Consolidated Financial Statements for Holding Companies

556

Board of Governors of the Federal Reserve System Instructions for Preparation of Consolidated Financial Statements for Holding Companies Reporting Form FR Y-9C Reissued March 2013

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Consolidated Financial Statements for Holding Companies

Board of Governors of the Federal Reserve System

Instructions for Preparation of

Consolidated Financial Statements forHolding Companies

Reporting Form FR Y-9C

Reissued March 2013

Contents forY-9C Instructions

Organization of the Instruction Book

The instruction book is divided into three sections:

(1) The General Instructions describing overall report-ing requirements.

(2) The Line Item Instructions for each schedule ofthe report for the consolidated holding company.

(3) The Glossary presenting, in alphabetical order, defi-nitions and discussions of accounting treatmentsunder generally accepted accounting principles(GAAP) and other topics that require more extensivetreatment than is practical to include in the line iteminstructions or that are relevant to several line itemsor to the overall preparation of these reports.

In determining the required treatment of particular trans-actions or portfolio items or in determining the defini-

tions and scope of the various items, the General Instruc-tions, the line item instructions, and the Glossary (all ofwhich are extensively cross-referenced) must be usedjointly. A single section does not necessarily give thecomplete instructions for completing all the items of thereports. The instructions and definitions in section (2) arenot necessarily self-contained; reference to more detailedtreatments in the Glossary may be needed. However, theGlossary is not, and is not intended to be, a com-prehensive discussion of accounting principles orreporting.

Additional copies of this instruction book may be obtainedfrom the Federal Reserve Bank in the district where thereporting holding company submits its FR Y-9C reports,or may be found on the Federal Reserve Board’s publicwebsite (www.federalreserve.gov).

FR Y-9C Contents-1Contents March 2013

GENERAL INSTRUCTIONS FOR PREPARATION OF FINANCIAL STATEMENTSFOR HOLDING COMPANIES

Who Must Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-1

A. Reporting Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-1

B. Exemptions from Reporting the Holding Company Statements . . . . . . . . . . . . . . . . . . . . . . . GEN-2

C. Shifts in Reporting Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-2

Where to Submit the Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-2

When to Submit the Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-3

How to Prepare the Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-3

A. Applicability of GAAP, Consolidation Rules and SEC Consistency . . . . . . . . . . . . . . . . . . GEN-3

Scope of the ‘‘consolidated holding company’’ to be reported in thesubmitted reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-3

Rules of consolidation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-3Reporting by type of office (for holding companies with foreign offices) . . . . . . . . . . . . . . GEN-4Exclusions from coverage of the consolidated report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-4

B. Report Form Captions, Non-applicable Items and Instructional Detail . . . . . . . . . . . . . . . . GEN-4C. Rounding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-5D. Negative Entries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-6E. Confidentiality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-6F. Verification and Signatures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-6G. Amended Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GEN-7

Contents

Contents-2 FR Y-9CContents June 2013

LINE ITEM INSTRUCTIONS FOR THE CONSOLIDATED FINANCIAL STATEMENTSFOR HOLDING COMPANIES

Schedule HI—Consolidated Income Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HI-1

Schedule HI-A—Changes in Equity Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HI-A-1

Schedule HI-B—Charge-Offs and Recoveries on Loans and Leases and Changesin Allowance for Loan and Lease Losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HI-B-1

Schedule HI-C—Disaggregated Data on the Allowance for Loan and Lease Losses . . . . . . . . HI-C-1

Notes to the Income Statement—Predecessor Financial Items . . . . . . . . . . . . . . . . . . . . . . . . . . . . .- ISnotes-P-1

Notes to the Income Statement—Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ISnotes-1

Schedule HC—Consolidated Balance Sheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-1

Schedule HC-B—Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-B-1

Schedule HC-C—Loans and Lease Financing Receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-C-1Schedule HC-D—Trading Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-D-1Schedule HC-E—Deposit Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-E-1Schedule HC-F—Other Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-F-1Schedule HC-G—Other Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-G-1Schedule HC-H—Interest Sensitivity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-H-1Schedule HC-I—Insurance-Related Underwriting Activities (Including Reinsurance) . . . . . . HC-I-1Schedule HC-K—Quarterly Averages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-K-1Schedule HC-L—Derivatives and Off-Balance Sheet Items . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-L-1Schedule HC-M—Memoranda . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-M-1Schedule HC-N—Past Due and Nonaccrual Loans, Leases, and Other Assets . . . . . . . . . . . . . . HC-N-1Schedule HC-P—Closed-End 1-4 Family Residential Mortage Banking Activities. . . . . . . . . . HC-P-1Schedule HC-Q—Financial Assets and Liabilities Measured at Fair Value . . . . . . . . . . . . . . . . . HC-Q-1Schedule HC-R—Regulatory Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-R-1Schedule HC-S—Servicing, Securitization, and Asset Sale Activities . . . . . . . . . . . . . . . . . . . . . HC-S-1Schedule HC-V—Variable Interest Entities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HC-V-1

Notes to the Balance Sheet—Predecessor Financial Items . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .- BSnotes-P-1Notes to the Balance Sheet—Other. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . BSnotes-1

Contents

FR Y-9C Contents-3Contents March 2013

GLOSSARY

Acceptances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 1

Accounting Changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 1

Accounting Errors, Corrections of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 3

Accounting Estimates, Changes in . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 3

Accounting Principles, Changes in . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 3

Accrued Interest Receivable Related to Credit Card Securitizations . . . . . . . . . . . . . . . . . . . . . . . GL- 3

Acquisition, Development, or Construction (ADC) Arrangements . . . . . . . . . . . . . . . . . . . . . . . . . GL- 4

Agreement Corporation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 4

Allowance for Loan and Lease Losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 4

Applicable Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 6

Associated Company . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 6

ATS Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 6

Bankers’ Acceptances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 6

Bank-Owned Life Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 8

Banks, U.S. and Foreign . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL- 9

Bill-of-Lading Draft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-11

Borrowings and Deposits in Foreign Offices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-11

Brokered Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-11

Brokered Retail Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-11

Broker’s Security Draft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-12

Business Combinations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-12

Call Option . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-14

Capital Contributions of Cash and Notes Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-14

Capitalization of Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Carrybacks and Carryforwards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Certificate of Deposit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Changes in Accounting Estimates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Changes in Accounting Principles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Commercial Banks in the U.S. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Commercial Letter of Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Commercial Paper . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Commodity or Bill-of-Lading Draft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Common Stock of Unconsolidated Subsidiaries, Investments in . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Continuing Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Contractholder . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Corporate Joint Venture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Corrections of Accounting Errors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Contents

Contents-4 FR Y-9CContents March 2012

Coupon Stripping, Treasury Receipts, and STRIPS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-16

Custody Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-17

Dealer Reserve Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-17

Deferred Compensation Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-17

Deferred Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-19

Defined Benefit Post Retirement Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-19

Demand Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-20

Depository Institutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-20

Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-20

Derivative Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-26

Discounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-31

Dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-31

Domestic Office . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-32

Domicile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-32

Due Bills . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-32

Edge and Agreement Corporation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-32

Equity-Indexed Certificates of Deposit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-33

Equity Method of Accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-34

Excess Balance Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-35

Extinguishments of Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-35

Extraordinary Items . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-36

Fails . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-36

Fair Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-36

Federal Funds Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-37

Federally-Sponsored Lending Agency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-38

Fees, Loan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-38

Foreclosed Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-38

Foreign Banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-40

Foreign Central Banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-40

Foreign Currency Transactions and Translation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-40

Foreign Debt Exchange Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-41

Foreign Governments and Official Institutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-42

Foreign Office . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-42

Forward Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-42

Functional Currency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-43

Futures, Forward, and Standby Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-43

Goodwill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-44

Hypothecated Deposit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-45

Contents

FR Y-9C Contents-5Contents March 2015

IBF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-45

Income Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-45

Insurance Commissions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-51

Insurance Premiums . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-51

Insurance Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-51

Intangible Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-51

Interest-Bearing Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-51

Interest Capitalization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-51

Internal-Use Computer Software . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-51

International Banking Facility (IBF) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-52

Investments in Common Stock of Unconsolidated Subsidiaries . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-53

Joint Venture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-53

Lease Accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-53

Letter of Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-54

Limited-Life Preferred Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-55

Loan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-55

Loan Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-56

Loan Impairment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-58

Loans Secured By Real Estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-59

Loss Contingencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

Mandatory Convertible Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

Market (Fair)Value of Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

Mergers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

Money Market Deposit Account (MMDA) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

Mortgages, Residential, Participations in Pools of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

NOW Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

Nonaccrual Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-61

Noninterest-Bearing Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-63

Nontransaction Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-63

Notes and Debentures Subordinated to Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-63

Offsetting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-63

One-Day Transaction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-64

Option . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-64

Organization Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-64

Other Real Estate Owned . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-64

Other-Than-Temporary Impairment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-64

Overdraft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-64

Participations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-65

Contents

Contents-6 FR Y-9CContents March 2015

Participations in Acceptances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-65

Participations in Pools of Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-65

Pass-through Reserve Balances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-65

Perpetual Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-65

Perpetual Preferred Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Policyholder . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Pooling of Interests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Pools of Residential Mortgages, Participations in . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Pools of Securities, Participations in . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Preauthorized Transfer Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Preferred Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Premiums and Discounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-66

Purchase Acquisition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-67

Purchased Impaired Loans and Debt Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-67

Put Option . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Real Estate, Loan Secured by . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Reciprocal Balances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Reinsurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Reinsurance Recoverables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Renegotiated ‘‘Troubled’’ Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Reorganizations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Repurchase Agreements to Maturity and Long-Term Repurchase Agreements . . . . . . . . . . . . . GL-69

Repurchase/Resale Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-69

Reserve Balances, Pass-through . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-71

Sales of Assets for Risk-Based Capital Purposes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-71

Savings Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-75

Securities Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-75

Securities Borrowing/Lending Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-77

Securities, Participations in Pools of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-77

Separate Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-77

Servicing Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-77

Settlement Date Accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-79

Shell Branches . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-79

Short Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-79

Standby Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-80

Standby Letter of Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-80

Start-Up Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-80

STRIPS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-80

Contents

FR Y-9C Contents-7Contents March 2015

Subordinated Notes and Debentures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-80

Subsidiaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

‘‘Super NOW’’ Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

Suspense Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

Syndications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

Telephone Transfer Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

Term Federal Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

Time Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

Trade Date and Settlement Date Accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-81

Trading Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-82

Transaction Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-83

Transfers of Financial Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-83

Traveler’s Letter of Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-88

Treasury Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-88

Troubled Debt Restructuring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-88

Trust Preferred Securities as Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-90

Trust Preferred Securities Issued . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-90

U.S. Banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-90

U.S. Territories and Possessions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-90

Valuation Allowance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-91

Variable Interest Entity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-91

When-Issued Securities Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-92

Yield Maintenance Dollar Repurchase Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . GL-92

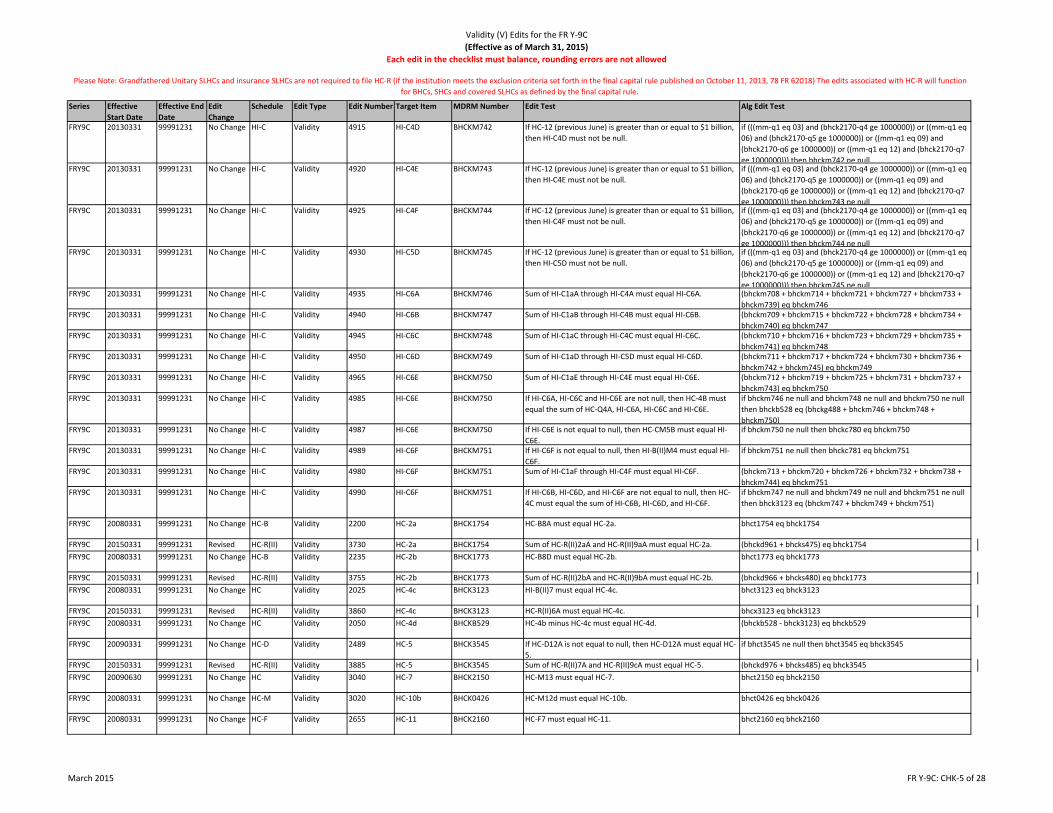

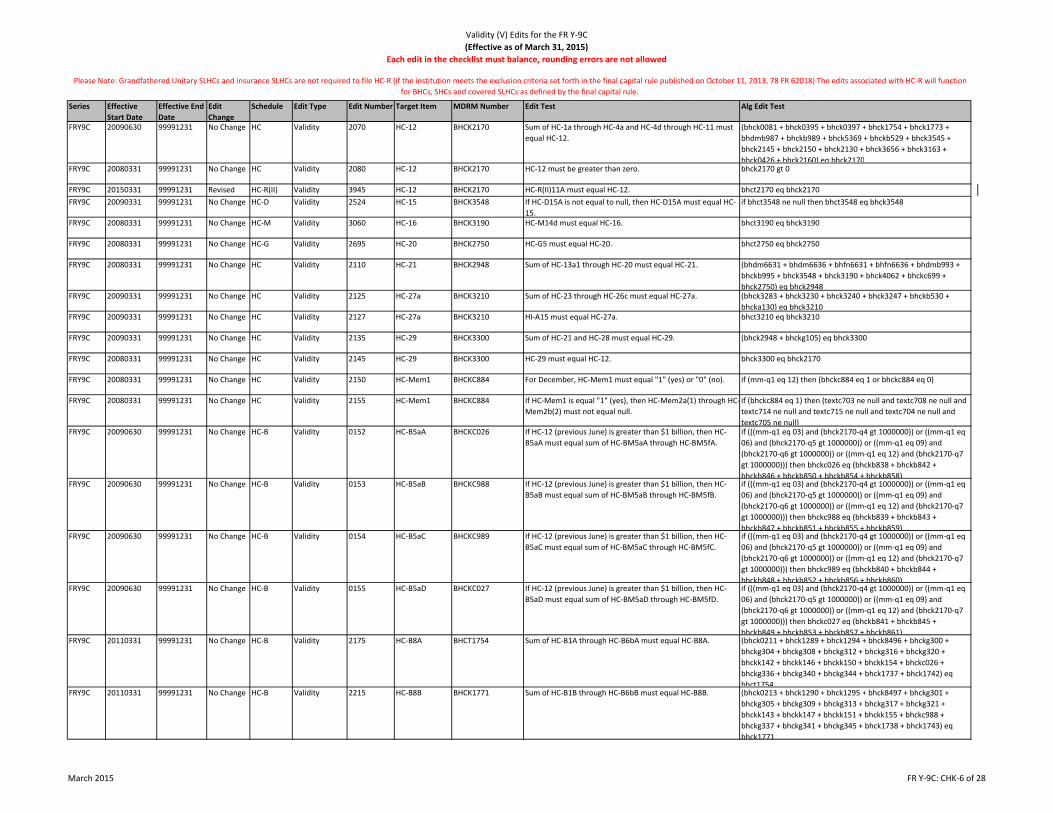

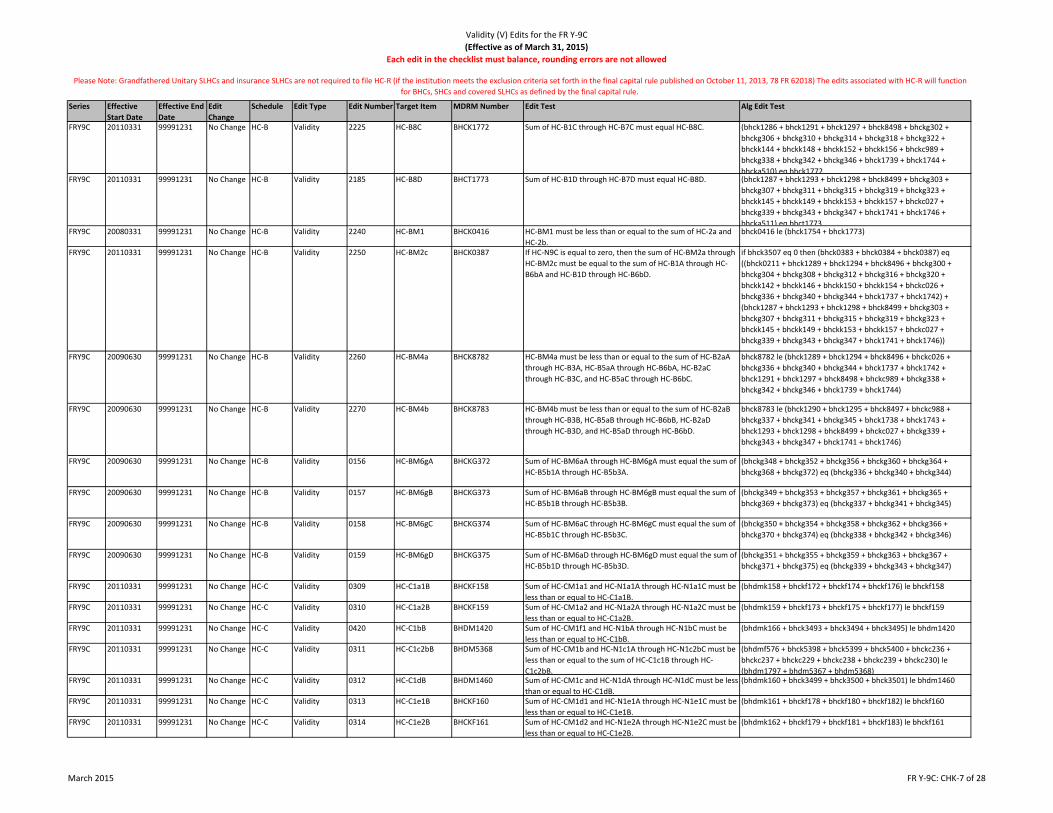

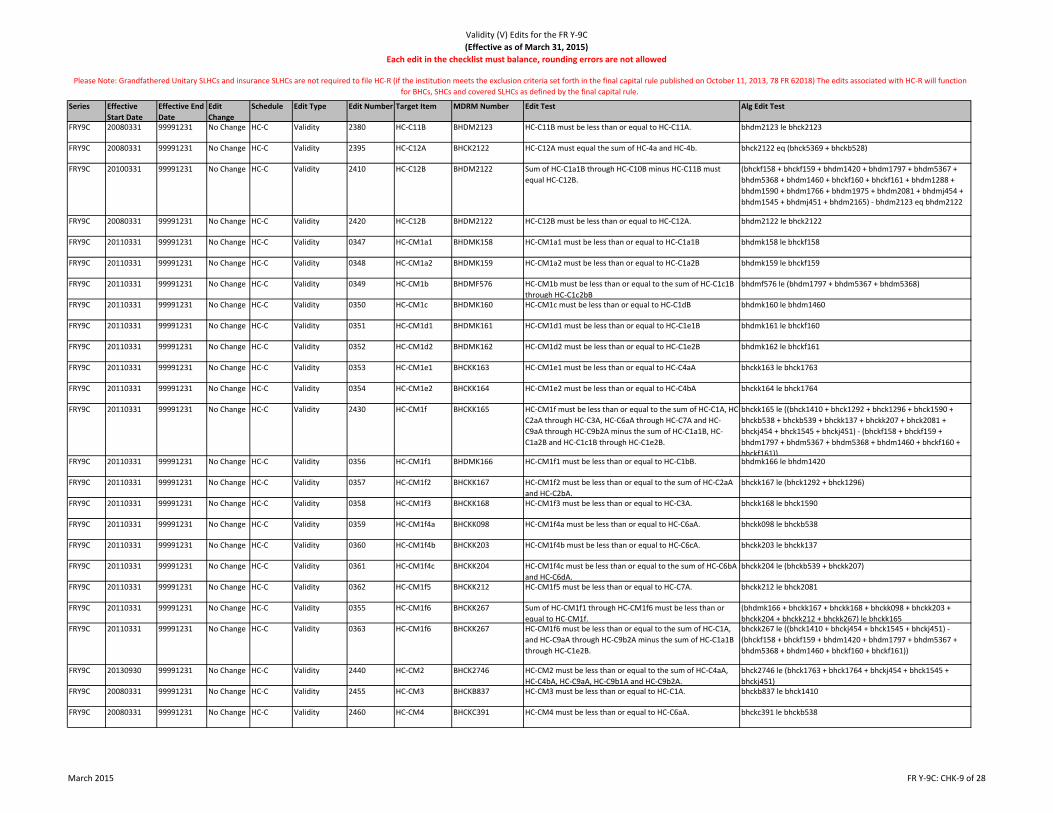

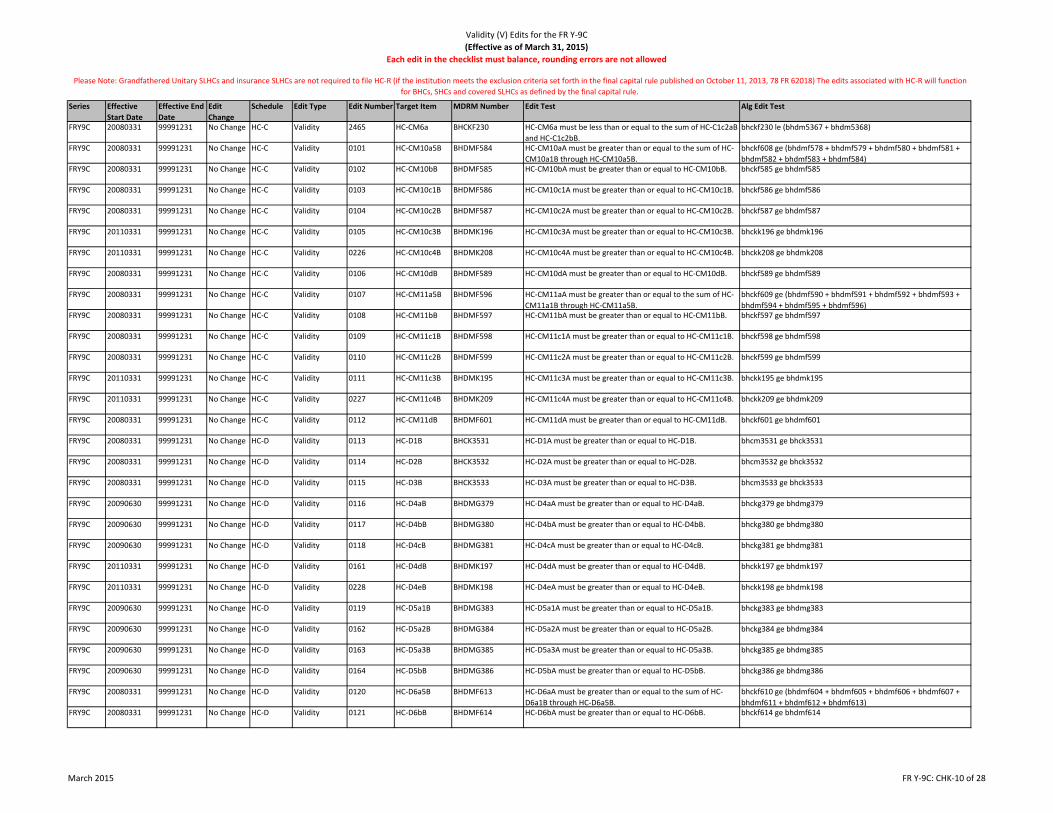

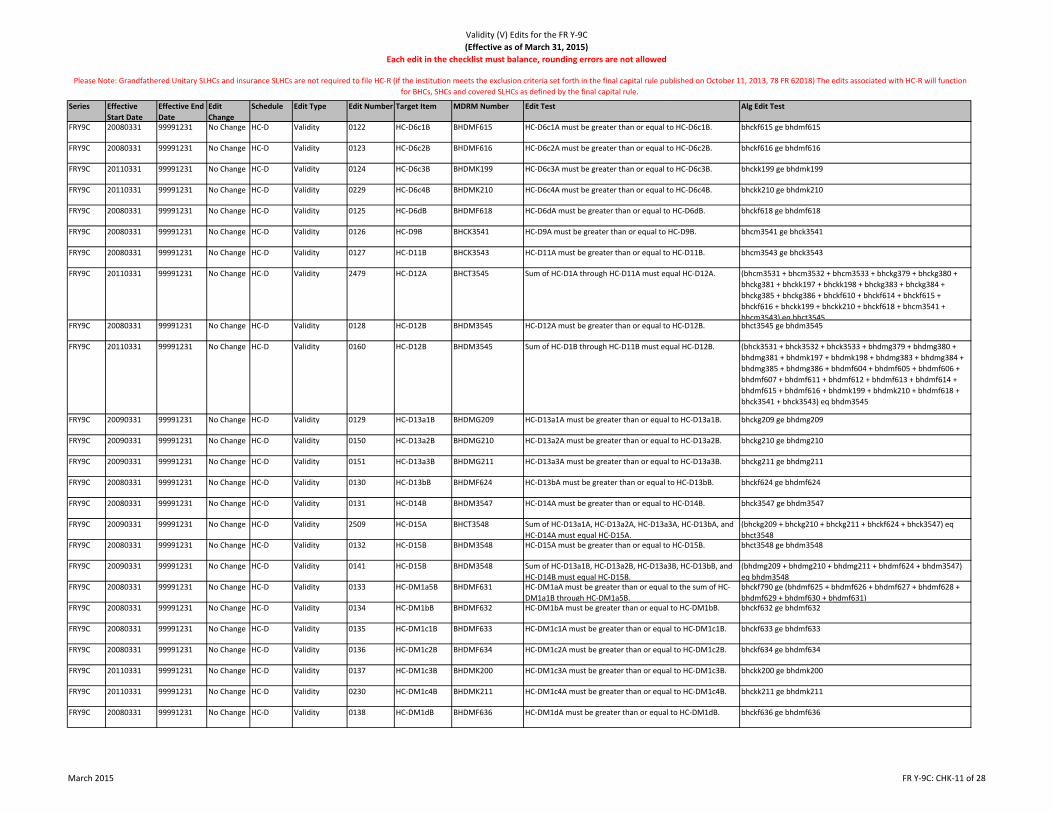

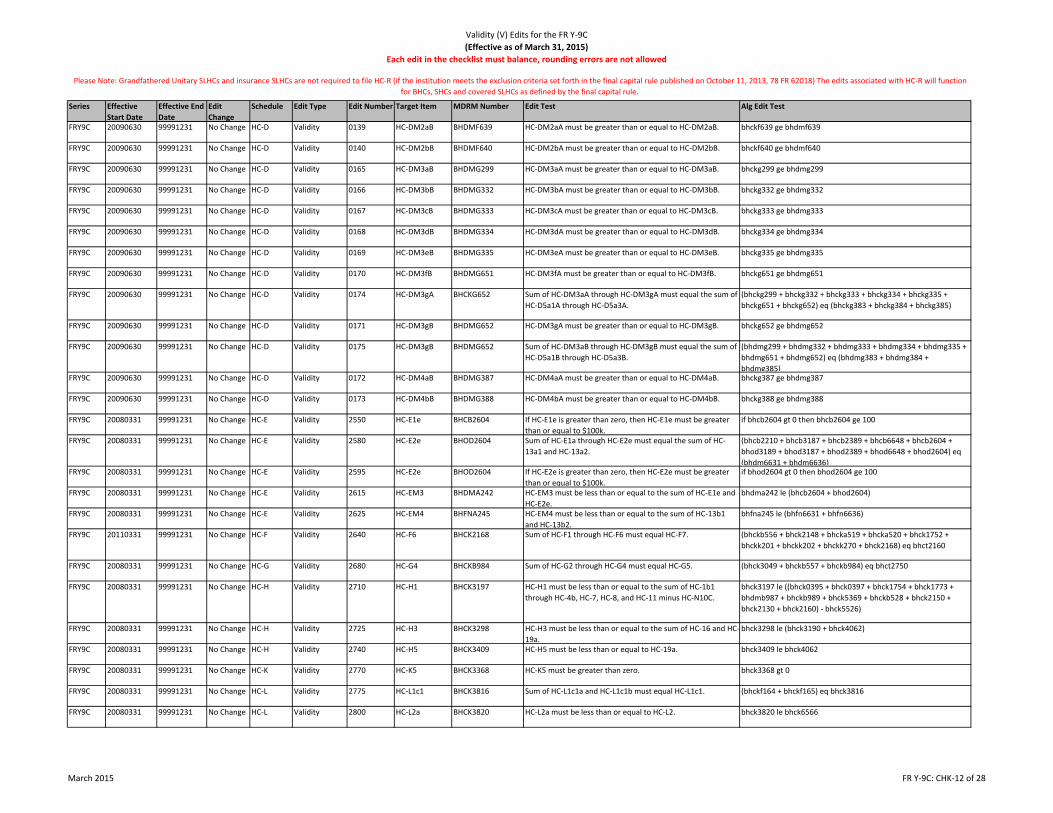

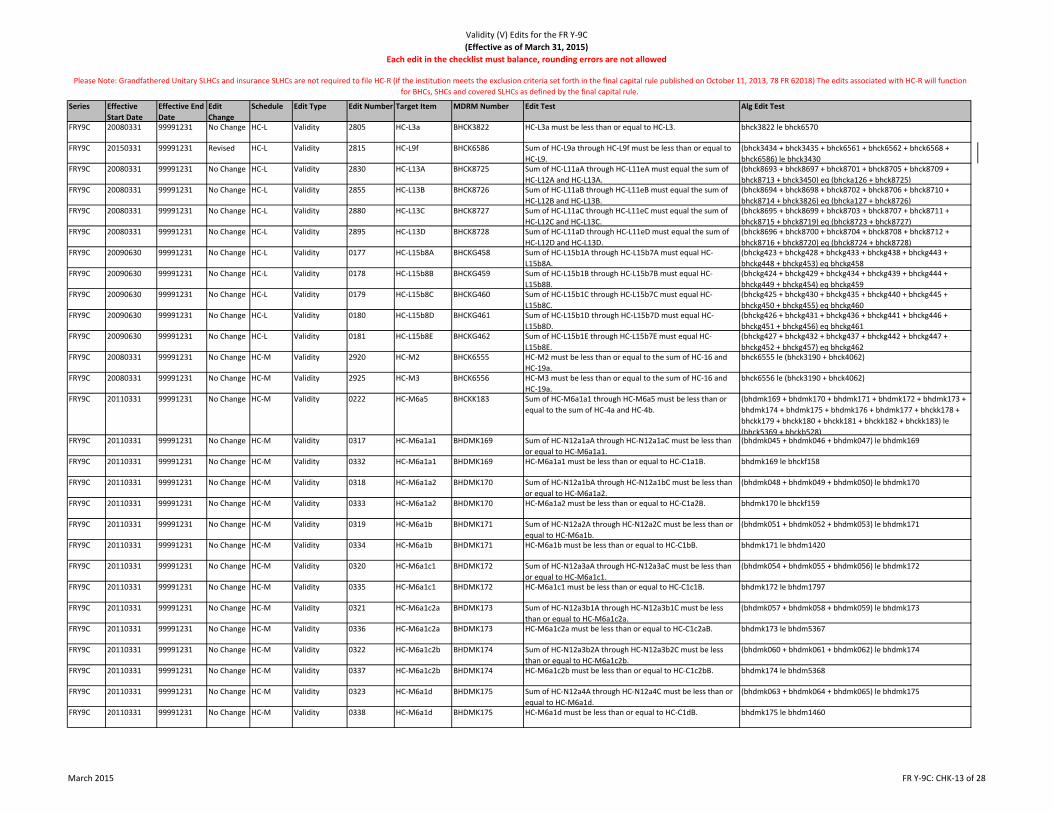

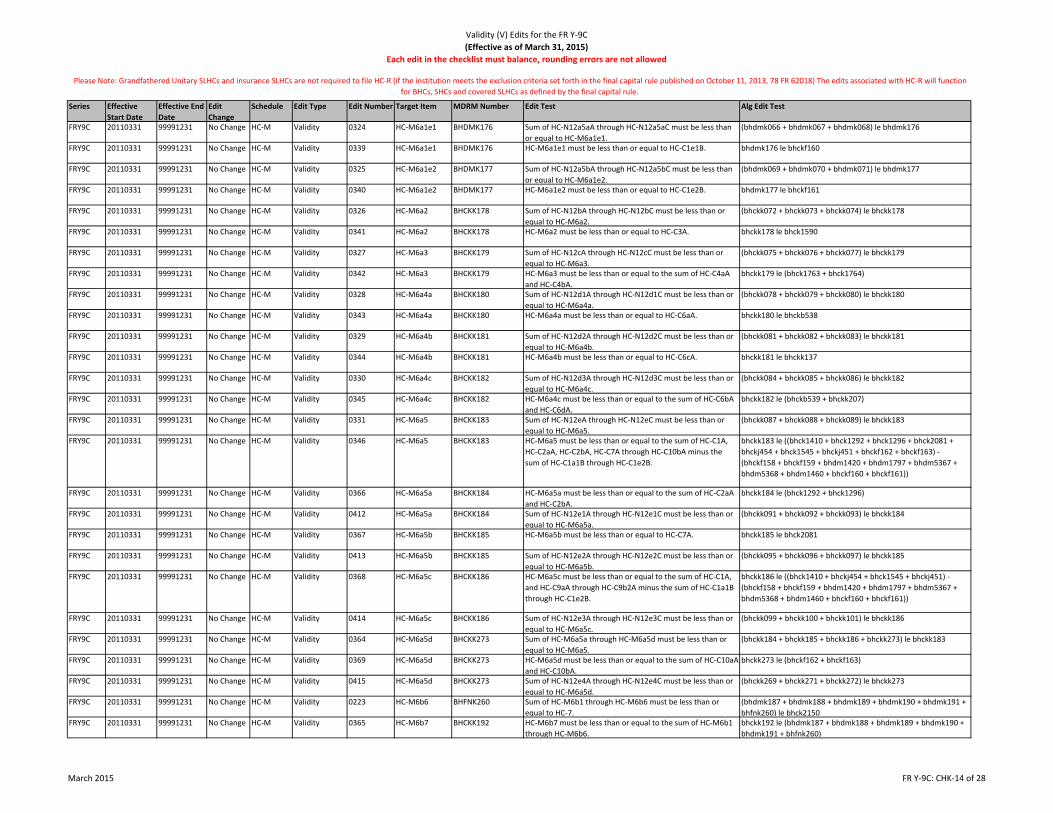

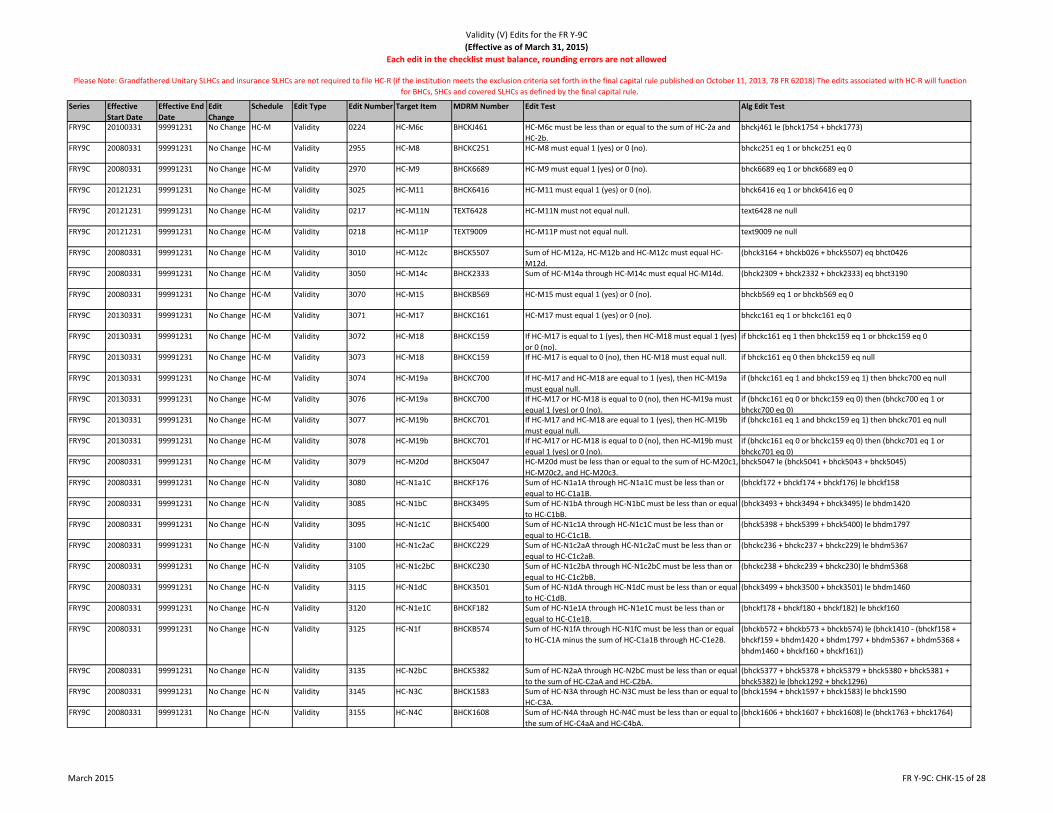

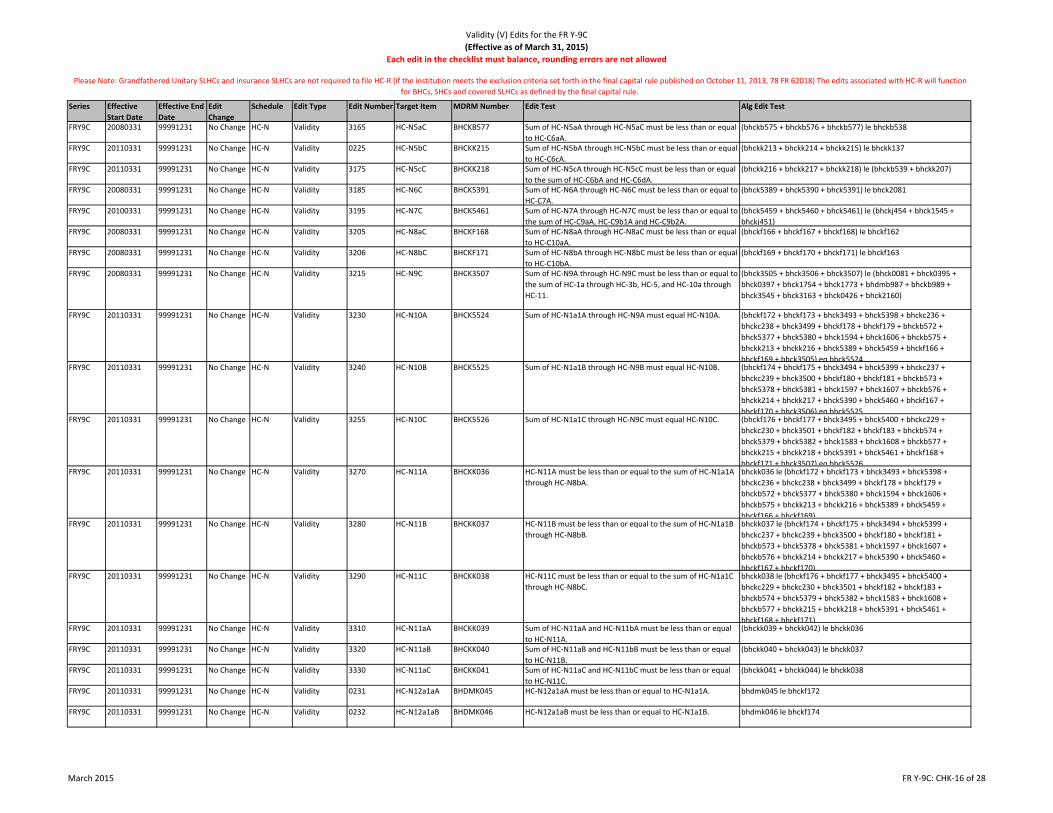

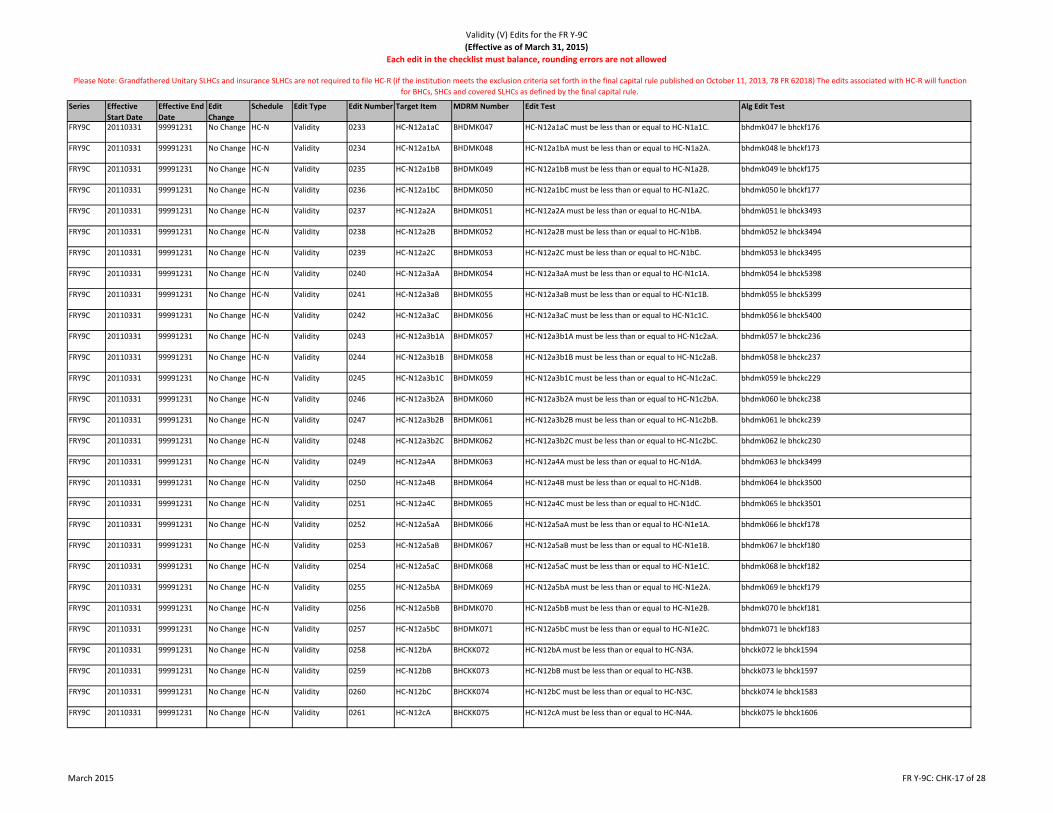

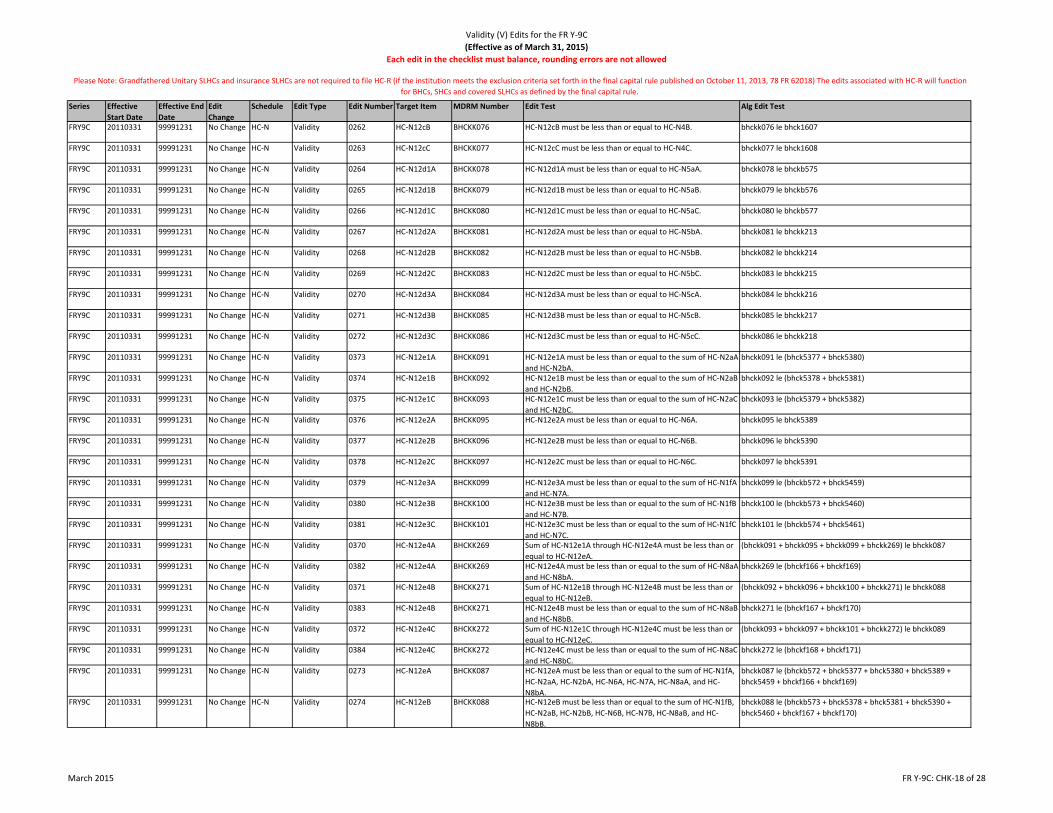

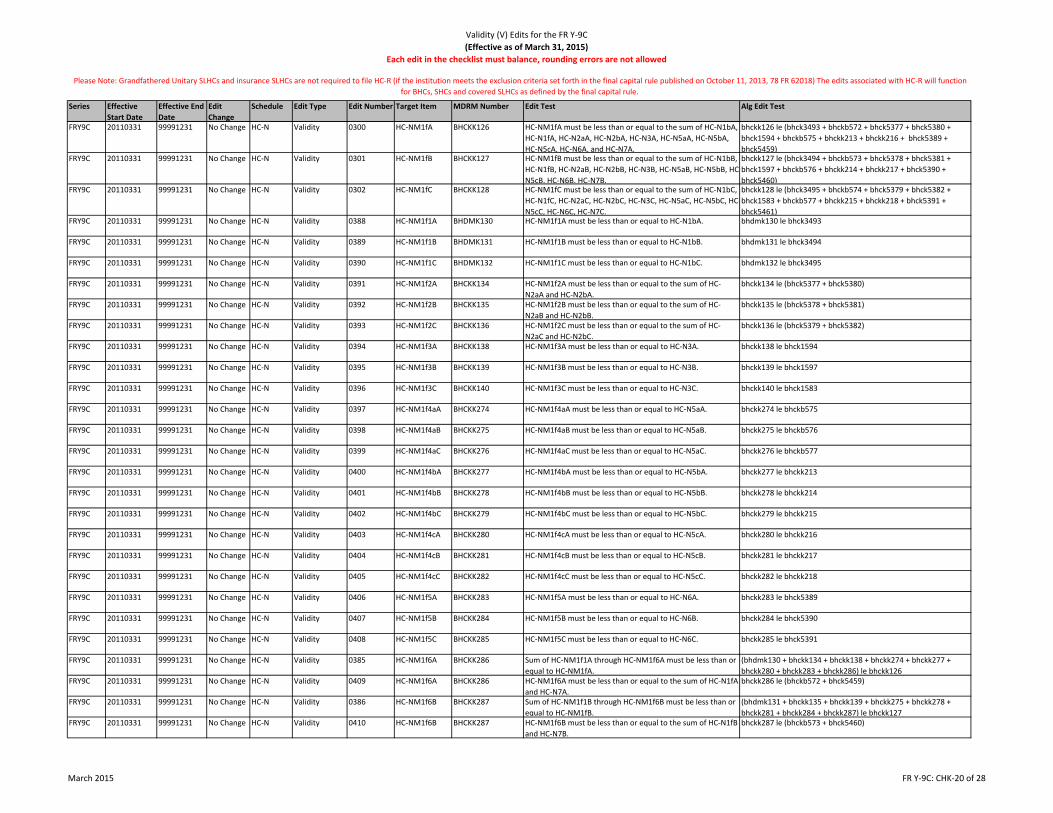

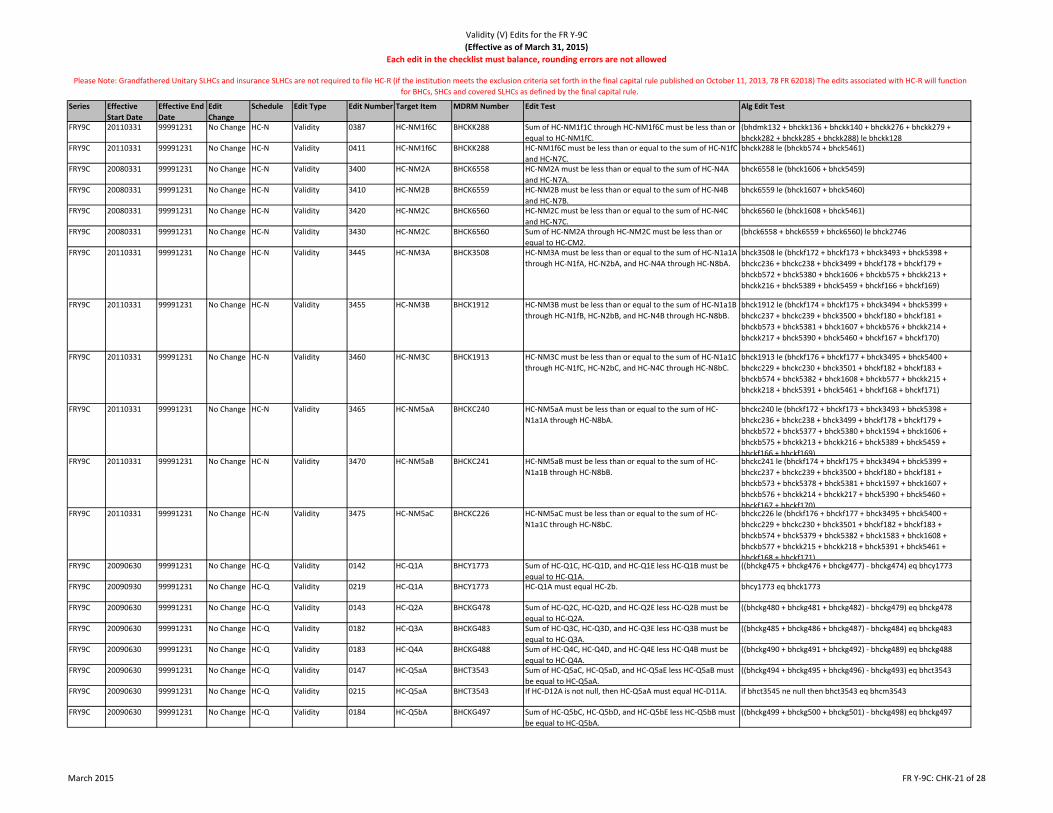

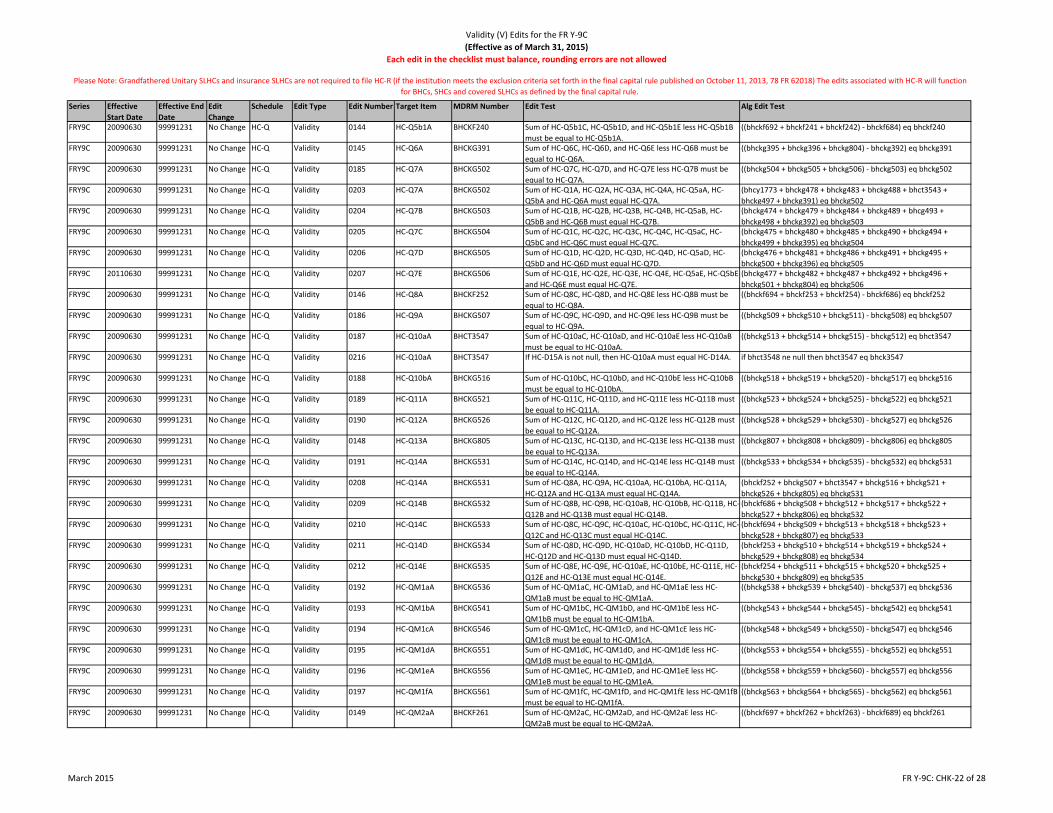

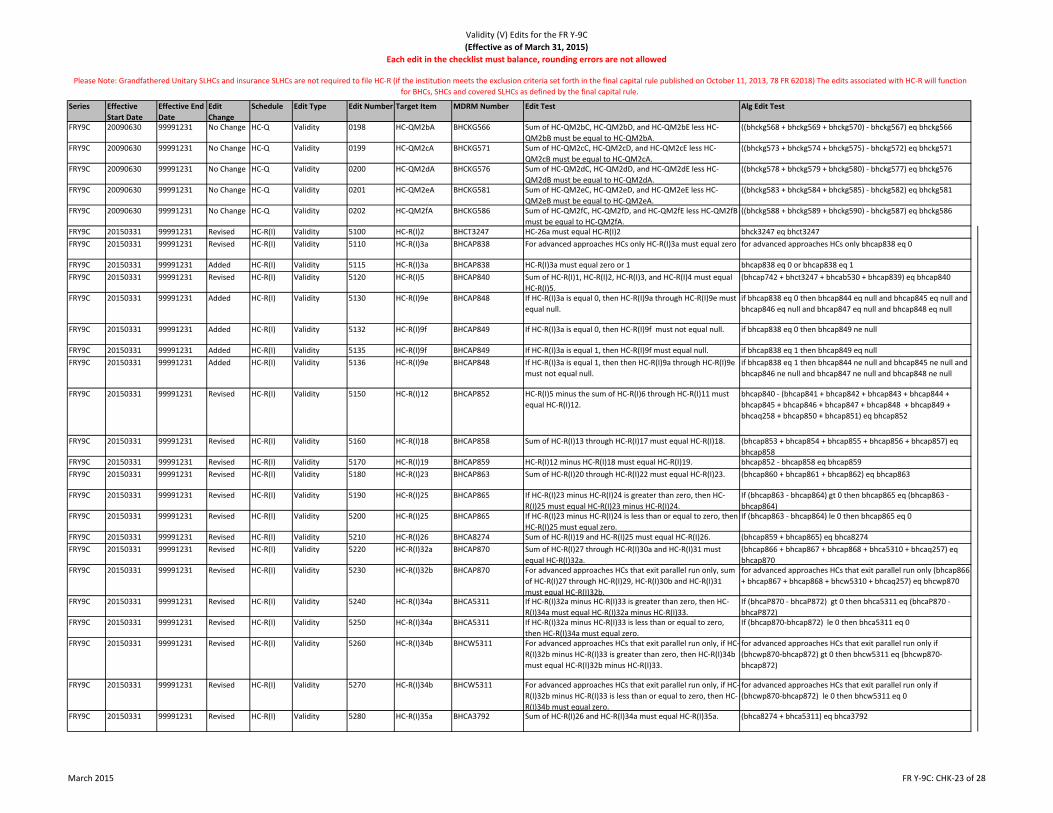

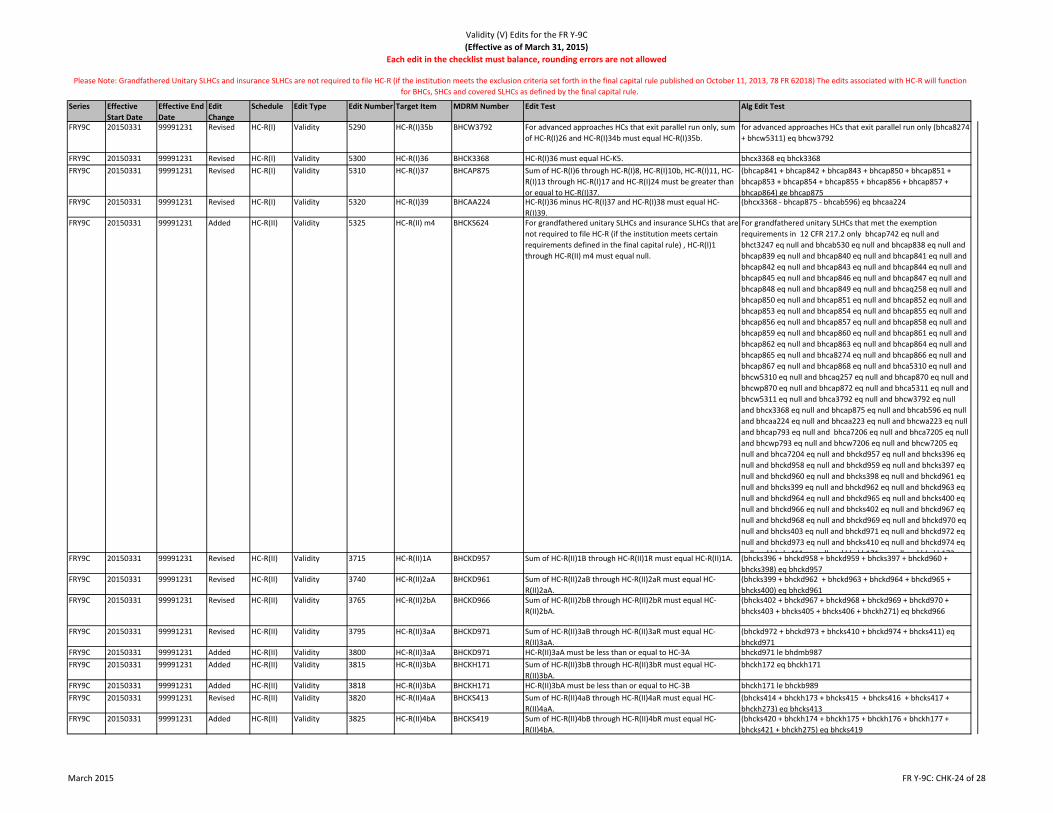

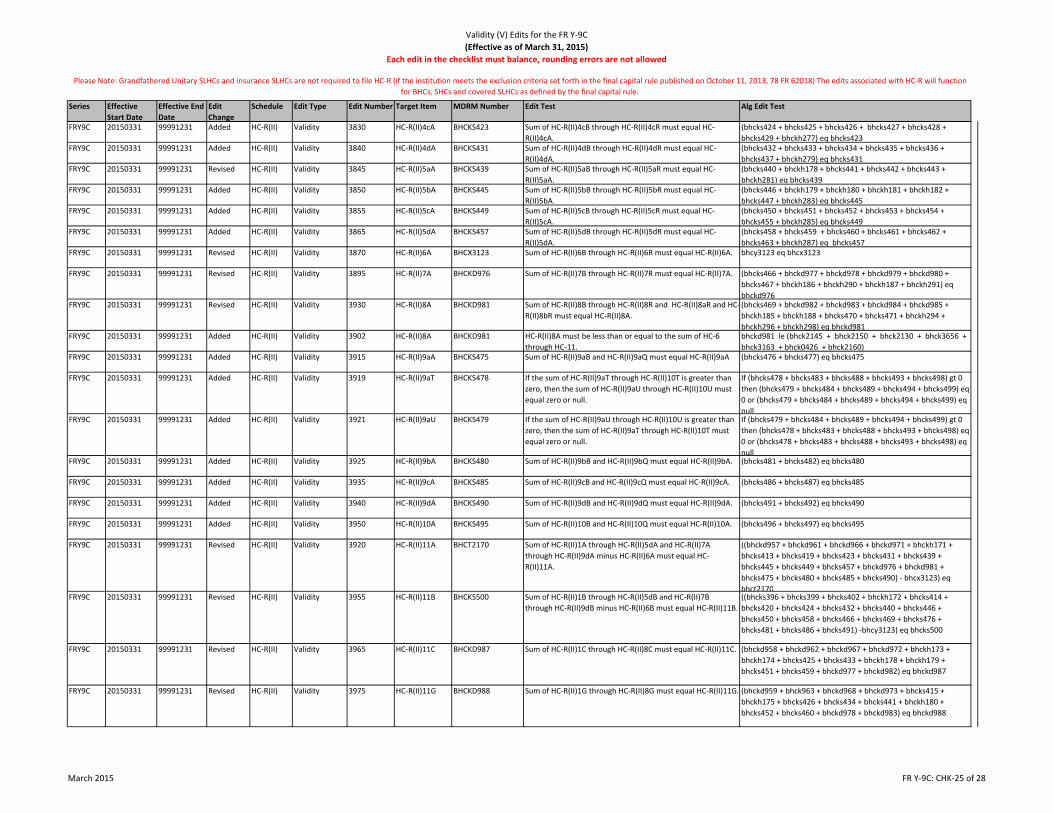

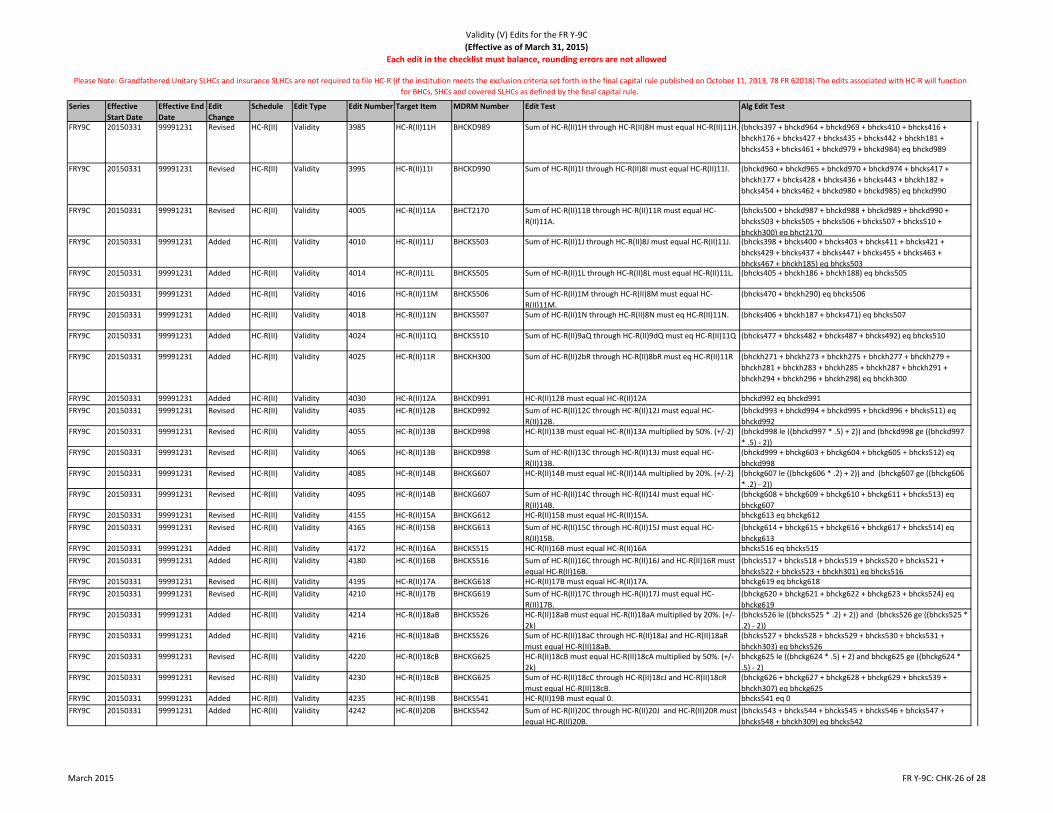

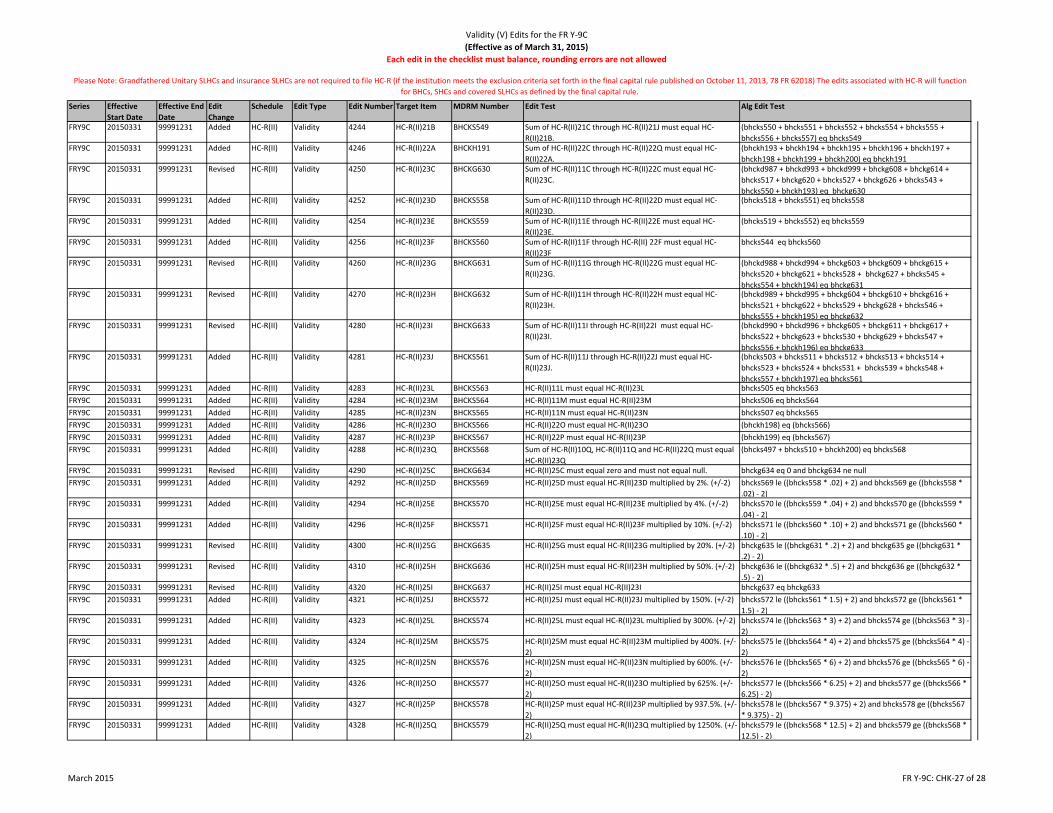

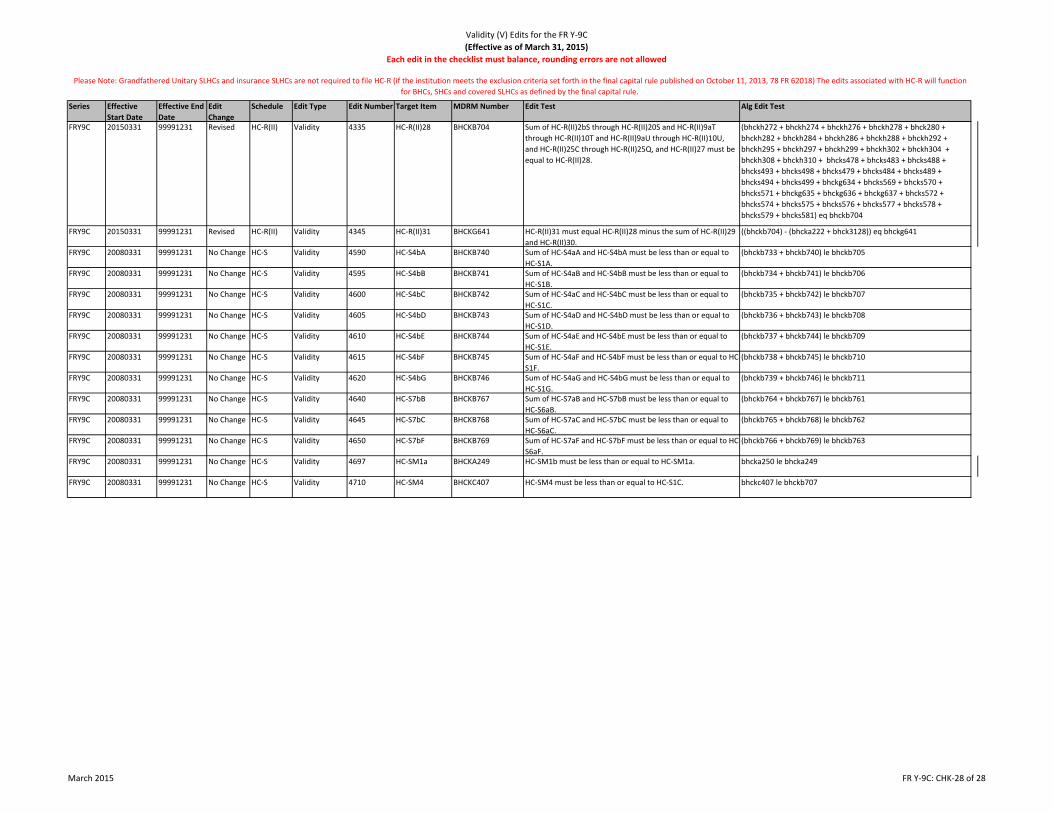

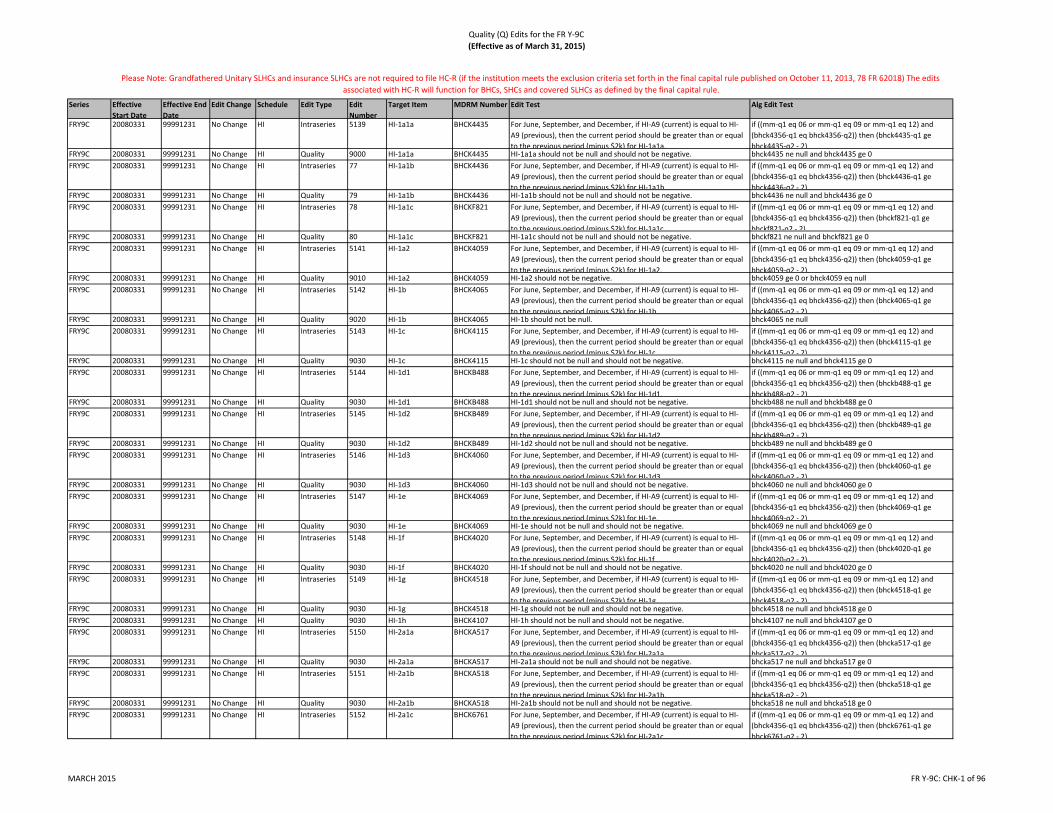

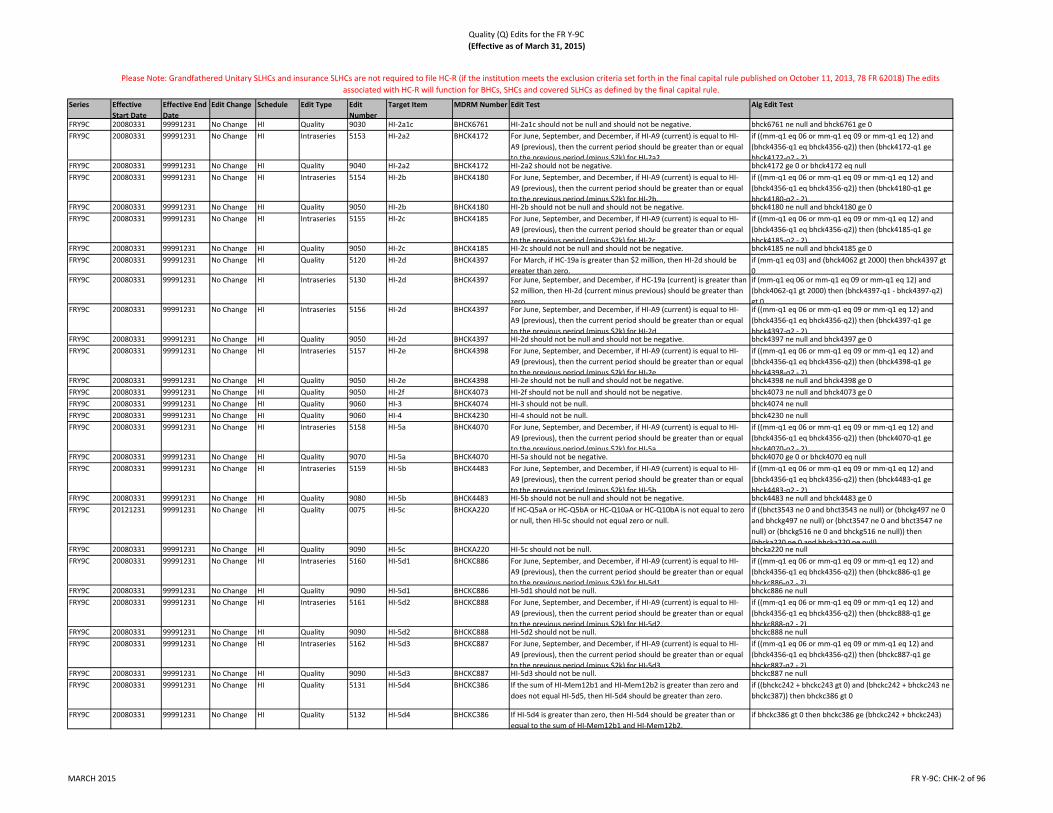

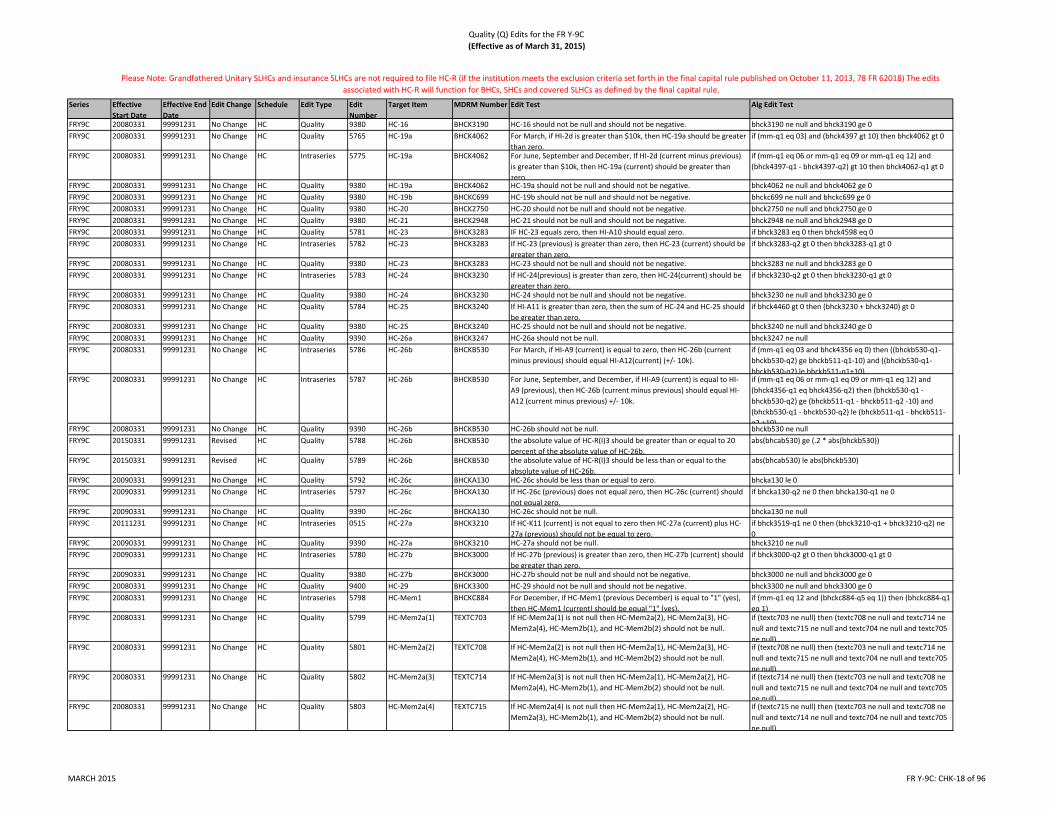

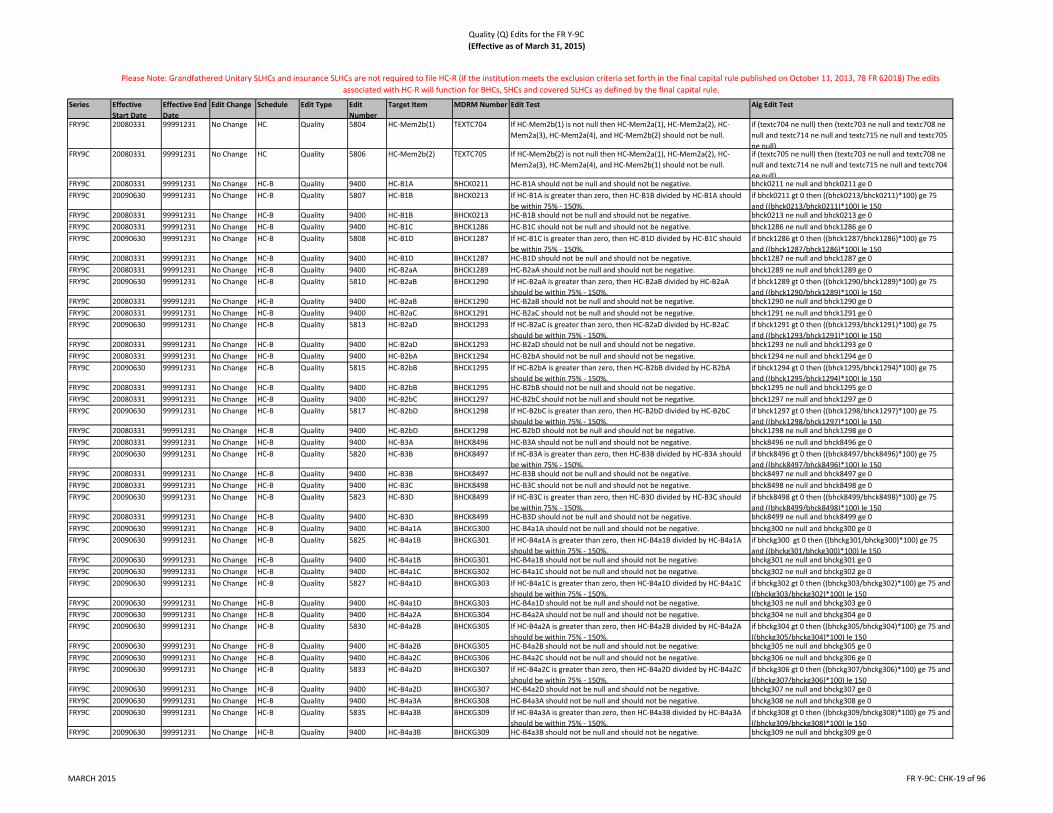

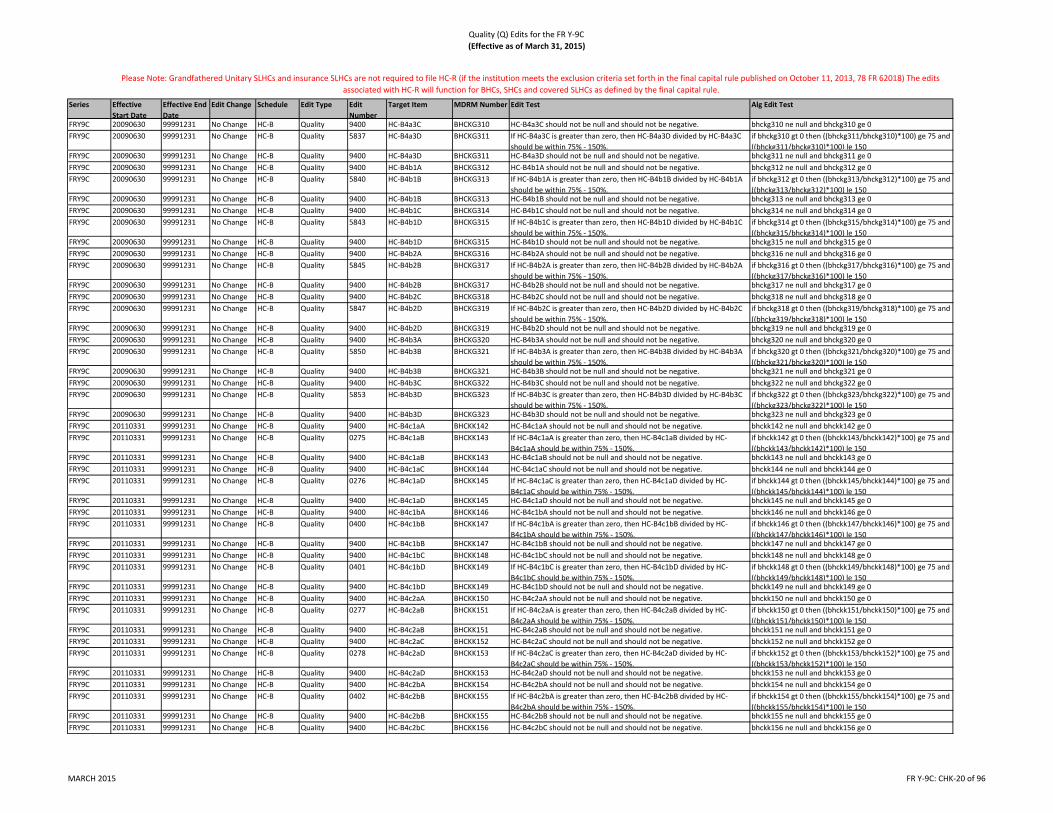

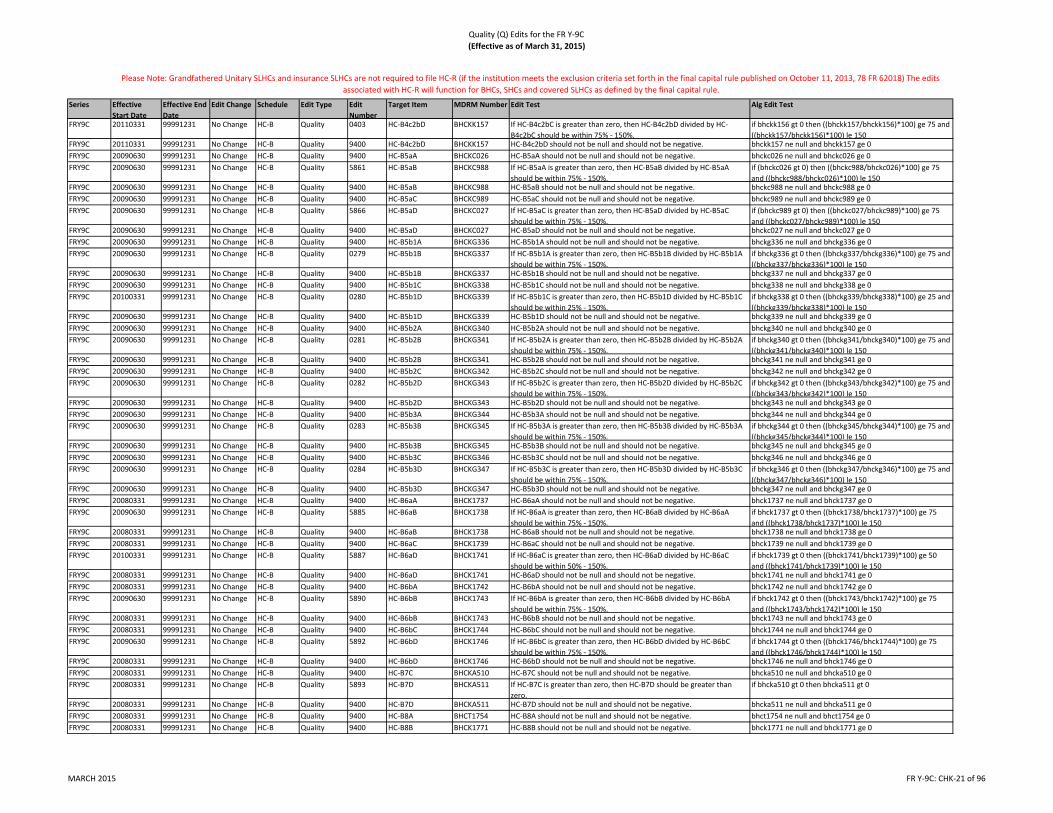

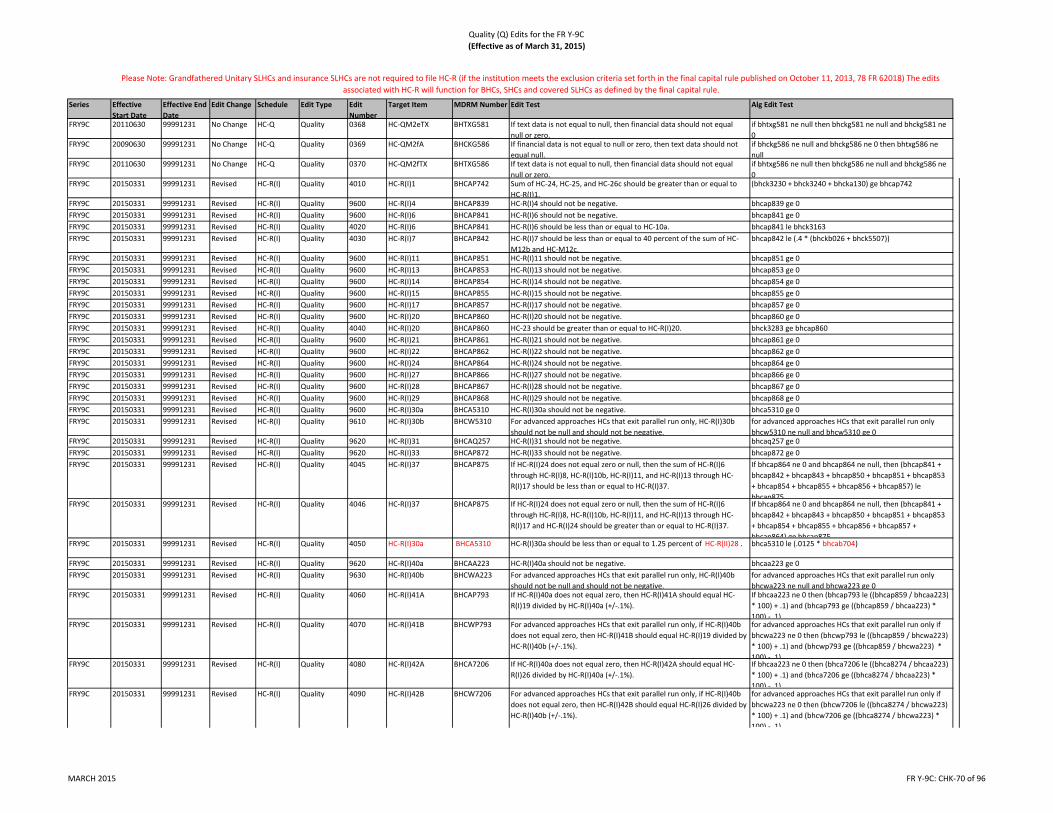

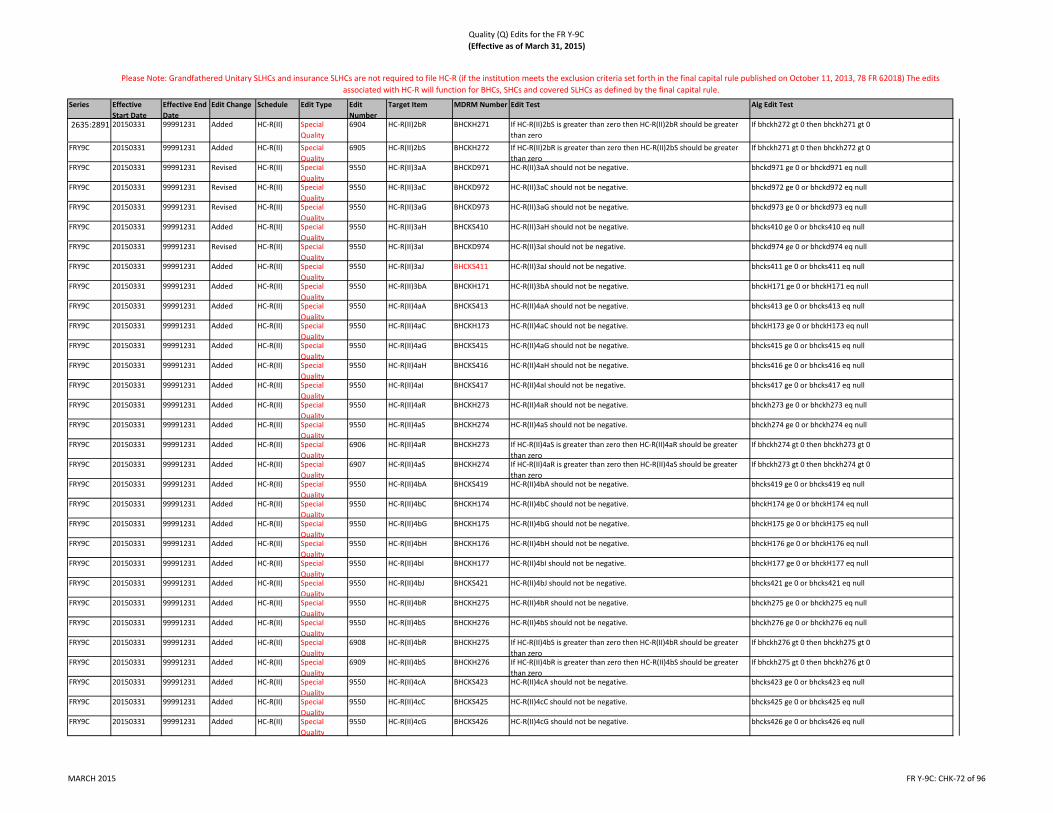

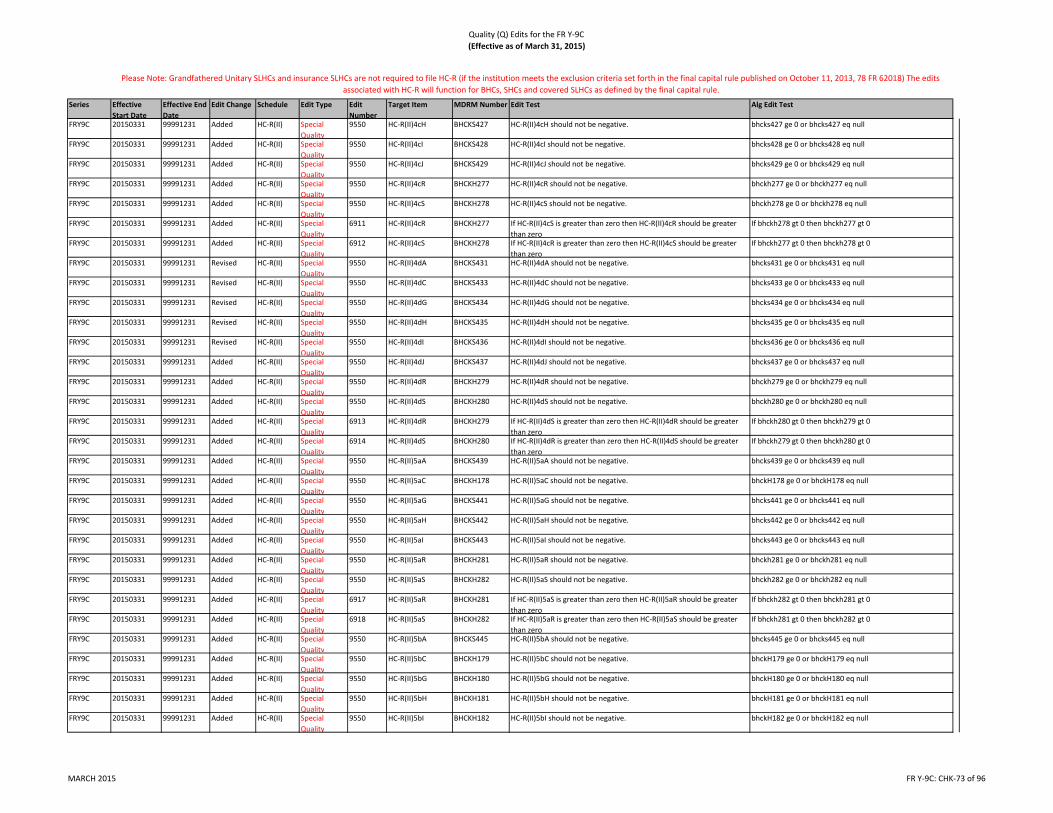

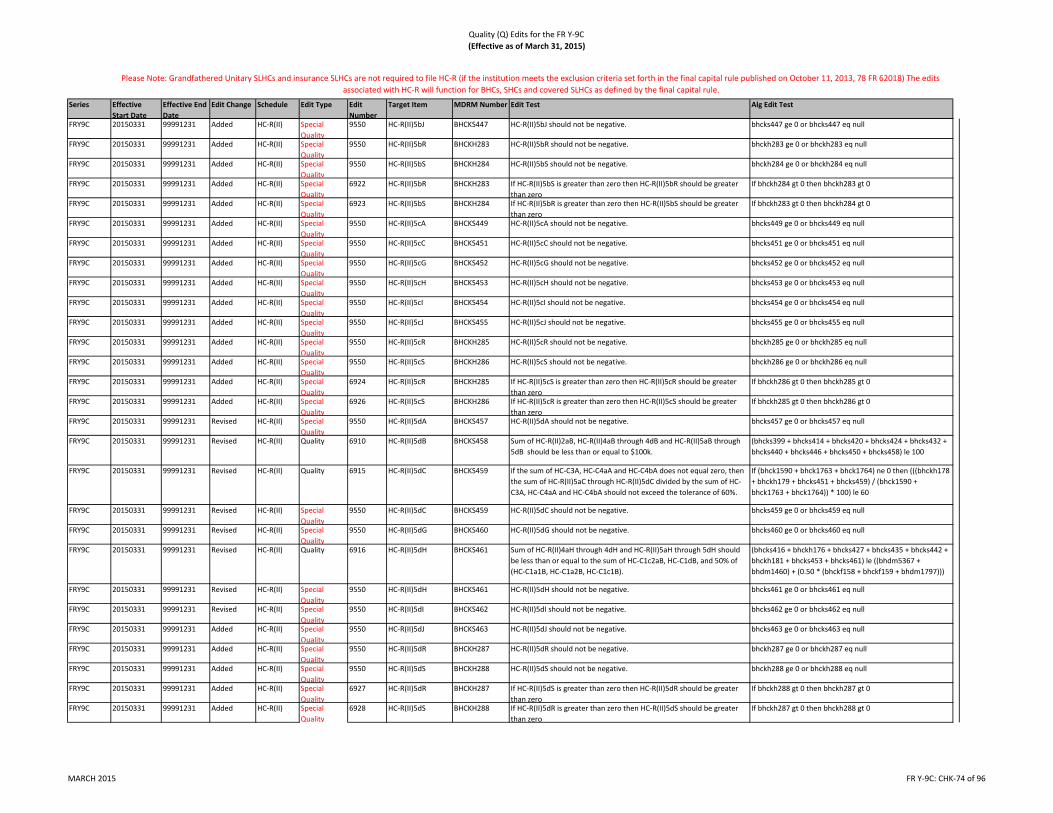

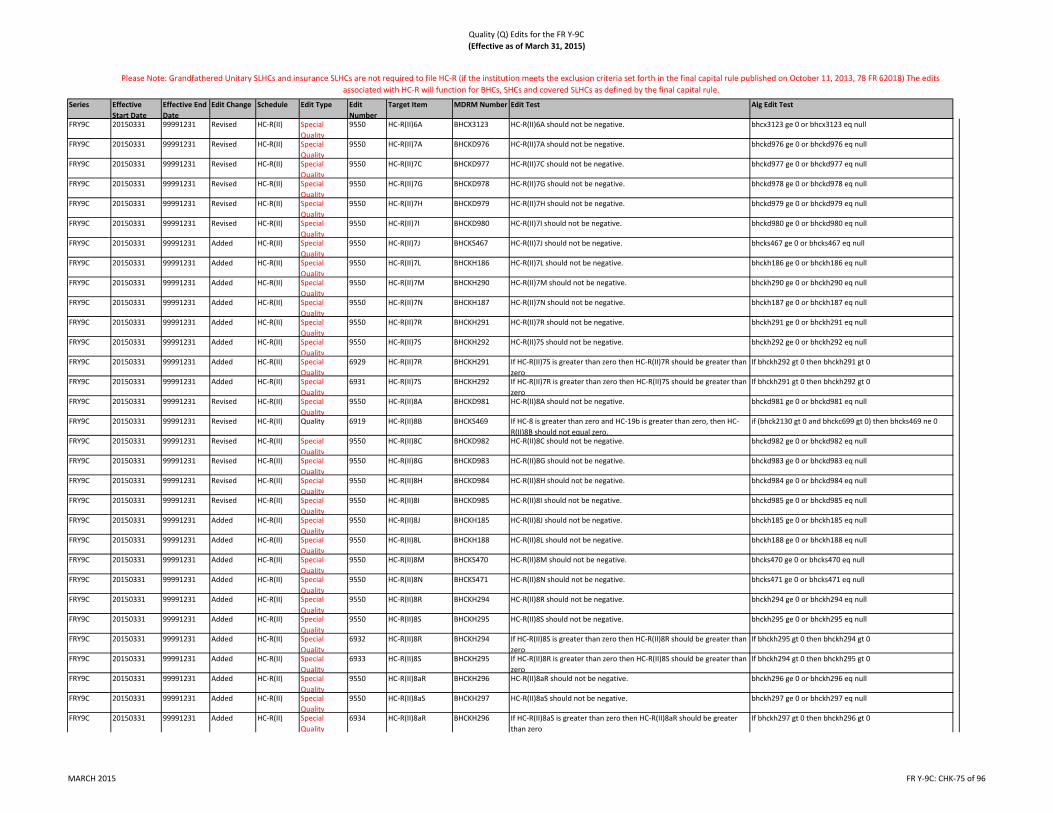

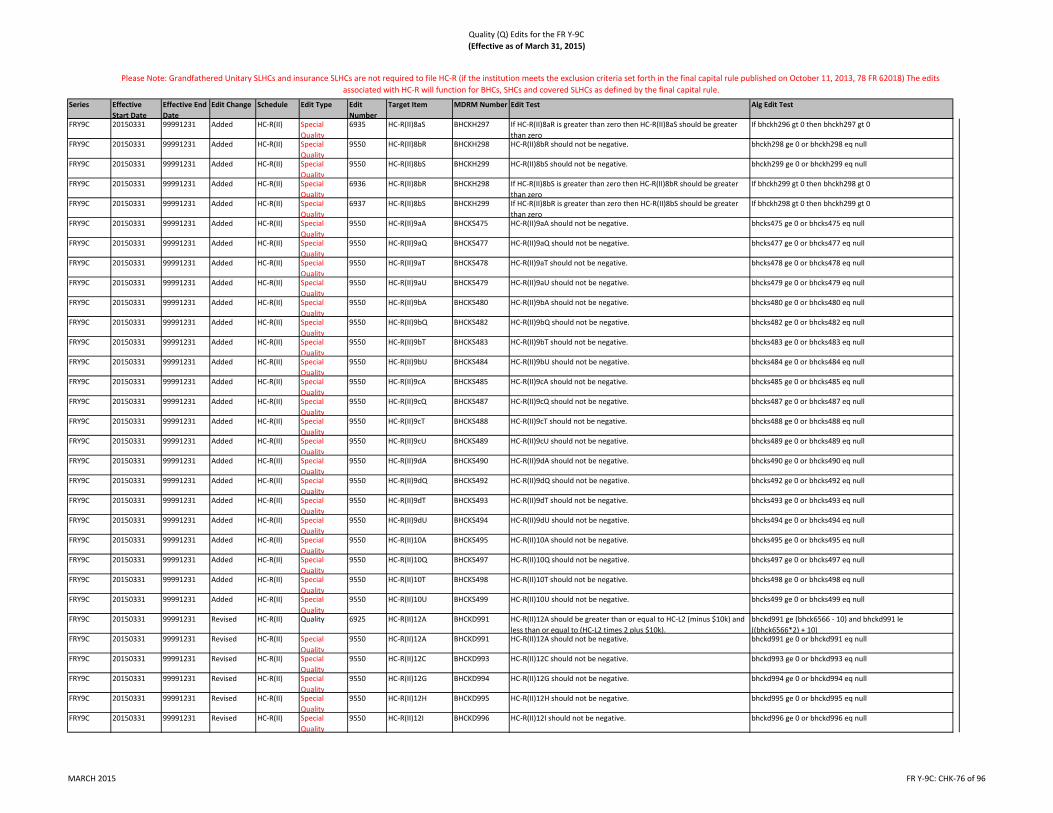

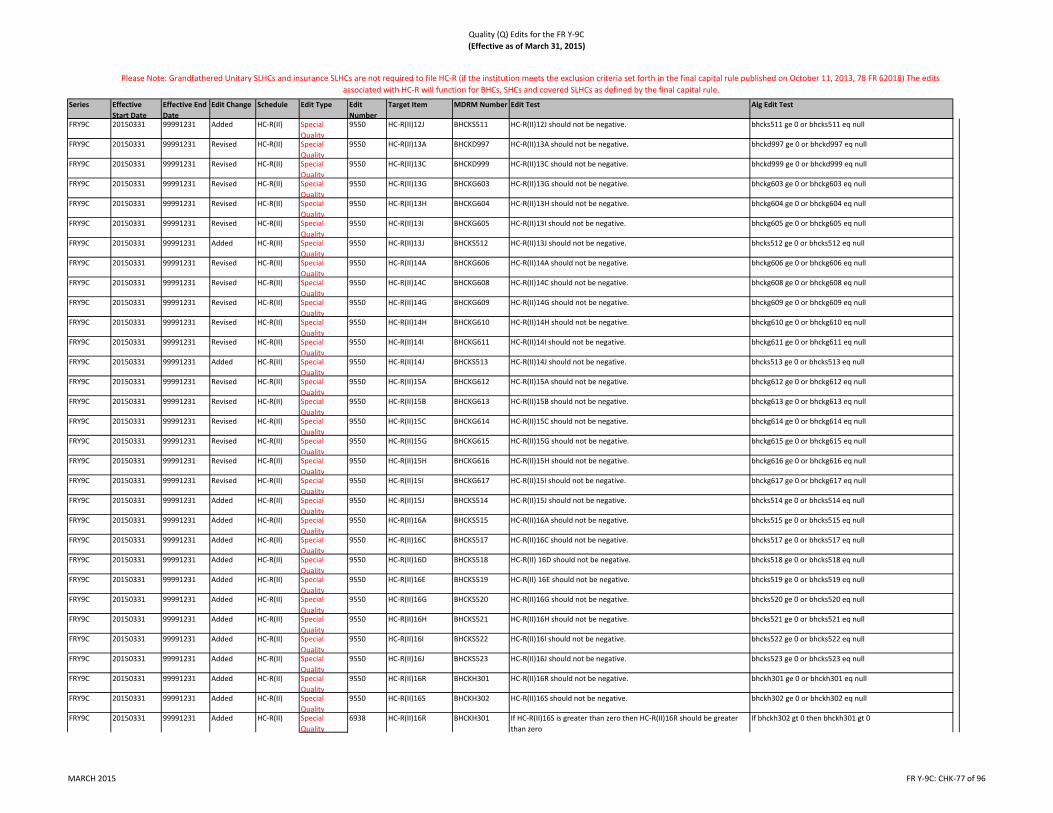

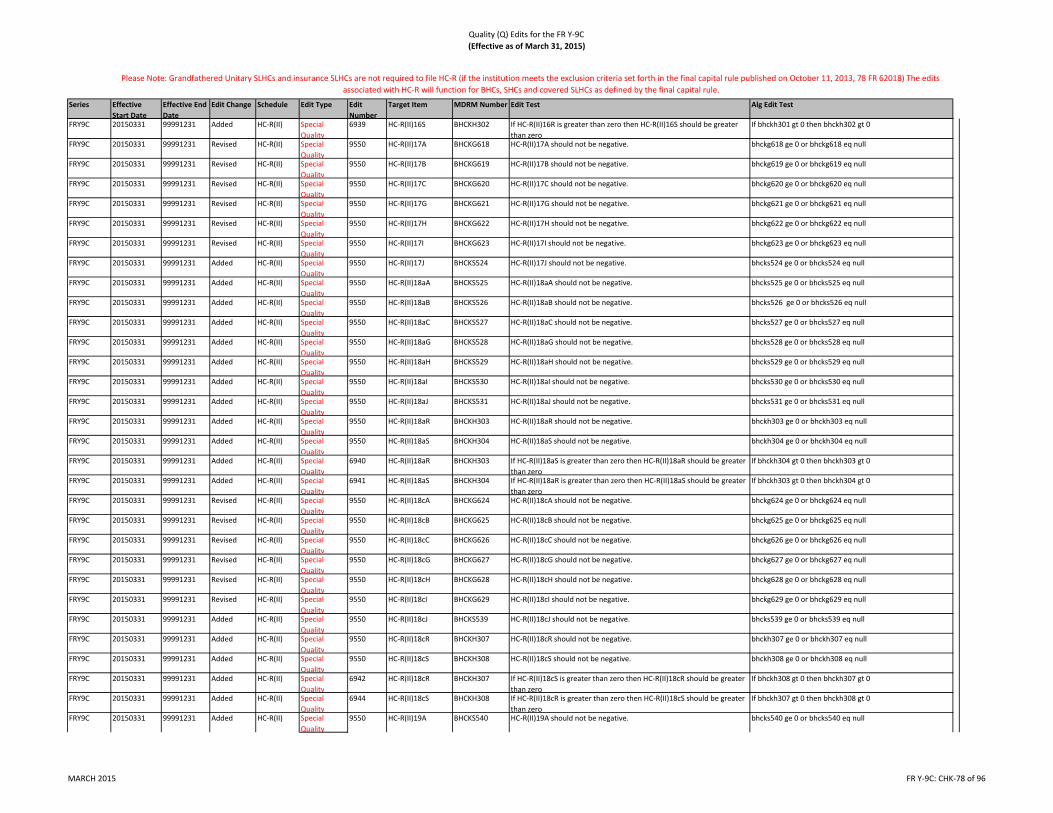

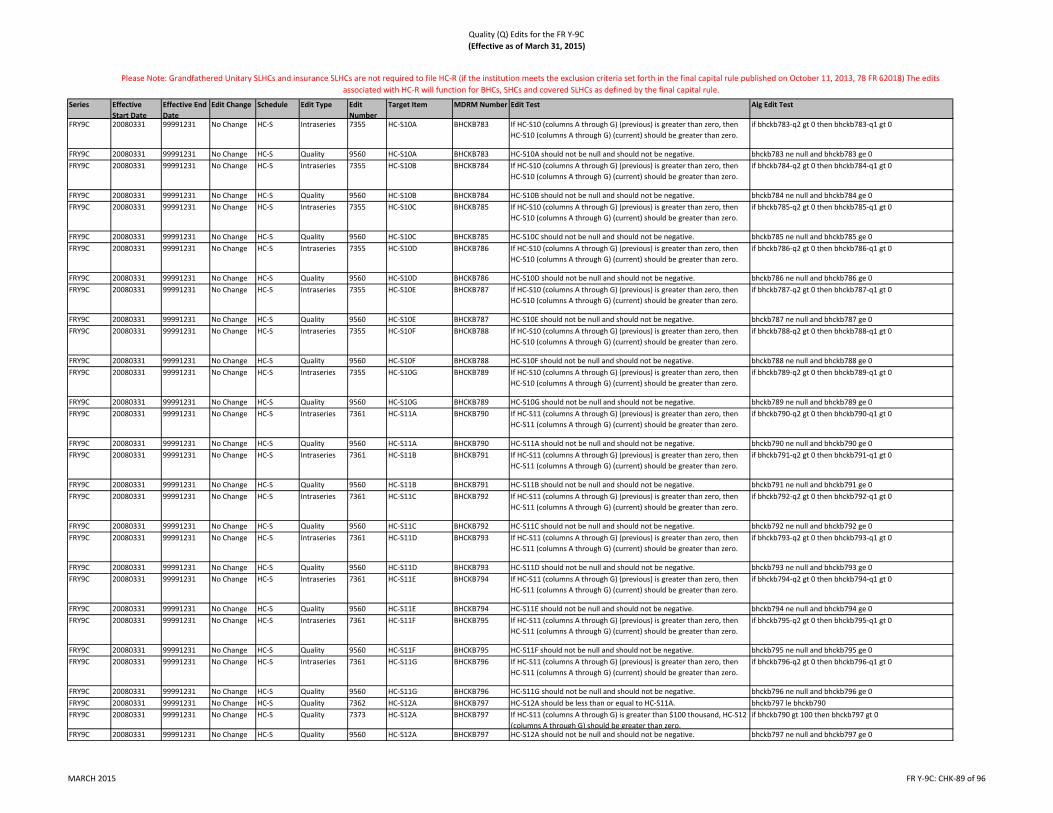

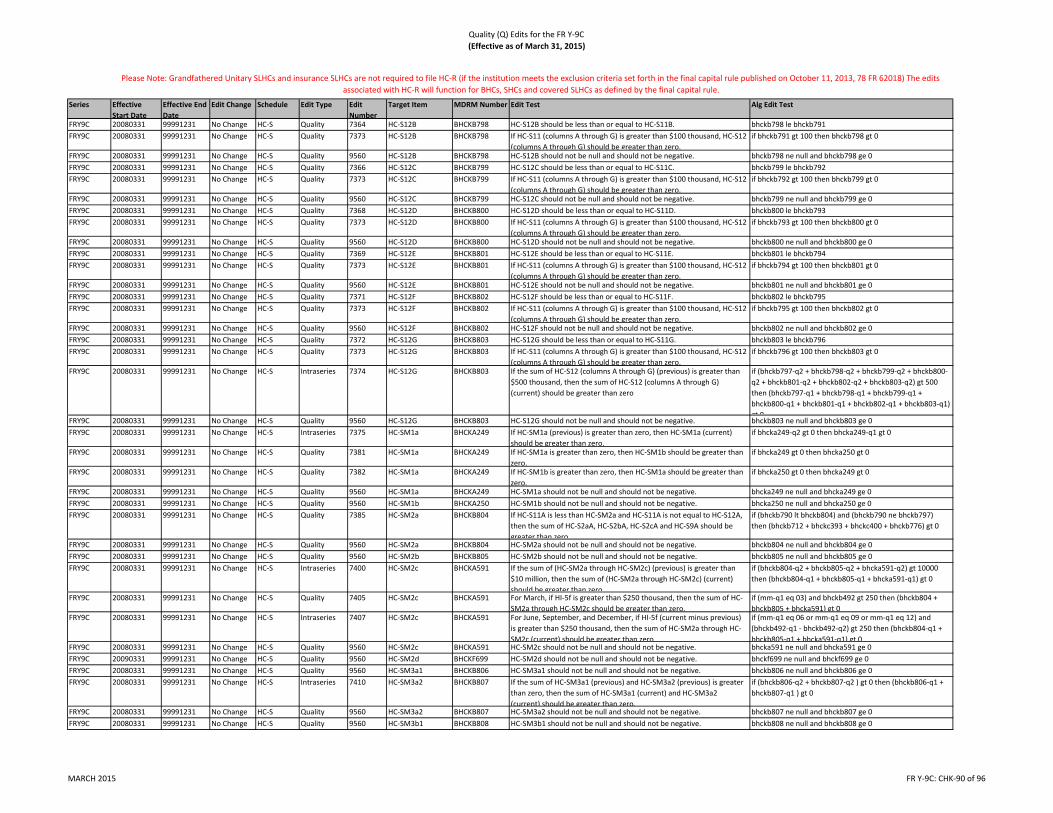

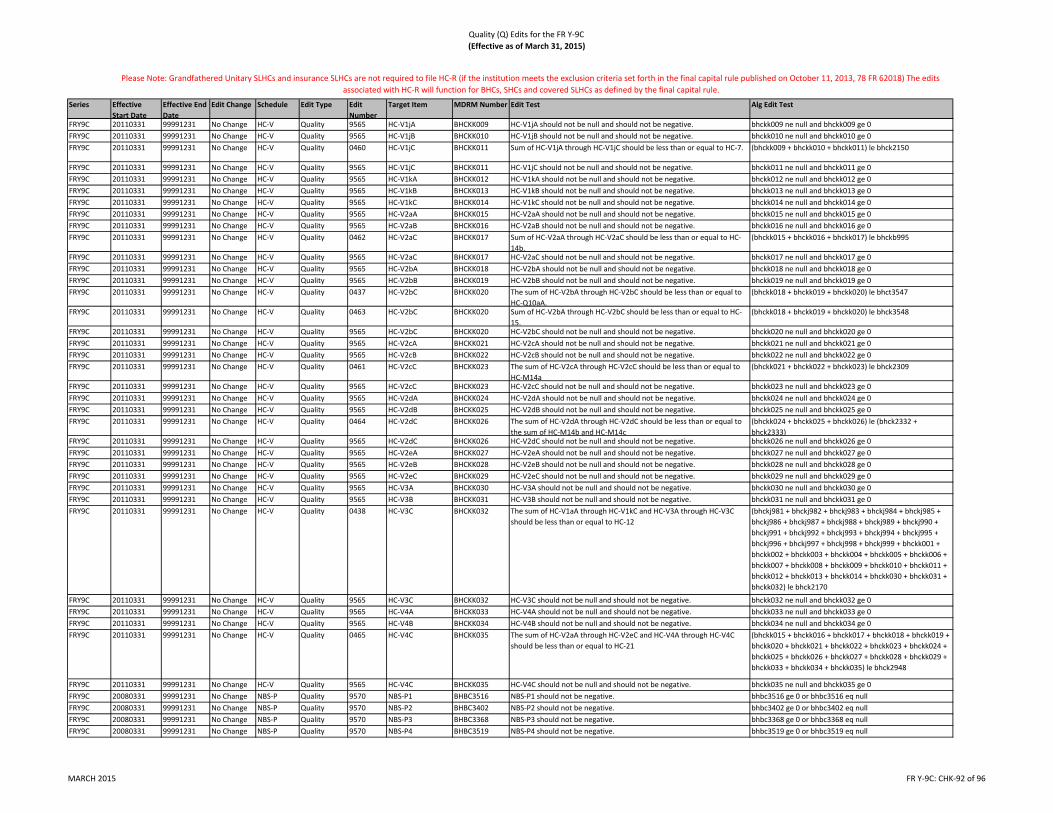

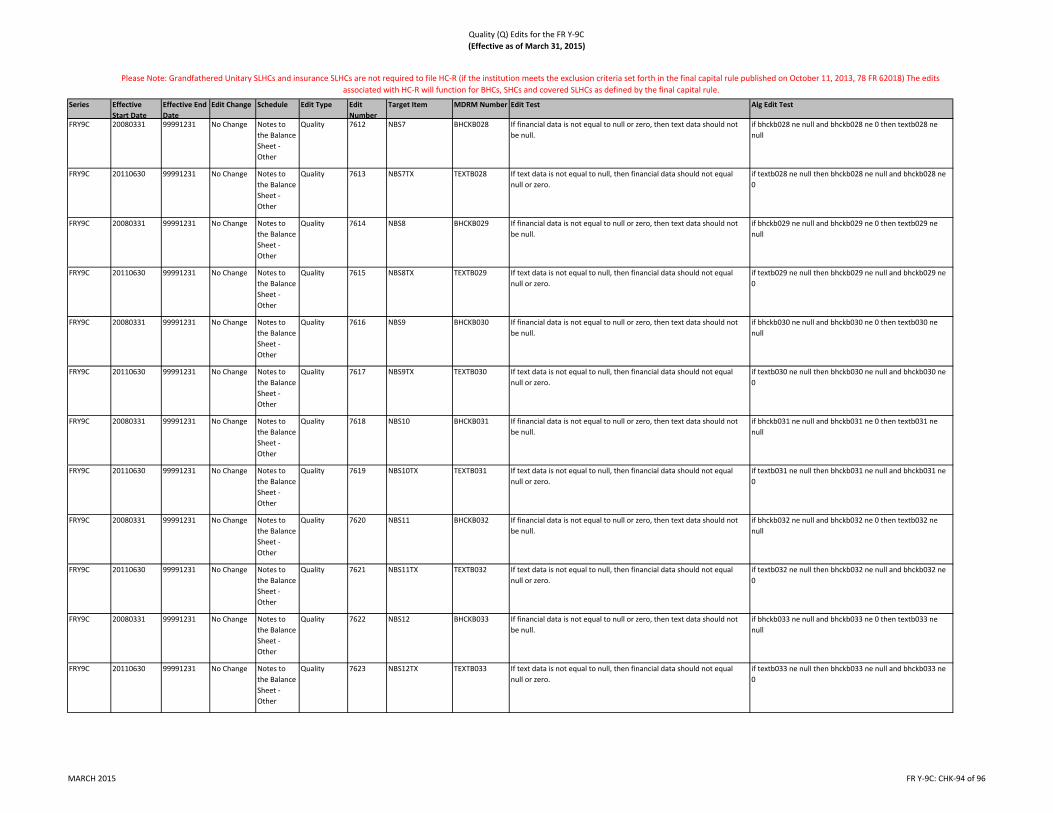

FR Y-9C Checklist for Verifying Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CHK-1

FR Y-9C Federal Reserve Edits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . EDIT-1

Contents

Contents-8 FR Y-9CContents March 2015

INSTRUCTIONS FOR PREPARATION OF

Financial Statements forHolding Companies

For purposes of this report, all references to ‘‘bank(s)’’ and ‘‘associated bank(s)’’ areinclusive of ‘‘savings association(s)’’ unless otherwise noted.

GENERAL INSTRUCTIONS

Who Must Report

A. Reporting Criteria

All bank holding companies, savings and loan holdingcompanies,1 and securities holding companies (collec-tively ‘‘holding companies’’) regardless of size, arerequired to submit financial statements to the FederalReserve, unless specifically exempted (see description ofexemptions below).

The specific reporting requirements for each holdingcompany depend upon the size of the holding company,or other specific factors as determined by the appropriateFederal Reserve Bank. Holding companies must file theappropriate forms as described below:

(1) Holding Companies with Total ConsolidatedAssetsof $1 billion or More. Holding companies with totalconsolidated assets of $1 billion or more (the top tierof a multi-tiered holding company, when applicable)must file:

(a) the Consolidated Financial Statements for Hold-ing Companies (FR Y-9C) quarterly, as of thelast calendar day of March, June, September, andDecember.

(b) the Parent Company Only Financial Statementsfor Large Holding Companies (FR Y-9LP) quar-terly, as of the last calendar day of March, June,September, and December.

Each holding company that files the FR Y-9Cmust submit the FR Y-9LP for its parent company.

For tiered holding companies. When holding com-panies with total consolidated assets of $1 billion, ormore, own or control, or are owned or controlled by,other holding companies (i.e., are tiered holdingcompanies), only the top-tier holding company mustfile the FR Y-9C for the consolidated holding com-pany organization unless the top-tier holding com-pany is exempt from reporting the FR Y-9C. If atop-tier holding company is exempt from reportingthe FR Y-9C, then the lower-tier holding company(with total consolidated assets of $1 billion or more)must file the FR Y-9C.

In addition, such tiered holding companies, regard-less of the size of the subsidiary holding companies,must also submit, or have the top-tier holding com-pany subsidiary submit, a separate FR Y-9LP foreach lower-tier holding company of the top-tierholding company.

(2) Holding Companies that are Employee Stock Own-ership Plans. Holding companies that are employeestock ownership plans (ESOPs) as of the last calendarday of the calendar year must file the FinancialStatements for Employee Stock Ownership Plan Hold-ing Companies (FR Y-9ES) on an annual basis, as ofDecember 31. No other FR Y-9 series form is required.However, holding companies that are subsidiaries ofESOP holding companies (i.e., a tiered holding com-pany) must submit the appropriate FR Y-9 series inaccordance with holding company reporting require-ments.

(3) Holding Companies with Total ConsolidatedAssetsof Less Than $1 billion. Holding companies withtotal consolidated assets of less than $1 billion mustfile the Parent Company Only Financial Statementsfor Small Holding Companies (FR Y-9SP) on a

1. Savings and loan holding companies (SLHCs) do not include any

trust (other than a pension, profit-sharing, stockholders’ voting, or business

trust) which controls a savings association if such trust by its terms must

terminate within 25 years or not later than 21 years and 10 months after the

death of individuals living on the effective date of the trust, and (a) was in

existence and in control of a savings association on June 26, 1967, or, (b) is

a testamentary trust. See Section 238.2 of the interim final rule for more

information.

FR Y9C GEN-1General Instructions March 2015

semiannual basis, as of the last calendar day of Juneand December.2

For tiered holding companies. When holding com-panies with total consolidated assets of less than$1 billion, own or control, or are owned or controlledby, other holding companies (i.e., are tiered holdingcompanies), the top-tier holding company must filethe FR Y-9SP for the top-tier parent company of theholding company. In addition, such tiered holdingcompanies must also submit, or have the holdingcompany subsidiary submit, a separate FR Y-9SP foreach lower-tier holding company.

When a holding company that has total consolidatedassets of less than $1 billion is a subsidiary of aholding company that files the FR Y-9C, the holdingcompany that has total consolidated assets of lessthan $1 billion would report on the FR Y-9LP ratherthan the FR Y-9SP.

The instructions for the FR Y-9LP, FR Y-9ES, and theFR Y-9SP are not included in this booklet but may beobtained from the Federal Reserve Bank in the districtwhere the holding company files its reports, or may befound on the Federal Reserve Board’s public website(www.federalreserve.gov/boarddocs/reportforms).

B. Exemptions from Reporting theHolding Company FinancialStatements

The following holding companies do not have to fileholding company financial statements:

(1) a holding company that has been granted an exemp-tion under Section 4(d) of the Bank Holding Com-pany Act; or

(2) a ‘‘qualified foreign banking organization’’ as definedby Section 211.23(a) of Regulation K (12 CFR211.23(a)) that controls a U.S. subsidiary bank.

Holding companies that are not required to file under theabove criteria may be required to file this report by theFederal Reserve Bank of the district in which they areregistered.

C. Shifts in Reporting Status

A top-tier holding company that reaches $1 billion ormore in total consolidated assets as of June 30 of thepreceding year must begin reporting the FR Y-9C and theFR Y-9LP in March of the current year, and any lower-tier holding companies must begin reporting the FRY-9LP in March of the current year. If a top-tier holdingcompany reaches $1 billion or more in total consolidatedassets due to a business combination, a reorganization, ora branch acquisition that is not a business combination,then the holding company must begin reporting the FRY-9C and the FR Y-9LP with the first quarterly reportdate following the effective date of the business combi-nation, reorganization, or branch acquisition, and anylower-tier holding companies must begin reporting theFR Y-9LP with the first quarterly report date followingthe effective date. In general, once a holding companyreaches or exceeds $1 billion in total consolidated assetsand begins filing the FR Y-9C and FR Y-9LP, it shouldfile a complete FR Y-9C and FR Y-9LP going forward(and any lower-tier holding companies should file acomplete FR Y-9LP going forward). If a holdingcompany’s total consolidated assets should subsequentlyfall to less than $1 billion for four consecutive quarters,then the holding company may revert to filing the FRY-9SP (and any lower-tier holding companies in thoseorganizations may revert to filing the FR Y-9SP).

Where to Submit the Reports

Electronic Submission

All holding companies must submit their completedreports electronically. Holding companies should contacttheir district Reserve Bank or go to www.frbservices.org/centralbank/reportingcentral/index.html for proceduresfor electronic submission.

2. The Reserve Bank with whom the reporting holding company files its

reports may require that a holding company with total consolidated assets

of less than $1 billion submit the FR Y-9C and the FR Y-9LP reports to

meet supervisory needs. Reserve Banks will consider such criteria includ-

ing, but not limited to, whether the holding company (1) is engaged in

significant nonbanking activities either directly or through a nonbank

subsidiary; (2) conducts significant off-balance-sheet activities, including

securitizations or managing or administering assets for third parties, either

directly or through a nonbank subsidiary; or (3) has a material amount of

debt or equity securities (other than trust preferred securities) outstanding

that are registered with the Securities and Exchange Commission.

In addition, any holding company that is not subject to the Federal

Reserve’s Capital Adequacy Guidelines, but nonetheless elects to comply

with the guidelines, are required to file a complete FR Y-9C and FR Y-9LP

report, and generally would not be permitted to revert back to filing the FR

Y-9SP report in any subsequent periods.

General Instructions

GEN-2 FR Y9CGeneral Instructions March 2015

When to Submit the Reports

The Consolidated Financial Statements for Holding Com-panies (FR Y-9C) are required to be submitted as ofMarch 31, June 30, September 30, and December 31. Thesubmission date for holding companies is 40 calendardays after the March 31, June 30, and September 30 as ofdates unless that day falls on a weekend or holiday(subject to timely filing provisions). The submission datefor holding companies is 45 calendar days after theDecember 31 as of date. For example, the June 30 reportmust be received by August 9, and the December 31 reportby February 14.

The term ‘‘submission date’’ is defined as the date bywhich the Federal Reserve must receive the holdingcompany’s FR Y-9C.

If the submission deadline falls on a weekend or holiday,the report must be received on the first business day afterthe Saturday, Sunday, or holiday. Earlier submission aidsthe Federal Reserve in reviewing and processing thereports and is encouraged. No extensions of time forsubmitting reports are granted.

The reports are due by the end of the reporting day onthe submission date (5:00 P.M. at each district ReserveBank).

How to Prepare the Reports

A. Applicability of GAAP, ConsolidationRules and SEC Consistency

Holding companies are required to prepare and file theConsolidated Financial Statements for Holding Compa-nies in accordance with generally accepted accountingprinciples (GAAP) and these instructions. All reportsshall be prepared in a consistent manner. The holdingcompany’s financial records shall be maintained in such amanner and scope so as to ensure that the ConsolidatedFinancial Statements for Holding Companies can beprepared and filed in accordance with these instructionsand reflect a fair presentation of the holding company’sfinancial condition and results of operations.

Holding companies should retain workpapers and otherrecords used in the preparation of these reports.

Subsequent Events

Subsequent events are events or transactions that occurafter the FR Y-9C balance sheet date, e.g., December 31,

but before the FR Y-9C report is filed. Consistent withASC Topic 855, Subsequent Events (formerly FASBStatement No. 165 ‘‘Subsequent Events’’), an institutionshall recognize in the FR Y-9C report the effects of allsubsequent events (not addressed in other ASC Topics)that provide additional evidence about conditions thatexisted at the date of the FR Y-9C balance sheet (Sched-ule HC) including the estimates inherent in the process ofpreparing the FR Y-9C report e.g., a loss that has beenincurred but not yet confirmed as of the FR Y-9C reportbalance sheet date.

Scope of the ‘‘consolidated holdingcompany’’ to be reported in the submittedreports

For purposes of this report, the holding company shouldconsolidate its subsidiaries on the same basis as it doesfor its annual reports to the SEC or, for those holdingcompanies that do not file reports with the SEC, on thesame basis as described in generally accepted accountingprinciples (GAAP). Generally, under the rules for con-solidation established by the SEC and by GAAP, holdingcompanies should consolidate any company in which itowns more than 50 percent of the outstanding votingstock.

Each holding company shall account for any investmentsin unconsolidated subsidiaries, associated companies,and those corporate joint ventures over which the holdingcompany exercises significant influence according to theequity method of accounting, as prescribed by GAAP.The equity method of accounting is described in Sched-ule HC, item 8. (Refer to the Glossary entry for ‘‘subsid-iaries’’ for the definitions of the terms subsidiary, associ-ated company, and corporate joint venture.)

Rules of Consolidation

For purposes of these reports, all offices (i.e., branches,subsidiaries, VIEs, and IBFs) that are within the scope ofthe consolidated holding company as defined above areto be reported on a consolidated basis. Unless the instruc-tions specifically state otherwise, this consolidation shallbe on a line-by-line basis, according to the captionshown. As part of the consolidation process, the results ofall transactions and all intercompany balances (e.g.,outstanding asset/debt relationships) between offices,subsidiaries, and other entities included in the scope of

General Instructions

FR Y9C GEN-3General Instructions December 2014

the consolidated holding company are to be eliminated inthe consolidation and must be excluded from the Consoli-dated Financial Statements for Holding Companies. (Forexample, eliminate in the consolidation (1) loans madeby the holding company to a consolidated subsidiary andthe corresponding liability of the subsidiary to the hold-ing company, (2) a consolidated subsidiary’s deposits inanother holding company consolidated subsidiary and thecorresponding cash or interest-bearing asset balance ofthe subsidiary, and (3) the intercompany interest incomeand expense related to such loans and deposits of theholding company and its consolidated subsidiary.)

Exception: For purposes of reporting the total assets ofcaptive insurance and reinsurance subsidiaries in Sched-ule HC-M, Memoranda, items 7(a) and 7(b), only, hold-ing companies should measure the subsidiaries’ totalassets before eliminating intercompany transactionsbetween the consolidated subsidiary and other offices orsubsidiaries of the consolidated holding company. Other-wise, captive insurance and reinsurance subsidiariesshould be reported on a consolidated basis as described inthe preceding paragraph.

Subsidiaries of Subsidiaries. For a subsidiary of a hold-ing company that is in turn the parent of one or moresubsidiaries:

(1) Each subsidiary shall consolidate its majority-ownedsubsidiaries in accordance with the consolidationrequirements set forth above.

(2) Each subsidiary shall account for any investments inunconsolidated subsidiaries, corporate joint venturesover which the holding company exercises signifi-cant influence, and associated companies accordingto the equity method of accounting.

Noncontrolling (minority) interests. A noncontrollinginterest, sometimes called a minority interest, is theportion of equity in a holding company’s subsidiary notattributable, directly or indirectly, to the parent holdingcompany. Report noncontrolling interests in the reportingholding company’s consolidated subsidiaries in ScheduleHC, item 27(b), ‘‘Noncontrolling (minority) interests inconsolidated subsidiaries.’’ Report the portion of consoli-dated net income reported in Schedule HI, item 12, that isattributable to noncontrolling interests in consolidatedsubsidiaries of the holding company in Schedule HI, item13.

Reporting by type of office (for holdingcompanies with foreign offices)

Some information in the Consolidated Financial State-ments for Holding Companies are to be reported by typeof office (e.g., for domestic offices or for foreign offices)as well as for the consolidated holding company. Whereinformation is called for by type of office, the informationreported shall be the office component of the consoli-dated item unless otherwise specified in the line iteminstructions. That is, as a general rule, the office informa-tion shall be reported at the same level of consolidationas the fully consolidated statement, shall reflect onlytransactions with parties outside the scope of the consoli-dated holding company, and shall exclude all transactionsbetween offices of the consolidated holding company asdefined above. See the Glossary entries for ‘‘domesticoffice’’ and ‘‘foreign office’’ for the definitions of theseterms.

Exclusions from coverage of theconsolidated report

Subsidiaries where control does not rest with the par-ent. If control of a majority-owned subsidiary by theholding company does not rest with the holding companybecause of legal or other reasons (e.g., the subsidiary is inbankruptcy), the subsidiary is not required to be consoli-dated for purposes of the report.2 Thus, the holdingcompany’s investments in such subsidiaries are not elimi-nated in consolidation but will be reflected in the reportsin the balance sheet item for ‘‘Investments in unconsoli-dated subsidiaries and associated companies’’ (ScheduleHC, item 8) and other transactions of the holding com-pany with such subsidiaries will be reflected in theappropriate items of the reports in the same manner astransactions with unrelated outside parties. Additionalguidance on this topic is provided in accounting stan-dards, including ASC Subtopic 810-10, Consolidation –Overall (formerly FASB Statement No. 94, Consolida-tion of All Majority-Owned Subsidiaries).

Custody accounts. All custody and safekeeping activities(i.e., the holding of securities, jewelry, coin collections,and other valuables in custody or in safekeeping forcustomers) should not to be reflected on any basis in thebalance sheet of the Consolidated Financial Statementsfor Holding Companies unless cash funds held by thebank in safekeeping for customers are commingled withthe general assets of the reporting holding company. In

General Instructions

GEN-4 FR Y9CGeneral Instructions December 2014

such cases, the commingled funds would be reported inthe Consolidated Financial Statements for Holding Com-panies as deposit liabilities of the holding company.

For holding companies that file financial statements withthe Securities and Exchange Commission (SEC), majorclassifications including total assets, total liabilities, totalequity capital and net income should generally be thesame between the FR Y-9C report filed with the FederalReserve and the financial statements filed with the SEC.

B. Report Form Captions, Non-applicableItems and Instructional Detail

No caption on the report forms shall be changed in anyway. An amount or a zero should be entered for all itemsexcept in those cases where (1) the reporting holdingcompany does not have any foreign offices; (2) thereporting company does not have any depository institu-tions that are subsidiaries other than commercial banks;or (3) the reporting holding company has no consoli-dated subsidiaries that render services in any fiduciarycapacity and its subsidiary banks have no trust depart-ments. If the reporting holding company has only domes-tic offices, Schedule HC, items 13(b)(1) and 13(b)(2),and Schedule HI, items 1(a)(2) and 2(a)(2) should be leftblank. If the reporting company does not have anydepository institutions that are subsidiaries other thancommercial banks, then Schedule HC-E, items 2(a)through 2(e) should be left blank. If the reporting com-pany does not have any trust activities, then Schedule HI,item 5(a) should be left blank. A holding companyshould leave blank memorandum items 9(a) through 9(d)of Schedule HI if the reporting holding company doesnot have average trading assets of $2 million or more(reported on Schedule HC-K, item 4(a)) as of the March31st report date of the current calendar year.

Holding companies who are not required to report Sched-ule HC-D or Schedule HC-Q may leave these schedulesblank. Savings and loan holding companies who are notrequired to report Schedule HC-L, item 7(c)(1)(a)through item 7(c)(2)(c), or all of Schedule HC-R mayleave these items blank.

There may be areas in which a holding company wishesmore technical detail on the application of accountingstandards and procedures to the requirements of theseinstructions. Such information may often be found in theappropriate entries in the Glossary section of theseinstructions or, in more detail, in the GAAP standards.

Selected sections of the GAAP standards are referencedin the instructions where appropriate. The accountingentries in the Glossary are intended to serve as an aid inspecific reporting situations rather than a comprehensivestatement on accounting for holding companies.

Questions and requests for interpretations of mattersappearing in any part of these instructions should beaddressed to the appropriate Federal Reserve Bank (thatis, the Federal Reserve Bank in the district where theholding company submits this report).

C. Rounding

For holding companies with total assets of less than $10billion, all dollar amounts must be reported in thousands,with the figures rounded to the nearest thousand. Itemsless than $500 will be reported as zero. For holdingcompanies with total assets of $10 billion or more, alldollar amounts may be reported in thousands, but eachholding company, at its option, may round the figuresreported to the nearest million, with zeros reported in thethousands column. For holding companies exercising thisoption, amounts less than $500,000 will be reported aszero.

Rounding could result in details not adding to their statedtotals. However, to ensure consistent reporting, therounded detail items should be adjusted so that the totalsand the sums of their components are identical.

On the Consolidated Financial Statements for HoldingCompanies, ‘‘Total assets’’ (Schedule HC, item 12) and‘‘Total liabilities and equity capital’’ (Schedule HC, item29), which must be equal, must be derived from unroundednumbers and then rounded to ensure that these two itemsare equal as reported.

D. Negative Entries

Except for the items listed below, negative entries aregenerally not appropriate on the FR Y-9C and should notbe reported. Hence, assets with credit balances must bereported in liability items and liabilities with debit bal-ances must be reported in asset items, as appropriate, andin accordance with these instructions. Items for whichnegative entries may be made, include:

General Instructions

FR Y9C GEN-5General Instructions December 2014

(1) Schedule HI, memorandum item 6, ‘‘Other non-interest income (itemize and describe the threelargest amounts that exceed 1 percent of the sum ofSchedule HI, item 1(h) and 5(m)).’’

(2) Schedule HI, memorandum item 7 ‘‘Other non-interest expense (itemize and describe the threelargest amounts that exceed 1 percent of ScheduleHI, items 1(h) and 5(m)).’’

(3) Schedule HI, item 5(e), ‘‘Venture capital revenue.’’

(4) Schedule HI, item 5(f), ‘‘Net servicing fees.’’

(5) Schedule HI, item 5(g), ‘‘Net securitizationincome.’’

(6) Schedule HI-A, item 12, ‘‘Other comprehensiveincome.’’

(7) Schedule HC, item 8, ‘‘Investments in unconsoli-dated subsidiaries and associated companies.’’

(8) Schedule HC, item 26(a), ‘‘Retained earnings.’’

(9) Schedule HC, item 26(b), ‘‘Accumulated othercomprehensive income.’’

(10) Schedule HC, item 26(c), ‘‘Other equity capitalcomponents. ’’

(11) Schedule HC, item 27(a), ‘‘Total holding companyequity capital.’’

(12) Schedule HC, item 28, ‘‘Total equity capital.’’

(13) Schedule HC-C, items 10, 10(a), and 10(b), on‘‘Lease financing receivables (net of unearnedincome).’’

(14) Schedule HC-P, items 5(a) and 5(b), on ‘‘Noninter-est income for the quarter from the sale, securitiza-tion, and servicing of 1–4 family residential mort-gage loans .’’

(15) Schedule HC-Q, memorandum item 2(a), ‘‘Loancommitments (not accounted for as derivatives).’’

(16) Schedule HC-R, Part I item 2, ‘‘Retained Earn-ings.’’

(17) Schedule HC-R, Part I item 3, ‘‘Accumulated OtherComprehensive Income (AOCI).

(18) Schedule HC-R, Part I item 9(a) ‘‘Net unrealizedgains (losses) on available-for-sale securities.’’

(19) Schedule HC-R, Part I item 9(b) ’’Net unrealizedloss on available-for-sale preferred stock classifiedas an equity security under GAAP and available-for-sale equity exposures.

(20) Schedule HC-R, Part I item 9(c) ‘‘Accumulated netgains (losses) on cash flow hedges.’’

(21) Schedule HC-R, Part I item 9(d) ‘‘Amounts recordedin AOCI attributed to defined benefit postretirementplans resulting from the initial and subsequentapplication of the relevant GAAP standards thatpertain to such plans.’’

(22) Schedule HC-R, Part I item 9(e) ‘‘Net unrealizedgains (losses) on held-to-maturity securities that areincluded in AOCI.’’

(23) Schedule HC-R, Part I item 9(f) ‘‘ Accumulated netgain (loss) on cash flow hedges included in AOCI,net of applicable income taxes, that relate to thehedging of items that a are not recognized at fairvalue on the balance sheet.

(24) Schedule HC-R, Part I item 10(a) Unrealized netgain(loss) related to changes in the fair value ofliabilities that are due to changes in own credit risk.

(25) Schedule HC-R, Part I item 10(b) ‘‘All other deduc-tions from (additions to) common equity tier 1capital before threshold-based deductions.’’

(26) Schedule HC-R, Part I item 12, ‘‘Subtotal,’’

(27) Schedule HC-R, Part I item 19, ‘‘Common EquityTier 1 capital’’

(28) Schedule HC-R Part I item 26, ‘‘Tier I Capital’’

(29) Schedule HC-R Part I item 35(a) and 35(b) ‘‘TotalCapital’’

(30) Schedule HC-R Part I item 38, ‘‘Other deductionsfrom (additions to) assets for leverage ratio pur-poses’’

(31) Schedule HC-R Part I item 41 through 44, Risk-based and leverage capital ratios, and

(32) Schedule HC-R Part II column B, ‘‘Adjustments toTotals Reported in Column A,’’ for the asset cate-gories in items 1 through 11’’

When negative entries do occur in one or more of theseitems, they shall be recorded with a minus (2) sign ratherthan in parenthesis.

General Instructions

GEN-6 FR Y9CGeneral Instructions March 2015

On the Consolidated Report of Income (Schedule HI),negative entries may appear as appropriate. Income itemswith a debit balance and expense items with a creditbalance must be reported with a minus (2) sign.

E. Confidentiality

The completed version of this report generally is avail-able to the public upon request on an individual basiswith the exception of any amounts reported in ScheduleHI, memoranda item 7(g), ‘‘FDIC deposit insuranceassessments,’’ for report dates beginning June 30, 2009,and in Schedule HC-P, item 7(a), ‘‘Representation andwarranty reserves for 1-4 family residential mortgageloans sold to U.S. government agencies and government-sponsored agencies,’’ and item 7(b), ‘‘Representation andwarranty reserves for 1-4 family residential mortgageloans sold to other parties.’’ However, a reporting holdingcompany may request confidential treatment for theConsolidated Financial Statements for Holding Compa-nies (FR Y-9C) if the holding company is of the opinionthat disclosure of specific commercial or financial infor-mation in the report would likely result in substantialharm to its competitive position, or that disclosure of thesubmitted information would result in unwarranted inva-sion of personal privacy.

A request for confidential treatment must be submitted inwriting prior to the electronic submission of the report.The request must discuss in writing the justification forwhich confidentiality is requested and must demonstratethe specific nature of the harm that would result frompublic release of the information. Merely stating thatcompetitive harm would result or that information ispersonal is not sufficient.

Information for which confidential treatment is requestedmay subsequently be released by the Federal ReserveSystem if the Board of Governors determines that thedisclosure of such information is in the public interest.

F. Verification and Signatures

Verification. All addition and subtraction should bedouble-checked before reports are submitted. Totals andsubtotals in supporting materials should be cross-checkedto corresponding items elsewhere in the reports. Before areport is submitted, all amounts should be compared withthe corresponding amounts in the previous report. If thereare any unusual changes from the previous report, a brief

explanation of the changes should be provided to theappropriate Reserve Bank.

Signatures. The Consolidated Financial Statements forHolding Companies must be signed by the Chief Finan-cial Officer of the holding company (or by the individualperforming this equivalent function). By signing thecover page of this report, the authorized officer acknowl-edges that any knowing and willful misrepresentation oromission of a material fact on this report constitutes fraudin the inducement and may subject the officer to legalsanctions provided by 18 USC 1001 and 1007.

Holding companies must maintain in their files a manu-ally signed and attested printout of the data submitted.The cover page of the Reserve Bank-supplied, holdingcompany’s software, or from the Federal Reserve’s web-site report form should be used to fulfill the signature andattestation requirement and this page should be attachedto the printout placed in the holding company’s files.

G. Amended Reports

When the Federal Reserve’s interpretation of how GAAPor these instructions should be applied to a specifiedevent or transaction (or series of related events or trans-actions) differs from the reporting holding company’sinterpretation, the Federal Reserve may require the hold-ing company to reflect the event(s) or transaction(s) in itsFR Y-9C in accordance with the Federal Reserve’sinterpretation and to amend previously submitted reports.The Federal Reserve will consider the materiality of suchevent(s) or transaction(s) in making a determinationabout requiring the holding company to apply the FederalReserve’s interpretation and to amend previously submit-ted reports. Materiality is a qualitative characteristic ofaccounting information that is addressed in FinancialAccounting Standards Board (FASB) Concepts State-ment No. 8, ‘‘Conceptual Framework for FinancialReporting,’’ as follows: ‘‘Information is material if omit-ting it or misstating it could influence decisions that usersmake on the basis of the financial information of aspecific reporting entity.’’ In other words, materiality isan entity-specific aspect of relevance based on the natureor magnitude or both of the items to which the informa-tion relates in the context of an individual entity’sfinancial report.

The Federal Reserve may require the filing of amendedConsolidated Financial Statements for Holding Compa-nies if reports as previously submitted contain significant

General Instructions

FR Y9C GEN-7General Instructions March 2015

errors. In addition, a holding company should file anamended report when internal or external auditors makeaudit adjustments that result in a restatement of financialstatements previously submitted to the Federal Reserve.

The Federal Reserve also requests that holding compa-nies that have restated their prior period financial state-ments as a result of an acquisition submit revised reportsfor the prior year-ends. While information to complete all

schedules to the FR Y-9C may not be available, holdingcompanies are requested to provide the ConsolidatedBalance Sheet (Schedule HC) and the ConsolidatedReport of Income (Schedule HI) for the prior year-ends.In the event that certain of the required data are notavailable, holding companies should contact the appropri-ate Reserve Bank for information on submitting revisedreports.

General Instructions

GEN-8 FR Y9CGeneral Instructions March 2015

LINE ITEM INSTRUCTIONS FOR

Consolidated Report of IncomeSchedule HI

The line item instructions should be read in conjunction with the Glossary and othersections of these instructions. See the discussion of the Organization of the InstructionBooks in the General Instructions. For purposes of these line item instructions, theFASB Accounting Standards Codification is referred to as ‘‘ASC.’’

General Instructions

Report in accordance with these instructions all incomeand expense of the consolidated holding company for thecalendar year-to-date. Include adjustments of accrualsand other accounting estimates made shortly after the endof a reporting period which relate to the income andexpense of the reporting period.

For purposes of this report, a savings and loan holdingcompany should report income from its savings associa-tion(s), nonbank subsidiary(s) and subsidiary savings andloan holding company(s) (as defined in section 238.2 ofRegulation LL) following the same guidelines andaccounting rules set forth in these instructions for allholding companies.

Holding companies that began operating during thereporting period should report in the appropriate items ofSchedule HI all income earned and expense incurredsince commencing operations. The holding companyshould report pre-opening income earned and expensesincurred from inception until the date operations com-menced using one of the two methods described in theGlossary entry for ‘‘start-up activities.’’

Business Combinations and Reorganizations − If theholding company entered into a business combinationthat became effective during the reporting period andwhich has been accounted for under the acquisitionmethod, report the income and expense of the acquiredbusiness only after its acquisition. If the holding com-pany entered into a reorganization that became effectiveduring the year-to-date reporting period and has beenaccounted for at historical cost in a manner similar to apooling of interests, report the income and expense of thecombined entities for the entire calendar year-to-date asthough they had combined at the beginning of the year.For further information on business combinations andreorganizations, see the Glossary entry for ‘‘businesscombinations.’’

Assets and liabilities accounted under the fair valueoption — Under U.S. generally accepted accountingprinciples (GAAP) (i.e., ASC Subtopic 825-10, FinancialInstruments – Overall (formerly FASB Statement No.159, The Fair Value Option for Financial Assets andFinancial Liabilities), ASC Subtopic 815-15, Derivativesand Hedging – Embedded Derivatives (formerly FASBStatement No. 155, Accounting for Certain HybridFinancial Instruments), and ASC Subtopic 860-50, Trans-fers and Servicing – Servicing Assets and Liabilities(formerly FASB Statement No. 156, Accounting forServicing of Financial Assets)), the holding companymay elect to report certain assets and liabilities at fairvalue with changes in fair value recognized in earnings.This election is generally referred to as the fair valueoption. If the holding company has elected to apply thefair value option to interest-bearing financial assets andliabilities, it should report the interest income on thesefinancial assets (except any that are in nonaccrual status)and the interest expense on these financial liabilities forthe year-to-date in the appropriate interest income andinterest expense items on Schedule HI, not as part of thereported change in fair value of these assets and liabilitiesfor the year-to-date. The holding company should mea-sure the interest income or interest expense on a financialasset or liability to which the fair value option has beenapplied using either the contractual interest rate on theasset or liability or the effective yield method based onthe amount at which the asset or liability was firstrecognized on the balance sheet. Although the use of thecontractual interest rate is an acceptable method underGAAP, when a financial asset or liability has a significantpremium or discount upon initial recognition, the mea-surement of interest income or interest expense under theeffective yield method more accurately portrays theeconomic substance of the transaction. In addition, insome cases, GAAP requires a particular method ofinterest income recognition when the fair value option iselected. For example, when the fair value option has been

FR Y-9C HI-1Schedule HI March 2013

applied to a beneficial interest in securitized financialassets within the scope of ASC Subtopic 325-40,Investments-Other – Beneficial Interests in SecuritizedFinancial Assets (formerly Emerging Issues Task ForceIssue No. 99-20, Recognition of Interest Income andImpairment on Purchased and Retained Beneficial Inter-ests in Securitized Financial Assets), interest incomeshould be measured in accordance with the consensus inthis issue. Similarly, when the fair value option has beenapplied to a purchased impaired loan or debt securityaccounted for under ASC Subtopic 310-30, Receivables– Loans and Debt Securities Acquired with DeterioratedCredit Quality (formerly AICPA Statement of Position03-3, Accounting for Certain Loans or Debt SecuritiesAcquired in a Transfer), interest income on the loan ordebt security should be measured in accordance with thisSubtopic when accrual of income is appropriate. Forfurther information, see the Glossary entry for “Pur-chased Impaired Loans and Debt Securities.”

Revaluation adjustments, excluding amounts reported asinterest income and interest expense, to the carryingvalue of all assets and liabilities reported in Schedule HCat fair value under a fair value option (excluding servic-ing assets and liabilities reported in Schedule HC, item10(b), “Other intangible assets,” and Schedule HC, item20, “Other liabilities,” respectively, and assets and liabili-ties reported in Schedule HC, item 5, ‘‘Trading assets,’’and Schedule HC, item 15, ‘‘Trading liabilities,’’ respec-tively) resulting from the periodic marking of such assetsand liabilities to fair value should be reported as “Othernoninterest income” in Schedule HI, item 5(l).

Line Item 1 Interest income.

Line Item 1(a) Interest and fee income on loans.

Report in the appropriate subitem all interest, fees, andsimilar charges levied against or associated with allassets reportable as loans in Schedule HC-C, items 1through 9.

Deduct interest rebated to customers on loans paid beforematurity from gross interest earned on loans; do notreport as an expense.

Include as interest and fee income on loans:

(1) Interest on all assets reportable as loans extendeddirectly, purchased from others, sold under agree-ments to repurchase, or pledged as collateral for anypurpose.

(2) Loan origination fees, direct loan origination costs,and purchase premiums and discounts on loans heldfor investment, all of which should be deferred andrecognized over the life of the related loan as anadjustment of yield under ASC Subtopic 310-20,Receivables – Nonrefundable Fees and Other Costs(formerly FASB Statement No. 91, Accounting forNonrefundable Fees and Costs Associated with Origi-nating or Acquiring Loans and Initial Direct Costs ofLeases) as described in the Glossary entry for ‘‘loanfees.’’ See exclusion (3) below.

(3) Loan commitment fees (net of direct loan originationcosts) that must be deferred over the commitmentperiod and recognized over the life of the related loanas an adjustment of yield under ASC Subtopic 310-20as described in the Glossary entry for ‘‘loan fees.’’

(4) Investigation and service charges, fees representing areimbursement of loan processing costs, renewal andpast-due charges, prepayment penalties, and feescharged for the execution of mortgages or agree-ments securing the holding company’s loans.

(5) Charges levied against overdrawn accounts based onthe length of time the account has been overdrawn,the magnitude of the overdrawn balance, or whichare otherwise equivalent to interest. See exclusion (6)below.

(6) The contractual amount of interest income earned onloans that are reported at fair value under a fair valueoption.

Exclude from interest and fee income on loans:

(1) Fees for servicing real estate mortgages or otherloans that are not assets of the holding company(report in Schedule HI, item 5(f), ‘‘Net servicingfees’’).

(2) Charges to merchants for the holding company’shandling of credit card or charge sales when theholding company does not carry the related loanaccounts on its books (report as ‘‘Other noninterestincome’’ in Schedule HI, item 5(l)). Holding compa-nies may report this income net of the expenses(except salaries) related to the handling of thesecredit card or charge sales.

(3) Loan origination fees, direct loan origination costs,and purchase premiums and discounts on loans heldfor sale, all of which should be deferred until the loan

Schedule HI

HI-2 FR Y-9CSchedule HI March 2013

is sold (rather than amortized). The net fees or costsand purchase premium or discount are part of therecorded investment in the loan. When the loan issold, the difference between the sales price and therecorded investment in the loan is the gain or loss onthe sale of the loan. See exclusion (4) below.

(4) Net gains (losses) from the sale of all assets report-able as loans (report in Schedule HI, item 5(i), ‘‘Netgains (losses) on sales of loans and leases’’). Refer tothe Glossary entry for ‘‘transfers of financial assets.’’

(5) Reimbursements for out-of-pocket expenditures (e.g.,for the purchase of fire insurance on real estatesecuring a loan) made by the holding company forthe account of its customers. If the holding company’sexpense accounts were charged with the amount ofsuch expenditures, the reimbursements should becredited to the same expense accounts.