Eo Siang Ee and Edmund Chua

47

Filling Up the Cracks: Reforming MediShield By: Eo Siang Ee and Edmund Chua

Transcript of Eo Siang Ee and Edmund Chua

Filling Up the Cracks: Reforming MediShield

By: Eo Siang Ee and Edmund Chua

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

1 of 24 | P a g e

Introduction

Singapore has a 3’M’ framework in place that has been institutionalized so that every

Singaporean is automatically enrolled in this national healthcare programme. Unlike most

developed countries in the west that utilize a defined benefit scheme, Singapore uses a defined

contribution scheme. This means that workers contribute a portion of their monthly wages to

their medical savings account and even their retirement account. In this way, our 3’M’ system

has continued to be fiscally sustainable and does not put immense strain on the government’s

fiscal budget.

This 3’M’ framework consists of i. Medisave, ii. MediShield and iii Medifund.

This framework was established gradually in response to the changing healthcare needs

of Singaporeans, the change in demographics, and also rising cost of medical care. Medisave was

established first in 1984, and it remains a compulsory medical savings plan. 7-9.5% of a person’s

income is contributed towards Medisave; the exact ratio depends on the worker’s age. The

contribution ratio increases as a worker ages. MediShield, on the other hand, was established in

1990 as a low cost catastrophic illness insurance plan that can be paid from Medisave or from a

policyholder’s own pocket. While all Singaporeans and Singapore Permanent Residents are

automatically enrolled in MediShield, there is also the option to opt-out of this insurance. Both

Medisave and MediShield are managed by Singapore Government’s Statutory Board: The

Central Provident Fund Board (CPF Board). As an added precaution, to prevent people from

falling through the cracks even with these two measures, the Medifund was established in 1993

as an endowment for needy patients. Medifund is the absolute last layer of protection and

patients can approach social workers in hospitals or community services centers to apply for

Medifund aid when they have depleted their own Medisave, and the immediate family members’

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

2 of 24 | P a g e

Medisave accounts. The underlying reason is that people should be responsible for their own

health and not depend on the government, unlike Britain, Singapore’s former colonial master that

has taken the path of universal healthcare with the establishment of the National Health Service

(NHS). The Singapore government therefore holds final discretion in allowing an applicant to tap

on Medifund for payment of healthcare expenditure1.

There is another ‘M’, which is ‘Managed Health’. Policyholders of MediShield can also

choose from a variety of life/health insurance policies in the private market to supplement the

existing coverage provided by MediShield. Premiums for some of these plans are payable

through an individual’s Medisave account2.

However, in spite of the above measures, there are still signs of people falling through the

cracks in the healthcare system. Examples include rising number of MediShield policy lapses,

non-working spouses who do not have MediShield insurance, higher out-of-pocket expenditure

on healthcare, etc. These disturbing developments have prompted Minister of Health, Mr. Gan

Kim Yong to announce that Singapore’s Healthcare System will undergo a review that involves

‘fundamental shifts’(Gan, 2013). Minister Gan highlighted three issues with the system and one

of which concerns the role of MediShield. In line with the government’s intention to stretch the

health dollar and give Singaporeans a greater peace of mind, our group has decided to undertake

a preliminary review on MediShield as highlighted by the Minister.

1 To qualify for medifund assistance, a person must fulfill all of the following criteria: i. Be a Singapore citizen, ii. Be a subsidized patient, iii. Receive treatment from a Medifund-approved institution, iv. The patient and family members must have difficulties affording the medical bill despite government subsidies, MediShield and Medisave. More details can be found at MOH website: http://www.moh.gov.sg/content/moh_web/home/costs_and_financing/schemes_subsidies/Medifund/Eligibility.html 2 These complementary insurance policies are known as Integrated Shield Plans (IP) that are sold by private insurers such as Great Eastern, NTUC Income, AIA, Aviva, and most major life insurance companies that operate with a license from the Monetary Authority of Singapore (MAS) in Singapore.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

3 of 24 | P a g e

Currently, Medishield premium payments increase with age; this is logical from an

actuarial perspective given that a person’s incidence of disease and frequency of hospitalization

increases with age. However, to do so for a government managed basic insurance is biased

against the elderly who have little or no income when they retire. With this backdrop, this paper

will critically examine, analyze and evaluate the appropriateness of MediShield based on the

ability to pay, and the effectiveness of MediShield in meeting the healthcare financing needs of

Singaporean and Permanent Resident (PR) patients in Singapore.

We intend to propose new improvements for MediShield that will address this issue and

other pertinent issues that affect the average Singaporean; such as rising out-of-pocket expenses,

and MediShield policy lapses.

Literature Review

There have been numerous research papers written in recent years about the healthcare

system in Singapore. ‘Medical savings account in Singapore: how much is adequate?’ (N.-C.

Chia & Tsui, 2005), highlights how it is insufficient to depend on just Medisave since a single

catastrophic or chronic illness may wipe out entire savings in the Medisave. Thus, there is the

need to use MediShield as a basic inexpensive insurance to shield the policyholder against

unforeseen illnesses. Chia and Tsui also propose that the claim limits and the age limit for

MediShield should be raised so that Singaporeans will still be able to enjoy the benefits of

medical insurance coverage in old age.

‘Feminization of Aging and Long Term Care Financing in Singapore’ (N. C. Chia, Lim,

& Chan, 2008), notes that life expectancy among Singaporeans is indeed rising, and the increase

is even more pronounced in females. The study is useful as it shows that healthcare expenses can

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

4 of 24 | P a g e

be quantified, and with the right tools and appropriate assumptions, it is possible to forecast

average healthcare expenses of the elderly. Rising longevity would also translate into rising

expected lifetime cost of healthcare among citizens. This raises the concern that current

Medishield premiums may be insufficient to provide healthcare coverage for policyholders in the

future.

In addition, an Honours Thesis was written on ElderShield, the government endorsed

insurance for the Elderly to guard against expensive palliative care (or Long Term Care, LTC)

‘Improving the adequacy of ElderShield: an actuarial perspective’.(Zeng & Chia, 2010). The

paper utilises the actuarial approach of which neither of us are trained in. However, in general,

the research paper provides evidence that insurance plans for the elderly and retirees have very

low adequacy ratios. This implies that the Eldershield policies are not worthwhile given the

premiums paid, and the potential pay-outs. This finding forms part of our underlying motivation

in understanding the insurance market so that premiums may be priced in a ‘fairer’ manner.

Methodology

From the above literature review, we note that there is indeed some scope for our

research on MediShield. Our policy memo acknowledges that changes in age and claim limits of

MediShield will be beneficial for the average Singaporean patient. However, in light of an aging

population where people are living longer and life expectancy is increasing, more needs to be

done.

In this paper, we will address 3 key issues: i) reducing the possibility of MediShield

policy lapses, ii) extending MediShield to families so that there is joint risk pooling, and iii) re-

structuring MediShield premiums so that premiums need not increase with age.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

5 of 24 | P a g e

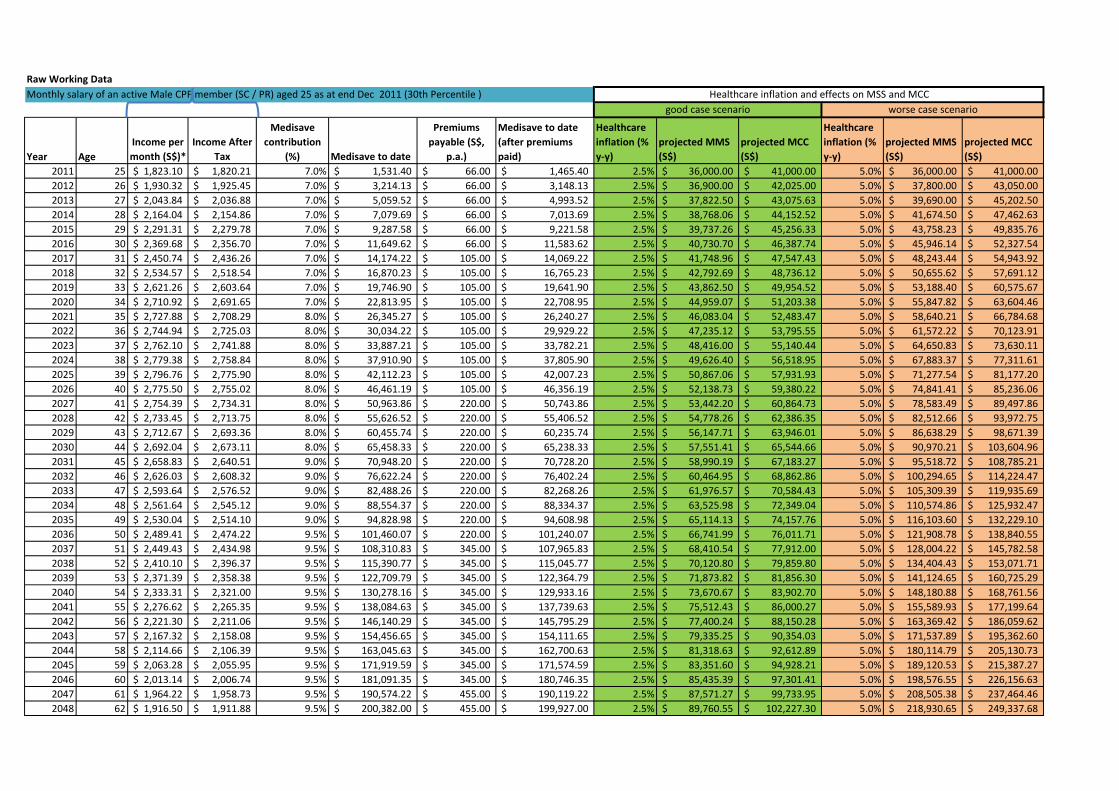

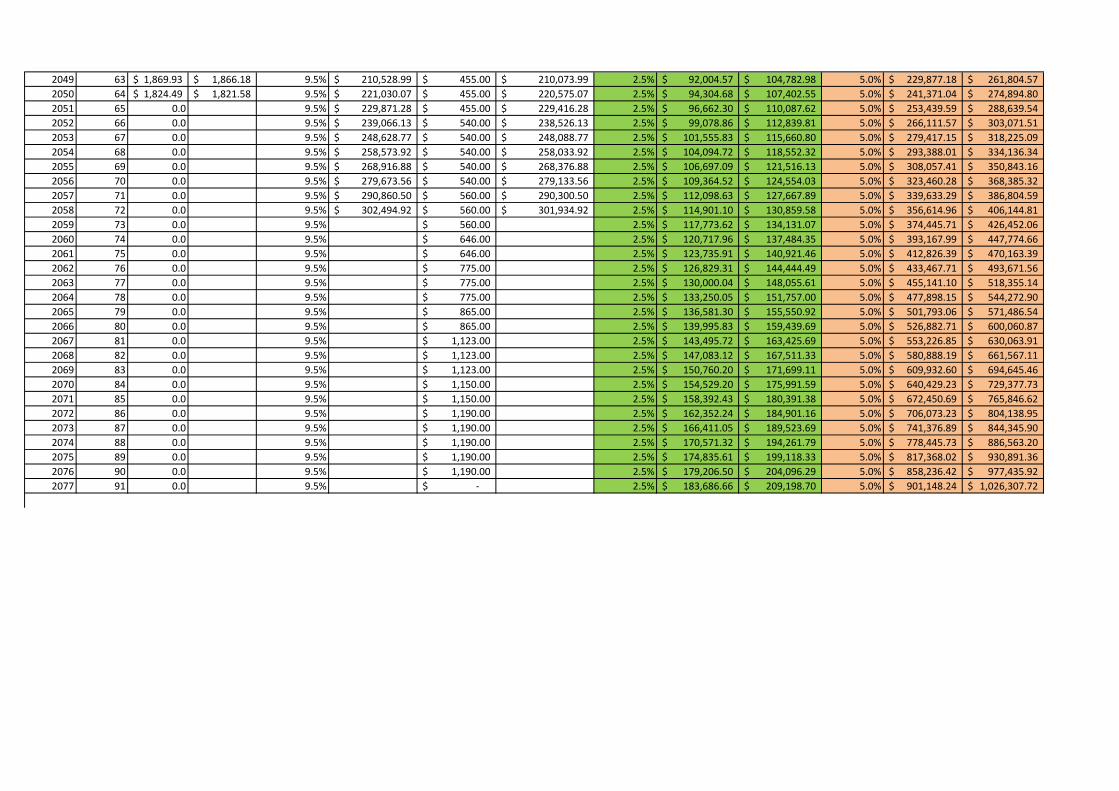

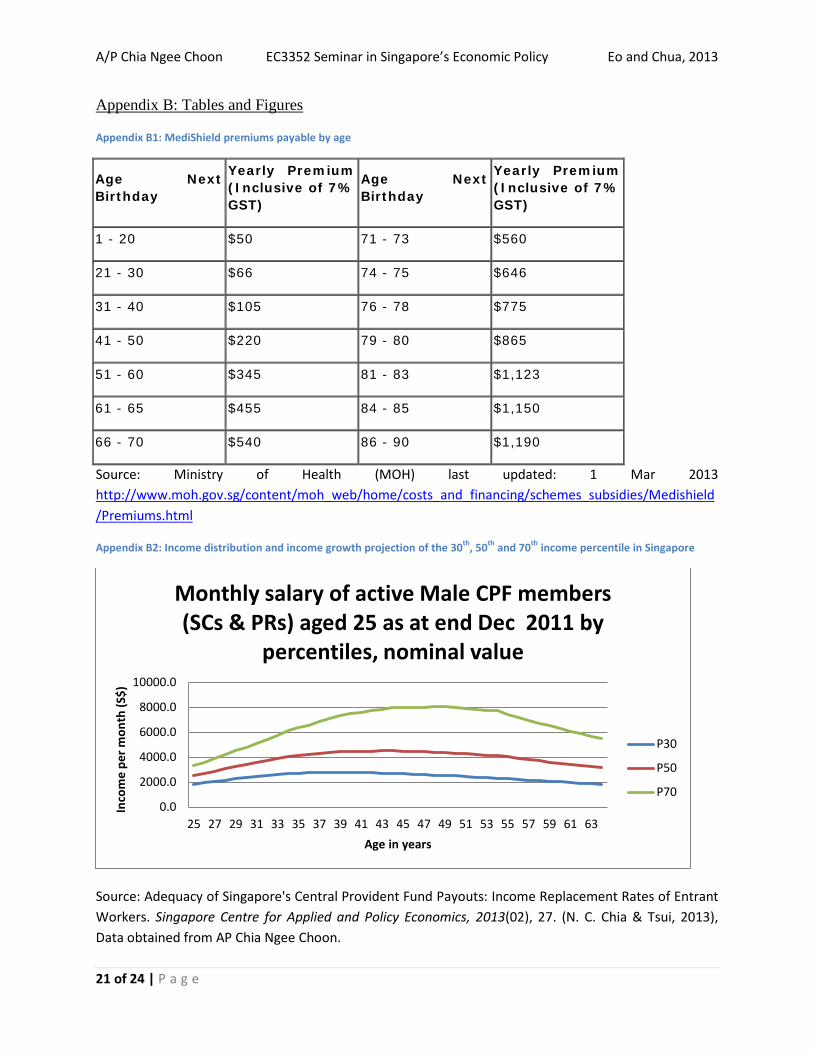

As mentioned, a person’s premium for MediShield increases with age. For example, the

premiums payable crosses the S$1000 mark when a person turns 81(refer to Appendix B1).

This has 2 implications. Firstly, a person’s income eventually declines as he/she ages. This is due

to the human capital effect and has been observed in workers in the USA, UK, Germany,

Netherlands, Denmark and Sweden (Bosworth, Burtless, & Steuerle, 2000). Appendix B2 shows

the nominal monthly income projection of the 30th, 50th and 70th percentile Singaporean male

workers from age 25 to 65. Secondly, incidence of chronic illnesses and diseases also increases

with age. Thus, MediShield insurance premiums become more expensive just when the need for

healthcare increases.

Therefore, the central idea in our policy recommendation is to keep the sum of all

premiums payable to CPF Board the same, so that the insurer is indifferent between the current

plan and the proposed plan. We aim to formulate the proposed plan using the present value (PV)

method. In this way, we adjust the premium paid by insures based on their income, by keeping

the total premiums paid up til age 65 the same.

i.e. 𝑃𝑉𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝=∑𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑖

(1+𝑝)𝑖401 𝑠𝑡𝑎𝑟𝑡𝑖𝑛𝑔 𝑓𝑟𝑜𝑚 𝑎𝑔𝑒 25,𝑎𝑛𝑑 𝑒𝑛𝑑𝑖𝑛𝑔 𝑎𝑡 𝑎𝑔𝑒 65.

• Keep PV constant with a constant discount rate of 4%3,

• Minimize 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑖𝑤𝑤𝑤𝑝𝑖

4 as a constant.

Since most people retire after 65 and are therefore without an active income, we also

propose that part of the retirement fund in CPF Life5 be used to pay for MediShield. CPF Life is

3 A constant discount rate of 4% will be used since this is the prevailing interest rate being guaranteed by the CPF Board on Medisave accounts. It will be unlike for people to be willing to prepay MediShield premiums if the returns to prepayment fall below what they would otherwise obtain if they would save in Medisave. 4 Since inflation will affect both ‘premiums’ and ‘wages’ in any given year, a simple 𝑝𝑝𝑝𝑝𝑝𝑝𝑝𝑝

𝑤𝑤𝑤𝑝𝑝 can be used as the

effect due to inflation is neutralized in both the numerator and the denominator.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

6 of 24 | P a g e

a relatively new initiative by CPF Board that attempts to pool all funds from the retirement

accounts of individuals and then distribute retirement monies to retirees on a monthly basis,

based on a define contribution framework. This CPF Life only comes into force when a person

reaches 55, or when retirement starts. Thus, to prevent MediShield insurance policies from

lapsing due to insufficient funds even after significantly lowering premium payments, it may be

necessary for people to set aside part of their payments from CPF Life, for the payment for

Medishield premiums after retirement.

Assumptions and Justifications

Firstly, our data only contains the projected income growth for the 30th percentile since

this is the group that deserves the most attention. We believe that the higher income deciles (i.e.

50P, 70P) will have sufficient financial capacity and information to make their own informed

private healthcare insurance purchases on top of the basic inexpensive MediShield. Moreover it

is reasonable to also assume that the higher deciles can also realize healthcare adequacy, if our

projection shows that our representative 30P worker can realize ‘healthcare adequacy’.

Healthcare adequacy is defined in this paper to be the ability to reach the Medisave Contribution

Ceiling (MCC) such that interest payments from Medisave accounts will be able to pay for

MediShield premiums in a person’s lifetime. Simulations are based on research on projected age

earning profiles of 30P income workers, conducted by AP. Chia Ngee Choon based on data

provided by the Ministry of Manpower.

5 For members born in or after 1958, you will be placed on CPF LIFE if you have at least $40,000 in your Retirement Account (RA) when you reach 55 or at least $60,000 when you are reaching your DDA. Members who are not placed on CPF LIFE can choose to join CPF LIFE anytime after reaching 55 and before they reach age 80.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

7 of 24 | P a g e

Secondly, we assume that a typical Singaporean/PR will not opt-out of MediShield at any

point in life. This should be a fairly reasonable assumption since 30th percentile workers may

find that the conventional insurance packages offered by the private sector may be priced beyond

their reach. It is therefore more affordable for them to stick with the CPF managed MediShield6.

We will also have to conclude that 30th percentile income group is sufficiently informed to know

that their income will not be enough to see them through a catastrophic/chronic illness and hence

will likely be more risk adverse. Following this logic, MediShield take-up rate should be close to

full capacity amongst the said income group.

Thirdly, basic projections assume full lifetime employment and no withdrawal from the

individual’s Medisave account. These assumptions may be unrealistic but they are necessary to

simplify calculations and projections. In the robustness test on healthcare adequacy, with

respected to increasing premiums, we will impose a discount factor of 0.85 on wages based on an

assumption of 85% employment density. (See Appendix A7)

Fourth, we assume that the average life expectancy of a Singaporean or PR is about 81

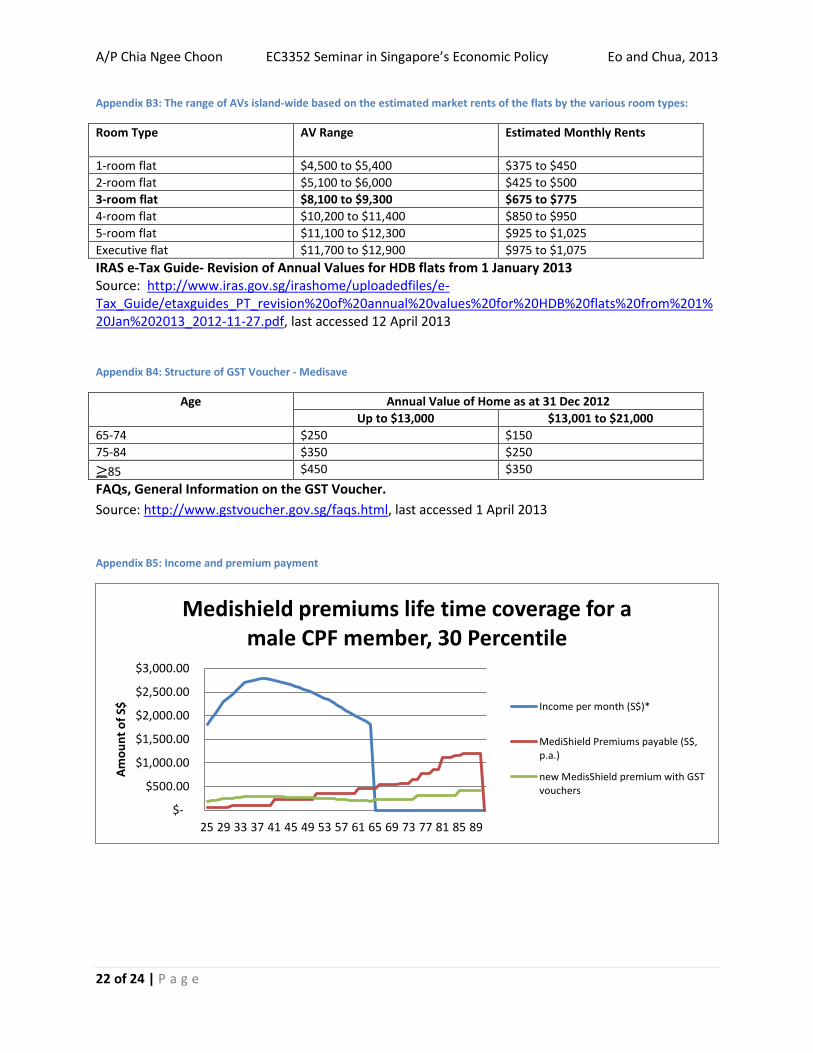

years. We also assume that a 30th income percentile male worker will be living in a 3 room flat.

It is fairly reasonable to suggest that a 30th income percentile worker will also marry a 30th

income percentile partner. This fourth assumption will have implications on the fifth assumption

that follows below, as household income is correlated to the type of Housing and Development

Board (HDB) flat a person resides in, and this in turn will determine the annual value (AV) of

the flat. The AV of the flat will then determine the amount of government transfers eligible by

the household. (See Appendix B3 and B4)

6 Unfortunately, CPF Board does not have a breakdown of the profile of MediShield policy holders who have not taken up the policy.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

8 of 24 | P a g e

Fifth, as partially mentioned above, a person’s income, especially for workers at the

lower deciles, will increasingly be affected by government transfers. Transfers may include the

Workfare Income Supplement (WIS)7, the Wage Credit Scheme (WCS) and a permanent yearly8

GST Voucher Scheme (from GST Voucher Fund). However, WIS will not be necessary n our

model as it only kicks in when income is less than or equal to S$1,700 9 per month. Our

representative 30P worker starts off with an income higher than $1,800 per month in 2011. As

for WCS, it is not useful to include the transfers into our projections as this scheme is temporary

as it only lasts for 3 years. Our model will factor in the GST Voucher Scheme instead, since it is

a permanent scheme that ensures certainty of rebate from the government even in unstable

economic times10. This presents an added advantage to our model as the effects of government

transfers to the individual will be stable since fluctuations in rebates are minimized.

The GST voucher comprises of 3 components: Cash transfers, Utility rebates (U-save),

and Medisave credit transfer. Of these 3 components, we will simplify projections yet again by

only considering the Medisave credit transfer to a person’s Medisave account. This is because

we are primarily concerned about whether our 30P worker will be able to retire with sufficient

healthcare savings and we fundamentally assume that the income of 30P workers will be so

stretched that they would not voluntarily make contributions to their Medisave accounts. On top

8 Point 1.2. “GST Voucher is a permanent Scheme, with benefits given out yearly.” http://www.gstvoucher.gov.sg/faqs.html#1.5, last access 1 April 2013 9In 2013, the WIS ceiling has been raised from $1,700 to $1,900. However, our calculation will be unaffected and will not change, we will still keep WIS out of our estimation since the data we use for the 30P worker was acquired in 2011 when the starting monthly wage at age 25 was $1,800. Source: http://mycpf.cpf.gov.sg/NR/rdonlyres/E78753A8-3D65-4FAD-A5FF-60C27FFDFC27/0/Budget2013WIS.pdf, last accessed 7 April 2013 10 Source: http://www.gstvoucher.gov.sg/faqs.html#1.5, last access 1 April 2013

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

9 of 24 | P a g e

of GST vouchers, the government had from time to time provided on off top ups to Medisave

accounts of Singaporeans. The Singapore government provides top-ups to citizens Medisave

accounts from time to time, however, this can be unpredictable. Therefore, in our model, we will

assume that there will not be any top-ups to the Medisave account of our representative worker.

Finally, we also assume no income mobility, across the lifetime of our representative

worker. In making these set of assumptions for accounting government transfers, the paper is

also conservative in its projections.

Evaluation of the Status Quo

There are 3 pertinent issues we have observed with the current MediShield system.

Firstly, the current MediShield premium structure makes it difficult for retirees to pay for

their MediShield insurance, and can be financially draining if these insures live beyond the

average life expectancy of 81 years. The problem is exacerbated by the fact that retirees may not

have an active income. Although it makes actuarial sense to design the payment structure of

MediShield premiums such that elderly citizens who are more likely to make insurance claims

pay more, such a policy is not socially equitable. Considering that the maximum coverage age of

Medishield may soon be increased from the current age of 90, it is highly likely that premiums

beyond the age of 90 may be further increased and this may put MediShield out of the reach of

Singaporeans who are living longer (MOH, 2012). While previous projections made for

Singaporeans in the 30th income percentile worker show that it is theoretically possible for

Singaporeans at the 30th percentile to have healthcare adequacy, this is contingent on two

unrealistic assumptions previously pointed out in assumption #3.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

10 of 24 | P a g e

Secondly, permanent disability at a young age may potentially affect healthcare

adequacy. CPF guarantees an interest rate of 4% on Medisave Accounts, and this relatively high

interest rate increases the effect of interest compounding. If policy holders are unable to work in

order to contribute to their Medisave, they may have difficulty in paying for their MediShield

premiums. They may stand to lose more and experience greater difficulty if they do not

accumulate sufficient amounts in their Medisave when they are still young. Thus, healthcare

adequacy at retirement is also dependent on the worker’s ability to sustain his CPF contributions

for his initial working years. Healthcare adequacy is also highly dependent on there being no

large withdrawals (cumulatively) made against the worker’s account. Both of these may be

compromised if the worker suffers from a major illness and the effects will be further

exacerbated if it results in the permanent disability of the worker. Such an event may also lead to

a double squeeze on a worker’s limited Medisave account 11 because of co-insurance and

deductibles on top of paying Medishield premiums.

Thirdly, healthcare adequacy of single income families may be threatened when house

wives who are not insured by Medisave fall sick("Channel News Asia," 2008). In a single

income family, if the house wife were to fall critically ill, the spouse may be at risk of healthcare

inadequacy because medical fees of housewives must be paid in full through their spouses’

Medisave account since the spouse’s MediShield policy only covers the policy holder and not

immediate family members. The alternative will be to tap on the government Medifund

endowment fund; however, this last layer of protection is accessible only when the family has

exhausted their health care savings. To exhaust healthcare savings in the form of Medisave and

11 It is difficult for people in the 30th percentile to accumulate large amounts of savings in their Medisave accounts in the earlier years of their work life.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

11 of 24 | P a g e

personal savings at a young age would severely risk the family’s healthcare adequacy at

retirement.

The following sections of this paper aim to address these problems that we have

identified with the MediShield system and we would also hope to provide some policy

suggestions which may help in mitigating the risk to healthcare adequacy.

Preventing Policy Lapses12

The exact number of people who lapse their policies is not known, however from

Minister of Health Gan Kim Yong’s answer in Parliament in September 2012, it is possible to

determine that less than 1% of policyholders encountered such an incident between 2006-2011.

According to the Ministry of Health, there were 3.5 million policy holders in 2011, this makes 1%

to be at most 35,000 people.

Even though MediShield is a basic insurance plan, it provides people with healthcare

coverage for up to 80% of their in-patient healthcare bills; we assume that the Medisave cap is

set at a level which ensures healthcare adequacy only if the retiree’s MediShield policy has not

lapsed. As mentioned earlier in our evaluation of the status quo, critical illnesses and disability at

a young age can lead to inability of workers to service their MediShield premiums. Furthermore,

the persistent nature of some illnesses like cancer and kidney failures, may mean that many

people who are not able to meet premium obligations will be doubly penalized since they will

most require medical coverage in future. 12 Between 2006 and 2011, less than 1% of MediShield policyholders suffered a policy lapse due to insufficient funds in their Medisave balance. Minister of Health Gan Kim Yong’s HealthSource:http://160.96.186.104/search/topic.jsp?currentTopicID=00077920-WA¤tPubID=00077935-WA&topicKey=00077935-WA.00077920-WA_1%2BhansardContent43a675dd-5000-42da-9fd5-40978d79310f%2B2, last accessed 7 April 2013.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

12 of 24 | P a g e

An alternative to the MediShield will be the Dependent’s Protection Scheme13, which

provides a basic payout to dependencies of insured workers in the event of death and disability.

However, it does not provide income substitution in the event of permanent disability. This

prevents workers from being able to continue servicing their MediShield premiums especially if

they do not have sufficient savings in their Medisave account to generate interest income. Hence

we believe that the government may want to include an optional (opt out) rider for waiver of

premium within the MediShield policy. Such a feature is common in private healthcare

insurances. At a cost (a small fraction of premiums), workers will be able to insure themselves

against medium (3 months) term to permanent incapacity to work. The waiver premium feature

acts as a safety mechanism to help the insured pay for the cost of their premiums over the period

of time in which they are unable to work. Further actuarial calculations will be required for us to

determine the exact cost this feature and we believe that there is room for more specialized

research in this area in the future.

Private life and health insurance policies often include such a rider and the cost of such a

rider would usually form only a small percentage of the cost of a policy’s monthly premium.

Even after making for a bold prediction that such a rider would require a 10% increase in

MediShield premiums, we can see from Appendix A2 that workers in the 30th percentile would

still be able to achieve healthcare adequacy. In essence such a rider acts as an insurance policy

which allows Singaporeans to pool their risk against low probability events that may lead to

medium term to permanent disability and if priced actuarially fairly, should in fact increase the

welfare of Singaporeans, assuming that Singaporeans are risk adverse.

13 DPS is an opt out insurance system that is linked to the CPF.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

13 of 24 | P a g e

Shared Payment of Premium within the Family

It is possible for family members to pay for each other’s medical expenditure through

their respective Medisave accounts; however while it is also possible for family members to pay

for the each other’s MediShield premiums using their respective Medisave accounts, many

Singaporean families do not do so and this is evident from the low level MediShield coverage

among housewives. This is a highly ironic setup and it creates asymmetric risk exposure among

Singaporean families due to two reasons. Firstly, while family risk pooling from Medisave

allows for risk sharing against chronic illnesses, it does not allow for risk sharing against

disability. In the presence of our previous policy, Singaporeans would be able to pool their risk

against disability. Hence the policy proposed in this section is aimed at reducing a second kind of

asymmetric risk which was described in our previous section as we were discussing about the

shortfalls of the MediShield system. Such an asymmetric risk is common among single income

families as the non-working spouse would not have CPF contributions required to pay for

MediShield premiums. To eliminate this asymmetric risk, we propose that MediShield account

of a Singaporean’s spouse is automatically activated to pay for their MediShield premiums,

whenever they do not have sufficient funds in their MediShield accounts to pay for their

premiums. Hence we propose a change from our opt in system of family copayment, to an opt-

out system, to ensure that lower income Singaporeans who would also tend to have less policies

awareness are still covered by MediShield even in the absence of Medisave contributions.

While it is possible of their spouses to help them pay for their premiums by voluntarily

topping up their Medisave accounts, lower income families which also tend to have lower

disposable incomes would tend to have less propensity to invest for the future. Risk pooling

within the family creates a second case of asymmetric risk where single income families in lower

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

14 of 24 | P a g e

groups are at a greater exposure to health related risks from housewives without MediShield

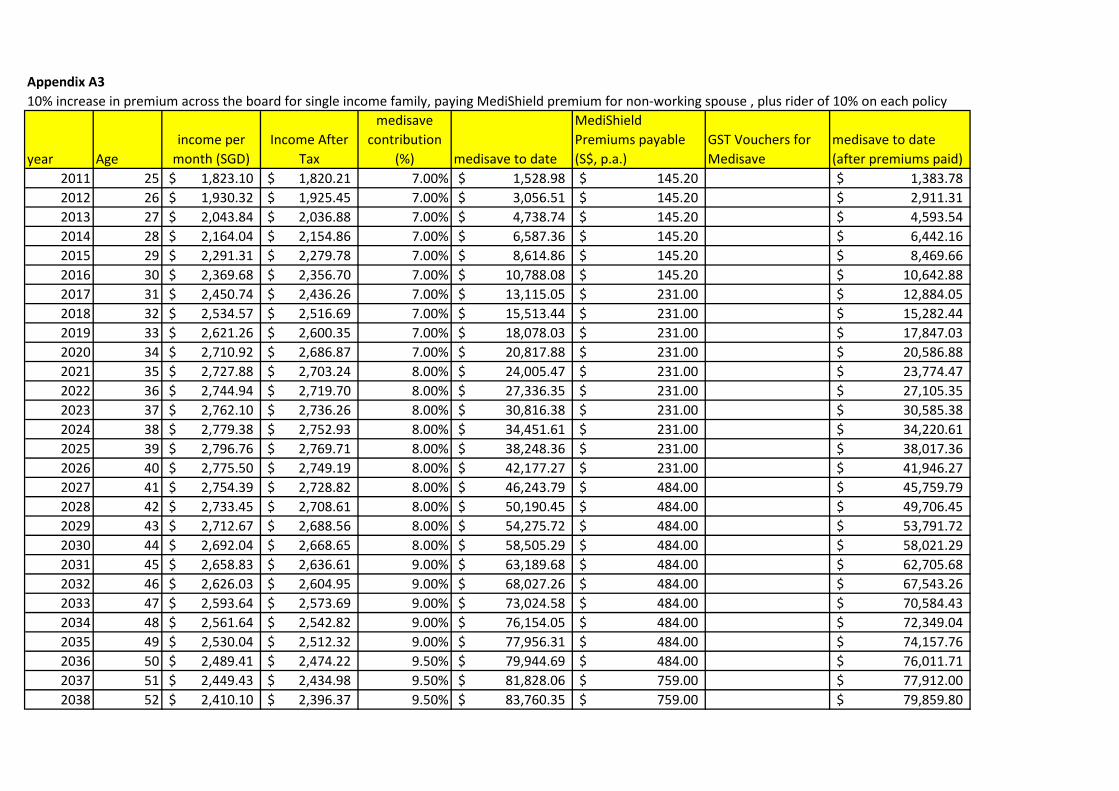

coverage. Projections made in Appendix A3 shows that it is possible for single income families

in the 30th percentile income group to achieve healthcare adequacy while paying MediShield

premiums for two members of the family.

Again, under the assumption that Singaporeans are risk adverse, this policy would benefit

lower income Singaporeans as it would allow them to eliminate the asymmetric risk present in

the status quo, without compromising on their short term disposable income. Because of the fact

that Singaporean families will ultimately have to bear the healthcare cost of spouses without

MediShield coverage it make sense to allow them to participate in risk pooling by making use of

funds from the same account that would be used to pay for medical expenditure of their family

members (See Appendix C). With coverage from Medisave, it will be unlikely that occurrence

of critical illness among young families create a financial cost that is so large that it prevents

young families from accumulating medical savings required to enjoy benefits of compounding

after they retire. This would in turn contribute to increasing the odds of post-retirement

healthcare adequacy among low income Singaporeans.

Based on the two policies that we have proposed, we conducted a robustness test on

healthcare adequacy for our representative single income family at the 30th percentile. By

applying a simplified discount over the lifetime salary of our representative single income

family, we find that even with the cost of our proposed rider and the additional cost of an extra

MediShield premium, we find that the healthcare adequacy of our low income workers are robust

to the extent that our representative family is able to take up to a 35% discount in wages without

having their healthcare adequacy compromised, assuming that no early withdrawals were made

to this single income family’s Medisave account. (See Appendix A3) This means that there is a

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

15 of 24 | P a g e

possibility that a single income family may also be able to pay for two sets of private integrated

insurance policies without jeopardizing their healthcare adequacy. However, due to the diverse

range of policies offered in the private market, we will not be evaluating the affordability of

these policies individually.

Ensuring Post-Retirement Healthcare Assurance

While the 2 measures that were proposed would help prevent MediShield policies from

lapsing as well as assist families in ensuring that they have sufficient post-retirement healthcare

savings, spells of unemployment caused by economic cycles during a Singaporean’s lifetime

may prevent low income Singaporeans from having sufficient healthcare savings. Low income

earners who start their career in part-time employment may also lack the early CPF contributions

needed to generate interest income to cover for increasing premiums in their later years.

In the unlikely situation where the sole breadwinner of the family retires without

sufficient Medisave savings to generate interest income for MediShield premiums14, we propose

an alternative payment structure for MediShield premiums to allow for ‘prepayment’ to be made

when workers are younger. The general idea of prepayment is to have the policyholder pay the

lifetime value of his policy up to and including a hypothetical maximum life span of 90 years,

before retirement at age 65.

Without using actuarial methods, we simplify our calculations by applying discounted

cash flow onto MediShield premiums. The purpose of this exercise is to propose alternative

payment structures for the MediShield premiums, where a greater weight of the payment is made

14 This may be caused when excessive withdrawals have been made by extended family member’s (e.g. siblings/parents, we define nuclear family here as one with a husband, wife and their children.), from the sole bread winner’s Medisave account.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

16 of 24 | P a g e

at the earlier stages of a workers life. We maintain the lifetime value of the MediShield

premiums, and we compute using the assumption of a 90 year life span. Prepayment creates

longevity risk for the insurer as insurers may have to provide subsidized premiums for people

who are living beyond their expected life spans. We have based our computations on an expected

life span of 90 years instead of Singapore’s average lifespan of 81 because of the higher risk of

critical illnesses above 82("The World Bank," 2013). Furthermore, we expect life expectancy of

Singaporeans to rise beyond 82. We also conduct discounted cash flow calculations based on an

interest rate of 4% which is provided by the CPF for Medisave. While we concede that there is a

possibility that interest rates may increase, we make a simplifying assumption that future

changes in interest rates would track changes in inflation rates and that long term real interest

rates remain constant. Considering that interest rates are at all-time low, a higher interest rate in

the future will only result in a decrease in the amounts of prepayment that has to be made to

sustain this policy and it would be beneficial to Singaporeans, without affecting the affordability

of this policy in the working years of Singaporeans when they will be required to make higher

premium payments.

While CPF Board faces longevity risk as Singaporeans may live beyond 90, CPF can also

be compensated by the pre-payment from Singaporeans who do not live past 90. Hence, in this

case, the insurer can act as an intermediary that allows all policyholders in the society to pool

longevity risk. To ensure that retirees in lower income groups are able to pay for their

MediShield premiums, there are 2 ways in which MediShield premiums can be structured. One:

design a system which places a higher financial burden on Singaporeans when they are younger

and free them up from having to pay for premiums after they retire or Two: design a system

where premiums paid after retirement tracks the amount transfers to Medisave that Singaporeans

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

17 of 24 | P a g e

will receive through GST vouchers. For the purpose of illustration, we will continue to model

these policies with our representative single income families at the 30th income percentile. To

ensure that affordability of MediShield can be maintained throughout the work life of a

Singaporean we would also seek to peg premiums to wages such that premiums form a fixed

proportion of our representative worker’s salary based on his age-earning profile.

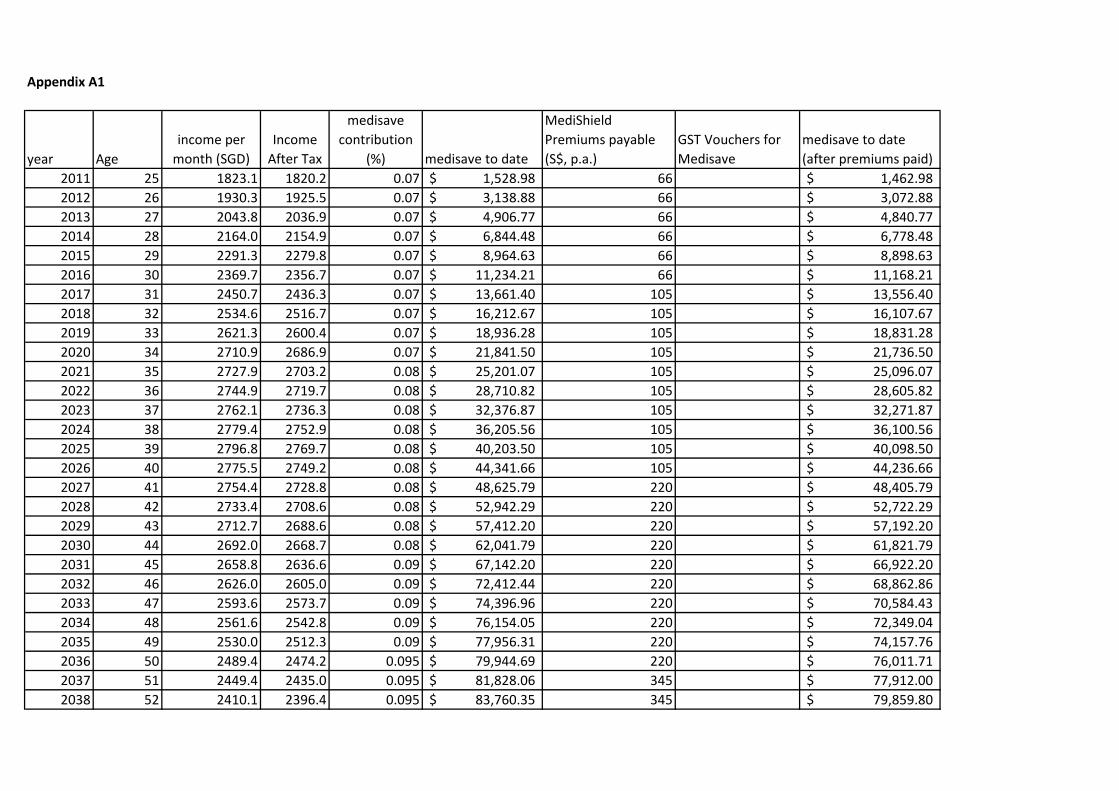

We have modeled our first policy proposal in Appendix A5 and we foresee that a

policyholder will have to contribute a constant 2.2% of his income towards medical insurance to

fund for 2 sets of MediShield policies with the additional rider of 10% each. This forms a very

small amount of a person’s income considering that contribution to the Medisave account is

minimally set at 7%. From the macro perspective we can also see that the MediShield policy also

has the potential of becoming a policy of redistribution as it may be possible to charge

MediShield premiums based on a person’s income. Under a redistributive policy where every

Singaporean pays fixed proportion of their income for medical insurance may result in a

contribution rate for MediShield premium to be significantly lower than 2.2% considering how

wages across the population increase at an increasing rate. This policy has a risk of being

unable to fulfill its redistributive purpose if higher incomes Singaporeans opt out of this system

and hence there may be a need to make this a mandatory health insurance policy. There will be

major implications with respect to this fundamental change as it will move our current system

into one which has a greater resemblance to the NHS. While we will not be advocating for such a

fundamental change in this paper, we believe that there will be room to evaluate such a policy in

a future paper.

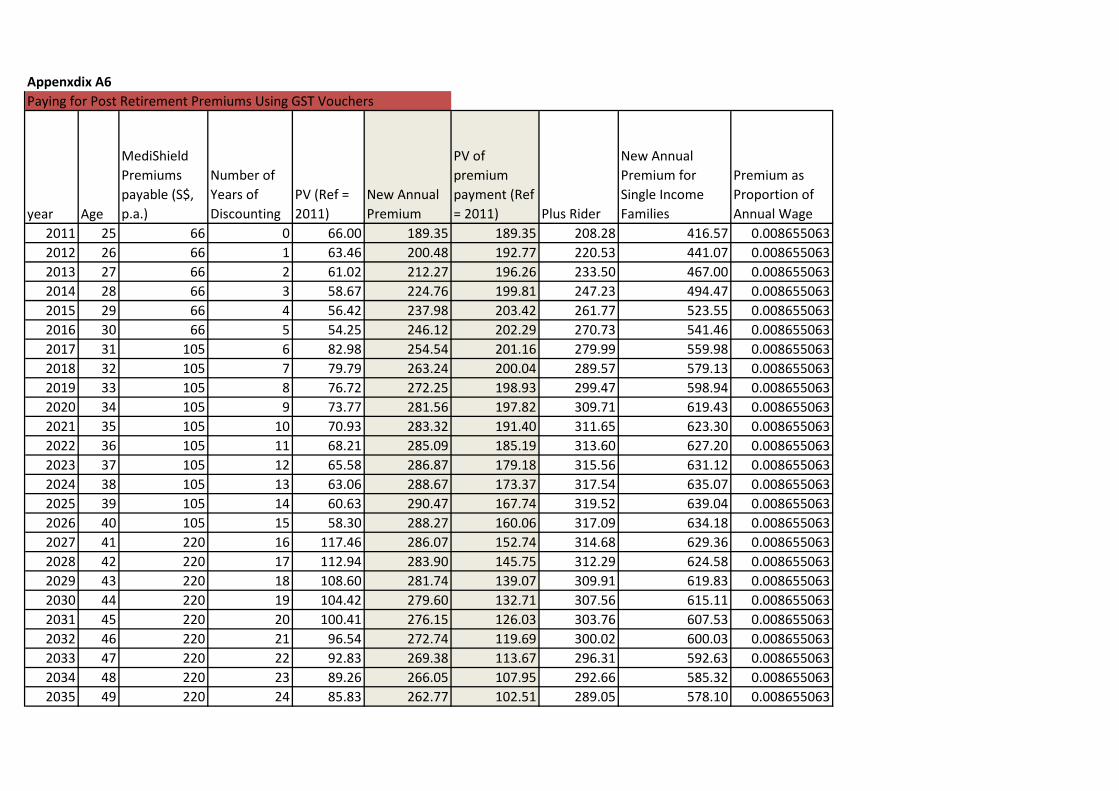

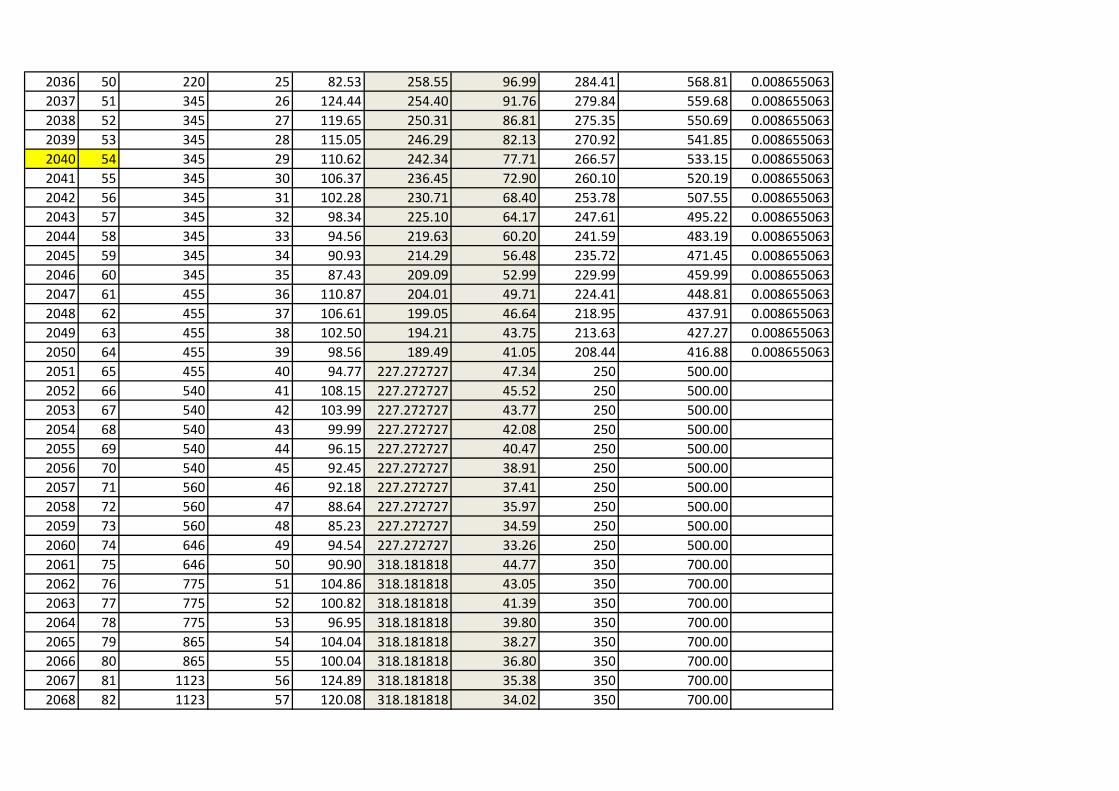

In our second model (see Appendix A6) where we rely on GST vouchers to pay for

MediShield contributions of our retirees, we find that the contribution as a proportion of income

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

18 of 24 | P a g e

is even smaller at less than 1%. MediShield is therefore affordable for the 30th income percentile,

even after allowing for a single income earner having to support his non-working spouse and an

additional rider of 10% on each policy. However the design of such a policy may seem

politically unpalatable to the general public as they may perceive the government as providing

GST vouchers on the one hand and taking it back with the other. This policy may also generate

unnecessary administrative cost within the civil service and this can be avoided by directly

transferring GST vouchers towards the medical insurance pool and providing a direct deduction

from the MediShield premiums of low wage Singaporeans who qualify for GST vouchers.

Looking Forward—Healthcare 2020

The theme of Healthcare 2020 is: Accessibility, Affordability and Higher Quality. Much

of the new initiative and plan is to brief up healthcare infrastructure in Singapore by opening new

hospitals in areas such as Jurong, Seng Kang, and also smaller community hospitals around the

island. More doctors will also be trained, with NTU Lee Kong Chian School of Medicine

accepting 500 medicine students and NUS increasing the number of medicine enrollment. For

the purposes of this paper, Healthcare 2020 can still be analyzed in the context of MediShield

premiums increments.

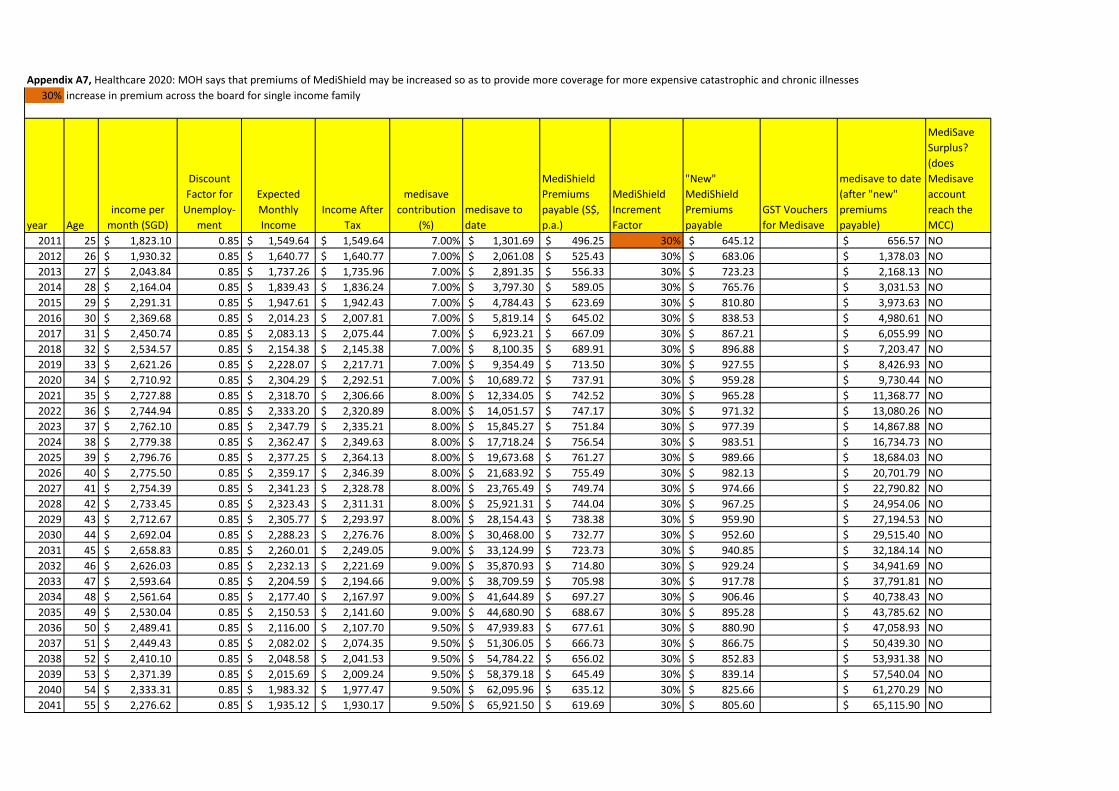

Our model will test how much MediShield premiums can increase before the worker is

unable to reach the MCC. We factor in an unemployment factor of 0.85; hence 85% of a

person’s lifetime, he will be unemployed due to unforeseen circumstances. The 30P

representative worker here is also the only income earner in the family, and he is paying for his

spouse’s MediShield premium on top of his, together with a rider of 10% on each policy.

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

19 of 24 | P a g e

From Appendix A7, it appears that the worker will still be able to reach the MCC at the

retirement age of 65 years even if MediShield premiums were to increase by 30% across the

board for all ages. This will provide the retiree with the maximum threshold of funds in his

Medisave for payment of healthcare bills and MediShield premiums. According to Minister of

Health Gan Kim Yong, for a high risk profile retiree at the age of 75, he can expect premium

increases of $240 annually(Gan, 2012). This is a 37% increase over his current premium of $646.

Whereas for a 45 year old MediShield policy holder, he can expect a $84 annual increase in

premium. This is a 38% increase over his current premium of $220. (See Appendix B1)

However, it should be cautioned that these premium increases are older policyholders with a

higher risk profile. It is still unlikely that there will be an indiscriminate across the board increase

in premiums of 30% since premium risk is lower when one is young.

By holding MediShield premium constant, we have also conducted another robustness

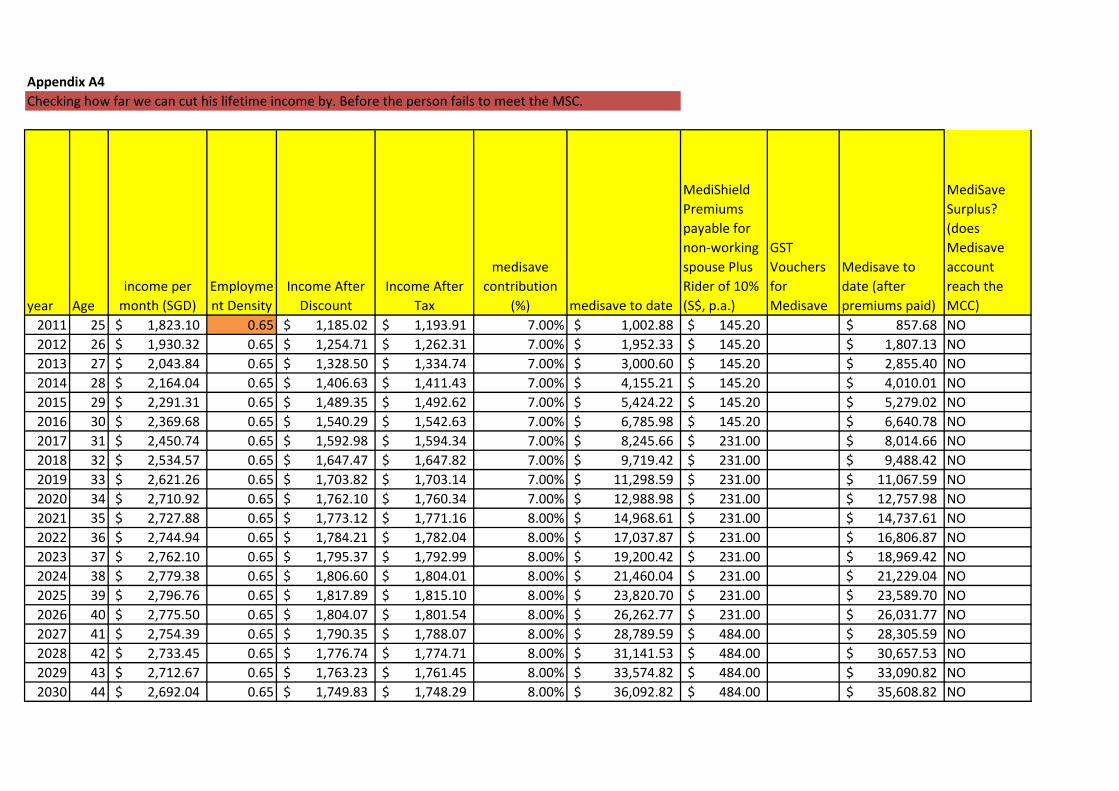

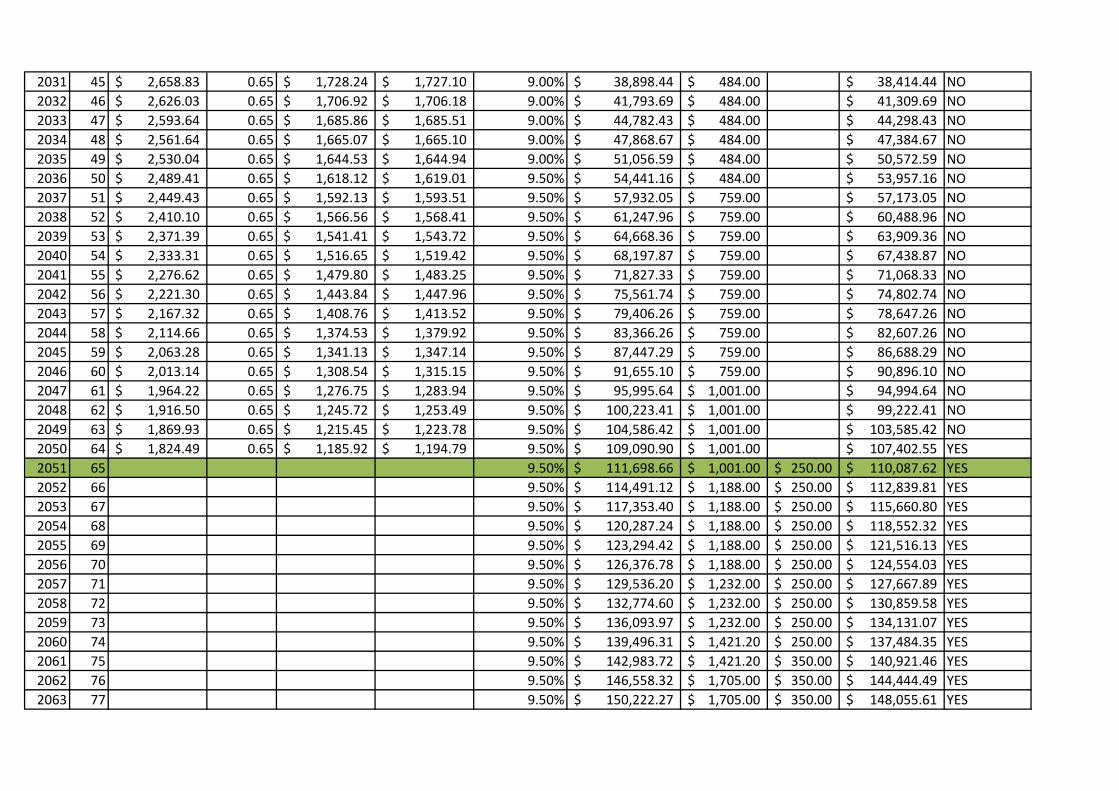

test (See Appendix A4) on our representative worker in a single income family and we find that

healthcare adequacy can still be achieved with an employment density of 65%.

Conclusion

The general approach to this research issue has been conservative and consistent with the

current government’s philosophy of healthcare financing: that is ensuring personal responsibility

and relying on current government transfers mechanisms. We acknowledge that the model is too

simplistic because it is riddled with unrealistic assumptions such as close to full lifetime

employment, full take up rate of policy, no withdrawals from Medisave account before

retirement, etc. However, it is still very much a viable working model, and provides a base from

which to work forward. Further research and enhancement can be made in the area of stochastic

so as to incorporate the uncertainties of being unemployed and withdrawing from the Medisave

A/P Chia Ngee Choon EC3352 Seminar in Singapore’s Economic Policy Eo and Chua, 2013

20 of 24 | P a g e

account. A good understanding of actuarial science should also be used to more accurately

predict the premiums payable due to varying life expectancies.

Overall, we have based our simulations on an arbitrarily estimated cost of the MediShield

rider as well as adjusted life expectancy for longevity risk pooling, we believe that more actuarial

based research and calculations have to be conducted to determine these actual numbers and we

see room for future research into these specific areas. With the accurate information on these

variables as well as detailed data on wage earning profiles of Singaporeans in the 10th and 20th

deciles, we would also seek to run similar simulations to determine the health care adequacy of

these lower income Singaporeans in future research. Such a research would also factor in the

impacts of the WIS scheme and can be used as a tool to evaluate the adequacy of the WIS

scheme. Overall, there can also be a third variation to our proposal of premium smoothing by

taking into consideration CPF Life and modeling it as post retirement income and we also see

room for future research in this direction where retirement adequacy is factored into

consideration.

Raw Working DataMonthly salary of an active Male CPF member (SC / PR) aged 25 as at end Dec 2011 (30th Percentile )

Year AgeIncome per month (S$)*

Income After Tax

Medisave contribution

(%) Medisave to date

Premiums

payable (S$, p.a.)

Medisave to date (after premiums paid)

Healthcare inflation (% y-y)

projected MMS (S$)

projected MCC (S$)

Healthcare inflation (% y-y)

projected MMS (S$)

projected MCC (S$)

2011 25 1,823.10$ 1,820.21$ 7.0% 1,531.40$ 66.00$ 1,465.40$ 2.5% 36,000.00$ 41,000.00$ 5.0% 36,000.00$ 41,000.00$ 2012 26 1,930.32$ 1,925.45$ 7.0% 3,214.13$ 66.00$ 3,148.13$ 2.5% 36,900.00$ 42,025.00$ 5.0% 37,800.00$ 43,050.00$ 2013 27 2,043.84$ 2,036.88$ 7.0% 5,059.52$ 66.00$ 4,993.52$ 2.5% 37,822.50$ 43,075.63$ 5.0% 39,690.00$ 45,202.50$ 2014 28 2,164.04$ 2,154.86$ 7.0% 7,079.69$ 66.00$ 7,013.69$ 2.5% 38,768.06$ 44,152.52$ 5.0% 41,674.50$ 47,462.63$ 2015 29 2,291.31$ 2,279.78$ 7.0% 9,287.58$ 66.00$ 9,221.58$ 2.5% 39,737.26$ 45,256.33$ 5.0% 43,758.23$ 49,835.76$ 2016 30 2,369.68$ 2,356.70$ 7.0% 11,649.62$ 66.00$ 11,583.62$ 2.5% 40,730.70$ 46,387.74$ 5.0% 45,946.14$ 52,327.54$ 2017 31 2,450.74$ 2,436.26$ 7.0% 14,174.22$ 105.00$ 14,069.22$ 2.5% 41,748.96$ 47,547.43$ 5.0% 48,243.44$ 54,943.92$ 2018 32 2,534.57$ 2,518.54$ 7.0% 16,870.23$ 105.00$ 16,765.23$ 2.5% 42,792.69$ 48,736.12$ 5.0% 50,655.62$ 57,691.12$ 2019 33 2,621.26$ 2,603.64$ 7.0% 19,746.90$ 105.00$ 19,641.90$ 2.5% 43,862.50$ 49,954.52$ 5.0% 53,188.40$ 60,575.67$ 2020 34 2,710.92$ 2,691.65$ 7.0% 22,813.95$ 105.00$ 22,708.95$ 2.5% 44,959.07$ 51,203.38$ 5.0% 55,847.82$ 63,604.46$ 2021 35 2,727.88$ 2,708.29$ 8.0% 26,345.27$ 105.00$ 26,240.27$ 2.5% 46,083.04$ 52,483.47$ 5.0% 58,640.21$ 66,784.68$ 2022 36 2,744.94$ 2,725.03$ 8.0% 30,034.22$ 105.00$ 29,929.22$ 2.5% 47,235.12$ 53,795.55$ 5.0% 61,572.22$ 70,123.91$ 2023 37 2,762.10$ 2,741.88$ 8.0% 33,887.21$ 105.00$ 33,782.21$ 2.5% 48,416.00$ 55,140.44$ 5.0% 64,650.83$ 73,630.11$ 2024 38 2,779.38$ 2,758.84$ 8.0% 37,910.90$ 105.00$ 37,805.90$ 2.5% 49,626.40$ 56,518.95$ 5.0% 67,883.37$ 77,311.61$ 2025 39 2,796.76$ 2,775.90$ 8.0% 42,112.23$ 105.00$ 42,007.23$ 2.5% 50,867.06$ 57,931.93$ 5.0% 71,277.54$ 81,177.20$ 2026 40 2,775.50$ 2,755.02$ 8.0% 46,461.19$ 105.00$ 46,356.19$ 2.5% 52,138.73$ 59,380.22$ 5.0% 74,841.41$ 85,236.06$ 2027 41 2,754.39$ 2,734.31$ 8.0% 50,963.86$ 220.00$ 50,743.86$ 2.5% 53,442.20$ 60,864.73$ 5.0% 78,583.49$ 89,497.86$ 2028 42 2,733.45$ 2,713.75$ 8.0% 55,626.52$ 220.00$ 55,406.52$ 2.5% 54,778.26$ 62,386.35$ 5.0% 82,512.66$ 93,972.75$ 2029 43 2,712.67$ 2,693.36$ 8.0% 60,455.74$ 220.00$ 60,235.74$ 2.5% 56,147.71$ 63,946.01$ 5.0% 86,638.29$ 98,671.39$ 2030 44 2,692.04$ 2,673.11$ 8.0% 65,458.33$ 220.00$ 65,238.33$ 2.5% 57,551.41$ 65,544.66$ 5.0% 90,970.21$ 103,604.96$ 2031 45 2,658.83$ 2,640.51$ 9.0% 70,948.20$ 220.00$ 70,728.20$ 2.5% 58,990.19$ 67,183.27$ 5.0% 95,518.72$ 108,785.21$ 2032 46 2,626.03$ 2,608.32$ 9.0% 76,622.24$ 220.00$ 76,402.24$ 2.5% 60,464.95$ 68,862.86$ 5.0% 100,294.65$ 114,224.47$ 2033 47 2,593.64$ 2,576.52$ 9.0% 82,488.26$ 220.00$ 82,268.26$ 2.5% 61,976.57$ 70,584.43$ 5.0% 105,309.39$ 119,935.69$ 2034 48 2,561.64$ 2,545.12$ 9.0% 88,554.37$ 220.00$ 88,334.37$ 2.5% 63,525.98$ 72,349.04$ 5.0% 110,574.86$ 125,932.47$ 2035 49 2,530.04$ 2,514.10$ 9.0% 94,828.98$ 220.00$ 94,608.98$ 2.5% 65,114.13$ 74,157.76$ 5.0% 116,103.60$ 132,229.10$ 2036 50 2,489.41$ 2,474.22$ 9.5% 101,460.07$ 220.00$ 101,240.07$ 2.5% 66,741.99$ 76,011.71$ 5.0% 121,908.78$ 138,840.55$ 2037 51 2,449.43$ 2,434.98$ 9.5% 108,310.83$ 345.00$ 107,965.83$ 2.5% 68,410.54$ 77,912.00$ 5.0% 128,004.22$ 145,782.58$ 2038 52 2,410.10$ 2,396.37$ 9.5% 115,390.77$ 345.00$ 115,045.77$ 2.5% 70,120.80$ 79,859.80$ 5.0% 134,404.43$ 153,071.71$ 2039 53 2,371.39$ 2,358.38$ 9.5% 122,709.79$ 345.00$ 122,364.79$ 2.5% 71,873.82$ 81,856.30$ 5.0% 141,124.65$ 160,725.29$ 2040 54 2,333.31$ 2,321.00$ 9.5% 130,278.16$ 345.00$ 129,933.16$ 2.5% 73,670.67$ 83,902.70$ 5.0% 148,180.88$ 168,761.56$ 2041 55 2,276.62$ 2,265.35$ 9.5% 138,084.63$ 345.00$ 137,739.63$ 2.5% 75,512.43$ 86,000.27$ 5.0% 155,589.93$ 177,199.64$ 2042 56 2,221.30$ 2,211.06$ 9.5% 146,140.29$ 345.00$ 145,795.29$ 2.5% 77,400.24$ 88,150.28$ 5.0% 163,369.42$ 186,059.62$ 2043 57 2,167.32$ 2,158.08$ 9.5% 154,456.65$ 345.00$ 154,111.65$ 2.5% 79,335.25$ 90,354.03$ 5.0% 171,537.89$ 195,362.60$ 2044 58 2,114.66$ 2,106.39$ 9.5% 163,045.63$ 345.00$ 162,700.63$ 2.5% 81,318.63$ 92,612.89$ 5.0% 180,114.79$ 205,130.73$ 2045 59 2,063.28$ 2,055.95$ 9.5% 171,919.59$ 345.00$ 171,574.59$ 2.5% 83,351.60$ 94,928.21$ 5.0% 189,120.53$ 215,387.27$ 2046 60 2,013.14$ 2,006.74$ 9.5% 181,091.35$ 345.00$ 180,746.35$ 2.5% 85,435.39$ 97,301.41$ 5.0% 198,576.55$ 226,156.63$ 2047 61 1,964.22$ 1,958.73$ 9.5% 190,574.22$ 455.00$ 190,119.22$ 2.5% 87,571.27$ 99,733.95$ 5.0% 208,505.38$ 237,464.46$ 2048 62 1,916.50$ 1,911.88$ 9.5% 200,382.00$ 455.00$ 199,927.00$ 2.5% 89,760.55$ 102,227.30$ 5.0% 218,930.65$ 249,337.68$

good case scenario worse case scenarioHealthcare inflation and effects on MSS and MCC

2049 63 1,869.93$ 1,866.18$ 9.5% 210,528.99$ 455.00$ 210,073.99$ 2.5% 92,004.57$ 104,782.98$ 5.0% 229,877.18$ 261,804.57$ 2050 64 1,824.49$ 1,821.58$ 9.5% 221,030.07$ 455.00$ 220,575.07$ 2.5% 94,304.68$ 107,402.55$ 5.0% 241,371.04$ 274,894.80$ 2051 65 0.0 9.5% 229,871.28$ 455.00$ 229,416.28$ 2.5% 96,662.30$ 110,087.62$ 5.0% 253,439.59$ 288,639.54$ 2052 66 0.0 9.5% 239,066.13$ 540.00$ 238,526.13$ 2.5% 99,078.86$ 112,839.81$ 5.0% 266,111.57$ 303,071.51$ 2053 67 0.0 9.5% 248,628.77$ 540.00$ 248,088.77$ 2.5% 101,555.83$ 115,660.80$ 5.0% 279,417.15$ 318,225.09$ 2054 68 0.0 9.5% 258,573.92$ 540.00$ 258,033.92$ 2.5% 104,094.72$ 118,552.32$ 5.0% 293,388.01$ 334,136.34$ 2055 69 0.0 9.5% 268,916.88$ 540.00$ 268,376.88$ 2.5% 106,697.09$ 121,516.13$ 5.0% 308,057.41$ 350,843.16$ 2056 70 0.0 9.5% 279,673.56$ 540.00$ 279,133.56$ 2.5% 109,364.52$ 124,554.03$ 5.0% 323,460.28$ 368,385.32$ 2057 71 0.0 9.5% 290,860.50$ 560.00$ 290,300.50$ 2.5% 112,098.63$ 127,667.89$ 5.0% 339,633.29$ 386,804.59$ 2058 72 0.0 9.5% 302,494.92$ 560.00$ 301,934.92$ 2.5% 114,901.10$ 130,859.58$ 5.0% 356,614.96$ 406,144.81$ 2059 73 0.0 9.5% 560.00$ 2.5% 117,773.62$ 134,131.07$ 5.0% 374,445.71$ 426,452.06$ 2060 74 0.0 9.5% 646.00$ 2.5% 120,717.96$ 137,484.35$ 5.0% 393,167.99$ 447,774.66$ 2061 75 0.0 9.5% 646.00$ 2.5% 123,735.91$ 140,921.46$ 5.0% 412,826.39$ 470,163.39$ 2062 76 0.0 9.5% 775.00$ 2.5% 126,829.31$ 144,444.49$ 5.0% 433,467.71$ 493,671.56$ 2063 77 0.0 9.5% 775.00$ 2.5% 130,000.04$ 148,055.61$ 5.0% 455,141.10$ 518,355.14$ 2064 78 0.0 9.5% 775.00$ 2.5% 133,250.05$ 151,757.00$ 5.0% 477,898.15$ 544,272.90$ 2065 79 0.0 9.5% 865.00$ 2.5% 136,581.30$ 155,550.92$ 5.0% 501,793.06$ 571,486.54$ 2066 80 0.0 9.5% 865.00$ 2.5% 139,995.83$ 159,439.69$ 5.0% 526,882.71$ 600,060.87$ 2067 81 0.0 9.5% 1,123.00$ 2.5% 143,495.72$ 163,425.69$ 5.0% 553,226.85$ 630,063.91$ 2068 82 0.0 9.5% 1,123.00$ 2.5% 147,083.12$ 167,511.33$ 5.0% 580,888.19$ 661,567.11$ 2069 83 0.0 9.5% 1,123.00$ 2.5% 150,760.20$ 171,699.11$ 5.0% 609,932.60$ 694,645.46$ 2070 84 0.0 9.5% 1,150.00$ 2.5% 154,529.20$ 175,991.59$ 5.0% 640,429.23$ 729,377.73$ 2071 85 0.0 9.5% 1,150.00$ 2.5% 158,392.43$ 180,391.38$ 5.0% 672,450.69$ 765,846.62$ 2072 86 0.0 9.5% 1,190.00$ 2.5% 162,352.24$ 184,901.16$ 5.0% 706,073.23$ 804,138.95$ 2073 87 0.0 9.5% 1,190.00$ 2.5% 166,411.05$ 189,523.69$ 5.0% 741,376.89$ 844,345.90$ 2074 88 0.0 9.5% 1,190.00$ 2.5% 170,571.32$ 194,261.79$ 5.0% 778,445.73$ 886,563.20$ 2075 89 0.0 9.5% 1,190.00$ 2.5% 174,835.61$ 199,118.33$ 5.0% 817,368.02$ 930,891.36$ 2076 90 0.0 9.5% 1,190.00$ 2.5% 179,206.50$ 204,096.29$ 5.0% 858,236.42$ 977,435.92$ 2077 91 0.0 9.5% -$ 2.5% 183,686.66$ 209,198.70$ 5.0% 901,148.24$ 1,026,307.72$

Appendix A1

year Ageincome per

month (SGD)Income

After Tax

medisave contribution

(%) medisave to date

MediShield Premiums payable (S$, p.a.)

GST Vouchers for Medisave

medisave to date (after premiums paid)

2011 25 1823.1 1820.2 0.07 1,528.98$ 66 1,462.98$ 2012 26 1930.3 1925.5 0.07 3,138.88$ 66 3,072.88$ 2013 27 2043.8 2036.9 0.07 4,906.77$ 66 4,840.77$ 2014 28 2164.0 2154.9 0.07 6,844.48$ 66 6,778.48$ 2015 29 2291.3 2279.8 0.07 8,964.63$ 66 8,898.63$ 2016 30 2369.7 2356.7 0.07 11,234.21$ 66 11,168.21$ 2017 31 2450.7 2436.3 0.07 13,661.40$ 105 13,556.40$ 2018 32 2534.6 2516.7 0.07 16,212.67$ 105 16,107.67$ 2019 33 2621.3 2600.4 0.07 18,936.28$ 105 18,831.28$ 2020 34 2710.9 2686.9 0.07 21,841.50$ 105 21,736.50$ 2021 35 2727.9 2703.2 0.08 25,201.07$ 105 25,096.07$ 2022 36 2744.9 2719.7 0.08 28,710.82$ 105 28,605.82$ 2023 37 2762.1 2736.3 0.08 32,376.87$ 105 32,271.87$ 2024 38 2779.4 2752.9 0.08 36,205.56$ 105 36,100.56$ 2025 39 2796.8 2769.7 0.08 40,203.50$ 105 40,098.50$ 2026 40 2775.5 2749.2 0.08 44,341.66$ 105 44,236.66$ 2027 41 2754.4 2728.8 0.08 48,625.79$ 220 48,405.79$ 2028 42 2733.4 2708.6 0.08 52,942.29$ 220 52,722.29$ 2029 43 2712.7 2688.6 0.08 57,412.20$ 220 57,192.20$ 2030 44 2692.0 2668.7 0.08 62,041.79$ 220 61,821.79$ 2031 45 2658.8 2636.6 0.09 67,142.20$ 220 66,922.20$ 2032 46 2626.0 2605.0 0.09 72,412.44$ 220 68,862.86$ 2033 47 2593.6 2573.7 0.09 74,396.96$ 220 70,584.43$ 2034 48 2561.6 2542.8 0.09 76,154.05$ 220 72,349.04$ 2035 49 2530.0 2512.3 0.09 77,956.31$ 220 74,157.76$ 2036 50 2489.4 2474.2 0.095 79,944.69$ 220 76,011.71$ 2037 51 2449.4 2435.0 0.095 81,828.06$ 345 77,912.00$ 2038 52 2410.1 2396.4 0.095 83,760.35$ 345 79,859.80$

2039 53 2371.4 2358.4 0.095 85,742.75$ 345 81,856.30$ 2040 54 2333.3 2321.0 0.095 87,776.49$ 345 83,902.70$ 2041 55 2276.6 2265.4 0.095 89,841.32$ 345 86,000.27$ 2042 56 2221.3 2211.1 0.095 91,960.89$ 345 88,150.28$ 2043 57 2167.3 2158.1 0.095 94,136.50$ 345 90,354.03$ 2044 58 2114.7 2106.4 0.095 96,369.48$ 345 92,612.89$ 2045 59 2063.3 2056.0 0.095 98,661.19$ 345 94,928.21$ 2046 60 2013.1 2006.7 0.095 101,013.02$ 345 97,301.41$ 2047 61 1964.2 1958.7 0.095 103,426.42$ 455 99,733.95$ 2048 62 1916.5 1911.9 0.095 105,902.85$ 455 102,227.30$ 2049 63 1869.9 1866.2 0.095 108,443.83$ 455 104,782.98$ 2050 64 1824.5 1821.6 0.095 111,050.90$ 455 107,402.55$ 2051 65 0.095 111,698.66$ 455 250 110,087.62$ 2052 66 0.095 114,491.12$ 540 250 112,839.81$ 2053 67 0.095 117,353.40$ 540 250 115,660.80$ 2054 68 0.095 120,287.24$ 540 250 118,552.32$ 2055 69 0.095 123,294.42$ 540 250 121,516.13$ 2056 70 0.095 126,376.78$ 540 250 124,554.03$ 2057 71 0.095 129,536.20$ 560 250 127,667.89$ 2058 72 0.095 132,774.60$ 560 250 130,859.58$ 2059 73 0.095 136,093.97$ 560 250 134,131.07$ 2060 74 0.095 139,496.31$ 646 250 137,484.35$ 2061 75 0.095 142,983.72$ 646 350 140,921.46$ 2062 76 0.095 146,558.32$ 775 350 144,444.49$ 2063 77 0.095 150,222.27$ 775 350 148,055.61$ 2064 78 0.095 153,977.83$ 775 350 151,757.00$ 2065 79 0.095 157,827.28$ 865 350 155,550.92$ 2066 80 0.095 161,772.96$ 865 350 159,439.69$ 2067 81 0.095 165,817.28$ 1123 350 163,425.69$ 2068 82 0.095 169,962.71$ 1123 350 167,511.33$ 2069 83 0.095 174,211.78$ 1123 350 171,699.11$ 2070 84 0.095 178,567.08$ 1150 350 175,991.59$ 2071 85 0.095 183,031.25$ 1150 450 180,391.38$

2072 86 0.095 187,607.03$ 1190 450 184,901.16$ 2073 87 0.095 192,297.21$ 1190 450 189,523.69$ 2074 88 0.095 197,104.64$ 1190 450 194,261.79$ 2075 89 0.095 202,032.26$ 1190 450 199,118.33$ 2076 90 0.095 207,083.06$ 1190 450 204,096.29$ 2077 91 0.095 0

Appendix A2

year Ageincome per

month (SGD)Income

After Tax

medisave contribution

(%) medisave to date

MediShield Premiums payable Plus Rider of 10%(S$, p.a.)

GST Vouchers for Medisave

medisave to date (after premiums paid)

2011 25 1,823.10$ 1,820.21$ 7.00% 1,528.98$ 72.6 1,456.38$ 2012 26 1,930.32$ 1,925.45$ 7.00% 3,132.01$ 72.6 3,059.41$ 2013 27 2,043.84$ 2,036.88$ 7.00% 4,892.76$ 72.6 4,820.16$ 2014 28 2,164.04$ 2,154.86$ 7.00% 6,823.05$ 72.6 6,750.45$ 2015 29 2,291.31$ 2,279.78$ 7.00% 8,935.48$ 72.6 8,862.88$ 2016 30 2,369.68$ 2,356.70$ 7.00% 11,197.03$ 72.6 11,124.43$ 2017 31 2,450.74$ 2,436.26$ 7.00% 13,615.87$ 115.5 13,500.37$ 2018 32 2,534.57$ 2,516.69$ 7.00% 16,154.40$ 115.5 16,038.90$ 2019 33 2,621.26$ 2,600.35$ 7.00% 18,864.76$ 115.5 18,749.26$ 2020 34 2,710.92$ 2,686.87$ 7.00% 21,756.20$ 115.5 21,640.70$ 2021 35 2,727.88$ 2,703.24$ 8.00% 25,101.44$ 115.5 24,985.94$ 2022 36 2,744.94$ 2,719.70$ 8.00% 28,596.28$ 115.5 28,480.78$ 2023 37 2,762.10$ 2,736.26$ 8.00% 32,246.83$ 115.5 32,131.33$ 2024 38 2,779.38$ 2,752.93$ 8.00% 36,059.40$ 115.5 35,943.90$ 2025 39 2,796.76$ 2,769.71$ 8.00% 40,040.57$ 115.5 39,925.07$ 2026 40 2,775.50$ 2,749.19$ 8.00% 44,161.29$ 115.5 44,045.79$ 2027 41 2,754.39$ 2,728.82$ 8.00% 48,427.29$ 242 48,185.29$ 2028 42 2,733.45$ 2,708.61$ 8.00% 52,712.97$ 242 52,470.97$ 2029 43 2,712.67$ 2,688.56$ 8.00% 57,150.82$ 242 56,908.82$ 2030 44 2,692.04$ 2,668.65$ 8.00% 61,747.08$ 242 61,505.08$ 2031 45 2,658.83$ 2,636.61$ 9.00% 66,812.82$ 242 66,570.82$ 2032 46 2,626.03$ 2,604.95$ 9.00% 72,047.00$ 242 68,862.86$ 2033 47 2,593.64$ 2,573.69$ 9.00% 74,396.96$ 242 70,584.43$ 2034 48 2,561.64$ 2,542.82$ 9.00% 76,154.05$ 242 72,349.04$ 2035 49 2,530.04$ 2,512.32$ 9.00% 77,956.31$ 242 74,157.76$ 2036 50 2,489.41$ 2,474.22$ 9.50% 79,944.69$ 242 76,011.71$ 2037 51 2,449.43$ 2,434.98$ 9.50% 81,828.06$ 379.5 77,912.00$

2038 52 2,410.10$ 2,396.37$ 9.50% 83,760.35$ 379.5 79,859.80$ 2039 53 2,371.39$ 2,358.38$ 9.50% 85,742.75$ 379.5 81,856.30$ 2040 54 2,333.31$ 2,321.00$ 9.50% 87,776.49$ 379.5 83,902.70$ 2041 55 2,276.62$ 2,265.35$ 9.50% 89,841.32$ 379.5 86,000.27$ 2042 56 2,221.30$ 2,211.06$ 9.50% 91,960.89$ 379.5 88,150.28$ 2043 57 2,167.32$ 2,158.08$ 9.50% 94,136.50$ 379.5 90,354.03$ 2044 58 2,114.66$ 2,106.39$ 9.50% 96,369.48$ 379.5 92,612.89$ 2045 59 2,063.28$ 2,055.95$ 9.50% 98,661.19$ 379.5 94,928.21$ 2046 60 2,013.14$ 2,006.74$ 9.50% 101,013.02$ 379.5 97,301.41$ 2047 61 1,964.22$ 1,958.73$ 9.50% 103,426.42$ 500.5 99,733.95$ 2048 62 1,916.50$ 1,911.88$ 9.50% 105,902.85$ 500.5 102,227.30$ 2049 63 1,869.93$ 1,866.18$ 9.50% 108,443.83$ 500.5 104,782.98$ 2050 64 1,824.49$ 1,821.58$ 9.50% 111,050.90$ 500.5 107,402.55$ 2051 65 9.50% 111,698.66$ 500.5 250 110,087.62$ 2052 66 9.50% 114,491.12$ 594 250 112,839.81$ 2053 67 9.50% 117,353.40$ 594 250 115,660.80$ 2054 68 9.50% 120,287.24$ 594 250 118,552.32$ 2055 69 9.50% 123,294.42$ 594 250 121,516.13$ 2056 70 9.50% 126,376.78$ 594 250 124,554.03$ 2057 71 9.50% 129,536.20$ 616 250 127,667.89$ 2058 72 9.50% 132,774.60$ 616 250 130,859.58$ 2059 73 9.50% 136,093.97$ 616 250 134,131.07$ 2060 74 9.50% 139,496.31$ 710.6 250 137,484.35$ 2061 75 9.50% 142,983.72$ 710.6 350 140,921.46$ 2062 76 9.50% 146,558.32$ 852.5 350 144,444.49$ 2063 77 9.50% 150,222.27$ 852.5 350 148,055.61$ 2064 78 9.50% 153,977.83$ 852.5 350 151,757.00$ 2065 79 9.50% 157,827.28$ 951.5 350 155,550.92$ 2066 80 9.50% 161,772.96$ 951.5 350 159,439.69$ 2067 81 9.50% 165,817.28$ 1235.3 350 163,425.69$ 2068 82 9.50% 169,962.71$ 1235.3 350 167,511.33$ 2069 83 9.50% 174,211.78$ 1235.3 350 171,699.11$ 2070 84 9.50% 178,567.08$ 1265 450 175,991.59$

2071 85 9.50% 183,031.25$ 1265 450 180,391.38$ 2072 86 9.50% 187,607.03$ 1309 450 184,901.16$ 2073 87 9.50% 192,297.21$ 1309 450 189,523.69$ 2074 88 9.50% 197,104.64$ 1309 450 194,261.79$ 2075 89 9.50% 202,032.26$ 1309 450 199,118.33$ 2076 90 9.50% 207,083.06$ 1309 450 204,096.29$ 2077 91 9.50% 0

Appendix A310% increase in premium across the board for single income family, paying MediShield premium for non-working spouse , plus rider of 10% on each policy

year Ageincome per

month (SGD)Income After

Tax

medisave contribution

(%) medisave to date

MediShield Premiums payable (S$, p.a.)

GST Vouchers for Medisave

medisave to date (after premiums paid)

2011 25 1,823.10$ 1,820.21$ 7.00% 1,528.98$ 145.20$ 1,383.78$ 2012 26 1,930.32$ 1,925.45$ 7.00% 3,056.51$ 145.20$ 2,911.31$ 2013 27 2,043.84$ 2,036.88$ 7.00% 4,738.74$ 145.20$ 4,593.54$ 2014 28 2,164.04$ 2,154.86$ 7.00% 6,587.36$ 145.20$ 6,442.16$ 2015 29 2,291.31$ 2,279.78$ 7.00% 8,614.86$ 145.20$ 8,469.66$ 2016 30 2,369.68$ 2,356.70$ 7.00% 10,788.08$ 145.20$ 10,642.88$ 2017 31 2,450.74$ 2,436.26$ 7.00% 13,115.05$ 231.00$ 12,884.05$ 2018 32 2,534.57$ 2,516.69$ 7.00% 15,513.44$ 231.00$ 15,282.44$ 2019 33 2,621.26$ 2,600.35$ 7.00% 18,078.03$ 231.00$ 17,847.03$ 2020 34 2,710.92$ 2,686.87$ 7.00% 20,817.88$ 231.00$ 20,586.88$ 2021 35 2,727.88$ 2,703.24$ 8.00% 24,005.47$ 231.00$ 23,774.47$ 2022 36 2,744.94$ 2,719.70$ 8.00% 27,336.35$ 231.00$ 27,105.35$ 2023 37 2,762.10$ 2,736.26$ 8.00% 30,816.38$ 231.00$ 30,585.38$ 2024 38 2,779.38$ 2,752.93$ 8.00% 34,451.61$ 231.00$ 34,220.61$ 2025 39 2,796.76$ 2,769.71$ 8.00% 38,248.36$ 231.00$ 38,017.36$ 2026 40 2,775.50$ 2,749.19$ 8.00% 42,177.27$ 231.00$ 41,946.27$ 2027 41 2,754.39$ 2,728.82$ 8.00% 46,243.79$ 484.00$ 45,759.79$ 2028 42 2,733.45$ 2,708.61$ 8.00% 50,190.45$ 484.00$ 49,706.45$ 2029 43 2,712.67$ 2,688.56$ 8.00% 54,275.72$ 484.00$ 53,791.72$ 2030 44 2,692.04$ 2,668.65$ 8.00% 58,505.29$ 484.00$ 58,021.29$ 2031 45 2,658.83$ 2,636.61$ 9.00% 63,189.68$ 484.00$ 62,705.68$ 2032 46 2,626.03$ 2,604.95$ 9.00% 68,027.26$ 484.00$ 67,543.26$ 2033 47 2,593.64$ 2,573.69$ 9.00% 73,024.58$ 484.00$ 70,584.43$ 2034 48 2,561.64$ 2,542.82$ 9.00% 76,154.05$ 484.00$ 72,349.04$ 2035 49 2,530.04$ 2,512.32$ 9.00% 77,956.31$ 484.00$ 74,157.76$ 2036 50 2,489.41$ 2,474.22$ 9.50% 79,944.69$ 484.00$ 76,011.71$ 2037 51 2,449.43$ 2,434.98$ 9.50% 81,828.06$ 759.00$ 77,912.00$ 2038 52 2,410.10$ 2,396.37$ 9.50% 83,760.35$ 759.00$ 79,859.80$

2039 53 2,371.39$ 2,358.38$ 9.50% 85,742.75$ 759.00$ 81,856.30$ 2040 54 2,333.31$ 2,321.00$ 9.50% 87,776.49$ 759.00$ 83,902.70$ 2041 55 2,276.62$ 2,265.35$ 9.50% 89,841.32$ 759.00$ 86,000.27$ 2042 56 2,221.30$ 2,211.06$ 9.50% 91,960.89$ 759.00$ 88,150.28$ 2043 57 2,167.32$ 2,158.08$ 9.50% 94,136.50$ 759.00$ 90,354.03$ 2044 58 2,114.66$ 2,106.39$ 9.50% 96,369.48$ 759.00$ 92,612.89$ 2045 59 2,063.28$ 2,055.95$ 9.50% 98,661.19$ 759.00$ 94,928.21$ 2046 60 2,013.14$ 2,006.74$ 9.50% 101,013.02$ 759.00$ 97,301.41$ 2047 61 1,964.22$ 1,958.73$ 9.50% 103,426.42$ 1,001.00$ 99,733.95$ 2048 62 1,916.50$ 1,911.88$ 9.50% 105,902.85$ 1,001.00$ 102,227.30$ 2049 63 1,869.93$ 1,866.18$ 9.50% 108,443.83$ 1,001.00$ 104,782.98$ 2050 64 1,824.49$ 1,821.58$ 9.50% 111,050.90$ 1,001.00$ 107,402.55$ 2051 65 9.50% 111,698.66$ 1,001.00$ 250.00$ 110,087.62$ 2052 66 9.50% 114,491.12$ 1,188.00$ 250.00$ 112,839.81$ 2053 67 9.50% 117,353.40$ 1,188.00$ 250.00$ 115,660.80$ 2054 68 9.50% 120,287.24$ 1,188.00$ 250.00$ 118,552.32$ 2055 69 9.50% 123,294.42$ 1,188.00$ 250.00$ 121,516.13$ 2056 70 9.50% 126,376.78$ 1,188.00$ 250.00$ 124,554.03$ 2057 71 9.50% 129,536.20$ 1,232.00$ 250.00$ 127,667.89$ 2058 72 9.50% 132,774.60$ 1,232.00$ 250.00$ 130,859.58$ 2059 73 9.50% 136,093.97$ 1,232.00$ 250.00$ 134,131.07$ 2060 74 9.50% 139,496.31$ 1,421.20$ 250.00$ 137,484.35$ 2061 75 9.50% 142,983.72$ 1,421.20$ 350.00$ 140,921.46$ 2062 76 9.50% 146,558.32$ 1,705.00$ 350.00$ 144,444.49$ 2063 77 9.50% 150,222.27$ 1,705.00$ 350.00$ 148,055.61$ 2064 78 9.50% 153,977.83$ 1,705.00$ 350.00$ 151,757.00$ 2065 79 9.50% 157,827.28$ 1,903.00$ 350.00$ 155,550.92$ 2066 80 9.50% 161,772.96$ 1,903.00$ 350.00$ 159,439.69$ 2067 81 9.50% 165,817.28$ 2,470.60$ 350.00$ 163,425.69$ 2068 82 9.50% 169,962.71$ 2,470.60$ 350.00$ 167,511.33$ 2069 83 9.50% 174,211.78$ 2,470.60$ 350.00$ 171,699.11$ 2070 84 9.50% 178,567.08$ 2,530.00$ 450.00$ 175,991.59$ 2071 85 9.50% 183,031.25$ 2,530.00$ 450.00$ 180,391.38$

2072 86 9.50% 187,607.03$ 2,618.00$ 450.00$ 184,901.16$ 2073 87 9.50% 192,297.21$ 2,618.00$ 450.00$ 189,523.69$ 2074 88 9.50% 197,104.64$ 2,618.00$ 450.00$ 194,261.79$ 2075 89 9.50% 202,032.26$ 2,618.00$ 450.00$ 199,118.33$ 2076 90 9.50% 207,083.06$ 2,618.00$ 450.00$ 204,096.29$ 2077 91 9.50% 0

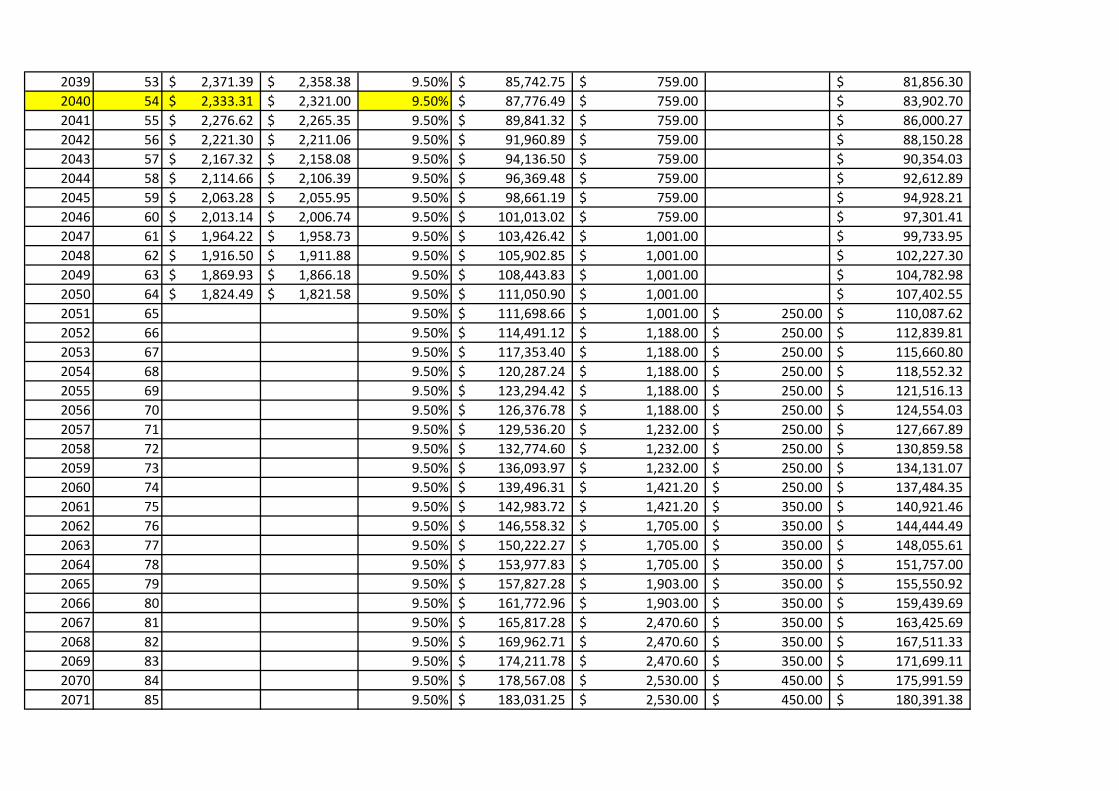

Appendix A4Checking how far we can cut his lifetime income by. Before the person fails to meet the MSC.

year Ageincome per

month (SGD)Employment Density

Income After Discount

Income After Tax

medisave contribution

(%) medisave to date

MediShield Premiums payable for non-working spouse Plus Rider of 10% (S$, p.a.)

GST Vouchers for Medisave

Medisave to date (after premiums paid)

MediSave Surplus? (does Medisave account reach the MCC)

2011 25 1,823.10$ 0.65 1,185.02$ 1,193.91$ 7.00% 1,002.88$ 145.20$ 857.68$ NO2012 26 1,930.32$ 0.65 1,254.71$ 1,262.31$ 7.00% 1,952.33$ 145.20$ 1,807.13$ NO2013 27 2,043.84$ 0.65 1,328.50$ 1,334.74$ 7.00% 3,000.60$ 145.20$ 2,855.40$ NO2014 28 2,164.04$ 0.65 1,406.63$ 1,411.43$ 7.00% 4,155.21$ 145.20$ 4,010.01$ NO2015 29 2,291.31$ 0.65 1,489.35$ 1,492.62$ 7.00% 5,424.22$ 145.20$ 5,279.02$ NO2016 30 2,369.68$ 0.65 1,540.29$ 1,542.63$ 7.00% 6,785.98$ 145.20$ 6,640.78$ NO2017 31 2,450.74$ 0.65 1,592.98$ 1,594.34$ 7.00% 8,245.66$ 231.00$ 8,014.66$ NO2018 32 2,534.57$ 0.65 1,647.47$ 1,647.82$ 7.00% 9,719.42$ 231.00$ 9,488.42$ NO2019 33 2,621.26$ 0.65 1,703.82$ 1,703.14$ 7.00% 11,298.59$ 231.00$ 11,067.59$ NO2020 34 2,710.92$ 0.65 1,762.10$ 1,760.34$ 7.00% 12,988.98$ 231.00$ 12,757.98$ NO2021 35 2,727.88$ 0.65 1,773.12$ 1,771.16$ 8.00% 14,968.61$ 231.00$ 14,737.61$ NO2022 36 2,744.94$ 0.65 1,784.21$ 1,782.04$ 8.00% 17,037.87$ 231.00$ 16,806.87$ NO2023 37 2,762.10$ 0.65 1,795.37$ 1,792.99$ 8.00% 19,200.42$ 231.00$ 18,969.42$ NO2024 38 2,779.38$ 0.65 1,806.60$ 1,804.01$ 8.00% 21,460.04$ 231.00$ 21,229.04$ NO2025 39 2,796.76$ 0.65 1,817.89$ 1,815.10$ 8.00% 23,820.70$ 231.00$ 23,589.70$ NO2026 40 2,775.50$ 0.65 1,804.07$ 1,801.54$ 8.00% 26,262.77$ 231.00$ 26,031.77$ NO2027 41 2,754.39$ 0.65 1,790.35$ 1,788.07$ 8.00% 28,789.59$ 484.00$ 28,305.59$ NO2028 42 2,733.45$ 0.65 1,776.74$ 1,774.71$ 8.00% 31,141.53$ 484.00$ 30,657.53$ NO2029 43 2,712.67$ 0.65 1,763.23$ 1,761.45$ 8.00% 33,574.82$ 484.00$ 33,090.82$ NO2030 44 2,692.04$ 0.65 1,749.83$ 1,748.29$ 8.00% 36,092.82$ 484.00$ 35,608.82$ NO

2031 45 2,658.83$ 0.65 1,728.24$ 1,727.10$ 9.00% 38,898.44$ 484.00$ 38,414.44$ NO2032 46 2,626.03$ 0.65 1,706.92$ 1,706.18$ 9.00% 41,793.69$ 484.00$ 41,309.69$ NO2033 47 2,593.64$ 0.65 1,685.86$ 1,685.51$ 9.00% 44,782.43$ 484.00$ 44,298.43$ NO2034 48 2,561.64$ 0.65 1,665.07$ 1,665.10$ 9.00% 47,868.67$ 484.00$ 47,384.67$ NO2035 49 2,530.04$ 0.65 1,644.53$ 1,644.94$ 9.00% 51,056.59$ 484.00$ 50,572.59$ NO2036 50 2,489.41$ 0.65 1,618.12$ 1,619.01$ 9.50% 54,441.16$ 484.00$ 53,957.16$ NO2037 51 2,449.43$ 0.65 1,592.13$ 1,593.51$ 9.50% 57,932.05$ 759.00$ 57,173.05$ NO2038 52 2,410.10$ 0.65 1,566.56$ 1,568.41$ 9.50% 61,247.96$ 759.00$ 60,488.96$ NO2039 53 2,371.39$ 0.65 1,541.41$ 1,543.72$ 9.50% 64,668.36$ 759.00$ 63,909.36$ NO2040 54 2,333.31$ 0.65 1,516.65$ 1,519.42$ 9.50% 68,197.87$ 759.00$ 67,438.87$ NO2041 55 2,276.62$ 0.65 1,479.80$ 1,483.25$ 9.50% 71,827.33$ 759.00$ 71,068.33$ NO2042 56 2,221.30$ 0.65 1,443.84$ 1,447.96$ 9.50% 75,561.74$ 759.00$ 74,802.74$ NO2043 57 2,167.32$ 0.65 1,408.76$ 1,413.52$ 9.50% 79,406.26$ 759.00$ 78,647.26$ NO2044 58 2,114.66$ 0.65 1,374.53$ 1,379.92$ 9.50% 83,366.26$ 759.00$ 82,607.26$ NO2045 59 2,063.28$ 0.65 1,341.13$ 1,347.14$ 9.50% 87,447.29$ 759.00$ 86,688.29$ NO2046 60 2,013.14$ 0.65 1,308.54$ 1,315.15$ 9.50% 91,655.10$ 759.00$ 90,896.10$ NO2047 61 1,964.22$ 0.65 1,276.75$ 1,283.94$ 9.50% 95,995.64$ 1,001.00$ 94,994.64$ NO2048 62 1,916.50$ 0.65 1,245.72$ 1,253.49$ 9.50% 100,223.41$ 1,001.00$ 99,222.41$ NO2049 63 1,869.93$ 0.65 1,215.45$ 1,223.78$ 9.50% 104,586.42$ 1,001.00$ 103,585.42$ NO2050 64 1,824.49$ 0.65 1,185.92$ 1,194.79$ 9.50% 109,090.90$ 1,001.00$ 107,402.55$ YES2051 65 9.50% 111,698.66$ 1,001.00$ 250.00$ 110,087.62$ YES2052 66 9.50% 114,491.12$ 1,188.00$ 250.00$ 112,839.81$ YES2053 67 9.50% 117,353.40$ 1,188.00$ 250.00$ 115,660.80$ YES2054 68 9.50% 120,287.24$ 1,188.00$ 250.00$ 118,552.32$ YES2055 69 9.50% 123,294.42$ 1,188.00$ 250.00$ 121,516.13$ YES2056 70 9.50% 126,376.78$ 1,188.00$ 250.00$ 124,554.03$ YES2057 71 9.50% 129,536.20$ 1,232.00$ 250.00$ 127,667.89$ YES2058 72 9.50% 132,774.60$ 1,232.00$ 250.00$ 130,859.58$ YES2059 73 9.50% 136,093.97$ 1,232.00$ 250.00$ 134,131.07$ YES2060 74 9.50% 139,496.31$ 1,421.20$ 250.00$ 137,484.35$ YES2061 75 9.50% 142,983.72$ 1,421.20$ 350.00$ 140,921.46$ YES2062 76 9.50% 146,558.32$ 1,705.00$ 350.00$ 144,444.49$ YES2063 77 9.50% 150,222.27$ 1,705.00$ 350.00$ 148,055.61$ YES

2064 78 9.50% 153,977.83$ 1,705.00$ 350.00$ 151,757.00$ YES2065 79 9.50% 157,827.28$ 1,903.00$ 350.00$ 155,550.92$ YES2066 80 9.50% 161,772.96$ 1,903.00$ 350.00$ 159,439.69$ YES2067 81 9.50% 165,817.28$ 2,470.60$ 350.00$ 163,425.69$ YES2068 82 9.50% 169,962.71$ 2,470.60$ 350.00$ 167,511.33$ YES2069 83 9.50% 174,211.78$ 2,470.60$ 350.00$ 171,699.11$ YES2070 84 9.50% 178,567.08$ 2,530.00$ 350.00$ 175,991.59$ YES2071 85 9.50% 183,031.25$ 2,530.00$ 450.00$ 180,391.38$ YES2072 86 9.50% 187,607.03$ 2,618.00$ 450.00$ 184,901.16$ YES2073 87 9.50% 192,297.21$ 2,618.00$ 450.00$ 189,523.69$ YES2074 88 9.50% 197,104.64$ 2,618.00$ 450.00$ 194,261.79$ YES2075 89 9.50% 202,032.26$ 2,618.00$ 450.00$ 199,118.33$ YES2076 90 9.50% 207,083.06$ 2,618.00$ 450.00$ 204,096.29$ YES

91

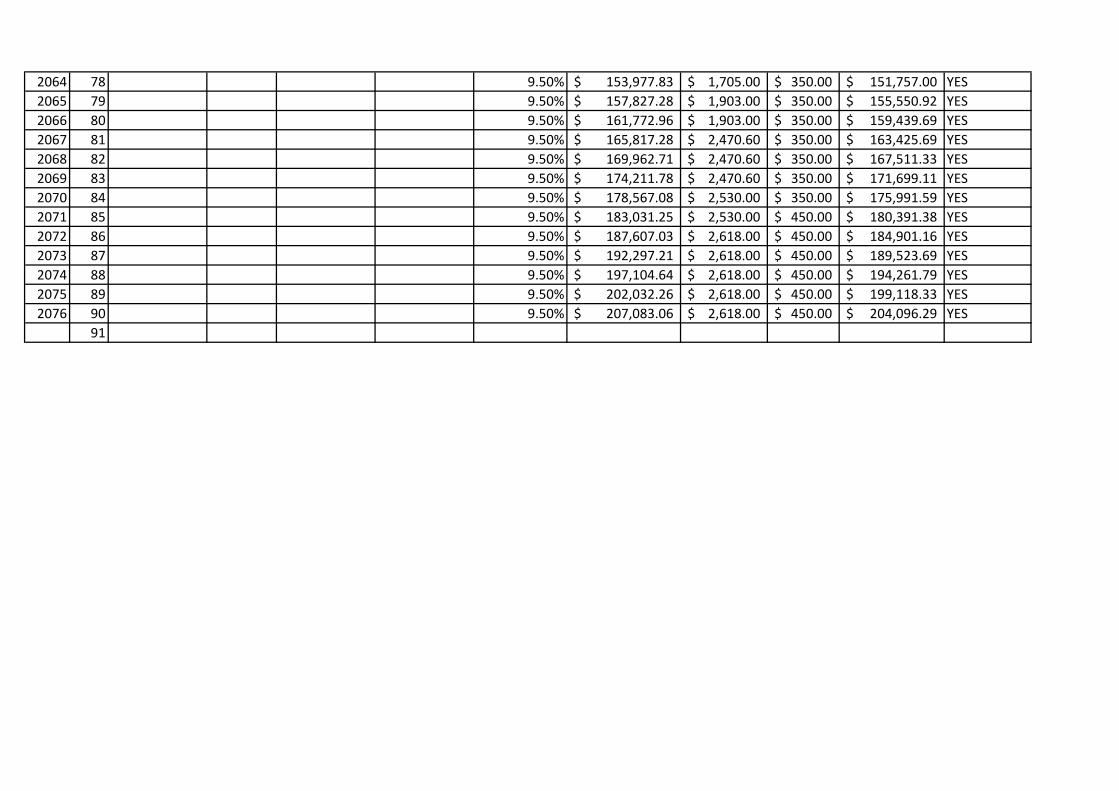

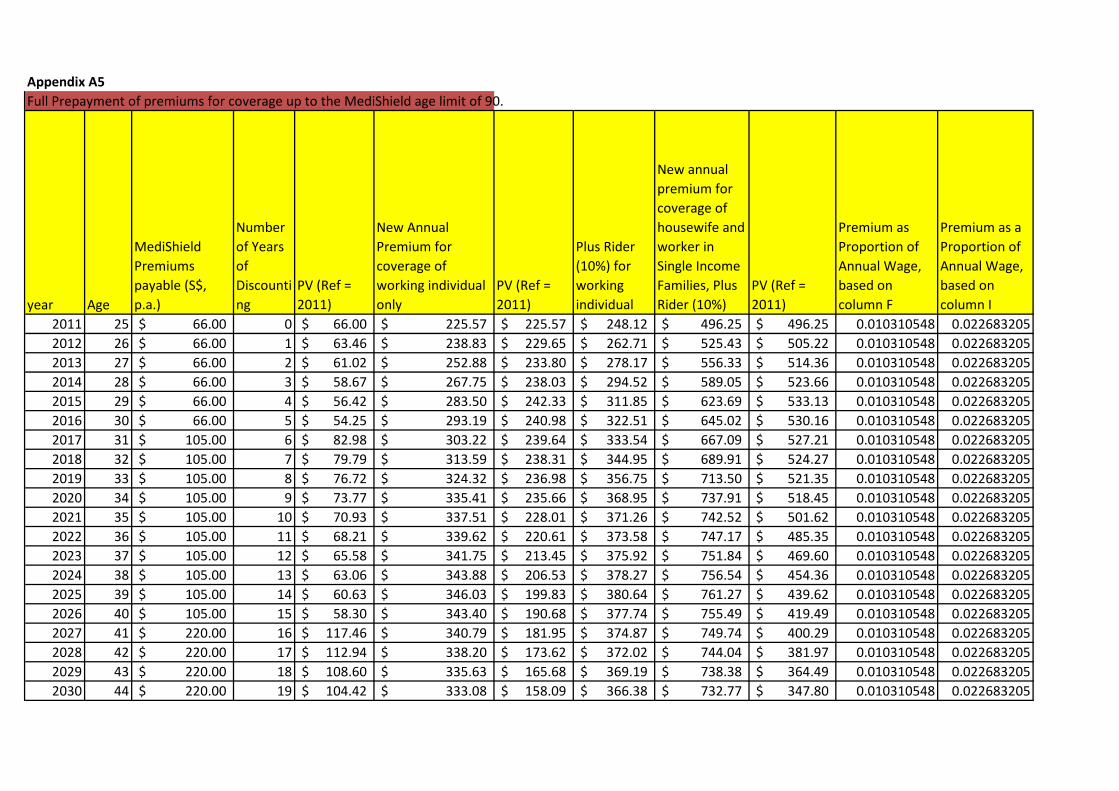

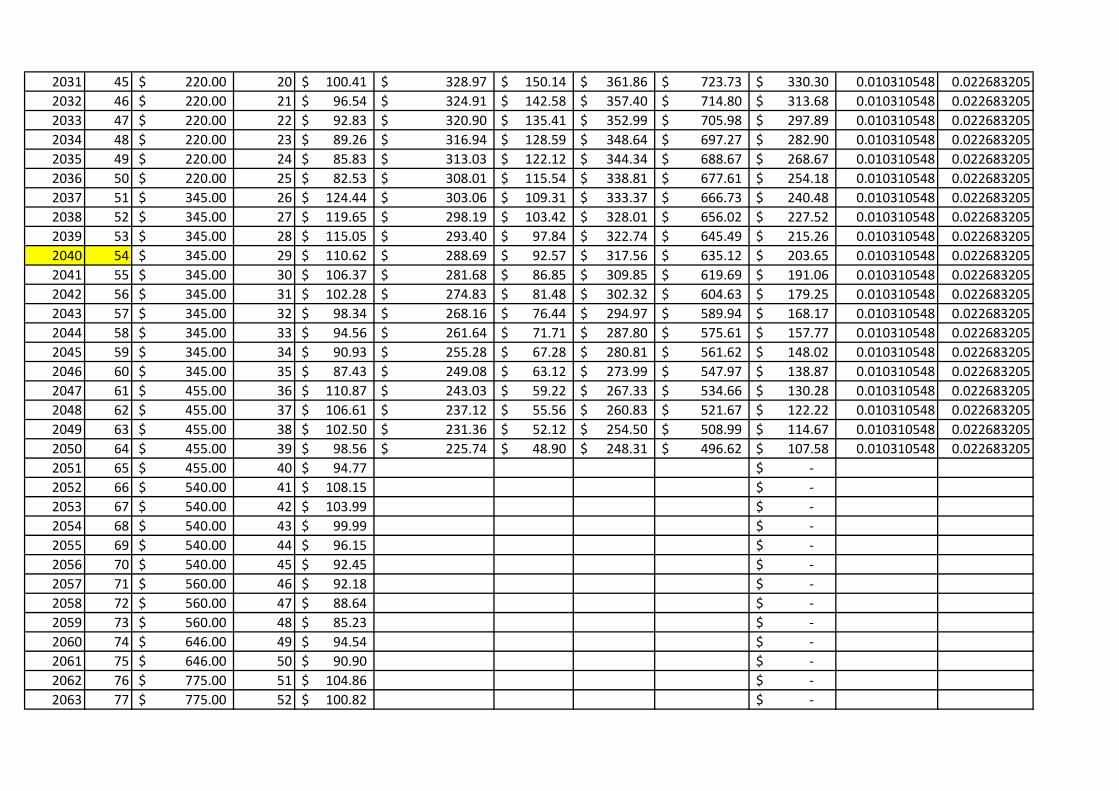

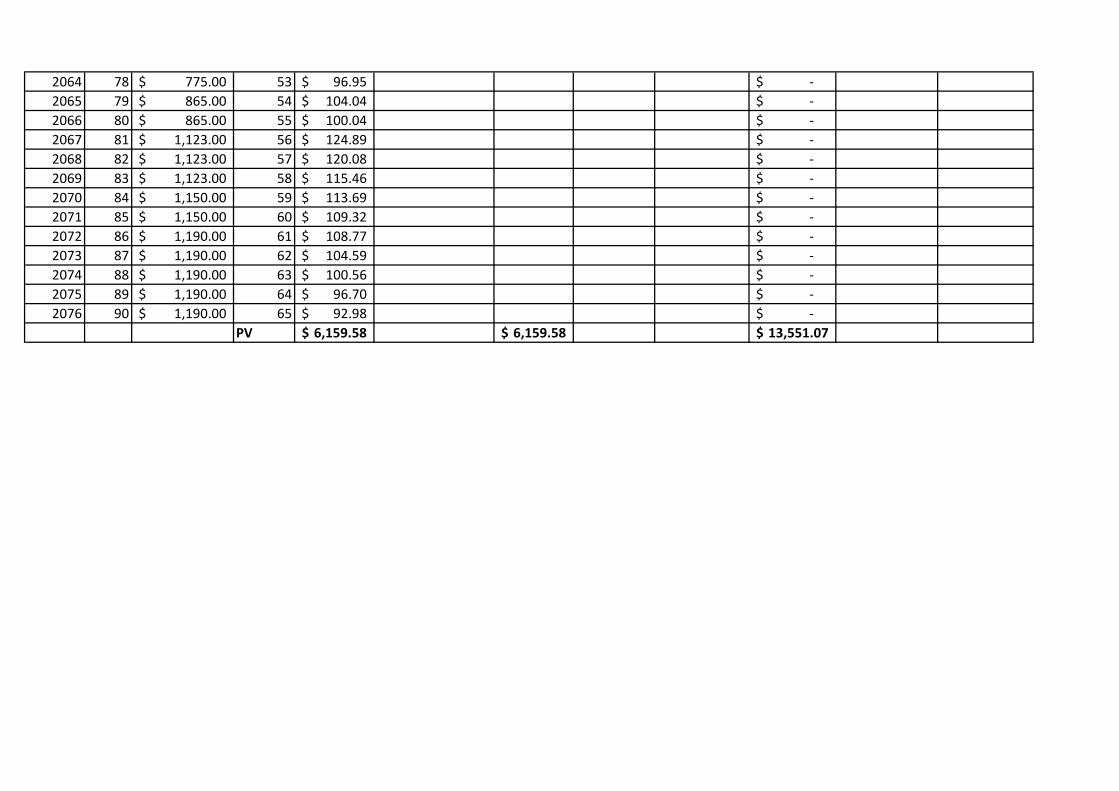

Appendix A5Full Prepayment of premiums for coverage up to the MediShield age limit of 90.

year Age

MediShield Premiums payable (S$, p.a.)

Number of Years of Discounting

PV (Ref = 2011)

New Annual Premium for coverage of working individual only

PV (Ref = 2011)

Plus Rider (10%) for working individual

New annual premium for coverage of housewife and worker in Single Income Families, Plus Rider (10%)

PV (Ref = 2011)

Premium as Proportion of Annual Wage, based on column F

Premium as a Proportion of Annual Wage, based on column I

2011 25 66.00$ 0 66.00$ 225.57$ 225.57$ 248.12$ 496.25$ 496.25$ 0.010310548 0.0226832052012 26 66.00$ 1 63.46$ 238.83$ 229.65$ 262.71$ 525.43$ 505.22$ 0.010310548 0.0226832052013 27 66.00$ 2 61.02$ 252.88$ 233.80$ 278.17$ 556.33$ 514.36$ 0.010310548 0.0226832052014 28 66.00$ 3 58.67$ 267.75$ 238.03$ 294.52$ 589.05$ 523.66$ 0.010310548 0.0226832052015 29 66.00$ 4 56.42$ 283.50$ 242.33$ 311.85$ 623.69$ 533.13$ 0.010310548 0.0226832052016 30 66.00$ 5 54.25$ 293.19$ 240.98$ 322.51$ 645.02$ 530.16$ 0.010310548 0.0226832052017 31 105.00$ 6 82.98$ 303.22$ 239.64$ 333.54$ 667.09$ 527.21$ 0.010310548 0.0226832052018 32 105.00$ 7 79.79$ 313.59$ 238.31$ 344.95$ 689.91$ 524.27$ 0.010310548 0.0226832052019 33 105.00$ 8 76.72$ 324.32$ 236.98$ 356.75$ 713.50$ 521.35$ 0.010310548 0.0226832052020 34 105.00$ 9 73.77$ 335.41$ 235.66$ 368.95$ 737.91$ 518.45$ 0.010310548 0.0226832052021 35 105.00$ 10 70.93$ 337.51$ 228.01$ 371.26$ 742.52$ 501.62$ 0.010310548 0.0226832052022 36 105.00$ 11 68.21$ 339.62$ 220.61$ 373.58$ 747.17$ 485.35$ 0.010310548 0.0226832052023 37 105.00$ 12 65.58$ 341.75$ 213.45$ 375.92$ 751.84$ 469.60$ 0.010310548 0.0226832052024 38 105.00$ 13 63.06$ 343.88$ 206.53$ 378.27$ 756.54$ 454.36$ 0.010310548 0.0226832052025 39 105.00$ 14 60.63$ 346.03$ 199.83$ 380.64$ 761.27$ 439.62$ 0.010310548 0.0226832052026 40 105.00$ 15 58.30$ 343.40$ 190.68$ 377.74$ 755.49$ 419.49$ 0.010310548 0.0226832052027 41 220.00$ 16 117.46$ 340.79$ 181.95$ 374.87$ 749.74$ 400.29$ 0.010310548 0.0226832052028 42 220.00$ 17 112.94$ 338.20$ 173.62$ 372.02$ 744.04$ 381.97$ 0.010310548 0.0226832052029 43 220.00$ 18 108.60$ 335.63$ 165.68$ 369.19$ 738.38$ 364.49$ 0.010310548 0.0226832052030 44 220.00$ 19 104.42$ 333.08$ 158.09$ 366.38$ 732.77$ 347.80$ 0.010310548 0.022683205

2031 45 220.00$ 20 100.41$ 328.97$ 150.14$ 361.86$ 723.73$ 330.30$ 0.010310548 0.0226832052032 46 220.00$ 21 96.54$ 324.91$ 142.58$ 357.40$ 714.80$ 313.68$ 0.010310548 0.0226832052033 47 220.00$ 22 92.83$ 320.90$ 135.41$ 352.99$ 705.98$ 297.89$ 0.010310548 0.0226832052034 48 220.00$ 23 89.26$ 316.94$ 128.59$ 348.64$ 697.27$ 282.90$ 0.010310548 0.0226832052035 49 220.00$ 24 85.83$ 313.03$ 122.12$ 344.34$ 688.67$ 268.67$ 0.010310548 0.0226832052036 50 220.00$ 25 82.53$ 308.01$ 115.54$ 338.81$ 677.61$ 254.18$ 0.010310548 0.0226832052037 51 345.00$ 26 124.44$ 303.06$ 109.31$ 333.37$ 666.73$ 240.48$ 0.010310548 0.0226832052038 52 345.00$ 27 119.65$ 298.19$ 103.42$ 328.01$ 656.02$ 227.52$ 0.010310548 0.0226832052039 53 345.00$ 28 115.05$ 293.40$ 97.84$ 322.74$ 645.49$ 215.26$ 0.010310548 0.0226832052040 54 345.00$ 29 110.62$ 288.69$ 92.57$ 317.56$ 635.12$ 203.65$ 0.010310548 0.0226832052041 55 345.00$ 30 106.37$ 281.68$ 86.85$ 309.85$ 619.69$ 191.06$ 0.010310548 0.0226832052042 56 345.00$ 31 102.28$ 274.83$ 81.48$ 302.32$ 604.63$ 179.25$ 0.010310548 0.0226832052043 57 345.00$ 32 98.34$ 268.16$ 76.44$ 294.97$ 589.94$ 168.17$ 0.010310548 0.0226832052044 58 345.00$ 33 94.56$ 261.64$ 71.71$ 287.80$ 575.61$ 157.77$ 0.010310548 0.0226832052045 59 345.00$ 34 90.93$ 255.28$ 67.28$ 280.81$ 561.62$ 148.02$ 0.010310548 0.0226832052046 60 345.00$ 35 87.43$ 249.08$ 63.12$ 273.99$ 547.97$ 138.87$ 0.010310548 0.0226832052047 61 455.00$ 36 110.87$ 243.03$ 59.22$ 267.33$ 534.66$ 130.28$ 0.010310548 0.0226832052048 62 455.00$ 37 106.61$ 237.12$ 55.56$ 260.83$ 521.67$ 122.22$ 0.010310548 0.0226832052049 63 455.00$ 38 102.50$ 231.36$ 52.12$ 254.50$ 508.99$ 114.67$ 0.010310548 0.0226832052050 64 455.00$ 39 98.56$ 225.74$ 48.90$ 248.31$ 496.62$ 107.58$ 0.010310548 0.0226832052051 65 455.00$ 40 94.77$ -$ 2052 66 540.00$ 41 108.15$ -$ 2053 67 540.00$ 42 103.99$ -$ 2054 68 540.00$ 43 99.99$ -$ 2055 69 540.00$ 44 96.15$ -$ 2056 70 540.00$ 45 92.45$ -$ 2057 71 560.00$ 46 92.18$ -$ 2058 72 560.00$ 47 88.64$ -$ 2059 73 560.00$ 48 85.23$ -$ 2060 74 646.00$ 49 94.54$ -$ 2061 75 646.00$ 50 90.90$ -$ 2062 76 775.00$ 51 104.86$ -$ 2063 77 775.00$ 52 100.82$ -$

2064 78 775.00$ 53 96.95$ -$ 2065 79 865.00$ 54 104.04$ -$ 2066 80 865.00$ 55 100.04$ -$ 2067 81 1,123.00$ 56 124.89$ -$ 2068 82 1,123.00$ 57 120.08$ -$ 2069 83 1,123.00$ 58 115.46$ -$ 2070 84 1,150.00$ 59 113.69$ -$ 2071 85 1,150.00$ 60 109.32$ -$ 2072 86 1,190.00$ 61 108.77$ -$ 2073 87 1,190.00$ 62 104.59$ -$ 2074 88 1,190.00$ 63 100.56$ -$ 2075 89 1,190.00$ 64 96.70$ -$ 2076 90 1,190.00$ 65 92.98$ -$

PV 6,159.58$ 6,159.58$ 13,551.07$

Appenxdix A6Paying for Post Retirement Premiums Using GST Vouchers

year Age

MediShield Premiums payable (S$, p.a.)

Number of Years of Discounting

PV (Ref = 2011)

New Annual Premium

PV of premium payment (Ref = 2011) Plus Rider

New Annual Premium for Single Income Families

Premium as Proportion of Annual Wage

2011 25 66 0 66.00 189.35 189.35 208.28 416.57 0.0086550632012 26 66 1 63.46 200.48 192.77 220.53 441.07 0.0086550632013 27 66 2 61.02 212.27 196.26 233.50 467.00 0.0086550632014 28 66 3 58.67 224.76 199.81 247.23 494.47 0.0086550632015 29 66 4 56.42 237.98 203.42 261.77 523.55 0.0086550632016 30 66 5 54.25 246.12 202.29 270.73 541.46 0.0086550632017 31 105 6 82.98 254.54 201.16 279.99 559.98 0.0086550632018 32 105 7 79.79 263.24 200.04 289.57 579.13 0.0086550632019 33 105 8 76.72 272.25 198.93 299.47 598.94 0.0086550632020 34 105 9 73.77 281.56 197.82 309.71 619.43 0.0086550632021 35 105 10 70.93 283.32 191.40 311.65 623.30 0.0086550632022 36 105 11 68.21 285.09 185.19 313.60 627.20 0.0086550632023 37 105 12 65.58 286.87 179.18 315.56 631.12 0.0086550632024 38 105 13 63.06 288.67 173.37 317.54 635.07 0.0086550632025 39 105 14 60.63 290.47 167.74 319.52 639.04 0.0086550632026 40 105 15 58.30 288.27 160.06 317.09 634.18 0.0086550632027 41 220 16 117.46 286.07 152.74 314.68 629.36 0.0086550632028 42 220 17 112.94 283.90 145.75 312.29 624.58 0.0086550632029 43 220 18 108.60 281.74 139.07 309.91 619.83 0.0086550632030 44 220 19 104.42 279.60 132.71 307.56 615.11 0.0086550632031 45 220 20 100.41 276.15 126.03 303.76 607.53 0.0086550632032 46 220 21 96.54 272.74 119.69 300.02 600.03 0.0086550632033 47 220 22 92.83 269.38 113.67 296.31 592.63 0.0086550632034 48 220 23 89.26 266.05 107.95 292.66 585.32 0.0086550632035 49 220 24 85.83 262.77 102.51 289.05 578.10 0.008655063

2036 50 220 25 82.53 258.55 96.99 284.41 568.81 0.0086550632037 51 345 26 124.44 254.40 91.76 279.84 559.68 0.0086550632038 52 345 27 119.65 250.31 86.81 275.35 550.69 0.0086550632039 53 345 28 115.05 246.29 82.13 270.92 541.85 0.0086550632040 54 345 29 110.62 242.34 77.71 266.57 533.15 0.0086550632041 55 345 30 106.37 236.45 72.90 260.10 520.19 0.0086550632042 56 345 31 102.28 230.71 68.40 253.78 507.55 0.0086550632043 57 345 32 98.34 225.10 64.17 247.61 495.22 0.0086550632044 58 345 33 94.56 219.63 60.20 241.59 483.19 0.0086550632045 59 345 34 90.93 214.29 56.48 235.72 471.45 0.0086550632046 60 345 35 87.43 209.09 52.99 229.99 459.99 0.0086550632047 61 455 36 110.87 204.01 49.71 224.41 448.81 0.0086550632048 62 455 37 106.61 199.05 46.64 218.95 437.91 0.0086550632049 63 455 38 102.50 194.21 43.75 213.63 427.27 0.0086550632050 64 455 39 98.56 189.49 41.05 208.44 416.88 0.0086550632051 65 455 40 94.77 227.272727 47.34 250 500.002052 66 540 41 108.15 227.272727 45.52 250 500.002053 67 540 42 103.99 227.272727 43.77 250 500.002054 68 540 43 99.99 227.272727 42.08 250 500.002055 69 540 44 96.15 227.272727 40.47 250 500.002056 70 540 45 92.45 227.272727 38.91 250 500.002057 71 560 46 92.18 227.272727 37.41 250 500.002058 72 560 47 88.64 227.272727 35.97 250 500.002059 73 560 48 85.23 227.272727 34.59 250 500.002060 74 646 49 94.54 227.272727 33.26 250 500.002061 75 646 50 90.90 318.181818 44.77 350 700.002062 76 775 51 104.86 318.181818 43.05 350 700.002063 77 775 52 100.82 318.181818 41.39 350 700.002064 78 775 53 96.95 318.181818 39.80 350 700.002065 79 865 54 104.04 318.181818 38.27 350 700.002066 80 865 55 100.04 318.181818 36.80 350 700.002067 81 1123 56 124.89 318.181818 35.38 350 700.002068 82 1123 57 120.08 318.181818 34.02 350 700.00

2069 83 1123 58 115.46 318.181818 32.71 350 700.002070 84 1150 59 113.69 318.181818 31.46 350 700.002071 85 1150 60 109.32 409.090909 38.89 450 900.002072 86 1190 61 108.77 409.090909 37.39 450 900.002073 87 1190 62 104.59 409.090909 35.95 450 900.002074 88 1190 63 100.56 409.090909 34.57 450 900.002075 89 1190 64 96.70 409.090909 33.24 450 900.002076 90 1190 65 92.98 409.090909 31.96 450 900.00

PV 6159.58 6159.58

Appendix A7, Healthcare 2020: MOH says that premiums of MediShield may be increased so as to provide more coverage for more expensive catastrophic and chronic illnesses30% increase in premium across the board for single income family

year Ageincome per

month (SGD)

Discount Factor for

Unemploy-ment

Expected Monthly Income

Income After Tax

medisave contribution

(%)medisave to date

MediShield Premiums payable (S$, p.a.)

MediShield Increment Factor

"New" MediShield Premiums payable

GST Vouchers for Medisave

medisave to date (after "new" premiums payable)

MediSave Surplus? (does Medisave account reach the MCC)