Contract Theory

740

CONTRACTTHEORY

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Contract Theory

CONTRACTTHEORY

CONTRACTTHEORY

PatrickBoltonand MathiasDewatripont

The MITPressCambridge,MassachusettsLondon,England

\302\251 2005 by the Massachusetts Institute of Technology.

All rights reserved. No part of this book may bereproduced in any form by any electronicor mechanical means (including photocopying, recording, or information storage andretrieval) without permission in writing from the publisher.

This book was set in Times Ten by SNP Best-set Typesetter Ltd., Hong Kong, and wasprinted and bound in the United States of America.

Library of Congress Cataloging-in-Publication Data

Bolton, Patrick, 1957-Contract theory / Patrick Bolton and Mathias Dewatripont.

p. cm.Includes bibliographical references and index.ISBN 0-262-02576-01.Contracts\342\200\224Methodology. I. Dewatripont, M. (Mathias) II.Title.

K840.B65 2004346.02'01\342\200\224dc22

2004055902

Contents

Preface xv

1 Introduction 11.1 Optimal Employment Contractswithout Uncertainty, Hidden

Information, or HiddenActions 41.2 Optimal Contractsunder Uncertainty 7

1.2.1Pure Insurance 81.2.2Optimal Employment Contractsunder Uncertainty 11

1.3 Information and Incentives 141.3.1AdverseSelection 151.3.2MoralHazard 20

1.4 Optimal Contracting with Multilateral AsymmetricInformation 251.4.1Auctions and Tradeunder Multilateral Private

Information 261.4.2MoralHazard in Teams,Tournaments, and

Organizations 271.5 TheDynamics of IncentiveContracting 30

1.5.1Dynamic AdverseSelection 311.5.2Dynamic MoralHazard 34

1.6 IncompleteContracts 361.6.1Ownershipand Employment 371.6.2IncompleteContractsand Implementation Theory 391.6.3BilateralContractsand Multilateral Exchange 40

1.7 Summing Up 42

Part I STATICBILATERALCONTRACTING 45

2 HiddenInformation, Screening 472.1 The Simple EconomicsofAdverseSelection 47

2.1.1First-BestOutcome:PerfectPriceDiscrimination 482.1.2AdverseSelection,LinearPricing, and Simple

Two-PartTariffs 492.1.3Second-BestOutcome:OptimalNonlinear Pricing 52

2.2 Applications 572.2.1CreditRationing 572.2.2Optimal IncomeTaxation 62

vi Contents

2.2.3Implicit Labor Contracts 672.2.4 Regulation 74

2.3 MoreThan TwoTypes 77

2.3.1Finite Number ofTypes 77

2.3.2Random Contracts 812.3.3A Continuum ofTypes 82

2.4 Summary 932.5 LiteratureNotes 96

HiddenInformation, Signaling 993.1 Spence'sModelof Educationas a Signal 100

3.1.1Refinements 1073.2 Applications 112

3.2.1CorporateFinancing and Investment Decisionsunder Asymmetric Information 112

3.2.2Signaling Changesin CashFlow through DividendPayments 120

3.3 Summary and LiteratureNotes 125

HiddenAction, MoralHazard 1294.1 TwoPerformanceOutcomes 130

4.1.1First-BestversusSecond-BestContracts 1304.1.2The SecondBestwith BilateralRisk Neutrality and

ResourceConstraints for the Agent 1324.1.3SimpleApplications 1334.1.4BilateralRisk Aversion 1354.1.5TheValue of Information 136

4.2 LinearContracts,Normally DistributedPerformance,and

Exponential Utility 1374.3 The Suboptimality of LinearContractsin the Classical

Model 1394.4 GeneralCase:TheFirst-OrderApproach 142

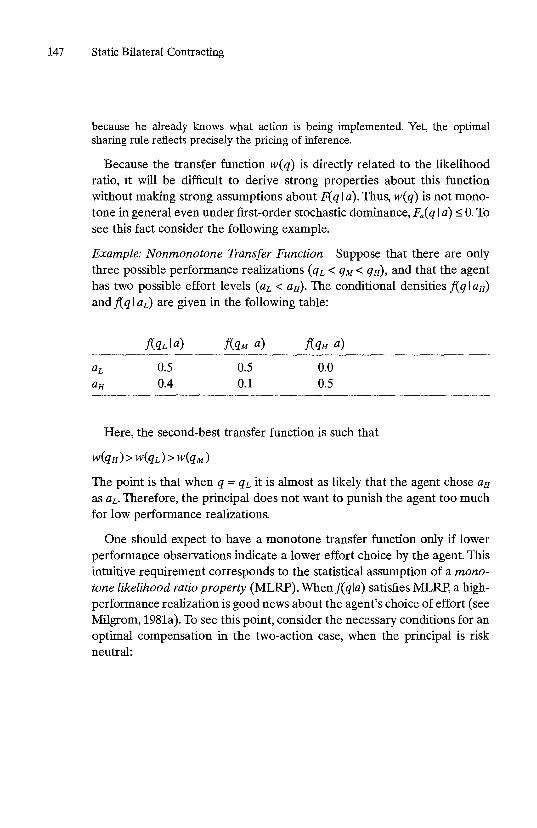

4.4.1Characterizingthe SecondBest 1424.4.2 When is the First-OrderApproachValid? 148

4.5 Grossmanand Hart'sApproachto the Principal-AgentProblem 152

4.6 Applications 157

vii Contents

4.6.1ManagerialIncentiveSchemes 1574.6.2The Optimality of DebtFinancing under Moral

Hazardand Limited Liability 1624.7 Summary 1684.8 LiteratureNotes 169Disclosureof Private CertifiableInformation 1715.1 Voluntary DisclosureofVerifiable Information 172

5.1.1Private, UncertifiableInformation 1725.1.2Private, CertifiableInformation 1735.1.3TooMuch Disclosure 1745.1.4Unraveling and the Full DisclosureTheorem 1755.1.5Generalizingthe Full DisclosureTheorem 176

5.2 Voluntary Nondisclosureand Mandatory-DisclosureLaws 1785.2.1Two Examplesof No Disclosureor Partial

Voluntary Disclosure 1795.2.2 Incentivesfor Information Acquisition and the

Role of Mandatory-DisclosureLaws 1805.2.3 No Voluntary DisclosureWhen the Informed

Party CanBeEither a Buyer or a Seller 1865.3 CostlyDisclosureand DebtFinancing 1905.4 Summary and LiteratureNotes 197Multidimensional IncentiveProblems 1996.1 AdverseSelectionwith Multidimensional Types 199

6.1.1An ExampleWhere Bundling IsProfitable 2006.1.2When IsBundling Optimal?A LocalAnalysis 2016.1.3Optimal Bundling: A GlobalAnalysis in the 2 x2

Model 2046.1.4GlobalAnalysis for the GeneralModel 212

6.2 MoralHazardwith Multiple Tasks 2166.2.1Multiple Tasksand Effort Substitution 2186.2.2Conflicting Tasksand Advocacy 223

6.3 An ExampleCombining MoralHazardand AdverseSelection 2286.3.1Optimal Contractwith MoralHazardOnly 2306.3.2Optimal Contractwith AdverseSelectionOnly 231

viii Contents

6.3.3Optimal Saleswith Both AdverseSelectionandMoralHazard 231

6.4 Summary and LiteratureNotes 233

Partn STATICMULTILATERALCONTRACTING 237

7 Multilateral Asymmetric Information: BilateralTrading andAuctions 2397.1 Introduction 2397.2 BilateralTrading 243

7.2.1 TheTwo-TypeCase 2437.2.2 Continuum ofTypes 250

7.3 Auctions with PerfectlyKnown Values 2617.3.1 OptimalEfficient Auctions with IndependentValues 2627.3.2 Optimal Auctions with IndependentValues 2657.3.3 Standard Auctions with IndependentValues 2677.3.4 Optimal Independent-ValueAuctions with a

Continuum ofTypes:The RevenueEquivalenceTheorem 271

7.3.5 Optimal Auctions with CorrelatedValues 2767.3.6 The Roleof Risk Aversion 2787.3.7 The Role ofAsymmetrically DistributedValuations 280

7.4 Auctions with Imperfectly Known Common Values 2827.4.1 TheWinner's Curse 2837.4.2 StandardAuctions with Imperfectly Known

CommonValues in the 2 x2 Model 2857.4.3 Optimal Auctions with Imperfectly Known

Common Values 2887.5 Summary 2907.6 LiteratureNotes 2927.7 Appendix: Breakdownof RevenueEquivalencein a 2 x3

Example 294

8 Multiagent MoralHazardand Collusion 2978.1 MoralHazard in Teamsand Tournaments 299

8.1.1UnobservableIndividual Outputs:The Needfor aBudget Breaker 301

ix Contents

8.1.2UnobservableIndividual Outputs:Using OutputObservationsto Implement the First Best 305

8.1.3ObservableIndividual Outputs 3118.1.4Tournaments 316

8.2 Cooperationor Competitionamong Agents 3268.2.1Incentivesto Helpin Multiagent Situations 3268.2.2Cooperationand Collusionamong Agents 331

8.3 Supervisionand Collusion 3388.3.1Collusionwith Hard Information 3388.3.2Application: Auditing 342

8.4 Hierarchies 3518.5 Summary 3608.6 LiteratureNotes 362

Part IDREPEATEDBILATERALCONTRACTING 365

9 Dynamic AdverseSelection 3679.1 Dynamic AdverseSelectionwith FixedTypes 367

9.1.1CoasianDynamics 3699.1.2Insuranceand Renegotiation 3799.1.3SoftBudgetConstraints 3849.1.4Regulation 388

9.2 RepeatedAdverseSelection:Changing Types 3969.2.1Banking and Liquidity Transformation 3979.2.2Optimal Contracting with Two Independent

Shocks 4029.2.3Second-BestRisk Sharing betweenInfinitely

LivedAgents 4089.3 Summary and LiteratureNotes 415

10 Dynamic MoralHazard 41910.1TheTwo-PeriodProblem 420

10.1.1NoAccessto Credit 42210.1.2MonitoredSavings 42610.1.3Free Savings and Asymmetric Information 429

10.2TheT-periodProblem:SimpleContractsand the Gainsfrom Enduring Relations 431

x Contents

10.3

10.4

10.5

10.610.7

10.2.1RepeatedOutput10.2.2RepeatedActions10.2.3RepeatedActions and Output10.2.4Infinitely RepeatedActions, Output, and

ConsumptionMoralHazardand Renegotiation10.3.1RenegotiationWhen Effort IsNot Observedby

the Principal10.3.2RenegotiationWhen Effort IsObservedby the

PrincipalBilateralRelationalContracts10.4.1MoralHazard10.4.2AdverseSelection10.4.3ExtensionsImplicit Incentivesand CareerConcerns10.5.1The Single-TaskCase10.5.2The Multitask Case10.5.3TheTrade-OffbetweenTalentRisk and Incentives

under CareerConcernsSummaryLiteratureNotes

433434435

447450

450

456461468468470470473475

481483484

Part IV INCOMPLETECONTRACTS 487

11 IncompleteContractsand Institution Design 48911.1Introduction: IncompleteContractsand the Employment

Relation 48911.1.1The Employment Relation 49011.1.2A Theoryof the Employment RelationBasedon

ExPostOpportunism 49111.2Ownershipand the Property-Rights Theoryof the Firm 498

11.2.1A GeneralFramework with ComplementaryInvestments 500

11.2.2A Framework with Substitutable Investments 51511.3Financial Structure and Control 521

11.3.1Wealth Constraints and Contingent AllocationsofControl 523

Contents

11.3.2Wealth Constraints and Optimal DebtContractswhen EntrepreneursCanDivert CashFlow 534

11.4Summary 54911.5LiteratureNotes 551

Foundations of Contracting with Unverifiable Information 55312.1Introduction 55312.2Nash and Subgame-PerfectImplementation 555

12.2.1Nash Implementation: Maskin'sTheorem 55512.2.2Subgame-PerfectImplementation 558

12.3TheHoldupProblem 56012.3.1SpecificPerformanceContractsand Renegotiation

Design 56312.3.2OptionContractsand Contracting at Will 56612.3.3DirectExternalities 57012.3.4Complexity 572

12.4ExPostUnverifiable Actions 57812.4.1Financial Contracting 57912.4.2Formal and Real Authority 585

12.5ExPostUnverifiable Payoffs 58812.5.1The Spot-ContractingMode 59112.5.2The Employment Relationand Efficient Authority 594

12.6Summary and LiteratureNotes 597

Markets and Contracts 60113.1(Static)AdverseSelection:Market Breakdownand

ExistenceProblems 60113.1.1The Caseof a SingleContract 60213.1.2The Caseof Multiple Contracts 604

13.2Contractsas a Barrier to Entry 60613.3Competitionwith BilateralNonexclusiveContractsin the

Presenceof Externalities 60913.3.1The Simultaneous Offer Game 61413.3.2The SequentialOfferGame 62313.3.3TheBidding Game:CommonAgency and Menu

Auctions 62813.4Principal-Agent Pairs 630

xii Contents

13.5Competitionas an Incentive Scheme 63613.6Summary and LiteratureNotes 641

APPENDIX 645

14 Exercises 647

References 687Author Index 709

SubjectIndex 715

To Our Families

Preface

Contracttheory, information economics,incentive theory, and organizationtheory have beenhighly successfuland activeresearchareas in economics,finance, management, and corporate law for more than three decades.Anumber of founding contributors have beenrewardedwith the Nobelprizein economicsfor their contributions in this generalarea,including RonaldCoase,HerbertSimon, William Vickrey, JamesMirrlees,GeorgeAkerlof,

JosephStiglitz, and MichaelSpence.There is now a vast literature relatingto contracttheory in leadingeconomics,finance, and law journals, and yeta relatively small number ofcorenotions and findings have found their way

into textbooks.The most recent graduate textbooks in microeconomics1devote a few chapters to basicnotions in incentive and information

economics like adverseselection,moral hazard, and mechanism design,but this

material servesonly as an introduction to theseenormoustopics.The goalof this bookis to providea synthesis of this huge area by

highlighting the common themes and methodologiesthat unite this field.Thebookcan serveboth as a complementary text for a graduate or advancedundergraduate coursein microeconomicsand for a graduate coursein

contract theory. Although we aim to provide very broad coverageof theresearchliterature, it is impossibleto do justiceto all the interestingarticles and all subfields that have emergedoverthe past30years.As a remedyagainst the most obvious gapsand omissions,we make a limited attempt to

providea short guide to the literature at the end of each chapter.Even if

this bookleavesout largeportionsof the literature, it still contains far toomuch material for evena full-semestercoursein contracttheory. Ourintention was to give instructors somediscretionoverwhich chapterstoemphasize and to leaveit to the students to do the background reading.

The bookalso presentsmethodologicalresults in the key applicationareaswherethey have beendeveloped,be they in laboreconomics,organization theory, corporatefinance,or industrial organization, for example.Inthis way, the bookcanalsoserveasa referencesourcefor researchersinterested in the very many applicationsof contract theory in economics.Thephilosophy of the bookis to stressapplicationsrather than generaltheorems, while providing a simplified yet self-containedtreatment of the keymodelsand methodologiesin the literature.

We owean immeasurableintellectual debt to our advisers,OliverHart,Andreu Mas-Colell,Eric Maskin, John Moore, and Jean Tirole.Their

1.See,for example, the books by Kreps (1990)and Mas-Colell,Whinston, and Green (1995).

xvi Preface

influence is visible on almost every page of this book.And although wehave not had the good fortune to have them as our advisers,theintellectual influence of Bengt Holmstrom, Jean-JacquesLaffont, Paul Milgrom,JamesMirrlees,and RogerMyersonhasbeenjust as important. Theinspiration and support of our coauthors,Philippe Aghion, ChristopherHarris,Ian Jewitt, Bruno Jullien, Patrick Legros,SteveMatthews, Patrick Rey,Alisa

Roell, Gerard Roland, Howard Rosenthal, David Scharfstein,Ernst-Ludwig von Thadden,MichaelWhinston, and Chenggang Xu, has beeninvaluable. In particular, PhilippeAghion and Patrick Rey have playedamajor role throughout the long gestationperiodof this book.

Over the years,every chapter of the bookhas beentested in theclassroom. We thank our students at ECARES(Universite LibredeBruxelles),Tilburg, Princeton,MIT,Helsinki, and the summer schoolsin Oberweseland Gerzenseefor their comments.We also thank Philippe Aghion andOliverHart for using our manuscript in their contract theory coursesatHarvard and for their feedback.We are grateful to Kenneth Ayotte, EstelleCantillon, Antonio Estache, Antoine Faure-Grimaud,Denis Gromb,ChristopherHennessy,Andrei Hagiu, JacquesLawarree,JoelShapiro,JeanTirole,and three anonymous MITPressreadersfor comments and advice.We are particularly grateful to KathleenHurley, Diana Prout, and EllenSklar for all their help in preparingthe manuscript. We are alsoenormouslygrateful to our editors,Terry Vaughn and John Covell,for their continuing

support and for making sure that we bring this project to completion.

Introduction

Economicsis often definedas a field that aims to understand the processby which scarceresourcesare allocatedto their most efficient uses,andmarkets are generally seenas playing a central role in this process.But,more fundamentally, the simple activity of exchangeof goodsand services,whether on organizedexchangesor outsidea market setting, is the basicfirst step in any productionor allocationof resources.For a long timeeconomic theory has beenable to analyze formally only very basicexchangeactivities like the barter of two different commoditiesbetween two

individuals at a given placeand point in time.Mostmicroeconomicstextbooks1begin with an analysis of this basicsituation, representingit in the classic\"Edgeworth box.\" A slightly more involved exchangesituation that canalsoberepresentedin an Edgeworth boxis betweentwo individuals trading atdifferent points in time. Simplelending, investment, or futures contractscanbe characterizedin this way. However,such a simple reinterpretationalreadyraisesnew issues,like the possibility of default or nondelivery bythe other party in the future.

Until the 1940sor 1950sonly situations of simple exchangeof goodsand serviceswere amenable to formal analysis.More complexexchangeactivities like the allocationand sharing of risk began to be analyzedformally only with the introduction of the idea of \"state-contingent\"commodities by Arrow (1964)and Debreu(1959)and the formulation of atheory of \"choiceunder uncertainty\" by von Neumann and Morgenstern(1944)and others.Thenotion of exchangeofstate-contingentcommoditiesgave a precisemeaning to the exchangeand allocationof risk. Preferenceorderings over lotteries provided a formal representation of attitudes

toward risk and preferencesfor risk taking. Theseconceptualinnovations

are the foundations of modern theories of investment under risk and

portfoliochoice.In the late 1960sand 1970syet another conceptualbreakthrough took

placewith the introduction of \"private information\" and \"hidden actions\"

in contractual settings.The notions of \"incentive compatibility\" andincentives for \"truth telling\" providedthe basicunderpinnings for the theory ofincentives and the economicsof information. Theyalsoprovidedthe first

formal tools for a theory of the firm, corporatefinance, and, moregenerally,

a theory of economicinstitutions.

1.See,for example,Part 4of the celebrated book by Mas-Colell,Whinston, and Green (1995).

2 Introduction

Finally, much of the existing theory of long-term or dynamic contractingwas developedin the 1980sand 1990s.Contractrenegotiation,relationalcontracts,and incompletecontractsprovidedthe first toolsfor an analysisof \"ownership\" and \"control rights.\" Thesenotions, in turn, completethefoundations for a full-fledged theory of the firm and organizations.

Thereare by now many excellentfinance and economicstextbookscovering the theory of investment under risk, insurance, and riskdiversification. As this is alreadywell-exploredterritory, we shall not provide any

systematic coverageof theseideas.In contrast,to date there are only a fewbookscovering the theory of incentives, information, and economicinstitutions, which is generally referredto in short ascontracttheory.2 Therehasbeensuch a largeresearchoutput on these topicsin the last 30years that

it is an impossibletask to give a comprehensivesynthesis of all the ideasand methodsof contracttheory in a single book.Nevertheless,our aim isto be as wide ranging as possibleto give a senseof the richnessof the

theory\342\200\224its core ideasand methodology\342\200\224as well as its numerous possibleapplicationsin virtually all fields of economics.

Thus, in this bookwe attempt to coverall the major topicsin contracttheory that are taught in most graduate courses.Part Istarts with basicideasin incentive and information theory like screening,signaling, and moralhazard.Part IIcoversthe lesswell trodden material of multilateral

contracting with private information or hidden actions.In this part we providean introduction to auction theory, bilateraltradeunder private information,and the theory of internal organization of firms. Part IIIdealswith long-term contractswith private information or hidden actions.Finally, Part IVcoversincompletecontracts,the theory of ownership and control,and

contracting with externalities.Exercisesare collectedin a specificchapter atthe end of the book.

There is obviously too much material in this bookfor any one-semestercoursein contracttheory. Rather than imposeour own preferencesand ourown pet topics,we thought that it would be better to coverall the mainthemesof contracttheory and let instructors pick and choosewhich partsto coverin depth and which ones to leaveto the students to read.

Consistentwith our goalofproviding broadcoverageof the field,we haveaimedfor a style ofexpositionthat favors simplicity overgenerality orrigor.

2.Seein particular the textbooks by Salanie (1997)and Laffont and Martimort (2002).

3 Introduction

Our primary goal is to illustrate the core ideas,the main methodsin their

simplest self-containedform, and the wide applicability of the centralnotions of contract theory. More often than not, researcharticlesin

contract theory are hard to penetrate evenfor a well-trained reader.We have

goneto considerablelengths to make the centralideasand methodsin thesearticlesaccessible.Inevitably, we have been led to sacrificegenerality toachievegreatereaseofunderstanding. Ourhope is that oncethe main ideashave beenassimilatedthe interestedreaderwill find it easierto read the

original articles.In the remainderof this chapterwe providea briefoverview of the main

ideasand topicsthat are coveredin the bookby consideringa singleconcrete situation involving an employer and an employee.Dependingon the

topicwe are interestedin we shall take the employerto bea manager hiringa worker, or afarmer hiring asharecropper,or evena company ownerhiringa manager. Throughout the bookwe discussmany other applications,andthis briefoverview should not be taken to be the leading applicationofcontract theory. Before we proceedwith a brief descriptionof the multiplefacetsof this contracting problem,it is useful to beginby delineating theboundariesof the framework and stating the main assumptions that apply

throughout this bdok.The benchmark contracting situation that we shall consider in this

bookis one between two parties who operate in a market economywith

a wen-functioning legal system. Under such a system, any contract the

parties decideto write will be enforcedperfectlyby a court, provided,ofcourse, that it doesnot contravene any existing laws. We shall assumethroughout most of the bookthat the contracting parties do not needto

worry about whether the courts are able or willing to enforce the termsof the contractprecisely.Judgesare perfectlyrational individuals, whoseonly concernis to stick as closelyas possibleto the agreed terms of thecontract.The penaltiesfor breachingthe contractwill be assumedto besufficiently severe that no contracting party will ever consider the

possibility of not honoring the contract.We shall step outsidethis framework

only occasionallyto consider, for example, the case of self-enforcingcontracts.

Thus, throughout this bookwe shall assumeaway most of the problemslegalscholars,lawyers, and judgesare concernedwith in practiceandconcentrate only on the economicaspectsof the contract.We shall beprimarily

interested in determining what contractual clausesrational economic

4 Introduction

individuals are willing to sign and what types of transactions they are willing

to undertake.If the transaction is a simple exchangeofgoodsor servicesfor money, we

shall beinterestedin the terms of the transaction.What is the priceperunit

the parties shall agree on? Doesthe contractspecifyrebates?Are therepenalty clausesfor late delivery?If so,what form do they take?And soon.Alternatively, if the transaction is an insurancecontract,we shall beinterested in detennining how the terms vary with the underlying risk, with therisk aversionofthe parties,orwith the private information the insureeor theinsurer might have about the exactnature of the risk. We beginby briefly

reviewing the simplest possiblecontractual situation an employer and

employeemight face:a situation involving only two parties,transacting only

once,and facing nouncertainty and no private information orhidden actions.

1.1Optimal Employment Contractswithout Uncertainty, HiddenInformation,or HiddenActions

Considerthe following standard bilateralcontracting problembetweenan

employerand employee:the employeehas an initial endowment of time,which she can keepfor herself of sell to the employeras labor services,becausethe employercan make productive use of the employee'stime.

Specifically,we can assume therefore that the parties'utility functions

dependboth on the allocationof employeetime and on their purchasing

power.Let us denotethe employer'sutility function as U(l, t) where/ is the

quantity of employeetime the employerhas acquiredand t denotes the

quantity of \"money\"\342\200\224or equivalently the \"output\" that this money canbuy3\342\200\224that he has at his disposal.Similarly, employeeutility is u(l, t), where/ is the quantity of time the employeehas kept for herselfand t is the

quantityof money that she has at her disposal.

Supposethat the initial endowment of the individuals is (lu i{)= (0,1)for the employer (hereafter individual 1) and (l2, i2) = (1> 0) for the

employee(hereafterindividual 2).That is,without any trade,the employergets no employeetime but is assumedto have all the money, while the

employeehas all of her time for herselfbut has no money.

3. Indeed, the utility of money here reflects the utility derived from the consumption of acomposite good that can bepurchased with money.

5 Introduction

Both individuals could decidenot to trade, in which casethey would

each achievea utility levelof U = U(0,1)and u = u(l,0),respectively.If,however,both utility functions are strictly increasingin both arguments and

strictly concave,then both individuals may be able to increasetheir jointpayoff by exchanging labor services/ for money/output. What will be theoutcomeof their contractualnegotiations?That is,how many hours ofworkwill the employeebe willing to offer and what (hourly) wagewill she bepaid?

As in most economicstexts, we shall assumethroughout this bookthat

contracting partiesare rational individuals who aim to achievethe highest

possiblepayoff. The joint surplus maximization problemfor bothindividuals can be representedas follows.If we denote by /,- the amount ofemployeetime actually consumedand by tt the amount of output consumedby eachparty i =1,2 after trade, then the partieswill solvethe following

optimization problem:

mzxU(!i,ti)+nu(!T,t2) (1-1)u,u

subjectto aggregateresourceconstraints:

k+h=k+h=land h+t2 =?i+?2=1Hereji canreflectboth the individuals' respectivereservationutility levels,U and u, and their relativebargaining strengths.

When both utility functions are strictly increasing and concave,themaximum is completelycharacterizedby the first-orderconditions

Ul+(iui=0=Ut+(Jict (1.2)which imply

Ui _ Ui

Ut ut

SeeFigure 1.1,whereindifferencecurvesare drawn.

In otherwords,joint surplus maximization is achievedwhen the marginalrates of substitution betweenmoney and leisurefor both individuals areequalized.

Thereare gains from trade initially if

Ui iii

Ut ut

6 Introduction

Figure 1.1Classical Edgeworth Box

Howthesegains are sharedbetweenthe two individuals is determinedby

/i.The employeegets a higher share of the surplus the higher /i is.Thehighest possibleutility that the employeecan get is given by the solutionto the following optimization problem:

maxu(l2, t2) subjectto \302\2437(1 -l2,l-t2)>U

Similarly, the highest payoff the employercan get is given by the solutionto

max\302\243/(/i,/i) subjectto u(l-ll,l-ti)>uThese extremeproblemscan be interpreted as simple bargaining gameswhereoneparty has all the bargaining powerand makesa take-it-or-leave-it offer to the other party. Note, however,that by increasingu in the

employer'sconstrainedmaximization problem or U in the employee'sproblemonecanreducethe surplus that either individual gets.Thus a givendivision of the surplus canbe parameterizedby either jj., U, or u,

dependingon how the joint surplus maximization problemis formulated.

7 Introduction

Throughout this bookwe shall representoptimal contracting outcomesas solutions to constrainedoptimization problemslike the two precedingproblems.We thus take as starting point the Coasetheorem(1960),that is,the efficient contracting perspective,as long as informational problemsarenot present.4Although this representationseemsquite natural, it isimportant to highlight that behind it lie two implicit simplifying assumptions.First,the final contractthe partiesend up signing is independentof the

bargaining processleading up to the signature of the contract.In reality it is likelythat most contractsthat we seepartly reflectprior negotiations and eachparty's negotiating skills.But, if the main determinants of contractsare the

parties' objectives,technologicalconstraints, and outsideoptions, then it isnot unreasonable to abstract from the potentially complexbargaining

gamesthey might be playing. At least as a first approach,this simplifying

assumption appearsto be reasonable.Second,as we have alreadymentioned,the other relevant dimension of

the contracting problem that is generally suppressedin the precedingformal characterizationis the enforcementof the contract.Without legalinstitutions to enforcecontractsmany gains from tradeare left unexploitedby rational individuals becauseone or both fear that the other will fail tocarry out the agreedtransaction.In the absenceof courtsor other modesof enforcement,a transaction betweentwo or morepartiescan take placeonly if the exchangeof goodsor servicesis simultaneous. Otherwise,the

party who is supposedto executeher trade last will simply walk away. In

practice,achieving perfectsimultaneity is almost impossible,so that

important gains from trademay remain unexploitedin the absenceof an efficientenforcementmechanism.

1.2Optimal Contractsunder Uncertainty

Thereis more to employment contractsthan the simple characterizationinthe previoussection.One important dimension in reality is the extent towhich employeesare insured against economicdownturns. In most

developedeconomiesemployeesare at leastpartially protectedagainst the risk

of unemployment. Most existing unemployment insurance schemesare

4. As we shall detail throughout this book, informational problems will act asconstraints onthe set of allocations that contracts can achieve.

Introduction

nationwide insurance arrangements, funded by employerand employeecontributions, and guaranteeing a minimum fraction of a laid-offemployee'spay over a imnimum time horizon (ranging from one year toseveralyearswith a sliding scale).A fundamental economicquestionconcerning these insurance schemesis how much \"business-cycle\" and other\"firm-specific\" risk should be absorbedby employersand how much by

employees.Should employerstake on all the risk, and if so,why? Onetheory, dating back to Knight (1921)and formalizedmore recentlybyKihlstrom and Laffont (1979)and Kanbur (1979),holdsthat employers(or\"entrepreneurs\") should take on all the risk and fully insure employees.Thereason is that entrepreneursare natural \"risk lovers\" and are bestable toabsorbthe risk that \"risk-averse\" employeesdo not want to take.

To be able to analyze this question of optimal risk allocationformallyone must enrich the framework of section1.1by introducing uncertainty.At one level this extensionis extremely simple.All it takes is theintroduction of the notions of a state of nature, a state space,and a state-contingent commodity. Arrow (1964)and Debreu(1959)were the first to

explorethis extension.Theydefine a state of nature as any possiblefuture

event that might affect an individual's utility. Thestatespaceis then simplythe set of all possiblefuture events, and a state-contingentcommodity is agood that is redefinedto be a new commodity in every different state ofnature. For example,a given number of hours of work is a different

commodity in the middle of an economicboom than in a recession.The difficulty is not in defining all thesenotions.The important

conceptual leap is rather to supposethat rational individuals are able to form acompletedescriptionof all possiblefuture eventsand, moreover,that allhave the samedescriptionof the state space.Once this commondescription is determined,the basiccontracting problemcan be representedlikethe precedingone,although the interpretation of the contractwill bedifferent. More precisely,it is possibleto represent a simple insurancecontract,which specifiestrades between the employerand employeein

different statesofnature, in an Edgeworth box.Beforedoing so,let usconsider a pure insurance problemwithout production.

Pure Insurance

Considerthe simplest possiblesetting with uncertainty. Assume that thereare only two possiblefuture statesof nature, 6L and 6H.Tobe concrete,let6Lrepresentan adverseoutput shock,or a \"recession,\"and 6Ha goodoutput

9 Introduction

realization,or a \"boom.\" For simplicity, we disregardtime endowments.Then the state of nature influences only the value of output eachindividual hasas endowment. Specifically,assumethe following respectiveendowments for each individual in eachstate:

(tw Jil)=(2,1), for individual 1(hH,hi)=(2,1), for individual 2

Thevariablefy thereforedenotesthe endowment of individual i in state ofnature dr Note that in a \"recession\"aggregateoutput\342\200\2242\342\200\224is

lowerthan in

a boom\342\200\2244.

Beforethe stateofnature is realizedeachindividual has preferencesoverconsumption bundles (tL, tH) representedby the utility functions V(tL, tH)

for the employerand v(tL, tH) for the employee.If the two individuals donot exchangeany contingent commodities,their

ex ante utility (beforethe state of nature is realized)is V = V(2,1)and v

= v(2, 1).But they can also increase their ex ante utility by coinsuring

against the economicrisk. Note,however, that someaggregaterisk isuninsurable: the two individuals can do nothing to smooth the differencein

aggregateendowments between the two states. Nevertheless,they canincreasetheir ex ante utility by poolingtheir risks.

As before, the efficient amount of coinsuranceis obtained when thefinal allocationsof eachcontingent commodity {{hL, t2{), (tm, ?2h)} are suchthat

VtL +livtL =0=VtH +/ivtH (1.3)

which implies

SeeFigure 1.2,whereindifferencecurvesare drawn.

It should be clearby now that the analysis of pure exchangeunder

certainty can be transposedentirely to the casewith uncertainty once oneenlargesthe commodity spaceto include contingent commodities.

However,to obtain a full characterizationof the optimal contracting

problem under uncertainty one needs to put more structure on this

framework. Indeed,two important elementsare hidden in the precedingcharacterizationof the optimal insurance contract:one is a descriptionof

10 Introduction

Slope=-

Figure 1.2Optimal Coinsurance

Allocation under optimalinsurance

-Initial

endowment: equalshares of output

-*-L

ex post utility once the state of nature has beenrealized,and the other isthe probability of eachstate occurring.

The first completeframework of decisionmaking under uncertainty,which explicitly specifiesthe probability distribution overstatesand the expost utility in eachstate,is due to von Neumann and Morgenstern(1944).It is this framework that is usedin most contracting applications.Interestingly,

eventhough there is by now a largeliterature exploring a wide rangeof alternative modelsof individual choiceand behaviorunder uncertainty,there have beenrelatively few explorationsof the implications for optimalcontracting of alternative modelsof behaviorunder uncertainty.

In the setup consideredby von Neumann and Morgenstern,individual

expost utility functions are respectivelyU(t) and u(f) for the employerandemployee,whereboth functions are increasingin t. If we callp,- e (0,1)the

probability of occurrenceof any particular state of nature dh the ex anteutility function is simply definedas the expectationover ex post utilityoutcomes:

V(f1L, t1H)=pLU(t1L)+pHU(t1H)

Introduction

and

v(t2L, t2H) =pLu{t2L) +pHu{t2H)

Theeasiestway of thinking about the probability distribution \\p,) is simplyas an objectivedistribution that is known by both individuals. But it is alsopossibleto think of {p;} as a subjectivebelief that is common to bothindividuals. In most contracting applicationsit is assumedthat all partiessharea common priorbeliefand that differencesin (posterior)probability beliefsamong the parties only reflect differencesin information. Although this

basic assumption is rarely motivated, it generally reflectsthe somewhat

vague idea that all individuals are born with the same\"view of the world\"

and that their beliefsdiffer only if they have had different life experiences.Recently, however, there have beensomeattempts to exploretheimplications for optimal contracting of fundamental differencesin beliefsamongcontracting parties.

It is instructive to consider the optimal insurance conditions (i.3)when the individuals' ex ante utility function is assumedto be the Von

Neumann-Morgensternutility function that we have specified.In that

casethe marginal rate of substitution between commodities1and 2 is

given by

Vu. _ Pl UVu.)VtH Ph U'(t1H)

As this expressionmakesclear,the marginal rate of substitution betweenthe two contingent commoditiesvarieswith the probability distribution.

Moreover,the marginal rate of substitution is constant along the 45\302\260 line,where t1L = t1H.

Optimal Employment Contractsunder Uncertainty

Using the framework of von Neumann and Morgenstern,let us comebackto the contracting problemof section1.1with two goods,leisure / and aconsumption good t, which canbe readily extendedto include uncertaintyas follows:

Let (liL, hO and (hit, hH) represent the two different state-contingenttime/output bundles of the employer,and (l2L, t2L) and (l2H, t2H) the two

different state-contingenttime/output bundles of the employee.Also let

(li}, Uj) denote their respectiveinitial endowments, (i =1,2;;'=L,H).Then

12 Introduction

the optimal insurance contractsignedby the two individuals canberepresented as the solution to the optimal contracting problem:

max[pLU(l1L, t1L)+pHU(l1H,t1H)]

subjectto

pMhL,hd +Phu(12h , hH) ^ u (1.4)and

k, +l2, < kj +h, for j=L,H

hj +12,< h, +t2j for ] =L,Hwhere

u =pLu(l2L, t2L)+pHu(l2H, t2H)

One important advantage of the von Neumann and Morgensternformulation is that an individual's attitude toward risk canbe easilycharacterizedby the curvature of the ex post utility function. Thus, if both

\302\243/(\342\200\242)

and u(-)are strictly concave,then both individuals are risk averseand want to sharerisk, whereasif both

\302\243/(\342\200\242)

and u(-) are strictly convex,then bothindividuals are risk loving and want to trade gambleswith eachother.

For now, supposethat both individuals are risk averse,so that their expost utility functions are strictly concave.Then the contract-maximizingjoint surplus is fully characterizedby the first-orderconditions:

Ui\\hjihj) _ ui\\hj,hi) /-i r\\

Ut(lij,tij) ut(l2ht2j)

1 ln lj constant across0/s (1-6)ui \\hi j h;)

ut\\l2l,hj)constant across9/s (1-7)

Condition (1.5)is the familiar condition for efficient trade ex post.Thismeansthat ex ante efficiencyis achievedif and only if the contractis alsoexpostefficient.We shall seethat when incentive considerationsenter into

the contracting problemthere is usually a conflict betweenex ante and expostefficiency

13 Introduction

Conditions(1.6)and (1.7)are conditionsof optimal coinsurance.Condition (1.7)is sometimesreferred to as the Borchrule (1962):optimalcoinsurance requiresthe equalizationof the ratio ofmarginal utilities ofmoneyacrossstatesof nature.

A risk-neutral individual has a constant marginal utility of money.Thus,if one of the two individuals is risk neutral and the other individual is risk

averse,the Borch rule says that optimal insurance requires that the risk-averseindividual must alsohave a constant marginal utility ofmoney acrossstatesof nature. In other words, the risk-averseindividual must getperfectinsurance.This is exactlythe solution that intuition would suggest.

To summarize, optimal contracting under uncertainty would resultin perfect insurance of the employeeagainst economicrisk only if the

employeris risk neutral. In general,however,when both employerand

employeeare risk averse,they will optimally sharebusinessrisk. Thus the

simple Knightian idea that entrepreneursperfectly insure employeesis

likely to hold only under specialassumptions about risk preferencesofentrepreneurs.An individual's attitude toward risk is driven in part by initial

wealth holdings. Thus it is generallyacceptedthat individuals' absoluteriskaversiontends to decreasewith wealth. If extremely wealthy individuals areapproximately risk neutral and poor individuals are risk averse,then onespecialcasewherethe Knightian theory would bea goodapproximation iswhen wealth inequalities are extremeand a few very wealthy entrepreneursprovidenearly perfectjobsecurity to a massofpooremployees.

It should be clearfrom this brief overview of optimal contracting under

uncertainty that the presumption of rational behaviorand perfectenforceability

of contractsis lessplausiblein environments with uncertainty than

in situations without uncertainty. In many contracting situations in practiceit is possiblethat the contracting partieswill beunable to agreeon acomplete descriptionof the state spaceand that, as a consequence,insurancecontractswill be incomplete.The rationality requirements imposedon the

contracting parties and the enforcementabilities assumedof the courtsshould bekept in mind as caveatsfor the theory of contracting when facedwith very complexactual contractualsituations wherethe partiesmay havelimited abilities to describepossiblefuture events and the courts havelimited knowledgeto be able to effectively stick to the original intentions

of the contracting parties.Another important simplifying assumption to bear in mind is that it is

presumed that each party knows exactly the intentions of the other

14 Introduction

contracting parties.However,in practicethe motives behind an individual's

willingness to contractare not always known perfectly.As a consequence,suspicionabout ulterior motives often may lead to breakdownofcontracting.

These considerationsare the subject of much of this bookand arebriefly reviewedin the next sectionsof this chapter.

1.3Information and Incentives

The precedingdiscussionhighlights that even in the best possiblecontracting environments, where comprehensiveinsurance contractscan bewritten, it is unlikely that employeeswill beperfectlyinsured againstbusiness risks.Thereasonis simply that the equilibrium priceofsuch insurancewould be too high if employerswerealsoaverseto risk.

Another important reasonemployeesare likely to get only limitedinsurance is that they needto have adequate incentives to work. If the output

producedby employeestends to be higher when employeesexertthemselves more, or if the likelihoodof a negative output shock is lower if

employeesare more dedicatedor focusedon their work, then economicefficiency requires that they receive a higher compensationwhen their

(output) performanceis better.Indeed,if their pay is independentofperformance and if their job security is not affectedby their performance,why

should they put any effort into their work? This is a well-understoodidea.Even in the egalitarian economicsystem of the former SovietUnion the

provision of incentives was a generally recognizedeconomicissue,and overthe years many ingenious schemeswere proposedand implemented toaddressthe problemofworker incentives and alsofactory managers'incentives. What was lesswell understood,however,was the trade-offbetweenincentives and insurance.How far should employeeinsurance be scaledbackto make way for adequatework incentives?Howcouldadequateworkincentives bestructured while preservingjob security as much aspossible?Theseremainedopenand hotly debatedquestionsoverthe successivefive-year plans.

Much of Part Iof this bookwill be devotedto a formal analysis of this

question.Twogeneraltypes of incentive problemshave beendistinguished.One is the hidden-information problem and the other the hidden-actionproblem.The first problemrefers to a situation where the employeemayhave private information about her inability or unwillingness to take on

Introduction

certaintasks.That is,the information about somerelevant characteristicsofthe employee(her distastefor certain tasks, her levelof competence)arehidden from her employer.The secondproblemrefers to situations wherethe employercannot seewhat the employeedoes\342\200\224whether she works ornot, how hard she works, how carefulshe is, and soon. In these situations

it is the employee'sactionsthat are hidden from the employer.Problemsof hidden information are often referred to as adverse

selection, and problemsofhidden actionsasmoral hazard.In practice,ofcourse,most incentive problems combine elements of both moral hazard andadverseselection.Also, the theoreticaldistinction betweena hidden-actionand a hidden-information problemcan sometimesbe artificial.

Nevertheless,it is useful to distinguish betweenthese two types of incentive

problems, in part becausethe methodologythat has beendevelopedto analyzetheseproblemsis quite different in eachcase.

AdverseSelection

Chapters2 and 3 provide a first introduction to optimal contractswith

hidden information. These chapters examineoptimal bilateral contractswhen one of the contracting parties has private information. Chapter 2explorescontracting situations wherethe party making the contractoffersis the uninformed party. Thesesituations are often referredto asscreeningproblems,sincethe uninformed party must attempt to screenthe different

piecesof information the informed party has.Chapter3 considerstheopposite situation wherethe informed party makesthe contractoffers.Thesesituations fall under the generaldescriptiveheading ofsignaling problems,asthe party making the offermay attempt to signal to the otherparty what it

knows through the type of contractit offersor other actions.The introduction of hidden information is a substantial breakfrom the

contracting problemswe have alreadyconsidered.Now the underlying

contracting situation requiresspecificationof the private information one ofthe partiesmight have and the beliefsof the other party concerningthat

information in addition to preferences,outsideoptions, initial endowments,a state space,and a probability distribution overstatesof nature.

In the contextof employment contractsthe type of information that mayoften beprivate to the employeeat the time ofcontracting is herbasicskill,

productivity, or training. In practice,employerstry to overcomethis

informational asymmetry by hiring only employeeswith some training or only

high schooland collegegraduates.

16 Introduction

In a pathbreaking analysis Spence(1973,1974)has shown how educationcan be a signal of intrinsic skill or productivity. The basicidea behind his

analysis is that more-ableemployeeshave a lowerdisutility of educationand therefore are more willing to educate themselves than less-ableemployees.Prospectiveemployersunderstand this and thereforeare willing

to pay educatedworkersmore even if educationperse doesnot add anyvalue.We review Spence'smodel and other contracting settings with

signaling in Chapter3.Another way for employersto improve their pool of applicants is to

commit to pay greater than market-clearingwages.This tends to attract

better applicants,who generally have betterjob opportunities and aremorelikely to do well in interviews. Sucha policy naturally gives risetoequilibrium unemployment, as Weiss (1980)has shown. Thus, as Akerlof, in his1970article,and Stiglitz, in many subsequentwritings, had anticipated,the

presenceof private information about employeecharacteristicscanpotentially explain at a microeconomiclevel why equilibrium unemploymentand other forms of market inefficienciescanarise.With the introduction ofasymmetric information in contracting problemseconomistshave at lastfound plausibleexplanationsfor observedmarket inefficienciesthat had

long eluded them in simpler settings of contracting under completeinformation.

Or at least they thought so.Understandably, given the importance of thebasiceconomicissue,much of the subsequentresearchon contracting under

asymmetric information has tested the robustnessof the basicpredictionsof market inefficienciesand somewhat deflatedearly expectationsabout ageneraltheory of market inefficiencies.

A first fundamental question to be tackledwas, Just how efficient cancontracting under asymmetric information be?The answer to this questionturns out to besurprisingly elegantand powerful. It is generally referredtoas the revelation principleand is one of the main notions in contracteconomics. The basic insight behind the revelationprincipleis that todetermine optimal contractsunder asymmetric information it sufficesto consideronly one contract for each type of information that the informed party

might have, but to make sure that each type has an incentive to selectonlythe contractthat is destinedto him/her.

Moreconcretely,consideran employerwho contractswith two possibletypes of employees\342\200\224a \"skilled\" employeeand an \"unskilled\" one\342\200\224and

who doesnot know which is which. The revelationprinciplesaysthat it is

17 Introduction

optimal for the employerto consideroffering only two employmentcontracts\342\200\224one destinedto the skilledemployeeand the other to the unskilledone\342\200\224but to make sure that each contractis incentive compatible.That is,that each type of employeewants to pick only the contractthat is destinedto her.Thus, accordingto the revelationprinciple,the employer'soptimalcontracting problemreducesto a standard contracting problem,but with

additional incentive compatibility constraints.As a way of illustrating a typical contracting problemwith hidden

information, let us simplify the previousproblemwith uncertainty with a simpleform of private information added.Supposefirst that employeetime and

output enter additively in both utility functions: define them as U[ccd(l-/)-t] for the employerand u(6l+ t) for the employee,where

\342\200\242 (1-/) is the employeetime soldto the employer,and / is the time the

employeekeepsfor herself;\342\200\242 t is the monetary/output transfer from the employerto the employee;\342\200\242 a is a positive constant; and\342\200\242 6measuresthe \"unit value of time,\" or the skill levelof the employee.

The variable 6 is thus the state of nature, and we assumeit is learnedprivately by the employee before signing any contract. Specifically, the

employeeknows whether sheis skilled,with a value of time 6H,or unskilled,with a value of time 6L < 6H.The employer,however,knows only that the

probability of facing a skilled employeeis pH.When the employerfacesa skilled employee,the relevant reservation

utility is uH = u(6H), and when he faces an unskilled employee,it is uL =u(6L)-5Assume that the employee'stime is more efficient when soldto the

employer;that is,assumea > 1.Then,if the employercouldalsolearn the

employee'stype, he would simply offer in state 0, a contractwith atransfer tj

= 6, in exchangefor all her work time (that is,1-/,\342\200\242

=1).Suchacontract would maximize production efficiency, and since the employee'sindividual rationality constraint, u(tj) > u(6j), would be binding under this

contract,it would maximize the employer'spayoff.When employee productivity is private information, however, the

employerwould not beableto achievethe samepayoff, for if the employeroffers a wage contract

t,-= 0, in exchangefor 1unit of work time, all

5. Indeed, in state6>;,

the employee's endowment l2]= 6r

18 Introduction

employeetypes would respondby \"pretending to be skilled\" to get the

higher wage 6H-Note that for the employee type to be truly private information it

must also be the casethat the employee'soutput is not observable.If it

were,the employercouldeasilyget around the informational asymmetryby including a \"money-back guarantee\" into the contract should the

employee'soutput fall short of the promisedamount. Assumptions similarto the nonobservability of output are required in these contractingproblems with hidden information. A slightly morerealisticassumption servingthe samepurposeis that the employee'soutput may be random and that

a \"no-slavery\" constraint prevents the employer from punishing the

employeeex post for failing to reach a given output target.If that is thecase,then an inefficient employee can always pretend that she was

\"unlucky.\" Even if this latter assumption is moreappealing,we shall simplyassumehere for expositionalconvenience(asis often done) that output isunobservable.

Under that assumption, the only contractsthat the employercan offerthe employeeare contractsoffering a total payment of t(l) in exchangefor

(1-/) units of work. Although this classof contractsismuch simpler than

most real-worldemployment contracts,finding the optimal contractsin theset of all (nonlinear) functions [t(l)}couldbe a daunting problem.Fortunately, the revelationprincipleoffersa key simplification. It saysthat all the

employerneedsto detennineisa menu of two \"point contracts\":(tL, lL) and

{tH, Ih), where,by convention, (tn /,) is the contractchosenby type j.Thereasonwhy the employerdoesnot needto specifya full (nonlinear)contract t([) is that each type of employeewould pick only one point on thefull schedulet(t) anyway. So the employermight as well pick that point

directly. However,eachpoint has to be incentive compatible.That is, type

6H must prefercontract(tH, lH) over(tL, lL),and type 6L contract(tL, lL)over(tH, Ih)-

Thus the optimal menu of employment contractsunder hiddeninformation canberepresentedas the solution to the optimal contracting problemunder completeinformation:

msLx{pLU[aeL(1-lL)-tL]+pHU[a6H(1-lH) -tH]}(/,,r,)

subjectto

u(iLeL+tL)>u(eL)

19 Introduction

and

u{iHeH+tH)>u{eH)

but with two additional incentive constraints:

u(lHOH+tH)^u(lLeH+tL)

and

u(iLeL+tL)>u(iH9L+tH)

The solution to this constrainedoptimization problem will produce themost efficient contractsunder hidden information. As this problemimmediately reveals,the addition of incentive constraints will in generalresultin lessefficient allocationsthan under completeinformation. In general,optimal contractsunder hidden information will be second-bestcontracts,which do not achieve simultaneously optimal allocative anddistributive efficiency.Much of Chapter2 will be devoted to the analysis of thestructure of incentive constraints and the type of distortions that resultfrom the presenceof hidden information. The generaleconomicprinciplethat this chapter highlights is that hidden information results in a form

of informational monopoly power and allocativeinefficienciessimilar tothose produced by monopolies.In the precedingexample,the employermight chooseto suboptimally employ skilled employees(by setting 1- lH

< 1)to be able to pay unskilled employeesslightly less.6In a nutshell, themain trade-off that is emphasizedin contracting problemswith hiddeninformation is one between informational rent extractionand allocativeefficiency.

6. Oneoption is to have a contract with allocative efficiency, that is, lH = lL = 0 and tH =tL = 6H.This leaves informational rents for the unskilled employee relative to her outsideopportunity. It may therefore be attractive to lower skilled employment (that is, set lH >

0)\342\200\224

at an allocative cost of (a -l)lH\342\200\224in

order to lower tL without violating the incentiveconstraint:

Intuitively, lowering skilled employment allows the employer to lower tH by a significantamount, since the skilled employee has a high opportunity cost of time. Therefore,

\"pretending

to beskilled\" becomeslessattractive for the unskilled employee (who has a lower

opportunitycost of time), with the result that a lower transfer tL becomescompatible with the

incentive constraint. The trade-off between allocative efficiency and rent extraction will bedetailed in the next chapter.

Introduction

If the presenceof hidden information may give rise to allocativeinefficiencies such as unemployment, it doesnot follow that public intervention

is warranted to improve market outcomes.Indeed,the incentive constraintsfacedby employersare alsolikely to be facedby plannersor publicauthorities. It is worth recallinghere that the centrally plannedeconomyof theSovietUnion was notoriousfor its overmanning problems.It may not havehad any official unemployment, but it certainly had huge problemsofunderemployment. Chapters7 and 13will discussat length the extent towhich market outcomesunder hidden information may be first- or second-best efficient and when the \"market mechanism\" may be dominated bysomebetter institutional arrangement.

Our discussionhas focusedon a situation where the employeehas aninformational advantage over the employer.But, in practice,it is often the

employerthat has more information about the value of the employee'swork. Chapter 2 also exploresseveral settings where employershave

private information about demandand the value ofoutput. As we highlight,these settings are perhaps more likely to give rise to unemployment.Indeed,layoffs can be seenas a way for employersto crediblyconveytotheir employeesthat the economicenvironment of their firm hasworsenedto the extent that pay cuts may beneededfor the firm to survive.

MoralHazard

Chapter 4 introducesand discussesthe other major classof contracting

problemsunder asymmetric information: hidden actions.In contrast tomost hidden information problems,contracting situations with hiddenactions involve informational asymmetries arising after the signing of acontract.In these problemsthe agent (employee)is not askedto choosefrom a menu of contracts,but rather from a menu of action-rewardpairs.

Contracting problemswith hidden actionsinvolve a fundamental

incentive problem that has long beenreferred to in the insurance industry asmoral hazard:when an insureegets financial or other coverageagainst abad event from an insurer she is likely to belesscarefulin trying to avoidthe bad outcomeagainst which she is insured.This behavioralresponsetobetter insurance arisesin almost all insurancesituations, whether in life,health, fire, flood,theft, or automobile insurance.When a persongetsbetterprotectionagainst a bad outcome,shewill rationally invest fewerresourcesin trying to avoid it. One of the first and most striking empiricalstudiesof

21 Introduction

moral hazard is that of Peltzman (1975),who has documentedhow theintroduction of laws compellingdrivers to wear seat beltshas resultedin

higher averagedriving speedsand a greaterincidenceof accidents(involving,

in particular, pedestrians).How do insurers deal with moral hazard? By charging proportionally

morefor greatercoverage,thus inducing the insureeto trade off thebenefits of better insurance against the incentive costof a greaterincidenceofbad outcomes.

Incentive problems like moral hazard are also prevalent in

employment relations.As is now widely understood,if an employee'spay and

job tenure are shieldedagainst the risk of bad earnings, then shewill worklessin trying to avoid theseoutcomes.Moralhazard on the jobwas one ofthe first important new economicissuesthat Sovietplannershad to contendwith. If they were to abolishunemployment and implement equaltreatment of workers, how could they also ensure that workerswould work

diligently? As they reluctantly found out, there was unfortunately nomiraclesolution. For a time ideologicalfervor and emulation of modelworkersseemedto work, but soonmajor and widespreadmotivationproblems arose in an economicsystem foundedon the separationof pay from

performance.Employerstypically respondto moral hazard on the job by rewarding

goodperformance(through bonus payments, piecerates,efficiencywages,stock options, and the like) and/or punishing bad performance(through

layoffs).As with insurancecompanies,employersmust trade off thebenefits of better insurance (in terms of loweraveragepay) against the costsinlowereffort provision by employees.The most spectacularform ofincentive pay seennowadays is the compensationof CEOsin the United States.Arguably, the basictheory of contracting with hidden actionsdiscussedinChapter 4 providesthe main theoreticalunderpinnings for the types ofexecutivecompensationpackagesseentoday.According to the theory, evenrisk-averseCEOsshould receivesignificant profit- and stock-performance-basedcompensationif their (hidden)actionshave a major impact on thefirm's performance.7

While it is easy to graspat an intuitive level that there is a basictradeoff betweeninsurance and incentivesin most employment relations, it is

7. Actual CEOcompensation packages have also shown someserious limitations, which the

theory has addressed too; more on this topic will follow.

22 Introduction

lesseasyto seehow the contractshould bestructured to besttradeoff effort

provision and insurance.Formally, to introduce hidden actions into the precedingemployment

problemwith uncertainty, supposethat the amount of time (1-/) workedby the employeeis private information (a hidden action).Suppose,inaddition, that the employeechoosesthe action(1-/) beforethe state ofnature

6j is realizedand that this actioninfluencesthe probability of the state ofnature:when the employeechoosesaction(1-/), output for the employeris simply 9H with a probability function pH[l-/],increasingin 1-/ (and 9L

with a probability function pL[l-/] =1-pH[l-/]).8Theusualinterpretation here is that (1-/) standsfor \"effort,\" and moreeffort produceshigher

expectedoutput, at cost1-/ for the employee,say.9 However,it is notguaranteed to bring about higher output, sincethe bad state of nature 6L maystill occur.Note that if output wereto increasedeterministically with effortthen the unobservability of effort would not matter becausethe agent'shidden effort supply couldbe perfectlyinferred from the observationofoutput.

Sinceeffort (1-/) is not observable,the agent canbecompensatedonlyon the basisof realizedoutput Q-r

The employeris thus restrictedto

offeringa compensationcontractt(6}) to the employee.Also the employermust

now take into accountthe fact that (1-/) will bechosenby the employeeto maximize her own expectedpayoff under the output-contingent

compensation schemet(6j). In otherwords, the employercannow make only abestguessthat the effort levelchosenby the employeeis the outcomeofthe employee'sown optimization problem:

(l-l)esLrgmsix{pL[l-l]u[t(eL)+l]+pH[l-l]u[t(6H)+l]}I

Therefore,when the employerchoosesthe optimal compensationcontract[t(6j)}to maximize his expectedutility, he must make sure that it is in the

employee'sbestinterest to supply the right levelof effort (1-/).In otherwords, the employernow solvesthe following maximization problem:

msix{pL[l-l]U[eL-t(eL)]+pH[l-l]U[9H-t(dH)]}

8.Where pff[-] (respectively pL[-]) is an increasing (respectively, decreasing) function of(1-0-9. For simplicity, we assume here that the opportunity cost of time for the employee isindependent of the state of nature.

23 Introduction

subjectto

pL[l-l]u[t(6L)+l]+pH[l-l]u[t(6H)+l]>u=u(l) (IR)and

(l-Qeaigmax{pdl-lMt{eL)+l]+pH[l-l]u[t(eH)+rft (IC)I

As in contracting problemswith hidden information, when the actionsupplied by the employeeisnot observablethe employermust take into

consideration not only the employee'sindividual rationality constraint but alsoher incentive constraint.

Determining the solution to the employerproblemwith both constraintsis not a trivial matter in general.Chapter4providesan extensivediscussionof the two main approaches toward characterizingthe solution to this

problem.For now we shall simply point to the main underlying idea that anefficient trade-offbetweeninsuranceand incentives involves rewarding the

employeemost for output outcomesthat are most likely to arisewhen sheputs in the requiredlevelofeffort and punishing her the most for outcomesthat are most likely to occurwhen sheshirks.Theapplicationof this

principlecangive rise to quite complexcompensationcontractsin general,often

morecomplexthan what we seein reality. There is one situation, however,wherethe solution to this problemis extremely simple:when the employeeis risk neutral. In that caseit is efficient to have the employeetake on all the

output risk so as to maximize her incentivesfor effort provision.That is,when the employeeis risk neutral, she should fully insure the employer.

One reason why this simple theory may predict unrealistically

complex incentive schemesis that in most situations with hidden actionstheincentive problem may be multifaceted.CEOs,for example,can takeactionsthat increaseprofits, but they canalsomanipulate earnings, or \"run

down\" assetsin an effort to boostcurrent earnings at the expenseof future

profits. Theycan alsoundertake high-expected-returnbut high-riskinvestments. It hasbeensuggestedthat when shareholdersor any otheremployerthus face a multidimensional incentive problem, then it may beappropriate

to respondwith both less \"high powered\"and simpler incentiveschemes.We exploretheseideasboth in Chapter6,which discusseshiddenaction problemswith multiple tasks, and in Chapter10,which considerslong-term incentive contracting problemswhere the employeetakesrepeated hidden actions.

24 Introduction

Chapter6 alsoconsidersmultidimensional hidden information problemsaswell asproblemscombining both hidden information and hidden actions.All these problemsraise new analytical issuesof their own and produceinteresting new insights. We providean extensivetreatment of someof themost important contracting problemsunder multidimensional asymmetricinformation in the researchliterature.

Part I of our book also discussescontracting situations with anintermediate form of asymmetric information, situations where the informed

party can credibly discloseher information if she wishes to do so.Thesesituations, which are consideredin Chapter 5, are mostly relevant for

accounting regulation and for the designof mandatory disclosurerules,which are quite pervasivein the financial industry. Besidestheir obvious

practicalrelevance,thesecontractualsituations are alsoofinterestbecausethey dealwith a very simple incentive problem,whether to discloseor hiderelevant information (while forging information is not an availableoption).Becauseof this simplicity, the contractualproblemsconsideredin Chapter5 offeran easyintroduction to the generaltopicof contracting underasymmetric information. One of the main ideasemerging from the analysis ofcontracting problemswith private but verifiable information is that

incentives for voluntary disclosurecan be very powerful. The basiclogic,which

is sometimesreferred to as the \"unraveling result,\" is that any sellerof agoodor service(e.g.,an employee)hasevery incentive to revealgoodinformation about herself,such as high test scoresor a strong curriculum vitae.

Employersunderstand this fact and expectemployeesto be forthcoming.If an employeeis not, the employerassumesthe worst. It isfor this reasonthat employeeshave incentivesto voluntarily discloseall but the worst

pieceof private verifiable information. This logicis so powerful that it isdifficult to seewhy there should bemandatory disclosurelaws. Chapter5discussesthe main limits of the unraveling result and explainswhen

mandatorydisclosurelaws might bewarranted.

Finally, it is worth stressingthat although our leadingexamplein this

introduction is the employment relation, each chapter contains severalother classicapplications,whether in corporatefinance, industrial

organization, regulation, public finance,or the theory of the firm. Besideshelpingthe readersto acquaint themselveswith the core conceptsof the theory,theseapplicationsare alsomeant to highlight the richnessand broadrelevance of the basictheory of contracting under private information.

25 Introduction

1.4Optimal Contracting with Multilateral Asymmetric Information

The contracting situations we have discussedsofar involve only one-sidedprivate information or one-sidedhidden actions.In practice,however,thereare many situations whereseveralcontracting partiesmay possessrelevant

private information or be calledto take hidden actions.A first basicquestion ofinterestthen iswhether and how the theory ofcontracting with

onesided private information extends to multilateral settings. Part IIof this

bookisdevotedto this question.It comprisestwo chapters.Chapter7 dealswith multilateral private information and Chapter8 with multilateral hidden

actions.Besidesthe obvioustechnicaland methodologicalinterest in

analyzing these more general contractual settings, fundamental economicissuesrelating to the constrainedefficiency of contractual outcomes,therole of competition, and the theory of the firm are alsodealtwith in thesechapters.

While the generalmethodologyand most of the core ideasdiscussedinPart I extend to the generalcaseof multilateral asymmetric information,there is one fundamental difference.In the one-sidedprivate information

casethe contractdesignproblemreducesto a problemof controlling theinformed party's response,while in the multilateral situation the

contracting problembecomesone of controlling the strategicbehaviorof severalparties interacting with each other.That is, the contract designproblembecomesone of designing a gamewith incomplete information.

One of the main new difficulties then ispredicting how the gamewill beplayed.Thebestway of dealing with this issueis in fact to designthecontract in such a way that eachplayerhas a unique dominant strategy. Thenthe outcomeof the game is easy to predict,sincein essenceall strategicinteractionshave then beenremoved.Unfortunately, however, contractswhereeachparty hasa unique dominant strategy aregenerally not efficient.Indeed,in a major result which builds on Arrow's (1963)impossibility

theorem,Gibbard (1973)and Satterthwaite (1975)have shown that it is

impossiblein generalto attain the full-information efficient outcomewhen

there are more than two possibleallocationsto choosefrom and when the

contracting parties'domain ofpreferencesisunrestricted (that is,when theset ofpossibletypes of eachcontracting party is very diverse).Rather than

stick to predictablebut inefficient contracts,it may then generally bedesirable to agree on contractswhere the outcomeis lesspredictablebut on

Introduction

average more efficient (that is, contracts where each party's responsedependson what the other contracting partiesare expectedto do).From atheorist'sperspectivethis isa mixed blessingbecausethe proposedefficientcontracts(or \"mechanisms,\" as they are often referredto in multilateral

settings) may besomewhat fragile and may not always work in practiceas the

theory predicts.

Auctions and Tradeunder Multilateral Private Information

Perhapsthe most important and widely studiedproblemofcontracting with

multilateral hidden information is the design of auctions with multiplebidders,each with his or her own private information about the value ofthe objectsthat are put up for auction.10Accordingly, Chapter7 devotesconsiderablespaceto a discussionof the main ideasand derivation of keyresults in auction theory, such as the revenue equivalencetheorem or the

winner's curse.The first result establishesthat a number of standardauctions yield the sameexpectedrevenueto the sellerwhen biddersare riskneutral and their valuations for the object are independently and

identicallydistributed. The secondidea refers to the inevitable disappointment

of the winner in an auction wherebiddersvalue the objectin a similar way

but have different prior information about its worth: when shelearns that

shewon shealsofinds out that her information ledher to be overoptimisticabout the value of the object.

In recentyearstherehasbeenan explosionof researchin auction theory

partly becauseof its relevanceto auction designin a number of important

practicalcases.Coveringthis researchwould requirea separatebook,and

Chapter7 can serveonly as an introduction to the subject.Auction designwith multiple informed biddersis by no means the only

example of contracting with multilateral hidden information. Another

leadingexample,which isextensively discussedin Chapter7, is trade in

situations whereeachparty hasprivate information about how much it valuesthe goodor the exchange.

A major economicprinciple emerging from the analysis of contractingwith one-sidedhidden information is the trade-offbetweenallocativeefficiency and extractionof informational rents.If the bargaining power lies

10.Despite its relative fragility, the theory of contracting with multilateral hiddeninformation has proved to beof considerable practical relevance, as for example in the design ofspectrum and wireless telephone license auctions (seefor example Klemperer, 2002).

Introduction

with the uninformed party, as we have assumed,then that party attemptsto appropriatesomeof the informational rents of the informed party at the

expenseof allocativeefficiency.But note that if the informed party (e.g.,the employeein our example)has all the bargaining powerand makesthecontractoffer,then the contracting outcomeis always efficient. So,if the

overriding objectiveis to achievea Pareto efficient outcome(with, say, nounemployment), then there appearsto be a simple solution when there is

only one-sidedhidden information: simply give all the bargaining powertothe informed party.

In practice,however,besidesthe difficulty in identifying who theinformed party is,there isalsothe obvious problemthat generally all partiesto the contractwill have somerelevant private information. Therefore,thenatural contracting setting in which to posethe question of the efficiencyof tradeunder asymmetric information and how it varieswith the

bargaining powerof the different parties isone of multilateral asymmetricinformation. A fundamental insight highlighted in Chapter7 is that the mainconstraint on efficient trade is not so much eliciting the parties'privateinformation as ensuring their participation.Efficient trade can (almost)always beachievedif the parties'participation isobtainedbeforethey learntheir information, while it cannot be achievedif participation is decidedwhen they alreadyknow their type.

Applying this insight to our labor contracting example,the analysis in

Chapter7 indicatesthat labormarket inefficiencieslike unemployment areto be expectedin an otherwisefrictionlesslabor market when employershave market power and employeesprivate information about their

productivity, or when there is two-sidedasymmetric information. It must bestressed,however, that policyintervention that is not basedon anyinformation superiorto that availableto the contracting partieswill not beableto reduceor eliminate these inefficiencies.But labor market policiesthat

try to intensify competitive bidding for jobsor for employeesshould lowerinefficienciescausedby hidden information.

MoralHazard in Teams,Tournaments, and Organizations

Contracting situations whereseveralparties take hidden actionsare oftenencounteredin firms and other organizations. It is for this reason that the

leading applicationof contracting problems involving multisided moralhazard isoften seento be the internal organization of firms and othereconomic institutions. Someprominent economictheorists of the firm like

28 Introduction

Alchian and Demsetz(1972)or Jensen and Meckling (1976)go as far asarguing that the resolution of moral-hazard-in-teamsproblems (whereseveralagentstake complementary hidden actions)is the raisond'etreofa firm. They contendthat the roleofa firm's ownerormanager is to monitor

employeesand make sure that they take efficient actionsthat are hiddento others.Hence,the analysis ofcontracting problemswith multisided moralhazard is important if only as an indirect vehiclefor understandingeconomic organizations and firms.

Accordingly, Chapter8 coversmultiagent moral hazard situations with aparticular focuson firms and their internal organization. To illustrate someof the key insights and findings coveredin this chapter,considerthesituation where our employernow contractswith two employees,A and B,eachsupplying a (hidden) \"effort\" (1- lA) and (1-lB).A key distinction in

contracting problemswith multisided moral hazard concernsthe measureofperformance:Iseach employee'sperformancemeasuredseparately,or isthere a single aggregatemeasureof both employees'contributions?

In the former case,when the output of eachemployeeis observableandis given by, say, 6A]with probability pAj and 6Bj with probability pBj, for ;'=L,H, the employer'sproblemis similar to the single-agentmoral hazardproblemdescribedearlier,with the new featurethat now the employercanalsobasecompensationon eachemployee'srelative performance:

9a, ~6b,

An important classof incentive contracting situations in which agentsarerewardedon the basisof how well they did relative to othersis rank-ordertournaments. Many sports contests are of this form, and promotionsofemployeesup the corporateladdercanalsobeseenas a particular form oftournament.

Thus, in our employment problemwith two employeesand observableindividual outputs, the employermay be able to providebetter incentiveswith lessrisk exposureto the two employeesby basing compensationonhow well they perform relative to each other.Thispossibility can be seenas one reason why firms like to provide incentives to their employeesthrough promotion schemes,appointing only the better employeesto

higher paying and more rewarding jobs.The reasonwhy relativeperformance evaluation improves incentivesis that when employeesare exposedto the same exogenousshocksaffecting their performance(changesin

demand for their output or quality of input supplies,say), it ispossibleto

29 Introduction

shieldthem against theserisks by filtering out the common shockfrom their

performancemeasure.Toseehow this works, think that the probability pA,

(iesp.,pBl)dependsnot only on individual effort (1-lA) [resp.,(1-lB)]but

also on a random variable that affectsboth agents.In this case,it makessenseto link an employee'scompensationpositively to her own