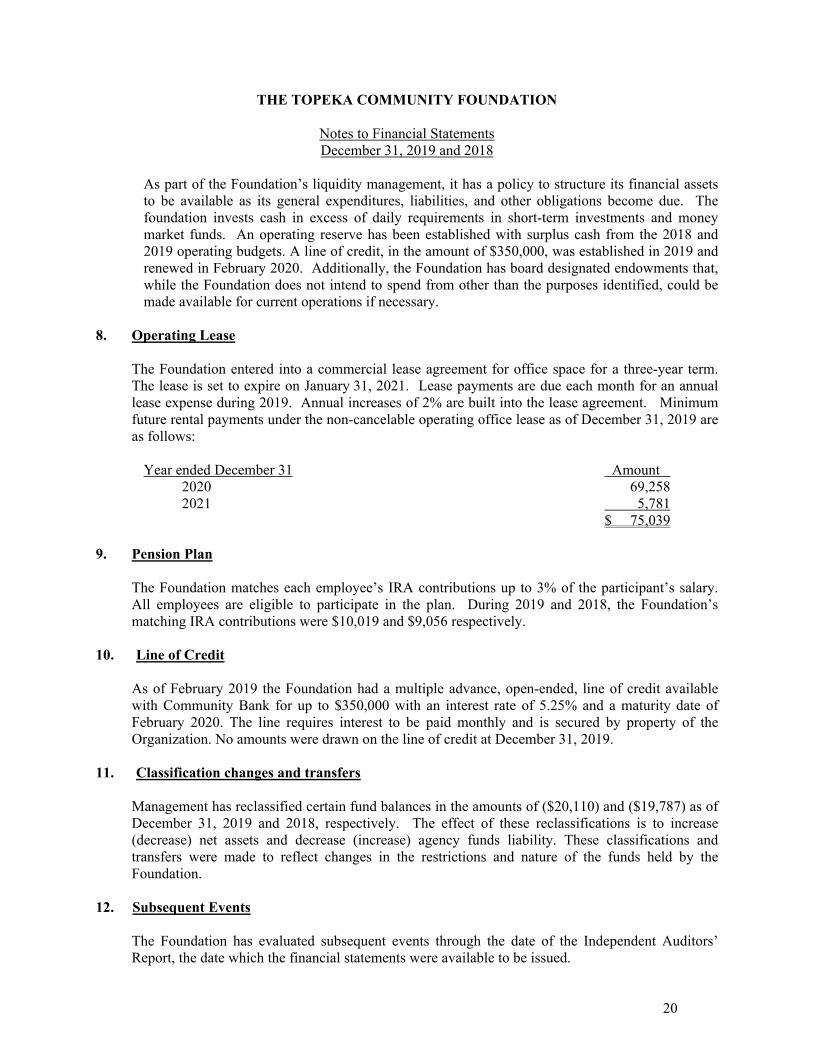

As part of the Foundation’s liquidity management, it has a policy to structure its financial assets to be available as its general expenditures, liabilities, and other obligations become due. The foundation invests cash in excess of daily requirements in short-term investments and money market funds. An operating reserve has been established with surplus cash from the 2018 and 2019 operating budgets. A line of credit, in the amount of $350,000, was established in 2019 and renewed in February 2020. Additionally, the Foundation has board designated endowments that, while the Foundation does not intend to spend from other than the purposes identified, could be made available for current operations if necessary.

8. Operating Lease

The Foundation entered into a commercial lease agreement for office space for a three-year term. The lease is set to expire on January 31, 2021. Lease payments are due each month for an annual lease expense during 2019. Annual increases of 2% are built into the lease agreement. Minimum future rental payments under the non-cancelable operating office lease as of December 31, 2019 are as follows:

Year ended December 31 Amount

2020 69,258 2021 5,781 $ 75,039

9. Pension Plan

The Foundation matches each employee’s IRA contributions up to 3% of the participant’s salary. All employees are eligible to participate in the plan. During 2019 and 2018, the Foundation’s matching IRA contributions were $10,019 and $9,056 respectively.

10. Line of Credit

As of February 2019 the Foundation had a multiple advance, open-ended, line of credit available with Community Bank for up to $350,000 with an interest rate of 5.25% and a maturity date of February 2020. The line requires interest to be paid monthly and is secured by property of the Organization. No amounts were drawn on the line of credit at December 31, 2019.

11. Classification changes and transfers

Management has reclassified certain fund balances in the amounts of ($20,110) and ($19,787) as of December 31, 2019 and 2018, respectively. The effect of these reclassifications is to increase (decrease) net assets and decrease (increase) agency funds liability. These classifications and transfers were made to reflect changes in the restrictions and nature of the funds held by the Foundation.

12. Subsequent Events

The Foundation has evaluated subsequent events through the date of the Independent Auditors’ Report, the date which the financial statements were available to be issued.

20

THE TOPEKA COMMUNITY FOUNDATION

Notes to Financial Statements December 31, 2019 and 2018

On January 30, 2020, the World Health Organization declared the coronavirus outbreak a "Public Health Emergency of International Concern" and, on March 11, 2020, declared it to be a pandemic. Actions taken around the world to help mitigate the spread of the coronavirus include restrictions on travel, quarantines in certain areas, and forced closures for certain types of public places and businesses. The coronavirus and actions taken to mitigate the spread of it have had and are expected to continue to have an adverse impact on the economies and financial markets of many countries, including the geographical area in which the Foundation operates. On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) was enacted to, amongst other provisions, provide emergency assistance for individuals, families and businesses affected by the pandemic. It is unknown how long the adverse conditions associated with the pandemic will last and what the complete financial effect will be to the Foundation. Accordingly, while management cannot quantify the financial and other impacts to the Foundation as of December 31, 2019, management believes that a material impact on the Foundation’s financial position and results of future operations is reasonably possible. Additionally, it is reasonably possible that estimates made in the Foundation’s financial statements have been, or will be, materially and adversely impacted in the near term as a result of these conditions.

21

Copyright © 2022 FDOKUMEN