How Credit Card Payments Increase Unhealthy Food Purchases: Visceral Regulation of Vices

Upload

khangminh22Category

view

1download

0

Optimising the use of Credit Card behaviour within risk scorecards

CSCXVI August 2019

Gergana AtanasovaChris Curtis

2 © Experian

Consumer Perspective- Have better understanding of their Credit Card

Portfolios. - Use it as a risk management tools.- Offer the right products to the right customers.

Commercial Perspective

The amount of Credit Card data collected in the recent years allows for more in-depth analysis of customers.

More DataThe variety of analytics techniques available in the recent

years allow for the development and implementation of new solutions.

Tools

Why Classifying Credit Card Users?

- Receive better products and services.- Increased product satisfaction.- Increased incentive to pay Credit Card debt.

3 © Experian

ContentsCredit Card data available within the UK Credit Bureau

Credit Card User Types

Classifying Customer Behaviour

Implementation

Results

4 © Experian

Credit Card data within the Credit Bureau

There are 60.1 million credit cards in the UK (January 2019)

The average number of credit cards per person is 1.7

Average credit card debt per household is £2,649 or £1,386 per person

In credit bureau a snapshot is used traditionally and therefore no information on statement balance/payments

Introduction of APACS data (behavioural Data Sharing) addressed this

5 © Experian

Behavioural Data Sharing (BDS) Overview

BDS is an account level database holding information supplied by credit card companies as part of CAIS

It includes up to six years of credit card information on statement balances, payments, cash advances,

promotional rates, credit card limits, balance transfers.

The information available allows for the investigation of customer behavior and finding patterns in their use

of credit cards.

6 © Experian

Delphi Generation

Gini Coefficients of Banking & Finance

Scores% Uplift in Gini

10 83.4 4.64%

9 79.7 1.66%

8 78.4 1.82%

7 77.0 N/A

Behavioural Data Sharing Usage

BDS data has been firstly introduced in the development of the Generation 10 Bureau Scores.

The addition of CC data in scorecards has resulted in improved scorecard discrimination (based on Gini

coefficient).

How can we make even more use of this data?

7 © Experian

Business-Driven Credit Card User Types Classification

8 © Experian

Credit Card Risk Groups Overview

Focus on Credit Card debt rather than overall

customer performance.

Investigation on how customers are using their

Credit Cards from raw BDS data.

Customers have been split into groups with different level of risk based on the Credit Card Usage in the

last 6 months.

The groups have been converted into an index

and aggregated on customer level by taking

the highest index for each customer.

9 © Experian

Credit Card Risk Groups Performance

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

700

750

800

850

900

950

1000

1050

1100

0 - No EligibleCC

1 - Inactive 2 - InfrequentUser

3 - Transactor 4 - RecentPromotional

balance

5 - PromotionalBalance

6 - PromotionalBalance - Roll

Over

7 - InfrequentRevolver

8 - Revolver 9 - HardcoreRevolvoer

% B

ad R

ate

Bure

au S

core

Average Bureau Score % Bad Rate

Higher bad rate for groups with lower Bureau score and lower bad rate for groups with higher Bureau score.

10 © Experian

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

low - 500 501 - 700 701 - 800 801 - 900 901 - 980 981 - 1020 1021 - 1050 1051 - 1080 1081 - 1120 1121 - high

Bad

Rat

e

Bureau Score 10% bands

Bad Rate across the Bureau Score bands

Bureau Score 1 - Inactive 2 - Infrequent User 3 - Transactor 4 - Recent Promotional Balance5 - Promotional Balance 6 - Promotional Balance - Roll Over 7 - Infrequent Revolver 8 - Revolver 9 - Hardcore Revolver

Credit Card Risk Groups Alignment

Around equal level of bad rate across the different groups in all bureau score bands

11 © Experian

Data-Driven Credit Card User Types Classification

12 © Experian

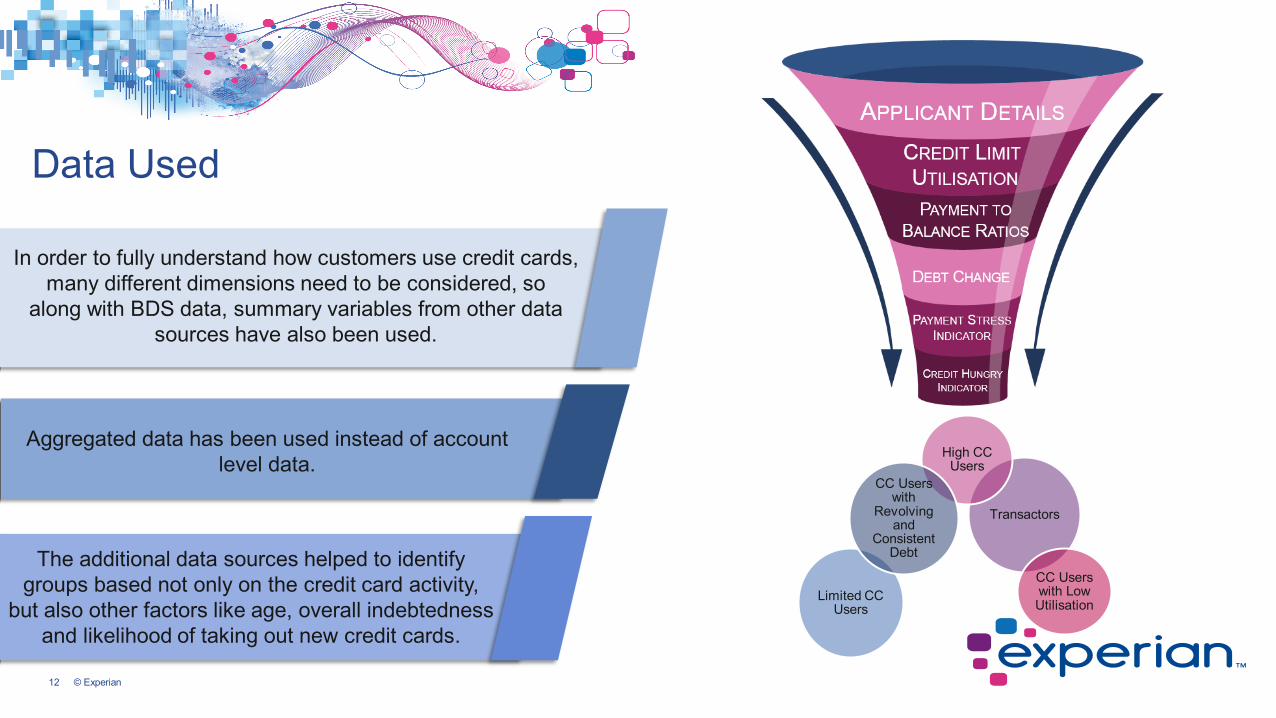

Data Used

Aggregated data has been used instead of account level data.

Transactors

Limited CC Users

High CC Users

CC Users with Low Utilisation

CC Users with

Revolving and

Consistent Debt

In order to fully understand how customers use credit cards, many different dimensions need to be considered, so

along with BDS data, summary variables from other data sources have also been used.

The additional data sources helped to identify groups based not only on the credit card activity,

but also other factors like age, overall indebtedness and likelihood of taking out new credit cards.

13 © Experian

An alternative method for segmenting customers based on the way they are using their credit cards.

Relatively simple approach and easy to understand compared to other classification methods.

Let data decides what groups of customers could be created without referring to known, or labelled

outcome.

The k-means algorithm groups similar data points together, forming clusters of customers that share

similar behavior.

K-means for Credit Card Users Classification

14 © Experian

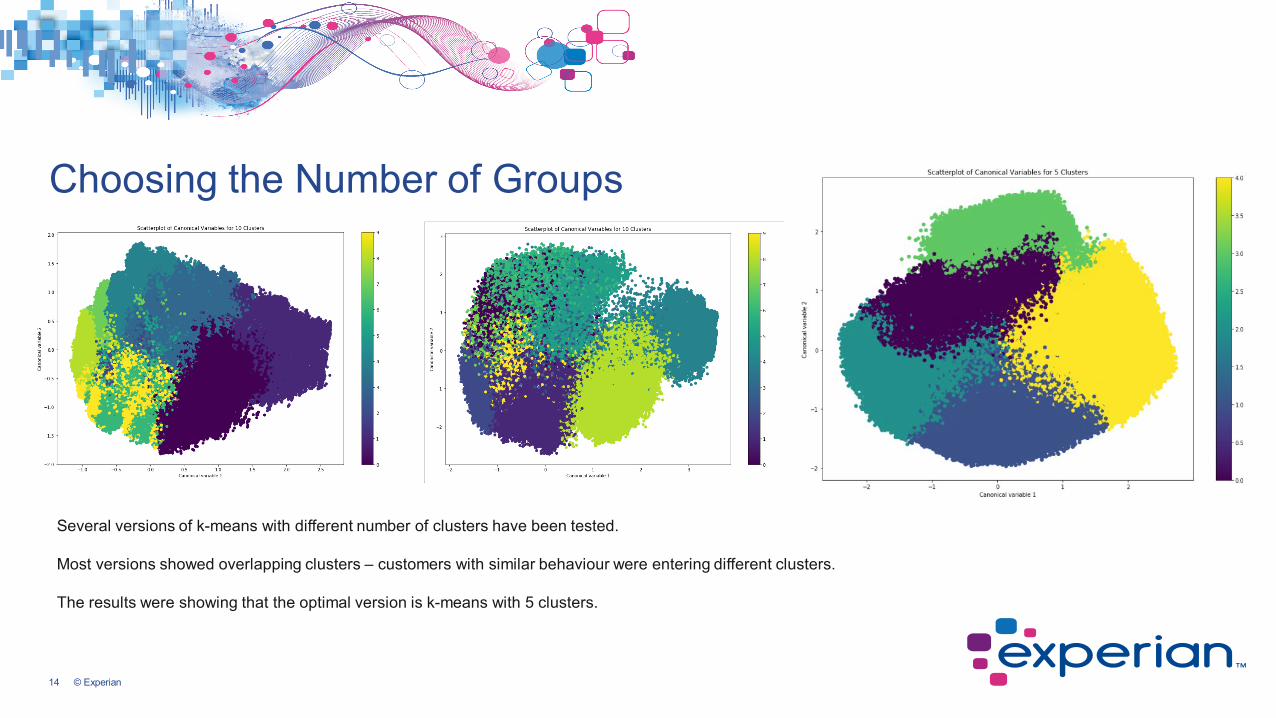

Choosing the Number of Groups

Several versions of k-means with different number of clusters have been tested.

Most versions showed overlapping clusters – customers with similar behaviour were entering different clusters.

The results were showing that the optimal version is k-means with 5 clusters.

15 © Experian

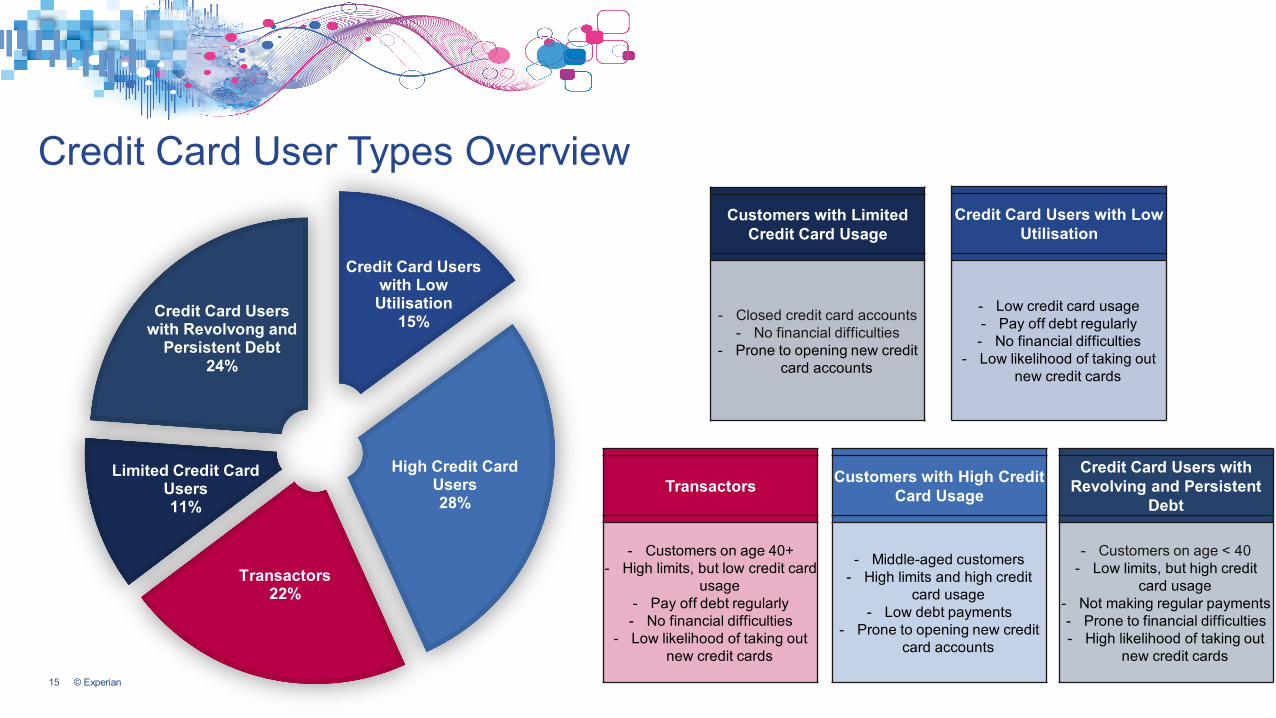

Credit Card User Types Overview

Credit Card Users with Low

Utilisation15%

High Credit Card Users28%

Transactors22%

Limited Credit Card Users11%

Credit Card Users with Revolvong and

Persistent Debt24%

Customers with Limited Credit Card Usage

- Closed credit card accounts- No financial difficulties

- Prone to opening new credit card accounts

Credit Card Users with Low Utilisation

- Low credit card usage- Pay off debt regularly- No financial difficulties

- Low likelihood of taking out new credit cards

Transactors

- Customers on age 40+- High limits, but low credit card

usage- Pay off debt regularly- No financial difficulties

- Low likelihood of taking out new credit cards

Customers with High Credit Card Usage

- Middle-aged customers- High limits and high credit

card usage- Low debt payments

- Prone to opening new credit card accounts

Credit Card Users with Revolving and Persistent

Debt

- Customers on age < 40- Low limits, but high credit

card usage- Not making regular payments- Prone to financial difficulties- High likelihood of taking out

new credit cards

16 © Experian

0.82% 3.13%6.27%

20.31%

37.22%

Transactors Low Utilisation High CC Use and BT Surfers

Limited CC Use Revolving and Persistent Debt

BAD RATE

1045 1066 918 876631

Transactors Low Utilisation High CC Use and BT Surfers

Limited CC Use Revolving and Persistent Debt

AVG BUREAU SCORE

£1,397 £142

£8,135

£193 £2,113

Transactors Low Utilisation High CC Use and BT Surfers

Limited CC Use Revolving and Persistent Debt

AVG BALANCE

11.15% 8.78%

30.29%

0.01%

18.83%

Transactors Low Utilisation High CC Use and BT Surfers

Limited CC Use Revolving and Persistent Debt

AVG CLU

Credit Card User Types Performance Statistics

17 © Experian

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%90.00%

low - 500 501 - 700 701 - 800 801 - 900 901 - 980 981 - 1020 1021 - 1050 1051 - 1080 1081 - 1120 1121 - high

Bad

Rat

e

Bureau Score 10% Bands

Bad Rate across the Bureau Score bands

Bureau Score Transactors Low Utilisation High CC Use Limited CC Use Revolving and Persistent Debt

Credit Card User Types Alignment

Different level of risk for the different Credit Card User Type groups across the Bureau score bands.

18 © Experian

Implementation

19 © Experian

Implementation with Random Forest

The testing showed that the k-means method can give different results when performed multiple times on the same data.

Therefore the unsupervised approach has been converted into supervised using a Random Forest model.

The Random Forest model predicts the probability of a customer being in any of the groups defined by the k-means method and assigns a customer to the group with highest probability.

Use k-means classification

method to determine the five

clusters

Take the assigned groups

Put them as an outcome

into a Random

Forest model

20 © Experian

Results

97% of the observations on the test sample have been correctly assigned to their actual group.

Group

Actual Groups

Low Utilisation

High CC Use Transactors Limited CC

Use

Revolving and

Persistent Debt

Pred

icte

d G

roup

s

Low Utilisation 95% 0% 2% 0% 1%

High CC Use 1% 96% 2% 0% 2%

Transactors 2% 2% 96% 0% 0%

Limited CC Use 0% 0% 0% 100% 0%

Revolving and

Persistent Debt

1% 2% 0% 0% 97%

21 © Experian

Conclusion

Different techniques could be used for the classification of Credit Card Users.

The output could be used in credit score modelling, or as a separate tool for risk management.

In the future Open Banking data for Credit Cards will provide more information but as this is used to ‘boost’ scores it may be of limited use for risk.

Copyright © 2022 FDOKUMEN