Do Joint Audits Improve Audit Quality? Evidence from Voluntary Joint Audits

35

Do Joint Audits Improve Audit Quality? Evidence from Voluntary Joint Audits MIKKO ZERNI ∗ , ELINA HAAPAMA ¨ KI ∗ , TUUKKA JA ¨ RVINEN ∗ and LASSE NIEMI ∗∗ ∗ Department of Accounting and Finance, University of Vaasa, PO Box 700, FI-65101, Finland; ∗∗ Department of Accounting, Aalto University School of Economics, Finland ABSTRACT This study examines whether the decision to voluntarily (i.e. without a statutory obligation) employ two audit firms to conduct a joint audit is related to audit quality. We use separate samples and empirical designs for public and privately held companies in Sweden, where a sufficient number of companies have a joint audit on a voluntary basis. Our empirical findings suggest that companies opting to employ joint audits have a higher degree of earnings conservatism, lower abnormal accruals, better credit ratings and lower perceived risk of becoming insolvent within the next year than other firms. These findings are robust to the use of a propensity score matching technique to control for the differences in client characteristics between firms that employ joint audits and those that use single Big 4 auditors (i.e. auditor self-selection). We also find evidence that the choice of a joint audit is associated with substantial increases in the fees paid by the client firm, suggesting a higher perceived level of quality. Collectively, our analyses support the view that voluntary joint audits are positively associated with audit quality in a relatively low litigious setting both for public and private firms. 1. Introduction In recent years, there has been increased concern regarding auditor independence, a necessity for audit quality. Calls for more regulation and governance to improve auditor independence have been made, with the ultimate goal of restoring trust in the quality of financial statement audits (Eilifsen and Willekens, 2008). A recent European Accounting Review iFirst Article, 1–35, 2012 Correspondence Address: Mikko Zerni, Department of Accounting and Finance, University of Vaasa, PO Box 700, FI-65101, Finland. Email: ZERMP@uwasa.fi Paper accepted by Laurence van Lent. European Accounting Review iFirst Article, 1–35, 2012 0963-8180 Print/1468-4497 Online/12/000001–35 # 2012 European Accounting Association http://dx.doi.org/10.1080/09638180.2012.678599 Published by Routledge Journals, Taylor & Francis Ltd on behalf of the EAA.

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Do Joint Audits Improve Audit Quality? Evidence from Voluntary Joint Audits

Do Joint Audits Improve AuditQuality? Evidence from VoluntaryJoint Audits

MIKKO ZERNI∗, ELINA HAAPAMAKI∗, TUUKKA JARVINEN∗

and LASSE NIEMI∗∗

∗Department of Accounting and Finance, University of Vaasa, PO Box 700, FI-65101, Finland;∗ ∗Department of Accounting, Aalto University School of Economics, Finland

ABSTRACT This study examines whether the decision to voluntarily (i.e. without astatutory obligation) employ two audit firms to conduct a joint audit is related to auditquality. We use separate samples and empirical designs for public and privately heldcompanies in Sweden, where a sufficient number of companies have a joint audit on avoluntary basis. Our empirical findings suggest that companies opting to employ jointaudits have a higher degree of earnings conservatism, lower abnormal accruals, bettercredit ratings and lower perceived risk of becoming insolvent within the next year thanother firms. These findings are robust to the use of a propensity score matching techniqueto control for the differences in client characteristics between firms that employ jointaudits and those that use single Big 4 auditors (i.e. auditor self-selection). We also findevidence that the choice of a joint audit is associated with substantial increases in the feespaid by the client firm, suggesting a higher perceived level of quality. Collectively, ouranalyses support the view that voluntary joint audits are positively associated with auditquality in a relatively low litigious setting both for public and private firms.

1. Introduction

In recent years, there has been increased concern regarding auditor independence,

a necessity for audit quality. Calls for more regulation and governance to improve

auditor independence have been made, with the ultimate goal of restoring trust in

the quality of financial statement audits (Eilifsen and Willekens, 2008). A recent

European Accounting Review

iFirst Article, 1–35, 2012

Correspondence Address: Mikko Zerni, Department of Accounting and Finance, University of Vaasa,

PO Box 700, FI-65101, Finland. Email: [email protected]

Paper accepted by Laurence van Lent.

European Accounting Review

iFirst Article, 1–35, 2012

0963-8180 Print/1468-4497 Online/12/000001–35 # 2012 European Accounting Associationhttp://dx.doi.org/10.1080/09638180.2012.678599Published by Routledge Journals, Taylor & Francis Ltd on behalf of the EAA.

example is the Green Paper ‘Audit Policy: Lessons from the Crisis’ of the Euro-

pean Commission, which is aimed at stimulating discussion on how to improve

audit regulation to increase audit quality (and audit market competition).1 The

Green Paper proposes several regulatory actions as possible remedies for the

alleged lack of market trust in auditor independence, such as joint audits,

auditor rotation, audit committees, and restrictions on the services that auditors

are allowed to provide to their clients. The focus of this study is on joint audits.

In the Green Paper, in some letters commenting on it, and in the financial press,

the idea of adopting joint audits has been raised as a potential way to enhance

audit quality and to stimulate audit market competition (see, for instance,

Andre et al., 2009, pp. 5-6; European Commission, 2010, pp. 15–16; Financial

Times, 2007; Herbinet, 2007a; Kauppalehti, 2011a, 2011b; Mazars, 2010). In a

joint audit, two different audit firms jointly form an opinion of a client’s financial

statements. Both audit firms are also jointly liable for the issued audit opinion.

Proponents of joint audits argue that joint audits have the potential to safeguard

auditor independence. For example, the audit firm Mazars conjectures that ‘[joint

audits are] an advanced form of governance of an audit enhancing in particular

independence and the auditors’ ability to stand their own ground in the event

of a difference of view with the audited entity’ (Mazars, 2010, Response to Euro-

pean Commission’s Green Paper, ‘Audit Policy: Lessons from the Crisis’, p. 31).

Opponents of mandating joint audits argue that joint audits increase the cost of

auditing with little effect on audit quality. The issue of adopting joint audits is

highly controversial. For instance, in their response letters to the Green Paper,

each of the Big 4 audit firms opposed mandatory joint audits while smaller

audit firms were generally in favour of such a requirement.

This study contributes to the audit literature by investigating the timely topic of

joint audits, addressing in particular the alleged benefits and costs associated with

joint audits.2 More specifically, we examine whether joint audits are associated

with audit quality and/or audit fees in a voluntary setting, which is fundamentally

different from previous studies related to a mandatory setting (e.g. Andre et al.,

2009; Francis et al., 2009; Gonthier-Besacier and Schatt, 2007; Piot, 2007;

Thinggaard and Kiertzner 2008). Our study relates to Sweden, where a sufficient

number of companies have a joint audit on a voluntary basis. The use of a volun-

tary setting is beneficial because it allows for the determination of the potential

effects of joint audits per se on audit quality and fees. Our study also contributes

to the recent stream of audit studies examining the effects of country-level insti-

tutional factors on auditing (e.g. Choi et al., 2008, 2009; Francis and Wang,

2008), as we study the potential effect of a voluntary joint audit on audit

quality in a relatively low litigious setting (Choi et al., 2008; Wingate, 1997).

The results from the empirical tests for public and privately held companies

separately suggest that companies employing voluntary joint audits have a

higher degree of earnings conservatism, lower abnormal accruals, better credit

ratings and lower risk forecasts of becoming insolvent within the next year

than other firms.3 For private firms, with a sufficiently large initial sample

2 M. Zerni et al.

(over 65,000 unique firms), we are able to address auditor self-selection by using

a propensity score matching technique and find that our results are robust in this

respect. We attribute the observed better credit ratings and more favourable risk

forecasts among privately held companies to a higher (perceived) assurance and/or insurance value of joint audits. Analyses of audit fees among the sample of

publicly listed firms show that joint audits are associated with considerably

higher fees. We interpret this fee premium for joint audits as an indication of

additional value for clients arising from the voluntary decision to hire two audi-

tors instead of one. Collectively, the empirical findings of our study support the

view that joint audits are positively associated with audit quality.

The structure of the paper is as follows. The next section reviews the relevant

literature and develops the hypotheses. Section 3 describes the data and the

matching procedure used for the sample of privately held firms. Section 4

describes the tests of earnings conservatism and reports the results. Sections 5

and 6 describe the tests used for abnormal accruals and credit risk, respectively.

Section 7 reports our results for audit fee tests, and Section 8 concludes the study.

2. Literature Review and Hypotheses Development

2.1. Joint Audits and Actual Audit Quality

Francis et al. (2009) examine auditor-pair choices and their effects on audit

quality in France, where joint audits are mandatory, and report evidence consist-

ent with an agency-driven demand to employ higher quality auditor pairs.4 They

also find that client firms employing higher quality auditor pairs have smaller

abnormal income-increasing accruals than the firms that do not use Big 4 auditors

(i.e. those that use two non-Big 4 auditors) and that this effect is strongest when

client firms use two Big 4 auditors.

At least three arguments suggest that joint audits would contribute positively to

audit quality, thereby giving credibility to financial statements. First, by appoint-

ing two different audit firms, the client firm allows audit firms to rotate, safe-

guarding auditor independence, but also retains the remaining auditor’s

knowledge and understanding of the client’s business operations, thereby avoid-

ing the potential downside of auditor rotation of a discontinuity in competence

(Carcello and Nagy, 2004). Second, the threat to auditor independence due to

economic bonding is likely to be a less significant issue with the joint audit

approach than it is with the single auditor approach. This is simply because, in

joint audits, the audit fees and lucrative consulting fees are distributed between

two different audit firms (i.e. there are lower fees at stake).5 Consequently, the

two different audit firms may take a stronger stand against pressure from the man-

agers and/or controlling owners and report their opinions on the clients’ accounts

more independently (Mazars, 2010; Zerni et al., 2010). Finally, it is ex ante less

likely that both Big 4 firms (or one Big 4 firm and one non-Big 4 firm) would sim-

ultaneously acquiesce to client pressure and not report the discovered breach(s)

Do Joint Audits Improve Audit Quality? 3

than that a single (Big 4) audit firm would do so. In essence, non-reporting of the

discovered breach(s) and willing to sign-off on financial statements that signifi-

cantly depart from GAAP would require three-party collusion.6 In a game-theor-

etic sense (Kargupta et al., 2007), the expected penalties of being caught for

substandard reporting are more likely to exceed its expected benefits for at

least one of the auditors in a joint audit setting compared with auditors in

single auditor engagements, increasing the likelihood of truthful reporting.

Opponents of mandatory joint audits present two main arguments that joint

audits do not increase audit quality. First, joint audits may suffer from a potential

‘free-rider problem’. This problem may occur if one of the auditors attempts to

‘shirk’ and rely on the other auditor’s effort during the audit. Second, it may

be difficult for two competitive audit firms to cooperate closely while conducting

the audit, resulting in insufficient information exchange. Competition between

auditors aiming to acquire a larger share of the business in the upcoming years

may hinder cooperation and even compromise audit quality because of insuffi-

cient information exchange. Moreover, accounting standards containing con-

siderable discretion can make cooperation difficult and lead to conflicts

(Neveling 2007). Thinggaard and Kiertzner (2008) report that after the abolition

of the mandatory two-auditor system in Denmark in 2004, 15 of the 63 (23.8%)

companies investigated retained two auditors in the next year.

In sum, the existing theories and models on audit production (e.g. Simunic,

1980) and quality (DeAngelo, 1981a, 1981b) examine single audit firm settings

and therefore are not applicable to settings in which two separate firms share

the work and legal liability of an audit. In addition, the few existing empirical

studies on joint audits relate to a mandatory setting. Thus, whether joint audits

improve earnings quality as compared with audits conducted by single audit

firms is an empirical question. Given the absence of convincing theories and

the above-discussed opposing views on the impacts of joint audits on audit

quality, we state our first hypothesis in null form:

H1: Joint audits are not significantly associated with audit quality.

2.2. Joint Audits and Perceived Audit Quality

According to financial theory, a higher credibility of financial information

reduces the cost of capital by reducing investors’ information risk (Botosan,

1997; Coles and Lowenstein, 1988; Jensen and Meckling, 1976; Lambert

et al., 2007). Datta et al. (1999) report evidence that firms lower their interest

rates by developing their reputations. The appointment of a high-quality, high-

reputation auditor(s) may thus help more efficiently to resolve contracting pro-

blems by reducing information risk about borrowers (Jensen and Meckling,

1976; Watts and Zimmerman, 1986). The increased credibility of the firms’ finan-

cial reporting would justify lenders and credit rating agencies considering auditor

choice when pricing debt contracts (Pittman and Fortin, 2004). Given that the

4 M. Zerni et al.

appointment of two separate audit firms instead of one signals ‘good news’ to the

market (Teoh and Wong, 1993; Titman and Trueman, 1986) about the client

firm’s financial reporting quality, we would expect joint audits to be associated

with lower perceived credit risk.

There are at least two complementary explanations as to why joint audits may

be perceived as of higher quality/value compared with single auditor audits.

First, as noted before, lenders and other users of financial statements consider

the probability that both auditors simultaneously acquiesce to client pressure to

be lower than the probability that either of them do so alone (i.e. higher assurance

value). The second explanation, the ‘insurance hypothesis’ (e.g. Wallace 1980),

predicts that audits are expected to add value by providing a type of implicit

insurance to investors. In the case of audit failure, investors can sue auditors to

recover their losses if an investment or credit loss results from misstated financial

statements. The auditor is deemed to be a ‘deep pocket’ because the audit firm

carries malpractice insurance and is often the only solvent defendant in a

lawsuit.7 Moreover, the larger the audit firm, the larger the insurance value or

‘bond of wealth’ from which to recover losses and, hence, the higher the value

of an audit (Dye, 1993). In the case of joint audits, the two audit firms together

by definition have deeper pockets (i.e. higher insurance value) than either of

them do alone.8 The deeper pockets of the two audit firms should be reflected

in a lower credit risk for investors providing funding for the audit client.

Consistent with the above viewpoints, Zerni et al. (2010) document both stat-

istically and economically significant equity discounts due to the entrenchment

problem9 for the clients of non-Big 4 auditors (i.e. the largest discount) and

Big 4 auditors (i.e. the second largest discount) but do not find a statistically sig-

nificant discount for the firms that employ joint audits. These findings are consist-

ent with the above explanations of the higher assurance and/or insurance value of

joint audits compared with single auditor audits. Our next two hypotheses add to

Zerni et al.’s (2010) findings by examining whether joint audits are associated

with a lower level of perceived credit risk and thus facilitate access to debt

capital. Formally, these hypotheses can be stated as follows:

H2a: Joint audits are associated with better credit ratings.

H2b: Joint audits are associated with more favourable risk forecasts of

insolvency.

3. Data Description

3.1. Public Company Sample

For listed Swedish companies, we obtain data from the Worldscope database and

combine those data with hand-collected data on auditor names, audit fees, and non-

audit fees from the annual reports available on the companies’ homepages. This

results in an initial sample of 1667 firm-year observations. Joint audits are

Do Joint Audits Improve Audit Quality? 5

identified directly from the issued audit reports, which in the case of joint audits are

signed by two engagement partners representing different audit firms. We elimin-

ate 91 observations by excluding the firms in the finance sector (SIC codes 6000-

6500) because of their distinct characteristics and because these firms are required

to employ joint audits by law. The number of (joint audit) observations varies

between different tests due to use of different subsamples, and limitations

arising from calculations of dependent and explanatory variables.

A professional association for authorised public accountants, approved public

accountants, and other highly qualified professionals in the accountancy sector in

Sweden (FAR) recommends the design in Figure 1 for the audit-fee-related foot-

note in the annual report.

The design recommended in the footnote reflects the Swedish tradition of fre-

quently employing joint audits. Among all Swedish non-financial publicly listed

firms the proportion of voluntary joint audits has been roughly 10%. For joint

audits, we aggregate the audit fees into single amounts because both audit

firms are jointly liable for the issued audit opinion.

3.2. Propensity Score Matched Private Company Sample

For privately held clients, we obtain most of the data from UC AB, a leading

Swedish business and credit information agency owned by the major Swedish

Figure 1. Recommended scheme for reporting audit and non-audit fees in footnotes forSwedish companies.

6 M. Zerni et al.

banks.10 In addition, we use data on firms where individual auditors are employed

to identify joint audits among remaining firms. These data are retrieved from

Revisorsnamnden (The Supervisory Board of Public Accountants), a governmen-

tal authority under the Ministry of Justice that handles all matters related to char-

tered accountants. Because only a few client firms hired joint audit pairs

composed of two non-Big 4 companies, we excluded these observations to sim-

plify our empirical models, reducing the number of interaction variables needed.

After excluding the finance sector and the observations with missing values

needed for our matching model, we identified 973 joint audit observations

from 191 different firms. For each of the above 973 treatment observations we

attempt to find as closely matched pair as possible through a propensity score

matching technique. Despite the number of joint audit observations varying

across different matched pair tests, the proportion of joint audits in each test is

always exactly 50% (please, refer also Note 15).

3.2.1. Matching procedure and propensity score matching model

A sufficiently large initial sample size of privately held firms (over 65,000 unique

firms)11 allows us to employ a propensity score matching technique12 to control for

the differences in client characteristics between the treatment group (i.e. the firms

employing joint audits) and the control group of single Big 4 auditor clients (Lawr-

ence et al., 2011; Lennox et al., 2012; Rosenbaum and Rubin, 1983). Propensity

score matching models match observations on the basis of the probability of under-

going treatment, which in our case is the probability of employing a joint audit.

Before estimating the matching model, we exclude all of the single audits con-

ducted by the non-Big 4 audit firms to further increase the comparability of the treat-

ment and control groups. We then match, without replacement, each Big 4 auditor

client with a joint audit client that had the closest predicted value (according to the

estimated logit model) within a maximum distance of 1%.13 Although the ‘greedy’

matching process reduces the number of observations available for subsequent ana-

lyses, it ensures that the scored distributions are close to identical between the treat-

ment and control groups (i.e. the firms employing joint audits and the Big 4 clients).

We use the following logit model to estimate the probability of employing joint

audits on the basis of prior auditor selection studies (e.g. DeFond, 1992; Francis

and Wilson, 1988; Johnson and Lys, 1990; Lennox, 2005) (firm and time sub-

scripts omitted):

PROB(JAUDIT) = a + b1SIZE + b2DTA + b3CONTROL

+ b4GROUP + b5LOGAGE + b6CASH + b7LOSS

+ b8CA CL + b9ROA + fixed effects

(1)

where the dependent variable JAUDIT is an indicator variable for the joint audit

decision. Explanatory variables are defined as follows: SIZE is the natural logar-

ithm of total assets; DTA is the ratio of debt to total assets; CONTROL is an

Do Joint Audits Improve Audit Quality? 7

indicator variable for the presence of a controlling shareholder with at least a 25%

stake of voting power; GROUP is an indicator variable for group affiliation;

LOGAGE is the natural logarithm of the client age in years; CASH is the ratio

of cash and cash equivalents to total assets; LOSS is an indicator variable for

accounting losses; CA_CL is the ratio of current assets to current liabilities;

and ROA is the return on assets. We also add indicator variables for the economic

sectors and different years.14

Using the 1% upper bound for the difference between propensity scores, we

were able to find a match for 597 joint audit observations from 135 different

firms between 2001 and 2007 resulting in a matched sample of 1194 firm-

years. However, because of missing values for variables used in our empirical

models, the final sample sizes in our tests are reduced to between 1160 and

848 firm-year observations.15

3.2.2. Results of estimating the propensity score matching model

Table 1 presents the results of the estimation model (1). As can be seen from

column (1) of Table 1, all of our chosen explanatory variables are significant pre-

dictors of the joint audit decision. The estimated magnitudes of the coefficients

indicate that client size, company age, group affiliation and the presence of a con-

trolling shareholder appear to be the most focal positive determinants of joint

audit selection. The return on assets, the leverage and the ratio of current

assets to total assets are all estimated to be significantly negative, but the magni-

tudes of their coefficients are considerably smaller compared with the above-

mentioned four variables. Finally, we find that accounting losses and liquidity

have positive impacts on the likelihood of employing a joint audit.

The estimated results reported in column (2) of Table 1 indicate that the match-

ing procedure balances the differences regarding all dimensions used in the pro-

pensity matching approach. The likelihood ratio test cannot reject the global

null hypothesis that all of the coefficients are zero (p-value ¼ 0.935). Hence,

given ‘perfect’ matching, the remaining differences between the two groups of

firms should reflect only the treatment effect, and a simple univariate t-test of

the differences in means should be sufficient to estimate the treatment effects

(Dehejia and Wahba, 2002; Heckman et al., 1997; Zhao, 2004). However, we

still use multivariate regressions to control for any potential remaining differences

in client characteristics between the treatment and control groups.

4. Multivariate Analysis: Earnings Conservatism

4.1. Earnings Conservatism Model Specification for Publicly Listed

Companies

Our first test uses the earnings conservatism framework of Basu (1997) to deter-

mine whether there are differences in timely loss recognition between the clients

of dual and single auditors. In this framework, positive annual stock returns are

8 M. Zerni et al.

used to indicate ‘good news’ whereas negative annual stock returns are assumed

to reflect ‘bad news’ in the current fiscal year. The premise of earnings conserva-

tism is that losses are recognised more quickly than gains, which are usually

deferred until they are realised. Accordingly, earnings conservatism exists if

the contemporaneous accounting earnings recognise bad news more quickly

than good news. Conservative earnings reduce the level of information asymme-

try and make earnings more useful for contracting purposes (e.g. LaFond and

Watts, 2008; Watts, 2003). By estimating the following model that builds on

Basu (1997), we test whether a firm’s choice of auditor affects the degree of con-

servatism:

EARN = b0 + b1R + b2DR + b3DR × R + b4JOINT + b5JOINT

× R + b6JOINT × DR + b7JOINT × DR × R + b8BIG + b9BIG

× R + b10BIG × DR + b11BIG × DR × R + b12LMV + b13P/B

+ b14DTA + fixed effects + 1

(2)

Table 1. Logit model for the joint audit decision used in the matching process.

JOINT JOINT

Matching Process After Matching

Variable Coef. Prob. Coef. Prob.

SIZE 0.4351 ∗∗∗ 0.0000 –0.2808 0.5240DTA –0.5430 ∗∗∗ 0.0000 0.0049 0.9832CONTROL 0.7860 ∗∗∗ 0.0000 –0.1904 0.1213GROUP 0.5941 ∗∗∗ 0.0000 –0.0240 0.8574LOGAGE 0.3213 ∗∗∗ 0.0000 0.0446 0.5067CASH 1.1899 ∗∗∗ 0.0000 0.1465 0.5670LOSS 0.2599 ∗∗∗ 0.0020 0.1012 0.5108CA_CL –0.0105 ∗∗∗ 0.0004 0.0016 0.6726ROA –0.3716 ∗∗∗ 0.0354 –0.0111 0.9723Intercept –12.495 ∗∗∗ 0.0000 –0.2808 0.5040Annual fixed effects? Yes NoEconomic sector fixed effects? Yes NoLikelihood ratio, x2 2,209.52 ∗∗∗ 3.62Nagelkerke R2 25.2% 0.4 %–2 Log Likelihood 9,463.78 ∗∗∗ 1,655.24N (# joint audits) 45,846 (973) 1,194 (597)

Notes:SIZE is the natural logarithm of total assets in thousands of Swedish kronor; DTA is the ratio of debt tototal assets; CONTROL is a dummy variable with a value of one if the firm has a controllingshareholder, otherwise zero; GROUP is a dummy variable with a value of one if the firm is affiliatedwith a group of companies, otherwise zero; LOGAGE is the natural logarithm of firm age in years;CASH is the ratio of cash and cash equivalents to total assets; LOSS is a dummy variable with a valueof one if earnings are negative, otherwise zero; CA_CL is the ratio of current assets to currentliabilities; ROA is the interest-adjusted return on opening total assets.

Do Joint Audits Improve Audit Quality? 9

where R is the buy-and-hold annual stock return (including dividends) and DR is

a dummy variable with a value of one if the return is negative, otherwise zero. We

add controls for firm size (LMV), leverage (DTA), and growth (P/B). However,

we omit the interactions with LMV, P/B and DTA to avoid multicollinearity pro-

blems. We include the year and industry-fixed effects and estimate the parameters

by adjusting the standard errors with respect to heteroscedasticity and within-firm

clustering (Rogers, 1993).

The standard Basu (1997) model includes the first four parameters in equation

(2). In the Basu framework, a positive sign on the coefficient on the interaction

variable DR ∗ R (b3) implies that accounting earnings recognise bad news

(timely loss recognition) more quickly than good news.16 The primary coeffi-

cients of interest are the interaction variables JOINT ∗ DR ∗ R (b7) and BIG ∗

DR ∗ R (b11), which measure the incremental effects of the decisions to

employ a joint audit or a single Big 4 audit firm on earnings conservatism relative

to clients of single non-Big 4 audit firms, respectively.

4.2. Specification of an Earnings Conservatism Model for Privately Held

Companies

Because private companies do not have stock returns, we rely on Ball and Shiva-

kumar’s (2005) metrics to examine the timeliness of loss recognition among pri-

vately held clients. Ball and Shivakumar’s (2005) approach builds on Dechow

et al.’s (1998) work and exploits the likelihood that timely loss recognition

occurs through accounting accruals. In particular, this approach hypothesises that

economic losses are more likely to be recognised on a timely basis in the form

of unrealised (i.e. non-cash) accrued charges against income whereas economic

gains are more likely to be recognised when they are realised (Ball and Shivakumar

2005). Following Ball and Shivakumar (2005), we estimate the following piece-

wise-linear model to examine whether a privately held client firm’s choice of

auditor affects the timely loss recognition through accounting accruals:

ACCR = b0 + b1DCFO + b2CFO + b3DCFO × CFO + b4JOINT

+ b5JOINT × CFO + b6JOINT × DCFO + b7JOINT × DCFO

× CFO + fixed effects + 1

(3)

where cash flow from operations (CFO) is measured as the earnings before excep-

tional and extraordinary items less accruals. We define accruals (ACCR) as the

change in current assets (less the change in cash and cash equivalents) from the

prior year minus the change in current liabilities (less the change in short-term

debt and the current portion of long-term debt) minus depreciation. We standardise

both the accruals and the cash from the operations by the beginning-of-period total

assets. DCFO is a dummy variable taking the value 1 if the cash flow (CFO) is

negative and zero otherwise. Similar to Dechow et al. (1998) and Ball and

10 M. Zerni et al.

Shivakumar (2005), we predict a negative coefficient for cash flows (b2). Losses

are hypothesised to be recognised faster via accruals than gains; hence, we

predict a positive incremental coefficient (b3) for negative cash flows. As in

Basu’s (1997) model, the primary coefficient of interest is the coefficient on the

interaction variable JOINT ∗ DCFO ∗ CFO (b7), which measures the incremental

effect of the choice of a joint audit on earnings conservatism relative to the single

Big 4 auditors.

4.3. Results for the Earnings Conservatism Tests

Table 2 reports the descriptive statistics for the variables used in our analyses of

earnings conservatism. Panel A reports the descriptive statistics for the sample of

public firms whereas panel B reports the descriptive statistics for the privately

held companies. Recall that no joint audits were conducted by two non-Big 4

firms in our analyses.17

Table 2. Descriptive statistics for the earnings conservatism tests.

Panel A: Public firm sample (N ¼ 1,257)

Variable Mean Std. Min 25 % Median 75 % Max

EARN –0.067 0.249 –0.509 –0.202 0.030 0.107 0.303R 0.141 0.597 –0.878 –0.241 0.104 0.423 2.750DR 0.411 0.492 0 0 0 1 1JOINT 0.103 0.303 0 0 0 0 1BIG a 0.898 0.301 0 1 1 1 1LMV 13.88 2.01 8.97 12.45 13.63 15.15 20.47P/B 2.99 3.75 0.21 1.29 2.12 3.42 72.74DTA 0.174 0.161 0 0.018 0.146 0.288 0.747

Panel B: Private firm sample (N ¼ 1,160)

ACCR –0.048 0.156 –0.718 –0.092 –0.020 0.079 0.706CFO 0.091 0.269 –0.954 –0.002 0.061 0.171 2.071DCFO 0.27 0.443 0 0 0 1 1JOINT 0.50 0.500 0 0 0.50 1 1

Notes:a Conditional on the firm employing a single-audit firm. EARN is defined as the earnings per share beforeextraordinary items scaled by the stock price at the beginning of the period; R is the annual raw stockreturn; DR is a dummy variable with the value of one if the annual raw stock return is negative, otherwisezero; JOINT is a dummy variable with a value of one if the client firm employs a joint audit, otherwisezero; BIG is a dummy variable with a value of one if the client firm employs a single Big 4 audit firm,otherwise zero; LMV is the natural logarithm of the market value of equity in thousands of Swedishkronor; P/B is the price-to-book ratio; DTA is the ratio of debt to total assets; and ACCR is the amount ofaccounting accruals divided by the opening total assets. Accruals are defined as the change in currentassets (less the change in cash and cash equivalents) from the prior year minus the change in currentliabilities (less the change in short-term debt and current portion of long-term debt) minus depreciation;CFO is measured as the earnings before exceptional and extraordinary items less accruals; and DCFO isa dummy variable with a value of one if cash flow (CFO) is negative, otherwise zero.

Do Joint Audits Improve Audit Quality? 11

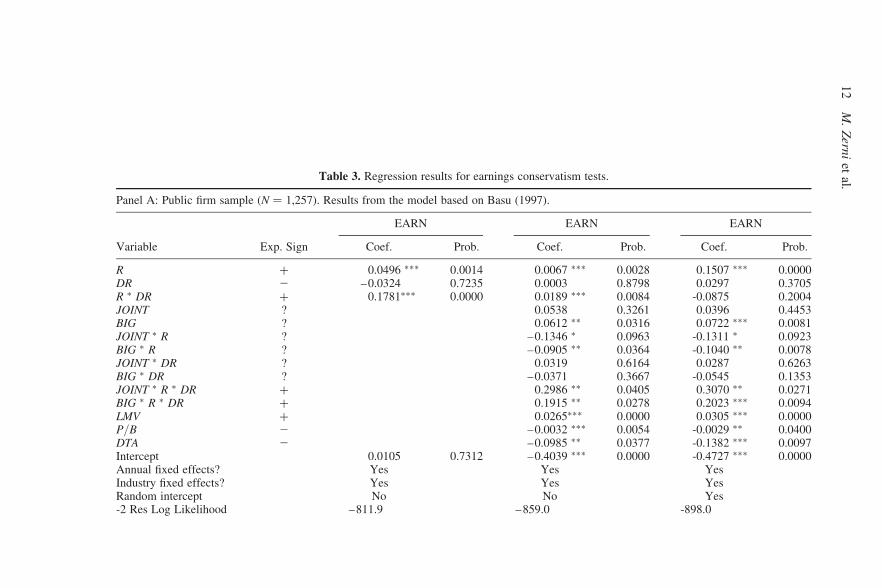

Table 3. Regression results for earnings conservatism tests.

Panel A: Public firm sample (N ¼ 1,257). Results from the model based on Basu (1997).

EARN EARN EARN

Variable Exp. Sign Coef. Prob. Coef. Prob. Coef. Prob.

R + 0.0496 ∗∗∗ 0.0014 0.0067 ∗∗∗ 0.0028 0.1507 ∗∗∗ 0.0000DR 2 –0.0324 0.7235 0.0003 0.8798 0.0297 0.3705R ∗ DR + 0.1781∗∗∗ 0.0000 0.0189 ∗∗∗ 0.0084 -0.0875 0.2004JOINT ? 0.0538 0.3261 0.0396 0.4453BIG ? 0.0612 ∗∗ 0.0316 0.0722 ∗∗∗ 0.0081JOINT ∗ R ? –0.1346 ∗ 0.0963 -0.1311 ∗ 0.0923BIG ∗ R ? –0.0905 ∗∗ 0.0364 -0.1040 ∗∗ 0.0078JOINT ∗ DR ? 0.0319 0.6164 0.0287 0.6263BIG ∗ DR ? –0.0371 0.3667 -0.0545 0.1353JOINT ∗ R ∗ DR + 0.2986 ∗∗ 0.0405 0.3070 ∗∗ 0.0271BIG ∗ R ∗ DR + 0.1915 ∗∗ 0.0278 0.2023 ∗∗∗ 0.0094LMV + 0.0265∗∗∗ 0.0000 0.0305 ∗∗∗ 0.0000P/B 2 –0.0032 ∗∗∗ 0.0054 -0.0029 ∗∗ 0.0400DTA 2 –0.0985 ∗∗ 0.0377 -0.1382 ∗∗∗ 0.0097Intercept 0.0105 0.7312 –0.4039 ∗∗∗ 0.0000 -0.4727 ∗∗∗ 0.0000Annual fixed effects? Yes Yes YesIndustry fixed effects? Yes Yes YesRandom intercept No No Yes-2 Res Log Likelihood –811.9 –859.0 -898.0

12

M.

Zern

iet

al.

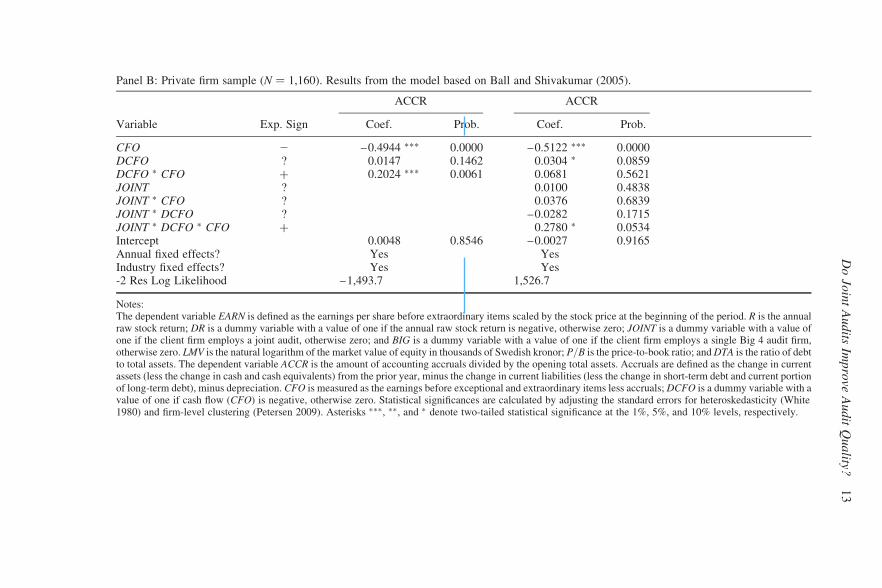

Panel B: Private firm sample (N ¼ 1,160). Results from the model based on Ball and Shivakumar (2005).

ACCR ACCR

Variable Exp. Sign Coef. Prob. Coef. Prob.

CFO 2 –0.4944 ∗∗∗ 0.0000 –0.5122 ∗∗∗ 0.0000DCFO ? 0.0147 0.1462 0.0304 ∗ 0.0859DCFO ∗ CFO + 0.2024 ∗∗∗ 0.0061 0.0681 0.5621JOINT ? 0.0100 0.4838JOINT ∗ CFO ? 0.0376 0.6839JOINT ∗ DCFO ? –0.0282 0.1715JOINT ∗ DCFO ∗ CFO + 0.2780 ∗ 0.0534Intercept 0.0048 0.8546 –0.0027 0.9165Annual fixed effects? Yes YesIndustry fixed effects? Yes Yes-2 Res Log Likelihood –1,493.7 1,526.7

Notes:The dependent variable EARN is defined as the earnings per share before extraordinary items scaled by the stock price at the beginning of the period. R is the annualraw stock return; DR is a dummy variable with a value of one if the annual raw stock return is negative, otherwise zero; JOINT is a dummy variable with a value ofone if the client firm employs a joint audit, otherwise zero; and BIG is a dummy variable with a value of one if the client firm employs a single Big 4 audit firm,otherwise zero. LMV is the natural logarithm of the market value of equity in thousands of Swedish kronor; P/B is the price-to-book ratio; and DTA is the ratio of debtto total assets. The dependent variable ACCR is the amount of accounting accruals divided by the opening total assets. Accruals are defined as the change in currentassets (less the change in cash and cash equivalents) from the prior year, minus the change in current liabilities (less the change in short-term debt and current portionof long-term debt), minus depreciation. CFO is measured as the earnings before exceptional and extraordinary items less accruals; DCFO is a dummy variable with avalue of one if cash flow (CFO) is negative, otherwise zero. Statistical significances are calculated by adjusting the standard errors for heteroskedasticity (White1980) and firm-level clustering (Petersen 2009). Asterisks ∗∗∗, ∗∗, and ∗ denote two-tailed statistical significance at the 1%, 5%, and 10% levels, respectively.

Do

Join

tA

ud

itsIm

pro

veA

ud

itQ

ua

lity?1

3

Our public firm sample includes a total of 129 joint audit observations from 28

unique firms (not tabulated). Panel A reveals that Big 4 firms dominate the

Swedish public company audit market, with a combined market share of single

auditor clients of 90%. The mean (median) annual raw stock return is 14.1%

(10.4%); furthermore, in approximately 41% of firm-years, the stock return is

negative, allowing for an examination of the asymmetric recognition of economic

gains and losses.

For privately held companies, the mean (median) amount of accruals is –0.048

(–0.020), with a range from –0.718 to 0.706. Furthermore, the mean (median)

operating cash flow is 0.091 (0.061), and the cash flow is negative in approxi-

mately 27% of observations.18 We conclude that there is a sufficient number of

observations with ‘bad news’ to capture the expected timely recognition of

losses in both of the earnings conservatism models.

Panel A of Table 3 reports the results for the Basu (1997) sample of public

companies whereas panel B reports the results for Ball and Shivakumar’s

(2005) measure of earnings conservatism.

As column 1 of Table 3 indicates, the standard Basu (1997) model appears to

work relatively well with the Swedish data. The estimated coefficient of the inter-

action DR ∗ R is positive and highly significant, which suggests more timely loss

recognition.

Column 2 reports our extension of the Basu model, which is defined in equation

(2). In column 3, we allow a firm-specific random intercept to control for the het-

erogeneity in firm characteristics that may affect the risk-return relationship. In

columns (2) and (3), the three-way interaction term ‘R∗DR∗JOINT’ (‘R∗DR∗BIG’)

tests the incremental earnings conservatism of the joint auditor (single Big 4

auditor) clients relative to the non-Big 4 auditors’ clients. The coefficient of the

interaction term ‘R∗DR∗JOINT’ is positive and significant at the 5% level. More-

over, the coefficient of ‘R∗DR∗BIG’ is positive and significant, although the mag-

nitude is lower. Collectively, these findings suggest that the clients of dual auditors

have the most conservative earnings while clients of single non-Big 4 auditors have

the least conservative earnings. In terms of earnings conservatism, the clients of

single Big 4 auditors appear to fall between these two classes.19

Panel B of Table 3 presents the results from the regression identified in

equation (3). As can be seen from column 1 of panel B, the estimated coefficient

on the interaction DCFO ∗ CFO is positive and significant at the 1% level. Thus,

the negative relationship between accruals and cash flow is less pronounced

during losses than during gains. In other words, the empirical evidence supports

the view that relative to gains, economic losses are recognised more quickly via

accruals.

Column 2 reports our extension of the model, which allows the asymmetric

recognition of unrealised gains and losses to vary between clients of single Big

4 firms and clients that employ joint audits. We find that the test variable JOIN-

T∗DCFO∗CFO is estimated to be significantly positive, which suggests that, on

average, the clients of dual auditors have more conservative earnings than their

14 M. Zerni et al.

propensity-score-matched counterparts. Overall, the results of the accruals-based

test, like those based on the Basu (1997) model, suggest that the client firms that

employ joint audits make more conservative reports than the clients of single

auditors. Joint liability essentially means that both auditors bear the (\,potentially)

incremental audit risk arising from the likelihood that the other auditor fails to

adequately perform its share of the audit work. One explanation for the increased

conservatism may thus relate to each auditor’s responses to information asymme-

try regarding the other auditor’s actions. In other words, each auditor responds to

the potential ‘free-rider problem’ by enforcing more conservative accounting

choices.

5. Multivariate Analysis: Abnormal Accruals

5.1. Abnormal Accruals Test Specifications

Our second set of tests employs abnormal working capital accruals as a proxy for

audit quality. For both the public and private samples, we define working capital

accruals (WA) as the change in the current assets (less the change in cash and cash

equivalents) from the prior year minus the change in current liabilities (less the

change in short-term debt and the current portion of long-term debt). We then

specify the abnormal working capital accruals (ABWA) as the actual accruals

minus the ‘expected’ accruals. To project the expected level of accruals, we

turn to an expectation model similar to that used by DeFond and Park (2001)

and Francis et al. (2009). In this approach, the level of expected accruals is

based on each firm’s prior-year linear relationship between sales and working

capital accruals.20 We calculate the expected accruals in the following manner:

Expected accruals = SALESt × (WAt−1/SALESt−1) (4)

We eliminated observations with extreme abnormal accruals values. In par-

ticular, observations were deleted if the absolute value of the abnormal

working capital accruals scaled by the lagged total assets was above 0.99

(0.71), which is approximately equivalent to deleting the top and bottom 2.5%

of the distribution for public (private) clients. Our multivariate models then

regress (absolute) abnormal accruals on our research variables and control vari-

ables based on prior studies in the field (e.g. Teoh et al., 1998; Becker et al.,

1998). Again, for reasons of data availability, we specify slightly different

models for public and private firms. For public firms, we estimate the following

model:

|ABWA| = a + b1SIZE + b2P/B + b3SALESG + b4OCF + b5LOSS

+ b6DTA + b7LAGWA + b8OVAR + b9JOINT + b10BIG

+ fixed effects + 1

(5a)

Do Joint Audits Improve Audit Quality? 15

where the dependent variable ABWA is the difference between the actual and

expected amounts of working capital accruals derived from model (4). Our vari-

ables of interest are JOINT and BIG, which are dichotomous variables that

respectively denote joint audits and single Big 4 audits. Our control variables

are based on prior studies that have addressed audit quality issues through

accruals-based measures. Large firms tend to have more stable revenue and

income streams. Larger firms also have more negotiating power in the event of

financial difficulties. Hence, we include the natural logarithm of total assets in

thousands of Swedish kronor (SIZE) to control for the expected negative relation-

ship between firm size and the magnitude of abnormal accruals. Matsumoto

(2002) shows that firms with growth prospects are more likely to be concerned

about missing their earnings benchmarks. For that reason, we include the

price-to-book ratio (P/B) and the growth in sales over the previous year

(SALESG) to control for the cross-sectional differences in growth prospects.

Kothari et al. (2005) argue that the estimated discretionary accruals are positively

correlated with firm performance. Thus, we measure firm performance using the

operating cash flow to total assets (OCF) variable. LOSS is a dummy variable

with a value of one if the client firm has negative earnings, otherwise zero. We

add the ratio of debt to total assets (DTA) because firms with high levels of

debt may struggle to avoid violating their debt covenants and may consequently

have greater incentives to manage their earnings (Becker et al., 1998; DeFond

and Jiambalvo 1994). We also include one-year lagged working capital accruals

to control for the reversal of accruals (LAGWA). However, the lagged value of the

accruals will likely capture the time-invariant factors omitted from DeFond and

Park’s (2001) expectation model for working capital accruals, which predicts that

the coefficient on LAGWA would be positive. We add the standard deviation of

sales over the years t–3 to t (OVAR) to control for potential errors in estimating

abnormal accruals that relate to the cross-firm differences in operating variability

(Hribar and Nichols, 2007).

Our model for private firms is similar to that for public firms (equation (5a)),

except that we have only one test variable (JOINT) and three additional control

variables. Specifically, we estimate the following model for our matched

sample of private firms:

|ABWA| = a + b1SIZE + b2LOGAGE + b3SALESG + b4OCF

+ b5LOSS + b6DTA + b7LAGWA + b8OVAR

+ b9TENURE + b10CASH + b11JOINT + fixed effects + 1

(5b)

where we include the following three additional controls. First, because older

firms are less likely to go bankrupt or violate their debt contracts, we add the

natural logarithm of firm age in years (LOGAGE) to the model (5b). Second,

TENURE denotes auditor tenure in years. Prior research has suggested that the

length of an auditor–client relationship may affect the auditor’s independence

16 M. Zerni et al.

and knowledge of its client (Johnson et al., 2002; Myers et al., 2003). To capture

this effect, we add a variable representing auditor tenure in years (TENURE) to

the model. Third, we add the ratio of cash to cash equivalents (CASH) into

equation (5b) to control for the cross-sectional differences in liquidity. The

other variables are as defined above.

5.2 Results for the Abnormal Working Capital Accruals Tests

Panel A of Table 4 reports the descriptive statistics for the variables used in the

tests for abnormal accruals among the publicly listed companies. The mean

(median) amount of absolute abnormal accruals among the sample of public com-

panies is 0.127 (0.069). A simple univariate t-test for the differences in means

suggests that the client firms employing joint audits have a lower level of absolute

abnormal accruals (untabulated). However, because these firms differ in many

other aspects (e.g. size), the unconditional descriptive evidence is limited.

Panel B reports the corresponding statistics for the privately held clients. Given

‘perfect’ matching as reported in Table 1, the remaining differences between the

two groups of firms should only reflect the treatment effect, and a simple univariate

t-test of the differences in means would be sufficient to estimate the treatment

effects (Dehejia and Wahba, 2002; Heckman et al., 1997; Zhao, 2004). According

to a t-test for the differences in means in the level of absolute abnormal accruals

(untabulated), the client firms that employ joint audits have a lower level of abnor-

mal accruals on average (p-value , 0.0001). Thus, the univariate evidence sup-

ports the view that joint audits are more effective at constraining earnings

management through the manipulation of accounting accruals than single Big 4

audit firms.

Panel A of Table 5 reports the results from our abnormal accruals models for

public firms (equation (5a)). The likelihood ratio test statistics for all of the

models indicate significance at the 1% level. As before, all the significance

levels of individual coefficients are reported as two-tailed p-values.

With respect to the absolute value of abnormal working capital accruals among

the public companies in column (1), we find that none of the auditor choice vari-

ables are significant in any of the tests. However, the opportunistic, income-

increasing application of GAAP is widely considered to more likely signal pro-

blems with auditor independence than the conservative application of GAAP.

Hence, we split the full sample into two sub-samples containing income-increas-

ing and income-decreasing abnormal accruals (i.e. ABWA . 0 and ABWA , 0)

and then estimate Model (3) separately for both sub-samples. The results of

these analyses are presented in Columns (2) and (3) of panel A. In column 2,

for the income-increasing abnormal accruals, the estimated coefficient of the

joint audit indicator is negative and significant at the 10% level (p-value ¼

0.0658). A negative sign indicates that the abnormal accruals of dual-auditor

clients are smaller on average (i.e. less income-increasing) than the accruals of

Do Joint Audits Improve Audit Quality? 17

single-auditor clients. For income-decreasing abnormal accruals, both auditor

choice variables are estimated to be insignificant.21

In sum, the results of the above analyses suggest that the employment of a joint

audit by public companies is associated with smaller income-increasing abnormal

working capital accruals and that the earnings of these companies are therefore

less likely to be affected by opportunistic firm insider discretion that overstates

earnings. These findings are also in good agreement with the results obtained

from tests for earnings conservatism.

Table 4. Descriptive statistics for variables used in abnormal accruals analyses.

Panel A: Public firm sample (N ¼ 858).

Variable Mean Std. Min 25 % Median 75 % Max

|ABWA| 0.127 0.155 0 0.027 0.069 0.166 0.984ABWA 0.020 0.199 –0.741 –0.060 0.009 0.080 0.984SIZE 13.98 2.03 8.89 12.51 13.66 15.15 19.35P/B 2.87 2.93 0.34 1.40 2.18 3.51 51.43SALESG 0.062 0.307 –0.962 –0.049 0.046 0.184 1.53OCF 0.047 0.160 –0.756 –0.001 0.077 0.130 0.445LOSS 0.156 0.363 0 0 0 0 1DTA 0.169 0.154 0 0.022 0.140 0.277 0.747OVAR 1.358 3.715 0.001 0.065 0.182 0.727 33.269JOINT 0.084 0.277 0 0 0 0 1BIG a 0.916 0.278 0 1 1 1 1

Panel B: Private firm sample (N ¼ 906)

|ABWA| 0.126 0.157 0.001 0.010 0.064 0.194 0.700ABWA –0.001 0.207 –0.674 –0.060 0.001 0.069 0.700SIZE 9.31 2.87 3.52 7.30 9.10 11.31 17.43LOGAGE 3.17 0.87 0.69 2.56 3.09 3.81 4.72SALESG 0.023 0.300 –0.984 –0.006 0.005 0.094 2.111OCF 0.086 0.233 –1.003 0.001 0.063 0.171 2.032LOSS 0.275 0.446 0 0 0 1 1DTA 0.687 0.278 0 0.510 0.773 0.910 1OVAR 0.286 1.071 0.000 0.002 0.013 0.089 10.646JOINT 0.500 0.500 0 0 0.500 1 1TENURE 6.01 4.06 1 2 5 9 17CASH 0.165 0.240 0.001 0.005 0.042 0.244 0.873

Notes:a Conditional on the firm employing a single-audit firm. ABWA is the amount of abnormal workingcapital accruals; SIZE is the natural logarithm of total assets in thousands of Swedish kronor; OCF isthe operating cash flow divided by the initial total assets; LOSS is an indicator variable for accountinglosses; SALESG is the growth in sales over the prior year; P/B is the price-to-book ratio; DTA is theratio of debt to total assets; OVAR is the standard deviation of sales in billions Swedish kronor over theyears t–3 to t; JOINT is a dummy variable with a value of one if the client firm employs a joint audit,otherwise zero; BIG is a dummy variable with a value of one if the client firm employs a single Big 4audit firm, otherwise zero; LOGAGE is the natural logarithm of firm age in years; and TENURE isaudit firm tenure in years. For joint audit observations we designate the value of the audit firm withlonger tenure; CASH is the ratio of cash and cash equivalents to total assets.

18 M. Zerni et al.

Table 5. Regression analysis of abnormal accruals.

Panel A: Public firm sample.

|ABWA| ABWA if ABWA ≥0 ABWA if ABWA ,0

VariableExp.Sign Coef. Prob. Coef. Prob. Coef. Prob.

SIZE 2 –0.0199 ∗∗∗ 0.0001 –0.0118 ∗ 0.0652 0.0165 ∗∗∗ 0.0023P/B + 0.0022 0.4857 –0.0035 ∗∗ 0.0335 0.0051 0.2130SALESG + 0.0904 ∗∗∗ 0.0002 0.1397 ∗∗∗ 0.0000 0.0245 0.5114OCF 2 –0.1825 ∗∗∗ 0.0060 –0.2411 ∗∗∗ 0.0061 –0.0279 0.6888LOSS + 0.0025 0.1798 0.0094 0.7133 0.0505 ∗∗ 0.0129DTA +/ 2 –0.1141 ∗∗∗ 0.0022 –0.1068 ∗∗∗ 0.0152 –0.0860 ∗∗ 0.0250LAGWA 2 –0.0039 0.9495 –0.5460 ∗∗∗ 0.0000 0.4064 ∗∗∗ 0.0000OVAR + 0.0043 ∗∗∗ 0.0028 0.0001 0.7285 0.0047 ∗∗∗ 0.0012JOINT ? –0.0258 0.3081 –0.0630 ∗ 0.0658 0.0158 0.6007BIG 2 –0.005 0.8374 –0.0203 0.4283 0.0091 0.7331Intercept 0.4535 0.0000 0.3101 ∗∗∗ 0.0001 0.3349 ∗∗∗ 0.0000Annual fixed effects? Yes Yes YesIndustry fixed effects? Yes Yes Yes-2 Res Log Likelihood –736.3 –345.8 –436.0N (# Joint audits) 858 (72) 465 (38) 393 (34)

Panel B: Private firm sample.

|ABWA| ABWA if ABWA ≥0 ABWA if ABWA ,0

VariableExp.Sign Coef. Prob. Coef. Prob. Coef. Prob.

SIZE 2 –0.0099 ∗∗∗ 0.0000 –0.0101 ∗∗∗ 0.0000 –0.0106 ∗∗∗ 0.0003LOGAGE +/ 2 0.0117 ∗∗ 0.0401 0.0091 0.2180 0.0136 0.1092SALESG + 0.0438 0.1363 0.2217 ∗∗∗ 0.0000 –0.0297 0.4662OCF 2 0.0798 ∗∗∗ 0.0077 0.1440 ∗∗∗ 0.0002 0.0463 0.2342LOSS + 0.0343 ∗∗∗ 0.0083 0.0487 ∗∗∗ 0.0039 0.0342 ∗ 0.0773DTA +/ 2 0.0202 0.2478 0.0433 ∗∗ 0.0256 –0.0006 0.9838LAGWA 2 0.0844 ∗∗∗ 0.0035 0.1286 ∗∗∗ 0.0028 0.0355 0.4010OVAR + –0.0018 0.5308 –0.0012 0.7260 0.0079 0.2802TENURE +/ 2 –0.0025 ∗∗ 0.0476 –0.0024 0.1127 –0.0028 0.1666CASH +/ 2 0.0433 ∗ 0.0710 0.0057 0.8309 0.0628 ∗ 0.0700JOINT ? –0.0784 ∗∗∗ 0.0000 –0.0685 ∗∗∗ 0.0000 –0.0846 ∗∗∗ 0.0000Intercept 0.2900 ∗∗∗ 0.0000 0.2623 ∗∗∗ 0.0000 0.3164 ∗∗∗ 0.0000Annual fixed effects? Yes Yes YesIndustry fixed effects? Yes Yes Yes–2 Res Log Likelihood –833.8 –501.0 –330.7N (# Joint audits) 906 (453) 472 434

Notes:The dependent variable ABWA is the amount of abnormal working capital accruals; SIZE is the naturallogarithm of total assets in thousands of Swedish kronor; P/B is the price-to-book ratio; SALESG is thegrowth in sales over the prior year; OCF is the operating cash flow divided by beginning total assets;LOSS is a dummy variable with a value of one if the earnings are negative otherwise zero; DTA is theratio of debt to total assets; LAGWA is the amount of total working capital accrual in year t–1; OVARis the standard deviation of sales in billions of Swedish kronor over the years t–3 to t; JOINT is adummy variable with a value of one if the client firm employs a joint audit, otherwise zero; BIG is adummy variable with a value of one if the client firm employs a single Big 4 audit firm, otherwise zero;LOGAGE is the natural logarithm of firm age in years; TENURE is audit firm tenure in years. For thejoint audit observations, we designate the value of the audit firm with longer tenure. CASH is the ratioof cash and cash equivalents to total assets. Statistical significance based on two-tailed tests at the 1%,5%, and 10% levels are denoted by ∗∗∗, ∗∗, and ∗, respectively.

Do Joint Audits Improve Audit Quality? 19

Panel B of Table 5 presents the results for estimating equation (5b) among the

sample of privately held clients. As in Panel A, we report the results for the absolute

abnormal accruals in column (1) whereas columns (2) and (3) report the results for

the income-increasing and income-decreasing abnormal accruals, respectively.

As seen in column (1), we find that the estimated coefficient on the joint audit

indicator is highly significant and negative. The estimated negative relationship

holds for both the income-increasing and income-decreasing observations,

suggesting that the employment of joint audits among private companies is

associated with smaller abnormal working capital accruals. Note that the inherent

limitation of the matching approach is a diminished ability to draw inferences

from the control variables. However, according to the estimated results in

panel B, abnormal accruals increase with sales growth, accounting losses and

lagged level of accruals, while decreasing with client size. The estimated positive

coefficient on the lagged value of accruals suggests that they capture the time-

invariant factors omitted from our expectation model for working capital

accruals. Overall, the results from the analyses of both the public and private

client companies suggest that joint audits decrease earnings manipulations

through accounting accruals, resulting in a higher actual audit quality.

6. Multivariate Analysis: Perceived Audit Quality

6.1. Empirical Test for Perceived Audit Quality

Our next analyses are designed to test whether the decision to employ a joint audit

affects the credit raters’ perception of the quality of audits. Given that we do not have

credit ratings or risk forecasts available for public firms, we cannot conduct these

tests for the public firm sample. However, we refer to the results of Zerni et al.

(2010) for evidence that joint audits for publicly-listed firms are perceived to be

of higher quality. Hence, these analyses are only conducted among privately-held

firms. We use credit ratings and forecasts of insolvency risk as our proxies for

perceived audit quality. We estimate the following two equations to test hypotheses

2a and 2b, i.e. whether the employment of a joint audit affects a client company’s

perceived credit risk and hence the cost and access to debt capital:

RATE = a + b1SIZE + b2ROA + b3CONTROL + b4LOSS + b5LOGAGE

+ b6CASH + b7DTA + b8JOINT + fixed effects + 1

(6a)

RISKFORE = a + b1SIZE + b2ROA + b3CONTROL + b4LOSS

+ b5LOGAGE + b6CASH + b7DTA + b8JOINT + fixed effects + 1(6b)

where RATE is UC AB’s risk rating for the client firm on a scale ranging from 1 to

5, with higher values indicating lower credit risks (model 6a is estimated as an

20 M. Zerni et al.

ordered logit model). RISKFORE represents UC AB’s risk forecast for client firm

insolvency in percentages ranging from 0.01 to 99%, with higher values indicat-

ing higher risk.22 The other variables are as previously defined.

6.2. Results for the Perceived Audit Quality Tests

Panel A of Table 6 presents the descriptive statistics for the variables used in the

tests for perceived audit quality. The sample that we use in these tests consists of

424 joint audit observations (92 unique firms) and their propensity-score-

matched pairs of firms audited by a single Big 4 auditor (control group), or in

total 848 observations. Descriptive statistics in Table 6 indicate that most of

the firms included in the sample have low levels of perceived credit risk. In par-

ticular, the mean (median) risk rating is 4.58% (5%) while the mean (median) risk

forecast of insolvency is 0.74% (0.2%), indicating a normal-to-low (low) per-

ceived credit risk. In our sample, the risk forecast for the probability that a

company will become insolvent within the next 12 months ranges from 0.1 to

32% (i.e. from a very low to a very high level of credit risk). A simple univariate

t-test for the differences in means (untabulated) suggests that the credit ratings are

better on average (p-value , 0.01) and risk forecasts are lower (p-value ¼

0.039) for clients employing joint audits compared with the control group.

Hence, the univariate evidence supports hypotheses 2a and 2b (i.e. that joint

audits reduce perceived credit risk and thus facilitate the firm’s access to credit

capital).

Panel B of Table 6 reports the results for the multivariate regressions that test

hypotheses 2a and 2b. Column (1) reports the regression results for equation

(6b) with risk forecast as the dependent variable, and column (2) reports the

results for the ordered logit model defined in equation (6a). All of the control

variables with the exception of the indicator variable for the presence of a

controlling shareholder (CONTROL) are estimated as significant with

expected signs. Specifically, the client firm’s size, age, liquidity and

profitability are estimated to be significantly positively (negatively) related to

the risk ratings (\,forecasts) issued by the credit rating agency. Moreover,

high financial leverage and accounting losses are associated with worse credit

ratings but are not estimated to have any significant effects on the risk forecasts

of insolvency.

Results regarding our test variable (JOINT) provide support to our hypoth-

eses 2a and 2b that joint audits enhance the outsiders’ perception of audit

quality. More specifically, JOINT is estimated to have a positive (negative)

effect on credit ratings (risk forecasts). Economically, the estimated coefficient

on the joint audit indicator in column (1) suggests that the credit rating

agency’s assessment of the probability that a company becomes insolvent

within the next 12 months is, on average, 10 basis points lower for joint

audit clients than for their propensity-score-matched counterparts of single

Big 4 auditor clients. We conclude that even after using propensity score

Do Joint Audits Improve Audit Quality? 21

Table 6. Tests of perceived audit quality

Panel A: Descriptive statistics for the perceived audit quality tests among private firms

(N ¼ 848)

Variable Mean Std. Min 25%tile Median 75%tile Max

RISKFORE 0.742 2.140 0.010 0.100 0.2000 0.680 32.00

RATE 4.58 0.77 1 4 5 5 5

SIZE 9.35 2.83 3.05 7.38 9.12 11.27 17.43

ROA 0.042 0.192 –0.752 –0.005 0.040 0.113 0.763

CONTROL 0.798 0.401 0 1 1 1 1

DTA 0.676 0.279 0 0.491 0.769 0.901 0.992

LOGAGE 3.12 0.92 0.69 2.48 3.04 3.78 4.72

LOSS 0.271 0.445 0 0 0 1 1

CASH 0.169 0.245 0.001 0.006 0.044 0.258 0.873

JOINT 0.500 0.500 0 0 0.500 1 1

Panel B: Multivariate results for the perceived audit quality tests among private firms (N ¼ 848)

RISKFORE RATE

Variable Exp. sign Coef. Prob. Exp. sign Coef. Prob.

JOINT – –0.1049 ∗∗ 0.0284 + 0.3505 ∗∗ 0.0463

SIZE – –0.0663 ∗∗∗ 0.0000 + 0.3195 ∗∗∗ 0.0000

ROA – –0.4798 ∗∗∗ 0.0011 + 1.3266 ∗∗∗ 0.0013

LOSS + 0.1659 ∗∗∗ 0.0083 – –0.5534 ∗∗∗ 0.0062

CONTROL – –0.0627 0.3662 + 0.0116 0.9565

DTA + 0.1514 ∗ 0.0685 – –0.6903 ∗∗ 0.0378

LOGAGE – –0.2138 ∗∗∗ 0.0000 + 0.8756 ∗∗∗ 0.0000

CASH – –0.5700 ∗∗∗ 0.0000 + 3.1958 ∗∗∗ 0.0000

Intercept1 2.4317 ∗∗∗ 0.0000 –7.2488 ∗∗∗ 0.0000

Intercept2 –5.6949 ∗∗∗ 0.0000

Intercept3 –3.7144 ∗∗∗ 0.0000

Intercept4 –2.4844 ∗∗∗ 0.0000

Annual fixed

effects

Yes Yes

Likelihood ratio,

x2

302.67 0.0000

Nagelkerke R2 36.8 %

-2 Log Likelihood 1,767.9 1,135.91

Notes:RISKFORE is the risk forecast issued for the client firm by the credit rating agency; RATE is the riskrating issued for the client firm by the credit rating agency; SIZE is the natural logarithm of total assetsin thousands of Swedish kronor; ROA is the interest adjusted return on the opening total assets;CONTROL is a dummy variable with a value of one if the firm has a controlling shareholder,otherwise zero; DTA is the ratio of debt to total assets; LOGAGE is the natural logarithm of firmage in years; LOSS is a dummy variable with a value of one if the earnings are negative, otherwisezero; CASH is the ratio of cash and cash equivalents to total assets; JOINT is a dummy variablewith a value of one if the client firm employs a joint audit, otherwise zero.

22 M. Zerni et al.

matching to control for potential endogeneity due to omitted client character-

istics, the evidence supports our hypotheses 2a and 2b that joint audits lower

outsiders’ perceived credit risk and thus facilitate the firm’s access to credit

capital.

7. Multivariate Analysis: Audit Fees

7.1. Audit Fees as a Proxy for Perceived Audit Quality

As a test of differences in perceived audit quality between joint audits and single

auditor audits among listed firms, we examine whether joint audits are associated

with higher audit fees. In a voluntary setting, an observed willingness to pay for

higher fees can be interpreted to indicate a higher perceived or experienced

quality of services (Moizer, 1997; Riley, 2001). In particular, clients may be

willing to pay more for joint audits if they perceive the market-assessed level

of quality associated with joint audits to be higher (cf. Yardley et al., 1992). In

other words, the client’s motivation to pay a premium may arise from the need

for a mechanism that signals ‘good news’ to the market (Teoh and Wong,

1993; Titman and Trueman, 1986). Voluntary joint audits may represent such

a mechanism.

We control for the relevant audit fee determinants identified in prior studies (e.g.

Choi et al., 2010; Craswell and Francis, 1999; Francis et al., 2005; Hay et al., 2006;

Niemi, 2004; Simunic, 1980; Zerni, 2012). We estimate the following model

by using the maximum likelihood principle from our unbalanced panel data:23

AFEES = a + b1SIZE + b2SQEMP + b3QR + b4ROA + b5DTA + b6INVREC

+ b7LOGNAS + b8LOSS + b9JOINT + b10BIG + fixed effects + 1

(7)

where the dependent variable AFEES is measured as the natural logarithm of the

audit fees; SQEMP represents the square root of the number of employees; QR

is the quick ratio; INVREC is the sum of the inventories and receivables divided

by total assets; and LOGNAS represents the natural logarithm of non-audit fees

in Swedish kronor that are paid to the incumbent auditor. The other variables are

as previously defined.

7.2. Results for the Tests of Audit Fees

Table 7 reports the descriptive statistics for the variables used in the analyses of

audit fees. The public company sample that we used in the audit fee tests includes

a total of 109 joint audits from 25 unique firms (untabulated).24 The average

(median) audit fee is 5.1 million (1.18 million) SEK while the mean (median)

ratio of non-audit fees to audit fees is 65.9% (46.7%). The Big 4 firms dominate

Do Joint Audits Improve Audit Quality? 23

the Swedish public company audit market as indicated by their 90.6% market

share of single auditor clients.

Table 7 also indicates that the audit fees paid to dual auditors are far from

equal, suggesting that one of the auditors tends to be mainly responsible for con-

ducting the actual audit planning and tests. However, the second auditor’s share

of the non-audit fee revenue is closer to that of the first auditor.25 Some clients

even purchase all their consulting services from the second auditor. Univariate

test statistics for differences in means (untabulated) indicate that the clients of

dual auditors pay significantly higher audit fees than the clients of single auditors

(p-value , 0.000).

Table 7. Descriptive statistics for variables used in audit fee tests (N ¼ 1,162).

Panel A: Public firm sample.

Variable Mean Std. Min 25% Median 75% Max

JOINT 0.094 0.292 0 0 0 0 1BIGa 0.906 0.292 0 1 1 1 1AFEE (MSEK) 5.09 11.79 0.03 0.50 1.18 3.70 130.00NAS (MSEK) 3.21 9.91 0 0.18 0.57 2.00 121.00FEERATIO 0.659 0.762 0 0.246 0.467 0.810 10.175SIZE 13.97 2.05 8.89 12.48 13.63 15.20 19.35SQEMP 48.71 64.07 1 13.82 25.37 52.53 465.82LOSS 0.163 0.369 0 0 0 0 1INVREC 0.355 0.188 0.001 0.213 0.356 0.485 0.931DTA 0.175 0.158 0 0.020 0.151 0.288 0.747ROA (%) –1.78 23.87 –133.36 –3.02 4.85 9.33 40.42QR 1.82 2.51 0.08 0.82 1.14 1.77 37.33

Panel B: Descriptive statistics on the distribution of fees among listed joint audit clients.

Variable Mean Std. Min 25% Median 75% Max

SHARE AFEES 0.228 0.138 0.032 0.095 0.213 0.337 0.495SHARE NAS 0.325 0.319 0 0.033 0.232 0.500 1

Notes:a Conditional on the firm employing a single-audit firm. JOINT is a dummy variable with a value ofone if the client firm employs a joint audit, otherwise zero; BIG is a dummy variable with a value ofone if the client firm employs a single Big 4 audit firm, otherwise zero; AFEE (MSEK) is the audit feesin millions of Swedish kronor paid to incumbent auditor(s); NAS (MSEK) is the non-audit fees inmillions of Swedish kronor paid to the incumbent auditor; FEERATIO is the ratio of non-audit fees toaudit fees. Regarding joint audits, we calculate the ratio on the basis of the fees paid to the incumbentauditor that receives a larger share of the audit fees; SIZE is the natural logarithm of the total assets inthousands of Swedish kronor; SQEMP is the square root of the number of employees; LOSS is adummy variable with a value of one if the earnings are negative, otherwise zero; INVREC is the sum ofthe inventories and receivables divided by total assets; DTA is the ratio of debt to total assets; ROA (%)is the interest-adjusted return on the opening total assets; QR is the quick ratio; SHARE AFEES is thesecond auditor’s share of the total audit fees; and SHARE NAS is the second auditor’s share of the totalnon-audit fees.

24 M. Zerni et al.

Table 8 reports the results obtained by regressing audit fees on a set of control

variables and the research variables identified in equation (7). Column (1) reports

the results obtained when using an indicator variable for the joint audits

while column (2) reports results for the firm-fixed effect-extension of Model

(equation (7)).26

As shown in Table 8, our empirical fee model is well specified, explaining a

considerable portion of the variation in fees (with an adjusted R-squared value

of roughly 90%). In both model specifications, most of the estimated coefficients

Table 8. Regression analysis of audit fees.

AFEES AFEES

Variable Exp. Sign Coef. Prob. Coef. Prob.

Experimental variablesJOINT ? 0.5703 ∗∗∗ 0.0062 0.9926 ∗∗ 0.0156BIG + 0.4466 ∗∗∗ 0.0011 0.5823 0.1528Control variablesSIZE + 0.5579 ∗∗∗ 0.0000 0.3290 ∗∗∗ 0.0000SQEMP + 0.0030 ∗∗∗ 0.0014 0.0030 0.2255QR 2 –0.0510 ∗∗∗ 0.0000 –0.0313 ∗∗∗ 0.0016ROA 2 –0.1200 0.3651 –0.0570 0.6740DTA + 0.0183 0.9294 –0.0075 0.9626INVREC + 0.5957 ∗∗ 0.0119 0.6864 ∗∗∗ 0.0036LOGNAS + 0.0344 ∗∗ 0.0272 0.0423 ∗ 0.0733LOSS + –0.1058 0.2449 0.1042 0.1495Intercept 5.4361 ∗∗∗ 0.0000 8.7188 ∗∗∗ 0.0000Annual fixed effects? Yes YesIndustry fixed effects? Yes NoFirm fixed effects? No YesaAdjusted R2 87.8 % 93.5 %–2 Res Log Likelihood 1904.6 1286.4N (# joint audits) 1,162 (109) 1,162 (109)

Notes:a Maximum likelihood methods do not compute the sums of squares. However, by calculating theresidual and total sums of squares, we can report the adjusted R-square statistics to facilitate thecomparability between related studies. The dependent variable AFEES is the natural logarithm ofaudit fees in Swedish kronor paid to the incumbent auditor(s); JOINT is a dummy variable with avalue of one if the client employs two or more audit firms to conduct a joint audit, otherwise zero;BIG is a dummy variable with a value of one if the auditor is a member of the Big 4 auditors,otherwise zero; SIZE is the natural logarithm of the total assets in thousands of Swedish kronor;SQEMP is the square root of the number of employees; QR is the quick ratio; ROA is the interest-adjusted return on the opening total assets; DTA is the ratio of debt to total assets; INVREC is thesum of the inventories and receivables divided by total assets; LOGNAS is the natural logarithm ofnon-audit fees in Swedish kronor paid to the incumbent auditor(s); LOSS is a dummy variable witha value of one if the earnings are negative, otherwise zero. Statistical significance based on two-tailed tests at the 1%, 5%, and 10% levels are denoted by ∗∗∗, ∗∗, and ∗, respectively. Furthermore,statistical significances are calculated by adjusting the standard errors for firm level clustering(Petersen 2009) and heteroskedasticity (White 1980). For simplicity, results for the fixed effectsare not reported.

Do Joint Audits Improve Audit Quality? 25

of control variables have the expected signs and are statistically significant. The

estimated coefficient of the joint audit indicator (JOINT) is positive and highly

significant (p-value , 0.01). Thus, the estimated results suggest that joint

audits are associated with significantly higher audit fees relative to single

auditor audits. Moreover, the Big 4 indicator (BIG) is estimated to be positive

and significant, suggesting that a Big 4 audit fee premium exists among the

clients of single auditors. However, the magnitude of the coefficient of the vari-

able JOINT is significantly larger than that of the variable BIG. The null hypoth-

esis in the LR-test for the equality of the parameter estimates is rejected at a level

lower than 0.001. The estimated results in column (1) suggest the following three-

level hierarchy of perceived audit quality: joint audits, single Big 4 audits and

single non-Big 4 audits. The magnitude of the economic effect of auditor

choice on audit fees is relatively large. Specifically, the estimated coefficients

in column (1) suggest that the clients of joint auditors pay on average 13.2%

(76.9%) cent higher audit fees than the clients of a single Big 4 (non-Big 4)

auditor.

In column (2), we attempt to control for unobservable firm heterogeneity by

including firm-fixed effects into the audit fee model.27 During our audit fee

sample period 2000–2006, 17 firms changed their status from single-firm audit

to joint audit or vice versa, allowing the use of fixed effect extensions. After con-

trolling for the unobservable, time-invariant, firm-specific characteristics, our

results are broadly consistent with the results reported in Column 1. Estimated

results show that the largest fee premium is attributable to joint audits. Consistent

with our main tests, the findings from our audit fee tests hence provide support for

the perceived higher quality of joint audits as compared with single auditor

audits.28

8. Conclusions

This study investigates whether a voluntary joint audit is related to actual and per-

ceived audit quality and the pricing of audit engagements in a relatively low liti-

gious setting, Sweden, where a sufficient number of client firms have voluntarily

(i.e. without a statutory obligation) opted to employ two audit firms to conduct a

joint audit, which allows studying this issue.

Our empirical findings indicate that the employment of a joint audit is associ-

ated with a higher degree of earnings conservatism for both public and private

firms. Joint liability essentially means that both auditors bear the (potentially)

incremental audit risk arising from the likelihood that the other auditor fails to

perform its share of the audit work. Hence, the increased conservatism may at

least partially be attributed to each auditor’s response to the information asymme-

try about the other auditor’s actions (i.e. the potential ‘free-rider problem’).

Moreover, it is less likely that the two audit firms simultaneously acquiesce to

client pressure in client-auditor negotiations on accounting choices, resulting in

a higher degree of auditor independence and ultimately audit quality. Consistent

26 M. Zerni et al.

with our findings on earnings conservatism, we also find evidence for both public

and private firms, suggesting that employing joint audits is associated with lower

income-increasing abnormal accruals and implying higher audit quality.

For private firms, we test and find evidence supporting the view that employing

two audit firms enhances the financial statement user’s perception of audit quality

proxied by credit ratings and risk forecasts of insolvency. This finding is consist-

ent with both the enhanced independence of joint audits and the insurance

hypothesis of auditing predicting that joint audits provide a better ‘insurance

value’ for providers of funding as two audit firms have ‘deeper pockets’ in the

event of an audit failure than either of them alone.

However, the decision to employ joint audits does not come without additional

costs. More specifically, our tests of audit pricing among publicly listed compa-