Financial Statements as at 31 December 2006 - Fineco

256

FinecoBank Banca Fineco S.p.A. Financial Statements as at 31 December 2006

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Financial Statements as at 31 December 2006 - Fineco

FinecoBank Banca Fineco S.p.A.

Financial Statements as at 31 December 2006

Contents

TABLE OF CONTENTS

Management Bodies 2

Report on Operations 4

Introduction to financial highlights 5

Financial highlights 6

Key figures 7

Macro-scenario: the economy and financial markets 8

Bank performance and key initiatives for the year 11

The activity of FinecoBank S.p.A. 17 Securities brokerage 18

Online 21 Financial Advisors Network 23

Mortgages 26 Salary guaranteed loans 27

Balance sheet figures 29

Regulatory capital and prudential requirements 41

Income statement figures 42

Operating structure 52 Human resources 52

Technology infrastructure 55 Internal control system 56

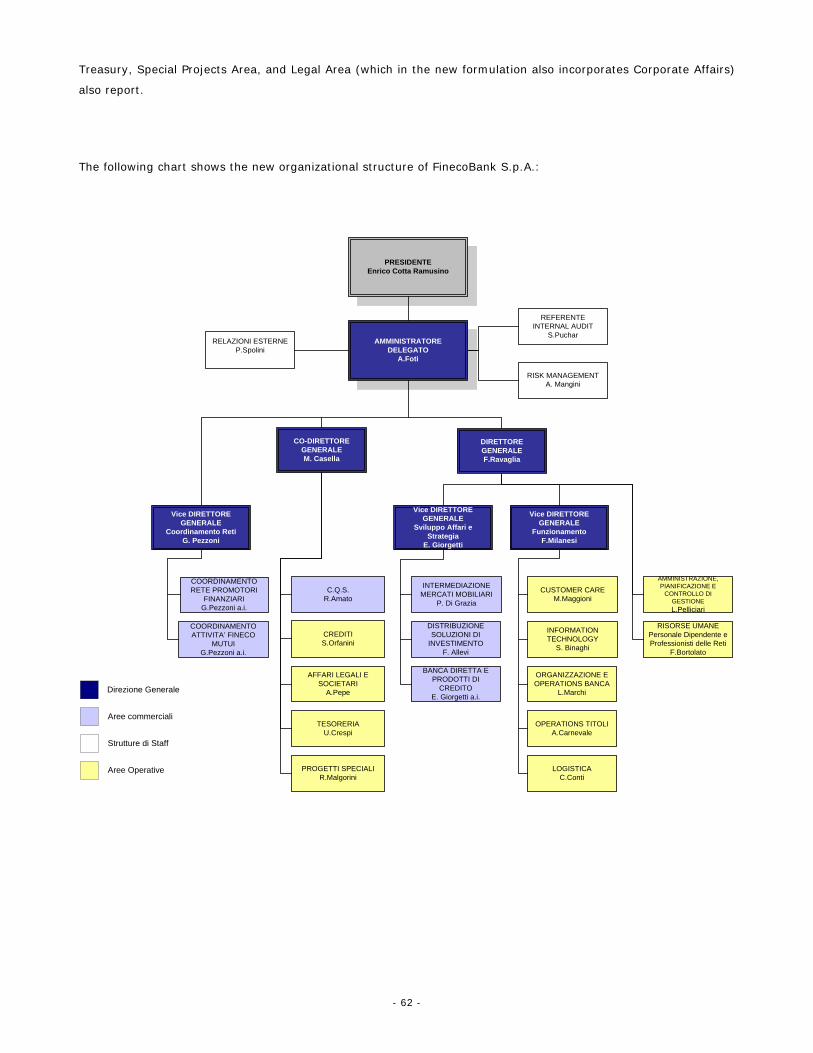

Risk measurement and control 57 Organizational structure 61

Document on Security Planning 63 Communications and external relations 63

Other information on operations 65 Securitization operations 65

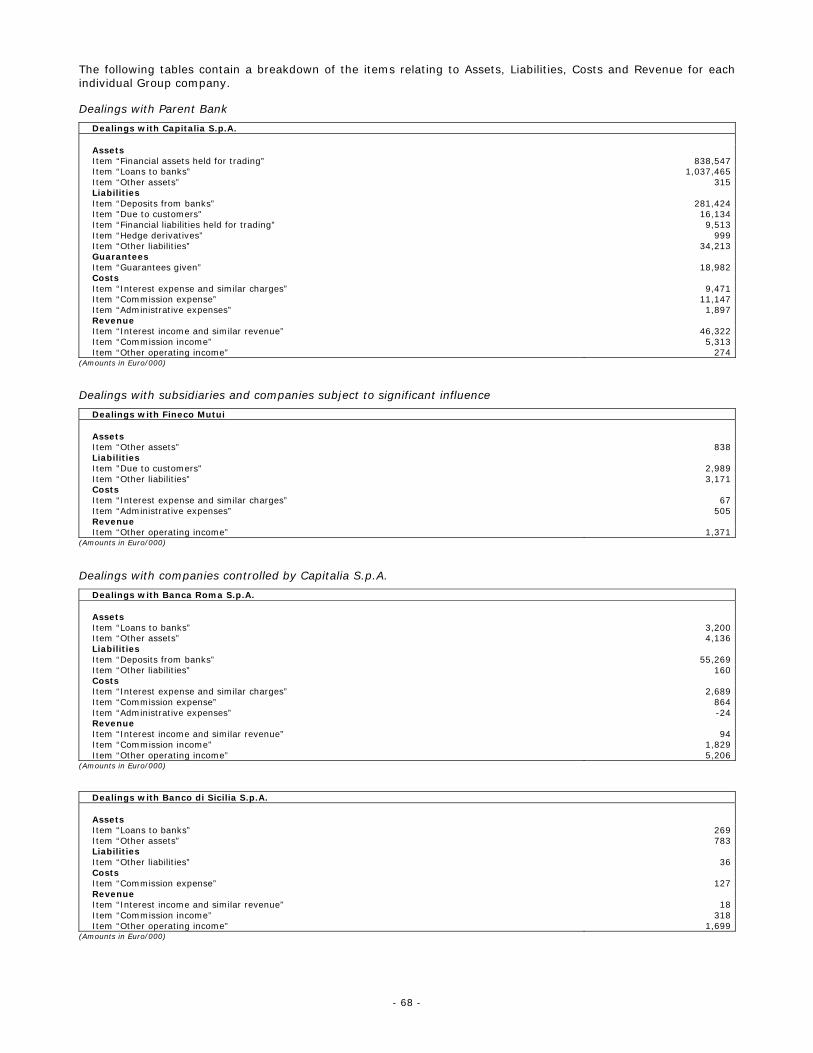

Dealings with the Parent Bank and other Group companies 67

Significant events occurring after year end and business outlook 72

Proposal for the approval of the financial statements and allocation of profits for the year 73

Reconciliation of income statement with reclassified income statement 74

Report of the Board of Statutory Auditors 75

Independent Auditors' Report 79

Bank financial statements 81

Balance sheet 82 Income statement 83

Statement of changes in shareholders' equity 84 Statement of cash flow 86

Notes 87

Part A - Accounting policies 89 Part B - Information on the balance sheet 107

Part C - Information on the income statement 147 Part D - Segment information 164

Part E - Information on risks and hedging policies 166 Part F - Information on shareholders' equity 243

Part G – Business combinations 247 Part H – Transactions with related parties 247

Part I - Payments based on own equity instruments 248

Appendix 249

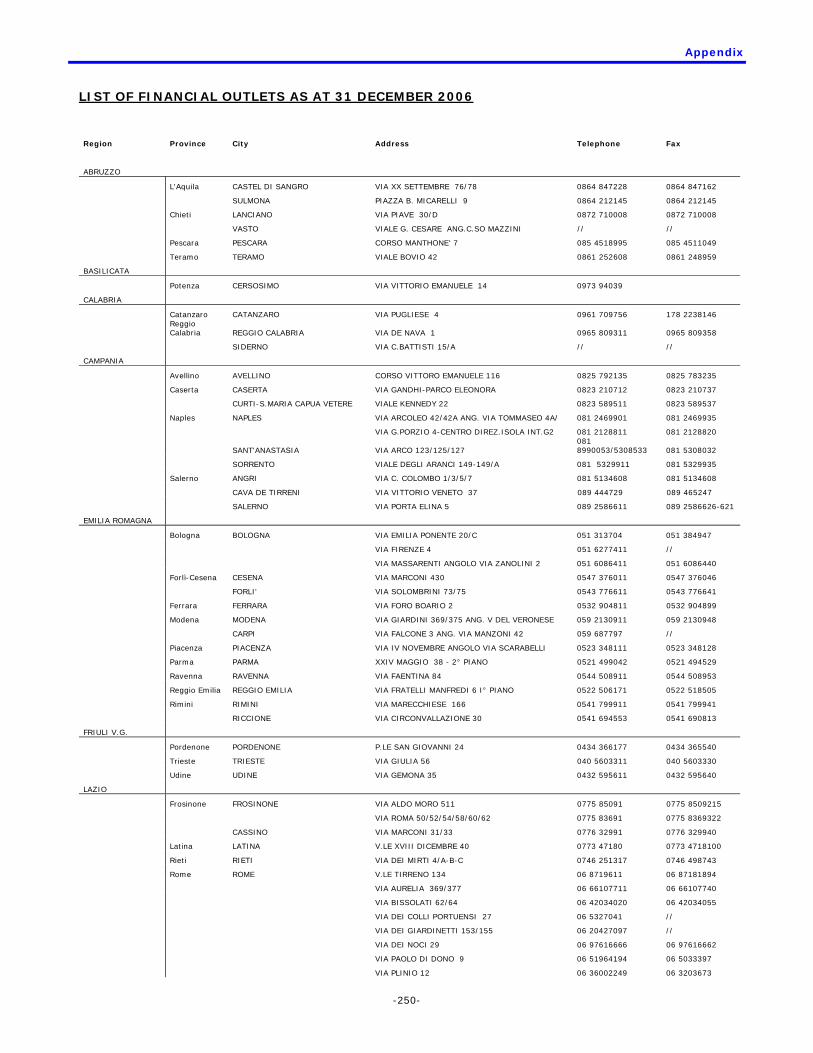

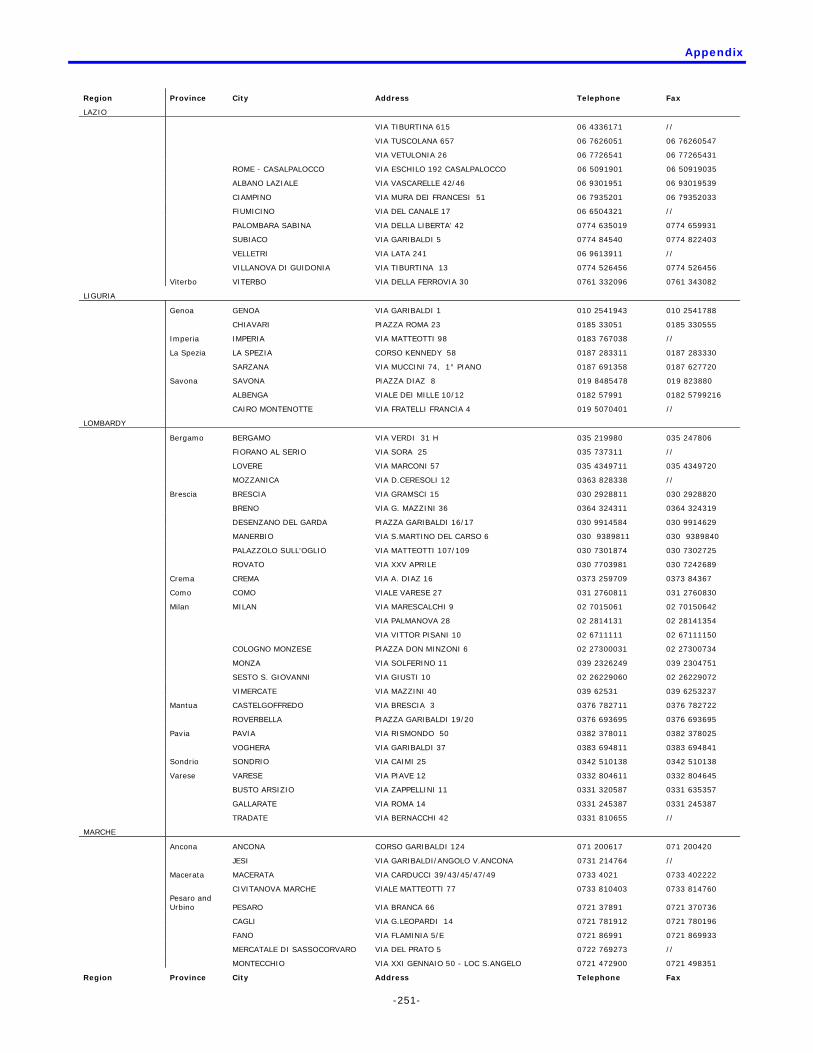

List of financial shops as at 31 December 2006 250

- 1 -

Share capital €199,850,987.49, fully paid-up, divided into 605,609,053 shares with a face value of €0.33, 99.99% of which is held by Capitalia S.p.A. and the remaining 0.01% by minority-interest shareholders. Registered office: Piazza Durante 11, 20131 Milan, Italy

“FinecoBank Banca Fineco S.p.A.”

in abbreviated form “FinecoBank S.p.A.”, or “Banca Fineco S.p.A.” or “Fineco Banca S.p.A.” Company controlled by Capitalia S.p.A., Gruppo Bancario Capitalia, Register of Banking Groups no. 3207.8,

Member of the Interbank Fund for the Protection of Deposits, Italian Banking Association Code 03015, Tax Code and Milan Register of Companies no. 01392970404 – R.E.A. (Economic and Administrative Index) no.

1598155, VAT no. 12962340159

- 2 -

Management Bodies

- 3 -

MANAGEMENT BODIES

Board of Directors

Chairman Enrico Cotta Ramusino Deputy Chairman Stefano Landi Chief Executive Officer Alessandro Foti Directors Giuseppe Colaiacovo

Michele De Capitani Donato Fontanesi Frederik Geertman Alfredo Malguzzi Emma Marcegaglia Fulvio Montipò Luigi Terzoli

Board of Statutory Auditors

Chairman Luigi Attilio Mazzocchi Statutory Auditors Antonio Passantino

Francesco Poddighe

Alternate Auditors Umberto Bocchino Luciano Masini

Management

General Manager Franco Ravaglia Assistant General Manager Michele Casella

Independent auditors Reconta Ernst & Young S.p.A. On 12 April 2006, an ordinary meeting of the Bank's shareholders: • increased the number of members of the Board of Directors from nine to eleven; acknowledged the resignation from the Board of Directors of Messrs. Francesco Bisesti, Angelo Brizi and Michele Casella; appointed the following new members of the Board of Directors: Giuseppe Colaiacovo, Michele Ferdinando De Capitani Da

Vimercate, Donato Fontanesi, Alfredo Malguzzi, Emma Marcegaglia and Fulvio Montipò.

- 4 -

Report

on Operations

- 5 -

INTRODUCTION TO FINANCIAL HIGHLIGHTS The separate financial statements of FinecoBank Banca Fineco S.p.A. (hereinafter referred to as

“FinecoBank S.p.A.”) as at 31 December 2006 have been prepared according to the indications provided by

the Parent Bank and in compliance with the valuation criteria established by the International Financial

Reporting Standards (IFRS) and International Accounting Standards (IAS) issued by the International

Accounting Standards Board (IASB) and endorsed by the European Commission under the procedure

envisaged in article 6 of Regulation (EC) no. 1606/2002 of the European Parliament and the Council of 19

July 2002. The Community Regulation has been fully applied in Italy following Italian Legislative Decree no.

38 of 28 February 2005, which came into force on 22 March 2005.

For a significant comparison between the figures from the income statement and balance sheet for 2006,

which incorporate new indications provided by the Parent Bank, and those for 2005, the income statement

and the balance sheet as at 31 December 2005 were reclassified to account for the following: • the change in the criteria for the accounting treatment of securities lending transactions to bring them in

line with those already adopted by the other Group companies;

• the reclassification of commission income from sums recovered on credit card service by FinecoBank

S.p.A. as issuer on behalf of other Group Banks. In 2005, the aforementioned recovered sums were

recognised with other operating income; in 2006, following the indication of the Parent Bank, these sums

were recognized with commission income as at June 2006, and with other operating income from July 2006

(following the transfer of credit card contracts to the Group Banks);

• the transfer of penalties for early redemption of loans classified as Loans & Receivables and measured at

amortized cost to net interest income;

Furthermore, subsequent to the application during 2006 of the provisions of the Bank of Italy contained in

the update to circular no. 49/1989 dated 1.12.2006, the tables in the notes were reclassified to account for

the following:

• the change in the representation of repurchase agreements to distinguish between transactions involving

securities owned by the Bank from transactions involving securities received by the Bank as part of

repurchase agreements;

• the change in the representation of interest income accrued on securities owned by the Bank involved in

repurchase agreements (previously recognised with interest income on financial assets held for trading and

currently recognised with interest income on financial assets sold but not eliminated).

The section “Financial Statements” contains the Bank’s financial statements as at and for the years ended

31 December 2006 and 31 December 2005 as prepared in accordance with IAS/IFRS.

The section “Accounting Standards” sets forth the relevant international accounting standards adopted in

preparing the accounts as at 31 December 2006.

The appendix contains a table reconciling the income statement items with those of the reclassified income

statement.

- 6 -

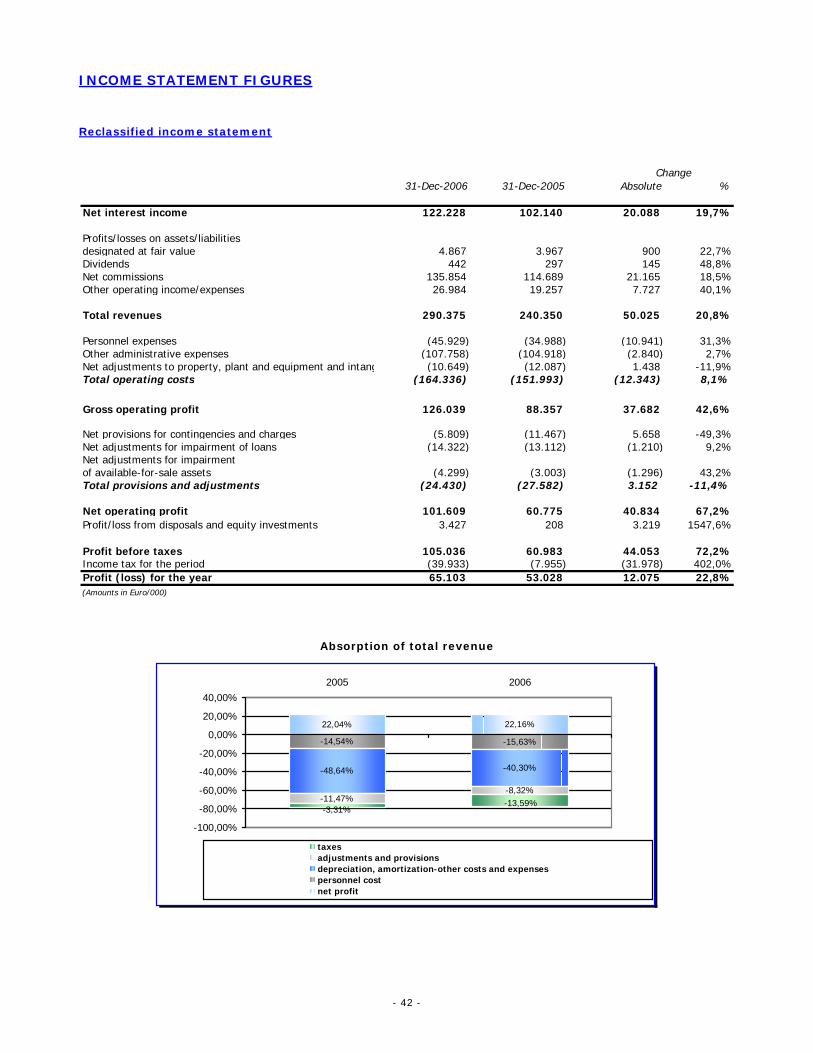

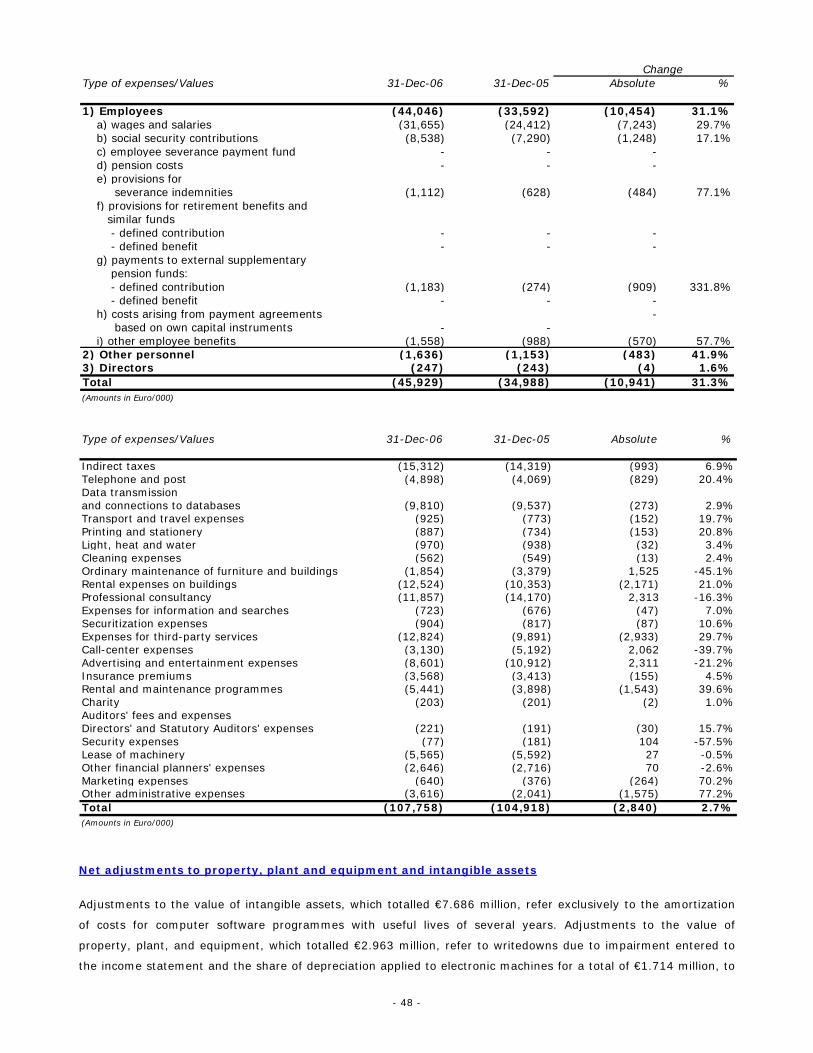

FINANCIAL HIGHLIGHTS Reclassified income statement

31-Dec-2006 31-Dec-2005 Absolute %

Net interest income 122.228 102.140 20.088 19,7%

Profits/losses on assets/liabilitiesdesignated at fair value 4.867 3.967 900 22,7%Dividends 442 297 145 48,8%Net commissions 135.854 114.689 21.165 18,5%Other operating income/expenses 26.984 19.257 7.727 40,1%

Total revenues 290.375 240.350 50.025 20,8%

Personnel expenses (45.929) (34.988) (10.941) 31,3%Other administrative expenses (107.758) (104.918) (2.840) 2,7%Net adjustments to property, plant and equipment and intangible assets (10.649) (12.087) 1.438 -11,9%Total operating costs (164.336) (151.993) (12.343) 8,1%

Gross operating profit 126.039 88.357 37.682 42,6%

Net provisions for liabilities and contingencies (5.809) (11.467) 5.658 -49,3%Net impairment adjustments of loans (14.322) (13.112) (1.210) 9,2%Net impairment adjustments of financial asset (4.299) (3.003) (1.296) 43,2%Total provisions and adjustments (24.430) (27.582) 3.152 -11,4%

Net operating profit 101.609 60.775 40.834 67,2%Profit/loss on disposal assets and from equity investments 3.427 208 3.219 1547,6%

Profit before taxes 105.036 60.983 44.053 72,2%Income tax for the period (39.933) (7.955) (31.978) 402,0%Profit (loss) for the year 65.103 53.028 12.075 22,8%(Amounts in Euro/000)

Change

Balance sheet

31-dic-06 31-dic-05 Absolute %

Ordinary customer loans (1) 6.137.252 5.875.945 261.307 4,4%Total assets 9.094.154 7.772.137 1.322.017 17,0%Direct funding from customers (2) 5.374.564 3.808.297 1.566.267 41,1%Indirect funding (3) 8.181.028 6.932.866 1.248.162 18,0%Total customer funding 13.555.592 10.741.163 2.814.429 26,2%Shareholders’ equity 313.196 254.814 58.382 22,9%(Amounts in Euro/000)

Change

(1) Ordinary customer loans consist of all loans to ordinary customers, including securitized loans that have not been re-entered to the financial statements; (2) Direct funding from customers includes overdrawn current accounts and repurchase agreements; (3) Indirect funding consists of the Bank’s own products and third-party products placed through the sales networks of FinecoBank S.p.A. The figures are net of liquidity from discretionary accounts.

- 7 -

KEY FIGURES Operating structure

31-dic-06 31-dic-05

No. Employees 763 688No. Financial planners 1.142 1.361No. Mortgage agents 215 165No. Operating financial shops 169 195

Balance sheet highlights

Composition 31-Dec-06 31-Dec-05

Customer loans/Total assets 75.17% 83.16%Financial assets/Total assets 10.75% 7.44%Customer loans/Customer deposits 88.34% 101.98%

31-Dec-06(*) 31-Dec-05

TIER 1 7.00% 8.21%Regulatory capital / Weighted assets - Total capital ratio 9.82% 9.94%

Risk ratios 31-dic-06 31-dic-05

Net non-performing loans / Customer loans 0.36% 0.26%Net doubtful loans / Customer loans 0.89% 0.55%

Income statement highlights Profitability ratios 31-Dec-06 31-Dec-05

ROE 20.79% 20.81%ROA 0.72% 0.68%Net interest income / Total revenues 42.09% 42.50%Profit from financial operations / Total revenues 1.68% 1.65%Net commissions on services, dividendsand other net income / Total revenue 56.23% 55.85%

Operating costs / Total revenues 56.59% 63.24%Net operating costs / Total net revenues 52.20% 59.10%

Legend Number of mortgage agents: Sales network of Fineco Mutui, on which FinecoBank S.p.A. relies to place its products. Number of operating financial shops: financial shops managed by the Bank and financial shops managed by financial planners. Shareholders' equity: share capital + share price premium + reserves + profit/loss for the year. ROE: net profit / shareholders’ equity at year-end. ROA: net profit / total assets at year-end. Classified loans: bad debts and substandard loans. Net operating costs: operating costs net of recovered expenses; Total net revenues: total revenues net of any sums recovered; (*) Regulatory capital and total weighted risk assets were calculated by applying current supervisory provisions on the basis of accounting figures prepared in accordance with international accounting standards. Regulatory capital and total weighted risk assets as at 31 December 2005 were calculated by applying supervisory provisions effective at the time on the basis of accounting figures prepared in accordance with Italian Legislative Decree no. 87/92.

- 8 -

MACRO-SCENARIO: THE ECONOMY AND FINANCIAL MARKETS

The macroeconomic scenario The world economy continued to expand in 2006. The divergences in the rate of GDP growth in the major industrial

areas narrowed: growth accelerated in the Eurozone and the United Kingdom, but slowed in the United States

reflecting the pronounced weakening in the poperty, and consolidatedin Japan. Emerging economies, especially China

and India, made a substantial contribution to global development expanding by close to 10%.

The persistence of the favorable phase of the business cycle and the rising prices of row materials caused consumer

price inflation to pick up the main industrial countries. In order to prevent inflationary pressures from impacting

longer term expectations, the central banks tightened their policy stances.

In Italy, 2006 closed with the highest growth in five years, with GDP expanding by 1.9%. This growth was driven

largely by domestic demand, with strong performance of investments in the first half of the year and household

consumption in the second. Investment was boosted by the recovery in industry associated with the continuation of

the restructuring and selection of companies; while consumption was supported by weak inflation growth, the partial

recovery of purchasing power in certain segments thanks to contract renewals and the positive trend in employment.

Exports also performed well, although their contribution to growth was offset by an equivalent rise in imports, which

reflected the jump in the prices of energy products. In cyclical terms, growth was fastest in the first and second

quarters of 2006, slowing in the second half of the year. The decelaration may be attributed largely to the

strengthening of the euro and the slowing of growth in the world economy.

Last year ended on a positive note for the main stock exchange, which consolidated the record levels achieved in the

past five and a half years and maintained their robust upward trend. The European stock market achieved the most

significant gains (approximately 19.6%), whereas the U.S. S&P 500 index ended the year up by about 12.2%. After a

long period of uncertainty, Tokyo investors began to buy again with a rally in the final weeks of the year that erased

earlier losses and enabled the stock market to post a gain for the year of about 7,2%.

Chart 1: Performance of equity market

Source: Datastream

- 9 -

Bank interest rates In the United States, the Federal Reserve (Fed) raised its target for the federal funds rate by 25 basis points four

times in the first half of 2006, bringing it up to 5.25% in June. With the emergence of signs of slowing growth in the

United States economy, the Fed interrupted the series of rate hikes in the second half of the year. In the Euro Area,

the strenthening of signs of recovery and the intensification of price strains prompted, the European Central Bank to

continue the monetary tightening started in December 2005. The minimum bid rate on main refinancing operations

and that on deposits at the ECB were raised by a quarter of a percentage point no fewer than five times, bringing the

rates to 3,5% and 2,5% respectively.

During 2006, bank interest rates were gradually raised in line with the increase in official rates. In particular, in

December the average 1-year lending rate applied by banks to households and businesses was 5.92%, up from

5.26% at the end of 2005. The average deposit rate for households and businesses also rose, ending the year at

1.45% (0.95% at the end of December 2005). The short-term spread consequently widened to 4.47% in December

(compared to 4.31% at the end of 2005 (Chart 2).

Chart 2: Performance of short-term bank interest rate spreads (in percent)

Source: Bank of Italy

Credit brokerage On par with the developments in the euro zone, direct funding with banks (deposits and bonds) grew rapidly,

although less so than in 2005 (annual growth-rate of 7.8% at the end of 2006 against 8.6% in 2005). The growth in

funding was boosted by the enduring preference for liquidity, despite the rise in official rates and the interes of

investors in low-risk bonds. Funding growth was driven by the recovery in repurchase agreements, which typically

offer higher yields than current accounts, and the continued strong growth of the bond segment (annual growth of

10.4% in December 2006).

Faced with loan growth that outpaced the increase in funding, in 2006 Italian banks increased their net external

liabilities abroad

- 10 -

The recovery in economic development that took place in the first half of 2006 supported the expansion of bank

lending: in December the growth rate of loans was up 11.2% year-on-year, compared to 8.6% in December 2005.

The pick-up in bank lending was mainly tied to demand from companies, which was more than enough to offset the

slight deceleration in loans to families associated with certain securitization operations, the cooling-off of the real-

estate market, and increasing interest rates. On a geographical basis, loans to, customers in Southern Italy expanded

especially rapid, driven by business lending, which grew at a rate nearly twice that of Italy’s Centre and North. Loans

to families also increased more rapidly in the South, despite slowing down from 2005.

Credit quality showed no signs of decline in 2006, benefiting from the brisk pace of economic activity, still-moderate

interest rates, and a further reduction of mark-up.

Assets under management Investments funds posted their worst results ever in 2006. Despite the improved performance of the markets over

the second half of the year, the net change in funding over the year was extremely negative, with asset outflows of

more than €17 billion.

The weakness of the mutual fund sector was tied in part to the performance of financial markets, which in the first

half of the year penalized the bond market and then the stock market against the backdrop of uncertainty

surrounding the expected performance of inflation and the degree of tightening of monetary policy. The industry

continued to register large asset outflows even after financial markets later turned bullish.

The performance of funding had a negative impact on the performance of assets invested in mutual funds. After a

period of rapid expansion recorded from February to April, total assets invested in the mutual funds industry slowed

once more, falling to 4.2% in December 2006 from 8.7% at the end of 2005. Roundtrip funds registered a positive

performance, although less so than the previous year (10.7% in December 2006, down from 23%), while the Italian

sector contracted sharply (down 7.7%, compared to an increase of 3.3% at the end of 2005) (Chart 4).

- 11 -

BANK PERFORMANCE AND KEY INITIATIVES FOR THE YEAR

Performance of balance sheet aggregates

In the trading area, FinecoBank S.p.A. confirmed its role as the number-one Italian broker for number of executed

orders, with a market share of 7.44% (source: Assosim), up from 7.19% in 2005. Traded volumes in the securities

market underwent significant growth, supported by the development of volumes traded on behalf of Capitalia

Group companies, as well as the consolidation of trading volumes generated by newly acquired customers over the

past few years.

Total customer fundung (direct plus indirect) came to €13,556 million, showing an increase of 26.2% compared to

the same period of the previous year. Direct funding (current accounts and repurchase agreements) held by retail

customers totalled €5,271 million as at 31 December 2006, against €3,749 million as at 31 December 2005,

posting an increase of 41% and confirming a growing trend. The number of current accounts in euro increased by

5.8% over the stock existing on 31 December 2005, bringing the total number of active current accounts up to

approximately 363.000. There was a significant increase in the number of credit cards (in terms of cards issued, net of expired cards),

which rose from 857,188 as at 31 December 2005 to 1,307,501 as at 31 December 2006 (up 52.5%), due in part

to cards issued on behalf of Capitalia Group Banks, for which FinecoBank S.p.A. serves as an issuer and provider of

processing and servicing.

The process of restructuring the financial planners distribution network moved forward with the rationalization of

sales shops (128 financial shops throughout all of Italy, with an additional 41 shops managed directly by Financial

Advisors) and the revision of the organizational structure and commission system. Development of the network’s

Information Technology systems continued, involving the installation of remote connections enabling a more

nimble production process, decreased costs, and greater loyalty by financial planners. As at 31 December 2006 the

distribution network consisted of 1,142 resources. With a total of over €9,473 million under management and

administration, the assets of the financial planners network grew by 22.9% compared to 31 December 2005. Of

this total, €4,784 million consisted of assets under management (up 15.2%).

Customer loans, including securitized loans, totalled €7,204 million. Loans to retail customers came to €6,137

million (up 4.4%). During 2006, FinecoBank S.p.A. continued to enact its strategy of expansion on the residential mortgage market

through its subsidiary Fineco Mutui S.p.A., focusing on the addition of new agents, the ongoing development of

geographical coverage, the shift in the composition of the product portfolio, and the improvement of business

processes, all of which were aimed at ensuring that the products offered by the Bank on the domestic market were

increasingly distinctive and innovative.

A total of 4,464 mortgage agreements were entered into during 2006, for a total of €541 million.

FinecoBank S.p.A. leads the market in the sector of loans secured bysalry guaranteed loans, with a total of €1,504

million in loans and an increase in loans issued of 24% over 2005.

- 12 -

Performance of income statement aggregates

Total revenues were up 21% over 2005, for a total of €290 million, due to the improvement of both net interest

income, which may be attributed largely to the increase in average volumes of funding and customer loans and the

diversification of financial investments, and the commissions spread, especially in the online trading and brokerage

area.

The positive performance of revenues from typical operations, along with the reduction of operating costs, had an

impact on profit before taxes, which came to more than €105 million, posting an increase of 72.2% over the same

period of the previous year.

Net profit came to €65 million, up 22.8% from 31 December 2005.

- 13 -

Main initiatives during the year

Early redemption of the Garda securitization transaction involving salary guaranteedloans

On 20 June 2006, as per the resolution of the Board of Directors passed on 22 February 2006 and following

authorization from the Bank of Italy, the Bank bought back the portfolio of loans secured by one-fifth of

salary totalling approximately €65 million, which had been sold on 30 March 2001 to the special vehicle

purpose Garda Securitisation S.r.l.. As provided in the securitization agreements, the "optional redemption"

clause, under which the special purpose vehicle had the option of early redemption of the entirety (and not

part) of the underlying assets, in the event that the amount of principal due on the class A and class B

notes was less than €61 million, or subsequent to the date of payment, 20 September 2005 had been

activated. Although there existed no formal obligation to activate the "early redemption" clause, it was in

the interest of FinecoBank S.p.A. to close out the operation in advance since the limited amount of the

bonds in issue did not justify the costs incurred to maintain the securitization operation.

Distribution of dividends by FinecoBank S.p.A.

On 2 May 2006 dividends were paid out on 605,609,053 shares, at the amount of €0.01 per share, as per

the resolution of the Shareholders’ Meeting passed on 12 April 2006.

Equity investments

On 20 February 2006 the Board of Directors approved the sale of the total equity investment in Ktesios

S.p.A., amounting to 4.5% of the latter’s share capital, following the offer received from a leading financial

company. The sale, which allows the Bank to maintain its current commercial agreements, was closed on 13

April 2006 and generated a capital gain of €2.5 million.

On 18 January 2006 the Board of Directors approved the agreement with the insurance company Net

Insurance S.p.A. for the purchase of an equity investment amounting to 15% of the latter's share capital

for a total price of €7,500,000. The agreement aims to establish a banking and insurance hub that will best

ensure adequate development of the Bank’s operations in the salary guaranteed loans sector in a scenario

of growing competition. During 2006, a 13.04% stake was acquired in the above insurance company in two

transactions:

1. the subscription for the reserved capital stock issue for a nominal value of €0.250 million with a

disbursement of €2.5 million;

2. the purchase of an additional 500,000 shares of stock of Net Insurance S.p.A. for a total price of €5

million.

On 27 June 2006 the Board of Directors resolved to accept the proposal advanced by the Parent Bank,

which during the meeting of its Board of Directors held on 21 June 2006 had moved to transfer equity

investments of a non-strategic nature to Capitalia Merchant as part of a reorganization of the Parent Bank’s

equity investments. Under these circumstances, Capitalia offered FinecoBank S.p.A. the option of selling its

equity investment in Agenzia di Pollenzo to Capitalia Merchant for its book value. The sale was closed on 28

July 2006.

Decrease in share capital due to cancellation of own shares

On 3 August 2006, in execution of the resolution passed by the Shareholders’ Meeting held on 13 March 2006, the

period of silence required by applicable law for opposition by creditors having expired, the Bank reduced its share

- 14 -

capital by €2,442,000 from €202,292,987.49 to €199,850,987.49 by cancelling 7,400,000 own shares with a face

value of €0.33 each. On 3 August 2006 the Bank also filed a notice of change in share capital with the Milan

Register of Companies, in addition to its new updated by-laws. Consequently, effective from 3 August 2006, the

Bank’s share capital stands at €199,850,987.49, divided into 605,609,053 shares with a face value of €0.33 each.

Issue of subordinated loan

On 20 February 2006 the Board of Directors authorized the exercise of the option for early redemption of

the following lower-tier II subordinated loans:

• €51.6 million, with maturity on 30 March 2010, subscribed by Bipop-Carire, Euribor 6 months + 1%.

• €1 million, issued by Banca Manager S.p.A. (a company that was incorporated into FinecoBank S.p.A. by

merger), with maturity on 29 December 2008, subscribed by Fineco S.p.A. (now Capitalia S.p.A.), Euribor 3

months + 0.90%.

The above-mentioned loans, in addition to not meeting the requirements for full calculation for regulatory

capital purposes, since their residual maturities were less 5 years, were particularly burdensome compared

to current market conditions.

Subsequent to authorization from the Bank of Italy, the Bank issued the following tranches of a subordinated loan

for a total of €100 million, authorized by the Board of Directors on 20 February 2006:

1. a first tranche of €50 million on 7 June 2006, subscribed by Fineco Finance Ltd. (board resolution of 20

February 2006);

2. a second tranche of €20 million on 7 September 2006, subscribed by Fineco Finance Ltd. (board resolution

of 20 February 2006);

3. a final tranche of €30 million on 7 December 2006, subscribed by Fineco Finance Ltd. (board resolution of 5

October 2006).

Transfer of contractual relationships pertaining to credit cards

On 27 June 2006 the Board of Directors resolved to transfer the contractual relationships pertaining to credit cards

from FinecoBank S.p.A. to the Group Network Banks (Bipop Carire Società per Azioni, Banca di Roma, Banco di

Sicilia) effective from 1 July 2006. The transaction was undertaken free of charge, since it may be considered a

modification of the legal form of the intercompany contractual structure that does not entail substantial change to

the roles and responsibilities of the companies involved or the associated economic returns. From a management

perspective, FinecoBank S.p.A., in its capacity as agent of the Network Banks, will continue to carry out the same

servicing tasks that it currently performs in its capacity as issuer.

The Business Continuity Project and Disaster Recovery Plan

At the meeting held on 14 December 2006, the Board of Directors approved the Bank's Business Continuity Plan in

accordance with Bank of Italy regulations and guidelines set by the Parent Bank.

The Business Continuity Plan, which derives from a project started in 2005 and completed in 2006, sets forth the

operating methods adopted by the bank to ensure continuity of service to customers and the banking system in

emergency situations.

Adjustment to comply with new regulatory requirements enabled the Bank to prepare effective measures for

restoring company processes to react to events that might lead to the unavailability of one or more vital aspects of

company function (technology, logistical infrastructure, human resources). The scope of the project included

processes with a direct or indirect impact on the business that would require prompt reactivation.

The aforementioned Plan shall be updated from time to time to keep pace with the evolution of the Bank's

operations.

- 15 -

Regulatory reporting

On 31 October 2006, assimilating the resolution of the Board of Directors of Capitalia passed on 7 September 2006,

and exercising the option afforded by article 152, subsection 8, of directive 2006/48/EC of 14.6.2006 pertaining to

the access to banking activity and the exercise thereof, which established the new prudential regime for banks and

banking groups, the Bank informed the Bank of Italy of its intention to continue to implement the prudential rules

currently effective throughout 2007.

On 11 December 2006 the Bank informed the Bank of Italy of its intention to implement the “Matrix Reconciliation

of IAS/IFRS Accounts” to its supervisory reporting from 31 December 2006 forwards, thereby waiving its right to

adopt reporting rules currently effective (known as the "two-track" system).

Commercial operations and development of new services and products

FinecoBank S.p.A. has continued its work aimed at consolidating and expanding the range of services it offers. The

Bank devoted particular attention to redefining processes in end-to-end terms more in line with customer

expectations and offering greater economic efficiency.

We provide a summary of the main products and services released in 2006 below:

Enhancement of the “news” section with the News Center and Google Research (news search engine with

Google's power, speed and ease-of-use);

Enhancement of operations on equities markets, involving the possibility of trading on the Dutch, Portuguese,

English, Swiss, and Spanish stock exchanges;

Ongoing enhancement of the offer of new segments of online funds: more than 1,400 funds from 30 of the

world’s best asset management companies;

New online mortgages section: possibility for the customer to apply for a mortgage online with exclusive

conditions or request contact and consulting with an agent from Fineco Mutui S.p.A. for information about the full

range of mortgages offered and the choice of a personalized solution;

Personal loans: limit of general-purpose loan reserved for employed customers raised to €30,000;

“ExtraCash Più”: possibility for all customers who have taken out an “ExtraCash" personal loan to combine their

current loans with a second loan;

Enhancement of the “Replay” section: addition of the option of automatic balancing of the ETF portfolio through

accumulation plans;

Expanded possibilities to request current account overdraft facilities: customers may apply for the granting of an

overdraft facility on their current accounts with a pledge on Capitalia AM funds or with a power of attorney to sell

stocks or bonds;

Trading on FOREX, the global currencies exchange: FinecoBank S.p.A. was the first Italian bank to offer its

customers the possibility of trading more than 50 cross currencies directly over the internet and integrated into

one single platform;

Fineco Mobile, a lighter version of the Fineco site that may be accessed from all mobile phones or palm-top

devices. Customers may use Fineco Mobile to trade, top up their telephone credit, order electronic funds transfers,

and access all information about their accounts directly from their mobile phones;

New online services that accompany services previously provided only by call centre such as the ordering of cash

and bankers’ drafts for collection at group affiliate banks (Banca di Roma, Banco di Sicilia e Bipop-Carire);

Introduction of a roll-on plan on the U.S. market to enable the degressive reduction of fixed commissions to

$8.95;

- 16 -

Current accounts for professionals: with the enforcement of Italian Decree Law no. 233/2006 of 4 July 2006,

FinecoBank S.p.A. offers professionals the possibility of opening a current account dedicated to managing their

professional activity;

Extension to all customers of Premium services (conditional orders, alerts, intraday graphs, interactive graphs,

technical analysis sheets) without access limitations or additional costs;

Trading by call centre on 10 new markets: beginning in September FinecoBank S.p.A. will expand the number of

markets on which customers may trade through the call centre to include Austria, Denmark, Finland, Greece,

Ireland, Norway, Spain, Sweden, Switzerland, and the UK.

- 17 -

THE ACTIVITY OF FINECOBANK S.P.A.

FinecoBank S.p.A. is a bank with a nearly exclusive focus on the retail customer segment.

It is a direct bank that offers the full banking, investment and lending services of traditional banks, while

distinguishing itself from the latter by its highly innovative nature.

The Bank’s innovative nature is expressed in two areas:

• the development of innovative businesses, such as, for example, online banking and trading services, an area in

which FinecoBank S.p.A. has played a leading role in launching the market, earning itself a position of leadership

at the national and European levels in the trading sector;

• the application of innovative methods to more traditional businesses, in which FinecoBank S.p.A. has gradually

established its distribution model – consider, for example, the retail lending sector, particularly the mortgage and

“one-fifth of salary” loans segments, in which FinecoBank S.p.A. has applied its innovative character to the

distribution model, which is largely founded on the activity of product marketing networks.

The following sections contain commentary on the main balance sheet indicators and figures of the Business Areas

into which the Bank’s operations are divided.

The Bank undertakes all of its activities with the aim of earning economic returns on the “industrial” management

of the businesses themselves, minimizing the financial risk profile thereof. The financial management of

FinecoBank S.p.A. tends towards risk management aimed at protecting the industrial returns on various

businesses and not assuming risk positions on its own account.

- 18 -

SECURITIES BROKERAGE – Trading Online

FinecoBank SpA trading area currently boasts a customer base with very strong loyalty to the Bank and significant

appreciation of the services it offers. The use of the internet channel, which allows customers to undertake trading transactions on the main financial

markets directly from their personal computers, has won clear approval from investors, especially from the most

active customer segments.

The positive financial markets scenario and the steady development of DMA (direct market access) products and

services, such as trading, are the driving factors behind the Bank’s growth and gradual acquisition of greater

market share on all brokerage segments throughout 2006. The Bank’s transversal development strategy, which

involves a single platform that is segmented and focused according to various use profiles, has fully satisfied

expectations. In further detail, 2006 was a decisive year for the personalization and improvement of the three

main brokerage platforms: web-based, java-based and mobile-based, with the latter fully redesigned and further

expanded to include new functions.

New products were released and the range of existing products offered was expanded:

enhancement of the “news” section with the News Center and Google Research (news search engine with

Google's power, speed and ease-of-use);

organization of online trading courses targeted at all Fineco customers;

enhancement of operations on equities markets, involving the possibility of trading on the Dutch, Portuguese,

English, Swiss, and Spanish stock exchanges;

new spot trading in currencies on the Forex market, making FinecoBank S.p.A. the first Italian bank to offer this

service with a focus on the retail market. Foreign exchange trading, which got underway in June 2006, has already

demonstrated significant growth rates and strong cross-selling and complementarity with the range of products

offered on the platform, thereby contributing to the stabilization of business flows deriving from equities and

derivatives markets;

ongoing enhancement of the offer of new segments of funds that may be purchased online;

extension to all Fineco customers of Premium services;

trading by call centre on 10 new markets;

availability of new order services (Forex trading and electronic funds transfers) on Fineco Mobile as well;

new version of the Book, a free platform in which orders may be entered and monitored, with the possibility of

access via Fast Order.

Value of orders executed in Euro(millions of euro)

0

20.000

40.000

60.000

80.000

100.000

120.000

2000 2001 2002 2003 2004 2005 2006

Value of orders executed on U.S. market

(millions of dollars)

0

2.000

4.000

6.000

8.000

10.000

12.000

2000 2001 2002 2003 2004 2005 2006

- 19 -

Fineco orders executed broken down by market (online only)

0 2.000.000 4.000.000 6.000.000 8.000.000 10.000.000

2004

2005

2006

Other markets Italy (MTA+AH) USA France Germany

Germany 41.522 43.592 86.189

France 31.888 27.275 67.033

USA 900.190 1.036.523 1.333.894

Italy (MTA+AH) 6.242.677 7.098.486 8.880.796

Other markets 0 0 5.909

2004 2005 2006

Average amount per Borsa Italiana order (online only)(euro/000)

6,21

10,0011,88

14,21

21,04

2002 2003 2004 2005 2006

Total value of Fineco orders executed (online only)

8.6

44

.01

9

8.0

15

.35

8

7.2

16

.27

7

8.2

05

.87

6

10

.37

3.8

21

2002 2003 2004 2005 2006

- 20 -

SECURITIES BROKERAGE - Brokerage The activity of the Trading and Brokerage Desk is largely oriented towards institutional customers (mutual funds,

small hedge funds, and high net worth individuals) who rely on the professional traders of FinecoBank S.p.A. in

order to obtain best execution. This activity is of fundamental relevance to the group as it represents the point

where fund managers and financial markets come together.

In 2006 the Bank consolidated past positive trends in trading activity, due in part to the level of operating

efficiency attained by the organization and the acquisition of new customers. Although the markets reached six-

year highs, as an asset class equities are still attractive because of trends in interest rates, which are at historically

low levels, and the enormous quantity of liquidity in circulation.

In 2006 new positions were created within the Trading and Brokerage Desk with the aim of enhancing and

transferring important accumulated knowledge and experience acquired. Sales structures dedicated to business

development were also enhanced in order to analyse and discover new opportunities.

- 21 -

ONLINE The Online Business Area has continued to pursue its mission of providing a wide range of banking and credit

services aimed at a target market of sophisticated customers who are open to innovation and take a critical yet

pragmatic approach to the consumption of financial services.

In 2006 the main activities in this area related to the planning and management of marketing campaigns aimed at

online target markets and word-of-mouth initiatives (“member gets member”) geared towards existing customers.

These complex initiatives are a combination of various aspects, including creativity, advertising, logistics and

monitoring.

ONLINE - Banking Deposits in the form of current accounts denominated in euro and foreign currencies totalled approximately €4,362

million as at 31 December 2006, against €3,355 million as at 31 December 2005, posting an increase of 30% and

confirming the growing trend.

The number of current accounts increased by 5.8% over the stock in existence as at 31 December 2005, bringing

the total to nearly 363 thousand active current accounts, driven by the opening of 50 thousand new current

accounts, and despite the closure of 30 thousand current accounts.

No. of current accounts and balance of direct deposits

1.7

91

.81

0

2.3

14

.91

3

2.9

52

.72

6

3.2

59

.08

7

3.7

48

.66

9

5.2

70

.62

7

32

.98

7

73

9.9

95

323.921310.211

4.792107.371

251.299

290.233

342.838

362.675

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

1999 2000 2001 2002 2003 2004 2005 2006

0

100.000

200.000

300.000

400.000

500.000

600.000

balance of direct deposits no. of current accounts

\

Direct deposits include overdrawn current accounts denominated in euro and foreign currencies and repurchase agreements with retail customers (SuperSave).

ONLINE - Credit cards During 2006, the indicators for the credit card segment posted positive results in line with the performance

recorded in 2005.

In particular, the number of holders of active credit cards with full payment of the balance at term increased by

16%, whereas the number of customers with credit cards with instalment payment plans (the revolving option)

rose by 7%.

Furthermore, the spending figure, which remains the main driver of profitability, increased by 22% over 2005, to

reach a total amount of approximately €950 million.

Spending with revolving credit cards represented 2.4% of the total.

- 22 -

Servicing activity provided on behalf of Group banks (Banca di Roma, Bipop, Banco di Sicilia) included the issue of

approximately 340 thousand new credit cards during 2006, bringing the total number of cards managed for the

Group to more than 810 thousand.

In this connection, it should also be noted that effective from 1 July, 2006 the Bank finalized the transfer of

contractual relationships en bloc in accordance with article 58 of Italian Legislative Decree no. 385/1993; the

purpose of this transfer was to transform the Network Banks from mere “placement agents” (their role until 30

June 2006) into “issuers” of payment cards under the Capitalia brand.

During 2006, FinecoBank S.p.A. accompanied its own cards, which were issued mainly on the VISA circuit, with new

credit cards, some of which relied upon the MasterCard circuit as well, while at the same time initiating the process

of gradual migration from magnetic strip to microchip technology.

No. of credit cards issued, net of expired cards

279.049 331.557 383.175495.324

812.177

335.878184.503

3.084209.988

474.013

2001 2002 2003 2004 2005 2006

Fineco cards Capitalia cards

Historical performance of total spending (cash and revolving)

92

4.3

00

70

4.4

24

61

3.9

40

47

1.5

93

34

5.5

79

14

8.7

35

23.022

8.205

2.233

11.956

14.185

16.313

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

1.000.000

2001 2002 2003 2004 2005 2006

0

5.000

10.000

15.000

20.000

25.000

cash spending revolving spending

(Amounts in Euro/000)

- 23 -

FINANCIAL PLANNERS NETWORK The purpose of the Financial Planners Network Business Area is to allow the Bank to cover a business segment that,

despite having reached a more advance stage of development, may nonetheless prove useful and synergetic to the

goal of completing the products and services offered by the Bank and the Group to which it belongs. Following the definitive transfer of the Financial Planners business division into FinecoBank S.p.A. and the thorough

process of revision of the Network’s hierarchy/organization and commissions carried out during 2005, in 2006 this

Business Area continued to make further investments aimed at fully exploiting the synergy between distribution

channels and the provision of personalized banking products and services.

The open architecture, which is based on multi-brand funds and investment certificates, was further expanded and

consolidated during 2006. This process allowed the Bank to support the growth of assets under management and

improve the quality of the customer portfolio. The advantages of the open architecture also translated into

increased satisfaction and loyalty of financial advisors.

- 24 -

Direct and indirect funding – Financial Planners Network

DIRECT FUNDINGCurrent acc. in euro, foreign currencies, and rep. 3.052.008 32,2% 2.276.417 29,5% 775.591 34,1%Total direct funding 3.052.008 32,2% 2.276.417 29,5% 775.591 34,1%

ASSETS UNDER MANAGEMENTDiscretionary accounts 324.173 3,4% 495.801 6,4% (171.628) -34,6%Mutual funds and and other Funds 3.454.962 36,5% 2.838.038 36,8% 616.924 21,7%Insurance products 821.658 8,7% 818.665 10,6% 2.994 0,4%Other assets under management 183.344 1,9% - 0,0% 183.344 -Total assets under management 4.784.138 50,5% 4.152.503 53,9% 631.634 15,2%

ASSETS UNDER ADMINISTRATIONGovernment securities, stocks and bonds 1.637.259 17,3% 1.277.595 16,6% 359.664 28,2%Total assets under administration 1.637.259 17,3% 1.277.595 16,6% 359.664 28,2%

Total direct / indirect customer funding 9.473.405 100,0% 7.706.514 100,0% 1.766.890 22,9%

% ChangeAbsolute change

% of Total31-dic-06 % of Total 31-dic-05

(Amounts in Euro/000)

The table provided above shows the stock of assets accumulated by the financial planners network as at 31

December 2006. With a total of more than €9,473 million in overall assets under management and administration

and direct deposits held with both FinecoBank S.p.A. and other Group Banks, the financial planners network

represents a significant asset. Indirect funding (FinecoBank S.p.A.)

ASSETS UNDER MANAGEMENTDiscretionary accounts 326.077 4,0% 504.299 7,3% (178.222) -35,3% of which cash 2.719 0,0% 7.470 0,1% (4.752) -63,6%Mutual funds and SICAVs 3.656.856 44,7% 3.003.737 43,3% 653.119 21,7%Insurance products 845.265 10,3% 822.667 11,9% 22.598 2,7%Other assets under management 185.429 2,3% - 0,0% 185.429 -Total assets under management 5.010.909 61,3% 4.330.703 62,6% 680.206 15,7%

ASSETS UNDER ADMINISTRATIONGovernment securities and bonds 808.198 9,9% 483.125 7,0% 325.073 67,3%Stocks 2.319.268 28,3% 2.098.970 30,3% 220.298 10,5%Other securities 42.653 0,5% 20.068 0,3% 22.585 112,5%Total assets under administration 3.170.119 38,7% 2.602.163 37,5% 567.956 21,8%

Total indirect customer funding 8.181.028 100% 6.932.866 100% 1.248.162 18,0%

% ChangeAbsolute change

% of Total31-dic-06 % of Total 31-dic-05

(Amounts in Euro/000) The table provided above sets out the figures for the stock of assets under management and administration of the

customers of FinecoBank S.p.A., whether the customers are linked to a financial advisor or are online customers.

The figures shown refer to the Bank’s own products and those of third parties placed online or through the Bank’s

sales networks.

Total indirect funding grew by more than €1,248 million over December 2005, posting a significant increase in the

area of mutual funds and foreign SICAVs (€653 million) and new structured certificates products (€185 million).

As at 31 December 2006 the distribution network consisted of 1,142 resources. A decrease of 219 resources was

recorded from the situation as at 31 December 2005.

The influx of new assets under management, net of disinvestment, came to approximately €567 million in 2006.

This influx may be broken down as follows: €503 million in funds of the Bank and third parties, €33 million in

insurance products, - €159 million in discretionary accounts, and €191 million in the new certificates.

During 2006, the range of funds offered for subscription online was significantly expanded through the placement

of the products of 11 new SICAVs (Henderson, Union, Capitalia IM, Sgam Fund and Sgam AI Equisys Fund, Merrill

- 25 -

Lynch Master Series, Mellon, Nordea, Pioneer Funds, Raiffeisen and Nomura) and one asset-management company

(Grifogest), which, along with the marketing of new segments of existing SICAVs or asset-management companies,

brought the total number of funds up to 1,700 representing 37 different brands, thereby expanding the range of

instruments available to the FinecoBank S.p.A. Network to meet the diverse needs of investors. The Bank also

began to market 14 structured investment certificates of various issuers, a real-estate fund, and open-ended

pension funds (Arca, Aletti Gestielle, Anima and Credit Agricole).

As at 31 December 2006 the distribution network was active throughout all of Italy, operating 128 financial shops

directly managed by the Bank, in addition to 41 shops managed by Financial Planners.

The rationalization of points of sale started during previous years continued throughout 2006, also in the light of

the combination of the distribution networks previously operated by the Group under the control of FinecoBank

S.p.A.

Assets under management – 2006 Performance (euro/000)

-16.

272

-19.

336

-14.

666

-7.3

19

-20.

308

-14.

653

-8.8

78

-9.0

43

-8.8

60

-17.

159

-17.

374 -5

.250

64.3

58 71.0

94

85.5

94

84.0

96

-15.

992

-10.

278

43.9

38

14.6

60

4.72

9

24.4

16

47.8

07

88.2

31

-1.6

33

2.74

1

4.43

0

4.31

4

5.46

2

4.19

7 12.1

59

-9 -18

-1.6

24

1.84

5

1.12

7

-40.000

-20.000

0

20.000

40.000

60.000

80.000

100.000Managed accounts (funds/securities) Funds Insurance Certificates

% Composition of Total Stock of Assets in Financial Planners Network as at 31 December

2006

49,5% 50,5%

1,9%

36,5%

8,7%

3,4%

Assets under administration/Current accountsManaged accounts (funds/securities)FundsInsuranceCertificates

% Composition of Total Stock of Assets in Financial Planners Network as at 31 December 2005

46,1%

36,8%

53,9%

10,6%6,4%

Assets under administration/Current accounts

Managed accounts (funds/securities)

Funds

Insurance

MORTGAGES

- 26 -

During 2006, FinecoBank S.p.A. continued to enact its strategy of expansion on the residential mortgage market

through its subsidiary Fineco Mutui S.p.A., focusing in particular on the addition of new agents, the steady

development of geographical coverage, the shift in the composition of the product portfolio and commissions, and

the improvement of business processes, all of which were aimed at ensuring that the products offered by the Bank

on the domestic market were increasingly distinctive and innovative.

As at 31 December 2006 the Bank had a multi-channel distribution structure consisting of 216 specialized agents

employed by Fineco Mutui S.p.A., 9 back-office structures, approximately 70 regional offices placed throughout all

of Italy, and more than 1,200 financial advisors a ble to indicate customers who are interested in taking out a

mortgage. FinecoBank S.p.A. further boasts a website that facilitates telephone and remote access to the Bank's

services, which include, in addition to providing information, the possibility of requesting and obtaining explanation

concerning mortgages through an exclusively online process.

It should be pointed out that among the regional offices must also be classified the new commercial shops opened

directly by agents, which are oriented towards optimizing geographical coverage under a variable cost

management model.

The Bank’s distribution system allowed it to issue approximately €541 million in mortgages and enter into 4,464

mortgage agreements during 2006.

The achievement of these results was made possible by the realization of a wide range of marketing,

communications, and organizational activities aimed at maximizing marketing and operational efficiency. In

particular, customers were provided with new products aimed at: creating a competitive advantage over other

industry players, consolidating the positions of leadership that the Bank has won for itself by expanding the range

of existing products and developing cross-selling between agents and financial planners.

Total outstanding mortgages as at 31 December 2006 came to €4,380 million, of which €2,065 million were in

portfolio, €1,952 had been sold but not eliminated from the balance sheet and the remaining €363 million had

been securitized.

As at 31 December 2006, subsequent to the redefinition of the product portfolio accomplished during the year,

FinecoBank S.p.A. Mortgages Business Area offered as many as 25 mortgage product families, with maturities

from 5 to 35 years, fixed and floating rates, with the option to switch to fixed rates, planned payments, and

flexible maturities.

During 2006, a total of €24 million in mortgages were sold at face value as part of a revolving mortgage facility. For further information on securitization operations, reference should be made to the chapter “Securitization

operations” and the Notes.

- 27 -

Performance of total stock

1.1461.694 1.863 2.065

1.264 2.3002.128 2.053 1.952

663408 388 363

1.847

693

Dec 04 Jun 05 Dec 05 Jun 06 Dec 06

Mortgages in portfolio Securitized mortgagesAssets sold but not eliminated

(Amounts in millions)

SALARY GUARANTEED LOANS Salary guaranteed loans issued in 2006 came to a total of €607 million in principal, against €490 million in 2005,

posting an increase of 23.7%.

Total outstanding salary guaranteed loans amounted to €1,504 million, of which €1,342 million were in portfolio

(of these €297 million were “delegated payment” loans), and €162 million were assets sold but not eliminated

from the balance sheet.

Number Amount issued

Salary guaranteed loans issued in 2006 34,356 606,871 Salary guaranteed loans issued in 2005 29,746 490,352

(Amounts in Euro/000)

With reference to the network of credit brokers, although the Bank has established relationships of full autonomy

with its credit brokers as required by applicable law, the development of information technology systems continued,

involving the installation of remote connections that led to a streamline production process, a reduction of internal

costs, and increased broker loyalty; 25 new connections were added in 2006, bringing the total number of

connections up to 69 at the end of 2006.

As part of the constant evolution of organizational processes and information systems, the Bank introduced

improvements that will allow it to combine ongoing technological development with the priorities and industrial

needs of this Business Area.

The Bank also completed processes aimed at improving the management of collections, with special attention on

facilitating the administration of securitization operations.

Cash held in the current accounts of the special vehicle purpose F-E Personal Loans, which came to a total of €9

million as at 31 December 2006, must also be considered as part of the category of assets sold but not eliminated

from the balance sheet.

4.109 4.230 4.305

3.804

4.380

- 28 -

During 2006, no new assignments of performing loans for securitization operations or revolving loan facilities were

undertaken. On 20 June 2006 the Bank closed the securitization operation that it had undertaken with the special vehicle

purpose Garda S.r.l. in advance of the term. For further information on securitization operations, reference should be made to the chapter “Securitization

operations” and the Notes.

(Amounts in millions)

Performance of total stock

650865

993

1.283 1.342

391

334267

214 162

107 79

209

Dec-04 Jun-05 Dec-05 Jun-06 Dec-06

Salary guaranteed loans in portfolio Assets sold but not eliminated

Salary guaranteed loans securitized

(Amounts in millions)

333410 389

468 437490

607

2000 2001 2002 2003 2004 2005 2006

Salary guaranteed loans

1.306 1.339 1.497

1.251

1.504

- 29 -

BALANCE SHEET FIGURES

ASSETS 31-Dec-2006 31-Dec-2005 Absolute %

10 Cash and cash equivalents 316 486 (170) -35,0%20 Financial assets held for trading 894.513 485.209 409.304 84,4%40 Available-for-sale financial assets 83.398 93.261 (9.863) -10,6%60 Loans to banks 1.088.915 514.161 574.754 111,8%70 Customer loans 6.835.626 6.463.671 371.955 5,8%80 Hedge derivatives 16.756 3.775 12.981 343,9%90 Adjustments to the value of financial assets

to be macro-hedged (+/-) (19.694) 3.830 (23.524) -614,2%100 Equity investments 1.118 1.118 -110 Property, plant and equipment 7.003 7.071 (68) -1,0%120 Intangible assets 32.791 34.775 (1.984) -5,7%

of which- goodwill 21.583 21.583 -

130 Tax assets 23.479 25.638 (2.159) -8,4%a) current - - - -b) prepaid 23.479 25.638 (2.159) -8,4%

140 Non-current assets and disposal groupsclassified as held for sale 145 145 -

150 Other assets 129.788 138.997 (9.209) -6,6%Total assets 9.094.154 7.772.137 1.322.017 17,0%(Amounts in Euro/000)

Change

LIABILITIES AND SHAREHOLDERS' EQUITY 31-Dec-2006 31-Dec-2005 Absolute %

10 Deposits from banks 796.985 858.059 (61.074) -7,1%20 Customer accounts 7.737.443 6.337.905 1.399.538 22,1%30 Debt securities in issue - 54.693 (54.693) -100,0%40 Financial liabilities held for trading 20.917 38.444 (17.527) -45,6%60 Hedge derivatives 4.580 15.962 (11.382) -71,3%80 Tax liabilities 8.272 6.201 2.071 33,4%

a) current 3.491 2.786 705 25,3%b) deferred 4.781 3.415 1.366 40,0%

100 Other liabilities 170.561 172.134 (1.573) -0,9%110 Employee severance payment fund 3.834 3.186 648 20,3%120 Provisions for contingencies and charges: 38.367 30.740 7.627 24,8%

b) other provisions 38.367 30.740 7.627 24,8%130 Valuation reserves 2.795 3.460 (665) -19,2%160 Reserves 45.446 (1.526) 46.972 3078,1%180 Share capital 199.851 202.293 (2.442) -1,2%190 Own shares (-) - (2.442) 2.442 -100,0%200 Net profit (loss) for the year 65.103 53.028 12.075 22,8%

Total liabilities and shareholders' equity 9.094.154 7.772.137 1.322.017 17,0%(Amounts in Euro/000)

Change

Financial assets (asset items 20 and 40) Financial assets may be broken down as follows:

Financial assets held for trading: this category includes the positive fair value measurement of derivatives

contracts held for trading, which came to €14.019 million, the positive measurement of commitments for

currencies and securities to be received and delivered, which totalled €0.354 million, in addition to stocks and

bonds classified as FVPL (fair value through profit or loss), for a total amount of €880.140 million, of which

€836.364 million pertained to bonds issued by the Parent Bank, Capitalia S.p.A.. The securities issued by the

Parent Bank are used for repurchase agreements with retail customers. The increase compared to 31 December

- 30 -

2005 may be attributed largely to the subscription of bonds denominated in euro and dollars issued by the Parent

Bank, Capitalia S.p.A. and used by FinecoBank S.p.A. in repurchase agreements;

Available-for-sale financial assets: this category consists exclusively of equity investments in companies over

which the Bank does not exercise control or a significant influence, whether directly or through its subsidiaries, and

totalled €8.262 million, in addition to senior and junior notes subscribed for as part of the Bank’s securitization

operations, for a total of €75.137 million. The junior notes subscribed for as part of the securitization operations

undertaken after 1 January 2002, which were represented in the accounts under customers loans, were eliminated

from the balance sheet.

During 2006, the junior notes issued by the special vehicle purpose Garda S.r.l. as part of the securitization of

“one-fifth of salary" loans were redeemed.

FinecoBank S.p.A. did not recognize financial assets under asset item 30, “Financial assets designated at fair

value” and item 50, “Held-to-maturity financial assets”.

31-dic-06 31-dic-05 Absolute %

Financial assets held for trading 894.513 485.209 409.304 84,4%Financial assets designated at fair value - - - -Available-for-sale financial assets 83.398 93.261 (9.863) -10,6%Held-to-maturity financial assets - - - -Total 977.911 578.470 399.441 69,1%(Amounts in Euro/000)

Change

Net loans to banks (asset item 60, liability item 10)

Type of transactions/Values 31-Dec-2006 31-Dec-2005 Absolute %

A. Loans to central banks - - - -1. Savings accounts - - - -2. Mandatory reserve - - - -3. Repurchase agreements - - - -4. Other - - - -B. Loans to banks 1.088.915 514.161 574.754 111,8%1. Current accounts and demand deposits 132.592 257.366 (124.774) -48,5%2. Savings accounts 939.526 248.165 691.361 278,6%3. Other loans: - - 3.1 Repurchase agreements 13.433 806 12.627 1566,6% 3.2 Finance leases - - - - 3.3 Other 1.800 5 1.795 35900,0%4. Debt securities - - 4.1 Structured securities 838 - 838 - 4.2 Other debt securities 726 7.819 (7.093) -90,7%5. Impaired assets - - - -6. Assets sold but not eliminated - - - -Total 1.088.915 514.161 574.754 111,8%(Amounts in Euro/000)

Change

- 31 -

Type of transactions/Values 31-Dec-2006 31-Dec-2005 Absolute %

1. Deposits from central banks - - - -2. Deposits from banks 796.984 858.059 (61.075) -7,1%2.1 Current accounts and demand deposits 171.723 221.891 (50.168) -22,6%2.2 Savings accounts 510.117 510.046 71 0,0%2.3 Loans 2.3.1 Finance leases - - - - 2.3.2 Other 113.304 126.122 (12.818) -10,2%2.4 Commitments to buy back - - own capital instruments - - - -2.5 Liabilities from assets sold but not eliminated 2.5.1 Repurchase agreements - - - - 2.5.2 Other - - - -2.6 Other payables 1.840 - 1.840 -Total 796.984 858.059 (61.075) -7,1%(Amounts in Euro/000)

Change

Loans to banks and deposits from banks in the form of current accounts and demand deposits consisted primarily

of reciprocal current accounts and lending between the Bank and Capitalia S.p.A., Bipop Carire Società per Azioni,

Banca di Roma and Banco di Sicilia.

The savings accounts recognized under assets consist of the deposit held with Capitalia for compulsory reserves,

with a book value of €83.661 million, in addition to short-term savings accounts held with Capitalia for a total of

€855.865 million.

The savings accounts recognized under liabilities consist of sums deposited by Capitalia S.p.A., with a book value

of €225.052 million, and by Banca Roma International, for a book value of €285.065 million.

The item “Other” under “Deposits from banks” consists exclusively of repurchase agreements involving securities

received as part of previous repurchase agreements.

Customer loans Customer loans, which came to a total of €6,835.626 million, may be broken down as follows:

€5,769.085 million in loans to ordinary customers; €679.504 million in repurchase agreements, of which €500.816 million with Fineco Finance Ltd.;

€154.873 million in securities lending;

€133.787 million in deposits held as collateral, initial margins, and variation margins with clearing systems in

relation to derivatives transactions;

€91.061 million in cash held in the current accounts for principal and interest of the special purpose vehicle due

to the impact of the recognition of loans sold but not eliminated from the balance sheet;

€0.910 million in relation to postal accounts;

€1.346 million in securities classified as Loans and Receivables;

€5.060 million in current accounts with institutional customers, of which €1.255 million in the current account

held with Fineco Finance Ltd.;

- 32 -

Type of transactions/Values 31-dic-06 31-dic-05 Absolute %

1. Current accounts 15.430 31.922 (16.492) -51,7%2. Repurchase agreements 834.377 828.194 6.183 0,7%3. Mortgages 2.057.282 1.681.279 376.003 22,4%4. Credit cards, personal loans and salary guaranteed loans 1.512.385 1.257.660 254.725 20,3%5. Finance leases - - - -6. Factoring - - - -7. Other transactions 144.864 141.501 3.363 2,4%8. Debt securities: 8.1 Structured 1.346 - 1.346 - 8.2 Other - - - -9. Impaired assets 58.999 34.694 24.305 70,1%10. Assets sold but not eliminated* 2.210.943 2.488.421 (277.478) -11,2%Total (book value) 6.835.626 6.463.671 371.955 5,8%(Amounts in Euro/000)

Change

* This item includes impaired assets in relation to loans sold but not eliminated from the balance sheet. Ordinary customer loans(Reclassified for management purposes) 31-dic-06 31-dic-05 Absolute %

Salary guaranteed loans and "delegated payment" loans 1.341.893 993.318 348.575 35,1%

Salary guaranteed loans and "delegated payment" loans sold but not eliminated 161.835 267.009 (105.174) -39,4%

Salary guaranteed loans and "delegated payment" loans sold - 79.168 (79.168) -100,0%Total salary guaranteed loans and "delegated payment" loans 1.503.728 1.339.495 164.233 12,3%Mortgages 2.064.503 1.693.125 371.378 21,9%Mortgages sold but not eliminated 1.952.483 2.128.937 (176.454) -8,3%Mortgages sold 362.928 408.076 (45.148) -11,1%Total mortgages 4.379.914 4.230.138 149.776 3,5%Current accounts 15.099 14.150 949 6,7%Use of credit cards 104.209 191.912 (87.703) -45,7%Personal loans and unsecured loans 93.989 78.349 15.640 20,0%Other loans 10.174 1.803 8.371 464,3%Non-performing loans 19.336 14.227 5.109 35,9%Non-performng loans sold but not eliminated 5.564 2.605 2.959 113,6%Non-performing loans sold 5.239 3.266 1.973 60,4%Total ordinary customer loans 6.137.252 5.875.945 261.307 4,4%(Amounts in Euro/000)

Change

For the purposes of evaluating the performance of ordinary customer loans from a management perspective, loans

sold but not re-entered to the balance sheet should be considered as belonging to the latter category. The total

amount of loans, which came to €6,137.252 million, posted growth of 4.4% compared to the same period of the

previous year. Total mortgage loans sold (€362.928 million), and non-performing loans sold (€5.239 million), unlike loans

recognized on the balance sheet, are entered gross of any specific and portfolio writedowns and are not recognized

at amortized cost. These loans, since they are not recognized on the balance sheet on the basis of the option

granted by IAS 39, are measured according to the criteria set forth in the section concerning securitization

operations, and the amortized cost criterion was not applied.

The item "Use of credit cards" decreased by 45.7% due to the transfer of contracts with customers holding credit

cards issued by FinecoBank S.p.A. on behalf of Bipop Carire, Banco di Sicilia, Banca di Roma and Capitalia, which

was executed on 1 July 2006.

- 33 -

Doubtful loans Doubtful loans (non-performing loans and problem loans held in portfolio and classified among loans sold but not

eliminated from the balance sheet), net of adjustments, came to a total of €61.180 million, an increase of 72.91%

over the €35.382 million recorded in December 2005; the classified loan portfolio represented 0.90% of total loans.

Net non-performing loans amounted to €24.900 million in the aggregate, up 47.92% over the €16.833 million

posted on 31 December, 2005. Of this category, 95.64% consisted of mortgage loans. Net non-performing loans

represented 0.36% of total cash loans. Net problem loans came to a total of €36.280 million; those pertaining to

mortgage loans made up €10.496 million of the total.

Net expired exposures stood at €9.327 million.

The following tables show the coverage ratios for doubtful loans, expressed as the ratio of total specific and

portfolio writedowns made (including interest on late payments deemed unrecoverable) to total gross exposures

(including written down interest on late payments).

Total doubtful loans gross of the writedown reserve

Category31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05

Non-performing loans 38.002 25.505 1.759 1.208 8.899 9.128 48.660 35.841Problem loans 12.361 13.493 25.489 6.311 1.710 738 39.560 20.542Total 50.363 38.998 27.248 7.519 10.609 9.866 88.220 56.383(Amounts in Euro/000)

Salary guaranteed loans and "delegated payment"

Mortgages Other loans Total

Total doubtful loans net of the writedown reserve

Category31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05

Non-performing loans 23.815 15.805 450 294 635 734 24.900 16.833Problem loans 10.496 11.991 25.184 6.299 600 259 36.280 18.549Total 34.311 27.796 25.634 6.593 1.235 993 61.180 35.382(Amounts in Euro/000)

Salary guaranteed loans and "delegated payment"

Mortgages Other loans Total

Coverage ratios for doubtful loans

Category31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05

Non-performing loans 37,33% 38,03% 74,40% 75,65% 92,86% 91,96% 48,83% 53,04%Problem loans 15,08% 11,13% 1,20% 0,18% 65,00% 64,92% 8,29% 9,70%Total 31,87% 28,72% 5,92% 12,31% 88,37% 89,94% 30,65% 37,25%

Salary guaranteed loans and "delegated payment"

Mortgages Other loans Total

Coverage ratios for performing and expired loans

Category31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05 31-dic-06 31-dic-05

Performing loans 0,19% 0,19% 0,30% 0,15% 1,05% 1,73% 0,24% 0,21%Expired loans 5,00% 0,19% 0,46% 0,11% 16,68% 5,75% 10,41% 2,53%Total 0,19% 0,19% 0,30% 0,15% 1,72% 1,85% 0,26% 0,22%

Salary guaranteed loans and "delegated payment"

Mortgages Other loans Total

- 34 -

Hedge derivatives (asset item 80 and liability item 60) and adjustment to the value of financial assets to be macro-hedged (asset item 90)

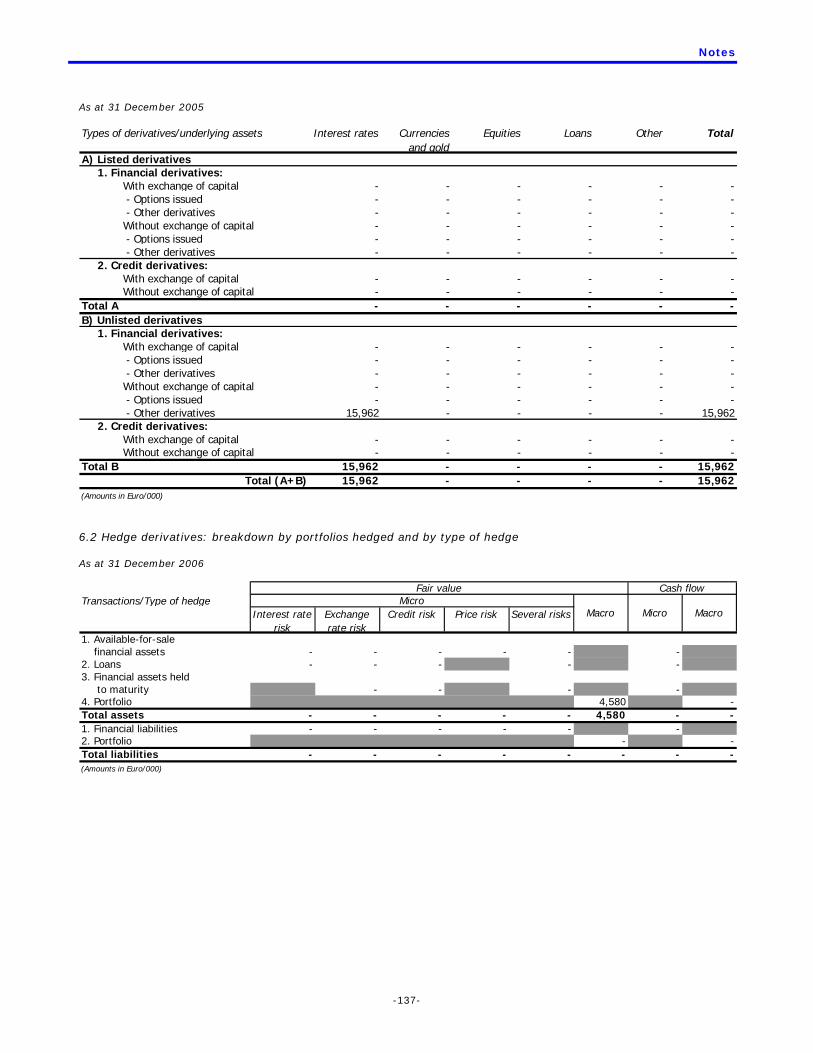

31-Dec-06 31-Dec-05 Absolute %

Hedge derivatives - assets 16,756 3,775 12,981 343.9%Hedge derivatives - liabilities (4,580) (15,962) 11,382 -71.3%Imbalance 12,176 (12,187) 24,363 -199.9%

Adjustments to the value of financial assetsto be macro-hedged (+/-) (19,694) 3,830 (23,524) -614.2%(Amounts in Euro/000)

Change

Hedge derivatives include positive and negative measurements of derivatives that the bank has entered into with

the purpose of macro-hedging against interest rate risk inherent in salary guaranteed loans and “delegated

payment” loans.

The increase in hedge derivatives, which totalled €24.363 million, and, consequently, the negative measurement

of salry guaranteed loans and “delegated payment” loans, amounting to €23.524 million, is to be attributed to the

raising of the interest rate curve, inasmuch as the relevant derivatives were IRSs involving the payment of a fixed

rate and the collection of a variable rate and fixed rate loans.

Equity investments and available-for-sale financial assets – (asset items 100 and 40) Equity investments have been classified into “Equity investments” and “Available-for-sale financial assets”.

The item “Equity investments”, with a balance of €1.118 million, includes the controlling interest in Fineco Mutui

S.p.A. and the stake held in the associated company Capitalia Investimenti Alternativi Sgr S.p.A. The item

“Available-for-sale financial assets”, totalling €8.262 million, includes the remaining equity investments in

companies over which the bank does not exercise either control or a significant influence, whether directly or

through subsidiaries.

The equity investment in Fineco Mutui S.p.A. is not consolidated in the separate financial statements of FinecoBank

S.p.A. since it is instead consolidated in the financial statements of the Parent Bank, Capitalia S.p.A..

Book value Book value

as at 31 Dec 06 % as at 31 Dec 05 %Ktesios S.p.A. - - 458 4,50%Net Insurance S.p.A. 8.189 13,04% - -Agenzia di Pollenzo S.p.A. - - 1.206 6,07%Monte Titoli S.p.A. 8 0,03% 8 0,03%Consorzio Patti Chiari 5 0,53% 5 0,53%Acroservizi S.p.A. 60 10,71% 60 10,72%Available-for-sale financial assets 8.262 1.737

Fin-Eco Investimenti Alternativi Sgr S.p.A. 258 5,00% 258 5,00%Fineco Mutui S.p.A. 860 100,00% 860 100,00%Equity investments 1.118 1.118Total 9.380 2.855(Amounts in Euro/000) Ktesios: on 13 April 2006 the Bank sold its entire equity investment in the company for a total of €3 million. The

capital gain on the sale came to a total of €2.542 million. During 2006, a total of €0.234 million in dividends were

collected, in addition to €0.203 million in earnings retained by Ktesios S.p.A..

- 35 -

Net Insurance: pursuant to the resolution passed by the Board of Directors on 21 July 2005, and on the basis of

the agreement signed with Net Insurance and shareholders on 5 August 2005, the Bank:

- subscribed to the reserved capital stock issue for a nominal value of €0.250 million and total amount of €2.5

million on 27 April 2006;

- purchased an additional 500,000 shares for a total price of €5 million on 9 May 2006.

The value of the equity investment was increased by €0.117 million for capitalizable costs directly related to the

purchase of the equity investment itself.

As at 31 December 2006 FinecoBank S.p.A. held 750,000 shares with a nominal value of €1.00 each, i.e. a percent

interest of 13.04%.

The valuation at fair value as at 31 December 2006 resulted in an increase in value of €0.572 million, which was

recognized to a specific shareholders' equity reserve.

Agenzia di Pollenzo: on 27 June 2006 the Board of Directors resolved to accept the offer advanced by Capitalia

S.p.A. to sell the full equity investment to Capitalia Merchant S.p.A.. On 28 July 2006 the Bank closed the deal,

collecting €1.206 million in payment, the equivalent of the book value of the equity investment.

Property, plant and equipment (asset item 110) Investments in electronic machines, which came to a total of €1.707 million, were primarily intended for use in

Bank branches. In particular, during 2006, a new office location was fitted out for the Business Continuity Project.

Investments in furniture, fittings and equipment were primarily intended for use in financial shops.

The book value of property, plant, and equipment includes the historical cost and the accumulated depreciation of

assets obtained under financial lease, as allowed by IAS 17.

Balance 01.01.2006

Investments in 2006

Other Changes-

Sales

Depreciation and

writedowns in 2006

Balance 31.12.2006

Buildings 3.456 - - (72) 3.384 EDP machines 1.918 1.707 (11) (1.714) 1.900 Furniture and fittings 950 689 - (611) 1.028 Plant and equipment 747 511 (1) (566) 691 TOTAL 7.071 2.907 (12) (2.963) 7.003