Equity Research - The Economic Times

31

Please refer to important disclosures at the end of this report Market Cap Rs24.9bn/US$334mn Year to Mar FY21 FY22E FY23E FY24E Reuters/Bloomberg GTIC IN / GATI.BO Revenue (Rs mn) 13,142 15,378 19,109 22,988 Shares Outstanding (mn) 123.0 EBITDA (Rs mn) 271 738 1,703 2,360 52-week Range (Rs) 212 / 84 Net Income (Rs mn) (2,429) 184 767 1,179 Free Float (%) 48.2 EPS (Rs) (19.9) 1.4 5.9 9.6 FII (%) 4.3 P/E (x) NM 145.9 35.0 21.5 Daily Volume (US$/'000) 3,120 EV/E (x) 100.7 36.0 15.1 10.2 Absolute Return 3m (%) 46.2 RoCE (%) 0.3 3.7 9.8 13.6 Absolute Return 12m (%) 123.0 Adjusted RoCE (%) 1.3 13.8 35.2 46.7 Sensex Return 3m (%) (2.9) RoE (%) (46.3) 3.3 12.2 15.8 Sensex Return 12m (%) 20.2 Adjusted RoE (%) NM 14.4 37.5 36.6 Equity Research January 24, 2022 BSE Sensex: 59037 ICICI Securities Limited is the author and distributor of this report Initiating coverage Logistics Target price Rs288 Shareholding pattern Jun ’21 Sep ’21 Dec ’21 Promoters 52.2 51.9 51.8 Institutional investors 2.7 4.0 5.5 MFs and others 1.5 1.7 1.2 FI/Banks 0.1 0.1 0.1 FIIs 1.2 2.3 4.3 Others 45.1 44.1 42.7 Source: NSE Price chart Gati Ltd. BUY Core business RoCE to reach ~50% in FY24E; initiate with BUY Rs202 0 50 100 150 200 250 Jan-19 Jul-19 Jan-20 Jul-20 Jan-21 Jul-21 Jan-22 (Rs) Research Analysts: Abhijit Mitra [email protected] +9122 6807 7289 Mohit Lohia [email protected] +91 22 6807 7510 Pritish Urumkar [email protected] +91 22 6807 7314 We initiate coverage on Gati with a BUY rating and target price of Rs288/share (30x FY24E P/E). Gati, along with Safexpress, TCI Express, Blue Dart, and Delhivery, remains one of the key organised express logistics players pan-India. Recent acquisition (CY19) by Allcargo has revived Gati’s corporate ambitions of reclaiming the best express logistics player status in the country. The actions taken, under the new management team, to stem past 7-8 years of market share loss appear promising. We concur with management vision of 3x revenue growth with improved margin profile over next three years. This will potentially allow expansion of profitability, earnings as well as valuations multiple over FY22E-FY24E. We studied the impending IPOs of new-age logistics players and their implied valuations – and we find Gati’s valuation much more nominal and conducive, given its underlying profitability and growth potential. Execution shortfalls, industry slack, heating-up of competition and corporate actions are key risks to our call. Transformation programme and new strategic direction to boost revenues ~3x and improve margins. Allcargo acquired Gati in CY19 (47% stake). It has also infused additional equity (~Rs 700mn including warrants). While revenues from the express business for Gati are comparable to TCI Express, Gati’s margins are significantly suppressed (management continues to guide for 12-14% EBITDA margins in express business). Post-acquisition, Allcargo started a transformation programme consisting of: i) de-levering meaningfully through non-core asset sales and pursuing asset-light business model (along with balance sheet cleanup), and ii) cost optimisation. Recent recruitment of CEO, Mr. Pirojshaw Sarkari (ex-MD of Mahindra Logistics), has allowed Gati to embark on a new strategic direction. Key targets are to grow the top line ~3x in three years (along with margin improvement expected from the transformation project) as Gati strives to establish itself as a logistics fulfillment company. We believe 3x revenue growth should be comfortably achievable in the proposed timeframe (3 years) given industry tailwinds, current scale, customer connect and focus on improving service delivery. Management has embarked on improving turnaround time through improved infrastructure. Two new transshipment hubs (in Ambala and Farukhnagar) have started operations while five more are under construction. With improving turnaround time, focus on digitisation and the diversity of existing customer relationships, management is confident of increasing wallet share as customer confidence on Gati’s service delivery improves. Efforts are also underway to: i) increase MSME penetration, and ii) target B2B retail market (music to our ears; for a listed express logistics play to target B2B e-commerce segment; market valuations of the platform providers, i.e. Indiamart, Udaan, Moglix, etc. have proliferated and Indian B2B e- commerce market is expected to reach US$1trn GMV by CY24 with current transport happening mostly through unorganised segment Link) B2B express market is also expected to double in the next five years, after a lacklustre run in the preceding five. INDIA

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Equity Research - The Economic Times

Please refer to important disclosures at the end of this report

Market Cap Rs24.9bn/US$334mn Year to Mar FY21 FY22E FY23E FY24E Reuters/Bloomberg GTIC IN / GATI.BO Revenue (Rs mn) 13,142 15,378 19,109 22,988 Shares Outstanding (mn) 123.0 EBITDA (Rs mn) 271 738 1,703 2,360 52-week Range (Rs) 212 / 84 Net Income (Rs mn) (2,429) 184 767 1,179 Free Float (%) 48.2 EPS (Rs) (19.9) 1.4 5.9 9.6 FII (%) 4.3 P/E (x) NM 145.9 35.0 21.5 Daily Volume (US$/'000) 3,120 EV/E (x) 100.7 36.0 15.1 10.2 Absolute Return 3m (%) 46.2 RoCE (%) 0.3 3.7 9.8 13.6 Absolute Return 12m (%) 123.0 Adjusted RoCE (%) 1.3 13.8 35.2 46.7 Sensex Return 3m (%) (2.9) RoE (%) (46.3) 3.3 12.2 15.8 Sensex Return 12m (%) 20.2 Adjusted RoE (%) NM 14.4 37.5 36.6

Equity Research January 24, 2022 BSE Sensex: 59037 ICICI Securities Limited is the author and distributor of this report

Initiating coverage

Logistics

Target price Rs288 Shareholding pattern

Jun ’21

Sep ’21

Dec ’21

Promoters 52.2 51.9 51.8 Institutional investors 2.7 4.0 5.5 MFs and others 1.5 1.7 1.2 FI/Banks 0.1 0.1 0.1 FIIs 1.2 2.3 4.3 Others 45.1 44.1 42.7

Source: NSE Price chart

Gati Ltd. BUY

Core business RoCE to reach ~50% in FY24E; initiate with BUY Rs202

0

50

100

150

200

250

Jan-

19

Jul-1

9

Jan-

20

Jul-2

0

Jan-

21

Jul-2

1

Jan-

22

(Rs)

Research Analysts:

Abhijit Mitra [email protected] +9122 6807 7289 Mohit Lohia [email protected] +91 22 6807 7510 Pritish Urumkar [email protected] +91 22 6807 7314

We initiate coverage on Gati with a BUY rating and target price of Rs288/share (30x FY24E P/E). Gati, along with Safexpress, TCI Express, Blue Dart, and Delhivery, remains one of the key organised express logistics players pan-India. Recent acquisition (CY19) by Allcargo has revived Gati’s corporate ambitions of reclaiming the best express logistics player status in the country. The actions taken, under the new management team, to stem past 7-8 years of market share loss appear promising. We concur with management vision of 3x revenue growth with improved margin profile over next three years. This will potentially allow expansion of profitability, earnings as well as valuations multiple over FY22E-FY24E. We studied the impending IPOs of new-age logistics players and their implied valuations – and we find Gati’s valuation much more nominal and conducive, given its underlying profitability and growth potential. Execution shortfalls, industry slack, heating-up of competition and corporate actions are key risks to our call. Transformation programme and new strategic direction to boost revenues ~3x and

improve margins. Allcargo acquired Gati in CY19 (47% stake). It has also infused additional equity (~Rs 700mn including warrants). While revenues from the express business for Gati are comparable to TCI Express, Gati’s margins are significantly suppressed (management continues to guide for 12-14% EBITDA margins in express business). Post-acquisition, Allcargo started a transformation programme consisting of: i) de-levering meaningfully through non-core asset sales and pursuing asset-light business model (along with balance sheet cleanup), and ii) cost optimisation. Recent recruitment of CEO, Mr. Pirojshaw Sarkari (ex-MD of Mahindra Logistics), has allowed Gati to embark on a new strategic direction. Key targets are to grow the top line ~3x in three years (along with margin improvement expected from the transformation project) as Gati strives to establish itself as a logistics fulfillment company.

We believe 3x revenue growth should be comfortably achievable in the proposed timeframe (3 years) given industry tailwinds, current scale, customer connect and focus on improving service delivery. Management has embarked on improving turnaround time through improved infrastructure. Two new transshipment hubs (in Ambala and Farukhnagar) have started operations while five more are under construction. With improving turnaround time, focus on digitisation and the diversity of existing customer relationships, management is confident of increasing wallet share as customer confidence on Gati’s service delivery improves. Efforts are also underway to: i) increase MSME penetration, and ii) target B2B retail market (music to our ears; for a listed express logistics play to target B2B e-commerce segment; market valuations of the platform providers, i.e. Indiamart, Udaan, Moglix, etc. have proliferated and Indian B2B e-commerce market is expected to reach US$1trn GMV by CY24 with current transport happening mostly through unorganised segment Link) B2B express market is also expected to double in the next five years, after a lacklustre run in the preceding five.

INDIA

Gati, January 24, 2022 ICICI Securities

2

Initiate with BUY and target price of Rs288/share. There are strong barriers to entry in the express logistics business, which don’t allow startups to make any meaningful dent in the industry or create pricing pressure. Further, operating with leased-out vendors (small fleet operators) in an environment where pressure of rails on road is relentless, has its own margin tailwind. Indian rail capex has increased ~3x over the past five years intensifying the rail to road shift; DFC will only further accelerate the shift – allowing increasingly better bargaining power for the road express logistics service providers. A comparison of costs with TCI Express underlines the potential margin improvement that Gati can embark upon. Recent strategic clarity on improving existing wallet share adds to our confidence and explains the valuation of 30x P/E on FY24E that we attribute to Gati.

Gati, January 24, 2022 ICICI Securities

3

TABLE OF CONTENT Gati is set to reclaim its pole position in Indian road express logistics .................... 4

History of Gati – The original proponent of road express in India ............................. 7

Ground express logistics is expected to witness 20% CAGR (CY20-CY25) .................. 8

New strategic direction ................................................................................................. 12

Allcargo Logistics: Strategic demerger with sharper focus on individual undertakings 17

Board of the company ................................................................................................... 18

Subsidiaries / Associates / JV ...................................................................................... 22

Audit and auditor’s opinion .......................................................................................... 23

Key related party transactions – cleaning up in progress ........................................ 24

Valuation methodology and key risks - Initiate with BUY ............................................. 26

Risks to investment thesis ............................................................................................ 27

Financial summary ........................................................................................................ 28

Index of Tables and Charts ........................................................................................... 30

Gati, January 24, 2022 ICICI Securities

4

Gati is set to reclaim its pole position in Indian road express logistics Gati, along with Safexpress, TCI Express and Blue Dart, remains one of the key express players pan-India. IT hardware, pharma and engineering companies remain prospective customers for Gati. Allcargo management acquired Gati in CY19 (47% stake). Allcargo has infused additional equity (~Rs 700mn including warrants). Per unit revenue for express business for Gati is similar to TCI E, but margins are significantly suppressed – management continues to guide for 12-14% margins in express. Company continues to de-lever meaningfully while undergoing cost optimisation and is set to reclaim its number one position in Indian road express space.

Chart 1: Gati in charts – past leader in express logistics (road) in India; trying to reclaim the position

Source: Company, I-Sec research

Chart 2: Surface express contributes 89% of FY21 top line, with key enterprise accounts contributing 52%, SME 26% and retail 22%

Source: Company, I-Sec research

Gati, January 24, 2022 ICICI Securities

5

Table 1: India’s leading end-to-end logistics solutions Services Description

Express Logistics (The main business)

Express Plus: A unique service that offers faster delivery compared to any average surface movement services. With direct route connectivity to major locations across India, one can save on time and ensure safety of shipments. Express A cost-effective surface cargo movement for shipments that have a time-definite delivery schedule. Premium Plus Specially designed service that promises delivery within 12 hours or before noon the next day, across all major ports in India. Premium A cost-effective service that assures delivery within 24 hours, 48 hours and more than 48 hours through multi-modal network across metros and non-metros in India.

Air Freight

Gati Air brings a dedicated air freight service built over 30 years of logistics and supply chain experience, and a commitment to moving cargo across India’s metros and non-metro cities alike. Gati’s experience along with network and tie-up with IndiGo Airlines, India’s largest airline, gives an edge when it comes to safely and efficiently moving cargo across India.

Cold Chain Solutions (Divested to Mandala capital)

Gati Kausar: A dedicated cold chain team, Gati Kausar, is India’s longest established cold chain service provider, with over 30 years of experience in cold chain distribution, offering temperature-sensitive shipments for consumer foods, pharmaceuticals, retail and agricultural goods. Gati’s promise of ‘Zero missed deliveries’ is backed by a fleet of over 200 refrigerated vehicles, ensuring the safe and timely delivery of perishable goods across India.

Gati, January 24, 2022 ICICI Securities

6

Source: Company, I-Sec research

Services Description

E-Commerce Solutions (Pivoted to mainly heavy parcel deliveries)

Gati E-Connect: This is a dedicated e-commerce logistics vertical and India’s first integrated e-commerce logistics solutions provider. Backed by Express Distribution, Gati E-Connect can reach over 99% of India’s districts to offer seamless last-mile delivery solutions.

Warehousing Solutions (3PL can drive the next leg of growth for Gati)

The supply chain management solutions feature over 65 warehouses across the country, including 3 e-fulfillment centres that cater to sectors like e-commerce, hospitality, healthcare and electronics, among others. Each warehouse is designed and built to meet global standards, equipped with dedicated team of experts backed by the latest tools, technologies and processes.

Gati, January 24, 2022 ICICI Securities

7

History of Gati – The original proponent of road express in India Gati was the original express distribution arm of Transport Corporation of India (TCI), which got demerged from the company in 1989. TCI subsequently formed another express logistics arm, TCI Express, which got demerged in CY16.

Back in 1997, Gati started express delivery for heavy shipments like AC and ATM machines for its clients like Blue Star and NCR Corporation.

ATM machines had a red tilting metre, which marked red if the machine slanted beyond a limit and the banks would reject such ATMs. Gati took up the challenge. While express cargo moved from Chennai to Delhi at Rs2-2.5/kg, Gati demanded Rs12/kg with a daring proposition ‘On-time delivery, else money back’. Gati also started Cash on Delivery (CoD) for Indian logistics. (Link) Gati started with 5,120 PIN codes and 15,400 remote ones. It also followed a hybrid model – allowing associates who functioned as entrepreneurs (in extra service locations), to make money with the number of packets handled.

Between CY10-CY13, business verticals such as consumer durables, apparel and textiles grew by a CAGR of 40%.

Gati partnered with Japanese Kintetsu Express (KWE) in CY12, where KWE invested Rs2.7bn and Gati retained 70% stake. Gati KWE Express eventually turned out to contribute 64% of Gati’s revenues and 48% of its EBITDA (at present, the express business forms 89% of top line).

However, the slowdown in the past few years was linked to Mr. Mahendra Agarwal (promoter, erstwhile MD) diverting his attention to a hydropower project in Sikkim and pledged his shares in Gati to invest in Amrit Jal Ventures. At the time of Gati’s stake sale to Allcargo, he had 2% stake left in the company. The deal by Allcargo also faced legal challenge from family members of Mr. Mahendra Agarwal

His son Manish Agarwal has in an interview stated how the Board was unwilling to optimise on employee costs – he cites it as one of the major drawbacks. (Link)

Gati also mixed up B2B express and B2C e-commerce, another instance where we have seen inherent lack of profitability of the B2C operations creating a drag on profitability.

In Dec’19, Allcargo Logistics bought controlling stake in Gati for Rs4.16bn and under the new leadership of Pirojshaw Sarkari, who has a track record of scaling up Mahindra Logistics India business and setting up UPS’ business in India, Gati’s prospects appear secure, in our view.

Gati, January 24, 2022 ICICI Securities

8

Chart 3: Events over the past 5 years lead to Allcargo’s acquisition of Gati and the start of a turnaround

Source: I-Sec research, Bloomberg

Ground express logistics is expected to witness 20% CAGR (CY20-CY25)

B2B express market deals with delivery of consignments with weights of between 10-2,000kgs. B2B express logistics providers operate a network of pick-up and delivery points and terminals where freight from different customers that is traveling in similar directions is consolidated. This consolidation leads to lower transportation costs for individual customers, while providing faster delivery times and greater flexibility. B2B express delivery typically entails turnaround times of 3-5 days, usually focused on smaller consignment sizes.

We believe ground express logistics is dominated by organised players. The factors that have helped a predominantly larger share for B2B express players are: changing customer expectations, e.g. brands and retailers with omni-channel operations increasingly need to match turnaround times of e-commerce players at affordable costs. Requirement of time-definite deliveries is also leading to increase in demand from pharma/chemicals/textiles (driven by higher exports) (critical shipments dictate supply chain requirements). Recovery in automobile demand, pick-up in BharatNet capex and impending spend in 5G implementation – all are expected to contribute to an uptick in B2B express business in India over the next 3-5 years.

Gati, January 24, 2022 ICICI Securities

9

Chart 4: B2B express market in India expected to take off

Source: Company Management highlights that the Indian B2B express industry is scheduled to grow from Rs135bn in FY20 to

Rs246bn in FY25 Correspondingly, the ground express segment where Gati is a major player is scheduled to increase from Rs115bn in FY20 to Rs217.7bn in FY25.

(These estimates are quite subdued when compared to what Delhivery has suggested in its DRHP; in Delhivery DRHP, estimates of the Express PTL – which we believe is a B2B express market – has been shown as US$3bn in FY20 and is expected to grow to US$9bn by FY26. It also states that organised players accounted for ~24% share of Express PTL in FY20, which is expected to rise to ~70% by FY26, growing at a CAGR of 45%).

From a current ~10% market share, management targets 15%. Latest CEO interviews point to Rs30bn of revenues in three years.

Table 2: Gati has lost market share, margins and fallen behind on all operating parameters with peers like TCI Express (Rs mn) FY17 FY18 FY19 FY20 FY21 TCI Express 7,503 8,851 10,238 10,320 8,440 Blue Dart 5,898 6,419 7,281 7,283 7,543 Delhivery 9,003 13,397 17,518 Spoton 4,924 6,500 7,000 7,700 Safexpress 9,968 11,099 12,690 15,698 17,631 Gati KWE 11,103 11,663 12,288 11,594 10,168 Combined topline NA 51,958 62,394 69,413 NA Safexpress market share 13.7 TCI Express Market share 9.0 Gati KWE market share 10.1 Gati KWE market share (among peers) 21.7 18.8 16.7 Addressable market 115,000 Source: I-Sec research

Gati, January 24, 2022 ICICI Securities

10

Gati’s revenue share as percentage of peer set revenues has declined from 21.7% in FY18 to 16.3% to FY20. The comparison with TCI Express highlights many areas of potential improvement and a significant scope of margin improvement possible in the coming years.

Key difference with TCI Express: Gati is a franchise-led model similar to Safexpress while TCI Express is an owned model. Key similarity being in the asset-light nature of business – Gati is selling land, which it used to own for future sorting centre expansion and has also followed TCI Express into selling all owned trucks.

New franchise policy drafted and ~20 new franchises onboarded under the new policy as part of operational improvement initiative.

Table 3: Comparison with TCI Express (Rs mn) FY19 FY20 FY21 Revenues TCIE 10,238 10,320 8,440 Gati 12,288 11,640 10,640 Volumes (te) TCIE 847,500 880,000 700,000 Gati 897,537 852,312 781,451 Realisations/te TCIE 12,080 11,727 12,057 Gati 13,691 13,657 13,616 EBITDA/te TCIE 1,404 1,378 1,919 Gati 788 619 512 Gross Margin (%) TCIE 26.4 28.9 32.8 Gati 29.5 30.2 27.3 Gross Margin (Rs/te) TCIE 3,191 3,384 3,961 Gati 4,040 4,128 3,711 Employee Costs as % of topline TCIE 8.4 9.9 10.3 Gati 12.2 12.9 12.2 Employee Costs Rs/te TCIE 1,013 1,157 1,248 Gati 1,671 1,760 1,664 Other Expense as % of topline TCIE 6.4 8.9 5.4 Gati 11.5 12.8 11.3 Other Expense (per te) TCIE 774 849 794 Gati 1,581 1,748 1,536 Source: I-Sec research Despite being a franchise-led model, Gati's expenses are higher than TCI Express on all counts. Management does not expect this gap to be filled when they have guided for 12% margin on the express business. Some of the expense items in Gati KWE look much higher (as a % of revenue) when compared to TCI Express, key line items being office maintenance and repairs, electricity expenses, automation/email expenses, repairs and maintenance. Even payment of rates and taxes and insurance is higher than TCI Express. Some of the elements can be attributed to past ownership of trucks by Gati KWE, some due to operating leverage and the rest on account of possible efficiencies that can be captured. We would like to see at least 2.5-3% reduction in other expenses for Gati KWE over the course of next 2-3 years.

Gati, January 24, 2022 ICICI Securities

11

Table 4: Other expenses show significant room for reduction (vis-à-vis TCI Express) Gati KWE TCI Express

Other Expense as % of Revenue FY17 FY18 FY19 FY20 Other Expense as % of Revenue FY17 FY18 FY19 FY20 FY21 Lease Rentals 4.7 5.1 5.4 4.8 Lease Rentals 2.7 2.5 2.6 3.0 3.5 Rates and Taxes 0.18 0.22 0.16 0.29 Rates and Taxes 0.05 0.05 0.04 0.03 0.06 Insurance 0.11 0.09 0.09 0.11 Insurance 0.02 0.03 0.02 0.04 0.06 Telephone expenses 0.3 0.3 0.1 0.1 Telephone expenses 0.2 0.1 0.1 0.3 0.2 Printing and Stationery 0.2 0.2 0.2 0.2 Printing and Stationery 0.2 0.1 0.2 0.3 0.2 Travelling expenses 0.6 0.6 0.5 0.5 Travelling expenses 0.8 0.9 0.9 0.9 0.2 Professional and Legal expenses 0.3 0.3 0.5 0.4 Professional and Legal expenses 0.0 0.0 0.0 0.0 0.0 Advertisement Expenses 0.2 0.4 0.3 0.2 Advertisement Expenses 0.0 0.1 0.1 0.1 0.1 Office Maintenance and Repairs 1.41 1.59 1.47 1.53 Office Maintenance and Repairs 0.98 0.69 0.64 0.64 0.65 Electricity Expenses 0.84 0.77 0.76 0.80 Electricity Expenses 0.31 0.25 0.26 0.31 0.32 Automation Network Expenses 0.46 0.46 0.46 0.44 Automation Network Expenses 0.24 0.17 0.16 - - Miscellaneous Expenses 0.87 0.86 0.78 0.71 Miscellaneous Expenses 0.43 0.30 0.32 0.48 0.25 Allowance for Doubtful receivables 0.6 - 0.0 0.7 Allowance for Doubtful receivables - - - - - Bad debts and irrecoverable balances written off 0.4 2.1 0.2 0.5 Bad debts and irrecoverable balances

written off 0.1 0.1 0.1 0.1 0.0

Less: - Provision for loss allowance in earlier years - 0.0 -0.2 -0.1 Less: - Provision for loss allowance in

earlier years - - - - -

CSR 0.1 0.0 0.1 0.1 CSR - 0.1 0.2 0.2 0.2 Donations 0.1 0.1 0.0 0.0 Donations 0.2 0.2 0.0 0.0 0.0 Repairs and Maintenance 0.59 0.63 0.61 0.75 Repairs and Maintenance 0.54 0.48 0.42 0.31 0.38 Consultancy 0.10 0.17 0.12 0.13 0.11 Conference and Seminar 0.05 0.17 0.13 0.18 0.10 Total 12.0 11.7 11.5 12.4 Total 7.0 6.5 6.4 7.2 6.6 Source: I-Sec research

Table 5: Comparison of ‘other expenses’ breakup (absolute) with TCI Express Gati KWE TCI Express

(Rs mn) FY17 FY18 FY19 FY20 (Rs mn) FY17 FY18 FY19 FY20 FY21 Lease Rentals 525 594 663 556 Lease Rentals 202 219 267 313 297 Rates and Taxes 20 26 20 33 Rates and Taxes 4 5 4 4 5 Insurance 12 11 11 13 Insurance 2 3 2 4 5 Telephone expenses 32 32 17 13 Telephone expenses 11 8 8 26 13 Printing and Stationery 25 25 29 29 Printing and Stationery 14 12 17 32 17 Travelling expenses 66 73 62 54 Travelling expenses 56 84 96 98 20 Professional and Legal expenses 36 36 59 52 Professional and Legal expenses 1 0 0 1 0 Advertisement Expenses 26 46 31 27 Advertisement Expenses 2 11 14 14 11 Office Maintenance and Repairs 157 186 181 178 Office Maintenance and Repairs 73 61 65 66 55 Electricity Expenses 93 90 94 93 Electricity Expenses 23 22 27 32 27 Automation Network Expenses 51 54 56 51 Automation Network Expenses 18 15 16 Miscellaneous Expenses 97 100 96 83 Miscellaneous Expenses 32 27 33 49 22 Allowance for Doubtful receivables 68 6 85 Allowance for Doubtful receivables Bad debts and irrecoverable balances written off 40 246 25 53

Bad debts and irrecoverable balances written off 7 5 6 15 3

Less: - Provision for loss allowance in earlier years 5 (25) (8)

Less: - Provision for loss allowance in earlier years

CSR 8 4 9 7 CSR 5 20 18 21 Donations 7 15 4 4 Donations 12 16 1 3 2 Repairs and Maintenance 66 73 75 87 Repairs and Maintenance 41 43 43 33 32 Consultancy 8 15 13 14 9 Conference and Seminar 4 15 13 19 9 Total 1,335 1,361 1,419 1,438 Total 525 575 656 747 556 Source: I-Sec research, Bloomberg

Gati, January 24, 2022 ICICI Securities

12

Comparison with peers on key parameters – significant improvement possible across parameters

Chart 5: Gati KWE revenue performance against peers

Chart 6: Gross margin performance

11,387 10,168

8,440

9,968

17,631

- 2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000

FY15 FY16 FY17 FY18 FY19 FY20 FY21

(Rs

mn)

Gati KWE TCI E Safe Express

31.0 29.9

23.1

32.9

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY15 FY16 FY17 FY18 FY19 FY20 FY21

(%)

Gati KWE TCI E

Source: Company data, I-Sec research. Source: Company data, I-Sec research.

Chart 7: EBITDA margin performance Chart 8: RoE performance

9.9

4.2

8.3

15.9

10.2 10.6

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY15 FY16 FY17 FY18 FY19 FY20 FY21

(%)

Gati KWE TCI E Safe Express

24.6

(2.3)

23.3 23.2

9.6

24.1

(5.0)

-

5.0

10.0

15.0

20.0

25.0

30.0

FY15 FY16 FY17 FY18 FY19 FY20 FY21

(%)

Gati KWE TCI E Safe Express

Source: Company data, I-Sec research. Source: Company data, I-Sec research.

Chart 9: RoCE performance

15.5

(0.4)

20.8 23.3

11.4

15.7

(5.0)

-

5.0

10.0

15.0

20.0

25.0

30.0

FY15 FY16 FY17 FY18 FY19 FY20 FY21

(%)

Gati KWE TCI E Safe Express

Source: Company data, I-Sec research.

New strategic direction

Gati, January 24, 2022 ICICI Securities

13

Key elements of the new strategic direction: 1. Reach 12% margin in express logistics.

2. Reach Rs30bn of top line in 3 years’ time (exit FY25E with a run-rate of Rs30bn). One can expect growth quarter over quarter hereon.

3. Become a fulfillment logistics company – bring predictability and visibility in express delivery and reduce inventory holding time for customers.

Levers for the next 12 months: 1. Digitisation -- Gati is building an in-house team.

2. Infrastructure -- Gati is building seven hubs.

3. People – Will continue to induct new talent.

Areas of growth 1. Key account growth: Large B2B players require surface and air express.

2. MSME: Should drive growth as well as yield management.

3. Retail: B2B retail segment targeted (Udaan, Indiamart come to mind). Shipment-wise numbers are small, but customer-wise numbers are large.

Allcargo seems (based on our interaction) clear about resurrecting the brand and concentrating in the express logistic business. The commitment to this strategy can be confirmed with the management selling and closing off other businesses including Gati-Kausar. Mr. Pirojshaw Sarkari (Phil) has been appointed as Gati’s new CEO. He envisions to make Gati the best express logistics company in India, but not the largest with immediate things on his roaster being hiring fresh talent, improving infrastructure and digitisation.

Infrastructure holds a big piece of the puzzle while growing an express logistic business. In general, it is all about how quickly the trucks can turn around and how reliable the infrastructure is for future opportunities. Gati has identified seven cities (Ambala, Fahrukhnagar, Bengaluru, Mumbai, Hyderabad, Indore, Nagpur) to build large hubs of which the Ambala and Farukhnagar hubs are already open. These hubs are being built for the future with automation and are set up with ‘Gati Nivas’ for the ground handlers.

Further, the management is putting its focus on digitisation as the Gati enterprise management system (GEMS) was developed 15 years ago, and needs to be developed for this age. GEMS 2.0 will have proactive notification, extra layer of analytics and machine learning. Gati’s largest competitors in B2B are Safexpress and TCI Express, with Delhivery (a B2C company) becoming a hybrid from the acquisition of Spoton.

Allcargo has initially put in a transformation project (should be over by Mar’22 as per management), hiring a multinational consulting firm (Alvarez & Marsal). Gati is being transformed into an asset-light company; all owned trucks are sold off and also all owned property is being sold off (company is looking for long-leased properties). Further, the company brought in digital payment system for end of the month billing and CoD.

Management is also putting its efforts in operational transformation. Basic operations of express logistics are made of two objectives: 1) trucks reach on time, and 2) are loaded

Gati, January 24, 2022 ICICI Securities

14

up to 85~90% of their capacity. Control towers for the trucks have been set up and the trucks are fitted with GPS, which are constantly monitored. The next step is network planning to load and unload trucks efficiently. Gati has a good reach in terms of percentage of PIN codes in India. Typical sorting centre of an express logistics company has ~5x loading docks than a usual warehouse as the job is to load and unload rather than store goods. Turnaround time (TAT) of a successful express logistics player should be above 95%; Gati’s TAT is hovering around 80-85% and the new hubs will take the TAT up to ~90%. (Link) Company’s expansion strategy is to focus on the MSME sector, with a strong network at the base and be able to reach smaller tier-2 and tier-3 towns and connect them to the rest of India.

Gati synergies with ECU Worldwide Gati is planning to set up distribution network for Allcargo’s global subsidiary, ECU Worldwide, in India and overseas. ECU brings cargo from all around the world to India; then a customs house agent of the receiver comes and clears the cargo – Gati sees an opportunity in this space. It is also looking at setting up positions in industrial parks that Allcargo is establishing across the country and then it may take up setting up network for ECU in the overseas market. Gati’s ambition is to set up logistical network wherever ECU ferries cargo. For all this to be realised, Gati is working on developing its infrastructure, investing in young talent and digitisation.

Surface Transshipment Centre (STC) at Allcargo Logistics Park at Farukhnagar (Gurugram) Company launched its largest STC spread over 0.15mn-sqft, connecting to all major national highways. This will offer customers the advantage of optimised supply chains, reduced dwell time, access to all major national highways and seamless connectivity into the country’s hinterlands. Further, the company plans to set up seven more such facilities, including Mumbai, Bengaluru, Hyderabad, Nagpur and Indore, in the next 15 months and 12 such hubs in the next three years.

Gati, January 24, 2022 ICICI Securities

15

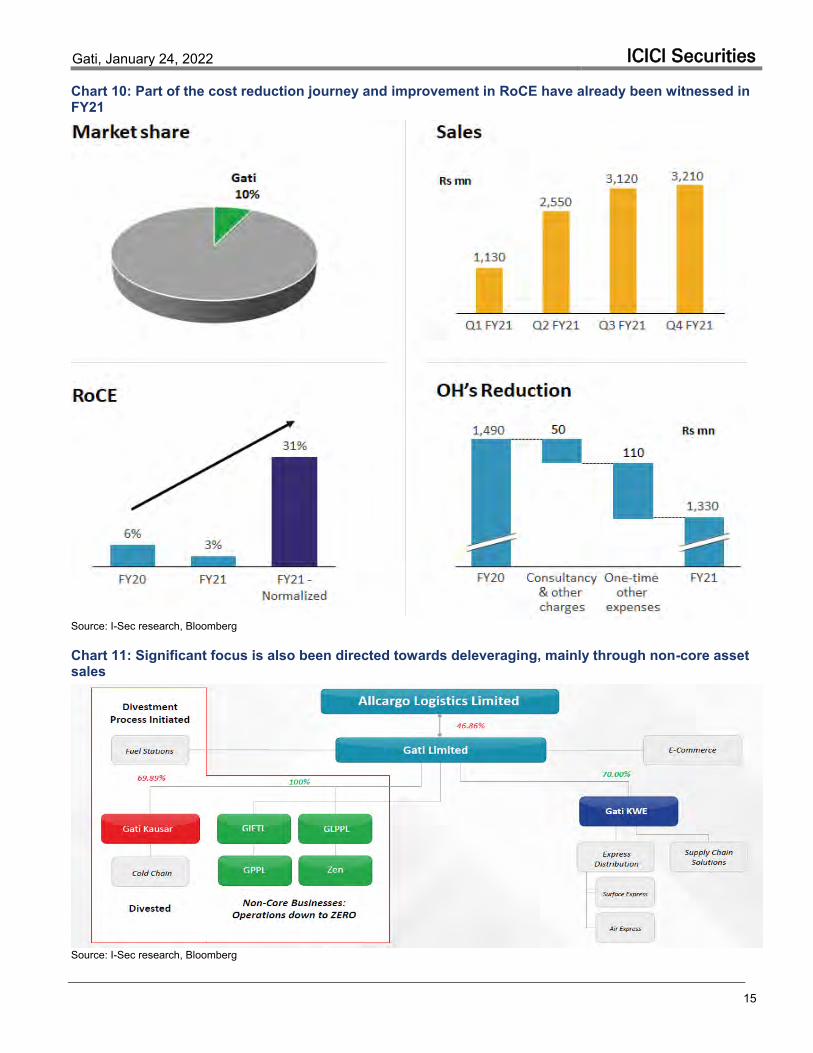

Chart 10: Part of the cost reduction journey and improvement in RoCE have already been witnessed in FY21

Source: I-Sec research, Bloomberg

Chart 11: Significant focus is also been directed towards deleveraging, mainly through non-core asset sales

Source: I-Sec research, Bloomberg

Gati, January 24, 2022 ICICI Securities

16

Chart 12: Net debt down to ~Rs1bn from Rs4bn from FY20

Source: I-Sec research, Bloomberg

Sale of cold chain (Rs1bn in debt reduction) and fuel retail business Rs1.6bn moved to assets held for sale leading to a drop in fixed assets. Has been monetising land and properties

to reduce debt 60% since Allcargo acquisition. Targeting zero debt. Monetised Rs600mn in the last year and another Rs1,500mn of non-core asset monetisation expected over the

next couple of years. Usage of Rs800mn infusion from Allcargo, Vivaad se Vishwas scheme -- Rs235mn paid. This has resulted

in contingent liability of Rs1.8bn reducing to low double-digit number. Rest will be gradually invested in the digital infrastructure.

Chart 13: Trying to create a better interface for customers – an effort that was core part of Gati 1.0

Source: I-Sec research, Bloomberg Salesforce implementation kicked off Customer portal redesign project in progress – in discussion with key service providers WhatsApp bot phase-2 launched – customer daily usage jumped 3x from Jan-Apr’21

Gati, January 24, 2022 ICICI Securities

17

Allcargo Logistics: Strategic demerger with sharper focus on individual undertakings

Allcargo has approved the demerger of its business units. Under the proposed scheme of demerger, equipment rental and real estate businesses will move to TransIndia and CFS/ICD (container freight stations / inland container depot) business into Allcargo Terminals Limited.

Allcargo Logistics. Allcargo will continue be the leader in the international supply chain, express logistics and contract logistics businesses with an increased focus on digitisation. This entity will continue to hold investment in Gati. Allcargo continues to grow full container load (FCL) mix (FCL has grown 7x in seven years and contributes majority of the volumes) in the business and expects to improve profitability though cost/productivity improvements (improvement in container utilisation) and procurement (better cargo visibility allowing better network utilisation). With higher volume growth, cost/productivity improvements, margins of the expanding FCL pie will counter the normalising freight environment (as and when that happens). There are other revenue levers that the management wants to develop, i.e. airfreight forwarding. Acquisition remains the key revenue driver for less than container load (LCL). Allcargo has completed three acquisitions in the recent past including Nordicon (Norway), which has helped consolidate market share (reaching 14% now from 12.5% earlier as the company launched a sales acceleration programme). Strategic acquisitions, where we feel management has already identified geographies and players, will continue to drive growth in this business. Organic growth can increase market share by 2%, and, along with inorganic acquisitions, market share can reach 17-18% as per management.

Allcargo Terminals. Allcargo Terminals will be the market leader in the CFS business in India and continue to expand its footprint in ICDs. The real estate for CFS/ICD has been transferred to TransIndia Logistics Park. Management believes there is a significant opportunity to grow in CFS and ICD businesses – specially in ICD along dedicated freight corridor (DFC). Allcargo has five CFS and one ICD at Dadri; recently they have completed the acquisition of Speedy (added two more CFS with one CFS at JNPT). These seven CFS facilities handle around 0.6-0.7mnteu. Acquisition of Speedy gives key advantages; second facility in JNPT with a complementary cargo mix. Allcargo facility in JNPT has a predominant import mix, while Speedy JNPT CFS has a predominant export mix. Speedy also has the closest CFS to JNPT.

TransIndia Logistics Park. Real estate business will comprise of a logistics park, land of CFS/ICD and the crane rental business (not a very prospective business as per management; they may exit it too). The capital employed here is Rs15bn. Logistics park business has high-quality assets leased out to Amazon, Flipkart, Decathlon, etc. Allcargo will create a portfolio of warehousing assets, hold the strategic assets and keep exiting the others based on regular assessment.

This will create a unique portfolio of best-in-class grade ‘A’ warehouses and other assets leased to marquee clients. The business will also hold shares in the JV with Blackstone. Post demerger, the business would have an opportunity to attract the right pools of capital as grade ‘A’ warehousing is in very strong demand, and capabilities of TransIndia will provide opportunities for robust growth.

Gati, January 24, 2022 ICICI Securities

18

Board of the company Table 6: Key changes in Board members in FY21

Source: I-Sec research

Name Category and Designation Remarks

Mr. Shashi Kiran Shetty Executive, Chairman & Managing Director Mr. Shashi Kiran Shetty was appointed as the Chairman of the Board and Managing Director of the Company w.e.f. July 24, 2020 and November 04, 2020 respectively.

Mr. Kaiwan Kalyaniwalla Non - Executive, Non-Independent Director Mr. Dinesh Kumar Lal Non - Executive, Independent Director Ms. Cynthia D’Souza Non - Executive, Independent Director Mr. Nilesh Shivji Vikamsey Non - Executive, Independent Director Mr. Nilesh Shivji Vikamsey was appointed as an Additional Independent

Director on the Board of the Company w.e.f. February 05, 2021. Mr. P N Shukla Non - Executive, Independent Director Mr. Yasuhiro Kaneda Non - Executive, Nominee Director Nominee Director being equity investor in GKEPL, represents Kintetsu

World Express (S) Pte Ltd. Mr. K L Chugh Non - Executive, Independent Director W.e.f. July 24, 2020, Mr. K.L. Chugh resigned from the Board due to age.

Mr. Mahendra Agarwal Executive, Managing Director, Founder & CEO (Promoter)

W.e.f. September 28, 2020, Mr. Mahendra Agarwal resigned from the Board pursuant to the Share Purchase Agreement entered by him along with two other Promoter group members with Allcargo Logistics Limited on December 05, 2019.

Mr. N Srinivasan Non - Executive, Independent Director W.e.f. January 01, 2021, Mr. N Srinivasan resigned from the Board due to age and related health issues.

Dr. P S Reddy Non - Executive, Independent Director W.e.f. July 08, 2020, Dr. P S Reddy resigned from the Board due to personal reasons.

Dr. Savita Date Menon Non - Executive, Independent Director W.e.f. October 12, 2020, Dr. Savita Date Menon resigned from the Board due to the transition of the Company into a new Management.

Mr. M.P. Bansal Non - Executive, Independent Director Mr. M.P. Bansal was appointed as an Independent Director on the Board of Company w.e.f. July 03, 2020, and w.e.f. March 04, 2021, he resigned from the Board due to personal reasons.

Mr. Adarsh Hegde Non - Executive, Non-Independent Director Mr. Adarsh Hegde was appointed as an Additional Director on the Board of Company w.e.f. July 03, 2020, and w.e.f. October 05, 2020, he resigned from the Board due to preoccupations and other professional commitments.

Mr. Jatin Chokshi Non - Executive, Non-Independent Director Mr. Jatin Chokshi was appointed as an Additional Director on the Board of Company w.e.f. July 03, 2020, and w.e.f. October 05, 2020, he resigned from the Board due to pre-occupations and other professional commitments.

Gati, January 24, 2022 ICICI Securities

19

Table 7: Current management profile Director Qualification / Experience Directorship in listed companies

Mr. Shashi Kiran Shetty Chairman and Managing Director

He is chairman of Allcargo Logistics, ECU Worldwide and Gati Ltd. He received a Doctorate in Literature from Mangalore University. Over the last 27 years, Mr. Shetty has built what is now India’s largest integrated logistics group. He has recently been appointed by, Ministry of Education as Chairman of the Society and Board of Governors of the National Institute of Industrial Engineering (NITIE), one of India’s premier engineering institutes. For his contribution to Belgian trade and industry, Mr. Shetty was awarded the Commander of the Order of Leopold II by King Philippe of Belgium in 2015.

Allcargo Logistics Limited (Promoter, Executive Director)

Mr. Nilesh Shivji Vikamsey Additional Independent Director

Mr. Vikamsey is Chartered Accountant and Senior Partner of Khimji Kunverji & Co LLP Chartered Accountants since 1985. A firm in practice since 1936, having over 80 years of experience in the areas of auditing, taxation, corporate & personal advisory services, business & management consulting services, due diligence, valuations, inspections, investigations, etc.

IIFL Finance Limited (Non-Executive, Independent Director) IIFL Wealth Management Limited (Non-Executive, Independent Director) Navneet Education Limited (Non-Executive, Non-Independent Director) Thomas Cook (India) Limited (Non-Executive, Independent Director PNB Housing Finance Limited (Non-Executive, Independent Director)

Mr. P N Shukla Independent Director

Mr. Shukla joined Indian Railway Traffic Service in 1976. He is a Rail Transport Operations & Logistics specialist. He completed M.Sc. in Physics & LLB from Allahabad University and graduated in business management.

Mr. Yasuhiro Kaneda Nominee Director

Mr. Yasuhiro Kaneda is a veteran in the logistics and freightforwarding industry; he has an experience of over 30 years. He is the managing director of KWE South East and South Asia Region. Mr. Kaneda holds a bachelor’s degree in commerce from Meiji University.

Mr. Kaiwan Kalyaniwalla Director

Mr. Kaiwan Kalyaniwalla, is a Solicitor and Advocate of the Bombay High Court. He has been in practice for over 34 years. He graduated from the University of Mumbai in Economics and Political Science and thereafter graduated as a Bachelor of Law (L.L.B) from the Government Law College. He also serves on the Board of public listed and private Indian and foreign companies and advises public and private sector corporates, multinational banks, transport and logistics companies and some of India’s largest property development companies and business houses. He is also on the investment committee of a SEBI registered real estate fund and NBFC and serves on the Board of a SEBI registered asset management trustee company.

Modern India Limited (Non-Executive, Independent Limited)

Ms. Cynthia D’Souza Independent Director

Ms. D’Souza’s experience spans over 44 years in the areas of general management, strategic planning, sales & marketing, and human resource management. Ms. D’Souza worked in very senior managerial positions in Coca Cola India Inc., Parke Davis-Warner Lambert – India, Eureka Forbes Ltd (a joint venture between Electrolux AB – Sweden and Forbes, Forbes & Campbell – India), Procter & Gamble and Tata Consultancy Services (the largest software company in India). Ms. D’Souza completed her graduation in psychology from Mumbai University in 1974 and master’s degree in human resources (including industrial psychology) from a premier institute in India in 1976 (Tata Institute of Social Sciences).

Allcargo Logistics Limited (Non-Executive, Independent Director)

Mr. Dinesh Lal Independent Director

Mr. Lal has four decades of experience in the shipping industry. He is renowned for his astute knowledge about the shipping industry. In the 45 years that he has been in the industry, he has held various positions such as Group Director-India, A P Moller-Maersk; Chairman, Gateway Terminals India Pvt Ltd; Director, Maersk Lanka; Director, Gujarat Pipavav Port Ltd; Director, Pipavav Railway Corporation Ltd; Managing Director, Safmarine; Trustee, Mumbai Port Trust; Trustee, Jawaharlal Nehru Port Trust – Mumbai; President, Nhava Sheva Ship Intermodal Agents Association; President; EU Chamber of Commerce; President, Indo-Belgium-Luxembourg Chamber of Commerce; and Chairman, Shipping Sub Committee - Mumbai Chamber of Commerce and Industry.

Raymond Limited (Non-Executive, Independent Limited)

Mr. Pirojshaw Sarkari Chief Executive Officer

Pirojshaw Sarkari is a Chartered Accountant and in his career trajectory, He has set up the UPS business and organisation in India and served as its managing director and country head till 2010. He then joined Mahindra Logistics as its CEO in 2010, where he built the team and fostered an organisational culture that resulted in the creation and growth of one of the largest and most successful 3PL businesses in India.

Gati, January 24, 2022 ICICI Securities

20

Source: I-Sec research

Table 8: Board structure

Source: I-Sec research

Table 9: Shareholding structure

Source: I-Sec research

Director Qualification / Experience Directorship in listed companies

Mr. G S Ravi Kumar Chief Information Officer

Mr. G.S. Ravi Kumar is an IT leader with over 30 years of demonstrated experience in strategising, planning, developing and implementing cutting-edge information technology solutions to address business opportunities. Prior to joining Gati Limited, he headed the Indian IT operations for a multinational, SHV Energy India Ltd., the world’s largest LPG company. He has been associated with Gati Limited as Chief Information Officer for over 19 years. He has played a major role in transforming the entire IT system of Gati Limited to be on par with the best in the industry. He was involved in successfully developing and implementing ‘Gati Enterprise Management System – GEMS’, a custom-developed ERP product for the express cargo industry.

Ms. T S Maharani Company Secretary & Compliance Officer

T.S. Maharani has over 20 years of experience handling compliance, secretarial, legal, finance and administration functions in the manufacturing industry, power sector and presently in the logistics sector. She is a qualified Company Secretary (FCS) with postgraduation in law (LLM), accountancy (MCOM) and business management (MBA).

Board has four independent directors out of 7 members. Key Committees Chairman Description Audit Committee Mr. Nilesh Shivji Vikamsey (Independent Director) 3 members with 2 Independent Directors Nomination & Remuneration Committee Mr. P N Shukla (Independent Director) 4 members with 2 Independent Directors Stakeholders Relationship Committee Ms. Cynthia D’Souza (Independent Director) 3 members with 1 Independent Directors CSR Committee Mr. Kaiwan Kalyaniwalla (Director) 3 members with 2 Independent Directors Risk Management Committee Mr. Nilesh Shivji Vikamsey (Independent Director) 2 members with 1 Independent Directors Finance Committee NA NA 0 Board Committees composed of 100% of Independent Directors Key Committees with Independent Chair Audit Committee, Nomination & Remuneration Committee, Risk Management Committee

Category Holding % Company Promoter / Promoter Group 51.9 FIIs 1.5 Banks / MFs / NBFC 0.1 Bodies Corporate 4.0 Individuals / HUF 36.4 NRIs 1.7 Foreign Corporate Bodies 3.6 IEPF 0.5 Clearing Members / Trusts 0.4 Foreign Nationals 0.0 Directors 0.0 Total 100.0

Gati, January 24, 2022 ICICI Securities

21

Chart 14: Quarterly shareholding structure

Source: I-Sec research, Bloomberg

Chart 15: Promoters’ holding and pledge

Source: I-Sec research, Bloomberg

17.8

%

14.7

%

7.8%

51.9

%

51.9

%

51.9

%

51.9

%

52.2

%

51.9

%

75.3

%

79.5

%

87.2

%

46.0

%

47.0

%

46.6

%

46.5

%

45.1

%

44.1

%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21Promoters Holding FIIs DIIs Public

17.8%14.7%

7.8%

51.9% 51.9% 51.9% 51.9% 52.2% 51.9%70.2%64.0%

34.1%

5.0% 5.0% 5.0% 4.8% 4.7% 4.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21

Holding Pledge (RHS)

Gati, January 24, 2022 ICICI Securities

22

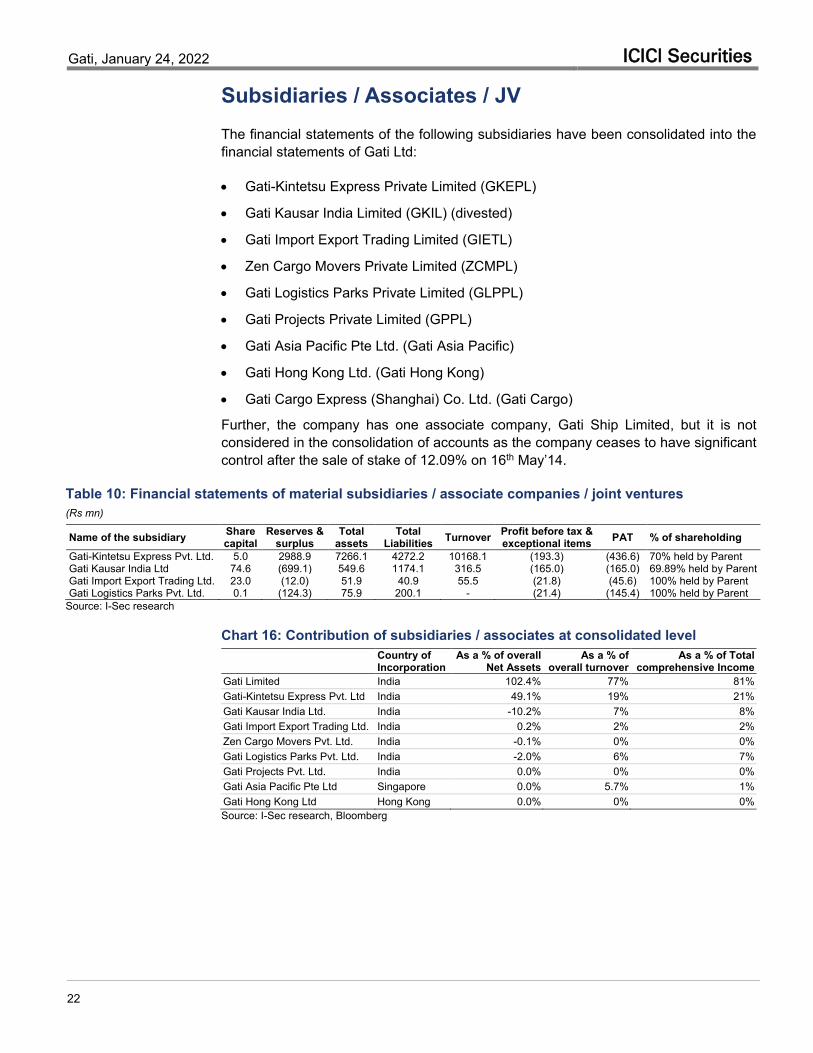

Subsidiaries / Associates / JV The financial statements of the following subsidiaries have been consolidated into the financial statements of Gati Ltd:

Gati-Kintetsu Express Private Limited (GKEPL)

Gati Kausar India Limited (GKIL) (divested)

Gati Import Export Trading Limited (GIETL)

Zen Cargo Movers Private Limited (ZCMPL)

Gati Logistics Parks Private Limited (GLPPL)

Gati Projects Private Limited (GPPL)

Gati Asia Pacific Pte Ltd. (Gati Asia Pacific)

Gati Hong Kong Ltd. (Gati Hong Kong)

Gati Cargo Express (Shanghai) Co. Ltd. (Gati Cargo)

Further, the company has one associate company, Gati Ship Limited, but it is not considered in the consolidation of accounts as the company ceases to have significant control after the sale of stake of 12.09% on 16th May’14.

Table 10: Financial statements of material subsidiaries / associate companies / joint ventures (Rs mn)

Source: I-Sec research

Chart 16: Contribution of subsidiaries / associates at consolidated level Country of

Incorporation As a % of overall

Net Assets As a % of

overall turnover As a % of Total

comprehensive Income Gati Limited India 102.4% 77% 81% Gati-Kintetsu Express Pvt. Ltd India 49.1% 19% 21% Gati Kausar India Ltd. India -10.2% 7% 8% Gati Import Export Trading Ltd. India 0.2% 2% 2% Zen Cargo Movers Pvt. Ltd. India -0.1% 0% 0% Gati Logistics Parks Pvt. Ltd. India -2.0% 6% 7% Gati Projects Pvt. Ltd. India 0.0% 0% 0% Gati Asia Pacific Pte Ltd Singapore 0.0% 5.7% 1% Gati Hong Kong Ltd Hong Kong 0.0% 0% 0% Source: I-Sec research, Bloomberg

Name of the subsidiary Share capital

Reserves & surplus

Total assets

Total Liabilities Turnover Profit before tax &

exceptional items PAT % of shareholding

Gati-Kintetsu Express Pvt. Ltd. 5.0 2988.9 7266.1 4272.2 10168.1 (193.3) (436.6) 70% held by Parent Gati Kausar India Ltd 74.6 (699.1) 549.6 1174.1 316.5 (165.0) (165.0) 69.89% held by Parent Gati Import Export Trading Ltd. 23.0 (12.0) 51.9 40.9 55.5 (21.8) (45.6) 100% held by Parent Gati Logistics Parks Pvt. Ltd. 0.1 (124.3) 75.9 200.1 - (21.4) (145.4) 100% held by Parent

Gati, January 24, 2022 ICICI Securities

23

Audit and auditor’s opinion Table 11: There are many potential areas of improvement including regularisation of old related party transactions, strengthening internal processes and systems

Year FY20 FY21 Auditor Singhi & Co. Singhi & Co. Report Qualified Qualified Qualification Basis for Qualified Opinion

Gati Kintetsu Express, has given operational advances to a few parties aggregating to Rs206.75mn (a provision of Rs21.85mn is been given) which is long overdue and full recoverability seems doubtful. But, the management is making necessary efforts to ensure collection of dues from those parties.

Gati Kausar India, has commitments of Rs83.77mn towards amended bond subscription agreement; however, absence of sufficient audit evidence in support of management assessment and pending final outcome of negotiation with the investors.

Gati Kintetsu Express: A recoverable of Rs14.09mn from an executive chairman towards managerial remuneration is outstanding in the books of FY20.

Material Uncertainty Related to Going Concern Gati Asia Pacific and one step-down subsidiary Gati HongKong Ltd incurred

a net loss of HKD13.02mn for the financial year ended 31st March 2020 and, as of that date, the subsidiary’s current liability and total liability exceeded its current assets and total assets by Rs1.50mn respectively. These events and conditions, indicate that a material uncertainty exists that may cast significant doubt on the subsidiary’s ability to continue as a going concern.

Gati Kausar India has incurred a net loss of Rs.141.60mn in FY20 and as of that date, the subsidiary’s accumulated losses amount to Rs924.10mn, which has resulted in complete erosion of the net worth of the said subsidiary, and the subsidiary’s current liabilities exceeded its current assets by Rs853.3mn. These conditions along with matters set forth in the said note, indicate the existence of a material uncertainty that may cast significant doubt about the subsidiary’s ability to continue as a going concern.

Emphasis of Matter Managerial remuneration paid to two executive directors of the company for

FY20 has exceeded the limit under section 197, schedule V of Companies Act 2013 by Rs40.3mn.

Qualification in Internal Financial Controls over Financial Reporting Subsidiary company’s internal financial controls related to contract

revenue mapping in IT systems is not operating effectively and resulting in inadequate control over process.

Subsidiary company does not have an effective integration between various functional software relating to sales and expenses resulting in weak internal control and reconciliation differences in Control Accounts.

Basis for Qualified Opinion Gati Kausar India, has commitments of

Rs83.77mn towards amended bond subscription agreement; however, absence of sufficient audit evidence in support of management assessment and pending final outcome of negotiation with the investors.

Material uncertainty related to going concern Gati Kausar has incurred a net loss of Rs165mn

in FY21 and accumulated loss of Rs1,098.2mn, which has resulted in complete erosion of the net worth; also, the subsidiary’s current liabilities exceed current assets by Rs958.2mn.

Emphasis of Matter Managerial remuneration paid to two executive

directors of the company (including one resigned in Sep’20) for FY21 has exceeded the statutory limit under Section 197, Schedule V of Companies Act 2013 by Rs27.5mn.

Qualification in Internal Financial Controls over Financial Reporting Subsidiary company’s internal financial

controls related to contract revenue mapping in IT systems is not operating effectively and resulting in inadequate control over process.

Subsidiary company does not have an effective integration between various functional software relating to sales and expenses resulting in weak internal control and reconciliation differences in Control Accounts.

Source: I-Sec research, Gati Annual report

Gati, January 24, 2022 ICICI Securities

24

Key related party transactions – cleaning up in progress Table 12: We see a progressive winding down of related party transactions as new management engages (Rs mn)

Source: I-Sec research; Gati Annual report

Related Party FY20 FY21 Remuneration Mr. Mahendra Agarwal (Left on Sep 20) 34.1 15.2 Mr. Bala Aghoramurthy (Left the company in FY22) 30.4 39.3 Mr. Adarsh Hedge 8.7 Mr. Rohan Mittal (Left the company in FY22) 4.3 Ms. T S Maharani 1.9 2.7 Rent Giri Roadlines & Commercial Trading * 64 32 Jaldi Traders & commerce house * 150 75 P.D. Agarwal Foundation * 13 25 TCI Telenet Solutions Pvt Ltd 36 16 Allcargo Logistics limited 15 Interest Expenses Mandala Agribusiness Investments II Ltd ** 333 345 Allcargo Logistics Limited 86 Premium on redemption of debenture Mandala Agribusiness Investments II Ltd ** 657 722 Solaflex Solar Energy Private Limited * 29 16 Manpower Expenses Gati Academy * 844 295 Management Fees Allcargo Logistics limited Sundry Debtors - Other Receivable Amrit Jal Ventures (Previously Sub) * 177 Provision Interest Receivable Amrit Jal Ventures (177) Gati Infrastructure Sada Mangder (Previously Sub) 39 Provision Interest Receivable- Gati Infrastructure Sada Mangder (39) Bala Aghoramurthy (Left the company in FY22) 10 Loans & Advances - Given Jaldi Traders & Commerce House * 570 TCI Highways Private Ltd (Holding Co) * 172 Less: Provision (22) Long term Borrowings Mandala Agribusiness Investments** 850 954 Investment held for sale Gati Ship Limited - Equity Shares (Associate) * 862 862 Less: Impairment (862) (862) Amrit Jal Ventures- OCDs * 346 346 OCD's Impairment (346) (346) Gati Infrastructure Sada Mangder (OCDs) * 99.3 OCD's Impairment -99.3 Corporate Guarantees given Gati Infrastructure * 236 Provision -236

Gati, January 24, 2022 ICICI Securities

25

Table 13: Significant balance sheet actions Air India Advance receivable includes Rs41mn due from Air India against which provision is made in FY21.

Provision towards advance – Related Parties

The group has total overdue advances given of Rs228.6mn to few parties in earlier years. Gati could not recover the agreed amount for which company has sent a legal notice to the said parties in FY20. Out of the amount receivable, the management had provided Rs21.8mn in FY20 and Rs225.6mn has been provided in FY21.

Gati Kausar 69.9% stake was sold to Mandala Capital in FY22. In FY21, decision was made not to draw down committed loan of Rs610mn (from the investors). GKIL has considered a provision of Rs3.1mn to be adequate to meet its obligations and is confident that no further financial obligations would dwell on GKIL.

Remuneration to previous management team

The managerial remuneration paid to the former Executive chairman and Managing Director (CMD) and current Deputy Managing Director of the subsidiary company, i.e., Gati Kintetsu Express Pvt Ltd., for FY21 exceeded the statutory limit by Rs27.5mn. The managerial remuneration paid to the former CMD and the Deputy MD of the subsidiary company, i.e., Gati Kintetsu Express Pvt Ltd. for FY20 has exceeded the statutory limit by Rs40.3mn. This excess remuneration has been waived off by the shareholders at AGM passing a Special Resolution. However, the waiver pertaining to the Executive CMD was conditional subject to the full refund of the excess of managerial remuneration paid to him for FY19 (amounting to Rs10.6mn) on or before 31st Jan’21. The same was recovered in full and hence the waiver of excess remuneration for FY20 was applicable.

Non-Core assets for monetisation

The group has identified certain non-core assets for monetisation. Rs588.9mn was realised in FY21 from sale of non-core assets and entire proceeds were used to discharge debt and other liabilities of the group.

Loss on Sale of Investments (Gati Asia Pacific)

The wholly-owned subsidiary, Gati Asia Pacific Pte Ltd (GAP), and its two stepdown subsidiaries ceased to be a subsidiary with effect from 16th Aug’20 after the transfer of investment to Allcargo, resulting in a loss of Rs112.7mn.

Source: I-Sec research; Gati Annual report

Gati, January 24, 2022 ICICI Securities

26

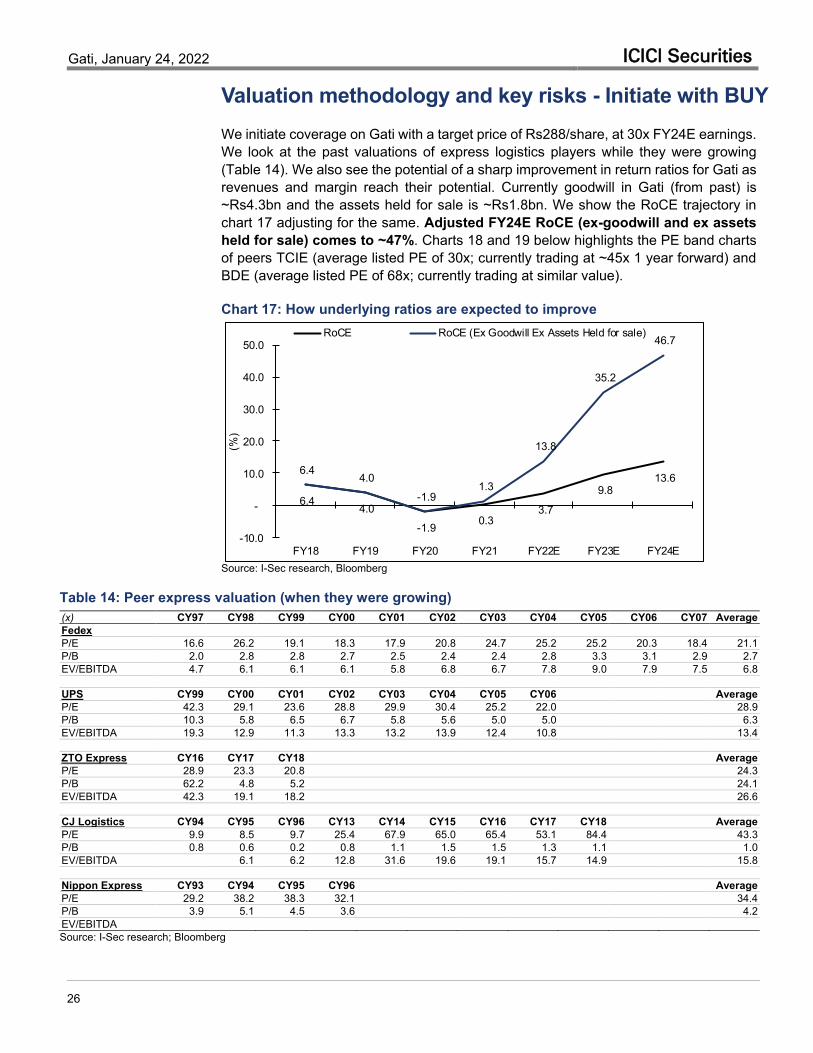

Valuation methodology and key risks - Initiate with BUY

We initiate coverage on Gati with a target price of Rs288/share, at 30x FY24E earnings. We look at the past valuations of express logistics players while they were growing (Table 14). We also see the potential of a sharp improvement in return ratios for Gati as revenues and margin reach their potential. Currently goodwill in Gati (from past) is ~Rs4.3bn and the assets held for sale is ~Rs1.8bn. We show the RoCE trajectory in chart 17 adjusting for the same. Adjusted FY24E RoCE (ex-goodwill and ex assets held for sale) comes to ~47%. Charts 18 and 19 below highlights the PE band charts of peers TCIE (average listed PE of 30x; currently trading at ~45x 1 year forward) and BDE (average listed PE of 68x; currently trading at similar value).

Chart 17: How underlying ratios are expected to improve

Source: I-Sec research, Bloomberg

Table 14: Peer express valuation (when they were growing)

Source: I-Sec research; Bloomberg

6.4 4.0

-1.9 0.3 3.7

9.8 13.6

6.4 4.0

-1.9 1.3

13.8

35.2

46.7

-10.0

-

10.0

20.0

30.0

40.0

50.0

FY18 FY19 FY20 FY21 FY22E FY23E FY24E

(%)

RoCE RoCE (Ex Goodwill Ex Assets Held for sale)

(x) CY97 CY98 CY99 CY00 CY01 CY02 CY03 CY04 CY05 CY06 CY07 Average Fedex P/E 16.6 26.2 19.1 18.3 17.9 20.8 24.7 25.2 25.2 20.3 18.4 21.1 P/B 2.0 2.8 2.8 2.7 2.5 2.4 2.4 2.8 3.3 3.1 2.9 2.7 EV/EBITDA 4.7 6.1 6.1 6.1 5.8 6.8 6.7 7.8 9.0 7.9 7.5 6.8 UPS CY99 CY00 CY01 CY02 CY03 CY04 CY05 CY06 Average P/E 42.3 29.1 23.6 28.8 29.9 30.4 25.2 22.0 28.9 P/B 10.3 5.8 6.5 6.7 5.8 5.6 5.0 5.0 6.3 EV/EBITDA 19.3 12.9 11.3 13.3 13.2 13.9 12.4 10.8 13.4 ZTO Express CY16 CY17 CY18 Average P/E 28.9 23.3 20.8 24.3 P/B 62.2 4.8 5.2 24.1 EV/EBITDA 42.3 19.1 18.2 26.6 CJ Logistics CY94 CY95 CY96 CY13 CY14 CY15 CY16 CY17 CY18 Average P/E 9.9 8.5 9.7 25.4 67.9 65.0 65.4 53.1 84.4 43.3 P/B 0.8 0.6 0.2 0.8 1.1 1.5 1.5 1.3 1.1 1.0 EV/EBITDA 6.1 6.2 12.8 31.6 19.6 19.1 15.7 14.9 15.8 Nippon Express CY93 CY94 CY95 CY96 Average P/E 29.2 38.2 38.3 32.1 34.4 P/B 3.9 5.1 4.5 3.6 4.2 EV/EBITDA

Gati, January 24, 2022 ICICI Securities

27

Chart 18: TCI Express PE Band chart Chart 19: Bluedart Express PE Band chart

Source: I-Sec research; Bloomberg Source: I-Sec research; Bloomberg

Risks to investment thesis Competition. Delhivery has acquired Spoton as they want to make a deeper dent in the express logistics industry. The addressable market that Delhivery has highlighted in its DRHP has potential of 45% CAGR for organised players between FY21-FY26E. The addressable market size is also much higher that what is being perceived by the traditional express logistics players as we have discussed on page 9. One reason of difference can be B2B e-commerce market, which can attribute scale to the operations of new-age startup looking for aggressive growth. This is an expanding market and GMV is expected to reach US$1trn in FY24 (Link) and the transport needs are majorly addressed by unorganised operators at present. There will be enough opportunities for everyone we feel.

Corporate action. Single biggest risk that we see can emanate from corporate restructuring. Gati should be left alone as a separate business to allow value unlocking and not be merged in Allcargo. We have asked this question repeatedly to management in various conference calls and management has been categorical in its assessment that Gati will be left as a separate business entity. Also, Allcargo is mindful of the current holding company discount that Gati attracts for Allcargo – as clarified by Mr. Shashi Kiran Shetty in latest investor interaction. As value unlocking starts happening in Gati, a revised structure will be thought of – we hope that the corporate action then is a demerger rather than a merger.

The process of acquiring the residual stake in Gati should be accelerated. We do expect the management to attempt buying out residual stake in Gati KWE and eventually merge Gati KWE in Gati. The acquisition and merger should happen before value unlocking. This, nevertheless, can relever the balance sheet.

Board has proposed an ESOP to allow suitable incentives to the management to ramp up the express business profitably. The same will come up for shareholder approval. We believe ESOP is a suitable incentivisation scheme for the new onboarded executive team (CEO and the recruitment he has done, including a new CFO who is expected to join from 1st Feb’22). Failure to suitably incentivise management can lead to attrition, especially given the increasing aspirations of new-age startups.

30x

20.0

25.0

30.0

35.0

40.0

45.0

Dec

-16

Mar

-17

Jun-

17O

ct-1

7Ja

n-18

Apr-1

8Ju

l-18

Oct

-18

Jan-

19M

ay-1

9Au

g-19

Nov

-19

Feb-

20M

ay-2

0Se

p-20

Dec

-20

Mar

-21

Jun-

21Se

p-21

Jan-

22

PE Average +1 StdDev -1 StdDev

68x

- 20.0 40.0 60.0 80.0

100.0 120.0 140.0 160.0 180.0 200.0

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16Ju

l-16

Jan-

17Ju

l-17

Jan-

18Ju

l-18

Jan-

19Ju

l-19

Jan-

20Ju

l-20

Jan-

21Ju

l-21

Jan-

22

PE Average +1 StdDev +1 StdDev

Gati, January 24, 2022 ICICI Securities

28

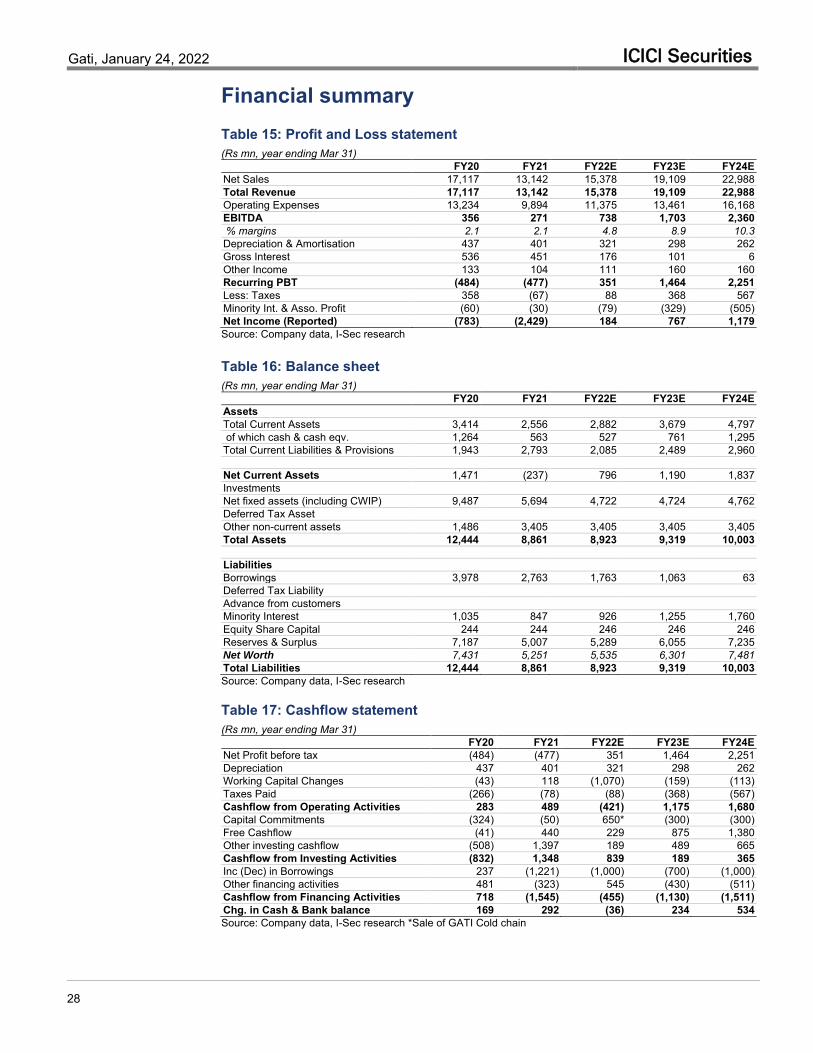

Financial summary Table 15: Profit and Loss statement (Rs mn, year ending Mar 31)

FY20 FY21 FY22E FY23E FY24E Net Sales 17,117 13,142 15,378 19,109 22,988 Total Revenue 17,117 13,142 15,378 19,109 22,988 Operating Expenses 13,234 9,894 11,375 13,461 16,168 EBITDA 356 271 738 1,703 2,360 % margins 2.1 2.1 4.8 8.9 10.3 Depreciation & Amortisation 437 401 321 298 262 Gross Interest 536 451 176 101 6 Other Income 133 104 111 160 160 Recurring PBT (484) (477) 351 1,464 2,251 Less: Taxes 358 (67) 88 368 567 Minority Int. & Asso. Profit (60) (30) (79) (329) (505) Net Income (Reported) (783) (2,429) 184 767 1,179 Source: Company data, I-Sec research

Table 16: Balance sheet (Rs mn, year ending Mar 31)

FY20 FY21 FY22E FY23E FY24E Assets Total Current Assets 3,414 2,556 2,882 3,679 4,797 of which cash & cash eqv. 1,264 563 527 761 1,295 Total Current Liabilities & Provisions 1,943 2,793 2,085 2,489 2,960 Net Current Assets 1,471 (237) 796 1,190 1,837 Investments Net fixed assets (including CWIP) 9,487 5,694 4,722 4,724 4,762 Deferred Tax Asset Other non-current assets 1,486 3,405 3,405 3,405 3,405 Total Assets 12,444 8,861 8,923 9,319 10,003 Liabilities Borrowings 3,978 2,763 1,763 1,063 63 Deferred Tax Liability Advance from customers Minority Interest 1,035 847 926 1,255 1,760 Equity Share Capital 244 244 246 246 246 Reserves & Surplus 7,187 5,007 5,289 6,055 7,235 Net Worth 7,431 5,251 5,535 6,301 7,481 Total Liabilities 12,444 8,861 8,923 9,319 10,003 Source: Company data, I-Sec research

Table 17: Cashflow statement (Rs mn, year ending Mar 31)

FY20 FY21 FY22E FY23E FY24E Net Profit before tax (484) (477) 351 1,464 2,251 Depreciation 437 401 321 298 262 Working Capital Changes (43) 118 (1,070) (159) (113) Taxes Paid (266) (78) (88) (368) (567) Cashflow from Operating Activities 283 489 (421) 1,175 1,680 Capital Commitments (324) (50) 650* (300) (300) Free Cashflow (41) 440 229 875 1,380 Other investing cashflow (508) 1,397 189 489 665 Cashflow from Investing Activities (832) 1,348 839 189 365 Inc (Dec) in Borrowings 237 (1,221) (1,000) (700) (1,000) Other financing activities 481 (323) 545 (430) (511) Cashflow from Financing Activities 718 (1,545) (455) (1,130) (1,511) Chg. in Cash & Bank balance 169 292 (36) 234 534 Source: Company data, I-Sec research *Sale of GATI Cold chain

Gati, January 24, 2022 ICICI Securities

29

Table 18: Key ratios (Year ending Mar 31)

FY20 FY21 FY22E FY23E FY24E Per Share Data (Rs) Basic EPS (6.4) (19.9) 1.4 5.9 9.6 Diluted EPS (6.0) (18.5) 1.4 5.8 9.0 Cash EPS (Fully Diluted) (2.4) (15.2) 3.9 8.1 11.1 OCF per share (Fully Diluted) 2.3 4.0 (3.2) 9.0 13.7 Book Value per share (Fully Diluted) 60.9 43.1 42.2 48.0 57.0 Growth YoY (%) Net Sales (8.1) (22.9) 17.0 24.3 20.3 EBITDA (62.2) (23.9) 171.9 130.7 38.6 PAT (465.9) 191.8 (110.7) 317.4 53.8

Valuation ratios P/E NM NM 145.9 35.0 21.5 P/CEPS NM NM 53.2 25.3 18.5 P/BV 3.4 4.8 4.9 4.3 3.6 EV / EBITDA 78.1 100.7 36.0 15.1 10.2 EV / FCF 859.9 123.3 19.1 18.3 11.7 Operating Ratios (%) Raw Material/Sales 77.2 75.3 74.0 70.4 70.3 Other Income / PBT (27.4) (21.8) 31.5 10.9 7.1 Effective Tax Rate (74.0) 13.9 25.2 25.2 25.2 NWC / Total Assets 11.8 (2.7) 8.1 8.8 10.2 Inventory Turnover NM NM NM NM NM Asset Turnover 137.0 148.3 173.9 214.4 252.9 Net D/E Ratio (x) 0.4 0.4 0.2 0.1 (0.0) Profitability Ratios (%) Rec. Net Income Margins (4.6) (18.5) 1.2 4.0 5.1 RoCE (1.9) 0.3 3.7 9.8 13.6 Adjusted RoCE (3.1) 1.3 13.8 35.2 46.7 RoNW (10.5) (46.3) 3.3 12.2 15.8 Adjusted RoNW* (24.7) (244.6) 14.4 37.5 36.6 EBITDA Margins 2.1 2.1 4.8 8.9 10.3 Source: Company data, I-Sec research * If Gati starts to pay dividend, this will improve further

Gati, January 24, 2022 ICICI Securities

30

Index of Tables and Charts

Tables Table 1: India’s leading end-to-end logistics solutions ......................................................... 5 Table 2: Gati has lost market share, margins and fallen behind on all operating parameters

with peers like TCI Express ............................................................................................. 9 Table 3: Comparison with TCI Express .............................................................................. 10 Table 4: Other expenses show significant room for reduction (vis-à-vis TCI Express) ...... 11 Table 5: Comparison of ‘other expenses’ breakup (absolute) with TCI Express ................ 11 Table 6: Key changes in Board members in FY21 ............................................................. 18 Table 7: Current management profile ................................................................................. 19 Table 8: Board structure ..................................................................................................... 20 Table 9: Shareholding structure .......................................................................................... 20 Table 10: Financial statements of material subsidiaries / associate companies / joint

ventures ......................................................................................................................... 22 Table 11: There are many potential areas of improvement including regularisation of old

related party transactions, strengthening internal processes and systems .................. 23 Table 12: We see a progressive winding down of related party transactions as new

management engages .................................................................................................. 24 Table 13: Significant balance sheet actions ....................................................................... 25 Table 14: Peer express valuation (when they were growing) ............................................. 26 Table 15: Profit and Loss statement ................................................................................... 28 Table 16: Balance sheet ..................................................................................................... 28 Table 17: Cashflow statement ............................................................................................ 28 Table 18: Key ratios ............................................................................................................ 29 Charts Chart 1: Gati in charts – past leader in express logistics (road) in India; trying to reclaim the

position ............................................................................................................................ 4 Chart 2: Surface express contributes 89% of FY21 top line, with key enterprise accounts

contributing 52%, SME 26% and retail 22% ................................................................... 4 Chart 3: Events over the past 5 years lead to Allcargo’s acquisition of Gati and the start of

a turnaround .................................................................................................................... 8 Chart 4: B2B express market in India expected to take off .................................................. 9 Chart 5: Gati KWE revenue performance against peers .................................................... 12 Chart 6: Gross margin performance ................................................................................... 12 Chart 7: EBITDA margin performance ................................................................................ 12 Chart 8: RoE performance .................................................................................................. 12 Chart 9: RoCE performance ............................................................................................... 12 Chart 10: Part of the cost reduction journey and improvement in RoCE have already been

witnessed in FY21 ......................................................................................................... 15 Chart 11: Significant focus is also been directed towards deleveraging, mainly through

non-core asset sales ..................................................................................................... 15 Chart 12: Net debt down to ~Rs1bn from Rs4bn from FY20 .............................................. 16 Chart 13: Trying to create a better interface for customers – an effort that was core part of

Gati 1.0 .......................................................................................................................... 16 Chart 14: Quarterly shareholding structure ......................................................................... 21 Chart 15: Promoters’ holding and pledge ........................................................................... 21 Chart 16: Contribution of subsidiaries / associates at consolidated level ........................... 22 Chart 17: How underlying ratios are expected to improve .................................................. 26 Chart 18: TCI Express PE Band chart ................................................................................ 27 Chart 19: Bluedart Express PE Band chart ........................................................................ 27

Gati, January 24, 2022 ICICI Securities

31

This report may be distributed in Singapore by ICICI Securities, Inc. (Singapore branch). Any recipients of this report in Singapore should contact ICICI Securities, Inc. (Singapore branch) in respect of any matters arising from, or in connection with, this report. The contact details of ICICI Securities, Inc. (Singapore branch) are as follows: Address: 10 Collyer Quay, #40-92 Ocean Financial Tower, Singapore - 049315, Tel: +65 6232 2451 and email: [email protected], [email protected].

"In case of eligible investors based in Japan, charges for brokerage services on execution of transactions do not in substance constitute charge for research reports and no charges are levied for providing research reports to such investors."

New I-Sec investment ratings (all ratings based on absolute return; All ratings and target price refers to 12-month performance horizon, unless mentioned otherwise) BUY: >15% return; ADD: 5% to 15% return; HOLD: Negative 5% to Positive 5% return; REDUCE: Negative 5% to Negative 15% return; SELL: < negative 15% return