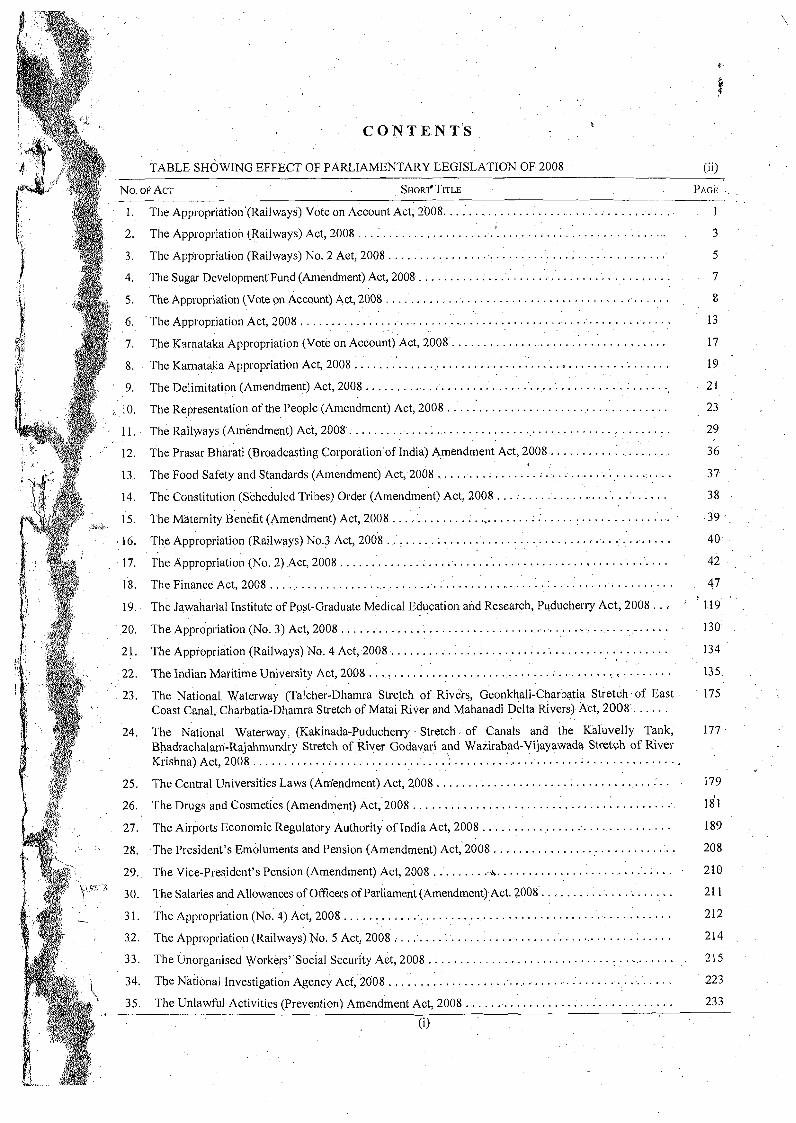

Download The file (11.65 MB) - Legislative Department

254

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Download The file (11.65 MB) - Legislative Department

*

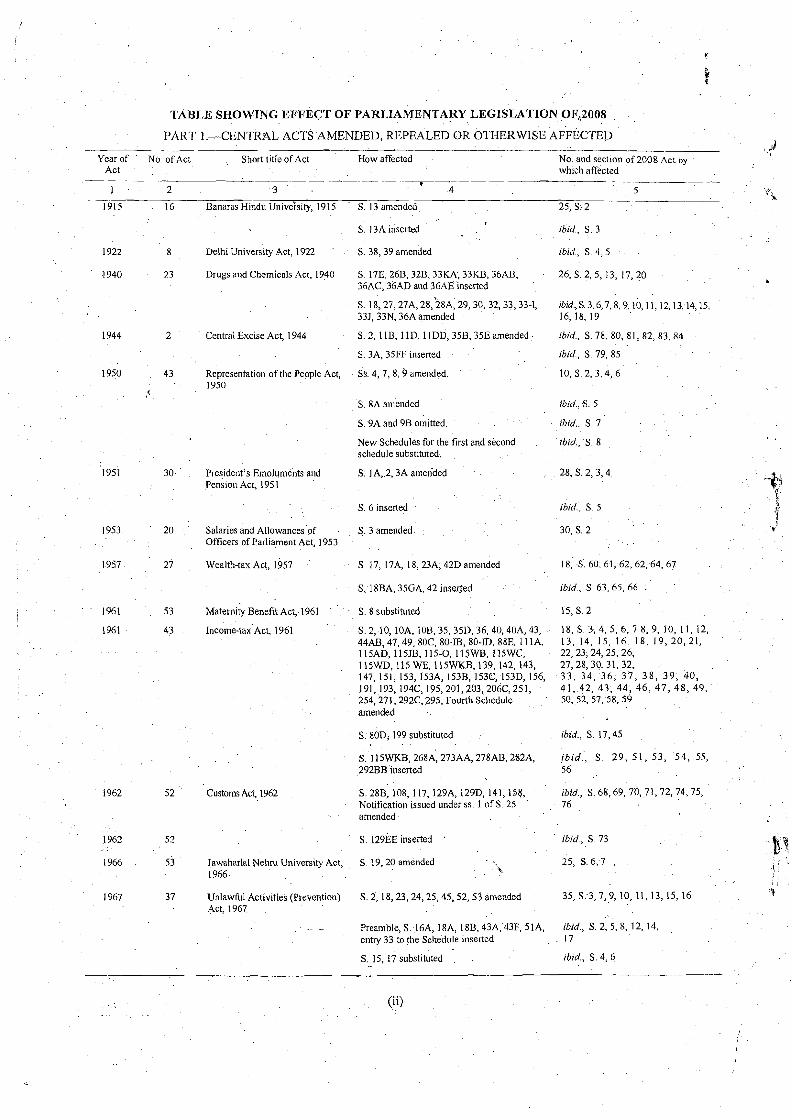

t TABLE SHOWING EFFECT OF PARLIAMENTARY LEGISLATION OF,2008

PART 1 .-CENTFWL ACTS AMENDED, REPEALED OR OTHERWISE AFFECTED

Year of No of Act Short tltle of Act How affected No and sectlon of 2008 A C ~ by P

Act which affected --

1 2 3 4 5 t

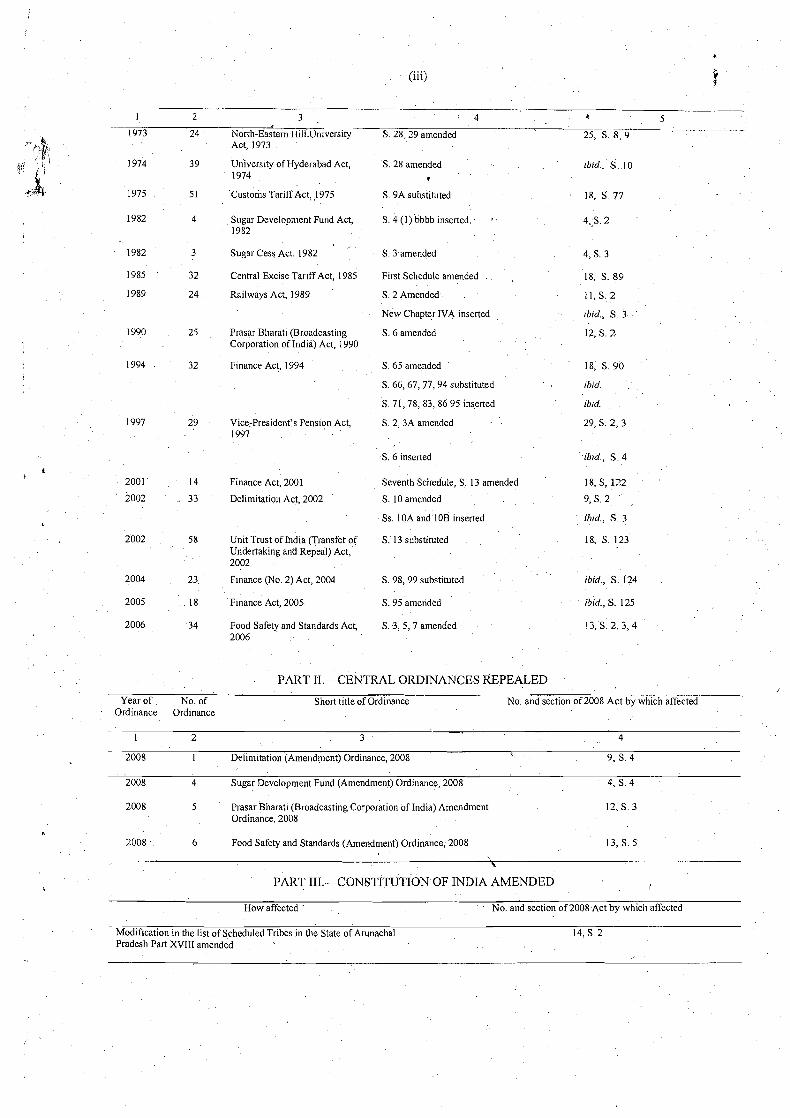

- -- < % 1915 16 Banaras Hlndu Unive'rs~ty, 1915 S 13 amended 25 , s 2

S 13A lnserted I

rbrd, S 3

1922 8 Delhl Unlvers~ty Act, 1922 S 38,39 amended rbrd, S 4,5

1940 23 Drugs and Chem~cals Act, 1940 S 17E, 26B, 32B, 33KA, 33RB, 36Al3, 26, S 2, 5, 13, 17, 20 36AC, 36AD and 36AE mserted

S 18,27,27A,28,28~, 29,30, 32.33,33-1, rbrd,S 3.6,7,8,9,10,11,12,13,14,15 33J, 33N, 36A amended 16, 18. 19

1944 2 Central Exclse Act, 1944 S 2, 1 lB, 1 lD, 1 IDD, 35B, 35E amended rbrd, S 78, 80, 81.82, 83.84

S 3A, 35FF lnserted rbrd, S 79, 85

1950 43 Representation of the People Act, SS 4,7, 8 ,9 amended 10, S 2,3,4, 6 1950

< S 8A a111ended rbrd, S 5

S 9.4 and 9B om~tted zbrd S 7

New Schedules for the first and second rbrd, S 8 schedule subst~tuted

1951 30 Pres~dent's Emolumenrs and S 1 A, 2,3A amended 28, S 2,3,4 Pension Act, 195 1 -$

1

S 6 inserted ~ b r d , S 5 3

8 1953 20 Salarles and Allowances of S 3 amended 30, S 2 9

Officers of Parliament Act, 1953

1957 27 Wealth-ta\: Act, 1957 S 17, 17A, 18,23A, 42D amended 18, S 60. 61, 62,62,64, 67

S, 18BA, 35GA, 42 ~nserted rbrd, S 63 65, 66 .

t 1961 53 Matern~ty Benefit Act, 1961 S 8 subst~tuted 15, S 2

1961 43 Income-tax Act, 1961 S 2, 10, IOA, IOB, 35,35D, 36, 40,40A, 43, 18, S 3, 4, 5, 6, 7 8, 9, 10, 11, 12, 44AB, 47,49,80C, 80-18, 80-ID, 88E. 1 11 A, 13, 14, 1 5 , 1 6 1 8, 1 9, 20,21, 115AD, 115JB, 115-0, 115WB, IlSWC, 22, 23, 24, 25.26, I15WD,115WE,I15WKB,139,142,143, 27,28,3031,32, 147, 151, 153, 153A, 153B, 153C, 153D, 156, 3 3 , 34 , 36 , 3 7 , 3 8 , 39 , 40, 191, 193, 194C, 195,201,203,206C,251, 41, 42, 43, 44, 46, 47 , 48, 49, 254,271,292C, 295, Fourth Schedule 50,52,57,58,59 amended

S. 80D, 199 substituted rbrd. S 17,45

SIISWKB,268A,273AA,278AB,282A, r b r d , S 2 9 , 5 1 , 5 3 , 5 4 , 5 5 , 292BB ~nserted 56

1962 52 Customs Act, I962 S 28B, 108, 117,129A, 129D, 141,158, rbrd, S 68.69, 70, 71.72, 74, 75, Nohficat~on lssued under ss 1 of S 25 76 amended

1962 52 S 129EE ~nserted ' rbrd, S 73

1966 53 Jawaharlal Nehw Untversity Act, S 19.20 amended 25, S 6 ,7 b!

1966 -'l \ I

' I

1967 37 Unlawful Act~vities (Prevention) S 2,18,23,24,25,45,52,53 amended 35, S 3,7,9, 10, 11.13, 15, 16 - % Act, 1967

- Preamble, S 16A, 18A, 18B, 4 3 4 43F, 5lA, ibrd, S 2,5. 8, 12, 14, entry 33 to the Schedule lliserted 17

S 15, 17 subst~tuted rbrd, S 4 ,6

.-

(ii)

1 2 3 4 k 5

1973 24 North-Eastern H~l l Un~vers~ty S 28,29 amended 25, S 8, 9 Act, 1973

1974 39 Un~vers~ty of Hyderabad Act, S 28 amended rbrd. S 10 1974 1

1975 51 Customs Tar~ff Act, J975 S 9A subst~tuted 18, S 77

4 Sugar Development Fund Act, 1982

3 Sugar Cess Act. 1982

1985 ' 32 Central Exc~se Tar~ff Act, :985

1989 24 Rallways Act, 1989

1990 25 Prasar Bbaratl (Broadcasting Corporat~on of India) Act, 1990

1994 32 Fmance Act, 1994

S 4 (1) bbbb inserted. 4,,S 2

S 3 amended 4 , s 3

F~rst Schedule amended 18, S 8 9

S 2 Amended 11, S. 2

New Chapter IVA lnserted rbrd, S 3

S 6 amended 12, S 2

S 65 amended 18, S 9 0

S. 66,67, 77,94 substituted

S. 71,78,83, 86 95 inserted

V~ce-Prestdent's Fens~on Act, S 2, 3A amended 1997

Finance Act, 2001 Seventh Schedule, S 13 amended

Del~m~tat~on Act, 2002 S 10 amended

Ss. 10A and 10B mserted

Un~t Trust of Ind~a (Transfer of S. 13 subst~tuted Undertakmg and Repeal) Act, 2002

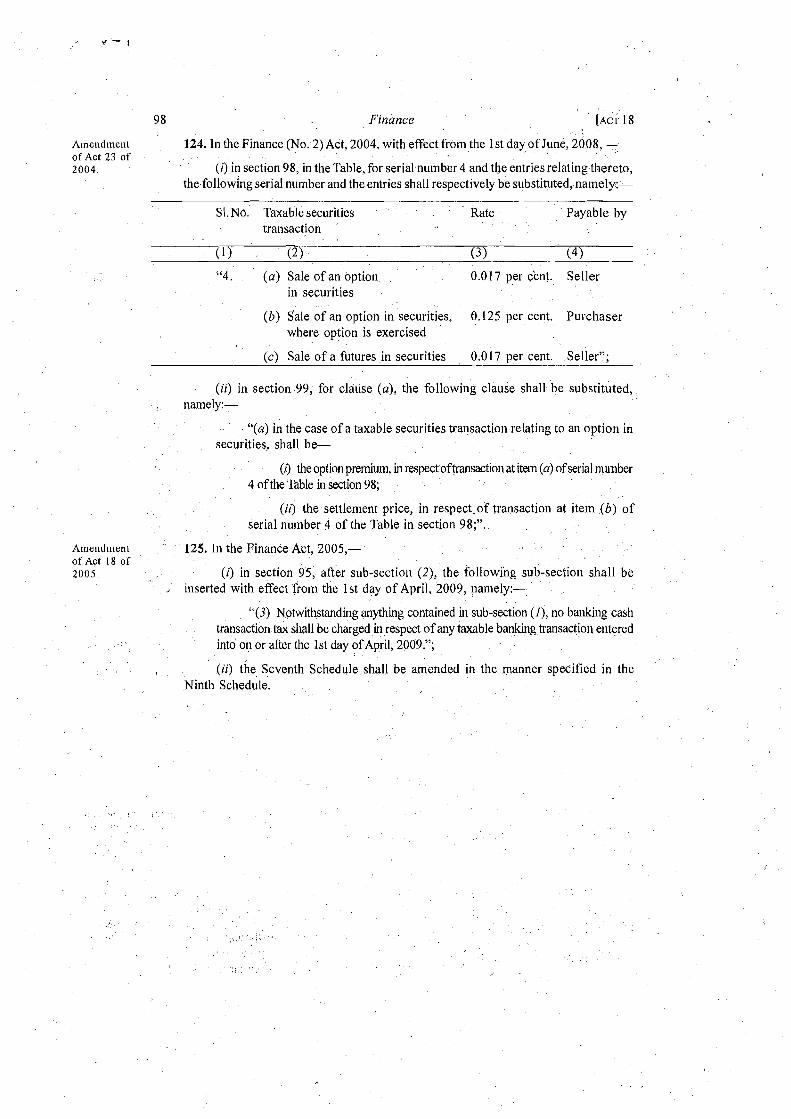

Fmance (No 2) Act, 2004 S 98,99 substituted

rbrd

r brd.

29, S 2, 3

18, S, 122

9, S. 2

ihrd., S. 3

18, S. 123

2005 18 Fmance Act, 2005 S. 95 amended rbrd, S. 125

2006 34 Food Safety and Standards Act, S 3, 5 , 7 amended 13,s 2 , 3 , 4 2006

PART 11.-CENTRAL ORDINANCES kEPEALED J

Year of No of Short title of Ordmance No and section of 2008 Act by wh~ch affected Ordinance Ordmance

2008 1 Delim~tat~on (Amendment) Ordmance, 2008 9 , s 4

2008 4 Sugar Development Fund (Amendment) Ord~nance, 2008 4.S 4

5 Prasar Bharatl (Broadcasting Corporation of Ind~a) Amendment Ordinance. 2008

2008 6 Food Safety and Standards (Amendment) Ordmance, 2008 1 3 , s 5

PART 111.-CONSTITUTION OF INDIA AMENDED

How affected ' No. and sectlon of 2008 Act by which affected

Modlficat~on ~n the 1st of Scheduled Trlbes in the State of Arunachal 14, S 2 Pradesh Part XVIII amended

>

w

I I

I

I

L

1

' i

\

I

I

I i

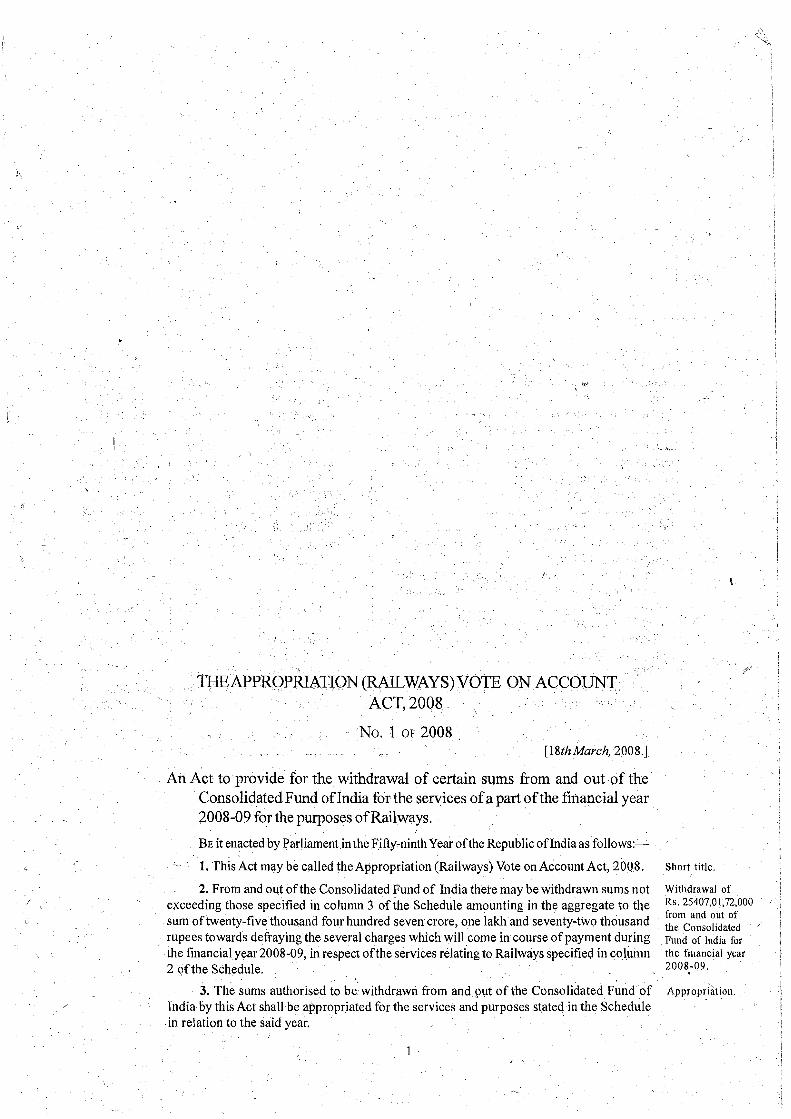

THE APPROP~IATION (RAILWAYS) VOTE ON ACCOUNT C

ACT,2008 , I

1

No. 1 OF 2008 [18th March, 2008.1 I

I An Act to provide for the withdrawal of certain sums from and out of the Consolidated Fund of India for the services of a part of the financial year 2008-09 for the purposes of Railways.

BE it enacted by Parliament in the FiRy-ninth year ofthe Republic of India as follows:-- - 1. This Act may be called the Appropriation (Railways) Vote on Account Act, 2008. Short title.

2. From and out of the Consolidated Fund of India thei-e may be withdrawn sums not Withdrawal of 1 exceeding those specified in column 3 of the Schedule amounting in the aggregate to the RS. 25407>013723000

from and out of sum of twenty-five thousand four hundred seven crore, one lakh and seventy-two thousand the ; rupees towards defraying the several charges which will come in course of payment during F U " ~ of for the financial year 2008-09, in respect ofthe services relating to Railways specified in column the financial year i

2008-09. 2 ofthe Schedule. I

3. The sums authorised to be withdrawn from and out of the Consolidated Fund of Appropr~ation I India by this Act shall be appropriated for the services and purposes stated in the Schedule 1

in relation to the said year. i I

1 I

J

,

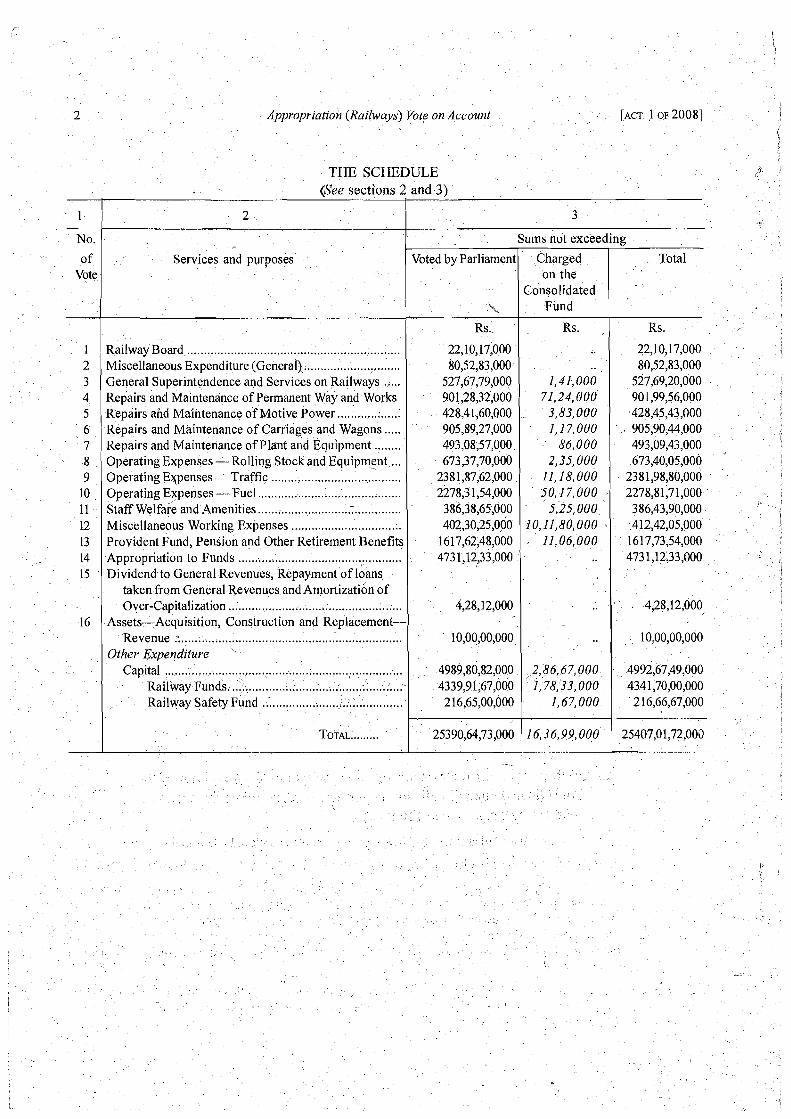

2 Appropriation (Rail~vays) Vote on Account [ACT 1 OF 20081

THE SCHEDULE i i

1

No.

of Vote

I 2 3 4 5 6 7 8 9

10 11 12 13 14 15

16

(See sections 2

2

Services and purposes

Railway Board .............................................................. Miscellaneous Expenditure (General) ............................. General Superintendence and Services on Railways ..... Repairs and Maintenance of Permanent Way and Works Repairs and Maintenance of Motive Power ................... Repairs and Maintenance of Carriages and Wagons ..... Repairs and Maintenance of Plant and Equipment ........ Operating Expenses - Rolling Stock and Equipment ... Operating Expenses - Traffic ....................................... Operating Expenses - Fuel ........................................... Staff Welfare and Amenities ........................................... Miscellaneous Working Expenses ................................. Provident Fund, Pension and Other Retirement Benefits Appropriation to Funds ................................................. Dividend to General Revenues, Repayment of lbans

taken from General Revenues and Amortization of ....................... Over-Capitalization ............................ ,

Assets-Acquisition, Construction and Replacement- Revenue .: ..................................................................

Other Expenditure Capital .....................................................................

Railway Funds. ................................................. Railway Safety Fund .........................................

TOTAL.. .......

and 3)

3

Total

Rs. r

22,10,17,000 80,52,83,000

527,69,20,000 90 1,99,56,000 428,45,43,000 905,90,44,000 493,09,43,000 673,40,05,000

2381,98,80,000 2278,81,71,000 386,43,90,000 412,42,05,000

1617,73,54,000 4731,12,33,000

. 4,28,12,000

10,00,00,000

4992,67,49,000 4341,70,00,000 2 16,66,67,000

- 25407,01,72,003

Voted by Parliament

k

Rs . 22,10,17,000 80,52,83,000

527,67,79,000 901,28,32,000 428,41,60,000 905,89,27,000 493,08,57,000 673,37,70,000

2381,87,62,000 2278,31,54,000 386,38,65,000 402,30,25,000

1617,62,48,000 4731,12,33,000

4,28,12,000

10,00,00,000

4989,80,82,000

Sums not exceeding

Charged on the

Consolidated Fund

Rs .

1,41,000 71,24,000

3,83,000 I, 17,000

86,000 2,35,000

ll,18,000 50,17,000

5,25,000 10,11,80,000 . 11,06,000

..

2,86,67,000 4339,91,67,000 I, 78,33,000 216,65,00,000 1 1.67,OOO

25390,64,73,000 16,36,99,000

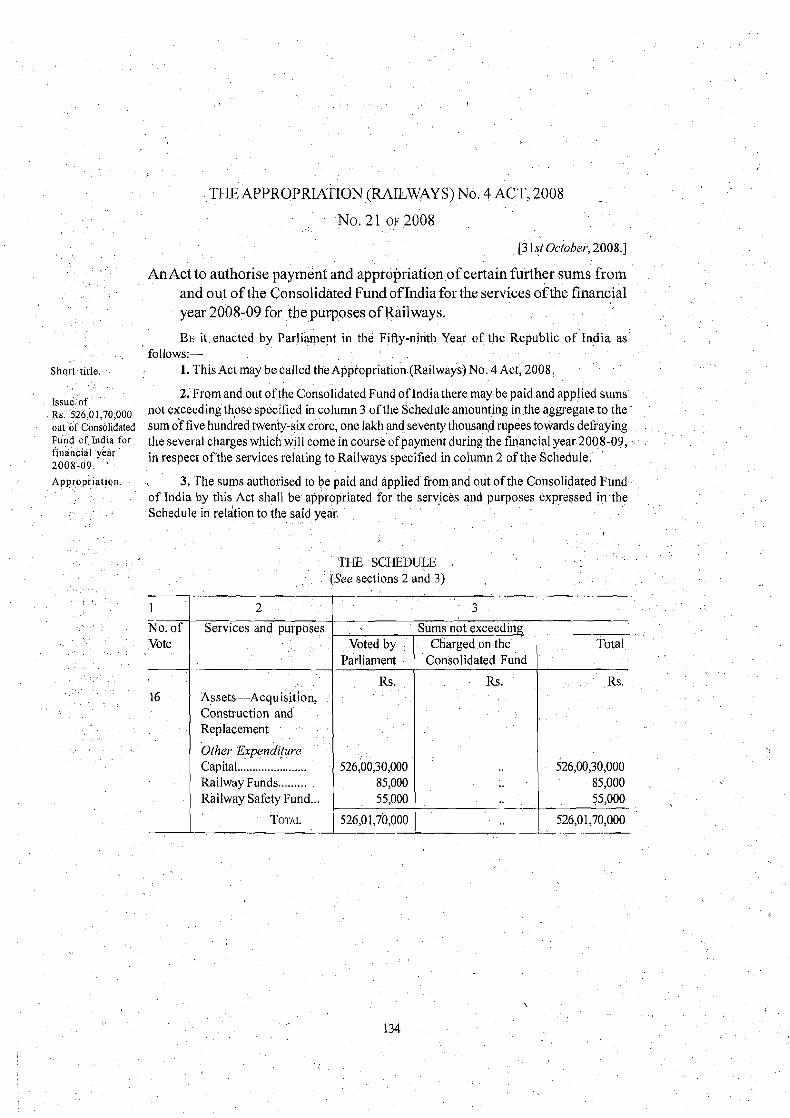

THE APPROPRIATION (RAILWAYS) ACT, 2008

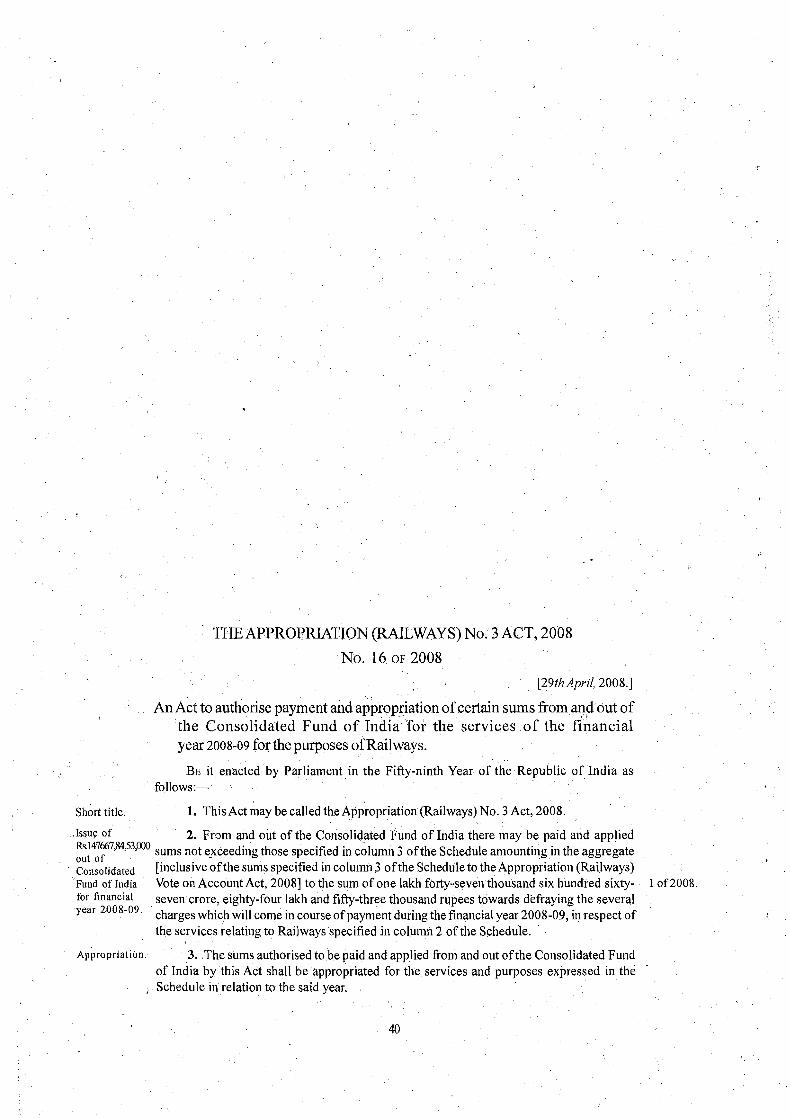

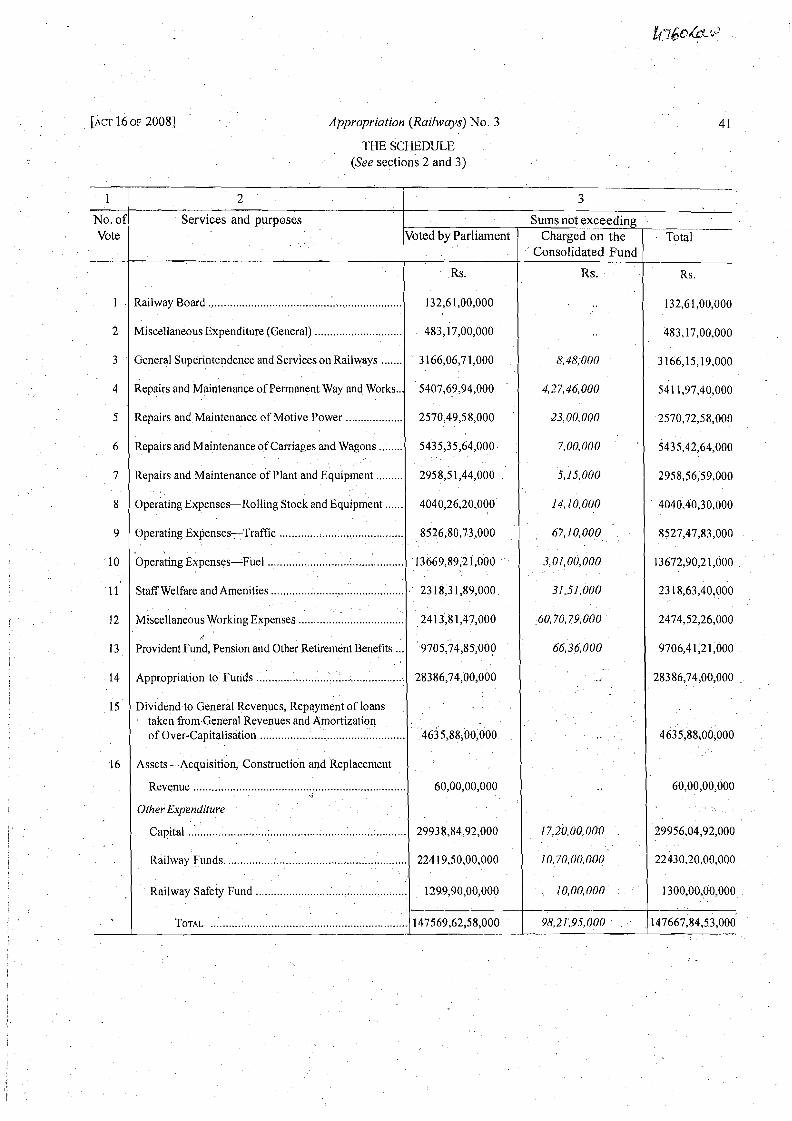

No. 2 OF 2008 \ [18th March, 2008.1

An Act to authorise payment and appropriation of certain fwther sums from and out of the Consolidated Fund of India for the services of the financial year

'

2007-08 for the purposes of Railways.

BE it enacted by Parliament in the Fifly-ninth Year of the Republic of India as follows:-

1. This Act may be called the Appropriation (Railways) Act, 2008. short title.

2. From and out ofthe Consolidated Fund of Indiathere may be paid and applied sums Issue of not exceeding those specified.in column 3 of the Schedule amounting in the aggregate to the Rs 2370154174,000

out of the sum oftwo thousand three hundred seventy crore, fifty-four lakhs and seventy-four thousand Consolidated rupees towards defraying the several charges which will come in course of payment during ~~~d of~ndia the finan~ial~year 2007-08, in respect ofthe services relating to Railways specified in column for the financial 2 of the Schedule. year 2007-08

3. The sums authorised to be paid and applied fiom and out of the Consolidated Fund Approprlatroll.

of India by this Act shall be appropriated for the services and purposes expressed in the Schedule in relation to the said year.

3

I I

Appropriation (Railways)

THE SCHEDULE I

1

No.

of Vote

3

4 5

8

10

12

13

14

15

16

, .

\

i

/

. *

8

(See sections 2

2

Services and purposes

General Superintendence and Services on Railways ..... Repairs and Maintenance of Permanent Way and Works

Repairs and Maintenance of Motive Power ................... Operating Expenses - Rolling Stock and Equipment .... Operating Expenses - Fuel ...........................................

< Miscellaneous Working Expenses ................................. Provident Fund, Pension and Other Retirement

Benefits ...................................................................... Appropriation to Funds , ............................................... Dividend to General Revenues, Repayment of loans

taken from General Revenues and Amo'rtization of

Over-Capitalisation .................................................... Assets-Acquisition, Construction and Replacement-

Other Expenditure

Capital ........................................................................ .......................................................... Railway Funds

Special Railway Safety Fund ......................................

TOTAL ,..... ,

1 > and 3) B

! 3

4

I

-bo

Total I I !

Rs. i 1

10,56,000 !

3,53,74,000 ;

96,000

6,33,000 i 12,85,42,000

\ i

61,85,19,000 i i I

6,55,000 I

1606,15,54,000

309,58,00,000

I

I

375,17,11,000

96,84,000 I

18,50,000 I

2370,54,74,000

I

Voted by Parliament

&.a

..

..

10,59,75,000

43,57,58,000

1606,15,54,000

309,58,00,000

,

365,00,00,000

..

..

Sums not exceeding

Charged on the

Consolidated Fund

Rs . 10,56,000

3,53,74,000

96,000

6,33,000

2,25.67,000

18,27,61,000 1

6,55,000

..

, 10,17,11,000

96,84,000

18,50,000 I

2334,90,87,000 35,63,87,000

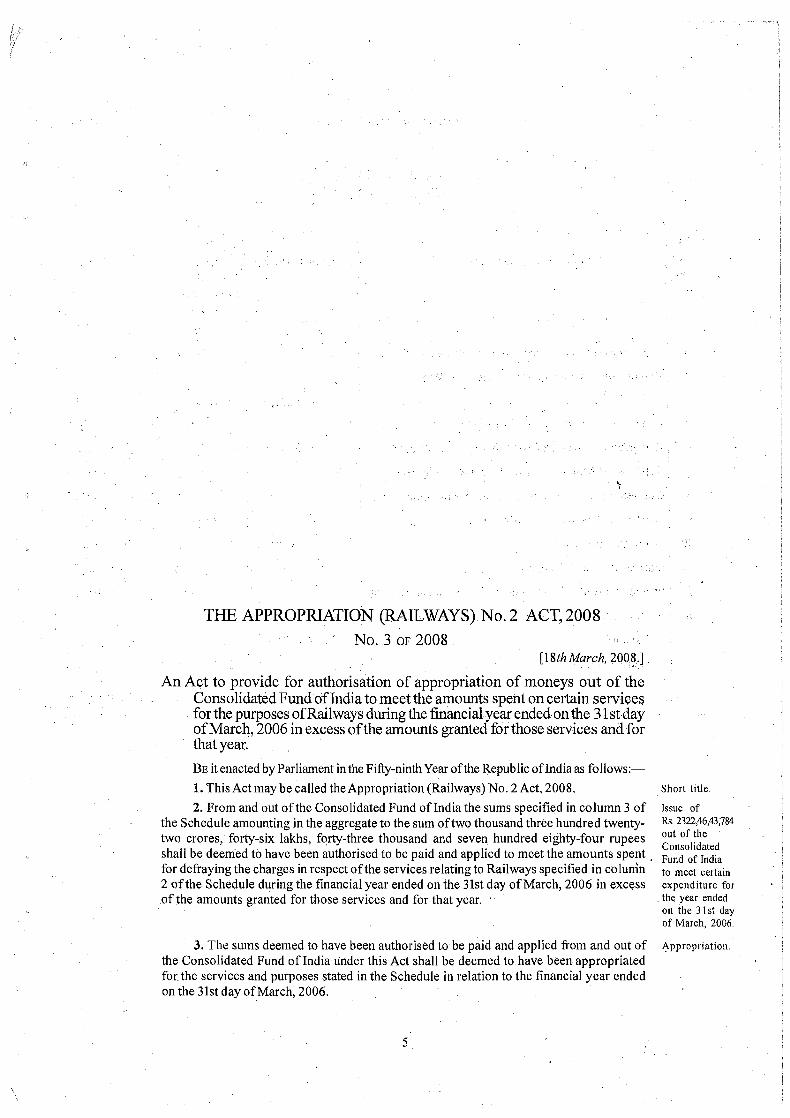

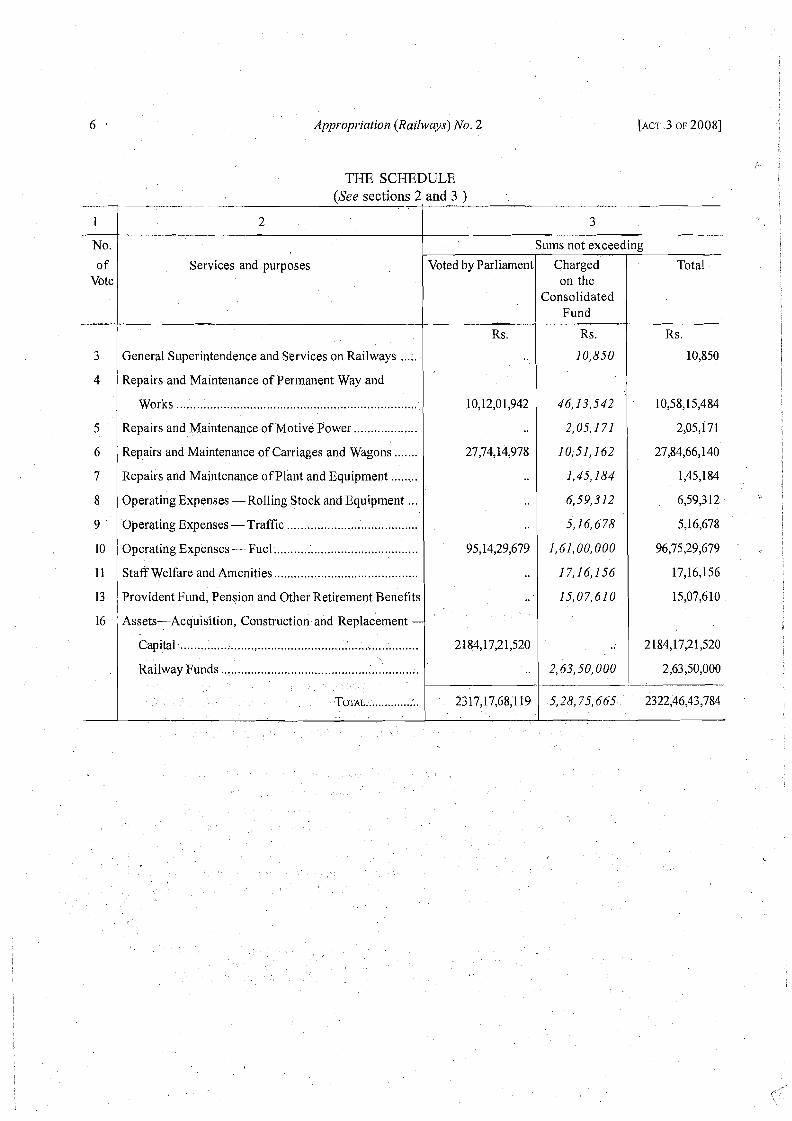

THE APPROPRIATION (RAILWAYS) No. 2 ACT, 2008 ' No. 3 OF 2008

[l8th March, 2008.1

An Act to provide for authorisation of appropriation of moneys out of the Consolidated Fund of India to meet the amounts spent on certain services for the purposes of Railways during the financial year ended on the 3 1 st day of March, 2006 in excess of the amounts granted for those services and for that year,

BE it enacted by Parliament in the Fifty-ninth Year of the Republic of India as follows:-

1. This Act may be called the Appropriation (Railways) No. 2 Act, 2008. Short title

2. From and out of the Consolidated Fund of India the sums specified in colu~nn 3 of Issue of

the Schedule amounting in the aggregate to the sum of two thousand three hundred twenty- 232W6P;J*4

two crores, forty-six lakhs, forty-three thousand and seven hundred eighty-four rupees Out

Consolidated shall be deemed to have been authorised to be paid and applied to meet the amounts spent Fund of India for defraying the charges in respect ofthe services relating to Railways specified in column to lneet certain 2 of the Schedule during the financial year ended on the 31st day of March, 2006 in excess expenditure for

of the amounts granted for those services and for that year. ' the year ended on the 3 1 st day of March, 2006

3. The sums deemed Lo have been authorised to be paid and applied fioin and out of b'ppropr~ation the Consolidated Fund of India under this Act shall be deemed to have been appropriated for the services and purposes stated in the Schedule in relation to the financial year ended on the 31st day of March, 2006.

6 * Appropriation (Railways) No. 2 [ACT .3 OF 20081

THE SCHEDULE (See sections 2 and 3 )

3 1 General Superintendence and Services on Railways ..... I . . I 10 ,8501 10,850

1

No.

of Vote

4 j Repairs and Maintenance of Permanent Way and 1 ' I i I

I . Works ............. .: ................................................... 1 10,12,01,942 1 46.13.542 ' 1 10,58,15,484

2

Services and purposes

5 1 Repairs and Maintenance of Motive Power ................... I

3

I 6 I Repairs and Maintenance of Carriages and Wagons .......

Sums not exceeding

........ 7 1 Repairs and Maintenance of Plant and Equipment I .. 1 1,45,184 1 1,45,184

Voted by Parliament

Rs .

11 1 Staff Welfare and Amenities ..................................... I . 1 17,16,156 1 17,16,156

Charged on the

Consolidated Fund

Rs.

8

9

13 1 Provident Fund, Pension and Other Retirement Benefits I

16 Assets-Acquisition, Construction and Replacement i

Total

Rs.

Operating Expenses - Rolling Stock and Equipment ... Operating Expenses -Traffic .......................................

10 Operating Expenses -Fuel ........................................... I

Capital ....................................................................... Railway Funds ...........................................................

TOTAL.. ............ .:.

2184,17,21,520

..

2317,17,68,119

2184,17,21,520

2,63,50,000 2,63,50,000

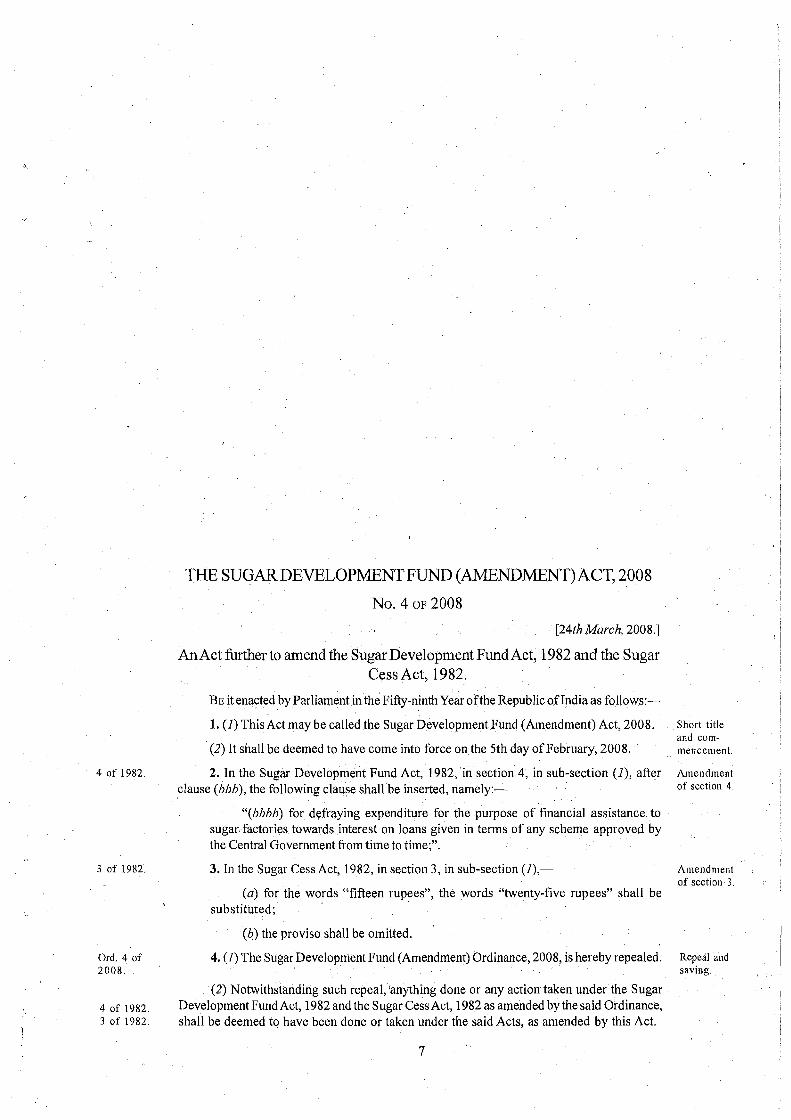

THE SUGAR DEVELOPMENT FUND (AMENDMENT) ACT, 2008

No. 4 OF 2008

[24th March, 2008.1

An Act further to amend the Sugar Development Fund Act, 1982 and the Sugar Cess Act, 1982.

BE it enacted by Parliament in the Fifty-ninth Year ofthe Republic of India as follows:-

1. (I) This Act may be called the Sugar Development Fund (Amendment) Act, 2008.

(2) It shall be deemed to have come into force on the 5th day of February, 2008.

4 of 1982. 2. In the Sugar Development Fund Act, 1982, in section 4, in sub-section (I), after clause (bbb), the following clause shall be inserted, namely:-

"(bbbb) for defraying expenditure for the purpose of financial assistance to sugar, factories towards interest on loans given in terms of any scheme approved by the Central Government from time to time;".

3 of 1982. 3. In the Sugar Cess Act, 1982, in section 3, in sub-section (I) ,-

(a) for the words "fifteen rupees", the words "twenty-five rupees" shall be substituted;

Ord. 4 of 2008.

(b) the proviso shall be omitted.

4. (1) The Sugar Development Fund (Amendment) Ordinance, 2008, is hereby repealed.

(2) Notwithstanding such repeal, anything done or any action taken under the Sugar J of ,982 Development Fund Act, 1982 and the Sugar CessAct, 1982 as amended by the said Ordinance, 3 of 1982. shall be deemed to have been done or taken under the said Acts, as amended by this Act.

Short title and com- mencement.

Amendment of sectlon 4.

Amendment of section 3 .

Repeal and saving.

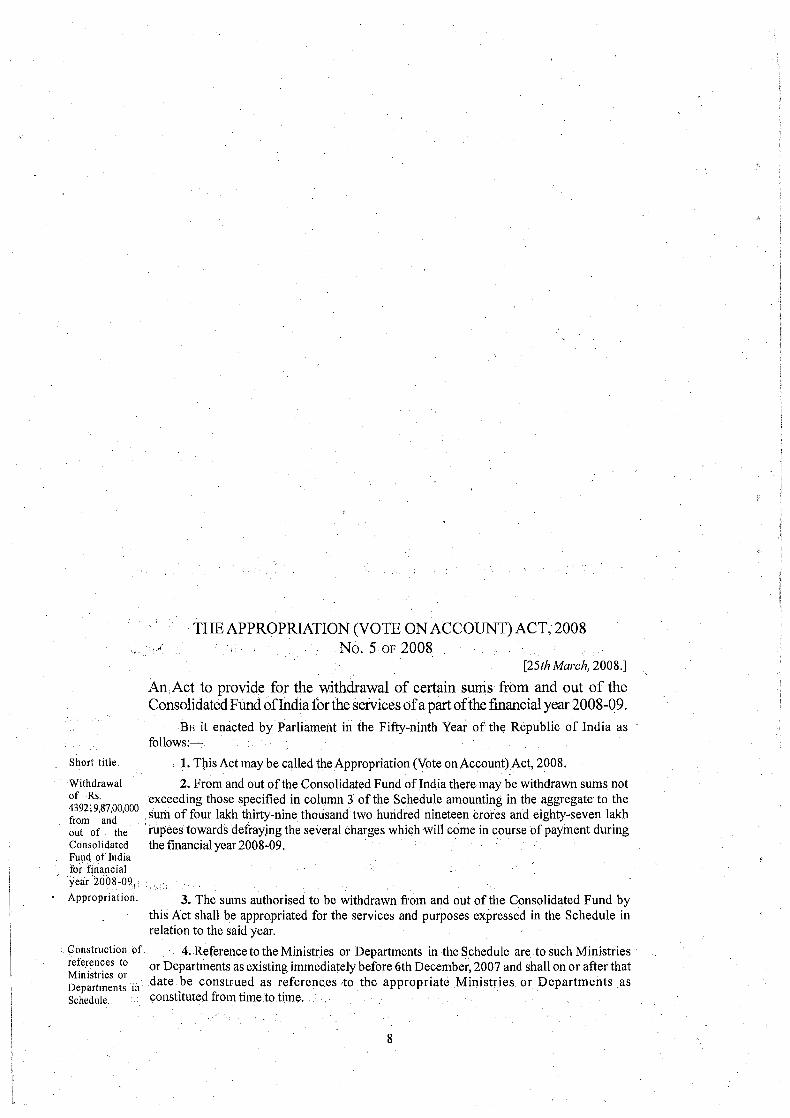

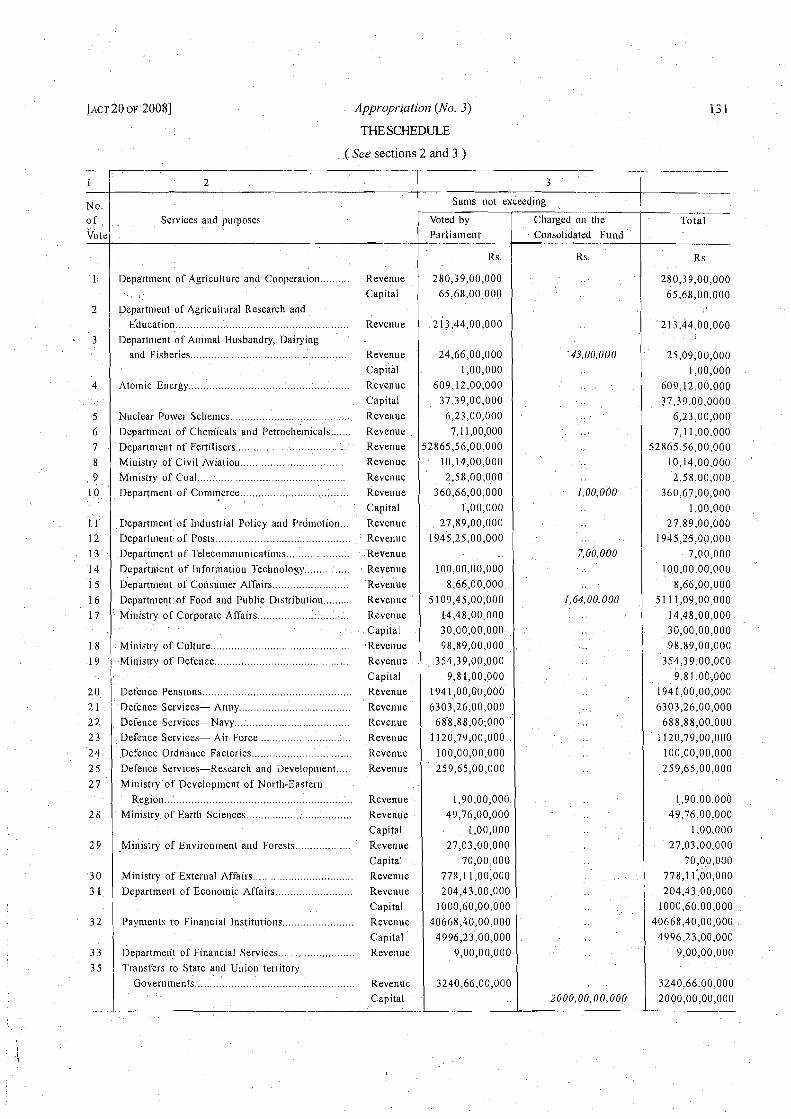

THE APPROPRIATION (VOTE ON ACCOUNT) ACT, 2008 No, 5 OF 2008

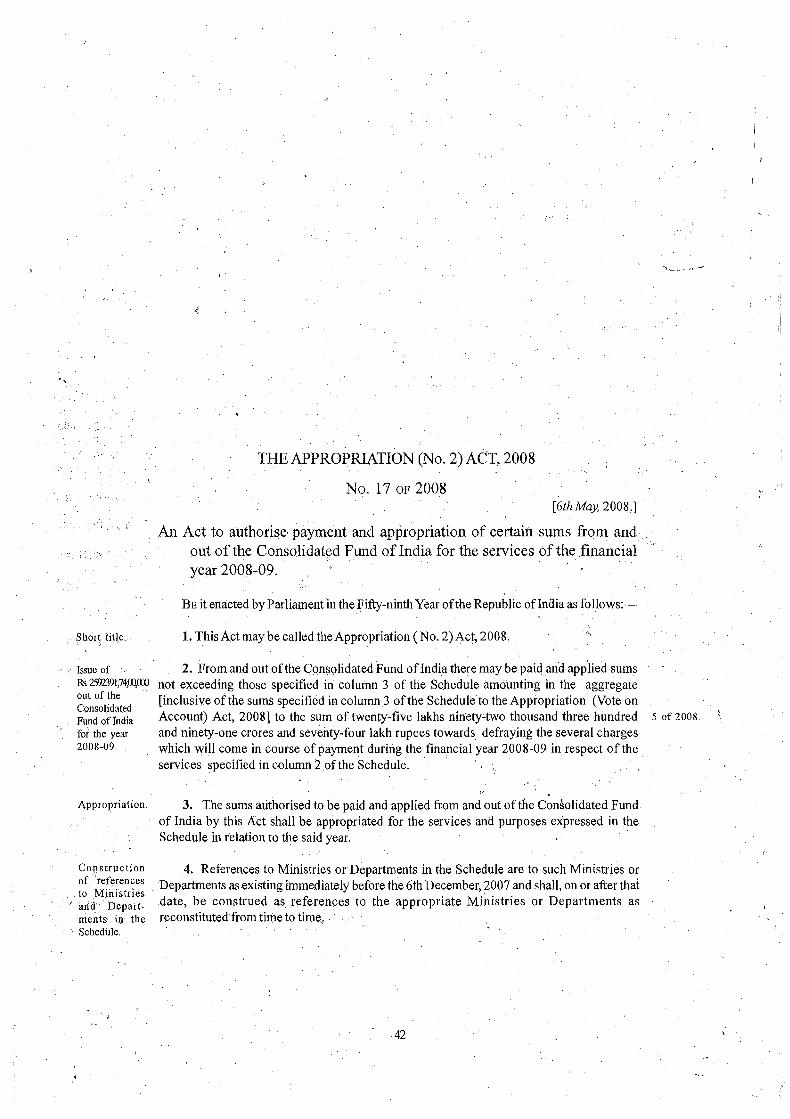

[25th March, 2008.1

An Act to provide for the withdrawal of certain sums from and out of the Consolidated Fund of India for the services of apart of the financial year 2008-09.

BE it enacted by Parliament in the Fifty-ninth Year of the Republic of India as follows:-

Short title 1. This Act may be called the Appropriation (Vote on Account) Act, 2008.

W~thdrawal 2. From and out of the Consolidated Fund of India there may be withdrawn sums not of RS exceeding those specified in column 3 of the Schedule amounting in the aggregate to the 439219's7'00'ooo sum of four lakh thirty-nine thousand two hundred nineteen crores and eighty-seven lakh from and out of the rupees towards defraying the several charges which will come in course of payment during Consol~dated the financial year 2008-09. Fund of Ind~a for financial year 2008-09. ,

Appropriation 3. The sums authorised to be withdrawn from and out of the Consolidated Fund by this Act shall be appropriated for the services and purposes expressed in the Schedule in relation to the said year.

construct lo^^ of 4. Reference to the Ministries or Departments in the Schedule are to such Ministries references or Departments as existing immediately before 6th December, 2007 and shall on or after that Ministries or Depart,nenls date be construed as references to the appropriate Ministries or Departments as Schedule. coilstitured froill tiine to time.

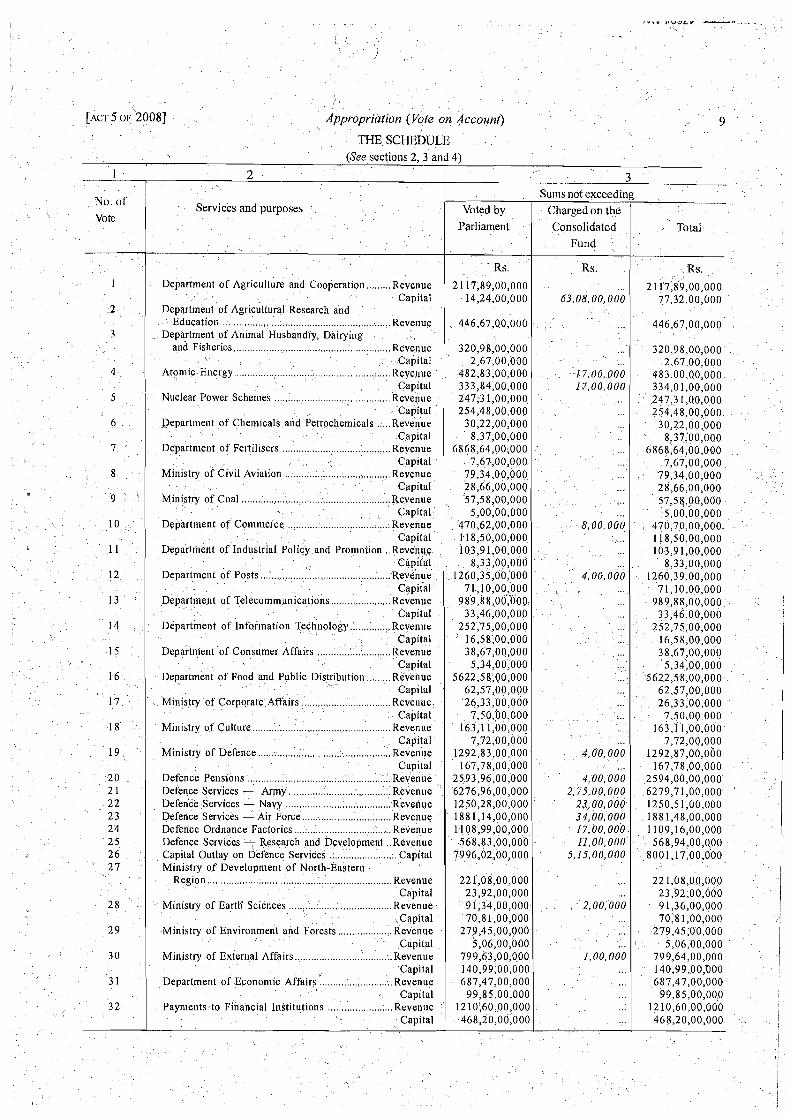

[ACT 5 OF 20081 Appropriation (Vote on Account) 9

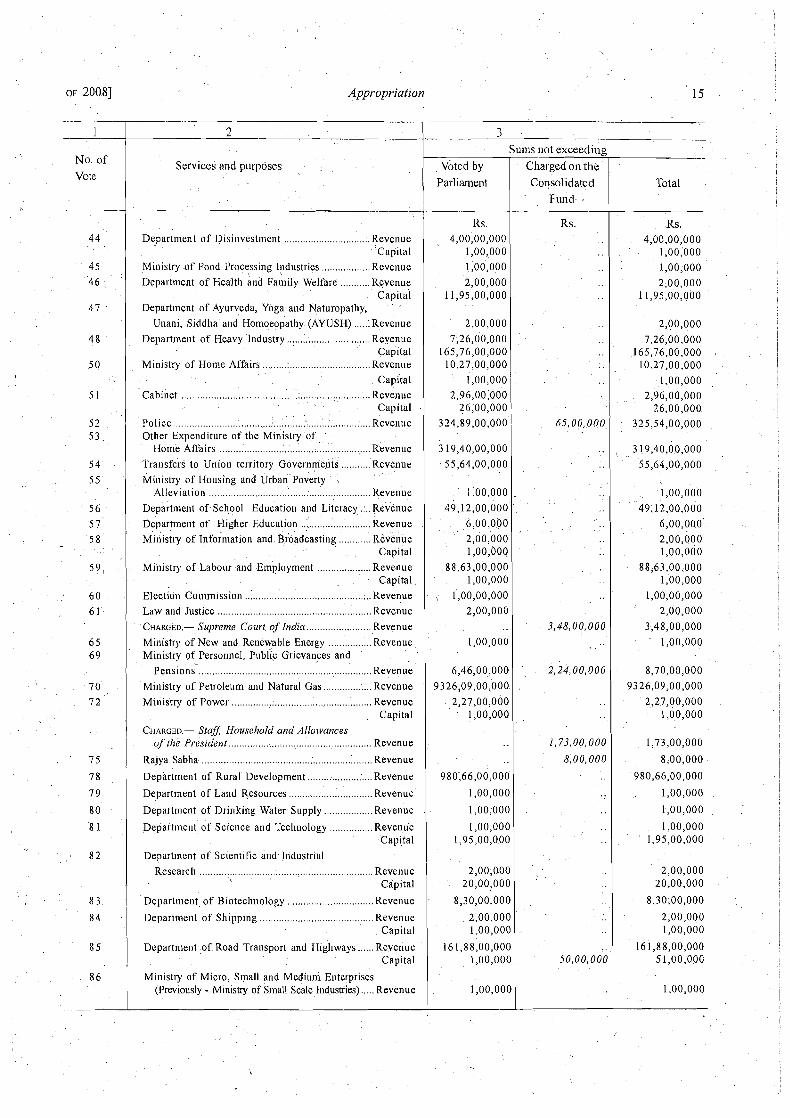

1

h o o f

vote

1

2

3

4

5

6

7

8

e 9

10

11

12

13

14

15

16

17

18

19

20 2 1 2 2 2 3 2 4 25 2 6 2 7

28

2 9

3 0

3 1

3 2

I

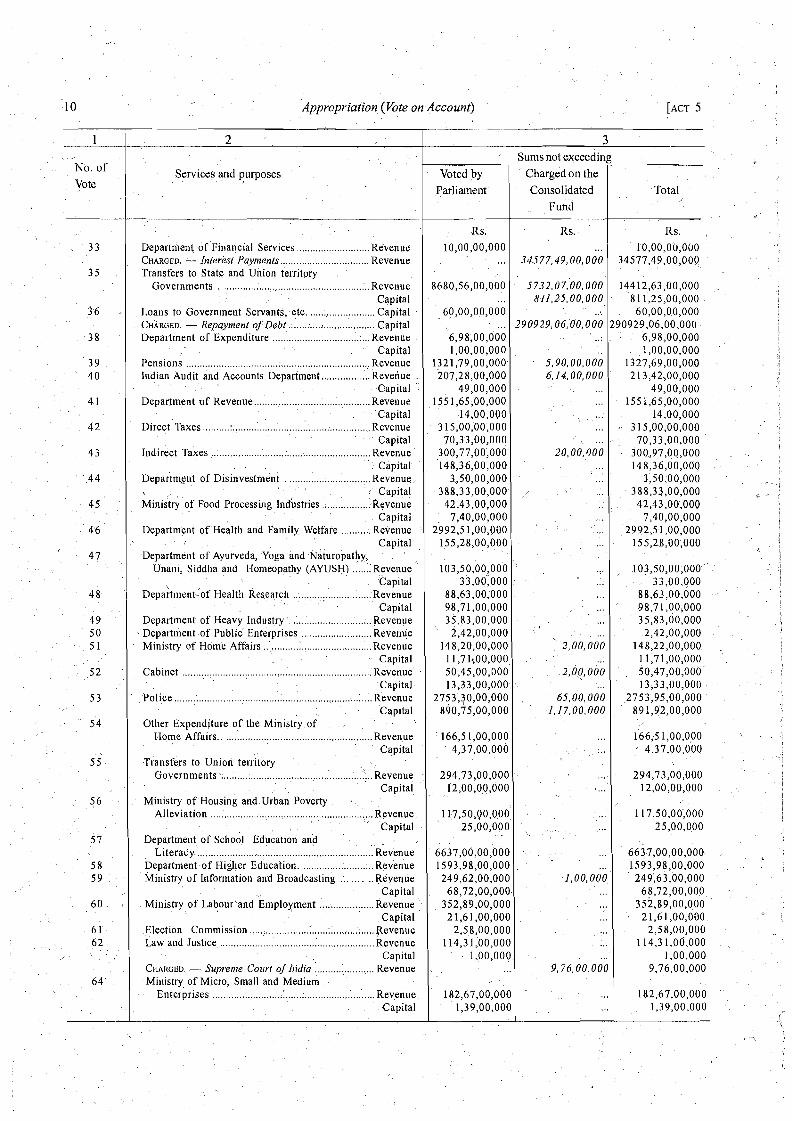

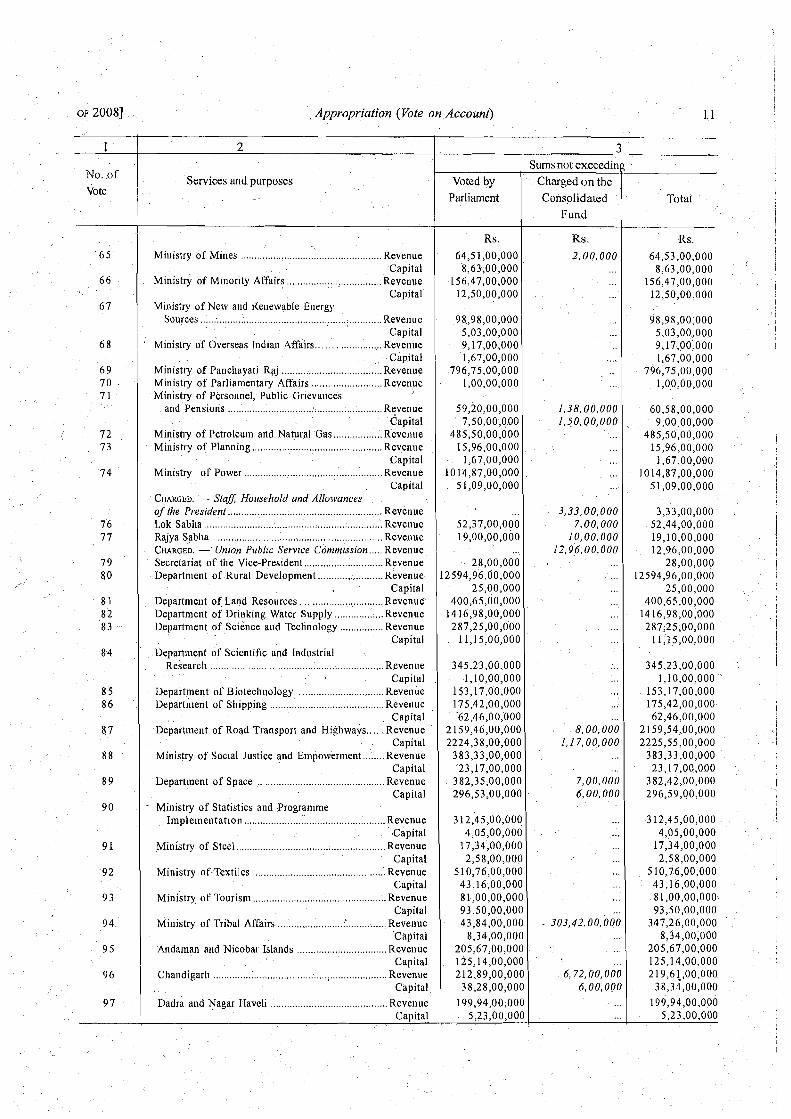

THE SCHEDULE (See sections 2,3 and 4)

2

Services and purposes

Department of Agr~culture and Cooperation . . Revenue Capital

Department of Agr~cultural Research and Educatior. . . . . . . . . . . . . . . . . . . . . . . . . . . . Revenue

Department of Animal Husbandry, D a i r y ~ ~ ~ g

Voted by Parliament

Rs.

21 17,89,00,000 14,24,00,000

446,67,00,000

. . . . . . . . . and F~sharies . . . . . . . . . . Revenue 320,98,00,000 i Cap~tal 2,67,00,000 Atonl~c Energy . . . . . . . ..... Revenue 482,83,00,000

Capital 333,84,00,000 Nuclear Power Schemes . . . . . . . .. Revenue 247,3 1,00,000

Capital 254,48,00,000 Qepartment of Chem~cals and Petrochemicals . Revenue 30,22,00,000

Cap~tal 8,37,00,000 Department of Fert~l~sers . . . . . . . . . . . . . . . . . . . . . Revenue 6868,64,00,000

Cap~tal 7,67,00,000 Ministry of Clv~l Av~at~on . . . . . . . . . . . . . . . . . . . . . . Revenue 79,34,00,000

Capital 28,66,00,000 Ministry of Coal . . . . . . . . . . . . . . . . . . . . . . . Revenue 57,58,00,000

Capital 5,00,00,000 Depart~neut of Commerce . . . . . . . . . . . . . ..Revenue 470,62,00,000

Capital 118,50,00,000 Department of Industrial Policy and Promoilon Revenue 103,91,00,000

Cap~tal 8,33,00,000 Departmeut of Posts . . . . . . . . . . . . . . . . . . . . . . . . . . . Revenue 1260,35,00,000

Capital 71,10,00,000 Department of Telecommunicat~ons .............. Revenue 989,88,00,000

Capital 33,46,00,000 Department of lnfor~nat~on Technology ........... .Revenue 252,75,00,000

Cap~tal 16,58,00,000 Department of Consumer Affa~rs ... ....I ............ Revenue 38,67,00,000

Capital 5,34,00,000 Department of Food and Public Distribution Revenue 5622,58,00,000

Cap~tal 62,57,00,000 . . . . . . . M1111stry of Corporate Affa~rs . Revenue 26,33,00,000

Cap~tal 7,50,b0,000 M~n~st ry of Culture . . . . . . . . Revenue 163,l 1,00,000

Cap~tal 7,72,00,000 M ~ n ~ s t r y of Defence . . . . . . . . . . . . . . . . . . . . . . Revenue 1292,83,00,000

Cap~tal 167,78,00,000 . . . . . . . . . . . . . . . . . . . . . . . Defence Pens~ons Revenue 2593,96,00,000

Defeqce Serv~ces - Army. . . . . . . . . . . . .Revenue 6276,96,00,000 Defence Services - Navy . . . . . . . . . . . . . . . . . . . . . Reve~iue 1250,28,00,000 Defence Serv~ces - Air Force. . . . . . . . . . . . . . . . .Revenue 188 1,14,00,000 Defence Ordnance Factor~es . . . . . . . . . . . . . . Revenue 1108,99,00,000 Defence Services - Research and Development Revenue 568,83,00,000 Capital Outlay on Defence Serv~ces .............. Cap~tal 7996,02,00,000 Ministry of Development of North-Eastern

Region . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Revenue 221,08,00,000 Capital 23,92,00,000

M~nistry of Earth' Sc~ences ...................... Revenue 91,34,00,000 , Cap~tal 70,81,00,000

Min~stry of Environment and Forests . . . . . . . . . .Revenue 279,45,00,000 Cap~tal 5,06,00,000

M ~ n ~ s t r y of External Affa~rs.. . ...... Revenue 799,63,00,000 Cap~tal 140,99,002000

Department of Econom~c Affa~rs . . . . . . . Revenue 687,47,00,000 Cap~tal 99,85,00,000

. . . . . . . . . . . . Paynlents to Financ~al lnst~tut~ons .Revenue 12 10,60,00,000 Cap~tal 468,20,00,000

3 Sums not exceeding

Charged o n the

Consolidated

Fund

Rs.

63,08,00,000

.

Total

Rs.

21 17,89,00,000 77,32,00,000

446,67,00,000

..

17,OO. 000 17,00,000

. .

...

...

... 8,OO. 000

. .

...

4,00,000

. .

..

4,0'0,000 . .

4,00,000 2,75,00,000

23,00,000 34,00,000 17.00,OOO 11.00,OOO

5,15,00,000

, 2,00,000 . .

... 1,00,000

..

320,98,00,000 2,67.00.000

483,00,00,000 334,01,00,000 247,3 1,OO.OOO 254,48,00,000

30,22,00,000 8,37,00,000

6868,64,00,000 7,67,00,000

79.34,00,000 28,66,00,000 57,58,00,000

5,00,00,000 470,70,00,000 11 8,50,00,000 103,9 1,00,000

8,33,00,000 1260,39,00,000

71,10.00,000 989,88,00,000

33,46,00,000 I

252,75,00,000 16,58,00,000 38,67,00,000

5,34:00,000 5622,58,00,000

62,57,00,000 26,33,00,000

7.50.00.000 163.1 1,00,000

7,72,00,000 1292,87,00,000

167,78,00,000 2594,00,00,000 6279,71,00,000 1250,51 ,OO,OOO 1881,48,00,000 1 109,16,00,000

568,94,00,000 1 8001,17,00,000

22 1,08,00,000 23,92,00,000 91,36,00,000 70,s 1,00,000

279,45,00,000 5,06,00,000

799,64,00,000 i

140,99,00,000 I

687,47,00,000 I 99,85,00,000 I

1210,60,00,000 468,20,00,000

L I

10 Appropriation (Vote on Account) [ACT 5

N o . o f , ' ~ ? : p u r p o s ~ s

Parliament Voted by

Rs.

10,00,00,000 ...

8680,56,00,000 ...

. 60,00,00,000 ...

. 6,98,'00,000 1 ,OO,OO,OOO

1321,79,00,000- 207,28,00,000

49,00,000 155 1,65,00,000

14,00,000 315,00,00,000

70,33,00,000. 300,77,08,OOO 148,36,00,000

3,50,00,000 388,33,00,000

42,43,00,000 7,40,00,000

2-992,s 1,00,000 155,28,00,000 . .

103,50,00,000 33.00,000

88,63,00;000 98,71,00,000

< 35,83,00,000 $,42,00,000

14 8,20,00,000 11,7.1+,00,000 50,45,00,000 13,33:00,000

2753,30,00,000 890,75,00,000

. 166,5 1,00,000 4,37,00,000

294,73,00,000 i2,00,00,000

11-7,50,~0,000' 25,00,000

..

. 6637,00,00,000 1593,98,00,000 249,62,00,000

68,72,00,000 352,89,00,000

21,61,00,000 2,58,00,000

114,3 I ;00,000 1.00,OOO

...

182,67,00,000 1,39,00,000

. .

, 33

3 5

36-

3 8

3 9 ' ' 40

4 1

42

4 3

4 4

45

46

' 47 ..

--

Department of Financial Services ........................... Revenue ................................ CHARGED. - Interest Payments Revenue

Transfers to State and Union territory . '

Governments . ........................................... Revenue Capital

Loans to Government Serva11ts;etc. ........................ Capital CHARGED. - Repayment of Debt ....... ; .... ; .................. Capital Department of Expenditure Revenue

. Capital Pensions ................................................................... Revenue Indian Audit and Accounts Depariment .................. Reveliue -

Capital .... ...................................... . Department ~f Revenue Revenue

Capital Direct Taxes .......... revenue

Capital Indirect Taxes ........................................................... Revenue

. Capital ~ e ~ a r t ~ e n t of Disinvestment .................... 1 .......... Revenue

, . . , , . . : Capital

............... . Ministry of Food Processing lnd'ustries .: : R ~ v e n u e Capital

Departmetit of ~ e a l t h and Fimily Welfare .........;. ~ e i e n u e . . Capital'

Department of Ayurveda, yoga a n d . ~ i t u r o p a t h ~ , Unani, Siddha and I-Iomeopatliy (AYUSH) ....... Revenue .

I Capital

3 Sums not exceeding

charged Consolidated o n the

Fund

Rs. ...

34577,49,00,000

5732,07,'00,000 811,25,00,000

... 290929,06,'00,000

. , . . . . . ...

5,90,00,000 6,14.00,000

. . . . . .

...

... ? .

. . . . .

... \

20,00,000 ... ... ... . . ... ...

. . . ...

... !

- . ... ... ... ... ... '

2,00,000 ... . . -

. . 2.00, 000 . *

... .,

. . 65,00,000 1,17,00,000

...

... . .

. . . .

...

...

... \ , ' ,

. . . ... :

. . ... 1 ,00 ,000

... . . . . .

... .....

.:. . . . .

9,76,00.000

...

...

Total

Rs . 10,00,00,000

34577,49,00,000

14412,63,00,000 81 1,25,00,000

60,00,0,0,000 290929,06,00,000

6,98,00,000 1,00,00,000

1327,69,00,000 21 3,42,00,000

49,00,000 . . 1551,65,00,0D0

14,00,000 315,00,00,000

70,33,001000 300,97,00,000 148,36,00,000

3;50,00,000 . 388,33,00,000

42,43,00,000 7,40,00,000

2992,51,00,000 155,28,00,000

.103,50,00,000~ 33,OO.OOO

88,63,00,000 . -

.98,7l,C!O,OOO 35,83,00,000

2,42,00,000 148,22,00,000.

1 1 ;71 ,OO,OOO ' . . . 50,47,00,000

13,33,00,000 .2753,95,00,000

891,92,00,000

166;s 1,00,000 4.37,00,000

. .

294,73,00,000 ~ 12,00,00,000

11,7,50,00~000 25,00,COO

6637,00,00,000. 1593,98,00,000 249;63,00,000

68,72,00,000 . 352,89,00,000

2 1,6 1 ,OO,OOO 2,58,00,000

1 14.3 1.00.000 1 ,OO,OOO

9,76,00,000

182,67,00,000 1,39,00,000

48 1

49 5 0 5 1

5 2

5 3

. ' 54

55

. .

5 6

57

5 8 59 . ,

. . 60

6 1 6 2

64 .

. .

Department- of Health Researct~ ............................. Revenue Capital

Department of Heavy industry Department -of Public fi~terprises ........................... Revenue Ministry of Home Affairs ..................................... ;..Revenue

Capital ................... ................................... . Cabinet .. ~ e v e n u e

Capital- .............. .... ............ . . . ..................... . Police : ..: : ~ i v e n u e

. Capital Other Expenditure qf the ~ i n i s t ; ~ of

. . Home Affairs.. ................................................ Revenue

Capital . Transfers to Union territory

.................. ................................. . Ciovernments. .. Revenue Capital,

Ministry o f ~ o u s i n ~ and Urban Poverty a

........................................................ Alleviation Revenue. , . Capital

Department o f school Education and ........................................................... Literacy: Revenue

.......................... Departmentof Higher Education. Revenue Ministry of Information and Broadcasting ....... ..Revenue

Capital .................... . Ministry of Labour'and Employment Revenue

Capital Election Commission ...................... : ....... : ...... : . . Revenue Law and Justice. Revenue

Capital CHARGED. -. Supre~iie Court of Itidia ...................... Revenue Ministry, of Micro, Small and Medium

Enterprises Revenue ,Capital

. Appropriation (Vote on Account)

No. o f

Vote Services and purposes

Sums not exceeding

Votcd by / C h a r g e d o n t h e

Millistry of Mines ............................................ Revenue Capital

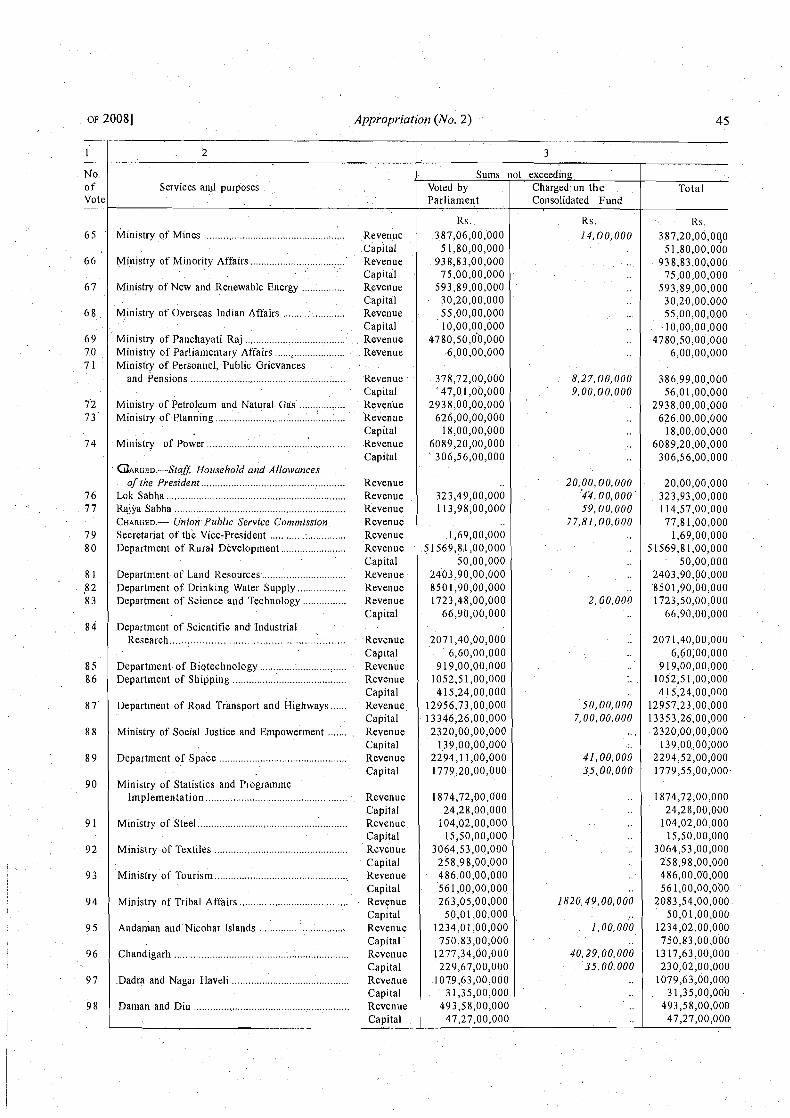

Ministry of Miuority Affairs ............................. .Revenue Capital

Ministry of New a~id Keuewable E~iergy Sources .................................................................. Revenuc . .

Capital . Ministry ofoverseas Indian Affairs ....................... Revenue capital

Ministry of Panchayati Raj .................................. Revenue Ministry of Parliamentary Affairs .......................... Revenue

-Ministry of Personnel, Public Grievai~ces and Pensions ..................................................... Revenue

Capital Ministry of Petroleum and Natural Gas .................. Revenue . Ministry of Planning ............................................. Revenue

Capital Ministry of Power Revenue

Capital CHARGED. - Stax Ho~rsehold and Allo~vances o f the President ........................................................ Revenue Lok Sabha .............................................................. Revenue Rajya Sabha .................... L..:. ............................. .Revenue CHARGED. - Union Public Service Commission ..... Revenue Secretariavof the Vice-president .......................... Revenue Department of Rural Development ............ : ........... Revenue

Capital Depart~iiei~t of Land Resources ............................... Revenue Department of Drinking, Water Supply .................. Revenue Department of Science aud Technology ................ Revenue

Capital Department of Scientific and Industrial

Research ....... Revenue Capital ,

Department of Biotechnology ........................... ~ e v e i i h e Department of Shipping .......................................... Revenue

Capital Department of Road Transport and Highways.. .... Revenue .

Capital Ministry of Social Justice and Empowerment ........ Revenue

Capital ' Department of Space ........................................... Revenue

Capital - Ministry of Statistics and Programme

.................................................... Impleine~ltation Revenue Capital

....................................................... Ministry of Steel Revenue Capital

... Ministry of2Textiles ...................................... Revenue 510,76,00,000 5 10,76,00,000'

... Capital 43,16,00,000 43,16,00,000

... Ministry of Tourism ............................................... Revenue 81,00,00,000 8 1 ,oo,oo,ooo

... Capital 93,50,00,000 93,50,00,000 . . - ................... ...... Ministry of Tribal Affairs A.. Revenue 43,84,00,000 303,42: 00,000 347,26,00,000

.... Capital 8,34,00,000 8,34,00,000 Andaman and Nicobar Islands .............................. Revenue 205,67,00,000 ... 205,67,00,000

Capital l25,I 4,00,000 ... 125,14,00,000 .............. Chandigarh revenue 212,89,00,000 6,72,00,000 21 9 ,6~ ,00:000

. . Capital, 38,28,00,000 6,OO;OOO 38,34,00,000 Dadra and Nagar Haveli ........................................... Revenue 199,94,00,000 . . . . 199,94,00.000

... 1 Capital 5,23,00,000 . . 5,23,00,000

To tal

Rs.

64,53,00,000 8,63,00,000

156,47,00,000 12,50,00,000

98,98,00;000 5,03,00,000 9,17100;000 1,67,00,000

796,75,00,000 1 ,OO,OO,OOO

60,58,00,000 9,00,00,000

485,50,00,000 15,96,00,000

1,67,00,000 1014,87,00,000

51,09,00,000

3,33,00,000 52,44,00,000 19,10,00,000

. 12,96,00,000 28,00,000

12594,96,00,000 25,00,000

400,65,00,000 14 16,98,00,000 287;25,00,000

Il~lS,OO,OOO

. 345;23.00,000 1,10,00,000 "

153,17,00,000 175,42,00,000 62,46,00,000

2.1 59,54,00,000 2225,55,00,000

383,33,00,000 23,17,00,000

3 82,42,00,000 296,59,00,000

312,45,00,000. . 4,05,00,000

17,34,00,000 2,58,00,000

Parliament 1 Rs.

. 64,51,00,000 8,63;00,000

156,47,00,000 12,50,00,000

98,98,00,000 5,03,00,000

. 9,17,00,000 1,67,00,000

796,75,00,000 I,OO,OO,ODO

59,20,00,000 ' 7,50,00;000

485,50,00,000 15,96,00,000

1,67,00,000 10 14,87,00,000

51,09,00,000

... 52,37,00,000 19,00,00,000

... - - 28,00,000

12594,96,00,000 25,00,000

400,65,00,000 14 16,98,00,000 287,25,00,000

11,15,00,000

345.23.00.000 ~1,10,00,000

153,17,00,000 175,42,00,000 -62,46,00,000

2 159,46,00,000 2224,38,00,000

3 83,33,00,000 '23,17,00,000

. 3 82,35,00,000 296,53,00,000

312,45,00,000 4,05,00,000

17,34,00,000 2,58,00,000

Consolidated

F u n d

Rs . 2,00 ,000

... . . . .

...

...

...

. . . . ..

' ...

1,38,00.000 l,SO,OO;OOO

.... - . ...

...

...

...

3,33,00,000 . 7,00,000

10 ,00 ,000 12,9:6,00,000

... , .

.

...

...

... . . . .

...

:..

...

...

. . . .

... 8,00,000

1.1 7,00,000 ...

7,00,000 6,00,000

. . .

...

...

...

Appropriation (Vote on Accourzt)

1 / 2 . +------ 3 Sums not exceeding j I 1 Voted by Services and purposes Chargedon the /

, Vote - 1 / Parliament 1 Consolidated I Toral I 1

I Fund

Rs. Rs; Rs. , - ,

9 8 Daman and Diu : .................. ..: ............................... Reveiiue 82,26,00,000 ... 82,26,00,000 Capital ' 7,88,00,000 . . . . 7,88,00,000

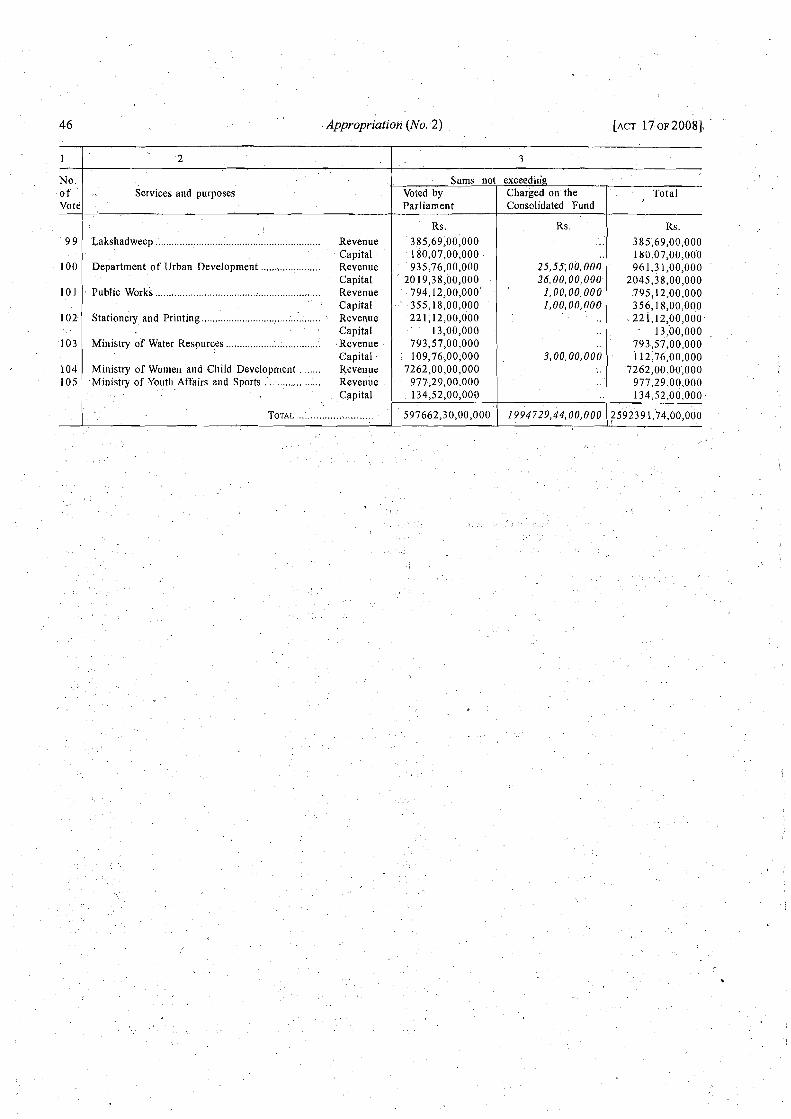

... 99 . Laksliadweep ........................................................... Revenue 64,28,00,$00 64,28,00,000 Capital 30,01,00,000 ... 30,Ol ,OO,OOO

Depart~ilent of Urban Develop~iient ...................... Revenue 191,04,00,000 4,26,00,1)00 195,30,00,000 Capital I 8 17,98,00,000 4,33,00,000 822,3 1,00,000

101 ....................................................... .

. I o 0 . 1 Public Works Revenue 132,35,00,000 17,00,000 132,52,00,000 Capital 59,20,00,000 17,00,000 59,37,00,000

102 Stationery and Pri~~ti l lg ................... ...l .............. Revenue . 36,85,00,000 ... 1 . 36,85,00,000 Capital 2,00,000 ... 2,00,000

'1 03 Ministry of Water Resources ................................... Revenue 132,26,00,000 . ' . . . 132,2$,00,000 Capital . 18,29,00,000 50,00,000 - 18,79,00,000.

104 ini is try of Women a"d Child Developlnent ........ Revenue 1209,50,00,000 . . . . . ' 1209,50,00,000~ ..................... 105 Ministry of Youth Affqirs and Sports Revenue 162,88,00,000 162,88,00,000 . . . .

... Capital 22,42,00,000 22,12,00.000

....................... TOTAL 106733,36.00.000 332486.53.1111.000 439219.87,00,000

. . ' _

. . . .

' ,

1

THE APPROPRIATION ACT, 2008

No. 6 OF 2008 \

[25th March, 2008.1

An Act to authorise payment and appropriation of certain further sums from and out of the Consolidated F i d of India for the services of the financial year

2007-08.

BE it enacted by Parliament in the Fifty-ninth year ofthe Republic of Indiaas follows:-

1. This Act may be called the Appropriation Act, 2008. Short title.

2. From and out of the Consolidated Fund of India there may be paid and applied Issue of

sums not exceeding those specified in column 3 of the Schedule amounting in the aggregate ~ 1 4 0 3 7 * ~ 9 1 , 0 0 . ~ out of the to the sum of one lakh forty thousand three hundred seventy-eight crores and ninety-one Consolidated

lakh rupees towards defraying the several charges which will come in the course of payment ~~~d of ~~d~~ during the financial year 2007-08 in respect of the services specified in column 2 of the for the Schedule. financial year

2007-08

3. The sums autliorised to be paid and applied from and out of the Consolidated Fund Approprlatlon

of India by this Act shall be appropriated for the services and purposes expressed in the Schedule in relation to the said year.

13

<

Appropriatioiz

THE SCHEDULE \

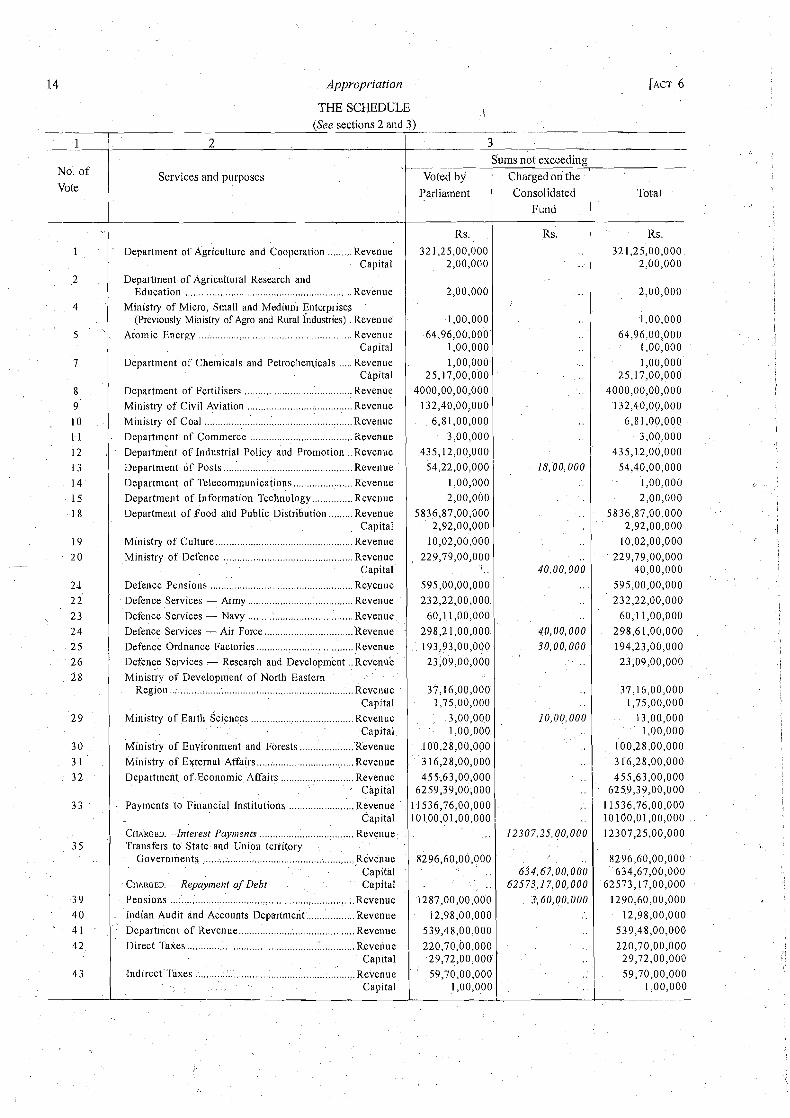

(See sections 2 and 3) I

1 1 2 I 3

No. o f

Vote Services and purposes Voted by

Parliament

1 Department of Agriculture and Cooperation ......... Revenue .

Capital 2 Department of Agricultural Research and --! Education ........................................................... Revenue

. ,

, .

Rs . 32 1,25,00,000

2,00,000

2,00,000

1 ,OO,OOO ,64,96,00,000

1,00,000 1,00,000

25,17,00,000 4000,00,00,000

132,40,00,000

6,8 1,00,000 3,00,000

435,12,00,000

4

5

7

8 9 ' 10 1- I 12 ,

13 14 I 5 18

19 2 0

. .-

25 22' 23

Sums not exceeding

Ministry of Micro, Small and ~ e d i u ~ l l Enterprises (Previously Ministry of Agro and Rural Industries) .Revenue

Atomic Energy .................... .. .............................. Revenue Capital

Department of Chemicals and Petroche~nicals ..... Revenue Capital

Department of Fertilisers ................................ Revenue Ministry of Civil Aviation . . ...................................... Revenue

................................................. Ministry of Coal Revenue . Department of Commerce ................................ Revenue

~ e ~ a r t m i n t of Industrial Policy and Promotion ..Revenue Department of Posts ............................................ Revenue Department of Telecom~nunications ...................... Revenue Department of Information Technology ............... Revenue Department of Food and Public,Distribution ......... Revenue

Capital Ministry of Culture ............................................. Revenue

Ministry of Defence ........................ ... ................ Revenue Capital

Defence Pensions .................................................. Reyenue Defence Services - Army ................................... Revenue Defence Services - Navy ....................................... Revenue

Charged on the

Consolidated

Fund

Rs. . .

. . .

. .

Total

- Rs.

321,25,00,000. 2,00,000

2,00,000

1,00,000 64,96.00.000

1,00,000 1,00,000

25,17,00,000' 4000,00,00,000

132,40,00,000

6,8 1 ,00,000 3,00,000

435,12,00,000 54,22,00,000 11~00,001 54,40,00,000 I

................................. . 24 1 Defence Services - Air Force Revenue ................................. 25 Defence Ordnance Factories Revenue,

26 ' Defence Services - Research and Development . . ~evenuk 2 8 in is try of Development of North Eastern , ,

......... ...... ........................................ Region ..; : :. Revenue capital

2 9 Ministry of Earth Scie~ices .................... .1 ............... Revenue Capital

.................... 3 0 ini is% of ~nvironment and Forests Revenue 3 1 Ministry of External Affairs .............................. Revenue

Departrnent of Economic Affairs ........... ; ............. ~ e v e n u e Capital

3 j 2 , 3 1 . Payments to Financial Institutions ...................... Revenue

1,00,000 2,00,000

5836,87,00,000 2,92,00,000

10,02,00,000 . 229,79,00,000

I

595,00,00,000 232,22,00,000

60,1.1,00,000 298,2 1,00,000

. 193,93,00,000 23,09,0'0,000

37,16,00,000 I ,75,00,000

3,00,000 ' . 1,00,000

100,28,00,000 3 16,28',00,000

455;63,00,000 6259,39,00,000

11536,76,00,000 10 100,01,00,000

' ,,

8296,60,00,000 . .

- .. 1287,00,00,000

. 12,98,00,000 539,48,00,000 220,70,00,000

, 29,72,00,000 . 59,70,00,000

1,00,000

3 5

39 40

4 1 ^ .

4 2

4 3

Capital

C H A R G E D . - ~ ~ ~ ~ Y ~ S ~ Paynlents ............... : ..... .. ......... Revenue, 'Transfers to State.and Union territory

Governinents Revenue Capital

CHARGED.- Repayment of Debt Capital Pensions ..................................................................... Revenue

. Indian Audit and Accounts Department: ...... .......... Revenue

Department of Revenue Revenue Direct f i xe s ................... L.... ............... . . . . . . Revenue

Capital Indircct 'Taxes :..........

Capital

1,00,000

..

.. 40,00,000

..

..

qO,OO,OOO 30,00,000

, 10.00,OOO

..

2,00,000 5836,87,00,000

2,92,00,000 10,02,00,000

229,79,00,000 40,00,000

595,00,00,000 232,22,00,000

60.1 1,00,000 298,6 1,00,000 194,23,00,000 23,09,00,000

37,16,00,000 1,75,00,000

13,00,000 1,00,000

100,28,00,000 3 16,28,00,000 1 155,63,00,000

.. 625.9,39,00,000

.. i 11536,76,00,000

..

12307,25,00,000

.. 634,67,00,000

62573,17,00,000 3;60,00.000

- .

. .

10100,01,00,000 12307,25,00,000

8296,60,00,000 634,67,00,000

62573,17,00,000 1290,60,00,000

12,98,00,000 539,48,00,000 220,70,00,000

29,72,00,000 59,70,00,000

I 1,00,000

Appropriation

--

Total

Rs. 4,00,00,000

. 1,OO;OOO

1,00,000 2,00,000

11,95,00,000

2,00,000

7,26,00,000 165,76,00,000

10,27,00,000 1,00,000

2,96,00,000 26,00,000

, 325,54,00;~00

319,40,00,000 55,64,00,000

1,00,000

49,12,00,000 6,00,000'. 2,00,000 1,00,000

88;63,00,000 l,OO,000

1,00,00,000 2,00,000

3,48,00,000

' 1,00,000

8,70,00,000 9326,09,00,000

2,27,00,000 1 ,OO,OOO

1,73,00,000

8,00,000

' 980,66,00,000

, l,OO,OOO

l,OO,OOO

1 ,OO,OOO 1,95,00,000

2,00,000 20,00,000

8,30,00,000

2,00,000 l,OO,OOO

161,88,00,000 51,00,000

. .

1,00,000

2' .

- - k x z i n g N o . o f lT=Fcs Vote and purposes Voted by Charged o n t h e

. . I Parliament Consolidated

Fund. , >.

Rs. Rs. 44 . . Department of Disi~iveslment ........................... :.Revenue 4,00,00,000

,Capital 1,00,000 45 -Ministry -of Food I'rocessing Illdustries .................. Revenue 1;00,000

. ........... 46 Department of Health and Family Welfare Revenue 2,00,000 Capital 11,95,00,000

47 Department of Ayurveda, Yoga and Naturopalhy, '

..... Unani, Siddha and' Homoeopathy (AYUSH) :Revenue 2,00,000 4 8 Department of Heavy Industry: .: ............................ Revenue 7,26,00,000

Capital 165,76,00,000 .. ......................................... 5 (3 Ministry of Home Affairs Revenue 10,27,00,000 ..

Capiial

1 ~ 0 0 , 0 0 0 i . . 5 1 Cabinet Revenue 2,96,00;000

, .

65 .00~000

. . .

. . . .

3,48,00,000

2,24,00,000

1,73,00,000

8,00,000

..

. .

. ,

50,00,000

52 5 3

. . 54 5 5

56 -

5 7 s ' 5 8

I , '

5 9 .

.; 6 0 . 6 1.

65 6 9

7 0 7 2 '

. . . . . .

. .

Capital Police .......................... : ......... ; . . . . . .................... Revenue Other Espenditure of the Minislry of

RomeAffairs ............................... .. ................ Revenue

........... ~ransfe ' rs to Union territory, Governments Revenue ~ilinistry of I-lousing and ~ r b a n ' ~ o v e & .,

Alleviation ........................................................... R e v e n u e

~ e ~ a r l i n e n t of Scl!ool Education and Literacy,.:..~e"'enue . Department of Higher Education ...................... .Revenue

. .

............ ~ i n i s t r ~ of 1nfo;mation and. Bkoadcasting ~ & n u e Capital

Ministry of Labour and Employment .................... Revenue , . Capital

............................................ Election Commission Revenue Law and Justice ......................... .. ..................... Revenue

CHARGED.- Supreme Court of India ........................ Revenue

............. . Ministry of New and Renewable Energy :..Revenue Ministry of Personnel, Public Grievances and

Pensions .............................................. R e v e n u e .................. Ministry of Petroleum and ~ a t u r a l Gas Revenue

Ministry of Power ..............I.....'........................... Revenue Capital

j c;+ARGEU.- Stag Household and Aiiolvances ...............

334,89,00,000 26'00'0001

319,40,00,000

55,64,00,000

. 1,00,000

49,12,00,000 6,00,000 2,00,000 1 ,OO,OOO

88,63,00,000 1,00,000

1,00,00,000 2,00,000

1,00,000

6,46,00,000

9326,09,00,000

. 2,27,00,000 l,OO,OOO

. .

980,66,00,000

1,00,000

. . 1 ,OO,OOO

1,00,000 1,95,00,000

2,00,000 2 O,OO,OOO

. 8,30,00,00'0

2,00,000 1,00,000

16 1,88,00,000 1 ,OO,OOO

1 ,OO,OOO

. . I of the Presidenl .............................. ... Revenue

7 5 1 Rajya Sabha 1 . . R e v e n u e . ..................................................

............. 7 8 1 Department of Rural Development :.........Revenue

7 9 Department of Land Resources ........................... Revenue

80 Department of Drinking Water Supply .................. Revenue

................ 8 1 Deparlment of Science and Technology Revenue Capital

8 2 Department 01' Scientific and~i~iclustrial

Research Revenue Capital

. . ............................. 8 3 1 . . Department, of Biotechl~ology Revenue

84 . 1 Depar tme~~l of Shipping .......................................... Revenue Capital

...... 85 1 Departnient of Road Transport and Highways Revenue Capital

8 6 Ministry of Micro, S~nall and Medium Enterprises ..... (Previously - Ministry of Small Scale Industries) Revenue

1

/

: 6 Appropriation [ACT. 6 OF 20081

1

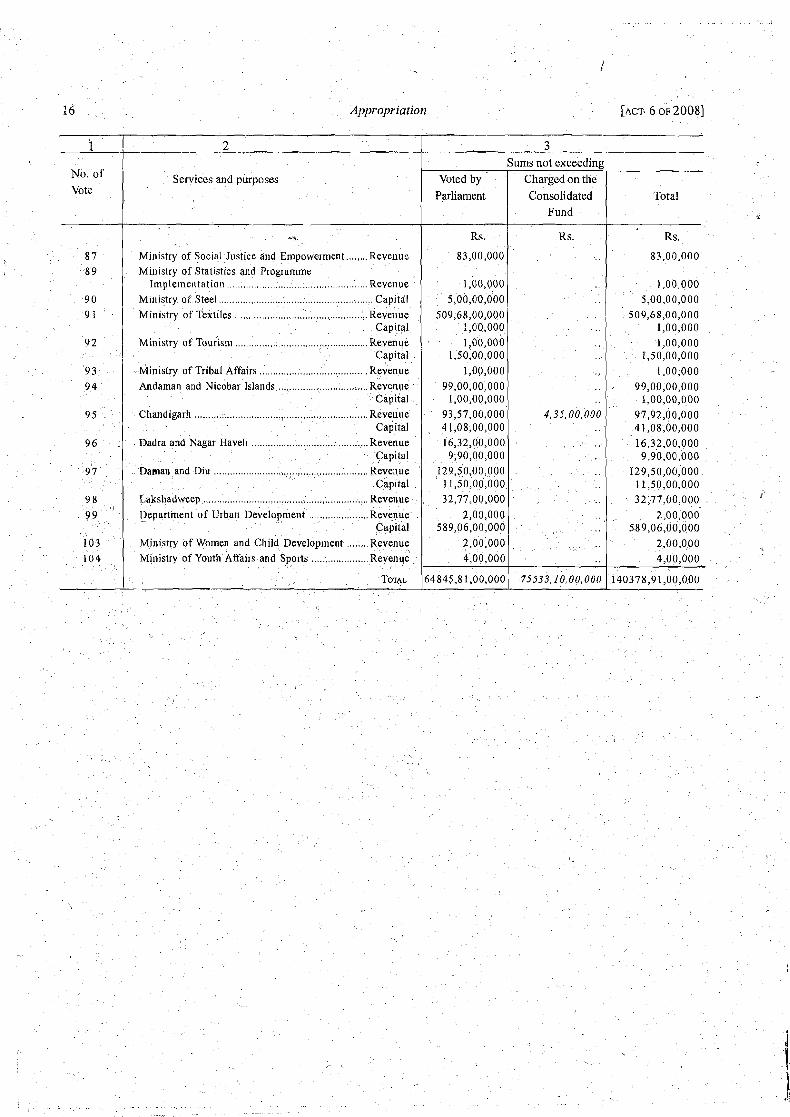

No. of

Vote

8 7 8 9

9 0 9 1

P 2 I 9 3 9 4

95

96 .

97

2

Services and purposes

di

Ministry of Soc~al Justice and Empowerment ....... Revenue Mlnlstry of S ta t~s t~cs and Programme

Imple~uentation . . . . . . . . . Revenue Min~stry of Steel . . . . . . . . . . . . . . . . . . . . . . Capllal

3

>

d

\

,!

Voted by Parliament

Rs,

83,00,000

1 ,OO,OOO 5,00,00,000

75533,10,00,000

32,77;00,000

2,00,000 589,06,00,000

2,00,000 4,00,000

64845,81,00,000

....................... ..................... I, / 1,akshadweep ,.., Revenue Department of Urban Development .............. ..Revenue

Capital

32,77,00,000 2,OO.OOO

589,06,00,000 2,00,000 4,00,000

140378,91,00,000

Min~stry of Textiles ............................... Revenue 1 509,68,00,000 Capital 1,00,000

Minsrry of Tourisni . . . . . . . . . . . . . . . . . . . . . . . . . . Revenue / 1,00,000

103 104

Sums not exceeding

Charged o n the

Consolidated

Fund

Us.

.

4,35,00,000

..

Capital

Ministry of Tribal Affairs .................................. .Revenue Andaman and Nicobar Islands .......................... .Revenue

Capital Chandigarli .................................................. .Revenue

Capital Dadra and Nagar Have11 ..................................... Revenue

Capital Dan~an and Diu .................................................. Revenue

Cap~tal

Ministry of Women and Child Develop~ilent ....... Revenue Mialstry of Youth Affairs and Sports ................. Revenue

TOTAL

l'otal

4

Rs . 83,00,000

1 ,00 000 5,00,00,000

509,68,00,000 1,00,000 1,00,000

1,50,00,000 1,OO 000

- 99,00,00,000 1,00,00,000

97,92,00,000 41,08,00,000 16,32,00,000

9,90,00,000 129,50,00,000

11,50,00,000

1.50,00,000 1,00,000

99,00,00,000 I ,OO,OQ,OOO

93,57,00,000 , 41,08,00,000

16,32,00,000 9,90,00,000

129,50,00,000 11,50,00,000

I THE KARNATAKA APPROPRIATION (VOTE ON ACCOUNT

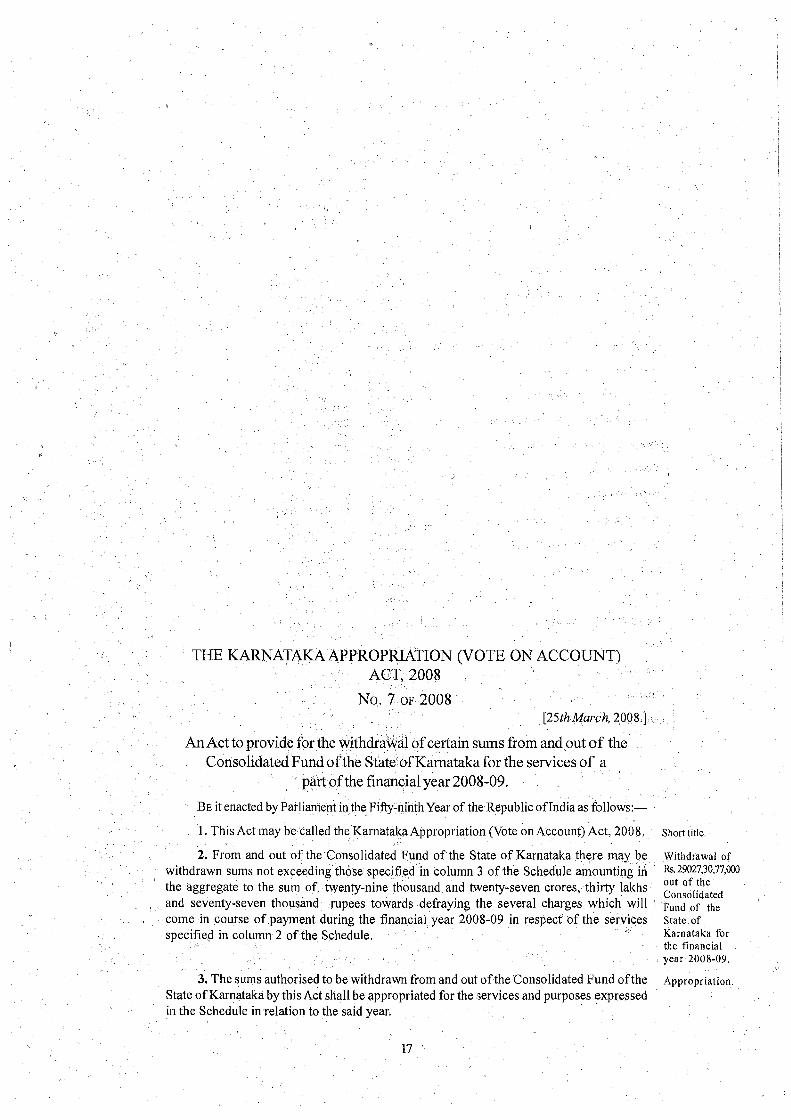

ACT, 2008 \

No. 7 OF 2008 [25th March, 2008.1

AnAct to provide for the withdrawal of certain sums from and out of the Consolidated Fund of the State of Karnataka for the services of a

part of the financial year 2008-09.

BE it enacted by Parliament in the Fifty-ninth year of the Republic of India as follows:-

I . This Act inay be called the Karnataka Appropriation (Vote on Account) Act, 2008. s~ lor t t~tle

2. From and out of the Consolidated Fund of the State of Karnataka there may be Withdrawal of withdrawn sums not exceeding those specified in column 3 of the Schedule amounting in 290273J.77NJ

out a f the the aggregate to the sum of twenty-nine thousand and twenty-seven crores, thirty lakhs Consolidated and seventy-seven thousand rupees towards defraying the several charges which will ~~~d of

, come in course of payment during the financial year 2008-09 in respect of the services State of

specified in column 2 of the Schedule. Karnataka for the financial year 2008-09.

3. The sums authorised to be withdrawn from and out of the Consolidated Fund of the Appropriation State of Karnataka by this Act shall be appropriated for the ;ervices and purposes expressed in the Schedule in relation to the said year.

17

18 Karnataka ~pp fo~r ia t i on (Vote on Account) [ACT 7. OF 20081

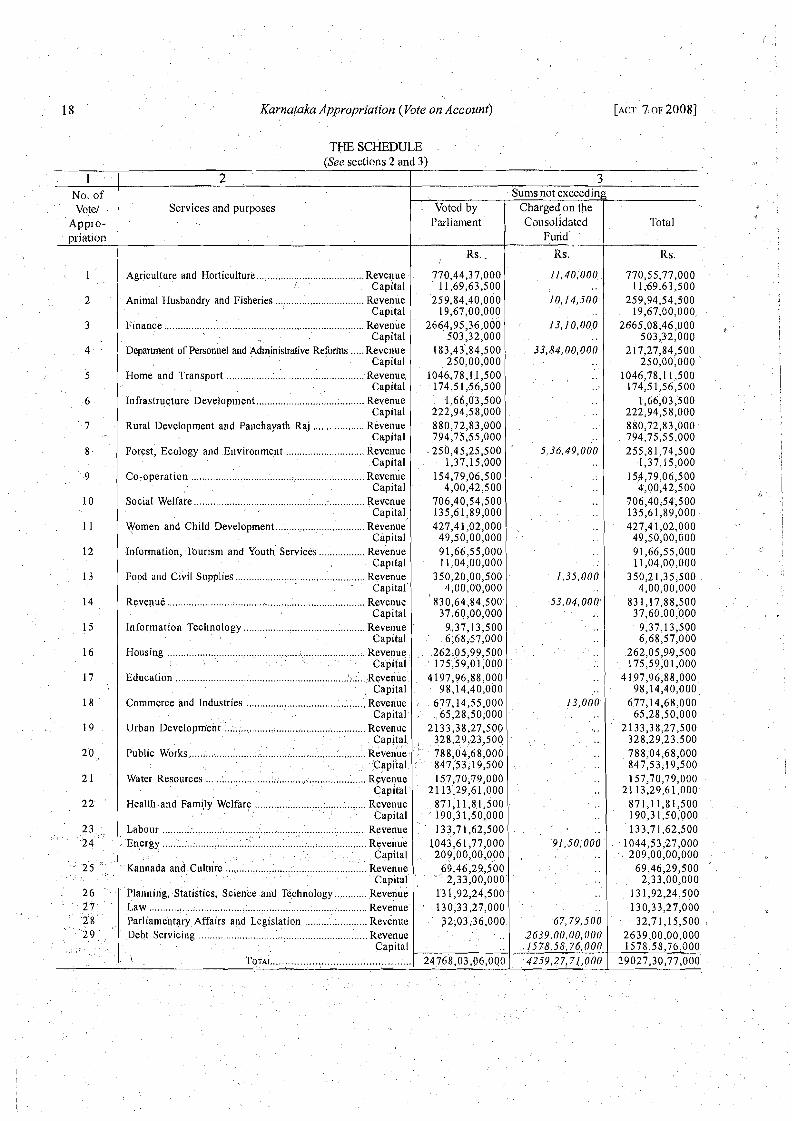

1 ' . No. of Vote/

Appro- priation

1 ~.

2

3

4 .

5

6

' 7

8 -

".9

10

11

12 '

13

14

15

16

17

18

. % 19

20,,,

2 1

. . 2 2

23 ... , r . ,

. . 2 4

. . ~ ... '25 . - , '

. . . . . .

. 26 .

" 2 7 " 2 8 '

. . . . . ' 29

. , . . . . .

. . . . . .

. . THE SCHEDULE (See sections 2 and

2 ppp--

Services and purposes e

Agriculture and' Horticulture ..................................... Revenue Capital

....................... ~ n i m a l Husbandry and Fisheries ...:...... Revenue Capital

Finance ........................................................................ Revenue Capital

Depamnent of Personnel and Administrative Refonns ..... Revenue Capital

Home and Transport ................. ; ........ .. .................. Revenue Capital

Infrastructure Development ........................................ Revenue Capital

~ u r a l .Development and Panchayath Raj ................... Revenue Capital

............................. Forest, Ecology and Environment Revenue Capital

Co-operation ............................:........:...................... R e v e n u e Capital

Social Welfare .............................. i....:.... .................. Revenue * . Capital,

.......... Women and Child Development ...................... : Revenue Capital

I~lformation, ,Tourism and Youth Services ................. ~ e v e n u e Capital

Food and civil Supplies ...................... ......................... Revenue ' ' Capital'

Reve~~ue ............................. .. ...................................... Revenue Capital

Information Technology .................... .. .................. Revenue Capital

.......................................... Housing . . . . . . . . . Revenue Capital',

Education Revenue >' Capital

Commerce and Industries .......................................... Revenue Capital

Urban Development ..: ..:.: .............. .... ............... Revenue Capital ? .

Public Works ......,:.. :.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Revenue. Capital

Water Resources ...... : .... : ........ .. '. ................................ Revenue Capital

....................... ........... Health ,and Family Welfare ..: Revenue . . Capital

Labour .......... : .......... .. ...... :: .................................. Revenue . . , ........ ..................... ........................................ Energy : :.' ~ e v e n u e

Capital , .

Kannada and Culture .................. : ........ ..l .................... Revenue Capital'

Planning, statistics, Science and Technology ............ ~ e v e n u e Law ................ : ....................... ..................... Revenue

........................ Parliamentary Affairs and Legislation ~ e v e n u e Debt Servicing Revenue

Capital . !

r > .............. ................ ~ O T A L ....

3)

Voted by Parliament

Rs. . I

770,44,37,000 11,69,63,500

259,84,40,000 19,67,00,000

2664,95,36,000 503,32,000

1 8 3,43',84,5 00 250,00,000

1046,78,1 1,500 174,s 1 ,.56.,500

1,66,03,500 222,94,58,000 880,72,83,000 794,75;55,000

. 250,45,25,500 1,37,15,000

154,79,06,500 4,00,42,500

706,40,54,500 135,61,89,000 427,41,02,000

49,50,00,000 91,66,55,000 11,04,00,000

350,20,00,500 , 4,00,00,000 830,64,84,500'

37,60,00,000 9.,37,13,500

. 6,68;57,000 , 262,05,99,500

175',59,01,000 41 97,96,88,000

98,14,40,000 . . 677,14,55,000 . 65,28,50,000

2133,38,27,500 , 328,29,23,500 ' 788;04,68,000 ' 847;53,19,500

157,70;79,000 21 13,29,61,000

87 1,l 1,81,500 .190,3 1,50,000

. 133,7 1,62,500 1043,6 1,77,000 209,00,00,000

69,46,29,500 , ' 2,33,00,000

13 1,92,24,500 . 130,33,27,000

32,03,36,000 ..

24768,03,06,000

3 -- Sums not exceeding

Charged o n the ~onso l ida t ed

F,und

Rs.

11,40.000,.

10,14,500

.' 13,10,000

33,84,00,000

, . .. .

. .

. . . ,.. .

5,36,49.000

.

..

. .

..

1.35.000

53,04,000' . .

. .

..

..

13,000 . . . .

. . . , . . .

. .

..

..

..

. .

.. \ . ..

91,50,000 , ..

.. ' . . . . .

67,79,500 .2639.00.00,000

. . . . 1578,58.76,000 .4259,27!71,000

. .

Total

Rs.

770,55,77,000 11;69,63,500

259,94,54,500 19,67,00,000,

2665,08,46,000 503,32,00G

217,27,84,500 250,00,000

1046,78,1 1,500 174,51,56,500

1,66,03,500 222,94,58,000 880,72,83,000 794,75,55,000 255,81,74,500

1,37,15,000 15,4,79,06,500

4,00,42,500 706,40;5.4,500 13,5,61,89,000 427,4 1,02,000

49,50,00,000 91,66,55,000 11,04,00,000

350;21,35,500 4,00,00,000

.83 1,17,88,500 37,60.00,000

9,37,13,500 6,68,57,000

262,05;99,500 175,59,01,000

41 97,96,88,000 98,14,40,000,

677,14,68,000 65,28,50,000

2133,38,27,500 328,29,23,500 788,04,68,000 847,53,19,500 157,70,79,000

21 13,29,61,000 871,11,81,500 190,3 1,50,'000 133,71,62,500

: 1044,53;27,000 ' 209,00,00,000

69,46,29,500 2,33,00,000

- 131,92,24,500 130,33,27,000

. . 32,71,15,500 2639,00,00,000 1578,5S,76,000

29027,30,77,000

\

I

THE KARNATAKA APPROPRIATION ACT, 2008 No. 8 OF 2008

I

[25th March, 2008.1 I

An Act to provide for the withdrawal of certain sums from and out of the I I

I

Consolidated Fund ofthe State ofKamataka for the services of a part I

of the financial year 2007-08. I

BE it enacted by Parliament in the Fifty-ninthyear of the Republic of India as follows:-

1. This Act may be called the Karnataka Appropriation Act, 2008. Short title

2. From and out of the Consolidated Fund of the State of Karnataka there may be W~thdrawal of

withdrawn sums not exceeding those specified in column 3 of the Schedule amounting in the 3311~013011~

aggregate to the sum of three thousand three hundred eleven crores, one lakh and one ~ ~ ~ ~ , ~ ~ ~ t e d thousand rupees towards defraying the several charges which will come in course of ~~~d of the payment duringthe financial year 2007-08 in respect ofthe services specified in column 2 of State of

the Schedule. Karnataka for the financ~al year 2007-08

3. The sums authorised to be withdrawn from and out of the Consolidated Fund of the Aeero~>rlatloll

State of Karnataka by this Act shall be appropriated for the services and purposes expressed in the Schedule in relation to the said year.

19

Karnataka Appropriation

THE SCHEDULE (See seciio~ls 2 and

1 I 2 No. of I

Services and purposes a . Appro- i priation

1 Agriculture and Horticulture .................................. Revenue Capital

2 Animal Husbandry and Fisheries ............................. Revenue 3 Finance ................................................. Revenue 4 , Department of Personnel and Administrat~vc

Reforms ..... :: ............. ......... ........... : . . . . . . Revenue . . 5 Home and Transport ......................................... Revenue

7 Rural Development and Panchyath Raj ................. Revenue

I , Capital 8 Forest, Ecology and Environment .......................... Revenue

c Capital 9 Co-operation ................................................... Revenue

Capital . I 0 Social Welfare ..................................................... Revenue

, . Capital 1.1 Women and Child Development .......................... ... Revenue

. . ............. 12 Information, Tourism and Youth, Services Revenue Capital

13 Food and Civil Supplies R e v e n u e Capital

......................... .................................. 14 Revenue .. Revenue .... . 15 Information Technology :....................................Revenue

16 Housing ...................... .: .......................................... Revenue Capital

17 Education ....... Capital

18 . Commerce and Industries ................................. Revenue Capital ,

19 Urban Development ................... .... Revenue 20 . . % ......................................................... Public Works Revenue

I . , Capital 2 1 Water Resources ........................ .................. Revenue

, , Capital ,

2 2 Health and Family Welfare ................... ... ........ Revenue . . . . . . - Capital

2 3 Labour ... Capital

< ,

24 Energy ...................... ... ................................... ~ e v e r k e . . Capital

2 5 Kannada and iCulture ............ : ................................ Revenue 2 6 Planning, Statistics, Science and Technology ........ Revenue .

................... .................................... 2 7 Law A......:.....:.... Revenue , . . .

. . . . . . . . . I . . . , ,Capital .

28 : Parliamentary Affairs and Legislation .................... Xevenue . .

29 . Debt Servicing :... ................................................. Reveuue . . . .

. . . . TOTAL . . . . ~.

. . . . . .

3)

. A (

Voted by ' Parliament

Rs. 232,28,52,000

7,60,00,000 13,74,65,000 3,53,00,000

,

7,70,21,000 75,90,00,000 84,7$,8 1,000 47,28,00,000

. . 9,77,02,000 4,00,00,000

288,l 1,55,000 4,68,57,000

63,24,94,000 36,25,00,000

2,48,70,000 ,I 1,84,53,000

4,73,36,000 53,57,67,000

1,62,93,000 52,69,93,000.

1,08,58,000 15,74,18,000

150,00,00,000 151,91,32,000

3,50,00,000 42,10,75,000 91,58,40,000 49,.98,00,000

' 11,62,98,000 .

563,35,45,000 43,87,20,000

602,80,65,000 50,10,'18,000

1 ; 115,88,00:000 22,63;06,000

, 9,86,97,000 . 150,'l 1,50,000

126,94,00,000 .

1,7 1 ,OO,OOO 85,60,08;000

7,38,00,000 ' 2,11,64,000

. . 5,0,00,000 . .

,3306,25,33,000

. .

3 1 sums ndt exceeding

Charged on ihe Consolidated

F U I I ~ --IT Rs. Rs.

232,28,52,000 7,60,00,000

' 13,74,65,000

I 3,53,00,000

2,22,50;000 9,92,71,000 75,90,00,000 84,74,81,000 47,28,00,000 .9,77,02,000 4,00,00,000

, 288,11,55,000 4,68;57,000

- 63,24,94,000 36,25,00,000

2,48,70,000 11,84,53,000 4,73,36,000 ' .

53,57,67,000 1,62,93,000

2,32,27,000 55,02,20,000

. .

. . . .

... .' - :: : . , '

.

',

. . . .': : 20,91,000

4,75,6S,UOO ' . . . ,

, .

1,08,58,000 15,74,18,000

150,00,00,000 15 1,91,32,000

3,50,00,000 42,10,75;000 91,58,40,000 49,98,00;000 11,62,98,000

563,35,45,000 43,'87,20,000

602,80,65,000 50,l0,18,000

115,88,00,000 22,63,06,000

9,86,97,000 150,l 1,50,000 126,94,00,000 ,

1,71 ,OO,OOO 85,60,08,000

7,38,00,000 ,2,11,64,000

50,00,000 "20,9 1,000

3311,01.01,000 4

.

. . *

THE DELIMITATION (AMEM)MENT) ACT, 2008

No. 9 OF 2008 [28th March, 2008.1

An Act further to amend the Delimitation Act, 2002.

BE it enacted by Parliament in the Fifty-ninth Year of the Republic of India as follows:-

1. ( I ) This Act may be called the Delimitation (Amendrnent)Act, 2008. Short title and commence-

(2) It shall be deemed to have come into force on the 14th day of January, 2008. ment

33 of 2002. 2. In section 10 of the Delimitation Act, 2002 (hereinafter referred to as the principal Amendment

Act),-- of sectlon 10

(I) in sub-section (4), the following proviso shall be inserted, namely:-

"Provided that nothing in this sub-section shall apply to the delimitation orders published in relation to the State of Jharkhand.";

(ii) in sub-section (li), for the words "within two years of the constitution of the Commission", the words "within a period not later than 3 1st day of July, 2008" shall be substituted.

111sertion of new sectio~ls 10A and 10B.

Deferment of delimitation in certain cases.

Delimitation Commission's order with

, respect to the State of

. Jharkhand not to' have any legal effect.

Repeal and savings.

22 Delimitation (Amendment) [ACT 9 OF 20081 I

3. After section 10 of the principal Act, the following sections shall be inserted, namely:-

"10A. (1) Notwithstanding anything contained in sections 4, 8 and 9, if the President is satisfied that a situation has arisen whereby the unity and integrity of India is threatened or there is a serious thrkat to the peace and public order, he may, by order, defer the delimitation exercise in a State.

- (2) Every order made under this section shall be laid before each House of

'-

Parliament.

10B. Notwithstanding anything contained in sub-section (2) of section 10, the final orders relating to readjustment of number of seats and delimitation of constituencies in respect of the State of Jharkhand published under the said section vide Order O.N. 63(E), dated 3OthApril,2007 and O.N. 1 l.O(E), dated 17thAugust, 2007 shall have no legal effect and the delimitation ofthe constituencies as it stood before the publication of the said Orders shall continue to be in force until the year 2026 in relation to every election tv the House of the People or to the Legislative Assembly, as the case may be, I

I held after the commencement of the Delimitation (Amendment) Act, 2008.".

4. (1) The Delimitation (Amendment) ordinance, 2008 is hereby repealed. Ord. 1 of 2008.

, (2) Notwithstanding such repeal, anything done or any action taken under the principal Act, as amended by the said Ordinance, shall be deemed to have been done or taken under the corresponding provisions of the principal Act, as amended by this Act. I

THE REPRESENTATION OF THE PEOPLE (AMENDMENT) ACT, 2008 No. 10 OF 2008

[28thMarch, 2008.1

An Act further to amend the Representation of the People Act, 1950. BE it enacted by Parliament in the Fifty-ninth Year of the Republic of India as

follows:- 1. (I) This Act may be called the Representation of the People (Amendment) Act,

2008. I

(2) It shall come into force on such date* as the Central Government may, by notification in the Official Gazette, appoint.

2. In section 4 bf the Representation ofthe People Act, 1950 (hereinafter referred to as the principal Act), for sub-section (S), the following sub-section shall be substituted, namely:-

"(5) Save as provided in sub-section (#), the extent of all parliamentary constituencies except the parliamentary constituencies in the States of Arunachal Pradesh, Assam, Jharkhand, Manipur and Nagaland shall be as determined by the orders of the Delimitation Commission made under the provisions ofthe Delimitation Act, 2002 and the extent ofthe parliamentary constituencies in the States of Arunachal Pradesh, Assam, Jharkhand, Manipur and Nagaland shall be as provided for in the Delimitation of Parliamentary and Assembly Constituencies Order, 2008 having regard to the provisions of sections 1 OA and 10B ofthe Delimitation Act, 2002.". 3. In section 7 of the principal Act,-

(i) in sub-section (IB), in clause (a), for the words "thirty-nine seats", the words "fifty-nine seats" shall be substituted;

* w.e.f. 16-4-2008 : Ede Notification No. S.O. 881(E), dated 16-4-2008.

23

Short iitle and commencement

Amendment of section 4.

Amendment of s e ~ t i o n 7.

Representation of the People (Amendment) [ACT 10

(ii) for sub-section (3), the following sub-section shall be substituted, namely:-

"(3) The extent of each assembly constituency in all the States and Union Territories except the assembly constituencies in the States ofArunacha1 Pradesh, Assam, Jharkhand, Manipur and Nagaland shall be as determined by the orders of the Delimitation Commission made under the provisions of the Delimitation Act, 2002 and the extent ofeach assembly constituency in the States of Arunachal 3 3 of 2002

Pradesh, Assam, Jharkhand, Manipur and Nagaland shall be as provided for in the Delimitation of Parliamentary and Assembly Constituencies Order, 2008 having regard to the provisions of sections 10A and 10B of the Delimitation Act, 2002.".

Amendment of section 8 4. In section 8 of the principal Act,-

(i) for sub-section ( I ) , the following sub-section shall be substituted, namely:-

" ( I ) Having regard to all the orders referred to in sub-section (5) of section 4 and sub-section (3 ) of section 7 relating to the delimitation of parliamentary and assembly constituencies in all States and Union Territories, except the States of Arunachal Pradesh, Assam, Jharkhand, Manipur and Nagaland, made by the Delimitation Commission and published in the Official Gazette, the Election Commission shall-

(a) after making such amendments as appear to it to be necessary for bringing up-to-date the description of the extent of the parliamentary and assembly constituencies as given in such orders, without, however, altering the extent of any such constituency;

(b) after taking into account the provisions of the Delimitation of Parliamentary and Assembly Constituencies Order, 1976, as made applicable pursuant to the orders made by the President under section 10A of the 3 3 of 2002

Delimitation Act, 2002 relating to delimitation ofparliamentary and assembly constituencies in the States of Arunachal Pradesh, Assam, Manipur and Nagaland, and the provisions of section 10B of the said Act relating to delimitation of parliamentary and assembly constituencies in the State of Jharkhand,

consolidate all such orders into one single order to be known as the Delimitation of parliamentary and Assembly Constituencies O~der , NO8 and shall send authentic copies of that Order to the Central ~overnment and t o h e Government of each State having a Legislative Assembly; and thereupon that Order shall supersede ail the orders referred to in sub-section (5) of section 4 and sub- section ( 3 ) of section 7 and shall have the force of law and shall not be called in question in any court.";

76 of 1972 (il) in sub-section (3) , for the words, brackets and figures "as provided in sub-

3 3 of 2002 section ( 5 ) of section 10 ofthe DelimitationAct, 1972", the words, brackets and figures "as provided in sub-section (5 ) of section 10 of the Delimitation Act, 2002" shall be

Insertion of new sectlon 8A substituted.

Delimitation of 5. After section 8 of the principal Act, the following section shall be inserted, namely:- Parl~amen tary and Assembly "8A. (I) Ifthe President is satisfied that the situation and the conditions prevailing Constituencies in thc States of in the States of Arunachal Pradesh, Assam, Manipur or Nagaland are'conducive for 3 3 of 2002 Arunachal the conduct of delimitation exercise, he may, by order, rescind the deferment order Pradesh, issued under the provisions of section 1OAof the Delimitation Act, 2002 in relation to Assam, Manipur or that State, and provide for the conduct of delimitation exercise in the State by the Nagnland Election Commission.

OF 20081 Representation of the People (Amendment) 25

(2) As soon as may be after the deferment order in respect of a State is rescinded under sub-section (I), the Election Commission may, by order, determine-

(a) the parliamentary constituencies into which such State to which more than one seat is allotted in the First Schedule shall be divided;

(6) the extent of each constituency; and

(c) the number of seats, if any, reserved for the Scheduled Castes or the Scheduled Tribes.

(3) As soon as may be after the deferment order in respect of a State is rescinded under sub-section (I), the Election Commission may, by order, determine-

(a) the assembly constituencies into which such State shall be divided for the purpose of elections to the Legislative Assembly of that State;

(6) the extent of each'constituency; and

(c) the nulnber of seats, if any, reserved for the Scheduled Castes or the Scheduled Tribes.

3 3 of 2002 (4)'~ubject to the provisions of sub-section (I), the Election Cominission shall, having regard to the provisions of the Constitution and the principles specified in clauses (c) and (d) of sub-section (I) of section 9 of the Delimitation Act, 2002 determine the parliamentary and assembly constituencies in the States of Arunachal Pradesh, Assam, Manipur andNagaland in which seats shall be reserved, if any, for the Scheduled Castes and the Scheduled Tribes.

(5) The Election Commission shall,-

(a) publish its proposals under sub-sections (2), (3) and (4) with respect to any State in the Official Gazette and also in such other manner as it thinks fit;

(6) specifL a date on or after which the proposals will be further considered by it;

(c) consider all objections and suggestions which may have been received by it before the date so specified;

(d) hold, for the purpose of such consideration, if it thinks fit s o to do, one or more public sittings at such place or places in such State as it thinks fit;

(e) after considering all objections and suggestions which may have been received by it before the date so specified, determine, by order, the delimitation of parliamentary and assembly constituencies in the State and also the constituency or constituencies in which seats shall be reserved, if any, for the Scheduled Castes and the Scheduled Tribes and cause such order to b e published in the Off~cial Gazette; and, upon such publication, the order shall have the force of law and shall not be called in question in any court and the Delimitation of Parliamentary and Assembly Constituencies Order, 2008 shall be deemed to have been amended accordingly.

(6) Every order made under sub-sections ( I ) and (2) and clause (e) of sub- section (5) shall be laid before each House of Parliament.

(7) Every order made under sub-sections (I) and (3) and clause (e) of sub- section (5) shall, as soon as may be after it is published under that sub-section, be laid before the Legislative Assembly of the State concerned.".

6. In section 9 of the principal Act, in sub-section (I), for clauses (a) and (aa), the following clauses shall be substituted, namely:-

Amendment of section 9.

"(a) correct any printing mistake in the Delimitation of Parliamentary and Assembly Constituencies Order, 2008 or any error arising therein from inadvertent slip or omission;

26 Representation of the People (Amendment) [ACT 10

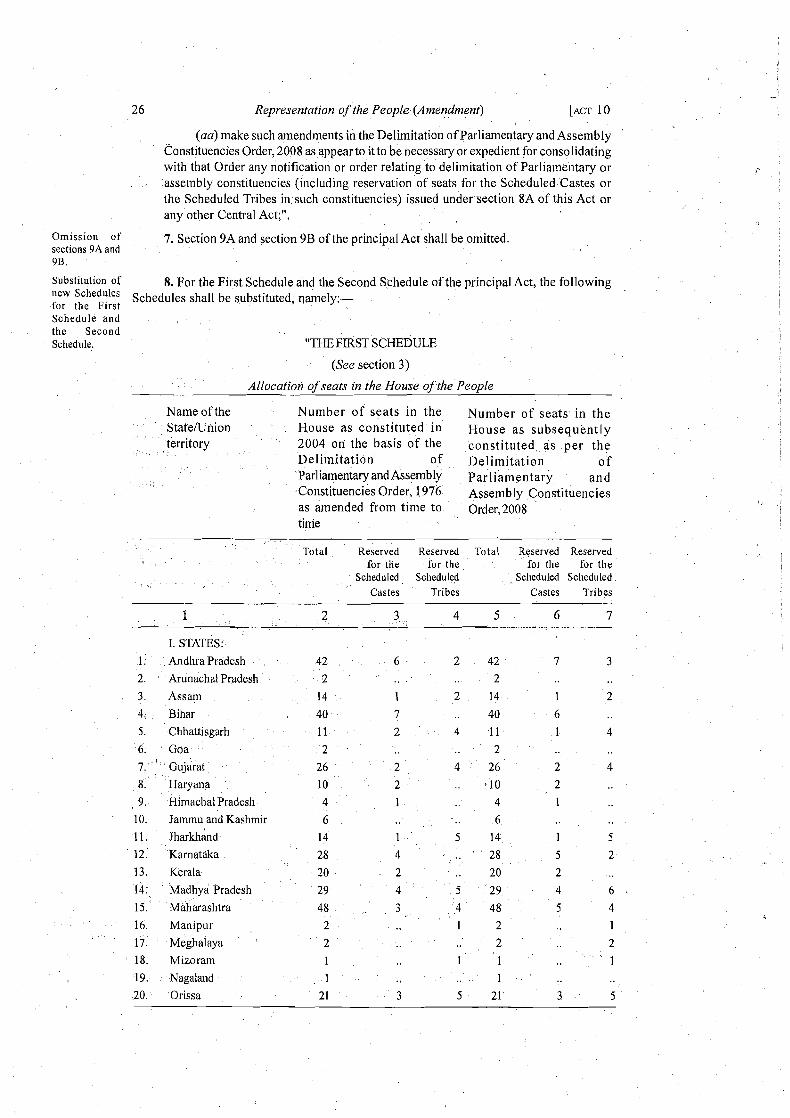

(aa) make such amendments in the Delimitation of Parliamentary and Assembly Constituencies Order, 2008 as appear to it to be necessary or expedient for consolidating with that Order any notification or order relating to delimitation of Parliainentary or assembly constituerlcies (including reservation of seats for the Scheduled Castes or I

the Scheduled Tribes in such constituencies) issued under section 8A of this Act or any other Central Act;".

Omission of sections 9A and 9B.

7. Section 9A and section 9B of the principal Act shall be omitted.

Substitution of 8. For the First Schedule and the Second Schedule of the principal Act, the following 'Iew Schedules shall be substituted, namely:- for the First Schedule and the Second Schedule. "THE FIRST SCHEDULE I

(See section 3)

Allocation of seats in the House of the People

Name of the Number of seats in the Number of seats in the Statefunion House as constituted in House as subsequently territory 2004 on the basis of the constituted as per the

Deliinitation of Deliinitation o f Parliamentary and Assembly parliamentary and Constituencies Order, 1976 Assembly Constituencies as amended from time to Order,2008 time

- Total Reserved Reserved Total Reserved Reserved

for the for the for the for the Scheduled Scheduled Scheduled Scheduled

Castes T r ~ b e s Castes T r ~ b e s

1 2 3 4 5 6 7

I. STATI~S: I . AndhraPradesh 42 6 2 42 7 3 2. Arunachal Pradesh 2 2

3. Assam 14 1 2 14 1 2

4. Bihar 40 7 .. 40 6

5. Chhattisgarh 11 2 4 11 1 4

6. Goa 2 2

7.' ' Gujarat 26 2 4 26 2 4 8. Haryana 10 2 .. 10 2

9. Himachal Pradesh 4 1 4 1

10. Jammu and Kashmir 6 6 11. harkh hand 14 1 5 14 1 5 12. Karnataka 28 4 . ' 28 5 2 13. Kerala 20 2 .. 20 2

14 Madhya Pradesh 29 4 5 29 4 6 %

15. Maharashtra 48 3 4 48 5 4

16. Manipur 2 1 2 1

17. Meghalaya 2 2 2 18. Mizoram 1 1 1 1 19. Nagaland 1 1

20. Orissa 21 3 5 21 3 5

OF 20081 Representation of the People (Amendment) 2 7

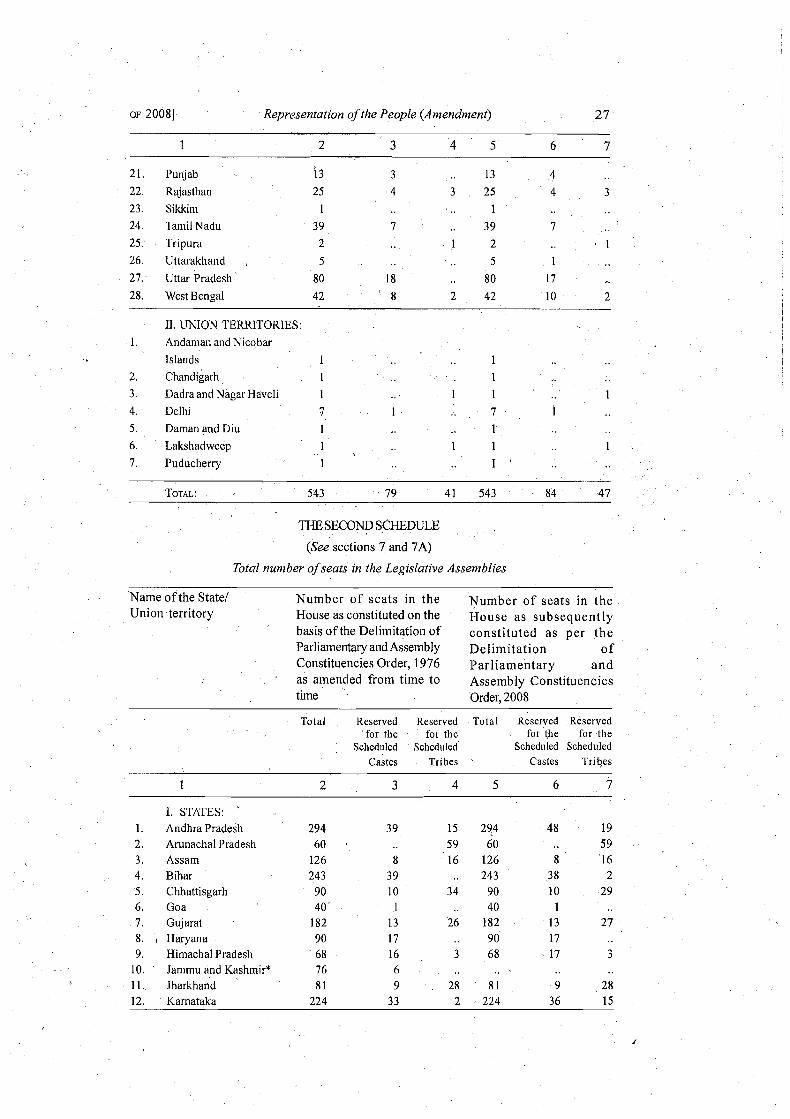

1 2 3 4 5 6 7

21. Punjab 13 3 .. 13 4 22. Rajasthan 25 4 3 25 4 3 23. Sikkim 1 1

24. Tamil Nadu 39 7 .. 39 7 25. Tripura 2 1 2 . 1

26. Uttarakhand , 5 5 1

27.- Uttar Pradesh 80 18 .. 80 17

28. West Bengal 42 8 2 42 10 2

11. UNION TERRITORIES: Andaman and Nicobar Islands Chandigarh Dadra and Nagar Haveli Delhi Daman and Diu Lakshadweep

Puducherry

THE SECOND SCHEDULE

(See sections 7 and 7 A )

Total number of seats in the Legislative Assemblies

Name of the State1 Union territory

Number of seats in the Number of seats in the House as constituted on the House as subsequently basis ofthe Delimitation of constituted as per the Parliamentary and Assembly Delimitation of Constituencies Order, 1976 Parliamentary and as amended from time to Assembly Constituencies time Order, 2008

Total Resewed Reserved Total Reserved Reserved for the for the for the for the

Scheduled Scheduled Scheduled Scheduled Castes Tribes Castes T r~bes

1 2 3 4 5 6 7

I. STATES: '

1. Andhra Pradesh 294 3 9 15 294 48 19 2. Arunachal Pradesh 60 59 60 59 3. Assam 126 8 16 126 8 16 4. Bihar 243 3 9 .. 243 3 8 2 5. Chhattisgarh 90 10 34 90 10 29 6. Goa 40 1 .. 40 1 7. Gujarat 182 13 26 182 13 27 8. Haryana 90 17 . . 90 17 9. Himachal Pradesh 68 16 3 68 17 3

10 Jammu and Kashmir* 76 6 1 1. Jharkhand 8 1 9 28 81 9 28 12. Karnataka 224 3 3 2 224 36 15

d

2 8 Representation of the People (Amendment) [ACT 10 OF 20081

1 2 3 4 5 6 7

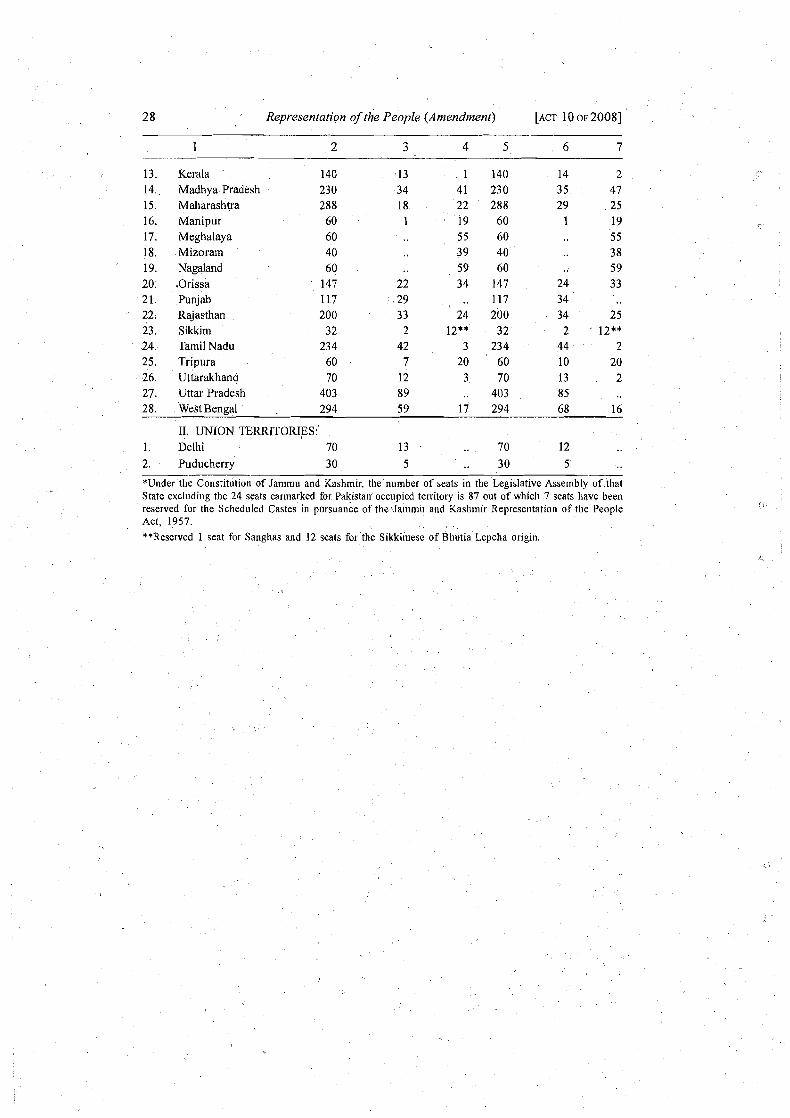

13. Kerala 140 13 1 140 14 2 14. Madhya Pradesh 230 34 41 230 3 5 47 15 Maharashtra 288 18 22 288 29 25 16. Manipur 60 1 19 60 1 19 17. Meghalaya 60 55 60 55 18. Mizoram 40 39 40 3 8 19. Nagaland 60 59 60 59 20. ,Orissa ' 147 22 34 147 24 3 3 21. Punjab 117 -29 .. 117 34 22. Raj asthan 200 3 3 24 200 34 25 23. Sikkim 32 2 12** 32 2 12** 24. Tamil Nadu 23 4 42 3 234 44 2 25. Tripura 60 7 20 60 10 20 26 Uttarakhand 70 12 3 70 13 2 27. Uttar Pradesh 403 89 .. 403 85 28. West Rengal 294 59 17 294 68 16

11. UNION TERRITORIES:' 1. Delhi 70 13 .. 70 12

2. Puducherry 30 5 .. 30 5

*Under the Constitut~on of Jammu and Kashmq the number of seats In the Leglslatlve Assetnbly of that State excluding the 24 seats earmarked for Pak~stan occupled territory IS 87 out of which 7 seals have been reserved for the Scheduled Castes in pursuance of the.Ja~nma and Kashm~r Representat~on of the People Act, 1957. **Reserved 1 seat for Sanglias and 12 seats for the Sikkimese of Bhutia Lepcha orig~n.

, <

THE RAILWAYS (AMEIVDNIENT) ACT, 2008 No. 11 OF 2008

[28th March, 2008.1

An Act m h e r to amend the Railways Act, 1989.

BE it enacted by Parliament in the Fifty-ninth year of the Republic of India as follows:- '