Export Costs of Visa Restrictions -the case of Russia

19

Export Costs of Visa Restrictions - the case of Russia How influence or not influence the visa restrictions the Russian export Topics in the Russian Economy (Aktuelle Forschungsfragen der internationalen Finanzpolitik) WIWISS_V_107046_13W Dénes Attila TORDAI Immatriculation number: 4761699 (ERASMUS)

-

Upload

uni-corvinus -

Category

Documents

-

view

2 -

download

0

Transcript of Export Costs of Visa Restrictions -the case of Russia

Export Costs of Visa Restrictions -

the case of Russia

How influence or not influence the visa restriction s the Russian export

Topics in the Russian Economy

(Aktuelle Forschungsfragen der internationalen Finanzpolitik)

WIWISS_V_107046_13W

Dénes Attila TORDAI

Immatriculation number: 4761699 (ERASMUS)

Contents

Introduction ........................................................................................................................................3

Model Analysis ...................................................................................................................................4

Short Analysis of the Basic Study .......................................................................................................5

Russian Export and Visa Restrictions ..................................................................................................8

The practice of the Russian visa regime ...........................................................................................8

Visa and trade with Commonwealth of Independent States ..............................................................8

Trade with visa-free countries .........................................................................................................9

Trade with the most important Western European partners ............................................................ 10

Trade with Central and Eastern European countries ....................................................................... 10

Other Possible Problems for Russian Firms ....................................................................................... 11

Competitiveness ............................................................................................................................ 11

Productivity .................................................................................................................................. 11

Cost to export ............................................................................................................................... 12

Diversification .............................................................................................................................. 12

Conclusion........................................................................................................................................ 14

Bibliography ..................................................................................................................................... 15

Appendix .......................................................................................................................................... 16

Introduction

Restriction on international trade, primarily in the form of non-tariff barriers, have multiplied

rapidly from the 1980s. In recent years, non-tariff barriers have increased, as tariffs have

fallen, primarily to the GATT, than the operation of World Trade Organization since 1995.

But the increasing use of protectionist trade policies raises national as well as international

issues. Non-tax measures imposed by governments to favor domestic over foreign suppliers.

Non-tariff measures such as quotas, voluntary export restraints, trade restraints, non-automatic

import authorizations, visa restrictions have significant effects. These “hard-core” non-tariff

measures are designed to reduce imports and, thereby, benefit domestic producers (Coughlin-

Wood, 1989).

As many observers have noted, international trade restrictions generally have costly national

consequences. Non-tariff barriers (NTBs) and other regulatory differences can have two main

effects. Non-tariff barriers can either increase the cost of doing business for firms (for

example visa regimes), or they can restrict market access. Traditional NTBs, like import

quotas, are an example where NTBs market access. In contrast, regulations that require

expensive reconfiguration of products for export are an example of cost raising NTBs (CEPR,

2013). Visa restrictions also can have a negative effect on market access, and as a non-tariff

restriction, can have an effect on the trade relations between countries.

The ongoing negotiation of the Transatlantic Trade and Investment Partnership (TTIP)

between the United States of America and the European Union also bring to focus the

importance of the non-tariff barriers, because not only the removing of the trade barriers being

negotiated, much more emphasis are on the non-tariff barriers (in the case of TTIP the

technical regulations, standards, approval procedures, bureaucracy). The reason is simple: the

economies could have substantial benefits from some liberalization of non-tariff barriers. Due

to the problems of collecting data on these barriers, a wide-scale impact of removing them are

hard to quantify. Some studies showed that removal of NTBs would generate 90 billion dollar

global gains or lowering the trade transaction costs by 1% would increase of $40 billion in

global welfare (Love-Lattimore, 2009). To estimate this gains is very difficult, but if we see,

that according to the World Trade Organization, Russia's share in the world total export was

2.88% in 2012, the benefits from the elimination of non-trade barriers could be billions of

dollars for the Russian economy and for the Russian companies. Therefore also it is

interesting and timely to analyze the role of visa restrictions to the export in Russia's point of

view. During this paper, I try to find the answer, how influence or not influence the visa

restrictions the Russian export.

Generally visa restriction are imposed by governments to control the inbound travel of non-

citizens, but also express the relationship between the countries. Visa restriction impose

significant burden on business and also private travelers, not only because of the cost of the

visa, but application process, personally on an embassy, consulate or via post, can take weeks

or month. Furthermore the visa in the passport may not guarantee to entering the country, but

there is a high probability, that you will be able to enter. The main problem of the visa

restriction, that the much of the international trade (and also investments) transaction requires

personal contact with the foreign partners, accordingly, visa regimes may impose extra costs

on business during the negotiations, render such physical contact more difficult restrict the

exchange of information, reputation building and business expansion in foreign countries.

Therefore bilateral trade activities are likely to be negatively affected by visa restrictions

(Neumayer, 2011; Kapelko-Volchkova, 2013).

Model Analysis

I found, that recently papers on analysis of international trade use two big types of model

during analyzing the trade: CGE model and the gravity-type model.

The CGE model is one of the most used quantitative methods to evaluate the impact of

economic and policy shocks and reforms in the economy. The CGE model is mostly used to

evaluate the effects of fiscal policy, climate change shocks, shocks in international prices and

trade policy, if the research question involves analyzing the static and dynamic, direct and

indirect, short and long term effects caused by the policy changes. The CGE approach is

especially useful when the expected effects of policy implementation are complex and

materialize through different transmission channels. The reason, why CGE model is not

suitable to analyze the impact of visa restriction to trade, is that CGE models perform

economic cost-benefit analysis for trade integration options, estimating aggregate effects not

only on trade, but production, employment, fiscal balance, household income and poverty and

inequality. Otherwise, it is a excellent model to evaluate effects at different levels (sectorial,

firm, household and geographic) and help for the governments, authorities to define trade

negotiation strategies (Inter-American Development Bank).

In contrast, the gravity model is a good choice to analyze the impact of the visa regimes to the

international and bilateral trade. Starting with Tinbergen in 1962, the gravity model has given

the base to literally thousands of publications and working papers covering the trade from a

wide variety of regions, time periods, and sectors. The gravity model was initially presented

as an intuitive way of understanding trade flows. In its most basic form, the gravity model can

be written as follows:

where the c term is a regression constant, the b terms are coefficients to be estimated, X

indicates exports from country i to country j, GDP is each country’s gross domestic product,

represents trade costs between the two countries, distance is the geographical distance

between them and is a random error term. "The name gravity comes from the fact that the

nonlinear form of equation 1a resembles Newton’s law of gravity: exports are directly

proportional to the exporting and importing countries’ economic “mass” (GDP), and inversely

proportional to the distance between them (not the square of the distance between them, as in

physics). In other words, gravity says that we expect larger country pairs to trade more, but

we expect countries that are further apart to trade less, perhaps because transport costs

between them are higher". Summarizing, the gravity model is a appropriate and a key tool for

economist and researchers to analyze the effects of trade policies. Regulatory policies, deep

political and institutional characteristics have been shown to influence trade as modeled in the

gravity framework (Shepherd, 2013).

Short Analysis of the Basic Study

Kapelko and Volchkova focused in their paper on the export costs of visa restriction, but first

of all I wanted to understand the problem, and watch after that it is a real problem, not only in

Russia but in the other parts of the world. Neumayer (2011) focused on the detrimental impact

of visa restrictions on bilateral trade and foreign direct investment. Neumayer also used a

standard gravity-type model, like Kapelko and Volchkova, but used partly different variables

in his model. As long as Kapelvo and Volchkova used visa, tariffs, WTO membership, GDP

PPP, Former Soviet Union membership, landlocked, contiguity and distance as variables, in

his more general model Neumayer used also contiguity and distance, and the colonial link is

very similar to the Former Soviet Union membership, but the additional variables are some

region, trade agreement, diplomatic representation, bilateral migrant stock, and finally the

visa, but separately on unilateral and bilateral level.

Neumayer (2011) finds, that both visa regimes, the unilateral and bilateral has a negative

effect on the bilateral trade between the countries. Without reciprocal visa restriction, when

just one country impose restriction, the bilateral trade estimated to be decreased

approximately 19%, and when both country have visa restriction, trade is estimated to be

reduced by up to 29%. Although the topic of FDI is not primary issue, but the fact, that the

effects of visa restrictions are essentially the same, the estimation shows an average 40%

decrease of FDI. The effects of visa restrictions on trade and investment are smaller than the

estimated effect of such restrictions on travel by visitors as reported by Neumayer, who finds

that visa restrictions could reduce travel by between 52 and 63 per cent. In Neumayer (2011)

the distance has also a negative correlation to trade, like in Kapelko and Volchkova (2013).

According to Neumayer (2011), one argue, that most trade business will be economically

profitable to compensate the trading partner for the costs of vista restrictions, but this

predication supposes the perfect information between the partners, which in the most cases is

lacking, and the potential gains will often only discovered after personal contact during

visiting the foreign partners. Generally, for developing countries even small additional costs

such (for example costs of visa regimes) can defeat the small profit margins of trade.

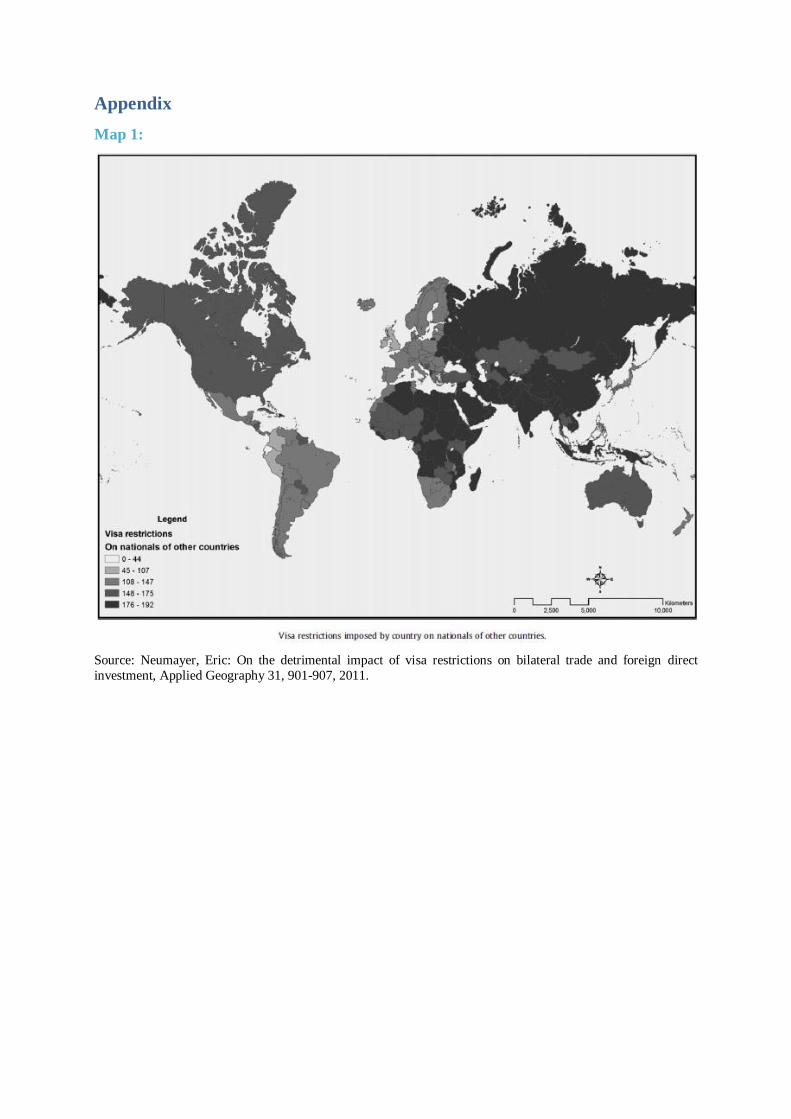

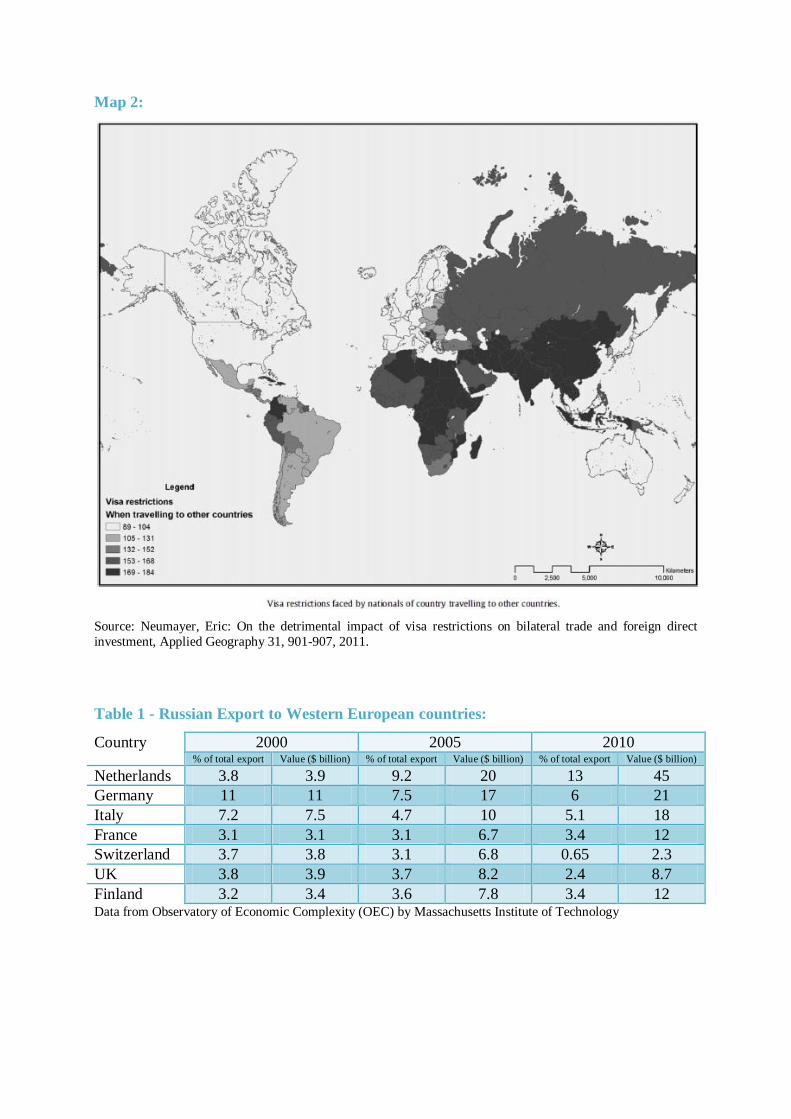

Map 1 and Map 2 show that Russia is strongly concerned with visa restrictions, also

restrictions imposed by country on national of other countries and nationals of country

travelling to other countries. In that case, the result of my basic paper is not surprise: the

probability of a Russian firm to export to visa restricted destinations is about 36 percent below

of the probability of export to visa-free destinations. The gap is higher, 40% for relationship

specific goods (logical, because they require special relationship between the buyer and the

seller) and with the 26% the non-relationship specific good are less influenced by visa

restrictions.

In their estimation Kapelko and Volchkova indicate that visa restrictions also have a negative

selection effect on destination choice and on export flows. The export values are lower at least

18% to countries with visa restrictions compared visa-free ones. The effects of visa regimes

are the large in the case of relationship-specific goods, and next to the negative probability of

exporting of relationship-specific goods, the export values are also lower by at least 50%,

compared to destinations without visa restrictions. But visa do not have effect on the value of

exports for non-relationship specific goods.

I want to add some critics and comments on the basic working paper by Kapelko and

Volchkova. I think that the selected variables fundamentally were good choices, the Former

Soviet Union membership dummy is an important factor, because of the common historical

background, and some of this countries have similar cultural history and similar language,

which make easier to close a business and a trade deal. However I miss a variable to

differentiate between the state owned enterprises and the private firms. It is clear, that the

working paper focused to all firms which exported at least one year between 2003 and 2010,

but the Russian export is dominated by state-owned enterprises.

I base my earlier statement about the domination of state-owned enterprises, that according to

the statistics of the World Trade Organization, oil-fuels and mining products with share of

71.3% dominate in the total export of Russia. According to EIA, Russia is the second-largest

producer of dry natural gas and third-largest liquid fuels producer in the world. Russia is also

a major exporter of oil and natural gas, and the Russian economy largely depends on energy

exports (economic growth is driven by energy exports and oil and gas revenues accounted for

52% of federal budget). Behind the majority of oil and exports stand a few robust state-owned

enterprises.

Six of the country’s ten largest companies operate in the oil and gas sector. Production and

transmission of gas in Russia are dominated by state-owned Gazprom, which is accounted for

about 75 % of Russian natural gas output. Russian oil production is dominated by five

companies that together produce about 80 % of oil production. Next to the state-owned

Rosneft-TNK-BP (account for about 40% of oil production) and Gazprom Neft the private

Lukoil and Surgutneftegaz are major players (Korhonen-Simola-Solanko, 2013). The Russian

government controls more than the half of the country's oil production, so adopt other

indicator for oil, gas and mineral companies also would be useful.

Russian Export and Visa Restrictions

The practice of the Russian visa regime

Russia has a reciprocal visa policy, which means, that the country has a similar policy with

respect to the citizens of another country as that country has with respect to Russian citizens.

It could be argument, that this reciprocity principle of Russian foreign policy is remunerative

or not, but next to the national and governmental pride probably the cost-benefit analysis

shows, that now it is the right policy. However, Neumayer (2011) finds, that the unilateral

visa can has a moderate negative effect (-19%) to trade on contrary bilateral visa (-29%), and

in long-term the other country can also change its own visa policy due to the positive effects.

Nowadays Russian citizen can visit 55 out of countries in the selected export destinations of

the basic working paper without visa requirements. From 2000 to 2010, in the 48 cases, it was

usually about visa abolishment, except five countries, Costa Rica, Czech Republic, Georgia,

Kyrgyzstan and Romania.

Visa and trade with Commonwealth of Independent States

Most of the members of the Commonwealth of Independent States (CIS) have no visa

restrictions with Russia. Armenia, Azerbaijan, Belarus, Kazakhstan, Moldova, Tajikistan and

Uzbekistan do not prevent the Russian citizens since 2000, only between Russia and

Kyrgyzstan and Turkmenistan is in effect visa obligation. Although the working paper by

Kapelko and Volchkova analyze the impact of visa restrictions from 2003 to 2010, analyze

the trade trends between Russia and the CIS from 2000 to 2012 can give comprehensive

picture. According to the database of Interstate Statistical Committee of the Commonwealth

of Independent States, the share of the CIS countries in the total Russian export was 13%,

which increased by 14% in 2005, and from 2005 it is continuously 15%.

Despite the positive correlation of contiguity, landlocked and Former Soviet Union indicators

and the visa-free regime, the share of the CIS countries from the total export of Russia do not

change dramatically from 2000 to 2012. Based on the database of CIS statistical bureau, from

2000 to 2012 the export to the CIS from Russia increased by an average of 18.23%, and the

export to the other countries of the world increased by 18.69%. This results strengthen the

outcome of my basic study, that there is an easier market access for Russian firms to market

of the former Soviet Union countries, but the visa-free status and the former historical

background do not have any effect on the value of the export. This result is somewhat

surprising.

Trade with visa-free countries

During my analysis in this and the next two parts I will use the data from Observatory of

Economic Complexity, which use the United Nations Comtrade Database. In this subsection I

will analyze the trade trends between the Russia and visa-free countries, primarily focus on

European countries and the Middle East, because of the distance variable and in same cases of

the former historical background after the second world war.

First I analyze Bulgaria, Bosnia And Herzegovina, Moldova and Serbia, but I am not going to

observe the trade between Montenegro and Russia, because the Russian export was $90

million in 2008, just the 0.022% of the total export of the country. The visa restriction was

cancelled against Russians in Moldova in 2000, in Bulgaria in 2001, in Bosnia And

Herzegovina in 2007 and in Serbia in 2009. The Russian export to Moldova was the 0.27%

($200 million) of the total export in 1999, but after the obliteration of the visa restriction, the

ratio of the export was 0.16% ($170 million) in 2000, 0.17% ($370 million) in 2005 and

0.16% ($580 million) in 2010, so the ratio do not increased, just the value of the export. One

year before Bulgaria cancelled the visa restrictions, the country's share of the Russian export

was 0.94% ($980 million), which reduced to 0.62% ($630 million) in the first visa-free year,

but in 2010 Bulgaria's share was 1.2% and $4.2 billion in value.

Bosnia And Herzegovina has a spectacular development in the Russian export after the

cancellation of the visa restrictions. In the first visa-free year, the country's share of the total

Russian export was only 0.058% ($180 million), but in 2010 was already 0.18% and $650

million in value. In the rate and amount Bosnia And Herzegovina does not play a major rule

in the Russian export, but it could be a positive example of the benefit of visa-free trade. We

can not say the same thing about Serbia, because there was no significant change in the

Russian export after 2008, when the Serbian share of total export of Russia was 0.75% ($3.1

billion), and in 2006 and in 2007 these data are as follows: 0.62% ($1.7 billion) and 0.5% (1.8

billion).

I do not find positive correlation also in the case of Egypt (visa-free from 2007) and Israel

(visa-free from 2008). The Russian export to Egypt was only the 0.81% ($ 2.5 billion) of the

total export, and the value of the export slightly increased to $3 billion in the next year, the

share from the total export decreased, in 2010 was 0.73% ($ 2.6 billion). After the Arab

Spring it could be an interesting question, what kind of role has the visa waiver status to

rebuild the international political and economical relations. In the case of Israel, the ratio of

the export was 0.52% ($2.1 billion) in 2008, 0.36% ($960 million) in 2009 and 0.46% ($1.6

billion) in 2010.

Trade with the most important Western European partners

The analysis the Russian export to the Western European countries made it clear, that not only

the visa requirements have serious influence to the trade changes, because all Western

European countries, also the non-European Union members have visa requirements to the

Russian citizens. However, from 2000 to 2010 there is a significant change in the destination

of the Russian export, without change of the visa regime.

In 2000 Germany was the most important western trade partner of Russia with 11% of the

total export and the value of $11 billion, ahead of Italy with 7.2% ($7.5 billion), and

Netherlands, France, Switzerland, UK and France was also important partner with their shares

between 3-4% (see Table 1). Already in 2005 Netherlands became the most important

European destination for Russian export with 9.2%, and its share increased to 13% in 2010.

Germany's and Italy's share fell between 2000 and 2010, though the volume of the Russian

export increased significant. The share of France and Finland essentially unchanged, the UK

decreased moderate, but Switzerland significant.

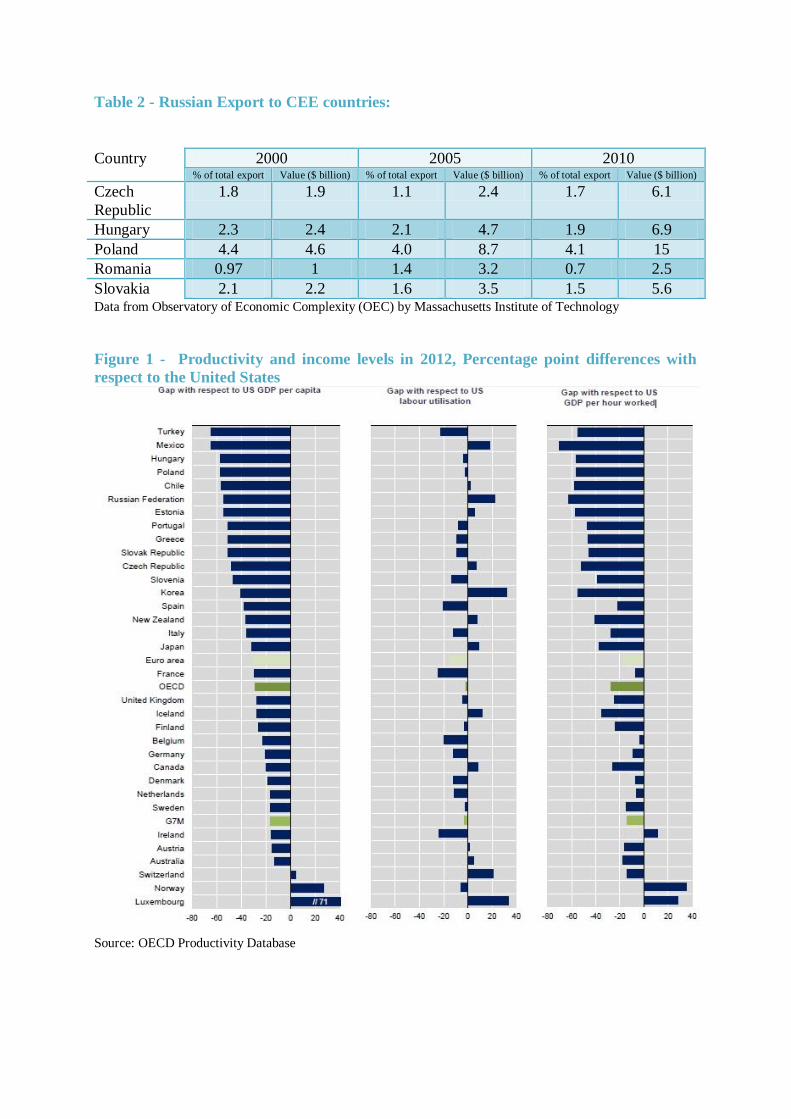

Trade with Central and Eastern European countries

After the analysis of the Russian export to the Western European countries, I look at the

Central and Eastern European countries curiosity, whether a similar trend could be observed. I

choosed Czech Republic, Hungary, Poland, Romania and Slovakia, and the results are

collected in Table 2.

Unlike the case of Western European countries, there are no significant changes in the

Russian export to the Central and Eastern European countries. Examining the export of Russia

from 2000 until 2010, we can observe a continuous, but no large-scale reduction in the CEE

share of the total export of Russia. Only Romania changed the visa regime during this period,

but the change in the share of the total export is not really remarkable. But the value of the

export to the CEE countries continuously increased for all countries. The explanation may be

that the most of the Russian export to this region is oil and gas, which dominate the total

export of Russia also. I think, that the mineral resources belong to the non-relationship

specific goods, because basically every host country has proper skills and infrastructure for

the processing, and the non-relationship specific goods are less affected by the visa

restrictions. Furthermore the politics and foreign policy play more important role in this topic.

Other Possible Problems for Russian Firms

Next to the visa requirements, there are more factor, which have major influence on the

Russian trade and export. I will explain in details the topics of competitiveness, productivity,

cost to export and diversification.

Competitiveness

In every year the World Economic Forum analyze the competitiveness of the countries in

their Global Competitiveness Report. In the 2013-2014 issue Russia take the 64th place,

improves by three positions since last year. The improvement is due to the satisfactory

macroeconomic environment, the low level of governmental debt, and the surplus in the

national budget. Other strength are the high level of education enrollment, a quite good

infrastructure and its large domestic market.

O the other hand, Russia continues to receive a poor evaluation of its public institution, a lack

of innovation capacity, furthermore the country suffers from inefficiencies in the goods, labor

and financial markets. The weak level of competition is due to inefficient anti-monopoly

policies, high restrictions on trade and foreign ownerships and a lack of trust in the financial

system.

Productivity

Productivity is the real value of output produced by a unit of labor in a unit of time, and it is

used to measure efficiency of the economy. The indicator varies across different countries, in

most cases refers to GDP produced per employed person. It can also measure output per

worker, output per filled job and output per hour worked. Figure 1 shows, that Russia has a

very modest position if we see the position of the country compared to the United States.

According to the OECD database, the gap compared to the US GDP per capita is close 60%,

and although the labor utilization is 20% better, the gap with respect to US GDP per hour

worked is more than 60% less. Russia should improve its performance in the case of labor

productivity.

An economy could be characterized by higher levels of competition pushes firms to improve

productivity and innovation. The World Bank study finds that productivity is a significant

factor in explaining export propensity in the sample of 19 countries, including Russia. They

described that the relationship between productivity and export tendency is likely explained

by the observation that improvements in productivity translate into improvements in offering

to the market. The improvements in productivity prepare the companies to compete in

international markets (World Bank, 2012).

Cost to export

The direct cost of starting export in Russia was $16 200 per month per foreign destination, if

the company decided to export their goods. Furthermore it takes at least months for a Russian

small or medium enterprise to become profitable of doing business abroad. Next to the

starting cost, Russian firms have to face with another high cost.

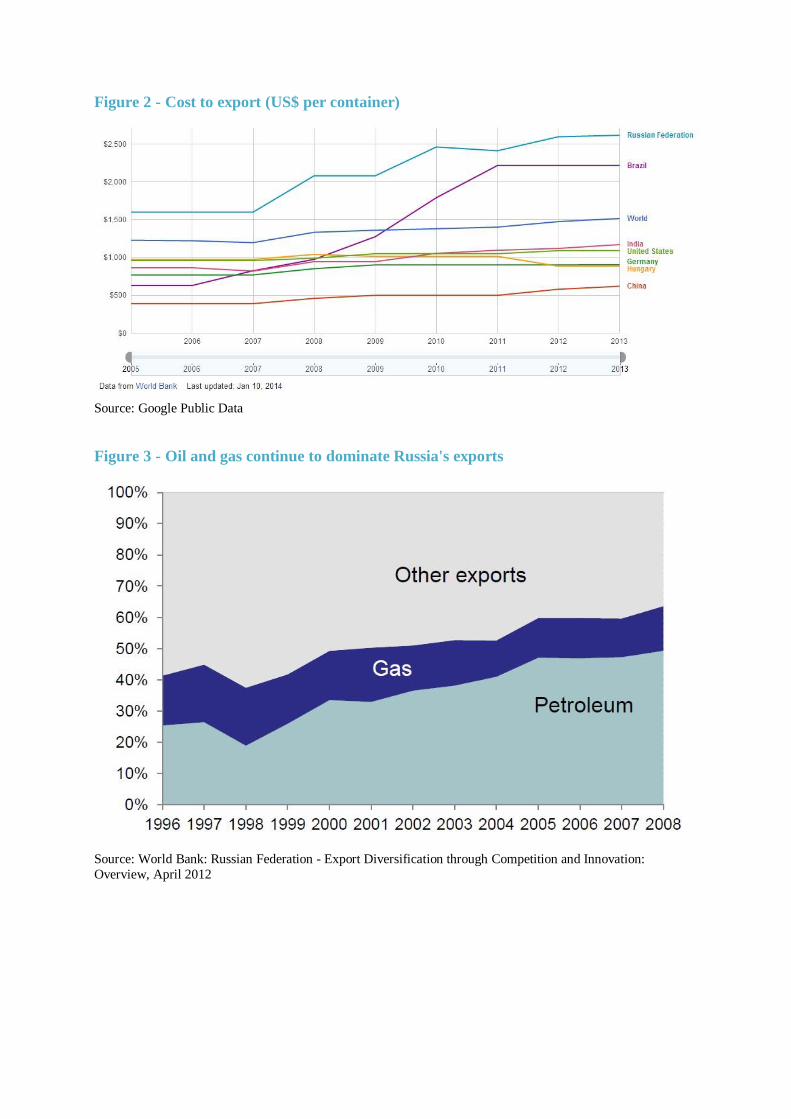

According to the World Bank, the cost to export (US$ per container) measures the fees levied

on a 6.1 meter-long container in U.S. dollars. These include costs for documents,

administrative fees for customs clearance and technical control, customs broker fees, terminal

handling charges and inland transport. The cost measure does not include tariffs or trade

taxes. Only official costs are recorded.

Figure 2 shows that Russian companies have significant disadvantage in this form of export

costs. To export one container was $2615 for a Russian firm in 2013, while the world average

was $1515. Russia has a serious disadvantage compare to the United States ($1090) and

Germany ($905), and among the BRIC countries Russia has the worst result, slightly ahead of

Brazil, but India perform close to the United States, and China with its $620 has a strong

position.

Diversification

Oil, fuels, gas and mining products dominate with the 71.3% share of the total export of

Russia, and behind the majority of oil and exports stand a few robust state-owned enterprises.

Although industries such as machinery, electronics, transportation equipment and chemicals

reached a combined growth rate in export value of 10 percent in the last decade, the mineral

resources continue to dominate, as Figure 3 shows. (World Bank, 2012).

Although the study from Kapelko and Volchkova mentioned that 48% of the 14 184 unique

Russian firms exported only in one year over the period 2003-2010, and another 20% of firms

exported in any two years over this period. The reason that the Russian exporters face

difficulties are not only the visa requirements, they can not maintain a permanent foreign

presence. In the period 1999-2009, 57 percent of export attempts to establish a foothold in a

market outside of Russia survived for more than two years, while in China the export survival

rate is over 70%, and Brazil and India also perform better than Russia. The low export

survival rate indicates a possible lack of international competitiveness in the non-oil and gas

sectors. In turn, International experience shows that the entry of new exporters has been a

driving force behind several export booms, and basically the oil and gas sectors spill-over

effect is weak (World Bank, 2012).

According to the World Bank study, Russia under-trade with China, India and several G8

countries, and the under-trading effect increase when the oil and gas sectors are excluded

from the model, and this phenomenon shows that Russia needs diversification in its export to

become more successful in the export. The first step could be to help to develop a healthy

domestic competition, because a better business environment allows firms to quickly adapt to

the market changes, improve the productivity and the competitiveness. Experience shows that

there are no magic recipe to promote export diversification, but without political support it is

unthinkable in Russia, and it needs changes in the incentive regime, in the state-owned

enterprise strategy.

Conclusion

The negative effect of visa restrictions to bilateral trade unquestionable, in general case and in

the case of Russian Federation. Primarily, its greatest negative effect is on relation specific,

instead of non-relationship specific goods. As a significant part of the Russian export is oil

and gas, which are in my view non-relationship specific goods, the visa restrictions has not so

great impact to the export of Russia. This statement strengthens that the Russian export is

dominated by the state owned enterprises (oil and gas sector), and in the case of export the

mineral resources the politics also plays a great role. During the analysis of the Russian export

to different countries there are examples for both cases of the effect of the visa regimes.

In addition, in some relation specific case the Russian government also strongly pressure on

other governments, in the last case the state-owned Rosatom won the a $ 3-4 billion dollar-

business in Hungary without tendering, to construct two new power units for Paks Nuclear

Power Plant. However, such pressure helps only for the state-owned and big private

companies.

If disregard the value of the export, the private owned Russian companies really faces with

high market access costs due to higher travel and visa costs, and due their low

competitiveness, the rate of return takes long time, problematic and questionable. Next to the

competitiveness, the productivity and the cost of export has also a negative influence on trade.

In addition, the visa regimes also have negative effect to support the diversification of the

Russian export, because the most of the small and medium enterprises are afflicted the most

by the visa costs.

To boost the number of the Russian exporter firms, which are able to export in the long run, it

is not enough to reduce the visa restrictions. It is necessary to improve the flexibility of the

Russian market and firms. With stimulating the competition in the domestic market, the

Russian companies could be more competitive abroad, which can improve equally the number

of the Russian export companies and the value of the export. To achieve this goals, the

Russian government may contribute with the transformation of the incentives, and tentatively

change some visa restrictions, which may lead to change the visa regime also by the other

country.

Bibliography

Centre for Economic Policy Research (CEPR): Reducing Transatlantic Barriers to Trade and

Investment - An Economic Assessment; Final Project Report, March 2013.

Coughlin, Cleins C. - Wood, Geoffrey E.: An Introduction to Non-Tariff Barriers to Trade,

Federal Reserve Bank of St. Louis Jurnal Review, Pages 32-46 January 1989.

http://research.stlouisfed.org/publications/review/89/01/Trade_Jan_Feb1989.pdf

Google Public Data:

http://www.google.com/publicdata/directory#!dp=Vil%25C3%25A1gbank

Inter-American Development Bank: Understanding a Computable General Equilibrium

Model, http://www.iadb.org/en/topics/trade/understanding-a-computable-general-equilibrium-

model,1283.html

Kapelkova, Natalia - Volchkova, Natalya: Export Costs of Visa Restrictions, Centre for

Economic and Financial Research at New Economic School, Working Paper No. 195, 2013.

Korhonen, Vesa - Simola, Heli - Solanko, Laura: Perspectives on Russia’s energy sector,

Bank of Finland, Institute for Economies in Transition, BOFIT Online, 2013 No. 3.

Love, Patrick - Lattimore, Ralph: “Protectionism? Tariffs and Other Barriers to Trade”, in

International Trade: Free, Fair and Open?, OECD Publishing, 2009.

Neumayer, Eric: On the detrimental impact of visa restrictions on bilateral trade and foreign

direct investment, Applied Geography 31, 901-907, 2011.

Observatory of Economic Complexity (OEC) by Massachusetts Institute of Technology:

http://atlas.media.mit.edu/

OECD Productivity Database: http://www.oecd.org/std/productivity-stats/

President of Russia: http://eng.kremlin.ru/transcripts/6527

Shepherd, Ben: The Gravity Model of International Trade: A User Guide; United Nations

publication, 2013

U.S. Energy Information Administration (EIA): Russia - Full Report, 2013.

http://www.eia.gov/countries/analysisbriefs/Russia/russia.pdf

World Bank: Russian Federation - Export Diversification through Competition and

Innovation: Overview, April 2012

World Bank Open Data: http://data.worldbank.org/

World Economic Forum: The Global Competitiveness Report 2013–2014

World Trade Organization, http://www.wto.org

Appendix

Map 1:

Source: Neumayer, Eric: On the detrimental impact of visa restrictions on bilateral trade and foreign direct

investment, Applied Geography 31, 901-907, 2011.

Map 2:

Source: Neumayer, Eric: On the detrimental impact of visa restrictions on bilateral trade and foreign direct

investment, Applied Geography 31, 901-907, 2011.

Table 1 - Russian Export to Western European countries:

Country 2000 2005 2010 % of total export Value ($ billion) % of total export Value ($ billion) % of total export Value ($ billion)

Netherlands 3.8 3.9 9.2 20 13 45

Germany 11 11 7.5 17 6 21

Italy 7.2 7.5 4.7 10 5.1 18

France 3.1 3.1 3.1 6.7 3.4 12

Switzerland 3.7 3.8 3.1 6.8 0.65 2.3

UK 3.8 3.9 3.7 8.2 2.4 8.7

Finland 3.2 3.4 3.6 7.8 3.4 12 Data from Observatory of Economic Complexity (OEC) by Massachusetts Institute of Technology

Table 2 - Russian Export to CEE countries:

Country 2000 2005 2010 % of total export Value ($ billion) % of total export Value ($ billion) % of total export Value ($ billion)

Czech

Republic

1.8 1.9 1.1 2.4 1.7 6.1

Hungary 2.3 2.4 2.1 4.7 1.9 6.9

Poland 4.4 4.6 4.0 8.7 4.1 15

Romania 0.97 1 1.4 3.2 0.7 2.5

Slovakia 2.1 2.2 1.6 3.5 1.5 5.6 Data from Observatory of Economic Complexity (OEC) by Massachusetts Institute of Technology

Figure 1 - Productivity and income levels in 2012, Percentage point differences with

respect to the United States

Source: OECD Productivity Database

Figure 2 - Cost to export (US$ per container)

Source: Google Public Data

Figure 3 - Oil and gas continue to dominate Russia's exports

Source: World Bank: Russian Federation - Export Diversification through Competition and Innovation:

Overview, April 2012