FDI BETWEEN EU MEMBER STATES: GRAVITY MODEL AND TAXES

16

FDI BETWEEN EU MEMBER STATES: GRAVITY MODEL AND TAXES 1 Paweł Folfas M.A. 2 Warsaw School of Economics Institute of International Economics Abstract Gravity models utilize the attractive force concept as an analogy to explain volume of trade, capital flows and migration among the countries of the world. A fundamental goal of my paper is to prove that direct investment flows between EU Member States are determined by standard variables included in gravity models such as: gross domestic products (total and per capita) of home and host economy and distance between them. In my gravity model of FDI I include not only geographic distance but also variables illustrating economic distance, namely: membership in euro area, cultural similarity, duration of membership in the EU (EC). Additionally, my model encompasses variables linked with tax policy of EU Member States. I prove that differences in corporate tax burdens determine FDI flows. States with simpler and lower taxes allure more direct capital. Especially, model confirms that European offshore financial centers: Cyprus, Luxembourg and Malta play a significant role in intra-EU direct capital flows. On one hand, my model includes time invariant variables, so the model with fixed effects is not proper. On the other hand, as individual effects might be correlated with some independent variables, model with random effects can be also not adequate. Consequently, I use Hausman-Taylor estimator. My FDI gravity model is based mainly on OECD and WDI databases concerning two last decades. Keywords: FDI, gravity model, the European Union, corporate taxes JEL codes: F14, F15, F21 1 Participation in ETSG 2011 Conference was financed from doctoral scholarship of National Science Centre (No. of agreement 3953/B/H03/2011/40). Text includes partial results of PhD research. 2 [email protected]

-

Upload

independent -

Category

Documents

-

view

6 -

download

0

Transcript of FDI BETWEEN EU MEMBER STATES: GRAVITY MODEL AND TAXES

FDI BETWEEN EU MEMBER STATES:

GRAVITY MODEL AND TAXES1

Paweł Folfas M.A.2

Warsaw School of Economics

Institute of International Economics

Abstract

Gravity models utilize the attractive force concept as an analogy to explain volume of

trade, capital flows and migration among the countries of the world. A fundamental goal of

my paper is to prove that direct investment flows between EU Member States are determined

by standard variables included in gravity models such as: gross domestic products (total and

per capita) of home and host economy and distance between them.

In my gravity model of FDI I include not only geographic distance but also variables

illustrating economic distance, namely: membership in euro area, cultural similarity, duration

of membership in the EU (EC). Additionally, my model encompasses variables linked with

tax policy of EU Member States. I prove that differences in corporate tax burdens determine

FDI flows. States with simpler and lower taxes allure more direct capital. Especially, model

confirms that European offshore financial centers: Cyprus, Luxembourg and Malta play a

significant role in intra-EU direct capital flows.

On one hand, my model includes time invariant variables, so the model with fixed

effects is not proper. On the other hand, as individual effects might be correlated with some

independent variables, model with random effects can be also not adequate. Consequently, I

use Hausman-Taylor estimator. My FDI gravity model is based mainly on OECD and WDI

databases concerning two last decades.

Keywords: FDI, gravity model, the European Union, corporate taxes

JEL codes: F14, F15, F21

1 Participation in ETSG 2011 Conference was financed from doctoral scholarship of National Science Centre (No. of agreement 3953/B/H03/2011/40). Text includes partial results of PhD research. 2 [email protected]

2

1. Background studies on gravity models of foreign direct investments

Gravity models appear as an adaptation of the law of universal gravitation3 for

socioeconomic phenomena. For the first time the law of gravitation was applied to social

science by Carey [1858, pp. 42, 88–90, 371–373, 465]. According to Carey phenomena in

physics and in social science are determined by similar laws and the gravitational attraction is

also present as a “molecular gravity in a society”. He claimed that more people in some area

means stronger “social attractive force” which is directly proportional to the “mass of people”

and inversely proportional to the distance (not only geographic, but also social or

psychological distance) between persons. Carey launched studies based on gravity models

which focused on determinants of masses’ behaviour, especially interdependence between

size of population, distance and attractive force between people. Gravity models became tools

in analyzing: size of migrations and trade, number of phone calls and number of passengers

and goods in transport. These studies concerned the attractive force between masses of people

living in different regions of single country4.

In 1960s gravity models were applied to analyzing international trade flows. Pioneers

in these studies were: Linemann [1963], Pöyhönen [1963], Pullainen [1963] and Tinbergen

[1962]. They were conducting independent and simultaneous studies which brought similar

results. However the most known is study proposed by Tinbergen who was announced as a

discoverer of gravity law (gravity equation) in international economics (see equation (1)).

(1) dij

bj

ai

ij DYY

CX

where notation is defined as follows:

Xij – international flow from reporter i (origin country) to partner j (destination country) or the

sum of the flows in both directions (for example: export, import or sum of export and import

values; size of migration, foreign direct investment, tourism),

Yi(j) – economic sizes of the two locations (for example: GDP, population, endowment of

labour, land or capital),

Dij – distance between the locations (usually between their economic centres),

3 In 1687, Newton proposed the law of universal gravitations which states states that every point mass in the universe attracts every other point mass with a force that is directly proportional to the product of their masses and inversely proportional to the square of the distance between them. 4 See for example: Ravenstein [1885], Reilly [1929], Stewart [1948], Converse [1949], Zipf [1949], Dodd [1950], Hammer and Ikle [1957].

3

G – gravitational constant,

a, b and d – elasticity of Xij to change in Yi, Yj and Dij.

Since Tinbergen’s study the gravity equation has been one of the most popular

empirical equations that has been successfully used to analyze the wide spectrum of

interactions in international economics. The gravity equation postulates that the amount of

flow between two locations increases in their economic sizes and decreases in the cost of

transportation between them as measured by the distance between economic centres of

locations.

However, there are many variables which can embody economic masses of locations.

In studies of bilateral trade and direct investment flows the economic size of the exporting and

importing countries are usually measured by gross domestic product. However economic size

can be also measured by: gross national product, gross domestic product and population, gross

domestic product per capita or endowment of production factors (absolute value or per

capita). Therefore, there are a number methods of measuring gross domestic products: in

current prices, in constant prices or in purchasing power parity. It is debatable which measure

is the most adequate for gravity models. In my opinion, as international flows of trade or

capital are measured in current prices, gross domestic product in current prices is the most

proper. Additionally, gross domestic products in PPP distort the difference between countries,

as their values are higher for developing countries and lower for developed economies

[Czarny, Folfas 2011, pp. 5– 6].

Distance in the law of universal gravitation illustrates resistance to attractive force

between point masses. In international economics resistance to gravity force between

locations is embodied by all factors which hamper international flows of goods, services,

capital, labour and technology. These factors can be divided in two groups: economic and

noneconomic. The first group encompasses: geographic distance between economic centres of

locations, adjacency, characteristics of geographic location (island, landlocked country),

cultural similarity (common languages, colonial links), volatility of exchange rates (common

currency, exchange rate regime), tariffs and nontariffs trade barriers, membership in

international organizations (free trade areas, custom unions, common markets, economic and

monetary unions) and the quality of infrastructure. The second group includes: regulations,

political conflicts and environmental barriers [Head 2000, pp. 5–10].

Moreover, there are a few candidates for dependent variable in gravity models.

Bilateral international flows can be illustrated by: export, import or sum of both of them. In

4

the case of international trade, exports value is not distorted by tariffs, nontariffs barriers and

cost of transport and insurance. However data concerning imports are more precise thanks to

the registration linked with customs duties (data concerning exports are usually based on tax

returns). Taking into consideration a sum of export and import is the most complete method,

however it meets difficulties with gaps in data. In the case of foreign direct investments and

other capital flows data concerning inflows are more precise than data concerning outflows,

which usually are riddled with gaps [Czarny, Folfas 2011, p. 7].

Popularity of gravity models in empirical studies concerning international trade in

goods and services and international movements of production factors has encouraged

economist to create theoretical foundations of gravity law, especially gravity model of

international trade. To the most important belong studies conducted by: Anderson [1979],

Bergstrand [1985, 1989], Helpman [1987], Deardoff [1998], Anderson and van Wincoop

[2003], Feenstra [2004], Haveman and Hummels [2004], Debaere [2005], Helpman, Melitz

and Rubinstein [2008]. The majority of mentioned authors conducted empirical studies of

bilateral trade based on different version of gravity models5.

Generally, gravity model is a kind of short-hand representation of supply and demand

forces. If Xij represents exports and if the country i is the origin, then Yi represents the amount

it is willing to supply. Meanwhile Yj represents the amount destination j demands, in other

words the amount of income country j spends on all goods from any source i. Big economies

with high income usually spend a lot of money on import. They are also able to allure quite

big share of other economies’ expenditures (so they are able to export a lot of goods) because

they produce goods in wide variety. Consequently, the amount of export is higher due to big

economic size at least of one partner [Head 2000, p. 3; Krugman, Obstfeld 2007, pp. 25–29].

Gravity model has become one of the most popular and successful analytical tool in

international economics, especially due to its high explanatory power and easily available data

in studies concerning international trade of goods. However, recently gravity model has

become very popular analytical tool also in explaining bilateral flows of capital, especially in

explaining determinants of foreign direct investments (FDI). Unfortunately construction of

FDI gravity models meets a number of additional obstacles. Firstly, the values of bilateral FDI

flows are available only for selected countries, mostly for developed countries (OECD, UE)

or countries from one region. Consequently, construction of FDI gravity models for all (even

the majority) countries of the world seems to be not possible. Secondly, FDI flows are

5 Studies based on gravity model of trade conducted by Polish economist – see for example Cieślik [2009], Cieślik, Michałek, Mycielski [2009] and Czarny, Śledziewska [2009].

5

vulnerable to single events (for example large cross-border mergers and acquisitions) what

may lead to irregularities disturbing gravity law. Instead of FDI flows, FDI stocks can be

used. However in my opinion FDI stocks as cumulative data are not adequate for independent

variables in model which describe values of GDPs or endowments of production factors only

in one year. Thirdly, there are negative values of FDI (disinvestments) which can also disturb

the regularity of gravity law. In my opinion these negative cannot be excluded from the

sample because it may lead to falsifying the results of empirical studies (disinvestments

account for 10–20% of all observations).

Despite of all mentioned difficulties, in the last ten years gravity models of FDI have

become very popular6. Apart from standards variables describing GDPs of host and home

country and geographic distance between economic centres of two locations, independent

variables in FDI gravity models illustrates issues such as:

endowment of physical and human capital (see Egger, Pffaffermayr [2004a]),

endowment pf labour force (see Bevan, Estrin [2004], Egger, Pffaffermayr [2004a, b],

Milner et al. [2004]),

quality of legal system (see Milner et al. [2004], Lada, Tchorek [2008]),

infrastructure – transport networks, number of phone calls (see Eggger, Pffaffermayr

[2004b], Roberto [2004], Portes, Rey [2005]),

investment risk and barriers, protection of foreign investors (see Bevan, Estrin

[2004]),

cultural similarity – common language, similarity in legal systems (see Buch et al.

[2003]),

taxation (see Egger, Pffaffermayr [2004b], Milner et al. [2004]),

bilateral trade, openness of economies (see Stone, Jeon [1999], Szczepkowska,

Wojciechowski [2002], Kumar, Zajc [2003], Bevan, Estrin [2004], Portes, Rey [2005],

Lada, Tchorek [2008]),

unemployment rate (see Roberto [2004], Szczepkowska, Wojciechowski [2002]), 6 Apart from gravity model bilateral FDI relations has been also scrutinized in other contexts. Desbordes, Vicard [2009] investigates the effect of implementation of bilateral investment treaties on bilateral stocks of foreign direct investment. They show that the effect of entry into force of bilateral treaty crucially depends on the quality of political relations between signatory countries; it increases FDI more between countries with tense relationships than between friendly countries. Therefore, Benassy-Quere, Coupet and Mayer [2007] investigate institutional determinants of FDI and find that the similarity of institutions between the host and home country raises bilateral FDI flows. Additionally, Choi [2004] examines the role of FDI in convergence of income level and growth. Panel analysis brings conclusion that income level and growth gaps between source and host countries decreases as bilateral FDI increases. Finally, UNCTAD [2007, pp. 19–22] includes studies concerning bilateral FDI relationships based on FDI intensity index – see also my paper from previous edition of ETSG [Folfas 2010b].

6

membership in international organizations (see Brenton et al. [1999], Buch et al.

[2003], Kumar, Zajc [2003], Lada, Tchorek [2008]),

education of labour force (see Kajmar, Zajc [2003], Eggger, Pffaffermayr [2004b],

Lada, Tchorek [2008]),

unit labour costs, average wages (see Szczepkowska, Wojciechowski [2002], Bevan,

Estrin [2004], Lada, Tchorek [2008]),

interests rates (see Bevan, Estrin [2004]),

development of financial markets (see Portes, Rey [2004], Lada, Tchorek [2008]),

bilateral investments treaties (see Egger, Pffaffermayr [2004b]),

exchange rates, common currencies (see Szczepkowska, Wojciechowski [2002], Lada,

Tchorek [2008])

expenditures on R&D (see Lada, Tchorek [2008]),

inflation rate, GDP deflator (see Szczepkowska, Wojciechowski [2002], Lada,

Tchorek [2008]).

The wide spectrum of independent variables appears as a symptom of high potential of

FDI gravity models and the perspective of their further development. As my empirical studies

focuses on FDI bilateral flows between EU–27 Member States, I pay attention to two groups

of determinants of FDI: investment creation effect (due to processes of integration in the old

continent) and corporate taxation. Firstly, investment creation effect means intensification of

FDI flows between countries participating in regional integration (see for example Baldwin,

Forslid and Haaland [1996], Motta, Norman [1996]). It is possible that membership in the EU

and in the euro area intensify flows of direct capital between EU Member States. Secondly,

there are significant disparities in corporate taxation between EU Member States. Differences

in taxes especially in corporate tax rates allure transnational corporations to use transfer

pricing in order to minimize total tax payments. Transfer pricing is directly linked with flows

of direct capital, especially to and from offshore financial centres7 (tax havens) such as:

7 Traditionally, tax haven is a country or territory where certain taxes (especially direct taxes such as: income taxes or inheritance taxes) are levied at a low rate or not at all. Tax havens allow non-residents to escape higher taxes in their country of residence. Particularly, liberal tax jurisidictions allure to establish foreign affiliates of transnational corporations (TNCs) originating from developed countries, where corporate taxes are much higher. According to the traditional approach tax havens can be divided into two groups: no-tax havens and low-tax havens. The first group encompasses: Bermuda, British Virgin Islands, Cayman Islands, Montserrat, Nauru and Turks and Caicos Islands. These tax havens impose nil taxes generally or impose taxes only on domestic incomes (the rule of no-tax-on-foreign-income). Low tax havens include: Andorra, Anguilla, Antigua and Barbuda, Aruba, Bahamas, Bahrain, Barbados, Belize, Cook Islands, Dominica, Gibraltar, Grenada, Guersney, Hong Kong (SAR of China), Isle of Man, Jersey, Liberia, Liechtenstein, Macau (SAR of China), Maldives, Marshall Islands, Mauritius, Monaco, Netherland Antilles, Niue, Panama, Samoa, Saint Lucia, Saint Kitts and Nevis, Saint Vincent and the Grenadines, Samoa, Seychelles, Tonga, US Virgin Islands, Vanuatu. However,

7

Cyprus, Luxembourg and Malta. Consequently, it is possible that differences in corporate tax

rates also intensify direct capital flows between EU Member States.

2. Data and methodology

In my study, I use bilateral direct investments flows between EU–27 Member States

based on data concerning FDI inflows into host economy (i) from home economy (j). The

sample covers the period 1990–20098. My gravity model is estimated in terms of natural

logarithms (ln) – see equation (2).

(2) ijtijijtijjtitijt cZDGDPGDPFDI lnlnlnln 3210

where notation is defined as follows:

i, j, t – indexes respectively for: host economy, home economy and year,

FDIijt – FDI inflow into host economy coming from home economy in year t,

GDPi(j)t – Gross Domestic Product of host economy (home economy) in year t,

Dij – geographic distance between economic centres of host and home economy (constant for

EU Member States during 1990–2009),

Zijt – vector of other variables which determines bilateral FDI flow;

cij – individual location-pair specific effect,

ijt – error term.

Including in my specification individual location-pair specific effect suggests

application one of the typical panel data based estimators, namely fixed or random effects

approach. However, the fixed effects approach is not adequate for models including time

invariant variables – for example distance, which is one of the fundamental variable. On the

contrary, random effects approach is available also for models with time invariant variables.

Additionally, this approach needs zero correlation between the individual effects and the traditional approach of tax haven is not enough. Contemporary name of tax havens is offshore financial centres (OFCs) and mean jurisdictions that make their living mainly by attracting foreign financial capital. They offer foreign business and well-heeled individuals not only low or no taxes, but also: economic and political stability, business- friendly regulation and laws, well-developed sector of services (especially in finance, banking and insurance), lack of constraints in capital flows and above all discretion. OFCs includes traditional tax havens but also countries (territorias) such as: Costa Rica, Cyprus, Malta, Dublin (Ireland), Labuan (Malaysia), Lebanon, Luxembourg, Singapore, Switzerland which has not been perceived as traditional tax havens. Geographically, OFCs can be divided into three groups: European OFCs, American OFCs and Asian (with Oceania) OFCs – see more The Economist [2007], Folfas [2008], Folfas [2010a]. 8 Before 1990s new EU–12 Member States had been cut off from substantial FDI inflows, consequently the first included year is 1990. Therefore, data for 2010–2011 has not been available yet (apart from some partial data).

8

independent variables in the model. Unfortunately, in my specification this assumption does

not hold. My model encompasses independent variables which characterize pair of host and

home economy (for example difference in corporate tax rates or simultaneous membership in

euro area). These kinds of variables are potentially correlated with individual effect,

consequently approach based on random effects is also not proper. In this situation there is

still one solution to be applied – Hausman-Taylor [1981] estimation method. It allows using

of both time-varying and time invariant variables and some of them can be endogenous in the

sense of correlation with individual effects, but remain exogenous with respect to error term

[Czarny et al. 2010, pp. 10–12].

Additional variables in my specification encompass variables linked with European

integration and corporate taxation in EU–27 Member States (a few of them are dummy

variables) – see equation (3).

(3)

ijtijcijOFCjtTaxitTaxijCultureijAccession

ijtEAijtEUjtgdpitgdpijDjtGDPitGDPijtFDI

7ln654

32ln1ln3ln2ln10ln

where notation is defined as follows: Abbreviation Description Data source

FDI Foreign direct investments inflows (current prices, USD)

OECD and Eurostat

GDP Gross Domestic Product (current prices, USD) The World Bank, WDI D Geographic distance between capitals (km) CEPII gdp Gross Domestic Product per capita (current prices,

USD) The World Bank, WDI

EU Dummy variable: 1 if both states belong to the EU and 0 otherwise (this variable incorporates EU enlargements)

Eurostat

EA Dummy variable: 1 if both states use euro as legal tender and 0 otherwise

Eurostat

Accession Dummy variable: 1 if both states join the EU in the same year and 0 otherwise

Eurostat

Culture Dummy variable: 1 if both states belong to the same group and 0 otherwise

Own classification including groups of EU Member States: (1) Celtic (IE, UK); (2) Mediterranean (CY, EL, IT, MT, PT); (3) Francophone and Benelux (BE, FR, LU, NL); (4) German (AT, DE, HU); (5) Slavonic (CZ, PL, SI, SK); (6) Baltic (EE, LT, LV); (7) Scandinavian (DK, FI, SE); (8) Other (BG, RO)

Tax Corporate tax rate (part of profit; if progressive tax average rate)

Eurostat

OFC Dummy variable: 1 if host or home economy is offshore financial centre (CY, LU, MT)

OECD and The Economist [2007] (list of tax havens/offshore financial centres)

9

Therefore I conduct empirical analysis for smaller sample which covers the period

2005–2009, however with additional independent variables linked with taxation9 - see

equation (4).

(4)

ijtijcjtTaxTotalitTaxTotaljtsTaxPaymentitsTaxPaymentjtTaxTimeitTaxTime

ijOFCjtTaxitTaxijCultureijAccession

ijtEAijtEUjtgdpitgdpijDjtGDPitGDPijtFDI

ln10ln9ln8

7ln654

32ln1ln3ln2ln10ln

where notation is defined as follows: Abbreviation Description Data source

TaxTime Total time required to fulfill all tax payments (hours) The World Bank, WDI TaxPayments Number of tax payments The World Bank, WDI TaxTotal Total costs due to tax payments (part of profit) The World Bank, WDI

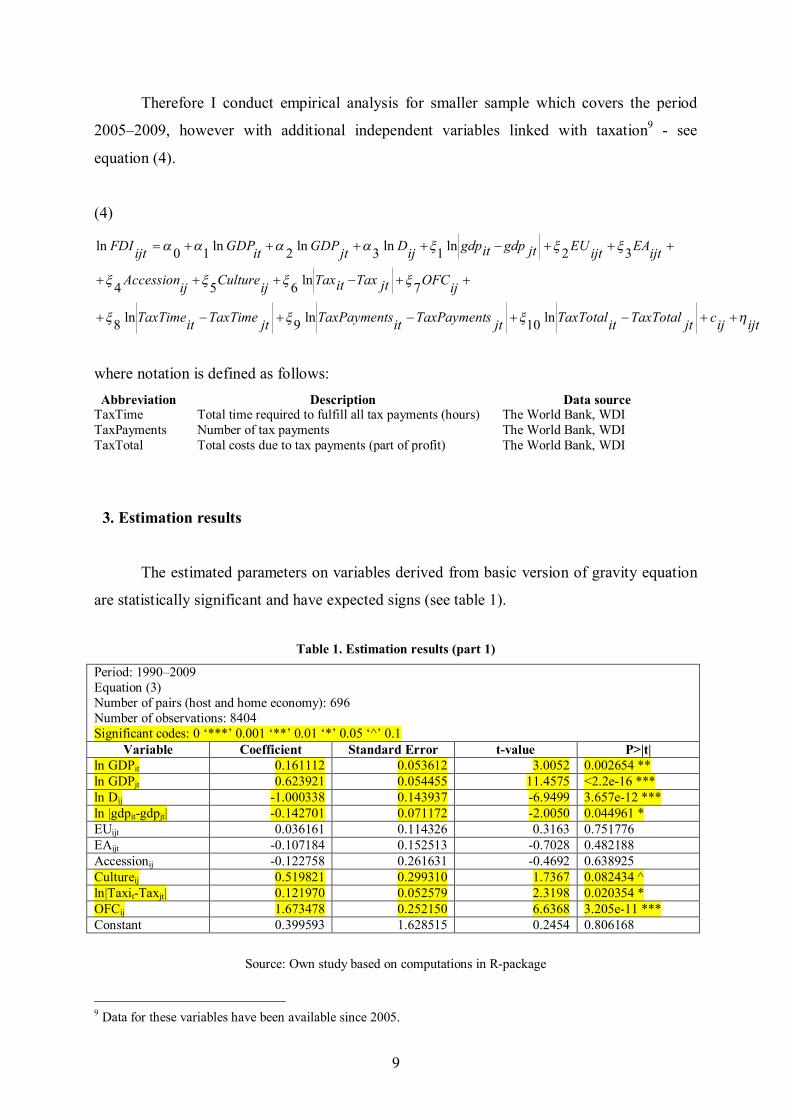

3. Estimation results

The estimated parameters on variables derived from basic version of gravity equation

are statistically significant and have expected signs (see table 1).

Table 1. Estimation results (part 1)

Period: 1990–2009 Equation (3) Number of pairs (host and home economy): 696 Number of observations: 8404 Significant codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘^’ 0.1

Variable Coefficient Standard Error t-value P>|t| ln GDPit 0.161112 0.053612 3.0052 0.002654 ** ln GDPjt 0.623921 0.054455 11.4575 <2.2e-16 *** ln Dij -1.000338 0.143937 -6.9499 3.657e-12 *** ln |gdpit-gdpjt| -0.142701 0.071172 -2.0050 0.044961 * EUijt 0.036161 0.114326 0.3163 0.751776 EAijt -0.107184 0.152513 -0.7028 0.482188 Accessionij -0.122758 0.261631 -0.4692 0.638925 Cultureij 0.519821 0.299310 1.7367 0.082434 ^ ln|Taxit-Taxjt| 0.121970 0.052579 2.3198 0.020354 * OFCij 1.673478 0.252150 6.6368 3.205e-11 *** Constant 0.399593 1.628515 0.2454 0.806168

Source: Own study based on computations in R-package

9 Data for these variables have been available since 2005.

10

The positive values of the estimated parameters on the GDP of both host and home

economy show that FDI flows are bigger between larger economies. However the estimated

coefficients are lower than in typical gravity model of international trade (values between 0.7

and 1.1). It can be caused by disinvestments and fluctuations in FDI inflows caused by single

events (for example large M&A). Therefore, the value of estimated parameter on the GDP of

home economy is much higher than value on the GDP of host economy. It suggests the higher

magnitude of home economy in bilateral FDI flows. As expected distance has negative impact

on bilateral FDI flows and also the impact of difference in GDP per capita is negative. It

proves that between similar economies FDI flows are more intensive.

Figure 1. FDI inflows into the EU–27 Member States vs. global FDI inflows (1990–2009, Mio. USD)

0

500000

1000000

1500000

2000000

2500000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Into EU-27 from World Global FDI inflows Into EU-27 from EU-27

Source: Own study based on UNCTAD’s and Eurostat’s data

All three variables linked with the European integration processes are not statistically

significant. There is no positive impact on FDI inflows when both host and home economy

belong to the EU, euro zone or both joined the EU (EC) in the same year. Firstly, it may

suggest that individual characteristics of host and home economies are more important for

bilateral FDI flows than participation in regional integration (weak investment creation

effect). Secondly, dummy variable might not be enough adequate for illustrating the results of

integration processes which is continuous, not discrete. Consequently, investment creation

effected linked with the EU-enlargement in 2004 and 2007 could have occurred earlier – for

example when new EU Member States joined free trade area, started accession negotiations

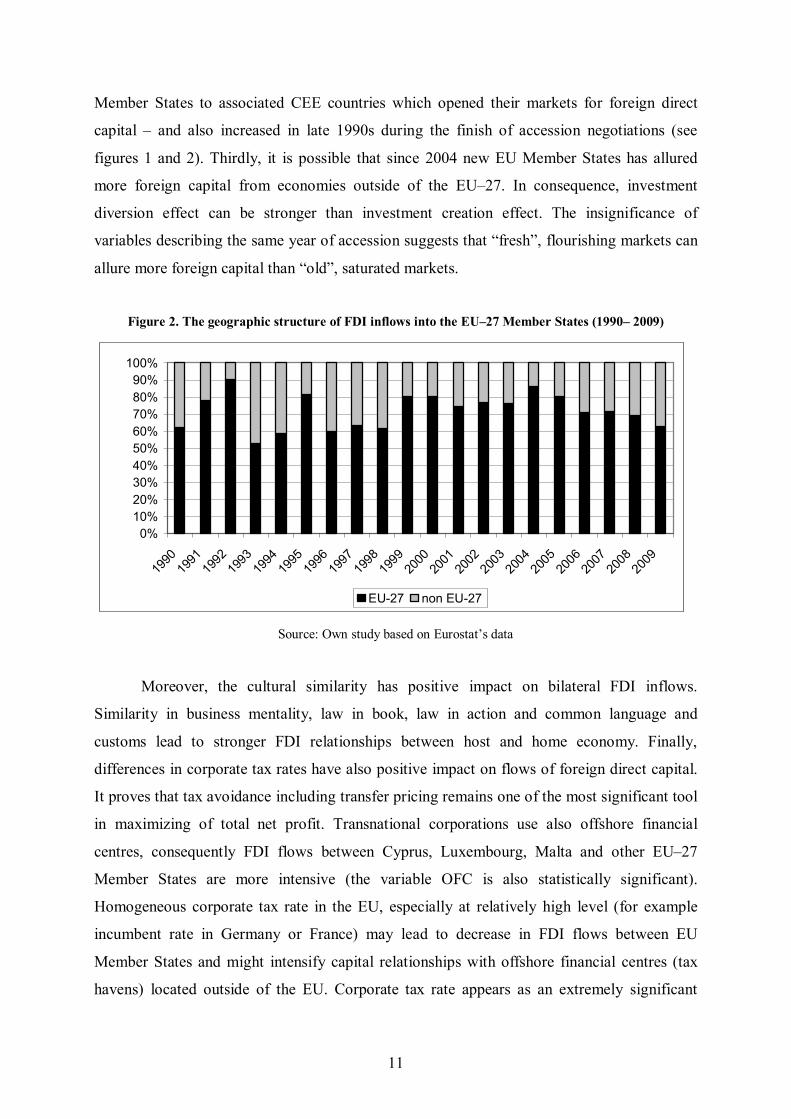

and so on. The share of FDI inflows to the EU–27 Member States coming from EU–27

Member States increased in early 1990s – probably due to intensive FDI flows from EU–15

11

Member States to associated CEE countries which opened their markets for foreign direct

capital – and also increased in late 1990s during the finish of accession negotiations (see

figures 1 and 2). Thirdly, it is possible that since 2004 new EU Member States has allured

more foreign capital from economies outside of the EU–27. In consequence, investment

diversion effect can be stronger than investment creation effect. The insignificance of

variables describing the same year of accession suggests that “fresh”, flourishing markets can

allure more foreign capital than “old”, saturated markets.

Figure 2. The geographic structure of FDI inflows into the EU–27 Member States (1990– 2009)

0%10%20%30%40%50%60%70%80%90%

100%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

EU-27 non EU-27

Source: Own study based on Eurostat’s data

Moreover, the cultural similarity has positive impact on bilateral FDI inflows.

Similarity in business mentality, law in book, law in action and common language and

customs lead to stronger FDI relationships between host and home economy. Finally,

differences in corporate tax rates have also positive impact on flows of foreign direct capital.

It proves that tax avoidance including transfer pricing remains one of the most significant tool

in maximizing of total net profit. Transnational corporations use also offshore financial

centres, consequently FDI flows between Cyprus, Luxembourg, Malta and other EU–27

Member States are more intensive (the variable OFC is also statistically significant).

Homogeneous corporate tax rate in the EU, especially at relatively high level (for example

incumbent rate in Germany or France) may lead to decrease in FDI flows between EU

Member States and might intensify capital relationships with offshore financial centres (tax

havens) located outside of the EU. Corporate tax rate appears as an extremely significant

12

instrument not only in domestic, but also in foreign economic policy. Therefore, it seems to

be a symbol of economic sovereignty within the EU.

Table 2. Estimation results (part 2)

Period: 2005–2009 Equation (4) Number of pairs (host and home economy): 643 Number of observations: 2706 Significant codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘^’ 0.1

Variable Coefficient Standard Error t-value P>|t| ln GDPit 0.201054 0.112678 1.7843 0.074369 ^ ln GDPjt 0.767659 0.110482 6.9483 3.697e-12 *** ln Dij -0.643572 0.223238 -2.8829 0.003940 ** ln |gdpit-gdpjt| 0.075379 0.250517 0.3009 0.763496 EUijt -0.268919 0.433840 -0.6199 0.535351 EAijt -0.245080 0.621024 -0.3946 0.693109 Accessionij 0.098786 0.543694 0.1817 0.855823 Cultureij 1.063568 0.490245 2.1695 0.030048 * ln|Taxit-Taxjt| 0.200297 0.178924 1.1195 0.262946 OFCij 2.035610 0.637526 3.1930 0.001408 ** ln|TaxTimeit-TaxTimejt|

-0.064335 0.097594 -0.6592 0.509763

ln|TaxPaymentsit-TaxPaymentsjt|

-0.088111 0.093801 -0.9393 0.347554

ln|TotalTaxit-TotalTaxjt|

-0.082067 0.226195 -0.3628 0.716742

Constant -6.393546 3.993103 -1.6011 0.109344

Source: Own study based on computations in R-package

According to the estimation of second model covering period 2005–2009 and

including additional variables linked with taxation, basic variables (GDPs and distance) are

statistically significant and the parameters display expected values (see table 2). Again

variables illustrating participation in regional integration are not statistically significant and

cultural similarity has positive impact on bilateral FDI flows. Therefore, in period 2005–2009

apart from transactions with OFC, all other taxation issues are not statistically significant for

flows of direct capital. These results confirms only up to a point the importance of tax

disparities and role of transfer pricing, however it is possible that the relatively small size of

sample has impact on estimation results. Additionally, disparities in corporate tax rates were

lower during period 2005–2009 than during last two decades.

13

4. Conclusions

Using gravity model I prove that direct investment flows between EU–27 Member

States are determined by variables such as: gross domestic products (total and per capita) of

home and host economy and distance between them. Therefore, other characteristics of

individual economies are more important for bilateral FDI flows than participation in the

regional integration. My estimation results confirm the sense of the EU motto In varietate

concordia10. In the case of FDI the variety appears to be more significant, especially

disparities in corporate tax rates intensify flows of direct capital. Moreover, cultural similarity

within groups of EU–27 Member States has also positive impact on FDI, what confirms the

magnitude of not strictly economic factors. To sum up, gravity model seems to be very useful

analytical tool and the further research based on it seems to be very lucrative.

References

1. Anderson J. E. [1979], A Theoretical Foundation for the Gravity Equation, „American Economic

Review”, Vol. 69, No. 1, pp. 106–116

2. Anderson J. E., van Wincoop E. [2003], Gravity with Gravitas: A Solution to the Border Puzzle,

“American Economic Review”, Vol. 93, No. 1, pp. 170–192

3. Baldwin R. E., Forslid R., Haaland J. I. [1996], Investment Creation and Diversion in Europe, “The

World Economy”, Vol. 19, No. 6, pp. 635–659

4. Benassy-Quere A., Coupet M., Mayer T. [2007], Institutional Determinants of Foreign Direct

Investment, “The World Economy”, Vol. 30, No. 5, pp. 764–782

5. Bergstrand J. H. [1985], The Gravity Equation in International Trade: Some Microeconomic

Foundations and Empirical Evidence, “Review of Economics and Statistics”, Vol. 67, No. 3, pp. 474–

481

6. Bergstrand J. H. [1989], The Generalized Gravity Equation, Monopolistic Competition and the Factor-

Proportions Theory in International Trade, “Review of Economics and Statistics”, Vol. 71, No. 1, pp.

143–153

7. Bevan A. A., Estrin S. [2004], The Determinants of Foreign Direct Investments into European

Transition Economies, „Journal of Comaparative Economics“, Vol. 32, No. 4, pp. 775–787

8. Brenton P., Mauro F. D., Lucke M. [1999], Economic integration and FDI: An Empirical Analysis of

Foreign Investments in the EU and in Central and Eastern Europe, “Empirica”, Vol. 26, No. 2, pp. 95–

121

9. Buch C. M., Kokta R. M., Piazolo D. [2003], Foreign Direct Investment in Europe: Is there Redirection

form the South to the East?, „Journal of Comaparative Economics“, Vol. 31, No. 1, pp. 94–109

10 United in diversity.

14

10. Carey H. C. [1858], Principles of Social Science, J.B. Lippincott & Co., New York

11. Choi Ch. [2004], Foreign Direct Investment and Income Convergence, “Applied Economics”, Vol. 36,

No. 10, pp. 1045–1049

12. Cieślik A. [2009], Bilateral Trade Volumes, the Gravity Equation and Factor Proportions, “Journal of

International Trade and Economic Development, Vol. 18, No. 1, pp. 37–59

13. Cieślik A., Michałek J.J., Mycielski J. [2009], Prognoza skutków handlowych przystąpienia do

Europejskiej Unii Monetarnej Polski przy użyciu uogólnionego modelu grawitacji, „Bank i Kredyt”,

Vol. 40, No. 1, pp. 69–88

14. Converse P.D. [1949], New Laws of Retail Gravitation, “Journal of Marketing”, Vol. 14, s. 379–384

15. Czarny E., Śledziewska K. [2009], Polska w handlu światowym, PWE, Warszawa

16. Czarny E., Śledziewska K., Witkowski B. [2010], Does monetary integration affect EU’s trade?,

http://www.etsg.org/ETSG2010/ETSG2010Programme.html

17. Czarny E., Folfas P. [2011], Modele Grawitacji jako Narzędzie Analityczne w Ekonomii

Międzynarodowej, Konferencja PITWIN, Kielce, mimeo

18. Deardoff A. V. [1998], Determinants of Bilateral Trade: Does Gravity Work in a Neoclassical World?

[in:] Frankel J. A. [ed.], The Regionalization of the World Economy, University of Chicago Press,

Chicago

19. Debaere P. [2005], Monopolistic Competition and Trade Revisited: Testing the Model without Testing

for Gravity, “Journal of International Economics”, Vol. 36, No. 3, pp. 249–266

20. Desbordes R., Vicard V. [2009], Foreign Direct Investment and Bilateral Investments Treaties: An

International Political Perspective, “Journal of Comparative Economics”, Vol. 37, No. 3, pp. 372–386

21. Dodd S. G. [1950], The Interactance Hypothesis. A Gravity Model Fitting Physical Masses and Human

Groups, “American Sociological Review”, Vol. 15, No. 2, pp. 245–256

22. Egger P., Pffaffermayr M. [2004a], Distance, Trade and FDI: A Hausman-Taylor SUR Approach,

“Journal of Applied Econometrics”, Vol. 19, No. 1, pp. 227–246

23. Egger P., Pffaffermayr M. [2004b], The Impact of Bilateral Investment Treaties on Foreign Direct

Investment, “Journal of Comparative Economics”, Vol. 32, No. 4, pp. 788–804

24. Feenstra R. C. [2004], Advanced International Trade: Theory and Evidence, Princeton University

Press, Princeton

25. Folfas P. [2008], Przenoszenie Działalności Gospodarczej do Rajów Podatkowych jako Strategia

Zarządzania Finansami Korporacji Transnarodowych: Motywy, Formy, Korzyści iZagrożenia, „Bank i

Kredyt”, Vol. 39, No. 12, pp. 15–30

26. Folfas P. [2010a], Offshoring to Tax Havens before and in the Time of Crisis: Role of Asian vs.

European and American Tax Havens, “Research Papers of Wrocław University of Economics”, No.

126, pp. 412–424

27. Folfas [2010b], The Intensity of Bilateral Relations In Intra-UE Trade and Direct Investments: Analysis

of Variance and Correlation, http://www.etsg.org/ETSG2010/ETSG2010Programme.html

28. Hammer C., Ikle F.C. [1957], Intercity Telephone and Airline Traffic Related to Distance and the

Propensity to Interact, “Sociometry”, Vol. 20, No.4, pp. 306–316

15

29. Hausman J. A., Taylor W. E. [1981], Panel Data and Unobservable Individual Effects, “Econometrica”,

Vol. 49, No. 6 , pp. 1377–1398

30. Haveman J., Hummels D. [2004], Alternative Hypotheses and the Volume of Trade: The Gravity

Equation and the Extent of Specialization, “Canadian Journal of Economics, Vol. 37, No. 1, pp. 199–

218

31. Head K. [2000], Gravity for Beginners, “The Canada – U.S. Border Conference”, Vancouver, (October

22, 2000)

32. Helpman E. [1987], Imperfect Competition and International Trade: Evidence from Fourteen Industrial

Countries, “Journal of the Japanese and International Economies, Vol. 1, No. 1, pp. 62–81

33. Helpman E., Melitz M., Rubinstein Y. [2008], Estimating Trade Flows: Trading Partners and Trading

Volumes, Quarterly Journal of Economics, Vol. 23, No. 2, pp. 441–487

34. Krugman P. R., Obstfeld M. [2007], Ekonomia międzynarodowa: teoria i polityka, Vol. 1, PWN,

Warszawa

35. Kumar A., Zajc K. [2003], Foreign Direct Investment and Changing Trade Patterns: The Case of

Slovenia, “Economic and Business Review for Central and South-Eastern Europe”, Vol. 5, No. 3, pp.

201–219

36. Lada K., Tchorek G. [2008], Przepływy bezpośrednich inwestycji zagranicznych a utworzenie strefy

euro, www.nbpnews.pl/r/nbpnews/Pliki_PDF/NBP/Publikacje/analityczne/LadaP.pdf

37. Linnemann H. [1963], An Econometric Study of International Trade Flows, North-Holland Publishing

Company, Amsterdam

38. Milner C., Reed G., Talernsgri P. [2004], Foreign Direct Investment and Vertical Integration of

Production by Japanese Multinationals in Thailand, „Journal of Comparative Economics”, Vol. 32, No.

4, pp. 805–821

39. Motta M., Norman G. [1996], Does Economic Integration Cause Foreign Direct Investments?,

“International Economic Review”, Vol. 37, No. 4, pp. 757–783

40. Portes R., Rey H. [2005], The Determinants of Cross-Border Equity Flows, “Journal of International

Economics”, Vol. 65, No. 2, pp. 269–296

41. Pöyhönen K. [1963], Towards a General Theory of International Trade, “Ekonomiska Samfundet

Tidskrift”, No. 16, pp. 69–78

42. Pulliainen K. [1963], A World Trade Study. An Econometric Model of the Pattern of Commodity Flows

in International Trade in 1948–1960, “Ekonomiska Samfundet Tidskrift”, No. 2, pp. 78–91

43. Ravenstein E. J. [1885], The Laws of Migration, „Journal of the Statistical Society of London”, Vol. 48,

No. 2, pp. 167–235

44. Reilly W. J. [1929], Methods for the Study of Retail Relationships, “University of Texas Bulletin”, No.

2944

45. Roberto B. [2004], Acquisition Versus Greenfield Investments: the Location of Foreign Manufactures

in Italy, “Regional Science and Urban Economics”, Vol. 34, No. 1, s. 3–39

46. Stewart J. Q. [1948], Demographic Gravitation: Evidence and Applications, “Sociometry”, Vol. 11, s.

31–58

16

47. Stone S. F., Jeon B. N. [1999], Gravity-Model Specification for Foreign Direct Investment: A Case of

Asia-Pacific Economies, “The Journal of Business and Economic Studies”, Vol. 5, No. 1, pp. 33–42

48. Szczepkowska A., Wojciechowski L. [2002] Możliwości wykorzystania modelu grawitacji do analizy

bezpośrednich inwestycji zagranicznych w Polsce [in:] Piech K., Szczodrowski G. [ed.], Przemiany i

perspektywy polskiej gospodarki w procesie integracji z gospodarką wiatową, Instytut Wiedzy,

Warszawa, pp. 267–282

49. Tinbergen J. [1962], Shaping The World Economy Suggestions for an International Economic Policy,

The Twentieth Century Fund, New York

50. The Economist [2007], A special report on offshore finance, “The Economist”, 24 February – 2 March

51. UNCTAD [2007], World Investment Report 2007: Transnational Corporations, Extractive Industries

and Development, New York and Geneva

52. Zipf G. K. [1949], Human Behaviour and the Principle of Least Effort: An Introduction to Human

Ecology, Addison-Wesley Press, Cambridge