Demand-Side Surveys for Financial Inclusion: - Squarespace

59

Bringing smart policies to life. 1 Guidance Note Demand-Side Surveys for Financial Inclusion: A practical, how-to guide based on the experience of AFI member countries

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Demand-Side Surveys for Financial Inclusion: - Squarespace

Bringing smart policies to life.

1

Guidance Note

Demand-Side Surveys for Financial Inclusion:

A practical, how-to guide based on the experience of AFI member countries

Bringing smart policies to life.

2

This report is dedicated to our dear colleague and friend

Raúl Hernández Cos, a tireless advocate for financial inclusion, comprehensive data collection, and improving the lives of the

poor in Mexico and around the world.

Bringing smart policies to life.

3

Contents Tables, figures, and boxes ............................................................................................................................. 4

Main Findings from AFI experience with demand-side surveys ................................................................... 6

Practitioners Notes: advice from the field .................................................................................................... 8

I. Introduction .......................................................................................................................................... 9

About this report....................................................................................................................................... 9

II. Part I: A solid working foundation ...................................................................................................... 11

a. Engaging stakeholders and working with partners ............................................................................. 12

Selecting the organization to implement the survey .......................................................................... 12

b. Budgeting and scope ........................................................................................................................... 14

c. Designing a policy-relevant survey ..................................................................................................... 17

III. Part II: Survey Design and Implementation .................................................................................... 19

a. Establishing a timeframe .................................................................................................................... 20

b. Gap analysis ........................................................................................................................................ 21

c. Approaches to survey design .............................................................................................................. 21

d. Sampling .............................................................................................................................................. 23

Probability Samples: simple random samples and clustered stratified samples ................................ 24

Sample size .......................................................................................................................................... 24

The sampling frame ............................................................................................................................ 25

Individual versus household sample and identifying the respondent ................................................ 26

Weighting ............................................................................................................................................ 27

e. Designing the questionnaire ............................................................................................................... 28

Modules and topics to include in the survey instrument ................................................................... 30

Length and organization of the questionnaire ................................................................................... 31

f. Piloting ................................................................................................................................................ 34

g. Training ............................................................................................................................................... 36

Ethics ................................................................................................................................................... 37

Nonsampling errors ............................................................................................................................ 38

Quality control and monitoring of field researchers .......................................................................... 39

IV. Part III: Analysis, dissemination, and making the best use of results ............................................. 42

a. Shaping data analysis ...................................................................................................................... 42

Bringing smart policies to life.

4

b. Dissemination ................................................................................................................................. 43

c. Examples of how data can be used to inform policy ...................................................................... 44

V. Conclusion ........................................................................................................................................... 46

Annex A: List of people interviewed ........................................................................................................... 47

Annex B: AFI Core Set.................................................................................................................................. 48

Annex C: Criteria for selecting a research house to implement a demand-side financial inclusion survey

.................................................................................................................................................................... 50

Annex D: Example of Gantt Chart for planning the timeframe of a survey ................................................ 52

Annex E: More technical information of sample size ................................................................................ 53

Annex F: Example of Kish Grid to randomly identify a respondent in the household ................................ 55

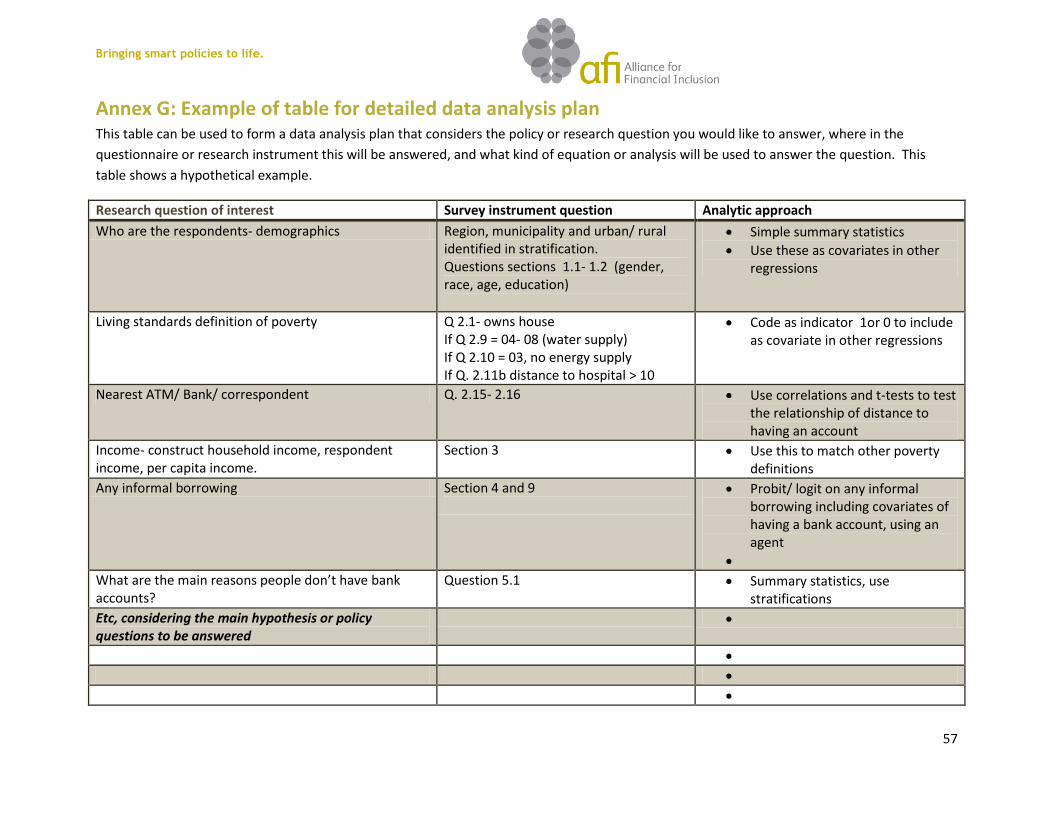

Annex G: Example of table for detailed data analysis plan ........................................................................ 57

References .................................................................................................................................................. 58

Tables, figures, and boxes Table 1: Example costs of country-led demand side surveys ..................................................................... 15

Table 2: Possible Survey Designs ................................................................................................................ 21

Table 3: The AFI Core Set ............................................................................................................................ 48

Figure 1: Defining the scope of a demand-side survey ............................................................................... 15

Figure 2: Process of survey design and implementation ............................................................................ 19

Figure 3: Steps used in Mexico's demand-side survey .............................................................................. 20

Figure 4: Levels of random selection in a sample of individuals ................................................................ 26

Figure 5: Five steps in questionnaire design ............................................................................................... 28

Figure 6: Possible structure for demand-side research instrument design ................................................ 33

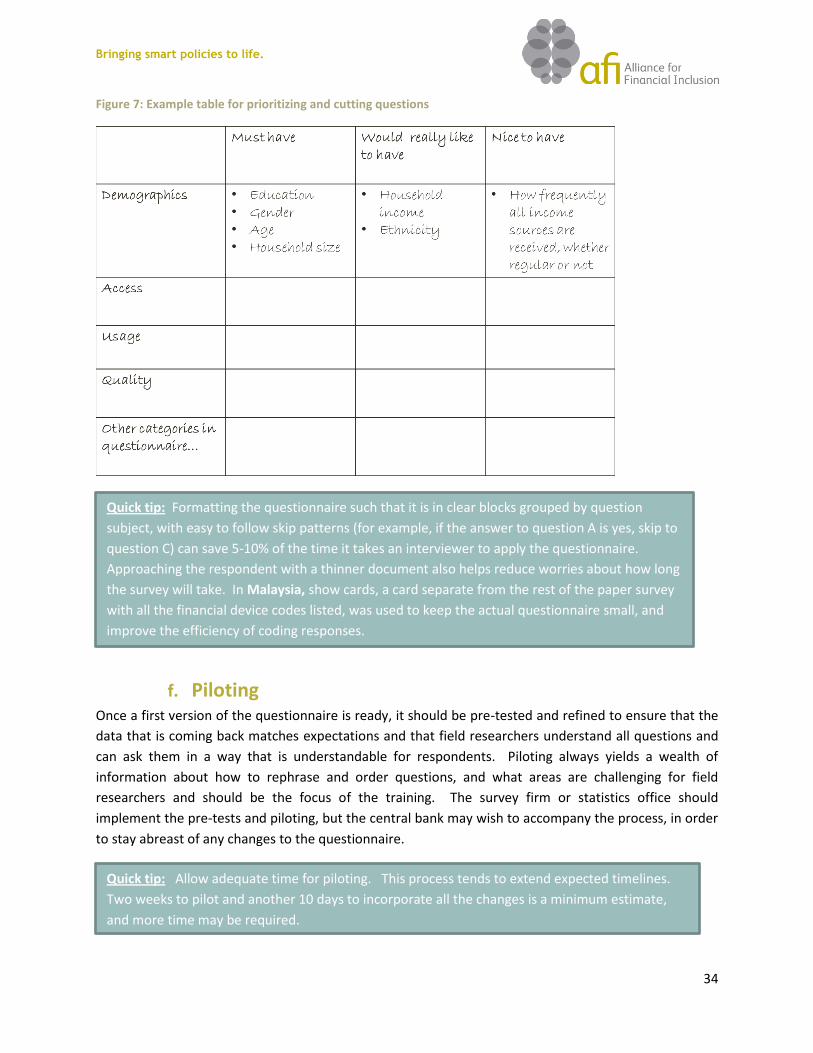

Figure 7: Example table for prioritizing and cutting questions ................................................................... 34

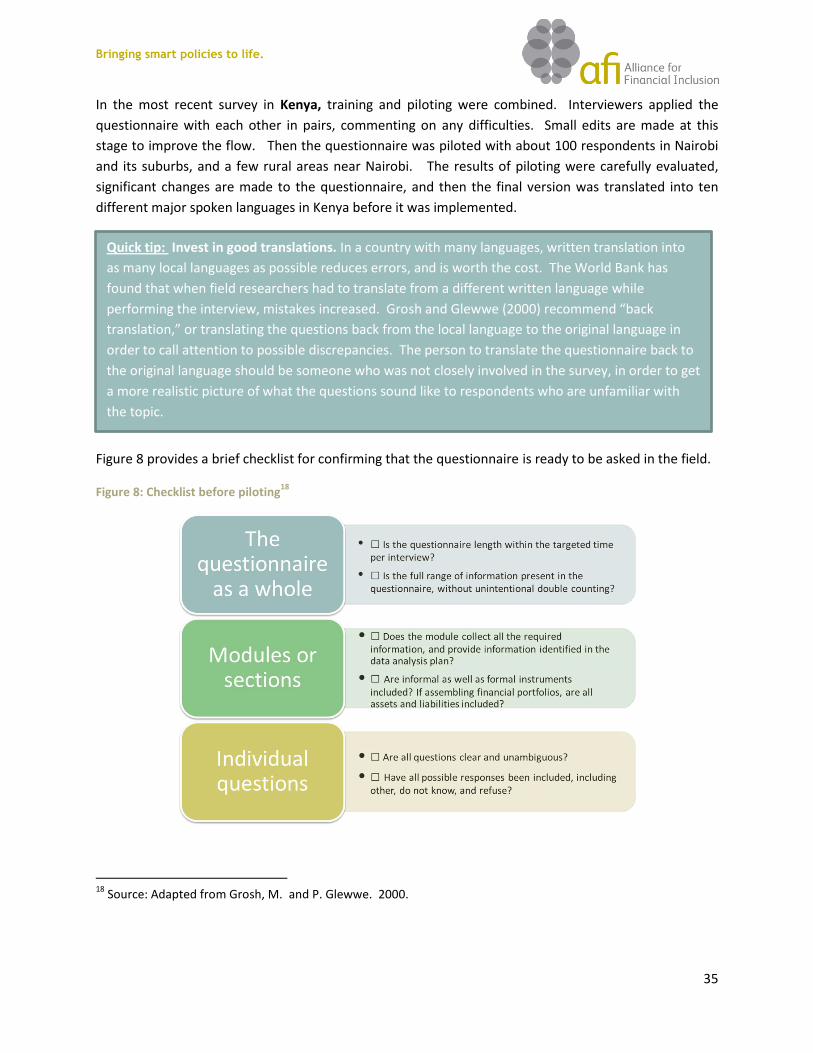

Figure 8: Checklist before piloting .............................................................................................................. 35

Figure 9: Use of financial services by Belarusian adults ............................................................................. 45

Box 1: FinMark Trust FinScope.................................................................................................................... 10

Box 2: Examples of management structures used to oversee the survey process .................................... 11

Box 3: Kenya’s Financial Access Partnership ............................................................................................... 12

Box 4: Selecting a research house or survey company ............................................................................... 14

Box 5: Policy questions guiding demand-side research in Malaysia ........................................................... 18

Box 6: Making Kenya’s FinAccess sustainable through fees to access data ............................................... 16

Box 7: Definition of key sampling terms ..................................................................................................... 23

Bringing smart policies to life.

5

Box 8: Alternative sampling approach when a household listing is not possible ....................................... 25

Box 9: Lessons from country experience in questionnaire design............................................................. 29

Box 10: Topics covered in the Mexico and Zambia questionnaires ............................................................ 30

Box 11: Informed consent ........................................................................................................................... 38

Box 12: Insuring anonymity in financial inclusion ....................................................................................... 38

Box 13: Reporting bias ................................................................................................................................ 39

Box 14: Verification and ensuring data quality ........................................................................................... 40

Box 15: Possible topics the survey firm could include in a field report ...................................................... 40

Box 16: Statistical programs for use in computing sampling errors ........................................................... 43

Box 17: Resources available from the Belarus survey of financial inclusion .............................................. 43

Bringing smart policies to life.

6

Main Findings from AFI experience with demand-side surveys Value of demand-side surveys

A demand-side survey is necessary to gain information on access, usage, and quality

of financial services in addition to information that banks and service providers can

provide.

A nationally-led survey is useful to supplement international data sets by delving into

specific policy questions pertinent to the country context.

Institutional arrangements

Clearly defining roles and having a working group with an appointed coordinator to

manage the survey helps ensure that the process goes smoothly.

Working with the national statistics institute, whether to execute the survey or to

design the sample, is useful, but not necessary for a successful survey.

Good data on market saturation, access among underserved populations, and

geographic patterns of financial inclusion is of interest to many diverse actors, and the

promise of this data can galvanize support for the survey.

Survey design and content

The first time a demand-side survey of financial inclusion is carried out in a country,

the focus should be on establishing a baseline of access to and use of financial

services, while subsequent waves can be focused on measuring progress.

Tailor the survey design— sample size, survey method, length of questionnaire — to

be reasonably implemented within the allocated budget.

Kenya, Tanzania, and Zambia have elected to survey repeated cross-sections of the

population at 2-3 year intervals, with interviews conducted with randomly selected

individuals within the selected households. The majority of the other countries

surveyed are planning a similar approach, although this may not be the best

methodology for all contexts.

Preparation

Plan the stratification, or divisions you want to include in the analysis, such as gender,

administrative units, urban and rural, etc. early on, from the time the sample is

designed.

Prioritize the main questions and themes to be explored in the survey at the onset,

and try to keep the scope narrow. Then group questions into modules or sections on

each topic.

Use qualitative work, such as focus group discussions and semi-structured interviews

to inform the questionnaire design.

Bringing smart policies to life.

7

Main Findings from AFI experience with demand-side surveys,

continued Implementation

Invest in translating the questionnaire into major local languages. Data quality

decreases when researchers have to translate on the spot.

Piloting the questionnaire is an essential step, and this step, along with the related

revisions and re-testing, often takes longer than expected.

It is wise for the central bank or other staff involved in the project to attend the field

researcher training and participate in piloting to ensure that all financial terms are

understood and questions are yielding the desired information.

The survey instrument itself should have a logic and flow, structured around a series of

sections or modules. This helps both the interviewer and the respondent understand

what is being discussed, and progress at a good pace.

Ethical considerations, such as preserving confidentiality and anonymity, are

important. In particular, respondents should provide informed consent, the risks and

benefits of the research should be carefully weighed, and that selection of subjects

should be fair, considering a just allocation of the costs and benefits of research.

Sampling and non-sampling error should be minimized.

Monitor data collection and verification closely, checking for irregularities.

Dissemination and use for policy

Dissemination costs can be significant, but there is a tendency to neglect these costs

that seem far down the line when planning the survey.

Consider innovative approaches to dissemination, such as workshops, TV and radio

distribution and publishing results internationally.

Use the survey to measure willingness to pay, demand for services, financial capability,

and other areas where regulation, policy, and changing incentives can make a

difference for financial inclusion.

Bringing smart policies to life.

8

Practitioners Notes: advice from the field

CNBV Mexico: “It is important to have an individual or office that will champion the

[survey] effort. It pays off to be inclusive, as a national survey on financial inclusion is a

big project. Now everyone is talking about the survey, so there is no need to promote it.”

Bank of Thailand: “The survey should be specific about whether it wants to understand

financial inclusion at a macro or micro and behavioral level. Although demographic and

economic variables need to be included, keep the survey focused on financial inclusion.”

Central Bank of Kenya: “It is important to focus on the common interests participating

actors may share. Banks, savings and credit cooperatives, MFIs and other market

participants have the desire to better understand potential markets and expand coverage

and market share. The government and development partners have an interest in

improving access, especially among the poor, and information is important to be able to

do this in terms of initiating reforms and/or policies that are evidence based. Academia

and research institutes have interests in the rich datasets to undertake more in-depth

analysis and gain further insights into the evolving financial access landscapes.”

Bank of Tanzania: “The lower the level of representation (e.g. national, regional, district,

etcetera), the bigger the sample and the more expensive the survey.”

“The survey should engage a wide range of stakeholders aiming at insuring stakeholders'

understanding of key issues such as sampling, questionnaire design and project

management. This secures "buy in" and maximizes the chances of stakeholders actively

using the data and analysis. This involvement also creates knowledge sharing and

learning at local level to feed back into subsequent surveys. (In Tanzania the stakeholders

in this survey are Bank of Tanzania, commercial banks, microfinance institutions,

government agencies, telephone companies).”

Bringing smart policies to life.

9

I. Introduction A well-functioning financial system is an important building block for economic growth and prosperity.

Fostering an inclusive financial system helps ensure that low-income people will share in the benefits of

growth, by being better able to access credit markets, smooth consumption, and plan for the future.

There has been remarkable international consensus about the importance of financial inclusion for

development in recent years. Regulators and other policymakers are learning about how they can

change laws and incentives in order to reduce barriers to financial inclusion in their countries. But in

order to know where we stand, to set the targets for where we are going, and to track progress along

the way, reliable data is needed.

In an important effort to galvanize support for harmonized financial inclusion data collection, the

Alliance for Financial Inclusion (AFI) has developed a Core Set of indicators, presented in Annex B of this

report. The AFI core set focuses on the access dimension of financial inclusion: the availability of

financial services, and the usage dimension: how many people are using these services and how often.

Indicators are currently being developed to measure the quality of financial products available and of

the overall environment to foster financial inclusion. When collecting data for the AFI Core Set and for

national objectives, especially related to access, policymakers can often collect fairly good data on the

supply of financial services from central bank supervision activities. But to quantify the fraction of

people using various savings and credit instruments1, to understand why some people do not have bank

accounts, and to delve into not just possession of products, but how often they are used and if they

meet clients’ needs, a demand-side survey— a survey of the population— is needed.

While the availability and comprehensive coverage of demand-side data from international datasets is

improving, governments stand to benefit significantly from designing a nationally tailored demand-side

survey of financial inclusion. Central banks and other regulatory authorities that support demand-side

surveys gain indispensable information that they can use as an evidence base on which to make policy

decisions.

This guidance note aims to provide practical advice on all steps required to successfully implement a

demand-side survey of financial inclusion, based on the experience of various Alliance for Financial

Inclusion (AFI) member countries that have recently implemented such a survey.

About this report

Members of the AFI Financial Inclusion Data Working Group (FIDWG) expressed interest in a document

synthesizing the experience and best practices for demand-side surveys at the working group meeting in

Livingstone, Zambia, in March 2012.2 Central bankers and other policymakers, primarily in developing

1 While central banks usually have information about the number of deposit and credit accounts, in many countries

it is not possible to determine which are multiple accounts held by the same individual, making a survey of consumers necessary to determine national access levels. 2 A subgroup to produce this report was formed at this meeting, chaired by Mr. Norbert Mumba at the Bank of

Zambia.

Bringing smart policies to life.

10

countries, are envisioned to be the primary audience for the report. This Guidance Note is based on the

experiences of Belarus, Kenya, Malaysia, Mexico, Tanzania, Thailand and Zambia, all of which have

carried out nationally representative surveys on financial inclusion. To inform the study, interviews

were carried out with staff working in the central banks, or with other officials who have been closely

involved in the survey implementation process in these seven countries. A list of people interviewed for

this report can be found in Annex A.

Background information about each of these surveys is helpful in framing the report. In Belarus the

National Bank worked closely with the Microfinance Center, a regional network in Central and Eastern

Europe and Asia based in Poland, to implement a baseline financial inclusion survey in early 2012. A

survey with a larger sample that will collect information about the barriers to financial access in all

regions of Belarus, allowing for supply and demand of financial services to be mapped in detail, will be

finalized in later in 2012. The Central Bank of Kenya (CBK) together with the Financial Sector Deepening

Trust (FSD Kenya) the Kenya National Bureau of Statistics (KNBS) have implemented demand-side

surveys, called FinAccess, in 2006 and 2009, and have another survey in the pipeline for late 2012.

Bank Negara Malaysia, the Central Bank of Malaysia, commissioned the first demand-side survey of

financial inclusion in 2011. Similarly, the Comición Nacional Bancaria y de Valores (CNBV) in Mexico

completed a national survey of financial inclusion in 2012. The Bank of Tanzania (BoT) has become

more involved with the FinScope survey there through the Financial Sector Deepening Trust Tanzania.

The third demand-side survey is planned for 2012. In Thailand, the Bank of Thailand initiated two

demand side surveys in 2006 and 2010, and has a third survey planned for 2013. The Bank of Zambia

supported the adaptation and implementation of a FinScope survey (see Box 1)3 there in 2005 and again

in 2009, under the Financial Sector Development Plan.

The report proceeds as follows: Part I provides guidance on how to establish strong working

partnerships between organizations implementing the survey, how to select the organization that will

implement the survey, how to tailor the survey to match the available budget, and how to craft a policy-

relevant survey. Part II provides guidance on survey design and implementation— including sampling,

questionnaire design, training fieldworkers, piloting, and supervision. Part III focuses on analysis,

dissemination, and using results for policymaking. A series of annexes offer examples of practical tables

and tools for use throughout the survey process.

3 More information available at : http://www.finscope.co.za/

Box 1: FinMark Trust FinScope

FinMark Trust FinScope Surveys

FinScope is a survey initiative of the South Africa- based FinMark Trust, supported by UK Aid. FinScope surveys

study perceptions and use of financial services among the adult population of a country. Nationally

representative surveys at the individual level, FinScope surveys cover attitudes, behaviors, and use of both

formal and informal financial instruments, with the aim of understanding the financial lives of the population.

To date, the surveys have been primarily implemented in Sub-Saharan Africa.

Bringing smart policies to life.

11

II. Part I: A solid working foundation In many countries, there is sufficient drive and interest in producing a nationally-led demand-side survey

of financial inclusion to garner the support of the government, industry, academics, and other relevant

stakeholders. In other countries, the central bank may need to do significant groundwork to convince

other institutional actors of the value of surveying consumers about their access to and use of financial

services. Regardless of the degree of commitment to the research effort, establishing solid working

relationships and clear roles early on in the process paves the way for a productive and seamless survey

management process.

Although the size of central banks staffs varies, designating a unit or office to support the demand-side

survey, where possible, can deliver considerable gains. The structures various central banks have

established to oversee the survey process are described in Box 2.

Box 2: Examples of management structures used to oversee the survey process

In Malaysia, the Development Finance and Enterprise Department (DFE) was responsible for supervising

the 2011 survey process, designing the questionnaire, and conducting the detailed analysis and report

writing.

In Kenya, the Financial Stability and Access Division of the Research Division of the Central Bank of Kenya

together with Financial Sector Deepening (FSD) Kenya and the Kenya National Bureau of Statistics (KNBS)

organize and manage demand side surveys on behalf of Financial Access Partnership (FAP).

In Mexico, the CNBV created a Financial Inclusion Data unit, which had the time and resources to manage

the demand-side survey conducted in 2011 and 2012.

In Zambia, the Bank of Zambia (BoZ) hosts the Financial Sector Development Plan (FSDP), which is also

under the purview of the Ministry of Finance. A Financial Sector Assessment Program in 2002 resulted in

the recommendation that Zambia collect demand-side data on financial inclusion, and a FSDP working group

was formed to manage this process.

In Belarus, a Deputy Chairman of the National Bank, the head of a special department, and two of their staff

were entrusted with the project. They also hired an external project manager who had significant expertise

in project management for financial inclusion, and was involved with various financial inclusion projects, the

Microfinance Center in Poland and AFI.

In Tanzania the Financial Sector Deepening Trust coordinates stakeholders for the demand-side survey.

Within the Bank of Tanzania, the Microfinance Unit within the Real Sector and Microfinance Department

manages the survey.

In Thailand, surveys have been used to understand more about the financial access situation, including a

focus on financial inclusion as a component of the Financial Sector Master Plan, a 5-year plan to enhance

efficiency, strength, and access of the Thai financial system.

Bringing smart policies to life.

12

a. Engaging stakeholders and working with partners

A strong organizational structure in the central bank, including designating one or two staff-members to

be fully dedicated to the process, is fundamental for the execution of a successful demand-side survey.

However, it is unlikely and perhaps unadvisable for the regulatory body to supervise implementation

entirely on their own. The central bank should engage other stakeholders, such as commercial banks,

academic researchers, experts, and other government agencies, in order to gain an audience for the

results and ensure the largest possible impact of the survey.

As the team from Mexico describes, a balance should be struck between being widely inclusive of

stakeholders in the design and implementation process, and maintaining a single point person or unit to

manage the survey efficiently. The Bank of Tanzania advises that the more local actors involved in the

process, the longer it will take.

In Malaysia, the survey team from Development Finance and Enterprise (DFE) Department compiled

inputs provided by various members of the Financial Inclusion Working Group (FIWG) in the Central

Bank of Malaysia to prepare the first drafts of the questionnaire. In Belarus, the National Bank looked

to the regional Microfinance Center in Poland to gain support and guidance through the survey process.

In Thailand, the five-year Financial Sector Master Plan provided a framework for designing the survey.

The Financial Access Partnership (FAP) in Kenya represents an institutionalized, enduring venture to

support a variety of financial inclusion initiatives. Box 3 describes the FAP in Kenya.

As more countries develop national strategies on financial inclusion, national-level alliances are likely to

form, such as the National Council on Financial Inclusion in Mexico or the National Financial Inclusion

Partnership in Brazil, and these structures can be a natural starting point for raising interest and

support, preparing a captive audience, and articulating the most pressing questions to be answered in a

demand-side survey.

Selecting the organization to implement the survey

Perhaps the most important partnership that will be formed is with the entity that will conduct the

survey itself. It is important to select a research institution that is competent, experienced, trustworthy,

and has the flexibility to work with the central bank and broader working group to ensure good data

collection and meet stakeholder expectations.

The Financial Access Partnership (FAP) is a public-private partnership in Kenya comprised of representatives

from government, industry, research institutes and the Financial Sector Deepening Trust Kenya (FSD Kenya),

which is a development partner. The FAP successfully implemented the 2006 and 2009 FinAccess Surveys, and

is planning the next iteration of the survey for late 2012. Kenyan regulators report that the success of the FAP

emerges from participants coming together around a shared goal of collecting more useful information on

financial access in the country.

Box 3: Kenya’s Financial Access Partnership

Bringing smart policies to life.

13

Selecting the organization that will execute the survey is likely to come down to a decision between the

national statistics institute and a private survey company or research house, or a combination of the two

working together. There are a number of advantages of involving the national statistics office, including:

Experience and technical know-how: National statistics offices often employ top statisticians,

sample design experts, and interviewers that have experience with nationally representative

surveys, such as the census. These offices have intimate knowledge of nationally representative

surveys in the country.

Access to national sample frame: In countries where there is a listing of household addresses

that is produced with each national census, the national statistics institute will have first-hand

access to this information. The address listing is usually needed to design the sample frame for

the financial inclusion survey.

Institutionalization: Working with the national statistics office offers the possibility that the

government will see the value of financial inclusion data, and add a demand-side survey to the

inventory of surveys that the national statistics office periodically performs.

Credibility and recognition: Respondents are accustomed to receiving visits from census

workers, and many more people have heard of the national statistics institute than any given

research house, increasing trust and possibly response rates.

In Mexico, the CNBV was able to engage the national statistics institute, Instituto Nacional de Estadística

y Geografía (INEGI), to implement their 2012 demand-side survey, and were pleased with the

implementation. Similarly, in Thailand the Bank of Thailand and the National Statistics Office (NSO)

carried out the survey once every three years in conjunction with other household surveys the NSO

conducts. Piggy-backing on existing surveys saved the Bank of Thailand considerable funds, and they

only ended up investing US$28,000 in the last survey. In Zambia, the national statistics office, the

Central Statistical Office (CSO), did not execute the survey, but did design a nationally representative

sample of 4,000 respondents, covering all nine provinces and targeting all residents aged 16 years and

above, the age at which Zambians are legally eligible to open a bank account.

Despite the benefits of working with the national statistics institute, the reality is that in many countries

these institutes are still building capacity. National statistics institutes may also already be juggling a full

schedule of surveys. In these cases, qualified survey firms with the capacity to undertake can be

contracted.

In Belarus, there are two main institutions that implement national polls: the Institute of Sociology at

the National Academy of Sciences, and the Belarusian State University. From these options, the

National Bank selected the Institute of Sociology at the National Academy of Sciences because they had

more experience in surveys on financial topics, and, unlike the university, they work all year round.

In Kenya the Kenya National Bureau of Statistics has been heavily involved in the research, participating

as a key member of the FAP. It provided the sample frames for the past two surveys and is currently

finalizing the new address listing for the next survey, which is being updated to consider changes in

administrative units in the country following the promulgation of the country’s new constitution in

Bringing smart policies to life.

14

2010, and using the new 2009 census data. The two previous FinAccess surveys were drawn using the

National Survey Sampling Evaluation Program (NASSEP) IV, which used 1999 census data and was also

based on the old administrative boundaries. FAP, however, contracts an independent research house

through competitive bidding to undertake field work but supervised by both the KNBS and the FinAccess

Secretariat.

The Bank of Tanzania also relied on the national statistics office to design the sample, but hired an

independent research house to carry out the survey. Based on Tanzanian experience, an either/or

decision between the statistics office and the survey company is not necessary, rather a collaborative

arrangement between National Bureau of Statistics (NBS), BoT, and the research house was an optimal

solution for survey implementation in Tanzania. The BoT felt that their established procurement

processes worked well to select a well-qualified research house. However, some central banks may wish

to consider additional factors alongside the standard government procurement rules. A template table

that can be used to evaluate firms is presented in Annex C. Box 4 details the Malaysia and Kenya

experience, and more information on the selection process.

Box 4: Selecting a research house or survey company

b. Budgeting and scope From modest to massive budgets, resources available for demand-side research on financial inclusion

vary. The cost of implementing a national survey also varies widely by country. But gaining valuable

In countries where the national statistics institute is occupied with either the national census or other research,

as was the case in Malaysia, Kenya, and Tanzania or does not have the capacity to implement the survey

themselves, a private survey company or research house can be selected through a competitive bidding

process. In addition to the national bidding procedures and rules, countries may wish to use or adapt the list of

criteria for selecting a research house in Annex C.

Bank Negara in Malaysia found that in selecting a research house, experience with nationally representative

surveys and familiarity with financial topics are important qualifications to consider.

In Kenya, FAP embraces the spirit of competitive bidding to improve on the quality of the survey. Towards this

end and in line with the laid out procurement procedures, a new research house was recruited and this is

expected to bring freshness and new approaches to the implementation process. The new research house

contracted for the third wave of the survey brought the idea of using tablet computers for data collection,

which will result in time and efficiency gains.

The Bank of Tanzania found that having the bank play a coordinating role between the National Bureau of

Statistics, the research house, the Technical Committee and other external advisors was essential to a

successful survey. For a geographically large country like Tanzania, with many stakeholders involved in the

survey, strong partnerships and monitoring is of paramount importance.

The Bank of Thailand found that having the NSO carry out the survey enhances the reliability of the data by

using a nationally representative sample, and provides the benefit of the accuracy of data collection through

the expertise of the NSO’s staff.

Bringing smart policies to life.

15

demand-side insights is still possible with a smaller budget. The essential points are that the research

design must take into account the resources available, and expectations must be adjusted accordingly.

In contrast, a survey for which the ambitions greatly exceed the budget is almost sure to fail. In

addition to the level of funding, the data already available and the research capacity in-country should

also be taken into account in defining the scope of the demand-side exercise, so as not to duplicate

efforts or waste resources on a data collection effort that is beyond the capabilities of researchers in the

country. Figure 1 shows this relationship.

Figure 1: Defining the scope of a demand-side survey4

Funds for the survey can be raised from government sources, contributions from banks and other

industry players, as well as from development partners. Table 1 gives the costs of various survey

efforts.

Table 1: Example costs of country-led demand side surveys

Country Year Sample size Cost5

Kenya 2006 4500 US$ 413,400

Kenya 2009 6500 US$ 551,000

Kenya 2013 TBD US$ 758,000

Malaysia 2011 2000 US$ 120,000

Belarus 2012 2500 Cost of two surveys together and National

Strategy was Belarus 2012 8000

4 Source: Adapted from Grosh, M. and P. Glewwe. 2000.

5 Value calculated in the year in which the survey was done. 2006 surveys in 2006 US dollars, etc.

Bringing smart policies to life.

16

US$291,500

Thailand 2010 11000 $28,000 because done

as an add-on to NSO

annual household

survey6

In Thailand, the Bank of Thailand was able to leverage the fact that the National Statistics Office was

already fielding a large-sample annual national survey to greatly reduce costs. Because the financial

access survey was added on to the NSO’s existing work, the cost for 11,000 interviews was only about

US$ 28,000. In Kenya, the FAP has opted to charge to access the FinAccess data in order generate

revenue for repeated surveys, as described in Box 6.

Box 5: Making Kenya’s FinAccess sustainable through fees to access data

The Bank of Tanzania found that the costs of ensuring national buy-in through consultation, and

dissemination are important to consider. While international surveys may not invest as much in local

consultation and dissemination in the country, the national demand-side survey should direct resources

towards these important steps in order to leverage the survey for the greatest possible impact.

If regulators wish to gain information about the consumer perspective, but do not have the budget to

launch a full-fledged, nationally representative survey, they may choose to reduce the sample size and

survey a particular segment of the population, such as poor and underserved populations, residents in a

major metropolitan area, or social transfer recipients, for example. Qualitative research can also be a

lower-cost alternative, and results of focus group discussions, for example, could be used to inform a

large, quantitative survey further down the road. Alternatively, financial inclusion questions can be

included in household consumption and budget surveys, or other research efforts that the government

6 Using an annual exchange rate of 31.7 Baht/ US$ in 2010

In order to generate revenue and contribute to sustainability of survey efforts, the FAP in Kenya decided to

charge token fees for accessing the FinAccess datasets. Masters students pay US$ 100, PhD students pay US$

300, and industry pays US$ 6000 to access the data set, although exceptions will be granted for needy

students. So far the CBK has raised 6 million Kenyan Shillings (about US$ 70,000) to help fund ongoing waves

of the survey.

Quick tip: Do not ignore national-level consultation and dissemination costs in budgeting. Dissemination is essential to affecting policy change and getting buy-in from private sector, academic, and other stakeholders.

Bringing smart policies to life.

17

already supports at regular intervals, allowing policymakers to track progress on key indicators without

having to fund an independent survey.7

The next section discusses strategies for ensuring that they demand-side survey answers policy

questions.

c. Designing a policy-relevant survey

Each regulatory body faces pressing financial inclusion policy questions—be they related to mobile

banking, use of cash versus electronic payments, agent banking, distance and perceived cost to access

financial services, use of informal financial tools, or many other issues. The demand-side survey offers

the valuable chance to obtain this targeted information and to employ it in evidence-based policy

making. All seven central banks interviewed for this report prioritized establishing a baseline level of

financial inclusion in the first demand-side survey implemented in the country. As stated in AFI (2010),

there are two high-level objectives for which data can be used to support policymaking:

1. Diagnosing the state of financial inclusion to help develop policy solutions, and

2. Monitoring the growth of financial inclusion to modify or create new policy reforms accordingly.

Belarus conducted a snapshot survey of 2500 people to gauge the overall condition of financial access in

the country in early 2012, and the results whet the appetite of policymakers for more data. The

National Bank and partners expanded the sample in a follow up survey later in 2012 to 8000 individuals,

in order to produce a detailed map of availability of financial services compared with use. National

Bank staff were so committed to the expansion of the survey that they opted not to go on a planned

study tour in order to use the money saved to fund the additional surveys.

Similarly, the Bank of Thailand emphasized that they wanted their survey to answer questions about the

macro picture of financial inclusion, and to be able to disaggregate this data at lower administrative

levels. The team focused on this objective rather than understanding micro-level behavior in their

national survey. Kenya and Zambia based their first surveys on the FinScope format, and have

continued to find the Financial Access Strand to be a useful metric in the country.

7 For example, the Central Bank of Brazil has delayed launching a demand-side survey until the national research

institute, Instituto Brasileiro de Geografia e Estatistica (IBGE), can conduct the survey, in the hopes that IBGE will be able to include financial inclusion research questions in its regular national information gathering efforts.

Quick tip: Do not let a small budget deter you from collecting demand-side information. Rather, scale back the scope. Thailand worked with the statistics office to spend less than US$ 30,000 on their survey, and Malaysia managed to implement a nationally representative survey for only US$ 120,000.

Bringing smart policies to life.

18

Box 5 gives more details on the policy questions Bank Negara Malaysia was able to answer by

conducting a demand-side survey.

Box 6: Policy questions guiding demand-side research in Malaysia

Once the institutional arrangements, budget, and scope, have been established, work can begin

planning the phases and timeframe of the research, and preparing the questionnaire itself.

Quick tip: The Financial Access Strand (FAS), developed by FinMark Trust for the FinScope surveys is a useful and internationally comparable measurement of financial inclusion. The Access Strand measures access across the formal-informal provider continuum, ranging from people who are served by formal institutions, to those who use only informal providers, and finally to those who

do not use any provider.

In Malaysia, Bank Negara Malaysia identified high-level objectives of the 2011 demand-side survey, including:

1. To develop an in-depth understanding of Malaysians’ access and use of financial services

2. To gauge whether low-income individuals have equal access to financial products

3. To assess the level of financial literacy among Malaysians, and their attitudes and behaviors with

respect to financial matters

4. To identify the gaps and needs of Malaysians to execute effective financial program in the long term

5. Establish a national baseline for level of financial inclusion

Some specific policy objectives of the survey were:

1. Benchmark willingness to pay for transactions at agents in order to inform Agent Banking Guidelines

2. Understand the penetration and interest by market segments in order to formulate strategies to

enhance usage of internet and mobile banking

3. Probe reception of microinsurance, asking, in which sectors, purposes, and for what type of products

is their demand for insurance, especially among low-income individuals

4. Better understand borrowing options and degree of indebtedness both among the general population,

particularly the low income individuals and microenterprises

Bringing smart policies to life.

19

III. Part II: Survey Design and Implementation Figure 2: Process of survey design and implementation

8

8 Source: Adapted from Yansaneh, I.S. 2005. “Chapter II: Overview of sample design issues for household surveys

in developing and transition countries. United Nations Statistical Division.

Sample design

1. Define target population and sampling frame

2. Define stratification variables for sample design

3. Design the sample- size, domains, stratification

4. Select respondent households from household listing

1. Clarify policy questions and assemble a questionnaire design team

Questionnaire

design

2. Identify modules or blocks around which to organize the questionnaire

5. Pre-test and pilot

3. Iterative revisions of questions and order

4. Expert review

Data collection

and

processing

1. Respondents selected at selected households

2. Data capture

3. Data verification, supervision and quality control

Data analysis

and

dissemination

1. Development of sample weights, code preparation, select statistical program

2. Data analysis

3. Variance estimation

4. Data entry

4. Field report and survey report

5. Produce and release report and public or paid-use file

DEFINE SURVEY OBJECTIVES

Bringing smart policies to life.

20

Once a strong foundation and clear objectives have been established, the team is ready to work towards

writing the instrument, designing the sample, and fielding the survey. Figure 2 shows the steps that are

often required throughout the research process, from defining clear objectives to creating a

dissemination strategy and publishing the report. Note that sample design and questionnaire design can

be done concurrently.

The Bank of Tanzania advises that once the questions for each sub-objective or theme have been

drafted, qualitative research to understand the market prior to the pilot can be used to inform the

possible replies and options.

a. Establishing a timeframe It is helpful to distill and consolidate the many steps in Figure 2. In Mexico, the CNBV identified seven

steps required to plan and implement the large-scale financial inclusion study there, and these steps are

shown in Figure 3.9 AFI member countries that have implemented demand-side surveys report that

taking adequate time, especially in the design stage, is imperative.

Figure 3: Steps used in Mexico's demand-side survey

Having a larger vision of the trajectory of the project, parceled into sequential steps, offers a useful

guiding framework and allows the team to keep the project on schedule. Planning the survey process

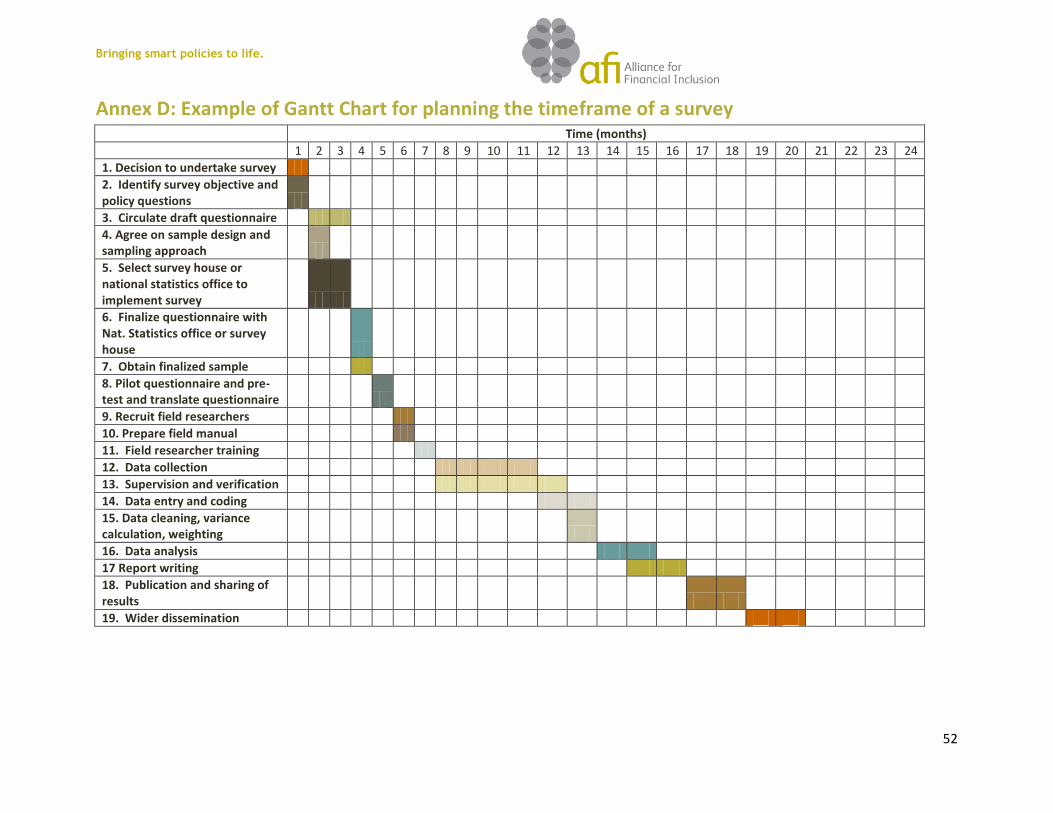

from beginning to end using a Gantt chart can help organize and map this process. Annex D provides an

example of a Gantt chart for hypothetical demand-side survey.

9 The differences between Figure 2 and 3 highlight that each country can define the phases to match their process.

Quick tip: Use qualitative research, such as focus groups and individual semi-structured interviews

to inform the questions and options in the quantitative survey. A large quantitative survey should

not have open ended questions, which make coding and analysis extremely difficult. In Tanzania,

qualitative research was useful in understanding how people speak about their financial behavior

to inform the wording and structure of the survey.

Quick tip: Consider any holidays, seasonal practices such as harvests, school holidays, elections, and

weather events such as monsoons or rainy seasons when planning the timing of the survey. Fielding

a survey when interviewers cannot travel or respondents are not at home can at best yield atypical

data and at worst jeopardize the collection of enough interviews.

Bringing smart policies to life.

21

The Bank of Thailand reported that the timeline to execute the project from start to finish improves

with each wave of the survey due to experience gained. In 2010 the process took about nine months,

not including data analysis and report writing.

b. Gap analysis When deciding to do a demand-side survey, the first step is to assess the information available from

existing sources. This process allows the central bank to determine the specific gaps and data needs.

IFC (2011) and IFC and CGAP (2011) are good starting points for identifying all the international data and

sources. In Mexico, the CNBV was able to delegate this task to a consultant, who completed the gap

analysis over the course of a few months. One person’s time dedicated to mapping existing data should

be sufficient. In Tanzania, the BoT found that if the demand-side survey is also intended to be useful

for the private sector, stakeholders must understand what data banks, telecoms, and other players

already have. Once the data needs have been clearly identified, agreeing on the best survey design to

obtain the desired information is a good next step.

c. Approaches to survey design

There are a variety of survey designs that can be employed in demand-side analysis, as portrayed in

Table 2, adapted from AFI (2010). Most AFI-member countries plan to undertake repeated cross-section

surveys, in order to be able to track progress in achieving financial inclusion without incurring additional

costs and challenges to response rate that are characteristic of panel surveys.10 In a repeated cross

section, it is useful to have a core of questions that do not change and are asked in exactly the same

way, so as to accurately measure change.

Table 2: Possible Survey Designs11

Type of survey

Definition Survey objective Examples

One-time cross section

Cross –section of the population is randomly selected and interviewed once

Snapshot of the current level of financial access

FinScope – In many countries there is not a specific intention to repeat the survey at a regular interval World Bank Living Standards Measurement Surveys- have only been implemented once in select countries

Repeated cross section

Cross-section of the population is randomly

Monitor progress of financial

FinScope South Africa- is repeated annually. FinScope Zambia has been

10

Finding the same respondents after years have passed can be challenging and costly. Panel data is very useful to more precisely measure causal impact, but the nonresponse rate in such surveys can be high. 11

Source: Adapted from AFI 2010.

Bringing smart policies to life.

22

selected and interviewed once. After an interval passes, another cross section of the population that has similar population characteristics when compared to the first is randomly selected and interviewed once.

inclusion over time. repeated about every three to four years FinAccess Kenya and the survey in Thailand -have been repeated twice and is to be repeated every three years Belarus, Mexico, and Malaysia – have so far undertaken one survey, although they plan to do a repeated cross section Global Findex- only carried out once thus far, planned to be annual

Panel or longitudinal study

The same households or individuals are interviewed multiple times at regular intervals.

Can be used to show causal impact of policy or other changes if the correct controls are included.

EEViH- (Mexico) household quality of life survey conducted with the same families every 3-4 years Townsend Thai Project household study beginning in 1997 with annual and monthly panels Financial diaries- research studies the cash flows and use of financial products in a household with fortnightly interviews over the course of one year12

In Malaysia, many questions from the first wave of the demand-side survey will be repeated in

subsequent waves, specifically questions on performance indicators for products and services provided

by the financial institutions and access levels. But some questions that were just needed for certain

policy purposes may be reviewed or dropped and new questions will arise as new policy issues become

pertinent. Indeed, as the financial access landscape can change quickly, questions and options must also

remain current. For example in Kenya, the 2006 survey did not include any questions about M-PESA or

other mobile money transfer facilities. These needed to be added to the 2009 survey, and the 2013

survey will need to add more questions about agent banking.

The sampling approach is a key component of survey design. The next section provides an overview of

key topics in sampling for demand side surveys.

12

In 2012-2013 Financial Diaries research is being carried out in Kenya, South Africa, India, Mexico, United States, and a modified version in Rwanda.

Bringing smart policies to life.

23

d. Sampling13 Policymakers will certainly engage experts to design the sample, but it is nonetheless valuable for

officials to obtain background knowledge on various sampling techniques and procedures. To

understand important elements of sample design, definitions of key terms will be useful. Box 7 provides

a list of key terms. 14

13

Some elements of this section are slightly technical, and can be skipped by readers who will outsource the sample design and do not need to supervise the process closely. 14

Source: Adapted from Lohr,1999. Sampling: Design and Analysis.

Box 7: Definition of key sampling terms

Observation unit- An object on which measurement is taken. In financial inclusion surveys, the observation

units are often individuals or households.

Target population- The complete collection of observations we want to study. In national demand-side

surveys this is often the adult population over 15 or 16 years old, small differences in the age of adults can

seriously affect the statistics that result.

Sample- A subset of a population.

Sampled population- The collection of all possible observation units that might have been chosen in a sample,

for example all adults in the country.

Sampling frame- The list of possible sampling units from which the sample can be selected. For a household

survey this is the list of all street addresses, for a small business survey this is the list of all businesses under a

certain size.

Enumeration area (EA)- The geographic area canvased by one census worker. The smallest division used in a

census.

Strata- Subgroups of interest to the research that are used in selecting the sample. In demand-side surveys

this might be the urban and rural populations, regions of a country, or income groups.

Sampling error- The margin of error, or the error that results from taking one sample instead of examining the

whole population.

Non-sampling error- Errors in the survey process, such as inaccuracy of responses, selection bias, or other

errors that cannot be attributed to sample-to-sample variability.

Representative- each sampled unit will represent the characteristics of a known number of people in the

country.

Bringing smart policies to life.

24

Probability Samples: simple random samples and clustered stratified samples

Probability samples are the most accurate type of samples for representative surveys. In a probability

sample, each population unit has a known, non-zero probability of selection into the sample.

The simple random sample (SRS) is the most simple sample design. In this methodology for a SRS of

sample size N, each subset of the population of size n has an equal chance of being selected. In a SRS no

members of the population are excluded a priori (including remote populations or regions in conflict),

and all have an equal chance of selection.

However, for practical reasons, most demand-side surveys use a clustered and stratified sample.

Clustered sampling is when clusters, such as census enumeration areas or villages, are selected in a first

tier selection before individuals are selected. Using clusters reduces the variation in the information

collected, but is much more practical in allowing interviewers to visit a smaller number of places and

stay there for a bit longer.

For stratification, the population is divided into groups, or strata, and then a random sample is taken

from each group proportional to the proportion of the population this group represents. Since elements

in the same strata are likely to be more similar than randomly chosen elements, the precision of

estimates increases in stratified samples.15 In demand-side surveys common strata include regions,

urban/rural, poor/ non-poor, and ethnic groups. This sampling approach allows for analyzing differences

among groups.

Sample size

In order to be able to accurately report on variables such as the number of adults with regulated

deposits and credit accounts, the sample of the financial inclusion survey should be nationally

representative, such that each interview can be backed out to represent a given proportion of the

population. A big question, then, is how large a sample is needed to create a nationally representative

survey? Annex E contains a more technical appendix on calculating sample size and an example of this

calculation for Belarus.

Even without getting into the math, it is useful to know that a good statistician can design a nationally

representative sample that is still manageable with a reasonable budget. On average, a sample size of

between 2000 and 3000 is usually sufficient for a nationally representative sample with some

stratification. The Central Bank of Malaysia had originally budgeted about US$ 150,000 for its demand-

15

Lohr, 1999 p. 24

Quick tip: If the central bank knows it wants to analyze the difference in financial access among

given populations, it is strongly recommended to include these characteristics as stratifications of

the sample, for example urban/ rural divisions or regions in the country. It is wise to define these

categories of interest early on in the survey design process, as they will have implications on

sample size, questionnaire design and resource allocation.

Bringing smart policies to life.

25

side survey, and ended up spending closer to US$ 120,000 because the research house was able to craft

a nationally representative sample with a smaller sample size than the project had originally budgeted

for (a sample of 2000 with the Malaysian population at 28.7 million in 2011). Larger samples are

needed as you add more layers of stratification and add representation at smaller administrative units.

For example, in Thailand, a sample size of 11,000 is statistically sufficient for a nationally representative

sample that can be disaggregated at lower administrative levels, with the Thai population at

approximately 65 million in 2010.

The sampling frame

The quality of the data obtained in a household survey often depends on the quality of the sample

frame. The seven countries interviewed for this note used a recent listing of household addresses in the

country, often from the most recent census, as the sample frame. In Kenya, the national sampling

frame is changing in 2012, as mentioned, due to the promulgation of the new constitution that changed

the administrative boundaries in the country and use of the new census data. Although FAP had

planned to field the next wave of the demand-side survey in 2011, it was postponed due to delays in

finalization of the development of the new NASSEP V which reflects the new administrative boundaries

and the new 2009 census data, as mentioned. Commendable progress has been made on this front and

the survey may be undertaken in the months of October and November 2012 once the frame is

finalized.

In some countries, a household address listing does not exist or is of such poor quality that it is unusable

for a large-scale survey. In such cases, small administrative units can be selected randomly, and a listing

can be done within these enumeration areas to select the households. However, the process of listing all

addresses, even in a subset of enumeration areas, is often very costly.

Box 8: Alternative sampling approach when a household listing is not possible

When a listing cannot be done, sampling may be carried out using a systematic or random walk approach. In

this methodology, enumeration areas (EA) are selected based on the chosen stratification. Then, using the

sample size of the survey, one can determine how many interviews should take place in each EA. For example,

if the survey has a sample size of 2000 individuals and 200 EA are selected to be visited, there should be 10

interviews in each to reach 2000 interviews. If the approximate number of households in an enumeration area

is known from the census, this number of households in the EA should be divided by 10, coming up with a

number x.1 Field researchers should then start in a designated place in the EA, and should visit every x houses

to conduct the interview.

This approach achieves similar results to selecting addresses randomly from a listing, as long as there are no

patterns in household blocks or formations of households in villages, although it is seen as less statistically

rigorous than using an address listing. When using this method researchers should be monitored carefully so

they do not stay from this pattern, which could result in bias. In a percentage of the EAs repeat visits should be

made to make sure the methodology is being followed.

Bringing smart policies to life.

26

Individual versus household sample and identifying the respondent

When defining the observation unit, an important consideration is whether to collect information about

the household or the individual. FinScope and most demand-side surveys done by AFI members thus far

have chosen the individual as the observation unit. This permits measurement of the number of adults

with regulated credit and deposit accounts in a country.

Note that if the head of household is interviewed, as is the best practice when collecting information

about the whole household, the individual data gained is not representative of the financial access of all

adults in the country, but is representative of the heads of households in the country. Furthermore, a

household-level survey will not be comparable with individual level surveys in other countries. Cull and

Scott (2009) performed an experiment using different interview designs in Ghana, and found that asking

the head of household about the household level information is nearly equally as reliable as asking all

household members about their individual use of financial services. Therefore, if doing a household

survey it is sufficient to interview the head of household.

If the interview will be at the individual level, the respondent must be selected randomly within the

household. Therefore, there will be three layers of randomization in the sample process, as depicted in

Figure 4. One drawback of surveys of individuals’ financial inclusion is that an individual who reports

only accounts in their name may understate their access, as he or she may have access to products that

are officially in the name of another household member.

Figure 4: Levels of random selection in a sample of individuals

Bringing smart policies to life.

27

The decision to interview randomly selected individuals or heads of households should also be driven by

the country context and policy. For example, if in the country, culturally, women or another group are

thought to have lower access levels, and this is a policy priority, individual-level surveys will do a better

job of capturing these differences. If the assumption is that households are run with equal benefit to all,

a household-level survey might give a more appropriate picture.

In Thailand, the 2006 survey interviewed heads of households about the entire household’s financial

instrument use. However, in the 2010 survey, the heads of the households were interviewed to assess

the level of his or her inclusiveness in financial services at the individual level. In this regard, the

information gained from the heads of the households was used to draw conclusions about the level of

inclusion among heads of households in the Thai population. Household level information was not

considered in 2010 because those heads of the households might not accurately know the financial

transactions of the other household members.

If the survey will be done at the individual level, one way to select a random adult is to list all the adults

in the household and choose the one who has the next birthday. However, AFI members have found

that in rural communities it is not uncommon for people not to know their date of birth. This also leaves

more temptation for fieldworkers to alter the “next birthday” to be someone who is more easily

accessible or already in the household at the time of the interview, so that they do not have to go back.

A more widely used method is the Kish table for random selection of a respondent. This grid uses the

number of people in the household and the number of the current interview in the enumeration area to

randomly select a household member. This method, which has been used by field teams in Kenya and

elsewhere, is explained with a sample table in Annex F.

Weighting

When the data is cleaned and ready for analysis it is incorrect to start calculating means and

percentages straight away: weights must be applied and used in the analysis. Therefore the

engagement of statisticians should continue through the analysis stage, and if the central bank or

regulatory authority is to be engaged in the analysis, it is important to bring someone on board who can

do calculations with weights.

Although this guidance note will not go into the details of weighting during analysis, it is important to

understand that observations will need to be weighted in order to gain representative estimates. The

weights in a nationally representative sample can be thought of as how many other people in the

country the individual represents. As Yaseneh (2005) describes in a guidance document on household

surveys in developing countries produced by the UN statistical division,

“Sampling weights are needed to compensate for unequal selection probabilities, for

nonresponse, and for known differences between the sample and the…population. The weights

should be used in the estimation of population characteristics of interest and also in the

estimation of the standard errors of the survey estimates generated.”

Bringing smart policies to life.

28

It is best to consider how the weighting will be done during the sampling design stage, although the final

weights can only be calculated after data collection to take into account nonresponse rates. Note that

questions about the household and questions about the individual will be weighted differently,

considering the number of households or individuals the respondent represents at the national level.

While the sample is being defined, central bank staff will likely be more substantially involved in the

questionnaire design, discussed in the next section.

e. Designing the questionnaire A well-designed questionnaire, also known as a survey instrument, can yield a wealth of information

about financial access, usage, and quality. But there will likely be a myriad of possible questions,

requiring the working group or steering committee to prioritize and improve useful, policy- and industry-

relevant questions, while eliminating less useful ones. The process of trimming down the survey

instrument will be easier if objectives are clearly identified early on in the process.

After the objectives are clearly identified, collecting the questions and forming the design team are

steps 1 and 2 to designing a strong questionnaire, as depicted in Figure 5.

Figure 5: Five steps in questionnaire design

Quick tip: Make sure the primary research objectives are defined and understood by all

contributors early on. Based on BoT experience in Tanzania, it is difficult to cut questions without a

clear prioritization ex-ante. Prioritization of subject areas to investigate should be done before the

questionnaire is designed.

Questionnaire

ready for pilot

testing, final

revision, and

translation

Bringing smart policies to life.

29

Forming a data analysis plan early on in the process also helps focus the objectives of the research, and

ensures that the team will have all the variables included that the team wishes to consider in the

analysis. An example of a table that can be used in the data analysis plan can be found in Annex E.

In step 3, organizing the survey instrument around modules, the themes of the questionnaire should be

grouped into sections, making it easier to organize and formulate the questions. In step 4, the actual

drafting of questions, it is important to use the most simple and clear way to phrase questions.

In Mexico, the CNBV learned in piloting that respondents had different understandings if seemingly

straightforward terms, like saving. When asked if they save, respondents thought only of bank accounts

instead of including the small amounts of money they may keep in the house, in tandas (savings groups),

or in physical assets. Asking “how do you keep your money?” worked better than asking, “Do you

save?” Box 8 provides additional advice on questionnaire design from AFI members.

While some central banks have found it useful to start from a model questionnaire, the Bank of

Tanzania warns that countries should be careful to clarify intellectual property issues and seek

permission to use an existing instrument. For example the FinScope surveys are propriety material of

FinMark Trust. As mentioned, the BoT found focus group discussions and other qualitative methods

extremely useful in designing an appropriate questionnaire. And while the 2009 survey was modeled on

other examples, the 2013 survey uses priorities set entirely by national stakeholders including the BoT,

National Bureau of Statistics, and Financial Sector Deepening Trust Tanzania.

Box 9: Lessons from country experience in questionnaire design

In Zambia and Tanzania, the FinScope core questionnaire was subsequently adapted to the respective country

contexts in close consultation with national stakeholders. In Tanzania qualitative research was done before

embarking on the quantitative survey, and information from focus groups and qualitative interviews was

invaluable in designing the instrument.

In Mexico the CNBV began by designing the survey instrument based on questionnaires from international

organizations, but the team now advises against doing this. The CNBV ended up starting fresh with a survey

instrument that was sufficiently simple, flowed naturally in Mexican Spanish, and was adequately tailored to

the country context.

In Kenya, the original questionnaire in 2006 was based on the FinScope survey from South Africa, but has

changed substantially since then to address the specific country context. The CBK shared a draft questionnaire

with AFI members of the data working group, and gained useful feedback and suggestions.

In Belarus, the National Bank drew on the experience and knowledge of researchers with the Microfinance

Centre, based in Poland, who had significant experience in studying financial access and microfinance. Since

the study was the first of its kind in Belarus, the country opted to start from this framework and adapt this

questionnaire to the local context.

In Malaysia, Bank Negara Malaysia saw that the comparative advantage of the research house is to tweak the

wording and order of the instrument, to make the survey more effective and manageable for the fieldwork.

Bringing smart policies to life.

30

Modules and topics to include in the survey instrument

The survey instrument itself should have a logic and flow, structured around a series of sections or

modules. This helps both the interviewer and the respondent understand what is being discussed, and

progress through it at a good pace. The questionnaire should include questions about demographic

characteristics that can be used as covariates in regressions, or simply to find averages for populations

of interest (women with an account, rural residents receiving remittances, etc.)

Mexican questionnaire structure

1. Section 1: Residents and Households in Dwelling

2. Section 2: Socio-demographic features of household members

3. Section 3: Socio-demographic features of the selected member

4. Section 4: Financial Capabilities and Income

5. Section 5: Informal and Formal Savings

6. Section 6: Informal and Formal Credit

7. Section 7: Insurance

8. Section 8: Retirement Savings Accounts

9. Section 9: Remittances

10. Section 10: Use of Financial Means

Topics in the Zambian Questionnaire

1. Access to, and usage of, formal and informal financial products and services

2. Household economic, financial and risk management

3. Financial discipline and knowledge

4. Attitudes to, and preference for, financial service providers

5. Features associated with products and providers

6. Asset accumulation patterns

7. Remittances

8. Access to, and usage of, technology

9. Psychographics and lifestyles

10. Business finance issues.

Categories of financial instruments in the Thai questionnaire

1. Savings

2. Loans

3. Credit cards

4. Payments transfer

5. Savings insurance

6. Other insurance

7. Government bonds

8. Private bonds, securities, and managed funds

9. Shares