Estimating the capital component of mental health care costs in the public sector

17

Administration and Policy in Mental Health Vol. 21, No. 6, July 1994 ESTIMATING THE CAPITALCOMPONENTOF MENTAL HEALTH CARE COSTS IN THE PUBLIC SECTOR Robert Rosenheck, M.D., Linda Frisman, Ph.D., and Michael Neale, Ph.D. ABSTRACT: This study describes methods for determining the cost of buildings and grounds in public sector facilities. Two methods for estimating the cost of capital (one using local office rents; the other based on estimates of the replacement cost of hospital buildings) are applied to six types of health care service at nine VA medical centers. Results indicate that capital costs for psychiatric inpatient care were about one-third those for surgical services and one-half those for medical services. Overall, capital costs add 6% to average inpatient costs and 4% to outpatient costs. The economic impact of innovative treatments on health care costs has become an increasingly important focus of mental health program evaluation, particularly in the evaluation of high cost treatments such as intensive case management or clozapine pharmacotherapy. In times of limited or shrinking mental health budgets, promising treatments must be judged as much by their cost efficiency as by their clinical effectiveness. The principal mechanism through which expensive mental health interventions have achieved cost offsets is by reducing inpatient utilization and associated costs (Bond, 1984; Dickey, Cannon, McGuire, & Gudeman, 1986; Weisbrod, 1983). Accurate estimation Robert Rosenheck, Linda Frisman, and Michael Neale are all with the VA Medical Center in Westhaven CT. Address for correspondence: Robert Rosenheck, Northeast Program Evaluation Center, VAMC, 950 Campbell Ave., West Haven, CT 06516. The authors thank Thomas McGuire, Ph.D., for his conceptual guidance for this article. Richard Frank, Ph.D., Paul Errera, M.D., and Boris Astrachan, Ph.D., provided valuable consultation. John Bonsall, Carl Lister, Stephanie Monroy, Stephen Hogel, and Robert Whiting helped with the interpretation of the VA data bases and accounting procedures. We are also grateful to the staffs at the nine Mental Health Initiative Sites. 493 1994 Human Sciences Press, Inc.

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Estimating the capital component of mental health care costs in the public sector

Administration and Policy in Mental Health Vol. 21, No. 6, July 1994

ESTIMATING THE CAPITAL COMPONENT OF MENTAL HEALTH CARE COSTS IN THE PUBLIC SECTOR

Robert Rosenheck, M.D., Linda Frisman, Ph.D., and Michael Neale, Ph.D.

A B S T R A C T : This study describes methods for de te rmining the cost of buildings and grounds in public sector facilities. Two methods for est imating the cost of capital (one using local office rents; the other based on estimates of the replacement cost of hospital buildings) are applied to six types of heal th care service at nine V A medical centers. Results indicate that capital costs for psychiatric inpat ient care were about one-third those for surgical services and one-half those for medical services. Overall , capital costs add 6% to average inpat ient costs and 4% to outpat ient costs.

The economic impact of innovative treatments on health care costs has become an increasingly important focus of mental health program evaluation, particularly in the evaluation of high cost treatments such as intensive case management or clozapine pharmacotherapy. In times of limited or shrinking mental health budgets, promising treatments must be judged as much by their cost efficiency as by their clinical effectiveness. The principal mechanism through which expensive mental health interventions have achieved cost offsets is by reducing inpatient utilization and associated costs (Bond, 1984; Dickey, Cannon, McGuire, & Gudeman, 1986; Weisbrod, 1983). Accurate estimation

Robert Rosenheck, Linda Frisman, and Michael Neale are all with the VA Medical Center in Westhaven CT. Address for correspondence: Robert Rosenheck, Northeast Program Evaluation Center, VAMC, 950 Campbell Ave., West Haven, CT 06516.

The authors thank Thomas McGuire, Ph.D., for his conceptual guidance for this article. Richard Frank, Ph.D., Paul Errera, M.D., and Boris Astrachan, Ph.D., provided valuable consultation. John Bonsall, Carl Lister, Stephanie Monroy, Stephen Hogel, and Robert Whiting helped with the interpretation of the VA data bases and accounting procedures. We are also grateful to the staffs at the nine Mental Health Initiative Sites.

493 �9 1994 Human Sciences Press, Inc.

494 Administration and Policy in Mental Health

of inpatient treatment costs has thus become important in mental health evaluation studies.

The growing emphasis on economic assessment in mental health program evaluation has fostered increasing sophistication in the methods used to esti- mate costs. A decade ago, Weisbrod and colleagues brought social costs to the attention of the mental health research community in a comprehensive cost- benefit study of the Madison model of community treatment (Weisbrod, Test, & Stein, 1980). Social cost analysis explicitly attends to costs that may be shifted

between parties (e.g., from state to federal governments or to patients' families) and indirect costs such as lost wages. While full social cost analyses were a rarity before Weisbrod's work was published, standard principles of cost- benefit research are now being applied to mental health cost studies with increasing frequency. Three of the most important of these principles are: 1) health care cost estimates must be based on analysis of the actual resources used to provide services, not on charges; 2) variation in the cost of specific services should be taken into account as much as possible, rather than relying on averages; and 3) "hidden" costs such as the opportunity cost of capital in publicly owned facilities should not be ignored, even though they may not be included in standard accounting procedures. This paper focuses on the estima- tion of capital costs.

The opportunity cost of land and buildings has been identified as a crucial variable that runs the risk of being neglected, particularly in studies of public facilities (McGuire, 1991). For the accountant, the cost of health care may be fully described through a summary of monthly expenditures and capital depre- ciation. A complete economic analysis requires that all resources that could be put to an alternative use be valued and considered as a cost. Government buildings and land are especially likely to be absent from the accountant's ledger because they are purchased through a one time expenditure of public revenues, with no further debt service payments by the agency using the building. Special efforts must be made to estimate their value. McGuire has recently underscored the importance of this issue, stating that " . . . mental health care is usually thought to be labor intensive, but for the seriously mentally ill treated in institutions just the opposite is true: much of the cost is in the form of land and buildings in which the ill are housed" (p. 383). He supports this contention by pointing out that in Weisbrod's pioneering study (1983), 30% of the cost of inpatient treatment was attributed to capital costs, and that even a small adjustment in the estimated annual cost of capital (from 8% to 4%) would have resulted in a change in the study's principal finding. In health care cost studies, and in public program planning, more generally, " . . . when the cost involves public facilities . . . the capital portion of the ledger potentially dominates the total" (Cannon, McGuire & Dickey, 1985).

The central methodological challenge in estimating capital costs in the public sector is the identification of the best (i.e., most valuable) alternative use to

Robert Rosenheck, Linda Frisman, and Michael Neale 495

which a facility could be put and determining its market value. Public facilities are rarely placed on the market and, as a result, indirect methods for approx- imating their value must be used. In the most detailed consideration of this problem published thus far, Cannon, McGuire and Dickey (1985) found that, depending on the method and assumptions employed to assess alternative use, there was wide a variation in the estimated capital cost of a state mental hospital in Boston, the Massachusetts Mental Health Center ( M M H C ) . In the absence of a clear best choice they indicated a preference for using a midpoint value among their results. In a subsequent report, the cost of capital an the M M H C was estimated to be a modest, but important, fraction of the total cost: 7.9% of inpatient costs ($9.80 per bed day of care) and 15.4% of quarterway house costs ($13.16 per bed day of care) (Dickey, et al., 1986). It can be further deduced from the data presented that use of alternative estimates for capital costs would not have affected the final results of their study. There is clearly a need for further examination of the methods used to estimate capital costs in public health care facilities, and of the impact of choosing one method over another on the results of mental health cost studies.

This paper presents cost data gathered for the evaluation of a multi-site Department of Veterans Affairs (VA) initiative in intensive case management, and addresses both methodological principles and specific procedures for esti- mating the capital component of health care costs in VA and, we expect, in other public mental health systems. This study goes beyond previous studies in five ways. First, unlike the studies of Weisbrod (1983) and Cannon et al. (1985), which concerned single institutions, this study addressed health care costs at multiple facilities, all located in the northeastern United States. Sec- ond, in addition to psychiatric inpatient services, we analyzed capital costs associated with five other types of health care service. Third, while previous studies incorporated the opportunity cost of the land on which medical facilities rest, they did not specifically consider the contribution of land to overall capital costs. In this study the value of land is independently considered for each facility. Fourth, special attention is paid to the allocation of capital resources to specific patient care services. While Cannon et al. (1985) meticulously detailed their approach to estimating the annualized capital value of the M M H C , they did not specify methods for distributing those costs to specific types of health care service (perhaps because use of capital was similar for various services). In VA medical centers or other general hospitals psychiatric, medical, and surgi- cal care are provided under a single roof, and differences in capital costs across services become more important. Finally, we pay explicit attention to the relative importance of capital costs as a portion of total inpatient and outpa- tient costs, and to variations in capital cost across different types of service, at different medical centers. Capital costs, at least in VA medical centers, may represent a relatively constant proportion of total inpatient and outpatient costs across facilities. If so, in circumstances in which detailed data are not readily

496 Administration and Policy in Mental Health

available, percentage estimates based on data presented here might be used with some justification.

METHODS

Study Sites

Nine Department of Veterans Affairs medical centers participated in the evaluation of a demonstration project in which high hospital users were treated with intensive case management, referred to in VA as Intensive Psychiatric Communi ty Care (IPCC). This initiative was based on treatment approaches described by Stein and Test (1980) and on rehabilitation principles proposed by other experts (Anthony, Cohen, & Farkas, 1991) in the community based care of the seriously mentally ill. The nine medical centers sponsoring the initiatives were located in major urban areas (the Bronx, Boston, Albany, and Buffalo), in smaller cities (Syracuse; West Haven, CT) and in suburban or rural areas (Brockton, MA; Canandaigua, NY; and Montrose, NY). Clinical data for this study were gathered from 1987-1991; cost information from 1989 is used throughout.

Opportunity Costs Associated with Medical Center Buildings and Land

As noted by Cannon et al. (1985), conventional accounting procedures do not provide an accurate assessment of the opportunity costs associated with public facilities such as VA medical centers. Since most of the hospitals involved in this study were constructed before 1949, and VA accounting procedures depreciate the cost of hospitals over 40 years, most of these hospi- tals were fully depreciated (i.e., their "book" value is zero). We agree with Cannon and her colleagues that the preferred method for evaluating the current opportunity cost associated with medical center buildings and grounds is to determine the fair market rental value of the extant facilities.

Estimating Opportunity Cost of Capital Using Rental Rates. Although rental rates for public facilities are not usually available, a proxy rental rate was obtained by questioning key informants (real estate agents, brokers or appraisers in each community) about rental rates for similar property. Using the real estate section of the local phone book, we contacted three or four key informants in each community and asked for information on current market rents for medi- cal office space similar to that at the local VA medical center. Estimates were obtained for unimproved office space, excluding the cost of furnishings or utilities. Where the estimates were divergent, a central value was employed. These rental estimates were subsequently used to estimate the opportunity cost of all medical center space used by each service, including both direct patient care space and indirect support service space.

Robert Rosenheck, Linda Frisman, and Michael Neale 497

The decision to use a single rental-based estimate to represent the value of space used by all services in the medical facility was carefully weighed. It could be argued that the value of the surgical service space, for example, is higher than the value of the psychiatric service space. Indeed, as discussed in the following section, surgery space is more costly to construct. To correctly assess opportunity costs, however, one must determine the best (highest priced) possible alternative use. If it would not be possible to rent or sell the building for the specialized use for which it was built (i.e., for providing surgical services), it is appropriate to use the next best alternative use, and to regard the extra cost of construction as sunk costs. For this study, it was not possible to state with certainty whether any of the additional costs associated with construction of specialized space could be recovered. However, given the paucity of new construction for medical facilities in the northeast, we decided that the best alternative use was as general medical office space.

Estimating Capital Costs Using Replacement Costs. An alternative approach, used here to validate the rental estimation method, uses the replacement cost of these VA medical centers. Capital cost as estimated by this method is equal to the annualized cost of replacing each facility, plus the annual depreciation of the involved buildings. The E.C. Boeckh Index, a proprietary compendium of cost estimates for various building types, was used to estimate the 1989 general hospital construction costs in each city involved in the study. Further adjust- ment to this basic hospital construction cost was made in consideration of the differential cost of replacing medical, surgical, psychiatric, nursing home, outpatient and non-patient care building space. A construction cost estimation index supplied by the Office of Cost Estimation in VA Central Office was used to make this adjustment. Annual depreciation was obtained from VA account- ing records.

While estimates based on rental values are presumed to incorporate the value of associated land, estimates of the replacement cost of VA medical centers required a specific additional assessment of land value. The number of acres of land owned by each medical center, the year of purchase, and the purchase price were obtained from federally mandated quarterly property assets reports. The shelter price component of the Consumer Price Index was then used to adjust the original purchase cost to 1989 levels (U.S. Bureau of Census, 1976, 1991).

The value of the land was then distributed back to medical center buildings on a square footage basis. The total space of each hospital in gross square feet (GSF) was obtained from the property assets report, and the ratio of total land area to hospital space was calculated. Multiplying the annual value of the land (in dollars per square foot) by this ratio, we obtained the value of the land per GSF of hospital space, which was then included in the replacement cost estimate.

498 Administration and Policy in Mental Health

Once the replacement cost per GSF was estimated (including adjustments for geographic locality, type of hospital space and the value of land), an estimate of return on capital was used to annualize replacement costs. A conventional way of determining the return on investment at a given point in time is to identify a standard measure of interest (e.g., the prime lending rate) and subtract a measure of inflation from it (e. g., the annual percent change in the consumer price index) (Samuelson & Nordhaus, 1985). Using this ap- proach the average return on investment in the United States, in 1989, was determined to be 6.07% (Samuelson & Nordhaus, 1985, pp. 478, 512). This estimate for return on capital is close to the 4 % figure recently advocated by McGuire (1991).

Allocating Costs to Specific Units of Service

Annualized capital costs, as determined by each of the above methods, were disaggregated and allocated to specific departments and to specific units of service. Three different types of information were used to calculate capital costs at the level of the unit of service: 1) the number of square feet of hospital space directly used in the delivery of patient care services by each clinical depart- ment; 2) an estimate of indirect (i.e., non-patient care) space used to support the delivery of those services; and 3) the number of units of service delivered annually by each service.

Allocation of the Rental Cost Estimate to Specific Units of Service. The formula used to determine the rental-based estimate of opportunity cost per unit of service is:

Capital Cost/Unit of Service = (DPCSA + ICSA) x (OC) UA

where,

DPCS A

ICS A OC

UA

= direct patient care space allocated to service A in (Net Square feet [NSF];

= indirect clinical space apportioned to service A (in NSF); = opportunity cost of hospital space ($/NSF); and = the number of units of service provided by service A.

Information on direct patient care space utilization by each service was obtained from the engineering service at each medical center. Since a service- by-service breakdown of outpatient space was not available at most hospitals, outpatient space had to be retained as an aggregate. The opportunity cost of medical center building space not used directly for patient care (i.e., indirect care space) was also allocated to specific patient care activities, through a two- step procedure: First, the total amount of indirect care space at each hospital was determined by subtracting the space used in direct clinical care from the total space of the hospital. Second, the indirect care space was allocated to

Roberl Rosenheck, Linda Frisman, and Michael Neale 499

specific departments in proportion to their share of other indirect costs, as determined by the VA Cost Distribution Report (CDR). The CDR is a facility-by-facility accounting record that identifies total expenditures and unit costs associated with all VA inpatient and outpatient health care services. Using standardized accounting procedures both direct health care costs (per- sonnel services, medications and supplies) and indirect costs (e. g., administra- tion, building maintenance, engineering service, building and equipment depreciation) are identified and distributed to specific health care programs. The indirect costs on the CDR provide a straightforward basis for apportion- ing indirect capital costs.

Allocation of the Replacement Cost Estimate to Specific Units of Service. Estimation of service-specific replacement costs is somewhat more complicated than estimat- ing rental-based opportunity costs because: 1) a specific replacement cost rate is used for each type of service, and 2) annual depreciation and the value of land are included.

Replacement costs per unit of service are thus calculated by the following formula, applying the service-specific replacement cost for each type of space:

(DPCS A X COSTA) + (ICSA) X COStls ) + LandCost X (DPCS A + ICSA) ) + D A

where,

DPCS A Cost A

ICS A = Costis =

Land Cost =

UA

D A

U A =

direct patient care space allocated to service A in (GSF); annualized replacement cost of space ($/GSF) for service A estimated using: a) the local Boeckh cost index for general hospital space, b) the VA Central Office index for specific types of hospital space and c) a 5.2% estimated return on capital; indirect clinical space apportioned to service A in (GSF); replacement cost of indirect care hospital space estimated using information similar to that used to estimate Cost A the estimated value of surrounding land per GSF of building space ($/GSF); annual depreciation of buildings used by service A; and the number of units of service provided by service A.

Using this formula capital cost per unit of service was estimated separately for each service, at each medical center.

(The unit of measurement conventionally used in estimates of replacement cost is Gross Square feet (GSF) as contrasted with Net Square Feet (NSF), the measure by which rental rates were determined. The net square footage of a

500 Administration and Policy in Mental Health

space refers only to the immediately useable space and excludes walls, hall- ways, stairs, etc. GSF, in contrast, is a measure of the entire covered space, i.e., the floors, walls, mechanical systems, and stairwells of each floor. A standard conversion factor, specific to hospital space, of 1.7 GSF per NSF (Hardy & Lammers, 1986) was used to convert NSF to GSF for these calcula- tions.)

Impact of Capital Costs of Total Cost Estimates

To evaluate the percentage increase in total health care cost resulting from capital cost, the value of all non-capital direct and indirect costs per unit of service was obtained from the C D R for each major service at the nine medical centers, and divided into the capital cost.

RESULTS

Opportunity Costs of Buildings and Land

Opportunity costs determined by both rental and replacement estimates are presented in Table 1. Rental estimates ranged from $8/NSF to $12.50/NSF with limited variation across sites (coefficient of variation = 0.15). Basic hospital replacement estimates (before adjusting for the cost of specific ser- vices), ranged from $I 26/GSF to $179/GSF and also showed limited variation (coefficient of variation = 0.12). The greatest degree of variation in cost was in the value of land, due to the wide range in the amount of land owned (from 7.4 to 200 acres; see Table 2) and the low cost of land in two rural settings, Canandaigua and Montrose, NY. On average the value of land represented less than 2 % of estimated replacement costs.

Estimated capital costs based on the rental method were lower than those based on the replacement cost method. The ratio of estimated rental costs/NSF to replacement costs/NSF ranged from 0.53 to 0.82 across sites (Table 1) with an overall ratio of 0.61.

Capital Costs Allocated to Specific Units of Service

Sections A and B on Table 3 show both direct patient care space and indirect space allocated to clinical services at the nine medical centers. The third section (C in Table 3) records the number of units of service provided by each service in each medical center (days of care for inpatient programs and clinic visits for outpatient services).

Using the formulae presented previously and the data presented in Tables 1 and 3, the capital costs per unit of service were calculated and are presented in Parts A and B of Table 4. Within service categories, variation across sites is modest for both the rental-based method (average coefficient of variation = 0.54) and the replacement cost method (average coefficient of variation =

TA

BL

E 1

E

stim

ated

Opp

ortu

nity

Cos

t of

Hos

pita

l B

uild

ings

, as

Det

erm

ined

by

Com

mun

ity

Ren

tal

Rat

es

and

Hos

pita

l R

epla

cem

ent

Cos

ts i

n 19

89,

by G

eogr

aphi

c L

ocat

ion

Alb

any

Bos

ton

Bro

ckto

n B

ronx

B

uffa

lo

Can

'dgu

a M

ontr

ose

Syra

cuse

W

. H

aven

Si

te M

ean

S.D

. of

Var

.

~A

nnua

l Ren

tal

Rat

e ($

/NS

F/Y

ear)

$1

0.00

$1

2.50

$8

.00

$10.

00

$8.0

0 $8

.00

$10.

00

$9.0

0 $8

.00

$9.2

8 $1

.44

bBui

ldin

g R

epla

cem

ent

Cos

t ($

/GS

F/Y

ear)

.$

126

$147

$1

47

$179

$1

32

$135

$1

70

$126

$1

42

$145

$1

7

cBui

ldin

g R

epla

cem

ent

Cos

t C

onve

rted

to

$/N

SF

/Yea

r $2

15

$250

$2

50

$304

$2

24

$229

$2

88

$214

$2

41

$246

$3

0

dVal

ue o

f L

and

per

N

SF

of

Hos

pita

l $4

.74

N/A

$1

2.68

N

/A

$2.6

2 $0

.38

$1.9

8 $4

.63

$6.9

5 $4

.85

$3.7

6

~A

nnua

lize

d R

epla

cem

ent

Cos

t ($

/NS

F/Y

ear)

(I

nclu

ding

Lan

d

Val

ue)

@ 6

.1%

C

ost

of C

apit

al

$13.

33

$15.

17

$15.

94

$18.

45

$13.

75

$13.

94

$17.

63

$13.

28

$15.

04

$15.

17

$1.7

6

Rat

io o

f R

enta

l C

ost/

A

nn

ual

ized

R

epl'

mn

t C

ost

0.75

0.

82

0.50

0.

54

0.58

0.

57

0.57

0.

68

0.53

0.

61

0.10

aBas

ed o

n in

terv

iew

s wit

h ke

y in

form

ants

. bH

ospi

tal c

onst

ruct

ion

cost

est

imat

es f

rom

Boe

chk'

s Ind

ex,

for

1989

. ~C

onve

rsio

n Fac

tor

from

Har

dy a

nd L

amm

ers

(198

6).

aOpp

ortu

nity

cos

t of l

and

from

Tab

le 2

. ~R

etur

n on

inv

estm

ent b

ased

on

1989

pri

me

lend

ing

rate

les

s the

per

cent

inc

reas

e of

CP

I (U

.S.

Bur

eau

of th

e C

ensu

s, 1

991)

0.15

0.12

0.12

N

"

0.77

~ g~

0.

12

0.17

TA

BL

E 2

A

nn

ual

ized

Val

ue

(Est

imat

ed O

pp

ortu

nit

y C

ost)

of

Lan

d A

ssoc

iate

d w

ith

VA

Med

ical

Cen

ters

a

Alb

an

y B

rock

ton

Buf

falo

C

anan

daig

ua

Mo

ntr

ose

Sy

racu

se

IV.

Hav

en

A.

Est

imat

e of

198

9 L

and

Val

ue/S

q.

Ft.

1.

T

otal

Acr

es

28.3

14

5.7

16.9

15

9.0

200.

0 7.

4 43

.7

2.

Lan

d P

urch

ase

Pri

ce

$376

,000

$1

,295

,000

$2

56,0

00

$32,

000

$306

,000

$2

67,0

00

$403

,000

3.

P

urch

ase

Dat

e 19

47

1949

19

47

1931

19

55

1952

19

48

4.

She

lter

Pri

ce I

nd

ex

5.55

5.

37

5.55

5.

32

5.06

5.

20

5.44

(P

urch

ase

to 1

989)

5.

19

89 L

and

Val

ue

$2,0

86,8

00

$6,9

54,1

50

$1,4

20,8

00

$170

,240

$1

,547

,442

$1

,387

,332

$2

,193

,126

6.

L

and

Val

ue/A

cre

$73,

739

$47,

729

$84,

071

$1,0

71

$7,7

37

$187

,477

$5

0,18

6

B.

Dis

trib

utio

n of

Lan

d V

alue

to

Pat

ient

Car

e S

pace

1.

H

ospi

tal

Spa

ce (

NS

F)

440,

179

548,

329

542,

730

442,

560

782,

168

299,

437

315,

636

2.

bLan

d S

q. F

t./P

atie

nt

2.8

11.6

1.

4 15

.6

11.1

4 1.

1 6.

0 C

are

Spa

ce (

NS

F)

3.

Lan

d V

alue

/Pat

ient

$4

.74

$12.

68

$2.6

2 $0

.38

$1.9

8 $4

.63

$6.9

5 C

are

Spa

ce (

NS

F)

aSee

text

for

sour

ces o

f dat

a. D

ata

are

inco

mpl

ete f

or B

osto

n an

d B

ronx

. bl

acr

e =

43,5

60 sq

. fe

et.

TA

BL

E 3

D

irec

t an

d I

nd

irec

t P

atie

nt

Car

e S

pac

e an

d U

nit

s of

Ser

vice

Alb

any

Bost

on

Bro

ckto

n B

ronx

Bu

ffalo

C

an'd

gua

Mon

tros

e Sy

racu

se

W.

Hav

en

A.

Dir

ect

Pat

ient

Car

e Sp

ace

(NSF

)/C

linic

al S

ervi

ce

Psyc

hiat

ry

25

,00

6

21

,74

8

80

,45

7

21

,33

1

18

,81

2

92

,49

2

14

1,3

18

1

0,5

35

4

4,0

82

M

edic

ine

68,5

01

85

,01

2

98

,06

3

33

,31

0

41

,80

6

10

,68

6

13

,98

1

45

,83

5

46

,20

2

Sur

gery

7

0,1

89

5

1,6

16

2

8,0

42

3

0,8

12

25

,293

0

0 2

8,1

35

31

,591

In

term

edia

te M

edic

ine

38

,01

8

0 19

,623

9

,18

8

19

,60

6

10

0,7

71

8

9,3

60

3

,91

5

31

,48

7

Nur

sing

Hom

e C

are

30,1

75

0 3

3,7

25

3

1,8

39

5

,64

3

31

,43

6

47

,13

1

14

,63

2

16,7

73

Out

pati

ent

Clin

ics

26

,59

9

23

,88

3

22

,26

4

18

,29

3

12,8

20

4,4

96

7

3,1

00

2

8,8

58

2

8,6

85

B.

Allo

catio

n of

Ind

irec

t P

atie

nt C

are

Spac

e (N

SF)/

Clin

ical

Ser

vice

C.

Psy

chia

try

9,32

6 3

,77

7

40

,95

8

11

,98

2

23

,08

1

25

,68

8

11

5,0

92

1

0,2

94

13

,432

M

edic

ine

48

,79

8

67

,82

7

94

,75

4

72

,12

7

138,

554

7,1

95

6

2,8

88

4

9,7

67

5

5,6

87

S

urge

ry

46

,97

8

43

,28

6

50

,49

4

52

,83

9

109,

139

0 0

40

,69

4

24

,09

9

Inte

rmed

iate

Med

icin

e 4

6,9

67

0

47

,26

1

39

,87

4

10

6,0

09

1

57

,38

1

15

3,4

41

36

,861

9,

533

Nur

sing

Hom

e C

are

8,21

6 0

9,59

1 3,

856

6,48

6 8

,43

0

21,8

53

2,16

2 2,

418

Out

pati

ent

Clin

ics

21

,40

6

15

,60

1

23

,09

7

19

,46

5

35,4

81

3,9

85

3

4,7

17

1

3,1

92

11

,647

~Uni

ts o

f Se

rvic

e/Y

ear

Psyc

hiat

ry

26

,25

2

19

,49

2

10

8,3

37

2

0,2

04

3

1,2

90

8

4,1

89

12

3,19

3 8

,96

3

46

,24

2

Med

icin

e 3

5,3

23

7

4,1

69

6

9,3

92

6

6,1

76

8

3,5

19

1

1,5

63

1

2,2

98

2

7,5

05

53

,281

S

urge

ry

22

,41

6

30

,48

0

14

,93

1

29

,59

7

31,3

57

0 0

15

,95

2

15,1

53

Inte

rmed

iate

Med

icin

e 3

0,0

48

0

33

,52

8

19

,54

7

39

,81

6

12

4,7

72

8

5,6

30

1

4,2

90

13

,483

N

ursi

ng H

ome

Car

e 33

,623

0

57

,74

2

39

,61

6

12

,52

1

35

,29

3

41

,53

9

3,4

50

3

2,0

97

O

utpa

tien

t C

linic

s 24

2,01

7 3

18

,36

7

38

0,7

05

4

00

,48

1

34

4,7

22

1

00

,19

4

15

6,3

62

1

87

,53

1

172,

356

aUni

ts of

serv

ice a

re b

ed d

ays o

f car

e for

inpa

tient

units

and

nurs

ing h

ome,

patie

nt vi

sits

for o

utpa

tient

clin

ics.

g.

2"

g~

kal

504 Administration and Policy in Mental Health

0.57). Higher degrees of variation for nursing home (0.84) and outpatient care (1.03) were attributable to extremely high values observed for nursing home care at the Syracuse VAMC (where a low workload was recorded) and for outpatient care at the Montrose VAMC (where there was an exceptionally high, and possibly erroneous, allocation of space to outpatient care). Capital costs varied considerably across services with capital costs for inpatient psychi- atry estimated to be 42% of the costs for surgery, about half the cost for medicine or intermediate medicine and 16 times the cost for outpatient care.

Capital Costs in Relation to Other Health Care Costs

Section A of Table 5 presents the non-capital cost for each type of health care service, including both direct and indirect costs, but excluding building depre- ciation. Capital costs, as determined by the rental estimation method, are a relatively small proportion of the value of VA health care, averaging 5-6% of inpatient costs and 4% of outpatient costs (Part B of Table 5).

Table 6 summarizes the average capital costs for each type of service, across all the hospitals involved in the study, using five different estimates: 1) the rent based estimate, 2) the replacement cost estimate using our empirical estimate of return on capital investment for 1989 (6.07 %), and 3) the replacement cost estimate using three other rates of return on capital (4 %, 7 %, and 9 %), those used by Cannon, McGuire and Dickey (1985) in their analysis. The rental- based cost estimate is almost identical to the replacement cost estimate when a 4 % rate of return on capital is used, but these estimates diverge as higher rates of return on capital are applied. It is notable, however, that, even at a 9 % rate of return on investment (a rate not achieved during the past two decades), capital costs in VA have only a modest effect on inpatient costs, increasing them by only 16%.

DISCUSSION

In this study we have presented a multi-step procedure for valuing and allocating the opportunity costs associated with public medical center buildings and grounds. The data have both methodological and substantive importance for cost studies in the mental health field.

Following Cannon, McGuire, and Dickey (1985), both community rental rates and replacement costs were used to estimate capital costs. In our study, however, estimates of the square foot value of buildings and land derived from these two methods were similar even though estimates were made indepen- dently for nine different hospitals. Real estate values in the study of Cannon et al. (1985) may have been particularly difficult to estimate in the Harvard Medical Complex in central Boston. Our findings were less clouded by un- usual market conditions. In addition, our use of a nationwide construction cost index and a specific estimate of return on investment also increased the

TA

BL

E 4

C

apit

al C

ost

Est

imat

es/U

nit

of S

ervi

ce (

Com

pari

son

of E

stim

ates

)

Std

. C

oeff

Alb

any

Bos

ton

Bro

ckto

n B

ronx

B

uffa

lo

Can

'dga

M

ontr

ose

Syra

cuse

W

. H

aven

Si

te M

ean

Dev

. V

at.

A.

Cap

ital

Co

st/U

nit

of

Ser

vice

(re

nt-b

ased

est

imat

e)

Psy

chia

try

$13.

08

$16.

37

$8.9

7 $1

6,49

$1

0.71

$1

1.23

$2

0.81

$2

0.91

$9

.95

$14.

28

$4.3

0 0.

30

Med

icin

e $3

3.21

$2

5.76

$2

2.23

$1

5.93

$1

7.28

$1

2.37

$6

2.50

$3

1.28

$1

5.30

$2

6.21

$1

4.55

0.

56

Sur

gery

$5

2.27

$3

8,92

$4

2.08

$2

8.26

$3

4.30

N

/A

N/A

$3

8.83

$2

9.40

$3

3.01

$1

4.36

0.

43

Inte

rmed

iate

Med

icin

e $2

8.28

N

/A

$15.

96

$25.

10

$25.

24

$16.

55

$28.

35

$25,

68

$24.

34

$23.

69

$4.5

0 0.

19

Nu

rsin

g H

om

e C

are

$11.

42

N/A

$6

.00

$9.0

1 $7

,75

$9.0

4 $1

6.61

$4

3.81

$4

.78

$13.

55

$11.

93

0.88

O

utp

atie

nt

Cli

nics

$1

.98

$1.5

5 $0

.95

$0.9

4 $1

.12

$0.6

8 $6

.90

$2.0

2 $1

.87

$2.0

0 $1

.79

0.90

B.

Cap

ital

Co

st/U

nit

of

Serv

ice

(rep

lace

men

t co

st-b

ased

est

imat

e: a

t 6.

07%

re

turn

on

inve

stm

ent)

P

sych

iatr

y 21

,75

22.5

6 18

.31

33.8

5 18

.09

21.9

2 47

.92

37.1

8 22

.43

$27.

11

$9.6

4 0.

36

Med

icin

e 51

.05

35.3

8 49

.11

34.6

8 29

.59

30,5

5 10

9.76

57

.32

41.2

1 $4

8.74

$2

3.41

0.

48

Sur

gery

95

.16

63.0

4 94

.77

66.6

4 60

.20

N/A

N

/A

77.9

9 85

.64

$67.

93

$28,

67

0.42

In

term

edia

te M

edic

ine

41.4

4 N

/A

29.2

7 48

.53

39.8

0 32

.69

59.6

6 35

.10

60.4

6 $4

3.37

$1

1.08

0.

26

Nu

rsin

g H

om

e C

are

18.5

8 N

/A

23.9

5 26

.29

13.5

5 17

.78

32.9

8 94

.39

11.5

0 $2

9.88

$2

5.24

0.

84

Ou

tpat

ien

t C

lini

cs

3.11

1,

95

1,88

2.

16

1.81

1.

32

15.1

8 3.

84

4.51

$3

,97

$4.0

9 1.

03

C.

Rat

io o

f re

ntal

-bas

ed e

stim

ate

to r

epla

cem

ent

cost

-bas

ed e

stim

ate

of c

apit

al c

ost

Psy

chia

try

0.60

0.

73

0.49

0.

49

0.59

0.

51

0.43

0.

56

0.44

0.

54

0.09

0.

16

Med

icin

e 0.

65

0.73

0.

45

0.46

0.

58

0.40

0.

57

0.55

0.

37

0.53

0.

11

0.21

S

urge

ry

0.55

0.

62

0.44

0.

42

0.57

N

/A

N/A

0.

50

0.34

0.

43

0.18

0.

42

Inte

rmed

iate

Med

icin

e 0.

68

N/A

0.

55

0.52

0.

63

0.51

0.

48

0.73

0.

40

0.56

0.

10

0.19

N

urs

ing

Ho

me

Car

e 0.

61

N/A

0.

25

0.34

0.

57

0.51

0.

50

0.46

0.

42

0.46

0.

11

0.24

O

utp

atie

nt

Cli

nics

0.

64

0.79

0.

51

0.44

0.

62

0.51

0.

45

0.53

0.

42

0.54

0.

11

0.21

N/A

= D

ata

not

avai

labl

e or

ser

vice

doe

s no

t ex

ist a

t th

at V

AM

C,

~z

g~

~m

TA

BL

E

5 N

on C

apit

al C

ost

s/U

nit

of

Ser

vice

an

d t

he P

erce

nt

Incr

ease

D

ue

to C

apit

al C

ost

s

W.

Site

St

d.

Coe

ff A

lban

y B

osto

n B

rock

ton

Bro

nx

Buf

falo

Can

'dgu

a M

ontr

ose

Syra

cuse

H

aven

M

ean

Dev

. of

Vat

.

A.

Non

Cap

ital

Cos

t (O

pera

ting

Exp

endi

ture

s E

xclu

ding

Dep

reci

atio

n fr

om t

he C

DR

) P

sych

iatr

y W

ards

$

21

9

$3

13

$

16

8

$3

32

$

20

0

$153

$2

02

$337

$

20

3

$2

36

$6

7 0.

28

Med

icin

e $

49

7

$5

93

$

58

3

$4

55

$

35

1

$344

$7

01

$522

$

62

0

$5

19

$1

14

0.22

S

urge

ry

$6

22

$

78

5

$9

01

$

62

6

$5

22

N

/A

N/A

$

66

7

$8

68

$

62

4

$265

0.

43

Inte

rmed

iate

Med

icin

e $

40

7

$6

22

$

32

6

$4

34

$

37

1

$305

$2

90

$5

67

$

39

6

$3

87

$8

3 0.

21

Nur

sing

Hom

e C

are

$147

N

/A

$97

$1

99

$

13

9

$106

$1

43

$261

$

10

2

$1

49

$5

2 0.

35

Out

pati

ent

Cli

nics

$6

7 $5

4 $4

1 $5

5 $5

8 $3

2 $4

3 $5

6 $7

9 $5

4 $1

3 0.

25

B.

Per

cent

Inc

reas

e in

Tot

al C

ost/

Uni

t of

Ser

vice

Due

to

Cap

ital

Cos

t/U

nit

of S

ervi

ce

Psy

chia

try

War

ds

6.0%

5.

2%

5.3%

5.

0%

5.4%

7.

3%

10.3

%

6.2%

4.

9%

5.8%

1.

4%

0.24

M

edic

ine

6.7%

4.

3%

3.8%

3.

5%

4.9%

3.

6%

8.9%

6.

0%

2.5

%

4.7%

1.

7%

0.36

S

urge

ry

8.4%

5.

0%

4.7%

4.

5%

6.6%

N

/A

N/A

5.

8%

3.4%

4.

5%

2.1%

0.

47

Inte

rmed

iate

Med

icin

e 7.

0%

N/A

4.

9%

5.8%

6.

8%

5.4%

9.

8%

4.5%

6.

1%

5.9%

1.

3%

0.23

N

ursi

ng H

ome

Car

e 7.

8%

N/A

6.

2%

4.5%

5.

6%

8.5%

11

.6%

16

.8%

4.

7%

7.5%

3.

2%

0.43

O

utpa

tien

t C

lini

cs

3.0%

2.

9%

2.3%

1.

7%

1.9%

2

~1

%

16.2

%

3.6%

2.

4%

3.7%

3.

7%

0.99

N/A

Dat

a not

ava

ilabl

e or

serv

ice d

oes n

ot e

xist

at th

is V

AM

C.

Robert Rosenheck, Linda Frisman, and Michael Neate 507

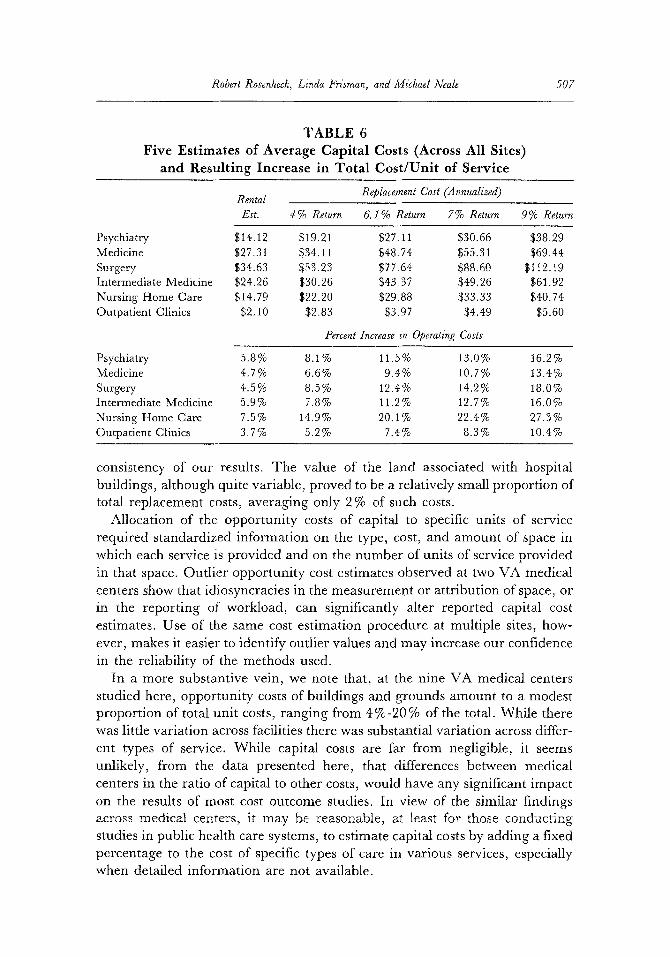

TABLE 6 Five Estimates of Average Capital Costs (Across All Sites)

and Resulting Increase in Total Cost/Unit of Service

Rental Replacement Cost (Annualized)

Est. 4% Return 6.1% Return 7% Return 9% Return

Psychiatry $14.12 $19.21 $27.11 $30.66 $38.29 Medicine $27.31 $34.11 $48.74 $55.31 $69.44 Surgery $34.63 $53.23 $77.64 $88.60 $112.19 Intermediate Medicine $24 .26 $30.26 $43.37 $49.26 $61.92 Nursing Home Care $14.79 $22.20 $29.88 $33.33 $40.74 Outpatient Clinics $2.10 $2.83 $3.97 $4.49 $5.60

Percent Increase in Operating Costs

Psychiatry 5.8% 8.1% 11.5 % 13.0% 16.2 % Medicine 4.7% 6.6% 9.4% 10.7% 13.4% Surgery 4.5% 8.5% 12.4% 14.2% 18.0% Intermediate Medicine 5.9% 7.8% 11.2% 12.7% 16.0% Nursing Home Care 7.5% 14.9% 20.l% 22.4% 27.3% Outpatient Clinics 3.7 % 5.2 % 7.4 % 8.3 % 10.4 %

consistency of our results. The value of the land associated with hospital buildings, although quite variable, proved to be a relatively small proportion of total replacement costs, averaging only 2% of such costs.

Allocation of the opportunity costs of capital to specific units of service required standardized information on the type, cost, and amount of space in which each service is provided and on the number of units of service provided in that space. Outlier opportunity cost estimates observed at two VA medical centers show that idiosyncracies in the measurement or attribution of space, or in the reporting of workload, can significantly alter reported capital cost estimates. Use of the same cost estimation procedure at multiple sites, how- ever, makes it easier to identify outlier values and may increase our confidence in the reliability of the methods used.

In a more substantive vein, we note that, at the nine VA medical centers studied here, opportunity costs of buildings and grounds amount to a modest proportion of total unit costs, ranging from 4%-20 % of the total. While there was little variation across facilities there was substantial variation across differ- ent types of service. While capital costs are far from negligible, it seems unlikely, from the data presented here, that differences between medical centers in the ratio of capital to other costs, would have any significant impact on the results of most cost outcome studies. In view of the similar findings across medical centers, it may be reasonable, at least for those conducting studies in public health care systems, to estimate capital costs by adding a fixed percentage to the cost of specific types of care in various services, especially when detailed information are not available.

508 Administration and Policy in Mental Health

It is of interest to compare our estimates of VA capital costs with estimates of capital costs among non-government health care providers for whom such costs are far less "hidden." It has been estimated that, in 1989, 8 % of total spending by U.S. hospitals was for capital expenses (including equipment), with 4.5 % for "fixed capital expenses," the category most comparable to the subject of this study (Herr, 1991). This estimate also fits with reports suggesting that between 1982 and 1985 total capital costs reimbursed by Medicare ranged from 7 % to 10% of all payments (Anderson & Ginsburg, 1983; Hemesath & Pope, 1989). Although the general similarity of these proportions might suggest a similar ratio of capital to operating costs, data have also been published to suggest a very wide range in the percentage of capital costs across facilities (Paschal, Klein, Bookman & Blanchard, 1987).

The VA data we have presented, while comparable to available data from other health care systems, have uncertain relevance beyond the VA system. In a comparative study of VA and non-VA hospitals, costs per case-mix adjusted inpatient day in VA were estimated to be about two-thirds of those in non-VA hospitals (Management Sciences Group, 1991). It would thus appear that while the ratio of capital costs to total costs is similar in VA and non-VA settings, the absolute value of annual capital costs may be somewhat less in VA.

A final comment is warranted about the potential for change in the oppor- tunity cost of public capital. In the highly volatile real estate market of recent years, the opportunity cost of publicly owned buildings, as estimated by the methods used here, has changed considerably, and in a direction opposite to the general rising trend of health care costs. Both rents for office space, and the estimated return on capital investments have been declining in the United States since their peak in 1982 (Passel, 1991). By 1989, office rents had lost 32 % of their 1982 value, after adjustment for inflation, and return on capital investments had declined 29%, from 8.6%, in 1982, to 6.1% 1989 (US Bureau of the Census, 1991). To the extent that capital costs do affect the result of cost benefit studies, the changing value of capital may alter the cost- effectiveness of an intervention over the years. In Weisbrod's 1980 study, for example, the experimental and control conditions differed in their total cost by only 6.5%. As demonstrated by McGuire (1991), a modest change in the estimated rate of return on capital would have changed the results of that study. Theoretically, a community-based program could therefore be cost effective at one point in time, but might lose its net cost effectiveness as the opportunity cost of capital changed. The question of whether findings from experimental studies can be generalized from the study sample to larger populations is a well recognized problem in experimental research (Cook & Campbell, 1979). In cost studies, especially where capital is concerned, the issue of generalizability over time may also be relevant, especially during periods of time, or in regions of the country, in which rapid economic change is occurring.

Robert Rosenheck, Linda Frisman, and Michael Neale 509

CONCLUSION

The annual cost of buildings and land in public sector hospitals emerges, in this study, as a notable but modest component of inpatient cost, and as a component that does not vary markedly from one VA facility to another. Such costs should be calculated and included in cost analyses whenever appropriate data are available, using methods comparable to those we have described here. However, our findings also suggest that, in the absence of site-specific data, a non-empirical estimate of opportunity costs based on a percentage of other operating costs (6% of inpatient costs and 4% of outpatient costs) may be acceptable for use with VA medical centers, if not with other public sector hospitals.

REFERENCES

Anderson, G., & Ginsburg, P.B. (1983). Prospective capital payments to hospitals. Health Affairs, 2, 52. Anthony, W., Cohen, M., & Farkas, M. (1991). Psychiatric rehabilitation. Boston: Center for Psychiatric

Rehabilitation. Bond, G.R. (1984). An economic analysis of psychosocial rehabilitation. Hospital and Community Psychiatry,

35, 356. Cannon, N.L., McGuire, T., & Dickey, B. (1985). Capital costs in economic program evaluation: The case

of mental health services. In J.S. Catterall (Ed.), Economic evaluation of public programs. New Direction in Program Evaluation, No. 26. San Francisco: Jossey-Bass.

Cook, T.D., & Campbell, D.T. (1979). Quasi-experimentation: Design and analysis issues for field settings. Skokie, IL: Rand McNally.

Dickey, B., Cannon, N.L., McGuire, T., & Gudeman, J. (1986). The quarterway house: A two-year cost study of an experimental residential program. Hospital and Community Psychiatry, 37, 1136.

Hardy, O.B., & Lammers, L.P. (1986). Hospitals: The planning and design process (2nd ed.). Rockville, MD: Aspen Publishers.

Hemesath, M., & Pope, G.C. (1989). Linking Medicare capital payments to hospital occupancy rate. Health Affairs, 8, 104.

Herr, W. (1991, April). Taking a deep breath over capital payments. Healthcare Financial Management. Management Sciences Group. (1991). A comparison of the operating costs and performance of VA and non-

federal hospitals: 1984-1988. Bedford, MA: Dept. of Veterans Affairs Management Sciences Group. McGuire, T.G. (1991). Measuring the economic costs of schizophrenia. Schizophrenia Bulletin, 17, 375. Paschal, W.E., Klein, R.A., Bookrnan, L.A., & Blanchard, T.P. (1987). Capital costs under Medicare

PPS: Exploring the myths and the reality. Federation of American Hospital Systems Review, May-June, p. 41. Passel, P. (1991, September 8). Surviving the real estate glut: Light at the end of the elevator shaft. New York

Times, Section 10, p. 1. Samuelson, P.A., & Nordhaus, W.D. (1985). Economics (12th ed.). New York: McGraw-Hill. Stein, L.I., & Test, M.A. (1980). Alternative to mental hospital treatment I: Conceptual model, treatment

program and clinical evaluation. Archives of General Psychiatry, 37, 392. U.S. Bureau of the Census. (1976). Historical statistics of the United States, colonial times to 1970. Washington,

DC: Author. U.S. Bureau of the Census. (1991). Statistical abstracts of the United States: 1991 (11 lth ed.). Washington, DC:

Author. Weisbrod, B.A. (1983). A guide to benefit-cost analysis, as seen through a controlled experiment in treating

the mentally ill. Journal of Health Politics & Law, 7, 808. Weisbrod, B.A., Test, M.A., & Stein, L.I. (1980). Alternative to mental hospital treatment II: Economic

benefit-cost analysis. Archives of General Psychiatry, 37, 400.