Financial Economics- CPP

50

Financial Economics- CPP Godfrey Ndlovu AERC January 1, 2021 Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 1 / 46

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Financial Economics- CPP

Financial Economics- CPP

Godfrey Ndlovu

AERC

January 1, 2021

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 1 / 46

Behavioural Finance

‘Financial markets are studied using models that are less narrow thanthose based on Von Neumann-Morgenstern utility theory and arbitrageassumptions’ Ritter, 2003- Click to link to paper

Definition

Behavioural Finance is the study of the way in which psychologyinfluences the behaviour of market practitioners, both at the individualand group level, and the subsequent effect on markets.

Originated in the 1970s, when academics turned to social psychology(neglected by economists)

I Economics has always been structured as a scienceI Most models built on Physics and Mathematics, however with alot of

puzzlesI In 1960s a revolution led by Professors Tversky, Kahneman,

Thaler,Barberis and Shleifer - mixed psychology with economics toexplain human interactions (solution to puzzles?)

.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 2 / 46

Behavioural Finance

‘Financial markets are studied using models that are less narrow thanthose based on Von Neumann-Morgenstern utility theory and arbitrageassumptions’ Ritter, 2003- Click to link to paper

Definition

Behavioural Finance is the study of the way in which psychologyinfluences the behaviour of market practitioners, both at the individualand group level, and the subsequent effect on markets.

Originated in the 1970s, when academics turned to social psychology(neglected by economists)

I Economics has always been structured as a scienceI Most models built on Physics and Mathematics, however with alot of

puzzlesI In 1960s a revolution led by Professors Tversky, Kahneman,

Thaler,Barberis and Shleifer - mixed psychology with economics toexplain human interactions (solution to puzzles?)

.Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 2 / 46

Behavioural Finance

Behavioural finance emerged primarily due to following;I Traditional finance could not explain some important factsI Response to the “arbitrage critique”I Developments in psychology - judgment and decision-making

Key Issues1 Prospect theory.2 The implications of investor overconfidence and misperceptions of

randomness.3 Sentiment-based risk and limits to arbitrage.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 3 / 46

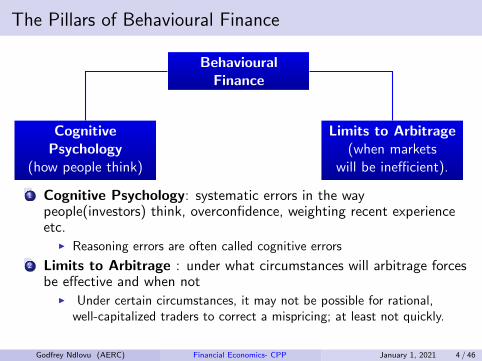

The Pillars of Behavioural Finance

BehaviouralFinance

CognitivePsychology

(how people think)

Limits to Arbitrage(when markets

will be inefficient).

1 Cognitive Psychology: systematic errors in the waypeople(investors) think, overconfidence, weighting recent experienceetc.

I Reasoning errors are often called cognitive errors

2 Limits to Arbitrage : under what circumstances will arbitrage forcesbe effective and when not

I Under certain circumstances, it may not be possible for rational,well-capitalized traders to correct a mispricing; at least not quickly.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 4 / 46

The Pillars of Behavioural Finance

BehaviouralFinance

CognitivePsychology

(how people think)

Limits to Arbitrage(when markets

will be inefficient).

1 Cognitive Psychology: systematic errors in the waypeople(investors) think, overconfidence, weighting recent experienceetc.

I Reasoning errors are often called cognitive errors

2 Limits to Arbitrage : under what circumstances will arbitrage forcesbe effective and when not

I Under certain circumstances, it may not be possible for rational,well-capitalized traders to correct a mispricing; at least not quickly.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 4 / 46

Emotional vs. Cognitive Biases

Emotional bias: distortion in decision making due to emotionalfactors, even if there is evidence to the contrary.

Cognitive bias : tendencies to think/behave in ways that can lead tosystematic deviations from a standard of rationality or ‘goodjudgement’

A cognitive bias is a pattern of poor judgement, often triggered by aparticular situation- can be changed via education. For this reasonmuch attention has been given to cognitive biases

Therefore decision making can be viewed to be on two extremes

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 5 / 46

Emotional vs. Cognitive Biases

Emotional bias: distortion in decision making due to emotionalfactors, even if there is evidence to the contrary.

Cognitive bias : tendencies to think/behave in ways that can lead tosystematic deviations from a standard of rationality or ‘goodjudgement’

A cognitive bias is a pattern of poor judgement, often triggered by aparticular situation- can be changed via education. For this reasonmuch attention has been given to cognitive biases

Therefore decision making can be viewed to be on two extremes

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 5 / 46

Emotional vs. Cognitive Biases

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 6 / 46

Economic Conditions for Market Efficiency

Some proponents of behavioural finance believe that investorcognitive errors cause market inefficiencies.

Recall key economic conditions for market efficiency:1 investor rationality,2 independent deviations from rationality, and3 arbitrage.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 7 / 46

Economic Conditions for Market Efficiency

Therefore for a market to be inefficient, all three conditions must beabsent, i.e.

1 There must many, many investors who make irrational investmentdecisions, and

2 The collective irrationality of these investors leads to an overlyoptimistic or pessimistic market situation, and

3 This situation cannot be corrected via arbitrage by rational,well-capitalized investors.

Whether these conditions can all be absent is the subject of a ragingdebate among financial market researchers.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 8 / 46

Behavioural Finance vs Conventional Finance

Conventional/Traditional Behavioural Finance

Rational individuals Some Not Fully RationalCorrect Bayesian Updating

Relax One or Both,-make processing mistakesChoices - Expected UtilityPerfect information Perfect information doesn’t existEfficient markets-quicklyabsorb information

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 9 / 46

Why Behavioural Finance

If we always behaved rationallyI No investor would ever sell stocks in a panic at the first sign of troubleI No investor would ever buy stocks (or other investments) based on

hunches, hot tips or media hypeI No investor would ever keep money in the bank instead of using it to

pay off high-interest credit card balances

Behavioural Finance provides an ‘overlay’ to the Standard Theoryunderstand ‘non-rational’ investor and market behaviours

Behavioural Finance argue that emotions and sentiment play a crucialrole in determining the behaviour of investors in the market place andvery often they act irrationally due to influence of psychologicalfactor.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 10 / 46

Behavioural Finance

Two categories of irrationalities:1 Investors do not always process information correctly and/or timely.

F Result: Incorrect probability distributions of future returns

2 Investors often make inconsistent or systematically suboptimaldecisions;even when given a probability distribution of returns

F Result: They have behavioural biases.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 11 / 46

Errors in Information Processing: Misestimating TrueProbabilities

1 Forecasting ErrorsOverweighting recent experiences.

2 OverconfidenceInvestors overestimate their abilities and the precision of theirforecasts. For example, for certain types of questions, answers thatpeople rate as “99% certain” turn out to be wrong 40% of the time.

3 ConservatismInvestors do not quickly update their beliefs and under-react to newinformation.

4 Sample Size Neglect and RepresentativenessInvestors make quick inferences on a pattern or trend from a smallsample.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 12 / 46

Behavioural Biases

Biases result in less than rational decisions, even with perfectinformation. This is due to;

Framing (or Frame Dependence)I Decisions affected by manner in which choices are described/modeled

(framed).I If an investment problem is presented in two different (but really

equivalent) ways, investors often make inconsistent choices. e.g. Howthe risk is described, “risky losses’ vs. “risky gains”, can affect investordecisions.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 13 / 46

Behavioural Biases- Mental accounting

It is a form of framing; people separate certain decisions

Associating the stock with its purchase price:-as the price of the stockchanges through time, gains and losses are obtained by comparing currentprice to the purchase price (i.e. mentally accounting for gains and losses)

Investors may segregate accounts or monies and take risks with their gainsthat they would not take with their principal (i.e. “house money effect”)

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 14 / 46

Behavioural Biases- Loss Aversion/Regret Avoidance

A further complication of mental accounting is loss aversion.Investors do not like losses, and they will engage in mentalgymnastics to reduce their psychological impactLoss Aversion: A reluctance to sell investments after they havefallen in value, a.k.a “breakeven” effect or “disposition effect”-tendency to sell a winning stock.If you suffer from Loss Aversion, you will think that if you can justsomehow “get even,” you will be able to sell the stock.

Contrast with risk aversion made earlier under modern finance

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 15 / 46

Behavioural biases- Prospect Theory

Investor utility depends on gains/losses from starting position, ratherthan levels of wealth

I Conventional view: Utility depends on level of wealth.I Behavioural view: Utility depends on changes in current wealth.

Figure: Conventional Utility Function

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 16 / 46

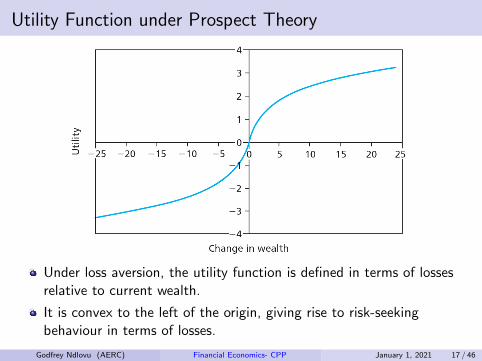

Utility Function under Prospect Theory

Under loss aversion, the utility function is defined in terms of lossesrelative to current wealth.

It is convex to the left of the origin, giving rise to risk-seekingbehaviour in terms of losses.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 17 / 46

Prospect Theory

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 18 / 46

Relaxes assumption of utility maximization- substitute with lossaversion

Investor are concerned more about relative changes in wealth thanabsolute changes- depends on area they are operation in

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 19 / 46

Limits to Arbitrage- Shleifer and Vishny (1997)

Behavioural biases would not matter for stock pricing if rationalarbitrageurs could fully exploit the mistakes of behavioural investors.(a claim of traditional finance)

Behaviourisms: in practice several factors limit the ability to profitfrom mispricing (Fundamental risk, Implementation costs, Modelrisk)

Limits to Arbitrage: The notion that, under certain circumstances,it may not be possible for rational, well-capitalized traders to correcta mispricing, at least not quickly. link

I Theory seeks to answer question: Why do arbitrage opportunitiesnot quickly disappear even if investors know how to exploitthem?

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 20 / 46

Fundamental Risk

Refers to the risk that new bad information arrives to the marketafter an investor has taken a long position on a security.

Theory suggests that this risk could be perfectly hedged by buying aclosely related product

However in practice substitutes are rarely perfect- thus limiting theability to remove all the fundamental risk.

Therefore, intrinsic value and market value may take too long toconverge“Markets can remain irrational longer than one can remain solvent.”

Example

Suppose you buy a certain number of ABSA shares believing it is under-priced.Then some unanticipated negative news drives the share price even lower.Theoretically one could hedge this firm-specific risk by shorting shares in anotherfirm, say, Nedbank. However, there is no guarantee that the price of Nedbankwill not fall if some firm-specific event triggers a decline in the price of ABSA- i.eyou are still vulnerable to bad news about the industry as a whole.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 21 / 46

Noise Trader Risk a.k.a Sentiment-based risk

Noise Trader: Someone whose trades are not based on information ormeaningful financially analysis- their collective action worsen a mis-pricing.

Noise trader risk introduced by De Long et al.(1990) and Shleifer &Vishny(1997)- it is the risk that the mis-pricing worsens in the short run, aspessimistic traders become even more pessimistic about the future.

Important because of its link to other agency problems.I Can force arbitrageurs, investors and professional managers fund

managers, to liquidate their positions early, bringing them unwantedand unnecessary steep losses

A.k.a resale risk (Shleiffer and Summers, 1990):-i.e. comes from theunpredictability of future resale prices. If it is high, investors will have acomparatively shorter time horizon because of fear to liquidate due toexogenous reasons.

A.k.a sentiment-based risk- i.e. the risk that price is influenced bysentiment (or irrational belief) rather than fact-based financial analysis.

Therefore, noise trader risk is additional risk to the systematic risk andunsystematic risk

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 22 / 46

Implementation Costs

Refer to transaction costs such as commissions, bid-ask spread,increased commissions for shorting securities, monetary costs, margininterest, or costs related to legal constraints and accounting issues,e.g money managers, such as pension fund and mutual fundmanagers, are not allowed to sell short.

These transactions costs and restrictions on short selling can limitarbitrage activity.

When fundamental risk(or firm-specific risk), noise trader risk, orimplementation costs are present, a mispricing may persist becausearbitrage is too risky or too costly.

Collectively, these risks and costs create barriers, or limits toarbitrage.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 23 / 46

Evidence of Limits to Arbitrage

As previously discussed, wide scope for arbitrage opportunities exist.

Relevant anomalies for the limits to arbitrage theory are thoseconcerning the relative prices of assets with closely related payoffs(Gromb and Vayanos, 2010)

1 Siamese twin stocks, with fairly identical dividend streams can tradeat significantly different prices.

2 Stocks of parent and subsidiary company can trade at prices suchthat the remainder of the parent company’s assets has negative value.

3 Newly issued on-the-run bonds can trade at significantly higher pricesthan older off-the-run bonds with fairly identical payoffs.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 24 / 46

Twin Shares

In 1907, Royal Dutch of the Netherlands and Shell of the UK agreedto merge and split profits on a 60-40 basis

Until 2005 firm maintained dual listing

Since 60% of the new company is Royal Dutch and 40% ShellTransport, if prices equal fundamental value, the market value ofRoyal Dutch equity should always be 1.5 times the market value ofShell equity.

Therefore, if the stock prices of Royal Dutch and Shell are not in a60-40 ratio, there is a potential arbitrage opportunity.

As shown in next slide there where daily deviations from the 60-40ratio of the Royal Dutch price to the Shell price.

I If the prices are in a 60-40 ratio- no deviation.I If there is a positive deviation- price of Royal Dutch is too high.I If there is a negative deviation-price of Royal Dutch is too low.

As shown there is a large (and persistent) deviations from the 60-40ratio.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 25 / 46

Royal Dutch and Shell 60-40 Price Ratio Deviations, 1962to 2004

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 26 / 46

Twin Shares

The mispricing above is a clear evidence of limits to arbitrage,I The shares are good substitutes- thus fundamental risk is nearly

perfectly hedged.I There are no major implementation costs since buying and shorting

shares of either company is relatively easy.

However, Thaler and Barberis argue that there is noise trader risk.I Investor sentiment causing one share to be undervalued relative to the

other could also cause that share to become even more undervalued inthe short term. .

We therefore conclude that arbitrage was limited- however there wereno profits for arbitrageurs

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 27 / 46

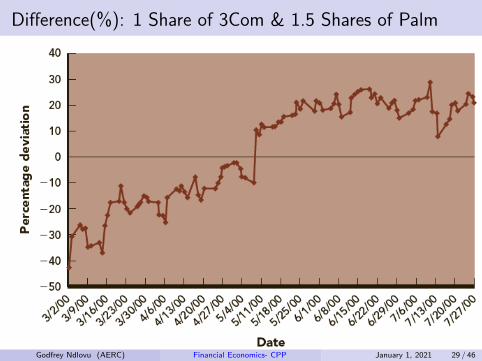

Equity-Curve out- The 3Com/Palm Mispricing

On March 2, 2000, a profitable provider of computer networkingproducts and services, 3Com, sold 5% of one of its subsidiaries to thepublic via an initial public offering (IPO)- Palm (now it is known aspalmOne).

For each share held in 3Com, one would receive 1.5 shares of Palm-therefore each 3Com share should be worth at least 1.5 times thevalue of each Palm share in the absence of arbitrage

As shown in the next slide, the market valued 3Com and Palm sharesin such that the non-Palm part of 3Com had a negative value forabout two months- March 2, 2000, until May 8, 2000

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 28 / 46

Difference(%): 1 Share of 3Com & 1.5 Shares of Palm

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 29 / 46

Index Effects

Share prices should not change upon inclusion in an index- since thefundamental values remained intact.

Empirical evidence by Harris and Gurel (1986) and Shleifer (1986),suggest that when a stock is added to an index, it jumps in price by3.5% (average), and this is often permanent.

I But when Yahoo was added to the index, its shares jumped by 24% ina single day!

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 30 / 46

Index Effects

Thaler and Barberis argue that this is not just mispricing butevidence of limited arbitrage

I An arbitrageur can exploit this mispricing by shorting a goodsubstitute for the stock being included in the index, and this entailsconsiderable risk.

I There is also noise trader risk- share price can continue to increase inthe short run, preventing the arbitrageur from closing the mispricing.

On the other hand, in some markets, institutional investors likemutual funds, pension funds and insurance companies, can only buyshares of companies that are part of an index like the JSE 40-therefore share price may increase due to increased demand whenthey become part of an index.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 31 / 46

Index effect- Wurgler and Zhuravskaya(2002)

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 32 / 46

Index effect- Wurgler and Zhuravskaya(2002)

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 33 / 46

Limits to arbitrage and investor rationality

Theory of limited arbitrage shows that if irrational traders causedeviations from fundamental value, rational traders will often bepowerless to do anything about it.

To explain these these deviations, behavioural models often assume aspecific form of irrationality based on a psychological of people’sbeliefs, and preferences

Research on this field is still growing

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 34 / 46

Limits to arbitrage towards a theoretical understanding-Gromb and Vayanos(1997)

Suppose there are two traded at time t = 0 and pay off at timet = 1, with payoff d

Aand d

Bdenote the mean, standard deviation

and correlation as d̄i , σi and ρ, respectively.

Assume, dA

and dB

are jointly normally distributed.

For simplicity, take exogenous both the price pB

of asset B at time,0,and the risk-less rate and set the former equal to asset B’s expectedpayoff d̄

Band the latter to zero.

There are two types of traders: outside investors and arbitrageurs.I Outside investor have inelastic demand for A and equal to u shares

(where u , the demand shock, can be positive or negative).I Arbitrageurs are competitive, risk averse, and maximize expected

utility of wealth in the next period

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 35 / 46

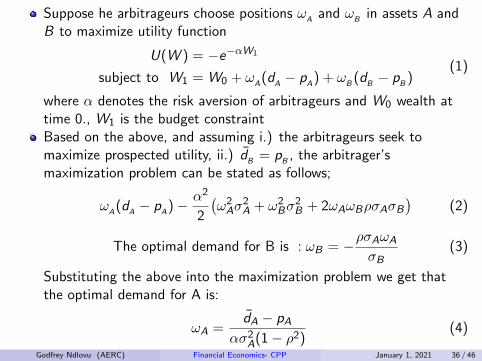

Suppose he arbitrageurs choose positions ωA

and ωB

in assets A andB to maximize utility function

U(W ) = −e−αW1

subject to W1 = W0 + ωA

(dA− p

A) + ω

B(d

B− p

B)

(1)

where α denotes the risk aversion of arbitrageurs and W0 wealth attime 0., W1 is the budget constraintBased on the above, and assuming i.) the arbitrageurs seek tomaximize prospected utility, ii.) d̄

B= p

B, the arbitrager’s

maximization problem can be stated as follows;

ωA

(dA− p

A)− α2

2

(ω2Aσ

2A + ω2

Bσ2B + 2ωAωBρσAσB

)(2)

The optimal demand for B is : ωB = −ρσAωA

σB(3)

Substituting the above into the maximization problem we get thatthe optimal demand for A is:

ωA =d̄A − pA

ασ2A(1− ρ2)(4)

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 36 / 46

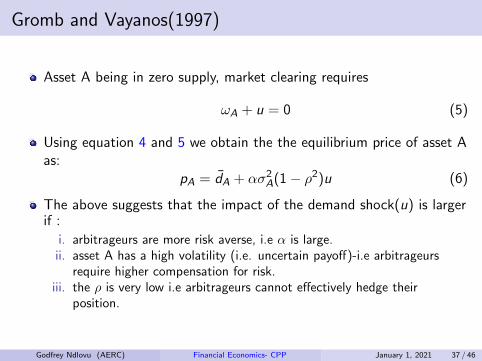

Gromb and Vayanos(1997)

Asset A being in zero supply, market clearing requires

ωA + u = 0 (5)

Using equation 4 and 5 we obtain the the equilibrium price of asset Aas:

pA = d̄A + ασ2A(1− ρ2)u (6)

The above suggests that the impact of the demand shock(u) is largerif :

i. arbitrageurs are more risk averse, i.e α is large.ii. asset A has a high volatility (i.e. uncertain payoff)-i.e arbitrageurs

require higher compensation for risk.iii. the ρ is very low i.e arbitrageurs cannot effectively hedge their

position.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 37 / 46

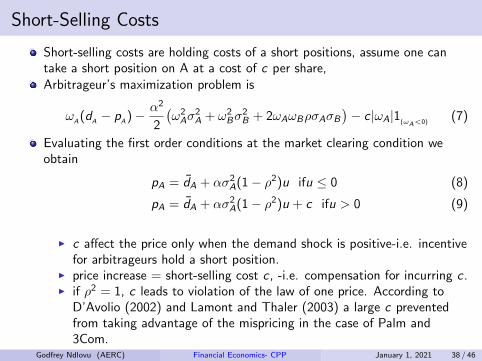

Short-Selling Costs

Short-selling costs are holding costs of a short positions, assume one cantake a short position on A at a cost of c per share,Arbitrageur’s maximization problem is

ωA(d

A− p

A)− α2

2

(ω2Aσ

2A + ω2

Bσ2B + 2ωAωBρσAσB

)− c |ωA|1(ωA<0)

(7)

Evaluating the first order conditions at the market clearing condition weobtain

pA = d̄A + ασ2A(1− ρ2)u ifu ≤ 0 (8)

pA = d̄A + ασ2A(1− ρ2)u + c ifu > 0 (9)

I c affect the price only when the demand shock is positive-i.e. incentivefor arbitrageurs hold a short position.

I price increase = short-selling cost c , -i.e. compensation for incurring c .I if ρ2 = 1, c leads to violation of the law of one price. According to

D’Avolio (2002) and Lamont and Thaler (2003) a large c preventedfrom taking advantage of the mispricing in the case of Palm and3Com.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 38 / 46

Behavioural Asset Pricing Model(BAPM)

BAPM adds a sentiment premium to the CAPM

re = rf + β(rm − rf ) + SP (10)

- SP- sentiment premium derived from analysts forecasts

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 39 / 46

Technical Analysis and Behavioural Finance

Technical Analysis: Using past price data and other nonfinancialdata to identify future trading opportunities (contrast withfundamental analysis).

Attempts to exploit recurring and predictable patterns in stock pricesI EMH proponents believe technical analysis cannot predict future

prices.I However, over the past, technical analysis has been thriving. Why?

Reasons Technical analysis works1 Investors can derive a number of successful technical analysis systems

by using historical security prices.F Past security prices easily fit into a wide variety of technical systems.F Technicians can continuously tinker and find methods that fit past

prices.F This is known as “backtesting”- but remember investment success is

all about future prices.)2 Technical analysis simply sometimes works.

F There are a large number of possible technical analysis systems.F Many of them will appear to work in the short run.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 40 / 46

Technical Analysis and Behavioural Finance

Technical Analysis: Using past price data and other nonfinancialdata to identify future trading opportunities (contrast withfundamental analysis).

Attempts to exploit recurring and predictable patterns in stock pricesI EMH proponents believe technical analysis cannot predict future

prices.I However, over the past, technical analysis has been thriving. Why?

Reasons Technical analysis works1 Investors can derive a number of successful technical analysis systems

by using historical security prices.F Past security prices easily fit into a wide variety of technical systems.F Technicians can continuously tinker and find methods that fit past

prices.F This is known as “backtesting”- but remember investment success is

all about future prices.)2 Technical analysis simply sometimes works.

F There are a large number of possible technical analysis systems.F Many of them will appear to work in the short run.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 40 / 46

Technical Anaylsis

A number of indicators have been used by technical analysts1 Market Sentiment Index(MSI)2 TRIN (TRaders INdex) (aka Arms)3 Confidence index

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 41 / 46

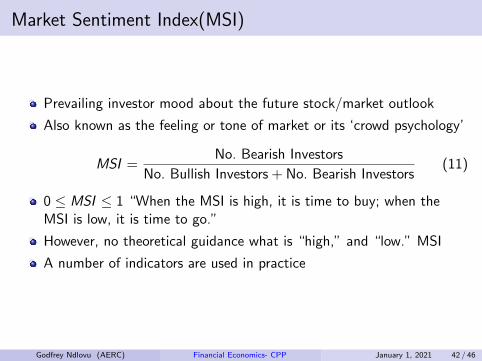

Market Sentiment Index(MSI)

Prevailing investor mood about the future stock/market outlook

Also known as the feeling or tone of market or its ‘crowd psychology’

MSI =No. Bearish Investors

No. Bullish Investors + No. Bearish Investors(11)

0 ≤ MSI ≤ 1 “When the MSI is high, it is time to buy; when theMSI is low, it is time to go.”

However, no theoretical guidance what is “high,” and “low.” MSI

A number of indicators are used in practice

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 42 / 46

TRIN (TRaders INdex) (aka Arms)

Flow of funds indicator, applied to broad market (eg. All share Index,or JSE40), to measure relative extent to which money is moving intoor out of rising and declining stocks

Ratio of average volume in declining issues to average volume inadvancing issues

Seeks to provide a more dynamic explanation of overall movements inthe composite value of stock market

Also known as the feeling or tone of market or its ‘crowd psychology’

Arms =Advancing issues/declining issues

Advancing volume/declining volume(12)

If Arms= 1- market is in balance- equal amount is moving into risingstocks and declining stocks

If Arms > 1,- there is more volume in declining stocks, i.e marketbearish

If Arms < 1- most trading activity is in rising stocks, i.e marketbullish

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 43 / 46

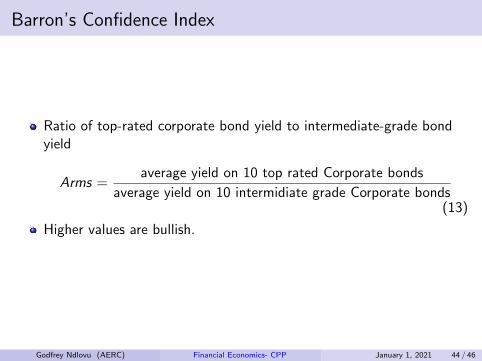

Barron’s Confidence Index

Ratio of top-rated corporate bond yield to intermediate-grade bondyield

Arms =average yield on 10 top rated Corporate bonds

average yield on 10 intermidiate grade Corporate bonds(13)

Higher values are bullish.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 44 / 46

The Future of Behavioural Finance

The death of Behavioral finance was predicted in 1999 by Thaler- oneof its founding fathers

However, Behavioral finance did not disappear instead it has foundnew applications in the financial markets.

After the subprime mortgage crisis of 2008, Behavioral finance andlimits to arbitrage in particular, has shown potential to deliver a moreuseful method of thought to evaluate the different regulations of thefinancial sphere.

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 45 / 46

Limits to Arbitrage- Contribution

The theory of Limits to Arbitrage has provided solutions to:I The equity premium puzzle -(Benartzi and Thaler (1995),

Sewell(2005), Thaler and Barberis (2002)I The conservatism principle of share prices- i.e.earning reflect bad news

more quickly than good news (Basu (1997)I Investors’ tendency to sell winning investments too soon and hold

investments for too long (Odean (1998)I Investor overconfidence- (Daniel, Hirshleifer and Subrahmanyam

(1998), Camerer and Lovallo (1999)I Herding behaviour financial markets (Wermers (1999)I Recently yielding insight into the effects of social networks (e.g.

Facebook Likes and good/bad tweets) on stock prices of publiclytraded companies- Karagozoglu and Fabozzi (2017)Liew andBudavari(2017), Liew and Wang(2016).

Godfrey Ndlovu (AERC) Financial Economics- CPP January 1, 2021 46 / 46