cover Tbank (10-03-14) copy - Thanachart Bank

284

ANNUAL REPORT 2013 THANACHART BANK PUBLIC COMPANY LIMITED SMART GROWTH

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of cover Tbank (10-03-14) copy - Thanachart Bank

ANNUAL REPORT 2013

THANACHART BANK PUBLIC COMPANY LIMITED

AN

NU

AL REPO

RT 2013 TH

AN

AC

HART BAN

K PU

BLIC

C

OM

PAN

Y LIM

ITED

SM

ART G

RO

WTH

900 Tonson Tower, Ploenchit Road, Lumpini,

Pathumwan, Bangkok 10330, THAILAND

Tel. +66 (0) 2655 9000 Fax +66 (0) 2655 9001

Thanachart Contact Center 1770

Thanachart Smartcar Call Center +66 (0) 2217 5555

www.thanachartbank.co.th

Registration No. 0107536001401

SMART GROWTH

002 FinancialHighlights

010 MessagefromtheBoardofDirectors

014 BoardofDirectorsThanachartBankPublicCompanyLimited

016 ManagementDiscussionandAnalysis

028 NatureofBusinessOperations

046 RiskFactors

058 CorporateSocialResponsibility(CSR)

068 ResponsibilitiesoftheBoardofDirectorsfortheFinancialReport

069 ReportoftheAuditCommittee

071 IndependentAuditor’sReport

073 FinancialStatementsandNotetoFinancialStatements

213 CorporateGovernance

224 InternalControlandRiskManagement

226 ReportoftheNominationandRemunerationCommittee

227 SupervisionandManagementStructure

236 BoardofDirectorsandManagementTeam

256 GeneralInformation

InvestmentofTBANKinOtherCompanies

TBANK’sReferences

OtherReferences

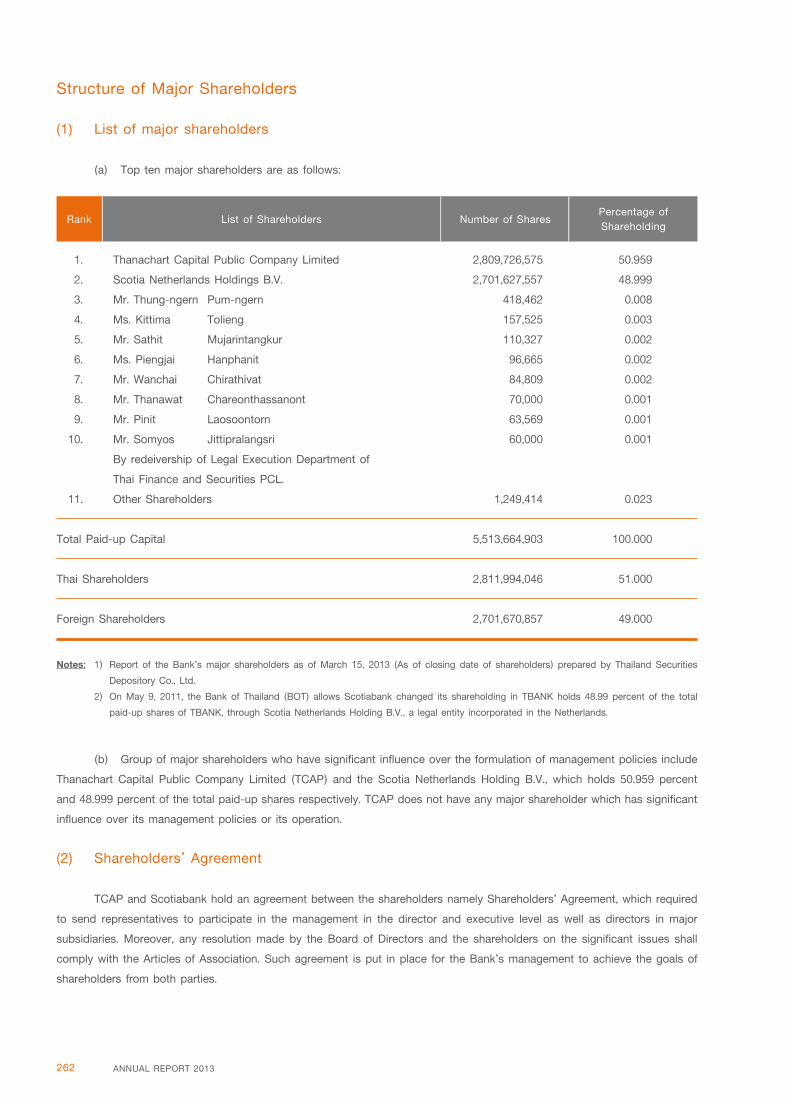

StructureofMajorShareholders

DividendPaymentPolicy

CompaniesinThanachartFinancialGroup

BranchesofTBANK

280 SummaryofSpecifiedItemsperform56-2in2013AnnualReport

“Investorscanlearnmoreontheissuingcompany’sannualstatement(Form56-2)

showninwww.sec.or.thortheBank’swebsite:www.thanachartbank.co.th” ThanachartGroupembracesitsenvironmentalresponsibilities

inthereductionofglobalwarmingandconsumptionofnaturalresources.

The2013AnnualReportusedpaperproducedfromfarmedtrees

andwasprintedwithsoy-basedink.

DesignedbyPlanGrafikCo.,Ltd. Tel.022772222

Four Strategic Intents for the Business Operation in 2014

1. We intend to accelerate growth in commercial and unsecured loans under prudent risk standards through

theprovisionofsuperiorserviceandfinancialadvicewhilemaintainingourdominantposition inauto lending.

2. We intend to improveour riskmanagementand reduceLICacrossallportfolios through focusedorigination,

riskbasedpoliciesanduseofmarketleadingtechnologyacrossthecreditcycle.

3. WeintendtoattractnewcustomersandgrowanddiversifyourfundingbasetomeetLCRrequirementsbyoffering

innovativesavings,insuranceandinvestmentproducts.

4. Weintendtohelpourclientssucceedfinanciallyandgrowourfeerevenuethroughrelationship-basedcrossselling

ofthefullsuiteoffinancialproductsandservicestailoredtomeettheirneeds.

Vision of Thanachart Group

To provide fully integrated financial solutions to our targeted customers’ complete financial needs by offering

thehighestqualityofproducts,servicesandadvice.

002 AnnuAl RepORT 2013

FInAncIAl hIGhlIGhTS

consolidated Separate financial statements

AsatandfortheyearendedDecember31

Operating results

(ThB Million)

Interestincome 53,887 48,736 44,052 34,781 21,470 50,549 46,331 29,386 21,397 20,934

Interestexpenses 27,234 25,556 19,636 11,566 6,736 26,489 25,371 14,797 7,375 6,791

Netinterestincome 26,653 23,180 24,416 23,216 14,734 24,060 20,959 14,589 14,022 14,143

Non-interestincome 25,826 12,098 9,465 8,695 17,571 22,958 10,902 6,454 3,322 2,053

Totalincome(1) 52,478 35,277 33,881 31,911 32,305 47,018 31,861 21,042 17,344 16,196

Non-interestexpenses 21,259 21,660 20,747 16,062 23,346 18,487 19,522 12,953 8,053 8,363

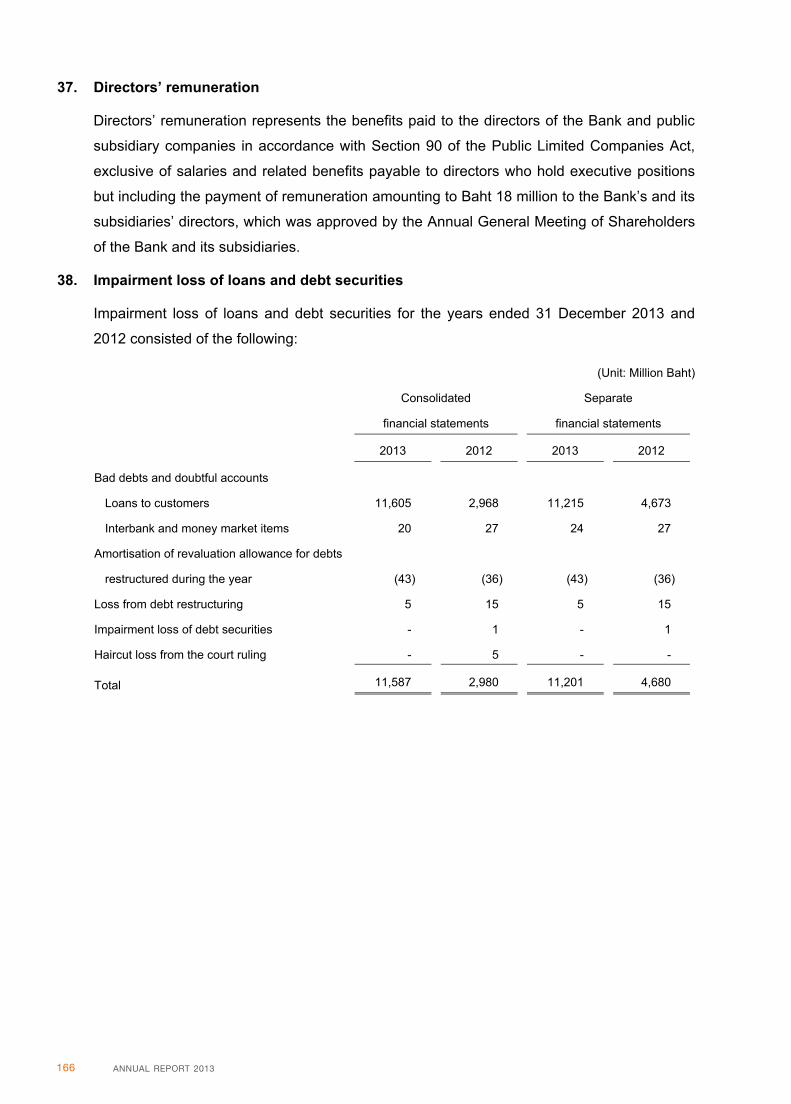

Baddebtanddoubtful 11,587 2,980 2,504 2,149 3,107 11,201 4,680 1,422 1,280 2,830

accounts(2)

Netincome(3) 15,385 8,354 7,671 8,777 4,056 14,113 6,855 6,668 5,719 3,547

Operating performance

Basicearningspershare(THB) 2.79 1.52 1.39 1.92 2.19 2.56 1.24 1.21 1.25 1.91

Returnonaverageassets 1.51 0.90 0.89 1.23 1.06 1.46 0.78 1.13 1.31 0.96

(ROAA)(Percent)

Returnonaverageequity 16.99 10.72 10.61 15.52 17.01 16.91 9.55 9.42 10.70 15.20

(ROAE)(Percent)

Interestspread(4)(Percent) 2.59 2.48 2.92 3.33 3.73 2.59 2.58 2.99 3.63 3.66

Costtoincomerationet 40.51 61.40 61.24 50.33 56.51 39.32 61.27 61.56 46.43 51.64

insurancepremiumincome(5)

(Percent)

Statement of financial position

(ThB Million)

Loans 790,017 754,063 635,220 606,851 285,515 750,494 723,023 616,713 326,549 282,577

Totalassets 1,038,349 1,018,620 886,060 873,203 432,970 990,724 953,209 878,053 482,063 413,878

Depositsandborrowings 811,308 776,521 690,336 707,605 356,496 799,186 769,677 729,121 374,883 357,664

Totalliabilities 941,109 934,435 810,526 800,809 405,098 901,572 875,708 807,169 415,327 387,523

Shareholders’equity(6) 96,218 83,330 74,848 72,183 27,811 89,153 77,501 70,884 66,737 26,355

Remark FinancialStatementAppearanceinaccordancewiththenotificationoftheBOTRe:thePreparationandAnnouncementofFinancialStatementsofFinancialInstitutions

dated28December2010orSorNorSor11/2010resultedinchangevariousitems.However,theBankanditssubsidiarieshaverevisedthefinancialstatementfortheyear2011

(exeptingY2010)foranalysisandcomparison

1. Interestincomeexcludesdividendincome

2. InterestexpenseincludescontributionfeetoDepositProtectionAgency

3. Non-interestincomeincludesfeepaidrelatedtoincomeandinsurance/lifeinsruanceexpenses

4. Non-interestexpenseexcludesfeepaidrelatedtoincome,insurance/lifeinsuranceexpenseandcontributionfeetoDepositProtectionAgency

5. Financialratiosarecalculatedondisclosurefinancialstatement

2013 2012 2011 2010 2009 2013 2012 2011 2010 2009

(Restated) (Restated)

003ThAnAchART BAnk puBlIc cOMpAny lIMITed

consolidated Separate financial statements

AsatandfortheyearendedDecember31

Asset quality

Loanstodepositsand 97.38 97.11 92.02 85.76 80.09 93.91 93.94 84.58 87.11 79.01

borrowingsratio(Percent)

NPL-grosstototalloans 4.23 4.10 5.58 5.60 2.57 3.09 2.63 2.74 2.26 2.49

(Percent)

NPL-nettototalloans(Percent) 2.19 2.05 2.64 2.48 0.58 1.69 1.35 1.45 0.57 0.59

Coverageratio(7)(Percent) 85.19 74.21 69.75 71.22 96.41 88.17 76.92 71.53 97.66 92.33

TotalallowancetoBOT 128.17 122.31 104.27 108.05 111.66 134.37 103.12 103.12 105.32 102.85

regulation(Percent)

Non-performingloans(NPL) 35,313 32,501 37,677 36,859 8,675 24,394 20,036 17,989 7,648 8,359

(THBMillion)

capital measures

TierIcapitalratio(Percent) 9.47 8.49 9.28 11.71 8.65

Totalcapitalratio(Percent) 14.80 13.99 13.72 14.75 14.10

Riskweightedassets(THBMillion) 747,992 724,801 664,103 609,277 273,366

common share information

Commonsharesoutstanding

(Millionshares)

-Average-basic 5,514 5,514 5,514 4,563 1,854 5,514 5,514 5,514 4,563 1,854

-Endofperiod 5,514 5,514 5,514 5,514 1,935 5,514 5,514 5,514 5,514 1,935

Bookvalue(THB) 17.45 15.11 13.58 13.09 14.38 16.17 14.06 12.86 12.10 13.62

Dividendspershare(THB) 0.37 0.35 0.40 0.56

Other information

Employees 15,358 15,193 16,298 16,846 9,368 13,286 13,642 14,152 7,871 7,470

Branches 621 630 676 256 256

Exchangebooth 54 55 79 89 92

DefinitionandFormula(1)Totalincome=Netinterestincome+Non-interestincome

(2)Includinglossondebtrestructuring

(3)Excludingminorityinterest/non-controllinginterest

(4)Interestspread=Yield-Costoffund

Yield=Interestincome/Averageearningassets

Earningassets=Interbankandmoneymarketfrominterestbearing+netinvestment+loans

Costoffund=Interestexpenses/Averagepayingliabilities

Payingliabilities=Totaldeposits+interbankandmoneymarketfrominterestbearing+totalborrowings

(5)Costtoincomeratio=Non-interestexpenses/Totalincome

(6)Excludingminorityinterest/non-controllinginterest

(7)Totalallowance/NPL

2013 2012 2011 2010 2009 2013 2012 2011 2010 2009

(Restated) (Restated)

The core mission of the Thanachart Group is to help our customers become better off

financially by providing customized solutions to meet their unique needs. With a foundation of

strong capital and liquidity, the full suite of financial products and market leading technology

and efficient processes, we are well positioned to deliver on our promise to customers

and generate sustainable growth and returns to all our stakeholders.

SMARTGROWTH

The key to our long term success is the quality and

service focus of our people. The Thanachart Group

is committed to strengthening our team through

ongoing investment in leadership, staff development,

accountability and empowerment of our teams

throughout the organization. With our staff

fully dedicated to serving our customers,

we look to the future with confidence.

peopleOUR STRenGTH

SMESHOP

INNoVATIoNOUR DRIVe

Customer needs are constantly evolving as is

the way they want to deal with their financial

services provider. In addition to innovative products

and services, clients increasingly look for new

and easier ways to obtain the services they need.

At the Thanachart Group, we are introducing

new services to increase customer convenience

and making substantial investments to improve

and expand our electronic channels and social

media access so that customers can bank with

us when it is best for them.

The financial services industry in Thailand is increasingly competitive with client needs

becoming ever more sophisticated. We are making substantial investments in our people,

processes and technology in order to allow us to efficiently meet customer needs and

control our operating costs and deliver long term sustainable growth to all our stakeholders.

effICIeNCyOUR GOAl

youOUR fOcUS

The Thanachart Group is committed to operating at the highest standards of ethics and good governance.

With our customers at the centre of all our activities, we actively participate in promoting the quality of life of

the Thai people and society. The Group also supports various activities that are beneficial for youth and which

promote our national culture for the sustainable growth of our organization and the society as a whole.

010 AnnuAl RepORT 2013

The banking industry in 2013 continued to face

challengesdue toslowinggrowth,higherconsumerdebt

and adjustments required to complywith extensive new

regulations.TheBankofThailandregulateslocalandforeign

commercialbanksoperatinginThailandandrequiresthemto

complywiththeBaselIIIGuidelineseffectiveon1January

2013,which increases capital and liquidity requirements.

This along with the promulgation of the Anti-Money

LaunderingAct(No.4),B.E.2556andtheCounter-Terrorism

FinancingActB.E.2556impactedbanks’activitiesaswell

asincreasesadministrativeandfinancingcostsinorderto

complywiththenewregulations.However,inthelongterm,

suchchangesshould reducesystemic risksandsupport

sustainablegrowthintheoveralleconomy.Despiteallthese

challenges,thebankingindustrystillgeneratedloangrowth,

thoughatalowerlevel,coincidingwiththeslowgrowthof

Thaieconomy.Thereduceddemandforautohirepurchase

loanswas apparent in the secondhalf of the year after

thematurityofthefirst-timecarbuyerincentiveprogram.

Bankdepositscontinuedtoexpandandwithstrongmarket

liquidity,westartedtoseeaneasingofthefiercepricing

competition seen in earlier periods. Of note, the overall

banking industry continued to demonstrate good credit

qualitywithimprovingreservecoverageandcapitalratios.

Dear Shareholders,

Inthepastyear,theglobaleconomybegantoemerge

afterthefinancialcrisiswithadvancedeconomiesstartingto

gainmomentum.TheUSeconomyshowedamodestrecovery

whichledtotheUSFederalReserve’sdecisiontobegin

reducingitsbondpurchasesundertheQuantitativeEasing

Program. Also, the EU economy experienced a fledgling

recovery,albeitatastillmodestpacewithhighunemployment

stillprevalentinmanycountries.Meanwhiletheeconomic

growthofAsiancountrieswasatagradualpaceunderpinned

bythegrowthinChina,andtheresumptionofgrowthin

Japandrivenbytheyen’sdepreciationandthegovernment’s

economicstimulusmeasures.Onthedomesticeconomic

front,theThaieconomicgrowthdeceleratedinthesecond

half of the year impacted by slowing growth in China,

theongoingpoliticalunrestwhichdelayed the launchof

thegovernment’sinfrastructuredevelopmentprogram,and

increasinghouseholddebt,allofwhichcombinedtoreduce

privatesectorconsumptionandinvestment.Moreover,export

growthperformedbelowthetarget,beingimpactedbythe

tepidglobaleconomyandtheBaht’sappreciationduring

thefirsthalfof2013.

(Mr. Banterng Tantivit)

Chairman

oftheBoardofDirectors

MeSSAGe FROM The BOARd OF dIRecTORS

011ThAnAchART BAnk puBlIc cOMpAny lIMITed

ForThanachartBank,2013wasayearofstrong

accomplishmentaswecontinuedtomoveforwardwithour

strategicoptimizationinitiativeswhileensuringwemeetthe

dailyneedsofourcustomersandgenerategoodresultsfor

ourshareholders.Ourprogresswasrecognizedaswewere

named“theFastestGrowingRetailBankThailand2013”

fromGlobalBanking&FinanceReviewand“theTrusted

Brand2013”fromReader’sDigestforourmarketleading

AutoHirePurchasebusiness.Earlierthisyear,wecompleted

thesaleof100-percentofThanachartLifeAssurancePlc.

to Prudential Life Assurance (Thailand) Plc. The capital

gain from this sale has further strengthenedour capital

base.With thecommencementof theexclusive15-year

bancassurance partnership, we have started distributing

PrudentialThailand’sgloballeadinglifeinsuranceproducts

throughourextensivebranchnetworkacrossthecountry.

Thisrelationshipenablesourwell-trainedstafftoprovide

betterproductsandservicestocustomerstomeettheirsavings

andprotectionneedsandhelpsincreaseourfeeincome.

During theyear,with thesupportofourstrategic

shareholder-the Bank of Nova Scotia, we made good

progressonourstrategicprioritiesandcontinuedtodeliver

keyinfrastructureandsystemimprovements(“Optimization

Initiatives”)throughouttheyear.Forexample,ourbranch

redesigned Sales & Service Program and Customer

RelationshipManagement tool continues to be launched

throughourbranchnetwork,retailCreditScoringhasbeen

launched and we are completing the Loan Origination

SystemwhichistobelaunchedinQ22014.Wecontinue

toreengineerkeybusinesslinesandprocessesincluding

ourCustomerContactCenter,HousingLoans,Commercial

Banking,Collectionsandothersinordertofurtherimprove

servicetocustomers.TheseOptimizationInitiativesimprove

our competitive position in many areas, enabling us to

providesuperiorcustomerexperience,increaseproductivity,

grow high-yielding loans, and increase fee incomewhile

maintainingourmarketdominance inautohirepurchase

business.Wealsodeliveredvariousprocessimprovements

in branches, auto hire purchase, telesales and Shared

Services,byadoptingtheSixSigmaprincipletostreamlineand

improve our processes. Numerous Strategic Sourcing

initiatives also play a key role in optimizing our supply

baseandreducingassociatedcosts.Inlinewithincreased

marketrisks,werealignedourriskmanagementandcredit

policiesforprudentriskmanagementwhilestrengtheningour

collections infrastructure through the launchofpredictive

dialertechnology.Inaddition,welaunchedseveralinnovative

(Mr. Suphadej poonpipat)

Chairman

oftheExecutiveCommittee

012 AnnuAl RepORT 2013

productsandservicessuchas‘Paperless’BankingforDeposit,

Withdraw,TransferandBillPaymentAISmPAYMasterCard

(on-lineshoppingwithpre-paidcard),ThanachartPay‘NGo

(newmobilepointofsalesservice),ElectronicJuristicPerson

CertificateIssuance,toenhanceconvenienceforcustomers.

Tofullysupportalloftheseinitiativesandweplacedstrong

effortinimprovingourhumancapitalbyretainingtalentand

developing leadership throughout the organization. As

detailed above,we have fully committed ourselves to be

“theDoingBank”,andtosupportthisthemeandincrease

marketawareness,welaunchedanewbrandinginitiativethis

yearwithstrongadvertisingandpromotionalsupportacross

allchannelswhichhasresultedinanincreaseinfavorable

awarenessofThanachartBank.

Intermsofperformance,wepostedasatisfactory

netprofitofTHB15,385millionin2013,bolsteredbythe

capitalgainfromthesaleofThanachartLifeAssurancePlc.

Excludingthisgainandextraprudentialreservessetasidein

linewithBoTguidelines,underlyingNetIncomeincreasedby

ahealthy21%in2013.Westronglyemphasizedefficiency

acrosstheorganizationwiththeincreaseininterestincome

attributabletogoodloangrowthaswellasimprovedinterest

spreadarisingfromtheefficientcostoffundsmanagement.

Meanwhile,feeincomeandotheroperatingincomewentup

thankstoimprovingcross-sellingandsynergiesgenerated

acrossallsubsidiariesunderthegroupresultingintheirimproved

performances.Finally,throughclosecontrolofdiscretionary

expensesandareduction infixedcosts(despiteongoing

investment in new processes and technology) from our

OptimizationInitiatives,totaloperatingcostsdecreasedby4%in

2013leadingtoastrongimprovementinourcosttoincomeratio.

2014isexpectedtobeachallengingyearfortheThai

bankingsector.Withuncertaintiesfrombothlocalandoverseas

markets,thegrowthofoverallbankingindustryisexpectedto

decelerate.Aprolongedpoliticalturmoilwillnotbeconducive

topublicandprivateinvestment,whilethetaperingofthe

QuantitativeEasingProgrambyUSFederalReservewillcause

arebalancingincapitalflowsandmayimpactmarketliquidity

andlongterminterestrates.Theexistinghighhouseholddebt,

asaresultofthere-buildingeffortsfollowingthedevastating

floodsandtheutilizationofgovernmentstimulusmeasures

includingthefirst-timecarbuyerprograminrecentyears,

has already impacted consumer credit demand and debt

servicingability.Finally,regulatorypressurewillcontinuewith

BaselIIIimplementationandtheimplementationtheForeign

AccountTaxComplianceAct(“FATCA”).

(Mr. Somjate Moosirilert)

ChiefExecutiveOfficer

andPresident

013ThAnAchART BAnk puBlIc cOMpAny lIMITed

ThanachartBankiswellpositionedtomeetthese

challengeswithstrongcapitalandliquidityandincreasingly

diversified opportunities for growth across the financial

servicesindustry.Inadditiontodetailed,customerfocused

business strategies, we will continue to implement our

OptimizationInitiativeswhichwillimproveourinfrastructure

and end-to-end processes across the Group. Most

importantly, these investments in state-of-art technology

andprocessredesignalongwithenhancedstafftraining

will enableus tosignificantly improvesalesproductivity

acrossallchannelsandallowustobuilddeepercustomer

relationships, better respond to their needs and offer

a differentiated customer experience. Through these

investmentsinourpeopleandinfrastructure,wewillcontinue

to accelerate growth in high-yielding products while

maintainingourdominantpositioninautolending.Moreover,

wehavestrengthenedourriskmanagementandwillreduce

creditcostsacrossallportfoliosthroughfocusedorigination,

riskbasedpoliciesanduseofmarketleadingtechnology

across the credit cycle. Simultaneously, we will attract

newcustomersandgrowanddiversifyourfundingbase,

particularlycurrentandsavingsaccountsatanappropriate

cost level,byoffering innovativesavings, insurance,and

investmentproducts.Wearealsodeterminedtohelpour

clientssucceedfinanciallyandgrowourfeerevenuethrough

relationship-basedcrosssellingofthefullsuiteoffinancial

productsandservicestailoredtomeettheirneeds.Lastbut

notleast,wewillpursueon-goingstrategicsourcingand

costmanagement initiativeswhile furtherdevelopingour

leadershipteamassstrategiccompetitiveadvantage.

Theadvancementsweachievedin2013aretheresult

of the focused commitment by all of staff to fulfill our

strategicintentsandsupportourcustomers.Thisunwavering

supportandloyaltyofourstaff,customers,partners,and

shareholdershasbeenasourceofenduringstrengthfor

ourBank.Wewill continue todrawon this strengthas

wemeetthechallengesaheadandarefullyconfidentof

abrighterfutureinthecomingyears.

(Mr. Brendan king)

ViceChairmanoftheExecutiveCommittee

andDeputyChiefExecutiveOfficer

014 AnnuAl RepORT 2013

BOARd OF dIRecTORS

ThAnAchART BAnk puBlIc cOMpAny lIMITed

10. Mr. Rod Michael

Reynolds

Director,

MemberoftheNomination

andRemunerationCommittee

1. Mr. Banterng Tantivit

Chairman

7. Mr. narong

chivangkur

IndependentDirector,

ChairmanoftheNomination

andRemunerationCommittee

4. Mr. Brendan George

John king

Director,

ViceChairmanoftheExecutive

Committee

015ThAnAchART BAnk puBlIc cOMpAny lIMITed

2. Mr. Suphadej

poonpipat

ViceChairman,Chairman

oftheExecutiveCommittee

5. Ms. Suvarnapha

Suvarnaprathip

Director,

ViceChairpersonof

theExecutiveCommittee

8. Mr. Sataporn

Jinachitra

IndependentDirector,

MemberoftheAuditCommittee,

MemberoftheNomination

andRemunerationCommittee

11. Mr. kobsak

duangdee

Director

9. Assoc. prof.

dr. Somjai

phagaphasvivat

IndependentDirector,

MemberoftheAudit

Committee

12. Mr. Alberto Jaramillo

Director

6. Mr. kiettisak

Meecharoen

IndependentDirector,

ChairmanoftheAudit

Committee

3. Mr. Somjate

Moosirilert

Director,

MemberoftheExecutive

Committee

016 AnnuAl RepoRt 2013

MAnAgeMent Discussion AnD AnAlysis

(Based upon operating results recorded in financial statements of 2013 comparing to that of 2012)

Major events in 2013

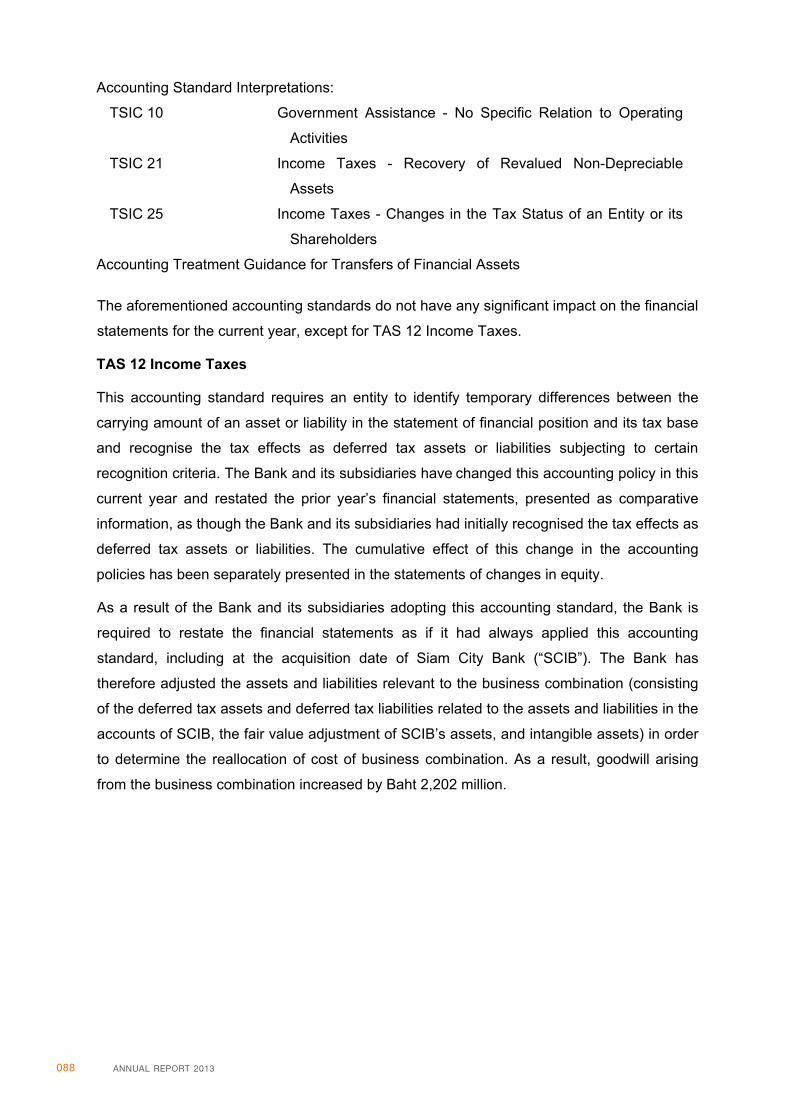

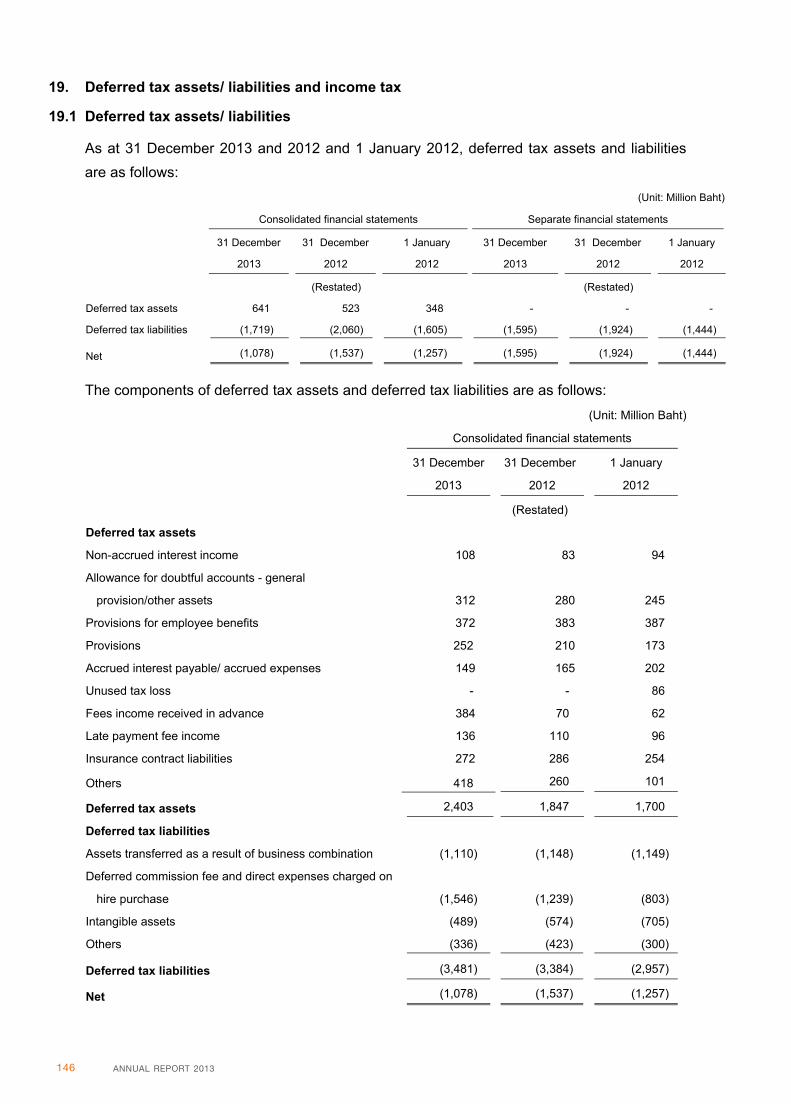

• As an accounting standard of TAS 12 Income Taxes became effective in 2013, Thanachart Bank Public Company

Limited (the Bank) and its subsidiaries were to ensure compliance with the aforementioned and, as a result, the Bank was

required to adjust the past records as if the standard had been applied throughout in the past including the period when

the acquisition of Siam City Bank Public Company Limited (SCIB) took place. Therefore, all items related to the merging i.e.

deferred tax assets concerning assets and liabilities in SCIB’s accounts, increase in fair value of SCIB’s assets, and intangible

assets, were to be adjusted to determine reallocation of cost of business combination which resulted in an increase in goodwill

of THB 2,202 million.

Furthermore, in adopting this accounting standard, the Bank and its subsidiaries were to adjust financial statements

as of December 31, 2012, which resulted in an increase in deferred tax assets and liabilities of THB 523 million and THB

2,060 million, respectively and consequently affected carry-over retained earnings of THB 1,167 million.

• On May 3, 2013, the Bank and Prudential Life Assurance (Thailand) Public Company Limited (Prudential) had signed

a 15-year Bancassurance Agreement. The Bank had transferred 328,500,000 of Thanachart Life Assurance Public Company

Limited (TLIFE)’s common shares, or 100 percent of total shares to Prudential and received a payment of THB 17,500 million

in return in accordance with the agreed terms. For a post-completion adjustment to be made to reflect the net asset value

as at the completion date and a further payment of THB 500 million were due in 12 months after the completion date.

The transaction would be recognized when the transfer of the shares and related payment are complete.

Gain on disposal of THB 12,216 million recorded in the consolidated financial statements and THB 13,128 million

in the separate financial statements were recognized in statements of comprehensive income for the year 2013. To be in

compliance with the accounting standard, TLIFE’s operating results, included in the consolidated statements, were separately

presented as “profit for the year from discontinued operations” item of 2013 and 2012. However, for Management Discussion

and Analysis, the item was recorded as non-interest income under item of other operating incomes. As for the analysis, the

item was excluded to reflect the true operating results of the Bank and its subsidiaries.

consolidated Financial statements were of tBAnK and its subsidiaries as follows:

Subsidiaries by mean of direct share-holding

SCIB Public Company Limited (formerly known as “Siam City Bank Public Company Limited”)

Thanachart Securities Public Company Limited

Thanachart Insurance Public Company Limited

Thanachart Life Assurance Public Company Limited

Thanachart Fund Management Company Limited

Thanachart Broker Company Limited

Thanachart Group Leasing Company Limited

Thanachart Management and Services Company Limited

Thanachart Legal and Appraisal Company Limited

Thanachart Training and Development Company Limited

017thAnAchARt BAnK puBlic coMpAny liMiteD

statement of comprehensive income 2013

increase/

(Decrease)

percentage

2012

Variance

Interest income 53,887 48,736 5,151 10.57

Interest expenses 27,234 25,556 1,678 6.57

Net interest income 26,653 23,180 3,473 14.99

Net fees and service income 6,903 5,070 1,833 36.15

Other operating income(1)

18,569 5,816 12,753 219.28

Other operating expenses(2)

21,259 21,660 (401) (1.85)

Profit (loss) before impairment loss of

loans and debt securities 30,865 12,406 18,459 148.80

Impairment loss of loans and debt securities 11,587 2,980 8,608 288.91

Profit (loss) before income tax 19,278 9,427 9,851 104.51

Income tax 4,031 2,076 1,955 94.20

Profit for the year from continuing operations 15,247 7,351 7,896 107.42

Profit for the year from discontinued operations 354 1,212 (858) (70.77)

Net profit 15,601 8,563 7,039 82.21

The Bank’s 15,385 8,354 7,031 84.16

Non-controlling interests’ 216 208 8 3.68

Earnings per share (baht) 2.79 1.52

Weighted average number of ordinary shares

(million shares) 5,513.66 5,513.66

TS Asset Management Company Limited

Siam City Life Assurance Public Company Limited

SCIB Service Company Limited

Ratchthani Leasing Public Company Limited

Subsidiary by mean of indirect share-holding

National Leasing Company Limited

overall operating Result

(Analysis comparing performance of 2012 and 2013 based on financial statements)

(Unit: THB Million)

Note: (1)

Operating income deducted by underwriting expenses

(2)

Excluding underwriting expenses

018 AnnuAl RepoRt 2013

The Bank and its subsidiaries had a net profit for

the year 2013 of THB 15,601 million, of which THB 15,385

million was the Bank’s; increased by THB 7,031 million or

84.16 percent comparing to the previous year as a result of

an extra profit from disposal of investment in a subsidiary

company by setting special provision. If excluded the item,

in 2013, the Bank’s net profit of Bank and its subsidiaries

would total THB 10,101 million; increased from the previous

year by THB 1,747 million or 20.91 percent. Changes in key

drivers of the business were as follows:

• Interest spread increased to 2.59 percent from

2.48 percent in the previous year. Yield on earning asset was

at 5.76 percent, decreased from 5.82 percent as a result of

policy interest adjustments; from 2.75 percent to 2.50 percent

during the 2nd

quarter of 2013 and again to 2.25 percent

during the last quarter of 2013. Yield decreased partially

because of ceasing of revenue recognition from non-

performing loans. Cost of fund was at 3.17 percent, decreased

from 3.34 percent as a result of efficient cost and liquidity

management that enhanced competitiveness by expanding

loan growth. The decrease in cost of fund was also a result

of the policy rate adjustments as aforementioned.

• Increase in non-interest revenue (excluding

special items) of 12.50 percent from banking and securities

fees, net profit from investment, and dividend income. Non-

interest income ratio in 2013 was at 33.80 percent and when

considered non-interest income to average asset to mitigate

impact of interest spread, the ratio was at 1.33 percent.

• Control and management of operating expenses

under the Cost Control policy, cost to income ratio in

2013 was at 52.80 percent, decreased from 61.40 percent

and when considered operating expense to average asset,

the ratio was at 2.08 percent.

• Credit cost in 2013 was at 0.78 percent (excluding

extra provision of the Bank and its subsidiaries), increased

from end of the previous year of 0.40 percent as a result

of loss on sales according to demand and supply condition

in the used-car market. As for non-performing loans as of

December 31, 2013, the amount totaled THB 35,313 million,

increased from the previous year of THB 32,501 million on

account of growth in hire purchase loan volume. The Bank

had formulated policies and management procedures to

ensure efficient debt collection. Furthermore, an increase

in non-performing loan, mainly attributed to major debtors,

was fully covered by the Bank’s reserve so that its financial

statements were not affected. NPL ratio was at 4.23 percent

comparing end of the previous year of 4.10 percent.

• Capital adequacy: the Bank’s total capital counted

following the Basel III requirements as of December 31,

2013 was THB 110,683 million, consisting of Tier I capital

(Common Equity Tier I and Additional Tier I) of THB 70,818

million and Tier II capital of THB 39,865 million. Capital

adequacy ratio was at 14.80 percent comparing to 13.99

percent as of the end of 2012. The Bank’s capital fund

included profit from operating result in the first half of 2013

and was affected by the changes from Basel II to Basel III

and dividend payment in April 2013.

net interest income

In 2013, the Bank and its subsidiaries had a net interest

income of THB 26,653 million, increased by THB 3,473 million

or 14.99 percent comparing to previous year. Total interest

income was of THB 53,887 million, increased by THB 5,151

million or 10.57 percent, while interest expense was of THB

27,234 million, increased by THB 1,678 million or 6.57 percent.

This result in interest spread to increase from the previous

year of 2.48 percent to 2.59 percent in 2013.

019thAnAchARt BAnK puBlic coMpAny liMiteD

non-interest income

Non-interest income comprised net fees and service

income, net underwriting income, and other operating income,

totaling THB 13,610 million; increased from the previous

year by THB 1,512 million or 12.50 percent. Non-interest

income ratio in 2013 was at 33.80 percent and when taking

Non-interest income to average asset into consideration to

mitigate impact from interest spread, the ratio was at 1.33

percent. Details of changes were as follows:

• Net fee and service income

The Bank and its subsidiaries earned from net

fee and service income an amount of THB 6,903 million,

increased by THB 1,833 million or 36.15 percent from growth

in customer base and more diversified financial products of

the Bank and subsidiaries. Total fee and service income was

THB 8,793 million, increased by THB 2,237 million or 34.13

percent, whereas total fee and service expense was of THB

1,890 million, increased by THB 405 million or 27.24 percent.

• Other operating income

Other operating income comprised net gain

(loss) from trading and foreign exchange transactions, net

profit from investments, shares of profit from investments in

associated companies under the equity method, dividend

income, profit from sales of property foreclosed and other

assets, underwriting income, and others. In 2013, total other

operating income was THB 6,707 million, decreased from the

previous year by THB 321 million or 4.56 percent mainly due

to disposal of investment in TLIFE, and was compensated

by fee income. An increase in profit from investment was

partially due to receipt of repayment from closing Vayupak

fund. Underwriting income, dividend receipt, and shares of

profit from investments in associated companies under the

equity method were still on an improving trend.

other operating expense

In 2013, other operating expense was THB 21,259

million, decrease by THB 401 million or 1.85 percent, as a

result of efficient cost control. Cost to Income Ratio was

at 52.80 percent, decreased from 61.40 percent and when

taking operating expense to average asset into consideration,

the ratio was at 2.08 percent.

impairment loss on loans and Debt

securities

In 2013, impairment loss on loans and debt securities

(excluding extra reserves of the Bank and its subsidiaries)

totaled THB 6,207 million. Credit cost was at 0.78 percent,

increased from the previous year of 0.40 percent as a result

of loss on sales due to demand and supply condition in the

used-car market.

020 AnnuAl RepoRt 2013

Assets

Cash 17,940 15,181 2,759 18.17

Interbank and money market items-net 69,697 71,963 (2,266) (3.15)

Investments-net 138,825 146,106 (7,281) (4.98)

Net loans to customers and accrued interest receivables 760,943 731,010 29,933 4.10

Property foreclosed-net 6,291 6,461 (170) (2.63)

Land, premises and equipment-net 8,037 8,292 (255) (3.08)

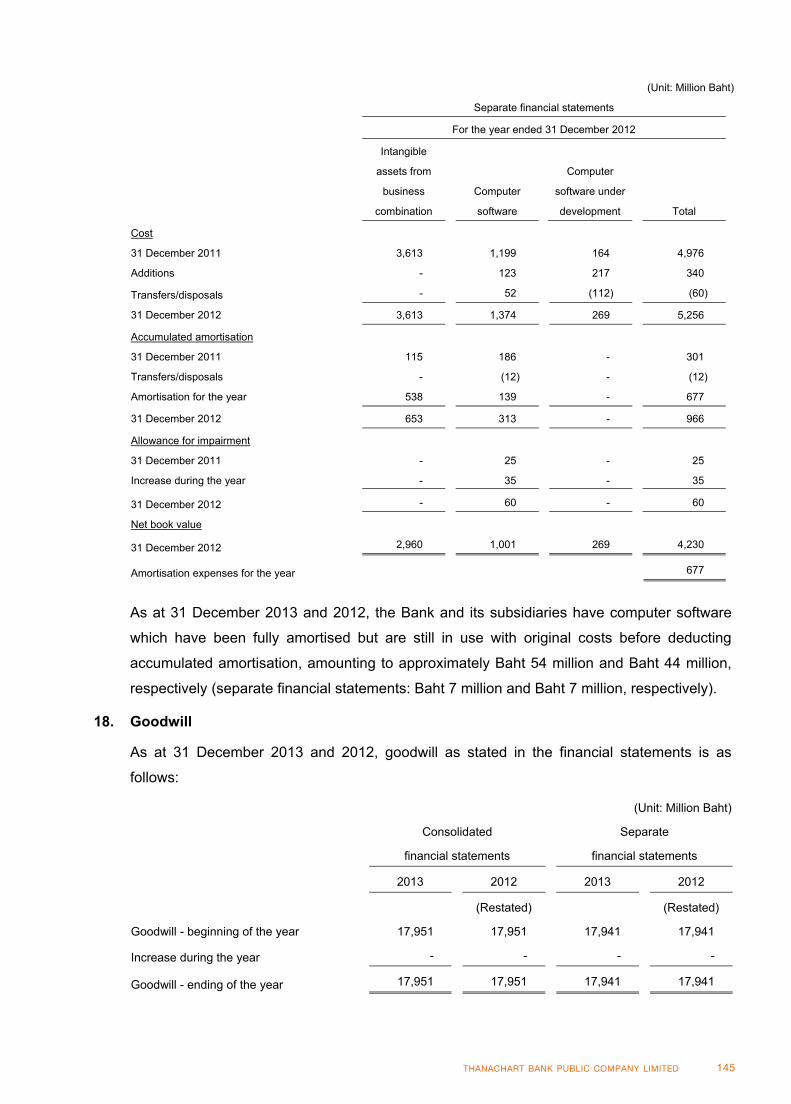

Goodwill 17,951 17,951 0 0.00

Other assets 18,665 21,656 (2,991) (13.81)

Total assets 1,038,349 1,018,620 19,729 1.94

Liabilities and equity

Deposits 719,079 698,372 20,707 2.97

Interbank and money market items-net 81,082 87,777 (6,695) (7.63)

Liability payable on demand 3,219 4,989 (1,770) (35.48)

Debt issued and borrowings 92,229 78,149 14,080 18.02

Provisions 3,146 2,976 170 5.71

Insurance contract liabilities 15,019 39,632 (24,613) (62.10)

Other liabilities 27,335 22,540 4,795 21.27

Total liabilities 941,109 934,435 6,674 0.71

Equity attributable to the Bank 96,218 83,330 12,888 15.47

Non-controlling interest of the subsidiaries 1,022 856 166 19.39

Total liabilities and equity 1,038,349 1,018,620 19,729 1.94

Financial position of the Bank and its subsidiaries’

The Bank and its subsidiaries’ total assets, as of December 31, 2013, was THB 1,038,349 million, increased from end

of 2012 by THB 19,729 million or 1.94 percent. The increase was mostly attributed to volume of loan to customers and net

interest receivables of THB 29,933 million or 4.10 percent as a result of growth in hire purchase business of 10.96 percent

from end of the previous year. Proportion of Retail and SMEs business volume was 69 : 31.

consolidated Balance sheet

consolidated Balance sheet

December 31,

2013

December 31,

2013

increase/

(Decrease)

increase/

(Decrease)

percent

percent

December 31,

2012

December 31,

2012

Variance

Variance

(Unit: THB Million)

(Unit: THB Million)

021thAnAchARt BAnK puBlic coMpAny liMiteD

Total liabilities of the Bank and its subsidiaries as of December 31, 2013 was THB 941,109 million, increased from the

previous year by THB 6,674 million or 0.71 percent. The increase was mostly accounted for the followings:

• Deposits of THB 719,079 million, increased by THB 20,707 million or 2.97 percent from end of 2012 as a result of

a deposit mobilization restructuring via financial products; Ultra Saving, short-term fixed deposits, fixed deposits with special

rates. Throughout the year, strategies for launching new product and interest rate were formulated to match the policy rate

and the market condition.

• Net Interbank and money market items of THB 81,082 million, decreased by THB 6,695 million or 7.63 percent as

a result of liquidity management of the Bank.

• Debt issued and borrowings of THB 92,229 million, increased by THB 14,080 million or 18.02 percent on account

of issuance of short-term debentures.

Shareholders’ equity as of December 31, 2013 was of THB 96,218 million, increased by THB 12,888 million or 15.47

percent from end of 2012. The increase was mainly attributed to profit from operations in 2013. Whereas, dividend payment was

made out of the 2012 net profit at a rate of THB 0.37 per share, amounting to a total dividend payment of THB 2,040 million.

Asset Quality

The asset quality was considered based on consolidated financial statements.

1. net loan to customers and accrued interest receivable

As of December 31, 2013, the Bank and its subsidiaries’ net loan to customers and accrued interest receivables

counted following the Bank of Thailand (BOT)’s regulations totaled THB 759,763 million, increased from end of 2012 by THB

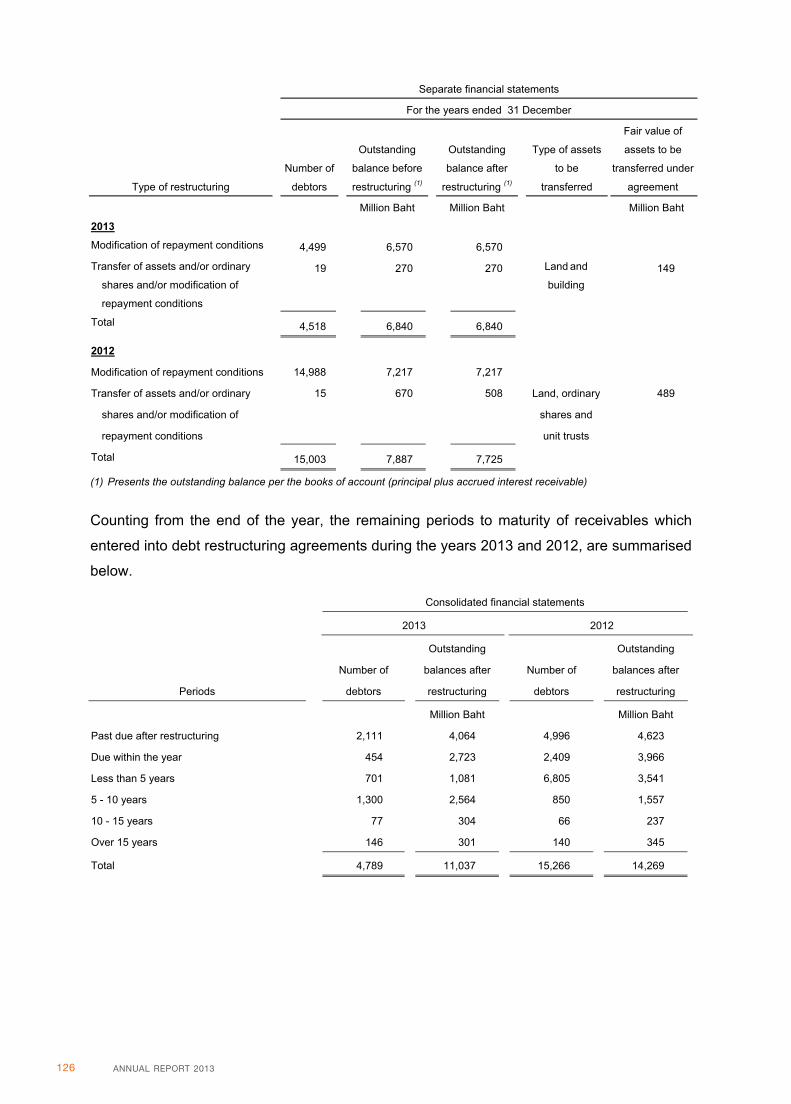

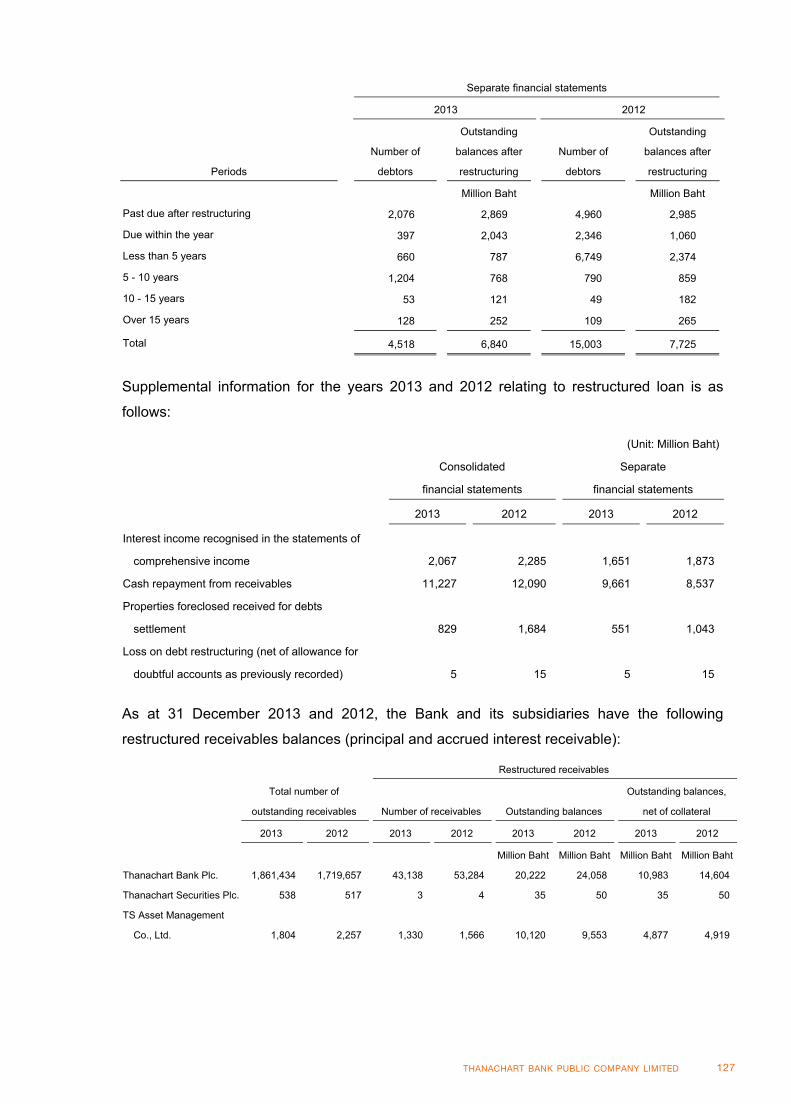

27,254 million or 3.72 percent. During the year 2013, the Bank and its subsidiaries had made debt restructuring agreements

with 4,789 debtors in various arrangements; amending terms of repayment, transferring assets and/or shares and/or amending

terms of repayment, of which outstanding before undergoing the debt restructuring program was approximately THB 11,303

million. The Bank and its subsidiaries had a total of 44,471 out of 1,863,776 debtors joined the debt restructuring program by

the end of 2013 of which their principal and accrued interest receivable amounting to THB 30,377 million.

Loan diversification

At the end of 2013, proportion of total loans comprised hire purchase of 55.71 percent, followed by housing loans

of 10.59 percent, manufacturing and commerce of 10.25 percent, public utilities and services of 8.64 percent, real estate and

construction of 6.41 percent, and others of 8.41 percent.

10.25%

Manufacturing

and Commerce

11.78%

Manufacturing

and Commerce

8.41%

Others

9.44%

Others

55.71%

Hire Purchase

52.63%

Hire Purchase

10.59%

Housing Loans 10.96%

Housing Loans

8.64%

Public utilities

and services

8.39%

Public utilities

and services

6.41%

Real Estate and

Construction

6.81%

Real Estate and

Construction

Loans to Customers Classified

by Type of Business in 2013

Loans to Customers Classified

by Type of Business in 2012

022 AnnuAl RepoRt 2013

2. loans to customers classified in accordance with the Bot’s regulation

As of December 31, 2013, the Bank and its subsidiaries had an outstanding of loan granted and accrued interest

receivable classified in accordance with the BOT’s guidelines of THB 759,763 million, increased from the previous year by

THB 27,254 million or 3.72 percent. Allowance for doubtful accounts, as of December 31, 2013, was set at THB 28,240 million

and total allowance for doubtful accounts to total loans and accrued interest receivable was 3.72 percent.

loans to customers and

accrued interest receivables December 31,

2013

December 31,

2013

December 31,

2012

December 31,

2012

Debt balance(1)

Allowance for doubtful accounts

Normal 689,679 671,590 7,163 4,834

Special mentioned 34,903 28,554 4,217 1,475

Substandard 6,133 5,273 2,705 3,535

Doubtful 9,324 4,529 5,125 2,393

Doubtful of loss 19,724 22,563 9,022 10,109

Total 759,763 732,509 28,232 22,346

Additional allowance for doubtful accounts 8 499

Total allowance for doubtful accounts 28,240 22,845

Ratio of total allowance for doubtful accounts to loans to customers and accrued

interest receivables (percent) 3.72 3.12

(Unit: THB Million)

Borrowers classified by the Bot’s regulations

Note: (1)

Debt balance/book value of normal and special mentioned accounts excluded accrued interest receivables.

023thAnAchARt BAnK puBlic coMpAny liMiteD

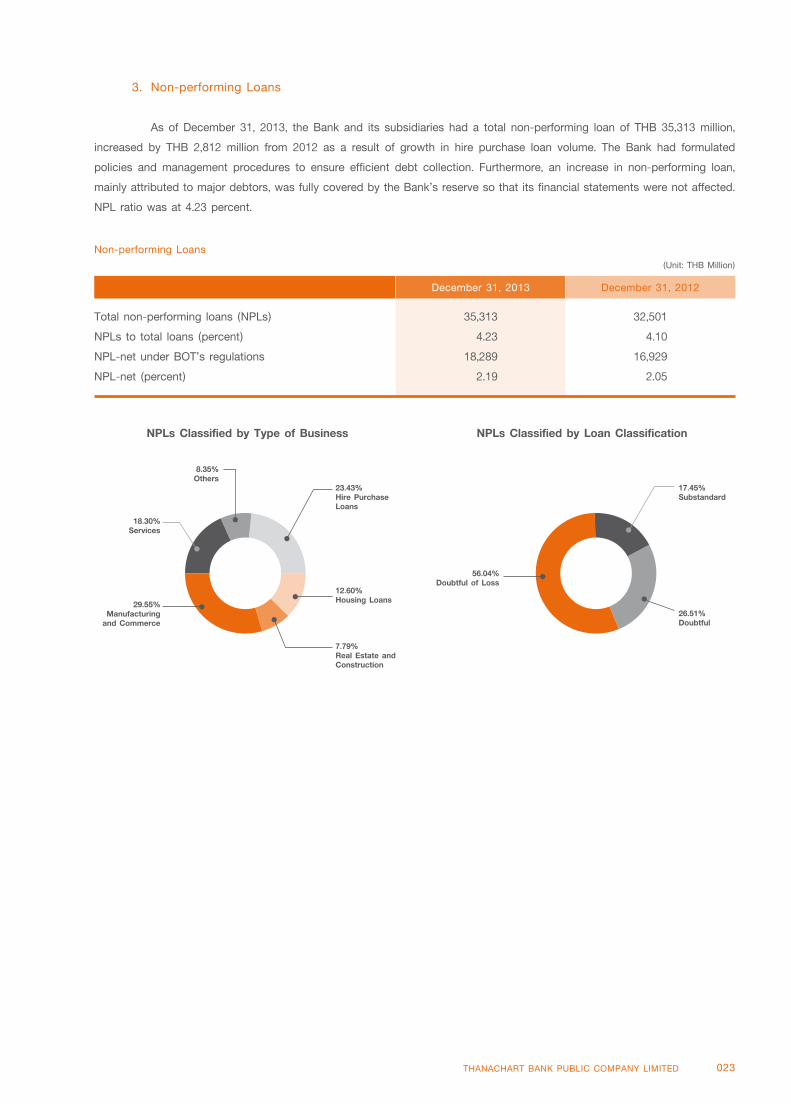

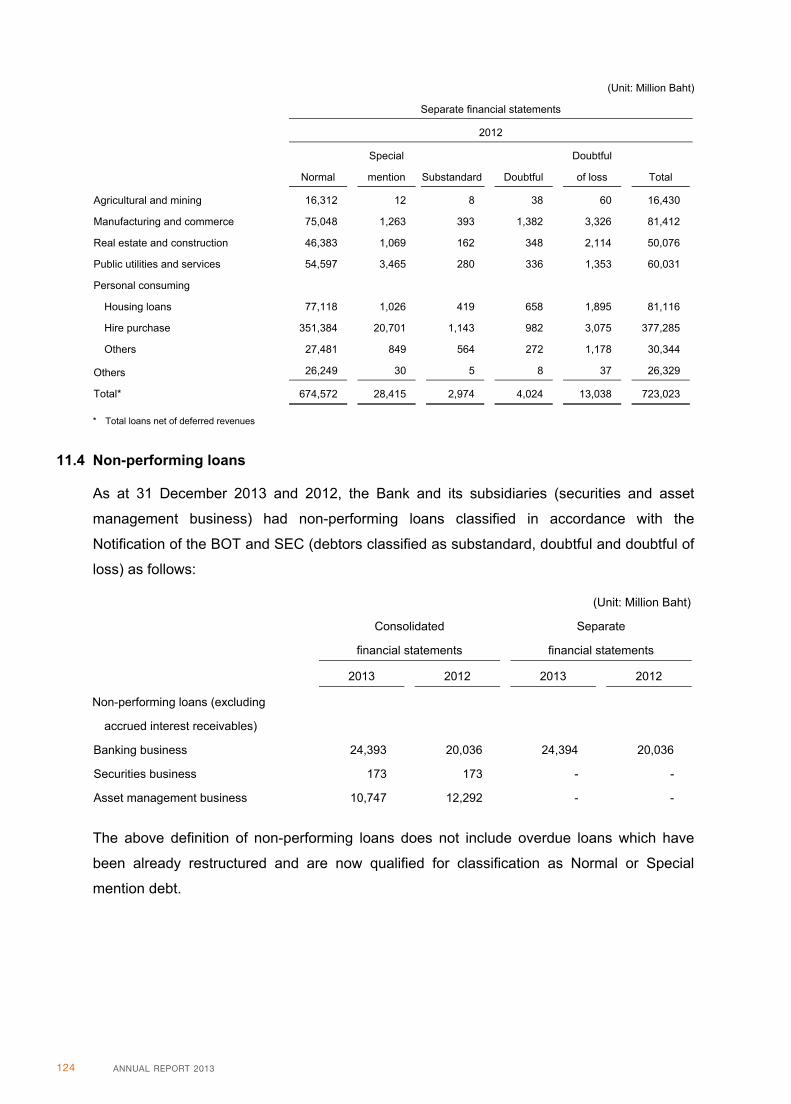

3. non-performing loans

As of December 31, 2013, the Bank and its subsidiaries had a total non-performing loan of THB 35,313 million,

increased by THB 2,812 million from 2012 as a result of growth in hire purchase loan volume. The Bank had formulated

policies and management procedures to ensure efficient debt collection. Furthermore, an increase in non-performing loan,

mainly attributed to major debtors, was fully covered by the Bank’s reserve so that its financial statements were not affected.

NPL ratio was at 4.23 percent.

December 31, 2013 December 31, 2012

Total non-performing loans (NPLs) 35,313 32,501

NPLs to total loans (percent) 4.23 4.10

NPL-net under BOT’s regulations 18,289 16,929

NPL-net (percent) 2.19 2.05

(Unit: THB Million)

non-performing loans

56.04%

Doubtful of Loss

26.51%

Doubtful

17.45%

Substandard

NPLs Classified by Type of Business NPLs Classified by Loan Classification

8.35%

Others

18.30%

Services

29.55%

Manufacturing

and Commerce

7.79%

Real Estate and

Construction

12.60%

Housing Loans

23.43%

Hire Purchase

Loans

024 AnnuAl RepoRt 2013

4. investment in securities

In 2013, the Bank and its subsidiaries had a total investment in securities of THB 138,254 million. A major

portion of approximately 63.32 percent was invested in government and state enterprises securities, followed by 22.49 percent

in private debt securities. After adding (deducting) allowance for change in values and impairment, net investment was

THB 138,825 million, decreased from 2012 of THB 146,106 million, Details were as follows:

type of investmentDecember 31,

2013

December 31,

2012percent percent

Debt securities

Government and state enterprise securities

• Trading 5,150 3.73 5,745 3.97

• Available-for-sale 71,398 51.64 55,220 38.16

• Held-to-maturity 10,986 7.95 21,756 15.03

Private debt securities

• Trading 5,266 3.81 5,683 3.93

• Available-for-sale 25,480 18.43 29,669 20.50

• Held-to-maturity 352 0.25 2,731 1.89

Foreign debt securities

• Trading 0 0.00 620 0.43

• Available-for-sale 14,691 10.63 11,485 7.94

• Held-to-maturity 0 0.00 0 0.00

Equity securities

Listed securities

• Trading 17 0.01 16 0.01

• Available-for-sale 987 0.71 7,062 4.88

Investment in receivables

• Held-to-maturity 2 0.00 5 0.00

Other investment 3,925 2.84 4,714 3.26

Total debt securities 138,254 100.00 144,706 100.00

Add (less): Allowance for change in value 594 1,456

Allowance for impairment (23) (56)

Total investment-Net 138,825 146,106

(Unit: THB Million)

securities investment classified by types of instruments

025thAnAchARt BAnK puBlic coMpAny liMiteD

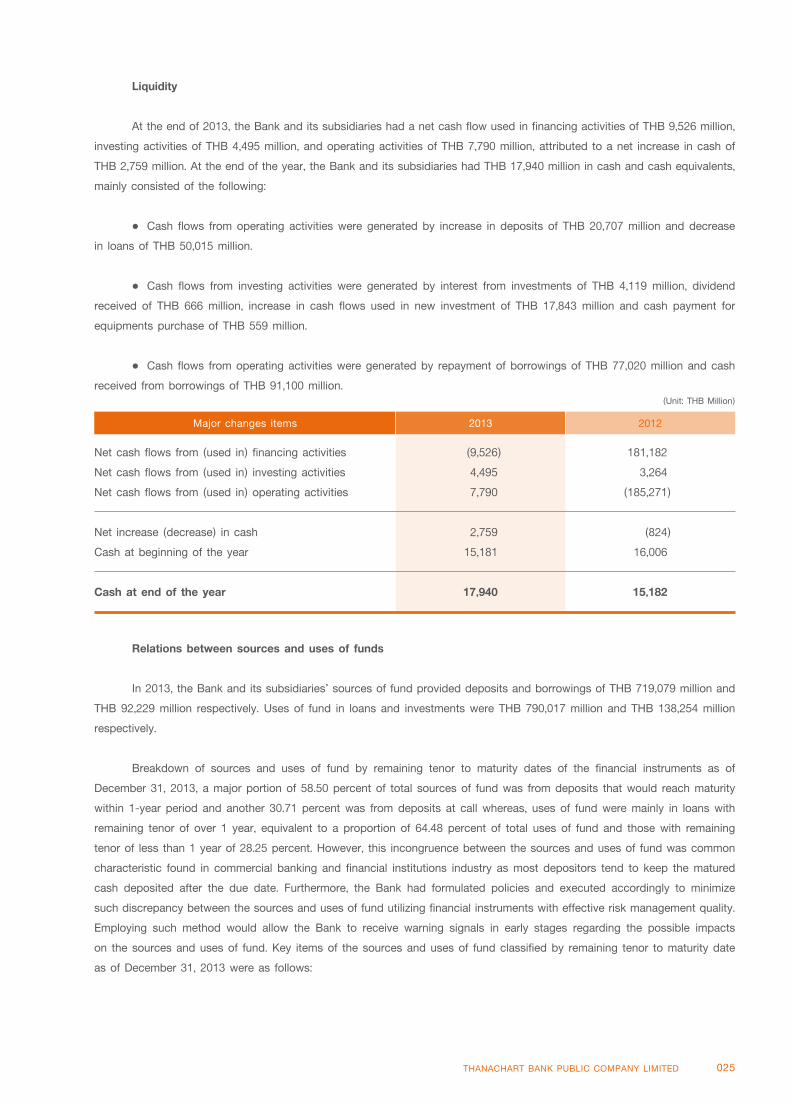

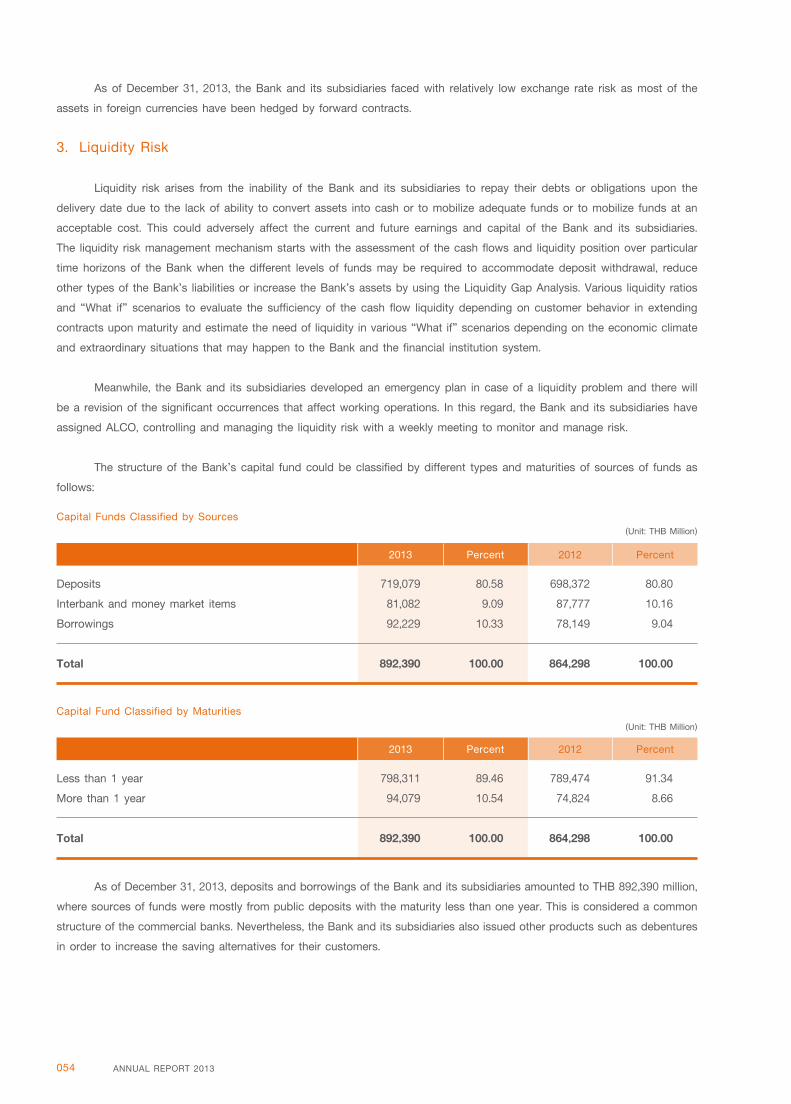

Liquidity

At the end of 2013, the Bank and its subsidiaries had a net cash flow used in financing activities of THB 9,526 million,

investing activities of THB 4,495 million, and operating activities of THB 7,790 million, attributed to a net increase in cash of

THB 2,759 million. At the end of the year, the Bank and its subsidiaries had THB 17,940 million in cash and cash equivalents,

mainly consisted of the following:

• Cash flows from operating activities were generated by increase in deposits of THB 20,707 million and decrease

in loans of THB 50,015 million.

• Cash flows from investing activities were generated by interest from investments of THB 4,119 million, dividend

received of THB 666 million, increase in cash flows used in new investment of THB 17,843 million and cash payment for

equipments purchase of THB 559 million.

• Cash flows from operating activities were generated by repayment of borrowings of THB 77,020 million and cash

received from borrowings of THB 91,100 million.

Relations between sources and uses of funds

In 2013, the Bank and its subsidiaries’ sources of fund provided deposits and borrowings of THB 719,079 million and

THB 92,229 million respectively. Uses of fund in loans and investments were THB 790,017 million and THB 138,254 million

respectively.

Breakdown of sources and uses of fund by remaining tenor to maturity dates of the financial instruments as of

December 31, 2013, a major portion of 58.50 percent of total sources of fund was from deposits that would reach maturity

within 1-year period and another 30.71 percent was from deposits at call whereas, uses of fund were mainly in loans with

remaining tenor of over 1 year, equivalent to a proportion of 64.48 percent of total uses of fund and those with remaining

tenor of less than 1 year of 28.25 percent. However, this incongruence between the sources and uses of fund was common

characteristic found in commercial banking and financial institutions industry as most depositors tend to keep the matured

cash deposited after the due date. Furthermore, the Bank had formulated policies and executed accordingly to minimize

such discrepancy between the sources and uses of fund utilizing financial instruments with effective risk management quality.

Employing such method would allow the Bank to receive warning signals in early stages regarding the possible impacts

on the sources and uses of fund. Key items of the sources and uses of fund classified by remaining tenor to maturity date

as of December 31, 2013 were as follows:

Major changes items 2013 2012

Net cash flows from (used in) financing activities (9,526) 181,182

Net cash flows from (used in) investing activities 4,495 3,264

Net cash flows from (used in) operating activities 7,790 (185,271)

Net increase (decrease) in cash 2,759 (824)

Cash at beginning of the year 15,181 16,006

Cash at end of the year 17,940 15,182

(Unit: THB Million)

026 AnnuAl RepoR

t 2013

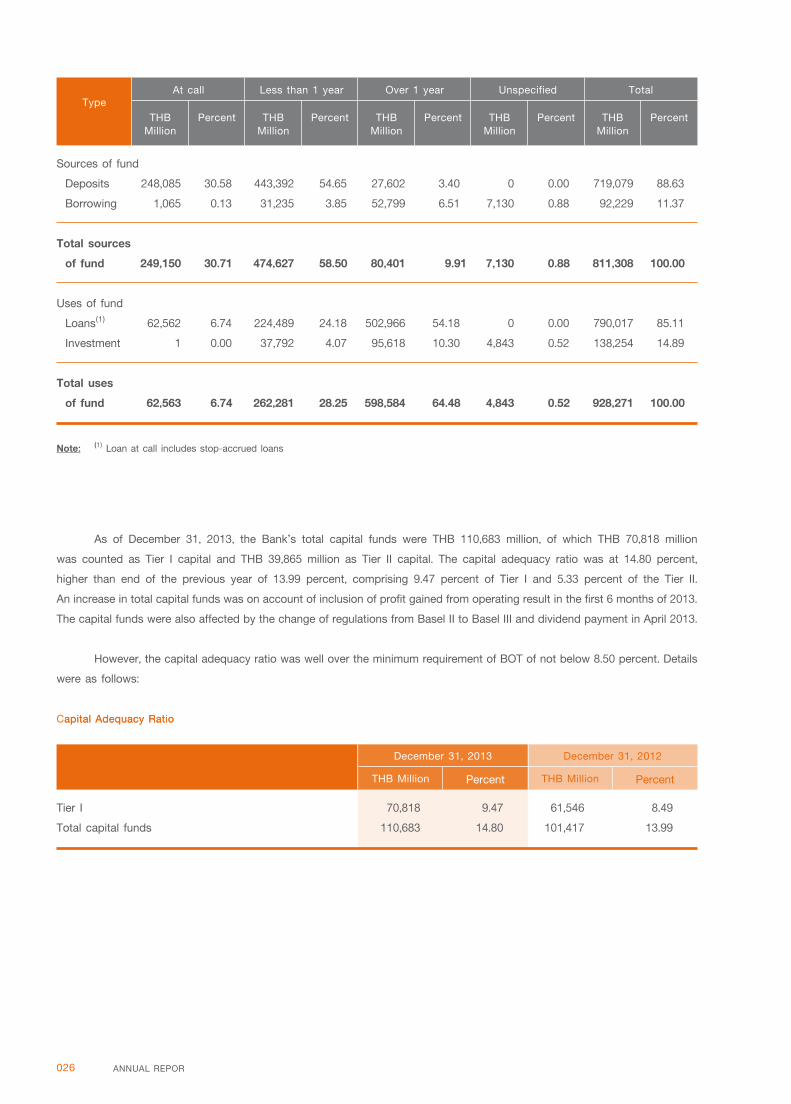

As of December 31, 2013, the Bank’s total capital funds were THB 110,683 million, of which THB 70,818 million

was counted as Tier I capital and THB 39,865 million as Tier II capital. The capital adequacy ratio was at 14.80 percent,

higher than end of the previous year of 13.99 percent, comprising 9.47 percent of Tier I and 5.33 percent of the Tier II.

An increase in total capital funds was on account of inclusion of profit gained from operating result in the first 6 months of 2013.

The capital funds were also affected by the change of regulations from Basel II to Basel III and dividend payment in April 2013.

However, the capital adequacy ratio was well over the minimum requirement of BOT of not below 8.50 percent. Details

were as follows:

capital Adequacy Ratio

December 31, 2013 December 31, 2012

thB Million Percent

thB

Million

type

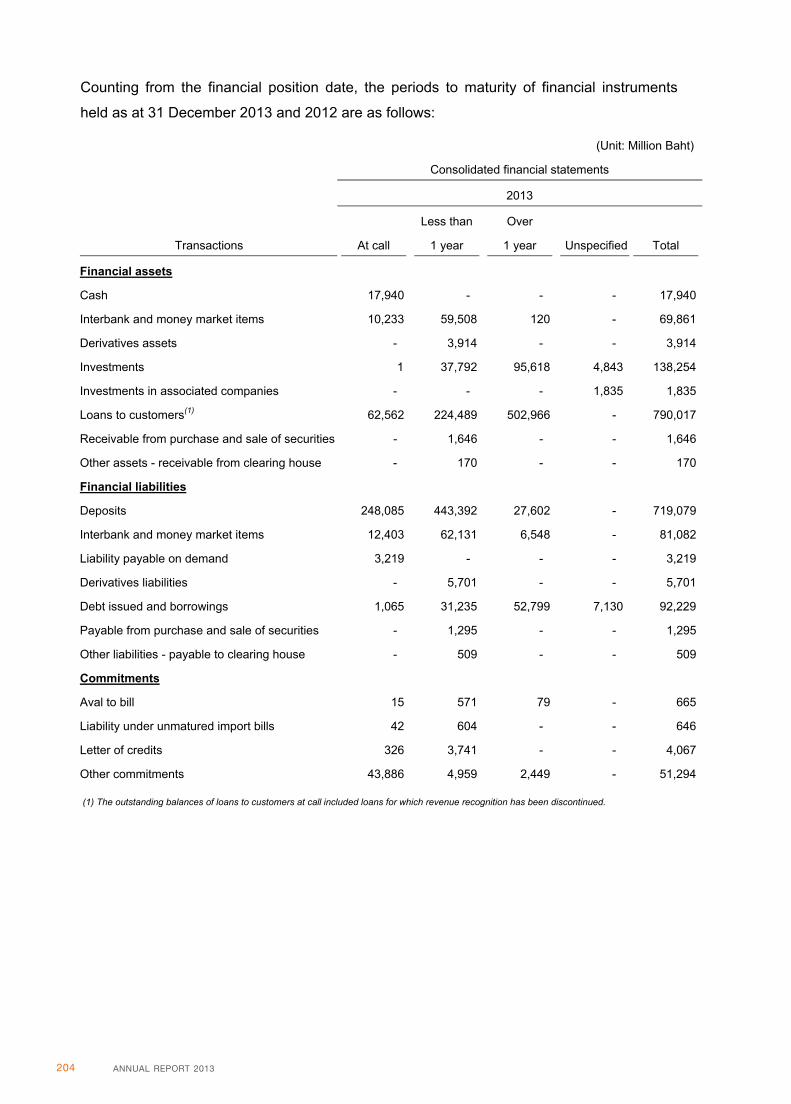

At call less than 1 year over 1 year unspecified total

percent thB

Million

percent thB

Million

percent thB

Million

percent thB

Million

percent

thB Million Percent

Tier I 70,818 9.47 61,546 8.49

Total capital funds 110,683 14.80 101,417 13.99

Sources of fund

Deposits 248,085 30.58 443,392 54.65 27,602 3.40 0 0.00 719,079 88.63

Borrowing 1,065 0.13 31,235 3.85 52,799 6.51 7,130 0.88 92,229 11.37

Total sources

of fund 249,150 30.71 474,627 58.50 80,401 9.91 7,130 0.88 811,308 100.00

Uses of fund

Loans(1)

62,562 6.74 224,489 24.18 502,966 54.18 0 0.00 790,017 85.11

Investment 1 0.00 37,792 4.07 95,618 10.30 4,843 0.52 138,254 14.89

Total uses

of fund 62,563 6.74 262,281 28.25 598,584 64.48 4,843 0.52 928,271 100.00

Note: (1)

Loan at call includes stop-accrued loans

apital Adequacy Ratio

39033

Typewritten Text

39033

Typewritten Text

39033

Typewritten Text

39033

Typewritten Text

39033

Typewritten Text

39033

Typewritten Text

Capital Adequacy

39033

Typewritten Text

39033

Typewritten Text

39033

Typewritten Text

39033

Typewritten Text

027thAnAchARt BAnK puBlic coMpAny liMiteD

thanachart securities public company

limited

Daily trading volume of TNS in 2013 was THB 4,074

million, a substantially increase from the daily trading volume

in the previous year of THB 2,711 million. The increase was

in line with the capital market condition. Market share in this

year was at 4.63 percent.

Net profit for the year ended December 31, 2013 was

THB 801 million, an increase of THB 338 million or 73.25

percent from the previous year. Total income amounted to

THB 2,403 million, an increase of 46.11 percent. The main

source of income came from brokerage income which totaled

to THB 1,828 million, fees and service income amounting

to THB 152 million, and interest income from margin loans

amounting to THB 205 million. On the other side, financial

costs and operating expenses were THB 1,410 million,

an increase of 33.73 percent from the previous year in line

with a growing business volume and income.

As at December 31, 2013, Net Capital Ratio (NCR)

was at 94.07 percent higher than the minimum requirement

of the SEC of 7.00 percent.

thanachart Fund Management company

limited

At the end of 2013, TFUND has asset under management

amounting to THB 134,410 million, an increase of THB 12,389

million or 10.15 percent from the end of 2012. Asset under

management comprised of 78.35 percent mutual funds, 7.83

percent provident funds, and 13.81 percent private funds.

For operating results of 2013, TFUND had a net profit

of THB 285 million, an increase of 145 million or 103.57

percent from the year 2012. This was mainly due to the

higher sales volume of equity fund and flexible fund than

that of 2012.

thanachart insurance public company

limited

TNI had a net profit for the year 2013 of THB 953

million, an increase of THB 337 million or 54.70 percent

from the year 2012. The key factors were given to a focus

on profitable products, claims management, and effective

cost management.

ts Asset Management company limited

In 2013, TS AMC has restructured debts in accordance

with policy and business plan of Thanachart Group. As at

December 31, 2013, TS AMC had a net profit of THB 404

million, due to the income from debt repayment of THB 850

million. Interest expenses amounted to THB 178 million while

income from selling properties foreclosed and other income

were THB 111 million. Operating expenses were THB 161

million and provision expenses amounted to THB 103 million.

However, TS AMC was able to restructure 257 loan accounts.

Income from debt restructuring was THB 819 million.

Ratchthani leasing public company limited

As at December 31, 2013, THANI had total assets of

THB 27,296 million, an increase of THB 8,081 million or 42.06

percent from the end of 2012. This was due to an expansion

of hire purchase loans, particularly from trucks. At the end of

2013, hire purchase loans of THANI recorded at THB 26,592

million, an increase of THB 7,933 million or 42.52 percent

from the end of 2012, accounted for 97.42 percent of total

assets. Total liabilities and shareholders’ equity were THB

24,072 million and THB 3,223 million respectively.

Net profit for the year 2013 amounted to THB 754

million, an increase of THB 277 million or 57.99 percent

from the previous year. Total income for the year 2013 was

THB 2,397 million, an increase of THB 814 million or 51.37

percent from the previous year. The increase was due to the

domestic automotive industry growth and the continuous hire

purchase loan base expansion of THANI. Interest expenses

were THB 917 million, an increase of THB 245 million

or 36.36 percent. The increase was due to an increase

in additional borrowings to support loan growth. Impairment

loss of loans of THANI was THB 269 million, an increase

of THB 188 million or 231.24 percent, due to the domestic

economic condition in the last quarter of 2013 showing

a clear sign of a slowdown and also the additional provision

provided in accordance with the large expansion of hire

purchase loan growth of THANI.

028 AnnuAl RepoRt 2013

nAtuRe oF Business opeRAtions

An overview of the Business operation

Thanachart Bank Public Company Limited (TBANK or the Bank) commenced its operation on April 22, 2002 with

Thanachart Capital Public Company Limited (TCAP) as the major shareholder. On December 21, 2006, the Bank of Thailand

(BOT) granted approval for TBANK and TCAP to form financial business group in consolidation and having TCAP as a parent

company.

In 2007, the Bank of Nova Scotia (Scotiabank) became our strategic partner by holding 24.98 percent of TBANK

shares, which later increased to 48.99 percent. The current major shareholders are TCAP and Scotiabank, and in 2011,

the Bank merged with Siam City Bank Public Company Limited (SCIB).

TBANK business structure, TCAP as a parent company, consists of two groups: 1) Financial Group and 2) Supporting

Group, which serves a full range of financial services through TBANK branch network and service outlet. It is strongly

committed to the good corporate governance principles.

Financial group

1. Thanachart Capital Public Company Limited (TCAP) operates as the holding company being a parent company of

Thanachart Financial Conglomerate.

2. Thanachart Bank Public Company Limited (TBANK) operates commercial banking business and other businesses

permitted by the BOT, such as life and non-life insurance broker, a provider of services relating to unit trust and securities

such as securities brokerage, proprietary trading, unit trust underwriting, mutual fund trustee service, provident fund custodian

service, debt instrument underwriting and trading, securities registrar, and gold derivative trading.

3. Thanachart Securities Public Company Limited (TNS) was permitted by the Ministry of Finance and the Office of

the Securities and Exchange Commission of Thailand (SEC) to operate the following activities:

3.1 TNS was granted a Full-Service License to operate securities businesses and related businesses such as

securities brokerage (domestically and internationally), securities underwriting, investment advisory service, securities borrowing

and lending, financial advisory service, unit trust underwriting and repurchasing, and securities registrar.

3.2 TNS was granted a Derivative Business Sor 1 License to engage in a full range of derivative businesses and

related businesses such as derivative brokerage and proprietary trading.

4. Thanachart Fund Management Company Limited (TFUND), which is a joint venture between TBANK (holding 75

percent of the total shares) and the Government Saving Bank (holding 25 percent shares), operates a full range of investment

management services in mutual fund management business, private fund and provident fund management business, and

investment advisory business.

5. Thanachart Insurance Public Company Limited (TNI) operates a non-life insurance business and a disaster

insurance business such as fire insurances, automobile insurances, marine and transportation insurances miscellaneous

insurance, and investment business.

6. Siam City Life Assurance Public Company Limited (SCILIFE) operates a life insurance business focusing on

middle and higher income customers who are interested in saving and health products. The Company’s sales channel includes

telelsales and broker.

7. Thanachart Group Leasing Company Limited (TGL) operates a hire purchase business of all automobile types.

029thAnAchARt BAnK puBlic coMpAny liMiteD

8. Ratchthani Leasing Public Company Lim-

ited (THANI) operates a hire purchase business and financial

lease business focusing on the segment of private used cars

and commercial cars such as pick-ups, taxis, tractors, and

trucks.

9. NFS Asset Management Company Limited

(NFS AMC) operates an asset management business by buying

or receiving transfers of NPLs and NPAs from financial

institutions in the Thanachart Group.

10. MAX Asset Management Company Limited

(MAX AMC) operates and asset management business by

buying or receiving transfers of NPLs and NPAs from other

financial institutions.

11. TS Asset Management Company Limited

(TS AMC) operates and asset management business by

buying or receiving transfers of NPLs and NPAs from SCIB

and TBANK.

supporting Business group

1. Thanachart Management and Services Company

Limited (TMS) provides services to the Group’s service staff.

2. Thanachart Broker Company Limited (TBROKE)

pursues Thanachart Group’s hire purchase customers to

insure their automobiles. TBROKE is also an automobile

insurance broker of TNI.

3. Thanachart Training and Development Company

Limited (TTD) organizes training activities for employees of

member companies of Thanachart Group.

4. SCIB Services Company Limited (SCIB Services)

provides general services to TBANK and companies in the

Group, such as janitor, security, delivery, car rental, car

drivers, and outsourcing service.

Business policy and strategies of thanachart

group

In 2014, Thanachart Group has determined its strategic

direction to become a fully integrated financial services

group capable of offering a full range of quality products

and services that cater to the financial needs of the customers

in an efficient manner. To achieve this goal, Thanachart Group

has set up its vision “To provide fully integrated financial

solutions to our targeted customers’ complete fianancial

needs by offering the highest quality products, services

and advice.”

Such vision was developed from three major

fundamentals which are providing fully integrated financial

services (Universal Banking) with TBANK being the main

services offering; focusing on satisfying our customers’

different needs (Customer Centric); and cooperating with

all departments to provide excellent services to customers

(Collaboration). The endeavor and accomplishment from

the three major fundamentals not only allowed Thanachart

Group to be a fully integrated financial services group with

highly successful in competition, but also is a key to drive

Thanachart Group to become one of Thailand’s leading banks

over the next three to five years.

Thanachart has adopted the professionalism and

innovation of Scotiabank and continuously develops its work

system such as CRM Tools for Sales and Service. This is

considered to be a significant tool to increase advisory

capacity, introduce products that match with customers

need, and increase the capacity of customer relationship

management that brings about customers satisfaction and

the Bank’s revenue.

Besides, Thanachart Group has communicated its

business strategy with all business units and employees

at all levels in order to have the same intent and vision in

accomplishing the goal. These Four Strategic Intents are

as follows:

1. To accelerate growth in commercial and unsecured

loan under prudent risk standards through the provision of

superior service and financial advice while maintaining our

dominant position in auto lending.

2. To improve our risk management and reduce LIC

across all portfolios through focused origination, risk based

policies and use of market leading technology across the

credit cycle.

3. To attract new customers and grow and diversify

our funding base to meet LCR requirements by offering

innovative savings, insurance and investment products.

4. To help our clients succeed financially and grow

our fee revenue through relationship-based cross selling of

the full suite of financial products and services tailored to

meet their needs

In order to ensure that all strategic intents and

purposes are progress in the same direction, Thanachart

Group came up with the CEO’s Focus Agenda, as a tool to

successfully pursue its goal.

030 AnnuAl RepoRt 2013

1. Financial Target: Meet or exceed our key financial

target of Net Income, Loan and NIR growth and Cost/Income

Ratio.

2. Customer Growth Initiatives: Complete our core

infrastructure improvements and end-to-end process

reengineering and ensure all sales channels and support

teams fully utilize the enhanced processed and tools to

improve customer service, cross sell and new customer

acquisition.

3. Operational Improvement: Continue with

Centralization and Shared Service initiative using best in

class technology and processes across key business lines

to improve service and reduce risk and cost.

4. Enhancing Human Capital Capabilities: Further

develop out leadership and strengthen our team through

focused leadership development, staff empowerment, and

accountabilities, cross functional transfers and targeted

training initiative.

5. Good Corporate Governance: Meet the highest

standards of good corporate governance that addresses the

need of all stakeholders and ensured full compliance with

all regulatory requirements.

6. Public Relations and Communications: Increase

TBANK’s positive brand perception and recognition with

strong customer service and innovative PR campaigns while

streamlining and improving internal communication

effectiveness.

shareholding structure of thanachart

group

Policy on Division of Operational Functions among

Member Companies of Thanachart Group

Being a parent company of Thanachart Financial

Conglomerate with a controlling interest (i.e. owning more

than fifty percent of issued and paid-up capital), TCAP has

adopted the following policies and approaches in managing

the member companies of the Group as follows:

Business policies

TCAP and TBANK are responsible for establishing

annual key business policies of Thanachart Group. Each

subsidiary is required to formulate business plans and

budgets for 3 - 5 years and submit them to the parent

company for consideration, in order to ensure that they are in

alignment with the established key business policies. The

business plans and budgets are also subject to evaluation

and review regularly. The objective is to ensure that the

business plans and budgets are in line with the changing

business conditions.

supervision of subsidiaries

The directors and high-ranking executives of TCAP

and TBANK are assigned to be the members of the Board

of Directors of the subsidiaries. The arrangement not only

enables TCAP and TBANK to assist the subsidiaries in

establishing their policies and in determining their future

direction, but also ensures the close supervision of the

subsidiaries’ business operations. Importantly, the Chief

Executive Officers of the subsidiaries are required to present

a monthly performance report to the Executive Committee

and the matters in the Executive Committee Meeting are than

reported to the Board of Directors of TBANK.

centralizing of support services

It is a policy of the Thanachart Group to centralize

specific functions of the support services into one company

which, then, is responsible for providing such services to

all other member companies of the Group. The purpose is

to maximize benefits within the existing resources including

expertise of operations staff and various information

technologies, and to reduce staffing costs. The centralized

support services available now within Thanachart Group

included information technology, human resource, systems

and internal regulatory development, internal audit, operation

control, business control, electronic services, administration

and procurement, legal and appraisal services, as well as

retail debt collections and collections brokerage.

internal control, audit, and corporate

governance of parent company and subsidiaries

Thanachart Group places strong emphasis on internal

control. The Group adheres to the principle of adequate and

appropriate internal control by establishing procedures for

business conducts, provision of services, and operations. The

Group also separates the duties and responsibilities of each

unit to allow internal examination of each other, based on

031thAnAchARt BAnK puBlic coMpAny liMiteD

a check and balance system. In addition, it puts in writing

the announcements as well as order mandates, rules and

regulations’ covering key business areas and operations, and

this information was also disclosed to all staff in such a way

that they can always study them to gain a full understanding.

A central unit at TBANK is responsible for preparing and

proposing the announcements, order mandates rules and

regulations of all member companies of the Group.

As regard to the internal audit, the internal audit

group is responsible for auditing the business operations

of all member companies of the Group, ensuring that they

comply with the regulations and the established work

systems. The internal audit group also assesses an adequacy

and effectiveness of an internal control system in operations

to ensure the use of resources and properties and prevention

or reduction of errors, damages in order in propose corrective

measures for improvement. In addition, the Thanachart

Group has established the Compliance Unit responsible for

closely monitoring changes of laws, notifications, and orders

related to the Group’s business affairs and operations and

disseminating the information to the staff. The Compliance

Unit is also responsible for ensuring that the conduct of

business affairs of the member companies of the Group is

in compliance with the legal requirements.

Moreover, the Audit Committee of each member

company of the Group is responsible for governing, controlling,

and auditing their respective business operations. The Audit

Committee is also allowed to carry out its duties and give

its opinions in an independent manner of the management

of each company. The purpose is to ensure that internal

control and audit systems are effective and that the financial

statements are properly reviewed.

As regard to the corporate governance, the Board of

Directors of TCAP and the companies in the Group place a

strong emphasis on the good corporate governance both at

the level of the Board of Directors and the level of various

Committees. Independent directors are appointed to the

Board of Directors and the Committees to provide effective

checks and balances on the powers of executive directors.

The established scope of responsibilities of the Board of

Directors and the Committees are also in line with the

principles of good corporate governance. In addition, the

Board of Directors of the TCAP and the subsidiaries have

established the corporate governance policy and the code

of conduct which the directors, executives, and staff of the

member companies of Thanachart Group are required to

adhere to. Focus is given to integrity, transparency, and

avoidance of any conflict of interest.

Risk management

TCAP ensured that the member companies of the

Group analyze and assess various risks of their business

operations and that the risks are properly managed in line

with the guidelines given by the authorities. In addition, TCAP

conducts an analysis of the key risks faced by the member

companies of the Group which may need direct financial or

management policy of the Thanachart Financial Conglomerate

is in line with the guidelines given by the BOT.

Relationship with business group of major

shareholder

Scotiabank is the leading international banking

institution with branches in 50 countries worldwide. It holds

48.99 percent of TBANK issued shares via Scotia Netherlands

Holding B.V., which is the juristic person in Netherlands.

Scotiabank is a strategic partner that helps to forge the

Bank’s capacity in fund business and management. It

passes on the knowledge of professionalism in banking

sector, risk management, information technology, and

expansion of TBANK services abroad through the network of

Scotiabank. Moreover, it sends representatives to participate

in the management in the director and executive level.

032 AnnuAl RepoRt 2013

chart of shareholding structure of thanachart group

As of December 31, 2013

thanachart capital public company limited

scotia netherlands holding B.V.

supporting Business

thanachart Broker company limited

thanachart training and Development

company limited

sciB services company limited

thanachart Bank

public company limited

MAX Asset Management

company limited

nFs Asset Management

company limited

commercial Banking Business Asset Management Business

48.99%

thanachart Management and services

company limited

100.00%

100.00%

100.00%

100.00%

50.96% 100.00% 83.44%

securities Business

100.00%

thanachart securities

public company limited

75.00%

thanachart Fund Management

company limited

Asset Management Business

insurance Business

thanachart insurance

public company limited

100.00%

siam city life Assurance

public company limited

100.00%

national leasing company limited

100.00%

ts Asset Management

company limited

100.00%

leasing Business

100.00%

thanachart group leasing

company limited

65.18%

Ratchthani leasing

public company limited

Financial Business

Note: 1. The above shareholdings include shares held by the related parties.

2. On May 9, 2012, the BOT granted approval for Scotiabank to adjust the shares holding structure of Thanachart Group, which holds

48.99 percent of issued shares via Scotia Netherlands Holding B.V., the registered juristic person in Netherlands.

033thAnAchARt BAnK puBlic coMpAny liMiteD

As of December 31

2013

thB Million percent thB Million percent thB Million percent

2012 2011

income structures of tBAnK and its subsidiaries

Income structures of TBANK and its subsidiaries based on the consolidated financial statements as of December 31,

2013, 2012, and 2011 are as follows:

table of income structures of tBAnK and its subsidiaries

Interest Income

Interbank and money market items 1,865 3.58 2,294 6.73 1,899 5.60

Investment for trading 457 0.87 480 1.41 78 0.23

Investment for debts securities 3,867 7.42 3,606 10.58 4,290 12.66

Loans 21,246 40.76 21,200 62.23 20,774 61.32

Hire Purchase and Financial Leases 26,452 50.75 21,156 62.11 17,011 50.21

Total Interest Income 53,887 103.38 48,736 143.06 44,052 130.02

Interest Expenses 27,234 52.25 25,556 75.02 19,636 57.95

Net Interest Income 26,653 51.13 23,180 68.04 24,416 72.07

Non-interest Income

Net Fees and Service Income 6,903 13.24 5,070 14.88 3,711 10.95

Gains on Trading and Foreign Exchange Transactions 531 1.02 664 1.95 891 2.63

Gains on Investments 13,081 25.10 312 0.92 712 2.10

Shares of Profit from Investments in Associated

Companies Accounted for Equity Method 415 0.80 150 0.44 156 0.46

Insurance Premium/Life Insurance Premium Income-Net 2,282 4.38 2,147 6.30 2,128 6.28

Dividend Income 562 1.08 397 1.17 708 2.09

Other Income 1,697 3.25 2,146 6.30 1,159 3.42

Total Non-interest Income 25,471 48.87 10,886 31.96 9,465 27.93

Net Operating Income 52,124 100.00 34,066 100.00 33,881 100.00

034 AnnuAl RepoRt 2013

Business operations of each Business

group

commercial Banking Business

TBANK operated its businesses in compliance with

the Financial Institutions Business Act and other relevant

notifications issued by the BOT. It acted as a non-life and

life insurance brokerage agent, an advisor and investment

unit distributor for mutual funds, trustee services for mutual

funds, custodian services for private funds, securities

brokerage, securities trading, debt instrument trading, securities

registrar, and a selling agent for gold derivatives.

As of December 31, 2013, TBANK had a total of 620

branches (excluding Tonson branch, the Headquarter), 54

foreign exchange booths (28 in-branches, and 26 stand-alone),

2,057 ATMs (Automatic Teller Machines), 2 Recycling

Machines, 46 CDMs (Cash Deposit Machine), and 127 PUMs

(Passbook Update Machine).

Group of Products and Services

TBANK improves and develops products to better

serve various needs of our customers. Its four main products

and services were as follows:

Group 1 Deposit Products

Characteristics

Deposit products are offered to customer, both

individuals and corporate. There are four major types of

deposit products which are saving deposit, fixed deposit,

current deposit, and foreign currency deposit.

Competitive Strategies

In 2013, TBANK focused on the expansion of small

and medium sized customer base as well as retail and corporate

customers in order to increase the number of customers who

used the Bank service as main bank. The Bank provides

variety of products through various sales channels amidst the

aggressive competition of other banking institutions especially

the Specific Financial Institution: SFIs, commercial banking

institutions, and as well as other product competitions such

as mutual fund and private debenture.

Apart from the success in providing deposit products,

the Bank has launched new financial products and service

to serve customer daily demand under the “Fixed Deposit”

program in July 2013, which customers can choose their

preferred deposit duration or maturity. For customers’

convenience, the Bank also provides “No slip deposit-

withdrawal and transfer” service in all branches across the

country.

Group 2 Lending Products

2.1 Corporate Loan

Characteristics

Corporate Loans are used to meet capital

requirements or enhance financial liquidity of businesses.

Customers can choose a variety of corporate loan services.

1) Corporate Banking Group To meet the

demand of large scale businesses, TBANK has developed

many types of products and services, including, inter alia,

several forms of loans such as flexible loan, Letter of

Guarantee, Project Finance, Trade Finance, Financial Advisory

Services, Debt and Capital Market such as issuance of

debentures for the purposes of funds mobilization and listing

on the Stock Exchange of Thailand as well as risk management

tools, particularly Interest Rate Swap (IRS) such as Forward

Contract and Foreign currency swap TBANK also provides

cash management facility to these customers through a range

of products that meet their individual requirements.

2) SME Commercial Banking SME Group

are products for small and medium-sized enterprises with

flexibility to serve the customers need include, inter alia,

Top Up facilities which are special loan limits to meet

working capital requirements of overdraft customers, letter