EU versus US regulation: Biotech

47

1 U.S. versus E.U. Biotechnology Regulations and Comparative Advantage: Implications for Future Conflicts and Trade By Gal Hochman, Gordon Rausser, and David Zilberman October 2008 1. Introduction In the 1990s, a new and important industry emerged; namely, the plant biotechnology industry. As the industry matured, US based firms became more dominant and their market shares increased. Although many former chemical companies in the US moved away from development of new chemicals into development of new biotechnology traits (e.g., Monsanto, followed by Pioneer/DuPont and Dow Chemical/Mycogen), European companies continued to heavily invest in chemicals well into the 21 st century (e.g., Syngenta, BASF, Bayers). The different patterns of investment in R&D caused the US firms to dominate the industry, and affected the two

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of EU versus US regulation: Biotech

1

U.S. versus E.U. Biotechnology

Regulations and Comparative Advantage:

Implications for Future Conflicts and

Trade

By

Gal Hochman, Gordon Rausser, and David Zilberman

October 2008

1. Introduction

In the 1990s, a new and important industry emerged; namely, the plant biotechnology industry.

As the industry matured, US based firms became more dominant and their market shares

increased. Although many former chemical companies in the US moved away from development

of new chemicals into development of new biotechnology traits (e.g., Monsanto, followed by

Pioneer/DuPont and Dow Chemical/Mycogen), European companies continued to heavily invest

in chemicals well into the 21st century (e.g., Syngenta, BASF, Bayers). The different patterns of

investment in R&D caused the US firms to dominate the industry, and affected the two

2

countries’ comparative advantage. Whereas the Europeans became more competitive in

agricultural chemicals, the US became more competitive in biotechnology.

In the United States, biotech crops under development are evaluated extensively before being

approved for commercialization. The specific regulatory process stems from the Regulation of

Biotechnology Products (1986) (Cast, 2007). Risks associated with biotechnology crops are

considered not to be fundamentally different from risks of conventionally derived products, and

regulation should be on a case-by-case bases. Regulation should, therefore, follow existing rules,

which provide adequate authority for regulation of biotechnology crops.

On the other hand, European Union efforts in the 1990s initially attempted to develop a uniform

EU-wide policy for approvals and trade in GM crops and foods, which was controversial in

several member states. Widespread media coverage of anti-GM activists helped move the issue

of GM foods quickly to the forefront of political debate in Europe. Increased representation of

the Green Party in member state parliaments and cabinets, as well as in the European Parliament,

ensured that these concerns would reflect national and European politics. Almost overnight,

GMOs became politically unpopular and politicians found it difficult to approve GM crops and

foods despite scientific reviews that should have ameliorated safety concerns.

By 1997, the effort to craft a uniform EU-wide policy on GMOs came apart. Despite EU

approvals for commercialization of several GM crops under Directive 90/220/EEC, a few

member states invoked a “safeguard clause” to ban the use of the approved GM crops in their

respective countries. In 1997, Austria and Luxembourg banned several EU-approved GM crops.

Over the next several years, additional bans on EU-approved crops followed in Austria, Italy,

Greece and Germany. While the Commission could have taken legal action to force compliance,

3

it chose not to do so. Europeans faced growing opposition to GM foods and a concern about an

inadequate regulatory system. In response to these concerns, the European Commission did not

approve any new GM foods or crops between 1998 and 2004, despite general scientific

consensus that they posed no food safety or environmental risks (Evenson, 2007). Regulation of

the introduction of biotechnology in Europe took a different approach than the United States;

whereas the Europeans adopted the ‘precautionary principle' toward the late 1990s, the United

States adopted the ‘substantial equivalence' principle.1

The decision to apply regulatory measures and the incentives of the different groups to influence

this decision is not, however, limited to a certain sector. Regulation is determined by a

bargaining process, which is political in nature and attempts to incorporate the well being of the

different groups affected by the proposed regulation. The challenge is to address different

incentives without slipping into protectionist policy. To keep political considerations at bay, and

to protect the public’s general interests (not the income of a well-connected sector), a

transparent and coherent methodology needs to be developed. The risk assessment model strives

to meet this challenge, as illustrated in Zilberman et al. 2008. Harmonizing the method used, not

the standard levels, seems to us a more promising approach.2 Harmonizing the methodology

introduces transparency to the decision process, while allowing nations to respond differently to

environmental and health risk.

1 The substantial equivalent approach measures, whether biotech food or crop shares similar health and nutritional characteristics with its conventional counterpart. Substantially equivalent biotech foods are determined to be as safe as their conventional counterparts. Not substantially equivalent products may still be safe, but must undergo a broader range of tests before approved for commercial use. The zero risk-tolerance regulatory regime, coined the precautionary principle, is a moral and political principle which states that if an action or policy might cause severe or irreversible harm to the public, in the absence of a scientific consensus that harm would not ensue, the burden of proof falls on those who would advocate taking the action. For more on the differences between the two regulatory regimes see Hochman et al. (2008). 2 See also Hochman et al. (2008).

4

In the paper, we extend political economic models to formally incorporate risk, and show that

setting of regulations in the biotech industry reflects political economic interactions, largely

driven in food safety regulations by comparative advantage. To this end, technical regulations

may be designed to discriminate against foreign suppliers both in their construction and in their

outcomes. They may be used to gain strategic international trade advantages for domestic firms

relative to foreign competitors. Regulation preserved and protected Europe’s comparative

advantage; regulation self-sustained the European chemical industry’s comparative advantage

and kept at bay investment in the emerging biotech industry.3 We further argue that regulation

spillover, particularly from the EU to developing countries, ill-served the developing countries

respective public interests.

Although the benefit from regulation is concentrated in a few sectors, the cost is dispersed across

continents, not only North America and Europe but also Africa and Asia. There are several

instances where the regulation in the United States and Europe is mimicked by developing

countries, not necessary for the right reasons. Some examples include Egypt, which created the

Agricultural Genetic Engineering Research Institute in 1989 to improve Egyptian crops. Yet,

despite successful field trials in 1997 with a genetically modified potato resistant to insect

damage, it never approved the potato for commercial production. The growing governmental

resistance in Africa to transgenic crops came into full bloom in 2002, when in the midst of a

severe draught that left 15 million people across seven countries facing a serious food deficit, the

government of Zimbabwe decided to turn away a 10,000 ton shipment of unmilled U.S. corn,

expressing an official concern that some of the genetically modified kernels might be planted

(Paarlberg 2008).

3 See also Graff and Zilberman (2008).

5

The balance of our paper is organized into four remaining sections. Biotech regulation in both

the European Union and the United States, as well as environmental and food safety concerns,

are described in Section 2. A conceptual framework illustrating how regulation has affected

production and trade is presented in Section 3, and Section 4 offers empirical support for the

arguments presented in the paper. The implication for policy, emphasizing the importance of

harmonizing methodology, and not the standards, is discussed in Section 5.

2. Background

Agricultural biotechnology applies modern knowledge in molecular and cell biology to produce

new and improved varieties of crops. It has transformed the production system of major field

crops such as soybeans, corn, cotton, and canola. Providing herbicide tolerance and insect

resistance as well as improved product quality, genetically modified crops have experienced a

high rate of adoption. Benefits come from increased yields, lower risk, reduced use of chemical

pesticides, gains from reduced tillage and other modified production practices, and savings in

management, labor, and capital improvement (Kalaitzandonkes 2003; Just, Alston, and

Zilberman 2006).

Over the last ten years, U.S. farmers have planted millions of acres of genetically modified

varieties of corn, cotton, and soybeans. In 2004, about 45% of corn, 85% of soybeans, and 76%

of cotton planted in the U.S. were genetically modified varieties. Since much of the corn and

soybeans harvested each year are processed into products like corn oil and lecithin, it is not

surprising that an estimated 75% of processed food sold in the United States contains ingredients

derived from genetically modified (GM) crops.

6

Notably, however, the adoption of biotechnology has varied across location, and was initially

concentrated in a small number of countries, partly due to regulatory regimes (Zilberman 2006;

James 2007). Agricultural biotechnology has recently begun to expand. In 2007, as a

consequence of consistent and substantial benefit from biotech and changes in the regulatory

regime in Europe, 114.3 million hectares (282.4 million acres) of biotech crops were planted by

12 million farmers in 23 countries. Still, the U.S. accounted for 50% of biotech production,

planting 57.7 million hectares to GM seed (James 2007).

2.1 Biotechnology and regulation

In the United States, the introduction of GM foods—foods derived from GM crops or containing

ingredients derived from GM crops—has not elicited strong public concern or widespread

opposition. Indeed, most Americans are unaware of the extent to which genetically modified

foods have been introduced into the marketplace. Europe, however, is a different matter. With

public confidence in food safety shaken by a series of food scares unrelated to GM foods,

including a serious outbreak of Mad Cow disease (Bovine Spongiform Encephalopathy),

European consumers are wary of GM foods.

European Union (EU) member states grow few GM crops (for instance, in 2003, France, the

largest wheat producer in Europe, grew less than 2 percent of world production whereas the

world largest producer by far, the United States, grew more than 40 percent – NUEweb 2008),

and very few (if any) foods carrying the required GM label appear to be available for sale in the

EU marketplace. Faced with popular opposition to GM foods and a concern about an inadequate

regulatory system, the European Commission did not approve any new GM foods or crops

between 1998 and 2004, despite general scientific consensus that they posed no food safety or

7

environmental risks (Evenson, 2007).4 In 2004, new EU laws went into effect providing for the

approval of GM crops, as well as GM food and feed, and establishing new requirements for

labeling and traceability.

Since then, the Commission has moved through a lengthy process to approve several GM crops,

as well as human food and animal feeds derived from GM crops. In June 2005, however, a

qualified majority of the Council of Ministers refused to lift certain EU member state bans on

GM products that had been approved by the Commission, creating new doubts about the viability

of an EU-wide policy on GM crops, foods and feeds.5

In the United States, risks associated with biotechnology crops are considered not to be

fundamentally different from risks of conventionally derived products, and regulation should be

on a case-by-case bases. Regulation should, therefore, follow existing rules which provide

adequate authority for regulation of biotechnology crops.

The Environmental Protection Agency (EPA) and the USDA-Animal and Plant Health

Inspection Service (USDA-APHIS) oversee the environmental safety of commercial releases of

biotech plants in the United States. The Endangered Species Act also applies to biotech plants.

The Food and Drug Administration (FDA) serves in a consultative manner on issues related to

food and feed safety issues, though regulation are pending that would make the consultation

process mandatory. The combined activities of EPA, USDA-APHIS, and FDA assess the

potential risks to human health and the environment through a comprehensive process prior to

the general release and potential commercial use of a biotech crop (see Appendix A). Biotech

products can be produced and sold only if no unacceptable risks are identified. After the biotech

4 See also Just et al. (2007), and reference therein. 5 For more on the regulatory regimes in the European Union and in the United States, see Hochman et al. (2008).

8

crop is approved for commercial use, government regulatory and monitoring mechanisms allow

products to be pulled from the market if new data relating to safety justify such action, although

no official mechanism for systematic post-commercial monitoring of biotech crops exists.

The goal of food policy regulations ought to be the provision, subject to resource constraints, of

readily available food with characteristics demanded by consumers in a manner that is minimally

distorting (Josling, Roberts, and Orden 2004). There is a strong economic rationale for food

safety regulation to respond to market failures, which in part include information asymmetries

that preclude consumers from making fully informed decisions. Food safety regulations can be

aimed at reducing risk of bad health outcomes or ensuring minimum quality. Some regulate the

content of food, such as the absence of disease or particular chemicals. Others regulate the

production process, mandating rinsing and cleaning or banning the use of chemical pesticides or

hormones. From an economic efficiency standpoint, content regulations are considered superior

to process regulations. They permit the achievement of desired food outcomes without limiting

the freedom of producers to use the most cost-effective processes.

There are a number of mechanisms by which countries regulate their food supplies. Quantity

restrictions, including bans, are a severe method and generally favored only if other mechanisms

are not feasible because of technical limitations. Technical standards provide conditions that

importers must meet to have access to markets. They may include limitations on the size and

weight of commodities or the use of specified processing technologies. While such standards can

be justified on health and safety grounds, they may also be used to shift the comparative costs of

producers and thereby discriminate against certain producers, such as those from a particular

country. Finally, regulation can also be classified as information requirements and include

mandates that food products disclose certain information, such as the presence of carcinogens or

9

other ingredients deemed hazardous to health. Information requirements may also limit the use of

voluntary claims about food products to ensure credible information is conveyed to consumers.

Claims of nutritional attributes, for instance, must be substantiated. In response to demand for

organic products, many governments have imposed standards with which producers must comply

if they are to receive government certification that products are organic.

Despite strong economic justification for the regulation of food safety, countries may choose

suboptimally restrictive food safety laws. Governments tend to be afraid of low-probability high-

risk events occurring. National governments often adopt a decision-making process that

considers the risk effects of policy, as well as the costs and benefits. Incremental reductions of

risk, therefore, may be favored regardless of the cost to domestic consumers and foreign

producers. Regulation may also be used by interest groups to extract rents. Producers may use

food regulation to reduce competition from imports. Consumer advocacy groups may use the

political process to achieve narrow agendas that are not consistent with the public interest. The

design of mechanisms that reduce the potential for food safety policy to be used for ulterior

purposes, like protectionism, is an important element of a regulation regime. It is estimated that

in 1995, $2.1 billion of U.S. exports were blocked by animal and plant safety regulations that had

little or no merit (Josling, Roberts, and Orden 2004).

Hypothetically, biotechnology may adversely impact food safety. It may introduce allergens and

toxins, and have a negative effect from the consumption of antibiotic-resistant marker genes and

viral-promoters genes used in the transformation process. Hypothetically, it may also negatively

impact environmental safety through gene transfer to related crops or wild species, and/or the

emergence of resistant pests. In practice, however, only gene flow became a real problem, and

only in a few local regions (2003-04 SOFA).

10

2.2 Gene Transfer

The transfer of genetic material and species among nations is central to the protection of natural

resources and human health. Such transfers can be intentional or accidental and can be

responsible for significant environmental and health benefits or for costly damage. For instance,

in many parts of the world, nutritional needs are primarily met by the cultivation of crops

intentionally introduced from other regions (Hoyt 1992). The United States is the leading

producer of corn and soybean, crops with origins in Mexico and China, respectively. On the

other hand, 80 percent of endangered species worldwide are threatened by invasive alien species,

which are responsible for nearly half of all invertebrate extinctions with known causes (Stein and

Flack 1996; Wilcove et al. 1998).

The two most material benefits of international gene and species transfer are their contributions

to food provision and chemical pest control reduction. As noted, much of the world’s food is

produced by crops that humans introduced from foreign lands. None of the staple crops in North

America are indigenous. The grasses that occupy U.S. pastureland were intentionally introduced

to provide better livestock grazing. Many of the fruits consumed today are the product of plant

breeding with genes from different regions. Genes from Andean corn, carefully bred in Mexico

City, ended a century-long effort to improve the nutritional content of corn and yielded modern

maize germ plasm. The assault of rusts on cereal crops has led to famine across human history.

An intense international effort to develop rust resistance in wheat has yielded a partial solution

and perhaps averted untold human misery. The work of transferring rust resistance in rice to

other cereals proceeds. Gene transfer will be integral to developing the agricultural productivity

gains necessary to feed a world of 10 billion people.

11

In addition to improving agricultural production, international species transfer can also benefit

the environment by offering alternatives to chemical pest control. The use of predator species to

control pest populations is fundamental to biological control, a relatively environmentally

friendly practice that uses natural methods to suppress pests. In many cases, predator species are

introduced to ecosystems. In other cases, indigenous predator populations are protected to

control pest populations. As environmental awareness has grown, demand for chemical-free

alternatives to pest control has increased. Alien species can be substitutes to chemical herbicides,

fungicides, and pesticides, which can cause wide-ranging changes in ecosystems by affecting

nontarget species and polluting water resources. For instance, several parasitoids were

successfully introduced in the United States to control the alfalfa weevil, itself an invasive alien

species from Europe. Absent biological control, the alfalfa weevil caused damage throughout the

United States and induced farmers to spray crops one or more times per year (Stoner 2006).

While species introductions can provide a valuable method of pest control, they can also backfire

and cause significant damage to ecosystems and native species. In some cases, biological control

has led to the extinction of native species, and in at least one case, the extinction of an entire

genus (Strong and Pemberton 2000).

Not all species and gene transfers are beneficial and many can be quite costly. Nonnative species

are spreading at faster and faster rates, imposing costs on the global economy on the order of

$1.4 trillion every year (Pimentel 2002). Despite the increasing rate of invasions, only 10 percent

of introduced species will become established, and only 10 percent of those will become pests

(Williamson 1996). Regardless, the spread of invasive alien species has altered ecosystems,

reduced biodiversity, endangered human health, fouled water sources, destroyed agricultural

land, and significantly altered the evolutionary process. These potential costs, combined with the

12

fact that an established invasive species can seldom be eliminated and that the extinction of

species threatened by invasives is irreversible, make the control of invasive species one of the

most critical issues facing the global community.

The spread of invasive species and the consequent homogenization of the earth’s ecosystems are

accelerating with the pace of movement of people and commodities across countries. Trade is the

primary pathway by which nonnative species are introduced to a region, often accidentally by

piggy-backing on traded commodities.

2.3 The environment

Nations may attempt to preserve environmental quality at home and abroad by intervening in

international trade via two primary mechanisms: enforcing process and production methods

(PPM) standards and blocking the importation of invasive species. Under existing trade

agreements, PPM standards can be used to influence environmental activities in foreign countries

and to reduce the effects of global environmental externalities so long as they do not discriminate

against particular producers. Intervention throughout the trade system can reduce the risk of

species invasion, though it may be combined with monitoring and control of the invaders.

In alien species and disease invasion management, governments seek policies that maximize

total social welfare, subject to many constraints. Policies should seek to balance the use of

incentives, monitoring, and control along the species-movement process. The ability to reject

imports prior to shipment, as well as reject imports and the impose fines at the border provide

importers with incentives to ensure their shipments are uncontaminated. After alien species have

entered the importing country, farmers can be subsidized to detect invasions and protect against

them. Monitoring to detect invasions can be done overseas, at the border, and within the country.

13

Control of invasive species includes treatment of shipments overseas and at the border, as well as

chemical spraying to control or eradicate populations within the country.

Cost-benefit analyses are typically used to determine which projects should be pursued. A

project should be undertaken if expected present value of a control or environmental project

exceeds or equals the expected present value of the cost of the project. A common response by

decisionmakers to the risk of invasion is to ban imports of any commodity that poses such a risk.

Such a response ignores the benefits of imports and invasive species themselves, and also

ignores less blunt policy options that may be available, such as control or financial incentives.

The determination of optimal policy response for species invasions is difficult for several

reasons, not the least of which is the difficulty of assigning value to nonmarketed environmental

services. The challenge of determining the full range of effects of invasions has yet to be

overcome in the literature. It is compounded by the diverse effects of invasions on other species

and the time-dependent magnitude of effects. Evaluation is further hindered by the endogeneity

of control dynamics. Risk of invasion and cost of invasion, for instance, are functions of human

impacts on ecosystems and human effort to reduce risk (Dalmazzone 2000). In general, lands

altered for agriculture or other uses are more susceptible to invasion and support fast growth of

invasive species. Mitigation and adaptation efforts, on the other hand, reduce invasion risk.

Besides the endogeneity of risk, the nature of invasion risk poses additional challenges. The

probability of invasion is typically low, but the consequences of invasion are quite high. A single

invasion can be calamitous. The power of expected utility is diminished with low-probability

catastrophic events (Chichilinsky 1998). People treat very unlikely events by either

overestimating their probabilities of realization or setting their probabilities to zero. Invasions are

14

also one-time events often independent of history, making estimation of probability density

functions impossible (Horan et al. 2002).

Because invasion is uncertain and a low-probability event, and because prevention efforts do not

stop invasions with certainty, it may be preferable to expend limited resources on control of

invasions once they occur. In some cases, it may be optimal to undertake considerable control

effort as soon as an invasion is detected in the hope of exterminating the invasive species before

exponential growth begins. In other cases, it may be optimal to try to maintain the invasive

species population at an acceptable level over an indefinite period of time.

While economics can address the market failures posed by species invasions, it is important to

realize the role of political institutions in determining responses to the problem. The Doha Round

was intended to address issues of food safety and the environment. In part, these objectives are

necessitated by the development of new technologies, new outbreaks of disease, and consumer

concerns. Increasingly, consumers are demanding greater levels of food safety and

environmental protection. The growing number of these regulations may be a response to

evolving consumer preferences, but they are also prone to political capture and may be used by

protectionists to reduce competitive pressure from imports. Policies can potentially be influenced

by consumers demanding cheap, safe food and domestic producers concerned about competition

and the availability of cheap inputs, as well as exporters, taxpayers, and environmentalists. The

principal food safety regulations related to trade involve attempts by importing countries to

reduce the risk of adverse health outcomes to acceptable levels. The most important

environmental regulations impacting trade include attempts by importing countries to reduce the

risk of alien species invasions and demand higher environmental quality provision in source

countries through the use of process and production methods (PPM) standards.

15

3. A conceptual framework

Using a multi-market approach to model the agriculture biotech and chemical industries, we

illustrate the benefits from biotech to the different groups. If (i) the chemical industry is not

diversifying its output to include biotech products and investing in genetic engineering, but

focusing only on chemicals, and (ii) the benefits to domestic consumers from biotech is small

(e.g., consumers in rich developed countries spend only a small percentage of their disposable

income on food), then a country does not benefit from biotech; a precautionary regulatory

regime, or even a preventive regime, maximizes the benefit to domestic producers while

imposing a very small cost on the country’s constituencies. Regulation preserves the chemical

industry’s market share, and therefore its profitability (as illustrated empirically in Section 4). On

the other hand, if a domestic biotech industry emerges and becomes a lucrative and dominant

industry, then a country will benefit from biotech and choose a more supportive regulatory

regime.

Formally, consider a product (e.g., staple crop seeds) that can be produced using two alternative

techniques: one uses genetic engineering and the other does not. If the seed is not genetically

modified, then to grow the crop agriculture chemicals are needed; the genetically modified crop,

on the other hand, does not require chemicals. Clearly, these assumptions oversimplify reality.

The conclusions, however, do not change if instead we assume genetically modified crops

consume less agriculture chemicals per hectare, when compared to the crop grown using

traditional techniques. Assume all markets are competitive – i.e., price equals marginal cost.

More specifically, farmers produce y units using two alternative technologies: traditional

technologies (denoted with subscript 0) and genetically engineered technologies (denoted with

subscript 1). Product y (e.g., staple crop) faces a price py and uses a subset of the variable inputs

16

with prices and . The subset of variable

inputs depends on the technology applied. A farmer that uses traditional production methods

consumes inputs x1 (e.g., agriculture chemicals), x2 and x3 (e.g., labor and land), as well as seeds

produced using traditional technology, s0; in other words, . On the other hand, a farmer

that uses the genetic modified technology utilizes only inputs s1, x2, and x3; in other words,

and . The aggregate profit for farmers using technology i for is

,

We assume the staple crop produced with genetic engineering is the same as the crop produced

using traditional technology.

The profit function of the seed producers is

whereas the profits of the agriculture chemical producers, x1, is

.

Now suppose prices in all industries in the sector are related through competition at the industry

level, and the introduction of genetically engineered traits reduces demand for variable input s0.

On the other hand, input purchased from other sectors, i.e., x2 and x3, are available in elastic

supply to the sector. The profit-maximizing levels of output and inputs, given prices, are

therefore , and , respectively.

17

Following the literature on multi-markets (Just and Hueth 1979; Alston and James 2002; among

others), we know that evaluating the welfare impact of such a change requires looking beyond

the buyers and sellers in market s0 and s1. Introducing seeds produced using genetically modified

techniques reduces quasi-rents to firms producing traditional seeds; it reduces the price to

traditional seeds. Using the envelope theorem, we know that

.

To compute the change in the producer surplus we integrate over the change in profits from

to :

The change in profits equals the change in the area under the equilibrium price and above the

supply curve. Because supply is upward slopping, a decline in prices implies . The

change in the producer surplus of genetically modified seed producers is clearly positive, and

equals their profits

In contrast to Just and Hueth (1979), the structure of the industry described in the paper is not

only vertical, it is also horizontal. The change in the price of seeds affects the agriculture

chemical industry, in addition to the farmers that grow the crop. The change in the producer

18

surplus of agriculture chemicals is computed using the envelope theorem, and assuming supply

for inputs x2 and x3 is elastic:

The computed change in chemical firms is

Biotech reduces demand for seeds produced using the traditional technology, which reduces

demand for chemicals.

Using similar techniques aggregate change in the farmers’ profits are

Integrating for a change from to implies

The change in profits equals the change in the area above the supply curve and below the

equilibrium price. Therefore, upon solving the difference equations, the change in welfare is

19

where the change in final consumer’s surplus is . The gains from biotech, however, are not

distributed between the two countries. Europe developed a strong chemical industry when the

United States developed a prosperous agriculture biotechnology industry. In what follows,

assume the industry producing the traditional technology is located in country F, whereas the

industry producing the genetically engineered technology is located in country H. Farmers are

distributed evenly between the two countries, and consumers are identical within and between

countries. Therefore

Moreover, because (i) the percentage of total expenditure on food in the developed world is

small, and (ii) the amount of genetically modified staple crops grown in Europe is small, in

contrast to the United States, the net welfare change from biotechnology is approximately

The United States stands to gain from agriculture biotech, much more than Europe does.

In figure 1 we depict an extreme scenario: only Europe produces chemicals and only the United

States produces genetically modifies seeds. The chemical industry, the seed markets, and the

staple crop market are depicted in the figures below. First, we describe the staple crop market in

Figure 1a. Let py denote the price of a unit of staple crop (e.g., the price of a bushel of corn), and

let y denote the quantity supplied. Let Sy denote the supply function of the staple crop, and Dy the

demand function. The market for staple crops is depicted in figure 1a, where superscript 0

20

denotes the equilibrium values prior to the introduction of genetically modified seeds (the black

curves) and superscript 1 denotes the equilibrium values after the introduction of genetically

modified seeds (the red curves). Biotechnology makes production more efficient, and therefore

the supply curve shifts down and to the right. Figure 1b depicts the market for agricultural

chemicals, where Sx denotes the supply function of the agricultural chemicals, and Dx the

demand function. The equilibrium price and quantity in the chemical market are px and x1,

respectively. Finally, Figure 1c depicts the market for traditional seeds, s0, and Figure 1d the

market for genetically modified seeds, s1. The notation follows the one used to construct Figures

1a and 1b.

Introducing genetically modified seeds (Figure 1d), affects the market for traditional seeds; it

reduces demand, and therefore the price, for traditional seeds (Figure 1c). The reduction in

traditional seeds, and the increase in genetically modified seeds that are more resilient to

pesticides and herbicides, reduces demand for chemicals. The demand function for agriculture

chemicals shifts down and to the left (Figure 1b). Introducing a more efficient technology to

produce staple crops implies that the supply of staple crops shifts down and to the right, the

economic surplus from producing and consuming staple crop increases (Figure 1a).

21

Px0

x10

Py0

Py1

y0 y1

PyPx

yx1

Figure 1b: The market for agricultural chemicals

Figure 1a: The market for staple crops

Px1

x11

Sx

Dx0

Dx1 Dy

Sy0

Sy1

22

Figure 1: Seeds, chemicals and staple crop

The country that wins the patent race benefits from the introduction of biotechnology. The

economic surplus of the country specializing in the traditional technology declines, whereas the

economic surplus of the country specializing in the new and more efficient technology increases.

The incentive to limit transgenic crops is then amplified if consumer surplus from staple crops is

very small, i.e., the amount spent on the staple crops is very small, especially given the

hypothetical health risk associated with consumption of genetically modified crops. Finally,

introducing a third country that does not produce agriculture chemicals but mimic EU’s

regulation (e.g., Africa), increases the global cost from banning transgenic crops.

Ps11

s11

Ps00

Ps01

s00

s01

1

Ps0

Ps1

s0s1

Figure 1d: The market for genetically modified seeds

Figure 1c: The market for traditional seeds

Ds1

Ss1

Ss0

Ds00

Ds01

23

The multi-market framework illustrates the economic incentives of the different groups in the

economy. Although global welfare is higher with biotechnology, EU's direct benefit is not clear;

especially given that food and environmental risks from biotech are not yet known.

While science and public health establish much of the intellectual foundation for intervention,

regulatory measures are the outcome of a bargaining process between the regulator and various

interest groups. This political process can affect the margin of safety and the computed benefit

from the regulatory measures.

Formally, the political process can be modeled as a cooperative game, à la Harsanyi (1963) and

Zusman (1976),6 or as a noncooperative game, à la Bernheim and Whinston (1986) and

Grossman and Helpman (1994). The fundamental assumption guiding both models is that any

individual affected by government policy has an incentive to influence the policymaker. Food

safety regulation affects the regulatory agency, consumers, farmers, the retail food sector,

incumbent firms, start-up firms and new entrants, and firms in competing sectors. The regulatory

measures, for example, affect consumer’s surplus from food consumption, CS, and the

agriculture biotech and chemical industries’ profits, π s1

and π x1 respectively. The regulatory

measures affect each group differently and therefore create different, and in many times

opposing, incentives. The regulator political economic objective function places different

weights on the different groups, where the chosen policy is constrained by the level of risk and

uncertainty a country is willing to put up with.

To keep political considerations at bay, and to maximize social welfare (not the income of a

well-connected sector), a transparent and coherent methodology needs to be developed. The risk

6 See also Rausser and Zusman (1998), and references therein.

24

assessment model strives to meet this challenge. If countries can agree on the model’s key

parameters, harmonizing the methodology used seems to us a more promising approach than the

standard levels (see Zilberman et al. 2008). It makes the decision process transparent, and yet

allows countries to choose the margin of safety, as long as the same margin is chosen for all food

and health related regulations.

In the context of transgenic crops, Zilberman (2006) argued that a major flaw in the current

regulatory process is that each new trait is evaluated separately, without taking alternatives into

account. Lichtenberg (2006), on the other hand, argued that uncertainty is the principle cause of

concern regarding these crops. This better understanding of policymakers' risk assessment, as

well as the realization that conducting risk assessment and risk-benefit analysis in isolation is

suboptimal, implies that incorporating economics into the risk assessment process is the

preferred alternative, either in a general equilibrium or in a partial equilibrium analysis.

To date, the pest and disease exclusion policies previously discussed have been developed

primarily on the basis of scientific risk assessment without economic analysis of the response of

importers to border enforcement policies. Existing policies are based on the reasoning that

increased enforcement effort will result in higher detection levels, or more specifically that

increased inspection will result in a higher number of interceptions and, in turn, higher

compliance. In addition to a deterrence effect under which importers respond to increased

enforcement with increased care, importers may respond in ways that yield unintended effects.

For example, importers may respond to the increased costs imposed by inspections by choosing

not to bring goods into a country, or they may ship a reduced amount. Moreover, different types

of firms are likely to respond to enforcement in different ways, affecting socially optimal

enforcement and social welfare.

25

Human behavior should be factored into the decision process. Consumers may respond to stricter

regulation by undertaking fewer personal safety measures (a similar effect is also observed in

insurance markets). They also react to safety information, although responses will vary by

consumer (e.g., Viscusi, Magat, and Huber 1987). Firm behavior should also be factored into the

decision process. Melcher (2003), for example, argues that firm compliance with regulatory

measures is imperfect. Monsanto and its partners, for example, violated federal regulation by

planting transgenic crops 44 times between 1990 and 2001.

4. The empirical analysis

Large technological innovations, as do smaller technical innovations, are usually invented and

commercialized not by the leading firms, but by firms that follow. The leading firms under-

invest in research and development (Grossman and Helpman 1991, Chapter 4). This conceptual

framework is used to explain business cycles in international trade. The agriculture

chemical/biotech industry is no exception.

One example is Monsanto, where in the 1980s’ sold mainly insecticides, herbicides, and

fungicides and operated the chemical business independent from the seeds industry. Monsanto

predicted that the agriculture chemical business would reach a plateau, and contemplated with

the idea that existing germplasm or seeds would be carriers of one or two useful foreign genes

(Charles 2001). During that time, Monsanto made a strategic decision: rather then attempting to

protect its chemical business, it embraced the vision in which chemicals would play a declining

but increasingly complementary role in agriculture (Hoover’s Company Records – In-depth

Records, June 27, 2006).

26

Monsanto, through mergers and acquisition it increased its seed capabilities and its abilities to

bring its seed products to the marketplace (see Figure 1A in Appendix B). Monsanto’s started

investing in plant biogenetics in the early 1980s. Although investing billions of US dollars in

research and development, Monsanto did not receive significant revenue from its biogenetics

research until it introduced the Roundup Ready trait for soybeans in 1996, 15 years after it began

investing in plant biogenetics.7

Monsanto leapfrog to become the leading firm in plant biogenetics. Monsanto’s expenses for

research and development were 509 million USD and 588 million USD for 2004 and 2005,

respectively (Monsanto 2005 10K, p.8). As a result of this commitment to innovation in plant

biogenetics, Monsanto’s biotech traits enjoyed 10 percent annual growth since being introduced

in 1996 (Monsanto Annual Reports).

Today, Syngenta is one of the largest agricultural chemical companies in the world, surpassing

Monsanto in revenue and sales.8 In 2005, Syngenta’s worldwide revenue totaled 8.1 billion USD.

Syngenta is a traditional chemical company formed through a series of acquisitions, where up till

recently its predecessors acquired biotechnology and agricultural seeds businesses, while

retaining their chemicals business and merged into one conglomerate. Novartis, a Syngenta

predecessor, was formed in 1996 by the merger of two of the world’s leading producers of

pesticides and herbicides, Ciba Geigy and Sandoz, each with histories going back to the 1800s.

Ciba Geigy was the first company to market and sell transgenic corn in the U.S.9 Both began

acquiring seed companies in the mid 1970s. In November 2000, Novartis Seeds merged with

AstraZeneca's agribusiness operations to form Syngenta. Figure 2A in Appendix B depicts the 7 http://www.monsanto.com/monsanto/layout/about_us/timeline/default.asp 8Syngenta 2005 Annual Report; Monsanto 2005 Annual Report. 9 http://www.syngenta.com/en/about_syngenta/time_prin.aspx and http://www.syngenta.com/en/about_syngenta/timeline.aspx.

27

various acquisitions and mergers that lead to today’s Syngenta. Figure 2, on the other hand,

depicts the ratio of investment in seeds to total investment in seeds and crop protection

(chemicals), which is substantially lower than the relative amount Monsanto invested in plant

transgenic. Other examples, summarized by a flowchart, and which include BASF, Du Pont and

Dow Chemicals presents a similar picture where these very successful companies began moving

toward the biotech industry only toward the beginning of the current century (Figures 1c to 1e in

Appendix B). US-based firms established a comparative advantage in the biotech industry. To

this end, Bayer, a leading chemical company, invested in crop protection 548, 500 and 506

million Euros, whereas it invested in plant science only 113, 114 and 116 million Euros in 2005,

2006, and 2007 respectively.10

When assessing the impact of regulation on biotech and trade in genetically modified crops and

agricultural Chemicals, we should first identify the winners and losers from the infant industry.

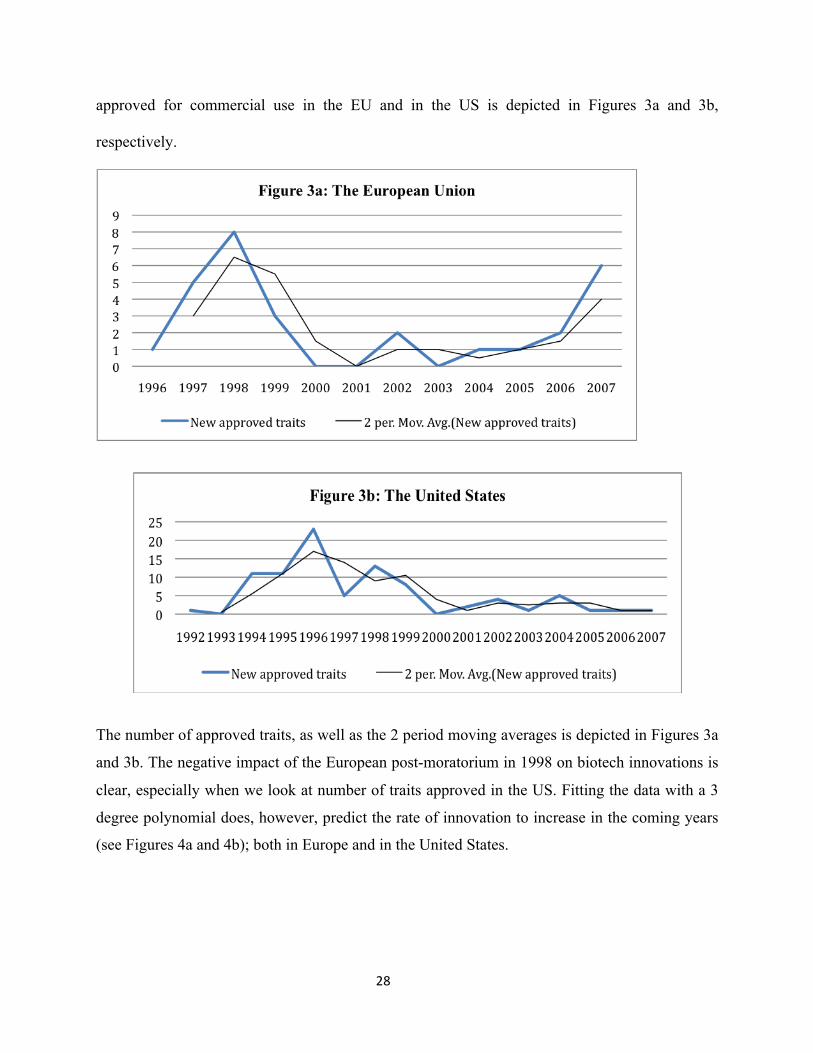

Using data on traits collected from the OECD BioTrack website (2008), we show that the

majority of traits came from firms with headquarters based in the U.S. The number of traits

10 Bayer Annual Reports.

28

approved for commercial use in the EU and in the US is depicted in Figures 3a and 3b,

respectively.

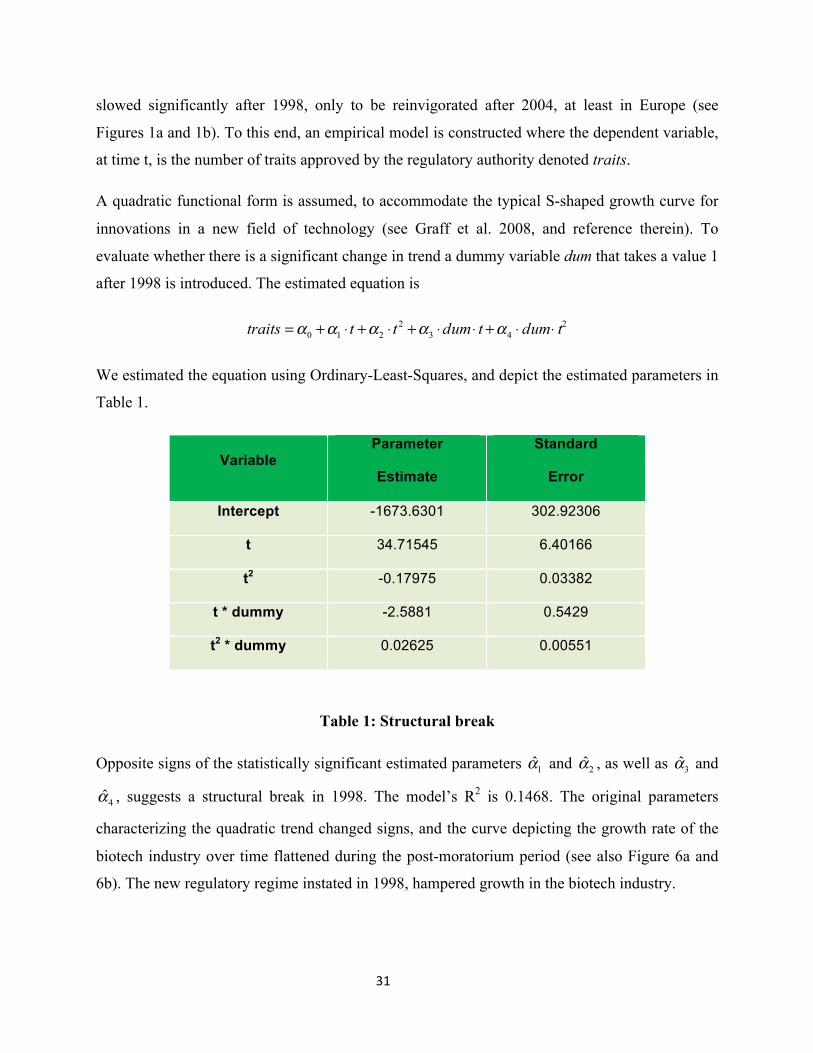

The number of approved traits, as well as the 2 period moving averages is depicted in Figures 3a

and 3b. The negative impact of the European post-moratorium in 1998 on biotech innovations is

clear, especially when we look at number of traits approved in the US. Fitting the data with a 3

degree polynomial does, however, predict the rate of innovation to increase in the coming years

(see Figures 4a and 4b); both in Europe and in the United States.

29

Whereas in Europe 44 percent of traits approved for commercial use originated in the United

States (38 percent came from Australia, and the rest from the European Union), in the United

States 66 percent came from U.S.-based firms. By 1997, the regulatory authority in the United

States approved 37 different traits for U.S.-based firms, but only 14 traits for European firms. By

the end of the 1990s, the success of U.S. firms in biotech placed them well ahead of the

competition, with followers more than several steps behind. Figures 5a and 5b depict the

accumulated number of traits approved in the EU and in the US, for EU and US based firms. In

Europe, during 1995 to 1997 the total number of traits for a European based firm was larger than

the total number for a US based firm (Figure 3a), although this difference is small when we look

at the US market (Figure 3b).

30

Figure 5a: Competition and traits – the EU

Figure 5b: Competition and traits – the US

The US-based firms are emerging toward the end of the 1990s with a clear competitive

advantage in the biotech industry. In 1998, a number of EU member states led by France vowed

to block approval of GM crops unless existing labeling and safety regulations were further

tightened. As a result, no new GM foods or crops were approved from 1998 through 2004,

constituting a de facto moratorium on GMO approvals while the EU was working to develop

new EU-wide legislation more acceptable to the member states.

The EU regulatory regime hampered progress in the biotech industry. Similar to Graff et al.

(2008), we identify a structural break in 1998. The change of the regulatory environment in

Europe severely dampened innovation in the biotech industry. The introduction of new traits

31

slowed significantly after 1998, only to be reinvigorated after 2004, at least in Europe (see

Figures 1a and 1b). To this end, an empirical model is constructed where the dependent variable,

at time t, is the number of traits approved by the regulatory authority denoted traits.

A quadratic functional form is assumed, to accommodate the typical S-shaped growth curve for

innovations in a new field of technology (see Graff et al. 2008, and reference therein). To

evaluate whether there is a significant change in trend a dummy variable dum that takes a value 1

after 1998 is introduced. The estimated equation is

We estimated the equation using Ordinary-Least-Squares, and depict the estimated parameters in

Table 1.

VariableParameter

Estimate

Standard

Error

Intercept -1673.6301 302.92306

t 34.71545 6.40166

t2 -0.17975 0.03382

t * dummy -2.5881 0.5429

t2 * dummy 0.02625 0.00551

Table 1: Structural break

Opposite signs of the statistically significant estimated parameters and , as well as and

, suggests a structural break in 1998. The model’s R2 is 0.1468. The original parameters

characterizing the quadratic trend changed signs, and the curve depicting the growth rate of the

biotech industry over time flattened during the post-moratorium period (see also Figure 6a and

6b). The new regulatory regime instated in 1998, hampered growth in the biotech industry.

32

Figure 6a: Number of approved traits – the EU

Figure 6b: Number of approved traits – the US

The impact of the European regulatory regime was not confined to trade between Europe and the

United States; it also substantially affected developing economies. Figure 7 depicts U.S. exports

for staple crops, which may be affected by traits approved for commercial use.

33

Figure 7: Staple crop exports to the US

The impact of the regulatory regime on the volume of trade affected U.S. agricultural exports.

Although agricultural production of staple crops has become much more competitive, regulation

and concerns in developing economies, which mimic European concerns, prevented the benefits

of biotech from spilling over to developing countries. The benefits of biotech do not reach those

who would have benefited the most from the new technology.

Despite strong economic justification for the regulation of food safety, countries may choose

overly restrictive food safety laws relative to conditions of optimality. Regulation may be used

by interest groups to extract rents. To this end, the chemical industry in Europe stands to lose the

most from the introduction of biotech. Transgenic plants have been developed for various

purposes, including resistance to pests, herbicides or harsh environmental conditions.

34

Figure 8: Exports from Europe to the US

Insecticides, fungicides and herbicides will be replaced by more resilient crops, which will

reduce demand for these chemicals. From 1999 to 2003, thee value of herbicides imported to the

United States from Europe increased, from 84,000 USD to 840,000 USD (see Figure 8).

Clearly, the agriculture chemical industry in Europe benefited enormously from the change in the

European regulatory regime. It not only curtailed competition within Europe, but it also

hampered future technological innovation and therefore future growth of the biotech industry.

Paarlberg (2008) argued that the urban elite in developing countries benefited from adopting

European's regulatory regime. Many developing countries dragged their feet and emphasized

food safety (Paarlberg 2002). By hiding behind food safety, they imposed restrictions which do

not make sense economically, although they do make sense politically. Although there might be

a hypothetical risk to consuming and growing GMO crops, there is a clear and immediate risk

from hunger in many of these countries. To this end, the European Union is by far the largest

donor to many of these countries. Figure 9 depicts aid from European countries, and contrast

35

these amounts with other donor countries. An interesting comparison, not done in the paper,

would be to compute the added value to Africa countries from reducing trade barriers to GMO

crops. The increased benefit can be used to reduce the amount of aid going into these countries.

Note that this scheme will distribute aid to rural populations, which need it the most, and not to

the urban elite.

Figure 9: Donor countries and amount donated11

5. Policy Discussion and Conclusion

Big technological changes require new policy choices, which are gradients between promotion

and prevention. Policies that accelerate the spread of plant transgenic can be termed

“promotional.” Policies that are neutral toward the new technology, intending neither to speed

nor to slow its spread are coined “permissive.” Policies that intend to slow the adoption of the

new technology, for various reasons, are coined “precautionary,” whereas policies that intend to

11 Source: IDS Online- DAC Database - Destination of Official Development Assistance and Official Aid - Disbursements (Table 2a).

36

block or ban entirely the spread of the new technology are called “preventive.”12 Using this

terminology, we now characterize the regulatory regimes in the European Union and in the

United States.

Specifically, in this paper we argue that regulation is a function of existing technology. The

current state of technology affects regulation, and regulation affects future innovations (see

Figure 10). Investment in research and development during the early stages of the biotech

industry established a comparative advantage to US-based firms. On the one hand, agriculture

chemical companies, located in the United States, recognized the potential of plant transgenic,

and invested aggressively in biotech. On the other hand, most of the research in biotech during

the early 1980s took place at land grant Universities in the US. To this end, internationally, the

public sector has generated 24% of the IP in agricultural biotechnology, much more than the

average number of IPs per industry generated by the public sector (Graff et al. 2003).

Differences in the pattern of investment led the agribusiness industry in the United States to

diverge from the traditional agriculture chemical industry, which led to two polar regulatory

regimes. Regulation in the US became permissive to biotech, whereas regulation in Europe

became precautionary. The precautionary regulatory framework reinstated in Europe in 1998,

kept progress in the biotech industry at bay and supported its domestic chemical industry – while

imposing a small cost on its constituencies.

12 See Paarlberg (2000).

37

Figure 10: Technological innovation and regulation

International trade has important effects on food safety and environmental preservation that

should be taken into account in the Doha Round of trade talks. From the spread of disease and

other biological material to the ability of trade partners to influence environmental and food

safety practices in source countries, the effects are wide-ranging and can be beneficial or quite

costly. Food safety and environmental regulation can efficiently solve market imperfections to

assure acceptable levels of risk to human health and protect valued natural resources. They can

also be used to protect producers from the competitive pressures of trade and thereby distort

trade considerably.

In terms of policy recommendations, we propose risk assessment as a framework for the efficient

regulation of trade with respect to food safety and environmental health risks. However, political

economy considerations may interfere with the implementation of efficient regulation. It is

38

important, therefore, to identify where the political economy has produced inefficient regulation

and to determine who wins and who loses. While the use of uniform standards would preclude

the subversion of safety regulations by interest groups, it would also reduce efficiency in the

presence of heterogeneity across countries. Rather than requiring all countries to follow the same

standards (and in effect value life, safety, and domestic environmental resources equally), we

suggest imposing a uniform decision process for countries to follow. To the extent that trading

countries can agree on a decision-making process that uses a risk assessment model and the best

available science and empirical findings, the capture of food safety and environmental regulation

by special interests and protectionists can be mitigated. Where politics is thought to have

overcome science, trade organizations should demand to know the decision rules that produced

suspect regulation. A decision rule that deviates from a consistent and rational procedure based

on the best available science should be easy to identify.

References

Alston, J.M. and James, J.S. “The Incidence of Agricultural Policy,” in Handbook of Agriculture Economics chapter 18 volume 2B, 1689 –1750, (2002)

Bernheim,BDandMDWhinston.“MenuAuctions,ResourceAllocationandEconomicInfluence.”

Quarterly Journal of Economics 101(1986):1‐31.

Charles, Daniel. Lord of the Harvest: Biotech, Big Money, and the Future of Food. 2001

Chichilnisky,G.1998.“TheEconomicsofGlobalEnvironmentalRisks,”InThe International Yearbook of

Environmental and Resource Economics 1998/9,eds.T.TietenbergandH.Folmer,Cheltenham: EdwardElgar.

Dalmazzone,S.2000.“EconomicFactorsAffectingtheVulnerabilitytoBiologicalInvasions,”InThe Economics of Biological Invasions,eds.C.Perrings,M.Williamson,andS.Dalmazzone,Cheltenham, UK:

EdwardElgarPublishing.

39

Evenson,RobertE.“StatusofAgriculturalBiotechnology:AnInternationalPerspective,”Chapter6inRegulating Agricultural Biotechnology: Economics and PolicyREJustJMAlstonandDZilbermanEditors

Springer,NewYork103‐123.

Graff, G.D. and Cullen, S.E. and Bradford, K.J. and Zilberman, D. and Bennett, A.B. “The public-private structure of intellectual property ownership in agricultural biotechnology” Nature Biotechnology, 21(9) 989 – 995, 2003

Graff,Greg,DavidZilbermanandAlanB.Bennett.“TheContractionofProductQualityInnovationinAgriculturalBiotechnology”2008

Grealy,R.David,KentJ.Bradford,LindaHall,RichardHellmich,AlanRaybould,JefreyWolt,andDavidZilberman."ImplicationsofGeneFlowintheScale‐upandCommercialUseofBiotechnology‐derived

Crops:EconomicandPolicyConsiderations,"CastIssuePaper,37(December,2007).

Grossman,GMandEHelpman.“Innovation and Growth in the Global Economy,”Cambridge,MA:MITPress,1991.

Grossman,GMandEHelpman.“ProtectionforSale.”The American Economic Review84(1994):833‐850.

Harsanyi,JC.“ASimplifiedBargainingModelforn‐personCooperativeGame.International Economic

Review4(1963):194–220.

Hochman,Gal,GordonRausser,SteveSextonandDavidZilberman.“AgriculturalbiotechnologyinCaliforniaandtheEU”CIGWorkingPaperNo.65,February2008

Horan,RD,CPerrings,FLupi,andEHBulte.“TheEconomicsofInvasiveSpeciesManagement:BiologicalPollutionPreventionStrategiesunderIgnorance:TheCaseofInvasiveSpecies.”American Journal of

Agricultural Economics84(2002):1303–1310.

Hoyt,E.1992.Conserving the Wild Relatives of Crops.IBPGR,IUCN,andWWF.

James,Clive."GlobalStatusofCommercializedBiotech/GMCrops:2007,"ISAAABriefNo.37,2007

Josling,T,DRobertsandDOrden.Food Regulation and Trade: Toward a Safe and Open Global Food System.PetersonInstituteforInternationalEconomics.Washington,D.C.2004.

Just,RichardE.,JulianM.AlstonandDavidZIlberman.Regulating Agriculture Biotechnology; Economics

and Policy.Eds.RichardJust,JulianM.AlstonandDavidZIlberman.SpringerScience+BusinessMedia,LLC.2006

Just,R.E.andHueth,D.L.“WelfareMeasuresinaMultimarketFramework,”The American Economic Review69(5)947–954,1979

40

Kalaitzandonakes, N. and Bijman, J. “Who is driving biotechnology acceptance?,” Nature Biotechnology, 21, 366 –369, 2003

Lichtenberg,E.“RegulatingofTechnologyintheContextofRiskGeneration.”Chapter14inRegulating Agricultural Biotechnology: Economics and PolicyREJustJMAlstonandDZilbermanEditorsSpringer,

NewYork,2006.243‐262.

MelcherR.“MonsantoBrokeU.S.Patentingrules44timesover12Years”St. Louis Post‐Dispatch,October18,2003.p.3ofBusinesssection.

NUEweb. http://www.nue.okstate.edu/.2008

Paarlberg,RobertL.“GoverningtheGMCropRevolution;PolicyChoicesforDevelopingCountries,”

Food, Agriculture, and the Environment,DiscussionPaper33,December2000

Paarlberg,RobertL.The Politics of Precaution: Genetically Modified Crops in Developing Countries.TheJohnHopkinsUniversityPress:BaltimoreandLondon.2001

Paarlberg,RobertL.Starved for Science: How Biotechnology is Being Kept Out of Africa.HarvardUniversityPress.2008

Pimentel,D.2002.“NonnativeSpeciesintheWorld,”InBiological Invasions: Economic and

Environmental Costs of Alien Plant, Animal and Microbe Species,ed.D.Pimentel,BocaRaton,FL:CRC Press.

Rausser,GordonandP.Zusman.Political Power and Endogenous Policy Formation,1998

SOFA: The State of Food and Agriculture 2003-04, FAO

SteinBAandSRFlack,eds.1996.America’s Least Wanted: Alien Species Invasions of U.S. Ecosystems.Arlington,Virginia:TheNatureConservancy.

Stoner,K.“ApproachestotheBiologicalControlofInsects.”NortheastRegionSustainableAgricultureResearchandEducation(SARE)andUniversityofMaineCooperativeExtension.2006.

Strong,DR.andRWPemberton.“BiologicalControlofInvadingSpecies:RiskandReform.”Science 16(2000):1969‐1970.

Viscusi,WK,WAMagatandJHuber.The RAND Journal of Economics18(1987):465‐479.

Wilcove,DS,DRothstein,JDubow,APhillipsandELosos.“QuantifyingThreatstoImperiledSpeciesin

theUnitedStates.”BioScience 48(1998):607–615.

Williamson,M.1996.Biological Invasions.London:ChapmanandHall.

Zusman,P.“TheIncorporationandMeasurementofSocialPowerinEconomicModels.”International Economic Review17(1976.):447–462.

41

Zilberman,D.“TheEconomicsofBiotechnologyRegulation.”Chapter12inRegulating Agricultural Biotechnology: Economics and PolicyREJustJMAlstonandDZilbermanEditorsSpringer,NewYork243‐

262.

Zilberman,David,GalHochmanandSteveSexton.“FoodSafety,Trade,andtheEnvironment,”WorldBankJune30,2008.

Appendix A

The following overview of the movement of biotech organisms through the U.S. regulatory

system is based on Cast (2007):

1) Research and Development (contained):

a. National Institutes of health (NIH) Guidelines for work with biotech organisms

b. Voluntarily adopted by many organizations, compulsory for recipients of NIH

grants.

2) Field Trials:

a. Proposed release must be approved by APHIS either under notification (for crops

and traits with great familiarity through direct experience; confidence of very low

risk) or permit (more restrictive; for less familiar crops and traits with potential

elevated risk – e.g., plants expressing pharmaceuticals or industrial proteins).

b. Trials may be inspected by APHIS or state department of agriculture officials.

c. Summary reports of trial must be submitted and APHIS promptly informed if

anything unusual occurs in the trial.

d. Gene flow and inadvertent environmental release must be minimized. (Trials must

be confined).

42

e. APHIS oversees storage and transport of seed to and from trial sites.

f. For plants expressing pesticidal proteins, an Experimental Use Permit (EUP) from

EPA is required if the trial exceed 10 acres (4 ha) in a calendar year.

g. Public notification and comment is required for an EUP, but not for pesticide field

trials generally.

3) General Environmental Release:

a. Applicants submit data to APHIS to allow determination of likely environmental

effects and the potential for the biotech organism to become a plant pest.

b. APHIS reviews data and solicit public comments.

c. APHIS determines whether to grant non-regulated status or impose other

conditions.

d. Non-regulated status required for general release, although regulated articles can

be grown commercially (but not for general release) under permits, with

restriction similar to field trials.

e. For plants expressing pesticides proteins, the EPA must grant the protein and the

material required for its production (promoters, marker genes, etc.) a registration

under Section III of FIFRA

4) Use as Food

a. As is done for all non-biotech foods, the FDA works through voluntary

consultation with the developer of the biotech crop to ensure that food safety

questions are addressed during development. The extent of consultation applied to

foods derived from biotech crops generally exceeds that undergone by any

conventional food.

43

b. Based on a favorable review of summary data and a presentation to FDA

scientists, the FDA issues a letter saying it has no further questions.

5) Post-commercialization

a. The USDA, the EPA, and the FDA have limited legal authority to demand

immediate removal from market should new and valid data bring into question the

safety of the product to human health or the environment. [USDA/APHIS/FSIS

ability in these areas is quite limited. This was the focus of much congressional

scrutiny in 2007 due to melamine contamination of pet food.] APHIS issuances of

non-regulated status are contingent on an ongoing requirement that unusual or

adverse events must be reported to APHIS even after a determination is issued.

Such new information can serve as the basis for modification or revocation of the

determination if APHIS warrants. Thus, the initial favorable determination for a

product does not give it a carte blanche release from any further oversight.

Appendix B

Each figure displays the acquisition, divestiture and merger activity with companies operating

within one or more of the following bio-life industries: chemicals, seeds,

pharmaceuticals/agrochemicals. In some cases, activity involving a company outside these areas

is also shown. The primary industry of each company is represented by the color of the

company’s title box in the figure. Additionally, the line connecting them shows the type of

activity taking place – acquisition, divestiture, joint venture or merger – as well as the

hierarchical relationship between different entities. Solid lines with arrows pointing in the

direction of the company of interest represent acquisitions, those pointing away from it,

divestitures. The acquisition and divestiture activity of Monsanto are tracked on two separate

44

figures. Dashed lines joining two companies represent joint ventures and lastly, solid lines

connecting one entity with another show one company to be the subsidiary of the other. In these

cases, the entity closer to the company of interest is the immediate parent of the other. Sources

relied upon primarily include the corporate websites of industry companies as well as the

database Thomson Financial Mergers & Acquisitions.

Confidential

16

¹http://www.monsanto.com/monsanto/layout/about_us/timeline/default.asp²Thomson Financial Mergers & Acquisitions3http://www.monsanto.com/monsanto/layout/media/04/11-16-04.asp

Agricultural assets(Icoria Inc.)

2005 Acquisition2

Seminis Inc.

2005 Subsidiary2

Interstate Seed Co. (Advanta Seeds)

2004 Acquisition2

Jacob Hartz Seed Co.

1982 Acquisition1

Continental PharmaSA

1986 Acquisition2

GD Searle & Co.

1985 Acquisition2

Heumann PharmaGmbH & Co Generica

KG1989 Acquisition2

Schiapparelli Searle

1992 Acquisition2

Syntex Corp-Oral-Contraceptive

Business1995 Acquisition2

Schwarz Pharma(Schwarz Pharma)

1997 Acquisition2

Pharmaceutical Division (Chemotecnica Sintyal

SA)

1997 Acquisition2

Exac Corp.

1987 Acquisition2

Defender Home Garden (Select Harvests Ltd.)

1992 Acquisition2

Diamonex Inc.

1992 Acquisition2

Devex SA

1992 Acquisition2

AES Polymer Tech. (Dow Chem. Co.)

1992 Acquisition2

Kelco Biopolymers (Merck & Co.)

1995 Acquisition2

Agracetus Inc. (W.R. Grace)

1996 Acquisition2

Corn States Hybrid

1997 Acquisition2

Calgene

1997 Acquisition1

Asgrow

1997 Acquisition1

Holden’s Foundation Seed

1997 Acquisition2

DeKalb

1998 Acquisition1

Cargill Inc.

1998 Acquisition2

Plant Breeding Int’l Cambridge Ltd.

1998 Acquisition2

Est. 19011

2000 Merger1

2000 Monsanto becomes subsidiary of Pharmacia Corp.1

Monsanto Pharmacia

American Seeds, Inc.

2004 Formation3

NC + Hybrids Inc.

2005 Acquisition2

2004 Acquisition3

Channel Bio Corp.

MonsantoToday

Pharmacia Corporation

2002 Spin-off of Phamacia Corp. Agriculture Bus. Division1

Monsanto

Sintefina

2005 Acquisition2

Limagrain Canada Seeds Inc.

2001 Acquisition2

GD Searle & Co.

Chemical

Seed

Chem./Seed

Other

Pharmaceut-Ical/Agrochem

¹http://www.monsanto.com/monsanto/layout/about_us/timeline/default.asp²Thomson Financial Mergers & Acquisitions3http://www.monsanto.com/monsanto/layout/media/04/11-16-04.asp

Agricultural assets(Icoria Inc.)

2005 Acquisition2

Seminis Inc.

2005 Subsidiary2

Interstate Seed Co. (Advanta Seeds)

2004 Acquisition2

Agricultural assets(Icoria Inc.)

2005 Acquisition2

Agricultural assets(Icoria Inc.)

2005 Acquisition2

Seminis Inc.

2005 Subsidiary2

Seminis Inc.

2005 Subsidiary2

Interstate Seed Co. (Advanta Seeds)

2004 Acquisition2

Interstate Seed Co. (Advanta Seeds)

2004 Acquisition2

Jacob Hartz Seed Co.

1982 Acquisition1

Jacob Hartz Seed Co.

1982 Acquisition1

Continental PharmaSA

1986 Acquisition2

Continental PharmaSA

1986 Acquisition2

GD Searle & Co.

1985 Acquisition2

GD Searle & Co.

1985 Acquisition2

Heumann PharmaGmbH & Co Generica

KG1989 Acquisition2

Heumann PharmaGmbH & Co Generica

KG1989 Acquisition2

Schiapparelli Searle

1992 Acquisition2

Schiapparelli Searle

1992 Acquisition2

Syntex Corp-Oral-Contraceptive

Business1995 Acquisition2

Syntex Corp-Oral-Contraceptive

Business1995 Acquisition2

Schwarz Pharma(Schwarz Pharma)

1997 Acquisition2

Schwarz Pharma(Schwarz Pharma)

1997 Acquisition2

Pharmaceutical Division (Chemotecnica Sintyal

SA)

1997 Acquisition2

Pharmaceutical Division (Chemotecnica Sintyal

SA)

1997 Acquisition2

Exac Corp.

1987 Acquisition2

Exac Corp.

1987 Acquisition2

Defender Home Garden (Select Harvests Ltd.)

1992 Acquisition2

Defender Home Garden (Select Harvests Ltd.)

1992 Acquisition2

Diamonex Inc.

1992 Acquisition2

Diamonex Inc.

1992 Acquisition2

Devex SA

1992 Acquisition2

Devex SA

1992 Acquisition2

AES Polymer Tech. (Dow Chem. Co.)

1992 Acquisition2

AES Polymer Tech. (Dow Chem. Co.)

1992 Acquisition2

Kelco Biopolymers (Merck & Co.)

1995 Acquisition2

Kelco Biopolymers (Merck & Co.)

1995 Acquisition2

Agracetus Inc. (W.R. Grace)

1996 Acquisition2

Agracetus Inc. (W.R. Grace)

1996 Acquisition2

Corn States Hybrid

1997 Acquisition2

Corn States Hybrid

1997 Acquisition2

Calgene

1997 Acquisition1

Calgene

1997 Acquisition1

Asgrow

1997 Acquisition1

Asgrow

1997 Acquisition1

Holden’s Foundation Seed

1997 Acquisition2

Holden’s Foundation Seed

1997 Acquisition2

DeKalb

1998 Acquisition1

DeKalb

1998 Acquisition1

Cargill Inc.

1998 Acquisition2

Cargill Inc.

1998 Acquisition2

Plant Breeding Int’l Cambridge Ltd.

1998 Acquisition2

Plant Breeding Int’l Cambridge Ltd.

1998 Acquisition2

Est. 19011

2000 Merger1

2000 Monsanto becomes subsidiary of Pharmacia Corp.1

Monsanto Pharmacia

2000 Merger1

2000 Monsanto becomes subsidiary of Pharmacia Corp.1

Monsanto Pharmacia

American Seeds, Inc.

2004 Formation3

NC + Hybrids Inc.

2005 Acquisition2

2004 Acquisition3

Channel Bio Corp.

American Seeds, Inc.

2004 Formation3

NC + Hybrids Inc.

2005 Acquisition2

NC + Hybrids Inc.

2005 Acquisition2

2004 Acquisition3

Channel Bio Corp.

2004 Acquisition3

Channel Bio Corp.

MonsantoToday

Pharmacia Corporation

2002 Spin-off of Phamacia Corp. Agriculture Bus. Division1

Monsanto

MonsantoToday

Pharmacia Corporation

2002 Spin-off of Phamacia Corp. Agriculture Bus. Division1

Monsanto

Sintefina

2005 Acquisition2

Sintefina

2005 Acquisition2

Limagrain Canada Seeds Inc.

2001 Acquisition2

Limagrain Canada Seeds Inc.

2001 Acquisition2

GD Searle & Co.

Chemical

Seed

Chem./Seed

Other

Pharmaceut-Ical/Agrochem

Chemical

Seed

Chem./Seed

Other

ChemicalChemical

SeedSeed

Chem./Seed

OtherOther

Pharmaceut-Ical/AgrochemPharmaceut-Ical/Agrochem

Figure 1. Monsanto’s M&A Activities—Acquisitions

Chemical

Seed

Chem./Seed

Other

Pharmaceut-Ical/Agrochem

MonsantoToday

¹http://www.monsanto.com/monsanto/layout/about_us/timeline/default.asp²Thomson Financial Mergers & Acquisitions3http://www.monsanto.com/monsanto/layout/media/04/11-16-04.asp

Pharmacia Corporation

2002 Spin-off of Phamacia Corp. Agriculture Bus. Division1

Icoria Inc. (agri-culture assets)2005 Acquisition2

Seminis Inc.

2005 Subsidiary2

Interstate Seed Co. (Advanta Seeds)

2004 Acquisition2

American Seeds, Inc.

2004 Formation3

NC + Hybrids Inc.

2005 Acquisition2

2004 Acquisition3

Channel Bio Corp.

Radiation Dynamics Mnf Division

1986 Sale2

NSC Technologies LLC

1999 Sale2

GD Searle & Co.

1985 Acquisition2

FRP Paper Chem. Div.

1986 Sale2

Cast and Blown Polyethylene Film Bus.

1989 Sale2

Form-Cor Board Bus.

1993 Sale2

Chlorinated Isocyanurate Bus.

1992 Sale2

Thermoplastic Elastomers Bus.

1991 Merger with Division of Exxon Corp. to form Advanced Elastomer Systems2

Animal Feed Ingredients Business

1990 Sale2

Fisher Controls

1995 Sale2

2000 Merger1

2000 Monsanto becomes subsidiary of Pharmacia Corp.1

Est. 19011

MonsantoPharmacia

Monsanto Electronics Materials