Partner Solicitation Language as a Reflection of Male Sexual ...

Upload

khangminh22Category

view

3download

0

Death of a Partner

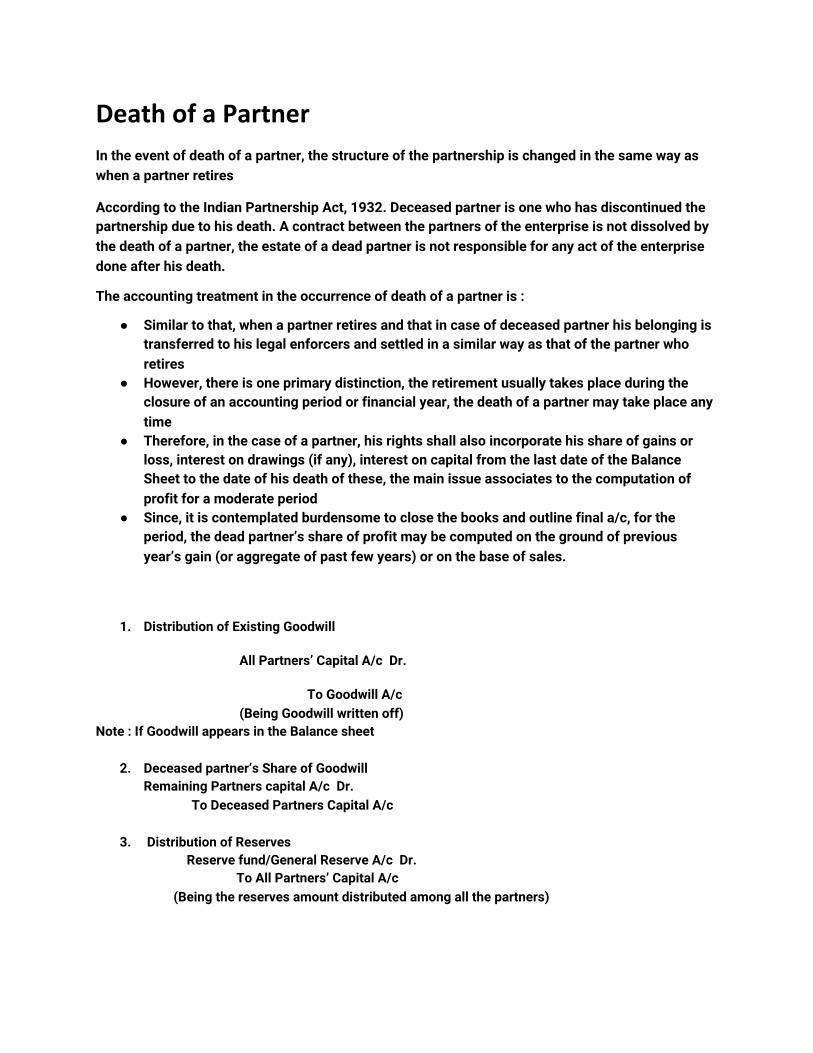

In the event of death of a partner, the structure of the partnership is changed in the same way as when a partner retires

According to the Indian Partnership Act, 1932. Deceased partner is one who has discontinued the partnership due to his death. A contract between the partners of the enterprise is not dissolved by the death of a partner, the estate of a dead partner is not responsible for any act of the enterprise done after his death.

The accounting treatment in the occurrence of death of a partner is :

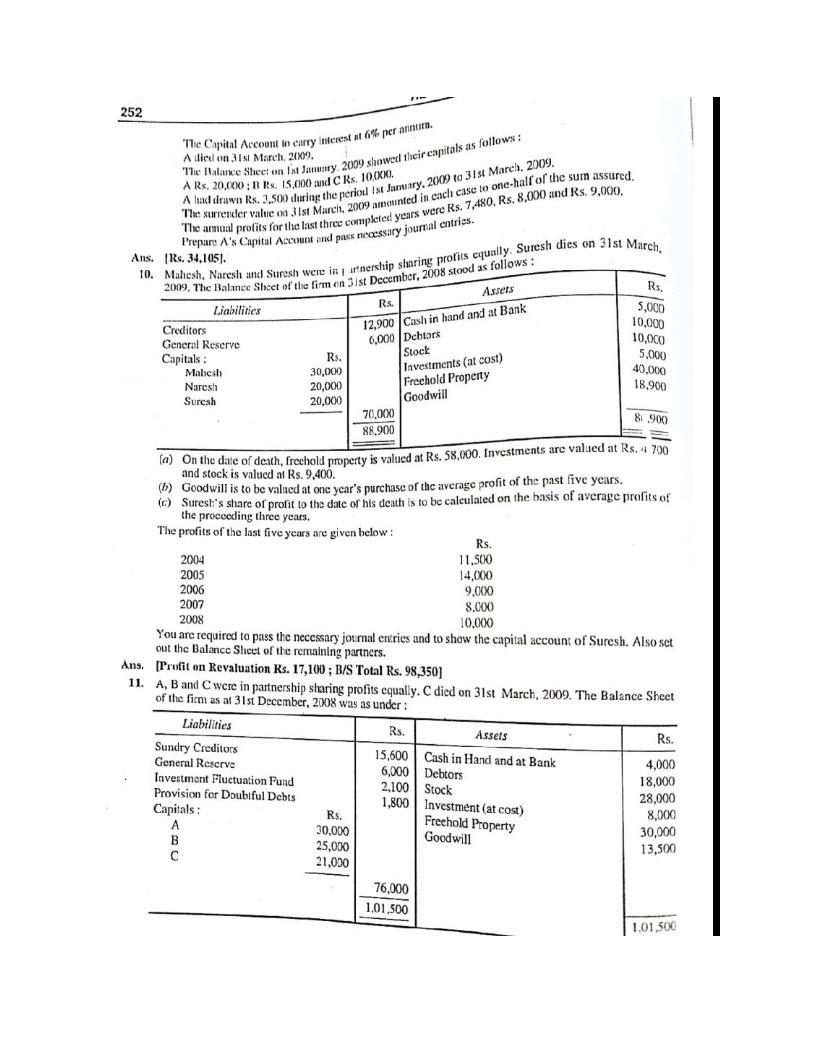

● Similar to that, when a partner retires and that in case of deceased partner his belonging is transferred to his legal enforcers and settled in a similar way as that of the partner who retires

● However, there is one primary distinction, the retirement usually takes place during the closure of an accounting period or financial year, the death of a partner may take place any time

● Therefore, in the case of a partner, his rights shall also incorporate his share of gains or loss, interest on drawings (if any), interest on capital from the last date of the Balance Sheet to the date of his death of these, the main issue associates to the computation of profit for a moderate period

● Since, it is contemplated burdensome to close the books and outline final a/c, for the period, the dead partner’s share of profit may be computed on the ground of previous year’s gain (or aggregate of past few years) or on the base of sales.

1. Distribution of Existing Goodwill

All Partners’ Capital A/c Dr.

To Goodwill A/c (Being Goodwill written off)

Note : If Goodwill appears in the Balance sheet

2. Deceased partner’s Share of Goodwill Remaining Partners capital A/c Dr.

To Deceased Partners Capital A/c

3. Distribution of Reserves Reserve fund/General Reserve A/c Dr. To All Partners’ Capital A/c (Being the reserves amount distributed among all the partners)

4. Distribution of Accumulated Losses All Partners’ Capital A/c Dr.

To Profit & Loss A/c

5. Distribution of Accumulated Profits Profit & Loss A/c Dr. To All Partners’ Capital A/c

Section 37 of the Partnership Act, the executive of the deceased partner would be entitled at their discretion either interest 6% per annum for the amount due from the date of death to the date of payment or to that portion of the profit that is earned by the firm with the amount due to the deceased partner.

1. Calculation of of deceased partner share of profits 2. Treatment of life policy or policies

1. Calculation of deceased partner share of profit: This can be determined either on the basis of time or turn over

a. On the basis of time: in this case it is assumed that the profit during the previous year has been earned uniformly in all months during the year, provided previous year is taken as the base for calculation of profits. Sometimes average profit for the past three or four years is taken as base rather than the previous year. Whatever base may be taken it is to be multiplied by the period for which the deceased partner remained in the and also by his profit sharing ratio at the time of his death.

b. On the basis of turnover: In this method, average past profit is divided into two portions, i.e., before the death and after the death on the basis of ratio of turnover to the date of death average turnover and then deceased partner share is calculated and credited to his capital account.

Journal Entry

Profit & Loss Suspense A/C…...Dr

To Deceased partners Capital A/C

(Being a deceased partner’s share in the profit credited to his capital account)

2. Treatment of life policy or policies: When a partner dies, his legal representatives are required to be paid a large sum of money which might affect the financial as well as working position of the partnership business. To provide funds to the legal representatives of the deceased partner generally A Joint life policy or individual life policies for partners might be taken. The premium for such policies is charged to the profit and loss account.Joint life policy is an asset of the firm and the deceased partner has a right to share any profits or losses on such policy. So the claim which is received by the firm on the death of a partner is divided among the partner and credited to their capital accounts in their profit sharing ratio. If the firm has taken individual life policies and the

premiums were charged to the profit and loss account then, the deceased partner has a right share the amount not only received from Life Insurance Corporation of India but also the surrender value which the other partners policies would acquire at the time of his death.

Journal Entry

a. For Joint life Policy

Joint Life Policy A/C Dr.

To, All Partner’s Capital A/c

b. For Individual Life policy

Insurance Policy A/c Dr.

To, All Partner’s Capital A/c

Problems:

1. A, B and C are partners in a firm sharing profits and losses in the ratio of 4:1. On April 2012 the capital of the partners were A - 50000: B- 40000. Profit and loss a/c of the firm for the year ended 31st March 2013 show the net profit of rupees 1,75,000. you are required to give the Profit and Loss appropriation account for the firm after taking into consideration the following adjustments:

1. Interest on capital at 5% per annum 2. Interest on these loan account of rupees 50000 for the whole year 3. Interest on drawings of partner at rate of 6% per annum 4. Drawing A- 15000; B- 10,000 5. Transfer 10% of the distributable profit before distribution to the Reserve fund of the firm.

(Answer: Profit - 1,51,425)

2. Amar and Bhanu are partners sharing profit and losses in the ratio of 3:2. Prepare Profit and

Loss appropriation account and capital account of partner for the year ending 31st December 2012.

1. Interest is payable on capital at the rate of 5% 2. Amar and Bhanu will get the remuneration @ 200 and 100 per month respectively 3. Interest is payable on loan contributed by Amar 4. loan given by Amar rupees 20000 on 1st July 2012 5. interest on drawings at the rate of 8% per annum 6. Amar withdrawn Rupees 6000 and Banu withdrawn rupees 4000 during the year 7. For the year ending 31st December 2012 the net profit of the firm is shown as Rs.70000

and the opening capital balances of Amar and Bhanu where Rs.50000and Rs. 40000 thousand respectively.

(Answer: Profit -61,700; capital a/c A- 85,680; B-63,720)

3. X Y and Z are partners in a firm with the capital of 40,000 ,24000 and 20000 respectively on 1st January 2018 . The partnership deed contains the following:

1. Interest on capital is to be charged at the rate of 5% 2. Interest on drawings at the rate of 4% per annum 3. X to get a salary of 400 per month 4. Y and Z get commission of 10% on the net profit. 5. profit and losses to be share up to 4500 in the ratio of 4:3:2 and above 4500 is equally. 6. The net profit of the firm for the year ended 31st December 2018 amounted to rupees 20500 and

the drawings of the partners are X -2400 Y- 1600 Z-1000. 7. prepare partners' capital account when the capitals are fixed and when the capital are

fluctuating.

(Answer: Profit -7,500; Fixed -X- 40000and 7,352; Y-24000and 4,118;Z-20000 and 4,030 Fluctuating X-47,352:Y-28,118;Z-24,030)

4. On January 2012 Mr author and Mr book enter into a partnership on the following terms:

o Mr Author and Mr Book are to contribute Capitals of of rupees 50000 and 30000 respectively

o profits and losses are shared in the ratio of 3 : 2 o Interest on capital is to be allowed at the rate of 5% per annum o Interest on drawings is to be charged at the rate of 2% per annum for the whole year o Mr. Author is to get a salary of Rs.500 per month o Mr. Book is to get a commission of 2% on the net profit before charging any of the above o 31st December 2012 the trading profit of the firm amounted to Rs.60000. o Mr. author withdraw Rs. 1000 and Mr. book withdraw Rs. 500 from the firm

You are required to prepare Profit and Loss appropriation account and capitals account of partners (i) Fixed (ii) Fluctuating (Answer: Profit -48,830; Fixed -Author- 50,000and 36,778; BooK-30,000and 21,722; Fluctuating Author -86,778: Book-51,722)

5. A and B are partners sharing profits and losses in the ratio of two third and one third respectively on 31st December 2011 the capital of a partnership was Rs.210000 of which Rs. 140000 contributed by A and Rs.70000 contributed by B.

On 31st December 2012 the following information was given to you as to the position of affairs The total combined capital was 2, 46,500. B had withdrawn rupees 3000. B had to be credited with Rs. 5000 At Special salary at the during the year 2012. Partners were to be credited with 5% interest on capital You are required to prepare Profit and Loss appropriation account and capital accounts of partner

(Answer: Profit -24,000; capital account’s A-1,63,000:B-83,500)

6. Arjun and Dev are Partners in a firm sharing profits and losses in the ratio of 3 :1. the profit and loss account of the firm for the year ended 31st March 2013 show the net profit of Rs. 75000. you are required to prepare the Profit and Loss appropriation account and Current account by taking the following information;

1. The partner's capital accounts Arjun Rs. 40000 Dev Rs.30000 2. interest on capital was to be calculated at the rate of 5% per annum 3. The current accounts of the partners at Rs.15000 Dev Rs. 10000 4. Partners Drawings amounted to Arjun Rs.10,000 and Dev Rs.7500 5. Interest on drawing is charged at the rate of 10% per annum at an average of 6 months 6. Partner salary Arjun Rs. 6000 and Dev Rs.4500 7. Arjun’s loan account Rs. 25000( the loan was contracted 2 years back)

(Answer: Profit -60,375; Current accounts: Arjun Rs. 59,281Dev Rs. 23,219)

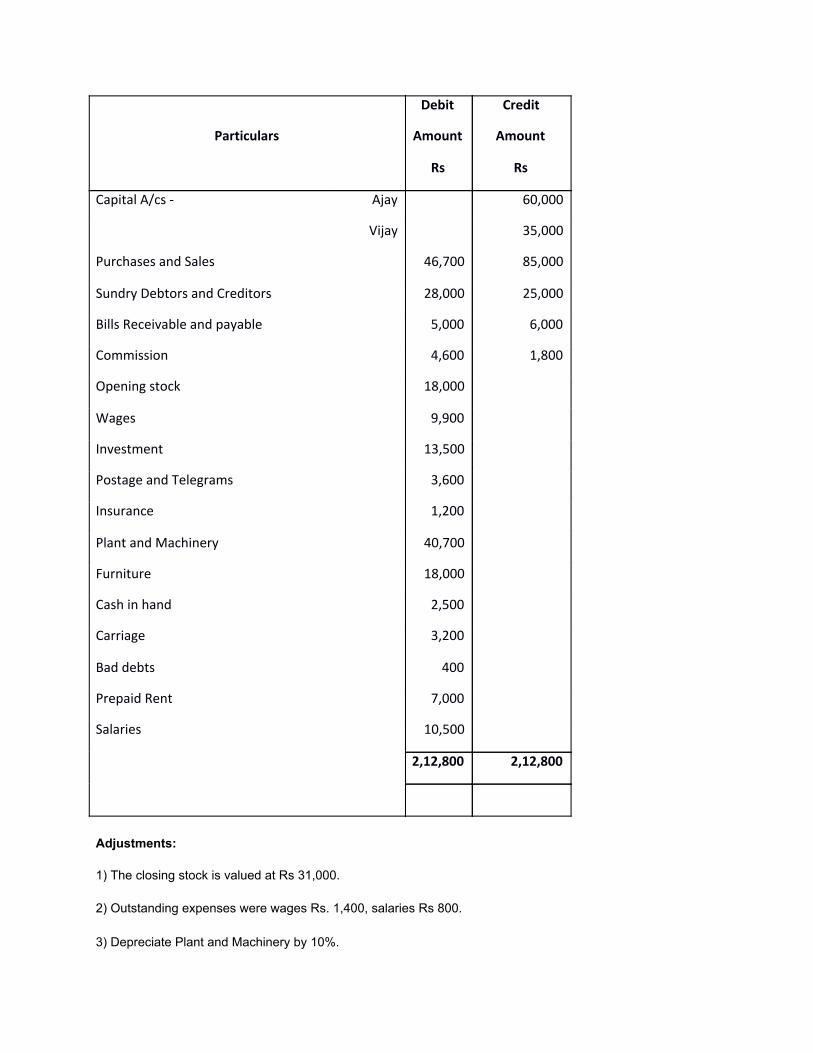

1. From the following Trading Balance of M/s Ajay and Vijay you are required to prepared Trading and Profit and Loss Account for the year ended 31st March, 2009 and Balance Sheet as on that date

Trial Balance as on 31st March, 2009

Adjustments:

1) The closing stock is valued at Rs 31,000.

2) Outstanding expenses were wages Rs. 1,400, salaries Rs 800.

3) Depreciate Plant and Machinery by 10%.

Particulars

Debit

Amount

Rs

Credit

Amount

Rs

Capital A/cs - Ajay 60,000

Vijay 35,000

Purchases and Sales 46,700 85,000

Sundry Debtors and Creditors 28,000 25,000

Bills Receivable and payable 5,000 6,000

Commission 4,600 1,800

Opening stock 18,000

Wages 9,900

Investment 13,500

Postage and Telegrams 3,600

Insurance 1,200

Plant and Machinery 40,700

Furniture 18,000

Cash in hand 2,500

Carriage 3,200

Bad debts 400

Prepaid Rent 7,000

Salaries 10,500

2,12,800 2,12,800

4) Insurance at Rs 500 is paid in advance.

5) Provide for further bad debts of Rs 1,500.

6) Commission due but not received Rs 1,200.

(ANSWER: Gross Profit:36,800; Net Profit: 13,630;B/S: 1,41,830)

2. Sanjay and Sudhir are partners sharing profit and losses in the ratio 3:2. The Trial Balance of the firm on 31st March, 2010 was follows:

Adjustments:

1) Stock on hand on 31st March, 2010 was at Rs 35,000.

2) Write off Rs 2,000, for further Bad debts and maintain R.D.D. at 5% on debtors.

3) Depreciate Land and Building at 5% and Machinery at 10%.

4) Outstanding expenses were wages Rs 2,000 and salary Rs 1,000.

5) Credit purchases amounted to Rs 4,000 were not recorded in the books of accounts.

6) Provide interest on Partners Capital at 5% p.a.

From the above Trial Balance and adjustments prepare Trading and Profit and Loss Account for the year ended 31st March, 2010 and Balance Sheet as on that data.

Trial Balance as on 31st March, 2010

Particulars Amount Rs Particulars Amount

Rs Opening stock 20,000 Capital A/cs- Sanjay 40,000 Purchases 30,000 Sudhir 30,000 Debtors 12,000 Sales 70,000 Wages 5,000 Sundry Creditors 21,000 Salaries 10,000 Bills payable 20,000 Land and Building 30,000 Discount 5,000 Plant and Machinery 25,000 Outstanding Rent 1,500 Furniture 16,000 Advertisement (for 2 years) 6,000 Bills Receivable 8,000 Insurance 2,000 Drawings- Sanjay 2,000 Sudhir 3,000 Cash in hand 5,500 Rent 10,000 Power and Fuel 3,000 1,87,500 1,87,500

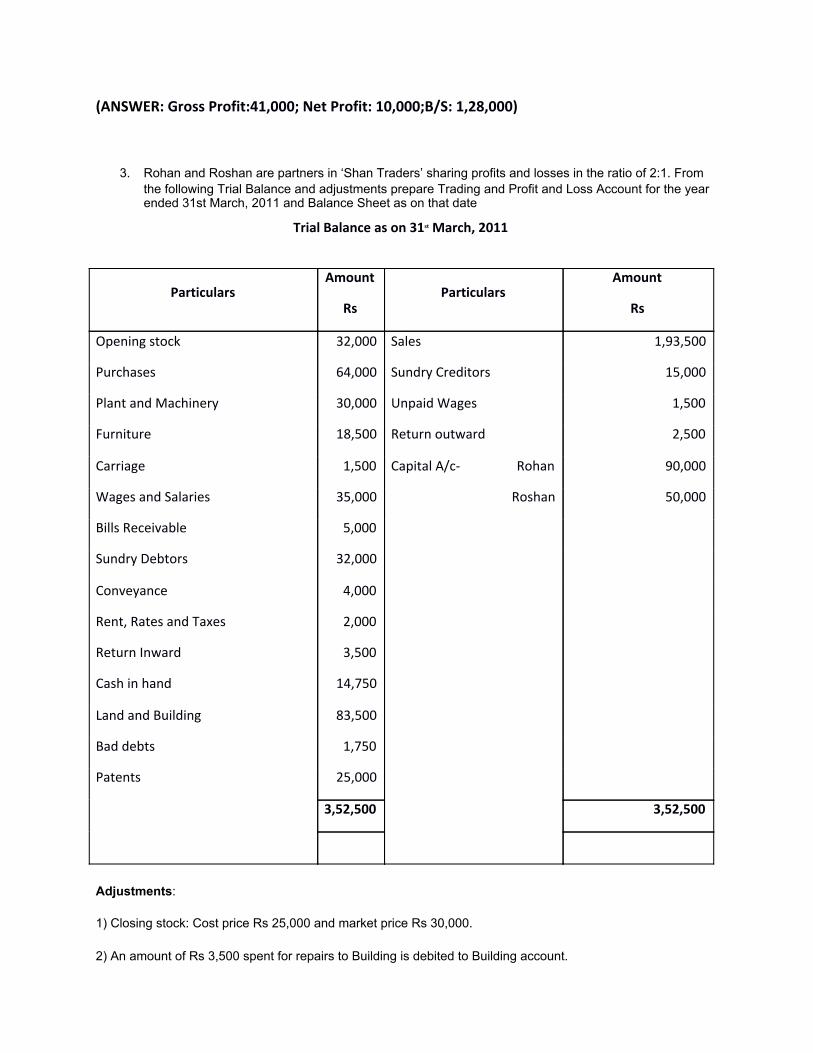

(ANSWER: Gross Profit:41,000; Net Profit: 10,000;B/S: 1,28,000)

3. Rohan and Roshan are partners in ‘Shan Traders’ sharing profits and losses in the ratio of 2:1. From the following Trial Balance and adjustments prepare Trading and Profit and Loss Account for the year ended 31st March, 2011 and Balance Sheet as on that date

Adjustments:

1) Closing stock: Cost price Rs 25,000 and market price Rs 30,000.

2) An amount of Rs 3,500 spent for repairs to Building is debited to Building account.

Trial Balance as on 31st March, 2011

Particulars Amount

Rs Particulars

Amount

Rs

Opening stock 32,000 Sales 1,93,500

Purchases 64,000 Sundry Creditors 15,000

Plant and Machinery 30,000 Unpaid Wages 1,500

Furniture 18,500 Return outward 2,500

Carriage 1,500 Capital A/c- Rohan 90,000

Wages and Salaries 35,000 Roshan 50,000

Bills Receivable 5,000

Sundry Debtors 32,000

Conveyance 4,000

Rent, Rates and Taxes 2,000

Return Inward 3,500

Cash in hand 14,750

Land and Building 83,500

Bad debts 1,750

Patents 25,000

3,52,500 3,52,500

3) Depreciate plant and Machinery and Building at 5% p.a.

4) Goods of Rs 750 taken by Roshan for this personal use.

5) Included in wages advances given to workers Rs 3,000.

6) Provide Rs 1,500 for bad and doubtful debts on Debtors.

(ANSWER: Gross Profit: 88,750; Net Profit: 70,500; B/S: 2,26,25 )

4. Given below is the Trial Balance of M/s Roma and Mona partnership firm. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2012 and Balance Sheet as on that date

Adjustments:

1) Stock on 31st March, 2012 was valued at Rs 80,000.

2) Goods of Rs 6,000 were sold and despatched on 27th March, 2012, but no entry was made in the books of accounts.

3) Write off Bad debts of Rs 4,000 and provide for R.D.D. at 5% on sundry debtors.

4) Provide reserve for discount on debtors at 2% and on creditors at 3%.

5) Outstanding wages Rs 4,000 and outstanding salaries Rs 3,066.

Trial Balance as on 31st March, 2012

Debit Balance Amoun

t Rs

Credit Balance Amount Rs

Stock on 1st April, 2011 52,000 Provident fund 50,000 Sundry Debtors 84,000 Interest on P.F. Investment 2,800 Bad debts 3,000 Sundry Creditors 84,000 Premises 78,000 Rent received 9,600 Salaries 28,000 Reserve for Doubtful Debts 2,000 Motor Vehicle 50,000 Discount received 3,600 Purchases 1,76,000 Sales 3,20,000 Provident Fund Investment

50,000 Capital A/c- Roma 50,000

Provident Fund contribution

5,500 Mona 50,000

Wages 22,000 Rent (for 10 months) 16,000 Office Expenses 5,000 Discount allowed 2,500 5,72,000 5,72,000

6) Depreciate Motor Vehicle at 5% p.a.

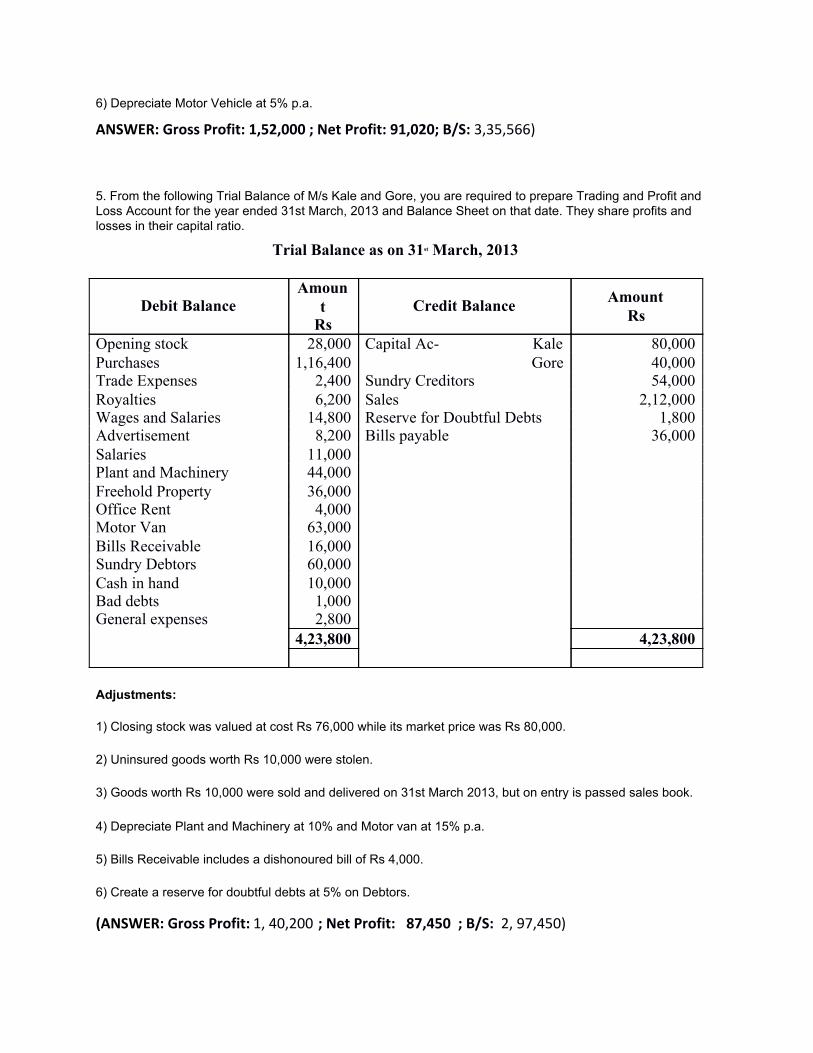

ANSWER: Gross Profit: 1,52,000 ; Net Profit: 91,020; B/S: 3,35,566)

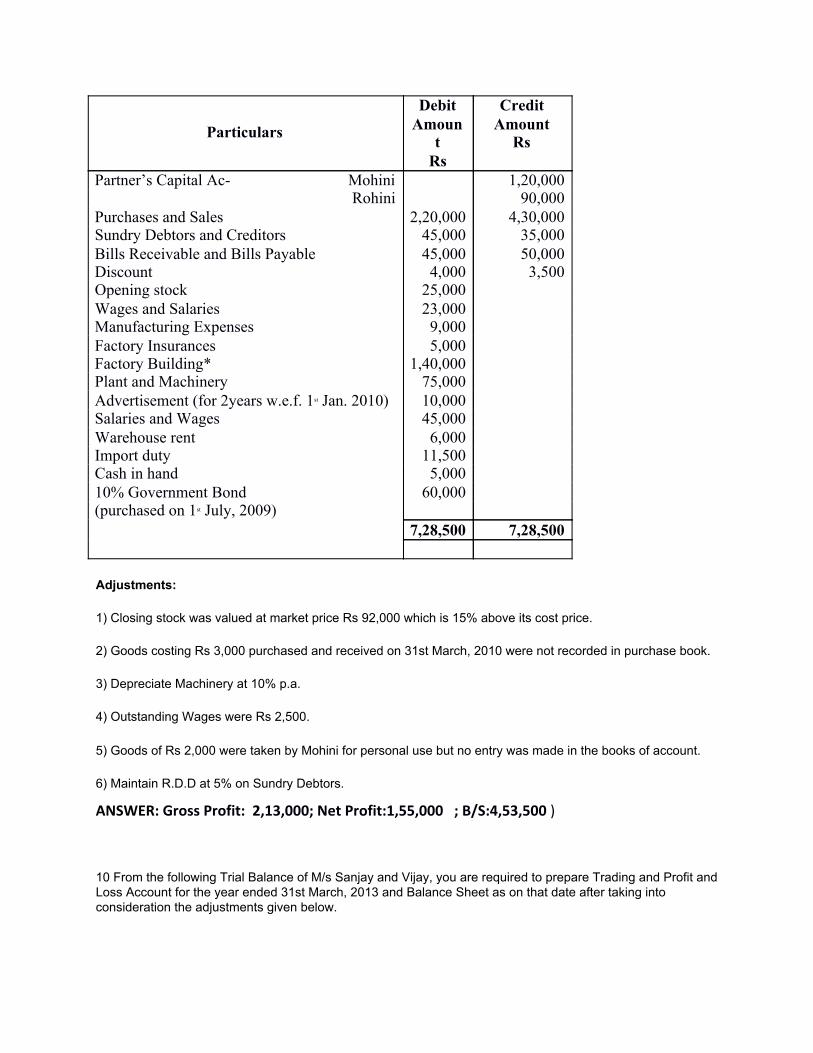

5. From the following Trial Balance of M/s Kale and Gore, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2013 and Balance Sheet on that date. They share profits and losses in their capital ratio.

Adjustments:

1) Closing stock was valued at cost Rs 76,000 while its market price was Rs 80,000.

2) Uninsured goods worth Rs 10,000 were stolen.

3) Goods worth Rs 10,000 were sold and delivered on 31st March 2013, but on entry is passed sales book.

4) Depreciate Plant and Machinery at 10% and Motor van at 15% p.a.

5) Bills Receivable includes a dishonoured bill of Rs 4,000.

6) Create a reserve for doubtful debts at 5% on Debtors.

(ANSWER: Gross Profit: 1, 40,200 ; Net Profit: 87,450 ; B/S: 2, 97,450)

Trial Balance as on 31st March, 2013

Debit Balance Amoun

t Rs

Credit Balance Amount Rs

Opening stock 28,000 Capital Ac- Kale 80,000 Purchases 1,16,400 Gore 40,000 Trade Expenses 2,400 Sundry Creditors 54,000 Royalties 6,200 Sales 2,12,000 Wages and Salaries 14,800 Reserve for Doubtful Debts 1,800 Advertisement 8,200 Bills payable 36,000 Salaries 11,000 Plant and Machinery 44,000 Freehold Property 36,000 Office Rent 4,000 Motor Van 63,000 Bills Receivable 16,000 Sundry Debtors 60,000 Cash in hand 10,000 Bad debts 1,000 General expenses 2,800 4,23,800 4,23,800

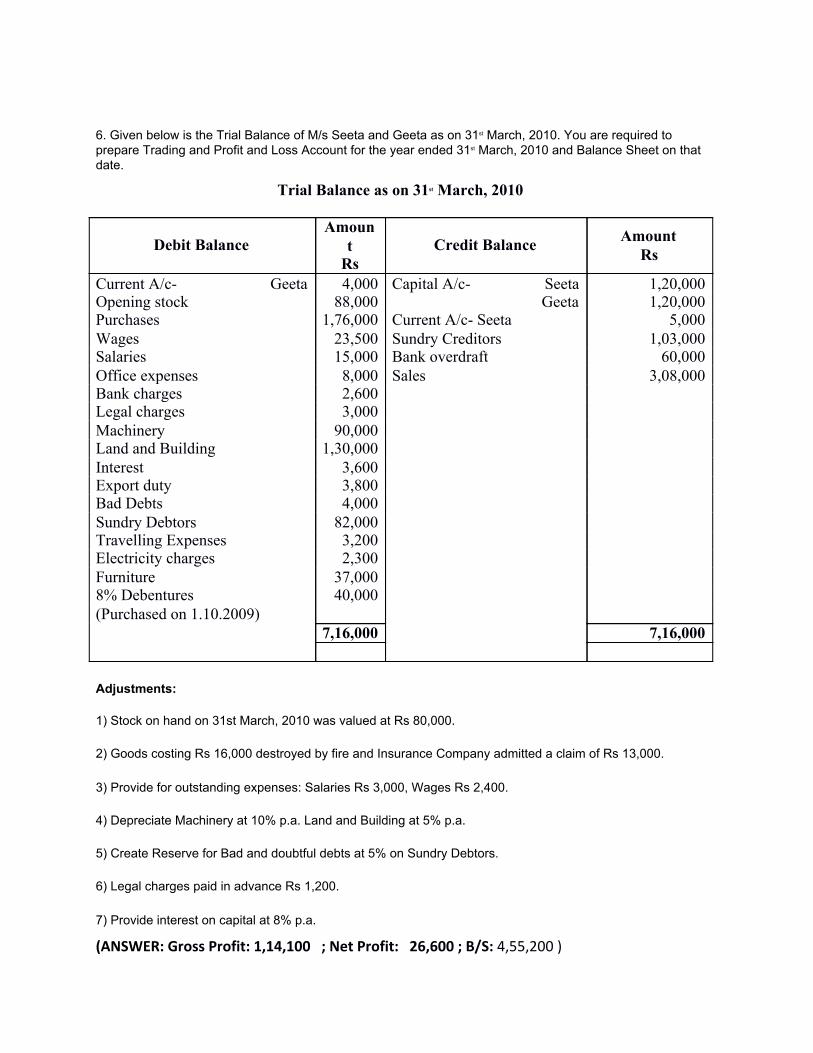

6. Given below is the Trial Balance of M/s Seeta and Geeta as on 31st March, 2010. You are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2010 and Balance Sheet on that date.

Adjustments:

1) Stock on hand on 31st March, 2010 was valued at Rs 80,000.

2) Goods costing Rs 16,000 destroyed by fire and Insurance Company admitted a claim of Rs 13,000.

3) Provide for outstanding expenses: Salaries Rs 3,000, Wages Rs 2,400.

4) Depreciate Machinery at 10% p.a. Land and Building at 5% p.a.

5) Create Reserve for Bad and doubtful debts at 5% on Sundry Debtors.

6) Legal charges paid in advance Rs 1,200.

7) Provide interest on capital at 8% p.a.

(ANSWER: Gross Profit: 1,14,100 ; Net Profit: 26,600 ; B/S: 4,55,200 )

Trial Balance as on 31st March, 2010

Debit Balance Amoun

t Rs

Credit Balance Amount Rs

Current A/c- Geeta 4,000 Capital A/c- Seeta 1,20,000 Opening stock 88,000 Geeta 1,20,000 Purchases 1,76,000 Current A/c- Seeta 5,000 Wages 23,500 Sundry Creditors 1,03,000 Salaries 15,000 Bank overdraft 60,000 Office expenses 8,000 Sales 3,08,000 Bank charges 2,600 Legal charges 3,000 Machinery 90,000 Land and Building 1,30,000 Interest 3,600 Export duty 3,800 Bad Debts 4,000 Sundry Debtors 82,000 Travelling Expenses 3,200 Electricity charges 2,300 Furniture 37,000 8% Debentures 40,000 (Purchased on 1.10.2009) 7,16,000 7,16,000

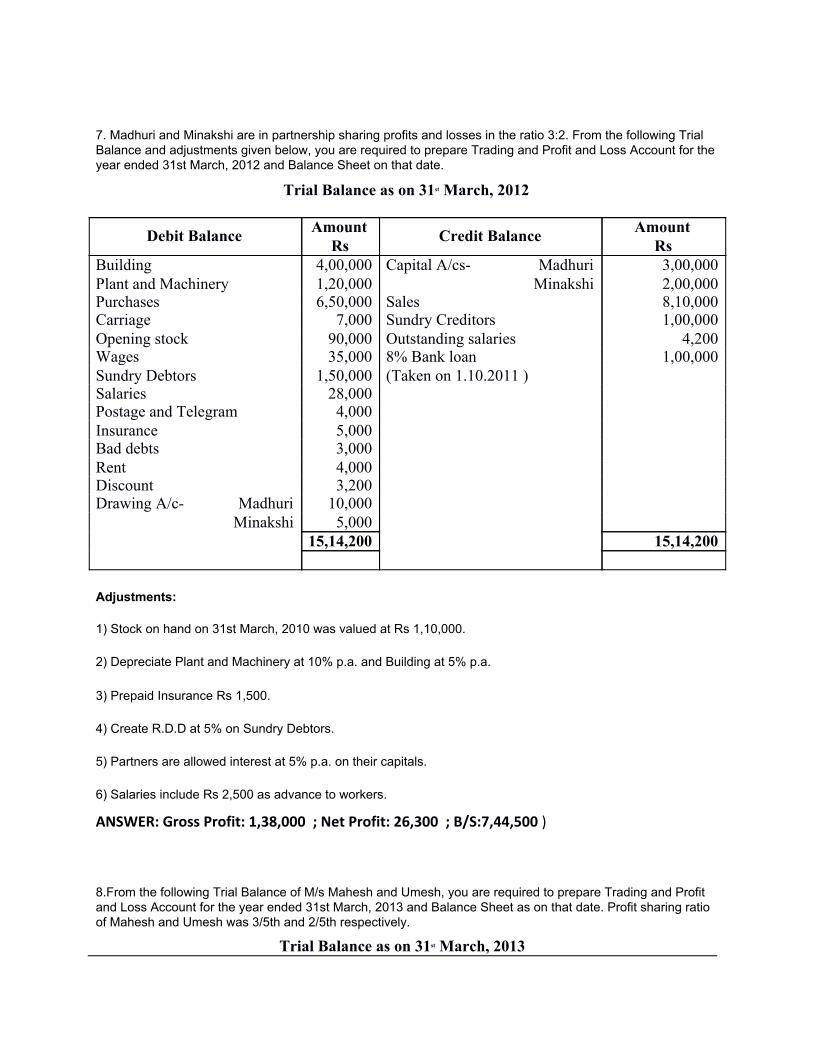

7. Madhuri and Minakshi are in partnership sharing profits and losses in the ratio 3:2. From the following Trial Balance and adjustments given below, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2012 and Balance Sheet on that date.

Adjustments:

1) Stock on hand on 31st March, 2010 was valued at Rs 1,10,000.

2) Depreciate Plant and Machinery at 10% p.a. and Building at 5% p.a.

3) Prepaid Insurance Rs 1,500.

4) Create R.D.D at 5% on Sundry Debtors.

5) Partners are allowed interest at 5% p.a. on their capitals.

6) Salaries include Rs 2,500 as advance to workers.

ANSWER: Gross Profit: 1,38,000 ; Net Profit: 26,300 ; B/S:7,44,500 )

8.From the following Trial Balance of M/s Mahesh and Umesh, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2013 and Balance Sheet as on that date. Profit sharing ratio of Mahesh and Umesh was 3/5th and 2/5th respectively.

Trial Balance as on 31st March, 2012

Debit Balance Amount Rs Credit Balance Amount

Rs Building 4,00,000 Capital A/cs- Madhuri 3,00,000 Plant and Machinery 1,20,000 Minakshi 2,00,000 Purchases 6,50,000 Sales 8,10,000 Carriage 7,000 Sundry Creditors 1,00,000 Opening stock 90,000 Outstanding salaries 4,200 Wages 35,000 8% Bank loan 1,00,000 Sundry Debtors 1,50,000 (Taken on 1.10.2011 ) Salaries 28,000 Postage and Telegram 4,000 Insurance 5,000 Bad debts 3,000 Rent 4,000 Discount 3,200 Drawing A/c- Madhuri 10,000 Minakshi 5,000 15,14,200 15,14,200

Trial Balance as on 31st March, 2013

Adjustments:

1) Stock on hand on 31st March, 2013 was valued at Rs 76,000.

2) Interest on partner’s capital at 5% p.a. was allowed.

3) Goods worth Rs 2,000 and Rs 1,500 withdrawn by Mahesh and Umesh respectively for their personal use.

4) Mahesh is entitled to get salary of Rs 6,500 and Umesh is to be given 20% commission on sales.

5) Rs 2,500 due from customer is not recoverable.

6) Depreciate Motor Van at 8% p.a. and Building at 7% p.a.

ANSWER: Gross Profit: 1,90,000 ; Net Profit: 1,09,660 ; B/S:5,86,960 )

9. Mohini and Rohini are in partnership firm sharing profits and losses equally. From the following Trial Balance and adjustments given below, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2010 and Balance Sheet as on that date.

Debit Balance Amoun

t Rs

Credit Balance Amount Rs

Investments 56,000 Capital A/c- Mahesh 1,62,000 Carriage 7,000 Umesh 1,08,000 Loose Tools 17,000 Current A/c- Mahesh 16,200 Building 1,50,000 Umesh 10,800 Salary 13,000 Sundry Creditors 99,000 Audit fees 8,500 Sales 4,20,000 Opening stock 83,000 Bank overdraft 56,400 Wages 7,500 Purchases 1,97,000 Motive Power 15,000 Bad debts 6,400 Printing and Stationery

4,000

Debtors 96,000 Cash at Bank 52,000 Machinery 72,000 Motor Van 88,000 8,72,400 8,72,400

Trial Balance as on 31st March, 2010

Adjustments:

1) Closing stock was valued at market price Rs 92,000 which is 15% above its cost price.

2) Goods costing Rs 3,000 purchased and received on 31st March, 2010 were not recorded in purchase book.

3) Depreciate Machinery at 10% p.a.

4) Outstanding Wages were Rs 2,500.

5) Goods of Rs 2,000 were taken by Mohini for personal use but no entry was made in the books of account.

6) Maintain R.D.D at 5% on Sundry Debtors.

ANSWER: Gross Profit: 2,13,000; Net Profit:1,55,000 ; B/S:4,53,500 )

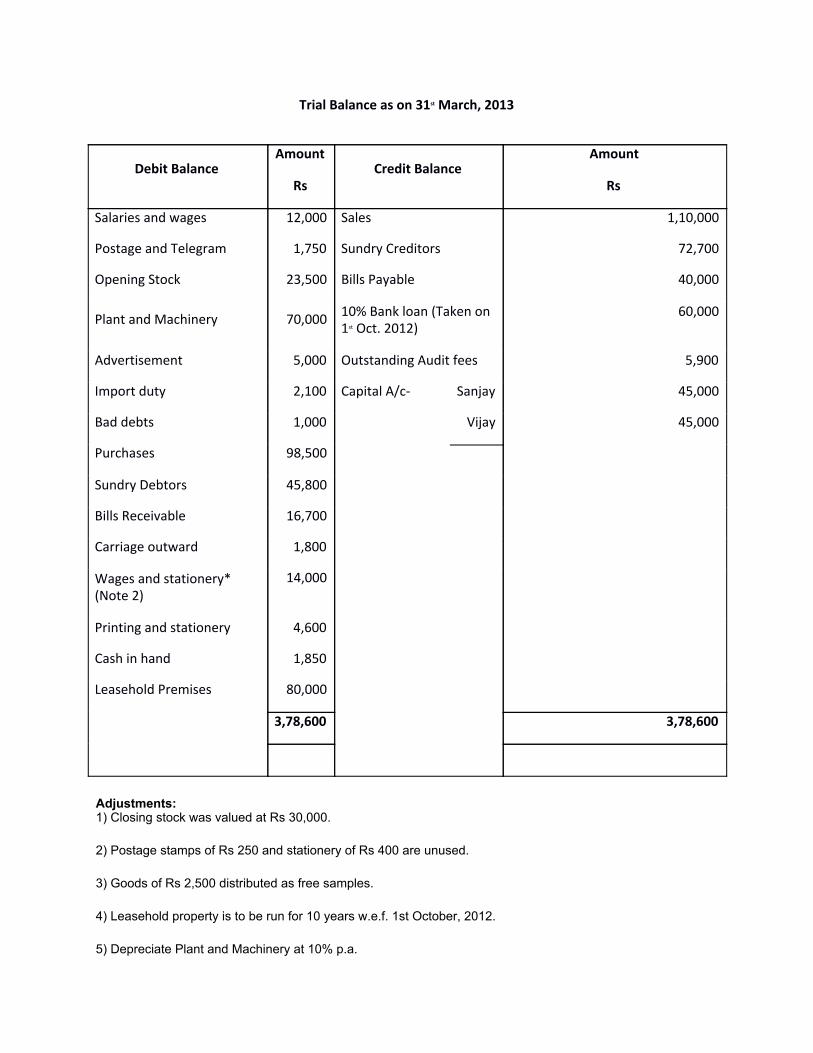

10 From the following Trial Balance of M/s Sanjay and Vijay, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2013 and Balance Sheet as on that date after taking into consideration the adjustments given below.

Particulars

Debit Amoun

t Rs

Credit Amount

Rs

Partner’s Capital Ac- Mohini 1,20,000 Rohini 90,000 Purchases and Sales 2,20,000 4,30,000 Sundry Debtors and Creditors 45,000 35,000 Bills Receivable and Bills Payable 45,000 50,000 Discount 4,000 3,500 Opening stock 25,000 Wages and Salaries 23,000 Manufacturing Expenses 9,000 Factory Insurances 5,000 Factory Building* 1,40,000 Plant and Machinery 75,000 Advertisement (for 2years w.e.f. 1st Jan. 2010) 10,000 Salaries and Wages 45,000 Warehouse rent 6,000 Import duty 11,500 Cash in hand 5,000 10% Government Bond 60,000 (purchased on 1st July, 2009) 7,28,500 7,28,500

Adjustments: 1) Closing stock was valued at Rs 30,000.

2) Postage stamps of Rs 250 and stationery of Rs 400 are unused.

3) Goods of Rs 2,500 distributed as free samples.

4) Leasehold property is to be run for 10 years w.e.f. 1st October, 2012.

5) Depreciate Plant and Machinery at 10% p.a.

Trial Balance as on 31st March, 2013

Debit Balance Amount

Rs Credit Balance

Amount

Rs

Salaries and wages 12,000 Sales 1,10,000

Postage and Telegram 1,750 Sundry Creditors 72,700

Opening Stock 23,500 Bills Payable 40,000

Plant and Machinery 70,000 10% Bank loan (Taken on 1st Oct. 2012)

60,000

Advertisement 5,000 Outstanding Audit fees 5,900

Import duty 2,100 Capital A/c- Sanjay 45,000

Bad debts 1,000 Vijay 45,000

Purchases 98,500

Sundry Debtors 45,800

Bills Receivable 16,700

Carriage outward 1,800

Wages and stationery* (Note 2)

14,000

Printing and stationery 4,600

Cash in hand 1,850

Leasehold Premises 80,000

3,78,600 3,78,600

6) Mr. Rajan, our customer become insolvent and could not pay his debts of Rs 1,500.

ANSWER: Gross Profit:4,400 ; Net LOSS: 39,100; B/S:2,32,500

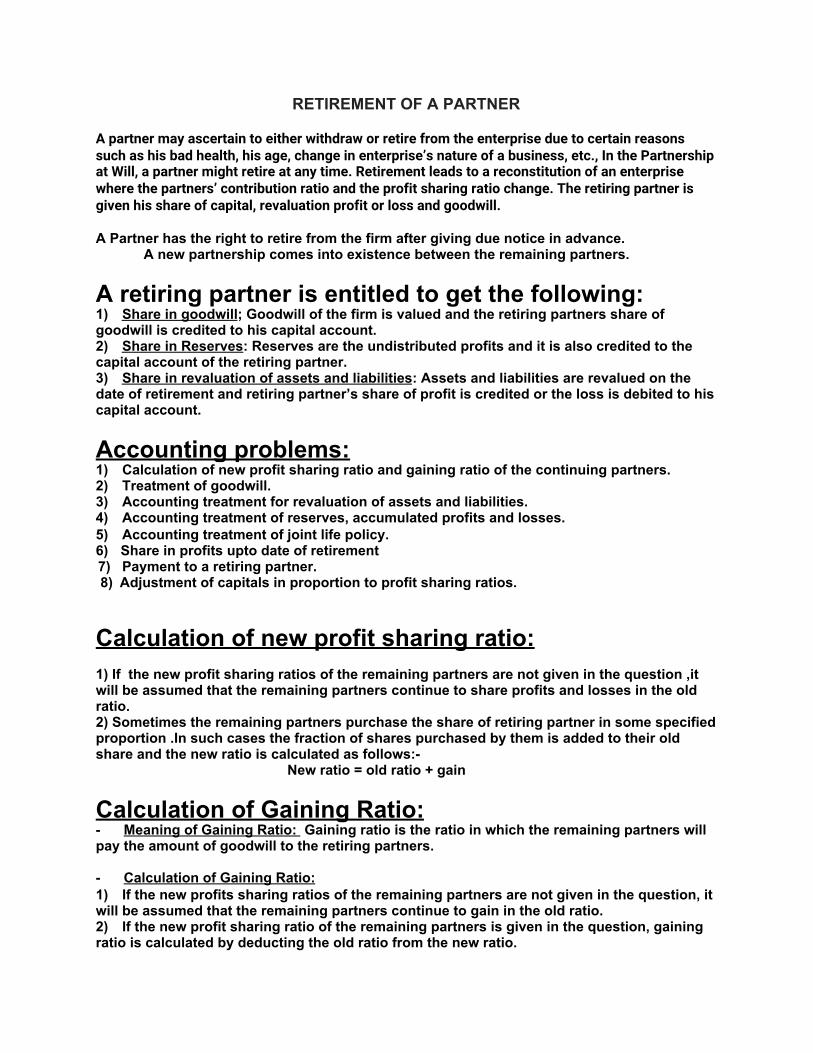

RETIREMENT OF A PARTNER A partner may ascertain to either withdraw or retire from the enterprise due to certain reasons such as his bad health, his age, change in enterprise’s nature of a business, etc., In the Partnership at Will, a partner might retire at any time. Retirement leads to a reconstitution of an enterprise where the partners’ contribution ratio and the profit sharing ratio change. The retiring partner is given his share of capital, revaluation profit or loss and goodwill. A Partner has the right to retire from the firm after giving due notice in advance. A new partnership comes into existence between the remaining partners.

A retiring partner is entitled to get the following: 1) Share in goodwill; Goodwill of the firm is valued and the retiring partners share of goodwill is credited to his capital account. 2) Share in Reserves: Reserves are the undistributed profits and it is also credited to the capital account of the retiring partner. 3) Share in revaluation of assets and liabilities: Assets and liabilities are revalued on the date of retirement and retiring partner’s share of profit is credited or the loss is debited to his capital account.

Accounting problems: 1) Calculation of new profit sharing ratio and gaining ratio of the continuing partners. 2) Treatment of goodwill. 3) Accounting treatment for revaluation of assets and liabilities. 4) Accounting treatment of reserves, accumulated profits and losses. 5) Accounting treatment of joint life policy. 6) Share in profits upto date of retirement 7) Payment to a retiring partner. 8) Adjustment of capitals in proportion to profit sharing ratios.

Calculation of new profit sharing ratio: 1) If the new profit sharing ratios of the remaining partners are not given in the question ,it will be assumed that the remaining partners continue to share profits and losses in the old ratio. 2) Sometimes the remaining partners purchase the share of retiring partner in some specified proportion .In such cases the fraction of shares purchased by them is added to their old share and the new ratio is calculated as follows:- New ratio = old ratio + gain

Calculation of Gaining Ratio: - Meaning of Gaining Ratio: Gaining ratio is the ratio in which the remaining partners will pay the amount of goodwill to the retiring partners. - Calculation of Gaining Ratio: 1) If the new profits sharing ratios of the remaining partners are not given in the question, it will be assumed that the remaining partners continue to gain in the old ratio. 2) If the new profit sharing ratio of the remaining partners is given in the question, gaining ratio is calculated by deducting the old ratio from the new ratio.

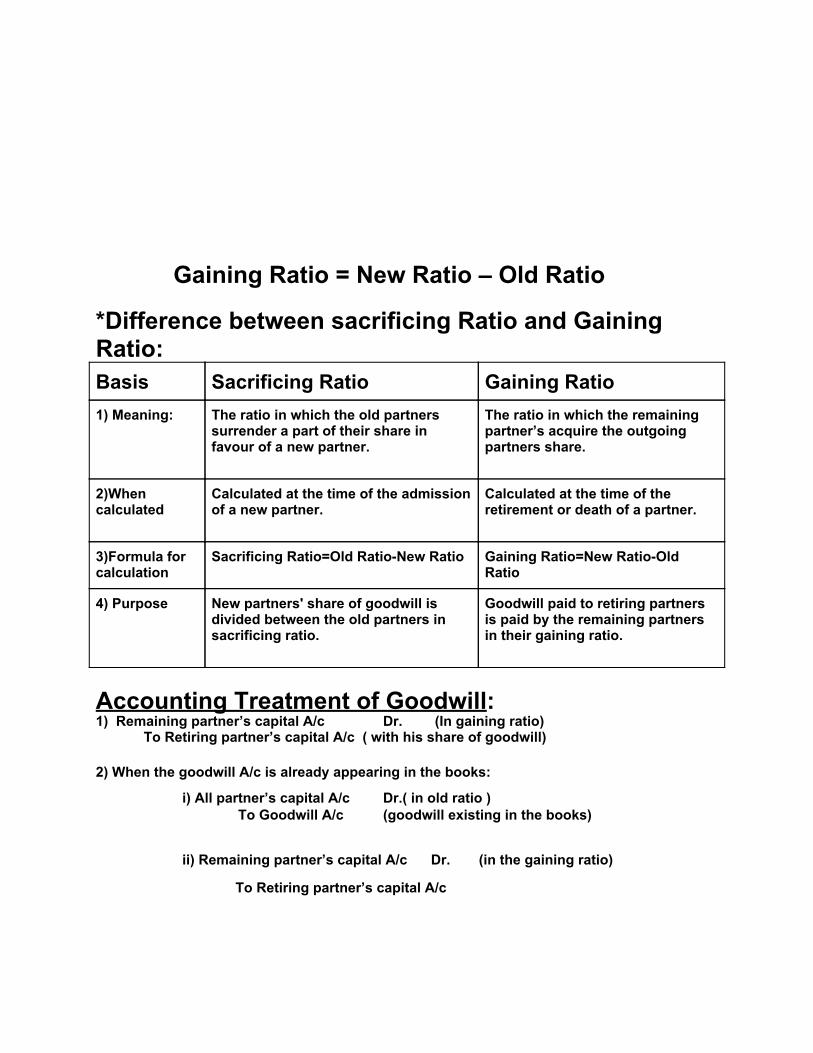

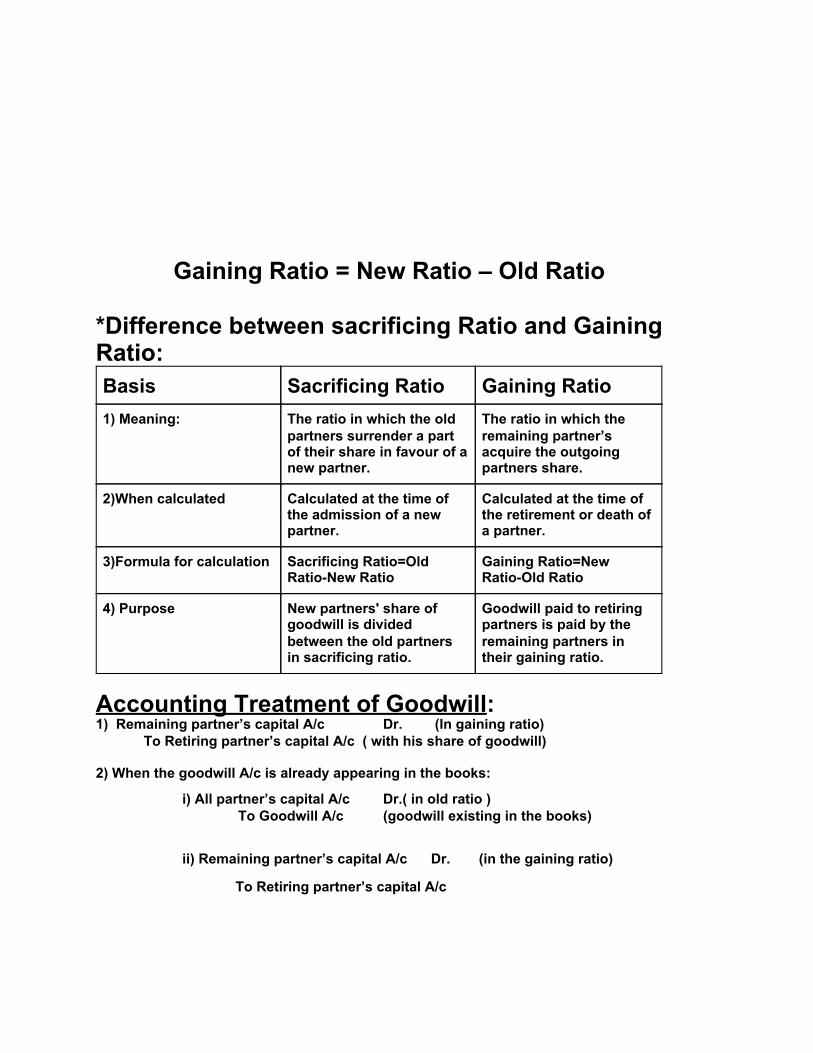

Gaining Ratio = New Ratio – Old Ratio *Difference between sacrificing Ratio and Gaining Ratio:

Accounting Treatment of Goodwill: 1) Remaining partner’s capital A/c Dr. (In gaining ratio) To Retiring partner’s capital A/c ( with his share of goodwill) 2) When the goodwill A/c is already appearing in the books: i) All partner’s capital A/c Dr.( in old ratio ) To Goodwill A/c (goodwill existing in the books) ii) Remaining partner’s capital A/c Dr. (in the gaining ratio)

To Retiring partner’s capital A/c

Basis Sacrificing Ratio Gaining Ratio

1) Meaning: The ratio in which the old partners surrender a part of their share in favour of a new partner.

The ratio in which the remaining partner’s acquire the outgoing partners share.

2)When calculated

Calculated at the time of the admission of a new partner.

Calculated at the time of the retirement or death of a partner.

3)Formula for calculation

Sacrificing Ratio=Old Ratio-New Ratio Gaining Ratio=New Ratio-Old Ratio

4) Purpose New partners' share of goodwill is divided between the old partners in sacrificing ratio.

Goodwill paid to retiring partners is paid by the remaining partners in their gaining ratio.

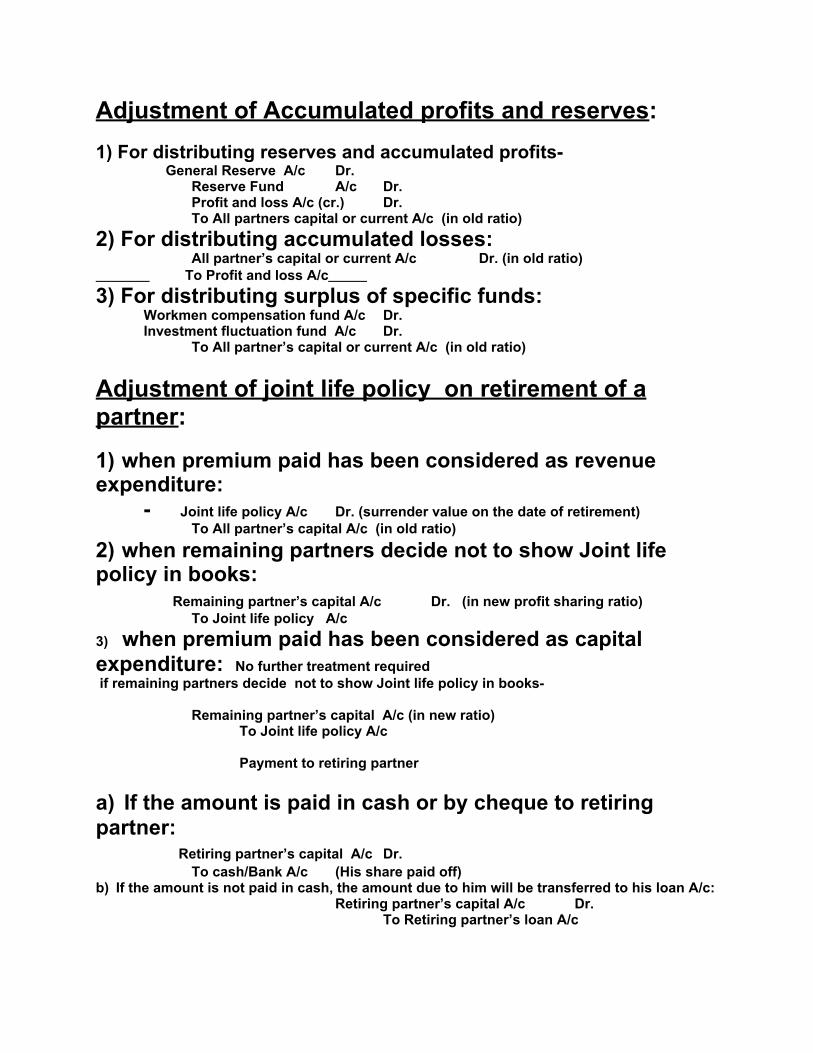

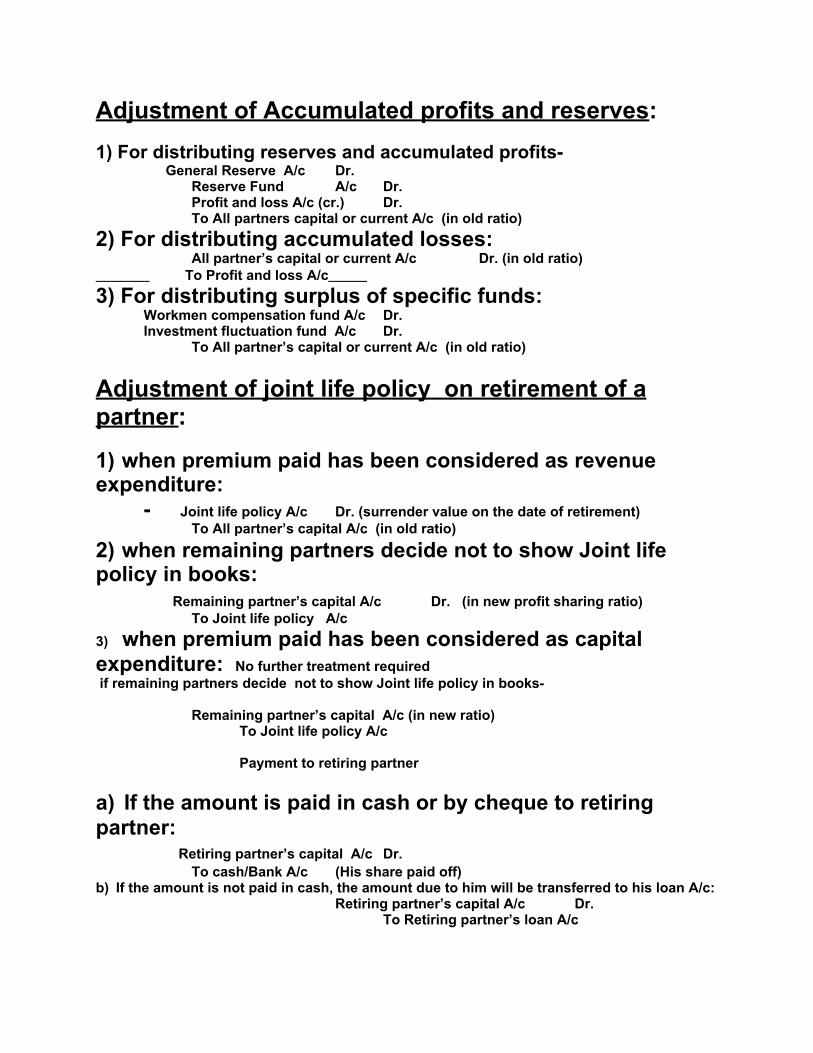

Adjustment of Accumulated profits and reserves: 1) For distributing reserves and accumulated profits- General Reserve A/c Dr. Reserve Fund A/c Dr. Profit and loss A/c (cr.) Dr. To All partners capital or current A/c (in old ratio) 2) For distributing accumulated losses: All partner’s capital or current A/c Dr. (in old ratio) To Profit and loss A/c 3) For distributing surplus of specific funds: Workmen compensation fund A/c Dr. Investment fluctuation fund A/c Dr. To All partner’s capital or current A/c (in old ratio) Adjustment of joint life policy on retirement of a partner: 1) when premium paid has been considered as revenue expenditure: - Joint life policy A/c Dr. (surrender value on the date of retirement) To All partner’s capital A/c (in old ratio) 2) when remaining partners decide not to show Joint life policy in books: Remaining partner’s capital A/c Dr. (in new profit sharing ratio) To Joint life policy A/c 3) when premium paid has been considered as capital expenditure: No further treatment required if remaining partners decide not to show Joint life policy in books- Remaining partner’s capital A/c (in new ratio) To Joint life policy A/c Payment to retiring partner a) If the amount is paid in cash or by cheque to retiring partner: Retiring partner’s capital A/c Dr. To cash/Bank A/c (His share paid off) b) If the amount is not paid in cash, the amount due to him will be transferred to his loan A/c: Retiring partner’s capital A/c Dr. To Retiring partner’s loan A/c

1.A and B are partners in a business sharing profits and losses as A 3/5ths and B 2/5ths.

Their Balance Sheet as on 1st January 2005 is given below:

B decides to retire from the business owing to illness and A takes it over and the following revaluation are made: (a) Goodwill of the firm is valued at Rs 15,000.

[ Answer: Revaluation loss – 4,425; B/S- 52,887; ]

2. The Balance Sheet of A, B and c who are sharing profits and losses in the proportion of

one-half, one-third and one-sixth, respectively, was as follows on 30th June 2002:

A retires from the business on 1st July 2002 and his share in the firm is to be ascertained on a

revaluation of the assets as follows:

Stock at Rs 20,000

Furniture Rs 3,000

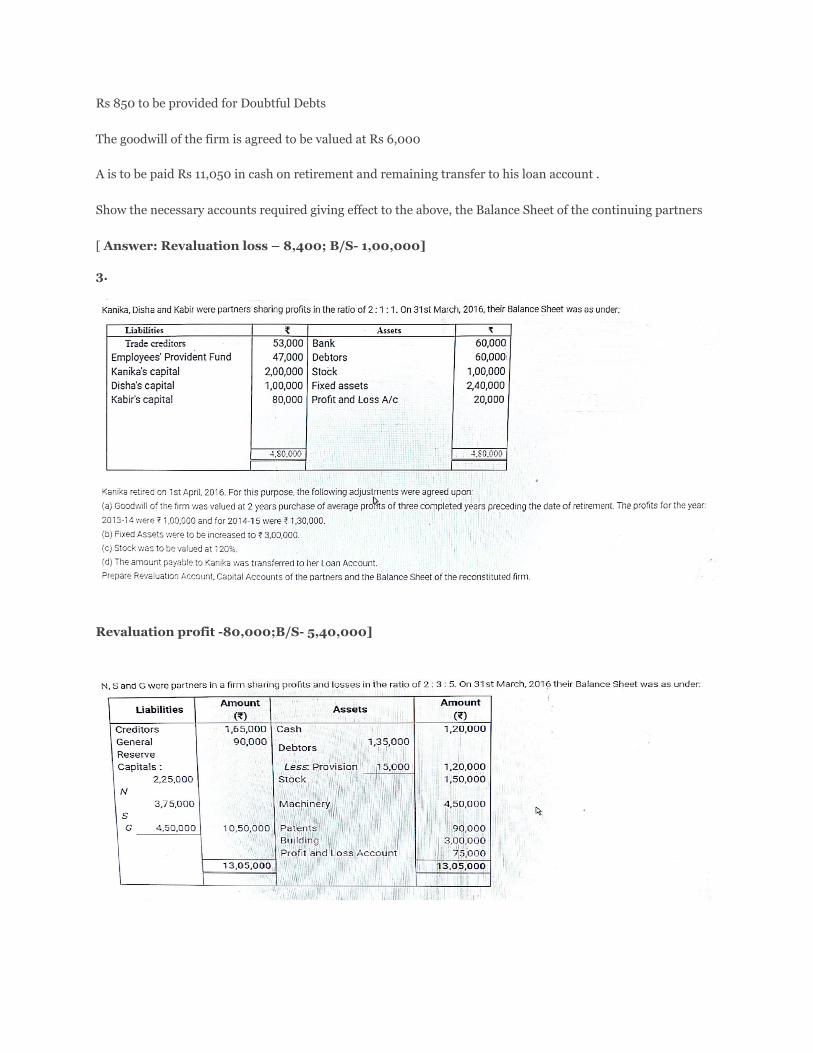

Plant and Machinery Rs 9,000

Buildings at Rs 20,000

Rs 850 to be provided for Doubtful Debts

The goodwill of the firm is agreed to be valued at Rs 6,000

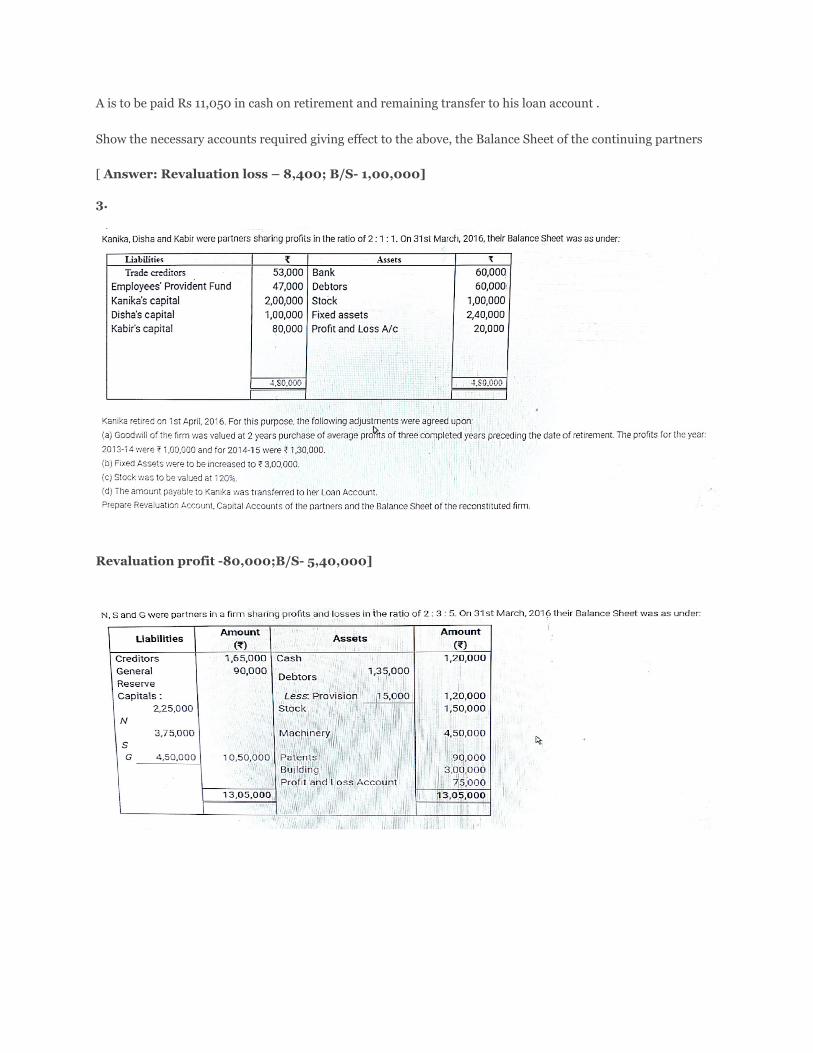

A is to be paid Rs 11,050 in cash on retirement and remaining transfer to his loan account .

Show the necessary accounts required giving effect to the above, the Balance Sheet of the continuing partners

[ Answer: Revaluation loss – 8,400; B/S- 1,00,000]

3.

Revaluation profit -80,000;B/S- 5,40,000]

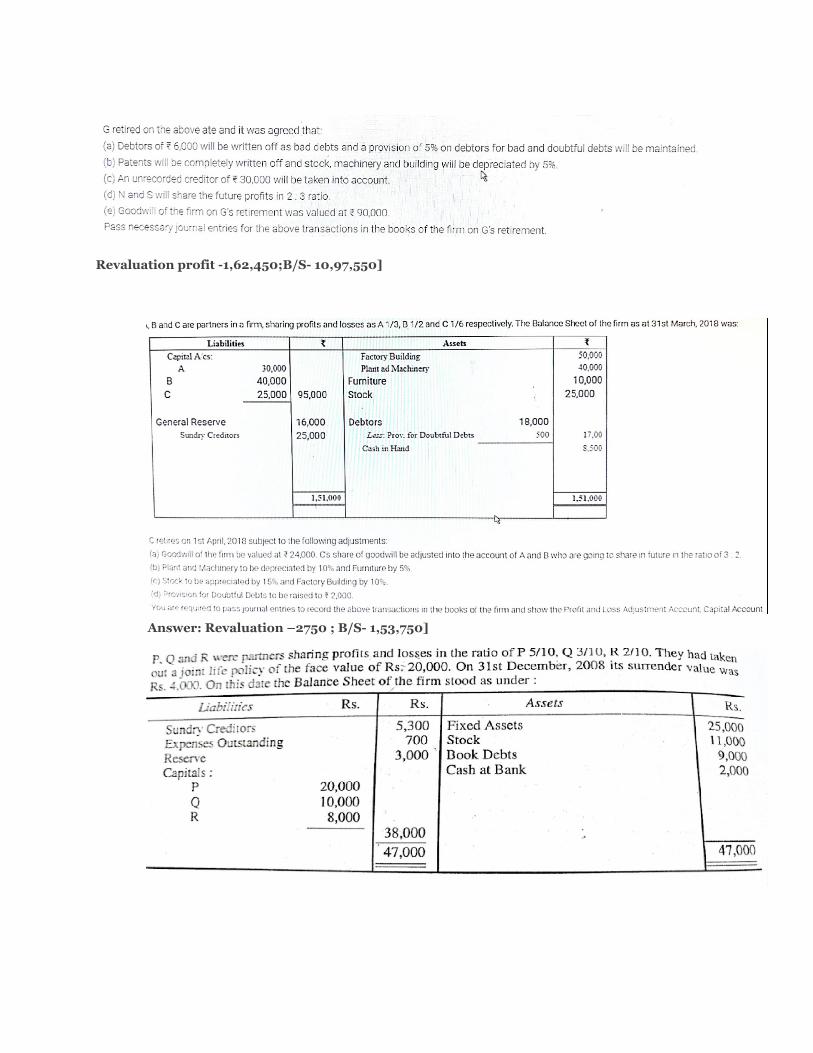

Revaluation profit -1,62,450;B/S- 10,97,550]

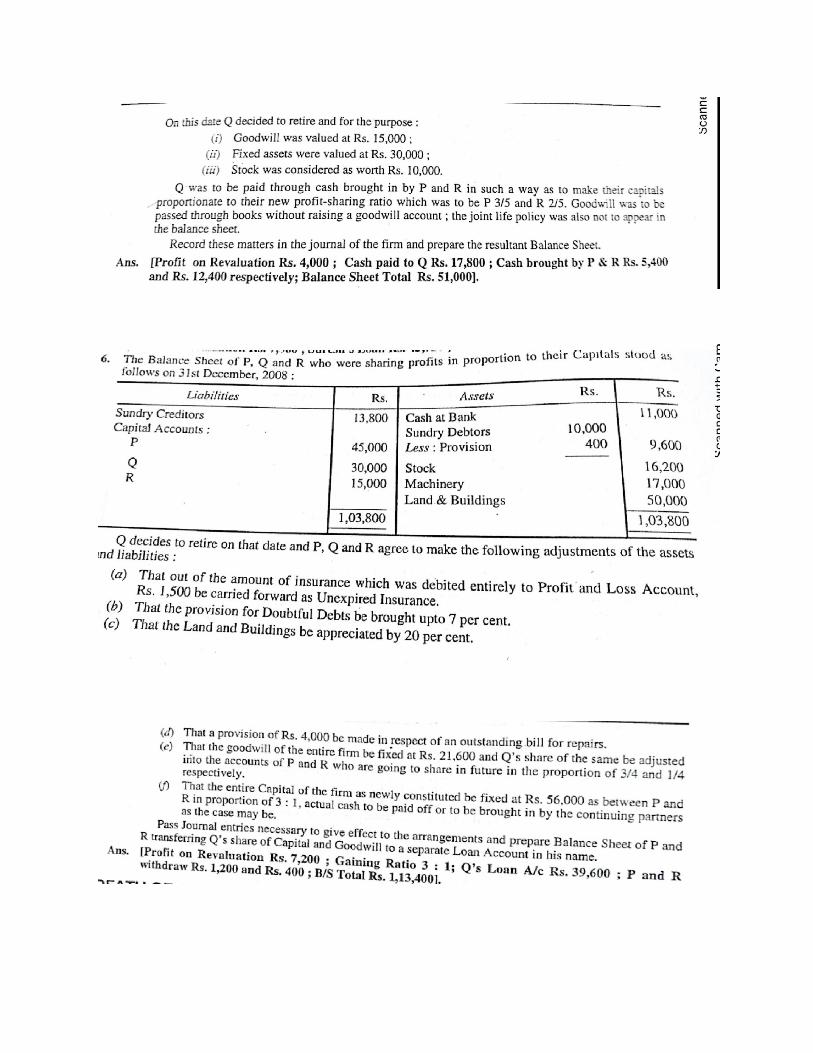

Answer: Revaluation –2750 ; B/S- 1,53,750]

Death of a Partner

In the event of death of a partner, the structure of the partnership is changed in the same way as when a partner retires

According to the Indian Partnership Act, 1932. Deceased partner is one who has discontinued the partnership due to his death. A contract between the partners of the enterprise is not dissolved by the death of a partner, the estate of a dead partner is not responsible for any act of the enterprise done after his death.

The accounting treatment in the occurrence of death of a partner is :

● Similar to that, when a partner retires and that in case of deceased partner his belonging is transferred to his legal enforcers and settled in a similar way as that of the partner who retires

● However, there is one primary distinction, the retirement usually takes place during the closure of an accounting period or financial year, the death of a partner may take place any time

● Therefore, in the case of a partner, his rights shall also incorporate his share of gains or loss, interest on drawings (if any), interest on capital from the last date of the Balance Sheet to the date of his death of these, the main issue associates to the computation of profit for a moderate period

● Since, it is contemplated burdensome to close the books and outline final a/c, for the period, the dead partner’s share of profit may be computed on the ground of previous year’s gain (or aggregate of past few years) or on the base of sales.

1. Distribution of Existing Goodwill

All Partners’ Capital A/c Dr.

To Goodwill A/c (Being Goodwill written off)

Note : If Goodwill appears in the Balance sheet

2. Deceased partner’s Share of Goodwill Remaining Partners capital A/c Dr.

To Deceased Partners Capital A/c

3. Distribution of Reserves Reserve fund/General Reserve A/c Dr. To All Partners’ Capital A/c (Being the reserves amount distributed among all the partners)

4. Distribution of Accumulated Losses All Partners’ Capital A/c Dr.

To Profit & Loss A/c

5. Distribution of Accumulated Profits Profit & Loss A/c Dr. To All Partners’ Capital A/c

Section 37 of the Partnership Act, the executive of the deceased partner would be entitled at their discretion either interest 6% per annum for the amount due from the date of death to the date of payment or to that portion of the profit that is earned by the firm with the amount due to the deceased partner.

1. Calculation of of deceased partner share of profits 2. Treatment of life policy or policies

1. Calculation of deceased partner share of profit: This can be determined either on the basis of time or turn over

a. On the basis of time: in this case it is assumed that the profit during the previous year has been earned uniformly in all months during the year, provided previous year is taken as the base for calculation of profits. Sometimes average profit for the past three or four years is taken as base rather than the previous year. Whatever base may be taken it is to be multiplied by the period for which the deceased partner remained in the and also by his profit sharing ratio at the time of his death.

b. On the basis of turnover: In this method, average past profit is divided into two portions, i.e., before the death and after the death on the basis of ratio of turnover to the date of death average turnover and then deceased partner share is calculated and credited to his capital account.

Journal Entry

Profit & Loss Suspense A/C…...Dr

To Deceased partners Capital A/C

(Being a deceased partner’s share in the profit credited to his capital account)

2. Treatment of life policy or policies: When a partner dies, his legal representatives are required to be paid a large sum of money which might affect the financial as well as working position of the partnership business. To provide funds to the legal representatives of the deceased partner generally A Joint life policy or individual life policies for partners might be taken. The premium for such policies is charged to the profit and loss account.Joint life policy is an asset of the firm and the deceased partner has a right to share any profits or losses on such policy. So the claim which is received by the firm on the death of a partner is divided among the partner and credited to their capital accounts in their profit sharing ratio. If the firm has taken individual life policies and the

premiums were charged to the profit and loss account then, the deceased partner has a right share the amount not only received from Life Insurance Corporation of India but also the surrender value which the other partners policies would acquire at the time of his death.

Journal Entry

a. For Joint life Policy

Joint Life Policy A/C Dr.

To, All Partner’s Capital A/c

b. For Individual Life policy

Insurance Policy A/c Dr.

To, All Partner’s Capital A/c

RETIREMENT OF A PARTNER A partner may ascertain to either withdraw or retire from the enterprise due to certain reasons such as his bad health, his age, change in enterprise’s nature of a business, etc., In the Partnership at Will, a partner might retire at any time. Retirement leads to a reconstitution of an enterprise where the partners’ contribution ratio and the profit sharing ratio change. The retiring partner is given his share of capital, revaluation profit or loss and goodwill. A Partner has the right to retire from the firm after giving due notice in advance. A new partnership comes into existence between the remaining partners.

A retiring partner is entitled to get the following: 1) Share in goodwill; Goodwill of the firm is valued and the retiring partners share of goodwill is credited to his capital account. 2) Share in Reserves: Reserves are the undistributed profits and it is also credited to the capital account of the retiring partner. 3) Share in revaluation of assets and liabilities: Assets and liabilities are revalued on the date of retirement and retiring partner’s share of profit is credited or the loss is debited to his capital account.

Accounting problems: 1) Calculation of new profit sharing ratio and gaining ratio of the continuing partners. 2) Treatment of goodwill. 3) Accounting treatment for revaluation of assets and liabilities. 4) Accounting treatment of reserves, accumulated profits and losses. 5) Accounting treatment of joint life policy. 6) Share in profits upto date of retirement 7) Payment to a retiring partner. 8) Adjustment of capitals in proportion to profit sharing ratios.

Calculation of new profit sharing ratio: 1) If the new profit sharing ratios of the remaining partners are not given in the question ,it will be assumed that the remaining partners continue to share profits and losses in the old ratio. 2) Sometimes the remaining partners purchase the share of retiring partner in some specified proportion .In such cases the fraction of shares purchased by them is added to their old share and the new ratio is calculated as follows:- New ratio = old ratio + gain

Calculation of Gaining Ratio: - Meaning of Gaining Ratio: Gaining ratio is the ratio in which the remaining partners will pay the amount of goodwill to the retiring partners. - Calculation of Gaining Ratio: 1) If the new profits sharing ratios of the remaining partners are not given in the question, it will be assumed that the remaining partners continue to gain in the old ratio. 2) If the new profit sharing ratio of the remaining partners is given in the question, gaining ratio is calculated by deducting the old ratio from the new ratio.

Gaining Ratio = New Ratio – Old Ratio *Difference between sacrificing Ratio and Gaining Ratio:

Accounting Treatment of Goodwill: 1) Remaining partner’s capital A/c Dr. (In gaining ratio) To Retiring partner’s capital A/c ( with his share of goodwill) 2) When the goodwill A/c is already appearing in the books: i) All partner’s capital A/c Dr.( in old ratio ) To Goodwill A/c (goodwill existing in the books) ii) Remaining partner’s capital A/c Dr. (in the gaining ratio)

To Retiring partner’s capital A/c

Basis Sacrificing Ratio Gaining Ratio

1) Meaning: The ratio in which the old partners surrender a part of their share in favour of a new partner.

The ratio in which the remaining partner’s acquire the outgoing partners share.

2)When calculated

Calculated at the time of the admission of a new partner.

Calculated at the time of the retirement or death of a partner.

3)Formula for calculation

Sacrificing Ratio=Old Ratio-New Ratio Gaining Ratio=New Ratio-Old Ratio

4) Purpose New partners' share of goodwill is divided between the old partners in sacrificing ratio.

Goodwill paid to retiring partners is paid by the remaining partners in their gaining ratio.

Adjustment of Accumulated profits and reserves: 1) For distributing reserves and accumulated profits- General Reserve A/c Dr. Reserve Fund A/c Dr. Profit and loss A/c (cr.) Dr. To All partners capital or current A/c (in old ratio) 2) For distributing accumulated losses: All partner’s capital or current A/c Dr. (in old ratio) To Profit and loss A/c 3) For distributing surplus of specific funds: Workmen compensation fund A/c Dr. Investment fluctuation fund A/c Dr. To All partner’s capital or current A/c (in old ratio) Adjustment of joint life policy on retirement of a partner: 1) when premium paid has been considered as revenue expenditure: - Joint life policy A/c Dr. (surrender value on the date of retirement) To All partner’s capital A/c (in old ratio) 2) when remaining partners decide not to show Joint life policy in books: Remaining partner’s capital A/c Dr. (in new profit sharing ratio) To Joint life policy A/c 3) when premium paid has been considered as capital expenditure: No further treatment required if remaining partners decide not to show Joint life policy in books- Remaining partner’s capital A/c (in new ratio) To Joint life policy A/c Payment to retiring partner a) If the amount is paid in cash or by cheque to retiring partner: Retiring partner’s capital A/c Dr. To cash/Bank A/c (His share paid off) b) If the amount is not paid in cash, the amount due to him will be transferred to his loan A/c: Retiring partner’s capital A/c Dr. To Retiring partner’s loan A/c

1.A and B are partners in a business sharing profits and losses as A 3/5ths and B 2/5ths.

Their Balance Sheet as on 1st January 2005 is given below:

B decides to retire from the business owing to illness and A takes it over and the following revaluation are made: (a) Goodwill of the firm is valued at Rs 15,000.

(b) Depreciate Machinery by 7.5% and Stock by 15%.

(c) A Bad Debts provision is raised against Debtors at 5% and a Discount Reserve against Creditors at 2.5%.

Journalise the above transaction in the books of the firm; prepare ledger accounts and the Balance Sheet of A.

[ Answer: Revaluation loss – 4,425; B/S- 52,887; ]

2. The Balance Sheet of A, B and c who are sharing profits and losses in the proportion of

one-half, one-third and one-sixth, respectively, was as follows on 30th June 2002:

A retires from the business on 1st July 2002 and his share in the firm is to be ascertained on a

revaluation of the assets as follows:

Stock at Rs 20,000

Furniture Rs 3,000

Plant and Machinery Rs 9,000

Buildings at Rs 20,000

Rs 850 to be provided for Doubtful Debts

The goodwill of the firm is agreed to be valued at Rs 6,000

A is to be paid Rs 11,050 in cash on retirement and remaining transfer to his loan account .

Show the necessary accounts required giving effect to the above, the Balance Sheet of the continuing partners

[ Answer: Revaluation loss – 8,400; B/S- 1,00,000]

3.

Revaluation profit -80,000;B/S- 5,40,000]

Revaluation profit -1,62,450;B/S- 10,97,550]

Answer: Revaluation –2750 ; B/S- 1,53,750]

B.COM SECOND YEAR

ODD SEM -III

ADVANCE ACCOUNTING –I

UNIT- I

Single Entry or Accounts from Incomplete Records

Introduction: Single Entry System is the oldest and most straightforward method of keeping records of financial transactions which does not exactly follow the principles of double entry system. They only maintain essential records. Under this method usually the personal accounts of the debtors and creditors are maintained and impersonal accounts may not be maintained in the books of accounts.

A single entry is a method in which each transaction is recorded only once. In other words, only one account is given debit or credit for each transaction. It is an incomplete double entry system, which does not give the complete picture of every transaction and thus it is also called accounts from incomplete records. There are two types of single entry: Pure Single Entry System: In this method, only the personal accounts are maintained and there is no information present, concerning the sales and purchases, cash in hand, and bank balance. Simple Single Entry System: In a simple single entry system, cash book is maintained along with the personal accounts . Quasi Single Entry System: In this system, subsidiary books such as sales book, purchases book, bills receivable book and bills payable book are maintained in addition to cash book and personal accounts. Single Entry System is simple and easy to maintain as it does not need any professional accountant to keep the records up to date. And so this system is quite helpful for small businesses and trades operated solely by individuals. Further, the system is quite economical. Definition of Single Entry system According to R.N. Carter, Single Entry cannot be termed as a system, and it is net based on any scientific system like Double Entry System. For this purpose, Single Entry is now-a-days known as preparation of accounts from incomplete records. Characteristics of Single Entry System

1. Suitability: The system is appropriate for small businesses, like sole proprietorship business and partnership firms, as they maintain records of cash and credit transactions only.

2. Profit or Loss: Profit earned or loss sustained is estimated, out of the information

available and so exact profits are not ascertained.

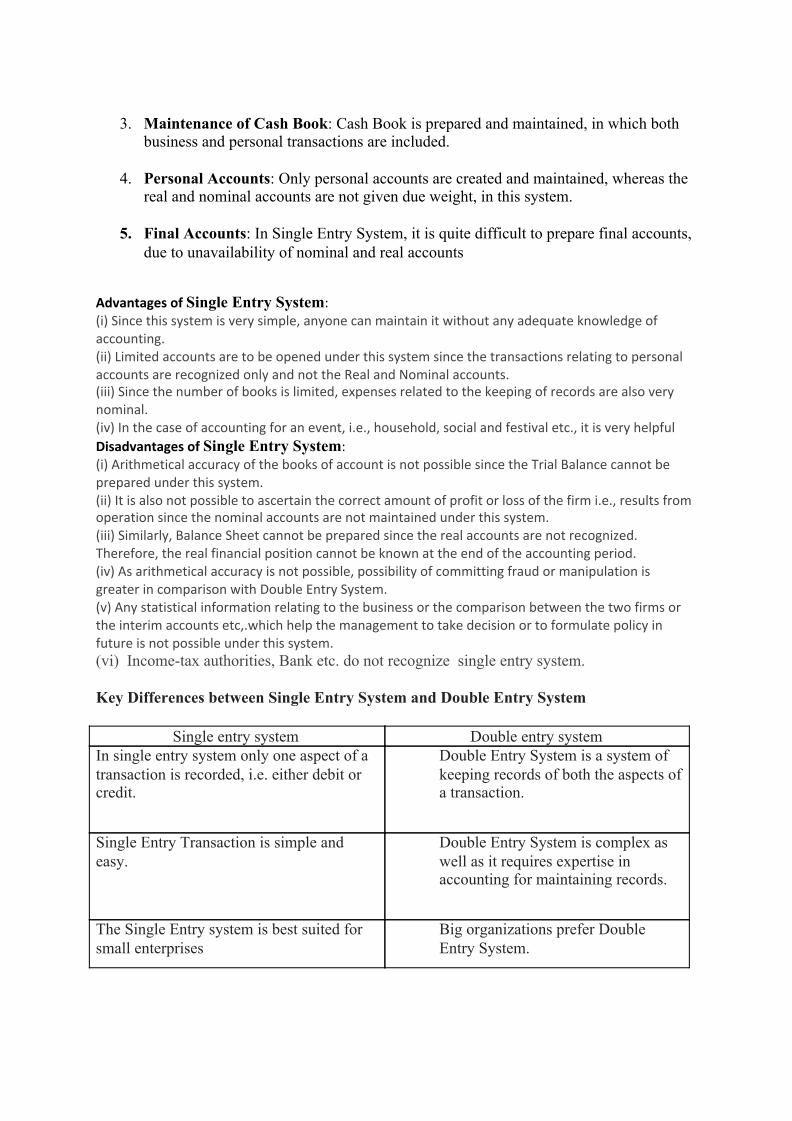

3. Maintenance of Cash Book: Cash Book is prepared and maintained, in which both

business and personal transactions are included.

4. Personal Accounts: Only personal accounts are created and maintained, whereas the real and nominal accounts are not given due weight, in this system.

5. Final Accounts: In Single Entry System, it is quite difficult to prepare final accounts,

due to unavailability of nominal and real accounts

Advantages of Single Entry System: (i) Since this system is very simple, anyone can maintain it without any adequate knowledge of accounting. (ii) Limited accounts are to be opened under this system since the transactions relating to personal accounts are recognized only and not the Real and Nominal accounts. (iii) Since the number of books is limited, expenses related to the keeping of records are also very nominal. (iv) In the case of accounting for an event, i.e., household, social and festival etc., it is very helpful Disadvantages of Single Entry System: (i) Arithmetical accuracy of the books of account is not possible since the Trial Balance cannot be prepared under this system. (ii) It is also not possible to ascertain the correct amount of profit or loss of the firm i.e., results from operation since the nominal accounts are not maintained under this system. (iii) Similarly, Balance Sheet cannot be prepared since the real accounts are not recognized. Therefore, the real financial position cannot be known at the end of the accounting period. (iv) As arithmetical accuracy is not possible, possibility of committing fraud or manipulation is greater in comparison with Double Entry System. (v) Any statistical information relating to the business or the comparison between the two firms or the interim accounts etc,.which help the management to take decision or to formulate policy in future is not possible under this system. (vi) Income-tax authorities, Bank etc. do not recognize single entry system.

Key Differences between Single Entry System and Double Entry System

Single entry system Double entry system In single entry system only one aspect of a transaction is recorded, i.e. either debit or credit.

Double Entry System is a system of keeping records of both the aspects of a transaction.

Single Entry Transaction is simple and easy.

Double Entry System is complex as well as it requires expertise in accounting for maintaining records.

The Single Entry system is best suited for small enterprises

Big organizations prefer Double Entry System.

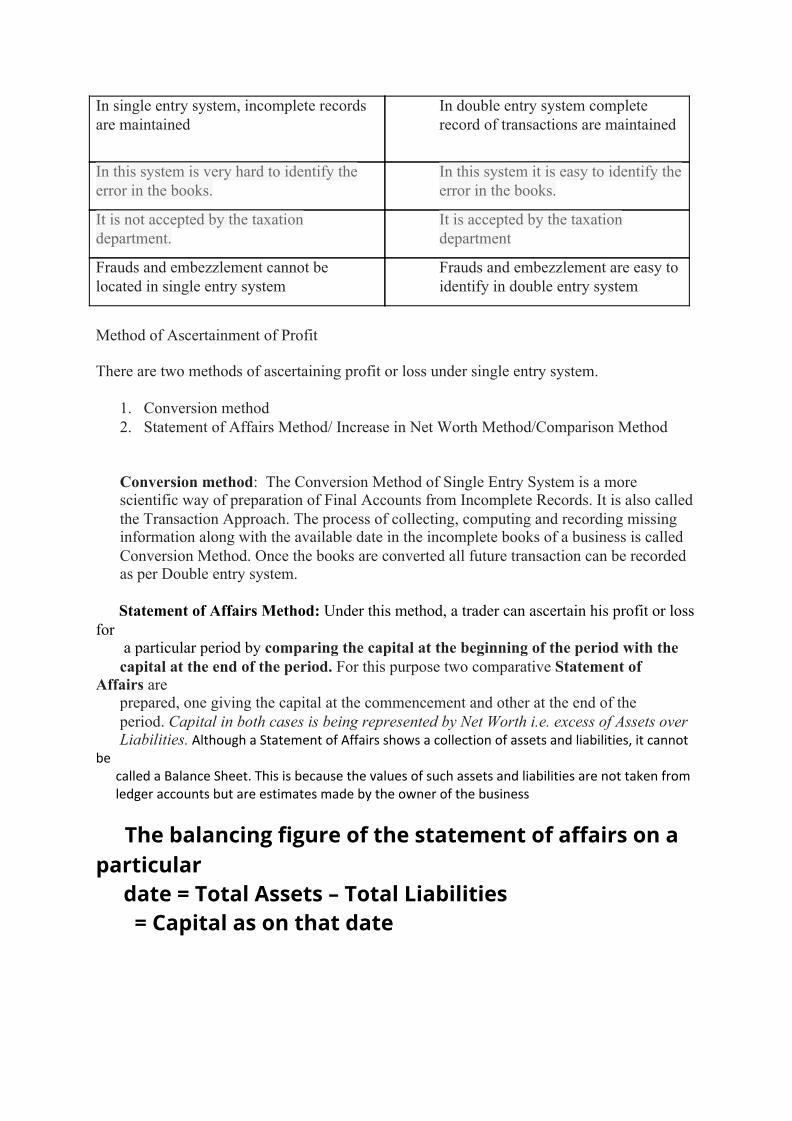

Method of Ascertainment of Profit

There are two methods of ascertaining profit or loss under single entry system.

1. Conversion method 2. Statement of Affairs Method/ Increase in Net Worth Method/Comparison Method

Conversion method: The Conversion Method of Single Entry System is a more scientific way of preparation of Final Accounts from Incomplete Records. It is also called the Transaction Approach. The process of collecting, computing and recording missing information along with the available date in the incomplete books of a business is called Conversion Method. Once the books are converted all future transaction can be recorded as per Double entry system.

Statement of Affairs Method: Under this method, a trader can ascertain his profit or loss for a particular period by comparing the capital at the beginning of the period with the capital at the end of the period. For this purpose two comparative Statement of Affairs are prepared, one giving the capital at the commencement and other at the end of the period. Capital in both cases is being represented by Net Worth i.e. excess of Assets over Liabilities. Although a Statement of Affairs shows a collection of assets and liabilities, it cannot be called a Balance Sheet. This is because the values of such assets and liabilities are not taken from ledger accounts but are estimates made by the owner of the business The balancing figure of the statement of affairs on a particular date = Total Assets – Total Liabilities = Capital as on that date

In single entry system, incomplete records are maintained

In double entry system complete record of transactions are maintained

In this system is very hard to identify the error in the books.

In this system it is easy to identify the error in the books.

It is not accepted by the taxation department.

It is accepted by the taxation department

Frauds and embezzlement cannot be located in single entry system

Frauds and embezzlement are easy to identify in double entry system

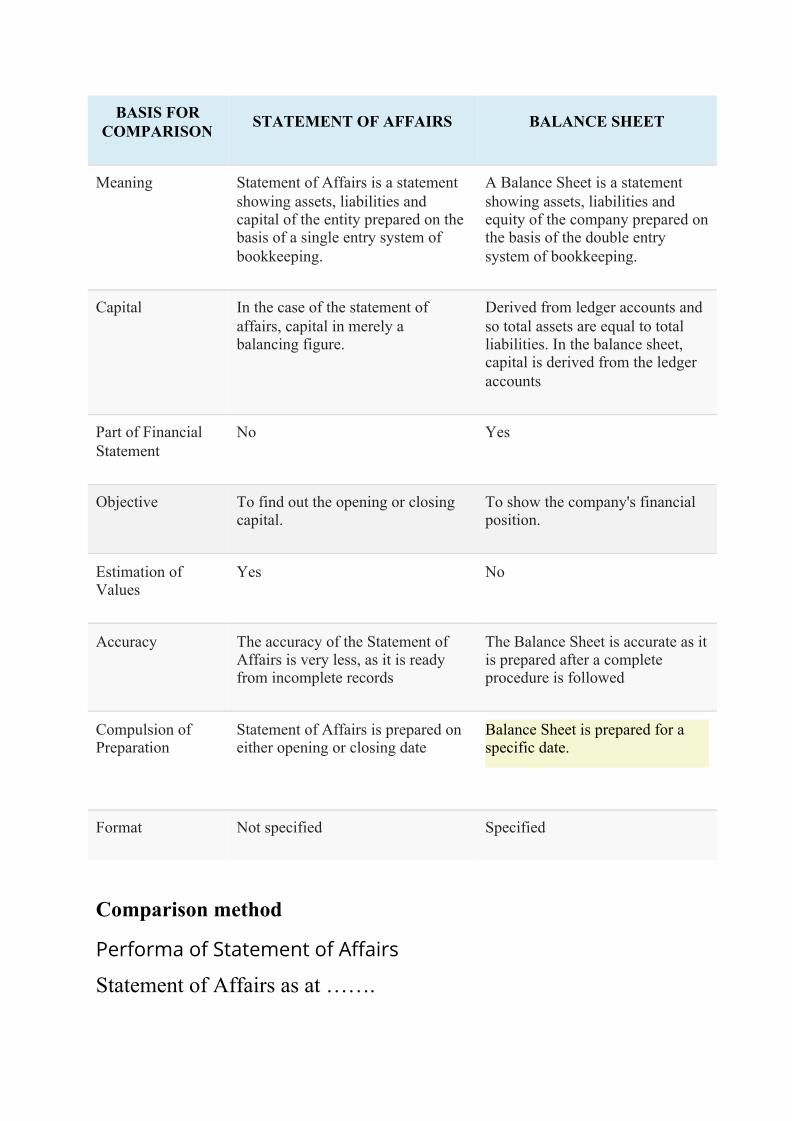

Comparison method

Performa of Statement of Affairs

Statement of Affairs as at …….

BASIS FOR COMPARISON STATEMENT OF AFFAIRS BALANCE SHEET

Meaning Statement of Affairs is a statement showing assets, liabilities and capital of the entity prepared on the basis of a single entry system of bookkeeping.

A Balance Sheet is a statement showing assets, liabilities and equity of the company prepared on the basis of the double entry system of bookkeeping.

Capital In the case of the statement of affairs, capital in merely a balancing figure.

Derived from ledger accounts and so total assets are equal to total liabilities. In the balance sheet, capital is derived from the ledger accounts

Part of Financial Statement

No Yes

Objective To find out the opening or closing capital.

To show the company's financial position.

Estimation of Values

Yes No

Accuracy The accuracy of the Statement of Affairs is very less, as it is ready from incomplete records

The Balance Sheet is accurate as it is prepared after a complete procedure is followed

Compulsion of Preparation

Statement of Affairs is prepared on either opening or closing date

Balance Sheet is prepared for a specific date.

Format Not specified Specified

Steps:

● Determine the Opening Capital by preparing the Statement of Affairs at the beginning of the year.

● Determine the Closing Capital by preparing the statement of affairs at the end of the year. ● Add drawings made by the proprietor to the closing capital during the year. ● Deduct the additional capital introduced by the owner during the year. ● Find out the Profit or Loss by deduction the opening capital from the adjusted closing

capital. ● If the adjusted closing capital exceeds the opening capital, it represents profit and vice versa.

Ascertainment of profit under single entry system:

Statement of affairs is a statement of all assets and liabilities as on a particular date. The difference between the two sides is regarded as capital-balancing figure. It is based on the equation Capital=Assets-Liabilities.

Statement showing the profit or loss made during the period

Capital at the end of the period xxxxxx Add : Drawing made during the period xxxxxx XXXX Less: Further Capital introduced during the period xxxxxx

XXXX xxxxxx Less: Capital at the beginning of the period Profit or loss made during the year XXXX

Liabilities Amount Assets Amount

Bills Payable xxxxx Land and Building xxxx

Creditors xxxxx Plant and Machinery xxxx

Outstanding Expenses xxxxx Furniture xxxx

Income received in advance xxxxx Stock xxxx

Capital (balancing figure) xxxxx Debtors/Bills Receivable xxxx

Cash and Bank xxxx

Prepaid Expenses xxxx

Accrued Income xxxx Total XXXXX

Total XXXXX

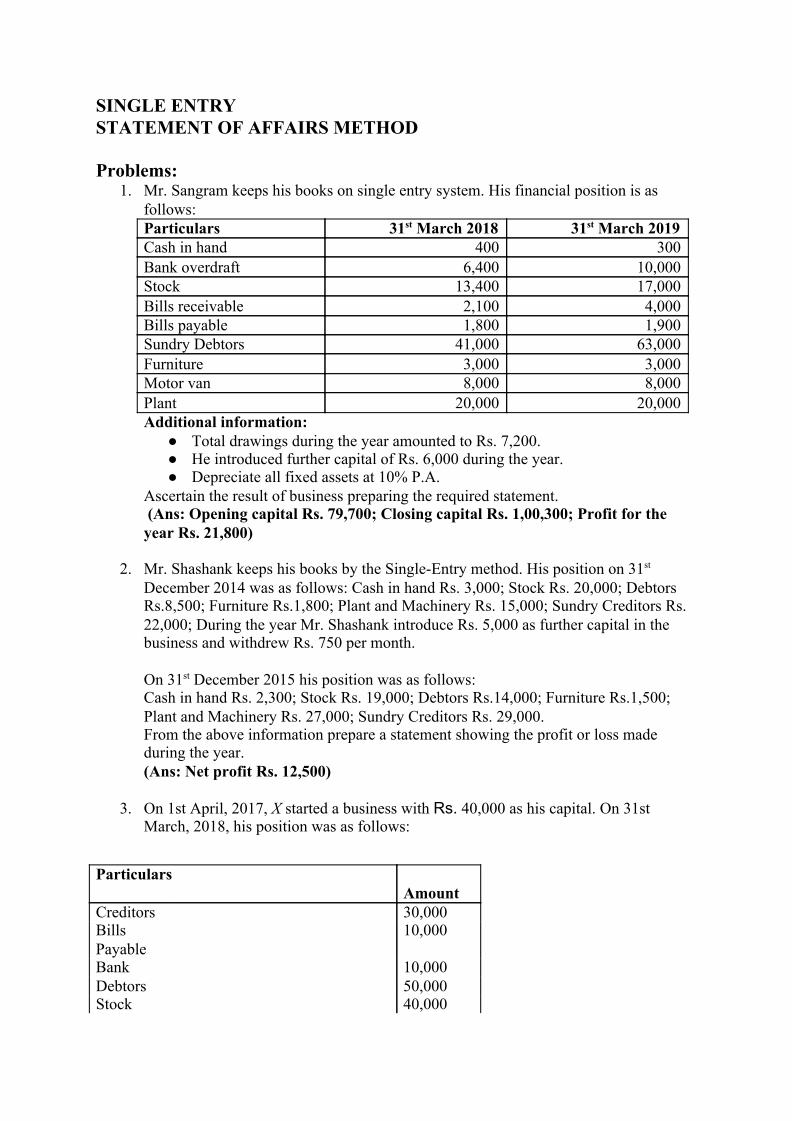

SINGLE ENTRY STATEMENT OF AFFAIRS METHOD Problems:

1. Mr. Sangram keeps his books on single entry system. His financial position is as follows:

Additional information: ● Total drawings during the year amounted to Rs. 7,200. ● He introduced further capital of Rs. 6,000 during the year. ● Depreciate all fixed assets at 10% P.A.

Ascertain the result of business preparing the required statement. (Ans: Opening capital Rs. 79,700; Closing capital Rs. 1,00,300; Profit for the year Rs. 21,800)

2. Mr. Shashank keeps his books by the Single-Entry method. His position on 31st December 2014 was as follows: Cash in hand Rs. 3,000; Stock Rs. 20,000; Debtors Rs.8,500; Furniture Rs.1,800; Plant and Machinery Rs. 15,000; Sundry Creditors Rs. 22,000; During the year Mr. Shashank introduce Rs. 5,000 as further capital in the business and withdrew Rs. 750 per month. On 31st December 2015 his position was as follows: Cash in hand Rs. 2,300; Stock Rs. 19,000; Debtors Rs.14,000; Furniture Rs.1,500; Plant and Machinery Rs. 27,000; Sundry Creditors Rs. 29,000. From the above information prepare a statement showing the profit or loss made during the year. (Ans: Net profit Rs. 12,500)

3. On 1st April, 2017, X started a business with Rs. 40,000 as his capital. On 31st March, 2018, his position was as follows:

Particulars 31st March 2018 31st March 2019 Cash in hand 400 300 Bank overdraft 6,400 10,000 Stock 13,400 17,000 Bills receivable 2,100 4,000 Bills payable 1,800 1,900 Sundry Debtors 41,000 63,000 Furniture 3,000 3,000 Motor van 8,000 8,000 Plant 20,000 20,000

Particulars Amount

Creditors 30,000 Bills Payable

10,000

Bank 10,000 Debtors 50,000 Stock 40,000

During the year 2017–18, X drew Rs. 24,000. On 1st October, 2017, he introduced further capital amounting to Rs. 30,000. You are required to ascertain profit on loss made by him during the year 2017–18. Adjustments: (a) Plant is to be depreciated at 10%. (b) A provision of 5% is to be made against debtors, Also prepare the Statement of Affairs as on 31st March, 2018. (Ans: Profit made during the year Rs. 84,700)

4. The following are the assets and liabilities of A at the end and beginning of the year 2008.

During the year A had withdrawn Rs. 5,000 in cash and Rs. 3,000 in goods from the business. He had also introduced Rs. 80,000 as additional capital. A machine costing Rs. 20,000 had been sold during the year for Rs. 18,000 and a new machine costing Rs. 50,000 was purchased in replacement. New furniture costing Rs. 2,500 was also purchased during the year.

Prepare a Statement of Profit or Loss the year ended 31-12-2008.

(Answer: Profit made during the year Rs. 28,000)

5. Hari maintains her books of account on Single Entry System. His books provide the following information:

Plant 68,000 Furniture 12,000

Particulars As on 31-12-2008 As 0n 1-1-2008

Land and Buildings 58,800 60,000 Plant & Machinery 1,20,000 96,000 Furniture & Fixtures 16,200 16,000 Stock in Trade 56,000 30,000 S. Debtors 3,10,000 2,80,000 S. Creditors 1,50,000 1,45,000 Loan from Bank 1,00,000 1,20,000 Outstanding Liabilities 80,000 90,000 Cash at Bank 30,000 34,000

Particulars 1st April, 2017

31st March, 2018

Furniture 2,000 2,000 Stock 28,000 30,500 Sundry Debtors 21,000 34,000 Cash 1,500 2,000 Sundry Creditors 17,500 19,000 Bills Receivable ... 3,000 Loan ... 5,000

His drawings during the year were Rs. 5,000 Depreciate furniture by 10% and provide a reserve for Bad and Doubtful Debts at 10% on Sundry Debtors. Prepare the statement showing the profits for the year.

(Answer: Profit made during the year Rs. 23,900)

6. Mr. Praveen Kumar a retailer, has not maintained proper books of account but it has been possible to obtain the following details:

Calculate the net profit for this year and draft the Statement of Affairs at the end of the year after noting that: (a) Shop Fittings are to be depreciated by Rs. 780. (b) He has drawn Rs. 100 per week for his own use. (c) Included in the Trade Debtors is an irrecoverable balance of Rs. 270. (d) Interest at 5% p.a. is due on the loan from Naresh but has not been paid for the year. Answer: Profit made during the year Rs. 3,960)

7. The following is the Statement of Affairs as at 31st march 2015 of Akshara and Bhayashree who are in partnership sharing Profit and Losses in proportions of 2/3 and 1/3 respectively. From the particulars given below prepare statement of profit as at 31st March 2016 and Statement of Affair as at that date.

Statement of Affairs as at 31st march 2015

Investments ... 10,000

Particulars Last Year

This Year

Trade Creditors 6,270 5,890 Loan from Naresh 5,000 5,000 Stock 12,350 11,980 Cash in Hand 570 650 Shop Fittings 7,250 7,800 Trade Debtors 5,280 4,560 Bank Balance 3,990 4,130

Liabilities Amount Assets Amount Capital: Akshara 20,000 Bhayashree 8,000

28,000

Land and Buildings 12,000

Bills payable 1,000 Plant & Machinery 4,000 Trade Creditors 12,000 Furniture 1,000 Stock 7,000

Trade Debtors 13,000 Bills Receivable 3,000 Bank Balance 990 Cash 10

The position as at 31st march 2016 was as follows:- Bank Balance 1,500; Cash Rs. 100; Trade Creditors Rs. 19,000; Bills payable Rs. 1,200; Trade Debtors Rs. 5,000; Bills Receivable Rs. 3,800; Stock Rs. 8,400; Akshara’s drawings during the year had been Rs. 3,000 and Bhayashree had drawn Rs. 1,200. Akshara withdrew the sum of Rs. 4,000 on 30th September from her capital account . Depreciate Machinery and Plant by 5%; Furniture by 10%; and allow interest on capital at the rate of 5% p.a. Ignore interest on Drawings. (Answer: Net Loss Rs. 5,800; Statement of Affairs total Rs. 35,500)

8. Mrs. Vandana runs a small printing firm. She was maintaining only some records, which she thought, were sufficient to run the business. On April 01, 2013, available information from her records indicated that she had the following assets and liabilities: Printing Press Rs. 5,00,000, Buildings Rs. 2,00,000, Stock Rs. 50,000, Cash at bank Rs. 65,600, Cash in hand Rs. 7,980, Dues from customers Rs. 20,350, Dues to creditors Rs. 75,340 and Outstanding wages Rs. 5,000. She withdrew Rs. 8,000 every month for meeting her personal expenses. She had also introduced Rs. 15,000 during the year as additional capital. On March 31, 2014 her position was as follows : Press Rs. 5, 25,000, Buildings Rs. 2,00,000, Stock Rs. 55,000, Cash at bank Rs. 40,380, Cash in hand Rs. 15,340, Dues from customers Rs. 17,210, Dues to creditors Rs. 65,680. Calculate the profit made by Mrs. Vandana during the year using statement of affairs method. (Answer: Capital(op) 7,63,590 (cl) 7,87,250 (balancing figure), Profit made during the year 1,04,660)

41,000 41,000

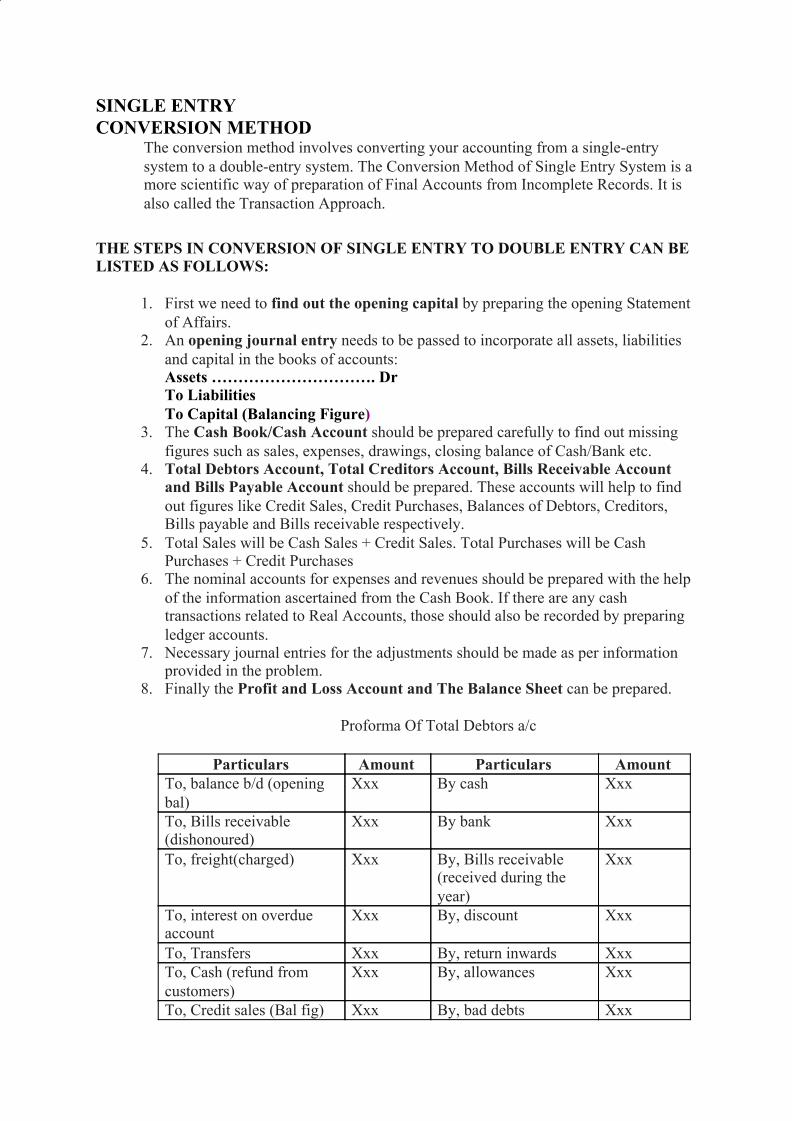

SINGLE ENTRY CONVERSION METHOD

The conversion method involves converting your accounting from a single-entry system to a double-entry system. The Conversion Method of Single Entry System is a more scientific way of preparation of Final Accounts from Incomplete Records. It is also called the Transaction Approach.

THE STEPS IN CONVERSION OF SINGLE ENTRY TO DOUBLE ENTRY CAN BE LISTED AS FOLLOWS:

1. First we need to find out the opening capital by preparing the opening Statement of Affairs.

2. An opening journal entry needs to be passed to incorporate all assets, liabilities and capital in the books of accounts: Assets …………………………. Dr To Liabilities To Capital (Balancing Figure)

3. The Cash Book/Cash Account should be prepared carefully to find out missing figures such as sales, expenses, drawings, closing balance of Cash/Bank etc.

4. Total Debtors Account, Total Creditors Account, Bills Receivable Account and Bills Payable Account should be prepared. These accounts will help to find out figures like Credit Sales, Credit Purchases, Balances of Debtors, Creditors, Bills payable and Bills receivable respectively.

5. Total Sales will be Cash Sales + Credit Sales. Total Purchases will be Cash Purchases + Credit Purchases

6. The nominal accounts for expenses and revenues should be prepared with the help of the information ascertained from the Cash Book. If there are any cash transactions related to Real Accounts, those should also be recorded by preparing ledger accounts.

7. Necessary journal entries for the adjustments should be made as per information provided in the problem.

8. Finally the Profit and Loss Account and The Balance Sheet can be prepared.

Proforma Of Total Debtors a/c

Particulars Amount Particulars Amount To, balance b/d (opening bal)

Xxx By cash Xxx

To, Bills receivable (dishonoured)

Xxx By bank Xxx

To, freight(charged) Xxx By, Bills receivable (received during the year)

Xxx

To, interest on overdue account

Xxx By, discount Xxx

To, Transfers Xxx By, return inwards Xxx To, Cash (refund from customers)

Xxx By, allowances Xxx

To, Credit sales (Bal fig) Xxx By, bad debts Xxx

Proforma Of Total Creditors A/c

Proforma Of Bills Receivable

Proforma Of Bills Payable a/c

By, balance c/d ( closing bal)

Xxx

Total Xxxxx Total xxxxx

Particulars Amount Particulars Amount To cash Xxx By balance b/d Xxxx To, Bank Xxx By cash (refund for

returns) Xxx

To Bills Payable(bills accepted during the years)

Xxx By, Bills payable (dishonoured)

Xxx

To, Return outwards Xxx By, Transfer Xxx To, discount received Xxx By, credit purchases

(balancing figure) Xxx

To, Allowances & Rebate

Xxx

To Transfers Xxx To, Balance c/d ( CLOSING BAL)

Xxx

TOTAL XXXX TOTAL XXXX

Particulars Amount Particulars Amount To, balance b/d (opening balance)

Xxx By, cash (B/R honoured during the year)

Xxx

To Totals debtors a/c (received during the year)

Xxx By, Total debtors a/c (dishonoured)

Xxx

By, balance c/d (closing balance)

Xxx

Total Xxx Total Xxx

Particulars Amount Particulars Amount To, total creditors a/c (dishonoured)

Xxx By, balance b/d (opening balance)

Xxx

To cash (B/P honoured during the year)

Xxx By, Total Creditors a/c (Acceptances given during the year)

Xxx

To, Balance c/d (closing balance)

Xxx

Problems

1. Opening balance of creditors 40,000 Closing balance of creditors 50,000 Payment made in cash 85,000 Discount received 2,000 . Debtors on April 01, 2013 50,000 Debtors on March 31, 2014 70,000 Cash received from debtors 60,000 Discount allowed 1,000 Bills receivable 30,000 Bad debts 3,000 The total debtors account will be prepared as follows : prepare total creditors and Debtors accounts. (Answer : Total Credit purchases 97,000; Credit sales 1,14,000)

2. Opening bills receivable 5,000, Opening bills payable 37,000, Bills receivable dishonored 2,000 Bills payable dishonored 66,750, Closing bills payable 52,000, Bills collected during the year 12,000, Closing bills receivable 4,000. Prepare bills receivable and payable account.

(Answer: balancing figure 13,000; 81,750)

3. Compute the amount of total purchases and total sales of Mr. Amit from the following information for the year ending on March 31,2014. Total debtors as on April 01, 2013 40,000; Total creditors as on April 01, 2013 50,000; Bills receivable as on April 01, 2013 30,000; Bills payable as on April 01, 2013 45,000; Discount received 5,000; Bad debts 2,000; Return inwards 4,000; Discount allowed 3,000 ; Cash sales 10,000; Cash purchases 8,000 ;Total debtors as on March 31, 2014 80,000 ;Cash received from debtors 1,00,000; Cash paid to creditors 80,000; Cash received against bills receivable 25,000 ;Payment made against bills receivable 40,000; Total creditors as on March 31, 2014 40,000; Bills payable as on March 31, 2014 50,000; Bills receivable as on March 31, 2014 35,000.

(Answer: Total purchases Rs. 1, 28,000; Total sales Rs. 1, 89,000)

4. Mr. Om Prakash did not keep his books of accounts under double entry system. From the following information available from his records, prepare profit and loss account for the year ending on March 31, 2014 and a balance sheet as at that date, depreciating the washing equipment @ 10%.

Summary of Cash :

Debits: Balance b/d Rs. 8,000 Cash sales Rs. 40,000 Received from debtors Rs. 30,000

Credits: Sundry expenses Rs. 6,000 Paid to creditors Rs. 20,000 Cartage Rs.2,000 Drawings Rs. 8,000Cash purchases Rs. 14,000 Balance c/d Rs. 28,000

Other information:

March 31, 2014

TOTAL XXX TOTAL XXX

Ans: GP: 50,300; NP: 40,600; B/S: 95,000)

5. A trader started business on 1st January, 2015 with a capital of Rs. 50,000. He kept only a cash book and a personal ledger. An analysis of the cash book for the year 2015 gave the following figures:

Receipt from debtors Rs.1,40,000; cash sales Rs.42,000; payment to creditors Rs.1,00,000; expenses paid Rs.22,000; personal drawings Rs.10,000; cash purchases Rs. 36,000. On 31st December, 2015 the stock in hand was valued at Rs.20,000 and the debtors and creditors were Rs.1,20,000 and Rs.1,10,000 respectively. You are required to prepare a profit and loss account for the year ended 31st December, 1991 and a balance sheet as on that date, after making a reserve of Rs.2,000 for bad and doubtful debts.

(Answer:Credit purchases: 2,10,000; Credit Sales: 2,60,000 ;Gross profit 76,000; Net profit 52,000; Balance Sheet 2,02,000) 6.From the below given information of Mr.Praveen Reddy who keeps his book on single entry system. Prepare Trading and Profit and Loss Account and Balance Sheet as on 31.12.2013

Receipt and Payments Account

March 31, 2013 Rs

March 31, 2014 Rs

Debtors 9,000 12,000 Creditors 14,400 6,800 Stock of materials 10,000 16,000 Washing equipment 40,000 40,000 Furniture 3,000 3,000 Discount allowed during the year

-- 1,400

Discount received during the year

-- 1,700

Receipts Amount Payments Amount

To Received from Debtors 50,000 By Balance b/d 8,000

To Cash Sales 30,000 By Interest on O.D 200

By Drawings 4,000

By Salaries 17,000

By Other Expenses 15,800

By Creditors 30,000

By Bank Balance 4,850

Other Information

Depreciate all the fixed assets by 5% and Provide 5% interest on capital. Rs. 3,000 for doubtful debts.

7. Mr. Bahadur does not know how to keep books of account. From his various records, the following particulars have been made available prepare the final Accounts, after providing for doubtful debts 5 per cent of debtors outstanding and depreciating the motor car @ 20 per cent. Balance Sheet as on April 1, 2013 Liabilities and Assets Amount Capital Rs. 92,500 ; Bills payable Rs.32,800; Creditors Rs.84,200 ;Debtors Rs.49,500; Bills receivable Rs.24,400; Cash in hand Rs.12,400 ;Motor Car Rs. 71,700; Stock Rs.51,500

By Cash in Hand 150

80,000 80,000

As on 1.1.2013 As on 31.12.2013

Stock 18,000 20,440

Creditors 16,000 11,000

Debtors 44,000 60,000

Furniture 2,000 2,000

Buildings 30,000 30,000

Receipts Amount Payments Amount

Balance b/d 12,400 Furniture 30,000

Receipt from debtors 1,15,000 Wages 9,400

Bills receivable 14,200 Purchases 40,500

Sales 1,03,000 Drawings 24,000

Bills payable 30,700

General expenses 20,700

Payment to creditors 80,800

Balance c/d 8,500

2,44,600 2,44,600

(iii) Other Information : Bills receivable drawn (received) Rs. 6,300; Discount to customers Rs.2,300; Discount from suppliers Rs. 700; Credit purchases Rs.29,600 ;Closing stock Rs. 41,700; Closing balance of debtor Rs.55,000; Closing balance of bills payable Rs.10,200.

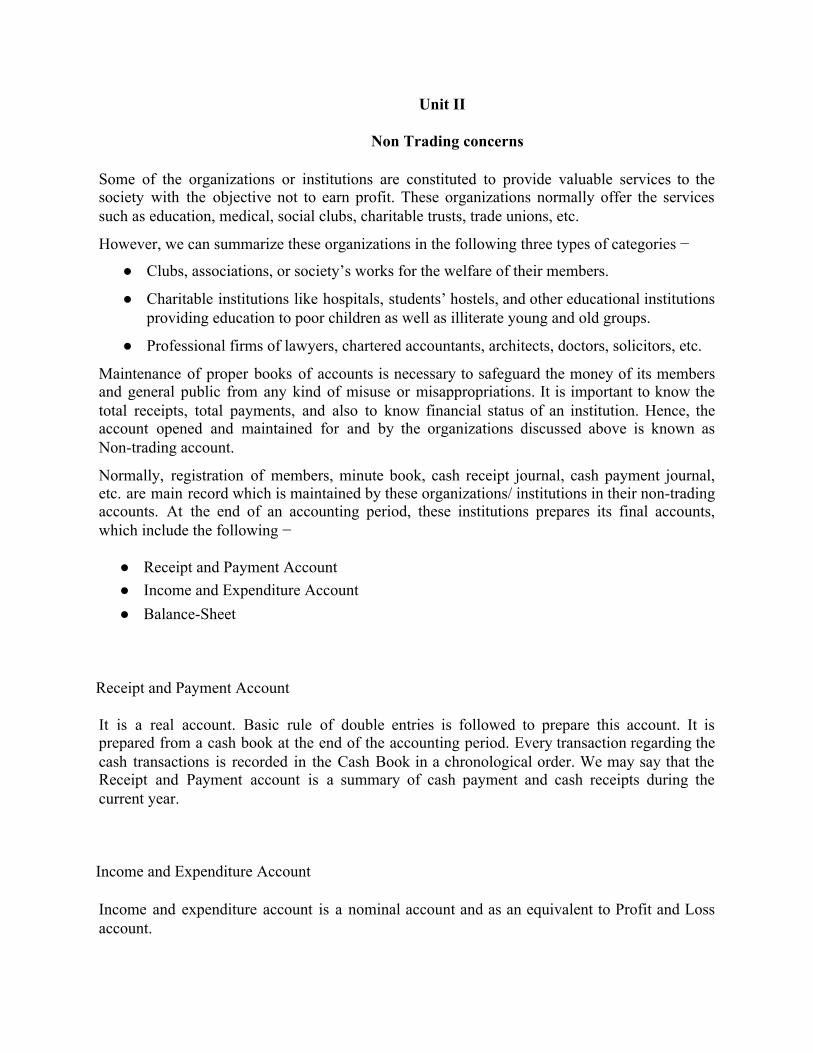

Unit II

Non Trading concerns

Some of the organizations or institutions are constituted to provide valuable services to the society with the objective not to earn profit. These organizations normally offer the services such as education, medical, social clubs, charitable trusts, trade unions, etc.

However, we can summarize these organizations in the following three types of categories −

● Clubs, associations, or society’s works for the welfare of their members.

● Charitable institutions like hospitals, students’ hostels, and other educational institutions providing education to poor children as well as illiterate young and old groups.

● Professional firms of lawyers, chartered accountants, architects, doctors, solicitors, etc.

Maintenance of proper books of accounts is necessary to safeguard the money of its members and general public from any kind of misuse or misappropriations. It is important to know the total receipts, total payments, and also to know financial status of an institution. Hence, the account opened and maintained for and by the organizations discussed above is known as Non-trading account.

Normally, registration of members, minute book, cash receipt journal, cash payment journal, etc. are main record which is maintained by these organizations/ institutions in their non-trading accounts. At the end of an accounting period, these institutions prepares its final accounts, which include the following −

● Receipt and Payment Account ● Income and Expenditure Account ● Balance-Sheet

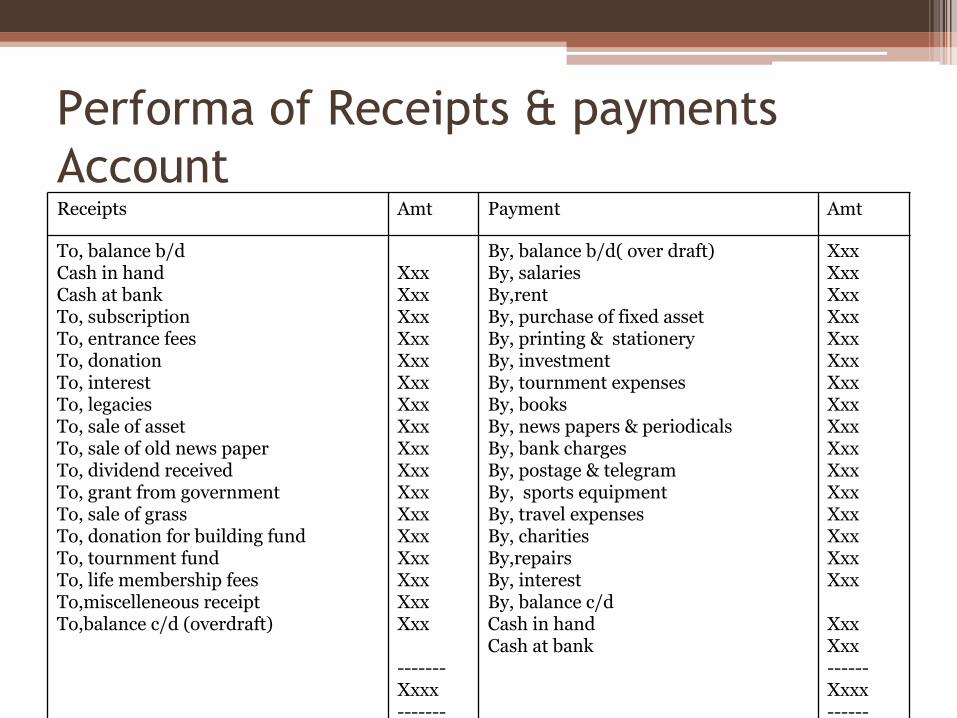

Receipt and Payment Account

It is a real account. Basic rule of double entries is followed to prepare this account. It is prepared from a cash book at the end of the accounting period. Every transaction regarding the cash transactions is recorded in the Cash Book in a chronological order. We may say that the Receipt and Payment account is a summary of cash payment and cash receipts during the current year.

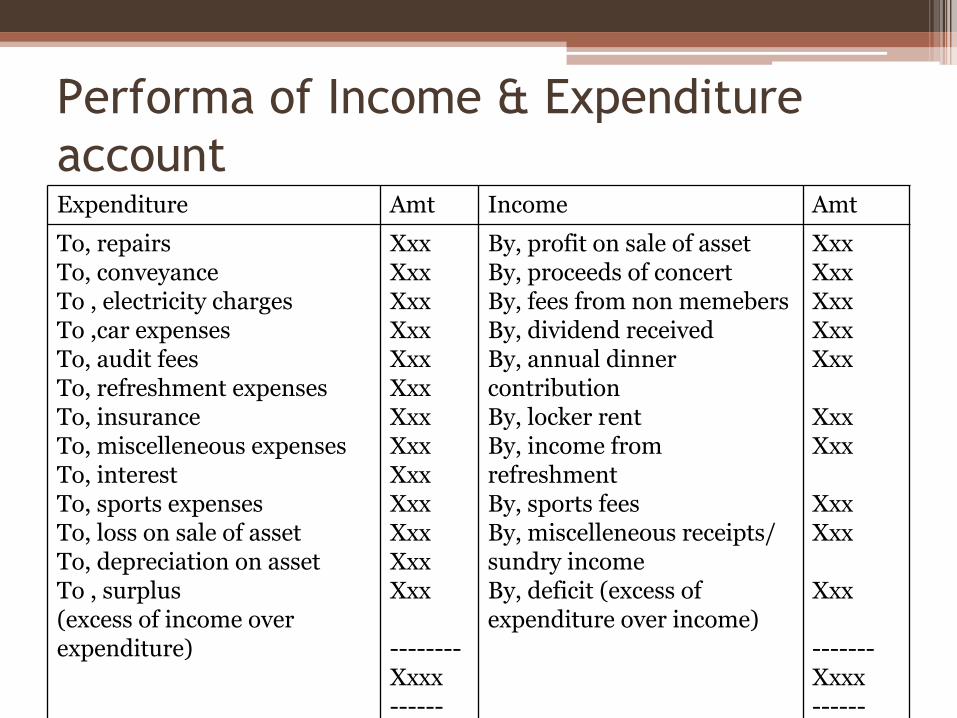

Income and Expenditure Account

Income and expenditure account is a nominal account and as an equivalent to Profit and Loss account.

The essential features of an income and expenditure account are as follows −

● Expenses and losses are recorded in the debit side of it and all incomes and gains are recorded on the credit side.

● Capital income and expenditure are excluded and revenue income and expenses are included in it.

● It is based on a mercantile system of accounting, therefore, the income and expenses related to preceding years or subsequent years are excluded while preparing the income and expenditure account.

● The credit balance of an income and expenditure account shows surplus. Further, excess of income over the expenditure and the debit balance of it show deficit i.e. excess of the expenditure over income.

● Only nominal accounts are considered in preparation of this account.

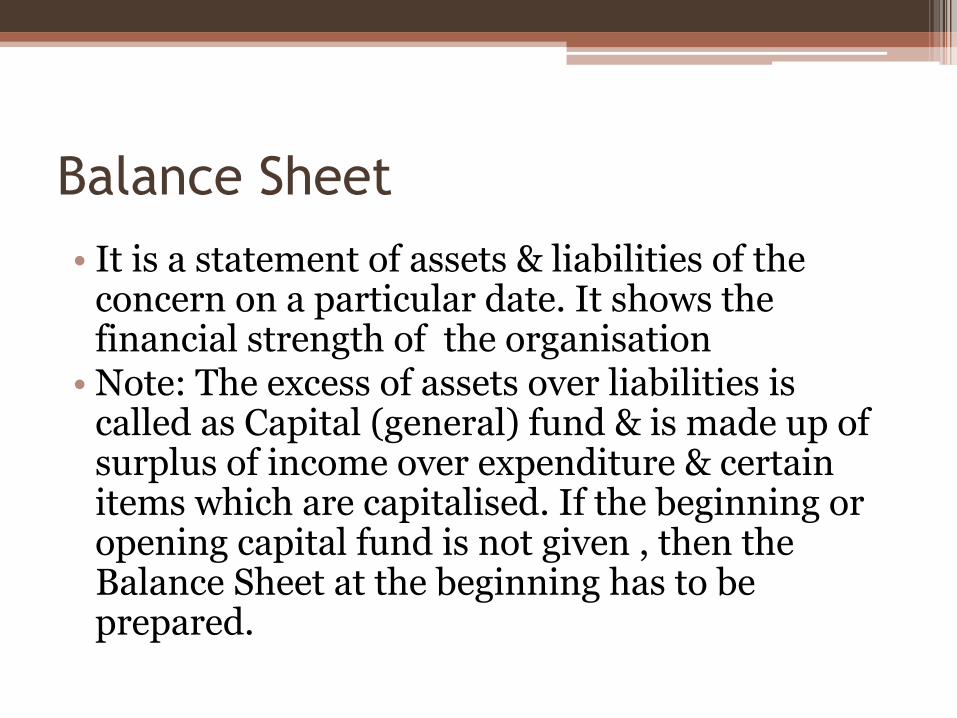

Balance Sheet

The date on which a balance sheet is prepared, particulars of all the assets and liabilities are recorded in the same manner as we do in any other profit making firms. Its capital fund is made up of surplus income over expenditure and other incomes capitalized in the given period of time. Sometimes, two balance sheets need to be prepared i.e.

● At the beginning of the accounting year to know the opening capital fund and ● At the end of the financial year to know the financial position of the organization.

There are certain peculiar items in the case of non-trading concerns, which require a special treatment −

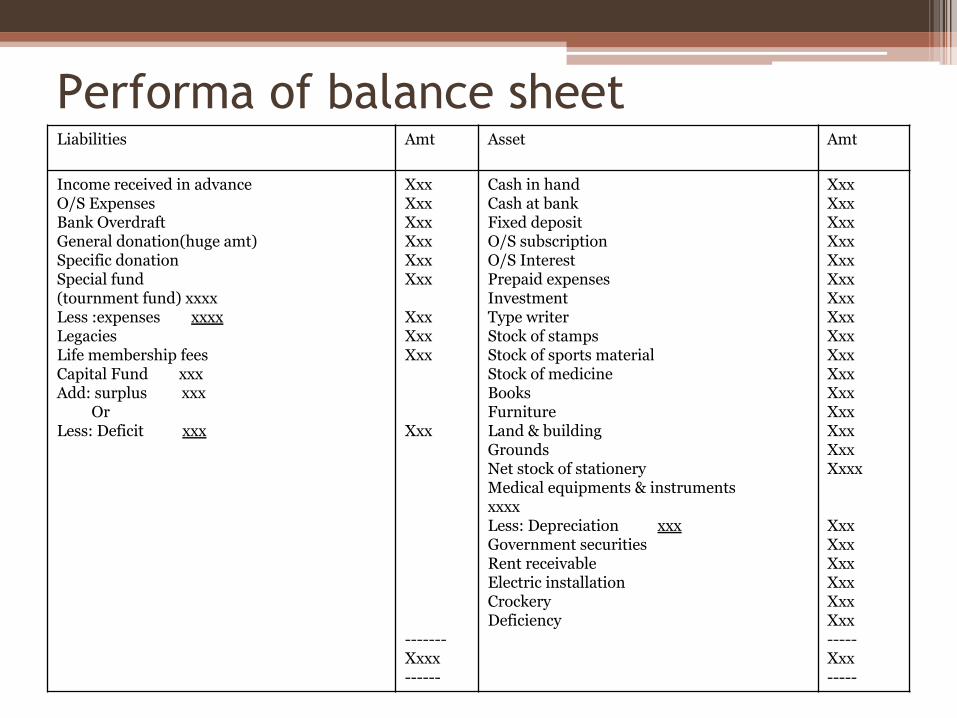

Donations Non-trading concerns may receive donations time to time. The treatment of donation depends upon nature of donation.

There are two types of donation as explained below −

● Specific Donation − Some donation may be received for any specific purpose, for example, for the construction of a room or building and then donation is termed as specific donation. The amount of such donation cannot be used for any other purpose. It should be shown on liabilities side of the Balance-sheet and used only for the same purpose it is meant for.

● General Donation − When a donation is received for a common purpose is termed as General Donation. If the amount of donation is small, it will be treated as recurring income and will be recorded in the credit side of income & expenditure account.

Donation of the big amount should be fairly treated as capital receipts and will be shown in the liabilities side of the Balance sheet. However, donation is of a small amount or a big amount may depend upon the size of a concern and amount.

Legacy Sometimes, as per the will of a person, an amount received is called as legacy. It is as good as donation. It is of a non-recurring nature, therefore should be treated as a capital receipt, and hence will appear in the liabilities side of a Balance sheet. However, it may also be treated as an income and may be taken to income & expenditure account.

Entrance Fees

A club or society usually charge admission fees or entrance fees for the membership. In case of club etc., admission fees or entrance fees usually charged as capital receipts, but in case of a hospital or educational institution, it is treated as a recurring income.

Life Membership Fees

The life membership fees may be taken from the members of institution only once in their lifetimes. On the basis of lifetime membership, members may enjoy certain benefits. Amount received as the Life Membership might be transferred to the “Life Membership Fees Account” of the institution and can be dealt in the accounts by any of the following methods −

● May be taken as liabilities side of a Balance sheet as Life Membership Fees.”

● Normal subscriptions of the members may be transferred from the Life Membership Fees account to the subscription account as an income and the balance may be carried forward to the following years.

● On the basis of average life of a member, the amount may be transferred to the income and expenditure account annually and rest will be carried forward towards the following years.

Sale of Scrap or Old Newspapers

Without any dispute, it will be treated as recurring income and will appear in the credit side of an income and expenditure account.

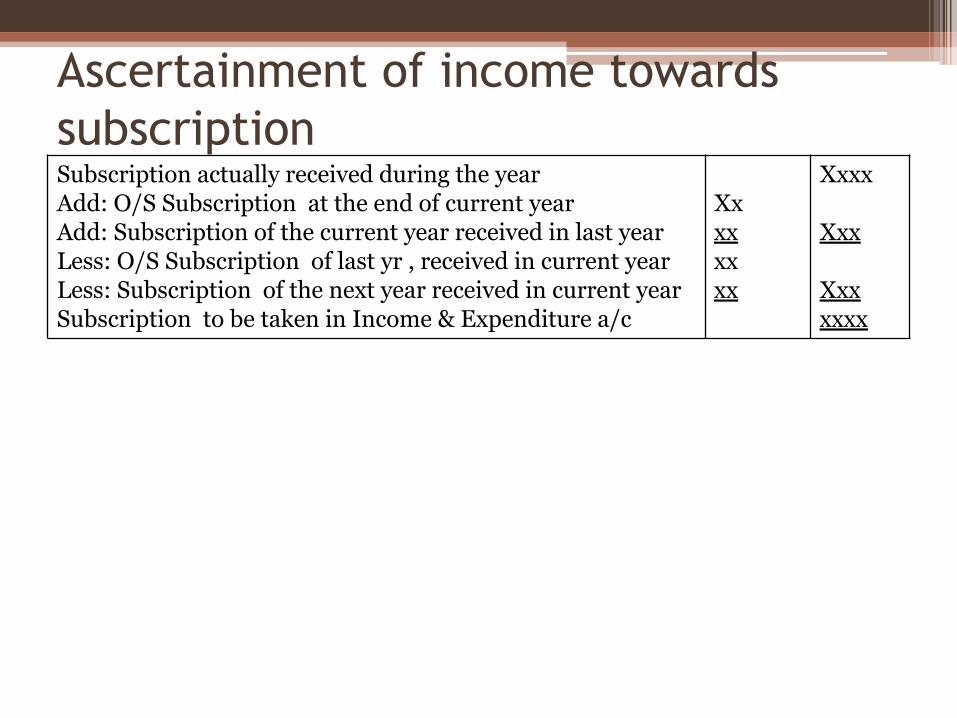

Subscription Subscription is the major source of an income for the non-trading concerns. Subscriptions are received from the members of a club or institution. A receipt and payment account records all the actual subscription received during the current year and an income & expenditure account shows the subscriptions, which relates to the current accounting period. Therefore, some adjustments require to calculate the subscription of the current year.

Special Funds Some special funds are created by the respective institutions for specific purpose. For example, a prize fund may be created to give the best player of the year award. Any income relating to those funds should be added to the funds and deficit, if any may be charged from the income & expenditure account.

Steps in the preparation of Receipt and Payment Account

1. Take the opening balances of cash in hand and cash at bank and enter them on the debit side. In case there is bank overdraft at the beginning of the year, enter the same on the credit side of this account.

2. Show the total amounts of all receipts on its debit side irrespective of their nature (whether capital or revenue) and whether they pertain to past, current and future periods.

3. Show the total amounts of all payments on its credit side irrespective of their nature (whether capital or revenue) and whether they pertain to past, current and future periods.

4. None of the receivable income and payable expense is to be entered in this account as they do not involve inflow or outflow of cash.

5. Find out the difference between the total of debit side and the total of credit side of the account and enter the same on the credit side as the closing balance of cash/bank. In case, however, the total of the credit side is more than that of the total of the debit side, show the difference on the debit as bank overdraft and close the account.

Steps in the Preparation of Income and Expenditure Account

Following steps may be helpful in preparing an Income and Expenditure Account from a given Receipt and Payment Account:

1. Pursue the Receipt and Payment Account thoroughly.

2. Exclude the opening and closing balances of cash and bank as they are not an income.

3. Exclude the capital receipts and capital payments as these are to be shown in the Balance Sheet.

4. Consider only the revenue receipts to be shown on the income side of Income and Expenditure Account. Some of these need to be adjusted by excluding the amounts relating to the preceding and the succeeding periods and including the amounts relating to the current year not yet received.

5. Take the revenue expenses to the expenditure side of the Income and Expenditure Account with due adjustments as per the additional information provided relating to the amounts received in advance and those not yet received.

6. Consider the following items not appearing in the Receipt and Payment Account that need to be taken into account for determining the surplus/ deficit for the current year : (a) Depreciation of fixed assets. (b) Provision for doubtful debts, if required. (c) Profit or loss on sale of fixed assets.

Unit IIIPartnership Final Accounts

Introduction to Partnership

Partnership is an association of two or more individuals who agree to share theprofits of a lawful business.

It is managed and carried on either by all or by any, or some of them acting for all.

The formation of partnership is easy and simple. Each member of such a group isindividually known as ‘partner’ and collectively the members are known as a‘partnership firm’.

1. Two or More Persons:

Section 11 of Indian Partnership Act, 1932 provides that the maximum number ofpersons a firm can have is 10 in case of partnership firm carrying on a bankingbusiness. In case of partnership firm carrying on any other business the number ofpartners can be 20.

2. Agreement:

A partnership comes into being through an agreement between persons who arecompetent to enter into a contract (e.g. Minors, lunatics, insolvents etc. not eligible).The agreement may be oral, written or implied.

3. Lawful Business:

The aim of a partnership firm should be profit-making by conducting only lawfulbusiness activities. Partnership business should be as per the law of land. Associationformed for conducting illegal actions like theft, black-marketing and smugglingcannot be called as partnership

4. Profit Sharing: