Indices and Index Notation Practice Questions 5.1 - Gill Books

Upload

khangminh22Category

view

0download

0

Factsheets index by titleClear and concise factsheets on business and personal issues

Accounting Standards Changes

Age Discrimination

Agency Workers Regulations

Annual Leave

Bribery Act 2010

Bring your own device

Business Motoring Tax Aspects

Business Plans

Business Structures Which Should IUse

Capital Allowances

Capital Gains Tax

Capital Gains Tax and the FamilyHome

Cars for Employees

Cash Basis for the Self Employed

Charitable Giving

Charities Trustees Responsibilities

Charities in Scotland TrusteesResponsibilities

Child Benefit Charge

Community Amateur Sports Clubs

Companies Tax Saving Opportunities

Company Secretarial Duties

Construction Industry Scheme

Corporation Tax QuarterlyInstalment Payments

Corporation Tax Self Assessment

Could I Really Make a Go of it

Credit Control

Data Security Access

Data Security Backup

Data Security Cloud andOutsourcing

Data Security Data Loss RiskReduction

Data Security Data Protection Act

Data Security General DataProtection Regulation

Data Security General DataProtection Regulation Preparation

Directors Responsibilities

Dismissal Procedures

Employee Expenses

Employer Supported Childcare

Employment Benefits

Enterprise Investment Scheme

Fixed Rate Expenses

Franchising

Fraud and How to Spot It

Grants

Health and Safety

Health and Safety Checklist

Homeworking Costs for the SelfEmployed

Homeworking and Tax Relief forEmployees

IR35 Personal Service Companies

Incorporation

Individual Savings Accounts

Inheritance Tax Avoidance PreOwned Assets

Inheritance Tax a Summary

Insuring Your Business

Internet and Email Access Policy

Land and Buildings Transaction Tax

Legal Working in the UK

Limited Liability Partnerships

Managing Absence

Micro Entity Accounting

Money Laundering High ValueDealers

Money Laundering and the Proceedsof Crime

National Insurance

National Minimum Wage

Non Domiciled Individuals

Occupational Pension SchemesTrustees Responsibilities

Payroll Basic Procedures

Payroll Real Time Information

Pensions Automatic Enrolment

Pensions Tax Reliefs

Pensions Tax Treatment on Death

Personal Tax Dividends and Interest

Personal Tax Self Assessment

Personal Tax When is Income Taxand Capital Gains Tax Payable

Preparing for Your Accountant

Property Investment Buy to Let

Property Investment Tax Aspects

Raising Finance

Recruitment Procedures

Recruitment ProceduresEmployment Law

Redundancy Procedures

Register of People with SignificantControl

Research and Development

Securing Business Success

Seed Enterprise Investment Scheme

Share Ownership for Employees EMI

Small Company Accounting

Social Enterprise Entity Structures

Sources of Finance

Stamp Duty Land Tax

Starting Up In Business

Statutory Pay

Statutory Residence Test

Taxation of the Family

Travel and Subsistence for Directorsand Employees

Trusts

VAT

VAT Annual Accounting Scheme

VAT Bad Debt Relief

VAT Cash Accounting

VAT Flat Rate Scheme

VAT Seven Key Points for the SmallerBusiness

Valuing Your Business

Venture Capital Trusts

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Accounting Standards ChangesDue to the introduction of new accounting standards,commonly referred to as ‘New UK GAAP’, the form andcontent of company accounts has changed.

The changes for non-small companies took effect foraccounting periods beginning on or after 1st January2015. In many instances companies will now show adifferent bottom-line profit or loss and a different total fornet assets on the balance sheet. These changes could alsolead to a higher or lower tax bill.

The extent of the changes will vary on a company bycompany basis. It will depend upon the nature of thecompany’s activities and the types of assets which it has.

This factsheet sets out the key changes and their impactand we would be happy to assist you in providing specificadvice for your company.

Large and medium sized companies

For these companies, the changes result from theintroduction of FRS 102 (‘Financial Reporting Standard102 – The Financial Reporting Standard applicable in theUK and Republic of Ireland’). FRS 102 replaces all existingaccounting standards.

The new standard must be applied for periodscommencing on or after 1 January 2015, though earlyadoption is possible.

Small companies

Previously small companies will have followed therequirements as per the Financial Reporting Standard forSmaller Entities (FRSSE).

The FRSSE however had a short shelf life and ‘smallentities’ will be moving to the recognition andmeasurement requirements of FRS 102 for periodscommencing on or after 1 January 2016. Although these‘small entities’ will have to account for balances andtransactions in the same way as larger entities there will bereduced disclosure requirements. This is commonlyreferred to as section 1A.

Certain small companies may qualify as micro-entities andcan choose to apply a new accounting standard: FRS 105 -The Financial Reporting Standard applicable to the Micro-entities regime which includes simplified accounting and

greatly reduced disclosure requirements. The qualificationas a micro entity, broadly requires a company to satisfytwo of the three criteria:

Current

Turnover £632,000

Total assets £316,000

Employees 10

At present to qualify as small, broadly, a company needsto satisfy two of the three criteria on an ongoing basis asset out in the table below. There are other criteria toconsider, and we would be pleased to discuss these inmore detail with you.

Current

Turnover £10.2m

Total assets £5.1m

Employees 50

The size criteria above is mandatory for periodscommencing on or after 1 January 2016 although earlieradoption is permissible in some situations.

The main areas in which FRS 102 willhave an impact on company accounts

FRS 102, including appendices, is less than 350 pages –significantly less than the existing accounting standardscontained within SSAPs and FRSs.

The main differences which may arise upon transition toFRS 102 are listed below. We can of course advise you onthe specific impacts for your business in far more detailand this list is not exhaustive.

• Taxation - one of the most important impacts will be onthe tax payable on profits. If the accounting profitsincrease or reduce as a result of a new accountingstandard, so could the tax payable. Changes to the

circumstances where deferred taxation is provided willoften mean more deferred taxation is included in theaccounts.

• Investment properties - there are some big changeshere including how to account for changes in valuationand potentially the actual value included in theaccounts.

• Goodwill (and other intangibles) – this is a complicatedarea with elements of judgment. If this affects you, werecommend contacting us for further information.

• Financial instruments - this is the technical name for anumber of items that appear in the accounts such ascash, debtors, creditors, loans payable and receivableand derivatives (the collective term for forwardexchange contracts, futures and interest rate swaps).The accounting for some of these items is broadly thesame however some accounting has changedsubstantially and will impact the values included in youraccounts. There could therefore be subsequent taximpacts.

• Related party disclosures - (non-small companies) thegood news here is that related party transactions canbe disclosed by category without the need for thenames of related parties. The bad news is that there is

additional disclosure required of ‘compensation of keymanagement personnel’. For small companies applyingsection 1A, only material related party transactionswhich are not concluded under normal marketconditions will need to be considered for disclosure.

• Numerous other areas including, but not limited to:accruing for outstanding holiday pay; spreading oflease incentives; changes to what are currently calledtangible fixed assets (such as land and buildings) butwhich become property, plant and equipment; changesin group accounts and changes to cash flowstatements.

How we can help

Implementing these new accounting standards (commonlyreferred to as ‘new UK GAAP’) may well be tricky anddecisions will need to be made in relation to choosingaccounting policies and complications on transition.

We will be very pleased to discuss the impact of FRS 102on your company and explain what will be required andwhen it will need to be done. If you would like to discussthese in more detail, please contact us.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Age DiscriminationThe Equality Act 2010 replaces all previous equalitylegislation, including the Employment Equality (Age)Regulations 2006. The Equality Act covers age, disability,gender reassignment, race, religion or belief, sex, sexualorientation, marriage and civil partnership and pregnancyand maternity. These are now called ‘protectedcharacteristics’.

The Act protects people of any age, however, differenttreatment because of age is not unlawful if you candemonstrate that it is a proportionate means of meeting alegitimate aim. Age is the only protected characteristicthat allows employers to justify direct discrimination.Employers need to ensure they have the appropriatepolicies and procedures in place to deal with agediscrimination and should raise awareness of it so thatacts of discrimination on the grounds of age can beprevented.

Discrimination

Discrimination occurs when someone is treated lessfavourably than another person because of their protectivecharacteristic.

There are four definitions of discrimination:

Direct Discrimination: treating someone less favourablythan another person because of their protectivecharacteristic

Indirect Discrimination: having a condition, rule, policyor practice in your company that applies to everyone butdisadvantages people with a protective characteristic

Associative Discrimination: directly discriminatingagainst someone because they associate with anotherperson who possesses a protected characteristic

Perceptive Discrimination: directly discriminatingagainst someone because others think they possess aparticular protected characteristic

Examples of Age Discrimination

An example of direct discrimination would be wheresomeone with all the skills and competencies to undertakea role is not offered the position just because theycompleted their professional qualification 30 years ago.Other examples could include refusing to hire a 40 yearold because of a company’s youthful image, not providing

health insurance to the over 50’s, colleagues nicknaming acolleague ‘Gramps’ and not promoting a 25 year oldbecause they may not command respect.

A business requiring applicants for a courier position tohave held a driving licence for five years is likely to beguilty of indirect discrimination. A higher proportion ofpeople aged between 40 and above will have fulfilled thiscriteria than those aged 25. Other examples of indirectdiscrimination could include seeking an ‘energeticemployee’, requiring 30 years of experience or askingclerical workers to pass a health test.

An example of perceived discrimination could be where anolder man who looks much younger than his years is notallowed to represent his company because the ManagingDirector thinks he is too young.

However, different treatment because of age is notunlawful if it can be objectively justified and you candemonstrate that it is a proportionate means of meeting alegitimate aim. For example, an employer might arguethat it was appropriate and necessary to refuse to recruitpeople over 60 where there is a long and expensivetraining period before starting the job. However, cost byitself is not capable of justifying such an action.

Harassment

Harassment on the basis of age is equally unlawful. Forexample, a mature trainee teacher may be teased andtormented in a school on the grounds of age during theteaching experience. If no action is taken by the headteacher, this may be treated as harassment. An employeemay be written off as ‘too slow’ or ‘an old timer’. This toocould be seen as harassment.

The Equality Act 2010 covered harassment by a thirdparty, making employers potentially vicariously liable forharassment of their staff by people they don’t employ.However, this has been repealed with effect from October2013, and employers will no longer have the risk of beingheld responsible if an external third party harasses anemployee. However, employers must continue to take 'allreasonable steps' to ensure that employees don’t sufferharassment at work; therefore it is recommended thatyour harassment policy still states that you show ‘zerotolerance’ towards such behaviour.

Recruitment

Employers must be aware of the significance of thelegislation at all stages in the recruitment process and toavoid breaking the age rules they should consider:

• removing age/date of birth from adverts for example:‘Trainee Sales Representatives.. envisaged age 21-30years’

• reviewing application forms to ensure they do not askfor unnecessary information about periods and dates

• avoiding asking for ‘so many years of experience’ in jobdescriptions and person specifications for example:‘graduated in the last seven years’

• avoiding using language that might imply a preferencefor someone of a certain age, such as ‘mature’,‘young’, ‘energetic’ or ‘the atmosphere in the office,although demanding, is lively, relaxed and young’

• ensuring that other visible methods are used to recruitgraduates as well as university milk rounds, to avoidlimiting opportunities to young graduates

• focusing on competencies to undertake a role and notmaking interview notes that refer to age considerations

• never asking personal questions nor make assumptionsabout health or physical abilities

• never ask health related questions before you haveoffered the individual a job.

Service related benefits

Employers are allowed to use a length of service criterionin pay and non-pay benefits of up to five years’ service.Benefits based on over five years service are also allowed ifthe benefit reflects a higher level of experience, rewardsloyalty or increases or maintains motivation and is appliedequally to all employees in similar situations. It is for theemployer to demonstrate that the variation in pay/benefitsover five years can be objectively justified.

Employers are recommended to review their pay andbenefits policies to ensure that they are based onexperience, skills and other non-age related criteria.

Redundancy

The existing statutory payment provisions remain in place.Employers can, as before, pay enhanced redundancypayments. However, to avoid discriminating, employersshould use the same age brackets and multipliers as usedwhen calculating statutory redundancy pay.

Retirement

The default retirement age and the statutory retirementprocedure were abolished from 6th April 2011.

Employers that wish to prescribe a compulsory retirementage may do so only if it is a proportionate means ofachieving a legitimate aim.

Action for employers

Employers need to undertake the following to ensure thatthey are not breaking the law:

• review equality policies

• review employee benefits

• review policies and procedures on retirement

• undertake equality training covering recruitment,promotion and training.

How we can help

We will be more than happy to provide you withassistance or any additional information required. Pleasecontact us for more detailed advice.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Agency Workers RegulationsRegulations which took effect from 1 October 2011 meanthat workers supplied to a company, or to any otherentity, by an agency will become entitled to receive payand basic working conditions equivalent to any directlyemployed employees after a 12 week qualifying period.

Guidance for businesses and otheremployers

Under the Agency Workers Regulations workers suppliedto a company (or to any other entity) by an agency willbecome entitled to receive pay and basic workingconditions equivalent to any directly employed employeesafter a 12 week qualifying period.

Where an agency worker is at the entity for less than 12weeks, a minimum break of more than six weeks betweenassignments with the same employer will be necessary forthe rights not to be available.

Supporting guidance

Guidance can be found on the GOV.UK website athttps://www.gov.uk/government/publications/agency-workers-regulations-2010-guidance-for-recruiters

Impact of the Regulations

As explained below, most of the additional work, andmuch of the risk and liability, will be the responsibility ofthe agencies but it seems certain that they will pass thecost on by way of higher fees.

More directly, where the 'Employer' (see below) hires stafffor more than the 12 week period, typically the costs ofhiring staff will be greater. The Employer will also need tomonitor the period of time the 'Agency Worker' has beenat their premises and there may be additional risks andcosts as a result.

Terms used in the Regulations

Much of the guidance uses terms such as ‘TemporaryWork Agency’ (the Agency supplying the workers), the‘Agency Worker’ and the ‘Hirer’ (being the entity orbusiness where the Agency Worker is working). In thissummary we have generally used the term ‘Employer/Hirer’when we mean the ‘Hirer’ although it is not strictly thecorrect legal term. We have also used the word ‘Agency’rather than ‘Temporary Work Agency’.

Rights of Agency Workers under theRegulations

Under the Regulations, from their first day working at theEmployer/Hirer, the Employer/Hirer will be required toensure that the Agency Worker can access what are called‘collective facilities’ such as canteens, childcare, transportservices, car parking, etc and that they are able to accessinformation on all job vacancies.

The Agency Worker’s rights are to ‘no less favourabletreatment’ in relation to these facilities, than that given toa comparable worker. A comparable worker is anemployee or worker directly employed by the employer.

Then, after 12 weeks in the same job, the ‘equal treatmententitlements’ described below come into force.

Equal treatment entitlements and the‘Qualifying Clock’

After completion of the 12 week qualifying period theAgency Worker is entitled to the same basic terms andconditions of employment as if they had been directlyhired by the Employer/Hirer. These would include:

• key elements of pay

• duration of working time

• night work

• rest periods

• rest breaks

• annual leave

• pregnant workers will be entitled to paid time off forantenatal appointments.

If a particular entitlement commences only after a periodof service, for example, additional annual leave arises afterone year of employment, then the entitlement would onlystart after one year plus 12 weeks.

The term ‘Qualifying Clock’ is used to illustrate theworking of the guidance.

The guidance refers to extensive anti-avoidance provisionspreventing a series of assignments being structured insuch a way as to prevent an Agency Worker fromcompleting the qualifying period and describes when theQualifying Clock can be reset to zero, where the clock‘pauses’ during a break, and where it continues to ‘tick’during a break.

The examples given are extensive but include, for example:

• the clock is reset to zero where an Agency Workerbegins a new assignment (and a new Employer/Hirer forthis purpose is closely defined) or there is a break ofmore than six weeks

• the clock would be paused for a break of no more thansix weeks and the worker returns to the same Employer/Hirer, or a break of up to 28 weeks because the workeris incapable of work because of sickness or injury

• the clock continues to tick as a result of breaks to dowith pregnancy, childbirth, maternity or paternity leave.

There are many more examples given in the BIS guidance.

Identification of basic working andemployment conditions and pay

Equal treatment covers basic working and employmentconditions included in the relevant contracts of directrecruits, which would normally mean terms and conditionslaid out in standard contracts, pay scales, collectiveagreements or company handbooks. Where available thiswould be the same pay, holidays, etc as if the AgencyWorker had been recruited as an employee or worker tothe same job. There does not have to be a comparableemployee (called a ‘comparator’) but it would be easier todemonstrate compliance with the Regulations where sucha person is available.

Pay is defined as including and excluding a number ofelements, most of which are shown below.

To be included in pay for this purpose:

• basic pay based on an annual salary equivalent

• overtime payments

• shift / unsocial hours allowances

• payment for annual leave

• bonus or commission payments

• vouchers or stamps with monetary value which are notsalary sacrifice schemes.

Not to be included:

• occupational sick pay

• occupational payments (agency workers will be coveredby Auto-enrolment which started to phase in fromOctober 2012)

• occupational maternity, paternity or adoption pay

• redundancy pay / notice pay

• majority of benefits in kind

• payments requiring an eligibility period of employment.

Working time and holiday entitlements

In addition to an agency worker’s existing rights under theWorking Time Regulations 1998, after 12 weeks, theworker becomes entitled to the same rights for workingtime, night work, rest periods and rest breaks, annualleave and overtime rates, as directly employed employees.

The guidance recognises that some Agency Workersalready receive these benefits from the date they join theEmployer/Hirer and mention as an example thatEmployers/Hirers often offer a lunch hour rather than theminimum 20 minute rest under the Working TimeRegulations. The guidance also includes a reminder thatthe statutory entitlement to paid holiday leave is 5.6 weeksper year.

Pregnant workers and new mothers

After the 12 week qualifying period pregnant workers willbe allowed paid time off for antenatal appointments andclasses and if they can no longer carry out the duties oftheir original assignment they will need to be foundalternative sources of work. If no such alternative work isavailable from either the Employer/Hirer or the Agency, theAgency should pay the pregnant woman for the remainingexpected duration of the assignment.

The provisions of the Equality Act also apply, meaning thatthere is a risk that either an Agency or the Employer/Hirercould be guilty of discrimination if a worker were toreceive less favourable treatment as a result of theirpregnancy or maternity.

If the nature of the assignment is such that there is a riskto the worker’s health and safety, the Agency will need toask the Employer/Hirer to carry out a workplace riskassessment, which they will need to do.

Permanent employment contract withthe Agency

If the Agency Worker has a permanent contract ofemployment with the Agency then the equal treatmentprovisions do not need to be complied with by theEmployer/Hirer.

Information likely to be requested by anAgency

To comply with these Regulations, agencies may need tocollect certain information from the Employer/Hirer beforean assignment begins. This is in addition to their existingobligations under what are known as the ConductRegulations 2010 and the Gangmasters LicensingRegulations (for the food, agricultural and shellfishsectors).

Where an assignment is likely to last for more than 12weeks, it will probably be good practice for the Agency toask for information at an early stage though theRegulations do not refer to any particular timescale.

Existing regulations require information about:

• hirer’s identity, business and location

• start date and duration

• role, responsibilities and hours

• experience, training, qualifications etc

• health and safety risk

• expenses.

The details now required to comply with the AgencyWorkers Regulations after the 12 week period are:

• basic pay, overtime payments, shift/unsocial hoursallowances and any risk payments

• types of bonus schemes

• vouchers with monetary value

• annual leave entitlement.

It is likely that the Agency will also ask for informationabout any day one entitlements which may be available,even though they are the responsibility of the Employer/Hirer.

Liability and remedies

The responsibility lies with the Employer/Hirer to provideday one entitlements and claims would probably beagainst the Employer/Hirer.

Claims with regard to basic working and employmentconditions could be against either the Employer/Hirer, orthe Agency, or against both, depending on the nature ofthe breach and whether, for example, the Employer/Hirerhad failed to provide information to the Agency. Claimswould be made to an Employment Tribunal if not resolvedthrough grievance procedures and/or possibly through theinvolvement of ACAS.

Employment Tribunals would be able to award financialcompensation or recommend action that should be taken.

How we can help

If you would like to discuss the implications of the newRegulations for your business in more detail please contactus.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Annual LeaveBackground

Under the Working Time Regulations 1998 (as amended),workers are entitled to paid statutory annual leave of 5.6weeks (28 days if the employee works five days a week).This basic entitlement is inclusive of bank holidays. Thisannual leave entitlement is now closer to that of workersin other European countries, where holiday allowance istypically more generous. Workers in Ireland are entitled to29 days; the highest minimum entitlement is in Austria at38 days.

Payment for annual leave

A worker is entitled to be paid in respect of any period ofannual leave for which they are entitled, at a rate of oneweek’s pay for each week’s leave. For employees withnormal working hours a week’s pay is the pay due for thebasic hours the employee is contracted to work. Anyregular contractual bonuses or allowances (except expenseallowances) which do not vary with the amount of workdone are also included.

Commission has previously not been included in thecalculation of holiday pay, however, following a ruling bythe European Court of Justice (ECJ) which was recentlyupheld by the Court of Appeal, when commission isrelated to the number of sales made whilst at work, itshould also be included in the calculation of holiday pay.There was a further appeal to the Supreme Court, whichwas not granted and employers will now be required tocomply with this ruling. The method of calculating suchpayments is not yet defined, but is likely to be an averageof previous months’ commission.

Guaranteed and non-guaranteed overtime should also beincluded along with regular voluntary overtimepayments. The difference between non-guaranteed andvoluntary overtime is that the employee is obliged to donon-guaranteed overtime if it is offered, but can turndown voluntary overtime. Where the voluntary overtime isirregular or ad hoc it does not need to be included unlessit extends for a sufficient period of time on a regular and/or recurring basis. This includes overtime regularly workedat certain points in the year for example at Christmas, aswell as frequently worked overtime throughout the year.These additional elements need only be included for thefour weeks of statutory leave required by European lawwhich is lower than the UK minimum of 5.6 weeks, it canbe excluded for any additional days above this.

Under the Regulations any statutory annual leave may notbe replaced by a payment in lieu, except on termination ofemployment. In such cases, a payment can be made forany untaken leave in the leave year that terminationoccurs. Payment may also be due for any carried over leavebecause of maternity/adoption leave or sickness.

Rolled up leave

The ECJ has ruled that it is unlawful for employers to rollup workers’ annual leave payments. In accordance withthis it is recommended that employers renegotiatecontracts involving such pay for existing workers as soonas possible so that payment for statutory annual leave ismade at the time when the leave is taken.

Requesting leave

Employees should be allowed to choose when they takesome of their leave although many employers do setcertain conditions, for example that only a certain numberof workers may take leave at the same time or thatworkers may not take more than a certain number ofconsecutive working days off in one go.

It is common for employers to have a procedure in placefor these instances and it should include the procedure fornotification. If this is excluded then the legal position isthat an employee requesting a period of leave must givenotice of at least twice the period of leave to his or heremployer. A similar arrangement of notice must be givenby the employer if they are requesting the employee totake leave at specific times.

First year of employment

Workers accrue their annual leave entitlement on a prorata basis during their first year of employment. This iscalculated in relation to the proportion of the employmentyear worked. Therefore, the annual leave entitlement willaccrue over the course of the worker’s first year ofemployment at the rate of 1/12 of the annual entitlement,starting on the first day of each month. If the calculationdoes not result in an exact number of days then the figurewill be rounded up to the nearest half day.

Annual leave and part time employees

Under the Regulations, time off for bank holidays shouldbe pro rated. Part time workers are currently entitled to5.6 weeks’ holiday, based on the hours a week that theywork, regardless of whether they work on days on whichbank holidays fall.

Contractual annual leave entitlement

An employer can increase a worker’s statutory annualleave entitlement via a contractual arrangement. In suchcases any unused additional annual leave may be carriedover to the next leave year. This is often a matter ofemployer discretion and will depend on the terms of thecontract.

Annual leave and maternity

An employee continues to accrue their statutory annualleave entitlement of 5.6 weeks and any additionalcontractual annual leave entitlement throughout bothordinary maternity leave (OML) and additional maternityleave (AML).

Sickness during holiday

Employees are now entitled to reclassify statutory holidayas sick leave if they fall ill whilst on prearranged statutoryholiday. This means that they are entitled to take thestatutory holiday they have missed at a later date. If theyare unable to take the rest of their statutory holiday thatholiday year they can carry it over to the next holiday year.If you offer more than 5.6 weeks holiday a year, you donot have to allow an employee to reclassify any additional

(contractual) holiday as sickness absence. However, youwill have to ensure that they can take their full statutoryholiday at other times. If you pay contractual sick pay, youcan minimise the scope for abuse by making contractualsick pay in these circumstances contingent on theemployee notifying you on the first day of illness that theyare ill and, possibly, requiring them to provide a medicalcertificate from the first day of their illness.

Employees who are on sick leave can ask their employer tore-classify their absence as statutory holiday in order toreceive holiday pay. If an employee on sick leave does notwant to take their outstanding statutory holiday beforeyour current leave year ends, they should be permitted tocarry it over into the next leave year. Employees returningfrom sick leave can take their statutory holiday entitlementfor the current year on their return but, if there isinsufficient time for them to take it, they should beallowed to carry it forward to the next leave year.

Recovery of overpayment of holiday

Employee contracts should make clear that if an employeetakes more holiday than he or she is entitled to during thecourse of a leave year, the company will be entitled torecover the overpayment of holiday pay by deducting itfrom the employee's wages or salary. It is advisable for thecompany to consult with the employee before making thededuction.

How we can help

We will be more than happy to provide you withassistance or any additional information required. Pleasecontact us for more detailed advice.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Bribery Act 2010The Bribery Act 2010 (the Act) applies across the UK andall businesses need to be aware of its requirements whichcame into effect on 1 July 2011.

The Act introduced a ‘corporate’ offence of ‘failure ofcommercial organisations to prevent bribery’. The defenceagainst this offence is to ensure that your business hasadequate procedures in place to prevent bribery. To helpensure this we recommend that, once you are familiarwith the requirements of the Act, you undertake a riskassessment for your own business and establishappropriate compliance procedures.

What action should you take?

• familiarise yourself with the guidance issued by theMinistry of Justice

• review the current activities of your business and assessthe risk of bribery occurring

• assess the strength of the measures that you currentlyhave in place to prevent bribery

• make any necessary updates to your staff handbooks:for example, your human resources manual

• consider whether specific anti-bribery staff training isrequired

• consider if changes are needed to other policies andprocedures, for example, expenditure approval andmonitoring processes

• communicate the changes that you have made to yourpolicies and procedures

• consider if you need to undertake any due diligenceprocedures.

The Bribery Act 2010

The Act replaces, updates and extends the existing UK lawagainst bribery and corruption. It applies across the UKand all UK businesses and overseas businesses carrying onactivities in the UK are affected.

The offences established by the Act are defined verybroadly and the Act has significant extraterritorial reach inthat it extends to acts or omissions which occur outside ofthe United Kingdom. Specific details about its jurisdictioncan be found in the detailed guidance referred to under‘Ministry of Justice guidance’ below, as well as in the Actitself.

What is bribery?

Bribery is a broad concept. In supplementary guidancepublished alongside the Act, it is very generally defined as‘giving someone a financial or other advantage toencourage that person to perform their functions oractivities improperly or to reward that person for havingalready done so. So this could cover seeking to influence adecision-maker by giving some kind of extra benefit tothat decision-maker rather than by what can legitimatelybe offered as part of a tender process.’

The key offences

Under the Act there are two general offences:

Active bribery – Section one of the Act prohibitsoffering, promising or giving a financial or otheradvantage (a bribe) to a person with the intention ofinfluencing a person to perform their duty improperly.

Passive bribery – Section two of the Act prohibits aperson from requesting, agreeing to receive or accepting abribe for a function or activity to be performed improperly.

In addition, there are two further offences that specificallyaddress commercial bribery:

Bribery of foreign public officials (FPO) – Section sixof the Act prohibits bribery of an FPO with the intention ofinfluencing them in their official capacity and obtaining orretaining business or an advantage in the conduct ofbusiness.

Failure of commercial organisations to preventbribery – Section seven of the Act introduces a strictliability offence that will be committed if:

• bribery is committed by a person associated with arelevant commercial organisation

• the person intends to secure a business advantage forthe organisation

• the bribery is either an active offence (section one ofthe Act) or bribery of an FPO (section six of the Act).

This means that a commercial organisation commits anoffence if a person associated with it bribes anotherperson for that organisation’s benefit. This ‘corporate’offence is the most significant and controversial change toexisting law and it is primarily this offence that you mustnow consider and prepare your business for as necessary.

It is important to note, however, that the Act also statesthat there is a defence available for commercialorganisations against failing to prevent bribery if they haveput in place ‘adequate procedures’ designed to preventpersons associated with them from bribing others on theirbehalf. The Secretary of State is required by the Act topublish guidance about such procedures.

Senior officers of an organisation can also be heldpersonally liable under the Act for other bribery offencescommitted by the organisation, i.e. the active and passivebribery offences as well as the bribery of an FPO, wherethe offence is proved to have been committed with their‘consent or connivance’.

‘Senior officer’ is widely defined in the Act to includedirectors, managers, company secretaries and other similarofficers, as well as those purporting to act in such acapacity.

Key definitions and terminology

Inevitably, in order to fully understand the requirements ofthe Act, it is necessary to be familiar with a number of keydefinitions.

Relevant commercial organisation

The corporate offence can be committed by a ‘relevantcommercial organisation’, which broadly includes:

• any body which carries on a business and isincorporated under, or is a partnership which is formedunder, any UK law, regardless of where it carries onbusiness

• any body corporate or partnership, wherever it isincorporated or formed, which carries on business inthe UK.

We will refer to those affected by this corporate offence as‘businesses’.

Persons associated

The corporate offence also refers to a person ‘associated’with a commercial organisation. While there is not anabsolute list of all who could be included, we are told thatthis is a person who performs services for, or on behalf of,the organisation, regardless of the capacity in which theydo so.

Accordingly, this term will be construed broadly and whileexamples are given of an employee, agent or subsidiary, itcould also cover intermediaries, joint venture partners,distributors, contractors and suppliers.

Guidance issued by the Ministry of Justice (see below)acknowledges that the scope of ‘persons associated’ isbroad and states that this is so as to ‘embrace the wholerange of persons connected to an organisation who mightbe capable of committing bribery’ on its behalf.

Improper performance

The passive and active bribery offences both refer to the‘improper performance’ of a function or activity. ‘Improperperformance’ covers any act or omission that breaches anexpectation that a person will act in good faith,impartially, or in accordance with a position of trust. Thisis an objective test based on what a reasonable person inthe UK would expect in relation to the performance of therelevant activity.

Ministry of Justice guidance

The Act requires the Secretary of State to publish guidancefor commercial organisations about procedures that theycan put in place to prevent persons associated with themfrom bribing. This is important guidance in respect ofproviding a defence against the ‘corporate offence’.

The Ministry of Justice (MoJ) has issued the followingformal, statutory guidance:

• The Bribery Act 2010 – guidance about procedureswhich relevant commercial organisations can put intoplace to prevent persons associated with them frombribing (section nine of the Bribery Act 2010). Whilstthe guidance is not prescriptive and does not set out anabsolute checklist of requirements for businesses tofollow, it does aim to clarify the practical requirementsof the legislation. Illustrative case studies, which do notform part of the guidance issued under section nine ofthe Act, are also included.

It has also produced non-statutory guidance for smallbusinesses, providing a concise introduction to how theycan meet the requirements of the Act:

• The Bribery Act 2010 – quick start guide.

• Insight into awareness and impact of the Bribery Act2010 among small and medium sized enterprises(SMEs).

Defending your business against failingto prevent bribery

As you can see from the legislation, all businesses willneed to pay some attention to the corporate offence offailing to prevent bribery. How much you will have to dowill depend on the bribery risks facing your business.

If a business can show that it had ‘adequate procedures’in place to prevent bribery then it will have a full defenceagainst the corporate offence. The meaning of ‘adequateprocedures’ is not defined in the Act and it is here that theMoJ statutory guidance should be considered.

This guidance requires procedures to be tailored to theindividual circumstances of a business, based on anassessment of where the risks lie. Therefore, what countsas ‘adequate’ will depend on the bribery risks faced by abusiness and its nature, size and complexity.

The MoJ guidance does recognise that the Act is not thereto impose the ‘full force’ of criminal law upon well runbusinesses for an isolated incident of bribery. It alsorecognises that no business is capable of preventing

bribery at all times. The ‘quick start’ guidance for smallerbusinesses comments that ‘a small or medium-sizedbusiness which faces minimal bribery risks will requirerelatively minimal procedures to mitigate those risks’.

How should you begin to determine the approach neededin your business? The MoJ guidance identifies six guidingprinciples for businesses wishing to prevent bribery frombeing committed on their behalf (see the panel below).These principles are not, however, prescriptive.

The six principles that should guide anti-bribery procedures

1. Proportionate procedures: A commercialorganisation’s procedures to prevent bribery bypersons associated with it are proportionate to thebribery risks it faces and to the nature, scale andcomplexity of the commercial organisation’s activities.They are also clear, practical, accessible, effectivelyimplemented and enforced.

2. Top-level commitment: The top-level managementof a commercial organisation (be it a board ofdirectors, the owners or any other equivalent body orperson) are committed to preventing bribery bypersons associated with it. They foster a culturewithin the organisation in which bribery is neveracceptable.

3. Risk assessment: The commercial organisationassesses the nature and extent of its exposure topotential external and internal risks of bribery on itsbehalf by persons associated with it. The assessmentis periodic, informed and documented.

4. Due diligence: The commercial organisation appliesdue diligence procedures, taking a proportionate andrisk based approach, in respect of persons whoperform or will perform services for or on behalf ofthe organisation, in order to mitigate identifiedbribery risks.

5. Communication (including training): Thecommercial organisation seeks to ensure that itsbribery prevention policies and procedures areembedded and understood throughout theorganisation through internal and externalcommunication, including training, that isproportionate to the risks it faces.

6. Monitoring and review: The commercialorganisation monitors and reviews proceduresdesigned to prevent bribery by persons associatedwith it and makes improvements where necessary.

Other important matters

Corporate hospitality

A potential area of concern under the Act is the provisionand receipt of corporate hospitality, promotional andother such business expenditure and how this might beperceived. While this may not be a significant issue for

your business, especially when you consider your own levelof such expenditure, it may be an important considerationfor others.

The MoJ guidance states: ‘Bona fide hospitality andpromotional, or other business expenditure which seeks toimprove the image of a commercial organisation, better topresent products and services, or establish cordialrelations, is recognised as an established and importantpart of doing business and it is not the intention of theAct to criminalise such behaviour. The Government doesnot intend for the Act to prohibit reasonable andproportionate hospitality and promotional or other similarbusiness expenditure intended for these purposes.’

The guidance goes on to say: ‘It is, however, clear thathospitality and promotional or other similar businessexpenditure can be employed as bribes.’

Facilitation payments

Facilitation payments, which are payments to induceofficials to perform routine functions they are otherwiseobligated to perform, are bribes and are therefore illegalunder the Act.

Penalties

The penalties associated with the Act are significant. Onconviction for one of the main bribery offences, anindividual may face up to ten years’ imprisonment and/oran unlimited fine. A business faces an unlimited fine.

The senior officers of a business could also be liable to aprison sentence if bribery was perpetrated with their‘consent or connivance’. Disqualification from acting as adirector for a substantial period of time could also arise.

Conclusion

The steps to be taken to prevent bribery will clearly varyfrom business to business and not all businesses will needto put in place complex procedures to deal with therequirements of the legislation. The supporting guidanceissued by the MoJ emphasises the need for a commonsense approach.

A key point noted in ‘quick start’ guidance is that ‘there isa full defence if you can show you had adequateprocedures in place to prevent bribery. But you do notneed to put bribery prevention procedures in place if thereis no risk of bribery on your behalf.’

How can we help

We believe the above summary will help you understandthe implications of the Bribery Act 2010. If you would liketo discuss the implications of the Act for you and yourbusiness in more detail please contact us.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Bring your own device (BYOD)Some employees will often prefer to use their ownpersonal mobile devices to access company networks/systems. However, this is potentially a security loopholewhich places the organisation at risk from reputationaldamage and legal proceedings.

Firms need to have a formal policy with regard to the useof personal devices at work.

Bring Your Own Device refers to this type of policy - whichdefines what mobile devices (if any), employees can use toaccess company networks/systems.

We consider how to structure such a policy, and what itmay contain.

Broadly what should a BYOD policycover?

Firms need a policy which sets out the devices which mayor may not be connected to a firms’ network; proceduresto ensure that non-approved devices can never be‘accidentally’ connected; and appropriate mechanisms inplace to maintain security over personal data which maybe stored on mobile devices.

Audit of existing devices and accessrights

The first step is to perform an audit of the currentsituation. Which devices use the network, and what for?

What does the law say?

As the employer (who is the data controller) there areobligations under the Data Protection Act 1998 (DPA) totake appropriate technical and organisational measuresagainst unauthorised or unlawful processing of personaldata and against accidental loss or destruction of, ordamage to, personal data.

There is a high risk that confidential corporate and clientdata can find its way onto personal devices – which areusually not very secure and can be easily lost/mislaid/stolen.

The risks of reputational damage

Imagine the scenario, an employee receives an email withan attachment containing a mailing list of all clients andtheir contact details which they open and save onto theirmobile device. If that device then goes missing the datastored on it could find its way into the public domain, orbe mis-used, or sold onto a competitor. What’s worse isthat the ICO will need to be notified of the loss of data, aswill each individual on that mailing list. This can causemajor reputational damage as well as a large financialpenalty.

Which devices are acceptable?

Having performed an audit, the second stage is to decidewhat to include or exclude from a BYOD policy, and this isusually done at device level.

Level Device

1 No devices (zero-tolerance)

2 A list of 'approved'devices

3 Any/all devices

1 - Zero-tolerance

This may be the quickest, easiest and simplest solution,but may not necessarily be the most pragmatic orpractical.

It may also serve to hinder rather than help someemployees perform certain tasks, which can lead to jobdissatisfaction and a lowering of morale.

So an outright ban could prove to be counter-productive.

It can also be quite difficult (and therefore expensive) tocontrol and police a zero-tolerance policy without strongnetwork security controls.

2 - Approved devices

This allows a set list of devices, or, devices with particularoperating software (e.g. iOS devices only or Android andWindows devices only).

The approved device approach can make it easier tomanage and control access, but may leave someemployees disadvantaged if their device is not covered. Itcan also be difficult to manage, as new models and newdevices emerge on a daily basis.

3 - Any device

This allows any device to be ‘plugged in’.

This approach is entirely opposite to zero-tolerance andallows any device to be ‘plugged in’ at any time.Advantages are a) for the employee who is not restrictedby device, and b) for the company which does not have tokeep updating a list of approved devices.

However, strong controls such as mobile devicemanagement systems need to be employed with this typeof approach.

An alternative option!

In an increasing trend, some firms have decided toabandon BYOD and have a zero-tolerance policy, in favourof providing devices to employees.

Which applications are acceptable?

The firm may wish to restrict access to certain applications– most often to email and internet access only. Full blownaccess to networks and applications should be avoidedwhere possible, other than from PCs or laptops and thenonly via trusted intranets or secure remote access tools.

Business v. private use

BYOD devices owned by an employee are likely to be usedfor both business and private purposes.

On the one hand the employee has to be confident thatthe company will not access personal material stored onthe device or use device monitoring tools, whilst on theother hand the company will want to protect corporateand client confidential information which may also bestored (or visible) on the device.

Employers also need to be aware that devices may be used(for personal purposes) not just by the employee, but alsoby other family members.

Wireless security

The easiest and quickest way for devices to be attached toa network is for employees to use their device to login to anetwork, wirelessly. Some firms publish their wireless keyto employees without realising that they are using the keyon all devices including personal devices.

So, one of the cheapest methods of providing devicesecurity is to make the wireless key very strong (i.e. difficultto remember), only available on request and only enteredinto the device by a member of the IT support team orother nominated individual. Thus control can bemaintained at device level relatively easily.

Device registration

Most current versions of network operating software(Windows and Mac) have inbuilt security tools which canbe used to maintain a list of 'approved' devices.

This is done through a registration process whereby thedevice is presented and registered on the network.

If a device gets mislaid or an employee leaves, the devicecan be blocked/removed from the list of registered devices.

Mobile device management(MDM)/Mobile applicationsmanagement (MAM)

A more expensive way of providing device security is to useMDM services – these may either be provided as part ofthe network operating software, or this service may beprovided by a third-party.

There are different levels of this type of service rangingfrom simple registration and device reset services, tosandboxing personal and corporate data – which willallow separate wiping of corporate data only.

Employees will have to agree/consent to whichever mobiledevice management system is used if they want to adoptBYOD.

Employees must also agree/consent if MDM software isused to monitor the device, the activities which aremonitored and whether or not geo-location is used.

Finally, employees will need to understand what willhappen to their own personal data stored on the device,in the event the device has to be disabled.

Data encryption

A BYOD policy in itself is not enough to provide sufficientsafeguards. All confidential/personal data must beencrypted. Just setting a document/spreadsheet as read-only, or creating a password to open the document/spreadsheet is not the same as encrypting the data.

Firms must assess what personal data is being transferredfrom and to which devices, perform a risk assessment ofthe chances of the data getting into the public domain,and then use appropriate encryption methods to protectthat confidential/personal data.

Other issues to consider

• Device password protection - Each BYOD device musthave a start-up password/pin and should lock if notactive for a specified number of minutes

• Mislaid devices – as part of the BYOD policy theemployee will need to know who to contact and whatwill happen to the device if it is mislaid (i.e. what datamight be wiped from the device)

• Cost – the firm may or may not agree to pay for certainmobile device charges

• Acceptable use policy – the firm will want to ensurethat any acceptable use policy also applies to BYODdevices

• Devices which have been rooted/jail-broken should notbe permitted

• Storage media – the firm may want to specify theapproach with regard to memory/SD cards.

Implementing the BYOD policy

BYOD can either be formulated as a separate policy, addedto an existing acceptable use policy, or added to anexisting Internet and email policy or social media policy.

Company devices, by default, will come under the scope ofBYOD.

Employees with their own personal devices should begiven the opportunity to opt-out or opt-in to the BYODpolicy -

• Opt-out - Decline to sign-up for the BYOD policy – inwhich case the employee will not be able to use anypersonal devices for work.

• Opt-in - Agree to sign-up for the BYOD policy – inwhich case their device will need to be registered onthe network and also, if applicable, with a mobiledevice management service.

See our summary for our 4 easy steps in defining andimplementing a BYOD policy.

Summary

It is important that the employer (who is the datacontroller) remains compliant with the DPA with regardsto the processing of personal data. In the event of asecurity breach, the employer must be able todemonstrate that all personal data stored on a particulardevice is secured, controlled or deleted. Having a BYODpolicy will go a long way towards meeting that objective.

4 steps to defining and implementing aBYOD

Step 1

Audit devices and usage

What devices are currently allowed onto the network?

What access rights do they have?

What applications do they use?

Step 2

Level of BYOD

Decide which level of BYOD is to be adopted –

1. No devices

2. Approved list

3. All/any devices

4. Define which applications are accessible to mobiledevices

Step 3

BYOD policy

Formulate and write the BYOD policy.

Make appropriate network infrastructure security changesand procure any additional services (such as MDM).

Decide if additional security is required such as dataencryption tools.

Define and communicate a date for implementing thepolicy.

Step 4

Implementation date

Remove all current devices.

Register approved devices.

Employees who own such devices sign BYOD.

How we can help

Please contact us if you require help in the following areas:

• Performing a security/information audit of corporate/client data and who and what access this data

• Defining a BYOD policy

• Implementing a BYOD policy and training staff.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Business Motoring - Tax AspectsThis factsheet focuses on the current tax position ofbusiness motoring, a core consideration of manybusinesses. The aim is to provide a clear explanation of thetax deductions available on different types of vehicleexpenditure in a variety of business scenarios.

Methods of acquisition

Motoring costs, like other costs incurred which are whollyand exclusively for the purposes of the trade are taxdeductible but the timing of any relief varies considerablyaccording to the type of expenditure. In particular, there isa fundamental distinction between capital costs andongoing running costs.

Purchase of vehicles

Where vehicles are purchased outright, the accountingtreatment is to capitalise the asset and to write off thecost over the useful business life as a deduction againstprofits. This is known as depreciation.

The same treatment applies to vehicles financed throughhire purchase with the equivalent of the cash price beingtreated as a capital purchase at the start with the additionof a deduction from profit for the finance charge as itarises. However, the tax relief position depends primarilyon the type of vehicle, and the date of expenditure.

A tax distinction is made for all businesses between anormal car and other forms of commercial vehiclesincluding vans, lorries and some specialist forms of carsuch as a driving school car or taxi.

Tax relief on purchases

Vehicles which are not classed as cars are eligible for theAnnual Investment Allowance (AIA) for expenditureincurred. The AIA provides a 100% deduction for the costof plant and machinery purchased by a business up to anannual limit. The amount of AIA available variesdepending on the period of the accounts. The currentamount of AIA is £200,000 and prior to 1 January 2016was £500,000.

Where purchases exceed the AIA, a writing downallowance (WDA) is due on any excess in the same period.The WDA available is currently at a rate of 18% or 8%depending on the asset. Cars are not eligible for the AIA,so will only benefit from WDA.

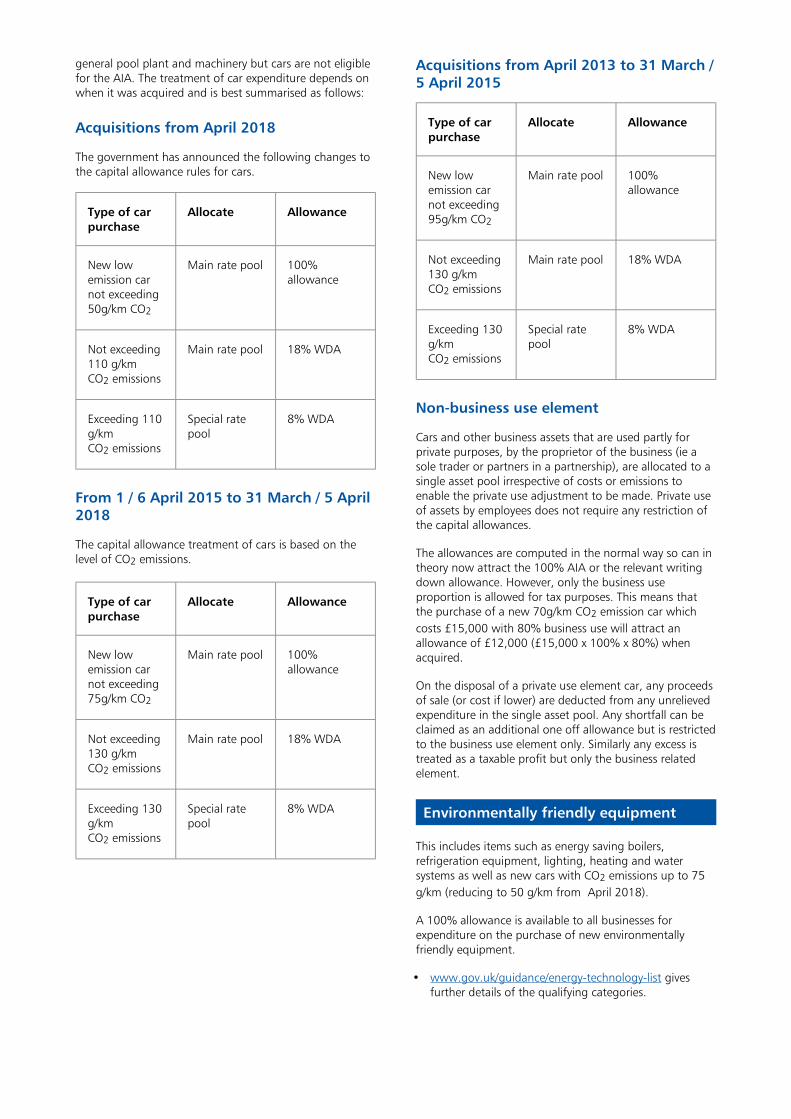

Capital allowance boost for low–carbontransport

A 100% First Year Allowance (FYA) is currently availablefor businesses purchasing zero-emission goods vehicles orgas refuelling equipment. Both schemes were due to endon 31 March 2018 but have been extended for a furtherthree years.

Writing Down Allowances (WDA)

The writing down allowance rates are 18% on the mainrate pool and 8% which applies to many higher emissioncars which are part of the special rate pool.

Complex cars!

The green car

Cars generally only attract the WDA but there is oneexception to this and that is where a business purchases anew car with low emissions - a so called 'green' car. Suchpurchases attract a 100% allowance to encouragebusinesses to purchase cars which are moreenvironmentally friendly. From April 2015 a 100% writeoff is only available where the CO2 emissions of the car donot exceed 75g/km (reducing to 50g/km from April 2018).The cost of the car is irrelevant and the allowance isavailable to all types of business.

When did you buy?

There have been significant changes to the basis of capitalallowances for car purchases and the tax relief thereon.The allowances due are determined by whether the carwas purchased

• from April 2018 (proposed)

• from April 2015 to April 2018

• or between April 2013 and April 2015.

The dates are 1 April for companies and 6 April forindividuals in business.

For purchases from April 2018:

The annual allowance is dependent on the CO2 emissionsof the car.

Cars with emissions between 51 – 110 gm/km inclusivewill qualify for main rate WDA.

Cars in excess of 110 gm/km are placed in the special ratepool and will qualify for an annual WDA of 8%.

The 100% first year allowance (FYA) will be available onnew low emission cars purchased (not leased) by abusiness is generally available where a car’s emissions donot exceed 50 gm/km.

If a used car is purchased with CO2 emissions of 50gm/kmor less, this will be placed in the main pool and will receivean annual allowance of 18%.

For purchases from April 2015 to April2018:

Cars with emissions between 76 – 130 gm/km inclusivecurrently qualify for main rate WDA.

Cars in excess of 130 gm/km are placed in the special ratepool and will qualify for an annual WDA of 8%.

The 100% first year allowance (FYA) available on new lowemission cars purchased (not leased) by a business isgenerally available where a car’s emissions do not exceed75gm/km.

If a used car is purchased with CO2 emissions of 75gm/kmor less, this will be placed in the main pool and will receivean annual allowance of 18%.

For purchases from April 2013 to April2015:

Cars with emissions between 96 – 130gm/km inclusivequalify for main rate WDA.

Cars in excess of 130 gm/km are placed in the special ratepool and will qualify for an annual WDA of 8%.The 100%first year allowance (FYA) available on new low emissioncars purchased (not leased) by a business is generallyavailable where a car’s emissions do not exceed 95 gm/km.

If a used car is purchased with CO2 emissions of 95gm/kmor less, this will be placed in the main pool and will receivean annual allowance of 18%.

Non-business

Any cars used by the self employed where there is partnon–business use will still be separately allocated to asingle asset pool. The annual allowance will initially beeither the current 18% or 8% depending on the CO2

emissions and then the available allowance will berestricted for the private use element.

Example

A company purchases two cars for £20,000 in its 12month accounting period to 31 March 2017. The dates ofpurchase and CO2 emissions are as follows:

White car Blue car

1 May 2016 1 May 2016

125 145

Allowances in the year to 31 March 2017 relating to thesepurchases will be:

White car (main poolas emissions less than130)

Blue car (special ratepool as emissionsmore than 130)

£20,000 @ 18% =£3,600

£20,000 @ 8% =£1,600

In the following year to 31 March 2018 the allowanceswill be:

White Blue

£16,400 @ 18% =£2,952

£18,400 @ 8% =£1,472

Disposals

Where there is a disposal of plant and machinery from themain or special rate pools any balance of expenditure,after taking into account sale proceeds, continues toattract the annual allowance.

Where there is a disposal of a car held in a single assetpool, the disposal proceeds are deducted from the balanceof the pool and a balancing allowance or a balancingcharge is calculated to clear the balance on the pool.

This applies to any cars used by the self employed withpart non business use whenever purchased.

What if vehicles are leased?

The first fact to establish with a leased vehicle is whetherthe lease is really a rental agreement or whether it is a typeof purchase agreement, usually referred to as a financelease. This is because there is a distinction between theaccounting and tax treatment of different types of leases.

Tax treatment of rental type operatingleases (contract hire)

The lease payments on operating leases are treated likerent and are deductible against profits. However wherethe lease relates to a car there may be a portiondisallowed for tax.

Currently a disallowance of 15% will apply for cars withCO2 emissions which exceed 130gm/km.

Example

Contract signed 1 April 2017 by a company:

The car has CO2 emissions of 136 gm/km and a£6,000 annual lease charge. The disallowed portionwould be £900 (15%) so £5,100 would be taxdeductible.

Tax treatment of finance leased assets

These will generally be included in your accounts as fixedassets and depreciated over the useful business life but asthese vehicles do not qualify as a purchase at the outset,the expenditure does not qualify for capital allowancesunless classified as a long funded lease. Tax relief isgenerally obtained instead by allowing the accountingdepreciation and any interest/finance charges in the profitand loss account – a little unusual but a simple solution!

Private use of business vehicles

The private use of a business vehicle has tax implicationsfor either the business or the individual depending on thetype of business and vehicle.

Sole traders and partners

Where you are in business on your own account and use avehicle owned by the business – irrespective of whether itis a car or van – the business will only be able to claim thebusiness portion of any allowances. This applies to capitalallowances, rental and lease costs, and other running costssuch as servicing, fuel etc.

Providing vehicles to employees

Where vehicles are provided to employees irrespective ofthe form of business structure – sole trader/partnership/company – a taxable benefit generally arises for privateuse. A tax charge will also apply where private fuel isprovided for use in an employer provided vehicle. For theemployer such taxable benefits attract 13.8% Class 1ANational Insurance.

Vans

No charge applies where employees have the use of a vanand a restricted private use condition is met. For details onwhat this means please contact us. Where the condition isnot met there is a flat rate charge per annum. Thesebenefits are £3,230 for the unrestricted private use plus anadditional £610 for private fuel 2017/18 (£3,350 and£633 for 2018/19).

How we can help

If you would like further details on any matter contained inthis factsheet please contact us.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Business PlansEvery new business should have a business plan. It is thekey to success. If you need finance, no bank manager willlend money without a considered plan.

It is one of the most important aspects of starting a newbusiness. Your plan should provide a thoroughexamination of the way in which the business willcommence and develop. It should describe the business,product or service, market, mode of operation, capitalrequirements and projected financial results.

Why does a business need a plan?

Preparing a business plan will help you to set clearobjectives for your business and clarify your thinking. Itwill also help to set targets for future performance andmonitor finances and profitability. It should help toprovide early warning for when you might need toreconsider the plan.

Always bear in mind that anyone reading the plan willneed to understand the essentials of your business quicklyand easily.

Contents

The business plan should cover the following areas.

• OverviewAn overview of your plans for the business and howyou propose to put them into action. This is the sectionmost likely to be read by people unfamiliar with yourbusiness so try to avoid technical jargon.

• DescriptionA description of the business, your objectives for it andhow you plan to achieve them. Include details of thebackground to your business for example how long youhave been developing the business idea and the workyou have carried out to date.

• PersonnelDetails of the key personnel including yourself and anyexternal consultants. You should highlight the skills andexpertise that these people have and outline how youintend to deal with any weaknesses.

• ProductDetails of your product or service and your UniqueSelling Point. This is exactly what its name suggests,something that the competition does not offer. Youshould also outline your pricing policy.

• MarketingDetails of your target markets and your marketing plan.This may form the basis for a separate, more detailed,plan. You should also include an overview of yourcompetitors and your likely market share together withdetails of the potential for growth. This is usually a veryimportant part of the plan as it gives a good indicationof the likely chance of success.

• PracticesYou will need to include information on your proposedoperating practices and production methods as well aspremises and equipment requirements.

• Financial forecastsThe plan should cover your projected financialperformance and the assumptions made in yourprojections. This part of the plan converts what youhave already said about the business into numbers. Itwill include a cash flow forecast which shows howmuch money you expect to flow in and out of thebusiness as well as profit and loss predictions and abalance sheet. Detailed financial forecasts will normallybe included as an appendix to the plan. As financialadvisers we are particularly well placed to help with thispart of the plan.

• Financial requirementsThe cash flow forecast referred to above will show howmuch finance your business needs. The plan shouldstate how much finance you want and in what form.You should also say what the finance will be used forand show that you will have the resources to make thenecessary repayments. You may also give details of anysecurity you can offer.

The future

Putting together a business plan is often seen as a one-offexercise undertaken when a new business is starting up.

However the plan should be updated on a regular basis. Itcan then be used as a tool against which performance canbe monitored and measured as part of the corporateplanning process. There is much merit in this as usedproperly it keeps the business focused on objectives andinspires a discipline to achieve them.

How we can help

We can look forward with you to help you put togetheryour best possible plan for the future.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken withoutconsulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by

the authors or the firm.

Business Structures - WhichShould I Use?

Having made the decision to be your own boss, it isimportant to decide the best legal and taxation structurefor your enterprise. The most suitable structure for you willdepend on your personal situation and your future plans.The decision you make will have repercussions on the wayyou are taxed, your exposure to creditors and othermatters.

The possible options you have are as follows.

Sole trader

This is the simplest way of trading. There are only a fewformalities to trading this way, the most important ofwhich is informing HMRC. You are required to keepbusiness records in order to calculate profits each year andthey will form the basis of how you pay your tax andnational insurance. Any profits generated in this mediumare automatically yours. The business of a sole trader is notdistinguished from the proprietor’s personal affairs so thatif there are any debts, you are legally liable to pay thosedebts down to your last worldly possession.

Partnership

A partnership is an extension of being a sole trader. Here,a group of two or more people will come together, pooltheir talents, clients and business contacts so that,collectively, they can build a more successful business thanthey would individually. The partners will agree to sharethe joint profits in pre-determined percentages. It isadvisable to draw up a Partnership Agreement which setsthe rules of how the partners will work together. Partnersare taxed in the same way as sole traders, but only ontheir own share of the partnership profits. As with soletraders, the partners are legally liable to pay the debts ofthe business. Each partner is ‘jointly and severally’ liablefor the partnership debts, so that if certain partners areunable to pay their share of the partnership debts thenthose debts can fall on the other partners.

Limited company

A limited company is a separate legal entity from itsowners. It can trade, own assets and incur liabilities in itsown right. Your ownership of the company is recognisedby owning shares in that company. If you also work forthe company, you are both the owner (shareholder) andan employee of that company. When a company

generates profits, they are the company’s property. Shouldyou wish to extract money from the company, you musteither pay a dividend to the shareholders, or a salary as anemployee. The advantage to you is that you can have abalance of these two to minimise your overall tax andnational insurance liability. Companies themselves paycorporation tax on their profits after paying your salary butbefore your dividend distribution. Effective tax planningrequires profits, salary and dividends to be consideredtogether.

There are many advantages as well as disadvantages tooperating through a limited company. We have a separatefactsheet on ‘incorporation’ which considers the relativemerits as well as the downsides of operating as acompany.

New companies can be purchased relatively cheaply in aready-made form usually referred to as ‘off the shelf’companies. There are additional administrative factors inrunning a company, such as statutory accountspreparation, company secretarial obligations and PAYE(Pay as You Earn) procedures. A big advantage of owninga limited company is that your personal liability is limitedto the nominal share capital you have invested.

Limited liability partnership

A limited liability partnership is legally similar to acompany. It is administered like a company in all aspectsexcept its taxation. In this, it is treated like a partnership.Therefore you have the limited liability, administrative andstatutory obligations of a company but not the taxationand national insurance flexibility. They are particularlysuitable for medium and large-sized partnerships.

Co-operative