Daniel Pindur Value Creation in Successful LBOs

27

Daniel Pindur Value Creation in Successful LBOs

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Daniel Pindur Value Creation in Successful LBOs

Daniel Pindur

Value Creation in Successful LBOs

GABLER EDITION WISSENSCHAFT

Daniel Pindur

Value Creation in Successful LBOs

With a foreword by Prof. Dr. Frank Richter

Deutscher Universitäts-Verlag

Bibliografische Information Der Deutschen NationalbibliothekDie Deutsche Nationalbibliothek verzeichnet diese Publikation in der Deutschen Nationalbibliografie; detaillierte bibliografische Daten sind im Internet über<http://dnb.d-nb.de> abrufbar.

1. Auflage September 2007

Alle Rechte vorbehalten© Deutscher Universitäts-Verlag | GWV Fachverlage GmbH, Wiesbaden 2007

Lektorat: Frauke Schindler / Anita Wilke

Der Deutsche Universitäts-Verlag ist ein Unternehmen von Springer Science+Business Media.www.duv.de

Das Werk einschließlich aller seiner Teile ist urheberrechtlich geschützt.Jede Verwertung außerhalb der engen Grenzen des Urheberrechtsgesetzesist ohne Zustimmung des Verlags unzulässig und strafbar. Das gilt insbe-sondere für Vervielfältigungen, Übersetzungen, Mikroverfilmungen und dieEinspeicherung und Verarbeitung in elektronischen Systemen.

Die Wiedergabe von Gebrauchsnamen, Handelsnamen, Warenbezeichnungen usw. in diesemWerk berechtigt auch ohne besondere Kennzeichnung nicht zu der Annahme, dass solcheNamen im Sinne der Warenzeichen- und Markenschutz-Gesetzgebung als frei zu betrachtenwären und daher von jedermann benutzt werden dürften.

Umschlaggestaltung: Regine Zimmer, Dipl.-Designerin, Frankfurt/MainGedruckt auf säurefreiem und chlorfrei gebleichtem PapierPrinted in Germany

ISBN 978-3-8350-0852-6

Dissertation Universität Ulm, 2006

Foreword V

Foreword

The empirical research contained in this book is unique. Daniel Pindur has put together a

database of successful LBO transactions in the European market from 1993 to 2004. Next to

insightful descriptive statistics of the representative sample, this database comprises purchase

and disposal prices, interim cash flows and capital structure information. The novelty and

granularity of this information enables the profound and first-time analysis of realized rates of

returns on individual transaction level, and, even more important, the analysis of the various

components and sources of such returns.

The covered successful LBO transactions generated significant returns to the buy-out firms.

Failed and unrealized LBO investments, which have to be taken into consideration for a

complete picture of LBO success rates as well, are not the topic of the present research. The

question is rather what buy-out firms and their investors can learn from successful LBO

transactions. Daniel Pindur provides answers to this question: an economic model of buy-out

firms decomposes the economic success of realized investments and serves as the framework

for identifying factors driving these components. Based thereupon the empirical work unveils

the magnitude of these components and their relative contribution to the economic success of

the covered transactions and reveals the relative importance of the various factors. Operational

improvements seem to be of utmost importance, i.e. the increase in earnings over the holding

period contributes by far most to value creation in these investments, with revenue growth

being most important followed by profitability improvements. Cash-flow generation, mainly

through discipline in capital expenditures and working capital management, comes next.

Finally, the buy-out firms, which conducted the transactions covered in the database, were to

some extent quite lucky, as they benefited substantially from multiple expansion during the

holding period, i.e. from the fact that multiples paid at entry were significantly lower than

multiples achieved at exit.

Furthermore, this book provides insightful and novel detail on various aspects and

characteristics of successful LBO transactions, such as for example transaction cost, the impact

of the divestiture mode and recapitalizations.

Findings presented in this book hence serve to much better understand the economics of

buy-out investments and contribute some transparency and objectivity to a currently heated

public debate regarding the economics of such investments. Further, buy-out firms will find

benchmarks, which they can use in order to assess value creation potential of companies they

are contemplating to invest in.

The same applies to industrial firms in the area of corporate strategy. Here, the “best-

owner” question gets addressed, which includes an assessment of the relative capability and

VI Foreword

willingness to enhance profitability. The underlying question is, whether the ownership

structure in the specific form of private equity makes a difference in terms of value creation

and returns. The results included in this book suggest that this can be the case if done right.

Prof. Dr. Frank Richter

Acknowledgements VII

Acknowledgements

The idea for this thesis developed while I was working in the Investment Banking Division

of Goldman Sachs and advising a buy-out firm on what was the largest German public-to-

private LBO transaction at that time. The question how buy-out firms create value in LBO

transactions had already attracted a lot of academic interest; however, related thorough,

quantitative empirical research did not seem to exist. Without having received access from

Goldman Sachs to a library of semi-public and confidential information booklets with raw

financial data on numerous LBO transactions, the novel empirical research as presented in this

book would clearly not have been possible. In this respect, special thanks go to Dr. Marcus

Schenck and Karl Skjelbred for their support.

Most importantly, I would like to thank my doctoral thesis supervisor Professor Dr. Frank

Richter who not only supported my ideas and intentions from the very beginning but who also

served as invaluable sounding board for stimulating and challenging academic discussions

throughout the development of this thesis. Also, I would like to acknowledge Professor Dr.

Kai-Uwe Marten from the University of Ulm and Professor Dr. Dirk Schiereck from the

European Business School, Oestrich-Winkel for serving as second and third referee for this

thesis.

Particularly, I want to thank my friends for their support; mainly by making my academic

leave a truly enjoyable and fun time.

I am deeply indebted to my parents who supported me in all respects throughout my

education in a unique and outstanding manner. This book is dedicated to them.

Dr. Daniel Pindur

Contents IX

Contents

Contents IX

Detailed Contents XI

List of Charts XVII

List of Tables XIX

Symbols XXIII

Acronyms XXVII

I. Introduction 1

A. On the Status of Research on Value Creation in LBOs 3

B. Shortcomings and Research Gap 21

C. Research Design to Assess Value Creation in LBOs 26

II. Preparatory Considerations for Value Creation Analysis in LBOs on Investment

Level 31

A. Research Object: Realized LBO Investments 31

B. Perspective: Equity Investors in LBOs 44

C. Objective Function: Value Creation in LBOs 52

III. Value Creation Analysis in the Context of the LBO Transaction Model 67

A. The LBO Transaction Model 67

B. Internal Perspective: FCF Effects 74

C. External Perspective: Variation in the Transaction Multiple 100

IV. Research Model, Derivation of Hypotheses and Operationalization of Variables 125

A. Research Model 125

B. Derivation of Hypotheses and Operationalization of Independent Variables 126

C. Operationalization of Dependent Variables 153

V. Empirical Analysis 161

A. Data Sample 161

B. Methodology 171

C. Independent Variables Descriptive Statistics 176

X Contents

D. Total Proceeds to Equity Investors 189

E. Relative LBO Performance Measures 235

VI. Conclusion 259

A. Components of/and their Relative Contribution to Value Creation Measures 259

B. Determinants of Value Creation in LBO Investments 263

C. Discussion and Outlook 267

Appendix 271

Bibliography 287

Detailed Contents XI

Detailed Contents

I. Introduction 1

A. On the Status of Research on Value Creation in LBOs 3

1. Theoretical Approaches to Analyzing Value Creation in LBOs 3

1.1 Neoclassic Financial Theory 4

1.2 Institution Economics 6

2. Empirical Work to Assess Value Creation in LBOs 10

2.1 Premia-Paid Analysis in Public-to-Private Transactions 11

2.2 Operational Performance Studies 14

2.3 Private Equity Performance Studies 17

B. Shortcomings and Research Gap 21

1. With Respect to the Research Object 21

2. With Respect to the Perspective of the Analysis 23

3. With Respect to the Notation of Value Creation 25

C. Research Design to Assess Value Creation in LBOs 26

II. Preparatory Considerations for Value Creation Analysis in LBOs on Investment

Level 31

A. Research Object: Realized LBO Investments 31

1. Defining Leveraged Buyouts 31

2. The LBO Investment Process 33

3. Modes of Entry for LBO Investments 35

3.1 Public-to-Private Entry (Going Private) 36

3.2 Private-to-Private Entry 37

4. Modes of Exit for LBO Investments 39

4.1 Private-to-Public Exit (Going Public) 40

4.2 Private-to-Private Exit 42

B. Perspective: Equity Investors in LBOs 44

1. The Concept of Sources and Uses in LBOs 44

XII Detailed Contents

2. Equity Financing Instruments 47

2.1 Common Stock 47

2.2 Quasi-Equity Financing Instruments 48

3. Debt Financing Instruments 50

3.1 Senior Debt 50

3.2 Subordinated Debt 50

C. Objective Function: Value Creation in LBOs 52

1. Total Proceeds to Equityholders in LBOs 53

2. Accounting for the Uncertainty of Total Proceeds or What’s the Right

Discount Rate 54

3. Value Creation Performance Measures 59

3.1 The Concept of Times Money 60

3.2 IRR as Timing-Adjusted Performance Measure 61

3.3 Alternative Performance Measures 64

III. Value Creation Analysis in the Context of the LBO Transaction Model 67

A. The LBO Transaction Model 67

1. Financial Leverage and the Variation in the Entity and Equity Market Value 67

2. Components of Total Proceeds to Equity Investors 69

3. Perspectives of Value Creation in LBOs 71

B. Internal Perspective: FCF Effects 74

1. Principal-Agent Theoretical Considerations 74

1.1 A Clarification of Agency Costs 75

1.2 Reducing Agency Costs in a LBO Governance Structure 82

2. Management Support 90

2.1 The Impact of the PE Fund and the LBO Organizational Form 90

2.2 Means of Equity Investor’s Operational and Strategic Involvement 92

3. Wealth Transfer Hypotheses 95

3.1 Wealth Transfer from Bondholders 95

3.2 Wealth Transfer from Employees 97

Detailed Contents XIII

3.3 Wealth Transfer from the Government 98

C. External Perspective: Variation in the Transaction Multiple 100

1. Conceptual Valuation Framework 101

1.1 The Risk-Neutral Valuation Theorem 102

1.2 The Binomial Cash Flow Model 102

1.3 Valuation with Multiples 105

2. From the Valuation to the Transaction Multiple 108

2.1 Market Timing, Supply and Demand and the Impact of the Capital

Market Environment 109

2.2 Information Asymmetries and Competition in the Divestment Process 116

IV. Research Model, Derivation of Hypotheses and Operationalization of Variables 125

A. Research Model 125

B. Derivation of Hypotheses and Operationalization of Independent Variables 126

1. Internal Perspective: FCF Effects 127

1.1 Agency Cost Reduction Related 127

1.2 Management Support Related 132

2. External Perspective: Variation in the Transaction Multiple 137

2.1 Conceptual Valuation Framework Related 137

2.2 Capital Market Environment Related 140

2.3 Information Asymmetries Related 143

3. Control Variables 146

C. Operationalization of Dependent Variables 153

1. Internal Perspective: FCF Effects 153

1.1 Operating Cash Flow 154

1.2 Net Investing Cash Flow 158

2. External Perspective: Variation in the Transaction Multiple 158

3. LBO Performance Measures 159

V. Empirical Analysis 161

A. Data Sample 161

XIV Detailed Contents

1. Investment Selection Criteria 162

2. Potential Sample Bias 166

3. Tests for Representativeness 168

B. Methodology 171

1. Financial Data 171

2. Statistical methods 174

C. Independent Variables Descriptive Statistics 176

1. Control Variables 176

2. Purely Internal Perspective Related 178

2.1 Agency Cost Reduction Related Aspects 178

2.2 Management Support Related 182

3. Purely External Perspective Related 183

3.1 Conceptual Valuation Framework Related Aspects 183

3.2 Capital Market Environment Related Aspects 185

3.3 Information Asymmetries Related Aspects 187

D. Total Proceeds to Equity Investors 189

1. The LBO Transaction Model 189

1.1 Financial Leverage and the Variation in the Entity and Equity Value 189

1.2 Components of Total Proceeds to Equity Investors 195

2. Internal Perspective: FCF Effects 200

2.1 Operating Cash Flow 200

2.2 Net Investing Cash Flow 213

2.3 Cumulated FCF Generation 214

2.4 Internal Perspective Intermediary Results 220

3. External Perspective: Variation in the Transaction Multiple 224

3.1 Descriptive Differences by Exit Mode 226

3.2 Variation in the Transaction Multiple of IPO Exited LBOs 227

3.3 Variation in the Transaction Multiple of Secondary Buyout Exited LBOs 231

3.4 External Perspective Intermediary Results 234

Detailed Contents XV

E. Relative LBO Performance Measures 235

1. Times Money Analysis 236

1.1 Times Money Descriptive Statistics and Decomposition 236

1.2 Separating Steady vs. Improved Operational Performance 239

1.3 Times Money and the Length of the Investment 240

2. Investment IRR Analysis 241

2.1 Investment IRR Descriptive Statistics 241

2.2 Investment IRR Sensitivity Analyses 246

2.3 Investment IRR Inferring Statistics 250

3. Alternative Performance Measures 252

3.1 Excess Investment IRRs 253

3.2 Standardized NPVs 253

3.3 LBO Performance Measure Correlation Analysis 256

VI. Conclusion 259

A. Components of/and their Relative Contribution to Value Creation Measures 259

B. Determinants of Value Creation in LBO Investments 263

C. Discussion and Outlook 267

Appendix 271

Bibliography 287

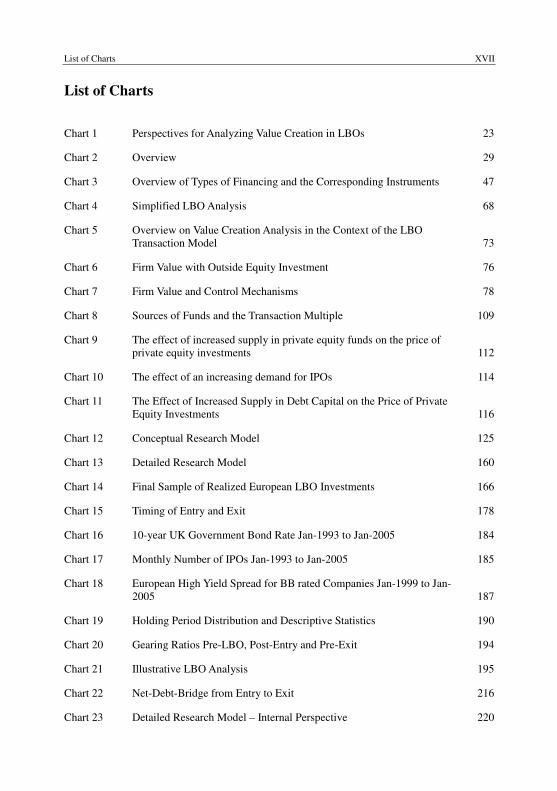

List of Charts XVII

List of Charts

Chart 1 Perspectives for Analyzing Value Creation in LBOs 23

Chart 2 Overview 29

Chart 3 Overview of Types of Financing and the Corresponding Instruments 47

Chart 4 Simplified LBO Analysis 68

Chart 5 Overview on Value Creation Analysis in the Context of the LBO

Transaction Model 73

Chart 6 Firm Value with Outside Equity Investment 76

Chart 7 Firm Value and Control Mechanisms 78

Chart 8 Sources of Funds and the Transaction Multiple 109

Chart 9 The effect of increased supply in private equity funds on the price of

private equity investments 112

Chart 10 The effect of an increasing demand for IPOs 114

Chart 11 The Effect of Increased Supply in Debt Capital on the Price of Private

Equity Investments 116

Chart 12 Conceptual Research Model 125

Chart 13 Detailed Research Model 160

Chart 14 Final Sample of Realized European LBO Investments 166

Chart 15 Timing of Entry and Exit 178

Chart 16 10-year UK Government Bond Rate Jan-1993 to Jan-2005 184

Chart 17 Monthly Number of IPOs Jan-1993 to Jan-2005 185

Chart 18 European High Yield Spread for BB rated Companies Jan-1999 to Jan-

2005 187

Chart 19 Holding Period Distribution and Descriptive Statistics 190

Chart 20 Gearing Ratios Pre-LBO, Post-Entry and Pre-Exit 194

Chart 21 Illustrative LBO Analysis 195

Chart 22 Net-Debt-Bridge from Entry to Exit 216

Chart 23 Detailed Research Model – Internal Perspective 220

XVIII List of Charts

Chart 24 Variation in the Transaction Multiple against Holding Period 225

Chart 25 Detailed Research Model – External Perspective 234

Chart 26 Times Money and its Relative Composition 237

Chart 27 Times Money and its Components against Holding Period 240

Chart 28 Investment IRR against Holding Period and Capital Invested 242

Chart 29 Distribution of IRRcm and Related Sensitivity 247

Chart 30 Distribution of IRRcRev and Related Sensitivity 248

Chart 31 Distribution of IRRcMrg and Related Sensitivity 249

Chart 32 Standardized Mean/Median NPVs against the Alternative Rate of Return 256

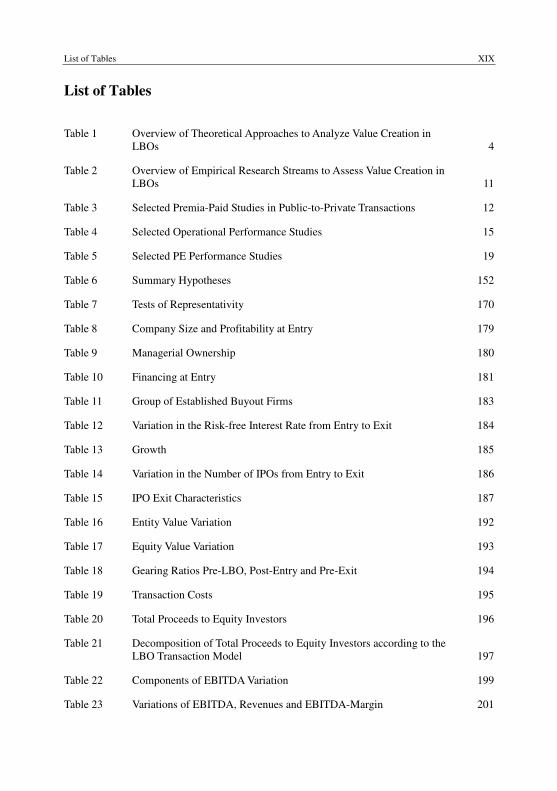

List of Tables XIX

List of Tables

Table 1 Overview of Theoretical Approaches to Analyze Value Creation in

LBOs 4

Table 2 Overview of Empirical Research Streams to Assess Value Creation in

LBOs 11

Table 3 Selected Premia-Paid Studies in Public-to-Private Transactions 12

Table 4 Selected Operational Performance Studies 15

Table 5 Selected PE Performance Studies 19

Table 6 Summary Hypotheses 152

Table 7 Tests of Representativity 170

Table 8 Company Size and Profitability at Entry 179

Table 9 Managerial Ownership 180

Table 10 Financing at Entry 181

Table 11 Group of Established Buyout Firms 183

Table 12 Variation in the Risk-free Interest Rate from Entry to Exit 184

Table 13 Growth 185

Table 14 Variation in the Number of IPOs from Entry to Exit 186

Table 15 IPO Exit Characteristics 187

Table 16 Entity Value Variation 192

Table 17 Equity Value Variation 193

Table 18 Gearing Ratios Pre-LBO, Post-Entry and Pre-Exit 194

Table 19 Transaction Costs 195

Table 20 Total Proceeds to Equity Investors 196

Table 21 Decomposition of Total Proceeds to Equity Investors according to the

LBO Transaction Model 197

Table 22 Components of EBITDA Variation 199

Table 23 Variations of EBITDA, Revenues and EBITDA-Margin 201

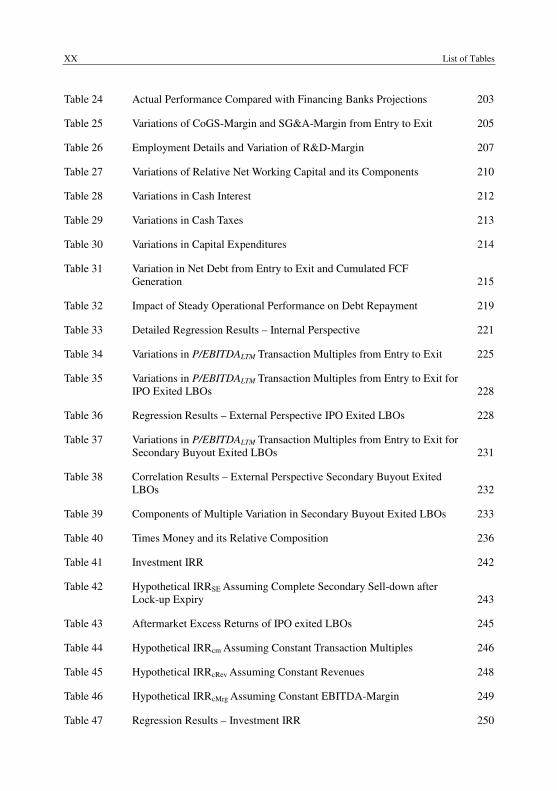

XX List of Tables

Table 24 Actual Performance Compared with Financing Banks Projections 203

Table 25 Variations of CoGS-Margin and SG&A-Margin from Entry to Exit 205

Table 26 Employment Details and Variation of R&D-Margin 207

Table 27 Variations of Relative Net Working Capital and its Components 210

Table 28 Variations in Cash Interest 212

Table 29 Variations in Cash Taxes 213

Table 30 Variations in Capital Expenditures 214

Table 31 Variation in Net Debt from Entry to Exit and Cumulated FCF

Generation 215

Table 32 Impact of Steady Operational Performance on Debt Repayment 219

Table 33 Detailed Regression Results – Internal Perspective 221

Table 34 Variations in P/EBITDALTM Transaction Multiples from Entry to Exit 225

Table 35 Variations in P/EBITDALTM Transaction Multiples from Entry to Exit for

IPO Exited LBOs 228

Table 36 Regression Results – External Perspective IPO Exited LBOs 228

Table 37 Variations in P/EBITDALTM Transaction Multiples from Entry to Exit for

Secondary Buyout Exited LBOs 231

Table 38 Correlation Results – External Perspective Secondary Buyout Exited

LBOs 232

Table 39 Components of Multiple Variation in Secondary Buyout Exited LBOs 233

Table 40 Times Money and its Relative Composition 236

Table 41 Investment IRR 242

Table 42 Hypothetical IRRSE Assuming Complete Secondary Sell-down after

Lock-up Expiry 243

Table 43 Aftermarket Excess Returns of IPO exited LBOs 245

Table 44 Hypothetical IRRcm Assuming Constant Transaction Multiples 246

Table 45 Hypothetical IRRcRev Assuming Constant Revenues 248

Table 46 Hypothetical IRRcMrg Assuming Constant EBITDA-Margin 249

Table 47 Regression Results – Investment IRR 250

List of Tables XXI

Table 48 Excess Investment IRRs 253

Table 49 Standardized NPVs 254

Table 50 LBO Performance Measure Correlation Analysis 257

Table 51 Predicted Signs of Coefficients for Internal Perspective Regression

Results 272

Table 52 Details for Size and Profitability Variables by Sub-samples 273

Table 53 Details for Managerial Ownership and Financing at Entry Variables by

Sub-samples 274

Table 54 Details for Entity and Equity Value and Leverage Variations by Sub-

samples 275

Table 55 Details for Total Proceeds and its Components by Sub-samples 276

Table 56 Details for Dependent Variables by Sub-samples – Internal Perspective 277

Table 57 Details for Independent Variables and Internal Perspective Dependent

Variables by Exit Modes 278

Table 58 Details for Transaction Multiples and their Absolute as well as Relative

Variations by Sub-samples – External Perspective 279

Table 59 Details for Times Money and its Components by Sub-samples 280

Table 60 Details for Realized Investment IRR and Hypothetical Investment IRRs

by Sub-samples 280

Table 61 Detailed Variations of EBITDA, Revenues and EBITDA-Margin 281

Table 62 Detailed Variations of CoGS-Margin and SG&A-Margin 281

Table 63 Additional Employment Details and Detailed Variation of R&D-Margin 282

Table 64 Detailed Variations of Relative Net Working Capital and its Components 282

Table 65 Detailed Variations of Capital Expenditures 283

Table 66 Independent Variables Correlation Matrix 284

Table 67 OLS Regression Premises Tests 284

Table 68 Regression Results – Hypothetical Investment IRRs 285

Symbols XXIII

Symbols

AccPay Accounts payable

AccRec Accounts receivable

B Firm-specific human capital costs of financial distress to management

C Operating cash flow

CF Cash flow

CI Capital Invested

CMgmt Change in (top) management during the holding period

CoGS Cost of goods sold

D Total debt; book value of total financial indebtedness

Dis Discount in an equity offering

Div Dividend

E[·] Expected value

EP[·] Expected value under the probability measure P

EQ[·] Expected value under the probability measure Q

E Equity value

EBIT Earnings before interest and taxes

EBITDA Earnings before interest, taxes, deprecation and amortization

Employment Number of employees

Employ-Mrg Personnel Cost as % of Sales

ER Excess return

ExpInd Experience Index

F Filtration

FCF Free cash flow available for distribution to debt- and equityholders

XXIV Symbols

I Investment costs

Int Net financial result

IntCash Cash effective net financial result

Inv End of period inventories

IRR Internal Rate of Return

L Leverage ratio defined as total debt (D) over EBITDALTM

Labor-Prod Labor productivity; defined as revenues per employee

Liq Liquidity

M Market portfolio

N Number of observations, sample size

ND Net Debt; total financial liabilities less cash and cash equivalents

P Purchase price

P/E Price–Earnings ratio

PI Profitability index

PME Public market equivalent

Rev Revenues

ROIC Return on invested capital

SG&A Sales, general and administrative expenses

Steady Investment (sample) without any acquisition and divestiture activity during

the holding period

T Point in time of the LBO exit transaction (exit)

Tax Tax expenses

TaxCash Cash effective tax expenses

TC Transaction costs

TP Total proceeds to equity investors in an LBO transaction

Symbols XXV

TS Total sources

U(·) Utility

V Entity value

W Wealth

X Amount

b Non-pecuniary benefits

d Down factor in a binomial model

g Growth rate

gP Subjective growth rate under the probability measure P

gQ Subjective growth rate under the probability measure Q

i Company index

j Index

k Alternative, comparable and available investment opportunity

l Gearing ratio defined as total debt over entity value

ln Natural logarithm

m Transaction multiple P/EBITDALTM

n Index

P Probability of occurrence under the probability measure P

Q Probability of occurrence under the probability measure Q

r Return

rf Risk-free rate of return

rk Rate of return of a comparable, alternative investment opportunity

rM Rate of return of the market portfolio

XXVI Symbols

t Point in time of the LBO entry transaction (entry)

u Up factor in a binomial model

~ Approximately

α Remaining LBO equity investors’ stake for a IPO exited investment

ß Beta

Aß Asset beta

Eß Equity beta

Lß Levered beta; beta of a partially debt financed company

ε Random variable; error term in a stochastic process

τ Tax rate

σ Standard deviation

2σ Variance

θ Reinvestment rate

λ Management’s relative ownership stake

General Notation

Throughout this thesis t indicates the entry point in time, T the exit point in time of the LBO

investment.

Negative values in tables are displayed in parentheses.

Prefix _ stands for the absolute difference of a variable at two different points in time; i.e.

tT VarVar − ; prefix g_ indicates the growth rate of a variable, i.e. varT-1 / vart-1 – 1; prefix c_

indicates the compounded annual growth rate of an investment, i.e. ( ) 1var/var12

11 −−− HPtT .

Consistently the suffix (i) cm refers to a constant P/EBITDALTM multiple at entry and at exit,

(ii) cRev to constant revenues throughout the holding period, and (iii) cMrg to constant

EBITDA-margin during the holding period.

Acronyms XXVII

Acronyms

APV Adjusted present value

CAGR Compounded annual growth rate

CAPM Capital asset pricing model

CE Continental Europe

CEO Chief executive officer

CFO Chief financial officer

CV Control Variable

DCF Discounted cash flow

DPI Distributed total value to paid-in capital

DV Dependent Variable

EI Equity investor

EURIBOR Euro Interbank Offered Rate

EVA Economic value added

EVCA European Venture Capital Association

GP General partner

HP Holding period

IAS International accounting standards

I/B/E/S Institutional brokers estimate system

IBO Institutional Buyout

IPO Initial Public Offering

IV Independent Variable

JoF Journal of finance

JoFE Journal of financial economics

XXVIII Acronyms

LBO Leveraged buyout

LIBOR London Interbank offered rate

LMBO Leveraged management buyout

LP Limited partner

LTM Latest twelve months

Max Maximum

MBO Management buyout

Md Median

Mgmt Management

Min Minimum

NAV Net asset value

NPV Net present value

NWC Net Working Capital

PC Primary component in an IPO

PE Private equity

PPE Plant, property and equipment

PV Present value

RADR Risk-adjusted discount rates

RNV Risk-neutral valuation

SC Secondary component in an IPO

SD Senior debt

SIC Standard industrial classification

SL Security Line

Std Standard deviation

Acronyms XXIX

SubD Subordinated Debt

S&P Standard & Poor’s

TCF Total cash flow

TM Times money, i.e. distribution to paid-in capital

TVPI Cumulative total value to paid-in capital

UK United Kingdom

US United States of America

US-GAAP United States Generally Accepted Accounting Principles

Var Variable

VC Venture Capital

VE Venture Economics

VIF Variance inflation factor

WACC Weighted average cost of capital

abs Absolute

cont. Continuous

e.g. For example, for instance (Latin exempli gratia)

et al. And others (Latin et alii)

f And the following page

ff And the following pages

i.e. That is to say, in other words (Latin id est)

inj Injection; in particular Einj additional equity injection by equity investors

na Not applicable

no. Number

p. Page

XXX Acronyms

pp. Pages

rel Relative

vol. Volume

vs. Versus