Effects of strategy and environment on corporate venture success in industrial markets

20

EFFECTS OF STRATEGY ANDENVIRONMENT ON CORPORATE VENTURE SUCCESS IN INDUSTRIAL MARKETS WILLIAM MING-HONE TSAI National Central University IAN C. MACMILLAN and MURRAY B. LOW The Wharton School The literature ident$es four importantfactors’ that determine the success EXECUTIVE of a corporate venture: culture, climate, and corporate support (Schon SUMMARY 1966; Kanter 1983; MacMillan, Block, and Subba Narasimha 1984; Fast and Pratt 1981; Roberts 1980; Maidique and Hayes 1984); structure and venturing effort (Burgelman 1983, 1985; Souder 1981; Maidique 1980; Block 1985; MacMillan and George 1985); planning, monitoring and eval- uation (Vesper and Holmdahll973, Quinn 1979; Fast 1981; Block and MacMillan 1985); and strategy and environment (Cooper 1979, 1983; Hobson and Morrison 1983; Biggadike 1979). This paper focuses on the last of the above issues. It seeks to explore the importance of environment and strategy for corporate venture success. At the broadest level, two theoretical perspectives have dominated the organization-environ- ment-strategy literature in recent years: population ecology and strategic adaptation. The population ecology perspective argues that organizational survival is determined by en- vironmental selection (Hannan and Freeman 1979.1984; Aldrich 1979; Greenfteld and Stricken 1986). Technological and demographic change results in “new resource sets” that provide opportunities for the expansion of existing, or the founding of new, organizations (Brittain and Freeman 1980). A shifting network of social linkages, both within and between existing firms, connects aspiring venture managerslentrepreneurs with resources and opportunities (Aldrich and Zimmer 1986). While managers develop and implement strategies, these strategies do not directly determine success. Instead, they are one of many sources of random variation that will be selected for, or against, by the environment. In contrast, the strategic adaptation perspective implies that new venture success is a function of the manager’s or entrepreneur’s ability to assess internal capabilities and environmental conditions for the purpose of developing and executing effective strategies (Andrews 1980; Porter 1980; Vesper 1980; Timmons 1982). The environment is viewed as a (major) constraint within which strategy is developed. Furthermore, environments are not immutable and are subject to negotiation and manip- ulation (Child 1972; Miles and Cameron 1982; MacMillan 1983). In recent years it has been acknowledged that both population ecology and strategic adaptation Address correspondence to Ian C. MacMillan, Snider Entrepreneurial Center, 4th Floor, Vance Hall, 37th and Spruce Streets, University of Pennsylvania, Philadelphia, PA 19104-6374. ‘See MacMillan (1986) for a more. complete review of this literature. Journal of Business Venturing 6, %28 0 1991 Elsevier Science Publishing Co., Inc., 655 Avenue of the Americas, New York, NY 10010 9

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Effects of strategy and environment on corporate venture success in industrial markets

EFFECTS OF STRATEGY

ANDENVIRONMENT ON

CORPORATE VENTURE

SUCCESS IN

INDUSTRIAL MARKETS

WILLIAM MING-HONE TSAI National Central University

IAN C. MACMILLAN and MURRAY B. LOW The Wharton School

The literature ident$es four importantfactors’ that determine the success EXECUTIVE of a corporate venture: culture, climate, and corporate support (Schon SUMMARY 1966; Kanter 1983; MacMillan, Block, and Subba Narasimha 1984; Fast

and Pratt 1981; Roberts 1980; Maidique and Hayes 1984); structure and venturing effort (Burgelman 1983, 1985; Souder 1981; Maidique 1980; Block 1985; MacMillan and George 1985); planning, monitoring and eval-

uation (Vesper and Holmdahll973, Quinn 1979; Fast 1981; Block and MacMillan 1985); and strategy and environment (Cooper 1979, 1983; Hobson and Morrison 1983; Biggadike 1979). This paper focuses on the last of the above issues. It seeks to explore the importance of environment and strategy for corporate venture success.

At the broadest level, two theoretical perspectives have dominated the organization-environ- ment-strategy literature in recent years: population ecology and strategic adaptation.

The population ecology perspective argues that organizational survival is determined by en- vironmental selection (Hannan and Freeman 1979.1984; Aldrich 1979; Greenfteld and Stricken 1986). Technological and demographic change results in “new resource sets” that provide opportunities for the expansion of existing, or the founding of new, organizations (Brittain and Freeman 1980). A shifting network of social linkages, both within and between existing firms, connects aspiring venture managerslentrepreneurs with resources and opportunities (Aldrich and Zimmer 1986). While managers develop and implement strategies, these strategies do not directly determine success. Instead, they are one of many sources of random variation that will be selected for, or against, by the environment.

In contrast, the strategic adaptation perspective implies that new venture success is a function of the manager’s or entrepreneur’s ability to assess internal capabilities and environmental conditions for the purpose of developing and executing effective strategies (Andrews 1980; Porter 1980; Vesper 1980; Timmons 1982). The environment is viewed as a (major) constraint within which strategy is developed. Furthermore, environments are not immutable and are subject to negotiation and manip- ulation (Child 1972; Miles and Cameron 1982; MacMillan 1983).

In recent years it has been acknowledged that both population ecology and strategic adaptation

Address correspondence to Ian C. MacMillan, Snider Entrepreneurial Center, 4th Floor, Vance Hall, 37th and Spruce Streets, University of Pennsylvania, Philadelphia, PA 19104-6374.

‘See MacMillan (1986) for a more. complete review of this literature.

Journal of Business Venturing 6, %28 0 1991 Elsevier Science Publishing Co., Inc., 655 Avenue of the Americas, New York, NY 10010

9

10 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

perspectives provides valuable insight. A new body of literature has emerged that attempts to reconcile these theories (Tushman and Anderson 1986; Van de Ven, Hudson and Schroeder 1984; Singh, House, and Tucker 1986; Aldrich and Auster 1986). This paper follows in this tradition and seeks to explore empirically the relative impact of strategy and environment on new corporate venture performance in

industrial markets.

STRUCTURE OF THE PAPER

This paper is the first of two. Both use data from the PIMS Start-up data base (STR4). The first paper is limited to an exploration of the relationships between environment, strategy, and performance at the initial stage of a new venture. The second paper builds upon the first and analyses the causal relationships, over time, among environment, strategy, com- petitive response, and performance.

The paper begins by proposing a simple conceptual model for understanding the relations between environment, strategy, and performance. This is followed by reviews of the organization theory, industrial organization economics, and strategy literatures, in order to identify the most salient dimensions of environment, strategy, and performance for a new venture. Some background is provided on the PIMS STR4 data base and variables are chosen to operationalize the model. Predictions are made regarding the relationships among specific variables, and a method for testing the model is chosen. The results are presented, followed by a general discussion that includes implications for practice.

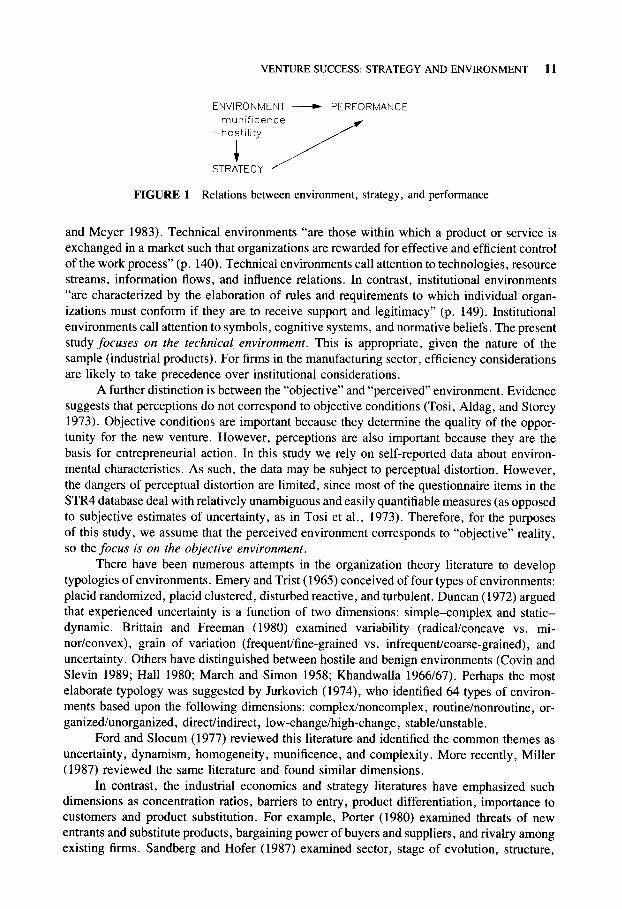

Figure 1 provides a simple model for conceptualizing the relations among environment, strategy, and performance. In keeping with the population ecology literature, it suggests that environmental conditions at the time of an organization’s founding will have a direct effect on performance. In keeping with the strategic adaptation literature, it suggests that choice of strategy will also have a direct affect on performance. Furthermore, choice of strategy will be influenced by the environmental conditions that exist at the time of founding.2 In the interest of brevity, however, this article will not deal directly with the relation between environment and strategy. This is reported briefly in Appendix A.

The purpose of this study is to answer the following question: What is the relative importance of environment and strategy for corporate venture performance?

THE ENVIRONMENT

During the last 20 years, a large multidisciplinary literature has emerged focusing on or- ganizational environments. This literature makes it clear that organizations face many dif- ferent kinds of environments. For example, organizational environments may be studied at different levels of analysis: organizational sets (Blau and Scott 1962; Evan 1966); populations of organizations (Hannan and Freeman 1979; Aldrich 1979); communities of organizations (Hawley 1950; Warren 1967; Astley and Van de Ven 1983); and functional organizational fields (Hirsch 1972; DiMaggio and Powell 1983; Scott and Meyer 1983). In this paper our focus is at the industry level. We are interested in the effect of firm entry under different industry conditions. We acknowledge, however, that other levels of analysis have been relatively understudied and may yield important insight (see, for example, Aldrich and Zimmer’s (1986) work on networks).

Another important distinction is between technical and institutional environments (Scott

‘The model does not consider feedback effects and the possibility that strategy may affect the environment. These issues are dealt with in the follow-on paper, where we examine the interaction, over time, among strategy, environment, competitive response, and performance.

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 11

ENVIRONMENT - PERFORMANCE

FIGURE 1 Relations between environment, strategy, and performance

and Meyer 1983). Technical environments “are those within which a product or service is exchanged in a market such that organizations are rewarded for effective and efficient control of the work process” (p. 140). Technical environments call attention to technologies, resource streams, information flows, and influence relations. In contrast, institutional environments “are characterized by the elaboration of rules and requirements to which individual organ- izations must conform if they are to receive support and legitimacy” (p. 149). Institutional environments call attention to symbols, cognitive systems, and normative beliefs. The present study focuses on the technical environment. This is appropriate, given the nature of the sample (industrial products). For firms in the manufacturing sector, efficiency considerations are likely to take precedence over institutional considerations.

A further distinction is between the “objective” and “perceived” environment. Evidence

suggests that perceptions do not correspond to objective conditions (Tosi, Aldag, and Storey 1973). Objective conditions are important because they determine the quality of the oppor- tunity for the new venture. However, perceptions are also important because they are the basis for entrepreneurial action. In this study we rely on self-reported data about environ- mental characteristics. As such, the data may be subject to perceptual distortion. However, the dangers of perceptual distortion are limited, since most of the questionnaire items in the STR4 database deal with relatively unambiguous and easily quantifiable measures (as opposed to subjective estimates of uncertainty, as in Tosi et al., 1973). Therefore, for the purposes of this study, we assume that the perceived environment corresponds to “objective” reality, so the focus is on the objective environment.

There have been numerous attempts in the organization theory literature to develop typologies of environments. Emery and Trist (1965) conceived of four types of environments: placid randomized, placid clustered, disturbed reactive, and turbulent. Duncan (1972) argued that experienced uncertainty is a function of two dimensions: simple-complex and static- dynamic. Brittain and Freeman (1980) examined variability (radical/concave vs. mi- nor/convex), grain of variation (frequent/fine-grained vs. infrequent/coarse-grained), and uncertainty. Others have distinguished between hostile and benign environments (Covin and Slevin 1989; Hall 1980; March and Simon 1958; Khandwalla 1966167). Perhaps the most elaborate typology was suggested by Jurkovich (1974), who identified 64 types of environ- ments based upon the following dimensions: complex/noncomplex, routine/nonroutine, or- ganized/unorganized, direct/indirect, low-change/high-change, stable/unstable.

Ford and Slocum (1977) reviewed this literature and identified the common themes as

uncertainty, dynamism, homogeneity, munificence, and complexity. More recently, Miller (1987) reviewed the same literature and found similar dimensions.

In contrast, the industrial economics and strategy literatures have emphasized such dimensions as concentration ratios, barriers to entry, product differentiation, importance to customers and product substitution. For example, Porter (1980) examined threats of new entrants and substitute products, bargaining power of buyers and suppliers, and rivalry among existing firms. Sandberg and Hofer (1987) examined sector, stage of evolution, structure,

12 W.M:H. TSAI, I.C. MACMILLAN AND M.B. LOW

disequilib~um, and barriers to entry. Hamb~ck (1983) examined concen~ation, infrequency of purchase, dollar importance, product dynamism, cost pressure, product sophistication, vulnerability, exports, demand instability, and market share instability.

Which of the environmental dimensions identified in the organization theory and industrial economics/strategy literatures are the most likely to affect new venture strategy and new venture performance? Clearly, there are no easy answers. However, this paper is concerned with the environment faced by a firm entering into an established product/market domain. In the spirit of the ecological model, we conceive of a firm entering a new domain as facing a situation similar to that faced by an organism attempting to enter an ecological niche that has already been occupied by competing organisms. In our opinion, there appear to be two characteristics of the environment that seem to get at the heart of the challenge to entry and that appear, also, to be gaining increasing recognition in the literature.

The first is the “munificence” of the environment (Staw and Szwajkowski 1975; Tussle and Gerwin 1980; Dess and Griser 1987; Yasai-Arkedeni 1989). This reflects the “quality” of the oppo~unity, as reflected by the degree of richness or sparseness of the niche being entered. In ecological terms this compares with the availability of nutrients in an ecological niche.

The second characteristic of the environment is its “hostility” (Grinyer, Al-bazazz, and Yasai-Arkedeni 1980; Miller and Friesen 1983; Covin and Slevin 1989). In ecological terms this compares with the population density of organisms competing for nutrients in the niche. This reflects the fierceness of competition that the firm encounters when it attempts to enter.

Some theorists have conceived of munificence and hostility as opposite ends of a continuum. While we acknowledge that the two concepts are related, we feel that there are good theoretical reasons to conceive of each as a separate dimension. Again, taking an ecological perspective: From the point of view of human beings, the plains of Africa are both munificent and hostile, whereas the plains of North America are munificent and benign, there being fewer predators, disease, and so on in North America than in Africa.

Munificence captures the structure and nature of the ~ffr~e~ being entered; hostility captures the strncture and nature of the firms competing for that market. Thus, some new venture opportunities have much more potential than others; and, holding the quality potential of the opportunity constant, some markets are more hotly contested than others. Obviously, the most favorable circumstance for a new venture is to pursue an op~~unity with high munificence under conditions of limited hostility. If this is the case, then our study should show that munificence and hostility are separately related to performance.

Having selected munificence and hostility as two key synthesizing dimensions of the environment for new ventures, our approach is to scan the variables in the PIMS data set to find the measures that best capture the quality of the op~~unity and the fierceness of competition.

STRATEGY

The concept of strategy, like that of environment, has been used to refer to a wide range of phenomena. Strategy means different things at different levels of analysis (Hofer and Schendel 1978); three such levels of strategy are corporate (product/market portfolio choices), business (choices of how to compete within a given product/market), and functional (choices of marketing, finance, m~ufact~ng strategies, and so on).

It is also possible to distinguish between strategies to achieve efficiency or effectiveness

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 13

(aimed at the technical environment: Porter 1980) and strategies to achieve legitimacy (aimed at the institutional environment: Selznick 1949; Macmillan and Jones 1986). Finally, it is possible to distinguish between “intended” and “realized” strategies (Mintzberg 1978) in a manner that is analogous to “perceived” and “objective” environments.

In this study we focus on the business level of analysis: how to compete within a given product/market area. Given the nature of our sample, we focus on strategies aimed at the technical environment. And our characterization of strategy is based on an exami- nation of actual, as opposed to intended, behavior.

Numerous authors have developed typologies of generic strategies. Porter (1980) distinguished between differentiation, cost leadership, and focus; Miles and Snow (1978) identified defenders, prospectors, analyzers, and reactors; Hofer and Schendel (1978) characterized six generic strategies: share increasing, growth, profit, market concentration and asset reduction, liquidation, and turnaround. Miller (1987) reviewed the work of these and other scholars (Hambrick 1983; Henderson 1979; Dess and Davis 1984) and con- cluded that the dimensions discussed repeatedly were product/service innovation, market- ing differentiation, breadth (niche vs. related diversification), and conservative cost con- trol (low cost, “harvester,” cost leadership). As Miller acknowledges it is not possible to say that these are the most important dimensions, but their frequent reference in the lit- erature suggests they are important to consider. Previous research specifically dealing with strategies for new ventures has found that aggressive entry is associated with success, as measured by market share and profitability (Biggadike 1979; Hobson and Morrison 1983; MacMillan & Day 1986). Therefore, when we attempt to operationalize strategy using the variables in the STR4 data base, some measure of entry aggressiveness will be con- sidered in addition to the other dimensions of strategy discussed above.

PERFORMANCE

Measuring performance is a complex problem in organizational studies (Lentz 1981; Kanter and Brinkerhoff 1981). The trade-offs between long-term and short-term profitability, and the recognition that organizations depend for survival upon the contributions of many con- sistuencies with varying criteria for performance, make traditional accounting measures of questionable value. Traditional accounting measures of performance such as return on in- vestment (ROI) or net profits are even more problematic when studying new ventures, since even successful start-ups often do not reach profitability for a considerable period of time (Biggadike 1979; Weiss 198 1). Furthermore, firms may engage in new ventures for purposes of acquiring new skills or technologies in order to keep strategic options available (Bowman and Hurry 1987), or in order that failed ventures may sow the seeds for future successes (Maidique and Zirger 1985).

The most basic measure of success for a new venture is survival, and much of the population ecology studies use the probability of organizational death as the dependent variable. We eschew this measure for several reasons. First, it provides no information about performance differences between surviving ventures. Second, it ignores the possibility that survival and performance may have different antecedents (Meyer and Zucker 1989). New venture researchers often use multiple measures of performance snch as sales growth, ROI, and market share gain (see Miller, Wilson, and Adams (1988) for a review of traditional measures and a suggested alternative). Percentage growth in sales is problematic for the first few years, because firms are starting from a position of no sales. Absolute dollar growth in sales is no more helpful unless one can control for industry and size of investment.

14 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

Relative ROI may be a more useful measure for comparing the success of new ventures, even though the firms would not be expected to achieve break-even within the first few years. It is important to realize, however, that ROI in the first two years may be largely an artifact of accounting practices designed to minimize taxes. For example, in some cases, start-up costs and R and D will be capitalized, while in other cases, they will be written off.

Market share gain may be the best measure of new venture performance available.3 As with growth in sales, market share gain measures the market acceptance of the new firm’s product. However, because the standard for comparison is the market and not the firm, share gain overcomes the problems associated with sales growth.

It is important to note, however, that the relationship between market share and profitability is a controversial one (Woo and Cooper, 1981; Buzzell, Gale, and Sultan 1975; Prescott, Kohli, and Venkatraman 1986), and in many cases, it has been argued that there are clear tradeoffs between the two (Gale and Branch 1982). So while market share may be the best measure of new venture performance available, it is important also to consider some indicator of profitability. In this study, we consider both share gain and profitability.

THE PIMS START-UP DATA BASE

The PIMS STR4 database contains data on 161 corporate ventures that market a “service or product that the parent company has not previously marketed and that required the parent company to obtain new equipment or new people or new knowledge” (Hobson & Morrison 1983). The ventures are divisions or profit centers, selling a distinct set of products or services within a well-defined industrial market and competitive setting. Recent studies based upon this database include MacMillan and Day (1986), and Lambkin (1988).

The pros and cons of the main PIMS database are well reported in the literature (Anderson and Paine 1978; Ramanujam and Venkatraman 1984; Woo and Cooper 1981; Hambrick, MacMillan, and Day 1982) and apply equally well to the STR4 database. While acknowledging information of the data base (respondents do not necessarily apply definitions in the same manner, and anonymity prevents correction and limitations of the AQD statistical analysis package) the general consensus is that PIMS data are of high quality and reliability. Moreover, the STR4 database is the largest and most comprehensive source of available data on corporate venturing.

Selection of Variables

The database contains several variables that portray environmental conditions prior to the firm’s entry into the market. From among those available, five environmental variables were chosen: three to measure munificence and two to measure hostility.

Measures of MunQicence

Life cycle stage of the product in the market being entered. In general, earlier life cycle stages are associated with better-quality opportunities (for reviews of the PLC literature,

3Miller, Wilson, and Adams (1988) correctly note that market share gain may be problematic for pioneering ventures. In such cases the successful pioneering firm would initially have 100% of the market, only to have this reduced as new firms entered. In our study, we are focusing on entry into established markets.

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 15

see Rink and Swan 1979 and Tellis and Crawford 1981). While there are some dangers associated with being too early into a market, these are outweighed by the reduced oppor- tunities (to establish market share and to benefit from long-run returns) associated with later life cycle stages.

Number of immediate customers. This variable measures the number of customers in the selected market to whom the firm can directly sell. Thus it is a proxy for market fragmentation.4 Higher levels of fragmentation of immediate customers make it more difficult for the new firm to reach its end users and is therefore associated with lower munificence.

Growth of market. A growing market is associated with increased opportunities. While growth and life cycle can be expected to be (negatively) related, there is an important distinction between the two.5 Growth measures the expansion of the market, while life cycle also measures how long the market can be expected to last.

Measures of Hostility

Market share of three largest competitors combined. This variable measures the extent to which the competitors are well entrenched. Well-entrenched competitors suggest a hotly contested market that will make it more difficult for the new entrant to get established.

Dependence of largest competitor on the market. A highly dependent competitor is likely to respond aggressively to the threat of a new entrant. Dependence of the largest competitor will be positively related to hostility.

Measures of Strategy

The STR4 data base has approximately 25 variables dealing with entry strategy. In order to control for industry, most of the variables are based upon comparisons with standard practices or competitors’ behaviors. Using the salient dimensions of strategy identified in the literature as guidelines, we selected the four variables that had the least problems of multicollinearity: relative product quality; relative promotion expenditure; relative price; and capacity as a

percentage of the served market. Relative product quality, promotion expenditure, and price each capture a critical

marketing dimension of entry strategy. Capacity as a percentage of the served market is a measure of the aggressiveness of entry, as well as an indicator of investment strategy.

EXPECTED ENVIRONMENTAL EFFECTS ON PERFORMANCE

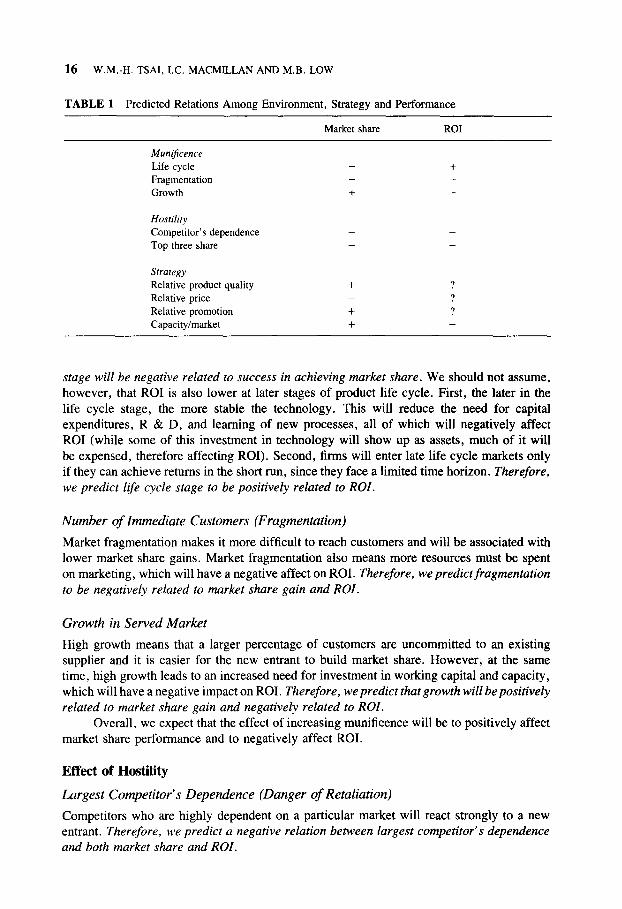

Effect of Munificence

Life Cycle

The later in the life cycle (holding growth constant), the more established the competitors and the more consumer resistance to switching. So, in Table I, we predict that life cycle

41deally, fragmentation should be measured by the number of immediate customers divided by market size. Unfortunately, number of customers and market size are both categorical variables in the STR4 database. As a result, it is not possible to divide one by the other without fundamentally distorting the data. While number of immediate customers may be an imperfect measure of fragmentation, we suggest that its shortcomings will not result in systematic bias.

‘In the actual data set, the correlation between growth and life cycle was - .15.

16 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

TABLE 1 Predicted Relations Among Environment, Strategy and Performance

Market share ROI

MuniJicence

Life cycle

Fragmentation

Growth

_ + _ -

+ -

Hostility Competitor’s dependence

Top three share

_ - _ -

Strategy Relative product quality

Relative price

Relative promotion

Capacity/market

+ ? _ ?

+ ?

+ _

stage will be negative related to success in achieving market share. We should not assume, however, that ROI is also lower at later stages of product life cycle. First, the later in the life cycle stage, the more stable the technology. This will reduce the need for capital expenditures, R & D, and learning of new processes, all of which will negatively affect ROI (while some of this investment in technology will show up as assets, much of it will be expensed, therefore affecting ROI). Second, firms will enter late life cycle markets only if they can achieve returns in the short run, since they face a limited time horizon. Therefore,

we predict life cycle stage to be positively related to ROI.

Number of Immediate Customers (Fragmentation)

Market fragmentation makes it more difficult to reach customers and will be associated with lower market share gains. Market fragmentation also means more resources must be spent on marketing, which will have a negative affect on ROI. Therefore, we predictfragmentation

to be negatively related to market share gain and ROI.

Growth in Served Market

High growth means that a larger percentage of customers are uncommitted to an existing supplier and it is easier for the new entrant to build market share. However, at the same time, high growth leads to an increased need for investment in working capital and capacity, which will have a negative impact on ROI. Therefore, we predict that growth will be positively

related to market share gain and negatively related to ROI. Overall, we expect that the effect of increasing munificence will be to positively affect

market share performance and to negatively affect ROI.

Effect of Hostility

Largest Competitor’s Dependence (Danger of Retaliation)

Competitors who are highly dependent on a particular market will react strongly to a new entrant. Therefore, we predict a negative relation between largest competitor’s dependence

and both market share and ROI.

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 17

Top Three Competitors’ Share (Competitors Well Established)

Well-entrenched competitors will make it more difficult for a new entrant to gain a foothold. Therefore, we predict a negative relation between top three competitors’ share and both

market share and ROI. Overall we expect that measurers tapping hostility will reflect a general depressing

effect on both performance and ROI as hostility increases.

EFFECT OF STRATEGY ON PERFORMANCE

Market Share

Predictions of the relationships between marketing strategy variables and market share are relatively straightforward. We predict relative product quality and relative promotion ex-

penditure to be positively related to market share gain, and relative price to be negatively related.

The relations between market share gain and investment in capacity compared to target market size is more complicated and draws attention to the danger of assumptions about causality. Investment in capacity can be viewed as an aggressive entry strategy that has been associated with market share gain (MacMillan and Day 1986). Alternatively, investment in capacity can be viewed as a reflection of expectations of success. Nevertheless, both ar- guments suggest a positive relationship between investment in capacity and market share gain. Therefore, we predict a positive relation between investment in capacity and market share gain.

Profitability

The relation between strategy and ROI are much more difficult to predict. This is because the relations of relative product, price, and promotion to ROI will depend upon the elasticity of demand with respect to quality, price, and promotion. For example, if demand is highly sensitive to quality differentials between product offerings, an investment in quality would result in a higher ROI. However, since it is expensive to achieve high quality, if these expenses are not compensated by significantly increased sales, the result will be to drive down ROI. The same argument applies for price and promotion. Unless we can control for elasticity of demand, no predictions are possible.

A clear prediction is possible for the effect of investment in capacity on ROI. While high capacity may improve ROI in the long term by taking advantage of economies of scale, in the short run (the first four years) it is unlikely that this advantage will be realized. Therefore, we predict a negative relation between investment in capacity and ROI.

METHODOLOGY

Environment, Strategy, and Performance

To explore the relations among environmental and strategic variables, a series of regressions were run. First, the munificence and hostility variables at the start of the venture were run separately against each of the performance variables after the venture had been going for two years. Then, the munificence and hostility variables were combined, and the regressions rerun. The purpose of this second step was to test the argument that munificence and hostility

18 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

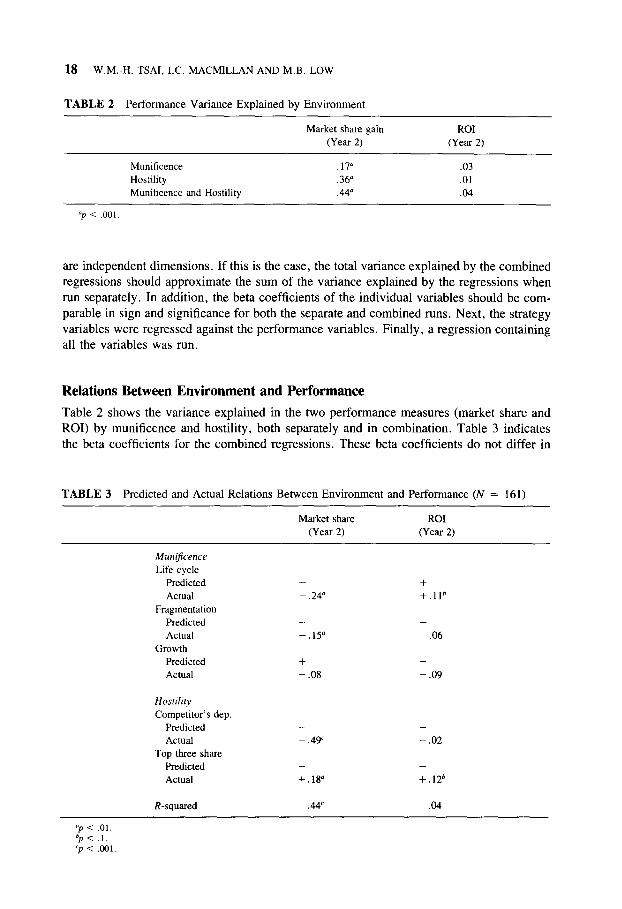

TABLE 2 Performance Variance Explained by Environment

Market share gain ROI (Year 2) (Year 2)

Munificence Hostility Munificence and Hostility

.17” .03

.36” .Ol

.44” .04

are independent dimensions. If this is the case, the total variance explained by the combined regressions should approximate the sum of the variance explained by the regressions when run separately. In addition, the beta coefficients of the individual variables should be com- parable in sign and significance for both the separate and combined runs. Next, the strategy variables were regressed against the performance variables. Finally, a regression containing all the variables was run.

Relations Between Environment and Performance

Table 2 shows the variance explained in the two performance measures (market share and ROI) by munificence and hostility, both separately and in combination. Table 3 indicates the beta coefficients for the combined regressions. These beta coefficients do not differ in

TABLE 3 Predicted and Actual Relations Between Environment and Performance (N = 161)

Munijcence

Life cycle Predicted Actual

Fragmentation Predicted Actual

Growth Predicted Actual

Market share (Year 2)

-

- .24”

-

-.15”

+ - .08

ROI (Year 2)

+ +.11b

_

.06

_

- .09

Hosriliry

Competitor’s dep. Predicted Actual

Top three share Predicted Actual

- _

- .49’ - .02

_ _

+.18” +.126

R-squared .44c .04

“p -c .Ol.

“p < .l. ‘p < .ccJl

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 19

an important way from the coefficients of the regressions when run separately (not reported here).

Tables 2 and 3 suggest that market share gain is significantly influenced by the en- vironment, whereas ROI is not. Furthermore, as can be seen from Table 3, with respect to market share, munificence and hostility are both important and independent dimensions. The latter conclusion is reached by observing that the variance explained by the separate regressions, nevertheless represents a substantial improvement in explanatory power. Fur- thermore, the betas of the separate and combined regressions are stable (not shown).

Discussion of Market Share Gains

Of the five predicted relations between environmental variables and market share, three are in the predicted direction and significant at the .Ol level or better.

We now discuss the results that were different from the predictions. Growth in served market was not significantly related to market share. One possibility

is that high-growth markets attract too many new entrants (Sahlman and Stevenson 1985) and, therefore, actually result in increased competition. It might be argued that high-growth, “glamour” markets should be avoided in favor of markets with more modest growth and a correspondingly lower profile. It might also be argued that the lack of a relation between market growth and share obtained is because growth prior to entry was measured, and this may reflect a timing problem. Clearly, the best time to get into the market is before the major growth, not the year after!

We also predicted that market share gain and top three competitors’ share (competitors well established) would be negatively related. Surprisingly, the results indicate they are strongly related in a positive direction. This outcome is hard to understand. Could it be that in cases where a few firms have a large share, a new firm would attempt entry only if it had a clear competitive advantage? Since we have controlled for retaliation (competitor’s dependence), a few clearly defined competitors might create an opportunity for the new firm to quickly gain share by astute positioning vis-a-vis the existing customers. Or could it be that markets that are dominated by a few large players who do not have high dependence on these markets are characterized by competitive complacency and are thus relatively easy to enter?

In summary, success in obtaining market share is strongly associated with entering early in the product life cycle, and avoiding fragmented markets and markets upon which the largest competitor is highly dependent. There are two counterintuitive findings: High- growth markets may not be desirable, because many others may be entering simultaneously; and provided that the danger of retaliation is low, entering markets that are dominated by a few well-entrenched firms may actually be advantageous, because this enables the new entrant to clearly position itself.

Discussion of ROI Perfomzance

As can be expected, the results for ROI are not as strong as those for market share. The relationships between life cycle, growth, and largest competitor’s dependence were all in the predicted direction.

The most surprising finding was that ROI was positively related to top three compet- itors’ share (competitors well entrenched). We offer the same explanation for this result as

20 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

TABLE 4 Predicted and Actual Relations Between Strategy and Performance

Market share

(Year 2)

ROI

(Year

2)

Relative product quality

Predicted

Actual

Relative price

Predicted

Actual

Relative promotion

Predicted

Actual

Capacity/market Predicted

Actual

R-squared .52” .lW

+ ? .25” - ,280

_ ? -.W -.llb

+ ? .29” .Ilb

+ - .53a .09

“p < .ool.

"p < .l.

'p -c .Ol.

we did for market share: If retaliation is unlikely, perhaps moves against clearly defined

competitors are easier to target effectively.

Relations Between Strategy and Performance

Table 4 shows the output for the four dimensions of strategy regressed on the two performance measures (market share and ROI). The results strongly suggest that strategy influences performance, particularly success in achieving market share.

All of the relationships between strategy and market share are in the predicted direction, and with the exception of relative price, all are highly significant.

The relations between strategy and ROI are less strong. The strongest relation is the negative correlation with relative product quality. We originally argued that this relation (as well as price and promotion) would be determined by the elasticity of demand. Therefore, we interpret the results as indicating that, in the short run, demand is not highly sensitive to changes in quality, and that the costs of achieving quality are not offset by greater revenues .6

It appears, however, that demand is somewhat sensitive to price. Higher prices have a negative effect on ROI, while lower prices have a positive effect. Relative expenditure on promotion also seems to have a small positive effect on ROI.

We predicted that investment in capacity would have a negative effect on ROI, at least during the short run, which is the focus of this study. The results indicate that the relationship is not significant. The explanation for this finding again raises the issue of causality. Although investment in capacity is likely to have a negative effect on ROI (par- ticularly in the short term), it is also true that in cases where high returns are expected,

6The negative relationship between product quality and ROI no longer holds by year four (partial correlation = 448, p = .30).

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 21

TABLE 5 Performance Variance Explained by Environment and Strategy

Market share ROI

Environment .44” .04

Strategy ,520 .lob

Environment and Strategy .63” .12b

“p < .ool “p < .05.

firms are more likely to invest in capacity. Therefore, it is not unreasonable to find an ambiguous relationship between investment in capacity and ROI.

In summary, product quality represents a major trade-off for new entrants, having a strong positive effect on market share but a strong negative effect on ROI.

On the other hand, price and promotion affect both performance variables in a similar fashion. Lower relative prices and higher relative promotion improve performance, both in ROI and market share gain.

Investment in capacity differs from the other strategy dimensions in that, in addition to being a measure of aggressive entry, it is also an indication of expectations of success. It is strongly related to gain in market share and ambiguously related to ROI.

Putting It All Together: Relations Among Environment, Strategy, and Performance

Table 5 shows the variance explained in the two performance measures (market share and ROI) by the environment and strategy variables, both separately and in combination. Table 6 indicates the beta coefficients for the combined regressions. With two exceptions,’ these beta coefficients do not differ in any substantive way from the coefficients of the regressions when run separately (compare Tables 3 and 4 with Table 6).

Table 5 indicates that performance is significantly related to both the environment and strategy. Despite the known relationship between environment and strategy (identified in Appendix I, Table Al), each contributes significantly to the explanation of performance variation. The results are much stronger for market share than for ROI. Table 6 indicates that with respect to market share, 2 of 3 measures of munificence, 1 of 2 measures of hostility, and 3 of 4 measures of strategy all significantly contribute to the explanation of variance in share gain. Furthermore, the signs of these relations are as predicted.

CONCLUSIONS

We are now in a position to answer the question laid out at the beginning of this paper. What is the relative importance of environment and strategy for new venture performance?

The results clearly indicate that both the environment and strategy are important for success in new corporate ventures, as measured by market share gain. In the combined regressions, both environment and strategy variables remain highly significant, making it impossible to identify one or the other as dominant. As expected, the relations within ROI

‘The relation between life cycle and ROI, which was marginally significant, is no longer significant; the relation between top three competitors’ share and market share is no longer significant.

22 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

TABLE 6 Regression Output: Performance as a Function of Munificence, Hostility, and Strategy

ROI Market share (Year

(Year 2) 2)

Munificence Life cycle

Fragmentation

Growth

Hostility Competitor’s dependence

Top three share

Strategy Relative product quality

Relative price

Relative promotion

Capacity/market

R-squared

- .16”

- .13”

.02

- .27’ .02

.13y - .29’ - .06 -.12b

.28’ .09

.3lC .07

.63’

- .03

.02

-.12b

.03

.07

.12‘+

“p i .Ol. “p < .l.

‘p < ,001.

“p < .os.

are much weaker and make it difficult to come to firm conclusions, although it appears that the strategy variables are somewhat more predictive.

While this study does not prove the strategic adaptation argument that managers can actively shape their venture’s success, it does leave the door open for such an argument, since quality, pricing, promotion, and capacity decisions are, typically, carefully considered, and not the result of random choice.

Market Share

In regard to the specific dimensions of strategy and the environment, and their relation to market share, we have observed two major findings:

1. Industries with late life-cycle stages, fragmented markets, and high competitor depen- dence should be entered with circumspection. As in previous studies, aggressive entry-in terms of expenditure on promotion and investment in capacity-seem to pay off in market share gain, at no cost in ROZ, while a trade-off must be made between the share gain and early ROI performance in the case of product quality.

Perhaps the most interesting findings were those that did not match our predictions:

High market growth-rates did not yield share gain-we suggest that high growth may also attract other new entrants or aggressive behavior of existing competitors. It appears that the time to enter a market is before it experiences high growth, not while it is underway.

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 23

4. A market dominated by few competitors with high market share need not be a handicap- there may be some advantages to having clearly defined competitors.

5. The results suggest that market share gain for new entrants is not achieved through lower

prices.

ROI

The strongest conclusion that can be reached about the effects on ROI is that a high-quality strategy will increase costs and depress ROI in the short term. It is important to note, however, that after four years, the negative effect of these early costs on ROI are dissipated, while the beneficial effect on market share continues.

In terms of theory, it appears that there is good reason to pay attention to the following constructs that appear in recent literature, at least as far as corporate ventures are concerned.

1. Aggressiveness of entry. There is clearly a high correlation between performance of ventures and aggressiveness of entry.

2. Munijcence of environment. The regressions of Table 3 and 6 suggest that if our selection of variables to measure munificence is acceptable, then munificence is a useful construct when thinking about corporate ventures entering into industrial markets. Munificence separately and meaningfully correlates with venture performance, particularly market share gain.

3. Hostility of environment. The regressions in Table 3 and 6 also suggest that the degree of hostility of the environment is important to consider for new ventures entering into existing markets.

4. Independence of the two constructs, hostility and muni$cence. An important finding is that munificence and hostility (as measured in this study) are related but independent constructs, as is evidenced by Table 2 and by Table A2 in Appendix 1.

Caveats

Several caveats are in order. First, the database contains only firms that have survived four years and is, therefore, not representative of all corporate start-ups. Second, all start-ups are corporate ventures of large firms, generally in the Fortune 1000. This raises the possibility that these firms could intimidate incumbents because of the depths of their resources. Third, in this study we examine success only as measured after the first two years. Initial success may not be a good predictor of long-term success. Fourth, owing to sample size limitations in the STR4 database, we limit our study to industrial product firms, and as a consequence, we do not know if the results will hold for firms in other sectors, especially consumer goods

and services.

REFERENCES Aldrich, H. 1979. Organizations and Environments. Englewood Cliffs, NJ: Prentice-Hall.

Aldrich, H., and Auster, E. 1986. Even dwarfs started small: Liabilities of age and size and their strategic implications. Research in Organizational Behavior 8: 165-98.

Aldrich, H., and Zimmer, C. 1986. Entrepreneurship through social networks. In D.L. Sexton and R.W. Smiler, eds., The Art and Science of Entrepreneurship (pp. 2-23). Cambridge, MA: Ballinger.

24 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

Anderson, C.R. and Paine, F.T. 1978. PIMS: A reexamination. Academy of Management Review 3602-611.

Andrews, K. 1980. The Concept of Corporate Strategy. Homewood, IL: Richard D. Irwin.

Astley, W.G. and Van de Ven, A.H. 1983. Central perspectives and debates in organizatianal theory. Administrative Science Quarterly 28:245-273.

Biggadike, R. 1979, The risky business of diversification. Harvard Business Review, May-June, 103- ill.

Blau, P.M., and Scott, W.R. 1962. Forma2 Organizations. San Francisco: Chandler.

Block, 2. 198.5. Concepts for corporate entrepreneurs. Proceedings of the Texas A&M Business Forum.

Block, Z., and MacMillan, I.C. 1985. The Paradox of Planning for New Ventures. Working paper: New York University Center for Entrepreneurial Studies.

Bowman, E.H., and Hurry, D. 1987. Strategic Options. Working Paper: Reginald Jones Center, The Wharton School.

Brittain, J.W., and Freeman, J. 1980. Organizational proliferation and density dependent selection. In J.R. Kimberly and R.H. Miles, eds., The Organizational Life-Cycle (pp. 291-338). San Francisco: Jossey-Bass.

Burgelman, R.A. 1983. A process model of internal corporate venturing in the major diversified firm. Adminisirat~ve Science Quarterly 28~223-244.

Burgelman, R.A. 1985. Managing the new venture division: Research findings and implications for strategic management. Strategic Management Journal 6(1):39-54.

Buzzell, R.D., Gale, B.T., and Sultan, R.G.M. 1975. Market share-A key to profitability. Harvard Business Review, Jan-Feb, 97-106.

Child, J. 1972. Organization structure, environment, and performance: The role of strategic choice. socioEogy* l(l):l-22.

Cooper, R.G. 1979. The dimension of industrial new product success and failure. Journal of Marketing 43:93-103.

Cooper, R.G. 1983. Most new products do succeed. Research Management, November-December, 20-25.

Covin, J.G.. and Slevin, D.P. 1989. Strategic management of small firms in hostile and benign environments. Strategic Management Journal lO( 1):7587.

Dess, G., and Davis, P. 1984. Porter’s generic strategies as determinants of strategic group membership and performance, Academy of Management Journal 26:467-488.

Dess, G.G., and Oriser, N.K. 1987. Environment, structure and consensus in strategy formulation: A conceptual integration. Academy of Management Review 12(2):3 13-330.

DiMaggio, P.J., and Powell, W.W. 1983. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review 48:147-160.

Duncan, R.B. 1972. Characteristics of organizational environments and perceived environmental uncertainty. Administrative Science Quarterly 17:3 13-327.

Emery, F,E., and Trist, E.L. 1965. The causal texture of organizational environments. Human Re- lations 1X:21-32.

Evan, W.M. 1966. The organization set: Toward a theory of interorganizational relations. In J.D. Thompson, ed., Approaches to Organizational Design (pp. 173-88). Pittsburgh: University of Pittsburgh Press.

Fast, N.D. 1981. Pitfalls of corporate venturing. Research Management, March 21-24.

Fast, N.D., and Pratt, S.E. 1981. Individu~ en~epreneu~hip and the large corporation. In KH. Vesper, ed., Frontiers of Entrepreneurshjp Research, pp. 443-450.

Ford, J.D., and Slocum, J.W. 1977. Size, technology, environment and the structure of organizations. Academy of Management Review 2561-575.

Gale, B.T., and Branch, B. 1982. Concentration versus market share: Which determines performance and why does it matter? Antitrust Bulletin 27:83-1(X.

Greenfield, S.M., and Stricken, A. 1986. ~n~epreneurship and Social Change. Lanham: Unive~i~ Press.

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 25

Grinyer, P., Al-bazazz, S., and Yasai-Arkedeni, M. 1980. Strategy, structure, the environment and financial performance in 48 U.K. companies. Academy of Management Journal 23(2): 193-220.

Hall, W.K. 1980. Survival strategies in a hostile environment. Harvard Business Review 59(5):75- 85.

Hambrick, D. 1983. An empirical typology of mature industrial-product environments. Academy of Management Journal 26(2):213-230.

Hambrick, D., MacMillan, I.C., and Day, D.L. 1982. Strategic attributes and performance in the BCG Matrix-A PIMS-based analysis of industrial-product businesses. Academy of Manage- ment, 25(4):December, 510-531.

Hannan, M.T., and Freeman, J. 1979. The population ecology of organizations. American Journal of Sociology 82:929-964.

Hannan, M.T., and Freeman, J. 1984. Structural inertia and organizational change. American Soci- ological Review 49~149-164.

Hawley, A. 1950. Human Ecology. New York: Ronald Press.

Henderson, B. 1979. Henderson on Corporate Strategy. Cambridge, MA: Abt Books.

Hirsch, P.M. 1972. Processing fads and fashions: An organization-set analysis of cultural industry systems. American Journal of Sociology 77~639-659.

Hobson, E.L., and Morrison, R.M. 1983. How do corporate start-up ventures fare? In J.A. Homaday, J.A. Timmons, and K.H. Vesper, eds., Frontiers of Entrepreneurship Research, pp. 390-410.

Hofer, C.W., and Schendel, D.E. 1978. Strategy Formulation: Analytical Concepts. St. Paul, MN: West.

Jurkovich, R. 1974. A core typology of organizational environments. Administrative Science Quarterly 19:380-394.

Kanter, R.M. 1983. The Change Musters. New York: Simon and Shuster.

Kanter, R.M., and Brinkerhoff, D. 198 1. Organizational performance: Recent developments in mea- surement. Annual Review of Sociology 7:321-349.

Khandwalla, P.N. 1976/77. Some top management styles, their context and performance. Organization and Administrative Sciences 7(4):2 l-5 1.

Lambkin, M. 1988. Order of entry and performance in new markets. Strategic Management Journal 9: 127-140.

Lentz, R.T. 1981. Determinants of organizational performance: An interdisciplinary review. Strategic Management Journal 2~131-154.

MacMillan, I.C. 1983. The politics of new venture management. Harvard Business Review 61:(6):8- 16.

MacMillan, I.C. 1986. Progress in research on corporate venturing. In. D.L. Sexton and R. W. Smilor, eds., The Art and Science of Entrepreneurship. Cambridge, MA: Ballinger.

MacMillan, I.C., Block, Z., and Subba Narasimha, P.N. 1984. Obstacles and experience in corporate venturing. In J.A. Homaday, F. Tarplay Jr., J.A. Timmons, and K.H. Vesper, eds., Frontiers of Entrepreneurship Research, pp. 34 l-63.

MacMillan, I.C., and Day, D.L. 1986. Corporate ventures into industrial markets: Dynamics of aggressive entry. Journal of Business Venturing 2(1):29-30.

MacMillan, I.C., and George, R. 1985. Corporate venturing: Challenges for senior managers. Journal of Business Strategy 5(3):34-44.

MacMillan, I.C., and Jones P.E. 1986. Strategy Formulation: Power and Politics. St. Paul, MN: West.

Maidique, M.A. 1980. Entrepreneurs, champions and technological innovation. Sloan Management Review, Winter, 59-75.

Maidique, M.A., and Hayes, R.H. 1984. The art of high-technology management. Sloan Management Review, Winter, 17-3 1.

Maidique, M.A., and Zirger, B.J. 1985. The new product learning cycle. Research Policy 14:299- 313.

March, J.G., and Simon, H.A. 1958. Organizations. New York: McGraw-Hill.

26 W.M.-H. TSAI, 1.C. MACMILLAN AND M.B. LOW

Meyer, M.M., and Zucker, L. 1989. Permanently Failing Organizations. Newbury Park: Sage.

Miles, R., and Cameron, K. 1982. CofJin Nails and Corporate Strategy, Englewood Cliffs, NJ: Prentice-Hall.

Miles, R.E., and Snow, C.C. 1978. Organizational Strategy, Structure, and Process. New York: McGraw-Hill.

Miller, A., Wilson, B., and Adams, M. 1988. Financial performance patterns of new corporate ventures: An alternative to traditional measures. Journal of Business Venturing 3(4):287-300.

Miller, D. 1987. The structural and environmental correlates of business strategy. Strategic Manage- ment Journal 855-76.

Miller, D., and Friesen, P.H. 1983. Strategy-making and environment: The third link. Strategic Management Journal 41221-235.

Minzberg, H. 1978. Patterns in strategy formulation. Management Science 247:934-948.

Porter, M. 1980. Competitive Strategy. New York: Free Press.

Prescott, J.E., Kohli, A.K., and Venkatraman, N. 1986. The market share-profitability relationship: An empirical assessment of major assertions and contradictions. Strategic Management Journal 7:377-394.

Quinn, J.B. 1979. Technological innovation, entrepreneurship and strategy. Sloan Management Re- view, Spring, 19-30.

Ramanujan, V., and Venkatraman, N. 1984. An inventory and critique of strategy research using the PIMS data base. Academy of Management Review 9(2): 138-151.

Rink, D. R., and Swan, J.E. 1979. Product life-cycle research: A literature review. Journal ofBusiness Research 78:219-242.

Roberts, E.B. 1980. New ventures for corporate growth. Harvard Business Review, July-August, 134-142.

Sahlman, W., and Stevenson, H. 1985. Capital market myopia. Journal ofBusiness Venturing 1(1):7- 30.

Sandberg, W.R., and Hofer, C.W. 1987. Improving new venture performance: The role of strategy, industry structure, and the entrepreneur. Journal of Business Venturing 2(1):5-28.

Schon, D.A. 1966. The fear of innovation. International Science and Technology 14:70-78.

Scott, W.R., and Meyer, J.W. 1983. The organization of societal sectors. In J.W. Meyer and W.R. Scott, eds., Organizational Environments: Ritual and Rationality. Beverly Hills, CA: Sage.

Selznick, P. 1949. TVA and the Grass Roots. Berkeley: University of California Press.

Singh, J.V., House, R.J., and Tucker, D.J. 1986. Organizational change and organizational mortality. Administrative Science Quarterly 3 1:587-611.

Souder, W.E. 1981. Encouraging entrepreneurship in the large corporations. Research Management, May, 18-22.

Staw, M., and Szwajkowski, B.E. 1975. The scarcity-munificence component of organizational en- vironments and the commission of illegal acts. Administrative Science Quarterly 20:345-354.

Tellis, G.J., and Crawford, C.M. 1981. An evolutionary approach to product growth theory. Journal of Marketing 45~125-132.

Timmons, J.A. 1982. New venture creation: Methods and models. In C.A. Kent, D.L. Sexton, and K.H. Vesper, eds., Encyclopedia of Entrepreneurship (pp. 126-138). Englewood Cliffs, NJ: Prentice-Hall.

Tosi, H., Aldag, R., and Storey, R. 1973. On the measurement of the environment: An assessment of the Lawrence and Lorsch environmental uncertainty questionnaire. Administrative Science Quarterly 18:27-36.

Tushman, M., and Anderson, P. 1986. Technological discontinuities and organizational environments. Administrative Science Quarterly 3 1:439-465.

Tussle, F.D., and Gerwin, D. 1980. An information processing model of organizational perception, strategy, and choice. Management Science 26(6):575-592.

Van de Ven, A.H., Hudson, R., and Schroeder, D.M. 1984. Designing new business startups: Entrepreneurial, organizational, and ecological considerations. Journal of Management 10(1):87- 107.

VENTURE SUCCESS: STRATEGY AND ENVIRONMENT 27

Vesper, K.H. 1980. New Venture Strategies. Englewood Cliffs, NJ: Prentice-Hall.

Vesper, K.H., and Holmdahl, T.G. 1973. How venture management fares in innovative companies. Research Management, May, 30-33.

Warren, R.L. 1967. The interorganizational field as a focus for investigations. Administrative Science Quarterly 12:396-419.

Weiss, L.E. 1981. Start-up businesses: A comparison of performances. Sloan Management Review 23(1):37-53.

Woo, C.Y., and Cooper, A.C. 1981. Strategies of effective low share businesses. Strategic Man- agement Journal 21301-318.

Yasai-Arkedeni, M. 1989. Effects of environmental scarcity and munificence on the relationship of context to organizational structure. Academy of Management Journal 32( 1): 131-156.

APPENDIX A: RELATIONS BETWEEN ENVIRONMENT AND STRATEGY

Table Al shows the variance explained in the four strategy dimensions by munificence and hostility, both separately and in combination. Table A2 presents the beta coefficients for the combined regressions. With one exception (the relationship between competitor’s de- pendence and quality was - .I8 and significant at the .05 level), these beta coefficients did not differ in a substantial way from the coefficients of the regressions when run separately (not reported here).

Tables Al and A2 indicate that all dimensions of strategy are significantly related to the environment. Furthermore, munificence and hostility are both important and independent dimensions. The latter conclusion is reached by observing that the variance explained in the combined regression approximates the sum of the variance explained by the separate regres- sions, and the betas of the separate and combined regressions are stable.

TABLE Al Strategy Variance Explained by Environment

Quality Price Promotion Capacity

Munificence Hostility

Munificence

and Hostility

.20*** .05* .05* .12***

.03+ .07** .05* .25***

.21*** .14*** .12** .32***

tp < .l.

*p < .05. **p < .Ol.

***p < .ool.

28 W.M.-H. TSAI, I.C. MACMILLAN AND M.B. LOW

TABLE A2 Relations Between Environment and Strategy

Munificence Life cycle

Predicted Actual

Fragmentation Predicted Actual

Growth Predicted Actual

Quality Price

- _

- .40” - ,215”

- ns -.11* .04

_ ns -.lY - .07

Promotion

+ - ,025

+ + .26”

+ -.040

Capacity

? - .09

_

- .21’

+ -.18’

Hostility Competitor’s Dependence

Predicted Actual

Top three share Predicted Actual

+ + - _

- .07 + .27” -.19’ - .36”

+ _ + -

.Ol -.12b +.17c + .26”

R-squared .21” .14” .12’ .32”

“p < ml. "p < .l.

‘p < .Ol.

“p < .os.