FILE C PY - World Bank Documents & Reports

117

Document of The World Bank FILE C PY FOR OFFICIAL USE ONLY Report No. 2745b-IN IND]IA SECOND SINGRAULI THERMALPOWfER PROJECT STAFF APPRAISAL REPORT April 25, 1980 Regional Projects Department South Asia Projects This document has a restricted distribution and may be used by recipients niry in mne pertormance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of FILE C PY - World Bank Documents & Reports

Document of

The World Bank FILE C PY

FOR OFFICIAL USE ONLY

Report No. 2745b-IN

IND]IA

SECOND SINGRAULI THERMAL POWfER PROJECT

STAFF APPRAISAL REPORT

April 25, 1980

Regional Projects DepartmentSouth Asia Projects

This document has a restricted distribution and may be used by recipients niry in mne pertormance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit = Rupee (Rs)Rs 1 Paise 100

US$1 = Rs 8.4 1/Rs 1 = US$0.1190 1/Rs 1 million = US$119,047.62 1/

MEASURES AND EQUIVALENTS

1 Kilometer (km) 1,000 meters (m) = 0.6214 miles (mi)1 Meter (m) = 39.37 inches (in)1 Cubic meter (m3) = 1.31 cubic yard (cu yd) = 35.35 cubic feet (ft)l1ectare (ha) 10,000 m2 = 2.471 acres (ac)l'Rilogram (kg) 2.2046 pounds (lb)1 Ton 1 metric ton = 2,200 lbs1 Kilocalorie (kcal) = 3.968 British thermal unit (Btu)1 Kilovolt (kV) = 1,000 volts (V)1 Kilovolt-ampere (kVA) = 1,000 volt-amperes (VA)1 Megawatt (MW) = 1,000 kilowatts (kW) = 1 million watts1 Gigawatt hour (GWh) = 1,000,000 kilowatt hours

ABBREVIATIONS AND ACRONYMS

APS - Annual Power Survey

BHEL - Bharat Heavy Electricals LimitedCANDU - Canadian Deuterium Uranium (Natural Uranium, Heavy

Water Reactor)CEA - Central Electricity AuthorityCWPC - Central Water and Power CommissionDESU - Delhi Electricity Supply UndertakingGOI - Government of IndiaGDP - Gross Domestic Product

HPSEB - Himachal Pradesh State Electricity BoardHSEB - Haryana State Electricity BoardHVDC - High Voltage Direct CurrentJKSEB - Jammu & Kashmir State Electricity BoardKfW - Kreditanstalt fuer WiederaufbauNHPC - National Hydro Power CorporationNTPC - National Thermal Power CorporationPERT - Programme Evaluation and Review TechniquePSEB - Punjab State Electricity BoardRAPS - Rajasthan Atomic Power StationREC - Rural Electrification Corporation LimitedREB - Regional Electricity BoardRSEB - Rajasthan State Electricity BoardSEB - State Electricity BoardTDO - Thermal Design OrganizationUNDP - United Nations Development ProgramUPSEB - Uttar Pradesh State Electricity Board

NTPC's FISCAL YEAR (FY)

April 1 - March 31

1/ Since September 25, 1975, the Rupee has been officially valued relativeto a basket of currencies. As these currencies are floating, the US$/Rsexchange rate is subject to change. Conversions in this report havebeen made at US$1 to Rs 8.4.

FOR OFFICIAL USE ONLYINDIA

SECOND SINGRAULI THERMAL POWER PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

I. THE POWER SECTOR ....................................... 1Background ............................................. 1Energy Resources ...................................... 1Past Bank Group Involvement in the Sector .... .......... 2Sector Institutions .................................... 3Existing Facilities - All India ........................ 5Power Supply/Demand Balance - All India .... ............ 6Future Development - All India ......................... 7Regional Demand and Supply - Northern Region .... ....... 8Future Integrated System Operation ..................... 9Bank Group's Strategy in the Sector ........ ............ 9

II. THE BENEFICIARY - NATIONAL THERMAL POWER CORPORATIONLIMITED ................................................ 13Legal Status and Authorities ........................... 13Organization and Management ............................ 14Training ............................................... 15Sale of Power from the Project .......................... 16Accounting Organization and Systems .................... 17Audit .................................................. 17

III. THE PROGRAM AND THE PROJECT ............................ 17The Program ............................................ 17The Project ......... ...... 18Estimated Cost ......................................... 18Project Financing ................... 19Engineering and Construction ........................... 19Procurement .......... .................................. 20Disbursements .......................................... 21Ecological Aspects ..................................... 21Project Risks ............ ... 22

IV. FINANCIAL ANALYSIS ..................................... 23Introduction ........... ... 23Future Earnings ........................................ 23Taxation ............ ................................... 24

This report is based on information provided by CEA, Department of Power inthe Ministry of Energy, NTPC and SEBs during an appraisal carried out byMessrs. B.C. Lynch, V. Antonescu, K.G. Jechoutek and A_E. Bailey (consultant)during May/June 1979.

This document hu a restricted distribution and may be used by recipients only in the performanceof their omcial duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

Table of Contents (continuation)

Page No.

Financing Plan FY1977-FY1987 ................................. 24Internal Cash Generation .--------------------.-.------ 26Future Finances ............................................ 26Borrowing Powers ................---------------- 28NTPC's Bulk Tariff .......................................... 28Regional Tariffs .------------------------------------------ 28Commercial Arrangements for Sale of NTPC Power .29Tariff Level and Marginal Cost .............................. 29

V. JUSTIFICATION . 30Project Definition .......................... 30Comparison of Alternative .30Benefits .................................................... 31

VI. AGREEMENTS REACHED AND RECOMMENDATION .33

ANNEXES

1. All India-Sales and Energy Data for 1969/70, 1974/75,1975/76, 1976/77, 1977/78 and 1978/79 .................... 34

2. Regional Demand and Supply; Energy Exchanges Among VariousSystems 1978/79; Schedule of Yearly Additions to ThermalGenerating Capacity; Comparative Demand Forecasts for UttarPradesh and Rajasthan - Northern Region .35

3. Sales and Energy Data for 1974/75 - 1978/79 - Northern Region 454. Power Supply Position 1976/77-1983/84 - Northern Region ..... 505. Tentative Demand Forecasts 1984/85 to 1988/89 - Northern

Region .516. Yearwise Capacity and Energy Allocation from the Singrauli

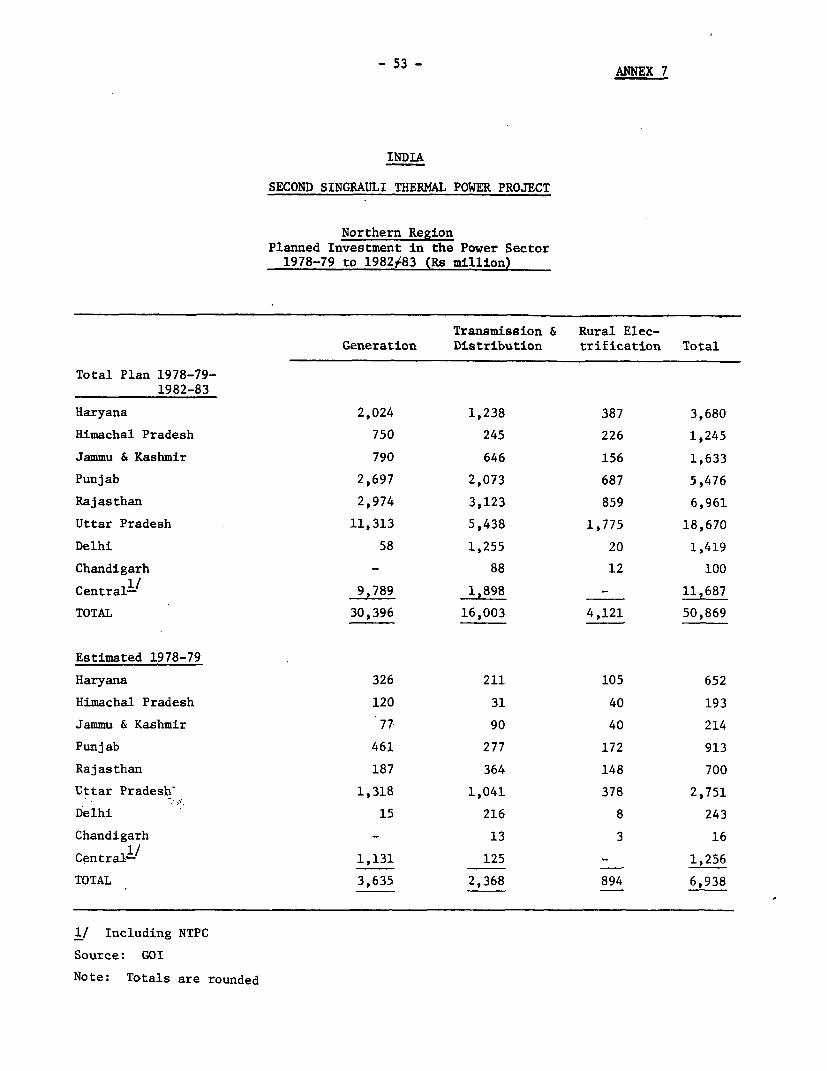

Development .527. Planned Investment in the Power Sector 1978/79 to 1982/83

- Northern Region .538. Suggested Terms of Reference for a Study to Prepare a

Least-Cost Power Development Program .549. Financial Position of the State Electricity Boards .5910. Terms of Reference of the Rajadhyaksha Committee on Power 6211. Organization Chart of NTPC .6412. Organization Charts of NTPC's Finance and Accounting

Organization .6713. Description of the Singrauli Development .6914. Project Cost Estimates .7215. Estimated Construction Schedule .7416. Estimated Schedule of Disbursements .7717. NTPC - Income Statements FY1979 through FY1991 .7818. NTPC - Source and Application of Funds FY1977 through FY1991. 80

- iii -

ANNEXES (continuation)

Page No.

19. NTPC - Condensed Balance Sheets FY1977 through FY1991 ....... 8220. Assumptions on Financial Projections ........................ 8321. Annual Rates of Return in Real Terms ........................ 8722. NTPC's Bulk Tariff (Northern Region) and Bulk Exchange

Tariffs in Northern Region ................................ 8823. Regional Marginal Cost Analysis of NTPC Operations .... ...... 9024. Definition and Cost of Alternative to the Project .... ....... 9625. Additional Transmission and Distribution Cost .... ........... 9726. Shadow Pricing of Costs and Benefits ........................ 9827. Structure of Operation and Maintenance Costs .... ............ 10028. Economic Benefits ........................................... 10129. Economic Costs - Second Singrauli Project and Alternative ... 10330. Economic Justification: Results ............................ 10531. Documents Available in the Project File ..................... 107

MAPS

IBRD - 14739RIBRD - 14517

INDIA

SECOND SINGRAULI THERMAL POWER PROJECT

I. THE POWER SECTOR

Background

1.01 Economic growth and improvement of the standard of living in Indiadepend critically on the development of the power sector. In the presentstage of economic development, the demand for power grows roughly twice asfast as the economy. Because the power industry is relatively capital inten-sive, its share in total fixed asset formation is increasing rapidly; thepower sector, which has made great strides in the last two decades, is todaythe largest economic sector in the country in terms of investments. The sheersize and increasing complexity of India's power sector, as well as economicconsiderations, necessitate an approach to system planning which, to a muchlarger extent than in the past, should concentrate on nationwide power devel-opment and aim at making use of economies of scale through construction oflarger, more efficient power stations and interconnected high voltage trans-mission systems.

1.02 The strategy of the Government of India (GOI) is to intensifycentralized planning of generation and'high voltage transmission with a viewto ultimately centralize control through a national grid with the operationof generating plant on a merit order basis. To this end, GOI establishedin 1975 two power generating companies, the National Thermal Power Corpora-tion (NTPC) and the National Hydro Power Corporation (NHPC) to construct andoperate large thermal and hydro power stations and associated transmission.Consultants have been engaged to assist the Central Electricity Authority(CEA) in undertaking a 400 kV system study to determine the configuration andparameters of the future interconnected national power system. GOI alsodecided to proceed with the construction of four large thermal power stationsof 1,100 MW to 2,100 MW capacity to be built in two stages, located on coalfields and supplying bulk power to the States via an interconnected 400 kVtransmission system. The construction of three such developments, the 2,000MW Singrauli, the 2,100 MW Korba and the 2,100 MW Ramagundam projects, hasbeen started with IDA/Bank financial assistance. This comprises 600 MW ofgenerating plant and transmission for each project (Credits 685-IN Singrauli,793-IN Korba, 874-IN and Loan 1648-IN Ramagundam). The second stage ofSingrauli, comprising two additional 200 MW units and two 500 MW units withassociated transmission facilities, is the subject of this report. An IDAcredit of US$300 million is proposed.

Energy Resources

1.03 India's main commercial energy resources are coal, oil, naturalgas and hydro power. There are also resources of nuclear fuels, principallyuranium and thorium, and India's power program includes the construction offurther "CANDU" type heavy water reactors using domestically produced natural

- 2 -

uranium as fuel. Two nuclear power stations have been constructed to dateand a third is under construction. Some geothermal energy sites have alsobeen identified, but the potential appears to be limited.

1.04 Coal is by far the most extensive indigenous fossil fuel; reservesare estimated at 83 billion tons of which some 21 billion tons have beenproven. Additionally, total reserves of lignite at the Neyveli field inTamil Nadu are estimated at around 2 billion tons. If low quality coal, e.g.,coal with high ash and moisture content, is excluded, the estimate of commer-cially usable coal and lignite is reduced to approximately 24 billion tonswhich, on a forecast countrywide usage, would be adequate for some 50 yearsunder current assumptions of economic growth.

1.05 By comparison with coal, proven reserves of oil are small. However,oil and gas exploration programs are still going on. Exploration and drill-ing activities to date have already proven an estimated 230 million tons onshore, and recent off-shore discoveries west of Bombay in the Arabian Sea haveled to delineation of fields with proven recoverable reserves of about 250million tons of crude oil and 30 billion cubic meters of natural gas. Otherreserves of natural gas, which are found in India both alone and in associa-tion with crude oil, are estimated at over 100 billion cubic meters.

1.06 The potential of hydroelectric power resources is estimated at70,000 MW of which some 11,000 MW has already been developed. A further4,700 MW is scheduled for commissioning by FY1984 (see Table 1.2) and some23,000 MW is currently under investigation or scheduled for investigation.Some 70% of the total potential is in the Northern and Northeastern regions.Additional emphasis on hydro power investments is planned.

1.07 Oil and natural gas have important alternative uses and it is un-likely that they will be a significant factor in the generation of electricpower. The Government intends, therefore, to base the development of generat-ing facilities for the foreseeable future on coal or lignite burning thermalstations and hydroelectric power stations and to gradually develop a smallnuclear program.

Past Bank Group Involvement in the Sector

1.08 The Bank has made nine loans to India for power projects amountingto US$334.5 million and IDA twelve credits totalling US$1,171 million. Ofthis amount US$870.5 million involves financing of generating plant; US$23million the purchase of construction equipment for the Beas hydroelectricproject; US$380 million the provision of high voltage transmission; and US$232million the purchase of rural electrification equipment. Nine loans andcredits for generating plant, the Beas project (Credit 89-IN) and the firstthree transmission projects (Loan 416-IN Credits 242-IN and 377-IN) have beencompleted. The Fourth Transmission Project (Credit 604-IN) is nearing comple-tion, and the whole credit amount of US$150 million has been committed. TheThird Trombay Thermal Power Project (Loan 1549-IN) was approved in April 1978.The Ramagundam Thermal Power Project (Credit 874-IN and Loan 1648-IN) and the

-3-

Second Rural Electrification Project (Credit 911-IN), are still in the preli-minary implementation stage and no disbursements have yet been made. Commit-ments to April 30, 1980 totalled some US$500 million on the four thermal powerplant projects (Singrauli, Korba, Ramagundam and Trombay) and US$150 millionon the two Rural Electrification Projects (Credits 572-IN and 911-IN).

1.09 The Singrauli, Korba and Trombay projects are on schedule. TheRamagundam Project, the Fourth Power Transmission Project and the First RuralElectrification Project are proceeding satisfactorily notwithstanding initialdelays in implementation and the substantial delay in preparation of specifi-cations and review of tenders for the more sophisticated load dispatch equip-ment in the case of the transmission project.

Sector Institutions

1.10 The principal agencies in the industry are: (i) the State Elec-tricity Boards (SEBs); (ii) the Atomic Energy Commission; (iii) the CentralElectricity Authority (CEA); (iv) Regional Electricity Boards; (v) the twoCentral Power Corporations (NTPC and NHPC); and (vi) the Rural ElectrificationCorporation Ltd (REC).

1.11 The SEBs are constituted by the State Governments under the provi-sions of the Electricity (Supply) Act, 1948, to promote the coordinateddevelopment of the generation, supply and distribution of electricity withintheir respective States in the most efficient and economical manner, and forthe control and regulation of other supply undertakings which are privatelicensees. These comprise municipal utilities such as Bombay Suburban Elec-tric Supply Undertaking, and private utilities, the largest of which are theTata Electric Companies, (Bombay), the Calcutta Electric Supply Company, andthe Ahmedabad Electric Supply Company. At the present time, the States effec-tively own or control well over 90% of electricity supply facilities. Whilethe SEBs are corporate entities in their own right and enjoy some autonomyin the management of their day-to-day operations, they are under the controlof their State Governments in such matters as policy, capital investment,tariff changes, borrowings, pay scales and personnel policies.

1.12 The CEA was formally created in 1950 with responsibility for devel-oping a national policy for power development and coordinating the activitiesof the various planning agencies involved in electricity supply. At thattime, it came under the Power Wing of the Central Water and Power Commission(CWPC). As a result of administrative changes introduced in October 1974,responsibility for power was transferred to the Ministry of Energy, which wascreated at that time to bring together ministerial responsibility for coal andpower. This involved the transfer of the Power Wing of the former CWPC to theCEA, which now comes under the Department of Power of the Ministry of Energyand is responsible for developing a sound national policy for the electricitysupply industry. The Department of Atomic Energy, which is directly responsi-ble to the Prime Minister, deals with nuclear power generation.

1.13 CEA's powers were enlarged through amendments to the generalprovisions of the Electricity (Supply) Act, 1948, which were enacted on

-4-

November 30, 1976. In addition to its general responsibilities for national

power policies, it is now responsible for the formulation and coordination

of plans for power development, optimization of investments in the power

sector for the whole country, development of interconnected system operation,

training of personnel and research and development. It includes specialist

engineering organizations which provide comprehensive project engineering

services to the electricity supply industry. The Thermal Department also

takes responsibility for monitoring the performance and maintenance records

of thermal power stations and for organizing the training of power stationpersonnel. The Economic and Commercial Department accumulates data on

economic, finance and accounting aspects of the power industry in India,

both at Center and State levels, with particular reference to the operations

of the SEBs. The emerging role of CEA in financial affairs is evidenced by

the conveying of statutory authority 1/ on it to formulate, in conjunction

with GOI, policy for the accounting treatment of depreciation of fixed assetsin the power sector in India. CEA is also playing a leading role in advising

State Governments on the measures to be taken to implement the amendments

to the financial provisions of the Electricity (Supply) Act, 1948, and isalso providing information to the various working panels of the RajadhyakshaCommittee (para 1.42). A recent major achievement for the CEA was the adop-

tion by the SEBs of a uniform system of commercial accounting, devised by it

over a period of time. This system, which applies to all SEB accounts fromApril 1979, brings uniformity to the procedures relating to the maintenanceof accounts, and, for the first time, enables direct inter-Board comparisonof financial results.

1.14 The SEBs and the other licensed electricity undertakings are

required to submit their investment proposals to the CEA for technical and

economic appraisal and to the Energy Division of the Planning Commission forinclusion in the Five Year Plan. The Planning Commission is responsible for

the allocation of Plan funds among the States and among sectors. Planning

of generation, transmission, and distribution development has traditionallybeen undertaken by each SEB for its own State rather than on a regional or

national basis. However, with the rapid growth of the power sector and with

the resultant increasing complexity of operation, GOI sees the necessity for

an integrated national approach to sector development.

1.15 Four Regional Electricity Boards (REBs), for the Northern, Southern,Eastern and Western regions, were established between 1964 and 1966 by common

resolution of the State and Central Governments, to help develop integratedpower systems in their respective regions, and thus prepare for the transition

from separate power systems at State level to regional systems and finally to

an interconnected national grid. The chairmanship of each REB is assumed inrotation by the Chairmen,of the SEBs within the region and they are staffed by

engineers seconded from their constituent SEBs. The general functions of theREBs are to plan integrated operation of the power systems in the region for

the maximum benefit of the region as a whole, coordinate overhaul and mainten-

ance programs, determine generation schedules to be followed and the power

1/ Amendment of Section 68 of the Electricity (Supply) Act, 1948.

-5-

available for transfer between States and determine a suitable tariff structurefor the transfer of power within the region. At present, the Boards functionmainly in an advisory role in relation to the SEBs.

1.16 NTPC and NHPC are at present not intended to take a leading rolein the generation and sale of power in the States. At the present time, theconstruction of four large central thermal power stations has been started asmentioned in paragraph 1.02. All of these developments are being constructedand will be operated by NTPC. NHPC will construct and operate large hydro-electric projects. A transmission wing has also been established in NHPC todesign and construct the 220 kV and 400 kV overhead transmission associatedwith hydro-projects, and any other transmission work which it might be commis-sioned to undertake. In most States, the SEB will continue for some time tobe the largest power undertaking.

1.17 REC was incorporated in July 1969 under the Indian Companies Act,1965, as a company wholly owned by GOI, under the general supervision of thethen Ministry of Irrigation and Power (now under the Ministry of Energy).REC's chief objective is to finance rural electrification schemes throughoutthe country, acting as a financial intermediary with technical expertise,and administering funds received primarily from GOI. It is REC's functionto ensure efficient allocation of these funds by establishing policies,procedures, and criteria for the formulation, approval and implementationof such schemes. In doing so, REC is directed to adopt a "project approach,"coordinating electrification with other inputs in rural development in orderto achieve increased agricultural production and overall economic development.

Existing Facilities - All India

1.18 The total installed generating capacity in the whole of India asof March 31, 1979 was just under 29,000 MW, including about 2,225 MW of non-utility capacity, mostly thermal, which is owned by major industrial consumersto meet their own needs. The generating capacity is shown in Table 1.1 below:

Table 1.1: INSTALLED GENERATING CAPACITY AS OF MARCH 31, 1979(MW)

Region Conventional Thermal Nuclear Hydro Total

Northern 3,773 220 3,718 7,711Western 5,204 420 1,770 7,394Southern 2,193 - 4,303 6,496Eastern 3,854 - 895 4,749North-eastern 188 - 146 334Andaman and NicobarLakshadweep 6 - - 6

Non-utility Capacity 2,225 - - 2,225

Total 17,443 640 10,832 28,915

Source: CEA.

- 6 -

1.19 Transmission is at 132 kV and 220 kV and, generally, load centersare interconnected by 132 kV and 33 kV subtransmission lines. Distributionvoltages are 11 kV and 415/240 V. The supply, in general, is reliable, butpower shortages, especially during the summer months, necessitate shutdownsand brownouts. System losses have been reduced in recent years but they arestill high accounting for about 20% of units sent out. This subject is underexamination by the "Rajadhyaksha Committee" (see para 1.42).

Power Supply/Demand Balance - All India

1.20 India's installed power generating capacity increased at an annualrate of 10.3% during the 1950s and 1960s while gross electricity generationgrew at just under 12% during this 20 year-period due to a better utilizationof the generating capacity. Although local and intermittent shortages didoccur during this period, system failures did not present a major problem.However, by the early 1970s, the supply situation had grown more serious andpotential unconstrained demand consistently outpaced supply in a number ofstates. This situation was due to several factors such as: failure to imple-ment projects in accordance with planned schedules; inadequate transmissiondevelopment; operating and maintenance problems leading to a low plant avail-ability factor of around 72%; inadequate budget allocation and the absence ofmonsoon rains, particularly during the early 1970s, leading to lower hydrooutput.

1.21 The shortage situation was most serious in 1974/75 and 1977/78 andis again extremely serious now, particularly in the Eastern Region. Theestimated deficit of energy throughout India in 1974/75 was about 11,000 GWh(14.1%); this fell to 8,600 GWh (10.3%) in 1975/76 and to 5,100 GWh (5.8%) in1976/77, but increased to 15,800 GWh (15.5%) in 1977/78. Data for 1978/79indicate that the deficit was of the order of 10%.

1.22 Power shortages, particularly in the industrial sector, have affectedthe output of the country and the cost in terms of industrial production fore-gone has been substantial (generally, energy restrictions fall on industry andthere is relatively little loss to the economy on account of power shortages ineither the residential or agricultural sectors). Lost value-added due to lostindustrial production because of power restrictions, could well be in theneighborhood of 3% of GDP. 1/

1.23 The growth of the power sector during the last 10 years and thepattern of consumption during this period is shown in Annex 1. Sales to agri-culture and irrigation have increased substantially during the 1970s, mainlybecause of the rural development programs. Industrial demand as a proportionof the total demand has declined, and there has been a small but steady increasein domestic demand. It is expected that this pattern of demand will continuewith a gradual improvement in the annual load factor.

1/ See: India, Economic Issues in the Power Sector, 1979 (World Bank ReportNo. 2335-IN, paragraph 68).

-7-.

Future Development - All India

1.24 The countrywide peak demand in 1977/78 was 15,520 MW; accordingto CEA's estimates, unconstrained demand was expected to increase to about20,300 MW by 1979/80, 18,600 MW of which are being met by available capacity.Installed capacity by 1979/80 was expected to reach about 31,900 MW of which29,700 MW would be utility plant with the balance of 2,200 MW non-utility.

1.25 The development program provides for an expansion of generatingcapacity during the five-year period 1979/80-1983/84, including the nuclearpower plants which are scheduled to come into operation during that period,by about 19,000 MW, so that the total planned installed capacity would beabout 45,000 MW by 1983/84. The additional capacity scheduled for commis-sioning during this period is shown in more detail in Table 1.2. Furthermore,the construction of some 15,000 km of 400 kV transmission lines is plannedto enable full integration of the regional systems and the evacuation of theoutput from the proposed large thermal power stations.

Table 1.2: SCHEDULE OF PLANNED ADDITIONS TO CAPACITY DURINGTHE PERIOD 1979/80-1983/84 /a

ConventionalThermal Nuclear Hydro Total

------------------- (MW) --------------------

Northern 2,900 455 1,300 4,655Western 5,270 - 521 5,791

Southern 2,100 470 2,310 4,880Eastern 2,710 - 305 3,015North-eastern 298 - 261 559

Total 13,278 925 4,697 18,900

/a Excludes non-utility capacity.

Source: CEA.

1.26 Table 1.3 shows the planned annual installed capacity aggregatingabout 45,600 MW in 1983/84, the available capacity, the peak load and theforecast of energy requirements and availability (not taking into accountdiversity). The data referring to the peak load and energy requirement in1978/79 show the demand constrained by supply. The estimated unsuppressedpower and energy demand would have been about 10% higher (see para 1.21).The forecasts of peak load and energy requirements are based upon continuousmonitoring of development trends during the preparation of the annual electricpower surveys of India. If the program of generation development can beachieved on time, the present shortage of energy would be eliminated from1982/83 on, but there would still be a capacity deficit through the five-yearperiod due to a low availability factor of generating plants. The peak avail-ability in India under present operating conditions, is around 60% of installedcapacity. This availability factor is expected to improve gradually as aresult of the development of system interconnection and the improvement ofmaintenance practices.

- 8 -

Table 1.3: INSTALLED CAPACITY, PEAK AVAILABILITY, PEAK LOAD,ENERGY AVAILABILITY, AND ENERGY REQUIREMENT

ALL-INDIA 1978/79-1983/84

1978/79 1979/80 1980/81 1981/82 1982/83 1983/84

Installed Capacity (MW) /a 26,741 29,734 33,009 35,585 40,804 45,590

Peak Availability (MW) 16,268 18,566 20,968 22,171 25,443 28,822

Peak AvailabilityFactor (%) 61 62 64 62 /c 62 /c 63

Peak Load (MW) 16,268 /b 20,348 22,443 24,717 27,334 30,068

Surplus (Deficit) (MW) - (1,782) (1,475) (2,546) (1,891) (1,246)

Energy Availability (GWh) 97,376 103,549 117,855 131,496 151,036 171,949

Energy Requirement (GWh) 97,376 /b 112,700 124,408 137,089 150,819 166,298

Surplus/(Deficit) (GWh) - (9,151) (6,553) (5,593) 217 5,651

Ia Excludes non-utility capacity.lb Demand constrained by supply.Ic Reduction in availability factor due to commissioning of hydro plant.

Source: CEA.

1.27 Table 1.3 also indicates that both peak load and energy requirement

are estimated to grow at an average annual rate of around 10% during the five

year period 1978/79-1983/84. The forecast capacity deficit decreases from

around 10% of the system load in 1979/80 to 4% in 1983/84 and the energy

availability exceeds energy demand by some 3% in 1983/84. These are varia-

tions which are less than the accuracy of any of the forecast data inputs, butthey demonstrate that, if anything, a case could be made for sanctioning morecapacity than presently planned for commissioning during the five-year periodending 1983/84, particularly since All-India data mask shortages in specificregions, which may develop due to insufficient interconnection.

Regional Demand and Supply - Northern Region

1.28 The major authorities supplying the Northern region are the UttarPradesh State Electricity Board (UPSEB), the Punjab State Electricity Board(PSEB), the Haryana State Electricity Board (HSEB), the Delhi ElectricitySupply Undertaking (DESU), the Rajasthan State Electricity Board (RSEB), theJammu and Kashmir State Electricity Board (JKSEB), and the Himachal PradeshState Electricity Board (HPSEB). NTPC operates the Government-owned 510 MWthermal station at Badarpur. Each of these authorities owns either totallyor partly generating facilities and (with the exception of NTPC) supplieselectricity to final consumers. Interchanges of temporary power surplus arecommon.

1.29 The Bhakra/Beas hydroelectric generating complex is jointly owned bythe SEBs of Punjab, Haryana, and Rajasthan. These SEBs draw energy from thi6facility in accordance with their ownership shares. In addition, energy issupplied on a contractual basis to "common pool consumers" such as part ofHimachal Pradesh, the Nangal Fertilizer Factory, Chandigarh, and Jammu andKashmir. The largest intra-regional transfers are recorded between the

- 9 -

Bhakra/Beas complex and its owners and bulk consumers, the second largesttransfer occurs from the Badarpur thermal power station to DESU. Annex 2describes the regional demand and supply situation in quantitative detail.49% of installed regional capacity is thermal, 48% hydro, and the remaindernuclear. This hides significant differences between States: only UPSEB,DESU and the Central Sector are not heavily dependent on hydro generatingfacilities. Installed capacity has been growing at a rate of about 13% p.a.in recent years--firm available capacity, however, only at 9% p.a., reflect-ing a falling availability percentage. Availability is expected to improveby 1983/84, by which time an additional 4,655 MW are expected to have beenadded to the existing capacity, most of it thermal and nuclear.

1.30 The region is less industrially oriented than the Indian average--only 52% of consumption is attributable to industry, compared to a nationalaverage of 66%. Agriculture, with its greatest burden on the supply system,is significantly more important than on an All-India basis. Energy consump-tion has been growing at an average annual rate of 14.5%, with fluctuationsdepending on hydro availability. Some reduction in technical losses has beenachieved (Annex 3).

1.31 Peak unconstrained capacity demand is expected to exceed availablecapacity for the foreseeable future: the anticipated shortfall will begrowing steadily to reach more than 1,100 MW in 1983/84. It is likely thatpersistent shortages will continue well beyond 1984 (Annexes 4 and 5). In1983/84, the capacity of the proposed project's first stage will be the equiv-alent of 7% of regional capacity. At the time of commissioning of the lastunit, the proposed project will represent about 3% of potential unconstrainedregional capacity demand (Annex 6). The shift of responsibility for powergeneration from SEBs to NTPC is reflected in the lower anticipated percentageof the SEBs' investment programs devoted to generating facilities (Annex 7).All supply authorities in the region had to impose restrictions on demandin 1978/79. Restrictions are widespread in Uttar Pradesh, imposing largecuts on capacity demand and energy consumption (Annex 2), mostly borne byindustry. Rotation of supply to rural areas is common, as is ad hoc loadshedding.

Future Integrated System Operation

1.32 With the increasing size of the power sector in India and its far-reaching impact on the country's economy, annual surveys and Five-Year Plansat the State level have become insufficient as a basis for power developmentplanning. The larger size of power plants, their consequent longer construc-tion period--on average six to eight years for thermal plants and eight toten years for hydro plants--as well as their gradual interconnection requirea long-range perspective for investment decisions on a regional and nationallevel.

1.33 Recognizing the need for coordinated power development throughoutthe country, provision was made in Credit 604-IN to help finance the costof consultants to study the technical, financial and economic aspects of along-term national plan for the sector. Such a plan should include, interalia, detailed demand forecasts, investigation of power generation schemes

- 10 -

to meet load growth requirements for a 15-20 year period (indicating costs andsequencing of investments to optimize resources), development of primary gridconfigurations, including the 400 kV system study which CEA has started butwhich has come to a temporary standstill mainly due to lack of overall plan-ning, coordination of power plans with plans for other sectors (determiningresource requirements), and recommendations on responsibilities and neededoperational policies at the State, regional and national levels (Annex 8).Such a study is an essential prerequisite for formulating sound policies forfuture development of the sector, and the Government has indicated its inten-tion to complete such a study by April 1982.

1.34 The operation of regional systems, which will be integrated in thefuture in a national grid, requires large numbers of personnel who would haveto be trained in the use of sophisticated load dispatch equipment and inter-connected systems operation. A UNDP project designed to assist CEA in devel-oping programs for training staff to operate the future load dispatch centerscame to a halt in 1977, primarily because of personnel problems, and lack ofcounterpart staff. GOI's plans to revise this project, in consultation withUNDP, were discussed during negotiations. These plans would form part of awider program for strengthening systems operation and training. The Associa-tion would be kept informed about the development of such program.

Bank Group's Strategy in the Sector

1.35 The Bank Group's strategy in its involvement in the Indian power

sector, has been one of co-operation with GOI in seeking solutions to themany difficult and politically sensitive problems which have confronted theIndian electricity supply industry since Independence. The sensitivity ofCenter-State relations, because of concurrent jurisdiction over the electri-city supply industry, has dictated that a policy of persuasion rather thanone of explicit leverage would produce better results.

1.36 The Bank Group's main objectives in the sector are:

(a) assistance in accelerating the installation of gene-rating capacity and promoting measures to improvethe operation and maintenance of existing plant 1/in order to gradually eliminate the prevailing powershortages in the country;

(b) assistance in introducing long-range system plan-ning on a nationwide basis which would assure imple-mentation of a least-cost power development program;

(c) promotion of appropriate measures with respect toimproving the sector organization and training; and

1/ This subject is dealt with in the terms of reference of both thesuggested Least-cost Power Development Study (Annex 8, para. 3) andthe Rajadhyaksha Committee (see para 1.42 and Annex 10).

- 11 -

(d) strengthening of the finances of the institutions involvedin the sector, particularly of the State Electricity Boards(SEBs), through setting of rate-of-return targets or levelsof self-financing and advising in designing of appropriatetariff systems.

1.37 Progress towards achieving the above goals has been hindered byconstitutional factors. Under the Electricity (Supply) Act 1948, power supplyis a concurrent subject. This means that the responsibility for supplyingelectricity is shared between the Central Government and the State Governments,requiring full agreement between the Center and the States for the implement-ation of most actions. The States operate, and develop, through their Elec-tricity Boards, most of the power facilities. The consequence of this arrange-ment in many instances has been a parochial approach where a national or atleast regional approach would have been more beneficial. On the other hand,it is debatable whether Central initiative could have been taken much furtherin the time available. The radical proposal which would have enabled powersystem generation and bulk supply to be exclusively a Central responsibility,would have meant a considerable upheaval and would have have raised fundamentalpolitical and constitutional issues going well beyond efficiency considerations.

1.38 Given these difficulties, results achieved so far have been encourag-ing. They are the following:

(a) with the establishment of the Regional Electricity Boards(REBs, para 1.15) and later of NTPC and NHPC, the firstimportant steps towards an improved organizational struc-ture of the power sector have been made. GOI intends togradually strengthen the authority of the REBs and toincrease their role of coordinating the SEBs in mattersof power development and operations;

(b) CEA was reorganized and had its powers enlarged throughthe amendment in 1976 of the Electricity (Supply) Act1948 (paras 1.12 and 1.13);

(c) a recent amendment of the financial provisions of theElectricity (Supply) Act 1948 requires that tariffs beset at levels sufficient to enable the SEBs to financefrom internal sources a reasonable proportion of theirinvestment programs;

(d) recently, SEBs in the Northern Region and the DelhiElectricity Supply Undertaking (DESU), have developedand partially implemented plans designed to restore thecovenanted rate of return of 9-1/2% (Credit 604-IN).These plans consist of tariff increases, rationalizationof manpower requirements and other cost effective measures;

(e) with a view to the reassessment of tariff policies,the majority of the SEBs have recently completed

- 12 -

tariff studies based on marginal cost pricing principles.The Bank Group's review of these studies recommended thestandardization of certain assumptions so as to producea uniform methodology for general application by all SEBs.To assist in this standardization process, CEA is establish-ing a specialist department to interact with the SEBs andto keep the Bank Group advised of future developments; and

(f) NTPC's generation/transmission construction program (paras3.01 and 3.02), which is in the process of staged implemen-tation with Bank Group assistance, will make an importantcontribution to the gradual elimination of the presentdeficit in the country's power balance. The proposedproject would help to continue this program.

1.39 There are two major remaining areas which have been the cause of con-

cern to the Bank Group and also have been the subject of continuing dialoguewith GOI. They are:

(a) the weakness of nationwide long-range planning for powerdevelopment; and

(b) the weak financial position of a number of SEBs which,for instance, have not always been able to achieve thecovenanted rate of return of 9-1/2%.

1.40 In the continued effort of the Bank Group in dealing with the long-range problems of the power sector in India, it was decided to concentrateon the above two areas. During appraisal and negotiations, discussions wereheld with CEA, NTPC and NHPC on the content of a long-range power developmentstudy designed to prepare a least-cost power development program, CEA's capa-bility to undertake such study with its own staff, and the possible need forconsultants' support (para 1.33). Agreements were reached during negotiationson the preparation of a least-cost development program based on the terms ofreference suggested by the Association.

1.41 From a commercial point of view, the financial performance ofseveral SEBs, the sole customers of NTPC, has been marginal (for detailedexplanation see Annex 9) and even in years when 9-1/2% rates of return wereachieved, a number of SEBs were not able to meet their debt service require-ments. 1/ There are several reasons for this unsatisfactory performance,

1/ However, in all States except one, excise taxes or duties are leviedon electricity sales. Including such taxes as a benefit to the States/SEBs increases the returns by up to 5 percentage points. Furthermore,a recently enacted GOI tax on kWh generated is also equivalent to areturn of about 2-3 percentage points. The total return in economicterms is therefore substantially higher than the commercial return to

the SEBs.

- 13 -

such as insufficient generating capacity which does not permit utilization ofthe market potential to the fullest extent, less than efficient operating of

existing plant, lack of monsoon rains in the Eastern Region leading to severeload shedding and blackouts, railroad and coal mine strikes resulting in insuf-ficient coal supply, and low tariff levels. In the Northern Region (supplyarea of the Singrauli station), the SEBs and the DESU have taken steps toredress the shortcomings (para 1.38d). The GOI representatives indicatedduring negotiations that these organizations were currently operating atlevels which are expected to achieve rates of return of at least 9.5%, netof taxes.

1.42 Indian authorities have recognized that with the rapidly expandingpower sector in the coontry, all aspects of the sector have to be reviewedand that satisfactory solutions have to be found for the various sector prob-lems. Consequently, GOI has established a high-level committee in November1978, known as the "Rajadhyaksha Committee", so called after the name of itsChairman. This committee, whose terms of reference are attached as Annex 10,has been assigned the task to examine and make recommendations for improve-ments of the following aspects of the power sector:

(a) power planning;

(b) project formulation and implementation;

(c) operation and maintenance;

(d) organization and management;

(e) finance, financial management and tariffs;

(f) rural electrification; and

(g) research and development.

Draft reports by the seven expert panels assembled for this purpose have beencompleted and are under review by the committee. The committee is expected tosubmit its findings to GOI during 1980. The Bank Group will continue to takean active interest in the committee's progress, and it is recognized that theBank Group may have to modify its approach to the problems of the Indian powersector in case the committee recommends approaches different from the presentBank Group approach, but equally acceptable. For example, one of the majorconcerns would be that consumers contribute more towards the cost of powersupply facilities through allowing their SEBs to generate internally a reason-able proportion of their capital investments.

II. THE BENEFICIARY - NATIONAL THERMAL POWER CORPORATION LIMITED

Legal Status and Authorities

2.01 NTPC, the beneficiary of the proposed credit was established in1975 under the Companies Act, 1956. The Electricity (Supply) Act, 1948, has

- 14 -

been amended to give the Corporation statutory recognition. NTPC is a companywholly owned by GOI under the general supervision of the Ministry of Energy.Its initial authorized share capital of Rs 1,250 million (US$149 million) wasincreased in May 1979 to Rs 3,000 (US$357 million). The Corporation has aBoard of Directors consisting of not less than four and not more than fifteen,some of whom are part-time.

2.02 The Companies Act, 1956, confers broad powers on NTPC to carry outits work. However, the tariffs to be applied, as well as, any changes in suchtariffs, its investment plans and annual capital budgets, have to be approvedby the Government. NTPC is also subject to periodic examination by theCommittee on Public Undertakings--a body established by GOI to monitor theperformance of public sector enterprises.

2.03 The main objectives for which the Corporation has been establishedare:

(i) to design, construct, and operate large central thermalpower stations and projects; and

(ii) to transmit and sell the power generated.

NTPC will initially own and operate the associated 400 kV transmission systemover which power will be distributed and sold in bulk to State ElectricityBoards. Later this system will be part of the 400 kV interconnected regionalsystem which will be integrated into the national grid.

2.04 NTPC's present program provides for the construction of four thermalpower stations, (Singrauli, Korba, Ramagundam and Farakka). It is also possi-ble that NTPC might ultimately take over the 510 MW Badarpur station nearDelhi (ultimate planned capacity 720 MW). Presently NTPC is in charge of theoperation of Badarpur on a management fee basis.

Organization and Management

2.05 NTPC's organization which at present is necessarily constructionoriented is shown in Annex 11, page 1. The complete range of managementsystems for all disciplines now under formulation are shown in Annex 11,pages 2 and 3. These are based on the philosophies explained in the NTPCpublication "Framework for Project Management" which was discussed with NTPCduring negotiations for the Ramagundam project and further reviewed by themission during appraisal. The organization is adequate.

2.06 NTPC has adopted a two-tier organizational structure: one at thecentral/corporate level and the other for the projects. In addition to theaccepted corporate level, activities such as the development and formulationof policies, and other services relevant to the projects, have been centralized;these are Technical Services, Contract and Procurement Services, QualityAssurance and Expediting and Project Management Services. Other departmentsat the central level are Corporate Planning and Marketing, Corporate Finance,Personnel and Administration.

- 15 -

2.07 The second tier, which embraces project activities, consists of aproject organization for each of the four power plants under construction.Each project organization is headed by a General Manager who is entrustedwith total responsibility for implementation of all aspects of the project'sconstruction program.

2.08 Good progress has been made in building up the organization since1975 when NTPC was established. The Chairman and Managing Director wasappointed in early 1976 and the number of staff appointed by February 29,1980, was 2,658 comprising 523 executives, 131 executives in training and2,006 non-executives. NTPC has also taken over the majority of the employeesof the Badarpur Project and Power Station (see para 2.04).

2.09 Present indications are that NTPC is developing along sound lines.It has a Chairman and Managing Director who is a competent administrator withan established reputation in the formation and development of large industrialundertakings. He has taken a great personal interest in developing a compre-hensive project management system as well as designing the organization andprocedures, while building up an establishment of highly motivated engineersand staff. Remarkable progress has been made in all activities in the fouryears since his appointement and providing this impetus can be maintained withno deterioration in management, NTPC should, with the assistance of consultants,be capable of handling the present large development program. Site organiza-tions are effectively functioning at the Singrauli, Korba and Ramagundam proj-ects. The centralized functions which, in addition to the corporate person-nel, are planning and finance, and provide the engineering, contracting andproject management input. They are organized to meet the project requirementsand to ensure an effective coordination of the projects under construction.

Training

2.10 NTPC is a young organization which is growing rapidly to meet thedemands of its large construction program. The next phase of expansion willinvolve the need to recruit and train operating staff. When all currentdevelopments have been completed and commissioned, NTPC's establishment willhave grown from a present 2,658 to a figure in the neighborhood of 10,000.The importance, therefore, of implementing training programs for the variousexpertises required during the construction and operational phases cannotbe too highly stressed.

2.11 Fortunately, NTPC has placed special importance on this aspect ofits organization, and training programs are being developed by the Corpora-tion which will, in due course, be backed by a training school equipped witha simulator, financed from funds of Credit 793-IN, and other modern facilitiesfor instructing and training the operating staff.

2.12 NTPC's training programs are presently concentrated on pre-operational spheres of activity such as Planning, Design, Construction andManagement. Some of the current major activities are:

- 16 -

(a) Professional engineering training for Executive Trainees(Engineering).

(b) Professional engineering training for Supervisory Trainees(Engineering).

(c) Management development programs.

(d) Seminars and lectures on selected topics.

(e) Familiarization courses for both accounting and managerialstaff on the accounting systems and procedures being imple-mented by NTPC's consultants.

Recruitment of young executive trainees is mainly from engineering graduatesbelonging to mechanical, electrical and civil disciplines on appointment,who are inducted into a one-year training program. The first group of youngexecutive trainees was recruited in February 1977, the second in December1977 and the third by mid-1978 comprising 35, 45 and 84 members respectively.The third group comprising 100 trainees was recruited during 1978 and joinedthe professional engineering training course which started on November 15,1978. The fourth group comprising 131 trainees was recruited in 1979 and thetraining was started on November 25, 1979. The training programs have beenwell designed to provide exposure to power stations under construction andoperation, equipment manufacturing plants, engineering descriptions and projectmanagement services. For these purposes, assistance is taken from a largefaculty of experienced engineers and managers selected from all over thecountry.

2.13 With the first 200 MW generating unit scheduled to commence commer-cial operation in FY1982, NTPC has finalized comprehensive plans for trainingoperational staff, particularly the non-supervisory staff, in the varioustechnical and non-technical trades, to provide foremen to the first two unitsat Singrauli. The manpower for these is being drawn from experienced staffas well as from fresh recruitment. Recruitment of manpower has commenced andkey personnel such as the station superintendent, are already in position.

2.14 On-the-job training has high priority. The methodology includesclassroom lectures, participation in group exercises and discussions sup-ported by direct reading, audio-visual presentations and plant visits.Overall training plans and arrangements at this time are satisfactory.

Sale of Power from the Project

2.15 GOI proposes to allocate 85Z of Singrauli's power to the SEBs ofUttar Pradesh, Punjab, Haryana, Rajasthan and the DESU, the remaining 15%being sold in accordance with priorities to be determined by CEA to Stateswith the greatest need. The Association has received undertakings from therespective SEBs and DESU confirming that they would take power in accordancewith agreed allocations, in aggregate not less than 85% of the output ofpower from the project.

- 17 7

Accounting Organization and Systems

2.16 NTPC and its management consultants report good progress in theplanning of NTPC's finance and accounting organization (Annex 12) and in thedesign and implementation of accounting systems and procedures. The designof systems for both the construction and operational phases of NTPC's activ-ities has been completed. Implementation of systems for the constructionphase is either complete or at an advanced stage both at the corporate centerat headquarters, and also at the sites, while the consultants' proposals forthe operational phase are at an advanced stage of discussion with management.To familiarize staff with the systems and procedures, training courses arebeing conducted by the consultants in conjunction with staff members fromNTPC's corporate cente'r.

2.17 Current problems being faced by NTPC and its consultants in build-ing up the accounting organization are: difficulties in obtaining adequatelyqualified staff; retaining staff at project sites, and the introduction oftighter controls in the management of materials on sites. This latter prob-lem will be resolved by the introduction of the systems for inventory controlwhich have been planned by management. These would include continuous stockchecking and the use of more sophisticated weighing and measuring facilities.The personnel problems are likely to be more difficult to resolve.

Audit

2.18 The audit of NTPC's accounts and records is undertaken by a profes-sional auditor appointed by the Company Law Audit Board, on the recommendationof the Comptroller and Auditor General of India. The auditor is normally amember of the Indian Institute of Chartered Accountants, and his audit reporton NTPC's financial statements is subject to comment by the Auditor General.The current auditor Messrs. V. K. Mehta and Company, Chartered Accountants,Delhi, has audited NTPC's accounts since its incorporation on November 7,1975, and their audit reports have expressed satisfaction at the state of thecompany's affairs during this period. It should be borne in mind that NTPC'sactivities will cover only project construction until FY1982 when power willbe sold for the first time. NTPC has already undertaken, in connection withprevious credits and loan, to submit to the Association/Bank audited financialstatements within seven months of the end of the fiscal year to which theyrelate, together with a certified report by the auditor, and a review of theaccounts by the Director of Commercial Audits. This has been restated inconnection with the proposed credit.

III. THE PROGRAM AND THE PROJECT

The Program

3.01 NTPC's present development program comprising the four centralthermal power stations Singrauli, Korba, Ramagundam and Farakka, with asso-ciated 400 kV transmission, is part of India's power development programwhich is described in paragraphs 1.24 through 1.27. The four power plants,

- 18 -

totalling 7,300 MW, have been located on coal fields, since it is more econo-

mical to transport electricity than coal to the load centers.

3.02 The first stages of the four central power stations consisting in

each case of 3 x 200 MW generating units and associated transmission are under

construction. The commissioning of the power plant units is scheduled between

February 1982 (first 200 MW unit at Singrauli) and July 1989 (last 500 MW

unit at Ramagundam).

The Project

3.03 The project represents the second stage of the Singrauli develop-

ment comprising two additional 200 MW units and two 500 MW units with asso-

ciated transmission totalling about 2,000 km of 400 kV lines. This extensionwould bring the power plant to its final installed capacity of 2,000 MW.

3.04 The Singrauli development which is described in detail in Annex 13

is being constructed on the fringe of the Rihand Reservoir close to the Sin-

grauli coal field deposit at Kota in the Mirzapur district of Uttar Pradesh(see attached maps).

Estimated Cost

3.05 The estimated cost of the project, excluding interest during con-

struction and duties and taxes, is about Rs 7,175 million (US$854 million).On the assumption that most of the contracts will be won by Indian suppliers,

the direct and indirect foreign currency costs are estimated at about Rs 1,199million (US$238 million) and the local currency costs at Rs 5,176 million

(US$616 million). The estimated costs of the principal features of the proj-ect are shown in Table 3.1 below, and in more detail in Annex 14.

Table 3.1: ESTIMATED COSTS

Local Foreign Total Local Foreign Total------Rs million ------ --------US$---------

Preliminary Works 2.7 - 2.7 0.3 - 0.3

Civil Works 449.3 7.7 457.0 53.5 0.9 54.4Electrical and MechanicalPlant 1,761.3 1,289.4 3,050.7 209.6 153.6 363.2

Coal Handling & Transportation 112.6 7.4 120.0 13.4 0.9 14.3Transmission (400 kV) 1,032.4 129.9 1,162.3 122.9 15.5 138.4

Sub-Total 3,358.3 1,434.4 4,792.7 399.7 170.9 570.6

Physical Contingencies 190.2 72.2 262.4 22.6 8.5 31.1Price Contingencies 1,217.9 467.3 1,685.2 145.0 55.7 200.7

Total 4,766.4 1,973.9 6,740.3 567.3 235.1 802.4

Engineering & Administration 409.2 25.2 434.4 48.7 3.0 51.7Project Cost (before Duties

& Taxes) 5,175.6 1,999.1 7,174.7 616.0 238.1 854.1

Duties & Taxes 505.9 - 505.9 60.2 - 60.2

Total Project Cost 5,681.5 1,999.1 7,680.6 676.2 238.1 914.3

Interest during Construction 528.4 - 528.4 62.9 - 62.9Total Financing Required 6,209.9 1,999.1 8,209.0 739.1 238.1 977.2

- 19 -

3.06 The estimates for the main items of equipment are based on thequotations received during 1977, 1978 and 1979 for similar types of plant andequipment for the first stage of the Singrauli and Korba developments, in thecase of the 200 MW units, and for the Trombay Project, in the case of the 500MW units. Prices were escalated to 1979 levels. Transmission costs areequally based on estimates received for the 400 kV transmission associatedwith the first stage of the Singrauli development and on the costs of 400 kVconstruction at various locations in India. Physical contingencies of 10% oncivil works, and of 5% on plant and transmission costs have been allowed toprovide for unforeseeable factors. In assessing price contingencies, it hasbeen assumed that fixed price contracts and contracts with ceilings on priceinflation for turbogenerators and boilers, as in the case of NTPC's three otherpower plants under construction, will also be obtainable in the case of theSecond Singrauli Project. Costs for equipment and erection have been escalatedat 6% for 1979, 10% for 1980, 7% for the years 1981-1983 and 5% for the yearsafter 1983. These assumptions have resulted in price contingencies of 24% forcivil works, 36% for supply and erection of electrical and mechanical equipment,32% for supply and erection of coal handling and transportation equipment, and31% for supply of materials and erection of the transmission system.

Project Financing

3.07 The proposed credit of US$300 million representing about 35% of thecost of the project (excluding duties and taxes and interest during construc-tion), should be applied to the CIF and/or ex-factory costs of plant andequipment, excluding the 2 x 500 MW turbogenerators and associated equipment.The latter would be financed by Kredit fuer Wiederaufbau (KfW) from Germanywhich has been requested by GOI, and in principle has agreed, to extend aloan of about US$100 million equivalent to support the proposed project infinancing the 500 MW turbo-generator units. Civil works, plant erection costs,inland transportation costs, interest during construction, duties and taxesand any other costs not financed from the credit and KfW, aggregating aboutUS$694 million, would be financed by GOI in the form of loan and equitycapital. Retroactive financing of up to US$15 million, to allow NTPC toexercise its option for a repeat order for the two 200 MW turbogenerators andboilers, is proposed.

Engineering and Construction

3.08 As in the case of the first stage, the second stage of the Singraulidevelopment comprises a number of major works which must be carefully coordi-nated to ensure efficient progress. The power plant is expected to be com-pleted by February 1987. The project construction schedule is shown in Annex 15.Much of the detailed power station engineering and design work carried out forthe first stage is applicable to the second stage. Under previous credits andloan granted for NTPC's program, consultants were appointed for the 200 MWunits to: (i) review NTPC's basic engineering and design; (ii) assist in themore sophisticated areas of design; and (iii) provide a back up review ofspecifications for generating units, boilers, transformers and other specifi-cations, as required by NTPC and the Association. NTPC has acquired adequateexperience in the area of design and engineering of 200 MW units, especially

- 20 -

from the first stage of the Singrauli power plant, and therefore there is no

need to appoint consultants for the engineering of the 200 MW units. As for

the 500 MW sets which are being installed for the first time in India, GOI and

NTPC have agreed during negotiations as a condition of effectiveness of the

proposed credit, to engage consultants acceptable to the Association to assist

in the design, the preparation of specifications and bidding documents and theevaluation of bids for the 2 x 500 MW part of the project.

3.09 NTPC, under its competent chairman, has developed a comprehensive

project management system, including program coordination and supervision of

construction of the power stations. However, in view of the magnitude of its

construction program, NTPC has agreed to conclude, as a condition of credit

effectiveness, all contractual arrangements for the employment of consultantsto review its project management and information systems and their initialimplementation.

3.10 Under the first Singrauli Project, GOI agreed to take the necessarysteps to make available adequate coal supplies for the 600 MW stage of thepower plant by the time the first generating unit shall have been commissioned.These measures should be extended under the proposed project for the finalinstalled capacity of the power plant. Agreements to this effect were reached

during negotiations.

Procurement

3.11 Procurement of all equipment to be financed from the proposed credit,

with the exception of the 200 MW units including turbogenerators and boilers,would be on the basis of international competitive bidding in accordance with

the Association's guidelines. For the procurement of the 200 MW turbo-generator

sets and boilers, the Association has agreed, in view of the expected cost and

time savings, that NTPC should exercise the option under the contract for thefirst Singrauli project, which was awarded after international competitivebidding. Documents for individual contracts above US$1,500,000 equivalentwould be subject to prior review by the Association. Bidding documents forsuch equipment, including tender analyses and recommendations for award ofcontracts, would be prepared by NTPC with the assistance of its consultants,

and approved by the Association. To facilitate contract coordination, theinvitation to tender for major plant contracts would be on a supply, deliverand erect basis. This could include civil works in certain cases where these

cannot be disassociated from the plant contract--i.e., coal handling, substa-

tion structures, transmission lines, but such civil works would not be financedfrom the proposed credit. Local manufacturers would be expected to bid forall categories of equipment. A domestic preference of 15% or the import duty,

whichever is less, would be applied in bid comparison for equipment contracts.

To prevent administrative procurement delays, in case the lowest evaluated

bidder is a foreign manufacturer, GOI agreed during negotiations that it wouldgrant import permissions for such items without further review by any agency

of the Government. There are competent local contracting firms in India and

also manufacturing facilities covering most of the equipment for the project.All goods not financed from the proposed credit (and from the KfW loan) willbe subject to local procurement procedures, which are satisfactory.

- 21 -

Disbursements

3.12 Disbursements from the proposed credit would be made against 100%of the cost of consultants retained for the 500 MW units (see para 3.08) andto review NTPC's project management systems (see para 3.09), and against thecost of the equipment to be financed from the proposed credit on the followingbasis:

(a) 100% of the ex-factory cost of equipment procured inIndia after international competitive bidding; and

(b) 100% of the foreign cost of equipment procured fromabroad.

Any balance of the credit not used after commitments have been made for allitems covered by the list of goods, could be used to purchase other electricaland mechanical equipment for the project, after obtaining the Association'sagreement. Retroactive financing of up to US$15 million is proposed for ex-penditures after August 1, 1979, made to allow NTPC to exercise its optionfor a repeat order for the two 200 MW turbogenerators and boilers (para 3.11).The estimated disbursement schedule is given in Annex 16.

Ecological Aspects

3.13 The ecological and environmental aspects of the project were dis-cussed during appraisal. GOI confirmed that the Singrauli development hadreceived the approval of the Indian National Committee on Environmental Plan-ning and NTPC agreed to comply with all environmental quality standardsprescribed by this committee in the design, construction and operation ofthe project.

3.14 As in the case of the first stage of the Singrauli development, theprincipal environmental problems with the proposed project are: (a) location,(b) stack emissions, (c) heat dissipation, and (d) ash disposal. These areoutlined below:

(a) Location. The proposed Singrauli power station is a pithead station and is situated far from any urban area.Accordingly, there are no problems other than the need toensure the health and environment of the operating staffwho will be housed in a residential area to be constructedsome 4 or 5 km from the power station.

(b) Stack Emissions. Electrostatic precipitators will be in-stalled and the stack will be of such a height that emittedparticulate matter will be spread over a sufficiently widearea to reduce the density of pollutants to an acceptablelevel. The sulphur content of the coal is in the range of0.3% to 0.6% which is low and does not present a pollutionproblem.

(c) Heat Dissipation. The cooling pond is designed to ensurethat its average temperature increase will not exceed 3%with the station under full operation. This would haveno adverse effect on fisheries.

- 22 -

(d) Ash Disposal. The ash will be pumped as a slurry, througha 5 km pipeline, to an ash dump area which has been reclaimedfrom the Rihand Reservoir. The area will be enclosed by abund, and together with a reserve area, will be adequate tocontain the ash output for the life of the power station.

3.15 With regard to the safety and occupational health of employees,safety regulations for power stations, to which all operating personnel mustconform, will be strictly enforced. As far as noise levels are concernedthe turbine hall of a modern steam turbine power station, which is the noisi-est area of the plant, has a sound pressure level of less than 90 decibelswhich is well below the maximum acceptable threshold for the normal 8 hour/day

shift worker.

Project Risks

3.16 The project represents one phase of an overall development programwhich comprises 7,300 MW of generating plant and some 7,000 km of 400 kVtransmission. It is part of a tightly designed program with plant and trans-mission coming in at phased intervals throughout the period 1982 through 1988.Maintaining this program on schedule requires careful coordination and expertsupervision at all levels. The principal risk is the possibility of slippagewhich could give rise to delayed commissioning of plant and loss of revenues.With a program of construction of this magnitude, there is no guarantee thatsome delays will not occur, but these will be kept to a minimum through care-ful coordination and supervision during construction and careful attention,when placing contracts, to the capability of manufacturers to meet the deliveryschedules.

3.17 Other risk areas are in engineering design, cost overruns and prob-lems of commissioning and operation during the early operational stage withresultant loss of revenues. There is also the risk of damage due to fire,explosion, etc., but this is covered by insurance provided by the respectivecontractors during the construction stage and by GOI through its self-insurancepolicy after commissioning.

3.18 These risks have been carefully assessed and the following safe-guards taken:

(a) NTPC is being assisted by consultants and sub-consultants, and this should minimize problemsdue to error at the engineering and design stage;

(b) Plant and equipment cost are based on similar workscurrently in progress in India; provision has beenmade for cost escalation and there should be littlerisk of any substantial cost overrun;

(c) a number of 200 MW generating units will have beenin operation for some years before the project iscommissioned, thus, providing experience and trainedmanpower for the project.

- 23 -

IV. FINANCIAL ANALYSIS

Introduction

4.01 Financial forecasts of NTPC's annual operations through FY91 arepresented in Annexes 17 through 19. The forecasts are based on a capitalinvestment program (Annex 18, page 2) which envisages the construction of fourlarge thermal power stations with a combined capacity of 7,300 MW, togetherwith almost 7,000 circuit kilometers of 400 KV transmission lines at a latestestimated cost of Rs 48 billion (US$5,714 million equivalent). The powerstations and transmission lines will be commissioned on a phased basis duringthe period February 1982 to July 1989.

4.02 Concurrently with this construction program, NTPC is responsible forthe operation and development of the Badarpur power station in Delhi. Thisinvolves directing operations of the 510 MW thermal generating plant (initial300 MW plus 210 MW extension constructed and commissioned by NTPC), and forconstruction of a further 210 MW extension already sanctioned and due forcommissioning in September 1981.

Future Earnings

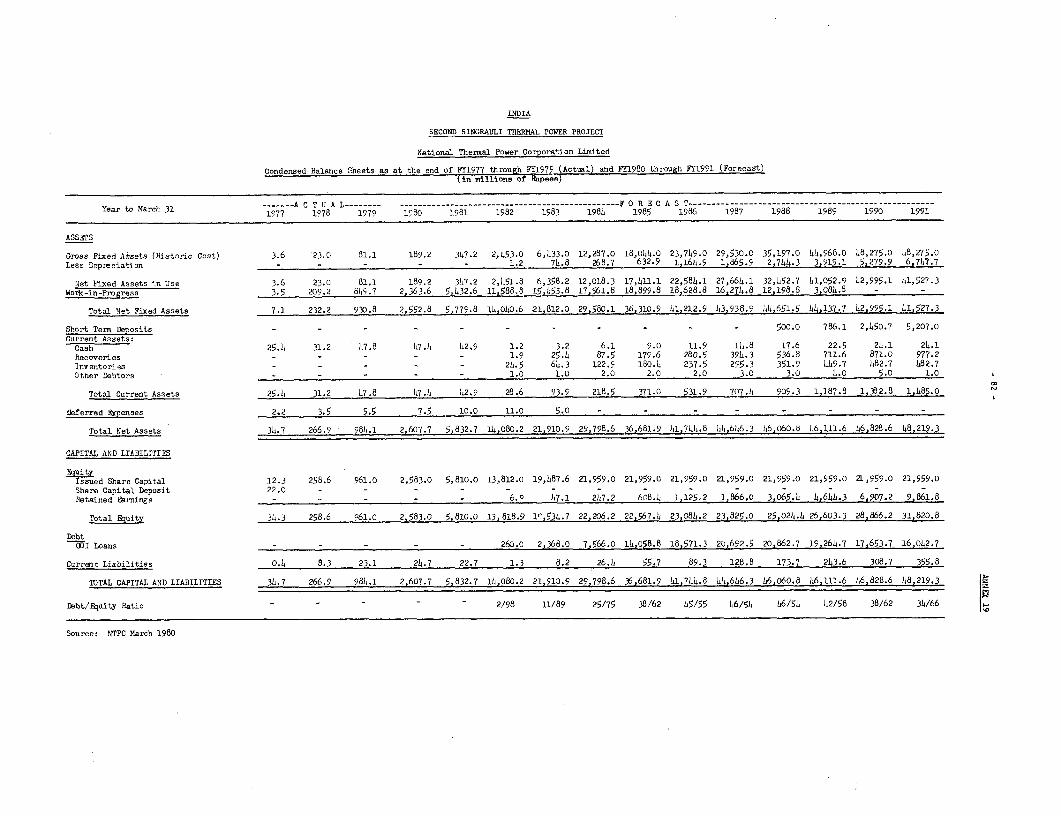

4.03 NTPC will become operational in February 1982 when its first 200 MWgenerating unit at Singrauli is expected to be commissioned. Additional gene-rating capacity scheduled for commercial operation during the succeeding sevenyear period, is set out in Annex 20, page 1, paragraph 2(a). NTPC's projectedearnings are based on the assumption that NTPC would supply bulk power at 400 kVto State Electricity Boards at a tariff level which would enable it to earn areasonable return on its investment. This was defined in connection withprevious credits and loan as being a tariff level sufficient to produce arate of return of not less than 9.5% on the book value of the average netfixed assets in service in FY1989 1/, and applied from the time of commis-sioning of the first generating unit in Singrauli in 1981/82 2/.

4.04 Several changes were necessary in, a number of assumptions underlyingNTPC's financial projections, because of: slippage in the commissioning datesof operating plant, release of GOI funds as equity capital in the earlieryears, followed by loan capital in later years and cost revisions in theoverall investment program. The effects of these changes are to:

1/ The first fiscal year in which all generating units at Singrauli wereprojected to operate at 5,500 hours a year.

2/ There are no requirements within India either statutorily or for commer-cial accounting purposes, to note fixed asset and depreciation data atcurrent price levels. The equivalent in real terms of a 9.5% rate ofreturn on an historic rate base in FY1989 is about 7.5%.

- 24 -

(a) increase the bulk selling price by 12% over the levelestimated at the Ramagunda appraisal, bringing it tojust over 29 paise/kWh;

(b) eliminate losses during the initial years of operation; and

(c) reduce by some 5% the overall cost of the investment program.

4.05 The income statement (Annex 17) shows the projected earnings per-formance for FY1982 through FY1991. Mainly because of a substantially reducedinterest charge, resulting from the revised financing arrangement referred toat paragraph 4.04, NTPC will become profitable in its first year of commercialoperation, FY1982. Earnings will rise rapidly thereafter, following the rapidcommissioning of plant from FY1984 through FY1989, and will reach the stipu-lated rate of return of 9.5% in FY1989, rising to 11.4% by FY1991. Internalresources will generously cover debt service requirements in the initial yearsFY1982-FY1986 and adequately thereafter.

4.06 The regulation of NTPC's annual earnings is a function imposed onGOI by the amendment to Section 75A of the Electricity (Supply) Act, 1948.Under the amendment, GOI is required to specify the quantum of annual surpluswhich should be earned so as to provide from internal resources a reasonablecontribution to capital investment, and to pay dividends on the equity capital.Under present assumptions, NTPC's internal resources would not be adequate tomeet these commitments until FY1988. During negotiations, GOI confirmed thatwhile NTPC's surplus would be regulated from the time NTPC became revenue earn-ing (FY1982) the appropriate amount of surplus would depend, in part, uponNTPC's future investment program at that time. It was thus premature to spe-cify a surplus at this stage. However, the 9.5% rate of return would beretained as a minimum requirement in FY1989 and thereafter.

4.07 As in earlier credits and loan, it has been restated for this pro-posed credit that NTPC would achieve in FY1989 and maintain thereafter arate of return not less than 9.5% on net fixed assets in operation, and toset tariffs from the time the first generating unit at Singrauli is commis-sioned, at levels not lower than estimated to achieve the required 9.5% rateof return in FY1989.

Taxation

4.08 NTPC is liable for income tax under the Indian Income Tax Acts.Because of the large capital expenditure program between FY1979 and FY1988liability to tax will not arise in the foreseeable future and a tax equaliza-tion reserve is not necessary.

Financing Plan FY1977-FY1987

4.09 The following table sets out the financing plan for the eleven-yearperiod FY1977 through FY1987 (the year during which the project is scheduledfor completion):

- 25 -

Table 4.1

Total TotalRs Million US$ Million x

Source of FundsInternal Cash Generation 6,426 765 14Less: Debt Service (3,083) (367) (7)

Deferred Charges (11) (1) -Working Capital Increase (579) (69) (1)

Net Internal Cash Generation 2,753 328 6Capital Raised:GOI Equity 21,959 2,614 48GOI Loans 13,413 1,611 29IDA Credits/IBRD Loan onlent /a 7,680 900 17Total 43,052 5,125 94

Total Sources 45,805 5,453 100

To Finance:Investment Program 45,805 5,453 100(incl. interest duringconstruction)

/a Includes the following:

Singrauli (Credit 685-IN) 1,290 150 3Korba (Credit 793-IN) 1,720 200 4Ramagundam (Credit 874-IN) 1,720 200 4Ramagundam (Loan 1648-IN) 430 50 1Second Singrauli ProposedCredit 2,520 300 5

7,680 900 17