Creating Capital Markets in Central and Eastern Europe

48

WORLD BANK TECHNICAL PAPER NUMBER 295 A. i'V'O Creating Capital Markets in Central and Eastern Europe Gerhard Pohl, Gregory T. Jedrzejczak, and Robert E. Anderson A ~~~~~~~~~ADT I 0 RONM I0~~~ ~i m4 - SANDJMANUFACTURINGINSTITU RE E__mbilON LAND TENURE-LMNG ST Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Creating Capital Markets in Central and Eastern Europe

WORLD BANK TECHNICAL PAPER NUMBER 295 A. i'V'O

Creating Capital Markets in Central andEastern Europe

Gerhard Pohl, Gregory T. Jedrzejczak,and Robert E. Anderson

A ~~~~~~~~~ADT

I 0 RONM

I0~~~

~i m4 - SANDJMANUFACTURINGINSTITURE E__mbilON LAND TENURE-LMNG ST

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

RECENT WORLD BANK TECHNICAL PAPERS

No. 213 Srivastava and Jaffee, Best Practicesfor Moving Seed Technology: New Approaches to Doing Business

No. 214 Bonfiglioli, Agro-pastoralism in Chad as a Strategyfor Survival: An Essay on the Relationship betweenAnthropology and Statistics

No. 215 Umali, Irrigation-Induced Salinity: A Growing Problem for Development and the Environimenit

No. 216 Carr, Improving Cash Crops in Africa: Factors Infliuencing the Productivity of Cotton, Coffee, and Tea Grown bySmallholders

No. 217 Antholt, Getting Readyfor tihe Tzventy-First Century: Tecinical Chtange and Instituitional Modernization in Agriculture

No. 218 Mohan, editor, Bibliography of Puiblications: Technical Department, Africa Region, July 1987 to December 1992

No. 219 Cercone, Alcohol-Related Problcms as ant Olbstacle to the Devclopmtctnt of Huma1nti Capital: Issues and Policy Options

No. 220 Kingsley, Ferguson, Bower, and Dice, Managing Urban Environmental Quality in Asia

No. 221 Srivastava, Tamboli, English, Lal, and Stewart, Conserving Soil Moist irr and Fertility in tlec Warm Seasonially Dry Tropics

No. 222 Selvarqtnam, Innovations in Higher Education: Singapore at the Competitive Edge

No. 223 Piotrow, Treiman, Rimon, Yun, and Lozare, Strategiesfor Family Planning Promotion

No. 224 Midgley, Urban Transport in Asia: An Operational Agendafor the 1990s

No. 225 Dia, A Governance Approach to Civil Service Reform in Sub-Saharan Africa

No. 226 Bindlish, Evenson, and Gbetibouo, Evaluation of T&V-Based Extension in Burkinia Faso

No. 227 Cook, editor, Involuntary Resettlement in Africa: Selected Papersfrom a Conference on Environment andSettlement Issues in Africa

No. 228 Webster and Charap, Thie Emergence of Private Sector Manufacturing in St. Petersburg: A Survey of Firms

No. 229 Webster, The Emergence of Private Sector Manufacturing in Hungary: A Survey of Firms

No. 230 Webster and Swanson, The Emergence of Private Sector Manufacturing in the Former Czech and Slovak FederalRepublic: A Survey of Firms

No. 231 Eisa, Barghouti, Gillham, and Al-Saffy, Cotton Production Prospectsfor the Decade to 2005: A Global Overview

No. 232 Creightney, Transport and Economic Performance: A Survey of Developing Countries

No. 233 Frederiksen, Berkoff, and Barber, Principles and Practicesfor Dealing with Water Resources Issues

No. 234 Archondo-Callao and Faiz, Estimating Vehicle Operating Costs

No. 235 Claessens, Risk Management in Developing Countries

No. 236 Bennett and Goldberg, Providing Enterprise Development and Financial Services to Women: A Decade of BankExperience in Asia

No. 237 Webster, Tlhe Emergence of Private Sector Manufacturing in Poland: A Survey of Firms

No. 238 Heath, Land Rights in Cote d'Ivoire: Survey and Prospectsfor Project Intervention

No. 239 Kirmani and Rangeley, International Inland Waters: Concepts for a More Active World Bank Role

No. 240 Ahmed, Renewable Energy Technologies: A Review of the Status and Costs of Selected Technologies

No. 241 Webster, Newly Privatized Russian Enterprises

No. 242 Barnes, Openshaw, Smith, and van der Plas, Wliat Makes People Cook with Improved Biomass Stoves?A Comparative International Review of Stove Programs

No. 243 Menke and Fazzari, Improving Electric Power Utility Efficiency: Issues and Recommendations

No. 244 Liebenthal, Mathur, and Wade, Solar Energy: Lessonsfrom the Pacific Island Experience

No. 245 Klein, External Debt Management: Ani Introduction

No. 246 Plusquellec, Burt, and Wolter, Modern Water Control in Irrigation: Concepts, Issues, and Applications

No. 247 Ameur, Agricultuiral Extension: A Step beyond the Next Step

No. 248 Malhotra, Koenig, and Sinsukprasert, A Survey of Asia's Energy Prices

No. 249 Le Moigne, Easter, Ochs, and Giltner, Water Policy and Water Markets: Selected Papers and Proceedings from theWorld Bank's Annual Irrigation and Drainage Seminar, Annapolis, Maryland, December 8-10, 1992

No. 250 Rangeley, Thiam, Andersen, and Lyle, International River Basin Organizations in Sub-Sahtran Africa

(List continues on the inside back cover)

WORLD BANK TECHNICAL PAPER NUMBER 295

Creating Capital Markets in Central andEastern Europe

Gerhard Pohl, Gregory T. Jedrzejczak,and Robert E. Anderson

The World BankWashington, D.C.

Copyright ©) 1995The International Bank for Reconstructionand Development/THE WORLD BANK

1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing August 1995

Technical Papers are published to communicate the results of the Bank's work to the development com-munity with the least possible delay. The typescript of this paper therefore has not been prepared in accor-dance with the procedures appropriate to formal printed texts, and the World Bank accepts no responsibili-ty for errors. Some sources cited in this paper may be informal documents that are not readily available.

The findings, interpretations, and conclusions expressed in this paper are entirely those of theauthor(s) and should not be attributed in any manner to the World Bank, to its affiliated organizations,or to members of its Board of Executive Directors or the countries they represent. The World Bank doesnot guarantee the accuracy of the data included in this publication and accepts no responsibility whatso-ever for any consequence of their use. The boundaries, colors, denominations, and other informationshown on any map in this volume do not imply on the part of the World Bank Group any judgment onthe legal status of any territory or the endorsement or acceptance of such boundaries.

The material in this publication is copyrighted. Requests for permission to reproduce portions of itshould be sent to the Office of the Publisher at the address shown in the copyright notice above. TheWorld Bank encourages dissemination of its work and will normally give permission promptly and,when the reproduction is for noncommercial purposes, without asking a fee. Permission to copy por-tions for classroom use is granted through the Copyright Clearance Center, Inc., Suite 910, 222Rosewood Drive, Danvers, Massachusetts 01923, U.S.A.

The complete backlist of publications from the World Bank is shown in the annual Index ofPublications, which contains an alphabetical title list (with full ordering information) and indexes of sub-jects, authors, and countries and regions. The latest edition is available free of charge from theDistribution Unit, Office of the Publisher, The World Bank, 1818 H Street, N.W., Washington, D.C. 20433,U.S.A., or from Publications, The World Bank, 66, avenue d'Iena, 75116 Paris, France.

ISSN: 0253-7494

All of the authors are with the World Bank. Gerhard Pohl is Chief of the Private Sector and FinanceTeam in the Europe and Central Asia/Middle East and North Africa Technical Department. Gregory T.Jedrzejczak and Robert E. Anderson are both Senior Private Sector Development Specialists on thatteam.

Library of Congress Cataloging-in-Publication Data

Pohl, Gerhard.Creating capital markets in Central and Eastern Europe / Gerhard

Pohl, Gregory T. Jedrzejczak, Robert E. Anderson.p. cm. - (World Bank technical paper, ISSN 0253-7494; no.

295)Includes bibliographical references (p. ).ISBN 0-8213-3370-41. Capital market-Europe, Eastern. 2. Capital market-Government

policy-Europe, Eastern. I. Jedrzejczak, Grzegorz. II. Anderson,Robert E. (Robert Edward), 1944- . Ill. Title. IV. Series.HG5430.7.A3P625 1995332'.0414'0947-dc20 95-32644

CIP

Contents

Foreword v

Acknowledgments vi

Sunmary vii

Introduction I

The Role of Capital Markets 3The joint-stock company as a transition device 4Western models 5Efficient financial systems 6Financial systems and corporate governance 6Control or arm's-length finance 7

Securities Trading Systems 8Order handling 9Market consolidation and competition 9Role of speculation 10Quote or order-driven markets 11Auction frequency 11Transparency 12Market stabilization 13

Clearing and Settlement 14Counterparty risk 14Alternative systems 15Legal form of securities 15Payment systems 15

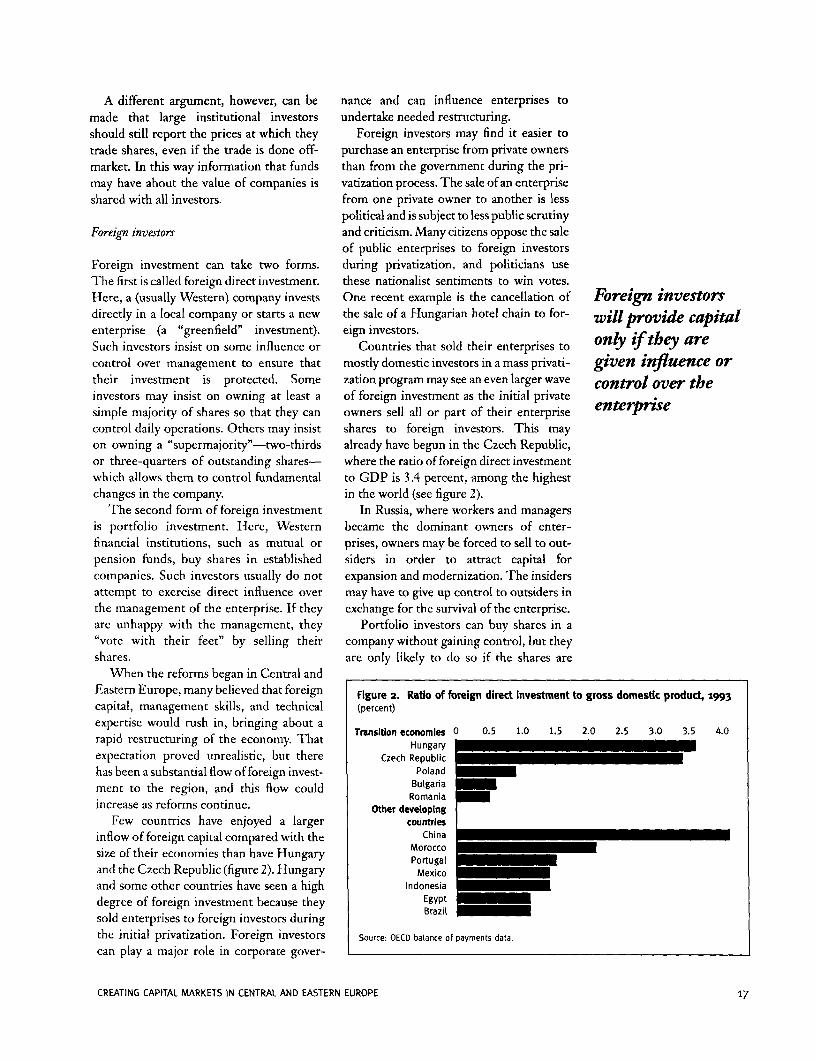

Perspectives of Market Participants 16Investment funds 16Foreign investors 17A trade cycle: an investor's perspective 18

Regulation of Capital Markets 20Institutions 20Regulatory models 20Company law 21Securities law 22Self-regulatory organizations 22

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE iii

Investrnent find regulation 23Impact of the tax system 24Regulatory challenges 25Costs of regulation 25Regulatory priorities 25

Country Studies 27Czech Republic 27Poland 2 8Russia 29

References 3 1

iv

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

Foreword

Some of the countries of Central and East- nomies of the region. Is the role merely toern Europe have made remarkable progress provide a convenient and low cost marketin privatizing their enterprises by transfer- for buying and selling shares? Alternatively,ring ownership from the state to private cit- will capital markets be a source of badlyizens. This has created millions of new needed new equity capital to help with theshareholders. It is estimated that more citi- restructuring of enterprises in the region?zens now own shares of enterprises in Rus- Will capital markets encourage managers ofsia than in the United States and Great enterprises to undertake the neededBritain combined. restructuring and discipline them if they do

This initial distribution of share owner- not, for example, through low share pricesship will change over time as millions of cit- or hostile takeovers?izens and financial institutions buy and sell The second question is how and to whatshares. The countries of Central and East- extent the governments in the regionern Europe need to develop the stock should encourage the development of capi-markets and related institutions such as bro- tal markets. A laissez faire approach wouldkerages, clearing and settlement organiza- be to let the market participants develop fortions, and regulatory agencies to handle the themselves the best institutions andlarge volume of share trading that is likely arrangements for trading shares. Stockto occur after privatization. In the not too exchanges will arise spontaneously as thedistant future, it is likely that the stock mar- need for them arises. A more activekets of Moscow, Prague, Poland, Budapest, approach would be for governments toand Kiev will become as important in their sponsor the creation of stock exchanges andeconomies as those of New York, London, establish the overall legal and regulatoryParis, Frankfurt, or Tokyo. framework. It is hoped that this paper can

This study attempts to answer two basic help governments in the region adoptquestions. The first question is the role of sound policies for the development of cap-capital markets in the new market eco- ital markets.

Anil SoodDirector

Technical DepartmentEurope and Central Asia

Middle East and North Africa Regions

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE V

Acknowledgments

The authors are World Bank staff in the tion practitioners from the region to sharePrivate Sector and Finance Team, Techni- ideas, experience, and technical know-how.cal Department for the Europe and Central Where appropriate, references are madeAsia and the Middle East and North Africa to papers presented at the conference. Theregions. This paper draws heavily on pre- views expressed here, however, are those ofsentations made at a conference titled "Cre- the authors and should not be considered aating Capital Markets in Central and consensus view of the participants orEastern Europe," held November 17-19, sponsors of the conference. The authors1994, in Prague, Czech Republic. The con- thank Claudia Morgenstern (Internationalference was sponsored by the World Bank Finance Corporation) and Robert Pardyand the Central and Eastern European and Paul J. Siegelbaum (World Bank) forPrivatization Network (CEEPN). The their helpful comments and suggestions.CEEPN was founded in 1991 by privatiza-

vi CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

Summary

With the privatization of so many state adopting a diversified financial system inenterprises in the countries of Central and which different institutions and marketEastern Europe, policymakers are asking practices compete. Due to limited availabil-themselves how and to what extent govern- ity of financial inforrnation and uncertaintyments should promote the development of about the success of companies, markets areformal capital markets. At this stage, that likely to be dominated by large financialessentially means markets for shares of institutions that have better access tocompanies. As in the case of mature stock information.markets, governments should put in place Stock marketstrncture. Traders should notthe necessary legal and regulatory frame- be required to use a single exchange, butworks to ensure fair, efficient, and transpar- multiple markets should not be encouraged.ent trading. The details (floor or electronic Government-imposed trading in a singletrading, single or multiple exchanges, and market may result in monopoly and ineffi-so on) will vary from country to country. ciency. The trading system best suited toExperience elsewhere and in the region, countries of the region is the call market-however, suggests that some issues are com- that is, buy and sell orders are accumulatedmon to all countries and that some obser- over a period and executed simultaneouslyvations can be made. when a market clearing price is established.

Sharebolder protection. There must be With the necessary safeguards, dual-func-clear and simple legal rules about creating tion broker-dealers should be allowed; suchand running joint-stock and public limited- speculators bring price stability to stockliability companies. These regulations markets. All trading should be transparent,should be embodied in new company law or with fast reporting of the size and price ofin a revised commercial code. Both pre- trades.suppose that other legislation is in place- Voucher funds. In countries with vouchercovering property rights, contracts, privatization programs, investment fundsbankruptcy, and so on. can play a major role in capital market

Wbich type offinancialsystem? Bank-based development and in the supervision andor market-based? In bank-based systems control of enterprises. Funds should bebanks are both lenders to and big share- encouraged to use their voting power toholders in corporations. Such exposure pro- improve management and to bring pressurevides the banks with board representation on enterprises to restructure. Fund man-and allows them to play a strong role in cor- agers and sponsors should be banned fromporate governance. In market-based finan- dealing in the shares of enterprises in whichcial systems shares are widely held by the the fund has a stake. Moreover, fundspublic either directly or indirectly through should not be allowed to corner the sharesmutual funds, pension funds, and insurance in any industry or market.companies. Corporate governance is exer- Regulation. Because many countries incised by selling shares in poorly performing Central and Eastern Europe aspire to joincompanies. Countries in the region, how- the European Union, they might considerever, can have the best of both worlds by adopting similar or compatible regulatory

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE Vii

regimes. These regulations would cover bodies similar to those set up under themany areas, including accounting and U.K. Financial Services Act.auditing standards, capital adequacy Enforcement. Governments must pursuerequirements for banks (and restrictions on and prosecute with vigor all fraud, theft,insider lending), regulations on investment insider trading, and other criminal acts byfunds, and enabling statutes on securities market participants.market intermediaries and self-regulatory

Viii CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

Introduction

Many enterprises in the countries of Cen- price. In a public companv the shares can betral and Eastern Europe have been trans- sold to the public, including small investors. Capital markets inferred to private ownership-ofteni as In a private or closely held company the some transitionjoint-stock companies whose shares can be shares may be sold only by one largebought and sold. An important postprivati- investor to another, and shares are rarely economies arezation issue for these countries is what the traded in organized markets. already larger thanrole of government should be in developing Successful mass privatization has created those in manycapital markets where these shares can be market capitalization in some countriestraded fairly and efficiently. that, relative to the size of their economies, Western countres

These markets include organized stock approaches or exceeds that in many indus- relative to the sizeexchanges and associated institutionis such trial countries (figure 1). Countries that of their econonziesas depositories and clearinghouses, over- have not used mass privatization typicallythe-counter markets, and informal markets. have a small market capitalization becauseParticipants include financial services fewer companies have been privatized.providers (such as brokers, dealers, banks, Measuring market capitalization is diffi-pension funds, and mutual funds), as well as cult in countries that have used mass priva-individual investors. tization, such as the Czech Republic and

We use the term capital market here to Russia, because shares of many companiesrefer to markets for shares (equities) of are not traded, are traded infrequently, orjoint-stock companies and do not deal with are traded outside organized markets.markets for other securities, such as bonds, Moreover, some companiies may still beoptions, or futures. Equities ire more partially owned by the state, and thus maniyirnportant than other types of securities at shares are not available for trade. And thesethis stage of capital market development in measures of market capitalization maythe region. By issuing shares, a company overemphasize the importance of capitalraises capital for modernization and expan- markets since shares are rarely traded.sion and gives new shareholders ownership Many think of organized stockrights to monitor and control the manage- exchanges as the principal market for trad-ment of the company, for example, by elect- ing shares, but exchanges are just one typeing the board of directors. In other words, of market. Trading that occurs outside anthe shareholders play the dominant role in organized exchange is sometimes calledcorporate governance. "off-market.' Tqhis term is misleading since

Market capitalization is the market value any trade ofshares occurs in a market ofoneof all shares in publicly traded companies-- form or another.in other words, the number of shares issued In organized or formal capital markets,by the company times the current market traders regularly meet in person or over a

In English, the term "capital" has come to mean all sources of finiance for enterprises. including bank loans, cor-porate debt, and suppliers credits. "Capital market" has become synonymous with the tern "finiancial market.' Inthis paper we use "capital" in its more traditional meaning-the resources that a -c.apitalist" contributes to oper-ate his or her business. In English, the terimis "equity" and "shares" are now used instead of this narrow meanfingof "capital." "Capital" still has this narrow Tiieaning in most European language-, however, and probably will bemore familiar to Central and Eastern European rcadcrs than "eqluity."

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

communications network to buy and sell ularly small, unsophisticated investors.shares according to the established rules of Lacking efficient fornal markets, share-that market. Such markets include stock holders have no choice but to trade onexchanges with a trading floor and over- informal markets.the-counter markets where traders deal Thus the central policy question iswith each other over telephones and com- whether and how the governments in theputer networks. transition economies should promote the

Informal markets cover all other markets development of formal capital markets towhere buyers meet sellers and arrange trade the shares of newly privatized enter-transactions. These markets might include prises. Several issues must be considered:individuals buying and selling on street cor- * What is the role of capital markets inners, selling through advertisements in allowing firms to raise needed capital for

Formal, organized newspapers or on bulletin boards, brokers restructuring through the sale of new

capital markets are standing outside factory gates offering to shares?likely to better serve buy shares distributed to workers in mass * Will capital markets encourage man-

privatization programs, or institutional agers to restructure and to increase prof-the public investors such as funds buying and selling itability? In other words, what is the role of

large blocks of shares over the telephone. these markets in corporate governance?These markets may trade many more shares * Should development of capital marketthan formal markets, especially in the early infrastructure and institutions occur earlystages of capital market development. in the transition so that a well-functioning

One weakness of these informal markets market can facilitate privatization, oris their lack of transparency. It is difficult to should this wait until after privatization?know the prices at which shares are being . What are the minimum legal rights oftraded because there is no formal reporting shareholders to receive profits earned bymechanism. This can lead to an inefficient the company and to control management?market where the same shares trade at dif- How should these rights be defined in com-ferent prices depending on the region of the pany law, and how can they be enforced?country, the size and sophistication of the * Should the government sponsor ortrader, the trader's access to inside informa- own exchanges, share registries, deposito-tion, and so on. ries, and clearing and settlement institu-

A second weakness is that these markets tions?are usually unregulated, and so there is S What is the best trading system to begreater scope for cheating investors, partic- used in an organized market? Should dif-

ferent systems be used depending on the

Figure i. Ratio of market capitalization to gross domestic product, 1993 type of trading?(percent) * Should trading be concentrated in a

single exchange, or should competing0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 snl xhne rsol optn

United Kingdom 0 exchanges be allowed or encouraged?United States Should trading be allowed outside officially

Japan recognized exchanges?Czech Republic _ SECOND WAVE ' Should the government or exchanges

Russia OTHERS attempt to stabilize prices of shares, and if

Slovakia 25 LARGEST so, how?Estonia i How can the government ensure that

Mongolia an efficient system is in place for transfer-Poland ring shares from seller to buyer and for

Hungary transferring payment from buyer to seller?Slovenia * How should the government regulateLithuania capital markets to improve their efficient

Note: Czech second wave capitalization extrapolated from first wave. Total Russian capitalization operation and reduce fraud? What model ofextrapolated from twenty-five largest traded companies, regulation is best suited to the transitionSource: Athors' estimates from data supplied by country officials and IFC 1994. econonmies?

2 CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

The Role of Capital Markets

The countries of Central and Eastern even in some industrial countries, such asEurope are moving rapidly to privatize state Germany orJapan, and will probably not be Creation of capitalenterprises and to remove government con- important in Central and Eastern Europe markets should nottrols over industry and commerce. Seventy for some time. Government securities,years of socialism have yielded overwhelm- including bonds, notes, and bills, however, take precendenceing proof of Adam Smith's views that mar- will grow in importance as governments over other, moreket forces are more efficient in solving most find better ways to finance their deficits. fundamentalproduction and distribution problems than Many new exchanges in the region trade market reformslarge organizations and administrative long-term government securities.controls. Capital markets include not only the

Large finns survive in market economies infrastructure to buy and sell securities (theonly where technological or other scale stock exchange, electronic trading system,economies outweigh the monitoring and or coffee house, as the case may be), butcontrol (principal-agent) problems inherent they also include the applicable rules (for-in managing large organizations through mal and informal) and the market partici-administrative controls. Transition econo- pants that buy, sell, or own suchmies have inherited large firms and organi- instruments and advise on corporate con-zations in almost every line of economic trol transactions (spinoffs, takeovers, man-activity. agement buyouts, mergers, acquisitions,

Privatization of existing state enterprises and so on).is only a first step in the restructuring of Most capital market activity in Centraltransition economies. If market reforms are and Eastern Europe is secondary marketto be successful, the privatized enterprises transactions-that is, transfers of owner-must be profoundly transformed. For ship of existing shares. Primary marketexample, they must stop producing unprof- activity-the mobilization of investmentitable products; adopt better design, pro- finance through the sale of new shares orduction, and marketing techniques; spin off other securities-is likely to remain com-nonessential activities into separate firms; paratively small.and invest in new products and production While the opening of stock exchangesfacilities. The current universe of a few has attracted much attention, these effortsthousand firms eventually will be replaced were largely symbolic. The most importantby a more diversified set of a few hundred steps toward creating capital markets liethousand firms. This cannot be done at elsewhere. These include:once, and restructuring will be a continuing * Adoption of a legal infrastructure forprocess. Capital markets-markets for private sector activity, including a companyownership and control rights over firmns and law that sets out standard contractualassets-will play an vital role in this restruc- arrangements for limited-liability compa-turing. nies owned by many small investors.

Banks loans are likely to continue to be * Incorporation of state enterprises asthe most important source of debt financ- joint-stock companies.ing for enterprises. Corporate bonds are 0 Transfer of ownership to private indi-not a major source of capital for enterprises viduals.

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE 3

The joint-stock company as a transition device institutions than in most other lines of eco-nomic activity. Directives of the European

The most important step is the removal of Union covering banking, mutual funds, andgovernment from commercial activities, investment services provide a useful guidethat is, the transfer of all state enterprises to to the minimum requirements that shouldprivate owners. Since most state enterprises be embodied in national legislation.are large, joint-stock corporations or public If company laws are clear and reasonablelimited-liability companies owned by many and if other necessary economic laws are inindividual shareholdcrs, they remain the place, restructuring can (and will) start. Butmost promising vehicles for fostering rapid this assumes that state enterprises have beenrestructuring of Central and Eastern Euro- transferred to the private sector and havepean economies. been cut off from government subsidies and

A good company While sales of a few firms to foreign- intervention. To ensure that hard budget

law should ensure investors may be feasible, more govern- constraints are imposed on privatizedthat managers act ments are realizing that a mass privatization enterprises, privatization should include

that managers act program. in which shares of enterprises are banks and other financial institutions earlyin the best interest transferred to the public for little or no pay- on.of sbareholders ment (for example, using vouchers), is the If company law is well designed,

most practical solution. investors can ensure that managers act inRcstricturing can be accelerated by their interest and will be disciplined if they

puttinig in place an appropriate capital mar- deviate too far from the objective of maxi-ket infrastructure that includes clear and mizing profits and thus shareholder wealth.simple legal rules about the creation and Monitoring of management can bemanagement of widely ownecl, joint-stock enhanced by promoting core investors (forcorporations (or public limited-liability example, voucher investment funds), bycompanies). These rules are normally making appropriate provisions for the rep-embodied in company law, but they pre- resentation of voting rights of small share-suppose that other elements of private eco- holders (proxies), and by forcing managersnomic law are in place, notably those to return periodically to lenders or to thegoverning property rights, contracts, capital market by providing them only withpledges (sectirity), and bankruptcy. short- or medium-term debt financing and

These laws may already exist in some requiring them to pay out profits as divi-Central and Eastern European countries in dends.old civil and commercial codes, but they Managers face other disciplines. Mostrequire exrensive revision. In other coun- important is competition in product mar-tries a new civil and commercial code, based kets. Where corporate governance is lax oron Western models, may be the simplest inefficient, product market competitionsolution. The conmiercial code should may force inefficient firms to shrink or exit,include rules about the creation and func- making room for more-efficient competi-tioning of at least three different types of tors. Low import barriers and stiff foreignfirms-partnerships, private limited-liabil- competition may bring even more pressureity companies, and pul)lic limited-liability to bear and stimulate higher efficiencycompanies. gains than domestic capital markets and

Dcpending on the extent of rules pro- good corporate governance. An essentialvided in these company laws, separate secu- complementary factor is the absence ofrities regulation may not be required. But government intervention and subsidies.tighter regulations than) those provided for Despite slow progress with privatization inpublic limited-liability companies are many Central and Eastern European coun-needed for banks and other financial service tries, some loss-making enterprises haveproviders (brokers, mutual funds, and so already begun significant restructuring byon), since there is more opportunity for reducing their work force once subsidiesfraud and impruldenit behavior in financial and bank lending have been curtailed.

4 CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

Western models same functions-collecting informationabout investment opportunities, monitor-

Financial systems are classified as bank- ing performance, and taking action on thisbased or market-based. Japan, Germany, information. WVhile capital markets areand most of Western Europe have bank- important, their role often is misunder-based systems, while the United States and stood.the United Kingdom have market-based Some of the most important but leastsystems. The main characteristics and com- understood features of financial systems inparative performance of these systems are market economies are:discussed in Walter (1993). * Retained profits are the dominant source

In bank-based financial systems banks are of enterprise finance in all market economies,both lenders to and shareholders in large accounting for 70 to 100 percent of net cor-joint-stock corporations. With substantial porate finance (investment funding, net of Countries are saidequity and debt exposure, banks act as accumulation of financial assets). Internal to have a bank-strong monitors. They have representation financing tends to be higher in the market-on boards of directors (and thus access to based systems (the lJnited States and thc based or a market-nonpublic information). Financial markets United Kingdom; table l). based financialtend to be smaller and less liquid, and trans- * Banks are the dominantsouzrce oJ erternal ys-temactions less transparent (at least to out- finance in all couintries. Over the past twentysiders). Bank control over corporations years, bank financing has been even higherneed not be based on shareholding alone. in the United Kingdom and the UnitedWV'here banks can engage in brokerage, States than in "bank-based" Germany. Onlytrust, or mutual fund business, they can Japan can still be characterized as a bank-exercise control by exercising voting rights based financial system.on behalf of small investors. Alternatively, * Veiy little netfinance is raised from seca-banks might write restrictive loan contracts rities mzarkets. In the United Kingdom andor lend only short term to retain influence the United States net equity issues haveover management decisions. been negative, as leveraged takeovers and

In market-based financial systems shares management buyouts have replaced sharesare held by the public either directly or with bank and corporate debt.through institutional investment vehicles, * Large firms rely increasingly on retainedsuch as mutual funds. Shares are actively earnings. Large firms often become finan-traded and corporate governance is exer- cial institutions in their own right. Smallercised by investors selling shares in poorly companies "go public" to raise risk capitalperforming companies. Poorly managed in equities markets, but larger firms arefirms may eventually become the target of a increasing financial leverage to lowerhostile takeover. One precondition for this financing costs (and strengthen manage-arrangement to be workable is extensive ment incentives).disclosure of reliable financial information. * This broad pattern also holds true for theHostile takeovers and leveraged buyouts emerging mark-et economiies of Asia and Latinare commonplace only in the United King-dom and the United States. Such takeovers Table 1. Sources of net corporate financing,reflect the absenice of insider controls on 1970-89(percent of net investment financing, excluding ac-management (for example, by large corpo- cumulation in financial assets)rate or financial stakeholders). In the United UnitedUnited States corporate control by financial Germany lapan Kingdom Statesinstitutions is severely restricted, not only internal 8a 69 97 91for banks but also for mutual funds and Bank 11 31 20 16insurance companies. Bonds -1 5 4 17

Shares 1 4 -10 -9Still, the differences between bank- and Trade credit -2 -8 -1 -4

market-based financial systems should not Other 10 o -8 -13be exaggerated. Both systems fulfill the Source: Corbett and lenkinson 1994.

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE 5

America. The recent wave of utility privati- Europe is their failure to stop the financingzation in these countries, however, has of losers, thereby reducing financing forbriefly raised securities issuance. This has potentially successful firms.significantly increased stock market capital-ization, but reflects primarily a shift in own- Financial systems and corporate governanceership, rather than additional investmentfinance. A country's corporate governance system is

* Cross-border portfolio investments bave determined not only by company and secu-become a major source of external finance for rities laws but also by the subtle interplayemerging market economies. Foreign portfolio between different parts of econornic legis-investors hold as much as 20 percent of all lation. Small differences in legal systemsshares in Malaysia, Mexico, and Thailand. can lead to large differences in control tech-

Initial offerings of While portfolio inflows are still small in niques, financial patterns, and the institu-securities are Central and Eastern Europe, they may tional structure of the financial system. In

become a major issue in the future. If port- the United States, for example, securitiesunlikely to be a folio investors are to be welcomed, com- markets play a big role in the financial sys-

major source of pany law and securities markets regulations tem, and nonfinancial corporations are the

new capital should be closely aligned with those of main monitors of management (FrankelWestern market economies. and Montgomery 1991). In Japan and Ger-

many, however, banks are the principalE]frientfinancial systemts monitors and wield considerable influence

over management appointments, particu-The main aim of a financial system is to larly for firms in distress (Charkham 1994).allocate financial resources to the best uses. The exclusive reliance on market disci-This is easier said than done, particularly in pline in the United States is not a naturalthe countries of Central and Eastern outcome. It is heavily influenced by restric-Europe because of the limited information tive banking laws that have prevented banksabout enterprises available to investors, and from owning nonfinancial corporations andlenders' lack of skills and experience. There from nationwide branching, brokerage, andare thousands, if not millions, of firms and underwriting of securities. Insurance com-investment opportunities in any economy panies and mutual funds also face severeat any time. Investors and lenders must restrictions on ownership stakes and activeredirect new capital away from 'losers" governance in corporations. Since manage-toward "winners" who have the greatest ment also controls the proxy voting processchance of success. In this regard, the biggest (and nominations to the board of directors),problem in the countries of the region is the this leaves only stock market "exit' by indi-lack of speed and vigor in dealing with the vidual investors as a corporate controllosers. Too much capital is still provided to mechanism. Once market discounts arefirms that have little chance of success. This large enough, other corporations (or extra-capital often takes the form of bank loans ordinarily rich individuals) are attracted toprovided under government direction or launch hostile takeover bids to replace man-pressure. agement.

Even firms that could be winners fail to There is lively debate among the devel-maximize their cash flow by cutting costs. In oped market economies about which sys-Western countries winners usually finance tem is more appropriate (Walter 1993).themselves more from internally generated Proponents of bank-based systems arguecash flow than from bank or market financ- that banks have better access to informationing (see table 1). Better information enables and can react more quickly to managerialfinancial institutions and markets to move shortcomings. Supporters of stock market-resources more quickly from poorly to well- based systems argue that these systems pro-managed companies and thus to speed eco- vide more financing to entrepreneurialnomic growth. The greatest weakness of firms and that bank-based systems are toothe financial systems in Central and Eastern conservative. They also point out the

6 CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

potential risks to the banking system if financing. Unsatisfactory performance canbanks become large owners of risky enter- only be sanctioned by selling shares. If bankprises, as well as the conflicts of interest lending is concentrated but share owner-between the role of banks as lenders to and ship dispersed, control may be exercised byowners of an enterprise. For example, there lenders while investors merely watch.are concerns in the Czech and Slovak Small differences in legal doctrines ofRepublics about banks controlling the large fairness may permit lenders to exercise con-voucher funds that in turn are major share- trol over firms in distress. Anglo-Americanholders of enterprises and banks. In Russia legal views are quite different from civil-lawthere is concern about "circular owner- countries in this regard. Such small differ-ship," in which enterprises own the banks ences in legal doctrine can lead to differentand the banks own the enterprises. financial market practices and structure (see

Empirical work has been unable to reject the discussion of "equitable subordination" Transitionthe hypothesis that banks are better corpo- in bankruptcy in Frankel and Montgomery economies shouldrate monitors than financial markets or that 1991).the existence of universal banks has a posi- Where are Central and Eastern Euro- incorporate the besttive impact on economic growth (Steinherr pean countries heading? Probably toward of both market-and Huveneers 1992). But the differences control-oriented finance, using contractual based and bank-between the two systems are small, and arrangements similar to those used by ven- based ofmany other factors (for example, educa- ture capital investors in the West. Suchtional systems) may be at work. investors will provide both capital and man- corporate

The choice is perhaps academic. It is agerial expertise but will insist on monitor- goverancepossible to have the best of both worlds by ing and, if necessary, controlling the gadopting a diversified financial system in management to protect their investment.which different types of institutions and As long as information is unreliable andmarket practices can compete. Put another disclosure limited, arms-length finance canway, there is no reason why banks should be work only when reliable and enforceablerestrained from participating in financial performance guarantees can be given. Liq-markets and corporate monitoring if they uid stock and corporate bond markets,are subject to appropriate prudential stan- widely dispersed ownership, and marketsdards (such as portfolio diversification, liq- for corporate control are thus unlikely touidity, and fiduciary rules). If banks, mutual develop soon.funds, or other financial institutions fail to A case in point is the Czech Republic.do a good job at corporate monitoring and Many early observers regarded widely dis-control, there is still the possibility of a persed ownership as the weak point of masstakeover by another (nonfinancial) corpo- privatization. The outcome showed theration, assuming that shareholders can be opposite. Nowhere else in the world (exceptconvinced of its merits. Few takeovers have perhaps in Japan) are core investors asoccurred in bank-based financial systems. prominent as is the Czech Republic, where

a dozen investment funds manage almostControl or arm'sr-length finance one-half of all shares on behalf of individual

investors.It is perhaps more useful to distinguish Control-oriented finance is more similarbetween "control-oriented" and "arm's- to the structures and instruments used inlength" financial practices than between the past. It is also easier to carry out becausebank- and market-based financial systems. it requires less development of related insti-If firms have core investors with significant tutions and skills such as brokers, organizedstakes (or proxy votes), management will be exchanges, auditors, lawyers, and financialunder more scrutiny. If share ownership is specialists. Large investors deal directlywidely dispersed, however, and solicitation with the managers of an enterprise, provideof proxy votes is controlled by manage- experts to evaluate the company, and canment, shareholder influence is small and trade with each other without benefit of annot much different from arm's-length bank organized exchange.

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE 7

Securities Trading Systems

A trading system is simply a mechanism by tions, commissions and market access wereStock exchanges which buyers and sellers are brought deregulated, computerized trading systems

around the world together and agree on prices so that a trade were introduced, and transaction cost,have adopted many in securities can take place. Securities mar- including taxes, were lowered.

kets are not unique in this regard since At the same time, the (then) Europeandifferent trading trading systems must exist for all services Community (EC) allowed greater freedomsystems and commodities in a market economy. for investors to trade on any exchange in the

Trading systems for securities can range EC. Exchanges in other European coun-from small investors trading on street cor- tries began to lose customers to the moreners to national stock exchanges using the efficient and cheaper London exchange,latest in computer technology. leading them to deregulate their markets

Organized stock exchanges tend to be and to improve their trading systems. Sincethe best type of market for small to many countries in Central and Easternmediumii-size trades of shares in large corn- Europe want eventually to join the (now)panies. Investors wishing to buy and sell European Union, EU trading systems andbigger block-s of shares, however, tend to regulatory regimes are useful examples fortrade directly with each other in informal them to follow.markets. In many countries (for example, Cohen and others (1986) discuss tradingthe Czech and Slovak Republics and Rus- practices before the Big Bang. Pagano andsia), most trading is done outside organiized Roell (1990) and H-luang and Stoll (1992)markets. Such trading will only move to an discuss trading practices in markets aroundorganized market if it offers a better service. the world. An easy-to-read description ofMature market economies offer a variety of the issues facing the U.S. capital marketstrading systems or markets. can be found in U.S. OTA (1990).

In establishing an organized market an Securities tradingis changingrapidlydueimportant issue is the structure of the to improvements in communications andtrading system or systems. The number of computer technology. Private exchanges-trading systems has increased due to dereg- not the government-should choose theulation, increase(d competition, and new most appropriate trading system. Officials,telecommunications and computer tech- however, must understand trading systemsnology. '[he first major deregulation to be able to exercise proper oversight andoccurred in the U.S. securities market in to create suitable regulation. Government1974. Then in 1986 came the "Big Bang" regulation also may influence the economicderegulation of the London securities mar- attractiveness and feasibility of differentket, which had a huge impact throughout trading systems.Europe. Before the Big Bang the London Trading systems can differ according to:Stock Exchange had relied on a privileged * Mlarket consolidation-a single stockgroup of market makers (called jobbers) to exchange versus a number of competingensure a smoothly functioning and stable stock exchanges and over-the-counter mar-market. After the Big Bang the exchange in kets.London-and eventually in most of Europe Auction timing-continuous markets-was opened to other financial institu- versus batched (or call) markets.

8 CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

* Functions of intermediaries-brokers * Duration. Limit orders usually have aversus dealers and market makers. fixed duration after which they expire.

* Entry restrictions-prohibiting banks Orders remain active until they are exe-or other financial institutions from engag- cuted, withdrawn, or expire.ing in direct market-making. * Volume. Trading systems often deal

* Transfer of securities-physical move- separately with small and large (block)ment of securities versus dematerialized orders.systems.

* Payment for securities-cash, check, or Market consolidation and competitionbank wire transfer.

Besides simply matching buyers with Securities often are traded in several mar-sellers, a well-functioning securities trading kets, and many countries have more thansystem provides four services to market par- one exchange. Transactions also can be con-ticipants: ducted off-market when a buyer and a seller

* Price discovery. Trading systems estab- trade directly or when buy and sell orderslish market prices that balance supply and are matched by a broker.demand for securities. Rapid dissemination Policymakers face some key decisions inof prices enhances transparency. determining the best kind of stock market

* Market stabilization. A large volume of structure (table 2). In the past twenty yearstrading (liquidity) and participation of there has been much debate concerning themany well-informed and well-capitalized benefits and drawbacks of consoLidating alldealers who are willing to engage in short- trades in a single exchange. Some expertsterm speculation leads to more predictable point out that, just as competition is bene-and stable prices. ficial in other markets, the competitive

* Market surveillance. Securities trading effects of multiple exchanges will lower thesystems can be used to monitor trades and costs of trading securities. Others point outto protect market participants from fraud that multiple exchanges have a detrimentaland manipulation. effect on market quality, volume of trade,

* Quality certification. Through mem- and price stability faced by individualbership and listing requirements, securities traders.trading systems can ensure minimum stan-dards of competence and integrity of mar-ket intermediaries (members) and of Tabte 2. Options and recommendations for stock market structuresecurities traded. Recom-

mendation Option Comment

Order bandling Fragmentation Traders should not be required to use av Integration single exchange, but multiple

Buy and sell orders to be executed on a secu- exchanges should be integrated to theextent possible to create a singlerities trading system can differ depending market.

on several factors, including: Single function brokers and dealers Broker-dealers are needed to ensure the* Price instructions. Orders are usually Sv Dual function broker-dealers. presence of speculative traders but

either limit orders or market orders. A limit create conflicts of interest.

order gives a miaximumn price for a buv order Dealer (quote-driven) market Unofficial speculators and dealersand a minimum acceptable price for a sell V Auction (order-driven) market should be allowed to participateorder. Market orders are executed at the in auctions to increase stability.best price offered by the market. V Discreet trading (call market) A call market is best until order flow

* Role of agent. Brokers simply act as Continuous trading increases to a level adequate forintermediaries, matching sell and buy continuous tradingorders at predefined prices and volumes. Opaque system (slow or no reporting) Transparency is increased in order-Dealers buy and sell securities for their own v Transparent system (fast reporting) driven markets. An issue is reporting

, , ~~~~~~~~~~~~~~~~~~~~~~~oF off-market transactions.account and may buy or sell at announcedprices to any investor who wishes to accept Source: Based on the presentation by Marco Pagano at the November 1994 Prague workshop on 'Creating

Capital Markets in Central and Eastern Europe' sponsored by the Central and Eastern Europe Privatizationtheir offer. Network and the World Bank.

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE 9

It is probably true that trading is more medium term, and result in similar pricesefficient and costs are lower if all buyers and for similar securities. The process of deter-sellers of a security are brought together in mining a market equilibrium price-thea single market. Trading of shares in a price discovery mechanism-is perhaps theparticular company may naturally consoli- most important but least understood func-date at a single exchange, resulting in a tion of securities trading systems. Price dis-more efficient market. But if this exchange covery depends on the design of a tradinghas high costs and poor service, traders system, including the extent of market con-should have the option of buying and sell- solidation, participation of intermediariesing through a competing exchange or off- acting as market makers, role of quotationsmarket. and orders, dissemination of information,

Some regulatory authorities or ex- costs of operation, and market growth rate.Forced changes have attempted to force consolida- Investors and traders can be divided into

consolidation of tion of trading in a single exchange. This two categories, though no investor is neces-has been done by forbidding cross-listing, sarily always one or the other. Long-term

trading may result by restricting in-house matching by bro- investors buy shares for price appreciation

in an inefficient kers, by requiring notification of the official and dividends and expect to hold the shares

monopoly exchange about off-exchange transactions for some time. Short-term investors, or(put-throughs), and by establishing a cen- speculators, buy and sell based on theirtralized depository of securities. expectation of a significant change in price

The efficiencies of consolidated trading over the near term and plan to hold themay be enjoyed even if more than one shares only for short periods. Speculatorsexchange exists. Each exchange can special- also are called dealers, jobbers, or special-ize in the shares of certain companies. For ists. We will use the term "market maker" ifexample, one exchange may specialize in the participant has an official role in thelarge companies, using a trading system exchange and "dealer" if the role is unoffi-most suitable for shares with heavy trading. cial.Another could specialize in small companies Market makers and dealers play a keyusing a trading system suitable for lightly role in price discovery and stabilization.traded shares. In Germany, steel and mining They actively buy and sell securities forstocks were traded mainly on the Dussel- their own account in response to expecteddorf exchange, while automobile and for- short-run fluctuations in the price of secu-eign stocks traded on the Frankfurt rities or changes in supply and demand.exchange. Systems also have been devel- Brokers buy or sell only on behalf of theoped to link different exchanges trading in ultimate investor. Broker-dealers do both.the same shares, thus producing a single Some exchanges have official marketnational market. makers. The role of market makers is to ini-

Russia is an interesting example in this tiate and drive the process of proposingregard. Because of its size, poor communi- equilibrium prices within a bid and offercations, and local or regional ownership of spread and to react to the response to thesemany companies, multiple regional prices. Market makers on the New Yorkexchanges will exist for some time. The Stock Exchange (called specialists) areissue is how these regional exchanges can be responsible for keeping trade of assignedintegrated over time to create a national securities liquid and orderly, which meansmarket for enterprises whose shareholders standing ready to buy and sell shares at a fairare not limited to a single region. price, if necessary. Market makers in the

London Stock Exchange and the U.S. NAS-Role of speculation DAQ are obliged always to give two quotes:

bid and ask.A well-functioning market is expected to set Dealers play an important, though unof-prices that maximize the volume of transac- ficial, role in exchanges without formaltions, are responsive to the changing mar- market makers (for example, in the call mar-ket environment, are stable over the kets commonly seen in Central and Eastern

10 CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

Europe). Dealers attempt to make a profit In order-driven markets (also called auc-by buying shares when a temporary excess tion markets) market participants revealsupply causes a price fall and by selling their orders to buy or sell at specific prices.shares when a temporary excess demand These markets can be continuous or call,causes a price increase. In doing so, dealers operated only by brokers, only by marketstabilize the market. Trading systems that makers, or by a mix of brokers and marketexclude dealers or other short-term specu- makers.lators have larger price swings. There are a number of arguments for

The trend in other countries is away order-driven markets. Depending on thefrom trading systems that rely on official patterns of supply and demand for shares,market makers to find the market price that they can provide a better price discoverybalances supply and demand. Instead all mechanism. In a quote-driven system, it istraders are allowed to make offers or orders. impossible for all orders to interact. This Sbort-terimDealers still participate in one form or argument is particularly valid for Central speculators bringanother and bring stability to the market. and Eastern European countries, with their . .

One question is whether brokers should thin and erratic markets. In addition, the stabtlity to capitalalso be allowed to be dealers, since such an new brokers in these countries may not marketsarrangement may produce a conflict of have adequate capital to act as dealers orinterest. Broker-dealers may put their own market makers, which would require theminterest as dealers ahead of the interest of to hold inventories of shares.clients for whom they act as broker. Forexample, a dealer may sell securities from Auction frequencyinventory to a client at a price above that atwhich the same securities could be pur- Auction markets can be call or continuouschased elsewhere. markets. In a call market buy and sell orders

The active involvement of dealers and are accumulated over a specific period andother speculators increases the efficiency executed simultaneously when a market-and stability of capital markets. Thus deal- clearing price is established-that is, wheners should be encouraged, especially in the the market is "called." In a continuous mar-early days of capital market development ket orders can be executed whenever bidwhen few participants may have the ability prices (buy order) and asking prices (sellor resources to be active speculators. Bro- order) cross, in other words, whenever thekers should be allowed to be dealers and buy order price exceeds the sell order price.dealers to be brokers, to encourage the par- The main advantage of call markets isticipation of dealers. But regulatory safe- their simplicity of price discovery and theguards are needed to avoid conflicts of ease of disseminating information tointerest between these two functions. investors. The timing of an order in a call

market is not as important because allQuote or order-driven markets orders brought to the market before call

time are treated equally. This is importantDifferences in the role of dealers and mar- for markets in Central and Eastern Europe,ket makers are most pronounced between where communications systems are poor.trading systems that rely on price quota- The advantage of continuous markets istions and systems that rely on orders. In that they allow traders to learn and adjust toquote-driven markets (also called dealer current market conditions from observationmarkets) market makers compete for orders of incoming orders, bid and ask quotations,by publishing bid (buy) prices and ask (sell) prices, and volume of transactions. As a re-prices. Thus the market maker is ready to suit decisions better reflect current (minute-accept orders on both sides of the market. to-minute) market conditions. ContinuousThe rules of the exchange determine the markets also guarantee execution of ordersextent to which dealers must reveal to the at the market price and trading withoutpublic any restrictions or volumes attached delay. Both features are particularly impor-to the proposed prices. tant for speculative investors.

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE 11

The main disadvantage of continuous Though most experts generally favormarkets is their vulnerability to manipula- transparency, some argue against it in cer-tion and abuse. This can happen when the tain cases. One is when the market relies onrecording of the time sequence of order market makers or specialists, in otherinflow and trading priority rules are impre- words, price- or quote-driven markets.cise and when rules of conduct of market Continuous quote-driven markets reportintermediaries are not enforced. Although best bid and ask quotations but not thecall markets are probably better suited to entire flow of orders. This is mainly due tothe needs and technological capacity of the the opposition of market makers, whocountries in the region, the two systems would lose a competitive advantage sincecan be used together. A call market may be they have better and earlier informationused for thinly traded shares or for orders than the rest of the market participants. It is

Call markets rather that have accumulated overnight. A con- argued that sharing this information with

than continuous tinuous, computer-assisted system may all participants would make it harder formarkets are best then be used during opening hours for market makers to bring order and liquidity

stocks with heavy trading of small or to the market.suited to the medium-size orders. A less formal system A second case involves large block trades.

countries of the involving negotiated trades may be neces- It is argued that such trades should not havesary for orders that are too large for the to be reported until some time after theyregion continuous system. take place-say, ninety minutes. The trader

may want to split up the large block intoTransparency smaller trades and would not want to dis-

close an early partial trade for fear that itA basic assumption of the theory of com- would cause a large price change in the mar-petitive markets is that they are fully trans- ket, to the trader's disadvantage. The issueparent and information is available free of of transparency is discussed in detail incharge. Securities markets are far from this IOSC (1992).ideal. The cost and availability of informa- The optimal degree of transparency maytion differ significantly from country to also depend on other factors, including:country. * Structure of the trading system. Call

Transparency can increase both the effi- markets will benefit little from online infor-ciency and fairness of securities markets. mation about prices and volumes, sinceComplete transparency would require such information cannot be used before theboth the disclosure of all bids, offers, and market is called. In highly automated con-orders before transactions takes place (pre- tinuous markets with computer-supportedtrade information) and the volume and trading, however, earlier access to informa-prices of transactions completed (posttrade tion (measured in seconds) can create sig-information). nificant gains.

Most trading systems report price and * Size of the market. With only a fewvolume of trades at the end of the day (clos- market makers, full transparency of theiring price), while a few report only price. positions can result in oligopolistic tradingPrice and volume information is available strategies, resulting in collusion amongthrough exchanges, newspapers, and televi- them against external traders (the public).sion. All major markets also provide online Informal and less-regulated marketsinformation about prices and volumes dominate trading in some countries of thethrough specialized domestic communica- region. One consequence is that sophisti-tions networks and international commer- cated traders and dealers who have bettercial networks, such as Dow-Jones and access to information about companies,Reuters. A few markets open their limit demand and supply conditions, and pricesorder books to the public at large, conceal- may earn substantial profits at the expenseing only the names of buyers and sellers. of less-sophisticated and less-informedThe most prominent are Toronto CATS investors. The long-term solution is toand the Tokyo Stock Exchange. increase the information available and to

12 CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

regulate to ensure equal treatmenlt for all intcgrating sLIbiiii-kets ;uol encritiragin-g

investors, market maikers or dilclers.II] selectilng aI tr.ldirig svstem11, there is

M-farket sutbilization often a tradcoff I wtweTCi 11n11e(dIMcv (t hc

abilitv to trade promptly) annd price stabil-

By one definition, a milarket is efficieit if thc it. (C ontilluons rit lirdi systcnis pro i(Iiprice ofa company's shares reflects all avail- imI1IediacI but, IccaUisC Of thiil tr:iedI rig.

able informnation about its fiuture operatioiis prices mla Ib unstable. lIn call ml lkets

and earnings. 'T'hus prices shoul(d change trailers 1m0ay have t, w 'a t foir an auctioll. but

only when new information becomes avaiil- the batching of iririieroLis orders will resultable. In reality share prices fluctuate simply in imore price stability. TIhin ttradingu andl

because of random increases in supply or price instability have led roost exchanges illdemand that have little to do with the ulider- Central and Eastern I auropc to a.dopt call AMarketlying fundamentals of a company's opera- auctions rather thlil co0nrinuous trading. stabilization shouldtions. One measure of a xvell-functioninig Some exchanigcs Nvith ()ntinonIs tradingmarket, however, is stable prices or prices systemosehaveintroduced pslicies toiultm1n pricethat do not fluctuate wil(ll. Since prices pric stabilitm. The,se policies;are risky, bow- manipulation ormust change when new informationl is avail- ever, because theyZ (c;anI ilitelfere II the ad- conntrolsable, however, it is difficult to judge whether justmcnt of priccs ti) ne equllibiulml ievels.

share prices are moving to a new equilib- If price instabilitN is a serioqus ipriolleiim the

rium level or fluctuating excessively, better choice niav Ie C to risc a c-all ma1cti()n.One prerequisite of an efficient aiid sta- Policics to Cnleiulrige price stabilirt

ble market is liquiditv. Liquidity can be includ:cmeasured by the relationship betvecn * Cpecial markct-oprning proccnrar. (ion-

money volume of trading and changes in tinuoius markets are only open durilig nor-

market prices. The greater the money vol- m3al business hours. -1 huse a;ch morning the

ume needed to cause a significant chainge in inarket iunst dcal wcith orders rcceived

the price ofa stock, the greater its liquidity. overnight. M1ost colitinlilouis marilets rise

In other words, random changes in supply proeidlurcs for setting i peniri.g prices that

and demand would not cause a large change resemble call markets. All rivernight ordecrs

in the price of shares in a liquid market. arc hatched, and in eqtuililiriuni price isLiquidity can be xiewed in terns of three established that .iaX1i1i7CS the voluirIe of

market characteristics: trade.D Depth-a market has depth if orders * Prict linuits. Imposing specific percent-

exist at prices above and below the current age limiits on the f1iuctuat1!i inf prices froi oequilibrium price. scssioii to sessiol Is the minost direct and

* Breadth-a market has breadth iflarge most widcelv ose(i instrmiienit of stihili7a-orders can be absorbed without large price tion. If the Iimiiit is rec1clced. officials an fur-

changes. tiher trades for a i ort pci-io d and 1 nav* Resiliencv-a market has resiliency if anilounce the "heavy" side of the market

price changes due to market imbala,nces (supply iir dcninani In Sonic c;ases traiingquickly attract new orders to the market oni may r(vcrt to a call iLnCtion. SnIch limits.the shortage side. however, shoul(d ii(it atte-mpt to pr( vei t

Ensuring sufficient liquidity should be fundamienital changcs in the ma;lrket cle;aringgone of the main considerations of miarket price. In such cases limnits tan he suspendedparticipants, policyrnakers, and regulators. to allow an adjustimliit to the nes ciluilib-Low liquidity may result from the small vol- riuLm1 price level.ume ofshares of publicly traded companies * Rfiusal no dcns- di:ualvilizing wrderk.the small population of investors. and the Sonie trailing systeliis lo uiot allow officildesire of investors to keep shares rathei niarkct imakers to place dcscalili-zing i-ders

than trade them. Market liquidity can bt on their own account--tom cxamnpic to scienhanced by such measures as widely andI when priccs aire fal1ling Ir IIto hui X hcmrquickly disseminating price infori:itaion, prices arc rising.

CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE 13

Clearing and Settlement

After a trade has been made, payment for completed because the buyer did not makeThe clearing and securities must be transferred from buyer the required payment.

settlement to seller and ownership transferred from In most exchanges the two parties areseller to buyer. Clearing refers to the typically brokers acting as intermediaries

organization tprocess of verifying the number and iden- for the ultimate investor. TIhus the brokersusually guarantees tity of shares in a particular transaction, the must be satisfied that their clients will meet

the performance of price and date of the trade, and the identity their obligations to either deliver the secu-both buyer and of the buyer and seller. Settlement involves rities or make pavment. If the ultimate

two steps-transferring payment from buyer or seller does not meet their obliga-seller buyer to seller and transferring legal own- tions, then the broker will in most cases be

ership of the shares from seller to buyer. If liable.these two steps are done simultaneously, WVhat assistance does the exchange orthe system is said to have achieved "deliv- the clearing and settlement organizationery versus payment." Serious problems can provide to guarantee the performance ofarise if one step occurs much before the the two parties to the trade? Because of theother. need to ensure the performance of the two

parties, there often is a close relationshipCounterparty risk between the stock exchange and the clear-

ing and settlement organization. TheThough clearing and settlement may exchange or its large members may own andappear to be merely administrative or ac- operate the organization.counting procedures, problems can arise if Trading is hindered without theone party to the deal does not live up to the assistance of the clearing and settlementagreement. The worst situation occurs organization because each party miust inde-when the ownership of the securities is pendently verify the creditworthiness of thetransferred but the payment is not made, or other. One party may refuse to participate inwhen the payment is made but the owner- a trade that has been arranged by theship is not transferred. The loss of one of exchange because of lack of confidence inthe parties could then equal the full value of the counterparty. The clearing and settle-the security traded. ment organization, in cooperation with the

Even if the trade is canceled because one exchange, can reduce this counterpartv riskparty does not meet its obligations, the in three ways. The first (and rarely used) isother party may still suffer. For example, a to require that both parties provide securi-seller may discover that the price of the ties and payment in advance of executingsecurity has fallen after the sale was agreed the trade. This is essentially what is done byto, or the buyer may discover that the price the RMS exchange in the Czech and Slovakhas risen. It is generally considered unac- Republics because it deals with many smallceptable for a stock exchange to have to can- investors who do not trade through brokers.cel a transaction because one party did not The second way is for the exchange ormeet its obligations. For example, the stock clearing and settlement organization toexchange cannot tell a seller some days after restrict participation by, for example,the trade was carried out that sale cannot be requiring that brokers meet certain capital

14 CREATING CAPITAL MARKETS IN CENTRAL AND EASTERN EUROPE

standards. This usually means that the paper certificates must be physically trans-clearing and settlement organization will ferred from the seller to the buyer.limit membership to the most reputable and * Paper certificates may be immobilizedcreditworthy brokers, dealers, and market in a central depository (for example, theparticipants. Nonmembers may participate Depository Trust Company in the Unitedonly through one of the members. The States). Share owners may be legally enti-member must then insure the creditworthi- tled to receive a paper certificate but areness of the nonmember. willing to leave them with a depository for

The third way is to organize a mutual easy trading.guarantee system whereby all members of * Shares may be "dematerialized" andthe clearing and settlement organization no paper certificates exist. The only proofagree to collectively stand behind the per- of ownership is ani entry in the database offormance of members. the central share registry. "Dematerialized"

A clearing and settlement organization is Clearing and settlement is simpler and or "immobilized"not required in off-market trades where the cheaper in the second and third cases.buyer and seller deal directly with each Either may be difficult to achieve, however, share certijcatesother. In such cases the two parties make because of outdated regulations, political are besttheir own arrangements for clearing and opposition, inadequate technology, and thesettlement and for satisfying themselves need for speed in privatization. The bestthat the other party will meet its obliga- compromise may be to recognize papertions. share certificates but to encourage a move

toward share depositories. This could beAlternative systemis done first for the largest investors (brokers,

dealers, funds, and banks) and eventuallyThe systems used by clearing and settle- for small investors, as happened in manyment organizations are complicated, vary WVestern countries.greatly from country to country, and are The Czech Republic and Russia illus-beyond the scope of this paper. A compre- trate some of the benefits and difficulties inhensive description of the various systems choosing a legal form forsecurities. Becauseappears in IOSC (1992a, b). the Czech Republic used a centralized com-

The Group of Thirty, a nonprofit orga- puterized system for its voucher auctions, itnization of market participants from thirty was relatively simple to register each share-industrial countries, has rnade recommen- holder in a central computer, thus avoidingdations on the operation of clearing and set- the need for paper certificates. In contrast,tlement systems that have become Russia's mass privatization program wasunofficial standards. These recommenda- decentralized because of the size of thetions are intended to ensure an efficient and country and because creating a central sharelow-risk system. Among the recommenda- registry would have slowed mass privatiza-tions: that final settlement occur within tion. The end result is a dematerialized sys-three days of the trade, that settlement be tem, but the registries are managed hy"delivery versus payment," that netting of enterprises and can be used to hinder ortransactions be considered, and that a cen- manipulate share trading.tral share registry or depository be used tothe maximum extent possible (for more Payment systemsdetails see Zhou 1991 and Pardy 1992).

Clearing and settlement must be closelyLegal formn of secir-ities integrated with a country's banking and

payment system. A poorly developed pay-'I'he system used for the transfer of securi- ment svstem may be the biggest obstacle toties depends greatly on the legal form of the development of capital markets. Thereownership. There are three options. is little point in striving for rapid transfer of