Ditc20082cer en

357

Transcript of Ditc20082cer en

Copyright © United Nations 2008All rights reserved

UNCTAD/DITC/2008/2

ISBN 978-0-9816619-0-2

Material in this publication may be freely quoted or reprinted as long as acknowledgementis provided with a reference to the source. A copy of the publication containing the quotationor reprint should be sent to the UNCTAD secretariat at: Palais des Nations,CH-1211 Geneva 10, Switzerland, and to the UNDP Special Unit for South-SouthCooperation, 1 UN Plaza, New York, NY 10017 USA.

This Report is the fruit of a collaborative effort that was led by UNCTAD and the UNDP SpecialUnit for South-South Cooperation and that included a team of experts from the collaborating UN agencies – UNCTAD, UNDP, UNESCO, WIPO and ITC – as well as internationalconsultants.

The designations employed and the presentation of material in this publication do not implythe expression of any opinion whatsoever concerning the legal status of any country,territory, city or area, or concerning the delimitation of its frontiers or boundaries.

The English version of the full report and the French and Spanish versions of its overview section are currently available on the Internet at the addresses indicated below:http://www.unctad.org/creative-economy and http://ssc.undp.org/creative_economy

ii C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

The world economy has clearly seen anextraordinary expansion in the past five years.This expansion has been more broadly basedthan ever before, allowing many developingcountries to benefit from it. Even some of theleast developed countries have been able to gen-erate average annual GDP growth of more than5 per cent, representing significant progress overthat made in the 1990s. Nevertheless, this pathof economic growth has not yet been sufficientto ensure the welfare and decent living standardsfor the large majority of people in the develop-ing world. Despite efforts to diversify theireconomies, 86 of 144 developing countries stilldepend on commodities for more than halftheir export earnings. Prevailing developmentstrategies have yet to succeed in generatingexpected levels of socio-economic developmentfor these countries. The challenge is to find fea-sible development options that take intoaccount their specific realities and in particulartheir scarcity of skilled labour, lack of basicinfrastructure and very low levels of foreigndirect investment. How to promote developmentthat is both sustainable and inclusive?

As economic models do not function inisolation, the time has come to go beyond economics and look for a more holistic develop-ment approach that considers their different cultural identities, economic aspirations, socialdisparities and technological disadvantages.Development strategies also must be updated inorder to cope with the far-reaching cultural andtechnological shifts under way in our society. Theworld needs to adapt to this new environment bybringing issues relating to culture and technologyinto the mainstream of economic developmentthinking. Achieving the Millennium DevelopmentGoals calls for dealing with cross-cutting development issues by introducing concertedmultidisciplinary policies and reinforcing policycoherence at the national and international levels.

Globalization and connectivity are newrealities that have brought profound changes inlifestyles worldwide. This is reshaping the overallpattern of cultural production, consumption andtrade in a world increasingly filled with images,sounds, texts and symbols. There is a clear need tobetter grasp the complex interactions among theeconomic, cultural, technological and socialaspects guiding the dynamics of the world econ-omy and the way people live in the twenty-firstcentury. In this era of transformation, creativityand knowledge are fast becoming powerful meansof fostering development gains.

In this context, the interface among cre-ativity, culture, economics and technology, asexpressed in the ability to create and circulateintellectual capital, has the potential to generateincome, jobs and export earnings while at thesame time promoting social inclusion, culturaldiversity and human development. This is whatthe emerging creative economy has alreadybegun to do as a leading component of eco-nomic growth, employment, trade, innovationand social cohesion in most advancedeconomies. The creative economy also seems tobe a feasible option for developing countries. Ifeffective public policies are in place, the creativeeconomy generates cross-cutting linkages withthe overall economy at macro and micro levels.It thus fosters a development dimension, offeringnew opportunities for developing countries toleapfrog into emerging high-growth areas of theworld economy.

This study is the first to present the perspectives of the United Nations on thisexciting new topic. The creative economy is anevolving concept centred on the dynamics of thecreative industries. There is no single definitionof the creative economy nor is there a consensusas to the set of knowledge-based economic activ-ities on which the creative industries are based.There is no one-size-fits-all recipe but rather, flexible

iiiC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Fore

word

Foreword

The creativeeconomy hasthe potential to generateincome and jobswhile promotingsocial inclusion,cultural diversityand humandevelopment

iv C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

and strategic choices to be made by national governments in order to optimize the benefits oftheir creative economies for development.

At the heart of the creative economy liethe creative industries. Loosely defined, the cre-ative industries are at the crossroads of the arts,culture, business and technology. In other words,they comprise the cycle of creation, productionand distribution of goods and services that useintellectual capital as their primary input. Today’screative industries involve the interplay of tradi-tional, technology-intensive and service-orientedsubsectors. They range from folk art, festivals,music, books, paintings and performing arts tomore technology-intensive subsectors such as thefilm industry, broadcasting, digital animationand video games, and more service-orientedfields such as architectural and advertising services.All these activities are intensive in creative skillsand can generate income through trade andintellectual property rights.

This Report provides empirical evidencethat the creative industries are among the mostdynamic emerging sectors in world trade. Overthe period 2000-2005, trade in creative goodsand services increased at an unprecedented aver-age annual rate of 8.7 per cent. World exportsof creative products were valued at $424.4 billion in 2005 as compared to $227.5 billionin 1996, according to preliminary UNCTADfigures. Creative services in particular enjoyedrapid export growth – 8.8 per cent annuallybetween 1996 and 2005. This positive trendoccurred in all regions and groups of countriesand is expected to continue into the nextdecade, assuming that the global demand forcreative goods and services continues to rise.

It is clear that developed countries stilldominate the global market for creative products.Nonetheless, many developing-country prod-ucts are already benefiting from the creative

industry boom, particularly in Asia.Unfortunately, however, the large majority ofdeveloping countries are not yet able to harnesstheir creative capacities for development. InAfrica, for instance, despite the abundance ofcreative talents, the creative potential remainshighly underutilized. The continent’s share inglobal trade of creative products remains mar-ginal at less than 1 per cent of world exportsdespite sharp increases. As is the case for otherdeveloping regions, this is a reflection of bothdomestic policy weaknesses and global systemic biases.

The policy-oriented analysis presented inthis Report represents an initial contribution todeveloping a better understanding of the keyissues underlying the creative economy and itsdevelopment dimension. The Report addressesthe challenge of assessing the creative economywith a view to informed policy-making by outlining the conceptual, institutional and policyframework in which this economy is flourishing.Given the multifaceted nature of the creativeeconomy, strategic choices for concerted interministerial policy action are crucial. Theimportant implications of multilateral processesin shaping policies for the creative economy alsowarrant consideration.

This Report is an example of coopera-tion inside the United Nations system, com-prising contributions from five internationalorganizations: UNCTAD, UNDP via itsSpecial Unit for South-South Cooperation,UNESCO, WIPO and ITC. It is a joint endeav-our that builds on complementarities in order toenhance the effectiveness of international coop-eration and policy coherence in this innovativefield. The creative economy is producing newopportunities for both developed and developingcountries, but the challenges ahead should not beunderestimated.

Fore

word

This Report provides empiricalevidence that thecreative industries

are among themost dynamic

emerging sectorsin world trade

The large majorityof developingcountries are

not yet able toharness their

creative capacitiesfor development

Supachai PanitchpakdiSecretary-GeneralUnited Nations Conference on Trade and Development

Kemal DervisAdministratorUnited Nations Development Programme

The Creative Economy Report 2008 is theresult of an initiative put forward by the part-nership between UNCTAD and the UNDPSpecial Unit for South-South Cooperation.This policy-oriented study is the main outputof the project, “Strengthening the CreativeEconomy in Developing Countries”, jointlycoordinated by Edna dos Santos-Duisenberg,Chief, UNCTAD Creative Economy andIndustries Programme, and FranciscoSimplicio, Chief, Division for KnowledgeManagement and Operations of the UNDPSpecial Unit for South-South Cooperation.

The Partnership expresses its sinceregratitude to Yiping Zhou, Director, UNDPSpecial Unit for South-South Cooperation,for his deep support to this initiative. Withouthis vision and commitment, this work wouldnot have materialized.

The Report was prepared under theleadership of UNCTAD and is a pioneeringexample of multi-agency cooperation reflectingthe work of the United Nations Multi-Agency Informal Group on CreativeIndustries in an effort to build upon comple-mentarities and enhance policy coherence onmatters relating to the creative industries andthe creative economy. It is the first report topresent the United Nations system-wide perspective on this innovative topic and itbrings together contributions from five collaborating bodies: the United NationsConference on Trade and Development (UNC-TAD), the United Nations DevelopmentProgramme (UNDP) Special Unit for South-South Cooperation, the United NationsEducational, Scientific and Cultural Organization(UNESCO), the World Intellectual Property

Organization (WIPO) and the InternationalTrade Centre (ITC).

The research and policy-oriented analysiswere carried out under the overall guidance of Edna dos Santos-Duisenberg, the main co-writer of this Report. The Report greatlybenefited from the invaluable academic insightsfrom Dr. David Throsby from MacquarieUniversity, Sidney, and Dr. Andrew Pratt fromthe London School of Economics, to whomthe team expresses its deep gratitude. TheMulti-Agency Group acknowledges and thanksthe contribution of the following team ofinternational consultants who provided inputsfor various chapters: Avril Joffe, PernilleAskerud, Ana Carla Fonseca Reis, David Diaz-Benevides and Sylvia Amaya Londoño.

The Partnership extends its profoundappreciation to all the colleagues from the collaborating organizations who participatedin this joint endeavour, in particular the mem-bers of the United Nations Multi-AgencyGroup. Acknowledgements are expressed to:Georges Poussin, Richard Engelhardt, SimonEllis, Lydia Deloumeaux and Guiomar AlonsoCano from UNESCO; Dimiter Gantchev,Wend Wendland, Brigitte Vezina and RichardOwens from WIPO; and Iris Hauswirth, Jean-Michel Pasteels and Kefalla Conte from ITC.

From UNCTAD, our special thanks goto the Head of the Central Statistics Branch,Henri Laurencin, and his team composed ofDavid Critsallo, Sanja Blazevic, Yoann Chaine,Mirco Moretti, Flavine Creppy and SoniaBlachier. Analytical inputs were also providedby Matfobhi Riba and Dimo Calowski.Comments were received from DianaBarrowclough, Yuefin Li and Susan Teltscher.

vC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Ackn

ow

ledgem

ents

Acknowledgements

vi C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Research assistance was provided by CarolinaQuintana as well as by Cheng Shang Li andSimon Alder, who were extremely devoted to thiswork during their internship with UNCTAD.

The Partnership also expresses its sinceregratitude to all those who kindly accepted ourinvitation to contribute with signed articles featuring concrete cases and/or their experi-ences in the creative economy as illustrated inthe boxes throughout the Report. These articleshelped to bring pragmatism to the policy-oriented analysis of this Report and evidence

for some of the empirical arguments.

The text was edited by Barbara Brewka,and Jennifer Bergamini designed the cover andthe layout of this publication.

Administrative and secretarial supportwas provided by Clisse Medeiros Ramos Perretfrom UNCTAD and Lourdes Hermosura-Chang and Ines Tofalo from the UNDPSpecial Unit for South-South Cooperation.

The Creative Economy Report 2008 wasfinanced by the UNDP Special Unit forSouth-South Cooperation.

Ackn

ow

ledgem

ents

viiC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

Contents

Foreword ..........................................................................................................................................iii

Acknowledgements ..........................................................................................................................v

Abbreviations and acronyms ........................................................................................................xix

PART 1. THE CREATIVE ECONOMY

Overview ............................................................................................................................................3

Chapter

1. Concept and context of the creative economy 9

1.1 Evolving concepts and definitions ........................................................................................91.1.1 Creativity ................................................................................................................................91.1.2 Creative goods and services..................................................................................................101.1.3 Cultural industries ................................................................................................................111.1.4 Cultural economics ..............................................................................................................111.1.5 Creative industries ................................................................................................................111.1.6 The UNCTAD classification of the creative industries ..............................................................121.1.7 The creative economy ..........................................................................................................151.1.8 The creative class and creative entrepreneurs........................................................................161.1.9 Creative cities ......................................................................................................................161.1.10 Creative clusters, networks and districts ................................................................................20

1.2 Major drivers of the creative economy worldwide..............................................................221.2.1 Technology ..........................................................................................................................221.2.2 Demand ..............................................................................................................................231.2.3 Tourism ................................................................................................................................23

1.3 The multiple dimensions of the creative economy ............................................................241.3.1 Economic aspects ................................................................................................................241.3.2 Social aspects ......................................................................................................................241.3.3 Cultural aspects....................................................................................................................261.3.4 Sustainable development ......................................................................................................26

1.4 The cross-cutting nature of creative industries..................................................................271.4.1 Need for concerted interministerial policies ............................................................................271.4.2 Need for dialogue with multiple stakeholders ........................................................................281.4.3 Need for institutional mechanisms ........................................................................................28

1.5 The creative economy in the developed world....................................................................28

viii C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

2. The development dimension 33

2.1 Policy implications: The Millennium Development Goals ..................................................33

2.2 The creative economy: Linkages and development implications ......................................352.2.1 Multifaceted aspects of the creative economy ........................................................................352.2.2 Cultural and technological linkages........................................................................................352.2.3 Social interactions ................................................................................................................36

2.3 Interface between traditional knowledge, arts and the creative economy ..........................36

2.4 Obstacles to the expansion of the creative economy ........................................................40

2.5 Shaping a model for enhancing the creative economy in developing countries ..............41

2.6 The creative economy in the developing world and transition economies ......................422.6.1 Africa ..................................................................................................................................432.6.2 The Asia-Pacific region ........................................................................................................462.6.3 Central Asia and the Middle East ..........................................................................................482.6.4 Latin America ......................................................................................................................502.6.5 The Caribbean ......................................................................................................................542.6.6 Eastern European economies in transition ..............................................................................56

PART 2. ASSESSING THE CREATIVE ECONOMY: ANALYSIS AND MEASUREMENT

3. Analysing the creative economy 61

3.1 The need for systematic analysis ........................................................................................61

3.2 Organization of the creative economy ................................................................................623.2.1 Organizational structures ......................................................................................................623.2.2 Operational matters ..............................................................................................................623.2.3 Locational issues ..................................................................................................................63

3.3 Economic analysis of the creative industries ........................................................643.3.1 Industrial organization analysis ..............................................................................................643.3.2 Value-chain analysis ............................................................................................................643.3.3 Inter-industry analysis ..........................................................................................................653.3.4 Locational analysis................................................................................................................663.3.5 Copyright and intellectual property ........................................................................................683.3.6 Contract theory ....................................................................................................................68

3.4 Structure of the creative industries ....................................................................................693.4.1 Predominance of small and medium-sized enterprises ..........................................................693.4.2 Large-scale corporate enterprises..........................................................................................713.4.3 Public or quasi-public cultural institutions ..............................................................................713.4.4 Individual artists and producers ............................................................................................71

3.5 Distribution and competition issues ..................................................................................723.5.1 Changing consumption patterns ..........................................................................................773.5.2 Creative industries and regulation..........................................................................................77

ixC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

3.6 An application of production-chain analysis: The music industry in sub-Saharan Africa ..........................................................................................................78

4. Towards an evidence-based assessment of the creative economy 81

4.1 Why we need a new information base and why it doesn’t already exist ..........................81

4.2 Towards a reliable benchmark for the creative economy ..................................................82

4.3 The challenge of building an operational model of the creative economy........................83

4.4 Measures: Their limitations and potential ..........................................................................844.4.1 Employment ........................................................................................................................844.4.2 Time use ..............................................................................................................................854.4.3 Trade and value added..........................................................................................................864.4.4 Copyright and IPR ................................................................................................................864.4.5 Public investment..................................................................................................................87

4.5 Implementation of a Culture Satellite Account ..................................................................89

4.6 Data sources and assessment tools: Why the current data are inadequate ................90

4.7 The case for a trade model for the creative industries using a product classification methodology ..................................................................................................91

4.8 Methodological basis for a unified measure of international trade of creative goods ....93

4.9 Main considerations ............................................................................................................96

PART 3. INTERNATIONAL TRADE IN CREATIVE GOODS AND SERVICES

5. International trade in creative goods and services: Global trends and features 101

5.1 Setting the scene ................................................................................................................101

5.2 Creative industries: A new dynamic sector in world trade ..............................................106

5.3 Global trends in world trade of creative goods and services ..........................................1075.3.1 Global trends in world exports ............................................................................................1075.3.2 Global trends in world imports ............................................................................................1095.3.3 Key players in the global market for creative goods ..............................................................110

5.4 Regional economic groups in world markets....................................................................112

5.5 Prospects for North-South and South-South trade in creative goods and services ............113

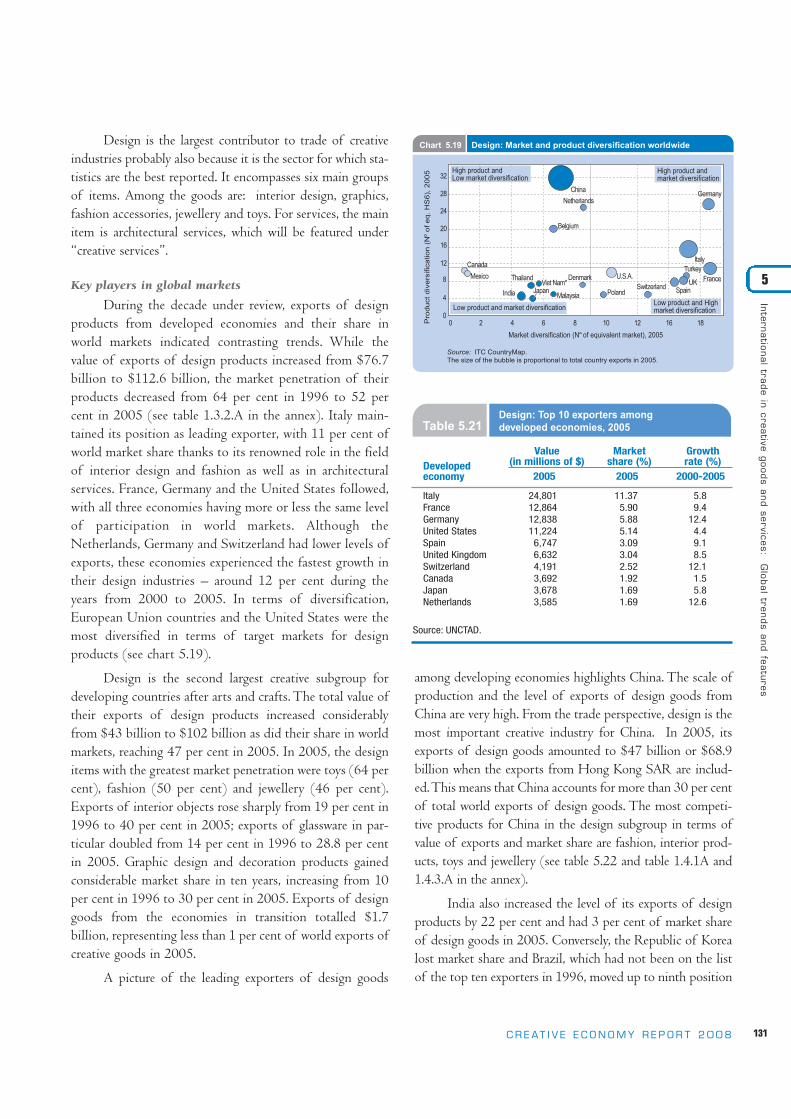

5.6 Global trends in international trade of creative industries, by subgroup ........................1145.6.1 Heritage ............................................................................................................................1145.6.2 Performing arts ..................................................................................................................1185.6.3 Visual arts ..........................................................................................................................1225.6.4 Audiovisuals ......................................................................................................................1245.6.5 Publishing and printed media ..............................................................................................1275.6.6 Design................................................................................................................................1295.6.7 New media ........................................................................................................................1325.6.8 Creative services ................................................................................................................134

x C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

5.6.9 Royalties and licence fees ..................................................................................................1355.6.10 Related industries ..............................................................................................................136

PART 4. THE ROLE OF INTELLECTUAL PROPERTY AND TECHNOLOGY

6. The role of intellectual property in the creative economy 141

6.1 Introduction ........................................................................................................................141

6.2 What are intellectual property rights? ..............................................................................142

6.3 Intellectual property and the creative industries ..............................................................1436.3.1 Geographical indications and appellations of origin ..............................................................144

6.4 Copyright and the creative economy ................................................................................1446.4.1 Exclusive rights ..................................................................................................................1456.4.2 Moral rights ........................................................................................................................1456.4.3 Related rights ....................................................................................................................1466.4.4 Exceptions and limitations to copyright ................................................................................1476.4.5 Enforcement of copyright ....................................................................................................148

6.5 The economics of copyright ..............................................................................................149

6.6 Contribution of the creative industries to the economy ..................................................149

6.7 Copyright, the creative industries and traditional cultural expressions..........................1516.7.1 Indigenous communities and new technologies ....................................................................152

6.8 Copyrights and new technologies......................................................................................154

6.9 Possible policy options ......................................................................................................155

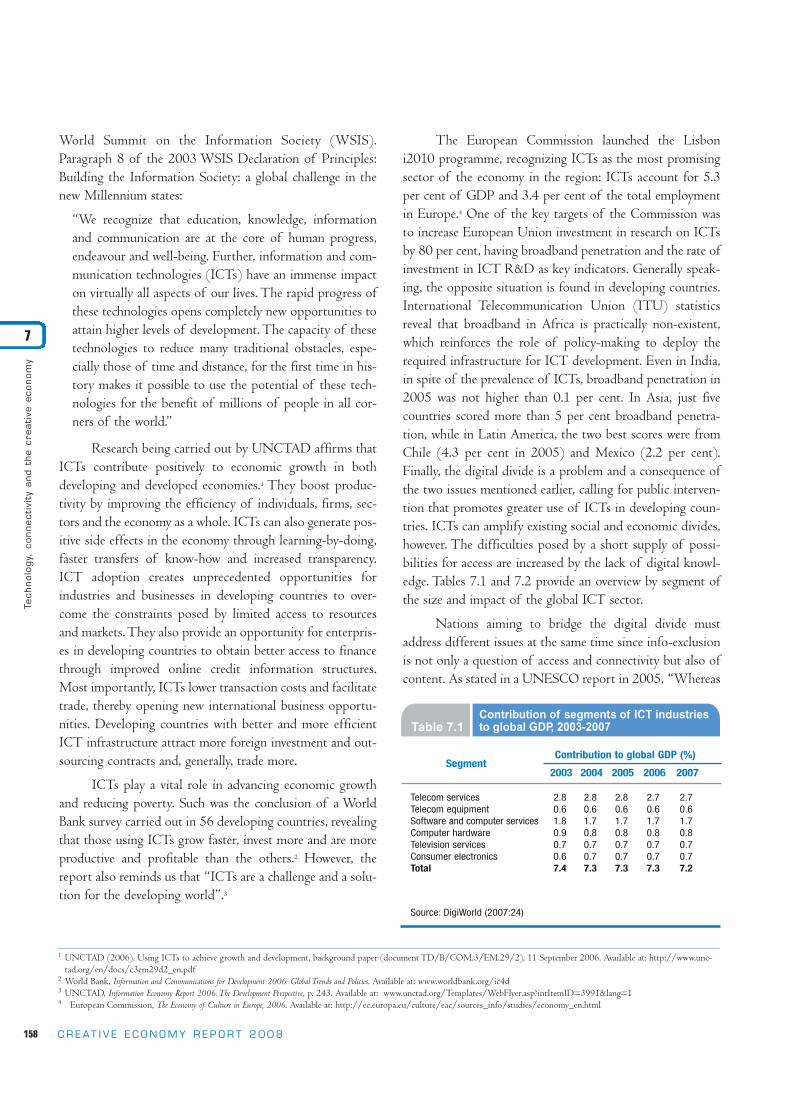

7. Technology, connectivity and the creative economy 157

7.1 Introduction ........................................................................................................................157

7.2 Connectivity and its wider impact ....................................................................................157

7.3 Measurement issues and creative content........................................................................160

7.4 ICTs and their impact on the creative economy................................................................162

7.5 Digitization ........................................................................................................................163

7.6 Convergence and new business models ..........................................................................163

7.7 Impact across the production chain ................................................................................165

7.8 Looking into the future ......................................................................................................168

PART 5. PROMOTING THE CREATIVE ECONOMY FOR DEVELOPMENT

8. Policy strategies for the creative industries 173

8.1 Introduction ........................................................................................................................173

8.2 The role of public policies ..................................................................................................174

8.3 The policy process ..............................................................................................................175

8.4 Policy directions..................................................................................................................1768.4.1 Provision of infrastructure....................................................................................................1768.4.2 Provision of finance and investment ....................................................................................1778.4.3 Creation of institutional mechanisms....................................................................................1788.4.4 Development of export markets ..........................................................................................1798.4.5 Protection of creators’ rights ..............................................................................................1808.4.6 Establishment of creative clusters........................................................................................1808.4.7 Institution of effective data-collection measures ..................................................................181

8.5 Target measures for enhancing creative capacities ........................................................1838.5.1 Non-formal sector ..............................................................................................................1838.5.2 Creative arts ......................................................................................................................1838.5.3 Small and medium-sized enterprises ..................................................................................1838.5.4 Public cultural institutions....................................................................................................1858.5.5 Corporate sector ................................................................................................................185

8.6 Tailoring policy action at the national level ......................................................................185

9. The international dimension of creative-industries policy 187

9.1 The international policy framework ..................................................................................187

9.2 UNCTAD: Creative industries on the economic and development agenda ......................1879.2.1 UNCTAD X: Audiovisual services ..........................................................................................1879.2.2 Third United Nations Conference on the Least Developed Countries: Music ..........................1899.2.3 UNCTAD XI: Creative industries – A turning point..................................................................1899.2.4 UNCTAD XII: From the creative industries to the creative economy ........................................190

9.3 WTO multilateral negotiations and implications for creative industries..........................1919.3.1 General Agreement on Trade in Services..............................................................................1919.3.2 Implications of multilateral and regional trade agreements for creative industries ........................1939.3.3 TRIPS Agreement................................................................................................................193

9.4 UNESCO cultural-diversity perspective ..............................................................................194

9.5 WIPO Development Agenda ................................................................................................196

9.6 UNDP: Engaging developing countries in the creative economy for development ................197

9.7 ITC: Creating business opportunities for creative industries ..........................................199

10. Lessons learned and policy options 201

10.1 Lessons learned ..................................................................................................................201

10.2 Major findings ....................................................................................................................20210.2.1 Definitions and concepts ....................................................................................................20210.2.2 Cross-cutting linkages ........................................................................................................20210.2.3 The creative economy in the developed world ......................................................................20310.2.4 The creative economy in the developing world ....................................................................20310.2.5 The value chain for creative products ..................................................................................203

xiC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

xii C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

10.2.6 Data issues ........................................................................................................................20410.2.7 Trade..................................................................................................................................20410.2.8 Connectivity and ICTs..........................................................................................................20510.2.9 Policy towards the creative economy ..................................................................................20510.2.10 International context............................................................................................................205

10.3 Policy options ......................................................................................................................20610.3.1 Role of governments ..........................................................................................................20710.3.2 Role of creative entrepreneurs ............................................................................................20810.3.3 Role of civil society and the place of strategic alliances ........................................................208

10.4 The way ahead ....................................................................................................................20910.4.1 Redefining priorities ............................................................................................................20910.4.2 Role of international cooperation..........................................................................................209

References ....................................................................................................................................211

LIST OF BOXES

1.1 A creative entrepreneur: Transforming ideas into successful business ..........................................171.2 The creative city ........................................................................................................................181.3 Cultural and creative clusters in China ........................................................................................211.4 Petra: A cultural trip ....................................................................................................................241.5 Cirque du Soleil: A very simple dream..........................................................................................251.6 Economics of the museum district of Paris ..................................................................................272.1 South-South sharing of creative experiences................................................................................362.2 Brazilian carnivals ......................................................................................................................382.3 Africa Remix: Africa speaking loudly, brightly and colourfully ........................................................432.4 Experience of the Shanghai Creative Industry Center....................................................................472.5 Guatemala: The economic contribution of culture ........................................................................512.6 Brand Jamaica as the home of reggae ........................................................................................552.7 The Bolshoi: A sublime gift to the world ......................................................................................573.1 Creative clusters ........................................................................................................................663.2 Broadcasting creativity blooms in South Africa ............................................................................723.3 Properties of creative industries ..................................................................................................753.4 Commercial practices and business models particular to the audiovisual and music industries ......76 4.1 Reality and numbers ..................................................................................................................87 4.2 Lessons from Uruguay ................................................................................................................976.1 Design as a key ingredient for growth........................................................................................1436.2 The Da Vinci Code case ............................................................................................................146 6.3 A collaborative approach to creativity and knowledge ................................................................1486.4 Jewellery: A magic marriage between tradition and contemporary design ..................................1536.5 Collective management of copyright ..........................................................................................155 7.1 When ICTs give rise to new business models ............................................................................165

7.2 Free and open-source software and the creative economy ........................................................167 7.3 Eurovision ................................................................................................................................1708.1 The Egyptian film industry: The waning of the “Hollywood of the East”? ......................................1788.2 Shanghai creative industries: The Chinese way ..........................................................................1818.3 Alphadi: The fashion caravan ....................................................................................................1848.4 Cultural policy in action: The Nairobi Plan of Action ....................................................................1869.1 Television and soap operas ......................................................................................................1889.2 Puppet planet ..........................................................................................................................1929.3 Cultural tourism: Impressions of the Peruvian experience ..........................................................1959.4 Nollywood: A creative response ................................................................................................1989.5 The Biennale of Contemporary African Art of Dakar: A contribution to economic and cultural

development in Africa ..............................................................................................................20010.1 Summary of key messages ......................................................................................................206

LIST OF TABLES

1.1 Classification systems for the creative industries derived from different models ............................131.2 Estimates of culture employment in selected creative cities ..........................................................201.3 Creative Cities Network ..............................................................................................................201.4 Workers in creative industries in the United States, 2003 ............................................................251.5 Contribution of the European cultural and creative sector to the European national economies ......291.6 Contribution of the cultural industries to GDP or GVA for five countries, various years ....................301.7 Contribution of the cultural sector to the national economies of eight European countries,

various years ..............................................................................................................................301.8 Comparison of contribution of creative/cultural sector with contributions of other sectors

for eight European countries (% of GDP)......................................................................................30 1.9 Estimates of the contribution of creative industries to GDP for five OECD countries........................312.1 Features of the African music industry ........................................................................................453.1 Value chain in the cultural industries in Canada, 2002 ................................................................654.1 Proposed categorization of creative goods ..................................................................................955.1 Goods and services of creative industries ..................................................................................1035.2 Creative goods: Exports, by economic group, 2005 ....................................................................1085.3 Creative goods: Exports, by economic group and region, 2000 and 2005 ..................................1095.4 Creative goods: Imports, by economic group, 1996 and 2005 ....................................................1095.5 Creative goods: Imports, by economic group and region, 2000 and 2005 ..................................110 5.6 Creative goods: Top 20 exporters worldwide, 1996 and 2005 ....................................................1105.7 Creative goods: Top 10 exporters among developed economies, 2005........................................1115.8 Creative goods: Top 10 exporters among developing economies, 2005 ......................................1125.9 Creative goods: Exports, by regional economic group, 1996 and 2005 ......................................1135.10 World exports of all creative-industry products (goods and services), by subgroup, 1996 and 2005 ......1155.11 Arts and crafts: Exports, by economic group and region, 2000 and 2005 ..................................1175.12 Arts and crafts: Top 10 exporters among developing economies, 2005 ......................................1175.13 Music: Exports, by economic group and region, 2000 and 2005 ................................................120

xiiiC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

xiv C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

5.14 Music: Top 10 exporters among developed economies, 2005 ....................................................1215.15 Music: Top 10 exporters among developing economies, 2005 ....................................................1215.16 Visual arts: Top 10 exporters among developed economies, 2005 ..............................................1245.17 Visual arts: Top 10 exporters among developing economies, 2005 ............................................124 5.18 Publishing and printed media: Top 10 exporters among developed economies, 2005 ..................1285.19 Publishing materials: Top 10 exporters among developing economies, 2005 ..............................128 5.20 Design: Exports, by economic group and region, 2000 and 2005 ..............................................130 5.21 Design: Top 10 exporters among developed economies, 2005....................................................1315.22 Design: Top 10 exporters among developing economies, 2005 ..................................................1325.23 New media: Exports, by economic group and region, 2000 and 2005 ........................................1335.24 New media: Top 10 exporters among developed economies, 2005 ............................................1335.25 New media: Top 10 exporters among developing economies, 2005 ............................................1345.26 Reported exports of creative services, 1996, 2000 and 2005 ....................................................1355.27 Royalties and license fees: World exports and imports, 1996, 2000 and 2005 ............................1366.1 Some results of the surveys based on the WIPO Guide ..............................................................1507.1 Contribution of segments of ICT industries to global GDP, 2003-2007 ........................................1587.2 ICT industries global market, by region, 2003-2007 ..................................................................1597.3 Internet penetration, by regional economic group, 2002-2006....................................................1597.4 Mobile phone penetration, by regional economic group, 2002-2006 ..........................................1607.5 Interconnected dimensions of digital life: Enablers, communications, content and transactions ....1607.6 Partnership on Measuring ICT for Development: Core ICT indicators ..........................................1617.7 Top 20 audiovisual companies worldwide and their 2004 turnover..............................................16410.1 Creative industries policy options ..............................................................................................207

LIST OF FIGURES

1.1 Creativity in today’s economy ........................................................................................................91.2 Interplay of the 5Cs: Outcomes of creativity + 4 capitals ..............................................................101.3 UNCTAD classification of creative industries ................................................................................142.1 Development dimension of the creative economy ........................................................................352.2 The creative nexus: The C-ITET model ........................................................................................413.1 Creative-industry value chain ......................................................................................................653.2 Simplified diagram of Porter’s model for clusters..........................................................................663.3 Stages of a music production chain in sub-Saharan Africa ..........................................................784.1 The creative chain ......................................................................................................................838.1 Funding flows to the cultural sector ..........................................................................................177

LIST OF CHARTS

5.1.a Creative industries: Exports of creative goods, by economic group, 2005 ....................................107 5.1.b Creative industries: Exports of creative services, by economic group, 2005 ................................1075.2 Evolution of world exports of creative goods and services, 1996-2005 ......................................1075.3.a Creative industries: Exports, by group, 1996 ..............................................................................108

Conte

nts

5.3.b Creative industries: Exports, by group, 2005 ..............................................................................1085.4 Share of economic groups in world exports of creative goods ....................................................108 5.5.a Imports of creative goods, by economic group, 1996, 2000 and 2005 ......................................1095.5.b Imports of creative goods, by group, 2005 ................................................................................1095.6 Creative goods: Exports from all developing countries, 1996 and 2005 ......................................1125.7 Heritage goods and services: Exports, by economic group, 1996 and 2005 ................................1165.8 Arts and crafts: Market and product diversification in world markets..........................................1165.9 Arts and crafts: Market and product diversification of developing economies ..............................117 5.10 Music: Exports, by economic group, 1996 and 2005..................................................................1205.11 Music: Market and product diversification of developing economies ............................................121 5.12 Visual arts: Exports, by economic group, 1996 and 2005 ..........................................................1235.13 Visual arts: Market and product diversification worldwide ..........................................................124 5.14 Audiovisuals: Exports, by economic group, 1996 and 2005 ........................................................1265.15 Audiovisuals: Market and product diversification worldwide ........................................................127 5.16 Publishing and printed media: Exports, by economic group, 1996 and 2005 ..............................1285.17 Publishing and printed media: Market and product diversification of developing economies ........1295.18 Design: Exports, by economic group, 1996 and 2005 ................................................................1305.19 Design: Market and product diversification worldwide ................................................................1315.20 Design: Market and product diversification of developing economies ..........................................132 5.21 New media: Exports, by economic group, 1996 and 2005..........................................................1335.22 New media: Market and product diversification worldwide ..........................................................134 5.23 Creative services: Exports, by economic group, 2005 ................................................................1355.24 Royalties and licence fees: World exports and imports, 1996, 2000 and 2005............................1365.25 Goods of related industries: Evolution of world exports, 1996 and 2005......................................137 6.1 Contribution of the creative industries to GDP ............................................................................1506.2 Contribution of groups of copyright-based industries to total of creative industries ......................150 6.3 Contribution of the creative industries to national employment....................................................151

STATISTICAL ANNEX

General explanatory notes....................................................................................................................226Distribution of developing economies by geographical region and economic grouping ............................232Distribution of developed economies and economies in transition by geographical region ......................234Distribution of economies by trade group..............................................................................................236

Part 1. Creative goods 238

1.1 Creative goods: Exports and imports, by economic group, region and country/territory,1996-2005..............................................................................................................................238

1.2.A Creative goods: Total world exports, by origin and product group, 1996, 2000 and 2005 ............2441.2.B Creative goods: Total world imports, by origin and product group, 1996, 2000 and 2005 ............2481.3.1.A Creative goods: Total world exports, by product group, 1996, 2000 and 2005 ............................2521.3.1.B Creative goods: Total world imports, by product group, 1996, 2000 and 2005 ............................253

xvC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

xvi C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

1.3.2.A Creative goods: Exports by developed economies, by product group, 1996, 2000 and 2005 ....2541.3.2.B Creative goods: Imports by developed economies, by product group, 1996, 2000 and 2005....2551.3.3.A Creative goods: Exports by developing economies, by product group, 1996, 2000 and 2005 ....2561.3.3.B Creative goods: Imports by developing economies, by product group, 1996, 2000 and 2005 ....2571.3.4.A Creative goods: Exports by economies in transition, by product group, 1996, 2000 and 2005 ....2581.3.4.B Creative goods: Imports by economies in transition, by product group, 1996, 2000 and 2005 ....2591.4.1.A Creative goods: Top 10 world exporters, by product group, 2005................................................2601.4.1.B Creative goods: Top 10 world importers, by product group, 2005 ..............................................2641.4.2.A Creative goods: Top 10 exporters among developed economies, by product group, 2005 ........2681.4.2.B Creative goods: Top 10 importers among developed economies, by product group, 2005 ..........2721.4.3.A Creative goods: Top 10 exporters among developing economies, by product group, 2005..........2761.4.3.B Creative goods: Top 10 importers among developing economies, by product group, 2005..........2801.4.4.A Creative goods: Top 10 exporters among economies in transition, by product group, 2005 ..........2841.4.4.B Creative goods: Top 10 importers among economies in transition, by product group, 2005..........2881.5.A1 Creative goods: Exports, by trade group, 1996-2005 ................................................................2921.5.A2 Creative goods: Exports, by trade group, as % of total exports of creative groups by all trade

groups, 1996-2005..................................................................................................................2931.5.B1 Creative goods: Imports, by trade group, 1996-2005 ................................................................2921.5.B2 Creative goods: Imports, by trade group, as % of total imports of creative goods by all trade

groups, 1996-2005..................................................................................................................293

Part 2. Creative services and royalties 295

2.1.A Categories of services that include creative industries: Exports of all creative services,by country/territory, 1996-2005 ................................................................................................295

2.1.B Categories of services that include creative industries: Imports of all creative services,by country/territory, 1996-2005 ................................................................................................297

2.2.A Categories of services that include creative industries: Exports of advertising, market research and public opinion polling services, by economic group and country/territory, 1996-2005 ..........299

2.2.B Categories of services that include creative industries: Imports of advertising, market research and public opinion polling services, by economic group and country/territory, 1996-2005 ..........300

2.3.A Categories of services that include creative industries: Exports of architectural, engineering and other technical services, by economic group and country/territory, 1996-2005 ....................301

2.3.B Categories of services that include creative industries: Imports of architectural, engineering and other technical services, by economic group and country/territory, 1996-2005 ....................302

2.4.A Categories of services that include creative industries: Exports of audiovisual and related services, by economic group and country/territory, 1996-2005 ..................................................303

2.4.B Categories of services that include creative industries: Imports of audiovisual and related services, by economic group and country/territory, 1996-2005 ..................................................304

2.5.A Categories of services that include creative industries: Exports of research and development services, by economic group and country/territory, 1996-2005 ..................................................305

2.5.B Categories of services that include creative industries: Imports of research and development services, by economic group and country/territory, 1996-2005 ..............................306

2.6.A Categories of services that include creative industries: Exports of personal, cultural and recreational services, by economic group and country/territory, 1996-2005................................307

2.6.B Categories of services that include creative industries: Imports of personal, cultural and

Conte

nts

recreational services, by economic group and country/territory, 1996-2005................................3092.7.A Categories of services that include creative industries: Exports of other personal, cultural

and recreational services, by economic group and country/territory, 1996-2005 ........................3112.7.B Categories of services that include creative industries: Imports of other personal, cultural

and recreational services, by economic group and country/territory, 1996-2005 ........................3122.8.A Categories of services that include creative industries: Exports of royalties and licence fees,

by economic group and country/territory, 1996-2005 ................................................................3132.8.B Categories of services that include creative industries: Imports of royalties and licence fees,

by economic group and country/territory, 1996-2005 ................................................................315

Part 3. Related industries 318

3.1 Related industries: World exports and imports, by economic group and country/territory,1996-2005..............................................................................................................................318

3.2.A Related industries: Exports, by origin and product group, 1996, 2000 and 2005 ......................3243.2.B Related industries: Imports, by origin and product group, 1996, 2000 and 2005 ......................3263.3.1.A Related industries: Total world exports, by product group, 1996, 2000 and 2005........................3283.3.1.B Related industries: Total world imports, by product group, 1996, 2000 and 2005........................3283.3.2.A Related industries: Exports of developed economies, by product group, 1996, 2000 and 2005....3293.3.2.B Related industries: Imports of developed economies, by product group, 1996, 2000 and 2005 ....3293.3.3.A Related industries: Exports of developing economies, by product group, 1996, 2000 and 2005 ....3303.3.3.B Related industries: Imports of developing economies, by product group, 1996, 2000 and 2005 ....3303.3.4.A Related industries: Exports of economies in transition, by product group, 1996, 2000 and 2005 ....3313.3.4.B Related industries: Imports of economies in transition, by product group, 1996, 2000 and 2005 ....331

xviiC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Conte

nts

xviii C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

xixC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Abbre

viatio

ns

and

acro

nym

s

ACP African, Caribbean and PacificANCOM Andean Common MarketAPEC Asia-Pacific Economic CooperationAPTA Asia-Pacific Trade Agreement (former Bangkok Agreement)ASEAN Association of Southeast Asian NationsBOP Balance of payments BSEC Black Sea Economic Cooperation OrganizationCACM Central American Common MarketCAFTA Central American-Dominican Republic Free Trade AgreementCARICOM Caribbean CommunityCD Compact discc.i.f. Cost, insurance and freightCIS Commonwealth of Independent StatesCOMESA Common Market for Eastern and Southern Africa (formerly PTA)COMTRADE Commodity Trade Statistics DatabaseCSA Cultural Satellite AccountDAC Development Assistance Committee (of OECD)DCMS Department of Culture, Media and SportDVD Digital versatile disc (formerly digital videodisc)EBOPS Extended Balance of Payments Services ClassificationECCAS Economic Community of Central African StatesECE Economic Commission for EuropeECO Economic Cooperation OrganizationECOWAS Economic Community of West African StatesEFTA European Free Trade AssociationESCAP Economic and Social Commission for Asia and the PacificESCWA Economic and Social Commission for Western AsiaEUROSTAT Statistical Office of the European Communitiesexcl. ExcludingFAO Food and Agriculture Organization of the United NationsFDI Foreign direct investmentf.o.b. Free on boardFOSS Free and open-source softwareFTA Free trade areaFTAA Free Trade Area of the AmericasG-77 Group of 77GATS General Agreement on Trade in ServicesGATT General Agreement on Tariffs and Trade

Abbreviations and acronyms

xx C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

GCC Gulf Cooperation CouncilGDP Gross domestic productGNP Gross national productGVA Gross value addedHIPCs Heavily indebted poor countriesIFPI International Federation of the Phonographic IndustryILO International Labour OrganizationIMF International Monetary FundIOM International Organization for MigrationIPR Intellectual property rightITC International Trade Centre ITU International Telecommunication UnionLAIA Latin American Integration AssociationLDC Least developed countryMDG Millennium Development Goal MERCOSUR Common Market of the SouthMFN Most-favoured nationMSITS Manual on Statistics of International Trade in ServicesNAFTA North American Free Trade Agreementn.e.s. Not elsewhere specifiedNGO Non-governmental organizationn.i.e. Not included elsewhereNPISHs Non-profit institutions serving householdsODA Official development assistanceOECD Organisation for Economic Co-operation and DevelopmentOECS Organisation of Eastern Caribbean StatesPRSP Poverty Reduction Strategy PaperR&D Research and developmentRMB RenminbiRTA Regional trade agreementSAARC South Asian Association for Regional CooperationSADC Southern African Development CommunitySAM Social accounting matrixSAR Special Administrative RegionSIDS Small island developing StateSITC Standard Industrial Trade ClassificationSMEs Small and medium-sized enterprisesSNA System of National AccountsTFYR The former Yugoslav Republic of MacedoniaTNC Transnational corporationTRIPS Trade-Related Aspects of Intellectual Property RightsUEMOA West African Economic and Monetary UnionUIS UNESCO Institute for StatisticsUMA Arab Maghreb UnionUN/DESA/SD United Nations Department of Economic and Social Affairs, Statistics DivisionUNAIDS Joint United Nations Programme on HIV/AIDS

Abbre

viati

ons

and

acro

nym

s

UNCTAD United Nations Conference on Trade and DevelopmentUNDP United Nations Development ProgrammeUNESCO United Nations Educational, Scientific and Cultural OrganizationUNHCR United Nations High Commissioner for RefugeesUNICEF United Nations Children’s FundUNWTO United Nations World Tourism OrganizationUSSR Union of Soviet Socialist RepublicsVCR Video cassette recorderWFP World Food ProgrammeWHO World Health OrganizationWIPO World Intellectual Property Organization WMO World Meteorological OrganizationWSIS World Summit on the Information SocietyWTO World Trade Organization

xxiC R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Abbre

viatio

ns

and

acro

nym

s

xxii C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

The Creative Economy 1PART

2 C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

In the contemporary world, a new devel-opment paradigm is emerging that links theeconomy and culture, embracing economic, cultural, technological and social aspects ofdevelopment at both the macro and micro levels. Central to the new paradigm is the factthat creativity, knowledge and access to infor-mation are increasingly recognized as powerfulengines driving economic growth and promot-ing development in a globalizing world.“Creativity” in this context refers to the formu-lation of new ideas and to the application ofthese ideas to produce original works of art andcultural products, functional creations, scientificinventions and technological innovations. Thereis thus an economic aspect to creativity, observ-able in the way it contributes to entrepreneur-ship, fosters innovation, enhances productivityand promotes economic growth.

Creativity is found in all societies andcountries – rich or poor, large or small,advanced or developing. The word “creativity”is associated with originality, imagination,inspiration, ingenuity and inventiveness. It isan inner characteristic of individuals to beimaginative and express ideas; associated withknowledge, these ideas are the essence of intel-lectual capital. Similarly, every society has itsstock of intangible cultural capital articulatedby people’s identity and values. Civilizationssince time immemorial have been aware ofthese concepts. However, the twenty-first century has seen a growing understanding ofthe interface between creativity, culture andeconomics, the rationale behind the emergingconcept of the “creative economy”.

The concept of the “creative economy”is an evolving one that is gaining ground in

3C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Ove

rview

Overview

Creativity, culture and economic development

The Creative Economy Report 2008 is the first study to present the United Nations perspective on this emerging topic. It is an initiative of the partnership between UNCTADand the UNDP Special Unit for South-South Cooperation. Furthermore, it is a pioneerexample of the work being undertaken by the Multi-Agency Informal Dialogue Group onCreative Industries.1 It brings together contributions from five relevant United Nationsbodies: UNCTAD, UNDP, UNESCO, WIPO and ITC. This collective effort not only contributesto building synergy and exploring complementarities but also is an effective way toadvance policy coherence and enhance the impact of international actions in the area ofthe creative economy and creative industries.

Creativity,knowledge and access toinformation arerecognized as powerfuldrivers ofdevelopment

1 This Group was set up by the Secretary-General of the United Nations Conference on Trade and Development (UNCTAD) in2004 in the context of preparations for the High-level Panel on Creative Industries and Development, held during the UNCTADXI Ministerial Conference. UNCTAD, as chair of the Group, convenes two meetings a year in Geneva. The work of the Group hasbeen revitalized with a view to promoting concerted international actions and joint initiatives by the United Nations family so asto enhance the contribution of the creative economy to development.

4 C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

contemporary thinking about economicdevelopment. It entails a shift from the conventional models towards a multidiscipli-nary model dealing with the interfacebetween economics, culture and technologyand centred on the predominance of servicesand creative content. Given its multidiscipli-nary structure, the creative economy offers a feasible option as part of a results-orienteddevelopment strategy for developing coun-tries. It calls for the adoption of effectivecross-cutting mechanisms and innovativeinterministerial policy action.2

For some people, the “creative economy”is a holistic concept dealing with complexinteractions between culture, economics andtechnology in the contemporary globalizedworld that is dominated by symbols, texts,sounds and images. Others are more scepticalabout this fashionable label, voicing concernsabout its overstated importance and the way itmay exacerbate cultural and technologicaldivisions. Against this background, the cre-ative economy has become a topical issue ofthe international economic and developmentagenda, calling for informed policy responsesin both developed and developing countries.

There is no unique definition of the“creative economy”. It is a subjective conceptthat is still being shaped. There is, however,growing convergence on a core group of activitiesand their interactions both in individual countries and at the international level.

The present Report adopts the UNCTADdefinition of the “creative economy”, whichcan be summarized as follows:

■ The creative economy is an evolving conceptbased on creative assets potentially generatingeconomic growth and development;

■ It can foster income generation, job creationand export earnings while promoting social

inclusion, cultural diversity and humandevelopment;

■ It embraces economic, cultural and socialaspects interacting with technology, intel-lectual property and tourism objectives;

■ It is a set of knowledge-based economicactivities with a development dimensionand cross-cutting linkages at macro andmicro levels to the overall economy;

■ It is a feasible development option callingfor innovative multidisciplinary policyresponses and interministerial action;

■ At the heart of the creative economy are thecreative industries.3

“Creative industries” can be defined as thecycles of creation, production and distributionof goods and services that use creativity andintellectual capital as primary inputs. Theycomprise a set of knowledge-based activitiesthat produce tangible goods and intangibleintellectual or artistic services with creativecontent, economic value and market objec-tives.4 Creative industries constitute a vast andheterogeneous field dealing with the interplayof various creative activities ranging from traditional arts and crafts, publishing, music,and visual and performing arts to more technology-intensive and services-orientedgroups of activities such as film, television andradio broadcasting, new media and design.The creative sector has a flexible and modularmarket structure that ranges from independentartists and small-business enterprises at oneextreme to some of the world’s largest conglomerates at the other.

Today, creative industries are among themost dynamic sectors in world trade. Over theperiod 2000-2005, international trade in cre-ative goods and services experienced anunprecedented average annual growth rate of8.7 per cent. The value of world exports of

Ove

rvie

w 2 UNCTAD Statement at the Second Meeting of the Ministers of Culture of the African, Caribbean and Pacific (ACP) Group of States, Santo Domingo, Dominican Republic, October 2006.

3 Definition by the UNCTAD Creative Economy and Industries Programme, 2005.4 UNCTAD definition further elaborated in chapter 1.

The creativeindustries are

at the heart of the creative

economy

The creative economy calls forinformed

policyresponses

creative goods and services reached $424.4billion in 2005, representing 3.4 per cent oftotal world trade, according to UNCTAD.Nowadays in the most advanced countries, thecreative industries are emerging as a strategicchoice for reinvigorating economic growth,employment and social cohesion. The so-called “creative cities” are proliferating inEurope and North America, revitalizing theeconomy of urban centres through culturaland social developments offering attractivejobs, particularly to young people. Theturnover of the European creative industriesamounted to 654 billion euros in 2003,growing 12.3 per cent faster than the overalleconomy of the European Union andemploying over 5.6 million people.5

A significant finding of the presentstudy is the evidence that some developingcountries, mainly in Asia, have started benefit-ing from the dynamism of the global creativeeconomy and are putting in place tailoredcross-cutting policies to enhance their creativeindustries. China, which is leading thisprocess, became the world’s leading producerand exporter of value-added creative products

in 2005. Nevertheless, the large majority ofdeveloping countries are not yet able to har-ness their creative capacities for developmentgains. The obstacles preventing these develop-ing countries from enhancing their creativeeconomies are a combination of domesticpolicy weaknesses and global systemic biases,issues addressed in the analysis of this Report.

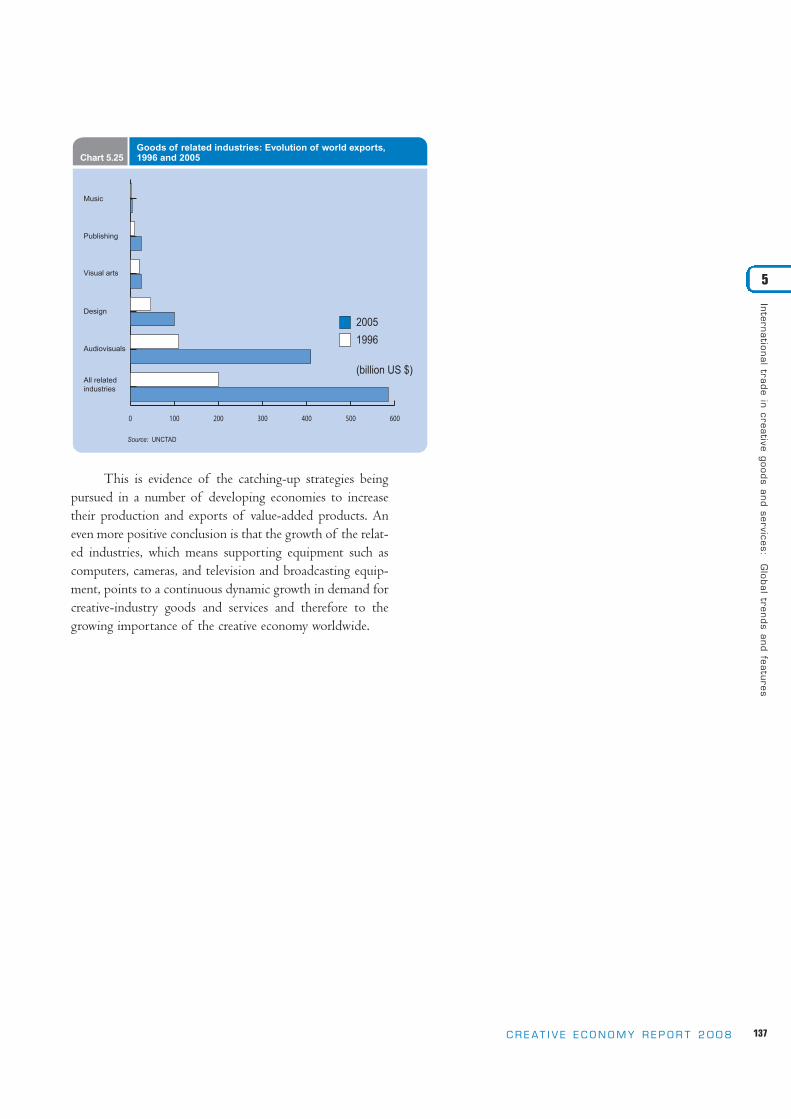

Another important conclusion of thisstudy is that developing-country exports ofrelated creative goods (including computers,cameras, television sets, and broadcasting andaudiovisual equipment) increased rapidly overthe period 1996-2005 from $51 billion to$274 billion.6 This spectacular growth isindicative of the catching-up strategies beingpursued in a number of developing countriesto increase their capacities to supply value-added products to global markets. Italso reaffirms the continually expandingdemand for creative products that rely onthese related industries for their distribu-tion and consumption. This ever-increasingdemand is further confirmation of the potentialof the creative economy to contribute to economic growth.

5C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

Ove

rview

5 See Economy of Culture in Europe, study prepared for the European Commission by KEA, European Affairs, Brussels, 2006.6 See also chapter 5.7 See Summary of High-level Panel on Creative Industries (document TD/L.379, 16 June 2004).

The creative industries accountfor 3.4 per cent of total worldtrade, withexports reaching $424.4 billion in 2005 and anaverage annualgrowth rate of 8.7 per cent during 2000-2005

The large majorityof developing countries are notyet able to harnesstheir creativecapacities

The development dimension of the cre-ative economy is the guiding principle of thisReport. Developing countries can furtherintegrate into the global economy by nurtur-ing their creative capacities and enhancing thecompetitiveness of their creative goods andservices in world markets, provided thatappropriate public policies are in place at thenational level and market imbalances can beredressed at the international level. In thisrespect, support for domestic creative indus-tries should be seen as an integral part of thepromotion and protection of cultural diversity.

Moreover, such diversity, because it is a globalpublic good, needs to be fully supported bythe international community.7

With the increasing knowledge intensityof the contemporary economy and the needfor innovation to maintain competitive advan-tage, it has become imperative for countries totap into their vast reserves of creativity. Thishas been made easier by rapid advances ininformation and communication technologies(ICTs), which are progressively linking coun-tries and regions worldwide. Opportunitiesare thus created for developing countries to

The development dimension

6 C R E AT I V E E C O N O M Y R E P O R T 2 0 0 8

access global markets for the products of theircreativity and cultural diversity in a way notpreviously possible – and to do so directly,without intermediaries. Nonetheless, the challenges are immense and should not beunderestimated.

Despite the richness of their culturaldiversity and the abundance of creative talent,the great majority of developing countries arenot yet fully benefiting from the enormouspotential of their creative economies toimprove development gains.8 These countrieshave been facing domestic and internationalobstacles that need to be fully understood andovercome through cross-cutting institutionalmechanisms and multidisciplinary policies. Inthis scenario, development strategies must beupdated to cope with the far-reaching cultural,economic and technological shifts that arereshaping society.