East Hampshire District Council Heat Techno-Economic ...

138

Report by: South East Wood Fuels Ltd Date: 17/03/2016 Version: Final 0.24 East Hampshire District Council Heat Techno-Economic Feasibility Studies Main Report

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of East Hampshire District Council Heat Techno-Economic ...

Report by: South East Wood Fuels Ltd

Date: 17/03/2016

Version: Final 0.24

East Hampshire District Council

Heat Techno-Economic Feasibility Studies

Main Report

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 2

Issued Version Control

Version Status Checked by Approved by

0.14 DRAFT Stewart Boyle Julian Morgan-Jones

0.20 DRAFT FINAL Matthew Morris Stewart Boyle

0.21 DRAFT FINAL Matthew Morris Stewart Boyle

0.22 DRAFT FINAL Matthew Morris Stewart Boyle

0.23 FINAL Matthew Morris Stewart Boyle

0.24 FINAL – Minor Edits Matthew Morris Stewart Boyle

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 3

1 EXECUTIVE SUMMARY

1.1 REPORT HIGHLIGHTS (PENNS PLACE, ALTON, WHITEHILL & BORDON)

1.1.1 Introduction EHDC commissioned this project after completion of the East Hampshire Heat Masterplan in 2015,

funded by DECC’s Heat Network Delivery Unit (HNDU). The Heat Masterplan concluded that three

heat loads provided sufficient potential to carry out further assessment to see if they were

technically and commercially viable.

This study is consistent with current EHDC Corporate and Energy Strategies which seek to expand

the contribution of renewable energy technologies in East Hampshire, to meet CO2 reduction

targets and stimulate economic development through green business expansion. The study is also

in keeping with the need to meet legally binding carbon reduction targets at a national level.

1.1.2 Technologies Of the wide range of low-carbon heat technologies assessed, three – biomass heating, gas-

Combined Heat and Power (CHP) and Ground Source Heat Pumps (GSHP) - are technically viable

(albeit with GSHP taking a more limited role). Biomass heating and gas-CHP are the two most

commercially viable options at this stage.

The three proposed heat network projects are all technically viable.

The heat networks combined offer an attractive £5 million investment with rates of return of

between 11% and 15% IRR.

The cumulative positive cash flow benefit for all three projects combined is £10.6 million over 20

years and £28.3 million over 40 years.

The Net Present Value (NPV) for the three projects is more than £3.1 million (20 years) and £5.2

million (40 years).

The results are robust under a wide range of sensitivity tests, except where the RHI is significantly

reduced or not available, and where import power prices fall by 25%.

The Penns Place/Taro Leisure Centre heat network could be installed in 2016, securing a 20-year

income stream of £800,000 from the Government’s RHI scheme.

All three projects offer attractive opportunities for an Energy Services Company (ESCo). If EHDC

took a prominent role in this ESCo, significant positive cash flows could be secured.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 4

Table 1: Summary of recommended modelling scenario technologies and costs for all three sites: Scenarios 2, 5 & 7

Heat (and Power)

demand Technology option Technology Scale Backup

Penns Place/Taro Leisure Centre

(Scenario 2)

2.7 million kWh(th) and 1.5 million kWh(e)

Biomass and CHP heat 450kW(th) biomass and

c.450,000kWh waste CHP heat

1

Gas boilers

Alton (Scenario 5)

3 million kWh (th) and 1 million kWh(e)

Biomass and CHP 400kW(th) biomass and

200kWe gas-CHP Gas boilers

Whitehill & Bordon

(Scenario 7 & 7A)

37 million kWh (th) and 17 million kWh(e)

Gas-CHP and biomass (GSHP for smaller

network)

2MWe gas-CHP + 2MWth biomass (and 1MWe gas-CHP and 4MW(th) biomass

variation)

Gas boilers

1.1.3 Study Results Table 2: Summary of modelling scenarios for all three sites: Scenarios 2, 5 & 7

Capital Costs

Cumulative cash flow benefit £ -

20yr

Cumulative cash flow benefit £ -

40yr

IRR % 20yr

IRR % 40yr

NPV £ 20yr

NPV £ 40yr

CO2 emission reduction (%)

Penns Place/Taro Leisure Centre

(Scenario 2) £550,000

£1.27 million

£1.3 million 14 14 £366,000 £338,000 62-72%

Alton (Scenario 5)

£760,000 £1.04

million £2.6 million 11 12 £220,000 £385,000 44-66%

Whitehill & Bordon

(Scenario 7 & 7A)

£3.75 million

£8.3 million £24.4

million 14 15

£2.46 million

£4.475 million

44-69%

Total £5 million £10.6

million £28.3

million n/a n/a

£3.05 million

£5.2 million

45-69% (8,000-13,000

tCO2/yr)

A detailed financial analysis was carried out for all projects, including sensitivity analysis to assess

how robust the results were. These were measured against a 7% IRR benchmark (the current rate

of return from EHDC’s property portfolio).

The three projects assessed under this study offer a £4.9 million investment opportunity in low-

carbon heat networks, with Internal Rates of Return (IRR) of between 11% and 15%.

The cumulative positive cash flow benefit is £10.6 million over 20 years (£28 million over 40 years).

The Net Present Value (NPV) for the three projects total more than £3 million over 20 years (£5.2

million over 40 years).

1.1.4 Risks and Opportunities The results are most sensitive to future grid electricity prices, as well as the availability and tariff

levels of the Renewable Heat Incentive (RHI). Large reductions in grid electricity prices under

current investment trends are unlikely.

1 Estimated, as metered data was not available.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 5

The results are resilient to the other sensitivity tests (i.e. variations in heat loads, gas and wood

chip prices, capital costs).

The technology risk is low for all three projects, and due to their direct involvement in both

buildings, the heat load risk is low for Penns Place-Taro Leisure Centre.

The Penns Place-Taro Leisure Centre heat network has a time limited opportunity to secure an

£800,000 index-linked RHI income stream over 20 years before the end of 20162.

The Alton project requires strong emphasis on the use of gas-CHP to become viable. A biomass

only investment with assumed lower rates of RHI support is not economic against the Council’s

current investment criteria (<7% IRR).

The Whitehill & Bordon Regeneration Project offers an attractive heat (and power) load and

density over time, and a combination ‘gas-CHP and biomass’ investment offers low-risk

technologies, strong CO2 reductions and an attractive rate of return. At this stage of development,

the heat load offers a ‘moderate’ risk to investment, as it will likely change from current estimates.

However a sensitivity test with 25% lower heat load reduced the IRR by only 2%.

1.1.5 Wider Economic and Environmental benefits EHDC has an Energy Strategy that seeks to grow the renewables sector in its district and meet

high CO2 reduction targets. There are wider economic and environmental benefits from investing

in the three projects. For example, they offer a potential wood fuel market of between 3,000 to

7,500 tonnes per annum. That is estimated to be worth between £270,000 and £700,000 of gross

income per year at current prices.

The three projects offer a combined CO2 reduction potential of 45-69% (8,160-13,165 tCO2/yr)

(see Table 2).

1.1.6 Governance of the Projects Governance of the three projects is critical, and this is explored for each of the projects in turn.

The projects would support the establishment of an Energy Services Company (ESCo).

The appetite of EHDC to take ownership of project design, fuel, capital and management risks will

determine the shape of the governance structure. This will also determine the extent of the

project value returns to EHDC and the wider community.

Based on the current level of risks and benefits, local authorities like EHDC would maximise

benefits by taking a leading direct role in the ESCo.

2 While final decisions over the RHI have not yet been announced by DECC, initial proposals by DECC to trade

associations indicate a preference to reduce biomass tariffs in 2017, while increasing relative support for heat pumps and biomethane (personal communication, Julian Morgan-Jones, WHA, 2016).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 6

1.2 HIGHLIGHTS: PENNS PLACE & TARO LEISURE CENTRE

1.2.1 Introduction The combined Penns Place offices and Taro Leisure Centre heat load offers an attractive

opportunity to develop a heat network.

A possible extension of the heat network to a 96 home development in Penns Field within the

next five years may allow a significant extension to the heat network.

1.2.2 Technologies The recommended heat network solution integrates a new 450kW biomass heating system with

either the existing CHP plant, or a new CHP plant in a few years’ time. A packaged boiler room

located close to the Taro Leisure Centre is recommended. This should have sufficient space

nearby to incorporate the biomass system, a new CHP plant and possible additional plant if the

housing development is connected to the heat network.

Given the age of the existing CHP plant, the fact that it is ‘over-sized’ and heat is being wasted, a

re-sized new CHP plant could be sited at the new boiler room site, with greater control over heat

inputs.

The technical aspects of this project are low risk and viable.

1.2.3 Study Results Table 3: Summary of modelling results for Penns Place/Taro Leisure Centre: Scenario 2

3

Capital Costs

Cumulative cash flow benefit £ -

20yr

Cumulative cash flow benefit £ -

40yr

IRR % 20yr IRR % 40yr NPV £ 20yr NPV £ 40yr CO2 savings

(% of benchmark)

£550,000 £1.27 million £1.26 million 14 14 £366,000 £338,000 62-72%

A detailed financial analysis was carried out. For an investment of £550,000 a 20-year rate of

return of 14% IRR is predicted.

A 20-year positive cash flow benefit of £1.27 million and a Net Present Value (NPV) of £366,000

are also predicted.

An extension of the heat network to a possible housing development in Penns Field is currently

too uncertain and risky to warrant extending the proposed heat network. However, a modest

level of ‘future proofing’ of a larger heat network could be achieved by ensuring there is enough

space for additional biomass boilers and CHP plant at the proposed packaged boiler plant room.

1.2.4 Risks and Opportunities The results are sensitive to the availability and tariff levels of the RHI. Without the current RHI

income stream the project is not viable.

The results are resilient to the other sensitivity tests (i.e. variations in heat loads, gas and wood

chip prices, capital costs).

The technology and heat load risks are low.

3 Figures are rounded.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 7

The Penns Place-Taro Leisure Centre heat network has a time limited opportunity to secure an

£800,000 index-linked RHI income stream over 20 years before the end of 2016. Without that

income stream the rates of return drop significantly to less than 7% IRR. This factor is a significant

driver for the Council in terms of potential investment in the project compared to its current

investment criteria.

1.2.5 Wider Economic and Environmental benefits There are wider economic and environmental benefits. For example, the project offers a potential

wood fuel market of 720 tonnes per annum. This is estimated to be around £75,000 gross income

at current prices.

The project offers a CO2 reduction potential of 62-72% (compared to a benchmark of gas boilers).

1.2.6 Governance of the Project The project lends itself to setting up an Energy Services Company (ESCo).

It is recommended that the Council is directly involved in the establishment of an ESCo and

consider the strengths of a private/public hybrid governance structure. This would maximise the

benefits for EHDC and the wider community.

Given the need to take an early decision over the project, an interim management solution would

be to tender and sign a ‘Design, Build and Operate’ contract with a specialist biomass-district

heating supplier for 3 to 5 years. When EHDC’s preferred approach for an ESCo is agreed and set

up, the management functions could then be taken over.

Figure 1: Provisional heat network pipe layout for Penns Place, Taro Leisure Centre and Penns Field

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 8

1.3 HIGHLIGHTS: ALTON SPORTS CENTRE

1.3.1 Introduction The proposed new Alton Sports Centre received outline planning permission in 2015 to replace

the existing facility. It offers an excellent heat network when combined with two smaller heat

loads at the nearby Cardiac Centre and 10 social housing apartments (The Gurdons).

A large 305 homes development nearby offers a potential larger heat network but the timing and

extent of this remains uncertain.

1.3.2 Technologies The recommended solution integrates a new 200kW(e) (300kW(th)4 gas-CHP unit with a 400kW

biomass heating system. Compared to standard gas heating, this offers a good combination of

strong financial returns with significant CO2 emission reductions.

1.3.3 Study Results Table 4: Summary of modelling results for Alton: Scenario 5

5

Capital Costs

Cumulative cash flow benefit £ -

20yr

Cumulative cash flow benefit £ -

40yr

IRR % 20yr IRR % 40yr NPV £ 20yr NPV £ 40yr CO2

emissions savings

£760,000 £1.04 million £2.6 million 11 12 £220,000 £385,000 44-66%

A detailed financial analysis was carried out. For an investment of under £760,000, an 11-12% IRR

is predicted.

The project has a 20-year positive cash flow benefit of £1.04 million (£2.6 million over 40 years)

and a NPV of £220,000 (£385,000 over 40 years).

1.3.4 Risks and Opportunities The financial results are most sensitive to the availability and tariff levels of the RHI, and grid

electricity prices. We think a large fall in electricity prices is unlikely.

The project assumes that 50% of the current ‘medium biomass tariff’ under the RHI is secured

(currently 5.2p/kWh (Tier 1)6. Without that income stream the rates of return drop by up to 6%

IRR, and only the gas-CHP option offers a decent rate of return (>12% IRR) when these factors are

considered.

The results are resilient to the other sensitivity tests (i.e. variations in heat loads, gas and wood

chip prices, capital costs).

The technology risks are low.

4 CHP heat and power ratios vary according to plant size and company offerings. Based on one company’s CHP range

where heat to power ratios vary between 1.07 and 2.17 and an average of 1.36, we have assumed 1.5. We accept this is a conservative figure that under-states the economic benefit of the CHP investment. 5 Figures are rounded.

6 See Footnote 2.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 9

1.3.5 Wider Economic and Environmental benefits There are wider economic and environmental benefits. For example, the project offers a potential

wood fuel market of 520 tonnes per annum. This is estimated to be worth around £54,000 gross

income at current prices.

The project offers a CO2 reduction potential of 46-66% (see Table 2).

1.3.6 Governance of the Project The project lends itself to setting up an ESCo.

It is recommended that the Council are directly involved in the establishment of an ESCo and

consider the strengths of a private/public hybrid governance structure. This would maximise the

benefits for EHDC and the wider community.

Figure 2: Provisional heat network pipe layout for new Alton leisure centre site and housing development

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 10

1.4 HIGHLIGHTS: WHITEHILL & BORDON

1.4.1 Introduction This project combines the projected heat loads for the proposed town centre, which is currently

due to be delivered between 2018 and 2021. The estimated combined heat (and power) loads for

housing, service and commercial buildings are attractive for heat network economics, and the

technical and financial aspects of the project are viable.

1.4.2 Technologies The recommended solution with a new heat network integrates a 2,000kW(e) (2,500kW(th)7 gas-

CHP unit with a 2,000kW biomass heating system. Compared to standalone gas heating and no

heat network, this offers a good combination of strong financial returns with significant CO2

emissions reductions. A variation on this with a higher emphasis on biomass was also assessed.

A more limited heat network, supplying around 1/8 of the total heat demand and heated by a

Ground Source Heat Pump (GSHP) system alongside a gas-CHP system offers promising rates of

return (c.15% IRR). While GSHP cannot supply the whole of the heat network, it is worth looking

at further.

1.4.3 Study Results Table 5: Summary of modelling results for Whitehill & Bordon: Scenario 7

Capital Costs

Cumulative cash flow benefit £ -

20yr

Cumulative cash flow benefit £ -

40yr

IRR % 20yr IRR % 40yr NPV £ 20yr NPV £ 40yr

CO2 emissions

savings (% of benchmark)

£3.75 million £8.3 million £24.4 million 14 15 £2.5 million £4.5 million 44-69%

With an investment of £3.7 million, a rate of return of 14-18% IRR is expected.

The project also shows a 20-year positive cash flow benefit of £8.28 million (£24 million over 40

years) and a NPV of £2.5 million (£4.5 million over 40 years).

1.4.4 Risks and Opportunities The financial results are robust under a range of sensitivity tests, except where grid electricity

prices drop by 25%. Sizing the CHP plant such that long-term contracts are entered into between

an ESCo and non-domestic building operators will be important in reducing risks. This will offer

secure financial flows for the project.

The project assumes that 50% of the current ‘large biomass tariff’ (which is currently just over

2p/kWh) under the RHI can be secured. Without that income stream, the rates of return drops by

2-3% (i.e. down to between 12-15% IRR).

7 CHP heat and power ratios vary according to plant size and company offerings. Based on one company’s CHP range

where heat to power ratios vary between 1.07 and 2.17 and an average of 1.36, we have assumed 1.5. We accept this is a conservative figure that under-states the economic benefit of the CHP investment.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 11

The project offers low risks for the Council and its partners, in that the technologies are well-

known, and that the heat network route can be installed at the same time as the town centre

development takes place.

An existing 1km heat network would offer potential cost savings through utilising the existing

Energy Centre and underground pipe routes for the new heat network.

No energy investments are risk-free. They critically depend on the assumptions made in the

modelling work, and the robustness of these under varying futures. The consultants have

deliberately adopted a conservative approach that is resilient to variations in price and cost

assumptions.

1.4.5 Wider Economic and Environmental benefits There are wider economic and environmental benefits. For example, the project offers a potential

wood fuel market of around 3,000 tonnes per annum. That is worth around worth around

£270,000 gross income at current prices.

Based on current technological and district heating network (DH) assumptions, the project offers a

CO2 reduction potential of 44-69% when compared to standard gas heating and imported grid

power.

1.4.6 Governance of the Project The project is attractive for the setting up an ESCo suitable for this project. Compared to a retrofit

district heating network in for example urban areas, this offers a much cheaper and less uncertain

investment.

It is recommended that a direct involvement in the ESCO by EHDC (or at least a hybrid public-

private sector run ESCO) be explored further with the Whitehill & Bordon Regeneration Company

as the development partner. This would allow as much of the project benefits to be retained for

EHDC and the wider community. While it is a larger and more complex project than the other two

projects in this study, with appropriate technical and commercial expertise from private sector

partners, the risks are manageable.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 12

Figure 3: Whitehill & Bordon structuring plan, showing details for the new town centre (within black dotted line) and position of existing gas-fired energy centre (red box). (Sources: Barton Willmore; SEWF Ltd).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 13

Contents

1 EXECUTIVE SUMMARY ..................................................................................................................................... 3

1.1 REPORT HIGHLIGHTS (PENNS PLACE, ALTON, WHITEHILL & BORDON) .................................................................................. 3 1.2 HIGHLIGHTS: PENNS PLACE & TARO LEISURE CENTRE ........................................................................................................ 6 1.3 HIGHLIGHTS: ALTON SPORTS CENTRE .............................................................................................................................. 8 1.4 HIGHLIGHTS: WHITEHILL & BORDON ............................................................................................................................ 10

2 HEAT TECHNO-ECONOMIC FEASIBILITY STUDIES ............................................................................................. 16

2.1 INTRODUCTION ......................................................................................................................................................... 16 2.2 EHDC ENERGY STRATEGY TARGETS .............................................................................................................................. 17 2.3 CURRENT DRIVERS FOR LOW-CARBON HEATING ............................................................................................................. 17 2.4 CARBON EMISSION REDUCTION TARGETS ...................................................................................................................... 18 2.5 TECHNOLOGY APPRAISAL SUMMARY ............................................................................................................................. 18 2.6 GAS PRICE UNCERTAINTY ............................................................................................................................................ 18 2.7 WHY SHOULD EHDC INVEST IN LOW-CARBON HEAT NETWORKS? ....................................................................................... 20 2.8 STUDY METHODOLOGY .............................................................................................................................................. 22 2.9 DEVELOPING THE MODELLING SCENARIOS ..................................................................................................................... 27

3 PENNS PLACE AND TARO LEISURE CENTRE ...................................................................................................... 30

3.1 INTRODUCTION ......................................................................................................................................................... 30 3.2 THE IMPACT OF FAÇADE REFURBISHMENT ON HEAT LOADS ................................................................................................. 31 3.3 ENERGY DATA .......................................................................................................................................................... 31 3.4 PENNS PLACE: NEW HOUSING ..................................................................................................................................... 31 3.5 TECHNOLOGY OPTIONS AND CHOICES ........................................................................................................................... 32 3.6 SCENARIOS DEVELOPED AND MODELLING RESULTS .......................................................................................................... 33 3.7 CONCLUSIONS .......................................................................................................................................................... 33 3.8 RECOMMENDATIONS ................................................................................................................................................. 34

4 ALTON LEISURE CENTRE .................................................................................................................................. 38

4.1 NEW LEISURE CENTRE AND BUILD STRATEGY ................................................................................................................... 38 4.2 ADDITIONAL HEAT LOADS ........................................................................................................................................... 38 4.3 TECHNOLOGY OPTIONS AND CHOICES ........................................................................................................................... 38 4.4 SCENARIOS DEVELOPED AND MODELLING RESULTS .......................................................................................................... 39 4.5 NEW HOUSING - LORD TRELOAR SITE ........................................................................................................................... 40 4.6 FINANCIAL MODELLING .............................................................................................................................................. 40 4.7 MODELLING RESULTS ................................................................................................................................................. 40 4.8 CONCLUSIONS .......................................................................................................................................................... 44 4.9 RECOMMENDATIONS ................................................................................................................................................. 44

5 WHITEHILL AND BORDON ............................................................................................................................... 45

5.1 INTRODUCTION ......................................................................................................................................................... 45 5.2 ENERGY DATA .......................................................................................................................................................... 46 5.3 TECHNOLOGY APPRAISAL AND SCENARIOS...................................................................................................................... 47 5.4 SCENARIOS AND MODELLING RESULTS .......................................................................................................................... 48 5.5 CONCLUSIONS .......................................................................................................................................................... 49 5.6 RECOMMENDATIONS ................................................................................................................................................. 50

6 OVERALL CONCLUSIONS AND RECOMMENDATIONS FOR ALL PROJECTS ......................................................... 54

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 14

7 GOVERNANCE AND THE IMPACT ON FINANCIAL ANALYSIS, PROJECT MANAGEMENT AND FUTURE SUCCESS

OF EACH PROJECT.................................................................................................................................................... 55

7.1 INITIAL CONCLUSIONS AND RECOMMENDATIONS OVER GOVERNANCE ................................................................................. 58 7.2 THE POTENTIAL PRIZE OF INVESTING IN LOW-CARBON HEATING NETWORKS ........................................................................ 60

8 CO2 EMISSION IMPACTS .................................................................................................................................. 61

9 BIOMASS FUEL REQUIREMENTS FOR ALL THREE SITES .................................................................................... 62

APPENDIX 1: HEAT NETWORKS AND LEISURE CENTRES IN EAST HAMPSHIRE: EHDC AND LEISURE CENTRE

OPERATORS PERSPECTIVE ....................................................................................................................................... 64

A1.1 ENERGY AND CARBON EMISSIONS ISSUES .................................................................................................................... 64

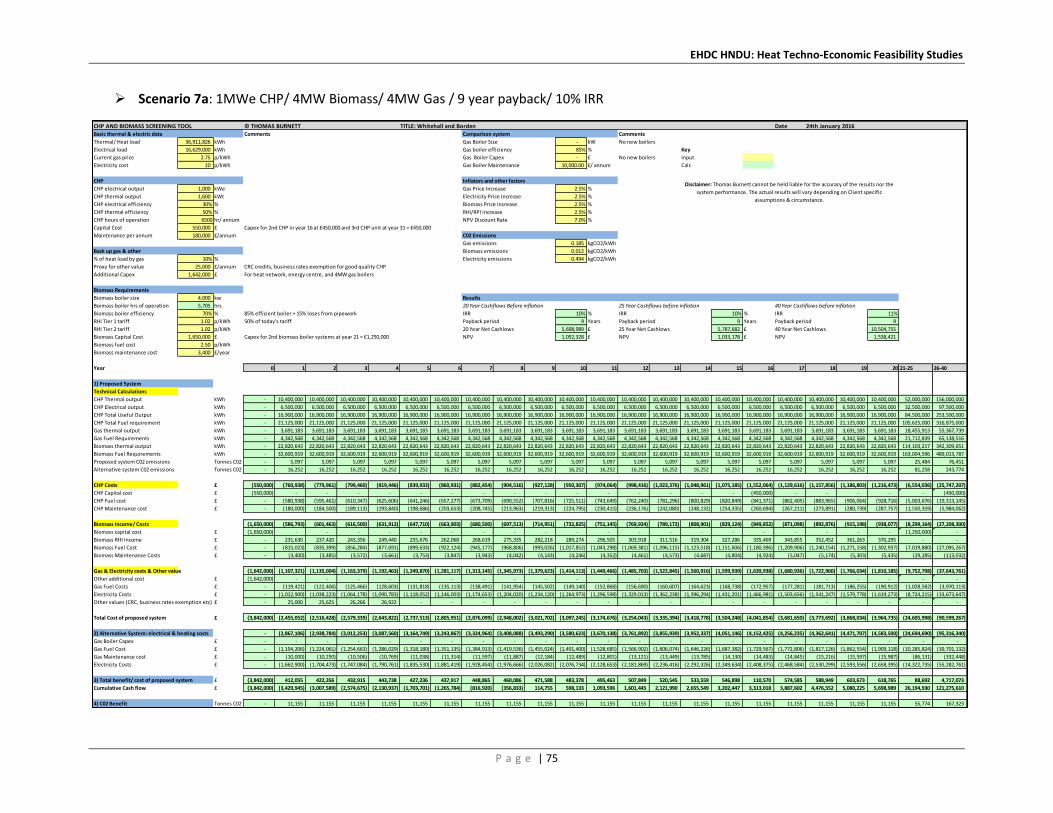

APPENDIX 2: SUMMARY OF FINANCIAL MODELLING RESULTS ................................................................................ 67

A2.1 MODELLING RESULTS: PENNS PLACE .......................................................................................................................... 67 A2.2 MODELLING RESULTS: ALTON ................................................................................................................................... 70 A2.3 MODELLING RESULTS: WHITEHILL & BORDON ............................................................................................................. 74

APPENDIX 3: PENNS PLACE AND TARO LEISURE CENTRE: SURVEY & ENERGY DATA ................................................ 77

A3.1 PENNS PLACE ......................................................................................................................................................... 77 A3.2 TARO LEISURE CENTRE SURVEY .................................................................................................................................. 81 A3.3 ENERGY DATA INTRODUCTION ................................................................................................................................... 82 A3.4 TECHNOLOGY OPTIONS AND CHOICES ....................................................................................................................... 100 A3.5 MODELLING SCENARIOS: SUMMARY OF KEY INPUTS .................................................................................................... 103 A3.6 PENNS FIELD: NEW HOUSING ................................................................................................................................. 103

APPENDIX 4: ALTON ENERGY DATA ....................................................................................................................... 105

A4.1 SURVEY ............................................................................................................................................................... 105 A4.2 ALTON LEISURE CENTRE: COMBINED HEAT AND POWER (CHP) ..................................................................................... 106 A4.3 NEW LEISURE CENTRE AND NEARBY ADDITIONAL HEAT LOADS ........................................................................................ 106 A4.4 BENCHMARK ENERGY DATA: DEVELOPMENT OF MODELLING SCENARIOS ......................................................................... 107 A4.5 TECHNOLOGY OPTIONS AND CHOICES ....................................................................................................................... 108 A4.6 SUMMARY OF TECHNOLOGY APPRAISAL .................................................................................................................... 109 A4.7 DEVELOPMENT OF MODELLING SCENARIOS................................................................................................................ 110

APPENDIX 5: WHITEHILL & BORDON: ENERGY DATA ............................................................................................. 111

A5.1 DATA ................................................................................................................................................................. 113 A5.2 TECHNOLOGY OPTIONS AND CHOICES ....................................................................................................................... 114 A5.3 SUMMARY OF TECHNOLOGY APPRAISAL (WHITEHILL & BORDON) .................................................................................. 116 A5.4 DEVELOPMENT OF SCENARIOS ................................................................................................................................. 117

APPENDIX 6: DISTRICT HEATING NETWORKS: TECHNOLOGY AND ISSUES ............................................................. 119

A6.1 DISTRICT HEATING INSULATED PIPEWORK ................................................................................................................... 119 A6.2 TYPICAL BELOW ROAD URBAN PIPEWORK AND SERVICES SET UP ...................................................................................... 119 A6.3 THE PRACTICAL ASPECTS OF LAYING PRE-INSULATED PLASTIC PIPEWORK ......................................................................... 121 A6.4 PIPEWORK TYPES: PLASTIC VS STEEL ......................................................................................................................... 122 A6.5 CIBSE HEATING NETWORK GUIDE ........................................................................................................................... 123 A6.6 HEAT NETWORK TECHNOLOGIES: CRITERIA FOR REVIEW AND ASSESSMENT ....................................................................... 124 A6.7 CAPITAL EXPENDITURE, GREEN ENERGY SUBSIDIES AND FUTURE ENERGY PRICES .............................................................. 132

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 15

APPENDIX 7: COMPARISON BETWEEN ECONOMIC ASSUMPTIONS USED IN PHASE I HNDU STUDY AND THIS STUDY

.............................................................................................................................................................................. 134

A7.1 GAS BOILER EFFICIENCY ......................................................................................................................................... 134 A7.2 BIOMASS BOILER EFFICIENCY .................................................................................................................................. 134 A7.3 BUILD RATE ......................................................................................................................................................... 134 A7.4 BOILER AND GAS-CHP SIZE .................................................................................................................................... 134 A7.5 CHP EFFICIENCY ................................................................................................................................................... 135 A7.6 BIOMASS FUEL COST ............................................................................................................................................. 135 A7.7 HEAT SALES PRICE ................................................................................................................................................ 135 A7.8 GAS PRICE ........................................................................................................................................................... 136 A7.9 ELECTRICITY PRICE ................................................................................................................................................ 136 A7.10 WHOLESALE PRICE OF ELECTRICITY (FROM GAS-CHP) ................................................................................................ 136 A7.11 OPERATION AND MAINTENANCE COSTS .................................................................................................................. 136 A7.12 NON-DOMESTIC CONNECTION CHARGES ................................................................................................................. 137 A7.13 DOMESTIC CONNECTION CHARGES ......................................................................................................................... 137

APPENDIX 8: INDICATIVE DESIGN FOR ENERGY CENTRE AT PENNS PLACE ............................................................. 138

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 16

2 HEAT TECHNO-ECONOMIC FEASIBILITY STUDIES

2.1 INTRODUCTION Of the eight opportunities identified as part of the heat mapping project in Phase 1 of this project8, East

Hampshire District Council (EHDC) has prioritised three sites for more in-depth feasibility assessment.

This report summarises the feasibility assessments for Penns Place, including the Taro Leisure Centre,

Alton Leisure Centre (and other nearby heat loads) and the Whitehill & Bordon regeneration project. Of

these, the Penns Place assessment is the most detailed, reflecting the perceived viability of the scheme

and the availability of background data, whereas the assessment at Alton and Whitehill and Bordon will be

in outline only.

This work has been developed in accordance with the EHDC’s Energy Strategy, which calls for a

commercial approach to drive increasing amounts of renewable energy generated and supplied in East

Hampshire. This Strategy identified the Heat Network Delivery Unit (HNDU), part of the Department of

Energy and Climate Change, as a potential funder of renewable heat research in the district. EHDC’s bid to

HNDU was successful and this has enabled the Council to continue with more detailed assessment of the

main renewable and low-carbon heat opportunities identified during Phase 1.

Figure 4: Phase I heat network opportunities (Peter Brett Associates, 2015)

The objective of the current project is to bring

forward schemes that have the same or better

financial returns compared to those that might be

realised from EHDC property investments, which are

currently estimated to be around 7% per annum.

The three Projects are:

Penns Place and Taro Leisure Centre

Alton Sports Centre (and nearby heat loads)

Whitehill and Bordon new Town Centre

It was agreed during the inception meeting (12th

Oct 2015) that 50% of the project effort should

focus on Penns Place (and the adjacent Taro leisure

centre), with 25% allocated to Whitehill & Bordon

and 25% to Alton.

This allocation of time was driven by the type of

feasibility work required (i.e. detailed at Penns Place,

outline only for Alton and Whitehill and Bordon).

8 Heat Masterplan for East Hampshire (Peter Brett Associates, 2015).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 17

The overall scope of this project is to:

Generate accurate energy data that can provide a solid foundation for future analysis and

investments.

To review technology options that offer viable, low-carbon and financially attractive heat (and

power if appropriate) options utilising decentralised heat networks.

To develop suitable scenarios utilising appropriate technologies with pragmatic and sensible

assumptions, and to carry out detailed financial appraisals.

To review options for possible governance of any viable projects thatemerge from this assessment.

To draw conclusions and make recommendations to EHDC.

2.2 EHDC ENERGY STRATEGY TARGETS The current energy strategy (2014-2020) focuses on carbon dioxide reduction and clean energy

generation from renewables. The Energy Centre and heat networks opportunity at Whitehill & Bordon is

considered to be of strategic importance to EHDC as it creates an opportunity to deliver a long-term

project with the potential for substantial income over future decades.

EHDC is prepared to invest in energy infrastructure from its reserves, prudential borrowing and also from

the £6.5M fund that will be created by the Whitehill & Bordon Section 106 agreement. Whilst this fund

will be used for a variety of measures, including water conservation, green space and sustainable

transport, a proportion has been allocated to a heat network if the decision to proceed is made.

Whilst the Whitehill & Bordon project is still some way into the future, the proposed mix of retail, leisure,

education, residential and health facilities would create a significant opportunity for distributed heating

and power.

Taylor Wimpey Dorchester will not only provide the space for an Energy Centre at Whitehill & Bordon but

will also be responsible for delivering utilities to building plots. Key questions relating to pipe networks,

energy consumers, timing and development phases are therefore critical for determining the viability of

energy infrastructure investments.

2.3 CURRENT DRIVERS FOR LOW-CARBON HEATING The interest in low-carbon heating is being driven by four important factors:

The regeneration project at Whitehill & Bordon, delivered through the Whitehill & Bordon

Regeneration Company led by Taylor Wimpey Dorchester, requires:

o Evidence of the efficacy of heat networks and business models for detailed planning

discussions and for future work.

o Space for an Energy Centre has been agreed and a Section 106 agreement has been

negotiated with some funds for heat networks included.

Investment at Penns Place EHDC offices has been undertaken to improve the energy efficiency of

the building. Additional investment is currently being considered by the Senior Management

Team and EHDC for the Taro Leisure Centre as part of a new 15 year contract for all Leisure Centre

facilities owned by EHDC.

o In addition a 96-unit housing development is planned to be built nearby at Penns Field.

Alton Sports Centre is being replaced, with outline planning already agreed.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 18

o Along with the new Sports Centre two small adjacent heat loads could also be supplied by

a low-carbon source and insulated heat pipework via a network.

o A 305 unit housing development is planned nearby.

The opportunity to reduce greenhouse gas emissions directly in EHDC owned and/or managed

buildings and via planning requirements at other development sites.

EHDC owns and also has access to woodland, and several biomass fuel supply chain studies have already

been completed. This includes a study by the Forestry Commission in 2011 which indicated, for example,

that significant wood fuel resources, around 120,000 cubic metres of wood per year are available within

20 km of Whitehill and Bordon (enough to heat at least 18,000 homes)9. The consideration of wood chip

based biomass heating in East Hampshire is therefore of considerable interest to EHDC, not only because

of the land and woodland owned by the Council, but also because of the role the Council could play in

bolstering the existing timber and wood fuel supply chains that already exist (or which are at an

embryonic stage).

2.4 CARBON EMISSION REDUCTION TARGETS EHDC have set out a clear target for a move towards 'carbon neutrality' by 2036 in the Whitehill & Bordon

development. Biomass (heating and power), heat pumps and solar power are three technologies

mentioned in this Master Plan document10.

2.5 TECHNOLOGY APPRAISAL SUMMARY A range of low-carbon heat technologies are potentially available for all three projects. We evaluated

these technologies set against the physical set up of each site, plus a range of other criteria. This appraisal

was carried out for each of the three sites (see Section 2.7.1).

2.6 GAS PRICE UNCERTAINTY All of the sites included in this study are on the gas network. As such, gas-based systems (boilers and CHP

units) are likely to play a key role in the financial analysis carried out.

A graph showing gas (and oil prices) over the past few decades should convince any energy analyst that

predicting prices more than a few years ahead a thankless task, where the credibility of these forecasts is

likely to be questionable. The UK Heren NBP Index (natural gas process) from 1997 to 2015 (see Figure 5)

varies between $2.1/mbtu (million British Thermal Units (mbtu)) and $10.6/mbtu with rapid price

variations of 50% to 100% in both directions in the space of a year or two. Making sense of these real

world market price variations and trying to model ahead 5, 10 and even 20 years ahead is therefore

fraught with difficulties and inherently risky.

9 Whitehill and Bordon: Woodfuel Supply Feasibility Study (Forestry Commission, 2011)

10 Whitehill and Bordon Eco-town Master Plan Summary, Revised May 2012.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 19

Figure 5: UK Heren NBP Index Natural Gas Prices 1997-2015

The assumption since 2008 that oil exporters would seek a fiscal break-even point when setting prices (or

production quotas that achieved similar ends) has been discredited since late 2014. At their November

2014 meeting, and despite falling prices and a growing surplus of production over demand, OPEC

(Organisation of the Petroleum Exporting Countries) decided to maintain high production quotas for a

range of reasons. Critically, a key driver was to maintain and increase market share, to drive higher cost

producers from the market or make them vulnerable to take-over, and to drive the hitherto burgeoning

US shale gas industry to the wall.

The outlook for gas demand and UK prices is highly complex and beyond the remit of this study to

describe and analyse in depth. However, with North Sea gas production levels continuing to fall, the UK is

essentially heavily reliant on natural gas imports from mainly Norway and Netherlands, and LNG imports

from Qatar. Prices will heavily depend on the attitude of OPEC, as and when it drives a number of shale

gas-oil and other higher cost producers from the market, plus the state of the Chinese and wider global

economy. In addition the impacts of the drive towards low carbon economies in the aftermath of the

Paris COP21 agreement may be felt over time.

Recent rapid changes in the oil and gas markets have made predicting future prices a significant dilemma.

Clearly gas price projections made even a few years ago are now wildly inaccurate and revisions have had

to be made (see Figure 6). There must hence be a significant degree of risk placed on all current gas price

projections, including those provided by DECC. As can be seen, in the space of just two years, DECC

forecasts for gas prices for the year 2020 have fallen by approaching 30%.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 20

Figure 6: Gas Price Forecasts (Source: DECC Fossil Fuel price Projections, September 2014)

For the purposes of this study we have assumed either status quo gas prices (increasing by annual RPI

only), or 2.5% per annum average price inflation for both gas and wood chip fuel. This may well be a

conservative assumption and we carried out sensitivity tests where gas prices increased by a further 25%.

2.7 WHY SHOULD EHDC INVEST IN LOW-CARBON HEAT NETWORKS? For EHDC, we suggest the following objectives may be important in deciding whether to invest in Whitehill

and Bordon (and the other two projects) and in guiding any ultimate decisions over governance if

investment takes place:

To counter-balance reducing Central Government Grants through secure and sustained future

revenue streams from low carbon investments, by accessing internal capital or very low cost

capital from other sources (e.g. PWLB).

In addition, to identify other sources of funding for renewable heat projects by, for example,

accessing EU funding (e.g. ERDF).

To encourage increased economic development in the District by making or attracting

investments into low-carbon initiatives that have a wider policy reach, for instance building local

skills capacity, and additional investment in supply chains for renewable energy and generating

new jobs (e.g. developing wood fuel supply hubs and chains).

To control and reduce energy costs internally through investments in energy efficiency and low-

carbon technologies.

To recycle revenues from successful investments locally in order to increase investment in

community and/or environmental projects.

To support the delivery of the Whitehill & Bordon Green Town Vision towards a low or zero

carbon future.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 21

To reduce carbon emissions from both EHDCs own estate, and other buildings to achieve

reductions and meet (or exceed) targets in line with internal targets, and also national carbon

reductions targets.

2.7.1 Technology Appraisal A range of technology options were assessed for each site. This involved considering technical viability,

whether the technology could be ‘fitted’ into the site, what integration issues the technology presented

and their financial viability. The summary for three sites is shown in table below.

It should be note that this appraisal was focused on the ability of a technology to generate useful heat at a

scale and cost that was suitable for the overall opportunity presented. Solar photovoltaics (PV), for

example, were therefore not considered, although they still could make a viable contribution to the

overall sustainability of the opportunities considered.

Moreover, solar PV can be integrated with hot water and heating systems via solar ‘switches’ that are

designed to divert power into heating hot water when excess solar PV energy is available (rather than it

being exported to the grid at a lower overall cost saving). This option should be considered, therefore, if

solar PV forms part of the overall solution at each site (n.b. this was not part of the scope of this study).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 22

Table 6: Summary of technology appraisal for all three sites

Project Technology

Option Technically

Viable Spatial Issues –

suitable? Integration

with existing?

Costs – attractive or

not?

Overall Assessment

Penns Place-Taro Centre

Solar HW Y – but limited

roof space N – roof not

strong enough Y

N – poor rate of return

No

GSHP

N – Temperature

output not suitable

N – playing fields not

suitable to dig up

N N No

Biomass Y

Y – space for energy centre and wood chip

delivery

Y Y Yes

Gas-CHP Y Y – one existing Y Y Yes

Alton

Solar HW

Y – could be integrated with

new Sports Centre

Y – new scheme

could design this in

N – poor rates of return

No

GSHP Y but spatial

needs make it not possible

No space for heat collection

Y but spatial issues

Y No

Biomass Y Y Y – space for

boilers and fuel store

Y Yes

Gas-CHP Y Y Y Y Yes

Whitehill & Bordon

Solar HW

Y – but not enough output

to make it worthwhile

Y – if roof space used

Y N – poor rates

of return No

GSHP

Y – but only for a small % of

heat and cooling load

N – only enough space for a

modest scheme Y

N – only for limited load

near space for heat

collection

Possible for smaller mini-

network

Biomass Y Y Y Y Yes

Gas-CHP Y Y Y Y Yes

2.8 STUDY METHODOLOGY In order to undertake the technical and financial assessments required for this study, the project team has

undertaken the following approach:

1. Surveys and meetings:

a. Study visits were undertaken at each of the three sites. In addition, several meetings

were held with EHDC officers at Penns Place.

b. At Penns Place this included extensive discussion with estates and facilities managers to

fully understand the condition of the buildings, how they are operated and the main

building services (i.e. boilers, CHP, air handling, air conditioning). This work was

facilitated by representatives of Places for People, the current facilities management

company responsible for the Taro Leisure Centre. The EHDC offices were also surveyed in

some detail to ascertain the likely impact on energy consumption following extensive

refurbishment of the main office facades.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 23

c. At Alton we again undertook a basic survey of the interior and exterior of the existing

leisure centre (again with Places for People). The grounds of the facility were also visited

to understand the relationship between the proposed new leisure centre and other

buildings in close proximity that might benefit from district heating. We also developed

energy data and scenarios for a projected 305 house development nearby.

d. We undertook a short visit to Prince Philips Barracks and the Technical Training Area (TTA)

at Whitehill & Bordon. At the former, we walked the area that will become the new town

centre. A representative of EHDC accompanied the visit and provided an overview of the

main development phases. During this visit we visited the existing (gas-based) energy

centre with an engineer from Carillion (n.b. this was not a scheduled meeting and access

was only gained by chance). This engineer provided useful information as to the route of

the existing district heating network and the capacity of the energy centre. This

information was critical in developing the scenarios for Whitehill & Bordon. Towards the

end of the project we received a brief status report on the quality of the existing

underground pipework via EHDC staff.

2. Energy data collection:

a. Data on electricity and gas consumption at Penns Place was received from both EHDC and

Places for People (for the Taro Leisure Centre). This data spanned five years and included

information on the volume and value (EHDC only) of energy used, along with other

information including VAT, levies, standing charges and so on. Despite a non-disclosure

agreement being in place, cost data for the Taro Leisure Centre was not provided. To

overcome this, the rates per unit for gas and electricity for the EHDC offices were applied

to the Taro data.

b. Data from the outline planning applications for new housing at Penns Field and the

former Lord Treloar Hospital site opposite Alton Leisure Centre were captured. These

documents contained information about the number of houses and their size from which

assumptions around energy use could be generated.

c. For Whitehill & Bordon, a number of outline planning and master planning documents

were consulted. In addition, EHDC provided several additional documents that provided

additional context and details relating to energy, sustainability and the deployment of

renewable energy technologies and district heating.

d. Information from two studies looking at the potential for wood fuel in East Hampshire

was also consulted.

e. References to the above documents, along with other sources of reference information,

have been made throughout this report.

3. Data analysis:

a. Data on gas and electricity consumption between 2011 and 2015 (gas) and 2006/7 and

2015/16 (electricity) was provided by EHDC for Penns Place, and by 'Places for People' for

the Taro Centre. For the other projects at Penns Field, Alton Sports Centre and associated

new housing, and Whitehill and Bordon, energy data was generated through appropriate

methodology and assumptions, and use of reports produced for planning purposes.

2.8.1 Energy Data Availability and Analysis

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 24

Our analysis for Penns Place and Taro Leisure Centre focused on the last five most recent years of

complete data, as follows:

Gas: 2011 to 2015

Electricity: 2010/11 to 2014/15

a. The data was aggregated and summarised in order to create an overview of the heat and

power loads and the cost per kWh of energy paid by the Council. Once completed, the

following additional processing steps were completed:

Extrapolation for missing data

Degree days correction

b. This process is described in more detail below. For the other projects we developed new

energy data based on information from a variety of sources (including planning

applications, master-planning and sustainability reports).

c. While daily or weekly metering data is not available for both sites, the pattern of heat and

power use is well known by users and energy managers at both sites.

d. Any missing data was filled in artificially by estimating missing months using averages and

proportions from previous years.

e. The heat load (based on the gas data and excluding any electrical heating) was corrected

for external temperatures using heating degree days. The full methodology for this

process is covered in Appendix 3.

f. The impact on the heat load for EHDC offices, caused by uprated windows and insulation,

was also factored in to the scenarios by modelling the estimated changes in heat loss.

Again, the detailed methodology for this is covered in Appendix 3.

g. For Penns Field, Alton Leisure Centre and Whitehill & Bordon we based our heat load

calculations, and subsequent scenarios, on data contained within planning applications

(and other related documents). We then applied standard rates for gas and electricity

used based on prevailing building regulations (e.g. 2013 Part L11; CIBSE Guide F12). This

produced a more consistent approach between all of the sites, rather than being based on

a range of assumption used by each developer (some of which were deliberately

overstated).

h. Energy cost data for Penns Place was based on the average gas and electricity prices (per

unit) from the EHDC data set. These prices were also applied to the Taro Leisure Centre

data set. Assumptions for the value of heat and power generated by the gas-CHP unit at

the Taro Leisure Centre were also based on EHDC costs per unit.

2.8.2 Financial appraisal methodology: The approach was as follows:

a. Select a representative ‘central case’ energy data set (heat and power) for the appraisal.

b. Model via a bespoke model the impact of investing in a range of new heat (mainly) and

power technologies such as biomass, gas-CHP and GSHP, to provide the heat and power

11

Approved Document L1A: Conservation of fuel and power in new dwellings, 2013 edition (HM Government, 2014). 12

Energy Efficiency in Buildings: CIBSE Guide F, 3rd

Edition (Chartered Institute of Building Services Engineers, 2012).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 25

required on site, when set against standard gas heating and fossil fuel based power from

the grid.

c. The quality of existing data for Penns Place and Taro Leisure Centre was good. We also

used prevailing prices for gas and power (adjusted for Whitehill & Bordon) as our central

price data for all three projects.

d. Capital expenditure (CAPEX): Estimated costs were derived from tenders, completed

projects, information from district heating and renewable energy specialists, and data

from supplier companies (as well as industry benchmark costs for items such as insulated

pipework)13.

e. The analysis is modelled through 20 years, 25 years and 40 year time periods. These are

typical ranges for this type of analysis. For the Penns Place/Taro Leisure Centre project

we have focussed much more on the 20-year time horizon as this is the time period when

the existing Renewable Heat Incentive (RHI) is available for biomass fuelled technologies.

f. Representative input costs for fuel and power (natural gas, wood chip, electricity), and

costs for operations and maintenance, including servicing, call-out, spares and major

rebuilds (in the case of CHP generally every 7-8 years), were gathered from suppliers and

recent tenders.

g. We then carried out cash flow modelling to produce Internal Rate of Return (IRR) and Net

Present Value (NPV) calculations for each project.

h. Based around the ‘central’ case for each modelling scenario we also carried out sensitivity

tests as follows:

i. Gas price variations +/-25% (n.b. we also modelled the most recent DECC gas

price data in several scenarios to asses to assess the impact of these)

ii. Wood chip price variations +/-25%

iii. Electricity price variations +/-25%

iv. Capital cost variations +/-25%

v. Variations in the level of RHI tariff likely to be available to the project, ranging

from full (current) tariff, to 50% of the current level and zero (i.e. no RHI available).

While the central case for Penns Place-Taro was assumed to be current full tariff

for medium biomass, for the other projects this was assumed to be 50% of this

tariff, with sensitivity tests at zero and 100% of existing tariffs.

i. The ‘benchmark’ test of 7% IRR was then used to gauge how investments compared to

those rates of return achieved by the existing EHDC property portfolio.

13

We have based the capital costs on typical ‘Design and Build’ tenders where specialist companies are used. Higher costs could occur where standard tendering using long-term framework supply companies are used (if these are in place).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 26

Table 7: Summary of financial model inputs

Input Standard Assumptions Variation Assumptions

Gas prices 2.75 p/kWh 2.50 p/kWh (Whitehill & Bordon) Wood Chip prices 3.00 p/kWh

Power prices 11.00 p/kWh 10.00 p/kWh (Whitehill &

Bordon)

NPV Discount Rate 7% †

O&M costs (for CHP includes spares, call-out + rebuild every 7-8 years)

Gas-CHP 5-7% of CAPEX pa Biomass 2-3% pa

Natural gas boilers 1% pa GSHP 1-2% pa

Inflation Rate 2.5%

all as per the standard assumption inputs

Gas price inflation Static or 2.5% pa real

Wood chip price escalation Static or 2.5% pa real

Power price escalation Static or 2.5% pa real Notes: † Based on the current IRR for the Council’s property portfolio. We accept that this is a relatively high discount rate for local authorities

but have left this as a conservatism.

2.8.3 Data Sources and Assumptions a. Gas, wood chip and power prices: Based on existing data for EHDC and commercial data.

b. Gas-CHP capital cost and servicing, spares, call-out and rebuild costs: Provided by a

major supplier (Cogenco) supplemented with data from other commercial sources14.

c. Biomass capital costs and servicing, spares and call-out costs: These were gained from a

range of recent tenders administered by SEWF (and others) which we have access to, as

well as quotes from several biomass boiler suppliers and servicing companies.

d. Future natural gas costs: We reviewed the data offered via DECC gas projections15 as well

as other sources such as World Bank and Deloitte. We also checked historical trends to

gauge whether future price projections were credible. While gas prices are important for

the economics of gas-CHP, where the difference in prices between gas inputs and power

outputs is critical, for biomass boiler system economics, it is the price margin differential

between gas and wood chip prices that is more important. Note that multiple annual gas

contracts are available, often in rolling three-year time periods, and this can provide a

good control of risks in this area.

e. Future heating fuel costs: We adopted steady gas and wood chip prices in real terms (i.e.

increased at RPI only) or modest escalating prices (e.g. +2.5% per annum for gas and

wood chip prices) which will slowly increase the margin between the two fuels over time.

For Penns Place and Taro Leisure Centre this will increase the existing 0.25p/kWh(th)

margin in favour of gas by a few % per annum.

f. Gas cost uncertainty: This is discussed in Section 2.6. After a review of options we used a

baseline assumption of steady state gas prices (increasing at RPI only) as well as testing at

2.5% price escalation, and for several of the scenarios, recent DECC gas projections.

g. Future wood chip prices: After modest real increases in prices from 2010-2014, prices

have steadied and in some cases fallen. Despite a reasonable surge in wood chip demand

14

Personal communication Mike King, Aberdeen Heat and Power (December 2015). 15

DECC Fossil Fuel price Projections (September 2014).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 27

for the biomass heating market, the big explosion of fuel demand expected under the RHI

has not taken place. There is hence a significant surplus in supply over current and

expected demand, and prices for the foreseeable future are expected to remain stable.

Multiple annual wood chip contracts are also available in the South-East market, and this

can again provide control of risks in this area. There are substantial wood resources across

the County and region and no indications of shortage which would substantially affect

prices.

2.9 DEVELOPING THE MODELLING SCENARIOS Based on the above inputs and assumptions, we developed a total of 10 main Scenarios which we used to

test out financial viability, matching up appropriate heat (and Power) loads and CO2 reduction impacts

(see Table 8). Of these 10 scenarios, one for each project site was recommended - Scenarios 2, 5 and 7.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 28

Table 8: Summary of financial scenarios

Scenario

(for 20, 25 and 40 years)

Technology Option Biomass/gas-CHP/Other

Central CAPEX Central Heat demand kWh

Fuel pricing

RHI Maintenance

Costs

1

Penns Place

Taro (inc. 50% CHP heat)+EHDC

Biomass takes over 95% of heat loads

Assumed biomass packaged boiler system based at Taro Centre and feeding into Taro and Penns Place

£500,000 and sensitivity test at +/-25%

Capex for 2nd biomass boiler at year 21 = £275,000 2.68M

kWh(th)

See

Table 7

Prevailing RHI tariffs as at Jan 2016

£2,800 per year and then index-

linked

2

Penns Place

Taro (inc. 100% CHP heat)

Lower demand for biomass heat due to rejected CHP heat being captured and used at no cost.

Biomass capacity reduced to 450 kW

£550,000

Capex for 2nd biomass boiler at year 21 = £245,000

£2,700 per year and then index-

linked

3 Penns Place-Taro and

96 homes

As above plus extra 200kW biomass capacity and pipework to the housing development at Penns Field

£1.21M

Capex for 2nd biomass boiler at year 21 = £375,000

4.9M kWh(th)

Prevailing RHI tariffs as at Jan 2016 for first

boiler but 50% of RHI tariff for 2nd boiler in 6

years’ time

£5,200 per year and then index-

linked

4

New Alton Sports Centre + Health Centre

and The Gurdons

2 x 400kW biomass boilers

Biomass provides 95% heat (gas the remainder)

£620,000 and sensitivity test at +/-25%

Capex for 2nd biomass boilers at year 21 = £375,000

3.09M kWh(th)

1.002M kWh(e)

Assume 50% current tariffs, then full and zero

£3,200 per year and then index-

linked

4A

As Scenario 4 but with 125kW(e) gas CHP

variation and smaller biomass

2 x 300 kW biomass boilers

125kW(e) and 200kW(th) heat gas CHP plant – working at 80% efficiency and for 5000 hours a year

£720,000 (£470K biomass + £170K CHP + £80K pipework)

Capex for 2nd biomass boilers at year 21 = £350,000

CAPEX for 2nd CHP in year 16 at £145,000 and 3rd CHP unit at year 31 = £150,000

50% of current and zero

£3,000 per year for biomass

£12,500 a year for CHP and then index-

linked for both

5 As Scenario 4 but with 200kW Gas CHP and

small biomass (400kW)

400kW biomass

200kW(e) Gas CHP unit

£760,000 includes 400kW biomass and gas CHP unit

Capex for 2nd biomass boiler at year 21 = £335,000

CAPEX for 2nd CHP in year 16 at £170,000 and 3rd CHP unit at year 31 = £180,000

£2,600 per year for biomass

£22,,000 for the CHP unit and then index-

linked for both

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 29

Scenario

(for 20, 25 and 40 years)

Technology Option Biomass/gas-CHP/Other

Central CAPEX Central Heat demand kWh

Fuel pricing

RHI Maintenance

Costs

6 As Scenario 4 plus new

Housing

3 x 400 kW biomass boiler

plus a 200kW(e) gas CHP plant working for c.5,000 hours

£3.75M

9.37M kWh (th) 2.53M kWh (e)

As above

50% of current and zero

£7,000/yr biomass +

£30,000/yr CHP

7

Whitehill & Bordon Town Centre

2MW Gas CHP and 2000kW biomass heat plus 3,000kW gas boilers

3.69M kWh(th);

16.63M kWh(e)

£6,500/yr biomass +

£110,000/yr CHP

7a Lower CHP/higher

biomass

1MW CHP

4MW biomass

4MW gas

£3.842M As per Scenario

7

CHP - £55,000 per year; biomass £12,500 per year and then index-

linked

As per Scenario 7

8 Part of Whitehill &

Bordon (limited network)

500kW(th) GSHP

200kW(e) gas CHP

600kW(th) gas boilers

CHP - £210,000 GSHP - £700,000

GSHP 3.35M kWh, 200kW

CHP plant 1.5M kW(th) and

1.0M kWh(e)

Tested at current GSHP tier 1 and Tier 2 RHI

tariffs

£3,500 per year GSHP and

£30,000 per year CHP

Notes: Green shading denotes recommended scenarios.

Of the multiple scenarios assessed, the recommended Scenarios offering the best rates of return linked to practical viability were Scenarios 2

(Penns Place-Taro), 5 (Alton) and 7 (Whitehill and Bordon).

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 30

3 PENNS PLACE AND TARO LEISURE CENTRE

3.1 INTRODUCTION Penns Place covers around 2.5 hectares and consists of the EHDC main offices and the Taro Leisure Centre.

A 96 unit domestic building programme has been mooted for Penns Field, the nearest point of which lies

approximately 250-300 metres from the leisure centre.

Penns Place is the main location for EHDC staff and consists of two interconnected office blocks. The Taro

Leisure Centre is located within 200 metres on the same site, and is separated from the council offices by

a car park and access roads.

The north and south Penns Place office buildings were constructed during the 1960s and have undergone

various changes, including the addition of a link building in the 1990s. The original buildings are poorly

insulated and the heat distribution system is a mix of mainly radiators and some electric heaters. Various

insulation measures have been planned and are due for completion in late 2015/early 2016. In

combination, these are expected to reduce energy consumption and increase comfort levels significantly.

The buildings also suffer from excess heat in the summer which is exacerbated by the lack of air

conditioning. The building facade consists of an aluminium frame with fibre glass inset panels. Insulation

behind some of these panels has been hampered by the presence of asbestos.

The Taro Leisure Centre was constructed in 1980s. The wet (pool) side was constructed first in the early

1980s and the dry side followed towards the end of the decade. It is of brick and steel construction. The

facility is open between 6am and 11pm seven days per week.

The Taro Centre was constructed in two phases. The dry side of the centre was completed in 1983 and the

wet side in 1996. The wet side houses the leisure and main pools and the cafe. The spa and sauna are

combined with the pool area. The pool water is maintained at 29 Celsius and the air temperature at 30

Celsius.

The Centre has three plant rooms:

Pool plant room:

o Large basement level room containing all of the infrastructure related to water treatment,

filtering and circulation for the wet side. Also contains a 125 kWe gas CHP engine and

associated switch gear.

o The plant room is susceptible to flooding and pumps are used to remove excess water.

o Surplus heat from the CHP unit is vented to the atmosphere via a heat exchanger at the

rear of the building.

Boiler plant room:

o Located at the opposite end of the building to the pool plant room. Total installed (gas

boiler) capacity is 475 kW.

Air handling plant room:

o The air handling unit includes a gas fired heater to condition the pool air. It also provides

condition air to other parts of the Centre.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 31

3.2 THE IMPACT OF FAÇADE REFURBISHMENT ON HEAT LOADS It was important to take into consideration the impact of the recent façade refurbishment on the total

energy demand for Penns Place. In combination, these works are likely to have a relatively large impact on

the kWh/m2 ‘result’ for North Block. For South Block the impact is likely to be lower due to the fact that

some glazing improvements have been in place for some time, plus the reduced opportunity to improve

the non-glazed parts.

Given that façade refurbishment can have a significant impact on heat demand, it was necessary to

develop different scenarios to take into account likely outcomes, as they affect the average heat demand

in kWh/m2. These are assumed to be 50% reductions for North Block and 10% reductions for South Block

(this is described fully in Appendix 3).

3.3 ENERGY DATA Our analysis of historical energy data has produced a set of inputs that will be used for the analysis of heat

network opportunities at Penns Place-Taro. These are summarised in the following table.

Table 9: Summary of annual heat and power inputs at Penns Place and Taro Leisure Centre

Current Heat Demand (kWh) Penns Place Taro Centre Total

Total annual average HDD corrected heat demand: 346,000 2,332,000 2,678,00016

Total annual average electricity demand: 416,000 1,050,000 (grid + CHP)

1,466,000

Cost per unit (p/kWh)

2015 cost per unit of gas (Excl. VAT): 2.75 2.75 n/a

2015 cost per unit of electricity (Excl. VAT): 11.31 11.31 n/a

5-year average cost per unit of gas (Excl. VAT): 2.37 2.37 n/a

5-year average cost per unit of electricity (Excl. VAT): 10.19 10.19 n/a

GHG (Kg CO2e)

Total annual average GHG emissions – gas: 64,000 428,000 492,000

Total annual average GHG emissions – electricity: 192,000 225,000 417,000

Total annual average GHG emissions – CHP electricity: n/a 260,000 260,000

GHG (Kg CO2)

Total annual average GHG emissions – gas: 12,000 427,000 439,000

Total annual average GHG emissions – electricity: 88,000 223,000 311,000

Total annual average GHG emissions – CHP electricity: n/a 258,000 258,000

Cost (£)

Total annual average cost of energy – gas: £8,400 £55,000 £63,400

Total annual average cost of energy – electricity: £42,300 £50,000 £92,300

of which CHP electricity £13,000 £13,000

Income (£)

Total annual average value of CHP electricity generation n/a £57,000 £57,000

Total annual average value of CHP heat generation n/a £21,000 £21,000

3.4 PENNS PLACE: NEW HOUSING A planning application17 for 96 homes at nearby Penns Field was used to derive a list of proposed

dwellings. We then applied a standard heat load per square meter of internal area to derive heat,

16

450,000 kWh(th) of the estimated ‘waste heat’ from the gas-CHP plant is excluded here.

EHDC HNDU: Heat Techno-Economic Feasibility Studies

P a g e | 32

electricity and hot water loads for each dwelling type. These loads were then aggregated to produce an

overall picture for the 96 dwellings proposed in the 2010 planning application. The results of this exercise

indicate a heat load of around 480,000 kWh of electricity and 1,914,712 kWh of heat per year. The

assumptions behind these figures are described in Appendix 3.