EAST VINCENT TOWNSHIP December 31, 2013 ROBERT C ...

39

EAST VINCENT TOWNSHIP December 31, 2013 ROBERT C. BEZGIN CERTIFIED PUBLIC ACCOUNTANT

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of EAST VINCENT TOWNSHIP December 31, 2013 ROBERT C ...

EAST VINCENT TOWNSHIP

December 31, 2013

ROBERT C. BEZGINCERTIFIED PUBLIC ACCOUNTANT

EAST VINCENT TOWNSHIP

DECEMBER 31, 2013

CONTENTS

Auditor's Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Management’s Discussion and Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . MD&A 1

Basic financial statements:

Government-wide Financial Statements:Statement of Net Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Statement of Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Fund Financial Statements:

Balance Sheet - Governmental Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Statement of Revenues, Expenditures and Changes in Fund

Balances - Governmental Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Reconciliation of the Statement of Revenues, Expenditures, and

Changes in Fund Balances of Governmental Funds to theStatement of Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Statement of Revenues, Expenditures and Changes in Fund Balances - Budget and Actual: General Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Statement of Net Assets - Fiduciary Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Statement of Changes in Fiduciary Net Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Statement of Net Assets - Proprietary Funds, Waste Water Services . . . . . . . . . . . . . 11Statement of Revenues, Expenses and Changes in Net Assets -

Proprietary Funds - Waste Water Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Statement of Changes in Cash Flows - Proprietary Funds Waste Water Services . . . . 13

Notes to Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Required Supplementary Information:Schedule of Funding Progress: Uniform and Non-Uniform Pension Plans . . . . . . . . . 29

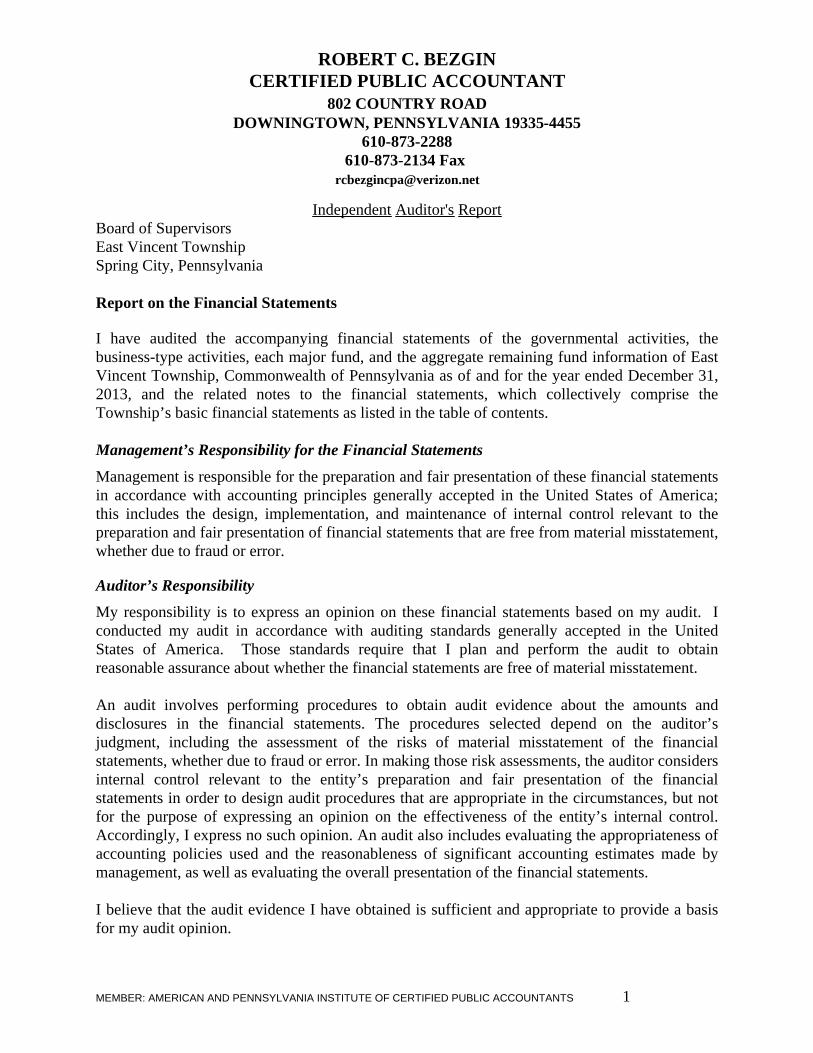

ROBERT C. BEZGINCERTIFIED PUBLIC ACCOUNTANT

802 COUNTRY ROADDOWNINGTOWN, PENNSYLVANIA 19335-4455

610-873-2288610-873-2134 Fax

Independent Auditor's ReportBoard of SupervisorsEast Vincent TownshipSpring City, Pennsylvania

Report on the Financial Statements

I have audited the accompanying financial statements of the governmental activities, thebusiness-type activities, each major fund, and the aggregate remaining fund information of EastVincent Township, Commonwealth of Pennsylvania as of and for the year ended December 31,2013, and the related notes to the financial statements, which collectively comprise theTownship’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statementsin accordance with accounting principles generally accepted in the United States of America;this includes the design, implementation, and maintenance of internal control relevant to thepreparation and fair presentation of financial statements that are free from material misstatement,whether due to fraud or error.

Auditor’s Responsibility

My responsibility is to express an opinion on these financial statements based on my audit. Iconducted my audit in accordance with auditing standards generally accepted in the UnitedStates of America. Those standards require that I plan and perform the audit to obtainreasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditor’sjudgment, including the assessment of the risks of material misstatement of the financialstatements, whether due to fraud or error. In making those risk assessments, the auditor considersinternal control relevant to the entity’s preparation and fair presentation of the financialstatements in order to design audit procedures that are appropriate in the circumstances, but notfor the purpose of expressing an opinion on the effectiveness of the entity’s internal control.Accordingly, I express no such opinion. An audit also includes evaluating the appropriateness ofaccounting policies used and the reasonableness of significant accounting estimates made bymanagement, as well as evaluating the overall presentation of the financial statements.

I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basisfor my audit opinion.

MEMBER: AMERICAN AND PENNSYLVANIA INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS 1

Unmodified Opinions

In my opinion, the financial statements referred to above present fairly, in all material respects,the respective financial position of the governmental activities, the business-type activities, eachmajor fund, and the aggregate remaining fund information of East Vincent Township,Commonwealth of Pennsylvania, as of December 31, 2013, and the respective changes infinancial position and, where applicable, cash flows thereof for the year then ended inaccordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that themanagement’s discussion and analysis and budgetary comparison information beginning onpages MD&A 1, and the Schedule of Funding Progress on Page 29 be presented to supplementthe basic financial statements. Such information, although not a part of the basic financialstatements, is required by the Governmental Accounting Standards Board, who considers it to bean essential part of financial reporting for placing the basic financial statements in an appropriateoperational, economic, or historical context. I have applied certain limited procedures to therequired supplementary information in accordance with auditing standards generally accepted inthe United States of America, which consisted of inquiries of management about the methods ofpreparing the information and comparing the information for consistency with management’sresponses to my inquiries, the basic financial statements, and other knowledge I obtained duringmy audit of the basic financial statements. I do not express an opinion or provide any assuranceon the information because the limited procedures does not provide me with sufficient evidenceto express an opinion or provide any assurance.

Other Information

My audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise East Vincent Township, Commonwealth of Pennsylvania’s basic financialstatements. The combining and individual non major fund financial statements are presented forpurposes of additional analysis and are not a required part of the basic financial statements.

The combining and individual non major fund financial statements are the responsibility ofmanagement and were derived from and relate directly to the underlying accounting and otherrecords used to prepare the basic financial statements. Such information has been subjected tothe auditing procedures applied in the audit of the basic financial statements and certainadditional procedures, including comparing and reconciling such information directly to theunderlying accounting and other records used to prepare the basic financial statements or to thebasic financial statements themselves, and other additional procedures in accordance withauditing standards generally accepted in the United States of America. In my opinion, thecombining and individual non major fund financial statements are fairly stated, in all materialrespects, in relation to the basic financial statements as a whole.

Robert C. Bezgin, CPA

Robert C. Bezgin, CPAJuly 8, 2014

MEMBER: AMERICAN AND PENNSYLVANIA INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS 2

1| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

East Vincent Township Management’s Discussion and Analysis

Fiscal Year Ended December 31, 2013 (Unaudited/Cash Basis)

Again East Vincent came through the year with a good financial picture. This analysis will show that measures taken have carried us through a difficult period and the signs that we saw at the end of 2012 are carrying forward. As 2013 ends we face the worst winter in decades yet in our midst a development of 42 single family homes and six condominiums has begun after it had languished in dormancy for over seven years; and our new, state-of-the-art sewer plant came on line. A 135 unit mixed-housing development with a daycare center has been given final approval and will commence in early spring. This is progress.

Overview

To gain a full understanding of our financial picture, this management report must be reviewed in concert with all of the tables and reports provided herein, particularly a report from our inde-pendent auditor and his financial statements.

The financial statements presented in management’s discussion offer rationale in decision-making and how these decisions affected East Vincent’s long-term goals. The audited financial statements reflect all assets and liabilities using the modified accrual method of accounting, however, management’s discussion and analysis uses the cash (or more realistic) method of ac-counting.

Government-Wide Financial Statements (The General Fund)

The first statements are township-wide in scope and reflect East Vincent’s finances as a whole and are presented in a similar manner to statements of any private-sector business or corporation. Also reported are proprietary funds. In 2010 the Elected Officials thought it in the best interest of the Township, the ratepayers and the taxpayers to dissolve the Municipal Sewer Authority and combine the operation of the sewer plants with the other services of municipal government. The sewage plants are now considered proprietary rather than component units and each plant is ac-counted within its own fund. The Veteran’s Center and Barton’s Meadows plants each have sep-arate funds and they are both separate from the general fund.

Basic services provided such as road maintenance, snow removal, maintenance and care of park-land, code enforcement, police services, emergency management, building inspection, general administration and the wastewater services (sewer) departments are considered government ac-tivities and represent services provided to our property owners and/or ratepayers.

2| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

Fund Financial Statements

Fund financial statements provide a more detailed look at specific activities and are used to track streams of revenue and expenditures for particular purposes. For example, the “liquid fuels” or State Highway Fund is restricted by law and audited by the Commonwealth. This is money that is collected by the state through gasoline taxes and passed on to us to be used solely for work performed in relation to roads. Other funds are for dedicated taxes for street lighting and fire hy-drants. There is also an Open Space Fund. As stated previously, funds are also typically divided into governmental or proprietary funds.

Examples of proprietary funds might be cemeteries, sewer systems, water or electric departments or in the case of the Commonwealth, liquor stores. They can generate revenue and are owned by the municipal entity. As of January 2011, the Municipal Sewer Authority was dissolved and the operations were taken in-house. It is now called Wastewater Services and is a township-run de-partment with accounting of its own, not a part of the general fund. It is reported here as a pro-prietary fund. Further, as there are two plants, each a separate cost-center, serving specific prop-erties, two distinct funds are maintained. An important difference is that proprietary uses are funded by those using the service and not all taxpayers. Thus, if you have street lights or fire hydrants you are taxed for them, if you do not have them you are not charged. If you are hooked into the public sewer system, you are billed for the service, if you have an on-lot system, you are not billed nor are your tax dollars used for the sewer facilities.

Governmental Funds

Municipal services are reported under Governmental Funds. The statements provide a detailed, short-term view of the operation of our local government and the services we provide. This in-formation helps us to determine whether there are greater or fewer financial resources available to finance future plans and how successfully we can to weather tough economic times or extreme emergencies.

The audited funds are reported using a method called modified accrual accounting which measures cash and all other financial assets that can readily be converted to cash. If there is sur-plus money left from one year it is available for use in the future. The relationship between gov-ernmental activities and government funds is described in a reconciliation included in the fund financial statements by our auditor.

Unlike State or Federal governments, East Vincent adopts a balanced budget in compliance with the requirements of the Commonwealth of Pennsylvania. Elected officials make decisions with input provided by the administration regarding needs and services to be offered based upon an-ticipated revenues. In accordance with law the proposed budget is advertised and made available for public review and comment prior to adoption at a public meeting before the end of the prior

3| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

year, though there is a process whereby changes can be made if it becomes necessary to do so. Also, newly elected officials may ‘reopen’ the budget.

Fiduciary Funds

The Elected Board of Supervisors is the trustee, or fiduciary, for our municipal employee’s pen-sion plans. There are two plans; one for uniformed employees (police) and the other for non-uniformed employees (everyone else). All such activities are reported in separate ‘Statements of Fiduciary Net Assets’ and ‘Changes in Fiduciary Net Assets.’ These statements are separate be-cause the funds are not available for Township use. It is our responsibility to ensure that these assets are specifically set aside and used only for their intended purposes. Again, this differs significantly from not only State and Federal governments but from the private sector where, while there are laws in place requiring certain funds to be set aside and segregated, never used for other purposes, it appears that blatantly ignoring these laws still hold no consequences.

Notes to Fund Statements

Notes provided by our auditor, a certified public accountant, offer additional essential infor-mation so that the data provided in the financial statements can be completely understood and transparent.

Government-Wide Financial Analysis

In compliance with the Government Accounting Standards Board (GASB), Statement #34 re-quirements, East Vincent changed its method of financial reporting in 2004 to reflect a manner more similar to that of the corporate world. Our completed audit along with this analysis pre-sents a more complete and professional picture of East Vincent finances.

Percent of Total

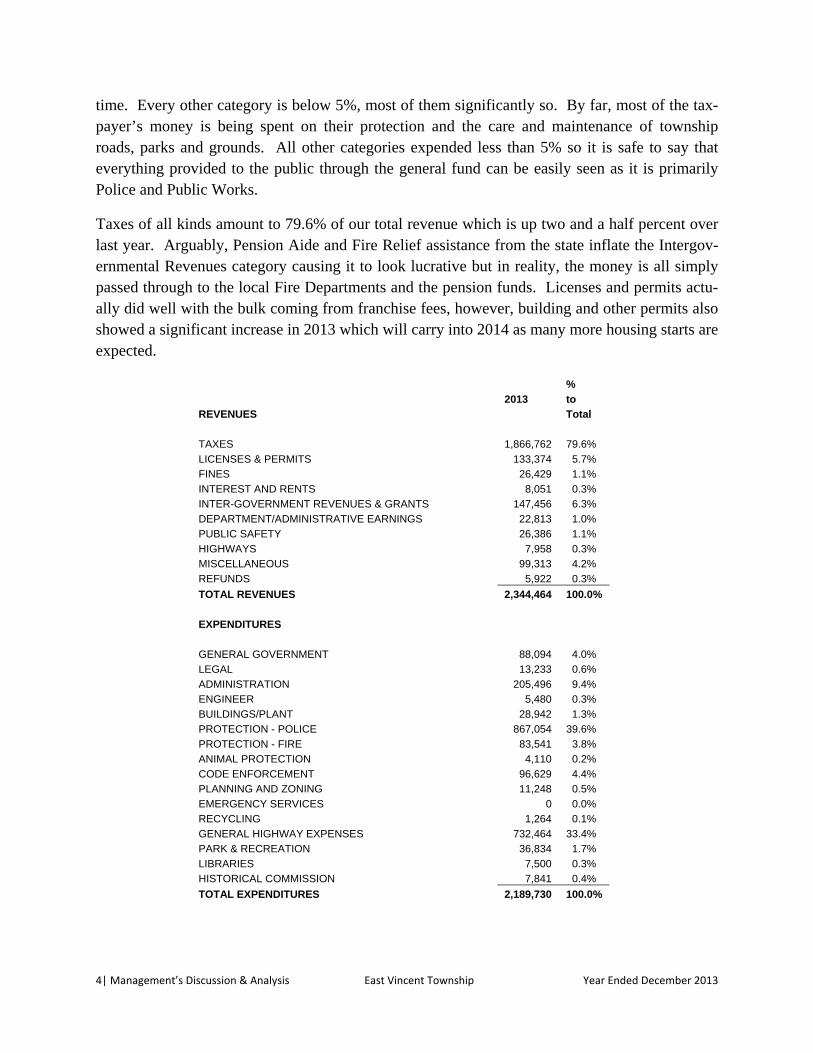

This table remains similar over the years and reflects the values and priorities of the elected offi-cials, management and the residents of the township. It is not uncommon for a police department to expend as much as 50% of municipal funds but our department comes in at 39.6%.

Public Works is just 6% less at 33.4%. This number would be slightly higher, however, due to an uncooperative, rainy summer much of our planned roadwork could not be completed. This is further evidenced by the fact that our bank balance for liquid fuels funds is normally at $70,000 or less at this time of year, however the balance as of January 1 is $251,721. This will be aug-mented by the state in the spring and it is our hope that a great deal of roadwork will be complet-ed this summer.

Administration is at a mere 9.3% which is too low and is beginning to show. More help is need-ed with administration, however where another person would work and specific duties must be developed. Possibly the answer is to restore a position that was reduced from full-time to part-

4| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

time. Every other category is below 5%, most of them significantly so. By far, most of the tax-payer’s money is being spent on their protection and the care and maintenance of township roads, parks and grounds. All other categories expended less than 5% so it is safe to say that everything provided to the public through the general fund can be easily seen as it is primarily Police and Public Works.

Taxes of all kinds amount to 79.6% of our total revenue which is up two and a half percent over last year. Arguably, Pension Aide and Fire Relief assistance from the state inflate the Intergov-ernmental Revenues category causing it to look lucrative but in reality, the money is all simply passed through to the local Fire Departments and the pension funds. Licenses and permits actu-ally did well with the bulk coming from franchise fees, however, building and other permits also showed a significant increase in 2013 which will carry into 2014 as many more housing starts are expected.

%

2013 to

REVENUES Total

TAXES 1,866,762 79.6%

LICENSES & PERMITS 133,374 5.7%

FINES 26,429 1.1%

INTEREST AND RENTS 8,051 0.3%

INTER-GOVERNMENT REVENUES & GRANTS 147,456 6.3%

DEPARTMENT/ADMINISTRATIVE EARNINGS 22,813 1.0%

PUBLIC SAFETY 26,386 1.1%

HIGHWAYS 7,958 0.3%

MISCELLANEOUS 99,313 4.2%

REFUNDS 5,922 0.3%

TOTAL REVENUES 2,344,464 100.0%

EXPENDITURES

GENERAL GOVERNMENT 88,094 4.0%

LEGAL 13,233 0.6%

ADMINISTRATION 205,496 9.4%

ENGINEER 5,480 0.3%

BUILDINGS/PLANT 28,942 1.3%

PROTECTION - POLICE 867,054 39.6%

PROTECTION - FIRE 83,541 3.8%

ANIMAL PROTECTION 4,110 0.2%

CODE ENFORCEMENT 96,629 4.4%

PLANNING AND ZONING 11,248 0.5%

EMERGENCY SERVICES 0 0.0%

RECYCLING 1,264 0.1%

GENERAL HIGHWAY EXPENSES 732,464 33.4%

PARK & RECREATION 36,834 1.7%

LIBRARIES 7,500 0.3%

HISTORICAL COMMISSION 7,841 0.4%

TOTAL EXPENDITURES 2,189,730 100.0%

5| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

The Budget vs Reality

Once again the year ended with a surplus. In all we ended 2013 spending $154,734 less than we brought in. This was due to a few different things. As previously stated, most of the roadwork was not completed due to rainy weather. In addition, a Cutler development of 42 single-family units came back to life after more than seven years of inactivity. Trails were waived for the de-velopment and that brought a $75,000 payment (in-lieu-of) to the township along with a $17,845 traffic contribution. These are found on the miscellaneous line. As is generally the case we planned to use $62,514 from reserves to balance the budget, however it was not necessary to transfer the money. Taxes came in 3.6% higher than planned and most of the categories did

2013 General Fund Budget Actual Balance %

From Reserves 62,813 0 62,813 0.0%

REVENUES

TAXES 1,801,248 1,866,762 -65,514 103.6%

LICENSES & PERMITS 125,250 133,374 -8,124 106.5%

FINES 25,000 26,429 -1,429 105.7%

INTEREST AND RENTS 12,000 8,051 3,949 67.1%

INTER-GOVERNMENT REVS & GRANTS 139,200 147,456 -8,256 105.9%

DEPARTMENT/ADMINISTRATIVE EARNINGS 13,820 22,813 -8,993 165.1%

PUBLIC SAFETY 5,750 26,386 -20,636 458.9%

HIGHWAYS 8,750 7,958 792 91.0%

MISCELLANEOUS 6,200 99,313 -93,113 1601.8%

INTERFUND TRANSFERS 221,639 0 221,639 0.0%

REFUNDS 100 5,922 -5,822 100.0%

TOTAL REVENUES 2,421,770 2,344,464 77,306 96.8%

EXPENDITURES

GENERAL GOVERNMENT 92,892 88,094 4,798 94.8%

LEGAL 24,500 13,233 11,267 54.0%

ADMINISTRATION 215,195 205,496 9,699 95.5%

ENGINEER 7,500 5,480 2,020 73.1%

BUILDINGS/PLANT 29,050 28,942 108 99.6%

PROTECTION - POLICE 904,881 867,054 37,827 95.8%

PROTECTION - FIRE 79,000 83,541 -4,541 105.7%

ANIMAL PROTECTION 5,394 4,110 1,284 76.2%

CODE ENFORCEMENT 96,852 96,629 223 99.8%

PLANNING AND ZONING 30,614 11,248 19,366 36.7%

EMERGENCY SERVICES 750 0 750 0.0%

RECYCLING 1,500 1,264 236 0.0%

GENERAL HIGHWAY EXPENSES 894,517 732,464 162,053 81.9%

PARK & RECREATION 26,800 36,834 -10,034 137.4%

LIBRARIES 7,500 7,500 0 100.0%

HISTORICAL COMMISSION 4,825 7,841 -3,016 162.5%

TOTAL EXPENDITURES 2,421,770 2,189,730 232,040 90.4%

TOTAL REVENUES 2,421,770 2,344,464 77,306 96.8%

TOTAL EXPENDITURES 2,421,770 2,189,730 232,040 90.4%

0 154,734 154,734

6| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

exceed expectations with the glaring exception of interest which remains stubbornly low. The police department gained an extra $16,700 covering a special venue. The largest single amount of savings came by way of our failure to transfer over $220,000 from our liquid fuels fund for roadwork. As explained earlier, the rainy summer precluded doing all the work that was origi-nally planned. In summary; almost $300,000 was not transferred in as budgeted and in spite of that we came in with 6.8% more on the bottom line.

On the expense side, Fire protection exceeded the budget but was entirely off set by the Inter-governmental Revenues and Grants category as this money is received from the state and passed through to the fire departments. The state sent us more and we sent the Fire Departments more.

Only a few categories ran in excess of budget: Park & Recreation by $10,000 and Historical Commission by $3,000. This was in large part due to a drifting insurance problem. Over the past few years, we were less and less diligent about proper allocation of our insurance costs. The budgets were based on the prior years and became less and less accurate until this year when with the help of our agent, we brought the amounts paid to their proper levels. The ‘proper level’ was not the budgeted number so we see a significant difference. In addition, Park & Recreation was given a grant and the go-ahead to do a Master Plan on 79 acres of parkland acquired by the Township. Though their overage is balanced by the grant, it was not budgeted and is reflected as a budget overage.

Money over Time

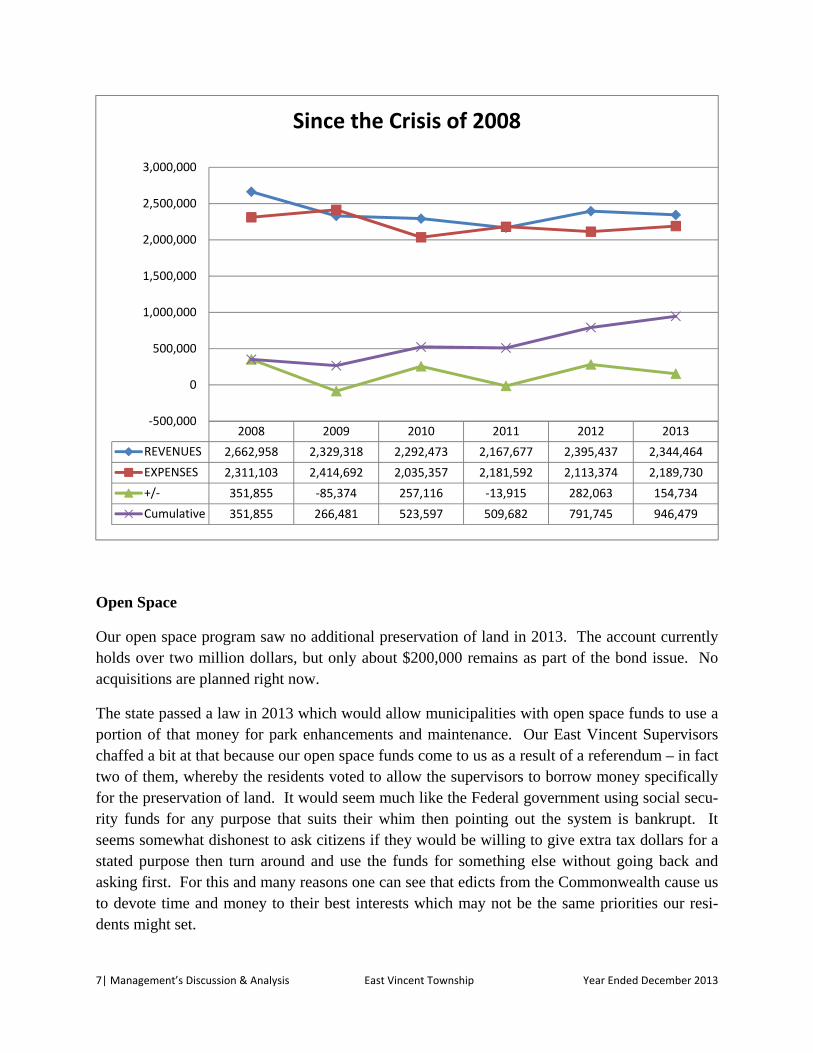

The upper graph in this chart depicts a comparison in revenues and expenditures over the past six years along with the lower graph with cumulative numbers showing that even though we took a hit in two of those years we banked almost $950,000 overall. As might be expected 2009 was our worst year, but in only two years of the past six we spent more than we brought in. That said, when we overspent it was with a three million dollar cushion in the bank – it was not reck-less spending; and it was accomplished in the face of the many towns, states and other entities crying for help, reorganizing and raiding pensions.

The surplus will help with upgrading our township facilities. The probability is that most of the funds will come from a bond issue but some will also be taken from reserves. These funds have helped us secure a very good bond rating and have also provided a sense of security when we experience severe and damaging weather. It has been helpful when our elected officials have been faced with a possibility and are not hampered by whether or not they have the cash on hand. This has been the only way we have overspent the budget, when the supervisors are met with an opportunity and they wish to take advantage of it but the opportunity comes from out-of-the-blue and has not been budgeted. This is precisely the kind of decision our elected officials are meant to make and it is greatly simplified when they don’t have to worry about the funding but only if it is the right thing to do.

7| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

Open Space

Our open space program saw no additional preservation of land in 2013. The account currently holds over two million dollars, but only about $200,000 remains as part of the bond issue. No acquisitions are planned right now.

The state passed a law in 2013 which would allow municipalities with open space funds to use a portion of that money for park enhancements and maintenance. Our East Vincent Supervisors chaffed a bit at that because our open space funds come to us as a result of a referendum – in fact two of them, whereby the residents voted to allow the supervisors to borrow money specifically for the preservation of land. It would seem much like the Federal government using social secu-rity funds for any purpose that suits their whim then pointing out the system is bankrupt. It seems somewhat dishonest to ask citizens if they would be willing to give extra tax dollars for a stated purpose then turn around and use the funds for something else without going back and asking first. For this and many reasons one can see that edicts from the Commonwealth cause us to devote time and money to their best interests which may not be the same priorities our resi-dents might set.

2008 2009 2010 2011 2012 2013

REVENUES 2,662,958 2,329,318 2,292,473 2,167,677 2,395,437 2,344,464

EXPENSES 2,311,103 2,414,692 2,035,357 2,181,592 2,113,374 2,189,730

+/‐ 351,855 ‐85,374 257,116 ‐13,915 282,063 154,734

Cumulative 351,855 266,481 523,597 509,682 791,745 946,479

‐500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Since the Crisis of 2008

8| Management’s Discussion & Analysis East Vincent Township Year Ended December 2013

Wastewater

In late 2010 the Elected Officials declared they would dissolve the Municipal Sewer Authority and bring the operation under general Township administration. No matter what costly im-provements we would have made to the plant, the usefulness would have been short-lived as the standards continue to get more rigid. Though there was a great capacity for the amount of sew-age the plant could handle, it was not efficient enough to get an end result that would satisfy the requirements of the Department of Environmental Protection. Consequently, bonds were issued and a new plant is very near completion. Due to a very severe increase in rates that were already high, the Veteran’s Center Plant saw a budget surplus last year and will be able to begin to reestablish a capital fund. This is critical because the pump stations are old and in need of up-grades.

The Barton’s Meadows Plant also enjoyed a small surplus at the end of 2013; however the over-haul of the plant last year has not brought the results that were hoped for. Our new operators are diligent and hard-working. We continue to work together to seek workable solutions.

Conclusion

In conclusion, East Vincent continues if not to thrive, certainly to sustain and maintain. Our elected officials continue to make considered, deliberate choices with a view to the future. Our residents on the whole are good volunteers and good citizens who maintain their properties and their responsibilities. In the coming year we look to continued improvement in operating our wastewater plants, and planning much needed municipal space.

Requests for information:

This report is intended to provide an overview of East Vincent Township’s finances for those with an interest in this matter. Questions concern-ing the information found in this report or requests for additional information should be directed to:

Township Manager, East Vincent Township 262 Ridge Road Spring City, PA 19475 or by calling 610-933-4424 or by e-mail at [email protected].

See footnotes to financial statements. 3

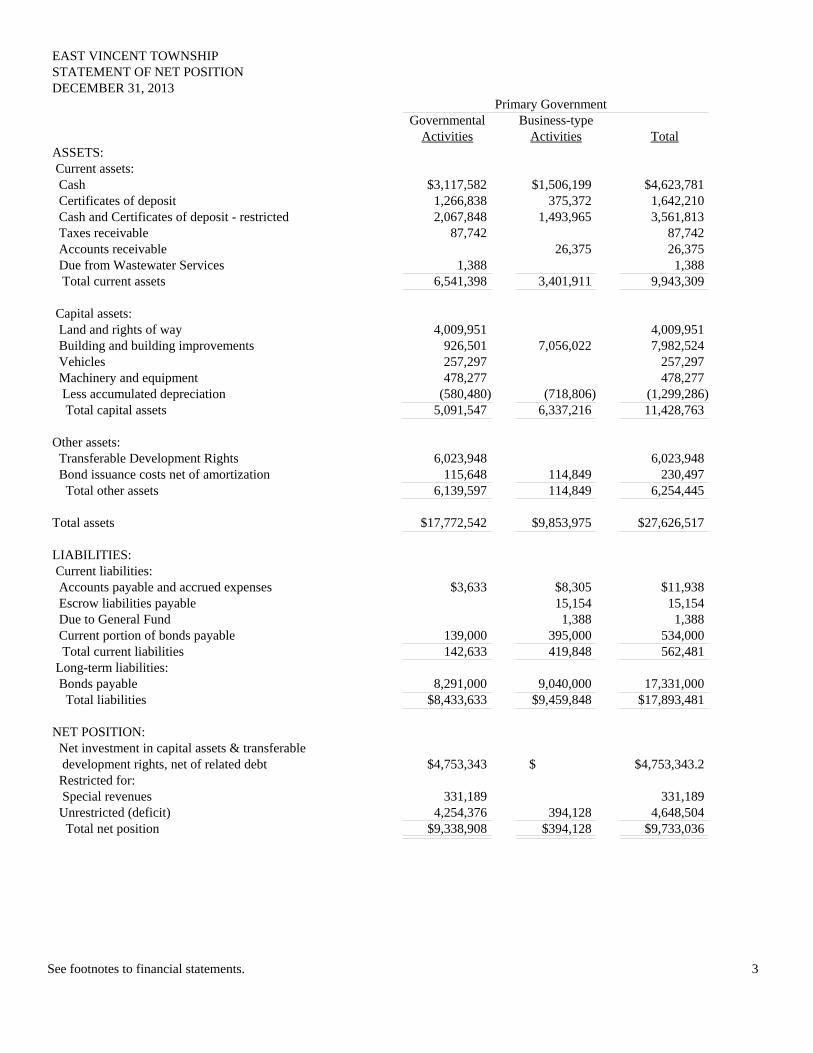

EAST VINCENT TOWNSHIPSTATEMENT OF NET POSITIONDECEMBER 31, 2013

Primary GovernmentGovernmental Business-type

Activities Activities TotalASSETS: Current assets: Cash $3,117,582 $1,506,199 $4,623,781 Certificates of deposit 1,266,838 375,372 1,642,210 Cash and Certificates of deposit - restricted 2,067,848 1,493,965 3,561,813 Taxes receivable 87,742 87,742 Accounts receivable 26,375 26,375 Due from Wastewater Services 1,388 1,388 Total current assets 6,541,398 3,401,911 9,943,309

Capital assets: Land and rights of way 4,009,951 4,009,951 Building and building improvements 926,501 7,056,022 7,982,524 Vehicles 257,297 257,297 Machinery and equipment 478,277 478,277 Less accumulated depreciation (580,480) (718,806) (1,299,286) Total capital assets 5,091,547 6,337,216 11,428,763

Other assets: Transferable Development Rights 6,023,948 6,023,948 Bond issuance costs net of amortization 115,648 114,849 230,497 Total other assets 6,139,597 114,849 6,254,445

Total assets $17,772,542 $9,853,975 $27,626,517

LIABILITIES: Current liabilities: Accounts payable and accrued expenses $3,633 $8,305 $11,938 Escrow liabilities payable 15,154 15,154 Due to General Fund 1,388 1,388 Current portion of bonds payable 139,000 395,000 534,000 Total current liabilities 142,633 419,848 562,481 Long-term liabilities: Bonds payable 8,291,000 9,040,000 17,331,000 Total liabilities $8,433,633 $9,459,848 $17,893,481

NET POSITION: Net investment in capital assets & transferable development rights, net of related debt $4,753,343 $ $4,753,343.2 Restricted for: Special revenues 331,189 331,189 Unrestricted (deficit) 4,254,376 394,128 4,648,504 Total net position $9,338,908 $394,128 $9,733,036

See footnotes to financial statements. 4

EAST VINCENT TOWNSHIPSTATEMENT OF ACTIVITIES Business-FOR THE YEAR ENDED DECEMBER 31, 2013 Type

Governmental Activities Activities TotalPolice andEmergency Codes and Public Parks and Debt Open Space Waste Water

Administration Services Engineering Works Recreation Service Acquisitions Total ServicesExpenses: Program expenses $339,985 $918,764 $106,504 $747,574 $50,713 $3,750 $16,198 $2,183,489 $543,130 $2,726,619 Depreciation 5,697 22,707 35,324 21,919 85,647 243,043 328,690 Amortization 7,228 7,228 6,380 13,609 Interest on debt 195,966 195,966 347,321 543,287 Total expenses 345,682 941,471 106,504 782,898 72,632 206,944 16,198 2,472,330 1,139,875 3,612,204

Program revenues: Charges for services 22,813 52,815 133,374 7,958 216,960 1,875,721 2,092,680 Operating grants and contributions 147,456 176,758 324,214 726,457 1,050,671 Total program revenues 170,268 52,815 133,374 184,716 0 0 0 541,174 2,602,178 3,143,351

Net (Expense) Revenue (175,414) (888,656) 26,870 (598,182) (72,632) (206,944) (16,198) (1,931,156) 1,462,303 (468,853)

General revenues: Taxes: Real estate 391,864 391,864 Per capita 39,211 39,211 Transfer 106,470 106,470 Earned income tax 2,001,992 2,001,992 Local services tax 63,992 63,992 Amusement tax 76,349 76,349 Investment earnings 10,090 16,900 26,990 Miscellaneous 105,235 20,361 125,596 Total general revenues 2,795,203 37,261 2,832,464

Change in net position 864,047 1,499,564 2,363,611

Net position - January 1, 2013 8,474,861 (1,105,436) 7,369,425

Net position - December 31, 2013 $9,338,908 $394,128 $9,733,036

See footnotes to financial statements. 5

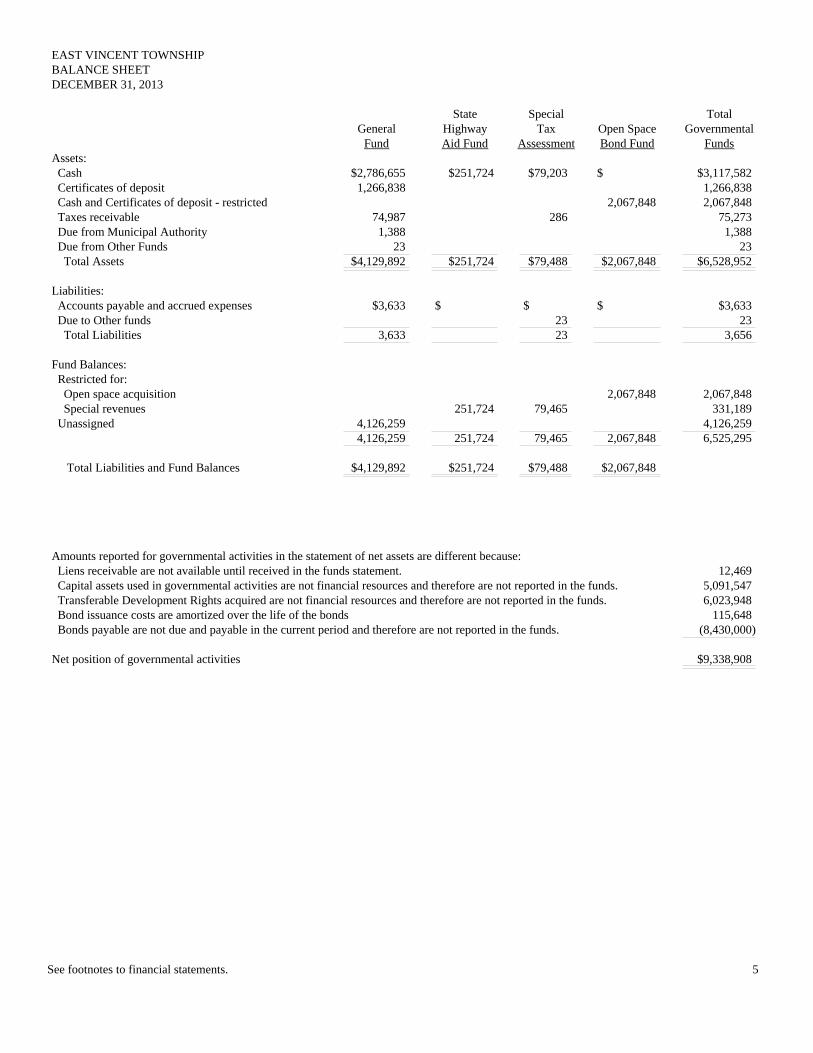

EAST VINCENT TOWNSHIPBALANCE SHEETDECEMBER 31, 2013

State Special TotalGeneral Highway Tax Open Space Governmental

Fund Aid Fund Assessment Bond Fund FundsAssets: Cash $2,786,655 $251,724 $79,203 $ $3,117,582 Certificates of deposit 1,266,838 1,266,838 Cash and Certificates of deposit - restricted 2,067,848 2,067,848 Taxes receivable 74,987 286 75,273 Due from Municipal Authority 1,388 1,388 Due from Other Funds 23 23 Total Assets $4,129,892 $251,724 $79,488 $2,067,848 $6,528,952

Liabilities: Accounts payable and accrued expenses $3,633 $ $ $ $3,633 Due to Other funds 23 23 Total Liabilities 3,633 23 3,656

Fund Balances: Restricted for: Open space acquisition 2,067,848 2,067,848 Special revenues 251,724 79,465 331,189 Unassigned 4,126,259 4,126,259

4,126,259 251,724 79,465 2,067,848 6,525,295

Total Liabilities and Fund Balances $4,129,892 $251,724 $79,488 $2,067,848

Amounts reported for governmental activities in the statement of net assets are different because: Liens receivable are not available until received in the funds statement. 12,469 Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds. 5,091,547 Transferable Development Rights acquired are not financial resources and therefore are not reported in the funds. 6,023,948 Bond issuance costs are amortized over the life of the bonds 115,648 Bonds payable are not due and payable in the current period and therefore are not reported in the funds. (8,430,000)

Net position of governmental activities $9,338,908

See footnotes to financial statements. 6

EAST VINCENT TOWNSHIPSTATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCESFOR THE YEAR ENDED DECEMBER 31, 2013

State Special TotalGeneral Highway Tax Open Space Governmental

Fund Aid Fund Assessment Bond Fund FundsRevenues: Taxes $1,837,310 $ $25,757 $804,341 $2,667,408 Licenses and permits 133,374 133,374 Fines 26,429 26,429 Interest income 8,051 46 19 1,975 10,090 Grants and Intergovernmental revenue 147,456 176,758 324,214 Departmental earnings 22,813 22,813 Public Safety 26,386 26,386 Highways 7,958 7,958 Miscellaneous Revenues 99,313 99,313 Refunds of prior year expenditures 5,922 5,922 Total revenues 2,315,012 176,804 25,775 806,316 3,323,908

Expenditures: General government 87,769 11,601 99,369 Legal 12,771 4,597 17,369 Administration 205,497 205,497 Engineer 5,480 5,480 Buildings 28,469 28,469 Police 859,802 859,802 Fire protection 83,541 83,541 Animal control 4,065 4,065 Code enforcement 96,587 96,587 Planning and zoning 9,916 9,916 Emergency services 0 0 Recycling 1,264 1,264 Public works 726,306 20,004 746,311 Park and recreation 35,372 35,372 Libraries 7,500 7,500 Historical and cemeteries 7,841 7,841 Debt services and bond issue discount / costs 329,966 329,966 Fiscal agent fees 3,750 3,750 Capital purchases 0 753,974 753,974 Total expenditures 2,172,180 0 20,004 1,103,888 3,296,073

Excess (deficit) of revenues over expenditures 142,832 176,804 5,771 (297,572) 27,835

Fund balances January 1, 2013 3,983,427 74,919 73,694 2,365,420 6,497,460

Fund balances December 31, 2013 $4,126,259 $251,724 $79,465 $2,067,848 $6,525,295

See footnotes to financial statements. 7

EAST VINCENT TOWNSHIPRECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, ANDCHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THESTATEMENT OF ACTIVITIESFOR THE YEAR ENDED DECEMBER 31, 2013

Excess (deficiency) of revenues over expenditures $27,835

Governmental funds report capital outlays as expenditures. However, in the statement of activities, the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which capital outlays ($782,618) exceeded depreciation ($85,647) in the current period. 696,971

Liens receivable are recognized as a receivable. However, in the statement of revenues, liens receivable are 12,469 recognized upon receipt.

Bond discount is amortized over the life of the bonds. Accordingly, amortization is recognized over the life of the bond. (7,228)

Principal payments are recognized as debt service in the statement of expenditures. However principal payments reduce the amount owed in the statement of net assets. 134,000

Change in net assets of governmental activities $864,047

See footnotes to financial statements. 8

EAST VINCENT TOWNSHIPSTATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCEBUDGET AND ACTUALFOR THE YEAR ENDED DECEMBER 31, 2013

General Fund

BudgetFavorable

Budget Actual (Unfavorable)Revenues: Taxes $1,801,248 $1,837,310 $36,062 Licenses and permits 125,250 133,374 8,124 Fines 25,000 26,429 1,429 Interest income 12,000 8,051 (3,949) Grants and Intergovernmental revenue 139,200 147,456 8,256 Departmental earnings 13,820 22,813 8,993 Public Safety 5,750 26,386 20,636 Highways 8,750 7,958 (792) Miscellaneous Revenues 6,200 99,313 93,113 Interfund Transfers 284,452 0 (284,452) Refunds of prior year expenditures 100 5,922 5,822 Total revenues 2,421,770 2,315,012 (106,758)

Expenditures: General government 92,892 87,769 5,123 Legal 24,500 12,771 11,729 Administration 215,195 205,497 9,698 Engineer 7,500 5,480 2,020 Buildings 29,050 28,469 581 Police 904,881 859,802 45,079 Fire protection 79,000 83,541 (4,541) Animal control 5,394 4,065 1,329 Code enforcement 96,852 96,587 265 Planning and zoning 30,614 9,916 20,698 Emergency services 750 0 750 Recycling 1,500 1,264 236 Public works 894,517 726,306 168,211 Park and recreation 26,800 35,372 (8,572) Libraries 7,500 7,500 0 Historical and cemeteries 4,825 7,841 (3,016) Other services & charges 0 0 Total expenditures 2,421,770 2,172,180 249,590

Excess of revenues over (under) expenditures $0 142,832 $142,832

Fund balance January 1, 2013 3,983,427

Fund balance December 31, 2013 $4,126,259

See footnotes to financial statements. 9

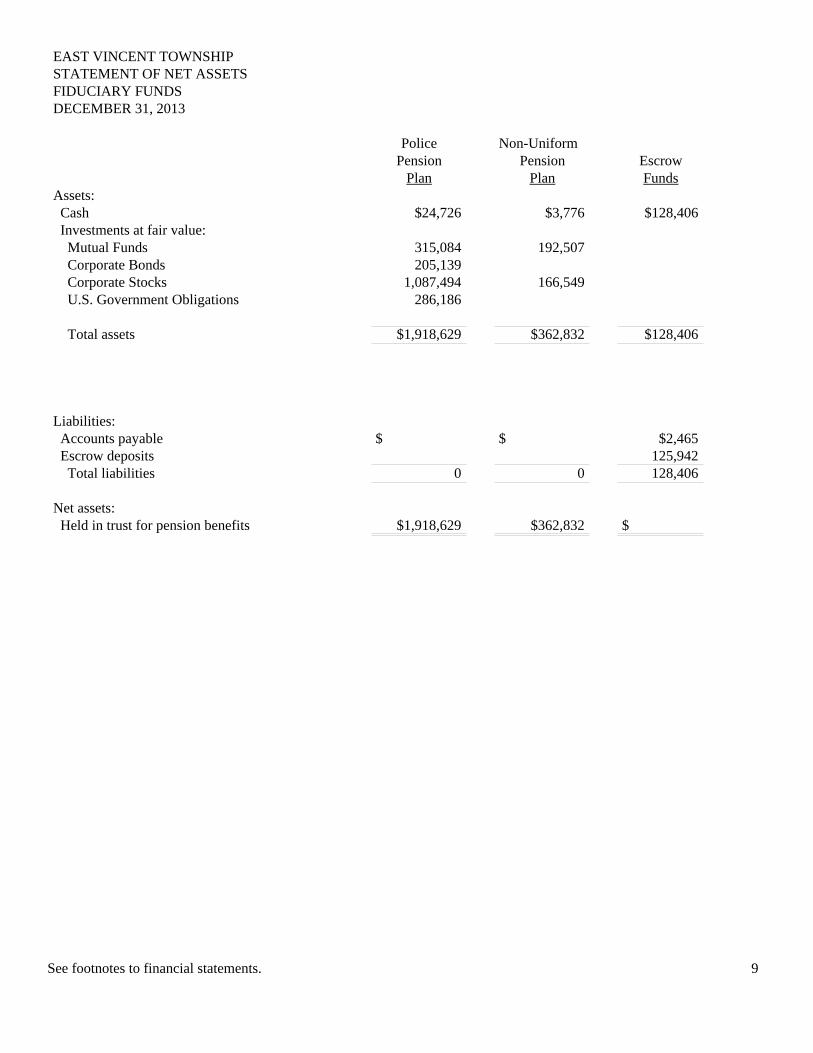

EAST VINCENT TOWNSHIPSTATEMENT OF NET ASSETSFIDUCIARY FUNDSDECEMBER 31, 2013

Police Non-UniformPension Pension Escrow

Plan Plan FundsAssets: Cash $24,726 $3,776 $128,406 Investments at fair value: Mutual Funds 315,084 192,507 Corporate Bonds 205,139 Corporate Stocks 1,087,494 166,549 U.S. Government Obligations 286,186

Total assets $1,918,629 $362,832 $128,406

Liabilities: Accounts payable $ $ $2,465 Escrow deposits 125,942 Total liabilities 0 0 128,406

Net assets: Held in trust for pension benefits $1,918,629 $362,832 $

See footnotes to financial statements. 10

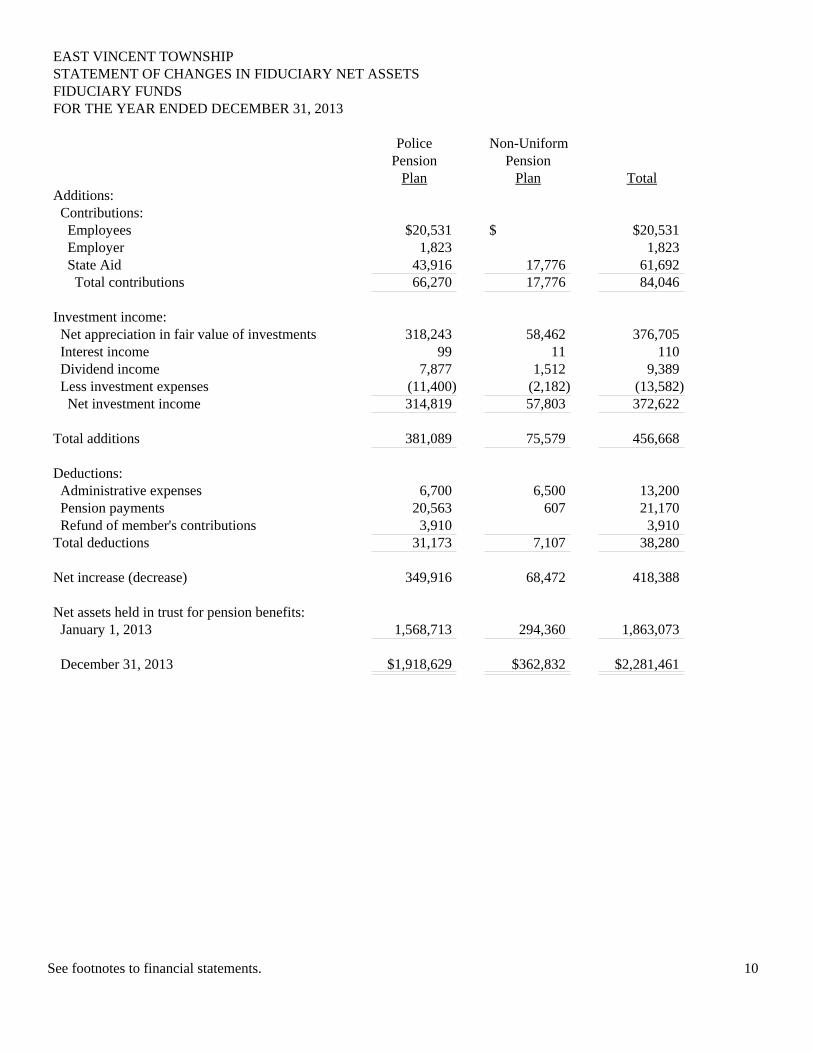

EAST VINCENT TOWNSHIPSTATEMENT OF CHANGES IN FIDUCIARY NET ASSETSFIDUCIARY FUNDSFOR THE YEAR ENDED DECEMBER 31, 2013

Police Non-UniformPension Pension

Plan Plan TotalAdditions: Contributions: Employees $20,531 $ $20,531 Employer 1,823 1,823 State Aid 43,916 17,776 61,692 Total contributions 66,270 17,776 84,046

Investment income: Net appreciation in fair value of investments 318,243 58,462 376,705 Interest income 99 11 110 Dividend income 7,877 1,512 9,389 Less investment expenses (11,400) (2,182) (13,582) Net investment income 314,819 57,803 372,622

Total additions 381,089 75,579 456,668

Deductions: Administrative expenses 6,700 6,500 13,200 Pension payments 20,563 607 21,170 Refund of member's contributions 3,910 3,910Total deductions 31,173 7,107 38,280

Net increase (decrease) 349,916 68,472 418,388

Net assets held in trust for pension benefits: January 1, 2013 1,568,713 294,360 1,863,073

December 31, 2013 $1,918,629 $362,832 $2,281,461

See footnotes to financial statements. 11

EAST VINCENT TOWNSHIPSTATEMENT OF NET ASSETSPROPRIETARY FUNDS - WASTE WATER SERVICESDECEMBER 31, 2013

Assets

Current assets: Cash and cash equivalents $1,506,199 Certificates of deposit 375,372 Restricted cash and cash equivalents 1,493,965 Receivables 26,375 Total current assets 3,401,911

Noncurrent assets: Capital assets: Office assets 900 Bartons Meadows plant and equipment 343,085 Southeast Veterans Center plan and equipment 6,712,037 Less accumulated depreciation (718,806) Net capital assets 6,337,216 Intangible assets: Bond issuance costs 133,990 Less accumulated amortization (19,141) Net bond issuance costs 114,849 Total noncurrent assets 6,452,064

Total assets $9,853,975

Liabilities Current liabilities: Accounts payable $8,305 Escrow liabilities payable 15,154 Due to general fund 1,388 Current portion of bonds payable 395,000 Total current liabilities 419,848

Noncurrent liabilities: Bonds payable 9,040,000 Total liabilities 9,459,848

Net Assets 394,128

Total liabilities and net assets $9,853,975

See footnotes to financial statements. 12

EAST VINCENT TOWNSHIPSTATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET ASSETSPROPRIETARY FUNDS - WASTE WATER SERVICESFOR THE YEAR ENDED DECEMBER 31, 2013

Barton VeteransMeadows Center Total

Operating Revenues: Sewer rents and tapping fees $156,708 $1,697,831 $1,854,539 Late charges 2,716 18,466 21,182 Miscellaneous income 562 19,799 20,361 Grants 726,457 726,457 Total operating revenues 159,986 2,462,553 2,622,539

Operating Expenses: Treatment: Chemicals 8,824 22,911 31,735 Equipment & repairs 12,182 5,668 17,850 Engineering 25,196 75,240 100,436 Electric 19,003 21,845 40,848 Sludge Removal & Water Hauling 18,434 18,434 Permit Fees 600 600 Contracted Operations 26,287 18,109 44,396 Collection: Equipment & repairs 263 15,532 15,795 Manholes 1,332 1,332 Electric 4,798 20,037 24,835 Operating supplies 3,319 1,396 4,715 Administration: Legal 8,130 28,949 37,079 Salaries 9,833 57,058 66,891 Payroll taxes 808 4,906 5,714 Employee benefits 3,065 17,316 20,382 Office Supplies 240 922 1,163 General Services 545 1,198 1,744 Property & casualty insurance 1,043 5,912 6,955 Audit 700 6,968 7,668 Postage & Phone 2,507 4,837 7,344 Miscellaneous 65 1,951 2,016 Engineering 16,689 25,954 42,642 Depreciation 26,030 216,712 242,743 Total operating expenses 169,529 573,787 743,316 Operating income (9,543) 1,888,766 1,879,223

Nonoperating income (expenses) Interest income 20 16,879 16,900 Interest expense (347,321) (347,321) Amortization (6,380) (6,380) Depreciation (30) (270) (300) Other expense (42,557) (42,557) Total nonoperating expenses (10) (379,649) (379,659)

Change in net assets ($9,553) $1,509,116 1,499,564

Net assets January 1, 2013 (1,105,436)

Net assets December 31, 2013 $394,128

See footnotes to financial statements. 13

EAST VINCENT TOWNSHIPSTATEMENT OF CASH FLOWSPROPRIETARY FUNDS - WASTE WATER SERVICESFOR THE YEAR ENDED DECEMBER 31, 2013

Increase (Decrease) in Cash and Cash Equivalents

Cash flows from operating activities: Receipts from customers $2,620,146 Payments to suppliers (481,095) Payments to employees (66,891) Net cash provided by operating activities 2,072,161

Cash flows from capital and related financing activities: Bond interest paid (347,321) Bond principal paid (390,000) Capital improvements made to sewer systems (5,508,326) Net cash used by capital and related financing activities (6,245,647) Cash flows from investing activities: Interest and trustee income 16,900 Investment in restricted cash and certificates of deposit 4,835,572 Net cash provided by investing activities 4,852,472

Net increase (decrease) in cash and cash equivalents 678,985

Cash and cash equivalents at beginning of year 827,213

Cash and cash equivalents at end of year $1,506,198

Reconciliation of operating income to net cash provided by operating activities: Operating income $1,879,223 Adjustments to reconcile operating income to net cash provided by operating activities: Depreciation 242,743 Nonoperating expenses (42,557) Change in assets and liabilities: Receivables (2,392) Accounts payable (3,546) Due to general fund (1,309)

Net cash provided by operating activities $2,072,161

1. East Vincent Township:

East Vincent Township (the "Township") is a second class township located in ChesterCounty, Pennsylvania. The Township is governed by a Board of Supervisors comprised of threeresidents. The Board of Supervisors is responsible for the administration, management andoperation of the Township. Members of the Board of Supervisors are elected for six year terms.Elections are held for one position every two years. The duties of the Board of Supervisorsinclude the adoption of the annual operating budget, capital improvements, maintenance ofroads, public safety, and planned development.

The Township’s financial statements are prepared in accordance with generally acceptedaccounting principles (GAAP). The Governmental Accounting Standards Board (GASB) isresponsible for establishing GAAP for state and local governments through its pronouncements(Statements and Interpretations). Governments are also required to follow the pronouncements ofthe Financial Accounting Standards Board (FASB) issued through November 30, 1989 (whenapplicable) that do not conflict with or contradict GASB pronouncements. The more significantaccounting policies established in GAAP and used by the Township are discussed below.

The Township’s financial statements are prepared in accordance with GovernmentalAccounting Standards Board (GASB) Statement No. 34, Basic Financial Statements-andManagement's Discussion and Analysis-for State and Local Governments (“GASB 34”).Significant aspects to GASB No. 34 include:

A management discussion and analysis section providing an analysis of the Township’soverall financial position and results of operations,

Financial statements prepared using full accrual accounting for all of the Township’sactivities,

A change in the fund financial statements to focus on the major funds.

The Township elected to implement the general provisions of the GASB 34 as of January1, 2004 and prospectively report infrastructure assets acquired after that date.

2. Summary of significant accounting policies:

A. Reporting Entity:

These financial statements present the Township (the primary government).

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

14

B. Basic Financial Statements—Government-Wide Statements

The Township’s basic financial statements include both government-wide (reporting theTownship as a whole), fund financial statements (reporting the Township’s major funds) andbusiness type activities. Both the government-wide and fund financial statements categorizeprimary activities as governmental activities. The Township’s general administrative services,State Highway Aid, Special Tax Assessment and Open Space Bond Fund are classified asgovernmental activities. Wastewater services are classified as a business-type activity.

The government-wide Statement of Net Position is reported on a full accrual, economicresource basis, which recognizes all long-term assets and receivables as well as long-term debtand obligations. The Township’s net position is reported in three parts: invested in capital assetsnet of related debt; restricted net assets; and unrestricted net assets. The Township first utilizesrestricted resources to finance qualifying activities.

The government-wide Statement of Activities reports both the gross and net cost of eachof the Township’s functions (police, fire, public works, etc.) and business-type activities(wastewater services). The functions are also supported by general government revenues(property, per capita, earned income taxes, certain intergovernmental revenues, fines, permitsand charges, etc.). The Statement of Activities reduces gross expenses (including depreciation)by related program revenues, operating and capital grants. Program revenues must be directlyassociated with the function (police, public works, community and youth services, etc.).Operating grants include operating-specific and discretionary (either operating or capital) grants.

The net costs are normally covered by general revenue (property, or earned income taxes,intergovernmental revenues, interest income, etc.).

The Township does not allocate indirect costs.

This government-wide focus is more on the sustainability of the Township as an entityand the change in the Township’s net position resulting from the current year’s activities.

C. Basic Financial Statements—Fund Financial Statements

The financial transactions of the Township are reported in individual funds in the fundfinancial statements. Each fund is accounted for by providing a separate set of self-balancingaccounts that comprises its assets, liabilities, reserves, fund equity, revenues andexpenditures/expenses. The various funds are reported by generic classification within thefinancial statements.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

15

The major governmental funds are as follows:

General Fund is the principal operating fund of the Township and accounts for all financialresources except those required to be in another fund.

State Highway Aid Fund accounts for all monies received under the State Highway LiquidFuels tax that are legally restricted to expenditures for roadway maintenance.

Special Tax Assessment Fund accounts for tax revenues received for street lights and firehydrants that are restricted to expenditures for such purposes.

Open Space Bond Fund accounts for monies budgeted by the Board of Supervisors for thepurchase of open space in the Township to be used to preserve and protect farmlands,parklands, and natural, historic and scenic resources.

Fiduciary Funds:

Fiduciary Funds are used to report assets held in a trustee or agency capacity for othersand therefore are not available to support Township programs. The reporting focus is on netassets and changes in net assets and are reported using accounting principles similar toproprietary funds.

Proprietary Funds:

Proprietary Funds are used to report fee for service activities. Effective January 1, 2011the Township began providing the waste water treatment services previously operated by theEast Vincent Municipal Authority. In anticipation of providing those services, the Townshipestablished the Waste Water Treatment Fund, secured bond financing and satisfied previous debtobligations of the Authority.

Governmental Fund Balances:

GASB Statement No. 34 as amended by GASB Statement No. 54 requires fund balancereported in the governmental fund balance sheet to be classified using a hierarchy basedprimarily on the extent to which a government is bound to honor constraints on the specificpurposes for which amounts in those funds can be spent. Governmental fund balance is to beclassified as:

• Non spendable fund balance - includes amounts that cannot be spent because they are notin spendable form or legally or contractually required to be maintained intact.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

16

• Restricted fund balance - includes amounts that are restricted to specific purposes (theuse of resources is constrained either by (a) external impositions by creditors, grantors,contributors, or laws or regulations of other governments or (b) impositions by law throughconstitutional provisions or enabling legislation).

• Committed fund balance - includes amounts that can only be used for specific purposespursuant to constraints imposed by formal action of the Board of Supervisors (for example,legislation, resolution, ordinance).

• Assigned fund balance - includes amounts that are constrained by the government’sintent to be used for specific purposes, but is not restricted or committed. Intent should beexpressed by (a) the governing body itself or (b) a body (a budget or finance committee, forexample) or official to which the governing body has delegated the authority to assignamounts to be used for specific purposes.

• Unassigned fund balance - represents fund balance that has not been assigned to otherfunds and that has not been restricted, committed, or assigned to specific purposes within thegeneral fund.

D. Basis of Accounting:

Basis of accounting refers to the point at which revenues or expenditures/expenses arerecognized in the accounts and reported in the financial statements. It relates to the timing of themeasurements made regardless of the measurement focus applied.

1. Accrual:

Governmental activities in the government-wide financial statements and the fiduciaryfund financial statements are presented on the accrual basis of accounting. Revenues arerecognized when earned and expenses are recognized when incurred.

2. Modified Accrual:

The governmental funds financial statements are presented on the modified accrual basisof accounting. Under the modified accrual basis of accounting, revenues are recorded whensusceptible to accrual; i.e., both measurable and available. “Available” means collectible withinthe current period or within 60 days after year end. Expenditures are generally recognized underthe modified accrual basis of accounting when the related liability is incurred. The exception tothis general rule is that principal and interest on general obligation long-term debt, if any, isrecognized when due.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

17

E. Financial Statement Amounts

1. Cash and Cash Equivalents:

The Township has defined cash and cash equivalents to include cash on hand, demanddeposits, and cash with fiscal agent. Additionally, each fund’s equity in the Township’sinvestment pool is treated as a cash equivalent because the funds can deposit or effectivelywithdraw cash at any time without prior notice or penalty.

2. Investments:

Investments, including pension funds, are stated at fair value, (quoted market price or thebest available estimate). Short term investments are reported at cost, which approximates fairvalue. Securities traded on a national or international exchange are valued at the last reportedsales price at current exchange rates.

3. Capital Assets:

Capital assets purchased or acquired with an original cost of $5,000 or more are reportedat historical cost or estimated historical cost. Contributed assets are reported at fair market valueas of the date received. Additions, improvements and other capital outlays that significantlyextend the useful life of an asset are capitalized. Other costs incurred for repairs and maintenanceare expensed as incurred. Depreciation on all assets is provided on the straight-line basis over thefollowing estimated useful lives:

Buildings 40-50 yearsWater and sewer system 40–50 yearsMachinery and equipment 5 yearsImprovements 10–20 years

GASB 34 requires the Township to report and depreciate new infrastructure assets.Infrastructure assets include roads, bridges, underground pipe (other than related to utilities),traffic signals, etc. These infrastructure assets are likely to be the largest asset class of theTownship. Neither their historical cost nor related depreciation has historically been reported inthe financial statements. The Township elected to implement the general provisions and theprospective infrastructure provisions (under the modified approach) of GASB 34 as of January 1,2004. Under the modified approach: eligible infrastructure assets are not required to bedepreciated as long as the Township manages the eligible infrastructure assets using an assetmanagement system that has the characteristics set forth below; and, the Township documentsthat the eligible infrastructure assets are being preserved approximately at (or above) a conditionlevel established and disclosed by the Township.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

18

To meet the first requirement, the asset management system should:

Have an up-to-date inventory of eligible infrastructure assets Perform condition assessments of the eligible infrastructure assets and summarize the results

using a measurement scale Estimate each year the annual amount to maintain and preserve the eligible infrastructure

assets at the condition level established and disclosed.

Accordingly, all expenditures made for those assets (except for additions and improvements) areexpensed in the period incurred. Additions and improvements to eligible infrastructure assets arecapitalized. Additions or improvements increase the capacity or efficiency of infrastructureassets rather than preserve the useful life of the assets.

4. Transferable Development Rights (“TDRs”):

TDRs allow ownership of the development rights on a privately owned parcel of land tobe separated from ownership of the parcel itself. These rights can then be transferred from thatproperty to another property in a different location. As a result of transferring the developmentrights, the landowner is restricted from developing his land, usually by means of a restrictivecovenant. The Township is allowed to sell development rights to a developer who seeks higherdensity than the current zoning allows at another location. If the Township sells TDRs, proceedsfrom the sale could then be used to purchase development rights of properties in areas that theTownship wants to protect from urban development. As of the date of these financial statements,the Township has no plans to sell the TDRs. However, should the Township decide to retire orabandon a TDR, the value of that TDR would be written off immediately. The value for theTDRs has been established as the original amount paid for the TDRs.

As of December 31, 2013 the Township holds the following TDRs:

$6,001,578203Total753,97430Styer

2,667,93976Olszanowski706,38431Keeley

1,052,26041Shantz$821,02125Roriquez

CostTDRs acquiredParcel

5. Revenues:

Substantially all governmental fund revenues are recorded when susceptible to accrual;i.e., both measurable and available. “Available” means collectible within the current period orwithin 60 days after year end. Property taxes are billed and collected within the same period inwhich the taxes are levied.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

19

6. Expenditures:

Expenditures are recognized when the related fund liability is incurred.

7. Interfund Activity:

Interfund activity is reported as either loans, services provided, reimbursements ortransfers. Loans are reported as interfund receivables and payables as appropriate and are subjectto elimination upon consolidation. Services provided, deemed to be at market or near marketrates, are treated as revenues and expenditures/expenses. Reimbursements are when one fundincurs a cost, charges the appropriate benefiting fund and reduces its related cost as areimbursement. All other interfund transactions are treated as transfers.

F. Use of estimates:

The preparation of the financial assets in conformity with generally accepted accountingprinciples requires management to make estimates and assumptions that affect the reportedamounts of assets and liabilities and disclosure of contingent assets and liabilities at the date ofthe financial statements and the reported amounts of revenues and expenditures during thereporting period. Actual results could differ from those estimates.

G. Budgetary Information

Annual budgets are adopted on a basis consistent with modified cash basis of accounting for the General Fund. All annual appropriations lapse at fiscal year end.

During November, the Township holds budget hearings for the purpose of receiving oraland written comments from interested parties in regard to the proposed budget for the followingyear. The Township makes available to the public its proposed operating budget for all funds.The operating budget includes proposed expenditures and the means of financing them. Theboard holds public hearings and a final budget must be prepared and adopted no later thanDecember 31 through the passage of an ordinance.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

20

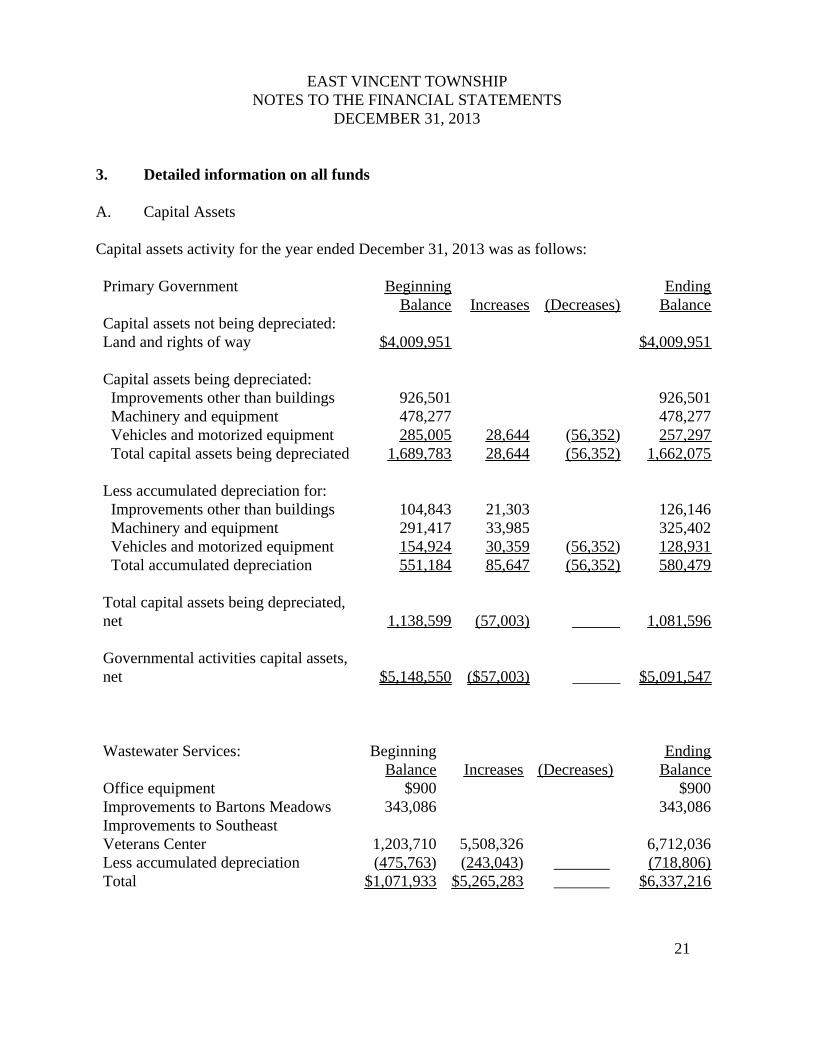

3. Detailed information on all funds

A. Capital Assets

Capital assets activity for the year ended December 31, 2013 was as follows:

$5,091,547 ______($57,003)$5,148,550Governmental activities capital assets,net

1,081,596 ______(57,003)1,138,599Total capital assets being depreciated,net

580,479(56,352)85,647551,184 Total accumulated depreciation128,931(56,352)30,359154,924 Vehicles and motorized equipment325,40233,985291,417 Machinery and equipment126,14621,303104,843 Improvements other than buildings

Less accumulated depreciation for:

1,662,075(56,352)28,6441,689,783 Total capital assets being depreciated257,297(56,352)28,644285,005 Vehicles and motorized equipment478,277478,277 Machinery and equipment926,501926,501 Improvements other than buildings

Capital assets being depreciated:

$4,009,951$4,009,951Land and rights of wayCapital assets not being depreciated:

EndingBalance(Decreases)Increases

BeginningBalance

Primary Government

$6,337,216 _______$5,265,283$1,071,933Total(718,806) _______(243,043)(475,763)Less accumulated depreciation 6,712,0365,508,3261,203,710

Improvements to SoutheastVeterans Center

343,086343,086Improvements to Bartons Meadows$900$900Office equipment

EndingBalance(Decreases)Increases

BeginningBalance

Wastewater Services:

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

21

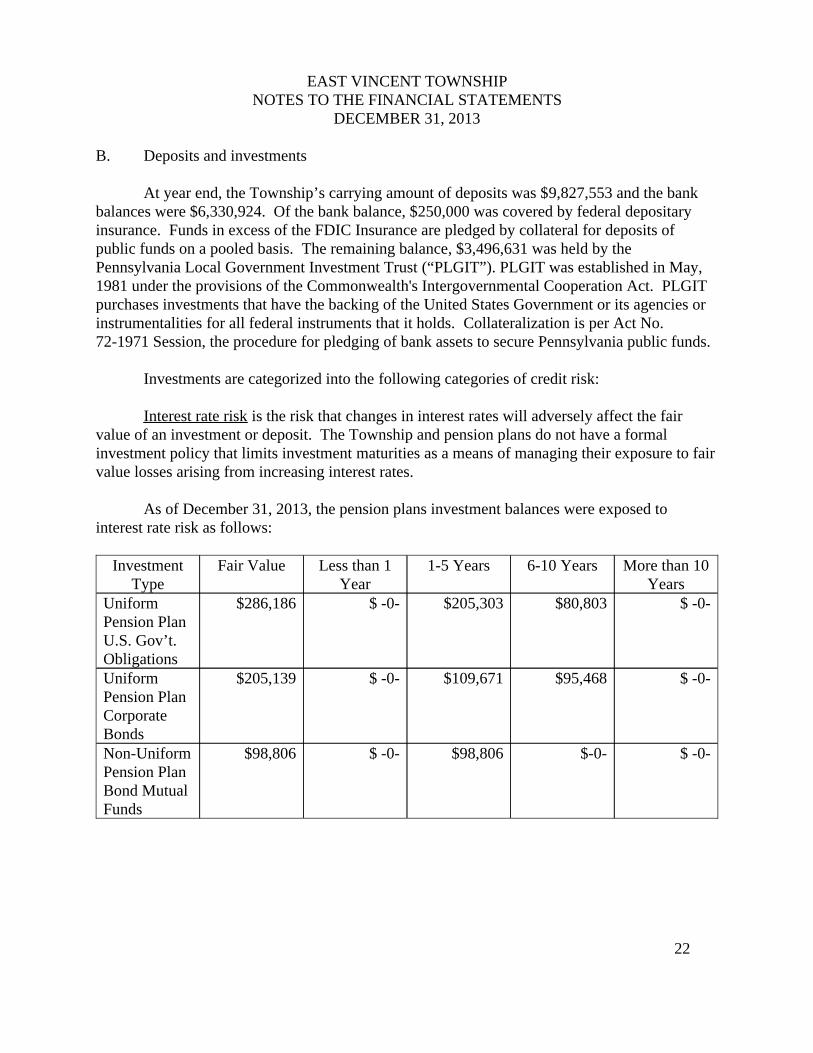

B. Deposits and investments

At year end, the Township’s carrying amount of deposits was $9,827,553 and the bankbalances were $6,330,924. Of the bank balance, $250,000 was covered by federal depositaryinsurance. Funds in excess of the FDIC Insurance are pledged by collateral for deposits ofpublic funds on a pooled basis. The remaining balance, $3,496,631 was held by thePennsylvania Local Government Investment Trust (“PLGIT”). PLGIT was established in May,1981 under the provisions of the Commonwealth's Intergovernmental Cooperation Act. PLGITpurchases investments that have the backing of the United States Government or its agencies orinstrumentalities for all federal instruments that it holds. Collateralization is per Act No.72-1971 Session, the procedure for pledging of bank assets to secure Pennsylvania public funds.

Investments are categorized into the following categories of credit risk:

Interest rate risk is the risk that changes in interest rates will adversely affect the fairvalue of an investment or deposit. The Township and pension plans do not have a formalinvestment policy that limits investment maturities as a means of managing their exposure to fairvalue losses arising from increasing interest rates.

As of December 31, 2013, the pension plans investment balances were exposed tointerest rate risk as follows:

$ -0-$-0-$98,806$ -0-$98,806Non-UniformPension PlanBond MutualFunds

$ -0-$95,468$109,671$ -0-$205,139UniformPension PlanCorporateBonds

$ -0-$80,803$205,303$ -0-$286,186UniformPension PlanU.S. Gov’t.Obligations

More than 10Years

6-10 Years1-5 YearsLess than 1Year

Fair ValueInvestmentType

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

22

Credit risk is the risk that an issuer or other counterparty to an investment will not fulfillits obligations. The Township and pension plans do not have a formal investment policy thataddresses credit risk. The credit risk of a debt instrument as measured by a nationallyrecognized statistical rating organization (Morningstar for bond mutual funds) is as follows:

$102,387$511,670TotalNot Available$3,581$20,345Money Market Funds

AA$98,806Bond Mutual FundsA$143,501Corporate Bonds

AA$61,638Corporate BondsAAA$286,186

U.S. Gov’t.Obligations

Credit Quality

Fair ValueNon-UniformPension Plan

Fair ValueUniform Pension PlanInvestment Type

U.S. Government obligations are not considered to have credit risk and do not require disclosureof credit quality.

Custodial credit risk is the risk that in the event of the failure of the counterparty to atransaction, the pension plan will not be able to recover the value of investment or collateralsecurities that are in the possession of an outside party. The Township and pension plans doe nothave a formal investment policy that addresses custodial credit risk. As of December 31, 2013,the pension plans had the following uninsured investment securities that are held by either thecounterparty or the counterparty's trust department or agent but not in the pension plan’s namethat were subject to custodial credit risk:

$286,186U.S. Gov’t. Obligations$205,139Corporate Bonds

$166,548$1,087,494Corporate Stocks

Fair Value Non-Uniform Pension Plan

Fair Value Uniform Pension PlanInvestment Type

Investments in external investment pools or in open-end mutual funds are not exposed tocustodial credit risk because their existence is not evidenced by securities that exist in physicalor book entry form. Securities underlying reverse repurchase agreements are not exposed tocustodial credit risk because they are held by the buyer-lender. The term securities as used inthis paragraph includes securities underlying repurchase agreements and investment securities.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

23

E. General Obligation Bonds Payable:

General Obligation Bonds are direct obligations issued on a pledge of the general taxingpower for the payment of the debt obligations of the Township. General Obligation Bondsrequire the Township to include in its annual budget such amounts from general revenues for thepayment (in each year bonds are outstanding) of interest and principal. The Township is incompliance with this requirement.

Arbitrage provisions of the Internal Revenue Act of 1986 require the Township to rebateexcess arbitrage earnings from bond proceeds to the federal government. The Internal RevenueAct of 1986 provides a small issue exemption if the amount of the proceeds are $5,000,000 orless.

Concentration of credit risk is the risk of loss attributable to the magnitude of theTownship’s or pension plan’s investment in a single issuer. Investments issued or explicitlyguaranteed by the U.S. government and investments in mutual funds, external investment pools,and other pooled investments are excluded from this requirement. The Township and pensionplans do not have a formal investment policy that addresses concentration of credit risk,however, as of December 31, 2013, no investments held by the pension plans represented morethan 5% of the net assets available for benefits.

Foreign currency risk is the risk that changes in exchange rate will adversely affect thefair value of an investment. The Township and pension plans do not have a formal investmentpolicy that addresses foreign currency risk, however, the Township and pension plans held noinvestments that were exposed to foreign currency risk as of December 31, 2013.

C. Receivables:

Receivables as of December 31, 2013 consist of:

$87,742Taxes$26,375Accounts

WastewaterServicesGeneral Fund

Receivables:

D. Property taxes:

The Township imposes a property tax of .9 mills on the assessed valuations determinedby the County of Chester. Property taxes are levied on March 1 of the calendar year. Propertytaxes are discounted 2% if remitted by May 1, due July 1, and penalized 10% if paid after July 1.Liens are filed for unpaid property taxes on March 1 of the following year.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

24

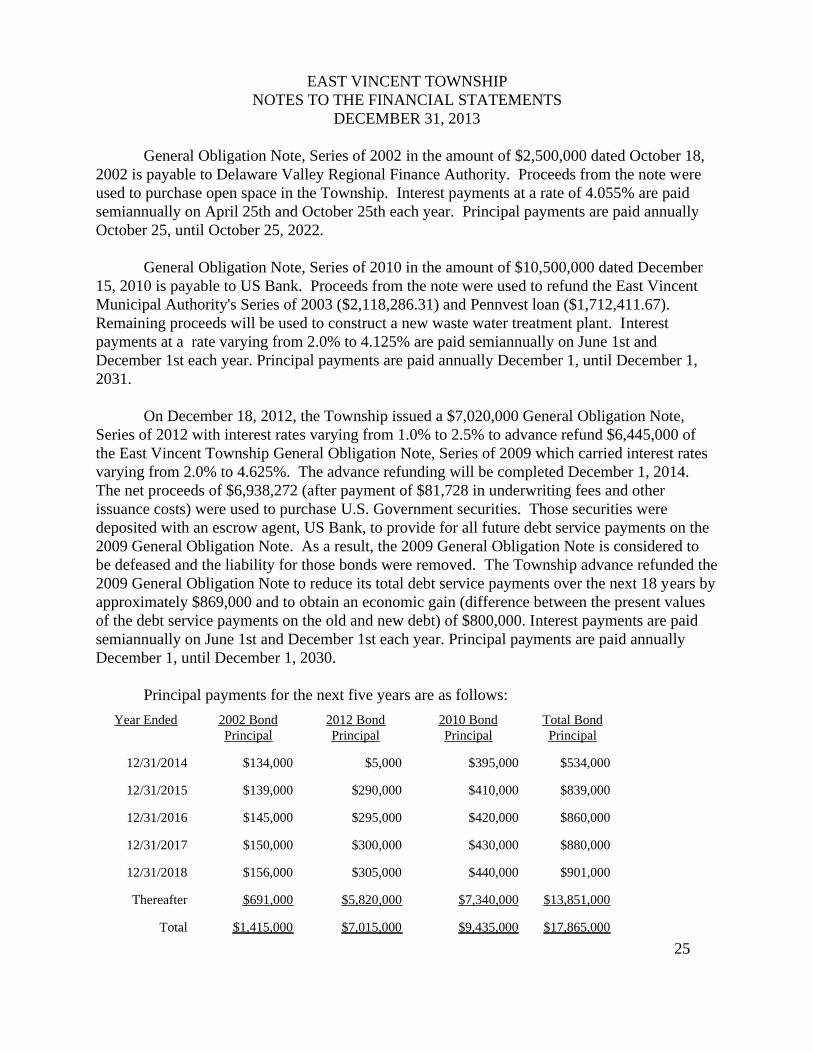

General Obligation Note, Series of 2002 in the amount of $2,500,000 dated October 18,2002 is payable to Delaware Valley Regional Finance Authority. Proceeds from the note wereused to purchase open space in the Township. Interest payments at a rate of 4.055% are paidsemiannually on April 25th and October 25th each year. Principal payments are paid annuallyOctober 25, until October 25, 2022.

General Obligation Note, Series of 2010 in the amount of $10,500,000 dated December15, 2010 is payable to US Bank. Proceeds from the note were used to refund the East VincentMunicipal Authority's Series of 2003 ($2,118,286.31) and Pennvest loan ($1,712,411.67).Remaining proceeds will be used to construct a new waste water treatment plant. Interestpayments at a rate varying from 2.0% to 4.125% are paid semiannually on June 1st andDecember 1st each year. Principal payments are paid annually December 1, until December 1,2031.

On December 18, 2012, the Township issued a $7,020,000 General Obligation Note,Series of 2012 with interest rates varying from 1.0% to 2.5% to advance refund $6,445,000 ofthe East Vincent Township General Obligation Note, Series of 2009 which carried interest ratesvarying from 2.0% to 4.625%. The advance refunding will be completed December 1, 2014.The net proceeds of $6,938,272 (after payment of $81,728 in underwriting fees and otherissuance costs) were used to purchase U.S. Government securities. Those securities weredeposited with an escrow agent, US Bank, to provide for all future debt service payments on the2009 General Obligation Note. As a result, the 2009 General Obligation Note is considered tobe defeased and the liability for those bonds were removed. The Township advance refunded the2009 General Obligation Note to reduce its total debt service payments over the next 18 years byapproximately $869,000 and to obtain an economic gain (difference between the present valuesof the debt service payments on the old and new debt) of $800,000. Interest payments are paidsemiannually on June 1st and December 1st each year. Principal payments are paid annuallyDecember 1, until December 1, 2030.

Principal payments for the next five years are as follows:

$17,865,000$9,435,000$7,015,000$1,415,000Total

$13,851,000$7,340,000$5,820,000$691,000Thereafter

$901,000$440,000$305,000$156,00012/31/2018

$880,000$430,000$300,000$150,00012/31/2017

$860,000$420,000$295,000$145,00012/31/2016

$839,000$410,000$290,000$139,00012/31/2015

$534,000$395,000$5,000$134,00012/31/2014

Total BondPrincipal

2010 BondPrincipal

2012 BondPrincipal

2002 BondPrincipal

Year Ended

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

25

4. Compensated absences:

The Township has implemented a compensated absences policy that permits employeesto accumulate a minimal amount of vacation with the requirement that the vacation be usedwithin the first three months of the new year. No sick days may be carried over.

5. Pension Plan:

Plan descriptions: The Township contributes to two single-employer defined benefitpension plans: Police Pension Plan, and Non-Uniform Pension Plan. The Police Pension Plan iscontrolled by the provisions of ordinance No. 180. The Non-Uniform Pension Plan is controlledby the provisions of ordinance No. 181. The plans are governed by the Township which isresponsible for the management of plan assets. The Police Pension Plan provides vesting,retirement, survivor and disability benefits to plan members and their beneficiaries. TheNon-Uniform Pension Plan provides vesting, normal retirement, survivor, and disability benefitsto plan members and their beneficiaries. Financial reports that include financial statements andrequired supplemental information for each plan are available from the Township.

Act 205: Act 205 of 1984, the “Municipal Pension Plan Funding Standard and RecoveryAct” initiated actuarial funding requirements for municipal pension plans. Under Act 205provisions, a municipal budget must provide for the full payment of the minimum municipalobligation (MMO) to each employee pension fund of the municipality. Act 189 of 1990amended Act 205 and redefined the calculation used to determine the MMO to employeepension funds. The MMO is now defined as the total financial requirements to the pension fund,less funding adjustments and estimated member contributions.

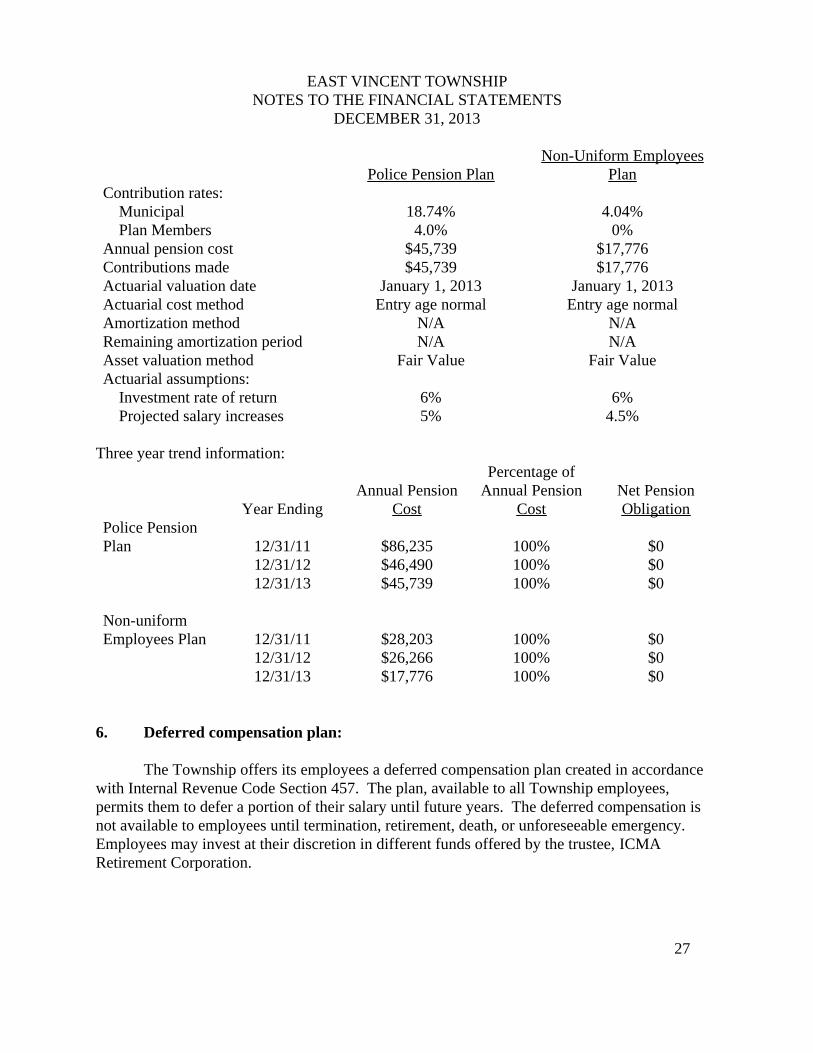

Funding Policy: As a condition of participation in the Police Pension Plan, full timepolice officers are required to contribute 4.0% of compensation to the Plan. The Townshipallocates State Aid received from the Commonwealth of Pennsylvania to the Plan. To the extentthat this funding is not adequate, the Township would then be required to contribute. Inaccordance with Act 205, the Township was required to contribute to the Plans for the year 2013.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

26

4.5%5% Projected salary increases6%6% Investment rate of return

Actuarial assumptions:Fair ValueFair ValueAsset valuation method

N/AN/ARemaining amortization periodN/AN/AAmortization method

Entry age normalEntry age normalActuarial cost methodJanuary 1, 2013January 1, 2013Actuarial valuation date

$17,776$45,739Contributions made$17,776$45,739Annual pension cost

0%4.0% Plan Members4.04%18.74%

Contribution rates: Municipal

Non-Uniform EmployeesPlanPolice Pension Plan

Three year trend information:

$0100%$17,77612/31/13$0100%$26,26612/31/12$0100%$28,20312/31/11

Non-uniformEmployees Plan

$0100%$45,73912/31/13$0100%$46,49012/31/12$0100%$86,23512/31/11

Police PensionPlan

Net PensionObligation

Percentage ofAnnual Pension

CostAnnual Pension

CostYear Ending

6. Deferred compensation plan:

The Township offers its employees a deferred compensation plan created in accordancewith Internal Revenue Code Section 457. The plan, available to all Township employees,permits them to defer a portion of their salary until future years. The deferred compensation isnot available to employees until termination, retirement, death, or unforeseeable emergency.Employees may invest at their discretion in different funds offered by the trustee, ICMARetirement Corporation.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

27

7. Contingencies:

East Vincent Township is the defendant in lawsuits arising principally in the normalcourse of operations. In the opinion of management, the outcome of these lawsuits is uncertain,the effect on the accompanying combined financial statements is uncertain and accordingly, noprovision for losses has been recorded.

9. Subsequent events:

The Township has evaluated events and transactions for potential recognition ordisclosure in the financial statements through July 8, 2014. No subsequent events have beenrecognized or disclosed.

EAST VINCENT TOWNSHIPNOTES TO THE FINANCIAL STATEMENTS

DECEMBER 31, 2013

28

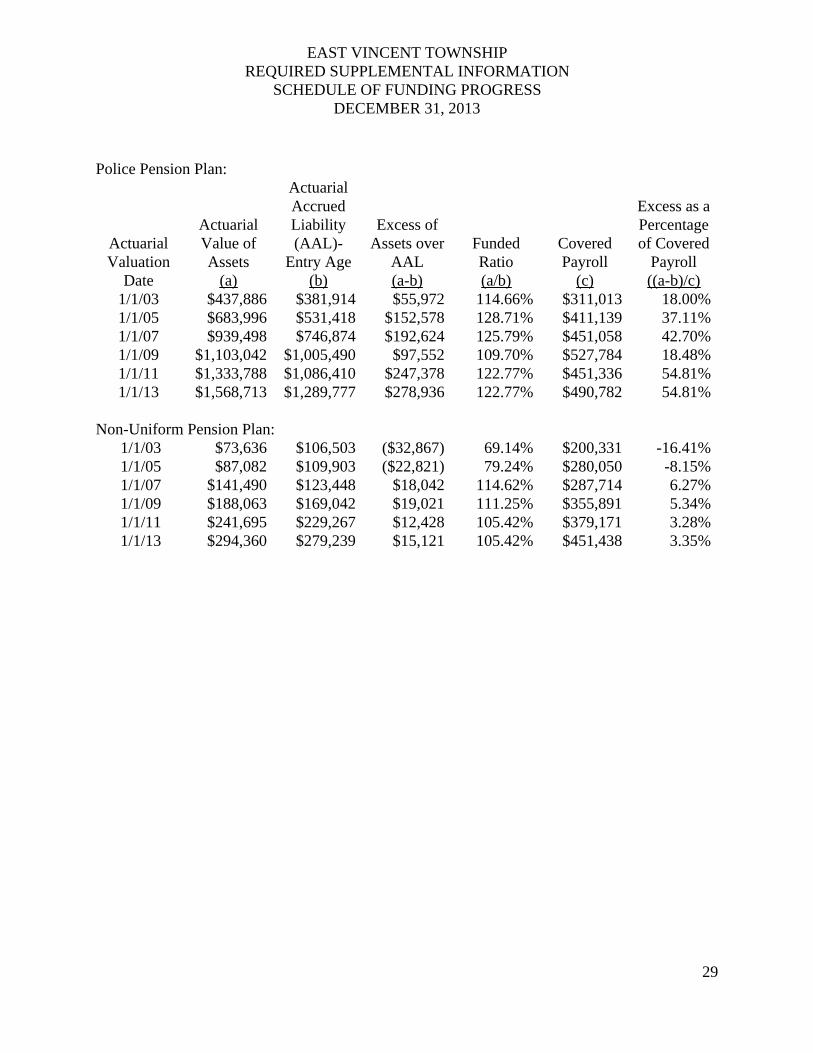

Police Pension Plan:

54.81%$490,782122.77%$278,936$1,289,777$1,568,7131/1/1354.81%$451,336122.77%$247,378$1,086,410$1,333,7881/1/1118.48%$527,784109.70%$97,552$1,005,490$1,103,0421/1/0942.70%$451,058125.79%$192,624$746,874$939,4981/1/0737.11%$411,139128.71%$152,578$531,418$683,9961/1/0518.00%$311,013114.66%$55,972$381,914$437,8861/1/03

Excess as aPercentageof Covered

Payroll((a-b)/c)

CoveredPayroll

(c)

FundedRatio(a/b)

Excess ofAssets over

AAL(a-b)

ActuarialAccruedLiability(AAL)-

Entry Age(b)

ActuarialValue ofAssets

(a)

ActuarialValuation

Date

Non-Uniform Pension Plan:

3.35%$451,438105.42%$15,121$279,239$294,3601/1/133.28%$379,171105.42%$12,428$229,267$241,6951/1/115.34%$355,891111.25%$19,021$169,042$188,0631/1/096.27%$287,714114.62%$18,042$123,448$141,4901/1/07

-8.15%$280,05079.24%($22,821)$109,903$87,0821/1/05-16.41%$200,33169.14%($32,867)$106,503$73,6361/1/03

EAST VINCENT TOWNSHIPREQUIRED SUPPLEMENTAL INFORMATION

SCHEDULE OF FUNDING PROGRESSDECEMBER 31, 2013

29