Did markets react efficiently to the 1994 Mexican peso crisis? Evidence from Mexican ADRS

10

ELSEVIER Journal of MULTINATIONAL FINANCIAL Journalof Multinational Financial Management MANAGEMENT 8 ( 1998) 39-48 Did markets react efficiently to the 1994Mexican peso crisis? Evidence from Mexican ADRS Ike Mathur *, Kimberly C. Gleason, Manohar Singh Depurtment of’ Finance, Southern Illinois University, Carbondale, IL 62901-4626, USA Received 30 June1997; accepted 30 January1998 Abstract The capital markets’ reaction to the 1994 Mexican peso crisis is examined in this paper. The transmission of news from the Mexican market to the US market is examined by using a sample of 29 Mexican ADRs trading in the US. Using event study methodology in a multivariate regression setting, we show that information is transmitted efficiently from one market to the other. The regression of the US dollar returns on the Mexican IPC Index on the dollar returns of a portfolio of Mexican ADRs trading in the US does not show any significant arbitrage opportunities on the event dates used in the study. However, excess returns are observed in the period subsequent to the event dates when the market model is used as the return generating process with the US index as the market index. This result indicates the possibility of deriving excess returns associated with trading the Mexican ADRs in days subsequent to the news disclosures. When both the US and the Mexican indices are employed simultaneously, both indices are significant in explaining returns on the Mexican ADR portfolio. 0 1998 Elsevier ScienceB.V. All rights reserved. JEL class$cation: F23; G15 Keywords: Mexican peso crisis; asset pricing 1. Introduction Despite seemingly optimistic economic prospects in the early part of the 1990s such as a budget surplus, a respectable privatization policy, rising capital inflows, and a falling government deficit, Mexico had begun a descent into a financial crisis that resulted in a severe devaluation of the peso by late 1994 (the peso crisis). Extensive analysis of the events preceding the peso crisis has uncovered several * Corresponding author. Fax: + I 618 453-5626; e-mail: [email protected] 1042-444X/98/$19.00 0 1998 Elsevier Science B.V. All rights reserved PII S1042-444X(98)00016-4

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Did markets react efficiently to the 1994 Mexican peso crisis? Evidence from Mexican ADRS

ELSEVIER

Journal of MULTINATIONAL FINANCIAL

Journal of Multinational Financial Management MANAGEMENT 8 ( 1998) 39-48

Did markets react efficiently to the 1994 Mexican peso crisis?

Evidence from Mexican ADRS

Ike Mathur *, Kimberly C. Gleason, Manohar Singh Depurtment of’ Finance, Southern Illinois University, Carbondale, IL 62901-4626, USA

Received 30 June 1997; accepted 30 January 1998

Abstract

The capital markets’ reaction to the 1994 Mexican peso crisis is examined in this paper. The transmission of news from the Mexican market to the US market is examined by using a sample of 29 Mexican ADRs trading in the US. Using event study methodology in a multivariate regression setting, we show that information is transmitted efficiently from one market to the other. The regression of the US dollar returns on the Mexican IPC Index on the dollar returns of a portfolio of Mexican ADRs trading in the US does not show any significant arbitrage opportunities on the event dates used in the study. However, excess returns are observed in the period subsequent to the event dates when the market model is used as the return generating process with the US index as the market index. This result indicates the possibility of deriving excess returns associated with trading the Mexican ADRs in days subsequent to the news disclosures. When both the US and the Mexican indices are employed simultaneously, both indices are significant in explaining returns on the Mexican ADR portfolio. 0 1998 Elsevier Science B.V. All rights reserved.

JEL class$cation: F23; G15

Keywords: Mexican peso crisis; asset pricing

1. Introduction

Despite seemingly optimistic economic prospects in the early part of the 1990s such as a budget surplus, a respectable privatization policy, rising capital inflows, and a falling government deficit, Mexico had begun a descent into a financial crisis that resulted in a severe devaluation of the peso by late 1994 (the peso crisis). Extensive analysis of the events preceding the peso crisis has uncovered several

* Corresponding author. Fax: + I 618 453-5626; e-mail: [email protected]

1042-444X/98/$19.00 0 1998 Elsevier Science B.V. All rights reserved PII S1042-444X(98)00016-4

40 I. Mathur et al. / Journal of Multinational Financial Management 8 ( 1VVXi 39-48

important contributing factors. Political unrest in the state of Chiapas and the assassination of a presidential candidate undermined investors’ confidence in the stability of the Mexican government and its ability to conduct domestic policy, leading to a capital outflow. Investors, unlike the Mexican government, also viewed the replacement of a substantial amount of short term debt with ‘Tesebonos’ -- securities convertible into US dollars at maturity - as an ominous sign regarding confidence levels in the fundamental value of the peso. By the end of 1994, investors fearing hyperinflation, default, or capital controls withdrew their money, resulting in the decline of Mexico’s foreign exchange reserves from $30 billion in 1993 to $5 billion by December 1994. In failing to recognize that the depletion of reserves represented a long term decline in the demand for Mexican assets by foreign investors, the Mexican government may not have anticipated the extent of the market’s reaction to a depreciation of the peso. (For additional details on the peso crisis see Espinosa and Russell, 1996; Kildegaard, 1996; Whitt, 1996.)

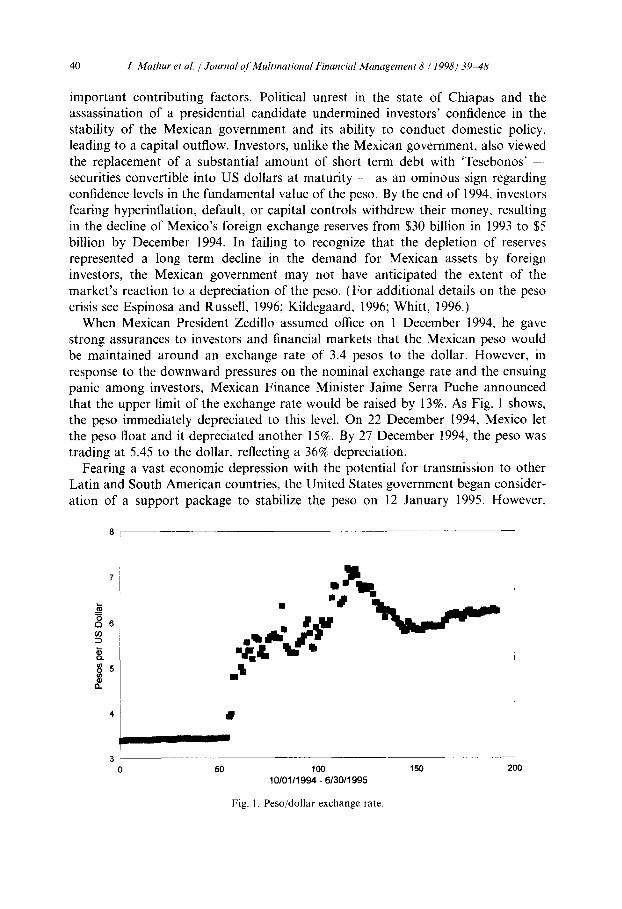

When Mexican President Zedillo assumed office on 1 December 1994, he gave strong assurances to investors and financial markets that the Mexican peso would be maintained around an exchange rate of 3.4 pesos to the dollar. However, in response to the downward pressures on the nominal exchange rate and the ensuing panic among investors, Mexican Finance Minister Jaime Serra Puche announced that the upper limit of the exchange rate would be raised by 13%. As Fig. 1 shows, the peso immediately depreciated to this level. On 22 December 1994, Mexico let the peso float and it depreciated another 15%. By 27 December 1994, the peso was trading at 5.45 to the dollar, reflecting a 36% depreciation.

Fearing a vast economic depression with the potential for transmission to other Latin and South American countries, the United States government began consider- ation of a support package to stabilize the peso on 12 January 1995. However,

1

l

3 i 0 50 100 150 200

10/0111994 -6/30/1995

Fig. 1. Peso/dollar exchange rate.

I. Math et al. / Journal of Multinational Financial Management 8 (1998) 39-48 41

Table 1 Events surrounding the peso crisis

Date Event

1 December 1994 19 December 1994

20 December 1994 22 December 1994 27 December 1994

President Ernest0 Zedillo takes office Finance Minister Jaime Serra Puche meets with business leaders regarding a change in the peso policy Official Mexican government announcement of devaluation Peso allowed to float Auction of dollar denominated Mexican government bonds fails to attract capital

12 January 1995 US government pledges support for peso stabilization plan 31 January 1995 Funds for US support package become available

infighting among various American political participants undermined these efforts, and it was not until 31 January that a support package of $20 billion was made available through the use of the Treasury’s Exchange Stabilization Fund. The relevant dates are summarized in Table 1.

By the time of the peso crisis, several Mexican firms were trading in the US in the form of American Depository Receipts (ADRs). A primary issue of ADRs is made by a US bank in lieu of the foreign shares that are physically deposited in trust with the bank’s foreign affiliate. After the primary issue, ADRs are traded in the US just like ordinary shares of US firms. Holding ADRs is a relatively easy way to invest in foreign securities because the ADR issuing bank acts as a transfer agent. The bank collects any dividends paid by the issuing firms and distributes them to the ADR holders after deducting applicable foreign taxes. It also informs ADR investors of any news regarding the shares such as exchange offers, recapitalization, and meeting notices. The price of an ADR reflects not only changes in value of its underlying foreign security but also currency shifts against the US dollar. US market conditions may also affect the price of an ADR because it is traded in the US.

ADR owners can convert ADRs into the underlying foreign currency shares subject to conversion fees. Similarly, investors in the foreign currency shares can convert their holdings into ADRs. Thus, any arbitrage opportunity between the prices of ADRs and their underlying securities quickly forces parity between the two categories of securities. If exchange rates are constant, then any changes in the underlying securities should be contemporaneously reflected in ADR prices. Similarly, foreign exchange rate changes should be contemporaneously reflected in the security prices. For example, if the price of the underlying security remains constant, but the Mexican peso depreciates from 4/$ to 5/$, then the price of a Mexican ADR should decline by 20%.

In the months subsequent to 20 December 1994, the Mexican peso depreciated substantially against the dollar. Mexican ADRs declined in price sharply, while the underlying securities suffered severe price fluctuations. Volatility of returns on both categories of securities increased sharply.

The reaction of investors to the development of the peso crisis has been examined

42 1. Mathur et al. /Journal qf’h4ultinational Financial Management 8 (1998) 39-48

from the perspective of trading activity of options on Telefonos de Mexico (Telmex) stock. Buttimer and Swidler (1998) examined Telmex options around the time of the devaluation of the Mexican peso and found that markets reacted quickly to the crisis. Furthermore, they found that the market perceived the devaluation as a temporary change in exchange risk as opposed to a permanent shift in equity risk.

The purpose of this paper is to examine whether financial markets reacted effi- ciently to the Mexican peso crisis of 1994. If markets are efficient, then changes in the prices of the underlying Mexican securities, coupled with changes in the Mexican/US exchange rate, should be contemporaneously reflected in the Mexican ADR securities.

We expect to make two contributions to the literature. First, we will demonstrate the extent to which shocks in a foreign exchange market are efficiently transmitted to interlinked securities in two countries. Second, by using Mexican and US indices in our model, we expect to shed light on the pricing factors associated with ADRs.

The results of this study show that capital markets did not provide any arbitrage opportunities during the peso crisis. The pricing mechanisms are such that once exchange rate fluctuations are taken into account, one could not arbitrage any price differences between Mexican ADRs trading in the US and their underlying securities trading in Mexico. However, the results suggest that there are overreactions when the ADR prices are considered vis-a-vis the US index. It appears that traders could have realized excess returns in the few days following the disclosure of significant news regarding the peso crisis.

2. Data and methodology

2.1. Data

The portfolio used in the analysis of the response of the ADRs to the peso crisis is constructed from the ADRs of the 29 Mexican firms listed on the NYSE or the NASDAQ for which daily returns from the CRSP tapes are available. The raw returns are used to form a time series of equally weighted portfolio returns from 1 November 1994 to 1 June 1995. Daily data for the Dow Jones Mexican Index and the Mexican IPC Index were obtained from various issues of the Wall Street Journal.

2.2. Estimation of returns

Returns from the perspective of an American investor are calculated as follows to take into account the changes in the exchange rate when calculating the return on the portfolio:

where Rf,j.t is the dollar adjusted return from buying the ith underlying share from country j, measured in the tth period; P&t and Prj.t-I are the foreign currency

1. Mathur et al. 1 Journal of’ Multinational Financial Management 8 (1998) 39-48 43

denominated prices for the ith underlying share from country j in periods t and t - 1, respectively; S,,, and S,,,- I are Mexico’s spot exchange rate expressed as dollars per peso for periods t and t - 1, respectively.

2.3. Event study

Standard event study methodology is used to identify cumulative average excess returns (CAERs) for the ADRs (Brown and Warner, 1985). Both the equally weighted and the value weighted CRSP indices were used in the analyses, with similar results. The return generating process is specified by the market model. Scholes-Williams betas are computed and the significance tests adjusted for cross- sectional dependence in the regression residuals.

2.4. Regression analysis

Binder (1985a,b) suggests that event day clustering and an industry or country induced correlation of returns can be addressed through the use of the multivariate regression model (MRM ) based on the Zellner ( 1962) SUR framework, which has been utilized, among others, by Cornett and Tehranian (1990) and Sundaram et al. ( 1992). The event period begins on 20 December 1994 and ends on 31 January 1995, when the US support package became available. Expectations of possible shifts in risk parameters during the event period and the post-event period are specifically recognized in the model. The following model is used in the study:

rjt =aj +a,i,D, +bjr,, +bj,Dormt +bj,,D,r,* + ‘f CkjDik +ej, i=l

where rjt = the rate of return on portfolio j for day t, in our model j = 1; rmt = the dollar rate of return on the Mexican IPC index; aj= the regression constant up to the agreement date; aj, = the shift in the regression constant in the post-event period; bj= the systematic risk coefficient of portfolio j; bj, = the shift in the systematic risk during event period; bj,, = the shift in the systematic risk during post-event period; D,= the shift dummy variable, 1 after the agreement, 0 up to the agreement date; D, = the shift dummy variable, 1 during event period, 0 otherwise; D, = the informa- tion dummy variable k for the ith event, 1 if the announcement or prior date, 0 otherwise; Ckj = the coefficient of information dummy variable k for portfolio j; n = the number of event dates analyzed; ejt = the stochastic error term for portfolio j.

The coefficients bj, bj,, and b,,, are estimated using the Scholes and Williams ( 1977) correction for non-synchronous data. Further, the White (1982) correction pro- cedure is used to control for heteroskedasticity.

The information dummy variable, Dik, assumes a value of one for the ith event and zero otherwise. To alleviate the problem of identifying the day of information release, the dummy variable takes the value one on the day prior to the event and on the event day.

A possible shift in the return generating process may be evident following the resolution of the Mexican peso crisis. Considering the ambiguity of the period of

44 I. Mathur et al. /Journal of Multinational Financial Management 8 (1998) 39-48

shift, it seems appropriate to consider the day when the US support package became available (31 January 1995) as the point of intervention because all uncertainty regarding the peso support was eliminated on this day. Thus, D, takes on the value of 1 for dates after 31 January 1995.

The specification of parameters in the equation defines the intercept term and systematic risk term following the agreement date as the sum of the u and uj,, and bj and b,,, respectively. A dummy variable D, is included in the model to isolate the shift in systematic risk during the event period. This allows for separate estimation of the systematic risk coefficient for the pre- and post-event periods. The standard significance of changes in the model parameters and information effects are measured by the t-statistics of the model coefficients.

2.5. Two jirctor regression analysis

The methodologies explained in the two previous sections may provide indications regarding the pricing of the Mexican ADRs vis-a-vis the US or the Mexican Index. However, they do not provide any indication of the extent to which Mexican ADRs trading in the US respond to the risk and return characteristics associated with either country’s index in the presence of the other index. This issue is addressed by estimating the following model proposed by Jorion and Schwartz (1986):

rjt = aj + bujrur + bmjrmt + ei,

where rjr is the dollar return on the portfolio of Mexican ADRs, and I’,, [rmt] is the dollar return on the US CRSP Equally Weighted Index [Mexican IPC Index].

3. Results

3.1. Event study results

The event study results are summarized in Table 2. For all dates and for many windows, we find significant CAERs. However, these CAERs are measured vis-a- vis the US index, which does not directly reflect peso devaluations. Thus, it is possible that the CAERs that we observe are a manifestation of the dynamics of the dollar/peso exchange rate and the pricing of the Mexican ADRs against the Mexican IPC Index rather than any measure of excess returns in the usual sense of the phrase.

One interesting point to note is that for events prior to the uncertainty resolution via the availability of the US support package, for three of the four dates - namely 20112194, 22112194, and 27112194 - a trader could have made significant excess returns by shorting Mexican ADRs following the announcement or disclosure of material information.

I. Mutlw et ul. i Journal of’ Multinutionul Financiul A4unugrment 8 (1998) 3% 48 45

Table 2 ADR cumulative average excess returns with US index

Event date CAERs for event windows (%)”

c-5, -2) (-1.0) C-1) (0) (+ I. +5)

Panel A: 20/12/1994 -6.26 (-2.68)***

Panel B: 221’12/1994 - I 1.92 (-5.08)***

Panel C: 27/12/1994 -22.19 (-9.55)***

Panel D: 12/01/1995 ~ 18.64 (-5.17)***

Panel E: 31:‘01.‘1995 -2.91 (-0.57)

-8.37 (-5.07) - 13.86 (-8.35)*** - I I .Y2 (-7.26)***

-7.97 (3.13)***

9.06 (2.500)**

-2.61 (2.23)**

-4.63 (~ 3.94)*** - I.89

(p1.65)* 5.71

(3.20)*** -9.03

(-3.53)***

-5.77 (-4.94)***

-9.24 (-7.87)*** - 10.04 (-g&4)***

2.21 (1.23) 18.09 (7.073)***

~ 19.61 (-7.51)***

-7.74 (-2.95)***

-6.18 (-2.38)**

- I .88 (-0.47)

I.30 (0.23)

***, **, * Significant at the I%, 5% and 10% levels, respectively. * CAERs - cumulative average excess returns ~~ indicate the average market-adjusted change over the event window in the market values of the sample firms. t-Statistics are given in parentheses.

3.2. Regression results

The dependent variable in the MRM is the return on the Mexican ADR portfolio. The market index is the dollar return on the Mexican IPC Index. If the market reacts efficiently to news and shocks are transmitted between markets quickly, then the Mexican stock market reaction to the various events of the Mexican peso crisis should be seamlessly transmitted to the Mexican ADRs trading on US markets. The regression results are summarized in Table 3. We note that none of the regression coefficients is significant. However, there is a shift in the post event beta, with the beta for the average ADR increasing by 0.39. These results indicate that on the informatin days the capital markets reacted efficiently to the peso crisis, resulting in no arbitrage opportunities between the Mexican ADRs trading in the US and their underlying Mexican stocks.

Table 3 Multiple regression results, r,, =u, +crj,D, +hjr,, +hi,D,r,, +hj,,D,r,, +X’;,, C,,D,, +c’,~

Constant Beta Information dummy variables

Overall Overall Event” Post b Di DZ 03 04 DS

PO.3574 0.653 -0.228 0.388 - I.005 -3.040 0.000 PO.175 I.766 (- 1.484) (1.497) (-0.514) (X597)* (-0.385) (&1.121) (0.807) (-0.070) (0.677) .Y= I I4

* Signihcant at 0.01 level. a Reports the change from overall during the event period. h Reports the change from overall during the post-event period

46 1. Mathur et al. /Journal qf Multinational Financial Management 8 (1998) 39-48

3.3. Two jbctor regression results

The results for the two-factor regression model are:

rjt = -0.42 + l.O6r,, + 0.65r,, i?=65.5% (- 1.69)* (l.w* (13.00)**

Both the US and Mexican indices influence returns for the Mexican ADR portfolio. However, the influence of the US index is larger than that for the Mexican index. The results show that Mexican ADRs are priced primarily in relation to the US index. The comparatively smaller coefficient for the Mexican index suggests that information is primarily assimilated to reflect that the ADRs are trading in the US market. The observed association creates the possibility of realizing risk-adjusted excess returns vis-a-vis the IJS index.

The results in this section validate the results reported previously. Since the Mexican ADRs are priced in relation to both the US and Mexican indices, the excess returns in Table 2 are consistent with results in this section.

4. Conclusion

The results of this study show that capital markets reacted efficiently to the Mexican peso crisis on the information days. Arbitrage opportunities between Mexican ADRs trading in the US and their underlying Mexican stocks did not exist during the unfolding and resolution of the peso crisis as evidenced by the results reported in Table 3. However, when Mexican ADRs are priced against the US index, it appears that there were opportunities to gain excess returns in the few days following the announcement or disclosure of significant news regarding the peso crisis. Thus, while the markets appear to be efficient in transmitting exchange rate shocks, the underlying security price dynamics across the two markets are not equally frictionless. In line with previously reported results, we find that the foreign exchange risk pricing mechanism seamlessly transmits information, while the under- lying stock market reactions may be more slow to take effect due to market segmenta- tion, capital controls and/or differences in structure and listing regulation across the two markets (Mitto, 1992).

Appendix A

The 29 Mexican ADRs utilized in this study

Grupo Indl. Maseca Grupo Iusacell Grupo Mexico Desarrollo Grupo Indl. Durango SA Grupo Radio Centro

I. Mathur et al. / Journul~f Multinational Financial Management 8 (I 998) 39-48 41

Grupo Financier0 Serfin Tram Maritima Mexico Tubos De Acero De Mexico Tolmex SA Telefonos De Mexico Banpais SA Grupo Elektra SA de CV Grupo Embotellador Mexico Vitro Sociedad Anonima Banca Quadrum SA Grupo Casa Autrey Grupo Sidek SA de CV Grupo Tribasa Grupo Televisa Cifra SA de CV Desc SA de CV Empresas ICA Sot Ctl Bufete Indl. Intl De Ceramica SA Grupo Simec Coca Cola Femsa De CV Cons G Grupo Dina Restaurant Hotlin Sas La Moderna

References

Binder, J.J., 1985a. On the use of the multivariate regression model in event studies. J. Accounting Research 23, 370-383.

Binder, J.J., 1985b. Measuring the effects of regulation with stock price data. Rand J. Economics 16. 167-183.

Brown, S.J., Warner, J.P., 1985. Using daily stock returns: The case of event studies. J. Financial Economics 14, 3-31.

Buttimer Jr., R.J., Swidler, S., 1998. The informational content of US listed options of foreign equity securities: The case of Telmex and the peso devaluation. J. Int. Financial Markets, Institutions & Money, in press.

Cornett, M.M., Tehranian, H., 1990. An examination of the impact of the Garn-St. Germain Depository Institutions Act of 1982 on commercial banks and savings and loans. J. Finance 45, 95-112.

Espinosa, M., Russell, S., 1996. The Mexican economic crisis: Alternative views. Federal Reserve Bank

of Atlanta Economic Review 81, 21-44. Jorion, P., Schwartz, E., 1986. Integration versus segmentation in the Canadian stock market. J. Finance

41, 6033613. Kildegaard, A., 1996. Liquidity, risk, and the collapse of the Mexican peso: A dynamic CGE interpreta-

tion. Southern Economic J. 96, 460-472. Mittoo. U.R., 1992. Additional evidence on integration in the Canadian stock market. Journal of Finance

47, 203552054.

48 I. Matlw et al. /Journal ~$Multinational Financial Management 8 (1998) 39-48

Scholes, M.. Williams. J.T., 1977. Estimating beta from nonsynchronous data. J. Financial Economics 5. 309-327.

Sundaram, S., Rangan, N., Davidson. W.N.. , 1111992. The market valuation effects of the Financial Institutions Reform, Recovery, and Enforcement Act of 1989. J. Banking and Finance 16. 1097-I 122.

White, H.. 1982. Instrumental variable regression with independent observations. Econometrica 50, 483m 500.

Whitt Jr., J.A.. 1996. The Mexican peso crisis. Federal Reserve Bank of Atlanta Economic Review 81, I-20.

Zellner. 1962. An efficient method of estimating seemingly unrelated regressions and tests of aggregation bias. Journal of the American Statistical Association 57. 348-368.