Introduction to Shipping Audits -101

52

Introduction to Shipping Audits - 101 Moore Stephens LLP, Singapore www.moorestephens.com.sg

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Introduction to Shipping Audits -101

Introduction to Shipping

Audits - 101Moore Stephens LLP, Singapore

www.moorestephens.com.sg

Shipping 101

• The Reasons for Sea Transport

• The Ship

• Types of Markets – Dry Bulk, Tankers, Liners,

• Major Trade Routes

• Practitioners in Shipping Business

• Basic Accounting and Auditing Implications

2

The Reasons For Sea Transport

www.moorestephens.com.sg

The Reasons for Sea Transport

• 90% of the world’s cargo is transported by sea.

• Concept of “Derived Demand” – i.e. demand for ships is

derived from the demand for the goods that they carry.

• Important to understand that shipping is generally divided by the

types of cargo these ships carry.

• Other than carrying goods from one country to another country,

goods can also be moved from one place to another within the

same country (especially when the country is made up of a

series of smaller islands)– this is known as “Coastal Shipping”.

Cabotage shipping refers to coastal shipping restricted by

certain countries to ships owned in that country, e.g. Indonesia

4

The Ship

www.moorestephens.com.sg

The Ship

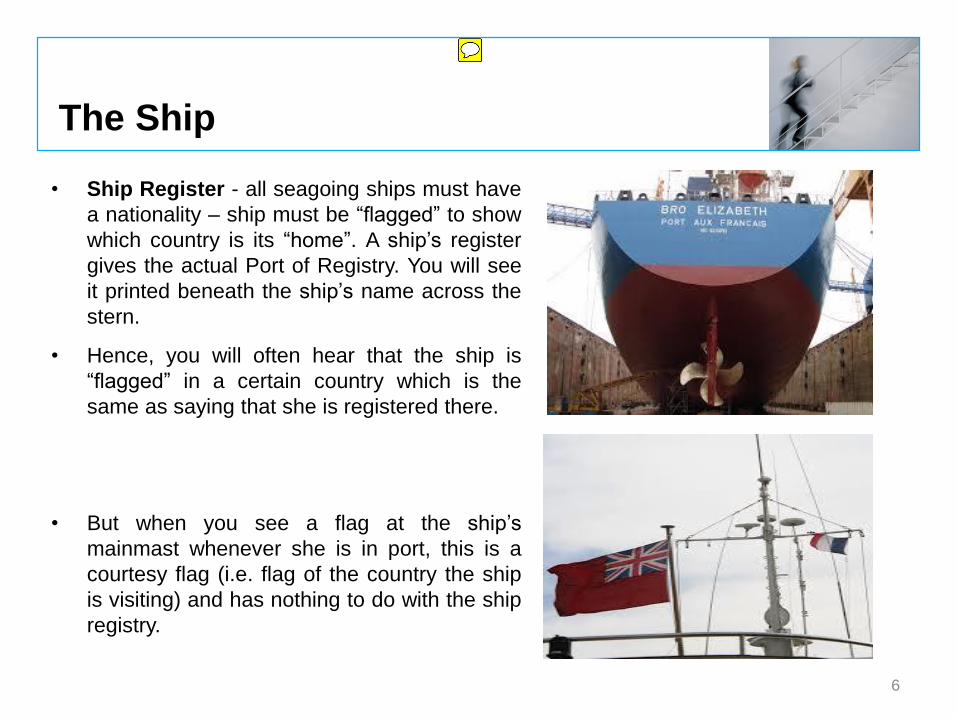

• Ship Register - all seagoing ships must have

a nationality – ship must be “flagged” to show

which country is its “home”. A ship’s register

gives the actual Port of Registry. You will see

it printed beneath the ship’s name across the

stern.

• Hence, you will often hear that the ship is

“flagged” in a certain country which is the

same as saying that she is registered there.

• But when you see a flag at the ship’s

mainmast whenever she is in port, this is a

courtesy flag (i.e. flag of the country the ship

is visiting) and has nothing to do with the ship

registry.

6

wuxiangchao

Sticky Note

phsyical sighting sometimes impractical. use confirmation via the registry see the minutes.

The Ship

• Ship Classification – this is the way a

ship obtains its “certificate of quality”.

This is needed before any insurer will

insure the ship or its cargo, no one will

also entrust their cargo to a ship without

it.

• Classification is provided by

Classification Societies, of which the

reputable ones are members of the

International Association of

Classification Societies (“IACS”).

7

The major classification societies as are

follows:

ABS – American Bureau of Shipping

BV – Bureau Veritas

DNV – Det Norske Veritas

GL – Germanischer Lloyd

IRS – Indian Register of Shipping

KR- Korean Register

LR – Lloyd’s Register

NK – Nippon Kaiji Kyokai

The Ship

• Size of Ship is based on tonnage.

• Gross Registered Tonnage (“GRT”) - The total enclosed space of the

vessel including machinery space and personnel accommodation, etc.

• Deadweight Tonnage (“DWT”) - how much weight a ship can safely carry.

It is the sum of the weights of cargo, fuel, fresh water, ballast water,

provisions, passengers, and crew.

• Light Displacement Tonnage (“LDT”) - Actual weight of an empty ship (i.e.

with no fuel, passengers, cargo, water, and other cargo on board). This is

used in calculating the estimated scrap value of a ship when applying the

prevailing market price of scrap steel. Scrap price for tankers and bulkers

can be different.

8

Major Segments in Shipping

www.moorestephens.com.sg

Dry Cargo Chartering Market

• Typical cargos in the dry bulk market include coal, iron ore, grains, fertilizers, steel and timber.

• Common vessels used are the handys, supramax, panamax, and capesizes (see Quick Reference Guide to Common Shipping Terms).

• The formal contract drawn up between the shipowner and the shipper is called the Charter Party.

10

Dry Cargo Chartering Market

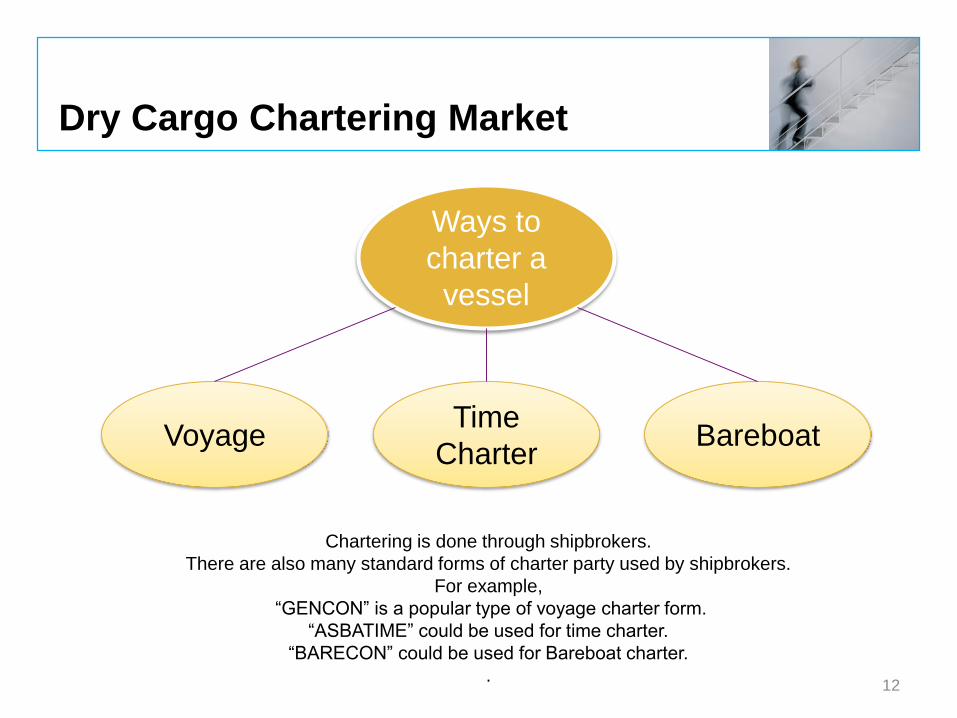

• There are 3 ways a ship can be chartered:

– Voyage charter : transport an agreed quantity of cargo from point A to B. Payment is by means of freight (US$/ton)

– Time charter: chartering of a vessel for a period of time and instead of paying freight per ton, the charterer pays hire rate per day (US$/day).

– Bareboat charter: An agreement under which the shipowner transfers management and control to charterers. The bareboat charter hire is usually quoted in US$/day.

11

Ways to

charter a

vessel

VoyageTime

CharterBareboat

Dry Cargo Chartering Market

12

Chartering is done through shipbrokers.

There are also many standard forms of charter party used by shipbrokers.

For example,

“GENCON” is a popular type of voyage charter form.

“ASBATIME” could be used for time charter.

“BARECON” could be used for Bareboat charter.

.

Voyage Charter

• In a voyage charter, much attention is paid to TIME.

• Laytime is the “allowed” time for loading/unloading of cargoes.

• Demurrage is payable by charterers at an agreed rate per day or pro rata to owners where time allowed for loading and/or discharging cargo has been exceeded.

• Despatch money is the bonus or reward given to charterer for taking less than the agreed time for loading/unloading.

• Sometimes, demurrage and despatch money are disputed which can lead to impairment loss of the receivables.

13

Time Charter

• In a time charter, the shipowner operates the vessel and provides the crew but the charterer tells the vessel where to go, what to do, and pays for all bunkers consumed, port charges, and loading/unloading costs.

• Time charter:

– No demurrage/despatch money

– Risks of still having to pay hire rate when bad weather or port strike causes delay in trip. If delay is caused by the ship breaking down then hire is not payable (i.e. “offhire”).

• Indicative rates are issued daily by the London-based Baltic Exchange, the Baltic Dry Index (“BDI”) provides an assessment of the price of moving the major raw materials by sea, taking in 23 shipping routes measured on a timecharter basis. BDI covers Handysize, Supramax, Panamax, and Capesize dry bulk carriers carrying a range of commodities including coal, iron ore and grain.

14

Tanker Chartering Market

• Tanker chartering market typically covers crude oil and oil products.

• Common vessels used are the panamax, aframax, VLCCs, product carriers, chemical carriers (see Quick Reference Guide to Common Shipping Terms).

• Freight is measured based on Worldscale (e.g.Worldscale 175 would mean 175% of the flat rate).

• There tends to be only one broker between the owner and the charterer (unlike dry bulk where there could be a charterer’s agent and owner’s broker)

• There are 2 distinct types of gas carried in ships as liquids:

– LNG (Liquid Natural Gas) : Ethane and Methane

– LPG (Liquid Petroleum Gas) : Propane and Butane15

Liners

• Liners are cargo ships that carry their entire load in truck-size intermodal containers.

• Liners runs on a scheduled service between ports (it conforms to an advertised schedule).

• Containers are measured in TEU (twenty feet equivalent unit).

• Slot chartering - voyage charter arrangement whereby the shipowner agrees to place a certain number of container slots at the charterer’s disposal (typically one TEU fits in a slot).

16

Liners

• The most important document in the liner business is the “Bill of Lading” (“B/L”) which is used as a receipt for cargo, as evidence of contract, and a document of title.

• The freight is paid by the shipper which includes the full cost of loading the cargo from the quay and unloading them at the port of destination.

• Companies such as Maersk, MSC and NOL are in the liner business.

17

Major Sea Routes

www.moorestephens.com.sg

Major Sea Routes

• Coal

– USA (e.g. Hampton Roads) to Europe and to Japan

– Australia (e.g. Newcastle-New South Wales) to Japan

• Iron Ore

– South America (e.g. Brazil) to Europe and the Far East

– Australia (e.g. Dampier) to Japan and to China

• Grain

– Canada (e.g. Great Lakes) to Europe

– South America (e.g. Argentina) to Europe and to China

• Oil

– Middle East to Europe and to Far East

– West Africa to Europe

19

Practitioners in Shipping Business

www.moorestephens.com.sg

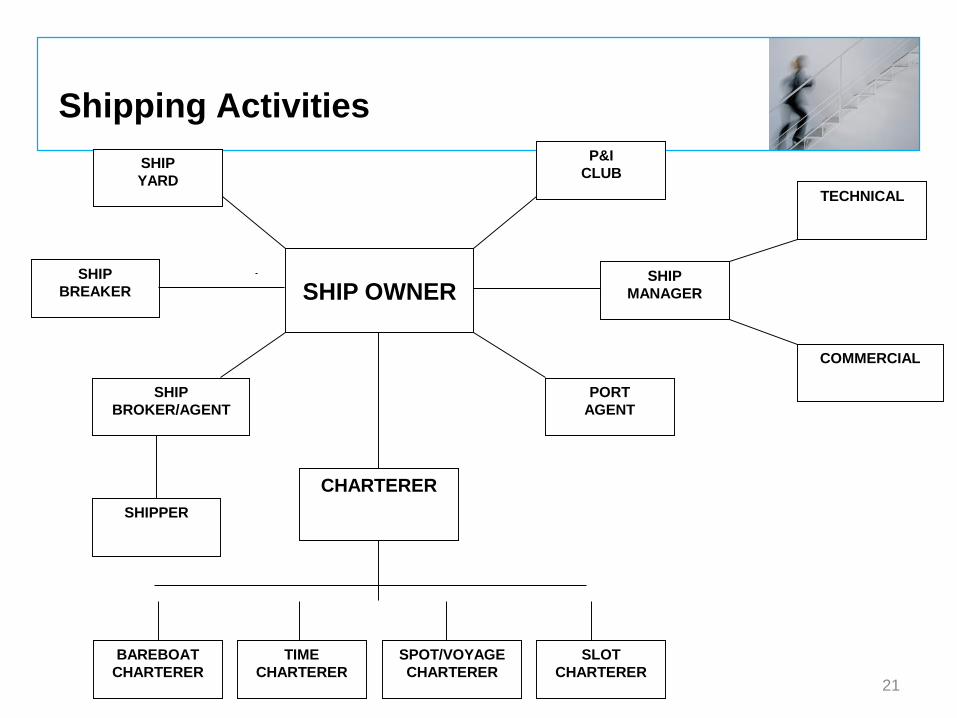

Shipping Activities

SHIP

YARD

SHIP

BREAKER

SHIP

BROKER/AGENT

SHIPPER

P&I

CLUB

TECHNICAL

PORT

AGENT

CHARTERER

SHIP OWNERSHIP

MANAGER

COMMERCIAL

BAREBOAT

CHARTERER

TIME

CHARTERER

SPOT/VOYAGE

CHARTERER

SLOT

CHARTERER21

Practitioners in the Shipping Business

Other than Shipowners and Charterers, core shipping practitioners can be grouped into 6 categories:

•Sale & purchase broking:

• involved in brokering the buying and selling of a vessel.

• S&P brokers have specialised knowledge and can be asked to act as ship valuers.

•Ship management:

• maintenance of a ship which includes crewing, storing, technical services, insurance and operations.

• Ship management operations may be organised in two ways. Either the shipowner manages the vessels in-house or the owner outsources this to an independent manager.

22

Practitioners in the Shipping Business

Other than Shipowners and Charterers, practitioners can be grouped into 6 categories:

•Liner agents : agents involved in the marketing of liner service, documentation of cargos, arrangements for loading and discharging of cargos. Many liner operators now have in-house liner agents

•Dry cargo chartering : brokers involved in finding dry cargo for the ship, or helping shippers with dry cargo find the right ship.

•Tanker chartering : brokers involved in finding liquid cargo for the ship, or helping shippers with liquid cargo find the right ship.

•Port agency : port agent looking after the interest of the vessel when the vessel calls at a port. Port agent provides the Statement of Factand also put together the disbursement account for submission to the owner.

23

Insurance Companies in the Shipping Industry

Marine insurance falls into 2 categories –

•Hull & Machinery Insurance

• Most famous provider of this type of insurance is Lloyd’s of

London

•Third Party insurance

• Includes the “P&I Clubs” (Protection & Indemnity Associations).

• P&I Club underwriters are shipowners who are members of the

P&I Club and they underwrite all insurance matters not covered

by the normal marine insurance, e.g. if there is an oil spill and

there are pollution fines, clean up costs,cargo loss etc.

24

Insurance Companies in the Shipping Industry

Loss Adjustor

A general average situation is when a common danger at sea threatens to

damage one or all of the parties involved in a voyage, and in order to prevent

the total loss of the voyage one party makes a sacrifice that saves the

voyage. Because this sacrifice has saved the interests of the other parties

they are then obligated to indemnify the party who made the sacrifice by

contributing to general average.

In the event of a general average incident, a loss adjuster will analyse the

events that took place, and he will assess the value of contribution of each

party who is obligated to contribute in a general average situation.

25

Basic Accounting and Auditing Implications

www.moorestephens.com.sg

Residual Values

• Current at balance sheet date

• Change in accounting estimate

27

Impairment

• Impairment review

• Indications of impairment

• Higher of carrying value and recoverable amount

• Recoverable amount

– Net selling price

– Present Value of future cash flows– Cash flows

– Discount rate

28

Impairment

• Impairment loss : Carrying Value > Recoverable amount

• Impairment loss recognised in profit and loss

• Asset carried at revalued amount

• Reversal of impairment loss

29

wuxiangchao

Typewritten Text

usually use cost method as the industry is fairly volatile if use revaluation, then values will change a lot

Valuation Basis

• Cost or valuation

• Valuation basis = current market value

• Entire class revalued

• Treatment of depreciation

• Revaluation reserve

• Downward valuation

30

wuxiangchao

Typewritten Text

Ship vault - app for list of vessels

Fleet Impairment

• Can we get broker valuations

• What are the caveats?

– Current valuation disclaimer– We cannot obtain more audit evidence than an expert is willing to

provide

– Spreads within valuations

– Divergence between valuations

31

Fleet Impairment

• “If there is no reason to believe that an asset’s value in use materially exceeds its fair value less costs to sell, the asset’s fair value less costs to sell may be used as its recoverable amount…” [para. 21, FRS 36]

• Vessel values ARE the market’s estimate of the present value of the future cash flows from vessel use, so the default position must be that Value In Use does not exceed market value

32

Fleet Impairment

• Recoverable amount is the higher of an asset’s fair value less costs to sell and its value in use

• Value in use is the present value of the future cash flows expected to be derived from an asset

33

Fleet Impairment

• When might VIU exceed market value?

– Long-term charter above market rates– What is the risk of charterer default?

–Can we get credit ratings?– Will the charterer try to renegotiate?

– Historical premium over market averages– Audit evidence?

– How material?

– ‘Unusual’ vessels

34

Fleet Impairment

• Methodology for charter premium

– Vessel value is sum of– Value of unfixed vessel, plus

– Present value of future charter income above future expected rates (eg. comparison with current fixtures or FFA rates to 2013)

35

Fleet Impairment

• Estimating future cash flows

– Projections must be based on “reasonable and supportable” assumptions

– “Greater weight shall be given to external evidence.” [Para. 33 (a), FRS 36]

– Assumptions that simply ignore current market perceptions cannot provide sufficient appropriate audit evidence

36

Fleet Impairment

• For companies with a valuation policy, must state at market even if not impaired

• However, does affect recognition of value changes

37

Newbuilding Impairment

• Issues basically identical to vessels, but

• Possibility of onerous contract if fall in value exceeds carrying value of newbuilding

• If onerous contract:

– Impair to zero

– Make provision

• Also consider availability of finance

38

Dry docking

• FRS 37 provisions

• Profit and loss

• Capitalise and write off

• Newly acquired vessels

• Allocation of cost

39

wuxiangchao

Typewritten Text

split up the vessels into various portions. Notional dry docking - split the cost to be dry docked

Borrowing Costs

• Capitalised interest

• Consistency

• Specific borrowing costs

40

Capital & Repairs

• Subsequent expenditure

• Repairs charged to income?

• Previously assessed standard of performance

• Extended life programmes

41

Breach of Covenants

• Read the covenants

• Is there a breach at the end of the year?

• If implication of breach is making amounts current, then any negotiations after balance sheet date have no effect on accounting treatment

• ‘Attitude’ of financiers irrelevant to disclosure per para. 74 FRS 1:

• “…An entity classifies the liability as current because it does not have an unconditional right to defer its settlement for at least twelve months…”

• ‘Attitude’ of financiers relevant to going concern

42

Breach of Covenant - Disclosure

• Even if arose during year, and even if remedied by end of year, must disclose all defaults of principal, interest, sinking fund or redemption terms [Para. 18 (a), FRS 107]

• For all other breaches of loan agreement during year, disclose where those breaches permitted the lender to demand accelerated repayment, unless remedied or renegotiated by end of year [Para. 19, FRS 107]

• Disclose details of all items in default at year end, and whether remedied, or renegotiated, before financial statements are issued [Para. 18 (b) & (c), FRS 107]

43

Onerous Contracts

- Present value of time charter revenue < Present value of operating costs.

- Provision for future losses.

44

wuxiangchao

Typewritten Text

like normal long term contracts that are onereous

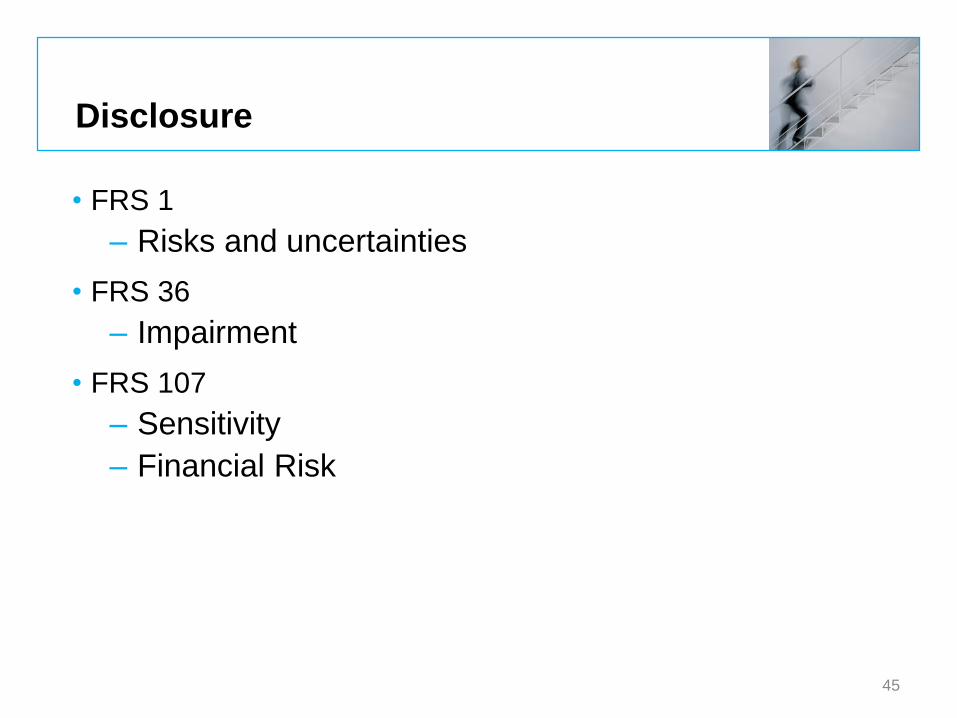

Disclosure

• FRS 1

– Risks and uncertainties

• FRS 36

– Impairment

• FRS 107

– Sensitivity

– Financial Risk

45

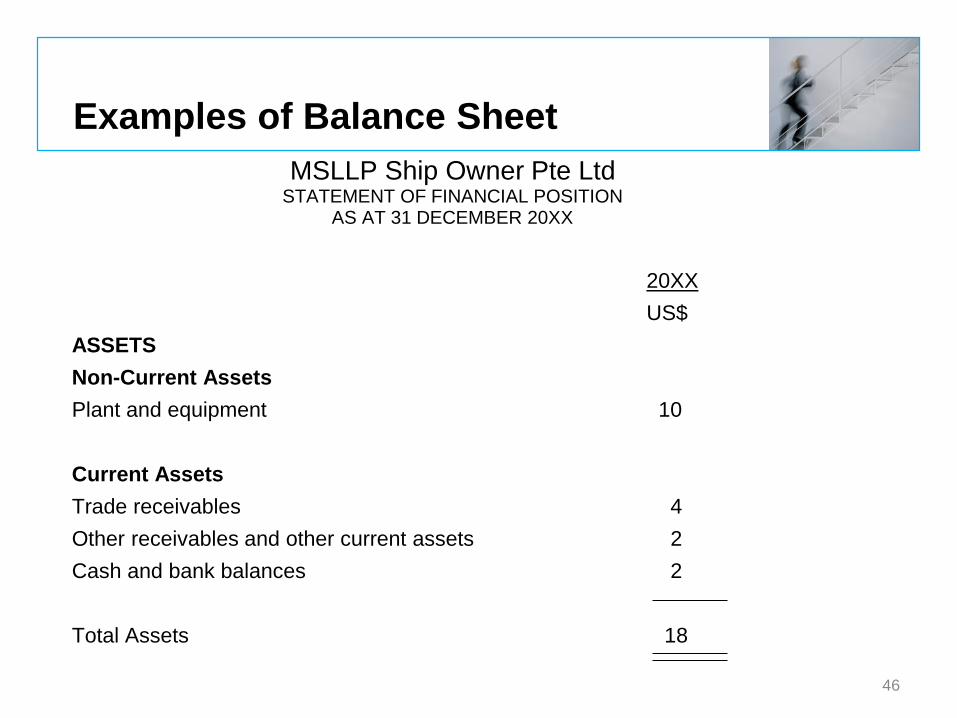

Examples of Balance SheetB/S

MSLLP Ship Owner Pte LtdSTATEMENT OF FINANCIAL POSITION

AS AT 31 DECEMBER 20XX

20XX

US$

ASSETS

Non-Current Assets

Plant and equipment 10

Current Assets

Trade receivables 4

Other receivables and other current assets 2

Cash and bank balances 2

Total Assets 18

46

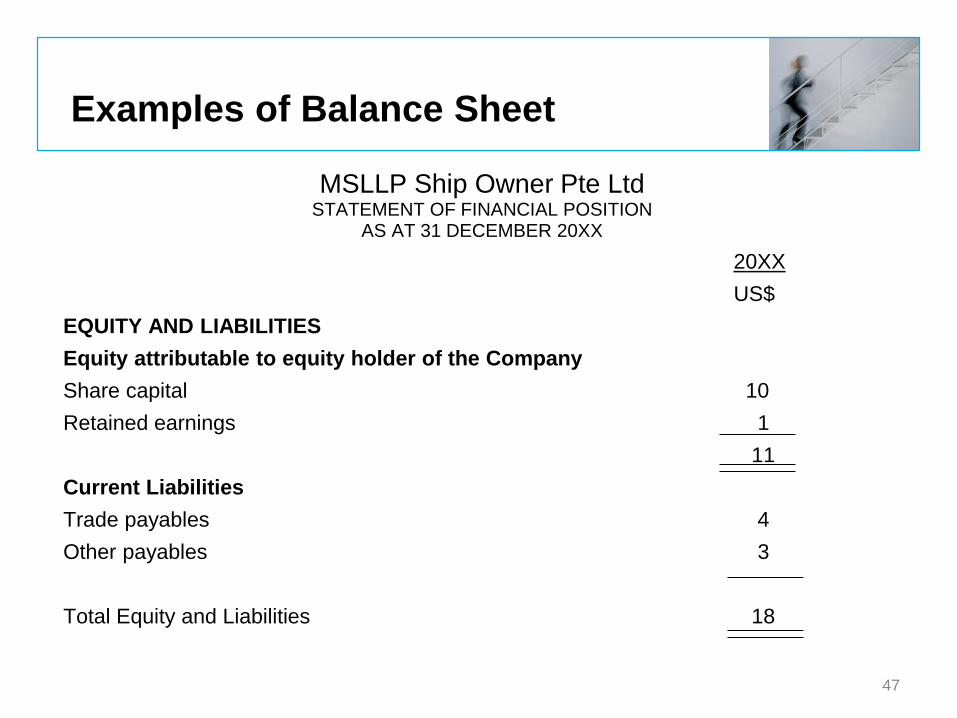

Examples of Balance SheetB/S

MSLLP Ship Owner Pte LtdSTATEMENT OF FINANCIAL POSITION

AS AT 31 DECEMBER 20XX

20XX

US$

EQUITY AND LIABILITIES

Equity attributable to equity holder of the Company

Share capital 10

Retained earnings 1

11

Current Liabilities

Trade payables 4

Other payables 3

Total Equity and Liabilities 18

47

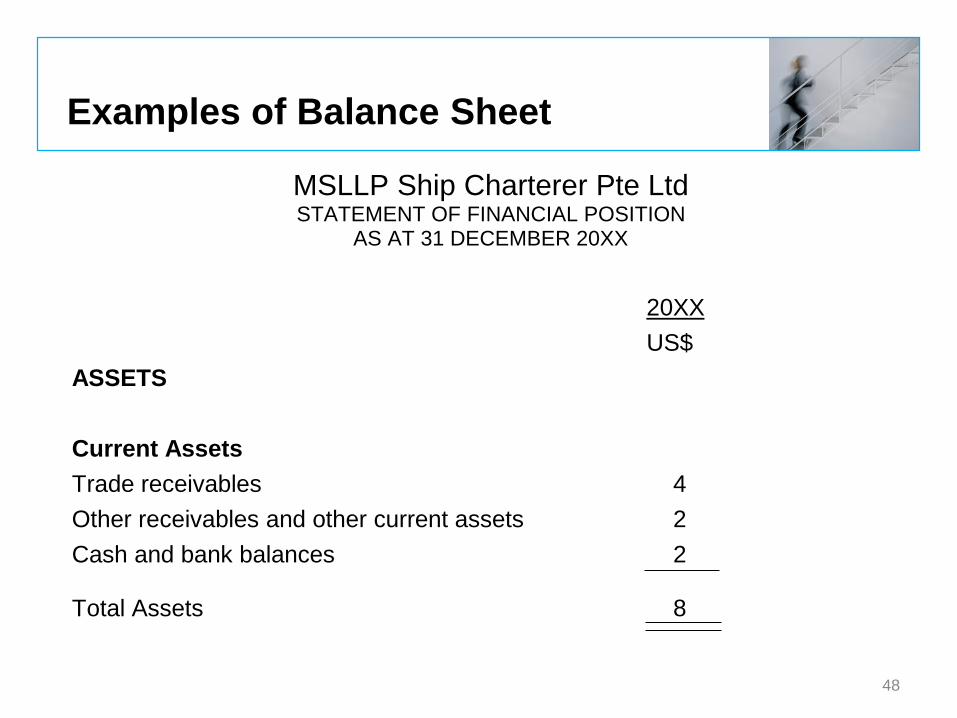

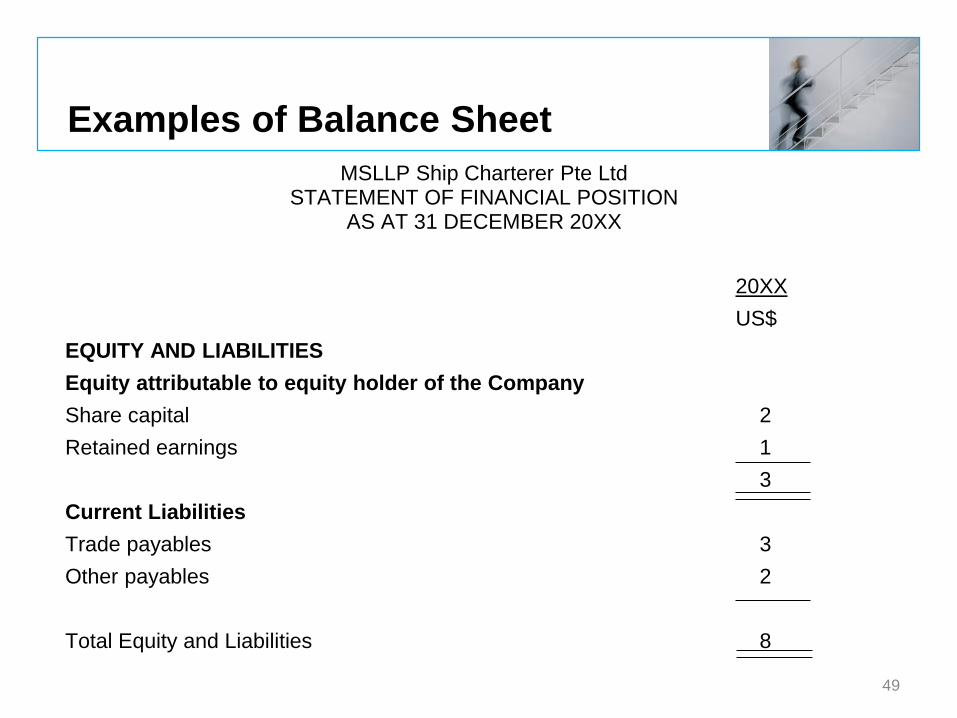

Examples of Balance SheetB/S

MSLLP Ship Charterer Pte LtdSTATEMENT OF FINANCIAL POSITION

AS AT 31 DECEMBER 20XX

20XX

US$

ASSETS

Current Assets

Trade receivables 4

Other receivables and other current assets 2

Cash and bank balances 2

Total Assets 8

48

Examples of Balance SheetB/S

MSLLP Ship Charterer Pte LtdSTATEMENT OF FINANCIAL POSITION

AS AT 31 DECEMBER 20XX

20XX

US$

EQUITY AND LIABILITIES

Equity attributable to equity holder of the Company

Share capital 2

Retained earnings 1

3

Current Liabilities

Trade payables 3

Other payables 2

Total Equity and Liabilities 8

49

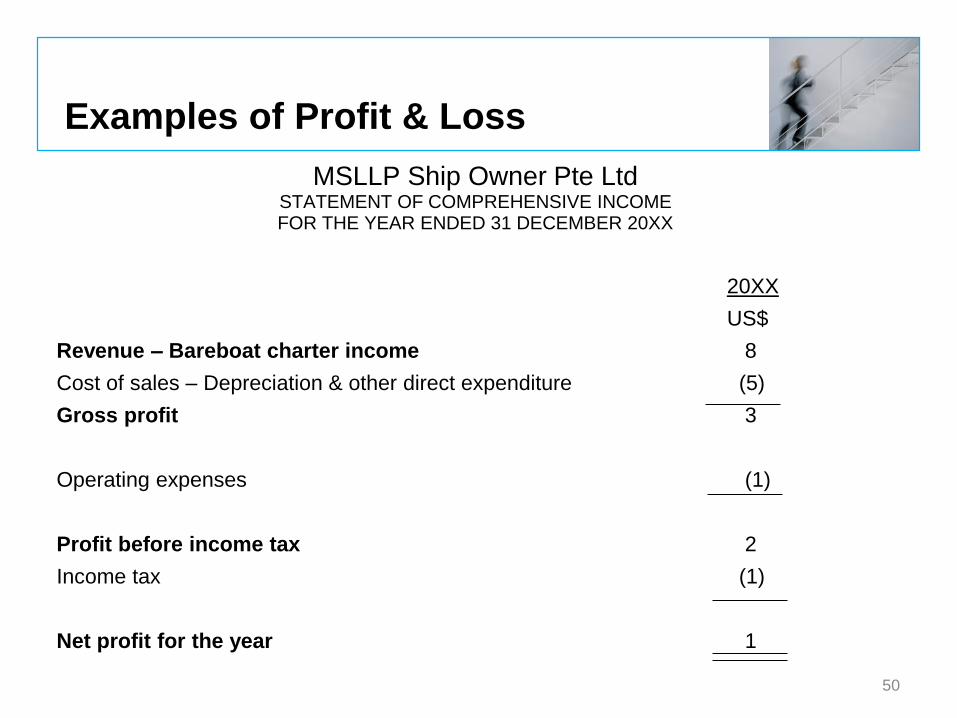

Examples of Profit & Loss

MSLLP Ship Owner Pte LtdSTATEMENT OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 20XX

20XX

US$

Revenue – Bareboat charter income 8

Cost of sales – Depreciation & other direct expenditure (5)

Gross profit 3

Operating expenses (1)

Profit before income tax 2

Income tax (1)

Net profit for the year 1

50

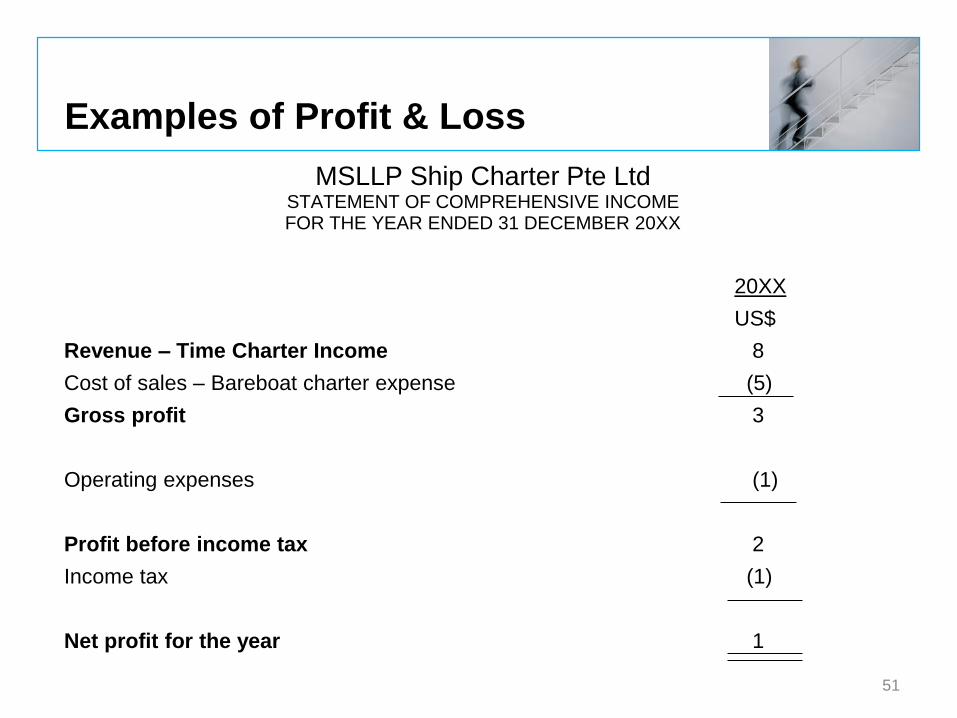

Examples of Profit & Loss

MSLLP Ship Charter Pte LtdSTATEMENT OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 20XX

20XX

US$

Revenue – Time Charter Income 8

Cost of sales – Bareboat charter expense (5)

Gross profit 3

Operating expenses (1)

Profit before income tax 2

Income tax (1)

Net profit for the year 1

51

Questions?

Thank you.

52

![[5437]-101 M.Sc ENVIRONMENTAL SCIENCE EVSC 101](https://static.fdokumen.com/doc/165x107/631d8020ec7900c0c80d1eb7/5437-101-msc-environmental-science-evsc-101.jpg)