Energy Sector Management Assistance Programme

100

:9w -:0ESMAP Energy Sector Management Assistance Programme bec. 129? Philippines Commercial Potential for Power Production from Agricultural Residues Report No. 157193 Results of a Joint Study by ESMAPand the Philippines Department of Energy Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Energy Sector Management Assistance Programme

:9w -:0ESMAPEnergy Sector Management Assistance Programme

bec. 129?

PhilippinesCommercial Potential for Power Production from

Agricultural ResiduesReport No. 157193

Results of a Joint Study by ESMAP and thePhilippines Department of Energy

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

JOINT UNDP / WORLD BANKENERGY SECTOR MANAGEMENT ASSISTANCE PROGRAMME (ESMAP)

PURPOSE

The Joint UNDP/World Bank Energy Sector Management Assistance Programme (ESMAP) waslaunched in 1983 to complement the Energy Assessment Programme, established three yearsearlier. ESMAP's original purpose was to implement key recommendations of the EnergyAssessment reports and ensure that proposed investments in the energy sector represented the mostefficient use of scarce domestic and external resources. In 1990, an international Commissionaddressed ESMAP's role for the 1990s and, noting the vital role of adequate and affordable energyin economic growth, concluded that the Programme should intensify its efforts to assist developingcountries to manage their energy sectors more effectively. The Commission also recommendedthat ESMAP concentrate on making long-term efforts in a smaller number of countries. TheCommission's report was endorsed at ESMAP's November 1990 Annual Meeting and promptedan extensive reorganization and reorientation of the Programme. Today, ESMAP is conductingEnergy Assessments, performing preinvestment and prefeasibility work, and providing institutionaland policy advice in selected developing countries. Through these efforts, ESMAP aims to assistgovermnents, donors, and potential investors in identifying, funding, and implementingeconomically and environmentally sound energy strategies.

GOVERNANCE AND OPERATIONS

ESMAP is governed by a Consultative Group (ESMAP CG), composed of representatives of theUNDP and World Bank, the governments and institutions providing financial support, andrepresentatives of the recipients of ESMAP's assistance. The ESMAP CG is chaired by the WorldBank's Vice President, Finance and Private Sector Development, and advised by a TechnicalAdvisory Group (TAG) of independent energy experts that reviews the Programme's strategicagenda, its work program, and other issues. ESMAP is staffed by a cadre of engineers, energyplanners and economists from the Industry and Energy Department of the World Bank. TheDirector of this Department is also the Manager of ESMAP, responsible for administering theProgramme.

FUNDING

ESMAP is a cooperative effort supported by the World Bank, UNDP and other United Nationsagencies, the European Community, Organization of American States (OAS), Latin AmericanEnergy Organization (OLADE), and countries including Australia, Belgium, Canada, Denmark,Germany, Finland, France, Iceland, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway,Portugal, Sweden, Switzerland, the United Kingdom, and the United States.

FURTHER INFORMATION

For further information or copies of completed ESMAP reports, contact:

ESMAPc/o Industry and Energy Department

The World Bank1818 H Street N.W.

Washington, D.C. 20433U.S.A.

Philippines:

Commercial Potential for Power Production fromAgricultural Residues

Results of a Joint Study by ESMAP and the PhilippinesDepartment of Energy

December 1993

Abbreviations and Acronyms

ANECs Affiliated Nonconventional Energy CentersBED Bureau of Energy DevelopmentBEU Bureau of Utilization1301 Board of InvestmentsCARP Comprehensive Agrarian Reform ProgramCNED Center for Nonconventional Energy DevelopmentDOE Departnent of EnergyDOST Departnent of Science and TechnologyDSM Demand side managementECC Energy Coordinating CouncilEDB Energy Development BoardERDC Energy Research and Development CenterESMAP Energy Sector Management ProgrammeGEF Global Environment FacilityGOP Government of the PhilippinesMOE Ministry of EnergyNASUTRA National Sugar Trading CorporationNCRD Nonconventional Resources DivisionNEA National Electrification AdministrationNCED Nonconventional Energy DivisionNEDP Nonconventional Energy Development ProgramNFA National Food AuthorityNPC National Power CorporationOEA Office of Energy AffairsP Philippine PesoPCA Philippine Coconut AuthorityPCIERD Philippine Council for Industry and Energy

Research and DevelopmentPNOC Philipine National Oil CompanyREC Rural Electric CooperativeSRA Sugar Regulatory AdministrationUNDP United Nations Development Program

Currency Equivalents

The Philippine currency is the peso (P). The exchange race used in this report is US$1 .00 = P 25.00

Weights and Measures

bbl - barrelbcf - billion cubic feetbcm - billion cubic metersbfoe - barrels of fuel oil equivalentha - hectareGWh - gigawatt-hour (I million kilowatt-hours)kcal - kilocalorie (3.97 British thermal units)kg - kilogram (2.2 pounds)km - kilometer (0.62 miles)kW - kilowattkWh - kilowatt-hourmcf - million cubic feetmloe - million litres of oil equivalent

immb - million barrelsmmbfoe - million barrels of fuel oil equivalentr - metric tonty - metric tons per yearMW - megawatttcd - tons of cane per daytcpy - tons of cane per yeartoe - tons of oil equivalent

Converlon Facton

I million tons of oil equivalent is

= 1.5 million tons of coal= 3 million tons of lignite= 1.l Ibcm of natural gas= 39.2bcf of natural gas= 12.WOOGWh of electricity

TABLE OF CONTENTS Page

FOREWORD ...........................

EXECUTIVE SUMMARY ....................... i

L.BACKGROUND......................... IIntroduction .. 1........................Energy Sector Overview .......................Current Power Situation.......................2The Case For Biomass Cogeneration.................. 3Objectives and Methodology of the Study ................. s

IL. THlE SUGAR SECTOR.......................6Sector Profile......................... 8Mill Operation......................... 8Cane Residue Availability .. 1...................iSector Segmentation .11..................... Investment Scenarios ....................... 12Results of the Economic and Financial Analysis...............13Implementation Issues.......................15

M. THE RICE SECTOR.......................17Sector Profile..........................17Biomiass Residue Availability.....................18

Potential Availability of Rice Hulls ................. 19Present Uses of Rice Hulls....................20

Sector Segmnentation ....................... 20Investment Scenarios ....................... 20Results of the Economic and Financial Analysis ............... 23Other Inplementation Constraints ................... 23

IV. THE COCONUT SECTOR.....................25Sector Profile..........................25

Area Planted and Production ................... 28Coconut Processing and Consumption.................28

Biomass Residue Availability.....................29Present Uses as Fuel......................30Non-Fuel Uses........................30

Sector Segmentation ....................... 31Coconut Oil Mills.......................31Coconut Desiccators......................31Coconut Production Sites .................... 32

Investment Scenarios ....................... 33Results of the Analysis.......................34Implernentation Issues.......................35

V. CONCLUSIONS AND RECOMMENDATIONS .......................... 36General Conclusions.36Sector Conclusions ............................................. 37Recommendations.39

ANNEXES

A. The Nonconventional Energy Development Program: An Evaluation ............... 41

B. Training on Economic Appraisal of Nonconventional Energy Projects ............... 48

C. Guidelines for Technology Selection ................................... 52

D. Data Tables ................................................... 56

E. Selected Spreadsheets ............................................. 71

FOREWORD

This report is one of the outputs of a technical assistance project to the Philippines Officeof Energy Affairs (OEA), now the Department of Energy (DOE), executed by the joint WorldBank/UNDP Energy Sector Management Programme (ESMAP) and financed by the NetherlandsGovernment. The activity entitled "Nonconventitnnal Energy Planning Technical Assistance" hadthree components: (a) an evaluation of OEA's nonconventional energy development program, (b)a training course on project economic appraisal and (c) a study of the potential for powerproduction using biomass residues. The study effectively commenced in November 1991.

The first component, a brief evaluation of program achievements, constraints and directions,was conducted by Dan Fallen-Bailey, Gregorio Kilayko and Nonnan Brown (consultants). Theoutput of this component was written by Ernesto Terrado and is presented as Annex A.

The results of the second cnmponent, a training program for staff of the NonconventionalResources Division of OEA and of the Affiliated Nonconventional Energy Centers of variousprovinces, are described in Annex B. The main resource person for this task was DonaldHertzmark (consultant).

The main body of this report comprises the bulk of the work done overall. Its purpose wastwofold. First, it aimed to determine the realistic potential for energy utilization of keyagricultural wastes in the country, namely residues of the sugar, rice and coconut processingindustries, given the prolonged power crisis. Second, and more importantly, it aimed to use theprocess of investigation as a hands-on training tool for OEA staff who previously have nevercarried out a study of similar complexity. Thus a local team consisting of OEA staff and localconsultants was forned in 1992 and interacted closely with the ESMAP team during the courseof the work. The local team, led by Conrado Heruela, Marites Cabrera and Eloida Balaniiento,conducted all field surveys, analyzed the data and performed most of the economic and financialcalculations. The local consultants were Fernando Corpuz (sugar sector), Levy Trinidad (coconutsector), Mauricio Valdez (rice sector) and Alberto Dalusong (power sector). Technicalsupervision was provided by Richard Stevenson, a Manila-based consultant.

Overall task managernent and technical backstopping were provided by Emesto Terrado andRobert Chronowski (consultant). The final report, based on a draft prepared by the Philippinesbased team, was written by Ernesto Terrado, Robert Chronowski and Gabriela Martin(consultant).

i

EXECUTIVE SUMMARY

Overview

Other than in the sugar industry, biomass has not received adequate attention as a potentialenergy resource by either the Government of the Philippines (GOP) or by major lenders mainlybecause of the relatively small energy production potential at any given project site. While thisis a legitimate issue froni the stand-point of regular project lending criteria, the aggregatepotential for economic energy production from this indigenous and renewable resource is clearlylarge enough to warrant more serious consideration.

The Philippines has an abundant supply of biomass resources in the form of agricultural cropresidues, forest residues, animal wastes, agro-industrial wastes, and aquatic biomass. Some oftherse resources are already being exploited. In 1992, biomass, principally bagasse burned in thesugar industry and coconut huskishell used by other industries, contributed about 11 percent ofthe total national energy supply mix, makling it the country's largest indigenous energy source.However, considerable biomass energy resources remain untapped and are treated as wastes.While the theoretical potential has always been recognized as considerable, the economic potentialfor energy production was, at the inception of the study, an unknown quantity. The Departmentof Energy requested assistance to determine the realistic potential for power production fromprocess residues in three major agro-industrial sectors: sugar, rice and coconut. One reason forthe interest is the the country's power sector situation, characterized by poor reliability,insufficient capacity to meet demand, rising electricity prices, and heavy reliance on importedfuels. Despite the already massive efforts to address the crisis by a variety of conventional powerprojects, it was thought important to also explore additional possibilities in less conventionalenergy production. The sugar, rice and coconut sectors examined in this report all haveagricultural waste byproducts that in most cases have minimal or even negative cost (factoriessometimes pay for waste disposal). Agro-industrial facilities in the country are generally agedand require replacement of equipment. There is tremendous renewed interest worldwide incogeneration projects that provide additional revenues to key industries.

At an estimated power purchase floor price of P1.80 per kWh, or an avoided electricity costfrom P2.00 (purchased electricity cost) to P2.50 per kWh (small diesel based captive electricityproduction with a commercial, heavily taxed diesel oil price) and possibly higher, there aresufficient revenues or savings potential to seriously consider investments in biomass-derivedpower generation in all three biomass residue sectors in the country. Also, along with the intentand provisions of recent private power legislation, there appears to be a real opportunity now forbiomass power project development that has not been possible in the past.

As finally determined by the study. however, the total potential for power production frombiomass residues in the three agro-industrial sectors is nowhere near the level required to fullyaddress the current power crisis in the country. Furthermore, because of the relatively largenumber of individual plants involved, only a small fraction of the potential can be developed inthe short-term to help alleviate the power shortage. Nevertheless, many of the biomass projectsthat were examined are cost-effective and present attractive investment opportunities. They mustbe viewed as energy efficiency investments that are in themselves worth doing because they areeconomically viable and environmentally beneficial.

ii

Objectives and Methodology of the Study

The principal objective of the study is to develop realistic estimates of lhe commercialpotential for power generation in thie Philippines from major bionlass residue in the sugar. riceand coconut processing/production industries. Based on techniical and statistical profiles preparedfor each sector by a Department of Energy (DOE) team, the industries were segmented into"clusters" or groupings by common characteristics such as size. and several sites were selectedfrom each cluster for the field surveys. The selections represent the ranges of sizes. types ofmills and sites in a particular cluster. The study teams from DOE surveyed the selected sites infield visits. Data sets of operational parameters were developed for a prototype mill or site thatwould most closely represent the particular cluster and enable a broader application of the resultsof the analyses. Economic and financial analyses were then conducted on each prototype millto screen the most promising cases.

The Sugar Sector

The processing se_tor of the sugar industry is composed of 39 mills (exclusive of 2inoperational mills) spread over 16 provinces. The bulk of the mills is concentrated in Negros,the "Sugar Bowl of the Philippines", which provides about 56 percent of the country's annualsugar production. The mills process from 500 tcd (tonnes of cane per day) to 10,800 tcd, for anaverage of 4,600 tcd. Bagasse, a by-product of sugarcane processing, is used as the principal fuelfor steam production in the sugar mills. Steam is utilized for power production and sugarprocessing. Investments to improve the efficiency of mill operations can result in excess bagassethat can be utilized to generate electricity for export to the grid.

Three investment scenarios were considered for each representative prototype mill. The firstscenario eliminates the current boiler makt-up steam and injection water input to the sugarprocessing steam header, and passes an equivalent amount of steam through a new or existingsteam turbine. The second scenario involves the replacement of old plant equipment with new,higher pressure and temperature boilers, and the corresponding topping cycle turbo generatorsets. The third scenario would add a new higher pressure boiler with a condensing-extractionsteam turbine-generator, allowing year round operation with the use of cane trash as asupplementary fuel. This scenario, for all intents and purposes, means putting up a stand-alonepower plant beside the sugar mill. The first two scenarios were limited in the analysis togeneration of surplus electricity only during the milling season. It is important to point out thatthe milling season does coincide with the dry season, such that surplus power is available whenthe hydro potential is at its lowest.

Some of the major conclusions drawn from the analysis are as follows:

a) The cases in the first or "bypass steam" scenario obtained the best rates of return, withfinancial IRRs ranging from 22 to 65 percent. The economics in actual cases may even bebetter, as the analysis uniformly assumed the purchase of additional turbo-generator capacityand associated equipment to utilize the excess bagasse.

b) The "topping cycle" approach of the second scenario, which involves high investments,does not appear to be viable for all mill sizes with electricity production during theprocessing season only.

iii

c) T'he stand-alone condenising cycle plant of the third scenario shows good potential formills of at least 700,000 tcpy capacity, with financial IRRs betweeni 26 and 31 percent. Onereason is the capability to operate year-round using a supplemential fuel such as cane trashor coal in lhe olT-season. The resuli of the analysis Illust be viewed as merely indicative.Only a plant-specific study can confirmii the feasibility of the complex assignment of benefitsand inputs between the stand-alone power plant and the sugar mill. 'he feasibility evaluationwould consider the bagasse and water as inputs from the mill, with electricity and steam asreturns to the mill. The benefiLs arising from use of thesc inputs and returns, the accountingof changes in personnel assignments, and possibly land lease clharges can be accounted forin multiple ways, depending on specific ownership/partnership arrangements.

d) Based on the results of this study, the sugar sector can be very conservatively describedas having the potential to contribute from 60-90 MW to grid supply from several individualprojects in the immediate term. The largest 15 sugar mills (each processing over 500,000tons of cane annually) would be the most likely contributors to this capacity goal. The totalinvestment requirement for financially viable projects would be at least US$ 112 million.

e) The above astimate of MW potential is very likely on the low side as the analysisassumed full investment costs in each case. In reality, many mills will already have thesurplus turbine-generator capacity required for Scenario l. and the investment will besignificantly below the assumed unit cost of capacity installed. Also, in a situation where anew bagasse boiler needs to be purchased anyway for sugar processing purposes when a millmodernizes, only the incremental cost for achieving the topping cycle pressure rating (andnot the total boiler cost) should be charged to electricity production. In that case, the toppingcycle will likely become a viable investment scenario because the boiler comprises the majorcost element in the total price for the topping cycle equipment. For example, if about halfof the mills that were screened out by the financial analysis in Scenario II are assumed torequire only half of the regular capital costs for the reasons cited, the total power potentialcould increase by an additional 25 MW.

f) There are few technical risks associated with the use of bagasse for surplus powerproduction. However, the need to employ higher steam pressures and temperatures does addsome O&M considerations not normally experienced by the sugar sector in the Philippines.This suggests that some type of improved skills will be required of the steam plant operatorsemployed for these projects.

g) The major barrier to cogeneration projects in Philippine sugar mills at this time, besidesthe presently poor financial condition of many mill companies, would appear to be the canesharing issue between the farmers and the mill owners. In general, the present system doesnot provide an incentive for the mills to invest in mill modernization projects, includingbagasse cogeneration projects for power export.

Rice Sector

In 1991, 3.42 million hectares of agricultural land were planted with rice, producing 9.67million tons, at an average yield of 2.82 tons per hectare. Rice husk or hull constitutes about 20percent of paddy. About 14,000 rice mills nationwide, most of them small, produce about 1.9million tons of rice husks annually. The Cono and Rubber Roll types of rice mills that were

iv

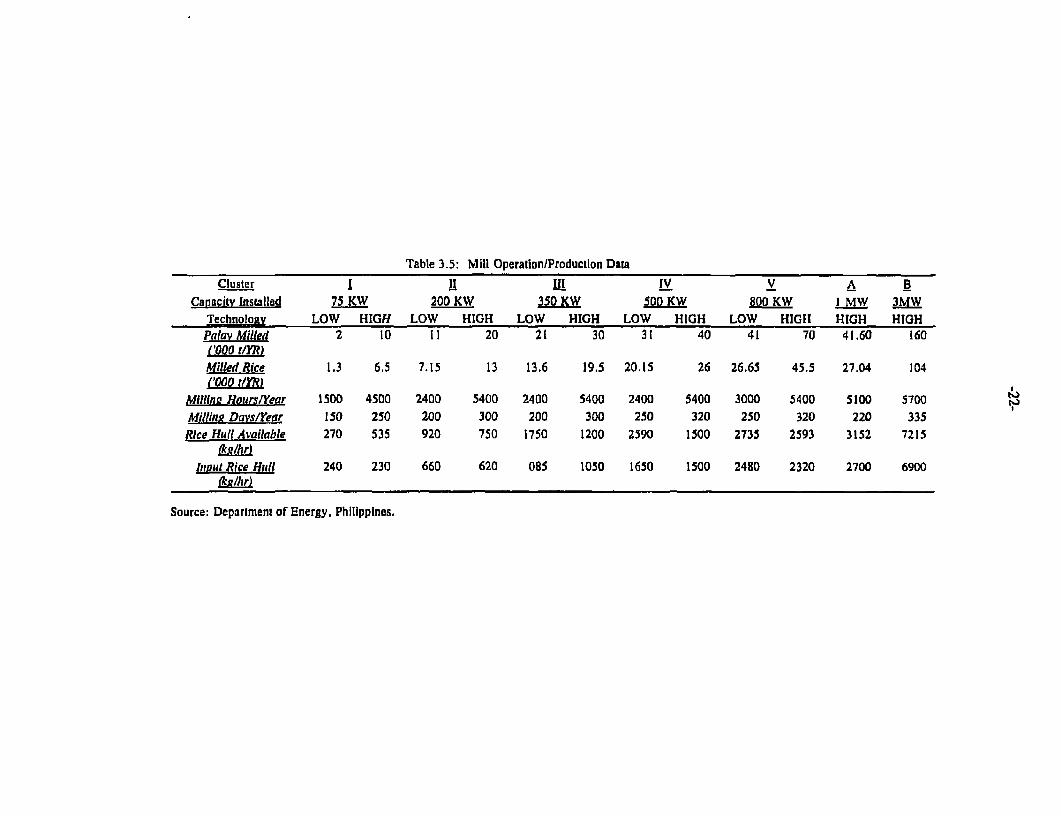

selected for the analysis constitute about 95 percent of total milling capacity. The cases selectedfor analysis involve the installation of a rice-hull fired power plant in a mill, ranging from a 75kW system for the smallest grouping (less than 11.000 tons paddy milled annually) to an 800 kWsystem for the largest mills (over 41,000 tois). In addition, it was determined from the surveyresults that it may be possible also to group rice mills under two types 01' schemes, such that themills in a cluster would contribute rice hulls to a common power plant. The schemes wouldproduce I and 3 MW, respectively. Only the systems above 500 kW are assumed lo generateenough surplus electricity for grid export. The rest would use the clectricity produced internally,displacing diesel-generated electricity. Specific conclusions concerning the rice sector analysisare:

a) Most of the potential projects with capacity of 350 kW and above (especially the high-tech option) have economic internal rates of return exceeding the discount rate of 15 percent.even with no revenues from ashl sales. These results indicate rice sector projects involvingat least 350 kW would warrant further investigation. Ash sales significantly improve theeconomics of all cases, raising the financial IRRs by 11-24 percent. This suggests the needto examine more closely the possibilities for marketing rice hull ash in the domestic andexport markets.

b) For simplicity in the analysis, the cogeneration option was not considered for the ricesector in this study, but the economics would be further improved if steam could be used forrice drying.

c) The economics of the investments depend strongly on the utilization of the electricityproduced. The locations of many of the rice mills are normally in areas with low powerdemand where the assumed 85 percent load factor will be difficult to attain.

d) Compared to bagasse, there is more technical risk with the use of rice hulls as boilerfuel because of the erosive nature of the rice hulls caused by their high silica content.Unless the equipment is properly specified and carefully operated and maintained, technicaldifficulties could lead to project failures. There would clearly be a need for more skilledmanpower in the rice mills to operate and mnaintain the power plant equipment.

e) Based on the results of the present study, the realistic potential aggregate contributionof rice hull-fired capacity is not likely to exceed 40 MW. Because of the large number ofinstaliations needed to achieve this amount, a progrum in the inmmediate term should targetno more than 10 MW total. Unless a significant rice hull ash market can be developed, itis not likely that off-shore entrepreneurs would participate in ventures to exploit this sector'sbiomass residue resource for energy production.

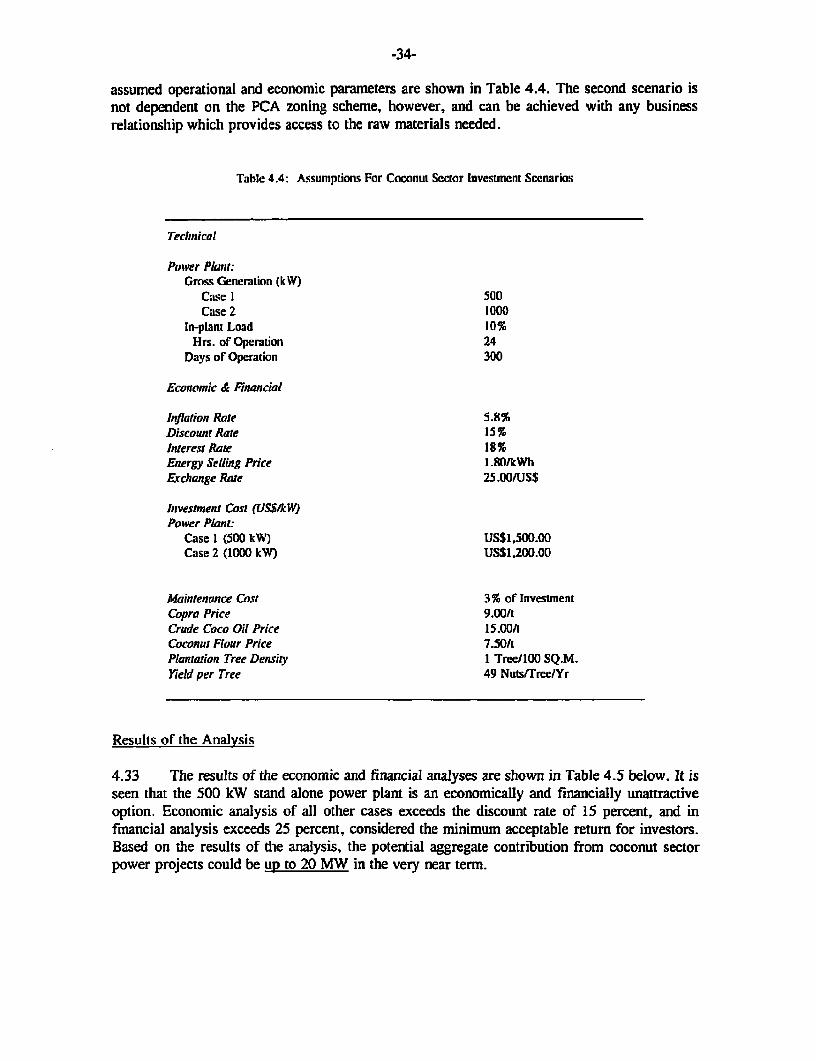

Coconut Sector

The coconut sector was the most difficult to deal with in the study because of theuncertainties regarding the structure of the Philippine coconut growing and processing industryand its markets. Although the original intent was to incorporate a cogenerating plant within anindividual coconut oil mill or a coconut desiccating plant, this was found to be not feasible forvarious technical reasons. It was decided instead to investigate two investnent scenarios: (a)installation of a power generating facility within a 7,500 ha. coconut plantation area, and (b)

v

installation of a power generating facility integrated with a 7,500 metric tons per year (tfyr)coconut oil mill. Based on biomass-fired power plant designs currently available in the market.two sizes, 500 kW and 1000 kWY, were examined for each of the two scenarios. Specificconclusions drawn from the analysis are:

a) The financial IRRs for the four cases range from 10 to 45 percent. which indicatespotential for proceeding to site specific analysis. The power plant integrated with an oil millhas a better return than the stand alone case because of a probable higher load factor, andthe higher value of the avoided purchase of eectr-city by the oil mill for self use. All of thecases assumed the implementation of the Philippine Coconut Authority (PCA) "nucleusestate" concept. However, any organizational or business arrangement giving the mill accessto 7500 ha of coconut production will yield the same result.

b) The analysis suggests that the power plants will have to be heavily base loaded toachieve sufficient IRRs. This appears unlikely in most rural areas. Integration of the powerplant with a coconut oil mill will only partially solve the load problem.

c) On the positive side, the remoteness of the potential power plant sites does suggest thatit may be possible on a site specific basis to negotiate a higher power sales rate than the P1.80 assumed for the analysis. Also, there are very few technical risks with implementingcoconut husk fired power projects, even in remote areas.

d) The concept of coconut husk-fired power stations is valid, but more analysis is neededto accurately define the potential of this sector. Unless the appropriate resources/load matchcan be made for the 500 kW and 1,000 kW cases, the aggregate power contribution fromthis sector will be minm=al. No doubt some viable sites can be identified, but it is likely thatthe aggregate potential contribution from this sector will be only about 20 MW.

Recommendations

The biomass power investments discussed in this report are expected to be undertaken mainlyby the private sector, once confirmed to be viable in specific situations. However, theGovernment has an important role to play in promoting the concept and facilitating theidentification and implementation of actual projects. Through its line agencies the DOE has beenimplementing a program for developing onconventional energy resources (see evaluation inArmex A). Given the urgency of the power crisis, it is recommended that grid-connected powergeneration opportunities using agricultural wastes be given priority attention in that program. Avariety of fiscal and other incentives for renewable energy projects already exist. The applicationof these incentives to the type of biornass projects discussed in this report should be clearlydefined and widely publicized. Information dissemination efforts are crucial in order to developawareness of investment opportunities in the three sectors.

It is recommended that the sugar industry, with its relatively better defined potential fordevelopment of surplus electricity generation capacity, should be targeted as the top sector forimmediate attention. The DOE, along with the Sugar Regulatory Administration (SRA), shouldhelp define the type of actions required to resolve the mill/farmer cane sharing issue in anequitable manner that provides the mill owners and their potential off-shore partners withsufficient incentive to make the substantial investments needed to develop the surplus power

vi

capacity. An arrangement is needed with all cane suppliers that will allow the millers to investin a surplus power project with some acceptable minimum revenue sharing liability. The marketleaders in the sugar industry are already involved in trying to define viable surplus powerprojects, and these activities should be fully supported as precedent setting projects. One usefularea of assistance would be in the pre-qualification of potential off-shore joint venture partnersto avoid wasting time and efforts of the mill owners.

For the rice sector, the market leaders should be identified and educational and awarenessbuilding activities should be directed toward them. This effort should be coordinated with theNational Food Authority (NFA) and its allied industry associations. As an immediate action, itis recommended that suitable demonstration projects involving selected mill sizes and types beidentified. Despite the failure of an earlier pilot project on rice-husk fired power production bythe NFA, technology advances and operational experience acquired in recent years, combinedwith a more favorable local climate for private power generation, warrant a re-investigation ofthis option. To the extent possible, DOE, through its line agencies should serve as a brokerbetween the market leaders with viable sites, the qualified equipment vendors, and the appropriatefinancing organizations to accelerate implementation of these pilot projects.

For the coconut sector, the potential for project investments is closely linked to theimplementation of the proposed sector decentralization program. The remoteness of the areaswhere the coconut husk resource is normally located implies low load factors and suggests thatthe most promising projects will be those integrated with an oil mill. Identification of precedent-setting projects in this sector must involve close cooperation between the DOE and the PhilippineCoconut Authority (PCA). It is recommended that one or two demonstration projects in carefullyselected sites be designed and assisted with financing arrangements, perhaps from bilateraldonors.

It is recommnended that the legal and contractual framework needed to facilitateimplementation of relatively small agricultural residue-fired power projects be clearly defined byDOE, starting with the adoption and publication of an appropriate standard power purchaseagreement for these types of projects. This should also include a clear delineation ofresponsibilities between the mills and the utility for interconnection and fault protectionrequirements.

In summary, given that the current national power supply deficit is in the order of 1,000MW, the total power potential of about 150 MW from agricultural biomass estimated by thisstudy is clearly not going to be a major solution to the energy problems of the Philippines, ineither the short or long term. It should be correctly viewed as a small but strategic part of thesolution, having good potential for economically and environmentally beneficial capacitycontributions. The present study has identified the specific mill situations and investmentconfigurations that will likely result in cost effective projects. Even in situations whereincremental power production from biomass projects are just sufficient for internal mill use, theycontribute to easing the power crisis by reducing total demand for grid supply. In addition, theprojects have the potential to contribute to the economic upliftment of the agro industries byproviding an additional revenue-generating activity and new opportunities for rural employment.

-1-

I. BACKGROUNDIntroduction

1.1 The Philippines has an abundant supply of biomass resources in the form of agriculturalcrop residues, forest residues, animal wastes, agro-industrial wastes, and aquatic biomass. Someof these resources are already being exploited. In 1992, biomass, principally bagasse burned inthe sugar industry, contributed about 11 percent to the total national energy supply mix, makingit the country's largest indigenous energy source. The bagasse, however, is not fully utilized,nor is its efficiency of use at an optimum level. Considerable biomass energy resources remainuntapped and are treated as wastes. The purpose of the present study is to examine the potentialfor new investment opportunities in the utilization of biomass residues for energy in thePhilippines. This study focusses on power generation potential from process residues in threemajor agro-industrial sectors: sugar, rice and coconut. From the perspective of industry, plantinvestments in power production from waste biomass would appear to be economically attractive,particularly when they coincide with a modernization program to replace aging equipment andimprove overall production efficiency.

1.2 Investigation of the energy potential of biomass resources is important given the currentpower situation in the country. The Philippines is in the midst of a worsening power crisis thathas affected local industries, the commercial sector and residential areas nationwide. Thegovernment is accelerating energy projects in a massive effort to solve the power crisis. Althoughsome have predicted that this effort, ironically, may result in surplus capacity in 3-5 years, thegovernment wishes to identify all possible options for power generation, including the use ofnonconventional sources of energy. The Department of Energy (DOE) has an ongoing programfor nonconventional energy development and, under that program, a priority is determiningwhether the economic potential of power production from biomass resources is significant.

Enerev Sector Overview

1.3 The Philippines remains highly dependent on foreign oil for its energy needs. In 1973,all oil was imported and accounted for 92 percent of the country's energy mix. At that time,national energy consumption was about 70 million barrels of fuel oil equivalent (MMBFOE). By1991, energy imports (oil and coal) had been reduced substantially but still accounted for 67percent of the total energy supply. Indigenous conventional energy accounted for about 21 percentof the energy mix, while approximately 13 percent came from nonconventional energy sources.

1.4 In 1991, 37 percent of total energy consumption was used for power generation.Oil-based generation provided 50 percent of total power produced in 1991. With respect to finalend-uses. the industrial and transport sectors accounted for the bulk of energy consumption, withshares of 37 percent and 47 percent, respectively, in 1991.

1.5 The Philippine energy outlook will be largely influenced by current energy patterns andthe course of future economic expansion. While the growth target for the gross domestic productwas scaled down in 1991, there is optimism that the economic recovery efforts will gain strengthin succeeding years. By the year 2000, national energy demand is projected to reach226.73 MMBFOE. almost double the 1991 volume. As noted in Figure 1. 1, oil will remain theleading energy source for the country, although its share is expected to decline.

-2-

Figure 1.1

Philippine Energy Mix

0. 7-

09

19.2

0 011 & G

EC.I m Hto a G.thkwr.l1 Nflonr.ntIon I

Source: Office of Encrgy Affairs (1993)

1.6 The government has embarked on an energy program calling for "sustained efforts inthe development of indigenous energy sources and the reduction of oil import dependence." Thekey institutions involved in the formulation and implementation of the energy program originallyconsisted of the Energy Coordinating Council (ECC) and its member agencies, namely: the Officeof Energy Affairs (OEA), the Philippine National Oil Company (PNOC), the National PowerCorporation (NPC), and the National Electrification Administration (NEA). Recently, OEA's coregave rise to the Department of Energy (DOE) and the ECC was abolished. DOE's mandateincludes formulation of the nation's energy policy and coordination of all energy programs.Promoting the use of biomass and other nonconventional energy sources also falls under theresponsibilities of the DOE, with programs in this area managed by the DOE's Non-ConventionalEnergy Division.

Current Power Situation

1.7 Power demand in the Philippines has grown sharply since 1987 (see Annex D, Figure 1)after the economy emerged from the recession of 1984-1985. Power demand continued toincrease until 1989 when the power infrastructure could no longer keep pace with economicgrowth. There has been no new baseload capacity commissioned since 1985.

-3-

1.8 Consequently, grid power supply has largely stagnated during the last four years. Theprivate sector has resorted to self generation using diesel- and bunker-fired diesel generator sets.Various estimates place this private capacity between 1,500 and 2,500 MW, much of it broughton-line under the tax- and duty-free importation incentive granted by the Board of Investments(BOI). In addition to industrial and commercial self-generation, there has been a significant risein household generation as seen in the brisk sales of small gasoline and diesel generator sets.

1.9 The power situation in the Philippines worsened further in 1992. Both the number andlength of power intermptions increased, particularly in the Luzon grid which represents abouttwo-thirds of total power consumption in the country. The MERALCO franchise area, whichaccounts for about half the total electricity sales in the country, faced brownouts in 1992 nearlyten times the 1991 level. Unserved energy due to brownouts was approximately 5 percent in1992.

1.10 In Mindanao, the power situation is even more severe. Heavy dependence on hydroresources and prolonged droughts have led to grid-wide load curtailmnents of 20 to more than 30percent. Only the Visayan sub-grids (i.e. Leyte-Samar and Negros-Panay) with access togeothemal energy have been spared these levels of brownouts. Cebu, which relies on coal anddiesel power plants, suffers fewer power interruptions than Manila.

1.11 To address the energy crisis, the Govermnent's power development program calls forregular baseload capacity projects and several "fast track" projects (essentially oil-based plants)designed to meet shortfalls in the immediate term. The total additional capacity from the fast tractprojects alone is about 800 MW, with a target commissioning date of summer 1993. The poweroutlook in the near future varies from grid to grid but overall - due to various technical,financial, institutional and political factors - there is a general lack of optimism that the officialtargets will be met. It is also widely recognized that the enormity of the power problem can onlybe addressed with private sector involvement.

The Case For Biomass Cogeneration

1.12 Cogeneration projects are an additional way to allow mobilization of private sectorresources to assist the government's power development program. Biomass cogeneration,involving residues generated from the processing of agricultural crops, seems particularlypromising with significant potential for excess power sales to the grid. The sugar industry, forexample, has been cogenerating since its earliest days, but mainly to meet in-plant power needs.Much of the sugarcane waste that remains after the milling season and is disposed throughincineration could be used to generate additional power.

1.13 There are several key factors that make cogeneration investments, using biomass orconventional fuels, attractive to the private sector in the Philippines.

0 Unreiable Power Supply. The discussion in the previous section on the current difficultiesof supplying power and the major fossil fuel response provide a strong argument for privatecompanies to venture into cogeneration. Meeting the large unserved demand and reversingthe debilitating effects of the shortage on both residential and productive sectors withimported fuel electricity generation, imply a high economic value for supply of additionalpower generated from an indigenous renewable energy resource.

-4-

o High Electriciy Costs. NAPOCOR is scheduled to install over eight hundred megawatts ofoil-fired gas turbines and diesel engines in 1993 to augment power capacities in Luzon andMindanao. These pealing units will in practice be operated as baseload power plants. Powertariff increases to recover the very high running costs of these systems have already beenimplemented. Furthermore, the Energy Regulatory Board has allowed MERALCO to recoveradditional costs related to system losses. Finally, NAPOCOR power tariffs are alreadyscheduled for restructuring towards long-run marginal costs. All of these measures willimprove the economics of alternative power supply.

a Proven Tecwology. Cogeneration has been used worldwide for nore than a hundred years.The current renewed interest in cogeneration has resulted not from technologicaldevelopments but from new perspectives taken by utilities in sourcing their power supplyfrom outside producers- Private power generation in the industrial setting has proven to betechnically and economically feasible.

1.14 Potential cogenerators with access to agricultural andlor by-product wastes have thefollowing additional motivating factors:

o Abwzdant low-cost fuel. The sugar, rice and coconut sectors considered in this report allhave access to agriwastes which are in most cases by-products of their production processes.These agriwastes have costs that are practically zero or even negaive as factories may payfor waste disposal.

o Aging Equipment. Many local applications of cogeneration and agriwaste utilization do notbegin to approach the efficiencies of late model equipment. For example, the average agefor boilers in the domestic sugar industry is 34 years. In several sugar mills steam generatingequipment has been in service for over 70 years. This equipment is ready for replacement,having been operated well beyond its expected economic life.

c Source of Process Heat/Steam. The establishment of a cogeneration power plant usingbiomass residues could provide a source of excess steam for ancillary process heating or saleto nearby steam users. The rice sector, in particular, could benefit from the availability ofa heat source for drying purposes. Paddy drying in the countryside remains dependent onsundying practices. This limits the capacity of the mills to process paddy during the rainyseason.

o Rual Employment Generaion. Many agricultural processing industries have close ties withthe community where they operate. Social objectives such as employment generation affectbusiness decisions of such industries. In the Hacienda Luisita project, for example, thecompany paid for costs to bale and transport field trash at equivalent to fuel oil on an energybasis. Aside from providing the cormmunity with an additional income opportunity, itdiscouraged the practice of burning the sugarcane in the fields for easier harvesting. Burntcane loses sucrose content very quickly and therefore has to be processed soon after beingbrought into the mill.

-5s-

Objectives and Methodologv of the Study

1.15 The principal objective of the study is to develop realistic estimates of the commercialpotential for power generation in the Philippines from major biomass residues in the sugar, riceand coconut processing/production industries. Whereas most previous studies of power potentialfrom agriwastes have examined the aggregate total of biomass residues available and theirtheoretical power potential, the present study aims to determine the conditions under whichbiomass cogeneration investments would be economically and commercially viable.

1.16 The study is a joint effort by ESMAP and the Philippine DOE. Selected staff of DOE-NCED were formed into three project teams. A chief technical adviser and several sectorconsultants provided guidance and technical support. One team each was assigned to study thesugar, coconut and rice production sectors. Technical and statistical profiles for each sector wereprepared. Based on these profiles, the industries were segmented into "rlusters" by commoncharacteristics such as size, and several sites were selected from each cluster for the field surveys.The selections represent a range of sizes, types of mills and sites in a particular cluster.

1.17 Detailed questionnaires were designed in order to gather a wide range of technical,operational and economic information for each sector. The questionnaires were pre-tested inselected plants and modified as needed. The project teams surveyed the selected sites in fieldvisits. After data review and random verification of the responses, data sets of operationalparameters were developed for a prototype mill or site that would most closely represent theparticular cluster. Economic and financial analyses were conducted on each prototype mill usingthe data sets as base conditions. Sensitivity analyses were subsequently carried out to detenminethe impact of changes in some key variables.

1.18 The study was a basic screening exercise for quantifying the potential contribution tothe power sector from 3 indigenous biomass resources. That a demand for the Kwh producedfrom the biomass resources will exist was assumed. No attempt was made to so any load flowstudies for the various electricity grids, and the boundary for the study analysis was set at thesubstation for transmission to the grid. The next logical steps would include the use of thisstudy's results to identify opportunities for site specific feasibility evaluation. These follow-upstudies would examine load flow implications, and the cost of transmnission in determining finalviability.

II. THE SUGAR SECTOR

Sector Profile

2.1 The Philippine sugarcane industry existed long before the Canlubang and San Carlosmills began producing centrifugal sugar in 1914. Chinese traders engaged in sugar barter salesduring the Spanish era with produce sourced from small animal-drawn mills scattered in Northemand Central Luzon, Panay, Mindoro and Negros Islands. In the 1960's the industry was bustlingwith activity as smaller mills merged, older ones were phased out, while larger, modeminstallations were established. Up to the middle 1970's around 15 factories were built. Raw sugarhas been the country's strongest export commodity.

2.2 After the 1974 termination of the Laurel-Langley Agreement which guaranteedPhilippine sugar a lucrative preferential US market, sugar's contribution to the national economygradually declined. In the 1930's, 55 percent of the Philippines' total foreign exchange earningscame from sugar. This fell to a mere 1.5 percent of GNP, averaged from 1980 to 1990. The mostsevere blows to the industry occurred in the mid- 1980's, as the mismanagement of NASUTRA(National Sugar Trading Corporation, the government's monopoly sugar trading entity) resultedin capital flight and a contraction in agricultural land allotted to cane. Coupled with low sugarprices in both domestic and export markets, this period almost spelled the end of the industry.

2.3 Since then, however, investor confidence has been restored and a consistent thoughgradual increase in production has become apparent during the past cropping seasons. Sugar isslowly regaining its importance in the national economy. As the annual U.S. sugar quota for thePhilippines has dwindled from 1.2 million tons to only about 0.2 million tons today, the industryis preparing for the eventual disappearance of this preferential market. About 80 percent ofproduction is now consumed in the domestic market. It is recognized that to improvecompetitiveness in the intemational free market, production costs have to be reduced by anindustry-wide modernization program. Replacement of aging inefficient boilers and powerequipment provide opportunities for cogeneration projects that would realize additional revenuesthrough the sale of excess power to the grid. Many sugar millers are keenly interested in thispossibility and some have initiated feasibility studies.

2.4 The sector currently supports about 5 million people, providing direct employment toover 530,000 workers in 39 milling districts. Already offering comparatively high wages to itsworkers, the industry also voluntarily contributes about P105 million annually for socio-economicimprovements directed at sugar workers. Furthermore, the industry also pays over P1 billion intaxes annually and provides a yearly subsidy amounting to about P60 million to the governmentregulatory agency, the Sugar Regulatory Administration (SRA).

2.5 The processing sector of the sugar industry is composed of 39 mills (exclusive of 2inoperational mills) spread over 16 provinces (see Fig. 2.1). The bulk of the mills isconcentrated in Negros, the "Sugar Bowl of the Philippines", which provides about 56 percentof the country's annual sugar production. The mills process from 500 tcd (tonnes of cane per day)to 10,800 tcd, for an average of 4,600 tcd. About 20 million tonnes of cane are ground annually,producing around 1.7 million metric tonnes of sugar. There are ten sugar refineries with acombined capacity rated at 87,000 50-kg bags refined per day or an annual throughput of roughly15 million 50-kg bags.

-7-

Figure 2.1IPRO3,

PHIUPPINES

LUNN LOCATION OF SUGAR MILLS AND.._.n REFINERIES

7 cEma'mammu* ^4~3~q a * 5SUGA I?EEI Sm.^CA.i mmMnwa V wm"

, .00-o"Wr oC e2 PmOI?NcAMIS

81~~~~ ~ - ouoe.

Ir C.E3.Wxcmim~.1_is .4a___c_a * r **t -SUe" e.. n

272 J~twm -A / DZ0 1x1

23Nw _._C - -

glRl- ~ ~ ~ ~ ~ ~ ~ ~~~4 _1 0 N -ls

CM CAAM NES a 0 a l: :fD2ve ~1 5 N| r-- -s . ~.

7 *.Zrrn._: cm J

24 SnwIEas&~~~~~~~~~~~~~~~~~~~~~~ Pf£1M E

hr NMw NrKa

U >4~SEEC sR A

-- ; C mw c

d ,J o lmc_ w

241 B ~"

I?USEtsN j :UUAItS

Su ~ ~ SE

- b-'p b g- VISAYrR >

~deda>;* rr f x ,,{ CDC9, .t

m.o CIi b-t ' ''"

C HE )IAQ

'It ," o Caeepm.X -

-8-

2.6 Approximately 30,000 sugarcane planters supply the mills with cane from a cultivatedarea of 371,000 hectares. Average yield per hectare is placed at 54 tonnes of cane, with atypical recovery of 4.58 tonnes of sugar.

Mill ODeration

2.7 Sugar Processing is a 24 hour per day, 7 day per week continous process during thecane season. The mills process cane at full rated capacity as long as sufficient cane can beobtained. Bagasse, a by-product of sugarcane processing, is used as fuel for steam productionin the sugar mills. Steam is utilized for power production and sugar processing. High pressuresteam from the boilers powers the mill's juice extractors, turbine-drives and prime movers forpower-generators and pumps. The exhaust steam from the equipment is then fed to the plant'sboiling house for use in juice heating, evaporation, vacuum pans, etc. It is difficult, however, toattain a satisfactory balance of power and process steam requirements in the system, mainly dueto the batch type operation of the boiling house. Hence, make-up steam is supplied through apressure reducing valve (automatically operated) which expands the steam isothermally from thehigh pressure main to the low pressure main. The condensate from the sugar processing cycleis pumped back to the boilers and the cycle is repeated. Figure 2.2 illustrates the standard steamcycle of a sugar rmill.

2.8 Philippine sugar mills, as anywhere in the global sugar industry, are not relied upontraditionally to supply electricity beyond their own processing needs. Electricity is generated formill use and the sugar plant operators are familiar with parallel operations of generators plusfiequency and voltage control and the skills needed for such operations are already present.Boiler and turbogenerator installed capacities are based tn rated cane input, with only the nonnalallowances for surplus. It is therefore typical to find mountains of bagasse accumulating outsidethe boiler house at the end of the week, and even more so at the close of the season. Because ofthis, the early steam boilers used by the industry also serve as incinerators to remove the bagasseand avoid costly disposal.

2.9 In recent years, the availability of excess bagasse worldwide has been increasinglyexploited by sugar producing countries to produce electricity for sale to the public grid, thusproviding an additional source of income for the mills and adding to the country's electricitysupply. For cc'untries like the Philippines which are plagued by power shortages, this opportunityis particularly important. Investment opportunities are further enhanced by the fact that much ofthe major equipment in local sugar mills has been in operation well beyond its economic life andis ready for replacement. The average age for boilers is 34 years and some steam generatingequipment has over 70 years of service (see Annex D, Table 1).

Cane Residue Availability

2.10 Biomass waste from the sugar industry is derived from two principal sources, the fieldand the factory. Bagasse, the main biomass waste used, is the residue remaining after juice isextrcted from the prepared sugarcane by the milling tandem. Bagasse comes out of the lasttwo-roller squeeze of the last mill, and is composed of particles averaging approximately 25 mm.Typically, bagasse contains 45-49 percent fiber, 49-52 percent moisture and 2-3 percent solublesolids (sucrose). Bagasse with 3 percent sucrose and 50 percent moisture has a calorific value of1789 kcal/kg.

STANDARD STEAM CYCLE OF PHILIPPINE SUGAR MILLS

Uve steam High pressure stoam Inornaily superteated)

Make.UPSteam

Boiler Boile;Fans GenoraTors PressureFeedwater GoeaosReducingPump Valve

(PAVI)

Make-up Water

I 12 *14 psig Low pressure sleam

t e -,UPRV2 '0

Evaporaltrs (11 st. 2nd, and 3rd effecl) 6 psgi (Vapor) +

___ __ t < 1 -

I I I I I I I ~~~~~~~~~~~~~~~~~Juice IvacuumIDeaeralorl L vp. Evap. EI ap I va EvaeaerpPns Other

aatorsI Ea.I .II Ea

Condensate---Pump

ExcessCondensate

-10-

2.11 Annual bagasse production by the sugar industry during the last ten years is given inTable 2.1. Most of this production ends up as boiler fuel in the mills, accounting for about 87percent of the sugar industry's total fuel mix in 1992, nr 851 million liters oil equivalent(MLOE). Supplementary fuels (bunker oil, wood, etc.) are also used, especially by mills withauxiliary processing plants (refinery, distillery) where the bagasse produced is not sufficient tosustain the additional steam and power requirements. Although there are alternative uses forbagasse, such as the production of particle board, activated carbon, newsprint, commercial andindustrial fuel etc., these have not been significant in the Philippines. Tnis is mainly due toeconomic reasons and the fact that the role of bagasse as fuel in sugar mills is viewed as the mostimportant. The bagasse does have a low density and low calorific value limiting its viabletransport distance.

Table 2.1: Ten-Year Summiary of Bagasse Production Data

Crop Year Gross Cane Milled Approximate Field Bagasse Fuel Oil EquivalentOt Area (Hat.) X (BBL)

1982-83 24,962,736 421,931 6,915,205 9,957,8951983-84 25,969,151 455,359 7,214,885 10,389,4351984-85 18,719,339 328,237 5,269,813 7,588,5301985-86 16,124,014 282,729 4,718,943 6,795,2771986-87 13,751,502 241,128 3,949,806 5687,7211987-88 15,663.605 274,656 4,500,687 6,480,9891988-89 19,375,44?. 339,741 5,522,816 7,952,8551989-90 19,352,218 339,334 5,660,011 8,150,4161990-91 20,499,044 359,443 5,801,407 8,354,0261991-92 22,815.603 370,718 6,539,043 9,416,222

Source: Annual Report, Production and Performance Report 1991-92, Sugar Regulatory Adniinisaion, Pbilippines.

2.12 In the Philippines, where harvesting is still far from being mechanized, cane is manuallycut and loaded. A good part of the cane's vegetative part remains in the field while a smallpercentage, about 2.5-3.0 percent, goes with the millable cane delivery. This field trash,popularly known as "barbojo" in Puerto Rico and "canciaja" in some districts in the NegrosIsland, is normally left on the land and then needs to be cleared in preparation for the nextcropping operation, ratoon or planting. Burning is used as the easiest and most economical modeof disposal.

2.13 This cane residue has been estimated at 11 to 21 tonnes per hectare, depending on thevariety and quality of growth. In Tarlac, where a cane trash utilization program documents fieldand cane handling operations, it has been established that on the average one hectare of plantedsugar yields 12 tonnes of residue, of which about 8 tonnes are recovered. Extrapolating thisamount to the present cane hectarage, there are potentially 3 million metric tonnes of trashavailable for use ir power generation. The available volume of cane trash far outweighs what isnormally obtained as excess bagasse in the mills. Moreover, the trash more nearly meets thecriteria set for ideal biomass fuel, namely low moisture content and high calorific value,availability and combustion characteristics. Available bagasse and field trash and their total fuel

-I 1-

equivalent in BFOE from the various mills during the 1991-92 crop year are shown in Annex D,Table 2. In Tarlac, it was established that the moisture content of a bale of trash comes from twoconstituents: the leaves of the tops and the young or dried stalks. While the percentage volumeof the latter is minimal (12-20%), the moisture content of the former is quite high (65-70%). Theresultant average moisture content is 26 percent as the trash arrives at the mill site. It is possibleto lower the moisture content through winnowing and sun drying. A tonne of field trash canprovide 2.938 million kcal or about 295 liters oil equivalent.

2.14 The main obstacle to economic utilization of cane trash is the collection process.Another is the need to transform the trash, which arrives at the mill site in bales, into a form orparticle size approximating that of bagasse in order to require little or no modification in theinstalled conveying and boiler feeding systems. Unlike the canciaia system in at least two millsin Negros, where whole trash bundles are manually fed to the boiler furnaces for efficientcombustion, the trash needs to pass through shredders or bale breakers.

Sector Segmentation

2.15 For the field surveys, the 39 sugar mills in the Philippines were ranked in terms of tonsof cane milled annually. This was selected as the principal variable for segmentation, rather thanthe theoretical capacity of the mill, because it determines the amount of bagasse available as fuelfor power generation. Figures for the last three milling years were averaged and the results wereused for ranking. The mills were then listed from the smallest (Barotac Sugar Mill), with anannual average throughput of 15 thousand metric tons of cane, to the largest sugar central(Victorias), milling an average of 2.3 million tons per year for the last three years (see AnnexD, Table "3 for the complete listing of sugar mills). The 39 mills were grouped into clusters A-E according to the ranges listed in Figure 2.3.

2-16 Of the total number of sugar mills in the Philippines, 10 mills (nearly 25%) are locatedin Luzon, of which 6 are sited in the north and 4 are in the south. Twenty-seven mills (70%)are from the Visayas Region with 18 (46%) situated in Negros, 5 (13%) in Panay and two eachin Cebu and Leyte (10%). Only 2 mills (5%) are on the island of Mindanao, at Davao andBukidnon. Both were included in the survey, one falling into Cluster A and the other into ClusterE.

2.17 Four representative mills were included in the smple selected for Cluster A, three eachfor samples from Clusters B, C and D, and two for a sample from Cluster E, for a total of 15representative respondents (see Annex D. Table 3). The samples within a size cluster were chosenfor their variety in geographical location. Although almost half of the total mill population islocated in Negros Island. the analysis did not confine itself to that area and reflects a diversesampling.

2.18 The field survey included four Luzon mills (27%). nine Visayas sugar centrals (60%)and the two Mindanao plants (13%). Cluster A includes two Luzon mills, and one each fromVisayas and Mindanao. Clusters B and C include two Visayas sugar centrals and one each fromLuzon. For D. which is composed of a total population of five plants, all in Negros. the analysisselected three. One Mindanao and one Visayas mill were selected from Cluster E.

-12-

Figure 2.3

Sugar Mil IsQ'.upd by AnnumI RloIe spse CepaIty

14 Cluster A: 10,000 -

12- 199,999i12-ii- Cluster B: 200,000 -_0 499,9991

* ~~~~~~~~~~~~~~~~~Cluster C: 500,000 -699,999it

* Cluster D: 700,OO

2 101 l l l ClusterE: > I1.0000 t

2

A c n 9iam m I I C lUotre

Investment Scenarios

2.19 After analysis of the collected data, a representative mill for each cluster was identifiedfor use in the economic and financial analyses. The initial the intent was to average the operatingdata from the surveyed samples for each cluster. However, several runs of the model developedby the team revealed that this method of averaging did not create a realistic set of characteristics.Therefore, it was decided that one prototvDe mill would be used to represent the whole cluster.This was done for all five clusters.

2.20 Three investment scenarios were considered for each representative prototype mill. Thefirst scenario eliminates the current boiler make-up steam and injection water input to the sugarprocessing steam header, and passes an equivalent amount of steam through a new or existingsteam turbine. In effect, this system uses the grid as a flywheel to absorb the surplus electricity,thereby generating additional revenues from the marginal power sales. This scheme will not applyto all mills, but could be an option for many, requiring no more than $500 capital investmentper kW installed if a new TG set is needed. This figure includes the necessary fault protectionand sub-station upgrade but not the cost of any new transmission lines.

2.21 The second scenario involves the replacement of some old plant equipment with new,more efficient machinery such as higher pressure and temperature boilers and the correspondingtopping-cycle turbo-generator sets. Back-pressure turbines are used and the existing turbo-generators are kept in service. Bagasse consumption is more efficient. The total cost is assumedto be $1500 per kW installed, including the substation but no transmission line costs.Alsoincluded in this amount are soft costs representing start-up capital, interest during constructionand financing fees at a maximum of 10 percent of project cost.

-13-

2.22 The third scenario adds a new higher pressure boiler with a condensing-extraction steamturbine-generator, allowing year round operation with the use of supplementary fuel. Bagasseconsumption is assumed to be even more efficient in this case. The scenario assumes thecollection and use of cane trash as a supplemental fuel to bagasse. This scenario, for all intentsand purposes, means putting up a stand-alone power plant beside the sugar mill. The costassumed for the installed new equipment is $2000 per kW, inclusive of soft costs and step uptransformer (substation). It does not include the cost of any new transmission lines.

2.23 Except for cases under the Third Scenario which allow year-round operation, all othercases are conservatively assumed to generate and export surplus electricity only during the millingseason as a base condition. Most sugar mills have back-pressure turbo-generator equipment andthere is no normal off-season operation of such equipment, whether or not surplus bagasse orcane trash may be available. The first case (Cluster A, Scenario I) is that of a small mill, usingthe by-pass steam approach with no investment in additional generating capacity. With theimposition of no off-milling season generation-, the case becomes irrelevant and is not includedin the analyses. All other cases have investments that result in the generation of surpluselectricity that is then exported to the grid at an assumed buyback price of P1.80/kWh. Todetermine an appropriate average buy back price, the ProjecL Team looked at both the contractualprice for the existing and proposed private power facilities, and at the reported energy chargecomponents of the the NPC bulk electricity sales tariffs for the Luzon, Cebu, Negros, Panay,Bohol and Leyte grids'. While the contractually agreed or proposed private power rates to bepaid by NPC during the contract period vary from P.1.252 to P.2.135 per KWH, the morerelevant current NPC energy charge components of their own tariffs range from P1.7193 toP1.9535 per K-WH, a much tighter range which results in an average energy charge of aboveP1.80 per KWH for each grid. The private power contracts, other than for the 2 hydra andgeothermal projects will include fuel adjustment and currency devaluation escalators that suggestan inevitable rising trend. The biomass projects will produce direct energy cost savings for NPCand, for screening purposes, the average NPC energy cost component should be considered asthe floor value per KWH produced from indigenous biomass resources. In specific cogenerationprojects in remote areas, buyback prices could be significantly higher. Project viability in allcases depends on how incremenital investment and 0 & M costs compare with the revenuesrealized from the sale of electricity.

Results of the Economic and Fir.-ncial Analysis

2.24 Operating data (including derived data) for each prototype mill as well as financial andeconomic data that were used in the analysis are shown in Annex D, Tables 4 and 5. In general,the number of operating days of the prototype mill increased with the size of the cluster to whichit belongs (i.e., from 114 days for Cluster A to 243 days for Cluster E), exet in the case ofthe prototype mill for Cluster C which had even fewer operating days than that for Cluster B.As mentiDoned earlier, the data used represent actual operating conditions of real mills. Theassumed capital investments range from acquisition of 500 kW additional turbo-generator capacityin the simplest cases to the installation of a 17.7 MW of new boiler! T-G system (Third Scenario,Cluster E) or investment costs of between $240,000 to $37.3 million. These costs compare with1992 equipment quotations for similar projects internationally.

' Staff Appraisal Report, Philippine Power Transmission and Rehabilitation Project, June 1993.

-14-

2.25 The results of the economic analysis are summarized in Table 2.2 below. The discountrate used was 15 percent. Foreign exchange costs and labor Losts were shadow priced usingcoefficients normally used by NEDA and IBRD in similar studies in the Philippines (see AnnexD). The results show that all cases under Scenario I (smallest capital investments) plus the casesfor Scenario lll, Clusters B, C, D and E (large capital investments but also large exportcapacity) provide acceptable economic rates of return. Note that mills in these clusters are locatedin regions with the longest milling seasons. All cases under Scenario 11 are uniformlyuneconomic, no doubt because of the much higher incremental capital investment compared toScenario I, coupled with the imposition of the condition of no electricity export during the off-milling season.

Table 2.2: Results of Economic and Financial AnalysisInternal Rates of Return (in percent)

Cluster A Cluster B Cluster C Cluster D Cluster E

Scenario IEconomic 24% 18% 24% 33%

Financial -- 37% 22% 37% 65%

Scenario 11Econormic -.2% 8% 5% 8% 12%Financial -10% 4% .9% 4% 12%

Scenario IIIEconomic 14% 17% 16% 19% 24%Financial 16% 22% 18% 26% 31%

2.26 The base case for financial analysis assumed project financing with 70:30 debt-equityratio, an 18 perc_nt interest rate and 10 years repayment term. An inflation rate of 5.8 percentwas assumed, as well as a tax holiday on the first 5 years of operation. These correspond topresent borrowing conditions for sugar industry projects in t.he country. The results of thefinancial analysis are sumnarized in Table 2.2. If the minimum acceptable financial rate of returnon investment is taken to be 25 percent in the Philippines, the cases that appear viable are allthose under Scenario 1, except cluster C, with an FIRR range of 37-65 percent, and Cluster Dand E under Scenario III, with FIRR between 26 and 30 percent. As in the economic analysisresults, all cases under Scenario II are not financially viable. Sensitivity analysis indicates thatthe viability of the above investments are strongly dependent on the length of the milling season,the capital investment costs and the buyback price for electricity. Cluster C mills that have anaverage size greater than Cluster B mills are shown to have lower rates of return because theprototype mill is in a region where the milling season is shorter (150 days as opposed to 180days for Cluster B). The stand-alone condensing system approach with year-round generation(Scenario III) has the best economics but relies on the use of cane trash for off-season fuel andon additional revenues from steam sales to the sugar mill. These factors are obviously highlysite-specific.

2.27 The above analyses indicate that the sugar sector has the potential to economicallycontribute up to 60-90 MW to grid supply, with about 85 percent due to mills employing thethird investment scenario. The investment requirement for financially viable projects would beat least US$ 112 million. About 15 large individual mills, each processing over 500,000 tonscane annually would be the most likely contributors. This number was obtained by considering

-15-

the "position" of the prototype mill in the size range of its cluster and then making ajudgernentas to the realistic number of mills that could implement the envisioned investment. Thisprocedure was also employed for the rice and coconut sectors and the resulting tables are includedin Annex D. The potential would be substantially larger if the topping-cycle scenario can haveextended operations beyond the cane processing season. This can only be defined by site-specificstudies, including approaches to bagasse storage, that would identify situations where idle sugarprocessing equipment could utilize excess bagasse for off-season operation at reduced load.

2.28 Even without off-season operation. the potential is likely to be larger than what theabove conservative analysis indicates. In the bypass steam approach (Scenario 1), it isconservatively assumed that each mill will purchase a new back-pressure turbine generator plusfault protection and control at about $500/kW of capacity. In reality, many mills already havesurplus turbine-generator capacity and the required investment will be significantly less. Theeconomics will be even better than the above results. The topping-cycle approach (Scenario 11)could become viable if the mill needs to purchase a new boiler for sugar processing purposes.In that case, only the incremental cost of achieving the topping-cycle pressure rating needs tobe charged to electricity production, not the full cost of the boiler. For example, if about halfof the mills that were screened out by the financial analysis in Scenario It are assumed to requireonly half of the regular capital costs for the reasons cited, the total power potential wouldincrease by about 25 MW (see Annex D).

Implementation Issues

2.29 An important issue which must be resolved before initiatives for grid power supply bythe sugar industry can make any substantial progress is the present sharing system between caneplanters and sugar mnill owners in the Philippines. Under this legislated arrangement, all producefrom cane consignment sent fir milling - sugar, molasses, bagasse and press cake - have to be"shared' by the planter and the miller, with the former getting 60 to 70 percent. Therefore, underthe existing law, 60-70 percent of any surplus bagasse produced at the sugar mill is still ownedby the planters. The planters could make a claim to a portion according to this formula of anyrevenues realized from electricity production using surplus bagasse, regardless of the incrementalinvestments made by the miller on power generation equipment.

2.30 For the time being, it is possible for an individual sugar mill to negotiate with theindividual farmers for an equitable sharing scheme for investments in bagasse cogeneration withsales of surplus power to the grid, because of the relative novelty of this type of venture and thelack of precedent. As the practice becomes more widespread, there are bound to be conflicts onthe sharing issue. It is clear that the solution must be institutionalized and not proceed on a millby mill basis. Congressional action may be required if sugar sector cogeneration projects are tobecome a widespread reality.

2.31 Sugar processing is seasonal in the Philippines with the season lasting from 3 to 8months. The sugar is harvested during the dry season which is important in any country that hashydroelectric capacity because the surplus power from the sugar industry would be available whenthe hydro potential is at its minimum. WhIe the sugar mill cogeneration facilities can be designedfor year round operation with a supplementary fuel, as in Scenario 3, it also has viable seasonalsupply options. The installation of any new equipment would be during the off-season, with littleor no impact on sugar production.

-16-

Environmental Issues

2.32 It is understood that new biomass combustion and power generation facilities must becapable of meeting much stricter emission limits than do existing industrial processing facilities.While biomass combustion does provide certain global greenhouse gas emissions benefits, thelocal environmental impact, especially for particulates can be significant. The installed cost perKW chosen for scenarios 2 and 3, and for the high tech options for rice and coconut residues thatare discussed later, are at the high end of the average cost for similar projects implementedrecently throughout the world. The high-end was deliberately used to allow for sufficientenviromnental control hardware to meet any new standards and to cover other such contingencies.

-17-

III. THE RICE SECTOR

Sector Profile

3.1 Rice is the main staple food of the Philippines and accounts for about 25 percent of bothtotal crop area total value of crop production in the country.

3.2 In 1991, 3.42 million hectares of agricultural land were planted with rice, producing9.67 million tons, at an average yield of 2.82 tons per hectare (see Table 3.1). The largestproduction areas harvested and highest yields per hectare are located in Central Luzon (Region3), Western Visayas (Region 6), Southern Tagalog (Region 4) and Cagayan Valley (Region 2).

3.3 Some 60 percent of the rice grain produced is grown in the wetter half of the year, fromJuly to December, while the remainder (40%) is grown during the drier months, from Januaryto June. About 55 percent of the planted area is classified as irrigated, 40 percent as lowlandrainfed and 5 percent as upland. Rice milling is a full year business, but all mills do notnecessarily have access to sufficient paddy to operate year round. This factor has been includedin the analysis done to support this study. Irrigated land can produce 5 crops of rice in 2 years.Yields per cropping season in the Philippines currently average about 2.8 tons per hectare. Thiscompares with about 2.0 tons per hectare in Thailand, 2.6 tons per hectare in Malaysia and 4.1tons per hectare in Indonesia.

Table 3.1: Rice Production. Area Harvested and Yield per Hectare

eion Rice Production Area Harvested Yield('000 metrico tans) ('0 ectares) itonslhetare)

CAR 152.56 59.33 2.57I 898.58 312.25 2.882 1,033.62 325.29 3.183 1,748.49 499.87 3-504 1,118.09 411.88 2.715 744.22 295.53 2.526 1,183.89 456.16 2.607 207.70 124.38 1.678 382.95 221.71 1.739 399.04 142.78 2.7910 531.78 170.11 3.1311 688.30 205.63 3.3512 584.05 200.04 2.92

Total 9,673.26 3.424.96 2.82

Source: National Food Authority

3.4 In the short term, the Philippine Agricultural Development Plan for 1991-1995 proposesan annual average growth rate target for rice production of 4.12 percent. This target growth rateis required in order to enable the Philippines to become self-sufficient in rice production by 1995,

-18-

taking into account population growth and expected increases in the per capita consumption rate.Irrigation development is expected to play a key role in raising rice production in the next 10years. However, actual attainment of these targets may well depend more on political andsocio-economic factors than on agronomic considerations.

Biomass Residue Availability

Potential Availability of Rice Hulls

3.5 Table 3.2 below shows the potentially available rice hulls by region. The percentage ofhusk (hull) in paddy varies widely, but 20 percent is a fair average. Using this figure, total ricehull production is about 1.9 million tons annually.

Table 3.2: Potntial Availability of Rice Hull

Region Rice Producdon Potential Rice Haul('000 metric tons) Available

('000 nmetric ons)

CAR 152.56 30.511 898.58 179.72

2 1,033.62 206.723 1,748.09 349.62

4 1,118.09 223.62

5 744.22 148.84

6 1,183.89 236.78

7 207.70 41.548 382.95 76.59

9 399.04 79.8110 531.78 106.36

11 688.30 137.6612 584.05 116.81

Total 9.673.26 1,934.65

Source: National Food Authority

3.6 Out of the potential rice hull available, only that produced by certain types of rice millscan be used in practice. In 1991, 13,704 rice mills were registered and licensed by the NationalFood Authority, representing an aggregate total capacity of 27,208 tons per hour. (See Figure3.1 for milling capacity by Province.)