Doing business in Morocco Contents

60

Doing business in Morocco March 2011

-

Upload

independent -

Category

Documents

-

view

7 -

download

0

Transcript of Doing business in Morocco Contents

Doing business in MoroccoMarch 2011

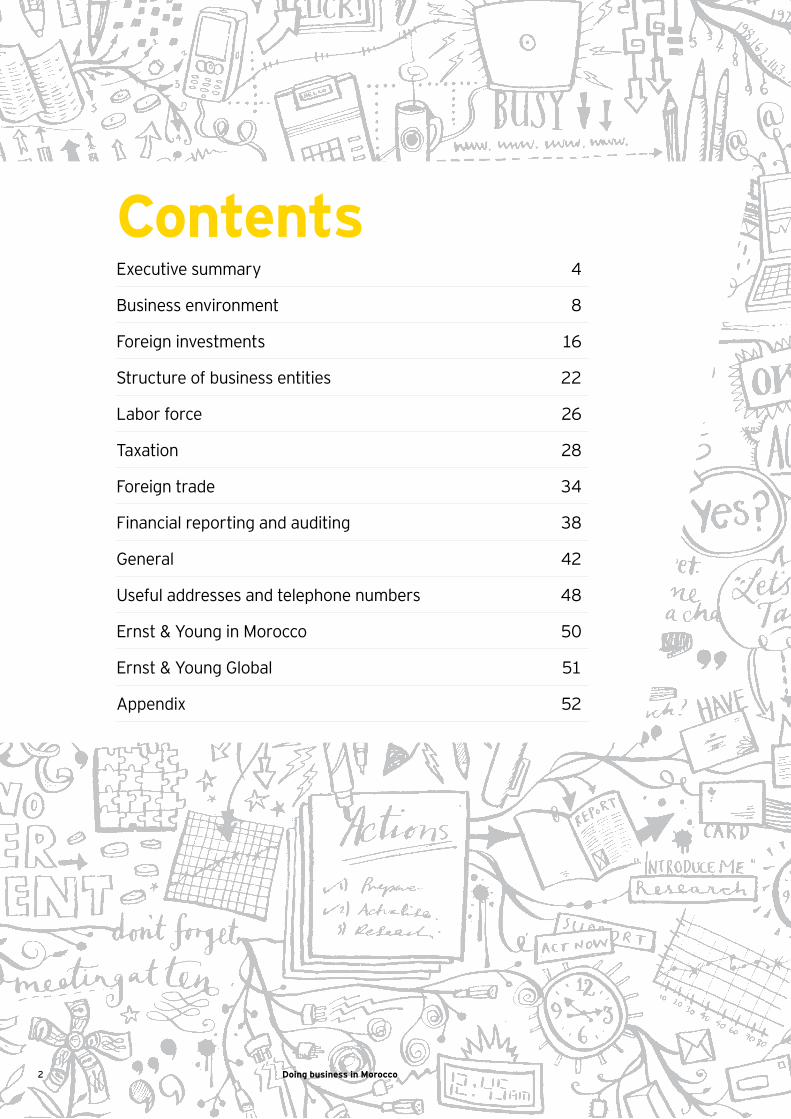

ContentsExecutive summary 4

Business environment 8

Foreign investments 16

Structure of business entities 22

Labor force 26

Taxation 28

Foreign trade 34

Financial reporting and auditing 38

General 42

Useful addresses and telephone numbers 48

Ernst & Young in Morocco 50

Ernst & Young Global 51

Appendix 52

2 Doing business in Morocco

Doing Business in Morocco is published by Ernst & Young Morocco. The book is intended to give the busy executive a quick overview of the business environment in Morocco. The authors of the book have made a sincere attempt to present the current picture of the country’s investment climate, taxation, forms of business organization, business and accounting practices etc., However, it may not represent a comprehensive account of resources on Morocco so that any concrete investment decision in the country can be taken purely going by it alone.

Making decisions about foreign operations is complex and requires an intimate knowledge of a country’s ever-changing commercial climate. There could be overnight changes in prospects in all areas discussed in this book due to several economic or political factors. Companies doing business in Morocco or planning to do so are advised to get current and detailed information from experienced professionals. This book reflects information current at March 2011.

Preface

3Doing business in Morocco

AEx

ecut

ive

sum

mar

y

4 Doing business in Morocco

5Doing business in Morocco

Executive summary

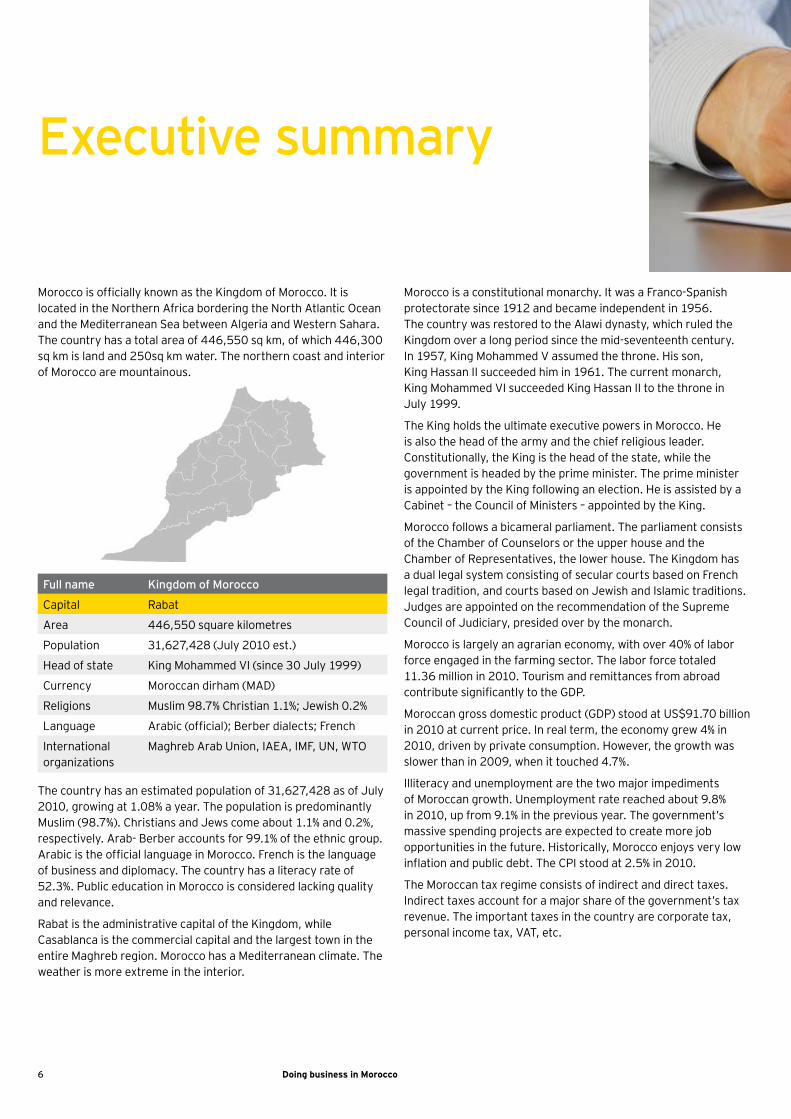

Morocco is officially known as the Kingdom of Morocco. It is located in the Northern Africa bordering the North Atlantic Ocean and the Mediterranean Sea between Algeria and Western Sahara. The country has a total area of 446,550 sq km, of which 446,300 sq km is land and 250sq km water. The northern coast and interior of Morocco are mountainous.

Full name Kingdom of Morocco

Capital Rabat

Area 446,550 square kilometres

Population 31,627,428 (July 2010 est.)

Head of state King Mohammed VI (since 30 July 1999)

Currency Moroccan dirham (MAD)

Religions Muslim 98.7% Christian 1.1%; Jewish 0.2%

Language Arabic (official); Berber dialects; French

International organizations

Maghreb Arab Union, IAEA, IMF, UN, WTO

The country has an estimated population of 31,627,428 as of July 2010, growing at 1.08% a year. The population is predominantly Muslim (98.7%). Christians and Jews come about 1.1% and 0.2%, respectively. Arab- Berber accounts for 99.1% of the ethnic group. Arabic is the official language in Morocco. French is the language of business and diplomacy. The country has a literacy rate of 52.3%. Public education in Morocco is considered lacking quality and relevance.

Rabat is the administrative capital of the Kingdom, while Casablanca is the commercial capital and the largest town in the entire Maghreb region. Morocco has a Mediterranean climate. The weather is more extreme in the interior.

Morocco is a constitutional monarchy. It was a Franco-Spanish protectorate since 1912 and became independent in 1956. The country was restored to the Alawi dynasty, which ruled the Kingdom over a long period since the mid-seventeenth century. In 1957, King Mohammed V assumed the throne. His son, King Hassan II succeeded him in 1961. The current monarch, King Mohammed VI succeeded King Hassan II to the throne in July 1999.

The King holds the ultimate executive powers in Morocco. He is also the head of the army and the chief religious leader. Constitutionally, the King is the head of the state, while the government is headed by the prime minister. The prime minister is appointed by the King following an election. He is assisted by a Cabinet – the Council of Ministers – appointed by the King.

Morocco follows a bicameral parliament. The parliament consists of the Chamber of Counselors or the upper house and the Chamber of Representatives, the lower house. The Kingdom has a dual legal system consisting of secular courts based on French legal tradition, and courts based on Jewish and Islamic traditions. Judges are appointed on the recommendation of the Supreme Council of Judiciary, presided over by the monarch.

Morocco is largely an agrarian economy, with over 40% of labor force engaged in the farming sector. The labor force totaled 11.36 million in 2010. Tourism and remittances from abroad contribute significantly to the GDP.

Moroccan gross domestic product (GDP) stood at US$91.70 billion in 2010 at current price. In real term, the economy grew 4% in 2010, driven by private consumption. However, the growth was slower than in 2009, when it touched 4.7%.

Illiteracy and unemployment are the two major impediments of Moroccan growth. Unemployment rate reached about 9.8% in 2010, up from 9.1% in the previous year. The government’s massive spending projects are expected to create more job opportunities in the future. Historically, Morocco enjoys very low inflation and public debt. The CPI stood at 2.5% in 2010.

The Moroccan tax regime consists of indirect and direct taxes. Indirect taxes account for a major share of the government’s tax revenue. The important taxes in the country are corporate tax, personal income tax, VAT, etc.

6 Doing business in Morocco

The major natural resources of the country are phosphates, iron ore, manganese, lead, zinc, marine products, salt etc. It is the world’s leading exporter of phosphates. Morocco has proven reserves of just 2 million barrels of oil and 43 billion cubic feet of gas. The country is a major importer of oil.

Analysts say the economy has a positive growth outlook in the medium to long term. The government’s continued thrust on education, tourism and energy infrastructure sectors will keep the momentum at a higher level. The fluctuations in the economic conditions of the European Union will have a strong impact on the Moroccan economy.

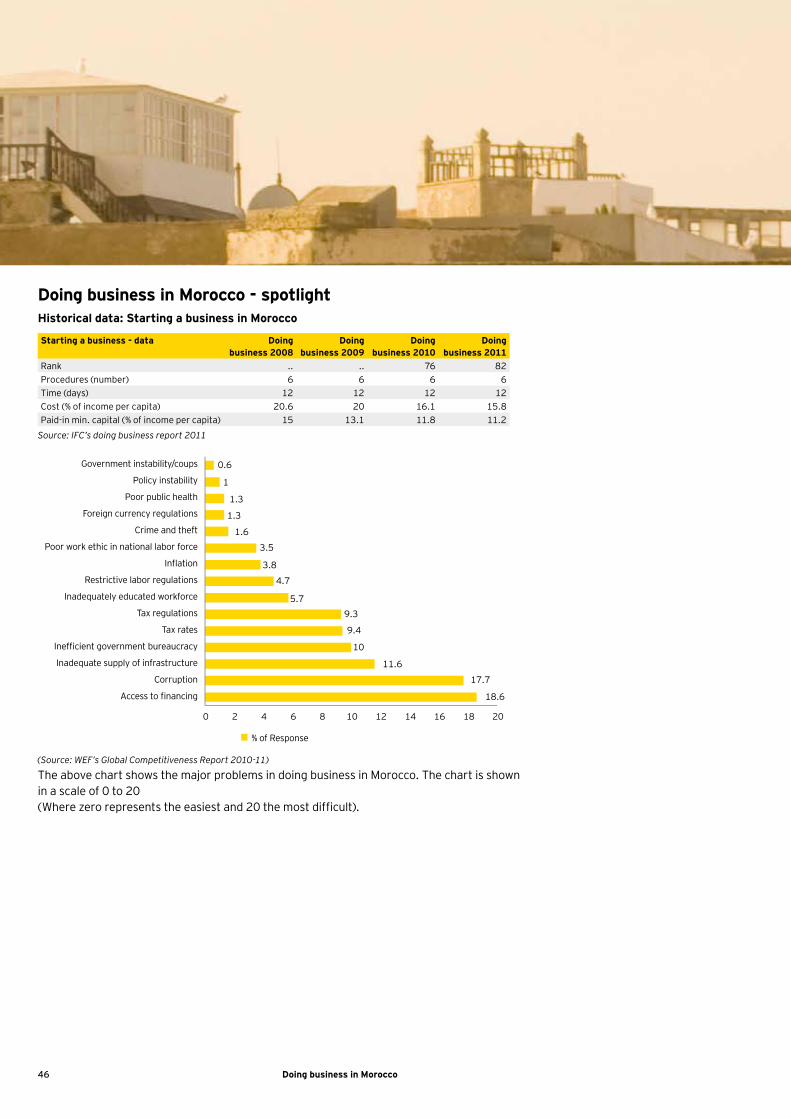

According to the Doing business report 2011 by International Financial Corporation, Morocco ranks 114 out of 183 countries in the world.

Morocco’s ranking in doing business out of 183 countries

Area Rank

Ease of doing business 114

Starting a Business 82

Dealing with construction permits

98

Registering property 124

Getting credit 89

Protecting investors 154

Paying taxes 124

Trading across borders 80

Enforcing contracts 106

Closing a business 59

Source: IFC’s Doing business report 2011(modified)

7Doing business in Morocco

BBu

sine

ss e

nviro

nmen

t

8 Doing business in Morocco

9Doing business in Morocco

Investment and business environmentMorocco’s economy is considered as a relatively liberal one, offering great investment opportunities to the private sector, both domestic and foreign. The country’s key sectors were opened up to foreign investments in 1990. The government’s reforms are aimed at projecting itself as an internationally competitive investment destination.

With a view to enhancing the attractiveness of Morocco, the government initiated a number of steps in the recent years. This includes the introduction of new laws and amendments or revision of the existing ones. This apart, Morocco concluded a number of free trade agreements (FTAs) with several countries, mostly advanced ones.

The government has undertaken numerous projects for the strategic liberalization of the Moroccan economy. Some of the major steps include:

Adoption of the Charter of investments to replace codes by • single sector

►Introduction of uniform law •

Tax advantages for investment•

►Encouragement of creativity through the adoption of legislation • on the protection of intellectual property and industrial property

Creation of Morocco industrial and commercial property•

►Convertibility for foreign investment•

Free repatriation of income from the investment operations •

►Retransfer the proceeds of liquidation or sale of their • investments

Liberalization of external financing•

Economic trends and performanceMorocco is a mid-sized economy with limited exposure to the global economy. But, the country maintains strong trade relations with the European Union (EU), especially France. France is its largest trading partner as well as the creditor. The sluggishness in the EU has impacted Morocco’s exports and inflow in the past couple of years.

Strengthening the business environment in Morocco is a policy goal of the government. Relaxing regulations to set up business was one of the positive steps toward this goal.

Macroeconomic stabilityThe economic reforms initiated by King Mohammed VI since 2003 have brought macroeconomic stability to the country. In 2005, the government launched a National Initiative for Human Development to alleviate poverty and underdevelopment. Improving education and job opportunities and reducing income disparity among the people are the major long-term challenges of Morocco.

The country’s textiles, electronic components, offshore services and tourism sectors are the priority sectors for foreign direct investment. The government is also keen on investment in the technology sector as well as research and development.

The government is confident of managing its fiscal position. The 2011 budget does not include any increases in tax rates. Reforming the subsidy system is a priority for the government. Rising international commodity prices can put strain on its public finances as it depends on imports for its energy needs.

The central bank, Bank al-Maghrib follows a benign policy rate of 3.25%, given the country’s slowing growth and inflation.

Business environment

10 Doing business in Morocco

Economic structure The economy is agrarian. The primary sector comprises agriculture, livestock farming and marine fisheries. The secondary sector consists of processing, industries, building and public works, mining and energy sectors. The tertiary sector is composed of tourism, transport and communication, commerce and other services.

Morocco - major economic indicators

For Morocco in 2010 Indicator value

GDP growth (constant prices, national currency) 4%

GDP (current prices, national currency) MAD 777.139 billion

GDP (current prices, US dollars) US$ 91.702 billion

GDP deflator 121.731 (index, base year as per country's accounts = 100)

GDP per capita (constant prices, national currency) MAD 19,967.48

GDP per capita (current prices, national currency) MAD 24,306.57

GDP per capita (current prices, US dollars) US$ 2,868.15

GDP (PPP), US dollars US$ 152.619 billion

GDP per capita (PPP), US dollars US$ 4,773.45

GDP share of world total (PPP) 0.21%

Implied PPP conversion rate 5.092

Inflation, average consumer prices (indexed to year 2000) 189.31 (index, base year 2000 = 100)

Inflation (average consumer price change %) 1.50%

Inflation, end of year (indexed to year 2000) 187.117 (index, base year 2000 = 100)

Inflation (end of year change %) 1.50%

Unemployment rate (% of labor force) 9.60%

Population 31.972 million

General government revenue (national currency) MAD 191.342 billion

General government revenue (% of GDP) 24.62%

General government total expenditure (national currency) MAD 217.374 billion

General government total expenditure (% of GDP) 27.97%

Total government net lending/borrowing (national currency) MAD −26.032 billion

Total government net lending/borrowing (% of GDP) −3.35%

Total government net debt (national currency) MAD 382.659 billion

Total government net debt (% of GDP) 49.24%

Total government gross debt (national currency) MAD 387.986 billion

Total government gross debt (% of GDP) 49.93%

Fiscal year gross domestic product, current prices MAD 777.139 billion

Current Account Balance (US Dollars) US$ -4.86 Billion

Current Account Balance (% GDP) -5.30%

11Doing business in Morocco

Financial sector

Banking The Moroccan banking closely follows the European banking system. The 1990s saw several reforms in the Moroccan financial sector. With the establishment of the banking law of 1993, the government wanted to fulfill the following main objectives:

The unification of the legal framework•

The creation of three institutions, namely The National • Council of Money and Savings (CNME), the Committee of Credit Establishments (CEC) and the Commission of Credit Establishments (CDEC)

The protection of lenders and borrowers by a range measures •

Reinforcement of the autonomy of the Central Bank and its • powers of control and supervision

A broadening of the field of control of the Bank al-Maghrib • (BAM) over off-shore banks, micro-credit associations and for certain establishments solely over matters of accounting and careful management

A complete overhaul of the composition and the attributions of • the CEC and the CNME

Obligation to introduce internal controls•

Widening of the role of the auditor•

Revision of the rules governing crisis management •

Reinforcement of protection of depositors•

Creation of a commission for the coordination of financial sector • supervising authorities

The 1993 Banking Law was replaced by a new banking law in 2006.

Banking supervisionBank al-Maghrib (BAM) is the central bank of Morocco. BAM is committed to reform the supervision of the financial sector. In October 2008, the IMF conducted an update of its Financial System Stability Assessment (FSSA), following its initiative in 2003. IMF concluded that Morocco complied with 21 out of the 25 Basel Core Principles (BCPs) for effective banking supervision.

According to IMF, following areas needed more attention of Moroccan authorities:

Supervisory approval of major acquisitions by banks •

Country and transfer risk•

Anti-money laundering and combating the financing of terrorism • framework

►Cooperation between home and host supervisors•

The new Banking Law 2006 enhanced central bank’s independence and supervisory role. It also provides for close coordination among financial sector supervisors. This led to the improvement of the regulatory framework for banking supervision. IMF also noted that Morocco made progress toward implementing the Basel II standardized approach to credit risk. Effective January 2010, the Moroccan banks are required to adopt International Financial Reporting Standards (IFRs).

The Moroccan banking sector includes 24 commercial banks.

Top banks

Attijariwafa Bank 1.

Banque Populaire du Maroc 2.

BMCE Bank 3.

BMCI 4.

Société Générale Maroc 5.

Crédit Agricole du Maroc 6.

Crédit du Maroc 7.

Crédit Immobilier et Hôtelie8.

Others

Arab Bank Maroc 9.

Banco Immobiliario & Mercantil de Marruecos 10.

Bank Al Amal 11.

Bex-Maroc 12.

Caisse Marocaine des Marches 13.

Citibank Maghreb 14.

Limar Bank Casa Union Marocaine de Banques 15.

Raw-Mat Bank 16.

Societe de Banque & de Credit17.

12 Doing business in Morocco

Insurance Morocco introduced a number of reforms in its insurance sector. With the US–Moroccan Free Trade Agreement (FTA), a number of US-based banking and insurance companies started operating in Morocco.

Insurance supervisionThe Insurance and Social Welfare Directorate (DAPS) is the regulator and supervisor of the insurance and reinsurance sector in the country. It functions under the Ministry of Economy and Finance.

According to the IMF’s FSSA report of 2003, Morocco has not fully complied with the Insurance Core Principles (ICPs), promulgated by the International Association of Insurance Supervisors (IAIS). .

Following are the weak areas of the sector:

Internal governance•

Internal control•

Asset and risk management•

Information sharing capacity of the regulator with foreign • supervisory agencies

In another report in July 2008, IMF observed that Morocco achieved much progress in the field, but there still persists some deficiencies in the area of licensing procedure.

The IMF wanted the country to enhance the independence of the regulator, and improve the licensing process.

Morocco’s sector expanded 14% (CAGR) in 2010. The total premium collected reached $2.76 billion last year. The insurance penetration comes to 3.0% of GDP.

Morocco’s insurance business environment indicators

Limits of potential returns Data

Non-life premiums (current year) US$1,962.9m

Non-life premium increase (5yr) $811.7m

Non-life penetration (current year) % 2.2%

Life premiums (current year) US$797.2m

Life premium increase (5yr) US$1,665.6m

Life penetration (current year) % 0.9%

GDP per capita US$2,932

Active population, % of total 63.7%

Data from BMI

Following are the major insurance companies operating in Morocco:

RMA Watanya Insurance •

AXA Assurance Maroc Insurance •

►Marocaine Vie Insurance •

CNIA Insurance •

Wafa Insurance •

Atlanta Insurance •

Zurich Insurance •

Sanad Insurance •

Morocco Non-Life Insurance Companies •

Wafa Insurance •

Sanad Insurance •

Atlanta Insurance •

CAT Insurance •

Zurich Insurance •

MAMDA Insurance•

Capital marketMorocco’s stock exchange (CSE) was established in Casablanca in 1929. It is the third largest stock market in Africa after Johannesburg and Cairo. The Ministry of Finance appoints a government commissioner to the CSE. The company’s shares are held by 17 brokerage firms. Trading is conducted on a central market and a block trade market basis. There is only one index known as ‘the index de la Bourse des Valeurs de Casablanca’.

In the third quarter of 2010, the MASI index rose 1% from the prior quarter and climbed 14% over the previous year. The volume of transactions increased 11.8% to 65.6 billion dirhams during the quarter. Market capitalization dropped to 538.2 billion dirhams showing a 5.5% decrease over the previous quarter. The price earning (PE) ratio of the Casablanca stock market stood at 17.7.

Securities regulation The Securities Commission (Conseil Déontologique des Valeurs Mobilières) is the market regulator in Morocco. The IMF’s FSSA in 2003 found inadequacy in the legal framework of the securities markets in the country. However, it endorsed the view that there was much progress in the regulatory and institutional aspects of supervision.

13Doing business in Morocco

Other findings of IMF are:

The market regulator has inadequate inspection and • enforcement powers

The political influence over the market regulator would affect its • operational independence

In response to these findings and recommendations, the government strengthened the market’s legal framework related to regulation and supervision. Six new laws were introduced and the market regulator’s authority over the stock exchanges was reinforced.

In an update of FSSA in 2008, IMF observed that the Moroccan authorities had planned measures to strengthen financial sector supervision, including granting full independence to the Securities Commission.

Regulatory bodiesThere are five main regulatory bodies in Morocco:

National Accounting Council 1. (Conseil National de la Comptabilité)

Bank al-Maghrib2.

Securities Commission 3. (Conseil Déontologique des Valeurs Mobilières)

Insurance and Social Welfare Directorate 4. (Direction des Assurances et de la Prévoyance Sociales)

The Institute of Chartered Accountants 5. (Ordre des Experts-Comptables)

Energy, minerals and other natural resourcesMorocco has proven reserves of just 2 million barrels of oil and 43 billion cubic feet of gas. There was no significant discovery in the country in the recent past. However, there are substantial infrastructure facilities in place to support an active natural gas and petroleum industry. This includes seaports, pipelines and refineries located near large cities.

Morocco has abundant natural resources. Phosphates, barite, clays, coal, cobalt, copper, fluorspar, gold, iron ore, lead, nickel, petroleum, salt, silver, talc and zinc are its main natural resources. Water is scarce in Morocco. It is a major constraint to the development of agriculture.

Morocco is the world’s third ranked producer of phosphates after China and the United States. It has about three-quarters of the

world’s estimated reserves of phosphates. The Kingdom controls about one-third of the international trade in phosphates and their derivatives. Obviously, the phosphate sector is the leading foreign exchange earner accounting for about 35% of foreign trade.

The country produces 17% of the world’s output of phosphate rock, 6% of the world’s output of barite, and 2% of the world’s output of cobalt, 2% of the world’s output of fluorspar and 1% of the world’s output of lead. Phosphate rock accounts for about 95% of the country’s volume of mining output.

Ongoing activities in mining

Natural gas In 2009, UK’s Dana Petroleum plc announced that it had made a significant natural gas discovery at Anchois. The Anchois-1 well is located about 40 km from the coast and was drilled to a total depth of 2,435 m. It was the first well drilled in the area. The preliminary estimates show about 2.8 billion cubic meters. Three other companies involved in exploration efforts in the area were Gas Natural S.A. of Spain, ONHYM and Repsol YPF, S.A. of Spain. Another UK company, Caithness Petroleum Ltd announced that it had interests in three exploration permits in Morocco.

CoalMorocco imports coal from Colombia, South Africa and the United States. Coal is used to power the electrical power stations at Jorf Lasar and Mohammedia. The state-owned company l’Office National de l’Electricité (ONE) is responsible for the generation, transmission and distribution of electrical power.

UraniumThe government encourages exploration for uranium. Morocco’s several uranium mineralization settings included paleochannel-type occurrences, granites with vein-type occurrences, and occurrences in sedimentary and metamorphic terrains. Areas, such as Haute Moulouya, Sirwa (Zgounder) and Wafaga are under investigation. Haute Moulouya and Wafaga have paleochannel deposits. Australia’s Toro Ltd. of had tenements in the Haute Moulouya area.

Solar energyThe government announced a large-scale solar energy project estimated to cost $9 billion. The Moroccan Agency for Solar Energy will supervise activities related to economic, financial and technical matters. The project is targeting 2,000 megawatts of capacity by 2020. Five sites had been identified and were located

14 Doing business in Morocco

in the southern region of Ouarzazate. The first power station was expected to be operational by 2015.

Major industriesMorocco has a growing industrial sector attracting foreign direct investment (FDI). Some of the preferred sectors for FDI include automotive, aeronautic, electronic, food processing, offshore activities and marine products. The countries industrial sector contributes an average 30% to GDP.

Mining industryMining industry is very significant to the Moroccan economy. Mineral concentrate production is dominated by the private sector. But phosphates sector is a state monopoly. The country is home to about a hundred mining companies, producing 20 different minerals. The Ministry of Industry Trade Energy and Mines is responsible for overseeing the mining industry in Morocco. Morocco’s mining industry continues to remain buoyant on the back of a dominant phosphate sector. It is the largest foreign exchange earner for Morocco.

Textiles and clothingMorocco is recognized as a leading producer of top quality leather goods and handcrafted cloth. The country developed many textile mills, producing large quantities of ready-to-wear accessories and clothing. Its textiles and clothing sector has a significant market in the European Union (EU). France imports about 27.6% of the ready-to-wear clothing, 46% of the hosiery and 28.5% of the basic textile produced by Morocco.

ManufacturingIn the manufacturing sector, the important industries are light consumer goods, particularly foodstuffs, beverages, textiles and metals, and leather products. There are certain heavy industries in the fertilizers, refining, automobile and tractor assembly, foundry work, asphalt and cement segments. There are several processed agricultural products and consumer goods, mostly for local consumption. The country exports canned fish and fruit, wine, leather goods, textiles and traditional Moroccan handicrafts. Overall, the manufacturing sector accounts for roughly one-sixth of the GDP.

TourismMorocco has achieved significant growth in the tourism sector. The country gets a large number of visitors from the EU, particularly France. The government enhanced its spending

on infrastructure in recent years. It also encourages private investment in the sector by extending incentives, such as long-term financing and tax exemptions.

AerospaceThe sector mostly based in Tangier and Casablanca has achieved tremendous growth in the recent past. Considering the low production cost, the sector is considered an ideal destination for foreign investment.

Call centers and outsourcingMorocco is fast becoming an attractive offshore services market. The government wanted to create 100,000 new jobs in the sector, by setting up special business zones. These zones are designed to offer lower overhead, simpler administration and abundant skilled human resources.

AgricultureNearly half the population is engaged in agriculture. The sector contributes about 16% of the GDP. The country’s agricultural sector is the largest in the region. Blessed with a long crop growing season and a relatively mild climate, Morocco is able to grow a large selection of vegetables and fruits. Lower labor cost and good communications and transportation systems are other positive factors. Morocco’s major agricultural exports include fruits, vegetables, olive oil, nuts and spices.

SeafoodMorocco is a leading exporter of sea food mostly to Japanese and European markets. The seafood processing industry accounts for about half of its total agriculture exports. The FTA between the US and Morocco offers many investment opportunities for Americans.

OutlookThe Government is expected to establish joint ventures with international companies, particularly in the natural gas and petroleum sectors. There are plans to privatize selected state-owned mining assets to boost the sector’s competitiveness. It is expected that the output of lead, silver and zinc will decline. Moroccan tin is expected to have good market on the face of growing demands from the electronic sector.

Morocco has also plans to launch a major independent power project (IPP), Al Wahda Combined Cycle Power Plant, at Safi near Casablanca. The government is expected to encourage foreign investment in the phosphate sector.

15Doing business in Morocco

CFo

reig

n in

vest

men

ts

16 Doing business in Morocco

17Doing business in Morocco

IntroductionForeign investment contributes substantially to Morocco’s growth. In 1990, the government opened almost all its sectors to foreign investment. Necessary steps were initiated to encourage foreign investors and to provide them with the same rights and advantages as local investors.

Morocco allows free repatriation of investments and investment returns, such as capital gains, dividends, interest or sales etc. Through periodic revisions of the Commercial Code, Company Law, the Labor Law etc., the Kingdom wants to establish an internationally competitive investment environment in the country.

In 1995, the government came up with an Investment Charter primarily to reduce investment cost and allowing free repatriation of investment and investment returns. The Charter came into effect in January1996.

The main objective of the Charter was to encourage private sector investment, both domestic and foreign, in Morocco. The Charter offers systematic access to all available benefits to the private sector. It contains specific incentives for large projects and makes provisions a one-stop investment agency to assist investors.

The other objectives of the Charter include:

A reduction in the tax on the capital goods required for • investment

The implementation of a preferential system favoring regional • development

The promotion of money markets•

The promotion of employment•

The promotion of exports•

A reduction in investment costs•

The protection of the environment.•

Exchange controlsThe current exchange-rate regime is a tightly managed one in the country. The local currency is pegged to a euro-dominated basket of currencies. Bank Al Maghrib believes that this system helped in anchoring the economy and keeping inflation low.

Economic operators in Morocco have free access to foreign currency, quoted by the Bank al-Maghrib, for convertibility of the Dirham and settlement of transactions. The sums payable for these operations required no authorization by the Foreign Exchange Office.

Morocco offers convertibility for:

Foreign trade operations and related costs •

Transfer of revenue from foreign investments•

Savings on income of natural persons of foreign nationality • residing in Morocco, and foreign technical support.

Foreign investors both resident and non-resident and Moroccans returning from abroad can have the freedom to:

Invest in projects with no prior formality with regard to exchange•

Transfer the revenue from these investments without • restrictions on amount or time (after paying duties and taxes in force in Morocco)

Retransfer the profits of transfers, liquidations or • unvested funds.

Foreign investments

18 Doing business in Morocco

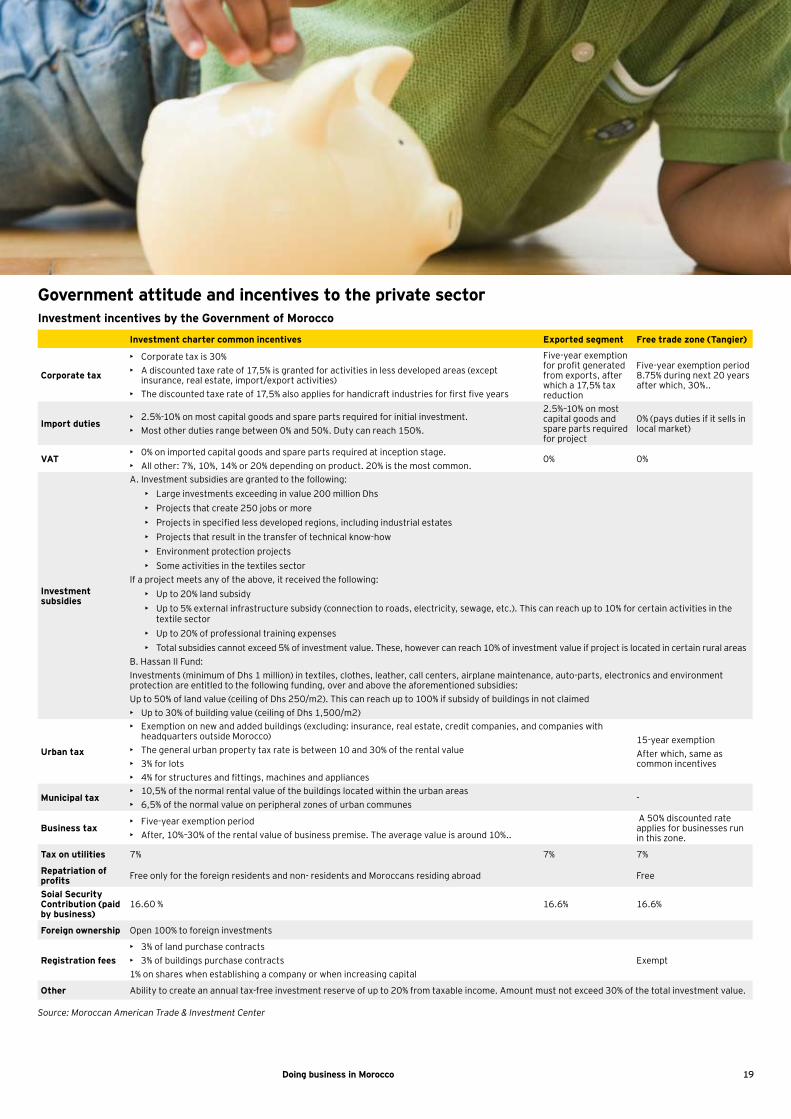

Government attitude and incentives to the private sectorInvestment incentives by the Government of Morocco

Investment charter common incentives Exported segment Free trade zone (Tangier)

Corporate tax

Corporate tax is 30%• A discounted taxe rate of 17,5% is granted for activities in less developed areas (except • insurance, real estate, import/export activities)The discounted taxe rate of 17,5% also applies for handicraft industries for first five years•

Five-year exemption for profit generated from exports, after which a 17,5% tax reduction

Five-year exemption period 8.75% during next 20 years after which, 30%..

Import duties2.5%-10% on most capital goods and spare parts required for initial investment.• Most other duties range between 0% and 50%. Duty can reach 150%.•

2.5%–10% on most capital goods and spare parts required for project

0% (pays duties if it sells in local market)

VAT0% on imported capital goods and spare parts required at inception stage.• All other: 7%, 10%, 14% or 20% depending on product. 20% is the most common.•

0% 0%

Investment subsidies

A. Investment subsidies are granted to the following:Large investments exceeding in value 200 million Dhs• Projects that create 250 jobs or more• Projects in specified less developed regions, including industrial estates• Projects that result in the transfer of technical know-how• Environment protection projects• Some activities in the textiles sector•

If a project meets any of the above, it received the following:Up to 20% land subsidy• Up to 5% external infrastructure subsidy (connection to roads, electricity, sewage, etc.). This can reach up to 10% for certain activities in the • textile sectorUp to 20% of professional training expenses• Total subsidies cannot exceed 5% of investment value. These, however can reach 10% of investment value if project is located in certain rural areas•

B. Hassan II Fund:Investments (minimum of Dhs 1 million) in textiles, clothes, leather, call centers, airplane maintenance, auto-parts, electronics and environment protection are entitled to the following funding, over and above the aforementioned subsidies:Up to 50% of land value (ceiling of Dhs 250/m2). This can reach up to 100% if subsidy of buildings in not claimed

Up to 30% of building value (ceiling of Dhs 1,500/m2)•

Urban tax

Exemption on new and added buildings (excluding: insurance, real estate, credit companies, and companies with • headquarters outside Morocco)The general urban property tax rate is between 10 and 30% of the rental value• 3% for lots• 4% for structures and fittings, machines and appliances•

15-year exemption After which, same as common incentives

Municipal tax10,5% of the normal rental value of the buildings located within the urban areas• 6,5% of the normal value on peripheral zones of urban communes•

-

Business taxFive-year exemption period• After, 10%–30% of the rental value of business premise. The average value is around 10%..•

A 50% discounted rate applies for businesses run in this zone.

Tax on utilities 7% 7% 7%

Repatriation of profits Free only for the foreign residents and non- residents and Moroccans residing abroad Free

Soial Security Contribution (paid by business)

16.60 % 16.6% 16.6%

Foreign ownership Open 100% to foreign investments

Registration fees3% of land purchase contracts • ►3% of buildings purchase contracts•

1% on shares when establishing a company or when increasing capitalExempt

Other Ability to create an annual tax-free investment reserve of up to 20% from taxable income. Amount must not exceed 30% of the total investment value.

Source: Moroccan American Trade & Investment Center

19Doing business in Morocco

Morocco has streamlined its legal framework to improve the business climate by encouraging more investment in the country. There are provisions of a number of operational instruments to support investments across sectors.

The objectives of these measures are:

Simplification and streamlining of administrative procedures•

►Guaranteed transfer of profits and earnings from sales including • added values

Lower cost of investment and taxes levels•

►Preferential treatment benefiting export enterprises•

Contract system granting additional advantages•

►Promotion of employment•

Legal environment of investment

Law on patent rights and intellectual property Morocco is a member of the World Intellectual Property Organization and signatory of the Bern Royalties Convention, the Paris Convention for Intellectual Property and universal royalties as well as the Brussels, Madrid and The Hague agreements.

The Moroccan Office of Patent and Commercial Property (OMPIC) enforces both national and international legislation.

The FTA with the US (June 2004) contains some of the strongest intellectual property protections in any free trade agreement.

The country has a relatively comprehensive regulatory and legislative system. In order to have the protection, intellectual property rights must be registered in both Casablanca and Tangier.

Patents An individual or legal entity can file an application for a patent with the Moroccan Patent Office in Casablanca. The Patent Office examines applications with regard to form only and not with regard to novelty or merit. Following this, the particulars of the application will be published in the Official Gazette. No opposition procedure is provided. Patents issued are valid for 20 years. Patents rights can be freely transferred to third parties. However, the transfer must be registered with the Patent Office in order to be effective against third parties..

TrademarksMorocco follows the international classification of goods for this purpose. The Trademark Office examines the trademark applications. Registered trademarks in the preceding year are published in a special trademark supplement of the Official Gazette. No opposition procedure is provided. A registered trademark is valid for 20 years and can be renewable for an additional 20-year period.

Transfer of trademark rights is allowed but needs to be registered with the Trademark Office within three months in order to be valid. Infringement of a registered trademark may be punishable under either the penal or civil laws of Morocco.

20 Doing business in Morocco

CopyrightMoroccan law provides copyright protection for the literary or artistic expression of an idea. There are no registration requirements to invoke such protection. A copyright confers upon the author two principal rights: a property right and an ethical right.

The property right gives the author the exclusive right to exploit the copyrighted work for pecuniary gain. This right extends throughout the author’s lifetime. Thereafter, it is transferred to the benefit of the author’s heirs for a period of 50 years.

Freedom of pricing and competitionLaw 6/99 guarantees the freedom of pricing through competition and free market access. It lifts all barriers and restrictions and promotes a competitive culture by enhancing transparency and fairness in business relationships.

Bilateral agreements with other countriesMorocco has signed bilateral agreements with more than 30 countries for:

►Protection and guarantee of investments•

►Avoidance of double taxation on income and capital•

Commercial courts Morocco’s legal system is non-discriminatory and is accessible to foreign investors. The government has designed its national legal structure to make the business culture conducive for both domestic and international business. There are commercial courts designed to facilitate the working environment more secure for domestic and foreign operators.

Commercial courts were established in 1998 to address the weakness in commercial proceedings. A system of commercial arbitration was also created in April 1998.

Protection of property rightsBy an amendment to the existing law, Morocco has brought into compliance with its TRIPS commitments in December 2004. The government has also passed a law permitting the development of a secondary mortgage market.

Tax system and trade agreementsMorocco had plans to progressively eliminate customs duties in order to create a free trade zone with the European Union by 2010. It already has a set of FTAs or PTAs with several countries such as the USA, Turkey and several Arab nations (Great Arab Free Trade Agreement).

21Doing business in Morocco

CSt

ruct

ure

of b

usin

ess

entit

ies

22 Doing business in Morocco

23Doing business in Morocco

Structure of business entitiesCompaniesFollowing are the different types of companies under the Moroccan Corporation law:

Public limited company •

►Private limited company•

Limited partnerships with shares•

►General and limited partnerships•

Joint ventures•

All these companies conform to the Western company forms of the same nomenclature. SA and SARL are the most common nomenclature..

The public limited company – ‘SA’ (Société Anonyme)Following are the basic characteristics of the SA:

A minimum of five shareholders is necessary to form a SA •

Share capital of a SA cannot be less than 3 million Dhs if the • company seeks public investment

Share capital will be 300,000 Dh if it does not seek public • investment

Shares are negotiable, freely transferable and tradable•

All the shareholders are responsible for the company’s liabilities • up to the extent their capital contribution

Share capital comprises contributions in kind or cash•

The minimum nominal value of the stock is fixed at Dh 100•

The SA is managed by one or more representatives from among • the shareholders

The private limited company -‘SARL’ (Société à Responsabilité Limitée)The SARL has the characteristics of both joint stock companies and partnerships at the same time.

Other characteristics of the SARL:

Minimum two members•

Must have a minimum capital of 10,000 MDh•

The shares must be of at least Dh 50 and of equal value •

Liability of shareholders is limited to the extent of their • shareholding

Members of the company need not to be registered merchants•

Must file a memorandum of association as part of its • incorporation process

The capital stock has to be fully described and paid up on the • formation of the company

Stock are not negotiable and should bear the same face value•

Transfer of share is possible only through contracts•

“Parts Sociales” may be transferred to third parties outside the • company only with the co-associates’ consent

The SARL may have a corporate style or business name•

The partnership (Société en Nom Collectif)The partnership is an agreement between at least two persons joining to trade under a corporate name.

Characteristics of the partnership are:

The deed of incorporation must be drawn up by a notarial deed • or under private seal

The partners are jointly and severally responsible for the • company’s debt

The limited co-partnership (Société en Commandite Simple)The limited co-partnership is governed by the same rules as the partnership. The exception is that there are two types of partners:

The administrative partner or partners who are responsible for • up to the total of their assets

Ordinary partners whose liability only extends to their level of • contribution

Joint venturesThe law recognizes joint ventures for the purpose of one or several commercial operations. Joint venture agreements are drawn up in the form and for the purpose agreed by the partners, and entail a joint sharing of income. They cannot undertake any legally binding action as they do not have legal status.

Others

Branch offices of foreign companiesThe Moroccan branch offices and subsidiaries of foreign companies are treated as independent legal entities.

The entities must submit details of the parent company, its representatives and its delegated powers. The parent company must submit its articles of incorporation as well as that of the branch when applying for its registration.

24 Doing business in Morocco

Sole proprietorshipsIn a sole proprietorship, the individual conducting the business is personally liable for the entity’s debts. The liability is to the extent of all business and personal assets. The promoter must register the company with the Commerce and the tax authority.

Governing documentsThere are some basic and replaceable rules for the internal management of a company. Companies need to have a separate constitution only if they want to modify or add the replaceable rules.

Certain rules are mandatory, while some special rules are designed for single shareholder and single director companies. The companies must have a registered office and an accountant’s office.

Role of directorsThe board of directors is the principal controlling body of the company. The board is appointed by the shareholders. There should be at least three directors for a public limited company, consisting of two ordinary residents in Morocco and one company secretary.

For proprietary companies, there should be at least one director, a resident in Morocco.

Directors have a statutory obligation to ensure that:

The annual financial report gives a true and fair view of the • financial position and performance of the company

The financial report has been prepared in accordance with • Moroccan accounting standards

The company will be able to pay its debts as and when they • become due and payable

The company safeguards its assets and maintains a complete • and adequate set of accounting records and statutory registers

Directors can face large fines or imprisonment for breaches of their duties. Under certain situations, they are also personally liable for the debts of the company.

Forming a company and disclosure obligationsAll listed companies intending to register securities for public sale must issue a prospectus that complies with the rules of the Company Law.

Those planning to invite public subscriptions may seek admission to the Casablanca Stock Exchange Ltd.

Continuous disclosure and periodic reporting requirements is a must for companies which are:

Listed on a stock exchange•

Raising funds from public•

Offering their securities for the acquiring a target company•

Issuing their securities under a compromise or scheme of • arrangement

Borrowing from market or financial institutions•

They need to publicly disclose all information having a potential influence on the price or value of their securities. Additionally, they should also lodge half-year financial reports.

All companies are bound to appoint auditors to annually report on their financial reports. The exceptions to the rule are small proprietary companies.

Shareholdings by non-residentsMoroccan companies are open to non-resident share holdings, with the exception of certain industries. Companies are not bound to disclose the names of non-resident shareholders and the amount of shares they own. The percentage of foreign ownership hardly affects the status of the company.

25Doing business in Morocco

Morocco’s labor force is about 11.36 million in 2010. About 40% of the labor force is engaged in the farming sector. The service and industry sectors account for about 35% and 25%, respectively.

Moroccan labor law and practice are based on French models. Article 14 of the Constitution gives workers the right to strike. Only unions with membership of 35% of the organization’s workforce can engage in collective bargaining. There are mandatory procedures governing the settlement of disputes.

The Ministry of Employment Social Affairs and Solidarity is responsible for employment and protection of workers’ rights. Occasionally, the Ministry may intervene, if the strategic interests are threatened.

Labor code (Code du travail) In 2004, the government launched a new labor code (Code du travail). The code underlines equal treatment under the law for its citizens.

The new labour law has come into effect on 7 June 2004. The law is in conformity with the recommendations of International Labor Organisation (ILO). The country ratified the ILO convention covering the right to organize and bargain collectively.

With the introduction of the labor code, the minimum employment age was raised from 12 to 15 to eliminate the chances of child labor, and the work week was reduced from 48 to 44 hours. Maximum daily working hours were fixed to 10 hours. A provision was made for payment of overtime for work beyond 10 hours.

According to the new labor code, the weekly break must consist of a minimum of 24 consecutive hours for all staff. All workers are entitled to a holiday after six months continuous employment.

The law stipulates that all workers must receive a seniority bonus equivalent of 5% of the wage after two years’ service, 10% after 5 years, 15 % after 12 years and 20% after 20 years’ service and 25% beyond.

The law not only modernized the previous texts regulating the labor market, it also gave room for more flexibility. Employers and employees can negotiate salaries freely. But, salaries should not be less than the minimum wage of Dh 9.66/hour for general sectors and Dh 50/day for the farm sector.

The new labor law outlined three modes of recruitment:

Indefinite duration contact (CDI)•

CDI is the most common contact and its termination by either party is subject to a notice.

Finite duration contract (CDD)•

Exceptional and cannot exceed 24 months•

Temporary work contract (CDT) •

This is applicable in seasonal activities and certain • traditional sectors. Also applies to replacement (suspension of a contract for instance) or increase of activity (all sectors).

ELa

bor f

orce

26 Doing business in Morocco

27Doing business in Morocco

FTa

xatio

n

28 Doing business in Morocco

29Doing business in Morocco

Taxation

Federal taxes and levies There are two types of taxes in Morocco; direct taxes and indirect taxes. Indirect taxes are the major source of tax revenue for the government.

Morocco follows a territorial tax system. Individuals with habitual residence in Morocco are liable to pay tax on their worldwide income. This applies to residents of all nationalities. Those without habitual residence in the country are taxable for income generated in Morocco.

The Moroccan tax system addresses the issue of double taxation partially by tax treaties or unilateral relief in the form of tax credit.

Income from agricultural is exempted from tax until the 31st December 2013. There are packages of tax incentives to attract foreign investors.

Corporate taxBoth resident and non-resident companies have to pay corporate tax on their Morocco-sourced income. Resident companies are those which are incorporated in Morocco or having their place of effective management in Morocco. All foreign corporations, with a permanent establishment in Morocco are subject to taxation on income arising locally.

By definition, corporations include:

Limited liability companies •

Limited partnerships by share •

General and limited partnerships in which at least one partner is • a corporate entity

Civil companies •

Branches of foreign corporations •

Public sector companies having profit-oriented activity •

Joint ventures having business-oriented activity•

General partnerships and limited partnerships in which all • partners are individuals can opt for corporate tax regime. Joint ventures in which all parties are individuals can also choose to do so.

Other features of corporate tax are:

All companies are liable to pay legal minimum tax (CM) • according to the higher amount between 1500 MAD or 0.5% of their annual turnover

There is a 36-month tax holiday related to the payment of the • legal minimum tax for new companies

The CM is based on turnover, income from interest, subsidies, • bonuses or donations received

The normal rate of corporate tax is 30% •

Leasing companies, banks and credit institutions are taxed • at 37%

Foreign entities in engineering, construction or assembly • projects relating to industrial or technical installations can opt for 8% tax, calculated on the total contract price net of VAT and similar taxes

Foreign companies that have elected for the 8% default taxation • must submit a declaration of their turnover before 1 April following each calendar year

Companies are taxed on the difference between their trading • income and expenditure

Business expenses incurred in the operation of the business are • generally deductible unless specifically excluded

Expenses not permitted include fines, penalties, interest on • shareholder loans where the stock is not fully paid up, and interest on shareholder loans in excess of the official annual interest rate

The calendar year is normally the fiscal year although a • company may opt for a different fiscal year

Accounts for income tax purposes must be filed within three • months after the end of the relevant accounting period

Corporate tax is payable in four equal instalments, based on the • prior year’s assessment

The actual amount payable is adjusted in the three months • following the end of the accounting period

30 Doing business in Morocco

Branch remittance tax A 10% branch remittance tax is imposed on profits remitted to the head office. Ordinary corporate tax rate will apply for the Moroccan sourced income of branches of foreign companies. For tax purposes, the branch of a foreign company will be treated as a separate entity.

Personal taxIndividuals with habitual residence in Morocco are liable to pay tax on their worldwide income. This applies to residents of all nationalities. Those without habitual residence in the country are taxable for income generated in Morocco. They are charged progressively at 10% to 38%..

Habitual residence status is determined by the:

Place of permanent abode•

Center of economic interest•

Duration of stay in the country exceeding 183 days within a • period of 365 days

The taxable income includes:

Salaries and wages•

Allowances •

Pension annuities•

Other employment benefits•

Investment income•

Property income •

Income derived from the carrying out of a business or profession•

Capital gains derived from the disposal of immovable property are generally subject to tax as part of the personal income of the individual.

Returns are to be filed each year before the 1st of March.

Income MAD Tax payable

0 – 30,000 Nil

30,001 – 50,000 10%

50,001 – 60,000 20%

60,001 – 80,000 30%

80,001 – 180,000 34%

Over 180,000 38%

Other features of personal tax:

Employers are bound to retain and pay any income tax due on • the salaries paid to their employees the previous before the end of the following month .

Individuals who receive incomes from non-wage sources must • file a tax declaration every year, before 1st March.

Net rental income is taxable under the general income tax (IGR) • at progressive rates.

A standard deduction of 40% of the gross rental income covers • the income-generating expenses in lieu of itemized deductions.

Individuals earning capital gains from selling property are • subject to tax on property profits.

Profits on the sale of property are taxable at 20% of any profit • but with a minimum tax of 3% of the sale price.

VATValue added tax or VAT is a non-cumulative tax levied at each stage of the production and distribution cycle. This binds suppliers of goods and services to add VAT to their net prices. In case the purchaser is also liable for VAT, input VAT may be offset against output VAT.

All goods except those taxed at other rates or those who are tax-exempt are subjected to a standard VAT rate of 20%. Tansport and electricity are taxed at 14%, while banking, credit, gas are taxed at 10% and water and pharmaceutical products are taxed at 7%.

There are two types of exemptions from VAT; the exemption VAT with the right to deduct the input VAT that applies for exports, agricultural material and equipment, fishing equipment and international transport services and the exemption without right to deduct the input VAT that applies for basic foodstuffs, newspapers.

There are four existing VAT rates:

The 7% rate

This rate applies with certain deductions, to sales and deliveries relating to widely consumed products; and deductions, to some professional services, including professional fees for lawyers, interpreters, doctors, other medical workers, etc.

The 7% rate

This rate is applied to banking and credit operations and also to gas.

31Doing business in Morocco

The 14% rate

This rate is applied to transport operations, tourist activities, catering operations provided by service providers to salaried personnel of the companies, to operations carried out by insurance brokers, agents and salesmen and certain foods products (tea, fats for human consumption, jams, fruits and fruits juices for jam factories and soluble coffee concentrates).

The 20% rate

This rate applies to taxable products and operations which are not subject abovementioned rates (7%, 10% and 14%)..

Specific taxes are applied to wines and precious metals (platinum, gold and silver).

Business taxIndividuals and enterprises that habitually do business in Morocco are liable to pay business tax. Business tax is applicable on machines and appliances that are used as integral parts of the establishment.

It consists of a tax on the rental value of business premises • (rented or owned) and a fixed amount based on the size and nature of the business

The tax rates range from 10% to 30% with exemption for the five • first years of activity.

Urban property tax This is the tax levied on the owners of real estate calculated on the rental value of the property.. Rental value is the basis of determining property tax. The rental value can be determined by the local tax authorities.

Properties occupied as a main or second residence are taxed at progressive rates as follows:

Tax base, MAD Tax payable

Up to 5,000 Exempted

5,001 – 20,000 10%

20,001 – 40,000 20%

Over 40,000 30%

Customs duties Most goods are subjected to import duty. Additionally, there will be VAT on the imported goods. Import license is required for goods having an impact on national production. The rates of import duties range between 2.5% and 10% for equipment, materials, parts and accessories.

Determination of taxable income

Capital gainA 10% tax is levied at source for payment of the following:

Dividends•

Capital interest•

Profit percentage•

Sums levied on profits to repay capital produced to stockholders or to buy over stocks

Surpluses from winding up augmented by reserves built up over • at least 10 years ago

Profits made in Morocco by establishments whose home office is • located abroad

The taxable gain is computed by deducting the following from the selling price:

Acquisition price and incidental cost•

Transfer costs•

Investment expenses•

Interest payments•

Capital gains from the sale of a property which has been the primary residence of the taxpayer are not subject to tax under some qualifications:

►The property has been the seller’s primary residence for at least • eight years

The property has been the seller’s primary residence for at least • four years on the day of the sale and the property area does not exceed 100 sqm and the profit does not exceed MAD250, 000

The profit made on one or more transfer by individuals within a • calendar year whose total value does not exceed MAD60, 000

If the property is used as a primary residence, only 25% of the assessed rental property value is subject to tax.

32 Doing business in Morocco

LossesCompanies are allowed to carry forward tax losses for a period of four years from the end of the loss-making accounting period. Portion of a loss that relates to depreciation can be carried forward indefinitely. Losses may not be carried back.

DividendsDividends received by corporate shareholders from taxable • Moroccan-resident entities must be included in business profits of the recipient company

But these dividends are 100% deductible in the computation of • taxable income

As of January 2008, the participation exemption in Morocco is • also applicable to dividend derived from foreign subsidiaries

The original participation exemption regime granted 100% • allowance to a Moroccan recipient company of Moroccan source dividends

Consolidated returnsConsolidated returns are not permitted. Each company must file its own return.

Interest deductionsInterest paid on loans and other debts is deductible to the extent it relates to borrowings made for income producing purposes.

Nevertheless, interests on debts related to partner account have to meet the following requirements for being deductible:

The share capital must be totally free,•

The amount of the debts must be less than the amount of the • share capital,

And the interest rate applies must be within the limit of the • maximum rate granted by the ministry of finance

Repatriation of profits and transfer pricingRepatriations to non-resident associates and controllers of Moroccan entities are mostly in the form of interest, dividends, management fees, service fees and royalties. These payments must be based on the market value of goods and services offered to the Moroccan company.

In case of excess remittance, the Moroccan company’s deduction claim will be disallowed. Transfer pricing rules will be applicable to all other transactions.

Foreign tax reliefAs mentioned, Moroccan residents are taxed on worldwide income. For all foreign taxes, they paid on such worldwide income, the Moroccan tax system compensates them through foreign tax credit in case of the existence of a Tax Treaty. This foreign tax credit cannot exceed the Moroccan tax otherwise payable in respect of the foreign-source income.

Withholding taxDividends paid to a non-resident are subject to a 10% withholding tax unless the rate is reduced under an applicable tax treaty.

Interest on loans obtained from a non-resident is subject to a 10% withholding tax.

Royalties paid to non-residents are subject to a 10% withholding tax unless the rate is reduced under an applicable tax treaty.

Registration feesThe registration fees are made up of fixed and proportional fees. The deadline for completing the registration formalities is generally 30 days from the date on which the document is drawn up. The tariffs vary between 1% and 6%.

Stamp dutyThere are three categories of stamp duty; dimension stamp duty, ad valorem stamp duty and special stamp duty.

Treaty and non–treaty withholding taxThe territorial principle for taxation, followed by the Moroccan government reflects its interest in attracting foreign investment. France is the Morocco’s first foreign investor, creditor and the first and leading trade partner.

Morocco has concluded about 43 treaties for the prevention of double taxation. Most of the treaty counterparties are developed countries. This includes Belgium, Canada, France, Germany, Italy, Luxembourg, the Netherlands, Norway, Romania, Spain, Sweden, Tunisia, the United Kingdom and the United States.

One feature is that most of the tax treaties are based on the OECD model and do not contain specific anti-abuse provisions. Reduced withholding tax rates are different for different treaties. The treaty with Sweden provides zero rates but this treaty has been terminated unilaterally by Morocco.

33Doing business in Morocco

GFo

reig

n tr

ade

34 Doing business in Morocco

35Doing business in Morocco

Foreign trade

Morocco is one of the world’s largest exporters of phosphate. The country also earns substantial export earnings from clothing and textiles, electric components, inorganic chemicals, transistors, crude minerals, fertilizers (including phosphates), petroleum products, citrus fruits, vegetables, fish crude, wine, services and tourism.

The country’s major imports are crude petroleum, textile fabric, telecommunications equipment, wheat, gas and electricity, transistors, plastics, motor vehicles, aircraft, manufacturing equipment and computer and software and hardware computer system.

The Government levies customs duties on imports of some. There are import and quarantine controls on certain goods, including certain drugs, animals, plants, food, firearms and motor vehicles. Most products imported are subject to import duties, the rates of which vary between 2.5% and 10% for equipment, materials, spare parts and accessories.

Goods imported under the investment convention or customs economic systems are exempted from import duty. Value added tax is also payable on goods imported into Morocco.

Imports shall be carried out under an importing agreement prepared in five copies and directly undersigned by the certified bank. Exceptions are for goods imported under the special regimes of the Customs.

Import agreements shall remain valid for six months beginning the day signed by the bank.

The Ministry of Foreign Trade issues the import licenses which remain valid for a maximum of six months.

Documents required for imports/exportsDocuments to be attached for the purpose of levying duties and taxes

Invoices corresponding to the goods for which complete • declaration has been submitted.

Bank certification mentioning the name of the bank paying • agent and the amount expressed in the invoiced currency, the exchange rate, and the reference information for the importation papers

Breakdown of the value of each article•

The exemption vouchers, if applicable•

Documents to be attached for the purpose of implementation of the customs regimes:

Certificates of originDocuments to be attached to ensure enforcement of the various pertinent laws, to the execution of which the administration lends its assistance

Import and export permits specific to each product and lifting • the prohibitions or restrictions stipulated in non-customs-related statutes

Exchange documents•

Import and export permits required as needed to further the • control of foreign trade.

Miscellaneous documents:As regards importation: shipping documents, such as bills of • lading, waybills, and trucking bills of lading

As regards exportation: notices of dockside delivery, receipt, • or consignment, or any other document in proof of delivery to customs for export of goods

Certificate of origin to cover preferred trade•

Packing lists citing the weight per parcel, the number and types • of goods

Documents in proof of inscription in the Trade Register, if • applicable

36 Doing business in Morocco

Payment of importation transactionsSecuring a deed of importation allows the goods to pass through • customs and the payment for the goods imported.

Payment must occur through the offices of the bank where • domiciliation takes place on behalf of the holder of the deed of importation.

Current provisions do not stipulate a deadline for payment for • imported goods.

Payment may take place only after the actual entry of the goods • into Morocco or upon submission of a certificate of shipment to Morocco.

Importers are authorized to transfer advance payments for the • importation of capital goods up to 40% of the FOB value of the goods to be imported

Imports and exports with countries having FTAs with Morocco are governed by respective FTAs.

37Doing business in Morocco

HFi

nanc

ial r

epor

ting

and

audi

ting

38 Doing business in Morocco

39Doing business in Morocco

Financial reporting and auditingAccording to the Best Practice report by estandard Forum, Financial Standard Foundation, Morocco achieved nearly overall compliance with international standards and codes. The country’s compliance in the area of macroeconomic policy and data transparency is reported to be relatively high.

Morocco is taking various steps in the area of institutional and market infrastructure, and making efforts to comply with the international standards. However, the progress drags in areas of accounting practices and payment systems. Morocco has enacted new laws that may lead to improving the regulatory framework for banking, securities and insurance supervision.

Macroeconomic policy and data transparency

Data disseminationAccording to the 2008 IMF Article IV Consultations report, Morocco meets specifications for timeliness, periodicity and coverage for all datasets. However, the country uses a periodicity flexibility option for its production index data and timeliness flexibility options for both production index and general government operations data. Overall, the compliance in the area is reported to be in progress.

Monetary transparencyThe monetary policy responsibility is vested with the central bank, Bank al-Maghrib (BAM). The Banking Law enacted (amendment) in 2006 enhanced the central bank’s autonomy and supervisory role.

Fiscal transparencyAccording to the IMF Report on the Observance of Standards and Codes (ROSC) of 2005, fiscal transparency in Morocco was generally guaranteed. The government follows a combination of strict controls to ensure the correctness of expenditures, adequate legal safeguards, and fiscal and accounting standards.

Setting accounting and auditing standardsSlow progress in accounting practice

Morocco has adopted a strict legal and regulatory framework to ensure compliance of auditing standards. In the early 1990s, the National Accounting Council (CNC) consolidated Morocco’s accounting standard setting initiated by the Ministry of Finance in 1986.

Further, the National Council of the Institute of Chartered Accountants developed a manual of professional standards for auditing of corporations in 1997. It was largely based on IFAC standards.

Bank al-Maghrib, the Securities Commission, and the Insurance and Social Welfare Directorate are responsible for compliance of accounting standards and publication requirements. The framework provides for a system of civil and criminal liability for violations of accounting rules by corporations.

World Bank ROSCIn 2002, the World Bank made an assessment of accounting and auditing practices in Morocco. According to the World Bank report on observance of standards and codes (ROSC), Morocco generally followed the accepted accounting standards (GAAP), which are conceptually different from International Accounting Standards (since renamed as International Financial Reporting Standards or IFRSs).

40 Doing business in Morocco

World Bank noted that the Moroccan accounting standards have improved significantly since the establishment of CNC, but there has been inadequate enforcement as well as non-compliance by corporations. This coupled with flawed standards-setting process has impaired further progress in the field. The teething problems of a relatively new system, inconsistency of the law and lack of effective supervisory mechanism are cited as other factors for this situation.

World Bank observed that the situation has been compounded by the absence of quality control by the Institute of Chartered Accountants. There is a lack of awareness of the importance of complying with professional auditing standards among most of the statutory auditors, it said.

The ROSC suggested reform agenda and a detailed action plan to improve the accounting and auditing framework in Morocco.

Remedial measuresOn the basis of the World Bank’s recommendations, Moroccan authorities developed an action plan to improve the financial reporting framework. According to reports, there are moves by the Central Bank of Morocco insisting all banks and similar financial institutions to use IFRSs. An International Monetary Fund (IMF) 2008 Article IV report confirmed that credit institutions in Morocco implemented IFRSs in January 2008.

The Moroccan Law on Stock Exchanges allows all non-banking companies listed on the Casablanca Stock Exchange, to follow either FRSs and Moroccan GAAP.

The Institute of Chartered Accountants promulgated professional auditing standards in 1998. The objective was to serve a system of reference for statutory and contractual audit engagements, additional engagements performed by statutory auditors, limited reviews, agreed-upon procedures, and compilations.

The general approach was largely consistent with IFAC International Standards on Auditing (ISA). However, the Moroccan auditing standards have not been updated. The standards are yet to incorporate some essential ISAs. For instance, auditing in a computer information systems environment was only partly incorporated into the Moroccan standards.

There are several factors that led to the noncompliance with the normative framework. These include absence of quality assurance mechanisms, lack of systematic training in professional standards, and lack of guidelines to facilitate their implementation.

Over all, Morocco strengthened investor protections by requiring greater disclosure by companies in their annual reports. Despite this, investors of listed companies are not satisfied with the quality of financial information published in the financial statements. Either, the publications may be late or the published data hardly meet the investors’ needs. This point to the responsibility of the board of directors, and they are subject to fines as high as MAD 1,000,000 or imprisonment of one to six months.

The World Bank recommended, among other things, full adoption of ISAs (now renamed as IFRs). In pursuant to closer ties with the EU, an EU–Morocco Action Plan was adopted on 27 July 2005. According to the plan, Morocco would take all necessary steps for the gradual adoption of ISAs. However, the European Commission observed on its Progress Report of 2006, that there had been little progress achieved with regard to building a modern legal and regulatory framework for auditing.

41Doing business in Morocco

IGe

nera

l

42 Doing business in Morocco

43Doing business in Morocco

General

Brief historyMorocco was a Franco-Spanish protectorate since 1912 until it gained independence in 1956. Following this, King Mohammed V of the Alawi dynasty assumed the throne. The Alawi dynasty had earlier ruled the Kingdom since the mid-seventeenth century till the European powers, such as France and Spain occupied the country. In 1961, King Hassan II succeeded King Mohammed V and the first general elections were held 1963.

In July 1999, the current monarch King Mohammed VI succeeded his father and it was a turning point for the Kingdom. King Mohammed VI initiated gradual liberalization and reform process. However, the political reform lagged the economic reform.

Geography, area, climateMorocco is located in the northwest of the African continent. It borders the North Atlantic Ocean and the Mediterranean Sea between Algeria and Western Sahara. The country occupies a strategic location along the Strait of Gibraltar (15 km).

Morocco has two coastlines spanning 3500 km. The total land area of the country comes to 446,550 sq km, consisting 446,300 sq km of land 250 sq km of water.

The northern mountains of Morocco are geologically unstable and subject to earth quakes and periodic droughts.

The country shares borders with Algeria (1,559 km), Western Sahara (443 km), Spain (Ceuta- 6.3 km) and, Spain (Melilla-9.6 km).

Rabat is the capital of Morocco, while Casablanca is the country’s commercial capital. Casablanca is the largest city in the Maghreb region also a leading port in Morocco. Tangier is another major port city of Morocco.

Morocco is bordered by Algeria to the east and the non-self-governing territory of the Western Sahara, over which it claims sovereignty, to the south. The administrative capital is Rabat, while the commercial capital – and largest town in the Maghreb region – is Casablanca.

Population, religion, languageMorocco’s population stood at 31,627,428 as of July 2010, with a growth rate of 1.08% a year. The birth rate in the country is 19.4 births/1000population, while the death rate is 4.74 deaths1000population.

The sex ratio is 0.97 male(s)/female. The average life expectancy is 78.9 years, reflecting a progressive improvement in living standards.

Arab- Berber is the single dominating ethnic group accounting for 99.1% share of the population. The main religions in the country are Muslims (98.7%), Christians (1.1%) and Jewish (0.2%).

Arabic is the official language in Morocco. French is the language of business and diplomacy. The country has a literacy rate of 52.3%.

Most people live west of the Atlas Mountains. The area is a 2,400- kilometer range of mountains starting off in northwest Africa and going through Morocco, Algeria and Tunisia.

Over two-thirds of Morocco’s poor live in rural areas. Urban population comes about 56% of the total population, and the rate of urbanization is an annual1.8% during 2005–2010. Rural to urban migration, especially among youth, adds to the country’s socioeconomic problems.

EconomyThe Kingdom of Morocco is a medium-income country. Its economy is ranked 61 in the world according to the International Monetary Fund (IMF). It is largely an agrarian economy, with over 40% of labor force engaged in the farming sector. Tourism and remittances from abroad contribute significantly to Moroccan GDP.

Morocco’s GDP reached US$91.70 billion in 2010 at current price. It reflects 4% growth in real terms. The growth was driven mostly by private consumption. However, the momentum slowed from 4.7% recorded in 2009.

Historically Morocco enjoys very low inflation. The CPI stood at an average 2.5% in 2010. The lower CPI was primarily due to subsidization of products by the government and its managed exchange rate policy. Morocco has low public debt and a stable financial system.

Illiteracy and unemployment are the two major impediments of Moroccan growth. The country has a literacy rate of 52.3%, while unemployment is about 9.8%. Despite the government’s reformative measures, major social challenges remain. More than a quarter of the population remains economically vulnerable. This prompted government to step up its spending on social development programs. These measures are expected to create more job opportunities and better household income going forward.

Analysts say the economy has a positive growth outlook in the medium to long term. The government’s continued thrust on education, tourism and energy infrastructure sectors will keep the momentum at higher levels in the future.

44 Doing business in Morocco

Government and political systemMorocco is a constitutional monarchy. Executive powers are vested with the King. The King is also the head of the army and the chief religious leader. The Kingdom of Morocco, constituting a part of the Great Arab Maghreb, is a Muslim Sovereign State. Realization of African unity is one of its objectives.

ExecutiveThe King is the head of the state, while the government is headed by the prime minister. Monarchy is hereditary. The prime minister is appointed by the King following an election. He is assisted by a Cabinet – the Council of Ministers – appointed by the King.

The current monarch, King Mohammed VI succeeded his father to the throne in 1999. The present prime minister, Abbas El-Fassi assumed office in September 2007.