Credit Reporting Knowledge Guide 2019

152

Credit Reporting Knowledge Guide 2019 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Credit Reporting Knowledge Guide 2019

Credit Reporting Knowledge Guide

2019

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

© 2019 The World Bank Group

1818 H Street NW Washington, DC 20433 Telephone: 202-473-1000 Internet: www.worldbank.org All rights reserved.

This volume is a product of the staff and external authors of the World Bank Group. The World Bank Group refers to the member institutions of the World Bank Group: The World Bank (International Bank for Reconstruction and Development); International Finance Corporation (IFC); and Multilateral Investment Guarantee Agency (MIGA), which are separate and distinct legal entities each organized under its respective Articles of Agreement. We encourage use for educational and non-commercial purposes.

The findings, interpretations, and conclusions expressed in this volume do not necessarily reflect the views of the Directors or Executive Directors of the respective institutions of the World Bank Group or the governments they represent. The World Bank Group does not guarantee the accuracy of the data included in this work.

Rights and Permissions

The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. The World Bank encourages dissemination of its work and will normally grant permission to reproduce portions of the work promptly.

All queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2422; e-mail: [email protected].

Photo Credits: World Bank Photo Library and Shutterstock.Com

Table of Contents

ICREDIT REPORTING KNOWLEDGE GUIDE 2019

ACRONYMS AND ABBREVIATIONS V

PREFACE VII

OVERVIEW IX

CHAPTER 1. THE IMPORTANCE OF CREDIT REPORTING SYSTEMS 11.1. The Role of Credit Reporting Systems 1

1.2. The Costs of Asymmetric Information 3

1.3. Key Concepts in Credit Information Sharing 4

1.4. Comprehensive (Positive and Negative) Information Sharing 6

1.5. Full-File Information Sharing 8

CHAPTER 2. CREDIT REPORTING SERVICE PROVIDERS 112.1. Functions of Credit Reporting Service Providers 12

2.2. Ownership Structures 17

2.3. Optimal Market Size 19

CHAPTER 3. THE EVOLUTION AND GROWTH OF CREDIT REPORTING SYSTEMS 253.1. The Evolution of Credit Reporting Systems 25

3.2. Factors Affecting the Growth of Credit Reporting Systems 26

3.3. Competition in the Credit Reporting Industry 31

3.4. Moving Forward: Expected Trends 37

CHAPTER 4. LEGAL AND REGULATORY FRAMEWORK 394.1. Licensing or Registration of CRSPs 41

4.2. Data Collection, Retention, Disclosure, and Security 41

II TABLE OF CONTENTS

4.3. Governance and Risk Management 45

4.4. Consumer Rights 46

4.5. Oversight and Enforcement 48

4.6. Alternative Dispute Resolution Mechanisms 49

4.7. Cross-Border Data Flows 55

CHAPTER 5. DEVELOPING CREDIT REPORTING SYSTEMS IN EMERGING MARKETS 575.1. Assessing Market Conditions 57

5.2. Changing Perceptions and Building Awareness 59

5.3. Ensuring Adequate Data Availability 62

5.4. Ensuring Financial Sustainability 66

5.5. Creating an Appropriate Business Model 66

5.6. Identifying Appropriate Technology Needs 69

5.7. Operational and Practical Considerations 72

CHAPTER 6. DEVELOPING VALUE-ADDED SERVICES 81

6.1. Automated Decision-Making Systems 81

6.2. International Industry Trends in Developing Value-Added Services 82

6.3. Products 84

6.4. The Use of Credit Information Data for Prudential Supervision 91

CHAPTER 7. CASE STUDIES 957.1. Reforming Credit Reporting Systems in Central Asia 95

7.2. The Role of Outreach and Financial Literacy in Mobilizing Credit Reporting System Reforms 98

7.3. Overcoming the Issue of Consent: Guyana’s Credit Bureau 99

7.4. Jamaica’s Experience in Licensing and Regulating Credit Bureaus 100

7.5. Establishing Credit Histories for Low-Income Women in India 103

7.6. Increasing the Coverage of Commercial Credit Reports and Using Alternative Sources of Data to Reach Underserved MSMEs in India 107

7.7. UEMOA: Pioneering a True Cross-Border Credit Information Sharing System 111

7.8. Credit Registry of the Bank of Italy 113

7.9. The AnaCredit Project 114

IIICREDIT REPORTING KNOWLEDGE GUIDE 2019

APPENDIXES 115Appendix 1. Contents of an Individual Credit Report 115

Appendix 2. Contents of a Commercial Credit Report 117

Appendix 3. General Principles for Credit Reporting and the International Committee for Credit Reporting (ICCR) 119

Appendix 4. World Bank Doing Business Surveys 120

Appendix 5. Examples of Specialized ADR service providers dealing with credit disputes 121

Appendix 6. Maps of Credit Registries and Credit Bureaus 123

REFERENCES 131

LIST OF BOXES Box 1.1. The Limitations of Negative-Only Reporting 8

Box 3.1. EFL Psychometrics and Creditinfo Psychometrics (Coremetrix) 29

Box 4.1. Quality of Data 42

Box 4.2. Issues Affecting Consent Regulation 43

Box 4.3. Equifax Data Breach: September 2017 46

Box 4.4. ADR Case Management by the South African Credit Ombud 52

Box 5.1. Errors in Consumers’ Credit Files* 63

Box 5.2. Outsourcing from the Czech Republic 68

LIST OF FIGURES Figure 1.1. Key Stakeholders in Credit Reporting Systems 4

Figure 1.2. Effect on Default Rates of Including Positive Information, United States 7

Figure 1.3. Effects on Default Rates of Including Positive Information, Argentina and Brazil 7

Figure 1.4. Effect on Approvals of Including Positive Information 7

Figure 1.5. Effect of Including Positive Information on Approvals among Retailers and Other Lenders 8

Figure 1.6. Effect on Default Rates of Increasing Number of Information Sources 9

Figure 1.7. Effect of Types and Sources of Information on Predictive Power 9

Figure 2.1. Data Subjects Covered by CRSP 12

Figure 2.2. Sources of Information for Privately Held Credit Bureaus 13

Figure 2.3. Information on Individuals Collected by Credit Bureaus 13

Figure 2.4. Sample History of Payments 14

Figure 2.5. Firm-Level Information Collected by Credit Bureaus 14

IV TABLE OF CONTENTS

Figure 2.6. Sources of Information for Credit Registries 15

Figure 2.7. Ownership Structures of Credit Bureaus 18

Figure 3.1. Growth of Consumer Credit Bureaus 32

Figure 3.2. Credit Bureau Coverage by Region 2017 32

Figure 3.3. Growth of Credit Registries 33

Figure 3.4. Credit Registry Coverage by Region, 2017 33

Figure 3.5. Credit Information Index 34

Figure 5.1. Average Time between Request and Release of Data 65

Figure 5.2. Qualities of a Strong Technical Partner 70

Figure 5.3. Common Delivery Modes for CRSPs 72

Figure 5.4. Key Items in Contracts/Agreements with Users and Data Providers 73

Figure 5.5. Sample Organizational Structure of a CRSP 74

Figure 5.6. Key Performance Indicators of a Credit Reporting Service Provider 77

Figure 6.1. Customer Life Cycle: Offering Value-Added Services 82

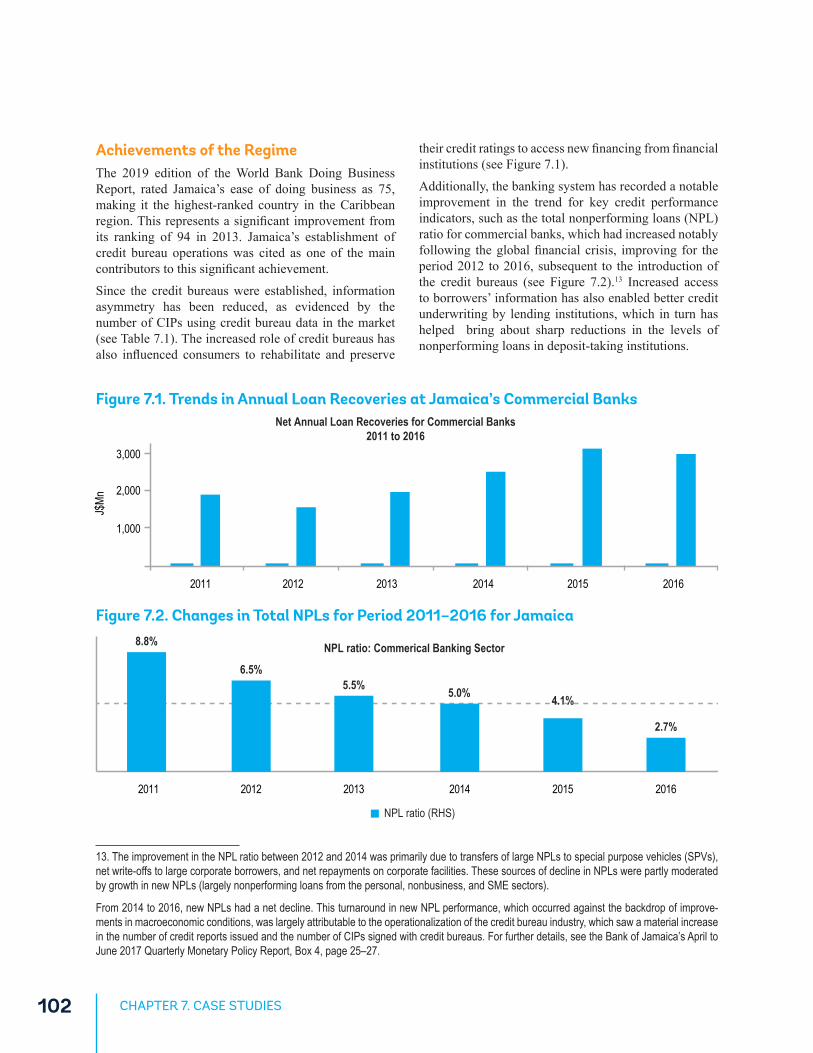

Figure 7.1. Trends in Annual Loan Recoveries at Jamaica’s Commercial Banks 102

Figure 7.2. Changes in Total NPLs for Period 2011–2016 for Jamaica 102

Figure 7.3. Commercial Credit Reporting India Project Pillars 108

Figure 7.4. Potential Alternative Data Sources for India’s Underbanked and Unbanked MSMEs 109

LIST of TABLESTable 1.1. Benefits of Comprehensive and Full-File Information Sharing 10

Table 2.1. Comparison of Credit Bureau Ownership Structures 20

Table 2.2. Differences Between the Various Types of CRSPs 21

Table 2.3. Credit Reporting and Collateral Regimes: Linkages and Synergies 23

Table 4.1. Rights and Obligations of CRSPs, Data Providers, Users, and Data Subjects 40

Table 4.2. Frequently Used Dispute Resolution Procedures 50

Table 5.1. Operational Phase Staffing 75

Table 5.2. Hypothetical Pricing Matrix for Credit Reporting Service Providers 76

Table 5.3. Hypothetical Profit and Loss Statement for a Consumer Credit Bureau 78

Table 7.1. Select Indicators for 2013–2016 for Jamaica 101

Table 7.2. Personal Data Points Need to Generate Credit Information Reports 105

Table 7.3. Trend of Credit Report Inquiries 110

Acronyms and Abbreviations

VCREDIT REPORTING KNOWLEDGE GUIDE 2019

ACAFI Azerbaijan and Central Asia Financial Infrastructure

AI artificialintelligence

API applicationprograminterface

AR augmentedreality

B2B business to business

B2G businesstogovernment

BCBS BaselCommitteeofBankingSupervision

BCEAO Banque Centrale des Etats de l’Afrique de l’Ouest

BOG BankofGuyana

BOJ BankofJamaica

CCR centralcreditregister

CIB CreditInformationBureau

CIBIL CreditInformationBureauLtd.(India)

CIC creditinformationcompany

CICRA CreditReportingAct(India)

CII CreditInformationIndex

CIP creditinformationprovider

CIR creditinformationreport

CRA CreditReportingAct(Jamaica)

CRSP creditreportingserviceprovider

EFT electronic funds transfer

EMV Eurocard,Mastercard,Visa(electroniccreditstandard)

VI ACRONYMS AND ABBREVIATIONS

ESCB EuropeanSystemofCentralBanks

F&M FinanceandMarkets(GlobalPractice)

fintech technology-enabledfinancialservices

FSAP FinancialSectorAssessmentProgram

G2G governmenttogovernment

GNI grossnationalincome

ICCR InternationalCommitteeonCreditReporting

IDG IFCDevelopmentGoals

IFC International Finance Corporation

IoT internetofthings

JLG jointliabilitygroup

KYC knowyourcustomer

MFI microfinanceinstitution

MFIN MicrofinanceInstitutionsNetwork

MIS managementinformationsystem

MSME micro,small,andmediumenterprises

NBFC nonbankingfinancialcompany

NCB nationalcentralbank

NIST NationalInstituteofStandardsandTechnology(UnitedStates)

NPL nonperformingloan

P2B person to business

P2G persontogovernment

P2P person to person

RBI ReserveBankofIndia

regtech regulatorytechnology

SHG self-helpgroup

SME smallandmediumenterprise

UEMOA Unionéconomiqueetmonétaireouest-africaine(WestAfricanEconomicand MonetaryUnion)

VAS value-addedservice

WAMU WestAfricanEconomicandMonetaryUnion

VIICREDIT REPORTING KNOWLEDGE GUIDE 2019

Preface

The Global Credit Reporting Program launched bythe International Finance Corporation (IFC) in 2001and later renamed Credit Information Solutions tobetter reflect the nature of its goal, has supported thedevelopment of credit bureaus and public registries inover 90 countries through a combination of analyticalandoperationalwork.Since the launch of the program, the World BankGrouphashelpedtodevelopfavorablecreditreportingenvironments in many countries around the worldand to implement reforms improving these countries’credit information systems. This third edition of theCredit Reporting Knowledge Guide,likethetwoearliereditions, disseminates knowledge on best practices increditreportingdevelopment,basedontheexperiencesoftheWorldBankGroup.Intheyearssincethepreviousedition (2nd ed., 2012), many nations have madegreat strides in credit reporting. In 2015, for example,Kenya and Uganda made large improvements byexpandingborrowercoverage(14.8percentoftheadultpopulation). Similarly, the credit bureaus or registriesin the Lao People’sDemocratic Republic,Mauritania,Rwanda, Uganda, and Vietnam expanded coverage toat least 5 percent of their adult populations. Between2014 and 2015, Afghanistan, the Comoros, Guyana,Lesotho,andtheSeychellesallestablishedanewcreditbureau or registry. Many countries improved theirregulatoryframeworksforcreditreporting:Latvia,TheBahamas and the Organization of English SpeakingCaribbeanStates (OECS), adoptedcreditbureau lawswith the aim of promoting responsible borrowingand lending while protecting the rights of borrowers;Namibia improved access to credit information bylegally guaranteeing borrowers’ rights to inspect their

owndata; andPeru fully implemented its new lawonpersonal data protection, requiring stronger safeguardsin administeringborrowers’ personal data. In addition,overthepastfewyears,nationsinSub-SaharanAfrica,theregionwiththelargestnumberofreforms,focusedon improving the availability of credit information: InRwanda, Zambia, and Zimbabwe, credit scoring wasintroducedasavalue-addedservicetobanksandotherfinancialinstitutionstosupporttheirabilitytoassessthecreditworthinessofpotentialborrowers.TheoriginalCredit Bureau Knowledge Guide(2006)anditssecondedition(2012)elaboratedontheWorldBankGroup’sknowledgegainedoverseveralyearsofrunningthe Global Credit Reporting Program and provided avarietyofstakeholders,primarilyinemergingmarkets,withacomprehensiveinformationresourcetohelpthemdevelop their own credit reporting systems.This thirdedition reflects on the experiences and lessons learnedinthelastsevenyears,withgreateremphasisoncreditreportingforbusinesses,theimpactofnewtechnologiesand data on credit reporting, and the development ofnew products and services catering specifically to theneeds of users and borrowers. In discussing how thecreditreportingarenaisadaptingtoarapidlychangingtechnologicalandfintechenvironment,theGuideseeksto align the adoption of these disruptive technologieswiththecoreBaliFintechagendaaroundenablingfintechwhile ensuring financial sector resilience, addressingrisks and promoting international cooperation. Severalnew case studies enhance the theoretical discussions,highlighting different aspects of developing creditreportingsystemsand the importanceof thesesystemstothecountriesimplementingandimprovingthem.

VIII PREFACE

UndertheguidanceofSebastianMolineusandMaheshUttamchandani, this Credit Reporting KnowledgeGuide was prepared by the Global Credit ReportingTeam within the World Bank Group’s Finance,Competitiveness & Innovation Global Practice.TheGuide was drafted by a team comprised of ShaliniSankaranarayanan and Guy Patrick Ewoukem Elat,with the support from theCredit Infrastructures teamof specialists: LuzMaria Salamina, OscarMadeddu,Fabrizio Fraboni, Colin Raymond, Pratibha Chhabra,Nina Pavlova Mocheva, Ghada O. Teima, andFredesvinda Fatima Montes. The authors would liketo thank colleagues in the World Bank Group for

their continuous support of the work of the CreditInformation Solutions Program and the preparationofthisGuide.1Wearealsogratefultothesupervisors,credit bureaus and registries around theworldwhosework and employees made the development andpublicationofthisGuidepossible.2

Theteamgratefullyacknowledgesthegenerousfinancialsupport of the Swiss State Secretariat for EconomicAffairs(SECO).We hope this Guide will prove both informativeanduseful to all thoseworking in the area of creditreportingdevelopment.

1. Contributors from World Bank Group’s Global Credit Reporting Team include Oscar Madeddu, Colin Raymond, Fabrizio Fraboni, Luz Maria Salamina, Hung Hoang Ngovandan, Shalini Sankaranarayan, and Fredesvinda Fatima Montes. Other important contributions were provided by Nina Pavlova Mocheva, Pratibha Chhabra and Renuka Madathiparambil. We also wish to acknowledge the feedback and inputs received from other WBG colleagues, including Matthew Saal, Sakshi Varma, Elaine MacEachern, Michael Terazi, David Medine, Robert Cull, Ata Can Bertay, Miriam Bruhn, Bilal Zia, and Mohamad Nazirwan.

2. We would like to acknowledge the kind contributions of Bank of Jamaica and Bank of Guyana in developing the respective case studies. We are grateful for the input received from the external peer reviewers: IMF (Arslanalp, Bidisha Das, Esha Chhabra, and Yingbin Xiao), Creditinfo (Stefano Stoppani and Ieva Bieliunaite), BIIA (Peter Sheerin and Neil Munroe), CRIF (Stella Lanzi, Vicenzo Resta, Venturi Emanuel, Parijat Garg, and Racemoli Valeria), and ACCIS (Enrique Velazquez). In addition, we would like to acknowledge the excellent editing assistance of Susan Boulanger. On design, layout, and production, we would like to thank Aichin Lim Jones and Amy Quach. We also would like to acknowledge Bruno Bonansea for producing the global and regional maps.

IXCREDIT REPORTING KNOWLEDGE GUIDE 2019

Overview

Since the first Knowledge Guide was written thirteenyearsago,globalfinancialmarketshavegrownbyleapsand bounds, leveraging a host of new technologiesanddata.Therapidgrowth in innovativeproductsandservicesisadirectresponsetothehugeunmetdemandfor financial services that the traditional financiallandscapehadbeenstrugglingtomeet.AccordingtotheWorldBank,approximately2billionadultsaroundtheworldstilllackabasicaccount(WorldBank2017).Somekeyobstacles tofinancial inclusionareaffordabilityoffinancialservices,distancetoprovider,lackoftrust,andpotentialborrowers’lackofnecessarydocumentation.More broadly, inadequate access to finance and creditcontinues to exert a critical constraint on economicdevelopment.Around2.5billionpeople lackaccess toformal financial services (World Bank 2015), and anestimated 70 percent of formal small- and medium-sized enterprises in developing economies are eitherunservedorunderservedby theformalfinancialsector(Stein, Ardic, and Hommes 2013). The total creditgap amounts to US$1.3 to US$1.6 trillion (US$700to US$850 billion excluding firms in OECD high-incomeeconomies)(Stein,Goland,andSchiff2010).Inemergingmarkets, an estimated 1.9 billion people areemployedintheinformalsectorassmallholderfarmers,household-basedentrepreneurswith retail shops, streetvendors, artisans, and other service providers (ILO2018).Adisproportionatepercentageofthispopulationofpotentialborrowersarewomen:Womenrepresent76percentoftotalborrowersfrommicrofinanceinstitutions(World Bank 2010). These populations generally relyon personal savings or loans from friends, family,or moneylenders to meet their businesses’ capitalrequirements. Being self-employed or part of the

informal sector, these workers frequently lack formalsalaryslipsorothertraditionalincomestatementsusedbylenderstoascertainwhetheraprospectiveborrowerpossesses a steady source of income with which toservicealoanorothercreditreliably.Withoutacceptableproofofincome,thesepotentialborrowersmustpossesscollateral—mostlyfixedassetssuchas land,buildings,and so on—before lenders will consider their creditapplications. Once again, disenfranchised, lower-income segments of the population frequently cannotmeet collateral requirements or provide relevant legaldocumentationregardingassets.Lenders, too, face several challenges in seeking toprovidecredit to thesepopulations.Lendersoften lacktheinformationnecessarytoassessthecreditworthinessofpotential customers, including reliable identificationfor individuals and businesses. In the absence ofautomated screening methods, the relative costs ofpersonal screening and due diligence are very high,while the loan amounts tend to be modest. Potentialcustomers are oftenwidely dispersed in rural areas inwhich lendersmaynotfind it cost effective tooperatebranch networks. With limited access to inclusiveand timely data, lenders face concerns that borrowersmight accumulate many loans from multiple lenders,potentially resulting in over-indebtedness on the partof borrowers and an unacceptably large portfolio ofnonperforming loanson thepartof lenders.Moreover,weak regimes for creditor and bankruptcy protection,coupled with unreliable property rights, often makeattemptsatcollateralcollectionineffective.In markets facing these challenges, credit reportingservice providers perform the crucial functions of

X OVERVIEW

gathering and distributing reliable credit informationacross the entire borrower population, thus improvingcreditor protection and strengthening creditmarkets. Ineffect,theneedforphysicalcollateralcanbereplacedby—or at least supplemented with—reputational collateral.Creditreportingserviceproviderscanreduceinformationasymmetry, thus reducing default rates, which in turnshouldresultinloweraverageinterestrates,customizedproductsandservices,enhancedcompetitioninthecreditmarket,andultimately,increasedaccesstocredit.The newly developing area of financial technology,known as fintech, provides an innovative approach todeliveringfinancialservicesindifferentmarketsaroundtheworld that reflects theactualorperceived inabilityof traditional lenders, including banks, microfinanceinstitutions,andevenmoneylenders,toprovideoptimalfinancialservices tounderservedorunservedborrowersegments. While the jury is still out on where thetraditional financial sector and the new fintech sectorwillmeetandwhat thisencounterwillmeanforcreditreportingasawhole,totheextentthatthesenewentrantsextend credit using whatever means available, theyshouldbeconsideredstakeholdersinthecreditreportingsystem, and the rules for sharing credit informationshouldgenerallyapplyequallytothesenewplayers.This third edition of theCredit Reporting Knowledge Guide,inthespiritoftheearliertwoeditions,continuesto disseminate knowledge on best practices in creditreporting development, based on the experiences ofthe World Bank Group. The original Credit Bureau Knowledge Guide(2006)andthesecondedition(2012)presentedknowledgegainedoverseveralyearsofrunningtheGlobalCreditReportingProgram,andtheyprovidedavarietyofstakeholders,primarilyinemergingmarkets,withacomprehensiveinformationresourcetohelpthemindeveloping their owncredit reporting systems.Thisthird edition reflects on the experiences and lessonslearnedoverthelastsevenyears,withemphasisoncreditreportingforbusinesses,theimpactofnewtechnologiesand data on credit reporting, and the development ofnew products and services catering specifically to theneedsofusersandborrowers.Severalnewcasestudiesenhancethetheoreticaldiscussions,highlightingvariousaspectsofdevelopingcreditreportingsystems.Chapter 1 introduces key concepts in credit reporting:Whyisaccesstocreditimportant?Whatarethefactorslimiting access to credit? How can credit reportingservicesimproveaccesstocredit,andwhatroledotheyplayinensuringfinancialstability?And,finally,whoarethekeyactorsincreditreportingsystems?Thechapter

examinestheproblemofasymmetricinformation:whenborrowersknowmoreabouttheirabilityandwillingnessto repay loans than do lenders. The chapter presentsevidence from empirical research that validates theimportanceofcreditreportingintheoverallagendaforaccesstofinance.Chapter2introducesthedifferenttypesofcreditreportingservice providers (CRSPs) that collect informationon borrowers’ credit histories from creditors andavailablepublicsources.Unlikecredit ratingagencies,CRSPsfocuson individualsandsmallbusinesses.Thethree basic types of CRSPs are credit bureaus, creditregistries, and commercial credit reporting companies.Each has its strengths and weaknesses, and no singletype is inherently better than the others for any givenmarket condition. Indeed, given adequate demand, thethreetypesofserviceproviderscancoexistinamarketunderavarietyofownershipstructuresorasingleentitycanprovide oneormore of the functions providedbythese different entities. Chapter 2 also discusses thecommercialcreditreportingspace,whichhadnotbeentreatedextensivelyinearliereditionsoftheGuide.Chapter 3 covers the evolution of the credit reportingindustry to today, including key trends now emergingandexternaltrendsaffectingitsdevelopment.Thesecondeditionof theGuide introduced theGeneralPrinciplesforCreditReporting,thefirstsetofuniversalstandardsforcreditreporting,developedbyataskforceledbytheWorldBankandtheBankforInternationalSettlements(see Appendix 3). Since the General Principles werereleased, the task force has been formalized as theICCR,andithassinceworkedondevelopingadditionalpublicationstoprovideguidanceonthevariousaspectsofcredit reportingsystems; thesearealsodescribed inthischapter.Recognitionhasbeengrowingregardingthevaluethatcreditreportingcanbringtomicro,small,andmediumenterprises(MSMEs),aswellastothesearchfor alternative data forms to enhance lenders’ abilityto serve borrowers lacking formal credit histories. Inadditiontodevelopments inconsumerandcommercialcreditreporting,greaterrecognitionhasbeengiventotheuseandimportanceofcreditreportingdataforprudentialsupervisionandregulation.Thischapterdiscusseshownewtechnologies,newbigdata,andrelatednewproductsandtoolshavethepotentialtotransformthecreditandthecreditreportingindustries,includingabalancedviewofthepotentialrisksanduncertaintiessurroundingthesenewtoolsandthechallengestheypose.Chapter4outlines the legal and regulatory frameworkoptions for credit reporting systems. The legal

XICREDIT REPORTING KNOWLEDGE GUIDE 2019

framework for credit reporting differs from country tocountry.Itmayincludeacombinationofcreditreportinglaws, banking laws, data protection laws, consumercreditprotectionlaws,faircreditgrantingandconsumercredit regulations, personal and corporate privacy andsecrecyprovisions,banksecrecylaws,andcommerciallaws.Creditreportingactivitiescananddotakeplaceintheabsenceofaclear legalandregulatoryframework;however, in the long run,bestpractice indicatescreditreporting systems benefit from a legal and regulatoryframeworkthatisclear,predictable,nondiscriminatory,proportionate, and supportive of data-subject andconsumer rights. As recognition grows that creditreporting systems are vital to strengthening financialinfrastructure and ultimately access to finance, moreandmorecountriesareincreasingtheireffortstocreatethe ideal legal and regulatory environment for theseactivities.Withtheincreasingavailabilityofdata—andoftechnologiestoharnessthepowerofthesenewdata—alsocomesincreasingrisksassociatedwithsafeguardingdataandtheunderlyingprivacyofthedatasubjects.Chapter5summarizestheWorldBankGroup’s15plusyears of experience in developing credit bureaus andcreditregistriesaroundtheworld.Thechapterpresentsvariousapproachestothedevelopmentofcreditreportingand discusses the business, technological, financial,

and other operational and practical considerations that a developing credit reporting service provider mustaddress. It also reflects on the World Bank Group’sexperienceinestablishingnewcreditreportingmarkets.Chapter 6 presents an overview of the value-addedservices typicallyofferedbyestablishedcreditbureausthrough the repurposing of algorithms and data andtheproductsandservicesofferedbycommercialcreditreportingcompanies.Theinformationprovidedbybothfinancial and nonfinancial institutions allows creditbureaustoprovidecomprehensiveanalysisofborrowercreditworthiness, information for portfoliomonitoring,and fraud detection. The chapter also discusses theuseofcredit reporting informationbyfinancialsystemsupervisors and regulators to perform prudentialsupervisionandsystemicriskmonitoringofaneconomyasawhole.Chapter 7 rounds out the theoretical discussions andpractical guidelines with nine case studies of recentdevelopmentsincreditreportingspanningtheglobe.Theobjectiveof thecasestudies is toprovidepractitionerswithrealexamplesofhowcreditreportingsystemshavedeveloped over time in variousmarkets, including thechallengestheyfacedandthesuccessestheyachieved.

XII DEVELOPING CREDIT REPORTING SYSTEMS IN EMERGING MARKETS

1CREDIT REPORTING KNOWLEDGE GUIDE 2019

The Importance of Credit Reporting Systems

Credit infrastructures, including credit reportingsystems, secured transactions and collateral registries,and insolvencyandbankruptcy regimes, are critical inanyeconomyforexpandingaccesstofinance,extendingfinancial inclusion, and supporting the developmentof stable financial systems. Broadly speaking, creditreportingsystemscomprisetheinstitutions,information,technologies, rules, and standards that enablefinancial intermediation. When comprehensive creditinfrastructures are available, efficient, and reliable, thecostoffinancialintermediationfalls;financialproductsand services become accessible to greater numbersof borrowers; and lenders and investors have greaterconfidenceintheirabilitytoevaluateandpricerisk(IFC2009). The information captured by credit reportingsystems is critical to ensuring stability in thefinancialmarkets.Accesstofinanceisanessentialcomponentofeconomicdevelopment and job creation. A host of studieshave shown a positive correlation between financialdevelopment and economic growth (Taivan and Nene2016). Well-functioning financial systems offer avarietyoffinancialproductsforsavings,credit,andriskmanagementtoawiderangeofpeopleandbusinesses.Access to financial services enables rural and urbanhouseholds tosmoothconsumptioncurvesandacquireessential services, including food,housing,health, andeducation(WorldBank2015).Micro,small,andmediumenterprises(MSMEs)requireaccesstofinancingtomeetshort- and long-term capital needs and to grow andexpandtheirbusinesses.Individual borrowers’ credit needs typically involvepersonal loans, auto loans, mortgage loans, student

loans,andothershort-termcreditneeds.Smallbusinessloans are generally necessary tomeetworking capitalrequirements, to maintain assets for production, or toexpand business operations. In the case of very smallbusinesses,thebusinessowner’spersonalfinancestendto be commingledwith the business’s finances, as theownermaydrawonpersonalfinancingsourcestofundthebusinessinitsearlystages.Accesstofinanceisalsocriticalforlargercorporationsandconglomerates,which,giventheirsize,performance,andassets,typicallymeetfundingrequirementsthroughcapital markets and other sources. Credit reportingsystems are less relevant for these businesses, aslenderstotheselargeentitiesrelyonavarietyofothersources of information when making credit-relateddecisions. This Guide focuses therefore more on thecreditneedsofindividualsandofthemicro,small,andmediumbusinesses thatstand tobenefitmost fromthedevelopmentofcreditreportingsystems.

1.1. The Role of Credit Reporting Systems Despite thetremendousneed,a largeproportionof theworld’spopulationlacksaccesstocredit.Worldwide,anestimated2.5billionpeoplearecurrentlywithoutformalfinancial services (World Bank 2015). In developedeconomies, approximately 90 percent of adults haveaccess to formal financial services, as compared with41 percent in emerging markets (Demirguc-Kunt andKlapper 2012). The World Bank Enterprise Surveysdatabase reports that, globally, 27 percent of firmsidentifyaccesstofinanceasamajorconstraint.ArecentreportbyIFCandtheSME(smallandmediumenterprise)

CHAPTER

1.

2 CHAPTER 1. THE IMPORTANCE OF CREDIT REPORTING SYSTEMS

Finance Forum found that 65 million enterprises— 40percentof formalMSMEs—haveanunmetfinanceneedof$5.2trillionayear,or1.4timesthecurrentlevelofMSMElending.Women-ownedbusinessescomprise28percentofMSMEsandaccountfor32percentoftheformalMSMEfinancegap(IFC2017).Access to credit is largely hindered by the lack ofsufficient information or information asymmetryregardingtheabilityofpotentialborrowerstorepaydebtsandby the lackofasupportingfinancial infrastructureto make such information available (Demirguc-KuntandKlapper2012).Over theyears, thebasicapproachto formal lending has remained traditional: Decisionsare based on subjective judgments about a borrower’spropensity to repay, supported by alternative risk-mitigating mechanisms, including group guarantees, arequirementfor(mostlyfixed)collateral,higherinterestrates,shorterfinancingterms,andsimilararrangements.In most markets, commercial lending traditionallyfocuses on large companies and select retail clientswithproven income, capacity to repay, and/or suitablecollateral.Thecreditneedsofsmallerentrepreneursandindividualborrowersareprimarilymetthroughinformalfinancialservicesandnonbankcredit.3

Microfinance continues to be an important sourceof access to credit and financial services for thevast majority of the global population unserved orunderserved by formal financial channels.The growthof the microfinance industry was driven in part byglobal recognition of its value as a development tooland inpart by its promotionbynationalgovernments,international development bodies, donors, and sociallyoriented investors. What started as a movement ledlargelybyNGOsandcooperativeshasrapidlyexpandedto include downstream lending by larger commerciallenders asmore emphasiswas placed on serving low-incomeconsumersandentrepreneursthroughlow-value,short-tenure loanswith flexible installment plans. Thenumberofborrowersservedbymicrofinanceinstitutions(MFIs) is estimated at around 130million (IFC). Thefield’sinitialrapidgrowthandhighreputationwasbuiltonstrongassetqualitycombinedwithlowdelinquencyrates;however,sometimeinthelate2000s,theindustrysuffered setbacks as portfolios deteriorated globally.The increasingportfolios-at-riskvalueswereattributedto inadequate risk management systems and controls,internal organizational weaknesses, lack of data

sharing with CRSPs, and excessive growth in narrowgeographies,combinedwithunhealthylendingpracticesthat affected borrower repayment incentives andbehaviors.These factors resulted inover-indebtedness,aswitnessed in severalmarkets, includingBosnia andHerzegovina, Cambodia, Egypt, India, Morocco, andPakistan(Lymanetal.2011).Small- and medium-size enterprise finance can bedistinguished frommicrofinance in two respects:First,itcoversawiderrangeofentrepreneurialclientele,andsecond, SMEs are often larger and therefore representa greater risk exposure than do microfinance clients.SMEsthusrequireamorein-depthcreditreviewprocessthandomicrofinanceclients.Still,SMEsoftenfallintothemiddlemarket:toobigfortraditionalmicrofinance,yettoosmallformainstreambanks.AccesstofinanceisakeyconstrainttoSMEdevelopmentand growth, especially in emerging markets. In theirearlystages,SMEsareoftenfinancedinternallybytheowner’ssavingsorearningsandbypersonalborrowingin theowner’sownname.Sustainedgrowth,however,usually requires external funding.A2003WorldBankstudy (Love and Mylenko 2003) that looked at datafrom 5,000 firms, across 51 countries, found that incountries without credit bureaus, 49 percent of smallfirms reported facing high financing constraints, asopposedto27percent incountries thatdidhavecreditbureaus. The study also found that in countries withcreditbureaus,theprobabilityofasmallfirmobtainingabankloanwas40percent,versus28percentincountrieswithout credit bureaus. Another World Bank studybasedondatafrom99developingcountriesfoundthatsmall firms are large contributors to total employmentandjobcreation,buttheirproductivitygrowthislowerthanthatoflargerfirms(Meghana,Demirguc-Kunt,andMaksimovic2011).ThestudyshowedthatSMEgrowthand productivity is hampered by inadequate financialinfrastructureandregulatoryenvironments(inadditiontootherobstacles),anditcalledonauthoritiestodesignpoliciestoovercomethesechallenges.Historically,smallbusinessborrowershaverepresenteda difficult-to-servemarket because of the traditionallyhigh cost of subjective credit evaluation. The SMEbusinessowner’spersonalfinancesareoftencomingledwith those of the business, and this distinction is notimmediately apparent to lenders. The difficulty inassessingthecreditworthinessofSMEbusinessescauses

3. This Guide discusses only the supply side of providing access to formal finance, but the demand side can also limit financial inclusion. The informal sector is sometimes unwilling to join the formal sector, which it can perceive as imposing greater tax burdens and regulatory burdens.

3CREDIT REPORTING KNOWLEDGE GUIDE 2019

lenderstoadoptprotectivemeasures,suchasimposinghigherinterestrates,requestingsubstantialcollateral,ordenyingcredittoSMEborrowersaltogether.SMEs typically look to internal andexternalfinancingmechanismstomeetworkingcapitalrequirementsand/ortofinancecapitalexpendituresandmaintenance.Intheabsenceof structured and cohesive informationon thecreditworthinessofSMEs,creditors relyonalternativefinancing, including heavy reliance on relationshiplending,collateralbasedlending,factoring,leasing,andothersimilarmeasures.Both lenders and SME borrowers are faced withchallenges,however,whenitcomestograntingandtakingcreditagainstcollateral.Thetwomainchallengesare:

● In most jurisdictions, the definition of collateralgenerally implies fixed/immovable assets, such asland and property, and ignores the moveable assetsmorecommonamongSMEs.Becausemoveableassetssuch as vehicles, equipment, and inventory are notconsidered formalcollateral, lendersareunwilling tograntcreditagainstthem.Intheemergingeconomies,78percentofthecapitalstockofbusinessenterprisesis typically in movable assets, such as machinery,equipment, or receivables, and only 22 percent isimmovableproperty(Safavian,Fleisig,andSteinbuks2006). Because most SME borrowers have moremovable than immovable collateral, they are unableto meet collateral requirements for securing a loan.Lendersloseoutaswell,astheyareunabletotapintothehugeborrowingbaseofSMEandmicroborrowerswithmovableassets,whichtendtobeunderutilizedorunrecognizedbylawasanassettype.

● Weak legal and regulatory frameworks concerningtheuseofcollateralcanpresentchallengestolendersattempting to collect debts. If legal enforcementmechanismsareweakorineffective,thecoststolendersof pursuing delinquent debtors increase. Faced withthepotentialofhighercoststoobtainalegalremedy,through either the judicial system or extrajudicialprocesses,lendersmaygrantcreditonlyatunfavorabletermstoSMEborrowersandmicroclientsormaydenycredittothesemarketsaltogether.

1.2. The Costs of Asymmetric InformationCredit markets are typically characterized by afundamentalproblem:asymmetricinformation(Stiglitz,and Weiss 1981), with borrowers knowing the oddstheywillrepaytheirdebtsmuchbetterthanlendersdo.The lender’s inability to accurately assess borrowers’

creditworthiness contributes to higher default ratesand smaller loan portfolios, which affect financialinstitutions’ profitability. Differentiating betweengood and bad clients becomes very difficult, almostimpossible,whencreditreportsarelacking.Withoutthisinformation, the risk of lending is higher, both raisingthecostsofborrowingandreducing theavailabilityofcredit, as lendershesitate to extend credit tounknownborrowersandseektooffsetthecostsofdefaultthroughhigherinterestrates.Lenders typically address these problems by requiringcollateraltocoverthelossintheeventofadefaultorbyinvestigatingaborrower’sabilitytorepay.Asmentioned,requiring collateral is often problematic, especially indevelopingcountriesandparticularlyinthecaseofnewfirms andMSMEs,which often lack significant assetsthatareformally(legally)recognizedasusablecollateral.Inthecaseofwomenborrowers,theproblemisfurtherexacerbatedaswomentypicallydonotholdfixedassetsintheirnames.Inaddition,thecoststolendersofseizingandliquidatingassetsusedascollateralcanbesignificantand the process lengthy.According to the 2019WorldBankDoingBusinesssurveyonenforcingcontracts,inmost developing economies it takes fromone to threeyears to enforce a contract, with costs reaching 25 to50percentofthedebt.Inextremecases,forexampleinGuinea-Bissau,ittakesonaveragefourandahalfyearstoenforceacontract,andinTimor-Lesteitmaycostupto164percentofthevalueoftheclaim.To investigate a borrower’s ability to repay, a lendermight hire investigators to check the borrower’sbackground,but this isalsoexpensive.Conducting in-depth background checks, while justifiable for largerloans,isnotalwayspossibleorcosteffectiveforsmallloans. Lack of low-cost information often restrictslenders’ ability to lend profitably to informal retail,micro,andsmallbusinessborrowers.Monitoringandscreeningborrowerbehavioroffersoneway tominimizeproblemsofasymmetric information.Past behavior is seen as a reliable predictor of futurebehavior. Banks in many countries, for example,commonly grant credit to a firm only after the firmhashadanaccountwithabankforatleastsixmonthsto a year, which allows the creditor bank to observethe firm’s cash flow. Similarly, the group lendingapproach, mostly used by microlenders, allows thelenders to provide loans to individual borrowerswho,through participation in the group, have developeda credit history with the lending institution. In theseexamples, thecredithistory—sometimes referred toas

4 CHAPTER 1. THE IMPORTANCE OF CREDIT REPORTING SYSTEMS

“reputational collateral”—minimizes the perception ofrisk,thusenablinganindividualorafirmtogainaccesstofinancing.Nonetheless,therelevanceofpastbehaviorshouldbeconsideredincontextsinceitcannotexplainallbehaviorandcouldbeirrelevantifadverseeconomicconditions change borrowers’ circumstances. Even agood borrower may default if faced with economichardshiporotheradversecircumstances.Credit reporting systems are those critical elementsof a country’s credit infrastructure that address theasymmetric information challenges characteristic ofmostlendingrelationships.Attheircore,creditreportingsystemsconsistofdatabasesofinformationondebtors,together with the institutional, technological, andlegal framework supporting the databases’ efficientfunctioning.Databaseoperatorsarebroadlycategorizedas (i) credit bureaus (consumer andcommercial),withthe primary objective of improving the quality andavailability of data so lenders and creditors canmakebetter-informed decisions, and (ii) credit registries,with the main objectives of assisting governments inbank supervision and of enabling regulated financialinstitutions to access data that can help improve thequalityoftheircreditportfolios(WorldBank2011;alsoseesection2.1inthisGuide).Credit reportingsystemshelpensurefinancial stabilitybyenablingmoreresponsibleaccesstofinance,andtheycanalsoplayaninstrumentalroleinexpandingaccesstocreditandothercredit-relatedservicestotheunderservedand unbanked. They facilitate lending processes byproviding lenders with objective information that canlead to reduced portfolio risk and transaction costsand expanded lending portfolios. By doing so, creditreporting systems enable lenders to expand access tocredit tocreditworthyborrowers, including individualswith thin credit files, particularly women borrowers;micro-entrepreneurs;andsmallandmediumenterprises.

1.3. Key Concepts in Credit Information SharingA credit reporting system comprises the institutions,individuals,rules,procedures,standards,andtechnologythatfacilitatetheflowofinformationrelevanttocreditagreement decision making (World Bank 2011).Developing an effective credit reporting system is alengthy process requiring sustained commitment fromall stakeholders. The entire process of setting up acredit reporting system—from initial discussions, to

publiceducationandworkon the legaland regulatoryframework,toactualsystemimplementation,includinguploading data and issuing the first credit report—may take between three and five years, if not longer.The credit information cycle of collecting, producing,storing,processing,distributing,andusing informationto support credit-granting decisions and financialsupervision involves a number of actors: individuals,MSMEs,CRSPs,dataproviders,authorities,regulators,and supervisors.Active participation by each of thesestakeholders is critical to ensuring the effectivenessofthecreditreportingsystem.Stakeholderparticipationisfurtherenhancedbygovernmentsupportforthesystemas awhole.These actors and their roles are shown inFigure1.1anddescribedbelow.

Credit Reporting Service Providers (CRSP)Creditreportingserviceproviders(CRSPs) are institutions that collect information on a borrower’s credit historyfromcreditorsandavailablepublicsources.TheCRSPcompilesinformationonindividualsand/orsmallfirms,including credit repayment records, court judgments,and bankruptcies, and creates a comprehensive creditreportthatitthensellstocreditproviders.CRSPsspecializeinmonitoringandscreeningborrowerFigure 1.1. Key Stakeholders in Credit Reporting Systems

Source: IFC 2017.

Credit Reporting

Service Providers

Authorities Regulators

Supervisors

Data Providers

Data Subjects

Users

5CREDIT REPORTING KNOWLEDGE GUIDE 2019

behavior to address issues of asymmetric information.Lenders share information accumulated through theirlending operations with a CRSP. The CRSP collates,validates,cross-checks,andaggregatesthisdataacrosslendersandthendisseminatescreditreports tolenders,generally on a reciprocal basis. Credit reports allowlenders to better assess credit risks, and they allowpotential borrowers with good payment histories tonegotiatemore favorable terms on credit applications.Lenders can therefore make better-informed lendingdecisions, thus not just avoiding loans to high-riskapplicants but also rewarding good payment behaviorwithbettertermsandconditions.CRSPs differ from credit rating agencies, such asStandard&Poor’s,Moody’s, andFitch,which collectfinancial information on large companies; conductdetailed analyses of those companies’ operations,finances,andgovernance;andthenissuecreditratings.CRSPs focus on smaller creditors, concentrating oncreditrepaymentrecordsandstatisticalanalysesoflargesamplesofborrowers,ratherthanonin-depthanalysesofindividualcompanies,toproducecreditscores.TheCRSPrunsandoperatesacredit reportingserviceonaday-to-daybasis.ACRSPcanbeacreditbureau,a credit registry, or a commercial credit reportingcompany (discussed further in chapter 2). The CRSPbears primary responsibility for ensuring the system’ssafetyandefficiency.TheCRSP’sdutiesaredischargedby theon-sitemanagement teamandoperational staff,whoseresponsibilitiesincludecollecting,validating,andmergingdata;producinganddispersingcreditreportstosubscribers and other users; implementing appropriategovernance arrangements; and handling personnelmatters. The CRSP, in the form of a credit bureau orcommercialcreditreportingcompany,isalsoresponsibleforthesustainabilityofoperations,includingincreasingmembership,developingnewandinnovativecustomer-focusedproductsandservices,reportingtoshareholders(where applicable), complying with regulatoryrequirements,anddealingwithconsumercomplaints.

Data Subjects: Consumers and Firms Data subjects are consumers, MSMEs, and largebusinesses whose data is collected, processed, andcollated into reports provided by the CRSP to itssubscribers or members. (The less cumbersome termconsumers is sometimes used in thisGuide to replacedata subjects.) Data subjects are the focus of lenders’efforts to assess the risks of default and nonpaymentbeforeapprovingnewloansoradvancingfurthercredit.

Data ProvidersDataprovidersplayakeyroleinthesuccessfuloperationof a CRSP since the CRSP relies on their proactivesupplyofinformation.Traditionaldataprovidersincludecommercial banks, other financial institutions, andcreditcard issuers.Nontraditionaldatasources includeretailers and utility providers. In addition, all privateandpublicentitiesthatcollectinformationonconsumersare potential data sources for CRSPs. For instance,a CRSP may have agreements with other parties toaccess databases on court judgments, information onunpaiddebts,personalidentityrecords,andregistriesofcollateral,suchasvehicles,realestate,andcompanies.Thefinanciallandscapehasbeenrapidlyevolvingoverthepastfewyearsasemerginginnovativetechnologiesenablefinancialservices(fintech)andalternativelenders.Among these players are alternative lenders likeTala,Kabbage,andothersthatderiveinsightsfrom“newdata”sources,suchasconsumerbehavioronsocialmediaandpayment platforms, and then make lending decisionsbasedontheseinsights.Aslenderswhoactivelyprovidecredit to consumers and small businesses, these newentitiescanalsobepotentialdataprovidersforCRSPswhentheyexchangeinformationwiththem.

UsersTheCRSPsproduceinformationofinteresttoavarietyof users.These users “query” or submit an inquiry totheCRSP on a data subject that has approached themforcredit.Users,alsoknownasmembersorsubscribersoftheCRSP,typicallyincludefinancialinstitutionsandnonbank creditors who contribute credit informationabouttheirowncustomers’accounts.Creditinformationmight also be of interest to other users, ranging fromfinancialsupervisorsandcentralbankstousersinothersectorsoftheeconomy,suchasemployers(particularlywhere a position involves significant financialresponsibility), insurers, or landlords (where legallypermitted).Inkeepingwiththeprincipleofreciprocity,only subscribers contributing information to theCRSPshouldreceivecreditinformationreportsfromit.SomeCRSPschargetheirusersmembershipfeesaswellasapay-per-usefee.

RegulatorsIn jurisdictions where credit reporting activities areregulated, the regulator is the authority with statutorypowers of supervision over credit reporting activitiesand services. Statutory powersmay include the powerto issue licenses and to create operational rules and regulations. The division of responsibilities among

6 CHAPTER 1. THE IMPORTANCE OF CREDIT REPORTING SYSTEMS

authorities for regulating and overseeing creditreporting systems varies depending on a country’slegaland institutional framework.Sourcesofauthorityand approaches to regulation and oversight may takedifferent forms.Anauthoritymayhave regulatory andoversight responsibility for a credit reporting systemprovider that is registered, chartered, or licensed asan entity fallingwithin a specific legislativemandate.The regulator may also have the power to stipulatecomplianceconditionsforCRSPs,topenalizethemforviolationsornoncompliance,ortocanceltheirlicenses.Credit reporting systems also may be overseen by anauthority that exercises customary or other forms ofresponsibility for oversight that does not derive froma specific legislative mandate. Once a CRSP is fullyoperational,theregulator’sroleistomonitorcompliance.In addition to direct regulation, CRSPs may also beindirectly subject to other laws, for example, businessor company law, consumer credit protection law, andinformation privacy law.As such, theymay also havecomplianceobligationsimposedbyotherregulators.A vastmajority of countries assign regulation of, andauthorityover,credit reportingservices to theircentralbanks. A few countries have a regulatory authorityspecifically dedicated to credit reporting, for example,theNationalCreditRegulatorinSouthAfrica.Inothercountries, a government agency assumes that role; forexample, theFederalTradeCommission in theUnitedStates had the authority to enforce the Federal CreditReportingAct(whichappliestocreditbureaus)aspartofitsmandatetoensureconsumerprotectionincreditandlendingpractices.Inaddition,asofSeptember30,2012,the U.S. Consumer Financial Protection Bureau hasbeenchargedwithmakingmarketsworkforconsumerfinancial products and services and with supervisingcreditbureaus(UnitedStates2012).Insomecountries(China,forexample),thecentralbankactsasboththeindustryregulatorandtheCRSPoperator.Despite the apparent conflict of interest, such systemsoperate reasonably well as long as the two functionsareundertakenbyseparatedepartmentsunderdifferentdirectorships: that is, the department issuing operatinglicensesandsupervisingcreditbureausisnotthesamedepartmentthatoperatesthecreditregistry.TheGeneralPrinciplesassumethatcreditreportingserviceproviderswiththesamefunction,whetherpublicorprivate,willbesubjecttothesamerules;thatis,alloperateonalevelplayingfield.

Sincethecorebusinessofcreditreportinginvolvestheflowofinformationthroughanetworkofstakeholders,credit reporting activities touch on sensitive issues,suchas theindividualprivacyrightsofconsumersandthe protection and security of the data subject’s data.A robust legal and regulatory framework covering allrelevant aspects of credit reporting is essential for thesound functioning of credit reporting systems. Thelegal and regulatory frameworksmay need to provideabalancedresolutionofthenaturaltensionbetweentheobjectivesofaccessingbroadsourcesofinformationforenhancedcredit reporting andofpreserving individualprivacy.Noclearconsensusexistsoverwhatconstitutesan optimal legal and regulatory framework for creditreporting.Inadditiontocontractualagreements,acleartrendworldwideistheenactmentoflawstohelpprotectprivacy and allow data subjects to access and correctinformationaboutthemselves.

1.4. Comprehensive (Positive and Negative) Information SharingToovercomeinformationasymmetriesincreditmarkets,credit reporting service providers collate personal andcredithistoryinformationfromavarietyofsourcesanddevelopcreditprofilesonborrowersthatenablelendersto make optimal lending decisions. Credit historyinformation can be divided into two broad categories:negativeinformationandpositiveinformation.Negativereporting includes only information pertaining tounfulfilled financial obligations, such as defaults,amounts in arrears, judgment orders on debts, andother adverse or negative information. Information ondelinquent debts that are eventually paid off usuallyremainsonfileandformspartof thecredithistoryforadefinedperiodoftime.Databaseswithnegative-onlydataaresometimesreferredtoas“blacklists.”Negative-onlydatabasesweredevelopedinitiallytohelplenderseffectivelyscreenandexcludehigh-riskborrowersthathadaccumulatedsignificantdebtexposure.Positive credit information contains favorableinformation on an individual’s open and closed creditaccounts.Informationsourcescouldinclude:debtratios,on-timepayments,creditlimits,accounttype,loantype,lending institution, detailed reports on the prospectiveborrower’s assets and liabilities, guarantees, debtmaturitystructure,andpatternofrepayments.Research has shown that comprehensive reportingsystems generate more accurate scores than negative-

7CREDIT REPORTING KNOWLEDGE GUIDE 2019

only systems. An analysis of Chile’s credit reportingsystem, a negative-only system with some positivedata elements, found that credit decisions based oncomprehensive information significantly outperformedthose based on negative-only information (Turner2010). Another study in the United States simulatedand compareddefault rates on loans approvedusing anegative-only credit scoring model with default ratesonloansbasedonascoringmodelusingbothnegativeand positive information.According to the study, thedefault rateon loansapprovedusing thenegative-onlysystem was 3.35 percent, whereas the default rate onloans approved using scores based on both positiveandnegative informationdropped to 1.9 percent, a 43percent decrease (Barron and Staten; see Figure 1.2).(Thefiguresshowthesimulatedcreditdefaultsassuminganacceptancerateof60percent.ThesimulationswerebasedondatainoneofthelargestU.S.creditbureaus.)AsimilarexercisewasconductedusingdatafromBrazilandArgentina,withsimilar results.Thatstudyshowedthat inclusion of positive information would haveproduced a 22 percent decrease in the default rate forArgentineanbanksanda45percentdecreaseindefaultratesforBrazilianbanks(Powelletal.2004;seeFigure1.3). Thus, including positive information in scoringmodelsproducesbetterpredictionsandimproveslenders’abilitytoseparategoodfromhigh-riskborrowers.Forabankwitha$100millionloanportfolio, this translatesintoanaveragesavingsofUS$830,000inArgentinaandUS$1.5millioninBrazil.

Figure 1.2. Effect on Default Rates of Including Positive Information, United States

Source: IFC, using Barron and Staten (2003) data.

Figure 1.3. Effects on Default Rates of Including Positive Information, Argentina and Brazil

Source: IFC, using Powell, Mylenko, Miller, and Majnoni (2004) data.

Figure 1.4. Effect on Approvals of Including Positive Information

Source: IFC, using Barron and Staten (2003) data.

Figure 1.4 shows how including positive informationincreasedapprovalratesby88percentinthesimulationusingdatafromtheUnitedStates.

NegativeInformation

Positive & NegativeInformation

3.35

1.9

00.51.01.52.02.53.03.54.0

Defau

lt Rate

s

43% Decrease in Defaults

45% Decline

22% Decline

Positive & Negative Information Negative Information

3.81

BrazilArgentina0

0.51

1.52

2.53

3.54

3.372.98

1.84

Defau

lt Rate

s

NegativeInformation

Positive & NegativeInformation

39.8

74.8

0

10

20

30

40

50

60

70

80

Appro

val R

ates

8 CHAPTER 1. THE IMPORTANCE OF CREDIT REPORTING SYSTEMS

To summarize, negative-only databases pose thefollowingproblems:

● Inasystemwherepositiveinformationisnotreported,aborrowercouldremainexcludedfromcreditaccess(for up to five years in some countries) based on asingle negative event, regardless of the borrower’scurrentpayment recordorotherpositive informationthatreflectsfavorablyontheborrower.

● Furthermore, in negative-only reporting systems,lenders have no credit information on prospectiveborrowers who have never defaulted, since noinformation on them is reported. Borrowers couldborrowfrommultiplesourcesandneverdefault,eveniftheyborrowfromonesourcetorepayanother.Inthelong run, this borrowing pattern is unsustainable, aswasseeninHongKongSARandKorea(seeBox1.1).

● The biggest disadvantage of a negative-only systemisthatitdoesnotacknowledgeborrowersthatpayalltheir dues andbills on time.Goodborrowers shouldbe rewarded for their good repayment behavior byreceiving access to better products and services onbettertermsandconditions.

Consumercreditbureausandcommercialcreditreportingcompanies collect positive credit information wherethe legal basis exists to do so and where the benefitsof such information sharing are generally known andappreciated.Creditregistriesmaycollectpositivecreditinformation, but the scope of such collection may belimited,asdiscussedinchapter2.Insomemarkets,creditbureausandcommercialcreditreportingcompaniesmayshare data with credit registries to support the micro-andmacroprudentialsupervisionfunction,andthiswillgreatlybeabettediftheseserviceprovidersalsocollectandsharepositivecreditinformation.ExamplesincludetheCzechRepublic,RepublicofKorea,Mexico,SlovakRepublic, Turkey, and the United Kingdom (IBRD2016). Inmarketswhere credit registries do not exist,comprehensive credit information sharing databases(consumer or commercial) can still provide invaluableinputs tofinancial sector supervisors and regulators inmeetingtheirmandateofensuringfinancialstability.

According to Doing Business 2019, approximately87 percent of all credit bureaus surveyed collectedand distributed both positive and negative information(WorldBank2019),oftenreferredtoas“comprehensivereporting.” Over 98 percent of all credit registriescollectedanddistributedboth.Regionalmapsinsection5oftheAppendixshowthenumberofcountriesaroundthe world that have adopted comprehensive creditreportingintheirrespectivejurisdictions.

1.5. Full-File Information Sharing Positiveandnegativeinformationcanbecollectedfromavarietyofsources.Credit reportingserviceproviderscollectinformationfrombothfinancialinstitutions,suchasbanksandcreditcardcompanies,andfromavarietyof nonfinancial institutions, such as utility companiesandcollateralregistries,aswellasfrompublicrecords,suchasbankruptcyrecords.

Figure 1.5. Effect of Including Positive Information on Approvals among Retailers and Other Lenders

Source: IFC, using Barron and Staten (2003) data.

Box 1.1. The Limitations of Negative-Only ReportingIn the late 1990s, Hong Kong SAR, China, and the Republic of Korea experienced a major increase in retail credit defaults as a result of the unfortunate combination of reckless lending and the unavailability of positive information. While both had negative credit information registries, positive information was not being shared, and lenders were unaware of the level of indebtedness of existing and prospective borrowers. As competition in the credit

card market increased and banks marketed credit cards more aggressively, many consumers accumulated several credit cards. Borrowers would typically open one credit card account and then open another to pay off the debt accumulated on the first credit card. This borrowing was unsustainable and resulted in a large number of credit card defaults. Following the crises, both countries moved to a system of positive credit reporting.

Retail Retail & Other Lenders

Appro

val R

ates

75.4

83.4

70

72

74

76

78

80

82

84

9CREDIT REPORTING KNOWLEDGE GUIDE 2019

Simulations using credit reporting data in the UnitedStates (Barron and Staten 2003; see Figure 1.5) alsofound thatsharingpositive informationderivedfromabroadercategoryofsourcesallowssignificantoperationalimprovements by lowering defaults or increasinglendingvolumes tonewcategoriesofborrowers. (Thefiguresshowthesimulatedcreditdefaultsassuminganacceptancerateof60percent.Thesimulations,basedondata fromoneof the largestU.S.creditbureaus, showthatalenderwithatargetapprovalrateof60percentwasabletoreducedefaultratesby38percent.Ifthedefaultrateisusedasatarget,thebankwouldbeabletoapprove11percentmore clients before reaching the targeted3percentdefaultrate.)Creditinformationsharingbenefitsbothsmallandlargeinstitutions.ThestudyusingdatafromArgentina(Powellet al. 2004) found that while small lenders do benefitmorethanlargelendersfromsharinginformation,largebanksalsobenefitfromasignificantdropindefaultsifpositive information isused.Although the resultsmayvaryfromcountrytocountryandfromlendertolender,bothanecdotalandavailableempiricalevidencesuggeststhatinformationsharinganduseofcreditscoringallowbothlargeandsmallbankstoreducedefaultratesand/orincreaselendingvolumessignificantly(seeFigure1.6).Insummary,creditreportscombiningbothpositiveandnegative information from both banks and nonbanklendershavethehighestpredictivepowerforcreditriskassessments.Bureausorcreditregistriesfragmentedbyindustrythatprovideonlynegativeinformationdeliverreports with less predictive power, often resulting ininaccuratecreditriskassessments(SeeFigure1.7).

Figure 1.6. Effect on Default Rates of Increasing Number of Information Sources

Source: IFC, using Barron and Staten (2003) data.

Figure 1.7. Effect of Types and Sources of Information on Predictive Power

Source: World Bank, Doing Business 2019.

Types of Information

Sources of Information

Positive & NegativeInformation

NegativeInformation

“Full” (Information Shared by Banks, Retailers, NBFIs)

“Fragmented” (e.g. Information Shared Among Banks Only or

Retail Only)

High Predictiveness

(e.g. U.S., U.K., India)

Lower Predictiveness (e.g. Botswana,

Ewatini)

Lower Predictiveness (e.g. Mexico,

Kuwait)

Lowest Predictiveness (e.g. Malaysia,

Botswana)

ResearchbyMartinezPeria,Soledad,andSingh(2014),usingdataonconsumercreditbureausthatalsocollectdataonfirms,looksattheimpactofcreditinformationsharing onfirmfinancing in a sample of 75,000firmsacross 63 countries from 2002 to 2013. The resultsshowedthatcreditinformationsharingincreasesaccesstofinanceforfirmsandimprovesthematurityofcreditextendedtofirms,thatis,financingforlongerthanayear.Suchfinancingmaybeimportantforfirmexpansionandasset acquisition in themedium term.Martinez Peria,Soledad,andSinghshowthatthegreaterthedepthandscopeofinformationshared,themorebeneficialthetermsforfirmsaccessingcredit.Reformofcreditinformationsharingenvironmentsparticularlystandstobenefitsmallfirmswithlessexperience,asectorgenerallyrelativelyopaquetolenders.One of the challenges of building credit informationsharingbasedon traditional lendingdata is that it cantendtoshutoutnewborrowersiftheylackformalcredithistories. These “thin file/no file” customers (oftenlow-income groups, women, or small- and medium-sizedenterprises)maynothavehadtheopportunity,ortheneed,toborrowpreviously,andtheirlackofcredithistorycanreducefuturecreditavailabilityandaccess.CRSPsattempttoreflectasubject’sbalancesheet,andthey often broaden the range of information gatheredto includenon-loan liabilities, suchasutilitycompanypayables and income information. These categoriestoomaybemissingfor lowincomeor informalsectorindividuals,however.Innovationssuchasthecollectionanduseofnon-creditfinancialtransactionsdata,socialmediaprofiles,paymentsdata,andpsychometricscouldexpandcustomercoverageandallowthebenefitsoffull-fileinformationsharingtoflowtoabroaderpopulation.

79% Decline

41% Decline

Small bankLarge bank

Defau

lt Rate

s

Information from a bank & bureau Information from a bank

1.31

2.22 2.42

0.52

0

0.5

1

1.5

2

2.5

10 CHAPTER 1. THE IMPORTANCE OF CREDIT REPORTING SYSTEMS

Table 1.1. Benefits of Comprehensive and Full-File Information SharingStakeholder Benefits

Lenders, creditors, alternative data providers

• Ability to see the client’s complete range of credit obligations, payments status, and level of indebtedness or over-indebtedness

• Ability to price risk appropriately and to provide customized products and services to meet clients’ specific needs

• Tools to proactively manage consumer accounts for credit line increases or decreases, payment terms, interest rates, etc.

• Ability to proactively manage collections by streamlining the collections process and maximizing collections by expending effort where most needed and where recovery rate is highest

Consumers • Enables consumers to establish “reputational collateral” based on credit histories, thus reducing the need for physical collateral

• Rewards consumers with on-time payments, no missed payments, and other good borrowing and repayment behavior; inspires creditors to offer them better terms of credit or higher credit lines

• Benefits consumers through reporting of non-traditional data like telephone bills, utility payments, etc., to the credit bureau; consumers with no formal relationships with banks or other creditors can show they meet other payment obligations responsibly and are worthy of credit

Regulators and supervisors • Allows regulators and supervisors to develop appropriate regulatory tools to assist in macro- and microprudential supervision

• Provides supervisors with the information necessary to support systemic risk monitoring and prudential supervision

11CREDIT REPORTING KNOWLEDGE GUIDE 2019

Credit Reporting Service Providers

The global credit reporting industry can be roughlydivided into three homogeneous, but not exclusive,groupings: credit bureaus, credit registries, andcommercial credit reporting companies.Thedatabasecontent, clientele, and associated services providedby these service providers can vary significantlyfrom country to country. Consumer credit reportingcompanies, referred to herein as credit bureaus, collectinformationonindividuals,includingsensitivepersonalinformationsuchasSocialSecurityNumbers(intheUS)andbankaccountnumbersandinformation.Thecompiledinformationismadeavailableonrequestto customers of the credit bureau for purposes ofcredit riskassessment,creditscoring,orothersimilarpurposes; consumer bureau customers include banksandotherfinancialinstitutionsthatevaluateindividualsforcredit.Credit registries generally support the state’s role as asupervisoroffinancialinstitutions.Loansaboveacertainamountmust,bylaw,beregisteredinthenationalcreditregistry,andinsomecases,creditregistrieshaverelativelyhighthresholdsforloanstobeincludedintheirdatabases.Creditregistriestendtomonitorloansmadebyregulatedfinancialinstitutions.Withthegrowthofconsumercredit,loanvaluethresholdshavebeenreducedorabolished,andinsomecountries(includingArgentina,Belgium,France,Italy, Peru, and Spain), the credit registry often offersproductsandservicessimilartothoseofcreditbureaus.Credit bureaus tend to cover smaller loans than creditregistries,andtheyoftencollectinformationfromawidevariety of financial and nonfinancial entities, including

retailers, credit card companies, and microfinanceinstitutions.Asaresult,datacollectedbycreditbureausare often more comprehensive and better geared toassessing and monitoring clients’ creditworthiness. Incontrast,creditregistrycoveragetendstobelimitedbythescopeofthedataproviders(regulatedlendersonly),and credit registries are often geared toward collectingsystem-wide informationformacroprudentialandotherpolicypurposes.Commercial credit reporting companies are creditreporting companies that collect information onbusinesses,includingsoleproprietorships,partnerships,and corporations. The compiled information is madeavailable on request to customers of the commercialreporting company for the purposes of credit riskassessment, credit scoring, or other similar purposes,suchastheextensionoftradecredit.Commercialcreditreporting company customers include banks and otherfinancial institutions that evaluate businesses for tradecreditorinsuranceforbusinesspurposes.Figure 2.1 shows the different data covered by theseentities. The three types of credit reporting serviceproviders have distinct differences in strengths andweaknesses,operatingmodels,andmarketsserved.Allthreeproviderscancoexistinagivenmarketbasedonthesizeofthemarket,marketpreferences,leveloffinancialdevelopment,andcreditculture.Someconsumercreditbureaus also provide commercial services (such asCRIF,Creditinfo,Experian);thus,itispossibletohaveoneentitycoveringbothservices.Nosinglesolutionismoreappropriatethananotherforanygivenmarket.

CHAPTER

2.

12 CHAPTER 2. CREDIT REPORTING SERVICE PROVIDERS

2.1. Functions of Credit Reporting Service Providers

Credit Bureaus CreditbureausprovidecreditinformationonindividualborrowersandMSMEstoawiderangeofcreditproviders.Theycollectinformationinastandardizedformatfromavarietyofcreditproviders,includingbanks,creditcardcompanies, telecommunications and utility companies,retail lenders, andothernonbankfinancial institutions.Theyalsocollectanddistributeawiderangeofpubliclyavailable information (such as court judgments,bankruptcy notices, and telephone directories) and/or facilitate access to third-party databases (such ascollateral registries, identification repositories, andtelephone directories). Other information may comefrom nontraditional sources, such as billing data fromgas, water, electricity, cable, telephone, internet, andotherservices,whichenablescreditbureaustocompilebetterandmorecomprehensivecreditreports.AccordingtotheWorldBankDoingBusinesssurvey,morethan45

Source: IFC.

Figure 2.1. Data Subjects Covered by Type of CRSP

Consumers Consumers, Micro, Small and Medium Businesses

Large Corporations

ConsumersCredit

Bureau

Consumer & Commercial

Credit Bureau

RatingsAgencies

percent of private credit bureaus included informationfrom utility providers, and more than 65 percentincluded information frommicrofinance institutions intheirdatabases(WorldBank2019;seeFigure2.2).ThisbroadeneddefinitionfordatasourcesbenefitsunbankedindividualborrowersandMSMEsbyenablingthemtobuild credit histories without necessarily having hadformal access to credit, thus overcoming the trap ofbeingineligibleforcreditduetolackofacredithistory.Oncedataiscollected,itiscross-checkedtoproduceacreditreportforeachindividualborrower,whichisthensoldtolenders.Thereportconstitutesacomprehensiveprofile of a borrower or potential borrower’s personalinformation and information on his or her creditaccounts. The personal information section usuallyincludes the borrower’s name, former names, nameofguarantor(s)ifany,identificationnumber(suchasSocialSecurity or other national identification number), dateof birth, addresses, employment information, alerts(suchasIDtheftreportedorsecurityfreezes),anddateoflastinformationupdate.Thecreditsummarysection

13CREDIT REPORTING KNOWLEDGE GUIDE 2019

typically contains informationonall of theborrowers’creditaccounts(bothopenandclosed),arecordofthestandingoftheaccounts(outstandingamount,pastdueamounts, andpaymentbehaviorhistory), and inquiriesmadeabouttheborrowerintherecentpast.Thereportsnormally also include repayment histories, notingpayments over 12 to 36 months (World Bank 2012). Figure2.3showsthetypesofinformationcreditbureauscollectonindividuals.

Figure 2.2. Sources of Information for Privately Held Credit Bureaus

Source: IFC calculation, based on Doing Business 2019 data.

Borrowers’credithistoriesareoftenrecordedintermsofthenumberofmissedpayments,usingaformatsimilartotheoneinFigure2.4.Thecreditreportalsoprovidesinformationoncollectionsmadeonoutstandingaccountsandanyavailablepublicrecords,suchascourtjudgmentsandbankruptcyrulings.Inmanycountries,creditreportsinclude a credit score, the statistical probability that aborrowerwillmakegoodonhisorherobligation,whichisbasedonanumberofcharacteristics(seesection6.3).

Figure 2.3. Information on Individuals Collected by Credit Bureaus

Source: IFC calculation, based on Doing Business 2019 data.

98 95

44

8577

86

39

93

3348

7695

80 82

0

20

40

60

80

100

120

Name o

f Indiv

idual

Name o

f Repo

rting

Institu

tion

Taxpaye

r ID

National

ID

Amount of

Periodic

Repaym

ents

On-time P

ayment

s

Individ

ual’s I

ncome &

Other P

ersona

l...

Type of

Loan

Interes

t Rate

of Loan

Bancrup

tcies

Number

of Defa

ults

Defaults

/Can

Celled D

ebts

Number

of Days

Loan Is

Past Due

Amount of

Arrears

% of

Cre

dit B

urea

us

97

5543

58

89

52

35

50

21

54

68

26 29

0

20

40

60

80

100

120

Priva

te No

. of P

rovide

rs:

Priva

te Co

m. Ban

ks

No. o

f Prov

iders:

Deve

opmen

t Ban

ks

Priva

te No

. of P

rovide

rs:

Cred

it Unio

n/Coo

ps.

Priva

te No

. of P

rovide

rs:

Finan

ce Co

rps

Priva

te No

. of P

rovide

rs:

Cred

it Card

Issu

ers

No. o

f Prov

iders:

Firm

s Prov

.

Loan

s/Trad

e Cred

itors

Priva

te Ins

t. Prov

iding

Inform

ation

: Reta

ilers

Priva

te No

. of P

rovide

rs:Micr

ofina

nce

Priva

te Ins

titutio

n Prov

iding

Info:

Public

Datab

ases

Priva

te No

. of P

rovide

rs:

Court

s

Priva

te Ins

titutio

n Prov

iding

Info:

Cred

it Bure

aus

Priva

te Ins

t. Prov

iding

Info:

Utilitie

s Prov

iders

No. o

f Prov

iders:

Public

Commerc

ial Ba

nks

% of

Cre

dit B

urea

us

14 CHAPTER 2. CREDIT REPORTING SERVICE PROVIDERS

Reports are usually available to lenders electronically,andmostmodernlargecreditorshavecreditinformationdata uploaded directly into their loan processingsystemsandoriginatingsoftware.Lenderspaythecreditbureau for credit reports through a subscription fee, afee-per-query with significant volume discounts, or acombinationofboth.Historically, credit bureaus only collected informationon individuals. In recent years, with the expansion ofsmall business lending and advances in informationtechnology,morecreditbureauscollateandsellreportson small businesses. In a recent World Bank survey(World Bank 2019), approximately 91 percent of the126 credit bureaus responding contained at least someinformation on firms. Approximately 35 percent ofreportingcreditbureausalsocollectedinformationfromtradecreditorsorfirmsprovidingsuppliercredit,whichis important in assessing a firm’s creditworthiness.Collecting information on both individuals andfirmswithin the same credit bureau has the benefit ofallowing a combined assessment of both a business

Figure 2.4. Sample History of Payments

History of Payments: Observation Periods2018 2017 2016

DNOSAJJMAMFJ DNOSAJ JMAMFJ DNOSAJ J

12113242111 1110113212121 1123145

Source: IFC.

and its owner. The credit history of a small businessowner is an important predictor of the credit risk ofthe small business, since small business owners oftenmix personal and business finances.Many individualspersonallyguaranteetheirbusinessloans.Insuchcases,however,allappropriatelawsandregulationsonprivacyrightsmustbeconsideredandrespected,andthebureaumustensure thatborrowers’personaldata isusedonlyfor thepermissible purposes specified in the legal andregulatoryframeworkandisprovidedonlytousersthatarelegallyallowedtoaccesssuchdata.

Credit Registries Historically, credit registries andcredit bureaus serveddifferentpurposes.Mostcredit registries startedoutasinternal databaseswithin a country’s central bank andwere,andinmanycasesstillare,usedasasupervisionmechanismtoidentifysystemicriskwithinthelendingportfolios of regulated financial institutions. As such,these databases focused primarily on large creditexposures, typically (according toWorld Bank DoingBusiness survey data) with a loan threshold value inexcessofUS$5,000,although,insomepartsofEurope,higherthresholdsapply:forexample,€25,000inFrance,€1million inGermany, and €30,000 in Italy. In 2010Mongolia’s credit registry eliminated the minimumthresholdforloansincludedinitsdatabase.Asaresult,the registry’s coverage doubled after just one year. InBrazil, a circular thatwent into force in2011 reducedtheminimumthresholdforloansreportedbythecentralbank’screditinformationsystemby80percent.

Source: IFC calculation, based on Doing Business 2019 data.

Figure 2.5. Firm-Level Information Collected by Credit Bureaus

91

7872

6370

32

1725 28 32

54 52

85 83

0102030405060708090

100Ty

pe of

Loan

Name

of R

eport

ingIns

titutio

n

Court

Judg

ments

Bank

ruptci

es

Bad C

heck

Lis

t

Utility

Paym

ent

Reco

rds

Finan

cial In

formati

on

on th

e Own

er(s)

Tax a

nd In

come

Asse

ts an

d Lia

bilitie

s

Field

of Bu

sines

s

Name o

f Owne

r

Taxpa

yer ID

Busines

s ID

Name o

f Firm

% of

Cre

dit B

urea

us

15CREDIT REPORTING KNOWLEDGE GUIDE 2019

Figure 2.6. Sources of Information for Credit Registries