customs modernization handbook - World Bank Document

356

CUSTOMS M ODERNIZATION H andbook THE WORLD BANK Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of customs modernization handbook - World Bank Document

CUSTOMSM O D E R N I Z AT I O N

H a n d b o o k

���������� ���������������������

THE WORLD BANK

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Administrator

31477

Customs ModernizationHandbook

CustomsModernization

Handbook

Editors

Luc De Wulf and José B. Sokol

THE WORLD BANK

Washington, D.C.

© 2005 The International Bank for Reconstruction and Development / The World Bank1818 H Street, NWWashington, DC 20433Telephone 202-473-1000Internet www.worldbank.orgE-mail feedback @worldbank.org

All rights reserved.A publication of the World Bank.

1 2 3 4 08 07 06 05

The findings, interpretations, and conclusions expressed herein are those of the author(s) and do not necessarilyreflect the views of the Board of Executive Directors of the World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors,denominations, and other information shown on any map in this work do not imply any judgment on the part of theWorld Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and PermissionsThe material in this work is copyrighted. Copying and/or transmitting portions or all of this work without

permission may be a violation of applicable law. The World Bank encourages dissemination of its work and willnormally grant permission promptly.

For permission to photocopy or reprint any part of this work, please send a request with complete information tothe Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA, telephone 978-750-8400,fax 978-750-4470, www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, World Bank, 1818 H Street NW, Washington, DC 20433, USA, fax 202-522-2422,e-mail [email protected]

Photo credits (clockwise): Australian Customs (upper right), Douane Francaise / M. Bonodot © (lower right),Chilean Customs Administration (lower left), Société Générale de Surveillance (upper left and backgroundphoto of people), Luc De Wulf (background photo of customs files).

Library of Congress Cataloging-in-Publication Data

Customs modernization handbook / edited by Luc de Wulf, José B. Sokol.p. cm.—(Trade and development series)

Includes bibliographic references and index.ISBN-0-8213-5751-4 (pbk.)1. Customs administration—Developing countries. I. Wulf, Luc de, 1942-

II. Sokol, José B. III. Series.

HJ7390.C86 2004352.4'48'091724—dc22 2004059856

Contents

Foreword ixAcknowledgments xiAbbreviations and Acronyms xiiiOverview xvii

PART I: CROSS-CUTTING ISSUES 1

1 STRATEGY FOR CUSTOMS MODERNIZATION 3Luc De Wulf

2 HUMAN RESOURCES AND ORGANIZATIONAL ISSUES IN CUSTOMS 31Luc De Wulf

3 LEGAL FRAMEWORK FOR CUSTOMS OPERATIONS AND ENFORCEMENT ISSUES 51Kunio Mikuriya

4 INTEGRITY IN CUSTOMS 67Gerard McLinden

5 MANAGING RISK IN THE CUSTOMS CONTEXT 91David Widdowson

PART II: LESSONS FROM A SELECT SET OF CUSTOMS REFORM INITIATIVES 101

6 POLICY AND OPERATIONAL LESSONS LEARNED FROM EIGHT COUNTRY CASE STUDIES 103Paul Duran and José B. Sokol

7 TWO DECADES OF WORLD BANK LENDING FOR CUSTOMS REFORM: TRENDS INPROJECT DESIGN, PROJECT IMPLEMENTATION, AND LESSONS LEARNED 127Michael Engelschalk and Tuan Minh Le

PART III: GUIDELINES ON ISSUES THAT AFFECT CUSTOMS’ OPERATIONAL TRADEFACILITATION 153

8 CUSTOMS VALUATION IN DEVELOPING COUNTRIES AND THE WORLD TRADEORGANIZATION VALUATION RULES 155Adrien Goorman and Luc De Wulf

9 RULES OF ORIGIN, TRADE, AND CUSTOMS 183Paul Brenton and Hiroshi Imagawa

10 DUTY RELIEF AND EXEMPTION CONTROL 215Adrien Goorman

v

11 TRANSIT AND THE SPECIAL CASE OF LANDLOCKED COUNTRIES 243Jean François Arvis

12 THE ROLE OF CUSTOMS IN CARGO SECURITY 265Luc De Wulf and Omer Matityahu

13 THE ROLE OF INFORMATION TECHNOLOGY IN CUSTOMS MODERNIZATION 285Luc De Wulf and Gerard McLinden

LIST OF BOXES, FIGURES, AND TABLES

BOXES1.1 Morocco Customs Gets Its Staff on Board for the Reform Program 171.2 An Example of Regional Leadership: The TTFSE Regional Steering Committee 21

Annex 1.C.1 The Steps to Release Goods From Time of Arrival 25Annex 1.C.2 The Philippines Time-Release Study: An Example to Follow 26

2.1 Staff Renovation in Bolivian Customs 342.2 Denmark: Integration of Customs and Tax Administration 392.3 Revenue Targets and Autonomy: Illustrations from Tanzania and Uganda 423.1 An Example of Obsolete Customs Legislation 523.2 Sample Checklist to Identify Provisions Requiring Amendment

or New Legislation under the Revised Kyoto Convention 593.3 Morocco’s Adoption of the Convention: A Success Story 603.4 Modernization of Customs Legislation in the Russian Federation 654.1 Leadership and Commitment: Key Issues and Questions 754.2 Regulatory Framework: Key Issues and Questions 764.3 Transparency: Key Issues and Questions 774.4 Automation: Key Issues and Questions 784.5 Modernization of Customs: Key Issues and Questions 794.6 Audit and Investigation: Key Issues and Questions 804.7 Code of Conduct: Key Issues and Questions 814.8 Are Low Salary Levels Really a Factor? 824.9 Human Resources: Key Issues and Questions 844.10 Morale and Organizational Culture: Key Issues and Questions 854.11 Relationship with the Private Sector: Key Issues and Questions 864.12 Lessons Learned from Customs Reforms to Control Corrupt Behavior 885.1 Managing Risk: Customs Valuation 986.1 Implementation of Customs Reform in Mozambique 1096.2 Information Technology in Turkey 1156.3 Import Verification in Peru 1176.4 Customs Cooperation with the Private Sector in Morocco and the Philippines 1236.5 Addressing Corruption in Uganda’s Independent Revenue Authority 1247.1 Diagnostic Framework—Three Project-Specific Cases 1337.2 Inadequacy of Performance Indicators: Project-Specific Cases 1367.3 Designing a Comprehensive Set of Performance Indicators: The Case of

Trade and Transport Facilitation Projects in Southeast Europe 1377.4 Integrated Approach in Process Management: The Case of the Tunisia Export

Development Project 1417.5 Increased Bank Emphasis on Coordination with Other Donors 142

vi Contents

7.6 Quality of Pre-Project Preparation and Design Matter: Two Project-SpecificCases 146

7.7 What Triggered the Modification of Project Objectives or Components 1477.8 Implementation Management Issues: The Case of the Senegal Development

Management Project 1488.1 Peru: Import Verification Program 1698.2 PSI Contract in Madagascar Introduces Targeted and Evolving Verification

Services 1739.1 Example of Restrictive Rules of Origin: The Case of EU Imports of Fish 1929.2 More Restrictive Rules of Origin: The Case of Clothing Under NAFTA Rules 197

10.1 Duty Relief and Exemption Regimes 21610.2 The Reform of Duty Relief Regimes in Morocco 22110.3 Fiji’s Duty Suspension Scheme 22210.4 The Passbook System in Nepal 22310.5 The Bangladesh Special Bonded Warehouse Facility 22410.6 Customs Administration of the Aqaba Export Processing Zone 22910.7 Thailand’s Move to Open Bond Arrangements 23210.8 Computer Application for Management of Investment Project Exemptions 23710.9 Reimbursement of Taxes and Customs Duties on Imported Petroleum

Products in Mali 23811.1 The Genesis of Transit Procedures in the Middle Ages 24611.2 General Requirements with Respect to Seals 24811.3 ASYCUDA Customs Operations in Zambia 25411.4 The SafeTIR 25811.5 The Unique Consignment Reference Number 25911.6 TTFSE Indicators 26312.1 Maritime Security Initiative at Panama Canal Waters 26913.1 IT System Procurement and Costs: Case Study—Turkey 29613.2 Morocco Case Study 29813.3 Customs ICT Deployment Case Study: Turkey 30213.4 Ghana Gateway Project Case Study 30513.5 Senegal Case Study 306

FIGURES1.1 Number of Declarations per Staff per Year in Southeastern Europe, 2002 165.1 Facilitation and Control Matrix 925.2 Compliance Management Matrix 945.3 Risk-Based Compliance Management Pyramid 967.1 Institutional Environment Assessment Framework 1389.1 Regional Trade Agreements in Eastern and Southern Africa 207

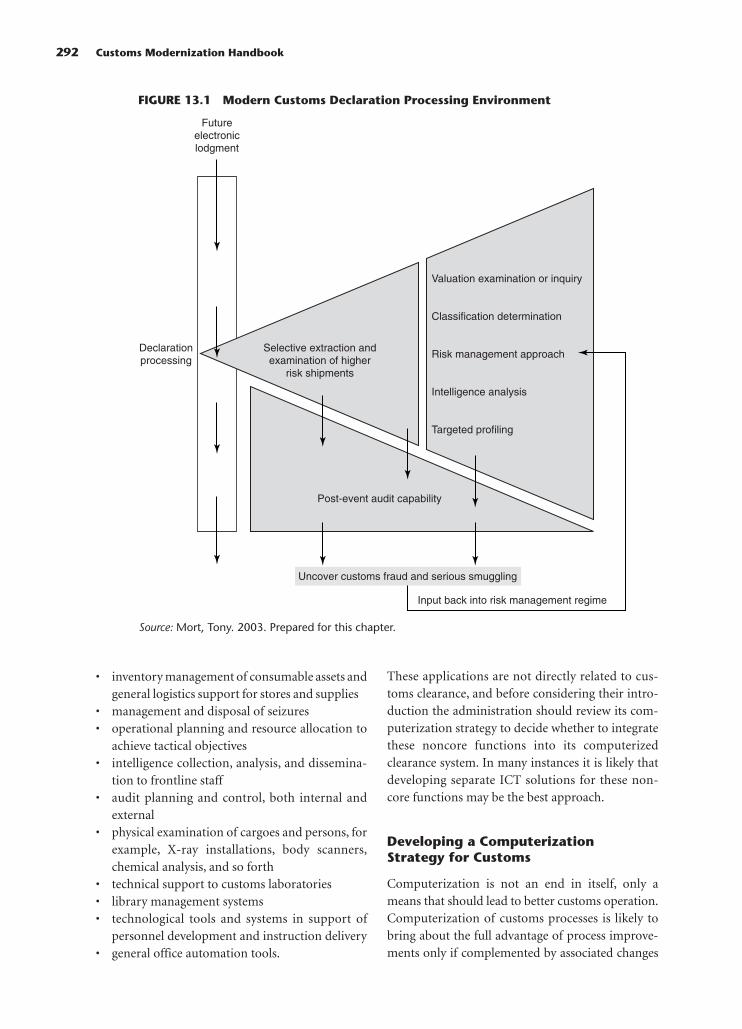

11.1 Typical Transit Operation 25211.2 The Sequence of the TIR Operations 25613.1 Modern Customs Declaration Processing Environment 292

TABLESAnnex 1.A.1 Customs Revenue as a Share of Tax Revenue in Selected Countries, 2001 23Annex 1.B.1 Collected Tariff Rates for Selected Countries, by World Region, 2001 24

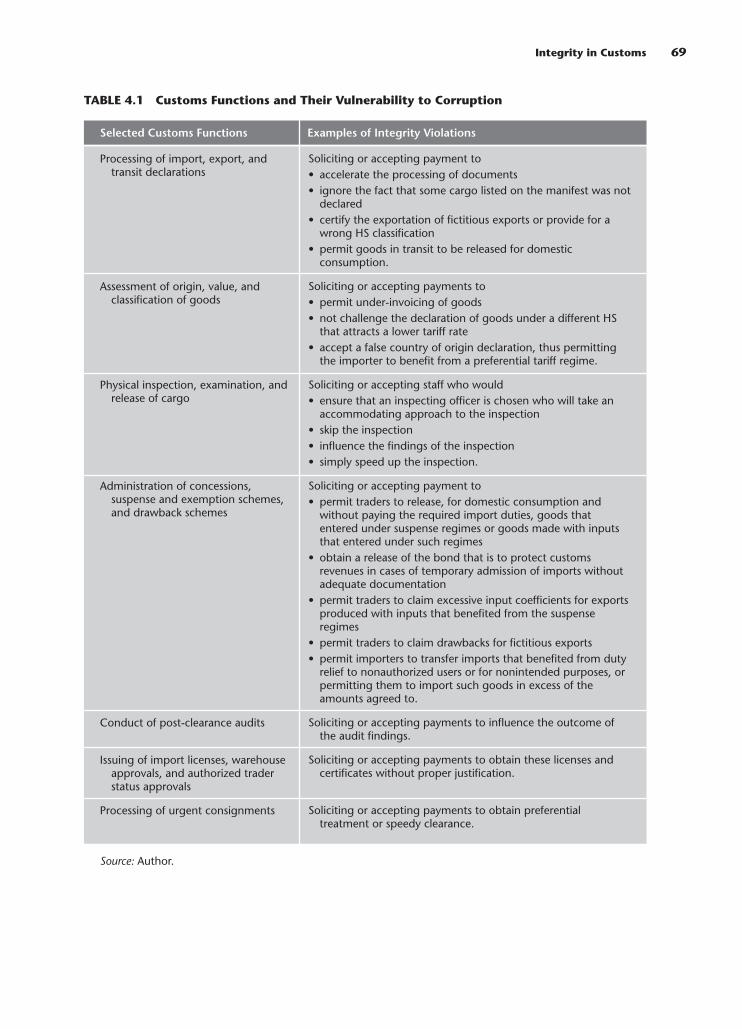

4.1 Customs Functions and Their Vulnerability to Corruption 694.2 Strategies to Reduce Corruption in Customs 73

Contents vii

5.1 Compliance Management Styles 956.1 Basic Economic Data, 2000 1066.2 Revenue Performance Before and After Customs Reforms 1066.3 Revenue Performance Before and After Customs Reforms 1206.4 Customs Processing Times 1217.1 Approved Amounts for Customs Components of Technical Assistance Projects,

1982–2002 1307.2 Distribution of Approved Operations with Customs Component by Project

Category, 1982–2002 1317.3 Pre-Project Diagnostic Analyses in Technical Assistance Projects, 1982–2002 1327.4 Summary of Objectives 1357.5 Performance Indicators 1367.6 Comprehensiveness of Project Design 1397.7 Summary of Suggested Rating of Outcomes of Customs Activities 1437.8 Correlation Estimation: A Summary 144

Annex 7.A.1 Distribution of Projects with Customs Components by Region, 1982–2002 149Annex 8.D.1 PSI Programs Operated by Members of the IFIA PSI Committee 178

9.1 Involvement of Customs in Issuing, Checking, and Providing Information on Preferential Certificates of Origin for Exporters 205

9.2 Resource Implications of Rules of Origin in Preferential Trade Agreements 2069.3 Overlapping Trade Agreements Cause Problems for Customs 208

Annex 9.A.1 Summary of the Different Approaches to Determining Origin 210Annex 9.B.1 Rules of Origin in Existing Free Trade and Preferential Trade Agreements 211

11.1 Transportation Costs from Main World Markets for Coastal and Landlocked Countries in Africa 245

11.2 General Provisions Applicable to Customs Transit as Codified by International Conventions 247

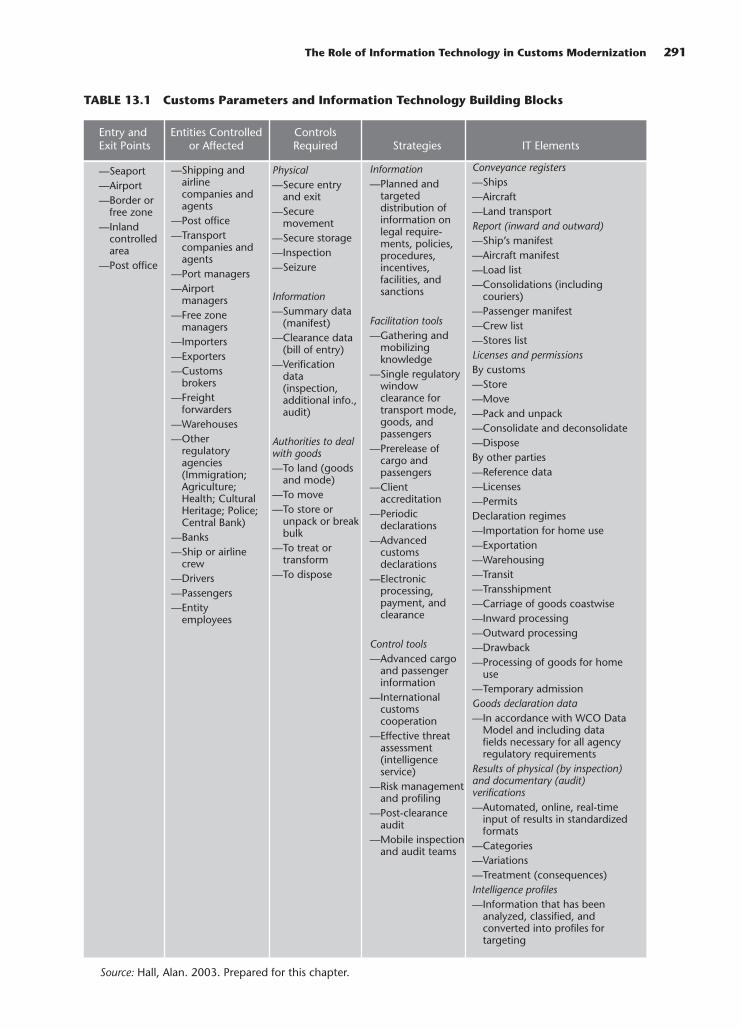

11.3 Transit Procedures without Facilitative Measures 24912.1 Selected Operational Practices to Enhance Cargo Security 27612.2 Technical Means to Assist Security Checks 27713.1 Customs Parameters and Information Technology Building Blocks 291

viii Contents

ix

Foreword

The experiences of recent decades have shown thatthe countries that have most successfully integratedinto the world economy also have tended to recordthe highest growth rates. This result should notcome as a surprise. Integration brings with itimproved allocation of resources, intensified com-petition, and pressures to raise productivity, as wellas exposure to new technologies, designs, and prod-ucts. With world trade growth expanding morethan twice as rapidly as world gross domestic prod-uct (GDP) over the past decade, the potentialrewards from participating in world trade are con-siderable. Increased trade openness, through lowerlevels of protection in developed and developingcountries, has contributed to this outcome. Never-theless, it is widely acknowledged that an opentrade regime will only foster trade integration whena range of complementary policies is in place.

One of the most important complementary poli-cies is to put in place a well functioning customsadministration that provides traders with transpar-ent, predictable, and speedy clearance of goods.Indeed, a poorly functioning customs administra-tion can effectively negate the improvements thathave been made in other trade-related areas.

For many countries, achieving efficiency andtransparency in customs operations remains a for-midable challenge. In 2002, over US$6.3 trillion ofgoods crossed international borders. Each one ofthose shipments passed through customs controlsat least twice—at entry and at exit. Customs serv-ices have often had to cope with these growingtrade volumes without any commensurate increasein staff or resources. In addition, customs adminis-trations continue to face changes to their operatingenvironment, which emphasize the need to adjustand modernize their processes. These include:

• more sophisticated and demanding clients,for example, traders who have investedsignificantly in modern logistics, inventorycontrol, manufacturing, and informationsystems

• greater policy and procedural requirementsassociated with international commitments

• proliferation of regional and bilateral tradeagreements, which significantly increase thecomplexity of administering border formali-ties and controls

• heightened security concerns and demands torespond to the threats posed by internationalterrorism and transnational organized crime

• widespread revenue fraud.

Many customs administrations are struggling tomeet the continually increasing demands and pri-orities placed on them.

During the last decade many countries devotedsubstantial resources to reforming and moderniz-ing their customs administrations, often withfinancial and technical support from internationalfinancial institutions and bilateral donors. TheWorld Bank, the World Customs Organization,the International Monetary Fund, the UnitedNations Conference on Trade and Development(the ASYCUDA program especially), and theRegional Development Banks have, for a longtime, been providing such support. As a result, anumber of customs administrations haveimproved their capacities. Yet, far too many stilloperate inefficiently and, to some extent, fail tofulfill their assigned objectives. Modernization ofcustoms is therefore likely to remain on the devel-opment agenda of many governments, and thedonor community will be called upon to continueits support for customs modernization.

In recognition of this, the Trade Department ofthe World Bank prepared this Customs Moderniza-tion Handbook to provide guidance to the manyorganizations and individuals involved in the prepa-ration and implementation of customs moderniza-tion projects. The Handbook draws on the lessonslearned from past successes and failures, both by theBank itself and a range of other organizations. It alsodraws on the collective experience of a wide range ofindividuals with extensive practical experience in

x Foreword

the field. The Handbook is complemented by a 2004World Bank publication of eight case studies ofcustoms modernization in developing countries—Customs Modernization Initiatives. These works, inconjunction with the recent IMF publicationChanging Customs, which focuses on the revenuemobilization function of customs administrations,provide the necessary tools for initiating and under-taking the process of customs reform.

The guidelines contained in the Handbook areaimed at several audiences. First, they are aimed atpolicymakers and national managers who are calledupon to take the lead in providing advice and guid-ance on the direction of reform efforts and securingthe necessary political support for such initiatives.Second, they are aimed at project managers,national as well as from the donor community, whoare required to design and implement customsmodernization projects. Third, they are aimed atstudents of trade facilitation, who will find in theHandbook the context and operational modalities

of an organization that plays a crucial role in theoverall trade logistics chain.

This Handbook is not intended to be encyclope-dic. It is deliberately selective. It avoids many tech-nical issues that are well covered in the many man-uals and guidelines provided by organizations suchas the World Customs Organization. Rather, itfocuses on the critical issues that need to beaddressed when designing and implementing effec-tive and sustainable modernization projects andrelated initiatives.

We at the World Bank hope that the CustomsModernization Handbook will help in the achieve-ment of the objective of helping policymakers toimplement the needed reform and overall modern-ization that will enable customs to fulfill its role inthe 21st century.

Danny M. LeipzigerVice President and Head of the Poverty

Reduction and Economic Management Network

Acknowledgments

This project would not have been possible withoutthe patience, understanding, and generous supportand contributions provided by many colleaguesand customs experts from national customs organ-izations, international organizations, and in theprivate consultancy business.

Larry Hinkle, Lead Specialist in the Bank’sAfrica Region, encouraged the initiation of thisproject, and the Africa Region provided financialsupport at its initiation. Ataman Aksoy and YvonneTsikata were instrumental in getting this projectlaunched.

Uri Dadush, Director of the Trade Department,gave this project priority status throughout itsdevelopment and provided his wisdom and guid-ance at the most critical stages. John Panzer, ourManager in the Trade Department, provided theteam with his unfailingly enthusiastic support andleadership and ensured the timely completion ofthe project.

The staff of the World Customs Organization,and especially its Deputy Secretary General,Mr. Kunio Mikuriya, who also acted as PeerReviewer, generously shared their operational expe-rience and their time with the editors andcontributed to several chapters. The staff of theInter-American Development Bank and of theInternational Monetary Fund also supportedthe project and provided advice and comments atvarious times during the preparation of the book.Our special appreciation goes to François Corfmatfrom the IMF who was a Peer Reviewer and whomade significant contributions to several chapters.All generously shared their insights and expertiseduring the process of defining the scope of theproject and provided guidance in its preparation.

The authors of the thirteen chapters contributedtheir expertise and showed great patience with themany demands placed on them by the editors. Ourdear late colleague Jit Gill contributed with hisadvice and comments with characteristic profes-sionalism and personal warmth. Special thanks are

xi

also due to the following colleagues and friendswho contributed to making this book possible:Amparo Ballivián (WB), Ed Campos (WB), Patri-cio Castro (IMF), Lee Deegan (Australian Customs,previously at the WCO), Antoni Estevadeordal(IDB), Bruno Favaro (UNCTAD), Odd Fjeldstad(Michelsen Institute), Alan Hall (consultant),Moshe Hirsch (Hebrew University Law School),Bernard Hoekman (WB), John Holl (consultant),Irene Hors (OECD), Darryn Jenkins (consultant),Peter Kalil (IDB), Holm Kappler (previously at theWCO), Joe Kelly (HM Customs and Excise), DavidKloeden (IMF), Michael Lane (consultant), PatriciaLaverly (OED), Bob Mall (WCO), Nick Manning(WB), Fabrice Millet (UNCTAD), Tony Mort(consultant), Mark Pearson (COMESA), JohnRaven (ICC), Will Robinson (WCO), GonzaloSalinas (WB), Edward Siaw (consultant), GrahamSmith (WB), Frederick Z. Stapenhurst (WB),Kati Suominen (IDB), Victor Thurony (IMF),Mashiho Yuasa (University of Michigan LawSchool), and Gianni Zanini (WB).

Our colleagues in the Trade Department of theWorld Bank strengthened our team and made sig-nificant contributions. Special thanks to MichelZarnowiecki who, in addition to being PeerReviewer, shared his technical expertise during thewhole process and significantly improved severalsections of the handbook. We also extend thisappreciation to Mr. Gerard McLinden (at the WCOuntil early 2004) who not only wrote several chap-ters but also contributed greatly to finalizing themanuscript. Finally, the project also benefited fromthe patient, professional, and extremely competentsupport provided by Melanie Faltas and Zeba Jetha.Special acknowledgment goes to Lili Tabada, whoundertook an enormous set of responsibilities,including preparing the desktop version, workingwith the publisher, and helping the team with hersuperb editing skills. She excelled in all these tasksand this project could not have been done withouther competent participation.

Abbreviations andAcronyms

ACI Advanced Cargo InformationACI Airports Council InternationalACP Africa, the Caribbean and the

PacificACP Autoridad del Canal de PanamáACV Agreement on Customs ValuationADCS Automated Data Collection SystemAfDB African Development BankAFTA Asian Free Trade AssociationAGOA African Growth and Opportunity

ActANZCERTA Australia New Zealand Closer

Economic Relations TradeAgreement

ANZSCEP Agreement between New Zealandand Singapore on a CloserEconomic Partnership

APEC Asia-Pacific Economic CooperationARA Autonomous Revenue AuthorityARO Agreement on Rules of OriginASAC Aviation Security Advisory

CommitteeASEAN Association of Southeast Asian

NationsASEZA Aqaba Special Economic Zone

AuthorityASYCUDA Automated System for Customs

DataATA Air Transport AssociationBDV Brussels Definition of ValueBGMEA Bangladesh Garments

Manufacturing and ExportAssociation

BIR Bureau of Internal RevenueBIVAC Bureau of Inspection Valuation

Assessment and ControlBOC Bureau of CustomsBOT Build-Operate-TransferBOT Bureau of TradeBOO Build, Operate, and OwnCA Crown AgentsCACM Central American Common MarketCAM Customs Assistance Mission

CARICOM Caribbean CommunityCAS Country Assistance StrategyCBI Cross-Border InitiativeCBP US Bureau of Customs and Border

ProtectionCCC Customs Cooperation CouncilCCO Central Customs OfficeCCP Central Control PointCEFACT United Nations Centre for Trade

Facilitation and Electronic BusinessCEPS Customs Excise and Preventive

ServicesCIF Cost, Insurance, and FreightCOMESA Common Market for Eastern and

Southern AfricaCRO Committee on Rules of OriginCSD Container Security DeviceCSI Container Security InitiativeCSTF Cargo Security Task ForceC-TPAT Customs–Trade Partnership Against

TerrorismDF Diagnostic FrameworkDFID Department for International

DevelopmentDSS Duty Suspension SchemeDTI Direct Trader InputEAC East African Cooperation EBA Everything but ArmsEC European CommunityECA Europe and Central AsiaECAC European Civil Aviation ConferenceECO Economic Cooperation

OrganizationECOWAS Economic Community of West

African StatesEDCS Electronic Data Collection SystemEDI Electronic Data InterchangeEEC European Economic CommunityEFT Electronic Funds TransferEFTA European Fair Trade AssociationEPZ Export Processing ZoneEU European UnionFAK Freight of all Kinds

xiii

FDI Foreign Direct InvestmentFOB Free on BoardFTA Free Trade AgreementFTZ Free Trade ZoneGAO General Accounting OfficeGATT General Agreement on Tariffs and

TradeGCMS Ghana Customs Management

SystemGCNet Ghana Community NetworkGDP Gross Domestic ProductGEP Global Economic Prospects GMS Greater Mekong SubregionGOIEC General Organization for Import

and Export ControlGOM Government of MozambiqueGSP General System of PreferencesGST General Sales TaxGVC GATT Valuation CodeHQ HeadquartersHRO Harmonized Nonpreferential Rules

of OriginHS Harmonized Commodity

Description and Coding SystemHWP Harmonization Work ProgramIACA International Air Carriers

AssociationIATA International Air Transport

AssociationICAC Independent Commission Against

CorruptionICAO International Civil Aviation

OrganizationICC International Chamber of

CommerceICMP International Customs

Modernization ProcessICR Implementation Completion

ReportICS Inspection and Control ServicesICT Information and Communications

TechnologiesIDB Inter-American Development BankIDI Institutional Development ImpactIFALPA International Federation of Airline

Pilots AssociationsIFIA International Federation of

Inspection AgenciesIGAD Intergovernmental Authority on

Development

ILO International Labor OrganizationIMF International Monetary FundIMO International Maritime

OrganizationIOC Indian Ocean CommissionIRU International Road Transport

UnionISPS International Ship and Port Facility

SecurityIT Information TechnologyITF International Transport Workers

FederationLDC Least Developed CountryMDCS Mobile Data Collection SystemMFN Most Favored NationMODAAC ASYCUDA++ Accounting ModuleMODTRS ASYCUDA++ National Transit

ModuleMOF Ministers of FinanceMOF Ministry of FinanceMPF Ministry of Planning and FinanceMTSA Maritime Transport Security ActMUB Manufacturing Under BondNAFTA North American Free Trade

AgreementNCTS New Computerized Customs

Transit SystemNGO Nongovernmental OrganizationNPR Nepalese RupeesNTB Nontariff BarriersNVOCC Nonvessel Operating Common

CarriersOECD Organisation for Economic

Co-operation and DevelopmentOED Operations Evaluation

DepartmentOP Operational PolicyOSC Operation Safe CommercePAD Project Appraisal DocumentPIN Personal Identification NumberPRA Port Risk AssessmentPRSP Poverty Reduction Strategy PaperPSI Preshipment InspectionPSR Project Status ReportPTA Preferential Trade AgreementRCDP Russian Customs Development

ProjectRFID Radio Frequency IdentificationRIFF Regional Integration Facilitation

Forum

xiv Abbreviations and Acronyms

Abbreviations and Acronyms xv

RMG Ready Made GarmentsRSC Regional Steering CommitteeRSO Recognized Security OrganizationRTCD Road Transit Customs DeclarationSAARC South Asian Association for

Regional CooperationSACU Southern African Customs UnionSAD Single Administrative DocumentSADC Southern African Development

CommunitySADOC Système de l’Administration des

Douanes et de l’Office des Changes;Computerized Support forCustoms Clearance

SAL Structural Adjustment Loans andCredits

SAR Staff Appraisal ReportSAT SatisfactorySBW Special Bonded WarehouseSCC State Customs CommitteeSDT Special and Differential TreatmentSECI South East Cooperation InitiativeSGS Societé Générale de SurveillanceSITPRO Simplifying International TradeSOLAS International Convention for the

Safety of Life at SeaSPARTECA South Pacific Regional Trade and

Economic Co-operation AgreementSSP Sector Strategy PaperSSP Shipper Security PlanSUNAT Superintendencia Nacional de

Administracion Tributaria; InternalRevenue Service

TA Technical AssistanceTAEPD Trade Assistance Evaluation Project

DatabaseTAL Technical Assistance LoanTAP Temporary Admission for Inward

ProcessingTARIC Tarif Integré de la Communauté;

The Integrated Tariff of theCommunity

TCCV Technical Committee on CustomsValuation

TCRO Technical Committee on Rules ofOrigin

THA Tanzania Harbors AuthorityTI Transparency InternationalTIMS Trade Information Management

SystemTIR Transport International

RoutierTRA Tanzania Revenue AuthorityTRACECA Transport Corridor Europe

Caucasus AsiaTRIE Transit Routier Inter-ÉtatsTRIPS Trade-Related Aspects of

Intellectual Property RightsTSA Transportation Security

AdministrationTTCA Transit Transport Coordination

AuthorityTTFSE Trade and Transport Facilitation in

Southeast EuropeUCR Unique Consignment

Reference UD Utilization DeclarationUDEAC Union Douanière des Etats de

l’Afrique CentraleUNCTAD United Nations Conference on

Trade and DevelopmentUNECE United Nations Economic

Commission for EuropeUNSAT UnsatisfactoryURA Uganda Revenue AuthorityUS United StatesUTRA Technical Unit for Restructuring

CustomsVAT Value Added TaxWBCG Walvis Bay Corridor GroupWCO World Customs OrganizationWEF World Economic ForumWTO World Trade OrganizationZRA Zambian Revenue Authority

xvii

OVERVIEW

This handbook aims to make a positive contributionto the efforts that many countries are undertaking tomodernize their customs administrations. Thehandbook views a competent and well-organizedcustoms service as one that successfully balances itsvarious responsibilities to ensure a high level ofcompliance with revenue objectives and regulatoryrequirements while at the same time intervening aslittle as possible in the legitimate movement ofgoods and people across borders.

The handbook recognizes that conditions differgreatly across countries, so that each customsadministration will need to tailor its modernizationefforts to national objectives, implementationcapacities, and resource availability. Nevertheless,meeting the modernization objectives will mostlikely require the adoption of the core principlesdiscussed in this handbook: adequate use of intelli-gence and reliance on risk management; optimaluse of information and communications technol-ogy (ICT); effective partnership with the privatesector, including programs to improve compliance;increased cooperation with other border controlagencies; and transparency through information onlaws, regulations, and administrative guidelines.

Success in customs modernization is, as impor-tantly, tied to the overall trade policy environment.Simple, transparent, and harmonized trade policiesreduce administrative complexities, facilitate trans-parency, and reduce the incentives and opportuni-ties for rent-seeking and corruption. Customsmodernization, therefore, also needs to be exam-ined from the broader and complementary per-spective of trade policy reform.

Improving Customs Processes Is Part of the TradeFacilitation Agenda

Trade facilitation measures need to complementtrade liberalization if countries are to increasetheir external competitiveness and become betterintegrated into the world economy. When theEuropean Community, introduced a common exter-

nal tariff in 1968 it quickly realized that to fully ben-efit from its common market, it needed to streamlinecustoms processes. In the same vein, the World TradeOrganization (WTO) in 1996—as part of the Singa-pore agenda—added trade facilitation to its negotia-tion agenda realizing that nontariff barriers, to whichexcessive customs costs belong, are at times moreimportant trade barriers than tariffs and prevent theachievement of trade liberalization objectives.

Trade involves goods crossing borders. Thisrequires that a number of procedures foreseen inthe national legislation be followed. Some of theseprocedures pertain to issues of security and stan-dards, while others deal with customs. Customsprocedures are governed by the national legislationand implemented by customs staff that operatemostly under the Ministry of Finance. Conformingto these procedures is not costless, but these costsare often excessive. It is not the intention of thehandbook to elaborate on inefficiencies nor todetail all the dysfunctionalities of customs organi-zations and customs operations, even though someof these are described in individual chapters, asintroduction on how best to remedy them. Yet, it istheir persistent recurrence and their impact on acountry’s competitiveness that prompted tradersand political leaders to seek out ways to make theircustoms organizations more effective and efficient.This handbook aims at assisting them in this ambi-tion. It must suffice, therefore, to briefly note themain inefficiencies that these reforms aim toaddress. First, outdated legislation may not clearlyestablish the authority of customs, may be out oftune with international commitment, may providefor inadequate transparency and predictability, andmay require complex procedures while preventingfull use of information technology and risk analy-sis. Second, customs staff may lack the competenceto interface with traders that operate in a constantlychanging and challenging business. Often theircompensation packages, including career manage-ment and training, are inadequate, so that moti-vating and retaining qualified staff is a major

challenge. Third, operational procedures are oftenexcessively and unnecessarily complex and open todiscretionary decisions while exporters have pooraccess to duty-free inputs. Fourth, customs all toooften makes insufficient use of available communi-cations and information technology, and thus is outof tune with modern business practices that rely onadvanced notification, direct trader input, andtracking devices. This increases costs to traders,opens the door to discretionary decisions, andundermines oversight and audit activities. Fifth,high levels of corruption characterize many a cus-toms agency, as is testified to in investors’ surveysand corruption indexes. Sixth, smuggling activitiesundermine revenue generation and impart unfairadvantages to unscrupulous traders, and under-mine the intended protection policies embedded inthe tariff structure. In sum, customs procedures areoften excessively time consuming, unpredictable,and weak in their revenue generation function.

Good Diagnostics Are the Key Starting Point

Customs operations consist of sets of interlockingprocesses. To be efficient and effective they need to beadapted to changing trade practices and modernmanagement approaches as well as reflect the variousobjectives of the country. Yet, customs practices inquite a few countries are not well attuned to thesecriteria. Rooted in long-standing traditions, they tendto delay the clearance of cargo and conduct operationsin a nontransparent manner. Experience shows thateffective customs modernization processes generallystart with good initial diagnostic work to identify theshortcomings of the existing system, to define a strat-egy for reform, and to mobilize stakeholder support.Successful modernization also requires a comprehen-sive approach, that is, an approach that encompassesall aspects of customs administration to address theissues identified, as well as an adequate sequencing ofactions. Strategies need to be realistic and should con-sider the country’s capacity to implement, the timethat is required, and the level of stakeholder and polit-ical support that is needed.

These reform efforts also need to be consistentwith the trade policies pursued and should have thecapacity to adapt to changing circumstances. Forexample, the emphasis on issues such as trade facil-itation and national security are now more preva-lent than in the past.

Human Resources Policies Need to Be at the Center of Customs Reforms

The task of customs has become increasingly diffi-cult because of the growing complexities of tradepolicy due to the proliferation of regional andinternational trade agreements, the greater sophis-tication of traders, and the multiple and shiftingobjectives imposed on customs. Security is now anew important challenge. Uniformity of customsoperations across the territory and across cargo cat-egories is important, and speedy release of goods iscrucial to supporting the competitiveness oftraders. There is also a need to adhere to interna-tional standards on value and classification, as wellas regional standards on rules of origin.

Good human resources management is thelinchpin to effective and efficient customs adminis-tration. This is too often neglected. The manage-ment of human resources is multifaceted. Itincludes recruitment, training, staff compensationand promotion, as well as enforcement. None ofthese tasks is easy, and often must be implementedin a constrained environment. These difficultiesshould not discourage the investigation of possiblenew initiatives and alternative approaches. How-ever, case studies do suggest that within these con-straints still much more attention should be givento human resources issues.

To address the constraints imposed on humanresources reforms by rigid and often outdated civilservice administration policies, many countrieshave pursued drastic organizational changes. Forexample, Autonomous Revenue Agencies (ARAs)have been established to avoid rigid civil servicerules, as well as to provide more financial auton-omy and greater flexibility in operational matters.However, experience has shown that creating anARA is no guarantee for success because they havetoo often been focused on providing better staffcompensation without sufficient attention to theother elements of customs operations that enhanceeffectiveness and efficiency. Also, quite a few ARAsfailed to maintain, over the longer term, the flexi-bility and the autonomy with which they were orig-inally established.

Another mechanism to implement reforms hasbeen the pursuit of management contracts with theprivate sector. Management contracts can indeedimprove aspects of customs operations if they are

xviii Overview

well designed and monitored. So far, these manage-ment contracts have largely been tested in uniquecircumstances in countries emerging from severeconflicts (Mozambique and Angola, for example)and where institutional capacity was exceedinglyweak. Engaging private service operators in thosecountries had the advantage of substantiallyimproving revenue performance in the short runand under difficult circumstances. The track recordfor transferring management capabilities to nation-als, however, is still being tested. Initial reports sug-gest that this has proven more difficult than origi-nally imagined.

Changes in the organizational structure of cus-toms can at times be instrumental to improvingperformance, as change can lift important opera-tional constraints. Evidence suggests, however, thatsuch changes will only have lasting effects if theycontribute to good human resources managementand better customs clearance practices.

An Adequate Legal Framework Is Important

The modernization of customs laws and regulationsand their supporting legal environment is an essen-tial component of the reform effort. In this area,countries can refer to (or adopt) the Revised KyotoConvention, which provides both the legal frame-work and a range of agreed on standards to improvecustoms operations with a view toward standardiz-ing and harmonizing customs policies and proce-dures worldwide. Countries that are signatories ofthe Convention can still tailor their policies and pro-cedures in specific ways to meet their unique legal,political, cultural, and economic requirements.

In many countries the Customs Code needs to bemodernized, especially to exclude noncore customselements, seek harmonization and compliance withagreed on international commitments, and ensuretransparency and predictability by providing basicinformation on matters such as rules, decisions,consultation mechanisms, and adequate appealsprocesses. A revised Code can also help trade facili-tation by supporting the use of risk managementpractices and by eliminating complex or redundantcustoms formalities that delay clearance and createopportunities for unnecessary discretionary inter-ventions. Finally, the Code should also grant ade-quate authority for customs to achieve its enforce-ment and compliance goals.

Improved Integrity Is Key to Promoting Investment and Growth

Customs is frequently perceived as being corrupt.To the extent that this is true, this image negativelyaffects the overall investment climate of the coun-try and the processing of international trade trans-actions. Corruption undermines the country’sexternal competitiveness and its attractiveness todomestic and foreign investment. If left unchecked,this image of corruption undermines the growthpotential of the country.

Customs is vulnerable to corruption because thenature of its work grants its officials substantialauthority and responsibility to make decisions thataffect the duty and tax liability of traders or theadmissibility of goods. High tariffs and complexregulations enhance opportunities and incentives.That many customs staff members are poorly paidadds to the problem.

The adoption of procedures that provide littlediscretion to customs staff and that have built-inaccountability mechanisms reduces both the oppor-tunity and incentive for corruption. In conjunctionwith improved trade policies, the first line ofdefense against corruption consists of implement-ing modern procedures that reduce face-to-facecontact between traders and customs officials andthat reduce the discretionary powers of customsofficials. In addition, providing adequate staff com-pensation, enhancing the risk of detection, andstrengthening the capacity to investigate and prose-cute breaches of integrity would go a long waytoward promoting integrity in customs. Most cus-toms managers are of the opinion that corruption issuch a prevalent phenomenon today that counter-measures would require the implementation of spe-cially designed policy efforts. This is the approachthat is promoted by the World Customs Organiza-tion and is incorporated into the Revised ArushaDeclaration on Integrity in Customs.

In looking to implement the key elements of theRevised Arusha Declaration, experience suggeststhat a good starting point is to conduct a compre-hensive assessment of the situation to identify theshortcomings that present opportunities for cor-ruption and to establish realistic priorities, as wellas practical objectives and activities, all leading toan integrity plan that should be a part of all com-prehensive customs reform efforts.

Overview xix

Risk Management Underpins Much of Modern Customs Practices

In an effort to achieve an appropriate balancebetween trade facilitation and regulatory control,customs administrations are generally abandoningtheir traditional, routine “gateway” checks and arenow applying the principles of risk managementwith varying degrees of sophistication and success.

Organizational risk refers to the possible eventsand activities that may prevent an organizationfrom achieving its objectives. Risks facing customsinclude the potential for noncompliance with cus-toms laws as well as the potential failure to facilitateinternational trade. Customs, like any other organi-zation, needs to manage its risks and do so whileinterfering as little as possible with the flow of legit-imate trade. There clearly is a trade-off betweencontrol and trade facilitation. Too much of onemakes it difficult to achieve the other. Customstherefore needs to apply a set of management pro-cedures that takes this into account. These proce-dures include the identification, analysis, evalua-tion, and mitigation of the risks that may affect theachievement of these objectives.

Basic risk management has always been funda-mental to customs operations, and has guided theformulation of antismuggling policies, the func-tioning of border controls to verify the movementsof goods and passengers, and the establishment ofdocumentary controls and physical inspection pro-cedures. However, in recent times the increasingcomplexity, speed, and volume of internationaltrade, fueled by technological advances that haverevolutionized global trading practices, have signifi-cantly affected the way in which customs authoritiesimplement risk management. This has led manycustoms administrations to adopt a more disci-plined and structured approach to managing risk.

Customs needs to evaluate the risks that are pre-sented by the nature of its operations. This includesthe need for customs to review its operational pro-cedures and assess where breaches of proceduresare likely to jeopardize the attainment of statedobjectives. Such assessment could be included inthe above-mentioned overall diagnostic exercise. Inother words, customs needs to provide a risk mapthat identifies the potential vulnerabilities of itsprocesses and determine how its procedures mayneed to be geared toward ensuring better realiza-

tion of its objectives. On the basis of the risk assess-ment, a risk containment strategy should bedefined. This implies that priorities would be set,operational details would be geared toward thesepriorities, and resources would be effectively andefficiently deployed. If smuggling turns out to be amajor problem, the strategy should reflect this, andborder posts and mobile inspection teams mayneed to be strengthened. If undervaluation is amajor problem, there may be a case for strengthen-ing the valuation unit and for increasing the num-ber of traders subject to post-clearance audit. If therisk is that goods tend to be misclassified to attracta lower tariff rate or are declared with lower unitcounts or weights, there may be a need to physicallyinspect the cargo. In any event, risk managementshould ease the controls on the less risky aspects oftrade and should focus on the part that representsthe greatest risk. This would reflect a balancedapproach between control and trade facilitation.

Customs Valuation Is a Core Customs Function

Customs valuation practices are subject to theWTO Agreement on Customs Valuation (ACV),which mandates that the customs value ofimported goods, to the greatest extent possible,should be the transaction value, that is, the pricepaid or payable for the goods. However, valuationfraud is frequently reported as a major problem indeveloping countries, and many of them still findthat implementing the ACV presents one of themost challenging aspects of customs work. Valua-tion work is particularly difficult in some countriesin which the reliability of commercial invoicestends to be poor, and where trade undertaken bythe informal sector and in second-hand goods issignificant. Also, many countries are still illequipped to undertake post-clearance audit.

Substantial efforts have so far been made toexplain the intricacies of the ACV to customs offi-cials of developing countries. Yet, most observersrealize that valuation reform, in the absence ofcomprehensive customs modernization programs,is likely to disappoint. A narrow focus on valuationwork will fail if reform takes place within an admin-istratively and technically ill-equipped customs.The reform elements that will benefit valuationwork must include the streamlining of operationalprocedures, the introduction of a modern customs

xx Overview

compliance improvement strategy based on a for-malized risk management strategy, the use of post-clearance audits, the development of a commercialintelligence capacity, and the adoption of appro-priate incentives and disincentives designed toprogressively increase the level of voluntarycompliance.

Direct technical assistance for improved valua-tion work might be more productive if such assis-tance were concentrated on the development ofvaluation databases, risk management systems, andpost-release review and audit. A valuation databaseshould be established and constantly updated toprovide customs with a practical tool for researchand risk management purposes. The valuationfunction in Customs could be strengthened by set-ting up an appropriate legal framework; establish-ing valuation control procedures based on selectivechecking, risk analysis and management, and post-release audit; establishing central and regional val-uation offices; and providing specialized training.

The hiring of preshipment inspection (PSI)companies may be useful in assisting customs withvaluation work during its initial reform stages,where capacity is being enhanced to carry out thevaluation function. However, if PSI services areused, care needs to be exercised to maximize theirutility and to ensure maximum consistency withthe WTO valuation principles. This handbookspells out a number of conditions that should beinvestigated when considering the adoption of PSIservices or when evaluating their contribution.

Rules of Origin Should Be Simplified

Determining the country of origin, or the “nation-ality,” of imported products is necessary for theapplication of basic trade policy measures such astariffs, quantitative restrictions, antidumping andcountervailing duties, and safeguard measures, aswell as for requirements relating to origin markingand public procurement, and for statistical pur-poses. Such objectives are met through the applica-tion of basic or nonpreferential rules of origin.Countries that offer zero or reduced duty access toimports from certain trade partners apply preferen-tial rules of origin. These differ most frequentlyfrom the nonpreferential ones. Preferential rulesare designed to ensure that only goods originatingfrom participating countries enjoy preferences.

However, rules of origin can be designed to restricttrade and, therefore, can and have been usedas trade policy instruments. The proliferation offree trade agreements with accompanying preferen-tial rules of origin is increasing the burden on cus-toms in many countries because the clearing ofpreferential trade is more complex than nonprefer-ential trade. This suggests that the trend towardmore preferential free trade agreements may con-flict with trade facilitation.

The determination of the country of origin ofproducts has, in the last few decades, become moredifficult as technological change, declining trans-port costs, and the process of globalization have ledto the splitting up of production chains and the dis-tribution of different elements in the production ofa good to different locations. The issue becomes,which one or more of these stages of productiondefine the country of origin of the good?

WTO members have so far failed to reach anagreement on the definition of rules of origin,despite efforts undertaken in the World CustomsOrganization (WCO) since 1995. Having harmo-nized rules of origin for nonpreferential purposeswould save time and costs to traders and customsofficers and provide for greater certainty and pre-dictability of trade. Harmonized rules would alsohelp avoid trade disputes that arise from uncertain-ties in the determination of the country of originwith regard to antidumping and countervailingduties, safeguard measures, and governmentprocurement decisions. In general, clear, straight-forward, transparent, and predictable rules oforigin, which require little or no administrative dis-cretion, will add less of a burden to customs thancomplex rules.

Good Duty Relief and Exemption Control SystemsAre Important

Customs may provide duty relief for some imports.This practice is mainly used for the importation ofinputs used for the manufacture of export prod-ucts. The justification for doing so is simple. Anyduty paid on these inputs would increase the cost ofthe exports and make these exports less competi-tive. In fact, following the widely accepted destina-tion principle of taxation, only goods destined fordomestic consumption should bear a tax burden.Duty relief for inputs that are directed toward the

Overview xxi

production of exports can be granted in two ways:either a suspense regime is applied and no dutiesfor imported inputs are paid at the point of import;or duties are paid and later refunded, when theproducts into which the inputs are incorporatedare exported. The WCO Revised Kyoto Conventionprovides guidelines on how this should be doneand these can be reflected in the Customs Code andtranslated in operational guidelines for importersand customs staff. However, experience shows thatmany developing countries have difficulty in prop-erly administering and monitoring duty relief andexemption regimes, resulting in abuse, fraud, andrevenue leakage. In the absence of smoothly operat-ing duty relief mechanisms, export manufacturershave to produce at higher cost than would be thecase if they had full and easy access to productioninputs at world prices.

Export manufacturers have a preference fortemporary admission systems, bonded warehouses,and export processing zones over duty drawback,especially when tariffs are high, when inflationerodes the duty refunds, and when interest rates forworking capital are high. The prepayment ofimport duties on inputs increases the productioncosts of the exporter. The drawbacks have all toooften been disbursed late, thus substantially erod-ing real value when inflation and financing costsare high. However, governments in most develop-ing countries require customs to focus on revenuecollection rather than trade facilitation and, there-fore, tend to prefer drawback to temporary admis-sion systems.

Managing duty relief schemes in a secure andcost effective way requires well-defined processesand controls. It requires that special mechanisms beput in place to ensure that claims for duty relief arelegitimate and correctly executed, and that goodsadmitted under duty suspense regimes are effec-tively incorporated in exports and not diverted forhome consumption.

The scope of duty exemptions should be limitedas much as possible as exemptions can be abused,thus leading to unfair competition and revenuelosses. Moreover, there are good economic andadministrative reasons for maintaining dutyexemptions only as required by international con-ventions and for noncommercial goods. Until theredundant exemptions are eliminated, customsshould devote adequate technological and man-

power resources to the control and monitoring ofsuch exemptions.

Customs Procedures Should Facilitate Transit

Poor transit procedures are a major obstacle to tradeand penalize many landlocked developing coun-tries. A transit system aims to facilitate the transportof goods through a customs territory, without levy-ing duties and taxes in the countries of departureand transit, in accordance with the destination prin-ciple of taxation that states that indirect taxes shouldonly be levied in the country of consumption. TheCustoms Code should provide transit-related legis-lation, failing which, transit should be regulated by abinding agreement between customs and the differ-ent parties affected by the transit operation.

The core provisions of a good transit systeminclude that the shipments be sealed at the point ofdeparture, that guarantees can be made available toensure the payments of duties and taxes if tradersdo not provide proof that the goods have left thecountry, and that customs has an information sys-tem that informs it when the goods have left thecountry so that the guarantee can be released. Inmany countries these core elements are either lack-ing or weak and should be the focus of any transitmodernization initiative.

Trade policies should recognize that customstransit is only one part of a wider range of policyissues that affect transit. These other issues pertainto many other participants and procedures, includ-ing cross-border vehicle regulations, visas for truckdrivers, insurance, police controls, and the qualityof infrastructure. Even if customs transit proce-dures are made effective and efficient, full tradefacilitation will require that these issues beaddressed. The TIR (Transit Routier Interna-tional—the international road transit procedures)and its network of national guaranteeing associa-tions offer the best current reference system.

Effective and efficient transit facilitation institu-tions such as corridor agreements can promoteactive cooperation between and among transit andlandlocked countries. Transit agreements areimportant in forming and shaping such coopera-tion, either at the bilateral, subregional, or regionallevel. Transit operations will benefit from goodpublic–private cooperation that can identify defi-ciencies in border-crossing procedures.

xxii Overview

Overview xxiii

Security Has Become an IntegralCustoms Objective

The emergence of international terrorism hascaused security to become a major issue for manygovernments, and customs administrations areincreasingly called upon to contribute to nationalsecurity objectives. In the past, many customsadministrations performed most of their preven-tive operations as goods arrived at seaports, air-ports, and land borders, based upon an entry decla-ration made at the time of importation. To providethe level of security that is required, governmentswill increasingly depend on information and riskassessments that are undertaken in advance of thearrival of the cargo in the country of destination.International conventions that apply to sea and airtransport provide for agreed upon mechanisms toenhance the security of these modes of transporta-tion—vehicles, cargo, and personnel—as well ashow these transport modes are operated. Severalnational governments, particularly that of theUnited States of America, have issued regulationsand have promoted private–public sector agree-ments to enhance security. These, again, are largelybased on the advance submission of informationand certification that the particular companiesadhere to a range of security standards. Such regu-lations are constantly being refined and imple-mented. Customs’ skill in assessing the informationthrough analytical processes, deployment ofresources, effective communication and decision-making, therefore, has become even more impor-tant than in the past.

Protecting society involves protection of theentire international trade supply chain fromthe moment the cargo leaves the export country tothe moment of arrival at the destination country.This changing environment requires an “all ofgovernment” approach. In this way, governmentscan use customs as a key resource in border secu-rity, using its experience of managing risks andknowledge of international trade as an importantelement of national security. Thus, customs canusefully complement the contributions made byother competent agencies, such as immigration,intelligence agencies, and those involved in policingmaritime, aviation, and land operations.

While security is of great importance to govern-ments and traders, customs has an equal responsi-

bility to facilitate legitimate trade. If applied cor-rectly, security can enhance facilitation by buildingbusiness confidence, increasing predictability, and,as a consequence, facilitating inward investment.However, the international community will needto monitor how specific security initiatives andadvance notice requirements will affect weakertrading partners, particularly those that use portsthat are not receiving technical assistance tostrengthen their security to the satisfaction of theports of destination. These traders may have diffi-culties in fully complying with the advance noticerequirements.

While it is not possible at this time to predict thetrade-related consequences of the heightened secu-rity agenda, it seems probable that the countriesthat feel vulnerable to terrorist attack will regardconsignments from certain countries as represent-ing a higher risk. In this regard, the level of integra-tion of the world economy is such that evencountries that are not directly involved in a conflictor subject to terrorist attack suffer losses in tradeand welfare as a result of increased security con-cerns and higher frictional costs of trade. For thosecountries with a high degree of reliance on trade(ratio of trade to GDP), including many developingcountries, the need for concerted action in thesecurity area becomes a key priority in the develop-ment agenda.

Information and Communications TechnologyPromotes Customs Modernization

An effective customs administration that lever-ages technology can benefit from improved trans-parency, greater efficiency, and enhanced security.However, the benefits that could be derived fromgreater reliance on ICT has at times been under-mined by the failure to streamline customs proce-dures, thus creating a process where outdated man-ual practices continue alongside computerizedpractices. Although ICT for customs administra-tion is not a panacea or an end in itself, it can pow-erfully contribute to effective customs administra-tion and operations when integrated into a broadermodernization effort.

To meet its mission, a customs administrationmust effectively integrate modern practices andprocesses with ICT-driven customs managementsystems. In doing so, customs should identify

xxiv Overview

realistic and practical targets and objectives that aretailored to its own specific circumstances. DesirableICT solutions are not necessarily the very latest andmost sophisticated ones available, but rather, theones that are most appropriate for the country’soperating environment, resource base, telecommu-nications infrastructure, and realistic developmentambitions. In any event, the ICT solution chosenmust assist customs in all its core business func-tions and must provide a platform that enablesachievement of its long-term vision.

In its choice of computer solutions, customs hasthe option of either developing a national systemthat is adapted to national needs, or acquiring anoff-the-shelf system. National solutions have theattraction of perfectly matching the specificrequirements of a given country, of developingnational computer skills, and of facilitating the sys-tem’s maintenance and development. Yet, suchnational solutions tend to be expensive, and it hasat times proven difficult for customs officials toconvey to the ICT technicians the complex transac-tions that need to be programmed. Off-the-shelfsolutions benefit from the fact that the variousmodules have been tested and avoid the need to“reinvent the wheel.” Where these solutions do notfully satisfy national needs, or where national cus-toms desires a variant of the solution offered, thereis the possibility of customizing the solution or ofadding on separate modules that interface with theoff-the-shelf solution. On balance, the handbookadvocates that policymakers take a hard look at off-the-shelf solutions before they consider designing anational solution.

ITC solutions tend to be expensive, even if theyenhance efficiency. Experience suggests that muchis to be gained from a well-balanced financing planfor the initial installation, maintenance, andupgrading, as well as financing plans to includeexternal and domestic resources. Also, procure-ment procedures should be transparent and shouldensure value for money by carefully weighing boththe technical and financial proposals.

Structure of the Handbook

This volume has three parts. The chapters in Part Icover cross-cutting issues that provide insights tothe key elements of a successful customs modern-ization strategy. The chapters discuss key organiza-tional issues that any customs service needs to dealwith and focus on the legal framework of customsand the issues of integrity and risk management.The chapters in Part II provide lessons from a selectset of customs reform initiatives as well as from theWorld Bank’s own experience with its support forcustoms reform. The chapters in Part III succes-sively discuss and provide guidelines on a numberof issues that affect customs operation and tradefacilitation. These are customs valuation, rules oforigin, duty relief and duty exemption regimes,transit, security, and the use of ICT.

Each of the 13 chapters begins with a shortintroduction or background section that isintended as a reader’s guide to the issues. This is fol-lowed by an analysis and discussion of the issues,then by the chapter’s main operational conclusionsand recommendations. Some chapters include anannex with a checklist of issues that need to beaddressed in the areas covered. Sections on furtherreading and references follow. The boxes includedin the chapters illustrate specific points or describespecific cases. Case studies are used to illustratepoints made in the chapters; the situation on theground may have since changed. Their usefulnessrests in illustrating that theory and guidelines canbe implemented. Many of these case studies andboxes were prepared by the editors of the hand-book, drawing on papers prepared for this projectand on the literature.

A companion volume titled Customs Modern-ization Initiatives: Case Studies, edited by Luc DeWulf and José B. Sokol, describes in some detail theexperiences and lessons learned from eight casestudies in customs modernization. It complementsthis handbook as it shows how in real life some ofthe issues described here were addressed.

1

Part I

Cross-CuttingIssues

3

1STRATEGY FOR CUSTOMS

MODERNIZATION

Luc De Wulf

TABLE OF CONTENTS

Objectives of Customs Operations 5

Contextual Factors Necessary for a SuccessfulCustoms Reform 7

Development of a Customs ModernizationStrategy 12

Implementation of a Customs ModernizationStrategy 20

Operational Conclusions 22

Annex 1.A Customs Revenue as a Share of TaxRevenue in Selected Countries,2001 23

Annex 1.B Collected Tariff Rates for SelectedCountries by World Region,2001 24

Annex 1.C Time-Release Methodology 24

Annex 1.D Physical Inspection as an Element ofRisk Management 27

Annex 1.E Checklist of Guidelines to Definea Customs ModernizationStrategy 29

Further Reading 29

References 30

BOXES

1.1 Morocco Customs Gets Its Staff on Board forthe Reform Program 17

1.2 An Example of Regional Leadership:The TTFSE Regional SteeringCommittee 21

1.C.1 The Steps to Release Goods fromTime of Arrival 25

1.C.2 The Philippines Time-Release Study:An Example to Follow 26

FIGURES

1.1 Number of Declarations per Staff per year inSoutheastern Europe, 2002 16

Research undertaken in recent years by the WorldBank and others shows that participation in worldtrade tends to boost growth, and that countries thathave integrated rapidly into the world economy alsotended to record the highest growth rates.1 This out-come should not come as a surprise. Integration

brings with it exposure to new technologies, designs,and products. It also enhances competition. Withworld trade growth expanding more than twice asrapidly as growth of world gross domestic product(GDP) over the past decade, the potential rewardsfrom participating in world trade are evident. Suchparticipation is predicated on the availability of goodquality products offered at competitive prices. In thisregard, a trade regime that tenders low protection todomestic producers contributes to the enhancement

1. Rapidly integrating countries experienced annual GDPgrowth three percentage points higher than slow integrators.Integration refers to trade integration as well as openness to for-eign direct investment (World Bank 1996).

of an economy’s competitiveness because it forcesdomestic producers to align their costs with those inthe rest of the world. Nevertheless, an open traderegime will only foster competitiveness when otheraccompanying policies are in place.

Over the past 20 years, average tariffs have beencut by half in developing countries and nontariffimport barriers have been sharply reduced (WorldBank 1996). Yet, for many developing countries, thishas not necessarily led to substantial trade integra-tion. Worse still, the poorest countries in the world,particularly those of Sub-Saharan Africa, lost mar-ket share during the 1990s. Such events were in partbrought about by the failure of developing countriesto produce the types of goods that would generatethe most rapid export growth. Another impedimentwas the maintenance by other countries of a rangeof import barriers to products that Sub-SaharanAfrican countries produce, including agriculturaland textile goods. Import barriers include exportsubsidies, high tariffs, and stringent rules of origin(see chapter 9). The issues of the cotton export sub-sidy granted by the United States and other agricul-tural export subsidies of the European Union (EU)and United States were a significant reason for thedisappointing results of the World Trade Organiza-tion (WTO) Ministerial Conference in Cancun in2003. A poorly functioning trade logistics environ-ment, as well as the combination of factors thatmake up the transaction costs—the cost of clearingcustoms, transport costs, noncustoms trade docu-mentation requirements, and unenforceability oflegal trade documents (World Bank 2003)—alsocontributed to the failure of many developing coun-tries to integrate successfully into the world econ-omy. High transaction costs, of which customsclearance costs are often an important element, maythus nullify the cost-reducing impact of trade liber-alization. Few customs services have managed toprovide exporters with the duty-free inputs neededto keep export prices competitive.2

The realization that customs services could beimproved has prompted many governments todevote substantial energy and resources to modern-ization. They have also mobilized external assistancein this endeavor. In response, bilateral and multilat-eral development agencies have supported manycustoms reform initiatives. International donors orfinancial institutions such as the European Union(EU), the International Monetary Fund (IMF), theInter-American Development Bank (IDB), theAfrican Development Bank (AfDB), the AsianDevelopment Bank (AsDB), the United NationsConference on Trade and Development (UNCTAD),and the World Bank (WB), have all been engaged incustoms strengthening operations. Bilateral donors,such as France, the United Kingdom, Japan, and theUnited States have also been active in providing suchsupport. In addition, the World Customs Organiza-tion (WCO) has made technical assistance (TA)available. A number of customs administrationshave improved their operations by taking advantageof this support. Yet, too many still operate ineffi-ciently, adding considerable costs to trading activi-ties while, at the same time, undermining the growthpotential of their economies.

This chapter outlines the main features of a cus-toms reform strategy and provides operationalguidelines that are likely to contribute to the suc-cess of such initiatives. It has been inspired by theknowledge of good practices; the World Bank’sown TA and project experiences (summarized inchapter 8); the approaches presented in a numberof TA reports that have been produced by diversecustoms experts and institutions, many of whichremain inaccessible to the general public; lessonslearned from several customs modernization ini-tiatives (chapter 7); and consultations with manycustoms officials and consultants who haveassisted in customs modernization initiatives. Thefirst section reviews the key objectives of customsmodernization initiatives. The second sectionspells out a number of contextual factors that needto be adequately addressed at the outset of areform process to enhance its chances for success.The third section defines the key steps in preparinga customs modernization strategy. The next sec-tion elaborates on implementing key issues of thestrategy. The final section provides some opera-tional conclusions.

4 Customs Modernization Handbook

2. A recent study of trade liberalization for a sample of countriesin Africa concluded “It is in the area of providing exporters withaccess to low tariffs and tax-free inputs that the progress of thesample countries has been the most disappointing. The samplecountries had made little progress in implementing timely reim-bursements to exporters of either import duties or value addedtax (VAT) on inputs.” (Hinkle, Herrou-Aragon, and Kubota2003, pp. 82–83.)

Objectives of Customs Operations

Customs administrations are expected to raise sub-stantial revenue, provide domestic producers withprotection, provide supply chain security, preventthe importation of prohibited or unsafe imports(for example, illegal weapons or out-of-date medi-cines), and combat the trade of narcotics throughthe implementation of laws and regulations that arein line with WTO commitments. Customs admin-istrations are expected to accomplish these objec-tives both effectively (by achieving them) and effi-ciently (at the lowest possible cost to the budgetand to the trading community) without compro-mising trade facilitation.

Evolution of Customs Role

The responsibilities of customs continue to evolve.Customs administrations are now increasinglyregarded as “the key border agencies” responsiblefor all transactions related to issues arising from theborder crossings of goods and people. Some ofthese functions are undertaken in close coopera-tion with other national agencies.3 The operationalguidelines of customs cannot give equal weight toall functions constantly; choices and priorities areinevitable in light of changing circumstances:

• Raising revenue has traditionally been high onthe agenda of governments, represented by theMinistry of Finance (MOF), because of the crit-ical importance of import duties as a source ofbudget revenue for many developing countries.Revenues from import duties for a sample ofAfrican countries accounted for just under 30percent of total tax revenue, on average. In com-parison, this share averaged 22 percent for coun-tries in the Middle East, 13 percent for LatinAmerican countries, and 15 percent for Asiancountries (see annex 1.A). While import tariffsare widely recognized as more distortionarysources of revenue than general sales andincome taxes, they remain important for historicreasons, and because they are relatively easy to

collect. Collection of VAT on imports constitutesanother major source of budget revenue. There-fore, a control mentality that ensures that allduties are assessed and paid has permeated cus-toms, irrespective of whether this causes delaysin the release of imports. With tariff ratesdeclining over time, customs revenues as a shareof the total budget revenues have also tended todecline in most countries; but customs revenuesare still a major concern of MOF officials. Thispriority has been reflected in many past customsreforms and TA initiatives.

• Import tariffs are meant to protect domesticproducers, who expect customs administrationsto ensure that all importers pay the officialimport taxes to ensure a level playing field. Onaverage, customs duties amount to 17 percent ofthe total import value in a sample of Africancountries, 12 percent in the Middle East, 10 per-cent in Asia and the Pacific, and 7 percent in theWestern Hemisphere (see annex 1.B).4 Increas-ingly, import tariffs are being seen as an instru-ment of protection rather than of raising budgetrevenue. This is clearly so in developed countrieswhere tariffs provide only a tiny share of totalrevenue and on average represent less than1 percent of overall import value. Import tariffsin developing countries are high, however, thushampering trade among developing countries aswell as the competitiveness of the countries’economies (Ebril, Stotsky, and Gropp 1999).

• Trade facilitation has attracted increasing inter-est in recent years as evidenced by the WTOCancún Agenda and the WCO Revised KyotoConvention. This interest has been broughtabout by an increasing commitment of govern-ments to pursue a private sector–orientedgrowth strategy, combined with increased pri-vate sector assertiveness and demands for bettergovernment services. Cost reductions to thetrader, derived from easier customs procedures,stem largely from the possibility of reducing

Strategy for Customs Modernization 5

3. See, for example, the International Convention on the Har-monization of Frontier Control of Goods (UNECE 1982) avail-able at http://www.unece.org/trans/conventn/harmone.pdf.

4. The IMF estimated these collection rates for a slightly differ-ent sample of countries for 1995. It appears that the rates fellslightly for the sample countries in Asia and the Pacific, but stag-nated and even rose slightly in Sub-Saharan Africa and MiddleEastern countries included in the sample (Ebril, Stotsky, andGropp 1999).

inventories and the amount of operations capi-tal, as well as the possibility for traders to satisfyincreasingly stringent “just in time” require-ments.

• Civil society is demanding better governanceand has identified customs services as particu-larly prone to harboring corrupt practices.Targeting customs for improvements fully rec-ognizes the fact that the integrity situationreflects the integrity of the greater society towhich the administration belongs.

• Over the years, customs administrations havereceived a mandate to protect society. This hasbeen included in the mandate of the WCO, toreflect the notion that most customs adminis-trations are responsible for preventing the cross-border movement of dangerous and unsafegoods. However, the security concern was ele-vated to new heights after the events of Septem-ber 11, 2001. The focus shifted from just importsto the entire supply chain, including exports.New procedures are being introduced and addi-tional safety measures are being prepared andimplemented.

Customs Role and Priorities in the 21st Century

It is difficult to predict the future role of any insti-tution, and there is no one correct or universallyapplicable response to anticipated trends in cus-toms, as each country will respond in ways that arebest suited to its needs, operating environment,national priorities, and cultural heritage. However,some general issues or themes are emerging thatsuggest the future role and priorities of customs.

First, in spite of declining tariff rates broughtabout by successive rounds of trade liberalization,the revenue mobilization and control functions ofcustoms are likely to remain substantial, for severalreasons: (a) the fiscal dependency on customs rev-enues is likely to linger for some time, in light of thedifficulty many developing countries encounter inbroadening their tax bases; (b) imports will proba-bly constitute a major tax base for levying VAT, andcustoms is well positioned to control the goods atthe time of importation; (c) customs will remainthe responsible agency to ensure that goods thatwere imported for other than home consump-tion are not diverted to such consumption; and(d) assessing VAT refunds on exported goods will

continue to require a high level of control overexported goods.

Second, in all countries, customs will continueto collect trade data for statistical and regulatorypurposes.

Third, customs will continue to be responsiblefor effective and efficient border management tofacilitate trade, a major contributor to the interna-tional competitiveness of nations. This will occurregardless of whether trade facilitation is formallyincorporated into multilateral trade negotiations.As such, harmonizing, simplifying, and effectivelycoordinating all national border managementrequirements and commitments will remain prior-ity responsibilities of customs.

Fourth, based on a heightened awareness of thethreat posed by international terrorism andtransnational organized crime, governments willrequire that customs administrations take on alarger role in ensuring national security and lawenforcement. To that effect, customs administra-tions are likely to institute a range of changes to sys-tems, procedures, and even administrative respon-sibilities to increase confidence in the level ofcontrol exercised over both imports and exports.Security checks will increasingly take place at thepoint of export in addition to the point of entry.