The Mexican economic crisis: alternative views

24

Federal Reserve Bank of Atlanta Economic Review 21 ew economic events succeed in capturing the sustained attention of both economic practitioners—policymakers, business economists, and press commentators—and academic economists. The ongoing economic crisis in Mexico is one of those events. Since the crisis broke out in December 1994, it has been the subject of innumer- able newspaper and magazine articles as well as a large number of academic papers. Most of the nonacademic analyses have tried to answer a question posed by the Wall Street Journal on July 6, 1995: “How could so many smart people on Wall Street, in Mexico City, and in Washington have been so blind to so many warnings?” This question captures the conventional wisdom about the crisis, which is that it was the inevitable result of funda- mental imbalances in the Mexican economy—imbalances that should have been obvious to informed observers and could have been corrected by rela- tively simple (though not necessarily painless) adjustments in Mexican eco- nomic policy. Most of the academic papers on the crisis have tried to identify the imbalances and the associated policy errors and to explain how and why they produced a crisis. We believe that many of these explanations for the Mexican economic crisis, both academic and nonacademic, are based on questionable assump- tions and dubious analysis. The principal purposes of this article are to iden- tify some of the major problems with the “conventional view” of the crisis and present an alternative view that seems more consistent with the evi- dence. Why look at alternative explanations? Economic science has not yet ad- vanced to the point of being able to identify a single, generally accepted ex- planation for most major economic issues or events. Understanding the he Mexican Economic Crisis: Alternative Views Marco Espinosa and Steven Russell Espinosa is a senior economist at the Federal Reserve Bank of Atlanta. Russell is an assistant professor of economics at Indiana University–Purdue University at Indianapolis. They thank Harold Cole, Frank King, Bobbie McCrackin, Will Roberds, Mary Rosenbaum, and Stephen Williamson for helpful comments and sugges- tions and John McCarthy for research assistance. F T T T

-

Upload

laaraucana -

Category

Documents

-

view

4 -

download

0

Transcript of The Mexican economic crisis: alternative views

Federal Reserve Bank of Atlanta Economic Review 21

ew economic events succeed in capturing the sustained attention ofboth economic practitioners—policymakers, business economists,and press commentators—and academic economists. The ongoingeconomic crisis in Mexico is one of those events. Since the crisisbroke out in December 1994, it has been the subject of innumer-

able newspaper and magazine articles as well as a large number of academicpapers. Most of the nonacademic analyses have tried to answer a questionposed by the Wall Street Journal on July 6, 1995: “How could so manysmart people on Wall Street, in Mexico City, and in Washington have beenso blind to so many warnings?” This question captures the conventionalwisdom about the crisis, which is that it was the inevitable result of funda-mental imbalances in the Mexican economy—imbalances that should havebeen obvious to informed observers and could have been corrected by rela-tively simple (though not necessarily painless) adjustments in Mexican eco-nomic policy. Most of the academic papers on the crisis have tried toidentify the imbalances and the associated policy errors and to explain howand why they produced a crisis.

We believe that many of these explanations for the Mexican economiccrisis, both academic and nonacademic, are based on questionable assump-tions and dubious analysis. The principal purposes of this article are to iden-tify some of the major problems with the “conventional view” of the crisisand present an alternative view that seems more consistent with the evi-dence.

Why look at alternative explanations? Economic science has not yet ad-vanced to the point of being able to identify a single, generally accepted ex-planation for most major economic issues or events. Understanding the

he Mexican Economic Crisis:

Alternative Views

Marco Espinosa and Steven Russell

Espinosa is a senior economistat the Federal Reserve Bank

of Atlanta. Russell is an assistant professor of economics at Indiana

University–Purdue Universityat Indianapolis. They thank

Harold Cole, Frank King,Bobbie McCrackin, Will

Roberds, Mary Rosenbaum,and Stephen Williamson for

helpful comments and sugges-tions and John McCarthy for

research assistance.

F

T T T

differences between alternative explanations for eco-nomic events is important for policymakers, who musttry to design policies that will address the problemsposed by these events. Frequently, the policies that arelikely to be successful if one explanation is correct arevery different from those that will succeed if anotherexplanation is closer to the truth.

Of course, alternative explanations that seem verydifferent from each other may in fact have a number ofcommon elements. For example, the alternative ac-count of the Mexican economic crisis presented in thisarticle resembles the conventional account in suggest-ing that the crisis may have been caused, at least inpart, by fundamental factors and may have been aggra-vated by mistakes in government policy. However, thecausal factors we identify and the policy mistakes weexpose are quite different from the ones emphasizedby most analysts. The article concludes by laying outsome changes in Mexican economic and financialpolicies that might make future crises less likely.While a few of these changes are similar to ones pro-posed by other commentators, some of the most im-portant recommendations have not been included inthe advice the proponents of the conventional viewhave offered the Mexican government.

The Mexican Economic Crisis

Prior to December 1994, the Mexican governmentbased its international economic policy on a strategyof exchange rate pegging.1 This strategy committedthe government to keeping the dollar value of theMexican peso inside a preannounced target zone andforced it to intervene in the foreign exchange marketwhenever market forces threatened to push the pesoexchange rate out of the zone. These interventions in-volved buying or selling financial assets payable indollars or other internationally convertible currencies.(The stock of these assets held by the government at agiven point in time constitutes its foreign exchange re-serves.) When the dollar value of the peso threatenedto fall below the lower boundary of the target zone, theMexican government sold dollar-denominated assetsin exchange for pesos, an action that increased the de-mand for pesos and prevented their dollar price fromfalling further.2

A serious problem for exchange rate pegging strate-gies is that if the market forces pushing the exchangerate lower are sufficiently strong and persistent, thegovernment’s rate-defending asset sales eventually ex-

haust its foreign exchange reserves. This is preciselythe situation that Mexico faced in the last two monthsof 1994, when the bottom dropped out of the pesomarket. The Mexican government intervened aggres-sively to try to keep the peso exchange rate fromfalling and by mid-December had sold $11 billionworth of reserve assets. Finally, on December 20 Mex-ico devalued the peso by 15 percent. Unfortunately,this action served only to increase the pace of the re-serve losses, and two days later the Mexican govern-ment felt compelled to give up its exchange ratetargeting policy and allow the peso to float against thedollar and other currencies. The peso immediately be-gan a rapid and dramatic depreciation. By early Jan-uary, its dollar value was almost 40 percent lower thanit had been in mid-December.

For Mexico, the devaluation of the peso markedthe beginning of a severe and persistent economic re-cession. By the end of 1995, Mexican real (inflation-adjusted) GDP had fallen by 7 percent, and theunemployment rate had increased from a precrisis lev-el of 4 percent to approximately 7 percent.3 A largenumber of private firms have failed, and the Mexicangovernment has been able to pay its debts only be-cause of financial aid from the International MonetaryFund (IMF) and the governments of the United Statesand Canada ($25 billion dollars’ worth to date). Do-mestic and foreign confidence in the prospects for theMexican economy has been shaken severely.

Conventional Explanations for the Crisis

Exchange Rate Policy. Many analysts believe thatthe Mexican economic crisis had been building forseveral years. According to this view, Mexico’s largeand persistent current-account deficits, which rosefrom $14.6 billion in 1991 to $28.8 billion in 1994, in-dicated that the Mexican peso was substantially over-valued. This overvaluation, it is argued, had to becorrected, and the longer the corrective measures wereput off, the harsher and more destabilizing they even-tually had to be. The blame for the overvaluation istypically placed on the Mexican government’s policyof pegging the peso exchange rate (see above). Au-thors such as Jeffrey Sachs, Aaron Tornell, and AndrésVelasco (1995) and Rudiger Dornbusch and AlejandroWerner (1994) argue that pegging an exchange rate aspart of an economic stabilization program makes senseonly for a short period of time; otherwise, “accumula-

22 Economic Review January/February 1996

tion of real appreciation . . . would ultimately risk thesuccess of the stabilization” (Sachs, Tornell, and Ve-lasco, 1995, 9; italics in original).

How are overvaluation, trade deficits, and econom-ic crises related? According to conventional macroe-conomic theory, an overvalued currency producescurrent account deficits by making a country’s exportsmore expensive and its imports cheaper and also by ar-tificially increasing the real value (at internationalprices) of incomes received in domestic money. Theresulting trade deficits must be financed by foreignborrowing—borrowing that cannot go on forever be-cause the overvaluation usually does not reflect any in-crease in the country’s ability to service its debts.Eventually, foreign lenders realize that the country’saggregate borrowing path is unsustainable and becomeunwilling to roll over their loans. The result is a re-serve outflow that is inevitably followed by a devalua-tion. The domestic price increases caused by thedevaluation, combined with the sudden withdrawal offoreign funds, produce a severe recession.

In some sense, the Mexican exchange rate crisis ac-tually began in March 1994, when political turmoil(discussed below) produced intense downward pres-sure on the market price of the peso and defending itsexchange rate peg cost the Mexican government a sub-stantial fraction of its foreign exchange reserves. Thegovernment’s unwillingness to devalue the peso duringthis episode has been frequently identified as a keyfactor leading to the crisis. Meanwhile, Mexico’s cur-rent-account deficit continued to widen: by December1994, it had reached $28.8 billion, which was 8 per-cent of the country’s GDP. (The comparable U.S. fig-ure was 3 percent.) To many analysts, this large tradedeficit was conclusive proof that peso overvaluationhad made foreign goods far too cheap and that a se-vere adjustment was imminent.

In evaluating this diagnosis of the cause of the cri-sis, it is important to bear in mind that large current-account deficits and heavy foreign borrowing can havecauses that do not involve currency overvaluation. Forexample, it is entirely possible for a developing coun-try to run large current account deficits because it of-fers attractive investment opportunities and lacksenough domestic savings to fund these opportunitiesinternally. As long as the investment projects are ulti-mately successful—as long as they produce returnslarge enough to service the foreign debts that providedthe funding for them—both the trade deficits and theforeign debts can persist indefinitely.4 This possibilityseems particularly relevant to the case of Mexico be-cause the country’s recent economic reforms, com-

bined with the negotiation of the North American FreeTrade Agreement (NAFTA), had led many U.S. ana-lysts to conclude that it had become a very promisingplace in which to invest. According to the IMF, from1990 to 1993 Mexico attracted $91 billion in net capi-tal inflows (1995, 53-55). Ratification of NAFTA inlate 1993, moreover, may have produced a substantialincrease in the availability of foreign funds.

Another problem with the conventional account ofthe crisis is that it is based on the rather woolly conceptof “overvaluation.” More specifically, the conventionalaccount is based on two possibly questionable premis-es: (1) that there is an equilibrium exchange rate withwhich the current exchange rate can be compared to

determine whether the currency in question is overval-ued and (2) that the value of this equilibrium exchangerate can be determined with some degree of accuracy.Many discussions of overvaluation seem to assume,with some circularity, that international macroeco-nomic equilibrium requires each country’s current ac-count to be in balance so that a country’s currency isovervalued whenever the country has a current ac-count deficit. Aside from the theoretical limitations ofthis assumption (see above), it is also questionable inpractice: for several years during the early 1980s, forexample, the U.S. dollar appreciated significantlyagainst most other major currencies at a time when theUnited States was running current account deficits ofunprecedented size.

Most other attempts to identify examples of overval-uation or measure their extent are based on the conceptof “purchasing-power parity” (PPP). Purchasing-powerparity is the principle that, other things being equal, aperson with a given quantity of domestic currencyshould be able to purchase the same quantity of goodsin the home country that he or she could purchase in a

Federal Reserve Bank of Atlanta Economic Review 23

In some sense, the Mexican exchange

rate crisis actually began in March 1994,

when political turmoil produced intense

downward pressure on the market price

of the peso.

foreign country if the domestic money were convertedinto foreign money at the current exchange rate. Sup-pose, for example, that an American with $100 can usethe foreign exchange market to convert the dollars into500 pesos and can use these pesos to buy 20 percentmore goods in Mexico than the $100 would buy in theUnited States. In this scenario, the dollar is overvaluedby 20 percent against the peso—or, equivalently, thepeso is undervalued by 20 percent against the dollar.Presumably, this sort of undervaluation will produceboth an increase in American purchases of Mexicangoods and a decrease in Mexican purchases of Ameri-can goods. If U.S.-Mexican trade were balanced initial-ly, the result should be that Mexico would run a tradesurplus with the United States.

There are a couple of serious problems with thisnotion of overvaluation, however. First, the PPP prin-ciple applies, strictly speaking, only to internationallytradable goods or services that can be transported be-tween countries at minimal cost and are not coveredby tariffs (import taxes) or export subsidies. Manygoods, and possibly most goods, do not meet these re-quirements. A person should not, for example, expectto be able to get haircuts in the United States for thesame exchangerate-adjusted prices that he or shewould pay in Mexico, as it is not really feasible formost Americans to travel to Mexican barbershops. Ahaircut is a classic example of a service that is essen-tially “nontradable.”5 And while the practical difficul-ties of international trade are less severe forautomobiles than for haircuts, neither should peopleexpect to be able to buy a U.S. car for the same pricein Mexico as in the United States. Cars are heavy andexpensive to transport, and the Mexican governmentimposes tariffs on imported automobiles.

A closely related problem with the PPP concept in-volves the fact that there are so many different goodswhose prices often change in different directions or in-crease/decrease at different rates. The typical solutionis to perform PPP calculations using price indexesbased on the prices of standard baskets of goods andservices in the relevant countries. However, both theitems and the quantities in a country’s standard basketvary significantly from country to country, and manyof the items in the baskets are either nontradable orquite costly to trade. Thus, the current consumer priceindexes (CPIs) for the United States and Mexico maynot be equal to each other, even if the two indexeshave the same base year and the average inflation ratesin the two countries have been equal since the baseyear, using an index based on a common basket of un-ambiguously tradable goods.

Perhaps the most widely used PPP-based approachto measuring currency values is “relative PPP,” whichassumes that if prices rise faster, on average, in countryA than in country B, then country A’s currency shoulddepreciate at a rate equal to the annual inflation differ-ential. In the case of the United States and Mexico, forexample, from 1991 to 1993 the Mexican inflation rate,as measured by Mexico’s CPI, averaged around 10 per-cent higher than the U.S. inflation rate as measured bythe U.S. CPI. According to the principle of relativePPP, the Mexican currency should have depreciatedagainst U.S. currency at an average rate of 10 percentper year. The fact that the actual rate of depreciationaveraged only 2.5 percent per year has led many ana-lysts to conclude that the Mexican peso was becomingincreasingly overvalued. (It should be noted, however,that during the year preceding the crisis—a periodwhen many analysts began warning that Mexican cur-rency was substantially overvalued—the peso depreci-ated against the dollar at a rate about 4 percent higherthan the Mexican-U.S. inflation differential.)

The relative-PPP concept suffers from the sameproblems as conventional or “absolute” PPP, plus animportant additional problem: relative PPP calcula-tions for a period implicitly assume that the currenciesin question were correctly valued at the beginning ofthe period. Suppose, for example, that Mexican cur-rency was substantially undervalued in 1990. Then thefact that the peso depreciated against the dollar during1991-93 at a rate lower than the Mexican-U.S. infla-tion differential may have reflected a gradual tendencyfor the peso’s dollar value to rise toward its “correct”level, rather than a tendency for the peso to become in-creasingly overvalued. Thus, unless the problem ofmeasuring absolute PPP can be solved, it is impossibleto place much faith in conclusions based on measure-ments of relative PPP.

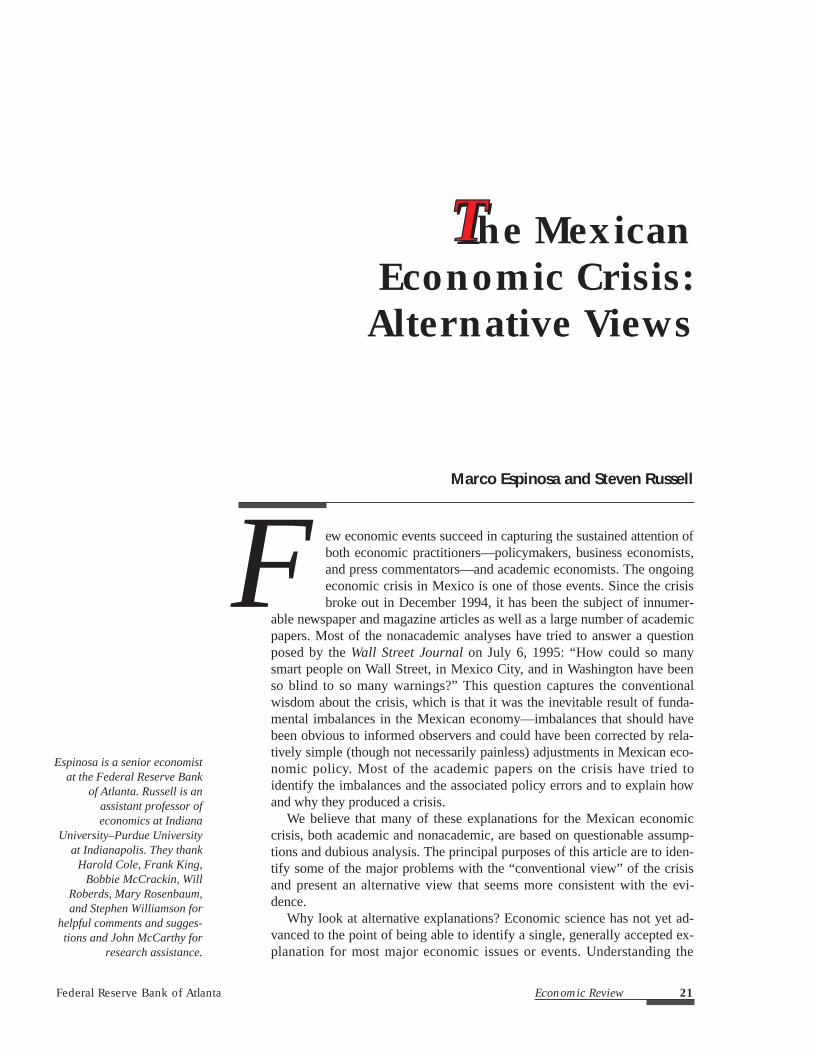

Mexico’s central bank, the Banco de Mexico, em-ploys an approach to relative PPP calculations that isbased on guidelines developed by the IMF. The ap-proach involves constructing a “real exchange rate” bycomparing labor costs in Mexico with those in othercountries. The following description of this approachis taken from one of the bank’s annual surveys of theMexican economy:

Its aim is very simple: to compare developmentsin labor costs in one country with those of itstrading partners, expressed in a common curren-cy. . . . If labor costs in one country, adjusted forproductivity, increase at a faster pace than itstrading partners, then its real exchange rate ap-

24 Economic Review January/February 1996

Federal Reserve Bank of Atlanta Economic Review 25

preciates and its external sector becomes lesscompetitive. . . . The 1978-1979 average waschosen as the base period, since it was consideredrepresentative of a suitable position of balancefor our external sector. Enough time had elapsed,since the 1976 devaluation, for us to reasonablyassume that the margin of undervaluation thatnormally follows the initial stages of an exchangerate adjustment had disappeared. Additionally,exports of manufactured goods showed a healthygrowth during this period and there was an up-swing in international reserves. (1993, 97)

The results the Mexican central bank obtains usingthis approach illustrate the sensitivity of relative-PPPcalculations to the choice of the base year. Althoughthe bank’s calculations confirm that the peso has ap-preciated in recent years relative to other currencies,they also suggest that by 1994 this appreciation hadnot yet succeeded in allowing the peso to regain therelative position it enjoyed during 1978-79.6 (SeeChart 1, which tracks Mexico’s relative unit laborcosts against those of its major trading partners.) In thebank’s view, the peso had indeed been undervalued in1990 and earlier years and remained undervaluedthroughout the period preceding the recent crisis.

While the validity of the bank’s choice of a base peri-od is certainly debatable, it seems clear that its staffsubjected the question to careful analysis—unlikemany commentators who have used the peso’s rela-tively low rate of depreciation during the early 1990sas the basis for casual criticism of the Mexican gov-ernment’s exchange rate management policies.

The economic importance of nontradable goods cre-ates other problems for relative-PPP calculations. Sup-pose, for example, that a country’s national income isgrowing faster than the incomes of other countries, per-haps because of a large inflow of foreign investment. Ifthis country’s markets are reasonably open to interna-tional trade, relative PPP can be expected to hold, atleast approximately, for its tradable goods. The pricesof its nontradables, however, are likely to be rising rela-tively rapidly: the rapid increase in domestic incomewill produce strong demand for nontradables, and thisdemand, unlike the demand for tradable goods, can besatisfied only out of domestic production. Becausenontradable goods have substantial weight in nationalprice indexes, the domestic CPI will rise faster than theCPIs of slower-growing countries. If the home coun-try’s exchange rate against these countries remainsconstant, the inflation differential will create the mis-taken impression that domestic currency is becoming

1980 1985 1990 1995

1978-79=100

20

60

100

140

180

1975

Chart 1Real Exchange Rate Based on Unit Labor Costs in the Manufacturing Industry, 1975–95

Source: Banco de Mexico.

26 Economic Review January/February 1996

Percentage

1980 1982 1984 1986 1988 1990 1992 1994

–8

–4

0

4

Source: Federal Reserve Bank of Atlanta using data from Banco de Mexico.

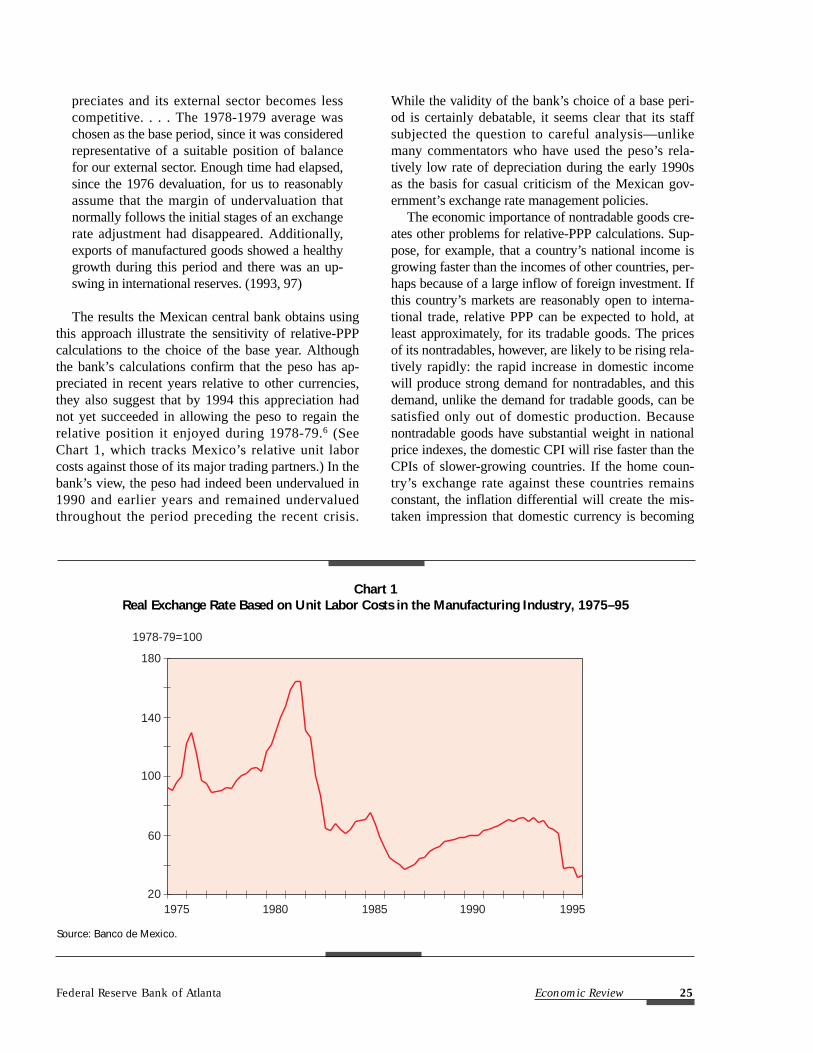

Chart 2Public Sector Operational Balance in Mexico, 1980–94

(As a percentage of GDP)

increasingly overvalued. It is worth noting, in this con-nection, that the 12.9 percent average inflation raterecorded in Mexico from 1990 to 1993 was dispropor-tionately due to nontradables: their prices rose at a 17.4percent average rate while the prices of tradables roseat an average rate of only 8.8 percent. The average dif-ferential between the Mexican tradables inflation rateand the U.S. inflation rate was around 3 percent duringthis period. Subtracting the latter figure from the aver-age rate of peso depreciation produces a relative-PPP-adjusted peso appreciation rate of only 5.8 percent,compared with the 14.4 percent rate yielded by a calcu-lation based on Mexico’s overall inflation rate.7

Bad Fiscal or Monetary Policy. Another popularclass of explanations for the Mexican economic crisisblames its outbreak on the malign effects of bad fiscalor monetary policy. At first glance, explanations of thissort seem rather puzzling. The most widely used indi-cator of the soundness of a country’s fiscal policy is thesize of its government budget deficit. By this indicator,Mexico appears to have been in fine shape (see Chart 2):its federal government reported budget surpluses from1990 to 1993, and its deficit for 1994 was only 0.5 per-cent of GDP. Similarly, the most popular indicator ofmonetary policy soundness is a country’s annual infla-tion rate. In Mexico, the annual inflation rate averaged

15.7 percent between 1990 and 1993, which is not highfor a developing country. In addition, the rate of infla-tion had been declining over time, reaching 8 percentin 1993 and 7 percent in 1994.

Fiscal Policy. In the case of fiscal policy, some ana-lysts argue that the budget numbers reported by theMexican government were misleading and that thegovernment was actually running substantial budgetdeficits. Sachs, Tornell, and Velasco comment that “inthe wake of the crisis, it has become fashionable toclaim that these numbers hide a part of the deficit,since starting in 1993 they omit the financial intermedi-ation activities of state and development banks” (1995,6). It should be noted, however, that in the long run theactivities of these institutions increase governmentexpenditures only if the loans are extended at below-market interest rates or are not ultimately repaid. Sachs,Tornell, and Velasco go on to point out that beginning in1993 “development banks must by law have an 8 per-cent capitalization ratio, must hold reserves against badloans and must lend to private banks on commercialterms” (6). Finally, even if all the funds raised by theseinstitutions are charged against the government budget,the 1994 budget deficit would not have exceeded 4 per-cent of GDP. It is hard to accept a figure of this magni-tude as an explanation for Mexico’s financial

Federal Reserve Bank of Atlanta Economic Review 27

meltdown. Deficits of this size are quite commonamong countries with relatively stable economies. Thegovernment of Italy, for example, regularly runs muchlarger budget deficits—8 percent of GDP in 1994.

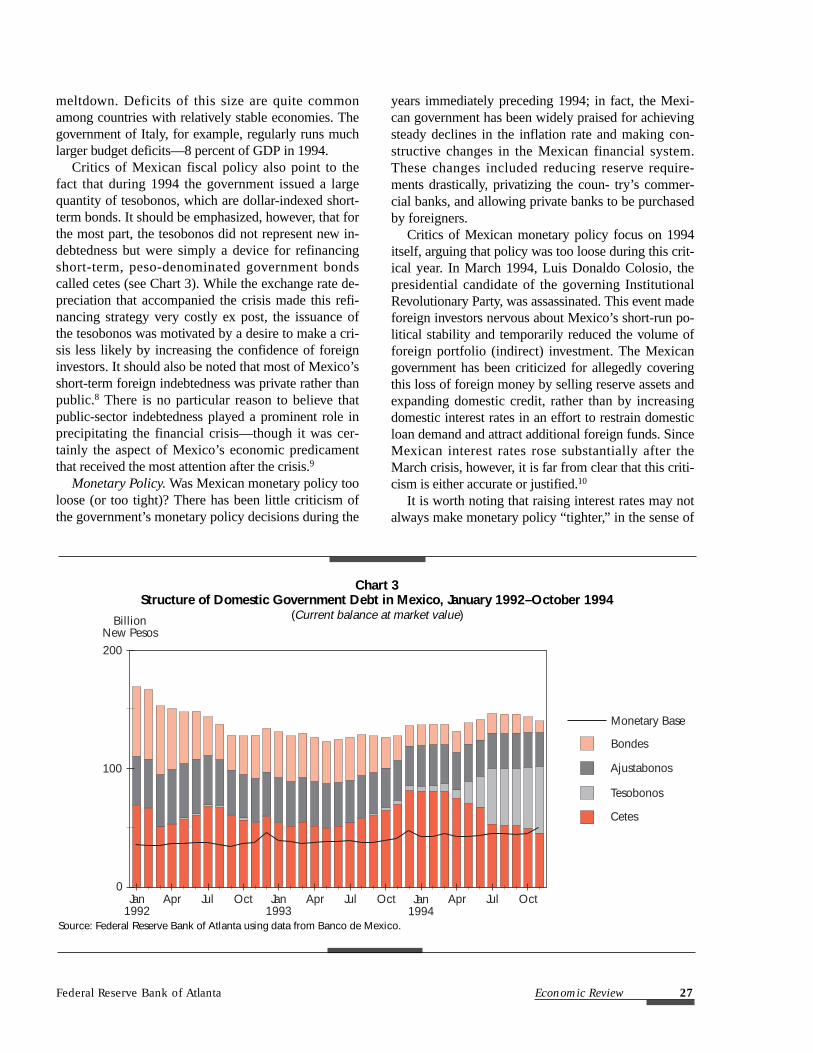

Critics of Mexican fiscal policy also point to thefact that during 1994 the government issued a largequantity of tesobonos, which are dollar-indexed short-term bonds. It should be emphasized, however, that forthe most part, the tesobonos did not represent new in-debtedness but were simply a device for refinancingshort-term, peso-denominated government bondscalled cetes (see Chart 3). While the exchange rate de-preciation that accompanied the crisis made this refi-nancing strategy very costly ex post, the issuance ofthe tesobonos was motivated by a desire to make a cri-sis less likely by increasing the confidence of foreigninvestors. It should also be noted that most of Mexico’sshort-term foreign indebtedness was private rather thanpublic.8 There is no particular reason to believe thatpublic-sector indebtedness played a prominent role inprecipitating the financial crisis—though it was cer-tainly the aspect of Mexico’s economic predicamentthat received the most attention after the crisis.9

Monetary Policy. Was Mexican monetary policy tooloose (or too tight)? There has been little criticism ofthe government’s monetary policy decisions during the

years immediately preceding 1994; in fact, the Mexi-can government has been widely praised for achievingsteady declines in the inflation rate and making con-structive changes in the Mexican financial system.These changes included reducing reserve require-ments drastically, privatizing the coun- try’s commer-cial banks, and allowing private banks to be purchasedby foreigners.

Critics of Mexican monetary policy focus on 1994itself, arguing that policy was too loose during this crit-ical year. In March 1994, Luis Donaldo Colosio, thepresidential candidate of the governing InstitutionalRevolutionary Party, was assassinated. This event madeforeign investors nervous about Mexico’s short-run po-litical stability and temporarily reduced the volume offoreign portfolio (indirect) investment. The Mexicangovernment has been criticized for allegedly coveringthis loss of foreign money by selling reserve assets andexpanding domestic credit, rather than by increasingdomestic interest rates in an effort to restrain domesticloan demand and attract additional foreign funds. SinceMexican interest rates rose substantially after theMarch crisis, however, it is far from clear that this criti-cism is either accurate or justified.10

It is worth noting that raising interest rates may notalways make monetary policy “tighter,” in the sense of

Monetary Base

Bondes

Ajustabonos

Tesobonos

Cetes

100

Jan1992

Jan1993

Jan1994

0

200

BillionNew Pesos

Apr Jul Oct Apr Jul Oct Apr Jul Oct

Chart 3Structure of Domestic Government Debt in Mexico, January 1992–October 1994

(Current balance at market value)

Source: Federal Reserve Bank of Atlanta using data from Banco de Mexico.

28 Economic Review January/February 1996

tending to produce lower inflation. Thomas Sargentand Neil Wallace (1981) point out that when real inter-est rates in a country exceed its real growth rate, high-er interest rates increase the cost of refinancing thegovernment’s debt and may eventually force it to re-spond by increasing the money growth and inflationrates in order to increase government revenues fromcurrency creation. If people understand this situation,moreover, increases in current interest rates can leadthem to expect higher inflation in the future, and thisexpectation can drive up the current inflation rate. Atthe time of the March 1994 crisis, real interest rates inMexico were already substantially higher than thecountry’s real growth rate, so it is possible that moreaggressive interest rate increases could actually havebeen counterproductive.

Alternative Explanations

Borrowing Constraints. We believe that bothMexico’s exchange rate policies and its fiscal andmonetary policies have been overemphasized as pos-sible causes of the financial crisis it experienced inlate 1994. In a recent paper, Andrew Atkeson andJosé-Víctor Ríos-Rull (1995) adopt a similar view,arguing that Mexico’s financial crisis could have oc-curred even though its exchange rate was not overval-ued and its precrisis monetary and fiscal policies werecredible in the sense of being potentially sustainablein the long run. In the formal model Atkeson andRíos-Rull present, the trade deficits Mexico runs be-fore the crisis are a rational response to the desire ofits people to achieve large increases in domestic in-vestment without giving up large amounts of currentconsumption. Because the investments in question areproductive in nature, the debts accumulated in thecourse of financing them can be serviced in the longrun. However, the amounts that Mexico’s private andpublic sectors can borrow are limited by externallyimposed “credit constraints.” When the country’s pri-vate or public borrowers reach the limits of theseconstraints, they can no longer increase their indebt-edness, even if the new debts in question are perfectlysound. Mexico’s trade account must henceforth bebalanced, and if it wishes to increase domestic invest-ment further it can do so only by reducing its pur-chases of consumption goods. According to Atkesonand Ríos-Rull, the Mexican financial crisis broke outbecause Mexico reached these borrowing limits inlate 1994.

While the analytical approach employed by Atke-son and Ríos-Rull has many appealing features, we arenot convinced that they have offered a useful explana-tion for the Mexican financial crisis. Perhaps thebiggest problem with the approach is its reliance on anexternally imposed credit constraint. Atkeson andRíos-Rull offer a number of possible explanations forthe existence of such constraints. They speculate, forexample, that these constraints may be imposed by in-vestors who recognize the difficulties of enforcingdebt collection in developing countries. The problem,of course, is that this sort of explanation explains toomuch: whenever a country suffers a financial crisis,the crisis can always be explained by assuming thatthe country has reached the limits of its borrowingconstraints. In addition, there seems to be little evi-dence indicating that the doubts investors may havehad about Mexico’s continued ability to service itsdebts were caused by concern about the size of thosedebts, as opposed to concern about Mexico’s overallpolitical stability or the ability of its government to de-fend its pegged exchange rate.

Another problem with the Atkeson and Ríos-Rullanalysis is that it does not explain the severity of the1994 financial crisis. In their model, the borrowingcountry knows in advance that it is approaching itsborrowing constraint. When it reaches the constraint,it calmly stops increasing its foreign indebtedness andbegins cutting back its consumption. There is no needfor dramatic declines in output or large increases inunemployment, and there is no reason for holders ofpreviously incurred debts to refuse to roll them over.In fairness to Atkeson and Ríos-Rull, one could viewtheir model as the precursor of a more sophisticatedmodel in which the country does not know preciselywhen it will approach the borrowing constraint. Thissort of model would presumably predict more eco-nomic dislocation after the limits of the constraint arereached. Nevertheless, the actual crisis created farmore economic disorder than even a more advancedmodel of this sort would seem capable of generating.

Finally, the Atkeson and Ríos-Rull story implies thatthe financial crisis broke out in 1994 simply becausethis happened to be the year in which the total volumeof Mexican foreign indebtedness reached the limits ofthe borrowing constraint. It is difficult to believe that itwas simply a coincidence that the crisis occurred at theend of a year distinguished by the most serious politicalturmoil Mexico has experienced in at least a decade.The political troubles that broke out during 1994 play akey role in the alternative explanation for the Mexicanfinancial crisis that is presented below.

Financial Panic. Our alternative explanation forthe Mexican financial panic is inspired by the similari-ty between the recent economic crisis in Mexico andsome economic crises in the U.S. historical experi-ence. As is the case with most historical analogies, thesimilarity between these two sets of events is not per-fect: some aspects of the historical U.S. situation werequite different from the situation facing modern Mexi-co, and some of the events that occurred in Mexico areoutside the range of U.S. experience. In addition, thefact that economists do not completely understand thecauses of the U.S. crises limits the degree to which thehistory of these crises can help explain the recentMexican crisis. Nonetheless, the degree of similaritybetween the circumstances and events of the two typesof crises seems substantial enough to make it useful tocompare them. In addition, examining the successesand failures of efforts by U.S. policymakers to solvethe problems posed by the U.S. crises can help identi-fy policies that may or may not be successful in Mexi-co. Finally, the comparison helps emphasize the pointthat crises of the type that Mexico experienced are notunprecedented and are not the result of unique failingson the part of the Mexican government or uniqueweaknesses in the country’s economy.

U.S. Financial Panics. During the late nineteenthand early twentieth centuries, the U.S. banking and fi-nancial system suffered recurrent crises that have be-come known as financial panics. A financial panicusually started because of the failure of one or moremajor commercial or financial institutions that wereheavily indebted to one or more large banks. Thebanks had financed the bulk of their loans by issuingchecking accounts, which are known formally as de-mand deposits. In the late nineteenth century, these de-posits could be redeemed on demand in gold dollars orin notes that were convertible on demand in gold dol-lars. As soon as the holders of these deposits heardabout the banks’ loan problems, they would rush toteller windows to withdraw their funds in the hope ofrecovering their money before similar demands byother depositors exhausted the bank’s funds andcaused them to fail. Depositors of other banks wouldobserve the runs and become concerned about the sol-vency of their own institutions. The runs might thenspread from bank to bank, from city to city, and fromregion to region. During a financial panic, this patternof contagion spread bank runs over all or a large partof the country.

A peculiar and distinctive feature of U.S. financialpanics was “suspensions of payments.”11 Panics usual-ly began, or gained momentum, in major U.S. cities—

most often New York, which was the country’s princi-pal financial center. When the banks in such a citywere confronted by a wave of panic-induced runs, theyrecognized that attempting to meet the runs by sellingassets would depress the asset market, causing them totake large losses or even driving them into bankruptcy.They typically responded by suspending payments—that is, by temporarily refusing to allow depositors towithdraw or transfer their funds.

While a suspension solved the immediate problemsof the banks in the city that initiated it, it usually creat-ed problems for banks elsewhere. Suspensions weredistressing to depositors because they lost access to

their funds, wholly or partially, for a period that some-times lasted weeks or months. As a result, if deposi-tors believed that their banks were likely to suspendpayments they would withdraw their funds as a pre-caution, even if they did not have any real concernsabout the banks’ solvency. Thus, fear of suspension re-placed fear of bankruptcy as a force driving runs. Forthis reason, once a suspension occurred in a single ma-jor city it typically spread nationwide within a fewdays. The financial disruption these nationwide pay-ments suspensions caused was very damaging to theeconomy and often produced (or at least contributed tothe severity of) economic recessions or depressions.12

Financial panics were extremely frustrating tothe nineteenth-century business community and tocontemporary economic policymakers because theadverse consequences of panics seemed entirely outof proportion to the seriousness of the events thattouched them off. The principal cause of this problemwas that panics spread so rapidly. Once a panic gotstarted, people were forced to make immediate deci-sions with little reliable information, and they often

Federal Reserve Bank of Atlanta Economic Review 29

Both Mexico’s exchange rate policies and

its fiscal and monetary policies may have

been overemphasized as possible causes

of the financial crisis it experienced in

late 1994.

found themselves responding less to their own judg-ments about the seriousness of situations than to theirfears about how other people might respond. Thus,New York bank depositors who participated in runs of-ten did so not because they believed that their bankswere insolvent but because they feared that with-drawals by other panicky depositors would drive thebanks into insolvency. Similarly, a suspension in NewYork would touch off a nationwide suspension not be-cause the banks in other cities were concerned abouttheir financial situations but because they feared that theevents in New York would cause their depositors to be-come concerned about their situations. Many of theirdepositors, in turn, would withdraw their deposits whenthey heard about the New York suspensions becausethey assumed that other depositors would react bywithdrawing their deposits, and so on.

Mexico’s Financial Situation. In our view, the recentfinancial crisis in Mexico was similar, in many ways, toa nineteenth-century U.S. financial panic. In order toexplore this similarity, it is necessary to describe a fewkey elements of Mexico’s economic and financial situ-ation during the period preceding the crisis.

To begin with, it is important to understand thatduring the late 1980s and early 1990s, Mexico hadchosen (intentionally or unintentionally) a develop-ment strategy of externally financed growth. Becauserapid economic growth requires large investments inplant, equipment, and technology, a key problem fac-ing any developing country is how to obtain the fundsnecessary to finance these investments. Many of thebiggest economic-growth success stories of the post-war period—Japan, Korea, and Taiwan, for example—chose internally oriented financing strategies. In thesecountries, most of the funds needed to finance domes-tic investments were provided (at least in the initialstages) by domestic savings.

Of course, internally based financing strategies re-quire the citizens of the countries in question to saverelatively large fractions of their incomes. In manyLatin American countries, the average level of house-hold income is so close to the subsistence level that itmay be unrealistic to expect households to increasetheir savings rates significantly.13 In addition, the gov-ernments of these countries may be unable or unwillingto ask their citizens to sacrifice current consumption inorder to finance investments whose rewards may notbe evident for many years. Consequently, these coun-tries have opted for externally based financing strate-gies—development strategies under which much ofthe funding for domestic investment comes from for-eign lenders and investors. The funds to repay these

lenders and investors are expected to come out of theprofits derived from the investment projects.

Mexico’s externally based financing strategy al-lowed the share of its GDP devoted to domestic invest-ment to rise from 20 percent to 23 percent from 1988to 1992, despite the fact that private savings fell fromroughly 18 percent of Mexican GDP to under 9 per-cent. Between 1990 and 1993, moreover, Mexico re-ceived $91 billion in net capital inflows (IMF 1995,53). Thus, in the years preceding the crisis an inflowof foreign funds allowed Mexico to enjoy substantialincreases in both consumption and investment.

Another important characteristic of Mexico’s finan-cial situation was the fact that a large fraction of thefunds it received from foreigners were provided on ashort-term basis. In 1993, at the peak of the foreign-investment inflow, only 32 percent of the foreignfunds went into the country’s stock market and onlyabout 13 percent was devoted to direct investment byforeign firms (Banco de Mexico 1995, 257). Most ofthe rest went into short-term debt issued by the Mexi-can government or by Mexico’s commercial banks;the banks, in turn, used much of this money to makeloans to Mexican firms engaged in investment pro-jects. In addition, while the Mexican government wasnot running large budget deficits, it was responsiblefor servicing the country’s national debt, which hadbeen accumulated during the 1970s and 1980s. Themagnitude of this debt had been reduced in recentyears, but it remained quite substantial. And whilemuch of the national debt was long-term in nature, agood deal of it took the form of short-term govern-ment bonds that had to be refinanced more or less con-tinually. Banco de Mexico reports that in 1992 theaverage maturity of outstanding Mexican governmentbonds was slightly longer than 400 days, or just overone year (1994, 160). In 1993 the average declined to300 days. It continued to fall in 1994, reaching 200days by the end of the year. In addition, even in 1993,the year that marked the peak of Mexico’s popularitywith investors, Mexican borrowers made only 33placements of long-term bonds (grossing $3.8 billion)on international financial markets, and only six ofthese involved private borrowers.

The last characteristic of Mexico’s economic situa-tion that is directly relevant to this discussion is its ex-change rate regime. As has already been noted, theMexican government was committed to an exchangerate peg that required it to sell reserve assets in the ex-change market whenever the peso’s dollar valuethreatened to fall below a prescribed level. The frac-tion of Mexico’s foreign debts that were denominated

30 Economic Review January/February 1996

in pesos had been increasing, and the exchange ratepeg also provided assurance to foreign holders of thesedebts that exchange rate depreciation would not drasti-cally reduce their dollar value. The reliability of thisassurance was a key factor determining the amount offoreign funds that were available to Mexican borrow-ers.

A Mexican Financial Panic. It is now possible todevelop the analogy between U.S. financial panics andthe Mexican financial crisis. The precrisis Mexicanbanks can be viewed as analogues of the U.S. banks ofthe late nineteenth century. The Mexican banks had is-sued a large quantity of short-term liabilities to for-eigners: these liabilities can be thought of as theanalogues of the demand deposits that were issued bythe nineteenth-century U.S. banks. Finally, the Mexi-can government’s exchange rate pegging regime canbe regarded as analogous to the legally required con-vertibility of nineteenth-century demand deposits.Just as demand-deposit convertibility guaranteednineteenth-century depositors that the value of theirdeposits was fixed in terms of gold, the exchange ratepeg guaranteed foreign investors that the value of theirpeso investments was fixed (or at least bounded be-low) in terms of U.S. dollars.

As has been noted, a U.S. financial panic usuallygot started because of bad news suggesting that loansmade by some U.S. banks might not be repaid, makingit difficult or impossible for the banks to cover theirdeposits. In Mexico, the “bad news” that triggered thefinancial crisis was somewhat less direct and took theform of political instability. Explaining the nature ofthese political problems will require a fairly extendeddigression.

Mexican Politics before and during 1994

Historically, Mexico’s political system has beensomewhat less stable than that of the United States.For the last sixty-five years, the Mexican governmenthas been dominated by a single political party, the In-stitutional Revolutionary Party, or PRI (see above). Al-though the PRI candidate has invariably won Mexicanpresidential elections, allegations of vote fraud haveplagued most of these victories, and the party is re-garded by a great many Mexicans as corrupt and unre-sponsive to their needs.14 From the point of view offoreign investors, however, the PRI appears to be asource of stability: during the last decade, at least, the

party has committed itself to a policy of respect forprivate property rights. Mexican or foreign firms en-gaged in investment projects have been able to operaterelatively unhindered by government interference, andthe party has enforced these firms’ promises to repayforeign lenders and investors. Many investors un-doubtedly fear that if there were a successful revolt inMexico, or even if the PRI candidate lost the presiden-tial election, the new government might change thecountry’s laws in ways that would interfere with manyMexican firms’ repayment of their debts, or it mightsimply refuse to assist in enforcing these debts. Simi-larly, the outbreak of civil war or widespread politicalviolence might make it impossible for many firms tooperate profitably and might divert government atten-tion and resources away from debt enforcement.

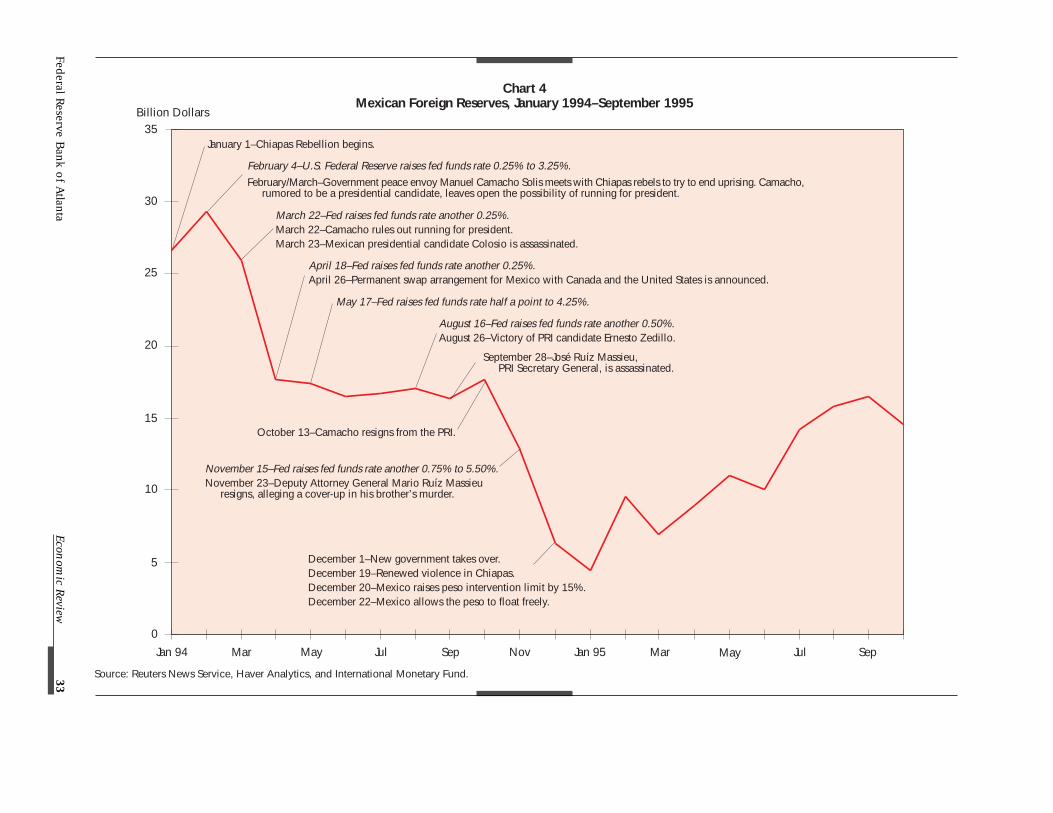

Under the Mexican constitution, a presidential elec-tion is scheduled every six years. The most recentelection occurred in late August of 1994. In early Jan-uary 1994, about nine months before the election, anarmed rebellion broke out among the Mayan Indianinhabitants of the province of Chiapas in extremesouthern Mexico. The participants in the rebellioncalled themselves Zapatistas after Emiliano Zapata, anearly-twentieth-century Mexican revolutionary hero.The rebellion was surprisingly successful, catching theMexican government off-guard and making headlinesworldwide. It was halted only after the governmentagreed to open high-level negotiations with rebelleaders. Three months later, in late March, the PRIpresidential candidate, Luis Donaldo Colosio, was as-sassinated. (See Chart 4 for a chronology of politicalevents and monetary policy actions during 1994). Al-though the motives for the assassination were not en-tirely clear, there were indications that it might havebeen the outgrowth of dissension inside the PRI. Noneof Colosio’s potential replacements enjoyed consensussupport within or outside the party, and the eventualchoice, Ernesto Zedillo, was an economist with littlepolitical experience. As a result, the assassinationraised the possibility that the PRI candidate might losethe election or that he might win the election but beunable to govern effectively.

The Colosio assassination set off a minor financialcrisis that preceded the major crisis by roughly ninemonths. This first crisis is instructive for understand-ing the second one. The assassination shook the confi-dence of foreign investors. As the foreign deposits ofthe Mexican banks were short-term and required semi-continuous refinancing, this loss of confidence createdimmediate difficulties for Mexican banks and putdownward pressure on the dollar price of the peso.

Federal Reserve Bank of Atlanta Economic Review 31

The government responded by selling large quantitiesof foreign exchange reserves and allowing domesticinterest rates to increase sharply. These moves seemedto be successful, in the sense that the government wasable to defend its peso peg without exhausting its for-eign exchange reserves (which were, however, greatlyreduced; see Chart 4).15

The March crisis was also similar to events thatsometimes occurred in the nineteenth-century UnitedStates. As was noted above, financial panics often gotstarted when bad news about the assets of one or morebanks in a major financial center disconcerted manydepositors and led to large withdrawals. The banks inthe affected center would respond to this situation byraising their deposit and loan interest rates sharply inan attempt to defend their cash reserves. Sometimesthis strategy would succeed, and the crisis would endbefore the reserves had been drawn down to a point atwhich the banks felt compelled to suspend convertibil-ity. Often, however, a near-crisis of this sort would bethe harbinger of a full-fledged crisis that would comeweeks or months later—a crisis that might result inboth a payments suspension and a financial panic. Inmany of these cases the events that ignited the secondcrisis seemed somewhat less serious than those thattouched off the first one. Apparently, investor confi-dence, once shaken, became fragile and more sensitiveto subsequent shocks.16

In the case of the recent crisis in Mexico, the possi-bility of renewed unrest in Chiapas cast a pall over theMexican election campaign. Nonetheless, the electiontook place in late August as scheduled and resulted in avictory for PRI candidate Zedillo. Both the Mexicanpublic and the foreign investment community beganwatching the Zedillo administration nervously for signsthat it was capable of pulling the PRI together and re-solving the troubles in Chiapas. During the monthsimmediately following the election, observers sawnothing to inspire confidence on either front. Just onemonth after the election, José Francisco Ruíz Massieu,the head of the PRI, was assassinated. In late Novem-ber Mario Ruíz Massieu, the brother of José Francisco,publicly accused the party’s leadership of organizing acover-up designed to prevent the identities and motivesof his brother’s killers from being revealed. Suspicionfell on Raul Salinas de Gortiari, the brother of ex-presi-dent Carlos Salinas de Gortiari, and there were pressreports of discord between the new president and hispredecessor. Meanwhile, the new government hadfailed to make any progress in negotiations with theZapatistas. (Its problems were complicated by the factthat Manuel Camacho Solis, a PRI leader and rival of

Zedillo’s who was the government’s chief negotiatorwith the rebels, had resigned shortly before the elec-tion.) In mid-December, the Zapatistas took up armsagain, and the government responded by sending alarge army detachment to Chiapas.

Genesis of Panic. In our view, the adverse politicalevents that occurred in the months following the Au-gust election, and particularly in November and De-cember, convinced many foreign investors that theZedillo government was not making much progressbringing the PRI or the country together and that thepotential for really serious political strife was high andrising. These investors responded by becoming in-creasingly reluctant to commit or recommit funds toMexico. The supply of foreign funds seems to havebegun to shift back in November, and the governmentwas again forced to sell large amounts of reserves. ByDecember 20 the reserves were nearly exhausted, andthe government responded by devaluing the peso by15 percent (see above).

The government’s decision to devalue the peso hadan effect on the Mexican financial system that wassimilar to the effect of a payments suspension on thenineteenth-century U.S. banking system. A suspensionby the banks in one U.S. city created expectations ofsuspensions elsewhere that would deprive depositorsin other cities of access to their funds; the peso devalu-ation created investor expectations of further devalua-tions that would greatly reduce the dollar value of theirassets. Nineteenth-century depositors responded to thethreat of suspension by rushing to their banks to with-draw their funds; modern foreign investors respondedto the threat of devaluation by refusing to roll overtheir securities and deposits. As most of the depositswere short-term, millions of dollars were drawn offevery day, producing a rapid deterioration in the gov-ernment’s reserve position and putting severe down-ward pressure on the dollar price of the peso. Withintwo days, the government was forced to give up its ex-change rate pegging strategy completely and allow thepeso to float. Its market value quickly fell by roughly40 percent against the U.S. dollar.

Ironically, in the weeks and months following thecrisis it became clear that the various threats to Mexi-can political stability were considerably less seriousthan they had appeared in November and December of1994. Although the PRI continued to be troubled bypolitical infighting and accusations of corruption, thesetroubles did not endanger the political dominance ofthe party or produce any challenge to the leadership ofPresident Zedillo. The Zapatistas, moreover, provedunable to expand their political base to the extent

32 Economic Review January/February 1996

Federal R

eserve Ban

k of A

tlanta

Econ

omic R

eview3

3

Billion Dollars

Jan 94 Mar May Jul Sep Nov Jan 95 Mar May Jul Sep

0

5

10

15

20

25

30

35January 1–Chiapas Rebellion begins.

February 4–U.S. Federal Reserve raises fed funds rate 0.25% to 3.25%.February/March–Government peace envoy Manuel Camacho Solis meets with Chiapas rebels to try to end uprising. Camacho,

rumored to be a presidential candidate, leaves open the possibility of running for president.

March 22–Fed raises fed funds rate another 0.25%.March 22–Camacho rules out running for president.March 23–Mexican presidential candidate Colosio is assassinated.

April 18–Fed raises fed funds rate another 0.25%.April 26–Permanent swap arrangement for Mexico with Canada and the United States is announced.

May 17–Fed raises fed funds rate half a point to 4.25%.

August 16–Fed raises fed funds rate another 0.50%.August 26–Victory of PRI candidate Ernesto Zedillo.

September 28–José Ruíz Massieu,PRI Secretary General, is assassinated.

October 13–Camacho resigns from the PRI.

November 15–Fed raises fed funds rate another 0.75% to 5.50%.November 23–Deputy Attorney General Mario Ruíz Massieu

resigns, alleging a cover-up in his brother’s murder.

December 1–New government takes over.December 19–Renewed violence in Chiapas.December 20–Mexico raises peso intervention limit by 15%.December 22–Mexico allows the peso to float freely.

Source: Reuters News Service, Haver Analytics, and International Monetary Fund.

Chart 4Mexican Foreign Reserves, January 1994–September 1995

necessary to foment unrest outside of Chiapas or exertsignificant leverage over the federal government. In ad-dition, despite the economic hardship created by the se-vere recession that followed the crisis, the governmentsucceeded in preserving labor peace—an accomplish-ment that allowed it to implement a number of austeri-ty measures. These measures, combined with financialassistance from the IMF, the United States, and Cana-da, enabled the government to continue to service itsdebts and to provide some assistance to the country’sdistressed private sector.

Unfortunately for Mexico, the fact that the politicalproblems that touched off the financial crisis were notas serious as they appeared at the time has done little tolimit the adverse economic effects of the crisis. The vul-nerability of the Mexican financial system to liquiditycrises has been convincingly demonstrated, and foreigninvestors consequently remain hesitant to recommittheir funds. While some of this reluctance may becaused by genuine doubts about the long-run politicalstability of Mexico, we suspect that most of it is due tofear that renewed political turmoil could spook enoughinvestors to provoke another liquidity crisis.

Before proceeding further, it is important to clarifyour views on the role of “fundamental” factors in pre-cipitating the Mexican crisis. The basic cause of the cri-sis was the political turmoil in Mexico that led foreignlenders to become concerned about the fate of their in-vestments. There was nothing irrational about this con-cern or about the decisions lenders made in response. Itis the nature of political crises, however, that they of-ten seem far more serious at the time they break outthan they do a few weeks or months later. As a result,it is important for a country whose social or economiccircumstances make it vulnerable to occasional politi-cal fireworks to structure its financial system in a waythat allows the system to remain stable until the smokecreated by the fireworks has cleared. The Mexicangovernment’s policy mistakes did not involve manag-ing the economy in a way that caused it to be out ofbalance under normal conditions; instead, they in-volved permitting (and, to some extent, encouraging)the development of financial institutions and practicesthat made the economy vulnerable to political shocks.

Again, considering the situation of the nineteenth-century United States may be insightful. At the time,the U.S. economy was based on a fractional-specie-reserve banking system that worked reasonably wellunder normal circumstances but was vulnerable to liq-uidity crises touched off by adverse economic shockssuch as large commercial failures or cyclical tradedownturns. The challenge for the U.S. government was

to develop a strategy for reforming and regulating thebanking system that reduced the system’s susceptibilityto these sorts of crises. Critics of Mexican economicpolicy might do well to reflect on the fact that it tookthe U.S. government roughly fifty years to developsuch a strategy and that its first attempt—the creationof the Federal Reserve System—was not entirely suc-cessful (see below).

Implications of the Financial Panic Explanation

A Floating Exchange Rate? The policy implica-tions of the conventional account of the Mexican fi-nancial crisis (see above) seem fairly straightforward.According to the conventional view, the crisis oc-curred because the Mexican government’s exchangerate pegging regime allowed the Mexican peso to be-come substantially overvalued. The overvaluation pro-duced a persistent (though necessarily temporary)disequilibrium in which Mexicans were consumingmore than could be justified by their incomes at inter-national prices. This overconsumption was financedby foreign borrowing and was reflected in Mexico’slarge trade deficit. The disequilibrium ended in De-cember 1994 when the government was no longer ableto defend its exchange rate peg because it had exhaust-ed its foreign exchange reserves. The peso was thenallowed to fall to a value that produced substantiallylower incomes and consumption for Mexicans. Pre-sumably, the Mexican government could prevent fu-ture problems of this sort by permanently abandoningits policy of exchange rate pegging and allowing thepeso to continue to float. The exchange rate wouldthen adjust to keep Mexico’s domestic consumption inline with its domestic income.

Because the financial panic explanation for the crisisalso gives a role to the collapse of the pegged exchangerate regime, one might think that its policy implicationswould be similar in nature. As has been noted, however,the financial panic explanation suggests that Mexico’sexchange rate policies have been overemphasized as acause of the crisis and that a more important cause wasthe short-term nature of Mexican borrowers’ liabilityportfolios. This difference in views is important becausecertain major implications of the conventional explana-tion are not implications of the financial panic explana-tion. In particular, the financial panic explanation doesnot necessarily imply that the Mexican peso was dra-matically overvalued. In addition, the panic explanation

34 Economic Review January/February 1996

does not interpret the fact that Mexico was runninglarge trade deficits as necessarily indicating that thecountry was borrowing or consuming at unsustainablerates. Nevertheless, the policy recommendations pre-sented below probably imply that even after the currentcrisis has passed Mexico still will have to accept some-what lower levels of borrowing and consumption.

Short-term liabilities were a problem for Mexicancommercial and financial institutions for the same rea-son that demand deposits were a problem for nineteenth-century American banks. Because demand depositscould be withdrawn at any time, the banks were veryvulnerable to bad news that shook depositors’ confi-dence in the value of their asset portfolios. There wasno way, short of concerted suspension, that they couldforce their depositors to wait weeks or months for anaccurate and dispassionate determination of the extentof their problems—a determination that would haverevealed, in most instances, no real grounds for seriousconcern. Similarly, the short-term nature of the de-posits of Mexican banks allowed large numbers of de-positors to withdraw their funds in response to badnews about Mexico’s political stability. Before the trueseriousness of the political situation could be dispas-sionately determined, the Mexican government hadexhausted its foreign exchange reserves and wasforced to devalue the peso. This decision further dis-concerted investors and intensified the outflow of for-eign funds.

A natural question that arises at this point is whyMexican financial institutions allowed themselves toacquire liability portfolios that made them so vulnera-ble to confidence shocks. The answer seems to lie inthe nature of the Mexican development strategy. Therelatively low rate of domestic savings discussed ear-lier forced the Mexican financial system to look toforeign countries for funds to finance domestic invest-ment. Moreover, both direct Mexican borrowers andthe country’s financial intermediaries were content torely on short-term foreign credit. Foreign short-termlenders had little reason to be concerned about thelong-run prospects of the projects their funds werebeing used to finance as it seemed certain that theMexican borrowers could continue to roll over theirshort-term deposits using short-term funds providedby further foreign lenders. As long as this was thecase, the deposits were perceived to have little defaultand the lenders were willing to purchase them at rela-tively low interest rates.

Long-term lenders would have recognized that theability of borrowers to repay their loans was depen-dent on the long-run success of the investment projects

and consequently was attended by a substantialamount of risk. They would have demanded higher in-terest rates to compensate themselves for this risk. Thecombination of higher interest rates and greater lenderrisk-consciousness would have forced Mexican firmsto scale back their investments, reducing both thefirms’ potential profits and the overall growth rate ofthe Mexican economy. However, neither these firmsnor the Mexican government was willing to acceptsuch a slowdown in the pace of development.

One potential source of risk whose existence wasgenerally recognized was exchange rate risk. Althoughthere was relatively little chance that the banks issuingthe deposits would default over horizons of three or sixmonths, under a floating exchange rate regime therewould have been significant risk of substantial declinesin the dollar value of the peso. After all, even for devel-oped countries exchange rate fluctuations of 10 percentor even 20 percent over short time horizons are not un-common. Lenders whose base currency was dollarswould have had to charge substantially higher interestrates to compensate themselves for the exchange raterisk. Presumably, the desire to avoid these interest costswas the reason the Mexican government began peggingthe exchange rate in the first place and was also thereason it continually assured investors that it had noplans to abandon or revise the policy. Of course, theexchange rate pegging scheme produced the samesorts of potential instabilities as the nineteenth-centuryguarantee of deposit convertibility: any threat that thepolicy might have to be abandoned, whether real orimagined, could produce a self-perpetuating outflow offunds and a financial/economic disaster.

In sum, the Mexican government’s policy of peg-ging the exchange rate appears to have been part of alarger strategy of making sure that short-term fundswere available to Mexico’s firms and governmentagencies in large quantities and at moderate interestrates. It is important to emphasize, however, that whilethe exchange rate peg increased both the benefits andthe risks of the Mexican development strategy, neitherthe benefits nor the risks would have disappearedwithout it. Clearly, even under a floating-rate regimeMexican firms and government agencies could haveobtained funds more cheaply in the short-term ratherthan the long-term credit market. Under floating rates,however, changes in the market value of the Mexicanpeso would have replaced changes in the reserve posi-tion of the Mexican government as potential factorstouching off a panic. Under a floating-rate regime, a sud-den loss of investor confidence would be immediatelyreflected in a sharp decline in the value of the Mexican

Federal Reserve Bank of Atlanta Economic Review 35

peso. This decline would reduce the dollar value ofMexican assets and disconcert foreign investors; itmight well become the cause of additional confidencelosses or create expectations of further depreciation inthe exchange rate. Either eventuality would lead to arapid drawdown of short-term foreign deposits andwould put further downward pressure on the peso. Asituation of this sort could easily degenerate into a self-reinforcing financial panic similar to the one Mexicoactually experienced. Thus, one could argue that undersome conditions a flexible exchange rate regime couldmake the Mexican financial system more vulnerable toa financial panic.

On balance, we think that a major financial crisiswould have been somewhat less likely under a floatingexchange rate regime. Under floating rates, an event orsequence of events disturbing enough to shake theconfidence of a large group of depositors might pro-duce a fairly gradual decline in the value of the peso,at least when the decline is compared with the abruptchanges that typically occur when countries adjusttheir exchange rate pegs. Declines of this sort mightnot disconcert less timid or better-informed depositorsto the extent necessary to touch off concerted runs. Atthe very least, there would no longer be any need forthe large, abrupt official devaluations that almost guar-antee runs and panic.17

On the other hand, unregulated foreign exchangemarkets are notoriously volatile: as noted above, swingsof 10 or 20 percent over periods of three months or lessare not uncommon, even for exchange rates betweenthe currencies of developed countries. In the relativelythin market for the currency of a less-developed coun-try like Mexico, the extent of the volatility is likely tobe much greater. Indeed, we suspect that one of theconsiderations that led the Mexican government toadopt a pegged exchange rate regime may have beenits belief that a floating exchange rate was more likelyto be a source of instability than a cure for it.

It is interesting, in this connection, to compare theMexican economic crisis with events that took place inthe United States shortly thereafter. Between Januaryand April 1995, the U.S. dollar depreciated by roughly20 percent against the Japanese yen and 13 percentagainst the German mark. Although there was muchdebate about the causes and consequences of the dol-lar’s relatively rapid loss in value against these twomajor currencies, no one seems to have feared that thesky was about to fall on the U.S. economy. In retro-spect this lack of concern seems to have been justified:the decline in the dollar’s exchange value did not pro-duce an economic recession, an episode of high infla-

tion, or a serious economic problem of any other sort.The dollar, moreover, has since regained all the groundit lost during this period.

In Mexico, the economic sky really did seem to fallafter the December devaluations. The first victim ofthe devaluations was Mexican financial markets,where interest rates skyrocketed and asset prices de-clined sharply. In the aftermath of the devaluations,moreover, most economic analysts became quite pes-simistic about the outlook for Mexico’s economy. Be-fore the crisis erupted, most private forecasts wereroughly consistent with the Mexican government’sreal GDP growth target of 3.8 percent. Afterwards,however, nearly every forecaster predicted a serious,extended recession that would be accompanied byhigh inflation. These predictions turned out to be cor-rect, at least qualitatively: during the year followingthe crisis, Mexico’s real GDP fell by 7 percent, and itsprice level rose by roughly 50 percent.

Policy Prescriptions

By now it should be clear that in our view the prin-cipal cause of the Mexican financial crisis was exces-sive reliance on short-term liabilities issued to foreigninvestors. What, if anything, could the Mexican gov-ernment have done to avoid this problem, and what canit do to prevent similar crises in the future? One mightargue that the problem will eventually solve itself asborrowers become more aware of the potential risks ofheavy reliance on short-term credit—risks that shouldnow be evident to everyone because of the crisis. How-ever, there are reasons to doubt that changes in privatebehavior stimulated by this crisis will be sufficient, inthemselves, to prevent future crises. The key problemis that when a Mexican financial institution issues addi-tional short-term debt, it increases not only its own refi-nancing risk but also the risk of a financial crisis thatwill affect many other financial and commercial insti-tutions. In the jargon of economists, issuance of short-term credit by one firm imposes external costs on otherfirms. A well-known principle of economic theorystates that unregulated markets cannot be expected tofind the most efficient solutions to problems involvingexternal costs and that there may therefore be a con-structive role for government intervention.

The external-cost problems of contemporary Mexi-can financial markets are not drastically different fromthe problems that confronted the U.S. financial systemof the nineteenth century. When a U.S. bank issued ad-

36 Economic Review January/February 1996

Federal Reserve Bank of Atlanta Economic Review 37

ditional demand deposits, it increased its own vulnera-bility to an idiosyncratic bank run, and it also increasedthe vulnerability of the U.S. financial system to a na-tionwide financial panic. Clearly, the experience gainedfrom past financial panics was not sufficient to moti-vate U.S. banks to rearrange their balance sheets inways that prevented future ones: panics continued tooccur roughly once every dozen years.

The U.S. government tried two basic strategies forpreventing financial panics. The first strategy, whichwas not entirely successful, was to create Federal Re-serve Banks to provide a lender of last resort for theprivate banking system.18 The second strategy, whichhas been quite successful (at least in preventing pan-ics) was to establish a system of federally adminis-tered deposit insurance. Unfortunately, neither of thesestrategies would seem to offer a viable solution to theproblems of the Mexican financial system. The short-term deposits that are in the most danger of being runoff are those supplied by foreigners who are very con-cerned about the dollar value of their peso-denominateddeposits. As Mexican government last-resort loanswould presumably be extended in pesos, large-scaleemergency lending would cause the peso to depreciatefurther against the dollar and would therefore create atleast as many problems as it solved. Similarly, in orderfor a deposit insurance system to be reassuring to for-eigners, it would have to guarantee the dollar value ofdeposits. Neither the Mexican government nor itsbanking system appear to have the financial resourcesnecessary to underwrite such a system.

In addition to last-resort lending and deposit insur-ance, the U.S. government tried several other strate-gies for reducing the vulnerability of the U.S. bankingsystem to financial panics. Two of these strategiesseem particularly relevant to a discussion of the Mexi-can financial situation. First, U.S. banks were prohibit-ed from purchasing corporate bonds or common stock.This prohibition was motivated, at least in part, by adesire to prevent volatile demand deposits from beingused to finance risky investment activities. Second, thepayment of interest on demand deposits was prohibit-ed. Part of the rationale for this prohibition was to dis-courage the issuance of demand deposits and reducetheir importance in the U.S. financial system.

In the case of Mexico, prohibiting banks from fi-nancing investment activities is probably not a realisticoption. It was possible in the United States only be-cause the U.S. financial system was sufficiently welldeveloped to allow investment-minded firms to seekfunds from other sources. In Mexico such alternativesare just beginning to emerge; almost all private credit

is intermediated through the banking system. Prohibit-ing or limiting interest on short-term liabilities is alsoprobably too drastic. The U.S. government felt free toprohibit banks from paying interest on demand de-posits because it was certain that the American publicwould continue to hold substantial quantities of thesedeposits for direct use as money or for related liquidi-ty-oriented reasons. It seems unlikely, however, thatmany foreigners rely on short-term deposits in Mexi-can banks as a source of liquidity. Consequently, an in-terest prohibition or limitation might cause this sourceof funds to dry up completely.

Reserve Requirements. The policy interventionproposed here is considerably less drastic. We suggest

that the Mexican government impose reserve require-ments on the short-term liabilities of banks and otherfinancial intermediaries and also on any direct (that is,unintermediated) short-term liabilities of Mexicanfirms. The reservable assets would be medium-termbonds (bonds with terms of five to ten years) issued bythe Mexican government.19 The new reserve require-ments would be graduated in a manner similar, in spirit,to the interest rate ceilings the U.S. government for-mer-ly imposed under Regulation Q: longer-term liabilitieswould have lower reserve ratios than shorter-term liabil-ities, and liabilities with terms longer than five years orso would have reserve ratios at or near zero.20

The purpose of these graduated reserve requirementswould be to discourage Mexican banks from issuingshort-term liabilities, without forbidding them to do so.Stated differently, the policy would provide Mexicanbanks with financial incentives to limit their exposureto institutional and systemic sources of refinancing risk.The lower reserve ratios on longer-term liabilitieswould give them a substantial interest-cost advantagerelative to short-term liabilities—an advantage that

The Mexican financial crisis can be seen as

an expectations-driven liquidity crisis that

shares many similarities with the financial

panics that afflicted the U.S. economy during

the late nineteenth century.

38 Economic Review January/February 1996

would allow Mexican financial institutions to issuelonger-term liabilities at rates that would increase theirrelative attractiveness to domestic and foreign in-vestors. The goal would be to increase the average termof Mexican domestic and foreign debts substantially,making the country’s financial system less susceptibleto liquidity crises. The policy would also help counter-act the external-cost problem with short-term liabilities.Under the policy, when a Mexican bank issued addi-tional short-term liabilities that marginally increasedthe susceptibility of the Mexican financial system topanics, the bank would also be allowing the Mexicangovernment to sell additional medium-term debt. Theaverage term of the government’s liability portfoliowould consequently increase, reducing its own vulner-ability to liquidity crises and increasing its ability toprovide emergency financial assistance to the country’sprivate sector.

As has been indicated, if this policy of reducing thecountry’s reliance on short-term debt were adopted, itwould not be without costs to Mexico. Interest rates ondebt would be higher than they would have been other-wise, and the amount of investment would be lower.21

As a result, in noncrisis periods the country wouldgrow somewhat more slowly than in the absence of thepolicy. However, the recent financial crisis and theeconomic recession that followed it have imposedhuge costs on the Mexican people. Consequently, ifthe reserve-requirement policy just outlined succeedsin materially reducing the probability of future crises,it may offer substantial net benefits to Mexico.