EUROMED AUDIOVISUAL III PROGRAMME Regional Capacity Development Support Unit IDENTIFICATION OF...

81

EUROMED AUDIOVISUAL III PROGRAMME Regional Capacity Development Support Unit IDENTIFICATION OF FINANCING TOOLS FOR FILM AND AUDIOVISUAL PRODUCTION AND THEIR PRACTICAL USE IN THE SOUTH MEDITERRANEAN REGION LINDA BEATH Senior short-term expert May 2012

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of EUROMED AUDIOVISUAL III PROGRAMME Regional Capacity Development Support Unit IDENTIFICATION OF...

EUROMED AUDIOVISUAL III PROGRAMME Regional Capacity Development Support Unit

IDENTIFICATION OF FINANCING TOOLS FOR FILM AND

AUDIOVISUAL PRODUCTION AND THEIR PRACTICAL USE IN THE

SOUTH MEDITERRANEAN REGION

LINDA BEATH Senior short-term expert

May 2012

2

Table of Contents SECTION I: Business Models for Film and Audiovisual Projects 4 SECTION II: Economics of the Business Models for the Film and Audiovisual Project 8 SECTION III: Future Economic Trends Affecting Film and Audiovisual Projects 12 SECTION IV: Types of Financing for Film and Audiovisual Projects 15

A: Subsidy Funding • National Funds 15 • Regional and Local Funds 17 • Pan-national Funds 19 • Specialised Territorial Funds 22

B: Tax Incentives 25

• Tax Exemption 25 • Tax Rebate 26 • Tax Credit 27 • Tax Shelter 29

C: Co-production 32 D: Television Funding for Independent Production 36

E: Presales 39

• Distribution 39 • International Sales 42 • Online Platforms 45

F: Advertising 47

• Sponsorship 47 • Product Placement 49 • Barter 52

G. Investment 55

• Equity Investment 55 • Deferrals 56 • Goods, Services and Facilities Support 58

H. Crowdsourcing 60

I. Awards, Grants and Prizes 63

3

SECTION V: Recommendations for the South Mediterranean Film and Audiovisual Production Sector 66 APPENDIX: Glossary of Film and Audiovisual Financing Terms 71

4

SECTION I

Business Models for the Film and Audiovisual Projects

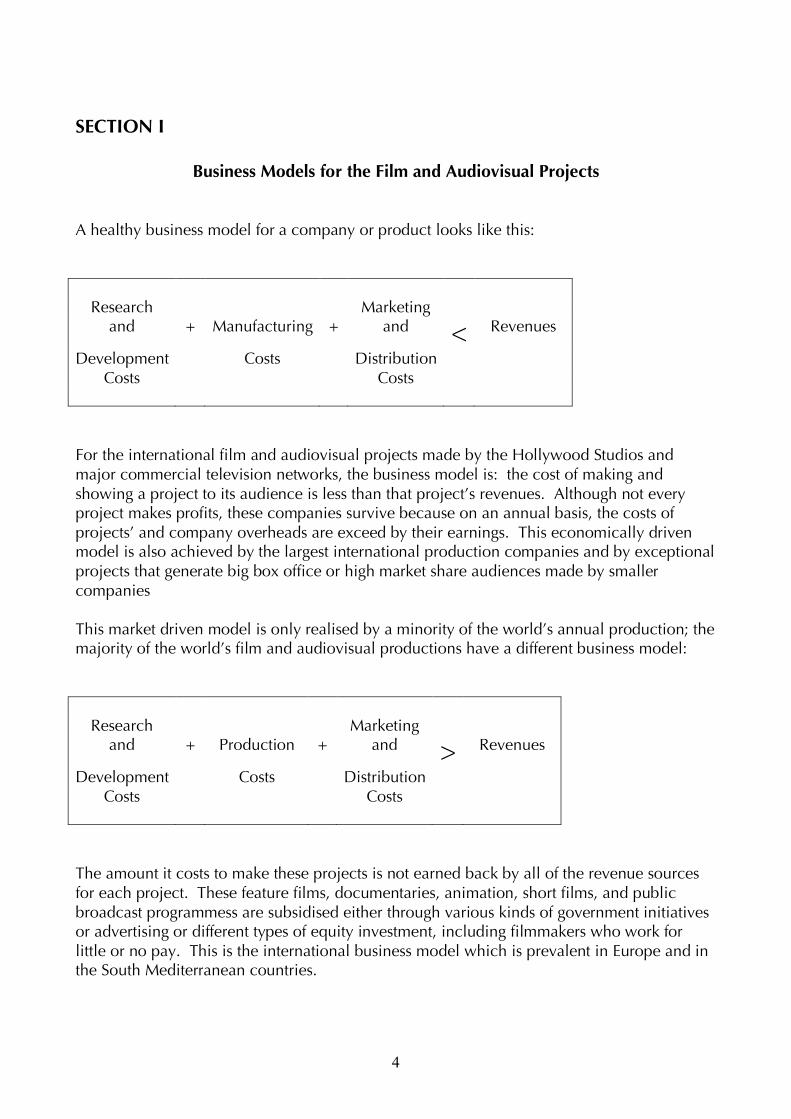

A healthy business model for a company or product looks like this:

Research Marketing and + Manufacturing + and < Revenues

Development Costs Distribution Costs Costs

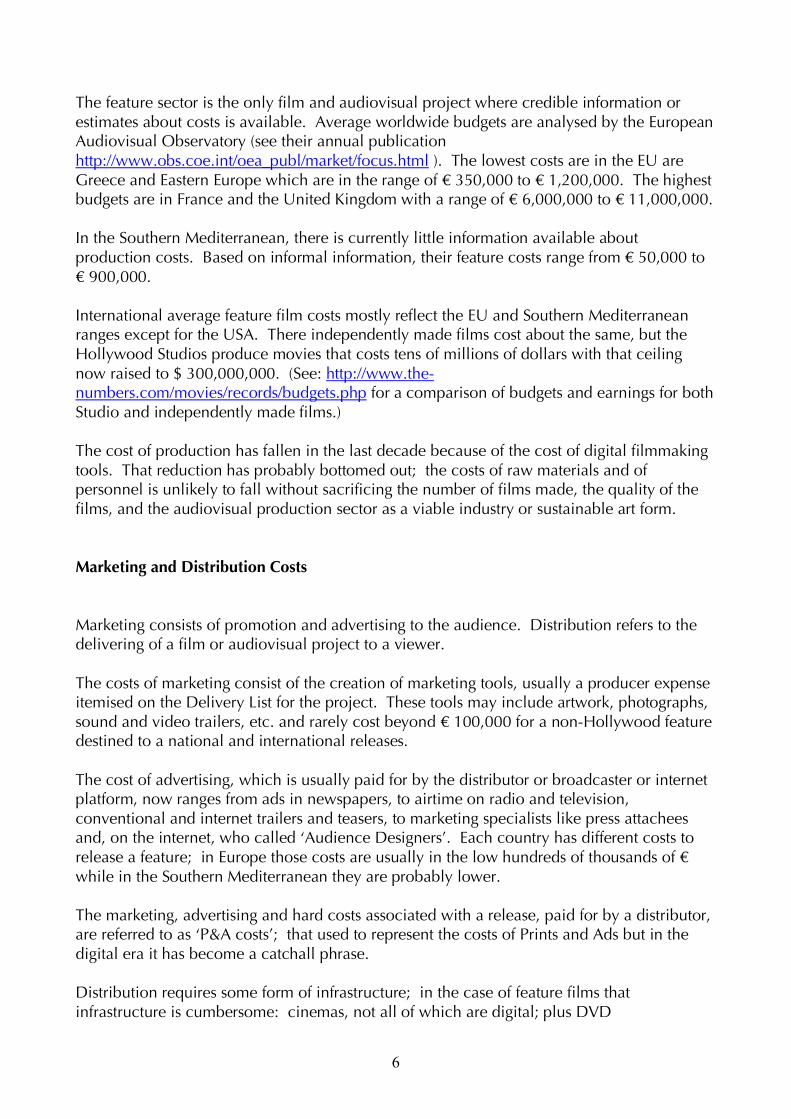

For the international film and audiovisual projects made by the Hollywood Studios and major commercial television networks, the business model is: the cost of making and showing a project to its audience is less than that project’s revenues. Although not every project makes profits, these companies survive because on an annual basis, the costs of projects’ and company overheads are exceed by their earnings. This economically driven model is also achieved by the largest international production companies and by exceptional projects that generate big box office or high market share audiences made by smaller companies This market driven model is only realised by a minority of the world’s annual production; the majority of the world’s film and audiovisual productions have a different business model:

Research Marketing

and + Production + and > Revenues

Development Costs Distribution Costs Costs

The amount it costs to make these projects is not earned back by all of the revenue sources for each project. These feature films, documentaries, animation, short films, and public broadcast programmess are subsidised either through various kinds of government initiatives or advertising or different types of equity investment, including filmmakers who work for little or no pay. This is the international business model which is prevalent in Europe and in the South Mediterranean countries.

5

The Four Stages of a Film or Audiovisual Project Business Model

Research and Development Costs There are three main types of production:

• drama – features, shorts, TV fiction • documentary and reality programmes • animation

Research and development follows different processes for the three categories. Drama is developed by writing scene by scene treatments or scripts. In the AngloSaxon countries and in Northern Europe, scripting feature films takes multiple drafts with up to 25 or 30 required in the most arduous countries (UK and USA). In the northern and southern Mediterranean, and most other non-English language countries, films are often made from the first, second or third draft with lower budgets projects sometimes shooting from treatments rather than full scripts. Documentaries are not developed by such a rigid and predictable process. After a period of research and a short treatment, part of the film is shot and edited, after which there is a rewrite period. This may repeat itself several times before completion. Animation dialogue scripts are written and recorded after a storyline has been agreed upon. Sketches, animated characters and backgrounds are done at the same time. Animation then starts and lasts for a much longer period of time than live action shooting and post production. Development budgets are high; at least two times the amount for other films and audiovisual project of the same length. Costs of research and development reflect the arduousness of the process: approximately 10% of the cost of a Hollywood movie is spent on development while in Europe it is closer to 3 or 4% of the total production costs. It is even lower in the rest of the world. Development is restricted by the amount of money available to filmmakers, but, in Europe particularly, there is concern that it is a false economy. There are significant and ongoing efforts by both MEDIA and local governments are working to increase the amount of money available for this part of the production process. Production Costs It is an understatement to say that the costs of making films and audiovisual projects varies widely. The costs vary with genre; animation is more expensive than live action drama which is more expensive than documentaries. The costs also vary by country and region. These costs include preproduction, production and post production as well as the costs associated with delivery.

6

The feature sector is the only film and audiovisual project where credible information or estimates about costs is available. Average worldwide budgets are analysed by the European Audiovisual Observatory (see their annual publication http://www.obs.coe.int/oea_publ/market/focus.html ). The lowest costs are in the EU are Greece and Eastern Europe which are in the range of € 350,000 to € 1,200,000. The highest budgets are in France and the United Kingdom with a range of € 6,000,000 to € 11,000,000. In the Southern Mediterranean, there is currently little information available about production costs. Based on informal information, their feature costs range from € 50,000 to € 900,000. International average feature film costs mostly reflect the EU and Southern Mediterranean ranges except for the USA. There independently made films cost about the same, but the Hollywood Studios produce movies that costs tens of millions of dollars with that ceiling now raised to $ 300,000,000. (See: http://www.the-numbers.com/movies/records/budgets.php for a comparison of budgets and earnings for both Studio and independently made films.) The cost of production has fallen in the last decade because of the cost of digital filmmaking tools. That reduction has probably bottomed out; the costs of raw materials and of personnel is unlikely to fall without sacrificing the number of films made, the quality of the films, and the audiovisual production sector as a viable industry or sustainable art form. Marketing and Distribution Costs Marketing consists of promotion and advertising to the audience. Distribution refers to the delivering of a film or audiovisual project to a viewer. The costs of marketing consist of the creation of marketing tools, usually a producer expense itemised on the Delivery List for the project. These tools may include artwork, photographs, sound and video trailers, etc. and rarely cost beyond € 100,000 for a non-Hollywood feature destined to a national and international releases. The cost of advertising, which is usually paid for by the distributor or broadcaster or internet platform, now ranges from ads in newspapers, to airtime on radio and television, conventional and internet trailers and teasers, to marketing specialists like press attachees and, on the internet, who called ‘Audience Designers’. Each country has different costs to release a feature; in Europe those costs are usually in the low hundreds of thousands of € while in the Southern Mediterranean they are probably lower. The marketing, advertising and hard costs associated with a release, paid for by a distributor, are referred to as ‘P&A costs’; that used to represent the costs of Prints and Ads but in the digital era it has become a catchall phrase. Distribution requires some form of infrastructure; in the case of feature films that infrastructure is cumbersome: cinemas, not all of which are digital; plus DVD

7

manufacturers, wholesellers and retailers; plus broadcasters and internet downloading or streaming sites. Television is more of an all-in-one marketing and distribution system that is cost effective, if limited in its reach. The internet is not limited in its territorial reach, it is a global distribution system, but it depends on audience ownership of comparatively expensive hardware and software as well as access to a server. Revenues Until the last decade there was a predictable, orderly marketplace in which to earn revenues with films and audiovisual projects. Unidirectional content distribution was clear with a distinct series of exclusive windows: For movies

• release in cinemas only for 3 to 6 months • DVD rentals and sales the following 6 months • a subsequent one year Pay TV window • a 2 to 5 year to 7 year free television window followed • specialised television channel window and second windows on free television

For other audiovisual projects, the windows were based on a television model

• several showings by the first broadcaster which commissioned the project • DVD rentals and sales after the first or second showing • broadcast by a second, smaller channel or network

While the US Studios and larger international media companies are still actively trying to retain this series of windows, the internet has upset their orderly marketplace. Legal operators and pirates alike are putting films on sites that allow downloading or streaming soon after production is complete. Companies handling smaller films and audiovisual projects are experimenting with simultaneous releases in cinemas, on television and on the internet. In 2011, bigger profit driven companies finally started challenging this convention, too, when Netflix announced it had bought the Pay TV rights to Dreamworks Animated films. This is the first time a Studio choose release on the internet over a traditional TV channel window but it is unlikely to be the last. The only certainty about revenue streams in the future is that there is no predictable model; confusion is increasing, and experimentation is evolving more slowly than most experts expected and in ways those experts did not predict.

8

SECTION II

Economics of the Business Models for the Film and Audiovisual Projects Introduction The South Mediterranean, like Europe, is dominated by American movies and TV programmes. Box office results and TV guides both confirm that economically, the US production companies, successfully operate on a market driven economic business model. This domination is reflected on the internet, with the USA leading statistics for computer use, broadband penetration and ownership of the major websites for audiovisual content on the web. The bottom line for a market driven business model in this industry means the bigger the audience, the more money for the project. The rest of the world’s producers are competing for the remainder of the marketplace. Often they are highly successful with their national audiences but international audiences are hard to win. With a concerted industry effort, nternet marketing and distribution may help grow these audiences. The market driven model infrequently works for international projects, so non-American films and audiovisual projects are made using different business models. Most involve combining subsidies, tax relief, broadcaster dependency and other smaller amounts from a variety of sources.

The USA’s Two Tier Film System Big Business The Hollywood Studios make films for the marketplace. They are large companies that exist to create profits for their shareholders so each film they greenlight is expected to earn back its costs from its revenues: domestic and international theatrical releases, DVD rentals and sales, television sales, internet earnings and a variety of ancillary rights. Not all of their films are profitable, so the Studios have found different ways to reduce production costs. They have been aggressively using tax credits around the world, lowering cast and crew fees by shooting outside their unions’ jurisdictions, hedging risk throught international presales, raising equity investment with or without tax shelter benefits and raising advertising monies early in the production process. The big American television networks and pay and cable organisations do the same, particularly with primetime drama. The US television sector is highly market driven, from networks through to local station syndication. Advertising time – commercials – are their main revenue source. Channel owners insure what they pay for content and operating overheads versus what they earn selling ads generates profits. The single exception is the PBS network which is also viewer supported via corporate funding raising and individual donations.

9

The Studios and the biggest American TV companies have been reluctant to embrace internet delivery of programmes to US computer users despite Amercia’s extensive broadband access. In their protectionist efforts, they also lead the international fight against piracy. As internet delivery numbers increase and as revenues become more significant, they are starting to follow companies like Netflix and Hulu into that marketplace. Even more reluctantly, they are beginning to create original content for it, too. The American Indies Independent filmmakers in the United States (in other words, those not affiliated to the Hollywood Studios and biggest television production companies) do not have access to subsidies beyond tax credits which approximately 35 states currently use to encourage shooting in their region. (That number has decreased recently with 9 states rescinding or not renewing the tax relief legislation in the past couple of years.) Independent US movies, shorts and documentaries are made on low budgets, including an increasing percentage of them made on micro budgets of under $ 250,000 per feature film, some as low as thousands or tens of thousands of dollars. Their go-to financing sources are a combination of credit, equity investment, deferrals or non-payment of cast and crew and some sponsorship, product placement and goods, services and facilities support. The America indies pioneered crowdfunding and now access over € 32,000,000 per year from just one of the bigger websites. Grants and financial prizes are highly competitive with thousands of applications for support at the National Endowment for the Arts, ITVS, etc. American independent filmmakers have assumed a more experimental approach to reaching their audience, they are now innovators. Marketing on the internet has become specialised with ‘audience designers’ and ‘producers of marketing and distribution’ being credited for building the brand of a film. They start the promotional effort before it is completed to attract audiences; releases are regional, local and self promoted; there is DIY and DIWO advice on the internet, at seminars and conferences and specialists that did not exist 5 years ago helping shape a new distribution sector. Streaming and downloading are being done on platforms like iTunes all the way to single websites for a film. The American independent filmmakers generally aim to earn money with their projects, but they rarely recover costs let alone make profits for their makers and financiers. Although the USA is the largest user of internet content, downloading and streaming, the independent producers of internet content including film and audiovisual projects cannot pay for their creations without advertisers – who are still only experimenting with their marketing budgets. Internet exploitation of features, television programmes, documentaries and shorts is growing in the United States, but the top numbers are still low; IndieWire recently sited $20,000 as the 2011 record high earnings for an independently produced feature.

10

International Film and Audiovisual Production Sectors: The Screen Industries While the American business models and financing are a study in extremes, the international industry is much more homogeneous, with the quantity of money involved being the sole variable. Until the end of the last century, international film and audiovisual production was subsidized. There was a simple trio of funders: a government subsidy plus a national – usually public – broadcaster plus a distributor. While the broadcasters accessed audiences and varying levels of market share, only the distributors and sales agents expected to earn revenues and make profits. The government subsidies usually gave soft loans – contracts that only required producers to share any revenues with them rather than guarantee repayment. In practice organisations from Telefilm Canada or the New Zealand Film Commission through to the world’s biggest, the CNC in France, had small, single digit percentage returns on their investments. The most successful recoupment of subsidy funds probably occurred at British Screen, which, during the 1980s, earned the unparalleled 25 to 50% of its expenditures back from the exploitation of its features. Co-production treaties started to be signed in the early 1970s and by the 1980s and 1990s, Europe was co-producing more than 20% of its feature films. Co-production now accounts for 100% of Belgian and Luxembourg features and almost as high a percentage in the Nordic countries. During the same period costs for prints, advertising and running exhibition chains climbed while, simultaneously, audiences numbers dropped. Distribution became economically less viable. With weaker distributors, investments in production, presales and sales numbers fell, too. Many single cinemas closed; most new cinema screens were constructed as part of a multiplex. During the same period, television audience numbers eroded with more viewing choices and changes in viewers’ tastes being blamed for dropping market share numbers. Advertisers responded with lower prices per commerical so the prices broadcasters paid per hour of programming fell, too. Starting in the 1980s, international producers were faced with a gap between the money they could raise from classic financing sources and the cost of their production. One response was under their control: they maintained or lowered their costs per production. Cheaper digital filmmaking tools and a lack of financial resources has kept the average cost of films fairly constant for over a decade. Even so, new sources of money had to be found. Europe and the AngloSaxon world responded to this crisis with different funding instruments: first national tax shelters which gave way to the less corruptible tax credits. France created a highly monitored tax relief system hybred with its credits and SOFICAs. Regional funding appeared and then expanded both in the number of funders and the amount of funding available. Previously banned product placement, sponsorship and advertising became viable

11

sources of money for producers. As well, some unique solutions were put into place like the more recent innovations: Italy’s tax shelter mechanism to encourage corporate investment and MEDIA subsidies for setting up and marketing VoD platforms so revenues to producers could increase. Even in the recent economic crisis, most countries which had them maintained or increased national support organisations for film and audiovisual production. Only now that is starting to unravel in the worst affected economies. The Irish Film Board has been cut for 2012 and it is expecting more reductions next year. Film Commissions and regional funds have blossomed almost everywhere in the EU and the AngloSaxon world and they are expanding into other regions including a few in the South Mediterranean and more in the Middle East. Politicians have caught on and now support the idea that inbound production provides many benefits including increased employment, particularly of younger people. The competition to bring foreigners in to shoot their movies locally is tough so economic incentives have had to become an essential to enticing them. In the South Mediterranean, very few of these newer funding sources – from tax incentives to regional funds – been adopted. In most countries, production has slowed or declined significantly. Digital, non-professional films are being made by unpaid filmmakers who have something to say; over all genres, budgets are very low. Shorts and documentaries as well as full length features are finding their way onto the internet but are not finding their way into more commercial outlets like cinemas and television. China has a fully subsidised and highly controlled industry with a market place that is so large that more native entrepreneurial investors are putting money into features. Private equity is also used in the Far East, India and Russia and. to a smaller extent, in Europe. Feature films, animated films, documentaries and shorts are subsidised in most South Mediterranean countries. There are government funds made available to promote production for cultural, artistic and/or economic reasons. Co-productions are important, particularly with the European Union. Funding sources usually include subsidies, various types of tax relief including tax-free production zones and private investment including deferrals. State funded production units still operate while state owned television provides some, albeit reluctant support to filmmakers. Distribution, while experiencing trouble to the north, is almost non-existent in most South Mediterranean countries outside Egypt and Israel. The home video market is saturated by pirated DVDs. The region’s television networks are still heavily into inhouse production plus foreign acquisitions. As a result of this combinations, there is not a significant revenue stream in domestic markets. While international festivals are celebrating more South Mediterranean features, documentaries and shorts, they are not yet selling to distributors; some specialist international sales companies are now hoping to change that. With so little access to market funds, to new forms of non-grant funding and with earnings hampered by its domestic market, the subsidisation of South Mediterranean production is fundamental to its existence.

12

SECTION III

Future Economic Trends Affecting Film and Audiovisual Projects Production costs have been kept low, and even lowered, for everything from short films to high end, multiple episode TV drama since digital filmmaking tools started appearing. Amateurs can access and use the same equipment as professionals. Viewer generated content made mostly by non-professional filmmakers fuels sites like YouTube, which in 2011, added 600 + videos per minute (or, to put it another way, 25 + hours were added to YouTube every 60 seconds, with some web analysts estimating it at twice that number). This low cost approach to filmmaking does not allow for an industry sector to function economically; production costs – particularly for personnel – will have to rise. That will only happen when the market place is less turbulent, when healthy business models are more prevalent, particularly when the internet generates fair prices for content and investment support for its creation. And none of that is likely to be accomplished in the short run. Feature film production and distribution is currently dependent on ‘old’ media companies and a ‘old’ media economics and methodology. The US studios are moving increasingly to making and releasing only blockbusters and franchises, with less room for the smaller and more intimate dramas they supported in the past. They are experimenting with new technological advances, like stereoscopic 3D but audiences seem to be first intrigued then quickly become tired of “gimmicks”. The independents in the States are developing a new way to get to their audiences using hybrid methods combining older but smaller marketing and distribution companies and increasingly heavy use of the internet. International governments are subsidising production which is paid for by a larger and larger number of financiers – some governmental, some market forces, talent deferrals and gradually increasing sponsorship and advertising. The national governments ability to continue investing significant amounts into film and audiovisual production sector is likely to come under review, particularly in the countries where the GNP is stalled or falling. As a global total national funding is likely to decrease in scope and size but regional funds will take up much of the loss. European distribution and marketing is being subsidised for its own feature productions. Most countries with a state subsidy also support international sales and marketing. There is some support for experimentation in internet social networking and audience building as well as training and investment in the cross pollinisation of the film production sector with the technology sector.

13

Television has undergone five major radical transformations since the early 1950s: from 1 to 3 major broadcasters per country, the number of channels more or less doubled when commercial broadcasters entered national markets in the 1970s. In the 1980s pay television and niche speacialty channels profilerated. In the 1990s boutiques of channels were delivered by cable and satellite. The number of channels on offer to each viewer increased, so that by the early 21st century, market share per programme – and therefore the price paid to purchase a programme – fell. From an international universe of a few channels to 10,000s of channels now targeted at national or territorial audiences, television is again poised to multiple itself. According to a long article in a recent New Yorker, internet television is likely to produce 100,000s of channels which are very highly specialised and which are aimed at global audiences, not local ones. A new internet channel (IPTV) can be set up for little money. They can be highly specialised with viable channels catering to knitters or white water rafters. These channels will use a limited number of hours of programming per day and will attract big enough numbers of international viewers that specialised advertisers – for knitting yarn, needles, patterns or for raft, paddle, and locations – which will support the channel profitably. In the first six months of 2012, YouTube is launching its first 100 internet television channels. The increase of potential buyers, albeit at lower prices per buyer, will open up possibilities for short, documentary and TV programme providers. Penetrating the new marketplace is going to demand that producers either acquire or hire a skillset, information and contacts which they do not now possess. The home video market is becoming less and less profitable. Time Magazine’s recent article on the 2011 entertainment industry numbers included this assessment: “But the DVD cash cow is nearly milked dry, as audiences go for cheaper downloading and streaming formats. Most signs point south, and some industry analysts predict catastrophe. “The business will never be the same again,” Harold Vogel, head of Vogel Capital Management and author of Entertainment Industry Economics: A Guide for Financial Analysis, told The Wrap late last year. “It’s not cyclical. This is a technological shift on a generational scale, and the long-term technology is distribution on the web — and that’s not ten years, that’s forever.” Currently, the cinema going audience is diminishing, the television universe is fragmenting with niche channels multiplying rapidly and DVDs are being phased out. All of the good, if confusing, news seems to begin and end with the wired marketplace. Active global internet users now exceed 2.1 billion people – more than 30% of the world’s population – according to to web traffic monitory company Pingdom. 710 computers are bought around the world every minute. Broadband penetration is no longer just a consumer concern but has become an essential service. YouTube is adding 600+ new videos per minute; that is 25+ hours of film and audi visual content every 60 seconds. Internet content is in search of a business model with positive – if still unique – examples starting to appear more regularly.

14

Predictions by the digital trade publication, PaidContent, estimate that a large percentage of revenues will be generated exclusively online by 2013 with internet portals contributing significant amounts of money for production of content by 2015. YouTube is already experimenting with investing in production with its first funds being put in the hands of the filmmakers who have generated hundreds of thousands, if not millions, of YouTube viewings. Development, production, marketing and distribution of film and audiovisual projects on the internet are heavily subsidised by advertisers and sponsors who are largely experimenting with a new medium. Or by the makers of the content, infrequently with the support of specialised and as yet experimental “digital funds” from their governments. Leading proponents of content for the internet and digital experts do not agree on what business models are, can be or will be. To paraphrase Wendy Bernfeld of Rights Stuff, “today’s business models can be summed up in one word: “confusion”. There are a number of possible models currently being discussed, used or tested by innovators:

• customers paying per view (or for each hit or click) • customers paying to own • customers paying subscriptions for services that provide access to a library of content • advertiser pays per customer view • advertiser pays for exposure • subsidised per view, per download or to own

The iTunes model (customer pays per unit to own content) has been duplicated worldwide by various types of platforms. Subscription based services are expanding and appear to be doing so profitably, with Netflix currently opening internationally. Advertising on the internet is increasing more rapidly than in any other medium. According to PaidContent, the amount of money spent on advertising in 2011 is $ 464 billion, of which 15.9 percent is spent on the internet. Online ad growth is outpacing other forms of advertising; it is 12% higher than the 2010 spend. Part of the credit for this growth is the improvement of more accurate methods to measure and then analyse the value of internet advertising for a brand. Advertising agencies still regard the internet as the “wild, wild west” – yes, a play on the ‘www.’ prefix for a website – but they are no longer as skeptical as they were 3 to 5 years ago. Customers, content viewers or users have made gaming on the internet – and across other platforms – highly profitable. Reuters forecasts that global revenues in 2011 would reach US $65 billion. However, customers, viewers and users are not yet supporting film and audiovisual projects in large enough numbers to represent a substantial revenue source let alone a potential source of financing. Most industry experts are counting on substantial, if not rapid, growth in this one area.

15

SECTION IV

Types of Financing for Film and Audiovisual Projects

A: Subsidy Funding

National Funds

What:

A public or semi-public body or government agency whose specific duties include providing funding to the film and audiovisual sector of a single country, for a range of activities.

Typical names: National Film Institute

National Film Fund

National Centre of Cinematography (and Image)

Ministry of Culture - AV or Cinema Department

How it works: Guidelines for eligible projects, production companies are made available to the film and audiovisual sector. Applications are required, usually by a set deadline, with proposed contents, proposed budgets and sometimes plans for reaching the audience. Producers generally are the only eligible applicant although some national funders will support writers or filmmakers directly in the early stages of development. All eligible applications are assessed, often by experts. Successful applicants sign contracts which include the amount of support, a schedule of payments and items or events to be met during and after production.

Funds available: Development and Research

Production Sometimes including auto-matic support based on prior performance

Post Production Sales & marketing, international promotion, festivals

Amounts: The annual budgets of National Funding bodies varies widely; in Europe in 2011 from as little as € 235,000 to as much as € 705,900,000.

Source of funds: The government allocates an amount per year from its Ministry of Finance or the national Treasury or from designated sources such as a specific tax, a percentage of state lottery sales, etc. There is usually an annual budget approval process as well as an annual performance review and financial

16

audit.

Where: Eligibility: Recoupment:

Generally available: South Mediterranean; all of the European Union countries (although this may change due to the global economic crisis); Latin America; East Asia; Anglophone countries, except the USA; some African countries south of the Sahara (which also include training initiatives). The agency establishes clear guidelines for eligibility including nationality of the production company, producer, writer and director, key cast and crew as well as projects including issues like genre, budget, content, length, etc. There are generally some exclusions: projects that are pornographic, graphically violent, xenophobic and/or those which exploit women or minorities. Co-productions are supported, usually because the countries involved grant formal approval under the terms of a treaty. Any financial investment by National Funds may be, but are not always, considered loans against a pro rata and pari passu proportion of all revenues earned by the film or audiovisual work. Some agencies also get a pro rata and pari passu share of the profits not earned by the creative team. There is no recoupment required in some countries (in Finland and Switzerland, for example).

Advantages: Direct aid for the film or audiovisual project, usually in the form of cash, of between 25% and 100% of the budget of film and audiovisual projects; support in the form of expertise for all stages from early development through to national and international sales

Disadvantages: The choice of projects is not based on automatic support but on the evaluation of perceived quality; national funding bodies are usually encumbered by rules, deadlines and limitations leading to frequent complaints of ‘too much bureaucracy’; governmental support can be withdrawn or reduced without notice

Examples: Centre Cinematographic Morocain; Egyptian National Film Centre; Swedish Film Institute; Ministero per i Beni e le Attività Culturali (MiBAC), Italia.

For more information:

There is a large article explaning public funding in detail at: http://www.obs.coe.int/oea_publ/funding/00002095.html

Links: Most funds have websites. The Korda Database of the European Audiovisual Observatory has gathered all of the links to European National Funding bodies: http://korda.obs.coe.int/ The CNC in France has an extensive website which is highly informative and which includes a large archive of past years’ activities: www.cnc.fr

17

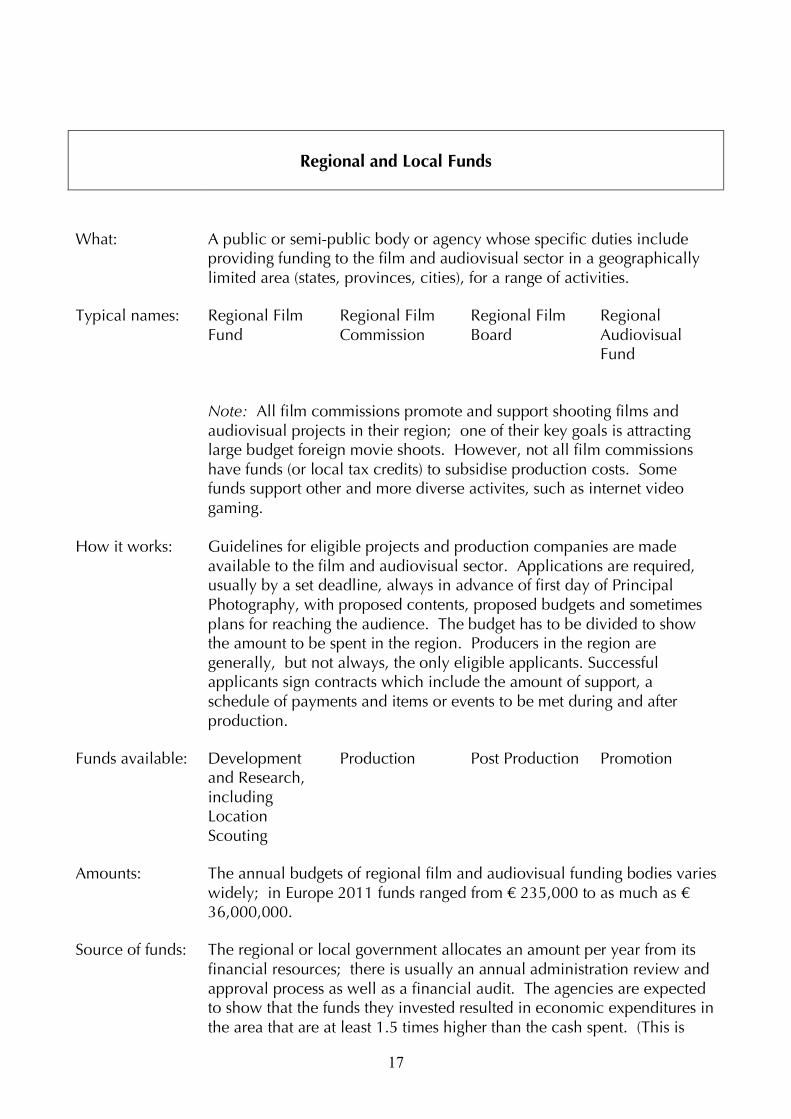

Regional and Local Funds

What:

A public or semi-public body or agency whose specific duties include providing funding to the film and audiovisual sector in a geographically limited area (states, provinces, cities), for a range of activities.

Typical names: Regional Film Fund

Regional Film Commission

Regional Film Board

Regional Audiovisual Fund

How it works:

Note: All film commissions promote and support shooting films and audiovisual projects in their region; one of their key goals is attracting large budget foreign movie shoots. However, not all film commissions have funds (or local tax credits) to subsidise production costs. Some funds support other and more diverse activites, such as internet video gaming. Guidelines for eligible projects and production companies are made available to the film and audiovisual sector. Applications are required, usually by a set deadline, always in advance of first day of Principal Photography, with proposed contents, proposed budgets and sometimes plans for reaching the audience. The budget has to be divided to show the amount to be spent in the region. Producers in the region are generally, but not always, the only eligible applicants. Successful applicants sign contracts which include the amount of support, a schedule of payments and items or events to be met during and after production.

Funds available: Development and Research, including Location Scouting

Production

Post Production Promotion

Amounts: The annual budgets of regional film and audiovisual funding bodies varies widely; in Europe 2011 funds ranged from € 235,000 to as much as € 36,000,000.

Source of funds: The regional or local government allocates an amount per year from its financial resources; there is usually an annual administration review and approval process as well as a financial audit. The agencies are expected to show that the funds they invested resulted in economic expenditures in the area that are at least 1.5 times higher than the cash spent. (This is

18

referred to as the ‘multiplier effect’.)

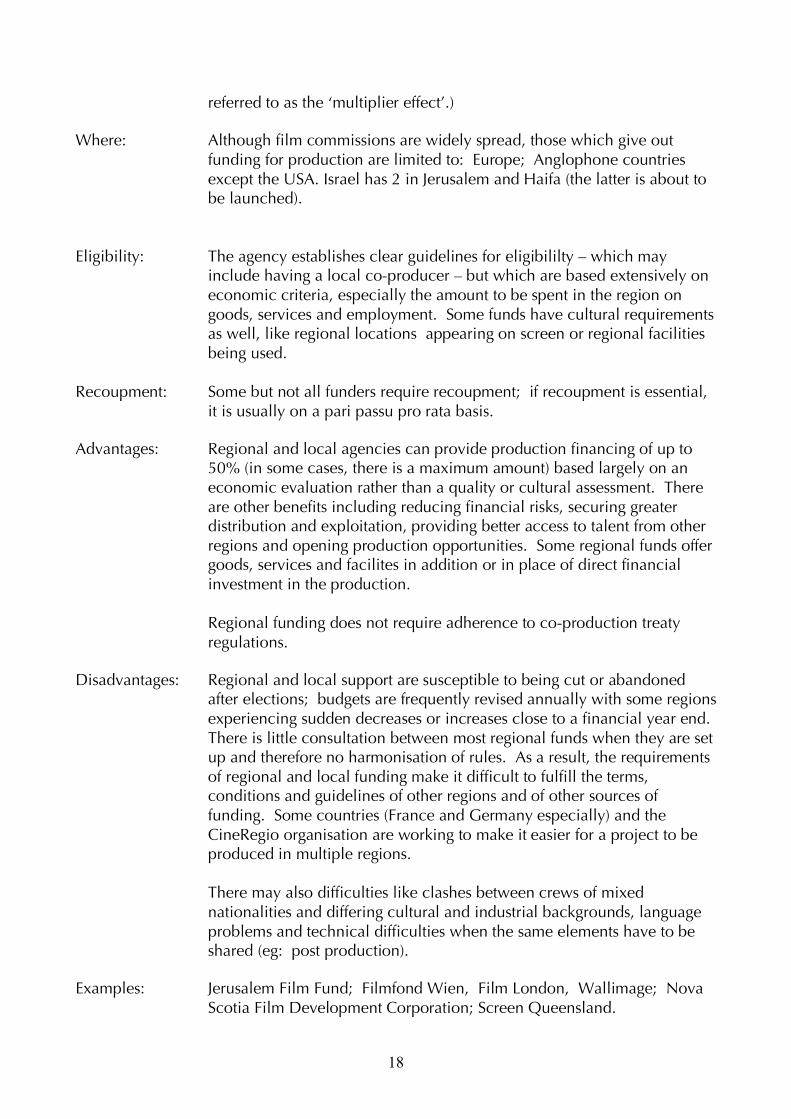

Where: Eligibility: Recoupment:

Although film commissions are widely spread, those which give out funding for production are limited to: Europe; Anglophone countries except the USA. Israel has 2 in Jerusalem and Haifa (the latter is about to be launched). The agency establishes clear guidelines for eligibililty – which may include having a local co-producer – but which are based extensively on economic criteria, especially the amount to be spent in the region on goods, services and employment. Some funds have cultural requirements as well, like regional locations appearing on screen or regional facilities being used. Some but not all funders require recoupment; if recoupment is essential, it is usually on a pari passu pro rata basis.

Advantages: Regional and local agencies can provide production financing of up to 50% (in some cases, there is a maximum amount) based largely on an economic evaluation rather than a quality or cultural assessment. There are other benefits including reducing financial risks, securing greater distribution and exploitation, providing better access to talent from other regions and opening production opportunities. Some regional funds offer goods, services and facilites in addition or in place of direct financial investment in the production. Regional funding does not require adherence to co-production treaty regulations.

Disadvantages: Regional and local support are susceptible to being cut or abandoned after elections; budgets are frequently revised annually with some regions experiencing sudden decreases or increases close to a financial year end. There is little consultation between most regional funds when they are set up and therefore no harmonisation of rules. As a result, the requirements of regional and local funding make it difficult to fulfill the terms, conditions and guidelines of other regions and of other sources of funding. Some countries (France and Germany especially) and the CineRegio organisation are working to make it easier for a project to be produced in multiple regions. There may also difficulties like clashes between crews of mixed nationalities and differing cultural and industrial backgrounds, language problems and technical difficulties when the same elements have to be shared (eg: post production).

Examples: Jerusalem Film Fund; Filmfond Wien, Film London, Wallimage; Nova Scotia Film Development Corporation; Screen Queensland.

19

Note: See Pan-National Funds for more information about the Doha Film Institute as well as the Dubai, Abu Dhabi and Screen Institute Beirut funds.

For more information:

There is a large article explaning public funding with references to regional funds at: http://www.obs.coe.int/oea_publ/funding/00002095.html

Links: In Europe, 37 regional funds are members of Cine Regio: http://www.cine-regio.org/

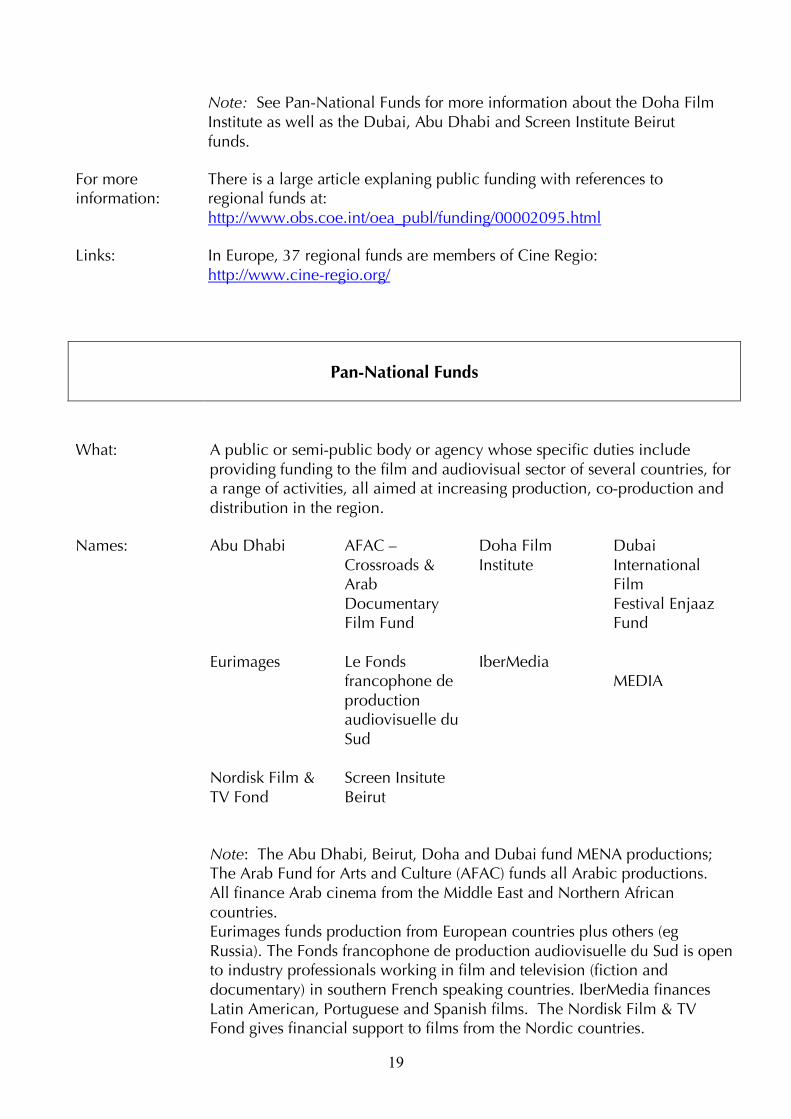

Pan-National Funds

What:

A public or semi-public body or agency whose specific duties include providing funding to the film and audiovisual sector of several countries, for a range of activities, all aimed at increasing production, co-production and distribution in the region.

Names: Abu Dhabi Eurimages Nordisk Film & TV Fond

AFAC – Crossroads & Arab Documentary Film Fund Le Fonds francophone de production audiovisuelle du Sud Screen Insitute Beirut

Doha Film Institute IberMedia

Dubai International Film Festival Enjaaz Fund MEDIA

Note: The Abu Dhabi, Beirut, Doha and Dubai fund MENA productions; The Arab Fund for Arts and Culture (AFAC) funds all Arabic productions. All finance Arab cinema from the Middle East and Northern African countries. Eurimages funds production from European countries plus others (eg Russia). The Fonds francophone de production audiovisuelle du Sud is open to industry professionals working in film and television (fiction and documentary) in southern French speaking countries. IberMedia finances Latin American, Portuguese and Spanish films. The Nordisk Film & TV Fond gives financial support to films from the Nordic countries.

20

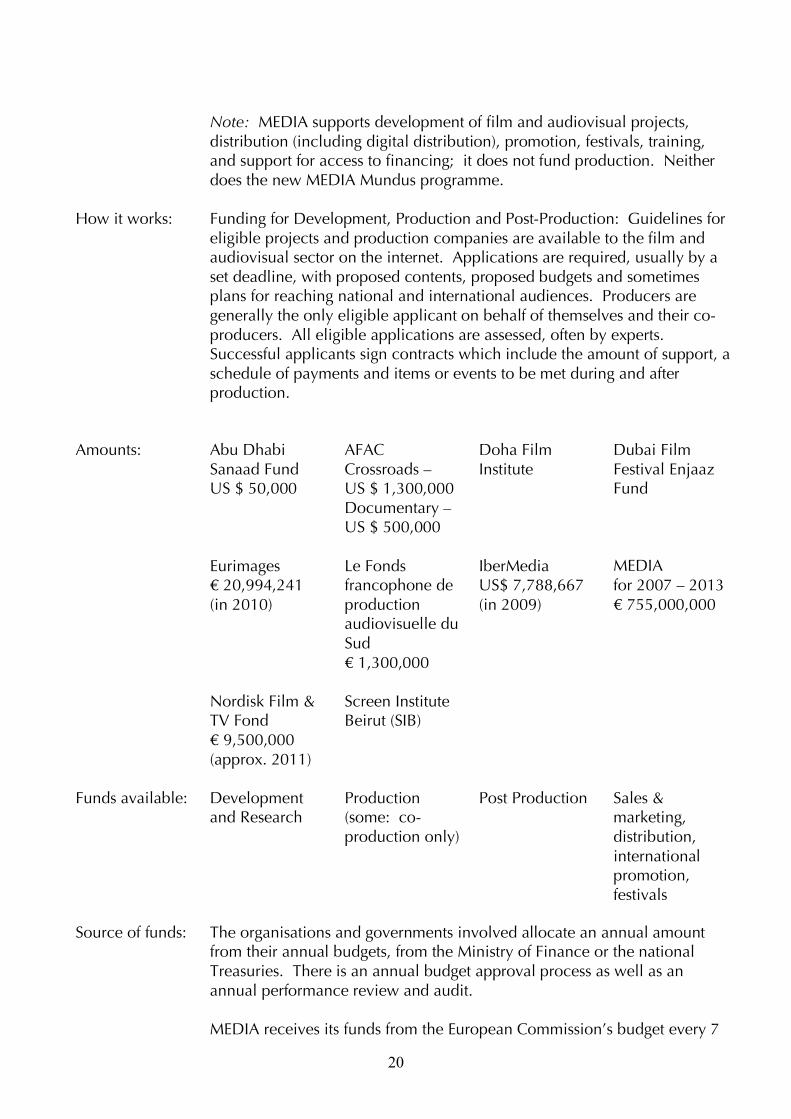

How it works:

Note: MEDIA supports development of film and audiovisual projects, distribution (including digital distribution), promotion, festivals, training, and support for access to financing; it does not fund production. Neither does the new MEDIA Mundus programme. Funding for Development, Production and Post-Production: Guidelines for eligible projects and production companies are available to the film and audiovisual sector on the internet. Applications are required, usually by a set deadline, with proposed contents, proposed budgets and sometimes plans for reaching national and international audiences. Producers are generally the only eligible applicant on behalf of themselves and their co-producers. All eligible applications are assessed, often by experts. Successful applicants sign contracts which include the amount of support, a schedule of payments and items or events to be met during and after production.

Amounts: Abu Dhabi Sanaad Fund US $ 50,000 Eurimages € 20,994,241 (in 2010)

Nordisk Film & TV Fond € 9,500,000 (approx. 2011)

AFAC Crossroads – US $ 1,300,000 Documentary – US $ 500,000 Le Fonds francophone de production audiovisuelle du Sud € 1,300,000 Screen Institute Beirut (SIB)

Doha Film Institute IberMedia US$ 7,788,667 (in 2009)

Dubai Film Festival Enjaaz Fund MEDIA for 2007 – 2013 € 755,000,000

Funds available:

Development and Research

Production (some: co-production only)

Post Production

Sales & marketing, distribution, international promotion, festivals

Source of funds: The organisations and governments involved allocate an annual amount from their annual budgets, from the Ministry of Finance or the national Treasuries. There is an annual budget approval process as well as an annual performance review and audit. MEDIA receives its funds from the European Commission’s budget every 7

21

years. The Nordisk Film & Television Fond receives 1/3 of its annual budget from the 5 Nordic Council countries, 1/3 from national film funders and 1/3 from Nordic broadcasters. Eurimages is funded by its 35 member countries as is Ibermedia by its 18 countries. The

Where: Eligibility: Recoupment:

Not available beyond the funds listed above. Note: In May 2010 at the Cannes Film Festival the International Organisation of La Francophonie (IOF) and the Federation of African Filmmakers (FEPACI) announed plans to start work on a Pan African Cinema Fund. A feasibility study was tabled at the Carthage Film Festival in 2010, including a name change to CineA. The African southern Mediterranean countries are instrumental in the effort to build this agency. There are two other pan national bodies being initiated: one for Africa under discussion by the OUA (Union Africaine), one for the Middle East with the Royal Film Commission of Jordan actively coordinating discussions and one from the Arab League. For Abu Dhabi, the AFAC, Doha, Dubai and the SIB the funds are restricted to Arab producers, some are geographically restricted to the Middle East and South Mediterranean. Co-production and distribution of films between the member countries of the agency are the essential requirements for all four European funds. The agency establishes clear guidelines for eligibililty including nationality of the production companies, co-producers, writer and director, key cast and crew as well as projects including issues like genre, budget, content, length, etc. MEDIA accepts applications from its member states’ film and audiovisual organisations with relevant experience for the activities requesting financial support. Financial investments in production by Pan-National Funds are loans against a pro rata and pari passu proportion of all revenues earned by the film or audiovisual work. These agencies also get a pro rata and pari passu share of the profits not earned by the creative team. Some of the funds give grants, for example, MEDIA does not require repayment.

Advantages: Direct aid for the film or audiovisual project, in the form of cash installments, of between 10% and 70% of the budget of film and audiovisual projects (with published maximum amounts which are low compared to average budgets); or financial support for development, distribution, promotion, festivals, film education and training, etc. Eligibility rules, guidelines and benefits are transparent, and applied the same way for all applicants; all contracts are the same for all recipients.

Disadvantages: The choice of projects is not based on automatic support but on the evaluation of perceived quality; Pan National funding bodies are have extensive rules and guidelines, and limitations leading to frequent complaints of ‘too much bureaucracy’; deadlines are infrequent; high proportion of signed financing required before applications can be

22

submitted; recoupment required for production funding. Links:

Abu Dhabi Sanad Fund: http://www.abudhabifilmfestival.ae/en/sanad/about-sanad AFAC: http://www.arabculturefund.org/ Doha Film Institute: http://www.dohafilminstitute.com/financing/guidelines Dubai International Film Festival Enjaaz Fund: http://www.dubaifilmfest.com/index.php/en/dubai_film_market/enjaaz/ Eurimages: http://www.coe.int/t/dg4/eurimages/default_en.asp Fonds francophone de production audiovisuelle du Sud (not available in English): http://www.francophonie.org/Fonds-francophone-de-production,28896.html IberMedia: www.programaibermedia.com/ MEDIA: http://ec.europa.eu/culture/media/index_en.htm One of its programmes that is relevant to the South Mediterranean, MEDIA Mundus, is a € 15,000,000 aimed at boosting international cooperation in the audiovisual industry. There is a brochure about its activities at: http://ec.europa.eu/culture/media/mundus/index_en.htm Nordisk Film & TV Fond: http://www.nordiskfilmogtvfond.com/ Screen Institute Beirut: http://www.screeninstitutebeirut.org

Territorial Support Funds

What:

A body or agency whose specific duties include providing funding to the film and audiovisual sector of its country, dedicates a portion of its budget to support productions between its national producers and co-producers from territories outside its own. Note: Unlike these funds for multiple countries, France has also pioneered the concept of “mini-treaties” which give up to 20% more than normal subsidy amounts to encourage more co-production with a single targetted country. There are three signed with Canada (for features, animation, television) and one with Germany.

23

Names: Aide aux cinemas du monde € 6,000,000

International Film Fund

SØRFOND € 500,000

Funds available: Development Production Post Production

Amounts: The annual budgets of the funds, if known, are listed above. The International Film Fund in Singapore limits per film investments to € 610,000.

Source of funds: These funds are a small, defined portion of the larger annual budget for production support or they are a fund (administered through, respectively, the CNC France, the Singapore Media Development Agency and the Norwegian Film Institute) that is allocated by one or more non-associated ministries of the government (Foreign Affairs, for example).

Where: Eligibility: Recoupment:

Limited availablity worldwide; these funds are valuable while they last, but are, often, also transient. These specialised funds establish clear guidelines for eligibililty tailored to the programme and its goals, including nationality of the production companies, producers, writers and directors, key cast and crew, facilities as well as projects including issues like genre, budget, content, length, etc. Co-production is a requirement; all the financing must go to a local producer, although applications may be able to be submitted by the non-national producer / rights owner. Singapore’s fund is eligible only to films with wide international marketability while the other funds are more interested in artistic quality and cultural importance. Any financial investment by these funds are considered either grants or loans against a pro rata and pari passu proportion of all revenues earned by the film or audiovisual work. The agency, if it takes a revenue share, also may get a pro rata and pari passu share of the profits not earned by the creative team.

Advantages: Disadvantages:

Direct aid for the film or audiovisual project, usually in the form of cash, of between up to a set amount or a % of the budget of film and audiovisual projects; support in the form of expertise for all stages from early development through to national and international sales. The requirement that the production is a treaty co-production means that the lead producer (non-nationals, usually), is obligated to work with a co-producer whose costs may be more expensive for all aspects of production than the producers’ costs; the lead producer is obligated to do certain of its work under the law, rules, conditions and industry practices of the co-producer.

Links:

Aide aux cinéma du monde:

24

http://www.cnc.fr/web/fr/international The 2012 call for applications is not yet up, but the 2011 information for the International Film Fund, Singapore, can be found at: http://www.smf.sg/BusinessCentre/Pages/IFF.aspx The Norwegian Film Institute’s SØRFOND: http://www.filmfrasor.no/en/news/2011/08/SORFUND-INTERWIEV-WITH-LASSE-SKAGEN

25

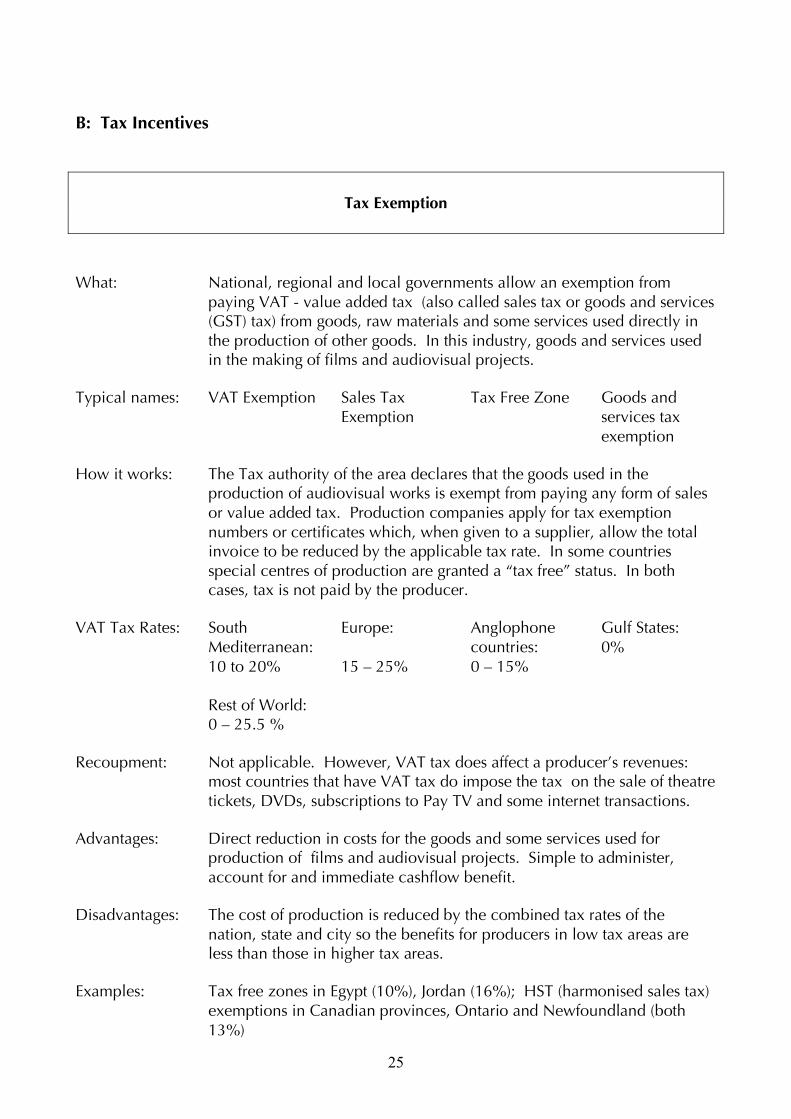

B: Tax Incentives

Tax Exemption

What: National, regional and local governments allow an exemption from

paying VAT - value added tax (also called sales tax or goods and services (GST) tax) from goods, raw materials and some services used directly in the production of other goods. In this industry, goods and services used in the making of films and audiovisual projects.

Typical names: VAT Exemption Sales Tax Exemption

Tax Free Zone Goods and services tax exemption

How it works: The Tax authority of the area declares that the goods used in the production of audiovisual works is exempt from paying any form of sales or value added tax. Production companies apply for tax exemption numbers or certificates which, when given to a supplier, allow the total invoice to be reduced by the applicable tax rate. In some countries special centres of production are granted a “tax free” status. In both cases, tax is not paid by the producer.

VAT Tax Rates: South Mediterranean: 10 to 20% Rest of World: 0 – 25.5 %

Europe: 15 – 25%

Anglophone countries: 0 – 15%

Gulf States: 0%

Recoupment:

Not applicable. However, VAT tax does affect a producer’s revenues: most countries that have VAT tax do impose the tax on the sale of theatre tickets, DVDs, subscriptions to Pay TV and some internet transactions.

Advantages: Direct reduction in costs for the goods and some services used for production of films and audiovisual projects. Simple to administer, account for and immediate cashflow benefit.

Disadvantages: The cost of production is reduced by the combined tax rates of the nation, state and city so the benefits for producers in low tax areas are less than those in higher tax areas.

Examples: Tax free zones in Egypt (10%), Jordan (16%); HST (harmonised sales tax) exemptions in Canadian provinces, Ontario and Newfoundland (both 13%)

26

For more information:

There is a large article explaning VAT and sales tax in detail at: http://en.wikipedia.org/wiki/Value_added_tax

Tax Rebate (aka Tax Refund)

What:

National, regional or local governments grant a company a rebate (a refund) for all or a portion of VAT - value added tax – paid on goods, services and faciliites used directly in the production of other goods; in this industry, in the production of films and audiovisual projects. Note: In some countries and regions, the term ‘tax rebate’ also refers to a Tax Credit.

Typical names: VAT Rebate VAT Refund

Sales Tax Rebate or Refund

Goods and Services Tax Rebate or Refund

How it works: The tax authority of a country or a region decrees that the goods, services and facilities used in the production of an audiovisual work will be collected but later returned to the producer. The supplier will invoice the producer for the cost plus the tax. All or a portion of the total VAT tax paid during production will be given back – refunded – to the production company by the tax authority. Production companies provide the tax authority accounts showing the total VAT tax paid. The tax authority then issues a cash refund or a credit note to the producer to use as payment of any monies due to the tax authority now or in the future. The credit note can be used to pay any forms of taxation, not just VAT including employee withholdings, or social charges (government health, unemployment or pension, for example).

VAT Tax Rates: The Southern Mediterranean: 10 to 20% Rest of World: 0 – 25.5 %

Europe: 15 – 25% (Hungary’s will be 27% in 2012)

Anglophone countries: 0 – 15%

Gulf States: 0%

Recoupment:

No.

Advantages: Direct reduction in costs for the goods, services and facilities used for production of films and audiovisual projects. Simple to administer and

27

to do the required accounting.

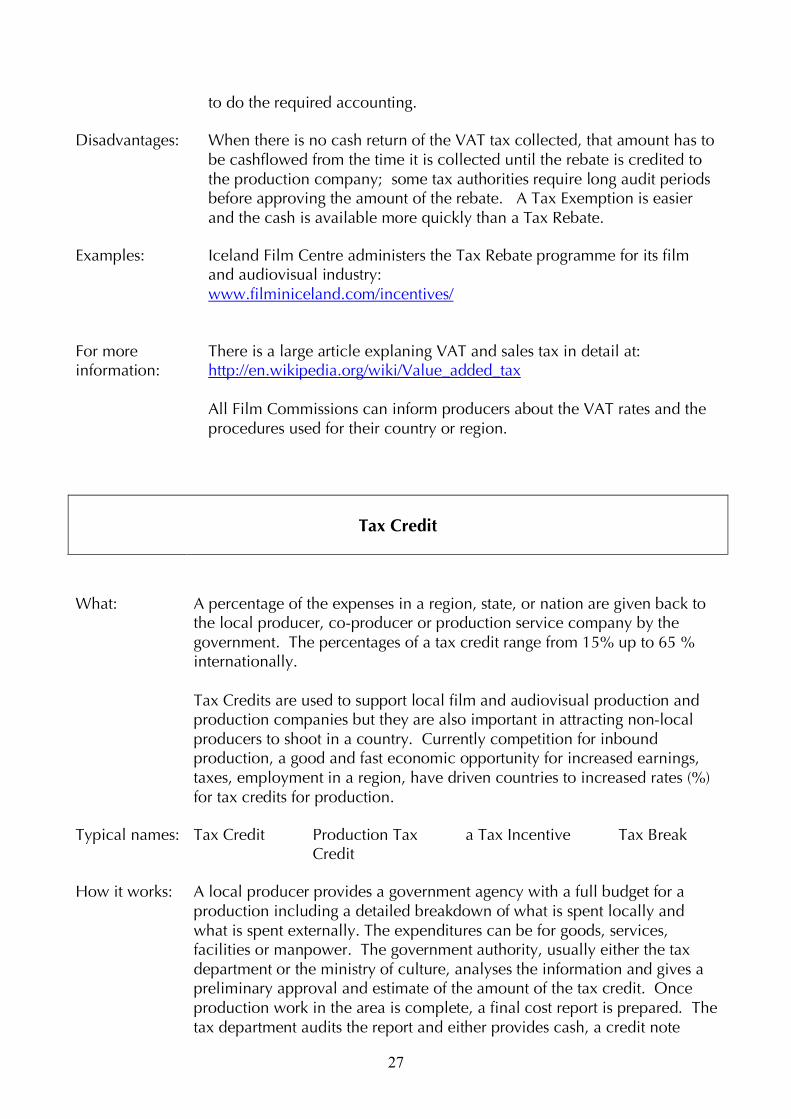

Disadvantages: When there is no cash return of the VAT tax collected, that amount has to be cashflowed from the time it is collected until the rebate is credited to the production company; some tax authorities require long audit periods before approving the amount of the rebate. A Tax Exemption is easier and the cash is available more quickly than a Tax Rebate.

Examples: Iceland Film Centre administers the Tax Rebate programme for its film and audiovisual industry: www.filminiceland.com/incentives/

For more information:

There is a large article explaning VAT and sales tax in detail at: http://en.wikipedia.org/wiki/Value_added_tax All Film Commissions can inform producers about the VAT rates and the procedures used for their country or region.

Tax Credit

What:

A percentage of the expenses in a region, state, or nation are given back to the local producer, co-producer or production service company by the government. The percentages of a tax credit range from 15% up to 65 % internationally. Tax Credits are used to support local film and audiovisual production and production companies but they are also important in attracting non-local producers to shoot in a country. Currently competition for inbound production, a good and fast economic opportunity for increased earnings, taxes, employment in a region, have driven countries to increased rates (%) for tax credits for production.

Typical names: Tax Credit Production Tax Credit

a Tax Incentive Tax Break

How it works: A local producer provides a government agency with a full budget for a production including a detailed breakdown of what is spent locally and what is spent externally. The expenditures can be for goods, services, facilities or manpower. The government authority, usually either the tax department or the ministry of culture, analyses the information and gives a preliminary approval and estimate of the amount of the tax credit. Once production work in the area is complete, a final cost report is prepared. The tax department audits the report and either provides cash, a credit note

28

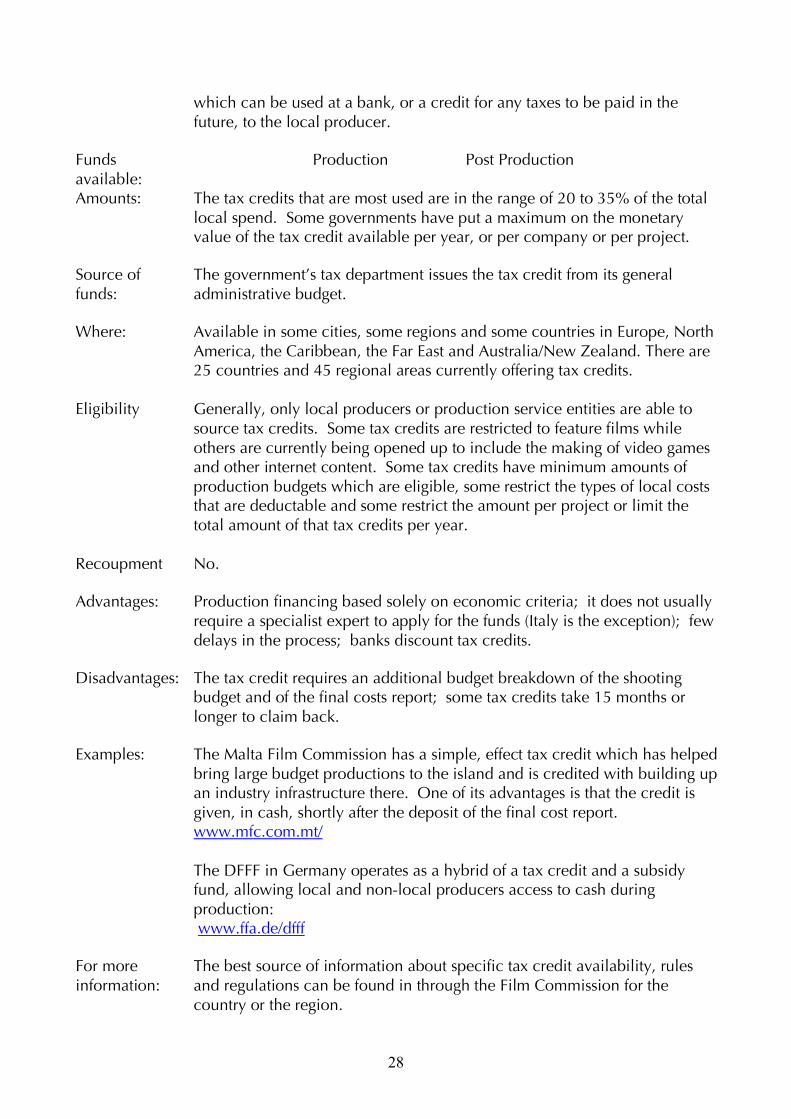

which can be used at a bank, or a credit for any taxes to be paid in the future, to the local producer.

Funds available:

Production

Post Production

Amounts: The tax credits that are most used are in the range of 20 to 35% of the total local spend. Some governments have put a maximum on the monetary value of the tax credit available per year, or per company or per project.

Source of funds:

The government’s tax department issues the tax credit from its general administrative budget.

Where: Eligibility Recoupment

Available in some cities, some regions and some countries in Europe, North America, the Caribbean, the Far East and Australia/New Zealand. There are 25 countries and 45 regional areas currently offering tax credits. Generally, only local producers or production service entities are able to source tax credits. Some tax credits are restricted to feature films while others are currently being opened up to include the making of video games and other internet content. Some tax credits have minimum amounts of production budgets which are eligible, some restrict the types of local costs that are deductable and some restrict the amount per project or limit the total amount of that tax credits per year. No.

Advantages: Production financing based solely on economic criteria; it does not usually require a specialist expert to apply for the funds (Italy is the exception); few delays in the process; banks discount tax credits.

Disadvantages: The tax credit requires an additional budget breakdown of the shooting budget and of the final costs report; some tax credits take 15 months or longer to claim back.

Examples: The Malta Film Commission has a simple, effect tax credit which has helped bring large budget productions to the island and is credited with building up an industry infrastructure there. One of its advantages is that the credit is given, in cash, shortly after the deposit of the final cost report. www.mfc.com.mt/ The DFFF in Germany operates as a hybrid of a tax credit and a subsidy fund, allowing local and non-local producers access to cash during production: www.ffa.de/dfff

For more information:

The best source of information about specific tax credit availability, rules and regulations can be found in through the Film Commission for the country or the region.

29

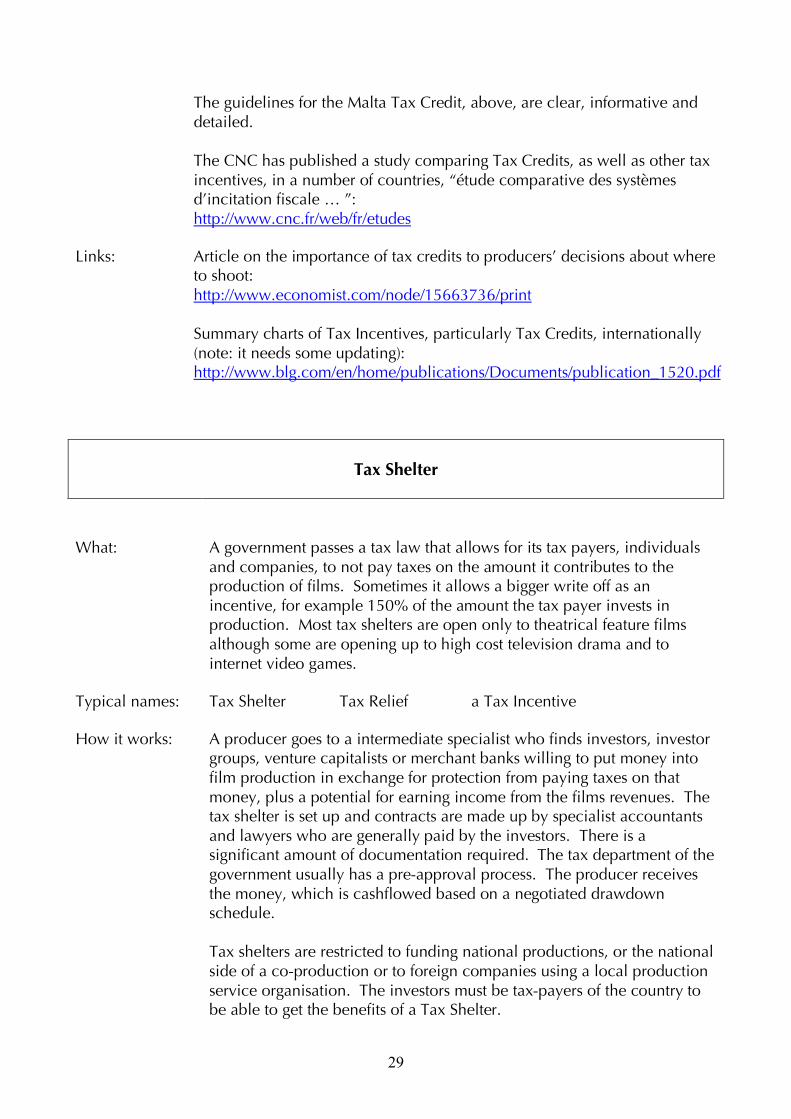

The guidelines for the Malta Tax Credit, above, are clear, informative and detailed. The CNC has published a study comparing Tax Credits, as well as other tax incentives, in a number of countries, “étude comparative des systèmes d’incitation fiscale … ”: http://www.cnc.fr/web/fr/etudes

Links: Article on the importance of tax credits to producers’ decisions about where to shoot: http://www.economist.com/node/15663736/print Summary charts of Tax Incentives, particularly Tax Credits, internationally (note: it needs some updating): http://www.blg.com/en/home/publications/Documents/publication_1520.pdf

Tax Shelter

What:

A government passes a tax law that allows for its tax payers, individuals and companies, to not pay taxes on the amount it contributes to the production of films. Sometimes it allows a bigger write off as an incentive, for example 150% of the amount the tax payer invests in production. Most tax shelters are open only to theatrical feature films although some are opening up to high cost television drama and to internet video games.

Typical names: Tax Shelter Tax Relief a Tax Incentive

How it works: A producer goes to a intermediate specialist who finds investors, investor groups, venture capitalists or merchant banks willing to put money into film production in exchange for protection from paying taxes on that money, plus a potential for earning income from the films revenues. The tax shelter is set up and contracts are made up by specialist accountants and lawyers who are generally paid by the investors. There is a significant amount of documentation required. The tax department of the government usually has a pre-approval process. The producer receives the money, which is cashflowed based on a negotiated drawdown schedule. Tax shelters are restricted to funding national productions, or the national side of a co-production or to foreign companies using a local production service organisation. The investors must be tax-payers of the country to be able to get the benefits of a Tax Shelter.

30

Funds available: Production

Post Production

Amounts: Tax shelters are generally restricted to an amount per project, usually between 15 and 30%.

Source of funds: The production funds come from investors which are profitable companies or wealthy individuals who do not want to pay taxes on a portion of their earnings in a given year. The governmental tax department allows the non-payment of taxes because of the shelter and it absorbs the reduction in revenue. The taxes paid by increased production activity makes up for this reduction.

Where: Eligibility: Recoupment:

Film tax shelters are not widely spread. They exist primarily in Europe and then only in Belgium. France, Ireland and Italy. National productions or approved co-productions within minimum and maximum budget levels; mostly feature films. Little to none. The government’s allowance of declaring more than 100% of the total value to the production (eg. 150%) is specifically meant to lower the investors’ risk.

Advantages: Direct aid for the film cashflowed according to pre-approved installments, of between 15% and 30% of the budget; little scrutiny of the script, cast and crew and other artistic aspects of the production; small recoupment, if any, from the film’s revenues.

Disadvantages: The amount of documentation and financial analysis is high; accounting on both sides is extensive. Film tax shelters have been tried and while many succeeded in igniting an expanded national industry in a short time, many also failed. The reasons for failure included the poor quality of the films, expanded production budgets and larger costs for specialists putting together the tax shelter; the lack of political will to support the film industry after its initial success. The tax shelters which exist now are highly regulated: Section 481 in Ireland has had two “gatekeepers” who maintain control of the applications; the few approved Sofica’s in France work within tight restrictions; and the Belgium tax shelter is the result of several years of experimentation and improvement. The Italian tax shelter is working but to a much lesser extent than its Tax Credit counterpart; it, too, has extensive requirements.

Examples: Belgium: Tax Shelter for Audiovisual Productions, France: SOFICAs Ireland: Section 481, Italy: Tax Shelter

For more

One of the clearest explanation of how a tax shelter works in the film

31

information:

industry is the Belgium publication listed below. While the procedures are similar to other countries, please note all of the numbers quoted may be unique to Belgium.

Links: Belgium’s relatively newer version of its tax shelter, which is aimed at “encouraging the production of audiovisual works and films” in the country. It generated €100,000,000 in funding for producers in 2011. There is a detailed brochure called “TAX SHELTER: Tax Incentives for Audiovisual Productions .be” that can be downloaded from the Publications site of: www.minfin.fgov.be France’s SOFICAs: www.ora-defiscalisation.com/placement-sofica.html Ireland: Section 481 www.irishfilmboard.ie Italy: www.anica.it

32

C: Co-production

Co-Production

What:

Two or more companies reach an agreement to produce a film or audiovisual work together, pooling resources, talent and funds. Informal co-productions can be negotiated between any types of companies. Formal or treaty co-productions adhere to the terms and conditions of a bilateral agreement which has been ratified by the governments of two countries, are approved by the relevant authority in both countries and receive ‘dual nationality’. This status allows the project to benefit from all of the subsidy funds, tax credits and quotas of both countries. There are trilaterial treaties (based on linguistically similar countries working together) and multilateral treaties (see below). Formal co-productions can be realised only by two or more production companies which meet local government requirements (tax status, residency, corporate legitimacy, etc). Treaties may cover one or more of: feature films, television drama, animation and documentaries but few cover digital media projects. Note: Co-production is an overused term: it may refer to any form of co-financing (a TV pre-sale, distribution advances or private equity). It may refer to any creative and financial collaboration between producers and broadcasters when production funds come from television sources. Internationally, co-financing arrangements are more popular than inter-governmental co-production agreements, in part to avoid the restrictions of treaty terms and conditions and, in part, because many sources of funds do not require adherence to a treaty nor do they require national approval.

How it works:

Two or more producers negotiate an agreement to work together to develop, finance and produce one film. The agreement is based on “the co-production ratio”:

% of investment from one producer =

% of budget spent by the same producer =

% of creative contribution by nationals of the same producer =

% of revenues that is returned to the same producer One of the producers is the lead producer while the others are co-

33

producers; the lead producer generally owns the underlying rights and has the higher percentage of the project (according to the ratio above). While the percentages of investment, budget and revenues are easily quantified, creative contribution is calculated using a point system that is set out in the relevant treaty. Points are allocated for key creators (writers, directors, actors, department heads, etc.) and sometimes for locations and / or production logistics. Treaty co-productions, which allow full access to national funds, quotas and tax incentives, require formal advance and post completion approval by the organisations in all the countries involved. These organisations are authorised by their government to approve co-productions (often the film institute, film centre or the ministry or government department responsible for cinema). The % share of a formal co-production is regulated by the minimums and maximums that are set out in the relevant treaty: typically either 20% or 30% is the least share and 70% or 80% is the maximum one producer can contribute. There is an exceptional 10% - 90 % share arrangement in Europe called “a financial only” co-production which allows the exchange of money but does not require any creative contribution by the minority producer.

Funds available: Development

Production

Post Production Sales & marketing (where support is offered nationally)

Amounts: Co-producers raise funds for the project from the financing sources available to them in their country. If the project is a treaty co-production, the minority co-producer has to raise at least 20 or 30 % of the budget of the project. (The treaties all have a clause which stipulates the minimum percentage.) Co-productions make up between 20 to 33% of the all productions of feature films in Europe. The amount contributed by minority co-producers has not been calcated but is estimated to be about 1/3 of the budget of a two country co-production and less if the project is a multiple country co-production. Canada, the country with most co-production treaties, paid for only 46% of the cost of its 27 co-produced features in 2009/2010 but 80% of its 34 long television drama co-productions.

Source of funds: Co-producers raise funds in their country from the financing sources available to them. There are special funds for co-productions in defined regions (Ibermedia, Eurimages, the Nordisk Film & TV Fond; see Pan National Funding for

34

more detailed information). France has also pioneered the concept of “mini-treaties” which give up to 20% more than normal subsidy amounts to encourage more co-production; there are three signed with Canada (features, animation, television) and one with Germany.

Where: Eligibility: Recoupment:

Bilateral co-production treaties exist in the Southern Mediterranean but not as extensively as in Europe. Bilaterial treaties have been signed by a large number of international countries. Trilateral treaties are rare but do exist between the German speaking countries in Europe: Germany, Austria and Switzerland. Two Pan-national treaties exist in Europe and Latin America (see below). Where a treaty exists, only recognised national production companies can apply for official co-production approval. Each co-producer recovers their recoupable cost of production first from their country and secondly from a share of revenues from the rest of the world. (In the event the country provides more funds than that country can earn back, the co-producers generally agree that one or more countries’ revenues will go to that co-producer.)

Advantages: There are three main reasons for producers to co-produce: access to more financing, access to more talent and access to other markets. Countries who sign co-production treaties and encourage the development of co-productions also believe that the intercultural exchange is important and beneficial.

Disadvantages: Co-productions, especially treaty ones, take longer; depending on the country and it funding system; it could be as little as three months longer (those regions where a major percentage of production is co-production, like Scandinavia) or as long as a year longer (the eastern and southern countries of Europe have few deadlines for national funding and take many months to assess applications and announce funding decisions). Terms and conditions for treaty co-productions are complex requiring some economic and creative compromises. There are added bureaucratic regulations required. Costs generally increase and if the producer fees and overheads are capped by funding authorities, they must be shared with co-producers. The needs and likes/dislikes of audiences of the co-production countries need to be addressed in the content and the casting.

Examples: Information regarding the financing and co-production of the following titles is available on the internet. Ranging geographically, from the South Mediterranean, to the South Mediterranean and Europe, to pan-European to Canada and Europe: Black Gold, Where Do We Go Now, Simon and the Oaks, The Whistleblower.

For more There is an EuroMed Audiovisual III census of Co-Production by Lucas

35

information: Rosant which contains a lot more facts, figures, treaties and case studies on the EuroMed Audiovisual III website.

Links:

The European Audiovisual Observatory has webpage about co-production with access links to several of its relevant databases at: http://www.obs.coe.int/about/oea/pr/coproduction.html European Convention on Cinematographic Co-Production Designed to encourage the development of film co-productions in Europe. This agreement allows most European countries to make treaty co-productions with each other (two, three or more countries for each project). Adherence to its terms and conditions is fundamental for support by the multinational production funding organisation Eurimages. The fulll Convention can be downloaded at: http://conventions.coe.int/Treaty/Commun/QueVoulezVous.asp?NT=147&CL=ENG There is a complete list of countries which have signed this agreement, updated regularly, at: http://conventions.coe.int/Treaty/Commun/ChercheSig.asp?NT=147&CM=8&DF=&CL=ENG

Acuerdo Latinoamericano de Coproducción Cinematográfica (Latin American Film Co-Production Agreement) Designed to encourage the development of film co-productions in Latin America. This agreement allows most Latin American countries to make treaty co-productions with each other (two, three or more countries for each project). Adherence to its terms and conditions is fundamental for support by the multinational production funding organisation Ibermedia. In Spanish: http://www.cinelatinoamericano.org/assets/docs/acuerdo_bol.pdf Background information and summary in English: http://www.ftaa-alca.org/wgroups/wgsv/sagreem/English/sv_p27.asp

36

D: Television Funding for Independent Producers

Broadcasters

What: Television broadcasters give producers financing, either in the form of

cash or goods, services and facilities, in exchange for the exclusive right to show a programme for an agreed period of time. Some broadcasters invest an additional amount of money in a project in exchange for the right to a percentage of all world wide revenues and profits. Broadcasters sometimes refer to their agreement with an independent producer as a “co-production” but this type of contract does not follow the same terms and conditions prescribed in formal co-production treaties. Broadcasters sometimes commission a programme by hiring the services of a producer to produce a the project on their behalf.

Typical names: TV Presale TV License Fee TV Equity Investment

TV Co-production

How it works: Commissioning editors are charged with assessing and acquiring certain kinds of programming (eg: features or movies of the week, drama series, factual, documentaries, children’s, etc.). Producers submit their project to the commissioning editor who, if his or her opinion is favourable, usually gives notes on changes required by the broadcaster during development. The contract department of the television station or network signs a development contract. Once development is complete, the budget, schedule and key cast and crew are approved by the broadcaster. Production contracts are signed by both parties. The producer then expects that the broadcaster will come on set during shooting, see and approve rushes and various cuts of the film. The broadcaster’s financing is usually given out in installment which are negotiated between the parties based on the cashflow projections for the project. The producer delivers the programme and all of the supporting materials outlined in the contract including a final cost report. Once that is approved the broadcaster’s financing is paid in full. Documentaries are usually commissioned in stages with input from the

37

broadcaster. Animation and series have more complex timelines for delivery to the broadcaster and a drawdown schedule with more installments for payment of the broadcaster’s funding.

Funds available: Development and Research

Production

Post Production Sales & marketing

Amounts:

Television broadcasters usually pay consistent amounts for similar projects regardless of the producer or the budget of the project. Price range from several million Euro for primetime drama for a major country’s top rated channel, to hundreds or thousands of Euro for a documentary for a specialised channel in a smaller country. Most producers can find out the normal price ranges for each broadcaster and for each type of programme. The typical deals change depending on the type of broadcaster. In order from larger amounts to smaller ones: public, commercial, specialised (or boutique) and finally the newer IPTV internet channels. If a broadcaster commissions a programme, it expects to pay the total production costs including the producer’s fees.

Source of funds: Television budgets come from license fees, government allocations and/or advertising. Some governments require that, in exchange for a television license, the broadcaster must support national independent production.

Where: Eligibility: Recoupment:

Available worldwide. The broadcaster determines eligibility. A pre-buy to show a project on the television channel or network is usually not recoupable; it is a simple pre-payment for license fees. If a broadcaster co-produces it may recoup all or a part of its financing and it may share in any profits; it depends on local industry practices. If a broadcaster puts up an equity investment, it will recoup this investment as well as have a share in profits; most broadcasters accept pari passu pro rata deals. If a broadcaster commissions a programme, the broadcaster owns it outright and the producer has no right to any revenues.

Advantages: Direct aid for the film or audiovisual project, in the form of cash or goods and services when needed, of between 10% and 100% of the budget of film and audiovisual projects; support in the form of expertise for all

38

stages from early development through to international sales; simple industry standard prices and contracts; a quarantee of a quality to all of the other financiers; a base upon which to sell other international broadcasters

Disadvantages: The choice of projects is not based on automatic support but on the evaluation of perceived quality; limited room to negotiate deals; few slots available for independently produced programming; broadcaster support can be withdrawn or reduced without notice (unless required by a government licensing agency for broadcasters)