DRAFT Discussion Paper, Employment Lands Official Plan ...

48

DRAFT DISCUSSION PAPER, EMPLOYMENT LANDS OFFICIAL PLAN REVIEW, BRADFORD WEST GWILLIMBURY PREPARED FOR THE CORPORATION OF THE TOWN OF BRADFORD WEST GWILLIMBURY September 1, 2016

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of DRAFT Discussion Paper, Employment Lands Official Plan ...

DRAFT DISCUSSION PAPER, EMPLOYMENT LANDS OFFICIAL PLAN REVIEW,

BRADFORD WEST GWILLIMBURY PREPARED FOR THE CORPORATION OF THE

TOWN OF BRADFORD WEST GWILLIMBURY

September 1, 2016

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

Table of Contents Executive Summary .............................................................................................................................. i

1 Introduction ................................................................................................................................... 1

1.1 Background and Objectives ............................................................................................................ 1

1.2 Approach ........................................................................................................................................ 2

2 Employment Lands Inventory ..................................................................................................... 3

2.1 Employment Land Characteristics .................................................................................................. 5

2.1.1 Artesian Industrial Park ............................................................................................................. 5

2.1.2 Reagens Industrial Park ............................................................................................................ 5

2.1.3 BWG Strategic Settlement Employment Area (“BWG SSEA”) ................................................. 5

2.1.4 Bradford By-Pass Employment Lands ...................................................................................... 6

2.2 Characteristics of Occupied Employment Lands in BWG .............................................................. 6

2.3 Supply of Vacant Employment Lands in BWG ............................................................................... 9

2.4 Summary ...................................................................................................................................... 11

3 Comparative Analysis ................................................................................................................ 12

3.1 Location and Transportation Analysis .......................................................................................... 13

3.2 Employment Clusters.................................................................................................................... 16

3.3 Skilled Labour Force ..................................................................................................................... 19

3.4 Supply of Vacant Employment Lands........................................................................................... 21

3.5 Industrial Property Tax Rates ....................................................................................................... 22

3.6 Industrial Development Charges .................................................................................................. 23

3.7 Summary ...................................................................................................................................... 23

4 Trend and Target Analysis ........................................................................................................ 24

4.1 Current Trends in Employment Lands Development ................................................................... 24

4.2 Business Type .............................................................................................................................. 25

4.3 Parcel size and Building Size ....................................................................................................... 25

4.4 Locational requirements ............................................................................................................... 26

4.5 Skills Labour requirements ........................................................................................................... 26

4.6 BWG Economic Development Strategy ........................................................................................ 26

5 Employment Land Demand ....................................................................................................... 28

5.1 Historic Employment Growth ........................................................................................................ 28

5.2 Employment Land Absorption ...................................................................................................... 30

5.3 Forecast Employment Growth ...................................................................................................... 32

5.4 Employment Growth on Employment Lands ................................................................................ 33

5.5 Employment Land Densities ......................................................................................................... 36

5.6 Market Contingency ...................................................................................................................... 38

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

5.7 Demand for Employment Lands ................................................................................................... 38

6 Land Needs ................................................................................................................................. 39

6.1 Employment Land Needs ............................................................................................................. 39

6.2 Population-Related Employment Land Needs ............................................................................. 40

7 Conclusions and Recommendations ....................................................................................... 41

7.1 Summary of Conclusions .............................................................................................................. 41

7.2 Recommendations – Land Supply Requirements ........................................................................ 42

7.3 Recommendations – Policy Development & Refinements ........................................................... 43

LIST OF FIGURES Figure 2-1: Location of Employment Area Lands in BWG ............................................................................ 4 Figure 2-2: BWG Occupied Employment Lands by Location and Land Use Designation (Gross Hectares) 6 Figure 2-3: BWG Occupied Employment Lands by Location and Zoning (Gross Hectares) ........................ 6 Figure 2-4: Average Employment Land Coverage by Location .................................................................... 7 Figure 2-5: Occupied Employment Lands by Type of Employment, BWG ................................................... 7 Figure 2-6: Employment Density ................................................................................................................... 8 Figure 2-7: Vacant GFA on Employment Lands, BWG ................................................................................ 8 Figure 2-8: BWG Vacant Employment Lands ............................................................................................... 9 Figure 2-9: BWG Developed and Vacant Employment Lands by Location, 2016 ...................................... 10 Figure 2-10: BWG Vacant Employment Land Supply by Land Use Designation, 2016 ............................. 10 Figure 2-11: BWG Vacant Employment Land Supply by Parcel Size, 2016 .............................................. 11 Figure 3-1: Study Area ................................................................................................................................ 13 Figure 3-2: Manufacturing LQ Relative to Ontario, BWG and Surrounding Study Area ............................. 17 Figure 3-3: Wholesale Trade LQ Relative to Ontario, BWG and Surrounding Study Area ........................ 17 Figure 3-4: Transportation & Warehousing LQ Relative to Ontario, BWG and Surrounding Study Area .. 18 Figure 3-5: Construction LQ Relative to Ontario, BWG and Surrounding Study Area ............................... 18 Figure 3-6: Unemployment Rate, BWG and Surrounding Study Area ....................................................... 19 Figure 3-7: Share of Population with Apprenticeship Certificate, College Diploma or University Degree .. 20 Figure 3-8: Vacant Employment Land Supply, BWG and Surrounding Study Area ................................... 21 Figure 3-9: Industrial Property Tax Rates, BWG and Surrounding Study Area .......................................... 22 Figure 3-10: Industrial Development Charges ($/sq.ft.), BWG and Surrounding Study Area .................... 23 Figure 4-1: Value of Goods and Services Produced in Manufacturing, Wholesale Trade and

Transportation and Warehousing, Ontario .................................................................................................. 24 Figure 5-1: Place of Work BWG by Industry, 2001 to 2011 ........................................................................ 29 Figure 5-2: Industrial New Construction Value, BWG ................................................................................. 30 Figure 5-3: Absorbed Industrial Land Parcels, BWG, 2002 to 2016 ........................................................... 31 Figure 5-4: BWG Absorbed Employment Lands ......................................................................................... 32 Figure 5-5: BWG Employment Forecast by Sector, 2011 to 2041.............................................................. 33 Figure 5-6: Commercial / Population-Related Employment Growth by Sector, 2016-2041 ....................... 35 Figure 5-7: Employment Growth on Employment Lands, BWG, 2016 to 2041 .......................................... 37 Figure 6-1: BWG Employment Land Needs ................................................................................................ 39

i

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

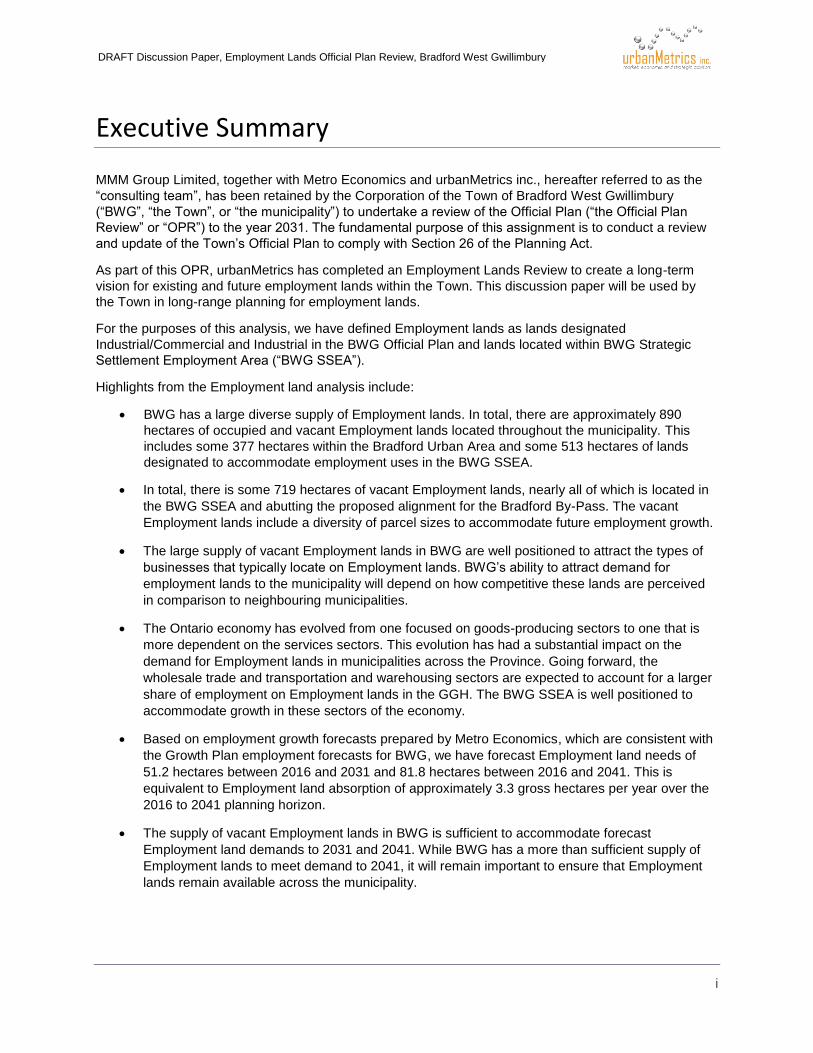

Executive Summary

MMM Group Limited, together with Metro Economics and urbanMetrics inc., hereafter referred to as the

“consulting team”, has been retained by the Corporation of the Town of Bradford West Gwillimbury

(“BWG”, “the Town”, or “the municipality”) to undertake a review of the Official Plan (“the Official Plan

Review” or “OPR”) to the year 2031. The fundamental purpose of this assignment is to conduct a review

and update of the Town’s Official Plan to comply with Section 26 of the Planning Act.

As part of this OPR, urbanMetrics has completed an Employment Lands Review to create a long-term

vision for existing and future employment lands within the Town. This discussion paper will be used by

the Town in long-range planning for employment lands.

For the purposes of this analysis, we have defined Employment lands as lands designated

Industrial/Commercial and Industrial in the BWG Official Plan and lands located within BWG Strategic

Settlement Employment Area (“BWG SSEA”).

Highlights from the Employment land analysis include:

BWG has a large diverse supply of Employment lands. In total, there are approximately 890

hectares of occupied and vacant Employment lands located throughout the municipality. This

includes some 377 hectares within the Bradford Urban Area and some 513 hectares of lands

designated to accommodate employment uses in the BWG SSEA.

In total, there is some 719 hectares of vacant Employment lands, nearly all of which is located in

the BWG SSEA and abutting the proposed alignment for the Bradford By-Pass. The vacant

Employment lands include a diversity of parcel sizes to accommodate future employment growth.

The large supply of vacant Employment lands in BWG are well positioned to attract the types of

businesses that typically locate on Employment lands. BWG’s ability to attract demand for

employment lands to the municipality will depend on how competitive these lands are perceived

in comparison to neighbouring municipalities.

The Ontario economy has evolved from one focused on goods-producing sectors to one that is

more dependent on the services sectors. This evolution has had a substantial impact on the

demand for Employment lands in municipalities across the Province. Going forward, the

wholesale trade and transportation and warehousing sectors are expected to account for a larger

share of employment on Employment lands in the GGH. The BWG SSEA is well positioned to

accommodate growth in these sectors of the economy.

Based on employment growth forecasts prepared by Metro Economics, which are consistent with

the Growth Plan employment forecasts for BWG, we have forecast Employment land needs of

51.2 hectares between 2016 and 2031 and 81.8 hectares between 2016 and 2041. This is

equivalent to Employment land absorption of approximately 3.3 gross hectares per year over the

2016 to 2041 planning horizon.

The supply of vacant Employment lands in BWG is sufficient to accommodate forecast

Employment land demands to 2031 and 2041. While BWG has a more than sufficient supply of

Employment lands to meet demand to 2041, it will remain important to ensure that Employment

lands remain available across the municipality.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

ii

It is also important to recognize that our employment land projections reflect Provincial

employment allocations within Simcoe County. Employment land absorption will ultimately

depend on a wide variety of factors such as the timing of the Bradford By-Pass and the ability of

the BWG SSEA lands to attract major tenants, which could act as a catalyst to future

development.

BWG has never had employment lands located along Highway 400, therefore, there may be

significant latent demand, beyond what is recognized in the Growth Plan employment allocations.

For these reasons, it is recommended that the municipality plan for employment land beyond

what is needed to 2041. Specifically, it will be important for the Town to protect Employment

lands located in the BWG SSEA, the Artesian and Reagens Industrial Parks and vacant

Employment lands located north of the proposed Bradford By-Pass for long-term employment

growth.

1

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

1 Introduction

MMM Group Limited, together with Metro Economics and urbanMetrics inc., hereafter referred to as the

“consulting team”, has been retained by the Corporation of the Town of Bradford West Gwillimbury

(“BWG”, “the Town”, or “the municipality”) to undertake a review of the Official Plan (“the Official Plan

Review” or “OPR”) to the year 2031. The fundamental purpose of this assignment is to conduct a review

and update of the Town’s Official Plan to comply with Section 26 of the Planning Act.

1.1 BACKGROUND AND OBJECTIVES In conducting the OPR, the consulting team have separated the analysis into three distinct phases. These

three phases are as follows:

Phase 1: Four Issues;

Phase 2: Policy Directions Report; and

Phase 3: New Official Plan Policies.

Collectively, these phases will form the OPR, which will guide and direct population and employment

growth in BWG through 2031.

Phase 1 of the OPR will involve ensuring conformity with recent Provincial planning policy and Council

priorities in four identified issue areas. This phase will also include Official Plan Amendments to

implement recommendations for these four issue areas. These four identified issues include:

Issue 1: Employment Lands

Issue 2: Growth and Population Distribution

Issue 3: Downtown Bradford Revitalization

Issue 4: Seniors Housing Options

The discussion paper provided herein represents Issue 1 in Phase 1 of the study. The purpose of this

discussion paper is to create a long-term vision for existing and future employment lands within the Town.

This discussion paper will be used by the Town in long-range planning for employment lands.

For the purposes of this analysis, we have defined Employment lands as lands designated

Industrial/Commercial and Industrial in the BWG Official Plan and lands located within BWG Strategic

Settlement Employment Area (“BWG SSEA”).

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

2

1.2 APPROACH In preparing this discussion paper, the following work steps have been undertaken:

Review of BWG Employment Land Inventory

This section of the analysis will review the existing and vacant Employment lands located in the

Town. This analysis will identify the characteristics of occupied Employment lands by location, parcel

size, land use designation and type of employment occupying the land. It will also examine the

location of Employment lands relative to complementary or sensitive land uses.

An important component of this analysis will also be the review of the supply of vacant Employment

lands within the municipality that are available to accommodate future employment growth. We will

categorize these vacant employment lands by location, parcel size, land use designation and the

availability of servicing.

Comparative Analysis

This section of the analysis assesses the competitiveness of Employment lands in BWG relative to

other local area municipalities. Variables considered in this analysis include the concentration of

employment compared to other local municipalities, land supply, property tax rates and development

charges.

Trend and Target Analysis

This section of the analysis reviews current trends in employment land development, including

business types, parcel and building size, and locational and skills requirements. We also comment on

the suitability of the employment land supply in BWG in terms of accommodating current and

anticipated future trends in Employment land demand.

Employment Lands Demand Analysis

Based on employment growth forecasts provided by Metro Economics and our own assumptions

regarding Employment land densities, we have forecasted demand for Employment lands to 2031

and 2041 within the municipality.

Demand and Supply Reconciliation

Based on the supply of vacant Employment lands and the Employment land demand projections, we

have determined the adequacy of the Employment lands supply in BWG to accommodate future

growth.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

3

2 Employment Lands Inventory

The BWG Official Plan identifies a variety of land uses across the municipality that are permitted to

accommodate industrial uses. We have generally defined these lands as “Employment lands”. These land

use designations include:

Industrial/Commercial;

Industrial;

Industrial – Industrial/Commercial;

Industrial Special Policy Area (Section 5.3.5.8); and,

Lands Subject to Minister’s Zoning Order.

Within the Industrial/Commercial land use designation, permitted uses include a full range of light

industrial uses, offices, conference and convention facilities, public institutional uses and

commercial/recreation uses. Also, limited convenience commercial uses may be permitted. Retail uses

are not be permitted within this land use designation, with the exception of products that are produced or

assembled on site, in which case up to 10% of the main building may be utilized as a retail outlet for such

products.

Within the Industrial designation, permitted land uses include manufacturing activities that could have a

detrimental physical or visual impact on adjacent uses. The Industrial land use designation provides

limited direction of the types of uses that are permitted.

The Zoning By-Law for BWG establishes a number of zones that permit industrial employment uses.

These include:

General Employment (M1);

Prestige Employment (M2);

Rural Employment (M3);

Extractive (MX); and,

Ministers Zoning Order.

The M1 and M2 zones generally apply to Employment lands located within the Bradford Urban Area and

Bond Head Urban Area, whereas the M3 and MX zones generally apply to lands located in the Rural

Area of the municipality.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

4

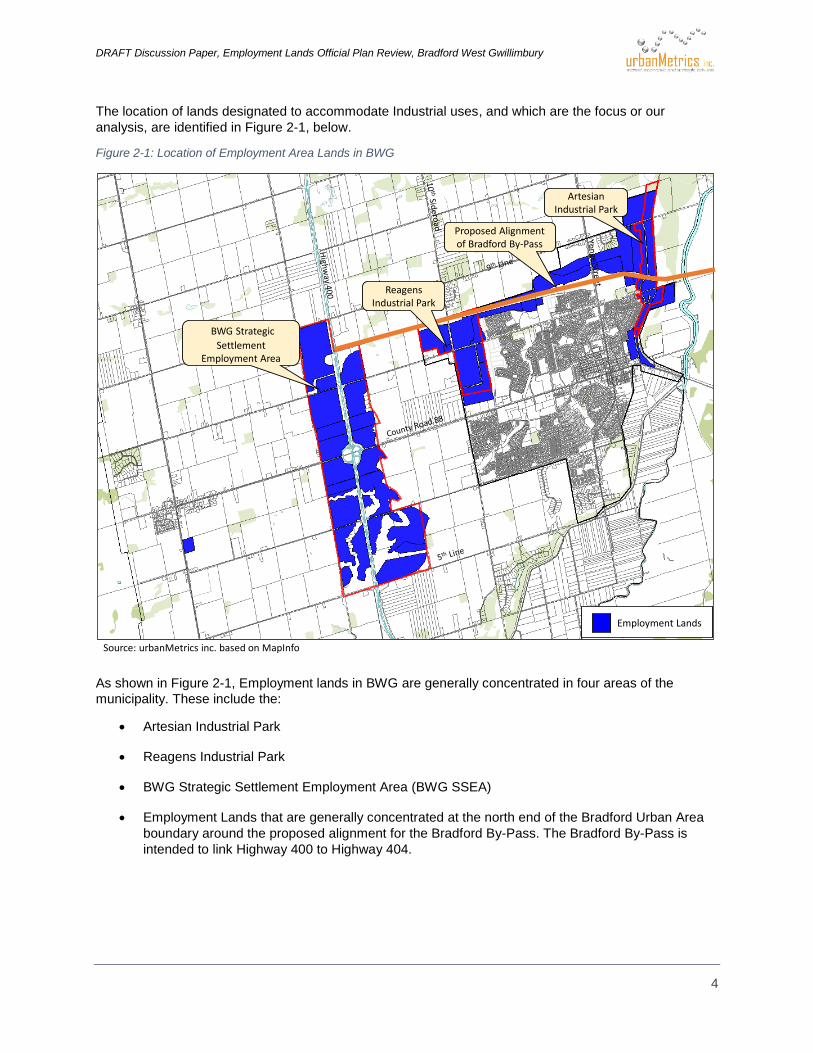

The location of lands designated to accommodate Industrial uses, and which are the focus or our

analysis, are identified in Figure 2-1, below.

Figure 2-1: Location of Employment Area Lands in BWG

As shown in Figure 2-1, Employment lands in BWG are generally concentrated in four areas of the

municipality. These include the:

Artesian Industrial Park

Reagens Industrial Park

BWG Strategic Settlement Employment Area (BWG SSEA)

Employment Lands that are generally concentrated at the north end of the Bradford Urban Area

boundary around the proposed alignment for the Bradford By-Pass. The Bradford By-Pass is

intended to link Highway 400 to Highway 404.

Source: urbanMetrics inc. based on MapInfo

Artesian Industrial Park

BWG Strategic

Settlement Employment Area

Employment Lands

Proposed Alignment of Bradford By-Pass

Reagens Industrial Park

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

5

2.1 EMPLOYMENT LAND CHARACTERISTICS This section of the discussion paper provides an overview of the supply of Employment lands in BWG

with respect to location, visibility and surrounding land uses.

2.1.1 Artesian Industrial Park The Artesian Industrial Park is located in the north eastern portion of the Bradford Urban Area. The

industrial park is 69.5 ha, and despite being the oldest industrial park in BWG, remains largely

undeveloped. Accessibility and visibility of the industrial park remain a challenge in attracting businesses,

as is access to 400-series highways. These factors have limited the types of business that have and will

likely locate in the industrial park.

The Employment lands in the Artesian Industrial Park are not constrained by any sensitive land uses. To

the east of the Industrial Park are lands designated as Open Space. Lands to the west of the Industrial

Park are currently vacant. While some of these lands are designated as Industrial/Commercial. Lands

further to the west are designated as Residential.

The majority of the businesses located in the Artesian Industrial Park are engaged in Commercial

Services and Construction. The Artesian Industrial Park is also characterized as having businesses with a

large amount of space dedicated to outdoor storage.

2.1.2 Reagens Industrial Park

The Reagens Industrial Park is located in the western portion of the Bradford Urban Area and is much

larger than the Artesian Industrial Park at 133.2 ha. The industrial park is connected to full municipal

services and also benefits from good access to Highway 400 via County Road 88.

The Reagens Industrial Park has experienced some difficulty with sensitive land uses located to the east.

This was a concern identified in the Economic Development Strategy1. In the Economic Development

Strategy, several property owners identified residential development encroaching to the east as a

potential challenge for the industrial park. While the open space buffer between the industrial and

residential uses has mitigated noise disturbances, other factors such as smells and safe

transportation/disposal of hazardous materials remains a challenge.

2.1.3 BWG Strategic Settlement Employment Area (“BWG SSEA”)

The BWG SSEA was designated under the provincial Growth Plan for the Greater Golden Horseshoe.

Land uses in the BWG SSEA are controlled by ministerial zoning orders. The BWG SSEA straddles

Highway 400 between Concession Rd. 9 in the north and Concession Rd. 5 in the south. While the BWG

SSEA is currently not serviced, there are plans to fully service the industrial park by late 2018.

Visibility and access to a major transportation corridor are important considerations when businesses

ultimately decide where to locate. As illustrated in Figure 2-1, the Employment lands subject to the

Minister’s Zoning Order have excellent visibility and access to Highway 400 and a potential future

interchange for the Bradford By-Pass.

While these lands have yet to be developed for employment purposes, it is less likely that there will be

significant challenges related to sensitive land uses than in the Bradford Urban Area, as the lands within

and surrounding the BWG SSEA consist of agricultural uses.

1 Town of Bradford West Gwillimbury Economic Development Strategy, Draft Final Report, October 2015, prepared by MDB Insight.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

6

2.1.4 Bradford By-Pass Employment Lands

The additional large cluster of Employment lands extends across the northern portion of the Bradford

Urban Area boundary. These Employments lands generally straddle the proposed alignment for the

Bradford By-Pass. While these lands are currently undeveloped, they represent long-term potential for

employment lands in the community should the proposed highway be developed.

2.2 CHARACTERISTICS OF OCCUPIED EMPLOYMENT LANDS IN BWG As part of this section of the discussion paper, we have analyzed the profile of developed Employment

lands in BWG by land use designation, zoning, parcel size, lot coverage and type of employment.

BWG has approximately 171 hectares of occupied Employment lands located in the Town. As shown in

Figure 2-2, the majority of the occupied Employment lands in BWG are designated as Industrial and are

located in the Artesian and Reagens Industrial Parks.

Figure 2-2: BWG Occupied Employment Lands by Location and Land Use Designation (Gross Hectares)

We have also examined the zoning on occupied Employment lands in BWG. Figure 2-3 shows that most

occupied lands in the Town are zoned M1.

Figure 2-3: BWG Occupied Employment Lands by Location and Zoning (Gross Hectares)

Industrial

Industrial /

Commercial

Lands Subject

to Minister's

Zoning Order TOTAL Percentage

Artesian Industrial Park 46.9 1.5 0.0 48.4 28%

Reagens Industrial Park 70.7 0.0 0.0 70.7 41%

BWG SSEA 0.0 0.0 23.2 23.2 14%

Other BWG 6.0 23.1 0.0 29.1 17%

TOTAL 123.5 24.6 23.2 171.3 100%

Percentage 72% 14% 14% 100%

Source: urbanMetrics inc. based on June 2016 inventory of Employment Lands.

M1 M2 M3 I C5

Lands Subject

to Minister's

Zoning Order TOTAL Percentage

Artesian Industrial Park 47.1 1.2 0.0 0.0 0.0 0.0 48.4 28%

Reagens Industrial Park 66.6 0.0 0.0 4.0 0.0 0.0 70.7 41%

BWG SSEA 0.0 0.0 0.0 0.0 0.0 23.2 23.2 14%

Other BWG 19.0 4.1 4.5 0.0 1.5 0.0 29.1 17%

TOTAL 132.7 5.3 4.5 4.0 1.5 23.2 171.3 100%

Percentage 77% 3% 3% 2% 1% 14% 100%

Source: urbanMetrics inc. based on June 2016 inventory of Employment Lands.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

7

The lot coverage ratio on Employment lands in BWG averaged 15% across the municipality. Coverage

was highest in the Reagens Industrial Park and somewhat lower in the Artesian Industrial Park. We

consider these lot coverage ratios to be very low. The low lot coverage ratios reflect lands being used for

outdoor storage and parking. For future planning purposes, we have assumed higher lot coverage ratios

on Employment lands.

Figure 2-4: Average Employment Land Coverage by Location

We have also estimated the share of Employment lands occupied by the various employment sectors.

These sectors include:

o Industrial - Employment primarily accommodated in low-rise industrial type buildings generally

located within business parks and industrial areas (i.e. Employment Area lands).

o Commercial / Population Related - Employment that primarily serves the resident population or

visitors, such as retail employment, as well as employment that typically occurs in office space

such as finance, insurance and real estate (FIRE), information and cultural services, professional,

scientific and technical services, and other business services.

o Institutional – Institutional employment also serves the resident population and includes jobs in

industries such as education, healthcare, and local government.

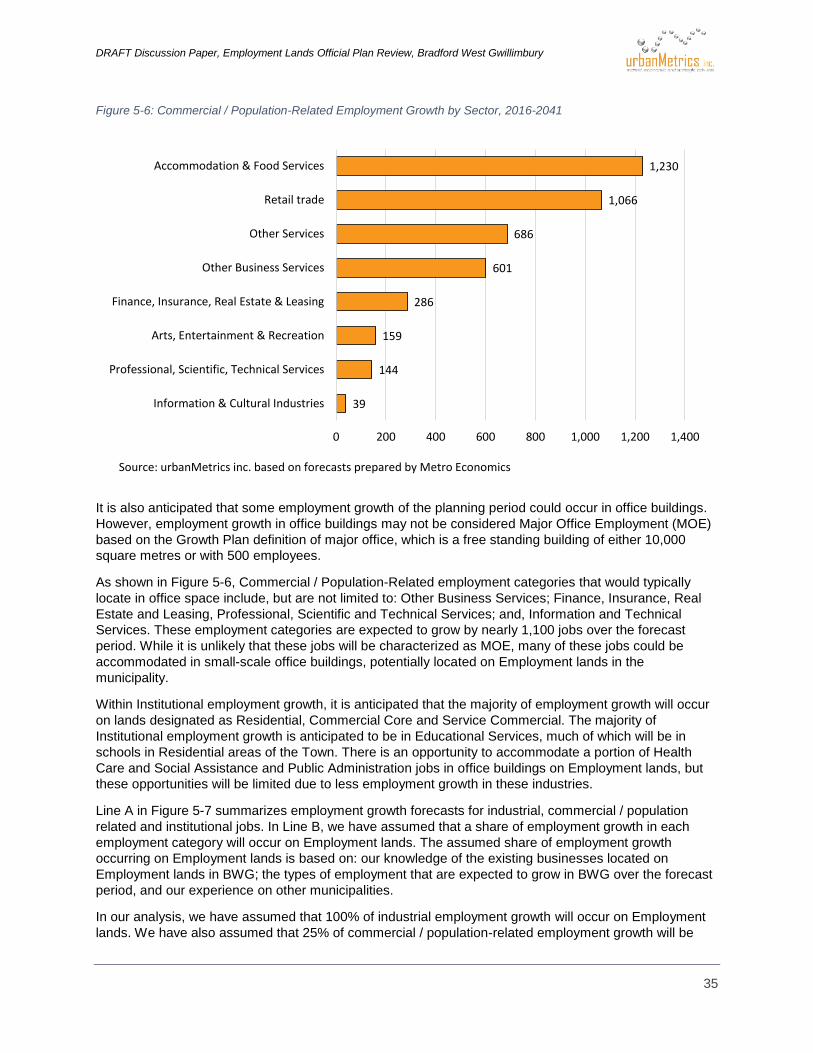

As shown in Figure 2-5, businesses engaged in

industrial employment account for nearly two-thirds

(64%) of occupied Employment lands in BWG.

Businesses engaged in commercial / population-related

employment is generally located in the Artesian

Industrial Park and consist of establishments such as

auto repair shops. The institutional component

represents the Bob Fallis Sports Centre located on Side

Road 10.

Coverage

Artesian Industrial Park 14%

Reagens Industrial Park 19%

Other BWG 10%

TOTAL 15%

Source: urbanMetrics inc. based on June 2016

inventory of Employment lands.

Industrial64%

Commercial / Population-

Related33%

Institutional3%

Source: urbanMetrics inc. based on June 2016 Employment Land Inventory

Figure 2-5: Occupied Employment Lands by Type of Employment, BWG

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

8

Based on the Employment land inventory conducted by urbanMetrics in June 2016 and data from the

2011 National Household Survey, we have calculated employment densities for industrial employment in

BWG. These densities range from a low of 400 square feet per employee in construction to a high of

1,450 square feet per employee in transportation, warehousing and wholesale trade.

Figure 2-6: Employment Density

BWG has approximately 262,000 square feet of vacant industrial Gross Floor Area (GFA) located on

Employment lands in the municipality. This represents a vacancy rate of 10.6%. Nearly all of the vacant

industrial GFA is located in the Reagens Industrial Park, and particularly in the former Faurecia industrial

building located at 100 Reagens Industrial Parkway.

We consider an industrial vacancy rate of 10.6% to be somewhat high in the Greater Toronto Area

(“GTA”) context. However, once the industrial building located at 100 Reagens Industrial Parkway is

occupied, the industrial vacancy rate in BWG would be approximately 3%, which is in line with the GTA

average.

Figure 2-7: Vacant GFA on Employment Lands, BWG

Density

(Sq.ft. Per

Employee)

Construction 400

Manufacturing 600

Transportation, Warehousing and Wholesale Trade 1,450

Source: urbanMetrics inc. based on 2011 NHS.

Vacant GFA Vacancy Rate

Artesian Industrial Park 29,712 4.0%

Reagens Industrial Park 191,607 13.6%

BWG SSEA 0 0.0%

Other BWG 41,140 13.4%

TOTAL 262,459 10.6%

Source: urbanMetrics inc. based on June 2016 inventory of

Employment lands.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

9

2.3 SUPPLY OF VACANT EMPLOYMENT LANDS IN BWG The supply and location of vacant Employment lands within BWG will be a significant factor in

determining how competitive the Town will be in attracting employment uses.

Figure 2-8 identifies the location of vacant Employment lands within the Town as of June 2016. As

shown, these lands are generally located throughout the Town with the largest concentrations located in

the BWG SSEA and lands abutting the proposed alignment for the Bradford By-Pass.

Figure 2-8: BWG Vacant Employment Lands

Vacant Employment Lands

Source: urbanMetrics inc.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

10

Figure 2-9 summarizes the supply of vacant Employment lands in BWG by industrial Park. Overall, as

shown, there is estimated to be a supply of approximately 719 hectares of vacant Employment lands in

the Town. This represents the net vacant supply of Employment lands and excludes environmentally

sensitive lands and internal infrastructure such as hazard lands, roads, stormwater ponds, easements,

etc. As shown, 89% of the vacant Employment land supply is located in the BWG SSEA or on lands

bordering the proposed Bradford By-Pass. The Artesian and Reagens Industrial Parks only account for

11% of the vacant Employment land supply, or approximately 76 hectares.

Figure 2-9: BWG Developed and Vacant Employment Lands by Location, 2016

Figure 2-10 identifies the vacant Employment land supply by Official Plan land use designation. It is

important that BWG maintain a healthy supply of vacant Employment lands within each land use category

to ensure that they can accommodate a variety of employment uses. As shown, the Employment land use

categories of Industrial, Industrial / Commercial, Industrial – Industrial / Commercial and Industrial Special

Policy Area account for 32% of the vacant Employment land supply. The remaining vacant Employment

lands are subject to the Minister’s Zoning Order.

Figure 2-10: BWG Vacant Employment Land Supply by Land Use Designation, 2016

The availability of a variety of parcel sizes will also be important in determining the future competitiveness

of BWG’s vacant Employment land supply. Transportation and Warehousing and Wholesale Trade type

uses will require large parcel sizes. Whereas, smaller manufacturing uses or construction type

businesses will likely require smaller Employment land parcels.

Developed Vacant Total

Percent

Vacant

Vacant

Percent of

Total

Artesian Industrial Park 48.4 20.5 68.8 30% 3%

Reagens Industrial Park 70.7 55.4 126.0 44% 8%

BWG SSEA 23.2 489.5 512.7 95% 68%

Other BWG 29.1 153.5 182.6 84% 21%

Total 171.3 718.8 890.1 81% 100%

Source: urbanMetrics and WSP, MMM Group Ltd.

Artesian

Industrial

Park

Reagens

Industrial

Park BWG SSEA Other BWG Total

Percent of

Total

Industrial 20.5 38.6 0.0 49.7 108.8 15%

Industrial / Commercial 0.0 13.1 0.0 60.6 73.7 10%

Industrial - Industrial / Commercial 0.0 0.0 0.0 36.9 36.9 5%

Industrial Special Policy Area 0.0 3.6 0.0 6.3 10.0 1%

Lands Subject to Minister's Zoning Order 0.0 0.0 489.5 0.0 489.5 68%

Total 20.5 55.4 489.5 153.5 718.8 100%

Source: urbanMetrics and WSP, MMM Group Ltd.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

11

Figure 2-11 illustrates that BWG has a healthy supply of Employment land parcels of various sizes. BWG

must ensure that it maintains a large supply of vacant Employment land parcels of various sizes to ensure

the long-term competitiveness of its Employment lands.

Figure 2-11: BWG Vacant Employment Land Supply by Parcel Size, 2016

2.4 SUMMARY BWG has a large diverse supply of Employment lands. In total, there are approximately 890 hectares of

occupied and vacant Employment lands located throughout the municipality. Highlights from the

Employment land analysis include:

Approximately two-thirds of Employment lands within the Bradford Urban Area are occupied. In

addition to Employment lands within the Bradford Urban Area, there are also 512 hectares of

lands designated to accommodate employment uses in the BWG SSEA.

Developed Employment lands in BWG accommodate a variety of employment uses, including

industrial, commercial / population-related and institutional. Based on our Employment land

inventory, industrial employment accounts for 64% of occupied Employment lands, followed by

commercial / population-related at 33%.

Within BWG, nearly all of the 719 hectares of vacant Employment lands are located in the BWG

SSEA and abutting the proposed alignment for the Bradford By-Pass. The vacant Employment

lands include a diversity of parcel sizes to accommodate future employment growth.

Vacant Land

Area (Ha)

Percent of

Total

Vacant

Employment

Land Parcels

Percent of

Total

Less than 1 ha 13.8 2% 40 29%

1 - 1.9 ha 35.6 5% 24 18%

2 - 4.9 ha 112.8 16% 35 26%

5 - 9.9 ha 114.8 16% 15 11%

10 ha and greater 441.8 61% 22 16%

Total 718.8 100% 136 100%

Source: urbanMetrics and WSP, MMM Group Ltd.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

12

3 Comparative Analysis

The large supply of vacant Employment lands in BWG are well positioned to attract a wide range of

businesses that typically locate on Employment lands. BWG’s ability to attract demand for employment

lands to the municipality will depend on how competitive these lands are perceived in comparison to

neighbouring municipalities. The location of BWG, at the southern edge of Simcoe County means that will

compete for business attraction and retention with municipalities in southern Simcoe County and

northwestern York Region.

In this section of the Discussion Paper, we have identified factors considered by businesses when

determining where to locate and how BWG compares to other local area municipalities. Variables

considered in our analysis include:

Locational Attributes of Employment Lands

Supply of Vacant Employment Lands

Access to Transportation (mainly Highway access)

Existing Types of Businesses in the Municipality

Skilled Labour Force

Property Tax Rates

Development Charge Rates

Based on these parameters, we have identified a study area for employment lands in BWG. Employment

lands in municipalities in our study area are expected to be most competitive with Employment lands in

BWG. Municipalities included in the Study Area include:

Barrie

Innisfil

Essa

New Tecumseth

King Township

East Gwillimbury

Newmarket

Aurora

Whitchurch-Stouffville

Vaughan

Georgina

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

13

These municipalities and the extent of the Study Area are identified in Figure 3-1.

Figure 3-1: Study Area

3.1 LOCATION AND TRANSPORTATION ANALYSIS All of the municipalities identified within the Study Area have employment lands that are located along or

in close proximity to a 400-series highway and are therefore directly competitive with Employment lands

in BWG. This section outlines the locational attributes of Employment lands in each municipality in the

Study Area.

City of Barrie

The City of Barrie has five Employment Areas within the old City of Barrie boundary, in addition to new

employment lands located in the lands annexed from Innisfil, which are located in the Salem Secondary

Plan. This secondary plan area includes approximately 170 gross hectares of employment lands

designated General Industrial and Highway 400 Industrial/Business Park.

Innisfil

Barrie

Essa

New Tecumseth

King

Vaughan

Whitchurch -Stouffville

Aurora

Newmarket

East Gwillimbury

Bradford West Gwillimbury

Source: urbanMetrics inc. based on MapInfo

Georgina

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

14

Nearly all employment lands in Barrie are located in close proximity to Highway 400. In fact, many of the

employment lands in Barrie are located adjacent to Highway 400 and therefore provide direct exposure to

passing vehicles.

Town of Innisfil

The largest concentration of employment lands in Innisfil are located in the Innisfil Heights Business Park,

which is a provincially designated employment area that straddles Highway 400. These lands total 320

hectares and are designated to accommodate a total of 7,700 highway commercial, general industrial and

business park jobs. These lands provide excellent visibility to passing vehicles and access to Highway

400 via Innisfil Beach Road. Work is underway to bring full municipal servicing to the business park.

Aside from the Innisfil Heights Business Park, additional employment lands in Innisfil consist of Rural

Industrial lands scattered throughout the municipality. These lands are generally built-out and are not

serviced.

Township of Essa

The Township of Essa has three concentrations of employment lands, the majority of which are located in

the rural area of the municipality and are not on municipal services. The largest concentration of serviced

employment lands in Essa are located in the Angus urban area, approximately one-third of which are

vacant. The employment lands in the Angus urban area are approximately 20 kilometres from a Highway

400 interchange and therefore do not have visibility or easy access to Highway 400.

Town of New Tecumseth

All employment lands in New Tecumseth are located in the three urban areas of Alliston, Beeton and

Tottenham. The urban area of Alliston accounts for the largest share of these employment lands within

the municipality.

Similar to Essa, the Town of New Tecumseth does not have direct access and exposure to a 400-series

Highway. However, this lack of highway exposure has not limited the ability of the municipality to attract

high profile businesses to its industrial lands. Despite the lack of highway exposure, employment lands in

the municipality have easy access to Highway 400 via Highway 89.

King Township

Employment lands in King Township are located in the three urban areas of King City, Nobelton and

Schomberg. The largest concentration of occupied employment lands are located in the Schomberg

urban area at the intersection of Highway 27 and Highway 9. The industrial park in Schomberg also

includes a large supply of vacant employment parcels to support future employment growth. The supply

of vacant employment lands in the urban areas of King City and Nobelton are limited.

Although the employment lands in King Township do not have direct exposure to a 400-series, all of the

employment lands have convenience access to Highway 400.

City of Vaughan

The City of Vaughan has a total of 28 employment areas. The majority of these employment areas are

located in close proximity and have access to Highway 400, Highway 407 and the proposed future

extension of Highway 427.

Among municipalities included in the Study Area for BWG, the City of Vaughan has the largest and most

diverse supply of employment lands.

Employment lands located south of Rutherford Road along Highway 400 and Highway 407 are generally

build-out, with only a few large vacant lots remaining. For employment lands located along Highway 400

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

15

north of Rutherford Road and employment lands located west of Highway 27, there are a large number of

vacant parcels available for development. However, many of these vacant lots remain unserviced and are

part of Vaughan’s long-term employment land supply.

Town of East Gwillimbury

Employment lands in East Gwillimbury are located in six designated Employment Areas in the Town.

Within these Employment Areas, the Town currently has a supply of approximately 500 hectares of

vacant Employment lands. A large supply of the vacant Employment lands in East Gwillimbury have

access and visibility to Highway 404.

Town of Newmarket

The largest concentration of employment lands in Newmarket are located adjacent to Highway 404. While

these lands have excellent access and visibility to the highway, nearly all employment lands in

Newmarket are built-out. The only significant concentration of vacant employment lands in Newmarket

are located in the Leslie South employment area between Davis Drive and Mulock Drive.

Town of Aurora

Employment lands in Aurora are located in six business parks, which combined account for nearly 400

net hectares of employment lands. The majority of the vacant employment lands in Aurora are located

adjacent to Highway 404. The location of these vacant employment lands provide excellent access and

visibility to Highway 404.

Town of Whitchurch-Stouffville –

Whitchurch-Stouffville has four employment areas, including Cardico, Gromley, Vandorf and Stouffville.

The Cardico, Gromely and Vandorf employment areas all have access and some exposure to Highway

404.

Town of Georgina

Employment lands in Georgina are located within both the urban and rural areas of the municipality. The

largest concentration of employment lands in the municipality is located in the Keswick Secondary Plan.

The Town of Georgina is also proposing a new business park along the planned Highway 404 Extension

at Glenwoods Avenue. These lands are proposed to be designated as Business Park in the Keswick

Secondary Plan.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

16

3.2 EMPLOYMENT CLUSTERS This section of the analysis has utilized Location Quotients (LQ’s) to compare the employment structure

in BWG with the municipalities in the Study Area. LQ’s are commonly used to identify the concentration of

employment activities and the relative strength in comparison to a regional economy. In this analysis, we

have calculated LQ’s by dividing the percentage of employment in a specific sector in a municipality by

total employment as a ratio of provincial employment in that sector.

Based on how LQ’s are derived, an LQ greater than 100% indicates that there is a concentration or

“cluster” of employment in a particular sector in comparison to the provincial average. Businesses cluster

together for a variety of reasons. When it comes to business sectors that typically locate on employment

lands, such as manufacturing, wholesale trade and transportation and warehousing, businesses cluster

together to take advantage of a pool of skilled labour, highway access, exposure to passing vehicles or

an abundance of large parcels of land.

An LQ equal to 100% indicates that the share of employment in a sector is the same as exists at the

provincial level. An LQ less than 100% indicates a concentration of employment in a particular sector that

is below the provincial average.

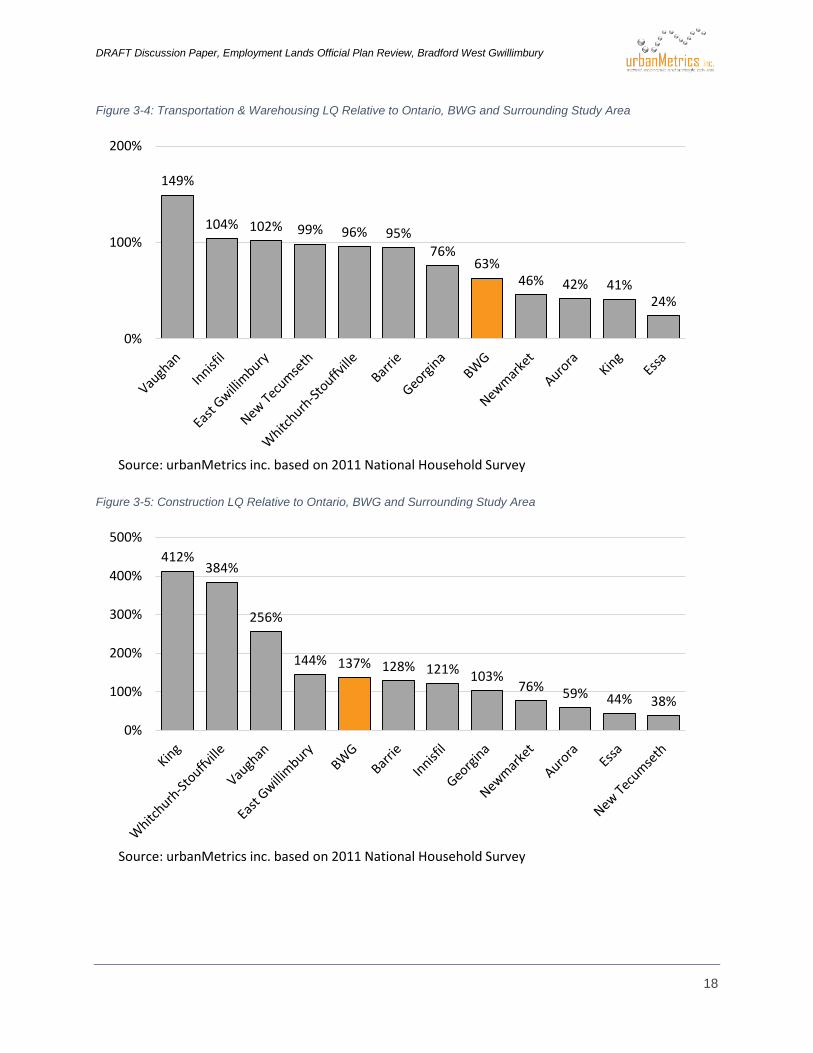

Figure 3-2 through Figure 3-5 summarizes LQ’s for BWG and other municipalities in the Study Area for

employment sectors that almost exclusively locate on Employment lands in business and industrial parks.

These sectors include manufacturing, wholesale trade, transportation & warehousing and construction.

Key findings from this analysis are as follows:

BWG has a cluster of manufacturing businesses located in the municipality. Aside from New

Tecumseth, which has a relatively high LQ due to the presence of the Honda facility, the LQ in

BWG is higher than other municipalities in the Study Area.

BWG also has a slight cluster of firms engaged in the construction sector. Most of these firms are

located in the Artesian Industrial Park in BWG.

The LQ analysis indicates that BWG has a relatively low concentration of wholesale trade and

transportation & warehousing companies relative to the provincial average and other

municipalities in the Study Area.

BWG’s lack of concentration in Wholesale Trade and Transportation and Warehousing is likely

related, in part, to the lack of convenient access to a 400-series Highway in the Artesian and

Reagens Industrial Areas. The opening of BWG SSEA lands located along Highway 400 would

likely attract a greater concentration of these types of businesses on Employment lands in the

municipality.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

17

Figure 3-2: Manufacturing LQ Relative to Ontario, BWG and Surrounding Study Area

Figure 3-3: Wholesale Trade LQ Relative to Ontario, BWG and Surrounding Study Area

359%

245%

204%

127% 124%104% 91%

74% 65% 56%28% 22%

0%

100%

200%

300%

400%

Source: urbanMetrics inc. based on 2011 National Household Survey

210%

139%

93% 88% 77% 75% 70% 69% 68%

35% 33%21%

0%

100%

200%

300%

Source: urbanMetrics inc. based on 2011 National Household Survey

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

18

Figure 3-4: Transportation & Warehousing LQ Relative to Ontario, BWG and Surrounding Study Area

Figure 3-5: Construction LQ Relative to Ontario, BWG and Surrounding Study Area

149%

104% 102% 99% 96% 95%76%

63%46% 42% 41%

24%

0%

100%

200%

Source: urbanMetrics inc. based on 2011 National Household Survey

412%384%

256%

144% 137% 128% 121% 103%76% 59% 44% 38%

0%

100%

200%

300%

400%

500%

Source: urbanMetrics inc. based on 2011 National Household Survey

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

19

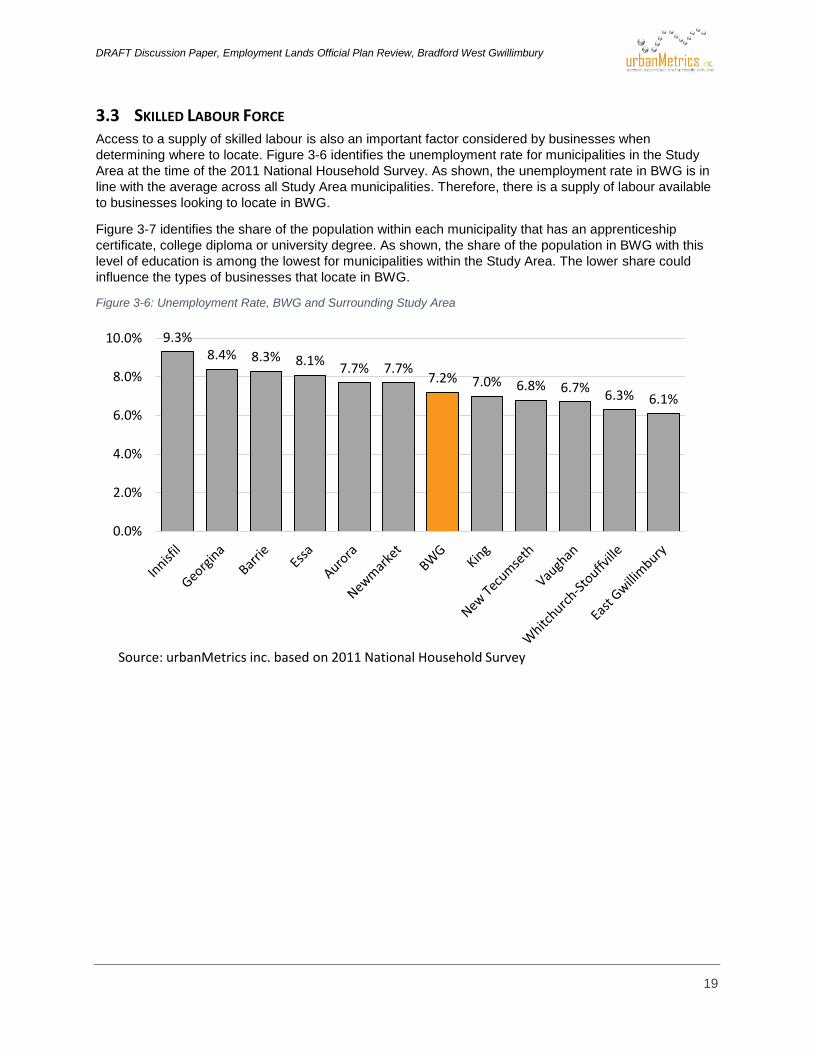

3.3 SKILLED LABOUR FORCE Access to a supply of skilled labour is also an important factor considered by businesses when

determining where to locate. Figure 3-6 identifies the unemployment rate for municipalities in the Study

Area at the time of the 2011 National Household Survey. As shown, the unemployment rate in BWG is in

line with the average across all Study Area municipalities. Therefore, there is a supply of labour available

to businesses looking to locate in BWG.

Figure 3-7 identifies the share of the population within each municipality that has an apprenticeship

certificate, college diploma or university degree. As shown, the share of the population in BWG with this

level of education is among the lowest for municipalities within the Study Area. The lower share could

influence the types of businesses that locate in BWG.

Figure 3-6: Unemployment Rate, BWG and Surrounding Study Area

9.3%8.4% 8.3% 8.1%

7.7% 7.7%7.2% 7.0% 6.8% 6.7%

6.3% 6.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Source: urbanMetrics inc. based on 2011 National Household Survey

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

20

Figure 3-7: Share of Population with Apprenticeship Certificate, College Diploma or University Degree

62% 60%57% 56% 55% 55%

51%48% 48% 46% 46% 45%

0%

15%

30%

45%

60%

75%

Source: urbanMetrics inc. based on 2011 National Household Survey

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

21

3.4 SUPPLY OF VACANT EMPLOYMENT LANDS Availability of vacant Employment lands is one of the most important locational factors for a business. As

such, we have summarized the supply of vacant Employment lands in each of the comparative

municipalities. As shown these municipalities have approximately 4,500 net hectares of vacant

Employment lands2. The City of Vaughan accounts for almost 30% of vacant Employment lands in these

municipalities.

The large supply of vacant employment lands in Vaughan has the potential to create challenges for the

other local municipalities in attracting employment uses. This is due to the proximity of Vaughan to

intermodal transportation hubs and Toronto’s Pearson International Airport.

Aside from Vaughan, BWG will also have to compete with other local municipalities that have a large

supply of vacant employment lands with access and exposure to 400-series highways. Therefore, BWG

will likely compete direction with municipalities such as East Gwillimbury, Barrie and Innisfil, as vacant

employment lands in these municipalities have similar locational attributes to vacant lands in the BWG

SSEA.

Figure 3-8: Vacant Employment Land Supply, BWG and Surrounding Study Area

2 Vacant employment land supply in the various municipalities is based on various dates.

1,296

719 682

418 399308

186 162 15483 75 34

0

500

1,000

1,500

Net Hectares

Note: Year of in which the supply was estimated is shown in brackets.Source: urbanMetrics inc. based on various sources.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

22

3.5 INDUSTRIAL PROPERTY TAX RATES Property tax rates for industrial properties are also a factor that impacts where a business decides to

locate. Figure 3-9 summarizes the industrial tax rate for municipalities in the Study Area. These property

tax rates include the municipal, regional and educational tax rates. As shown, the tax rate for an industrial

property in BWG is amongst the highest in the Study Area. It is notable that municipalities in Simcoe

County have the highest industrial property tax rates, while municipalities in York Region have the lowest.

It is also important to note that these property tax rates are applied to the assessed value of a property.

What will be important to a business when determining where to locate is the final tax bill, which is the

industrial tax rate applied to the assessed value of the property. Since the assessed value of an industrial

property in Simcoe County is lower than a comparable property in York Region, it will affect the final tax

bill. Therefore, while the industrial property tax rate in Simcoe County municipalities is higher than York

Region municipalities, the final tax bill would likely be similar.

Figure 3-9: Industrial Property Tax Rates, BWG and Surrounding Study Area

3.0% 3.0% 2.9% 2.8%2.5% 2.4%

2.2% 2.2% 2.2% 2.2% 2.1% 2.0%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Source: urbanMetrics inc. based on various sources

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

23

3.6 INDUSTRIAL DEVELOPMENT CHARGES The industrial development charge rate in a municipality may also impact how competitive a municipality

is in attracting businesses to employment lands, as it will impact how much it will cost a business to build

a new facility in the municipality.

As shown in Figure 3-10, the industrial development charge in BWG is among the lowest for the

municipalities in the Study Area. These development charges include the municipal, regional and

educational rates per square foot. The development charge for BWG in Figure 3-10 is for industrial

development in the Bradford Settlement Area. The development charge for industrial buildings in the

Bond Head Settlement Area and the BWG SSEA is slightly lower at $18.16 per square foot.

Figure 3-10: Industrial Development Charges ($/sq.ft.), BWG and Surrounding Study Area

3.7 SUMMARY BWG is one of the only municipalities in the Study Area that did not have Employment lands with

access to a 400-series highway. The addition of the BWG SSEA, which has direct access and

exposure to Highway 400, will greatly enhance the ability of BWG to attract businesses engaged

in Wholesale Trade and Transportation and Warehousing.

The supply of vacant Employment lands in BWG will also be important in attracting businesses to

the municipality. BWG accounts for approximately 16% of vacant Employment lands among

municipalities in the Study Area.

BWG also has non-residential development charges that are among the lowest for municipalities

in the Study Area. The low development charges and an abundance of Employment lands with

access to Highway 400 will be important in attracting businesses to the municipality.

$28.6$25.7 $25.7 $24.8 $24.5

$22.4 $21.5 $20.7 $19.7 $19.4

$13.9$12.1

$0

$5

$10

$15

$20

$25

$30

$35

Source: urbanMetrics inc. based on various sources

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

24

4 Trend and Target Analysis

4.1 CURRENT TRENDS IN EMPLOYMENT LANDS DEVELOPMENT The Ontario economy has evolved from one focused on goods-producing sectors to one that is more

dependent on the services sectors. This evolution has had a substantial impact on the demand for

Employment lands in municipalities across the Province. In some municipalities in the GTA, there has

been a shift towards growth in Major Office Employment (MOE) on Employment lands. Whereas, in

municipalities that have not attracted Major Office Employment, absorption of Employment lands has

slowed.

The three main sectors in the economy that have contributed to demand for Employment lands in are the

manufacturing, wholesale trade and transportation and warehousing sectors.

The manufacturing sectors continues to play a significant role in the Ontario economy, accounting of

nearly 13% of the value of all goods and services produced in the Province. However, the value of goods

produced by the manufacturing sector is down significantly from the late 1990’s, when it accounted for as

much as 20% of Provincial output. While the manufacturing sector will continue to play a significant role in

the Ontario economy, the role of sectors such as wholesale trade and transportation and warehousing are

becoming more significant.

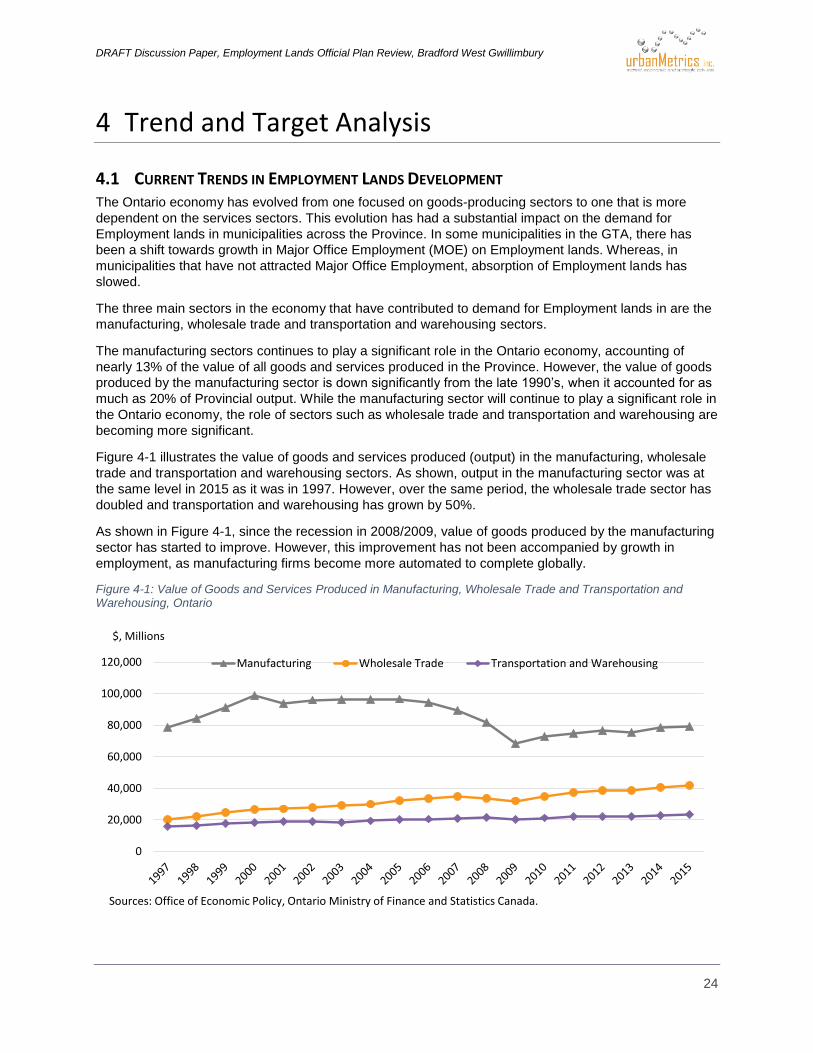

Figure 4-1 illustrates the value of goods and services produced (output) in the manufacturing, wholesale

trade and transportation and warehousing sectors. As shown, output in the manufacturing sector was at

the same level in 2015 as it was in 1997. However, over the same period, the wholesale trade sector has

doubled and transportation and warehousing has grown by 50%.

As shown in Figure 4-1, since the recession in 2008/2009, value of goods produced by the manufacturing

sector has started to improve. However, this improvement has not been accompanied by growth in

employment, as manufacturing firms become more automated to complete globally.

Figure 4-1: Value of Goods and Services Produced in Manufacturing, Wholesale Trade and Transportation and Warehousing, Ontario

0

20,000

40,000

60,000

80,000

100,000

120,000 Manufacturing Wholesale Trade Transportation and Warehousing

$, Millions

Sources: Office of Economic Policy, Ontario Ministry of Finance and Statistics Canada.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

25

Needless to say, these changes in the regional economy will have an impact on the demand for the type

and location of employment lands across the Province and in BWG. The following section outlines the

impact these changes in the regional economy are likely to have on the types of businesses locating in

employment areas, the parcel size and building size desired by these new businesses, locational

requirements and skills requirements of businesses competing in this “new economy”.

The remainder of this section identifies trends in demand for Employment lands based on business types,

parcel and building size, locational requirements and skills requirements.

4.2 BUSINESS TYPE Businesses engaged in manufacturing, wholesale trade, and transportation and warehousing continue to

account for the majority of business types located on Employment lands in various municipalities,

including BWG.

In recent years, industrial employment growth is being driven by growth in the goods movement sectors

such as wholesale trade and transportation and warehousing. This is consistent with the increasing

contribution of these sectors to the Provincial economy.

Among traditional manufacturing type businesses, sectors that have seen their contribution to Provincial

GDP expand over the past decade include:

Food, Beverage & Tobacco Products;

Plastic and Rubber Products;

Transportation Equipment;

Primary Metal & Fabricated Metal Products; and

Other Manufacturing, which includes businesses engaged in the making of furniture, medical

equipment and supplies, jewellery, sporting goods, toys, office supplies and other products.

In recent years, businesses engaged in non-industrial sectors have accounted for a growing share of

Employment land absorption. For example, in larger urban communities, such as Vaughan, Richmond Hill

and Markham, there has been a trend towards office development locating in prestige employment areas.

The trend towards office development on Employment lands has been slow to migrate north of Vaughan.

Therefore, over the planning horizon for the BWG Official Plan, there is not expected to be strong

demand for Employment lands to accommodate office uses.

4.3 PARCEL SIZE AND BUILDING SIZE The recent trend towards businesses engaged in wholesale trade and transportation and warehousing is

anticipated to impact the size of parcels and buildings that are likely to be demanded within employment

areas. For example, the increasing importance of wholesale trade and transportation and warehousing,

has and will continue to influence the parcel and building sizes sought by these businesses. These types

of businesses tend to favour large warehouse facilities and therefore are attracted to large greenfield

lands that are priced competitively.

As industrial land prices in GTA municipalities continue to rise, it is expected to result in land extensive

sectors such as wholesale trade and transportation and warehousing companies moving further north of

the GTA to find more appropriate parcel sizes and more affordable land prices. This trend will likely

benefit lands located in the BWG SSEA.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

26

4.4 LOCATIONAL REQUIREMENTS The locational requirements of businesses vary by sector. For example, in York Region, the vast majority

of employment growth has occurred in the southern municipalities of Vaughan and Markham. This strong

employment growth is tied to the increasing number of major office buildings locating on Employment

lands in these municipalities and the proximity of these municipalities to intermodal facilities.

As noted earlier, the types of businesses that are likely to be attracted to the BWG SSEA are those

engaged in wholesale trade and transportation and warehousing. Businesses engaged in these sectors

tend to be concentrated close to intermodal terminals such as Pearson International Airport or the

intermodal facilities in Vaughan. As a result, in recent years, there has been strong demand for

Employment lands in the southern municipalities in York Region. However, as the employment land

supply in these municipalities becomes more constrained and land prices increase, there will inevitably be

pressure to move further north for less expensive land.

Access to 400-Series highways is also an important consideration for businesses engaged in wholesale

trade and transportation and warehousing. The Employment lands in the BWG SSEA appear poised to

benefit from the movement towards larger parcel sizes with access to 400-series highway.

Within the Artesian Industrial Park, it is anticipated that vacant Employment lands will continue to appeal

to more localized businesses or firms engaged in construction that require outdoor storage space. The

significant cluster of manufacturing firms in the Reagens Industrial Park is anticipated to help attract these

types of firms to this area of the municipality.

4.5 SKILLS LABOUR REQUIREMENTS Access to skilled labour is increasing becoming an important consideration for businesses when

determining where to locate. With manufacturing, and transportation and warehousing increasingly

becoming automated, there has been an increased demand for a skilled workforce.

As demonstrated earlier in the locational quotient analysis, BWG already has a large concentration of its

labour force employed in the manufacturing sector, which may be important in attracting these types of

businesses to BWG. However, it was also demonstrated in the previous sector is this discussion paper

that BWG has a somewhat lower share of its labour force with an apprenticeship certificate, college

diploma or university degree. The relatively lower share of skilled labour in BWG could also have an

impact on the types of businesses that choose to locate in the municipality.

4.6 BWG ECONOMIC DEVELOPMENT STRATEGY In October 2015, MDB Insight prepared the Town of Bradford West Gwillimbury Economic Development

Strategy, hereafter referred to as the Economic Development Strategy. The purpose of this Economic

Development Strategy was to optimize BWG’s economic development capacity over the next five year

period. Based on BWG’s existing strengths, the Economic Development Strategy recommends that the

Town focus on attracting the following industries:

Food Processing;

Materials Manufacturing; and,

Transportation, Logistics and Warehousing

In the Economic Development Strategy, MDB Insight emphasized the importance of the BWG SSEA in

attracting businesses in each of these identified sectors, as this area is expected to accommodate a

significant share of the Town’s future employment growth.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

27

Recent trends in employment land development highlighted in the previous section of this discussion

paper are positive for BWG’s ability to attract the types of businesses identified in the Economic

Development Strategy to employment lands within the municipality.

Based on the Economic Development Strategy and the characteristics of businesses engaged in food

processing, materials manufacturing and transportation, logistics and warehousing, the available

Employment lands in BWG are well suited to accommodate these types of uses.

For example, based on the Economic Development Strategy, businesses engaged in food processing

require skilled labour, a variety of parcel sizes and willing partners. BWG has all of these.

In addition to the types of employment uses that are identified in the Economic Development Strategy,

recent events such as the decision by Magna International Inc. to move its global headquarters to a site

near King City could act as a catalyst for future Employment land absorption in BWG based on the

proximity of these two municipalities.

BWG is well positioned to capitalize of the changing landscape for employment lands in the GGH.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

28

5 Employment Land Demand

5.1 HISTORIC EMPLOYMENT GROWTH BWG’s has experienced robust employment growth in recent years, expanding by nearly 1,700 jobs

between 2001 and 2011 (Figure 5-1). This represented average annual growth of approximately 2.6% per

year, which significantly outpaced the provincial average of 0.7% over the same period. Despite strong

employment growth, BWG continues to be a net exporter of jobs to neighbouring municipalities. Although

there were 15,145 employed residents in BWG in 2011 there were only 7,500 jobs in the municipality.

The manufacturing sector remains the backbone of the BWG economy, accounting for nearly 1 in 4 jobs

in the municipality in 20113. While manufacturing has been challenged across the province over the past

decade, the manufacturing sector in BWG has been quite resilient. Between 2001 and 2011, BWG added

nearly 800 new manufacturing jobs, at a time when the province of Ontario lost nearly 280,000 jobs in this

sector.

Businesses engaged in the construction sector have also added jobs over the 10 year period between

2001 and 2011. Despite the strength of the wholesale trade and transportation and warehousing sectors

across the GGH, employment in these sectors in BWG was essentially flat between 2001 and 2011. The

lack of employment growth in these sectors is likely related, in part, to an insufficient supply of suitable

sites for these uses over this period in BWG.

Figure 5-1 illustrates the recent shift in the Provincial economy identified in the previous section of the

Discussion Paper. In BWG, between 2001 and 2006, the manufacturing sector accounted for the majority

of employment growth across the municipality. However, between 2006 and 2011, growth in

manufacturing employment stalled. In fact, between 2006 and 2011, the service sectors, specifically retail

trade, accommodation and food services and health care and social assistance, accounted for all

employment growth in the municipality.

3 Based on employed persons with a usual place of work and who work at home.

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

29

Figure 5-1: Place of Work BWG by Industry, 2001 to 2011

2001 2006 2011

Growth

2001 to 2011

585 500 375 -210

0 0 0 0

30 15 20 -10

265 340 445 180

1,180 2,025 1,975 795

2,060 2,880 2,815 755

255 290 250 -5

555 725 955 400

260 255 225 -35

65 45 110 45

140 185 145 5

70 75 105 35

345 185 210 -135

0 10 0 0

155 160 255 100

460 575 550 90

415 515 650 235

60 90 100 40

510 325 490 -20

360 370 380 20

90 150 275 185

3,740 3,955 4,700 960

5,810 6,835 7,500 1,690

Note: Numbers may not add to totals due to rounding.

Source:

Accommodation and food services

Other services (except public administration)

Public administration

Sub-total Services-Producing Sectors

TOTAL

urbanMetrics based on 2001 and 2006 Census of Canada and 2011 National Household Survey.

Professional, scientific and technical services

Management of companies and enterprises

Administrative and support, waste

management and remediation services

Educational services

Health care and social assistance

Arts, entertainment and recreation

Wholesale trade

Retail trade

Transportation and warehousing

Information and cultural industries

Finance and insurance

Real estate and rental and leasing

Agriculture, forestry, fishing and hunting

Mining and oil and gas extraction

Utilities

Construction

Manufacturing

Sub-total Goods-Producing Sectors

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

30

5.2 EMPLOYMENT LAND ABSORPTION Figure 5-2 summarizes the value of new industrial construction in BWG over the 2002 to 2013 period. As

shown, new industrial construction activity in BWG was very buoyant in the early part of the 2000s. This is

consistent with strong Employment land absorption in BWG during this period, most notably in the

Reagens Industrial Park, which saw the construction of new industrial buildings to accommodate

companies such as Dortec Industries, Spectra Aluminum Products, Landini Canda and Cericola Farms.

However, with the onset of the recession in 2008, the value of new industrial construction in BWG

declined significantly. More recently, new industrial construction values have increased slightly with the

addition of a second building for Array Canada in the Reagens Industrial Park.

Figure 5-2: Industrial New Construction Value, BWG

Figure 5-3 illustrates the location of absorbed Employment land parcels in BWG between 2002 and 2016.

As shown, nearly all of the Employment land absorption in BWG has occurred within the Artesian and

Reagens Industrial parks. In total, absorbed parcels accounted for 35.1 hectares over the 14 year period,

or approximately 2.5 hectares per year. However, as shown in Figure 5-3 absorption was strongest during

the 2002 to 2008 period and has since slowed. During the 2002 to 2008 period, average annual

Employment land absorption was approximately 5.0 hectares per year, declining to 0.2 hectares per year

during 2008 to 2012 during the recession, and since improving slightly to 1.0 hectares per year during

2012 to 2016. However, it is notable that some of the absorption that occurred during 2012 to 2016 was

for staff parking and storage in the Artesian Industrial Park.

0

5,000

10,000

15,000

20,000

25,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: urbanMetrics inc. based on Town of Bradford West Gwillimbury Development Charge Background Study and Proposed By-Law, Consolidated Report, September 15, 2014, prepared by Watson & Associates Economists Ltd.

Dollars ($000)

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

31

Figure 5-3: Absorbed Industrial Land Parcels, BWG, 2002 to 2016

Source: urbanMetrics inc.

Absorbed 2002-2008 = 30.2 ha

Absorbed 2008-2012 = 1.0 ha

Absorbed 2012-2016 = 3.8 ha

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

32

Figure 5-4 summarizes various statistics for absorbed Employment land parcels in BWG between 2002

and 2016. As shown, the Reagens industrial park accounted for 74% of absorbed Employment lands in

BWG between 2002 and 2016. Absorbed parcels in the Reagens Industrial Park also had the highest lot

coverage at 23% during 2002 to 2016. By comparison, coverage for absorbed parcels in the Artesian

Industrial Park was quite low at 9%. This was due to some parcels being absorbed for on-site storage or

parking.

Approximately one-third (32%) of absorbed parcels during the 2002 to 2016 period were less than one

hectare in size. While there were only two absorbed parcels greater than 5 hectares, these parcels

accounted for about 40% of the absorbed land area in BWG.

Figure 5-4: BWG Absorbed Employment Lands

5.3 FORECAST EMPLOYMENT GROWTH As part of the OPR, Metro Economics has prepared population and employment growth forecasts for the

Town. These employment forecasts tie in with the 2031 employment forecasts for BWG in Schedule 7 of

the Growth Plan and are extended to 2041 by Metro Economics. In preparing these forecasts, Metro

Economics has forecast employment for 18 industry categories, which have then been aggregated by

urbanMetrics for the purposes of forecasting demand for Employment lands within the municipality.

Schedule 7 of the Growth Plan identifies total employment forecasts that are to be achieved by each

municipality in the Simcoe Sub-Area, which includes BWG. These Schedule 7 forecasts indicate that

BWG is expected to achieve 18,000 jobs by 20314. To plan for employment land needs, we have broken

down the employment forecasts into the following sub-categories:

o Primary – This generally includes employment in the rural areas of municipalities, primarily

agriculture.

4 Includes people with a usual place of work in BWG, BWG residents working at home and people with no fixed place of work.

Absorbed

Land Area

(Ha)

Building

Floor Space

Average

Coverage

Artesian Industrial Park 7.8 75,377 9%

Reagens Industrial Park 26.0 633,937 23%

Other Employment Lands 1.3 24,559 18%

Total 35.1 733,873 19%

Parcels % of Parcels Area (Ha)

Less than 1 ha 6 32% 3.1

1 to 4.9 ha 11 58% 18.3

5 ha and Larger 2 11% 13.7

Total 19 100% 35.1

Source: urbanMetrics and WSP, MMM Group Ltd.

Absorbed Parcels 2002-2016

DRAFT Discussion Paper, Employment Lands Official Plan Review, Bradford West Gwillimbury

33

o Industrial - Employment primarily accommodated in low-rise industrial type buildings generally

located within business parks and industrial areas (i.e. Employment Area lands).

o Commercial / Population Related - Employment that primarily serves the resident population,