Estimating, Tenderin.. - engbookspdf.net – Free Engineering ...

268

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Estimating, Tenderin.. - engbookspdf.net – Free Engineering ...

Macmillan Buildingand Surveying SeriesSeries Editor: Ivor H. Seeley

Emeritus Professor, Nottingham Trent UniversityAccountingand Finance for Buildingand Surveying AR. JenningsAdvanced Building Measurement, second edition Ivor H. SeeleyAdvanced Valuation Diane Butler and David RichmondApplied Valuation, second edition Diane ButlerAsset Valuation Michael RaynerBuilding Economics, fourth edition Ivor H. SeeleyBuilding Maintenance, second edition Ivor H. SeeleyBuilding Maintenance Technology Lee How Son and George C.S. YuenBuilding ProcurementAlan E.TurnerBuilding Project Appraisal Keith HutchinsonBuilding QuantitiesExplained, fourth edition Ivor H. SeeleyBuilding Surveys, Reports and Dilapidations Ivor H. SeeleyBuilding Technology, fifth edition Ivor H. SeeleyCivil Engineering ContractAdministration and Control, second edition Ivor H. SeeleyCivil Engineering Quantities, fifth edition Ivor H. SeeleyCivil Engineering Specification, second edition Ivor H. SeeleyCommercial Lease Renewals - A Practical GuidePhilip Freedman and Eric F. ShapiroComputers and Quantity Surveyors AJ. SmithConflicts in Construction- Avoiding, managing, resolving Jeff WhitfieldConstructability in Building and Engineering Projects A Griffith and A.C. SidwellConstruction Contract Claims Reg ThomasConstruction LawMichael F. JamesContractPlanning and Contract Procedures, thirdedition B. CookeContractPlanning CaseStudies B. CookeCost Estimation ofStructures in Commercial Buildings Surinder SinghDesign-Build Explained D.E.L.JanssensDevelopment Site Evaluation N.P. TaylorEnvironment Management in Construction Alan Gr iffithEnvironmental Science in Building, thirdedition R. McMullanEstimating, Tendering and Bidding for Construction AJ. SmithEuropean Construction - Procedures and techniques B. Cooke and G. WalkerFacilities Management Alan ParkGreenerBuildings- Environmental impact ofpropertyStuart JohnsonHousingAssociations Helen CopeHousing Management- Changing Practice Christine Davies (Editor)Information and Technology Applications in Commercial Property Rosemary Feenan

and Tim Dixon (Editors)Introduction to Building Services, second edition Christopher A Howard and Eric F.

CurdIntroduction to Valuation, thirdedition D. RichmondMarketing and Property People Owen BevanPrinciples of Property Investment and Pricing, second edition W.O. FraserProject Managementand Control David Day

(continued)

Property Finance David IsaacProperty Valuation Techniques David Isaac and Terry SteleyPublic Works Engineering Ivor H. SeeleyResource Management for Construction M.R. CanterQuality Assurance in Building Alan GriffithQuantity Surveying Practice Ivor H. SeeleyRecreation Planning and Development Neil RavenscroftResource and Cost Control in Building Mike CanterSmall Building Works Management Alan GriffithStructural Detailing, second edition P. NewtonSub-Contracting under the}CTStandard Forms ofBuilding Contract jennie PriceUrban Land Economics and Public Policy, fifth edition P.N. Balchin, j.L. Kieve and

G.H.BullUrban Regeneration R.just and D. WilliamsUrban Renewal- Theory and Practice Chris Couch1980 }CTStandard Form of Building Contract, second edition R.F. FellowsValue Management in Construction B. Norton and W. McElligott

Series Standing OrderIf you would like to receive future titles in this series as they are published, you canmake use of our standing order facility. To place a standing order please contact yourbookseller or, in case of difficulty, write to us at the address below with your nameand address and the name of the series. Pleasestate with which title you wish tobegin your standing order . (If you live outside the United Kingdom we may not havethe rights for your area, in which casewe will forward your order to the publisherconcemed.)

Customer ServicesDepartment, Macmillan Distribution LtdHoundmills, Basingstoke, Hampshire, RG21 2XS, England.

Estimating, Tendering andBidding for Construction

Theory and Practice

Adrian J. SmithDepartment of Building and Construction

City University of Hong Kong

~MACMILLAN

© A.J. Smith 1995

All rights reserved. No reproduction, copy or transmission ofthis publication may be made without written permission.

No paragraph of this publication may be reproduced, copied ortransmitted savewith written permission or in accordance withthe provis ions of the Copyright, Designs and Patents Act 1988,or under the terms of any licence permitting limited copyingissued by the Copyright Licensing Agency, 90 Tottenham Court Road,London W1 P 9HE

Any person who does any unauthorised act in relation to thispublication may be liable to criminal prosecution and civilclaims for damages.

First published 1995 byMACMILLAN PRESS LTDHoundmills, Basingstoke, Hampshire RG21 2XSand LondonCompanies and representativesthroughout the world

ISBN 978-1-349-13632-2 ISBN 978-1-349-13630-8 (eBook)DOI 10.1007/978-1-349-13630-8

A catalogue record for this book is availablefrom the British Library

10 9 8 7 6 5 4 3 2 104 03 02 01 00 99 98 97 96 95

Typeset by Ian Kingston Editorial Services, Nottingham

Contents

Preface xi

1 Estimating and Tendering - Some Contextual Factors 11.1 Introduction 11.2 The Construction Industry 11.3 The Construction Client 21.4 Economics of the Construction Market 51.5 Sources of Construction Work 81.6 The Theory of the Firm 101.7 References 12

2 The Estimating Process 142.1 The Place of Estimating in the Competitive Tendering Process 142.2 The Process of Estimating 162.3 The Place of the Estimator in the Contractor's Organisation 172.4 Skills and Training 182.5 Management of the Estimating and Tendering Process-

An Overview 192.6 Examination of the Tender Documents 202.7 Establishment of a Programme for Estimate and

Tender Preparation 212.8 Site Visit 222.9 Analysis of Prime Cost and Provisional Sums 232.10 References 23

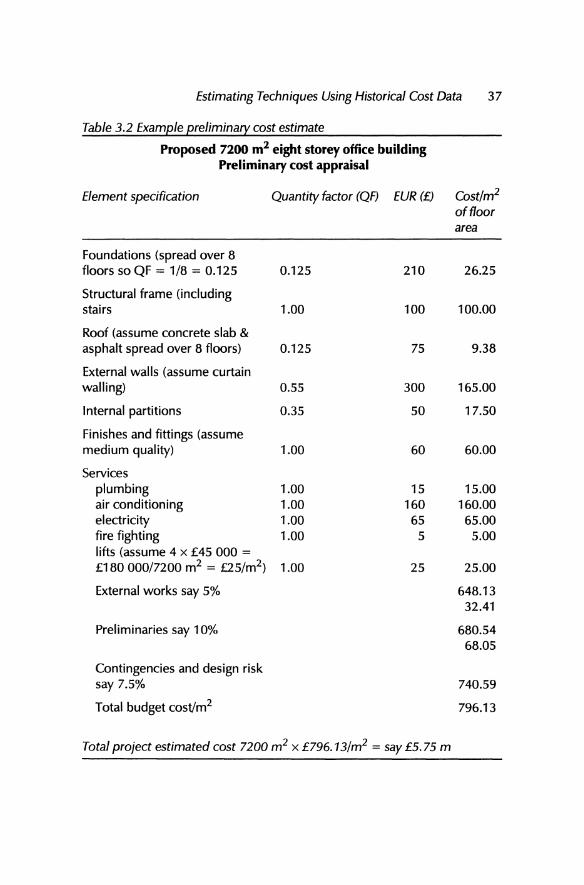

3 Estimating Techniques Using Historical Cost Data 243.1 Introduction 243.2 Cost Per Functional Unit 253.3 Costs Per Unit of Floor Area 263.4 Updating of Costs from Previous Schemes to a Common Base 28

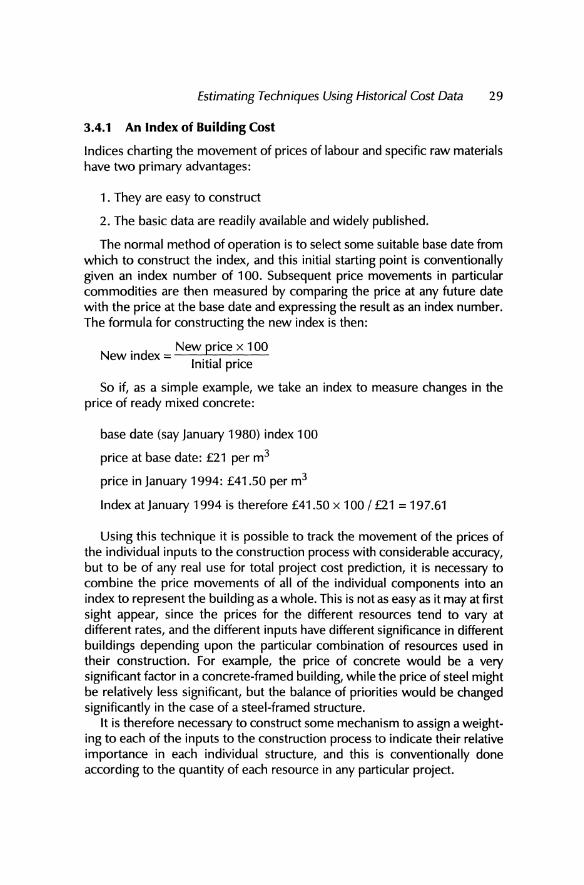

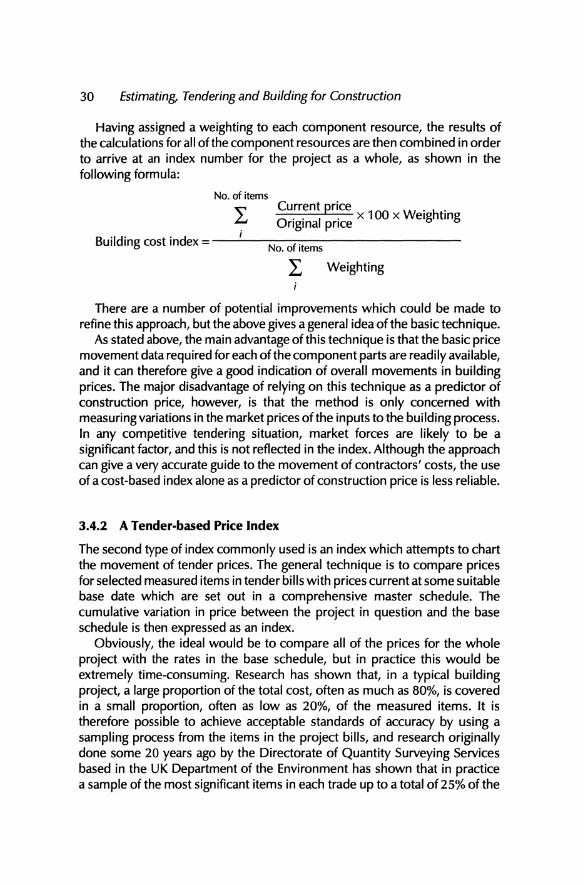

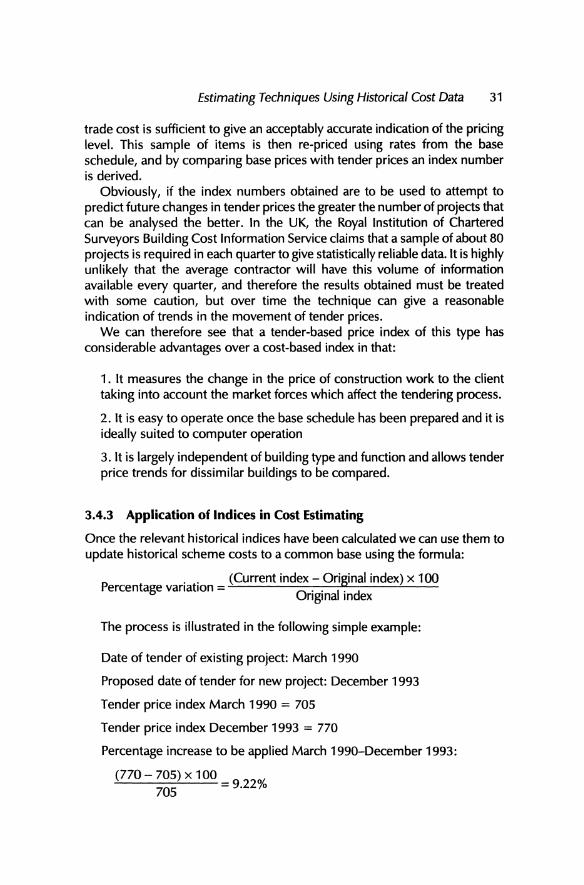

3.4.1 An Index of Building Cost 293.4.2 A Tender-based Price Index 303.4.3 Application of Indices in Cost Estimating 31

v

vi Contents

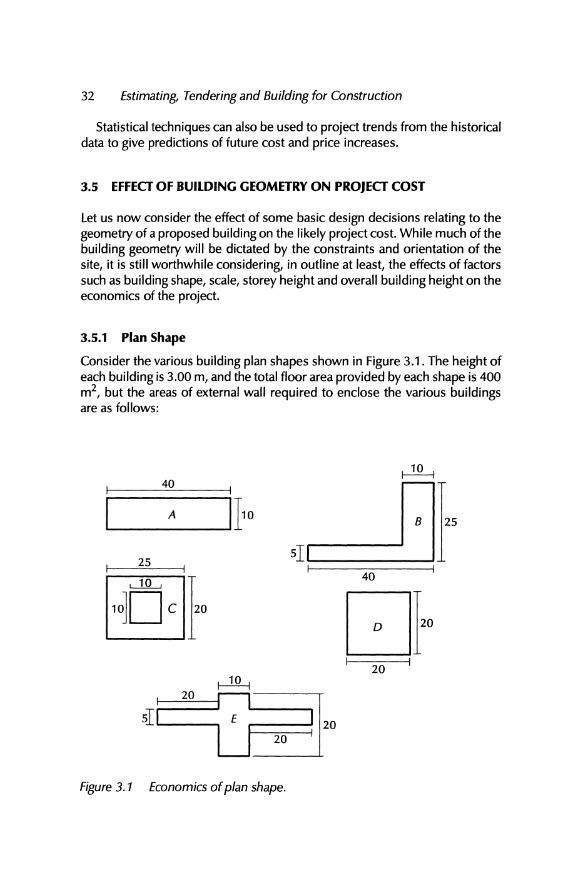

3.5 Effect of Building Geometry on Project Cost 323.5.1 Plan Shape 323.5.2 Effects of Scale (Size) 333.5.3 Storey Heights 343.5.4 Building Height 34

3.6 Improving the Accuracy of the Data 353.7 Elemental Cost Estimating 363.8 Contingency Allowances 383.9 Accuracy of Early Cost Forecasts 383.10 References 39

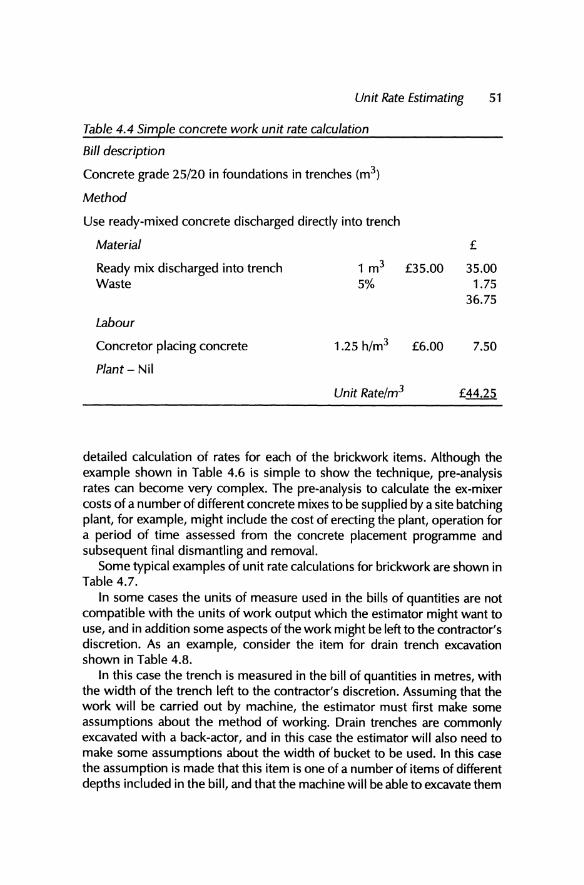

4 Unit Rate Estimating 404.1 Introduction 404.2 Net or Gross Pricing 404.3 Resource Costs 41

4.3.1 The Cost of labour 414.3.2 Estimating the Productivity of labour 434.3.3 The Cost of Materials 484.3.4 The Cost of Plant 49

4.4 Synthesis of Unit Rates 504.5 Accuracy of Unit Rates 564.6 References 57

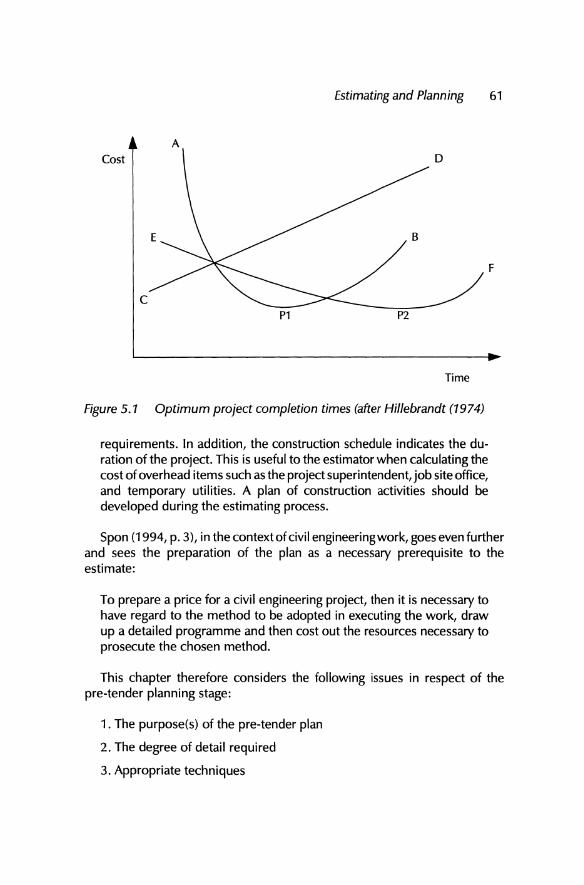

5 Estimating and Planning 595.1 Introduction 595.2 The Relationship Between Time and Cost 595.3 The Purpose of the Pre-Tender Plan 625.4 Degree of Detail Required in the Pre-Tender Plan 635.5 Planning Techniques 65

5.5.1 Bar or Gantt Charts 655.5.2 Network Analysis 655.5.3 line of Balance 66

5.6 Who Prepares the Programme? 665.7 Method Statements 675.8 References 68

6 Operational Estimating 696.1 Introduction 696.2 Preparation of an Operational Estimate : Some Examples 706.3 Advantages and Disadvantages of Operational Estimating 726.4 Converting the Operational Estimate to Bill Rates 756.5 Method-Related Charges 786.6 References 80

Contents vii

7 Subcontractors 817.1 Introduction 817.2 Types of Subcontractor 82

7.2.1 Nominated Subcontractors 827.2.2 Named Subcontractors 837.2.3 Domestic Subcontractors 83

7.3 Advantages and Disadvantages to the Main Contractor 847.4 Subcontract Enquiries 867.5 Contractual Relationships 87

7.5.1 Nominated Subcontractors 877.5.2 Named Subcontractors 897.5.3 Domestic Subcontractors 89

7.6 Settling the Subcontract Price 907.7 Incorporation of Domestic Subcontractors' Prices into the

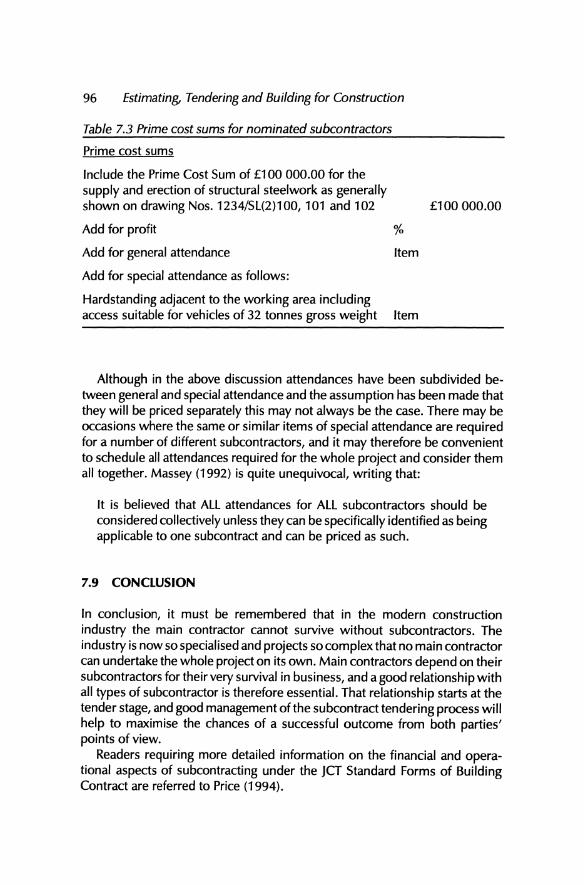

Main Project Estimate 947.8 Attendances 947.9 Conclusion 967.10 References 97

8 Pricing Preliminaries 988.1 What are Preliminaries? 988.2 Fixed and Time-Related Charges 998.3 General Project Details 1038.4 Contractual Matters 1048.5 Employer's Requirements 1048.6 Contractor's General Cost Items 1068.7 Works by Persons Other than the Main Contractor or

Subject to Instruction 1148.8 References 115

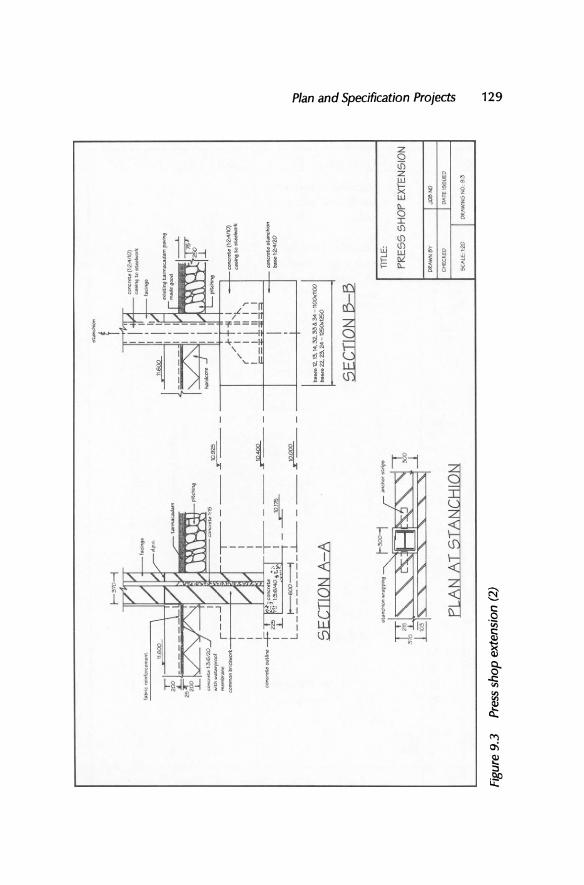

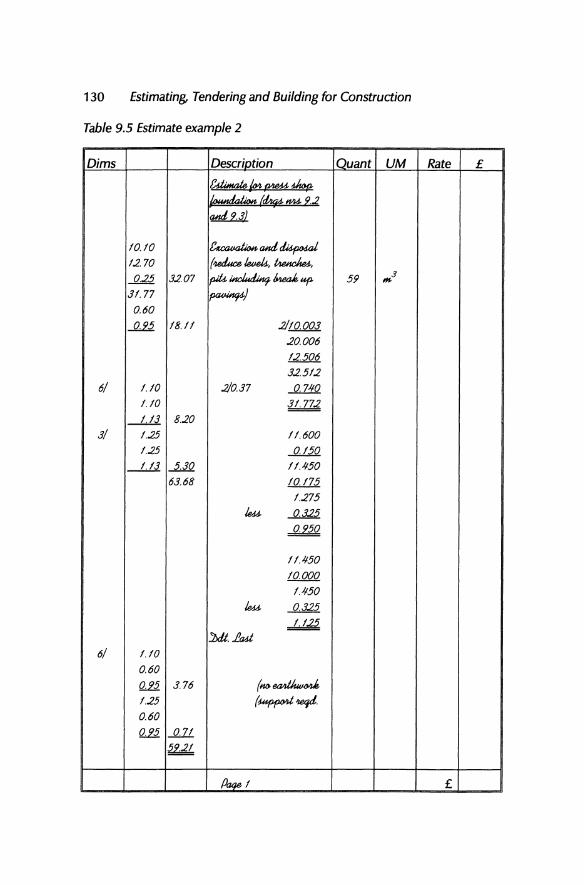

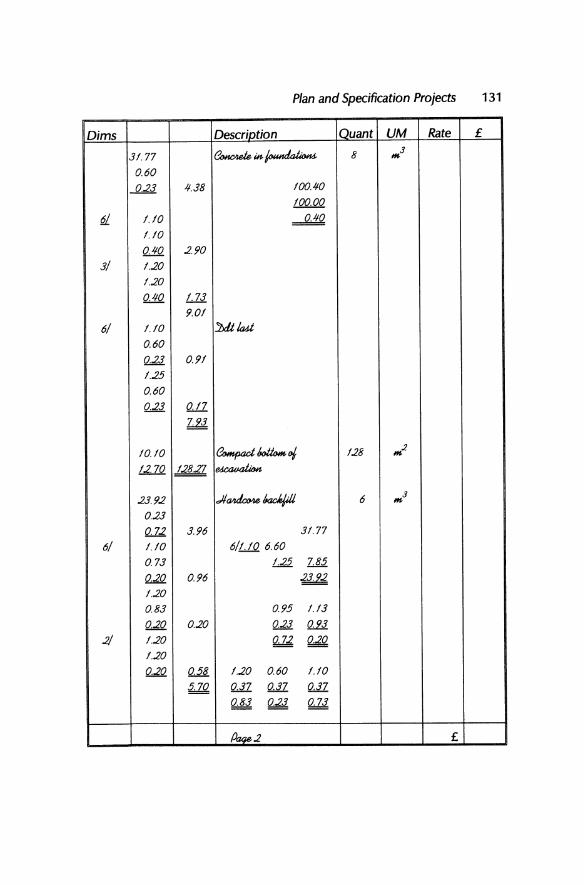

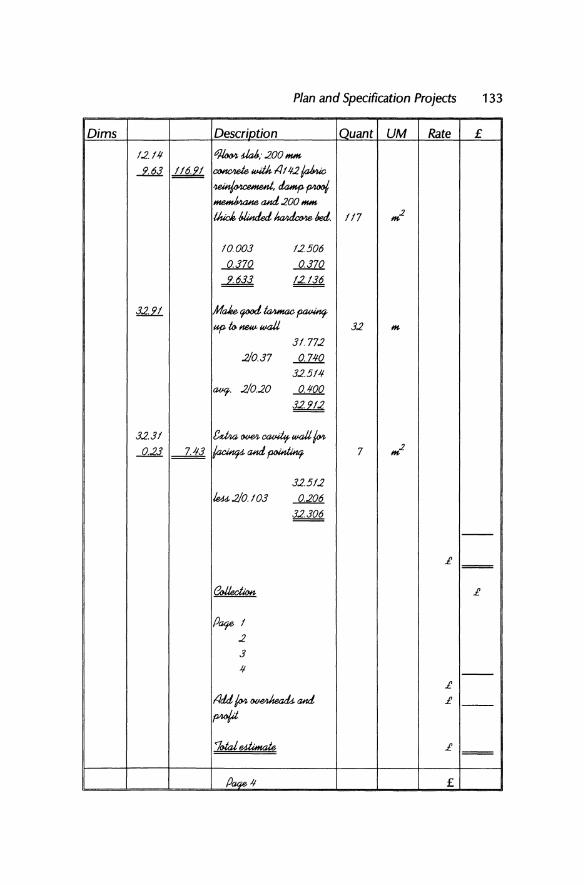

9 Plan and Specification Projects 1169.1 Introduction 1169.2 Tender Documentation 1179.3 Types of Specification 1189.4 Risk 1199.5 Builder's Quantities 121

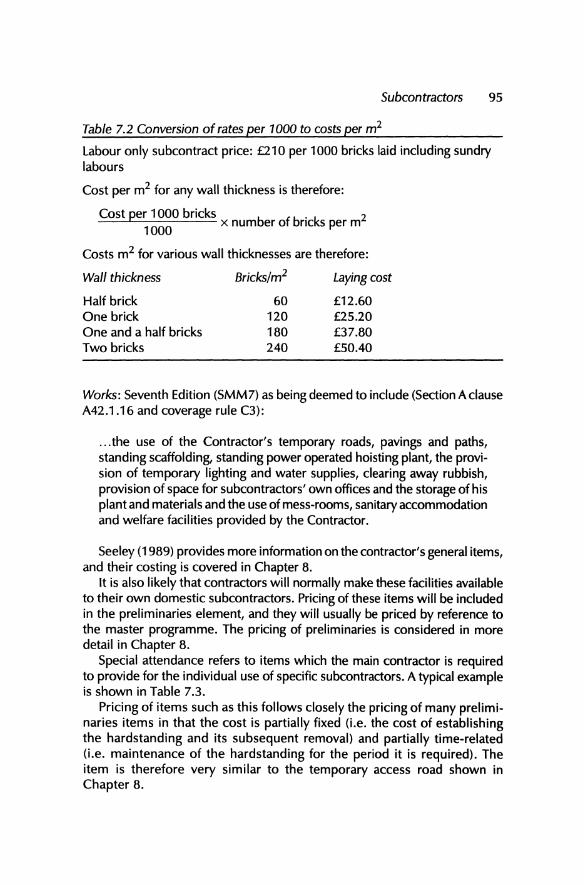

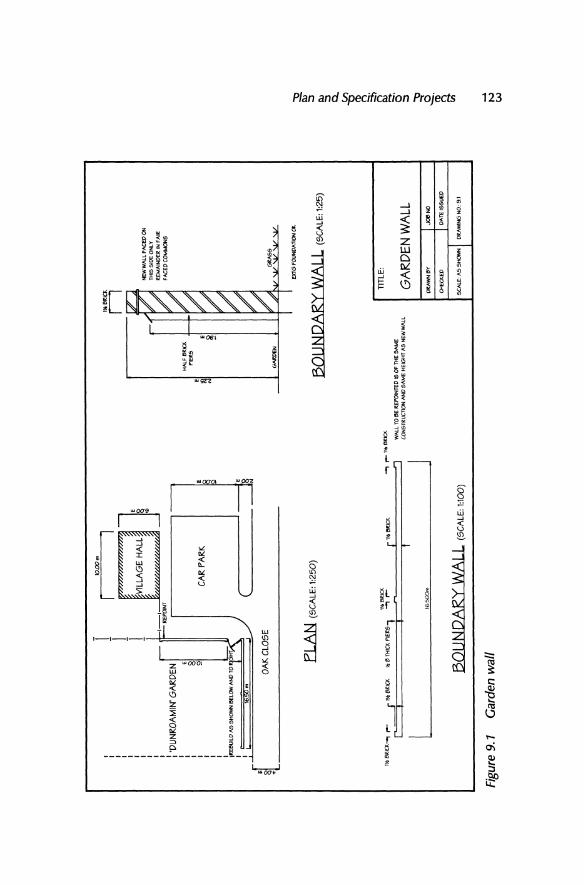

9.5.1 Example 1: Garden Wall 1229.5.2 Example 2: Foundation to Press Shop Extension 127

9.6 References 134

10 Overheads, Profit and Project Financing 13510.1 Introduction 13510.2 Indirect Costs 135

viii Contents

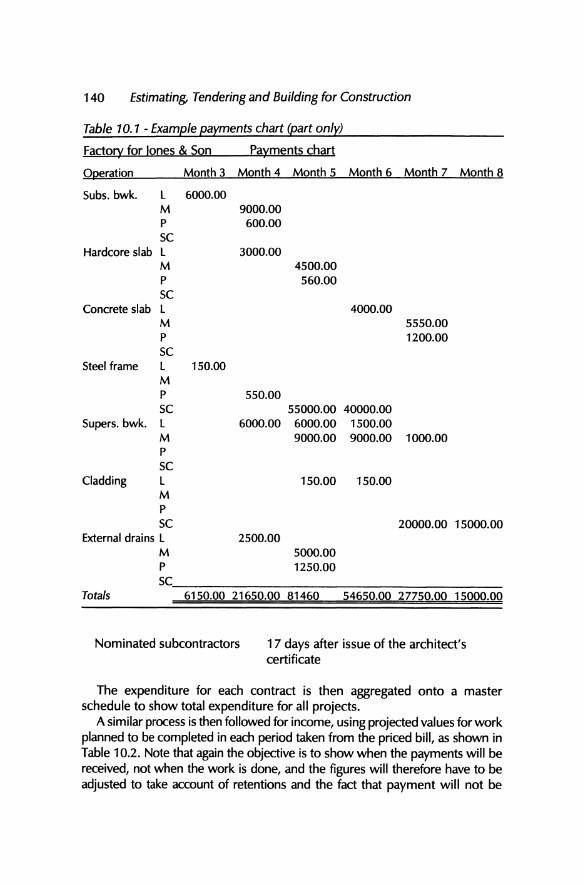

10.3 Overheads10.4 Financial Planningand Baseline Profit10.5 Project Finance10.6 Cash Flow Forecasting10.7 Sources of Project Finance

10.7.1 Internal Finance10.7.2 Financial Institutions10.7.3 Merchant Banks

10.8 Typesof Project Finance10.8.1 Bridging Finance10.8.2 Mortgages10.8.3 Non-Recourse Loans

10.9 References

136136138139141141142142142142142143143

11 Adjudication and Bid Submission 14411.1 Introduction 14411.2 The Estimator's Report 14611.3 Bid Submission and Presentation 14711.4 Submission of the Priced Bill 14811.5 Front End Loading 14911.6 'Item Spotting' 15011.7 Back End Loading 15011.8 Maximising the Net PresentWorth of the Cash Flow 15111.9 Conclusions 15111.10 Summary 15211.11 References 153

12 Riskand Uncertainty in Estimating and Tendering 15412.1 Introduction 15412.2 The Nature of the Construction Business 15412.3 Risk and Uncertainty 15612.4 RiskEvaluation 15812.5 Aspects of Human Decision-Making 16012.6 Risks and Uncertainties to be Considered in the

Estimating Process 16212.6.1 Project Risk 16212.6.2 Risks Posed by the Client and the

Professional Team 16712.6.3 Risks and Uncertainties Inherent in the

Contractor's Tendering and Estimating Process 17012.7 Conclusions 17112.8 References 171

Contents ix

13 Bidding Strategies 17313.1 Introduction 17313.2 The Tendering Process 17313.3 Acceptance or Rejection? 17313.4 Setting the Bid Price 17713.5 Factors Generally Consideredby Contractors when Bidding 17813.6 Bidding Models 18013.7 The Probability Approach 18113.8 Econometric Models 18613.9 Regression Models 18713.10 Conclusions 18813.11 References 189

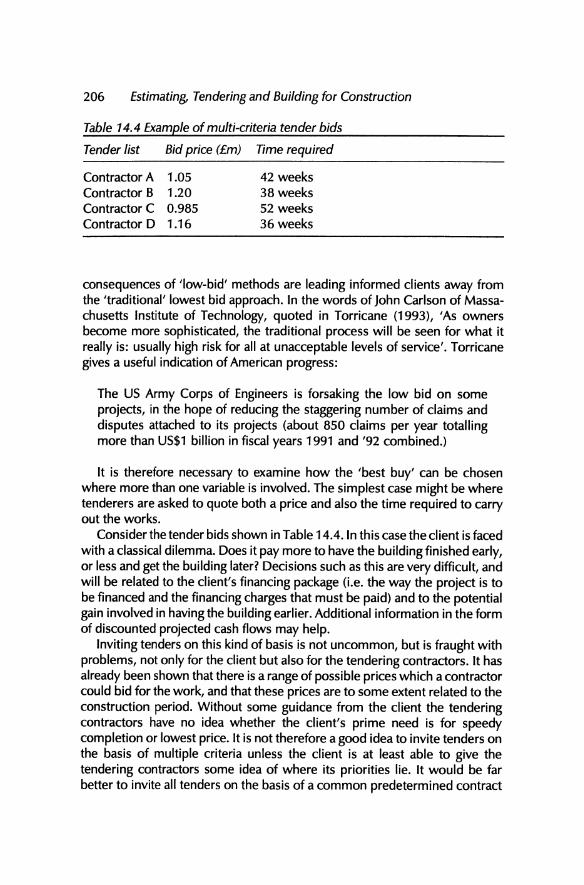

14 The Competitive Tendering Process -A Client's View 19114.1 Introduction 19114.2 The Client's Objectives 19114.3 Tendering Practice 19214.4 Identification and Selection of Suitable Contractors 19514.5 How Many Contractors? 19514.6 Prequalification 19614.7 Financial Models 19714.8 Integrated Models 19914.9 Models Using Advanced Mathematical Techniques 20214.10 Current Developments 20314.11 Choosing the Best Buy 20314.12 Choosing the BestBuy when Multiple Criteriaare Involved 20514.13 Feedback 20914.14 Conclusion 20914.15 References 209

15 Consortium and Joint Venture Bidding 21215.1 Introduction 21215.2 joint Ventures and Consortia 21315.3 Advantages of a joint Venture or Consortium Arrangement 21415.4 Requirements for a Successful joint Venture 21815.5 Potential Problem Areas for joint Venture Agreements 220

15.5 .1 Management Issues 22015.5.2 Commercial Issues 222

15.6 Project Financing 22315.7 Conclusion 22515.8 References 225

x Contents

16 Computers in Estimating16.1 Introduction16.2 Computers in Estimating16.3 Why Use Computers for Estimating?16.4 AvailableOptions

16.4.1 General PurposeSoftware16.4.2 Purpose-Written Software16.4.3 Off the Shelf Estimating Packages

16.5 Choosing the Right Package16.6 Management of the System16.7 Tendering16.8 Expert Systems16.9 Integrated Systems16.10 References

Index

227227227228229229234234235238241241243245

247

Preface

This book is about the twin processes of estimating and tendering forconstruction work. Unlike many other texts on the same subject it is notintended to be a compendium of estimators' labour constants, neither doesit set out to describe in minute detail the calculation of unit rates for everyconstruction trade. Although the mechanics of the estimating and tenderingprocess are considered, they are considered only in sufficient detail for thegeneral principles to be understood in the context of the process as a whole .Instead, this book attempts to explore estimating and tendering as a holisticprocess in the wider context of construction management and constructioneconomics .

The objectives of this book are therefore twofold: firstly to provide a textcovering rather wider aspects of estimating and tendering than has normallybeen the case in the past, and secondly to review recent research in the lightof its application to UK estimating and tendering practice. In this respect Ihave drawn upon research published in various parts of the world, includingthe UK, America, Australia and Hong Kong.

The book is primarily aimed at those students who already have a basicgrounding in the mechanics of estimating. It covers awide range of subjectsand I am well aware that some areasaretreated more superficially than others.This is partly deliberate and partly imposed by pressures of space, but I haveattempted to give extensive references wherever possible, in the hope thatthese might stimulate and assist the research of those wishing to pursueaspects of the subject to a greater depth. I hope the book might also be ofinterest to practitioners in the field.

Hong KongDecember 1994

xi

Adrian Smith

1 Estimating and Tendering Some Contextual Factors

1.1 INTRODUCTION

Most construction works are let on the basis of some form of competition, inwhich the quoted price for the work usually plays a large part. It is thereforeobvious that, for a construction company to thrive, it must have the ability toforecast the likely cost of proposed construction work, and thus at leastbeableto establish a baseline figure from which a price can bequoted to the client.

The twin processes of estimating and tendering are thus very important, butbefore considering them in detail it will be useful to look atsome ofthe contextualfactors which govern the environment in which the construction company hasto operate, and in doing so gain a feel for some of the problems involved. Thesefactors will include the organisation of the construction industry, the nature ofconstruction clients and the way construction work is procured, and the economic framework within which the constituent firms operate.

1.2 THE CONSTRUCTION INDUSTRY

The construction industry throughout the world is, in many ways, unique ineconomic terms. Briscoe (1988, p. 10), for example, says:

While there are many economic characteristics which the constructionindustry experiences in common with other sectors, there remain anumber of features which set it apart.

The same view is expressed slightly differently by Hillebrandt (1984, p. 1):

. . .the construction industry has characteristics that separately are sharedby other industries but in combinat ion appear in construction alone.

The industry is also very diverse. In terms of its constituent firms, at thelowest end of the scale it is essentially local in character, with large numbers

1

2 Estimating, Tendering and Building for Construction

of very small firms concentrating mainly on domestic scale work, generallyrepairs and renovations. It then runs through a continuum of progressivelylarger organisations to very large international construction companies operating all over the world. Construction is also characterised by a high degreeof specialisation, with many firms specialising in specific parcels of work,although the products of the industry as a whole, the completed constructionprojects, are more often bought by clients as complete entities. During theproduction phasethis situation gives rise to the need for a management layer,the main contractor, whose major task is to integrate, control and coordinateall of the various inputs required in order to deliver the whole completedconstruction project to the client.

A further distinction is that, compared with most other industries, theindividual products of the construction industry are relatively few in number,but each is of comparatively high value, and, despite various attempts overthe years towards standardisation, virtually all major construction projects areto a large extent, individual bespoke solutions to particular and specificproblems . Everyseparateconstruction project is carried out on a different site,and it is likely that each site will pose different problems for the constructioncontractor in terms of access, geography, geology, working conditions etc.Each construction site becomes, in effect, a temporary 'factory', the purposeof which is to produce the very restricted range of products comprising theparticular construction project, and which is then dismantled and removedon completion of the work.

The temporary nature of the production facility, and the fact that eachproject is a unique solution to a particular problem, also gives rise to 'peopleproblems'. In many cases the people involved in the design and constructionprocesseswill be different from one construction project to another. In otherwords, the construction 'team' must be formed anew for each new project,and must very quickly go through all of the usual 'team-building' processes ifit is to operate as an efficient working organisation.

All of these factors pose considerable problems for the contractor whenattempting to fix a price for construction work. Although some commentators(e.g.Adrian, 1982), haveseenconstruction contractors asapart of manufacturingindustry, there are in fact marked differences. Unlike most other industr ies, theuniqueness of construction projects and the temporary nature of the organisations required to complete them give rise to considerable uncertainty whenattempting to forecast what the cost of the works will actually be.

1.3 THE CONSTRUCTION CLIENT

In addition to the problems posed by the uniqueness of each of the industry'sproducts, the construction contractor must also cope with the problemsposed by the fact that construction is an industry which is essentially c1ient-

Estimating and Tendering - Some Contextual Factors 3

led. Most construction projects arise as a direct result of prospective clientsapproaching the industry rather than as a result of the industry marketing itsproducts. This is not to say that individual firms do not market themselves;they obviously do, but the marketing is generally intended to differentiate theservice offered by them from others in the field, to persuadeclients who havealready decided that they may need the servicesof the industry to select theirparticular company instead ofothers in the samefield, rather than to persuadethe general public to buy the products the industry produces. The majorexception to this, and the closest the construction industry gets to massproduction and a large consumer market, is in speculative housing, but eventhen total sales to each customer will be small, with little opportunity forrepeat business.

The construction industry has many different types of client, ranging from'experienced' clients with a detailed and intimate knowledge of the construction industry and with large and ongoing programmes of work (e.g. government and other public authorities) through to those 'na"ive' clients, oftenprivate individuals, who may build only occasionally; maybeonly once in theirlives. Clients embark on construction work for different reasons. Examplesmight include property or development companies looking for investment orto make a profit from the saleor letting of completed buildings, industrial andcommercial clients looking to provide themselves with facilities for carryingout their business, private individuals looking to provide themselves withsomewhere to live, and public sector clients looking to procure public works.Although each of these different types of client has different motives forbuilding, and all therefore have their different priorities and differing expectations of the construction industry, they do all have some things in common:

1. To every client the particular construction project is usually extremelyimportant. Powell (1980, p. 1) puts it rather well:

Everybuilding ever built arose from acarefully premeditated decisionwhich was usually of the utmost importance to the person who madeit.

2. For most clients any construction work represents a large investment inboth time and money.

3. All clients rely to a greater or lesserextent on the construction team (thecontractors and consultants) that they employ to solve their problems forthem. Experienced clients, that is those who build regularly and haveconsiderable experience of the construction industry, may often, althoughnot by any means always, be able to analyseand articulate their problemsfor themselves, but on the other hand, especially in the caseof those natveclients who have little or no experience of construction, the role of the

4 Estimating, Tendering and Building for Construction

construction team will also include helping them to identify what theirproblems actually are.

4. No matter how good the drawings and the models are, many clients,even some of the most experienced, will have difficulty in visualising whatthe completed project will look like and how well it will work, and thereforehow likely it is that it will actually meet their needs, until the project isconstructed.

In addition, because construction is a costly and lengthy process, eachconstruction project is essentially a 'one shot' activity. Each and every construction project has only one chance to satisfy the client, and yet a numberof studies over the years have purported to show that the constructionindustry in general, and in particular in the UK, has a poor record in thisrespect. Fine (1987), for example, while admittedly presenting a somewhatextreme view, still paints a disturbing picture :

...the estimating and planning tools in use in the construction industry,for the last few score of years, are failing too regularly for comfort....Almost every major project fails: Motorways, Ports, Tunnels, Dams,Power Utilities, Ships,Military Installations, Space Stations, Aircraft andChemical Plants fail to be completed according to estimate. This is notan English disease. This is a world catastrophe.

While things have undoubtedly improved in recent years, there is still astrong likelihood that the completed work will either be late and/or will costmore than the client was originally led to believe. There are, in some parts ofthe world, considerable problems with quality control, and there is even apossibility that the completed work may fail in some way to satisfy the client'sfunctional needs. If the completed project does seriously fail to satisfy theclient's needs it will almost certainly be very difficult and very costly to makenecessarymodifications.

Construction clients also demand progressively shorter contract periods,thus leading to the need for a greater degree of pre-contract planning bycontractors. Unfortunately, however, this same time pressure also tends tomean that in many cases the pre-contract design work is incomplete at thetime tenders are invited. In addition to adding to the degree of uncertaintyposed by the project from the construction contractor's point of view, thisoften gives rise to the needfor variations during the course of the work. Theseareextremely disruptive, particularly when the contractor is working to a tighttime-scale, andconsequently often give rise to expensive claims for additionalpayment. Clients are not likely to be very pleased if, on completion of theproject, they are asked to pay large sums of money as a result of variations

Estimating and Tendering - Some Contextual Factors 5

which were necessary because of problems which were avoidable at thedesign stage.

In the light of all of the above, the prime objective of all constructionclients ought to be to seek to maximise the chances that the constructionteam they choose will be able to offer the best possible solution to theirproblem in terms of their particular required combination of functionalperformance, t ime, cost and quality. Although each of these four criteriawill carry different weight for particular clients on particular schemes, it islikely that in their attempts to secure the best all-round solution mostclients will want to compare several different alternatives, and this thenimplies some form of competition . It is perhaps unfortunate, but nonetheless a fact, that on many, perhaps the majority of, projects in the past thiscompetition has been largely limited to price, with a number of contractorseach submitting bids for the work and the winning contractor usually beingthe one who has submitted the lowest price.

In the past competition has tended to be limited to the constructioncontract itself, with professional firms (architects, engineers, quantity surveyors etc.) being appointed to carry out the pre-contract work on the basis ofsome generally agreedscaleof fees,but more recently it hasbecomethe normfor clients to seek competitive fee bids from their professional consultants aswell.

In the light of the above, it is apparent that, in addition to the problems ofproject uniqueness ment ioned above, construction contractors submittingcompetitive tenders also have to cope with the demands of a commercialmarket place.The problems and risks areobvious, but Park(1979, p. 37) sumsup the problems rather well :

Under the competitive bidding system, the contractor is forced to makea 'short sale' of his resources. In effect he is sellingafinished commodity- a building for example - which he does not yet have and which doesnot even exist at the time the sale is made. The contractor is gamblingthat he will, within a prescribed time, be able to furnish the end productat the price originally set.

It might therefore be appropriate to look briefly at the economics of theconstruction market .

1.4 ECONOMICS OF THE CONSTRUCTION MARKET

In general economic terms the construction market is characterisedby a largenumber of sellers (i.e. construction firms) competing for acomparatively smallnumber of relatively high-value orders, and it is a characteristic of this type ofmarket that prices tend, in the main, to be market-led.

6 Estimating, Tendering and Building for Construction

Given a perfect market, economic theory tells us that a further characteristic of compet itive markets of this type would be that the market mechanism is essentially self-regulating, i.e, if there are too many firms chasing toofew orders then prices will tend to fall. Eventually, the less efficient will fail tosecure enough work at a price which enables them to remain profitable, andif this situation continues they will leave the industry. This process will, intheory, continue until the number of firms in the market-place, the marketprice and the amount of work available are again in balance. Conversely, ifthe demand for construction services exceeds available capacity then pricesand hence profit levels will be seen to rise and more firms will be attracted toenter the market until the status quo is again reached.

In the construction industry, however, such perfect market conditionsrarely if ever apply, and the market does not therefore behave in precisely theway that the economic theory predicts that it should. One of the main reasonsfor this is that construction is a long-term business. Even for so-called 'fasttrack' projects, the time-scale for most major construction work, from theinitial inception and feasibility study, through final completion and occupat ionof the building, to completion of the final account is likely to be measured inyears.

The construction market as a whole therefore has considerable kineticenergy, and assuminga policy of non-intervention by government, in generaltends to lag behind movements in the economy as a whole. The effect of thisis that, in a recession, the construction sector may still appear to be strongand moving ahead even though the remainder of the economy is slowingdown, and conversely when the economy as a whole begins to recover thelengthy lead times required to commence major construction projects resultsin construction appearing to be weak when the economy as a whole appearsto be gaining momentum .

Given these circumstances it is very difficult for the construction market toadjust quickly to changes in demand. Note the need here to distinguishbetween 'demand' and 'need'. While there might appear to be an obviousneed for considerable construction in order to improve social and livingconditions in many parts of the world, the need will only be translated intoan economic demand for the construction industry when someone is willingto pay for the work.

While the fragmented nature of the industry does, to some extent, give theadvantagethat the industry can cope fairly well with a fluctuating demand inthe short term, if the demand fluctuations become too large or occur tooquickly the construction market asa whole becomes very unstable and pricesbecome erratic and difficult to predict. We have already seen that the industryreacts comparatively slowly to conditions of falling demand, and if demandfalls relatively quickly there may be a considerable period of lower thanexpected tender prices as the same number of firms compete increasingly

Estimating and Tendering - Some Contextual Factors 7

more fiercely for the available work. Construction, aswe have also alreadyseen, tends to be a highly fragmented and specialised business, and firmscannot easily switch their resources to operate in other markets . They willtherefore tend only to leave the industry as a last resort; that is, they willtend to try to hang on for as long as possible, usually by progressivelyreducing the profit margins included in new tenders wh ile at the same timeattempting to reduce direct costs to a minimum, often by shedding staff,in the hope that things will improve. If demand continues to fall, or evenremains static at low levels, then eventually the market mechanism willcome into play and the less competitive, least efficient firms will be forcedto leave the industry. This phase will generally occur some considerabletime (certainly some months, and perhaps even years) after the initial fallin market demand began.

The effect of this is that, for a period, the industry 's production capacity islikely to grossly exceed the amount of work available, and, in the case of asevere fall in demand, the reluctance of individual firms to leave the market,except asa last resort, may mean that a substantialnumber of firms eventuallyall leave the industry at the same time. A substantial proportion of the siteworkforce w ill attempt to move to other industries. The eventual collapse ofthe industry, when it does eventually come, may therefore appear to be bothsudden and dramatic.

On the other hand, however, if demand begins to rise relatively quicklyfrom some stable level, the reverse applies. Since construction is a businessrequiring specialised technical knowledge and skills, it is not easy for newfirms to enter the market quickly. In addition, it is not easyto expandthe poolof skilled labour required rapidly, particularly if many skilled workers haveestablished themselves in other industries. As demand rises, therefore, twothings tend to happen:

1. Because construction is a long-term activity, existing firms will bereluctant to expand and new firms will be reluctant to enter the industryuntil they can be fairly sure that the increase in demand will be sustainedfor a reasonable period of time. The capacity of the existing firms isexceeded and the tender prices and profit levels of those firms already inthe industry will tend to rise. The industry might expect to experience asubstantial period of higher than expected tender prices. In addition,because firms can afford to be more selectiveabout the kind of work theyare prepared to take on, the rise in tender prices for particularly complexor difficult projects may be even higher than the average for the market asawhole. At the extreme casethere isa dangerof localconstruction marketsmoving towards a situation where the number of contractors is comparatively small in comparison with the number of projects on offer, with theconsequent dangers of price fixing, collusion on tender prices etc.

8 Estimating, Tendering and Building for Construction

2. Large numbers of relatively unskilled or semi-skilled workers are recruited into the industry to cope with the increased demand. Qualitystandards and industrial productivity tend to fall.

Eventually,of course, the market mechanism will againoperate: more firmswill enter the industry and/or the capacity of existing firms will be deliberatelyexpanded and the statusquo will again be restored . Note, however, that, inthe case of major fluctuations in demand, a substantial period of stabledemand levels may be required before the status quo can be restored , thesupply and demand sides of the industry will again be in balance, and themarket price for construction work will again become reasonably predictable.

It can therefore be seen that, if the construction industry is to remainhealthy, there is a need for the average demand for construction work to beat least reasonably predictable and hopefully relatively constant. We haveclearly seen that major fluctuations of demand with in a comparatively shorttime-scale or extended periods of demand uncertainty may give rise to seriousproblems in matching demand and supply and thus in predicting the marketprice for construction work.

Given the above it would seem that some method of predicting the possiblefuture fluctuations in demand for construction work might be a useful tool forcontractors to use in their forward planning. Most analyses of this type arebased on some type of historical projection, supplemented by some form ofsubjective 'expert' judgement, but Oshabajo and Fellows (1991) have shownthat it is possible to take advantage of the fact that changes in constructiondemand generally lag behind the fluctuations in other key economic indicators, principally, it seems, changes in interest rates. They go on to formulatea mathematical model which, they claim, is appropriate for short-term forecasts of between three and four quarters.

1.5 SOURCES OF CONSTRUCTION WORK

Traditionally, most construction work has been let by competitive tender. Theprocess is therefore controlled to a large extent by the industry's clients, themarket customers, who invite contractors to tender in competition with eachother. On the other hand, the service providers, the sellers in the market-place,take a generally passive role in that they normally have to wait for customers tocome to them. While it is, of course, possible for them to improve their chancesof being asked(i.e, being includedon tender lists) by various forms of advertising(although recent research by Preece (1994) appears to show that few firms doeventhis effectively),the traditional contracting market is largelydemand-led andthe conventional commercial practices of attempting to increase sales throughadvertisingand promotion generallydo not havethe same effect as is the case inindustries like manufacturing.

Estimating and Tendering - Some Contextual Factors 9

Contractors have attempted to overcome this problem in a number ofways:

1. The growth of property-owning democraciesin the developed world hasencouraged speculative housing for sale on the open market. This aspectof construction is the closest the construction industry gets to producingconsumer goods, and in this sector of the market many of the basic rulesof economics which apply to manufacturing industry do apply. Otherspeculative developments may include offices, industrial parks etc., butinvolvement in speculative development is a two-edged sword. On the onehand, contractors may be able to use their own speculative buildingventures to even out their demand for contract work, but on the other handthe contractor or its partners must finance the whole cost of the development, including the land purchase, from inception until the first units arelet or sold. The cash flow for this type of project therefore may be far lesspredictable than that for a project won in competition , where the employerwill usually pay for work completed on a monthly basis. The process canalso be risky, since successdependsupon the contractor gambling that theproperty market will continue to rise and that there will be a market for theproduct at an acceptable price when the work is completed . While thelong-term trend is undoubtedly upward, in the short term the propertymarket can be very fickle, particularly in times of recession.

2. Most contractors will attempt to cultivate a number of regular clientswho are likely to provide them with a regular programme of work on anegotiated basis. In these cases the contractor will typically attempt todifferentiate its service from others available in the market-place on thebasis of observable criteria, such as reliability, quality of workmanship,speed of construction or rapidity of response, as well as price, and oncesuch clients have been secured the contractor will usually be prepared towork very hard to keep them. Such arrangements are often in the area ofrout ine maintenance or repair, but may also include new works, althoughthey will not generally be major projects.

3. Some contractors have attempted to improve their market share byproviding a system of 'single point' responsibility for clients, usuallythrough the use of 'design and build'-type packages, often linked to aguaranteed maximum price arrangement, where the contractor takes fullresponsibility for both the design and construction of the works. In the pastthese packages have tended to be generally limited to fairly simple typesof building, but the technique is now beginning to be widely used for anumber of complex building types. Macniel (1992), for example, describesthe development of a £32 million design and build scheme for a majorhospital in Scotland. Some commentators (for example Fellows and Lang-

10 Estimating, Tenderingand Building for Construction

ford (1993) and Yates (1994)) , predict that an increasing volume ofconstruction work worldwide will be procured through this route in thefuture.

4. Some contractors have attempted to create their own constructionmarket, usually as part of a larger consortium. The basis of these schemesis that projects are identified which would normally be considered aspublicworks, and where a worthwhile income is likely to arise, but where thegovernment or other authority involved does not have the resources tocarry them out. Typical examples might be highway works , such as roads,bridges or tunnels, which can be operated on a toll basis, or more complexfacilities such as power stations, where the power generated can be soldto an existing power supply authority. The projects are designed andconstructed by the consortium, using private capital, and in return theconsortium is given a concession to operate the utility for some futureperiod. At the end of the concession period possession of the utility istransferred to the relevant public authority. Projectsof this type are knownby a number of acronyms, generally variants of build/operate/transfer(BOT), and are becoming very popular. Examples of recently completedsuccessful BOT projects include the Channel Tunnel between Britain andFrance and the Dartford bridge, while the Hong Kong Cross HarbourTunnel and the Shajiao 'B' power station in southern China representexamples of successful BaTs which have almost reached the end of theirconcession periods. Although the concept might appear to be new, Walker(1993) reports that the first true BOT project was probably the SuezCanal.The potential returns to the consortium may be high but the risks may begreat.

1.6 THE THEORYOF THE FIRM

Conventional economic theory tells us that all firms will attempt to keep costsand income in equilibr ium by assessing likely demand for their producttogether with the market price for the goods produced, and gearing supplycapacity to suit. It might therefore be helpful to look at how well this theoryapplies to the construction industry.

All firms, including construction firms, have some fixed costs, which theyhave to pay whether or not they produce anything at all, and some variablecosts, which are directly related to the volume of output. In construction, theamount of fixed costs varies according to the nature of the firm. In the caseof a general contractor, which relies on subcontracting most of its work, fixedcosts may be relatively low, perhaps only comprising office rental, staffsalaries, provision of company cars and the cost of financing any workingcapital. On the other hand, an excavation and earthworks contractor, for

Estimating and Tendering - Some Contextual Factors 11

example, might have a large amount of capital tied up in expensive plant, withan associated plant yard, workshops etc.

The problem with fixed costs is that they tend to rise in steps. A certainlevel of fixed cost might be adequatefor acertain rangeof production capacity,and when the end point of the range is reached a further increase in capacitywill require that fixed costs increase by a larger amount than a marginalincrease in production would justify. The revised level of fixed costs thenapplies for the next range of production, and so on. Fixed costs may also bedifficult to adjust quickly, and changes in fixed costs therefore tend to beconsidered only in the medium to long term. This means that if we plot theshort-term costs of a firm against production capacity,we find that the curveis U-shaped, with the bottom of the U representing the optimum productionlevel, where the cost per unit of production is at its lowest. Cost per unit ofproduction at low levels of production tends to be high, falls to a minimumat some optimum production capacity, and tends to rise againwhere production approaches the high end of the range.

It is therefore obvious that to maximise profits for a given product pricelevel the firm needs to operate asclosely aspossible to the optimum unit cost.This is very difficult to do in the construction market, where demand ispotentially so unpred ictable, but the short-run cost curve will be unique foreach firm , and in theory at least it is important that all firms know what theircost per unit of output actually is. An example of the calculation of short-runcost curves is given in Hillebrandt (1985).

Each company will have its own short-run cost curve, which will indicatewhat the total value of production ought to be for maximum profitability. Atany instant in time, therefore, each firm will be in a different trading position,but all firms ought to be attempting to maintain their product ion at theoptimum. What then ought to be the effect of this on tender prices?

For firms operating towards the left-hand end of the curve, i.e. withproduction levels below the optimum, costs per unit of production are high.In the short run they must attempt to increase production in order to drivecosts per unit down; in a construction tendering situation that would meansubmitting lower prices and thus hopefully winning more work, but the pricemust never fall below the firm 's minimum cost level. If the minimum cost atwhich the firm can tender is still above the market price (i.e. if it is still notsuccessful in obtaining work) then it must attempt to reduce fixed costs inorder to move its optimum level of production closer to what it canrealisticallyachieve.

Firms operating towards the right-hand end of the short-run curve, however, ought only to tender at a rate which represents a true reflection of theirunit costs. Such costs will normally be higher than the market rate, since theywill usually be tendering against firms operating at or below optimum capacity. It is therefore less likely that they will be successful, but if they are

12 Estimating, Tenderingand Building for Construction

successful then they will have secured the work at a price which allows themto cover their true costs. If they do get the work then they may gain valuableintelligence about the state of the competition, and this may help them todecide whether or not they should plan for expansion and an increase in f ixedcosts in the long run.

But how do firms know when they are operating at optimum efficiency?The classical theoretical economics answer is usually thought to be given bythe use of marginal analysis techniques. Marginal analysis compares theincrease in revenue generated from the last small rise in output (the marginalrevenue) w ith the relevant costs of production (the marginal cost) . Normally,of course, for afirm in a healthy trad ing situation marginal revenue will exceedmarginal cost, but the difference between the two will tend to decrease as thefirm approaches the limit of its fixed resources. As soon as marginal costexceeds marginal revenue the firm is no longer efficient, and the firm istherefore operating at maximum efficiency (i.e. the fixed resources of the firmare being used to their maximum) when marginal cost and marginal revenueare equal.

This techn ique works well in manufacturing industry, whereoutputvolumecan be fairly closely monitored, controlled and varied in the short term, but ithas been pointed out by several commentators (for example Rutter (1993»that construction does not work like that. Construction projects are generallylarge,generally indivisible, and generally w ill each individually comprise a highproportion of the firm's turnover, so the concept of marginal analysis as aprecision decision analysis tool in deciding whether or not to tender for newwork does not operate very well. The difficulties involved in applying thetechniques developed for use in manufacturing engineering to the construction industry have caused many firms simply to ignore economic analysisaltogether, but this risks throwing away the potential benefits aswell. Standardeconomics techniques, such asmarginal analysis, can give an idea of the firm'sefficiency, but the nature of the construction business means that it is verydifficult to use such techniques with any great degree of precision.

1.7 REFERENCES

Adrianj .l .A. (1982) Construction Estimating:AnAccountingandProductivityApproach,Reston Publishing Company, Reston, Virginia.

BriscoeG. (1988) The Economics of the Construction Industry, Mitchell, London.Fellows R. and Langford D. (1993) Marketing and the Construction Client, Chartered

Instituteof Building, London.Fine B. (1987) 'Kitchen sink economics and the construction industry', in Building,

CostModellingandComputers (ed. Brandon P.S.), E. & F.N. Spon, London.Hillebrandt P.M. (1984) Analysis of the British Construction Industry, Macmillan,

London.

Estimating and Tendering - Some Contextual Factors 13

Hillebrandt P.M. (1985) Economic Theory and the Construction Industry, 2nd edn,Macmillan, London.

Macn iel l- (1992) 'An aesthetic treat', Building, 14 August 1992.Oshabajo A.a. and Fellows R.F. (1991) 'Investigation of leading indicators for the

predict ion of UK contractor's workloads (total new orders)', in Management,Qualityand Economics in Building, (eds, BezalgaA. and BrandonP.), E.& F.N.Spon,London.

Park W.R. (1979) Construction Bidding for Profit, Wiley, New York.Powell CG. (1980) An Economic History of the British Construction Industry,

Architectural Press, London.Preece C (1994) 'Promoting construction for competitive advantage', Chartered

Builder, july/August 1994, pp. 7-9, Chartered Institute of Building, London.Rutter G. (1993) Construction economics : is there such a thing?, Construction paper

No. 18, Chartered Institute of Building, London.Walker CT. (1993) 'BOT Infrastructure: Anatomy of Success', MSc Dissertation, City

Polytechnic of Hong Kong.Yates j.K. (1994) 'Construction competition and competit ive strategies', Journal of

Management in Engineering, Vol. 10, No.1, American Societyof Civil Engineers.

2 The Estimating Process

2.1 THE PlACE OF ESTIMATING IN THE COMPETITIVE TENDERINGPROCESS

The traditional methods of construction procurement in most parts of theworld all generally involve some form of competition between a number ofcontractors, with price usually playing a major part in the selection of thecontractor eventually chosen to carry out the work. Contractors thereforeneed some reliable method of forecasting prices, and therefore likely costs,for future construction work.

Historically, in the competitive tendering situation, the price forecastingtechnique most commonly used has closely followed that used in industriessuch as manufacturing engineering. The process is essentially a linear one, inwhich the contractor first calculates the cost of all of the inputs to the project(i.e. the total cost of the labour, materials, plant, subcontract work etc.required to complete the project; in economic jargon the 'factors of production'), and to this total is added some figure to cover overheads and profit,often in the form of a percentage, to give the price which will be quoted tothe client. The total cost of the inputs to the process is usually termed theestimate , and the price quoted to the client is usually termed the tender. Thepreparation of the estimate is therefore seen asa mainly technical and factualoperation (CIOB (1983), for example, defines estimating as 'the technicalprocess of predicting costs of construction '), and is usually carried out by aspecialist estimator.

The tender, on the other hand, represents 'The sum of money, time andother conditions required by the tenderers to carry out the work' (CIOB,1983). The tendering process must therefore take into account the contractor's assessment of prevailing market conditions, in other words an assessment of what price the market will bear, and the calculation of the tenderfigure has therefore been seen as a largely subjective commercial management decision. It has conventionally been assumed that the tender will bebased on the estimate. CIOB (1983, p. 3), for example, defines tendering asa'...separateand subsequentcommercial function based upon the estimate'.Theprocess ofconvertinganestimate into atender isusuallytermedadjudication.

14

The Estimating Process 15

Some commentators, for example Fine (1975) and Ostwald (1992), pointout that the validity of the above approach is sometimes questioned on thebasis that, in a free market, the link between cost and market price for anygoods is at best a tenuous one. The same point is reinforced by Ashworth andSkitmore who, reporting previous research, comment that :

As a consequence of the theoretical considerations and observed behaviourof contractors in a competitive environment it is not surprising to findreferences to pricesbeing unrelated to performance or costsof construction.

One example of this phenomenon which is often quoted in constructionis that of speculative housing, where the selling price of the product isgoverned strongly by market demand, and where the price the prospectivepurchasers are willing (or able) to pay may often bear little or no relationshipto the actual costs incurred by the builder. It is held by some that, by extension,the same argument should apply to other sectors of the construction market.If, for example, a hotel chain wishes to build a new hotel, its commercialassessment of the viability of the scheme must include a maximum figure forconstruction costs beyond which the project would not be commerciallyfeasible. It is therefore this figure which represents the maximum market pricewhich it would be willing to pay for the construction work, and consequentlythe figure which the lowest tenderer should be aiming to predict.

The difference in practical terms, of course, between the two examplesquoted above, is that houses, both new and old, are a commodity which iswidely traded on an open market. The market price of new houses - theirvalue to prospective purchasers - is therefore relatively easyfor the contractorto assess, and it can then pitch its selling price according to the market valueof similar units. In the case of bespoke construction works, such as theconstruction of a new hotel, however, the market is much less open and thetrue market value for any particular project is much more difficult to determine. In this case the only person who knows the real commercial value ofthe construction project is the hotel developer. In the case of a competitionbased solely on price, therefore, the hotel developer is effectively offering toauction the opportunity to construct the project to the lowest bidder. Anexcellent discussion of the economic concepts of cost, price and value andthe relationship between them is given in Raftery (1991, Ch. 2) .

The issue of consideration of the market price will be discussed in moredetail in a later chapter, but it is evident that, however the market price isdetermined, construction companies tendering for work still need to knowwhat their own direct costs for the project will be, if only to give their own'bottom line' below which it would not be economic for them to carry outthe work. The process of estimating is therefore of fundamental importance.

16 Estimating, Tendering and Building for Construction

2.2 THE PROCESS OF ESTIMATING

It can clearly be seen from the above that the ability to estimate the likelycost of proposed future construction work reliably is a fundamental requirement for any construction contractor. The estimator's prediction oflikely cost will, at the very least, form an important part of the informationavailable to management when establishing the tender price. In addition,if the tender is successful and the contractor is to obtain the anticipatedfinancial return, then the estimate must also effectively become the contractor's budget for construction of the works, and must also provide thebasis for the contractor's post-contract costing and valuation systems. It istherefore obvious that every estimate must be compiled in a systematicway, and the information upon which it is based should be as factual aspossible. The most variable items are likely to be factors such asproductionrates, materials wastage etc., and the most reliable source of data forfactors such as these ought to be from recorded company data derivedfrom site feedback or work study exercises. Unfortunately, such data arefrequently not available, and estimators are therefore frequently forced tofall back on their own skill and experience. Ashworth and Skitmore reportthat, in the United Kingdom at least:

Estimators'standardoutputs arecontained and secretly guarded in their'black book'. They are only rarely ever amended or revised.... A majorreasongivenwhy estimatorsdisassociatethemselves from site feedbackisdue to the poor recording systemsemployed by contractors and hencea lack of confidence in the data provided.

But we havealreadyseen that the estimate is a forecast of future events. Itis subject to considerable uncertainty, and it is perhaps for this reason thatestimating, particularly in a competitive tendering situation, is considered bysome to be 'more an art than a science' (Adrian, 1982, pAl. Fine (1974) wenteven further and described estimating as:

.. .like witchcraft: it involves people foretelling situations about whichthey can have little real knowledge

and it is perhaps with this thought in mind that Ashworth and Skitmorecomment that:

Builders' estimating has, in the past, had its own mystique, withthe result that certain processes discussed both in the classroomand in the estimator's office are found to have little practicalrelevance.

The Estimating Process 17

Estimating is not therefore the precise technical and analytical processwhich many theorists would have us believe. Estimating must be, to a largeextent, asubjective process, and the estimator canneverhope to predict actualcosts precisely, but the degree of accuracy sought must at least attempt tosatisfy two basic criteria:

1. The sums of money allowed in the estimate must be at least high enoughto cover the direct cost of the work.

2. The overall tender figure must be low enough to be competitive.

Ashworth and Skitmore report that most estimators areconvinced that theyare able to consistently estimate to within ±S%, but that research indicatesthat this figure may be over ly optimistic.

2.3 THE PlACE OF THE ESTIMATOR INTHE CONTRACTOR'SORGANISATION

From a purely technical point of view the estimator's main funct ion is toattempt to forecast the probable prime cost of construction work with theassistance of the tender documents (bill of quantities, specifications anddrawings), while maintaining an awarenessof the stipulations and constraintsof the Conditions of Contract, and in so doing to predict the probable finalcost to the contractor of completing the project. But this simple technical viewruns the risk of undervaluing the estimator's contribution to the process as awhole. Ayres (1984, p. 18), for example, sees the estimator's input almostlyr ically as a fundamental turn ing point in the project's progress from dreamto reality:

Any building is a dream until construct ion is started. The architect hasa picture on paper, but it is only a picture until the contractor transformsthat picture into a solid, three dimensional structure. The estimator isthe one who translates that pictu re into cold hard dollars. Lines on adrawing or phrases in a specif ication can be changed for the cost of aneraser, but when an estimator sayshewill furnish abuilding for aspecificsum of money, it is a final action and the first step in the transformationof a dream into a solid object.

Taking into account the implications for the production stage, if the tendershould be successful, of any assumptions made in the estimate, it is obviousthat the estimator cannot accomplish this taskalone.Theprocessof producingan estimate, particularly on larger projects, cannot be seen as a singleoperation carried out by one single individual. If estimators are to be effectivethey must work in close liaison with other personnel, who will in due course

18 Estimating, Tendering and Building for Construction

be responsible for planning the work, for procuring the necessary plant andmaterials and for carrying out the work on the site.

A 'team approach', at least during the early stages of project appreciation, including buyer, project planner, construction manager and plantmanager, as well as the estimator, will assist in identifying and analysingpotential problem areas which might not be apparent to an estimatorworking in isolation and which, in turn, might not be considered untilconstruction works had commenced on site, at wh ich point it wouldusually be too late to take corrective action. During the project appreciationstage the team should also consider, evaluate and make decisions aboutfactors such as the proposed construction programme, alternative methods of construction and site layout.

It is sometimes said that the major funct ion of the estimator is to obtainwork, and there is sometimes a tendency to blame the estimator if the pricesquoted by the contractor aretoo high. If the firm is short ofwork, the estimatoris frequently told to 'sharpen his pencil'. This is, in the majority of cases, bothunfair and counter-productive . The procurement of work is a managementresponsibility. While it is true that the main reason for preparing the estimateis to help in the procurement of new work, the estimator's function is simplyto make a prediction of the probable cost of the work to the contractor, andone of the most important factors must be consistency of approach. Davies(1980) sums up the issue rather well:

Ensurethe estimating team is consistent. Consistency and reliabil ity arethe key characteristicsneeded in estimators . When considering a tenderthe first essential is to haveconfidence in the estimated prime cost andbe reassured that it has been prepared on a basis consistent with theestimates looked at yesterday, last week and last month, and that thisbasis produces as accuratea forecast as can reasonably be expected inthe face of many uncertainties.

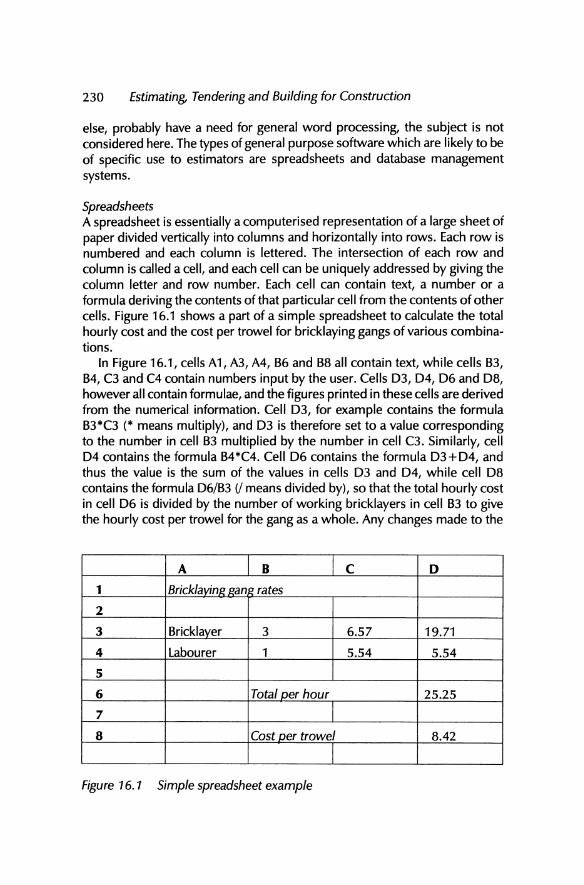

2.4 SKILLS ANDTRAINING

In the UK estimating is not generally considered to be a separate professionin its own right, and estimators tend to be drawn from a variety of differentbackgrounds within the construction industry. There are, in the UK, no formaleducation or training courses for estimators, and therefore most of theirknowledge has to be gained through experience. The situation is, however,different in other parts of the world. In the USA, for example, the AmericanSociety of Professional Estimators provides construction industry estimatorswith a formal professional framework, includ ing a published code of ethics,and also sponsors estimating education through scholarships and participation in a variety of educational programmes.

The Estimating Process 19

While a good grounding in construction technology is essential, it is alsoimportantthatyoung estimators spend areasonable periodon siteobservinghowthings are actually done in order to supplement, and perhapscomplement, theirtheoretical knowledge of how things ought to be done. The following, compiledfrom a variety of published sources, are generally accepted to be the mostimportant technical skills which a good estimator should possess:

1. The ability to read, quickly understand and summarise both written andgraphical technical documentation.

2. Well-developed organisational and communication skills .

3. Good numerical and analytical skills.

4. The ability to visualise the project in three dimensions from two-dimensional drawings.

5. A good grasp of quantity surveying construction measurement skills .

6. A good understanding of labour and equipment performance, and theability to recognise those unusual situations where the 'standard' allowances no longer apply.

7. A clear understanding of the commonly used Conditions of Contract.

8. Creativity and imagination.

2.5 MANAGEMENT OF THE ESTIMATING AND TENDERING PROCESS- AN OVERVIEW

Management of the estimating and tendering process will usually involve thefollowing activities:

1. Decision to tender

2. Examination of the tender documents

3. Establishment of a programme for estimate and tender preparation

4. Site visit

5. Analysis of prime cost and provisional sums

6. Preparation of outline method statements and production programme

7. Subcontractors' and suppliers' enquiries

8. Estimation of the direct costs

9. Estimate appraisal and adjud ication

20 Estimating, Tendering and Building for Construction

10. Assembly of the bid documentation and submission of the tender

Some of these stages are essent ially management decisions, and aredealt w ith in detail elsewhere in this book. Specifically, stage 1, thedecision to submit a tender, is covered in Chapter 13, and stage 9,estimate appraisal and adjudication , and stage 10, assembly of the biddocumentation in are covered in Chapter 11. In addition, stage 6, thepreparation of method statements and production programme, is dealtwith separately in Chapter 5, and stage 7, subcontractors and suppl iers,in Chapter 7.

The remainder of the aboveactivities comprise those management activities usually dealt with by the estimator, and are considered here.

2.6 EXAMINATION OF THE TENDER DOCUMENTS

The tender documents usually comprise a selection of the project drawings, the specification , the Conditions of Contract, and, for larger projects,the bill of quantities. A close examination of the tender documents isessential, f irst of all to ensure that all of the documents have been received,but secondly to gain a thorough grasp of the work required. It is essentialthat all staff involved in the estimating process have a thorough understanding of the project if the estimating process is to be successful.

A further reason for a close examination of the tender documents isto gain an impression of the appropriateness of the Conditions ofContract as compared with the completeness of the design . Some Formsof Contract and some Standard Methods of Measurement assume thatthe design is virtually complete at the time of tender, and the degree ofuncertainty and risk faced by the contractor may be cons iderably increased if this is not the case, especially where a bill of quantitiespurports to give accurately measured quantit ies for the work. A moredetailed consideration of the risks posed by incomplete design is included in Chapter 12.

When examining the documents, the estimator should also be particularly on the lookout for :

1. Any amendments to the standard Conditions of Contract.

2. Non-standard payment or retention provisions.

3. Project time -scale and any associated liquidated damages requirements .

4. Provision of bid or performance bonds.

5. Unusual insurance requirements.

The Estimating Process 21

6. Any discrepanciesbetween the variousdocuments,for examplebetweenthe drawings and the bill of quantitiesor between the specificationand thedrawings.

7. Clear and unambiguous specifications and bill of quantit ies.

8. Any outstanding information required.

The time available for the estimator to carry out this task is usuallyvery limited, but it is only through this close and detailed scrutiny ofthe project documentation that estimators and their colleagues will beable to form judgements about possible methods of construction, buildability, likely construction programme and the degree of risk involvedin the project.

Once this initial examination is completed, or perhaps sometimes inparallel with it, the estimator needsto identify andabstractfrom the bills thosesections of the work which it is envisaged will be subcontracted, and also toabstract details of all of the major materials required, together with their totalquantities.

In addition to a study of the project tender documents, there is a widevariety of 'standard' documents which may apply to the works. Perhapsthe most important among these, from the estimator's point of view, arethe various standard methods of measurement for construction work incommon use, and the various standard forms of contract in use in theindustry. Some combination of these standard documents often forms oneof the main planks upon which the framework of the project procurementmethodology is based, and may be referred to in the tender documentation, but copies will rarely be provided. These documents include important information about the contractor's general obligations and, in the caseof Standard Methods of Measurement, about items of work which theestimator will be deemed to have included in his estimate, but which willnot be explicitly quantified in the bill of quantities. It is therefore mostimportant that the estimator should be thoroughly familiar with their scopeand contents.

2.7 ESTABLISHMENT OF A PROGRAMME FOR ESTIMATE ANDTENDER PREPARATION

The estimator w ill usually act as the manager of the estimate productionprocess, and will be responsible for coordinating the work of colleagues. Theestimator will therefore be responsible for establishing the necessary keydates to allow the estimate to be prepared within the time available. It isperhaps worth noting that the time allowed for preparationof a typical tenderfor a project basedon a bill of quantities is usuallya maximum of only four or

22 Estimating, Tendering and Building for Construction

five weeks, and this crucial activity will typically represent perhaps only asmall proportion, perhaps one th irtieth or less, of the overall projecttime-scale.

The following dates must be clearly established as early as possible :

1. Latestdate for dispatch of enquiries for materials, plant and subcontractors' work

2. Latest date for receipt of quotations

3. Finalisation of the method statement

4. Completion of pricing

5. Adjudication meeting

6. Tender submission

2.8 SITE VISIT

For most projects a site visit will be essential in order to gain an accurateimpression of the site and its surroundings. Among the more importantconsiderations should be:

1. General site particulars, including soil and groundwater, location andtopography, any existing structures, condition and present use of anybuildings abutting the site, availability of drainage and other public utilityservices, areas available for materials storage, site hutting etc., site access,police regulations and parking restrictions, security and likelihood of theftand vandalism, and trees to be protected.

2. Location of the nearest town, travelling distance, public transport links,possible accommodation for workforce etc.

3. Location of suitable tips, charges.

4. Demolition works and possible salvageable materials.

5. Local labour, subcontractors and materials suppliers .

6. Possibility of complaints regarding noise, dust and other pollution.

7. Weather conditions.

Photographsshould be takenof the site, showing access,relevant buildingsand other structures, and any other important features. The use of a standardpro forma such as that given in CIOB (1983) may be a useful way to ensurethat all the relevant detail is collected.

The Estimating Process 23

2.9 ANALYSIS OF PRIME COST AND PROVISIONAL SUMS

Provisional sums are sums of money included to cover work which, at thetime the tender documents are prepared, cannot be adequatelydescribed andmeasured. In the caseof a bill of quantities measured in accordancew ith theStandard Method ofMeasurement for Building Works, 7th edn (SMM7) in theUK, prov isional sums must be identified as being for either 'defined' or'undefined' work. 'Undefined' work is work which mayor may not berequired, whereas 'defined' work is work which is known to be required, butwhich cannot be adequately measured and described at the time the bills areprepared. One important point arising from this is that preliminaries andoverheads costs included in the tender must cover defined work, but do nothave to cover undefined work.

Prime cost sums are sums of money inserted into project documentationto cover work to be completed by subcontractors and suppliers who will bechosen by the architect or engineer to complete certain specified parcels ofwork.

Relevant issues to do w ith the pricing of work in connection with primecost sums are considered in detail in Chapter 7, but an early analysis of theapproximate total proportion of the project value covered by prime cost andprovisional sums will be useful to the estimator in gaining a 'feel' for theproject as a whole .

2.10 REFERENCES

Adrian j .j .A. (1982) Construction Estimating, Reston Publishing Co, RestonVA.Ashworth A., and Skitmore R.M. Accuracy in Estimating, Occasional Paper No. 27,

Chartered Institute of Building, London.Ayres C. (1984) Specifications for architecture, engineering and construction, second

edition, McGraw Hill, USACIOB (1983) CodeofEstimating Practice, The Chartered Institute of Building, London.Davies F.A.W. (1980) 'Preparation and settlement of competitive lump sum tenders

for building works', in The Practice of Estimating, The Chartered Institute ofBuilding, London.

Fine B. (1974) 'Tendering Strategy, Building, 25 October 1974, pp. 115-21.Fine B. (1975) 'Tendering Strategy', in Aspectsof the Economics of Construction, (ed.

Turin D.A.), Macmillan, London.Ostwald P.F. (1992) Engineering Cost Estimating, 3rd edn, Prentice-Hall, Englewood

Cliffs Nj .Raftery j . (1991) Principles of Building Economics, BSP Professional Books, United

Kingdom.

3 Estimating TechniquesUsing Historical Cost Data

3.1 INTRODUCTION

A wide rangeof techniques exists for the forecasting of construction costs andprices, ranging from, at one extreme, simple unit cost-based predictions, tocomplex analytical estimating techniques at the other. The particular technique chosen in each case, and the degree of accuracy of the resultingprediction, will depend to a very large extent on the amount and quality ofinformation about the proposed building which is available at the time.

Research by Fortune and Lees (1994) shows that the majority of early stagecost estimating techniques in current use are still concerned primarily withinitial capital cost, despite a growing pressure from academics for a deeperconsideration of estimating systems wh ich deal with the whole life cost ofprojects . The major techniques in common use, in increasing order of potential accuracy, are therefore:

1. Cost per funct ional unit

2. Cost per unit of floor area

3. Elemental cost estimating

4. Analytical estimating

The first three techniques generally make use of historical data, and areusually used for early stagecost predictions at various stages throughout thedesign process. While these early stage techniques (or variations of them)have long been used by contractors for smaller projects, usually those basedon plans and specifications, they are now beginning to become more widelyused for larger projects, particularly with the present shift towards design andbuild-based approaches to construction procurement, where the design maybe incomplete at the time of the bid submission. Nonetheless, use of thesetechniques, and collection of the necessary data to support them, is more

24

Estimating Techniques Using Historical Cost Data 25

usually considered to be part of the quantity surveyor's construction economics function, and it would perhaps be more usual for contractors to seekadvicefrom specialist quantity surveyors in the preparation of estimates of this typewhere complex projects are concerned. These historical cost-based techniques are therefore considered here in outl ine only, and those seeking a moredetailed treatment of the subject should refer to a specialised text on construction economics, such as Seeley (1995) or Ferry and Brandon (1991).

The fourth technique, analytical estimating, makes use of current cost dataand is the approach most often used by contractors in the competitivetendering situation. Analytical methods are dealt with separately in detail inChapters 4-6.

3.2 COST PER FUNCTIONAL UNIT

One way of forecasting the probable cost of a proposed new building, perhapsthe easiest, would be to look at how much similar buildings have cost in thepast. If, for example, a contractor has previously built aschool of acertain sizeand level of specification, and is lucky enough to be invited to build anotherschool of similar size and specification but on a different site, it ought, in theabsence of any detailed design information for the new building, to bepossibleto use the historical cost data from the first scheme to give a reasonablyaccurate prediction for the construction cost of the new project. The datawould of course need to be adjusted for the effects of time (cost inflation) anddifferent site and market conditions, but nevertheless the data should besufficient to give a reasonably accurate guideline estimate for the cost of thenew building.

It is, however, rare to get two schemes that are exactly the same, and if weare to consider the use of historical data of this type we are therefore forcedinto a position where the best we can hope for is to find one or more previousschemes which are, in some respects, similar to the proposed project, andsomehow to adjust the cost data to suit the new scheme.

Perhapsthe simplest way is to express the historical costs in terms of somefunctional unit. In the caseof a school, for example,costscould be expressedperpupil place, or in the case of a hospital in terms of cost per bed. Using this veryrough and ready analysis the historical costs of a number of previous schemes,each suitably adjusted for time, can be combined and usedto prepareearly stagecost estimates for the construction of similar buildings in the future. Theestimateswill, of course, be subject to a large margin of error, perhaps as much as ±30%,but may nevertheless be useful in setting outline budgets.

This, and the other following price forecasting techniques described, arefairly well developed in the case of build ing projects, but much less so for civilengineering, since the costs for this type of work are considered to be muchmore dependent upon the detailed programme and working methods to be

26 Estimating, Tendering and Building for Construction

used. There has consequently been a tendency to postpone any attempt atdetailed estimating until the tendering stage, relying up to that point onestimates prepared on a simple 'cost per mile lkrnl' basis. According to Spon(1994 , p. 3):

The result has been a growing pressure on the part of project sponsorsfor an improvement in budgetary advice, so that a decision to commitexpenditure to a particu lar project is then taken on fi rmer grounds. Theabsence of a detailed pricing method during the pre-contract phase alsoinhibits the accurate cost ing of alternative designs and regular costchecking to ensure that the design is being developed within theemployer's budget.

3.3 COSTS PER UNIT OF FLOOR AREA