The Effects of Corporate Governance on Bank Financial Performance

Journal of Entrepreneurship in Emerging EconomiesFinancial marketization and corporate venturing in China: The impact ofprovincial-level institutions on the pharmaceutical sectorWeiqi Dai Ilan Alon Hao Jiao

Article information:To cite this document:Weiqi Dai Ilan Alon Hao Jiao , (2015),"Financial marketization and corporate venturing in China",Journal of Entrepreneurship in Emerging Economies, Vol. 7 Iss 1 pp. 2 - 22Permanent link to this document:http://dx.doi.org/10.1108/JEEE-01-2015-0001

Downloaded on: 17 February 2015, At: 07:45 (PT)References: this document contains references to 69 other documents.To copy this document: [email protected] fulltext of this document has been downloaded 7 times since 2015*

Access to this document was granted through an Emerald subscription provided byToken:JournalAuthor:C5FFC29B-D86D-41B7-9E6F-75E2978C8201:

For AuthorsIf you would like to write for this, or any other Emerald publication, then please use our Emeraldfor Authors service information about how to choose which publication to write for and submissionguidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comEmerald is a global publisher linking research and practice to the benefit of society. The companymanages a portfolio of more than 290 journals and over 2,350 books and book series volumes, aswell as providing an extensive range of online products and additional customer resources andservices.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of theCommittee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative fordigital archive preservation.

*Related content and download information correct at time ofdownload.

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

Financial marketization andcorporate venturing in China

The impact of provincial-level institutions onthe pharmaceutical sector

Weiqi DaiSchool of Business Administration,

Zhejiang University of Finance & Economics, Hangzhou,People’s Republic of China

Ilan AlonDepartment of International Business, Rollins College,

Winter Park, Florida, USA, and

Hao JiaoBusiness School, Beijing Normal University, Beijing,

People’s Republic of China

AbstractPurpose – The paper aims to empirically examine the role of intra-national institutions in businessperformance. In particular, the article develops hypotheses regarding financial marketization andbusiness venturing with organizational slack and political connections as moderating variables.Design/methodology/approach – The authors choose listed firms from the pharmaceuticalindustry in China and focus on the period of 2001-2009. Results from the Hausman specification testindicate that the random effects model is appropriate for data. Because the dependent variable isdichotomous, the random effects logistic regression technique in Stata is used. To check the robustnessof the estimation, the random-effects Tobit regression technique in Stata is also used. Overall, modelsare robust and statistically significant.Findings – It was found that the level of regional financial sector marketization is positivelyassociated with the likelihood of engaging in corporate venturing by firms within the region. Moreover,it was found that organizational slack significantly decreases the institutional influence on corporateventuring.Originality/value – This study is one of the first to theorize and empirically test the impact ofintra-national institutions on corporate venturing in China’s pharmaceutical industry. Institutionsmatter more when organizational slack is low. Firms in the pharmaceutical industry in China do notseem completely dependent on political connections for business venturing and use organizationalslack to buffer against (adverse) institutional change.

Keywords China, Guanxi, Manufacturing industries, Corporate venturing, Financial marketization,Intra-national institutions

Paper type Research paper

This research is supported by grants from National Natural Science Foundation of China (Project# 71202173; Project # 71132007). The financial support from the program of China ScholarshipCouncil (201308330363) is also acknowledged.

The current issue and full text archive of this journal is available on Emerald Insight at:www.emeraldinsight.com/2053-4604.htm

JEEE7,1

2

Received 4 January 2015Revised 13 January 2015Accepted 13 January 2015

Journal of Entrepreneurship inEmerging EconomiesVol. 7 No. 1, 2015pp. 2-22© Emerald Group Publishing Limited2053-4604DOI 10.1108/JEEE-01-2015-0001

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

1. IntroductionIn this paper, we link intra-national institutions (marketization of the environment) andpolitical connections and organizational slack (organizational resources) with businessperformance (in the form of corporate venturing) in the emerging market of China’spharmaceutical industry. We focus on corporate venturing because it is regarded as aneffective way of revitalizing obsolete firm operations, building new capabilities andachieving strategic renewal (Zahra and Hayton, 2008; Burgers et al., 2009; Covin andMiles, 2007) and has stimulated the interest from both business and academic worldover the past decades (Yang et al., 2013; Thornhill and Amit, 2001). Corporate venturingrefers to setting up new business within or outside the incumbent organizations(Sharma and Chrisman, 1999) and involves organizational systems, processes andpractices that create business in existing or new fields, markets or industries(Narayanan et al., 2009; Sharma and Chrisman, 1999; please refer to Narayanan et al.(2009) work for a comprehensive review of corporate venturing).

Among the key antecedents of corporate venturing are organizational factors such asresources (Burgelman and Valikangas, 2005; Chiu et al., 2012) and contextual factorssuch as the institutional framework for raising money. To date, most of the research oncorporate venturing is still focused on North American settings (Narayanan et al., 2009),leading to a lack of our understanding of corporate venturing in other institutionalframeworks. Little research exists on the broader institutional factors that have bearingon the occurrence of corporate venturing. Given that institutions are rules of games of asociety and firms are not immune from their influence (North, 1990), it is imperative toexamine how institutions exert their influence on corporate venturing and howorganizational factors interact with institutions to affect corporate venturing.

We contribute to the literature of corporate venturing not only by looking at China asan emerging market but also by empirically examining the impact of intra-nationalinstitutional variations in the financial sector on corporate venturing. We argue thatfinancial marketization at the provincial level enables corporate venturing. We furthersuggest that two organizational resources moderate this relationship: politicalconnections and organizational slack.

To build our model, we rely on two streams of research: institutional theory (North,1990) and resource dependence theory (RDT). These two streams of research allow us todevelop a more complete explanation linking environmental and organizationalresources with corporate venturing.

With the inception of institution-based view, the tenets of this theory were primarilytested at the country level (Chan et al., 2010). In other words, prior studies primarilyexamined the between-country institutional influences on firm strategies andperformance in different host countries (Makino et al., 2004), little is known about howwithin-country institutional differences affect firm strategies and performance indifferent regions within a host country, with only a few exceptions (Nguyen et al., 2013).More importantly, prior cross-country research was somewhat difficult to isolate theinfluence of institutions from those of culture and history when delineating theinstitutional framework of a country (Meyer and Nguyen, 2005), resulting in concernsover the content validity of measurement. To separate institutions’ influence on firmstrategies from that of national culture and history, we rely on significant variations ininstitutional development within a large and complex emerging country, i.e. China, toexamine how a firm’s corporate venturing strategy is facilitated or inhibited by regional

3

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

institutions. Powell (1996) postulates, the more critical issues in advancing the institutionaltheory are to understand how, under what circumstance and in what ways institutionsmatter. In response to his call, we seek to understand when and how intra-nationalinstitutions matter for corporate venturing.

RDT suggests that firms are dependent on external resources for survival andprosperity (Pfeffer and Salancik, 1978). As resources emanate from the environment andare a source of power, firms devise strategies to control key resources (those that arecritical and scarce) and reduce uncertainty and dependence on others’ sources of power.The customer is the ultimate resource on which firms depend and from which they cangenerate financial returns. Based on RDT, the firm is an open system, subject to theexternal environment, which must acquire resources to reduce uncertainty (Lin et al.,2014).

In general, there are three sources for obtaining capital for corporate venturing:through internally generated means, through government connections and/or throughthe banks. As provinces liberalized banks and have allowed them to act according tomarket principles, these banks became more responsive to the needs of local companiesand have lent based on their creditworthiness and the merits of their proposed ventures/projects. Banking reform in China has not been applied uniformly and, thus, localvariations in the institutional environment of lending can be observed. Therefore, ourmain effect hypothesis is a positive association between financial marketization andcorporate venturing.

In this paper, we analyze two specific, key firm-specific resources, especiallyimportant in the capital-intensive pharmaceutical industry in China (IBIS WorldIndustry Report, 2014). These firm-specific factors moderate the impact of institutions,the marketization of banks, on corporate venturing. Using RDT, we suggest that firms’resources including political connections and organizational slack, reduce the impact ofbank marketization. Firms that are able to leverage their other sources of capital are lessdependent on the market reforms of the banking sector.

In the context of the overall institutional environment, political connections is seen asa form of clientelism and corruption, leading to inefficient redistribution of resources insociety (Ozcan and Gunduz, 2014). Clientelism is a political exchange between a politicalleader and a firm, where the firm “buys” the services of the politician in exchange forfavorable conditions and support. Ties between business and political elites mayundermine democratic reform (Ozcan and Gunduz, 2014). The impact of politicalconnections on business venturing is, thus, important not only competitively for the firmbut also from a more macro social, political and economic points of view.

To sum up, we argue that varying financial liberalization has had a positive effect oncorporate venturing among provinces in China, but this effect has been undermined bypolitical connections and organizational slack. In Section 2, we develop the hypotheses.This is followed by methods in Section 3, results in Section 4 and conclusions anddiscussion in Section 5).

2. Theoretical frameworkAs mentioned in our introduction, we rely on two streams of research: institutionaltheory and RDT. This theoretical linking has been encouraged by Hillman et al.’s (2009,p. 1,418) meta-analysis review of RDT, in which they ask “do institutional forcesinfluence what form of dependency reducing strategies firms use?”. We suggest two

JEEE7,1

4

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

firm-specific dependency-reducing strategies moderating the impact of financial reformand test for their moderating impacts.

Given that there is a lack of fully developed institutional framework supportingmarket transactions in emerging economies such as China, critical resource allocations(e.g. financial resource) are coordinated by the government. In China, governmentaffects firms through institutions in two ways: through government connections andthrough policy initiatives and regulations. While the former maybe company/industryspecific, the latter affects all companies operating in the area. A feature of emergingeconomies is “institutional void” which means there is a lack of fully developed (formal)institutional infrastructures that support economic transactions (Khanna and Palepu,1997; Peng and Luo, 2000). In China, political connections often fill the void in theinstitutional environment. When the rules are unclear, knowing and influencing the rulemakers can have positive impact on performance. Drawing upon the institution-basedtheory, RDT and prior research on corporate venturing, intra-national financialliberalization is our main effect, and organizational slack as well as political connectionspresent our moderating variables. In the next sub-sections, we hypothesize a directrelationship between regional institutional variations and indirect impact of politicalconnections and organizational slack.

2.1 Financial marketizationWe start by examining the main effect, regional financial institutions, on corporateventuring, proposing that the effect should be straight and simple: positive impact offinancial liberalization. Echoing the call from Powell (1996), this paper seeks tounderstand when and how institutions matter in the context of emerging economies. Ina large and complex economy setting, firms’ corporate venturing activities areresponding to the development of market-supporting institutions. The market reformsof the financial sector will enable financing of worthwhile corporate ventures and, in thecase of China, lower the reliance of firms on the government or internal resources forfinancing.

As the institution-based view suggests, a firm’s strategic choice is not onlyconstrained by industrial dynamics and firm resources but also by more boardervariables such as institutions (Peng, 2002). Indeed, no one would deny that institutionsmatter for strategic choice, as no firms are able to be immune from the influence ofinstitutions (Peng, 2002). Therefore, it is imperative to know what types of institutionsare of importance in investigating the antecedents of corporate venturing.

Prior research claims that innovation and entrepreneurship are encouraged in adeveloped financial market (Lamoreaux, 1994). In the case of corporate venturing,institutions regarding financial market, in particular the marketization level of regionalfinancial sector, are of great importance, in that financial resources are indispensable inimplementing corporate venturing strategy, whereas the level of regional financialmarketization determines, to a large extent, the availability and cost of externalfinancing for firms within a specific region. Specifically, almost all firms amass financialresources for their corporate venturing from both inside and outside.

With fixed amount of internal resources, the amount of financial resources that couldbe gathered for a firm depends on the availability of external financial resources. Withinregions with higher levels of financial marketization and more opening-up of thefinancial sector, the number of rival financial institutions such as banks is bigger and

5

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

the competitions among them are more intensified, leading to more availability offinancial resources and lower cost of using the financial credit. Hence, corporateventuring activities by firms within the region are more likely to occur due to favorablefinancial supports. In contrast, firms within regions with lower-level financialmarketization are less likely to engage in corporate venturing due to limited access tofinancing and higher financing costs. As a result, the financial marketization as a formalinstitution associated with financial market within a specific region plays importantroles in determining the availability of financial resources and the cost of using them,and, in turn, it does matter for firms to conduct corporate venturing activities. Firmslocated in regions with more market-based financial institutions are likely to engage incorporate venturing activities. Therefore, we predict that:

H1. There is a positive relationship between provincial financial marketization andcorporate venturing.

2.2 Political connectionsAs North (1990) claims, there are two types of institutions, namely, formal institutionsand informal institutions. Informal institutions will play salient roles once if the formalones are not fully developed. Political connections are a way to deal with the informaleconomy, salient in emerging markets. The nexus of business and politics relationsshould be viewed in the context of a broader institutional context (Ozcan and Gunduz,2014). As North (1990) claims, the formal and informal institutions are substitutes toeach other. Filling the institutional void, informal institution comes into place whenformal institution are weak or non-existent (North, 1990). As a type of informalinstitution (Zhou, 2013; Xin and Pearce, 1996), political connections substitute formalmarket institutions and facilitate the resource acquisitions by firms.

One of the features of emerging economy country is “institutional void” (Peng andLuo, 2000) – the market-supporting institutions are not fully developed. As a result,resource allocation is not fulfilled completely by the market mechanism. Instead, manyresources, especially critical resources, are allocated by all levels of governments.Indeed, governments still hold substantial key resources such as land, financial subsidy,as well as the approvals or access to some regulated industries that are inseparable incarrying out corporate venturing activities in emerging economies. Because ofinstitutional voids, companies in emerging markets are particularly likely to invest inpolitical connections. To gain critical resources, firms have to turn to the governmentsand ask for their favor and assistance.

In China, institutional development is both purposeful and directed, going throughperiod of liberalization starting in 1978 (Yang and Stoltenberg, 2014). Despite theunder-developed market-supporting institutions, firms with political connections arestill able to access critical resources with assistance from governments. As a result,political connections functions as a conduit for firms to access financial resources andact as a substitution mechanism that renders the formal institutions less important.Accordingly, we have to consider the impact of political connections as well inexamining how corporate venturing responses to financial marketization.

Political connections are widespread among corporations, especially large ones(Faccio, 2006). The impact of political connections on firm competitiveness, businessperformance, survival and growth has been studies in both developed (Goldman et al.,2009) and developing countries (Johnson and Mitton, 2003), with results that are

JEEE7,1

6

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

inconsistent in both significance and directionality (Ozcan and Gunduz, 2014). Someresearchers claim that the relationship between political connections and businessperformance is both positive and significant (Ozcan and Gunduz, 2014; Faccio, 2006);others claim no relationship (Blumentrit, 2003); while some even claim a negativerelationship (Boubakri et al., 2008). In the USA, Timothy Geithner-related firmsexperienced abnormal returns (Acemoglu et al., 2010).

The inconsistencies in the results between political connections and businessperformance maybe due to institutional differences. Political connections tied to aparticular regime may experience problems during a regime change. Johnson andMitton (2003) showed how political connection to Prime Minister Mahathir Mohamadhad significant, positive impact on stock market performance during the Asian financialcrisis. Misfortune can follow a political regime change, as seen anecdotally in manylarge capital-intensive, resource-based industry deals. Ties to political regimes in Asiaduring the financial crisis proved to be politically risky (Alon and Kellerman, 2001).Political connections matter more when power is concentrated and in non-democraticregimes (Ozcan and Gunduz, 2014).

Political connections can be seen from the point of view of RDT. RDT suggests thatas firms attempt to reduce uncertainty and interdependence from government (andother key resources on which they depend), the firm will help re-create its environmentthrough political action (Pfeffer and Salancik, 1978). Research has shown that firms aremore likely to engage in political action, such as making political connections toinfluence policy, when firms are dependent on the government (Meznar and Nigh, 1995;Birnbaum, 1985). Industries that depend on the government or are more sensitive topolitical action and regulation are likely to invest in political action and connections.Mullery et al. (1995) found a similar pattern of political action by firms facingcomparable regulatory and political environment. This suggests that there might beisomorphic pressure for firms to react in similar ways (DiMaggio and Powell, 1983).

In emerging markets in particular, the government is a key resource to the firm, bothdirectly through funding, buying or facilitation the sales, or, indirectly, throughpreferential treatment and regulations. Firms which are dependent on government as akey resource will invest in political connections. While the personal connections withpolitical leaders as a salient social capital are critical for firms even in developedcountries (Sun et al., 2012; Siegel, 2007), they are almost paramount in emergingeconomies (Wu et al., 2013). Pfeffer and Salancik (1978) suggested that companiespurposefully appoint directors who have the ability to manage the politicalinterdependencies.

In China, guanxior personal connection plays important roles in coordinating andregulating economic transactions (Xin and Pearce, 1996) and therefore is regarded as atype of an informal institution. Much has been written on the role of guanxi in thepromotion of business in China, where the government may exert much influence in keysectors (Alon, 2003a, 2003b). Among various types of personal connections, politicalconnections are critical for firms, in that governments still hold considerable power overthe resource allocations and economic development. Despite insufficient formalinstitutions or institutional void, firms with various political connections are able toconduct business smoothly by resorting to the supports from governments via politicalconnections. Lin et al. (2014) found, from a sample of 105 Chinese new ventures, thatpolitical ties were positively related to performance, while business ties were not.

7

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

The social connections with political leaders or political connections function as agreat conduit to exchange information and to promote the mutual understanding of eachother, leading to emotional attachments between firms and political leaders. With theinformation symmetry and emotional attachment, political leaders are more aware offirm’s needs and are more confident in their future, thereby more willing to support thesefirms by financial or other possible means. Arguably, firms with more extensivepolitical connections are more likely to gain resources from governments (Li and Zhang,2007), reducing the dependence on other resources.

Previous studies on political connections reviewed above suggest that the causalpattern may not be simple and direct and dependent on “institutional voids”. Given thatinstitutions play a significant role in the promotion of political connections, we suggestthat political connection moderates the impact of financial marketization. Financialliberalization may not have the same strong positive impact on firms that are alreadyconnected. Their connections may act as an obstacle to desired results from formalpolicy action. The existence of political connections may directly decrease the need forcorporate venturing. Investments in political connections may substitute the need forsome investments in new businesses. Firms with political connections with access tocapital from informal institutions may not need formal market institutions. If cheap orfree capital is available through guanxi, why should the firm pay “market prices”. Theimpact of marketization of financial institutions on corporate venturing is likely to belower when political connections exist. Therefore, in the case of corporate venturing, theexistence of political connections decreases the importance of formal financialinstitutions and reduces their impacts on corporate venturing activities by firms.Accordingly, we propose:

H2. Political connections will negatively moderate the relationship between themarketization of financial institutions and corporate venturing

2.3 Organizational slackAs customers are the ultimate resource, they generate profits which improve thefinancial condition of the company, creating organizational slack. In a sense, profit fromoperations can finance new venture creation. Organizational slack is defined as a pool ofresources in excess of the necessity of current organizational operations (Nohria andGulati, 1996). Organizational slack refers to the resources in excess of the necessitiesrequired by daily operations of a firm (Bourgeois, 1981). In other words, organizationalslack is the resource controlled by a firm but is not put into firm operations (Dimick andMurray, 1978).

As an important organizational variable, organizational slack attracted numerousscholarly investigations. Prior research examines the influence of organizational slackon a variety of firm outcomes, such as firm financial performance (George, 2005),innovation (Singh, 1986) and internationalization (Lin, 2014) and so on. Overall, priorstudies treat organizational slack as an independent variable and maintain that it isrelevant to numerous organizational outcomes.

Organizational slack affects corporate venturing directly, both positively andnegatively. First, as Hambrick and Snow (1977) and Bourgeois (1981) suggest, thepresence of organizational slack provides firms with the capability to experiment withnew strategies such as launching new products, entering new markets and so on(Hambrick and Snow, 1977; Bourgeois, 1981). Not surprisingly, organizational slack is

JEEE7,1

8

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

able to fuel corporate venturing activities by supplying resources needed in establishingor acquiring new businesses or investing in nascent firms (Yiu and Lau, 2008). As aresult, firms with sufficient slack resources depend less on external financing inimplementing corporate venturing strategies and, in turn, the institutions governing theavailability of external financing are not able to exert much influence on their decisionson corporate venturing strategy. On the other hand, some researchers conjecture that themanagement is likely to become over optimistic about their future with redundantresources (George, 2005). This over-optimism about the future and desire to limit riskamong the top managers may lead to less corporate venturing, and the overall,long-term deterioration of the firm’s competitive positioning. As such, the direct impactof organizational slack on corporate venturing can be either positive or negative.

More recently, organizational slack was treated as a contingent variable which is ableto moderate a variety of relationships, such as the link between technological diversityand innovation performance (Huang and Chen, 2010), as well as the link betweencreative workforce density and innovation performance (Chen and Huang, 2010).Following these studies, we maintain that organizational slack can isolate the firm fromthe external fluctuations in the environment, including the political and institutionalenvironment. Firms that do not need external financing may not be as impacted byfinancial reforms of the banks, and the effect of the policy will, thus, be less salient. Assuch, we predict that:

H3. Organizational slack will negatively moderate the relationship between themarketization of financial institutions and corporate venturing

3. Method3.1 DataTo ensure the internal validity and mitigate the unobservable heterogeneity problem,we use sample firms from a single industry, the pharmaceutical industry, in China.Corporate venturing is common in both China and this industry, in particular. Thisindustry in China is also highly regulated, requiring political action as suggested byRDT. In China’s pharmaceutical industry, legislative compliance requirements arestringent, highly politicized and subject to a plethora of product, manufacturing anddistribution restrictions (IBIS World Industry Report, 2014). Government in China’spharmaceutical industry, thus, has an influential role on the venturing and success offirms in the sector.

To mitigate the threat of unobservable heterogeneity, as well as confounding effects ofindustry-level variables, we choose firms from a single industry to increase the internalvalidity. Our sample for this study consists of listed firms from the pharmaceutical industryin China. As a function of China’s rapid economic growth, the country’s pharmaceuticalindustry has also experienced a surge over the past decade.

From 2001 to 2008, the Chinese pharmaceutical industry grew at a compoundedannual growth rate of 20 per cent (Li et al., 2009). It is among the first to implement theopening-up policy and attracted foreign direct investments from multinational firms.Currently, top 20 pharmaceutical multinational firms all set up their joint ventures orsubsidiaries in China, resulting in increased domestic competitions in this industry. Togain competitive advantages, domestic pharmaceutical firms, in particular listedpharmaceutical firms, in China implemented corporate venturing strategies by settingup new production lines or investing in new drug development projects initiated by

9

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

research institutions (White and Liu, 2001), as well as acquiring external pharmaceuticalfirms. For instance, Renhe Pharmacy (stock code: 000650) acquired 100 per cent stockshare of Jiangxi Yuxin Pharmaceutical Limited through one of its subsidiaries inSeptember 2013. The widely spread corporate venturing activities in China’spharmaceutical industry provide us with an ideal setting to investigate the corporateventuring phenomenon.

Moreover, as the largest emerging economy, China features significant regionaldifferences in terms of the cultural and social background and economicdevelopment, as well as institutional framework (Atsmon et al., 2011; Kwon, 2012).In particular, the development of institutional framework is uneven among regionsin China due to heterogeneous historical, social and economic backgrounds.Meanwhile, as a transition economy as well, China still has various types ofstate-owned enterprises in parallel with the rapid development of domestic privatefirms (i.e. POEs). Therefore, using Chinese firms located in various regions withheterogeneous institutional backgrounds and highly diverse political connections isappropriate for examining the effects of institutions, political connections and theirinteractions on corporate venturing.

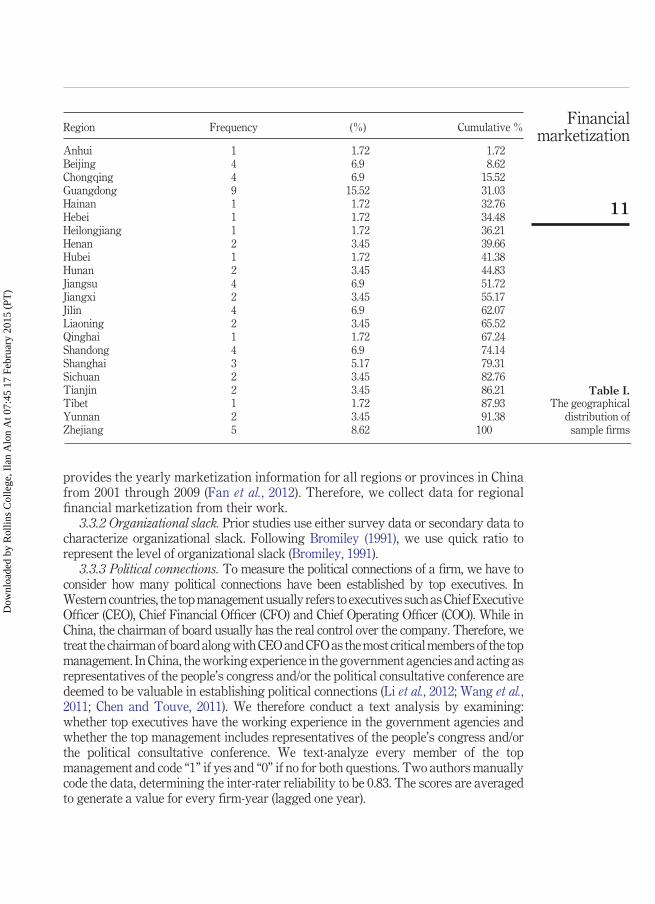

We initially find 84 firms in the pharmaceutical industry that are listed on theShanghai and Shenzhen Stock Exchange according to the industry category issued byChina Securities Regulatory Commission in 2001. We primarily collect data from theCSMAR Solution, a frequently used database developed and maintained by the GTA ITCo., Ltd. In addition, we use annual reports issued by listed companies, official Websites, as well as other public information, to supplement the data draw from the CSMARSolution. We focus on the time period of 2001-2009, in that the data for all variablesduring this period could be gathered comprehensively. We exclude some listedcompanies that are not able to provide comprehensive information from 2001 through2009, leading to a sample of 58 firms with 522 observations. The remaining sample firmsare based in 22 provinces in China, as shown in the Table I.

3.2 Dependent variable3.2.1 Corporate venturing. We code the dependent variable manually by reading theannouncements by listed companies every year regarding corporate venturingactivities. In a particular year, we code “1” for a company if it has an announcementconcerning establishing a subsidiary and/or investing in nascent firms. We code “0” ifsuch an announcement is absent. We find the corporate venturing is not a yearlyhappened phenomenon. Instead, most of the sample firms announce a corporateventuring event every 2-3 years. Accordingly, the dependent variable is a non-normaldistributed variable with many “0” values.

3.3 Independent and moderating variables3.3.1 Financial marketization. As a key component of regional institution framework,regional financial marketization represents the competition intensity of financialsector within a specific region in China and the extent to which the bank loans areallocated according to the credits or merits of borrowers. The higher level offinancial marketization, the more intense of competitions among financialinstitutions within the region and loans or credits are more likely allocated toborrowers with higher efficiency. The Marketization Index by Fan et al. (2012)

JEEE7,1

10

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

provides the yearly marketization information for all regions or provinces in Chinafrom 2001 through 2009 (Fan et al., 2012). Therefore, we collect data for regionalfinancial marketization from their work.

3.3.2 Organizational slack. Prior studies use either survey data or secondary data tocharacterize organizational slack. Following Bromiley (1991), we use quick ratio torepresent the level of organizational slack (Bromiley, 1991).

3.3.3 Political connections. To measure the political connections of a firm, we have toconsider how many political connections have been established by top executives. InWestern countries, the top management usually refers to executives such as Chief ExecutiveOfficer (CEO), Chief Financial Officer (CFO) and Chief Operating Officer (COO). While inChina, the chairman of board usually has the real control over the company. Therefore, wetreat the chairman of board along with CEO and CFO as the most critical members of the topmanagement. In China, the working experience in the government agencies and acting asrepresentatives of the people’s congress and/or the political consultative conference aredeemed to be valuable in establishing political connections (Li et al., 2012; Wang et al.,2011; Chen and Touve, 2011). We therefore conduct a text analysis by examining:whether top executives have the working experience in the government agencies andwhether the top management includes representatives of the people’s congress and/orthe political consultative conference. We text-analyze every member of the topmanagement and code “1” if yes and “0” if no for both questions. Two authors manuallycode the data, determining the inter-rater reliability to be 0.83. The scores are averagedto generate a value for every firm-year (lagged one year).

Table I.The geographical

distribution ofsample firms

Region Frequency (%) Cumulative %

Anhui 1 1.72 1.72Beijing 4 6.9 8.62Chongqing 4 6.9 15.52Guangdong 9 15.52 31.03Hainan 1 1.72 32.76Hebei 1 1.72 34.48Heilongjiang 1 1.72 36.21Henan 2 3.45 39.66Hubei 1 1.72 41.38Hunan 2 3.45 44.83Jiangsu 4 6.9 51.72Jiangxi 2 3.45 55.17Jilin 4 6.9 62.07Liaoning 2 3.45 65.52Qinghai 1 1.72 67.24Shandong 4 6.9 74.14Shanghai 3 5.17 79.31Sichuan 2 3.45 82.76Tianjin 2 3.45 86.21Tibet 1 1.72 87.93Yunnan 2 3.45 91.38Zhejiang 5 8.62 100

11

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

3.4 Control variables3.4.1 Firm age. Prior research claims that older firms will be less likely to engage incorporate venturing activities due to organizational inertia (Burgers et al., 2009). As aresult, we control for the firm age in the regression model.

3.4.2 Firm scale. Prior research shows that the firm size has negative effects oncorporate entrepreneurial intensity (Zahra, 1996) and thus we control for it by using thenatural logarithm of total sales, lagged one year.

3.4.3 Ownership types. Following Delios et al. (2006), we divide firm ownership typesinto two categories, namely, state-owned and private-owned, by identifying the ultimateownership identities of sample firms and using one dummy variable “state-owned” tocontrol for differentiate ownership identities of sample firms.

3.4.4 Past performance. Past performance is also controlled for because when a firmperforms well, it tends to engage in entrepreneurial activities with increased slackresources (Zahra, 1996). Firm performance is an important antecedent to corporateventuring and is likely to affect the intensity of corporate venturing by firms (Zahra andHayton, 2008). Accordingly, we include a control variable, past performance, in theregression model. Following Zahra (1996), we select the return on assets (ROA) laggedone year as the indicator of past firm performance.

3.4.5 Year effects. Our sample period is 2000 through 2009. To control for potentialtemporal effects, we included a dummy variable for each year (Certo and Semadeni,2006).

4. ResultsBecause the data for this study were organized into a pooled cross-sectional time seriesdataset, with multiple observations per firm and over nine years, we usedcross-sectional time series regression analyses to estimate our models. Results from theHausman (1978) specification test indicates that the random-effects model is appropriatefor our data. Moreover, the dependent variable is dichotomous (as described above) andtherefore we used the random effects logistic regression technique in Stata (“xtlogit,”with clustering on a firm) to estimate all models (Certo and Semadeni, 2006). To checkthe robustness of the estimation, we also used the random-effects tobit regressiontechnique in Stata (“xttobit,” with clustering on a firm)[1]. The models have explanatorypower, as measured by the log likelihood and Weld chi-square and robustness withrespect to alternative model and statistical method specifications.

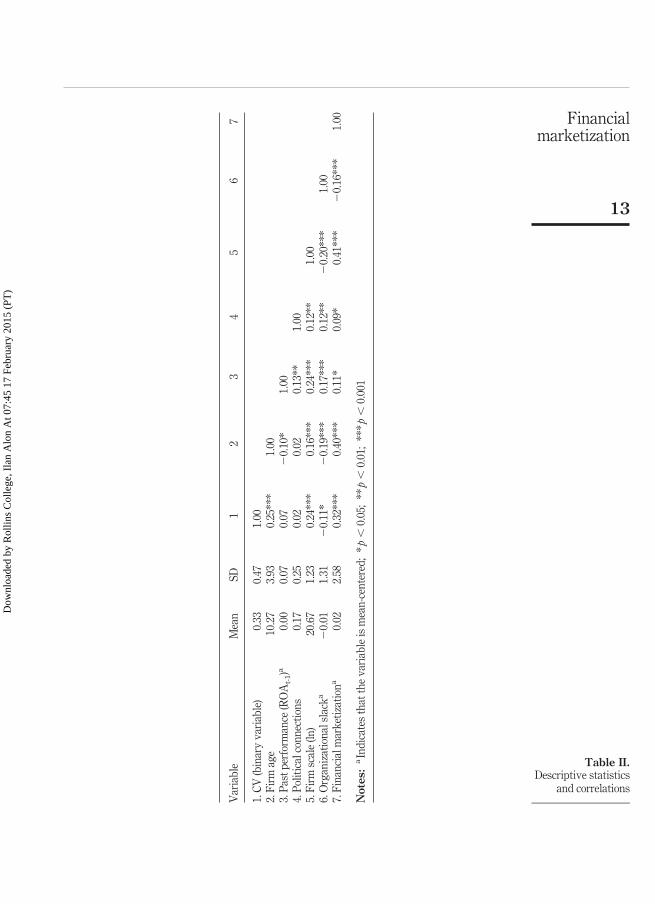

Table II presents the descriptive statistics and correlations for the variables in thisstudy. The correlations among independent variables are all below 0.45, suggesting thatthe multicollinearity is not problematic.

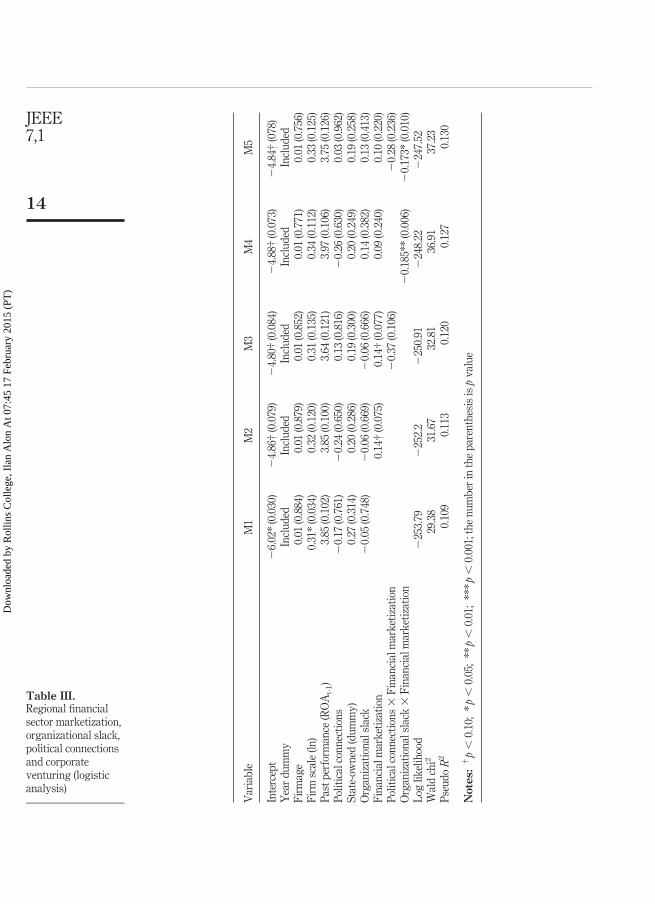

We run five model permutations (M1-M5). M1 is the base model including controlvariables, but excluding our hypothesized relations. M2 introduces the main effect:financial marketization. M3 adds the moderating impact of political connections. M4replaces the moderating impact of political connections with organizational slack.Finally, M5 presents the full model with all variables, control, main effect andmoderating. Table III presents the random-effects logistic regression results for theanalyses in which we test the influence of regional marketization of the financial marketand organizational slack, as well as political connections on corporate venturingactivities (H1-H3).

JEEE7,1

12

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

Table II.Descriptive statistics

and correlations

Var

iabl

eM

ean

SD1

23

45

67

1.CV

(bin

ary

vari

able

)0.

330.

471.

002.

Firm

age

10.2

73.

930.

25**

*1.

003.

Past

perf

orm

ance

(RO

At-

1)a

0.00

0.07

0.07

�0.

10*

1.00

4.Po

litic

alco

nnec

tions

0.17

0.25

0.02

0.02

0.13

**1.

005.

Firm

scal

e(ln

)20

.67

1.23

0.24

***

0.16

***

0.24

***

0.12

**1.

006.

Org

aniz

atio

nals

lack

a�

0.01

1.31

�0.

11*

�0.

19**

*0.

17**

*0.

12**

�0.

20**

*1.

007.

Fina

ncia

lmar

ketiz

atio

na0.

022.

580.

32**

*0.

40**

*0.

11*

0.09

*0.

41**

*�

0.16

***

1.00

Not

es:

aIn

dica

tes

that

the

vari

able

ism

ean-

cent

ered

;*p

�0.

05;

**p

�0.

01;

***p

�0.

001

13

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

Table III.Regional financialsector marketization,organizational slack,political connectionsand corporateventuring (logisticanalysis)

Var

iabl

eM

1M

2M

3M

4M

5

Inte

rcep

t�

6.02

*(0

.030

)�

4.86

†(0

.079

)�

4.80

†(0

.084

)�

4.88

†(0

.073

)�

4.84

†(0

78)

Yea

rdu

mm

yIn

clud

edIn

clud

edIn

clud

edIn

clud

edIn

clud

edFi

rmag

e0.

01(0

.884

)0.

01(0

.879

)0.

01(0

.852

)0.

01(0

.771

)0.

01(0

.756

)Fi

rmsc

ale

(ln)

0.31

*(0

.034

)0.

32(0

.120

)0.

31(0

.135

)0.

34(0

.112

)0.

33(0

.125

)Pa

stpe

rfor

man

ce(R

OA

t-1)

3.85

(0.1

02)

3.85

(0.1

00)

3.64

(0.1

21)

3.97

(0.1

06)

3.75

(0.1

26)

Polit

ical

conn

ectio

ns�

0.17

(0.7

61)

�0.

24(0

.650

)0.

13(0

.816

)�

0.26

(0.6

30)

0.03

(0.9

62)

Stat

e-ow

ned

(dum

my)

0.27

(0.3

14)

0.20

(0.2

86)

0.19

(0.3

00)

0.20

(0.2

49)

0.19

(0.2

58)

Org

aniz

atio

nals

lack

�0.

05(0

.748

)�

0.06

(0.6

69)

�0.

06(0

.666

)0.

14(0

.382

)0.

13(0

.413

)Fi

nanc

ialm

arke

tizat

ion

0.14

†(0

.075

)0.

14†

(0.0

77)

0.09

(0.2

40)

0.10

(0.2

20)

Polit

ical

conn

ectio

ns�

Fina

ncia

lmar

ketiz

atio

n�

0.37

(0.1

06)

�0.

28(0

.236

)O

rgan

izat

iona

lsla

ck�

Fina

ncia

lmar

ketiz

atio

n�

0.18

5**

(0.0

06)

�0.

173*

(0.0

10)

Log

likel

ihoo

d�

253.

79�

252.

2�

250.

91�

248.

22�

247.

52W

ald

chi2

29.3

831

.67

32.8

136

.91

37.2

3Ps

eudo

R2

0.10

90.

113

0.12

00.

127

0.13

0

Not

es:

†p

�0.

10;

*p�

0.05

;**

p�

0.01

;**

*p�

0.00

1;th

enu

mbe

rin

the

pare

nthe

sis

isp

valu

e

JEEE7,1

14

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

H1. Suggests that the regional financial marketization (institution) in which firmsare embedded in has positive effects on the corporate venturing by firms.Controlling for the year effects, firm age, scale, political connections,organizational slack, as well as past performance by firms, we find in theModels 2 and 3 of Table III that the financial marketization (institution) ispositively and significantly associated with corporate venturing (coeff � 0.14,p � 0.10). Thus, H1 is supported.

H2. Suggests that firms with more political connections are less likely to engage incorporate venturing activities. In Model 3 of Table III, we find that whilepolitical connections predictably negatively moderates the relationshipbetween financial marketization (institution) and corporate venturing, thecoefficient is not significant at 0.10 level (coefficient � �0.37, p � 0.10).Therefore, H2 is not supported. Political connections did not have a consistentor significant direct effect on corporate venturing either.

H3. Suggests that firms with more organizational slack are less likely to engage incorporate venturing activities. In Models 4 and 5 of Table III, we find thatorganizational slack negatively and significantly moderates the relationshipbetween financial marketization (institution) and corporate venturing(coefficient � �0.19, p � 0.01). Therefore, H3 is supported. It should be notedthat when organizational slack is present and interactive, it nullifies thesignificance of financial marketization.

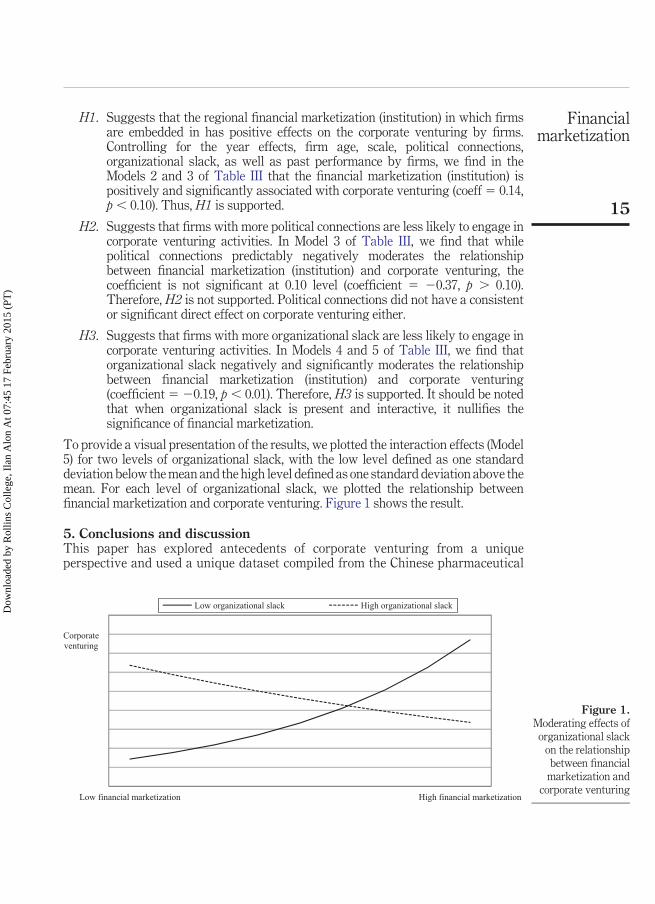

To provide a visual presentation of the results, we plotted the interaction effects (Model5) for two levels of organizational slack, with the low level defined as one standarddeviation below the mean and the high level defined as one standard deviation above themean. For each level of organizational slack, we plotted the relationship betweenfinancial marketization and corporate venturing. Figure 1 shows the result.

5. Conclusions and discussionThis paper has explored antecedents of corporate venturing from a uniqueperspective and used a unique dataset compiled from the Chinese pharmaceutical

noitazitekramlaicnanifhgiHnoitazitekramlaicnanifwoL

Corporate venturing

Low organizational slack High organizational slack

Figure 1.Moderating effects oforganizational slack

on the relationshipbetween financial

marketization andcorporate venturing

15

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

industry. We hypothesized that organizational slack (internal financial resource)and political connections will dampen the positive impact of banking financialreform on business venturing. In a sense, we suggested that financial reform’simpact on corporate venturing is undermined by political connections and the firm’sown financial success.

Our hypotheses were partially confirmed, and the model as a whole is significant.The main effect hypothesis relating financial marketization to corporate venturing wassignificant. We find that the occurrence of corporate venturing activities by firms variesacross different levels of financial marketization, and this relationship weakens with themoderating effect of organizational.

5.1 Theoretical contributionsThe pronounced impact from the institutions in which a firm is embedded in oncorporate venturing is substantiated within a large and complex emerging economysetting. We develop a model of corporate venturing using both institution theory andRDT, using both environmental- (financial marketization) and company-specific(political connections and organizational slack) variables. The framework, as a whole,performs well statistically, as evidenced by the log likelihood and Wald chi matrices. Bylooking at provincial data, we make a contribution to the study of intra-nationalinstitutional influences on business practices. The interaction effects highlight that theextent to which institutions affect firm strategic choice is hinged at least in part on firmcontextual factors. These results respond to the call made by Powell (1996) that we haveto tackle more difficult questions of how and when institutions matter and in what waysso as to advance institutional theory (Powell, 1996). The revealed antecedents can beused in future studies and expanded upon by examining different regions, industriesand measures.

From RDT point of view, our study suggests that political connections do notco-determine with institutions the firm-specific business venturing. In other words,whether a firm has political connections does not affect its new venture creation, directlyor indirectly. Firm venturing activities are more dependent on the institutionalenvironment than on its own political connections. Organizational slack, on the otherhand, co-determines venturing. Firms using internal resources depend less oninstitutions. This may suggest that firms may seek to be less reliant on the externalenvironment and more self-reliant on its own financial ability. If financial limitations arenot a concern for a firm, government financial liberalization policy will not have itsintended effect on business creation and renewal.

5.2 Policy implicationsGovernments in emerging markets often attempt to develop market-supportinginstitutions for economic development. As corporate venturing is an element ofeconomic renewal and growth, policymakers have an interest to stimulate it.

As our results show, the financial institutions play pivotal roles in determining theavailability and cost of external financing and therefore are driving forces of corporateventuring. Consequently, local governments need to make efforts to building up morefavorable financial institutions so as to promote the venturing activities by firms withintheir jurisdictions. Our research suggests that the marketization of financial institutionsis largely an effective tool. However, these policy actions can be mitigated and nullified

JEEE7,1

16

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

if the company has other means to obtain power, resources and financial means. Whilewe hypothesized on two such organizational variables (political connections andorganizational slack), only one has shown to be statistically significant: organizationalslack. Our empirical results indicate that organizational slack is indeed an importantfirm-level contingent variable that merits scholarly attentions. For government policy tobe effective, organizational slack should be low. This may suggest that liberalizationmay be most effective in financially restrictive industries, where markets can fill theinstitutional void.

5.3 Managerial implicationsThis paper also has managerial implications. With the implementation of reform andopening-up policy since 1978, China achieved an average annual growth rate ofapproximately 10 per cent in terms of gross domestic product and became thesecond-largest economy in the world, acting as the growth engine of the world over thepast three decades. Nevertheless, the growth achieved was primarily in fixed assetsinvestment and exports. Both methods are not sustainable with the financial and debtcrisis, which, since 2008, affected the world. China’s economy must rebalance byreducing its reliance on investment and increasing consumption (Huang, 2013). As aresult, Chinese firms have to make efforts to adapt to such transformation by catering todomestic demand. One way to achieve this is through corporate venturing, wherebyfirms set up new businesses and/or invest in nascent firms to tap the potential of newmarket demands.

As for firms with limited organizational slack and/or political connections,location decisions should be made cautiously if they were intended to engage incorporate venturing by securing external financing. Firms have to make sure thatfinancial institutions are favorable by careful due diligent investigations. Drawingon the data from China’s pharmaceutical industry, we find that firms do respond tofinancial marketization in terms of corporate venturing and the effects ofinstitutions on corporate venturing do vary across firms with different level oforganizational slack.

5.4 Limitations and future researchThis study is specific for a single industry (pharmaceutical) and a single emergingmarket (China), and the generalizability is thus limited. Future studies may extend thisarticle to include more industries and countries and, thus, increase the generalizability.It would also allow for a test of international institutional differences. Studies that cancombine both intra-national and international institutions and show their interactionswill greatly enhance our understanding of institutional impacts.

Business venturing is only a single performance variable and the focus of thisinvestigation. Financial performance, abnormal returns, sustainability and others maybe explored in future research. While various performance variables may be related,their antecedents and impact may be different.

While the political connections variable showed the hypothesized direction, thevariable was not significant. Previous research suggests that in emerging economysetting, political connections as informal institution substitutes formal institutions(Zhou, 2013). Our results suggest that formal rules may, in fact, substitute informalpractices. In other words, Chinese do not necessarily like guanxi, but have to use it in the

17

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

absence of formal institutions. When these institutions become available, the role ofpolitical connections may not be as significant. Future research should attempt differentmeasures of political connections, along with their impact on different organizationaloutcomes (sales, internationalization, profits, etc.).

Note1. Similar results, available upon request.

ReferencesAcemoglu, D., Johnson, S., Kermani, A., Kwak, J. and Mitton, T. (2010), The Value of Political

Connections in the United States, National Bureau of Economic Research, Cambridge, MA.Alon, I. (2003a), Chinese Culture, Organizational Behavior and International Business

Management, Praeger Publishers, Westport, CT.Alon, I. (2003b), Chinese Economic Transition and International Marketing Strategy, Praeger

Publishers, Westport, CT.Alon, I. and Kellerman, E.A. (2001), “How cultural factors led to risky antecedent market

conditions and the 1997 Asian economic crisis”, in Jay Choi, J. (Ed.), Asian Financial CrisisFinancial, Structural and International Dimensions, Emerald Group Publishing,pp. 439-457.

Atsmon, Y., Kertesz, A. and Vittal, I. (2011), “Is your emerging-market strategy local enough?”,McKinsey Quarterly, April, pp. 50-61.

Birnbaum, P.H. (1985), “Political strategies of regulated organizations as functions of context andfear”, Strategic Management Journal, Vol. 6 No. 2, pp. 135-150.

Boubakri, N., Cosset, J.-C. and Saffar, W. (2008), “Politically connected newly privatized firms”,Journal of Corporate Finance, Vol. 14 No. 5, pp. 654-673.

Bourgeois, L. (1981), “On the measurement of organizational slack”, Academy of ManagementReview, Vol. 6 No. 1, pp. 29-39.

Bromiley, P. (1991), “Testing a causal model of corporate risk taking and performance”, Academyof Management Journal, Vol. 34 No. 1, pp. 37-59.

Burgelman, R.A. and Valikangas, L. (2005), “Managing internal corporate venturing cycles”, MITSloan Management Review, Vol. 46 No. 4, pp. 26-34.

Burgers, J.H., Jansen, J.J., Van den Bosch, F.A. and Volberda, H.W. (2009), “Structuraldifferentiation and corporate venturing: the moderating role of formal and informalintegration mechanisms”, Journal of Business Venturing, Vol. 24 No. 3, pp. 206-220.

Certo, S.T. and Semadeni, M. (2006), “Strategy research and panel data: evidence andimplications”, Journal of Management, Vol. 32 No. 3, pp. 449-471.

Chan, C.M., Makino, S. and Isobe, T. (2010), “Does subnational region matter? Foreign affiliateperformance in the United States and China”, Strategic Management Journal, Vol. 31 No. 11,pp. 1226-1243.

Chen, C.-J. and Huang, Y.-F. (2010), “Creative workforce density, organizational slack andinnovation performance”, Journal of Business Research, Vol. 63 No. 4, pp. 411-417.

Chen, Y. and Touve, D. (2011), “Conformity, political participation and economic rewards: the caseof Chinese private entrepreneurs”, Asia Pacific Journal of Management, Vol. 28 No. 3,pp. 529-553.

Chiu, Y.C., Tseng, W.K. and Liaw, Y.C. (2012), “Firm resources and corporate venturinginvestment”, Canadian Journal of Administrative Sciences, Vol. 29 No. 1, pp. 40-49.

JEEE7,1

18

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

Covin, J.G. and Miles, M.P. (2007), “Strategic use of corporate venturing”, EntrepreneurshipTheory and Practice, Vol. 31 No. 2, pp. 183-207.

Delios, A., Wu, Z.J. and Zhou, N. (2006), “A new perspective on ownership identities in China’slisted companies”, Management and Organization Review, Vol. 2 No. 3, pp. 319-343.

DiMaggio, P.L. and Powell, W.W. (1983), “The iron cage revisited: institutional isomorphism andcollective rationality in organizational fields”, American Sociological Review, Vol. 48 No. 2,pp. 147-160.

Dimick, D.E. and Murray, V.V. (1978), “Correlates of substantive policy decisions in organizations:the case of human resource management”, Academy of Management Journal, Vol. 21 No. 4,pp. 611-623.

Faccio, M. (2006), “Politically connected firms”, American Economic Review, Vol. 96 No. 1,pp. 369-386.

Fan, G., Wang, X. and Zhu, H. (2012), NERI INDEX of Marketization of China’s Provinces 2011Report, Economic Science Press, Beijing.

George, G. (2005), “Slack resources and the performance of privately held firms”, Academy ofManagement Journal, Vol. 48 No. 4, pp. 661-676.

Goldman, E., Rocholl, J. and So, J. (2009), “Do politically connected boards affect firms value?”,Review of Financial Studies, Vol. 22 No. 6, pp. 2331-2360.

Hambrick, D.C. and Snow, C.C. (1977), “A contextual model of strategic decision making inorganizations”, Academy of Management 1977 Proceedings of the InternationalConference, Kissimmee, FL, pp. 109-112.

Hausman, J.A. (1978), “Specification tests in econometrics”, Econometrica: Journal of theEconometric Society, Vol. 46 No. 6, pp. 1251-1271.

Hillman, A.J., Withers, M.C. and Collins, B.J. (2009), “Resource dependence theory: a review”,Journal of Management, Vol. 35 No. 6, pp. 1404-1427.

Huang, Y. (2013), “China’s great rebalancing: promise and peril”, McKinsey Quarterly, June,pp. 34-36.

Huang, Y.-F. and Chen, C.-J. (2010), “The impact of technological diversity and organizationalslack on innovation”, Technovation, Vol. 30 No. 7, pp. 420-428.

IBIS World Industry Report (2014), “Pharmaceutical Manufacturing in China, IBIS WorldIndustry Report”, pp. 1-38.

Johnson, S. and Mitton, T. (2003), “Cronyism and capital controls: evidence from Malaysia”,Journal of Financial Economics, Vol. 67 No. 2, pp. 351-382.

Khanna, T. and Palepu, K. (1997), “Why focused strategies may be wrong for emerging markets”,Harvard Business Review, Vol. 75 No. 4, pp. 41-48.

Kwon, J.-W. (2012), “Does China have more than one culture?”, Asia Pacific Journal ofManagement, Vol. 29 No. 1, pp. 79-102.

Lamoreaux, N. (1994), Insider Lending: Banks, Personal Connections and Economic Developmentin Industrial New England, Cambridge University Press, New York, NY.

Li, B., Wu, S. and Lui, C. (2009), China Pharmaceuticals: Time to Look at the Neglected China DrugSector, Morgan Stanley Research, New York, NY.

Li, H. and Zhang, Y. (2007), “The role of managers’ political networking and functional experiencein new venture performance: evidence from China’s transition economy”, StrategicManagement Journal, Vol. 28 No. 8, pp. 791-804.

19

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

Li, W., He, A., Lan, H. and Yiu, D. (2012), “Political connections and corporate diversification inemerging economies: evidence from China”, Asia Pacific Journal of Management, Vol. 29No. 3, pp. 799-818.

Lin, W.-T. (2014), “How do managers decide on internationalization processes? The role oforganizational slack and performance feedback”, Journal of World Business, Vol. 49 No. 3,pp. 396-408.

Lin, Y.-H., Chen, C.-J. and Lin, B.-W. (2014), “The roles of political and business ties in newventures: evidence from China”, Asian Business & Management, Vol. 13 No. 5, pp. 411-440.

Makino, S., Isobe, T. and Chan, C.M. (2004), “Does country matter?”, Strategic ManagementJournal, Vol. 25 No. 10, pp. 1027-1043.

Meyer, K.E. and Nguyen, H.V. (2005), “Foreign investment strategies and sub-national institutionsin emerging markets: evidence from Vietnam”, Journal of Management Studies, Vol. 42No. 1, pp. 63-93.

Meznar, M.B. and Nigh, D. (1995), “Buffer or bridge? Environmental and organizationaldeterminants of public affairs activities in American firms”, Academy of ManagementJournal, Vol. 38 No. 4, pp. 975-996.

Mullery, C.B., Brenner, S.N. and Perrin, N.A. (1995), “A structural analysis of corporate politicalactivity an application of MDS to the study of intercorporate relations”, Business & Society,Vol. 34 No. 2, pp. 147-170.

Narayanan, V., Yang, Y. and Zahra, S.A. (2009), “Corporate venturing and value creation: a reviewand proposed framework”, Research Policy, Vol. 38 No. 1, pp. 58-76.

Nguyen, T.V., Le, N.T. and Bryant, S.E. (2013), “Sub-national institutions, firm strategies and firmperformance: a multilevel study of private manufacturing firms in Vietnam”, Journal ofWorld Business, Vol. 48 No. 1, pp. 68-76.

Nohria, N. and Gulati, R. (1996), “Is slack good or bad for innovation?”, Academy of ManagementJournal, Vol. 39 No. 5, pp. 1245-1264.

North, D.C. (1990), Institutions, Institutional Change and Economic Performance, CambridgeUniversity Press, New York, NY.

Ozcan, G. and Gunduz, U. (2014), “Political connectedness and business performance: evidencefrom Turkish industry rankings”, Business and Politics, Vol. 16 No. 4, pp. 1-33.

Peng, M.W. (2002), “Towards an institution-based view of business strategy”, Asia Pacific Journalof Management, Vol. 19 Nos 2/3, pp. 251-267.

Peng, M.W. and Luo, Y. (2000), “Managerial ties and firm performance in a transition economy: thenature of a micro-macro link”, Academy of Management Journal, Vol. 4 No. 3, pp. 486-501.

Pfeffer, J. and Salancik, G.R. (1978), The External Control of Organizations: A ResourceDependence Perspective, Harper and Row, New York, NY.

Powell, W.W. (1996), “Commentary: on the nature of institutional embeddedness: labels vsexplanation”, Advances in Strategic Management, Vol. 13, pp. 293-302.

Sharma, P. and Chrisman, J. (1999), “Toward a reconciliation of the definitional issues in the fieldof corporate entrepreneurship”, Entrepreneurship: Theory and Practice, Vol. 23, pp. 11-27.

Siegel, J. (2007), “Contingent political capital and international alliances: evidence from SouthKorea”, Administrative Science Quarterly, Vol. 52 No. 4, pp. 621-666.

Singh, J.V. (1986), “Performance, slack and risk taking in organizational decision making”,Academy of Management Journal, Vol. 29 No. 3, pp. 562-585.

Sun, P., Mellahi, K. and Wright, M. (2012), “The contingent value of corporate political ties”,Academy of Management Perspectives, Vol. 26 No. 3, pp. 68-82.

JEEE7,1

20

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

Thornhill, S. and Amit, R. (2001), “A dynamic perspective of internal fit in corporate venturing”,Journal of Business Venturing, Vol. 16 No. 1, pp. 25-50.

Wang, H., Feng, J., Liu, X. and Zhang, R. (2011), “What is the benefit of TMT’s governmentalexperience to private-owned enterprises? Evidence from China”, Asia Pacific Journal ofManagement, Vol. 28 No. 3, pp. 555-572.

White, S. and Liu, X. (2001), “Transition trajectories for market structure and firm strategy inChina”, Journal of Management Studies, Vol. 38 No. 1, pp. 103-124.

Wu, J.F., Li, S.L. and Li, Z.J. (2013), “The contingent value of CEO political connections: a study onIPO performance in China”, Asia Pacific Journal of Management, Vol. 30 No. 4,pp. 1087-1114.

Xin, K.K. and Pearce, J.L. (1996), “Guanxi: connections as substitutes for formal institutionalsupport”, Academy of Management Journal, Vol. 39 No. 6, pp. 1641-1658.

Yang, X. and Stoltenberg, C.D. (2014), “A review of institutional influences on the rise of made inChina multinationals”, International Journal of Emerging Markets, Vol. 9 No. 2, pp. 162-180.

Yang, Y., Nomoto, S. and Kurokawa, S. (2013), “Knowledge transfer in corporate venturingactivity and impact of control mechanisms”, International Entrepreneurship andManagement Journal, Vol. 9 No. 1, pp. 21-43.

Yiu, D.W. and Lau, C.M. (2008), “Corporate entrepreneurship as resource capital configuration inemerging market firms”, Entrepreneurship Theory and Practice, Vol. 32 No. 1, pp. 37-57.

Zahra, S.A. (1996), “Governance, ownership and corporate entrepreneurship: the moderatingimpact of industry technological opportunities”, The Academy of Management Journal,Vol. 39 No. 6, pp. 1713-1735.

Zahra, S.A. and Hayton, J.C. (2008), “The effect of international venturing on firm performance: themoderating influence of absorptive capacity”, Journal of Business Venturing, Vol. 23 No. 2,pp. 195-220.

Zhou, W.B. (2013), “Political connections and entrepreneurial investment: evidence from China’stransition economy”, Journal of Business Venturing, Vol. 28 No. 2, pp. 299-315.

Further readingBlumentritt, T. (2003), “Foreign subsidiaries’ government affairs activities: the influence of

managers and resources”, Business & Society, Vol. 42 No. 2, pp. 202-233.

Guerrero, M. and Pena-Legazkue, I. (2013), “The effect of intrapreneurial experience on corporateventuring: evidence from developed economies”, International Entrepreneurship andManagement Journal, Vol. 9 No. 3, pp. 397-416.

About the authorsWeiqi Dai is an Associate Professor of strategy and entrepreneurship in the School of BusinessAdministration at Zhejiang University of Finance & Economics, China. He obtained his PhD inbusiness administration from Zhejiang University, China. His research interests include corporateentrepreneurship, inter-firm networking and institutional theory.

Ilan Alon is Cornell Chair of International Business and Founding Director of The China &India Centers at Rollins College. He is also a research scholar at Georgetown University. Alon isalso Editor-in-Chief of International Journal of Emerging Markets (Emerald). Alon’s researchfocus is on China yielded numerous research articles and the following books: The Globalizationof Chinese Enterprises (Palgrave, 2008), Biographical Dictionary of New Chinese Entrepreneursand Business Leaders (Edward Elgar Publishing, 2009), China Rules: Globalization and PoliticalTransformation (Palgrave, 2009), A Guide to the Top 100 Companies in China (World Scientific,

21

Financialmarketization

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

2010), Entrepreneurial and Business Elites of China (Emerald, 2011), Chinese InternationalInvestments (Palgrave, 2012).

Hao Jiao earned his PhD from Fudan University, China, and is an Associate Professor ofstrategy, innovation and entrepreneurship in School of Economics and Business Administrationat Beijing Normal University, Beijing, China. His research interests include strategy, managementof innovation and technology and organizational behaviors within the context of emergingmarkets. He has published well over 40 articles in referred academic journals such as Journal ofProduct Innovation Management, Academy of Management Perspectives, Journal of ChineseEntrepreneurship, Frontier of Business Research in China, Management World, among others.Hao Jiao is the corresponding author and can be contacted at: [email protected]

For instructions on how to order reprints of this article, please visit our website:www.emeraldgrouppublishing.com/licensing/reprints.htmOr contact us for further details: [email protected]

JEEE7,1

22

Dow

nloa

ded

by R

ollin

s C

olle

ge, I

lan

Alo

n A

t 07:

45 1

7 Fe

brua

ry 2

015

(PT

)

Copyright © 2022 FDOKUMEN