Emerging Third World Multinationals: A Case Study of the Foreign Operations of Singapore Firms

16

Emerging Third World Multinationals: A Case Study of the Foreign Operations of Singapore Firms RAJ AGGARWAL AbstrQct This paper forms the first systematic examination of the foreign o'peratiotl5 of Singapore in dustrial and commercial finns listed on the Stock Exchange of Singapore. It was found that out of a total of such firms, nearly four out of five have" foreign operations, and more than three out of fiye have operations in countries ot her than in Singapore and Malaysia. This is a remarkably high propor- ( io n givenrChe opportunities available for reinvestment in a rapidly growing inrernaJ market. Whiie most of these rcrc:ign investments were in [he other countries in the Southeast region, Singapore lirms are also beginning to undertake significant foreign investments i.r. devc:ioped :oumries. Thus, while very few Singapore firms are true multinationals. a significant proportion have extensive investme!llS in operating affiliates in foreign countries. introduction Multinational corporations (MNCs) have historically be en considered indig!nou s 10 the: more economicaJly advanced countries, and virtua lly all studies of th e economic and poiiticaJ impact of these e:1terprise:s have proce:" ded from that premise. While this notion regarding the native habitat of the MNCs was quite accurate in the past and remains large ly so today. a growing number of exceptions - in the form of companies investing abroad and conducting inter· nationaJ operations from bases in lcss..jevdoped and newly industrialized countries (LDCs and NICS) - are being noted. The data which has been accumulated on these NIC multinationals is still sketchy I but some observers of the international business sC:i1e have posiled that these fir ms constitute a signiflcam ascending force. and that their emergence may have profound effects upon the pattern of interna ti onal business activity. as well as upon political and economic relationships among nation·states. As an example. it has been contended that MNCs from developed countries such as the United States, Japan, and Western Europe are facing increasing levels of competition from newly industrializing country multinational companies (NICMNCs), especially in other developing countries. I " Such an assessmeilt of the potent ia l impact oi the NICMNCs is based largeiy upon the idea that these firms possess several inh erent advantages V LNi-vis multinational companies from the countries and that those advantag!s 193 From: Contemoorary Southeast Asia 7(No. 3, Decembe,' 1985).

Transcript of Emerging Third World Multinationals: A Case Study of the Foreign Operations of Singapore Firms

Emerging Third World Multinationals: A Case Study of the Foreign Operations of Singapore Firms

RAJ AGGARWAL

AbstrQct

This paper forms the first systematic examination of the foreign o'peratiotl5 of Singapore industrial and commercial finns listed on the Stock Exchange of Singapore. It was found that out of a total of fifty~two such firms, nearly four out of five have" foreign operations, and more than three out of fiye have operations in countries ot her than in Singapore and Malaysia. This is a remarkably high propor(ion givenrChe opportunities available for reinvestment in a rapidly growing inrernaJ market. Whiie most of these rcrc:ign investments were in [he other countries in the Southeast .~ia region, Singapore lirms are also beginning to undertake significant foreign investments i.r. devc:ioped :oumries. Thus, while very few Singapore firms are true multinationals. a significant proportion have extensive investme!llS in operating affiliates in foreign countries.

introduction

Multinational corporations (MNCs) have historically been considered indig!nous 10 the: more economicaJly advanced countries, and virtually all studies of the economic and poiiticaJ impact of these e:1terprise:s have proce:"ded from that premise. While this notion regarding the native habitat of the MNCs was quite accurate in the past and remains largely so today. a growing number of exceptions - in the form of companies investing abroad and conducting inter· nationaJ operations from bases in lcss..jevdoped and newly industrialized countries (LDCs and NICS) - are being noted. The data which has been accumulated on these NIC multinationals is still sketchy I but some observers of the international business sC:i1e have posiled that these firms constitute a signiflcam ascending force. and tha t their emergence may have profound effects upon the pattern of interna tional business activity. as well as upon political and economic relationships among nation·states. As an example. it has been contended that MNCs from developed countries such as the United States, Japan, and Western Europe are facing increasing levels of competition from newly industrializing country multinational companies (NICMNCs), especially in other developing countries. I "

Such an assessmeilt of the potent ia l impact oi the NICMNCs is based largeiy upon the idea that these firms possess several inherent advantages VLNi-vis multinational companies from the dev~oped countries and that those advantag!s

193

From: Contemoorary Southeast Asia 7(No. 3, Decembe,' 1985).

I f

194

are being butlrcssed by certain political and ideological movementS which make the NICMNCs more "acceptable" as international direct investors. Considerable emphasis is also placed upon the formal or informaJ aJ1iances which exist between these enterprises and their respective home governments in expanding and projecting their rising innuence in the international ousiness arena .1

The nrst pan of this paper consists of a brief g.lobal survey of the re::nt growth and current status of the NICMNCs. It dea ls with the scope and character

. of their international operations and with the chara:teristic.s of geographic areas in which these emerging multinationals operate. In this pan, the information on the

"nature and characteristics of the worldwide activities of these enterprises is used to compare the activities of the NICMNCs with the activities and characteristies of multinationals based in developed countries. Tne second part of this paper examines the nature of the foreign operations of Singapore-based industrials - a group of companies thai have not been studied in published li lerature . The paper concludes with a discussion of some of the implications of the find ings.

Recent Growth oj NICMNCs

Early multinational finns such as the British and Dutch East Indian trading . companies have often been seen as an outgrowth of the technological and economic lead enjoyed by the European colonial powers over other nations althat time. In the post· World War II era, the economic and technological leadership passed from the European colonial powers to the United States. Consequently, the post-World War II era saw the emergence and dominance of multinational firms from the United States with a decline in the relative size and importance of most of the now mature multinationals from the former colonial powers.

Thus, for much of the post-World War II e:-a. the international business system was dominated by multinational firms headquartered in the United States and in 1966 American direct investment alone ac:ounted for well over half the worJd total. However. as Europe and Japan have rebuilt their post~war economies and their technological sophistication, the now-maturing United States multinationals have begun to face increasingly stiff competition and challenge from the new European and 1 apanese multinational firms. The American hegemony diminished in the 19705 as firms based in Western Europe and Japan aggressively expanded their international activities and even the United States market becam.e a competitive battleground. .

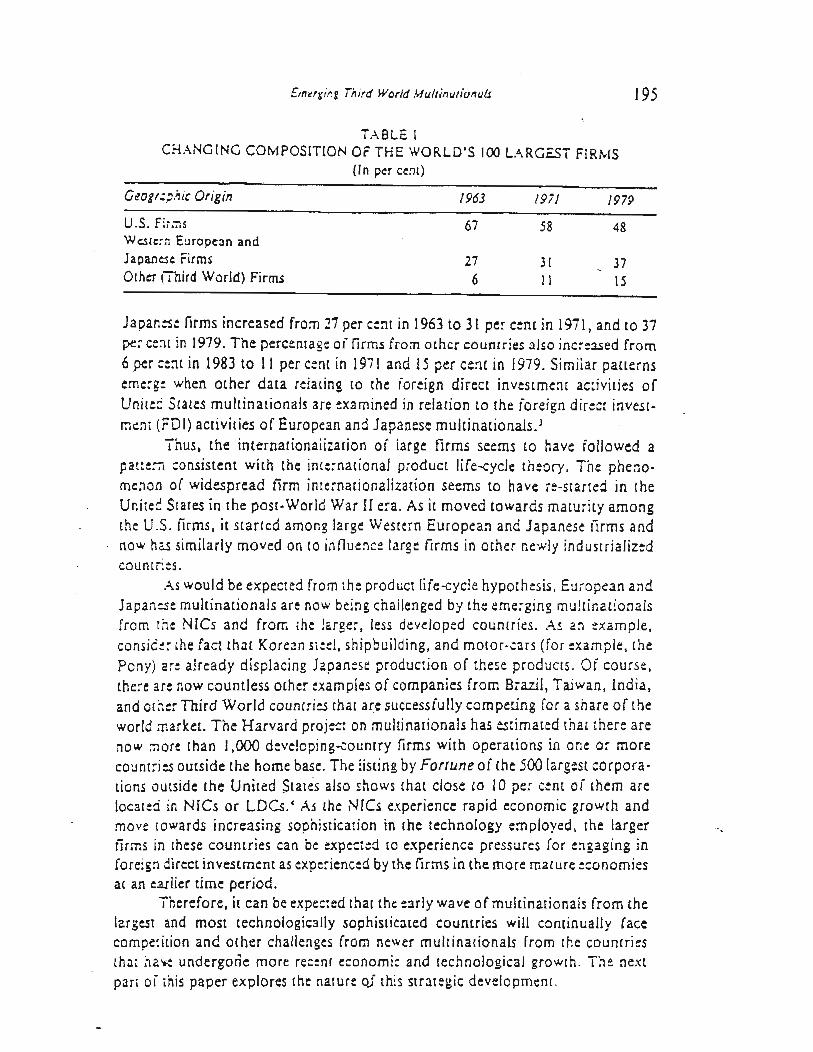

While multinationals from America, Western Europe, and Japan have been vying for market.pQ.sitions worldwide. multinationals based in other. countries that are usually classified as being pan of the Third Worlo have emerged as serious con· tenders in the marketplace. Table I summarizes the results of a Conference Board srudy of the changing composition of the 100 largest firms in the world.

According to this study, the proportion of United States firms in the world's 100 largest industrial corporations declined from 67 per cent in 1963 to 58 per cent in 1971 and to 48 per cent in 1979, while the proportion of Wester~ E.uropean and

TABLE I CHANGING COMPOSITION Of THE WORLD'S 100 LARGEST FIRMS

(In per cent)

CI!Olr;;.1ic Origin 196) 1971 1979

U.S. Fi,;::, 67 58 48 Wes[~~:; Europe3n and Japanese Firms 27 )1 37 Other (Third World) Firms 6 I I 15

195

Japar,ese firms increased from 27 per cent in 1963 to 3 I per cent in 19i I, and to 37 pe: ce:1t in 1979. The percentage oi firms from other countries also inc!'e!l.Sed from 6 per :ent in 1983 to II per cent in 1971 and IS per cent in 1979. Similar patterns eme:-g: when other data reiating [0 the foreign direct investment ac:ivilies of Vnice:: States multinationals are examined in relation to the foreign dire=~ invesrment (FDI) activities of European and Japanese multinationals.'

Thus, the internadonaiization of large firms seems to have follo wed a patte::-I :::onsistent with the ime:nationaJ product Iife--cycJe theory. The phenome:lon of widespread firm ime:nadonalization seems to have fe-Staned in the Unite::: States in the postwWorid War II era, As it moved towards maturity among the U.S, firms, it started among large Western European and Japan!!s~ rirms and now has similarly moved on to innuence large firms in other newly industrialized countr.es.

As would be expected from the product life<ycle hypothesis, European and Japanese multinationals are now being challenged by the eme:ging multinationals from the NICs and from the larger. less developed countries. As an example, comiC:: the fact that Korean sieel. shipbuilding, and mator·.:ars (for example, [he Pony) are already displacing Japanese production of these products. Of course, there are now countless other examples of companies from Brazil, Taiwan. India, and otner Third World coumri:s rhat az:e successfully compeung for a share of the world market. The Harvard projoot on multinationals has estimated thatther, are now :nore than 1,000 deve!oping...:ounrry firms with operations in one or more countries outside the home base. The listing by Fortune of the 500 larg'st corporations outside the United StateS also shows that close (0 10 per cem oi them are located in NICs or LDCs.· As [he NICs e:-:perience rapid economic growth and move towards increasing sophistication in the technology employed, the larger firms in these countries can be: expe:ted to experience pressures for e:lgaging in foreign direct investment as experienced by the firms in the more manue :,onomies at an e3Ilier time period.

Therefore. it can be expe:::ed that the early wave of multinationais from the largest and most technologically sophisticated countries will continually (ace compe~jtion and other challenges from newer muhinarionals from the cQumries that ;'a.e undergone more re:::O( economic and technologital growth. The next pan oi this paper explores the nature oj this strategic development.

196 I?oj Allorwol

The Nature 0/ NTCMNw. P:-e .... ious studies on the hature of the NICMNC pheno~ menan can be subdivided into three categori~s. The first category focuses on the overall features ofNICMNCs ir. 2 given country. such as the study of NICMNCs in Thaiiand. NICMNCs from Hong Kong. Korea, and India. and other small countries and Latin Ameri:a are examined by the second category of studies. The third :ategory of studies eJ:.amine the N1CMNC phenomenon in gene~aL' Previous rmarch on NICMNCs has focused primarily on their overall characmistics especially with regard to th:ir growth pallerns and their geographic and industry concentration . Preliminary results of a comparative analysis of this literature indicates that while NICMNCs are similar to MNCs from developed countri., in many r~pects. they also have ceitain unique characteristics.

Motives for foreign dir!':t investment that N1CMNCs sha r: with other ' MNCs include the restrictd opportunities (or domestic growth because of antitrust and market siz~ reaSO!1S and the need to protect export markets. In contrast to othe, MNCs, NICMNCs usually receive aid and encouragement from the home country government to unci::r.ak~ foreign investment. Their investment strategy is gene:,al ly characterized by the :oncentration of investment in countries that are geographically and culturally close to the home country, with the forma tion of joint v~ntures with local and oth:r investors as an overwhelming mode of foreign ' affiliates. Most foreign operations of NICMNCs emphasize low..:ost, labourintensive. smaller-scale op::'2.tions using mostly intermediatc-Ievel technology' serving markets that would be considered too small or hostile in most ta.5es for developed country MNCs. Whiie in a number of countries NICMNCs were also considered less of a threa: to host government objectives than were developed country MNCs, it should b: nO!ed that the former have not completely escaped the poiiticai risks of e:r:propriation or fo rced sale of equity even at this early stage of their gro\.\:th cycle.

Thus. it se:ms dear from this preliminary literature survey that a significant number of NICMNCs are feding the same press~res and urges to move into the international arena that MNC.s from developed countries have experienced, and that they are pursuing this course with considerable perspicacity and elan. The rapid growth of their ove:seas a:tivities attests to the vigour and effectiveness of their efforts and adds more weight to the proposition that the emergence of the NICMNCs is a development which definitely merits the attention of everyone canc:rned with multinational business enterprise and the international economy, 'Con· sequently, it has been contencied that just as in the 1970. we saw the emergence of MNCs from developed countries other than the United Stales, the 1980. is likely to witness the eme~gence ofMNCs frem countries that art and may still be considered to be Third World countries.

Outward Fordgn In'll~lmtn( and (he Singaport Economy

Singapore. originally calltd lOT emasek" or sea town. is an island dty·s12te with a population of about 2.5 million and an estimated i983 GNP (gross national

£mrrliflf Third World MII/(iflllrior:3Is 197

proQuct) of abo'ut USSI5 billion. It is a managed free-<nterprise economy where lhe government plays an important role not only in e:::or.omic planning but also as a major owner oflarge segments of the economy. The government owns a number of major listed and unlisted companies through its holding companies such as Temasek Holdings, Sheng·li Holdings and MND Hoidings. Examples of major companies in which the gove:nment has a controlling interest include financial institutions such as the Deveiopmont Bank of Singapc:: (DBSJand the Post Office Savings Bank (POSB), and industrial firms such as the giant Kopper Group, Semb.wang Shipyards, .Ne?tune Orient Lines, Sing."ore Airlines, National Iron anei'Steel, Intraca, and othe:s, In addition, the gavernmeni owns all of the utilities and other economic infrast:uc:ure in Sjngapore. It is a major force in the propeny market through the Housing aod Development Boarj, and the Urban Redevelop· ment Authority. Nevenhei~ss. in sharp contrast to the: situation in most other countries. Singapore Go .... e:.liT.ent-owned companies are dynamic, innovative and profitable. Singapore cominu:s to provide an ex:~:!ent environme:u for freeenterprise market~rive~ gove:nment and private ente:prises and its economy has managed to compile a re:::arKable re~ord of economi: growth.

Singapore's 1983 p-e: ::3pita GNP of over six. thousand U.S. dollars is second only to Japan in ail oi A.sia. Singapore is OJ.: of the world's largest oil refining centres. a major 5uppiier of eJe::uonic ::ompc::.ems to the world market. a major centre in this region for marine construclion. and ship-repairing, and an international financial c::r.(:e oi growing importance. furthermore, thl! Singapore economy is expected [0 continue to have one of the :tighest growth rates in the world o .... er the next twO dl!:.J.de.s . 6

Thus, Singapore, th: !ion city, is an attrac:ive and dynamic business setting and its government has attrac:ed a large amount oi inward foreign investment from other coumries. With a ~apidly growing and dyr.amic internal market why should Singapore-based nr;;:,s invest in foreign operat:ons especially since foreign markets can also be served ihrough exports and by li,::nsing arrangements with local producers? The next se::ion attempts to answe: :his question.

Motives by Singapore Companies 10 invesl Overseas. One of the primary reasons why Singapore·based firms :night want to invest ove:s~as is the limited size of the local market for their produ::s. In addition. while a n:.!:nber of its ioreign markets can be served by exports from Singapore. there are a number of problems in depending solely on thisstrate;y. One problem is that of possible protective actions by the foreign host gove:nmeot by imposing tariiis, ,uotas, or other non-tariff barriers to impede impons and to ge:1erale or prote::t local employment. As an example, it is the announc!c policy of [he Indonesian Government 10 reduce its economic dependence on Singapore·based firms and, in the rece:ll past. even the industrialized countries have s;aned erecting highe: walls oi prote~tionism. ":\no{h~r problem arising irom dependence on expons;o service foreign markels is the limited ability of such a tirm ,0 monilor .lna ml!~ t ':vmpe[ition from lower-cos! local prOOUt:ers.

198

Moreoyer. sinc: the majori!y of the world's trade consists of movements of goods and services among affiliates of the same company. a Singapore company rna ... indeed be able to in:;!!s: its exports ir it has direct investments overseas. An additional advantage of ior::g:n direct investments is thai as productive capacity and the silt of a firm in:::2!!s. it can take advantage of economies of scale in administration, marketing. finance, and research and development. As an example. corporate adminis::ative costs can be spread over a larger volume of output 3.! can the cosu or developing a market strategy or the floatation costs of financing. The same can 0. said for the research and development cosu of developing and introducing a ne .... product.

A second reason 'g,'hy Singapore-based companies may want to invest overseas is their desire to ob~ain access to cheaper sources of raw material. labour, and an environment of jow:r taxes and fewer government regulations. Thus. Singapore companies may go overseas \0 satisfy the ne:d for rdiable sources of raw materials and an incre2.5 i!1,g n~d for access to labour that is cheaper than that available in Singapore. In ore:!" to ensure steady supplies of raw materials in the face of shortages or other market disruptions. a company must own and control the source of its raw mate:ial!. Ownership of the sources of raw material also gives a company other advant2g~ traditionally associated with vertical integration. such as ~te, quality control and higher overall profit levels. For Singapore·based companies, inve5tment in scurc~ of raw material would generally mean under~ taking foreign invc:stme:n. Singapore companies may a150 invest in countries (such as Hong Kong) that ha"e lower taxes and fewer government regUlations. An additional reason for und!:":.aking foreign investment is that Singapore labour costs are rising rapidly. making a number of industries too high cost for Singapore, Companies in Singapore are also increasingly facing shortages of certain categories of labour, especially in (he uoskilled or less educated categories. Furthennore, Singapore companies using foreign guest workers face a particular problem since the Singapore Govenune-::! has adopted a policy to reduce and ultimately eliminate the use of foreign Workd. Those companies engaged in labour-intensive indus· tries must, therefore. shiP. production overseas to countries with cheaper and more available labour in orde, to remain competitive. This has already been the case for a numo.r of textile compani ... An added advantage of undertaking foreign direct investment can be ac::s.\ to a wider variety of financing sources including sub· sidized financing desi~!'d to encourag~ investment in panicular areas Dr

industries. ' A third major rt'ason why Singapore~based companies may find it useful 10

undertake foreign inves.m~nt5 is to better exploit their comparative advantage in serving the markets of the oeighbouring countries. Betause of their geographic and culturai proximity. Singapore·based companies may find that they have better knowledge and skills for serving the markets in other Southeast Asian countries than do finns from other develop<d or developing countries. In addition. foreign investments by Singapore firms may be facilitated in the other countries of this region where the ethnic Chinese community is active in business and. thus, offers

£mrr:itlr Tilird World ,'.flJl/inQ/lotl::!.! 199

Ihe possibililY of a local partner '.'jth a very simiiar operating style and approach to business as the Singapore firm. Thus. Singapore·based firms can also profitably form three-way joint ventures wilh firms from such countries and from the industrialized countries to serve Ihe ;;-;a:ke:s in the Southeast Asia region.

A fourth r,ason for Singapore. based firms to invest overseas is their need for acquiring reliable soure:s oi new technology and market imelJigene •. These reasons are particularly true for foreign investments in the developed l!1:onomies. While some technology" may be acquired by Ihe Singapore economy when advanced country multinational :irms invest in Singa.pore, consistent access to higher levels of technology that wiil make and keep Singapore companies eompetilive in global markets can bc::s{ :,e acquirc::d through ownership of appropriate (smaJl. high-technology) firms ic .he advanc~d countries. Fortunately, in many cases the entrepreneurs - s.an::s oi such companies - are looking for investors. In se:king high technology for .h::r j~:nkonduclor incus[r)" firms from Japan and even South Korea and Taiwan have found that making equity investments in small high-technology firms is one :Ji :~e best ways and pe:haps Ihe only way in some cases, to acquire [he technology :h!y need. Rec::u reporr.s indicate that Singapore is also e3cOuntering diificulty :n upgrading its ele-:t:onics industry and the only way out may be for its firms to ,ogage in such FDI.'

Another reason for making investr.lents in such advanced counlry firms is to acquire the knowledge and sbls to compete effe::ively and consistently in the dynamic and ever changing mark,,, 0 f these advanced ,ountries. Thus. in addition to the technical knowledge and ;nanagerial skills th~t a Singapore company can acquire from such an acquisition. it also acquires a continuing source of market inteIligence thac may contribute :owards irs abjjjry [0 prole=1 and develop irs expon markets. The need to make invcs:m:nts in advanced :ountry firms is panicularly urgent in view of the announc::: )~:alegy of the Singapore Govemmeor to upgrade the level of technology being u,,:j by business and industry in Singapore.

Fifthly. in undenaking for::::gn direct inyestm::lt. Singapore firms will also be abl, to diversify the poiiticaL economic, and business risks they face if th,y limit themselves to only one markc: or :oumry. Adve~se developments are unlikely (0

lake plac: simultaneously in many tiirrerem countries and. lhus, while business in one country (say, Singapore) may be bad it rna)' be much bener in another country so thal (he overall performance of the Jirm is protec;ed from 'he swings in anyone country's political, economic, and business environment.

, Another reason why Singa;lcre companies may have overseas investments is that many of them are, or untii :ecently were, managed by expatriate European managers and in many cases w"e part of a European multinational firm. These companies have become Singapore firms as the foreign OWDers and, in many cases, [he foreign managers were replaced by Singapore citizens starting in [he late 1950s.

Lastly, if Singapore· based companies have to continue to compete effectively in the global market plac:" .:speeially against countries such as Hong Kong. Taiwan and South Karel the y :nus! make ior~ign direct investments in other countries in order to acquire th;: r.1any advantages ai being multinationals such as

200 Rtlj AtlDl'wol

those in Hong Kong. South Korea and Taiwan. These advantages include access to larser markets and to lower cost raw material. capital. labour and technology. as weli as the increased. ability to ride out and overcome tides of protectionism and other barriers'to export markets. Furthermore, as pointed out above, a multi· national firm can achieve iewer overall costS through its many opportunities to rationalize ove:- more than one market and country its production. marketing, and finance. Most or those ad\'an:agos cannot be obtained through expons or Iic:nsing arrangements.

FDI by Singapore Industriais

Research Design and Daro Sources. T~is section will examine the foreign direct inv'!stm'!:1t5 of Singapore·b2sd industrial firms listed on the Stock E:lCchange of Singapore (SES). The ioc:Js will be on overseas industrial and commercial invest-

.) m:m$ :-at~:r than O\,::-S:2.$ inv:$tments in properly. finance, plantations or other non~jndustrial ar!2..5 . Such 2. iocus should make this study more comparabie to other studies of FDl and is more likely to contribute to our understanding or the nature and proc=ss or roreign direct investment by a firm.

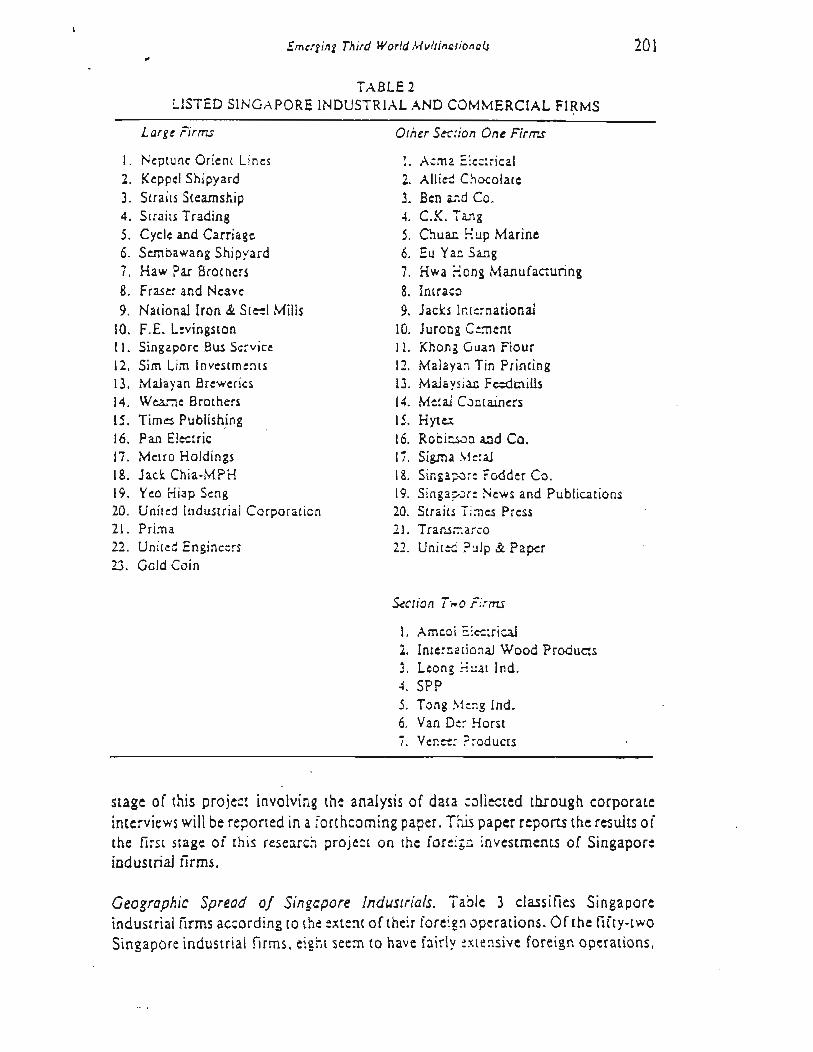

There are a total of seventy-two companies listed on the SES which are incorpora ted in Singapore ood classified as industrial or commercial firms. Of th:se seventy-two, twenty-four are large companies since they were among the one hundred companies with the Ia:gest assel5listed on the SES at 31 December 1983. Thirty-six additional industrial and commercial firms are listed in section one of the SES, while the re:T.aining twelve are listed in section tWO.

Thus. these se\'enty~two listed industria! and commercial firms can be c!assified into twenty-iour iaige firms. thirty-six medium-sized firms and twelve small firms. Howeve:, twelve or the seventy-two are foreign-owned firms and an additional eight compani .. a" actually only portrolio investors with no operating armiates. Thus. there remain tiftY-IwO Singapore-based industrial and commercial firms that are listed on the SES (see Table 2). Th .. e firms form the group that is the rocus or this study.

Dala sourc=s used ror this research project involved coliecting both primary and secondary data. No official statistics are available from the Singapore Govern· ment regarding roreign investments by Singapore companies. especially since no official approval is required for such investments. Thus, all overall figures for Singapore FDl provided in Ihis paper come from host governments. Another source of se::ondary cara used in the first stage of -this Study is the business and general press such as ihe Slrait! Times, Busin ess Times, the Asian Wall Slreet Journal. Insight. Singaport Business. and the Far Eastern Economic Review. Secondary data were also colleOld from the Stock behange of Singapore publications and corporate annual reports. For the second stage of this research project, primary data are beingcolle:ted in a series of inter.tiews with company officials, accounting firms. bankers, and government officials. The results of the seeond

I. 2. 3. 4. 5. 6. 7. 8. 9.

10. II. 12. 13. 14. 15. 16. 17. 18. 19. 20. 21. 22.

23.

EmUI;'" Third World MlI ltingrioll:ls

TABLE 2 LISTED SINGAPORE INDUSTRIAL AND COMMERCIAL FIRMS

Lar't! Firms

Neptune Orienl Lines Keppel Shipyard Straits Steamship Straiu Trading Cycle and Carriage Sembawang Ship~' ard

Haw Par Brothers Frase: and Ne:lve National!ron & Ste<1 Mills F.E. Levingston Singapore Bus Se:vice Sim Lim Investments Malayan Breweries Wear<1e Brothers Timc:s Publishing Pan Electric Me~ro Holdings Jack Chia·MPH Yeo Hiap Seng Unite:llndustrial Corporaticn Prima United Engineers Gold Coin

Ollter 5«:ion One Firms

I. Ac:ne E:e::rical 2. Allie::! Chocolare 1. Ben ... ,d Co. 4. C.K. T~'''i 5. Chuac. :-tup Marine 6. Eu Yan Sang 7. Hwa r:ong Manufacturing 8. Inlraco 9. Jacks lra::national

10. Juroag C:."Oent II. Khoni Cuan Flour 12. Mala )'an Tin Printing 13. Malaysia Fe:dmiUs 14. Me:al C~otainers 15. Hyte;(

16. Robi::.s.:>o and Co. Ii. Sigma .\1e:aJ 18. Singa;:.ore Fodder Co. 19. Sinpyvr: News and Publications 20. Straits T::ne.s Press 2l. Trans:;:arco 21. United ?'Jlp &:. Paper

~clion T.,.·o firms

I. Amcoi ::e::rical 2, Inte:-cational Wood Products 3. Leong :-:':.:at Ind. 4. SPP 5. Tong ~l,"g Ind. 6. Van De~ Horst I. Vene-:: ?~OdUCIS

201

Slage of Ihis project involving Ihe analysis of data :ollected Ihrough corporate interviews will be re_oned in a fOrlhcoming paper. This paper reporu the resullS oi the first stage oi this rc:sc;uc:: projc::t on the [or::;o investments of Singapore industrial firms.

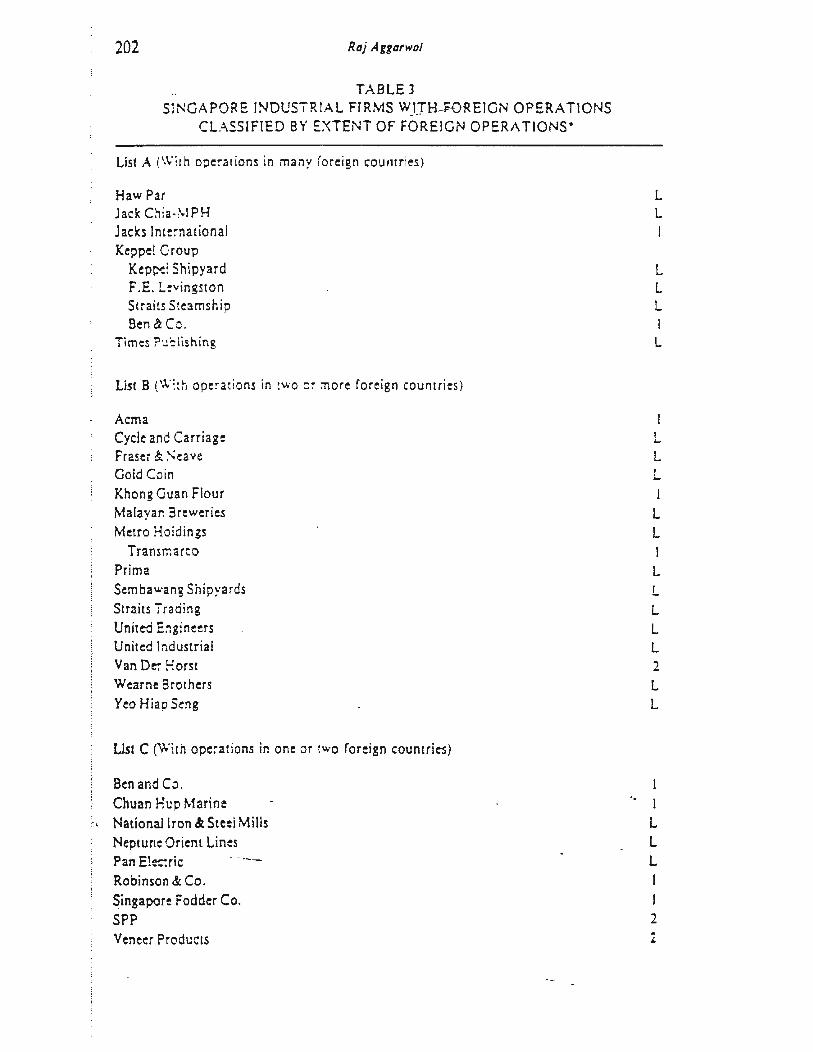

Geographic Spread o[ Singapore Industrials. Taole 3 classifies Singapore industria! firms according [0 the extent of their fore:g!1 operations. Of the fifty-two SingapQre industrial nrms. eight see:n to have fairly "!~tensive foreign operations,

202 Raj Aggarwal

TABLE J SINGAPORE INOL'STRIAL FIRMS WIJ<UDREIGN OPERATIONS

CLASSIFIED BY "X TENT OF FOREIGN OPERATIONS'

List A (\Virh operations in many (oreign coulltries)

Haw Par Jack. C~ia·,\lPH Jacks lm!!'national Keppe! Group

Kepp<; Shipyard F,E, L:vingston Straits Steamship Be" & Co.

Times P'..:i:lishing

List B (\\:::h operations in twO 0: :nore foreign countries)

Acma Cycle and Carriage Fraser & :-';eave Gold Coin Khong C-uan Flour Malayan 3reweries Metro Hoidings

Tramr.:arc:o Prima Semba\.\rang Ship~'ards Straits Trading United E::gineers United Industrial Van De:- Horst Wearne Sralhers Yeo Hiap Seng

Ust C (\\'ith ope:ations in onl! or iWO foreign counuie-s)

Ben and Co. Chuan Hup Marine National Iron & Steel MiUs Neptune Orient Lines Pan Ele:!ric Robinson & Co. Singapore Fodder Co. SPP Veneer Products

'.

L L I

L L L

L

I L L L I

L L

L L L L L 2 L L

L L L

2 2

t·III'·'~ ltl t TiUNJ IV""" ,\lIII(IfI"li"fllIl.~

TA3LE J - (,·onrinued)

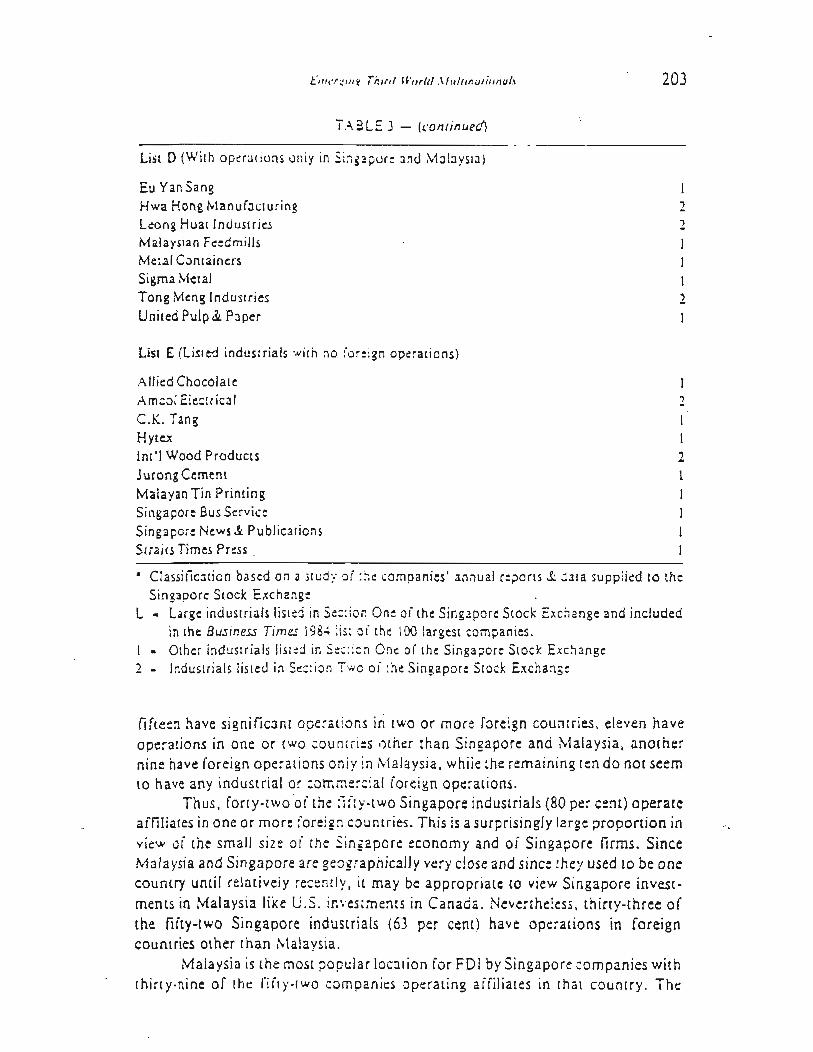

List D (With opl!ratioos ulliy in Si:;ppur: Jnu MJIJ.ysi:l.)

Eu Yan Sang Hwa Hong ManufJL"lUring Leong Huat Induslries Mala ysian Fc::dmills Me:al C.Jnlainers Sigma Metal Tong ;'.-1eng Industries Uni(ed Pulp& P,per

list £ (Listed industrials ...... ith no (or:ign op!:rations)

Allied Chocolate Amcoi E:c::tric ll C.K. Tang Hytex 1m 'J Wood Products JUfong Cement Malayan Tin Printing Singapore Bus Service Singapore News &. Publicltions Suai{s Times Pn:ss .

203

1 2

1

! 1

• Classiiic3tion based on a Hudy oi :~c: companies' an~ua! r: ;lo rts J.: j31<! supplied to the Singapore Stock Exchange

L .. Large industrials lisld in St::::ion Ort! oi the Singapore Stock Exchange and induded in the Business Times ! 98~ ;i5~ ci the 100 largest companies. Other industrials Jis:d in Se:;;:cn One of the Singapore Stock Exchange

2 Industrials listed in S~-:::ion Two o j t h~ Singapore SIOC);. Exchan;:

(jfte~:l have significanl ope:alions in two or more foreisn couiHrie.s , eleven have operations in one or (WO ~ou ntri e:s '1the.r than Singapore and Malaysia, another nine have foreign operations cniy in Malaysia, whiie ~h: remain ing ten do nO{ seem to have any industrial or :otr.m!:-:iai foreign op~:alions.

Thus, (any-two 'oi the :ii:y-twQ Singapore industrials (80 per cent) operate affiliates in one or more fore:g:1 countries. This is a surprisingly large proportion in view oi [he small size oi the Singapore economy and of Singapore firms. Since Maiaysia and Singapore H e ge::>grapnicaiJ y very close and since ~h"y used 10 be one coumry until relative iy re::ntly , it may be appropriale to view Singapore investments in Malaysia like U. S. in· .. estme:-us in Canada. Neve!'the!ess , thirty-three of !he fiity-!wo Singapore industrials (63 per cent) have opeca(ions in foreign countries other than Malaysia.

Malaysia is the most ~opu!ar iocrllion for FDI by Singapore companies with thirty-nine of the fifty-two companies operating airiliates in that country. Th~

"

204 Raj Aggarwal

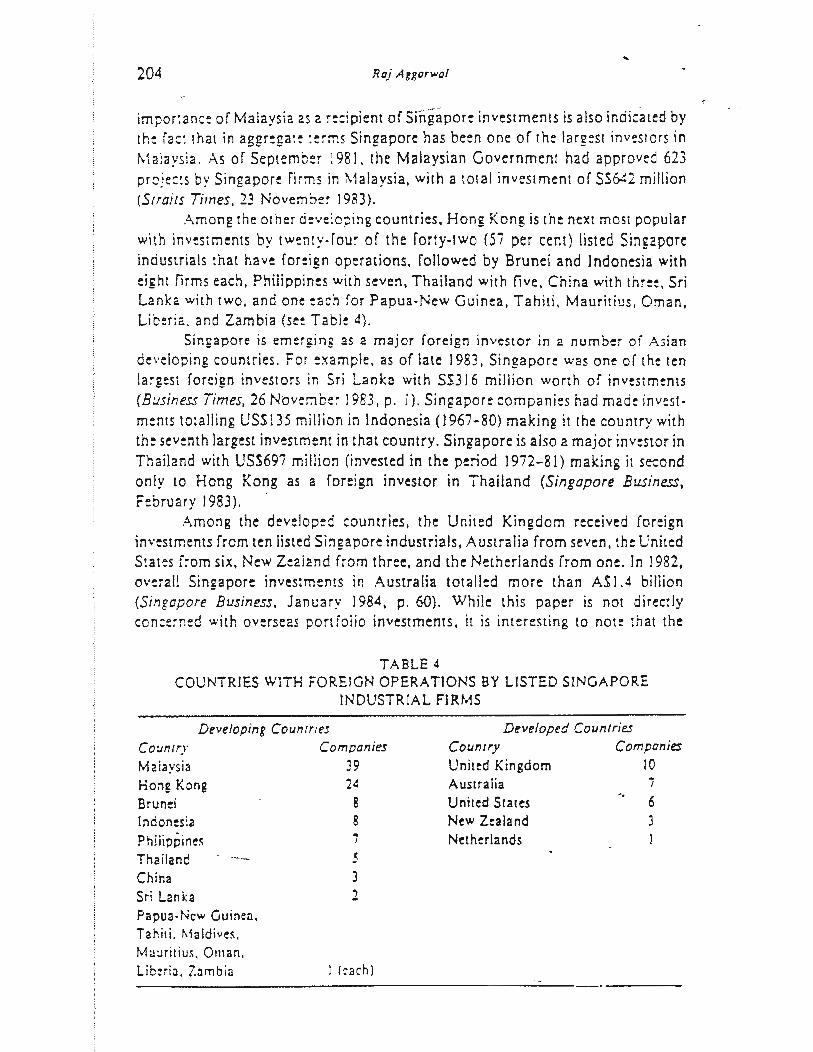

impor:anc! of Malaysia as a f:!:ipiem ofSin-g-aporeinvestments is also indicated by the fa:: 1ha! in aggregate :er:m Singapore has been one of the largest investors in Malays:a. As of September :981. the Malaysian Government had approved 623 pfcje:!S by Singapore fir:ns in Malaysia, with a tolal inveslmem of 55642 million (Straits Times, 23 November 1983).

Among the other developing countries. Hong Kong is the next most popular with investments by twenty-four of the forty-two (5i per cent) listed Singapore industrials that have foreign operations. followed by Brunei and Indonesia with eight lirms each, Philippines with seven, Thailand with five, China with three, Sri Lanka with two, and one each for Papua~New Guinea, Tahiti, Mauritius, Oman, Liber,a, and Zambia (s« Table 4)_

Singapore is emerg.ing as a major foreign investor in a number oi Asian developing countries. For example, as of late J983, Singapore was one of the ten la~gest foreign inveslors in Sri Lanka with S.$3 J 6 million worth of investments (Business Times, 26 Nove:71b" 1983. p. iJ. Singapore companies had made investments totalling USSI35 million in Indonesia (1967-80) making it the country with th! sev!nth largest investment in that country. Singapore is also a major inv!stor in Thailand with USS69i million (invested in the period 1972-81) making it ,,,,ond only to Hong Kong a, a foreign investor in Thailand (Singapore Business, February 1983).

Among the developed countries, the United Kingdom received foreign investments from ten listed Singapore industrials, Australia from seven, the United States from six, New Zealand from three, and the Netherlands from one. In 1982, Qv!;-all Singapore inves:mems in Australia totalled more than ASlA bi!lion (Singapore Business. January 1984, p.60), While this paper is not directly con:::-ned with overseas ponioiio investments, it is interesting to note that the

TABLE, COUNTRIES WITH FOREIGN OPERATIONS BY LISTED SINGAPORE

INDUSTRIAL FIRMS

Developing Counlfles Co:,mlry Malaysia Hong Kong Brunei Indono:s:a PhijjPl;ine~ Thailand - ----

China Sri Lanka Papua-New Guineil. Tahiti. MaJdive~, M,1Uritim, Oman. Lib:ri<l. Z:lmbia

Companies 39 2' 8 8 . , ! J 2

t (,,,hi

Developed Countries Country Companies United Kingdom 10 Australia i United Stales New Zealand Netherlands

6 l

Emtrtrnt Third World Mullinrwoflais 205

Government or Singapore Investment Corporation had over USSIS billion invested Overseas (mainly in the United States) in .arly 1983 (Fortune. 21 March 1983). Its investments indude U.S. property. liquid debt instruments, and Ie" than 5 per cent ownership or a number of large compani!s. Thus, as this brief review suggests, Singapore firms are engaging in consid:,.:I. for.1gn-investment that is nowing in a direction opposite to that indicated by traditional theories oi ioreign direct investment. . ~ .

'. A review of the geographic spread of the for.:gn operations of Singapore industrials indicalcs thai the Soulheast Asian region. and in particular Malaysia, has received the most attention. Only very minor investments have be:n made: in the Middle·East or Africa. Among the developed ,"untries, Australia and New Zealand because of the proximity in geography and similarity in business and legal practices have received significant Singapore private :nvestmencs as has the United Kingdom which also has a similar business and leg!.i system. Anothe:, example: of significant reverse foreign investment is the Unite: States sine: it is the largest trading partner for Singapore and is also se.:n as a s~urc: of new technoiogy.

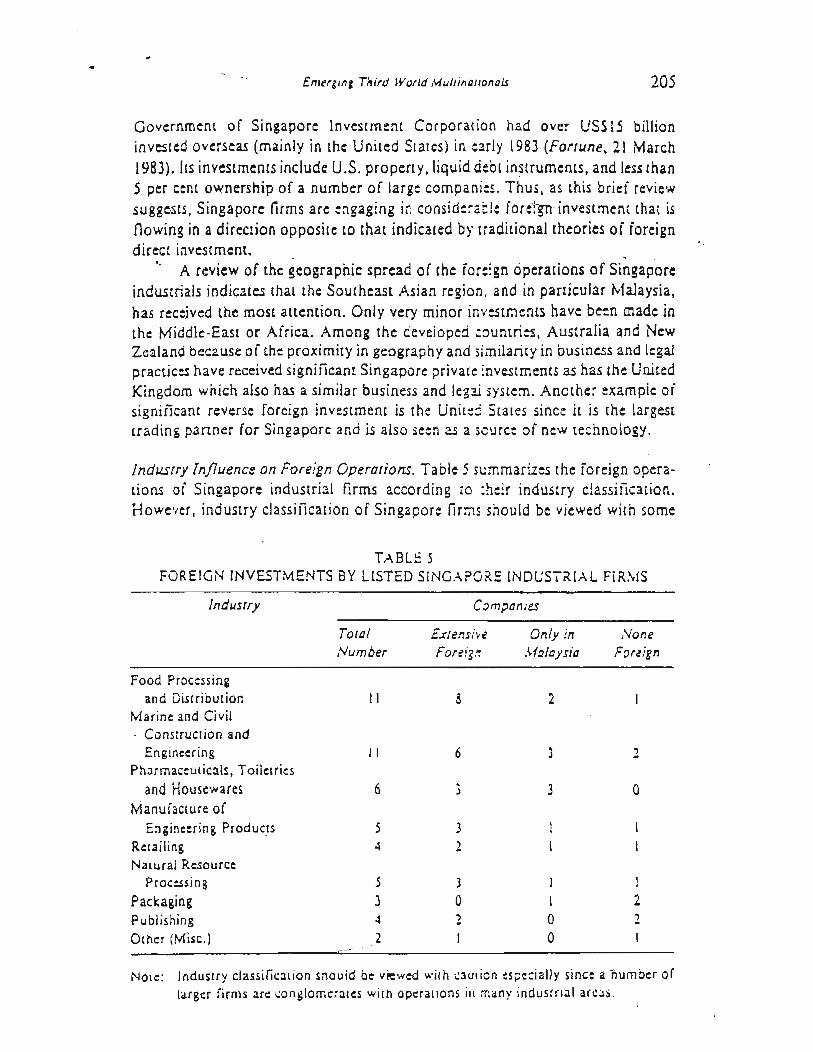

induscry In;7uence on Foreign Operations. Table 5 summarizes the foreign operations of Singapore industrial firms according to :heir industry c!assiiic:uion. However, industry classiiic3lion of Singapore firms should be viewed with some

TAB LE 5 FOREIGN INVESTMENTS BY LISTED SINGA?ORE INDUSTRIAL FIR~fS

induSlry C,mpanles

TOlal EXfe!fSi'''c Only in None Number For{il·-: .I..iaiaysia FOf(ign

Food Processing and Distribution II 8 2

Marine and Civil Construction and Engineering II 6 1 1

Pharmaceuticals, Toiletries

and Housewares 6 ; J 0 Manufacture of

E:lgineering ProducIS l J Retailing • 1 Natural Resource

Proc:ssing l 1 I I Packaging 1 0 t 2 Publishing 4 2 0 1 Other (Misc.) 2 0

Note: Indusuy classificltion should be viewed ..... i'h caution ~spe::ially since a number of larger firms an: .:ong!omC::-Ju::s with opc:ralions ill :nany ind ustr ial arC:1S .

'.

206 Raj Anarwal

caution. especially since the: larger firms are conglomerates and conduct business in many dirrerent industry categories. Thus. a rirm·sindustry classification in this section refers only to what :3n be considered to be its mnjor line or business.

One or the two major industries with the most international ope:-::ltions is Food ?~ocessi[1g and Dis::-ibution with ten of the eleven firms in this group ope:-ating in a roreign country and eight of the te~ in countries cthe:- than Singapore and Malaysia. The other major industry with "'tensive foreign opera· tions is :he Marine and Civil E'gineering and ConstrucIion Industry with nine or the eleven firms operating overseas and six of the e!even in foreign countries other than Malaysia. Singapore has :.he loeational advantage for the Marine Engineering and Se:-vice lndustry and some of its largest industrials are engaged in this business suc::ssfully competing for Ih:ir niche of t.he market wilh firms like twkDermotl and Brown and Root from the developed countries tha t have extensi ve o ~:;""a t io n s

in Singapore. Similarly, be:a~~e of the large domestic market for Civil E:1glne::-ing and Construction. Singapore companies in this industry, such as the .\1arine Engine::-ing and Construction Industry. have been able to develop the krlOw!edge and skills that give them the firm specific advantages necessary to undertake successful a·nd profitable fore:gn operations.

Two other industries with significant fore ign operations are the Pharmaceuticals, Toiletries and Housewares Industry an~. the Engineering Products Manu facturing Industry. Firms in these industries seem to have' acquired the knowledge and skills to survive and compele in the most sophislicate-:j marKet for these products in the Southeast Asia region and. therefore . are able to use these skills suc::ssfully in the othe~ countries of the region to maimain an advantage over other firms. Some firms;n these industries have: also made: inVeSlme:1!S in the developed countries, perhaps in order to acquire a reliable source of marke~ inteJ· ligen" and high technology, Firms in the Retailing and the Natural Resource Processing Industries also se-::n to be motivated by similar factors when investing overseas.

While Singapore firms have started undertaking extensive FD I, they are still early in the learning curve for FDI and not an foreign operations have be::1 succe.ss~ ful. One Singapore.based furniture company with foreign operations. the Le~ Wah group, has gone bankrupt. Whiie the exact causes are unclear and may evel'l involve rraud. it has been alleged that the company failed partly because or an 0.", expan· sion of its European and U.S. retail operations.' As another example. by 1981. of · the 44 projects from Singapore companies approved by the Sri Lankan Govern· me:1!, only half or 22 project5 were in operation. The others had eilhe:- failed or were ne"er started (Singapore Business. February 1983. p. 59).

Conclusions

This study forms the first syslematic examination of the foreign investments of listed Singapore industrial orms. A limitation or this study is that il did not examine the roreign operations of lisled non~induslrial firms or [hose of unlisted

I:'ml'f,,\i fll: Third IVorlrl .\fllltilillill"wl, 207

firms. II has :llso nOI examined whether there an! -dirrerences in the nature or foreign investmentS by governme:lI-owned and private firms based in Singapore. Future research could be direcled to ovc:rcome these limil31ions.

While not as extensive as those by Hong Kong nrms, foreign investments by Singapore ind~strial firms are fairly common and <Xlensive.-Ma{aysia seems to be the niost popular site for such investmc:ms. but more than three out of c'/ery five listed Singapore industrial firms have also invested in other foreign countries. .~ For.eign dire::::t investments se:m 10 serve a numbe;- of goals for these companies including the need to exploit their lirm-spe;:iiic adyantages especially in the neighbouring countries, and to seek reliable and less e.'pensive sources of labour, raw materials and technology. Singapore :ompanies have made an exc:He:u and impressive starr in an activity that is be::oming more important as Singapore cominues to grow as the business ccnlr: for this region of the world.

Thus, while only a few Singapore:. industrial firms can be considered to be true multinationals, a significan t proportion have extensive inveslme:1tS in operating afiiiiares in many foreign countries, These ::w Singapore MNCs se~m to have some striking similarities to older MNCs. However, they also se.", to have some ve.ry significant characteristics that may give ~he:n a comparative advantage over the traditional MNCs from indunriaiized c;)umries. As an exam pie, pre· liminary research seems to indicate that Singapore MNCs operate with lower overheads compared to Western MNCs and can be:!er exploit small" foreign markm, Such advantages could mean Ihat the Sir.gJpore MNCs may be able to operate !nore successiully in the high growth areas oi the Third World than can the traditional MNCs.

The challenges for international bus iness posed by the emergence oi these new :ViNCs from Singapore and other NICs include the challenge oi continued efforts (0 understand [he nature of Ihese new ~t~Cs and their competitive advantages. For example, the developed cour.i.ries fa;:: the chaJlenge oi de':eloping viable and effective corporate sn'ategie~ and public policies to accommodate this new but rapidly growing phe:1omenon.

NOTES .AND RE,=RE~C=S

• While lhis re$e:lrch was conducted as pan oi my Fulbright Rescr:::h Fellowship. Ihe: vie:'''''s e,\pre$sed

he: re: lre mine alone:, This paper re:?orts only the in itial findinu oi Ine research projeci anc . lhe:erore. 'he resuhs and conc:iulians presented he:e are only leru31 jve and ;na ~' oe modified as Ihe: rcseatch project progresses, This paper has benefilc:t1 (rom Ihe ::omme::u by !v1r . AUan Palhmarajan and ~1r. Roben Booker on an :!3tlier draf!. Any re::naining errors are:, howeve:, soieiy my responsibility,

I. Se~ , for e.umple. Oavid A, Hce:lan and W.J. K«aan . "The Ri$e of Ihe Third World MuJlimll ionals··, Har\"urd Businefs Reviel" (January.F ~bruary 1979); 101 -9: 5 , Lll l., "Oc\" c1 opin~ Counwe1 _as Expon~n_ of l,n~i:l1 -Teehnolo~y", R.!ItrJf"h PuliC'), I} (19g0[ ; ~.\-!1: PC'let O ' Brien , "The New !l.luhinal iunah : Develop i n~ C.,)unlt y Firms in Inll:rn:uional ,\IJriws",

"'1II 11f~)' (A upt;,1 1980): 303-)6; lee SHlil h·, "I\ ur:l 'S Ch.all en~: 10 JJp:I;n" • F"~l/l tIf: , 6 F cOru:l;rr

208

1984, pp. 94-104; and P. Stre-=:en. "Multinationals Rhisi!cd", Financt! and ~ytlapmenl 16. no. 2 (June 19791: 39-42.

2. Se:, for t:l:3mple. Raj Agg:lrwai ;nd!. Khera. "Strategic Planning ror Western Dire-:: Investment in Deve!oping Countries: Re:llifi~ for Growth Markeu". Mid-A tfantk Journal 0/ Business ::1. no.'~ !Summer 1983): 1_1.4: He:nan .and Keegan. op. cit.: Lal!. ap. cit.: Raj Aggarwai and James K. Weekly, "Foreig" Oper2!!OnS or Third World Muhinalionals: A Lilerature Re ... iew and Analysis of Indian Companies", )OlJrrTQ( oj D~\JI'!Ioping Areas (October 1982); Raj Aggarwal, "The Challenge of Third World Multinationals: A New SIB It of the Product life Cyc:!e of Multinationals" in Advanca ill Compararivt! Manolt!mt!nt. editedby Richard N. Farmer (Gre"!nwich, Conn.: JAI Pre!.S. 198.t), pp. 103·:1.

J.The conrerence Board. 171f! World'; Multinationais; A Globel C"all~ng~ (New York: The Board. 1981).

4. Louise T. Wells. Jr., Titird Wo,fe ,\.{ultinat;ol'lais (Cambridge, Mass.: MIT Pres!, 1983). S. See, ror ~:'!ample. O. LeC: .. w, "Dire-:l Investment by Firms from Less Develope-:! Counfrie~".

Oxford E:Ol1omic Pc~n (Nove:nbe~ 1977): 442-S7; L.T, Wells. "Foreign lnvestme:1! from Hong: Kong", C"lumbia JourMal 0/ 'riI",ld Eusi,,~~ (Spring 1978): 39-49; K. Ghymn, "~1u!tinafional E:'1te~prises from Developing Countries: The Experience of Korea", Journal of /flft'flafional Busine:.s Studits (Fall 19801: JC.:-~: T. Agmon and C.P. Kindleberger. eds., Multlnafiol1r1is from Sma/! Counffie.r (Cambridge. ,'"1m,: .\.fIT Pre1ll, 1977); Aggarwal and Week.ly, 01'. cit.: C.F. Diaz Alejandro. "Foreign Dire=! Inv~tme:'1.t by Lacin Americans", in Agmon and Kindlet>erger, 01'. ci:.: H~nan and Keehan, cp. e:t.: La!!, cp, tit.; and Street en, 01', cit.

6. See, for example. R.F. Jansse::, "Sewcomers scramble to the lummi!", Wall Slrul )outnar, 20 AI'ri! 19~!, p. I: A. Jon~, "Wh:=-e Adam Smith mett! Conrudu~", Forbes, 19 Dt-;e:-nber 1983, PI'. IIJ-N: and Kasper Wolfgang, "Innovation and Growth in Developing Countries". UMBC Economic R~vitw 19. no, 2 (l98)}: 4-11.

7, For details see. (or e~ample, S. Robod: and K. Simmonds. lnttrnational 8u.sint:lS and Mu/rinalioflat Enttrpristl (Home .... ood.lllinois: Richard D. Irwin. 1983); Jones Age!!. "Subsidy to Caoilai Through Tv: Jncentiv~ in the ASEAN Countries: An Application of [he CoS{ oi Capilal ApI'roach Under Infla.lionary C~ndilion$". Sinra"or~ £(O!70mic R~vi~w 28, no. 2 (Oc:oe.er 1983): 98·1:3: and Dan Usher; "The E:onomie of Tax Incentives to Encourage Investme:1C in Less Developed Countries". Journai of ~vtlo"mtn{ Economics (1917).

8. See. ror e:l:ampie. A. Spaeth. "Singapore Encountering Difficully Upgrading Its E!emonics Industry", AJian Wall Sl'~' Journal WuKly. ) January 1983. p. 8; "Scill learning :0 learn the tricks," Economist, 28 April !98-4, ~. 7~: and Lillian Chew. "Firs! Singapore-owned compuler plant e!o~es.", Straits Ttmtl, :1 ~ay 1984,\). 19.

9, Tee Fo~ Seng. "Tak.in! credit for 3 good loan'" S;ntaporr Bal1tinJ. Finonct, and lfUlJ'an~. 19M (Singapore: nmes Directories. 1984), p. 17.

Raj AuarwaJ i3 PtOr~sor or Business Administration al the Univet!i!y crToledo, Toledo. Ohio. USA, :and was Fulbright R~rch Fellolll lithe Institute of Southeast A3ian Studies.

,