Deepak Nitrite Limited (DNL) - Anand Rathi

18

Anand Rathi Research Time Horizon – 12 Months May 11, 2017 Mar-17 Dec-16 Sep-16 Jun-16 Promoter 46.5% 52.0% 52.0% 52.0% Institutions 26.0% 17.4% 14.1% 14.0% Others 27.5% 30.6% 34.0% 34.0% Total 100% 100% 100% 100% Source: Company, Anand Rathi Research, Bloomberg V A L U E P I C k (In ₹ Mn.) FY-16 FY-17 FY-18E FY-19E Net Sales 13,729 13,604 15,313 30,130 EBITDA 1,663 1,382 2,220 4,595 EBITDA Margin 12.1% 10.2% 14.5% 15.3% PAT 627 978 984 2,386 EV/Sales 1.4 1.5 1.3 0.7 EV/EBITDA 11.7 13.8 8.6 4.2 P/E (x) 29.0 18.6 18.5 7.6 Price Performance CY14 CY15 CY16 YTD Absolute 172% -10% 25% 51% Relative 134% -9% 21% 32% Analyst: Narendra Solanki [email protected] Relative stock performance (Aug’15=100) CMP: ₹139 Target: ₹179 Shareholding Pattern (as on Mar’17) Key Data Bloomberg Code DN IN NSE Code DEEPAKNTR BSE Code 506401 Sector Chemicals Industry Basic & Diversified Chemicals Face Value (₹) 2.0 BV per share (₹) 55 Dividend Yield (%) 0.9% 52 Week L/H(₹) 71 / 149 Market Cap. (₹ Mn.) 18,169 Deepak Nitrite Limited (DNL) 80 100 120 140 160 180 200 220 Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17 Nifty 500 DDEEPAKNTR

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Deepak Nitrite Limited (DNL) - Anand Rathi

Anand Rathi Research

Time Horizon – 12 Months

May 11, 2017

Mar-17 Dec-16 Sep-16 Jun-16

Promoter 46.5% 52.0% 52.0% 52.0%

Institutions 26.0% 17.4% 14.1% 14.0%

Others 27.5% 30.6% 34.0% 34.0%

Total 100% 100% 100% 100%

Source: Company, Anand Rathi Research, Bloomberg

V

A

L

U

E

P

I

C

k

(In ₹ Mn.) FY-16 FY-17 FY-18E FY-19E

Net Sales 13,729 13,604 15,313 30,130

EBITDA 1,663 1,382 2,220 4,595

EBITDA Margin 12.1% 10.2% 14.5% 15.3%

PAT 627 978 984 2,386

EV/Sales 1.4 1.5 1.3 0.7

EV/EBITDA 11.7 13.8 8.6 4.2

P/E (x) 29.0 18.6 18.5 7.6

Price Performance CY14 CY15 CY16 YTD

Absolute 172% -10% 25% 51%

Relative 134% -9% 21% 32%

Analyst: Narendra [email protected]

Relative stock performance (Aug’15=100)

CMP: ₹139

Target: ₹179

Shareholding Pattern (as on Mar’17)

Key Data

Bloomberg Code DN IN

NSE Code DEEPAKNTR

BSE Code 506401

Sector Chemicals

Industry Basic & Diversified Chemicals

Face Value (₹) 2.0

BV per share (₹) 55

Dividend Yield (%) 0.9%

52 Week L/H(₹) 71 / 149

Market Cap. (₹ Mn.) 18,169

Deepak Nitrite Limited (DNL)

80

100

120

140

160

180

200

220

Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17

Nifty 500 DDEEPAKNTR

2 Anand Rathi Research

Established in 1970s by Mr. C.K. Mehta (Founder & Chairman), Deepak Nitrite Limited (“DNL”) is an Indian chemical manufacturing company.Enjoys a leading market position in most of its products in the domestic as well as global markets.

DNL is on of the leading global player for several niche chemical products like Xylidines, Cumidines, Oximes & Colour Intermediates andcaters to several industries - Colorants, Petrochemicals, Agrochemicals, Rubber, Pharmaceuticals, Paper, Textile, Detergents, Fine &Specialty Chemicals, etc.

DNL currently operates its businesses with three main SBUs namely Bulk Chemicals segment, Fluorescent & whitening agents segment andFine & speciality segment each contributing 56%, 20% and 24% to the revenues respectively.

During the latest quarterly results ending March-17 the company has reported revenues of ₹3254 million as against ₹3408 millions, a de-growth 4.5%. The de-growth was mainly due to temporary shut down of its manufacturing facilities in Hyderabad and Roha which hassubsequently restarted production gradually. As per the management the capacity utilisation should reach at normal levels by May-17.

On profitability front, the company’s EBITDA margins stood 12.1% at ₹393 million in Q4-FY17 as against 13.7% at ₹466 million and its PATmargins stood 6.4% at ₹208 million as against 6% at ₹206 million in Q4-FY17. The margins were also lower due to the shutdown which led toincrease in operational costs due to lower utilisations. On normalised basis the company’s operating margins would have been higher in thecurrent quarter due to improved product mix.

DNL has recently increased its focus on adding high value products and moving higher in the value chain to improve its profitability in longterm. As a result the company has renamed its Bulk chemicals segment to Basic chemicals segment and Fluoroscent & whitening segment toperformance products segment.

DNL is undertaking a greenfield expansion plan at Dahej, Gujarat for manufacturing phenol (2,00,000 ton/year) and acetone (1,20,000T/year). The project is already under execution and is expected to complete by Dec-17. Due to India’s dependent heavily on the imports dueto lack of domestic production capacity and imposition of around 7.5% cumulative anti-dumping duties, the macro scenarios for thedomestic market looks promising for DNL.

The company has already incurred around ₹4750 million towards the project. The total revised capex for this project stands at ₹14,000millions to be funded by 60 : 40 debt to equity ratio for which financial closure has already achieved.

We re-initiate our coverage on Deepak Nitrite Limited with a BUY rating and a target price of ₹179 per share.

A well known chemical company with proven track record in chemicals sector.

Deepak Nitrite Limited (DNL)

3 Anand Rathi Research

Q4-FY17 Results (Consolidated)

Source: Company, Anand Rathi Research

Deepak Nitrite Limited (DNL)

(In ₹ mn) Q4-FY17 Q4-FY16 Chg FY17 FY16 Chg

Net Sales 3,254 3,408 -4.5% 12,216 13,357 -8.5%

Operating Expense 2,861 2,941 -2.7% 10,764 11,690 -7.9%

EBITDA 393 466 -15.6% 1,451 1,667 -12.9%

Other Income 3 8 39 15

Depreciation 107 103 423 395

EBIT 290 372 -22.0% 1,068 1,288 -17.1%

Interest 83 78 309 374

PBT 207 294 -29.6% 759 913 -16.9%

Tax 41 88 388 262

Exceptional Items 42 - 750 -

PAT 208 206 0.9% 1,120 652 72.0%

Margins Q4-FY17 Q4-FY16 Chg BPS FY17 FY16 Chg BPS

Operating Margin % 12.1% 13.7% -159 11.9% 12.5% -60Net Margin % 6.4% 6.0% 34 9.2% 4.9% 429

4 Anand Rathi Research

Spread across key chemical hubs of the country…

Manufacturing Facilities

Source: Company, Anand Rathi Research

Nitration

Alkylation

Nox Absorption

Hydrogenation

Sulphonation

Condensation

Diazotisation

Oxidation

Expertise in multiple chemical processes

Deepak Nitrite Limited (DNL)

5 Anand Rathi Research

…offering products throughout key chemical value chain.

Business Segments

Source: Company, Anand Rathi Research

Fine & Specialty Chemicals Basic ChemicalsPerformance

Products

Deepak Nitrite Limited (DNL)

6 Anand Rathi Research

With revenue well distributed over products and geographies.

Source: Company, Anand Rathi Research

Colour, 58%Agro, 22%

Fuel Additives, 17%

Pharma, 1% Others, 2%

Europe48%

U.S.23%

China8%

Others21%

Product wise revenues (FY-16)Segment wise revenues (FY-17)

Exports geography wise revenues (FY-16)Domestic vs Exports revenues (FY-17)

Deepak Nitrite Limited (DNL)

Basic Chemicals51%

Fine & Speciality Chemicals

29%

Performance Products

20%

Domestic61%

Exports39%

7 Anand Rathi Research

Basic and Specialty segments performance remain stable to positive…

Fine & Specialty Chemicals

Source: Company, Anand Rathi Research

Basic Chemicals Segment

Basic Chemicals segment contributed almost 52% to revenues of DNL’s high volume segment consisting of manufacturing of both organic &

inorganic chemicals that are made to standard specifications. While on margins front its average EBIT margins for the financial year ending March-

17 stood at 14% as against 12% in FY-16.

This SBU can be further classified under Nitro Toluene, Ortho Toluene and Inorganic Chemicals such as Sodium Nitrites & Sodium Nitrates. DNL

plans to leverage on its cost leadership to enhance volumes & drive profits in this segment. The company also plans to increase contributions from

its high value products within the segment.

The Fine & Specialty Chemicals segment contributing around 30% to revenues in FY-17 including niche products that require greater value

addition and is segregated into Specialty Chemicals, Xylidines, Oximes, Cumidines, Nitro Oxylene amongst others.

These products are customized as per customer specifications and find application in the manufacture of agrochemicals, pharmaceuticals,

pigments, paper, hair colour, etc. TheEBIT margins for this segment in FY-17 stood at 24% as against 25% in Fy-16.

Deepak Nitrite Limited (DNL)

8%

11%

13%

16%

18%

-

600

1,200

1,800

2,400

Q1-FY16 Q2-FY16 Q3-FY16 Q4-FY6 Q1-FY17 Q2-FY17 Q3-FY17 Q4-FY17

Revenues ₹ Mn. EBIT % (RHS)

11%

17%

23%

29%

35%

-

350

700

1,050

1,400

Revenues ₹ Mn. EBIT % (RHS)

8 Anand Rathi Research

…while performance products segment remains muted with green shoots visible.

Performance Products Segment

Source: Company, Anand Rathi Research

Performance products segment (Fluorescent Whitening Agents) contributed around 19% to revenues is an application

chemical and is commonly known as Optical Brightening Agent (OBA). DNL is a fully integrated manufacturer of FWA.

OBA has wide applications in varied industries - Paper, Detergents, Textiles, Coating Applications in Printing & Photographic

Paper the products in this segment can be customized into liquid or powdered form, as per the customer’s requirements.

The segment has reported a volume de-growth of 5% in FY-17 due to unplanned Hyderabad plant shutdown. However,

change in product mix towards application in textiles and detergents and widening its focus to include additional markets

and end-user industries is expected to achieve accelerated volume growth going ahead.

Deepak Nitrite Limited (DNL)

-15%

-10%

-5%

0%

-

225

450

675

900

Q4-FY15 Q1-FY16 Q2-FY16 Q3-FY16 Q4-FY6 Q1-FY17 Q2-FY17 Q3-FY17 Q4-FY17

Revenues ₹ Mn. EBIT % (RHS)

9 Anand Rathi Research

New capacity expansion to lead revenue growth…

Phenol & Acetone Project

Source: Company, Anand Rathi Research

DNL is currently in process to set up its new production unit for producing Phenol and Acetone at Dahej. The

project is being set up with technological tie up with KBR (USA), a licensor of phenol production process.

The company has already achieved financial closure and preliminary engineering work has also been completed

at the site. As of March-17, an amount of ₹4,750 million has already been invested for the Cumene plant which

will serve as a feedstock.

The project execution is progressing within scheduled timelines and is expected to get operationalized by

December 2017. Revenues from this project is expected to be reported in Q4-FY17 onwards.

Deepak Nitrite Limited (DNL)

10 Anand Rathi Research

…presenting DNL an opportunity to make inroads into domestic markets.

Source: Company, Anand Rathi Research

Deepak Nitrite Limited (DNL)

11 Anand Rathi Research

We expect DNL to almost add ₹1,600 to ₹1,700 million through new project going ahead.

Revenue estimates (₹ Mn.)

DNL with its new Phenol project at Dahej coming online by Q4-FY18, the top line for the company is expected to be almost get

doubled by FY-19E. Due to India’s dependent heavily on the imports due to lack of domestic production capacity and imposition of

around 7.5% cumulative anti-dumping duties, the macro scenarios for the domestic market looks promising for DNL.

We have in our projections for the new project have assumed utilisation levels at 65% in FY-19E and with this we expect DNL to

report around ₹1,300-1,400 million in sales from phenol and acetone combined.

On margins front we expect DNL to improve its margins gradually over next two years and further increase in margins in FY-19E on

back of phenol project.

Source: Company, Anand Rathi Research

EBITDA & EBITDA margin estimates

Deepak Nitrite Limited (DNL)

10%

12%

13%

15%

16%

-

1,200

2,400

3,600

4,800

FY-15 FY-16 FY-17 FY-18E FY-19E

EBITDA (₹ Mn.) EBITDA Margins (RHS)

-

9,000

18,000

27,000

36,000

FY-15 FY-16 FY-17 FY-18E FY-19E

Traditional Sales (₹ Mn.) Phenol Project Sales (₹ Mn.)

12 Anand Rathi Research

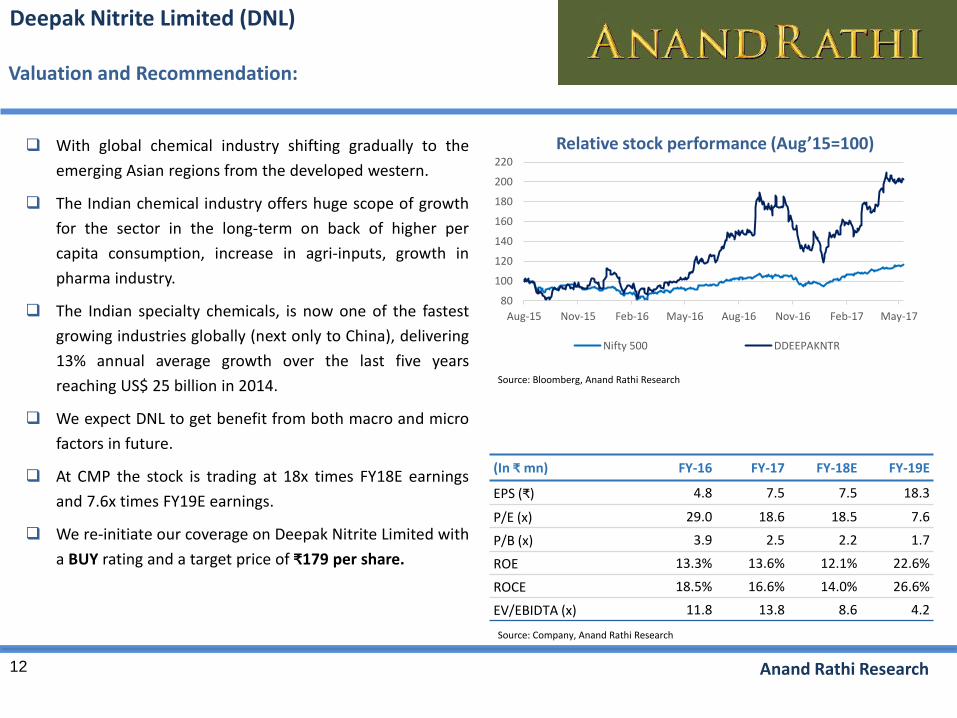

With global chemical industry shifting gradually to the

emerging Asian regions from the developed western.

The Indian chemical industry offers huge scope of growth

for the sector in the long-term on back of higher per

capita consumption, increase in agri-inputs, growth in

pharma industry.

The Indian specialty chemicals, is now one of the fastest

growing industries globally (next only to China), delivering

13% annual average growth over the last five years

reaching US$ 25 billion in 2014.

We expect DNL to get benefit from both macro and micro

factors in future.

At CMP the stock is trading at 18x times FY18E earnings

and 7.6x times FY19E earnings.

We re-initiate our coverage on Deepak Nitrite Limited with

a BUY rating and a target price of ₹179 per share.

Relative stock performance (Aug’15=100)

Valuation and Recommendation:

Source: Bloomberg, Anand Rathi Research

Source: Company, Anand Rathi Research

(In ₹ mn) FY-16 FY-17 FY-18E FY-19E

EPS (₹) 4.8 7.5 7.5 18.3

P/E (x) 29.0 18.6 18.5 7.6

P/B (x) 3.9 2.5 2.2 1.7

ROE 13.3% 13.6% 12.1% 22.6%

ROCE 18.5% 16.6% 14.0% 26.6%

EV/EBIDTA (x) 11.8 13.8 8.6 4.2

Deepak Nitrite Limited (DNL)

80

100

120

140

160

180

200

220

Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17

Nifty 500 DDEEPAKNTR

13 Anand Rathi Research

Margins FY-16 FY-17 FY-18E FY-19E

Sales Growth % 3.4% -0.9% 12.6% 96.8%

Operating Margin % 12.1% 10.2% 14.5% 15.3%

Net Margin % 4.6% 7.2% 6.4% 7.9%

Consolidated Financials:

Source: Company, Anand Rathi Research

(In ₹ Mn.) FY-16 FY-17 FY-18E FY-19E

Liabilities

Equity Share Capital 233 261 261 261

Reserves & Surplus 4,496 6,910 7,893 10,279

Total Shareholder's Funds 4,729 7,171 8,154 10,541

Minority Interest - - - -

Long-Term Liabilities 1,589 2,383 3,183 3,183

Other Long-term Liabilities 77 107 107 107

Deferred Tax Liability 566 657 657 657

Short-term Liabilities 5,980 7,731 6,813 13,405

Total 12,941 18,048 18,914 27,892

Assets

Net Fixed Assets 6,297 9,398 13,975 20,233

Long-Term L&A 797 1,701 1,701 1,701

Non Current Investments 28 27 27 27

Other Non-Current Assets 9 0 0 0

Current Asset 5,812 6,923 3,211 5,932

Total 12,941 18,049 18,914 27,892

(In ₹ Mn.) FY-16 FY-17 FY-18E FY-19E

Net Sales 13,729 13,604 15,313 30,130

Operating Expense 12,066 12,222 13,092 25,535

EBITDA 1,663 1,382 2,220 4,595

Other Income 20 49 77 90

Depreciation 395 427 599 836

EBIT 1,288 1,004 1,697 3,850

Interest 397 341 331 535

Misc. items - 705 - -

PBT 891 1,368 1,366 3,314

Tax 262 388 382 928

Minority Interest (2) (1) - -

PAT 627 978 984 2,386

Deepak Nitrite Limited (DNL)

14 Anand Rathi Research

The company’s business is exposed to crude oil price.

Any substantial delay in its new project at Dahej may impact our projections negatively.

Key Risks:

Deepak Nitrite Limited (DNL)

15 Anand Rathi Research

Rating and Target Price history:

Date Rating Target Price (₹) Share Price (₹)

30-Aug-16 BUY 161 101

19-Nov-16 BUY 161 94

16-Feb-17 BUY 145 102

11-May-17 BUY 179 139

DNL rating detailsDNL rating history & price chart

Source: Bloomberg, Anand Rathi Research Source: Bloomberg, Anand Rathi Research

NOTE: Prices are as on 11th May 2017 close.

Deepak Nitrite Limited (DNL)

80

100

120

140

160

180

200

220

Aug-15 Nov-15 Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17

Nifty 500 DDEEPAKNTR

16 Anand Rathi Research

Disclaimer:

Research Disclaimer and Disclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014

Anand Rathi Share and Stock Brokers Ltd. (hereinafter refer as ARSSBL) (Research Entity, SEBI Regn No. INH000000834, Date of Regn. 29/06/2015) is a subsidiary of the

Anand Rathi Financial Services Ltd. ARSSBL is a corporate trading and clearing member of Bombay Stock Exchange Ltd, National Stock Exchange of India Ltd. (NSEIL),

Multi Stock Exchange of India Ltd (MCX-SX), United stock exchange and also depository participant with National Securities Depository Ltd (NSDL) and Central

Depository Services Ltd. ARSSBL is engaged into the business of Stock Broking, Depository Participant, Mutual Fund distributor.

The research analysts, strategists, or research associates principally responsible for the preparation of Anand Rathi Research have received compensation based upon

various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues.

General Disclaimer: - This Research Report (hereinafter called “Report”) is meant solely for use by the recipient and is not for circulation. This Report does not

constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The

recommendations, if any, made herein are expression of views and/or opinions and should not be deemed or construed to be neither advice for the purpose of

purchase or sale of any security, derivatives or any other security through ARSSBL nor any solicitation or offering of any investment /trading opportunity on behalf of

the issuer(s) of the respective security (ies) referred to herein. These information / opinions / views are not meant to serve as a professional investment guide for the

readers.No action is solicited based upon the information provided herein. Recipients of this Report should rely on information/data arising out of their own

investigations. Readers are advised to seek independent professional advice and arrive at an informed trading/investment decision before executing any trades or

making any investments. This Report has been prepared on the basis of publicly available information, internally developed data and other sources believed by ARSSBL

to be reliable. ARSSBL or its directors, employees, affiliates or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy

and reliability of such information / opinions / views. While due care has been taken to ensure that the disclosures and opinions given are fair and reasonable, none of

the directors, employees, affiliates or representatives of ARSSBL shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary

damages, including lost profits arising in any way whatsoever from the information / opinions / views contained in this Report. The price and value of the investments

referred to in this Report and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide

for future performance. ARSSBL does not provide tax advice to its clients, and all investors are strongly advised to consult with their tax advisers regarding taxation

aspects of any potential investment.

Continued…

Deepak Nitrite Limited (DNL)

17 Anand Rathi Research

Disclaimer:

Contd…

Opinions expressed are our current opinions as of the date appearing on this Research only. We do not undertake to advise you as to any change of our views expressed in this Report. Research Report may differ between ARSSBL’s RAs and/ or ARSSBL’s associate companies on account of differences in research methodology, personal judgment and difference in time horizons for which recommendations are made. User should keep this risk in mind and not hold ARSSBL, its employees and associates responsible for any losses, damages of any type whatsoever.

ARSSBL and its associates or employees may; (a) from time to time, have long or short positions in, and buy or sell the investments in/ security of company (ies) mentioned herein or (b) be engaged in any other transaction involving such investments/ securities of company (ies) discussed herein or act as advisor or lender / borrower to such company (ies) these and other activities of ARSSBL and its associates or employees may not be construed as potential conflict of interest with respect to any recommendation and related information and opinions. Without limiting any of the foregoing, in no event shall ARSSBL and its associates or employees or any third party involved in, or related to computing or compiling the information have any liability for any damages of any kind.

Details of Associates of ARSSBL and Brief History of Disciplinary action by regulatory authorities & its associates are available on our website i. e. www.rathi.com

Disclaimers in respect of jurisdiction: This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject ARSSBL to any registration or licensing requirement within such jurisdiction(s). No action has been or will be taken by ARSSBL in any jurisdiction (other than India), where any action for such purpose(s) is required. Accordingly, this Report shall not be possessed, circulated and/or distributed in any such country or jurisdiction unless such action is in compliance with all applicable laws and regulations of such country or jurisdiction. ARSSBL requires such recipient to inform himself about and to observe any restrictions at his own expense, without any liability to ARSSBL. Any dispute arising out of this Report shall be subject to the exclusive jurisdiction of the Courts in India.

Copyright: - This report is strictly confidential and is being furnished to you solely for your information. All material presented in this report, unless specifically indicated otherwise, is under copyright to ARSSBL. None of the material, its content, or any copy of such material or content, may be altered in any way, transmitted, copied or reproduced (in whole or in part) or redistributed in any form to any other party, without the prior express written permission of ARSSBL. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of ARSSBL or its affiliates, unless specifically mentioned otherwise.

Contd…

Deepak Nitrite Limited (DNL)

18 Anand Rathi Research

Disclaimer:

Contd.

Statements on ownership and material conflicts of interest, compensation - ARSSBL and Associates

Sr. No.

Statement

Answers to the Best of the knowledgeand belief of the ARSSBL/ itsAssociates/ Research Analyst who ispreparing this report

1ARSSBL/its Associates/ Research Analyst/ his Relative have any financial interest in the subject company? Nature of Interest (if applicable), is givenagainst the company’s name?. NO

2

ARSSBL/its Associates/ Research Analyst/ his Relative have actual/beneficial ownership of one per cent or more securities of the subject company, at theend of the month immediately preceding the date of publication of the research report or date of the public appearance?. NO

3ARSSBL/its Associates/ Research Analyst/ his Relative have any other material conflict of interest at the time of publication of the research report or atthe time of public appearance?. NO

4 ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation from the subject company in the past twelve months. NO

5ARSSBL/its Associates/ Research Analyst/ his Relative have managed or co-managed public offering of securities for the subject company in the pasttwelve months.

NO

6ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for investment banking or merchant banking or brokerageservices from the subject company in the past twelve months. NO

7

ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for products or services other than investment banking ormerchant banking or brokerage services from the subject company in the past twelve months. NO

8ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation or other benefits from the subject company or third party inconnection with the research report. NO

9 ARSSBL/its Associates/ Research Analyst/ his Relative have served as an officer, director or employee of the subject company. NO

10 ARSSBL/its Associates/ Research Analyst/ his Relative has been engaged in market making activity for the subject company. NO

Deepak Nitrite Limited (DNL)