Daily Credit Briefing - UniCredit Research

21

14 November 2018 Credit & Credit Strategy Research Daily Credit Briefing UniCredit Research page 1 See last pages for disclaimer. Credit Market Snapshot Synthetic indices traded sideways during the day and tightened somewhat into the close yesterday. The iTraxx Main narrowed 0.5bp to 71bp, while the iTraxx FinSen narrowed 1bp to 89bp. The Crossover was unchanged at 294bp. Cash bonds continued their widening trend. In contrast to the day before, when widening was concentrated in a few sectors and was mostly driven by few single-name issues, it was very broad yesterday. The iBoxx Non- Financials widened 2-3bp across all sectors. Hybrids widened 4bp to 246bp and High Yield was 6bp wider at 361bp. The iBoxx Non-Financials Senior index stands at 57bp, while Financials widened 3.5bp to 62bp. European stock indices recovered part of their losses from Monday. The Euro STOXX 50 index was up by about 1% with positive momentum coming into the market when US exchanges opened. However, by the end of the US trading session, the S&P 500 had given up all its gains and closed marginally down. In terms of sector distribution, Automobiles & Parts (+2.0%) and Technology (+1.7%) were among the major winners. Government bond markets were little changed yesterday at the end of the day. BTP yields increased during the day (10Y by 7bp to 3.51%) but recovered all losses by the close. Preliminary German GDP reading released this morning showed a 0.2% qoq contraction in the third quarter, down from 0.5% increase in the previous quarter. This compares with consensus expectations of a 0.1% contraction. Later this morning, 3Q18 eurozone GDP will be out; consensus expects +0.2%. In addition, UK and US inflation data for October are scheduled to be released later today. Earlier this year, US President Trump threatened to impose tariffs of as much as 25% on imports of foreign-made cars. Companies have warned that such tariffs would also hurt the US economy and could disrupt the global auto industry. According to media reports, the Trump administration will hold off for now on imposing new tariffs on automobile imports as top officials weigh revisions to a report on the national security implications. The Auto sector within the Nikkei 225 is up 1.7% this morning. This morning, Asian equities are more or less unchanged amid Chinese macro data releases that suggest stabilization. Industrial production grew 5.9% yoy in October, slightly more than expected, and fixed investment rose 5.7% yoy, up from 5.4% in the month before. However, retail sales grew only 8.6%, which was slower than 9.2% growth in the previous month. In Japan, preliminary 3Q18 GDP was released showing the economy contracted for the second time on a quarterly basis this year after several natural disasters. According to the preliminary data, Japan’s economy contracted 0.3% from the previous quarter, in line with expectations and after expanding at an (upwardly revised) rate of 0.8% in the second quarter. However, consensus expects recovery in the fourth quarter with 0.3% growth qoq. Dr. Philip Gisdakis (UniCredit Bank, Munich) +49 89 378-13228 [email protected] Investment Grade INDUSTRIALS p2 Alstom 2Q18/19 results strong, but EC investigation intensifies AUTOS p3 LeasePlan Underlying net result for 3Q18 up by 6.0%, and Lincoln Finance's interest coverage is down to 2.9x, from 3.0x qoq TMT p4 Vodafone Releases slightly better-than-expected 1H18/19 results CONSUMER p5 BAT Thoughts on WSJ article reporting that US regulators plan to pursue a ban on menthol cigarettes Merck KGaA Strong 3Q18 operting profit key figures - adjusted forecast for 2018 - focus remains on deleveraging BANKS p14 Berlin Hyp 9M18 operating results before taxes and profit transfer up 15% to EUR 85.8mn High Yield HIGH YIELD p7 Codere Reports good 3Q18, keeps outlook unchanged Jaguar Land Rover Moody's downgrades to Ba3 with negative outlook Peugeot Fitch upgrade to IG Telecom Italia Board of directors dismisses CEO CMC di Ravenna Rating downgrade to CC at S&P, remains on watch negative Gamenet Group Reports 9M18 in line with our estimates Nidda Healthcare Bain Capital and Cinven announce the final result of their public delisting tender offer Nordex Reports 9M18 results, narrows FY18 guidance Quick links Market Data Page Rating Actions Recent Credit Research Publications

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Daily Credit Briefing - UniCredit Research

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 1 See last pages for disclaimer.

Credit Market Snapshot

Synthetic indices traded sideways during the day and tightened somewhat into the close yesterday. The iTraxx Main narrowed 0.5bp to 71bp, while the iTraxx FinSen narrowed 1bp to 89bp. The Crossover was unchanged at 294bp. Cash bonds continued their widening trend. In contrast to the day before, when widening was concentrated in a few sectors and was mostly driven by few single-name issues, it was very broad yesterday. The iBoxx Non-Financials widened 2-3bp across all sectors. Hybrids widened 4bp to 246bp and High Yield was 6bp wider at 361bp. The iBoxx Non-Financials Senior index stands at 57bp, while Financials widened 3.5bp to 62bp.

European stock indices recovered part of their losses from Monday. The Euro STOXX 50 index was up by about 1% with positive momentum coming into the market when US exchanges opened. However, by the end of the US trading session, the S&P 500 had given up all its gains and closed marginally down. In terms of sector distribution, Automobiles & Parts (+2.0%) and Technology (+1.7%) were among the major winners.

Government bond markets were little changed yesterday at the end of the day. BTP yields increased during the day (10Y by 7bp to 3.51%) but recovered all losses by the close.

Preliminary German GDP reading released this morning showed a 0.2% qoq contraction in the third quarter, down from 0.5% increase in the previous quarter. This compares with consensus expectations of a 0.1% contraction. Later this morning, 3Q18 eurozone GDP will be out; consensus expects +0.2%. In addition, UK and US inflation data for

October are scheduled to be released later today. Earlier this year, US President Trump threatened to impose tariffs of as much as 25% on imports of foreign-made cars. Companies have warned that such tariffs would also hurt the US economy and could disrupt the global auto industry. According to media reports, the Trump administration will hold off for now on imposing new tariffs on automobile imports as top officials weigh revisions to a report on the national security implications. The Auto sector within the Nikkei 225 is up 1.7% this morning.

This morning, Asian equities are more or less unchanged amid Chinese macro data releases that suggest stabilization. Industrial production grew 5.9% yoy in October, slightly more than expected, and fixed investment rose 5.7% yoy, up from 5.4% in the month before. However, retail sales grew only 8.6%, which was slower than 9.2% growth in the previous month. In Japan, preliminary 3Q18 GDP was released showing the economy contracted for the second time on a quarterly basis this year after several natural disasters. According to the preliminary data, Japan’s economy contracted 0.3% from the previous quarter, in line with expectations and after expanding at an (upwardly revised) rate of 0.8% in the second quarter. However, consensus expects recovery in the fourth quarter with 0.3% growth qoq.

Dr. Philip Gisdakis (UniCredit Bank, Munich) +49 89 378-13228 [email protected]

Investment GradeINDUSTRIALS p2

Alstom 2Q18/19 results strong, but EC investigation intensifies

AUTOS p3

LeasePlan Underlying net result for 3Q18 up by 6.0%, and Lincoln Finance's interest coverage is down to 2.9x, from 3.0x qoq

TMT p4

Vodafone Releases slightly better-than-expected 1H18/19 results

CONSUMER p5

BAT Thoughts on WSJ article reporting that US regulators plan to pursue a ban on menthol cigarettes

Merck KGaA Strong 3Q18 operting profit key figures - adjusted forecast for 2018 - focus remains on deleveraging

BANKS p14

Berlin Hyp 9M18 operating results before taxes and profit transfer up 15% to EUR 85.8mn

High Yield

HIGH YIELD p7

Codere Reports good 3Q18, keeps outlook unchanged

Jaguar Land Rover Moody's downgrades to Ba3 with negative outlook

Peugeot Fitch upgrade to IG

Telecom Italia Board of directors dismisses CEO

CMC di Ravenna Rating downgrade to CC at S&P, remains on watch negative

Gamenet Group Reports 9M18 in line with our estimates

Nidda Healthcare Bain Capital and Cinven announce the final result of their public delisting tender offer

Nordex Reports 9M18 results, narrows FY18 guidance

Quick links Market Data Page Rating Actions Recent Credit Research Publications

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 2 See last pages for disclaimer.

Industrials

Alstom (Underweight) Event Alstom (Baa2s/--/--) reported 2Q18/19 results that showed strong operating momentum

in the first half of its fiscal year. Orders received came to EUR 7.1bn, exceeding the EUR 3.2bn as of 1H17/18. The order backlog was up to EUR 38.1bn compared to EUR 35.0bn in1H17/18. Sales were up 23% in organic terms to EUR 4.0bn. The book-to-bill ratio came to a very strong 1.8x. EBIT was up 58% to EUR 285mn, bringing the margin to 7.1% in 1H18/19,compared to 5.4% in the prior-year period. Sales growth was strong in all regions, with Europe (50% of sales) up 16% yoy, Americas (18% of sales) up 10%, Asia/Pacific (11% of sales) up 9% and Middle East/Africa (21% of sales) up 53%. Despite the higher EBIT, FCF was down yoy at EUR 172mn compared to EUR 227mn in 1H17/18, due in large part to a WC swing. The company said that it had spent EUR 212mn of EUR 300mn in planned“transformation capex” so far. Net debt came to EUR 280mn as of 30 September 2018, compared to EUR 255mn as of 31 March 2018, and the company had cash on the balance sheet of EUR 1.4bn. Alstom confirmed its previous outlook for the fiscal year and expectssales to reach EUR 8mn with an adjusted EBIT margin of 7%.

Expected development of credit profile/rating

Citing several people who have seen the European Commission’s (EC) list of concerns, Politico reported yesterday that EC antitrust officials have set out a long set of objections tothe Siemens/Alstom merger. The article reports that the EC has concluded the deal is“incompatible” with the EU’s internal market and is likely to lead to higher prices for a range of rail services. Approving the deal is likely to require significant concessions that could be unacceptable to the two parties. We think it therefore looks much less likely that the deal will be approved than it did a few months ago, when the parties expressed optimism after the EC opened an in-depth (Phase 2) antitrust investigation into the transaction. In its 1H18/19 results release, Alstom acknowledged receiving a Statement of Objections from the EC andsaid that it is working with the EC to “explain the rationale and benefits of the proposedcombination”. Alstom still expects the transaction to close in 1H19.

Name recommendation We expect further news on the mobility JV with Siemens to be the primary spread driver for ALOFP rather than quarterly results. Considering that ALOFP trades only slightly wider than SIEGR, we think that ALOFP spreads are currently pricing in a successful conclusion to the rail merger. ALOFP also trades tighter than comparably rated SUFP and ABBNVX, which have also reported strong quarterly results. We therefore see the relative value of ALOFP as unattractivecompared to key peers and we reiterate our underweight recommendation on the name.

Jonathan Schroer, CFA (UniCredit Bank, Munich) +49 89 378-13212 [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 3 See last pages for disclaimer.

Autos

LeasePlan (Marketweight); Lincoln Finance (Hold) Event LeasePlan’s (Baa1s/BBB-p/BBB+s) 3Q18 results showed an underlying net result that was

down by 48.1% (+6.0% excluding EUR 73mn for Turkey fleet impairments) yoy to EUR 74mn (EUR 147mn). The company’s serviced fleet grew 6.8% to 1.82mn vehicles and revenue grew by2.9% in 3Q18 to EUR 2,391mn. Lease & Additional Services income in 3Q grew 0.9% to EUR 1,640mn or 1.6% on a constant FX basis due to growth in the fleet and increased uptake of services. Vehicle Sales and End-of-Contract Fees were up 7.6% to EUR 751mn. LeasePlan’s liquidity and capital positions remain strong, with a liquidity buffer of EUR 4.6bn (EUR 4.9bn qoq) consisting of cash balances, as well as access to its committed revolving credit facility and a CET 1capital ratio of 17.9% (vs. 17.3% qoq), well above regulatory requirements. According toBloomberg on 12 October, LeasePlan withdrew its IPO as the stock market climate worsened and investors obviously sought a discount compared to ALD’s valuation, according to an article in Dutch newspaper Het Financieele Dagblad.

Expected development of credit profile/rating

Lincoln Finance (LINCFI) is a holding/financing vehicle set up with the acquisition of LeasePlan. At3Q18, Lincoln Finance (source: www.lincoln-financing.com) had a total cash balance of EUR 822mn (EUR 276mn on an interest reserve account [IRA], EUR 35mn on an interest coverage account [ICA] and EUR 511mn of further cash balances). The combined IRA and ICA balance ofEUR 311mn represents 2.9x (compared to 3.0x qoq) the annual interest expense of the senior secured notes, which is above the 2.5x minimum. LeasePlan has declared an interim dividend ofEUR 171.4mn, or 60% of its reported net income in 1H18 (9M18 dividend cash-out: EUR 120.1mn). Details on Lincoln Finance and LeasePlan can be found in our 14 December Credit Report.

LPTY RELATIVE TO AUTO AND FSV IBOXX INDICES LPYT IN THE AUTO FINANCE BOND UNIVERSE

Source: iBoxx, Bloomberg, Markit, UniCredit Research

Name recommendation LeasePlan has four euro-denominated bonds outstanding in the iBoxx Financial Services index and EUR 1.5bn in maturing bonds in 2019. We continue to have a marketweight recommendation on LeasePlan, given that its cash curve is trading slightly wider than that of similarly rated European auto-finance bonds such as RCI Banque’s RENAUL (Baa1p/BBBs), but tighter than PSABFR (Baa1s/BBBs). We are keeping our hold recommendation on LINCFI bonds as any price upside is limited. Both LINCFI (B1/BB+/BB-) bonds have high coupons but are callable from 15 April 2018. As the IPO was withdrawn, a call now seems less likely for the LINCFI 7.375% 4/21 (USD 400mn) and LINCFI 6.875% 4/21 bonds, which is positive for buy-and-hold investors in these bonds.

Dr. Sven Kreitmair, CFA (UniCredit Bank, Munich) +49 89 378-13246, [email protected]

0

10

20

30

40

50

60

70

80

90

100

Nov-17 Feb-18 May-18 Aug-18 Nov-

bp

LPTY 0.75% 10/22 LPTY 1% 5/21

LPTY 1% 4/20 LPTY 1% 5/23

ALDFP 0.875% 7/22 iBoxx € Automobiles & Parts

iBoxx € Financial Services

FC 1.355% 2/25

LPTY 0.75% 10/22

LPTY 1% 5/21

LPTY 1% 4/20

LPTY 1% 5/23

0

20

40

60

80

100

120

140

160

180

200

0 1 2 3 4 5 6 7 8

bp

mDur

FCEB_Cash FC_Cash FCABNK_Cash GMFIN_Cash

RCI_Cash VWFS/VWL VWB PSABFR_Cash

LPTY_Cash OPELFN_Cash

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 4 See last pages for disclaimer.

TMT

Vodafone (Marketweight) Event Vodafone’s (Baa1cwn/BBB+n/BBB+s) 1H18/19 results are broadly in line with expectations.

The company has increased its FCF outlook on the basis of further cost reductions and the creation of a virtual-tower company has added a deleveraging option. In 1H18/19, reported group revenue decreased by 5.5% to EUR 21.8bn (Bloomberg consensus: EUR 22.1bn), primarilydue to foreign-exchange headwinds and impacts from the adoption of IFRS 15 and the sale of Vodafone Qatar. The group’s organic service revenue fell by 0.5% in 2Q18/19 (consensusestimate: -0.6%; and compared to +0.3% in 1Q18/19, 1.4% in 4Q17/18, excluding a legal settlement in Germany, 1.1% in 3Q17/18, 1.3% yoy in 2Q17/18 and 2.2% yoy in 1Q17/18).Overall, Europe Consumer service revenue, excluding UK handset financing, declined by 0.6% in 1H, with fixed growth of 3.6% offset by a mobile decline of 2.1%. The company claims that, excluding Spain, Italy and a drag from UK, handset financing service revenues grew by 3.0%, with fixed growing 6.1% and mobile 1.8%. However, the situation in Italy did not improve (organic service revenue growth in 1Q was -6.5%, in 2Q -6.3%), and in Spain, it worsened meaningfully (organic service revenue growth in 1Q was -2.2%, and in 2Q, it was -7.2%) alongside still-declining service revenues in the UK (organic service revenue growth in 1Q was -4.9%, and in 2Q, it was -5.1%). Group-adjusted EBITDA was down 4.2% yoy to EUR 7.08bn (Bloomberg consensus:EUR 7.03bn), reflecting foreign-exchange headwinds, a lower benefit from handset financing in theUK and a regulatory settlement in the UK in the prior year. Organic adjusted EBITDA grew 2.9%(excluding handset financing and settlements), significantly faster than service revenue due to theoperating-cost-reduction program “Fit for Growth”. Consequently, the group’s adjusted EBITDAmargin improved by 0.3pp, to 30.8%, or 1.3pp on an organic basis. Free cash flow pre-spectrum was EUR 0.9bn, EUR 0.4bn lower than in the prior year, mainly due to lower adjusted EBITDA andhigher capital creditor outflows – and partly offset by lower capital additions. Net debt was up from EUR 29.6bn at 31 March 2018 to EUR 32.1bn at 30 September 2018, as free-cash-flow generation (EUR 0.9bn) and proceeds from Verizon loan notes of EUR 2.1bn were offset by FY18final dividend payments (EUR 2.7bn), spectrum purchases (EUR 1.0bn) and a net cash outflow toIndia from Vodafone Group of EUR 0.8bn, in connection with the Vodafone Idea transaction.

Expected development of credit profile/rating

Vodafone has slightly lifted its full-year guidance for FY18/19. It now expects adjusted organicEBITDA to grow by around 3% in FY18/19 (at the mid-point of its prior guidance of between 1% and 5%), excluding the impact of UK handset financing and the significant benefit in theprior year from regulatory settlements in the UK and a legal settlement in Germany. Based onguidance FX rates, and under IAS 18 accounting standards, this implies an adjusted EBITDArange of EUR 14.3-14.5bn (previously EUR 14.15-14.65bn) for FY18/19. The capex-to-revenue ratio is to remain in the mid-teens, excluding capex related to the Gigabit Investment Plan in Germany. The group now aims to achieve a reduction in operating expenses of at least EUR 1.2bn in Europe and Common Functions by FY21 (compared to FY18) on an absolute organic basis, including savings of around EUR 400mn in FY19. Hence, Vodafonenow aims to generate pre-spectrum FCF of around EUR 5.4bn (versus previously “at least EUR 5.2bn”) after all capex and before M&A and restructuring costs – and based on guidance FX rates as well as by achieving the mid-point of its EBITDA guidance range. Moreover, Vodafone confirmed somehow recent speculation in the market that the company is going toestablish a tower company to manage 58,000 (mobile) towers across Europe.

Name recommendation We are keeping our marketweight recommendation on Vodafone bonds. Overall, we view the results as moderately positive for VOD bonds, as the company confirmed its EBITDA outlook and increased its FCF guidance (based on cost reductions) despite a weak or worsening trend in Italy and Spain. Moreover, the company is making progress on the potential partial disposal of its tower assets. We think this should help it further stabilize its leverage at the mid-BBB rating level (assuming the proposed transaction with Liberty Globalis approved). Current VOD bond spreads are already priced in the mid-BBB range, in our view. For further information, see our Credit Flash on Vodafone, published yesterday.

Stephan Haber, CFA (UniCredit Bank, Munich); +49 89 378-15192; [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 5 See last pages for disclaimer.

Consumer

BAT (Overweight), Imperial Brands (Overweight) Event At the beginning of this week, Bloomberg and WSJ reported that the US regulator

plans to pursue a ban on menthol cigarettes. In our view, there is no certainty that a ban will be implemented and it would take years to implement (UniCredit estimate up tofive years). In our view, the recent spread widening after the WSJ report mainly for BAT seems to be an overreaction by the market. BAT (Baa2s/BBB+s/BBBs) and Imperial Brands (Baa3s/BBBs/BBBs) would be impacted by the US FDA plan. BAT’s USD 59bnReynolds American deal in 2016 means about 40% of sales now come from the US. BAT is exposed to menthol products sold in the US, which accounts for about a quarter of the company’s earnings (source Bloomberg). Newport is BAT’s largest menthol brand and accounts for about 40% of US sales, according to Bloomberg. According to Bloomberg, about 15% of Imperial Brands profits comes from US menthol products.

Expected development of credit profile/rating

Tobacco companies like BAT and Imperial Brands are trying to manage the steady decline oftheir traditional cigarette businesses and use the cash flow to develop faster-growing alternative products like those in the vapor segment. A menthol ban would impact its traditional business. In our view, BAT’s strategy to enhance its leading position in the vapor segment, with Vype andVuse inherited from Reynolds, as well as to proactively develop its presence in the heatingtobacco products space via glo, should pay off in the medium term. From 2018, we estimate that BAT will be able to progressively ramp up its overall next-generation offer, but will not meet its original target of GBP 1bn. Nevertheless, the contribution of alternative products to profitability will remain marginal in 2018 and 2019. Imperial manages a diversified portfolio of tobaccoproducts, encompassing cigarettes, fine-cut tobacco, papers, cigars and snus. Imperial continues to work on next generation products through Fontem Ventures, a non-tobacco subsidiary focused on the company's growth in the e-vapour sector though its blu brand.

All three big rating agencies have a stable outlook on the names. Due to the remaining uncertainty surrounding the FDA proposal to ban menthol cigarettes, we assume there will be no rating action or outlook revision in the short-term. We estimate slight deleveraging for BAT (adjusted net leverage in FY17: 5.4x, UniCredit calculation) and Imperial Brands (adjusted net leverage in FY17: 3.5x, UniCredit calculation) in 2018 and 2019. We assume that BAT and Imperial Brands will be able to sustain strong cash flow generation.

TOBACCO SNAPSHOT (ISSUES DENOMINATED IN EUR) Z-SCORE 1 MONTH

Source: iBoxx, UniCredit Research

Name recommendation We confirm our overweight recommendation on Imperial Brands and BAT after recent spreadwidening. Over the last two days, BAT senior issues denominated in EUR have widened by 15bp to 25bp and IMBLN senior issues denominated in EUR have widened by around 2bp to 8bp.

Dr. Silke Stegemann, CEFA (UniCredit Bank, Munich), +49 89 378-18202, [email protected]

BATSLN 3.625% 11/21

BATSLN 0.875% 10/23

BATSLN 2.25% 1/30

BATSLN 1.25% 3/27

BATSLN 1.125% 11/23

BATSLN 4.875% 2/21

BATSLN 2.75% 3/25

BATSLN 2.375% 1/23

BATSLN 2% 3/45

BATSLN 1% 5/22

BATSLN 4% 7/20

BATSLN 3.125% 3/29

IMBLN 2.25% 2/21IMBLN 0.5% 7/21

IMBLN 1.375% 1/25

IMBLN 5% 12/19

IMBLN 3.375% 2/26

PM 1.875% 11/37

PM 0.625% 11/24

PM 1.875% 3/21PM 1.75% 3/20

PM 2.875% 3/26PM 2.75% 3/25

PM 2% 5/36PM 2.875% 5/24

PM 3.125% 6/33PM 2.875% 5/29

PM 2.75% 3/25

iBoxx € Personal & Household

Goods

0

50

100

150

200

250

0 5 10 15 20

bp

mDur

BAT

IMBLN

PM

iBoxx_PHG

0 0.5 1 1.5 2 2.5 3 3.5 4

PM 1.875% 11/37

IMBLN 5% 12/19

PM 2.75% 3/25

IMBLN 2.25% 2/21

PM 2.875% 3/26

iBoxx € Personal & Household Goods

IMBLN 1.375% 1/25

PM 2.875% 5/29

PM 3.125% 6/33

BATSLN 2% 3/45

BATSLN 2.25% 1/30

BATSLN 1.25% 3/27

BATSLN 2.75% 3/25

BATSLN 3.625% 11/21

BATSLN 1.125% 11/23

Z-Score

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 6 See last pages for disclaimer.

Merck KGaA (Marketweight) Event This morning, Merck KGaA (Baa1s/As/--) reported key 3Q18 results showing operating

profit above market expectations. Merck raised its sales outlook for 2018 andconfirmed its forecast for the development of organic EBITDA pre for 2018.Management maintains its focus on further deleveraging, which is credit-positive. In 3Q18, group sales rose by 6.6% to EUR 3.7bn (3Q17: EUR 3.5bn). Organically, sales grew very strongly, by 8.8%. The Healthcare business delivered very strong organic sales growthof 9.9% in 3Q18. EBITDA pre, the key financial indicator, grew organically by 3.7%, thanks mainly to Healthcare and Life Science. However, significant negative FX effects of -9.5% caused EBITDA pre to decrease by 5.9% to EUR 963mn (3Q17: EUR 1,023mn). EBITDA pre at Healthcare decreased in 3Q18 by 3.9% to EUR 381bn (3Q17: EUR 397mn). Negative foreign exchange effects of -7.7% canceled out organic growth of 3.8%. The Life Science business generated very strong organic growth of 9.8%. Including negative foreign-exchange effects of -1.4%, net sales rose by 8.5% to EUR 1.5bn (3Q17: EUR 1.4bn). All three Life Science business units contributed to organic growth.

Expected development of credit profile/rating

Merck has confirmed its organic EBITDA pre forecast for full-year 2018. Following strong organic sales growth in 3Q18, Merck now expects an organic net sales increase of 4% to 6% (previously 3% to 5%) over 2018. Furthermore, Merck continues to assume a moderately negative foreign-exchange impact of -3% to -5% in comparison with 2017, and also expects high exchange-rate volatility in 4Q18. Overall, taking into account the treatment of the Consumer Health business as a discontinued operation, Merck forecasts group net sales in a range of between EUR 14.4bn and EUR 14.8bn in 2018 (previously: EUR 14.1bn to EUR 14.6bn; 2017: EUR 14.5bn).

At 30 September 2018, net financial debt was down by more than EUR 500mn. At EUR 10.2bn, it was slightly higher than at FYE 2017 (EUR 10.1bn) but lower yoy(30 September 2017: EUR 11.1bn). At 3Q18, net leverage reported was 2.5x (2017: 2.3x). Management underlined that deleveraging remains its focus to ensure a strong investment-grade rating and financial flexibility. It says cash flow will be used to drive down leverage to below 2.0x net debt/EBITDA pre in 2018. Management ruled out larger acquisitions (> EUR 500mn) in 2018.

Name recommendation We confirm our marketweight recommendation on Merck KGaA and await further details inthe conference call today. We still prefer MRKGR perps [Baa3s/BBB+s/-] over seniors. Our preferred bond is the MRKGR 3.375% perp.

Dr. Silke Stegemann, CEFA (UniCredit Bank, Munich) +49 89 378-18202 [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 7 See last pages for disclaimer.

High Yield

Codere (Buy) Event Codere (B2s/Bs/--) reported a good set of 3Q18 results, including a decline in revenue of

11.2% yoy to EUR 356mn, while company-adjusted EBITDA improved by 3.4% yoy to EUR 70.8mn. Its adjusted EBITDA margin improved to 19.9% (from 17.0%), mainly driven by a pickup in its LatAm margin.

By geography, Mexico, with an increase by 9% yoy to EUR 26.1mn, was the strongest contributor to group EBITDA, while that of Argentina dropped by 33% to EUR 22.9mn. InSpain, adjusted EBITDA grew to EUR 7.9mn, from EUR 6.0mn, whereas that of Italy grew to EUR 6.5mn, from EUR 4.8mn.

On the back of inflation in Argentina, Codere started to accrue results there, according to its inflation accounting in 3Q18. Codere reported the inflation adjustment as an operating expense and added it back to company-adjusted EBITDA – this is a neutral position in cash flow, to our understanding.

Company-adjusted FCF declined to EUR 1.2mn (down from EUR 11.4mn in 3Q17) on the back of EUR 43.6mn of growth capex. On a 9M18 basis, growth capex increased by EUR 5.3mn, to EUR 57.2mn, mainly on the back of new product agreements, via which the company acquired a selection of leased slot products to improve operational and financial returns.

Expected development of credit profile/rating

Ahead of today’s conference call, scheduled for 16:00 CET, we expect the company to keep a relatively stable credit profile over the upcoming year – i.e. one that is broadly in line with our projection for its adj. net debt/EBITDA ratio (of around 3x [UniCredit-adjusted]). Codere’s main operating downside is still associated with the challenging macroeconomic environment in Argentina. Management confirmed its year-end guidance for adjusted EBITDA of around EUR 280-285mn and added that “final numbers will depend on the evolution of the Argentinepeso until year-end”.

In terms of liquidity, Codere reported having a relatively stable cash position YTD of around EUR 102mn in 3Q18 and that it had used around EUR 17mn of the available EUR 95mn in its SSRCF.

Name recommendation We are keeping our buy recommendation on (and continue to see value in) the CDRSM 6.75% 11/21 (first call 10/18), which is trading at a Z-spread of around 880bp. We recommend a switch out of LHMCFI 6.25% 10/23 (first call 6/20 – bond rating: B2/B+), which is trading at a Z-spread of around 484bp.

Mehmet Dere (UniCredit Bank, Munich) +49 89 378 11294 [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 8 See last pages for disclaimer.

Jaguar Land Rover (Hold) Event Moody’s downgraded Jaguar Land Rover (JLR; Ba3n/BBwn/BB+n) by one notch to Ba3

with negative outlook reflecting JLR's continued weak operating performance in 1H18/19 (ending March 2019), which was below Moody's expectations, and results in financial metrics that are well below the Ba2 rating category. The negative outlook reflects the significantchallenges JLR faces to quickly turn around the negative performance trend against the heightened market risks regarding sizably weaker Chinese market demand, headwinds from rising input costs and fuel prices, potential adverse impacts from the outcome of the Brexit negotiations, according to Moody’s.

Expected development of credit profile/rating

For our comment on JLR’s 2Q results and its transformation plan please refer to our Daily Credit Briefing, 1 November. JLR’s adjusted net (gross) debt/EBITDA (UniCredit Research)increased to 3.1 (6.3x) in 1H18/19 from 1.4x (3.8x) qoq, but we take comfort from JLR’s strong liquidity and its transformation plan, including positive margins in FY19/20. For our model, please refer to our Euro High Yield & Crossovers publication, 21 September.

WE RECOMMEND A SWITCH FROM THE EXPENSIVE USD 4.5% 10/27 BOND TO CHEAPER GBP BONDS OR THE EUR 1/26

Source: Bloomberg, UniCredit Research

Name recommendation JLR reported October sales (see company report) that were down by 4.6% yoy (January-October: -4.0%). Retail sales in October in the UK went up by 46.9%, and they increased in North America by 24.1% on the back of the new I-Pace and E-Pace and refreshed Range Rover and Range Rover Sport. Sales in China decreased by 49.0%, as market conditions remain challenging amid tariff changes and continued trade tensions with the US, which areimpacting consumer confidence and automotive purchases. Sales also declined in Europe(13.5%) due to ongoing diesel uncertainty, and sales were 4.0% lower yoy in Overseas markets.

We keep our hold recommendation on JLR bonds at current elevated spread levels. Positive inflection points for the bonds could include improving monthly retail sales releases, marginsand/or a softer Brexit scenario. In terms of relative value across currencies, the GBP 2021/22 and EUR 1/26 bonds look most attractive and the USD 10/27 bond looks least attractive (see left chart above). The TTMTIN 4.125% 12/18 (USD 700mn) will mature soon and the 5.625% 2/23 (USD 500mn) has been callable since 1 February 2018 at 102.813. In its 3Q call, JLR said that FCF would remain negative for FY18/19 and 19/20, which might lead to furtherrefinancing transactions.

Dr. Sven Kreitmair, CFA (UniCredit Bank) +49 89 378-13246 [email protected]

TTMTIN 4.5% Jan-26

TTMTIN 2.2% Jan-24 TTMTIN 4.5%

Oct-27TTMTIN 5.625% Feb-23

TTMTIN 3.5% Mar-20

TTMTIN 4.25% Nov-19

TTMTIN 4.125% Dec-18

TTMTIN 3.875% Mar-23

TTMTIN 5% Feb-22

TTMTIN 2.75% Jan-21

-300

-200

-100

0

100

200

300

400

500

600

700

0 1 2 3 4 5 6 7

Z-S

prea

d in

bp

(FX

-adj

ust

ed)

mDur

EUR USD GBP

0

100

200

300

400

500

600

Nov-17 Feb-18 May-18 Aug-18 Nov-

bp

JAGLN 2.2% 1/24 JAGLN 4.5% 1/26 iBoxx EUR HY BB

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 9 See last pages for disclaimer.

Peugeot (Buy); Faurecia (Hold) Event After Peugeot (Ba1p/--/BBB-s) released 3Q18 group revenues (see the comment in our

HY Daily from 25 October ), Moody’s recently changed its outlook to positive from stable, and now Fitch has upgraded Peugeot to BBB- with stable outlook, i.e. to IG. The upgrade reflects the continuous improvement of PSA's financial profile since 2013-2014, with key credit ratios now firmly in line with the 'BBB' rating category. Fitch believes that financial metrics have become more resilient against the next cyclical slowdown in the group's mainEuropean markets and that this mitigates the company’s moderately weaker business profile compared with investment grade peers. Fitch expects profitability and leverage to weaken moderately in the medium term, but it expects credit metrics to remain largely commensurate with the rating and to display less volatility than in the past.

Expected development of credit profile/rating

At Moody’s, Peugeot’s ratings could come under upward pressure should 1. PSA generate positive FCF despite anticipated restructuring cash outflows; 2. leverage (debt/EBITDA) fall sustainably below 2.0x; 3. profitability be restored to an EBITA margin at or above 5%sustainably; 4. the company's liquidity profile remain solid. The agency added that upward pressure on the ratings has increased significantly given that in 2017 and based on LTM June2018 PSA’s metrics have been in line with these expectations.

In 1H18, adjusted automotive gross debt (UniCredit Research) improved to 2.2x, compared to2.5x yoy, and FFO/debt improved to 32% versus 22%. We note that there has beenspeculation in the past about a French diesel probe fine (see 11 September 2017 Daily Credit Briefing). For further details on the OV takeover, see our 6 March 2017 Credit Flash. For details on Peugeot’s credit profile and our financial model, see our most recent Euro High Yield & Crossovers publication (21 September).

Name recommendation Despite the upgrade to IG at Fitch, Peugeot’s bonds will not yet enter the iBoxx IG index, butthey are now CSPP-eligible, at least in terms of the ratings requirement. Nevertheless, we keep a buy recommendation on Peugeot’s and a hold recommendation on fully-consolidated Faurecia’s (Ba1s/BB+s/BB+s) bonds. We think that the upgrade to IG at Moody’s is highly likely if Peugeot can keep its current metrics. In this context, however, the fully-consolidated Faurecia recently announced an acquisition of Clarion for EUR 1.1bn, which will also increase the leverage at Peugeot slightly after closing (see our Daily Credit Briefing dated 29 October). This is why Faurecia’s cash curve trades around 100bp wider than Peugeot’s. Nevertheless, the Opel Vauxhall (OV) integration has been performed better than expected so far, and Peugeot now has a larger and more-diversified business profile. We also like that Peugeot has no revenue exposure to North America. Therefore, direct risks from the Trumpadministration’s tariffs are low.

Nevertheless, Peugeot’s 2023-25 bonds are already trading close to IG benchmark bonds(maybe with a 20bp premium to the low-BBB rated ZFFNGR cash curve). Peugeot has only EUR 430mn in bond maturities in 2019.

Dr. Sven Kreitmair, CFA (UniCredit Bank, Munich) +49 89 378-13246 [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 10 See last pages for disclaimer.

Telecom Italia (Sell) Event Telecom Italia’s (TIM, Ba1s/BB+p/BBB-n) board of directors has dismissed (by a

majority vote) TIM’s CEO, Amos Genish, from all his duties. A new board meeting will beconvened on 18 November to appoint a new CEO.

Expected development of credit profile/rating

We note that currently TIM’s board of directors consists of ten members nominated by Elliott and five members nominated by Vivendi. Moreover, Amos Genish was appointed as CEO ofTIM, and the CEO’s strategy was approved by TIM’s board at a time when the majority of the board of directors was nominated by Vivendi. Although Elliott has stated in the past that it fully supports Amos Genish and his strategy for TIM, it looked obvious that Elliott had a differentstrategy in mind, which the fund had set out in a presentation.

Bloomberg reports, citing people familiar with the matter, that three people are on the shortlist of TIM’s Chairman, Fulvio Conti, to become TIM’s next CEO: Two of them are alreadymembers of TIM’s board of directors, nominated by Elliott: Alfredo Altavilla (who for years worded alongside Fiat Chrysler Automobiles NV CEO Sergio Marchionne) and Luigi Gubitosi(a former Wind SpA CFO). The third potential candidate is Stefano de Angelis, who led TIMBrasil from May 2016 to July 2018.

Hence, we are not surprised about this management change. We expect it change to lead to a strategy change/adjustment at Telecom Italia. In the above-mentioned presentation, Elliottproposes a structural separation of TIM’s fixed network (TIM NetCo), in which TIM might hold a share of 25% to 75%. A meaningful stake in Sparkle would also be sold and the 60% stake in INWIT would be further monetized, according to the proposal. The 67% stake in TIM Brazil would be kept or possibly combined with local peers to strengthen TIM’s internationalpresence. Last but not least, Elliott aims to reinitiate dividend payments of TIM.

We have already stated in the past that, in our view, a spin-off and partial sale of TI’s fixednetwork would likely reduce synergies within TI. Moreover, we assume that existing TITIMbonds would, in total, remain with the remaining TI business (excluding the fixed network) and that the network business would likely be structured to receive investment-grade ratings, i.e. the remaining TI business might be rated weaker, as the business profile of a “pure” telecomsretail business profile is generally seen to be weaker than a telecoms infrastructure business.For this reason, we think that a spin-off and partial sale of TI’s fixed network would likely be credit negative for TI. Last but not least, we think that it is too early for TI to start paying dividends if the company wants to return to investment grade.

On Sunday, Italian Deputy Premier Luigi Di Maio said in an Italian television interview that he wanted a “single Italian player” to make internet and broadband available to everyone. To us this sounds as if the Italian government would like to have one fixed-network companyorganize the fiber network rollout and which would treat all retailers/unbundlers fairly/evenly. A network company controlled by TIM (controlled by whomsoever) might not offer thisindependence. Moreover, the Italian government would like to have some control over such a strategic asset. Via a spin-off of TIM and the merger of Enel’s Open Fiber into TIM NetCo, theItalian government might get what it may have been aiming for for quite some time.

Name recommendation We are keeping our sell recommendation on TITIM bonds. Our sell recommendation shouldbe interpreted as an underweight recommendation given the size and importance of TITIMbonds in the iBoxx HY NFI index. Especially after the Italian 5G spectrum auction, an upgradeof TI to investment grade is no longer a realistic upside scenario in the short term and the factthat TI recently did not reaffirm its leverage target underpins this. TITIM bonds already trade at BB spread levels. However, we expect the management turmoil combined with ashareholder dispute to be negative for TIM’s operating performance. This would already be negative in a normal market environment, but in a difficult market environment – the macroeconomic and political environment has become more challenging and the situation inthe Italian telecoms market is also challenging – it is even worse that management’s focus is distracted. Stephan Haber, CFA (UniCredit Bank, Munich), +49 89 378-15192, [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 11 See last pages for disclaimer.

CMC di Ravenna (Sell) Yesterday evening, S&P downgraded the rating on CMC from B- to CC. The rating

remains on watch negative. The downgrade is due to CMC having indicated last Friday thatit will not pay the coupon for the CMCRAV 23s on time, i.e. on 15 November 2018 (see ourrelated comment here). Unexpectedly, S&P stated that it would downgrade the rating further if CMC does not make the EUR 9.75mn semi-annual coupon payment within the 30-day grace period (we initially reported a 15-day grace period, which it is for the RCF) and/or if CMC were to “pursue a distressed exchange or other restructuring within the next few months”.

The downgrade to below the B area by S&P (so far still B3 with negative outlook at Moody’s) might still result in some “forced sellers” of the CMCRAV bonds today and we keep a sell recommendation on CMC di Ravenna. We continue to expect CMC to have sufficient cashresources to make the coupon payment and avoid a default at this stage but expect management to await the (restructuring) plan presented by advisors before deciding on the next steps by 24 November 2018 (i.e. within 15 days of the 9 November press release).

Christian Aust, CFA (UniCredit Bank, London)+44 207 826-6054 [email protected]

Gamenet Group (Hold) Gamenet Group (B1s/B+s/--) reported 9M18 results that were in line with our estimates,

including revenues down by 1.9% yoy to EUR 442mn and EBITDA up by 14.4% yoy toEUR 66mn (compared to our estimates of EUR 447mn and EUR 64mn). The growth in EBITDAwas mainly due to sports betting, where the company continued to benefit from the low payout trend, the benefits of vertical integration and the opening of new venues as well as a positiveVLT impact. On a stand-alone basis, it reported a company adjusted net debt/EBITDA ratio of 2.0x, up from 1.9x, and it reported leverage of 2.7x on a pro-forma basis, including the GoldBet acquisition (recall that the company closed the transaction in October).

In terms of current trading, we understand from the conference call that the betting payoutwas less positive in October, without providing further guidance on the future, whilemanagement indicated that it will continue with its distribution insource strategy in the coming year. Regarding the headlines in the Italian press concerning a potential 50bp increase in gaming machine taxes, management estimates an impact of around EUR 5-7mn on its full year EBITDA, depending on the degree to which it can offset the impact with the reduction inVLT payout. However, management added that the payout reduction is currently capped by the product mix in gaming machines rather than consumer behavior, i.e. the low availability ofgames with a low payout.

We keep our hold recommendation on the name in light of the results, which we view asuneventful. We also note that, given the regulatory environment, the company’s dividend policy as well as our expectation of further opportunistic bolt-on acquisitions in the Italian market (vertical integration), we see limited deleveraging potential for the company going forward. Nevertheless, our recommendation is supported by a stable to strong gaming consumer demand environment in Italy. We recommend switching out of GAMENT bonds into TCGLN 3.875% 7/23 (bond rating: B1/B+/BB-). For the latter name we see some deleveraging potential next year, as we expect some normalization in the operating environment and despite our expectation of higher fuel cost for the airlines business.

Mehmet Dere (UniCredit Bank, Munich)+49 89 378 11294 [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 12 See last pages for disclaimer.

Nidda Healthcare (Hold) Nidda Healthcare [B2s/B+s/BB-wn], controlled by funds of Bain Capital and Cinven,

announced the final result of its public delisting tender offer for the remaining Stada (previously not rated) shares. Approximately 28.29% of the share capital and the voting rights of Stada was tendered during acceptance period. Together with the shares already owned and following settlement of the offer, which will occur at the latest on 28 November 2018, Bain Capital and Cinven will hold approximately 93.61% of the share capital and voting rights of Stada.

In September 2017, Bain and Cinven (Nidda Healthcare) took over Stada (previously not rated) for an EV of approximately EUR 5.4bn. Nidda BondCo GmbH owns Stada through thesub-holding Nidda Healthcare Holding GmbH. Nidda BondCo GmbH is the TopCo of the restricted group and the issuer of the senior notes. On 31 October 2018, Fitch placed Nidda Bondco GmbH’s rating of B+ on rating watch negative (RWN). Fitch assumes that theacquisition of outstanding shares under the implemented public delisting tender offer couldlead to a higher financial leverage over the next three years.

On 16 October, Nidda Healthcare Holding GmbH and Nidda BondCo GmbH announced that they had obtained committed financing for the delisting offer by their subsidiary, NiddaHealthcare GmbH. Assuming that all remaining Stada shares are tendered, the total offercosts are estimated at approximately EUR 1,792.5mn. Financing is secured for the delisting offer through a mix of debt and equity funding. Investment funds managed or advised by BainCapital and Cinven have agreed to indirectly provide equity contributions and/or shareholder loans or similar instruments to fund a portion of the offer costs. There are also undrawncommitments available under its existing senior facilities agreement.

We confirm our hold recommendation on Nidda Healthcare and await an announcement of the final funding mix. Stada is a highly leveraged company (UniCredit adjusted net leverage at 1H18: 5.8x; NiddaBondCo and existing Stada debt). The delisting tender offer and the intention of the sponsors to own 100% of Stada is already reflected in the current spread levels, in our view. Hold the STADAH 3.5% 9/24 trading at 97.8/98.9 and STADAS 5% 9/25trading at 94.5/95.5.

Dr. Silke Stegemann, CEFA (UniCredit Bank, Munich)+49 89 378-18202 [email protected]

Nordex (Hold) Nordex (B3s/Bs/--) has reported its 9M18 results, which showed that sales dropped in 9M18

to EUR 1.8bn from EUR 2.3bn in 9M17 while the EBITDA margin was 4.0% (7.8% in 9M17). Nordex’s EBITDA dropped to EUR 71.4mn from EUR 181.9mn. Management lowered itsguidance for FY18 to the lower end of its previous range.

The company had an order intake in Turbines of 3,070MW, up by 169% yoy. Service salesincreased by 14% yoy to EUR 258mn at an EBIT margin of 18.1% (based on “alignment segment reporting”), and they amounted to 14.6% of group sales in 9M18. Regarding its order backlog, the company reported an increase of 186% to EUR 3.1bn in Turbines, and it reported an increase of 15% yoy to EUR 2.2bn in Service .

Nordex’s net debt amounted to EUR 162mn in 9M18, up from EUR 60mn in FY17, while thecompany-adjusted net debt/EBITDA increased to 1.8x from 0.3x in FY17 (and up from 1.4x in 1H18). Nordex says that the leverage ratio increased due to lower 12M rolling EBITDA, butthe company expects it to decline again in 4Q18.

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 13 See last pages for disclaimer.

Management narrowed its guidance for FY18 to the lower end of the range, which includes sales of EUR 2.4-2.6bn and an EBITDA margin of 4-5%. The working capital ratio is expected to be below 5%. The capex outlook remains unchanged at around EUR 110mn.

While we are concerned about the outlook as well as the increase in the company-adjusted net debt/EBITDA to 1.8x and the negative FCF, we positively note the sizeable order backlog.According to Bloomberg data, the price of NDXGR 6.5% 2/23 dropped by around 4 priceyesterday. We keep our hold recommendation on the name.

Mehmet Dere (UniCredit Bank, Munich)+49 89 378 11294 [email protected]

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 14 See last pages for disclaimer.

Banks

Berlin Hyp (Marketweight) Event 9M18 results presentation

Berlin Hyp (Aa2s/--/A+s) reported an operating results before income taxes and profit transfer of EUR 85.8mn in 9M18, up from EUR 74.1mn in 9M17. New lending includingextensions stood at EUR 4.8bn in 9M18, which was slightly down from 5.1bn in 9M17. Berlin Hyp also managed to expand its network within the Savings bank group with a new business volume of EUR 1.9bn attributable to savings banks. This was significantly up from EUR 844mn in 9M17. Berlin Hyp allocated EUR 92.5mn for general banking risks (up from EUR 30mn in 9M17). Net interest income increased by more than 7% yoy to EUR 259mn. This increase reflects the increase in its average mortgage portfolio and special effects, including the pro-rata waiver of the interest payable of EUR 14.8mn for TLTROs. Net commission income of EUR 16.4mn was significantly below the previous year’s figure of EUR 29.1 million. This is due to the adjustment of the mapping of processing fees in the wakeof the rulings by the German Federal Court of Justice (BGH) concerning loan processing fees. The CET1 ratio declined from 12.5% as of FYE 2017 to 11.8% as of 30 Sep 2018. This decline is attributable to the high volume of new business. Outlook 2018: Berlin Hyp expects FY18 results before profit transfer to be in line with FY17 results.

Expected development of credit profile/rating

We view these results as credit neutral. New business volume remains at high levels, and the higher profitability will support the bank in adapting to higher regulatory capitalrequirements resulting from Basel IV in the coming years.

Name recommendation Seniors of Berlin Hyp trade at very tight levels, reflecting the strong credit fundamentals ofBHH and its membership in the institutional protection scheme of the German savings bank sector. The senior non-preferred bond BHH 0.5% 9/23 (A2/--/A+) trades only 15bp above senior preferred bond BHH 0.375% 8/23 (Aa2/--/A+), which itself trades 27bp above the covered bond BHH 0.125% 10/23 (Aaa/--/--). Given the very high MREL stock of BHH (68% of RWAs), in our view senior preferred bond spreads could move closer towards the coveredbond spreads on a relative basis.

SENIOR SNAPSHOP GERMAN BANKS

Source: iBoxx, UniCredit Research

Dr. Michael Teig (UniCredit Bank, Munich), +49 89 378-12429, [email protected]

DB SP

BHH SP

DB SNP

DB COV

CMZB SNP

CMZB COV

CMZB SP

BHH COV

BHH SNP

-50

0

50

100

150

200

250

0 2 4 6 8 10 12 14

bp

mDur

<date>

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 15 See last pages for disclaimer.

Market Data Page IBOXX YIELD BY ASSET CLASS

current 1D 1W MTD YTD

Sovereigns 0.96 0.01 0.01 0.04 0.39

Germany 0.03 0.01 -0.01 0.03 -0.01

SSA 0.41 0.00 0.00 0.02 0.18

Covered 0.34 0.01 0.00 0.02 0.19

Non-Financials 1.09 0.02 0.01 0.05 0.34

Financials 1.19 0.04 0.02 0.02 0.50

High Yield NFI 4.24 0.08 0.12 0.07 1.42

Source: iBoxx, UniCredit Research

INTEREST RATE CURVES

current 1D 1W MTD YTD

Euribor 6m -0.32 0.00 0.00 0.00 0.01

EUR Swap 2Y -0.12 0.00 0.01 0.00 0.03

EUR Swap 5Y 0.34 0.00 -0.02 -0.01 0.03

EUR Swap 10Y 0.96 0.00 -0.02 0.00 0.07

USD Libor 6m 2.86 0.00 0.02 0.06 1.02

USD Swap 5Y 3.13 -0.04 -0.07 0.00 0.88

USD Swap 10Y 3.21 -0.04 -0.08 0.00 0.81

Source: Bloomberg, UniCredit Research

ASW SPREAD CURVES BY ASSET CLASS CORPORATE IBOXX AND ITRAXX HISTORY

Source: iBoxx, UniCredit Research

IBOXX ASW SPREADS BY SECTOR

current 1D 1W MTD YTD

Non-Financials 67 +2.7 +2.7 +4.5 +32.1

Automobiles & Parts 97 +3.6 +9.6 +7.6 +58.7

Chemicals 36 +2.0 +0.1 +2.2 +17.0

Construction & Materials 69 +2.5 -1.4 +1.9 +40.3

Food & Beverage 47 +3.1 +1.6 +3.8 +20.5

Health Care 52 +2.2 +0.8 +3.5 +20.4

Industrial Goods & S. 73 +3.0 +5.6 +7.4 +41.1

Media 70 +2.1 +1.2 +6.2 +29.4

Oil & Gas 57 +3.3 +2.4 +3.0 +26.6

Personal & Household G. 52 +3.0 +5.9 +7.1 +19.3

Retail 60 +2.4 +1.8 +4.4 +33.4

Technology 28 +2.2 +1.3 +3.4 +16.5

Telecommunications 75 +2.6 +1.2 +6.2 +27.9

Travel & Leisure 54 +2.6 +0.5 +2.1 +17.7

Utilities 75 +2.3 +0.8 +2.1 +34.7

HY Non-Financials 361 +6.2 +9.8 +4.9 +115.5

Consumers 384 +6.0 +14.5 +6.0 +166.0

Energy 280 +2.5 +3.9 -2.8 +86.7

Industrials 361 +6.6 +5.4 +0.9 +101.4

TMT 359 +6.5 +12.0 +10.5 +89.9

Financials 87 +3.9 +3.5 +2.8 +45.6

Banks 69 +3.5 +1.6 +1.1 +38.2

Insurance 189 +4.9 +12.2 +5.3 +87.1

Financial Services 75 +7.6 +11.9 +15.0 +41.1

Source: iBoxx, UniCredit Research

IBOXX ASW SPREADS BY STRUCTURE/QUALITY

current 1D 1W MTD YTD

Non-Financials 67 +2.7 +2.7 +4.5 +32.1

IG Senior 57 +2.6 +2.2 +4.0 +28.0

IG Hybrids 246 +4.0 +11.9 +10.8 +99.5

AAA 7 +1.9 -0.1 +4.1 +5.4

AA 14 +2.0 +0.1 +2.5 +8.0

A 43 +2.7 +3.4 +5.2 +21.9

BBB 90 +2.9 +2.8 +4.3 +43.2

BB 294 +5.8 +12.4 +5.2 +103.0

B 572 +4.5 +0.8 +4.2 +121.7

CCC 862 +1.7 +41.9 +21.8 +183.7

Financials 87 +3.9 +3.5 +2.8 +45.6

IG Senior 62 +3.5 +2.1 +2.9 +36.3

IG LT2 135 +5.5 +4.1 +1.8 +61.2

AAA 24 0.0 -0.1 -0.2 -1.5

AA 19 +1.7 +0.1 +1.7 +12.1

A 58 +4.1 +3.3 +3.6 +30.7

BBB 156 +4.6 +5.3 +4.8 +81.1

BB 358 +4.0 +1.3 -7.2 +135.8

B 623 +2.6 -7.7 -7.4 +157.0

CCC 1007 +4.3 +11.5 -2.7 +368.3

Source: iBoxx, UniCredit Research

COV

DBR

FNL

NFI

SSA

-100

-50

0

50

100

150

0 5 10 15 20

Sen

ior A

SW

(b

p)

mDur

20

30

40

50

60

70

80

90

100

110

120

Nov-17 Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18

Sp

rea

d (b

p)

iBoxx Non-Fin iTraxx Europe 5Y

iBoxx Fin Sen iTraxx Fin Sen 5Y

<date>

UniCredit Research page 16 See last pages for disclaimer.

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

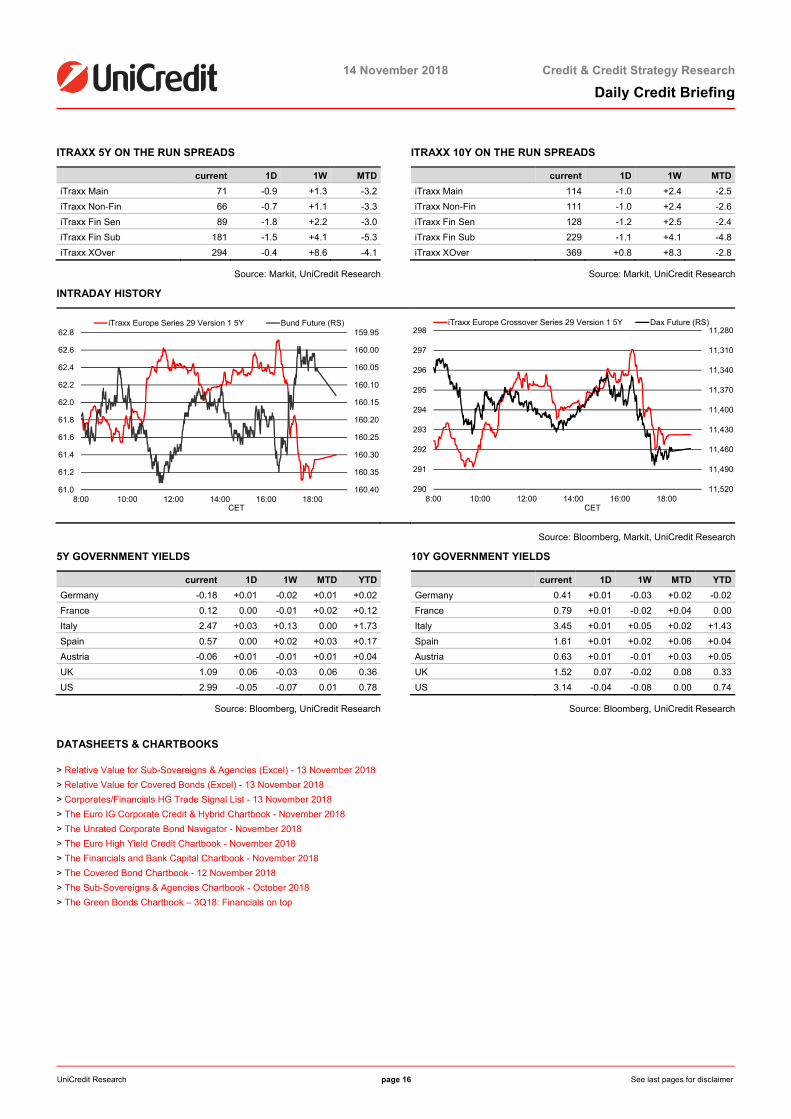

ITRAXX 5Y ON THE RUN SPREADS

current 1D 1W MTD

iTraxx Main 71 -0.9 +1.3 -3.2

iTraxx Non-Fin 66 -0.7 +1.1 -3.3

iTraxx Fin Sen 89 -1.8 +2.2 -3.0

iTraxx Fin Sub 181 -1.5 +4.1 -5.3

iTraxx XOver 294 -0.4 +8.6 -4.1

Source: Markit, UniCredit Research

ITRAXX 10Y ON THE RUN SPREADS

current 1D 1W MTD

iTraxx Main 114 -1.0 +2.4 -2.5

iTraxx Non-Fin 111 -1.0 +2.4 -2.6

iTraxx Fin Sen 128 -1.2 +2.5 -2.4

iTraxx Fin Sub 229 -1.1 +4.1 -4.8

iTraxx XOver 369 +0.8 +8.3 -2.8

Source: Markit, UniCredit Research

INTRADAY HISTORY

Source: Bloomberg, Markit, UniCredit Research

5Y GOVERNMENT YIELDS

current 1D 1W MTD YTD

Germany -0.18 +0.01 -0.02 +0.01 +0.02

France 0.12 0.00 -0.01 +0.02 +0.12

Italy 2.47 +0.03 +0.13 0.00 +1.73

Spain 0.57 0.00 +0.02 +0.03 +0.17

Austria -0.06 +0.01 -0.01 +0.01 +0.04

UK 1.09 0.06 -0.03 0.06 0.36

US 2.99 -0.05 -0.07 0.01 0.78

Source: Bloomberg, UniCredit Research

10Y GOVERNMENT YIELDS

current 1D 1W MTD YTD

Germany 0.41 +0.01 -0.03 +0.02 -0.02

France 0.79 +0.01 -0.02 +0.04 0.00

Italy 3.45 +0.01 +0.05 +0.02 +1.43

Spain 1.61 +0.01 +0.02 +0.06 +0.04

Austria 0.63 +0.01 -0.01 +0.03 +0.05

UK 1.52 0.07 -0.02 0.08 0.33

US 3.14 -0.04 -0.08 0.00 0.74

Source: Bloomberg, UniCredit Research

DATASHEETS & CHARTBOOKS

> Relative Value for Sub-Sovereigns & Agencies (Excel) - 13 November 2018

> Relative Value for Covered Bonds (Excel) - 13 November 2018

> Corporates/Financials HG Trade Signal List - 13 November 2018

> The Euro IG Corporate Credit & Hybrid Chartbook - November 2018

> The Unrated Corporate Bond Navigator - November 2018

> The Euro High Yield Credit Chartbook - November 2018

> The Financials and Bank Capital Chartbook - November 2018

> The Covered Bond Chartbook - 12 November 2018

> The Sub-Sovereigns & Agencies Chartbook - October 2018

> The Green Bonds Chartbook – 3Q18: Financials on top

159.95

160.00

160.05

160.10

160.15

160.20

160.25

160.30

160.35

160.4061.0

61.2

61.4

61.6

61.8

62.0

62.2

62.4

62.6

62.8

8:00 10:00 12:00 14:00 16:00 18:00CET

iTraxx Europe Series 29 Version 1 5Y Bund Future (RS)11,280

11,310

11,340

11,370

11,400

11,430

11,460

11,490

11,520290

291

292

293

294

295

296

297

298

8:00 10:00 12:00 14:00 16:00 18:00CET

iTraxx Europe Crossover Series 29 Version 1 5Y Dax Future (RS)

<date>

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 17 See last pages for disclaimer.

Rating Actions

Issuer Sector Agency Rating From To

CMC di Ravenna (CMCRAV) Industrials High Yield S&P Issuer Credit Rating B- *- CC *-

Jaguar Land Rover (JAGLN) Consumers High Yield Moody's Senior Unsecured Debt Ba2 Ba3

Outlook STABLE NEG

Peugeot (PEUGOT) Consumers High Yield Fitch Senior Unsecured Debt BB+ BBB-

Outlook POS STABLE

Source: Rating Agencies, Bloomberg, UniCredit Research

Recent Credit Research Publications

Date Title Sector/Region Analyst

13 Nov 18 » Daily Credit Briefing Tobacco, Industrial Goods & Services, Utilities, Construction & Materials, Technology, Health Care, Corporates, Banks, Energy

Dr. Silke Stegemann, Gianfranco Arcovito, Christian Aust, Stephan Haber, Dr. Sven Kreitmair, Mehmet Dere, Dr. Michael Teig, Dr. Philip Gisdakis, Dr. Stefan Kolek

» Credit Flash - Vodafone: A sigh of relief Telecommunications, Corporates Stephan Haber

» Credit Report - Garrett Motion: Initiation of coverage Corporates, Automobiles & Parts Dr. Sven Kreitmair

» Securitization Market Watch - Regulatory topics to create uncertainty

Holger Kapitza

12 Nov 18 » Daily Credit Briefing Corporates, Oil & Gas, Chemicals, Industrial Goods & Services, Automobiles & Parts, Technology, Health Care, Banks, Insurance, Energy, Construction & Materials

Christian Aust, Mehmet Dere, Dr. Sven Kreitmair, Stephan Haber, Dr. Silke Stegemann, Dr. Michael Teig, Natalie Tehrani Monfared, Dr. Stefan Kolek

» Credit Flash - LEG Immobilien: 3Q results robust and in line with expectations

Real Estate Holger Kapitza

Source: UniCredit Research

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 18 .

Disclaimer Our recommendations are based on information obtained from, or are based upon public information sources that we consider to be reliable but for the completeness and accuracy of which we assume no liability. All estimates and opinions and projections and forecasts included in the report represent the independent judgment of the analysts as of the date of the issue unless stated otherwise. This report may contain links to websites of third parties, the content of which is not controlled by UniCredit Bank. No liability is assumed for the content of these third-party websites. We reserve the right to modify the views expressed herein at any time without notice. Moreover, we reserve the right not to update this information or to discontinue it altogether without notice.

This analysis is for information purposes only and (i) does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any financial, money market or investment instrument or any security, (ii) is neither intended as such an offer for sale or subscription of or solicitation of an offer to buy or subscribe for any financial, money market or investment instrument or any security nor (iii) as an advertisement thereof. The investment possibilities discussed in this report may not be suitable for certain investors depending on their specific investment objectives and time horizon or in the context of their overall financial situation. The investments discussed may fluctuate in price or value. Investors may get back less than they invested. Changes in rates of exchange may have an adverse effect on the value of investments. Furthermore, past performance is not necessarily indicative of future results. In particular, the risks associated with an investment in the financial, money market or investment instrument or security under discussion are not explained in their entirety.

This information is given without any warranty on an "as is" basis and should not be regarded as a substitute for obtaining individual advice. Investors must make their own determination of the appropriateness of an investment in any instruments referred to herein based on the merits and risks involved, their own investment strategy and their legal, fiscal and financial position. As this document does not qualify as an investment recommendation or as a direct investment recommendation, neither this document nor any part of it shall form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Investors are urged to contact their bank's investment advisor for individual explanations and advice.

Neither UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank AG Vienna Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch nor any of their respective directors, officers or employees nor any other person accepts any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

This analysis is being distributed by electronic and ordinary mail to professional investors, who are expected to make their own investment decisions without undue reliance on this publication, and may not be redistributed, reproduced or published in whole or in part for any purpose.

Responsibility for the content of this publication lies with:

UniCredit Group and its subsidiaries are subject to regulation by the European Central Bank

a) UniCredit Bank AG (UniCredit Bank, Munich or Frankfurt), Arabellastraße 12, 81925 Munich, Germany, (also responsible for the distribution pursuant to §34b WpHG). The company belongs to UniCredit Group. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany.

b) UniCredit Bank AG London Branch (UniCredit Bank, London), Moor House, 120 London Wall, London EC2Y 5ET, United Kingdom. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany and subject to limited regulation by the Financial Conduct Authority, 12 Endeavour Square, London E20 1JN, United Kingdom and Prudential Regulation Authority 20 Moorgate, London, EC2R 6DA, United Kingdom. Further details regarding our regulatory status are available on request.

POTENTIAL CONFLICTS OF INTERESTS

Alstom 8a; BAT 8a; Faurecia 8a; Imperial Brands 8a; Merck KGaA 8a; Nordex 8a; Peugeot 3, 8a; Telecom Italia 3, 8a; Vodafone 3, 8a Key 1a: UniCredit Bank AG and/or any related legal person owns at least 2% of the capital stock of the analyzed company.

Key 1b: The analyzed company owns at least 2% of the capital stock of UniCredit Bank AG and/or any related legal person.

Key 2: UniCredit Bank AG and/or any related legal person has been lead manager or co-lead manager over the previous 12 months of any publicly disclosed offer of financial instruments of the analyzed company, or in any related derivatives.

Key 3: UniCredit Bank AG and/or any related legal person administers the securities issued by the analyzed company on the stock exchange or on the market by quoting bid and ask prices (i.e. acts as a market maker or liquidity provider in the securities of the analyzed company or in any related derivatives).

Key 5: The analyzed company and UniCredit Bank AG and/or any related legal person have concluded an agreement on the preparation of analyses.

Key 6a: Employees or members of the Board of Directors of UniCredit Bank AG and/or any other employee that works for UniCredit Research (i.e. the joint research department of the UniCredit Group) and/or members of the Group Board (pursuant to relevant domestic law) are members of the Board of Directors of the analyzed company. Members of the Board of Directors of the analyzed company hold office in the Board of Directors of UniCredit Bank AG (pursuant to relevant domestic law). The application of this Key 6a is limited to persons who, although not involved in the preparation of the analysis, had or could reasonably be expected to have access to the analysis prior to its dissemination to customers or the public.

Key 6b: The analyst is on the Supervisory Board/Board of Directors of the company they cover.

Key 8a: UniCredit Bank AG and/or any related legal person hold a net long position exceeding 0.5% of the total issued share capital of the issuer.

Key 8b: UniCredit Bank AG and/or any related legal person hold a net short position exceeding 0.5% of the total issued share capital of the issuer.

UniCredit S.p.A. acts as a Specialist or a Primary Dealer in government bonds issued by the Italian or Greek Treasury, and as market maker in government bonds issued by the Spain or Portuguese Treasury. Main tasks of the Specialist are to participate with continuity and efficiency to the governments' securities auctions, to contribute to the efficiency of the secondary market through market making activity and quoting requirements and to contribute to the management of public debt and to the debt issuance policy choices, also through advisory and UniCredit Bank AG research activities. UniCredit S.p.A. Registered Office in Rome: Via Alessandro Specchi, 16 - 00186 Roma Head Office in Milan: Piazza Gae Aulenti 3 - Tower A - 20154 Milano, Registered in the Register of Banking Groups and Parent Company of the UniCredit Banking Group, with. cod. 02008.1; Cod. ABI 02008.1 - Competent Authority: Commissione Nazionale per le Società e la Borsa (CONSOB)”. UniCredit Bank AG acts as a Specialist or Primary Dealer in government bonds issued by the German or Austrian Treasury. Main tasks of the Specialist are to participate with continuity and efficiency to the governments' securities auctions, to contribute to the efficiency of the secondary market through market making activity and quoting requirements and to contribute to the management of public debt and to the debt issuance policy choices, also through advisory and research activities.

RECOMMENDATIONS, RATINGS AND EVALUATION METHODOLOGY

Company Date Recommendation Analyst Company Date Recommendation Analyst ALOFP 16/07/2018 Underweight Jonathan Schroer JAGLN 14/08/2018 Sell Sven Kreitmair BATSLN 22/01/2018 Overweight Silke Stegemann JAGLN 21/02/2018 Hold Sven Kreitmair CDRSM 15/02/2018 Buy Mehmet Dere LINCFI 14/12/2017 Hold Sven Kreitmair CMCRAV 16/10/2018 Sell Christian Aust LPTY 05/10/2018 Marketweight Sven Kreitmair CMCRAV 09/05/2018 Hold Christian Aust LPTY 14/12/2017 Overweight Sven Kreitmair CMCRAV 19/01/2018 Buy Christian Aust NDXGR 19/04/2018 Hold Mehmet Dere EOFP 26/10/2018 Hold Sven Kreitmair PEUGOT 24/07/2018 Buy Sven Kreitmair GAMENT 17/10/2018 Hold Mehmet Dere PEUGOT 11/04/2018 Hold Sven Kreitmair GAMENT 11/09/2018 Restricted Mehmet Dere PEUGOT 09/03/2018 Restricted Sven Kreitmair GAMENT 28/05/2018 Hold Mehmet Dere STADAH 21/09/2018 Hold Silke Stegemann GAMENT 16/04/2018 Restricted Mehmet Dere VOD 09/05/2018 Marketweight Stephan Haber GAMENT 15/02/2018 Sell Mehmet Dere VOD 05/02/2018 Underweight Stephan Haber JAGLN 01/11/2018 Hold Sven Kreitmair Overview of our ratings

You will find the history of rating regarding recommendation changes as well as an overview of the breakdown in absolute and relative terms of our investment ratings on our website http://www.disclaimer.unicreditmib.eu/credit-research-rd/Recommendations_CR_e.pdf.

14 November 2018 Credit & Credit Strategy Research

Daily Credit Briefing

UniCredit Research page 19 .

Note on the evaluation basis for interest-bearing securities:

Recommendations relative to an index: For high grade names the recommendations are relative to the "iBoxx EUR Benchmark" index family, for sub investment grade names the recommendations are relative to the "iBoxx EUR High Yield" index family.

Marketweight (MW): We recommend having the same portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is equal to the total return of the index.

Overweight (OW) : We recommend having a higher portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is greater than the total return of the index.

Underweight (UW): We recommend having a lower portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is less than the total return of the index.

Outright recommendations:

Hold (H): We recommend holding the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is equal to the yield.

Buy (B): We recommend buying the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is greater than the yield.

Sell (S): We recommend selling the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is less than the yield.

We employ three further categorizations for interest-bearing securities in our coverage:

Restricted (R): A recommendation and/or financial forecast is not disclosed owing to compliance or other regulatory considerations such as a blackout period or a conflict of interest.

Coverage in transition (T): Due to changes in the research team, the disclosure of a recommendation and/or financial information are temporarily suspended. The interest-bearing security remains in the research universe and disclosures of relevant information will be resumed in due course.

Not rated (NR): Suspension of coverage.

Trading recommendations for fixed-interest securities mostly focus on the credit spread (yield difference between the fixed-interest security and the relevant government bond or swap rate) and on the rating views and methodologies of recognized agencies (S&P, Moody’s, Fitch). Depending on the type of investor, investment ratings may refer to a short period or to a 6 to 9-month horizon. Please note that the provision of securities services may be subject to restrictions in certain jurisdictions. You are required to acquaint yourself with local laws and restrictions on the usage and the availability of any services described herein. The information is not intended for distribution to or use by any person or entity in any jurisdiction where such distribution would be contrary to the applicable law or provisions.

If not otherwise stated daily price data refers to pre-day closing levels and iBoxx bond index characteristics refer to the previous month-end index characteristics.

Coverage Policy A list of the companies covered by UniCredit Bank is available upon request.

Frequency of reports and updates It is intended that each of these companies be covered at least once a year, in the event of key operations and/or changes in the recommendation.

SIGNIFICANT FINANCIAL INTEREST UniCredit Bank AG and/or other related legal persons with them regularly trade shares of the analyzed company. UniCredit Bank AG and/or other related legal persons may hold significant open derivative positions on the stocks of the company which are not delta-neutral.

UniCredit Bank AG and/or other related legal persons have a significant financial interest relating to the analyzed company or may have such at any future point of time. Due to the fact that UniCredit Bank AG and/or any related legal person are entitled, subject to applicable law, to perform such actions at any future point in time which may lead to the existence of a significant financial interest, it should be assumed for the purposes of this information that UniCredit Bank AG and/or any related legal person will in fact perform such actions which may lead to the existence of a significant financial interest relating to the analyzed company.

Analyses may refer to one or several companies and to the securities issued by them. In some cases, the analyzed companies have actively supplied information for this analysis.

INVESTMENT SERVICES The analyzed company and UniCredit Bank AG and/or any related legal person concluded an agreement on the provision of investment services in the previous 12 months, in return for which the Bank and/or such related legal person received a consideration or promise of consideration or intends to do so. Due to the fact that UniCredit Bank AG and/or any related legal person are entitled to conclude, subject to applicable law, an agreement on the provision of investment services with the analyzed company at any future point in time and may receive a consideration or promise of consideration, it should be assumed for the purposes of this information that UniCredit Bank AG and/or any related legal person will in fact conclude such agreements and will in fact receive such consideration or promise of consideration.

ANALYST DECLARATION The author’s remuneration has not been, and will not be, geared to the recommendations or views expressed in this study, neither directly nor indirectly.

ORGANIZATIONAL AND ADMINISTRATIVE ARRANGEMENTS TO AVOID AND PREVENT CONFLICTS OF INTEREST To prevent or remedy conflicts of interest, UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank AG Vienna Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch have established the organizational arrangements required from a legal and supervisory aspect, adherence to which is monitored by its compliance department. Conflicts of interest arising are managed by legal and physical and non-physical barriers (collectively referred to as “Chinese Walls”) designed to restrict the flow of information between one area/department of UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank AG Vienna Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch, and another. In particular, Investment Banking units, including corporate finance, capital market activities, financial advisory and other capital raising activities, are segregated by physical and non-physical boundaries from Markets Units, as well as the research department. In the case of equities execution by UniCredit Bank AG Milan Branch, other than as a matter of client facilitation or delta hedging of OTC and listed derivative positions, there is no proprietary trading. Disclosure of publicly available conflicts of interest and other material interests is made in the research. Analysts are supervised and managed on a day-to-day basis by line managers who do not have responsibility for Investment Banking activities, including corporate finance activities, or other activities other than the sale of securities to clients.

ADDITIONAL REQUIRED DISCLOSURES UNDER THE LAWS AND REGULATIONS OF JURISDICTIONS INDICATED

You will find a list of further additional required disclosures under the laws and regulations of the jurisdictions indicated on our website http://www.cib-unicredit.com/research-disclaimer.