DCM Shriram Limited - Anand Rathi

18

Anand Rathi Research Time Horizon – 12 Months February 8, 2018 Source: Company, Anand Rathi Research, Bloomberg V A L U E P I C k Analyst: CA Saurabh Joshi [email protected] Relative stock performance (Feb’17=100) CMP: ₹546 Target: ₹745 Shareholding Pattern (as on Dec’17) DCM Shriram Limited Key Data Ticker (Bloomberg) DCMS IN NSE Code DCMSHRIRAM BSE Code 523367 Sector Diversified Industry Diversified Face Value (₹) 2.0 BV per share (₹) 156 Dividend Yield (%) 1.07% 52 Week L/H(₹) 269 / 628 Market Cap. (₹ mn.) 88216 Dec-17 Sep-17 Jun-17 Mar-17 Promoter 63.9% 63.9% 63.9% 63.9% Institutions 13.3% 12.4% 11.8% 11.8% Others 22.8% 23.7% 24.4% 24.3% Total 100% 100% 100% 100% 80 120 160 200 240 Nifty 500 DCM Shriram (In ₹ mn) FY-16 FY-17 FY-18E FY-19E Net Sales 57,805 57,885 73,579 81,317 EBITDA 5,020 7,690 11,510 13,505 EBITDA Margin 8.7% 13.3% 15.6% 16.6% EPS (₹) 18.6 34.0 50.7 59.3 EV/Sales 1.6 1.6 1.3 1.1 EV/EBITDA 17.0 11.3 7.8 6.6 P/E (x) 29.4 16.1 10.8 9.2 Price Performance CY15 CY16 CY17 YTD Absolute -12% 53% 161% -3% Relative -11% 50% 125% 0%

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of DCM Shriram Limited - Anand Rathi

Anand Rathi Research

Time Horizon – 12 Months

February 8, 2018

Source: Company, Anand Rathi Research, Bloomberg

V

A

L

U

E

P

I

C

k

Analyst: CA Saurabh [email protected]

Relative stock performance (Feb’17=100)

CMP: ₹546

Target: ₹745

Shareholding Pattern (as on Dec’17)

DCM Shriram Limited

Key Data

Ticker (Bloomberg) DCMS IN

NSE Code DCMSHRIRAM

BSE Code 523367

Sector Diversified

Industry Diversified

Face Value (₹) 2.0

BV per share (₹) 156

Dividend Yield (%) 1.07%

52 Week L/H(₹) 269 / 628

Market Cap. (₹ mn.) 88216

Dec-17 Sep-17 Jun-17 Mar-17

Promoter 63.9% 63.9% 63.9% 63.9%

Institutions 13.3% 12.4% 11.8% 11.8%

Others 22.8% 23.7% 24.4% 24.3%

Total 100% 100% 100% 100%

80

120

160

200

240

Nifty 500 DCM Shriram

(In ₹ mn) FY-16 FY-17 FY-18E FY-19E

Net Sales 57,805 57,885 73,579 81,317

EBITDA 5,020 7,690 11,510 13,505

EBITDA Margin 8.7% 13.3% 15.6% 16.6%

EPS (₹) 18.6 34.0 50.7 59.3

EV/Sales 1.6 1.6 1.3 1.1

EV/EBITDA 17.0 11.3 7.8 6.6

P/E (x) 29.4 16.1 10.8 9.2

Price Performance CY15 CY16 CY17 YTD

Absolute -12% 53% 161% -3%

Relative -11% 50% 125% 0%

2 Anand Rathi Research

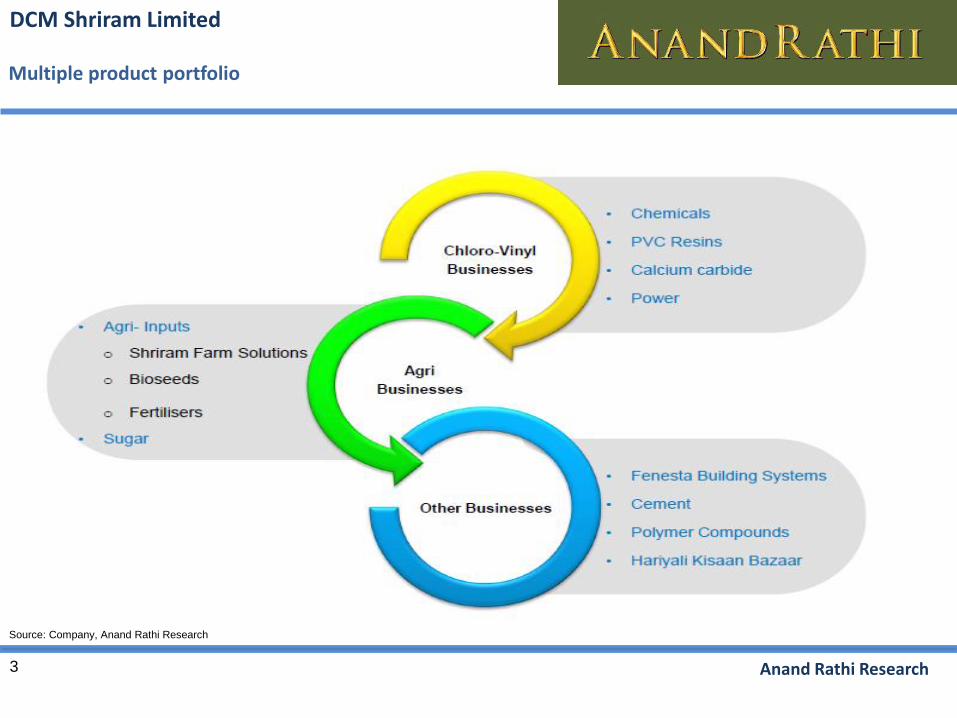

DCM Shriram Ltd is a spin-off from the trifurcation of the reputed erstwhile DCM Group. The company’s businessportfolio consists of Chloro-Vinyl Business, Agri-Rural Business and other Value-Added Businesses. It is amongst oneof the most cost efficient producers of products and services in all its businesses and has been continuously strivingfor operational efficiency.

DCM Shriram, across its various businesses is strategically diversified yet operationally integrated company. Someof the businesses feed others, thereby lowering operation costs and making DCM Shriram a highly competitiveplayer.

The announced expansion initiatives in Chloro-Vinyl and Sugar businesses amounting to INR 1,200 crores areprogressing well. According to the management, these projects are expected to be commissioned in the next twofiscal years and substantially augment the growth prospects of the company.

The continued focus of the Govt. on agriculture & infrastructure is expected to fuel growth of the agricultural & PVCindustry in India.

Recent increase in import duty on all types of sugar (raw sugar, refined or white sugar) from the present 50 per centto 100 per cent, which is aimed at curbing cheaper import, should help the Indian sugar industry in betterrealisation. We expect company to get benefit from both macro and micro factors in future.

We expect DCM Shriram business to report a revenue CAGR of 18.5 % over the two financial years. The increase inrevenue going ahead to be due to higher capacity utilisation, new capacity expansion and better realisations goingforward.

We initiate our coverage on DCM Shriram Limited with a BUY rating and a target price of ₹745 per share.

A leading business conglomerate with diversified business portfolio

DCM Shriram Limited

3 Anand Rathi Research

DCM Shriram Limited

Multiple product portfolio

Source: Company, Anand Rathi Research

4 Anand Rathi Research

Charting a new growth path in a new era

Year History & Milestones

1992 Expansion of Power from 40 MW to 70 MW

1994 Textile Rationalisation

1996 Commissioned Shriram Alkali & Chemicals, Bharuch

1997 Started Sugar Business Ajbapur Plant

1998 Started Energy Services Business

2002 Acquired Majority Control of Bioseed Global

2002 Started Hariyali Kisaan Bazaar

2002 Acquired Rupapur Sugar Plant

2003 Launched Fenesta UPVC Windows

2005 Capacity Expansion of PVC, Carbide, Chlor-Alkali, Cement & Power

2006 Established New Sugar Plants at Loni & Hariawan

2007 100 % Takeover of Bioseed

2007 Divested Swatantra Bharat Mills

2009 Doubled the Capacity of Chlor Alkali Plant, Bharuch

2011 Set up Bioseed Indonesia

2014 Started JV with Axiall, Launched Shriram Axiall Pvt. Ltd.

2016 Introduction of S/4HANA

2017 Doubled Capacity at Bharuch Facility

DCM Shriram Limited

Source: Company, Anand Rathi Research

5 Anand Rathi Research

DCM Shriram Limited

Strategically diversified yet operationally integrated

Shriram Fertilisers & ChemicalsKota

Fenesta Building Systems Bhiwadi, Chennai &

Hyderabad

Source: Company, Anand Rathi Research

Shriram Alkali & Chemicals Bharuch

SSP Production UnitKapasan & Chittaurgarh

Shriram BioseedHyderabad

( Also Present in Vietnam, Philippines & Indonesia )

Sugar Production UnitsAjbapur, Rupapur, Hariawan & Loni

6 Anand Rathi Research

DCM Shriram Limited

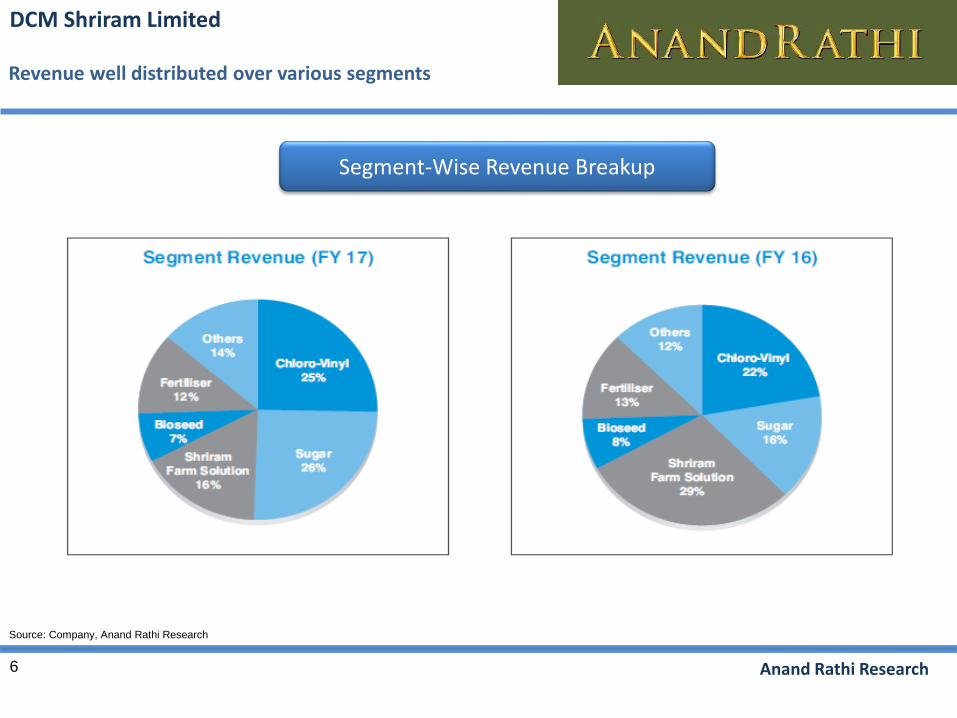

Revenue well distributed over various segments

Segment-Wise Revenue Breakup

Source: Company, Anand Rathi Research

7 Anand Rathi Research

Capacity expansion projects in various segments

Source: Company, Anand Rathi Research

DCM Shriram Limited

Chloro-Vinyl

Company is undertaking capacity expansion at Kota (84 TPA) and Bharuch (146 TPA). Bharuch expansion is expected to be completed by Q1 FY20 and Kota by Q3 FY20. The company expects to sustain on the 100 % capacity utilization achieved by the end of Q3 FY18 at Bharuch.

Sugar

Distillery plant at Hariawan unit (150 KLD) will be commissioned by the end of Jan 18. The company has also approved expansion of Sugar capacity by 5,000 TCD, which includes a distillery of 100 KLD and power Co-gen (34 MW). These projects are likely to be completed by Q3 FY19 and distillery by Q3 FY20.

8 Anand Rathi Research

Capacity addition in the high margin Chloro Vinyl

will boost margin significantly

Normal Monsoon will have significant impact on the revenue stream of Agri-

Input business

Generation of strong cash flow helping the company to reduce debt gradually in

FY18 and FY19.

New Distillery project at Hariawan to aid growth in

the sugar segment

Divestment of loss making Hariyali Kisan Bazar business will lead to

further improvement in the return ratios

DCM Shriram Limited

Multiple growth levers

9 Anand Rathi Research

DCM Shriram Limited

Source: ACMA, Company, Anand Rathi Research

Higher GDP growth to augment demand in chlor-alkali industry

Chlor-Alkali Industry

The Chlor- Alkali industry in India has 35 operating units with a combined installed capacity of 3.7 million Tons per annum of Caustic Soda.

The domestic demand for Caustic Soda and Chlorine in 2016-17 is estimated to be about 3.6 million TPA and 2.9 million TPA respectively.

The demands of both the products are linked to the Indian GDP growth because these products are considered as the building blocks of various other industries.

As GDP is poised for a higher growth, the demand of these products is also expected to increase.

10 Anand Rathi Research

India's PVC resin installed capacity currently stands at

around 1.4 million TPA.

Domestic demand has been growing steadily and has

reached to 2.95 million TPA in FY 17, up 9.3% over last

year.

The gap in demand and supply, which currently

stands at 54.5% of our total demand, is being met by the import of PVC resin.

The continued focus of the Govt. on building

infrastructure is expected to fuel growth of the PVC industry in India over the

next few years.

Indian PVC demand is expected to grow at a CAGR

of 8 to 10% for the next 5 years.

DCM Shriram Limited

Government focus on building infra to fuel growth of PVC industry

11 Anand Rathi Research

DCM Shriram Limited

Financial Estimates

Source: Company, Anand Rathi Research

We expect company to report a revenue CAGR of 18.5 % over the two financial years.

The increase in revenue going ahead to be due to higher capacity utilisation, new capacity expansion and better

realisations going forward.

On profitability front, we expect company to report operating margins around 15.6 % in FY18E and 16.6 % in

FY19E.

Better product mix, improving overall equipment efficiencies and persistence towards cost optimization will

result in delivering good operating margins going forward.

Source: Company, Anand Rathi Research

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

10,000

30,000

50,000

70,000

90,000

FY-15 FY-16 FY-17 FY-18E FY-19E

Revenue Estimates

Sales (₹ Mn.) Sales growth

0%

5%

10%

15%

20%

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY-15 FY-16 FY-17 FY-18E FY-19E

EBITDA & EBITDA Margin Estimates

EBITDA (₹ Mn.) EBITDA Margins (RHS)

12 Anand Rathi Research

Company working towards research led expansion of

its crop portfolio and product offerings, which is

expected to provide growth prospects over the

medium-to-long term

New Distillery project at Hariawan to aid growth in the

sugar segment

Government focus on building infra to fuel growth of

PVC industry and higher GDP growth to augment

demand in chlor-alkali industry

We expect company to get benefit from both macro

and micro factors in future.

At CMP the stock is trading at 10.8x times FY18E

earnings and 9.2x times FY19E earnings.

We initiate our coverage on DCM Shriram Limited with

a BUY rating and a target price of ₹745 per share.

Relative stock performance (Feb’17=100)

Valuation and Recommendation:

Source: Bloomberg, Anand Rathi Research

Source: Company, Anand Rathi Research

DCM Shriram Limited

80

120

160

200

240

Nifty 500 DCM Shriram

Particulars FY-16 FY-17 FY-18E FY-19E

EPS (₹) 18.6 34.0 50.7 59.3

P/E (x) 29.4 16.1 10.8 9.2

P/B (x) 4.2 3.5 2.6 2.1

ROE 14.4% 21.8% 24.6% 22.3%

ROCE 17.8% 22.6% 26.8% 25.1%

EV/EBIDTA (x) 17.0 11.3 7.8 6.6

EV/Sales (x) 1.6 1.6 1.3 1.1

13 Anand Rathi Research

Consolidated Financials:

DCM Shriram Limited

Source: Company, Anand Rathi Research

(In ₹ mn) FY-16 FY-17 FY-18E FY-19E

Net Sales 57,805 57,885 73,579 81,317

Operating Expense 52,785 50,195 62,069 67,812

EBITDA 5,020 7,690 11,510 13,505

Other Income 436 489 441 488

Depreciation 980 1,137 1,425 1,721

EBIT 4,477 7,041 10,527 12,271

Interest 854 714 832 945

Misc. items - - - -

PBT 3,623 6,327 9,694 11,327

Tax 619 804 1,454 1,699

Minority Interest 13 (7) - -

PAT 3,018 5,517 8,240 9,628

Margins FY-16 FY-17 FY-18E FY-19E

Sales Growth % 2.5% 0.1% 27.1% 10.5%

Operating Margin % 8.7% 13.3% 15.6% 16.6%

Net Margin % 5.2% 9.5% 11.2% 11.8%

(In ₹ mn) FY-16 FY-17 FY-18E FY-19E

Liabilities

Equity Share Capital 326 326 326 326

Reserves & Surplus 20,583 24,951 33,191 42,818

Total Shareholder's Funds 20,909 25,277 33,517 43,145

Minority Interest 22 21 21 21

Long-Term Liabilities 2,575 4,722 4,722 4,722

Other Long-term Liabilities 1,720 1,886 1,886 1,886

Deferred Tax Liability (145) (801) (801) (801)

Short-term Liabilities 27,987 27,318 32,737 37,975

Total 53,069 58,422 72,082 86,948

Assets

Net Fixed Assets 17,855 20,793 24,854 28,771

Long-Term L&A 1,060 596 596 596

Non Current Investments 353 380 380 380

Other Non-Current Assets 530 597 597 597

Current Asset 33,272 36,058 45,656 56,605

Total 53,069 58,422 72,082 86,948

14 Anand Rathi Research

As company has a direct impact of rainfall so unseasonal rains could impact Agri-Input Business which would impact the

company’s sales. So timely and normal rainfall is essential for agrochemical companies to post good performance.

Rise in energy costs as a result of rising international and domestic coal prices, freight, duties and levies, will increase

the cost of production which can impact the margin adversely.

Key Risks:

DCM Shriram Limited

Source: Company, Anand Rathi Research

15 Anand Rathi Research

Rating and Target Price history:

Date Rating Target Price (₹) Share Price (₹)

8-feb-18 BUY 745 546

DCM Shriram rating detailsDCM Shriram rating history & price chart

Source: Bloomberg, Anand Rathi Research Source: Bloomberg, Anand Rathi Research

NOTE: Prices are as on 8th feb 2018 close.

DCM Shriram Limited

80

120

160

200

240

Nifty 500 DCM Shriram

16 Anand Rathi Research

Disclaimer:

Research Disclaimer and Disclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014

Anand Rathi Share and Stock Brokers Ltd. (hereinafter refer as ARSSBL) (Research Entity, SEBI Regn No. INH000000834, Date of Regn. 29/06/2015) is a subsidiary of the

Anand Rathi Financial Services Ltd. ARSSBL is a corporate trading and clearing member of Bombay Stock Exchange Ltd, National Stock Exchange of India Ltd. (NSEIL),

Multi Stock Exchange of India Ltd (MCX-SX), United stock exchange and also depository participant with National Securities Depository Ltd (NSDL) and Central

Depository Services Ltd. ARSSBL is engaged into the business of Stock Broking, Depository Participant, Mutual Fund distributor.

The research analysts, strategists, or research associates principally responsible for the preparation of Anand Rathi Research have received compensation based upon

various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues.

General Disclaimer: - This Research Report (hereinafter called “Report”) is meant solely for use by the recipient and is not for circulation. This Report does not

constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The

recommendations, if any, made herein are expression of views and/or opinions and should not be deemed or construed to be neither advice for the purpose of

purchase or sale of any security, derivatives or any other security through ARSSBL nor any solicitation or offering of any investment /trading opportunity on behalf of

the issuer(s) of the respective security (ies) referred to herein. These information / opinions / views are not meant to serve as a professional investment guide for the

readers.No action is solicited based upon the information provided herein. Recipients of this Report should rely on information/data arising out of their own

investigations. Readers are advised to seek independent professional advice and arrive at an informed trading/investment decision before executing any trades or

making any investments. This Report has been prepared on the basis of publicly available information, internally developed data and other sources believed by ARSSBL

to be reliable. ARSSBL or its directors, employees, affiliates or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy

and reliability of such information / opinions / views. While due care has been taken to ensure that the disclosures and opinions given are fair and reasonable, none of

the directors, employees, affiliates or representatives of ARSSBL shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary

damages, including lost profits arising in any way whatsoever from the information / opinions / views contained in this Report. The price and value of the investments

referred to in this Report and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide

for future performance. ARSSBL does not provide tax advice to its clients, and all investors are strongly advised to consult with their tax advisers regarding taxation

aspects of any potential investment.

Continued…

DCM Shriram Limited

17 Anand Rathi Research

Disclaimer:

Contd…

Opinions expressed are our current opinions as of the date appearing on this Research only. We do not undertake to advise you as to any change of our viewsexpressed in this Report. Research Report may differ between ARSSBL’s RAs and/ or ARSSBL’s associate companies on account of differences in research methodology,personal judgment and difference in time horizons for which recommendations are made. User should keep this risk in mind and not hold ARSSBL, its employees andassociates responsible for any losses, damages of any type whatsoever.

ARSSBL and its associates or employees may; (a) from time to time, have long or short positions in, and buy or sell the investments in/ security of company (ies)mentioned herein or (b) be engaged in any other transaction involving such investments/ securities of company (ies) discussed herein or act as advisor or lender /borrower to such company (ies) these and other activities of ARSSBL and its associates or employees may not be construed as potential conflict of interest with respectto any recommendation and related information and opinions. Without limiting any of the foregoing, in no event shall ARSSBL and its associates or employees or anythird party involved in, or related to computing or compiling the information have any liability for any damages of any kind.

Details of Associates of ARSSBL and Brief History of Disciplinary action by regulatory authorities & its associates are available on our website i. e. www.rathi.com

Disclaimers in respect of jurisdiction: This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of orlocated in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which wouldsubject ARSSBL to any registration or licensing requirement within such jurisdiction(s). No action has been or will be taken by ARSSBL in any jurisdiction (other thanIndia), where any action for such purpose(s) is required. Accordingly, this Report shall not be possessed, circulated and/or distributed in any such country or jurisdictionunless such action is in compliance with all applicable laws and regulations of such country or jurisdiction. ARSSBL requires such recipient to inform himself about and toobserve any restrictions at his own expense, without any liability to ARSSBL. Any dispute arising out of this Report shall be subject to the exclusive jurisdiction of theCourts in India.

Copyright: - This report is strictly confidential and is being furnished to you solely for your information. All material presented in this report, unless specifically indicatedotherwise, is under copyright to ARSSBL. None of the material, its content, or any copy of such material or content, may be altered in any way, transmitted, copied orreproduced (in whole or in part) or redistributed in any form to any other party, without the prior express written permission of ARSSBL. All trademarks, service marksand logos used in this report are trademarks or service marks or registered trademarks or service marks of ARSSBL or its affiliates, unless specifically mentionedotherwise.

Contd…

DCM Shriram Limited

18 Anand Rathi Research

Disclaimer:

Contd.

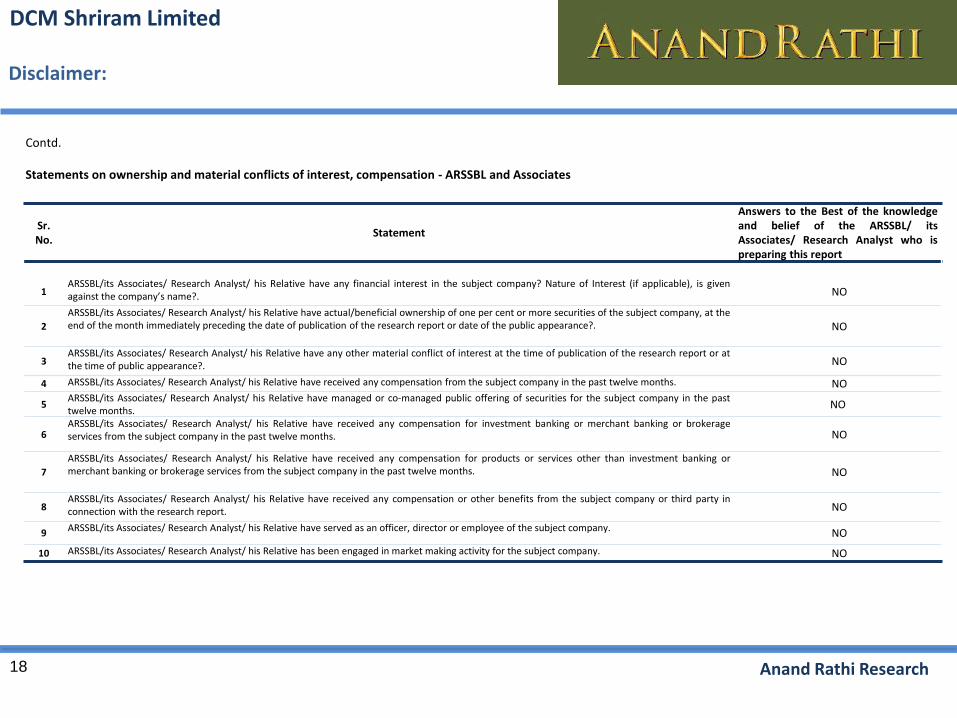

Statements on ownership and material conflicts of interest, compensation - ARSSBL and Associates

Sr. No.

Statement

Answers to the Best of the knowledgeand belief of the ARSSBL/ itsAssociates/ Research Analyst who ispreparing this report

1ARSSBL/its Associates/ Research Analyst/ his Relative have any financial interest in the subject company? Nature of Interest (if applicable), is givenagainst the company’s name?. NO

2

ARSSBL/its Associates/ Research Analyst/ his Relative have actual/beneficial ownership of one per cent or more securities of the subject company, at theend of the month immediately preceding the date of publication of the research report or date of the public appearance?. NO

3ARSSBL/its Associates/ Research Analyst/ his Relative have any other material conflict of interest at the time of publication of the research report or atthe time of public appearance?. NO

4 ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation from the subject company in the past twelve months. NO

5ARSSBL/its Associates/ Research Analyst/ his Relative have managed or co-managed public offering of securities for the subject company in the pasttwelve months.

NO

6ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for investment banking or merchant banking or brokerageservices from the subject company in the past twelve months. NO

7

ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for products or services other than investment banking ormerchant banking or brokerage services from the subject company in the past twelve months. NO

8ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation or other benefits from the subject company or third party inconnection with the research report. NO

9 ARSSBL/its Associates/ Research Analyst/ his Relative have served as an officer, director or employee of the subject company. NO

10 ARSSBL/its Associates/ Research Analyst/ his Relative has been engaged in market making activity for the subject company. NO

DCM Shriram Limited

![Lawrie v Carey DCM and Anor [2016] NTSC 23 PARTIES](https://static.fdokumen.com/doc/165x107/632542fc051fac18490d2d4b/lawrie-v-carey-dcm-and-anor-2016-ntsc-23-parties.jpg)