Corporate Governance and Accounting Conservatism: Evidence from the Banking Industry

23

Corporate Governance and Accounting Conservatism: Evidence from the Banking Industry Stergios Leventis, Panagiotis Dimitropoulos, and Stephen Owusu-Ansah* ABSTRACT Manuscript Type: Empirical Research Question/Issue: In this paper, we empirically investigate whether US listed commercial banks with effective corporate governance structures engage in higher levels of conservative financial accounting and reporting. Research Findings/Insights: Using both market- and accrual-based measures of conservatism and both composite and disaggregated governance indices, we document convincing evidence that well-governed banks engage in significantly higher levels of conditional conservatism in their financial reporting practices. For example, we find that banks with effective governance structures, particularly those with effective board and audit governance structures, recognize loan loss provisions that are larger relative to changes in nonperforming loans compared to their counterparts with ineffective governance structures. Theoretical/Academic Implications: We contribute to the extant literature on the relationship between corporate gover- nance and quality of accounting information by providing evidence that banks with effective governance structures practice higher levels of accounting conservatism. Practitioner/Policy Implications: The findings of this study would be useful to US bank regulators/supervisors in improv- ing the existing regulatory framework by focusing on accounting conservatism as a complement to corporate governance in mitigating the opaqueness and intense information asymmetry that plague banks. Keywords: Corporate Governance, Accounting Conservatism, Asymmetric Timeliness, Banking Institutions, Earnings Quality INTRODUCTION I n this paper, we investigate whether US listed com- mercial banks that have effective corporate governance structures engage in conservative financial reporting. We document evidence suggesting that well-governed banks significantly engage in higher levels of conditional account- ing conservatism. For example, we find that banks with effective governance structures report loan losses in a time- lier manner than those with ineffective governance struc- tures. We also find that banks with particularly effective board and audit governance structures provide for loan losses that are larger relative to changes in non-performing loans compared to their counterparts. While prior studies (e.g., Cohen, Dey, & Lys, 2008; He, El-Masry, & Wu, 2008; Lobo & Zhou, 2006; Zhou, 2008) have investigated the effect of corporate governance structures on the quality of accounting information, they have focused exclusively on nonfinancial/industrial firms, leaving the financial sector largely unexplored. However, Nichols, Wahlen, and Wieland (2009) investigate the effect of equity ownership structure of both privately held and publicly traded banks on conservative reporting, but their analysis was limited only to the era before the passage of the Sarbanes-Oxley Act (SOX) of 2002. Beasley, Carcello, Her- manson, and Neal (2010) observe less or no discernible, systematic variation among firms in their governance char- acteristics following the passage of SOX. This led Carcello, *Address for correspondence: Stephen Owusu-Ansah, Department of Accountancy, College of Business and Management, University of Illinois Springfield, One Univer- sity Plaza, MS UHB 4093, Springfield, IL 62703-5407, USA. Tel: 1 217 206 8254; Fax: 1 217 206 7543; E-mail: [email protected] or [email protected] 264 Corporate Governance: An International Review, 2013, 21(3): 264–286 © 2013 Blackwell Publishing Ltd doi:10.1111/corg.12015

Transcript of Corporate Governance and Accounting Conservatism: Evidence from the Banking Industry

Corporate Governance and AccountingConservatism: Evidence from theBanking Industry

Stergios Leventis, Panagiotis Dimitropoulos, andStephen Owusu-Ansah*

ABSTRACT

Manuscript Type: EmpiricalResearch Question/Issue: In this paper, we empirically investigate whether US listed commercial banks with effectivecorporate governance structures engage in higher levels of conservative financial accounting and reporting.Research Findings/Insights: Using both market- and accrual-based measures of conservatism and both composite anddisaggregated governance indices, we document convincing evidence that well-governed banks engage in significantlyhigher levels of conditional conservatism in their financial reporting practices. For example, we find that banks witheffective governance structures, particularly those with effective board and audit governance structures, recognize loan lossprovisions that are larger relative to changes in nonperforming loans compared to their counterparts with ineffectivegovernance structures.Theoretical/Academic Implications: We contribute to the extant literature on the relationship between corporate gover-nance and quality of accounting information by providing evidence that banks with effective governance structures practicehigher levels of accounting conservatism.Practitioner/Policy Implications: The findings of this study would be useful to US bank regulators/supervisors in improv-ing the existing regulatory framework by focusing on accounting conservatism as a complement to corporate governance inmitigating the opaqueness and intense information asymmetry that plague banks.

Keywords: Corporate Governance, Accounting Conservatism, Asymmetric Timeliness, Banking Institutions, EarningsQuality

INTRODUCTION

I n this paper, we investigate whether US listed com-mercial banks that have effective corporate governance

structures engage in conservative financial reporting. Wedocument evidence suggesting that well-governed bankssignificantly engage in higher levels of conditional account-ing conservatism. For example, we find that banks witheffective governance structures report loan losses in a time-lier manner than those with ineffective governance struc-tures. We also find that banks with particularly effectiveboard and audit governance structures provide for loan

losses that are larger relative to changes in non-performingloans compared to their counterparts.

While prior studies (e.g., Cohen, Dey, & Lys, 2008; He,El-Masry, & Wu, 2008; Lobo & Zhou, 2006; Zhou, 2008) haveinvestigated the effect of corporate governance structures onthe quality of accounting information, they have focusedexclusively on nonfinancial/industrial firms, leaving thefinancial sector largely unexplored. However, Nichols,Wahlen, and Wieland (2009) investigate the effect of equityownership structure of both privately held and publiclytraded banks on conservative reporting, but their analysiswas limited only to the era before the passage of theSarbanes-Oxley Act (SOX) of 2002. Beasley, Carcello, Her-manson, and Neal (2010) observe less or no discernible,systematic variation among firms in their governance char-acteristics following the passage of SOX. This led Carcello,

*Address for correspondence: Stephen Owusu-Ansah, Department of Accountancy,College of Business and Management, University of Illinois Springfield, One Univer-sity Plaza, MS UHB 4093, Springfield, IL 62703-5407, USA. Tel: 1 217 206 8254; Fax:1 217 206 7543; E-mail: [email protected] or [email protected]

264

Corporate Governance: An International Review, 2013, 21(3): 264–286

© 2013 Blackwell Publishing Ltddoi:10.1111/corg.12015

Hermanson, and Ye (2011:5) to call for further examinationof the relationship between governance characteristicsand accounting outcomes in the post-SOX environment.However, Adams and Mehran (2003) had earlier noted asystematic difference in governance structures betweenbanks and industrial firms, suggesting that governancestructures may be industry-specific. Hence, our motivationis to deepen our understanding of the association betweencorporate governance structures and the accounting out-come of conservatism in the post-SOX era, using the UScommercial banking sector as a case study.

It is imperative to study the association between corporategovernance and accounting conservatism in the bankingindustry in that the former is particularly important for banksdue to their complexities, intense information asymmetries,opaqueness and contracting peculiarities coupled with thefailure of several prominent US banks due to corporate gov-ernance lapses.1 Effective governance structures are essentialto achieving and maintaining public trust and confidence inthe banking system, which are critical to the proper function-ing of the banking sector and the economy as a whole.Ineffective governance structures, on the other hand, maycontribute to bank failures, which can pose significant publiccosts and consequences due to their potential impact on anydeposit insurance scheme and the possibility of broader mac-roeconomic implications such as contagion risk and impacton payment systems. In addition, ineffective governance canlead markets to lose confidence in the ability of a bank toproperly manage its assets and liabilities, including deposits,which could in turn trigger a bank run or liquidity crisis(Basel Committee on Banking Supervision, 2006).

Accounting conservatism, which ensures the exercise ofcaution in financial accounting and reporting under condi-tions of uncertainty, complements corporate governance inthat it constrains managerial opportunism, mitigates agencyproblems, and enables efficient contracting in the presenceof asymmetric information (Ahmed & Duellman, 2007; Ball& Shivakumar, 2005; Basu, 2005; García Lara, García Osma,& Penalva, 2009).

Using a sample of 315 US listed commercial banks overthe seven-year period, 2003–2009, we document that bankshaving effective governance structures engage in higherlevels of conditional accounting conservatism. For example,relative to banks having ineffective governance structures,those with effective governance structures report loan losses(“bad news”) in a timelier manner, and provide for loanlosses that are larger relative to changes in non-performingloans. Additional tests show that our findings are robust tothe use of market- and accrual-based measures of condi-tional conservatism and several sensitivity tests with respectto different specifications of the empirical models andresearch design.

We contribute to the extant literature in two ways. First, weprovide empirical evidence that, in spite of having uniquegovernance challenges, banks with effective board and auditgovernance structures, as opposed to effective executive anddirector compensation and ownership policies and antitake-over provisions, practice higher levels of conditional account-ing conservatism. Second, we extend García Lara et al. (2009)and Nichols et al. (2009). Using a sample of nonfinancialfirms, García Lara et al. (2009) examine the association

between corporate governance and accounting conservatism.Unlike their study, ours uses a sample of financial firms –commercial banks. For Nichols et al. (2009), while they inves-tigate the effect of equity ownership structure of privatelyheld and publicly traded banks on conditional conservatismin the pre-SOX era, we add to their work by investigating theeffect of corporate governance on conditional conservatismby publicly listed banks during the post-SOX era.

We organize the rest of the paper as follows. We reviewthe extant literature and develop our hypotheses in the nextsection by first describing the particularities of corporategovernance of banks and the problems they pose comparedto those of generic firms. We then follow this by discussingthe concept of accounting conservatism and end the sectionby reviewing the relevant literature associating corporategovernance with accounting conservatism. We describe thesample selection procedure and our research design in thethird section. We present the empirical findings and performrobustness checks in the fourth section. We conclude thepaper in the last section.

LITERATURE REVIEW AND HYPOTHESESDEVELOPMENT

Corporate Governance of BanksThere is yet to be a generally accepted definition of corporategovernance. However, for our purpose, we adopt the muchbroader definition of corporate governance that is very muchin line with the understanding of banking supervisors, asembodied in the Basel Committee on Banking Supervision’s(2006) guidance, which states that from

a banking industry perspective, corporate governance involvesthe manner in which the business and affairs of banks aregoverned by the board of directors and senior managementwhich, inter alia, affects how they: (1) set corporate objectives;(2) operate the bank’s business on a day-to-day basis; (3) meetthe obligation of accountability to their shareholders and takeinto account the interests of other recognized stakeholders(including, inter alia, supervisors, governments and deposi-tors); (4) align corporate activities and behavior with the expec-tation that banks will operate in a safe and sound manner andin compliance with applicable laws and regulations; and (5)protect the interests of depositors.

As noted, effective governance structures are essential toachieving and maintaining public trust and confidence inthe banking system, which are critical to the proper func-tioning of the banking sector and an economy as a whole.While banks are similar to nonfinancial/industrial firms asthey all have stockholders, debt holders, board of directors,and competitors, banks have unique governance structuresthat are different from industrial firms (Adams & Mehran,2003). First, banks are opaque and more complex than non-financial firms (Levine, 2004). Although information asym-metries plague all sectors of an economy, Furfine (2001) findevidence suggesting that information asymmetries are morepronounced in the banking sector. For example, the qualityof bank loans is not readily observable, while the quality ofassets of industrial firms is more easily discernible by thirdparties (Mülbert, 2009). Morgan (2002) finds that bond ana-

CORPORATE GOVERNANCE AND ACCOUNTING CONSERVATISM 265

Volume 21 Number 3 May 2013© 2013 Blackwell Publishing Ltd

lysts disagree more substantially over bonds issued by banksthan those issued by nonfinancial firms. The greater infor-mational asymmetries between insiders and outsiders inbanking make it very difficult for diffuse equity and debtholders to monitor bank managers. In terms of incentivecontracts, the informational asymmetries make it more dif-ficult to design contracts that align managers’ interests withthose of bank stockholders. Levine (2004) argues that whenoutcomes are difficult to measure and easy to influence inthe short run, managers will find it easier to manipulatepay-offs from compensation packages. Further, the opaque-ness of banks weakens competitive forces that, in otherindustries, help discipline managers through the threat oftakeover. Levine (2004) argues that takeovers are less likelyto be effective when insiders have much better informationthan potential purchasers. Prowse (1997) finds that hostiletakeover is rare in the banking sector even in the industrial-ized countries.

Second, banks are heavily regulated and are subject tosupervisory actions because of their importance to theeconomy and as a source of fiscal revenue as well as theopacity of their assets and activities. Of course, banking is notthe only regulated industry. Nevertheless, even countries thatintervene less in other sectors tend to impose elaborate andextensive regulations on banks. Greater government regula-tions adversely distort the behavior of bankers and inhibitstandard corporate governance processes. At the extreme,governments own banks, and when the government is theowner, it changes the character of the governance of banks(Levine, 2004). In some cases, governments restrict the con-centration of bank ownership and the ability of outsiders topurchase a substantial percentage of bank equity stockwithout regulatory approval (Levine, 2004). By prohibitingconcentrated equity ownership in banks, a corporate gover-nance mechanism for dealing with the inability of diffuseequity holders to exert effective corporate control is lost.Another example of regulatory effect on governance ofbanking firms is the structure of executive compensation.Stock-based compensation schemes motivate managers toundertake more value-enhancing decisions (see Core, Guay,& Larcker, 2003), but regulators would also want to considerhow stock options affect risk taking. Thus, although in indus-trial firms stock options are used to incentivize managers tocreate value, as well as to protect the creditors of distressedfirms, their use in financial firms may conflict with policyobjectives that seek to protect the non-shareholding stake-holders such as depositors and taxpayers.

Third, banks have a different capital structure from otherfirms. Banks tend to have very little equity relative to otherfirms (Mehran, Morrison, & Shapiro, 2011). While it is notuncommon for some industrial firms to be financed almostentirely by equity, banks normally receive 90 percent ormore of their funding from debt (Macey & O’Hara, 2003:97).Thus, they are highly leveraged due to customers’ deposits(Andres & Vallelado, 2008). In addition, banks’ liabilities arelargely in the form of deposits, which are available to theircreditors/depositors on demand, while their assets often arein the form of loans that take longer to mature. Thus, banksare different because of their liquidity production function(i.e., the mismatch in the term structure of banks’ assets andliabilities). Banks’ leveraged capital structures affect their

risk-taking behavior. Depending on the situation, bank man-agers and stockholders benefit from the greater flexibility inrisk shifting. Thus, because remuneration of bank managersis partly performance-based, the managers are easily able tochange the banks’ risk profile to meet the agreed performancetargets. On the other hand, stockholders are able to exploitcreditors (depositors and debt holders) by opportunistic (expost) switch to riskier business strategies (Mülbert, 2009).

Fourth, while the establishment of deposit insurancefunds (such as the US Federal Deposit Insurance Corpora-tion insurance fund in 1933 in response to the devastatingeffects of the Great Depression) has been effective in pre-venting bank runs and keeping the failure of individualbanks from affecting the larger economy, implementation ofsuch funds has a regulatory cost – it gives stockholders andmanagers of insured banks incentives to engage in excessiverisk taking. According to Macey and O’Hara (2003), thismoral hazard occurs for two reasons: (1) banks are able tofoist some of their losses onto other healthy banks, whosecontributions to the insurance fund are used to pay offdepositors of failed banks, and eventually taxpayers whosefunds replenish the insurance funds when they are depleted,and (2) deposit insurance premiums are unrelated to,or would not fully compensate, the insurance fund forincreased risk posed by a particular bank. Thus, depositinsurance induces banks to rely less on uninsured creditorswith incentives to monitor and more on insured depositorswith no incentives to exert corporate governance.

Fifth, the existence of deposit insurance schemes removesany incentive that insured depositors have to control exces-sive risk-taking behavior of banks because their funds areprotected regardless of the outcomes of investment strate-gies that the banks may pursue. Thus, government-imposeddeposit insurance schemes diminish depositors’ incentive tomonitor banks and to demand interest payments commen-surate with the risks of the banks (Keeley, 1988; Santos,2001). Also, deposit insurance increases the incentives forbank owners to increase risk because of lower capital-to-asset ratios (Levine, 2004).

Sixth, deposit insurance schemes increase the risk of fraudand self-dealing in the banking industry by reducing incen-tives for monitoring (Macey & O’Hara, 2003). Researchshows that 175 of 286 bank failures occurring between 1990and 1991 in the US were caused by insider lending (Jackson& Symons, 1999). Macey and O’Hara (2003) assert that suchproblems are more pronounced in the banking sectorbecause a large portion of banks’ assets are held in highlyliquid form. Thus, deposit insurance reduces the incentivesof depositors to monitor banks, which directly hinders cor-porate governance.

In sum, the uniqueness of banks, as described above, actsto exacerbate the multiple agency conflicts faced by banksand to reduce the effectiveness of some of the governancemechanisms for mitigating these conflicts.

Accounting ConservatismConservatism is an important valuation concept in account-ing (Sterling, 1970). It requires caution when measurement isuncertain (Epstein & Jermakowicz, 2007). Conservatism isdefined as “accountants’ tendency to require a higher degree

266 CORPORATE GOVERNANCE

Volume 21 Number 3 May 2013 © 2013 Blackwell Publishing Ltd

of verification for recognizing good news than bad news infinancial statements . . . earnings reflects bad news morequickly than good news” (Basu, 1997:4).2 It requires a higherverifiability threshold for recognizing gains than losses(Basu, 1997). Conservatism benefits financial statement usersby constraining managerial opportunism, mitigating agencyproblems associated with managerial investment decisions,and enabling efficient debt agreements in the presence ofasymmetric information (Ahmed & Duellman, 2007; Ball& Shivakumar, 2005; Basu, 2005; García Lara et al., 2009).Further, conservative accounting commits managers to moretimely reporting of “bad news” (as economic losses) thanthat of “good news” (as economic gains), and as a result, aidsoutsiders in efficient valuation of their claims (Lafond &Watts, 2008).

García Lara et al. (2009) state that conservatism producesaccounting numbers that are used in contracts to reduceagency costs. They explain that conservative accountingreduces the tendency of managers with short-term horizonsto invest in negative-net present value (NPV) projects in twoways. First, as argued by Ball and Shivakumar (2005), itmakes managers aware that they will not be able to defer therecognition of losses to the future. Second, it imposes greatercosts to biasing financial reports upwards (Guay & Verrec-chia, 2006). Thus, conservatism can be used as a device tomotivate managers to cut losses earlier and abandon poorlyperforming projects (García Lara et al., 2009).

Conservative accounting also facilitates the monitoring ofdebt contracts that can be written based on conservativenumbers, triggering violations of debt covenants faster (Ball& Shivakumar, 2005; Watts, 2003). Conservative accountingincreases contracting efficiency by limiting the control rightsof loss-making managers and by timely proving these rightsback to stockholders and creditors (Watts, 2003).

Accounting conservatism can also lessen litigation risk.This is because the asymmetric recognition requirements foreconomic gains and losses are closely linked to asymmetriesin the loss function of directors and auditors, where over-stating (understating) net assets or earnings is more (less)likely to generate litigation costs (García Lara et al., 2009).Evidence in the auditing literature suggests that lawsuitsagainst auditors are more likely to be related to overstate-ment of earnings or net assets (Kellogg, 1984; St Pierre &Anderson, 1984) or cases of significant income-increasingabnormal accruals (Heninger, 2001).

Accounting conservatism is particularly important forbanks due to their complexities, intense informationasymmetries, opaqueness, and contracting particularities(Furfine, 2001; Levine, 2004). Regulators favor conservativeaccounting and reporting by firms to avoid criticisms whenfirms become insolvent (Watts, 2003). Indeed, centralbankers prefer banks to practice accounting conservatism bysetting aside higher loan loss provisions during economicupturn (Turner, 2010).

Corporate Governance and AccountingConservatismCorporate governance structures are put in place to addressagency problems that arise from the separation of ownershipand control (Jensen & Meckling, 1976) and from information

asymmetry between contracting parties by efficiently moni-toring management and contracts, respectively. Conserva-tism produces accounting numbers that are used in contractsto mitigate agency costs (García Lara et al., 2009). Lafondand Watts (2008) argue that conservatism reduces informa-tion asymmetry by restricting managers’ incentive andability to manipulate financial reporting. García Lara et al.(2009) also posit that effective governance structures willfavor implementation of conservative accounting choices.Thus, corporate governance and accounting conservatismare closely related and both are important in reducingagency costs associated with contracting (García Lara et al.,2009; Lim, 2011).

A literature review suggests that there are two competingviews on the relationship between accounting conservatismand corporate governance. One view is that the relationship isnegative (substitution view) in that the demand for conser-vatism is greater in situations where agency costs are morepronounced. Hence, ineffective governance structures willrequire higher levels of conservative accounting. Chi, Liu,and Wang (2009) document empirical evidence consistentwith this view. The alternative view is that the relationship ispositive (complementary view) in that effective governancestructures result in better monitoring of management andhence will favor the implementation of conservative account-ing. The available empirical evidence in support of the alter-native view is mixed. Thus, while the results of earlier studies(e.g., Ahmed & Duellman, 2007; Beekes, Pope, & Young, 2004;García Lara et al., 2009) provide strong evidence, those of themost recent studies (e.g., Lim, 2011) provide only weak evi-dence that firms having certain governance structures engagein more conservative reporting.

We hold the view that corporate governance complementsconservatism in facilitating contracting in that, as Lim (2011)argues, corporate governance promotes the adoption ofconservatism in financial reporting as it is costly or nearlyimpossible to write and enforce complete contracts toresolve all agency issues (Fama & Jensen, 1983), and manag-ers retain adequate discretion to manipulate accountingnumbers. Given that banks are plagued by intense informa-tion asymmetry and a higher degree of accounting conser-vatism is needed to reduce the likelihood of managers’manipulation and to enhance the quality of accountinginformation (Lafond & Watts, 2008), we therefore hypoth-esize that:

Hypothesis 1. Ceteris paribus, banks having effective corporategovernance structures engage in higher levels of conditionalconservative accounting and reporting practices.

To better align our empirical proxies for effective corpo-rate governance structures with the theoretical propositions,we also develop specific hypotheses for different dimen-sions of governance structures being tested, namely, bestpractices pertaining to board of directors, audit, executiveand director compensation and ownership, and antitakeoverprovisions.

Board Governance Structures and Accounting Conser-vatism. The board of directors is the cornerstone of an orga-nization’s monitoring and control systems. Ahmed and

CORPORATE GOVERNANCE AND ACCOUNTING CONSERVATISM 267

Volume 21 Number 3 May 2013© 2013 Blackwell Publishing Ltd

Duellman (2007), Beekes et al. (2004), and Bushman, Chen,Engle, and Smith (2004) document a positive associationbetween board effectiveness and accounting conservatism.On the contrary, less effective boards (dominated by insid-ers, with weak monitoring incentives, etc.) are likely toprovide greater opportunities for managers to use moreaggressive (less conservative) financial reporting (Ahmed& Duellman, 2007). This assertion is corroborated by Xie,Davidson, and DaDalt (2003), who provide evidence thatactivities of boards and the financial sophistication of theirmembers constrain the likelihood of managers engaging inearnings management. Hence, we hypothesize that:

Hypothesis 1a. Ceteris paribus, banks having effective boardgovernance structures engage in higher levels of conservativefinancial reporting.

Audit Governance Structures and Accounting Con-servatism. Another dimension of corporate governancestructures that mitigates agency costs is an effective auditoversight function. Xie et al. (2003) argue and find that auditcommittees whose members are both independent andfinancial experts are able to restrain aggressive accountingbehavior that manifests in less earnings management andmore conditional conservative reporting. Corroborating theabove findings of Xie et al. (2003), Krishnan and Visvanathan(2008) find that audit committees consisting only of account-ing experts positively associate with accounting conserva-tism. Therefore, we hypothesize that:

Hypothesis 1b. Ceteris paribus, banks having effective auditgovernance structures engage in higher levels of conservativefinancial reporting.

Executive Compensation and Ownership Plans andAccounting Conservatism. Accounting numbers are mostlyused in top executive compensation contracts to shield man-agement incentive compensation from market-wide fluctua-tions in equity values that are beyond their control (Sloan,1993). As a consequence, managers have the tendency tomanage firms’ earnings because accounting numbers affecttheir wealth (Balsam, 1998). However, conservative financialreporting mitigates this agency problem by penalizingmanagers for their failures (economics losses) in a timelymanner, but postpones rewards for their successes (eco-nomic gains) until realized, thereby curtailing managers’incentives and ability to overstate the value they create(Ramalingegowda & Yu, 2012). Thus, conservative account-ing aligns the interests of managers and shareholdersthrough its impact on accounting earnings measures that arefrequently used in management compensation contracts(Iyengar & Zampelli, 2010).

With respect to managerial equity ownership, Shuto andTakada (2010) suggest that managers respond to two oppos-ing forces and that the relationship between ownership andaccounting conservatism depends on which of the forcesdominates at a certain range of managerial equity owner-ship. The incentive alignment force prevails at both low andhigh ownership levels, and at these levels, managers havethe incentive to act in line with outsider equity holders’interest. Thus, at low and high levels of managerial equity

ownership, the relationship between managerial ownershipand accounting conservatism is negative, as managerialownership at these levels results in more severe agencyproblems, thereby increasing the demand for accountingconservatism. Findings reported by both LaFond and Roy-chowdhury (2008) and Shuto and Takada (2010) are consis-tent with the implication of the incentive alignment force.The second is the management entrenchment force, whichprevails when managerial ownership is at the intermediatelevel. At this managerial ownership level, managers havegreater control over the firm with the consequence that theytend to act in their own private interests (Morck, Shleifer, &Vishny, 1988). Thus, at the intermediate ownership level, therelationship between managerial ownership and accountingconservatism is positive. Shuto and Takada (2010) findempirical evidence consistent with the implications of themanagement entrenchment force.

While the results of the extant literature is mixed, onlyLaFond and Roychowdhury (2008) examine managerialownership from the perspective of accounting conservatismand find that the former is negatively related to the latter, assuggested by the interest alignment force. Therefore, wehypothesize that:

Hypothesis 1c. Ceteris paribus, banks having effective execu-tive compensation and ownership plans engage in low levels ofconservative financial reporting.

Antitakeover Provisions and Accounting Conservatism.Antitakeover provisions (or takeover protection) weaken(s)the efficacy of the external governance device of takeoverthat disciplines managers who indulge in opportunisticbehavior or the perceived threat of which provides incen-tives for managers to act in the interests of stockholders(Fama, 1980). However, the extant literature suggests thatthe relationship between takeover protection and earningsquality – an attribute of which is timely loss recognition thatcomplies with accounting conservatism – can be explainedby three theories, namely entrenchment, interest alignment,and quiet life, albeit with contradictory outcomes. Theentrenchment theory argues that takeover protectionentrenches incumbent managers (Manne, 1965), which, inturn, incentivizes them to engage in opportunistic earningsmanagement – the flip side of conservatism. Thus, theentrenchment theory suggests a negative relationshipbetween takeover defense and accounting conservatism. Onthe other hand, both the interest alignment and quiet lifetheories propose a mitigating effect on earnings manage-ment. Thus, the alignment theory emphasizes that takeoverprotection aligns the long-term interests of managers andthose of shareholders (Knoeber, 1986), which, in turn, miti-gates managers’ incentives to opportunistically manageearnings. The quiet life theory states that managers have apreference for a quiet life (Bertrand & Mullainathan, 2003)and that takeover protection alleviates their concerns aboutlosing the quiet life upon takeover, and thus mitigates theirincentives to engage in aggressive accounting behavior.Thus, both the interest alignment and quiet life theoriessuggest that takeover defense is positively related toaccounting conservatism. Zhao and Chen (2008) find that theexistence of staggered boards of directors, a proxy for

268 CORPORATE GOVERNANCE

Volume 21 Number 3 May 2013 © 2013 Blackwell Publishing Ltd

enhanced takeover protection, is associated with timelierrecognition of losses. Thus, the evidence suggests that take-over protection allows managers to enjoy the quiet life andso mitigates managers’ inclination to manage earnings.Based on the above review and because our measure ofeffective takeover defenses favorably views firms that do notavail themselves of available takeover devices such as poisonbills, we hypothesize that:

Hypothesis 1d. Ceteris paribus, banks having effective takeoverpolicies engage in higher levels of conservative financialreporting.

DATA AND METHODOLOGY

Data Collection ProcedureOur sample consists of US listed commercial banks duringthe seven-year period, 2003–2009. During this period in theUS, commercial banks among other public corporationswere subject to a major regulatory change, namely, theimplementation of the SOX, which mandates the adoption ofprudent corporate governance principles to mitigate agencyproblems between managers and stockholders. Our initialsampling frame consists of 560 banks, which are listed in theUS stock exchanges. We exclude those banks with incom-plete accounting data in the Thomson ONE Banker database.We also exclude development, cooperative, export-import,and investment banks from the sampling frame. These pro-cedures resulted in 421 commercial banks with full account-ing data surviving for the period of investigation, 2003–2009.Further, we delete 106 banks with incomplete governancescores in the RiskMetrics database. This procedure resultedin a balanced sample of 315 commercial banks with com-plete end-of-year information, yielding 2,205 firm-yearobservations.

Measuring Corporate Governance EffectivenessWe use an externally determined corporate governancecomposite index by the RiskMetrics Group, Inc., the Corpo-rate Governance Quotient, as our measure of effectivecorporate governance in monitoring management. Becausethe Corporate Governance Quotient is a relative measure,3 weinterpret a higher Corporate Governance Quotient as beingmore effective than a lower Corporate Governance Quotient.The Corporate Governance Quotient consists of 67 internaland external corporate governance best practices topics (seethe Appendix for the details). The information for the com-putation of the Corporate Governance Quotient is sourcedfrom publicly available disclosure documents (i.e., proxystatement, form 10-K, form 8-K, etc.), press releases, andcorporate websites, which are then reviewed and verifiedby corporate governance analysts of Institutional Share-holder Services. RiskMetrics Group, Inc.’s Corporate Gover-nance Quotient is considered the world’s leading corporategovernance rating solution, and it is designed on thepremise that good corporate governance ultimately resultsin increased shareholder value. Thus, the Corporate Gover-nance Quotient measures the overall effectiveness of corpo-rate governance structures employed by a firm. The

Corporate Governance Quotient is widely used in practice andhas been used as a proxy for corporate governance inseveral prior studies (e.g., Agarwal, Chomsisengphet, Liu,& Rhee, 2007; Anderson & Gupta, 2009; Bauer, Eichholtz, &Kok, 2010; Brown & Caylor, 2009; Cornelius, 2005; Epps &Cereola, 2008).

Given the inherent limitations of composite measures ofcorporate governance (see Larcker, Richardson, & Tuna,2007), we also use Corporate Governance Quotient sub-indicesto emphasize different dimensions of corporate governancein our analyses, as in prior research (see, e.g., Aggarwal, Erel,Stulz, & Williamson, 2009; Beltratti & Stulz, 2012; Doidge,Karolyi, & Stulz, 2007). The disaggregated Corporate Gover-nance Quotient sub-indices are broadly classified into four,namely Board of Director, Audit, Executive and Director Com-pensation and Ownership, and Antitakeover Provisions. Thevalues of the sub-indices range from one to five, with thehigher values indicating higher degrees of effectiveness. Forexample, if a firm incorporates in a state without antitake-over provisions, or opts out of such protections of the state ofincorporation, it is viewed favorably and awarded fivepoints under the Antitakeover Provisions sub-index, becauseantitakeover provisions are designed to reduce the power ofthe market for corporate control in disciplining the firm. Theuse of this approach enables us to identify which corporategovernance structures are more relevant to financial firmsgiven their uniqueness, and how those governance struc-tures affect conservative financial reporting in the bankingindustry.

Measuring Accounting ConservatismWe measure accounting conservatism in three different waysbecause “it is difficult to test its level through a singlemeasure or even a number of measures” due to the absenceof a generally acceptable definition of conservatism (Givoly& Hayn, 2000). Our first measure of accounting conservatismis based on Basu’s (1997) reverse regression model betweenEarnings and Returns. Basu (1997) argues that earnings incor-porate publicly available “bad news” (as losses) morequickly than it does with “good news” (as gains) underconservatism, leading to asymmetric timeliness in news rec-ognition. Basu (1997) introduces a Dummy Variable in hismodel, based on the assumption that earnings are morehighly correlated with market returns in periods of depres-sion of stock market prices than in periods of prosperity inthe capital market. This dummy variable takes the value ofone when returns are negative (“the bad news”) or zerowhen returns are positive (“the good news”).

In spite of the widespread use of Basu’s (1997) model, thevalidity of its differential timeliness coefficient has beenquestioned (see, e.g., Dietrich, Muller, & Riedl, 2007; Givoly,Hayn, & Natarajan, 2007; Patatoukas & Thomas, 2011).Nevertheless, some recent studies (e.g., Ball, Kothari, &Nikolaev, 2011; Ettredge, Huang, & Zhang, 2012) have alsoreported evidence on the usefulness of the Basu model.Either way, our use of alternative measures of conditionalconservatism might minimize any potential bias of the Basumodel. Therefore, we investigate whether well-governedbanks engage in more conservative reporting by estimatingthe following modified Basu (1997) model:

CORPORATE GOVERNANCE AND ACCOUNTING CONSERVATISM 269

Volume 21 Number 3 May 2013© 2013 Blackwell Publishing Ltd

Earnings b b Return b Dummy b Return Dummyb Governance b

= + + + ∗+ +

0 1 2 3

4 55

6 7

Governance Dummyb Governance Return b Governance Dummy

∗+ ∗ + ∗ ∗ RReturn

b Control b Yr Dummies e+ + +− −8 12 13 19 _ [1]

The variables in Model [1] are operationally defined inTable 1. The coefficients on Return (b1) and Return * Dummy(b3) capture more timely recognition of losses relative to therecognition of gains to contemporaneous “good news” and“bad news,” respectively. Contextually, a positive b3 is anindication of accounting conservatism. Because conservatismreporting delays recognition of “good news,” this laggedeffect may appear as a persistent shock, therefore the inter-cept b0 is expected to have a positive sign. In other words, ifconservatism affects earnings downwardly, the intercept isexpected to have a positive sign. The coefficient on Dummy,b2, is explained as a reversal of the previous year’s marketinformation in the light of current value decreases. When b2

is positive, over-provisioning is reversed as a prior yearadjustment, and when b2 is negative, deferred income rec-ognition is scaled down (Raonic, McLeay, & Asimakopoulos,2004). If banks with effective corporate governance engagein conservative reporting, they would recognize losses moretimely than recognizing gains. If such were the case, thecoefficient on Governance * Dummy * Return, b7, would besignificantly positive.

We control for Size with the natural logarithm of totalassets of each bank. LaFond and Watts (2008) argue thatdemand for conservatism is less for large firms because theyusually produce more publicly available information and areable to use a variety of information dissemination tech-niques. Givoly et al. (2007) find that asymmetric timelinessof earnings for large firms differs significantly from thatof small firms. In contrast, Callen, Segal, and Ole-Kristian(2010) argue that large firms face lower operational uncer-tainty and therefore demand greater accounting conserva-tism. Consequently, since the relationship between size andthe degree of conservatism is ambiguous ex ante, we cannotpredict the sign of the Size variable.

We control for the effect of Risk on conservatism by includ-ing Tier 1 capital ratio4 in Model [1]. We make no prediction,however, about the sign of its coefficient. Further, we controlfor bank profitability measured as Operating Cash Flow.Profitable firms tend to use more conservative accounting(Ahmed & Duellman, 2007). Consequently, we expect thecoefficient on Operating Cash Flow to be positive. We alsocontrol for Growth Opportunities measured as the ratio ofmarket-to-book value of equity. Roychowdhury and Watts(2007) and LaFond and Roychowdhury (2008) argue that themarket-to-book ratio reflects the composition of equityvalue, which is determined by the investment opportunitiesof the firm and the past asymmetric timeliness of earnings.Therefore, we expect Growth Opportunities to have a positiveassociation with conservatism. Following Ghosh and Moon(2005), Gul, Sun, and Tsui (2003), Gul, Tsui, and Dhaliwal(2006), Park and Pincus (2001), and Teoh and Wong (1993),we control for the External Audit Quality by including adummy variable coded one for Big-4 audit firms or zero fornon-Big-4 audit firms.

Our second measure of accounting conservatism is thetimeliness with which Loan Loss Provisions are recognized by

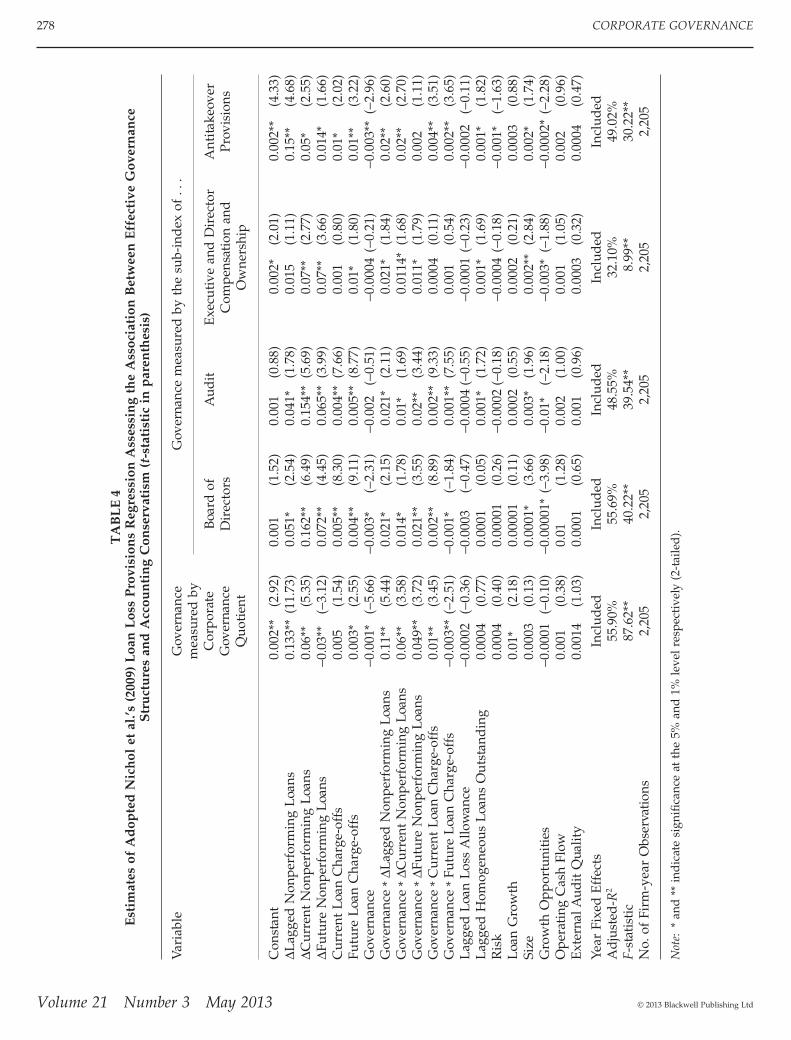

banks relative to changes in nonperforming loans (nondis-cretionary indicators of possible future credit losses).Nichols et al. (2009) argue that a bank’s loan loss accountingreflects its credit risk management behavior and can createsubstantial information asymmetry between managementand stockholders. Additionally, a bank’s loan loss account-ing has a material effect on its earnings and requires asubstantial degree of management discretion. Loan Loss Pro-visions are accrued expenses reflecting management’scurrent period assessment of the level of future loan lossesof a bank’s loan portfolio. Hence, bank managers’ preferencefor conservative reporting can be inferred from how theyaccount for Loan Loss Provisions. Thus, banks that engage inconservative accounting would recognize Loan Loss Provi-sions that are larger and on a more timely basis relative tochanges in nonperforming loans (Liu & Ryan, 1995; Nicholset al., 2009). To test for the differences in the timeliness withwhich poor- and well-governed banks recognize Loan LossProvisions, we follow Nichols et al. (2009) by associating LoanLoss Provisions with changes in Lagged Nonperforming Loans,Current Nonperforming Loans, and Future NonperformingLoans. We also control for differences in Lagged Loan LossAllowance, Current Loan Charge-offs, Future Loan Charge-offs,and Lagged Homogeneous Loans Outstanding, and the presentlevels of both Risk and Loan Growth. Further, we create inter-active terms between changes in Lagged NonperformingLoans, Current Nonperforming Loans, Future NonperformingLoans, Current Loan Charge-offs, Future Loan Charge-offs, andGovernance. We also include the variables controlled for inModel [1], except for Risk, which is already an independentvariable in Model [2]. Thus, we estimate the following modelfrom Ball and Shivakumar (2005) as adopted by Nicholset al. (2009):

Loan Loss Provisions c c Lagged NonperformingLoans c Curr

= ++

0 1

2

ΔΔ

eent Nonperforming Loans

c Future Nonperforming Loans c C

+ +3 4Δ uurrent LoanCharge offs c Future Loan Charge offs c Govern

- -+ +5 6 aance

c Governance Lagged Nonperforming Loansc Governanc

+ ∗+

7

8

Δ ee Current Nonperforming Loans

c Governance Future Nonpe∗

+ ∗ΔΔ

9 rrforming Loans

c Governance Current Loan Charge offsc

-+ ∗

+10

11GGovernance Future Loan Charge offsc Lagged Loan Loss All

∗+

- 13 oowance

c Lagged Homogenous Loans Outstanding c Riskc

+ ++

12 14

15

LLoan Growth c Control c Yr Dummies e _+ + +− −16 19 20 26 [2]

All variables in Model [2], which were in Model [1],are defined as previously and those newly introducedin the former are also operationally defined in Table 1.For Model [2], our primary predictions are that the coeffi-cients c7, c8, and c9, on Governance * DLagged NonperformingLoans, Governance * DCurrent Nonperforming Loans, andGovernance * DFuture Nonperforming Loans, respectively, willbe positive, indicating that well-governed banks recognizelarger or more timely loan loss provisions relative to changesin nonperforming loans than banks with weak governancestructures. Consistent with prior research, we expect thecoefficients c1, c2, c3, c4 and c5 on DLagged NonperformingLoans, DCurrent Nonperforming Loans, DFuture NonperformingLoans, Current Loan Charge-offs, and Future Loan Charge-offs,

270 CORPORATE GOVERNANCE

Volume 21 Number 3 May 2013 © 2013 Blackwell Publishing Ltd

TABLE 1Summary Statistics of the Variables (n = 2,205)

Variable Operational definition Mean Median Std. dev. Min. Max.

Earnings Earnings per share deflated by the stockprice at the beginning of the fiscalyear

-0.03 0.01 0.92 -0.05 0.41

Return The annual buy and hold stock returnover the fiscal year

2.72 0.13 30.12 -99.33 69.02

Dummy Indicator variable coded 1 in the case ofbad news (when return is negative)or 0 in case of good news (whenreturn is positive)

0.48 0.00 0.45 0.00 1.00

Corporate GovernanceQuotient

A bank’s effective corporate governancecomposite index developed byRiskMetrics Group, Inc.

0.58 0.59 0.15 0.01 1.00

Board of Directors A bank’s effective board governancestructures sub-index developed byRiskMetrics Group, Inc.

3.11 3.00 1.40 1.00 5.00

Audit A bank’s effective audit governancestructures sub-index developed byRiskMetrics Group, Inc.

3.33 3.00 1.42 1.00 5.00

Executive and DirectorCompensation andOwnership

A bank’s effective executive anddirectors compensation andownership policies sub-indexdeveloped by Risk Metrics Group,Inc.

3.28 3.00 1.44 1.00 5.00

Antitakeover Provisions A bank’s antitakeover provisionssub-index developed by RiskMetricsGroup, Inc.

3.03 3.00 1.41 1.00 5.00

Cash Flow Dummy Indicator variable coded 1 if operatingcash flow is negative and 0 otherwise

0.06 0.00 0.24 0.00 1.00

Total Accruals Difference between income before taxesand operating net cash flows, anddeflated by lagged total assets

-0.01 -0.004 0.03 -0.79 0.30

Size Natural logarithm of year-end totalassets

60.33 67.62 30.34 5.10 140.85

Risk Natural logarithm of Tier 1 risk-basedcapital ratio, which is the percentageof a bank’s capital to its risk-weighted assets

4.74 4.85 1.12 -4.02 10.89

Operating Cash Flow Ratio of operating net cash flows tolagged total assets

0.01 0.01 0.03 -0.30 0.80

Growth Opportunities Ratio of market value to book value ofequity

1.30 1.42 10.31 -0.03 5.69

External Audit Quality Indicator variable coded 1 if a bank isa client of a Big-4 audit firm or 0otherwise

0.37 0.00 0.48 0.00 1.00

Loan Loss Provisions Ratio of loan loss provisions to laggedtotal loans

0.005 0.002 0.01 -0.02 0.09

Nonperforming Loans Ratio of non-performing loans to laggedtotal loans

0.01 0.01 0.01 0.00 0.12

DNonperforming Loans Ratio of the annual change ofnon-performing loans to lagged totalloans

0.003 0.002 0.005 -0.12 0.12

CORPORATE GOVERNANCE AND ACCOUNTING CONSERVATISM 271

Volume 21 Number 3 May 2013© 2013 Blackwell Publishing Ltd

respectively, to have positive signs. We expect the DLaggedNonperforming Loans, DCurrent Nonperforming Loans, andDFuture Nonperforming Loans to be positively related to LoanLoss Provisions because increases in nonperforming loanswill require higher loan loss provisions (Kanagaretnam,Krishnan, & Lobo, 2010). We also expect both the CurrentLoan Charge-offs and Future Loan Charge-offs to be positivelyrelated to Loan Loss Provisions because, as explained byBeaver and Engel (1996), loan charge-offs can provide infor-mation about future charge-offs.

We expect banks with high Lagged Loan Loss Allowance tohave lower Loan Loss Provisions in the current period, if banksthat are over-reserved recognize lower provisions in the nextperiod (Liu & Ryan, 2006). Similarly, we expect banks withhigh Lagged Homogeneous Loans Outstanding to have lowerLoan Loss Provisions in the current period, because banks thathave higher percentage of homogeneous loans in their port-folio recognize lower provisions later in the lives of the loans(Liu & Ryan, 2006). On the contrary, we expect a positiveassociation between Loan Loss Provisions and Risk because,when banks take greater risk in their portfolios, they maintainhigher capitalization levels to absorb future potential losses.An increase in Loan Growth may create an increase in Loan LossProvisions, thus we expect the coefficient on Loan Growth tohave a positive sign (Nichols et al., 2009).

While the Nichols et al. (2009) model is able to capture theextent of delay in recognizing expected losses, it requires theuse of time-series data that at times constrain sample sizeand, as a consequence, bias coefficient estimates (Beatty &Liao, 2011). Nevertheless, this model is appropriate forthe current research because timely recognition of loan lossprovisions is a significant financial reporting issue inbanking.

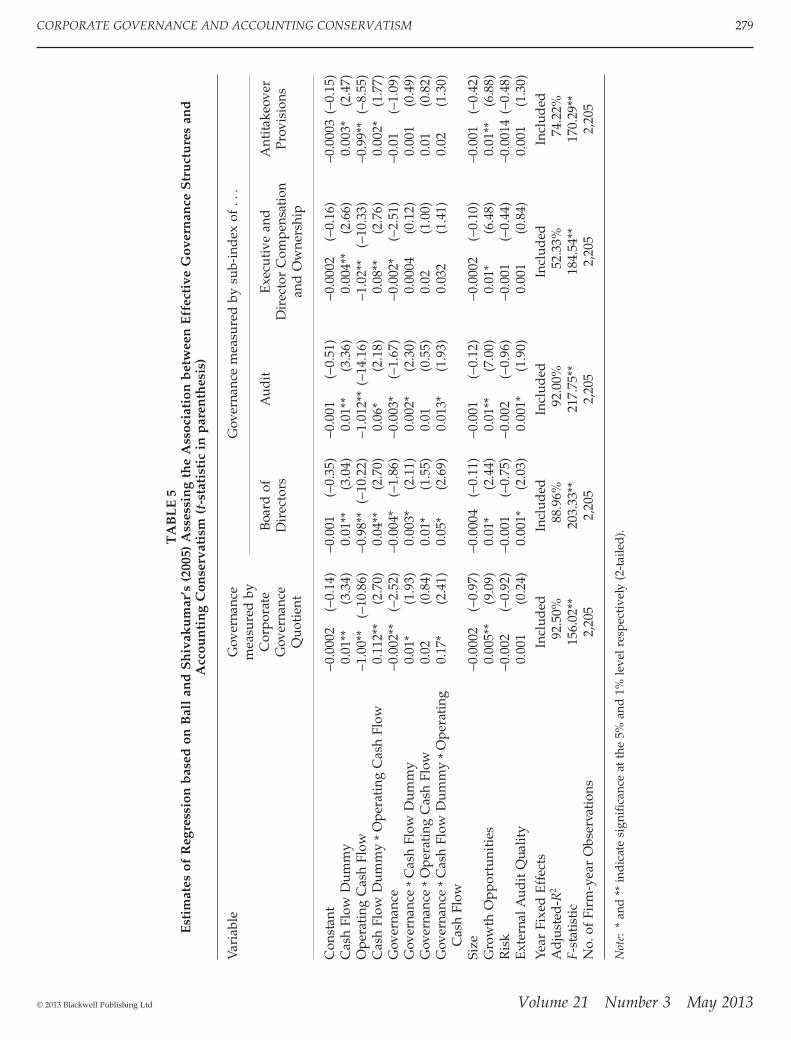

Our third and final proxy for conditional conservatism isbased on Ball and Shivakumar’s (2005) accrual-based model,which relates accruals to cash flows. It has an advantage of

not being a market measure, which cannot be biased bymarket inefficiencies. Ball and Shivakumar (2005) argue thatDechow’s (1994) finding that earnings negatively correlatewith operating cash flows is less pronounced in periods of“bad news” because of the asymmetric verification require-ments for recognizing gains and losses in income. Theyargue further that the asymmetric recognition of gains andlosses also creates asymmetry in accruals. Thus, economiclosses are likely to be recognized in a timelier mannerthrough unrealized accruals, while economic gains are rec-ognized when realized and are, in effect, accounted for on acash basis (Ball & Shivakumar, 2005; García Lara et al., 2009).This implies that any revision in current period’s cash flows(originating from revaluation of loans and other risk invest-ments made by the banks) is positively correlated withcurrent revisions in expected future cash flows. Ball andShivakumar (2005) argue that timely gain and loss recogni-tion is based on expected, not realized, cash flows and isachieved through accruals. They argue further that timelygain and loss recognition remains a source of positive cor-relation between accruals and current cash flows, and thiscorrelation seems to be greater in the case of losses. To testthe asymmetry in accruals and its association with corporategovernance, we estimate an augmented Ball and Shivakumar(2005) model, where the independent variables are inter-acted with Governance and the effects of Size, Growth Oppor-tunities, Risk, and External Audit Quality are controlled (as inModel [1]). Thus:

Total Accruals d d Cash Flow Dummy d OperatingCash Flow d

= + ++

0 1 2

3CCash Flow Dummy Operating Cash Flowd Goverance d Governa

∗+ +4 5 nnce Cash Flow Dummy

d Goverance Operating Cash Flow d Gov∗

+ ∗ +

6 7 eernance CashFlow Dummy Operating Cash Flow d Control

d

∗∗ +

+− 8 11

122 18− +Yr Dummies e_ [3]

TABLE 1 Continued

Variable Operational definition Mean Median Std. dev. Min. Max.

Loan Loss Allowance Loan loss allowance deflated by laggedtotal loans

0.02 0.01 0.005 0.01 0.08

Lagged HomogeneousLoans Outstanding

Ratio of homogeneous (consumer andinstalment) loans to total loans for theprevious year

0.19 0.14 0.17 0.00 0.95

Loan Charge-offs Loan charge-offs deflated by laggedtotal loans

0.21 0.07 1.92 -1.21 86.86

Loan Growth Annual growth in loans estimatedas total loans for the current yeardivided by total loans in the previousyear

0.76 0.84 2.05 0.002 83.13

Operating Performance Earnings before extraordinary itemsand taxes deflated by lagged totalassets

0.01 0.01 0.01 -0.102 0.03

Leverage Ratio of total debt to common stock 0.16 0.17 0.10 0.07 0.71Intangible/Total Assets Ratio of intangible assets to total assets 0.09 0.09 0.01 0.013 0.14

272 CORPORATE GOVERNANCE

Volume 21 Number 3 May 2013 © 2013 Blackwell Publishing Ltd

As in Model [2], all old variables are defined as previouslyand new ones introduced in Model [3] are operationallydefined in Table 1.

We expect the coefficient on Operating Cash Flow, d2, in theabove model to be significantly negative, because accrualsand operating net cash flows are contemporaneously andnegatively related (Dechow, 1994), and that on Cash FlowDummy * Operating Cash Flow, d3, to be significantly positivein the presence of conservative reporting. The coefficient onGovernance, d4, is expected to be negative because firms witheffective governance structures report less accruals. Addi-tionally, because firms with effective governance structuresengage in accounting conservatism, we expect the coefficienton Governance * Cash Flow Dummy * Operating Cash Flow, d7,to be significantly positive.

EMPIRICAL FINDINGS

Descriptive and Correlation AnalysesTable 1 also presents the summary statistics of the variablesused in our tests. The mean Loan Loss Provisions of the banksin our sample is 0.5 percent of their total loan portfolio, whilethe mean Nonperforming Loans is about 0.7 percent, and themean DNonperforming Loans is 0.3 percent. Loan Loss Allow-ance is 1.5 percent of total loans, indicating that the banks areeffective in evaluating loan risk. The proportion of LaggedHomogeneous Loans Outstanding granted by the banks in oursample represents about 19 percent of their total loan port-folio. While the banks reported mean Earnings of –0.027,they achieved mean Return of 2.71 during the sample period.The effectiveness of the banks’ governance structuresappears to be modest, as the mean Corporate GovernanceQuotient is 57.8 percent. The sub-indices for Board of Direc-tors, Audit, Executive and Director Compensation and Owner-ship, and Antitakeover Provisions, which are anchored on a1–5 scale, have mean values greater than three, indicatingthat our sample banks have average effective governancestructures.

About 47 percent of the banks experience negative stockreturns during the sample period, as indicated by the meanof the Dummy variable. The mean of the External AuditQuality variable equals 36.5 percent, indicating that a littleover one-third of the banks in our sample are audited by aBig-4 audit firm. The mean Risk is 4.74, suggesting that oursample banks are adequately capitalized as their Tier 1capital ratio exceeds the US federal bank regulators’ bench-mark of 4 percent. The sample banking firms managed togenerate, on average, an operating cash flow that equals 1.3percent of their total assets. Only a small percentage of thebanks (6.3 percent) reported negative cash flows duringthe period of investigation, as evidenced by the mean of theCash Flow Dummy variable.

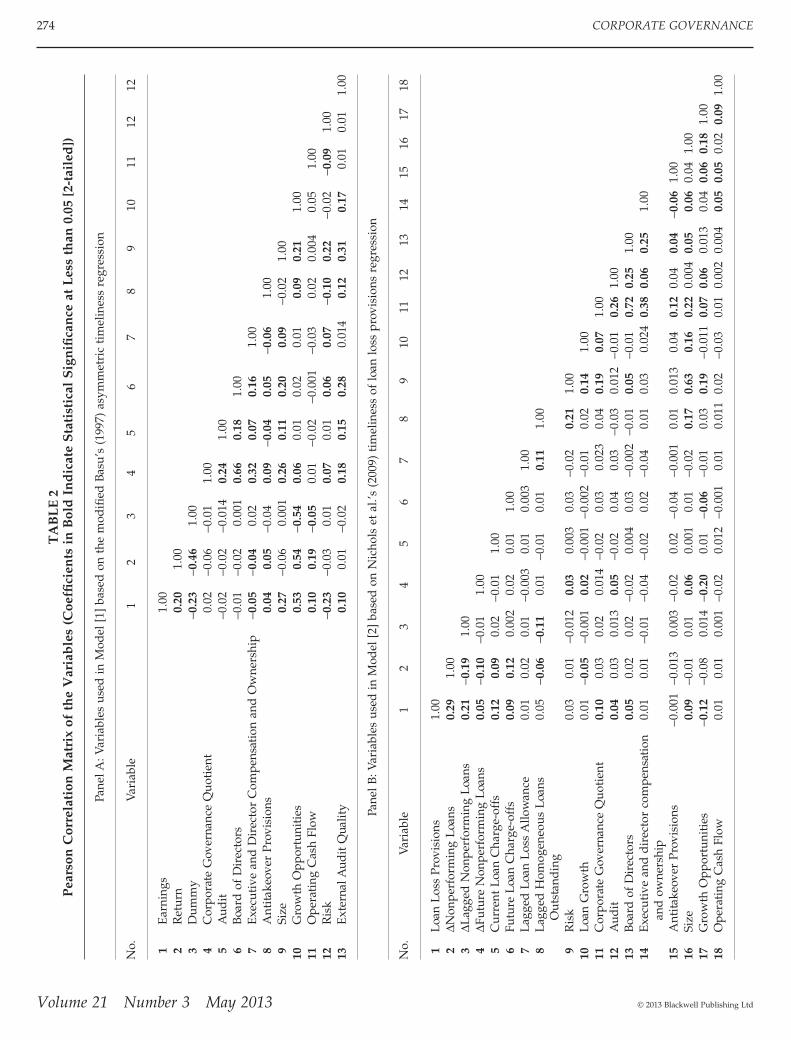

Panel A of Table 2 presents the Pearson pairwise corre-lation coefficients for the independent variables in Model[1]. Earnings correlates significantly (p < 0.05) and posi-tively with Returns, Size, Growth Opportunities, OperatingCash Flows, and External Audit Quality, but negatively withRisk. Corporate Governance Quotient correlates significantlywith Size, Growth Opportunities, Risk and External Audit

Quality, indicating that banks with effective governancestructures tend to be large in size, have increased growthopportunities, are less risky, and are audited by Big-4 auditfirms. Also, Corporate Governance Quotient has a positivesignificant correlation with each of its sub-indices. Further,while large banks (in terms of total assets) are associatedsignificantly (p < 0.05) with effective board, audit, andexecutive and director compensation and ownership gov-ernance structures, banks with increased growth opportu-nities are not likely to adopt antitakeover policies(p < 0.05).

Panel B of Table 2 presents the Pearson pairwise correla-tion coefficients for the independent variables in Model [2].The Loan Loss Provisions variable correlates positively andsignificantly (p < 0.05) with DLagged Nonperforming Loans,DCurrent Nonperforming Loans, DFuture Nonperforming Loans,Current Loan Charge-offs, and Future Loan Charge-offs. Thesefindings provide initial evidence of conservatism in the rec-ognition of Loan Loss Provisions, and are similar to thosereported by Nichols et al. (2009). Thus, Loan Loss Provisionsin year t reflects the anticipated level of loan losses based oninformation about non-performing loans during the previ-ous, present, and even future periods. In addition, the LoanLoss Provisions variable correlates positively with the Corpo-rate Governance Quotient, suggesting that well-governedbanks report higher levels of loan loss provisions. The rela-tionship between Loan Loss Provisions and the sub-indices ofBoard of Directors and Audit governance structures is positiveand significant, indicating that banks with both effectiveboard and audit governance structures recognize higherlevels of loan loss provisions.

Panel C of Table 2 reports the correlation coefficients forthe independent variables in Models [3], which is based onBall and Shivakumar’s (2005) model. The relationshipbetween Total Accruals and Operating Cash Flows is signifi-cantly negative (p < 0.05), suggesting that accruals and oper-ating net cash flows are contemporaneously negativelyrelated (Dechow, 1994). The Total Accruals variable alsorelates significantly (p < 0.05) and positively with bothGrowth Opportunities and Risk, indicating that banks withgrowth opportunities and those that are less risky seem toreport higher levels of accruals.

In addition to the Pearson pairwise correlation coefficientsfor the independent variables, we compute variance inflationfactor (VIF) for each independent variable in the threemodels. The untabulated findings show none of the VIFmeasures is more than 4, suggesting that multicollinearity isnot a serious problem with our data. However, the Gover-nance variable has the highest VIF of 3.55 in Model [1] whenthe dependent variable is measured by the governance sub-index of Executive and Director Compensation and Ownership.Also, the control variable of Size in Model [2] has the highestVIF of 3.61 when the Executive and Director Compensation andOwnership sub-index of governance serves as the dependentvariable. Further, we observe that the Cash Flow Dummy hasthe highest VIF of 3.98 in Model [3] when the dependentvariable is measured by Corporate Governance Quotient.

Overall, none of the pairwise correlation coeffici-ents as well as the VIF measures is above their theoreti-cal thresholds, suggesting no serious multicollinearityproblems.

CORPORATE GOVERNANCE AND ACCOUNTING CONSERVATISM 273

Volume 21 Number 3 May 2013© 2013 Blackwell Publishing Ltd

TA

BL

E2

Pea

rson

Cor

rela

tion

Mat

rix

ofth

eV

aria

ble

s(C

oeffi

cien

tsin

Bol

dIn

dic

ate

Sta

tist

ical

Sig

nifi

can

ceat

Les

sth

an0.

05[2

-tai

led

])

Pane

lA:V

aria

bles

used

inM

odel

[1]

base

don

the

mod

ified

Basu

’s(1

997)

asym

met

ric

tim

elin

ess

regr

essi

on

No.

Vari

able

12

34

56

78

910

1112

12

1E

arni

ngs

1.00

2R

etur

n0.

201.

003

Dum

my

-0.2

3-0

.46

1.00

4C

orpo

rate

Gov

erna

nce

Quo

tien

t0.

02-0

.06

-0.0

11.

005

Aud

it-0

.02

-0.0

2-0

.014

0.24

1.00

6B

oard

ofD

irec

tors

-0.0

1-0

.02

0.00

10.

660.

181.

007

Exe

cuti

vean

dD

irec

tor

Com

pens

atio

nan

dO

wne

rshi

p-0

.05

-0.0

40.

020.

320.

070.

161.

008

Ant

itake

over

Prov

isio

ns0.

040.

05-0

.04

0.09

-0.0

40.

05-0

.06

1.00

9Si

ze0.

27-0

.06

0.00

10.

260.

110.

200.

09-0

.02

1.00

10G

row

thO

ppor

tuni

ties

0.53

0.54

-0.5

40.

060.

010.

020.

010.

090.

211.

0011

Ope

rati

ngC

ash

Flow

0.10

0.19

-0.0

50.

01-0

.02

-0.0

01-0

.03

0.02

0.00

40.

051.

0012

Ris

k-0

.23

-0.0

30.

010.

070.

010.

060.

07-0

.10

0.22

-0.0

2-0

.09

1.00

13E

xter

nalA

udit

Qua

lity

0.10

0.01

-0.0

20.

180.

150.

280.

014

0.12

0.31

0.17

0.01

0.01

1.00

Pane

lB:V

aria

bles

used

inM

odel

[2]

base

don

Nic

hols

etal

.’s(2

009)

tim

elin

ess

oflo

anlo

sspr

ovis

ions

regr

essi

on

No.

Vari

able

12

34

56

78

910

1112

1314

1516

1718

1L

oan

Los

sPr

ovis

ions

1.00

2DN

onpe

rfor

min

gL

oans

0.29

1.00

3DL

agge

dN

onpe

rfor

min

gL

oans

0.21

-0.1

91.

004

DFut

ure

Non

perf

orm

ing

Loa

ns0.

05-0

.10

-0.0

11.

005

Cur

rent

Loa

nC

harg

e-of

fs0.

120.

090.

02-0

.01

1.00

6Fu

ture

Loa

nC

harg

e-of

fs0.

090.

120.

002

0.02

0.01

1.00

7L

agge

dL

oan

Los

sA

llow

ance

0.01

0.02

0.01

-0.0

030.

010.

003

1.00

8L

agge

dH

omog

eneo

usL

oans

Out

stan

din

g0.

05-0

.06

-0.1

10.

01-0

.01

0.01

0.11

1.00

9R

isk

0.03

0.01

-0.0

120.

030.

003

0.03

-0.0

20.

211.

0010

Loa

nG

row

th0.

01-0

.05

-0.0

010.

02-0

.001

-0.0

02-0

.01

0.02

0.14

1.00

11C

orpo

rate

Gov

erna

nce

Quo

tien

t0.

100.

030.

020.

014

-0.0

20.

030.

023

0.04

0.19

0.07

1.00

12A

udit

0.04

0.03

0.01

30.

05-0

.02

0.04

0.03

-0.0

30.

012

-0.0

10.

261.

0013

Boa

rdof

Dir

ecto

rs0.

050.

020.

02-0

.02

0.00

40.

03-0

.002

-0.0

10.

05-0

.01

0.72

0.25

1.00

14E

xecu

tive

and

dir

ecto

rco

mpe

nsat

ion

and

owne

rshi

p0.

010.

01-0

.01

-0.0

4-0

.02

0.02

-0.0

40.

010.

030.

024

0.38

0.06

0.25

1.00

15A

ntita

keov

erPr

ovis

ions

-0.0

01-0

.013

0.00

3-0

.02

0.02

-0.0

4-0

.001

0.01

0.01

30.

040.

120.

040.

04-0

.06

1.00

16Si

ze0.

09-0

.01

0.01

0.06

0.00

10.

01-0

.02

0.17

0.63

0.16

0.22

0.00

40.

050.

060.

041.

0017

Gro

wth

Opp

ortu

niti

es-0

.12

-0.0

80.

014

-0.2

00.

01-0

.06

-0.0

10.

030.

19-0

.011

0.07

0.06

0.01

30.

040.

060.

181.

0018

Ope

rati

ngC

ash

Flow

0.01

0.01

0.00

1-0

.02

0.01

2-0

.001

0.01

0.01

10.

02-0

.03

0.01

0.00

20.

004

0.05

0.05

0.02

0.09

1.00

274 CORPORATE GOVERNANCE

Volume 21 Number 3 May 2013 © 2013 Blackwell Publishing Ltd

TA

BL

E2

Con

tinu

ed

Pane

lC:V

aria

bles

used

inM

odel

[3]

base

don

Ball

and

Shiv

akum

ar’s

(200

5)re

gres

sion

No.

Vari

able

12

34

56

78

910

1112

1To

talA

ccru

als

1.00

2O

pera

ting

Cas

hFl

ow-0

.54

1.00

3C

ash

Flow

Dum

my

0.29

-0.3

71.

004

Cor

pora

teG

over

nanc

eQ

uoti

ent

-0.0

120.

030.

031.

005

Aud

it0.

02-0

.02

0.01

0.24

1.00

6B

oard

ofD

irec

tors

-0.0

02-0

.001

0.08

0.66

0.18

1.00

7E

xecu

tive

and

Dir

ecto

rC

ompe

nsat

ion

and

Ow

ners

hip

0.01

-0.0

3-0

.03

0.32

0.07

0.16

1.00

8A

ntita

keov

erPr

ovis

ions

-0.0

030.

02-0

.03

0.09

-0.0

40.

05-0

.06

1.00

9Si

ze0.

020.

130.

030.

240.

110.

200.

09-0

.02

1.00

10G

row

thO

ppor

tuni

ties

0.10

0.08

-0.0

20.

030.

014

0.02

0.01

0.09

0.22

1.00

11R

isk

0.14

-0.0

40.

200.

090.

010.

060.

07-0

.10

0.31

0.15

1.00

12E

xter

nalA

udit

Qua

lity

-0.0

30.

004

0.00

10.

220.

150.

280.

014

0.11

0.32

0.08

0.02

1.00

CORPORATE GOVERNANCE AND ACCOUNTING CONSERVATISM 275

Volume 21 Number 3 May 2013© 2013 Blackwell Publishing Ltd

Evidence of Accounting Conservatism

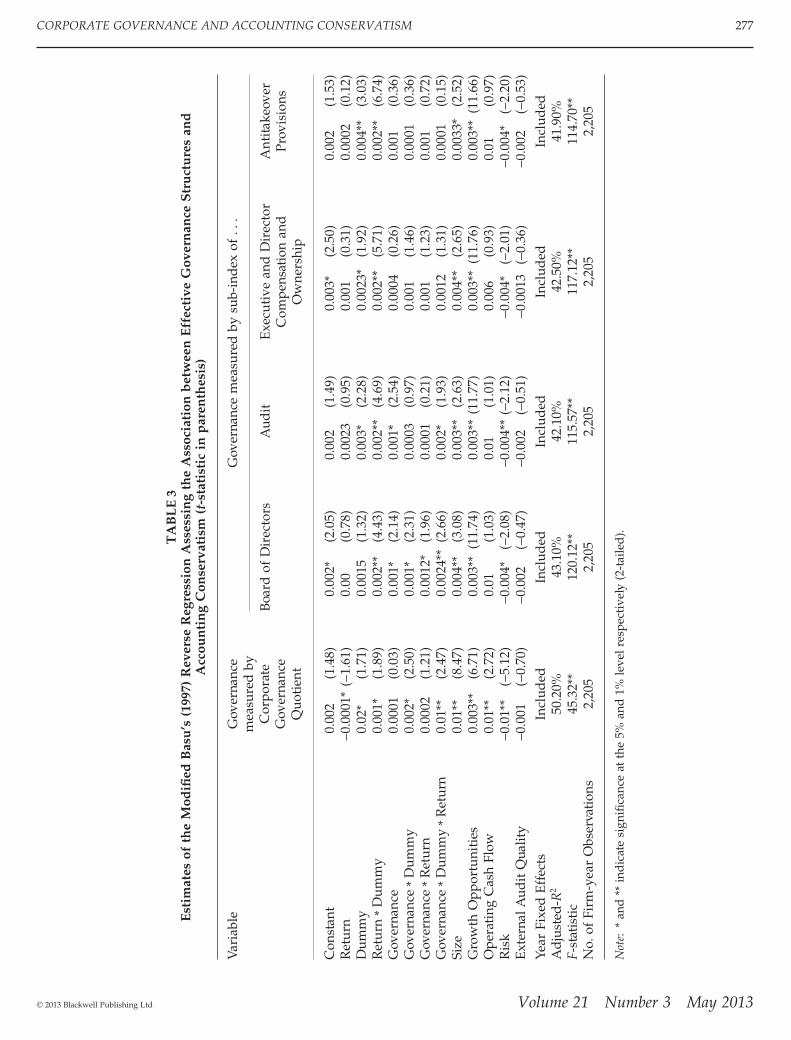

We present the estimates of Model [1] in Table 3. The coeffi-cient on Return * Dummy, b3, is significantly positive forboth the composite governance index (t = 1.89, p < 0.05)and all the governance sub-indices (p < 0.01), which indi-cates evidence of conservatism. Also, the coefficient onGovernance * Dummy * Return, b7, is positive and highly sta-tistically significant in all cases except for the sub-indices ofExecutive and Director Compensation and Ownership and Anti-takeover Provisions. These findings suggest that banks havingeffective overall governance structures engage in higherlevels of conservatism. More specifically, banks with effec-tive Board of Directors and Audit governance structures areassociated with higher levels of conservatism. Thus, exceptfor Hypotheses 1c and 1d, those for 1, 1a, and 1b are sup-ported by the empirical data. The finding for Corporate Gov-ernance Quotient is consistent with García Lara et al. (2009),who also document that effective governance is associatedwith higher levels of accounting conservatism. The findingsfor the sub-indices of Board of Directors and Audit gover-nance structures are consistent with Hypotheses 1b and 1c,and those documented by Xie et al. (2003) and Ahmed andDuellman (2007). Except for the sub-index of Board of Direc-tors, the coefficient on Dummy, b2, is positive and significantin all cases, suggesting that US banks recognize “bad news”more quickly in earnings. Also, the coefficient on Return, b1,is negative and significant only for the regression having theCorporate Governance Quotient as its dependent variable(t = -1.61, p < 0.001), suggesting that accounting conserva-tism affects earnings. This finding contradicts the evidencereported by García Lara et al. (2009). Overall, the findings ofthe main variables of interest confirm our expectation thatbanks with effective governance structures engage in higherlevels of conservative accounting.

The control variable of Size has a positive and highly sig-nificant coefficient in all cases, suggesting that large banksdemand a greater degree of conservatism by recognizing“bad news” in earnings on a timely basis. The coefficient onGrowth Opportunities has significant positive signs in allcases. Finally, the coefficient on the Risk variable is negativeand significant.

We report the estimates of Model [2] in Table 4. Asexpected, the coefficients on both DLagged NonperformingLoans (c1) and DCurrent Nonperforming Loans (c2) are positiveand statistically significant, at least, at the 0.05 level in allcases except for the governance sub-index of Executive andDirector Compensation and Ownership. These findings are con-sistent with evidence reported by Nichols et al. (2009), indi-cating that poorly governed banks recognize loan lossprovisions in a timelier manner relative to changes inpresent and past non-performing loans, thus exercising ahigher degree of accounting conservatism. The conservativereporting persists with DFuture Nonperforming Loans in allcases except for the Corporate Governance Quotient, whosecoefficient, c3, is negative and significant, indicating thatpoorly governed banks are either less conservative withfuture non-performing loans or they have the tendency torecognize loan loss provisions only when they are fullyrealized. Consistent with our expectations, the coefficientson both Governance * DCurrent Nonperforming Loans, c8, and

Governance * DFuture Nonperforming Loans, c9, are statisticallysignificant in all cases except for the governance sub-indexof Antitakeover Provisions, suggesting that banks with effec-tive governance structures do recognize larger loan lossprovisions and in a timely manner. Further, the coefficientsc10 and c11 on Governance * Current Loan Charge-offs andGovernance * Future Loan Charge-offs, respectively, are posi-tively significant (p < 0.01) in all but two cases, indicatingthat well-governed banks report larger loan charge-offs forthe current and future periods compared to their poorlygoverned counterparts (Nichols et al., 2009). Overall, thefindings reported in Table 4 for either the governance com-posite index, Corporate Governance Quotient, or the gover-nance sub-indices are consistent with our expectations.Thus, our empirical findings are consistent with the theo-retical propositions in Hypotheses 1, 1a, 1b, 1c, and 1d. Ofthe control variables included in Model [2], only Size andGrowth Opportunities are statistically significant (p < 0.05) inthe cases of the governance sub-indices.

Finally, Table 5 presents the estimates of Model [3], whichtests whether the asymmetry in the treatment of gains andlosses also creates an asymmetry in accruals. The coefficienton Operating Cash Flow, d2, is significantly negative (p < 0.01),indicating a negative association between accruals and cashflows. This finding is similar to that reported by García Laraet al. (2009). As predicted, the coefficient on Cash FlowDummy * Operating Cash Flow, d3, is significantly positive, atleast, at the 0.05 level in all cases except for the sub-index ofExecutive and Director Compensation and Ownership, indicat-ing that the negative relationship between accruals and cashflow is less pronounced when cash flow is negative. In otherwords, the positive findings imply a positive contempora-neous relationship between cash flows and accruals in “badnews” periods (i.e., accrued losses are more probable inperiods of negative cash flows [García Lara et al., 2009]). Thefinding for the Corporate Governance Quotient is consistentwith the assertion of both Ball and Shivakumar (2005) andGarcía Lara et al. (2009) that asymmetrically more unreal-ized losses are recognized via accruals than unrealizedgains. Consistent with our expectation, the coefficient onGovernance, d4, is negative and statistically significant in allbut one case, signifying the negative association betweeneffective corporate governance structures and total accruals.The coefficient on the interactive term between Governanceand Cash Flow Dummy, d5, is positive and statistically signifi-cant (p < 0.05) in all cases except for the governance sub-indices of Executive and Director Compensation and Ownershipand Antitakeover Provisions. This finding corroborates evi-dence reported by García Lara et al. (2009). However, weinterpret the statistically positive coefficient in all cases,except for the sub-indices of Executive and Director Compen-sation and Ownership and Antitakeover Provisions, that banksthat have effective governance structures but generate nega-tive operating cash flows tend to report more total accruals.Consistent with our expectation that banks with effectivecorporate governance structures engage in accountingconservatism, the coefficient on Governance * Cash FlowDummy * Operating Cash Flow, d7, is positive and statisticallysignificant (p < 0.05) for Corporate Governance Quotient andthe governance sub-indices of Board of Directors and Audit,supporting Hypotheses 1, 1a, and 1b. These findings suggest

276 CORPORATE GOVERNANCE

Volume 21 Number 3 May 2013 © 2013 Blackwell Publishing Ltd

TA

BL

E3

Est

imat

esof

the

Mod

ified

Bas

u’s

(199

7)R

ever

seR

egre

ssio

nA

sses

sin

gth

eA

ssoc

iati

onb

etw

een

Eff

ecti

veG

over

nan

ceS

tru

ctu

res

and

Acc

oun

tin

gC

onse

rvat

ism

(t-s

tati

stic

inp

aren

thes

is)

Vari

able

Gov

erna

nce

mea

sure

dby

Cor

pora

teG

over

nanc

eQ

uoti

ent

Gov

erna

nce

mea

sure

dby

sub-

ind

exof

...

Boa

rdof

Dir

ecto

rsA

udit

Exe

cuti

vean

dD

irec

tor

Com

pens

atio

nan

dO

wne

rshi

p

Ant

itake

over

Prov

isio

ns

Con

stan

t0.

002

(1.4

8)0.

002*

(2.0

5)0.

002

(1.4

9)0.

003*

(2.5

0)0.

002

(1.5

3)R

etur

n-0

.000

1*(-

1.61

)0.

00(0

.78)

0.00

23(0

.95)

0.00

1(0

.31)

0.00

02(0

.12)

Dum

my

0.02

*(1

.71)

0.00

15(1

.32)

0.00

3*(2

.28)

0.00

23*

(1.9

2)0.

004*

*(3

.03)

Ret

urn

*D

umm

y0.

001*

(1.8

9)0.

002*

*(4

.43)

0.00

2**

(4.6

9)0.

002*

*(5

.71)

0.00

2**

(6.7

4)G

over

nanc

e0.

0001