The performance of de novo commercial banks: A profit efficiency approach

Upload

khangminh22Category

view

0download

0

Master Thesis

TAMTA PUTURIDZE

Brno

2021

Supervisor: Dagmar Vagnerova Linnertova

Financial Markets

FACULTY OF ECONOMICS AND ADMINISTRATION

Cross sectional analysis of commercial banks performance

operating in Georgia

Bibliographic record

Author: Tamta Puturidze Faculty of Economics and Administration

Masaryk University Department of Finance

Title of Thesis: Cross Sectional analysis of commercial banks performance operat-ing in Georgia

Degree Programme: Financial Markets

Field of Study: Financial Markets

Supervisor: Dagmar Vagnerova Linnertova

Year: 2021

Number of Pages: 78

Keywords: Commercial bank, valuation, ratios, analysis

Abstract

This master thesis analysed the financial performance of two systematically important commercial banks in Georgia for the financial year 2020. Selected banks were measured and compared to each other with the following parametres comprising: capital adequacy, assets quality, earnings, liquidity and different financial ratios. In addition some relevant stock valuation models were applied to compute fair value of their stocks and give recommendations for investment percpetive.

Declaration

I certify that I have written the Master’s Thesis ’’Cross sectional analysis of commercial banks operating in Georgia’’ by myself under the supervision of Dagmar Vagnerova Lin-

nertova and I have listed all the literature and other sources in accordance with legal reg-ulations, Masaryk University internal regulations, and the internal procedural deeds of Ma-

saryk University and the Faculty of Economics and Administration.

Brno, .......................................

Tamta Puturidze

Acknowledgement

I would like to give a sincere thanks to my supervisor Ing. Dagmar Vagnerova Linnertova, Ph.D. for her guidanc, as well as for providing necessary information and the direction. I would also like to express my gratitude to my mother Dodo Davituliani for her continuous moral support and motivation during all my life and studies.

Šablona DP 2.0.1 (9. ledna 2018) © 2014, 2016, 2018 Právnická fakulta Masarykovy univerzity

Table of content

List of Figures 11

List of Tables 12

List of equations 13

List of Terms and Abbreviations 14

Introduction 17

1 Economic overview 18

2 Banks Business model 24

2.1 Bank Regulatory Environment in Georgia ..................................................................... 25

2.1.1 Pillar 1 and capital buffer requirements ................................................................................ 25

2.1.2 Pillar 2 Requirements............................................................................................................ 28

3 Theory of valuation 30

3.1 Bank Valuation.......................................................................................................................... 30

3.2 Financial ratios .......................................................................................................................... 32

3.3 Valuation Models ..................................................................................................................... 32

4 Fundamental analysis of TBC and BGEO 37

4.1 Implications of COVID-19 ................................................................................................... 37

4.2 Georgia Banking Industry Analysis .................................................................................. 40

4.2.2 Porter’s Five Forces Analysis .............................................................................................. 45

4.3 Business Model of TBC and BGEO ................................................................................. 47

4.3.2 Market Share Analysis ............................................................................................................. 51

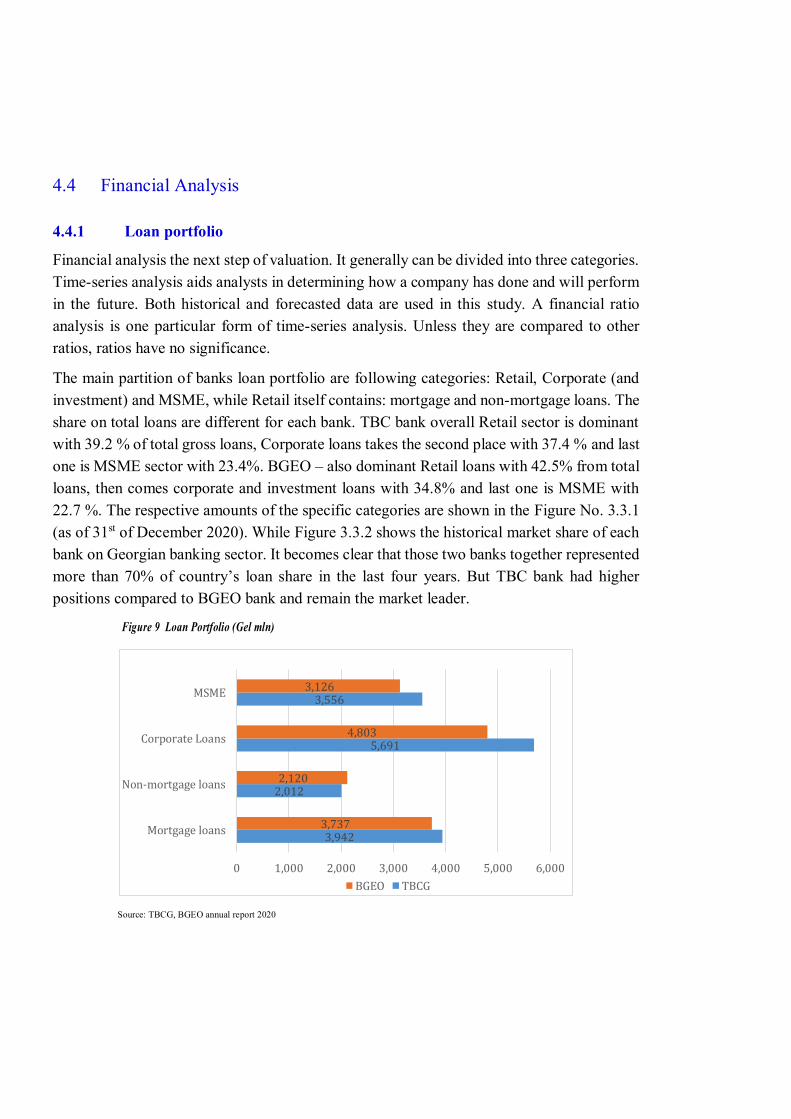

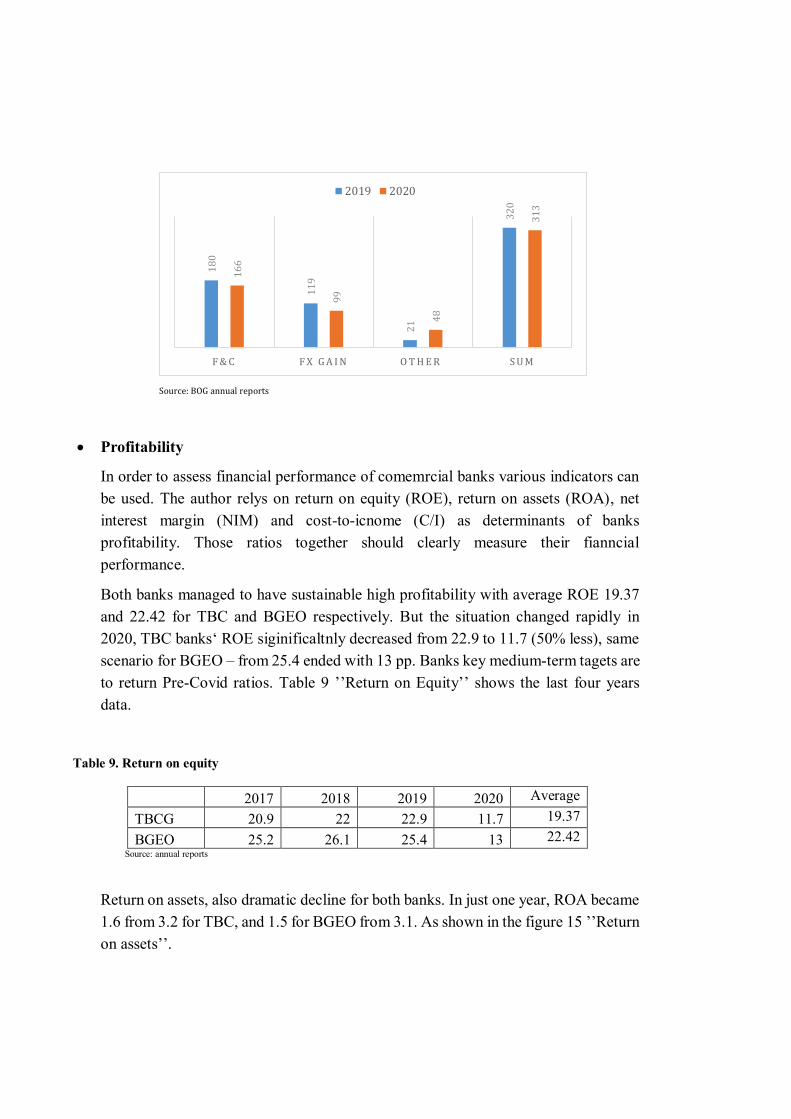

4.4 Financial Analysis .................................................................................................................... 54

4.4.1 Loan portfolio ................................................................................................................. 54

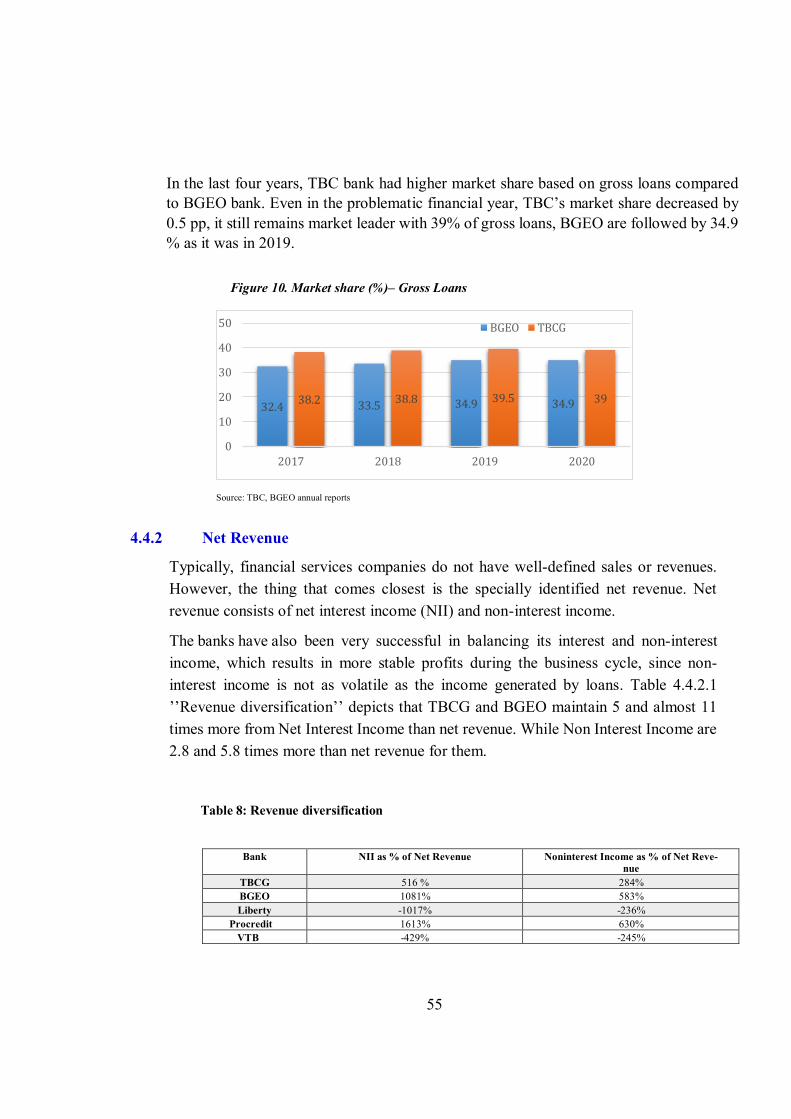

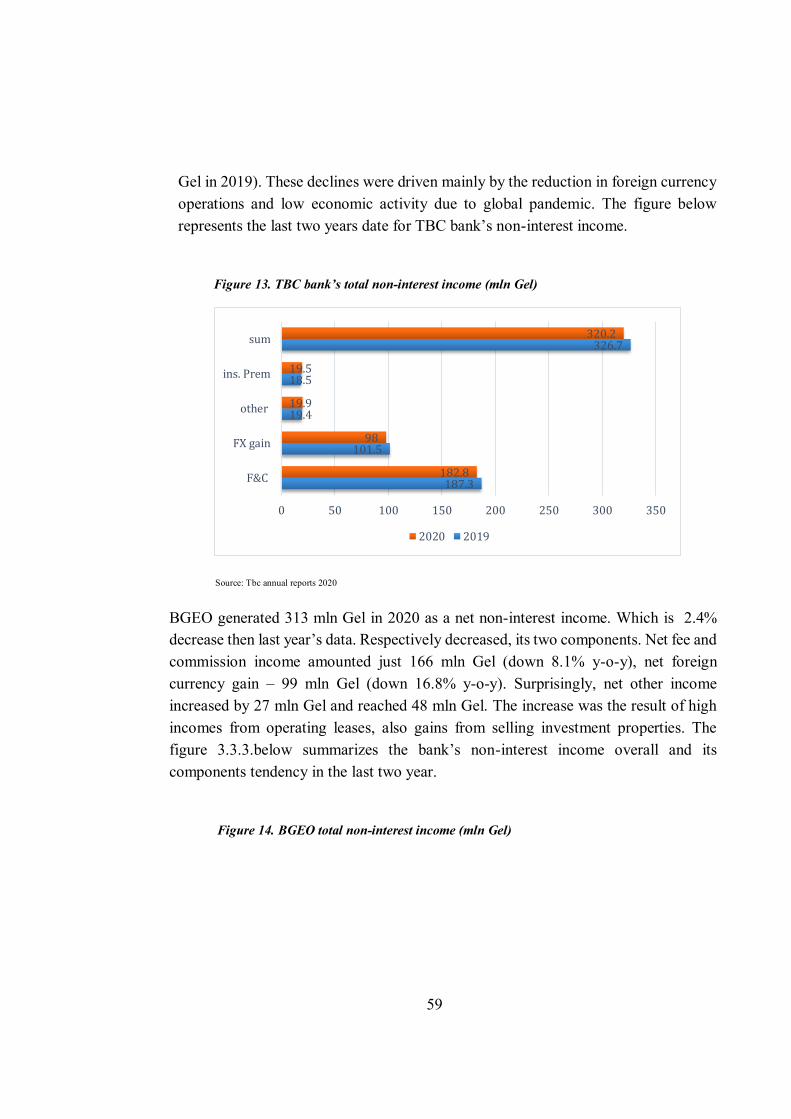

4.4.2 Net Revenue .................................................................................................................... 55

4.4.3 Operating expenses ....................................................................................................... 63

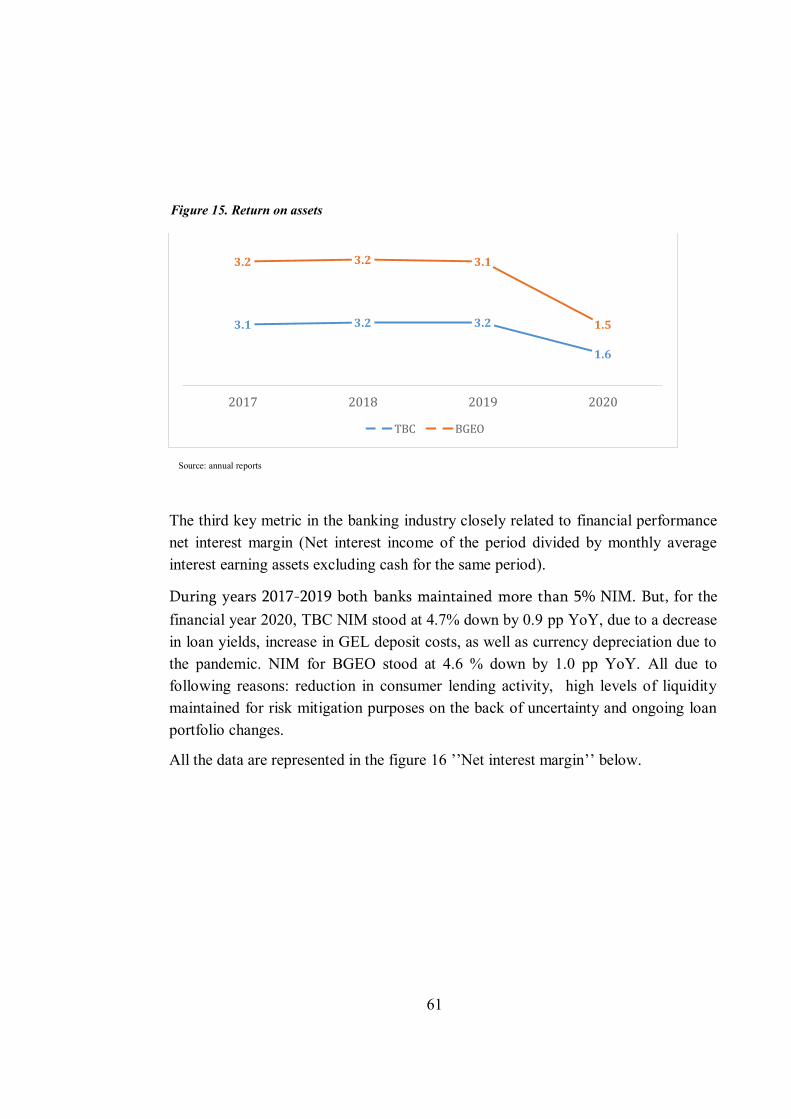

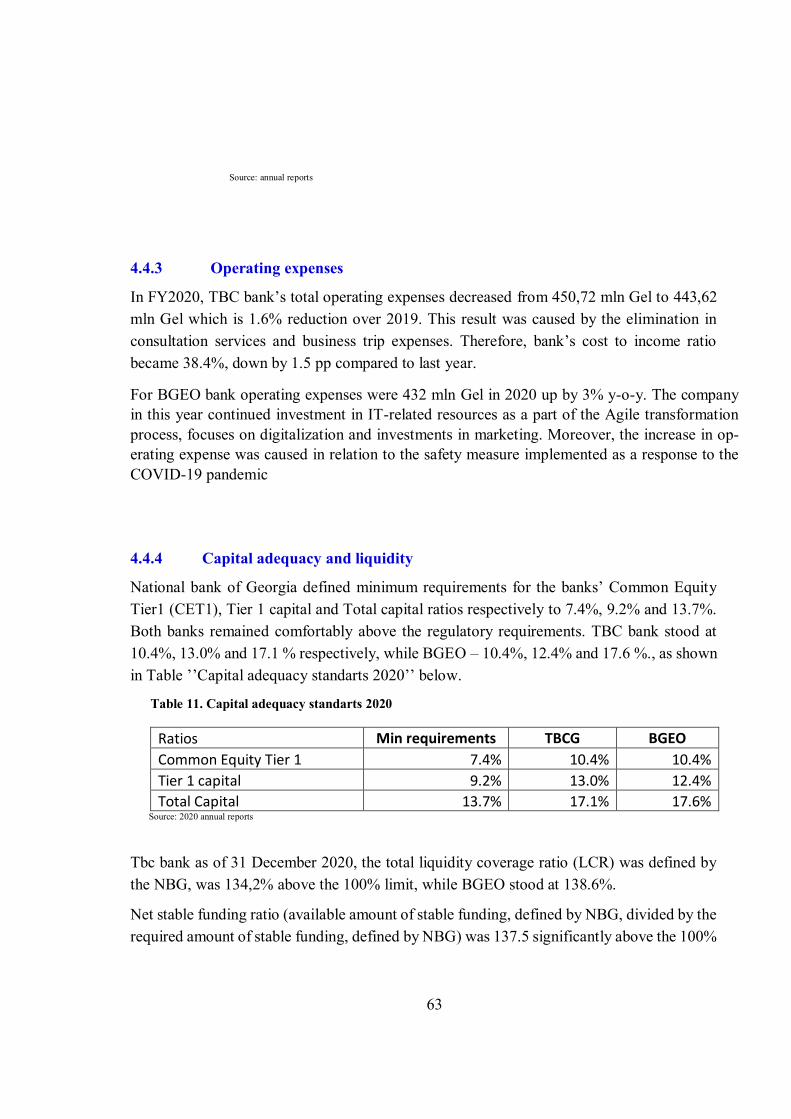

4.4.4 Capital adequacy and liquidity ................................................................................. 63

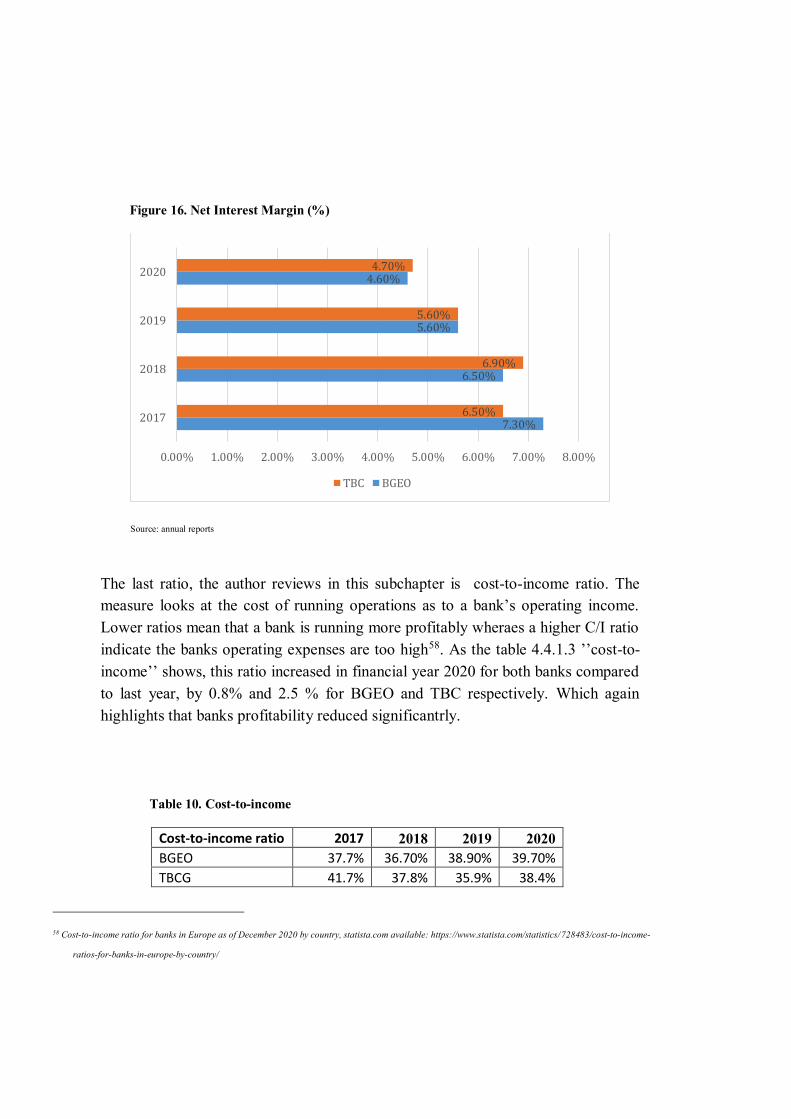

4.4.5 Dividend Policy .............................................................................................................. 64

5 Valuation 66

5.1 FCFE ............................................................................................................................................. 66

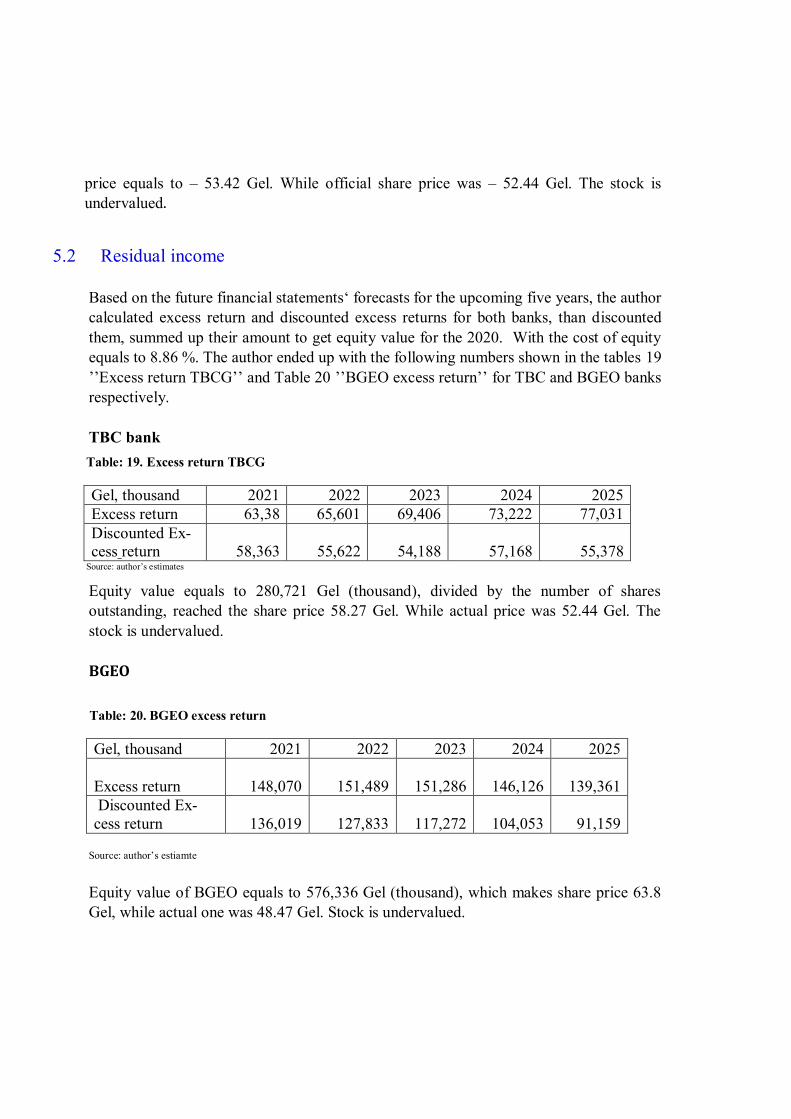

5.2 Residual income ........................................................................................................................ 68

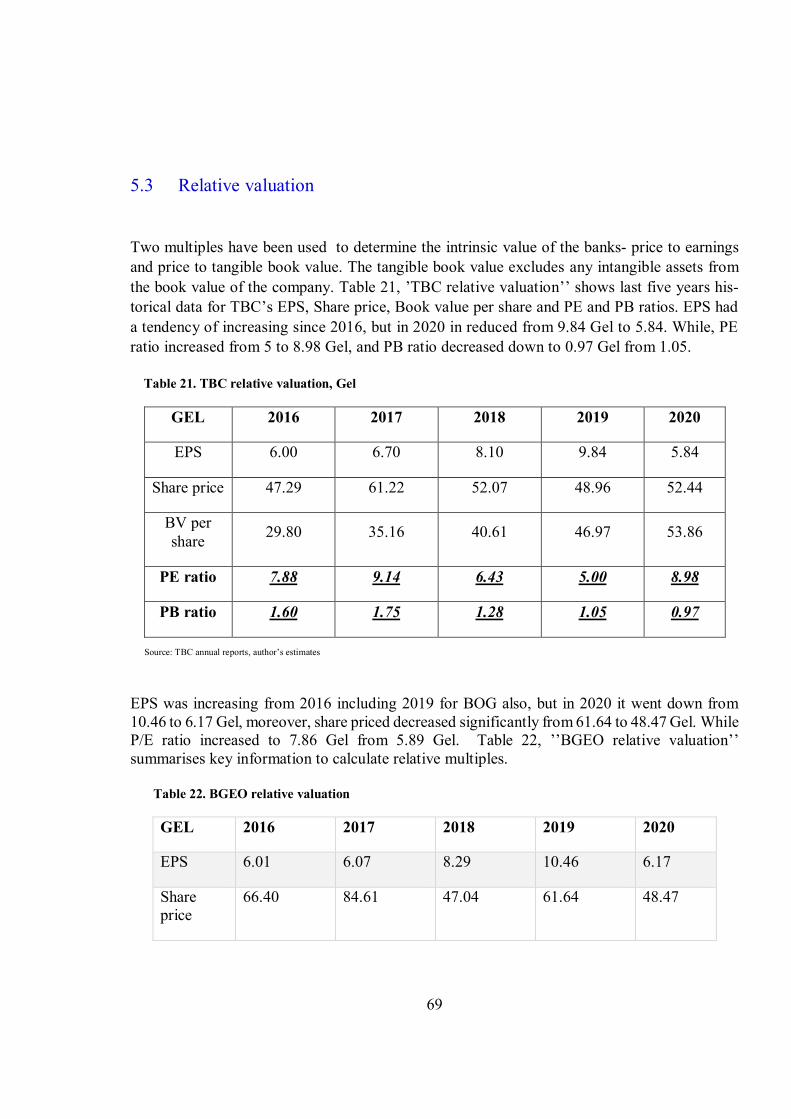

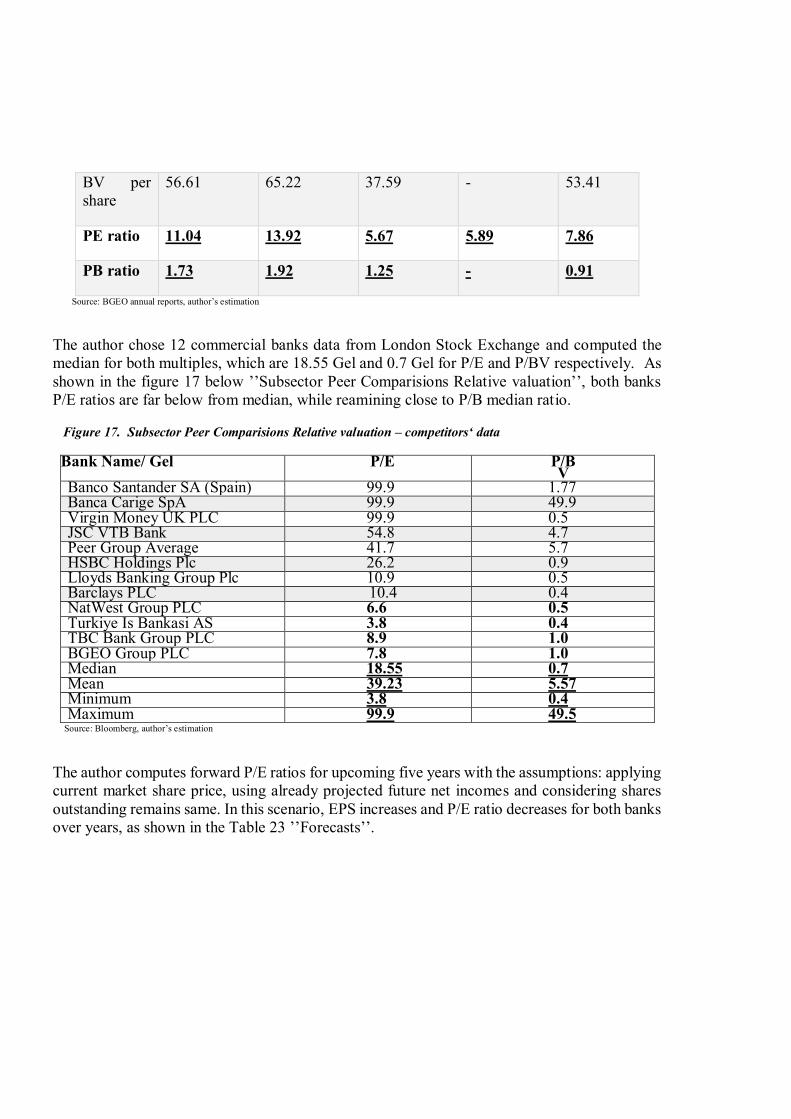

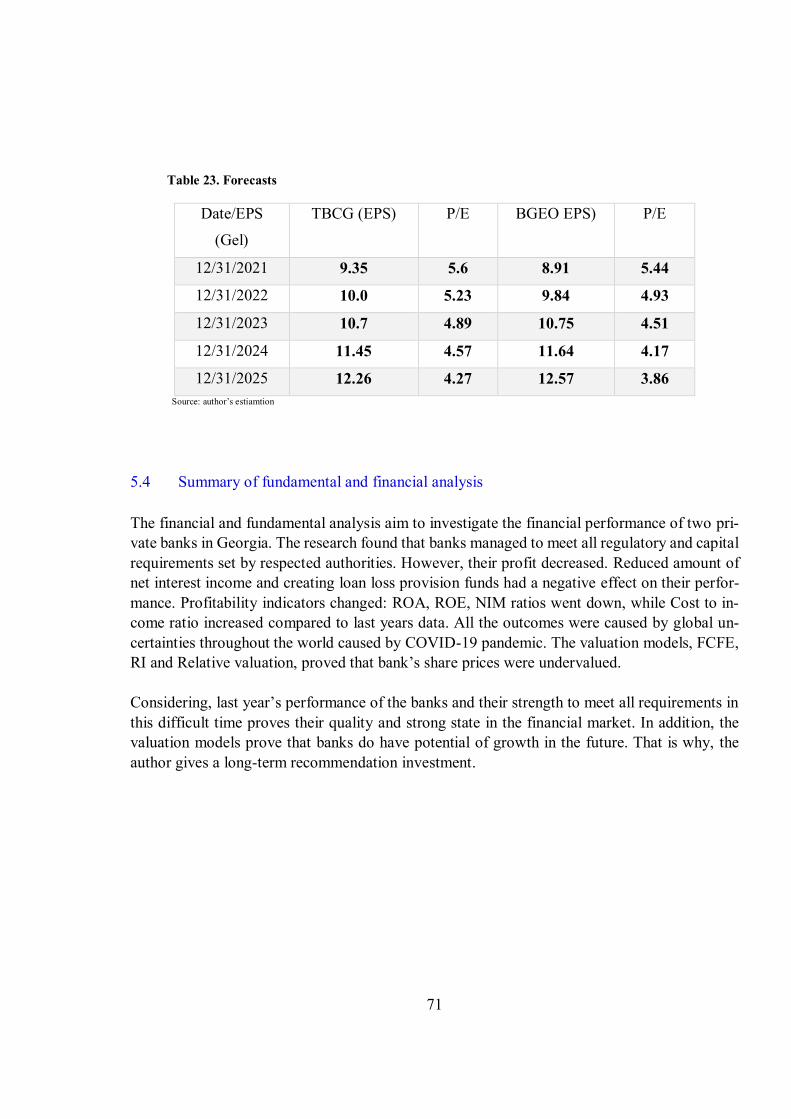

5.3 Relative valuation ..................................................................................................................... 69

5.4 Summary of fundamental and financial analysis .......................................................... 71

Conclusion 72

References 74

11

List of Figures

FIGURE 1. GDP ANNUAL GROWTH RATE (ANNUAL %) .............................................................. 19 FIGURE 2. FOREIGN DIRECT INVESTMENTS (MLN USD) ........................................................... 20 FIGURE 3. GDP PER CAPITA GROWTH (ANNUAL %) .................................................................. 21 FIGURE 4. MONETARY POLICY INTEREST RATE DYNAMICS ........................................................ 22 FIGURE 5. PROFITABILITY RATIOS OF BANKING SECTOR............................................................ 44 FIGURE 6: DEPENDENCE ON LOANS RELATED INCOME .............................................................. 51 FIGURE 7: MARKET SHARE ANALYSIS ....................................................................................... 52 FIGURE 8: DEPOSITS FUNDING ................................................................................................. 53 FIGURE 9 LOAN PORTFOLIO (GEL MLN) .............................................................................................. 54 FIGURE 10. MARKET SHARE (%)– GROSS LOANS ..................................................................... 55 FIGURE 11. NET INTEREST INCOME (THOUSANDS, GEL) ........................................................... 56 FIGURE 12. NON INTEREST INCOME (THOUSANDS, GEL) ........................................................... 58 FIGURE 13. TBC BANK’S TOTAL NON-INTEREST INCOME (MLN GEL) ......................................... 59 FIGURE 14. BGEO TOTAL NON-INTEREST INCOME (MLN GEL) .................................................. 59 FIGURE 15. RETURN ON ASSETS ............................................................................................... 61 FIGURE 16. NET INTEREST MARGIN (%) .................................................................................. 62 FIGURE 17. SUBSECTOR PEER COMPARISIONS RELATIVE VALUATION – COMPETITORS‘ DATA ... 70

List of Tables

TABLE.1 SYSTEMIC BUFFER REQUIREMENTS ........................................................................... 27 TABLE 2. KEY FINANCIAL INDICATORS OF THE GEORGIAN BANKING SECTOR (GEL BILLION) .... 41 TABLE 3. AVERAGE INTEREST RATE ON COMMERCIAL BANK LOANS ......................................... 42 TABLE 4. AVERAGE INTEREST RATE ON COMMERCIAL BANK DEPOSITS ..................................... 42 TABLE 5. PROFITABILITY OF THE INDUSTRY............................................................................. 43 TABLE 6. INTEREST MARGIN FOR GEORGIAN BANKS ................................................................ 44 TABLE 7. NON-PERFORMING LOANS ........................................................................................ 45 TABLE 8: REVENUE DIVERSIFICATION...................................................................................... 55 TABLE 9. RETURN ON EQUITY ................................................................................................. 60 TABLE 10. COST-TO-INCOME .................................................................................................. 62 TABLE 11. CAPITAL ADEQUACY STANDARTS 2020 ................................................................... 63 TABLE 12. LIQUIDITY STANDARTS .......................................................................................... 64 TABLE 13. BOG DIVIDEND INFORMATION ............................................................................... 65 TABLE 14. DIVIDEND INFORMATION. ....................................................................................... 65 TABLE 15. FORECASTS............................................................................................................ 66 TABLE 16. COMPONENTS OF VALUATION ................................................................................. 66 TABLE 17. FCFE (BGEO) ...................................................................................................... 67 TABLE 18. FCFE (TBCG) ...................................................................................................... 67 TABLE: 19. EXCESS RETURN TBCG ........................................................................................ 68 TABLE: 20. BGEO EXCESS RETURN ......................................................................................... 68 TABLE 21. TBC RELATIVE VALUATION, GEL ........................................................................... 69 TABLE 22. BGEO RELATIVE VALUATION ................................................................................ 69 TABLE 23. FORECASTS............................................................................................................ 71

13

List of equations

EQUATION 1. FCFE ................................................................................................................ 33 EQUATION 2. GROWTH RATE ................................................................................................... 34 EQUATION 3. EQUITY VALUE .................................................................................................. 35 EQUATION 4. EXCESS RETURN ................................................................................................. 35 EQUATION 5. PRICE TO EARNINGS RATIO.................................................................................. 35 EQUATION 6. PRICE TO BOOK RATIO ........................................................................................ 36

List of Terms and Abbreviations

Gel Georgian Lari

Basel II International Convergence of Capital Measurement and Capital Standarts

Basel III Third Basel Capital Accord

BGEO Bank of Georgia

CAR Capital Adequacy Ratio

CAPEX Capital Expenditures

CEO Chief Executive officer

CET1 Common Equity Tier 1

CoE Cost of equity

C/I Cost-to-income

DDM Dividend Discound Model

DPS Dividend per share

EPS Earnings per share

EU European Union

FCFE Free cahs-flwo to equity

FDI Foreign Direct Investmetns

GDP Gross Domestic Product

GEO Georgia

GRAPE General Risk Assessment Program

IMF International Monetary Fund

LCR Liquidity Coverage Ratio

NBG National Bank of Georgia

NII Net interest income

NIM Net Interest Margin

15

NPL Non-performing loan

NSFR Net Stable Funding Ratio

P/B Price to book value

P/E Price to earnings

PV Present value

RI Residual income

ROA Return on Assets

ROE Return on Equity

RWA Risk Weighted Assets

TBC TBC PLC

T1 Tier 1 Capital

UK United Kingdom

US United States

WC Working Capital

17

Introduction

The banking sector is critical to the stability of financial markets and has a direct effect on the economy’s success. This is especially true for Georgia where other financial market representa-tives are not developed and banking sector remains key driver. Commercial banks have under-gone various regulatory reforms and changes since establishment. All together aiming to make them way more adequately capitalized and strong for the sake of depositors, creditors and for the whole economy. The purpose of this master thesis ’Cross sectional analysis of commercial banks operating in

Georgia’’ is to evaluate two domestic commercial banks’ financial performance and value their stocks. Both are operating in the same industry, listed on London Stock Exchange which make them easier for comparison. The theoretical part of the thesis starts with country’s economic overview with the help of vari-

ous indicators: GDP growth, Inflation rate, Foreign Direct Investments etc. Then comes descrip-tion of banking industry where author focuses on the regulatory and capital requirements set for commercial banks as they determine their operations and set boundaries. After that it is explained relevant valuation models solely for financial institutions. In the practical part the author firstly analyses overall country’s banking industry and then fo-

cuses on the selected banks. An attention is given to the banks’ business models’, their profita-bility and capital adequacy ratios, costs, dividend policies and, most importantly stock valuation models computation process. Also, it is explained implications of Covid-19, set by government or bank that made changed in their regulation requirements. In the end, the author summarises the banks’ financial performance, compares them to each other, declares own opinion about the firms’ future development and gives recommendations.

1 Economic overview

The first chapter of the thesis starts with reviewing the economic development of Georgia and analysing current state. The author aims to give overall idea of the environment banking sector operates in. For that reason different ratios and indicators will be mentioned.

Georgia is located at the crossroads of Europe and Asia, which makes it an unique geographic advantage for market integration with the rest of the world, including the European Union.

It takes the 7th place globally on Ease of Doing Business1, second place for starting a business and twelfth place in Economic Freedom Index2. All this positive ranking make the country attractive for investors. Overall country has BB/Negative rating according to Fitch, while Moody gives it Ba2/Stable rating. Up this moment Georgia has a developing economy.

In its thirty years old of independence, there were implemented many economic reforms, country faced rapid growths but still has not fully addressed the major economic challenges: poverty and high unemployment rate. While the national unemployment rate makes 18.5%3 in 2020, youth unemployment reaches more than 40% in some of the regions. According to World Bank4, poverty (national measure) declined to 19.5 percent in 2019, almost half its 2007 rate, as a result of better governance and sound macroeconomic policies. However, in the country has not been created enough jobs, and still many Georgians have to continue working in low-productivity agricultural jobs or leave the country to find relatively high paid ones.

After its independence from the Soviet Union in 1991, Georgia has once again become a place for competing interests. A variety of factors played a role in Georgia’s

economic collapse in the 1990s. Civil war, corruption, terrorism, a complete lack of knowledge about the market environment, hyperinflation, and the oil crisis all played a role in this situation, making it difficult to pick out the most damaging factor5. It took

1 Available at: https://openknowledge.worldbank.org/bitstream/handle/10986/32436/9781464814402.pdf, page 16

2 Available at: https://www.fraserinstitute.org/studies/economic-freedom-of-the-world-2019-annual-report

3 Available at: https://www.geostat.ge/ka/modules/categories/683/dasakmeba-umushevroba

4 Available at: https://www.worldbank.org/en/country/georgia/overview#1

5 The Economic History of Independent Georgia, Forbes Georgia, available at: https://forbes.ge/the-economic-history-of-independent-georgia/

19

four years the economy after independence to start creative positive GDP geowth rate. Figure 1.’’GDP annual growth rate’’ clearly shows that GDP growth began only after

1995 year, it took four years the economy to put positive growth rate.

Figure 1. GDP annual growth rate ( %)

Source: the world bank data6

In 1995 GDP increased by 2.6 %, while in 1996-1997, GDP had already increased by 10.6%, which was due to relatively stable political environment, the end of war and the monetary reforms implemented in September of 19957 when Georgian national currency Lari replaced the coupon (the currency of Soviet Union). According to national statistical office of Georgia, by 1996-1997, Georgian exports increased by 57%. 2004-2007 year was a rapid economic growth period. The rate of crime and corruption significantly decreased, regulations implemented by the government motivated business.

6 Online, Available at: https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2019&locations=GE&start=1991

7 Online, Available at: https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2019&locations=GE&start=1991

-50.00

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

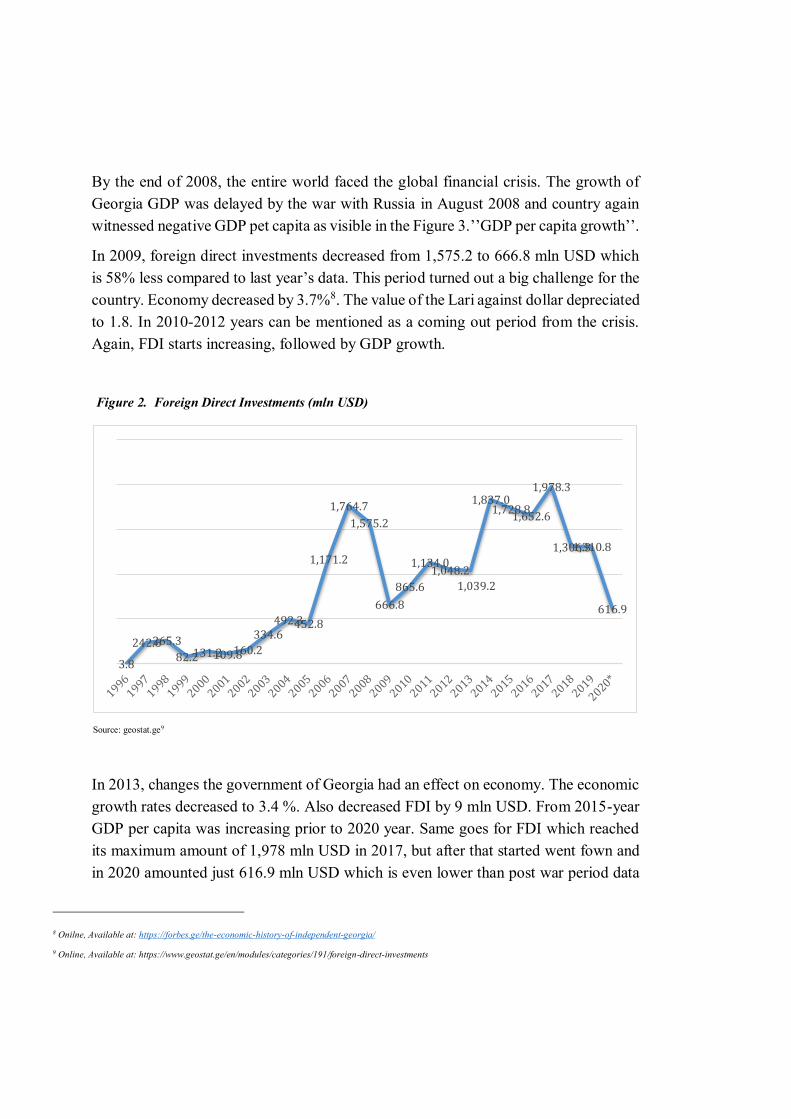

By the end of 2008, the entire world faced the global financial crisis. The growth of Georgia GDP was delayed by the war with Russia in August 2008 and country again witnessed negative GDP pet capita as visible in the Figure 3.’’GDP per capita growth’’.

In 2009, foreign direct investments decreased from 1,575.2 to 666.8 mln USD which is 58% less compared to last year’s data. This period turned out a big challenge for the

country. Economy decreased by 3.7%8. The value of the Lari against dollar depreciated to 1.8. In 2010-2012 years can be mentioned as a coming out period from the crisis. Again, FDI starts increasing, followed by GDP growth.

Figure 2. Foreign Direct Investments (mln USD)

Source: geostat.ge9

In 2013, changes the government of Georgia had an effect on economy. The economic growth rates decreased to 3.4 %. Also decreased FDI by 9 mln USD. From 2015-year GDP per capita was increasing prior to 2020 year. Same goes for FDI which reached its maximum amount of 1,978 mln USD in 2017, but after that started went fown and in 2020 amounted just 616.9 mln USD which is even lower than post war period data

8 Onilne, Available at: https://forbes.ge/the-economic-history-of-independent-georgia/

9 Online, Available at: https://www.geostat.ge/en/modules/categories/191/foreign-direct-investments

3.8

242.6265.3

82.2131.2109.8160.2

334.6492.3452.8

1,171.2

1,764.7

1,575.2

666.8

865.6

1,134.01,048.2

1,039.2

1,837.01,728.8

1,652.6

1,978.3

1,306.31,310.8

616.9

21

in 2009. The completion of the South Caucasus Pipeline Expansion (the gas pipeline linking Azerbaijan and Turkey), the transition of many businesses to domestic ownership, and debt repayments between related companies are all contributing to the decline. FDI still remained the largest source of currency inflows despite the fall10.

In 2019 Georgian Lari faced another pressure. A Russian ban on direct flights to and from Georgia has been in force since July 2019. Due to the restrictions, some political uncertainties inflation has risen from 2.6 percent in 2018 to 6.4 percent in September 2019.

Figure 3. GDP per capita growth (annual %)

Source: the world bank data11

Georgia’s real GDP decreased by (-6.1 %) in 2020 due to COVID-19 related lock-down and restrictions throughout the year. Annual inflation dropped to 2.4% in December, from 3.8% in previous months. During 2020, NBG maintained a moderately tight monetary policy to anchor inflation mainly by refinance rate.

The main tool for the monetraty policy was refinance rate. The monetary policy committee’s decisions on monetary policy rate adjustments are based on real and

expected economic and financial market developments. If forecast inflation exceeds the target inflation rate, the NBG will tighten monetary policy by raising the policy

10Online, availbale at: https://www.ebrd.com/transition-report, country assessment Georgia,

11 Available at: https://data.worldbank.org/indicator/NY.GDP.PCAP.KD.ZG?end=2019&locations=GE&start=1986&view=chart

-50.00

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

rate to counteract a potential price spile. As a result, aggregate demand falls, resulting in a decline in aggregate price levels. The NBG, on the other hand, would follow an expansionary monetary policy by lowering the refinancing rate when aggregate demand is poor and current inflation expectations are below the goal. Reduced monetary policy rates translate into lower loan interest rates, which boosts credit to the economy and boosts aggregated demand.

As shown in the Figure 4.’’ Monetary policy interest rate dynamics’’ interest rate responds to the economic events happening in the country. The highest percentage was announced in May after the first total lockdown, the rate decreased just by 0.5 pp throughout the year and reached the year minimum level in the end of financial year -8%.

Figure 4. Monetary policy interest rate dynamics

Source: NBG12

12 Monetary Policy Rate statistical data. Available at: https://www.nbg.gov.ge/index.php?m=306&lng=eng

0.00

2.00

4.00

6.00

8.00

10.00Interest rate %

23

During the economic recession, government and NBG implemented many reforms, measures, trying to help businesses and households. The extension of IMF program also played a significant role in this process.

The gradual easing of the existing sanctions is expected to accelerate Georgia's economic recovery in 2021. Restrictions, vaccinations, strengthened domestic and international sentiments, and continued fiscal stimulus are all on the horizon. Nonetheless, the COVID-19 pandemic remains one of the most significant uncertainties in the development forecast.

2 Banks Business model

TBC Bank Group PLC (TBC Bank) and Bank of Georgia PLC (BGEO) are industry-leading systematically important banks in Georgia. To appraise such companies, first is needed to understand the theoretical basis of their business models.

A bank is profit seeking organization, which always plays a major part in the economy. In general, it is differentiated three types of banks: commercial banks, universal banks and investments banks. They do differ from each other by the functions and operations. The author below reviews the commercial bank, since the institutions that are valued belong to this category.

A commercial bank is a financial institution which performs the functions of accepting deposits from the general public and giving loans for investment with the aim of earning profit13. Besides those two main operations, commercial banks can offer customers other services: like trust operations, investment and financial advices and etc. Net interest income (NII) is the most significant revenue item for the majority of commercial banks. They do benefit from charging big interest rates on loans while paying low interest rate on deposits. The difference between the mentioned interest rates is called interest spread, is often tracked by analysts14. The related metric is net interest margin (NIM), which is a main metric in the industry.

Commercial banks’ profitability is influenced by a number of factors. The interest rates

that a bank pays on deposits and charges on loans are the most important. Naturally, not all of the issued loans are completely paid. As a result, every bank must be ready for the potential losses and set aside loan loss provisions. Loan loss provisions, also known as credit loss provisions, are a type of risk expense. Operating expenses are the third main group, with wages, salaries, and employee benefits typically ranking first.

13 Commercial Bank: Definition, Function, Credit Creation and Significances. Economic Discussion [online]. 2013 [cit. 2017-02-21]. Available at

http://www.economicsdiscussion.net/banks/commercial-bank-definition-function-credit-creation-and-significances/607 14 Commercial Bank: Definition, Function, Credit Creation and Significances. Economic Discussion [online]. 2013 [cit. 2017-02-21]. Available at

http://www.economicsdiscussion.net/banks/commercial-bank-definition-function-credit-creation-and-significances/607

25

2.1 Bank Regulatory Environment in Georgia

Banks amass large sums of money from both individual and corporate customers, which can be put at risk because of the financial institution’s financial difficulties. For that reason, a regulator, normally the national bank or another official body, establishes strict risk thresholds that banks must not exceed. Banking supervision is carried out by the National Bank of Georgia to promote financial stability. Articled 96 and 96 of Georgia’s

Constitution, as well as the Organic Law of Georgia ’’On the National Bank of Georgia,’’

the ’’Law on the Activities of Commercial Banks,’’ and other related laws, describe the

National Bank of Georgia’s mandate.

The National Bank of Georgia conducts risk-based supervision within framework of the General Risk Assessment Program. This process is regulated by the ‘’Rule on

General Risk Assessment Program (GRAPE)’’. GRAPE entails assessment of risk

levels of commercial banks according to the following risk categories: credit risk, liquidity risk, market risk, operating risk, business model and profitability risk, as well as considering the macroeconomic environment, group structure and corporate governance. Furthermore, GRAPE considers a bank’s potential access to resources in the case of risks of being realized15.

2.1.1 Pillar 1 and capital buffer requirements

Capital requirements for commercial banks are defined by Basel III standards, namely Regulation 575/2013 adopted on 26 June 2013 by the European Parliament and Commission, and Directive 2013/36/EU16. The Third Basel Agreement applies majority of countries all over the world.

BASEL III is a comprehensive reform designed to improve banking sector supervision and risk management. It based on the prior document International Convergence of Capital Measurement and Capital Standards, also known as BASEL II. Three pillars make up the Basel Framework. Calculations of regulatory capital requirements for credit, industry, and operating risk are implemented in Pillar 1. Pillar 2 lays out the

15 GRAPE, available at: https://www.nbg.gov.ge/uploads/publications/grape/grape_f.pdf, page 7

16 Capital Adequacy Standards, available at: https://www.nbg.gov.ge/index.php?m=698

steps the bank should take to determine its capital adequacy, as well as the mechanism that a regulator should use when evaluating the risks that banks take. Pillar 3 defines transparency standards with the aim of promoting market discipline. There are some parts that will be extensively discussed because they have a significant impact on bank’s core business and intrinsic value.

According to the amendments to’’the Regulation on Capital Adequacy Requirements

for Commercial Banks’’ Pillar 1 minimum requirements have become compatible with

the framework established by Basel Committee of Banking Supervision. Conservation buffer in the amount of 2.5% which used to be merged with minimum requirements, has been separated from the minimum capital requirements (Common Equity Tier 1, Tier 1 and Total Regulatory Capital respectively being 7%, 8.5% and 10.5%). Therefore, updated minimum capital requirements are: 4.5%, 6% and 8% for Common Equity Tier 1, Tier 1 and Total Regulatory Capital respectively17.

Another important explanation why financial services business are valued differently than non-financial corporations is because of capital requirements. The criteria influence not just how a bank works, but also how much equity it must hold to satisfy the requirements.

From an economic standpoint, Tier 1 Capital must possess the characteristics of shareholders’ equity. Tier 1 Capital must be able to withstand future losses while also

allowing the bank to operate. Common Equity Tier 1 and Additional Tier 1 are the two subcategories. Equity in the commons Tier 1 or core capital is the highest quality capital since it can withstand any losses

The aim of regulators is to keep banks well-funded because they are typically deeply entrenched in the economy. As a result, banks are normally required by the regulatory body to maintain specific capital ratios that are higher than the set threshold. In other words, Common Equity Tier 1 must always be at least 4.5 percent of risk-weighted assets (RWA).

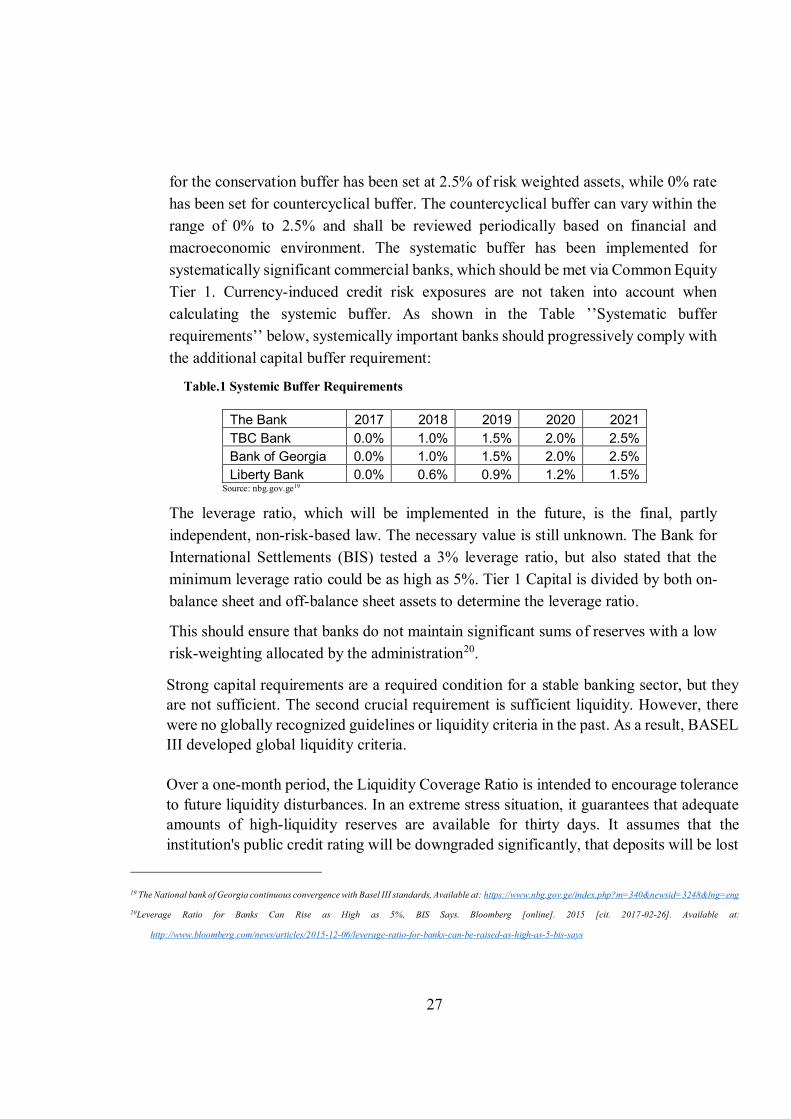

Furthermore, besides above-mentioned changes, banks are required to hold additional so-called Combined Buffer through Common Equity Tier 1. The combined buffer consists of the conservation, the countercyclical and the systematic buffers18. Rate

17 Supervisory Plan of The National Bank of Georgia With Regard To COVID-19, available at: https://www.nbg.gov.ge/index.php?m=340&newsid=3901&lng=eng

18 The National bank of Georgia continuous convergence with Basel III standards, available at: https://www.nbg.gov.ge/index.php?m=340&newsid=3248&lng=eng

27

for the conservation buffer has been set at 2.5% of risk weighted assets, while 0% rate has been set for countercyclical buffer. The countercyclical buffer can vary within the range of 0% to 2.5% and shall be reviewed periodically based on financial and macroeconomic environment. The systematic buffer has been implemented for systematically significant commercial banks, which should be met via Common Equity Tier 1. Currency-induced credit risk exposures are not taken into account when calculating the systemic buffer. As shown in the Table ’’Systematic buffer

requirements’’ below, systemically important banks should progressively comply with the additional capital buffer requirement:

Table.1 Systemic Buffer Requirements

The Bank 2017 2018 2019 2020 2021 TBC Bank 0.0% 1.0% 1.5% 2.0% 2.5% Bank of Georgia 0.0% 1.0% 1.5% 2.0% 2.5% Liberty Bank 0.0% 0.6% 0.9% 1.2% 1.5%

Source: nbg.gov.ge19

The leverage ratio, which will be implemented in the future, is the final, partly independent, non-risk-based law. The necessary value is still unknown. The Bank for International Settlements (BIS) tested a 3% leverage ratio, but also stated that the minimum leverage ratio could be as high as 5%. Tier 1 Capital is divided by both on-balance sheet and off-balance sheet assets to determine the leverage ratio.

This should ensure that banks do not maintain significant sums of reserves with a low risk-weighting allocated by the administration20.

Strong capital requirements are a required condition for a stable banking sector, but they are not sufficient. The second crucial requirement is sufficient liquidity. However, there were no globally recognized guidelines or liquidity criteria in the past. As a result, BASEL III developed global liquidity criteria. Over a one-month period, the Liquidity Coverage Ratio is intended to encourage tolerance to future liquidity disturbances. In an extreme stress situation, it guarantees that adequate amounts of high-liquidity reserves are available for thirty days. It assumes that the institution's public credit rating will be downgraded significantly, that deposits will be lost

19 The National bank of Georgia continuous convergence with Basel III standards, Available at: https://www.nbg.gov.ge/index.php?m=340&newsid=3248&lng=eng

20Leverage Ratio for Banks Can Rise as High as 5%, BIS Says. Bloomberg [online]. 2015 [cit. 2017-02-26]. Available at:

http://www.bloomberg.com/news/articles/2015-12-06/leverage-ratio-for-banks-can-be-raised-as-high-as-5-bis-says

in part, and that the institution's assets will be liquidated, other serious concerns include the lack of unsecured wholesale financing.

Second, in order to comply with the net stable funding ratio, a bank must maintain a minimum number of stable sources of funding. The aim is to reduce the risk of a bank's liquidity status being seriously impacted by threats to its normal sources of funding. Supervisors, understandably, use a range of reporting methods to detect possible problems before they become severe21. The current global trend pushes banks to diversify their funding sources, which should help them maintain adequate liquidity at all times. As a result, the gap between banks financed by deposits and those funded by bond issuances is closing.

2.1.2 Pillar 2 Requirements

Commercial banks, in compliance with the Basel III system, can keep capital adequacy reserves for certain threats that aren't properly protected under Pillar 1. The National Bank of Georgia adopted the "Rule on Additional Capital Buffer Requirements for Commercial Banks within Pillar 2" with the aim of formalizing and establishing this structure.

Pillar 2 capital requirements, in compliance with this law, include requirements for an unhedged currency driven credit risk buffer, which was previously included in Pillar 1. The Unhedged Currency Exposure Buffer is a macroprudential shield against the systemic risk of dollarization. The addition of this buffer emphasizes the National Bank of Georgia's plan to gradually reduce banking system dollarization, resulting in a more robust banking system that can withstand external shocks. In addition, the Pillar 2 system specifies a capital buffer for credit portfolio concentration risk (both name and sectoral concentration risk), a net stress-test buffer based on supervisory stress-test outcomes, and a net GRAPE buffer set calculated by the NBG supervisory mechanism – General Risk Assessment Program (GRAPE).

It's important to note, that capital buffers under Pillar 2 should be proportionately incorporated in capital requirements. Therefore, 56% of capital required under Pillar 2 should be held through Common Equity Tier 1, while 75% through Tier 1 capital

21 Basel III summary, IBM (online) 2015 (cit. 2021-05-16). Available at: https://www.ibm.com/docs/en/bfmdw/8.8?topic=accord-basel-iii-summary

29

instruments22. Commercial banks have been granted sufficient timeframes to comply with these criteria.

As a result of the changes to capital adequacy requirements, when a commercial bank breaches the new total capital requirement, the combined buffer requirement is considered to be breached first. In such cases, distribution of own equity instruments, including dividend distributions, is prohibited under the updated ‘'Regulation on

Capital Adequacy Requirements for Commercial Banks." prohibited.

Furthermore, because of a sudden devaluation of currency that triggers a mechanical increase in risk weighted assets, the total capital requirement calculated under Pillar 2 may be temporarily decreased, for a period of one year. The specific amount of capital that will be used to minimize the capital requirement must be measured using the bank's methodology and approved by the NBG. This technique must be followed when calculating capital amounts by commercial banks. If a commercial bank's capital is reduced further than the methodology allows, the bank will fail to meet the combined buffer threshold and will be subject to dividend payment and other restrictions.

22 The National bank of Georgia continuous convergence with Basel III standards, available at: https://www.nbg.gov.ge/index.php?m=340&newsid=3248&lng=eng

3 Theory of valuation

After getting useful theoretical information about the country’s economic state and regulatory frameworks, the author in this chapter starts explaining key valuation models which are implied in the practical part of the thesis. For evaluating the financial performance of the banks and comparison well known financial ratios are calculated, then Porter’s five forces analysis are

used. Lastly the cross-sectional analysis concludes with valuation.

3.1 Bank Valuation

In general, any financial service firms it can be a bank, insurance company or something else, have different valuation technique compared to other profit seeking companies. When valuing a bank, the unique business model and operational activities must be considered. The differences between financial statements and activities are examined in this chapter. Bank valuation models are discussed in the second part of the chapter.

According to Damodaran23, there are four differences in financial service firms compared to others in the market that can create considerable issues in valuation: regulatory framework, accounting rules, definitions of debt and reinvestment.

Regulation

Financial companies are strictly regulated throughout the world. Considering their influence on the market it is quite needed. Besides the general Basel committee decisions, each country’s regulatory institute imposes different requirements related to capital ratios, investment opportunities, merges, and acquisition procedures or even the entrance of a new firm into the market. Overall, those restraints serve to protect banking sector itself, then customers and shareholders interests too. While analyzing financial services firms, the one must be aware all the regulations that govern their operations. Otherwise it can lead to a serious discrepancy

According Rules

The products, services (any financial instruments) financial firms offer to the customers often does not have fixed value. Their prices change depending on the

23 Valuing financial Sevices firms. NYU Stern (online). 2009 (cit. 2021-05-05). Availabe at: http://people.stern.nyu.edu/adamodar/pdfiles/papers/finfirm09.pdf

31

market performance. Therefore, for the accounting purposes marking assets to market value has been an established practice, well before other firms even started talking about fair value accounting24. Another peculiarity for bank’s bookkeeping is creating

loan loss provisions. Since there is no general rule regarding this amount, banks define amounts individually. Depending on the type of financial firm, it can create more for potential losses or way less and use it for reinvestment. Understanding, the accounting rule of the company you are evaluating is also quite important

Debt

Again, because of the essence of financial firms’ operations their definition of debt is different from typical case. Debt is a source for further operations, banks take excess capital from one part and turn it into a product -loan for another part. This is the easiest product. They do not account deposits as debts. If so the operating income for a bank should be measured prior to interest paid to depositors, which would be problematic25.

Reinvestment

As mentioned above, national authorities control where financial firms invest and how much. While reinvestment is needed for the future growth, it can be quite challenging to measure two required variables for computation: net capital expenditures (CAPEX) and working capital (WC). Financial firms usually invest in intangible assets and not in property, plant and equipment. Which are recorded as operational expenses in cash flow statement. When it comes to WC, the difference between current assets and current liabilities, a significant portion of a bank’s balance

sheet will fall under one of these categories and the number may have no relationship to reinvestment for growth. That is the reason we need to make some adjustments for valuation.

24 Valuing Financial Service Firms. NYU Stern [online]. 2009 [cit. 2021-05-05]. Available at: http://people.stern.nyu.edu/adamodar/pdfiles/papers/finfirm09.pdf p 6 25 Valuing Financial Service Firms. NYU Stern [online]. 2009 [cit. 2021-05-05]. Available at: http://people.stern.nyu.edu/adamodar/pdfiles/papers/finfirm09.pdf, p 8

3.2 Financial ratios

From the perspective of future investments usually investors are interested in the ratios which give them Therefore, their financial performance is important step in the analysis process. Prof-itability can be clearly measured with the following ratios: Return on Assets (ROA), Return on Equity (ROE) and Net Interest Margin (NIM). The author briefly describes their importance and idea’s below. ROA is the result of net profit divided by total assets. ROA indicates the ability of a bank to generate profit from its total assets, how profitably a commercial bank uses its resources. The higher the ROA, the more efficiently the resources are used by the bank26. ROE is the second important ratio, representing the relation of the bank profit to its total equity. A bank with a high value of ROE is capable of creating an internal cash flow. Therefore, the higher the ROE, the more profitable the company is in terms of making a profit27 NIM is the difference between the bank’s income and its expense related to interest such as

difference between the difference between the interest income received and the interest expense paid to a lender regarding his/her deposits28.

3.3 Valuation Models

Comparing the implied and actual share prices is the simplest step in the valuation process. Knowing how much an asset is worth and how that value is determined is important for making informed decisions29. Many assumptions are made in valuation models, but they should be sup-ported by data or logical explanations. Otherwise, the results cannot be trusted. The emphasis of this study is on valuing two banks for the intent of a future investment. The author theoretically

defines following valuation models: free cash flow to equity (FCFE), excess return and rel-

ative valuation and then compute TBC and BGEO banks’ value.

26 Nguyen, A. H., Nguyen, H. T., & Pham, H. T. (2020). Applying the CAMEL model to assess performance of commercial banks: empirical evidence from

Vietnam. Banks and Bank Systems, 15(2), 177. p179 27 Nguyen, A. H., Nguyen, H. T., & Pham, H. T. (2020). Applying the CAMEL model to assess performance of commercial banks: empirical evidence from Vietnam. Banks and Bank Systems, 15(2), 177. p179 28 Nguyen, A. H., Nguyen, H. T., & Pham, H. T. (2020). Applying the CAMEL model to assess performance of commercial banks: empirical evidence from

Vietnam. Banks and Bank Systems, 15(2), 177. p179 29 What is Valuation? NYU Stern [online]. 2014 [cit. 2021-05-05]. Available at: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/background/valintro.htm

33

It is recommended that the three statements model (Income Statement, balance sheet, cash flow statement) be created in order to be able to build way more advanced models. An analyst actually forecasts how the company's financial statements will appear in the future, discounting anticipated future cash flows, dividends, or some other metric used in valuation. This is referred to as financial modeling30.

Free Cash Flow to Equity

The common Free Cash Flow to Equity (FCFE) approach is particularly useful for valuing banks because it considers the fact that banks can generate value from their liabilities.

For some factors, using cash flow as a basis for measuring profits of owners as dividend income potential for bank owners is inappropriate:

In the banking industry, the statement of cash flows is not appropriate for identifying sources for shareholders, such as dividends, which can only be paid from actual net income after tax, not from the movement of cash (cash flow).

Shareholders do not have fair access to bank and company income; in the bank, there is no issue with cash supply to shareholders due to the existence of the vast majority of assets and liabilities; however, other types of companies can produce large discrepancies between cash flow and profits in the sense that the business produces profits but not enough cash flow

Differences between interest income and cost, as well as payments for services, are the key sources of income in banking.

Interest income and cost, as the most significant component of their income and capital growth, or its renewal, must be taken into consideration when avluing financial institutions. The calculation of FCFE in banks and financial institutions can be implemented in the following way:

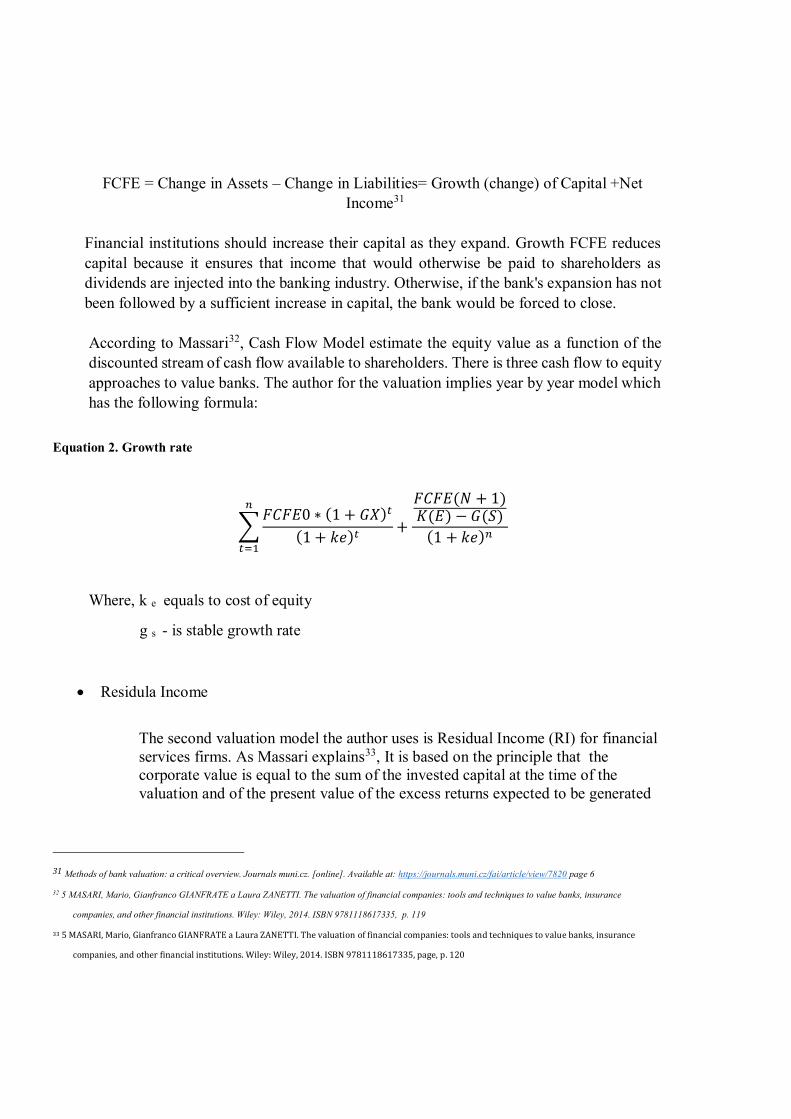

Equation 1. FCFE

30 What is Financial Modelling CFI. 2021 [cit. 2021-05-05]. Available at: https://corporatefinanceinstitute.com/resources/knowledge/modeling/what-is-financial-

modeling/

FCFE = Change in Assets – Change in Liabilities= Growth (change) of Capital +Net Income31

Financial institutions should increase their capital as they expand. Growth FCFE reduces capital because it ensures that income that would otherwise be paid to shareholders as dividends are injected into the banking industry. Otherwise, if the bank's expansion has not been followed by a sufficient increase in capital, the bank would be forced to close. According to Massari32, Cash Flow Model estimate the equity value as a function of the discounted stream of cash flow available to shareholders. There is three cash flow to equity approaches to value banks. The author for the valuation implies year by year model which has the following formula:

Equation 2. Growth rate

∑𝐹𝐶𝐹𝐸0 ∗ (1 + 𝐺𝑋)𝑡

(1 + 𝑘𝑒)𝑡+

𝐹𝐶𝐹𝐸(𝑁 + 1)𝐾(𝐸) − 𝐺(𝑆)

(1 + 𝑘𝑒)𝑛

𝑛

𝑡=1

Where, k e equals to cost of equity

g s - is stable growth rate

Residula Income

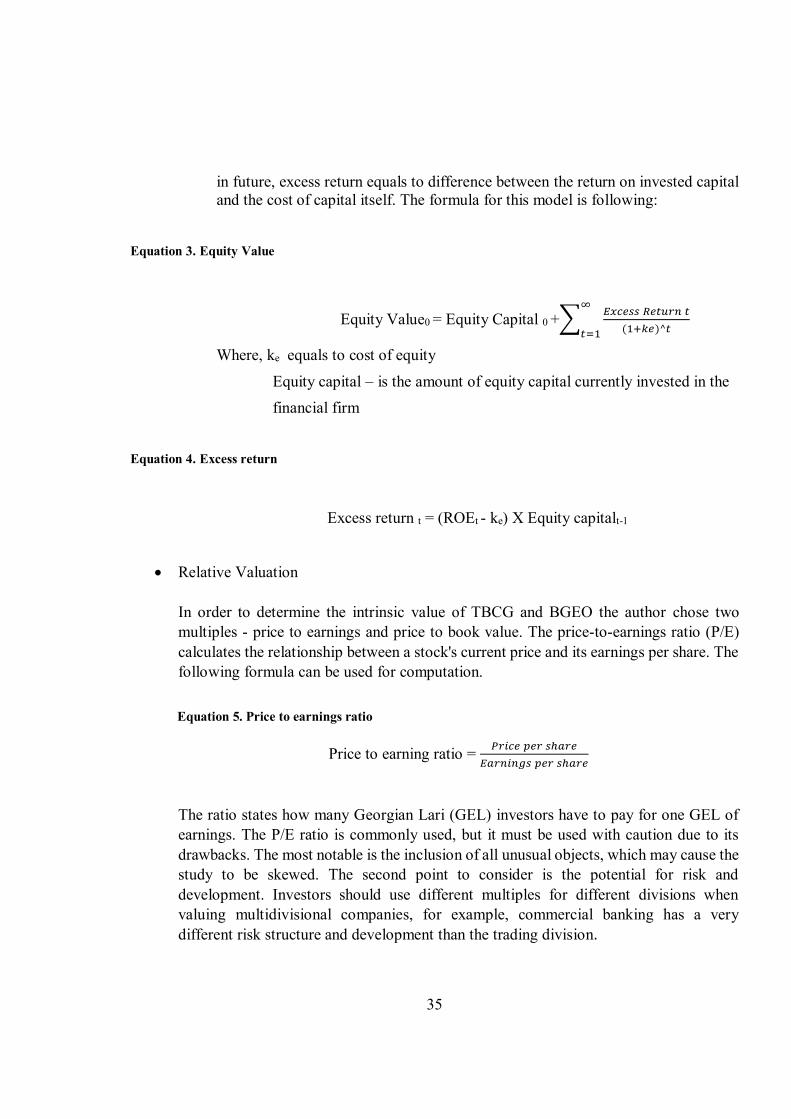

The second valuation model the author uses is Residual Income (RI) for financial services firms. As Massari explains33, It is based on the principle that the corporate value is equal to the sum of the invested capital at the time of the valuation and of the present value of the excess returns expected to be generated

31 Methods of bank valuation: a critical overview. Journals muni.cz. [online]. Available at: https://journals.muni.cz/fai/article/view/7820 page 6

32 5 MASARI, Mario, Gianfranco GIANFRATE a Laura ZANETTI. The valuation of financial companies: tools and techniques to value banks, insurance

companies, and other financial institutions. Wiley: Wiley, 2014. ISBN 9781118617335, p. 119

33 5 MASARI, Mario, Gianfranco GIANFRATE a Laura ZANETTI. The valuation of financial companies: tools and techniques to value banks, insurance

companies, and other financial institutions. Wiley: Wiley, 2014. ISBN 9781118617335, page, p. 120

35

in future, excess return equals to difference between the return on invested capital and the cost of capital itself. The formula for this model is following:

Equation 3. Equity Value

Equity Value0 = Equity Capital 0 +∑𝐸𝑥𝑐𝑒𝑠𝑠 𝑅𝑒𝑡𝑢𝑟𝑛 𝑡

(1+𝑘𝑒)^𝑡

∞

𝑡=1

Where, ke equals to cost of equity

Equity capital – is the amount of equity capital currently invested in the financial firm

Equation 4. Excess return

Excess return t = (ROEt - ke) X Equity capitalt-1

Relative Valuation In order to determine the intrinsic value of TBCG and BGEO the author chose two multiples - price to earnings and price to book value. The price-to-earnings ratio (P/E) calculates the relationship between a stock's current price and its earnings per share. The following formula can be used for computation.

Equation 5. Price to earnings ratio

Price to earning ratio = 𝑃𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

The ratio states how many Georgian Lari (GEL) investors have to pay for one GEL of earnings. The P/E ratio is commonly used, but it must be used with caution due to its drawbacks. The most notable is the inclusion of all unusual objects, which may cause the study to be skewed. The second point to consider is the potential for risk and development. Investors should use different multiples for different divisions when valuing multidivisional companies, for example, commercial banking has a very different risk structure and development than the trading division.

Price-to-book ratio (P/B) measures the relationship between the current price of a stock and the book value per share. Four factors influence the P/B ratio. The higher the growth rate, the higher the return on equity, the higher the dividend ratio, or the lower the cost of equity, the higher the P/B ratio34. Owing to the close relationship between the market value of equity and the book value of equity, which is primarily a result of banks' asset marked to market accounting process, financial services companies are often priced using the P/B ratio.

The standard computation is described by the formula below35.

Equation 6. Price to book ratio

𝑃𝑟𝑖𝑐𝑒 𝑡𝑜 𝑒𝑎𝑟𝑛𝑖𝑛𝑔𝑠 𝑟𝑎𝑡𝑖𝑜= 𝑃𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

𝐵𝑜𝑜𝑘 𝑣𝑎𝑙𝑢𝑒 𝑝𝑒𝑟 𝑠ℎ𝑎𝑟𝑒

34 Price-Book Value Ratio: Definition. NYU Stern [online]. 2012 [cit. 2017-02-21]. Available at http://people.stern.nyu.edu/adamodar/pdfiles/eqnotes/pbv.pdf

35 Overview: Making sense of the price-to-book value ratio. Market Realist [online]. 2014 [cit. 2021-05-05]. Available at http://marketrealist.com/2014/08/overview-

making-sense-price-book-value-ratio/

37

4 Fundamental analysis of TBC and BGEO

The practical part of the thesis is focused on cross sectional analysis of TBC and BGEO banks. In the first place the author conducts a systematic macroeconomic study. Since, banks are highly vulnerable to a number of macroeconomic factors, which cannot be overlooked. The importance of business-specific problems and individual company valuation is emphasized below.

4.1 Implications of COVID-19

During 2020, Georgia, like most countries of the world, faced Covid-19 pandemic which caused the recession in global economies. Economic downtown had a significant impact on banking sector as well, mainly by increasing loan provisions and consequently effecting the banks’ profitability. This became the main driver of Georgian banking sector’s negative

performance for the period. That is the reason implications of COVID-19 can not be missed.

The COVID -19 pandemic has tested the resilience and character of banking sector. The sector was directly affected by three following factors:

Measures implemented by the Georgian Government to address the COVID-19 crisis, including the economic lockdown

Measures introduced by the National Bank of Georgia (NBG) in response to the COVID-19 crisis, and

Actions implemented by the individual banks to address the COVID-19 crisis.

The Government anti-crisis stimulus plan.

The Government announced a series of support measures designed to mitigate the negative economic impact of COVID-19. The Government’s revised 2020 budget document was

approved by Parliament in June 2020. The revised budget incorporates the fiscal parameters agreed with the IMF, US$1.5 billion in donor funding and fiscal stimulus measures for businesses and households affected by the coronavirus pandemic. Business support is at 3.8% of GDP and social assistance is at 2.7% of GDP in 2020 revised budget document, similar

fiscal support package in 2021 is expected to reach Gel 1.247 million, 2.3 percent of 2021 GDP36.

Georgian authorities have mobilized US$3.0 billion financing from the International Monetary Fund (the “IMF”) and other international partners (US, EU, World Bank, KFW, AFD, EBRD, EIB, ADB, etc.) to respond effectively to the COVID-19 pandemic associated economic crisis. Of this funding, US$1.5 billion is earmarked for the public sector and US$1.5 billion for the private sector. The IMF’s financing is c.US$576.4 million37, of which US$200 million was already disbursed to the budget.

Georgia successfully contained the first wave of the pandemic by introducing tight lockdown measures, including a curfew and a ban on transportation in 2Q20. From mid-May, businesses gradually reopened, but international flights resumed only to a limited number of countries from August 2020. A surge in COVID-19 cases in autumn resulted in further lockdown measures put in place in the retail and hospitality sectors at the end of November 2020, as well as a curfew and a ban on public transportation, while avoiding a full-scale lockdown for other areas of the economy, unlike in April-May. The Government responded to the pandemic with higher healthcare spending, a social assistance package for individuals, as well as tax exemptions and various funding mechanisms for businesses, and stimulus plans for some sectors of the economy. This was financed with the support of international donors, as the ongoing IMF programme and trust in the Government’s continued prudent

macroeconomic policymaking enabled the authorities to mobilize significant donor funding Georgia’s economy contracted by an estimated 6.5% y-o-y in 4Q20, reversing the recovery in 3Q20, on the back of the second wave of the COVID-19 cases and the new restrictions introduced by the Government. Domestic demand moderated due to the restrictions on mobility, as well as other restrictions introduced in large cities at the end of November 2020. Despite deceleration, the banking sector loan portfolio growth remained robust, increasing by 9.1% y-o-y on a constant currency basis, minimizing the second wave impact of the pandemic on the economy. Importantly, remittances continued to grow and were up 15.7% y-o-y in 4Q20. This, along with an improved trade deficit and The NBG interventions, stabilized the local currency at the end of December 2020. International reserves increased to US$ 3.9 billion as at 31 December 2020, largely reflecting the increased donor funding. The NBG maintained a moderately tight monetary policy to anchor inflation expectations

36 Onilne, available at: https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19#G

37Online, available at: https://www.imf.org/en/News/Articles/2020/11/10/pr20336-georgia-imf-staff-concludes-virtual-review-mission

39

and limit any pass-through impact from local currency depreciation. Annual inflation dropped to 2.4% in December 2020 from 3.8% in previous months, mainly reflecting utility subsidies by the Government for low-energy consumers. Notably, on 12 February 2021, Fitch Ratings affirmed Georgia's sovereign credit rating at BB, supported by strong governance and business environment indicators as well as consistent and credible policy framework underpinning Georgia's relative resilience to shocks.

NBG Policy

The NBG was implementing countercyclical measures to support the financial stability of the banking system and to ensure the provision of financial support to sectors of the economy affected by the current turmoil. The measures included a significant reduction in capital adequacy requirements and standby liquidity support incentives. In addition, the NBG coordinated the creation of respective loan loss provisions across the system. In relation to capital adequacy requirements, this means:

Combined buffer - the conservation buffer requirement of 2.5% of risk-weighted assets has been reduced to 0% indefinitely38

Allowing banks to use the conservation buffer (currently at 2.5pp on CET1) and 2/3 of the CICR buffer resulted in the release of 1.0-2.0% of capital across our CET1, Tier 1 and Total CAR

Leaving open the possibility of releasing all pillar 2 buffers (remaining 1/3 CICR, HHI and Net Grape buffers) in the range of 1.0-4.0% of capital across our CET1, Tier 1 and Total CAR

NBG requested the Georgian banks to create general provisions under the local accounting basis in the first quarter of 2020; this accounting basis is that used for calculation of capital adequacy ratios. The specific quantum of the provision reflects the NBG’s current

expectation of estimated credit losses on the lending book of the banking system for the entire economic cycle, given current economic expectations. The NBG considers the banking system capital ratios to be sufficiently in excess of the expected minimum capital requirements, to be able to absorb this upfront general provision, whilst maintaining sufficiently comfortable buffers over the required minimum capital ratios.

38 Onilne, Available at: https://bankofgeorgiagroup.com/storage/news/National%20Bank%20of%20Georgia%20supervisory%20plan%20-%20COVID-19.pdf

In relation to liquidity requirements, the NBG has introduced a swap program for US$ 200 million, with an annual spread of 9%.39

Bank policies and outcomes

To respond to the pandemic outbreak in spring 2020, the banks introduced a number of protocols and a comprehensive Business Continuity Plan aimed at mitigating the negative impact on businesses, employees, customers and communities. They have implemented measures to reduce physical interactions to prevent the virus spread, whilst maintaining the full banking capability required to support and assist their customers. This included fully moving back office staff to working from home, significantly ramping up the capacity of the call center, temporarily closing the customer service support areas of Express branches (mostly re-opened in June), implementing a three-month grace period on principal and interest payments on all retail loans, also for all their individual and MSME customers as well as those corporate customers whose business is the most exposed in the current situation, applying more stringent risk assessment procedures during the lending process, incentivizing the offloading of customer activity to digital channels through the temporary removal of fees on transactions executed through their mobile and internet banking platforms, among others. In the fourth quarter of 2020, following the emergence of the second wave of the COVID-19 cases, the banks again adjusted accordingly, moving a large part of their back office staff to remote work and reintroducing two-week shifts for certain departments and the front office staff.

4.2 Georgia Banking Industry Analysis

The financial sector is one of the most developed areas of the Georgian economy. In total, the sector currently consists of 15 privately owned commercial banks40, 39 mi-crofinance organisations, six brokerage companies, private pension funds (owned by insurance companies), deposit insurance fund. The financial system is biased towards

39 TBC bank, annual report 2019, available at: https://www.tbcbank.ge/web/documents/10184/411010/JSC+TBC+Bank+MRA+2019.pdf/a36335a9-aab7-488c-

b838-a6e3435f4daf page 10

40 NBG.gov.ge. available at https://www.nbg.gov.ge/index.php?m=403

41

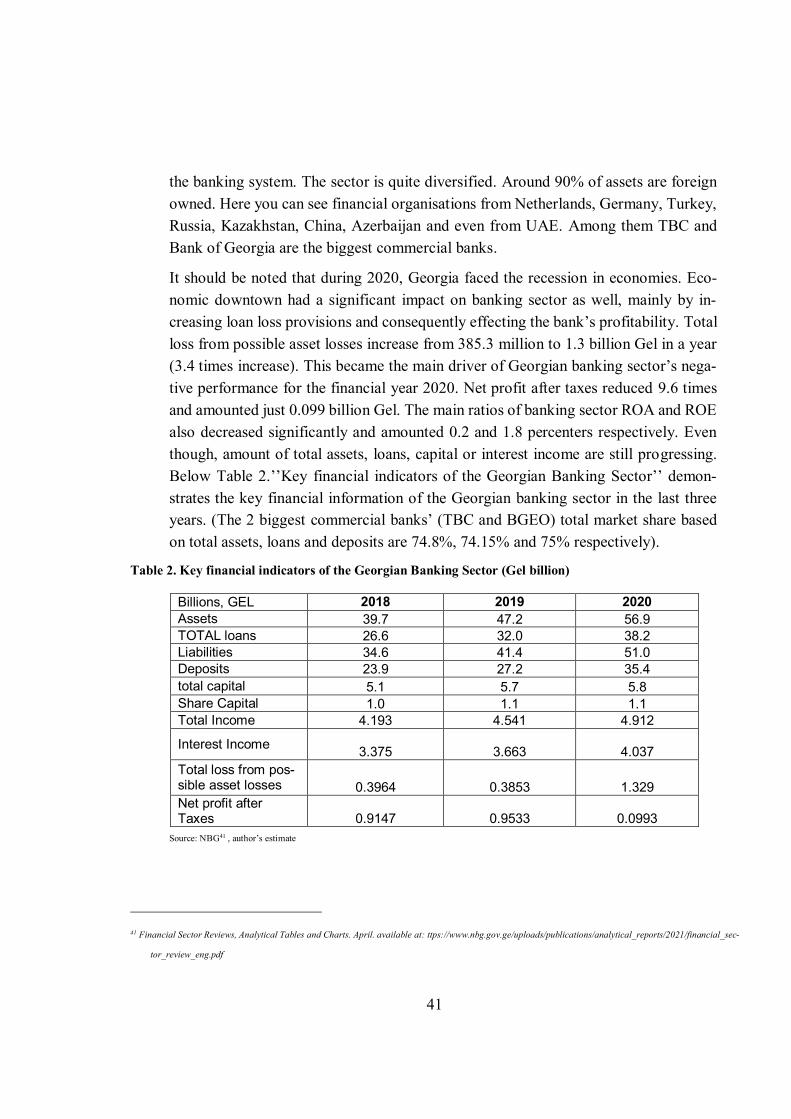

the banking system. The sector is quite diversified. Around 90% of assets are foreign owned. Here you can see financial organisations from Netherlands, Germany, Turkey, Russia, Kazakhstan, China, Azerbaijan and even from UAE. Among them TBC and Bank of Georgia are the biggest commercial banks.

It should be noted that during 2020, Georgia faced the recession in economies. Eco-nomic downtown had a significant impact on banking sector as well, mainly by in-creasing loan loss provisions and consequently effecting the bank’s profitability. Total loss from possible asset losses increase from 385.3 million to 1.3 billion Gel in a year (3.4 times increase). This became the main driver of Georgian banking sector’s nega-

tive performance for the financial year 2020. Net profit after taxes reduced 9.6 times and amounted just 0.099 billion Gel. The main ratios of banking sector ROA and ROE also decreased significantly and amounted 0.2 and 1.8 percenters respectively. Even though, amount of total assets, loans, capital or interest income are still progressing. Below Table 2.’’Key financial indicators of the Georgian Banking Sector’’ demon-

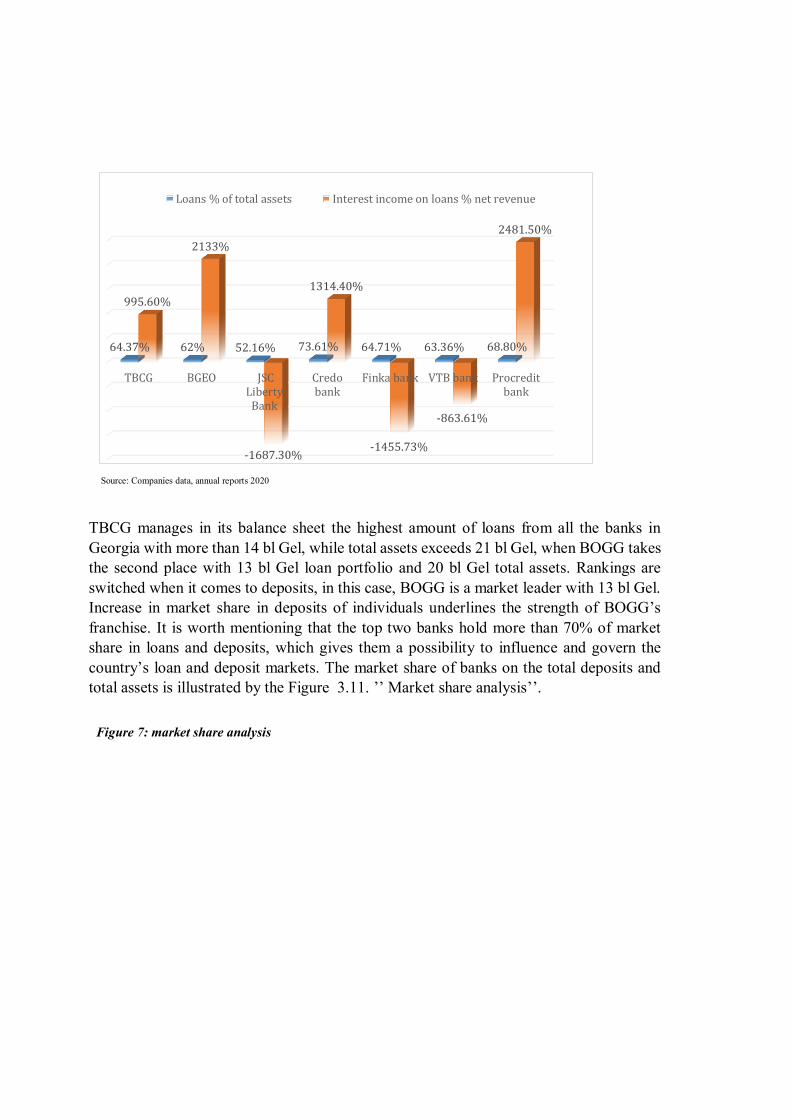

strates the key financial information of the Georgian banking sector in the last three years. (The 2 biggest commercial banks’ (TBC and BGEO) total market share based on total assets, loans and deposits are 74.8%, 74.15% and 75% respectively).

Table 2. Key financial indicators of the Georgian Banking Sector (Gel billion)

Billions, GEL 2018 2019 2020 Assets 39.7 47.2 56.9 TOTAL loans 26.6 32.0 38.2 Liabilities 34.6 41.4 51.0 Deposits 23.9 27.2 35.4 total capital 5.1 5.7 5.8 Share Capital 1.0 1.1 1.1 Total Income 4.193 4.541 4.912

Interest Income 3.375 3.663 4.037 Total loss from pos-sible asset losses 0.3964 0.3853 1.329 Net profit after Taxes 0.9147 0.9533 0.0993

Source: NBG41 , author’s estimate

41 Financial Sector Reviews, Analytical Tables and Charts. April. available at: ttps://www.nbg.gov.ge/uploads/publications/analytical_reports/2021/financial_sec-

tor_review_eng.pdf

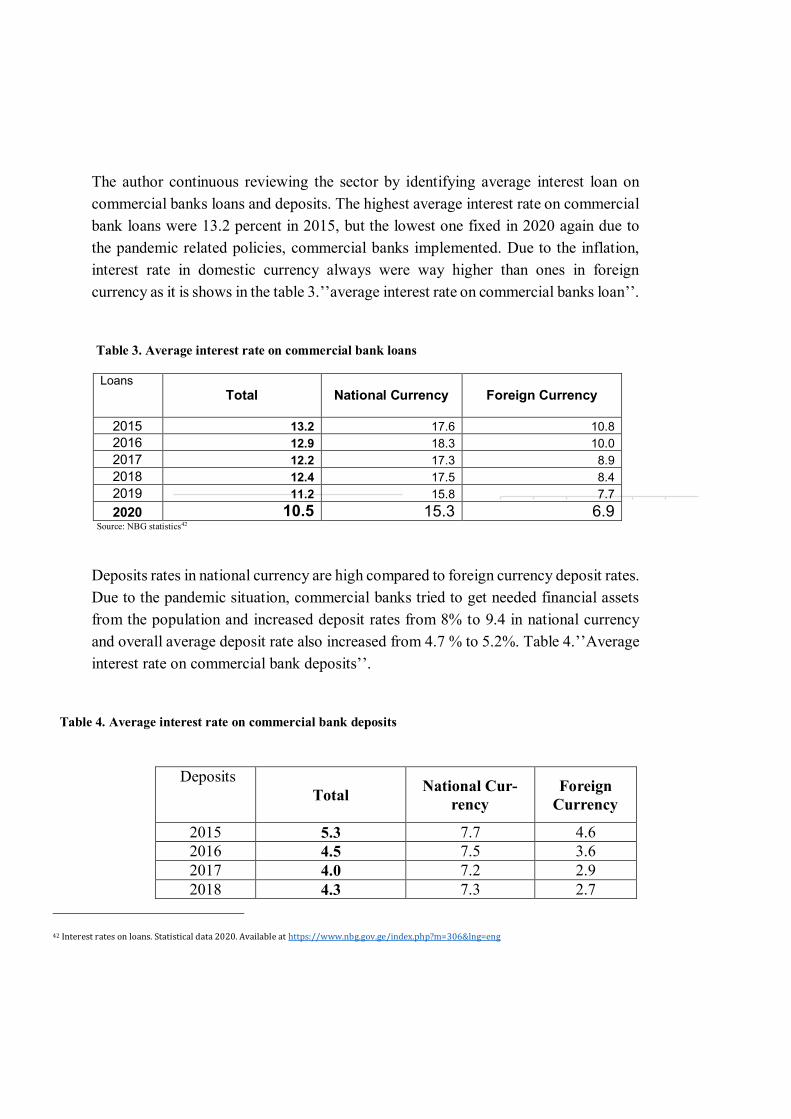

The author continuous reviewing the sector by identifying average interest loan on commercial banks loans and deposits. The highest average interest rate on commercial bank loans were 13.2 percent in 2015, but the lowest one fixed in 2020 again due to the pandemic related policies, commercial banks implemented. Due to the inflation, interest rate in domestic currency always were way higher than ones in foreign currency as it is shows in the table 3.’’average interest rate on commercial banks loan’’.

Table 3. Average interest rate on commercial bank loans

Loans

Total National Currency Foreign Currency

2015 13.2 17.6 10.8 2016 12.9 18.3 10.0 2017 12.2 17.3 8.9 2018 12.4 17.5 8.4 2019 11.2 15.8 7.7 2020 10.5 15.3 6.9

Source: NBG statistics42

Deposits rates in national currency are high compared to foreign currency deposit rates. Due to the pandemic situation, commercial banks tried to get needed financial assets from the population and increased deposit rates from 8% to 9.4 in national currency and overall average deposit rate also increased from 4.7 % to 5.2%. Table 4.’’Average

interest rate on commercial bank deposits’’.

Table 4. Average interest rate on commercial bank deposits

42 Interest rates on loans. Statistical data 2020. Available at https://www.nbg.gov.ge/index.php?m=306&lng=eng

Deposits

Total National Cur-rency

Foreign Currency

2015 5.3 7.7 4.6 2016 4.5 7.5 3.6 2017 4.0 7.2 2.9 2018 4.3 7.3 2.7

43

Source: NBG statistics43

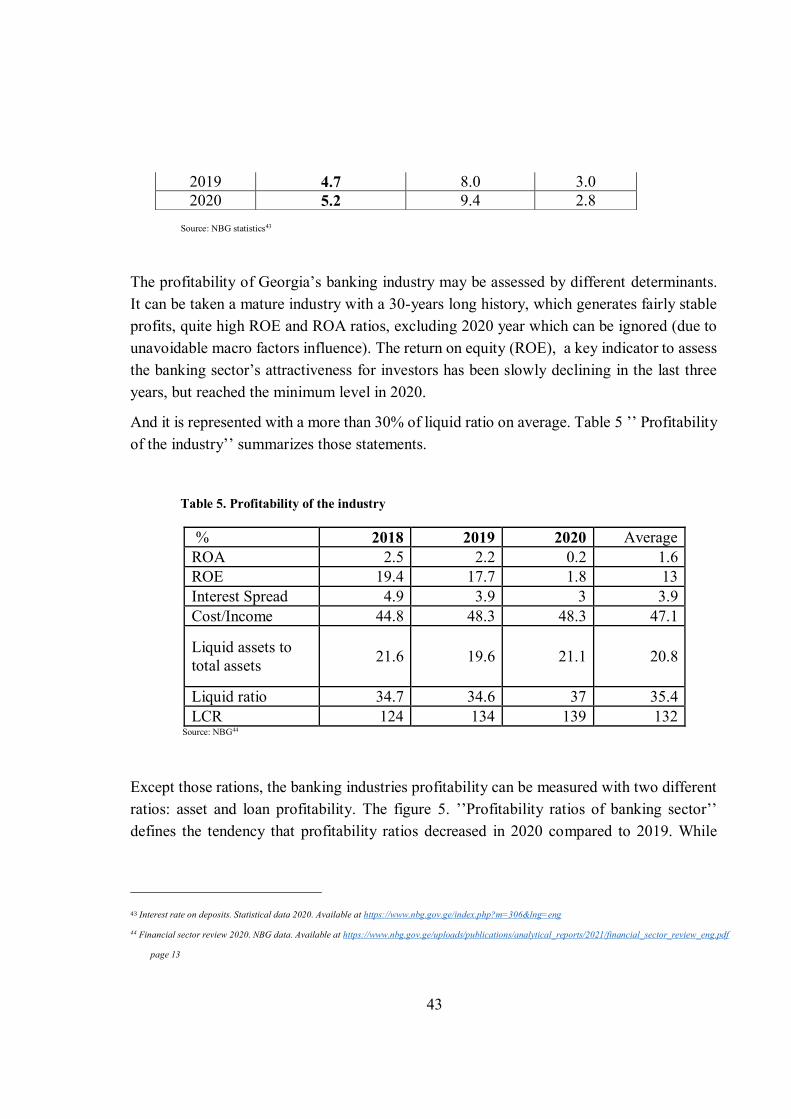

The profitability of Georgia’s banking industry may be assessed by different determinants. It can be taken a mature industry with a 30-years long history, which generates fairly stable profits, quite high ROE and ROA ratios, excluding 2020 year which can be ignored (due to unavoidable macro factors influence). The return on equity (ROE), a key indicator to assess the banking sector’s attractiveness for investors has been slowly declining in the last three

years, but reached the minimum level in 2020.

And it is represented with a more than 30% of liquid ratio on average. Table 5 ’’ Profitability of the industry’’ summarizes those statements.

Table 5. Profitability of the industry

% 2018 2019 2020 Average ROA 2.5 2.2 0.2 1.6 ROE 19.4 17.7 1.8 13 Interest Spread 4.9 3.9 3 3.9 Cost/Income 44.8 48.3 48.3 47.1

Liquid assets to total assets 21.6 19.6 21.1 20.8

Liquid ratio 34.7 34.6 37 35.4 LCR 124 134 139 132

Source: NBG44

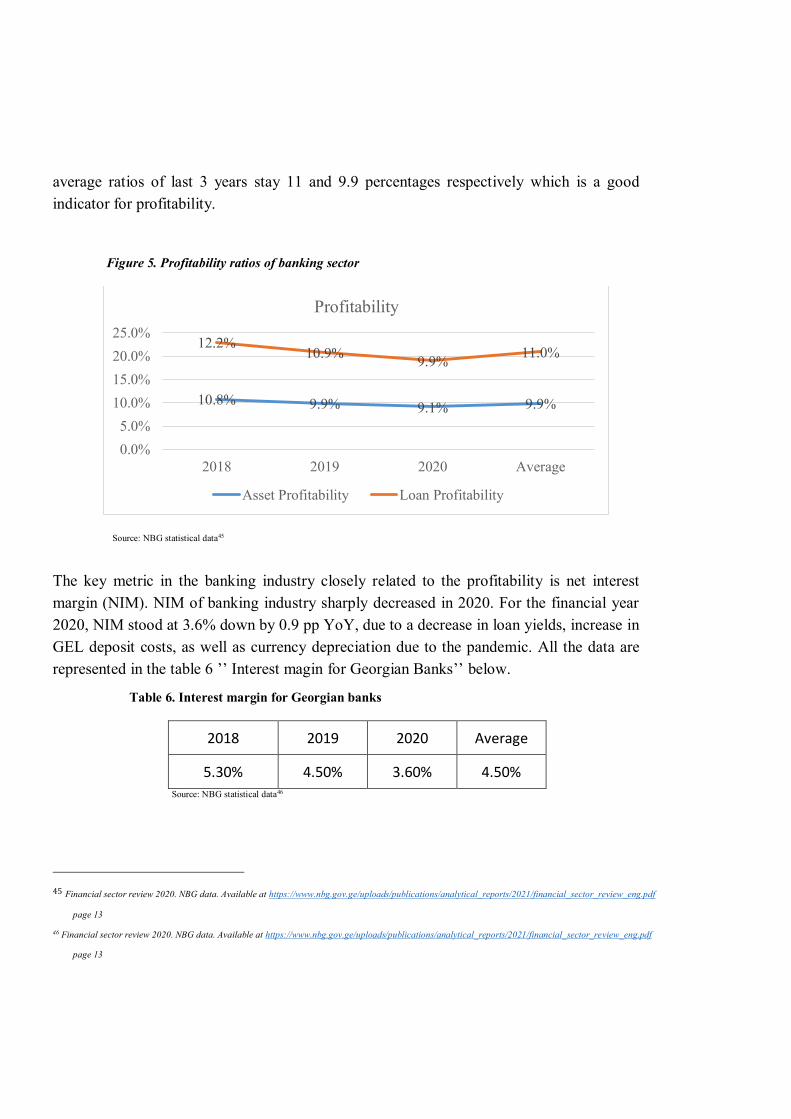

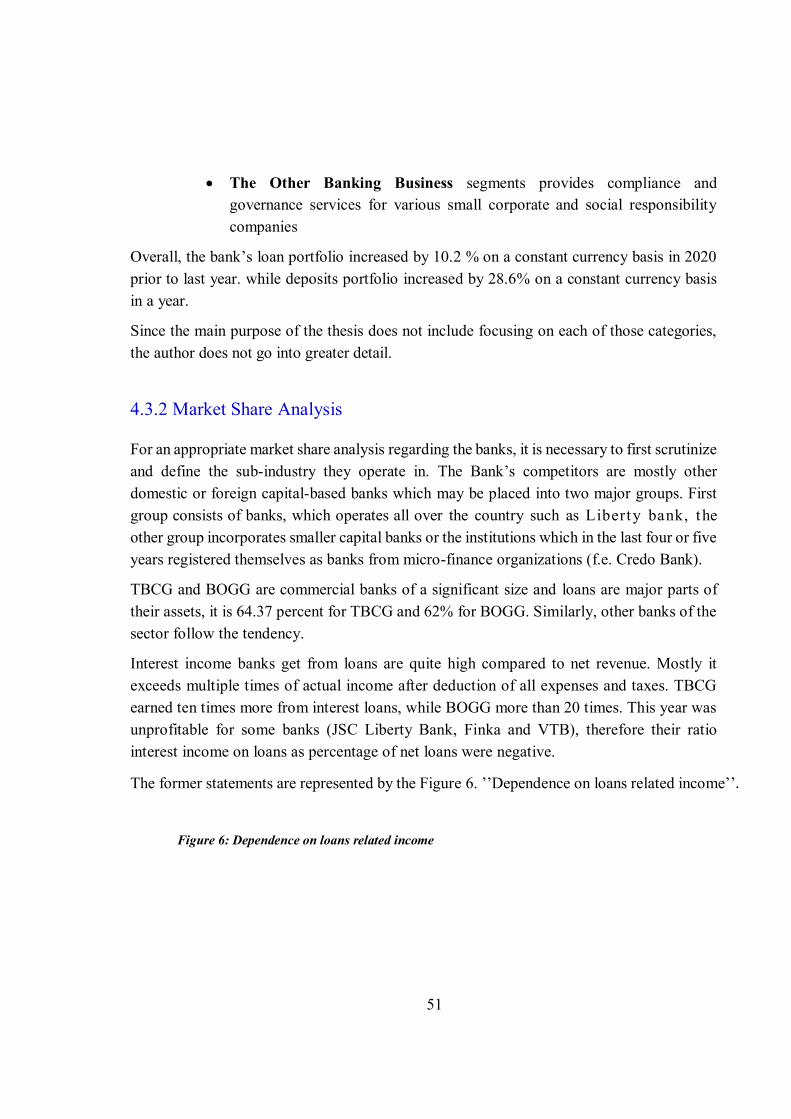

Except those rations, the banking industries profitability can be measured with two different ratios: asset and loan profitability. The figure 5. ’’Profitability ratios of banking sector’’

defines the tendency that profitability ratios decreased in 2020 compared to 2019. While

43 Interest rate on deposits. Statistical data 2020. Available at https://www.nbg.gov.ge/index.php?m=306&lng=eng

44 Financial sector review 2020. NBG data. Available at https://www.nbg.gov.ge/uploads/publications/analytical_reports/2021/financial_sector_review_eng.pdf

page 13

2019 4.7 8.0 3.0 2020 5.2 9.4 2.8

average ratios of last 3 years stay 11 and 9.9 percentages respectively which is a good indicator for profitability.

Figure 5. Profitability ratios of banking sector

Source: NBG statistical data45

The key metric in the banking industry closely related to the profitability is net interest margin (NIM). NIM of banking industry sharply decreased in 2020. For the financial year 2020, NIM stood at 3.6% down by 0.9 pp YoY, due to a decrease in loan yields, increase in GEL deposit costs, as well as currency depreciation due to the pandemic. All the data are represented in the table 6 ’’ Interest magin for Georgian Banks’’ below.

Table 6. Interest margin for Georgian banks

2018 2019 2020 Average

5.30% 4.50% 3.60% 4.50%

Source: NBG statistical data46

45 Financial sector review 2020. NBG data. Available at https://www.nbg.gov.ge/uploads/publications/analytical_reports/2021/financial_sector_review_eng.pdf

page 13

46 Financial sector review 2020. NBG data. Available at https://www.nbg.gov.ge/uploads/publications/analytical_reports/2021/financial_sector_review_eng.pdf

page 13

10.8% 9.9% 9.1% 9.9%

12.2%10.9% 9.9% 11.0%

0.0%5.0%

10.0%15.0%20.0%25.0%

2018 2019 2020 Average

Profitability

Asset Profitability Loan Profitability

45

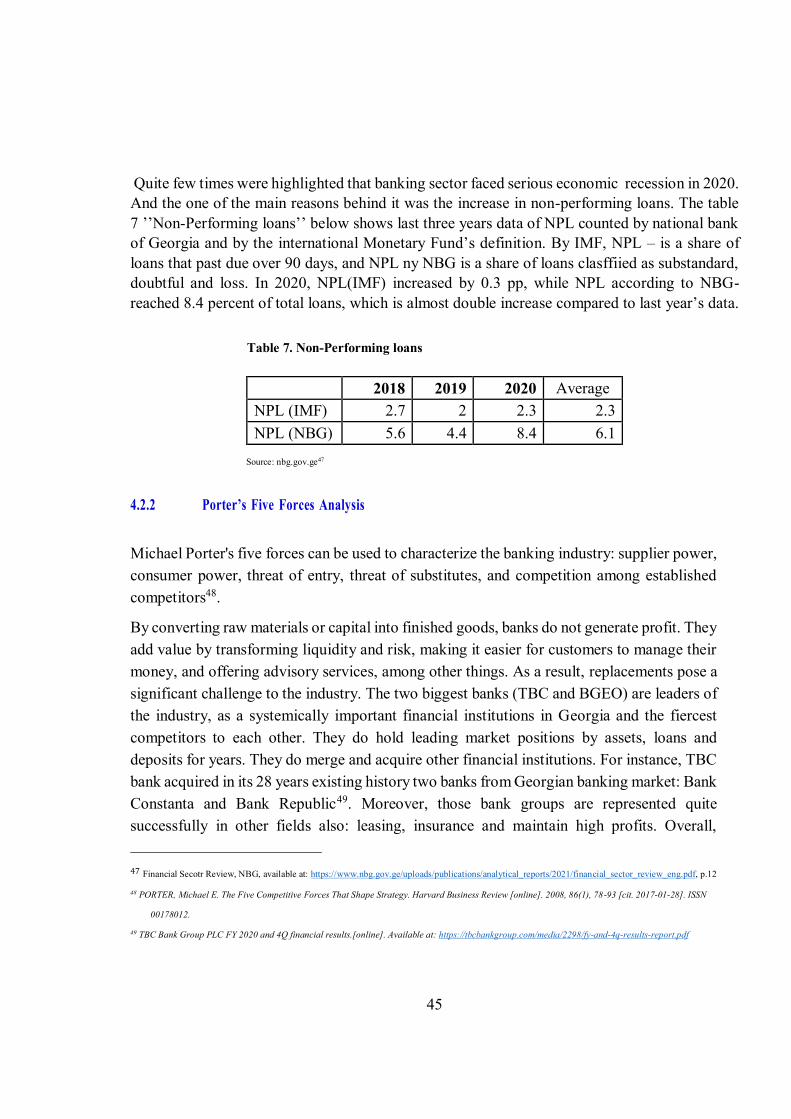

Quite few times were highlighted that banking sector faced serious economic recession in 2020. And the one of the main reasons behind it was the increase in non-performing loans. The table 7 ’’Non-Performing loans’’ below shows last three years data of NPL counted by national bank

of Georgia and by the international Monetary Fund’s definition. By IMF, NPL – is a share of loans that past due over 90 days, and NPL ny NBG is a share of loans clasffiied as substandard, doubtful and loss. In 2020, NPL(IMF) increased by 0.3 pp, while NPL according to NBG- reached 8.4 percent of total loans, which is almost double increase compared to last year’s data.

Table 7. Non-Performing loans

Source: nbg.gov.ge47

4.2.2 Porter’s Five Forces Analysis

Michael Porter's five forces can be used to characterize the banking industry: supplier power, consumer power, threat of entry, threat of substitutes, and competition among established competitors48.

By converting raw materials or capital into finished goods, banks do not generate profit. They add value by transforming liquidity and risk, making it easier for customers to manage their money, and offering advisory services, among other things. As a result, replacements pose a significant challenge to the industry. The two biggest banks (TBC and BGEO) are leaders of the industry, as a systemically important financial institutions in Georgia and the fiercest competitors to each other. They do hold leading market positions by assets, loans and deposits for years. They do merge and acquire other financial institutions. For instance, TBC bank acquired in its 28 years existing history two banks from Georgian banking market: Bank Constanta and Bank Republic49. Moreover, those bank groups are represented quite successfully in other fields also: leasing, insurance and maintain high profits. Overall, 47 Financial Secotr Review, NBG, available at: https://www.nbg.gov.ge/uploads/publications/analytical_reports/2021/financial_sector_review_eng.pdf, p.12

48 PORTER, Michael E. The Five Competitive Forces That Shape Strategy. Harvard Business Review [online]. 2008, 86(1), 78-93 [cit. 2017-01-28]. ISSN

00178012.

49 TBC Bank Group PLC FY 2020 and 4Q financial results.[online]. Available at: https://tbcbankgroup.com/media/2298/fy-and-4q-results-report.pdf

2018 2019 2020 Average NPL (IMF) 2.7 2 2.3 2.3 NPL (NBG) 5.6 4.4 8.4 6.1

competition and entrance of strong players are welcomed in the industry. But being in the same level as those two banks are quite challenging for any other banks even though they are domestic or foreign capital founded ones.

Money is, in essence, the most liquid and transferable of all financial instruments. If a consumer takes out a loan, the commodity, the loan itself, is nearly identical regardless of which bank offers it. The customer is given a certain amount of money and is required to repay it. The interest rate is the most significant variable. Other considerations, such as the branch office's proximity or a previous relationship with the bank, may be taken into account. Customers, on the other hand, almost always believe and know that they have a choice. As a result, market differentiation is extremely difficult.

As a result of the internet's rise, customers' bargaining power has greatly increased. Switching banks takes just a few minutes, and customers can quickly compare the terms and conditions of various banks. An individual does not pose a serious risk to a bank. Customers who shop in stores, on the other hand, have a lot of bargaining power. Since NII is traditionally the most important source of revenue for commercial banks. Corporate and high-net-worth individuals have more individual bargaining power because the loss of large accounts would have a greater impact on the bank's profitability. The asset management industry is unusual in that the loss of a single well-known customer will result in large withdrawals.

The bargaining power of suppliers cannot be measured all at once. Bank suppliers are divided into two groups based on their religious differences. Depositors (those who provide capital) make up the first category, while workers make up the second (supplying labor). The former party's situation is identical to that of the customers' bargaining power.

Employees usually do not have a lot of bargaining power. Individual vendors, with the exception of executives, have little influence over the bank's operations and policy, and labor union representation is low.

Georgia's banking sector is fiercely competitive. Essentially, any customer who requires banking services already has them. As a result, new consumers must be attracted from rivals. That, however, is prohibitively costly. Banks aim to sell as many items to their customers as possible. The behavior is due to two factors. For starters, more sold goods imply more income for the bank. Second, the higher a customer's switching costs are, and the less likely he is to accept a competitor's bid, the more goods he has.

47

Strict regulation, capital requirements, and the length of time required to develop brand identity and operations reduce the danger of new entrants to a bare minimum. TBC and BGEO, two financial behemoths, have been in existence for decades. In less than a decade, every new entrant has a very low chance of seriously threatening their spot.

To summarize, the Georgian banking industry is competitive, with suppliers and consumers wielding only moderate influence. However, due to the unique characteristics of capital, the sector as a whole is very unique. New entrants face a tough start due to the stringent regulatory criteria.

4.3 Business Model of TBC and BGEO

After analyzing the country’s banking sector, the author focuses on two systematically

important banks. The valuation process cannot be taken completed without first understanding their business descriptions by reviewing key operating categories. Later on, this chapter values and compares their economic conditions.

TBC Bank Group PLC

TBC Bank Group PLC (or the Group) was founded in 1992 and is headquartered in Tbilisi, Georgia. TBC Bank Group PLC was incorporated on 26 February 2016 as the ultimate hold-ing company for JSC TBC Bank Georgia50. TBC Bank became the parent company of JSC TBC Bank Georgia on 10 August 2016, following the Group’s restructuring. TBC Bank suc-cessfully listed on the London Stock Exchange’s premium listing segment on 10 August

2016. TBC Bank is a constituent of the FTSE 250 Index and MSCI United Kingdom Small Cap Index. It is also a member of the FTSE4 Good Index Series.

The company through its subsidiaries, provides banking, leasing, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan. Its main home affiliates are: TBC Leasing, TBC Pay, and TBC Capital. TBC

50 Online, Available at tbcbankgroup.com/about-us/history/

Bank is the largest banking group in Georgia, where 99.5% of its business is concentrated, with a 38.2% market share by total assets (GEL 22,557.8 million).

Overall, TBC Bank offers various current/settlement accounts, and term deposits; mortgage, consumer, retail, and corporate loans, as well as loans for micro, small, and medium enterprises; credit cards, credit lines, letters of credit, and guarantees; and money transfer and currency exchange services. The company also provides motor, travel, personal accident, credit life and property, business property, liability, cargo, and agro insurance products; finance leasing; payment services; and corporate advisory, debt and equity capital markets, brokerage, investment research, PR and marketing, real estate management, computer and software, and postal services. In addition, it offers internet and mobile banking services.

But the key segments for the company can be divided into four categories: Retail, Corporate, and Micro, Small and Medium Enterprises segments.

Retail Banking

TBC Bank serves 2.6 million customers51. Which is 90% of the adult population of the country. They offer banking products to their clients and a full range of services focusing on digital distribution channels. Retail banking is divided into ‘’mass’’ retail and personal banking which allows offering

comfortable banking services to each customer. Moreover, bank offers multi-channel services to digital distribution channels to affluent customers with a focus that includes Internet and mobile banking services with improved features as well as well expanded capabilities of the call center.

The segment’s gross loans amounted 5,954 ml Gel in the end of the 2020

financial year with a bias to the mortgage loans mostly (66%), which formed approximately 39.4 % of market share. This is 2% growth rate with at constant currency compared to last year’s data. While Retail Banking deposits amounted

7,255 ml Gel and got 39.5% of market share. Which means 2% growth rates at constant currency prior to the last year52.

Corporate Banking

51 Key business segments. FY 2020 and 4Q Investor Presentation. Available at https://tbcbankgroup.com/media/2295/fy-and-4q-2020-investor-presentation.pdf

page 25

52 FY 2020 and Q4 2020 results report. TBC bank. available at: https://tbcbankgroup.com/media/2298/fy-and-4q-results-report.pdf page 17

49

Bank has a well-diversified loan portfolio serving 3.7 thousands clients and includes all major field of economy: Energy and utilities, real estate, food industry, hotels and recreation, construction healthcare, trade, agriculture, financial services, metallurgy and mining industry, auto-tech service, oil and gas and etc. It includes full range of core and supplementary products.

The segments gross loans reached 5,691 ml Gel at the end of financial year 2020 which is 38.6% of market share and means 2.8 % of growth at constant currency prior to last year. While corporate banking deposits amounted 3,940 ml Gel, 34.5 % of market share and 1.4 % growth at constant currency compared to last year53.

Micro, Small and Medium Enterprises (MSME)

In the country, 62% of newly registered legal entities choose TBC Bank. Diversified MSME portfolio with strong dynamics in Agriculture Hotel & Leisure and Trade. It serves 160.3 thousand clients which makes it the leading partner bank for MSMEs.

The segments gross loans amounted 3,556 ml Gel in the end of 2020 which means 2% growth rate at constant currency prior to last year. MSME deposits reached 1,378 ml Gel and got also 2% growth rate at constant currency prior to 2019 year54.

Bank of Georgia Group PLC

Bank of Georgia Group PLC (Bank of Georgia group or BOGG) was established in 1994. It is a UK incorporated holding company55 As of 31 December 2020, the principal shareholder of the Bank was JSC BGEO Group, owning 79.78% of the Bank’s shares. Bank of Georgia

Group plc (admitted to premium listing segment of the Official List of the UK listing Authority and to trading on the London Stock Exchange plc under ticker BGEO.

53 Key business segments. FY 2020 and 4Q Investor Presentation. Available at https://tbcbankgroup.com/media/2295/fy-and-4q-2020-investor-presentation.pdf

page 13

54 Key business segments. FY 2020 and 4Q Investor Presentation. Available at https://tbcbankgroup.com/media/2295/fy-and-4q-2020-investor-presentation.pdf

page 13

55 Annual report 2020. Bog.ge . available at https://bankofgeorgiagroup.com/reports/annual page 2

The company operates through Retail Banking, Corporate and Investment Banking, BNB, and other Banking Business segments.

The Retail Banking segment offers consumer loans, mortgage loans, overdrafts, credit cards, and other credit facilities; funds transfer and settlement services; and customers’ deposits for individuals and legal entities

under the Express, Bank of Georgia, and SOLO brands. Retail banking Gross loans amounted 9.0 bl Gel in the end of 2020 and means 65.2 % of gross loans of the bank56